WELLNESS FOREVER MEDICARE LIMITED - BSE

372

DRAFT RED HERRING PROSPECTUS Dated September 30, 2021 (This Draft Red Herring Prospectus will be updated upon filing with the RoC) Please read Section 32 of the Companies Act, 2013 Book Built Offer WELLNESS FOREVER MEDICARE LIMITED Our Company was originally incorporated as ‘Wellness Forever Medicare Private Limited’ , a private limited company under the Companies Act, 1956, Mumbai, Maharashtra, pursuant to a certificate of incorporation da ted February 8, 2008, issued by the Registrar of Companies, Maharashtra at Mumbai. Subsequently, our Company was converted into a public limited company pursuant to a resolution passed by our Shareholders at an extraordinary general meeting held on July 9, 2021 and a fresh certificate of incorporation dated August 5, 2021 was issued by the RoC consequent upon conversion, recording the change in the name of our Company to “Wellness Forever Medicare Limited”. For details of changes in name and registered office of our Company since incorporation, see “History and Certain Corporate Matters”, beginning on page 176. Registered and Corporate Office: 7 th Floor, Wing A, Empire Plaza, IT Park, LBS Marg, Vikhroli (West), Mumbai 400 083, Maharashtra India Contact Person: Nidhi Vora, Company Secretary and Compliance Officer; Tel: +91 22 4354 1722 E-mail: [email protected]; Website: www.wellnessforever.com Corporate Identity Number : U24239MH2008PLC178658 OUR PROMOTERS: ASHRAF MOHAMMED BIRAN, GULSHAN HARESH BAKHTIANI AND MOHAN GANPAT CHAVAN INITIAL PUBLIC OFFER OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹ 2 EACH (“EQUITY SHARES”) OF WELLNESS FOREVER MEDICARE LIMITED (“COMPANY” OR “ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹ [●] PER EQUITY SHARE FOR THE FRESH ISSUE) (“OFFER PRICE”) AGGREGATING UP TO ₹ [●] MILLION COMPRISING OF A FRESH ISSUE OF [●] EQUITY SHARES AGGREGATING UP TO ₹ 4,000.00 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO 16,044,709 EQUITY SHARES, COMPRISING OF UP TO 720,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY ASHRAF MOHAMMED BIRAN, UP TO 720,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY GULSHAN HARESH BAKHTIANI, UP TO 120,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY MOHAN GANPAT CHAVAN (COLLECTIVELY, “THE PROMOTER SELLING SHAREHOLDERS”); AND UP TO 14,484,709 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY PERSONS REFERRED TO IN ANNEXURE A (REFERRED TO AS THE “OTHER SELLING SHAREHOLDERS”, TOGETHER WITH THE PROMOTER SELLING SHAREHOLDERS, THE “SELLING SHAREHOLDERS”, AND SUCH EQUITY SHARES, THE “OFFERED SHARES”) AGGREGATING UP TO ₹ [●] MILLION (“OFFER FOR SALE”, AND TOGETHER WITH THE FRE SH ISSUE, THE “OFFER”). THE FACE VALUE OF EQUITY SHARES IS ₹ 2 EACH. THE PRICE BAND AND THE MINIMUM BID LOT SHALL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS AND WILL BE ADVERTISED IN ALL EDITIONS OF [●], AN ENGLISH NATIONAL DAILY NEWSPAPER, ALL EDITIONS OF [●], A HINDI NATIONAL DAILY NEWSPAPER AND REGIONAL EDITION OF [●], A MARATHI NEWSPAPER, MARATHI BEING THE REGIONAL LANGUAGE OF MAHARASHTRA, WHERE OUR REGISTERED OFFICE IS LOCATED, WITH WIDE CIRCULATION, AT LEAST TWO WORKING DAYS PRIOR TO THE BID/OFFER OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR THE PURPOS E OF UPLOADING ON THEIR RESPECTIVE WEBSITES IN ACCORDANCE WITH SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2018, AS AMENDED (THE “SEBI ICDR REGULATIONS”). In case of any revision in the Price Band, the Bid/Offer Period will be extended by at least three additional Working Days after such revision in the Price Band, subject to the Bid/Offer Period not exceeding 10 Working Days. In cases of force majeure, banking strike or similar circumstances, our Company may, for reasons to be recorded in writing, extend the Bid/Offer Period for a minimum of three Working Days, subject to the Bid/Offer Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, shall be widely disseminated by notification to the Stock Exchanges, by issuing a public notice, and also by indicating the change on the respective websites of the Book Running Lead Managers and at the terminals of the Syndicate Members and by intimation to Designated Intermediaries and the Sponsor Bank, as applicable. The Offer is being made through the Book Building Process, in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (“ SCRR”) read with Regulation 31 of the SEBI ICDR Regulations and in compliance with Regulation 6(2) of the SEBI ICDR Regulations, wherein not less than 75% of the Offer shall be allocated on a proportionate basis to Qualified Institutional Buyers (“ QIBs”, the “QIB Portion”), provided that our Company may, in consultation with the Book Running Lead Managers, allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis in accordance with the SEBI ICDR Regulat ions (“Anchor Investor Portion ”), of which one-third shall be reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price. Further, 5% of the QIB Portion (excluding Anchor Investor Portion) (“Net QIB Portion”) shall be available for allocation on a proportionate basis only to Mutual Funds, and the remainder of the Net QIB Portion shall be available for allocation on a proportionate basis to all QIBs, including Mutual Funds, subject to valid Bids being received at or above the Offer Price. However, if the aggregate demand from Mutual Funds is less than 5% of the Net QIB Portion, the balance Equity Shares available for allocation in the Mutual Fund Portion will be added to the remaining Net QIB Portion for proportionate allocation to QIBs. Further, not more than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not more than 10% of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All potential Bidders (except Anchor Investors) are required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective ASBA accounts(including UPI ID in case of RIBs using the UPI Mechanism) if applicable, in which the corresponding Bid Amounts will be blocked by the SCSBs or under the UPI Mechanism, as the case may be, to the extent of respective Bid Amounts. Anchor Investors are not permitted to participate in the Offer through the ASBA process. For details, see “ Offer Procedure” beginning on page 338. RISKS IN RELATION TO THE FIRST OFFER This being the first public Offer of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ₹ 2. The Floor Price, Cap Price and Offer Price should not be considered to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares nor regarding the price at which the Equity Shares will be traded after listing. GENERAL RISK Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended or approved by the Securities and Exchange Board of India (“ SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “ Risk Factors” beginning on page 26. OUR COMPANY’S AND THE SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospe ctus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission or inclusion of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, each of the Selling Shareholders, severally and not jointly, accept responsibility for and confirm only the Selling Shareholder statements expressly made by such Selling Shareholder in this Draft Red Herring Prospectus to the extent of information specifically pertaining to itself and respective portion of its Offered Shares and assumes responsibility that such statements are true and correct in all material respects and not misleading in any material respect. The Selling Shareholders assume no responsibility for any other statements, including without limitation, any and all statement made by or relating to our Company or the other Selling Shareholders or in relation to our Company’s business in this Draft Red Herring Prospectus. LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the Stock Exchanges. Our Company has received ‘in-principle’ approvals from BSE and NSE for the listing of the Equity Shares pursuant to their letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered to t he RoC in accordance with Section 26(4) and 32 of the Companies Act 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus up to the Bid/Offer Closing Date, see “Material Contracts and Documents for Inspection” beginning on page 363. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER IIFL Securities Limited 10th Floor, IIFL Centre Kamala City, Senapati Bapat Marg Lower Parel (West), Mumbai 400 013 Maharashtra, India Tel: +91 22 4646 4600 E-mail: [email protected] Website: www.iiflcap.com Investor Grievance ID: [email protected] Contact person: Mukesh Garg/Nishita Mody SEBI Registration Number: INM000010940 Ambit Private Limited Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013 Maharashtra, India Tel: +91 22 6623 3000 E-mail: [email protected] Website: www.ambit.co Investor Grievance ID: [email protected] Contact person: Nikhil Bhiwapurkar / Miraj Sampat SEBI Registration Number: INM000010585 DAM Capital Advisors Limited (Formerly IDFC Securities Limited) One BKC, Tower C, 15 th Floor, Unit No. 1511, Bandra Kurla Complex, Bandra (East), Mumbai 400 051 Maharashtra, India Tel: +91 22 4202 2500 E-mail: [email protected] Website: www.damcapital.in Investor Grievance ID: [email protected] Contact person: Gunjan Jain SEBI Registration Number: MB/INM000011336 HDFC Bank Limited Investment Banking Group Unit No. 401 & 402, 4 th Floor, Tower B, Peninsula Business Park, Lower Parel, Mumbai 400 013, Maharashtra, India Tel: +91 22 3395 8233 E-mail: [email protected] Website: www.hdfcbank.com Investor Grievance ID: [email protected] Contact Person: Harsh Thakkar / Ravi Sharma SEBI Registration Number : INM000011252 Link Intime India Private Limited C 101, 247 Park L.B.S Marg Vikhroli (West), Mumbai 400 083 Maharashtra, India Tel: +91 22 4918 6200 E-mail: [email protected] Website: www.linkintime.co.in Investor Grievance ID: [email protected] Contact Person: Shanti Gopalkrishnan SEBI Registration Number : INR000004058 BID/OFFER PROGRAMME BID/OFFER OPENS ON * [●] BID/OFFER CLOSES ON ** [●] * Our Company in consultation with the Book Running Lead Managers may consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor Bid/Offer Period shall be one Working Day prior to the Bid/Offer Opening Date. ** Our Company in consultation with the Book Running Lead Managers may consider closing the Bid/Offer Period for QIBs one Working Day prior to the Bid/Offer Closing Date in accordance with the SEBI ICDR Regulations.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of WELLNESS FOREVER MEDICARE LIMITED - BSE

