Bahasa

Halaman

Hukum

A study on Savings and Investment Patterns

of Women in Bangalore

Submitted in partial fulfillment of the requirements for the degree of

Master of Philosophy in Management

by

Iyer Anusha Srinivasan

(Roll No. 1130004)

Supervisor:

Dr. Ganesh L

Associate Professor

Institute of Management

CHRIST UNIVERSITY, BANGALORE

2012

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

i

ACKNOWLEDGEMENT

I take this opportunity to express my gratitude to the people who made it possible for me to

complete this dissertation.

I express my sincere gratitude to my guide, Dr Ganesh L for his step by step guidance throughout

the research. Even though the time span within which the research had to be conducted was short,

he ensured that the research was conducted in a meticulous and procedural manner.

I am extremely thankful to Ms. Keerti Mallela, Research Assistant, Christ University for

selflessly helping me with Data Analysis.

My heartfelt gratitude to my parents for the sacrifices they made to facilitate me complete this

course and to my husband for his constant support.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

ii

DECLARATION

I, Iyer Anusha Srinivasan, hereby declare that the dissertation, entitled “A study on Savings

and Investment Patterns of Women in Bangalore” submitted to Christ University, in partial

fulfillment of the requirements for the award of the Degree of Master of Philosophy in

Management is a record of original and independent research work done by me during 2011-2012

under the supervision and guidance of Dr.Ganesh L of Christ University Institute of

Management, and it has not formed the basis for the award of any

Degree/Diploma/Associateship/Fellowship or other similar title to any candidate of any

University.

Date: Signature of the candidate

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

iii

CERTIFICATE

This is to certify that the dissertation, entitled “A study on Savings and Investment Patterns of

Women in Bangalore” submitted to Christ University, in partial fulfillment of the requirements

for the award of the Degree of Master of Philosophy in Management is a record of original

research work done by Ms. Iyer Anusha Srinivasan during the period 2011-2012 of her study in

the Institute of Management at Christ University, Bangalore, under my supervision and

guidance and the dissertation has not formed the basis for the award of any

Degree/Diploma/Associateship/Fellowship or other similar title to any candidate of any

University.

Date: Dr. Ganesh L

Associate Professor

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

iv

APPROVAL OF DISSERTATION

The Dissertation entitled “A study on Savings and Investment Patterns of Women in

Bangalore” by Iyer Anusha Srinivasan is approved for the degree of Master of Philosophy in

Management

Examiners:

1. ___________________ ___________________

2. ___________________ ___________________

3. ___________________ ___________________

Chairman:

___________________ (Seal)

Date: ___________

Place: __________

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

v

ABSTRACT

Economic growth of a nation is driven by savings and its transformation into investment. In the

last three decades, Indian economy has emerged as one of the fastest growing economies of the

world. Households are the biggest contributors to India’s savings rate; their savings equal 23

percent of India’s GDP. Though the percentage of savings by household sector in financial assets

is increasing year on year, what is worrying is that only around half of the household savings in

India are invested in financial instruments. Knowledge about saving and investment preferences,

gender-wise, will help to design effective investment instruments. Another area that requires

further examination is the role that a woman plays in influencing aggregate savings and

investment.

Till the last decade, considering the low earning potential of women to earn, save and invest, not

much research has been conducted on this subject. The coming decade, is going to see more and

more women getting higher education and aiming for heavy pay cheque jobs. There is an urgent

need to understand the savings and investment pattern of women, so as to frame policies and

develop financial products exclusively for women. Another reason for understanding the savings

and investment pattern of women is that, though they are good savers, they are unable to convert

all their savings into investments. They do not invest as much as the men do.

According to Barber (2001) though women are not active investors, they make more profits than

men when they trade because by trading more, men hurt their performance more than women.

Preda (2001) comments that women are always excluded from financial discussions, on the

explicit ground that they cannot understand investments. According to Chachoria (2000) women

are the next generation financial decision makers and they should be targeted from a financial

perspective. She suggests that marketing for financial products should be done differently for

women.

Through this study an attempt is made to understand the savings and investment pattern of

women. The factors which influence their investment decision making are identified. As 60

percent of women in India are house wives , they have been included in this study . The Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

vi

variations in the investment pattern between working and non-working with respect to socio-

demographic attributes have been analyzed.

The sample size consisted of 225 women, who regularly save and invest. The study was

conducted in the city of Bangalore. Convenience sampling was used for the purpose of data

collection. Data was collected through questionnaires and was subjected to descriptive and

inferential analysis.

The major findings of the research are:

The most important reason why a woman saves is because of a “Precautionary” motive.

Saving money in Bank and in the house kitty (saving at home) are the most preferred

saving avenues.

Even though non-working women don’t have direct income of their own, they are able to

save a minimum of 5 to 10 percent from their household savings.

Safety of the principal is regarded as a very important criterion before investing, as

opposed to instruments with low initial investment.

The main motive behind investing is to fulfill their personal and financial goals. They also

recognize the importance of multiplying savings through investment.

Gold is the most preferred investment instrument, followed by real estate, insurance

products, bank deposits, chit funds, mutual funds, bonds, post office deposits, shares and

SIP.

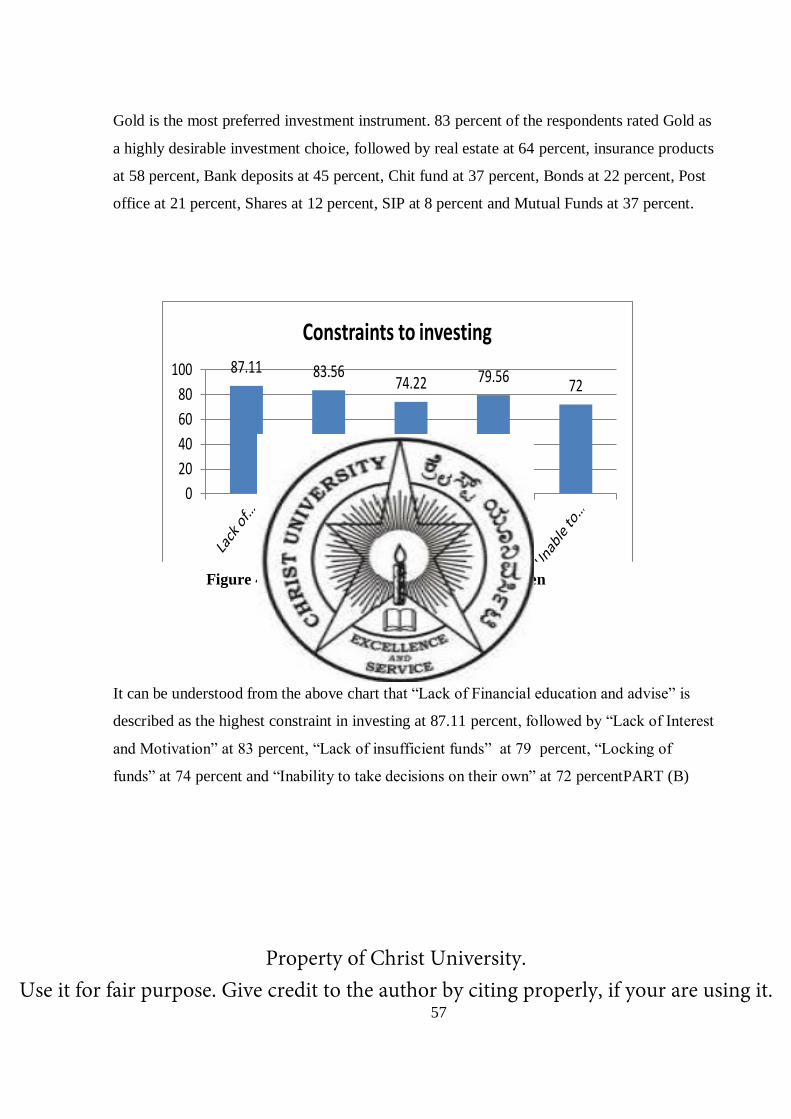

The highest constraint in investing is found to be lack of awareness and advice. This

bursts a common myth: In India women are not able to invest as they are not able to take

decisions on their own. Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

vii

Occupation of a working woman has bearing over the choice of traditional investments

but has no effect over the choice of risky instruments. It can also be said that education

plays a role in the choice of risky instruments for a non-working women, however for the

safe- traditional investments, education has no bearing. Also, irrespective of the

occupational status (working or non-working) for safe –traditional instruments, age does

not play a role, whereas for risky instrument it plays a role.

The study will help the financial institutions in designing exclusive instruments for women and to

the Government in coming up with new policies for utilizing women’s savings for the betterment

of the economy.

