Various sources of funds for business Highlighting their Advantages and Disadvantages

30

JOMO KENYATTA UNIVERSITY OF AGRICULTURE AND TECHNOLOGY MSc. PROJECT MANAGEMENT HEPM 3108: ACCOUNTING AND FINANCIAL MANAGEMENT Individual Assignment Topic: Various sources of funds for business Highlighting their Advantages and Disadvantages Presenter: Joshua Kibiti M’Aburi – Reg. No: HD317-C004-0789/2015 Presented to: Mr. Terer (Lecturer) Date: March 2015

Transcript of Various sources of funds for business Highlighting their Advantages and Disadvantages

i

JOMO KENYATTA UNIVERSITY OF AGRICULTURE AND TECHNOLOGY

MSc. PROJECT MANAGEMENT

HEPM 3108: ACCOUNTING AND FINANCIAL MANAGEMENT

Individual Assignment

Topic: Various sources of funds for business Highlighting their Advantagesand Disadvantages

Presenter: Joshua Kibiti M’Aburi – Reg. No: HD317-C004-0789/2015

Presented to: Mr. Terer (Lecturer)

Date: March 2015

ii

Contents

Page 1.0 Sources of funds for business, their Advantages and Disadvantages

1

1.1 Long Term sources of business financing........................1a) Equity Shares..................................................1

b) Retained earnings..............................................2c) Preference Shares..............................................3

d) Debentures.....................................................4e) Loan from Financial Institutions...............................5

f) Loan from Banks................................................6g) Sale-lease back................................................7

1.2 Medium – Term sources of business financing....................8a) Public deposits................................................8

b) Lease financing................................................9c) Hire purchase:................................................10

1.3 Short Term sources of business finances.......................11a) Bank overdraft................................................11

b) Trade Credit..................................................12c) Factoring.....................................................13

d) Commercial paper..............................................14e) Mortgage /remortgage on a property............................15

f) Funds from investors of shareholders..........................15g) Grants or loans from Government or other organizations........15

h) Venture capital or business angels............................162.0 References 17

i

QUESTION: DISCUSS SOURCES OF FUNDS TO BUSINESS HIGHLIGHTING THEIR

ADVANTAGES AND DISADVANTAGES

1.0 Sources of funds for business, their Advantages and

Disadvantages

1.1 Long Term sources of business financing

Issue of shares

The capital obtained by issue of shares is also known as share

capital. The capital of a company is divided into small units

called shares. Each share has its nominal value. For example, a

company can issue 1million shares of Ksh. 10 each for a total

value of Ksh. 10million. The person holding the share is known as

shareholder. There are two types of shares normally issued by a

company; these are equity shares and preference shares. The money

raised by issue of equity shares is called equity share capital,

while the money raised by issue of preference shares is called

preference share capital.

a) Equity Shares

Equity shares are the most important source of raising long term

capital to a business or a company. Equity shares represent the

ownership of a company and thus the capital raised by issue of

such shares is known as ownership capital or owner’s funds.

1

Equity share capital is a prerequisite to the creation of a

company. Equity shareholders do not get a fixed dividend but are

paid on the basis of earnings by the company. They are referred

to as ‘residual owners’ since they receive what is left after all

other claims on the company’s income and assets have been

settled. They enjoy the reward as well as bear the risk of

ownership. Their liability, however, is limited to the extent of

capital contributed by them in the company. Further, through

their right to vote, these shareholders have a right to

participate in the management of the company.

Advantages Disadvantagesi) The equity shares are suitable

for investors who are willing

to assume risk for higher

returns;

ii) Payment of dividend to the

equity shareholders is not

compulsory. Therefore, there is

no burden on the company in

this respect;

iii) Equity capital serves as

permanent capital as it is to

be repaid only at the time of

liquidation of a company. As it

stands last in the list of

claims, it provides a cushion

i) Investors who want steady

income may not prefer

equity shares as equity

shares get fluctuating

returns;

ii) The cost of equity

shares is generally more

as compared to the cost of

raising funds through

other sources;

iii) Issue of additional

equity shares dilutes the

voting power, and earnings

of existing equity

shareholders;

2

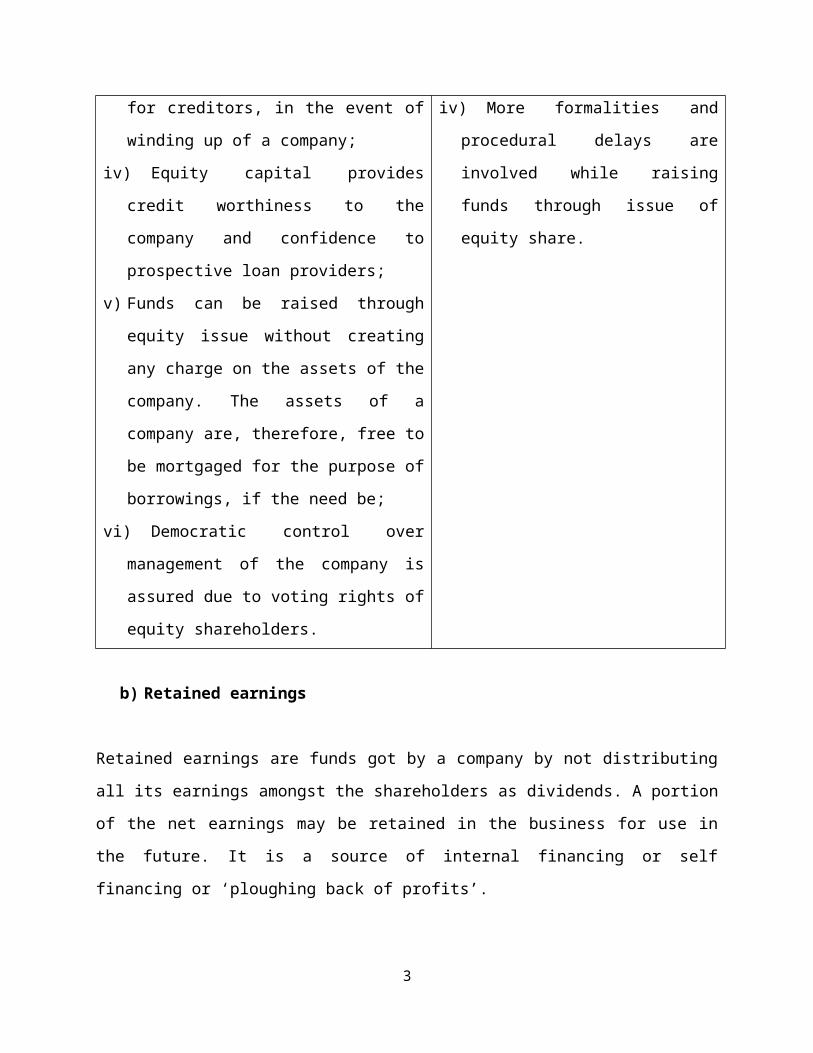

for creditors, in the event of

winding up of a company;

iv) Equity capital provides

credit worthiness to the

company and confidence to

prospective loan providers;

v) Funds can be raised through

equity issue without creating

any charge on the assets of the

company. The assets of a

company are, therefore, free to

be mortgaged for the purpose of

borrowings, if the need be;

vi) Democratic control over

management of the company is

assured due to voting rights of

equity shareholders.

