“"Nature, Knowledge and Enlightenment: Ansel Adams and Fiat Lux”

The Fundamental Value of Non-Fiat Anonymous DigitalPayment Methods: Coining a (Bit of) Theory toDescribe and Measure the Bitcoin Phenomenon.

Greg Hunter∗ and Craig Kerr

PRELIMINARY AND INCOMPLETE.PLEASE DO NOT QUOTE OR CITE WITHOUT PERMISSION.

COMMENTS WELCOME.

July 8, 2015

Abstract

This paper discusses the determinants of a Non-Fiat Anonymous Digital PaymentMethod’s (N-FAD) value and investigates how the use of N-FAD’s could theoreti-cally affect monetary policy on fiat currency. The investigation illuminates a uniquecharacteristic of money that is not widely discussed in the economic literature, whichdistinguishes commonly accepted methods of payment from N-FAD’s. Using a sim-ple augmented quantity equation-type model, we are also able to construct a roughestimate of the amount of goods and services purchased with bitcoin in the U.S.

∗Greg Hunter: California State Polytechnic University - Pomona. Email: [email protected] Kerr: California State Polytechnic University - Pomona. Email: [email protected]

1

1 Introduction

In Economics, the value of an item is defined by its opportunity cost - the next best alterna-

tive forgone. To facilitate comparisons of value, it is standard practice to express opportunity

cost in currency units or money. For many goods and services, market prices exist and the-

ory suggests that these prices are good approximations of the value of the marginal unit

consumed by individuals. When the items of interest are not widely traded or are abstract,

then typically some related market price is used as an approximation. For example, the

value of a persons time is often approximated using his wage rate.

In the case of money itself, this approach is problematic because it is the unit of account.

In addition, money is also a store of value and a medium for exchange. Thus far, economists

have identified two species of money: commodity and fiat.1 Examples of commodity money

are gold, silver, gems, sea shells, salt, and cigarettes. Commodity money is distinguished

from fiat money because it has an intrinsic value separate from its value as money. Fiat

money is created by an act of law by a government that designates a token that has little or

no intrinsic value as such. The key feature of fiat money is that it can be used to pay taxes.

Prior to the development of fiat currency governing authorities (e.g., monarchs) would

demand tax payments in commodities. However, with a fiat currency the government desig-

nates all tax obligations in units of the currency and demands that the payments be made in

currency. If a taxpayer does not have the financial resources (i.e., money) to pay his tax obli-

gations, the government typically seizes the taxpayers property and auctions the property

to get the money to pay the obligation. The ability of fiat currency to satisfy government

payment requests represents an additional source of demand for fiat currency not shared by

other forms of money, in particular, N-FAD’s.

Although publicly available digital transaction records are available for many popular

N-FAD’s currently in use, the data do not include the purpose of the transactions. Thus,

1In a working paper, [14] categorizes monies according to not only their intrinsic value, but also accordingto their scarcity being absolute or contingent on a decision maker, thus deriving four species of money. Whatthe author denotes “synthetic commodity” money is what this paper refers to as non-fiat anonymous digitalpayment methods.

2

it is not possible to directly observe the value of goods and services purchased via NFAD’s.

Many transactions are individuals transferring potentially undeclared funds abroad avoiding

fees paid via traditional means. In addition, as is common practice with users masking the

flow of finances, many transactions are individuals transferring wealth among their many

virtual wallets to make tracing the value of any incoming wealth extremely difficult.

The remainder of this paper discusses the demand determinants of N-FAD’s and how

the characteristics of the currency’s supply protocols are likely to influence demand for the

currency. We also construct an estimate of the amount of purchases made using the most

widely used N-FAD, bitcoin2, using ran augmented quantity equation.

2 N-FAD Demand

N-FAD’s are money, but they are neither commodity money nor legal tender (i.e., fiat cur-

rency). So, what are the functional components of N-FAD’s that have given rise to its

demand? As previously stated, money is defined by three characteristics. It is: (i) a unit of

account, (ii) a store of value, and (iii) a medium of exchange. An asset with these charac-

teristics generates three demand components: transactions demand, precautionary demand,

and speculative demand. However, transactions demand makes up the greatest source of

demand for most currencies. The discussion that follows applies to all NFAD’s, however, we

will focus mainly on the most widely adopted NFAD, bitcoin.

