Dialogues Between Paradise Lost and the Novels of Salman ...

Upload

khangminh22Category

view

0download

0

Strategic Customer Management

Relationship marketing and customer relationship management (CRM) can be jointly utilised

to provide a clear roadmap to excellence in customer management; this is the first textbook to

demonstrate how this can be done. Written by two acclaimed experts in the field, the book

shows how a holistic approach to managing relationships with customers and other key

stakeholders leads to increased shareholder value. Taking a practical, step-by-step approach,

the authors explain the principles of relationship marketing, apply them to the development

of a CRM strategy and discuss key implementation issues. The book’s up-to-date coverage

includes the latest developments in digital marketing and the use of social media. Topical

examples and case studies from around the world connect theory with best global practice,

making this an ideal text for both students and practitioners keen to keep abreast of changes in

this fast-moving field.

Dr Adrian Payne is a Professor of Marketing in the Australian School of Business at the

University of New South Wales.

Dr Pennie Frow is Associate Professor of Marketing and Director of the Master of Marketing

Programme at the University of Sydney Business School, Australia.

Visit the Companion Website at www.cambridge.org/payneandfrow to find valuable learningmaterials, including:

For lecturers

� Instructor’s Manual, including recommended Harvard Business School case studies� Full set of PowerPoint slides that can be adapted for your course� A bank of multiple choice questions to test student learning

For Students

� Links to useful sites on the web� Sample chapter

‘Adrian Payne and Pennie Frow have written the best guide to understanding customer

relationship management strategy. They have provided an excellent framework and illustrate

it with a rich set of cases that both students and managers would profit from reading.’

Philip Kotler, S. C. Johnson & Son Distinguished Professor of International Marketing,

Kellogg School of Management, Northwestern University

‘Relationship Marketing and CRM have until now been treated as two separate processes, even

though all the evidence points to the fact that most CRM systems fail because of a lack of

understanding of customer needs. Adrian Payne and Pennie Frow have brought the two

domains together under a title which makes sense – Strategic Customer Management –

which from the very beginning should have been the whole purpose of CRM.’

Malcolm McDonald, Emeritus Professor, Cranfield School of Management, Cranfield

University, and Chairman, Brand Finance PLC

‘Strategic Customer Management is the most comprehensive treatise on Customer Centric

Marketing. It provides insightful understanding of how to create value for customers and

also for the company. I congratulate Adrian Payne and Pennie Frow for an outstanding

contribution to both marketing discipline and practice.’

Jagdish N. Sheth, Charles H. Kellstadt Chair of Marketing, Goizueta Business School,

Emory University

‘This book is a comprehensive guide to building shareholder value through long-lasting

relationships with all kinds of customers.’

James Heskett, Baker Foundation Professor Emeritus, Harvard Business School, and

author of The Culture Cycle

‘Strategic Customer Management takes a thorough, relational approach to the customer. By

integrating relationship marketing with CRM and adding a service perspective on business, it

goes far beyond conventional marketing books. It provides a comprehensive approach to how

a firm can understand and manage customers in the contemporary competitive environment,

where traditional marketing models are increasingly less effective.’

Christian Grönroos, Professor of Service and Relationship Marketing, Hanken School of

Economics, Finland

‘As Peter Drucker says, “There is only one definition of business purpose: to create a customer.”

If you agree with Drucker, and desire a competitive advantage, consider the strategic funda-

mentals and execution techniques outlined in Strategic Customer Management: Integrating

Relationship Marketing and CRM’.

Jim Guyette, President and CEO Rolls-Royce, North America

Strategic CustomerManagementIntegrating Relationship Marketing and CRM

Adrian PaynePennie Frow

CAMBR IDGE UN IVER S I T Y PR E S S

Cambridge, New York, Melbourne, Madrid, Cape Town,Singapore, São Paulo, Delhi, Mexico City

Cambridge University PressThe Edinburgh Building, Cambridge CB2 8RU, UK

Published in the United States of America by Cambridge University Press, New York

www.cambridge.orgInformation on this title: www.cambridge.org/9781107649224

© Adrian Payne and Pennie Frow 2013

This publication is in copyright. Subject to statutory exceptionand to the provisions of relevant collective licensing agreements,no reproduction of any part may take place without the writtenpermission of Cambridge University Press.

First published 2013

Printed and bound in the United Kingdom by the MPG Books Group

A catalogue record for this publication is available from the British Library

Library of Congress Cataloging-in-Publication DataPayne, Adrian.Strategic customer management : integrating relationship marketing and CRM /Adrian Payne, Pennie Frow.pages cm

Includes bibliographical references and index.ISBN 978-1-107-01496-1 – ISBN 978-1-107-64922-4 (pbk.)1. Customer relations – Management. I. Frow, Pennie. II. Title.HF5415.5.P395 2013658.8012–dc23

2012036778

ISBN 978-1-107-01496-1 HardbackISBN 978-1-107-64922-4 Paperback

Additional resources for this publication at www.cambridge.org/payneandfrow

Cambridge University Press has no responsibility for the persistence oraccuracy of URLs for external or third-party Internet websites referred toin this publication, and does not guarantee that any content on suchwebsites is, or will remain, accurate or appropriate.

,

To Christopher

,

,

CONTENTS

List of Figures page xiAcknowledgements xv

Part I Introduction 1

1 Strategic customer management 3

Part II Relationship marketing 37

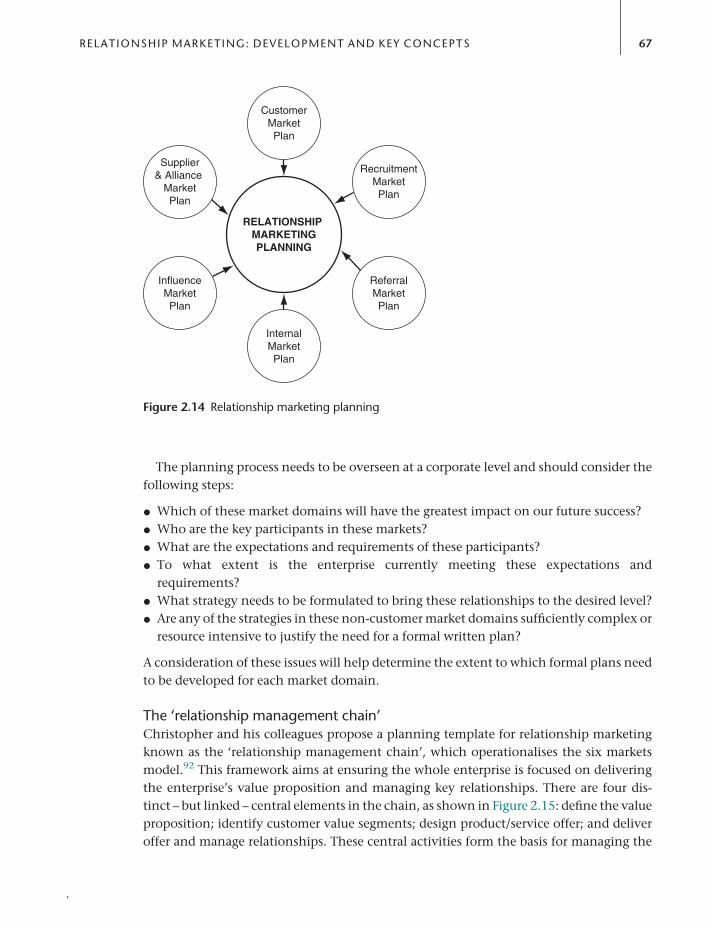

2 Relationship marketing: Development and key concepts 39Case: 2.1 Myspace – The rise and fall 72Case: 2.2 PlaceMakers – success factors in the building supplies sector 75

3 Customer value creation 79Case: 3.1 British Telecommunications (BT) – creating new customer valuepropositions 108

Case: 3.2 Zurich Financial Services – building value propositions 111

4 Building relationships with multiple stakeholders 116Case: 4.1 AirAsia spreads its wings 144Case: 4.2 The City Car Club, Helsinki – driving sustainable car use 148

5 Relationships and technology: Digital marketing and social media 152Case: 5.1 Hippo in India – using Twitter to manage the supply chain 197Case: 5.2 Blendtec – the ‘will it blend’ viral marketing initiative 201

Part III Customer relationship management: Key processes 205

6 Strategy development 207Case: 6.1 Tesco – the relationship strategy superstar 251Case: 6.2 Samsung – from low-cost producer to product leadership 256

