Vocabulary Learning Strategies of Chinese International Students in Japan

Upload

khangminh22Category

view

1download

0

Country Profile 2006

Zambia This Country Profile is a reference work, analysing the country�s history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit�s Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at www.eiu.com/schedule The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-7300

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

LUSA

KA

LUSA

KA

Livi

ng

sto

nLi

vin

gst

on

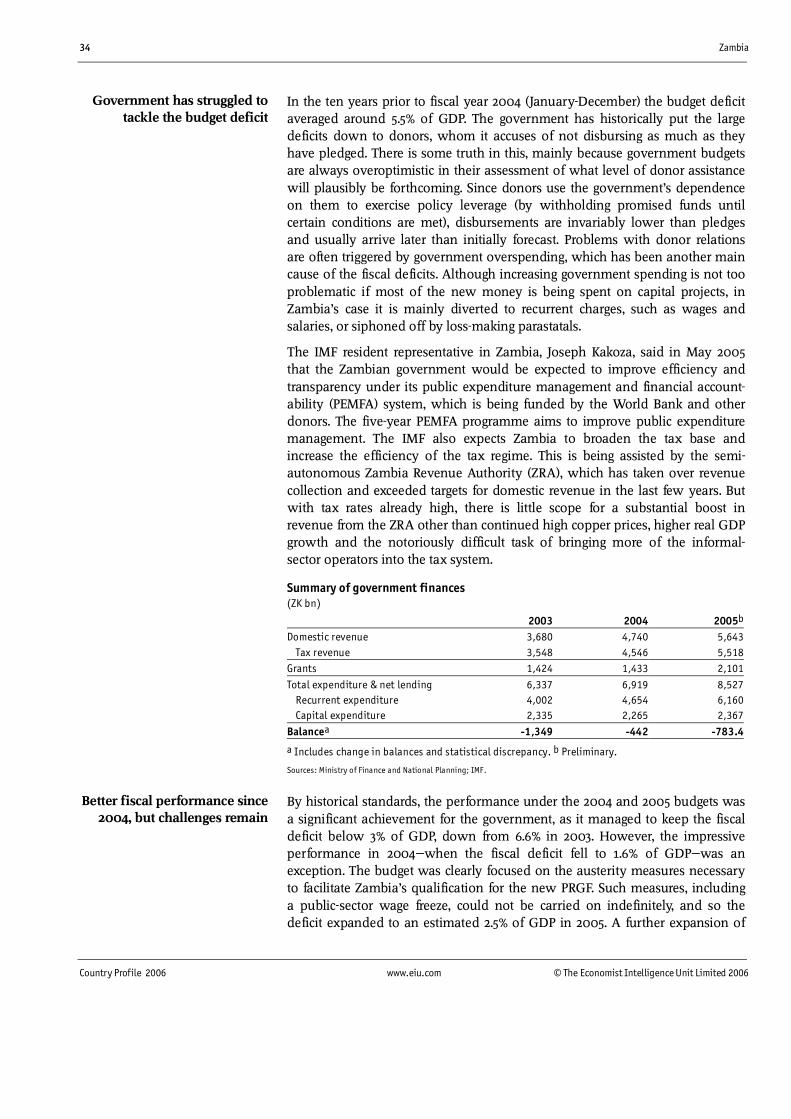

LUSA

KA

Kas

ama

Kas

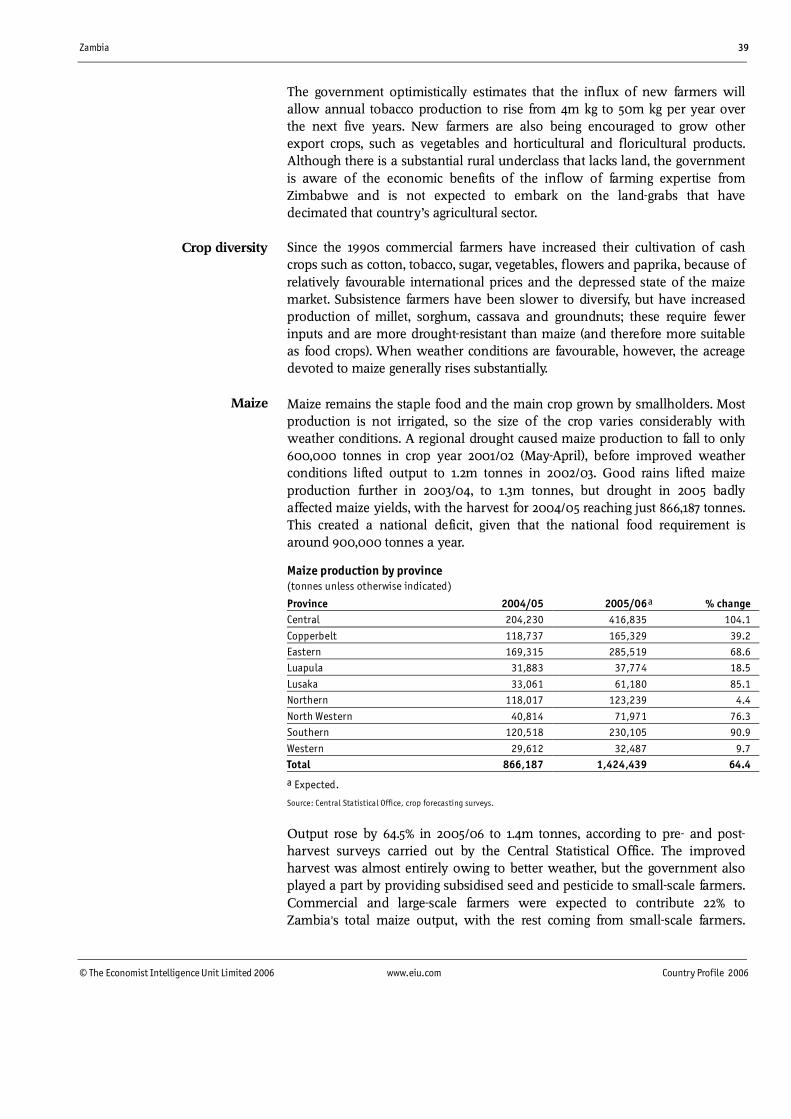

ama

Kas

ama

Kit

Kit

we

we

Kit

we

Mu

fuli

rau

fuli

raCh

ing

ola

Chin

go

laM

ufu

lira

Livi

ng

sto

ne

Chin

go

la Luan

shya

Kab

we

Kab

we

Kab

we

Nd

ola

do

laN

do

la

Kaf

ue

Kaf

ue

Cho

ma

Cho

ma

Kal

om

oK

alo

mo

Maz

abu

kaM

azab

uka

Kaf

ue

Mo

nze

Mu

lob

ezi

Kaz

un

gu

laK

azu

ng

ula

Kaz

un

gu

la

Mo

ng

uM

on

gu

Mo

ng

u

Sen

ang

a

Kao

ma

Kao

ma

Kao

ma

Zam

bez

i

Solw

ezi

Solw

ezi

Solw

ezi

Mw

inil

uM

win

ilu

ng

an

ga

Mw

inil

un

ga

Chil

ilab

om

bw

eCh

ilil

abo

mb

we

Chil

ilab

om

bw

e Kap

iri M

po

shi

Sere

nje

Sere

nje

Sere

nje

Mp

ika

Man

saM

ansa

Kaw

amb

wa

Kaw

amb

wa

Man

sa

Sam

fya

Nch

elen

ge

Nch

elen

ge

Nch

elen

ge

Chie

ng

iKap

uta

Kaw

amb

wa

Mp

oro

koso

Mp

oro

koso

Luw

ing

uLu

win

gu

Mp

oro

koso

Mb

ala

bal

a

Iso

kaIs

oka

Mb

ala

Iso

ka

Nak

on

de

Nak

on

de

Nak

on

de Ch

ama

Cham

a

Kak

um

bi

Kak

um

bi

Cham

a

Lun

daz

i

Kak

um

bi

Chip

ata

Chip

ata

Chip

ata

Kat

ete

Kat

ete

Kat

ete

Peta

uke

Peta

uke

Peta

uke

Chin

sali

Mp

ulu

ng

u

Luw

ing

u

Mu

mb

wa

Mu

mb

wa

Mu

mb

wa

Kal

abo

Cho

ma

L. K

ari

ba

Itez

hi-

Tezh

i Da

mL.

Ca

ho

ra B

ass

a

Kal

om

o

Sesh

eke

Maz

abu

kaCh

iru

nd

uCh

iru

nd

uCh

iru

nd

u

Luan

gw

aLu

ang

wa

Luan

gw

a

Nam

wal

aN

amw

ala

Nam

wal

a

ZA

MB

IA

ZIM

BA

BW

E

AN

GO

LA

NA

MIB

IA BO

TSW

AN

A

DE

MO

CR

ATI

C R

EP

UB

LIC

OF

CO

NG

O

TAN

ZAN

IA

MA

LAW

I

MO

ZAM

BIQ

UE

Zambezi R.

Kab

om

poR.

Luen

a

R.

Lu

anginga

R.

Lungwe-B

u ngu

R.

Zam

bezi

R.

Zam

bezi

R.

Zam

bezi

R.

Luangwa

R.

L. B

an

gweu

lu

L. M

wer

u

Lake

Tan

gan

yika

Ka

fue

R.

Kafu

eR

.

. R al upauL

Ka

riba

Da

m

July

20

06

Mai

n r

ailw

ay

Mai

n r

oad

Inte

rnat

ion

al b

ou

nd

ary

Mai

n a

irp

ort

Cap

ital

Maj

or

tow

n

Oth

er t

ow

n

© T

he

Eco

no

mis

t In

tell

igen

ce U

nit

Lim

ited

20

06

0 k

m10

02

00

30

0

0 m

iles

150

100

50

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Comparative economic indicators, 2005

Gross domestic product(US$ bn)

Sources: Economist Intelligence Unit estimates; national sources.

0.0 5.0 10.0 15.0 20.0 25.0

Lesotho

Malawi

Swaziland

Zimbabwe

Namibia

Mauritius

Mozambique

Zambia

Botswana

Tanzania

Angola

South Africa

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Malawi

Tanzania

Zimbabwe

Mozambique

Zambia

Lesotho

Angola

Swaziland

Namibia

Mauritius

South Africa

Botswana

0.0 5.0 10.0 15.0 20.0 25.0

Namibia

Lesotho

South Africa

Tanzania

Mauritius

Swaziland

Mozambique

Botswana

Malawi

Zambia

Angola

Zimbabwe

-10.0 -5.0 0.0 5.0 10.0 15.0 20.0

Zimbabwe

Malawi

Lesotho

Swaziland

Mauritius

Namibia

Botswana

South Africa

Zambia

Tanzania

Mozambique

Angola

Gross domestic product(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Consumer prices(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product per head(US$)

Sources: Economist Intelligence Unit estimates; national sources.

