![1 22nd Report – Subject Committee – II (2017-18] - Tripura ...](https://static.fdokumen.com/doc/165x107/6317746471e3f2062906ca43/1-22nd-report-subject-committee-ii-2017-18-tripura-.jpg)

Bahasa

Halaman

Hukum

GOVERNMENT OF INDIAMINISTRY OF TEXTILES

OFFICE OF THE TEXTILE COMMISSIONERPOS'[ BAC NO. 11500 : MUMBAI - 400 020

t.-mail : atufs.mu m-textiles ,ln: Fax : 022-22004693

F.No. 12(7)/'IAMC/ATUFSiz021/TUFS/ ? I Date -o$/0712021.

Subiect:- Minutcs of the 22nd Technical Advisory Monitorins CommitteeMecting (TAMC) under A-TUFS heldon0 021.

Sir i Ma'am,

'fhe undersigned is directed to enclose herewith Minutes of the 22'd Technical

Advisory Monitoring Committee Meeting (TAMC) under A-TUFS held on 05/01/2021 under

the chairmanslrip of the -lextile commissioner for kind pelusal and necessary action.

To,

AIIM oITAMC M

Conv to :

1. PS to'l \.C. :- For kind information.

2. PA to DDC / A.Tx.C. / Jt.Tx.C's.

3. Shli Anil Kumar K.C.,Under Se cletary to the GOI, MOT, New Delhi.

4. Mis. Silr er Touch Technologies Ltd., (Ws. STTL) .

Yours faithfully,

3(th6( Usha Pralhad Pol )

Deputy Director Ceneral (DDG)

$cbsitc : wrvrv,txcindia.sov.in / www.ministryoftextiles.gov'in

Enclosures :- As above.

Minutes of the 2l,t meeting of TAMC held on 02.03.2021 were circulated to all

members. As no comments/suggestions were received from the members of TAMC, the

minutes are treated as final.

Asen No.02: Review of Progress of TUFSFund allocation and Expenditure undcr TUFS in 2021'22 (as on 30.06.2021):tl

{ in Crore

# Schcme Allocation Claims approved includingBG cases

Fund Released

I MTUFS

700(BE)

0.00

2 RTUFS 0.00 0.00

J RRTUFS 8.88 8.88

1 ATUI-S 53.51 45.72

) MMS 5.17 3.0

TOTAL 67.56 57.60

b. ATUFS (position as on 30.06.2021): The total subsidy cap available { 5151 Crore

UIDs are being auto generated w.e.f. 9th August 2019. As on 30.06.2021, total 11669

UIDs with provisional subsidy { 3556.58 Cr. have been generaled.

The progress is placed before the Committee for information.

Asenda No. 03: Inclusion of lending agencies under ATUFS

(i). Request of Rabobank (cooperative Rabobank u.A.) 20,{F Towet A Pemrnsula Business

Park Senapati Bapat Marg Lower Parel Mumbai 400013 as per para 2'5 of revised

Resolution ofATUFS for inclusion as lending agency under ATUFS is approved by the

Competent Authority.

(ii). Request of Co-operative bank of Rajkot Ltd. Sahakar Sarita Panchnath Road, Rajkot-360001 (Gujrat) as per paru 2.5 of revised Resolution of ATUFS for inclusion as

lending agency under ATUFS is approved by Competent Authority.Page 1 of 8

3d{u)P

Minutes of 22nd meeting of Technical Advisory-cum-Monitoring committee (TAMC) fordiscussing issues relating to ATUFS and Previous versions of TUFS held at 04.00 pm on

osth Juty 2021.

22nd meeting of the Technical Advisory-cum-Monitoring Committee (TAMC) on

Amended Technology Upgradation Funds scheme (ATUFS) and Previous versions ofTUFSwas held at 04.00 pm on 05'h h]Jy 2021, through Video Conferencing mode under the

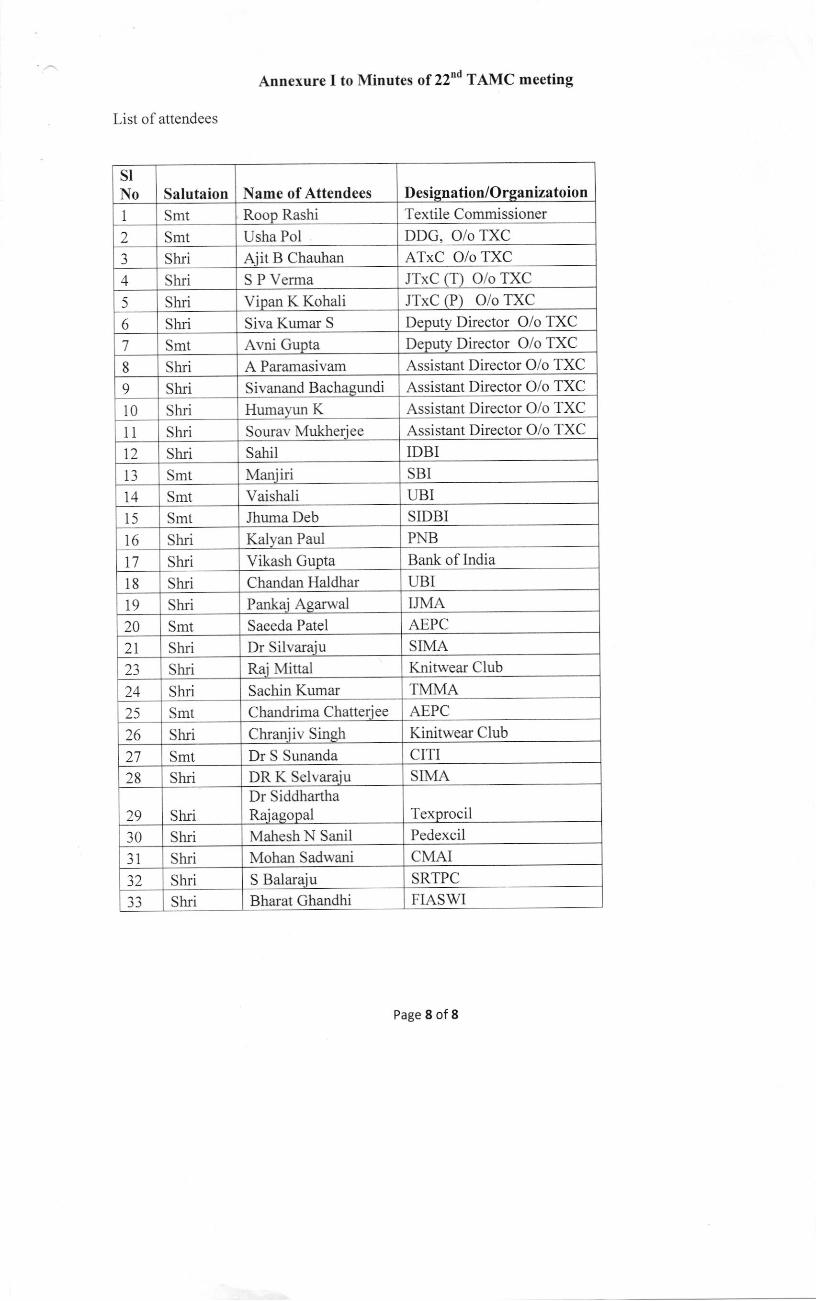

chairpersonship of Ms.Roop Rashi, Textile Commissioner. The list of participants is enclosed

at Annexure-I.

