Bahasa

Halaman

Hukum

“This presentation contains general information regarding the business and strategies of BK Brasil Operações e Assessoria a Restaurantes

S.A. and its controlled companies (“BK”). The information contained herein is in summarized form and does not purport to be complete. Due

to this fact, one cannot rely in its completeness or accuracy and no representations or warranties, implicit or explicit, is made concerning as

to the completeness or accuracy of the information contained herein.

This presentation contains forward-looking statements, which involves risks and uncertainties and should not be construed as a guarantee

of future performance. Investors should be aware that such forward-looking statements may be affected by current or future facts or

expectations regarding our industry, our market share, our reputation, business, financial situation and perspectives. Although we believe

that the forward-looking statements and estimates are based in reasonable assumptions, they are subject to several risks and uncertainties

and were made only based on information currently available to us, and, therefore, we cannot guarantee future results.

The above mentioned considerations are not exhaustive and other risks and uncertainties may cause results that may be substantially

different from those contained in the forward-looking statements. Due to the abovementioned uncertainties, no investment decision

should be made relying only on these forward-looking statements. This presentation should not be construed as recommendation to

potential investors.”

162

639

801

661 950

1,393 1,784

2,348

61 86 134 211 288

9.2% 9.1% 9.6% 11.8% 12.3%

2014 2015 2016 2017 2018

NET REVENUES ADJUSTED EBITDA ADJUSTED EBITDA MARGIN

• Burger King opened its first restaurant in Brazil in 2004, and currently has more than 793 restaurants in the country(1) (3)

• 20-year Master franchisee with exclusive rights to develop and manage Burger King and Popeyes brands in Brazil

• Significant market share gains since 2011

• 2nd player in burger and 3rd largest QSR in number of restaurants

• Largest restaurant operator in the country

• Market leader in brand preference on target segment (2)

• Clear growth and expansion opportunities

• Elected best Burger King LatAmfranchisee in 2017

• First Popeyes openings in Brazil Owned restaurants Franchisees

RESTAURANTS (1) (3)

OVERVIEW

FINANCIAL HIGHLIGHTS

GEOGRAPHIC FOOTPRINT (1) (3)

SOURCE: Ipsos Brasil/ BK Brasil / Note: 1. As of December 20182-4º Quarter of 2018: Burger King has achieved 37% of consumers preference for Fast Food brand within 18 to 34 years old target with significant difference versus 27% of the most important competitor in a online trademark monitoring study conducted by Ipsos at Burger King's request. The study was conducted in October, November and December of 2018 in the metropolitan areas of: SP, RJ, BH, CTB, POA, SAL and BSB, with 815 consumers of fast food in the last 2 months. The results consider 95% of confidence level, and 495 cases in the 18-34 y.o. target. / 3. Does not include dessert centers / 4. Excludes pre-operating expenses, expenses related to M&A, impairment and SOP expenses. / 5. Includes 8 Popeyes restaurants opened in 4Q18

BKBRASIL

SHAREHOLDING STRUCTUREOWNED RESTAURANTS(3)

71

2872

2542

447

64

12

626

4

(5)

(4)

(5)

7.8% 7.5% 4.9% 69.9%9.9%

Others

12 113 190 293419 480 526

639²

127110

123128

112121

171162

139223

313421

531601

697801

2011 2012 2013 2014 2015 2016 2017 2018

BUILDING FOUNDATIONS (2011 – 2013) GAINING SCALE (2014 – 2016) CONTINUOUS IMPROVEMENT (2017 onward)

• Getting the right people on-board

• Net opening of 149 owned restaurants

• Acquisition of 41 restaurants (1 franchisee)

• SAP implementation

• First debenture issuance – R$150 mm

• Net opening of 240 owned restaurants

• Acquisition of 50 restaurants (4 franchisees)

• Expansion to new regions

• Sub-franchisee project

• Enhanced focus on operational efficiency

• Two CRA(1) issuances totaling R$300 mm

• IPO at B3 (Novo Mercado), with a capital increase of R$0.8 billion

• Acquisition of 1 franchisee with 51 restaurants and 20 dessert centers

• New POS platform implemented

• Roll-out of new platforms: mobile app, delivery, self-order kiosks

• Increasing focus on free standing and dessert center openings

• Exclusive right to develop, franchise and operate POPEYES® restaurants in Brazil for 20 years.

Owned restaurants Franchisees

NOTE: 1. CRA is a registered and freely traded debt security / 2. Includes 8 Popeyes restaurants opened in 4Q185

THE RELATIONSHIP WITH RBI/BK CORPORATION IS GUIDED BY THE MASTER FRANCHISEE AND DEVELOPMENT AGREEMENT (“MFDA”)

SUMMARY OF MFDA ECONOMICS KEY MFDA ASPECTS

• Service fee on net sales

BK CORPORATION

BK BRASILLEGACY

FRANCHISEES(Pre 2011)¹

SUB-FRANCHISEES

(Post 2016)

• Royalties on net sales

• Franchise fee per opening

• 20+20-year agreement post-opening (restaurant level)

• Royalties on net sales

• Franchise fee per opening

• Royalties on net sales

• Franchise fee per opening

• Royalties on net sales

• Franchise fee per opening

BKB IS FULLY COMPLIANT WITH THE MFDA

RIGHTS

• A 20-year MFDA agreement with BKC: signed in 2011 and may be extended for another 20 years

• Exclusive right to develop, open and operate Burger King restaurants in Brazil

• Right to manage the advertising fund in Brazil

• Right of establishing required and optional menu items, proving that all Core Menu items are offered at the restaurants and all products / suppliers are approved by BKC

• BKB can operate other brands in Brazil that do not offer hamburger or sandwich as main component of its gross sales

• Target of minimum number of restaurants to build and operate

OBLIGATIONS

SOURCE: BK BrasilNote: 1. Restaurants owned by franchisees that have an agreement with Burger King Corporation pre-2011

6

7

POSITIVE DEMOGRAPHICS AND FAVORABLE

SECTOR DYNAMICS

STRONG BRAND WITH UNIQUE ATTRIBUTES

UNIQUE MANAGEMENT

MODEL AND EXCELLENCE IN

EXECUTION

SIGNIFICANT AVENUES FOR GROWTH AND

EXPANSION IN BRAZIL

EXPERIENCED MANAGEMENT

TEAM

DEVELOPMENT OF POPEYES IN

BRAZIL

8

DEMOGRAPHIC FACTORSSOCIO-ECONOMIC FACTORS

• ~50% of Brazilians fall within Burger King’s target market (A / B / C1) (1)