239.5

266.8

Zambia 1

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Contents

Zambia

3 Basic data

4 Politics 4 Political background 5 Recent political developments 10 Constitution, institutions and administration 12 Political forces 15 International relations and defence

18 Resources and infrastructure 18 Population 19 Education 20 Health 22 Natural resources and the environment 23 Transport, communications and the Internet 26 Energy provision

28 The economy 28 Economic structure 29 Economic policy 35 Economic performance 37 Regional trends

37 Economic sectors 37 Agriculture 41 Mining and semi-processing 43 Manufacturing 44 Construction 45 Financial services 46 Other services

47 The external sector 47 Trade in goods 49 Invisibles and the current account 49 Capital flows and foreign debt 50 Foreign reserves and the exchange rate

52 Regional overview 52 Membership of organisations

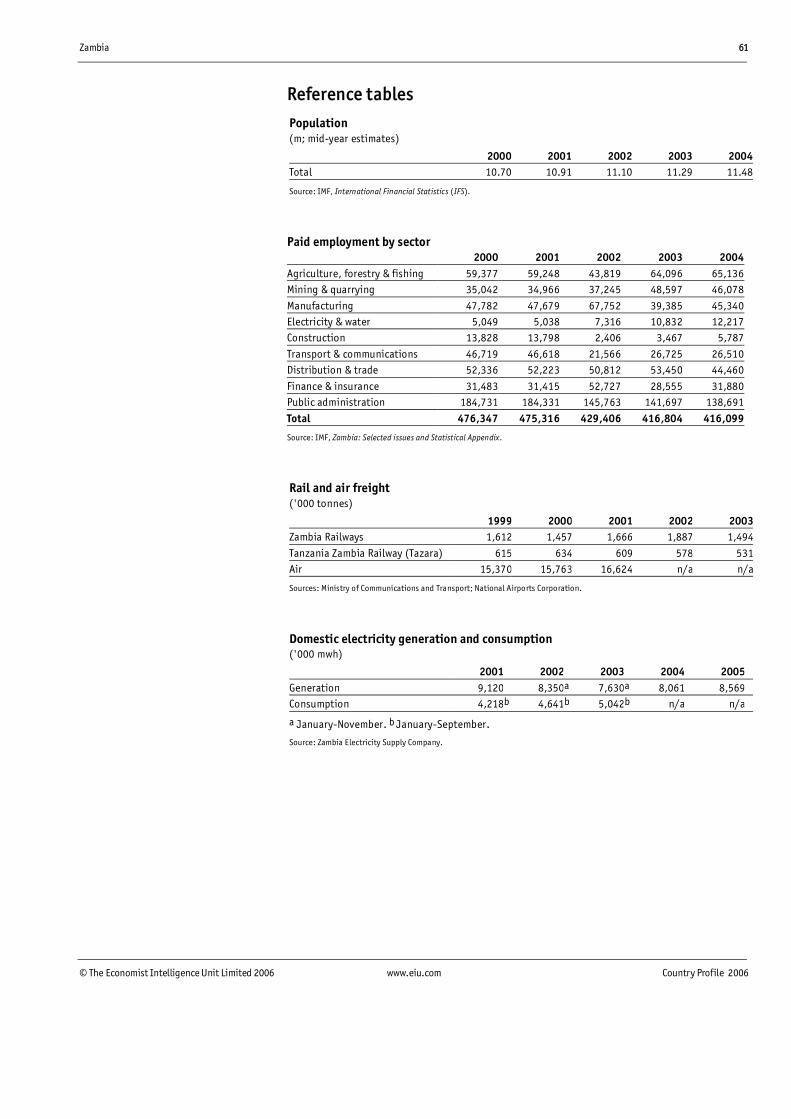

59 Appendices 59 Sources of information 61 Reference tables 61 Population 61 Paid employment by sector 61 Rail and air freight 61 Domestic electricity generation and consumption

