Unsecured Creditors Do Not Need to Be the Losers - 2022 ...

199

ABI panel at National Conference of Bankruptcy Judges Annual Meeting Indianapolis, October 8, 2021 Unsecured Creditors Do Not Need to Be the Losers Moderator: Hon. Kevin J. Carey (Ret.), Hogan Lovells US LLP, Philadelphia, PA Presenters: Cullen Drescher Speckhart, Cooley LLP, Washington, D.C. Edward T. Gavin, Gavin/Solmonese LLC, Wilmington, DE David M. Posner, Kilpatrick Townsend & Stockton LLP, New York

-

Upload

khangminh22 -

Category

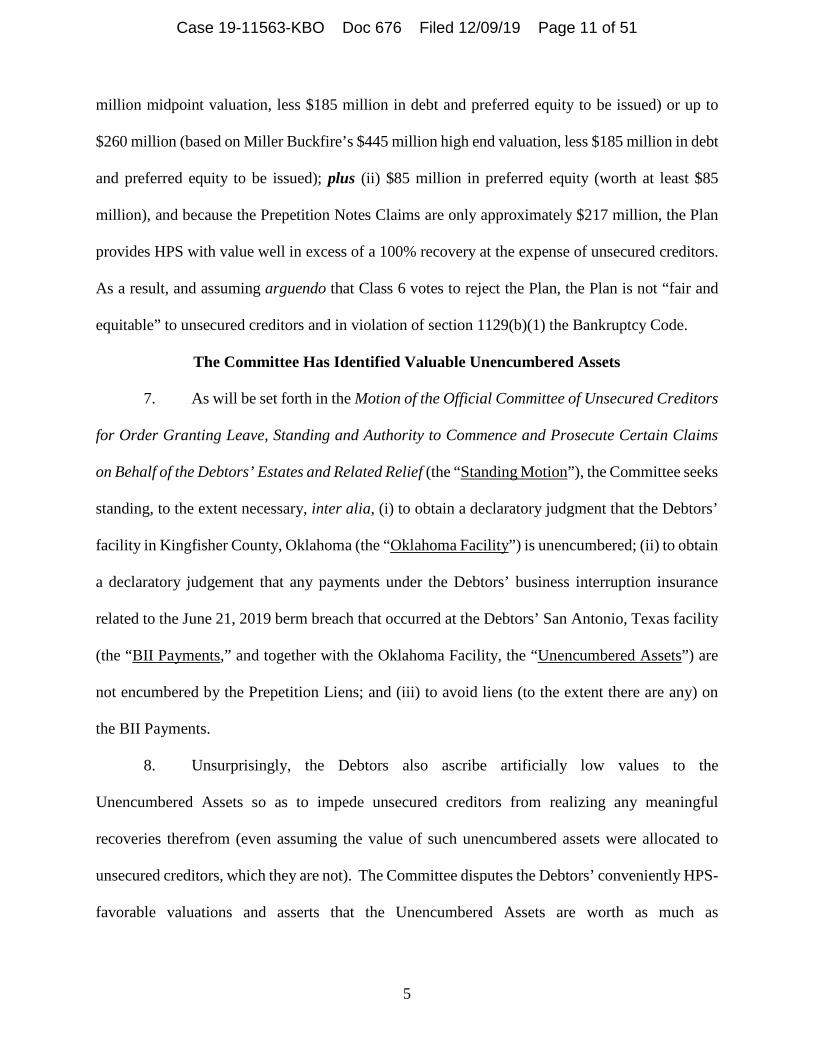

Documents

-

view

1 -

download

0

Transcript of Unsecured Creditors Do Not Need to Be the Losers - 2022 ...

ABI panel at

National Conference of Bankruptcy Judges Annual Meeting

Indianapolis, October 8, 2021

Unsecured Creditors Do Not Need to Be the Losers

Moderator:

Hon. Kevin J. Carey (Ret.), Hogan Lovells US LLP, Philadelphia, PA

Presenters:

Cullen Drescher Speckhart, Cooley LLP, Washington, D.C.

Edward T. Gavin, Gavin/Solmonese LLC, Wilmington, DE

David M. Posner, Kilpatrick Townsend & Stockton LLP, New York

In re: Country Fresh Holding Company Inc., et al.

Objection of the Official Committee of Unsecured Creditors

to Emergency Motion for Entry of an Order (A) Authorizing

and Approving the Debtors’ Key Employee Incentive Plan

and (B) Granting Related Relief

IN THE UNITED STATES BANKRUPTCY COURT

FOR THE SOUTHERN DISTRICT OF TEXAS

HOUSTON DIVISION

§

In re: § Chapter 11

§

COUNTRY FRESH HOLDING COMPANY

INC., et al.,

§

§

Case No. 21-30574 (MI)

§

Debtors.1 § (Jointly Administered)

§

OBJECTION OF THE OFFICIAL COMMITTEE OF UNSECURED

CREDITORS TO EMERGENCY MOTION FOR ENTRY OF AN

ORDER (A) AUTHORIZING AND APPROVING THE DEBTORS’ KEY

EMPLOYEE INCENTIVE PLAN AND (B) GRANTING RELATED RELIEF

TO THE HONORABLE MARVIN ISGUR, UNITED STATES BANKRUPTCY JUDGE:

The Official Committee of Unsecured Creditors (the “Committee”) of the above

captioned debtors and debtors in possession (the “Debtors”), by and through its undersigned

proposed counsel, Kilpatrick Townsend & Stockton LLP, hereby files its objection (the

“Objection”) to the Emergency Motion for Entry of an Order (A) Authorizing and Approving the

Debtors’ Key Employee Incentive Plan and (B) Granting Related Relief [Dkt. No. 275] (the

“Motion”),2 filed by the Debtors, and shows the Court as follows:

1 The Debtors in these Chapter 11 cases and the last four digits of each Debtors’ taxpayer identification

number are as follows: Country Fresh Holding Company Inc. (7822); Country Fresh Midco Corp. (0702);

Country Fresh Acquisition Corp. (5936); Country Fresh Holdings, LLC (7551); Country Fresh LLC

(1258); Country Fresh Dallas, LLC (7237); Country Fresh Carolina, LLC (8026); Country Fresh

Midwest, LLC (0065); Country Fresh Orlando, LLC (7876); Country Fresh Transportation LLC (8244)

CF Products, LLC (8404) Country Fresh Manufacturing, LLC (7839); Champlain Valley Specialty of

New York, Inc. (9030); Country Fresh Pennsylvania, LLC (7969); Sun Rich Fresh Foods (NV) Inc.

(5526); Sun Rich Fresh Foods (USA) Inc. (0429); and Sun Rich Fresh Foods (PA) Inc. (4661). The

Debtors’ principal place of business is 3200 Research Forest Drive, Suite A5, The Woodlands, TX,

77381.

2 All capitalized undefined terms used herein shall have the meanings ascribed to them in the Motion.

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 1 of 11

2

PRELIMINARY STATEMENT

1. The Debtors propose to “incentivize” the KEIP Participants for work already

performed. Beyond vague and conclusory statements, the Motion fails to provide any evidence

that the KEIP Participants need to be incentivized beyond the payment of their already

substantial salaries ranging from or that the proposed “incentive” metrics

will truly incentivize the KEIP Participants to perform above and beyond their already existing

job responsibilities, which they will have already performed when this Motion is heard by the

Court. In fact, this Court is scheduled to hear this Motion on the same date that the Court will be

asked to approve a sale, which predicates a substantial portion of the proposed KEIP.

2. The KEIP must be viewed in the appropriate context according to the facts of this

case. Here, the proposed KEIP will further enrich these senior executives at the expense of other

creditors of the Debtors’ estates, including general unsecured creditors who may receive nothing

from these potentially administratively insolvent estates. As discussed below, the various

proposed ranges for incentive payments in the KEIP are neither very challenging nor difficult to

attain, and thus are not incentivizing. The Debtors’ argue that “properly incentivizing,

compensating and rewarding the Debtors’ key employees at this critical juncture is in the best

interests of the Debtors, the Debtors’ estates, and all parties in interest.” However, should this

Motion be approved, the KEIP Participants will be paid for work already completed. The

Debtors fail to explain (and the Committee cannot see) any reason that the KEIP is in the best

interests of the Debtors’ estates at this juncture. While the Committee understands the concept

of rewarding hard working employees for meeting challenging performance metrics during a

chapter 11 process, the KEIP, as currently proposed, does not meet the requirements of sections

503(c)(1) or 503(c)(3) of the Bankruptcy Code.

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 2 of 11

3

BACKGROUND

3. On February 15, 2021 (the “Petition Date”), the Debtors filed their voluntary

petitions for relief under Chapter 11 of Title 11 of the United States Code (the “Bankruptcy

Code”). The Debtors are continuing in possession of their property and operating their businesses

pursuant to sections 1107 and 1108 of the Bankruptcy Code. No trustee or examiner has been

appointed.

4. The Committee was constituted by the United States Trustee on February 25,

2021.

5. On March 12, 2021, the Debtors filed the Motion in which they seek approval of

the key employee incentive plan (the “KEIP”) for five members of their management team (the

“KEIP Participants”).

