Webinar - Non-performing loans_23-out_Deck.pdf - Deloitte

85

Non-Performing Loans? Respond to thrive post-moratorium October 23 rd 2020

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Webinar - Non-performing loans_23-out_Deck.pdf - Deloitte

Non-Performing Loans? Respond to thrive post-moratorium

October 23rd 2020

Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A. 2

Agenda

Challenges for the real economy or challenges for the banking sector? 9AM - 10:15 AM

Q&A and closing

Webinar foundations - the prospects of NPL ecosystem• Joaquim Paulo, Deloitte• Nuno Martins, Caixa Geral de Depósitos

Challenges for the real economy – the “Day after”• Tom Simmons, Deloitte UK

The Portuguese case – script for the banking sector• Álvaro Nascimento, Católica Porto Business School

Challenges for the real economy – the “Day after”

Tom Simmons, Economist | 23rd October 2020

4Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Lockdowns drive huge contraction in second quarter GDP

Real GDP

Source: Refinitiv Datastream

H1 overall mobility vs GDP

5Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Monetary and fiscal stimulus have supported activity and financial markets

Source: Refinitiv Datastream

Source: OECD

Substantial fiscal support has been announced since the pandemic began: Official estimates of fiscal support

USD, trillionsCentral bank balance sheet, total assets

Lending to non-financial corporates

Central bank policy rates

Source: Refinitiv Datastream

Source: Refinitiv Datastream

% of 2019 GDP

6Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Strong initial recovery

Third quarter bounce:

• Fiscal stimulus

• Monetary stimulus

• Low infection rates – lagged impact of lockdowns

• Pent up demand

Composite Markit / NBS PMIs

Source: Refinitiv Datastream

7Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

But the recovery is slowing and faces significant headwinds - COVID-19 infections are rising

New daily COVID-19 cases

Source: Refinitiv Datastream

COVID-19 new daily deaths

Source: Refinitiv Datastream

Per million of the population, 7 - day averagePer million of the population, 7 - day average

8Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Unemployment set to rise

Euro area unemployment rate and hours worked

Source: Refinitiv Datastream Source: Refinitiv Datastream

% of workforce

US unemployment rate

9Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Consumer confidence has fallen sharply

Euro area consumer confidence

Source: Refinitiv Datastream Source: Refinitiv Datastream

UK & US % of disposable income, euro area gross savings rate

Household savings rates

10Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Significant headwinds for corporates

• Lower demand

• Higher levels of debt

• Operating below capacity due to restrictions

• Uncertainty

A relative majority of companies expect to get back to pre-crisis levels in one-year’s time at the earliest.Based on the information you have so far, when do you expect your company to return to a pre-crisis level of revenue generation?*

Source: Deloitte European CFO Survey

11Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Prospects vary significantly by industry

Some sectors are coming back to pre-crisis levels at a more rapid pace.Based on the information you have so far, when do you expect your company to return to a pre-crisis level of revenue generation?

Source: Deloitte European CFO Survey

12Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Corporates are prioritising defensive balance sheet strategies

Corporate priorities in the next 12 months% of CFOs who rate each of the following as a strong priority for their business in the next 12 months

Source: Deloitte CFO Survey

13Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

When are regions expected to return to pre-crisis levels?

Source: Consensus Forecasts

When Are Regions Expected to Regain Lost Output?Asia Pacific Already on the Way;Western Europe to Return to Pre-Crisis Levels in 2023

14Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Interest rates lower for longer

Expect 3m interest rates by December 2021

Source: Refinitiv Datastream

15Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Euro area banks expect credit standards to tighten in Q3

Banks expect credit standards for enterprises to tighten considerably in the third quarter, which is reported to be related to the expected end of state guarantee schemes for loans in some large euro area countries. – ECB euro area bank lending survey

ECB bank lending survey: tightening/easing lending standards to corporates

Source: Refinitiv Datastream

16Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Corporate bond spreads have recovered, despite ongoing downgrades

Spread of BBB corporate bonds yields over government bonds

Source: Refinitiv Datastream Source: Refinitiv Datastream

Equity indices

17Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Government debt has risen sharply, bond yields remain low

Euro area government debt

Source: IMF

10 year bond yields in the euro area

Source: Refinitiv Datastream

18Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

1. 2020 likely to see biggest downturn in centuries

2. Easing of lockdown, pent up demand, stimulus = bounce back

3. Momentum has slowed over recent weeks with rising infections, restrictions

4. Corporates and households face lower income and rising debt burdens

5. Headwinds from scarring, debt, caution, social distancing

6. 2 years before economy returns to pre-crisis GDP

7. Central banks countered initial financial stress and supported asset prices, but credit conditions may tighten

Summary

19Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

For a fresh view on economics subscribe to our weekly email…just Google:

Deloitte Monday Briefing

To follow the latest health and economic data Google & bookmark:

Deloitte Covid Monitor

Follow economics with Deloitte

NPL ecosystem in Portugalwebinar, Deloitte23 de Outubro de 2020Porto, CPBS, Álvaro Nascimento ⓒ

FactoryofNPLsRisk&Return in the Portuguese Corporation

21

purposeis there hidden value to unlock in Portuguese corporations?

Where: St. Barbara’s Church in Kutna Hora. Czech RepublicAbout: Fibonacci spiral, Golden Ratio