Key words: Savings, Investment, Women, Working Women, Non-working women

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

viii

Table of Contents

1. Introduction

1.1 Savings and Investment in the present Indian Economy………………………………….2

1.2 Importance of Women as savers and Investors …………………………………………..4

1.3 Present position of women in India with regard to savings and investments……………..8

1.4 Challenges faced by Women in Saving and Investing…………………………………...11

1.5 Genesis of the problem…………………………………………………………………...12

1.6 Need and Relevance of the study………………………………………………………...14

1.7 Scope of the study………………………………………………………………………..16

1.8 Limitations……………………………………………………………………………….16

1.9 Chapeterization…………………………………………………………………………...16

2. Review of Literature

2.1 Review of Studies………………………………………………………………………...17

2.1.1 Studies regarding nature and pattern of savings……………………………………...18

2.1.2 Studies regarding nature and pattern of investment…………………………………27

2.2 Research Gap…………………………………………………………………………….31

3. Research Methodology

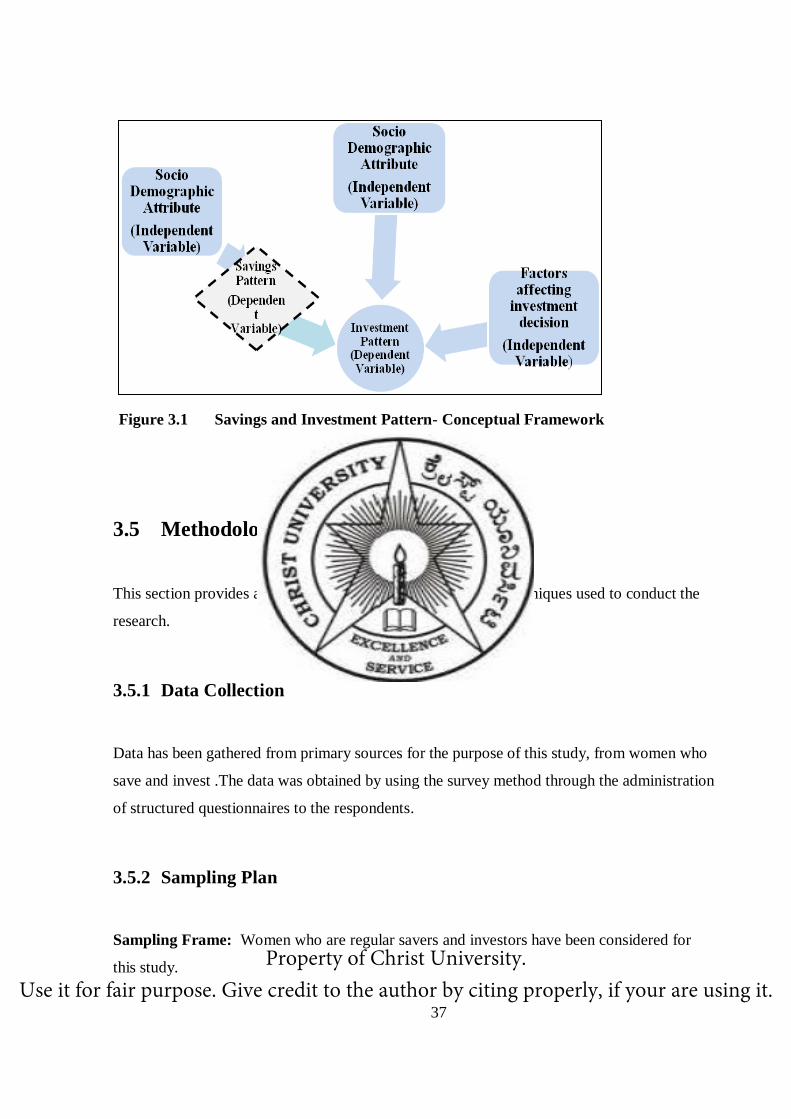

3.1 Statement of the problem…………………………………………………………………33

3.2 Research Objective……………………………………………………………………….33

3.3 Research Hypothesis……………………………………………………………………...34

3.4 Theoretical Framework…………………………………………………………………...37

3.5 Methodology……………………………………………………………………………..37

3.5.1 Data Collection……………………………………………………………………….37

3.5.2 Sampling Plan………………………………………………………………………..37

3.5.3 Survey instrument…………………………………………………………………….38

3.5.4 Reliability of the instrument………………………………………………………….38 Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

ix

3.5.5 Scaling techniques……………………………………………………………………38

3.5.6 Statistical techniques…………………………………………………………………38

3.6 Operational Definitions…………………………………………………………………..40

3.7 Variables………………………………………………………………………………….41

3.8 Limitations………………………………………………………………………………..41

4 Analysis and Interpretation

4.1 Demographics of the Respondents……………………………………………………….44

4.2 Savings and Investment patterns of Women……………………………………………..45

4.2.1 Savings pattern ………………………………………………………………………...45

4.2.2 Investment pattern ……………………………………………………………………..52

4.3 Factor Analysis………………………………………………………………………….58

4.3.1 Factor Analysis for Independent Variables…………………………………………….58

4.3.2 Factor Analysis for Dependent Variables………………………………………………61

4.4 Variance in Investment pattern among working and non-working women……………..75

4.4.1 Differences in frequency of investing across socio-demographic attributes………....76

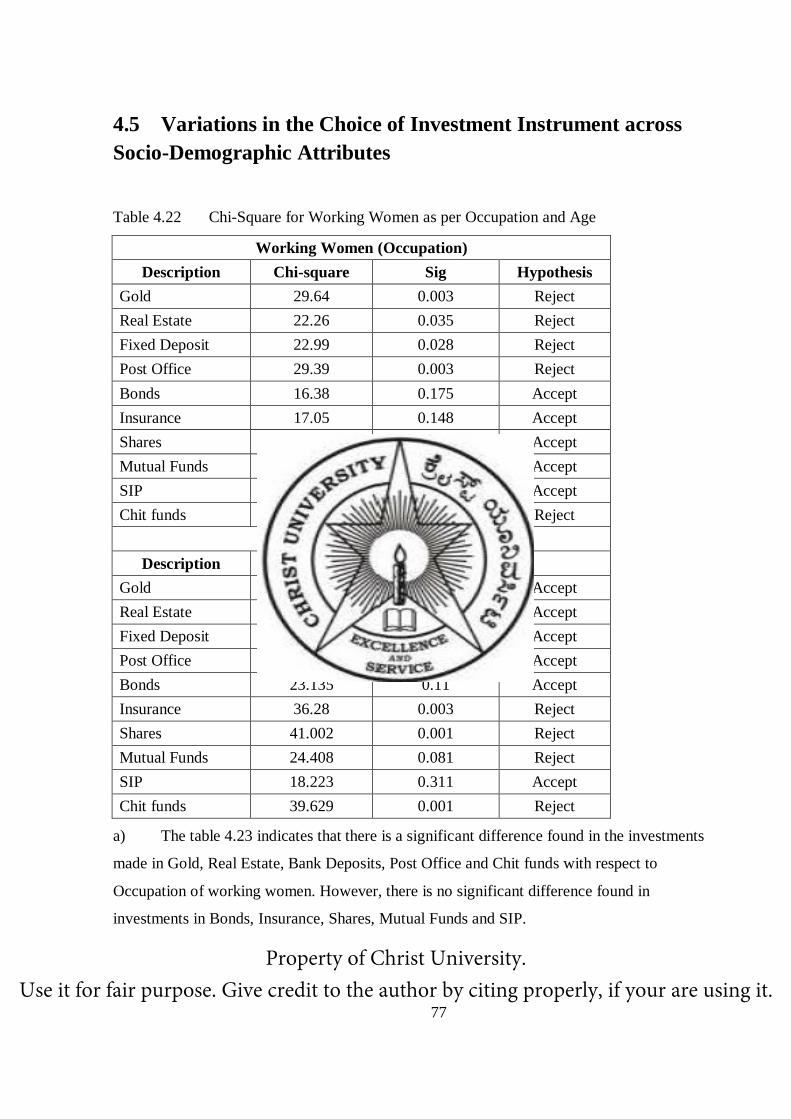

4.5 Variations in the choice of instrument across socio-demographic attributes…………..76

4..6 Descriptive statistics……………………………………………………………………77

5. Summary and Conclusion

5.1 Need and Rationale of the study………………………………………………………..90