• Since 2005, 50 million households entered Burger King’s target market

• Food has become an entertainment and leisure destination

• Increase of female participation in the workforce

• 85% of the Brazilian population lives in urban areas (179 million inhabitants)

• 37 million people live in the country’s ten largest cities

• The hectic urban lifestyle requires city-dwellers to spend more time away from home

• Increasing number of single households should boost out-of- home food expenditure in Brazil

INCREASING NUMBER OF SINGLE HOUSEHOLDS On par with the USA as of 1965 and with

Chile as of 2007

SOURCES: Euromonitor, IBGE, PNAD / Note: 1. Average household income per social class – A: R$20,888; B1: R$9,254; B2: R$4,852; C1: R$2,705; C2: R$1,625; D-E: R$768

Percentage of single households (%)

9

9.1% 9.1% 11.1% 13.1% 15.0%

9.6% 11.0% 14.9% 19.8% 24.3%

25.2%27.4% 28.0% 27.6% 27.8%

1997 2001 2007 2012 2017

11.9%10.1% 9.9%

8.3% 8.1%

Chickenfast food

Burger Fast Food FullService

Total FoodService

R$86bnR$419bn

FOOD SERVICE MARKET SHARE FAST FOOD MARKET SHARE FOOD SERVICE SEGMENT CAGR (2011-17)

BURGER IS ONE OF THE FASTEST-GROWING SEGMENTS IN THE BRAZILIAN FAST FOOD SECTOR

Number of Restaurants in Brazil (2018)

9%91%

Independent Fast Food Chained Fast Food

Chained fast food

represents 63% in the US

BURGER KING IS THE 3RD LARGEST FAST FOOD COMPANY IN BRAZIL, WITH FIRST OPENING IN 2004BRAZILIAN FAST FOOD OUTLETS BY TYPE

THE BRAZILIAN FAST FOOD MARKET IS LARGELY FRAGMENTED AND DOMINATED BY INDEPENDENT PLAYERS

SOURCES: Euromonitor and Geofusion and companies (for number of restaurants in Brazil)

21%

39%

28%5%

7%

Fast food Bars / CoffeesFull-service Self serviceOthers

Burger King Rank in Brazil Fast Food

2013 6th

2017 3rd

10

2,159

968793

559393 351 312

218 15657 8

1992 1979 2004 1952 1981 1999 1988 1993 1989 1975 2018

1%

12%

35%

52%

Chicken fast food Burger

Bakery Others

INDULGENT TASTY FLAME-GRILLEDHAVE IT

YOUR WAYMADE-TO-ORDER FREE

REFILL

AUTHENTIC EXPERIENCE

11

FAST FOOD

C+37%AB

63%

C+39%AB

61%

35 to 4423%

45+18%

15 to 34 59%

35 to 4424%

45+23%

15 to 3454%

Male49%

Female51%

Male52%

Female48%

More AB Social Class¹

Younger(15-34 years)

Democratic

SOURCES: GS&NPD | CREST® Brasil (2018)Note: 1.Average household income per social class – A: R$20,888; B1: R$9,254; B2: R$4,852; C1: R$2,705; C2: R$1,625; D-E: R$768

12

95

95

84

52

33

POSITIVE EVOLUTION OF BRAND PYRAMID – INCREASINGLY POSITIVE AWARENESS LEVEL, WITH ROOM TO INCREASE FREQUENCY

BRAND PYRAMID COMPARISON (%)

Preferred

Trial

ConsidersBra

nd

Aw

are

ne

ss

Awareness

Last Month

2015

91

88

71

31

17

4Q16

92

88

75

35

22

4Q17

95

89

83

46

29+29% +32% +14%

SOURCES: SOURCES: Online trademark monitoring study conducted monthly by Ipsos at Burger King's request, with a sample base of 840 cases, calculated in December 2015, Q4’16, Q4’17 and Q4’18, respondents profile: Men / Women, 18-55 y.o., in the metropolitan areas of São Paulo, Rio de Janeiro, Belo Horizonte, Curitiba, Porto Alegre, Brasília and Salvador with a confidence level of 95%.

13

4Q18

SOURCE: BK Brasil

GENERATE TRAFFIC AND TASTING OF NEW PRODUCTS

REINFORCE FUNCTIONAL PRODUCTS ATTRIBUTES

INCREASE EMOTIONAL ENGAGEMENT WITH THE BRAND THROUGH UNIQUE TERRITORIES

14

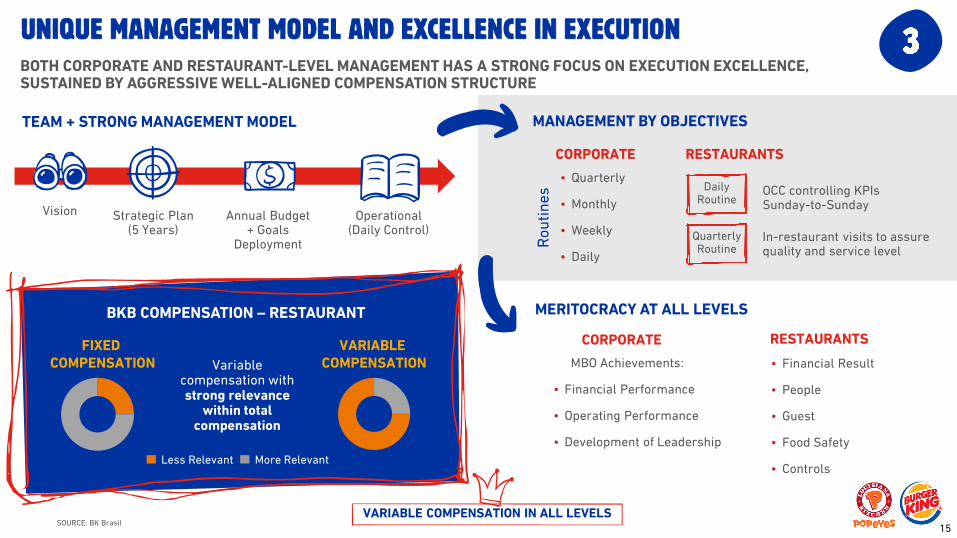

Vision

BOTH CORPORATE AND RESTAURANT-LEVEL MANAGEMENT HAS A STRONG FOCUS ON EXECUTION EXCELLENCE, SUSTAINED BY AGGRESSIVE WELL-ALIGNED COMPENSATION STRUCTURE

MBO Achievements:

• Financial Performance

• Operating Performance

• Development of Leadership

• Financial Result

• People

• Guest

• Food Safety

• Controls

CORPORATE RESTAURANTS

VARIABLE COMPENSATION IN ALL LEVELS

Less Relevant More Relevant

Variable compensation with strong relevance

within total compensation

FIXED COMPENSATION

VARIABLE COMPENSATION

MANAGEMENT BY OBJECTIVES

• Quarterly

• Monthly

• Weekly

• Daily

CORPORATE RESTAURANTS

OCC controlling KPIs Sunday-to-Sunday

Daily Routine

In-restaurant visits to assure quality and service level

Quarterly RoutineR

ou

tin

es

MERITOCRACY AT ALL LEVELS

TEAM + STRONG MANAGEMENT MODEL

Strategic Plan (5 Years)

Annual Budget + Goals

Deployment

Operational (Daily Control)

SOURCE: BK Brasil

BKB COMPENSATION – RESTAURANT

15

SPEED OF SERVICE – NPS (%)

OVERALL CLIENT SATISFACTION – NPS (%)

SOURCE: BK Brasil16

32.0% 34.3% 38.7%45.8%

57.3%67.8% 75.9%

2012 2013 2014 2015 2016 2017 2018

5.4% 9.3%19.4%

30.2%45.3%

56.9%64.0%

2012 2013 2014 2015 2016 2017 2018

ORGANIC EXPANSION

IMPROVEMENT IN SSS AND PROFITABILITY, LEVERAGING ON TECHNOLOGY

ADDITIONAL GROWTH OPPORTUNITIES

NEW RESTAURANT OPENINGS

FOCUS ON FREE-STANDING AND DESSERT CENTERS

SUB-FRANCHISEES EXPANSION

6.5%SSS

(2018)

50 bpsEBITDA Mg. Expansion

(2018)

MOBILE APP

SELF-ORDER KIOSKS

DELIVERY

NEW POS AND SALES TABLET

• 162 RESTAURANTS OPERATED BY LEGACY

FRANCHISEES AND SUB-FRANCHISEES

• ACQUISITION OF 51 RESTAURANTS FROM ONE LEGACY FRANCHISEE (IN 2Q18)

FURTHER CONSOLIDATION OF EXISTING FRANCHISEES

ABILITY TO LEVERAGE PLATFORM TO DEVELOP OTHER FOOD CONCEPTS

SELECTIVELY

OPPORTUNITIES IN NEW BRANDS

SOURCE: BK Brasil 17

148356

FREESTANDINGS

DESSERTCENTERS

REV CONSTRUCTION MONITORING

APPROVED POS SUPPLY CHAIN & AGREEMENTS

LAYOUT OF RESTAURANT TRAINING PLATFORM

IN 2016 BKB CREATED THE SUB-FRANCHISE PROJECT IN ORDER TO LEVERAGE ITS ORGANIC EXPANSION

ACTIVE RESTAURANT PORTFOLIO MANAGEMENT

Restaurant not performing well

(i.e. mature restaurants with negative 4-Wall

EBITDA) Established three years ago, the Committee determines

measures to be implemented in order to increase

restaurant’s profitability

• Suitability to sub-franchisee

• Restaurant location

• Profitability evolution

RationaleRestaurant starts performing well

Restaurant continues not

performing well

Sub-franchisee conversion

Restaurant closes

Profitability Committee

SU

B-F

RA

NC

HIS

EE

RATIONALE STRONG CONTROL OF THE FRANCHISEE OPERATION

Increase national footprint – open restaurants in BKB’s non-target markets

Take advantage of fiscal benefits (“SIMPLES”) and operate restaurants that would not meet BKB’s required returns

Accelerate brand awareness in markets where BKB would take longer to reach

SOURCE: BK Brasil18

THE MAIN OBJECTIVE OF TECNOLOGY USAGE IS TO IMPROVE CONSUMER EXPERIENCE IN ALL INTERACTIONS WITH THE BRAND, AND TO ENABLE A BETTER COMPREHENSION OF OUR CLIENT’S WISHES AND BEHAVIOR

SOURCE: BK Brasil

CRM

WI -FI

SELF-ORDER KIOSK

MOBILE APP

SALES TABLET

DELIVERY

CHAT BOT

Builds channel, develops payment methods and helps to understand customer behavior

Improves experience and increases average ticket

Improves experience and collects client data

Develops loyalty program and builds stronger relationship with clients

Improves experience andpromotes friendly interaction

Takes the Burger King experience to client’s house and workplace

Increases digital contact and improves communication

19

WI-FI

+180 restaurants

SOURCE: BK Brasil*Active users: unique users who opened the app at least once on the last 28 days

DELIVERY• +100 restaurants

• Incremental sales

MOBILE APP

Next steps:Roll out to all restaurants;Media investment to support the roll out

• Downloads: +9million• Active users*: +2million

• Digital coupons

SALES TABLET• +400 restaurants

• Higher average ticket

SELF-ORDER KIOSK• +12 restaurants

• Higher average ticket

20

BK APP

Guests are able to order Burger King from anywhere

RESTAURANTS MAP

Map with the location of restaurants nearby

AUTHENTIC EXPERIENCE

Have it your way

PROFITABILITY IMPROVEMENTImproves average ticket

SELF ORDER & PAY

• Feature allows users to order and pay directly through the app

• Guests have more autonomy in the purchase without having to wait in line

MAIN OBJECTIVES

• Improve guest experience

• Communicate new functionalities

• Digitalcouponing

• National roll-out • Enhance CRMwith Big Data

21

22

BEVERAGE OPTIONS: free refill, beer and natural juice

SELF-ORDER KIOSKS in all restaurants

DESSERTS PLATFORM:ice creams, milk shakes and pies

DIGITAL MENU BOARDin all restaurants

CHICKEN SANDWICH PLATFORM developed locally

23

BK BRASIL SIGNED A MASTER FRANCHISE AND DEVELOPMENT AGREEMENT (MFDA) WITH POPEYES® IN BRAZIL, FURTHER SOLIDIFYING ITS LEADING POSITIONING IN THE QSR INDUSTRY IN THE COUNTRY

BURGER KING® Brazil POPEYES®

Significant improvement in brand awareness and preference over past years

More than 793 restaurants in Brazil

2nd largest global chicken QSR brand, with +3,100 restaurants worldwide

Unique brand, with a differentiated product based on a 300-year old culinary tradition

RATIONALE

Chicken is the most consumed protein in Brazil

Leverage on BK Brasil existing capabilities, infrastructure and scale

Attractive opportunity to further optimize capital allocation

Diversification in a profitable, scalable and sizable business

2nd player in Burger and 3rd

largest QSR in number of restaurants

24

More than 8 restaurants in Brazil

SINCE BEING FOUNDED IN 1972 IN NEW ORLEANS, LOUISIANA, POPEYES HAS BROUGHT THE HEART AND SOUL OF LOUISIANA COOKING TO THE WORLD

