Bahasa

Halaman

Hukum

AN ASSESSMENT OF INTERNET BANKING SERVICE QUALITY

by

MASOPHA NEHEMIA MOLAPO

Short dissertation

Submitted in partial fulfilment of the requirements of the degree

MASTER COMMERCII

in

Business Management

at

UNIVERSITY OF JOHANNESBURG

STUDY LEADER: Mr C. SCHEEPERS

October 2008

JOHANNESBURG

i

Abstract

Extensive studies have been done in the past on measuring service quality where the

service is delivered on a face-to-face encounter. This study assesses and measures

online service quality where there is no face-to-face encounter. The service quality

measures are particularly on Internet Banking service. The research problem has

been stated as the lack of insight into customer perceptions on Internet Banking

service quality by management in South African banks. The purpose of this study was

to explore customers’ perceptions on key electronic service dimensions or factors of

Internet Banking service quality. The primary objective of the study was to have an

insight into how Internet Banking customers in South Africa perceive their respective

banks’ performance on pre-defined electronic service quality dimensions. The

secondary objective was to determine if there was any difference in Internet Banking

service quality perception based on age, gender, or primary bank offering the service

(service provider).

Even though online shopping and Internet Banking are online services there are

subtle differences between the two services. With online shopping there is a physical

item that gets traded and in Internet Banking only services are traded. It is for this

reason that the original E-S-Q instrument was slightly adjusted. Some of the

dimensions that were excluded from the original E-S-Q instrument include flexibility,

price knowledge and customization

Given the purpose and objectives of the study a quantitative approach was taken as

the major research approach for the study. The sampling design was a non-

probability sampling one because the convenience method of sampling was used.

The survey population was all online banking users, utilizing services from South

African banks. A slightly revised electronic service quality (E-S-Q), a service quality

measurement instrument, was used in this study. Data was collected via a web based

self administered survey. The original E-S-Q instrument measured customer service

quality from an online shopping experience point of view. This study aimed at

gleaning respondents’ perceptions on key Internet Banking service dimensions.

The study involved collecting primary data through a structured survey questioning

which was followed by statistical analysis of the data. The objective was to generalise

about online banking customers’ perceptions on the quality of Internet Banking

ii

service. To collect primary data the Internet survey method was used. In essence, the

combination of the quantitative approach and the survey method was utilised in this

study.

The findings and conclusion of the study is that the overall respondents’ perception on

Internet Banking service quality was a satisfactory one. The Internet Banking service

quality perceptions are not influenced by who the service provider is, age or gender.

Respondents’ perceptions were neutral or indifferent on the responsiveness service

quality dimension. Lastly there were five dimensions that the respondents evaluated

Internet Banking service quality on, that of efficiency, performance, security,

responsiveness and contact.

iii

Declaration of Original Work

AFFIDAVIT: MASTER’S AND DOCTORAL STUDENTS TO WHOM IT MAY CONCERN

This serves to confirm that I Masopha Nehemia Molapo

ID Number 6112025743086

Student number 200610108 enrolled for the

Qualification: M.Com

Faculty: Business Management

Herewith declare that my academic work is in line with the Plagiarism Policy of the

University of Johannesburg which I am familiar with. I further declare that the work

presented in the minor dissertation is authentic and original unless clearly indicated

otherwise and in such instances full reference to the source is acknowledged and I do

not pretend to receive any credit for such acknowledged quotations, and that there is

no copyright infringement in my work. I declare that no unethical research practices

were used or material gained through dishonesty. I understand that plagiarism is a

serious offence and that should I contravene the Plagiarism Policy notwithstanding

signing this affidavit, I may be found guilty of a serious criminal offence (perjury) that

would amongst other consequences compel the UJ to inform all other tertiary

institutions of the offence and to issue a corresponding certificate of reprehensible

academic conduct to whomever requests such a certificate from the institution.

Signed at Johannesburg on this 17 day of March 2009. Signature__________________________________ Name: Masopha Molapo STAMP COMMISSIONER OF OATHS Affidavit certified by a Commissioner of Oaths This affidavit conforms with the requirements of the JUSTICES OF THE PEACE AND COMMISSIONERS OF OATHS ACT 16 OF 1963 and the applicable Regulations published in the GG GNR 1258 of 21 July 1972; GN 903 of 10 July 1998; GN 109 of 2 February 2001 as amended.

iv

Acknowledgements

First and foremost I would like to thank my saviour, the Almighty God, for His love and

guidance, for granting me the strength to persevere and the ability to succeed.

Secondly I would like to express my sincere gratitude to my wife Thuso, my children

Khanyapa, Thato and Refiloe, for their love, understanding and patience they gave

me when I could not spend quality time with them during my studies. I am also

thankful to my brothers and sisters for the encouragement and support they gave me

during these trying times.

Lastly I would also like to express my gratitude to the following persons:

• Mr. Cor Scheepers for his supervision, advice, guidance and support.

• Professor Adele Thomas for her encouragement and continued drive in

assisting me to complete this dissertation.

• My friends, colleagues, business partners and my family for being available as

a sounding board in the process of writing this dissertation.

• My language editor, Mr Patrick Radebe, for his editorial work on this document.

• All those who participated in the survey, without whom this study would not

have been possible.

• University of Johannesburg statistical services (STATKON) for assisting me in

designing, hosting the online survey and completing the statistical analysis.

v

TABLE OF CONTENTS Page

Abstract.......................................................................................................................i

Declaration of Original Work................................................................................... iii

Acknowledgements.................................................................................................. iv

Chapter ONE..............................................................................................................1

INTRODUCTION.........................................................................................................1

1.1 Background of the study ...............................................................................1

1.1.1 Historical background .............................................................................1

1.1.2 Banking and technology..........................................................................2

1.1.3 Internet service quality ............................................................................3

1.1.4 Internet Banking......................................................................................4

1.2 Problem statement: .......................................................................................5

1.3 Objective / purpose .......................................................................................6

1.4 A brief outline of the research methodology..................................................6

1.4.1 The research methodology .....................................................................6

1.4.2 The research population .........................................................................6

1.4.3 The sampling method .............................................................................6

1.4.4 Data Collection........................................................................................6

1.5 An outline of the remainder of the dissertation..............................................7

1.6 Conclusion ....................................................................................................8

Chapter TWO .............................................................................................................9

LITERATURE REVIEW ..............................................................................................9

2.1 Introduction. ..........................................................................................................9

2.2 Traditional Services ....................................................................................10

2.2.1 Definition and characteristics of services ..............................................10

2.2.2 Traditional service quality......................................................................11

2.2.3 SERVQUAL ..........................................................................................16

2.2.4 Traditional banking service quality ........................................................17

2.3 Electronic Services (e- Services) ................................................................18

2.3.1 Definition and characteristics of e-Services ..........................................18

2.3.2 Electronic Service quality ......................................................................20

2.3.3 Understanding and measuring e-Service quality...................................23

2.4 Online systems quality ................................................................................24

2.4.1 Definition of online systems quality .......................................................24

2.4.2 Characteristics of online systems quality ..............................................25

vi

2.4.3 Measuring online systems quality .........................................................26

2.5 Internet Banking..........................................................................................30

2.5.1 Definition of Internet Banking................................................................30

2.5.2 Characteristics of Internet Banking .......................................................30

2.5.3 Internet Banking Service quality............................................................33

2.5.4 Measuring Internet Banking service quality...........................................35

2.6 Conclusion ..................................................................................................35

Chapter THREE .......................................................................................................38

RESEARCH METHODOLOGY.................................................................................38

3.1 Introduction .................................................................................................38

3.2 Research design .........................................................................................38

3.3 Research population ...................................................................................39

3.4 Sampling .....................................................................................................41

3.4.1 Sampling methodology..........................................................................41

3.4.2 Sample size ..........................................................................................42

3.5 Research instrument ...................................................................................43

3.6 Data Collection............................................................................................44

3.7 Data Analysis ..............................................................................................45

3.8 Ethical Considerations ................................................................................46

3.9 Conclusion ..................................................................................................47

Chapter FOUR .........................................................................................................48

PRESENTATION OF RESULTS ..............................................................................48

4.1 Introduction. ................................................................................................48

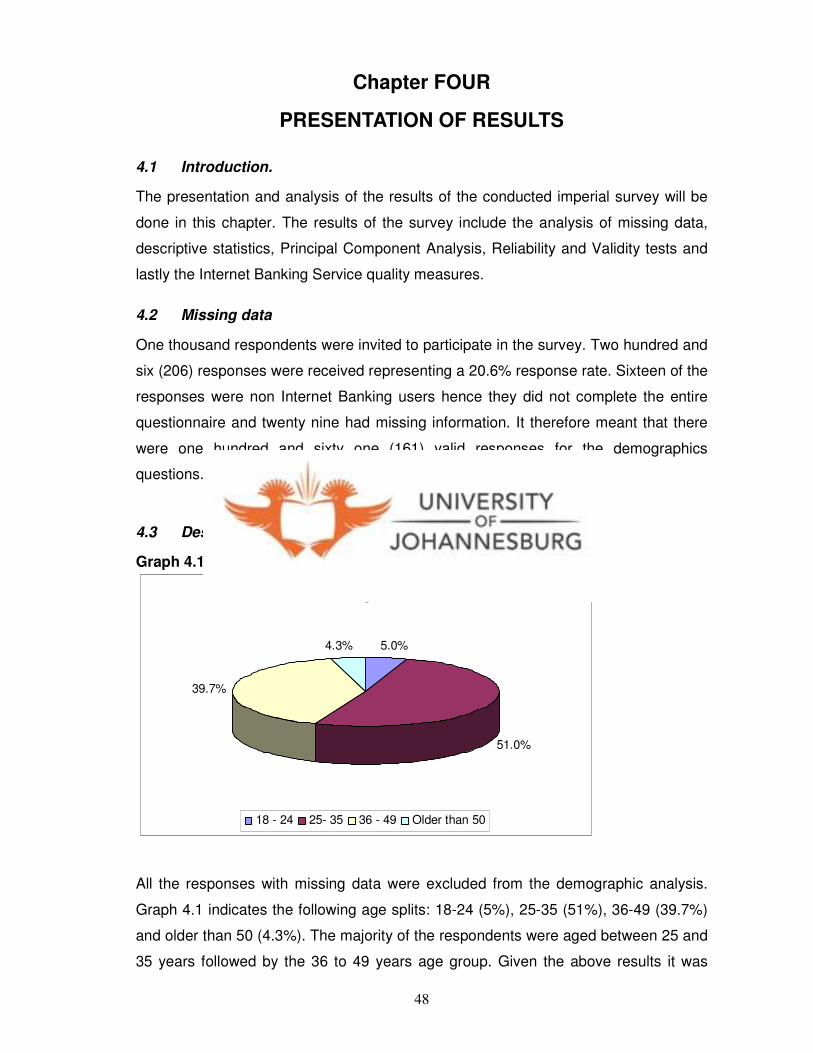

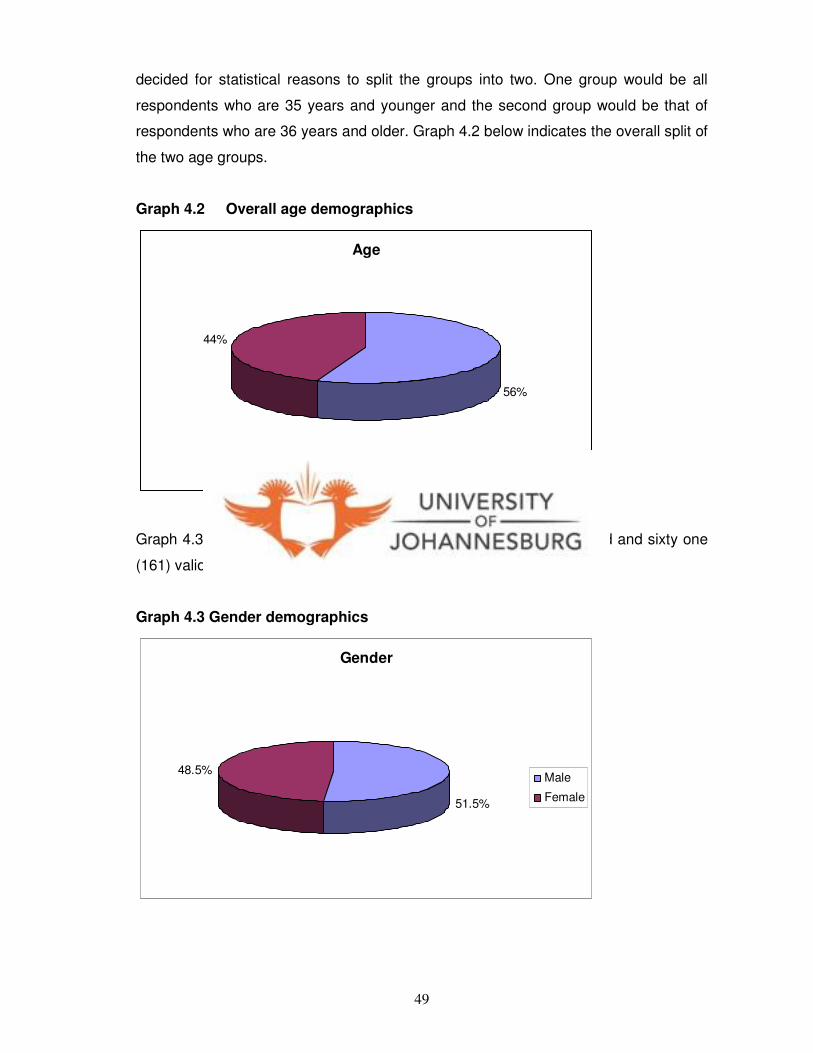

4.2 Missing data................................................................................................48

4.3 Descriptive Statistics ...................................................................................48

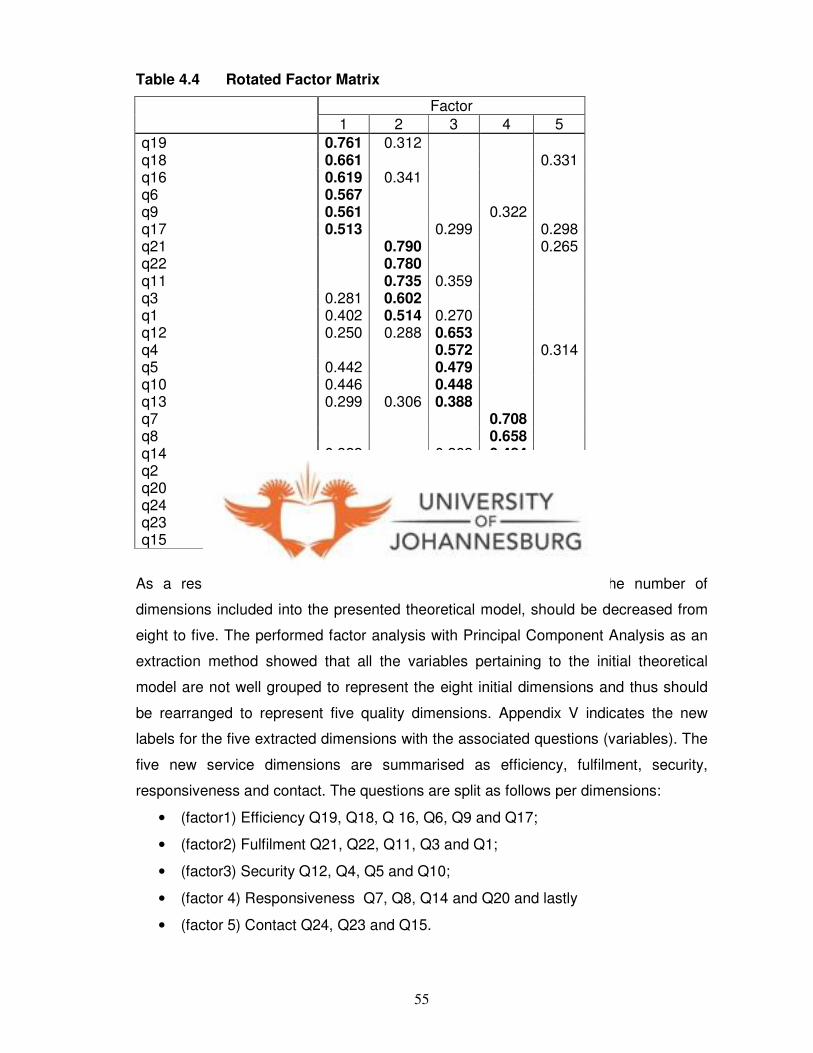

4.4 Principal Component Analysis ....................................................................51

4.5 Reliability and Validity Tests .......................................................................56

4.6 Internet Banking service quality measures .................................................58

Chapter FIVE............................................................................................................69