22

viewpointFinancial Intermediaries are

enablers, weaving threads that link investors and

corporations.Where: Farolim de Felgueiras, Porto. Portugal

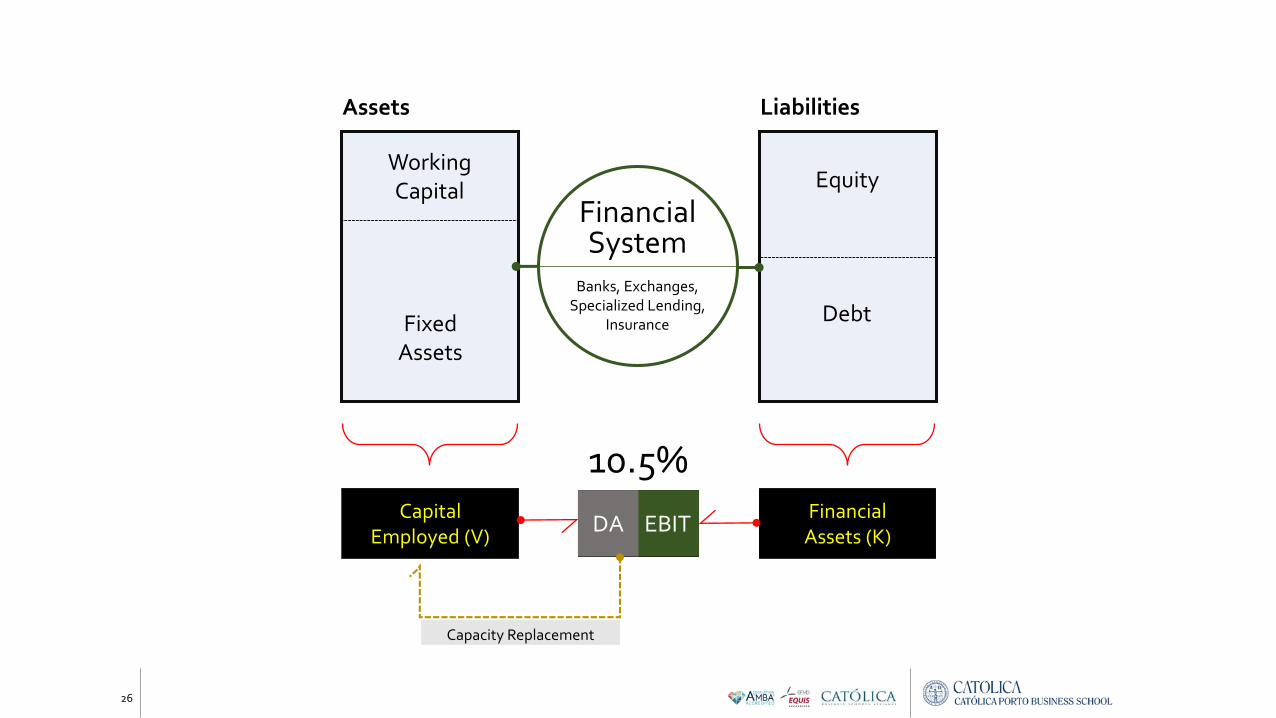

Working Capital

Cash Conversion

TechCapital

Production Technology

23

From a financial (not

managerial) perspective, we can

represent the corporation as a

portfolio of assets (i.e.,

microeconomics capital)

essential for production, which

needs to be funded.

The CorporationToolkit

About: Operations behind blind walls (opaque transactions), Coase (1937)

24

Financial Markets and

Institutions exist to perform

two basic functions: [1] serve

the payments system; and [2]

intermediate savings and

investments.

The Financial SystemToolkit

Where: Chicago Mercantile Exchange floor, 1997Author: Andreas Gursky | https://www.andreasgursky.com/en/works/1997/chicago-mercantile-exchange

Householdssavings

CorporationsInvestment

RiskManagement

25

brokers

RiskManagement

✕

investment trusts

investment banks

Rating agencies

Financial Systempoolingandscreening

26

Equity

Debt

Liabilities

Working Capital

Fixed Assets

Assets

Capital Employed (V)

Financial Assets (K)

Financial System

Banks, Exchanges, Specialized Lending,

Insurance

EBITDAEBITDA

Capacity Replacement

10.5%

27

insightCorporations offer

returns far lower than required, given business

risk exposures.

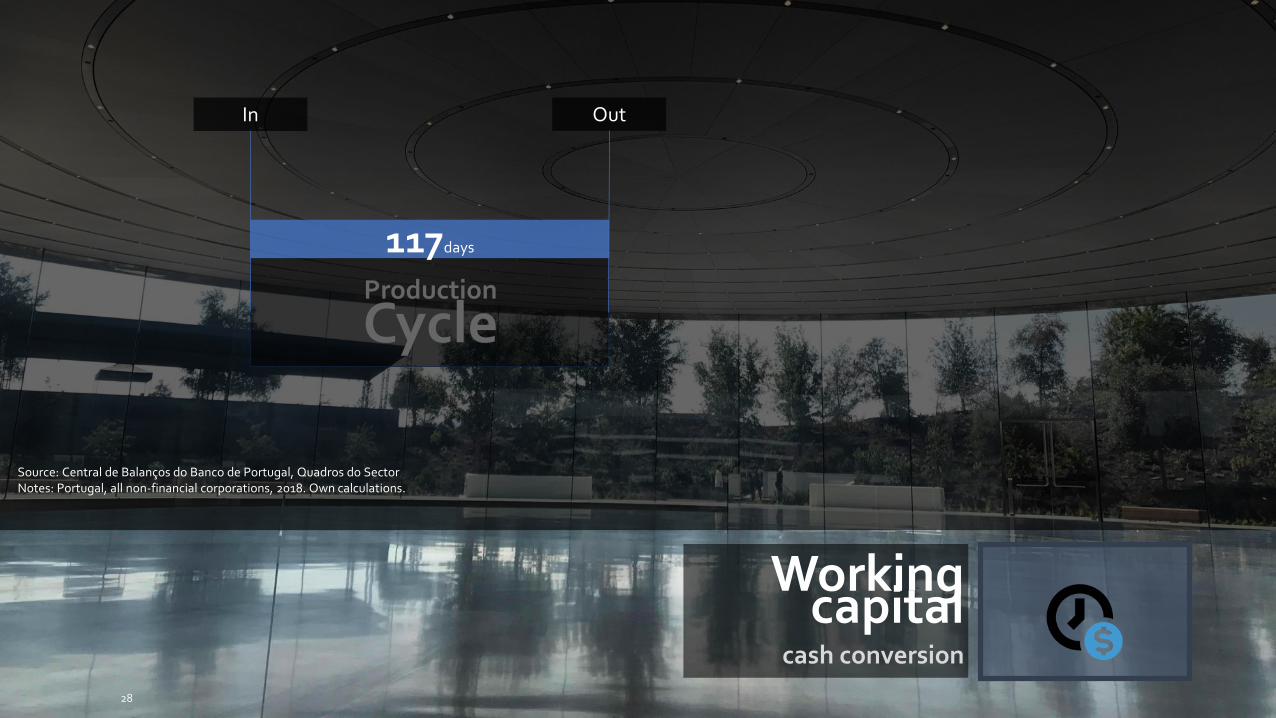

Production

Cycle

28

117days

In Out

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

Workingcapital

cash conversion

Workingcapital

cash conversion

117days

In Out

Collection(receivables)