At the outset, the Chairperson extended a warm welcome to all the participants and

requested Ms. Usha Pralhad Pol, Deputy Director General to take up item-wise agenda for

deiiberations before the committee. The agenda-wise decisions of TAMC are as follows:

Agenda No.01: Confirmation of the minutes of the 2I't TAMC meeting held on

02.03.2021

0.00

manufacturers under ATUFS

As per the decision of 4th IMSC, feedback to be taken from various clusters for formulating a

detailed procedure to be followed for enlistment of accessories/spares manufacturers.

Accordingly, feedback has been sought however no reply received from the Industry / Textile

Associations / cluster representatives due to prevailing pandemic situation in country.

This Office implements procedure for enlistment of machinery manufacturers as per TAMC

directions. In the 4th IMSC it was directed to this Offrce that extant procedure for enlistment ofmachine/accessory manul'acture to be reviewed in consultation with Dio of Revenue, D/o

Commerce and D/o Hearry Industry however due to the prevailing pandemic situation in the

country this could not be executed.

process lbr enlistment of accessories/spares manufactures under ATUFS is intricate / detailed,

since OEM (Original Equipment Manufacturers) enlisted is exhaustive. However, as the

Accessories/sparei Manufacturers being exhaustive in number in terms of respective

manulacturing field / segment, so in order to enlist them it wouid be time taking besides taking

into consideration in aligning them with the OEM.

It is also to clarify that there are huge number of accessories/spares manufacturers in India and

abroad, many of them are limited with infrastructure compared to main machinery

manufacturing units.

Moreover, cost ol the accessories are calculated to maximum @ 20Y, of the basic cost of the

main machinery and sub'sidy is also very less compared to the main machines. The enlistment

of these types of manulbcturers is practically not possible. Hence, the accessories/spares

manuf'acturing units may be considered under ATUFS without the condition of enlistment ofmanufacturers.

Decision of TAMC: The Committee ratitied the inclusion of the above 02 lending agencies

under ATUFS.

Asenda No. 04: Relaxation of enlistment of Accessories/ Spare parts /attachments of

ision of TAMC: Aller detailed deliberation I AMC members unanimously recommended

that the cost of accessories / spares may be considered under ATUFS without the condition ofenlistment of Accessories/ spares manufacturers. Recommendation involves modification rn

GR, the Committee recommended for taking up the matter with MoT.