INTERPRETATION OF RESULTS ...........................................................................69

5.1 Introduction. ................................................................................................69

5.2 Findings ......................................................................................................69

5.3 Findings linked to the literature ...................................................................70

5.3.1 Characteristics of service ......................................................................70

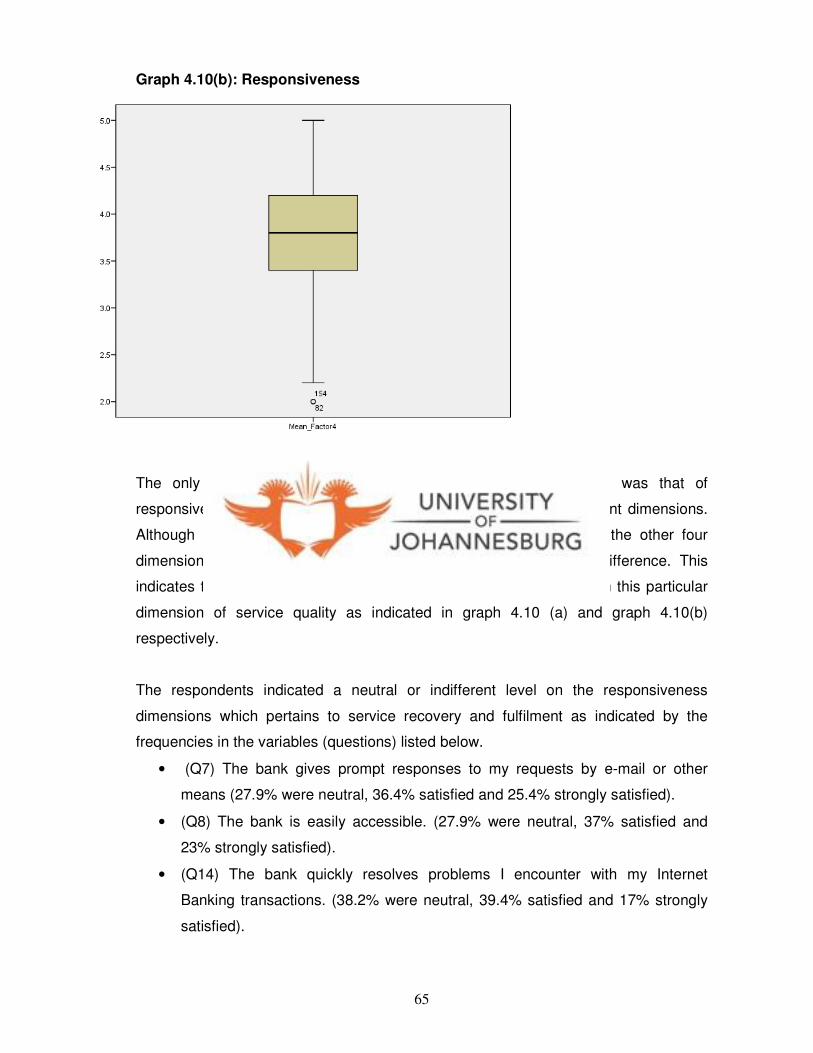

5.3.2 Responsiveness in service recovery.....................................................70

vii

5.3.3 GAPS model .........................................................................................71

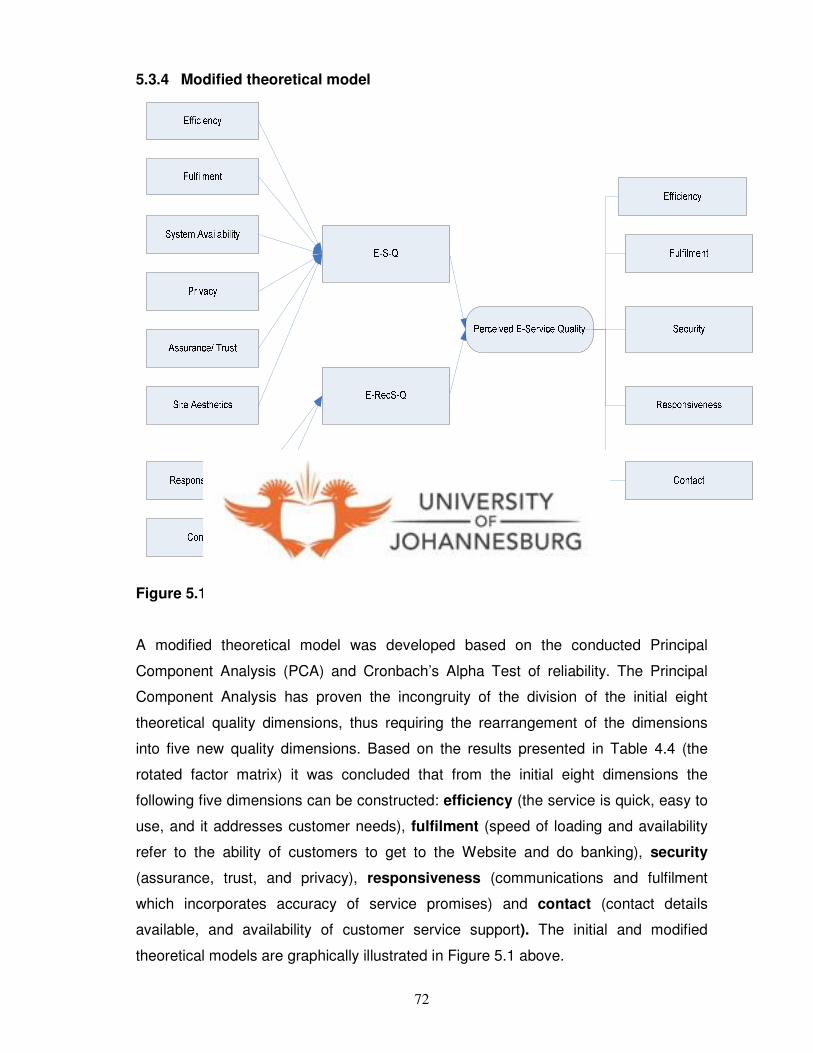

5.3.4 Modified theoretical model ....................................................................72

5.4 Limitations to the study ...............................................................................73

5.5 Conclusion ..................................................................................................73

Chapter SIX..............................................................................................................74

CONCLUSION AND RECOMMENDATIONS ...........................................................74

6.1 Summary of research objectives and major findings...................................74

6.2 Recommendations ......................................................................................75

6.3 Suggestions for further study ......................................................................76

REFERENCES..........................................................................................................77

APPENDICES...........................................................................................................81

viii

List of Tables Page

Table 2.1: WebQual 4.0 Instrument ......................................................................... 27

Table 2.2: E-S-Q instrument .................................................................................... 28

Table 2.3:E-RecS-Qual............................................................................................ 29

Table 2.4: Retail banking services and distribution channels................................... 32

Table 2.5: Service dimensions and related categories............................................. 35

Table 4.1: KMO and Bartlett’s Tests ........................................................................ 51

Table 4.2:Communalities of the twenty four variables.............................................. 52

Table 4.3: Total Varience explained......................................................................... 53

Table 4.4: Rotated Factor Matrix.............................................................................. 55

Table 4.5: Cronbach’s Alpha scores ........................................................................ 57

Table 4.6: Potential Maximum Validity Coefficient ................................................... 57

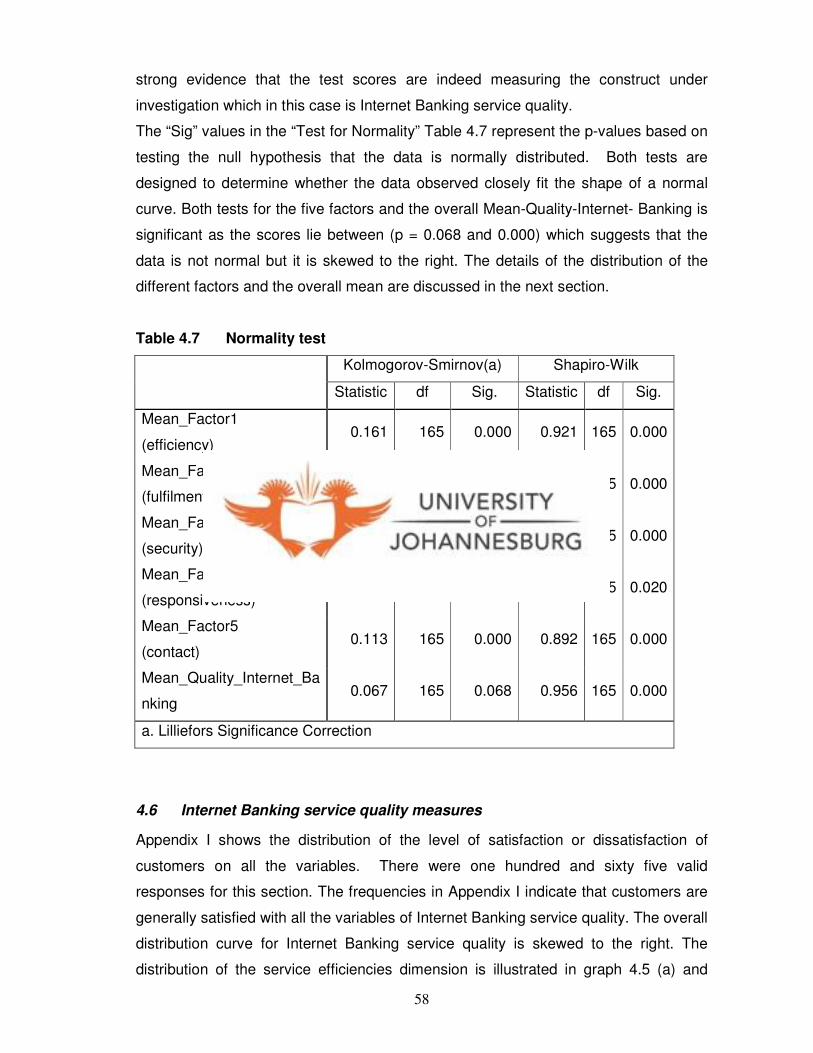

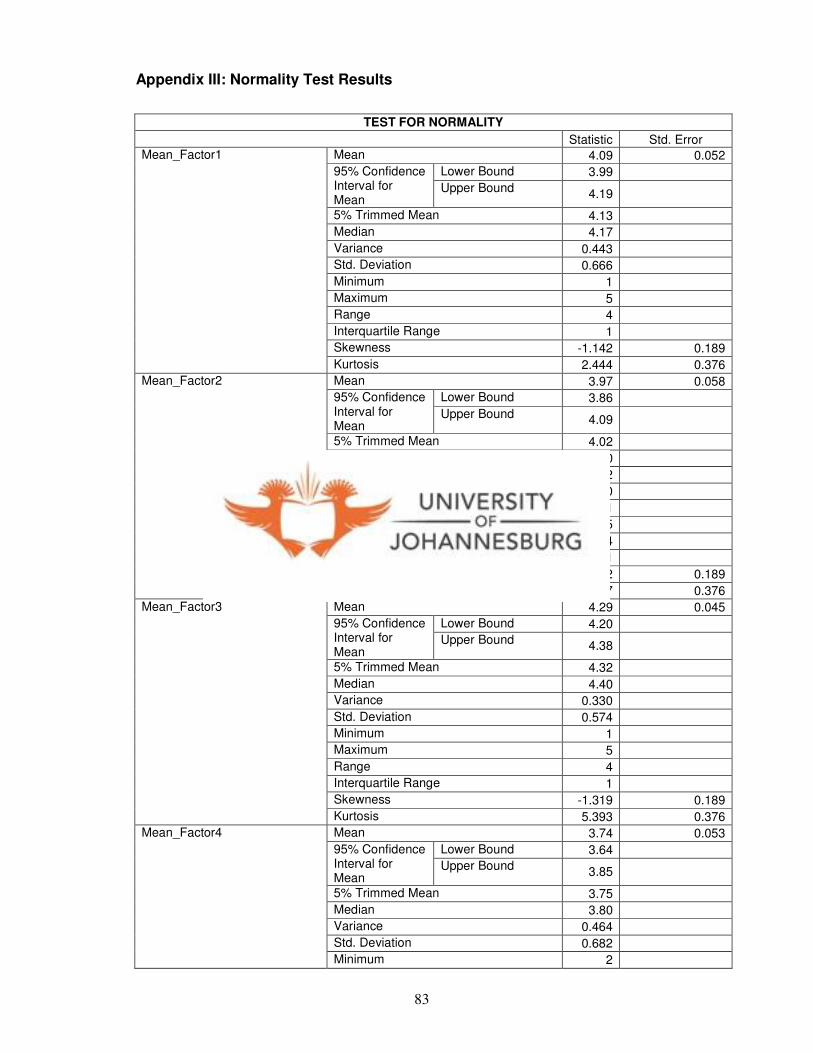

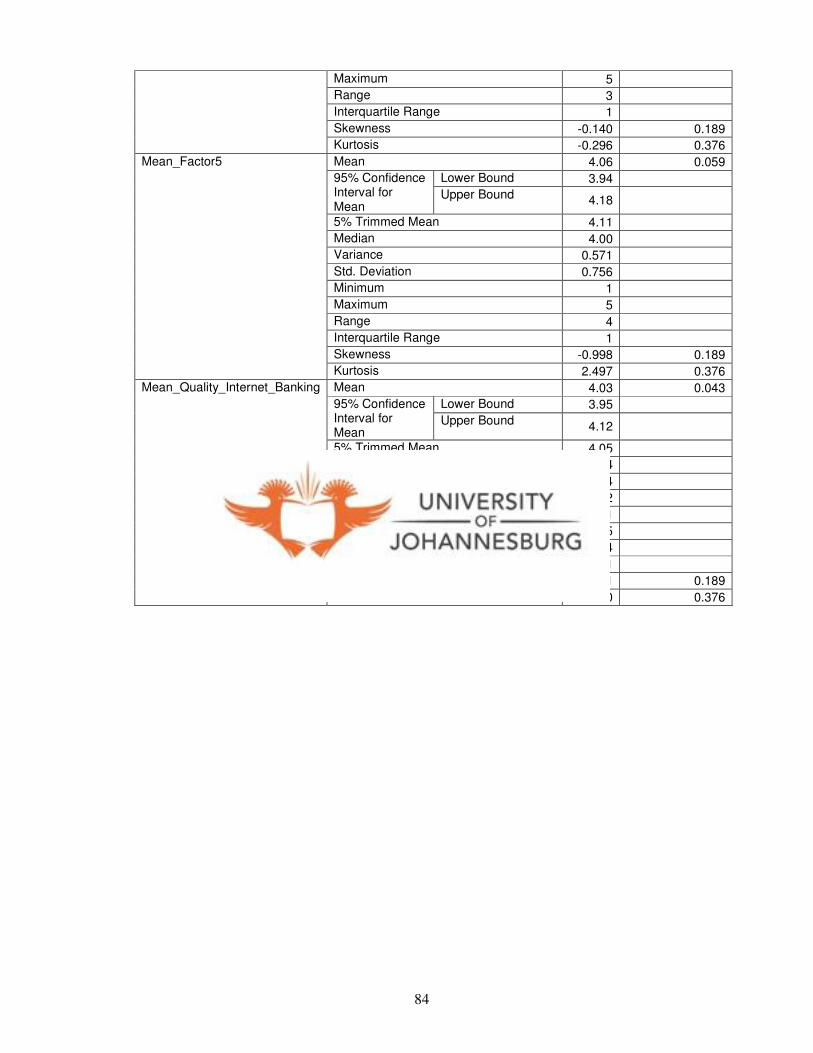

Table 4.7: Normality Test......................................................................................... 58

Table 4.8: ANOVA T-Test for Age............................................................................ 66

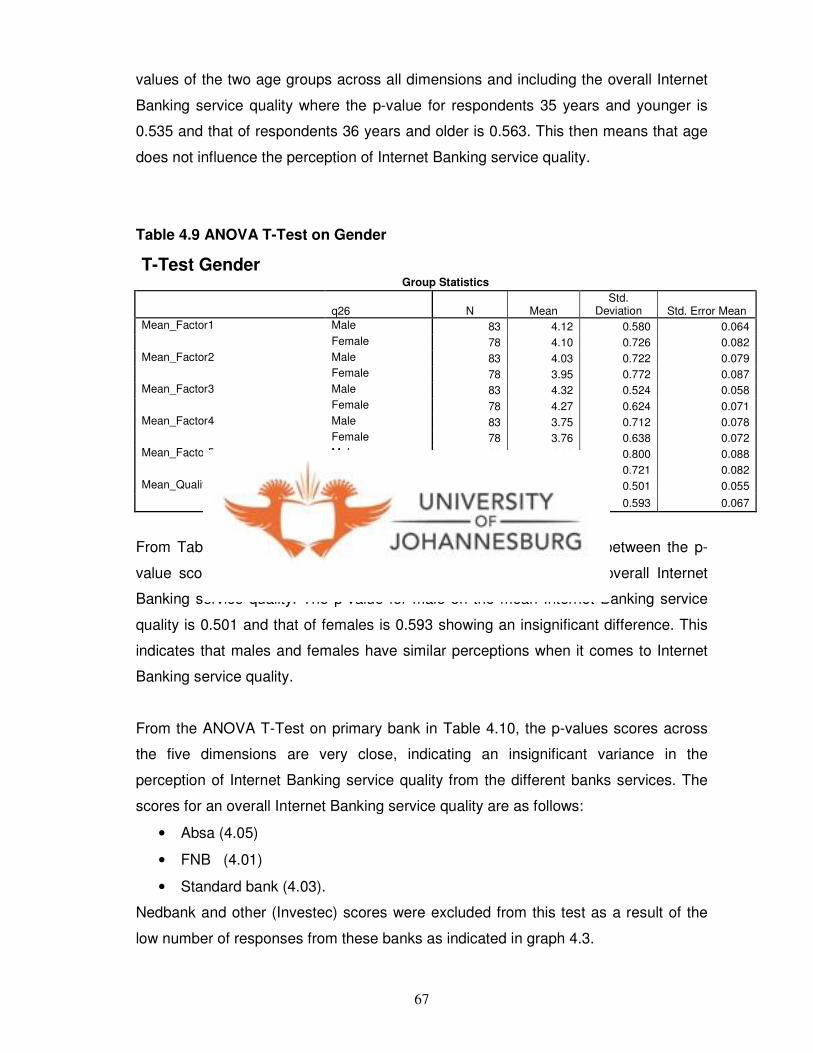

Table 4.9: ANOVA T-Test for Gender ...................................................................... 67