2.1 Transactions Demand

In the case of N-FAD’s currently available, the ability of the currency to function as a means

of transactions (i.e., medium for exchanging goods and services) has been the main barrier

to wide-scale adoption. Currently, purchases of general goods and services made using the

most widely accepted N-FAD, bitcoin, is expanding. According to blockchain.info [1], there

were between 162,000 to 188,000 transactions a day in May 2015 worth approximately $37

2When referring to bitcoin or Bitcoin, we follow the convention and [5] in using a lowercase “b” for thecurrency and an uppercase “B” for the payment system.

3

to $44 million dollars. Although the amount of these transactions that were purchases of

goods and services is unknown, what is known is that the largest retail acceptor of bitcoin,

Overstock.com, is selling an average of $15,000 a day worth of goods via bitcoin purchases

[2]. However, the majority of transactions are likely not for traditional goods and services

as [5] presents evidence that the majority of small (less than $100 in value) transactions are

attributable to Satoshi Dice, a popular online gambling service.

Bitcoin users encounter a number of difficulties that users of other forms of money do

not. For instance, bitcoin is not widely accepted as a form of payment in the day-to-day

real economy and it is unlikely that governments will accept bitcoin as form of payment for

government payment requests (e.g., tax obligations) in the near future. As a result, one

would predict that transactions demand for bitcoin among the general populace is likely

to be weak until established currency markets develop to allow regular exchanges between

bitcoin and broadly used fiat currencies.

At the moment, there are also significant costs associated with establishing Bitcoin ac-

counts and trading that discourage most people from transacting in bitcoin. One must first

obtain a virtual wallet to store the bitcoin or purchase online storage at an additional fee.

If the currency is stored on a physical drive via a virtual wallet, the entire amount will be

permanently lost in the case of a drive failure. This initial technological hurdle requires an

investment of time to understand Bitcoin trading protocols.

There is also a risk-assessment hurdle, which requires a new user to delve into contempla-

tion regarding the risks of government (public) seizure and theft (private seizure) of Bitcoin

assets. On July 26th, 2011, the third largest bitcoin exchange (Bitomat) permanently lost

all of its customers’ bitcoin when its servers were reset[8]. When the largest bitcoin ex-

change, Mt. Gox, was hacked for a second time in 2013, it lost 850,000 of its customer’s

bitcoin ($460 million). The Department of Homeland Security also seized $5 million from

Mt. Gox’s U.S. bank account because the company had not registered with the government

as a money transmitter causing individuals with bitcoin stored on Mt. Gox’s servers to lose

4

access to their assets.[11] Also, as pointed out in [16], there is currently no form of insurance

comparable to the deposit insurance provided to bank customers.

Lastly, the current tax treatment of Bitcoin greatly increases the cost of using NFAD’s

for law-abiding citizens. The Internal Revenue Service (IRS) declared bitcoin a “convertible

virtual currency”, which implies that it should be treated as property for tax purposes. For

example, if an individual purchased a bitcoin for $400 and spent the entire bitcoin after it

had appreciated to $500, he would owe taxes on the $100 appreciation [15]. On the other

hand, the treatment of N-FAD’s as property by the IRS may actually be a positive sign for

their users as it implies that the U.S. government is unlikely to declare them illegal according

to the Stamp Payments Act of 1862, which states

Whoever makes, issues, circulates, or pays out any note, check, memorandum,

token, or other obligation for a less sum than $1, intended to circulate as money

or to be received or used in lieu of lawful money of the United States, shall be

fined under this title or imprisoned not more than six months, or both.[4]

The technological hurdles and seizure risk uncertainty of N-FADs can be summed up by

saying that the general transactions demand for them is likely to be weak for the time being

due to increased set up costs and risk relative to standard fiat currency. Moreover, with

a currency such as bitcoin, whose value fluctuates widely, risk assessment for the general