6. If approved, the proposed KEIP will potentially pay close to to five of

the Debtors’ employees, specifically, the Chief Executive Officer, the Chief Financial Officer,

the Executive Vice President of Operations, the Executive Vice President Food Safety & Quality

Assurance, and the Executive Vice President Human Resources. As senior officers of the

Debtors, the KEIP Participants are insiders within the meaning of section 101(31) of the

Bankruptcy Code.3

7. As set forth in the Motion, the proposed payment of a KEIP bonus is based upon

certain metrics. First, the Debtors propose to provide an award to KEIP Participants based upon

the Debtors’ fill rate4, which will be benchmarked at (the “Fill Rate Incentive”). If the

Debtors’ fill rate is in the aggregate through the conclusion of the Sale, the Debtors will

3 The Debtors acknowledge that all five KEIP Participants “are or may be considered ‘insiders’ under the

Bankruptcy Code.” Motion ¶ 9.

4 According to the Debtors, the fill-rate for customer orders is the basis upon which the Debtors are paid.

If the Debtors’ do not meet their fill-rate, they are penalized through a backup penalty charge or reduced

payment.

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 3 of 11

4

award the KEIP Participants a bonus that is 25% of their base salary. Such an award will result

in a $445,000 payment to the KEIP Participants.

8. Second, the Debtors propose to provide an award to the KEIP Participants tied to

the total price of the sale (the “Sale Incentive”), which will award the KEIP Participants

collectively $123,550 for every additional in proceeds above the current Stalking

Horse Bid. An aggregate cap of $492,500 will apply to the Sale Incentive, limiting the total

award for each KEIP Participant, with the exception of the CEO. The CEO will receive no less

than $100,000 upon the sale of the Debtors that the Debtors’ secured lenders have allegedly

agreed to fund from their distribution should an overbid not yield sufficient proceeds. The

$492,500 cap does not apply to the CEO’s award under the Sale Incentive.

9. The Debtors propose to measure the award for the Fill Rate Incentive and Sale

Incentive at the Sale closing and will pay such awards “as soon as practical after the Sale

closing.” Motion ¶ 20.

OBJECTION

10. Section 503(c)(3) controls whether the Court should approve Debtors’ proposed

KEIP. “Section 503(c) was enacted to limit a debtor’s ability to favor powerful insiders

economically and at estate expense during a chapter 11 case.” In re Pilgrim’s Pride Corp., 401

B.R. 229, 234 (Bankr. N.D. Tex. 2009). In other words, through section 503(c)(3), Congress

sought to “eradicate the notion that executives were entitled to bonuses simply for staying with

the Company through the bankruptcy process.” In re Hawker Beechcraft, Inc., 479 B.R. 308,

312-13 (Bankr. S.D.N.Y. 2012) (internal citations omitted); see also In re Dana Corp., 358 B.R.

567, 575 (Bankr. S.D.N.Y. 2006) (discussing the legislative history of section 503(c) of the

Bankruptcy Code). To make that determination, courts often look at historical performance

under proposed performance metrics and whether the targets will be difficult to achieve. See In

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 4 of 11

5

re Velo Holdings, Inc., 472 B.R. 201, 210-11 (Bankr. S.D.N.Y. 2012) (noting that the Debtors

had yet to meet the proposed incentive program targets). The goals should be more like “half

court flings at the buzzer” than “layups” or “free throws.” Hawker Beechcraft, 479 B.R. at 313 n.

7. Thus, debtors bear a burden by the preponderance of the evidence that insider bonus programs

are truly incentives and not retentive in nature. In re Residential Capital, LLC, 478 B.R. 154, 170

(Bankr. S.D.N.Y. 2012).

11. In evaluating any proposed incentive plan, the first consideration is whether it is

merely a disguised retention plan, the approval of which is governed by the strict requirements of

section 503(c)(1) of the Bankruptcy Code, rather than the more liberal provisions of section

503(c)(3) of the Bankruptcy Code. The Committee submits that, in this case, the proposed KEIP

is a disguised retention plan designed to benefit a small subset of already well-compensated

insiders for work already performed. Specifically, the KEIP Participants’ salaries range from

. Courts recognize that debtors often mischaracterize retention programs

as incentive programs to evade the heightened scrutiny of section 503(c)(1). See In re Velo

Holdings Inc., 472 B.R. at 209 (“Attempts to characterize what are essentially prohibited

retention programs as ‘incentive’ programs in order to bypass the requirements of section

503(c)(1) are looked upon with disfavor”); In re Hawker Beechcraft, Inc., 479 B.R. at 312 (“the

threshold question . . . is whether the KEIP is a true incentive plan, or instead, a disguised

retention plan.”). As such, this Court must examine the proposed KEIP and determine whether

its KEIP metrics are “designed to motivate insiders to rise to a challenge or merely report to

work.” Hawker Beechcraft, 479 B.R. at 313.

12. For a KEIP to be truly incentivizing, it should be tied to significant and

challenging metrics. See, e.g., In re Dana Corp., 358 B.R. at 583 (approval of incentive plan

where performance metrics were “difficult targets to reach and [were] clearly not ‘lay-ups’”);

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 5 of 11

6

US2008 18245505 5

Hawker Beechcraft, 479 B.R. at 313-15 (rejection of a bonus plan where lowest level of

performance metrics were “well within reach”). Additional work and requirements placed on

insiders caused by the commencement of a chapter 11 case are not sufficient reasons for

increased pay. See In re Residential Capital, LLC, 478 B.R. 154, 168 (Bankr. S.D.N.Y. 2012).

(“[w]hile it is no doubt true that the requirements of these chapter 11 cases and the proposed

assets sales have altered or increased the work of insiders, such would also be true in virtually all

chapter 11 cases; section 503(c) requires more than increased responsibilities to justify increased

pay for insiders.”). Yet, this type of additional work is exactly what the Debtors seem to rely

upon in trying to justify the payment of over in KEIP incentive payments to the five

insiders.

A. Fill Rate Incentive

13. The Debtors have entirely failed to meet their burden with respect to the Fill Rate

Incentive. The Debtors note that during the first week of these chapter 11 cases, the Debtors met

a fill rate. The Debtors fail to provide any other historical information sufficient for this

Court, the Committee and other parties in interest to determine that the proposed fill rate

metric is an appropriate target.

14. Additionally, at the time of the hearing for approval of the Sale, the Debtors will

likely know whether they will achieve a fill rate from the Petition Date through the

closing of the Sale, as the closing is required to occur on or before April 8, 2021 consistent with

the milestone set forth in the Final Order (I) Authorizing the Debtors to Obtain Postpetition

Financing, (II) Authorizing the Debtors to Use Cash Collateral, (III) Granting Liens and

Providing Superpriority Administrative Expense Claims, (IV) Granting Adequate Protection to

Prepetition Secured Parties, (V) Modifying Automatic Stay, and (VI) Granting Related Relief

(the “Final DIP Order”) [Dkt. No. 335]. See Final DIP Order ¶ 24. Approval of the KEIP at the

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 6 of 11

7

March 25, 2021 hearing cannot be said to properly incentivize the KEIP Participants, who will

already know whether or not the fill rate target is likely to be achieved. Accordingly, the

Fill Rate Incentive should be removed from the KEIP.

B. Sale Incentive

15. Under the Sale Incentive, the Debtors propose to award the KEIP Participants

collectively $123,550 for every additional in proceeds above the current Stalking

Horse Bid. An aggregate cap of $492,500 will apply to the Sale Incentive, limiting the total

award for each KEIP Participant, with the exception of the CEO. The CEO will receive no less

than $100,000 upon the sale of the Debtors assets, as the Debtors’ secured lenders have allegedly

agreed to backstop this amount from their distribution should an overbid not yield sufficient

proceeds. The $492,500 cap does not apply to the CEO’s award under the Sale Incentive.

16. The Committee objects to providing the KEIP Participants with incentive payouts

simply for entry by this Court of an order approving the sale of the Debtors’ assets (which is

expected to occur soon) and the subsequent closing of such sale. That simply is not

incentivizing. The Debtors argue that it is “critical” that they implement the KEIP

“immediately” to ensure that the KEIP Participants “continue to meet the extraordinary

challenges confronting the Debtors during these chapter 11 cases and to ensure the highest

and best value for the Sale.” Yet, the KEIP Participants will be rewarded simply because a

bidder determines in its own business judgment to increase its bid. Moreover, the Motion

was filed at a time during which the Debtors anticipated that multiple bids for portions or

substantially all of the assets would be received. In addition, many of the functions that the

Debtors allege the KEIP Participants are being asked to perform are functions that, upon

information and belief, the Debtors’ Chief Restructuring Officer is also performing. The

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 7 of 11

8

Sale Incentive is not challenging when the Debtors and their management team were already

aware that a competitive auction would likely be held.

17. In sum, the APA with Stellex/CF Buyer (US) LLC and Stellex/CF Buyer (CN)

Inc. (collectively, “Stellex”) was negotiated and executed prior to the bankruptcy filings, so the

KEIP Participants should not need to be incentivized for work that has already been done

prepetition in connection with the APA. Moreover, under the KEIP, the Debtors’ CEO will

receive $100,000 for the mere closing of the proposed Sale to Stellex; hardly an incentive to

maximize value of the Debtors’ estates. Further, the proposed incentive payments that are tied to

each increase of the sale price of the Debtors’ assets appear to be readily achievable

as the Debtors are already aware of multiple bids that have been made for the Debtors’ assets.