63days

Payment(supplyers)

72days

109days

29

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

Tech Capital

production & technology

Productivity |Innovation | Balance

socialcontracting

Final Goods and Services

Production Parts and Services

Labour

Workerslabour markets

Supplyersmarkets for inputs

Customersmarkets for goods

Machinery and Equipment

Capital markets

Funding

30

valuesharing

Capital Employed

Production & Technology

Labour

Workerslabour markets

Production Parts and Services

Supplyersmarkets for inputs

Machinery and Equipment

Fundingcapital markets

Final Goodsand Services

31Productivity |Innovation | Balance

socialcontracting

Equity (4.2%)

Loans (1.6%)

Taxes (1.3%)

Supplyersmarkets for inputs

Final Goodsand Services

Workerslabour market

Fundingcapital markets

52,5% 22,3%

14,2%

Customersmarkets for goods

11,0%

32

Capital Employed

Production & Technology

Productivity |Innovation | Balance

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

Society

Lenders

Owners

valuesharing

33

Capital Employed

Production & Technology

Productivity |Innovation | Balance

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

Equity (4.2%)

Loans (1.6%)

Taxes (1.3%)Society

Lenders

Owners

onReturnCapitalEmployed

6.7%

34

Capital Employed

Production & Technology

Productivity |Innovation | Balance

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

Equity (4.2%)

Loans (1.6%)

Taxes (1.3%)Society

Lenders

Owners

onReturnCapitalEmployed

4.3%

2014

balance sheets

35

Investing

36

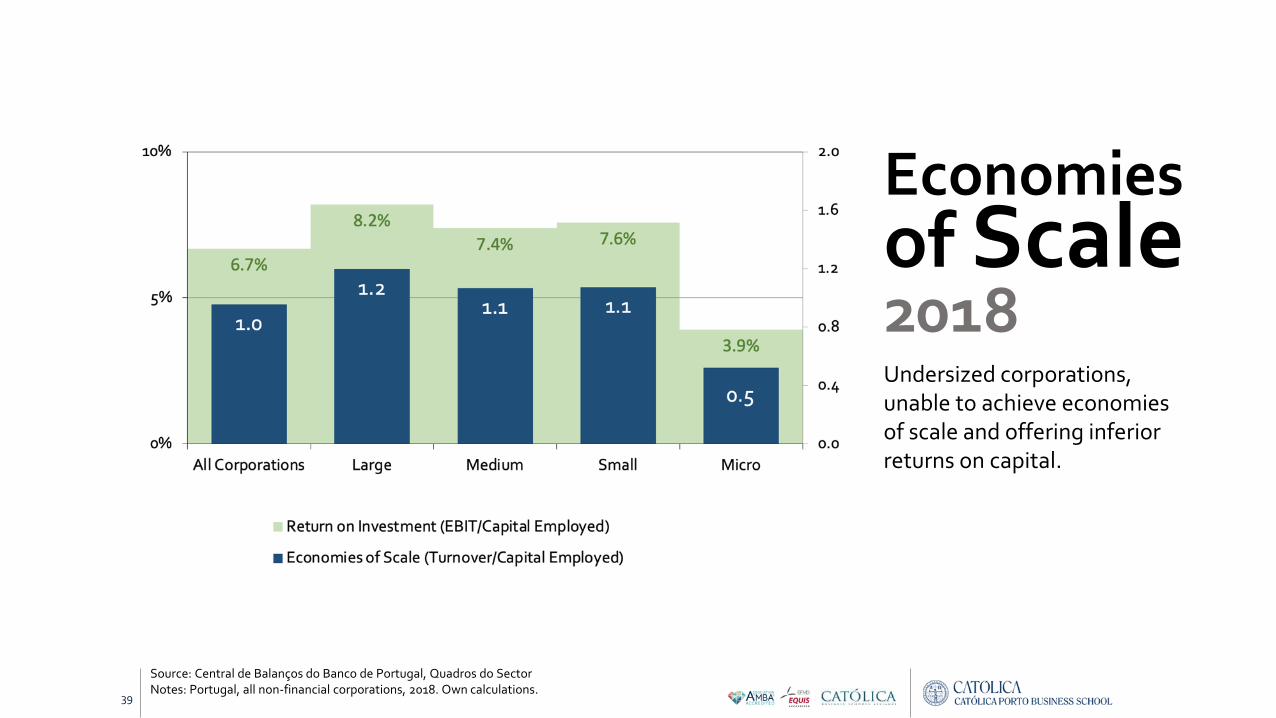

Return on CapitalEmployed2018Too small returns for too many small corporations: micro firms account for 16% of revenue and 26% of capital employed; small and medium perform alike.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

37

410bi,€

Capital Employed

449kAll Corporations

Too Many… Too Small

Micro corporations account for almost 30% of overall capital

employed: similar to large corporations, yet only (less

than) half profitable!

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

&NOTProfitable!

38

Return on CapitalEmployed2014+2.4pp

change ’10-14

+2.6% +1.3% +2.3% +3.3%

Strong improvement for largeand small corporations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2014. Own calculations.

Return on Capital Employed(percentage points, chg. ‘10-14)

39

Economies of Scale2018Undersized corporations, unable to achieve economies of scale and offering inferior returns on capital.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

40

Economies of Scale2014Excessive capital employed, high fixed costs, and suboptimal operational leverage shown in low levels of profitability.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2014. Own calculations.

32.2

41.8

36.4

28.0

22.0

134.2

152.5

134.2

94.6

151.7

0

50

100

150

200

250

0

10

20

30

40

50

All Corporations Large Medium Small Micro

GVA per worker (left scale)

Turnover per worker (right scale)

Capital Employed per worker (right scale)

41

ProductivityPuzzles[labour]2018Large corporations make better use of labour resources than any other. Yet, Large and Medium sized firms are equally productive (when normalized by capital).

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. Values as thousand of euros.

+14%

0.274 0.271 0.296Productivity of Capital(GVA/Capital Employed)

+14%

28.3

40.9

34.2

24.9

15.2

142.1

189.5

140.5

95.8

139.6

0

50

100

150

200

250

0

10

20

30

40

50

All Corporations Large Medium Small Micro

GVA per worker (left scale)

Turnover per worker (right scale)

Capital Employed per worker (right scale)

42

ProductivityPuzzles2014Overall, firms optimized usage of capital and labour: small and medium sized posted labour productivity gains; while the larger decreased capital employed without loss in GVA.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2014. Own calculations. Values as per thousand of euros.