DRAFT RED HERRING PROSPECTUS Dated September 30, 2021

(This Draft Red Herring Prospectus will be updated upon filing with the RoC)

Please read Section 32 of the Companies Act, 2013 Book Built Offer

WELLNESS FOREVER MEDICARE LIMITED Our Company was originally incorporated as ‘Wellness Forever Medicare Private Limited’ , a private limited company under the Companies Act, 1956, Mumbai, Maharashtra, pursuant to a certificate of incorporation da ted February 8,

2008, issued by the Registrar of Companies, Maharashtra at Mumbai. Subsequently, our Company was converted into a public limited company pursuant to a resolution passed by our Shareholders at an extraordinary general meeting held on July 9, 2021 and a fresh certificate of incorporation dated August 5, 2021 was issued by the RoC consequent upon conversion, recording the change in the name of our Company to “Wellness Forever Medicare Limited”. For details of changes in name and registered office of our Company since incorporation, see “History and Certain Corporate Matters”, beginning on page 176.

Registered and Corporate Office: 7th Floor, Wing A, Empire Plaza, IT Park, LBS Marg, Vikhroli (West), Mumbai 400 083, Maharashtra India

Contact Person: Nidhi Vora, Company Secretary and Compliance Officer; Tel: +91 22 4354 1722 E-mail: [email protected]; Website: www.wellnessforever.com

Corporate Identity Number: U24239MH2008PLC178658

OUR PROMOTERS: ASHRAF MOHAMMED BIRAN, GULSHAN HARESH BAKHTIANI AND MOHAN GANPAT CHAVAN

INITIAL PUBLIC OFFER OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹ 2 EACH (“EQUITY SHARES”) OF WELLNESS FOREVER MEDICARE LIMITED (“COMPANY” OR “ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹ [●] PER EQUITY SHARE FOR THE FRESH ISSUE) (“OFFER PRICE”) AGGREGATING UP TO ₹ [●] MILLION COMPRISING OF A FRESH ISSUE OF [●] EQUITY SHARES AGGREGATING UP TO ₹ 4,000.00 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO 16,044,709 EQUITY SHARES, COMPRISING OF UP TO 720,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY ASHRAF MOHAMMED BIRAN, UP TO 720,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY GULSHAN HARESH BAKHTIANI, UP TO 120,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY MOHAN GANPAT CHAVAN (COLLECTIVELY, “THE PROMOTER SELLING SHAREHOLDERS”); AND UP TO 14,484,709 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION BY PERSONS REFERRED TO IN ANNEXURE A (REFERRED TO AS THE “OTHER SELLING SHAREHOLDERS”, TOGETHER WITH THE PROMOTER SELLING SHAREHOLDERS, THE “SELLING SHAREHOLDERS”, AND SUCH EQUITY SHARES, THE “OFFERED SHARES”) AGGREGATING UP TO ₹ [●] MILLION (“OFFER FOR SALE”, AND TOGETHER WITH THE FRESH ISSUE, THE “OFFER”). THE FACE VALUE OF EQUITY SHARES IS ₹ 2 EACH. THE PRICE BAND AND THE MINIMUM BID LOT SHALL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS AND WILL BE ADVERTISED IN ALL EDITIONS OF [●], AN ENGLISH NATIONAL DAILY NEWSPAPER, ALL EDITIONS OF [●], A HINDI NATIONAL DAILY NEWSPAPER AND REGIONAL EDITION OF [●], A MARATHI NEWSPAPER, MARATHI BEING THE REGIONAL LANGUAGE OF MAHARASHTRA, WHERE OUR REGISTERED OFFICE IS LOCATED, WITH WIDE CIRCULATION, AT LEAST TWO WORKING DAYS PRIOR TO THE BID/OFFER OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR THE PURPOSE OF UPLOADING ON THEIR RESPECTIVE WEBSITES IN ACCORDANCE WITH SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2018, AS AMENDED (THE “SEBI ICDR REGULATIONS”). In case of any revision in the Price Band, the Bid/Offer Period will be extended by at least three additional Working Days after such revision in the Price Band, subject to the Bid/Offer Period not exceeding 10 Working Days. In cases of force majeure, banking strike or similar circumstances, our Company may, for reasons to be recorded in writing, extend the Bid/Offer Period for a minimum of three Working Days, subject to the Bid/Offer Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, shall be widely disseminated by notification to the Stock Exchanges, by issuing a public notice, and also by indicating the change on the respective websites of the Book Running Lead Managers and at the terminals of the Syndicate Members and by intimation to Designated Intermediaries and the Sponsor Bank, as applicable.

The Offer is being made through the Book Building Process, in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”) read with Regulation 31 of the SEBI ICDR Regulations and in compliance with Regulation 6(2) of the SEBI ICDR Regulations, wherein not less than 75% of the Offer shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIBs”, the “QIB Portion”), provided that our

Company may, in consultation with the Book Running Lead Managers, allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis in accordance with the SEBI ICDR Regulations (“Anchor Investor Portion”), of which one-third shall be reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price. Further, 5% of the QIB Portion (excluding Anchor Investor Portion) (“Net QIB Portion”) shall be available for allocation on a proportionate basis only to Mutual Funds, and the remainder of the Net QIB Portion shall be available for allocation on a proportionate basis to all QIBs, including Mutual Funds, subject to valid Bids being received at or above the Offer Price. However, if the aggregate demand fr om Mutual Funds is less than 5% of the Net QIB Portion, the balance Equity Shares available for allocation in the Mutual Fund Portion will be added to the remaining Net QIB Portion for proportionate allocation to QIBs. Further, not more than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional

Bidders and not more than 10% of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All potential Bidders (except Anchor Investors) are required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective ASBA accounts(including UPI ID in case of RIBs using the UPI Mechanism) if applicable, in which the corresponding Bid Amounts will be blocked by the SCSBs or under the UPI Mechanism, as the case ma y be, to the extent of respective Bid Amounts. Anchor Investors are not permitted to participate in the Offer through the ASBA process. For details, see “Offer Procedure” beginning on page 338.

RISKS IN RELATION TO THE FIRST OFFER

This being the first public Offer of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ₹ 2. The Floor Price, Cap Price and Offer Price should not be considered to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares nor regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISK

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention

of the investors is invited to “Risk Factors” beginning on page 26.