5.2 Review of Literature…………………………………………………………………….91 Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

x

5.3 Research Gap…………………………………………………………………………….91

5.4 Statement of the Problem………………………………………………………………..92

5.5 Research Objectives…………………………………………………………………...…92

5.6 Sampling plan…………………………………………………………………………....93

5.8 Survey Measurement……………………………………………………………………..93

5.9 Statistical Techniques…………………………………………………………………….93

5.10 Variables………………………………………………………………………………..94

5.11 Summary of findings……………………………………………………………………94

5.11.1 Savings pattern of women…………………………………………………………….94

5.11.2 Investment pattern of women…………………………………………………………95

5.11.3 Inferential Analysis……………………………………………………………………97

5.12 Implications of the Research……………………………………………………………99

5.13 Suggestions and Recommendations…………………………………………………...100

5.14 Scope for further Research…………………………………………………………….101

5.15 Limitations of the study………………………………………………………………..101

5.16 Conclusions……………………………………………………………………………102

Appendix

Questionnaire……………………………………………………………………………….103

References…………………………………………………………………………………. 108

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

xi

List of Tables

1.1 Percentage of savers by gender…………………………………………………………..9

1.2 Percentage of investor households by gender…………………………………………....9

1.3 Percentage of other households by gender……………………………………………….9

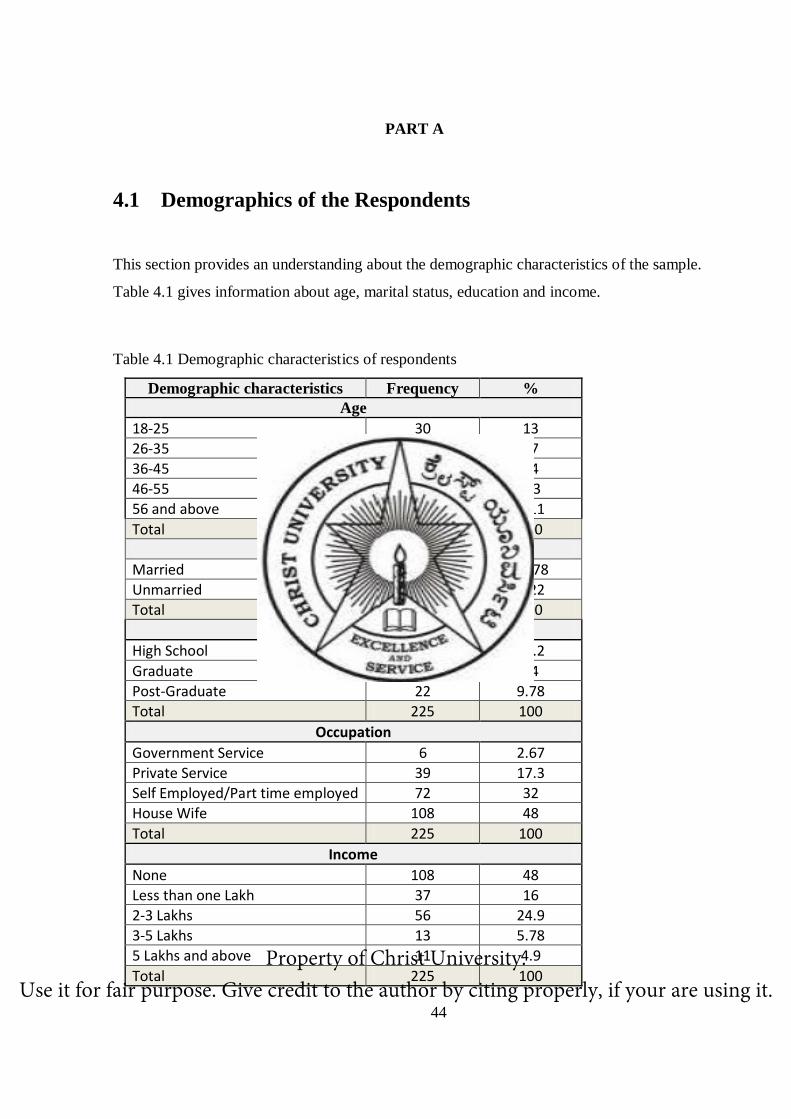

4.1 Demographic Characteristics of the Respondents……………………………………….44

4.2 Descriptive statistics for savings pattern of women…………………………………….46

4.3 Descriptive statistics for sources of saving and amount saved each month…………….50

4.4 Investment pattern …………………………………………………………………… ..53

4.5 KMO Bartlett’s Test for Independent Variables…………………………………………59

4.6 Communalities…………………………………………………………………………..59

4.7 Rotated Component Matrix……………………………………………………………..60

4.8 KMO Bartlett’s Test for Dependent Variables………………………………………….62

4.9 Communalities…………………………………………………………………………..62

4.10 Rotated Component Matrix…………………………………………………………….63

4.11 Karl Pearson’s Correlation ……………………………………………………………..65

4.12 Model Summary for Zero Risk Instrument…………..………………………………...66

4.13 Analysis of Variance for Zero Risk Instrument………………………………………..67

4.14 Co-efficients of Regression for Zero Risk Instrument…………………………………67

4.15 Model Summary for High Risk Instrument…………………………………………….69 Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

xii

4.16 Analysis of Variance for High Risk Instrument………………………………………..69

4.17 Co-efficients of Regression for High Risk Instrument…………………………………70

4.19 Model Summary for Low Risk Investment…………………………………………….72

4.20 Analysis of Variance for Low Risk Investment………………………………………..72

4.21 Co-efficient of Regression for Low Risk Investment…………………………………73

4.22 Differences in frequency of investing………………………………………………….76