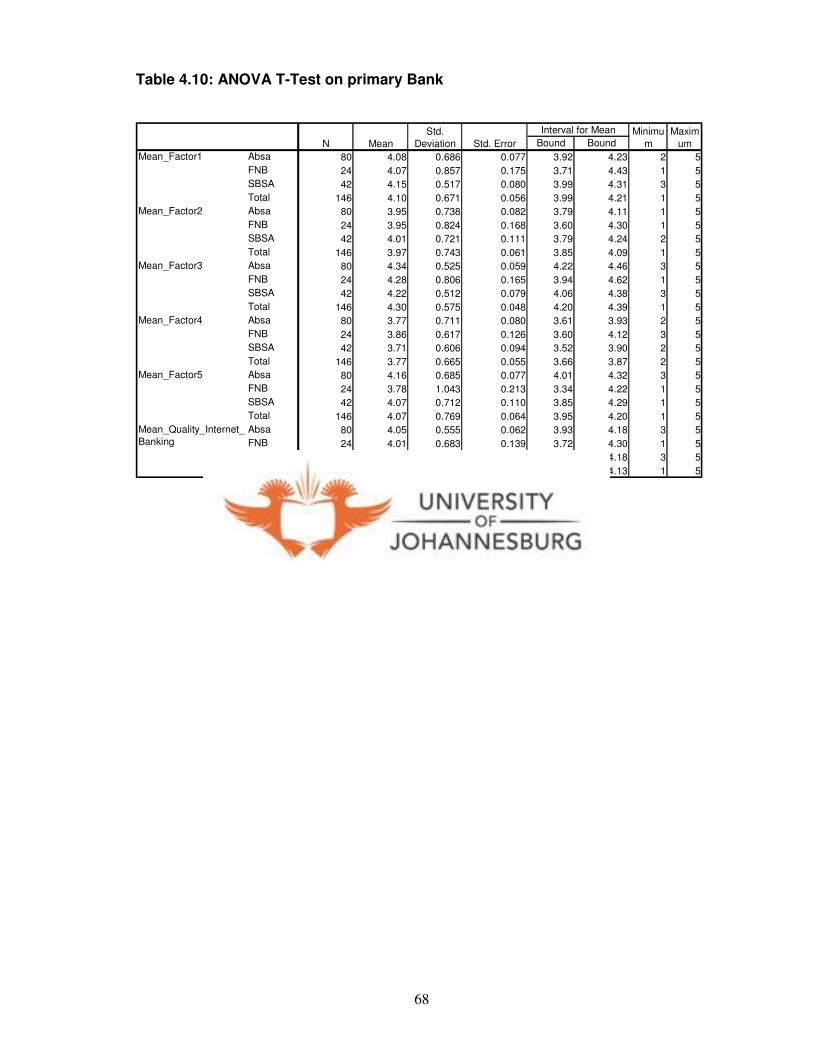

Table 4.10:ANOVA T-Test for primary bank ............................................................ 68

ix

List of Figures Page

Figure 2.1: GAPS model of service quality .............................................................. 13

Figure 2.2: Extended GAPS model if service quality................................................ 14

Figure 2.3:Possible levels of customer expectations ............................................... 15

Figure 2.4:Inherent characteristics of systems......................................................... 19

Figure 2.5: Conceptual model for understanding quality.......................................... 20

Figure 2.6: e-Service quality model.......................................................................... 22

Figure 2.7: Conceptual model for e-SQ ................................................................... 24

Figure 2.8: Website Portal Quality ........................................................................... 25

Figure 2.9: Changes in the banking sector .............................................................. 31

Figure 2.10:Internet Banking perceived qulaity model ............................................. 34

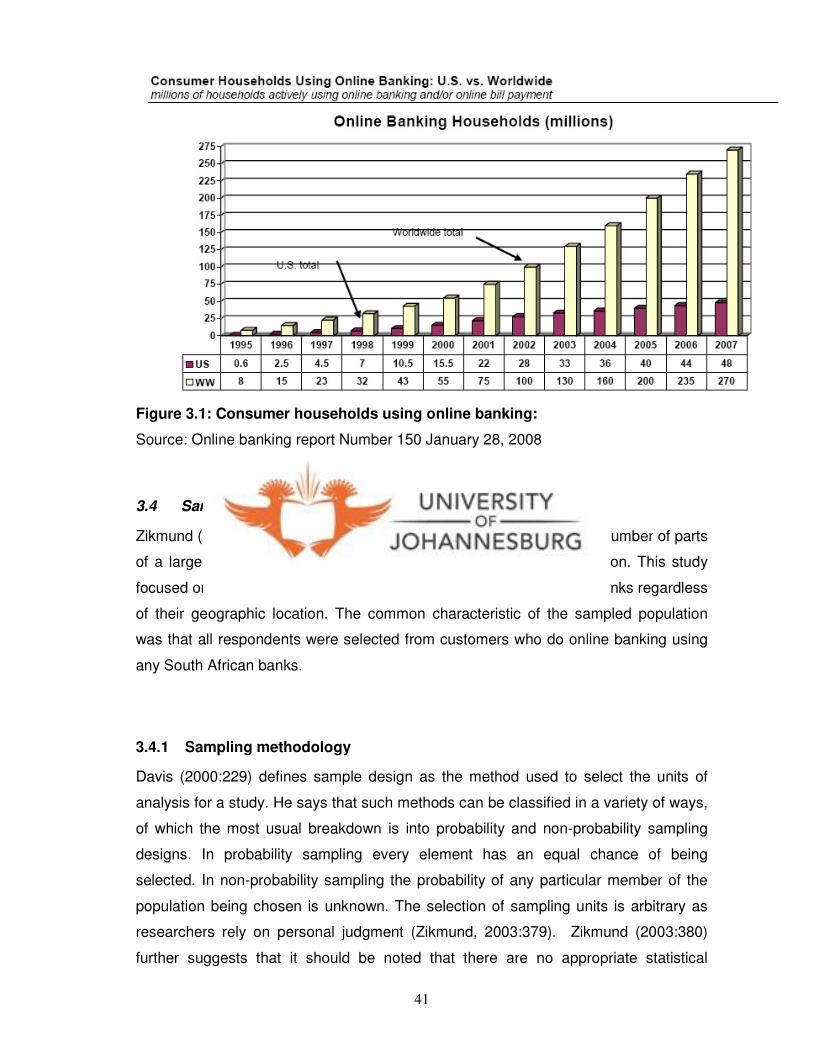

Figure 3.1: Consumer households using Internet Banking ...................................... 41

Figure 5.1: Initial and modified theoretical model..................................................... 72

Appendices

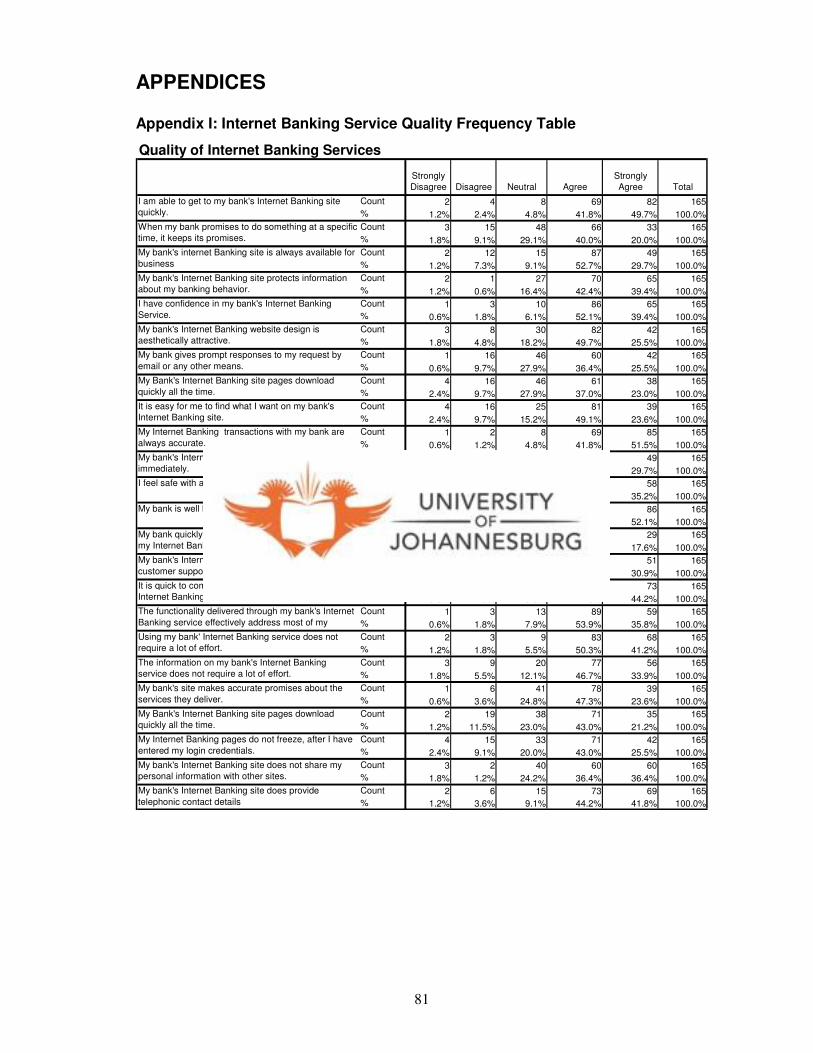

Appendix I: Internet Banking Service Quality Frequency Table ................................ 81

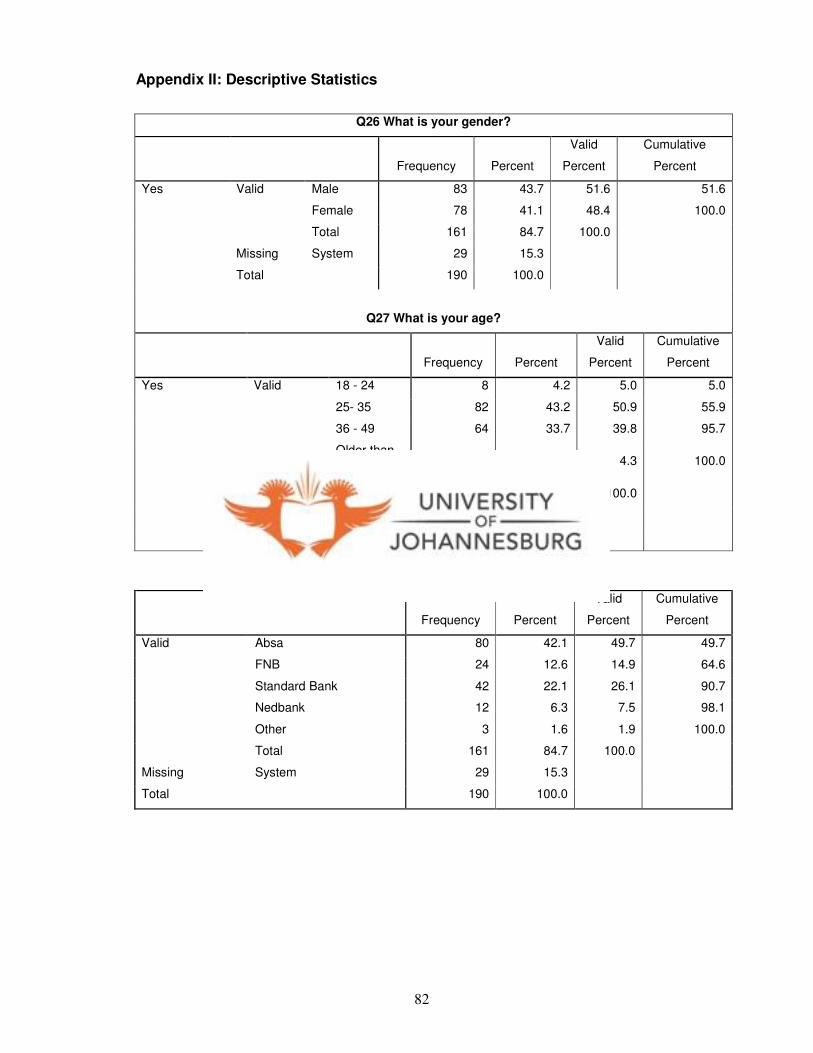

Appendix II: Descriptive Statistics ............................................................................. 82

Appendix III:Normality Test results ...........................................................................83