OUR COMPANY’S AND THE SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospe ctus contains all information with regard to our Company and the Offer, which is material in the context

of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission or inclusion of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, each of the Selling Shareholders, severally and not jointly, accept responsibility for and confirm only the Selling Shareholder statements expressly made by such Selling Shareholder in this Draft Red Herring Prospectus to the extent of information specifically pertaining to itself and respective portion of its Offered Shares and assumes responsibility that such statements are true and correct in all material respects and not misleading in any material respect. The Selling Shareholders assume no responsibility for any other statements, including without limitation, any and all statement made by or relating to our Company or the other Selling Shareholders or in relation to our

Company’s business in this Draft Red Herring Prospectus. LISTING

The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the Stock Exchanges. Our Company has received ‘in-principle’ approvals from BSE and NSE for the listing of the Equity Shares pursuant to

their letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered to the RoC in accordance with Section 26(4) and 32 of the Companies Act 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus up to the Bid/Offer Closing Date, see “Material Contracts and Documents for Inspection” beginning on page 363.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER

IIFL Securities Limited

10th Floor, IIFL Centre Kamala City, Senapati Bapat Marg Lower Parel (West), Mumbai 400 013 Maharashtra, India

Tel: +91 22 4646 4600 E-mail: [email protected] Website: www.iiflcap.com Investor Grievance ID: [email protected] Contact person: Mukesh Garg/Nishita

Mody SEBI Registration Number: INM000010940

Ambit Private Limited

Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013 Maharashtra, India

Tel: +91 22 6623 3000 E-mail: [email protected]

Website: www.ambit.co Investor Grievance ID: [email protected]

Contact person: Nikhil Bhiwapurkar / Miraj Sampat SEBI Registration Number: INM000010585

DAM Capital Advisors Limited

(Formerly IDFC Securities Limited) One BKC, Tower C, 15th Floor, Unit No. 1511, Bandra Kurla Complex, Bandra (East), Mumbai 400 051

Maharashtra, India Tel: +91 22 4202 2500 E-mail: [email protected] Website: www.damcapital.in Investor Grievance ID:

[email protected] Contact person: Gunjan Jain SEBI Registration Number: MB/INM000011336

HDFC Bank Limited

Investment Banking Group Unit No. 401 & 402, 4th Floor, Tower B, Peninsula Business Park, Lower Parel, Mumbai 400 013,

Maharashtra, India Tel: +91 22 3395 8233 E-mail: [email protected] Website: www.hdfcbank.com Investor Grievance ID:

[email protected] Contact Person: Harsh Thakkar / Ravi Sharma SEBI Registration Number: INM000011252

Link Intime India Private Limited

C 101, 247 Park L.B.S Marg Vikhroli (West), Mumbai 400 083 Maharashtra, India

Tel: +91 22 4918 6200 E-mail: [email protected] Website: www.linkintime.co.in Investor Grievance ID:

[email protected] Contact Person: Shanti Gopalkrishnan SEBI Registration Number: INR000004058

BID/OFFER PROGRAMME

BID/OFFER OPENS ON* [●]

BID/OFFER CLOSES ON** [●]

* Our Company in consultation with the Book Running Lead Managers may consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor Bid/Offer Period shall be one Working Day prior to the Bid/Offer Opening Date.

** Our Company in consultation with the Book Running Lead Managers may consider closing the Bid/Offer Period for QIBs one Working Day prior to the Bid/Offer Closing Date in accordance with the SEBI ICDR Regulations.

(This page is intentionally left blank)

i

TABLE OF CONTENTS

SECTION I: GENERAL ..............................................................................................................................................................................2

DEFINITIONS AND ABBREVIATIONS ..............................................................................................................................................2 SUMMARY OF THIS DRAFT RED HERRING PROSPECTUS.................................................................................................... 12 CERTAIN CONVENTIONS, PRESENTATION OF FI NANCIAL, INDUSTRY AND MARKET DATA ............................ 20 NOTICE TO INVESTORS ...................................................................................................................................................................... 22 FORWARD-LOOKING STATEMENTS............................................................................................................................................. 24

SECTION II: RISK FACTORS .............................................................................................................................................................. 26

SECTION III: INTRODUCTION .......................................................................................................................................................... 55

THE OFFER ............................................................................................................................................................................................... 55 SUMMARY OF FINANCIAL INFORMATION ................................................................................................................................ 57 GENERAL INFORMATION.................................................................................................................................................................. 61 CAPITAL STRUCTURE......................................................................................................................................................................... 69 OBJECTS OF THE OFFER..................................................................................................................................................................... 91 BASIS FOR OFFER PRICE .................................................................................................................................................................. 100 STATEMENT OF SPECIAL TAX BENEFITS................................................................................................................................. 102

SECTION IV: ABOUT OUR COMPANY ......................................................................................................................................... 105

INDUSTRY OVERVIEW ..................................................................................................................................................................... 105 OUR BUSINESS ..................................................................................................................................................................................... 153 KEY REGULATIONS AND POLICIES ............................................................................................................................................ 171 HISTORY AND CERTAIN CORPORATE MATTERS ................................................................................................................. 176 OUR MANAGEMENT .......................................................................................................................................................................... 181 OUR PROMOTERS AND PROMOTER GROUP............................................................................................................................ 194 OUR GROUP COMPANIES ................................................................................................................................................................ 197 DIVIDEND POLICY.............................................................................................................................................................................. 200

SECTION V: FINANCIAL INFORMATION .................................................................................................................................. 204

RESTATED CONSOLIDATED FINANCIAL INFORMATION.................................................................................................. 204 OTHER FINANCIAL INFORMATION............................................................................................................................................. 289 FINANCIAL INDEBTEDNESS .......................................................................................................................................................... 290 CAPITALISATION STATEMENT .................................................................................................................................................... 293 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

.................................................................................................................................................................................................................... 294

SECTION VI: LEGAL AND OTHER INFORMATION .............................................................................................................. 308

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS.................................................................................... 308 GOVERNMENT AND OTHER APPROVALS ................................................................................................................................ 312 OTHER REGULATORY AND STATUTORY DISCLOSURES .................................................................................................. 313

SECTION VII: OFFER INFORMATION ......................................................................................................................................... 331

TERMS OF THE OFFER....................................................................................................................................................................... 331 OFFER STRUCTURE............................................................................................................................................................................ 336 OFFER PROCEDURE ........................................................................................................................................................................... 338 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ............................................................................. 354

SECTION VIII: DESCRIPTION OF EQUITY SHARES AND TERMS OF ARTICLES OF ASSOCIATION .......... 356

SECTION IX: OTHER INFORMATION.......................................................................................................................................... 363

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION....................................................................................... 363

DECLARATION ....................................................................................................................................................................................... 365

ANNEXURE A........................................................................................................................................................................................ 370

2

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

This Draft Red Herring Prospectus uses certain definitions and abbreviations which, unless the context otherwise indicates or

implies, or unless otherwise specified, shall have the meaning as provided below. References to any legislation, act, regulation,

rules, guidelines or policies shall be to such legislation, act, regulation, rules, guidelines or policies as amended, supple mented

or re-enacted from time to time, and any reference to a statutory provision shall include any subordinate legislation made from

time to time under that provision.

The words and expressions used in this Draft Red Herring Prospectus but not defined herein shall have, to the extent applicable,

the same meaning ascribed to such terms under the SEBI ICDR Regulations, the Companies Act, the SCRA, the Depositories

Act and the rules and regulations made thereunder. Further, Offer related terms used but not defined in this Draft Red Herring

Prospectus shall have the meaning ascribed to such terms under the General Information Document.

Notwithstanding the foregoing, the terms used in “Basis for Offer Price”, “Statement of Special Tax Benefits”, “Industry

Overview”, “Key Regulations and Policies”, “Financial Information”, “Outstanding Litigation and Material Developments”

and “Description of Equity Shares and Terms of Articles of Association” beginning on pages 100, 102, 105, 171, 204, 308 and

356, respectively, shall have the meaning ascribed to them in the relevant section.