1972

Founded in New Orleans, Louisiana as “Chicken on the Run”

1976Popeyes begins franchising; opens ~500 locations over the next 10 years

1999

Popeyes surpasses US$1B in system-wide sales for the first time

2008Popeyes name changes to “PopeyesLouisiana Kitchen”

2011

Popeyes opens it 2000th store in Memphis, TN

2017RBI Acquires Popeyes

2018“First POPEYES openings in Brazil”

25

OVER

3,100

26

12 HOURS MARINATED AND HAND BATTERING AND BREADING ARE KEY FACTORS THAT DEMONSTRATE POPEYES COMMITMENT TO QUALITY AND FRESHNESS

CULINARY INTEGRITY BRAND AUTHENTICITYBOLD INNOVATION

• Fresh Prep• 12-hour marination• Hand Battered & Breaded

in restaurant• Proprietary recipe

• Unique Flavor Trends• Special Chicken Cuts• Distinct Sauces & Sides• Differentiated Menu

• Louisiana Heritage• Origin Story Credibility• 7 nations formed a unique

culture

THE POPEYES DIFFERENCE LEADS TO:Taste Preference, Higher Quality Perception & Brand Authenticity

27

45% 46% 47% 46% 48%

41% 40% 39% 39% 38%

14% 14% 14% 14% 14%

2013 2014 2015 2016 2017

Chicken Beef and Veal Pork

28.4 32.6 35.5 39.5 45.554.2

63.671.7 78.9 83.1

0.2 0.2 0.2 0.20.3

0.40.5

0.60.6

0.7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Other Fast Food

Chicken Fast Food

PROTEIN CONSUMPTION BY CATEGORY - BRAZIL(Million of metric tons)

19.5

28.6 32.435.7 39.7

45.854.6

63.872.3 79.5 83.8

17%19.9 20.0 19.5 20.2

FAST FOOD MARKET ESTIMATES - BRAZIL(BRL billion)

CONSUMER TREND KEY MFDA ASPECTS

• More than 90% of consumers intend to increase or maintain Chicken QSR consumption in the future

• Top 3 attributes for Chicken QSR: • Quality of chicken• Taste• Value proposition

• QSR chicken market in Brazil remains considerably underpenetrated vs. other countries

• Currently, there are very few chicken QSR players to serve guest demand

• Mainly concentrated in the Southeast and South regions of Brazil, mostly in Sao Paulo

SOURCE: USDA, Euromonitor, A.T. Kearney28

RIGHTS

• A 20-year MFDA agreement with Popeyes

• Exclusive right to develop, franchise and operate POPEYES® restaurants in Brazil

• Right to manage the advertising fund in Brazil

• Payment of royalties and contribution to marketing fund in line with levels paid for BURGER KING® brand

OBLIGATIONS

• Annual target of minimum number of restaurants to build and operate

• Opening targets will gradually accelerate over the years, achieving a potential of more than 300 restaurants in the first 10 years of contract

29

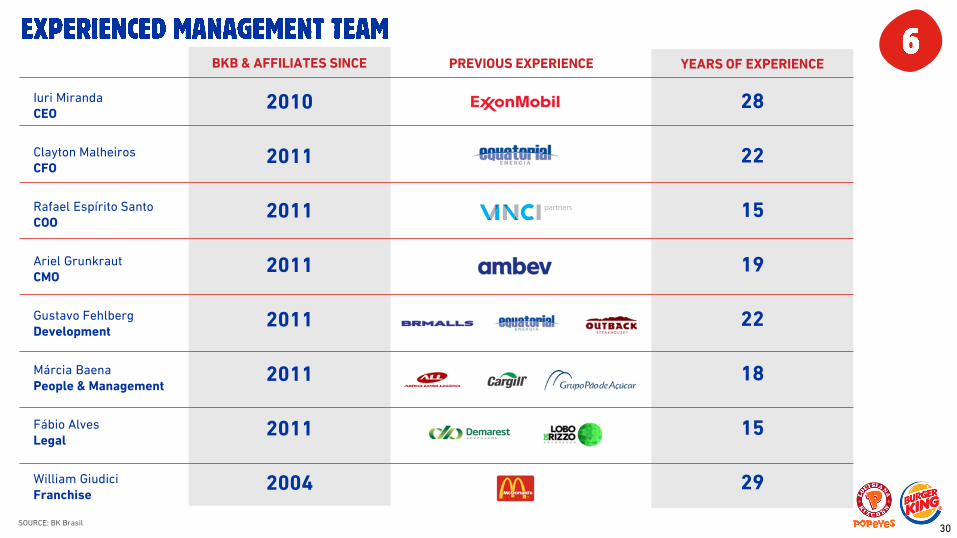

YEARS OF EXPERIENCE

28

22

15

19

22

18

15

29

BKB & AFFILIATES SINCE

2010

2011

2011

2011

2011

2011

2011

2004

Iuri MirandaCEO

Clayton MalheirosCFO

Rafael Espírito SantoCOO

Ariel GrunkrautCMO

Gustavo FehlbergDevelopment

Márcia BaenaPeople & Management

Fábio AlvesLegal

William GiudiciFranchise

PREVIOUS EXPERIENCE

SOURCE: BK Brasil30

COMMITTEE PERIODICITY OVERVIEW DIRECTORS

Sales Weekly Approval / analysis of sales for new restaurants COO / CMO / Development

Engineering Weekly Approval of project layouts for own and sub-franchises restaurants and remodeling Development

Investments Weekly Approval of new restaurants, both own and sub-franchises, and candidates for sub-franchisees CEO / CFO / COO / Development

Building Weekly Approval of the construction company for new restaurants Development

Projects Monthly Monitoring of the monthly evolution of Capex of projects approved for the year (ex-capex of restaurants) Development

Profitability Monthly Monitoring of restaurants below profitability (following specific PDCAs)CEO / CFO / COO / CMO / Development

Monitoring Monthly Analysis and monitoring of restaurants opened for up to 3 months COO / Development

Auditing Monthly Discussions on corporate governance, statutes, and policies -

G&A Management Monthly Detailed monitoring of the evolution and forecast of corporate G&A All

Compensation Semiannually Discussions on stock-option, promotions and compensation CEO

Cash Flow Monthly Monitoring of current and forecasted cash position, investments, debt amortization schedule, and overall liquidity CFO