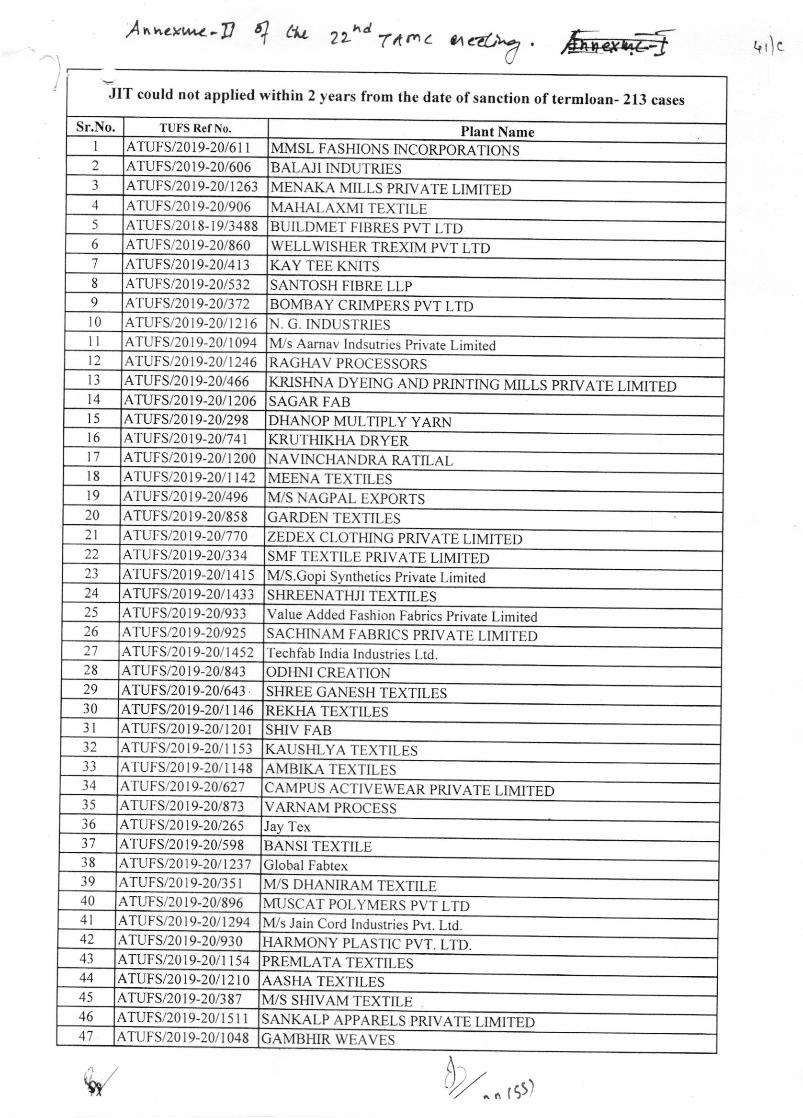

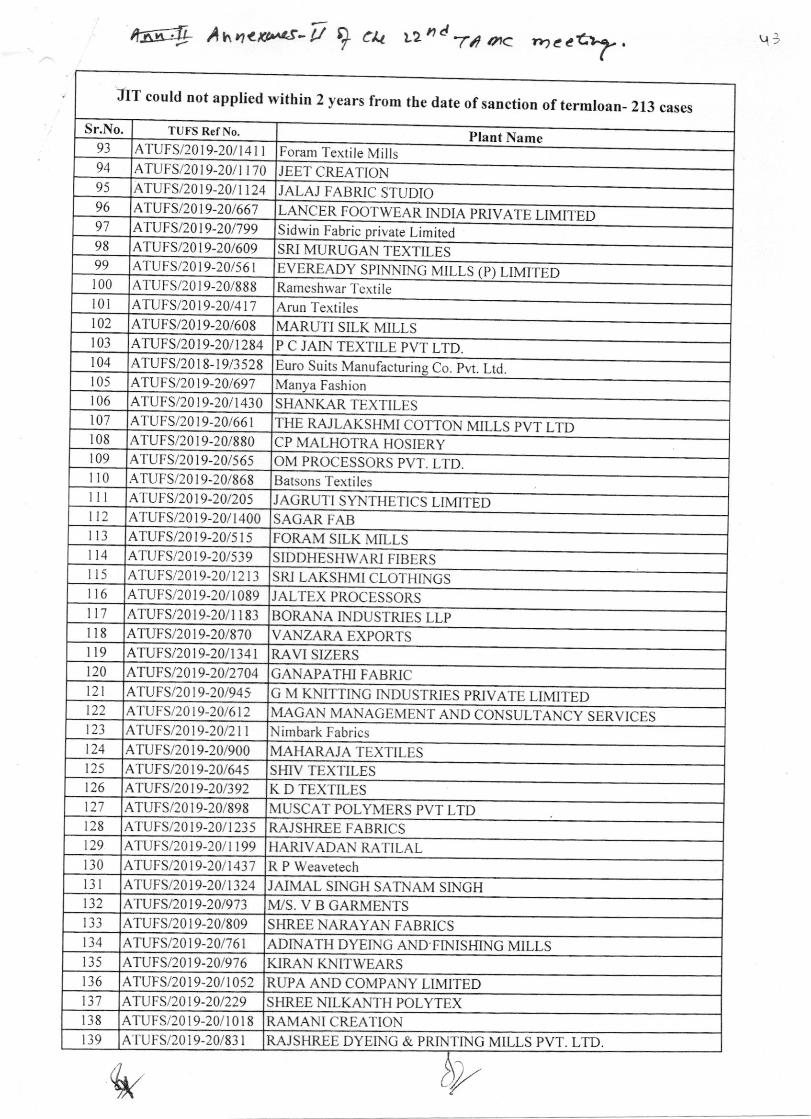

Asenda No.l05- Condoni ng delay of timeline for UID and JIT

2218 unit which could not submit JIT request within 2 years from the date of sanction ofTermloans were recommended in 19th TAMC for condoning delay due to covlD pandemic to

IMSC. Further representations have been received for condoning delay due the same reasons

hence additional 213 may also be considered (list of213 )at Anncrurc-II

The committee may deliberate and recommend the delay of condonation to IMSC.

Decision of TAMC: The Committee deliberated and recommended for condoning delay ofd in l9h TAMC to213 cases listed at Annexure -II in addition to the 2218 cases recommende

the forthcoming IMSC.

Decisions of ITC for ratification bv TAMC

Page 2 of 8

3g@t @

Enlistment of 19 machinery manufacturers & 8 authorized agents as per Annexure- IIIrecommended by the Intemai Technical committee in its 19 & 20s Meeting placed before the

Committee for ratification.

Agenda No.6: Enlistment of machinery manufacturer & Authorized agents

Page 3 of 8

3diltb

In the I 5tl' TAMC meeting it was decided that in absence of manufacturer name on the

Consideration of Logo and name of the brand found on machine plate in absence of name ofmachine manufacturer under ATUFS machine and only the logo of manufactue is found on

machine plate, the manufacturer should submit a note detailing their branding exercise,

marketing practices and share their authentic logo. The intemal Technical Committee (ITC)

may then take a view on a case to case basis considering the explanation submitted by the

manufacturer. Accordingly, Powerloom Development Cell has now submitted the

clarifications of the machinery manufacturer I\4/s. Qingdao Wanchun Machinery Co., China

lorwarded by M/s. Kailash Process, Surat for the consideration of ITC.

in respect of M/s. Kailash Process, Surat and also the details of the

marketing practices and authentic logo submitted by the Manufacture M/sMachinery Co., China. It was also observed that the logo is found on the

as well as the photos ol the machine plate submitted by the JIT.

In view of the above, the competent authority has a doubt that if IVVs. Zhejiang Taitan Co Ltd.,

China is a machinery manufacturer then why have they procured machines from other

manufacturer i.e. M/s. Shenzhen Lisu Import and Exports Co. Ltd. China and supplied to the

units afler fixing their name plate.

Dccision Taken in the 19th ITC: The Committee verified the documents submitted by PDCbranding exercise,

. Qingdao Wanchuncommercial invoiceHence, Committee

recommended the case.

Decision of TAMC: The Committee deliberated and recommended to follow the same

protocol where the machinery manufacturer name is not available.

Asenda No. 8: PDC have vide Note dt. 22t0312021 have forwarded the details ofdiscrepancies found in the supply of rapier looms by lWs. Zhejiang Taitan Co., Ltd.,China under Stand up India of PowerTex India Scheme.

Case-I : In the Certificate Country of origin, the origin/exporter is M/s. Zhejiang Taitan co.

Ltd-, China and Invoice is issued by lrif/s. Zhejiang Taitan Co. Ltd., China. The name of the

Manufacturer found on machine plates is M/s. Zhejiang Taitan Co' Ltd., China.

Case-II : In the Certificate Country ol Origin, the origin/expo(er is IWs. Shenzhen Lisu

t.port'ara Exports Co. Ltd., China, Invoice is issued by N{/s. Zhej iang Taitan Co. Ltd.'

china. The name of the Manufacturer found on machine plates is IWs. Zhej iang Taitan co.Ltd.. China. Instead of M/s. Shenzhen Lisu Import and Exports Co. Ltd. China

Decision of TAMC: The Committee ratified inclusion of 19 machinery manufacturers and 08

Authorised agents recommended by ITC enclosed at Annexure -III.

Asenda No. 7: Consideration of Logo of Manufacturer found on machine plate in the

absence of name of machine manufacturer under MMS-RRTUFS.

Accordingly, PDC has now requested that the matter may be discussed in the ITC meeting to

deliberate as to wherher the machinery supplied by lvl/s. Zhejiaag Taitan co Ltd., chinashould be considered for subsidy under Stand-up India Scheme'

Decision taken in lgth ITC: After due deliberation the ITC reconfirmed that Zhejiang Taitan

Co. Ltd., China is a textile machinery manufacturer. However, as regards to country of originissues the concemed section may decide at their level.

Decision of TAMC: The Committed has agreed to the decision of ITC that Zhejiang TaitanCo. Ltd., China is a textile machinery manufacturer. However, as regards to country of originissues , concerned section may decide at their level based on clarification provided by machine

suppliers.

Asenda No. 09: TUFS cell have vide Note dt.231312021 forwarded the case of a unit who has

purchased a PLC controlled fully automatic Mercerizing machine with caustic recovery Plant

(MC 02-A-3). From the photographs, it is observed that the caustic recovery plant is supplied

by one manufacturer i.e Unitop Aquacare and separate machine serial number is also given by

the manulacturer who is enlisted only for manufacturing and supply of RO system not forcaustic soda recovery plant. The Mercerizing machine is supplied by another manufacturer i.e

M/s. Yamuna Machine works Ltd, However the invoice is raised by IWs. Yamuna Machineworks Ltd only and therein the description of the machine is mentioned that as fully automatic

mercerizing machine with caustic recovery Plant. Both the Machine suppliers are enlisted

under ATUFS. In view of the above, decision on the eligibility of Mercerizing Machine withcaustic recovery plant may be taken which was purchased from 02 suppliers i.e main part from

one supplier and caustic recovery plant from another suppli but with single invoice.

Decision Taken in the 19th ITC: The Committee noted that under the TUF Scheme, onlvPLC controlled fully automatic Mercerizing machine with caustic recovery Plant is allowed.

As such machines purchased separately (standalone) i.e. mercerizing machine from one

manut'acturer and caustic recovery plant from another manufacturer is not eligible

Decision of TAMC: The Committee has agreed to the decision of ITC that complete machine

purchased from single machinery manufacturer as per ATI-iFS specification will be considered

ior subsidy benefits under the scheme except Technical Textile items as per 3'o IMSC

decision.