iv) More formalities and

procedural delays are

involved while raising

funds through issue of

equity share.

b) Retained earnings

Retained earnings are funds got by a company by not distributing

all its earnings amongst the shareholders as dividends. A portion

of the net earnings may be retained in the business for use in

the future. It is a source of internal financing or self

financing or ‘ploughing back of profits’.

3

The profit available for ploughing back in an organisation depends on

many factors like net profits, dividend policy and age of the

organisation.

Advantages Disadvantagesi) Retained earnings is a

permanent source of funds

available to an organisation;

ii) It does not involve any

explicit cost in the form of

interest, dividend or

floatation cost;

iii) As the funds are generated

internally, there is a greater

degree of operational freedom

and flexibility;

iv) It enhances the capacity of

the business to absorb

unexpected losses;

v) It may lead to increase in the

market price of the equity

shares of a company.

i) Excessive ploughing back

may cause dissatisfaction

amongst the shareholders

as they would get lower

dividends;

ii) It is an uncertain source

of funds as the profits of

business are fluctuating;

iii) The opportunity cost

associated with these

funds is not recognized by

many firms. This may lead

to sub-optimal use of the

funds.

c) Preference Shares

The capital raised by issue of preference shares is called

preference share capital. The preference shareholders enjoy a

preferential position over equity shareholders in two ways:4

(i) Receiving a fixed rate of dividend, out of the net

profits of the company, before any dividend is declared

for equity shareholders; and

(ii) Receiving their capital after the claims of the company’s

creditors have been settled, at the time of liquidation.

In other words, as compared to the equity shareholders, the

preference shareholders have a preferential claim over dividend

and repayment of capital. Preference shares resemble debentures

as they bear fixed rate of return. Also as the dividend is

payable only at the discretion of the directors and only out of

profit after tax, to that extent, these resemble equity shares.

Thus, preference shares have some characteristics of both equity

shares and debentures. Preference shareholders generally do not

enjoy any voting rights. A company can issue different types of

preference shares.

Advantages Disadvantagesi) Preference shares provide

reasonably steady income in the

form of fixed rate of return

and safety of investment;

ii) Preference shares are useful

for those investors who want

fixed rate of return with

comparatively low risk;

iii) It does not affect the

control of equity shareholders

i) Preference shares are not

suitable for those

investors who are willing

to take risk and are

interested in higher

returns;

ii) Preference capital

dilutes the claims of

equity shareholders over

assets of the company.

5

over the management as

preference shareholders don’t

have voting rights;

iv) Payment of fixed rate of

dividend to preference shares

may enable a company to declare

higher rates of dividend for

the equity shareholders in good

times;

v) Preference shareholders have a

preferential right of repayment

over equity shareholders in the

event of liquidation of a

company;

vi) Preference capital does not

create any sort of charge

against the assets of a

company.

iii) The rate of dividend on

preference shares is

generally higher than the

rate of interest on

debentures.

iv) As the dividend on these

shares is to be paid only

when the company earns

profit, there is no

assured return for the

investors. Thus, these

shares may not be very

attractive to the

investors;

v) The dividend paid is not

deductible from profits as

expense. Thus, there is no

tax saving as in the case

of interest on loans.

