Unnat Nagar Dairy A Case Study Marketing Management-II Table of Content P Particulars Page Number...

32

Unnat Nagar Dairy A Case Study Marketing Management- II Presented By: Siddhartha Singh Solanki-07 XISS-Marketing/case study/Finance-1 Page 1

Transcript of Unnat Nagar Dairy A Case Study Marketing Management-II Table of Content P Particulars Page Number...

Unnat Nagar Dairy A Case Study

Marketing Management-II

Presented By:

Siddhartha Singh Solanki-07

XISS-Marketing/case study/Finance-1 Page 1

George toppo-09 Monica Hembrom-10 Sonal E. Tirkey-11 Chandan Kumar-13 Ashish Shankar-14

XISS-Marketing/case study/Finance-1 Page 2

Table of Content

Particulars

Page Number

Objective of the case study

3

Introduction 4

Unnat Nagar District 5

Milk Consumption Pattern in the district

6

Bottle Vending System 7

Bulk Vending system 8-9

Cost analysis 10-20

Summary of cost analysis

21

Value analysis 22

Suggestions and Recommendations

23

XISS-Marketing/case study/Finance-1 Page 3

OBJECTIVE OF THE CASE STUDY

In the Given Case study, Unnat Nagar Dairy is using Bottle

Vending System to distribute milk. But Mr. Praful Sardesai ,

the General Manager, argues that the Bottle vending system is

causing certain issues in terms of Money Collection,

Adulteration, Economy. Thus to come out of this he suggested

new method of distribution i.e Bulk Vending System.

Therefore, our objective is to bring out the causes that are

causing the issues in Bottle Vending Distribution System ,

analyze the Bottle Vending distribution with Bulk Vending

distribution and give suggestions and recommendations.

XISS-Marketing/case study/Finance-1 Page 4

INTRODUCTION

In Late 1975, Mr. Praful Sardesai, the General Manager of UnnatNagar Dairy was deliberating on the possibility of delivering the major supply of milk to the Unnat Nagar city through automatic bulk vending machine. The dairy had been supplying milk to the city of Unnat Nagar for over 15 years, first only by collecting and distributing milk from village’s cooperative societies and later by processing and pasteurizing the same milk.

Initially the dairy was operated by Unnat Nagar District Cooperative Milk Producers Union, Limited; in 1965 the dairy itself started the operation. Intially the dairy supplied milk and ghee to the citizen of Unnat Nagar.

In the case study, various parameters to examine the benefits and issues of the currently used Bottle Vending distribution system have been discussed and various benefits and limitationsof Bulk vending system have been discussed by various stakeholders.

The case study has also given the expected projection of milk supply and requirements of distribution facilities, which will

XISS-Marketing/case study/Finance-1 Page 5

be helpful to analyze the two different distribution methods under the purview of Future Plan.