Agenda No. l0 : TUFS Cell have lbrwarded the case of a unit which has purchased ACinvertor driven PLC based Fabric inspection machine with fault analyzer and report generator

and length measuring and cutting device (MC 02-71) . RO has confirmed the specification ofthe machine that the fault analyser is based on manual observation' ln this regard, the

eligibility olthe machine may be confirmed.

Decision Taken in the lgth ITC: The Committee noted that under the TUF Scheme only

PLC based Fabric inspection machine with fault artalyzer and report generator and length

measuring and cutting device is allowed. As such fabric inspection machine without fault

analyser cannot be considered under the Scheme

Decision of TAMC: The Committee has agreed to the decision of ITC that the fabricinspection machine without fault analyzer and report generator and length measuring and

cutting device cannot be considered under the ATUF Scheme.

Page 4 of 8

3Url,tla{

Asenda No. 11 : A unit (M/s. Ramayani Creations, Alwar - ATUFS/2018-19/1290) has

Karl Mayer India Pvt Ltd, Ahmedabad and invoice also issued by them. However as per the

name plate photos of the machine submitted by the JIT, the machine manufactuler name

mentioned as Mis. Karl Mayer (China) Ltd, China. Both the manufacturers are enlisted,

however as per the Name plate, the machine seems to be imported and as per the invoice the

machine is supplied by the indigenous enlisted machine manufacturer and hence the matter

may be placed in the ITC for confirming the eligibility of the machine.

Decision Taken in the lgth ITC: The Committee noted that this can be a'High Sea Sale'

case as the invoice for an imported machine is being raised by an Indian company. As such it

cannot be permitted

Decision of TAMC: The Committee has noted the above observation and recommended to

purchased machine MC 01-C-5 - (High speed computerised warping

with minimum closed creel capacity of 200 and minimum speed of 100

place it before the sub-committee for decision on the claim after due verificationterm loan sanction (RRTUFS / ATUFS), mode of purchase (Direct i Subsidiary

machine for knittingMts/ Min ) from M/s.

of period ofCo. / High

Seas Sale / Authorised agent) etc., as per the GR ofATUFS.

Asenda No. 12 : M/s. Alps Industries Ltd vide representation dated 01.03.2021 has requested

to consitler the Electronic Jacquards for l0oh capital subsidy under M-TUFS The unit has

refenedi. Circular No.5 (2006-2007) dated 06.02.2007 which was force under TUFS

from the period 01.04.1999 to 31.03.2007.ii. Circular No.2 (201 1-2012 Series) dated 29.07.2011 which was force under R-

TUFS from the period 28.04.2011 to 31.03.2012.

As per M-TUFS in Annexure D-l under heading "/is/ of machinery eligible forWeat ing/Knitting units under TUF scheme", the Jacquard & Dobby on Standalone basis is

tisted in Annexuie D-l -b (15). The machines listed in Annexure D-l of M-TUFS are eligible

for 5% IR.

Dccision Taken in the 19th ITC: The said Circular No.5 (2006-2007) dated 06.02.2007 doesThe jacquard is an

taken by this offrceconsider Jacquard

machine for 10% CS also

Decision of TAMC: The Committee has agreed to the decision of ITC and rejected the

request of the unit to consider their claim for l0% Capital Subsidy (CS)

Asenda No. 13 : IWs. Alps Industries Ltd vide representation dated 01.03.2021 has requested

to consider Electrical Installation under M-TUFs by giving the reference of Circular No. 2(2011-12 series) dated 29.07 .2011.

The para-l(ii) olthe said Circular dated 29.07.2011 is reproduced below

Covcra e of elect rical installations under TUFS w.e.f' 0l .04.2007."T'he Committee observed lhat electrical installations were covered in the erstwhile

not apply in this case as it not an essential component of the machine.

accessory for weaving machine. Hence ITC is of the view that the decision

earlier is valid and there is no technicality applicable in their claim to

TUFS, but were omitted when the modified TUFS was announced w.eJ. 01.04.2007 and this

omission was rectifie(l in the 2nd meeting of TAMC held on 25.07.2008. Committee also

obserted thdt rtnancial implication of coverage of electrical installations w.e.f. 01.04.2007 is

Page 5 of 8

3s;b

not significant and lherefore decided that coverage of electrical inslallations should be

ejlective.from the beginning tf rhe moililied TUFS, i.e. 01.04-2007. "

tn eaaitionat Agenda No.7 of the 2nd meeting of TAMC held on 25.07.2008, the committee

decided that the electrical installations may be allowed with other specified investments upto

25% ofthe cost of machinery under para3.3(2) (i) on TUFS. The same was included at Para-

1() vide Circular No.4 (2008-2009 Series) dated 28.07.2008.

Decision Taken in the 19th ITC: The TAMC decision was already communicated to all

lending agencies and on that basis the lending agencies must have submitted the claim with

proper due diligence as was required under the scheme. In case the bank has not calculated the

imount the claims are being re-visited through special JITs for release of their due payment ifany. Hence, appropriate action may be taken accordingly by their Bank.

Decision of TAMC: The committee has agreed to the decision of ITC.

Agenda No. 14 : Request for Inclusion of Marketing/sales/export house of machinery

manufacturers, those are raising invoices on behalf of them.a) M/s. DMS DILMENLER MAKINA ve TAKSTIL SAN. TIC. A.S' TURKEY

(enlisted ar sr. No. 388 in Amexure III has requested to include lvus. DILMENLERMAKINE PAZ. SAN. VE TIC LTD. STI as a Marketing/Sales company.

In the application letter M/s. DMS DILMENLER MAKINA ve TAKSTIL SAN' TIC'

A.S, TURKEY has mentioned that they are manufacturing unit and sell machines in

domestic & international market through their marketing company lvl/s. DILMENLERMAzuNE PAZ. SAN. VE TIC LTD. STI' Their Machines have name plate ofmanufacturing unit & commercial invoice and other such documents are raised by

marketing unit. In support of their claim legal proof of documents like commercial

balance sheet, financial audit report and pa(nership documents are submitted.

Decision Taken in the 20th ITC: From the documents submitted by the unit it cannot be

ascertained whether IWs DILMENLER MAKINE PAZ. SAN. VE TIC LTD. STI iS A

subsidiary / marketing company of lvf/s. DMS DILMENLER MAKINA ve TAKSTIL SAN.

TIC. A.S, TURKEY. Therefore, M/s. DILMENLER MAKINE PAZ. SAN. VE TIC LTD'

STI.. cannot be considered as a marketing company / subsidiary of lWs. DMS DILMENLERMAKINA VE TAKSTIL SAN. TIC. A.S, TURKEY.

Dec ision of TAMC: The committee has agreed to the decision of ITC.

M/s. Fong's National Dyeing and Finishing Machinery (Macao CommercialOffshore) Co., ( enlisted at sr. No. 143 in Annexure II ) has requested to includeM/s. Fong's National Engineering (Shenzhen) Co., Ltd. as a Manufacturing Unit.