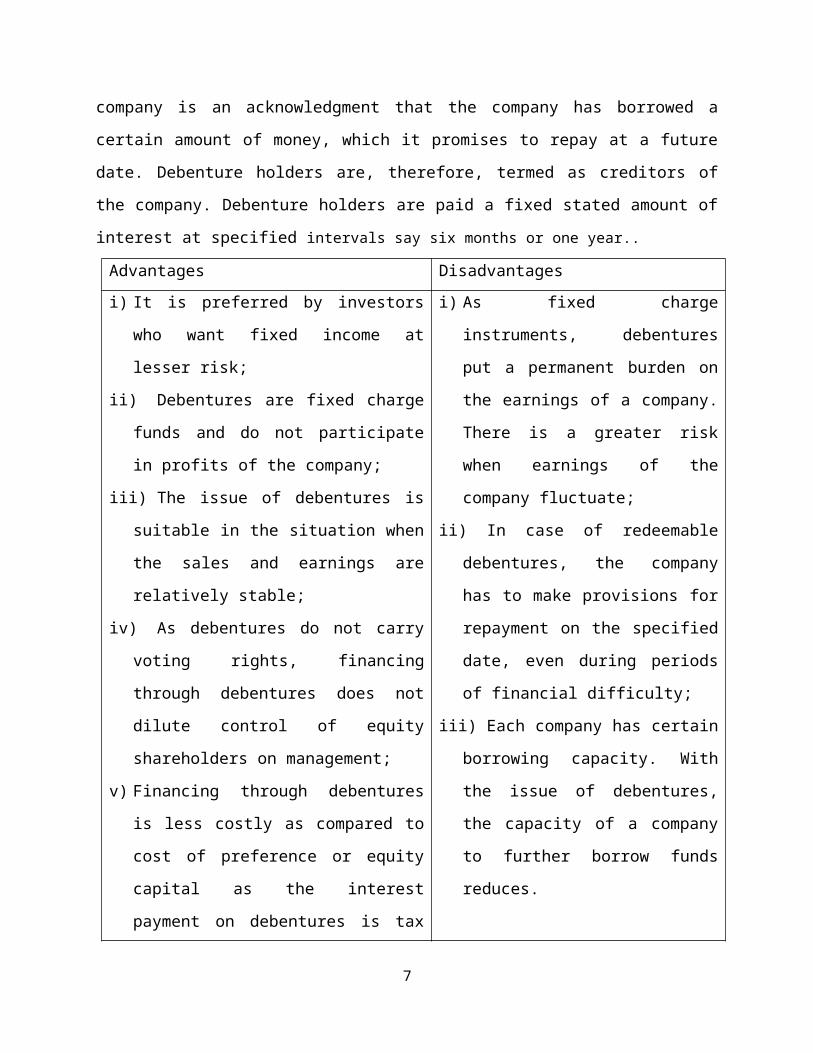

d) Debentures

Debentures are an important instrument for raising long term debt

capital. A company can raise funds through issue of debentures,

which bear a fixed rate of interest. The debenture issued by a

6

company is an acknowledgment that the company has borrowed a

certain amount of money, which it promises to repay at a future

date. Debenture holders are, therefore, termed as creditors of

the company. Debenture holders are paid a fixed stated amount of

interest at specified intervals say six months or one year..

Advantages Disadvantagesi) It is preferred by investors

who want fixed income at

lesser risk;

ii) Debentures are fixed charge

funds and do not participate

in profits of the company;

iii) The issue of debentures is

suitable in the situation when

the sales and earnings are

relatively stable;

iv) As debentures do not carry

voting rights, financing

through debentures does not

dilute control of equity

shareholders on management;

v) Financing through debentures

is less costly as compared to

cost of preference or equity

capital as the interest

payment on debentures is tax

i) As fixed charge

instruments, debentures

put a permanent burden on

the earnings of a company.

There is a greater risk

when earnings of the

company fluctuate;

ii) In case of redeemable

debentures, the company

has to make provisions for

repayment on the specified

date, even during periods

of financial difficulty;

iii) Each company has certain

borrowing capacity. With

the issue of debentures,

the capacity of a company

to further borrow funds

reduces.

7

deductible.

e) Loan from Financial Institutions

The government has established a number of financial institutions

all over the country to provide finance to business

organisations. These institutions are established by the central

as well as state governments. They provide both owned capital and

loan capital for long and medium term requirements and supplement

the traditional financial agencies like commercial banks. As

these institutions aim at promoting the industrial development of

a country, these are also called ‘development banks’. In addition

to providing financial assistance, these institutions also

conduct market surveys and provide technical assistance and

managerial services to people who run the enterprises. This

source of financing is considered suitable when large funds for

longer duration are required for expansion, re-organisation and

modernisation of an enterprise.

Advantages Disadvantages(i)Financial institutions provide

long-term finance, which are

not provided by commercial

banks;

(ii) Besides providing funds, many

of these institutions provide

financial, managerial and

(i) Financial institutions

follow rigid criteria for

grant of loans. Too many

formalities make the

procedure time consuming

and expensive

(ii) Certain restrictions

8

technical advice and

consultancy to business firms;

(iii) Obtaining loan from

financial institutions

increases the goodwill of the

borrowing company in the

capital market. Consequently,

such a company can raise funds

easily from other sources as

well;

(iv) As repayment of loan can be

made in easy installments, it

does not prove to be much of a

burden on the business;

(v)The funds are made available

even during periods of

depression, when other sources

of finance are not available.

such as restriction on

dividend payment are

imposed on the powers of

the borrowing company by

the financial

institutions;

(iii) Financial

institutions may have

their nominees on the

Board of Directors of the

borrowing company thereby

restricting the powers of

the company.

f) Loan from Banks

Commercial banks occupy a vital position as they provide funds

for different purposes as well as for different time periods.

Banks extend loans to firms of all sizes and in many ways, like,

cash credits, overdrafts, term loans, purchase/discounting of

bills, and issue of letter of credit. The rate of interest

charged by banks depends on various factors such as the

9

characteristics of the firm and the level of interest rates in

the economy. The loan is repaid either in lump sum or in

installments. Bank credit is not a permanent source of funds.

Though banks have started extending loans for longer periods,

generally such loans are used for medium to short periods. The

borrower is required to provide some security or create a charge

on the assets of the firm before a loan is sanctioned by acommercial bank.

Advantages Disadvantagesi) Banks provide timely assistance

to business by providing funds

as and when needed by it.

ii) Secrecy of business can be

maintained as the information

supplied to the bank by the

borrowers is kept confidential;

iii) Formalities such as issue of

prospectus and underwriting are

not required for raising loans

from a bank. This, therefore,

is an easier source of funds;

iv) Loan from a bank is a

flexible source of finance as

the loan amount can be

increased according to business

needs and can be repaid in

i) Funds are generally

available for short

periods and its extension

or renewal is uncertain

and difficult;

ii) Banks make detailed

investigation of the

company’s affairs,

financial structure etc.,

and may also ask for

security of assets and

personal sureties. This

makes the procedure of

obtaining funds slightly

difficult;

iii) In some cases, difficult

terms and conditions are

10

advance when funds are not

needed.

imposed by banks. For the

grant of loan. For

example, restrictions may

be imposed on the sale of

mortgaged goods, thus

making normal business

working difficult.