2 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

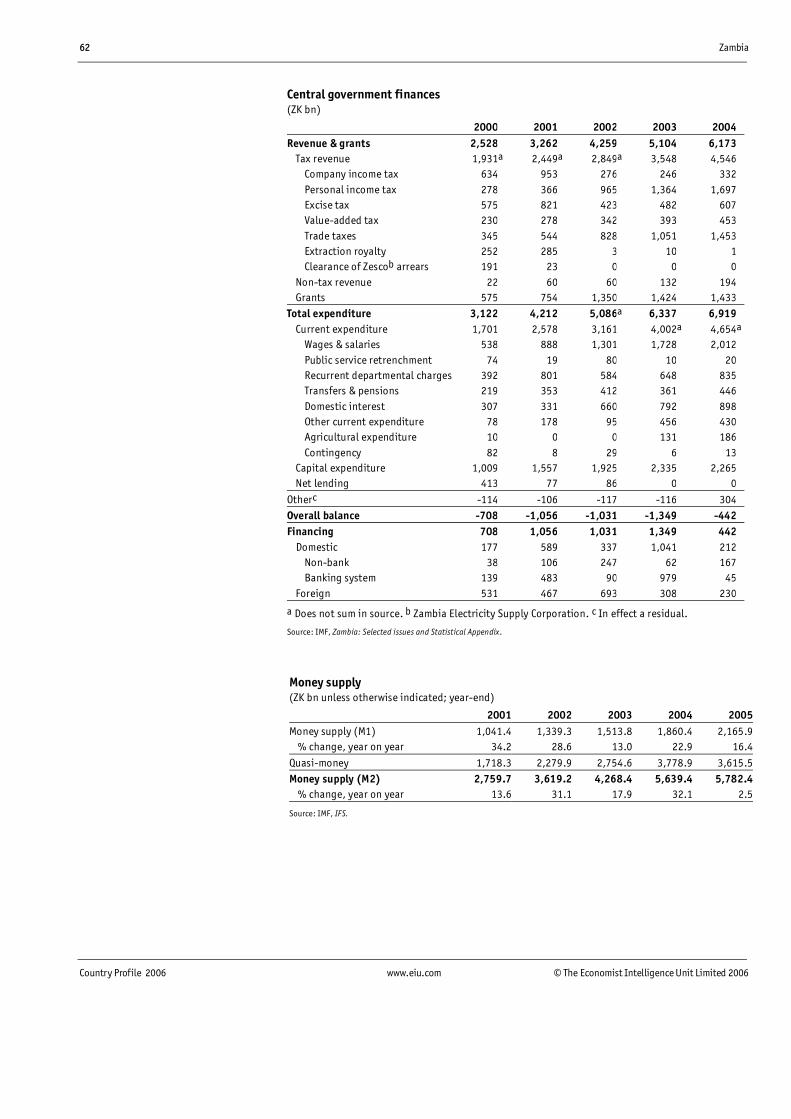

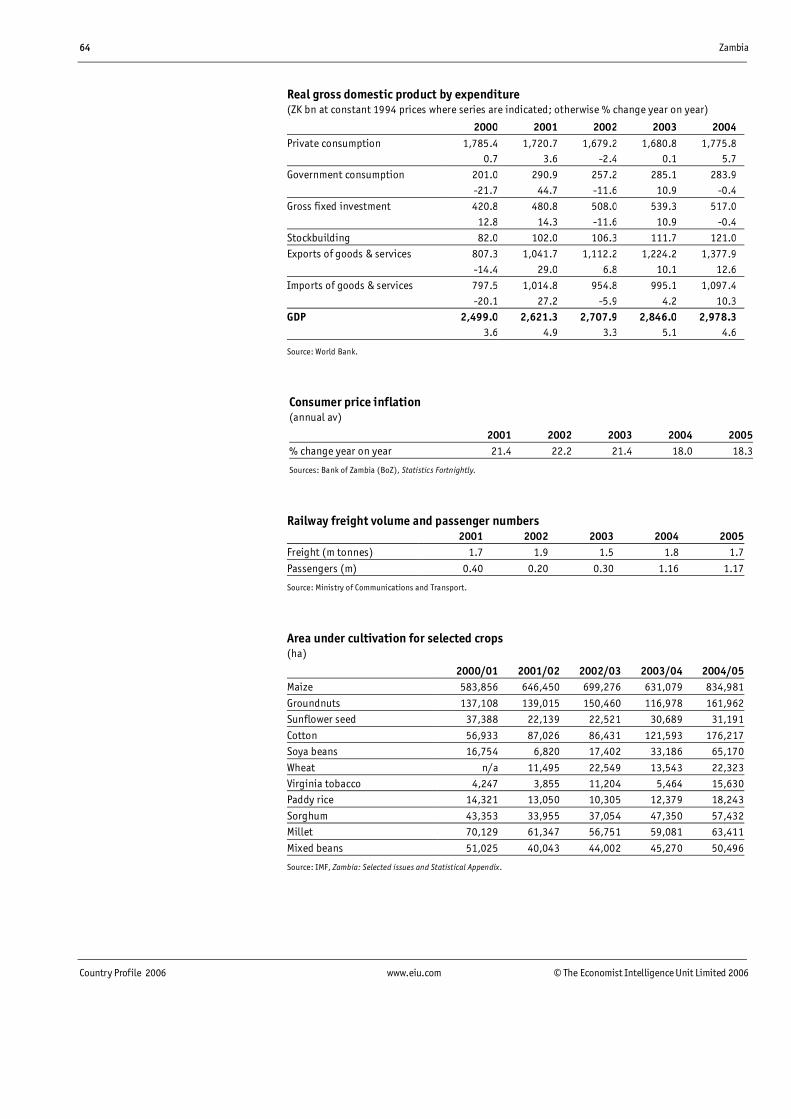

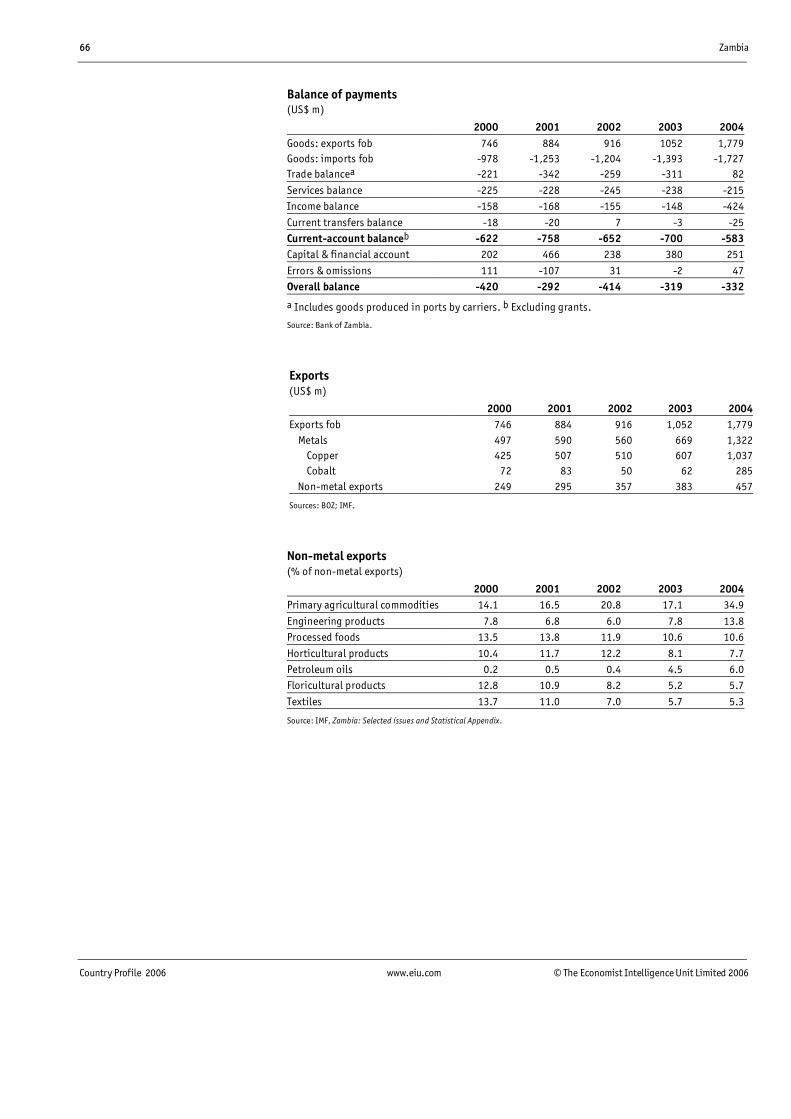

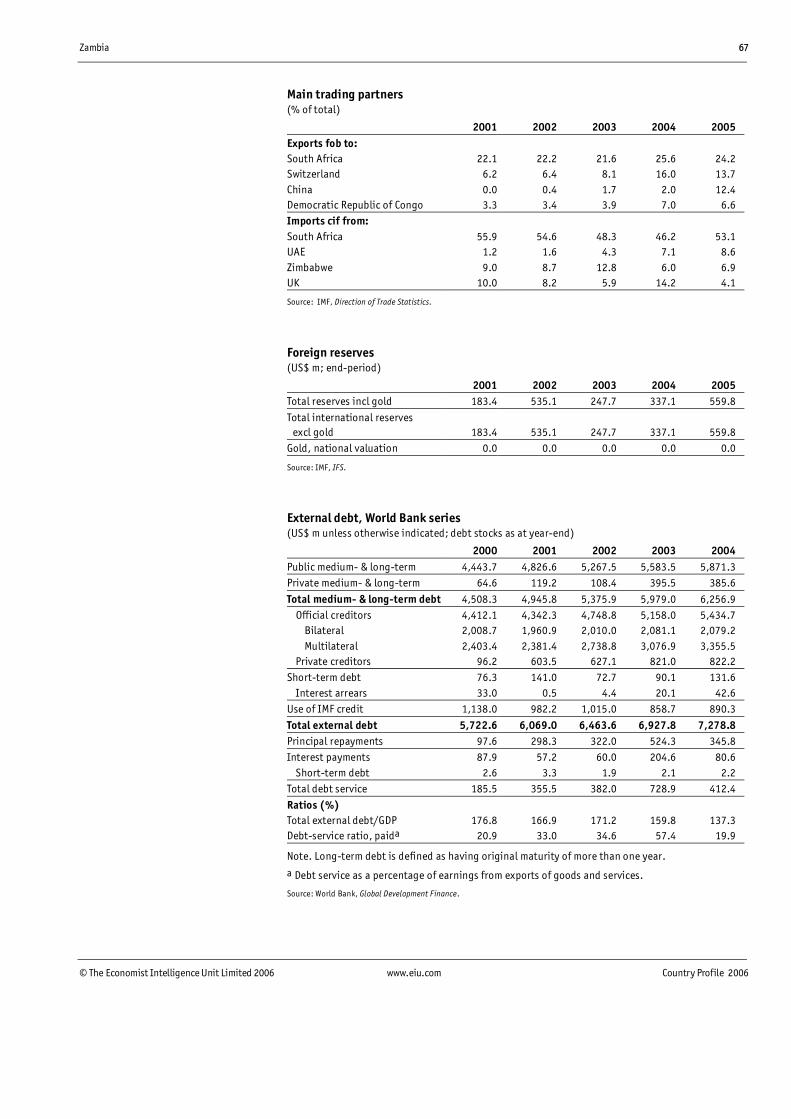

62 Central government finances 62 Money supply 63 Interest rates 63 Gross domestic product 63 Nominal gross domestic product by expenditure 64 Real gross domestic product by expenditure 64 Consumer price inflation 64 Railway freight volume and passenger numbers 64 Area under cultivation for selected crops 65 Copper and cobalt production 65 Stockmarket indicators 65 Index of industrial production 66 Balance of payments 66 Exports 66 Non-metal exports 67 Main trading partners 67 Foreign reserves 67 External debt, World Bank series 68 Net official development assistance 68 Exchange rates

Zambia 3

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Zambia Basic data

752,612 sq km

11.48m (2004, IMF mid-year estimate)

Population in �000, 2000 (Economist Intelligence Unit estimates based on actual data from the 1990 census and regional growth rates from the 2000 census)

Lusaka (capital) 1,432 Ndola 536 Kabwe 512 Kitwe 373 Chingola 173 Mufulira 156 Luanshya 152 Livingstone 103

Tropical, cool on high plateaux

Hottest month, October, 18-31°C; coldest month, July, 9-23°C (average daily minimum and maximum); driest month, August, 0 mm average rainfall; wettest month, December, 231 mm average rainfall

English (official), Nyanja, Bemba, Tonga, Lozi and other local languages

Metric system

Kwacha (ZK)=100 ngwee. Average exchange rate in 2005: ZK4,464:US$1. Exchange rate on July 20th 2006: ZK3,600:US$1

2 hours ahead of GMT

January 1st (New year), Good Friday, Easter Monday, May 1st (Labour day), May 25th (Africa day), first Monday (Heroes' day) and Tuesday (Unity day) in July, October 24th (Independence day), December 25th-26th (Christmas).

Population

Main towns

Climate

Weather in Lusaka (altitude 1,277 metres)

Measures

Currency

Time

Public holidays

Land area

Languages

4 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Politics

Zambia is a republic, in which the president, who is elected every five years by universal suffrage, wields considerable power. The largest party in the National Assembly, the legislature, is the Movement for Multiparty Democracy (MMD), which has held power since 1991. It was last re-elected in December 2001, when the party�s candidate at the concurrent presidential election, Levy Mwanawasa, was elected to serve the first of a possible two five-year terms. Mr Mwanawasa has had to work hard to maintain his grip on power as splits have appeared in the MMD, with his rivals seeking to replace him. He faces another challenge from his own ill health�he suffered a stroke in early 2006�but seemingly remains determined to contest the next presidential election, due in the second half of 2006.

Political background

The British explorer, David Livingstone, travelled through Zambia in the mid-19th century, followed by European settlers keen to farm. With the assistance of British troops, the British South Africa Company (BSAC) established control over Zambia, then called Northern Rhodesia, by 1911, and soon appropriated prime agricultural land for white settlers, removing locals to �native reserves� on inferior land. The British Colonial Office took control of Northern Rhodesia in 1924. Shortly afterwards, large-scale copper mining began in Copperbelt province. As urban areas developed and the demand for food rose, settlers appropriated more land and established Zambia�s major commercial farms. Indirect rule was introduced in 1929, requiring chiefs to collect state taxes. After 1945 the chiefs, known as native authorities, acquired additional responsibilities for rural development. Educational opportunities were expanded to meet the demands of the growing local elite, from which was drawn Zambia�s post-war political leadership.

In 1953 Britain federated Northern Rhodesia, Southern Rhodesia (now Zimbabwe) and Nyasaland (now Malawi), but the federation was opposed by independence movements and finally collapsed in 1963. An election in Northern Rhodesia in October 1962 produced a coalition government of Kenneth Kaunda�s United National Independence Party (UNIP) and Harry Nkumbula�s African National Congress (ANC). The coalition fell apart in 1963 and UNIP won an outright victory in the subsequent election. The independent state of Zambia was created on October 24th 1964, and Mr Kaunda was its first president. Multiparty politics was permitted until 1972, when Mr Kaunda instituted a one-party state. Zambia was badly affected by regional instability in the 1970s. In the 1980s Zambia suffered economically for its part in attempts by South Africa�s neighbours to isolate that country�s apartheid regime.

Criticism of Mr Kaunda�s government by business and trade unions intensified in the late 1970s as economic decline set in. There was a coup attempt in 1980 and a series of strikes in 1981, after which several trade union leaders, including the next state president, Frederick Chiluba, were arrested and detained. The

Early years

Independence in 1964

Growing internal dissent and economic decline

Zambia 5

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

economic situation deteriorated in the 1980s and the government sought IMF assistance. However, IMF policies, including the removal of the maize subsidy, provoked riots. Alarmed, the government restored the subsidy, nationalised milling companies and denounced the Fund. The government broke with the IMF in 1987 and embarked on its own, ultimately unsuccessful, economic recovery programme.

Buoyed by electoral victory in 1988, the government attempted limited economic liberalisation, but a reduction in the maize subsidy led to renewed riots and strikes. Mr Kaunda eventually bowed to popular pressure and lifted the ban on opposition parties in December 1990. An umbrella grouping, the MMD, whose members had little in common other than their opposition to Mr Kaunda�s continued rule, was founded shortly afterwards, and quickly attracted a mass following. The MMD, led by Mr Chiluba, won a landslide victory in the 1991 presidential and legislative elections on a low turnout, judged free and fair by international observers. The MMD government soon distanced itself from its trade union support base and embraced donor-advised structural adjustment policies, including a wide-ranging privatisation pro-gramme.

A new Constitutional Amendment Act of 1996 weakened judicial powers and excluded Mr Kaunda from contesting the presidential election, by stating that anyone running for president had to have been born in Zambia and have Zambian parents (Mr Kaunda�s parents were Malawian). Most opposition parties rejected the new constitution and boycotted the November 1996 general election, with the result that the MMD and Mr Chiluba were re-elected on a low turnout. Following an attempted military coup (lasting only two hours) on October 28th 1997, the government imposed a state of emergency until March 1998. Senior politicians, including Mr Kaunda, were arrested, accused of treason and detained for several months, but were later released. The MMD won local elections in December 1998, again on a low turnout. Mr Kaunda resigned as UNIP president in March 2000.

Recent political developments

Mr Chiluba�s campaign to run for a third term�the constitutional limit is two five-year terms�and his refusal to allow other MMD members to campaign to stand as the party�s candidate in the 2001 presidential election caused major divisions within the party during 2000 and 2001. Despite strong opposition from civil society groups, the MMD formally reappointed Mr Chiluba as party president at a special party convention in April 2001�opponents of the third term within the party were barred from attending the convention. Public opinion remained strongly against a third term, and in May 2001 Mr Chiluba announced that he would not stand for the presidency, while at the same time dismissing the cabinet ministers who were opposed to his third term, including the vice-president, Christon Tembo. Most of the sacked ministers subsequently formed a new party, called the Forum for Democracy and Development (FDD).