7 Enterprise value creation 261Case: 7.1 Coca-Cola in China – bringing fizz to the Chinese beverages market 289Case: 7.2 Sydney Opera House – exploring value creation strategies 292

8 Multi-channel integration 299Case: 8.1 TNT – creating the ‘perfect’ customer transaction 341Case: 8.2 Guinness – delivering the ‘Perfect Pint’ 346

,

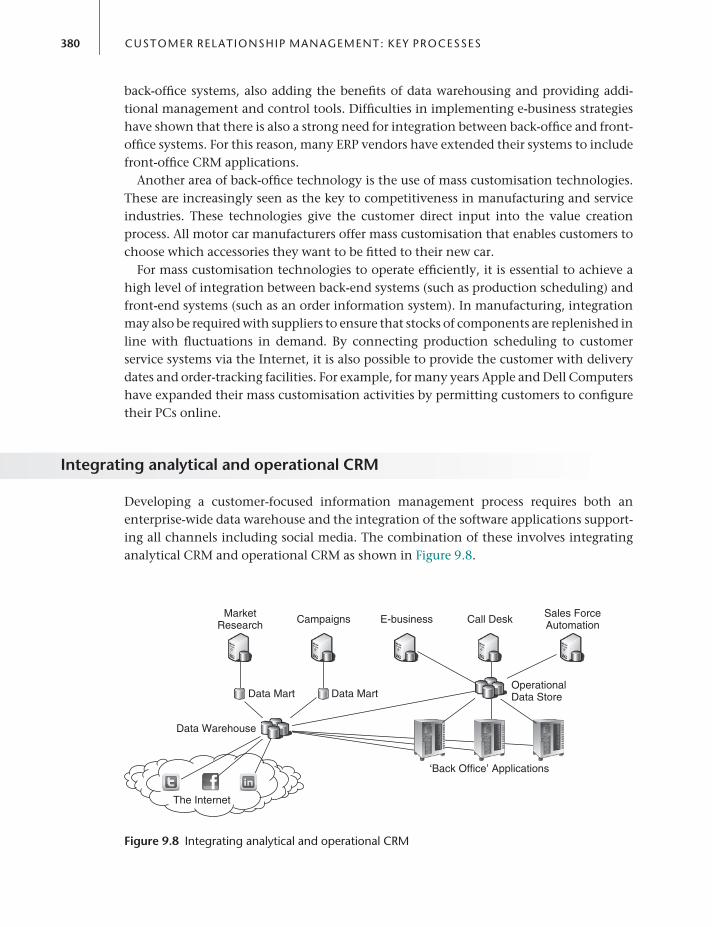

9 Information and technology management 350Case: 9.1 Royal Bank of Canada – building client service commitment 390Case: 9.2 The DVLA – innovating with CRM in the public sector 392

10 Performance assessment 397Case: 10.1 Sears – the service profit chain and the Kmart merger 428Case: 10.2 The Multinational Software Company – driving results with a metricsdashboard 432

Part IV Strategic customer management implementation 435

11 Organising for implementation 437Annex: The comprehensive CRM audit 478Case: 11.1 Nationwide Building Society – fulfilling a CRM vision 488Case: 11.2 Mercedes-Benz – building strategic customer management capability 491

Notes 497Index 520

x CONTENTS

,

FIGURES

1.1 The domain of strategic customer management page 41.2 The development of the marketing discipline 51.3 Size of the service sector as percentage of GNP for different countries 81.4 Service-dominant logic – key foundational premises 101.5 Marketing as a matching process 131.6 Relationship marketing strategy 141.7 The relationship marketing mix 151.8 The transition to relationship marketing 171.9 The CRM continuum 25

1.10 The CRM Strategy Framework 302.1 Alternative approaches to relationship marketing 412.2 Transaction marketing and relationship marketing 432.3 Marketing as a functional activity – the command and control organisational

structure 442.4 The shift from a vertical organisational focus to a horizontal focus 452.5 The shift from functions to processes 462.6 The transaction marketing ‘stage’ 472.7 The connection between quality, customer service and marketing 482.8 The relationship marketing ‘stage’ 502.9 Four categories of customer loyalty 55

2.10 Types of relationships 572.11 The six markets framework 602.12 The Gant USA brand – the Pyramid Sportswear value web 622.13 Some examples of social networks 632.14 Relationship marketing planning 672.15 The relationship management chain 683.1 The total value offer 823.2 Using the supplementary services checklist – a personal lines insurance example 833.3 The customer relationship ladder of loyalty 873.4 General Electric’s appliance contact centre website 883.5 grumbletext.com website home page 913.6 Brand image study: Coke versus Pepsi 933.7 Examples of value propositions for various industries 983.8 Value map for the airline industry – past and present 993.9 Value proposition checklist 101

,

3.10 The value delivery system 102Case study 3.1, figure 1 Zurich Financial Services value proposition framework 1134.1 The six markets model 1184.2 The customer market domain 1214.3 The referral market domain 1244.4 The supplier/alliance market domain 1284.5 The influence market domain 1304.6 The recruitment market domain 1334.7 The internal market domain 1374.8 BAA – a review of key market participants in the six market domains 1404.9 The six markets radar chart 141

4.10 RSPB relationship marketing radar chart 1424.11 Referral market audit for an accounting firm 143Case study 4.1, figure 1 AirAsia – summary of its strategy 1475.1 Projected growth of digital marketing in the US to 2016 1555.2 Estimates of sales of personal computers, smartphones and tablets to 2016 1615.3 Projected growth of the Internet 2005–2015 1635.4 Evolution of the World Wide Web 1645.5 Estimated online retail sales as a percentage of total retail sales in 2016 1665.6 The social media ecosystem 1745.7 The social media landscape 2012 1755.8 Social networks where B2B and B2C brands are most active in US 1845.9 Forrester Research Technographics® segmentation 186

5.10 Social media strategy framework 1875.11 Paid, owned and bought media 1945.12 Reach and control of the three media types 195Case study 5.1, figure 1 The Hippo story 198Case study 5.1, figure 2 Examples of Hippo ‘Tweets’ 199Case study 5.1, figure 3 Hippo ‘Excellence in Hunger Fighting’ certificate 200Case study 5.2, figure 1 Screenshot of CEO Dickson about to ‘blend’ an iPhone 203Case study 5.2, figure 2 Blendtec’s integration across digital channels 203Case study 5.2, figure 3 The Blendtec social media strategy 2046.1 The CRM Strategy Framework 2116.2 Best practices in making vision and values work 2166.3 A framework for industry analysis 2196.4 Alternative strategies based on differentiation and cost 2226.5 Value disciplines for market leaders 2246.6 Balance marketing effort directed at the ‘customer’ 2306.7 Levels of segmentation emphasis 2346.8 Review of product/service and market/customer segment options 2406.9 The danger of ‘current focus’ 240

6.10 Starbucks’ wireless Internet initiative 241

xii L IST OF FIGURES

,

6.11 The CRM strategy matrix 2436.12 Transition paths for CRM 248Case study 6.1, figure 1 Tesco strategy wheel 253Case study 6.1, figure 2 The Market Leaders framework for UK supermarkets 2557.1 Customer profitability analysis 2637.2 Customer segment data template for ‘United Electricity plc’ 2677.3 Profit impact of a 5 percentage point increase in customer retention for selected

businesses 2697.4 Profit projections for improved retention at ‘United Electricity plc’ 2707.5 Expenditure on customer acquisition and customer retention 2717.6 Customer retention improvement framework 2737.7 Team-based relationship management 2787.8 The ACURA framework 2797.9 ACURA model cross-selling template for a supermarket 280

7.10 Calculation of customer lifetime value 2837.11 A conceptual framework for value co-creation 2858.1 Alternative industry structures in terms of channel participants 3028.2 Market structure map 3078.3 General characteristics of the different channel options 3108.4 The Schiphol Airport website: www.schiphol.com 3178.5 The Schiphol Airport ‘mobile’ website: www.schiphol.mobi 3188.6 The Schiphol Airport iPhone app 3198.7 Understanding the nature of customer encounters 3228.8 The emotional reservoir of goodwill 3258.9 Channel chain analysis for personal computers 332