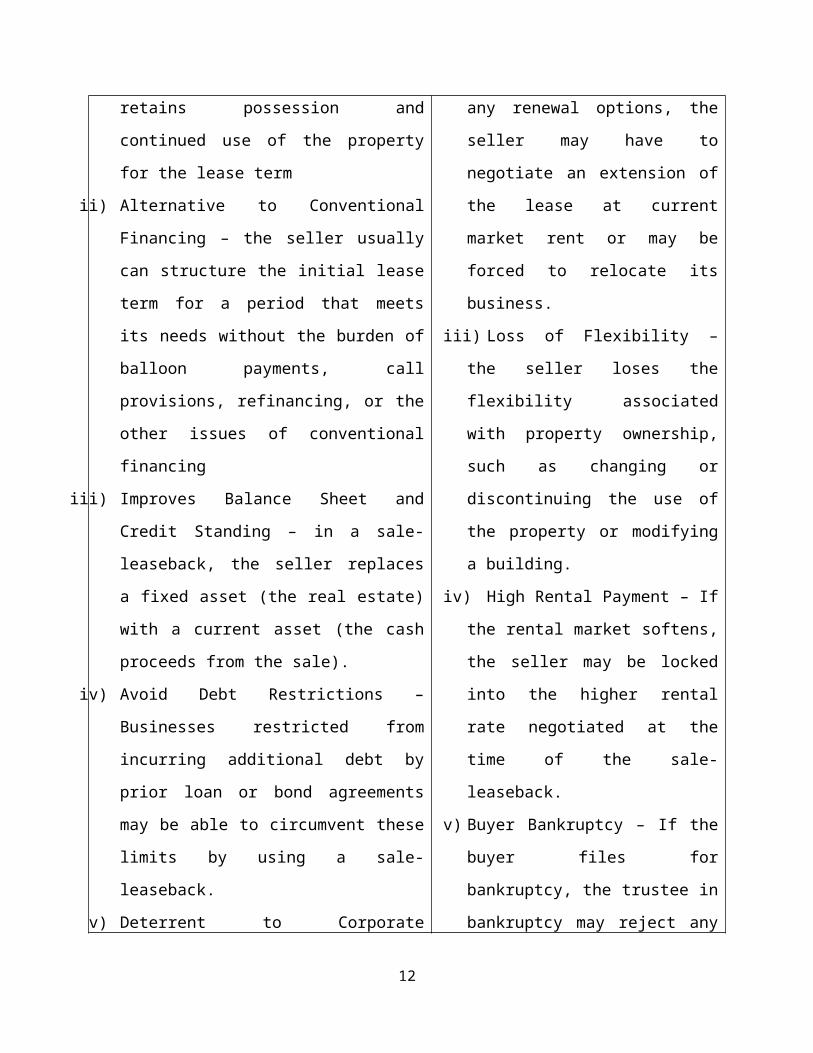

g) Sale-lease back

This involves a firm selling its assets or property to an

investment company. Simultaneously with the sale, the property is

leased back to the seller for mutually agreed-upon period,

usually 20 to 30 years. The business thus can use the asset

without purchasing it and can use the revenue earned from its

sale for other purposes. The sale-leaseback may include either or

both the land and the improvements. Lease payments typically are

fixed to provide for amortization of the purchase price over the

term of the lease plus a specified return rate on the buyer’s

investment.

Seller

Advantages Disadvantagesi) Converts Equity into Cash – the

seller regains use of the

capital that otherwise would be

tied up in property ownership;

at the same time, the seller

i) Loss of Residual Property

Value – seller transfers

title to the buyer.

ii) Possible Relocation – At

the end of a lease without

11

retains possession and

continued use of the property

for the lease term

ii) Alternative to Conventional

Financing – the seller usually

can structure the initial lease

term for a period that meets

its needs without the burden of

balloon payments, call

provisions, refinancing, or the

other issues of conventional

financing

iii) Improves Balance Sheet and

Credit Standing – in a sale-

leaseback, the seller replaces

a fixed asset (the real estate)

with a current asset (the cash

proceeds from the sale).

iv) Avoid Debt Restrictions –

Businesses restricted from

incurring additional debt by

prior loan or bond agreements

may be able to circumvent these

limits by using a sale-

leaseback.

v) Deterrent to Corporate

any renewal options, the

seller may have to

negotiate an extension of

the lease at current

market rent or may be

forced to relocate its

business.

iii) Loss of Flexibility –

the seller loses the

flexibility associated

with property ownership,

such as changing or

discontinuing the use of

the property or modifying

a building.

iv) High Rental Payment – If

the rental market softens,

the seller may be locked

into the higher rental

rate negotiated at the

time of the sale-

leaseback.

v) Buyer Bankruptcy – If the

buyer files for

bankruptcy, the trustee in

bankruptcy may reject any

12

Takeovers – Undervalued real

estate on a company’s books

often serves as a target for

corporate raiders. A timely

liquidation through a sale-

leaseback transaction may serve

as a deterrent, providing

management with funding to

resist the takeover. In

addition, a long-term lease is

not as inviting to raiders as

undervalued real estate.

vi) Avoids Usury Limitations –

Because a sale-leaseback is not

considered a loan, state usury

laws do not apply; a buyer in a

sale-leaseback can earn a

higher rate of return on its

investment than if it had made

a conventional mortgage loan to

the property owner

agreement to renew the

leaseback or the seller’s

option to purchase the

property.

vi) Higher Cost of Financing

– The interest rate is

higher than what the owner

would pay through

conventional mortgage

financing.

1.2 Medium – Term sources of business financing

a) Public depositsThe deposits that are raised by organisations directly from the public

are known as public deposits. Rates of interest offered on public

deposits are usually higher than that offered on bank deposits. Any13

person who is interested in depositing money in an organisation can do

so by filling up a prescribed form. The organisation in return issues

a deposit receipt as acknowledgment of the debt. Public deposits can

take care of both medium and short-term financial requirements of a

business. The deposits are beneficial to both the depositor as well as

to the organisation. While the depositors get higher interest rate

than that offered by banks, the cost of deposits to the company is

less than the cost of borrowings from banks. Companies generally

invite public deposits for a period up to three years.

Advantages Disadvantagesi) The procedure of obtaining

deposits is simple and does not

contain restrictive conditions

as are generally there in a

loan agreement;

ii) Cost of public deposits is

generally lower than the cost

of borrowings from banks and

financial institutions;

iii) Public deposits do not usually

create any charge on the assets

of the company. The assets can

be used as security for raising

loans from other sources;

iv) As the depositors do not have

voting rights, the control of

the company is not diluted.

i) New companies generally

find it difficult to raise

funds through public

deposits;

ii) It is an unreliable source

of finance as the public

may not respond when the

company needs money;

iii) Collection of public

deposits may prove

difficult, particularly

when the size of deposits

required is large.