Perhaps most importantly, at the time of the scheduled hearing on the Motion, the auction will be

over, and the Debtors will know whether the Sale Incentive targets have been achieved. Where

the KEIP Participants themselves will know exactly what their award related to the Sale

Incentive will be at the time of the Debtors’ request for approval of the proposed KEIP, such

Sale Incentives cannot possibly be designed to properly incentivize. In sum, based on the

foregoing, the Committee submits that the Sale Incentive should be totally eliminated from the

KEIP.

CONCLUSION

18. The Debtors have the burden of proving by a preponderance of the evidence that

the KEIP is an incentive plan. See In re Dana Corp., 351 B.R. 96, 100 (Bankr. S.D.N.Y. 2006).

The Debtors have failed to establish that the KEIP Participants will work above and beyond their

fulfillment of their pre-existing employment and/or fiduciary duties. See In re GT Advanced

Techs., Inc., No. 14-11916-HJB, 2015 WL 5737181, at *6 (Bankr. D.N.H. Sept. 30, 2015) (“the

Insiders seek bonus compensation for doing a job they are already obligated to do—to right the

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 8 of 11

9

ship”). Indeed, the KEIP seeks to “incentivize” the KEIP Participants for work they have

already substantially performed. In addition, the scope and cost of the KEIP is neither

reasonable nor fair as the KEIP Participants may receive over in the aggregate in

addition to the base salaries they continue to collect. The Committee submits that such KEIP

awards are inappropriate and far from fair or reasonable in a case where a portion of the KEIP

awards are all but guaranteed and where unsecured creditors may not receive any recovery.

Lastly, the Debtors have failed to prove that the various proposed targets for the Fill Rate

Incentive and Sale Incentive are truly difficult metrics to establish and thus incentivizing. In

fact, if approved, the KEIP would provide $100,000 to the CEO simply for the closing of the

Sale already contemplated by the Stalking Horse Bid. In the absence of meaningful or

challenging targets that would truly provide a benefit to these estates, the proposed KEIP payouts

cannot be characterized as a true incentive plan and should not be approved. The Debtors have

failed to meet their burden in showing that the KEIP is properly structured to actually incentivize

the KEIP Participants to meet certain difficult targets. Accordingly, this Court should find the

KEIP to be retentive and not incentive-based and therefore deny approval thereof.

RESERVATION OF RIGHTS

19. The Committee reserves any rights as to the Motion and any further amendment

to the Motion that may be filed in these cases. The Committee further reserves the right to

amend, modify, or supplement this Objection at any time.

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 9 of 11

10

WHEREFORE, the Committee requests that the Court deny the Debtors’ Motion and

grant such other and further relief as is appropriate.

Dated: March 23, 2021 By: /s/ Paul M. Rosenblatt

KILPATRICK TOWNSEND & STOCKTON LLP Patrick J. Carew, Esq.

State Bar No. 24031919

2001 Ross Avenue, Suite 4400

Dallas, TX 75201

Telephone: (214) 922-7155

Facsimile: (214) 279-5178

Email: [email protected]

-and-

KILPATRICK TOWNSEND & STOCKTON LLP Todd C. Meyers, Esq. (admitted pro hac vice)

Paul M. Rosenblatt, Esq.

1100 Peachtree Street NE, Suite 2800

Atlanta, GA 30309-4528

Telephone: (404) 815-6321

Facsimile: (404) 541-3373

Email: [email protected]

-and-

KILPATRICK TOWNSEND & STOCKTON LLP Kelly E. Moynihan, Esq. (admitted pro hac vice)

The Grace Building

1114 Avenue of the Americas

New York, NY 10036

Telephone: (212) 775-8700

Facsimile: (212) 775-8800

Email: [email protected]

Proposed Counsel for the Official Committee of

Unsecured Creditors

Case 21-30574 Document 376 Filed in TXSB on 03/23/21 Page 10 of 11

In re: Emerge Energy Services LP, et al.

Objection of the Official Committee of Unsecured Creditors to Debtors’

Motion (I) Pursuant to 11 U.S.C. §§ 105, 361, 362, 363 and 364

Authorizing the Debtors to (A) Obtain Senior Secured Priming

Superpriority Postpetition Financing, (B) Grant Liens and Superpriority

Administrative Expense Status, (C) Use Cash Collateral of Prepetition

Secured Parties and (D) Grant Adequate Protection to Prepetition

Secured Parties; (II) Scheduling a Final Hearing Pursuant to Bankruptcy

Rules 4001(b) and 4001(c); and (III) Granting Related Relief

IMPAC - 6339100V.2 08/10/2019 10:21 PM

UNITED STATES BANKRUPTCY COURT

FOR THE DISTRICT OF DELAWARE

In re:

EMERGE ENERGY SERVICES LP, et al.,1

Debtors.

)

)

)

)

)

)

)

)

Chapter 11

Case No. 19-11563 (KBO)

Jointly Administered

Hearing Date: August 14, 2019 at 11:00 a.m.

Re: Docket Nos. 20 and 64

OBJECTION OF THE OFFICIAL COMMITTEE OF UNSECURED CREDITORS TO

DEBTORS’ MOTION (I) PURSUANT TO 11 U.S.C. §§ 105, 361, 362, 363 AND 364

AUTHORIZING THE DEBTORS TO (A) OBTAIN SENIOR SECURED PRIMING

SUPERPRIORITY POSTPETITION FINANCING, (B) GRANT LIENS AND

SUPERPRIORITY ADMINISTRATIVE EXPENSE STATUS, (C) USE CASH

COLLATERAL OF PREPETITION SECURED PARTIES AND (D) GRANT

ADEQUATE PROTECTION TO PREPETITION SECURED PARTIES; (II)

SCHEDULING A FINAL HEARING PURSUANT TO BANKRUPTCY RULES 4001(b)

AND 4001(c); AND (III) GRANTING RELATED RELIEF

The Official Committee of Unsecured Creditors (the “Committee”) of the above captioned

debtors and debtors in possession (the “Debtors”), by and through its undersigned proposed

counsel, Kilpatrick Townsend & Stockton LLP and Potter Anderson & Corroon LLP, hereby files

this objection (the “Objection”) to the Debtors’ Motion (I) Pursuant to 11 U.S.C. §§ 105, 361,

362, 363, and 364 Authorizing the Debtors to (A) Obtain Senior Secured Priming Superpriority

Postpetition Financing, (B) Grant Liens and Superpriority Administrative Expenses Status, (C)

Use Cash Collateral of Prepetition Secured Parties and (D) Grant Adequate Protection to

Prepetition Secured Parties; (II) Scheduling a Final Hearing Pursuant to Bankruptcy Rules

4001(b) and 4001(c); and (III) Granting Related Relief [D.I. 20] (the “DIP Motion” and the DIP

1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification

number, are: Emerge Energy Services LP (2937), Emerge Energy Services GP LLC (4683), Emerge Energy

Services Operating LLC (2511), Superior Silica Sands LLC (9889), and Emerge Energy Services Finance

Corporation (9875). The Debtors’ address is 5600 Clearfork Main Street, Suite 400, Fort Worth, Texas

76109.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 1 of 22

¨1¤{/_3(* !¢«

1911563190810000000000001

Docket #0162 Date Filed: 08/10/2019

2

IMPAC - 6339100V.2 08/10/2019 10:21 PM

financing facility contemplated therein, the “DIP Facility”).2 In support of this Objection, the

Committee respectfully states as follows:

PRELIMINARY STATEMENT3

1. The DIP Lenders, who are one in the same as the Prepetition Secured Parties, are

seeking to provide a DIP Facility consisting of new-money and roll-up loans as a means to

effectuate their pre-negotiated Restructuring Support Agreement (the “RSA”), which will turn over

substantially all of the reorganized Debtors’ equity to the Prepetition Secured Parties. Pursuant to

the proposed Plan and attendant RSA, even if the Prepetition Secured Parties are determined to be

oversecured, the Prepetition Secured Parties are slated to receive, among other things, 95% of the

reorganized Debtors’ equity (and possibly 100% of the equity) and broad sweeping releases, all

within eighty-five (85) days of the Petition Date. Unsecured creditors, in contrast, are slated to

share in 5% of the reorganized Debtors’ equity and out-of-the-money warrants, but only if such

creditors vote in favor of the Plan. While objections to the Plan contemplated by the RSA are for

another day, the Debtors’ overall strategy for these cases—which is undoubtedly driven by the

DIP Lenders/Prepetition Secured Parties—is to run roughshod over unsecured creditors at

lightning speed leaving existing management and the lenders with virtually all of the potentially

significant upside to the business while unsecured creditors owed as much as $300 million or more

(when rejection damages are added to the pot) are left with at most a few pockets full of sand.

2. As discussed herein, the DIP Facility is inextricably tied to the RSA in that they

each contain, among other things, value-destructive cross-defaults. For example, if the Debtors

2 Capitalized terms used herein but not otherwise defined herein shall have the meaning ascribed to them

in the DIP Motion.