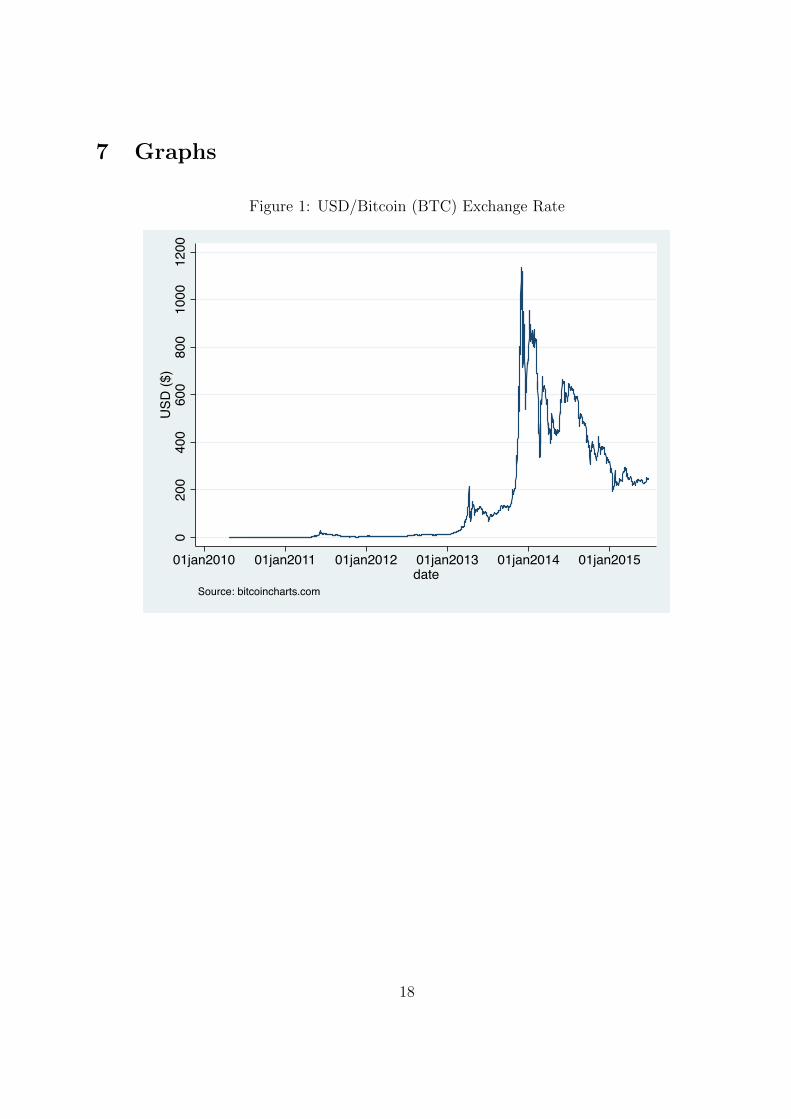

populace is very difficult. Figure 1 displays the US dollar/bitcoin exchange rate for the last

two years.3 Within this time frame alone, the value of a unit of bitcoin (BTC) has gone from

approximately $45 to almost $1200 only to briefly sink below $200 and then rise back to just

under $300. According to [7], this volatility can be largely attributed to many short-lived

bubbles in the valuation of bitcoin and three bubbles lasting 66 days or longer. Unless the

uncertainty in bitcoin’s ability to serve as a storer of value subsides, transactions demand is

likely to not exist at all for the general population.

In addition to consumers and investors, merchants also have an incentive to favor N-FAD’s

over fiat to avoid fees paid to financial institutions. According to the Federal Reserve’s 2013

3Reported values are exchange rates on the exchange Bitstamp at the close of the day.

5

Payments Study, there were 122.8 billion non cash payments made in 2012, with a total value

of $79.0 trillion. Banks, credit card associations (Visa, American Express, etc), and credit

card processors charge fees for maintaining the financial infrastructure to process payments

on behalf of consumers and merchants. These fees act as a an additional tax, driving a wedge

between the prices consumers pay and the prices merchants receive.

Merchants that provide the option of purchasing their goods and services using N-FAD’s

can avoid fees paid to traditional financial intermediaries and keep more of the revenue they

receive from consumers. To avoid the risks associated with a highly volatile exchange rate,

merchants can utilize services that instantly exchange N-FADs for fiat for a small transaction

fee of 1% or $0.15 for transactions that are $15 or less [3]. This fee is considerably less

than those paid when transacting with credit cards, which include interchange fees that are

typically a few percentage points of the transaction value and other flat fees for use of the

credit card’s payment system. In addition, [10] find preliminary evidence that some online

retailers accepting bitcoin may be passing on what they save in avoided fees to consumers,

which should serve to increase transactions demand.

Even in the face of technological hurdles, the use of Bitcoin has been rising. The phe-

nomenon of increasing bitcoin demand despite its increased risk must be largely due to the

other two potential sources of demand: precautionary and speculative demand.

2.2 Precautionary Demand

Precautionary demand for money comes from holding an asset in anticipation of some con-

tingency. In the case of N-FAD’s, this appears to be a central component of their appeal.

By definition the transactions carried out using N-FAD’s are anonymous.4 Currently, Bit-

coin allows for anonymity between transacting (i.e., primary) parties and social (i.e., third

party) anonymity. The appeal of holding bitcoin in the event that an anonymous primary

party transaction becomes necessary depends on the likelihood of such an event arising. For

4All transactions of bitcoin between virtual wallets are recorded in a public ledger. Therefore, the trans-actions are anonymous so long as users keep their wallet ID private. Since the fixed cost of creating a newwallet is essentially zero, many users who value the anonymity create a new wallet for every transaction.