14

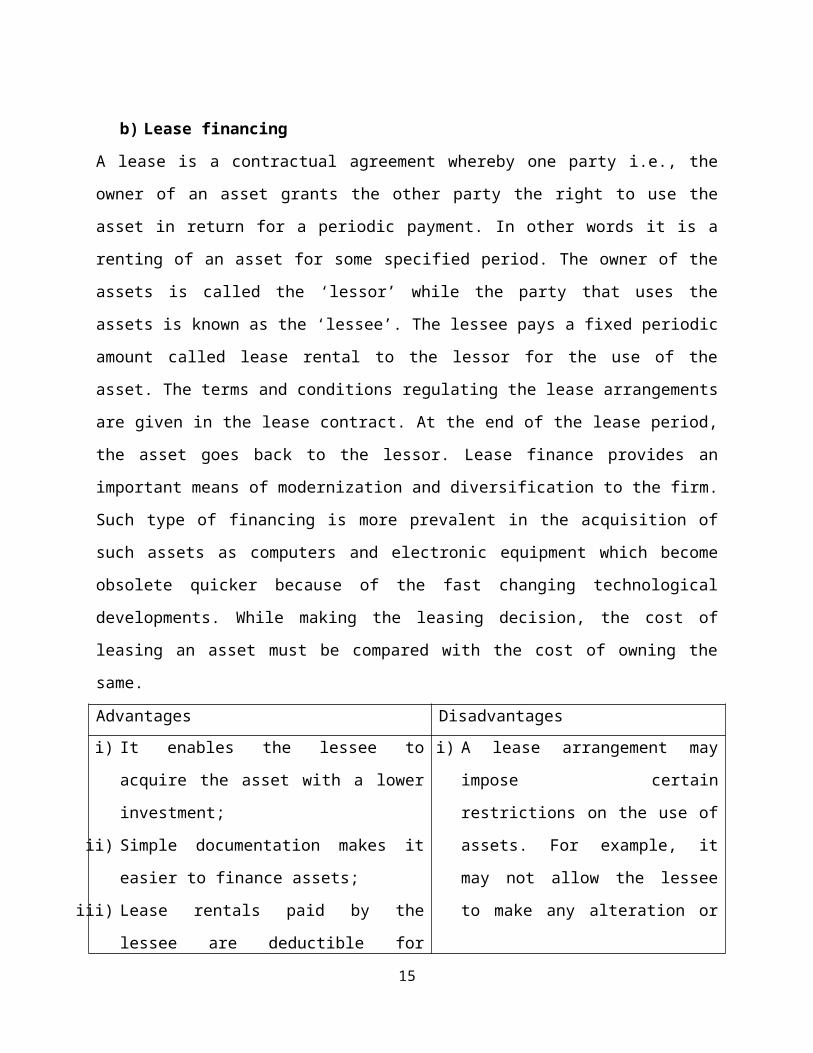

b) Lease financing

A lease is a contractual agreement whereby one party i.e., the

owner of an asset grants the other party the right to use the

asset in return for a periodic payment. In other words it is a

renting of an asset for some specified period. The owner of the

assets is called the ‘lessor’ while the party that uses the

assets is known as the ‘lessee’. The lessee pays a fixed periodic

amount called lease rental to the lessor for the use of the

asset. The terms and conditions regulating the lease arrangements

are given in the lease contract. At the end of the lease period,

the asset goes back to the lessor. Lease finance provides an

important means of modernization and diversification to the firm.

Such type of financing is more prevalent in the acquisition of

such assets as computers and electronic equipment which become

obsolete quicker because of the fast changing technological

developments. While making the leasing decision, the cost of

leasing an asset must be compared with the cost of owning the

same.

Advantages Disadvantagesi) It enables the lessee to

acquire the asset with a lower

investment;

ii) Simple documentation makes it

easier to finance assets;

iii) Lease rentals paid by the

lessee are deductible for

i) A lease arrangement may

impose certain

restrictions on the use of

assets. For example, it

may not allow the lessee

to make any alteration or

15

computing taxable profits;

iv) It provides finance without

diluting the ownership or

control of business;

v) The lease agreement does not

affect the debt raising

capacity of an enterprise;

vi) The risk of obsolescence is

borne by the lesser. This

allows greater flexibility to

the lessee to replace the

asset.

vii) Usually the maintenance of the

asset is done by the leasing

firm.

modification in the asset;

ii) The normal business

operations may be affected

in case the lease is not

renewed;

iii) It may result in higher

payout obligation in case

the equipment is not found

useful and the lessee opts

for premature termination

of the lease agreement;

and

iv) The lessee never becomes

the owner of the asset. It

deprives him of the

residual value of the

asset.

v) The total cost of leasing

may end up higher than the

purchasing of asset

c) Hire purchase: It involves purchasing an asset paying for it over a period of time.

Usually a percentage of the price is paid as down payment and the rest

is paid in instalments for the period of time agreed upon. The

business has to pay an interest on these instalments.

Advantages Disadvantages

16

i) Convenience in Payment – the

buyer is greatly benefited as

he has to make the payment in

installments.

ii) Increased Volume Of Sales –

this system attracts more

customers as the payment is to

be made in easy installments.

This leads to increased volume

of sales.

iii) Increased Profits – Large

volume of sales ensures

increased profits to the

seller.

iv) Encourages Savings –It

encourages thrift among the

buyers who are forced to save

some portion of their income

for the payment of the

installments. This inculcates

the habit to save among the

people.

v) Helpful For Small Traders –

this system is a blessing for

the small manufacturers and

traders. They can purchase

i) Higher Price – A buyer has

to pay higher price for

the article purchased

which includes cost plus

interest. The rate of

interest is quite high.

ii) Artificial Demand – Hire

purchase system creates

artificial demand for the

product. The buyer is

tempted to purchase the

products, even if he does

not need or afford to buy

the product.

iii) Heavy Risk – the seller

runs a heavy risk under

such system, though he has

the right to take back the

articles from the

defaulting customers. The

second hand goods fetch

little price.

iv) Difficulties in Recovery

of Installments – It has

been observed that the

sellers do not get the

17

machinery and other equipment

on installment basis and in

turn sell to the buyer charging

full price.

vi) Earning Of Interest – the

seller gets the installment

which includes original price

and interest.

vii) Lesser Risk – from the point

of view of seller this system

is greatly beneficial as he

knows that if the buyer fails

to pay one installment, he can

get the article back.

installments from the

purchasers on time.

v) Break Up Of Families – the

system puts a great

financial burden on the

organisations which cannot

afford to buy costly and

luxurious items.

1.3 Short Term sources of business finances

a) Bank overdraftBank overdraft is a facility given by banks to its business customers.

Through this facility the customers can overdraw their accounts to a

greater value than the balance in the account. The overdrawn amount is

agreed in advance with the bank manager. The bank assigns a limit to

overdraw from the account and the business can meet its short term

liabilities by writing cheques to the extent of limit allowed.