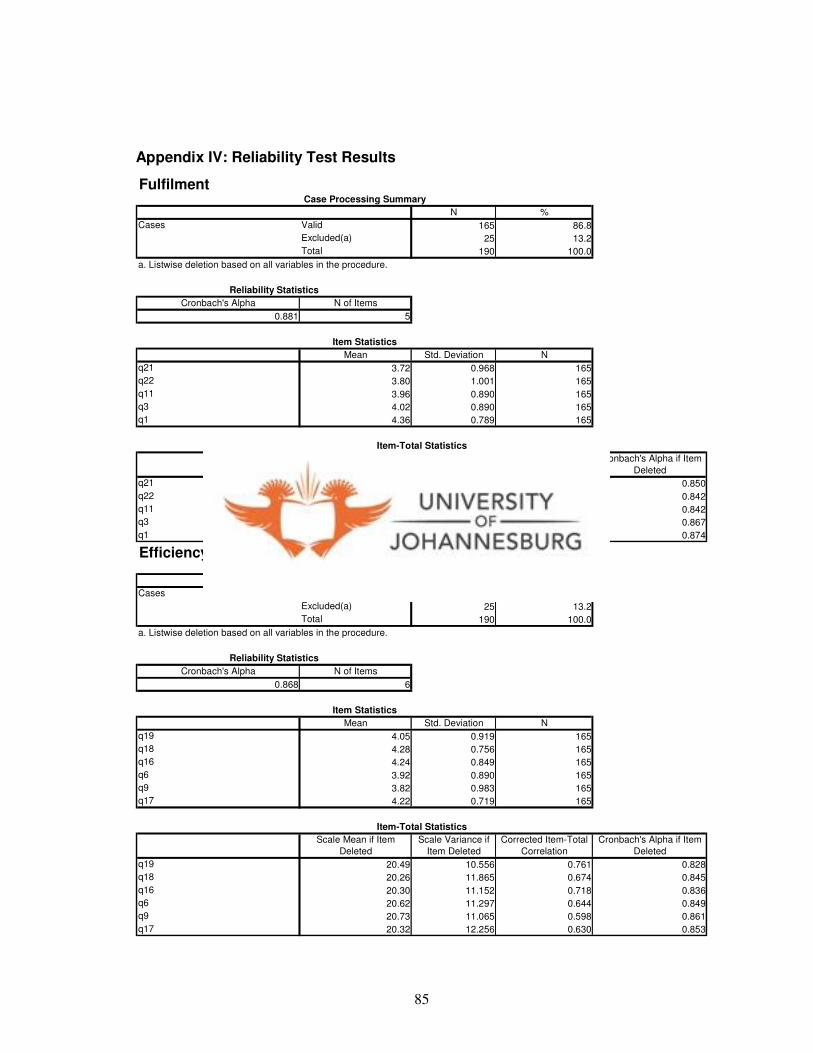

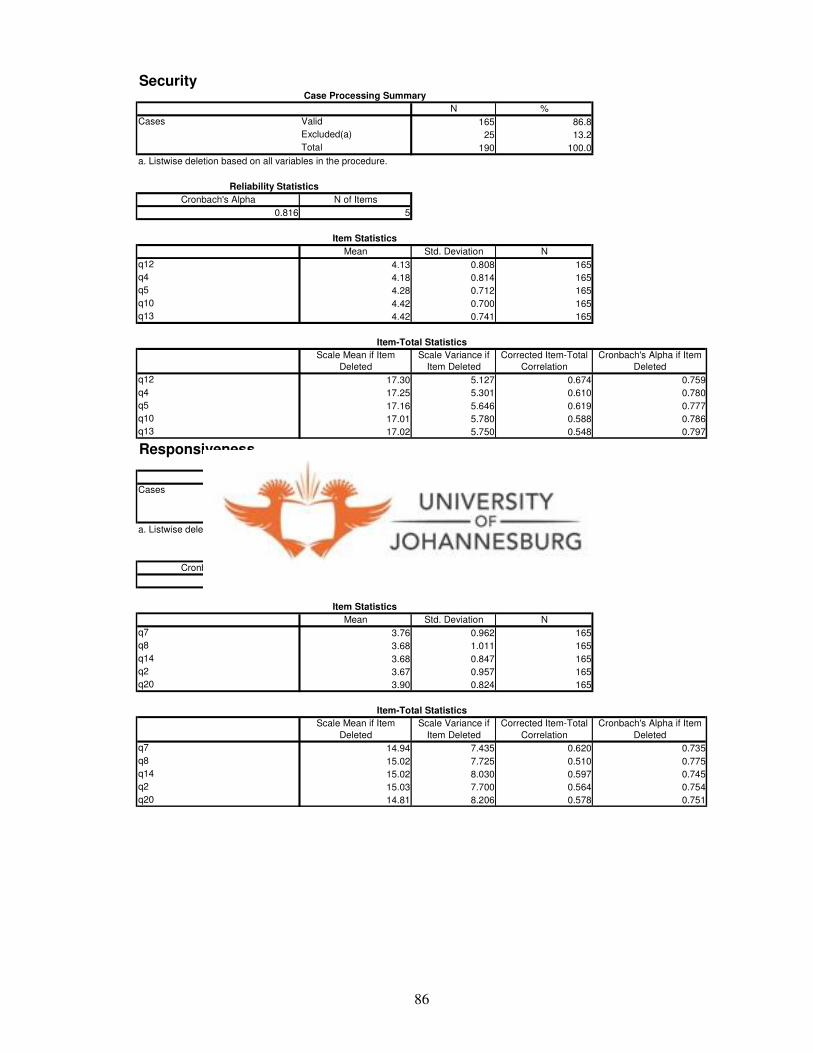

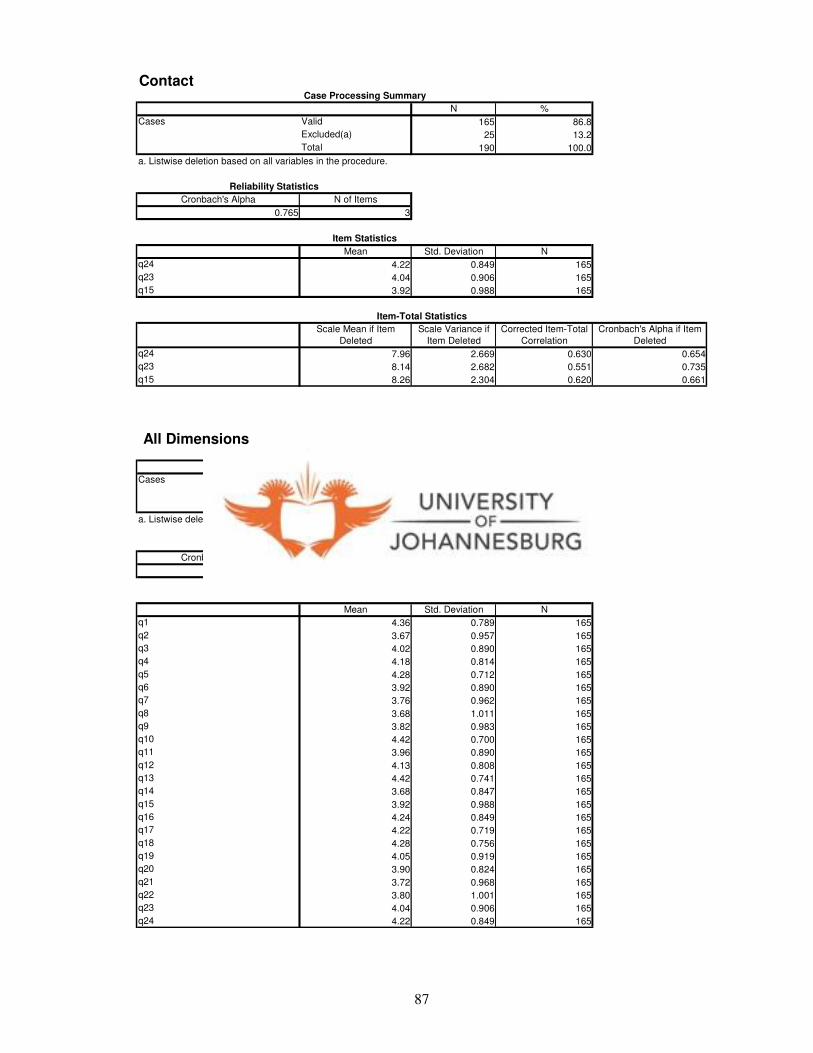

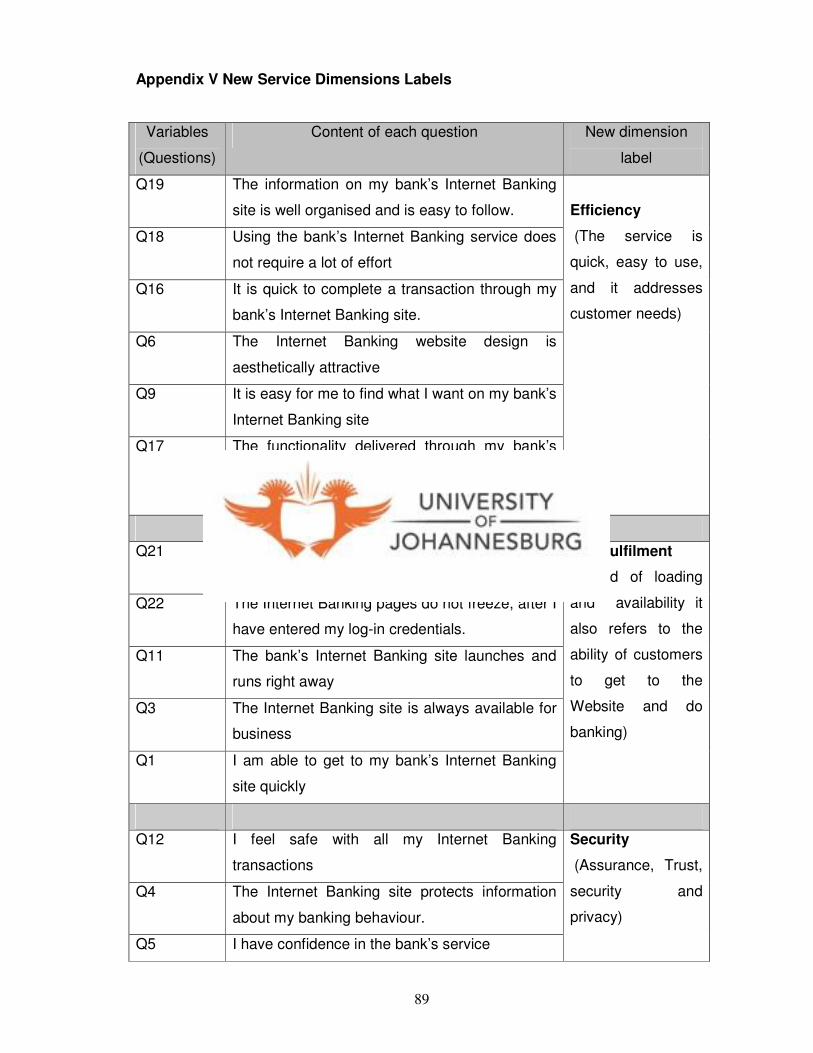

Appendix IV: Reliability Test results.......................................................................... 85

Appendix V:New Service Dimensions Labels ........................................................... 89

Appendix VI:The Kruskal-wallis Test......................................................................... 91

Appendix VII:Survey Covering Letter........................................................................92

Appendix VIII:The Survey Questionnaire..................................................................93

1

Chapter ONE

INTRODUCTION

1.1 Background of the study

The Internet emerged as a key competitive arena for the future of financial services

hence it came as no surprise when banks and brokers flocked to the Web. The use of

the Internet makes it possible for banks to offer a number of home banking services

24 hours a day (Möls, 1998:331). According to Sayar and Wolfe (2007:123) the term

Internet Banking is used to describe the case where banks’ customers conduct

banking transactions on the Internet.

1.1.1 Historical background

According to Singh (2004:187) banking in South Africa has its roots in both the British

and Dutch traditions. The British and the Dutch influence led to the existence of

Standard Bank and Nedbank respectively. The year 1998 saw the consolidation of

United, Volskas and TrustBank into a single brand as Absa adopted a new corporate

identity. As a result, four major banks, Standard Bank, Nedbank, Absa and First

National Bank emerged. These banks dominate the South African retail banking

sector (Singh, 2004:188).

Internet Banking in South Africa started in 1996. The start was fairly slow, but

consumers were attracted to the convenience, safety and low costs of online banking.

Absa was the first to offer online services and was followed by Nedcor with Standard

Bank, First National Bank and Mercantile Bank being the last to follow (Singh,

2004:190). Below are some of the key milestones in the history of Internet Banking:

• May 1995: Wells Fargo (USA), already on the Web, offered online access to

statements

• November1995: NBS became the first South African bank on the Web, offering

only a brochure on its site, with no clickable links.

• October 1996: Absa became the first South African bank to offer personal

banking details online.

• February 1997: Nedbank became the first South African bank to allow online

transactions.

2

• December 1997: Wells Fargo became the first online banking service to sign-

up 400 000 customers.

• July 2001: South Africa’s first standalone bank 20Twenty was launched with

the backing of Saambou and 40 000 customers signed up in the first six

months.

• July 2003: UK based Standard Chartered Bank signed an agreement to

acquire 20Twenty as part of its entry into the retail banking space in South

Africa.

• May 2004: Absa reached the 450 000 online banking customer mark

(Goldstuck, 2004:23).

1.1.2 Banking and technology

The Internet emerged as a key competitive arena for the future of financial services

hence it came as no surprise when banks and brokers flocked to the Web. The use of

the Internet makes it possible for banks to offer a number of home banking services

24 hours a day (Möls, 1998:331). The Internet is not merely a medium of information

delivery in a passive sense. Due to the necessary participation of the consumer in

using the Internet, it also serves as a means of service delivery. The Internet, along

with other means of home banking services, has dramatically changed the distribution

channel of the structure of banks. New partnerships and electronic commerce product

announcements have become a daily routine for financial services industry. The

momentum to move to Web-based business models is increasing and the traditional

distinction amongst the service providers is blurring (Sweeny & Lapp, 2004:276).

Singh (2004:187) supports this notion by stating that in South Africa business is being

revolutionised every day as a result of the influence of the Internet. He further

maintains that organisations have become leaner, meaner, more profitable and more

competitive. Some existing organisations have moved from brick-and-mortar format to

clicks-and-mortar format, whilst others have adopted a more conservative approach

and have both physical and virtual presence.

Bradley and Steward (2003:272) are of the opinion that the banking sector, which has

been characterised by its tried and tested processes of service delivery, is greatly

affected by the environmental change. The authors assert that competition is

escalating for both traditional players and new entrants because of deregulation,

changing consumer behaviour and needs, globalisation and Information Technology.

3

The financial sector is one of the business areas that has been most affected by the

spread of new technologies, particularly the Internet. These technologies have not

only had a bearing on the internal organizational processes, but have also had a

sizeable influence on the way in which financial institutions interrelate with their

customers (Flavian, Guinalίu & Torres, 2006:406). The Internet has been accepted as

a new addition to the traditional way of doing business. Banking organisations have

progressed a long way in the use of the Internet, with most banks offering transaction

services over the Internet (Sohail & Shaikh, 2008:58). O’Neill, Palmer and Wright

(2003:281) reckon that the winners in the online search market space will be those

who consistently provide compelling, user friendly and responsive online service

experiences. They further suggest that specific research on the identification of

attributes that work together to create effective online services experience is lacking.

1.1.3 Internet service quality

Sweeney and Lapp (2004:276) argue that following the proliferation of e-commerce

and the Internet there has been an increasing interest in the evaluation of Websites.

Ibrahim, Joseph, and Ibeh (2006:476), add that the challenging business environment

in the financial services market in the UK and beyond has also resulted in more

pressure on the banks to develop and utilise alternative channels with a view of

attracting more customers and improving customer perceptions. According to Ibrahim

et al. (2006:476) “not enough is known regarding how customers perceive and

evaluate electronically delivered services”. Service quality research has

overwhelmingly focused on customer expectations. The importance-performance

analysis (IPA) approach is built around customer perceived importance of quality

attributes and attributes of performance, the interplay of which suggests strategies for

service improvement and satisfaction management (Ibrahim et al., 2005:479).

Rowley (2006:339) is of the view that service experience associated with electronic

environments is very different from a service experience that is mediated through a

human service agent. Zeithaml (2002:135) defines electronic service quality (E-S-Q)

as an extent to which a Website facilitates efficient and effective shopping, purchasing

and delivery. Zeithaml’s (2002:135) research on electronic service quality indicates

that E-S-Q has seven dimensions that form two scales: a core E-S-Q scale and a

recovery scale. Four dimensions - efficiency, reliability, fulfilment and privacy form the

4

core E-S-Q scale that can be used to measure customer perceptions of service

quality. According to Zeithaml (2002:136) the other three dimensions become salient

when online customers run into problems. These three dimensions are

responsiveness, compensation and contact. These three dimensions were

conceptualised by the research as constituting E-S-Q recovery. Jun and Cai

(2001:276) identified seventeen dimensions under three categories of Internet

Banking service quality. These dimensions included:

• Customer service quality: reliability, responsiveness, competence, courtesy,

credibility, access, communication, understanding, collaboration and continuous

improvements

• Online system quality: content, accuracy, ease of use, timeliness, aesthetics, and

security.

• Banking service product quality: one dimension of product variety.

Broderick and Vachirapornpuk (2002:332) in their study on Internet Banking service

quality agreed that the management implication for their study arises in two areas:

firstly within the service interface and secondly, with the management of increased

customer role. From a service setting point of view they argued that at the outset

customers might use service setting cues more in judging service quality, because of

the lack of tangible cues that are available in Internet formats. Broderick and

Vachirapornuk (2003:333) further purport that one feature of customer interaction is

not confined to Internet transactions, but involves a lot of other interfaces. Customer

scripts also operate between the service setting and the service encounter, as when

customers seek to solve problems with service setting by contacting personnel. This

study will focus on assessing Internet Banking service quality dimensions. From the

set of identified dimensions the study will establish how the South African banks are

performing as perceived by their customers.

1.1.4 Internet Banking

Internet Banking, at a basic level, is defined as the setting up of a Web page by a

bank to give information about its products and services. At a more advanced level it

is defined as provisioning of facilities such as accessing accounts, funds transfer and

buying financial products or services online (Sathye, 1999:524). According to Sayar

5

and Wolfe (2007:123) the term Internet Banking is used to describe the case where

banks’ customers conduct banking transactions on the Internet. In the contemporary

context, this mainly implies the usage of computers, and digital TV’s for accessing

internet branches.

Internet Banking refers to a service offered by banks that allows account holders to

access their account data via the Internet. In order to take advantage of the Internet

Banking, an account holder would need to meet several technological requirements,

such as having a personal computer with Internet access and a web browser. If these

conditions are satisfied Internet Banking can be performed from anywhere in the

world. Thus, Internet Banking facilitates direct access to account details; enables

transfer of funds; allows for multiple bills payments, and performs an array of other

transactions (Sayar & Wolfe, 2007:124).

1.2 Problem statement:

The challenging business environment in the financial services market resulted in

more pressure on banks to develop and utilise alternative delivery channels, with a

view to attracting more customers and improving customer perceptions and

encouraging loyalty. Internet Banking is among the channels that were developed and

implemented. Banks have invested heavily in introducing and making Internet

Banking service functionality rich, with an objective of improving customer satisfaction

and loyalty, ultimately contributing positively to income and profits.

The challenge for teams of software designers, marketers and experts in human-

computer interaction, (amongst others), is to create a business model that not only

increases productivity and enhances bottom line performance, but one that also seeks

to add value for customers, employees and suppliers alike (O’Neill et al., 2003:293).

Research Problem:

Management in South African banks, do not have an insight into how their customers

perceive and evaluate Internet Banking service quality.

6

1.3 Objective / purpose

This study aims to explore customers’ perceptions on Internet Banking service quality

dimensions or factors. This will be done with the following objectives in mind:

• Have an insight into how Internet Banking customers in South Africa perceive and

evaluate their respective banks’ performance on pre-defined Internet Banking

service quality dimensions.

• Determine if there are any differences in perceptions of Internet Banking service

quality based on gender, age or primary bank.

1.4 A brief outline of the research methodology

1.4.1 The research methodology

The survey method was used to collect primary data for this study. Electronic

interactive media was employed, as respondents were contacted via e-mail and

directed via a URL to take a self-administered questionnaire online. Zikmund

(2003:198) defines electronic interactive media as “a communication media that

allows an organization and the audience to interact using digital technology”. This

method was chosen as it was inexpensive and could reach a wide sample of the

survey population with ease.

1.4.2 The research population

The survey population was a sample of customers that do banking online with any of

the South African banks.

1.4.3 The sampling method

Convenience sampling was used to sample the population. This was a non-probability

sampling design

1.4.4 Data Collection

Data was collected using an Internet survey. The survey was a self-administered

questionnaire posted on a web-site. This made it possible to reach a large number of

respondents and secure confidential answers quickly and cost-effectively.

7

Respondents were invited by e-mail to participate in the survey. This ensured that the

respondents’ feedback was captured at the time when the responses were submitted.

1.5 An outline of the remainder of the dissertation

Chapter one: Introduction

This chapter provides a background to the study, in which the environment within

which the research is undertaken is described. Concepts such as Internet Banking

and service quality are introduced. The problem statement, which flows from the

background, is also stated in this chapter. The objective(s) of the research in

addressing the research problem are then identified

Chapter 2: Literature review

The chapter reviews related literature on Internet Banking. The literature offers

guidance to the tentative solutions to the problem. It addresses concepts such as

traditional services, electronic services, online system quality, Internet Banking

services and instruments like SERVQUAL and E-S-Q for quality of service

measurements.

Chapter 3: Research Methodology

This chapter will explain the research design chosen and the rationale behind such a

choice. It will focus on the research population, the sampling techniques to be used

and the sample size. It will further elaborate on the research instruments used and

data collection and analysis including validity and reliability of the research instrument.

Chapter 4: Presentation of research results

The chapter will focus on providing the main findings of the study, the insights gained

in relation to the research objectives.

Chapter 5: Interpretation of research results

The chapter will analyse and interpret research results and link them to the reviewed

literature. The chapter will conclude by giving a statement on limitations of the study.

8

Chapter 6: Conclusions and recommendations

The chapter will give a summary of the research objectives and major findings.

Recommendations and suggestions for further research will also be outlined in this

chapter.

1.6 Conclusion

Chapter one served as an introduction to the study, outlining the problem statement,

the research objectives and the research methodology were discussed. In chapter two

a review of the related literature will be done. The review will include an explanation of

what service quality, service and electronic service are. The chapter will undertake to

offer insights into service quality dimensions. The other concepts to be discussed

include SERVQUAL and E-S-Q as instruments used to measure traditional service

quality and electronic service quality respectively.

9

Chapter TWO

LITERATURE REVIEW

2.1 Introduction.

O’Sullivan, Edmond and ter Hofstede (2002:3) define a service in its simplest form, as

an action which involves transferring value, performed by one entity on behalf of the

other. According to Zeithaml, Bitner and Gremler (2006:6) the broad definition of

service implies intangibility as a key determinant of whether an offering is a service or

not. The International Organization for Standardization (ISO) describes a service as

part of the total production concept. A service is generated by a process and the

customer outcome is created in this process. In the case of a service as compared to

a product the customer is present and affects the results in terms of added value and

quality (Edvardsson, 1998:142).

Service quality can be viewed in a structured and integrated way called the GAPS

model of service quality. Zeithaml, Bitner and Gremler (2006:33) depict the GAPS

model as consisting of the customer and provider gaps. The customer gap is the

difference between the customer expectations and perceptions. To close the all

important gaps, the GAPS model suggests that the other four gaps, referred to as

provider gaps, need to be closed. According to Zeithaml et al., (2006:34) the gaps

occurring within the organization providing the service include:

• Gap1 is about not knowing what customers want.

• Gap2 refers to not selecting the right service designs and standards.

• Gap3 refers to not delivering to service designs and standards.