In the application Ietter M/s. Fong's National Dyeing and Finishing Machinery(Macao Commercial Offshore) Co., has mentioned that they are marketing unit for

selling machines in domestic & international market of its manufacturing unit M/s.

Fong's National Engineering (Shenzhen) Co., Ltd.. Their Machines have name plate

of manufacturing unit & commercial invoice and other such documents are raised by

marketing unit.

Suggestion - Similar case, i.e. M/s. Fukuhara Industrial and Trading Co. Ltd., Japan

who not involved in manufacturing activity and doing the sales division of entire

Fukuhara Group. As such after due deliberation, 15th ITC and subsequent 21't TAMCPage 6 of 8

h

3diiia

was recornmended that }vvs. Fukuhara Industrial and Trading co. Ltd as a sales office

of the Manufacturing i.e. Mis. Precision Fukuhara Works Ltd', Japan'

Decision Taken in the 20'h ITC: Based on the annual report submitted by the unit and after

due deliberation the Committee decided that IWs. Fong 's National Dyeing and Finishing

Decision of TAMC: The committee has agreed to the decision of ITC'

Asenda No. 15 : TUFS cell have vide their Note d:.25l5l2\2l have forwarded the following

Agenda Point for decision of iTC" u. I\rlls. Yamuna Machine works Ltd., Valsad has sold "Form Finishing Range" and PLC

based Multi chamber Stenter Machine during the same period. However the machine

plutes ."". to be different from one another. The machine manufacturer has confirmed

ihat both the name plates have been supplied by them only'

b. M/s. Jupiter Comtex Pvt. Ltd., has sold "lndigo Dyeing Range and High Speed

w".pi,gmachinewithyarnTensionControtduringthesameperiod.Howeverthe.u.|,irr. plates seem to be different from one another. The machine manufacturer has

conllrmed that both the name plates have been supplied by them only

Decision iaten in tne 20th ItC: -Since

the matter is related to machine identity and its

@ised that the claimed machine of both lr4/s. Yamuna

Machinl Works Ltd., Valsad and M/s. Jupiter Comtex Prt. Ltd., appears to be. eligible as per

ATUFS guidelines. However, guidelines for lollowing standard branding practice needs to be

circulatei to all enlisted manufacturers / uploaded on Tx'C office website'

Decision of TAMC: The committee has agreed to the decision of ITC Further, guidelines for

ilC*r"g rt*d.d branding practice n""ds to be circulated to all enlisted manufacturers /

uploaded on Textile Commissioner OfTice website'

Machinery (Macao Commercial offshore) co., as Marketing Unit and l\[/s. Fong',s

National il,ngio...ing (Shenzhen) co., Ltd.. as the Manufacturing Unit. The invoice for the

machinery m"an,tactured by IVI/s. Fong's National Engineering (Shenzhen) co., Lrd., will be

raised by M/s. Fong's National Dyeing and Finishing Machinery (Macao Commercial

Oltihorei Co. The maluer is placed in the TAMC meeting ratification of the modification'

Asenda No. 16 : TUFS cell have vide rcre dt. 151412021 forwarded a case where instead of

_h".*,1.u.t*"name;manufacturegroupnameisindicatedonthenameplate.Eventhoughthe manulacture M/s. Zhejian Rifa Textili Machinery corporation Ltd has infbrmed that Mis'

ihejian Rifa Textile Machinery Tech co. Limited is. their subsidiary unit the plate should

invariablv mention the manufacture name i.e. N4/s. Zhejian Rifa Textile Machinery Tech Co'

Oe.irion Tnrcn io tl" ZOtn fI.C, after due deliberation the committee requested ATUFS

@eet / Annual Report as proof for subsidiary unit from the

nanufacturer, fbr enlisting M/s. M/s. Zhejian Rifa Textile Machinery Tech Co as a subsidiary

unit of M/s.Decision of

Zhej ian fufa Textile MaTAMC: The committee

chinery Corporation Ltd.has agreed to the decision of ITC

Meeting ended with a vote of thanks to the Chair.

Page 7 of 8

3arutv

List of attendees

Annexure I to Minutes of 22'd TAMC meeting

Page 8 of 8

SINo Salutaion Name of Attendees Designation/Organizatoion

1 Smt Roop Rashi Textile Commissioner

2 Smt Usha Pol DDG, O/o TXC

3 S hri Ajit B Chauhan ATxC O/o TXC

I Shri S P Verma JTxC (T) O/o TXC

5 shd Vipan K Kohali JTxC (P) O/o TXC

6 shd Siva Kumar S Deputy Director O/o TXC

7 Smt Avni Gupta Deputy Director O/o TXC

8 Shri A Paramasivam Assistant Director O/o TXC

9 shd Sivanand Bachagundi Assistant Director O/o TXC

l0 shd Humal'un K Assistant Director O/o TXC

11 Slui Sourav Mukherjee Assistant Director Oio TXC

t2 shd Sahil IDBI

i3 Smt Maniiri SBI

1,1 Smt Vaishali UBI

15 Smt Jhuma Deb SIDBI

l6 shd Kalyan Paul PNB

17 Shri Vikash Gupta Bank of India

18 Slui Chandan Haldhar UBI

19 shd Parkaj Agarwal IJMASaeeda Patel AEPC

21 Shri Dr Silvaraju SIMA

-a) shi Raj Mittal Knitw-ear Club

24 Shri Sachin Kumar TMMA

25 Smt Chandrima Chatterjee AEPC

26 shd Ctuaniiv Singh Kinitwear Club

27 Smt Dr S Sunanda CITI

28 shd DR K Selvaraj u SIMA

29 SluiDr SiddharthaRaiagopal Texprocil

30 Shri Mahesh N Sanil Pedexcil

31 shd Mohan Sadwani CMAI

J, Shri S Balaraju SRTPC

J-) Shri Bharat Ghandhi FIASWI

I

L

I

I20 Snrt

I

I

^d

JIT could not applied within 2 years from the date ofsanction of termloan- 213 cases

/r'acvv"t-p tl t{L 2L c') t

Plant NameI ATUFS/2019-20/61 I MMSL FASHIONS INCOR?ORATIONS) ATUFS/2019-20/606 BALAJI INDU'TRIES, ATUFS/20 l9-20l I 263 MENAKA MILLS PRryATE LIMITED"l ATUFS/201 9-201906 MAHALAXMI TEXTILE) ATUFS/201 8- l913488 BUILDMET FIBRES PVT LTD6 ATUFS/20 I 9-20l860 WELLWISHER TREXIM PVT LTD7 ATUFS/2019-20/413 KAY TEE KNITS8 ATUFS/2019-20/532 SANTOSH FIBRE LLP9 ATUFS/2019-20t3'72 BOMBAY CRIMPERS PVT LTDIO ATUFS/2019-20/12 t6 N. G. INDUSTRIESll ATUFSi20 t 9-20l 1094 M/s Aamav Indsutries Private Limitedt: ArUFS/20t9-20/t246 RAGHAV PROCESSORSr3 ATUFS/2019-20t466 KRI D C PRTV ITSHN AN PRIN INT MI LL S T LE IM EDt4 ATUFSt20t9-20n206 SAGAR FABl5 ATUFS/2019-20/298 DHANOP ML]LTIPLY YARNt6 ATUFS/201 9-201741 KRUTHIKHA DRYERl7 ATUFSi20l9-20/ 1200 NAVINCHANDRA RATILALl8 ATUFS/2o19-20/1 142 MEENA TEXTILESl9 A'ruFS/20t9-20t496 M/S NAGPAL EXPORTS20 ATUFS/2019-20/858 GARDEN TEXTILES2l ATUI--S/201 9-20l770 ZEDEX CI,OTHING PRIVATE LIMITED22 ATUFS/201 9-20l3 34 SMF TEXTILE PRIVATE LIMITED23 ATUFS/2019-20/t415 I\4/S.Go iS nthetics Private Limired