3 Capitalized terms used but not otherwise defined in the Preliminary Statement shall have the meanings

ascribed to them below.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 2 of 22

3

IMPAC - 6339100V.2 08/10/2019 10:21 PM

attempt to exercise the fiduciary out under the RSA, such action would trigger an event of default

under the RSA which, in turn, triggers a default under the DIP Facility. With this structure in

place, approval of the DIP Facility would render the restructuring set forth in the RSA and the

related Plan a fait accompli.

3. As if that were not enough, the Prepetition Secured Parties will also use the DIP

Facility to, among other things, (a) effectuate a “creeping” roll-up of as much as $66.7 million in

prepetition debt; (b) relend such rolled-up amounts to the Debtors with the same protections that

are afforded to new-money DIP loans; (c) encumber all previously unencumbered property on

account of both the new-money loans and the Roll-Up Loans, including (i) the assets of Emerge

Services Finance Corporation (“ESFC”), a Debtor that was not subject to any of the Prepetition

Debt or the Prepetition Liens; and (ii) assets encumbered by the Prepetition Secured Parties’

Prepetition Liens that are subsequently avoided; (d) eliminate the risk of a cram-down by way

of the proposed Roll-Up Loans; (e) receive payment of all professional fees without any cap; (f)

receive payment of excessive DIP fees for minimal new money loans; (g) lock these cases into

overly restrictive milestones; and (h) obtain sections 506(c) and 552(b) and marshaling waivers.

All of this relief, if granted, would be overreaching, unnecessary and unduly prejudicial to

unsecured creditors. Indeed, unless the one-sided Interim Order (and presumably Final Order) is

modified to address the issues and objections raised herein, entry of the Final Order may deprive

unsecured creditors of substantial unencumbered value less than one month after the

commencement of these chapter 11 cases.

4. Adding insult to injury, the Interim Order (and presumably the proposed Final

Order) also inappropriately restricts the Committee’s ability to discharge its fiduciary duties by,

among other things, providing an inadequate Challenge Period during which the Committee must

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 3 of 22

4

IMPAC - 6339100V.2 08/10/2019 10:21 PM

not only investigate the Prepetition Secured Parties’ liens and claims but also causes of action or

claims against such parties (which parties appear to have hand-picked a special committee that

makes all restructuring-related decisions for the Debtor)4; and (b) seek and obtain standing to

commence a challenge5. These restrictions prevent the Committee from validating the Prepetition

Secured Parties’ position that they have enforceable and valid liens on substantially all of the

Debtors’ assets and asserting any claims or causes of action against the Prepetition Secured Parties.

5. Prior to filing the Objection, the Committee engaged in negotiations with the

Debtors and the Prepetition Secured Parties in an attempt to resolve the Committees issues with

the Final Order. While such negotiations hopefully remain ongoing, the parties were not able to

agree to the form of a Final Order, which necessitated the filing of this Objection.

6. For the reasons set forth herein, the Court should condition approval of the DIP

Motion on a final basis upon the Debtors substantially revising the Final Order and DIP Credit

Agreement so as to address the serious concerns discussed in this Objection including: (a) the

overreaching liens and superpriority claims in connection with the Roll-Up Loans; (b) the proposed

encumbrance of avoidance proceeds, claims under the Debtors’ D&O insurance policies,

commercial tort claims, and any proceeds or property of the foregoing; (c) the cross-defaults

between the RSA and DIP Facility; (d) the truncated Challenge Period and related terms; (e) the

4 Prior to the Petition Date, the board of directors of Emerge Energy Services GP LLC (which is wholly

owned by the Debtors’ ultimate equity owner, Insight Equity) delegated the powers to approve and

implement the terms of the proposed restructuring to a special restructuring committee of the board created

pursuant to the RSA (the “Special Restructuring Committee”). The Special Restructuring Committee

consists of two members that were appointed by the Debtors from a slate of candidates acceptable to the

Noteholders, who are one in the same with the DIP Lenders. See Declaration of Bryan M. Gaston,

Restructuring Officer of the Debtors, in Support of Chapter 11 Petitions and First Day Pleadings [D.I. 14]

(the “First Day Declaration”) at ¶ 33. 5 The Committee’s professional fee budget related to all challenge efforts is limited to $35,000.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 4 of 22

5

IMPAC - 6339100V.2 08/10/2019 10:21 PM

restrictive case milestones; (f) the proposed section 506(c), 552(b), and marshaling waivers; and

(g) the excessive DIP Fees.

BACKGROUND

7. On July 15, 2019 (the “Petition Date”), the Debtors commenced voluntary cases

under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”). The Debtors

continue to operate their businesses and manage their properties as debtors in possession pursuant

to sections 1107(a) and 1108 of the Bankruptcy Code.

8. On July 17, 2019, the Court entered its Interim Order (I) Authorizing Debtors (A)

to Obtain Postpetition Financing Pursuant to 11 U.S.C. §§ 105, 361, 362, 363, and 364 and (B)

to Utilize Cash Collateral Pursuant to 11 U.S.C. § 363, (II) Granting Adequate Protection to

Prepetition Secured Parties Pursuant to 11 U.S.C. §§ 361, 362, 363, 364 and 507(b) and (III)

Scheduling Final Hearing Pursuant to Bankruptcy Rules 4001(b) and (c) (the “Interim Order”)

[D.I. 64].

9. On July 30, 2019, pursuant to Section 1102 of the Bankruptcy Code, the United

States Trustee for the District of Delaware appointed the Committee [D.I. 111]. The Committee

consists of the following five members: (i) Trinity Industries Leasing Company; (i) The

Andersons, Inc. an Ohio Corporation; (iii) Iron Mountain Trap Rock Co.; (iv) Greenbrier Leasing

Company, LLC; and (v) BMT Consulting Group, LLC.

10. On July 30, 2019, the Committee selected Kilpatrick Townsend & Stockton LLP

and Potter Anderson & Corroon LLP as its proposed co-counsel. On August 2, 2019, the

Committee selected Province, Inc. as its proposed financial advisor and Miller Buckfire as its

proposed investment banker.

11. The objection deadline for the DIP Motion was originally August 7, 2019 at 4:00

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 5 of 22

6

IMPAC - 6339100V.2 08/10/2019 10:21 PM

p.m. (ET). The Debtors agreed to extend the objection deadline for the Committee to August 1,

2019 at 11:59 p.m. (ET). A hearing to approve the DIP Motion on a final basis is scheduled for

August 14, 2019 at 11:00 a.m. (ET).

OBJECTION

12. Courts routinely recognize that “[d]ebtors in possession generally enjoy little

negotiating power with a proposed lender, particularly when the lender has a prepetition lien on

cash collateral.” In re Defender Drug Stores, Inc., 145 B.R. 312, 317 (9th Cir. BAP 1992). As a

result, courts are hesitant to approve financing terms that are considered harmful to an estate and

its creditors. See, e.g., In re Ames Dep’t Stores, Inc., 115 B.R. 34, 40 (Bankr. S.D.N.Y. 1990)

(noting that “the court’s discretion under section 364 is to be utilized on grounds that permit

reasonable business judgment to be exercised so long as the financing agreement does not contain

terms that leverage the bankruptcy process and powers or its purpose is not so much to benefit the

estate as it is to benefit a party-in-interest”). Thus, while certain favorable terms may be permitted

as a reasonable exercise of the debtor’s business judgment, bankruptcy courts have not approved

financing arrangements that convert the bankruptcy process from one designed to benefit all

creditors to one designed for the sole (or primary) benefit of the lender. See, e.g., Ames, 115 B.R.

at 38; (citing In re Tenney Vill. Co., 104 B.R. 562, 568 (Bankr. D.N.H. 1989)) (holding that the

terms of a postpetition financing facility must not “pervert the reorganizational process from one

designed to accommodate all classes of creditors . . . to one specially crafted for the benefit” of

one creditor).

13. The Interim Order, and presumably the Final Order, includes a number of

provisions that (a) prejudice the rights and powers that the Bankruptcy Code confers on the Court,

the Debtors, and the Committee, (b) unjustifiably benefits the DIP Lenders/Prepetition Secured

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 6 of 22

7

IMPAC - 6339100V.2 08/10/2019 10:21 PM

Parties at the expense of the Debtors’ unsecured creditors, and (c) are likely to give the DIP

Lenders/Prepetition Secured Parties undue control over these cases.

I. The Liens and Claims on Account of the Roll-Up Loans Are Unwarranted and

Overreaching

14. The Committee recognizes that roll-ups are approved by courts in certain situations

based upon the unique facts and circumstances of a case. Here, however, the DIP liens and

superpriority claims related to the Roll-Up Loans are overreaching and detrimental to all creditors,

save the DIP Lenders/Prepetition Secured Parties. As discussed above, the DIP Facility

contemplates a “creeping roll-up” of the Prepetition Revolving Credit Obligations from cash

proceeds from the sale of any Prepetition Collateral or the proceeds from receivables. Such rolled

up amounts will then be deemed borrowed by the Debtors on a dollar-for-dollar basis under the

DIP Facility. Despite the Roll-Up Loans being characterized as DIP borrowings, the economic

reality of the Roll-Up Loans is that they are tantamount to the consensual use of cash collateral.