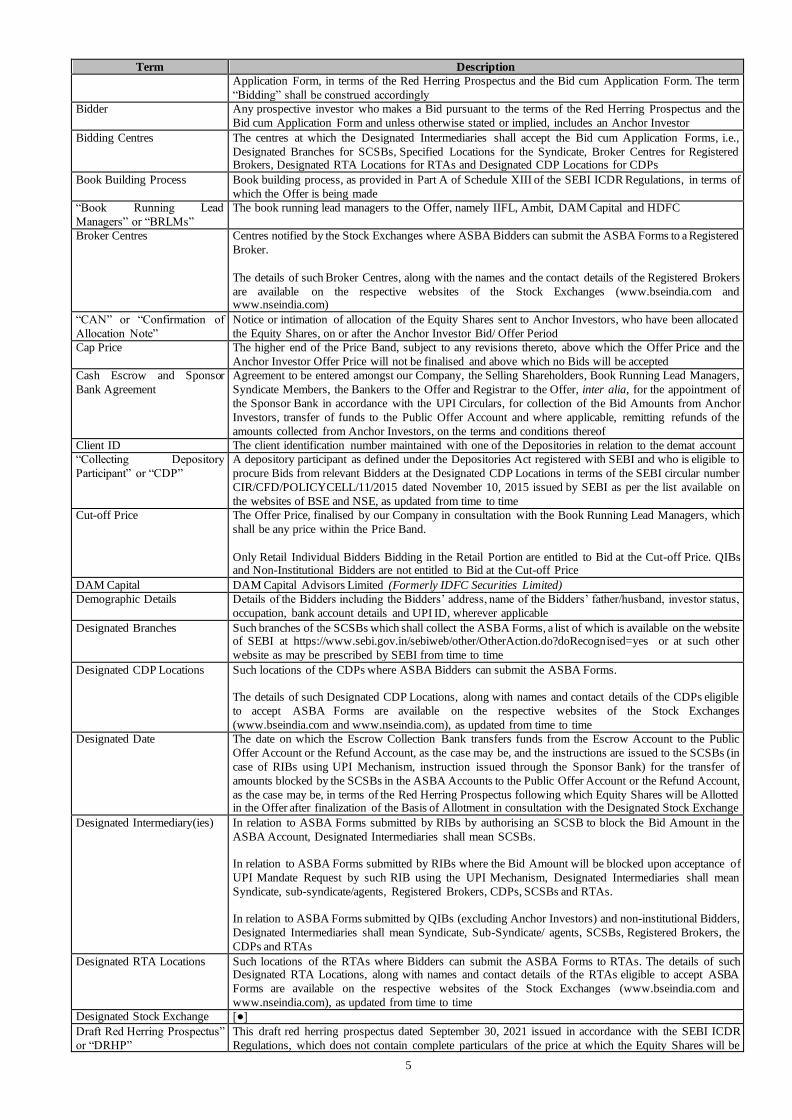

General Terms

Term Description

“our Company” or “the Company”

Wellness Forever Medicare Limited, a public limited company incorporated under the Companies Act, 1956 and having its Registered and Corporate Office at 7th Floor, Wing A, Empire Plaza, IT Park, LBS

Marg, Vikhroli (West), Mumbai 400 083, Maharashtra, India

“we”, “us” or “our” Unless the context otherwise indicates or implies or except in terms of our Restated Consolidated Financial Information, refers to our Company together with our Subsidiaries

Company Related Terms

Term Description

Amendment cum Termination

Agreement

Amendment cum termination agreement dated September 30, 2021 entered into among the parties to the

SHA (defined hereinafter)

“Articles of Association” or

“AoA”

Articles of association of our Company, as amended

Audit Committee The audit committee of our Board, constituted in accordance with the applicable provisions of the

Companies Act, 2013 and the SEBI Listing Regulations, and as described in “Our Management –

Committees of our Board of Directors – Audit Committee” on page 185

“Auditors” or “Statutory Auditors”

Statutory auditor of our Company, namely, Deloitte Haskins & Sells LLP

“Board” or “Board of

Directors”

Board of directors of our Company, as described in “Our Management”, beginning on page 181

Business Transfer Agreement Business transfer agreement dated September 2, 2021, pursuant to which the e-commerce business along

with operation, development and maintenance of the website www.wellnessforever.com and “Wellness

Forever” mobile application (including assets, contracts, employees, liabilities and intellectual property) has been transferred to Wellness Forever HealthTech Private Limited on a slump sale basis

Class A equity shares Class A equity shares of face value of ₹10 each of our Company

Class A1 equity shares Class A1 equity shares of face value of ₹10 each of our Company

Class A2 equity shares Class A2 equity shares of face value of ₹10 each of our Company

Class A3 equity shares Class A3 equity shares of face value of ₹10 each of our Company

Company Secretary and

Compliance Officer

The company secretary and compliance officer of our Company, Nidhi Vora. For details, see “Our

Management”, beginning on page 181

Corporate Social

Responsibility Committee

Corporate social responsibility committee of our Board, constituted in accordance with the applicable

provisions of the Companies Act, 2013, and as described in “Our Management – Committees of our Board

of Directors – Corporate Social Responsibility Committee” on page 189

Director(s) Directors on the Board as described in “Our Management”, beginning on page 181

Equity Shares Equity shares of face value of ₹ 2 each, of our Company

ESOP 2018 Wellness Forever Employee Stock Option Plan 2018

ESOP 2020 Wellness Forever Employee Stock Option Plan 2020

ESOP 2021 Wellness Forever Employee Stock Option Plan 2021

Executive Director(s) Executive director(s) on our Board, as described in “Our Management”, beginning on page 181

Group Companies Companies identified as ‘group companies’ of our Company in terms of Regulation 2(1)(t) of the SEBI

ICDR Regulations, namely, RDPL, PBPL, SDPPL and IHPL

IHPL IPC Healthcare Private Limited

Independent Directors Independent directors on our Board, as described in “Our Management”, beginning on page 181

IPO Committee IPO committee of our Board

“Key Managerial Personnel” or “KMP”

Key managerial personnel of our Company identified in accordance with Regulation 2(1)(bb) of the SEBI ICDR Regulations, as described in “Our Management – Key Managerial Personnel” on page 192

3

Term Description

“Memorandum of Association”

or “MoA”

Memorandum of association of our Company, as amended

Nomination and Remuneration

Committee

Nomination and remuneration committee of our Board, constituted in accordance with the applicable

provisions of the Companies Act, 2013 and the SEBI Listing Regulations, and as described in “Our

Management – Committees of our Board of Directors – Nomination and Remuneration Committee” on

page 188

Non-Executive Directors Non-executive directors on our Board, as described in “Our Management”, beginning on page 181

Other Selling Shareholders Persons listed in Annexure A

PBPL Pinnacle Biomed Private Limited

Promoters The promoters of our Company, namely Ashraf Mohammed Biran, Gulshan Haresh Bakhtiani and Mohan

Ganpat Chavan. For details, see “Our Promoters and Promoter Group”, beginning on page 194

Promoter Group Persons and entities constituting the promoter group of our Company in terms of Regulation 2(1)(pp) of

the SEBI ICDR Regulations, as disclosed in “Our Promoters and Promoter Group”, beginning on page

194

Promoter Selling Shareholders Ashraf Mohammed Biran, Gulshan Haresh Bakhtiani, and Mohan Ganpat Chavan

RDPL Rahul Distributors Private Limited

Registered and Corporate

Office

7th Floor, Wing A, Empire Plaza, IT Park, LBS Marg, Vikhroli (West), Mumbai 400 083, Maharashtra

India

“Registrar of Companies” or

RoC”

Registrar of Companies, Maharashtra at Mumbai

Restated Consolidated Financial Information

Restated consolidated financial information of our Company and its Subsidiary i.e. Amore Health Essentials Private Limited (collectively referred to as “Group”) comprising of the restated consolidated

statement of assets and liabilities as at March 31, 2021, March 31, 2020 and March 31, 2019, the restated

consolidated statement of profit and loss (including other comprehensive income), the restated

consolidated statement of cash flows and the restated consolidated statement of changes in equity for the

years ended March 31, 2021, March 31, 2020 and March 31, 2019 and the summary of significant accounting policies and explanatory notes, prepared in terms of the requirements of Section 26 of Part I of

Chapter III of the Companies Act, the SEBI ICDR Regulations and the Guidance Note on Reports in

Company Prospectuses (Revised 2019) issued by the ICAI, as amended from time to time.