8.10 Interactions shift to new channels 3338.11 Transaction costs per sales channel 3348.12 Strengths of sales & marketing channels 3358.13 Channel alternatives based on cost and the complexity of sale 3388.14 Channel mix change matrix for customers, employees and partners 339Case study 8.1, figure 1 The ‘perfect customer transaction’ at TNT 342Case study 8.1, figure 2 TNT strategy map 343Case study 8.1, figure 3 TNT customer promise 344Case study 8.1, figure 4 Specific TNT customer promise: ‘We promise to look after you’ 3449.1 The knowledge hierarchy 3539.2 The CRM strategy matrix 3549.3 Technology levels for CRM 3589.4 Tactical database and decision support systems 3599.5 Data marts 3619.6 Enterprise data warehouse 3629.7 Integrated CRM solutions 3649.8 Integrating analytical and operational CRM 380

L IST OF FIGURES xiii

,

9.9 The Cloud cube model 3839.10 Timing of technology delivery 386

Case study 9.1, figure 1 DVLA customer segmentation 395Case study 9.1, figure 2 DVLA databases and CRM system 39610.1 The linkage model 39910.2 Key drivers of shareholder results 40010.3 Shareholder value measures 40410.4 CMAT performance benchmarking for ‘United Bank’ 40910.5 Commonly used key marketplace metrics 41410.6 The service profit chain 41610.7 Simplified success map for Sears, Roebuck 41810.8 Success map based on the balanced scorecard 41910.9 Example of a CRM dashboard 420

10.10 Marketing Executive Dashboard 42110.11 Sales Manager Dashboard 42210.12 Sales Representative’s Dashboard 42310.13 Comparison of CRM performance to business performance 424Case study 10.1, figure 1 The revised employee-customer-profit chain at Sears 429Case study 10.1, figure 2 The IT transformation at Sears 430Case study 10.1, figure 3 Sears, Roebuck – selected performance measures,

1992–1998 431Case study 10.2, figure 1 Dashboard illustration 43411.1 Present and proposed emphasis on CRM processes in a retail bank 44811.2 Classification matrix for issues identified in CRM audit 45011.3 The McKinsey ‘Seven S’ framework 45211.4 CRM change management issues 45311.5 Orange’s CRM vision 45511.6 IT’s view of marketing 45711.7 Marketing’s view of IT 45711.8 Framework for project management 45911.9 CRM vendors’ profiles on evaluation criteria 464

11.10 Examples of CRM executive development programmes 473Case study 11.2, figure 1 Integrating customer, retailer and distributor relationships 493

xiv L IST OF FIGURES

,

ACKNOWLEDGEMENTS

The development and publication of this book would not have been possible withoutthe help of many people. We wish to acknowledge the assistance and support of not onlythe organisations and people listed below, but also the numerous executives who havegenerously given up their time to share issues relating to relationshipmarketing and CRMimplementation in their businesses.In particular, wewish to thank the following organisations for their support: Accenture,

BT, BroadVision, Detica, IBM, Royal Mail, Oracle, Pegasystems Inc., SAS, Salesforce.com,Teradata, TNT, Nationwide Building Society, Vectia Ltd. and Unisys.Our very special thanks is due to David Fagan, who commented on many aspects of

the book. Also many thanks to Bob Barker and Alistair Sim, who made special contribu-tions to Chapter 9, to Heather Albrecht for her insights on digital marketing and SueAlmeida for her contribution to Chapter 5. Also, to Andrew Dickson and Jon Chidley,who helped with the development of the CRM audit in Chapter 11. We also wish tothank Kaj Storbacka of the University of Auckland and his colleagues at Vectia Ltd. (nowTalent Vectia), who generously shared their insights and contributed towards some of theconcepts developed in this book.Many researchers and scholars at other institutions and practitioners have contributed

to our thinking in this area. In particular, we would like to thank Martin Christopher atCranfield School ofManagement, David Ballantyne at Otago University, Christian Grönroosat Hanken School of Economics, Finland, Don Shultz at Northwestern University, EvertGummesson at Stockholm University School of Business, Jagdish Sheth at EmoryUniversity and Flemming Poulfelt at Copenhagen Business School. Also, thanks are due toClive Humby, Don Peppers, Martha Rogers and Ron Swift – pioneers who have made greatadvances in the areas of relationship marketing and CRM.Special thanks are due to Simon Knox, Lynette Ryals and Hugh Wilson of Cranfield,

Reg Price of MirrorWave and Pat LaPointe of MarketingNPV for contributing case studies.All the case studies in this book remain the copyright of the authors and are used herewiththeir permission. Anyone who wishes to use the cases should contact the authors forpermission to reproduce case material. Anyone who wishes to use extracts from the textshould contact the publisher for permission.We alsowish to recognise thework of our colleagues involved in relationshipmarketing

and CRM at Cranfield University. Our journey in this area started with a rewarding andongoing collaboration over more than two decades ago with Martin Christopher andDavid Ballantyne. We acknowledge the contribution of present and former colleagues atCranfield including:Moira Clark, HughDavidson, SimonKnox,MalcolmMcDonald, Stan

,

Maklan, Roger Palmer, Helen Peck, Joe Peppard, Lynette Ryals and HughWilson. Parts ofour co-authored works are drawn onwithin this book.We are also grateful for the supportof our colleagues and students at the University of New South Wales and The Universityof Sydney. Finally, we thank Paula Parish and her colleagues at Cambridge UniversityPress for their great support and enthusiasm.

xvi ACKNOWLEDGEMENTS

,

Part I

Introduction

,

,

1 Strategic customer management

The strategic management of customer relationships is a critical activity for all enterprises. Themeans of effectively managing relationships with customers are typically addressed under theheadings of relationship marketing and customer relationship management (CRM), to namebut two terms used to describe the management of customer relationships. Resources appliedto such relationship management initiatives are substantial and growing. For example, globalexpenditure just on CRM activity has been estimated to exceed US $100 billion when CRM-related implementation services are considered.Since the early 1980s, relationship marketing has become the topic of great interest to both

marketing scholars and marketing practitioners. In the increasingly mature and complexmarkets of the twenty-first century, organisations have learned that building relationshipsand sustaining them is usually more important than activities focusing on customer acquis-ition. Much of the recent interest in relationship marketing has evolved from the work under-taken in industrial marketing and services marketing in this period, although antecedents ofrelationship marketing can be traced back to ancient times. The importance of the topic ofrelationships in marketing is now undisputed.In the early 2000s, in conjunction with the rapid rise in the use of information technology by

enterprises, CRM made a high-profile entry into the corporate world as businesses saw thepotential of implementing relationship marketing strategies through IT. Companies started torecognise how CRM could provide enhanced opportunities to use data and information tobetter understand customers and to implement relationship-based strategies. CRM built onthe philosophy of relationshipmarketing with the objective of utilising information technologyto develop a closer fit between the needs and characteristics of customers and the organisa-tion’s product and service offering.

In this chapter, we outline the development of themarketing discipline to place the conceptsof relationship marketing and CRM in context. We explain the transition from transactionmarketing to relationship marketing. We define both relationship marketing and CRM andexplain the similarities and differences between them. Finally, we provide an overview of thestructure of the book.

The domain of strategic customer management

Over the past three decades relationship marketing, CRM and other approaches forsystematically managing relationships such as one-to-one marketing have developedsignificantly. However, there is considerable confusion in the academic and managerial

,

literatures about how they differ and what the implications might be of using eachapproach for effective customer management. The terms relationship marketing andCRM have been used interchangeably1 despite the fact that many, including us, agreewith Zablah, Bellenger and Johnston,2 who argue that relationship marketing and CRMare different phenomena and a clear distinction should be made between them.In a recent review of the conceptual differences between the terms CRM and relationship

marketing and customer management we define these terms and highlight key differencesbetween them, as shown in Figure 1.1.3 These brief definitions, developed from the academicliterature and field-based researchwith executives, help clarify the distinction between theseterms. In Chapters 2 and 6 we explore the implications of these definitions further.

Relationship marketing involves the strategic management of relationships with multiplestakeholders. This is a view increasingly supported within the relationship marketingliterature (e.g., Christopher, Payne and Ballantyne;4 Doyle5 and Gummesson6).Srivastava, Shervani and Fahey define CRM as an activity that addresses all aspects of

identifying customers, developing customer insight and building customer relation-ships.7 Boulding and his colleagues develop a similar definition emphasising the integra-tion of processes across the many areas of the firm.8 Thus, CRM involves the strategicmanagement of relationships utilising, where appropriate, technological tools.