Notwithstanding this important distinction, the DIP Lenders are requesting that the Roll-Up Loans

be afforded the same DIP liens and superpriority claims as if they were new money financing, but

they are not.

15. If the DIP liens and superpriority claims on account of the Roll-Up Loans are

approved as currently proposed, the Roll-Up Loans will encumber all of the Debtors’

unencumbered assets, namely (a) assets of the Debtor obligors under the Prepetition Secured Debt

that were previously unencumbered; (b) encumbered assets that become unencumbered as a result

of a successful Challenge by the Committee (or any other party); and (c) the assets of ESFC, a

Debtor that was not previously subject to any of the Prepetition Debt or the Prepetition Liens.

Such a result would essentially guarantee that unsecured creditors will not see a penny on account

of the Debtors’ unencumbered assets.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 7 of 22

8

IMPAC - 6339100V.2 08/10/2019 10:21 PM

16. Given that these cases were clearly commenced for the benefit of the Prepetition

Secured Parties/DIP Secured Parties, the DIP Lenders’ efforts to scoop up all of the Debtors’

unencumbered assets on account of the Roll-Up Loans is overreaching and inconsistent with the

protections afforded to the use of cash collateral, which is all that is being provided by the so-

called Roll-Up Loans. Accordingly, the Committee objects to the DIP Lenders being granted any

DIP liens or superpriority claims on account of the Roll-Up Loans on any unencumbered assets

except to secure a superpriority adequate protection claim for diminution in value, if any, provided

that the Debtors are required to marshal encumbered assets before unencumbered assets. These

superpriority adequate protection claims and the new money portion of the DIP Facility are the

only claims that can properly be secured by any unencumbered assets.

II. The DIP Liens and Superpriority Claims and Adequate Protection Liens and

Claims on Account of the New Money Loans Should Not Encumber Avoidance

Proceeds, Commercial Tort Claims, Claims Under the Debtors’ D&O

Insurance Policies, or Proceeds or Property of the Foregoing

17. The Committee objects to the DIP Lenders being granted any DIP liens and

superpriority claims or adequate protection liens and claims on avoidance proceeds, commercial

tort claims, claims under the Debtors’ D&O Insurance Policies, and proceeds or property of the

foregoing, even to secure the new money and superpriority diminution in value claims.

18. With respect to the proposed liens and claims on avoidance proceeds, such relief is

fundamentally at odds with the unique purposes served by avoidance actions. Avoidance actions

are distinct creatures of bankruptcy law designed to benefit, and ensure equality of distribution

among, general unsecured creditors. See Official Comm. of Unsecured Creditors of Cybergenics

Corp. v. Chinery (In re Cybergenics Corp.), 226 F.3d 237, 244 (3d Cir. 2000), rev’d en banc, 330

F.3d 548 (3d Cir. 2003) (identifying underlying intent of avoidance powers to recover valuable

assets for estate’s benefit); In re Tribune Co., 464 B.R. 126, 171 (Bankr. D. Del. 2011) (noting

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 8 of 22

9

IMPAC - 6339100V.2 08/10/2019 10:21 PM

“that case law permits all unsecured creditors to benefit from avoidance action recoveries”). The

Debtors have not provided any justification for the extraordinary grant of liens on avoidance

proceeds, or for the potential payment of superpriority claims with the proceeds of avoidance

actions. To the contrary, there is no legal basis for this Court to grant the DIP Lenders a lien on

avoidance proceeds. Accordingly, avoidance proceeds should be wholly excluded from the DIP

Collateral and reserved for the benefit of the Debtors’ unsecured creditors. With respect to any

DIP liens and superpriority claims or adequate protection liens and claims against the Debtors’

D&O insurance policies and commercial tort claims, those assets were likely unencumbered

prepetition and they should continue to remain unencumbered postpetition for the benefit of

unsecured creditors who, under the existing Plan, may receive no recovery whatsoever.

III. The Cross-Default Provisions in the DIP Facility and RSA Give the DIP

Secured Parties Undue Control Over These Cases

19. The fiduciary out is illusory because, should the Debtors determine that an

alternative restructuring proposal is in the best interest of the estates and terminate the RSA, the

DIP Lenders may (a) declare an event of default under the DIP Facility immediately, without

notice, application or motion, hearing before or order of the Court, (b) declare all obligations under

the DIP Facility immediately due and payable, (c) immediately terminate and restrict any right of

the Debtors to use cash collateral; and (d) upon five days’ written notice, exercise all rights and

remedies, including foreclosure upon the DIP Collateral, without further notice or order from the

Court. See DIP Credit Agreement §§ 10.7(c) and 11.1(a), Interim Order at ¶ 14(d). Accordingly,

any termination of the RSA and as a result, the DIP Facility—even if consistent with the exercise

of the Debtors’ fiduciary duties—would result in dire consequences for these estates and its

stakeholders.

20. Furthermore, although the RSA does not contain a “no-shop” provision, the

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 9 of 22

10

IMPAC - 6339100V.2 08/10/2019 10:21 PM

existence of the cross-defaults and tight case milestones effectively creates a restrictive “no-shop”

provision. Indeed, the First Day Declaration makes no mention of the Debtors looking outside of

their own capital structure with regard to an in-court restructuring of the Debtors’ balance sheet

and business operations. Rather, the First Day Declaration provides that the Debtors and their

restructuring advisors engaged with only Insight Equity (the Debtors’ ultimate equity owner) and

the Prepetition Secured Parties. See First Day Declaration at ¶ 32. Why now, with a cross-default

looming over any exercise of the Debtors’ fiduciary out, would the Debtors “shop” for

restructuring alternatives, if they have not apparently done so to date? Furthermore, even if the

Debtors were to exercise their fiduciary out, they are still liable for the breach of the RSA: “no

termination of this Agreement shall relieve any Party from liability for its breach or non-

performance of its obligations hereunder prior to the date of such termination.” RSA at ¶ 6(e).

Therefore, approval of the Final Order in its current form would be tantamount to (a) approving

the assumption of the RSA without compliance with the provisions of section 365 of the

Bankruptcy Code; and (b) confirming a plan of reorganization without compliance with the

provisions of section 1129 of the Bankruptcy Code.

21. For the foregoing reasons, this Court should deny the DIP Motion to the extent that

the DIP Facility provides cross-defaults with the RSA and effectively nullifies the Debtors’

fiduciary out, improperly granting control of these cases to the Prepetition Secured Parties/DIP

Secured Parties. At a minimum, in the event a DIP default is triggered as a result of the Debtors

exercising their fiduciary out, the DIP Lenders’ exercise of remedies should not extend beyond the

ability to terminate lending. For the DIP Lenders to be able to exercise “all remedies”, including

the ability to foreclose, is inappropriate and value-destructive.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 10 of 22

11

IMPAC - 6339100V.2 08/10/2019 10:21 PM

III. The Proposed Adequate Protection Package is Unwarranted

22. The Interim Order provides an overly generous adequate protection to the

Prepetition Secured Parties in the form of (a) all accrued and unpaid interest and fees at the default

rate, as provided under the Prepetition Revolving Credit Agreement; and (b) all reasonable and

documented fees, out-of-pocket expenses, and disbursements incurred by the Prepetition Secured

Parties, without any cap. See Interim DIP Order at ¶ 18(d). However, it is not clear that the

Prepetition Secured Parties are oversecured, a necessary predicate for the payment of postpetition

interest. See In re Residential Capital, LLC, 508 B.R. 851, 853 (Bankr. S.D.N.Y. 2014) (“The

Bankruptcy Code entitles oversecured creditors to postpetition interest[.]”) (emphasis added). In

fact, the Dunayer Declaration states that, “Houlihan has concluded, however, that the going-

concern value of the Debtors’ assets fall significantly short of the total outstanding obligations

under the Prepetition Facilities.” See Declaration of Adam Dunayer in Support of Motion (I)

Pursuant to 11 U.S.C. §§ 105, 361, 362, 363, and 364 Authorizing the Debtors to (A) Obtain Senior

Secured Priming Superpriority Postpetition Financing, (B) Grant Liens and Superpriority

Administrative Expenses Status, (C) Use Cash Collateral of Prepetition Secured Parties and (D)

Grant Adequate Protection to Prepetition Secured Parties; (II) Scheduling a Final Hearing

Pursuant to Bankruptcy Rules 4001(b) and 4001(c); and (III) Granting Related Relief at ¶ 9 [D.I.

21] (the “Dunayer Declaration”)6.

23. For these reasons, the Committee requests that the Final Order exclude any payment

of postpetition interest to the Prepetition Secured Parties until a final determination is made as to

(a) the value of the Debtors’ assets; and (b) the validity of the Prepetition Liens. At a minimum,

6 By the filing of this Objection, the Committee is not agreeing with the value conclusion contained in the

Dunayer Declaration and expressly reserves the right to contest same.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 11 of 22

12

IMPAC - 6339100V.2 08/10/2019 10:21 PM

the Committee requests that the default rate not be utilized in calculating the postpetition interest

payments and that the Final Order make clear that any adequate protection payments be subject to

recharacterization as payments on principal in the event the Prepetition Lenders are undersecured.