Risk Management Committee The risk management committee of our Board, constituted in accordance with the applicable provisions of the SEBI Listing Regulations, and as described in “Our Management – Committees of our Board of

Directors – Risk Management Committee” on page 187

Selling Shareholders Collectively, the Promoter Selling Shareholders and the Other Selling Shareholders

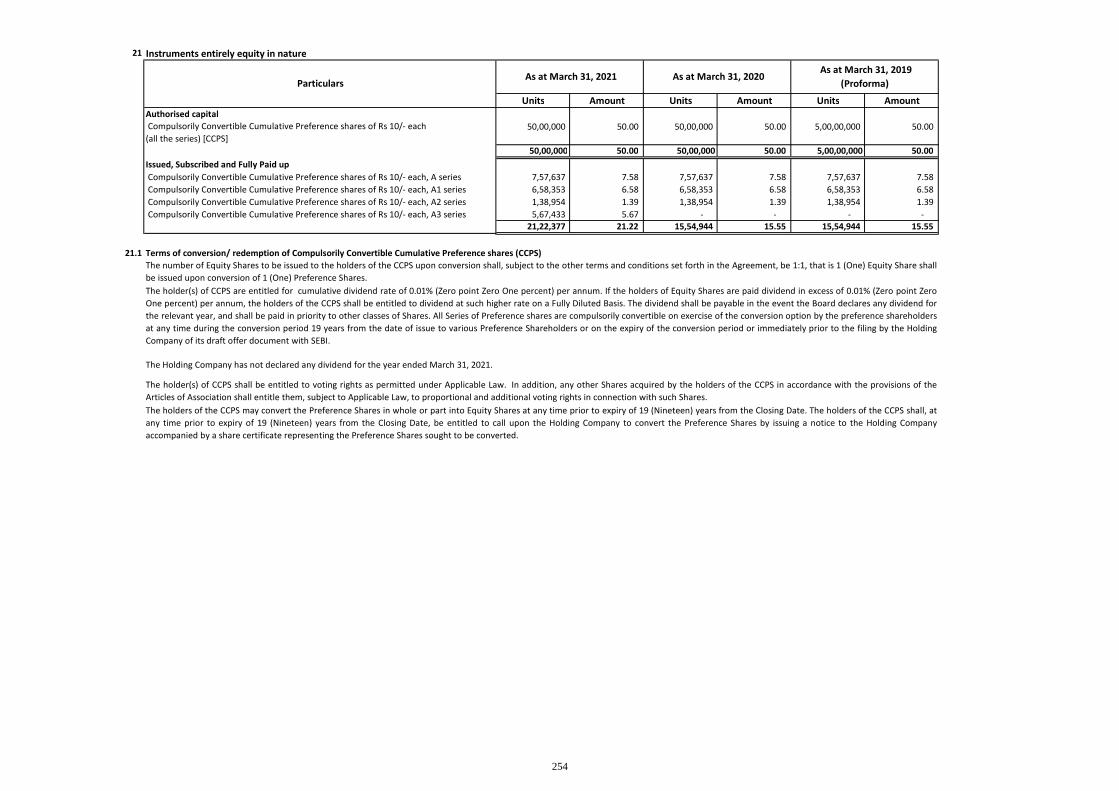

Series A CCPS Series A compulsorily convertible preference shares of face value of ₹10 each of our Company

Series A1 CCPS Series A1 compulsorily convertible preference shares of face value of ₹10 each of our Company

Series A2 CCPS Series A2 compulsorily convertible preference shares of face value of ₹10 each of our Company

Series A3 CCPS Series A3 compulsorily convertible preference shares of face value of ₹10 each of our Company

SHA/ Shareholders’

Agreement

Shareholders’ Agreement dated September 29, 2014 entered into among our Company, Promoters, Ramesh

Shantilal Mehta and certain other Shareholders, as amended by the amendment agreement dated May 12,

2015, addendum to the Shareholders’ Agreement dated July 26, 2016, second addendum to the Shareholders’ Agreement dated November 21, 2017, third addendum to the Shareholders’ Agreement

dated July 17, 2019

Shareholders Holders of Equity Shares of our Company from time to time

SDPPL Shreeji Distributors Pharma Private Limited

SPA 2017 Share Purchase Agreement dated November 21, 2017 entered into among our Company, Promoters, certain Shareholders and persons purchasing the equity shares

SPA 2019 Share Purchase Agreement dated July 17, 2019 entered into among our Company, certain Promoters,

certain Shareholders and persons purchasing the equity shares

Stakeholders’ Relationship

Committee

Stakeholders’ relationship committee of our Board, constituted in accordance with the applicable

provisions of the Companies Act, 2013 and the SEBI Listing Regulations, and as described in “Our

Management – Committees of our Board of Directors – Stakeholders’ Relationship Committee” on page

189

Subsidiaries The subsidiaries of our Company, namely Amore Health Essentials Private Limited and Wellness Forever

HealthTech Private Limited

Offer Related Terms

Term Description

Abridged Prospectus Abridged prospectus means a memorandum containing such salient features of a prospectus as may be

specified by the SEBI in this behalf

Acknowledgement Slip The slip or document issued by the relevant Designated Intermediary to a Bidder as proof of registration

of the Bid cum Application Form

“Allot” or “Allotment” or

“Allotted”

Unless the context otherwise requires, the allotment of Equity Shares to the successful Bidder pursuant to

the Fresh Issue and transfer of Offered Shares pursuant to the Offer for Sale to the successful Bidders

Allotment Advice A note or advice or intimation of Allotment, sent to the successful Bidders who have been or are to be

Allotted the Equity Shares after the Basis of Allotment has been approved by the Designated Stock

Exchange

Allottee A successful Bidder to whom the Equity Shares are Allotted

4

Term Description

Ambit Ambit Private Limited

Anchor Investor A Qualified Institutional Buyer, applying under the Anchor Investor Portion in accordance with the requirements specified in the SEBI ICDR Regulations and the Red Herring Prospectus and who has Bid

for an amount of at least ₹100 million

Anchor Investor Allocation

Price

The price at which Equity Shares will be allocated to the Anchor Investors in terms of the Red Herring

Prospectus and the Prospectus, which will be decided by our Company in consultation with the Book Running Lead Managers during the Anchor Investor Bid/Offer Period

Anchor Investor Application

Form

The application form used by an Anchor Investor to make a Bid in the Anchor Investor Portion and which

will be considered as an application for Allotment in terms of the Red Herring Prospectus

Anchor Investor Bid/Offer

Period

One Working Day prior to the Bid/ Offer Opening Date, on which Bids by Anchor Investors shall be

submitted and allocation to the Anchor Investors shall be completed

Anchor Investor Offer Price The final price at which the Equity Shares will be Allotted to the Anchor Investors in terms of the Red

Herring Prospectus and the Prospectus, which will be a price equal to or higher than the Offer Price but not

higher than the Cap Price.

The Anchor Investor Offer Price will be decided by our Company in consultation with the Book Running Lead Managers

Anchor Investor Portion Up to 60% of the QIB Portion which may be allocated by our Company in consultation with the Book

Running Lead Managers, to the Anchor Investors on a discretionary basis in accordance with the SEBI ICDR Regulations.

One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid

Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price, in

accordance with the SEBI ICDR Regulations

Application Supported by

Blocked Amount” or “ASBA”

An application, whether physical or electronic, used by ASBA Bidders to make a Bid and authorizing an

SCSB to block the Bid Amount in the ASBA Account and will include applications made by RIBs using

the UPI Mechanism where the Bid Amount will be blocked upon acceptance of UPI Mandate Request by RIBs using the UPI Mechanism

ASBA Account A bank account maintained with an SCSB by an ASBA Bidder, as specified in the ASBA Form submitted

by ASBA Bidders for blocking the Bid Amount mentioned in the relevant ASBA Form and includes the account of an RIB which is blocked upon acceptance of a UPI Mandate Request made by the RIBs using

the UPI Mechanism

ASBA Bid A Bid made by an ASBA Bidder

ASBA Bidders All Bidders except Anchor Investors

ASBA Form An application form, whether physical or electronic, used by ASBA Bidders to submit Bids, which will be considered as the application for Allotment in terms of the Red Herring Prospectus and the Prospectus

Bankers to the Offer Collectively, Escrow Collection Bank, Public Offer Account Bank, Sponsor Bank and Refund Bank, as the

case may be

Basis of Allotment Basis on which Equity Shares will be Allotted to successful Bidders under the Offer and which is described

in “Offer Procedure”, beginning on page 338

Bid Amount The highest value of Bids indicated in the Bid cum Application Form and, in the case of RIBs Bidding at

the Cut off Price, the Cap Price multiplied by the number of Equity Shares Bid for by such RIBs and

mentioned in the Bid cum Application Form and payable by the Bidder or blocked in the ASBA Account

of the ASBA Bidder, as the case may be, upon submission of the Bid. Bid cum Application Form Anchor Investor Application Form or the ASBA Form, as the context requires

Bid Lot [●] Equity Shares and in multiples of [●] Equity Shares thereafter

Bid/Offer Closing Date Except in relation to any Bids received from the Anchor Investors, the date after which the Designated

Intermediaries will not accept any Bids, which shall be published in all editions of [●], an English national

daily newspaper, all editions of [●], a Hindi national daily newspaper and regional edition of [●], a Marathi

newspaper, Marathi being the regional language of Maharashtra, where our Registered Office is located, each with wide circulation.