XISS-Marketing/case study/Finance-1 Page 6

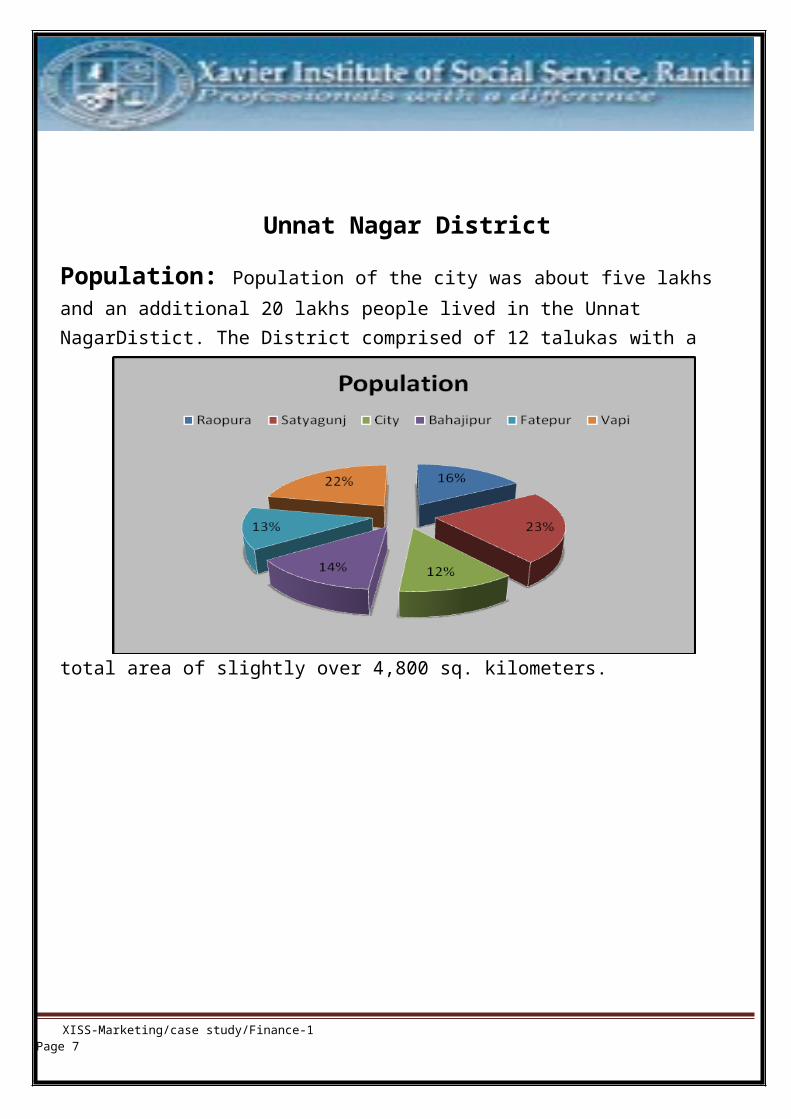

Unnat Nagar District

Population: Population of the city was about five lakhs and an additional 20 lakhs people lived in the Unnat NagarDistict. The District comprised of 12 talukas with a

total area of slightly over 4,800 sq. kilometers.

XISS-Marketing/case study/Finance-1 Page 7

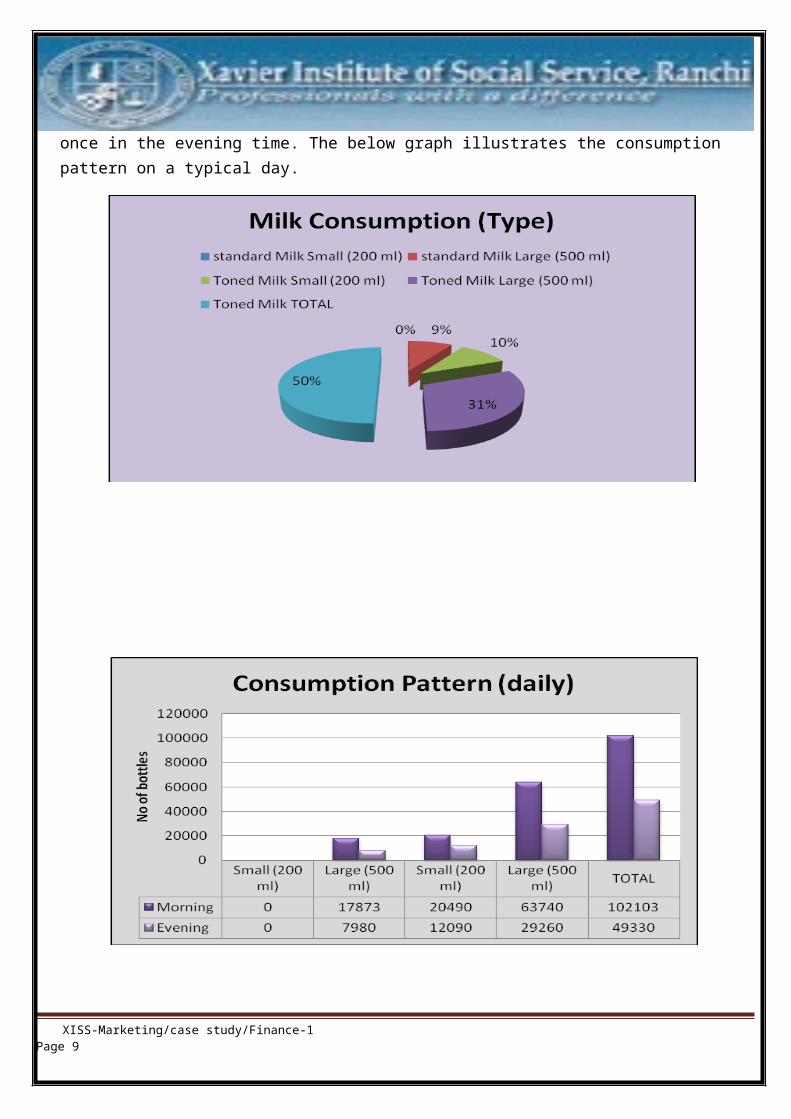

Milk Consumption Pattern in the District

Unnat Nagar Dairy supplies milk through Bottle Vending System. Under this 200ml and 500 ml of bottles are supplied once in the morning and

XISS-Marketing/case study/Finance-1 Page 8

once in the evening time. The below graph illustrates the consumption pattern on a typical day.

XISS-Marketing/case study/Finance-1 Page 9

Bottle Vending SystemAdvantages:

Oldest distribution system in the region. Distribution system is as per the consumption pattern

of the district, as most consumers link their milk purchase to the morning and evening tea prepration.