IV. The Challenge Period and Related Terms Constrain the Committee’s Ability

to Appropriately Discharge its Fiduciary Duties

24. The DIP Facility contains substantial constraints on the ability of the Committee to

discharge its fiduciary duties. Specifically, the terms of the Interim Order limit the time during

which the Committee may investigate a litany of liens and claims related to the Prepetition Secured

Parties, file a motion to obtain standing, obtain the requisite standing, and commence a challenge

to (60) calendar days after the appointment of the Committee (the “Challenge Period”)7. This

timeframe is unacceptable and unworkable because the Challenge Period applies not only to the

liens and claims of the Prepetition Secured Parties (the “Prepetition Lien Matters”), but also any

claims or causes of action that may be asserted against the Prepetition Secured Parties (i.e., lender

liability claims and claims related to a valuation of the Debtors’ assets) (the “Prepetition Claim

and CoA Matters”). Given that the Interim Order (and presumably the Final Order) includes a

broad sweeping plan-like release of the Prepetition Secured Parties, the Committee, the only estate

fiduciary who has not granted such a release, must have a reasonable amount of time to investigate

whether such a release is appropriate or whether there are viable claims or causes of action against

such parties.8 See Interim Order at ¶ 7.

7 The Committee was appointed on July 30, 2019. Sixty (60) calendar days from the appointment of the

Committee is September 28, 2019. See Interim Order at ¶ 26. 8 The Committee also objects to the proposed investigation budget, which is currently set at $35,000.

Interim Order at ¶ 27. This provision clearly seeks to shield the Prepetition Secured Parties, who are also

the DIP Secured Parties, by unduly limiting the resources available to the Committee to investigate potential

claims against such parties. Therefore, the Committee requests that an additional $40,000 be made

available to the Committee for its analysis of Prepetition Lien Matters and that no cap be placed on the

Committee’s investigation into the Prepetition Claim and CoA Matters

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 12 of 22

13

IMPAC - 6339100V.2 08/10/2019 10:21 PM

25. The Committee also objects to the requirement that it obtain standing prior to the

expiration of the Challenge Period if it wishes to pursue a challenge. See Interim Order at ¶ 26.

The process by which the Committee may obtain standing to pursue such a cause of action will

likely take a reasonable amount of time. As such, and given the proposed case milestones and thin

investigation budget for the Committee, the Committee should not be required to expend the time

and expense necessary to obtain standing prior to commencing a challenge. Indeed, courts have

previously approved financing agreements that grant standing to creditors’ committees without the

need for a standing motion. See, e.g., In re Phoenix Payment Sys., Inc., No. 14-11848 (Bankr. D.

Del. Sept. 3, 2014); In re Am. Safety Razor, LLC, No. 10-12351 (Bankr. D. Del. Aug. 27, 2010) at

¶ 6; see also In re Quebecor World (USA) Inc., No. 08-10152 (Bankr. S.D.N.Y. Apr. 1, 2008) ¶

21; In re Dana Corp., Case No. 06-10354 (Bankr. S.D.N.Y. Mar. 29, 2006) ¶ 25.9

26. In light of the complexity of these cases and the speed at which they are progressing,

the Committee requests that the Final Order be revised such that: (a) the Challenge Period for the

Prepetition Lien Matters be 90 days from the appointment of the Committee; (b) the Challenge

Period for the Prepetition Claim and CoA Matters be through and until the later of (i) 90 days from

the appointment of the Committee; and (ii) the hearing to confirm a chapter 11 plan; (c) the

investigation budget be increased to $75,000 for Prepetition Lien Matters only and that no cap be

placed on the Committee’s investigation into the Prepetition Claim and CoA Matters; and (d) the

Committee be granted automatic standing to commence a Challenge or, alternatively, that upon

the filing of a standing motion, the Challenge Period be automatically tolled until three (3) business

days after this Court rules on such motion.

9 In the event the Committee is required to obtain standing, the Challenge Period should be automatically

tolled upon the filing of a standing motion until three (3) business days after this Court rules on such motion.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 13 of 22

14

IMPAC - 6339100V.2 08/10/2019 10:21 PM

V. The DIP Milestones Must by Extended by at Least Thirty (30) Days

27. Pursuant to the milestones set forth in the DIP Credit Agreement and RSA:

within 37 days of the Petition Date, the Debtors shall have a hearing to approve the

Disclosure Statement Hearing (the “Disclosure Statement Hearing Deadline”);

within 60 days of the Petition Date, the Debtors shall have filed a motion seeking rejection

of any railcar leases designated by the Debtors and with the consent of the Required

Lenders (as defined in the DIP Credit Agreement);

within 35 days after the Disclosure Statement Hearing Deadline, the Debtors shall have a

hearing to seek confirmation of the Plan (the “Confirmation Hearing Deadline”); and

within the earlier of (i) 15 days after the Confirmation Deadline; and (ii) 100 days after the

Petition Date, the Effective Date of the Plan shall have occurred.

See DIP Credit Agreement § 6.16; RSA Term Sheet at Appendix I.

28. The Committee, which was formed only 11 days ago, should have an opportunity

to, among other things, vet the Debtors’ prepetition marketing efforts; independently test the

market for interest in the Debtors’ assets; understand and analyze the go-forward business plan;

perform a valuation analysis; investigate the Prepetition Secured Parties’ alleged liens and claims;

investigate potential claims against the Prepetition Secured Parties, including claims related to the

apparent mandate that the board abdicate its duties in favor of hand-picked proxies for the

Prepetition Secured Parties; understand the prepetition negotiations and analyses regarding entry

into the RSA; analyze tax-related issues that may be driving the structure of the Plan; analyze the

insider releases contained in the Plan; and analyze other Plan provisions including the rationale for

inexplicably providing consideration to equity despite the woeful consideration provided to

general unsecured creditors.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 14 of 22

15

IMPAC - 6339100V.2 08/10/2019 10:21 PM

VI. The Waivers of Sections 506(c) and 552(b) of the Bankruptcy Code and

Related Provisions are Unwarranted and Not Supported by the Record

29. The Debtors are seeking a waiver of the estates’ right to surcharge collateral

pursuant to section 506(c) of the Bankruptcy Code, as well as a marshaling waiver and a waiver

of the estates’ right under section 552(b) of the Bankruptcy Code. These waivers are entirely

inappropriate at this time, and in any event, not justified by the record.

A. Surcharge Rights Under Section 506(c) Should Not be Waived

30. The Interim Order provides that subject to entry of the Final Order, neither the DIP

Collateral nor Prepetition Collateral shall be subject to any surcharge pursuant to section 506(c) of

the Bankruptcy Code. See Interim Order at ¶ 16. Section 506(c) of the Bankruptcy Code is a rule

of fundamental fairness for all parties in interest and provides that secured creditors shall share the

burden of satisfying administrative expenses where funds are expended for the purpose of

preserving and selling their collateral. Section 506(c) ensures that the cost of liquidating a secured

lender’s collateral is not paid from unsecured recoveries. See, e.g., Precision Steel Shearing v.

Fremont Fin. Corp. (In re Visual Indus., Inc.), 57 F.3d 321, 325 (3d Cir. 1995) (stating, “section

506(c) is designed to prevent a windfall to the secured creditor”). As such, the Debtors’ unilateral

waiver of Bankruptcy Code section 506(c) would eliminate a further avenue of recovery for the

Debtors’ estates and foist the costs of the Debtors’ reorganization onto unsecured creditors.

31. By waiving the estates’ section 506(c) rights, the Debtors are agreeing to pay for

any and all expenses associated with the preservation and disposition of the collateral of the DIP

Secured Parties and the Prepetition Secured Lenders. Here, such a waiver is highly inappropriate

given that these cases are being run as a vehicle for the exclusive benefit of the Prepetition Secured

Parties. Indeed, if these cases proceed according to the RSA as currently proposed, the Prepetition

Secured Parties will reap almost all of the benefit of these cases with unsecured creditors being

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 15 of 22

16

IMPAC - 6339100V.2 08/10/2019 10:21 PM

relegated to a de minimis recovery, if any. Courts have routinely rejected similar surcharge waivers

under these circumstances. See In re AFCO Enters., Inc., 35 B.R. 512, 515 (Bankr. D. Utah 1983)

(“When the secured creditor is the only entity which is benefited by the trustee’s work, it should

be the one to bear the expense. It would be unfair to require the estate to pay such costs where

there is no corresponding benefit to unsecured creditors.”); see also Transcript of Hearing at 20-

21, In re Mortgage Lenders Network USA, Inc., No. 07-10146 (PJW) (Bankr. D. Del. Mar. 27,

2007) [D.I. No. 346]; Transcript of Hearing at 212-13, In re Energy Future Holdings Corp., No.

14-10979 (CSS) (Bankr. D. Del. June 5, 2014) [D.I. No. 3927]; Hartford Fire Ins. Co. v. Norwest

Bank Minn., N.A. (In re Lockwood Corp.), 223 B.R. 170, 176 (B.A.P. 8th Cir. 1998).