ATUFS/2019-20/ 1433 SHREENATHJI TEXTILES25 ATUFS/2019-20/933 Value Added Fashion Fabrics private Limited

ATUFSt20l9-20/925 SACHINAM FABRICS PRIVATE LIMITED27 ATUFSi20r 9-20l1452 Techfab lndia Industries Lrd28 ATUFS/2019-20/843 ODHNI CREA'TION

ATUFS/20t9-701643 SHREE GANESH TEXTILES30 ATUFS/2019-20i 1146 REKI]A TEXTILES

ATUFS/20 I 9-20l1201 SHIV FAR32 ATUFS/2o19-20/l 153 KAUSHLYA TEXTILESl3 ATUFSi20l9-20/l 148 AMBIKA TEXTILES31 ATUFSt20t9-20/627 AMPUS ACTIVEWEAR PRIVATE LIMITEDC

l5 ATUFS/20 r 9-20l873 VARNAM PROCESS36 ATUFSt20t9-20t265 Ja Tex37 ATUFS/20 I 9-20l598 BANSI TEXTILE

ATUFSI20)9-20/1237 Global Fabtex39 ATUFS/20I9-20l3 s I M/S DHANIRAM TEXTILE,10 ATUFS/2019-20/896 MUSCAT POLYMERS PVT LTD.11 ATUFS/2019-20/l294 M/s Jain Cord Indusrries Pvt. Ltd42 ATUFS/20 I 9-201930 HARMONY PLASTIC PVT, LTD43 ATUFS/2o19-20i I 154 PREMLATA TEXTILES

ATUFS/2019-20/12 t0 AASHA TEXTILESATUFS/2019-20/3 87 M/S SHIVAM TEXTILEATUFS/2o19-20/l5l l SANKALP APPARELS PRIVATE LIMITEDATUFS/2019-20/ I 048 GAMBHIR WEAVES

V, h)/^^,srt

Sr.No. TUI'S RefNo.

DYEINC

26

t8

lu

Lzs

tx

144I qs

146l*

l*',,.U 6l ct tz"'T,trr- t)-tIr{rlcfa c.

JIT could not applied within 2 years from the date of sanction of termloan- 213 cases

Plant NameSr.No, TUFS Ref No

VEER TRENDATUFS/2019-20/436PRATIK TEXTILESATUFS/2019-20/ 1502

SONI FABzuCSATUFS/2o19-20/l1l I

M.P KNITTING5l ATUFS/2019-20/55 8

NYS JAI MAA VAISHNO DEVI ENTERPRISES52 ATUFS/2019-20/796IWs. Kamal ProcessATUFS/2019-20i 1384

S.K.L. EXPORTSATt'FS/2019-20/I13751

MAIIALAXMI FABRIC MILLS (A LNIT OF MAHALAXMI RUBTECH

LTD)ATI-,'FS/2019-20/8655

VANDNA TEXTILESATUFS/2019-20/l 14456

RAVI TEXTILE INDUSTzuES51 ATUFS/2019-20/501SANDEEP WEAVERS PVT LTD58 ATUFS/2019-20/ I32 I

KHl]SHBU YARNS59 A',tuFS/2019-20/23 8

SHARMAN SPINNING MILLS PVT. LTDATUFS/2or9-2011313GOPINATHJI CREAIIONATUFS/2019-20/63 8

SHIV TEXTILESATUFS/2019-20/ 1258

PRAMOHI SONSATUFSi20l9-20i l44lJindal Poly Films Limited64 ATUFS/2019-20/5 70

OPUS APPARELSATUFS/2019-20/100365

SRI RAMESH GAARMENTATUFS/2019-20i 152066

MEET TEXATIJFS/2019-20/ I I 78

SANGAM FASTIION PRIVATE LIMI'I'EDATU F S/2019-20/760

M/S FALAK TEXTILEATUFS/20 l9-20l3 89

PIot No.5 l, Sector-32, Gur on, Haryana - 122001ATUFS/20 r 9-20l69070

M/S. MAA PADMAVATI EXIMA tUFS/2019-20/4677lSHREE RAM FASH]ONATUFSl20l9-20192672

are lsoctave aATUFS/2019-20/ 1245

M/S AMARJYOI'I FASHIONS PVT LTD11 ATUFS/2019-20/1002G'l'EX Fabrics Private LimitedA',tuFS/20 r9-20196I15

Hariom Pol acks LimitedATUFS/2017-18/183KALINDI FABRICSATUFS/2019-20/13 3671

SAI RAJ CREATIONATUFS/2019-20/670G M KNITTING INDUSTRIES PRIVATE LIMITEDA'luFSl20t9-20194719WEBTEX INDUSTRIESATUFSt2019-20143'780EVELINE tN'TERNA'IIONALATUFSi20l9-20/6938lSwan Medicot LLPATUFSi20l9-20/857M/s Kanodia International Pvt. LtdATUFS/2019-20/1516COMPASS FASHIONATUFS/20 r 9-20l1396SHREESHAKTI SYN BAGS PRIVATE LIMITED85 ATr.J FS/2019-20/245

KPM PROCESSING MILL P LTD86 ATUFS/20 r 9-20l1369M/s Wilhelm Textiles lndia Private Limited87 ATUFS/2019-20/1020DHARM BHAKTI TEXTILESATUFS/2019-20/527M/S KEVAL TEXTILEATUFS/2019-20/390n9

GANESH LAXMI PROCESSORS PRIVATE LIMITEDATUFS/20r 8- 19/361790KTM Textile Co orationATUFS/2019-20i 149691

TALAVIA TEXTILES92 ATUFS/2019-20i434

'1/'

13

l+sa4eIso

ls:

t 60-I 6r

,6,63

t--I o/T6sf6,

76

I- ?s

18,l- s3

l- s4

188

ndAanqts- U ? CK L2 7A .7< ft)ec"7 qj

TUFS Ref No. PIant Name93 ATUFS/20 r 9-20l l4 I I Foram Textile Mills91 ATUFS/2ot9-20lt 170 JEET CREATION95 ATUFS/2019-20/t 124 JALAJ FABRIC STUDIO96 ATUFSt20t9-20t667 L N EC R oF oTWE R ND PzuV TE L MITED97 ATUFSt20t9-20/799 Sidwin Fabric rivate Limited98 ATUFS/201 9-201609 SRI MURUCAN TEXTILES99 ATUFS/2019-20i56 I ( )E ERE YAD PS ININN MG LL S L IM llT D100 ATUFS/20 l9-20l888 Rarneshwar l'extiler0l ATUFS/20t9-20/4t1 Arun l'extiles102 ATUFSi20l9-201608 MARUTI SILK MILLS103 ATUFSt20t9-20il284 P C JAIN TEXTILE PVT LTD.104 ATUFS/2018-t9/3528 fauE Sro u Mts uan C tur Co Pvt L dl'tg