We also introduce a third term, customer management, which represents that part of CRMwhich involves the more tactical management of customer interactions and transactions.These three activities relationship marketing, CRM and the more tactical activity of

customer management collectively represent the domain of strategic customer management.We consider that the lack of clear definitions and understanding of these different, butclosely related, activities has negatively impacted the successful implementation of rela-tionship marketing and its more technological cousin CRM. In the following chapters weelaborate on these short descriptions in much more detail. As the title of this book

CRM:Strategic management ofrelationships with customers,involving appropriate use of technology

CRM

Relationship Marketing:Strategic management ofrelationships with all relevantstakeholders

RELATIONSHIPMARKETING

Customer Management:Implementation andtactical management ofcustomer interactions

CUSTOMERMANAGEMENT

Figure 1.1 The domain of strategic customer management

4 INTRODUCTION

,

suggests, we focus primarily on strategic aspects that relate to relationship marketing andCRM and we do not address the tactical management of customer transactions (i.e.,‘customer management’) in detail.To set the development of relationship marketing and CRM in context, we now review

the development of the marketing discipline.

The development of the discipline of marketing

Although marketing has its origins in the earliest forms of commerce, the widespreadacceptance of the marketing concept by enterprises is relatively recent. The modernadoption of the marketing concept can be traced to the substantial period of growthfollowing the Second World War. The adoption of marketing was especially prevalentin large US companies over this period. Little marketing literature was published prior tothe 1950s.Since the 1950s the formal study of marketing has focused on an evolving range of

marketing sectors and foci, as shown in Figure 1.2. The emergence and development ofthese sectors do not coincide exactly with the decades show in Figure 1.2. However, thesedecades broadly represent the starting point of substantive research and the appearance ofacademic and practitioner publications relating to these sectors.In the 1950s marketing interest was primarily focused on consumer goods, following

the rise in consumer demand at the conclusion of the Second World War. The emergingconsumer goods companies quickly became recognised as sophisticated marketers andwere the first companies to develop formal marketing plans. Most of the academicliterature on marketing around this period focused on consumer goods businesses andespecially fast moving consumer goods.

1950s 1960s 1970s 1980s 1990s

MajorAreas of

MarketingFocus

Consumer Marketing

Industrial Marketing

Non-Profit & Social Marketing

ServicesMarketing

Strategic Customer Management:• Relationship Marketing• CRM

2000s 2010s

Figure 1.2 The development of the marketing discipline

STRATEGIC CUSTOMER MANAGEMENT 5

,

In the 1960s increased attention started to be directed towards industrialmarkets. Booksand articles on industrial marketing started to appear and make distinctions betweenconsumer marketing and industrial marketing. Specialised marketing textbooks andjournals addressing industrial markets started to appear. Much of this work focusedespecially on selling to business customers and later led to substantive work in the areaof key account management.In the 1970s considerable academic effort was placed on the area of non-profit or

societal marketing. This required marketers operating in the not-for-profit sector to revisetheir thinking as such organisations did not have commercial enterprises’ motive ofprofit. Further, they typically had more than one ‘market’ to serve. For example, amuseum or charity had to undertake marketing activities directed at the attraction offunds from donors as well as undertaking marketing activities directed at customers.In the 1980s attention started to be directed at the services sector, an area ofmarketing

that had received remarkably little consideration despite its importance to the overalleconomy of most developed countries at that point in time. Since then, in NorthAmerica and Western Europe in particular, there has been a steady and unrelentingdecline in traditional manufacturing industries. Their place has been taken by numer-ous service-based enterprises that have been quick to spot the opportunities created byorganisational needs, increased personal affluence and raised lifestyle expectations ofthe population.By the 1990s a newmarketing area, relationshipmarketing, became the subject ofmuch

attention. Relationship marketing, as a term, appears first to have been introduced in theacademic literature in 1983 at an AmericanMarketing Association conference by LeonardBerry. He described relationship marketing as ‘attracting, maintaining and . . . embracingcustomer relationships’.9 Shortly afterwards, two further articles addressing customerrelationships were published by Theodore Levitt10 and Barbara Bund Jackson.11 Thesearticles were influential in emphasising the need to understand different types of relation-ships and the extent to which relationship or transaction-oriented approaches are appro-priate. However, it was not until the 1990s that the first book on relationship marketingappeared, published by one of the current authors and his colleagues.12 From this period,a substantive flow of academic and practitioner articles started to appear.

In the early 2000s the term CRM or customer relationship management emerged. Weuse the term ‘emerged’, as a review of the literature on CRM does not disclose where theterm was first used in a publication. CRM is increasingly found at the top of corporateagendas today. Companies large and small across a variety of sectors are embracing CRMas amajor element of corporate strategy for two important reasons: new technologies nowenable companies to target chosen market segments, micro-segments or individual cus-tomers more precisely, and new marketing thinking has recognised the limitations oftraditional marketing and the potential of more customer-focused, process-based strat-egies. CRM is a business approach that seeks to create, develop and enhance relationshipswith carefully targeted customers in order to improve customer value and corporateprofitability and thereby maximise shareholder value. CRM is often associated withutilising information technology to implement relationship marketing strategies. As

6 INTRODUCTION

,

such, CRM unites the potential of new technologies and new marketing thinking todeliver profitable, long-term relationships.

From themid-2000s we have seen the rise of a new relationship-focused phenomenon –

social media. Social media is a dynamic phenomenon. The rapid acceptance of socialmedia platforms such as Facebook and Twitter – which are largely consumer-orientedplatforms – and LinkedIn – which is primarily a business-oriented platform – is unparal-leled in the history of marketing. Social media has important implications for strategiccustomer management which we consider at various points throughout this book. It isalso a highly turbulent sector as characterised by the rise and fall of Myspace, which isdiscussed in a case study at the end of Chapter 2.Social media has already had an important impact on relationship marketing and

CRM and this will increase substantially in the next decade. However, social media,in our view, does not represent one of the major areas of marketing focus illustratedin Figure 1.2. Rather its use has significant implications for the development ofrelationship marketing strategies and the implementation of CRM initiatives.Collectively, relationship marketing and CRM – together with the appropriate use ofsocial influence marketing strategies – constitute the area of strategic customermanagement.

The growth of the service economy

The rise of the service sector has had an important and continuing influence on bothrelationship marketing and CRM. As noted above, there has been a steady decline intraditional manufacturing industries over a long period. This transition is such that todaymore than 70 per cent of most Western economies are now in the service sector, whethermeasured in terms of income or numbers employed. Figure 1.3 shows estimates of thesize of the service sector as a percentage of gross national product (GNP) for differentcountries. These statistics, published by the US Central Intelligence Agency,13 showthe dramatic transformation of the global service landscape. Hong Kong leads theworld with 92 per cent of its economy in the service sector. China’s economy a fewdecades ago was principally an agricultural economy. The service sector in China hasgrown by 191 per cent over the last 25 years. Today, services represent over 44 per centof China’s GNP.Some observers refer to this shift to a services economy as the ‘second industrial

revolution’. As individuals spend greater proportions of their income on services includ-ing travel, entertainment and leisure, postal and communication services, restaurants,personal health and grooming and the like, the service sector responds by creatingbusinesses and jobs. This growth in services has obvious and important implications forrelationshipmarketingwhere customer relationships and service employees are especiallycritical.Further, the distinction between services and manufactured products has become

increasingly blurred as many manufacturing companies have seen the opportunity to

STRATEGIC CUSTOMER MANAGEMENT 7

,

add services to their portfolios.14 Many manufacturing organisations now have substan-tial service businesses with companies such as Rolls-Royce and IBM standing out as twoexemplar organisations that have embraced services. Both these organisations haveachieved huge growth in the services component of their businesses.Rolls-Royce, the jet engine manufacturer, introduced their ‘power by the hour’ initia-

tive which provides airline operators with a service which involves a fixed engine main-tenance cost over an extended period of time. Rolls-Royce retains ownership of theengines and airline operators are assured of an accurate cost projection by buying‘power by the hour’ with guaranteed performance standards. They also avoid the costsassociated with unexpected engine breakdowns. Service revenue accounts for over 53 percent of Rolls-Royce’s annual revenues and it is now the world’s second largest manufac-turer of aircraft engines, behind General Electric.IBM, a company once primarily involved inmanufacturing largemainframe computers

and later personal computers has significantly increased the share of its business derivedfrom services. IBM has shifted its focus from commoditised hardware to higher-marginservices and software. This is being achieved by both organic growth and purchase of

China

India

South Korea

Argentina

Russia

Brazil

Finland

Australia

Germany

Canada

New Zealand

Spain

Netherlands

Singapore

Italy

Japan

Denmark

United States

United Kingdom

France

Hong Kong

44%

55%

58%

60%

62%

68%

68%

71%

71%

71%

71%

72%

72%

73%

73%

76%

76%

77%

77%

79%

92%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

World Average: 63%

Figure 1.3 Size of the service sector as percentage of GNP for different countries

8 INTRODUCTION

,

service businesses like the consulting division of PricewaterhouseCoopers. IBM’s GlobalServices organisation is the world’s largest business and technology services provider. It isthe fastest growing part of IBM, with over 190,000 workers serving customers in morethan 160 countries.Theodore Levitt, who was recognised as one of the world’s leadingmarketing experts,

commented that ‘everybody is in service’. He pointed out that all industries are inservices, although some have a greater or lesser service component than other indus-tries.15 Services scholar Evert Gummesson makes a similar point when he points outthat: ‘The former special case of the service sector has now become the universal case.’16

It follows that to consider service as being confined only to service industries is nolonger appropriate.