Advantage Disadvantage

i) No need for collaterals or

security.

i) Interest rates are usually

variable and higher than bank

18

ii) More flexible and the

overdraft amount can be

adjusted every month

according to needs.

loans

ii) Cash flow problems can

arise if the bank asks for

the overdraft to be repaid at

a short notice.

b) Trade Credit

Trade credit is the credit extended by one trader to another for

the purchase of goods and services. Trade credit facilitates the

purchase of supplies without immediate payment. Such credit

appears in the records of the buyer of goods as ‘sundry

creditors’ or ‘accounts payable’. This can range from 1 week to

90 days depending upon the type of business and industry.Tradecredit is commonly used by business organisations as a source of

short-term financing. It is granted to those customers who have

reasonable amount of financial standing and goodwill. The volume and

period of credit extended depends on factors such as reputation of the

purchasing firm, financial position of the seller, volume of

purchases, past record of payment and degree of competition in the

market. Terms of trade credit may vary from one industry to another

and from one person to another. A firm may also offer different credit

terms to different customers.

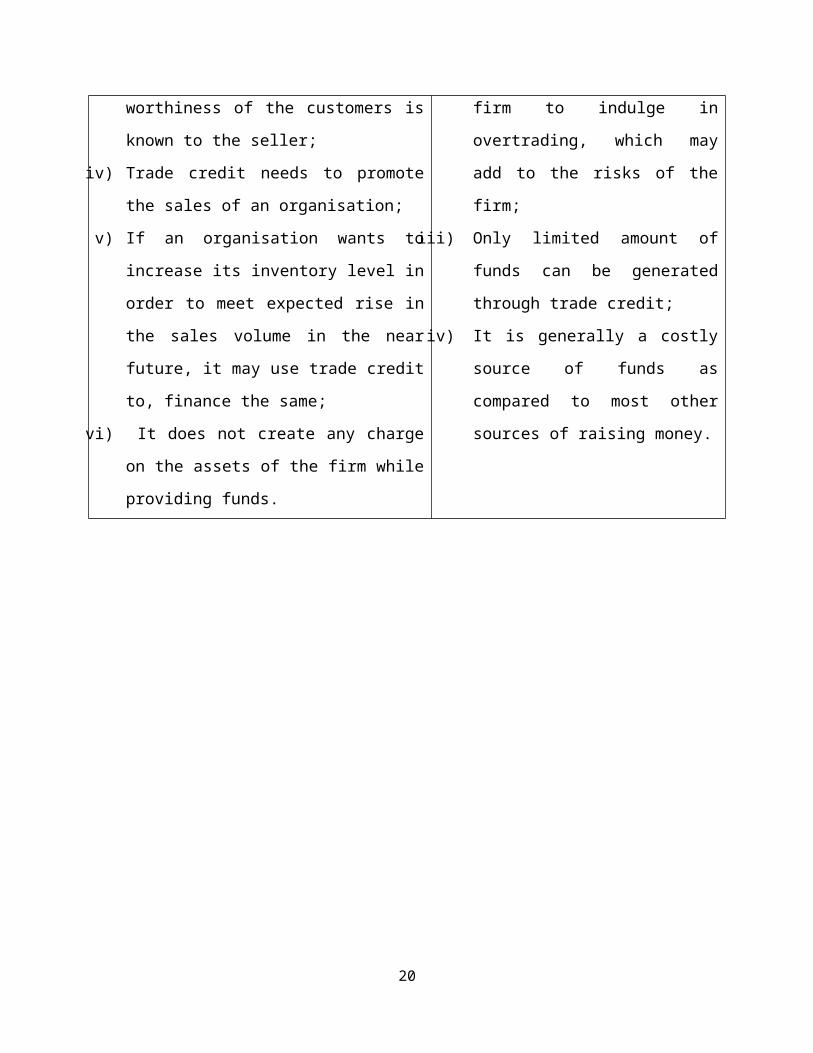

Advantages Disadvantagesi) No interest has to be paid

ii) Trade credit is a convenient

and continuous source of funds;

iii) Trade credit may be readily

available in case the credit

i) The business may not get

cash discounts

ii) Availability of easy and

flexible trade credit

facilities may induce a19

worthiness of the customers is

known to the seller;

iv) Trade credit needs to promote

the sales of an organisation;

v) If an organisation wants to

increase its inventory level in

order to meet expected rise in

the sales volume in the near

future, it may use trade credit

to, finance the same;

vi) It does not create any charge

on the assets of the firm while

providing funds.

firm to indulge in

overtrading, which may

add to the risks of the

firm;

iii) Only limited amount of

funds can be generated

through trade credit;

iv) It is generally a costly

source of funds as

compared to most other

sources of raising money.

20

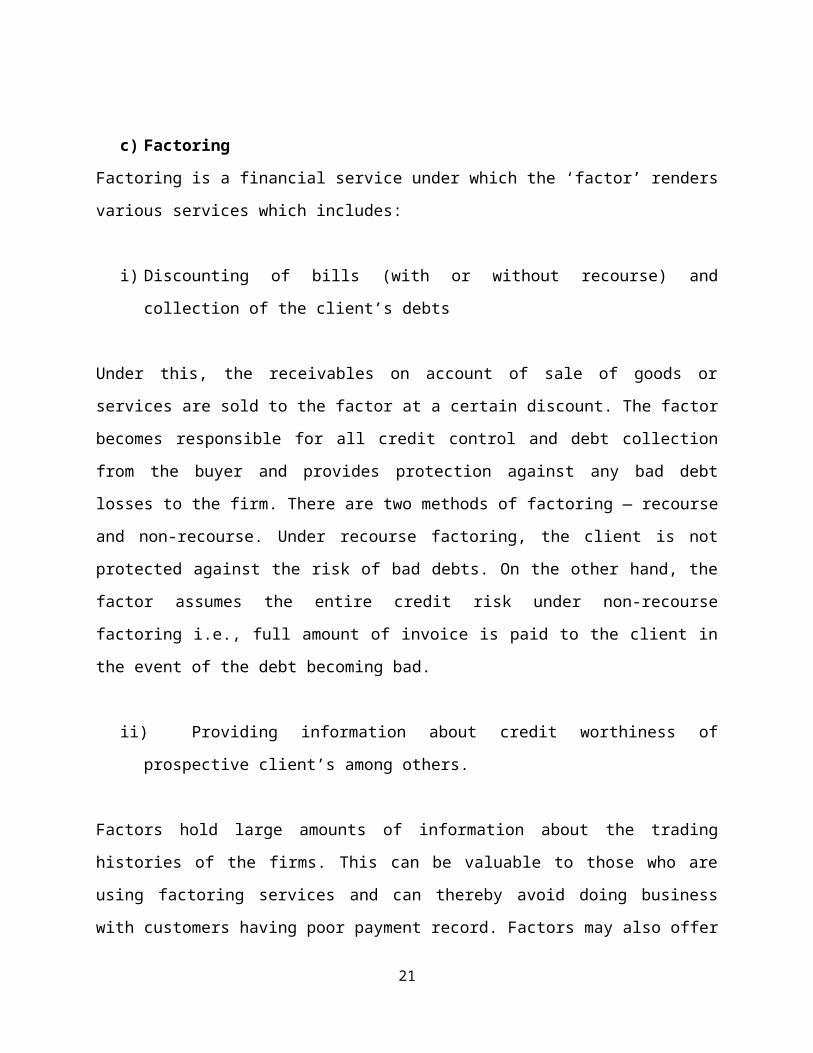

c) Factoring

Factoring is a financial service under which the ‘factor’ renders

various services which includes:

i) Discounting of bills (with or without recourse) and

collection of the client’s debts

Under this, the receivables on account of sale of goods or

services are sold to the factor at a certain discount. The factor

becomes responsible for all credit control and debt collection

from the buyer and provides protection against any bad debt

losses to the firm. There are two methods of factoring — recourse

and non-recourse. Under recourse factoring, the client is not

protected against the risk of bad debts. On the other hand, the

factor assumes the entire credit risk under non-recourse

factoring i.e., full amount of invoice is paid to the client in

the event of the debt becoming bad.

ii) Providing information about credit worthiness of

prospective client’s among others.

Factors hold large amounts of information about the trading

histories of the firms. This can be valuable to those who are

using factoring services and can thereby avoid doing business

with customers having poor payment record. Factors may also offer

21

relevant consultancy services in the areas of finance, and

marketing, among others. The factor charges fees for the services

rendered.

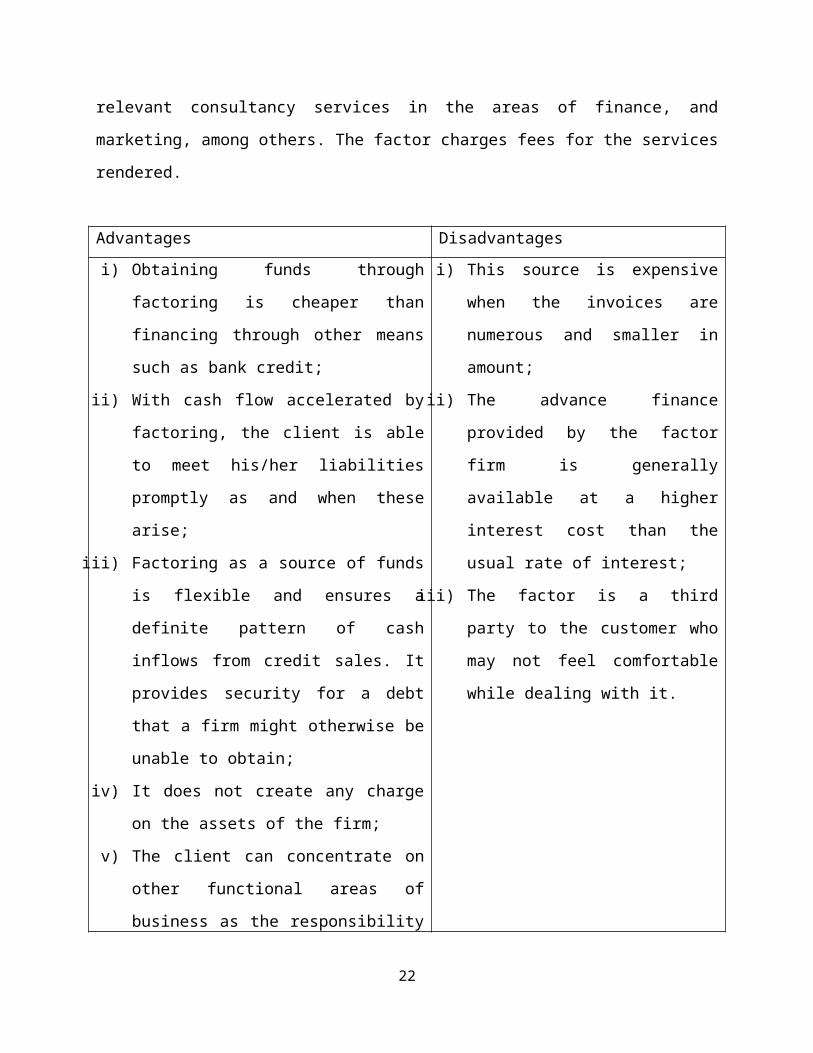

Advantages Disadvantagesi) Obtaining funds through

factoring is cheaper than

financing through other means

such as bank credit;

ii) With cash flow accelerated by

factoring, the client is able

to meet his/her liabilities

promptly as and when these

arise;

iii) Factoring as a source of funds

is flexible and ensures a

definite pattern of cash

inflows from credit sales. It

provides security for a debt

that a firm might otherwise be

unable to obtain;

iv) It does not create any charge

on the assets of the firm;

v) The client can concentrate on

other functional areas of

business as the responsibility

i) This source is expensive

when the invoices are

numerous and smaller in

amount;

ii) The advance finance

provided by the factor

firm is generally

available at a higher

interest cost than the

usual rate of interest;

iii) The factor is a third

party to the customer who

may not feel comfortable

while dealing with it.

22

of credit control is

shouldered by the factor.

d) Commercial paper

Commercial Paper emerged as a source of short term finance in

India in the early nineties. Commercial paper is an unsecured

promissory note issued by a firm to raise funds for a short period,

varying from 90 days to 364 days. It is issued by one firm to other

business firms, insurance companies, pension funds and banks. The

amount raised by CP is generally very large. As the debt is totally

unsecured, the firms having good credit rating can issue the CP. Its

regulation comes under the purview of the Reserve Bank of India.