Mr Chiluba�s third-term bid splits the MMD

Rebirth of multiparty politics in 1990s

The MMD is re-elected in 1996

6 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

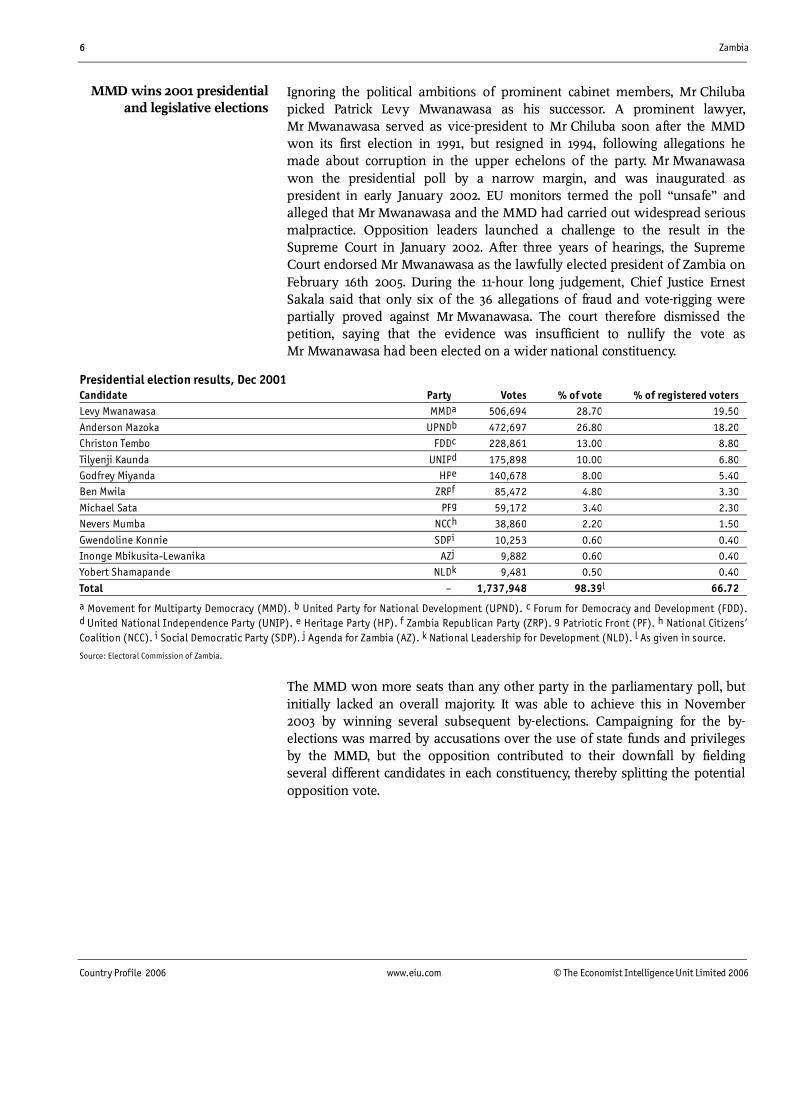

Ignoring the political ambitions of prominent cabinet members, Mr Chiluba picked Patrick Levy Mwanawasa as his successor. A prominent lawyer, Mr Mwanawasa served as vice-president to Mr Chiluba soon after the MMD won its first election in 1991, but resigned in 1994, following allegations he made about corruption in the upper echelons of the party. Mr Mwanawasa won the presidential poll by a narrow margin, and was inaugurated as president in early January 2002. EU monitors termed the poll �unsafe� and alleged that Mr Mwanawasa and the MMD had carried out widespread serious malpractice. Opposition leaders launched a challenge to the result in the Supreme Court in January 2002. After three years of hearings, the Supreme Court endorsed Mr Mwanawasa as the lawfully elected president of Zambia on February 16th 2005. During the 11-hour long judgement, Chief Justice Ernest Sakala said that only six of the 36 allegations of fraud and vote-rigging were partially proved against Mr Mwanawasa. The court therefore dismissed the petition, saying that the evidence was insufficient to nullify the vote as Mr Mwanawasa had been elected on a wider national constituency.

Presidential election results, Dec 2001 Candidate Party Votes % of vote % of registered voters

Levy Mwanawasa MMDa 506,694 28.70 19.50

Anderson Mazoka UPNDb 472,697 26.80 18.20

Christon Tembo FDDc 228,861 13.00 8.80

Tilyenji Kaunda UNIPd 175,898 10.00 6.80

Godfrey Miyanda HPe 140,678 8.00 5.40

Ben Mwila ZRPf 85,472 4.80 3.30

Michael Sata PFg 59,172 3.40 2.30

Nevers Mumba NCCh 38,860 2.20 1.50

Gwendoline Konnie SDPi 10,253 0.60 0.40

Inonge Mbikusita-Lewanika AZj 9,882 0.60 0.40

Yobert Shamapande NLDk 9,481 0.50 0.40

Total � 1,737,948 98.39l 66.72

a Movement for Multiparty Democracy (MMD). b United Party for National Development (UPND). c Forum for Democracy and Development (FDD). d United National Independence Party (UNIP). e Heritage Party (HP). f Zambia Republican Party (ZRP). g Patriotic Front (PF). h National Citizens� Coalition (NCC). i Social Democratic Party (SDP). j Agenda for Zambia (AZ). k National Leadership for Development (NLD). l As given in source.

Source: Electoral Commission of Zambia.

The MMD won more seats than any other party in the parliamentary poll, but initially lacked an overall majority. It was able to achieve this in November 2003 by winning several subsequent by-elections. Campaigning for the by-elections was marred by accusations over the use of state funds and privileges by the MMD, but the opposition contributed to their downfall by fielding several different candidates in each constituency, thereby splitting the potential opposition vote.

MMD wins 2001 presidential and legislative elections

Zambia 7

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Distribution of parliamentary seats Dec 2001 election End-Jun 2006 ChangeMovement for Multiparty Democracy 77 85 +8United Party for National Development 49 41 -8United National Independence Party 13 12 -1

Forum for Democracy & Development 12 11 -1Heritage Party 4 2 -2

Patriotic Front 1 2 +1Independent 1 1 �Zambia Republican Party 1 0 -1

Vacant 0 4 +4

Note. The president can appoint up to eight members of parliament (MPs). Mr Mwanawasa has appointed all these from the MMD.

Sources: Electoral Commission of Zambia; Economist Intelligence Unit.

Once in office, Mr Mwanawasa embarked on a wide-ranging and high-profile anti-corruption drive, primarily targeting senior civil servants and politicians of the Chiluba era, including Mr Chiluba himself, who was charged with 264 counts of theft and diversion of state funds. The trial soon ran into problems, with the director of public prosecutions (DPP) removed from office after allegedly meeting one of the accused. A new DPP has attempted to restructure the trials, and on October 11th 2004 Mr Chiluba pleaded not guilty to fresh charges of corruption involving the theft of US$488,000 of public money�a much smaller amount than the millions of dollars that he was originally accused of stealing. Despite the restructuring of the trials, they have continued to drag on and much of the electorate has come to see the ongoing attempts to prosecute Mr Chiluba as little more than a political witch-hunt. Moreover, the slow progress made has left Mr Mwanawasa vulnerable to the charge that by concentrating on high-profile corruption cases he has failed to broaden the corruption fight to junior government officials. Although less dramatic, low-level corruption within the civil service remains endemic, and it is this type of graft that has much more of an impact on people�s everyday lives.

Patronage, state and civil society

Zambian political history has been relatively stable compared with many other states in Sub-Saharan Africa. No government has been overthrown by a coup d�état and in-fighting has been generally played out without recourse to arms, often ending up in the courts, where verdicts are in most cases accepted. Zambian politics is, however, based on patronage: leaders reward supporters with jobs and contracts to retain them and to enhance their own power, the result of which is the systematic use of the public purse for private ends. There is also turmoil every time the government changes, as new patronage networks are established as old ones are dismantled. Beneficiaries of the outgoing patronage networks are reluctant to let go, partly in fear of prosecution, and this seems to have been the reason for Frederick Chiluba�s third-term presidential bid. The public has long grown tired of the political elite looting state assets, and this has contributed to widespread electoral apathy. Patrick Levy Mwanawasa�s ongoing anti-corruption campaign was an attempt to harness public hostility to corruption to his own advantage, but an apparent lack of political will to reform

Mr Chiluba is charged with corruption

8 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

the patronage system means that Mr Mwanawasa�s campaign could well backfire on him.

Mr Mwanawasa attempted to strengthen the position of himself and the MMD by co-opting members of the opposition. He brought numerous opposition politicians into the MMD, offering many of them lucrative positions in the cabinet. The twin aim of this policy appeared to be to make the MMD more representative�therefore widening its appeal to the public�and also to strengthen the MMD by gaining more seats in parliament while at the same time weakening the opposition parties. The policy was initially successful as the public�s perception of the MMD improved while opposition influence in parliament was curtailed. However, the seeds were sown for future problems for Mr Mwanawasa. The appointment of opposition figures ahead of those already in the MMD caused divisions within the president�s party. Also, those politicians joining the MMD often did so out of their desire to increase their political influence, ambitions that would prove a threat to the president.

In mid-March 2005 Nevers Mumba�who had been previously co-opted by Mr Mwanawasa from the National Citizens' Coalition party�announced that he intended to challenge the president for the leadership of the MMD at the party convention, which was scheduled for May. However, Mr Mumba was unable to take part in the contest, as he was promptly sacked from the MMD. Mr Mumba was dismissed for improper conduct and bringing the party�s name into disrepute after he accused Mr Mwanawasa of involvement in graft. Although Mr Mumba did break party rules by going to the media with corruption allegations, his sacking also served to remove a political rival, as well as upholding MMD rules and regulations. The MMD convention was deferred to July so that a tribunal could investigate the allegations of corruption. The tribunal subsequently cleared Mr Mwanawasa of any corruption, saying that Mr Mumba�s accusations were based on hearsay.

Mr Mumba was not to be the only challenger to the president�s position. On July 12th 2005 a former vice-president, Enoch Kavindele, announced his intention to challenge Mr Mwanawasa�s leadership at the MMD convention. Mr Kavindele was eventually defeated by Mr Mwanawasa during the elections at the convention. However, Mr Kavindele claimed that the poll was rigged, an allegation that the MMD hierarchy dismissed. Although poll-rigging is impossible to prove, the list of delegates was altered numerous times in the run-up to the convention, with supporters of Mr Mwanawasa being added and many of those opposed to him removed. Thus, although Mr Mwanawasa won the leadership contest comfortably, the political manoeuvring involved in securing the vote seems to have divided the MMD even further.

With presidential and legislative elections due in the second half of 2006, political tensions have been building. The announcement that on March 30th Mr Mwanawasa had been rushed to the UK for medical treatment after he suffering a minor stroke served to add much confusion to the political scene. The president's illness has raised concerns over the president's ability to run for a second five-year term of office in the presidential election. The seriousness of the stroke has been downplayed by the government, with Mr Mwanawasa

Mr Mwanawasa co-opts the opposition

The president works hard to maintain his grip on power

Mr Mwanawasa suffers a stroke

Zambia 9

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

himself insisting that he is perfectly capable of continuing to lead the country. However, there remain suspicions that the stroke was actually more serious, which were fuelled by the fact that the president delegated a number of state functions to the vice-president, Lupando Mwape. Nonetheless, Mr Mwanawasa has repeatedly reiterated his intention to contest the election. If he were to stand down, which is regarded as unlikely, an upsurge in in-fighting within the MMD can be expected as members compete for the presidential candidacy of the party. This would in almost any other situation hand the opposition a significant boost; however, they are currently facing their own problems.

The 2006 election hopes of the opposition suffered a major blow following the death of the leader of the United Party for National Development (UPND), Anderson Mazoka, in May. Mr Mazoka died at the age of 63 in a South African hospital after kidney complications. As well as leading the UPND, Zambia's largest opposition party, Mr Mazoka was the favourite to become the presidential candidate for the United Democratic Alliance (UDA), a coalition of the country's three largest opposition parties, of which the UPND is a member. Mr Mazoka had enjoyed a national profile following his narrow defeat to Mr Mwanawasa in the 2001 presidential election, and represented a real threat to the president at the 2006 election. Those standing to replace Mr Mazoka include the UPND vice-president, Sakwiba Sikota, and a wealthy businessman, Hakainde Hichilema. Delegates of the UPND convened in mid-July to elect the new leader, with Mr Hichilema declared the winner later in the month. However, the poll was marred by controversy, with Mr Sikota claiming that vote-buying was widespread. Mr Sikota subsequently left the UPND along with a number of his supporters, and is believed to be in the process of forming a new party.