The service-dominant logic of marketing

Peter Drucker, the management guru, once said that the greatest danger in times ofturbulence is not the turbulence; it is to act with yesterday’s logic. Since the 1980s, thedominant logic of marketing has been increasingly challenged by newer perspectivesincluding relationshipmarketing, qualitymanagement, market orientation, servicesmar-keting and brand relationships. These more recent frames of reference have challengedmarketing and identified limitations in the traditional ‘goods-dominant logic’ of market-ing. A common theme in this work is that the dominant logic of marketing is shiftingfrom the exchange of tangible goods to the exchange of intangibles such as skills, knowl-edge and processes.This view has been increasingly recognised since the publication of Stephen Vargo and

Robert Lusch’s award-winning research on service-dominant (S-D) logic.17 This researchprovides a new perspective on service. Vargo and Lusch argue that services are moreprevalent than goods and that goods need to be considered as a ‘medium’ for a firm’sservice. They consider all enterprises are in the business of providing service. Service-dominant logic makes an important distinction between ‘service’ (singular) and ‘services’(plural). In the service-dominant logic literature, ‘service’ involves a process, while theplural term ‘services’ indicates intangible units of output.Enterprises that produce goods only, such as an automobile manufacturer, are in fact

creating a service for their customers – in this case a ‘service’ that enables customers to gofrom ‘point A’ to ‘point B’. Many of the issues addressed by Vargo and Lusch haveappeared previously within the services and relationship marketing literatures.However, what they present in their research is an important integration of many of theconcepts and principles relevant to relationship marketing. They identify ten founda-tional premises, shown in Figure 1.4.18

These foundational premises are not a set of ‘rules’; instead they represent a developingand collaborative effort to create a bettermarketing-grounded understanding of value andexchange. Central to this work is the recognition of the need for a shift from a firmperspective to a customer perspective. S-D logic emphasises that companies need to

STRATEGIC CUSTOMER MANAGEMENT 9

,

become continuous learning organisations working more closely with their customersand that communication with customers should be characterised by conversation anddialogue. By adopting this perspective the customer shifts from being a passive audienceto an active player who is engaged more deeply in joint value creation. This idea ofmarketing as a facilitator and structurer of mutual creation of value with customers isgaining increased credence.From a goods-dominant logic perspective, enterprises produce products and customers

buy them.With a service-dominant logic, customers engage in dialogue and interaction with their

suppliers during product design, production, delivery and consumption. The termsco-creation or co-production are increasingly used to describe this dialogue and interac-tion. Service-dominant logic suggests that value starts with the supplier understandingcustomer value-creating processes and learning how it can support customers to co-createvalue.The foundational premises of service-dominant logic have important implications for

relationship marketing and CRM. In the next section we discuss the transition fromtransaction marketing to relationship marketing that is captured within several of these

Foundational Premise Explanation & CommentFP1 Service is the fundamental basis of

exchange.The application of operant resources (knowledge andskills), ‘service’, as defined in S-D logic, is the basis for allexchange. Service is exchanged for service.

FP2 Indirect exchange masks the fundamentalbasis of exchange.

Because service is provided through complex combinationsof goods, money, and institutions, the service basis ofexchange is not always apparent.

FP3 Goods are a distribution mechanism forservice provision.

Goods (both durable and non-durable) derive their valuethrough use – the service they provide.

FP4 Operant resources are the fundamentalsource of competitive advantage.

The comparative ability to cause desired change drivescompetition.

FP5 All economies are service economies. Service (singular) is only now becomingmore apparent withincreased specialisation and outsourcing.

FP6 The customer is always a co-creator ofvalue.

Implies value creation is interactional.

FP7 The enterprise cannot deliver value, butonly offer value propositions.

Enterprises can offer their applied resources for valuecreation and collaboratively (interactively) create valuefollowing acceptance of value propositions, but cannotcreate and/or deliver value independently.

FP8 A service-centred view is inherentlycustomer oriented and relational

Because service is defined in terms of customer-determined benefit and co-created it is inherently customeroriented and relational.

FP9 All social and economic actors are resourceintegrators.

Implies the context of value creation is networks of networks(resource integrators).

FP10 Value is always uniquely andphenomenologically determined by thebeneficiary

Value is idiosyncratic, experiential, contextual, andmeaning laden.

Figure 1.4 Service-dominant logic – key foundational premises

10 INTRODUCTION

,

foundational premises. Later in the bookwe return to examine some implications of otherfoundational premises relating to value, co-creation and value propositions.

From transaction marketing to relationship marketing

The development of interest in relationshipmarketing some two decades ago was not somuch the discovery but a rediscovery of an approach which has long formedthe cornerstone of many successful businesses. This approach emphasises the develop-ment and enhancement of relationships over the entire customer life-cycle rather thanfocusing on new customer acquisition. As industries have matured, there have beenchanges in market demand and competitive intensity that have resulted in a shift fromtransaction marketing to relationship marketing. Over the past half century the waywe think about marketing and the way that it is practised have altered substantially.Marketing thinking has progressed from a functionally based ‘make and sell’ philoso-phy to cross-functional orientation in which the capabilities of the enterprise focusaround creating and delivering customer value to target market segments. To placerelationship marketing in context, we now trace the development of the concept ofthe marketing mix and the transition from transaction-based marketing to currentrelationship-based marketing.The 1950s represents the starting point of modern marketing. Textbooks of substance

started to appear during this period and by the mid-1950s Borden published the firstexposition of the concept of the marketing mix. His list consisted of 12 elements, includ-ing product plan, price, branding, channels of distribution, personal selling, advertising, promo-tions, packaging, display, fact-finding and analysis, servicing, and physical handling.19 Theseelements represented ingredients or variables which themarket could use to ‘mix’ into anintegrated marketing plan or marketing programme.In 1960 McCarthy developed the best-known representation of the marketing mix

consisting of the ‘4Ps’ model of marketing.20 He simplified Borden’s original list of 12elements into just four elements:

* Product – the product or service being offered* Price – the price charged and terms associated with its sale* Promotion – the communications programme associated with marketing the product or

service* Place – the distribution and logistics function involved in making a firm’s products and

services available.

The shorthand of the ‘4Ps’ of product, price, promotion and place was used to describe thelevers that, if pulled appropriately, would lead to increased demand for the company’soffer. The objective of this ‘transactional’ approach tomarketing was to develop strategiesthat would optimise expenditure on the marketing mix in order to maximise sales.Over time, the marketing mix concept gained considerable acceptance and the ‘4Ps’

were considered to capture the key elements ofmarketing. However, it has been argued by

STRATEGIC CUSTOMER MANAGEMENT 11

,

some that simplifying the original list has resulted in a seductive sense of simplicity whichmay lead to neglect of some key relevant elements. As a result, many authors have addedto the basic ‘4Ps’ framework. Lists of additional marketing mix elements have been addedwhich extend the ‘4Ps’ framework to five, seven and even 11 key elements which shouldbe considered in the marketing mix. Several authors have argued that a different market-ing mix is needed for services, while others have suggested different elements for specificsectors such as professional services.However, before considering the marketing mix and criticisms of it further, it is impor-

tant to recognise that the marketing mix must not be seen in isolation. Some academicsadopt a verymyopic view of themarketingmix by discussing it in isolation to relationshipmarketing and strategic marketing perspectives.A marketing programme not only involves the marketing mix but it also needs to

consider the externalmarket forces and is concernedwith amatching process that ensuresalignment of the marketing mix with these market forces. Thus the marketing processcomprises three elements:

* The marketing mix – the important internal elements or ingredients that make up anorganisation’s marketing programme

* Market forces – external opportunities or threats in themarkets inwhich an organisationengages

* Amatching process – the strategic andmanagerial process of ensuring that themarketingmix and internal policies are appropriate to the market forces.