6

consumers that place a high value on privacy, the desire to carry out financial transactions

using N-FAD’s will always be present.

In the case of the general public, the necessity of transactions requiring primary party

anonymity is likely to be small. However, for parties involved in illicit transactions anonymity

reduces the risk of sanctions from legal authorities. In determining the strength of precau-

tionary demand for illicit transactions for N-FAD’s, economic theory suggests that the par-

ties involved in illicit transactions will balance the risk of sanctions involving transactions

in other forms of money against the transactions cost, risk of sanctions, and risk of seizure

using N-FAD’s.

2.3 Speculative Demand

The demand for bitcoin depends on assessing a wide variety of risks that are not well-

understood, which leads to speculation. Speculation in this context means assessing risks

for which common source of data and techniques have not been established. The speculative

demand component of N-FAD demand is due to optimistic assessments of widescale adoption

in light of the risks previously mentioned, which would lead one to conclude that the value

of bitcoin will likely rise in the future. There is also speculation regarding the ability of the

Bitcoin protocol to generate a hedge against inflation or a general anticipated decrease in

the value of widely accepted fiat currencies. The inflation risk speculation associated with

bitcoin is due to the widely accepted belief that the stock of bitcoin is fixed by the algorithm

used to create and track the currency.

Assuming the stock of bitcoin is fixed and that no modifications to the algorithm could

be undertaken5, there is a critical trade-off that the Bitcoin developers likely did not antici-

pate. Namely, that the inflation hedging properties of the currency could potentially distort

the central bank’s control over price levels and thus magnify the risks associated with public

seizure (this is a main result of the model presented in Section 3). As the inverse relationship

5Hypothetically, if a single entity were to control over half of the Bitcoin network’s computing power,it could change the supply of bitcoin. However, the simulations run in [12] show this to be a practicalimpossibility.

7

between the inflation hedging property of bitcoin and the probability of public seizure be-

come well-accepted, one may expect that the precautionary motives for holding bitcoin as a

medium for illicit transactions would decrease, which will lead to a decrease of the currency’s

value. In what follows, we formally model the relationship between the supply of an N-FAD

and a central bank’s ability to control inflation with monetary policy by augmenting the

quantity equation. The theoretical work below is not inteded to fully model the dynamics of

an ecomony with multiple currencies. Its main purpose is simply to illustrate the potential

effect of an N-FAD on the central bnak’s ability to control inflation. Its secondary purpose

is to derive a rough estimate of the goods and services purchased with the most widely used

N-FAD, bitcoin.

3 Model

Imagine a closed economy with no fiscal government, no stochastic disturbances, and only

two payment methods: fiat currency (f) and an N-FAD (n). By introducing a second cur-

rency to the traditional quantity theory of money described in [9] where real output is

assumed determined by exogenous forces, such as a Walrasian equilibrium, we can derive an

augmented quantity equation6.

Mf · Vf + εfMn · Vn = Pf ·Qf + εfPn ·Qn, (3.1)

where Mj, Vj, Pj, and Qj are the money supply, velocity, price level, and quantity of output

purchased for currency j ∈ {f, n} and εf is the exchange rate of fiat per unit N-FAD. Written

in this way, both sides of Equation 3.1 are in terms of the fiat currency.

Assuming that there is purchasing power parity between the two currencies and that

the stock of real output is divided between the two payment methods gives the additional

restrictions below:

Pf = εfPn (3.2)

6details are discussed in the appendix.

8

Q = Qf +Qn (3.3)

With the above constraints, Equation 3.1 can be written as

Mf · Vf + εfMn · Vn = Pf · (Qf +Qn) (3.4)

Taking the total differential of Equation 3.4 and assuming that the velocity of monies do

not change yields:

∆Mf = V −1f [∆Pf (Qf +Qn) + Pf (∆Qf + ∆Qn)−∆εfMnVn − εf∆MnVn] (3.5)

Dividing both sides by Mf and making use of Equations 3.2, 3.3, and Mf =PfQf

Vf, we can

derive a new equation describing money supply growth in the presence of a second currency

mf = πf + gf + (πf + gn − ef −mn)Qn

Qf

(3.6)

where mi = ∆Mi

Mi,gi = ∆Qi

Qi, for i = {f, n}, πf =

∆Pf

Pf, and ef =

∆εfεf

.