+2% +6% +12%Labour Productivity Gain(GVA per worker, chg. ‘10-14)

Capital Productivity Gain(GVA/Capital, chg. ‘10-14) +27% +11% +13%

43

Valuesharing[wages]

2014-18Similar employee remuneration in large and medium sized firms, despite higher labour average productivity in the former.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations. Own calculations. Values as thousand of euros.

18.2

21.4 21.1

17.4

12.917.1

21.2 20.2

16.4

11.5

0.0

5.0

10.0

15.0

20.0

25.0

All Corporations Large Medium Small Micro

Compensation per Employee,2018

Compensation per Employee,2014

44

sharing Gains[capital]2014-18Productivity gains use to increase remuneration of capital, while labour was kept approximately constant, except micro and small firms: is labour a fixed cost?

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations. Own calculations. Values as thousand of euros.

45

usage of Capital2018All corporations decreased capital employed between 2014 and 2018, on average. Exception to micro firms. Yet, overall capital employed in the Portuguese corporate world increased.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2014. Own calculations. Values as thousand of euros.

1.131.06

1.15 1.16 1.19

1.02

0.860.95 0.99

1.08

0.0

0.5

1.0

1.5

0.0

0.5

1.0

1.5

All Corporations Large Medium Small Micro

Capital Employed (all corporations) | Base 100: 2014

Capital Employed (average corporation) | Base 100: 2014

114.4 11.9 1.7Corporation Size(avg., mi. €, 2018) 0.9 0.3

28.6%

17.6%

31.9%36.1% 34.6%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Working Capital Technological Capital

46

CapitalEfficiency[cash cycle&capacity]

2018Capital Employed structure kept stable during ‘14-18, signalling better resource allocation: [1] improved cash conversion cycle; [2] higher technological productivity.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. Values as thousand of euros.

47

after-taxReturn2018The after-tax return on Capital Employed increased as compared to 2014, not only because of productivity gains, but also because the tax wedge decreased.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. Values as thousand of euros.

6.7%

8.2%

7.4% 7.6%

3.9%5.1%

6.5%5.7% 5.7%

2.7%

0%

5%

10%

0%

5%

10%

All Corporations Large Medium Small Micro

Return on Investment (EBIT/Capital Employed)

After-Tax Return on Investment (EBIT–Taxes/Capital Employed)

20.7% 23.0% 25.0%Tax Burden(avg. corporate rate) 23.8% 30.7%

48

Too Many… Too Small& Profitable!Too Much

Capitaldespite adjustment during ‘14-18!

49

6.7% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% 16.9% 15.6% 14.2% 12.8% 11.5% 10.1% 8.8% 7.4% 6.1% 20%

15% 15.7% 14.4% 13.0% 11.6% 10.3% 8.9% 7.6% 6.2% 4.9% 15%

10% 14.5% 13.2% 11.8% 10.4% 9.1% 7.7% 6.4% 5.0% 3.7% 10%

5% 13.3% 12.0% 10.6% 9.2% 7.9% 6.5% 5.2% 3.8% 2.5% 5%

0% 12.1% 10.8% 9.4% 8.0% 6.7% 5.3% 4.0% 2.6% 1.3% 0%

-5% 10.9% 9.6% 8.2% 6.8% 5.5% 4.1% 2.8% 1.4% 0.1% -5%

-10% 9.7% 8.4% 7.0% 5.6% 4.3% 2.9% 1.6% 0.2% -1.1% -10%

-15% 8.5% 7.2% 5.8% 4.4% 3.1% 1.7% 0.4% -1.0% -2.3% -15%

-20% 7.3% 6.0% 4.6% 3.2% 1.9% 0.5% -0.8% -2.2% -3.5% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

ho

ck

Employee Compensation Adjustment

after-COVID resilience

Returns on Investment (EBIT/Capital Employed) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes).

Easily return to 2014!

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

4.3%

gross return on capital employed ´14

balance sheets

50

Funding

51

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % of total assets.

71%Technological

Capital53%Debt

29%Working

Capital47%Equity

0%

25%

50%

75%

100%

Capital Employed

FinancialAssets

5.1%

after corporate tax

enoughReturn?

52

Capitalfinancing2018On average there is not big difference between large and small corporations regarding the structure of financing (i.e., capital structure).

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % of total assets.

53

Capitalfinancing2014-18All corporations are financially more robust in 2018, as compared to 2014 (asset sales used to pay back loans and decrease financial leverage).

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % of total assets.

52.9% 53.7% 52.2%48.4%

55.2%

0%

25%

50%

75%

100%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Debt ('14) Equity (´14)

Debt ('18) Equity ('18)

54

Debt’financing2018Currently banks are responsible for financing less than 20% of total corporate assets (i.e., capital employed). Overall, debt contracts have an average interest rate of 3.3% (quite likely, the cost of bank loans is higher).

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % of total assets.

18.0%10.8%

26.1% 24.6%16.7%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Debt (banks & credit institutions) Debt (bonds) Debt (owners & others) Equity

55

cost ofDebt2018Implicit interest rates paid on debt reflect financing options available and managers’ choices: small and micro corporations resort to highly collateralized debt contracts (i.e. leasing) and borrowing from shareholders.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

2.8%

3.2%3.4%

3.1%

1.8%2.1%

2.5% 2.6%2.3%

1.3%

0%

1%

2%

3%

4%

0%

1%

2%

3%

4%

All Corporations Large Medium Small Micro

gross cost of debt after-tax cost of Debt

56

cost ofEquity2018Available return left for equity holders is, on average 8.4%. Large corporations offer a 200bp excess return over small and medium sized corporations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

2.8%

3.2%3.4%

3.1%

1.8%8.4%

11.1%

9.1% 8.9%

4.4%

0%

4%

8%

12%

16%

0%

1%

2%

3%

4%

All Corporations Large Medium Small Micro

gross cost of debt, left-hand scale

Return on Equity (Earnings/Equity), right-hand scale

57

cost ofEquity2014Available return left for equity holders in 2014 was just 1.9%. High financial leverage then, not enough to offset high interest rates and low (labour and capital) productivity effects.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

4.1%

4.9%4.6%

4.3%

2.7%

1.9%

3.9%

5.7%

3.8%

-2.5%

-4%

0%

4%

8%

12%

-2%

0%

2%

4%

6%

All Corporations Large Medium Small Micro

gross cost of debt, left-hand scale

Return on Equity (Earnings/Equity), right-hand scale

58

requiredwacc2018Equity Risk Premium (ERP) for Portugal estimated to be 10% (Damodaran, 2020). Assume the average corporation beta to be 1.0 (well diversified portfolio). Difficult for PE to invest in medium and small Portuguese corporations.