Consumers are not required to bring their containers. Conveninet for higher income group. Unsold milk is returned to the plant so fresh milk is

available at the time of purchase.

Issues and Causes:

IiI Issues

Causes

Delay of payment by milk centres operators

Operators have to deposit the money collected in bank.

Problem of Adulteration

Expected cause is somemalpractice going on either during transportation or in the milk centres.

Reduction in Bottle Declining condition of XISS-Marketing/case study/Finance-1 Page 10

life plant machinery

Extra cost of alumininum caps

When bottles return toplant caps are lost.

Losses due to return of milk

Due to 0.4%-0.5% loss in fat

Only 20% sales of small bottle milk

Min. Bottle size is 200ml

Bulk Vending System Advantages:

Cost saving on bottles and on its losses due to

breakage.

Cost saving on aluminium caps.

Cost saving on crates.

Cost saving on number of vehicle needed for distribution.

Cost saving on comission paid to intedepended contractors

to sell milk.

Cost saving on unsold milk.

XISS-Marketing/case study/Finance-1 Page 11

Elimination of pilferage and adulteration of milk.

24*7 availability of fresh milk.

Less selling price of Rs. 1.80/lit as compared to Rs.

1.90/lit through Bottle vending distribution.

Elimintion of the problem of delay in payment.

Will save the investment required in the new bottling

plant, which has an expected life of 3 to 5 more years.

XISS-Marketing/case study/Finance-1 Page 12

Issues and Causes:

IiI Issues

Causes

Fixed amount of milk being dispensed

For each token inserted machine will dispense 500 ml of milk

Customer has to carry hi/her own container

Bulk vending machine

Extra Manpower required

One operator will be required to operate bulk vending centres

Greater convenience tothe customer

Because of 24*7 availability of milk

Would not appeal to High Income Group

They have to come to the milk centre with their own container tocollect milk.

Maintenance Frequent maintenance will be required to run the machine

XISS-Marketing/case study/Finance-1 Page 13

smoothly

Long Downtime Because of power failure

XISS-Marketing/case study/Finance-1 Page 14

ANALYSISa. Cost Analysis

In cost analysis we will compare the “Total Annual Expense” of the two system of distribution-

Bottle Vending Distribution System

Bulk Vending Distribution System

Given Data-

Particulars Quantity ReferencePer day supply of milk (1974-75)(In Lit)

64414Exhibit-1

Per Day Production Of milk (In Lit)

65000-75000 Exhibit-5 Foot Note

No of Booths 231 Exhibit-2No of Pilot vending machine 10 Future PlansNo of Trucks 22 Distribution

ArrangementNo of bottles used daily 151433 Exhibit 1Each crates consist of 24 bottles Distribution

ArrangementCost of 500 ml of bottle 1.10 Economy of

DistributionAverage Breakage of bottle/day

1% Economy of Distribution

Average milk distribution inmilk centres

300 lit/day Distribution Arrangement

commission of contractor 2 paisa/ litsales

Distribution Arrangements

Expected Life of Bottles80 days

Economy of Distribution

Expected Life of Bottling Plant from 1975 3-5 years Bulk Vending

Cost Associated with Bottle Vending(INR)

Fixed Cost

Depreciation on Plant 10% Exhibit 5 foot XISS-Marketing/case study/Finance-1 Page 15

structure and rolling stock noteMaintenance annual

15%Exhibit 5 foot note

Interest on capital15%

Exhibit 5 foot note

AT 1974-75 capacity, investment cost of bottle used 1750000 Exhibit 5At 1974-75, Investment cost of creates 70,000 Exhibit 5At 1974-75, Investment cost of distribution truck 18,80,000 Exhibit 5At 1974-75 , Investment costof milk cabin 2,30,000 Exhibit 5Investment cost of washer, filler etc 6,00,000 Exhibit 5

Running costs(Rs/Day)

Steam, water, electricity 2,500 Exhibit 5Detergent 120 Exhibit 5Labour 600 Exhibit 5Foil For Caps 1,200 Exhibit 5Truck (Salaries, & Fuel) 1,200 Exhibit 5Losses due to return/breakage 1,700 Exhibit 5

XISS-Marketing/case study/Finance-1 Page 16

Particulars Quantity ReferenceCost Associated with Bulk

Vending(INR)Fixed Cost

Depreciation on Plant structure and rolling stock 10%

Exhibit 5 foot note

Maintenance annual15%

Exhibit 5 foot note

Interest on capital15%

Exhibit 5 foot note

Each Vending Machine (1000 lit capacity) 1,00,000 Exhibit 6Each Tanker 2,25,000 Exhibit 6

Running costs(Rs/Day)

Each Bulk Vending MachineElectricity 20 Exhibit 6Maintenance & Clearing 3 Exhibit 6Machine attendant cum salesman 30 Exhibit 6