Equation 3.6 implies that with an N-FAD, the monetary authority needs to additionally

monitor the growth of the economic activity carried out with the N-FAD, the change in

the exchange rate, and the change in the N-FAD money supply.7 Furthermore, these new

variables affecting monetary policy are all weighted according to the proportion of goods and

services purchased with the N-FAD. Note that if no purchases are made with the N-FAD,

Qn = 0, Equation 3.6 reduces to the traditional relationship between money supply and

inflation.

The main point of this exercise is to show that N-FAD’s, have the potential to undermine

the ability of central bank monetary authorities to carry out their principle objective - price

stabilization. Of course if bitcoin were to remain the main N-FAD of choice in the economy,

the supply of N-FADs would become relatively fixed once all bitcoin were mined as the

7Of course nothing up to this point in the model has distinguished the N-FAD from the fiat currency. Wehave simply assumed two currencies in a single economy.

9

algorithm is designed to have an absolute maximum amount (mn = 0). In this case, the lack

of control over the fiat inflation rate would then be only due to the fraction of purchases

made with the N-FAD, the growth of N-FAD purchases, and the exchange rate.

3.1 Measuring Purchases Made with N-FADs

Regardless of the rules under which the N-FAD changes in supply, the monetary authority

overseeing the fiat currency will be have to adjust their policies according to the amount

of purchases made with the N-FAD. Estimating such a measure is a difficult task since the

purpose of many N-FADs in use is to mask what is being purchased along with the parties

involved.

Although every transaction of bitcoin from one virtual wallet another is recorded in a

public record, the purpose of the transaction (sale of a good, illicit money laundering, etc)

is not. However, with the additional assumption that the velocity of money for N-FAD’s

is equal to that for fiat, the we are able to calculate an estimate of how much goods and

services were purchased with N-FAD’s using our simple model.

The quantity equation must hold for each currency. Specifically, MnVn = PnQn or

Qn = MnVnPn

. Assuming purchasing power parity holds and that the velocity of money is

the same across currencies, we can write the quantity of goods and services purchased with

N-FADs as

Qn =MnVfεfPf

(3.7)

which can be calculated using publicly available data. Although many N-FADs have surfaced

since 2008, bitcoin continues to hold the lion’s share of the market for N-FADs. In fact, as

of the writing of this paper, Bitcoin’s market capitalization is $3.5 million while the distant

second ranked currency, Ripple, has only $0.4 million in market capitalization and all of the

other N-FADs have a market capitalization under $70,000. As such, we approximate our

calculation of Qn by using data solely on bitcoin. Proceeding in this manner, Mn and εf are

10

easily obtained from bitcoincharts.com, for Vf we use the average value of velocity of M2

money provided by the Federal Reserve8, and Pf is measured by the CPI.