4.23 Chi-square for working women (Occupation and Age)………………………………..77

4.24 Chi-square for non-working women (Education and Age)…………………………….78

4.24 Variations in Investment pattern of Working Women (Occupation)…………………..80

4.25 Variations in Investment pattern of Non-Working Women (Education)………………83

4.26 Variations in Investment pattern of Working Women (Age)…………………………..86

4.27 Variations in Investment pattern of Non working women (Age)………………………88

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

xiii

List of Figures

3.1 Conceptual Framework………………………………………………………………….38

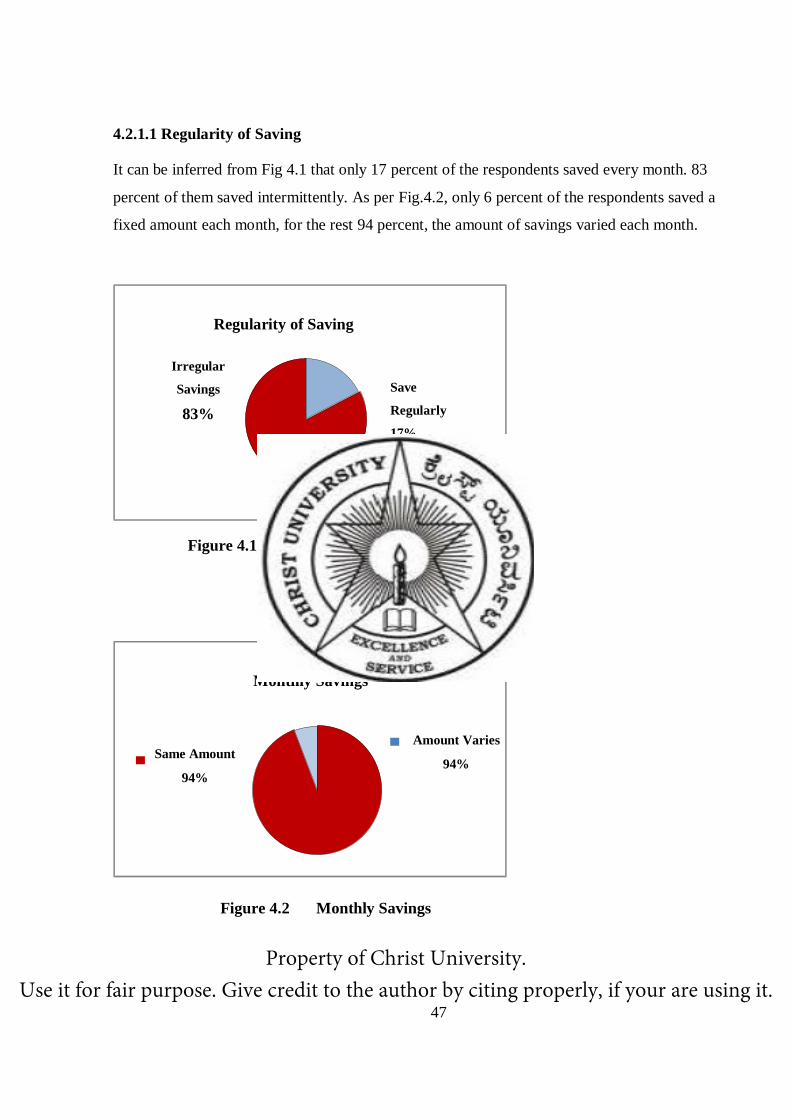

4.1 Regularity of saving……………………………………………………………………..48

4.2 Monthly savings…………………………………………………………………………48

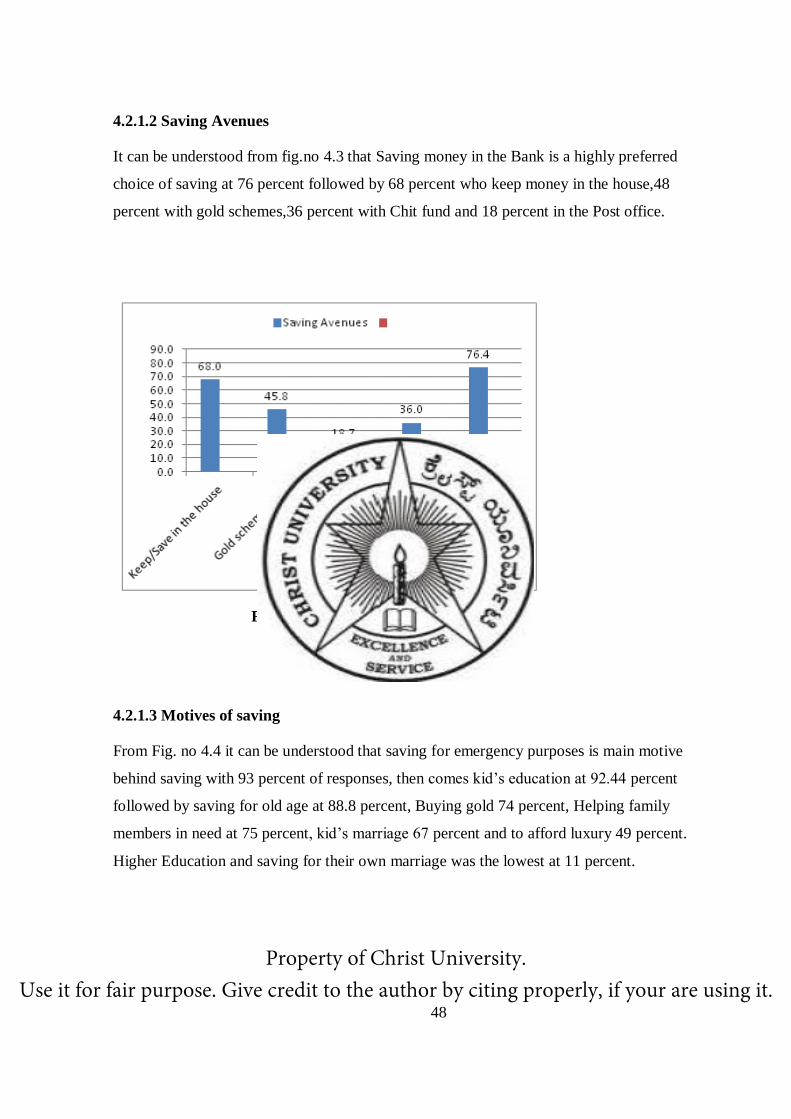

4.3 Saving Avenues………………………………………………………………………….49

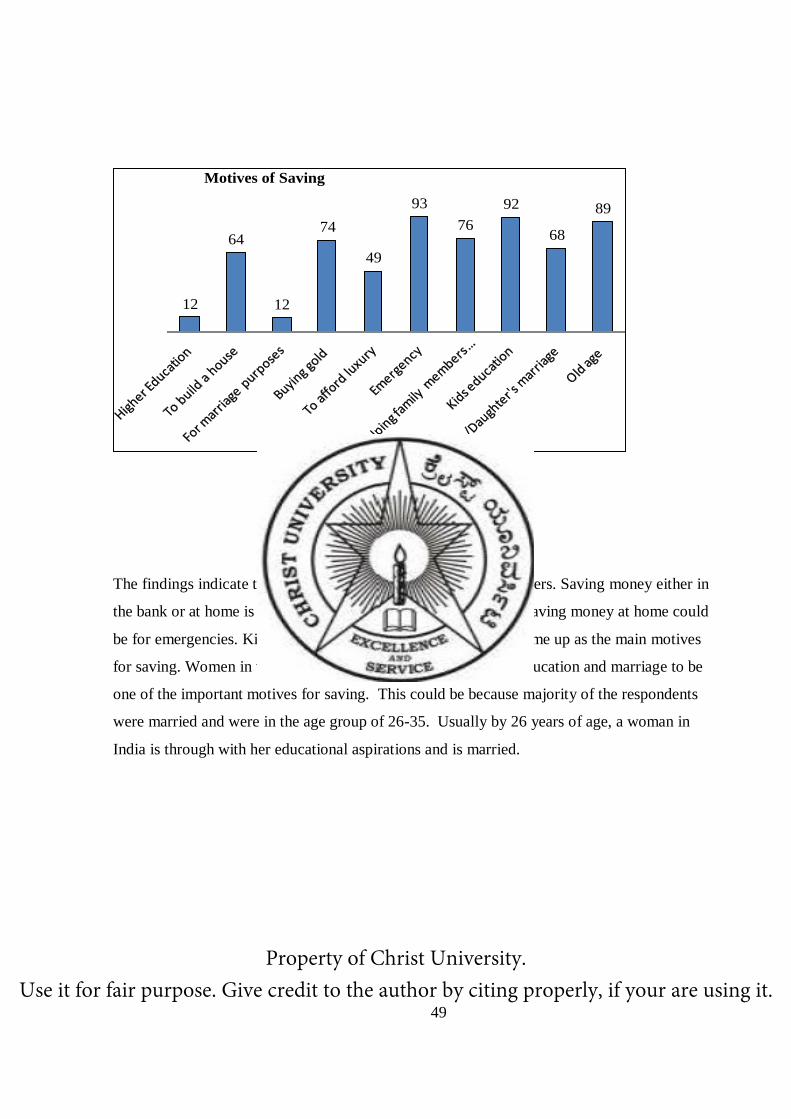

4.4 Motives of Saving……………………………………………………………………….50

4.5 Sources of saving- Working women…………………………………………………….52

4.6 Sources of saving- Non-working women………………………………………………..52

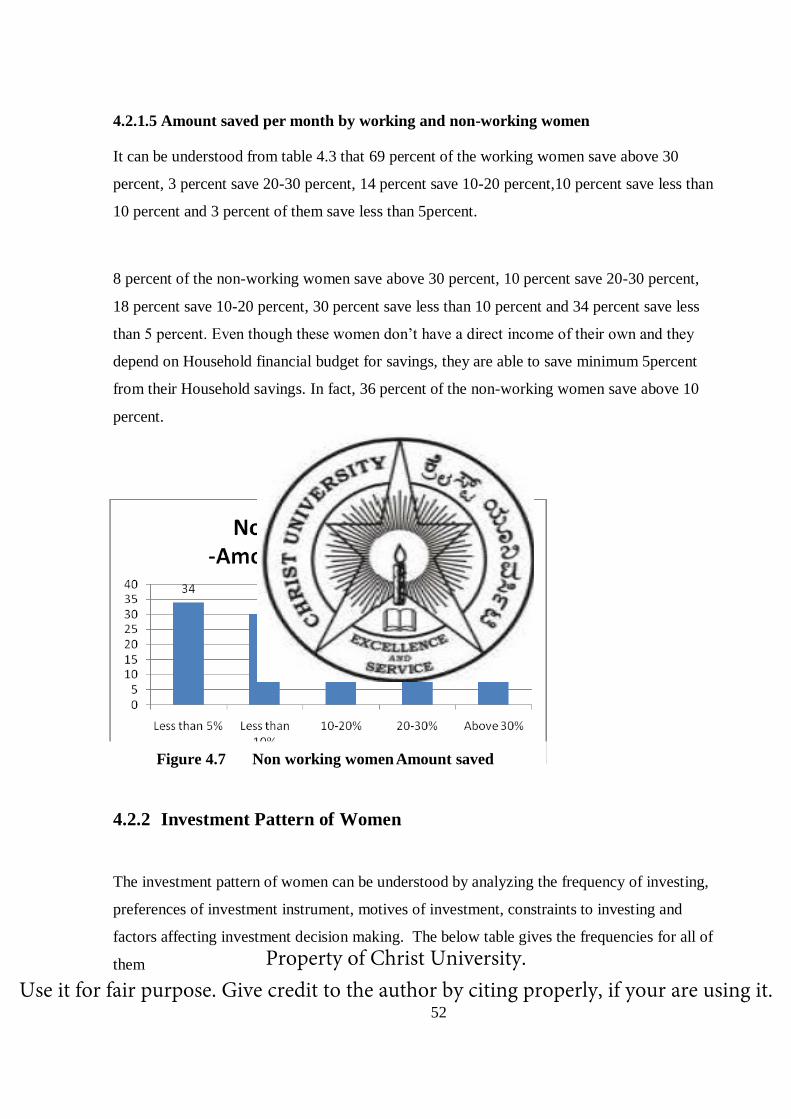

4.7 Amount saved by non-working women…………………………………………………53

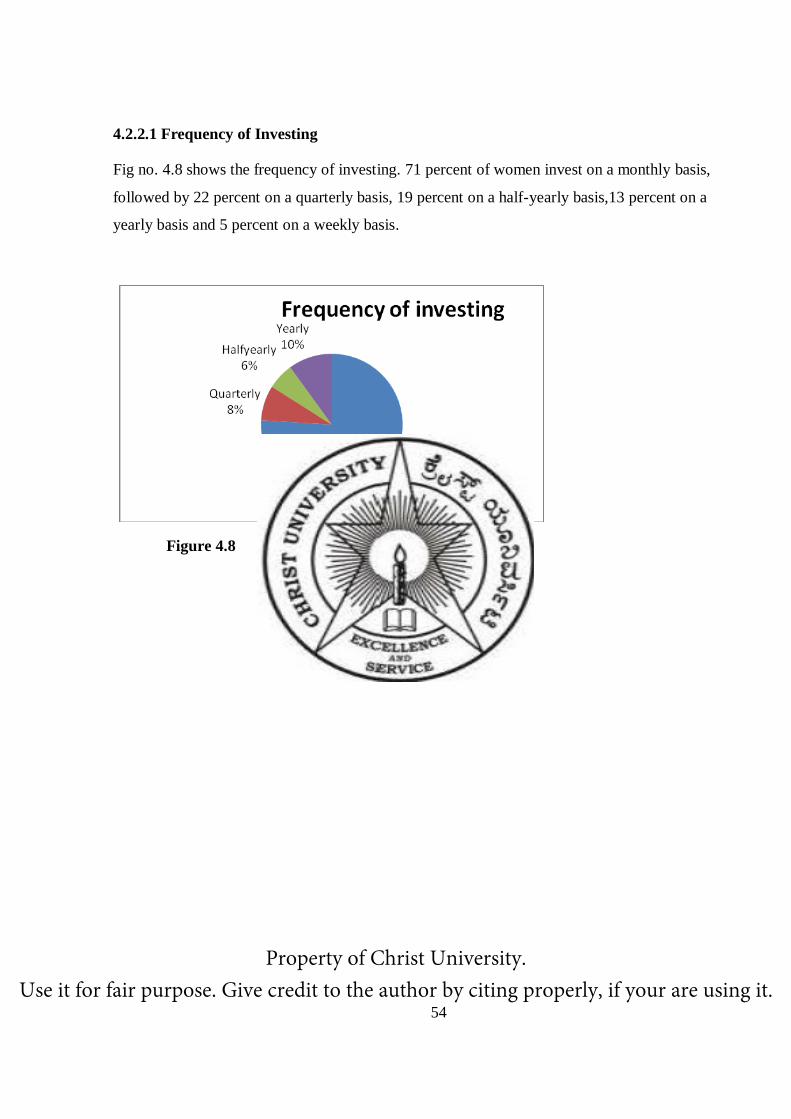

4.8 Frequency of investing…………………………………………………………………..55

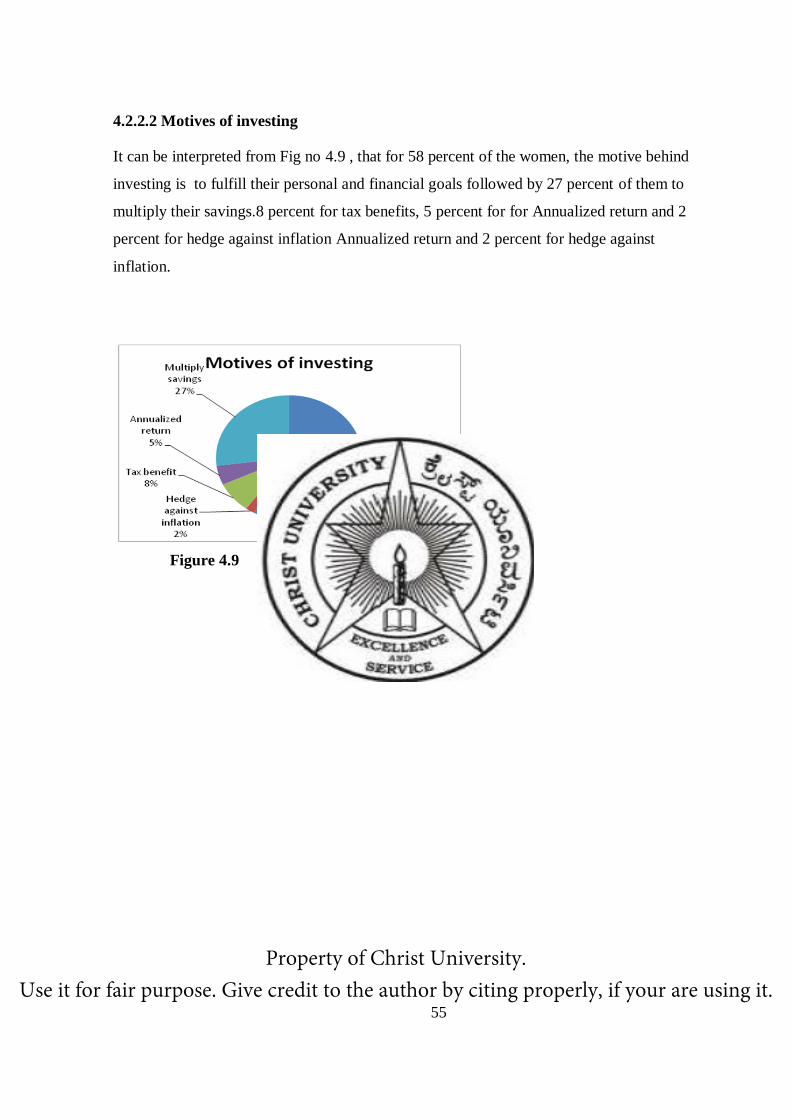

4.9 Motives of investing……………………………………………………………………..56

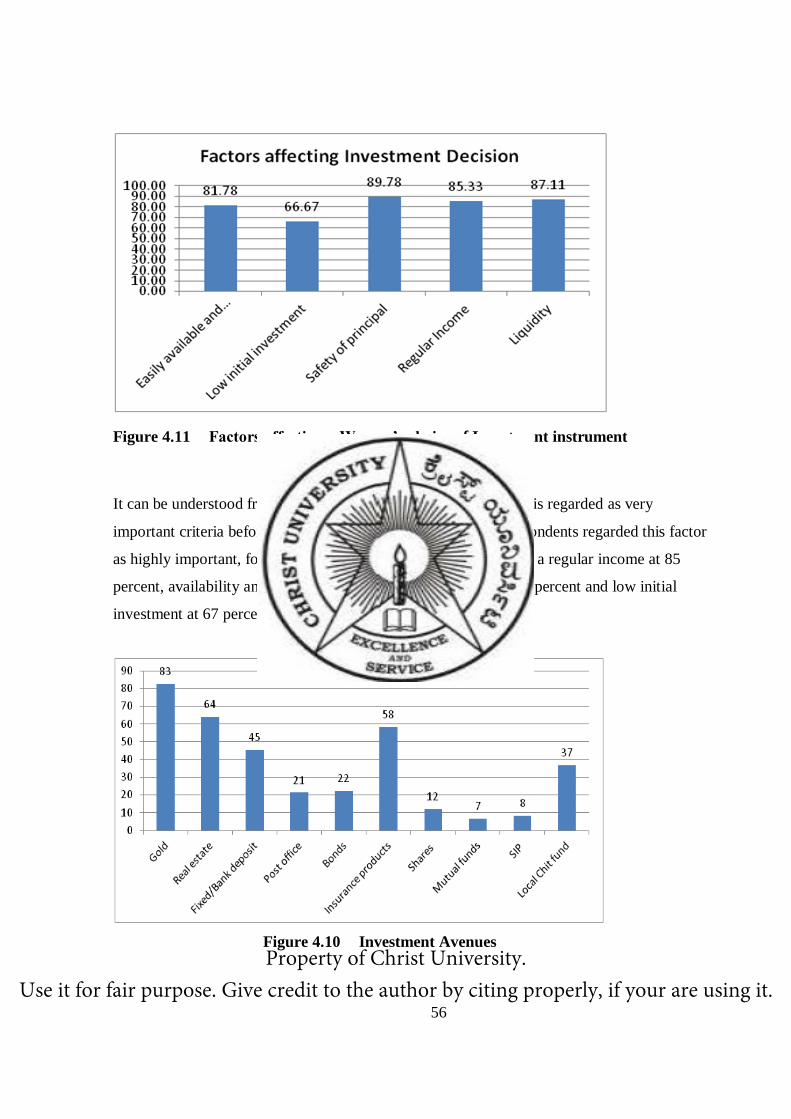

4.11 Factors affecting a woman’s choice of investment………………………………………57

4.12 Investment Avenues……………………………………………………………………..57.

4.13 Histogram for Zero Risk Investment…………………………………………………….69

4.14 Normal P Plot for Zero Risk Investment………………………………………………. .69

4.16 Histogram for High Risk Investment……………………………………………………72

4.17 Normal P Plot for High Risk Investment………………………………………………...72

4.18 Histogram for Low Risk Investment…………………………………………………….74

4.19 Normal P Plot for Low Risk Investment…………………………………………………75

Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

xiv

List of Abbreviations

1. ABS: Ability to save

2. CSO: Central Statistics office

3. FLCC: Financial Literacy Counseling Center

4. GDS: Gross Domestic Savings

5. GDP: Gross Domestic Product

6. HIES: Household Integrated Economic Survey

7. ITS: Incentives to save

8. MIMAP: The Micro Impact of Macro and Adjustment Policies in India

9. NCAER : National Council of Applied Economic Research

10. ROSCAS :Rotating savings and credit associations

11. NCAER : National Council of Applied Economic Research

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

Chapter 1

1Introduction

This chapter discusses the importance of savings and investment in the Indian economy,

importance of women as savers and investors, the present position of women with regard to

investing, the challenges they face and the qualities they posses for becoming a good investor.