Our Company in consultation with the Book Running Lead Managers may, consider closing the Bid/Offer

Period for QIBs one Working Day prior to the Bid/Offer Closing Date in accordance with the SEBI ICDR

Regulations. In case of any revision, the extended Bid/Offer Closing Date shall also be notified on the websites of the Book Running Lead Managers and at the terminals of the Syndicate Members and

communicated to the Designated Intermediaries and the Sponsor Bank, which shall also be notified in an

advertisement in the same newspapers in which the Bid/Offer Opening Date was published, as required

under the SEBI ICDR Regulations

Bid/ Offer Opening Date Except in relation to any Bids received from the Anchor Investors, the date on which the Designated

Intermediaries shall start accepting Bids, which shall be published in all editions of [●], an English national

daily newspaper, all editions of [●], a Hindi national daily newspaper and regional edition of [●], a Marathi

newspaper, Marathi being the regional language of Maharashtra, where our Registered Office is located,

each with wide circulation

Bid/ Offer Period Except in relation to Anchor Investors, the period between the Bid/ Offer Opening Date and the Bid/ Offer

Closing Date, inclusive of both days, during which prospective Bidders can submit their Bids, including

any revisions thereof

“Bid” or “Bidding” An indication to make an offer to subscribe to the Equity Shares at a price within the Price Band (i) by an

ASBA Bidder during the Bid/ Offer Period pursuant to submission of the ASBA Form, or (ii) by an Anchor

Investor during the Anchor Investor Bid/ Offer Period, pursuant to submission of the Anchor Investor

5

Term Description

Application Form, in terms of the Red Herring Prospectus and the Bid cum Application Form. The term

“Bidding” shall be construed accordingly

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring Prospectus and the

Bid cum Application Form and unless otherwise stated or implied, includes an Anchor Investor

Bidding Centres The centres at which the Designated Intermediaries shall accept the Bid cum Application Forms, i.e.,

Designated Branches for SCSBs, Specified Locations for the Syndicate, Broker Centres for Registered Brokers, Designated RTA Locations for RTAs and Designated CDP Locations for CDPs

Book Building Process Book building process, as provided in Part A of Schedule XIII of the SEBI ICDR Regulations, in terms of

which the Offer is being made

“Book Running Lead

Managers” or “BRLMs”

The book running lead managers to the Offer, namely IIFL, Ambit, DAM Capital and HDFC

Broker Centres Centres notified by the Stock Exchanges where ASBA Bidders can submit the ASBA Forms to a Registered

Broker.

The details of such Broker Centres, along with the names and the contact details of the Registered Brokers

are available on the respective websites of the Stock Exchanges (www.bseindia.com and www.nseindia.com)

“CAN” or “Confirmation of

Allocation Note”

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who have been allocated

the Equity Shares, on or after the Anchor Investor Bid/ Offer Period

Cap Price The higher end of the Price Band, subject to any revisions thereto, above which the Offer Price and the

Anchor Investor Offer Price will not be finalised and above which no Bids will be accepted

Cash Escrow and Sponsor

Bank Agreement

Agreement to be entered amongst our Company, the Selling Shareholders, Book Running Lead Managers,

Syndicate Members, the Bankers to the Offer and Registrar to the Offer, inter alia, for the appointment of

the Sponsor Bank in accordance with the UPI Circulars, for collection of the Bid Amounts from Anchor

Investors, transfer of funds to the Public Offer Account and where applicable, remitting refunds of the

amounts collected from Anchor Investors, on the terms and conditions thereof

Client ID The client identification number maintained with one of the Depositories in relation to the demat account

“Collecting Depository

Participant” or “CDP”

A depository participant as defined under the Depositories Act registered with SEBI and who is eligible to

procure Bids from relevant Bidders at the Designated CDP Locations in terms of the SEBI circular number

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI as per the list available on

the websites of BSE and NSE, as updated from time to time

Cut-off Price The Offer Price, finalised by our Company in consultation with the Book Running Lead Managers, which

shall be any price within the Price Band.

Only Retail Individual Bidders Bidding in the Retail Portion are entitled to Bid at the Cut-off Price. QIBs and Non-Institutional Bidders are not entitled to Bid at the Cut-off Price

DAM Capital DAM Capital Advisors Limited (Formerly IDFC Securities Limited)

Demographic Details Details of the Bidders including the Bidders’ address, name of the Bidders’ father/husband, investor status,

occupation, bank account details and UPI ID, wherever applicable

Designated Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which is available on the website of SEBI at https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes or at such other

website as may be prescribed by SEBI from time to time

Designated CDP Locations Such locations of the CDPs where ASBA Bidders can submit the ASBA Forms.

The details of such Designated CDP Locations, along with names and contact details of the CDPs eligible

to accept ASBA Forms are available on the respective websites of the Stock Exchanges

(www.bseindia.com and www.nseindia.com), as updated from time to time

Designated Date The date on which the Escrow Collection Bank transfers funds from the Escrow Account to the Public

Offer Account or the Refund Account, as the case may be, and the instructions are issued to the SCSBs (in

case of RIBs using UPI Mechanism, instruction issued through the Sponsor Bank) for the transfer of

amounts blocked by the SCSBs in the ASBA Accounts to the Public Offer Account or the Refund Account,

as the case may be, in terms of the Red Herring Prospectus following which Equity Shares will be Allotted in the Offer after finalization of the Basis of Allotment in consultation with the Designated Stock Exchange

Designated Intermediary(ies) In relation to ASBA Forms submitted by RIBs by authorising an SCSB to block the Bid Amount in the

ASBA Account, Designated Intermediaries shall mean SCSBs.

In relation to ASBA Forms submitted by RIBs where the Bid Amount will be blocked upon acceptance of

UPI Mandate Request by such RIB using the UPI Mechanism, Designated Intermediaries shall mean

Syndicate, sub-syndicate/agents, Registered Brokers, CDPs, SCSBs and RTAs.

In relation to ASBA Forms submitted by QIBs (excluding Anchor Investors) and non-institutional Bidders,

Designated Intermediaries shall mean Syndicate, Sub-Syndicate/ agents, SCSBs, Registered Brokers, the

CDPs and RTAs

Designated RTA Locations Such locations of the RTAs where Bidders can submit the ASBA Forms to RTAs. The details of such Designated RTA Locations, along with names and contact details of the RTAs eligible to accept ASBA

Forms are available on the respective websites of the Stock Exchanges (www.bseindia.com and

www.nseindia.com), as updated from time to time

Designated Stock Exchange [●]

Draft Red Herring Prospectus”

or “DRHP”

This draft red herring prospectus dated September 30, 2021 issued in accordance with the SEBI ICDR

Regulations, which does not contain complete particulars of the price at which the Equity Shares will be

6

Term Description

Allotted and the size of the Offer, including any addenda or corrigenda thereto

Eligible FPI(s) FPI(s) that are eligible to participate in the Offer in terms of applicable law and from such jurisdictions outside India where it is not unlawful to make an offer / invitation under the Offer and in relation to whom

the Bid cum Application Form and the Red Herring Prospectus constitutes an invitation to purchase the

Equity Shares

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an offer or invitation under the Offer and in relation to whom the ASBA Form and the Red Herring Prospectus will constitute an invitation

to subscribe to or to purchase the Equity Shares

Escrow Account(s) Account(s) to be opened with the Escrow Collection Bank and in whose favour the Anchor Investors will transfer money through NACH/direct credit/NEFT/RTGS in respect of the Bid Amount when submitting

a Bid

Escrow Collection Bank Bank which is a clearing member and registered with SEBI as a banker to an issue under the SEBI BTI Regulations and with whom the Escrow Accounts will be opened, in this case being [●]

First Bidder or Sole Bidder Bidder whose name shall be mentioned in the Bid cum Application Form or the Revision Form and in case

of joint Bids, whose name shall also appear as the first holder of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, subject to any revision(s) thereto, not being less than the face value of

Equity Shares, at or above which the Offer Price and the Anchor Investor Offer Price will be finalised and

below which no Bids will be accepted

Fresh Issue Fresh issue of up to [●] Equity Shares aggregating up to ₹ 4,000.00 million by our Company

Fugitive Economic Offender An individual who is declared a fugitive economic offender under Section 12 of the Fugitive Economic

Offenders Act, 2018

“General Information

Document” or “GID”

The General Information Document for investing in public issues prepared and issued in accordance with

the SEBI circular no. SEBI/HO/CFD/DIL1/CIR/P/2020/37 dated March 17, 2020, suitably modified and

updated pursuant to, among others, the circular (SEBI/HO/CFD/DIL2/CIR/P/2020/50) dated March 30, 2020 issued by SEBI and the UPI Circulars, as amended from time to time. The General Information