32. While the Committee suspects that the Debtors are hopeful (or perhaps cautiously

optimistic) that the budget captures all of the expenses that will be incurred in the administration

of these cases, there can be no assurance at this early juncture that the administrative expenses of

these cases will be paid by the Debtors in the ordinary course. Furthermore, if an event of default

is called under the DIP Facility, the budgeted amounts that were incurred and not paid at such time

could remain unpaid. For these reasons, the Court should not approve a section 506(c) waiver at

this time.

B. The Equities of the Case Exception Under 552(b) and Marshaling Rights Must

be Preserved

33. The Debtors’ willingness to waive their rights under section 552(b) is, at best,

premature. The Court should also not permit a section 552(b) waiver before allowing parties in

interest – including the Committee – to properly examine the “equities of the case”. See Sprint

Nextel Corp. v. U.S. Bank Nat’l Ass’n (In re TerreStar Networks, Inc.), 457 B.R. 254, 272-73

(Bankr. S.D.N.Y. 2011) (denying request for 552(b) waiver as premature because factual record

was not fully developed). If unencumbered assets are used to increase the value of the secured

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 16 of 22

17

IMPAC - 6339100V.2 08/10/2019 10:21 PM

creditors’ collateral, unsecured creditors should be able to argue that such value inures to them,

and not to secured creditors. See In re Metaldyne, No. 09-13412 (MG) 2009 WL 2883045, at *6

(Bankr. S.D.N.Y. June 23, 2009) (holding, in the context of a proposed 552(b) waiver, that “the

waiver of an equitable rule is not a finding of fact…and the Court, in its discretion, declines to

waive prospectively an argument that other parties in interest may make”); see also In re iGPS Co.

LLC, No. 13-11459 (KG) 2013 WL 4777667, at *5 (Bankr. D. Del. July 1, 2013) (no waiver of

the “equities of the case” exception with respect to creditors committee). In the alternative, any

section 552(b) waiver should be subject in all respects to the Committee’s challenge rights.

34. The Debtors also should not waive any rights with respect to the marshaling

doctrine in the Final Order. Such favorable treatment, which would enable the Prepetition Secured

Parties to “cherry pick” the collateral they want to liquidate most expeditiously is unwarranted

under the circumstances of these cases where the DIP Lenders are receiving excessive fees and

liens on assets previously unencumbered prepetition. Accordingly, marshalling rights should be

preserved for the Committee.10 See, e.g., In re Newcorn Enters. Ltd., 287 B.R. 744, 750 (Bankr.

E.D. Mo. 2002) (granting unsecured creditors’ committee derivative standing to bring marshaling

claim against secured lender, and thereby increase payout to unsecured creditors, where debtor

refused to do so); Official Comm. Of Unsecured Creditors v. Hudson United Bank (In re America’s

Hobby Ctr., Inc.), 223 B.R. 275, 287 (Bankr. S.D.N.Y. 1998) (“[S]tanding in the shoes of the

debtor in possession, the Committee can assert [marshaling] claim.”).

10 As noted above, marshaling should be required before the new money portion of the DIP Facility and

Adequate Protection Claims are satisfied from previously unencumbered assets, including assets

encumbered by the Prepetition Secured Parties’ prepetition liens that are subsequently avoided.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 17 of 22

18

IMPAC - 6339100V.2 08/10/2019 10:21 PM

VII. The Proposed DIP Fees are Excessive

35. In the context of a $35 million new money DIP Facility, the proposed DIP fees are

excessive and should be reduced. The proposed DIP fees include:

Commitment Fee: 1.00%

Closing Fee 3.00%

DIP Fee (if DIP replaced) 5.00%

36. With these fees in place, the “all in” financing cost is effectively 18%. It is self-

evident that these fees, which are for a DIP facility that furthers the DIP Lenders’ agenda of

effectuating the restructuring set forth in the RSA, are excessive and insulting from the perspective

of unsecured creditors who are slated to receive a de minimis recovery, if any. At a bare minimum,

the Committee requests that the 5% DIP Fee be reduced to 2.5%.

VIII. Other Objectionable Provisions

37. The Committee also objects to the provisions referenced below and requests that

the Final Order be amended accordingly. The Committee notes that by objecting to these

provisions in bullet point format, the Committee is by no means suggesting that these objections

are either technical or minor in nature.

Deposit/Security Accounts. The Final Order should make clear that with respect to deposit

or securities accounts being within the “control” of the Prepetition Secured Parties, the

term “control” is as defined in the Uniform Commercial Code. See Interim Order at ¶ 6(d).

Release. The plan-like release is overbroad for a DIP financing order and should be

stricken. See Interim Order at ¶ 7.

Indemnity. The indemnity provisions in favor of the DIP Agent and DIP Lenders needs to

be limited to their respective capacities as such. See Interim Order at ¶ 8(f).

Section 364(e) Good Faith Finding. The Debtors’ stipulation that the DIP Obligations are

deemed to have been extended by the DIP Secured Parties in good faith, as that term is

used in section 364(e) of the Bankruptcy Code, needs to be subject to the Committee’s

challenge rights. See Interim Order at ¶ 8(f).

Material Modifications. Any material modifications, amendments, updates and

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 18 of 22

19

IMPAC - 6339100V.2 08/10/2019 10:21 PM

supplements to the Approved Budget need to be subject to further Court approval. See

Interim Order at ¶ 8(i).

Remedies Notice Period. The Remedies Notice Period should be elongated to five business

days’ notice. See Interim Order at ¶ 14(d).

Information Rights. The Committee should receive the same reporting at the same time as

the DIP Lenders. See Interim Order at ¶ 18(e).

Use of Proceeds/Carve-Out. The Interim Order prohibits the use of proceeds or access to

the Carve-Out for efforts related to: (i) “preventing, hindering, or otherwise delaying the .

. . enforcement or realization on the [Prepetition Debt];” and (ii) “seek[ing] to modify any

of the rights and remedies granted to the Prepetition Secured Parties, the DIP Agent . . .

under this Interim Order”. See Interim Order at ¶¶ 11(k) and 27. The Final Order should

include an overarching provision providing that nothing in the order shall limit the use of

proceeds or the Carve Out with respect to fees and expenses incurred by the Committee in

contesting the DIP Motion prior to entry of the Final Order, contesting the Disclosure

Statement, Plan, or credit bid, or any other action adverse to the Prepetition Secured

Parties/DIP Secured Parties other than investigating or asserting a challenge.

Limitation of Liability. The limitations of liability in favor of the DIP Agent and DIP

Lenders needs to be limited in their respective capacities as such. See Interim Order at ¶

31.

Credit Bidding. The Committee echoes the objection from Market and Johnson, Inc., Stout

Excavating Group LLC, and A-1 Excavating, Inc. [D.I. 134] regarding the Prepetition

Secured Parties’ ability to credit bid their claims without properly accounting for possible

senior liens such as Prior Permitted Liens. See Interim Order at ¶ 38.

Section 503(b)(9) Claims. So as to ensure administrative solvency, the DIP Lenders should

fund a segregate account not subject to the control or liens of the DIP Secured Parties or

the Prepetition Secured Parties with funds sufficient to pay all allowed claims arising under

section 503(b)(9) of the Bankruptcy Code.

IX. Objectionable Provisions in DIP Credit Agreement

38. The Committee also objects to the provisions in the DIP Credit Agreement

referenced below and requests that as a condition to approval of the DIP Motion, the DIP Credit

Agreement be revised accordingly.

Roll-Up Loans. The terms Pre-Petition Loans and Prior Lender Obligations encompasses

the entirety of the Prepetition Debt, not just the Prepetition Revolver Obligations. So as to

be consistent with the DIP Motion, Interim Order, and proposed Final Order, the DIP Credit

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 19 of 22

20

IMPAC - 6339100V.2 08/10/2019 10:21 PM

Agreement needs to be clear that the Roll-Up only applies to the Prepetition Revolver

Obligations. See DIP Credit Agreement § 6.16.

Cross-Defaults. As the entire of the Prepetition Debt is not being rolled-up, the Credit

Parties will have indebtedness of more than $250,000 and, as a result, are susceptible to

triggering the cross-default provisions at section 10.11. See DIP Credit Agreement § 10.11.

Prohibition Language. The DIP Credit Agreement should not “prohibit any effort” by the

Debtors, the Committee or other party to prime or create pari passu liens. While such

efforts may trigger an event of default under the DIP Credit Agreement, this provision

should not be the equivalent of a restriction under contempt upon Court approval of the

DIP Motion and attendant DIP Credit Agreement. See DIP Credit Agreement § 7.2.

Corporate Governance Default. An event of default should not be triggered if (i) the charter

for the Special Committee is terminated or the Special Committee is dissolved; (ii) the

chief restructuring officer for the General Partner is terminated or replaced; and (iii) the

“[operational consultant]” engaged by the Special Committee is terminated or replaced;

and (iv) the Permitted Holders or the board of directors of the General Partner fail to

support the Approved Chapter 11 plan. See DIP Credit Agreement § 10.19

DIP/RSA Cross Defaults. For the same reasons discussed in this Objection, the DIP Credit

Agreement needs to remove the cross-defaults with the RSA, especially as it relates to the

Debtors’ exercising their fiduciary out. If the cross defaults remain as-is, the fiduciary out

is effectively illusory. See DIP Credit Agreement §§ 10.7(c) and 11.1(a).