• Gap4 is about not matching performance to promise

The literature review will look into the definition of traditional service, service quality,

banking service quality and service quality measurements. This will then lead to a

discussion on electronic service, service quality and electronic service measurements.

The majority of definitions for electronic service use the Internet and/ or workflows as

a conduit to new revenue or task completion. Web services have also been described

as an aggregation of functionality with a single façade and published for the purpose

of use (O’Sullivan et al. 2002:3). To conclude the literature review an important

10

discussion on online systems will be undertaken. Internet Banking service will be

defined and its characteristics outlined.

2.2 Traditional Services

2.2.1 Definition and characteristics of services

Zeithaml et al. (2006:4) simply describe services as deeds, processes and

performances, whilst Baron and Harris (2003:4) concur that services are processes

that occur over time. There are three fundamental aspects of service: process,

people, and physical evidence. Compatible to the simple definition is that services

include all economic activities whose output is not a physical product and is

consumed at the time it is rendered. In the broad definition of service, intangibility is

the key determinant of whether an offering is, or is not a service (Baron & Harris,

2003:5). According to Zeithaml and Bitner (1996:5) while the statement on

intangibility being the key determinant of service is true, it is also true that few are

purely intangible or totally tangible. Services tend to be more intangible than

manufactured products. The latter products tend to be more tangible than services.

Bateson and Hoffman (1999:9) agree that it is difficult to define a pure good product

or service. A pure service assumes that there is no “goods” element to the service that

the customer receives. In reality most services contain some “goods” element in them

(Bateson & Hoffman, 1999:9). Zeithaml et al. (2006:21) summarises the

characteristics of services that distinguish it from products as intangibility,

heterogeneity, simultaneous production and consumption as well as perishability.

• Intangibility

The distinguishing characteristic of services is intangibility because services are

performances or actions rather than objects, they cannot be seen, felt, tasted or

touched in the same manner one can touch and feel physical goods (Zeithaml et al.

2006:22). Baron et al. (2003:19) indicate that the intangibility of services often

increases the risk for the purchaser. Some services are perceived to be riskier than

others depending on whether they are high in search, experience, and credence

factors. Baron and Harris (2003:19) describe these factors as:

o A service that is high in search factors is the one about which customers

can get some (prior) information as to what they will receive.

o A service that is high in experience factors is one that customers must try

out (experience) before they can decide whether or not it is a great deal.

11

o A service that is high in credence factors is one that is difficult to evaluate

even after experiencing it.

• Heterogeneity

No two services will precisely be alike because they are performances frequently

rendered by humans (Zeithaml et al., 2006:22). Baron and Harris (2003:20) say

organisations providing services know that no two service provisions are exactly the

same, whatever the attempts to standardise them. The quality of any service will vary

when offered by different employees, probably at different times of the day.

• Simultaneous rendering and consumption

To receive the benefit of the service, the consumer must be part of the system. It thus

becomes impossible to store a service (Bateson & Hoffman, 1999:12). This situation

of simultaneous rendering and consumption means that the consumer is present while

the service is being rendered and thus views and may even take part in the rendering

process. In simultaneously rendering and consumption of service, customers will

interact with one another during the service rendering process and thus may affect

one another’s experiences (Zeithaml et al., 2006:23). Baron and Harris (2003:20) refer

to this characteristic of service as inseparability.

• Perishability

According to Zeithaml et al. (2006:23) perishability refers to the fact that services

cannot be saved, stored resold or returned.

2.2.2 Traditional service quality

Imrie, Cadogan and McNaughton (2002:10) describe service quality as an antecedent

of consumer assessment of value. Examples of behaviours motivated by favourable

service quality assessment are re-purchase intentions, loyalty and word of mouth.

Kang and James (2004:267) point out that the construct of service quality as

conceptualised in the services marketing literature centres on perceived quality,

defined as a consumer’s judgement about an entity’s overall excellence. Kang and

James (2004:268) further suggest that the “perceived service quality model” replaces

the product features of a physical product in the consumption of services. The

technical aspect (what service is provided) and the functional aspect (how the service

is provided) are the two dimensions that Kang and James (2004: 268) identified.

12

Santos (2003:234) argue that there are two main conceptualisations of service quality

that exist – one based on disconfirmation approach, and the other based on the

performance-only approach. Oliver (1980:461) points out that expectations are

thought to create a frame of reference about which one makes a comparative

judgement. This means that outcomes poorer than expected (negative

disconfirmation) are rated below this reference point, whereas those better than

expected (a positive disconfirmation) are rated above the base. Service quality was

therefore understood to be a measure of how well the service level delivered matched

customer expectations.

Bateson and Hoffman (1999:340) argue that the two concepts of customer satisfaction

and service quality are intertwined. One plausible explanation is that satisfaction

assists customers in revising service quality perceptions. Bateson and Hoffman

(1999:340) describe the logic for this position as follows:

• Consumer perception of the service quality of a firm with which no prior

experience exists is based on the consumer’s expectations.

• Subsequent encounters with the service firm lead the consumer through the

disconfirmation process and further revise the perceptions of service quality.

• Each additional encounter with the service firm further revises or reinforces

service quality perceptions.

• Revised service quality perceptions modify future consumer purchase

intentions towards the service firm.

Baron and Harris (2003:136) describe perceived service quality as the degree and

direction of the gap between consumer perceptions and expectations of service. In

the GAPS model as described by Zeithaml et al. (2006:46) this refers to the customer

gap 5 - the gap between the expected service and the perceived service. Baron and

Harris (2003:136) further describe consumer satisfaction as a function of the

similarities between the consumers’ expectations and the perceived performance of

the purchaser.

13

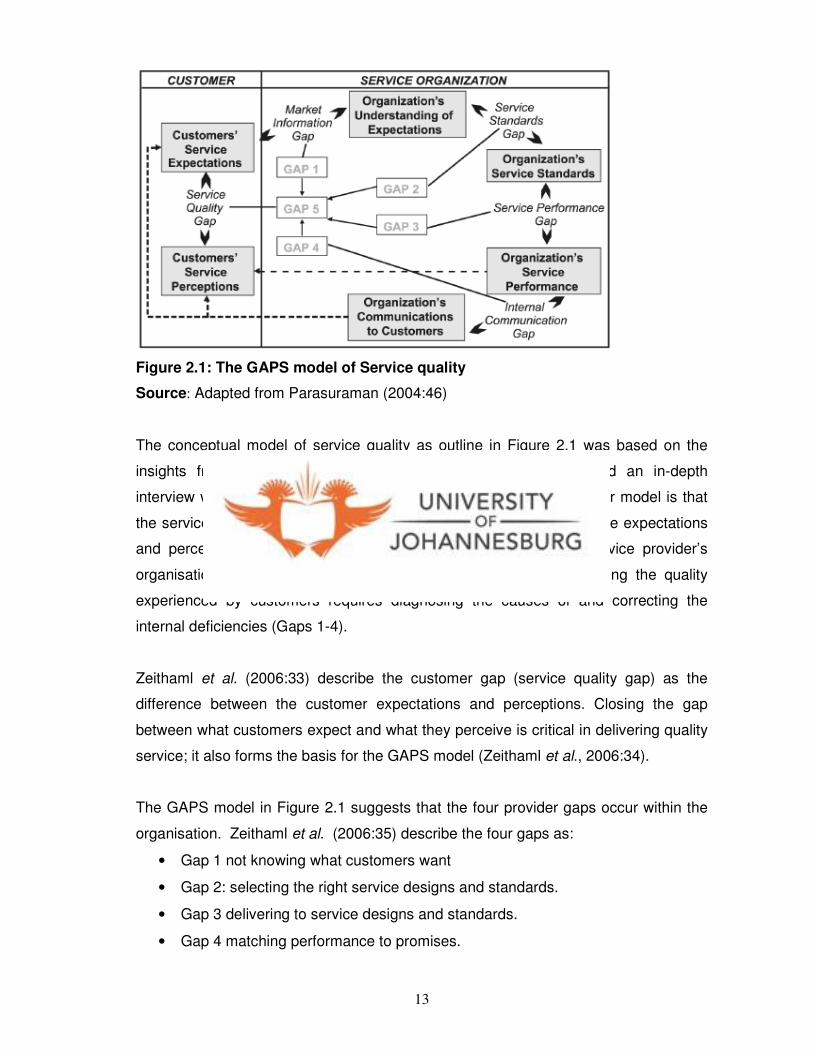

Figure 2.1: The GAPS model of Service quality

Source: Adapted from Parasuraman (2004:46)

The conceptual model of service quality as outline in Figure 2.1 was based on the

insights from extensive focus group research with customers and an in-depth

interview with executives in various sectors. The primary thesis of their model is that

the service quality shortfall Gap 5 (the gap between customers’ service expectations

and perceptions) is a result of a series of shortfalls within the service provider’s

organisation (Parasuraman, 2004:45). This then means that improving the quality

experienced by customers requires diagnosing the causes of and correcting the

internal deficiencies (Gaps 1-4).

Zeithaml et al. (2006:33) describe the customer gap (service quality gap) as the

difference between the customer expectations and perceptions. Closing the gap

between what customers expect and what they perceive is critical in delivering quality

service; it also forms the basis for the GAPS model (Zeithaml et al., 2006:34).

The GAPS model in Figure 2.1 suggests that the four provider gaps occur within the

organisation. Zeithaml et al. (2006:35) describe the four gaps as:

• Gap 1 not knowing what customers want

• Gap 2: selecting the right service designs and standards.

• Gap 3 delivering to service designs and standards.

• Gap 4 matching performance to promises.

14

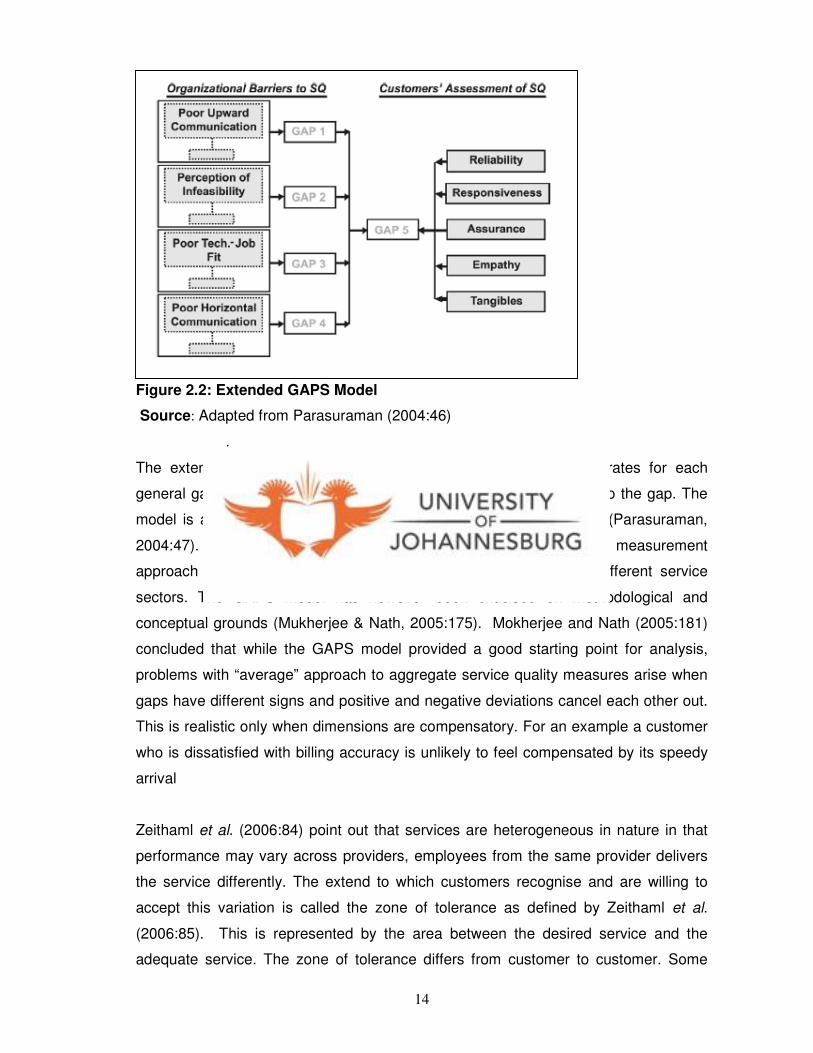

Figure 2.2: Extended GAPS Model

Source: Adapted from Parasuraman (2004:46)

.

The extended Gaps model as shown in Figure 2.2 above enumerates for each

general gap a list of organisational deficiencies that could contribute to the gap. The

model is a useful starting point for diagnosing and closing the gaps (Parasuraman,

2004:47). The GAPS model has emerged as the most popular measurement

approach of service quality and has been extensively applied in different service

sectors. The GAPS model has however been criticised on methodological and

conceptual grounds (Mukherjee & Nath, 2005:175). Mokherjee and Nath (2005:181)

concluded that while the GAPS model provided a good starting point for analysis,

problems with “average” approach to aggregate service quality measures arise when

gaps have different signs and positive and negative deviations cancel each other out.

This is realistic only when dimensions are compensatory. For an example a customer

who is dissatisfied with billing accuracy is unlikely to feel compensated by its speedy

arrival

Zeithaml et al. (2006:84) point out that services are heterogeneous in nature in that

performance may vary across providers, employees from the same provider delivers

the service differently. The extend to which customers recognise and are willing to

accept this variation is called the zone of tolerance as defined by Zeithaml et al.

(2006:85). This is represented by the area between the desired service and the

adequate service. The zone of tolerance differs from customer to customer. Some

15

customers have narrow zones of tolerance, requiring a tighter range of service from

providers and others have a greater range of service (Zeithaml et al., 2006:86).

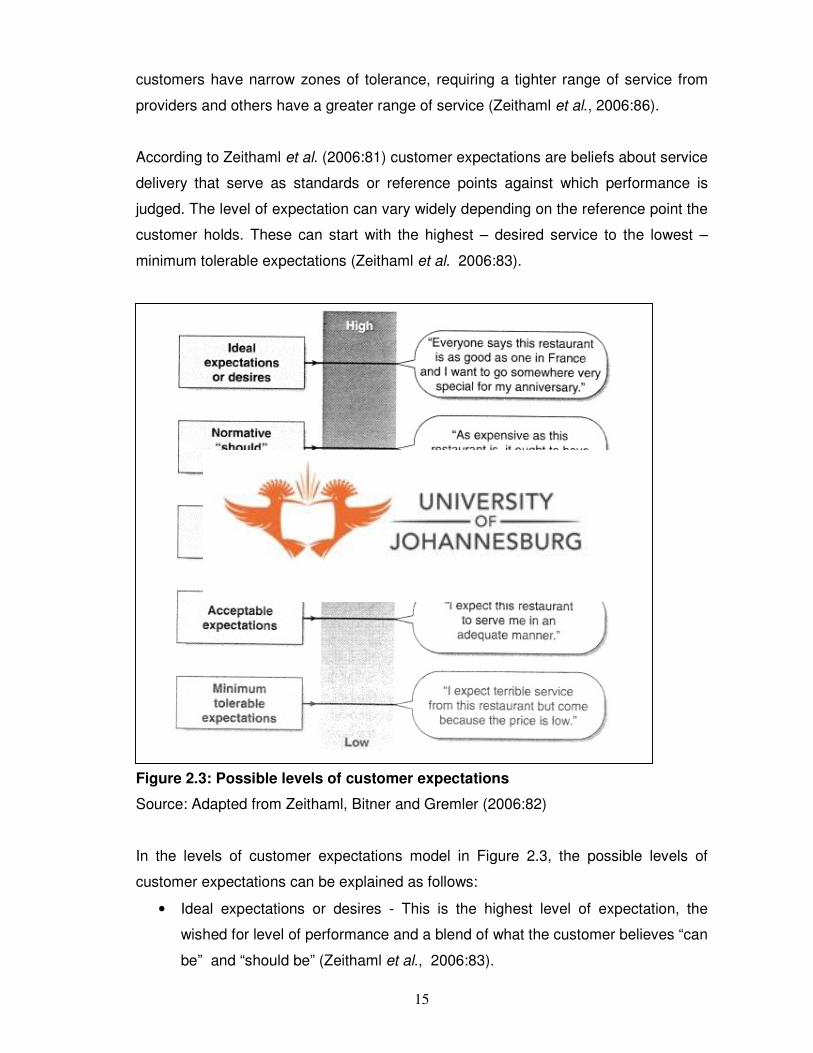

According to Zeithaml et al. (2006:81) customer expectations are beliefs about service

delivery that serve as standards or reference points against which performance is

judged. The level of expectation can vary widely depending on the reference point the

customer holds. These can start with the highest – desired service to the lowest –

minimum tolerable expectations (Zeithaml et al. 2006:83).

Figure 2.3: Possible levels of customer expectations

Source: Adapted from Zeithaml, Bitner and Gremler (2006:82)

In the levels of customer expectations model in Figure 2.3, the possible levels of

customer expectations can be explained as follows:

• Ideal expectations or desires - This is the highest level of expectation, the

wished for level of performance and a blend of what the customer believes “can

be” and “should be” (Zeithaml et al., 2006:83).

16

• Normative (“Should”) expectation: an example of this expectation would be: as

expensive as this restaurant is, it ought to have excellent food for service.

• Experience-based norms: this refers to an expectation based on past

experience. For example, “In most cases this restaurant is very good, but when

it gets busy the service is slow”.

• Acceptable expectation: an example of an acceptable expectation would be: “I

expect this restaurant to serve me in an adequate manner”.

• Minimum tolerable expectation: This is the extreme side of the desired service

as it relates to the bottom level of performance acceptable to the customer

(Zeithaml et al., 2006:83).