Advantages Disadvantagesi) A commercial paper is sold on

an unsecured basis and does not

contain any restrictive

conditions;

ii) As it is a freely transferable

instrument, it has high

liquidity;

iii) It provides more funds compared

to other sources. Generally,

the cost of CP to the issuing

firm is lower than the cost of

commercial bank loans;

iv) A commercial paper provides a

i) Only financially sound and

highly rated firms can

raise money through

commercial papers. New and

moderately rated firms are

not in a position to raise

funds by this method;

ii) The size of money that can

be raised through

commercial paper is

limited to the excess

liquidity available with

the suppliers of funds at

23

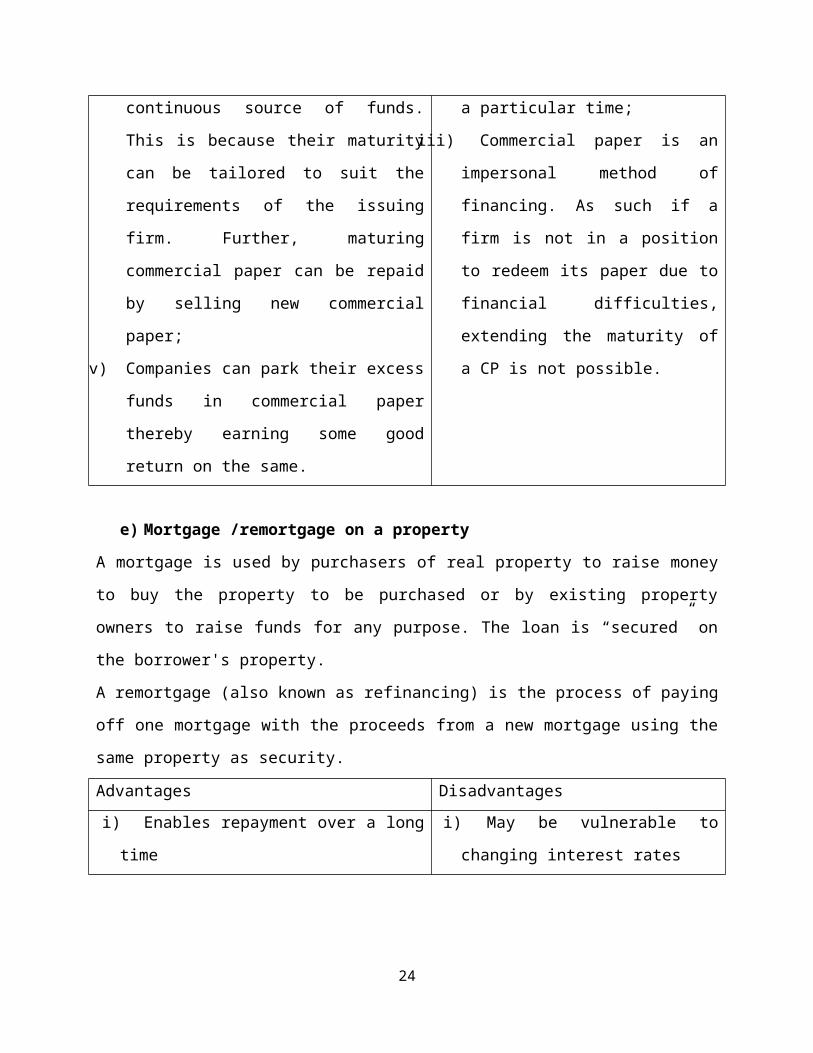

continuous source of funds.

This is because their maturity

can be tailored to suit the

requirements of the issuing

firm. Further, maturing

commercial paper can be repaid

by selling new commercial

paper;

v) Companies can park their excess

funds in commercial paper

thereby earning some good

return on the same.

a particular time;

iii) Commercial paper is an

impersonal method of

financing. As such if a

firm is not in a position

to redeem its paper due to

financial difficulties,

extending the maturity of

a CP is not possible.

e) Mortgage /remortgage on a property

A mortgage is used by purchasers of real property to raise money

to buy the property to be purchased or by existing property

owners to raise funds for any purpose. The loan is “secured” on

the borrower's property.

A remortgage (also known as refinancing) is the process of paying

off one mortgage with the proceeds from a new mortgage using the

same property as security.

Advantages Disadvantagesi) Enables repayment over a long

time

i) May be vulnerable to

changing interest rates

24

f) Funds from investors of shareholders

Advantages Disadvantagesi) Potentially more funds

available

ii) Enables large scale

investment

i) May be expensive to set up

ii) Shared control

iii) Share values can rise

and fall, affecting the

company value

g) Grants or loans from Government or other organizations

Grants are non-repayable funds or products disbursed by one party

(grant makers), often a government department, corporation,

foundation or trust, to a recipient, often (but not always) a

nonprofit entity, educational institution, business or an

individual. In order to receive a grant, some form of "Grant

Writing" often referred to as either a proposal or an application

is required.

Advantages Disadvantagesi) Grants not repayable

ii) Loans often cheaper than

banks

i) Usually limited in size

ii) Use may be restricted

25

h) Venture capital or business angels

Venture capital is a type of funding for a new or growing

business. It usually comes from venture capital firms that

specialize in building high risk financial portfolios. With

venture capital, the venture capital firm gives funding to the

startup company in exchange for equity in the startup. This is

most commonly found in high growth technology industries like

biotech and software. It is provided in the interest of

generating a return through an eventual realization event such as

an initial public offer (IPO) or trade sale of the company.

Advantages Disadvantagesi) May give tax benefit to

investors

i) Needs clear exit strategy

for investor

ii) Shared control

26

2.0 References

Alexander, G. J., Jones, J. D., & Nigro, P. J. (1996). Report on

the OCC/SEC survey of mutual fund investors. Washington, DC:

Of ce of the Comptroller of the Currency and the U. S.fi

Securities and Exchange Commission.

Alexander, G. J., Jones, J. D., & Nigro, P. J. (1997). Investor

self-selection: evidence from a mutual fund survey.

Antle, R. and Garska, S. J. (2003) Financial Accounting 2nd

Edition. Thomson South – Western

Managerial and Decision Economics 18(Special Issue, Nov.–Dec.),

719–729. Crenshaw,A.B.

(1996,May19).Beforeriskingthemoney,investin nancialliteracy.TheWfi

ashingtonPost,pp. H1, H4.

Saleemi, N. A. (2008). Financial Accounting Simplified. Saleem

Publications Ltd, 2nd Edition, reprinted 2008.

The Journal of International Financial Management & Accounting,

New York University’s Stem School of Business, Salomon Center.

Updegrave, W. L. (1996). Fund investors need to go back to

school. Money (February) 98–100.

Williams, J. (2005). Financial and Managerial Accounting:

Business Decisions – 13th edition. McGraw – Hill.

27