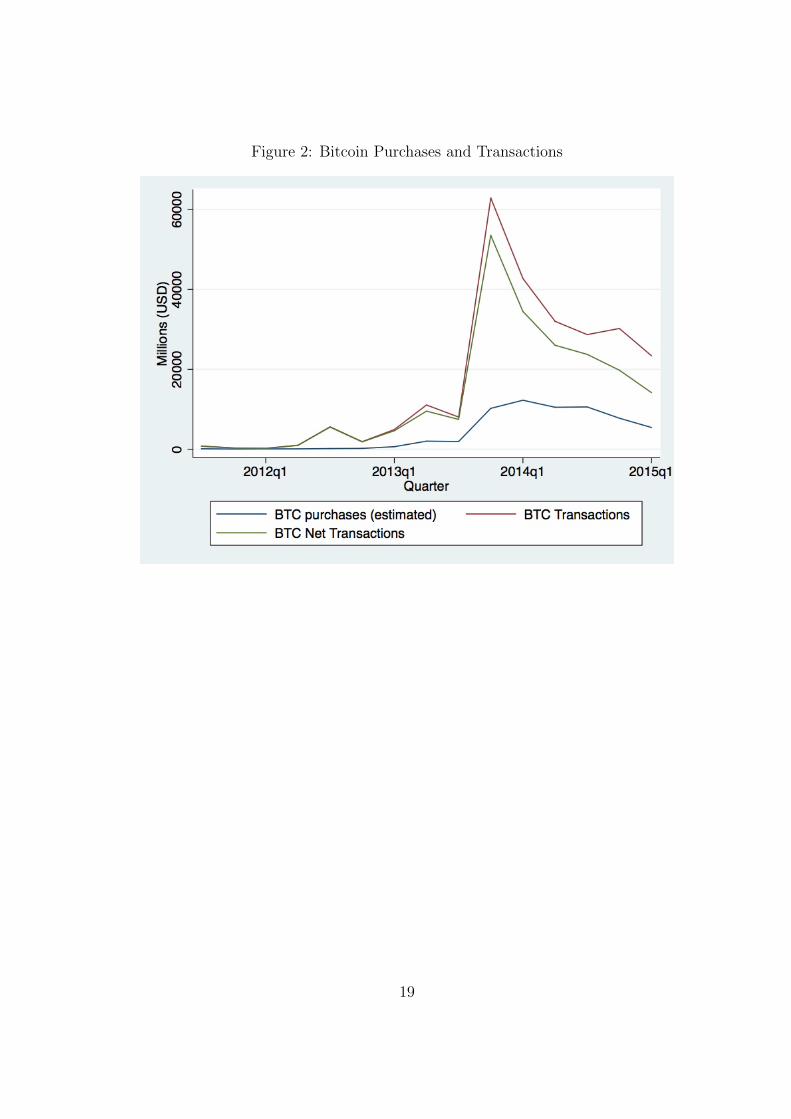

We display our estimates of bitcoin purchases of goods and services converted to millions

of U.S. 2008 dollars as well as actual transactions (transfers of bitcoin from one wallet to

another) and transactions net of trades for fiat for comparison in Figure 2. The transactions

data come from blockchain.info, which takes the data directly from the public ledger, and the

net transactions are calculated by adding up all recorded transactions of bitcoin for currency

on the all the exchange markets listed on bitcoincharts.com and subtracting them from the

total amount of transactions.9 In this way we remove a large portion of transactions that

we can confirm were not for goods and services but for other (sometimes fiat, sometimes

N-FAD) currency.

Although we do not observe what was purchased with each transaction and therefore

cannot directly comment on how well the model predicts purchases made with bitcoin, the

estimated purchases series does fluctuate in harmony with the net transactions measure.

The remaining net transactions not accounted for by our estimated purchases of goods and

services would include payments of debt, trades for fiat not occurring on the exchanges,

and of course transactions between wallets owned by the same individual or entity meant

to obfuscate the movement of funds. The latter has the potential to make up a substantial

portion of net transactions. For example, if a bitcoin user purchased a good or services

worth 100BTC, he may pay 500BTC and have the change (400BTC) paid back to separate

wallets to mask his activity. The recorded transactions would be 900BTC even though only

100BTC of goods or services were purchased.10

8Although our model assumes velocity is constant while the M2 measure of velocity does change overour time period, its variation is not great. Replacing the average value in our time frame with a quarterlymeasure measure does not alter our predictions substantially.

9The trade data on bitcoincharts is self-reported by the exchanges and so is not guaranteed to containall currency trades. In particular, it will not include currency trades that occurred between private partiesnot using exchanges.

10[5] provides an alternative measure of bitcoin used to purchase goods and services. The authors measurehow active wallets are as a function of the period of time between transactions. One could then potentiallycalculate a direct estimate of the number of times a bitcoin changes wallets for the purpose of purchase versesthe purpose of masking transactions. The drawback of this method is that it would involve assumptions onwhat type of behavior is likely masking activity.

11

Not all purchases carried out with bitcoin occur in the U.S. Since the net transaction

volume in Figure 2 measures all transactions regardless of geography, the graph is an upper

bound of potential purchases of goods and services using bitcoin in the U.S. Another point

to consider is the emergence of alternative N-FAD’s (sometimes referred collectively to as

“altcoins”). Specifically, the second and third largest N-FAD’s by market capitalization (as

of the writing of this paper), Ripple and Litecoin, started to gain significant market share

in 2013 although their acceptance by merchants is significantly less than that of bitcoin.

Therefore the difference between net transactions of all N-FAD’s (not just bitcoin) and our

predicted purchases of goods and services using N-FAD’s is likely a little more than what we

observe in Figure 2.

With these caveats in mind, our calculations suggest that purchases of goods and services

via N-FAD’s ranged from approximately $42 million to $13 billion between 2011 and 2015.

4 N-FAD and Monetary Policy

The simple model provided above can also calculate how much the presence of the N-FAD

distorts the monetary authority’s ability to target inflation. With the presence of the N-

FAD, inflation will no longer increase one-for-one with an increase in the money supply but

rather it will increase proportionately with money supply according to the fraction of goods

and services purchased with the fiat currency. Solving Equation 3.6 for πf and taking the

partial derivative with respect to the fiat money supply, we have

∂πf∂mf

=Qf

Qf +Qn

. (4.1)

The more the economy switches from using fiat to the N-FAD, holding Q constant, the less

control the monetary authority will have over inflation in fiat prices. We calculate Equation

4.1 by using our estimates of Qn and real GDP as our measure of Qf .