Economic growth of a nation is driven by savings and its transformation into investment.

Savings made by one section of the society can be lent to another section where there might

be a need for money for production purposes. This type of saving-investing cycle creates

economic growth across many sections of the society and results in job creation. By

increasing savings within the country, the dependence on foreign direct investment reduces.

Generally, when savings rate of a country are high, the investments increase and the economy

grows. But if investment opportunities are not identified within the country, the savings flow

out of the country. If savings are hidden in homes or used to buy Gold or Real Estate they

don’t get channeled into investments by businesses.

One thing which becomes very clear is the fact that there is a pressing need to study savings

and investment side by side for all strata of the society in order to turn valuable savings into

productive investment.

The following chapter discusses the importance of savings and investment in the Indian

economy, importance of women as savers and investors, the present position of women with

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

2

regard to investing, the challenges they face and the qualities they posses for becoming a good

investor.

1.1 Savings and Investment in the present Indian Economy

Aggregate saving is an important source of funds for domestic investment and economic

growth of a country. Likewise, savings is also important at the household level for fulfilling

the immediate requirements of the family members, for old age and to leave bequests to

children. In simple terms, ‘Saving’ is the money left over from income after the consumption

needs of a person are satisfied. Saving is a critical variable in economic growth hence its role

as a determinant of economic growth has been emphasized by classical economists like Adam

Smith and David Ricardo in Wealth of Nations (1776) and On the Principles of Political

Economy and Taxation (1817) respectively. In the formation of physical assets and capital of

a developing economy like India, household saving plays a major role. Not only is the volume

of saving of household sector important but the form in which it is held is also equally

important.

Since independence, savings and investment have been considered as two very important

macro-economic variables in promoting economic growth of India. In the last three decades,

Indian economy has emerged as one of the fastest growing economies of the world. India is

amongst the highest savers among the emerging market economies. Gross Domestic Saving

(GDS) of the Indian economy constitutes savings of public, private, corporate and household

sectors. India reported a 33.7 percent gross domestic savings as a percentage of Gross

Domestic Product (GDP) in fiscal year 2010 as its economy picked up pace following the

economic slowdown in 2009The economic slowdown in 2009 saw gross domestic savings fall

to 32.2 percent of the GDP, down from 36.9 percent in 2008. While the household share of

gross domestic savings declined from 74 percent to 69.6 percent of total gross domestic

savings, household savings showed overall improvements, contributing INR 15,361 billion in

gross domestic savings, up from INR 13,310 billion in 2008-2009

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

3

Households are the biggest contributors to India’s savings rate; their savings equal 23 percent

of India’s GDP. This sector occupies a position of dominance over the other institutional

sectors like private corporate sector and the public sector in terms of generating saving. It

comprises of individuals, non-government non-corporate enterprises of farm business and

non-farm business like sole proprietorships and partnerships, and non-profit institutions.

According to data given by CSO, financial assets constituted 50.2 percent of household

savings in 2009-10, and have remained around these levels for the past four years; financial

savings were merely 10.7 percent in 1950-51. Saving in physical assets, which had a

whopping share of 89.3 percent of total household saving in 1950-51, has come down to 49.8

percent by 2009-10, reflecting growing monetization of the economy.

Though the percentage of Savings by household sector in financial Assets is increasing year

on year, what is worrying is that only around half of the household savings in India is invested

in financial instruments. This is also an important reason for the low level of financial

deepening in the country. As per RBI report (2010), only 1 percent of these savings in India

are invested in the Capital Markets. The majority of the savings are invested in physical assets

like Real Estate, Gold, Currency or Bank Deposits. If the savings continue to be invested this

way without building up the necessary infrastructure or industries, the future economic

development of the nation will be hampered.

The Planning Commission has pointed out that to achieve 9 percent GDP growth in the 12th

Plan, gross capital formation GFC (investments) need to be raised to 40 percent of the GDP in

the 12th Plan from 35.8 percent in 2009-10. The ability to finance this level of capital

formation depends largely on domestic savings. India has had 8-9 percent growth in the past,

but this could not be sustained as the economy ran into capacity constraints leading to

overheating. Therefore, to achieve and sustain a high growth rate, capacity needs to be scaled

up and for this, domestic savings need to be raised by about 5 percentage points in the next

five years. This underscores the importance of stepping up financial savings in the economy.

While addressing a conference in Mumbai, Reserve Bank of India Governor D. Subbarao said

that there is a need to raise the level of national savings and channel those savings into Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

4

investment for a double-digit and inclusive growth rate to take place. A large share of

domestic savings is held in the form of physical assets like land and gold.

To reverse this situation the household sector needs to be encouraged to increase its savings in

the form of financial assets such as equities, insurance, pension products, etc. The Reserve

Bank of India has introduced Financial Literacy and Counseling Centers (FLCC) to provide

consumers with the tools to make better credit choices (Reserve Bank of India, 2008). They

have also targeted schoolchildren to cultivate financial literacy at an early stage via interactive

websites (Reserve Bank of India, 2007). There is a need to increase the Individual’s trust in

financial markets. One another way is by increasing the Household saving rate.

Indian Economy with its population accounting for 16.0 per cent of the global population, is

expected to benefit from the ‘demographic dividend’, as huge pool of younger population

enter into the labor force and gainfully employed in production, generating a larger national

income and high household saving rate. For capitalizing on demographic dividend, targeting

urban population seems to be a perfect choice. However, the task does not look to be very

easy. In an exercise conducted by NCAER, to know the composition of Savers, non savers

and investors from various cities of India, it was found that only 20.75 percent of urban

population consists of Investors. The rest 79.25 percent of them are non investors. This data

clearly shows that though the urban population, which we can safely assume to be better

educated, is lagging behind in undertaking investments. Studies point out that it is Risk

appetite and financial awareness of individuals which play a major role in determining the

Investment profile of the Urban Investor.

1.2 Importance of Women as Savers and Investors

According to Centre for Development Informatics, in the coming decade there will be a rise in

levels of women’s employment. Some reasons which substatiate this optimism are: India’s

IT/BPO exports have increased from USD 105 million in 1989-1990 to 50.41 billion in 2008-

09. The software and services segment accounted for 40.61 billion, or 55 percent. In a recent Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

5

Indian study domestic IT turnover by a Dutch economic information agency (EVD) predicts

USD 50 billion for 2012. The development of the Indian IT industry is closely linked with

improvement of the country’s (higher) education system, combining technical and analytical

(mathematic) skills and English language abilities. As per World Bank edstats, females

constitute about 40 percent of all students currently enrolled in institutions of higher education

and it may be estimated that yearly 40-50,000 of these “new” IT professionals will be female.

In an effort to recruit more women employees, some companies are offering 25 percent

bonuses for female employee referrals and many companies have started providing child care

facilities to women under the Factories Act of 1948 . Thus, compared to the previous years, in

the coming decade, women will have more disposable income.

The consumer base in India consisting of educated women in urban cities is growing

immensely. Year on year the sale for Diamonds, Gold, Women’s Apparels, Imported beauty

products, footwear etc has been increases. Urban Women in India have purchasing power

with or without earning.Whether they earn by themselves or use their pocket money, or

household expenditure money, they are buyers. This gives a small hint : Women have money.

In the words of Delia Passi Smalter, founder of Medelia Communications, “Women currently

make or influence up to 85 percent of all consumer purchases, so isn’t it the time you started

marketing all products to them?” With increasing literacy amongst women, slow

disappearance of joint family system in the urban cities of India, men have started consulting

women for many decisions of the household including financial decisions. Whether working

or not working, the urban woman gets to influence the financial decisions of her household.

Thus they should be targeted from a financial perspective.

Saving for future emergencies has been an inherited and intrinsic quality of a woman. All

over the world women are known for their saving habits. In all cultures, mother’s teach their

daughters to save money for a rainy day. The oldest find of a money box dates from 2nd

century B.C. Greek colony Priene, Asia Minor, and features the shape of a little Greek

temple with a slit in the pediment. Money boxes of various forms were also excavated

in Pompeii and Herculaneum, and appear quite frequently on late ancient provincial sites,

particularly in Roman Britain and along the Rhine (Hurschmann 2009). Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

6

Women in India are no different when it comes to savings. They usually save from their

salaries or household budget. They save for meeting emergencies or for specific goals.

Available evidence suggests that in India even young girls are more likely to save than boys,

although they are less likely to save in a bank. For example, findings of a study of adolescents

residing in the slums of Allahabad, Uttar Pradesh, India, indicate that although girls were less

likely than boys to work for pay, they were more inclined to save; and although more girls

than boys saved, a larger percentage of boys than girls saved in a formal banking institution

(Sebastian, Grant and Mensch, 2004).

As per Sibley & Law (2008) , men tend to be more optimistic than women about their

household’s ability to meet its financial obligations. This is probably because fewer men than

women have a realistic understanding of the household’s actual financial situation. Nearly

three quarters of women state that their household sometimes — or always — struggles to pay

bills and repay loans whereas less than half of men consider this to be a problem. A revealing

difference is that five times more men than women stated they do not know how well their

household is meeting its current financial commitments. Women are also more diligent at

managing household expenditures than men. They are three times more likely than men to

keep household records and are significantly more likely than men to check that household

bills and accounts are correct. Not only do more women budget than men, but women are

twice as likely to keep a written record of household income and expenditure as men.

Though women understand the importance of saving better than men, they are unable to

invest in great numbers. One reason could be that they, as mentioned above , save for a rainy

day. Hence the top priority in a woman’s mind when she invests is “Security of money”.

Thus, she is most of the times Risk averse when it comes to picking up of Investments.

Though the Risk averse nature of a woman is regarded as the greatest drawback for successful

investing in way it turns out to be their greatest strengths while investing

Of all the stereotypes about the sexes, perhaps the most enduring is that men are better with

money unless the contest is spending it. However, a research on the ways each gender earns, Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

7

saves, and invests shows that women often come out ahead of men. A host of reasons why

women can be good investors are presented.

1. Women take the long view and they set goals

For most women, investment is a means of achieving life goals Goff (2003). Men want to get

rich. Women want to send their kids to college, build a house, etc. Belsky (2000) believes

that, since they match their investments with their goals, they tend to be more practical while

taking an investment decision.

2. Women sweat the details and do homework before investing

Female investors spend 40 percent or more time researching stocks than males do. They also

pay more attention to the general operations of the companies that they're putting their money

into. The result: Women -only investment clubs earn close to 7 percent more a year than all-

male groups do ( Goff 2003).