ATUFS/2019-20t697 Manya FashionATUFSi20 r9-20l1430 SHANKAR TEXTILES

107 ATUFS/2019_201661 ETH LARAJ SK N,{H C TTo No MILL PS T TL DATUFS/20 I 9-20l880 CP MALHOTRA HOSIERY

109 ATUFS/2019-20/56s OM PROCESSORS PVT. LTDil0 ATUFS/2019-20/868 Batsons Textiles

ATUFS/2019-20/205 JACRUTI SYNTHETICS LIMITEDll2 ATUFS/20 l9-20l 1400 SAGAR FABlt3 ATUFS/2019-20/5 I 5 FORAM SILK MILLSl4 ATUFS/201 9-20l53 9 SIDD}{ESHWARI FIBERSIl5 A]'UFS/2019-20/ l2 t 3 SRI LAKSHMI CLOTHINGS

ATUFS/20 l9-20l I 089 JALTEX PROCESSORSATUFS/2019-20/l 183 BORANA INDUSTRIES LLP

ll8 ATUFS/2019-20/870 VANZARA EXPORTSll9 ATUFSi20l9-20/1341 RAVI SIZERSr20 ATUFSl20t9-20t2704 GANAPATHI FABRIC121 ATUFS/2019-20/945 GMKNITTINC INDUSTRIES PRIVATE LIMITEDt22 A't'uFSt20t9-20t6t2 I.,GMA N M N G E1\{ TN ND C No US TL N SCY Rti I EC S

ATUFSt20l9-20/2tt Nimbark FabricsATUFSi20l9-20i900 MAHARAJA TEXTILESA1'UFS/2019-20/645 SH]V TEXTILESATUFS/2019-20/392 K D TEXTILESATUFS/20 l9-201898 MUSCAT POLYMERS PVT LTDATUFSi20l9-20/1235 RAJSHREE FABRICS

129 ATUFS/2019-20/l199 HARIVADAN RATILAL130 ATUFSt20l9-20fi437 R P Weavetech

ATUFS/2019-20n324 JAIMAL SINGH SATNAM SINGHATILTSlz0t9-20/973 It,S. V B GARMENTSATUFS/2019-20/809 SHREE NARAYAN FABRICSATUFSt20t9-20t761 ADINATH DYEING AND FINISHING MILLSATUFS/2019-20/976 KIRAN KNITWEARSATUFS/2019-20/ I 052 RUPA AND COMPANY LIMITED

137 ATUFSt2019-20/229 SHREE NILKANTH POLYTEXATUFS/2019-20i l0l8 RAMANI CREATIONATT.JFS/201 9-20l83 I RAJSHREE DYEING & PRINTING MILLS PVT. LTD.

q*

JIT could not applied within 2 years riom the date of sanction of termroan- 213 cases

108

ln

r36

ts.N"

t l05

I to6

Iur

t ---; .;-I l)

awtl<

lvaI rztI rzr

trxI r:zI rrrInqI t3s

t l3s

f 13,

JIT could not applied rvithin 2 years from the date ofsanction of termloan- 213 cases

Sr.No. TtrFS Ref No. Plant Name1,10 ATUFS/20 l9-20l43 5 VEER PRABHUI11 ATUFS/20t9-20/733 Radha Tex

ATUFS/2019-20/ I 056 MANJU TEXTILESATUFS/201 9-201280 Chhabra Fashions

144 ATUFS/2019-20/605 JAYCO SYNTTIETICS145 ATUFS/20t9-20/124 SU PARSHWA TEXPRNT LLPl4t) ATUFS/2019-201723 IlS ERL GRA II ti UK l'L PEX RIN 1' PS T t-

,ID

141 ATUFS/201 9-20l 1280 KUMAR GRAPHICS148 ATUFS/20 l9-20i285 Jash Rayon149 ATUFS/2o19-20/l 190 NIRVAN SILK MILLS PRIVATE LIM ITEDi50 ATUFS/2018- I9l3422 AVADAT TRENDZ PRIVATE LIMIT I]D151 ATUFS/20 r 9-20l53 5 M/s. COTWIN KNITTINGt52 ATUFS/20l9-20ll 186 SONA TEXTILESl5l ATUFS/2019-20/270 JALARAM TEXTILES154 ATUFS/201 9-20l450 SR-EEPRryA EXPORTS PVT LTD

ATUFS/2019-20/ 1057 SANDHYA TEXTILES156 ATUFSt20t9-20t37 Darshan S ntheticst51 ATUFS/2oI9-20lt310 UK tJD NK PIT ROC St-. PS RI T LE ITEIM D158 ATUFSt20l9-20t474 Parmeshwari CreationI59 ATUFS/201 9-20l I 8 Navin Fashionr60 ATUFS/2019-20i 53 8 ACV PRODUCTS PRTVATE LIMITED

ATUFS/2019-20t t 426 HEMKUNT INDUSTRIESATUFS/2019-20/t 173 Kru a Textiles

l6i ATUFS/20t9-20t644 SHAKTI'IEXTILESATUFSt20t9-20t12s4 BHUMI TEXTILES

165 ATUFStz0t9-20t674 HIIT LRAJ K HMIS oC o'tT MN L SL I),f

t.TDr66 ATUFS/2019-20/ I 368 KPM PROCESSINC MILL P LTD161 ATUI-'S/2018- l9l3766 BINAL TEXTILES168 ATUFS/201 9-201668 M/s. Bakson lnd169 ATUFS/2019-20/969 Selvam Processt70 ATUFS/2019-20t64 Dream Pol kt'7 1 ATUFSt20t9-?0t663 A. K. KNITWEARS112 ATUFS/201 9-20l705 Vrundavan Textile173 ATUFS/201 9-20ll 062 SATUI'A I'EX1-ILISt]4 ATUFS/2019-20/1337 ICAPOOR INDUSTRIES LTD175 ATUFS/2019-20/l I l2 SATYA FABRICSt16 ATUFS/2019-20/105 I TIRUPATI TEXTIT-ES117 ATUFS/2019-20t607 J K TEXBOND PRIVATE LIMITED

ATUFS/20 r 9-20l407 ANISHA THE COLOUR CO.179 ATUFS/2019-20/344 JAY JAY GARMENTSt80 ATUIiS/20 I 9-20l 1039 TARUN ENTERPRISESt8t ATUFS/2019-20/903 NAVALNIT TEXTILE182 ATUFS/2019-20/ 1243 tsSBR OVERSEAS LLP183 ATUFS/20 l9-20l1 080 M/s. D Paradise Tex184 ATUFS/20 l9-20i574 BHAGWATI WARPINGr85 ATUFSt20t9-20/L141 ADITI SILK MILLS PVT LTDr86 ATUFSt2019-20t964 POOJA TEX

*snext* -I I ", L>h/ TAlnL 4u0a

qA?