12

In addition, any increase in the supply of the N-FAD will increase inflation in fiat terms

for any fixed growth of fiat money supply. We can similarly show this by solving the partial

derivative of Equation 3.6 solved for πf with respect to the N-FAD money supply,

∂πf∂mn

=Qn

Qf +Qn

, (4.2)

which is simply 1 − ∂πf∂mf

. Given the small amount of purchases made with bitcoin relative

to those made with fiat, the estimates for Equation 4.1 and 4.2 are very close to 1 and 0

respectively in every quarter of our time period. In addition, when all bitcoin are mined and

the money supply no longer increases, bitcoin will no longer affect fiat denominated inflation

via Equation 4.2. However, if other N-FAD’s become widely used and/or have non-fixed

money supplies, their money supply could potentially be a concern for central banks aiming

to control inflation. We conclude that as of today, the presence of N-FAD’s, or at least

bitcoin, is likely not yet interfering with monetary policy but theoretically has the potential

to do so.

Lastly, consider inflation tax avoidance as motivation for using N-FAD’s. By symmetry

of our model, it follows that

∂πn∂mf

=Qf

Qf +Qn

(4.3)

so that the introduction of the N-FAD will not completely protect users from the inflation

tax imposed by the central bank as is ideal for many N-FAD creators and users. It will,

however, dampen the effect with the dampening being proportional to the economic activity

carried out via the N-FAD. More to the point, N-FAD’s will require widescale adoption before

one of the purported benefits of their existence can be realized. Since N-FAD purchases are

extremely small relative to overall economic activity in the U.S., current users are unlikely

to feel any protection from inflation.

13

5 Discussion

The introduction of N-FAD’s into financial markets has created new ways of transferring

wealth without the use of a centralized monetary authority. In addition, users of N-FAD’s

enjoy a degree of anonymity not available when conducting financial transactions using fiat

currencies. Part of the motivation for creating an N-FAD is to avoid monetary authorities’

ability to deflate the value of currency held by increasing the money supply. What we show

with our simple model is that the widescale adoption of N-FAD’s would help consumers

avoid the inflation tax, but it would also dampen the monetary authority’s ability to control

inflation of prices denominated in fiat.

In the absence of N-FADs (Qn = ∆Qn = 0), Equation 3.6 collapses to the traditional

money supply/inflation relationship and the essence of a straight-forward price stabilization

policy is preserved. However, what Equation 3.6 highlights is that the presence of an N-

FAD with a fluctuating rate of exchange makes a price stabilizing policy more difficult to

implement.

Given that the demand for bitcoin is currently derived from a relatively small number

of individuals who can overcome the fixed costs of entering and understanding the N-FAD

market, the likelihood of public interference prior to wide-spread transacting may be likely.

With the recent IRS notification that N-FAD transactions are taxable, those using N-FADs

for illicit transactions can add tax evasion to their list of legal offenses. When those using

bitcoin realize that the precautionary motive (i.e., the need for avoiding sanctions associated

with illicit transactions) is no longer valid because of the high probability of public seizure

and increasing punishments, they may abandon the currency and the value of bitcoin would

dramatically decrease if these users are the majority.

Bitcoin and other N-FAD’s have already begun to suffer attacks from established financial

institutions. In April of 2014, the lobbying firm Peck Madigan Jones registered five employees

to lobby Congress on virtual currencies on behalf of Mastercard [6]. Credit card companies

charge fees to businesses when customers make purchases using credit or debit cards. They

stand to potentially lose a significant portion of their market share in financial transaction

14

services to N-FAD’s, which come with little to no fees for usage. The state of New York

is also, at the time we write this paper, proposing legislation to enforce strict regulation

of any person or business that makes use of virtual currency including the maintenance

of transaction and personal information of all customers making purchases with virtual

currencies for ten years [13].

However, there are parities outside of consumers who have much to gain from the presence

of N-FAD’s. Merchants may have an even stronger demand for N-FAD’s than consumers.

With $79 trillion dollars transacted in 2012 via non-cash payments, even a small reduction

in fees paid by merchants by switching to N-FAD’s could reap trillions of dollars of savings.

Since merchants collectively have much to gain from avoiding credit card fees, one may

expect a movement for merchants to protect the legality of N-FAD’s.

While the regulation and adoption of N-FAD’s continues to increase, according to our

estimates the current amount of goods and services purchased with N-FAD’s is extremely

small relative to total GDP of the U.S. economy. In the first few years of existence, we

estimate that the purchase of goods and services in the U.S. economy using N-FAD’s ranged

from $42 million to $13 billion. Thus, it is unlikely that N-FAD’s will soon interfere with

monetary policy although they do posses the ability to do so given widescale adoption.