BOARD OF DIRECTORS

COMPLIANCE

• Audit committee with external independent auditor

• Bi-annual FCPA compliance and annual audit by big 4 accounting firm

• Anonymous whistleblower channel

• Internal controls and effective monitoring + extension to vendors

GUILHERME LINS“Chairman”

Marcelo Penna

Renato Ribeiro

Bruno Zaremba

Rodrigo Galindo

Marcos Grodetzky

Joshua Kobza

INDEPENDENT

31

32

104 164 159 19530462

53 5363

52

166217 212

258

356

2014 2015 2016 2017 2018

RESTAURANT BREAKDOWN (QUARTERLY)

DESSERT CENTERS BREAKDOWN (QUARTERLY)DESSERT CENTERS BREAKDOWN (ANNUAL)

RESTAURANT BREAKDOWN (ANNUAL)(# of restaurants) (# of restaurants)

(# of dessert centers) (# of dessert centers)

+380 restaurants

+190 dessert centers

Owned FranchiseesSOURCE: BK Brasil33

195 201 243 261 30463 65 37 44

52258 266 280 305356

4Q17 1Q18 2Q18 3Q18 4Q18

235341 382 413 48417

2430 32

32

41

5468 81

115

128

112121

171162

421531

601697

793

2014 2015 2016 2017 2018

MALL FREE STANDING IN LINE FRANCHISEE

293 419 480 526 639

TOTAL OWNED RESTAURANTS

413 413 461 465 484

32 3231 32 3281 8391 97 115171 181 134 142

162697 709 717 736 793

4Q17 1Q18 2Q18 3Q18 4Q18

526 528 583 594 639

TOTAL OWNED RESTAURANTS

61 86134

211

2889.2% 9.1% 9.6%11.8% 12.3%

2014 2015 2016 2017 2018

661 950

1.3931.784

2.3482,9% 5,3%

9,9%13,8%

6,5%

2014 2015 2016 2017 2018

(R$ mm, %) (R$ mm, %)

(R$ mm) (R$ mm)

NET REVENUE AND SAME-STORE SALES GROWTH (ANNUAL) NET REVENUE AND SAME-STORE SALES GROWTH (QUARTERLY)

ADJ. EBITDA(1) AND ADJ. EBITDA MARGIN (QUARTERLY)ADJ. EBITDA(1) AND ADJ. EBITDA MARGIN (ANNUAL)

CAGR14-18: +47.5%

+310bps

SOURCE: BK Brasil1 Excludes pre-operanting expenses related to M&A, impairment and SOP expenses

34

523 483 537 611

718

16,2%10,3%

0,0%8,2% 7,1%

4Q17 1Q18 2Q18 3Q18 4Q18

83

36 49

77

125

15,9%

7,5%9,2%

12,6%

17,5%

4Q17 1Q18 2Q18 3Q18 4Q18

70 264 275

(706)

(324)0.5x

3.1x2.1x

(3.4x)

(1.1x)

2014 2015 2016 2017 2018

(R$ mm, xEBITDA) (R$ mm, xEBITDA)

(R$ mm, %) (R$ mm, %)

NET DEBT AND NET DEBT / ADJ. EBITDA(1) (ANNUAL) NET DEBT AND NET DEBT / ADJ. EBITDA(1) (QUARTERLY)

NET INCOME AND NET MARGIN (QUARTERLY)NET INCOME AND NET MARGIN (ANNUAL)

SOURCE: BK Brasil1 Excludes pre-operanting expenses related to M&A, impairment and SOP expenses

35

(706) (636)

(223) (236) (324)

(3,4x)(2,9x)

(1,0x) (1,0x) (1,1x)

4Q17 1Q18 2Q18 3Q18 4Q18

(35.9) (36.8)

(93.5)

3.8

128.0 -5.4% -3.9%

-6.7%

0.2%5.5%

2014 2015 2016 2017 2018

21,8 8,8 8,6

27,0

83,6 4,2%

1,8% 1,6%

4,4%

11,6%

4Q17 1Q18 2Q18 3Q18 4Q18

(R$ mm)

(R$ mm)

CAPEX (ANNUAL) CAPEX (QUARTERLY)

OPERATING CASH FLOW

ACQUISITION OPENINGS, EQUIPMENT AND OTHERS

SOURCE: BK Brasil

ACQUISITION OPENINGS, EQUIPMENT AND OTHERS

36

69 45 58 89146

404

462

4Q17 1Q18 2Q18 3Q18 4Q18

+111.1%

(R$ mm)