The market forces comprise a number of areas which need to be considered, including:

* The customer – buying behaviour in terms of motivation to purchase, buying habits,environment, size of market and buying power of customer segments. This includes aconsideration not just of direct customers but also, where appropriate, customers’customers.

* The industry setting – the motivations, structure, practice and attitudes of industryparticipants including, retailers, intermediaries and any other members of the supplychain.

* Competitors – a company’s position and its activities are influenced by the structure ofthe industry and the nature of direct and indirect competition.

* Other key stakeholders – there are a wide range of external stakeholders which may havean impact on an enterprise and its customers. These include the media, governmentand regulatory bodies and other influencers that can impact marketing activities andcompetitive practices. These key stakeholders are addressed in detail in Chapter 4.

The task of executives chargedwith developing amarketing programme is to assemble theelements of a marketingmix to ensure the best match between the internal capabilities ofthe enterprise and the external market environment. A key issue in the marketing pro-gramme is the recognition that the elements of themarketingmix are largely controllableby managers within the organisation, and that the market forces in the external environ-ment are, to a large extent, uncontrollable. The success of a marketing programme

12 INTRODUCTION

,

depends primarily on the degree of match between the external environment and theorganisation’s internal capabilities and resources.The marketing programme can thus be characterised as a matching process, and this

is especially important in a relationship context. The extent to which different enter-prises develop a good match or a poor match between the external market forces andtheir marketingmix varies greatly. This is shown in Figure 1.5. A key issue to recognise isthat these external market forces are not stable. The forces can alter quickly anddramatically, as shown by the impact of deregulation, increased regulation and theemergence of new forms of competition. The escalating consumer interest in sustain-ability, the rise of social media, the global financial crisis, continuing wars and globalconflict, and competition from unexpected sources are just some of the issues con-fronting organisations today. Changes in these forces create both marketing opportu-nities and marketing threats. Thus marketing executives need to monitor the externalenvironment constantly and be prepared to adjust their marketing mix to create abetter match with market opportunities.

However, viewing the marketing mix in isolation from marketing strategy is not theonly issue related to the conventional marketing mix. The marketing mix concept hasbeen challenged by a number of academics. Amongst the criticisms, observers argue thatthe marketing mix: is too internally focused on what the business wants; it is more suitedto fastmoving consumer goods than industrial products and services; it is too functionallyoriented; it does not consider repeat purchase and relationship building; it fails to takeinto account themechanisms of word-of-mouth advocacy and referralmarketing; and it isnot sufficiently strategically oriented.

Our principal criticism is that in addition to being viewed in isolation to the marketingstrategy, themarketingmix elements are heavily focused on customer acquisition and arethus not relationally oriented. The ‘4Ps’model oversimplifies themore complex process ofwinning and keeping customers. Further marketing mix elements need to be added toaddress issues of keeping and growing customers. In Figure 1.6 we identify three furthermarketing mix elements – people, processes and customer service – which are primarilyconcerned with customer retention rather than acquisition. This has similarities to a

Poor Match

Market ForcesMarketing Mix Market Forces Marketing Mix

Good Match

Figure 1.5 Marketing as a matching process

STRATEGIC CUSTOMER MANAGEMENT 13

,

marketing mix for services developed by Booms and Bitner21 except we highlight thecriticality of customer service to a relationship marketing mix and argue that the physicalevidence dimension discussed by these authors is more appropriately viewed as a sub-element of the product element of the marketing mix.All these elements are essential in building a relationship marketing strategy. It should

be emphasised that the traditional elements of product, price promotion and place are notsolely concerned with ‘customer winning’. Nor are the elements of people, processes andcustomer service only concerned with ‘customer keeping’. However, it is clear that thetraditional marketing mix elements are mainly concerned with ‘making the offer’.During our professional careers we have come across many businesses that execute the

‘4Ps’ of the marketing mix very well, yet fall down in the areas of processes, people andcustomer service. This is especially evident in service businesses such as restaurants or thehospitality sector where a product may be excellent, the location convenient and thepricing reasonable, yet the businesses fail in terms of broken back-office processes, poorcustomer service and disinterested or rude staff. This is also evident in product markets.Research shows that customers purchasing a car would prefer to have a problem car withgood service, than a good car and problems with service. Customers know that a cardealership with good service will pull out all the stops to ensure the problems with the carare rectified. The more enlightened car distributors recognise the relationship value ofretained customers over a lifetime. If the average customer purchases a car every fouryears, they are likely to buy around ten cars or more over their lifetime. If a customerpurchases all his or her cars, servicing of these cars, all accessories and car insurance, thismay represent as much as $500,000 worth of business over that customer’s lifetime. Byadopting this principle Carl Sewell, a well-known US car dealer, built a chain of cardealerships which became a business with revenues of over $1 billion.The original concept of the ‘4Ps’ of the marketing mix was formulated with the objec-

tive of manipulating and exploiting market demand. It emerged from a period of unpre-cedented growth and prosperity in the US and was heavily oriented towards fast movingconsumer goods. We do not agree with some extreme academics that dismiss the market-ingmix as no longer relevant. Rather we endorse the more balanced view of our colleagueEvert Gummesson, who points out the role of themarketingmix has changed from being

RelationshipMarketing

‘Customer Winning’Elements

• Product

• Pricing

• Promotion

• Place

• People

• Processes

• Pro-active customer

service

‘Customer Keeping’ Elements

Figure 1.6 Relationship marketing strategy

14 INTRODUCTION

,

one of the founding parameters of marketing to being one of the contributing parametersto relationships, networks and interaction.22 While the marketing mix concept needs tobe extended to consider the context of relationship marketing, it still has importance indeveloping a relationally oriented marketing strategy.However, the dangers of failing to adopt a relationship orientation in developing the

marketing mix may lead to firms becoming supplier-oriented rather than customer-oriented. As Gummesson points out:

In practice, however, the 4P approach has led to a manipulative attitude to people. If we justselect the right measures in the right combination and with the right intensity, the consumerwill buy; it is amatter of putting pressure on the consumer . . .Weoften know little of what is inthe mind of consumers, how they think and feel, and what their motives are. It is more of astimulus-responsemodel, similar to the fisherman’s relationship to fish. If we improve the bait,the fish will bite and it is hooked. How the fish feels about it has been less considered.23

The expanded relationship marketing mix, consisting of the seven elements outlined inFigure 1.7, represents a key element in the shift from a transactional approach to a relation-ship approach inmarketing by recognising the criticality of people, processes and customerservice. This figure illustrates how each of the elements is interconnected. Each of theserelationship marketing mix elements interacts with each other and they should be devel-oped so that they aremutually supportive in obtaining the best possiblematchbetween theinternal and external environments of the organisation. Essential to avoiding the manip-ulative approach inherent in the ‘4Ps’ approach, as identified by Gummesson, is placinghigh emphasis on the relational elements of people, customer service and processes.

In developing a marketing mix strategy, marketers also need to consider the relation-ships between the elements of themix. It has been pointed out that there are three issues toconsider.24 These include:

Promotion Price

Place People

Product

Processes

CustomerService

Figure 1.7 The relationship marketing mix

STRATEGIC CUSTOMER MANAGEMENT 15

,

* Consistency, where there is a logical and useful fit between two or more elements of themarketing mix

* Integration, which involves an active harmonious interaction between the elements ofthe mix

* Leverage, which involves a more sophisticated approach and is concerned with usingeach element to best advantage in support of the total marketing mix.

Thus, effective relationshipmarketing is based on the choice and design ofmarketingmixelements that are mutually supportive and leveraged together so that synergy is achievedand customer value is co-created. Each of the elements of the marketing mix, and theirsub-elements, needs to focus on supporting each other in terms of consistency, integra-tion and leverage, reinforcing the positioning and delivery of the product or servicerequired by the market segment (or segments) that is being targeted. In developing arelationally based marketing mix strategy, we also need to consider the impact of eachmarketing mix element on the different market segments selected. We return to considermarket segmentation in Chapter 6.