Important recent events

February 2003

Frederick Chiluba is arrested and charged with corruption and theft. He is later released on bail. Opposition politicians are brought into the cabinet.

November 2003

The Movement for Multiparty Democracy (MMD) secures a parliamentary majority for the first time by winning six out of seven by-elections held over the previous month. Mr Chiluba�s corruption trial begins and goes badly for the government.

February 2004

Public-sector workers hold their first one-day strike for 16 years in protest at the public-sector pay freeze announced in the 2004 budget.

June 2004

The IMF resumes lending under a new three-year US$320m poverty reduction and growth facility (PRGF), triggering financial pledges from other donors.

October 2004

Mr Chiluba pleads not guilty to fresh charges of corruption. However, the amounts of money purportedly stolen are much smaller than previously alleged, leading many Zambians to question the real motives behind the corruption case.

The chief opposition leader dies

10 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

February 2005

After three years of hearings, the Supreme Court dismisses an opposition petition to nullify the results of the 2001 presidential election.

March-July 2005

The president, Levy Mwanawasa, faces down two leadership challenges. He remains in power, but at the cost of deepening the divisions within his party.

March 2006

Mr Mwanawasa suffers a stroke. Despite the president's assurances that he is fit enough to remain in power, doubts remain.

May 2006

Mr Mwanawasa assents to a new Electoral Act Amendment Bill, which does not include contentious issues raised by the opposition and civil society that would level the electoral playing field. The chances of success for the opposition at the 2006 presidential and legislative elections are dealt a further blow when the popular opposition leader, Anderson Mazoka, dies.

July 2006

The United Party for National Development (UPND) begins to disintegrate as the election to choose a new leader ends in acrimony, with a number of party members resigning.

Constitution, institutions and administration

Zambia is a constitutional republic. The current constitution, the third, dates from 1996, and was passed by legislators despite hostility from opposition parties, human rights groups, churches trade unions, the free press, lawyers� associations and others. The new constitution circumscribed the power of the judiciary and increased the powers of the president to remove High Court judges. The presidency is a powerful post, offering great scope for patronage, and the incumbent enjoys wide executive and discretionary powers. Com-petition between politicians for the presidency is intense, and generally eclipses policy differences between parties. The president must seek re-election after five years and can serve only two terms. Since Mr Chiluba�s attempt to run for a third term was defeated in 2001 the two-term rule appears likely to remain.

The 1996 constitution strengthened the formal powers of the unicameral legislature, the 158-seat National Assembly. However, MMD parliamentarians have rarely challenged their government, with the notable exception of their opposition to Mr Chiluba�s third-term bid. For nearly one year after the 2001 election, no party had an overall majority in the National Assembly. However, opposition parties failed to muster sufficient unity to disturb the government�s legislative programme, and the government soon managed to build itself a majority in parliament, thereby neutralising the potential threat the Assembly had briefly posed.

Presidency confers widespread powers

Zambia 11

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

The president�s office dominates government. Mr Mwanawasa has demon-strated how the powers of appointment it bestows can be used to bolster the incumbent�s position, even when his original mandate and support base is weak. After the president�s office, the Ministry of Finance and National Planning is the most powerful in the government, driving economic policy and relations with donors, although, under Mr Mwanawasa, the president�s office has asserted greater control over this. Policy implementation by line ministries is generally weak because of severe capacity problems, which are exacerbated by the brevity of so many ministerial terms, which make it hard for ministers to master their briefs. The quality of senior civil servants varies between ministries, with the Ministry of Finance and National Planning seen as the most technically competent. However, the large number of HIV/AIDS cases has reduced skill levels throughout government, and hinders skills transfer, reducing the already limited effectiveness of government.

Constitutional review

A constitutional review commission (CRC) appointed by the president, Levy Mwanawasa, began work in August 2003. In early July 2005 the CRC published its interim report and draft constitution. In the draft, the CRC recommended adopting the constitution through a constituent assembly representing a cross-section of Zambians. A constituent assembly is popular with civil society and the opposition as they have little faith that a constitution approved via a parliament that is dominated by the ruling Movement for Multiparty Democracy (MMD) would serve the people rather than the governing politicians. Mr Mwanawasa and the MMD had long held out against the calls for a constituent assembly; they had cited the cost implications, but an ulterior motive appears to have been Mr Mwanawasa's fears that he might not win a second term should a popular new clause on the election of the president be implemented. Many educated Zambians want the next president to be elected through a 50%-plus-one voting system instead of the current first-past-the post or simple-majority system. However, in February 2006 Mr Mwanawasa, backed down and agreed to adopt the new constitution through a constituent assembly in the face of mounting public pressure. As well as representing a triumph for the opposition and civil society groups, Mr Mwanawasa's climb-down could actually be a shrewd move on the part of the president. His move will appeal to voters, who will credit him with listening to their requests, but it will also buy him some time to delay the constitution's implementation until after the presidential and legislative elections due in the second half of 2006. Mr Mwanawasa said that the government would facilitate the creation of a constituent assembly through amendments to the current constitution, but warned that no shortcuts would be taken. In addition, a referendum will have to be conducted to ask Zambians formally how they want a new constitution to be adopted, and this will be a relatively lengthy process. Mr Mwanawasa's determination to follow correct procedure in adopting the new constitution should go some way towards avoiding the controversy that has surrounded previous constitutions, and the opposition and civil society will therefore find it difficult to argue against his thorough approach. However, it also means that a new constitution will not be in place in time for the next elections, thus vastly improving

President�s office and Ministry of Finance lead government

12 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Mr Mwanawasa's chances of securing a second and final term in office under the existing voting system.

Despite some questionable judgements in high-profile political cases, the spirited judiciary has managed to preserve its independence from the executive and legislature. The strength and independence of the justice system is being seriously tested by the trial of Mr Chiluba. In dismissing the DPP after what from the government�s perspective was a bad start to the trial, Mr Mwanawasa went beyond what is allowed by the constitution. Although a legal tribunal recommended the DPP�s reinstatement, relations with Mr Mwanawasa had deteriorated to the point where this was not possible, so the DPP was retired with full benefits. Further pressure may be exerted on judicial independence if the government becomes concerned that it will fail to secure a conviction against Mr Chiluba. There are also doubts that the judicial system can properly handle the substantial, politically sensitive caseload.

Since 1996 Zambia has officially adopted Christianity as the state religion. Although most Zambians are Christian, there are also substantial Muslim and animist minorities. Nonetheless, church-based groups wield some authority and much of the population appears to trust their advice rather than that of the politicians. However, the involvement of church leaders in politics is growing�Mr Mumba, the former vice-president and presidential aspirant, is a Pentecostal pastor�which may diminish this trust in the long term.

Political forces

The MMD was created in December 1990 as a loose alliance united around the aim of ousting the then president, Kenneth Kaunda, and UNIP, and more broadly of modernising domestic politics. Members espousing a neo-liberal economic agenda gained control of the MMD shortly before the 1991 election and consolidated their position once the party was in power. For over a decade, the MMD remained neo-liberal in outlook, but the ardour of its faith has waned considerably in recent years; Mr Mwanawasa espouses old-fashioned state intervention and central planning. Particularly during the final years of Mr Chiluba�s rule, the distinction between the state, the party and senior MMD members became increasingly blurred, making it hard to discern any clear ideology in much of government policy and leading to increasingly endemic corruption.

Like most other Zambian parties, the MMD is not overtly ethnically based, but ethnicity does play a role. Mr Chiluba is a Bemba, and Bemba people (from Copperbelt, Luapula and Northern provinces) have been influential in the MMD in the past. This influence is resented by other ethnic groups, particularly from the south, and was a factor in their vote for opposition parties in the 2001 elections. Mr Mwanawasa grew up in the Copperbelt�his father is a Lamba from this region and his mother is a Lenje from the central province. Bemba influence in the MMD has waned since he came to power, and the ethnic groups that make up the Tonga tribe, including the Lenje, are becoming increasingly powerful. Ethnic balances within the party swing because the

The MMD is the dominant party

The judiciary is mostly independent

Zambia is officially Christian

Zambia 13

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

president tends to appoint people from his ethnic group to strategic government positions.

Last five election results

Year Winning party

2001 MMD

1996 MMD

1991 MMD

1988 UNIP a

1983 UNIP a

a Sole party.

Source: Economist Intelligence Unit.

In recent times, a number of Mr Mwanawasa�s actions have widened divisions in the party. In particular, supporters of Mr Chiluba have been alienated by the anti-corruption campaign, while many of the party rank and file are annoyed at being deprived of access to patronage following a clampdown by Mr Mwanawasa for the purposes of saving the party, and the state, money. Some party members are also aggrieved about the number of opposition politicians that the president has appointed to the cabinet. The political manoeuvring of Mr Mwanawasa as he attempts to maintain his grip on power has further alienated some members.

In recent years there have been upwards of 30 registered parties in Zambia, and their fragmented nature has played into the hands of the MMD, as they split the opposition vote at elections. This was evident in the 2001, polls when opposition parties won over 50% of the parliamentary seats and opposition presidential candidates received around 70% of the votes cast. With an eye on the approaching 2006 elections, many prominent opposition members of parliament have recognised that this fragmentation will severely reduce their chances of coming to power, leading to much political manoeuvring within the opposition during late 2005 and into 2006. On March 1st 2006 Zambia's three largest opposition parties agreed to field a single presidential candidate, in what represented the most potent threat to Mr Mwanawasa's re-election. The United Party for National Development (UPND), the Forum for Democracy and Development (FDD) and the United National Independence Party (UNIP) agreed to come together under the banner of the United Democratic Alliance (UDA), and said that they intended to pick their presidential candidate at a joint congress later in the year.

Opposition alliances have featured before in Zambian politics, but no major coalition has ever survived long enough to contest elections. The problem remains that few, if any, opposition leaders are willing to stand down in order to support another opposition candidate, owing to the personalities involved and the widespread ambition to ascend to the powerful position of president. It did look as though things would be different for the UDA, with the leader of the UPND (the largest of the coalition members), Anderson Mazoka, being the clear favourite to become the presidential candidate. Mr Mazoka was a close runner-up to Mr Mwanawasa in the 2001 presidential election and enjoyed a

Divisions threaten the MMD hegemony

Opposition coalitions form ahead of the 2006 elections

The death of Anderson Mazoka threatens the UDA

14 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

national profile, something that the other members of the UDA lacked. However, in May 2006 Mr Mazoka died in a South African hospital following kidney complications. This has thrown the UPND and UDA into confusion, with the battle to succeed Mr Mazoka ending in acrimony and numerous members leaving the party. The UPND, and consequently the UDA, have been severely weakened as a result.

Parliament�s failure to effectively hold the MMD to account has contributed to the growth in civil society groups. The largest of these is the Oasis Forum, which is comprised of leading civil society organisations, church groups and the Law Association of Zambia, and was instrumental in the failure of Mr Chiluba�s third-term bid. The authorities attempted to ban the Oasis Forum in June 2004 for operating without registration, something that the heads of the forum, and many other Zambians, saw as a deliberate attempt by the govern-ment to silence one of its largest critics. The stand-off eventually resulted in the government backing down, as the forum and other civil society organisations mobilised much public support.