17533947

404

221 198

743

2016 2017 2018

166.5

304.7

61.5

67.2 13.4 (84.1)68.6 11.5

Operating CashFlow 2017

Operationalresult

Net financialresult

Depreciationand

amortization

Interest,charges and

others

Change inworking capital

Change in otherassets /

liabilities

Operating CashFlow 2018

37

SOURCE: BK Brasil39

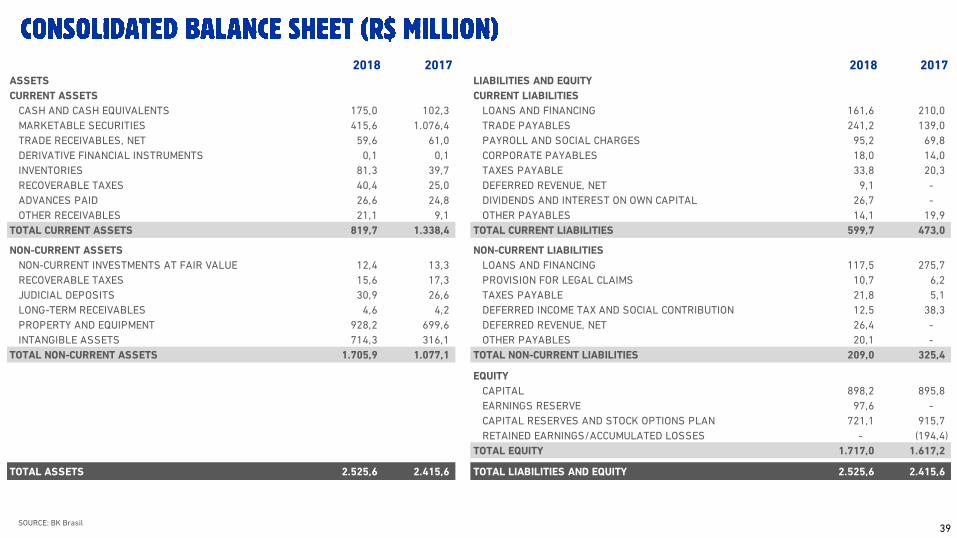

2018 2017 2018 2017ASSETS LIABILITIES AND EQUITY

CURRENT ASSETS CURRENT LIABILITIES

CASH AND CASH EQUIVALENTS 175,0 102,3 LOANS AND FINANCING 161,6 210,0

MARKETABLE SECURITIES 415,6 1.076,4 TRADE PAYABLES 241,2 139,0

TRADE RECEIVABLES, NET 59,6 61,0 PAYROLL AND SOCIAL CHARGES 95,2 69,8

DERIVATIVE FINANCIAL INSTRUMENTS 0,1 0,1 CORPORATE PAYABLES 18,0 14,0

INVENTORIES 81,3 39,7 TAXES PAYABLE 33,8 20,3

RECOVERABLE TAXES 40,4 25,0 DEFERRED REVENUE, NET 9,1 -

ADVANCES PAID 26,6 24,8 DIVIDENDS AND INTEREST ON OWN CAPITAL 26,7 -

OTHER RECEIVABLES 21,1 9,1 OTHER PAYABLES 14,1 19,9

TOTAL CURRENT ASSETS 819,7 1.338,4 TOTAL CURRENT LIABILITIES 599,7 473,0

NON-CURRENT ASSETS NON-CURRENT LIABILITIES

NON-CURRENT INVESTMENTS AT FAIR VALUE 12,4 13,3 LOANS AND FINANCING 117,5 275,7

RECOVERABLE TAXES 15,6 17,3 PROVISION FOR LEGAL CLAIMS 10,7 6,2

JUDICIAL DEPOSITS 30,9 26,6 TAXES PAYABLE 21,8 5,1

LONG-TERM RECEIVABLES 4,6 4,2 DEFERRED INCOME TAX AND SOCIAL CONTRIBUTION 12,5 38,3

PROPERTY AND EQUIPMENT 928,2 699,6 DEFERRED REVENUE, NET 26,4 -

INTANGIBLE ASSETS 714,3 316,1 OTHER PAYABLES 20,1 -

TOTAL NON-CURRENT ASSETS 1.705,9 1.077,1 TOTAL NON-CURRENT LIABILITIES 209,0 325,4

EQUITY

CAPITAL 898,2 895,8

EARNINGS RESERVE 97,6 -

CAPITAL RESERVES AND STOCK OPTIONS PLAN 721,1 915,7

RETAINED EARNINGS/ACCUMULATED LOSSES - (194,4)

TOTAL EQUITY 1.717,0 1.617,2

TOTAL ASSETS 2.525,6 2.415,6 TOTAL LIABILITIES AND EQUITY 2.525,6 2.415,6

40

2018 2017 VAR %NET OPERATING REVENUE 2,348.3 1,783.8 31.6%

GROSS REVENUE FROM SALES 2,541.8 1,917.7 32.5%

GROSS REVENUE FROM SALES DEDUCTIONS (206.1) (148.1) 39.2%

GROSS REVENUE FROM SERVICES 14.3 15.1 -5.1%

GROSS REVENUE FROM SERVICES DEDUCTIONS (1.7) (0.8) 100.0%

COST OF GOOD SOLD (891.3) (687.9) 29.6%

GROSS PROFIT 1,457.0 1,096.0 32.9%

TOTAL SELLING EXPENSES (1,219.7) (935.2) 30.4%

PERSONNEL EXPENSES (404.5) (308.2) 31.2%

ROYALTIES AND MARKETING FUND (215.8) (160.1) 34.8%

EXPENSES WITH OCCUPANCY AND UTILITIES (280.2) (221.9) 26.3%

PRE-OPERATING EXPENSES (9.7) (6.1) 57.7%

DEPRECIATION AND AMORTIZATION (125.1) (110.2) 13.5%

OTHER SELLING EXPENSES (184.4) (128.7) 43.3%

TOTAL GENERAL AND ADMINISTRATIVE EXPENSES (110.5) (95.5) 15.8%

GENERAL AND ADMINISTRATIVE EXPENSES (84.2) (66.4) 26.8%

DEPRECIATION AND AMORTIZATION (8.0) (9.5) -15.5%

EXPENSES WITH MERGER AND ACQUISITIONS (6.7) (2.1) 219.9%

GAIN (LOSS) FROM WRITE-OFF OF PROPERTY, EQUIPMENT AND IMPAIRMENT (7.1) (12.2) -41.9%

GAIN (LOSS) ON CLAIMS 0.0 0.3 -98.7%

COST OF STOCK OPTION PLAN (4.5) (5.5) -18.7%

PROFIT (LOSS) BEFORE FINANCIAL INCOME 126.8 65.3 94.2%

FINANCIAL RESULTS 10.9 (56.3) -

FINANCIAL EXPENSES (44.6) (84.7) -47.3%

FINANCIAL INCOME 55.5 28.4 95.3%

PROFIT (LOSS) BEFORE INCOME TAX AND SOCIAL CONTRIBUTION 137.7 9.0 -

INCOME TAX AND SOCIAL CONTRIBUTION (9.7) (5.2) 85.3%

CURRENT (35.5) - -

DEFERRED 25.8 (5.2) -

NET INCOME FOR THE PERIOD 128.0 3.8 -

1Q16 2Q16 3Q16 4Q16NET OPERATING REVENUE 308.2 325.2 350.9 409.0

GROSS SALES REVENUE 333.8 351.9 380.8 433.5

SALES REVENUE DEDUCTIONS (28.0) (29.8) (32.4) (27.8)

GROSS REVENUE FROM SERVICE RENDERED 2.6 3.2 2.7 3.6

SERVICE REVENUE DEDUCTION (0.2) (0.2) (0.1) (0.3)

COST OF GOOD SOLD (117.8) (125.5) (133.6) (149.4)

GROSS PROFIT 190.5 199.7 217.3 259.6

TOTAL SELLING EXPENSES (182.2) (183.5) (199.8) (210.7)

PERSONNEL EXPENSES (58.9) (62.0) (66.4) (65.6)

ROYALTIES AND MARKETING FUND (30.8) (32.4) (34.1) (38.5)

EXPENSES WITH OCCUPANCY AND UTILITIES (43.9) (36.3) (45.2) (44.6)

PRE-OPERATING EXPENSES (1.2) (1.1) (1.3) (2.6)

DEPRECIATION AND AMORTIZATION (20.1) (24.2) (23.7) (26.2)

OTHER SELLING EXPENSES (27.4) (27.6) (29.1) (33.1)

TOTAL GENERAL AND ADMINISTRATIVE EXPENSES (13.9) (14.8) (18.1) (29.3)

GENERAL AND ADMINISTRATIVE EXPENSES (10.5) (11.2) (14.0) (21.6)