Principles of relationship marketing

By the start of the twenty-first century many basic tenets of marketing were increasinglybeing questioned. The marketplace now is vastly different from that of the previouscentury. Numerousmarkets havematured in the sense that growth is low or non-existent,resulting in increased pressure on corporate profitability. Consumers and customers aremore sophisticated and less responsive to traditional marketing pressures, particularlyadvertising. They are computer literate and there is a very high utilisation of the Internetas well as a high engagement in social media. Greater customer choice and convenienceexists as a result of the globalisation of markets.Some two decades ago Philip Kotler pointed to the future. He proposed a new view of

organisational performance and success based on relationships, whereby the traditionalmarketing approach – including the marketing mix – is not replaced, but is instead‘repositioned’ as the toolbox for understanding and responding to all the significantplayers in a company’s environment. He outlines the importance of the relationshipapproach to stakeholders:

The consensus in . . . business is growing: if . . . companies are to compete successfully in domesticand global markets, they must engineer stronger bonds with their stakeholders, including cus-tomers, distributors, suppliers, employees, unions, governments and other critical players in theenvironment.Commonpractices such aswhipsawing suppliers for better prices, dictating terms todistributors and treating employees as a cost rather than an asset, must end. Companies mustmove from a short-term transaction-orientated goal to a long-term relationship-building goal.25

Kotler’s comments underscore the need for an integrated approach for understanding thedifferent stakeholder relationships. In many large industrial enterprises, marketing is still

16 INTRODUCTION

,

viewed as a set of related but compartmentalised activities that are separate from the rest ofthe company. Relationship marketing seeks to change this perspective by managing thecompeting interests of customers, staff, shareholders and other stakeholders. It redefinesthe concept of ‘a market’ as one in which the competing interests are made visible andtherefore more likely to be managed effectively.The development of this broader wave of marketing thinking by marketing academics

and practitioners has influenced the perceived role of marketing in business. In effect,marketing is given lead (but not sole) responsibility for strengthening the firm’s marketperformance. In our earlier work26 we have progressively refined our view of relationshipmarketing. In particular, we identify that relationship marketing:

* requires a focus on relationships rather than transactions* represents a shift from functionally based marketing to cross-functionally based

marketing* demands full attention being placed on the creation of value to customers* is an approach which addresses multiple ‘market domains’, or stakeholder groups – not

just the traditional customer market* involves a shift from marketing activities which emphasise customer acquisition to

marketing activities which emphasise customer retention as well as acquisition.

We now provide a short overview of these principles of relationship marketing. In laterchapters we explore these principles and their implications in greater detail.

An emphasis on relationships

The transition from traditional, ‘transactional’ marketing to relationship marketing isdepicted in Figure 1.8. Relationshipmarketing emphasises two important issues. First, youcan only optimise relationships with customers if you understand and manage

Emphasis on customer retention &multiple market domains

Emphasis oncustomer acquisition &customer market domain

Functionallybased

marketing

Cross-functionallybased

marketing

Relationshipmarketing

Transactionmarketing

Figure 1.8 The transition to relationship marketing

STRATEGIC CUSTOMER MANAGEMENT 17

,

relationships with other relevant stakeholders. Most businesses appreciate the critical roletheir employees play in delivering superior customer value, but other stakeholders mayalso play an important part. Second, the tools and techniques used in marketing tocustomers, such as marketing planning and market segmentation, can also be usedequally as effectively in managing non-customer relationships. We explore the natureof this emphasis on non-customer relationships in more detail in Chapter 4.Figure 1.8 shows some key distinguishing characteristics of relationshipmarketing. The

first is an emphasis on customer retention and extending the ‘lifetime value’ of customersthrough strategies that focus on retaining targeted customers. The second is a recognitionthat companies need to develop relationships with a number of stakeholders, or ‘marketdomains’, if they are to achieve long-term success in the customer marketplace. The thirdfeature of relationship marketing is that marketing is seen as a pan-company or cross-functional responsibility and not solely the concern of the marketing department.

An emphasis on a cross-functional approach to marketing

For a long time, marketing strategies have been developed within functionally basedmarketing departments. As a result, the marketing strategies developed often do nottake into account their organisation-wide implications. The problem is that they arefunctionally focused not market-focused. They typically seek to optimise the use ofinputs and hence are budget driven, rather than seeking to optimise around outputs andhence be market driven. Rarely do they consider the interrelationship of differentshareholders.To succeed inmanaging themultiple stakeholders effectively, marketingmust be cross-

functional. David Packard, co-founder of Hewlett-Packard, is reported to have said that‘marketing is too important to be left to the marketing department’. His comment couldbe interpreted in a number of ways, but we understand it as a call to bring marketing outof its functional silo and extend the concept and the philosophy of marketing acrossthe business enterprise. In practice, a cross-functional approach to marketing requiresan organisational culture and climate that encourages collaboration and cooperation.Everyone within the business must understand that they perform a role in servingcustomers, be they internal or external customers. Thus, relationship marketing involvesintegrating activities undertaken within a marketing department with those undertakenin other functional departments. In particular, relationship marketing requires integrat-ing quality, customer service and marketing. We address these issues in more detail inChapter 2.

An emphasis on creation of value for customers

Relationship marketing involves placing special attention on the creation of value forcustomers. There are two types of customer value. First, there is the value that customerscreate for the enterprise. Second, there is the value that the enterprise creates for custom-ers. In many organisations the focus appears to be on the former type of customer value

18 INTRODUCTION

,

rather than the latter. Such organisations are principally concerned with extractingmoney from the customer, with relatively little attention paid to the value that is createdfor customers.The value that an organisation can create for customers should be an early consider-

ation in relationship marketing. If this is addressed satisfactorily, long-term profitabilityand future value for the enterprise will follow. In Chapter 3 we consider value creation forcustomers. Later, in Chapter 7, we consider value creation for the enterprise.

An emphasis on multiple markets

Relationship marketing focuses marketing action on multiple stakeholder markets. The‘six markets stakeholder model’ developed by Payne, Ballantyne and Christopher27 is oneof a number of models that provide a structured approach for reviewing the role of anextended set of stakeholders. Themodel identifies six key groups, ormarket domains, thatcontribute to an organisation’s effectiveness in themarketplace. These comprise customermarkets, influencer (including shareholder) markets, recruitment markets, referral mar-kets, internal markets and supplier/alliance markets.Eachmarket domain is made up of a number of key participants. Customer markets, for

example, may include wholesalers, intermediaries and consumers, while influencer mar-kets may comprise financial and investor groups, unions, industry and regulatory bodies,business press andmedia, user and evaluator groups, environmental groups, political andgovernment agencies and competitors. Relationship marketing recognises that multiplemarket domains can directly or indirectly affect a business’s ability to win and keepprofitable customers. We return to explore these market domains in greater detail inChapter 4.

An emphasis on retention of profitable customers

Maximising the lifetime value of customers is a fundamental goal of relationship market-ing. In this context we define the lifetime value of a customer as the future flow of netprofit, discounted back to the present, that can be attributed to a specific customer.Adopting the principle of maximising customer lifetime value forces the organisation torecognise that not all customers are equally profitable and that it must devise strategies toenhance the profitability of those customers it seeks to target.Loyal customers are an intangible asset that adds value to the balance sheet. They

represent the goodwill earned by the brand. Domino’s Pizza chain in the US, forexample, estimates that a customer who purchases one pizza for $5 may represent anet worth of approximately $5,000 over the ten-year life of a Domino franchise. Loyaland repeat customers not only contribute revenue by returning again and again topurchase from the same company or brand, but act as advocates, referring new cus-tomers and reducing acquisition costs. The retention of profitable and potentiallyprofitable customers is a key consideration in the development of relation-based strat-egies in CRM.

STRATEGIC CUSTOMER MANAGEMENT 19

,

Important trends in relationship marketing and CRM

Before discussing CRM and how it differs from relationshipmarketing, it is appropriate toreflect on some key trends which have led to both the adoption of relationshipmarketingand the rapid rise of CRM as a management approach in large enterprises. These trendshelp explain further why there has been such a sustained and increasing interest inrelationship marketing and CRM. They include:

* marketing being undertaken on the basis of relationships* the realisation that customers are a business asset and not simply a commercial audience* the transition in structuring organisations, on a strategic basis, from functions toprocesses* the recognition of the benefits of using information proactively rather than solely

reactively* the greater utilisation of technology in managing and maximising the value of

information* the acceptance of the need for trade-off between delivering and extracting customer value* the development of one-to-one marketing approaches.