(l- trz

155

l6l

178

I t4z

I ra:

t62

t r64-

tartc1,/,/.0 + ,U .rL'l Ttat- occl*<6 'qfl

JIT could not applied within 2 years from the date ofsanction of termloan- 213 cases

Sr.No. TUFS RefNo. Plant NameATUFS/2o19-20/lt3 Mehar Prints

188 ATUF S/2019-20i 1255 Harikrishna Sizersr89 ATUFS/2018- l9l3764 S R AY DYE GIN M LL PS RIV LTE M T DE190 ATUFSl20t9-20t1407 RAMESHWAR FAB191 ATUFS/2019-20/394 MARVIN FASHION192 ATUFS/20 t8- 19/3751 OM FAB

ATUFS/201 9-20l r 149 PRACHI TEXl'ILES194 ATUFS/20 r9-20l307 llindustan Di195 ATUFS/2019-20/79 Abhi Creationst96 ATLTIS/2O19-20/1139 GOKILAA GAARMENTS197 ATUFS/2019-20/919 J B }ASHIONS LIMITED

ATUFS/2019-20/ I 086 Nakoda Prints199 ATUFS/2019-20/ ls7 ack LimitedKan ur Plasti200 ATlLTS/2019-20t927 SHREE KzuSHNA FASHION201 ATUFS/2019-20/212 Ka Fabrics

ATUFS/20t 8-19/3750 Abha Fabrics203 ATUFSt20t9-20t629 LAXMI TEXTILES204 A'tuFs/20t9-20n344 RASHAM KNITWEARS205 ATUFS/2019-20i613 M/s. Riba Textiles Ltd.206 ATUFS/2019-20t649 MEENAR POLYDYED YARNS LTD207 ATUFSt20t9-20/846 SANGAM FASHION PRIVATE LIMITED208 ATUFSt20t9-20/1269 SHIVASAA APPARELS PRIVATE. LIMITED

ATUFS/2019-20/780 S. K. FABATUFS/2019-20/5 85 INDER SANDIIU IMPEX PRIVATE LIMITEDDAVATUFS/2019-20/6s 1 VIRA CREATIONSATUFSi20l9-20/ I I l9 PRIME PROCESSORSATUFSt20t9-20t462 Shri Gimar Fabrics

187

Fab

202

I rrl

198

I 2os

I zroT 2llI ztz[rr3

u//,k

x

Ar'n-* -J/\ €1"

A ^r,LY,* -gT gqd

27 T0lta

List of Machinery Manufacturers / Authorized Agent recommended in the lgth ITC meetings.

\

)!

Sr.No.Name of the

Manufacturer/Aqent Recommended for the Eligible machinery

MC-3-W-16, MC-3-H-14, MC-3-t-l I

2M/s. Erhard+Leimer (lndia)Private Limited.. Ahmedabad MC-2-H-87

JlWs. Teccno Caare Engineers.,Tirupur.

MC-2-8, MC-2-41

4 M/s. Satya Group., Valsad. MC-3-D-6

) M/s. Fimat SRL, ItalyMC-2- l. MC-2-24. MC-2-46

6IWs. Veith Svstem GmbHGermany.

MC-4-54

7 M/s Orox Croup Srl, Italy. MC-4-2t,MC-4-20

IvUs. Macpi S.P.A. PressingDivision. ltaly.

MC-4-23,MC-4-26,MC-4 -27,MC-4-28,MC-4-3 I,MC-4-4 r,MC-4 -42,MC-4-66,MC-74,MC-4-90,MC-4-9 I

MC -2-29,MC-2-50,MC-2-3 l,MC-2-54,MC-4-88

10.N4/s. Keumyong MachineryCo.,Ltd. Korea.

MC-l-C-t

M/s. Hansa Industrie-MixerGmbH & Co.Kg. Germany.

MC-2-80

12.N,l/s. Mobase SunStar Co.,Ltd.Korea.

MC-4-47

M./s. Daekwang MachineryCo.,Ltd. Korea.

MC-3-h- r4

M/s. Nova Inter Tech Co. Ltd.,Thailand.

MC-2-46

lWs. Toyoti IndustriesCorporation, Japan.

MC- l -3-(i), MC-l -3-(ii)

M/s. Hashima Vietnam Co.,Ltd.Vietnam. (subsidiary unit of IWsHashima Co. Ltd, Japan)

MC-4-22, MC-4-28

17.Hashima (S) Pte.,Ltd. Singapore.(Sales Unit of Hashima Japan &Vietnam)

MC-4-22, MC-4-28

0r\

iI

I

I

l. MVs. NLK Engineering. Kolkata.

I

I

8.

I I

I

I

l

le. tvl/s. Salvade Srl, Italy.

I ll.

r3. i

,0. I

,, I

t6.

I

r8.

N,l-ls. Yancheng Heng Xin Foreign

Trade Corp.Ltd. China. (Auth.

Agent of M/s. Changshu Signal

Nonwoven Equipment Co., China)

Recommended with l0% Agent Commissionto be deducted

M/s. Sanj Textile P*.,Ltd. Delhi.(Auth. Agent of trfls. XinchangZhengbao Textile Machinery Co.

China)

Recommended with 20o/o Agent Commissionto be deducted

t2 ^dAa c.lou -!. ? Ttot ^"!'?

List of Machinery Manufacturers / Authorized Agent recommended in the 20 s ITC meetings

5o/o

t^}-Ja

\

SR.

NO.

NAME OF THE UNIT ELIGIBLE TEXTILEMACHINECOVERED LINDERWHICH ANNEXUREOF ATUFS

MOU FOR

AUTHORIZEDAGENT WITH % OF

COMMISSION

I M/s. Centpro Engineering Pvt Ltd.Pune, Maharashtra,

MC-2-9

) M/s. Shang Hsing Machinery Co.,Ltd

Taiwan.

MC-2-59,MC-2-63,MC-2-77

) lvlls. Mah Tech. Chennai. (Auth. Agent

of IvUs.DMS Dilmenler Makine Ve

Tekstil San. Tic. A.s. Turkey)

1 M/s. Epson India Private Limited.Banglore (Auth. Agent of IWs. Seiko

Epson Corporation Limited. Japan)

s%

5 M/s.Zheijiang Allwell lntelligentTechnology Co.,Ltd. China. (Auth.

Agent of N4/s. Wenzhou AllwellMachinery Share Co.,Ltd. China)

6 lrrUs. OM Satya Exim Prt.,Ltd. Surat

(Auth. Agent of Quanzhou Bushuo

Machinery Co.,Ltd. China)

I

t9.I

I

I

I

I

I

I

I

I

5o/o

I

I

4a4eX,.-t -p 4La22 7lil?c zt.cc% \81 c

\\'N

7 M/s. IIGM Pvt. Ltd. New Delhi. (Auth.Agent of M/s. Gerber TechnologyLLC. USA)

5%

8 N4./s. Jean Lab Co., Mumbai (Auth.Agent of M./s. Pioneer Udyog., Delhi)

7%

I

I

I

I I

i

Top Related

Copyright © 2022 FDOKUMEN