DEPRECIATION AND AMORTIZATION (2.5) (2.5) (2.2) (2.1)

EXPENSES WITH MERGER AND ACQUISITIONS (0.6) (0.7) (0.8) (0.7)

GAIN (LOSS) FROM WRITE-OFF OF PROPERTY, EQUIPMENT AND IMPAIRMENT (0.2) (0.3) (1.0) (4.5)

GAIN (LOSS) ON CLAIMS 0.0 (0.1) (0.0) (0.1)

COST OF STOCK OPTION PLAN - - - (0.3)

PROFIT (LOSS) BEFORE FINANCIAL INCOME (5.6) 1.4 (0.6) 19.7

FINANCIAL RESULTS (18.1) (19.3) (16.9) (46.2)

FINANCIAL EXPENSES (29.2) (35.6) (22.5) (54.8)

FINANCIAL INCOME 11.2 16.2 5.6 8.6

PROFIT (LOSS) BEFORE INCOME TAX AND SOCIAL CONTRIBUTION (23.7) (18.0) (17.5) (26.5)

INCOME TAX AND SOCIAL CONTRIBUTION 1.7 (1.4) (2.2) (5.4)

CURRENT (259.0) (100.0) (1.0) -

DEFERRED 1.7 (1.4) (2.2) (5.4)

NET INCOME (LOSS) (22.1) (19.4) (19.7) (32.0)

SOURCE: BK Brasil41

1Q17 2Q17 3Q17 4Q17NET OPERATING REVENUE 389.9 428.4 443.0 522.5

GROSS SALES REVENUE 421.8 452.1 479.0 564.8

SALES REVENUE DEDUCTIONS (34.4) (27.3) (39.9) (46.5)

GROSS REVENUE FROM SERVICE RENDERED 2.6 3.8 4.2 4.5

SERVICE REVENUE DEDUCTION (0.1) (0.2) (0.3) (0.3)

COST OF GOOD SOLD (150.1) (162.2) (170.0) (205.6)

GROSS PROFIT 239.8 266.2 273.0 316.9

TOTAL SELLING EXPENSES (222.8) (225.2) (236.7) (250.5)

PERSONNEL EXPENSES (76.0) (71.6) (79.5) (81.1)

ROYALTIES AND MARKETING FUND (37.7) (41.7) (42.6) (38.0)

EXPENSES WITH OCCUPANCY AND UTILITIES (53.0) (54.5) (55.3) (59.2)

PRE-OPERATING EXPENSES (0.5) (1.0) (1.3) (3.3)

DEPRECIATION AND AMORTIZATION (23.6) (24.4) (27.9) (34.3)

OTHER SELLING EXPENSES (31.9) (32.0) (30.1) (34.6)

TOTAL GENERAL AND ADMINISTRATIVE EXPENSES (19.2) (18.0) (22.4) (35.8)

GENERAL AND ADMINISTRATIVE EXPENSES (16.4) (14.3) (14.9) (20.7)

DEPRECIATION AND AMORTIZATION (1.8) (1.7) (3.9) (2.2)

EXPENSES WITH MERGER AND ACQUISITIONS (0.4) (0.3) (0.8) (0.7)

GAIN (LOSS) FROM WRITE-OFF OF PROPERTY, EQUIPMENT AND IMPAIRMENT (0.8) (1.7) (0.4) (9.4)

GAIN (LOSS) ON CLAIMS 0.2 - 0.1 0.0

COST OF STOCK OPTION PLAN - - (2.6) (2.9)

PROFIT (LOSS) BEFORE FINANCIAL INCOME (2.2) 23.1 13.9 30.6

FINANCIAL RESULTS (15.8) (14.6) (18.7) (7.2)

FINANCIAL EXPENSES (24.0) (18.6) (27.0) (15.1)

FINANCIAL INCOME 8.2 4.1 8.3 7.9

PROFIT (LOSS) BEFORE INCOME TAX AND SOCIAL CONTRIBUTION (18.1) 8.5 (4.8) 23.4

INCOME TAX AND SOCIAL CONTRIBUTION (1.9) (1.6) (0.1) (1.6)

CURRENT - - - -

DEFERRED (1.9) (1.6) (0.1) (1.6)

NET INCOME (LOSS) (20.0) 6.9 (4.9) 21.8

SOURCE: BK Brasil42

1Q18 2Q18 3Q18 4Q18NET OPERATING REVENUE 482.5 536.9 610.9 718.1

GROSS SALES REVENUE 523.3 578.7 662.9 776.9

SALES REVENUE DEDUCTIONS (43.7) (45.0) (55.1) (62.3)

GROSS REVENUE FROM SERVICE RENDERED 3.3 3.5 3.5 4.1

SERVICE REVENUE DEDUCTION (0.4) (0.4) (0.4) (0.5)

COST OF GOOD SOLD (185.2) (205.2) (228.4) (272.5)

GROSS PROFIT 297.3 331.6 382.5 445.6

TOTAL SELLING EXPENSES (265.8) (292.7) (316.3) (344.9)

PERSONNEL EXPENSES (89.7) (100.4) (105.5) (108.9)

ROYALTIES AND MARKETING FUND (45.3) (47.5) (57.3) (65.6)

EXPENSES WITH OCCUPANCY AND UTILITIES (64.0) (64.3) (72.7) (79.3)

PRE-OPERATING EXPENSES (0.9) (0.7) (2.5) (5.6)

DEPRECIATION AND AMORTIZATION (27.7) (31.6) (31.3) (34.5)

OTHER SELLING EXPENSES (38.2) (48.1) (47.1) (51.1)

TOTAL GENERAL AND ADMINISTRATIVE EXPENSES (28.6) (27.1) (26.6) (28.2)

GENERAL AND ADMINISTRATIVE EXPENSES (23.7) (21.8) (23.3) (15.4)

DEPRECIATION AND AMORTIZATION (1.9) (2.1) (2.0) (2.1)

EXPENSES WITH MERGER AND ACQUISITIONS (0.9) (1.6) (0.6) (3.6)

GAIN (LOSS) FROM WRITE-OFF OF PROPERTY, EQUIPMENT AND IMPAIRMENT (1.1) (0.5) 0.4 (6.0)

COST OF STOCK OPTION PLAN (1.1) (1.1) (1.1) (1.1)

PROFIT (LOSS) BEFORE FINANCIAL INCOME 2.9 11.9 39.6 72.5

FINANCIAL RESULTS 8.0 (2.5) 2.3 3.0

FINANCIAL EXPENSES (11.6) (13.2) (9.4) (10.5)