3. Women keep a close eye on household finances

Generally more wives than husbands handle the bill paying- hence they know exactly how

much cash flow is needed and where the budget can be nipped and tucked. (Goff 2003)

4. Women aren't afflicted with remote control disease

Once a woman buys a stock, she doesn't let go of it on a whim. So, she ends up earning more

in the market. (Goff 2003)

5. Women possess metaknowledge and manage overconfidence

Metaknowledge is an appreciation of what we do know and what we do not know may be

more important than primary knowledge. Women admit ignorance while taking investment

decisions. Thus they seek help. They also keep overconfidence at bay. Russo (1992). Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

8

6. Women are Rational

Women stick to their investments. They can see through the emotional haze and weigh the

evidence in a detached way. Emotion and investing do not mix. Rothschild, Baruch,

Templeton, Buffett and others all understood that one should establish investment principles

that they believe in, stick to them and remain undaunted by the hysterical bleating of the

markets

7. Women are Risk Averse

Neurobiological research suggests that high testosterone levels lead to a greater sense of and a

higher likelihood of taking risks, a combination that can be toxic when it comes to securities

trading. Since the percentage of testosterone is less in women, they tend to take less risky

decisions.

Women are blessed with innate abilities to be a good saver and investor. The flip side is that

they are good spenders also. With more income in their hand, they become powerful savers

and spenders. Thus, their savings and investment is something that the economy can look

forward to.

1.3 Present Position of Women in India with regard to Savings

and Investments

Due to the increased disposable income ,even savings generated by women will increase in

the future. But, whether are they equipped to save and whether the savings will materialize

into investment is a question less pondered.Going by the current statistics from the National

Council of Applied Economic Research ‘s Report on “How Households Save and Invest :

Evidence from NCAER Household Survey (July 2011), it is understood that women lag much

behind ,when it comes to savings and investment

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

9

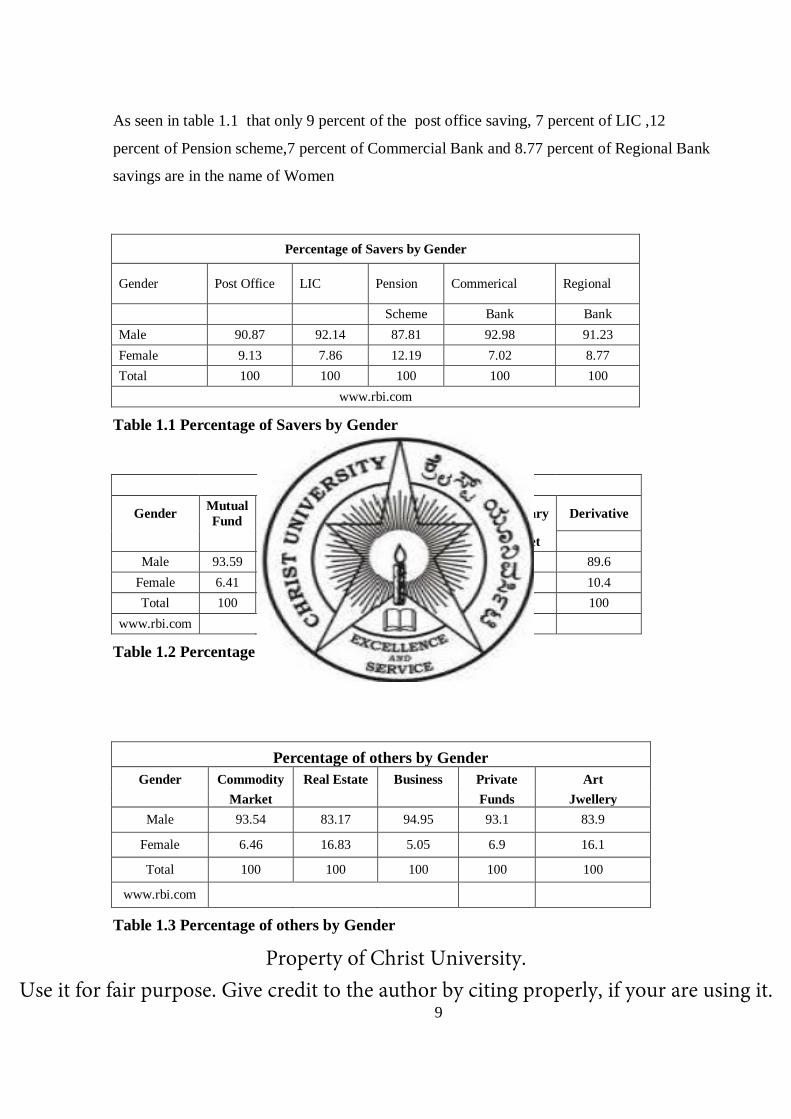

As seen in table 1.1 that only 9 percent of the post office saving, 7 percent of LIC ,12

percent of Pension scheme,7 percent of Commercial Bank and 8.77 percent of Regional Bank

savings are in the name of Women

Percentage of Savers by Gender

Gender Post Office LIC Pension Commerical Regional

Scheme Bank Bank

Male 90.87 92.14 87.81 92.98 91.23

Female 9.13 7.86 12.19 7.02 8.77

Total 100 100 100 100 100

www.rbi.com

Table 1.1 Percentage of Savers by Gender

Percentage of Investors by Gender

Gender Mutual

Fund

Bond

only Debentures IPO Secondary Derivative

Market

Male 93.59 92.55 94.42 96.43 94.77 89.6

Female 6.41 7.45 5.58 3.57 5.23 10.4

Total 100 100 100 100 100 100

www.rbi.com

Table 1.2 Percentage of Investors by Gender

Percentage of others by Gender

Gender Commodity Real Estate Business Private Art

Market

Funds Jwellery

Male 93.54 83.17 94.95 93.1 83.9

Female 6.46 16.83 5.05 6.9 16.1

Total 100 100 100 100 100

www.rbi.com

Table 1.3 Percentage of others by Gender

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

10

As seen in table 1.2 and table 1.3 that barring investment in Derivatives, Art Jewellery and

Real Estate which are at 10.40 percent, 16.10 percent,and 16.83 percent respectively the rest

of them are under 10 percent. The numbers are not flattering.

There is still a silver lining and optimism that investment will pick up in the women category.

Women in urban India, are far more educated than the rural areas, hence have started

contributing their thoughts and finances in the financial decisions of the household. They save

in Banks and Postoffices and invest in Mutual funds, Shares and Bonds. As most of them are

Computer literates, they are keen about investing in Stock Market. Some fairly educated

women, working and non-working both trade online and make good money. They invest in

equity of reputable companies.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

11

1.4 Challenges faced by Women in Saving and Investing

Some of the constraints which stop women from investing successfully are presented below:-

1. Risk Aversion

A considerable stream of research suggests that women are more risk averse than men in

financial situations (Bajtelsmit, Bernasek, & Jianakoplos, 1999; Halek & Eisenhauer, 2001;

Hallahan, Faff, & McKenzie, 2004).Results about gender differences in risk taking in the

financial arena (Croson and Gneezy, 2009; Eckel and Grossman, 2003) are more nuanced. A

general tendency for greater risk aversion among women has been observed as early as

childhood (Hargreaves & Davies, 1996; Kass, 1964). It can also be believed that the

biological differences in women should be held responsible for their risk aversion (Olsen,

2001). This reason ranks number one as constraint for successful investing.

2. Financial Illetracy

A leading explanation for this behavior is that women are not financially literate—they lack

sufficient information about financial concepts and instruments to make informed financial

decisions. A growing literature has evaluated both the state of financial literacy and the

effectiveness of financial education programs aimed at improving financial decision-making.

Women have identified Financial Illiteracy as the main reason why they don’t fare as well as

men when it comes to investment planning. Lusardi (2008)

3. Feminine Mentality

Many women consider purchase of financial services as a masculine activity (Burton, 1995).

While they are single they, save and invest for their marriage. But once they get married, they

think planning for the future is a husband's job. The fact that they may not be able to continue

working and earning throughout their lives, stops them from long term investment planning.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

12

4. Math Anxiety

Math anxiety is “a feeling of tension, apprehension, or fear that interferes with math

performance”. Related to this is gender and mathematics as women are thought to develop

anxiety towards mathematics and sciences when they become more interested in social

relations in their teen years. It is thought that women experience more anxiety in mathematics

as a group than men and this has also been suggested in regards computer programming who

explore computing and gender and especially have done experiments relating gender and

anxiety. (Copper, etal 2003). People who suffered from math anxiety as teen-agers often have

trouble making investment decisions later life, according to a survey by Dreyfus Corp. and the

national Center for Women and Retirement Research. The mail survey of nearly 1,300 people

found that those who were uncomfortable with math in their youth often put off personal

financial decisions for fear of making mistakes. Since as teenagers, women develop more

math anxiety than men (Dar-Nimrod & Heine, 2006), it can be concluded that, this may be

one of the reasons for them not turning out to be successful investors.

1.5 Genesis of the Problem

Inorder to chanelize the household Savings to productive Investment avenues, it becomes very

important to motivate and encourage women to invest in financial assets. The Government

,Banks and other Financial institutions are taking steps in this direction. Surveys are

undertaken to understand the Savings and Investment Pattern along with the Risk profile of

Individuals . Financial Literacy programmes are also undertaken by the Reserve Bank of

India to educate people in the Financial domain. However, these programmes and surveys

target the earning members of the household, which most of the times turn out to be a male

member. In houses where both the couples are earning , most of the times, it is the male

member’s Income, Saving and Investment which is reported. Housewive’s Savings or

Investment don’t get reflected in any of the surveys.

But, there are few reasons for not giving enough preference to women in such studies. Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

13

1. Since 1971, there has been a stabilization of women’s employment. The International

Labor Organization database shows no rise in women’s economic activity rates for India

1972-2002. These data show 31 percent of women working in 1970, 31 percent in 1980, 27

percent in 1990, and 30 percent for India in 2000. In other words there has been no

substantial change. Since women don’t have a regular income, it makes no point in taking

their perception or opinion about Savings and Investment. Perhaps this was the most

important reason why the focus for Savings and Investment have not been on women.

2. Women in India take breaks from employment for taking care of household

responsibilities, which suggests intermittent earning tenure.Thus more often, the financial

responsibility is on the shoulders of the Male members of the family. In such a situation, it

hardly makes sense to take opinion of the wife

3. Women are always excluded from financial discussions, on the explicit ground that

they cannot understand investments .(Prada ,2001)

4. A common myth that women don’t have a say in the Financial decisions of the

household.