2.2.3 SERVQUAL

SERVQUAL is a multidimensional scale used to capture customer perceptions and

expectations of service quality. The SERVQUAL scale was first published in 1988 and

has undergone numerous improvements and revisions since then. The scale currently

contains twenty one perception items that are distributed across five service quality

dimensions (Zeithaml et al., 2006:154). Parasuraman (2004:46) indicates that building

on key insights from qualitative research, the research team launched a series of

empirical studies to develop, test and refine a scale for measuring service quality as

perceived by customers. These qualitative studies gave birth to SERVQUAL, a five

dimensional, two part instrument. The first and the second parts measure customer

expectations and perceptions respectively along a variety of service attributes

grouped into five dimensions of reliability, responsiveness, assurance, empathy and

tangibles. The SERVQUAL instrument, though very valuable, is believed to be just

one approach for assessing service quality (Parasuraman, 2004:48).

One criticism of SERVQUAL has been the point that the instrument mainly focuses on

the service delivery process (Kang & James, 2004:266). The other criticism by

Oppewal and Vriens (2000:154) is that SERVQUAL does not provide good measures

of the importance of service attributes and dimensions. SERVQUAL grounded in the

GAPS model, measures service quality as the calculated difference between

customer expectations and the performance perceptions of a service encounter.

Cronin and Taylor (1992:56) challenged this approach and developed the SERVPERF

scale which directly captures customers’ performance perceptions in comparison to

17

their expectations of service encounter. A qualitative method of measuring service

quality includes techniques such as interviews, focus groups, customer role-play and

observation. These provide insight into the mindset of customers and are highly

subjective. Quantitative surveys can be administered either face-to-face or customers

may be left to do these on their own. The confirmation-disconfirmation paradigm has

been extensively incorporated into surveys (O’Neill et al., 2003:283). O’Neill et al.

(2003:284) further suggest that as consumers evaluate the levels of the service’s

performance, they typically cannot help but compare that performance to what they

expected. In turn, these expectations provide a baseline for the assessment of a

customer level satisfaction.

2.2.4 Traditional banking service quality

Using the critical incident technique Johnston (1995:65) made the following

conclusions in his study on the determinants of service quality satisfiers and

dissatisfiers amongst bank customers:

• Some determinants of quality predominate over others.

• For the personal customer of the bank, the main sources of satisfaction are

attentiveness, responsiveness, care and friendliness. The main sources of

dissatisfaction are integrity, reliability, responsiveness, availability and

functionality.

• The sources of dissatisfaction are not necessarily the obverse of sources of

satisfaction.

• The intangible aspects of the staff-customer interface have significant effects,

both negative and positive, on service quality.

• Responsiveness is the crucial determinant of quality, as it is the key component

in providing satisfaction and the lack of it is a major source of dissatisfaction.

• Reliability is predominantly a source of dissatisfaction not satisfaction.

Johnston (1995:62) in his study used eighteen service quality attributes:

attentiveness, responsiveness, care, availability, integrity, friendliness, courtesy,

communications, competence, functionality, commitment, access, flexibility,

aesthetics, cleanliness, comfort and security.

18

Bahia and Natel (2000:86) used an alternative measure on service quality by

proposing seven dimensions of which some were covered by the SERVQUAL scale.

These included effectiveness and assurance, access, price, tangibles, place, service

portfolio and reliability. Oppewal and Vriens (2004:158) used twenty eight attributes

including four service quality dimensions to evaluate service quality. The four

dimensions included accessibility, competence, accuracy and tangibles.

2.3 Electronic Services (e- Services)

2.3.1 Definition and characteristics of e-Services

Buckley (2003:455) defines e-Service as the electronic provision of a service to

customers whilst Santos (2003:234) describes e-Service as the provision of

consumers with a superior experience with respect to the interactive flow of

information. Rowley (2006:341) on the other hand brings in a different perspective of

e-Service by defining it as deeds, efforts or performances whose delivery is mediated

by information technology (including the Web, information kiosks and mobile devices)

and such includes the service element of e-tailing, customer support , service and

service delivery. In e-Service the customer’s interaction or contact with the

organisation is through the technology, such as Websites. e-Service encounter is the

initial landing on the home page until the requested service has been completed or

the final product has been delivered and is fit for use (Bucley, 2003:456). During an e-

Service encounter, customers have to rely on only two senses, that of sight and

sound, whereas the traditional service experience can use all senses. e-Service is

described as a relative impoverished experience, due to the absence of face to face

interaction, which is seen as central to relationships development (Rowley 2006:341).

From all the definitions of e-Service discussed the following characteristics standout:

• There is an interactive flow of information between the customer and the

service provider.

• This customer interaction is mediated through some kind of information

technology.

• The service is a virtual one and there is no face-to-face interaction.

• Customers have to rely on only two senses that of sight and sound during the

interaction.

19

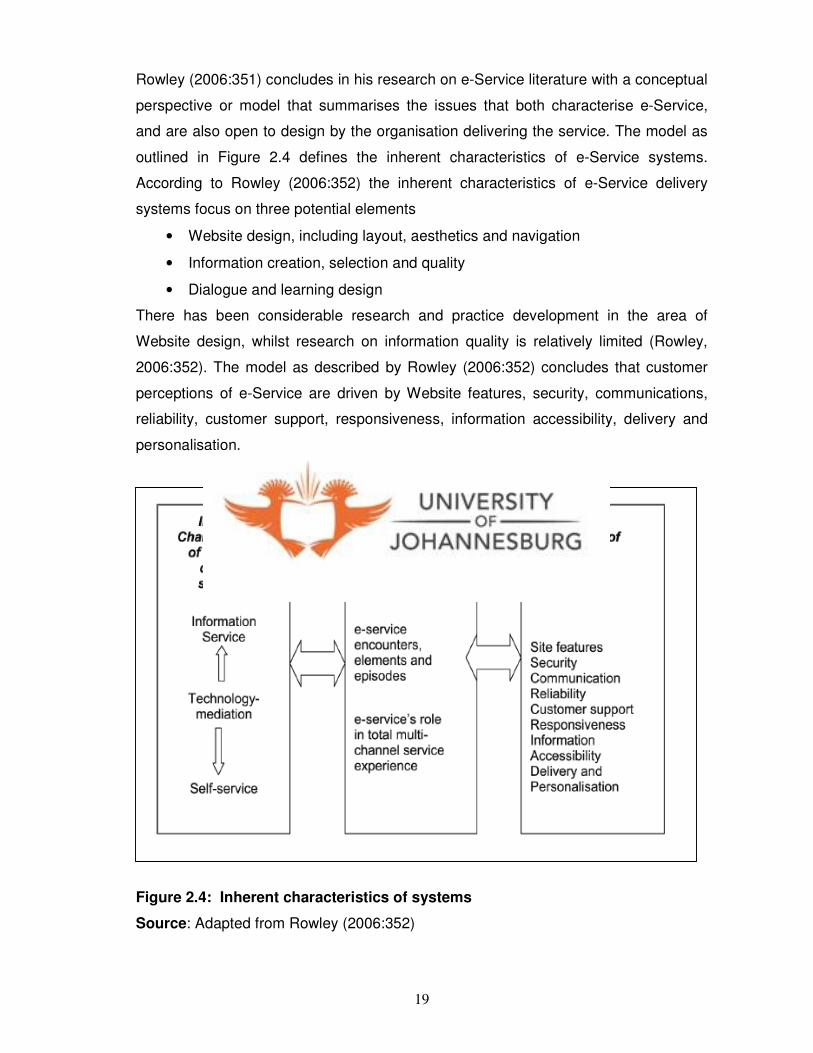

Rowley (2006:351) concludes in his research on e-Service literature with a conceptual

perspective or model that summarises the issues that both characterise e-Service,

and are also open to design by the organisation delivering the service. The model as

outlined in Figure 2.4 defines the inherent characteristics of e-Service systems.

According to Rowley (2006:352) the inherent characteristics of e-Service delivery

systems focus on three potential elements

• Website design, including layout, aesthetics and navigation

• Information creation, selection and quality

• Dialogue and learning design

There has been considerable research and practice development in the area of

Website design, whilst research on information quality is relatively limited (Rowley,

2006:352). The model as described by Rowley (2006:352) concludes that customer

perceptions of e-Service are driven by Website features, security, communications,

reliability, customer support, responsiveness, information accessibility, delivery and

personalisation.

Figure 2.4: Inherent characteristics of systems

Source: Adapted from Rowley (2006:352)

20

The first box in Figure 2.4 summarizes the issues that both characterise e-Service and

are also open to design by the organisation delivering the service. The second box

includes differentiating factors. This means that one service system and experience

are different from the next in terms of scope and nature. The third box is concerned

with the customers’ perceptions of the experience of e-Service and derives from work

on e-Service quality dimensions. It summarizes and identifies some of the dimensions

that customers use in their evaluation of e-Service experiences (Rowley, 2006:352).

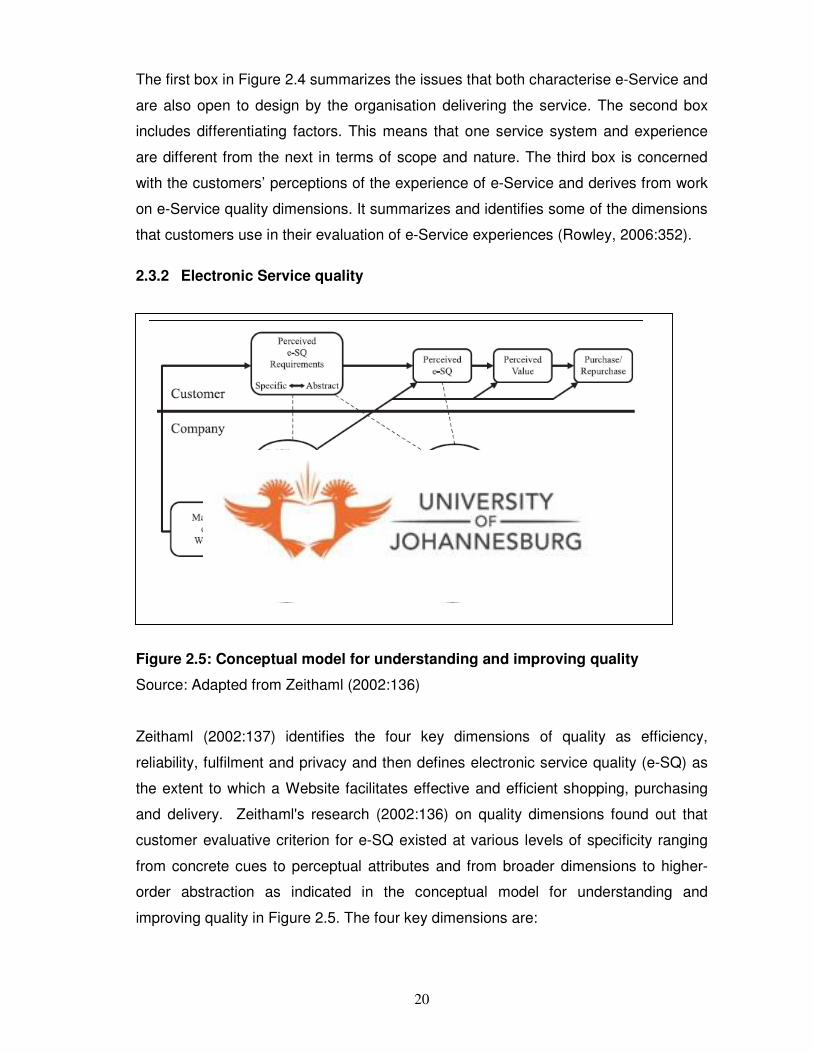

2.3.2 Electronic Service quality

Figure 2.5: Conceptual model for understanding and improving quality

Source: Adapted from Zeithaml (2002:136)

Zeithaml (2002:137) identifies the four key dimensions of quality as efficiency,

reliability, fulfilment and privacy and then defines electronic service quality (e-SQ) as

the extent to which a Website facilitates effective and efficient shopping, purchasing

and delivery. Zeithaml's research (2002:136) on quality dimensions found out that

customer evaluative criterion for e-SQ existed at various levels of specificity ranging

from concrete cues to perceptual attributes and from broader dimensions to higher-

order abstraction as indicated in the conceptual model for understanding and

improving quality in Figure 2.5. The four key dimensions are:

21

1. Efficiency – refers to the ability of customers to get to the Website, find their

desired product and information associated with it and check-out with minimal

effort.

2. Fulfilment incorporates accuracy of service promises, having products in stock

and delivering the products in the promised time.

3. Reliability is associated with the technical functioning of the site, particularly the

extent to which it is available and functioning properly.

4. The privacy dimension includes assurances that shopping behaviour and

information is secured.

The recovery-SQ scale includes the personal service aspects:

1. Responsiveness measures the ability of a company to provide appropriate

information to customers when a problem occurs, have mechanisms for

handling returns and providing online guarantees.

2. Compensation is the dimension that involves receiving money back.

3. Contact points. So that customers should be able to speak to a live service

agent in times of problems.

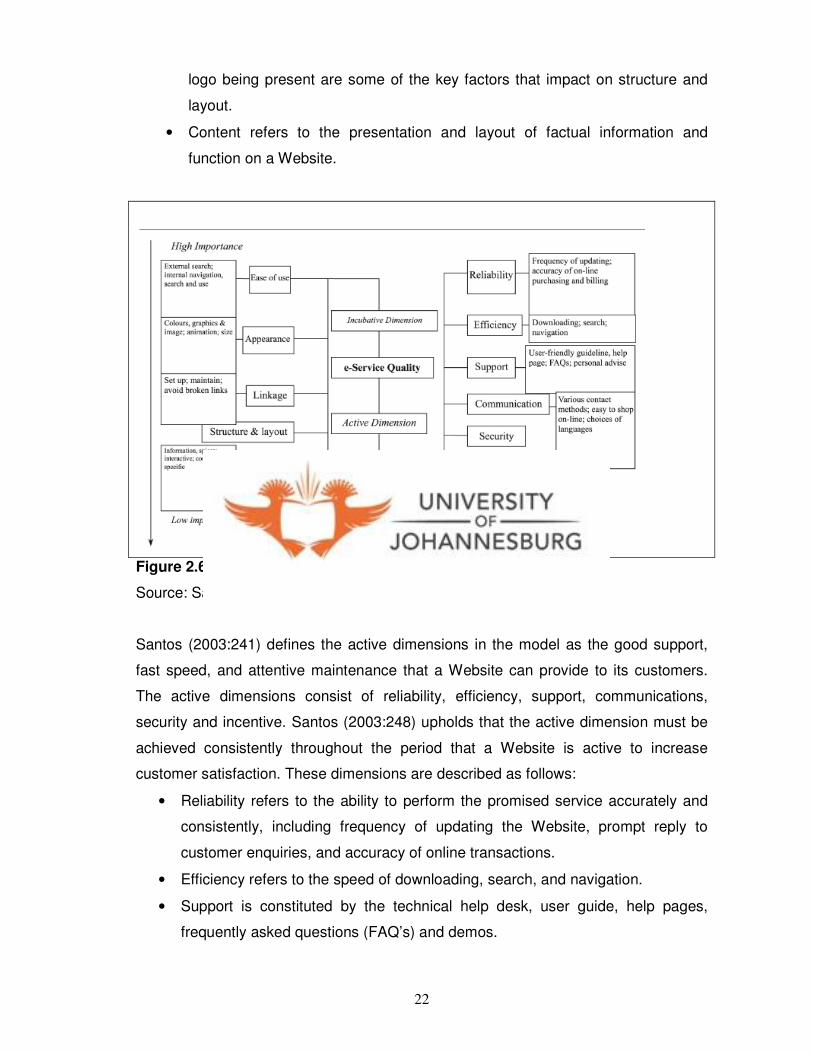

According to Santos (2003:238) there are two dimensions that determine e-Service

quality, the incubative and active dimensions as indicated in the model of e-Service in

Figure 2.6. The incubative dimension lists the determinants of a Website daily hit rate

and the time length any visitor stays on the Website as ease of use, appearance,

linkages, content and layout. Santos (2003:239) defines these determinants as

follows:

• Ease of use is defined as how easy the Website is for customers to conduct

external search in cyberspace and internal navigation and search within the

Website.

• Appearance is defined by Santos (2003:239) as the proper use of colour,

graphics, images and animations, together with the appropriate size of the

Web pages. Appearance is usually the first thing observed by Web users.

• Linkages refer to the number and quality of links that a Website offers.

• Structure and layout refers to the organisation and presentation of a Website’s

content and information. This structure is characterised by simplicity clarity,

consistent layout, good use of frame, provision of a site map that allows users

to skip sections that are of no interest, a clear listed menu, and the company

22

logo being present are some of the key factors that impact on structure and

layout.

• Content refers to the presentation and layout of factual information and

function on a Website.

Figure 2.6: A model of e-Service quality

Source: Santos (2003:239)

Santos (2003:241) defines the active dimensions in the model as the good support,

fast speed, and attentive maintenance that a Website can provide to its customers.

The active dimensions consist of reliability, efficiency, support, communications,

security and incentive. Santos (2003:248) upholds that the active dimension must be

achieved consistently throughout the period that a Website is active to increase

customer satisfaction. These dimensions are described as follows:

• Reliability refers to the ability to perform the promised service accurately and

consistently, including frequency of updating the Website, prompt reply to

customer enquiries, and accuracy of online transactions.

• Efficiency refers to the speed of downloading, search, and navigation.

• Support is constituted by the technical help desk, user guide, help pages,

frequently asked questions (FAQ’s) and demos.

23

• Communications is defined as keeping the customers properly informed and

communicating with them in a language they can understand. Communications

in e-Service consists of online communications (e-mails and chat rooms) and

traditional communications methods (telephone, fax and postal mail.

• Security refers to the freedom from danger, risk, or doubt (including financial

insecurity) during the service process.

• Incentive is the encouragement given by Web providers to consumers to

browse and use the Website.

2.3.3 Understanding and measuring e-Service quality

Parasuraman, Zeithaml and Malhorta (2005:230) on their research on electronic

service quality (E-S-Q) a multiple item scale for assessing electronic service quality

came up with the five managerial implications:

• Efficiency and fulfilment were the most critical and important facets of the

Website service quality. Of the four E-S-Q dimensions, customers’

assessments of a Website on these two dimensions had the strongest

influence not only on the overall quality perceptions but also on perceived value

and loyalty intentions.