59

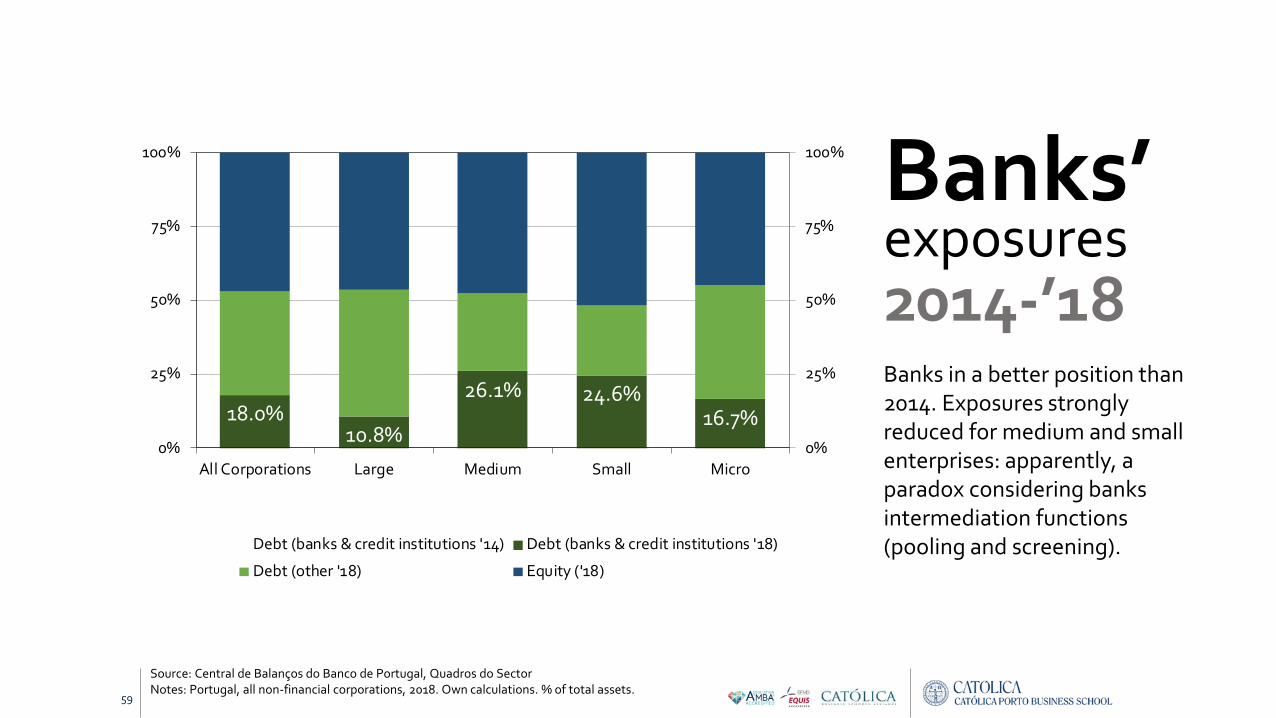

Banks’exposures2014-’18Banks in a better position than 2014. Exposures strongly reduced for medium and small enterprises: apparently, a paradox considering banks intermediation functions (pooling and screening).

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % of total assets.

18.0%10.8%

26.1% 24.6%16.7%

0%

25%

50%

75%

100%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Debt (banks & credit institutions '14) Debt (banks & credit institutions '18)

Debt (other '18) Equity ('18)

loans to corporations, 2018Financing Assets and Banks’ Exposures, Portugal

Equity

Debt

Liabilities

Reserves

Loans

Deposits

Equity

Investments Funding

Banking Book

Loans and Deposits

216.8bi,€

All-corporations (loans: 185.5bi; and others: 31.3bi).

73.7bi,€

Gross Lending to non-financial corporations (18.0% of firms’ total assets).

60

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: 1bi=1ooo million euros

34%

52.9%

Working Capital

Capital Employed

Assets

28.6%

loans to corporations, 2014Financing Assets and Banks’ Exposures, Portugal

Equity

Debt

LiabilitiesAssets

61

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: 1bi=1ooo million euros

220.2bi,€

All-corporations (loans: 191.8bi; and others: 28.4bi).

87.8bi,€

Gross Lending to non-financial corporations (24.2% of firms’ total assets).

40%

Banking Book

Loans and Deposits

60.6%

–16%

cumulative growth ’10-14

–6.2pp

debt share chg. ’10-14

Reserves

Loans

Deposits

Investments Funding

Equity

+0.5pp

working capital chg. ’10-14

Capital Employed

Working Capital

28.1%

capital structure and debt holders, 2018Financing Assets and Banks’ Exposures, Portugal: large corporations

Fonte: Central de Balanços do Banco de Portugal, Quadros do SectorNotas: utiliza-se como convenção 1bi=1ooo milhões de euros

62

Equity

Debt

Liabilities

Working Capital

Capital Employed

Assets

Banking Book

Loans and Deposits

53.7%

17.6%

Reserves

Loans

Deposits

Investments Funding

Equity73.9bi,€ 14.9bi,€

10.8%

45.7bi,€

Other (Parent Co. & Owners)

13.3bi,€

Bonds

9.7% 33.2%

59.8%

78.0bi,€11.8% 16.0bi,€

9.5% 36.2%

17.4%

x.x%

x.xbi,€

x.x%

x.xbi,€

2014 figures

2018 figures

capital structure and debt holders, 2018Financing Assets and Banks’ Exposures, Portugal: medium-sized corporations

Fonte: Central de Balanços do Banco de Portugal, Quadros do SectorNotas: utiliza-se como convenção 1bi=1ooo milhões de euros