But more than the above reasons, one concept in the Keynesian system of Saving, can be

blamed for excluding women from such studies: “Only those receiving income are "allowed"

to spend or to save.” Savings do result from income, but the fact that individuals who don’t

earn cannot save is not the truth. Walter C. Neale in his article “Who Saves? The Rich, the

Penniless, and Everyone Else” (1999) argues about this concept. Answering the question:

Who is “allowed” to save? leads to another question “Who is allowed to Spend” Thus one

who is allowed to spend can save. Going by this proposition, even housewives who don’t

earn, but get money to spend, can surely save. Studies of savings mobilization show that

economically active poor people, including women in the informal sector, can and do save but

they require services that are close to home, that do not require large opening balances or

regular deposits. In order to respond to these needs while recovering costs, institutions

recognize that they must employ innovative low-cost delivery channels (Hirschland, 2006;

Rutherford, 2006) But more importantly marketing for financial products should be done

differently for women.(Chachoria,2000) Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

14

It is in the benefit of the nation, if steps are taken to consider the savings of women, working

or non working and channelize them into productive investments. One more compelling fact

is that a quiet revolution has been altering greatly the mortality tables of many low-income

countries. Women are much more likely to be alone in old age, and elderly women are more

likely to be poor. The percentage of the female population over age 85 who are widows is

more than 85 percent compared to about 45 percent for men. An analysis of the National

Long Term Care Study data from 1984, 1989 and 1994 indicated that 20 percent of the

residual life expectancy at age 65 for men and 30 percent of the residual life expectancy at age

65 for women were spent in a state of chronic disability. Inflation affects people who live

longer more than those who live a shorter period so overall it is a greater issue for women. Its

impact grows over time.

1.6 Need of the Study

In order to formulate appropriate theories and policies to boost aggregate saving and

investment of the nation, it is important that economic planners have a true and fair idea about

the nature and volume of saving and investment, the behavior of people towards saving and

investment and the method by which saving can be improved for investment decisions. They

also need to know about the motives of saving and investment in order to frame policy

appeals accordingly. Knowledge about saving and investment preferences gender wise, will

help to design and implement saving and investment instruments which will effectively

stimulate investment. Sustained research in this field thus becomes imperative in order to

understand the patterns of savings and capital formation in our country.

Except for a few household surveys in the late 90s, very few studies estimate the profile of

households' saving and investment for both rural and urban areas in India. The Micro Impact

of Macro and Adjustment Policies in India (MIMAP) survey in 1996 and the detailed report

on "Household Savings and Investment Behavior in India in 2003" by EPW Research

Foundation and NCAER was an attempt in this direction. Although these studies describe

India's saving performance in detail, they do not sufficiently describe the analytical

framework of households' decision-making determinants and the factors that determine the

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

15

propensity to save and invest, which are important from a policy perspective. One area that

requires further examination is the role that women play in influencing aggregate saving and

investment.

Till the last decade, considering the low potential of women to earn, save and invest, not

much research has been conducted on this subject. Government surveys, policies, financial

awareness, marketing of financial products etc has been very less focussed towards woman.

The kind of enthusiasm shown by agencies and Governement for women’s development,

health, education, is yet to be seen in the subject motivating women to save and invest.

Marketing is heavily done on television ,radio or magazines for products that are bought by

women. Information regarding Women’s health or education, self-employment etc., is also

provided to them with wide coverage. However, except for Life Insurance there are very few

advertisements on investment products, financial services etc., targeting women.

The coming decade, is going to see more and more women getting higher education and

aiming for heavy pay cheque jobs. There is an urgent need to understand the savings and

investment pattern of women, so as to frame policies and develop financial products

exclusively for women. As 60 percent of women in India are house wives, they cannot be left

out of this study since they also get to save. Since working and non-working women have

different styles of living, earning and spending, their patterns differ. There is a need to bring

out these differences so that , accordingly financial products and programmes may be

designed. Above all, factors which influence them to save and invest have to be higlighted.

This study is an attempt to understand the above mentioned paradigms in depth.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

16

1.7 Scope of the Study

The study focuses on financial saving and investment of women of Bangalore. The variables

tested in the empirical study are occupation, educational qualification, and age. The factors

that affect women’s investment making decision are identified. Through analysis the

differences are identified between working and non-working women with regard to their

savings and investment pattern.

1.8 Limitations

The major limitations of this study are with respect to the time frame within which the

research had to be carried out and the sample size from which it would be difficult to draw

accurate conclusions on the entire women population. The results may not be free from biased

figures as some of the responses may include deliberate falsification and incomplete

information.

1.9 Chapterization

The second chapter gives an insight into the literature reviewed for the area under study,

followed by the third chapter that provides details of the methodology used for the purpose of

this research. The fourth chapter deals with analysis and interpretation of data gathered for

the study and the last chapter summarizes the entire report, discusses the implications of the

study, the suggestions made and the conclusion arrived at the end of the study.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

17

Chapter 2

2Review of Literature

The review of literature gives a fair idea about the work done in the subject area, the views

and observations made by different researchers and the gaps which need to be filled. In order

to understand and solve the research problem in question, it becomes important to get an

understanding of the various methodologies used by other researchers. During the process of

reviewing the past literature, various perceptions about the subject and concepts within the

subject get surfaced. This gives a direction to address the research problem from different

viewpoints. Several attempts have been made to explore the nature of Savings and Investment

done by people of various nationalities, cultures and age groups.

2.1 Review of Studies

The review of literature has been divided into two broad categories.

1. Studies regarding the nature and pattern of Savings

2. Studies regarding the nature and pattern of Investment

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

18

2.1.1 Studies Regarding Nature and Pattern of Savings

In an effort to study the saving patterns of people and the factors influencing the reasons for

saving and investment Anbarasu et al (2011), conducted a study on 1655 people of

Tiruchirappali city. Data was primarily collected through a questionnaire. The variables

considered were age, number of children, beliefs, opinions, Educational qualification and

income. Data was analysed through Econometric Analyses, Chi Square and Regression. It was

found that, out of all factors Educational Qualification played a major role for saving. Another

observation made was that people are not precise about their return and they invest their

savings carefully. The reasons for savings include Education, marriage, building a new house

and medical expenses. The amount of money saved depends on the Income level.

The socio economic and demographic factors influencing savings of various income groups

has been explored by Rehman (2011). For that purpose, data has been collected from 107

households of Multan from lower, middle and higher income group following per capita

income method. Life cycle hypothesis proposed by Ando and Modigliani in 1963 forms the

base of the study. The variables used were socio-economic and demographic in nature. It was

concluded that education, children’s educational expenditure, family size, liabilities and value

of house are reducing factors while total dependency rate and income are inducing factors for

household savings of lower income groups. Savings of middle income group was found to be

positively related to total dependency rate and total income was inversely affected by

children’s educational expenditures, liabilities, marital status, size of land holdings, and value

of house.

Dupas and Robinson (2011) conducted experiments on the participants to find whether there

was any effect of mental accounting on the psychology of saving. In one such experiment,

participants were provided with a simple metal box with a lock and key and a deposit slit in

the top. Just providing the box increased health savings by 68 percent. Based on interviews

with participants, it was concluded that this effect was due to mental accounting- meaning that

with the funds set aside, it was easier to refuse requests or it would limit consumption. It was Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

19

found that the respondents felt less obligated to share funds with others when they were in the

box.

Based on primary data collected from one hundred households selected from three villages

from the state of Kerala (India), Unny (2010) tries to find the determinants of saving. After

running Regression on the data, he finds that the Level of income, value of assets and level of

education of the head of the household positively influence savings whereas number of male

children, number of earners and dependency ratio has negative influence. Among the

occupational groups, households engaged in non-farm sector have higher propensity to save.

The number of female children has been believed to have a positive influence on savings in

India due to dowry system. However; in this study this factor shows a negative influence.

Copur(2010) explored saving behavior of Turkish families in Ankara, Turkey. Data was

drawn from 600 families from the city of Ankar. This study used a trans-created adaptation of

the NCC 1172: The Complex Nature of Saving: Psychological and Economic Factors to

establish a better understanding of saving behaviour.The independent demographic variables

consisted of gender, age, education, work, marital status, and income; Willingness to Take

Financial Risks: Financial Socialization and Negative Financial Events. Results indicated that

the vast majority of Turkish families were not saving and not willing to take any financial

risk. More than half of the participants did not discuss finance with their parents when they

were growing up. Majority of the families reported that over the past year their family’s

spending exceeded their income and the current economic situation significantly impacted

more than half of the families’ saving behavior and attitudes. Most of the families indicated

that their parents were savers while they were growing up. Interestingly, families who

reported both parents were savers while they were growing up were less likely to be saving

than those who reported neither were savers. An important finding was that having experience

of negative financial events in the last two years was significantly related to the likelihood of

saving.

The study undertaken to assess the level of financial literacy among people residing in Delhi

and National Capital Region (NCR) who invest in different financial instruments, like Post

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

20

Office Savings Scheme, Mutual Funds, Life Insurance, Stock market etc indicated that the

financial literacy of investors was different for different financial instruments. Around 96

percent of them had knowledge about Banks, 30 percent had knowledge about National

Savings Certificate & Public Provident Fund, 98 percent of the investors knew about Life

Insurance, 92 percent of the investors knew about Mutual Funds but only 24 percent preferred

them. A Chi-square analysis has been conducted to understand whether financial literacy is

found to be affected by age, income and educational level of the individuals. The results

indicated that there is a relationship between Financial literacy and income, however no

relationship between age and educational level. Seth (2010)

Using a sample composed of 167 individuals in Bangkok, Termprasertsakul (2009), explores

the associations between the saving behavior of individuals and variables, including

demography, perceived risks, and desired benefits. The demographic variables included

gender, age, marital status, employment status, education attainment, monthly income, and

number of dependants, public medical care program membership, company’s health insurance

provision, and spending behavior. The data was collected using self-administered

questionnaires in a survey. Chi-square tests were conducted to test the hypotheses of the

associations between saving behavior and independent variables .The research showed that,

all of the demographic variables, except gender, support the hypotheses of the association

with saving behavior in terms of saving method selection. It means that there is no difference

in the way men and women save.

Boring (2007) attempts to analyze the Household Savings Behavior in Uganda, using the

Finscope 2006 national survey data. Binomial probit models have been used and thereafter

probit regressions are run to test a number of characteristics ranging from education to trust in

financial institutions to attitudes about life in General. Findings suggest that the age of the

respondent (not just the age of the head of household), literacy, higher education, formal

sector employment, entrepreneurial activity, and attitudes about life’s current state to be the

determinants of saving behavior. It was also found that the marital status and whether or not

the respondent is solely responsible for the household financial decisions are statistically Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

21

insignificant regarding whether or not to save but quite important regarding institutional

choice.

To analyze the relationship between savings and age structure, Demery & Duck (2006) used

data derived from the FES, an annual cross-sectional survey of around 7,000 UK households.

Results point out that household data exaggerate savings rates of young adults and the elderly

whilst underestimating those of 45- to 60-year-olds. The individual saving rates follow more

closely the 'hump shape' of the life-cycle model, although the savings rates of the elderly

remain positive for some ages. It was also observed that there is a sample selection bias when

data refers to households and not individuals because most surveys provide consumption and

income data only at the household level.

Chowa (2006) investigates savings performance among participants in a matched savings

program in Uganda, modeled after the Individual Development Accounts (IDAs) in the

United States. Comparison of savings behavior by gender, level of education, marital status,

and type of work was performed. Participants save for a minimum of six months, and an

incentive is provided to them. After successfully reaching the savings goal the participants

had to purchase productive assets that could be used to generate income. The data sample size

for the analysis was 145. Average Monthly Net Deposit (AMND) was used as the dependent

variable in the analysis. This variable was used to measure the savings performance of

participants The AMND was calculated by adding total deposits plus interest (net of fees)

minus total unmatched withdrawals, divided by the number of months of participation The

results indicate that both male and female participants were saving in the project. However,

women were found to be saving more than their male counterparts across education,

employment, and type of work.