• The systems availability facet of the Websites was also critical contributor to

customers’ perceptions of overall quality, value and loyalty intentions.

• Privacy was the least critical of the four E-S-Q dimensions

• The three service recovery dimensions (responsiveness, compensation, and

contact) and the perceptual attributes they contain imply service aspects that

mirror aspects of traditional service quality (ready access to company

personnel, solving customers’ problems)

• The E-S-QUAL and electronic recovery of service quality ( E-RecS-Q) are

generic scales, intended for obtaining a global (as opposed to transaction-

specific) assessment of a Website service quality.

The dimensions on which customers assess electronic service quality (e-SQ) are:

access, ease of navigation, efficiency, customization/personalization, security/

privacy, responsiveness, assurance/ trust, price knowledge, aesthetics, reliability,

flexibility and efficiency. Each of the mentioned general dimensions has a number of

specific attributes (Parasuraman, 2004:50). Parasuraman (2004:50) adds that the

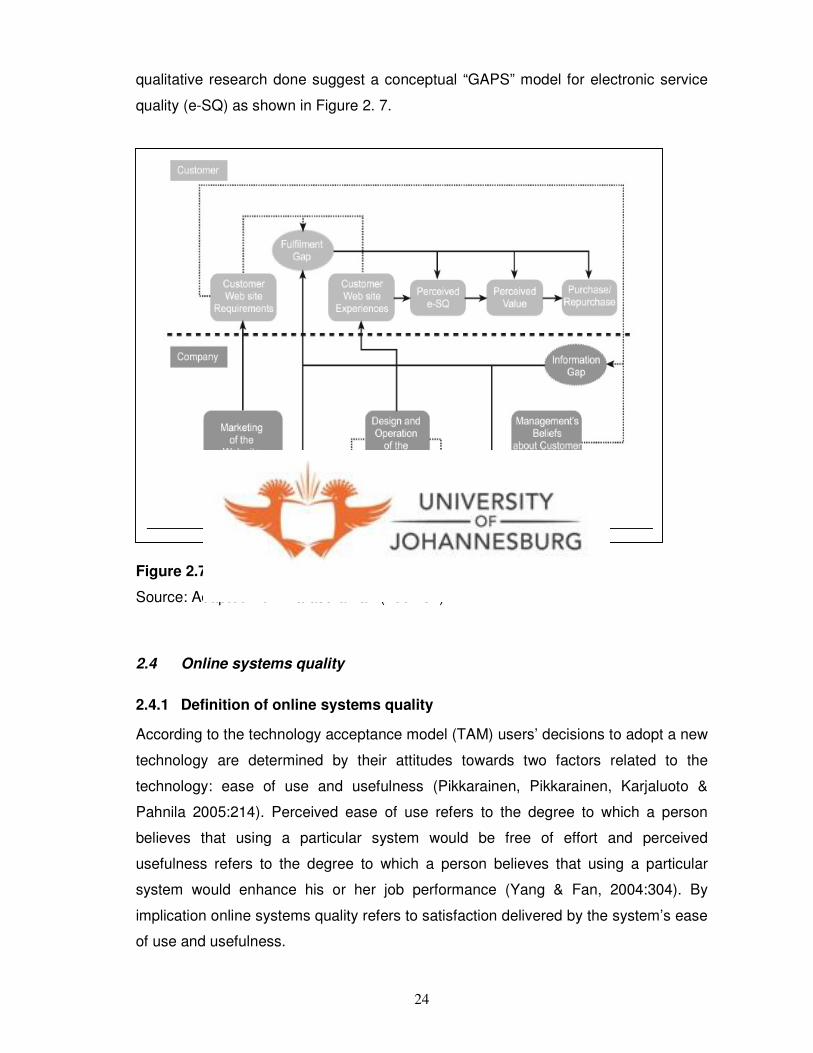

24

qualitative research done suggest a conceptual “GAPS” model for electronic service

quality (e-SQ) as shown in Figure 2. 7.

Figure 2.7: Conceptual GAPS model for E-S-Q

Source: Adapted from Parasuraman (2004:51)

2.4 Online systems quality

2.4.1 Definition of online systems quality

According to the technology acceptance model (TAM) users’ decisions to adopt a new

technology are determined by their attitudes towards two factors related to the

technology: ease of use and usefulness (Pikkarainen, Pikkarainen, Karjaluoto &

Pahnila 2005:214). Perceived ease of use refers to the degree to which a person

believes that using a particular system would be free of effort and perceived

usefulness refers to the degree to which a person believes that using a particular

system would enhance his or her job performance (Yang & Fan, 2004:304). By

implication online systems quality refers to satisfaction delivered by the system’s ease

of use and usefulness.

25

2.4.2 Characteristics of online systems quality

Figure 2.8: Website portal quality

Source: Adapted from Zeithaml et al. (2006:83)

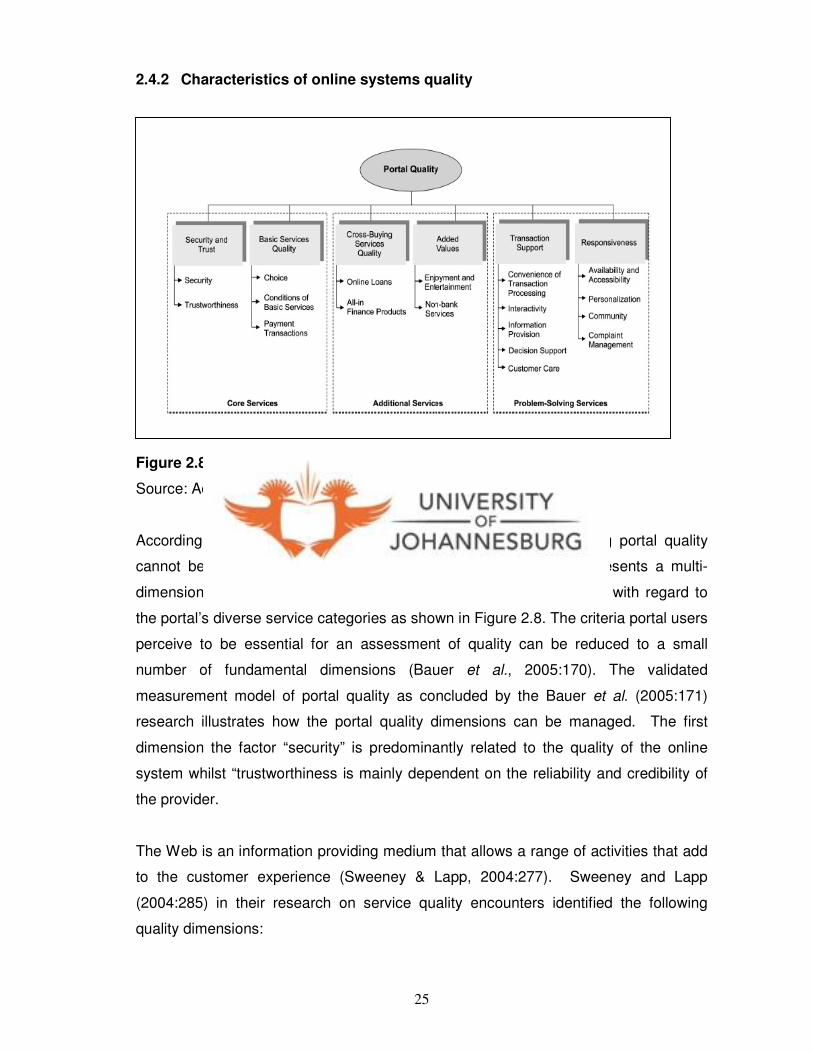

According to Bauer, Hammerschmidt and Falk (2005:172) e-banking portal quality

cannot be described as a one dimensional customer rating. It represents a multi-

dimensional construct that is composed of partial quality judgements with regard to

the portal’s diverse service categories as shown in Figure 2.8. The criteria portal users

perceive to be essential for an assessment of quality can be reduced to a small

number of fundamental dimensions (Bauer et al., 2005:170). The validated

measurement model of portal quality as concluded by the Bauer et al. (2005:171)

research illustrates how the portal quality dimensions can be managed. The first

dimension the factor “security” is predominantly related to the quality of the online

system whilst “trustworthiness is mainly dependent on the reliability and credibility of

the provider.

The Web is an information providing medium that allows a range of activities that add

to the customer experience (Sweeney & Lapp, 2004:277). Sweeney and Lapp

(2004:285) in their research on service quality encounters identified the following

quality dimensions:

26

1. Ease of use which deal with the following factors:

• Instructions and explanations on the web

• Structural design

• Navigational systems

2. Content

• Depth of content

• Correctness and accuracy of the content

• Presentation appropriateness

3. Process

• Control of the process

• Speed

The empirical results from the Bauer et al. research (2005:172) support the

understanding of portals as integral solutions representing a bundle of various

services and functions. Based on this research, aspects such as depth of service

range and possibility of opening accounts online or call back buttons and prompt

responses to questions, are important drivers leveraging overall service quality in an

effective manner.

2.4.3 Measuring online systems quality

Yang and Fang (2004:305) hold that: “since consumers’ use of Internet-based

services can be viewed as similar to the adoption of new technology, ease of use and

usefulness are important factors in evaluating online service quality.” Dimensions of

online service quality such as information content, customization, reliability, and

response also have significant effects on perceived ease of use and perceived

usefulness, which in turn influences the attitude towards using the portal site,

behavioural intention to reuse portal sites and actual portal site use (Yang & Fang,

2004:305).

27

Table 2.1: The WebQual 4.0 Instrument

Source: Adapted from Barnes and Vidgen (2003:299)

According to Barnes and Vidgen (2003:298) WebQual is based on quality function

deployment (QFD) which is a structured process that provides a means to identify and

carry the voice of the customer through each stage of the product or service

development. The standard WebQual 4.0 instrument in Table 2.1 consists of 23

questions with usability, information quality and service interaction as the main

categories.

The original electronic service quality (E-S-Q) scale was used to measure Website

service quality. The Table 2.2 below represents the original E-S-Q scale dimensions

with related questions (variables).

28

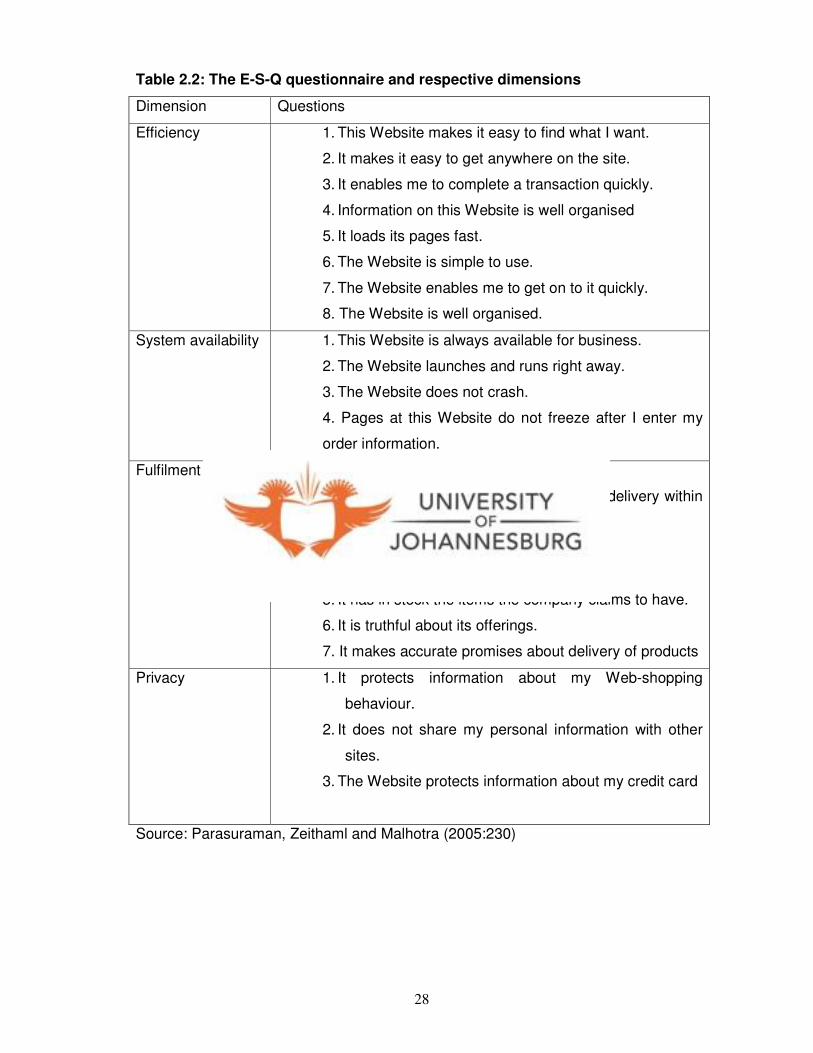

Table 2.2: The E-S-Q questionnaire and respective dimensions

Dimension Questions

Efficiency 1. This Website makes it easy to find what I want.

2. It makes it easy to get anywhere on the site.

3. It enables me to complete a transaction quickly.

4. Information on this Website is well organised

5. It loads its pages fast.

6. The Website is simple to use.

7. The Website enables me to get on to it quickly.

8. The Website is well organised.

System availability 1. This Website is always available for business.

2. The Website launches and runs right away.

3. The Website does not crash.

4. Pages at this Website do not freeze after I enter my

order information.

Fulfilment 1. It delivers orders when promised.

2. This Website makes items available for delivery within

suitable time frame.

3. It quickly delivers what I order.

4. It sends out the orders I ordered.

5. It has in stock the items the company claims to have.

6. It is truthful about its offerings.

7. It makes accurate promises about delivery of products

Privacy 1. It protects information about my Web-shopping

behaviour.

2. It does not share my personal information with other

sites.

3. The Website protects information about my credit card

Source: Parasuraman, Zeithaml and Malhotra (2005:230)

29

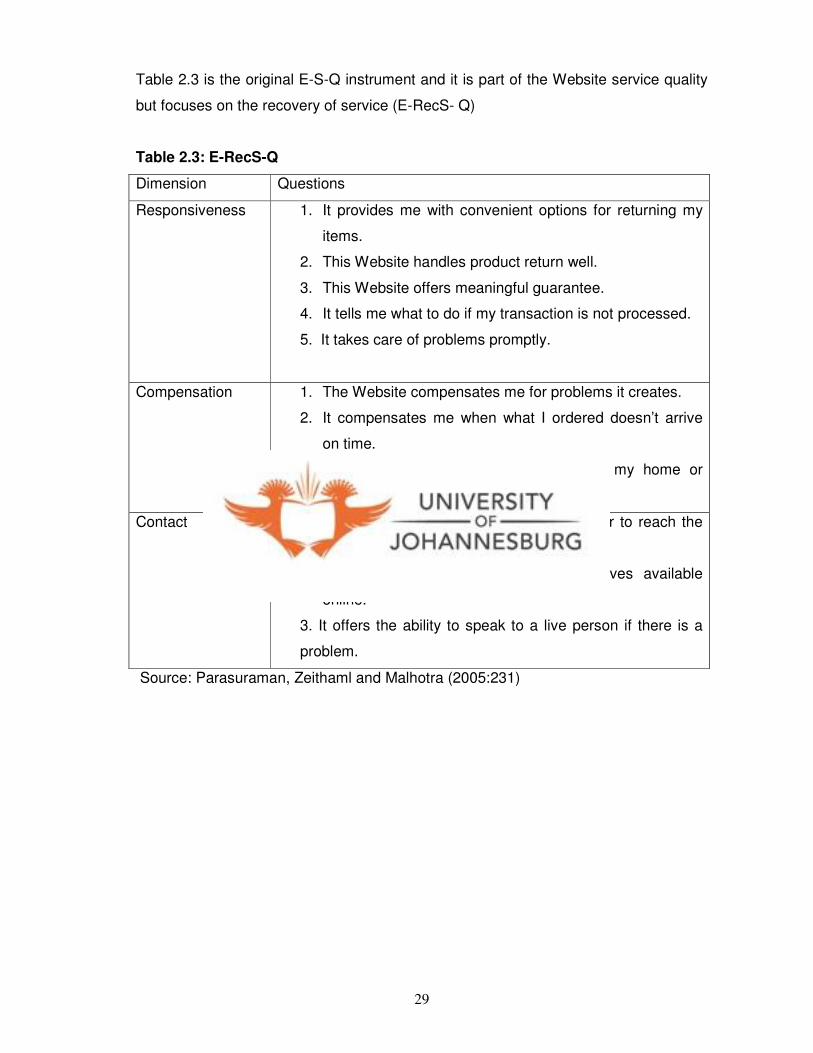

Table 2.3 is the original E-S-Q instrument and it is part of the Website service quality

but focuses on the recovery of service (E-RecS- Q)

Table 2.3: E-RecS-Q

Dimension Questions

Responsiveness 1. It provides me with convenient options for returning my

items.

2. This Website handles product return well.

3. This Website offers meaningful guarantee.

4. It tells me what to do if my transaction is not processed.

5. It takes care of problems promptly.

Compensation 1. The Website compensates me for problems it creates.

2. It compensates me when what I ordered doesn’t arrive

on time.

3. It picks up items I want to return from my home or

business.

Contact 1. The Website provides a telephone number to reach the

company.

2. The Website has customer representatives available

online.

3. It offers the ability to speak to a live person if there is a

problem.