63

Equity

Debt

Liabilities

Working Capital

Capital Employed

Assets

Banking Book

Loans and Deposits

52.2%

31.9%

Reserves

Loans

Deposits

Investments Funding

Equity42.5bi,€ 21.3bi,€

26.1%

18.1bi,€

Other (Parent Co. & Owners)

3.1bi,€

Bonds

3.8% 22.3%

59.7%

42.2bi,€31.3% 24.3bi,€

2.6% 20.6%

37.8%

x.x%

x.xbi,€

x.x%

x.xbi,€

2014 figures

2018 figures

capital structure and debt holders, 2018Financing Assets and Banks’ Exposures, Portugal: small-sized corporations

Fonte: Central de Balanços do Banco de Portugal, Quadros do SectorNotas: utiliza-se como convenção 1bi=1ooo milhões de euros

64

Equity

Debt

Liabilities

Working Capital

Capital Employed

Assets

Banking Book

Loans and Deposits

48.4%

36.1%

Reserves

Loans

Deposits

Investments Funding

Equity34.9bi,€ 17.8bi,€

24.6%

15.3bi,€

Other (Parent Co. & Owners)

1.9bi,€

Bonds

3.8% 22.3%

56.2%

34.9bi,€32.6% 21.6bi,€

2.6% 20.6%

38.7%

x.x%

x.xbi,€

x.x%

x.xbi,€

2014 figures

2018 figures

capital structure and debt holders, 2018Financing Assets and Banks’ Exposures, Portugal: micro corporations

Fonte: Central de Balanços do Banco de Portugal, Quadros do SectorNotas: utiliza-se como convenção 1bi=1ooo milhões de euros

65

Equity

Debt

Liabilities

Working Capital

Capital Employed

Assets

Banking Book

Loans and Deposits

55.2%

34.6%

Reserves

Loans

Deposits

Investments Funding

Equity65.5bi,€ 19.8bi,€

16.7%

44.8bi,€

Other (Parent Co. & Owners)

0.9bi,€

Bonds

0.7% 37.7%

65.0%

65.1bi,€25.1% 25.9bi,€

0.1% 37.8%

32.9%

x.x%

x.xbi,€

x.x%

x.xbi,€

2014 figures

2018 figures

66

Banks’exposures2018Overall banks decreased lending to corporations in Portugal, therefore still shielded from economic downturn, except if compelled to build up their exposures (moratorium period)…

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. Values as of million euros.

16 022

24 279

21 575

25 941

14 897

21 232

17 78019 788

0

10 000

20 000

30 000

0

10 000

20 000

30 000

Large Medium Small Micro

Bebt (banks & credit institutions '14)

Debt (banks & credit institutions)

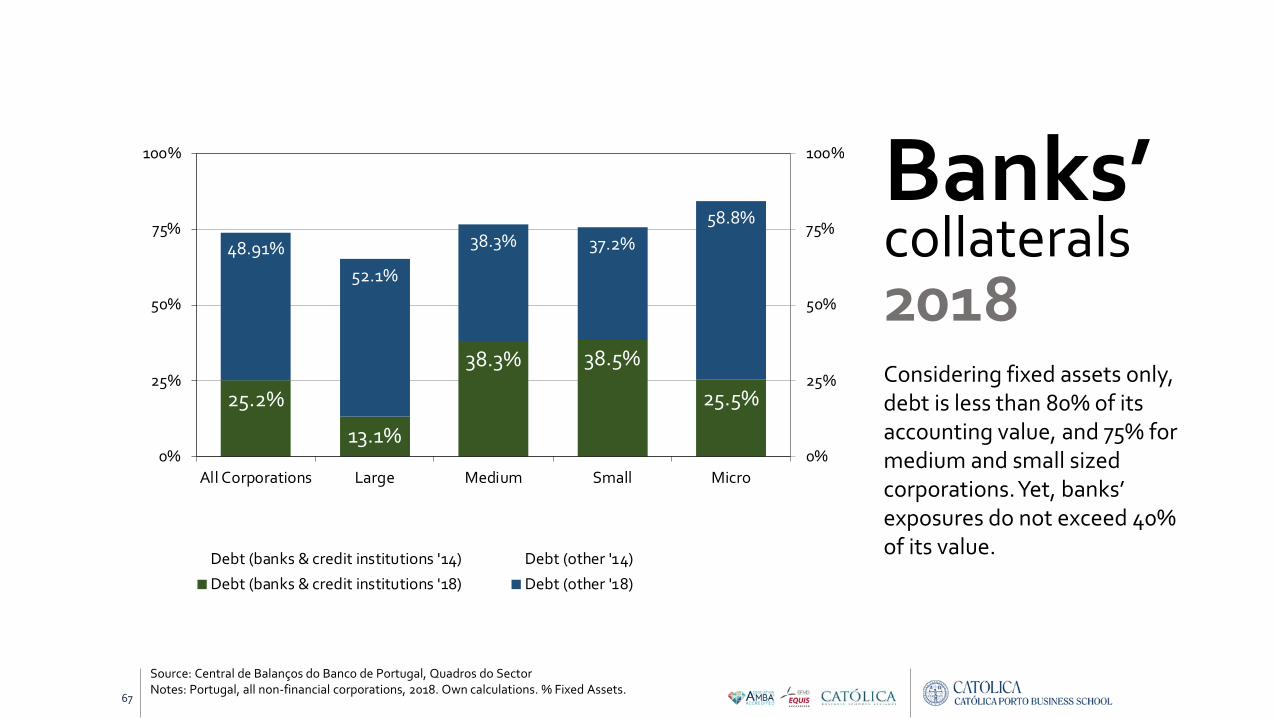

67

Banks’collaterals2018Considering fixed assets only, debt is less than 80% of its accounting value, and 75% for medium and small sized corporations. Yet, banks’ exposures do not exceed 40% of its value.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % Fixed Assets.

25.2%

13.1%

38.3% 38.5%

25.5%

48.91%

52.1%

38.3% 37.2%

58.8%

0%

25%

50%

75%

100%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Debt (banks & credit institutions '14) Debt (other '14)

Debt (banks & credit institutions '18) Debt (other '18)

68

Banks’potential risks

2018What if we restore the 2014 level of bank loans per firm, assuming 2018 fixed assets? From a “real estate value” perspective, things do not look much different now…

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % Fixed Assets.