Case Milestones. For the same reasons discussed in this Objection, each of the milestones

contained in the DIP Credit Agreement need to be extended by at least thirty (30) days.

See DIP Credit Agreement § 6.16.

RESERVATION OF RIGHTS

The Committee reserves its respective rights, claims, defenses, and remedies, including,

without limitation, the right to amend, modify, or supplement this Objection, to seek discovery,

and to raise additional objections during any further hearing on the DIP Motion.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 20 of 22

21

IMPAC - 6339100V.2 08/10/2019 10:21 PM

CONCLUSION

WHEREFORE, the Committee respectfully requests that the Court (i) condition entry of

an order approving the DIP Motion on a final basis unless the Final Order and DIP Credit

Agreement are modified as requested in this Objection; and (ii) granting such other and further

relief as the Court deems just and proper.

[Remainder of Page Intentionally Left Blank]

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 21 of 22

IMPAC - 6339100V.2 08/10/2019 10:21 PM

Dated: August 10, 2019

Wilmington, Delaware

Respectfully submitted,

POTTER ANDERSON & CORROON LLP

/s/ L. Katherine Good

Jeremy W. Ryan (DE Bar No. 4057)

Christopher M. Samis (DE Bar No. 4909)

L. Katherine Good (DE Bar No. 5101)

Aaron H. Stulman (DE Bar No. 5807)

1313 North Market Street, Sixth Floor

P.O. Box 951

Wilmington, DE 19801

Telephone: (302) 984-6000

Facsimile: (302) 658-1192

Email: [email protected]

-and-

KILPATRICK TOWNSEND & STOCKTON LLP

Todd C. Meyers

David M. Posner

Kelly Moynihan

The Grace Building

1114 Avenue of the Americas

New York, NY 10036

Telephone: (212) 775-8700

Facsimile: (212) 775-8800

Email: [email protected]

-and-

KILPATRICK TOWNSEND & STOCKTON LLP

Lenard M. Parkins

700 Louisiana Street, Suite 4300

Houston, TX 77002

Telephone: (281) 809-4100

Facsimile: (281) 929-0797

Email: [email protected]

Proposed Counsel to the Official Committee of Unsecured

Creditors of Emerge Energy Services LP, et al.

Case 19-11563-KBO Doc 162 Filed 08/10/19 Page 22 of 22

In re: Brookstone Holdings Corp., et al.

Objection of the Official Committee of Unsecured Creditors to Debtors’ Motion for Entry

of an Order Approving Certain Bidding Protections for the Sale of Certain Assets to Blue Star Alliance, LLC

{BAY:03350798v1}

IN THE UNITED STATES BANKRUPTCY COURTFOR THE DISTRICT OF DELAWARE

--------------------------------------------------------------X

In re:

BROOKSTONE HOLDINGS CORP., et al.,1

Debtors.

(Chapter 11)

Case No. 18-11780 (BLS)

Jointly Administered

Hearing Date: September 6, 2018 at 11:00 a.m. (ET)Obj. Deadline: September 5, 2018 at 4:00 p.m. (ET)(extended for Committee)

--------------------------------------------------------------XOBJECTION OF THE OFFICIAL COMMITTEE OF

UNSECURED CREDITORS TO DEBTORS’ MOTION FOR ENTRYOF AN ORDER APPROVING CERTAIN BIDDING PROTECTIONS

FOR THE SALE OF CERTAIN ASSETS TO BLUESTAR ALLIANCE, LLC

The Official Committee of Unsecured Creditors (the “Committee”) of Brookstone

Holdings Corp., and its affiliated debtors and debtors-in-possession (the “Debtors”), by and

through its undersigned proposed counsel, hereby submits this objection (the “Objection”) to the

Debtors’ motion [D.I. 287] (the “Motion”)2 for entry of an order approving proposed bidding

protections (the “Bidding Protections”) for the sale of the Debtors’ intellectual property assets to

a newly-formed subsidiary or affiliate of Bluestar Alliance, LLC (“Bluestar”). In support of the

Objection, the Committee respectfully represents as follows:

1 The Debtors, along with the last four digits of each Debtor’s tax identification number, are:Brookstone Holdings Corp. (4638), Brookstone, Inc. (2895), Brookstone Company, Inc. (3478),Brookstone Retail Puerto Rico, Inc. (5552), Brookstone International Holdings, Inc. (8382), BrookstonePurchasing, Inc. (2514), Brookstone Stores, Inc. (2513), Big Blue Audio LLC (N/A), BrookstoneHoldings, Inc. (2515), and Brookstone Properties, Inc. (2517). The Debtors’ corporate headquarters andthe mailing address for each Debtor is One Innovation Way, Merrimack, NH 03054.

2 Capitalized terms not expressly defined herein shall be given the meanings ascribed to them inthe Motion.

Case 18-11780-BLS Doc 319 Filed 09/05/18 Page 1 of 6

{BAY:03350798v1} 2

OBJECTION

A. ABG Should Be Designated the Stalking Horse Bidder

1. Over the past 10 days, the Debtors received multiple proposals for stalking horse

designation from Bluestar and Authentic Brands Group (“ABG”)3:

Date Received BidForm

Bidder Cash Purchase Price Purchased Assets

August 24 LOI ABG $35 million Intellectual Property

August 28 LOI 4

August 30 LOI ABG $41 million IP/$36 millionGoing-Concern

Intellectual Property orGoing-Concern

August 31 LOI Bluestar $43 million Intellectual Property5

September 2 LOI ABG $50 million Intellectual Property orGoing-Concern

2. Over the past 36 hours, both Bluestar and ABG have each submitted proposed

asset purchase agreements (“APAs”) memorializing and documenting their stalking horse bids.

The bid submitted by Bluestar provides for the purchase of the Debtors’ intellectual property

3 True and correct copies of the ABG and Bluestar LOI’s are annexed hereto in chronological order asExhibits B through F.

4 With respect to a potential going-concern transaction, August 28 bid provides:

”

5 With respect to a potential going-concern transaction, Bluestar’s August 31 bid provides: “As part ofour bid, we will also consider, in conjunction with the Company, a restructuring transaction that providesthat the post-restructured Company operates as a going concern (i.e. we will consider keeping 40-50stores open, and will work with the company and third parties to review all options). If we do not keep atleast 40-50 stores open, we will provide the Debtors (or a post-effective date trust, the format to be at theDebtors’ option) with a guaranteed cash payment of $100,000 on January 2, 2020, and $100,000 onJanuary 2, 20211. In addition, we will also evaluate, and will consider implementing, any alternativetransaction proposed by any other bidder in conjunction with a sale of the IP and related assets.”

Case 18-11780-BLS Doc 319 Filed 09/05/18 Page 2 of 6

{BAY:03350798v1} 3

assets for a cash purchase price of $43 million. The Bluestar bid makes only vague reference to

a potential going-concern transaction, while remaining silent on the assumption of liabilities

related to the Debtors’ real property and payment of cure costs.6

3. The APA submitted by ABG provides for an alternative IP or going-concern

transaction (which election shall be made no later than September 19, 2018) for the purchase of

the Debtors’ intellectual property assets or a going-concern purchase of the company. A copy of

the APA is annexed hereto as Exhibit A. The purchase price for either transaction is $50

million. The APA submitted by ABG expressly contemplates an assumption of liabilities related

to the Debtors’ real property and payment of cure costs for Assumed Contracts in the event of a

going-concern transaction, and provides for the purchase of limited causes of action related to

Assumed Contracts only.

4. The APA submitted by ABG is the superior bid. Not only does it provide for $7

million of additional cash consideration, but it represents the best and perhaps only chance of a

going-concern transaction that could preserve a significant portion of the Debtors’ mall and

airport stores, an ongoing business relationship with the Debtors’ vendors and landlords, and

jobs for hundreds of the Debtors’ employees. Moreover, having previously stewarded a going-

concern purchase of Aéropostale, a retailer currently operating more than 500 retail stores that

was once on the brink of chapter 11 liquidation, ABG has an established track record in

executing retail going-concern transactions. Under these circumstances, the Committee submits

that the best interests of these estates will be served by designating ABG as the stalking horse

bidder. Through this designation, creditors can be assured that over the next several weeks,

6 The Bluestar bid provides for payment of a token $200,000 over the next several years if it doesnot purchase the assets as a going concern. The Committee is not aware of Bluestar having had anyadvanced discussions with landlords or retail partners.

Case 18-11780-BLS Doc 319 Filed 09/05/18 Page 3 of 6

{BAY:03350798v1} 4

ABG will be provided with information and resources on a wide range of going-concern issues,

including mall and airport inventory levels, store closing strategy, leasehold monetization,

license review, inventory replenishment strategies, and workforce review, which must be

analyzed and resolved on this expedited sale timeline.

5. While the most recent ABG bid was technically submitted after the deadline set

forth in the Bidding Procedures, the ABG bid should be accepted because it is a superior bid and

no parties would be prejudiced by its acceptance. Further, the bid deadline can be extended by

the Debtors. See Bidding Procedures, § XVI (“Notwithstanding any of the foregoing, the

Debtors and their estates, in consultation with the Consultation Parties, and with the consent of

the DIP Administrative Agent, which consent shall not be unreasonably withheld, and consistent