Document shall be available on the websites of the Stock Exchanges and the Book Running Lead Managers

HDFC HDFC Bank Limited

IIFL IIFL Securities Limited

Monitoring Agency [●]

Monitoring Agency

Agreement

Agreement to be entered between our Company and the Monitoring Agency

Mutual Fund Portion 5% of the Net QIB Portion, or [●] Equity Shares which shall be available for allocation to Mutual Funds

only on a proportionate basis, subject to valid Bids being received at or above the Offer Price

Net Proceeds Proceeds of the Fresh Issue less our Company’s share of the Offer expenses. For further details regarding the use of the Net Proceeds and the Offer expenses, see “Objects of the Offer” beginning on page 91

Net QIB Portion QIB Portion less the number of Equity Shares Allotted to the Anchor Investors

Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders and who have Bid for Equity Shares for an

amount of more than ₹200,000 (but not including NRIs other than Eligible NRIs)

Non-Institutional Portion The portion of the Offer being not more than 15% of the Offer consisting of [●] Equity Shares which shall be available for allocation on a proportionate basis to Non-Institutional Bidders, subject to valid Bids being

received at or above the Offer Price

Non-Resident Person resident outside India, as defined under FEMA

Offer The initial public offer of [●] Equity Shares comprising of the Fresh Issue and the Offer for Sale

aggregating up to ₹ [●].

Offer Agreement Agreement dated September 30, 2021 entered amongst our Company, the Selling Shareholders and the

Book Running Lead Managers, pursuant to which certain arrangements have been agreed to in relation to

the Offer

Offer for Sale The offer for sale of the Offered Shares, at the Offer Price aggregating up to ₹ [●] offered for sale by the

Selling Shareholders in the Offer

Offer Price The final price at which Equity Shares will be Allotted to ASBA Bidders in terms of the Red Herring

Prospectus and the Prospectus. Equity Shares will be Allotted to Anchor Investors at the Anchor Investor Offer Price, which will be decided by our Company, in consultation with the Book Running Lead

Managers, in terms of the Red Herring Prospectus and the Prospectus.

The Offer Price will be decided by our Company in consultation with the Book Running Lead Managers,

on the Pricing Date in accordance with the Book Building Process and the Red Herring Prospectus

Offer Proceeds Collectively, the proceeds of the Fresh Issue which shall be available to our Company and the proceeds

of the Offer for Sale which shall be available to the Selling Shareholder. For further information about

use of the Offer Proceeds, see “Objects of the Offer” beginning on page 91

Offered Shares Up to 16,044,709 Equity Shares aggregating up to ₹ [●] million being offered for sale by the Selling

Shareholders in the Offer for Sale

Price Band The price band of a minimum price of ₹ [●] per Equity Share (Floor Price) and the maximum price of ₹[●]

per Equity Share (Cap Price) including any revisions thereof.

The Price Band and the minimum Bid Lot size for the Offer will be decided by our Company in consultation

with the Book Running Lead Managers, and will be advertised, at least two Working Days prior to the Bid/Offer Opening Date, in all editions of [●], an English national daily newspaper, all editions of [●], a

Hindi national daily newspaper and regional edition of [●], a Marathi newspaper, Marathi being the

regional language of Maharashtra, where our Registered Office is located, each with wide circulation and

shall be made available to the Stock Exchanges for the purpose of uploading on their respective websites

7

Term Description

Pricing Date The date on which our Company, in consultation with the Book Running Lead Managers, will finalise the

Offer Price

Prospectus The prospectus to be filed with the RoC on or after the Pricing Date in accordance with Section 26 of the

Companies Act, 2013 and the SEBI ICDR Regulations containing, inter alia, the Offer Price that is

determined at the end of the Book Building Process, the size of the Offer and certain other information,

including any addenda or corrigenda thereto

Public Offer Account Bank account to be opened with the Public Offer Bank, under Section 40(3) of the Companies Act, 2013

to receive monies from the Escrow Account and ASBA Accounts on the Designated Date

Public Offer Bank Bank which is a clearing member and registered with SEBI as a banker to an issue and with which the Public Offer Account will be opened, in this case being [●]

QIB Portion The portion of the Offer (including the Anchor Investor Portion) being not less than 75% of the Offer

comprising [●] Equity Shares which shall be allocated to QIBs (including Anchor Investors), subject to valid Bids being received at or above the Offer Price or Anchor Investor Offer Price (for Anchor Investors).

Our Company, in consultation with the Book Running Lead Managers may allocate up to 60% of the QIB

portion to Anchor Investors on a discretionary basis

Qualified Institutional Buyers

or QIBs or QIB Bidders

Qualified institutional buyers as defined under Regulation 2(1)(ss) of the SEBI ICDR Regulations

Red Herring Prospectus or RHP

The red herring prospectus to be issued by our Company in accordance with Section 32 of the Companies Act, 2013 and the provisions of the SEBI ICDR Regulations, which will not have complete particulars of

the Offer Price and the size of the Offer, including any addenda or corrigenda thereto. The Red Herring

Prospectus will be filed with the RoC at least three Working Days before the Bid/Offer Opening Date and

will become the Prospectus upon filing with the RoC after the Pricing Date

Refund Account(s) Account to be opened with the Refund Bank(s), from which refunds, if any, of the whole or part of the Bid

Amount to the Bidders shall be made

Refund Bank(s) Bank(s) which is a clearing member and registered with SEBI as a banker to an issue under the SEBI BTI Regulations and with whom the Refund Account will be opened, in this case being [●]

Registered Brokers Stock brokers registered with SEBI and the stock exchanges having nationwide terminals, other than the

members of the Syndicate and eligible to procure Bids in terms of the SEBI circular number CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI

Registrar Agreement Agreement dated September 30, 2021 entered by and amongst our Company , the Selling Shareholders and

the Registrar to the Offer, in relation to the responsibilities and obligations of the Registrar to the Offer pertaining to the Offer

“Registrar and Share Transfer

Agents” or “RTAs”

Registrar and share transfer agents registered with SEBI and eligible to procure Bids from relevant Bidders

at the Designated RTA Locations as per the list available on the websites of BSE and NSE, and the UPI Circulars

“Registrar to the Offer” or

“Registrar”

Link Intime India Private Limited

“Retail Individual Bidder(s)”

or “RIB(s)”

Individual Bidders, who have Bid for the Equity Shares for an amount not more than ₹200,000 in any of

the bidding options in the Offer (including HUFs applying through their Karta and Eligible NRIs)

Retail Portion Portion of the Offer being not more than 10% of the Offer consisting of [●] Equity Shares which shall be

available for allocation to Retail Individual Bidders (subject to valid Bids being received at or above the

Offer Price), which shall not be less than the minimum Bid Lot subject to availability in the Retail Portion,

and the remaining Equity Shares to be Allotted on a proportionate basis

Revision Form Form used by the Bidders to modify the quantity of the Equity Shares or the Bid Amount in any of their

ASBA Form(s) or any previous Revision Form(s), as applicable.

QIB Bidders and Non-Institutional Bidders are not allowed to withdraw or lower their Bids (in terms of

quantity of Equity Shares or the Bid Amount) at any stage. Retail Individual Bidders can revise their Bids during the Bid/ Offer Period and withdraw their Bids until Bid/ Offer Closing Date

Self-Certified Syndicate

Bank(s) or SCSB(s)

The banks registered with SEBI, which offer the facility of ASBA services, (i) in relation to ASBA, where

the Bid Amount will be blocked by authorising an SCSB, a list of which is available on the website of SEBI at www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=34 and updated

from time to time and at such other websites as may be prescribed by SEBI from time to time, (ii) in relation

to RIBs using the UPI Mechanism, a list of which is available on the website of SEBI at

https://sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=40 or such other

website as may be prescribed by SEBI and updated from time to time.

Applications through UPI in the Offer can be made only through the SCSBs mobile applications (apps)

whose name appears on the SEBI website at

www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=43. Details of nodal

officers of SCSBs, identified for Bids made through the UPI Mechanism, are available at www.sebi.gov.in.