6 Appendix

Consider a closed economy with no fiscal government, no stochastic disturbances, and only

two payment methods: fiat currency (f) and an N-FAD (n). The model can be described by

C

P= f

(Y

P, r

)(6.1)

I

P= g(r) (6.2)

Y

P=C

P+I

P(6.3)

15

Y

P= y0 (6.4)

MDj = Pj · `j

(Y

P, r, εf

)for j ∈ {f, n} (6.5)

MSj = hj(r) (6.6)

MDj = MS

j (6.7)

Pf = εfPn (6.8)

Equations 6.1 through 6.4 are self-contained and combine to yield

y0 = f (y0, r) + g(r), (6.9)

which in principle can be solved for r = r0. Plugging this value into Equation 6.5 and

combining with the result with Equations 6.6 and 6.7 yields

hf (r0) ≡M f = Pf · `f (y0, r0, εf ) (6.10)

and

fn(r0) ≡Mn = Pn · `f (y0, r0, εf ), (6.11)

which can be solved for in terms of prices

Pf = θf (εf ) (6.12)

and

Pn = θn(εf ) (6.13)

16

Finally, Equations 6.12 and 6.13 combined with 6.8 can be used to determine εf . Plugging

this value back into Equations 6.10 and 6.11, multiplying and dividing both sides of each

equation by y0, and replacing `j(y + 0, r0) with its velocity equivalent 1Vj

, we have

MfVf = Pfy0 (6.14)

and

MnVn = Pny0 (6.15)

or

εfMnVn = εfPny0 (6.16)

Adding Equations 6.14 and 6.16 will yield Equation 3.1.

17

7 Graphs

Figure 1: USD/Bitcoin (BTC) Exchange Rate

020

040

060

080

010

0012

00U

SD ($

)

01jan2010 01jan2011 01jan2012 01jan2013 01jan2014 01jan2015date

Source: bitcoincharts.com

18

Figure 2: Bitcoin Purchases and Transactions

19

References

[1] url: http://www.blockchain.info.

[2] url: http://moneymorning.com/2014/08/15/check-out-how-many-overstock-sales-are-done-using-bitcoin/.

[3] url: https://support.coinbase.com/customer/portal/articles/585625-what-is-coinbase-and-how-much-does-it-cost-to-use-.

[4] 18 U.S.C. §336. 1862.

[5] Anton I Badev and Matthew Chen. “Bitcoin: Technical Background and Data Analy-sis”. In: (2014).

[6] Perianne Boring. SEC’s Investor “Warning” On Bitcoin Could Stifle Innovation. url:http://www.forbes.com/sites/perianneboring/2014/05/09/secs-investor-

warning-on-bitcoin-could-stifle-innovation/.

[7] Adrian Cheung, Eduardo Roca, and Jen-Je Su. “Crypto-currency bubbles: an applica-tion of the Phillips-Shi-Yu (2013) methodology on Mt. Gox bitcoin prices”. In: AppliedEconomics 47.23 (2015), pp. 2348–2358.

[8] Kyt Dotson. Third Largest Bitcoin Exchange Bitomat Lost Their Wallet, Over 17,000Bitcoins Missing. url: http://siliconangle.com/blog/2011/08/01/third-

largest-bitcoin-exchange-bitomat-lost-their-wallet-over-17000-bitcoins-

missing/.

[9] Milton Friedman. “A theoretical framework for monetary analysis”. In: The Journalof Political Economy (1970), pp. 193–238.

[10] Stephanie Lo and J Christina Wang. “Bitcoin as money?” In: Federal Reserve Bank ofBoston (2014).

[11] Robert McMillan. The Inside Story of Mt. Gox, Bitcoin’s $460 Million Disaster. url:http://wired.com/2014/03/bitcoin-exchange.

[12] Satoshi Nakamoto. “Bitcoin: A peer-to-peer electronic cash system”. In: Consulted1.2012 (2008), p. 28.

[13] New York State Department of Financial Services Proposed New York Codes, Rules,and Regulations. Title 23 Chapter 1 Part 200.

[14] George Selgin. “Synthetic Commodity Money”. In: Working Paper (2013).

[15] U.S. Department of the Treasury. Notice 2014-21. IRS Publication. Internal RevenueService, 2014.

[16] David Yermack. Is Bitcoin a Real Currency? Tech. rep. National Bureau of EconomicResearch, 2013.

20

Copyright © 2022 FDOKUMEN