Main political figures

Levy Mwanawasa

Inaugurated as president in January 2002 following a flawed poll that left him with the weakest mandate ever received by a Zambian head of state. Mr Mwanawasa has attempted to bolster his position since taking office by spearheading an anti-corruption campaign that has pitted him against Frederick Chiluba (who chose him as the presidential candidate of the Movement for Multiparty Democracy, MMD) and co-opting members from opposition parties. Although initially successful in gaining him support, his actions have alienated many within the party, threatening his continued leadership. Ill-health in the first half of 2006 has raised questions over his ability to contest the 2006 elections, but the president remains adamant that he is healthy enough.

Frederick Chiluba

Zambia�s president from 1991 to 2001, he failed to secure the constitutional change required to allow him to stand for the presidency a third time. A former trade union leader, he came to power amid great expectations, but left it with a poor record. During his term in office Mr Chiluba became one of the richest people in Zambia, and is now on trial for a number of offences of theft by a public servant. The legal process has dragged on for several years, and it will be difficult to produce a paper trail that proves the former president�s guilt. He retains considerable popularity among some of the Bemba ethnic group.

Ng'andu Magande

Appointed finance minister in July 2003, Mr Magande is a technocrat who has never before held political office. He worked previously as the secretary-general of the African, Caribbean and Pacific (ACP) group of states, leaving him with solid connections throughout the developing world and the donor community. Since assuming office, Mr Magande has said that he is opposed to further privatisation, and has hinted at increased economic intervention to enable the state to resume a �leading role� in the economy. His actions, such as the public-sector pay freeze in

Civil society groups have a growing role

Zambia 15

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

2004, indicate that, despite this populist rhetoric, he is aware of the importance of keeping donors happy.

Godfrey Miyanda

A former army general and Zambian vice-president, Mr Miyanda has emerged as an unblemished politician with a respectable track record, and leads the opposition Heritage Party (HP). He has a reputation of being a firm believer in good and clean political governance. This has earned him great respect among Zambians, and he is now being seen as a credible prospect in the 2006 presidential election.

Michael Sata

Leader of the Patriotic Front (PF) and a former minister without portfolio in Mr Chiluba�s last government. Mr Sata was influential in the expulsions of his cabinet colleagues who were opposed to a Chiluba third term, but resigned from the MMD to form the PF after Mr Chiluba ignored him and appointed Mr Mwanawasa as his successor. The PF has only two seats in parliament but is influential outside the National Assembly, where Mr Sata's populist politics are increasing his profile, and his rallies have attracted big crowds.

Nevers Mumba

Mr Mumba was expelled from the MMD after he accused Mr Mwanawasa of graft. Although his Reform Party currently has no seats in the National Assembly, he enjoys significant backing from many within his influential Bemba ethnic group. Although not expected to pose a major challenge in the 2006 presidential election, Mr Mumba could cause an upset if large numbers of the Bemba ethnic group turn away from the MMD.

Vernon Mwaanga

Mr Mwaanga is the information and broadcasting minister, and is an influential figure who helped Mr Mwanawasa plan and execute his successful 2001 election campaign. A trained diplomat, Mr Mwaanga is seen as a political manipulator who keeps the MMD intact whenever it is in trouble. However, in what was seen as a shift in the leadership power base to younger members of the party, Mr Mwaanga lost his position as MMD national secretary at the party's 2005 convention, and his power within the party may be waning.

Fred M�membe

Editor of the influential privately owned daily newspaper, The Post. Mr M�membe has played a key role in exposing corruption in Zambia since the The Post began publication in 1991, and it remains the most credible newspaper in the country.

International relations and defence

South Africa�s ruling party, the African National Congress (ANC), is an old ally of Mr Kaunda and has not shown any affection for the MMD. The South African government is, however, relieved that Mr Chiluba is no longer president and relations between Mr Mwanawasa and the South African president, Thabo Mbeki, are cordial, though hardly warm. The two have been consulting on the peace process in the Democratic Republic of Congo (DRC) and Mr Mwanawasa has expressed support for the New Partnership for Africa�s Development (Nepad), co-led by Mr Mbeki. The substantial trade imbalance between Zambia

South Africa is relieved at Mr Chiluba�s departure

16 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

and South Africa is a permanent strain on relations. However, the ratification in 2001 of a trade protocol between the Southern African Development Community (SADC) and the Southern African Customs Union (SACU), guaranteeing Zambian producers access to the South African market, should ease tensions in the medium term.

The end of the civil war in Angola in April 2002 benefited the whole region, not least Zambia, which then had over 200,000 Angolan refugees (many of whom have now returned home). However, Zambia still hosts DRC refugees and endures constant incursions by DRC militia to scavenge for food or commit armed robbery, but the government managed to stay neutral in the war and at no time deployed troops in the country, bucking the regional trend.

Outside of the region, international relations revolve largely around aid and debt. The country is heavily aid-dependent, meaning that relations with donor governments and multilateral agencies are of constant significance. Donor conditions for aid were essentially economic in the 1980s and 1990s, but to these were added a variety of governance criteria following the completion of the privatisation of ZCCM in March 2000. The IMF and bilateral donors suspended much of the budgetary support scheduled for 2003 in protest at the government�s fiscal laxity. Although lending resumed in mid-2004, donors will be vigilant as far as governance issues are concerned. There was strong support for Mr Mwanawasa�s anti-corruption drive, but donors are becoming increas-ingly wary at the lack of progress.

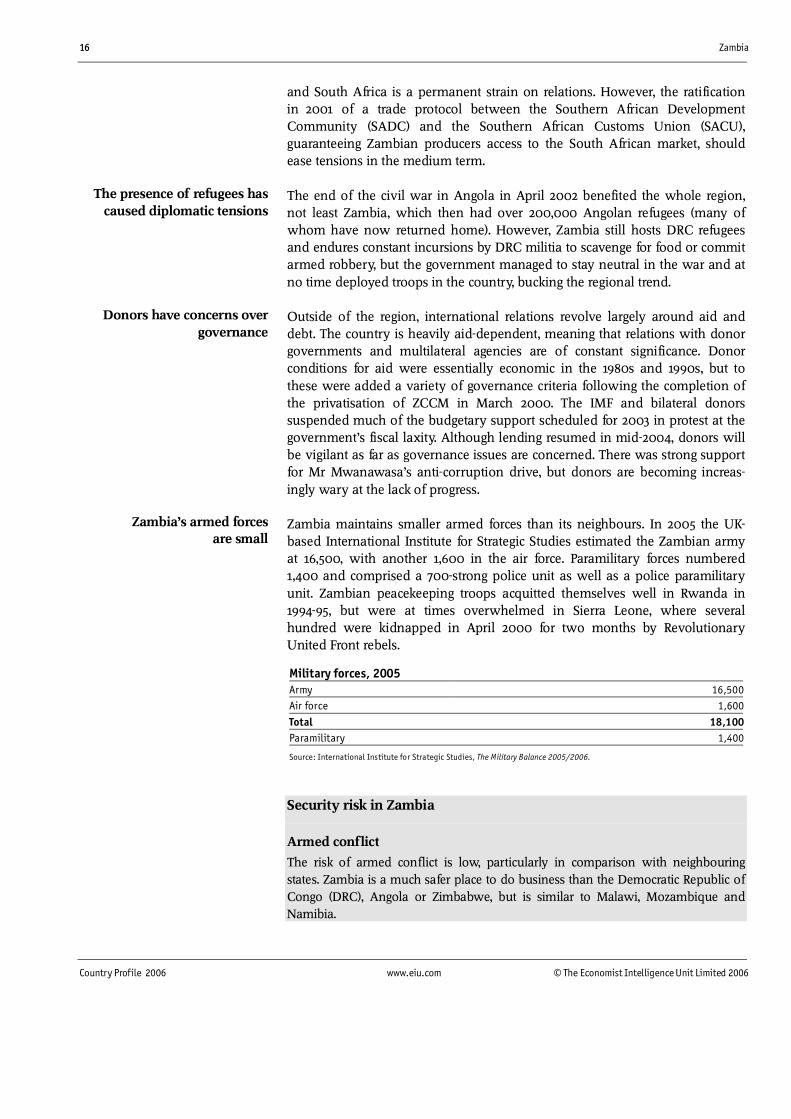

Zambia maintains smaller armed forces than its neighbours. In 2005 the UK-based International Institute for Strategic Studies estimated the Zambian army at 16,500, with another 1,600 in the air force. Paramilitary forces numbered 1,400 and comprised a 700-strong police unit as well as a police paramilitary unit. Zambian peacekeeping troops acquitted themselves well in Rwanda in 1994-95, but were at times overwhelmed in Sierra Leone, where several hundred were kidnapped in April 2000 for two months by Revolutionary United Front rebels.

Military forces, 2005 Army 16,500Air force 1,600

Total 18,100Paramilitary 1,400

Source: International Institute for Strategic Studies, The Military Balance 2005/2006.

Security risk in Zambia

Armed conflict

The risk of armed conflict is low, particularly in comparison with neighbouring states. Zambia is a much safer place to do business than the Democratic Republic of Congo (DRC), Angola or Zimbabwe, but is similar to Malawi, Mozambique and Namibia.

The presence of refugees has caused diplomatic tensions

Zambia�s armed forces are small

Donors have concerns over governance

Zambia 17

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Unrest and demonstrations

Zambia�s politics are sufficiently pluralistic for there not to have been much call or support for internal armed opposition. Zambia has experienced a few coup d�état attempts by disaffected soldiers, but none have come anywhere near seizing power. Political mobilisation tends to require financial or other inducements and at most political rallies there is a �rent-a-crowd� element. These groups can also be deployed to rough up their opponents or stage noisy and intimidating demonstrations from time to time, particularly in the capital, Lusaka, but these are not generally deployed against foreign-owned businesses. Workers� grievances and protests against specific companies occasionally turn violent.

Violent crime

Unemployment and poverty are entrenched and state capacity to fight low-level crime is weak. Private security companies, many of which are of South African origin, are growing. Personal day-to-day security is still generally good, and except occasionally during periods of political unrest (such as the run-up to national elections) and outside traditional danger zones, such as taxi ranks, Lusaka and other towns are generally safe during the day. Caution at night is advised when in any urban area. The police chief, Ephraim Mateyo, initiated a crackdown on violent crime in 2005, with a number of notorious criminals subsequently arrested or killed. However, Mr Mateyo was forced to disband a crack anti-robbery squad at the biggest police station in Lusaka, after evidence surfaced that some policemen were con-niving with criminals to rob residents. Some policemen were subsequently arrested and charged with aggravated robbery, although corruption persists. An amnesty for people who were holding military firearms�many of which had entered Zambia during the periods of war in Angola and DRC�has also had a favourable impact on violent crime, although the exercise was suspended after police ran out of funds to compensate people who were turning in guns.

Organised crime and kidnapping

Organised crime does operate in the country, often as part of a regional network. Hijacked South African cars, for example, are regularly brought to Lusaka for sale or to be broken up for spare parts. Money-laundering is also prevalent, although the implementation of tough anti-money-laundering rules by the Bank of Zambia (the central bank) has had an impact. The president, Levy Mwanawasa, supports the tough stance on international terrorism of the US president, George W Bush, and has publicly pledged to enact laws that will make it difficult for people involved in clandestine activities to operate in Zambia. Kidnapping is rare, and few businesses say that organised crime is a major problem. Instead, businesses stress that their main concerns are corruption and embezzlement, primarily from within companies.