33.2%

17.3%

52.9% 54.9%

36.7%

48.91%

52.1%

38.3% 37.2%58.8%

0%

25%

50%

75%

100%

0%

25%

50%

75%

100%

All Corporations Large Medium Small Micro

Debt (other '14)

Debt (banks & credit institutions '14)

Debt (other '18)

Simulated Debt (banks & credit institutions '18)

69

after-COVID resilience

Returns on Equity (Earnings/Equity) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes) and debt contractual obligations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

8.4% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% 24.9% 22.8% 20.6% 18.4% 16.2% 14.0% 11.8% 9.6% 7.4% 20%

15% 23.0% 20.8% 18.6% 16.4% 14.2% 12.1% 9.9% 7.7% 5.5% 15%

10% 21.1% 18.9% 16.7% 14.5% 12.3% 10.1% 7.9% 5.7% 3.5% 10%

5% 19.1% 16.9% 14.7% 12.6% 10.4% 8.2% 6.0% 3.8% 1.6% 5%

0% 17.2% 15.0% 12.8% 10.6% 8.4% 6.2% 4.0% 1.9% -0.3% 0%

-5% 15.2% 13.1% 10.9% 8.7% 6.5% 4.3% 2.1% -0.1% -2.3% -5%

-10% 13.3% 11.1% 8.9% 6.7% 4.5% 2.4% 0.2% -2.0% -4.2% -10%

-15% 11.4% 9.2% 7.0% 4.8% 2.6% 0.4% -1.8% -4.0% -6.2% -15%

-20% 9.4% 7.2% 5.0% 2.8% 0.7% -1.5% -3.7% -5.9% -8.1% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

ho

ck

Employee Compensation Adjustment

1.9%

average return on equity ‘14

70

Bottompotential risks

2018There are more than 220 thousand corporations – half of the Portuguese corporate world – with a return (EBIT as % revenues) to financing less than 3.3%, just enough to pay debt holders!

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % Fixed Assets.

506.8% 6.7% 6.8% 6.9% 7.2%

3.3%

4.2% 3.9% 3.7%3.1%

0%

5%

10%

0%

5%

10%

All Corporations Large Medium Small Micro

Return on Revenue (mean) Return on Revenue (median)

71

after-COVID resilience

Returns on Equity (Earnings/Equity) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes) and debt contractual obligations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

2.0% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% 21.8% 18.9% 16.1% 13.2% 10.3% 7.4% 4.6% 1.7% -1.2% 20%

15% 19.7% 16.9% 14.0% 11.1% 8.2% 5.4% 2.5% -0.4% -3.3% 15%

10% 17.6% 14.8% 11.9% 9.0% 6.1% 3.3% 0.4% -2.5% -5.4% 10%

5% 15.5% 12.7% 9.8% 6.9% 4.0% 1.2% -1.7% -4.6% -7.5% 5%

0% 13.4% 10.6% 7.7% 4.8% 2.0% -0.9% -3.8% -6.7% -9.5% 0%

-5% 11.4% 8.5% 5.6% 2.7% -0.1% -3.0% -5.9% -8.8% -11.6% -5%

-10% 9.3% 6.4% 3.5% 0.6% -2.2% -5.1% -8.0% -10.9% -13.7% -10%

-15% 7.2% 4.3% 1.4% -1.4% -4.3% -7.2% -10.1% -12.9% -15.8% -15%

-20% 5.1% 2.2% -0.7% -3.5% -6.4% -9.3% -12.2% -15.0% -17.9% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

hock

Bottompotential risks 50220k

firms

72

Bottompotential risks

2018There are more than 110 thousand corporations with a negative return (EBIT as % revenues) to financing!

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations. % Fixed Assets.

25

73

after-COVID resilience

Returns on Equity (Earnings/Equity) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes) and debt contractual obligations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018. Own calculations.

-15.0% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% 1.4% -1.5% -4.3% -7.2% -10.1% -12.9% -15.8% -18.7% -21.6% 20%

15% 0.2% -2.7% -5.6% -8.4% -11.3% -14.2% -17.1% -19.9% -22.8% 15%

10% -1.1% -3.9% -6.8% -9.7% -12.6% -15.4% -18.3% -21.2% -24.1% 10%

5% -2.3% -5.2% -8.1% -10.9% -13.8% -16.7% -19.6% -22.4% -25.3% 5%

0% -3.5% -6.4% -9.3% -12.2% -15.0% -17.9% -20.8% -23.7% -26.5% 0%

-5% -4.8% -7.7% -10.5% -13.4% -16.3% -19.2% -22.0% -24.9% -27.8% -5%

-10% -6.0% -8.9% -11.8% -14.7% -17.5% -20.4% -23.3% -26.2% -29.0% -10%

-15% -7.3% -10.1% -13.0% -15.9% -18.8% -21.6% -24.5% -27.4% -30.3% -15%

-20% -8.5% -11.4% -14.3% -17.1% -20.0% -22.9% -25.8% -28.6% -31.5% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

hock

Bottompotential risks 25110k

firms

74

after-COVID resilience

Returns on Equity (Earnings/Equity) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes) and debt contractual obligations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, large non-financial corporations, 2018. Own calculations.

Bottompotential risks 25

300largecorporations!

-6.9% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% 12.8% 9.8% 6.8% 3.7% 0.7% -2.3% -5.3% -8.4% -11.4% 20%

15% 10.9% 7.9% 4.8% 1.8% -1.2% -4.2% -7.3% -10.3% -13.3% 15%

10% 9.0% 6.0% 2.9% -0.1% -3.1% -6.1% -9.2% -12.2% -15.2% 10%

5% 7.1% 4.0% 1.0% -2.0% -5.0% -8.1% -11.1% -14.1% -17.1% 5%

0% 5.2% 2.1% -0.9% -3.9% -6.9% -10.0% -13.0% -16.0% -19.0% 0%

-5% 3.2% 0.2% -2.8% -5.8% -8.9% -11.9% -14.9% -17.9% -21.0% -5%

-10% 1.3% -1.7% -4.7% -7.7% -10.8% -13.8% -16.8% -19.8% -22.9% -10%

-15% -0.6% -3.6% -6.6% -9.7% -12.7% -15.7% -18.7% -21.7% -24.8% -15%

-20% -2.5% -5.5% -8.5% -11.6% -14.6% -17.6% -20.6% -23.7% -26.7% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

ho

ck

Employee Compensation Adjustment

75

after-COVID resilience

Returns on Equity (Earnings/Equity) after a shock in production (VAB), considering mitigating circumstances (layoff and furlough schemes) and debt contractual obligations.