Share Escrow Agent The share escrow agent to be appointed pursuant to the Share Escrow Agreement namely, [●]

Share Escrow Agreement Share escrow agreement to be entered into between our Company, the Selling Shareholders and the Share Escrow Agent in connection with the transfer of Equity Shares under the Offer for Sale by the Selling

Shareholders for the purposes of credit of such Equity Shares to the demat accounts of the Allottees in

accordance with the Basis of Allotment

Specified Locations Bidding Centres where the Syndicate shall accept ASBA Forms from Bidders

Sponsor Bank [●], being a Banker to the Offer, appointed by our Company to act as a conduit between the Stock

Exchanges and NPCI in order to push the mandate collect requests and / or payment instructions of the

8

Term Description

RIBs using the UPI Mechanism and carry out other responsibilities, in terms of the UPI Circulars

Stock Exchanges Collectively, BSE Limited and National Stock Exchange of India Limited

“Syndicate” or “Members of

the Syndicate”

Collectively, the Book Running Lead Managers and the Syndicate Members

Syndicate Agreement Agreement to be entered amongst our Company, the Selling Shareholders, the Book Running Lead

Managers, the Registrar and the Syndicate Members, in relation to collection of Bids by the Syndicate

Syndicate Members Intermediaries (other than the Book Running Lead Managers) registered with SEBI who are permitted to carry out activities including accepting bids, applications and as an underwriter, namely, [●]

Systemically Important Non-

Banking Financial Company

Systemically important non-banking financial company as defined under Regulation 2(1)(iii) of the SEBI

ICDR Regulations

Technopak Technopak Advisors Private Limited

Technopak Report Report titled “Industry Report on Pharmacy Retail in India” dated September 28, 2021, issued by Technopak and which has been commissioned and paid for by our Company

Underwriters [●]

Underwriting Agreement Agreement to be entered amongst our Company, the Selling Shareholders and the Underwriters to be

entered into on or after the Pricing Date but prior to filing of the Prospectus with the RoC

UPI Unified payments interface which is an instant payment mechanism, developed by NPCI

UPI Circulars SEBI circular no. SEBI/HO/CFD/DIL2/CIR/P/2018/138 dated November 1, 2018, SEBI circular no.

SEBI/HO/CFD/DIL2/CIR/P/2019/50 dated April 3, 2019, SEBI circular no.

SEBI/HO/CFD/DIL2/CIR/P/2019/76 dated June 28, 2019, SEBI circular no.

SEBI/HO/CFD/DIL2/CIR/P/2019/85 dated July 26, 2019 SEBI circular no. SEBI/HO/CFD/DCR2/CIR/P/2019/133 dated November 8, 2019, SEBI circular no.

SEBI/HO/CFD/DIL2/CIR/P/2020/50 dated March 30, 2020, SEBI circular no.

SEBI/HO/CFD/DIL2/CIR/P/2021/2480/1/M dated March 16, 2021, SEBI circular no.

SEBI/HO/CFD/DIL1/CIR/P/2021/47 dated March 31, 2021, SEBI circular no.

SEBI/HO/CFD/DIL2/P/CIR/2021/570 dated June 2, 2021 and any subsequent circulars or notifications issued by SEBI in this regard

UPI ID ID created on the UPI for single-window mobile payment system developed by the NPCI

UPI Mandate Request A request (intimating the RIB by way of a notification on the UPI linked mobile application as disclosed

by SCSBs on the website of SEBI and by way of an SMS on directing the RIB to such UPI linked mobile

application) to the RIB initiated by the Sponsor Bank to authorise blocking of funds on the UPI application

equivalent to Bid Amount and subsequent debit of funds in case of Allotment

UPI Mechanism The bidding mechanism that may be used by an RIB in accordance with the UPI Circulars to make an

ASBA Bid in the Offer

UPI PIN Password to authenticate UPI transaction

Wilful Defaulter A company or person, as the case may be, categorised as a wilful defaulter by any bank or financial

institution or consortium thereof, in accordance with the guidelines on wilful defaulters issued by the RBI

Working Day(s) All days on which commercial banks in Mumbai are open for business provided however, with reference

to (a) announcement of Price Band and (b) Bid/Offer Period, the term Working Day shall mean all days,

excluding Saturdays, Sundays and public holidays, on which commercial banks in Mumbai are open for business and (c) the time period between the Bid/Offer Closing Date and the listing of the Equity Shares

on the Stock Exchanges, “Working Day” shall mean all trading days of the Stock Exchanges, excluding

Sundays and bank holidays, as per circulars issued by SEBI

Technical/Industry Related Terms or Abbreviations

Term Description

“Average order value” or “AOV”

Average cost of an order per bill at our stores

“Average Operating EBITDA” Average Operating EBITDA per store computed as Operating EBITDA for the financial year divided by

average store count for the financial year (Average store count for the year = Store count at the beginning

of the year + Store count at the end of year)/2)

“Average store level

profitability”

Total income less purchases of stock-in-trade, changes of stock-in-trade, employee benefit expense and

other expenses (including rent) store during a given year for all stores operating divided by the average

number of stores in operation.

“B&M stores” Brick and mortar stores

“CAGR” Compounded Annual Growth Rate (as a %)

“C&F” Carry-forward

“Cluster Saturation Model” Cluster Saturation model focuses on maximising the store count in a particular area before expanding in

other geography.

For more details, see “Industry Overview” on page 105.

“CNS” Central nervous system

“COGS” Cost of goods sold

“CPOE” Computerised physician order entry

“CRM” Customer relationship management

“Drugs and Cosmetics Act” or

“DCA”

Drugs and Cosmetics Act, 1940

“Drugs and Cosmetics Rules” Drugs and Cosmetics Rules, 1945

9

Term Description

“EBITDA” or “Operating

EBITDA”

Aggregate of restated profit/(loss) after tax, tax expense, finance cost, depreciation and amortisation

“EBITDA margin” EBITDA divided by total income

“eBR” Electronic batch records

“E-Commerce Marketplace” The E-Commerce marketplace are tech driven platforms with a wide variety of product offering including

of products like electronics, fashion, furniture, home furnishings, and cosmetics.

For more details, see “Industry Overview” on page 105.

“ERP” Enterprise resource planning

“FDI” Foreign Direct Investment

“F&G” Food and Grocery

“FMCG” Fast-moving consumer goods

“FMHG” Fast-moving health goods

“FSSAI” Food Safety and Standards Authority of India

“GPO” Group purchase organisation

“GST” Goods & Services Tax

“Hyperlocal Model” Hyperlocal Model is an inventory light model where the e-pharmacy only provides the online infrastructure

and logistics support.

For more details, see “Industry Overview” on page 105.

“Inventory-led Model” In an inventory-led model the inventory of goods and services is owned by the retail company, which are

sold to the customers directly.

For more details, see “Industry Overview” on page 105.

“KSM” Key starting materials

“THE” Total health expenditure

“MRP” Maximum retail price

“NCD” Non-communicable disease

“NLEM” National list of essential medicine

“NPPA” National Pharmaceutical Pricing Authority

“OTC” Over-the-counter

“PDS” Packaging, distribution and storage

“PG Charge” Payment Gateway cost

Pharmacy Act Pharmacy Act, 1948

“R&D” Research and development

“ROA” Return on assets calculated as net profit after tax divided by total average assets

“ROCE” Return on capital employed calculated as profit before interest and tax divided by total assets less current

liabilities

“Sales margin” Revenue from operations less purchases of stock-in-trade and changes in inventories of stock-in-trade divided by revenue from operations

“Same store sales growth” Total sales generated by existing stores over a year compared to the previous year

“Share of private and premium

label in total sales”

Total private and premium label sales divided by total store sales

“SFA” Sales force automation

“SKU” Store keeping units

“Store numbers state wise and

region wise”

Total sales per state/region divided by net income

“Store level profitability

margin”

Total income less purchases of stock-in-trade, changes of stock-in-trade, employee benefit expense and

other expenses (including rent)) during the year for all stores operating divided by the total revenue for stores operating

“Store level revenue” Store sales

“SWOT” Strength, Weakness, Opportunity, and Threats

“Vintage wise sales at stores” Total sales grouped by opening year for the store

“VMN” Vitamin, mineral and nutrient

“ZEDC” Zero Error Distribution Center

Conventional and General Terms or Abbreviations

Term Description

₹/Rs./Rupees/INR Indian Rupees

AIFs Alternative Investments Funds, as defined in, and registered under the SEBI AIF Regulations

AGM Annual general meeting

BSE BSE Limited

Category I AIF AIFs who are registered as “Category I Alternative Investment Funds” under the SEBI AIF Regulations

Category II AIF AIFs who are registered as “Category II Alternative Investment Funds” under the SEBI AIF Regulations