18 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Resources and infrastructure

Population

The 2000 census put the total population at 9.89m. Domestic and international estimates of the population more recently are sparse and often inconsistent. The IMF and the World Bank estimate of a total population of 11.48m for 2004 appears the most plausible, given what is known about population growth rates. Annual population growth averaged 2.9% during the 1990s, compared with 3.1% in the 1980s, and the growth rate has continued to decline more recently. The main reason for the falling population growth rate is the effect of HIV/AIDS, which is expected to reduce annual population growth to 2% by 2010. Annual population growth in the Copperbelt during the 1990s was just 0.8% owing to migration to other areas as a result of the economic crisis in the province. Population growth in Lusaka over the same period was much higher, averaging 3.5% a year, reflecting the city�s continued attraction, despite its chronic jobs shortage. Urbanisation is a growing problem in Zambia (as is the case in most less-developed countries): rural-to-urban migrants create pressure on employment structures, housing needs and security.

The population is young and getting younger. Some 45% is aged under 15 years and this segment continues to show a greater annual percentage increase than any other. The Copperbelt is Zambia�s most urbanised and populous province, followed by Lusaka. Around 62% of Zambians live in rural areas.

About one-half of the population is in some form of employment. Income distribution is highly skewed, with the majority earning very little while a minority makes a comfortable living. Subsistence agriculture is the biggest single employer, but data for this category are scarce and unreliable. However, it is estimated that around 2m people are subsistence farmers. Informal trading is believed to employ over 1m, but is under-represented in official statistics.

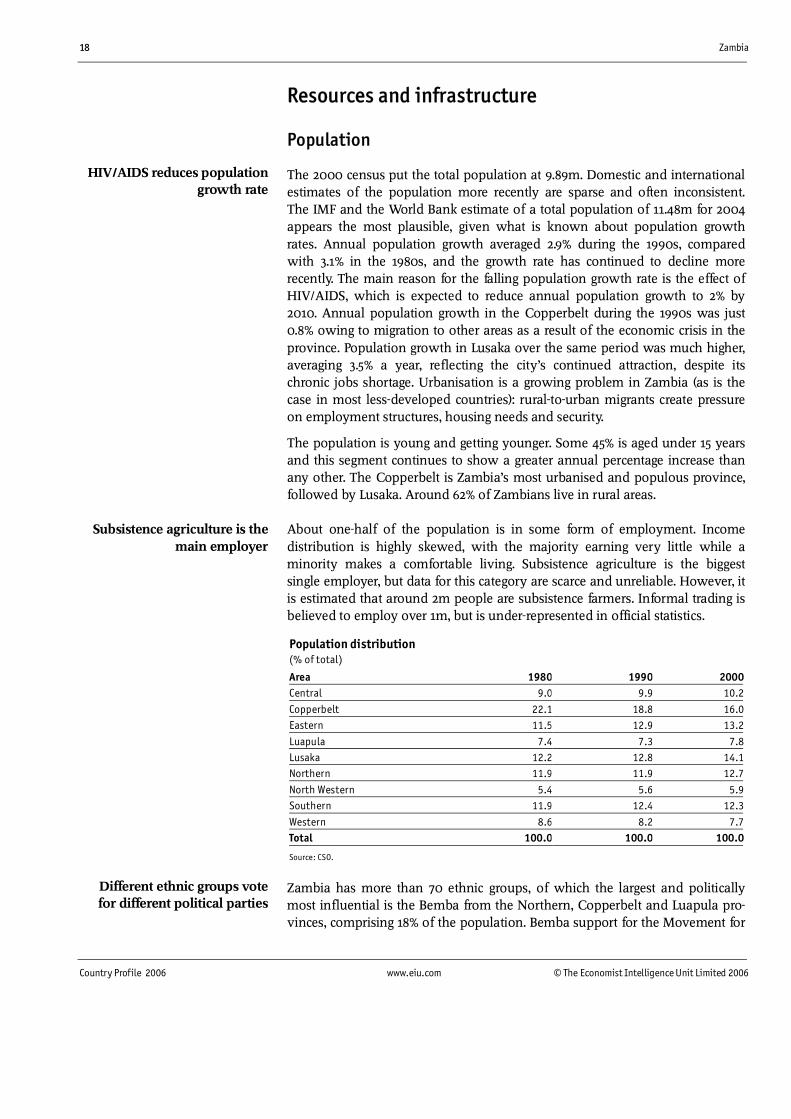

Population distribution (% of total)

Area 1980 1990 2000Central 9.0 9.9 10.2

Copperbelt 22.1 18.8 16.0Eastern 11.5 12.9 13.2

Luapula 7.4 7.3 7.8Lusaka 12.2 12.8 14.1Northern 11.9 11.9 12.7

North Western 5.4 5.6 5.9Southern 11.9 12.4 12.3

Western 8.6 8.2 7.7Total 100.0 100.0 100.0

Source: CSO.

Zambia has more than 70 ethnic groups, of which the largest and politically most influential is the Bemba from the Northern, Copperbelt and Luapula pro-vinces, comprising 18% of the population. Bemba support for the Movement for

HIV/AIDS reduces population growth rate

Subsistence agriculture is the main employer

Different ethnic groups vote for different political parties

Zambia 19

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Multiparty Democracy (MMD) was solid in the early 1990s, but has fragmented considerably over the past few years, owing to the different ethnic background of the president, Levy Mwanawasa. Around 10% of the population are Tonga people from the Southern province, who are strong supporters of the United Party for National Development (UPND). The Nyanja from the Eastern province, who are also numerous in Lusaka, mostly support the United National Independence Party (UNIP). The Lozi from the Western province are the only group to show strong support for secession from the country (to join their fellow Lozi members in Namibia�s Caprivi strip, which, together with Zambia�s Western province, formed the majority of the old kingdom of Barotseland).

Education

Recent poverty assessment surveys show a consensus among education users that during the 1990s access to education and its perceived value deteriorated. The trends are mixed regarding quality. Almost every child of primary school age attended school in the mid-1980s. User fees were introduced in the 1990s to generate funds to improve quality, but households have increasingly removed children from school as a poverty-coping strategy and attendance fell. In 2002 the government introduced a free basic education policy, supported by the con-struction of more schools, which led to an upturn in primary school enrolment.

In 2005 the government continued to implement the free basic education policy, as well as increasing intervention to remove barriers to education for orphans and vulnerable children. According to Treasury data, pupil enrolment at basic level (grade 1-9, ages 7-15) rose by 13.1% compared with 2004. Male enrolments accounted for 51.2% of total basic school enrolments. Basic-level school enrolment is now approaching 100%. However, the national average completion rate in 2005 was just 42.7%, compared with 38.5% in 2004, indicating that problems still exist. Enrolments at high-school level rose by 5.9% in 2005 from 158,238 in 2004. The increase was partly owing to an expansion in the number of high schools to 322, from 319 in 2004. Access to high schools is still limited, as the gross enrolment ratio was just 21.7% in 2005. The gross enrolment ratio for girls was lower, at 19.4%, compared with that for boys, at 24.1%.

Enrolment at basic school level 2003 2004 2005 % change, year on yeara

Female 1,101,949 1,218,611 1,390,028 14.1

Male 1,184,666 1,300,530 1,458,329 12.1Total 2,286,615 2,519,141 2,848,357 13.1

a 2005 compared with 2004.

Source: Ministry of Education

The number of teachers at basic school level fell by 7.4% in 2005 from 45,761 in 2004. The Ministry of Education has estimated the national basic school requirement for teachers at 48,357, which implies a shortfall of 5,595. The national pupil-teacher ratio in basic schools was 55.3 in 2005, up from 52.6 in 2004, against a national recommended ratio of 45. The northern province had the highest pupil-teacher ratio of 70.8, whereas the capital, Lusaka, had the lowest ratio, at 42.8. Teacher numbers are falling owing to the incidence of

Educational access has improved in recent years

Efforts are made to increase teacher numbers

20 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

HIV/AIDS and the lure of better-paid jobs abroad. Teacher morale is also a problem. Salaries have not kept pace with inflation and are lower in real terms than a decade ago. A lack of skills transfer through the school system is also of significant concern.

In an attempt to remedy the deficit of teachers, the government has stated that it intends to employ 7,000 additional teachers in 2006, plans that were initially mooted in 2005 but which were not implemented. The government is funding the process from the monies saved from debt relief, although doubts remain as whether enough teachers can actually be found in Zambia. To attract and retain more teachers the government intends to improve their conditions of service, particularly those working in rural areas where teacher retention is a major problem. Progress is slowly being made, with the share of the budget going towards education increasing in recent years. According to IMF and government data, the share of education in the discretionary budget rose to 26.9% in 2006 from 18.5% in 1999.

Zambia has two universities, the University of Zambia (UNZA) in Lusaka and the Copperbelt University (CBU) in Kitwe. According to the education ministry, total enrolment at the two public universities increased by 14.7% to 12,900 in 2005 from 11,245 in 2004. Enrolment at UNZA rose by 13.4%, while enrolment at the CBU rose by 18.2%. UNZA accounted for 71.7% of total enrolments in 2005, and the CBU accounted for 28.3%. To some extent this reflects the success of a government loan scheme, introduced in 2004. Under this scheme, students obtain loans from the government to pay for their tuition and upkeep at the universities. Nevertheless, the two universities continue to face staffing problems and heavy indebtedness to utility firms and other suppliers of goods and services. In 2005 the government released ZK4.9bn (US$1.1m) to UNZA and ZK2.3bn to the CBU for rehabilitation works, but the funds fell short of the requirements for improving infrastructure at the two institutions.

The emphasis at university level remains on the arts and social sciences, with fewer than 40% of graduates studying technical, scientific, medical, agricultural or managerial subjects. However, away from the universities, the Technical, Vocational and Entrepreneurship Training (TEVET) institutions continued to experience growth in 2005, in terms both of the number of institutions and of the level of enrolment. The number of institutions providing technical and vocational training rose to 319 in 2005, from 315 in 2004. Total enrolment in these institutions rose by 5.4% to 27,986 in 2005.

Health

Health provision is faced with a double crisis of declining resources and a growing disease burden, particularly because of HIV/AIDS (although malaria is still the main killer). Key health indicators, including life expectancy, are falling owing to poor nutrition and infant mortality, both of which are worse today than a decade ago. Average life expectancy rose from 40 years in 1964 to 54 in the mid-1980s, but has since declined to an estimated 37.5 years in 2003. The UN Development Programme�s Human Development Report 2005 ranks Zambia 166th out of 177 countries in its Human Development Index (HDI), placing it

Higher-education enrolment grows

Key health indicators are worsening

Zambia 21

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

between Malawi and the Democratic Republic of Congo. Zambia�s HDI score has declined since 1985, and is now 16% lower than in 1975.

The government has made better healthcare a priority in recent budgets, with large planned spending increases in 2006. In June 2006 the government announced plans to spend ZK651bn on recruitment of new doctors and also to lure back home nearly 300 doctors who are working in developed countries. Currently in Zambia, of the 2,300 doctors required only 646 are available, and of the 16,732 nurses needed only 6,096 are working domestically. In addition to raising the numbers of medical personnel, the government also scrapped user fees in rural clinics in April 2006. The ending of the fees is one of the first benefits to flow from debt relief granted to Zambia under the multilateral debt relief initiative, initiated by the G8 group of industrialised nations.

According to the IMF, procedures and mechanisms for the procurement of drugs have been tightened to improve accountability and transparency. Scandals have in the past affected the procurement of drugs, with millions of US dollars in Treasury funds often diverted to other purposes or squandered by some senior officials. Zambian authorities agreed with donors in 2004 that the Central Board of Health would be in charge of all procurement of medical drugs, and that the company�in which the government has a major interest�should provide quarterly procurement reports to enable the tracking of drug purchases.