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, large non-financial corporations, 2018. Own calculations.

Bottompotential risks 25

100kmicrocorporations!

-13.3% -40% -30% -20% -10% 0% 10% 20% 30% 40%

20% -3.2% -5.1% -7.0% -8.9% -10.8% -12.7% -14.6% -16.5% -18.4% 20%

15% -3.9% -5.8% -7.7% -9.6% -11.5% -13.4% -15.3% -17.2% -19.1% 15%

10% -4.5% -6.4% -8.3% -10.2% -12.1% -14.0% -15.9% -17.8% -19.7% 10%

5% -5.1% -7.0% -8.9% -10.8% -12.7% -14.6% -16.5% -18.4% -20.3% 5%

0% -5.7% -7.6% -9.5% -11.4% -13.3% -15.2% -17.1% -19.0% -20.9% 0%

-5% -6.4% -8.3% -10.2% -12.1% -14.0% -15.9% -17.8% -19.7% -21.6% -5%

-10% -7.0% -8.9% -10.8% -12.7% -14.6% -16.5% -18.4% -20.3% -22.2% -10%

-15% -7.6% -9.5% -11.4% -13.3% -15.2% -17.1% -19.0% -20.9% -22.8% -15%

-20% -8.2% -10.1% -12.0% -13.9% -15.8% -17.7% -19.6% -21.5% -23.4% -20%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

VA

B s

hock

76

enterprise classification

Source: Central de Balanços do Banco de Portugal, Quadros do SectorNotes: Portugal, all non-financial corporations, 2018.values as million of euros.

2018 2014 2018 2014 2018 2014

All Corporations 6.8 6.3 0.871 0.777 0.913 0.895

Large 750.2 701.5 137.056 136.841 114.423 132.938

Medium 88.9 89.0 12.701 12.009 11.923 12.506

Small 18.4 18.3 1.871 1.817 1.744 1.757

Micro 2.0 2.0 0.155 0.134 0.297 0.275

Number of employees Annual Turnover Employed Capital

77

practices

Managing

Productivity and profitability depend on management practices“Management Practice” scores

78

Source: Bloom, Genakos, Sadun & Reenen, 2012Notes: international study on management practices in 20 countries around the world, comprising companies ranging between 100 e 5000 employees. Portugal is represented with 247 firms | management scores on a scale from 1 (min) to 5 (max).

2,67

2,71

2,71

2,73

2,87

2,90

3,02

3,02

3,02

3,23

3,35

Índia

Brasil

China

Grécia

Portugal

Polónia

França

Itália

Reino Unido

Alemanha

Estados Unidos

20

1918

1714

128

76

31 “In the United States, a plant at the 90th percentile has

labor productivity 4x a plant at the 10th percentile

(Syverson, 2004), total factor productivity is 2x.”

Portugal & Greece…recall:

United States Brazil

79

Source: Van Reenen, John (2017). “Management and the Wealth of Nations”. World Bank Empirical Management Conference, Washington.

management istechnology

A positive relationship between management practices (scores), productivity, and economic development and growth.

Corporate performance…depends on management practices

In the United States, a plant at the 90th percentile has labor productivity 4x a plant at the 10th percentile (Syverson, 2004), total factor productivity is 2x

Fonte: Bloom, Genakos, Sadun & Reenen, 2012Source: international study on management practices in 20 countries around the world, comprising companies ranging between 100

e 5000 employees. Portugal is represented with 247 firms | management scores on a scale from 1 (min) to 5 (max).

Brasil

0.2

.4.6

.8

De

nsi

ty

1 2 3 4 5management

Total Factor Productivity: 2x

Labour Factor Productivity: 4x

80

81

0 1 2 3 4 5

Vestuário

Metalomecânica

Couro e Calçado

Edição e Impressão

Máquinas industriais

Carvão e Petróleo

Texteis

Instrumentos de Precisão

Papel

Borracha e Plásticos

Produtos Químicos

Electrónica

Alimentação e Bebidas

Mobiliário

Transportes

Metalúrgicas

Cerâmicas

Madeira

23

3431

27

352

92

238

26

302

836

20

25

3733

322

4

Source: Bloom, Genakos, Sadun & Reenen, 2012Notes: international study on management practices in 20 countries around the world, comprising companies ranging between 100 e 5000 employees. Portugal is represented with 247 firms | management scores on a scale from 1 (min) to 5 (max).

82

• prevalência por modelos de propriedade e de governo

• “Management Practice” scores

2,53

2,70

2,93

2,97

2,97

3,01

3,13

3,30

Founder

Family owned, family CEO

Managers

Family owned, external CEO

Private Individuals

Government

Private Equity

Dispersed Shareholders

Portugal

2,64

2,77

2,94

3,14

2,95

2,74

3,21

3,24

Founder

Family owned, family…

Managers

Family owned, external…

Private Individuals

Government

Private Equity

Dispersed Shareholders

Total 20 países

Source: Bloom, Genakos, Sadun & Reenen, 2012Notes: international study on management practices in 20 countries around the world, comprising companies ranging between 100 e 5000 employees. Portugal is represented with 247 firms | management scores on a scale from 1 (min) to 5 (max).

corporations

investors

83

Non-Performing Loans? Respond to thrive post-moratoriumChallenges for the real economy or challenges for the banking sector?

© 2020 For more information, contact Deloitte Corporate Finance, S.A. 84

Next session: Recovery instruments and the Investors’ narrative

October 30th – from 9AM to 10:15AM

Q&A and closing

Webinar reloaded - NPL ecosystem at a glance• Joaquim Paulo, Deloitte Portugal• Susana Bento, Deloitte Portugal

The outbreak of recovery instruments• Andrew Grimstone, Deloitte UK• Ricardo Reis, Deloitte Portugal• Jorge Marrão, Deloitte Portugal

Voice to investors: a new narrative?• Benjamin Collet, Deloitte UK• André Nunes, Whitestar• Martim Avillez Figueiredo, Core Capital

© 2020 For more information, contact Deloitte Corporate Finance, S.A.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our network of member firms in more than 150 countries and territories serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 312,000 people make an impact that matters at www.deloitte.com.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.