Marketing on the basis of relationships

The shift in marketing focus from increasing the number and value of transactions togrowing more effective and profitable relationships with customers and other key stake-holders has had a profound impact on business enterprises. Marketing on the basis ofrelationships concentrates attention on building customer value in order to retain cus-tomers, a topic we examine in Chapter 7. By building on existing investments in productdevelopment and customer acquisition, firms can generate potentially higher revenueand profit at lower cost.Marketing on the basis of transactions, by contrast, involves greaterfinancial outlay and

risk. Focusing on single sales involves winning the customer over at every sales encounter,a less efficient and effective use of investment.Relationship marketing also produces significant intangible benefits. The prominence

given to customer service encourages customer contact and customer involvement. As aresult, firms can learn more about customers’ needs and build this knowledge into futureproduct and service delivery. Clearly, customer encounters that end once the transactionis completed, and with only a record of purchase details for reference, do not offer thesame wealth of opportunities for service and relationship enhancement that enduringcustomer relationships do.

Viewing customers as business assets

This focus on the ‘relationship’ rather than the ‘transaction’ is evident in the emergentview that customer relationships represent key business assets. The implication is thatrelationships with customers can be selectively managed and further developed to

20 INTRODUCTION

,

improve customer retention and profitability. This represents a significant departure fromthe more traditional view that customers are simply a commercial audience that need tobe ‘broadcast to’ by a range of advertising and other promotional activities. One aspect ofa company’s market value is future profit stream generated over a customer’s lifetime.If customers are viewed as business assets then the company will focus on growingthese business assets and their market value. CRM stresses identifying the most profitablecustomers and building relationships with them that increase the value of this businessasset over time.

Organising in terms of processes

Over the past decade, companies have increasingly realised the advantages of organisingin terms of processes rather than functions. Process-oriented firms retain their functionalexcellence in marketing, manufacturing and so on, but recognise that processes are whatdeliver value to the customer as well as to the supplier. A process is essentially any discreteactivity, or set of activities, that adds value to an input. In the modern marketplace,customers rarely seek an ‘isolated’ product; they alsowant immediate delivery, guaranteedwarranty and ongoing service support. The product or service offer has therefore becomemultifaceted; the culmination of cross-functional expertise.Process integration and cross-functional collaboration are defining strengths of both

relationshipmarketing andCRM.We discuss the shift from functional to cross-functionalfocus in greater detail in Chapter 2. The integration of key processes forms a critical part ofCRM. Later in this chapter we provide an overview of the five key cross-functionalprocesses that constitute ‘The CRM Strategy Framework’. In Part III of this book, a chapteris developed devoted to each of these five CRM processes.

From reactive to proactive use of information

With an ever-expanding wealth of options on offer, customers are faced with increasinglypersonalised choices. The move from ‘mass market’ to ‘mass customisation’ in marketinghas created a buyer’s market. Empowered to choose (and to refuse), customers exerttremendous influence over the actions of supplying organisations. Their weapons are adiminished sense of loyalty and a greater propensity to switch to organisations that canpromise (and deliver!) something better. This is particularly true in e-commerce, wherecustomers can change their minds at the click of a button and savvy competitors canquickly redefine or refine their offers to gain a greater slice of customer share.To increase customer satisfaction and reduce customer attrition, businesses must know

their customers (and competitors) like never before, using this knowledge proactively.Improvements in knowledge-gathering and knowledge-sharing activities within andacross organisations have greatly enhanced access to information and the insights thatunderpin the creation of customer value. The rapid rise of socialmedia provides importantadditional opportunities for gaining insight into existing and potential customers.Customer service operations and, in particular, call centres often focus mainly on

STRATEGIC CUSTOMER MANAGEMENT 21

,

‘reactive’ relationships with customers. Experience has shown, however, that carefullydesigned ‘proactive’ customer-centric initiatives can be much more effective and reward-ing. For example, proactive customer support operations do not wait for complaints to beregistered but actively seek to uncover and remedy customer dissatisfaction. They recog-nise that customers often never lodge a complaint and simply take their business else-where. Similarly, proactive call centres now research prospective, current and lapsedcustomers, feeding valuable information to cross-functional customer information andmanagement teams.

Balancing the value trade-off

Crucially, the concept of relationship marketing highlights the trade-off between deliver-ing and extracting customer value. Relationships are built on the creation and delivery ofsuperior customer value on a sustained basis. There has been an increasing emphasis incompanies regarding the need to create an appropriate balance between the value offeredto customers and the value received in return and to recognise how this may need to bevaried across different customer segments.In a sense, optimising the value trade-off means marrying the aforementioned princi-

ples of relationship marketing with current trends implicit in CRM. For example, groceryshoppers are increasingly turning to the convenience of the Internet for their weeklyshopping. More sophisticated e-shoppers are demanding online options that will allowthem to compare prices among similar products, select items based on the nutritionalinformation provided by manufacturers and check out new products.

Developing ‘one-to-one’ marketing

As markets become increasingly competitive and consumers and organisations seekincreasingly specific solutions to their needs, markets fragment into ever smaller seg-ments. Consultants Don Peppers and Martha Rogers have suggested that we may haveto address ‘segments of one’ in some markets where the customer and the supplier ineffect create a unique and mutually satisfactory exchange process.28

The increasing ubiquity of the Internet has proven to be a powerful tool for involvingboth business-to-consumer (B2C) and business-to-business (B2B) customers in the mar-keting process, enabling a one-to-one dialogue rather than relying on mass communica-tions. The unique capabilities of the Internet allow marketers to capture the anonymousbehaviour necessary to be able to answer the question, ‘What does each customer want?’CRM has a key role to play in developing such one-to-one relationships. CRM systems

and processes enable a company to commit tomemory each relevant customer encounterand to recall all past encounters with that customer at every future association. In effect,the capture of customer data, the interpretation of data analyses and the dissemination ofresultant customer knowledge become natural and automatic functions of the organisa-tion. How well CRM fulfils this role depends very much on how CRM is defined andadopted within the organisation concerned.

22 INTRODUCTION

,

A definition of relationship marketing

The previous discussion of relationshipmarketing and its principles shows it covers a widelandscape of topics. In Figure 1.1 and in the accompanying discussion we gave briefdefinitions of the terms relationship marketing, CRM and customer management. Wenow provide a more formal definition of relationship marketing.The first formal definition in the academic literature appears to have been made by

Berry, who defined relationship marketing as ‘attracting maintaining . . . and embracingcustomer relationships’.29 However, as we noted earlier and expand on in much greaterdetail in Chapter 2 and Chapter 4, relationship marketing is concerned with a broader setof stakeholders than just the firm–customer dyad.

Given that relationship marketing is regarded more as a general philosophy with manyvariations, rather than a completely unified concept,30 it is not surprising that there aremany definitions of relationship marketing. Harker31 documents 28 definitions of rela-tionship marketing, Dann and Dann suggest there are approximately 50 published defi-nitions of relationship marketing32 and Agariya and Singh consider 72 definitionsassociated with relationship marketing.33 Drawing on our own and others’ conceptuali-sations of relationship marketing, we define relationship marketing as follows:

Relationship marketing is an umbrella concept concerned with the identification of the appropriaterelationships to have within a network of customers and other key stakeholders and then initiating,developing, extending, maintaining or ceasing interactions with these actors, based on the types ofrelationships that are desired. These relationships can be considered on a continuum ranging from anintimate partnership-type relationship, through to having no relationship at all with a given actor. Theconcept involves an enterprise offering value propositions which represent promises of value andmaintaining relational exchanges aimed at co-creation of mutual value, long-term profitability andshareholder value.

Customer relationship management (CRM)

The trends outlined above help explain why both relationship marketing and CRM havebecome so important.However, the problem facedbymanyorganisations, both indecidingwhether to adopt CRM and in proceeding to implement it, stems from the fact that thereremains a great deal of confusion about what constitutes CRM. As a result, organisationsoften view CRM from a limited perspective or adopt CRM on a fragmented basis.This confusion surrounding CRM may be explained by:

* the lack of a widely accepted and clear definition of its role and operation within theorganisation

* an emphasis on information technology aspects rather than its benefits in terms ofbuilding relationships with customers