On a study on different cultures of household structures and saving patterns, De Laiglesia &

Morrisson (2006), finds that family relations shape saving institutions. Policies can alter

saving incentives and create the conditions for household structures themselves to change. It

was found that in many African countries, where men and women have different roles in

managing family finances, Roscas (rotating savings and credit associations) are often all-

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

22

female. This gender segregation allows women to render their savings illiquid, and even to

hide them from their partners. This allows women to save more in order to pay for school fees

and uniforms, or to buy kitchen ware and furniture. They are then better equipped to resist

pressures to draw on them when disagreements about saving and consumption choices erupt

in the couple. Another finding is that Polygamy plays a role in the amount savings done.

Wherever polygamy exists, men must pay an important bride-price to her father. This practice

diverts savings away from productive investment.

To examine the pattern of saving among cooperative farmers in southwestern Nigeria,

Adeyemo & Bamire (2005) collected data from 400 farmers. The data was analyzed using

descriptive statistics and multiple regression technique. Two functional forms, the linear and

Cobb-Douglas were fitted to the data. The model had savings as the dependent variable while

family size, gross income, cooperative experience, distance to the nearest bank, age, level of

education, source of initial capital, technology level, total consumption and household living

expenses were independent variables. Results show that cooperative farmers in southwestern

Nigeria are mostly males, literate and of average age of 47 years. Different factors influenced

their saving and investment patterns. Income, loan repayment and amount of money borrowed

were significant variables that influenced saving patterns. Age and loan repayment positively

influenced savings pattern while family size recorded a negative influence. Also it was found

that the farmers increase their savings, as they grow old. Though this negates the life cycle

hypothesis of savings, which claims that a person would be expected to save up to a point and

then start dissaving as he grows old, the results obtained show that most farmers in the study

area are not too old and therefore tend to save to cater for their household.

In order to understand how married women use their economic resources, Schmeer (2005),

uses data from Cebu, Philippines. This study finds that the more income women earn and

control; the more households spend on food. Multiple regression analysis has been used to

assess the effect of women's resource position on food expenditures, controlling for the

individual, house-hold, and community characteristics. One important point that surfaces is

that, providing employment opportunities may not be sufficient if women must relinquish

control over their earnings. For women, in better off households, improving their financial Property of Christ University.

Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

23

management skills may increase the likelihood that household income will be turned over to

them and thus be used to improve child welfare.

Ahmad and Asghar (2004) estimated saving function based on HIES (1998-99) primary data

in Pakistan. 8933 rural and 5374 urban respondents were chosen from the survey. It was

found that saving was directly influenced by income, employment status, age square and sex

of rural and urban respondent. Wealth, dependency ratio, and age of the respondents were

found negatively affecting savings of rural and urban respondents

After exploiting data collected from the first wave of the SAVE panel, specifically collected

to understand economic, psychological and sociological determinants of saving, Börsch-

Supan & Essig (2003) study the savings patterns of Germans. The findings suggest that nearly

everyone - whether in the middle income bracket or richer - saves substantial amounts in old

age. The research points out that 40 percent of German households save regularly a fixed

amount. About 25 percent of German households plan their savings and have a clearly defined

savings target in mind. Most of German household saving is in the form of contractual saving,

such as saving plans, whole life insurance and building society contracts. This makes the flow

of saving rather unresponsive to economic fluctuations, such as income shocks. Most

households prefer to cut consumption if ends do not meet. In particular the elderly do not like

to use credit cards, and they eschew debt.

In order to examine the determinants of private saving in the process of economic

development, in India during the period 1954 -1998, Athukorala (2002). The data obtained

was compiled from various publications like National Accounts Statistics, Government of

India, Economic Survey & Reserve Bank of India, Monthly Bulletin The methodology

involved the estimation of a saving rate function derived within the life cycle framework

while paying attention to the structural characteristics of a developing economy. It was found

that the saving rate rises with both the level and the rate of growth of disposable income and

the magnitude of the impact of the former is smaller than that of the latter. The real interest

rate on bank deposits has a significant positive impact, but the magnitude of the impact is

modest. Public saving seems to crowd out private saving, but less than proportionately,

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

24

suggesting that public policy can influence the national saving rate. Among the other

variables considered, the spread of banking facilities in the economy and the rate of inflation

seem to have a positive impact and changes in the external terms of trade and migrant

remittances a negative impact on private saving

Khandker (2000) does an econometric analysis on the household survey data from three

villages of Bangladesh where micro-credit programme had been in operation for three years

or more. One of the observations made was that, women were saving more in such micro-

borrowing programmes and that the informal finance impact is more pronounced for men than

for women. Also by offering membership and opportunities for borrowing, many microcredit

programmes have been able to mobilize savings (largely involuntary) from their poor and

women members, who are not considered net savers by traditional financial institutions

For exploring the saving behavior of rural industry households, Brata (1999), collected

information from 93 respondents by conducting survey of small industries in Bantul Sub

district in 1996. In the survey, he found that respondents were more interested in keeping

financial assets than real assets as their savings. They preferred to save their financial assets in

non-banking institutions like co-operations, credit unions etc. It was concluded that Income,

Education, Sex and Industry type were found to have direct significant impact on savings

Baden (1996) examines gender issues in relation to financial liberalization and financial

sector reform. The objective of the study is to demonstrate that processes of financial

liberalization and financial sector reform are not gender-neutral and that, therefore, gender

analysis has a place in the design and implementation of financial sector restructuring. The

findings suggest that women have less access to formal sector’s financial savings facilities

than men and women hold real assets in different forms. Men’s financial assets are more

likely to be in interest bearing accounts, whereas women’s savings are often in forms where

no interest accrues or else is held as real assets.

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

25

Panikar (1992) has studied the rural household saving pattern in few villages of two states in

India, namely Kerala and Tamil Nadu. The study was conducted with an objective of looking

into the levels of saving and the manner of its disposition and to identify the factors

underlying the rates of saving. Data was collected from 300 households. Variables like

Income of the household, consumption, expenditure, indebtness, physical investment and

financial investment were introduced apart from the basic socio-economic variables. Data was

analysed using Multiple regressing, Chi-square tests and Anova. The study found that a high

proportion of saving was absorbed in unproductive assets leading to a vicious circle of low

income and low saving.

During an analytical review of the literature on saving capacity of rural households in India,

Desai (1981) found that the existing literature has neglected “incentives to save” (ITS)

hypothesis of savings behavior. After reviewing the estimates of rural household savings

published by Reserve Bank of India (1954), he reveals the fact that there has been a

pessimistic assumption about the saving capacity of rural households in India. Most studies

have considered the “ability to save”(ABS) hypothesis alone. He says most of the studies are

Keynesian and hence consider only current income as a measure of ABS. He agrees with

Bhatty et al (1977) on the thought that the Keynesian framework of savings which assumes

that the decisions to consume and save-invest are independent, does not work for rural

household savings

Repetto & Shah (1975) studied the demographic and other influences on long term saving

behavior in India. The data for the study was collected from surveys conducted in the Kaira

district of Maharashtra from 1930 to 1965. It was found that large family size has a depressing

effect on long term household saving rate also. The study also revealed that sons in rural India

serve as substitute assets in households.

In an attempt to study the saving behavior of Indonesian households, Kelley and Williamson

(1968) run a regression analysis on per capita household saving against per capita household

income for five household age groups. They have found that the age of the head of the

household is an important determinant of household saving in rural areas and that the average

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

26

and marginal saving rates rise with the share of agricultural income and the presence of

positive interaction between wealth and saving.

Johnson and Chiu (1968) ran time series regression for household saving on household

income and private saving on private income for 30 countries includes developed and

developing countries. Majority of the results show a positive correlation between saving and

income. These results suggest that at best both household saving and private saving are

proportional to household income and private income respectively.

With the purpose of throwing some light on the saving behavior of urban Indian households,

Ramanathan (1969) collected data from 600 households from Delhi. Data was collected on

components of income, net worth and saving, qualitative information on past and expected

income-change, liquid assets, debts, the extent of visitors to the households, occupation of

head, family size, number of earners, age, education of head, home-ownership status,

expenditure on durable goods and dowries, motives for and attitudes toward saving, etc The

effects of income and net worth on saving are examined in detail for different socio-economic

sub-groups. The results say that in- come and net worth significantly influence the level of

saving. Contrary to the studies in advanced countries, home-owners had a much lower saving-

income ratio than renters although the former had a slightly higher average income. A major

reason for this may be the uncommonness of amortized mortgages in India, with no

contractual commitment to save till the age of 45 savings steadily increased and then started

dropping. After the age of 65, again increases. The author attributes this to the joint family

system in India.

While describing the use of modern banks by women in SriLanka, Dissanaike (1968) finds

that women prefer informal sources of saving and lending that afford them more flexibility. In

addition to gold SriLankan women have adopted informal group savings method called

“seetu”, where each contributes to a common fund that is then given to one member each

month. In a bid to attract women, banks offer pawning facilities .Some rural banks have even

begun to design loan schemes to accept jewellery as a collateral in order to draw more women

to their doorstep. One of the reasons found for financial exclusion of women is that in male

Property of Christ University. Use it for fair purpose. Give credit to the author by citing properly, if your are using it.

27

dominated societies, particularly in south Asia, men traditionally handle cash and investible

funds, even when the funds arise from women’s economic activity. Another observation made

is that, it is very difficult for a poor woman to walk into a fancy looking commercial bank to

get a loan due to lack of confidence, moreover banks lack the patience to deal with their

ignorance. The very process of going to a bank in town neglecting the whole days work is not

a happy choice.

2.1.2 Studies regarding nature and pattern of Investment.

Issahaku (2011) conducted a study that was based on a microeconomic approach of estimating

the determinants of financial saving and investment in one of the most deprived district

capitals in Ghana, Nadowli.Primary data were collected from sixty households in Nadowli.

Questionnaires were designed so as to facilitate the collection of data from households about

saving and investment. Stratified random sampling technique has been used to ensure that the

various occupational groupings were fairly represented. A multiple linear regression model

adapted from Rogg (2000) and Kibet et al (2009) has been fitted into investment. The

independent variables were Age, Education, and Occupation, number of Dependents, Income,

Assets and Saving with the dependent variable being Investment. The study reveals that there

is propensity to save and invest in Nadowli in spite of low income and the factors that drive

Saving and Investment are occupation, expenditure, assets and saving.s

To gain knowledge about key factors that influence investment behavior among men and

women, Kabra et al (2010) conducted a study based on primary data collected from 700

individuals who invest regularly. A four page questionnaire consisting of six subscales was

used. In the first subscale, demographic information such as age, gender, marital status, region

to which they belong, profession, individual income levels were sought. In the remaining five

subscales, questions were designed to measure the investment pattern of individuals on the

five variables viz. investing background, opinion leadership, duration of investment,

awareness of investments, and security. Later the statements under these variables were

reduced into smaller number of manageable variables by exploring common dimensions