To assist in the fight against HIV/AIDS, anti-retroviral drugs (ARVs) began to be provided free from 2005. This raised the number of people on ARVs to nearly 40,000 in early 2006, but the government still failed to attain its target of 100,000 by December 2005. The problems are more to do with the stigma attached to the illness than to problems with availability of medicine. The government is utilising debt relief savings to provide the free drugs, as well as large grants from the World Bank, the UN and the US government.

HIV infection may have peaked

In common with neighbouring states, the Zambian population suffers from high levels of HIV infection. The impact on the economy has been severe: workers� absen-teeism rates have increased, and skills are not being passed on from one generation to another. The latest estimate from the Joint UN Programme on HIV/AIDS (UNAIDS) is that 17% of adults aged 15-49 are HIV-positive (this is broadly in line with the government�s estimate), down from 21.5% in 2001. The decline is the result of a number of factors, including a government public awareness campaign, which coincided with the launch of a national council and secretariat to co-ordinate the fight against AIDS in November 2002. The provision and expansion of community-based care has also been an important factor. However, the decline in prevalence is also a reflection of the death rate among the HIV population.

Free anti-retroviral therapy is now available

The government is attempting to improve things

22 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

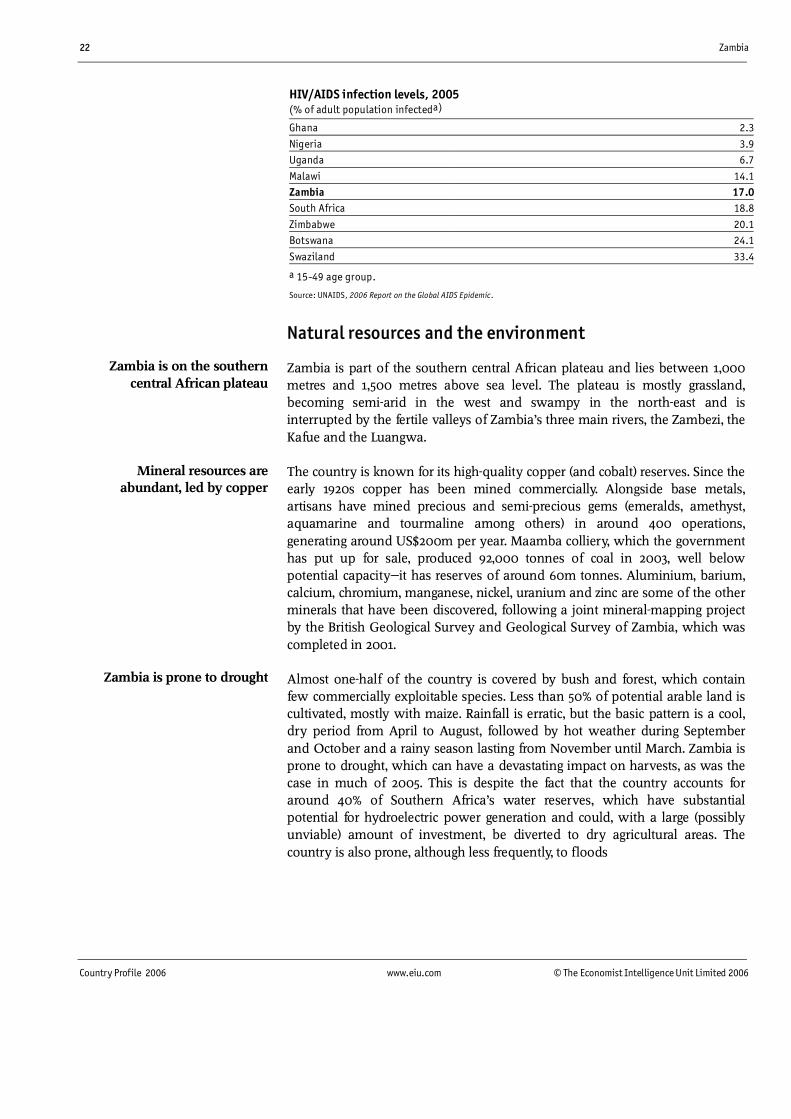

HIV/AIDS infection levels, 2005 (% of adult population infecteda)

Ghana 2.3

Nigeria 3.9Uganda 6.7

Malawi 14.1Zambia 17.0South Africa 18.8

Zimbabwe 20.1Botswana 24.1

Swaziland 33.4

a 15-49 age group.

Source: UNAIDS, 2006 Report on the Global AIDS Epidemic.

Natural resources and the environment

Zambia is part of the southern central African plateau and lies between 1,000 metres and 1,500 metres above sea level. The plateau is mostly grassland, becoming semi-arid in the west and swampy in the north-east and is interrupted by the fertile valleys of Zambia�s three main rivers, the Zambezi, the Kafue and the Luangwa.

The country is known for its high-quality copper (and cobalt) reserves. Since the early 1920s copper has been mined commercially. Alongside base metals, artisans have mined precious and semi-precious gems (emeralds, amethyst, aquamarine and tourmaline among others) in around 400 operations, generating around US$200m per year. Maamba colliery, which the government has put up for sale, produced 92,000 tonnes of coal in 2003, well below potential capacity�it has reserves of around 60m tonnes. Aluminium, barium, calcium, chromium, manganese, nickel, uranium and zinc are some of the other minerals that have been discovered, following a joint mineral-mapping project by the British Geological Survey and Geological Survey of Zambia, which was completed in 2001.

Almost one-half of the country is covered by bush and forest, which contain few commercially exploitable species. Less than 50% of potential arable land is cultivated, mostly with maize. Rainfall is erratic, but the basic pattern is a cool, dry period from April to August, followed by hot weather during September and October and a rainy season lasting from November until March. Zambia is prone to drought, which can have a devastating impact on harvests, as was the case in much of 2005. This is despite the fact that the country accounts for around 40% of Southern Africa�s water reserves, which have substantial potential for hydroelectric power generation and could, with a large (possibly unviable) amount of investment, be diverted to dry agricultural areas. The country is also prone, although less frequently, to floods

Zambia is on the southern central African plateau

Mineral resources are abundant, led by copper

Zambia is prone to drought

Zambia 23

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Transport, communications and the Internet

Transport costs are high, partly because Zambia is land-locked, but also because of inefficiencies and structural weaknesses in the transport network. Transport costs are estimated to account for 60-70% of the cost of production for many goods. This is higher than the regional average and damages the competitive-ness of exports. Government policy is to reverse the trend of the decay of transport infrastructure, particularly for roads, and the government intends to direct substantial funds to this end. The government�s policy of extending private-sector involvement to the rail network is already far advanced and is set to continue.

Beira in Mozambique is the nearest major port to Zambia and is linked by rail to Lusaka via Harare, the capital of Zimbabwe. Further away, but far better equipped and also accessible by rail, is Durban in South Africa. Zambia uses Mpulungu port on Lake Tanganyika to export to the Great Lakes region, although the volumes are not substantial owing to weak demand. Mpulungu is in a poor state and is not connected to Zambia�s rail network, but is in the process of rehabilitation. The Tanzania Zambia Railway (Tazara) is the main route for the transportation of Zambia�s copper cathode to Europe, China and the US via the port of Dar es Salaam, but has recently been losing market share to Beira and Durban. The decline in trade through Dar es Salaam has put pressure on Tazara (1,860 km of track), which was built in 1975 with Chinese assistance. Tazara is a classic parastatal, where overstaffing, weak management and poor wages have long kept industrial relations combative and service delivery poor. A private-sector participation options study was concluded in 2005 for the management of Tazara. The outright privatisation of Tazara and the formation of a joint venture between the private sector and the government were among options recommended, but the process on either front is expected to be slow.

A 20-year concession to manage Zambia Railways (with 685 miles of track) was signed in February 2003 by a consortium of two South African companies, New Limpopo Bridge Projects Investments (NLPI) and Spoornet. However, the government has recently recommended a comprehensive review of the management concession, following regular complaints raised against the concessionaire regarding poor service and lack of improvement.

The government awarded a private company, Northwest Railways, tax rebates totalling US$35m in May 2006 in a bid to speed up implementation of the rail link between Zambia and Angola, which is key to ensuring faster access to world markets for Zambia�s copper. Northwest Railways was exempted from paying customs duty on imported equipment. The project envisages a 685-km railway line running north-west from Zambia�s mining hub in the Copperbelt province to join Angola�s Benguela railway. The railway line will be constructed in three phases:

• it will initially connect the Copperbelt town of Chingola to Solwezi in the North-Western province;

Transport costs are too high

Exports are sent via ports in neighbouring countries

South Africans manage Zambia Railways

A rail link to Angola is planned

24 Zambia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

• during phase two, the line will be extended to a new mine at Lumwana in the North-Western province; and

• the final phase will connect the line to Angola�s Benguela railway, itself expected to undergo refurbishment.

The chairman of Northwest Railways, Enoch Kavindele, said that discussions had made progress with the Development Bank of Southern Africa (DBSA) and the Industrial Development Corporation (IDC), which were keen to finance the project. Construction work was expected to commence once the Environ-mental Council of Zambia (ECZ) had approved an environmental impact assessment plan.

Zambia has an estimated 23,000 miles of roads, of which about 4,100 miles are tarred. The road network is in a dire state. In 1998 the National Roads Board (NRB) launched a US$1bn investment programme for the road sector, to run for ten years. The first phase closed at the end of 2002. Expenditure on the road network has risen as a result of the programme. However, there has been considerable underspend because of a shortage of funds. In addition, in some cases money earmarked for road maintenance and upgrading has been embezzled. However, according to government figures the NRB targets for end-2002�when 45% of tarred roads and 15% of feeder roads were supposed to be in good condition�were attained.

The government is now focusing on institutional reforms. The Roads Development Agency (RDA), the National Road Fund Agency (NRFA) and the Road Safety Agency (RTSA), which were created in 2004, all became operational in 2005. The government also commenced the process of working on a new partnership policy that will allow the private sector to be involved in construction, rehabilitation and maintenance of infrastructure in collaboration with the public sector.

Zambia has fully privatised its air services, following the liquidation of the loss-making Zambia Airways in 1994. There are at least 17 private airlines, but Zambian Airways, formed in 1999, has become the de facto national carrier, although it only operates within the region. A variety of African airlines fly to Lusaka, but only British Airways and South African Airways operate inter-continental flights. There is little practical competition and airfares in and out of Zambia are expensive. There are 144 airports or aerodromes in Zambia. The National Airports Corporation manages the four international airports: Lusaka, Livingstone, Ndola and Mfuwe. Flight services have increased in recent years, particularly through Ndola, reflecting the revival in copper mining.

Embezzlement compromises road investments

Zambian Airways operates international routes

Zambia 25

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Aircraft movements (take-offs and landings; no. unless otherwise indicated)

2004 2005

Airport DomesticInter-

national Total Domestic Inter-

national TotalTotal

(% change)Lusaka 13,014 8,453 21,467 13,530 7,783 21,313 -0.7Ndola 3,042 2,673 5,715 3,601 2,331 5,932 3.8

Livingstone 1,857 4,294 6,151 2,252 4,643 6,895 12.1Mfuwe 2,753 840 3,593 3,235 969 4,204 17

Total 20,666 16,260 36,926 22,618 15,726 38,344 3.8

Source: National Airports Corporation.