FINANCIAL INCOME 19.6 10.7 11.7 13.5

PROFIT (LOSS) BEFORE INCOME TAX AND SOCIAL CONTRIBUTION 10.9 9.4 42.0 75.5

INCOME TAX AND SOCIAL CONTRIBUTION (2.1) (0.8) (14.9) 8.1

CURRENT (1.4) (0.1) (13.0) (21.0)

DEFERRED (0.6) (0.8) (1.9) 29.1

NET INCOME (LOSS) 8.8 8.6 27.0 83.6

SOURCE: BK Brasil43

2018 2017CASH FLOW FROM OPERATING ACTIVITIES 304.7 166.5

CASH GENERATED BY OPERATING ACTIVITIES 321.8 263.8

EARNINGS (LOSS) BEFORE INCOME TAX AND SOCIAL CONTRIBUTION 137.7 9.0

DEPRECIATION AND AMORTIZATION OF PROPERTY AND EQUIPMENT AND INTANGIBLE ASSETS 133.1 119.7

INTEREST, CHARGES, EXCHANGE DIFFERENCES AND MONETARY VARIATIONS (7.6) 67.4

OTHERS 58.5 67.6

CHANGES IN ASSETS AND LIABILITIES

TRADE RECEIVABLES,NET 8.5 (27.3)

INVENTORIES (39.4) (8.9)

RECOVERABLE TAXES (12.0) (2.0)

ADVANCES PAID (1.5) (16.1)

TRADE AND RENTAL PAYABLES 96.6 58.6

PAYROLL AND SOCIAL CHARGES (10.1) (11.1)

PAYMENT OF INTEREST ON LOANS AND FINANCINGS (30.8) (68.2)

OTHERS CHANGES IN ASSETS AND LIABILITIES (28.4) (22.3)

NET CASH USED IN INVESTING ACTIVITIES 6.0 (1,208.4)

PURCHASES OF PROPERTY AND EQUIPMENT (321.4) (172.2)

PURCHASES OF INTANGIBLE ASSETS (17.5) (25.6)

CONSIDERATION PAID ON THE ACQUISITION OF INVESTMENTS (360.9) -

INVESTMENT IN MARKETABLE SECURITIES (722.9) (1,304.9)

REDEMPTION OF MARKETABLE SECURITIES 1,428.7 294.4

NET CASH USED IN FINANCING ACTIVITIES (238.1) 887.3

CAPITAL CONTRIBUTED IN THE PERIOD 2.4 890.1

SHARE PREMIUM INCREASE, NET OF ISSUANCE COSTS - 178.8

SHARES ISSUANCE COSTS (4.7) (48.6)

PAYMENT OF LOANS AND FINANCINGS (PRINCIPAL) (235.7) (121.3)

PAYMENT OF CONTINGENT CONSIDERATION AND PAYABLES FOR ACQUISITION OF SUBSIDIARIES - (11.6)

INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 72.6 (154.6)

OPENING BALANCE OF CASH AND CASH EQUIVALENTS 102.3 256.9

CLOSING BALANCE OF CASH AND CASH EQUIVALENTS 175.0 102.3 SOURCE: BK Brasil44

EBITDA AND ADJUSTED EBITDA¹

NET DEBT AND LEVERAGE

SOURCE: BK Brasil Note: 1- Adjusted EBITDA is a non-accounting measure adopted by the Company, which corresponds to EBITDA adjusted by pre-operating expenses, expenses with mergers and acquisitions mergers, and other expenses, which the Company’sManagement believes are not part of the normal course of business and/or distort any analysis of the Company’s operating performance, including: (i) write-off of property and equipment (damages, obsolescence, gain (loss) from asset divestment andimpairment); and (ii) costs with the stock option plan)

45

EBITDA - R$ MILLION 4Q18 4Q17 VAR % 3Q18 VAR % 2018 2017 VAR %NET INCOME FOR THE PERIOD 83.6 21.8 283.2% 27.0 209.4% 128.0 3.8 -

(+) FINANCIAL INCOME (LOSS) (3.0) 7.2 - (2.3) 29.0% (10.9) 56.3 -

(+) DEPRECIATION AND AMORTIZATION 36.6 36.4 0.4% 33.3 9.8% 133.1 119.7 11.2%

(+/-) INCOME TAX AND SOCIAL CONTRIBUTION (8.1) 1.6 - 14.9 - 9.7 5.2 85.3%

EBITDA 109.0 67.0 62.7% 72.9 49.6% 260.0 185.0 40.5%

EBITDA MARGIN 15.2% 12.8% 240bps 11.9% 330bps 11.1% 10.4% 70bps

(+) OTHERS EXPENSES* 6.0 9.4 -35.6% (0.4) - 7.1 11.9 -40.4%

(+) COST OF STOCK OPTION PLAN 1.1 2.9 -61.7% 1.1 -0.1% 4.5 5.5 -18.7%

(+) MERGE AND ACQUISITION EXPENSES 3.6 0.7 453.4% 0.6 464.5% 6.7 2.1 219.9%

(+) PRE-OPERATING EXPENSES 5.6 3.3 68.4% 2.5 126.9% 9.7 6.1 57.7%

ADJUSTED EBITDA 125.4 83.3 50.6% 76.7 63.4% 288.0 210.7 36.7%

ADJUSTED EBITDA MARGIN 17.5% 15.9% 160bps 12.6% 490bps 12.3% 11.8% 50bps

*Include write-off of property and equipment (damages, obsolescence, gain (loss) from asset divestment and impairment).

1

NET DEBT - R$ MILLION DEC/18 DEC/17 VAR % SEP/18 VAR %LOANS AND FINANCINGS 279.1 485.7 -42.5% 409.9 -31.9%

CURRENT 161.6 210.0 -23.1% 278.9 -42.1%

NON-CURRENT 117.5 275.7 -57.4% 131.1 -10.3%

CASH AND CASH QUIVALENTS AND MARKETABLE SECURITIES 602.9 1,192.0 -49.4% 646.2 -6.7%

CASH AND CASH EQUIVALENTS AND MARKETABLE SECURITIES (CURRENT) 590.6 1,178.7 -49.9% 633.4 -6.8%

MARKETABLE SECURITIES (NON-CURRENT) 12.4 13.3 -7.0% 12.8 -3.4%

NET DEBT (323.8) (706.3) -54.2% (236.3) 37.0%

ADJUSTED EBITDA (12M) 288.0 210.7 36.7% 245.9 17.1%

NET DEBT/ TOTAL ADJUSTED EBITDA (12M) (1.1x) (3.4x) 2.2x (1.0x) (0.2x)

Top Related

Copyright © 2022 FDOKUMEN