Source: Parasuraman, Zeithaml and Malhotra (2005:231)

30

2.5 Internet Banking

2.5.1 Definition of Internet Banking

According to Sayar and Wolfe (2007:123) the term “Internet Banking” from a

customer’s perspective is used to describe the case where banks’ customers conduct

banking transactions on the Internet. In the contemporary context, this mainly implies

the usage of computers, but also allows for other possible devices like mobile phones

and digital TVs (Sayar & Wolfe, 2007:123). Internet Banking presents the industry

with an electronic and remote distribution channel. It represents an electronic

marketplace whereby consumers may conduct their financial transactions on a virtual

level (Bradley & Steward, 2003:272). Internet Banking refers to a service offered by

banks that allows account holders to access their account data via the Internet. In

order to take advantage of Internet Banking, an account holder would need to meet

several technological requirements, such as having a personal computer with Internet

access and web browser. If these conditions are satisfied, Internet Banking can be

performed from anywhere in the world. Thus, Internet Banking facilitates direct access

to account details, enables transfer of funds, allows for multiple bills payments, and

performs an array of other transactions.

2.5.2 Characteristics of Internet Banking

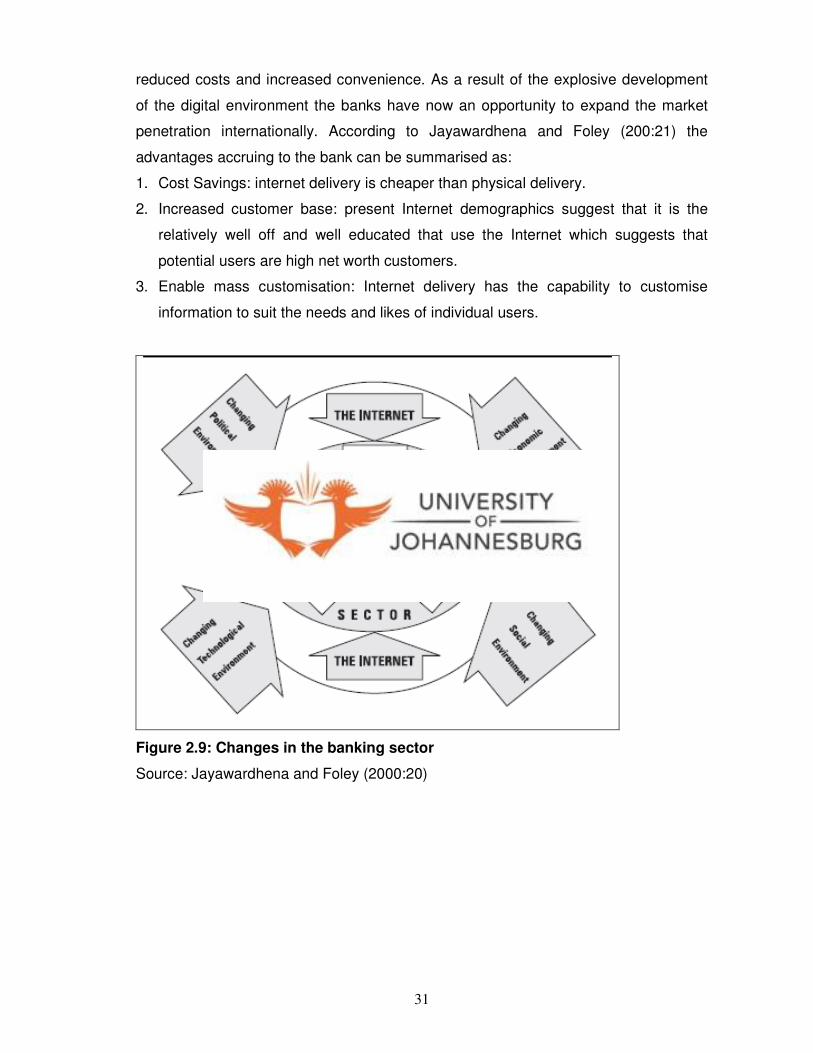

Jayawardhena and Foley (2000:19) in Figure 2.9 explain that the developments in

technology have dominated the revolution in the banking sector. The world-wide

expansion in technologies for connections has supported increased globalisation of

capital flows and financial organisations. The successful implementation and

development of online banking are influenced by the quality and security of Internet

network, the level of Internet knowledge of the population, the government support, as

well as the Internet strategy of the bank and the quality/ reliability of online banking

services (Gurau, 2002:294). Jayawardhena and Foley (2000:20) further state that

traditional banking is characterised by physical decentralisation, with branches

scattered around populated areas providing an ubiquitous presence. The rationale

behind such branch investment is the need to distribute the banking services.

Jayawardhena and Foley (200:21) indicate that the properties of Internet are the key

reasons why it is an ideal medium for delivery of banking products and services.

Gurau (2002:285) concurs that by using the Internet people can access their bank

accounts and conduct transactions twenty four hours a day, seven days a week with

31

reduced costs and increased convenience. As a result of the explosive development

of the digital environment the banks have now an opportunity to expand the market

penetration internationally. According to Jayawardhena and Foley (200:21) the

advantages accruing to the bank can be summarised as:

1. Cost Savings: internet delivery is cheaper than physical delivery.

2. Increased customer base: present Internet demographics suggest that it is the

relatively well off and well educated that use the Internet which suggests that

potential users are high net worth customers.

3. Enable mass customisation: Internet delivery has the capability to customise

information to suit the needs and likes of individual users.

Figure 2.9: Changes in the banking sector

Source: Jayawardhena and Foley (2000:20)

32

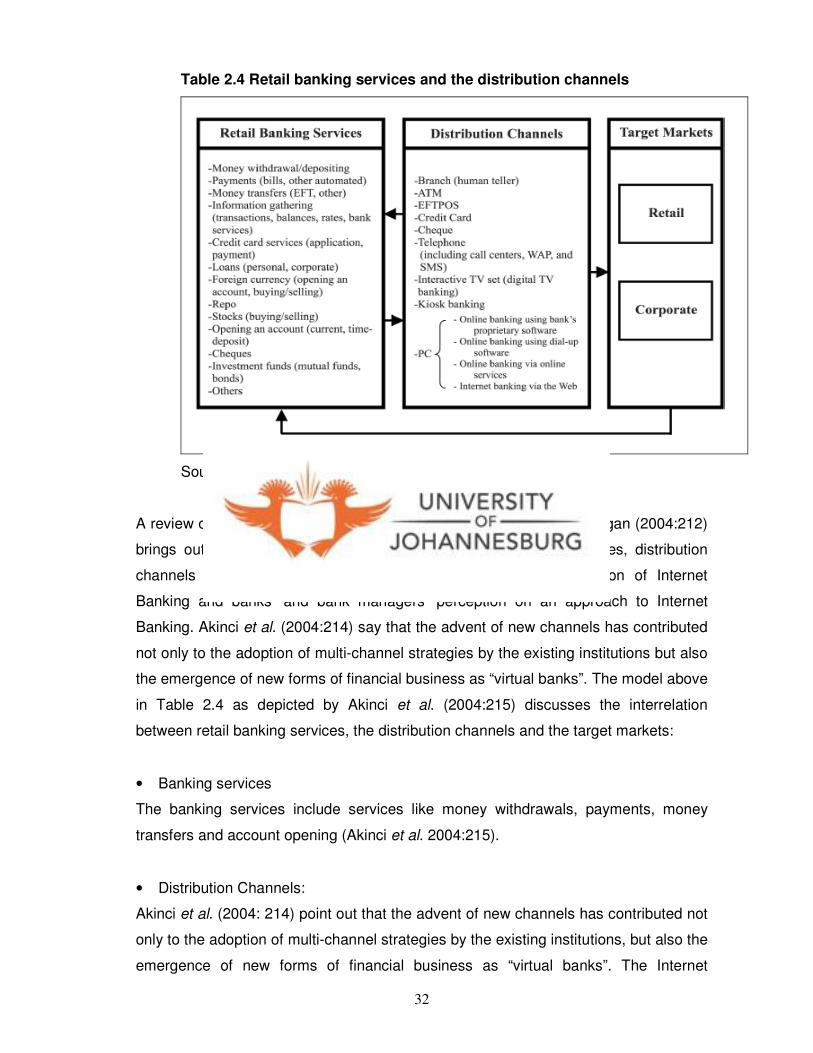

Table 2.4 Retail banking services and the distribution channels

Source: Akinci, Aksoy and Atilgan (2004:215)

A review of the literature on Internet Banking by Akinci, Aksoy and Atilgan (2004:212)

brings out four interrelated areas identified as: retail banking services, distribution

channels for the services, consumer attitudes towards the adoption of Internet

Banking and banks’ and bank managers’ perception on an approach to Internet

Banking. Akinci et al. (2004:214) say that the advent of new channels has contributed

not only to the adoption of multi-channel strategies by the existing institutions but also

the emergence of new forms of financial business as “virtual banks”. The model above

in Table 2.4 as depicted by Akinci et al. (2004:215) discusses the interrelation

between retail banking services, the distribution channels and the target markets:

• Banking services

The banking services include services like money withdrawals, payments, money

transfers and account opening (Akinci et al. 2004:215).

• Distribution Channels:

Akinci et al. (2004: 214) point out that the advent of new channels has contributed not

only to the adoption of multi-channel strategies by the existing institutions, but also the

emergence of new forms of financial business as “virtual banks”. The Internet

33

influences the future distribution channel structure in two ways. Firstly, it is in itself a

new distribution channel for financial service. The costs of using it are different from

those of other available distribution channels. Secondly, the Internet influences

consumers many of whom invest time and money in becoming PC literate and getting

to know the Internet (Möls, 1998:332)

• Target Market

The extent to which customers switch to Internet Banking is mainly determined by

each individual’s expectations regarding security, accuracy, transaction speed, user

friendliness, user involvement and convenience, all of which are components of

“perceived usefulness” (Sayar & Wolfe, 2007: 125).

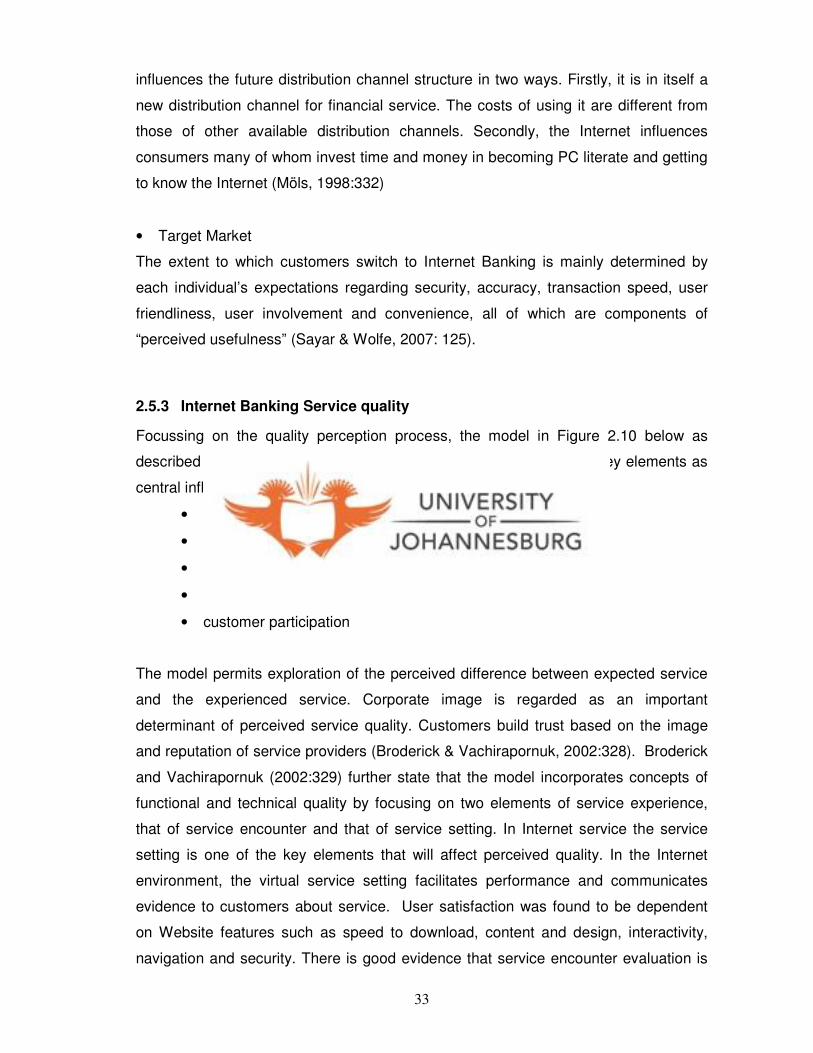

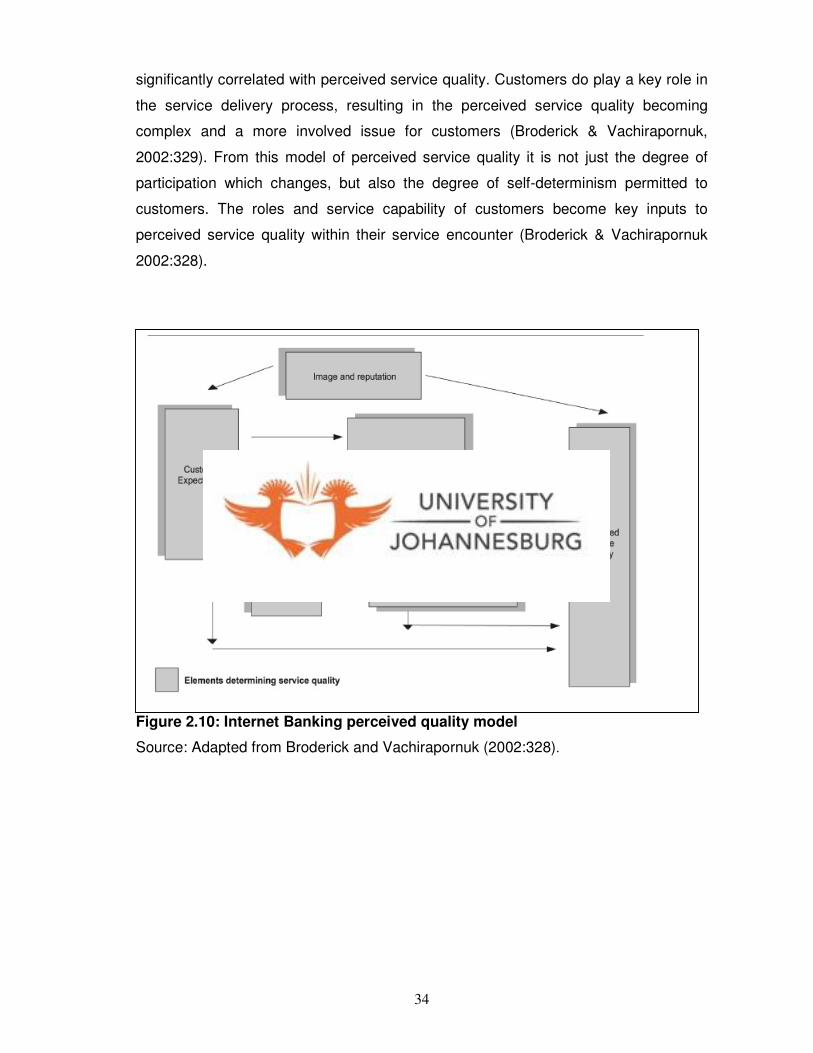

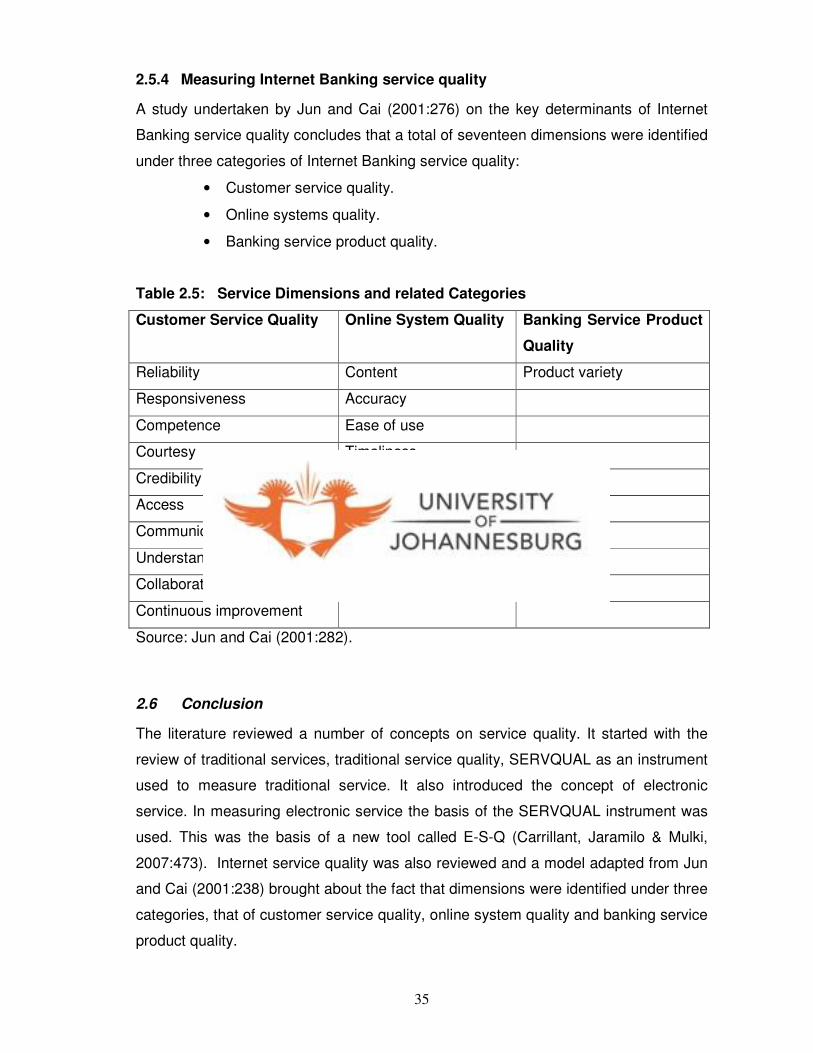

2.5.3 Internet Banking Service quality

Focussing on the quality perception process, the model in Figure 2.10 below as