Each TankerSalaries 40 Exhibit 6Fuel 400 Exhibit 6

Assumptions Made

a. Total Production=Total sales

b. Cost of Each truck, crates, bottle calculated @ 1974-75 Investment cost as actual cost is not given

c. Standby stock of bottle = daily avg. breakage of 1%

d. Depreciation is calculated using Fixed Installment Method OR Straight Line Method

e. All fixed and Running cost are calculated per liter of milk sold/produced

f. Average Cost to fill up bottles lost due to breakage =Rs 1.0 (as price of 500ml of bottle given 1.10)

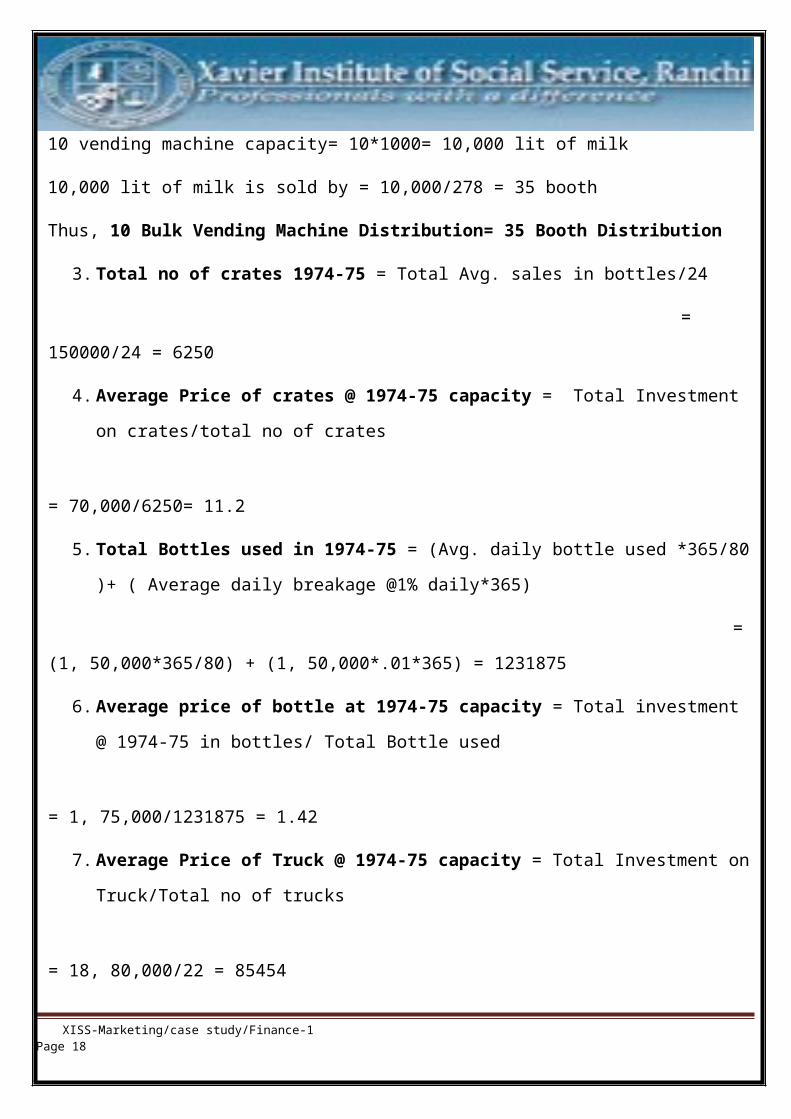

Initial Calculations (All cost in inr)

1. Average daily supply of milk (Lit)= Daily Average daily supply

of milk/No of Booth

= 64414/231= 278 lit./Day

2. As we have to compare two system of distribution using pilot

lot of 10 vending machine, that will be equal to no. of booth:

XISS-Marketing/case study/Finance-1 Page 17

10 vending machine capacity= 10*1000= 10,000 lit of milk

10,000 lit of milk is sold by = 10,000/278 = 35 booth

Thus, 10 Bulk Vending Machine Distribution= 35 Booth Distribution

3. Total no of crates 1974-75 = Total Avg. sales in bottles/24

=

150000/24 = 6250

4. Average Price of crates @ 1974-75 capacity = Total Investment

on crates/total no of crates

= 70,000/6250= 11.2

5. Total Bottles used in 1974-75 = (Avg. daily bottle used *365/80

)+ ( Average daily breakage @1% daily*365)

=

(1, 50,000*365/80) + (1, 50,000*.01*365) = 1231875

6. Average price of bottle at 1974-75 capacity = Total investment

@ 1974-75 in bottles/ Total Bottle used

= 1, 75,000/1231875 = 1.42

7. Average Price of Truck @ 1974-75 capacity = Total Investment on

Truck/Total no of trucks

= 18, 80,000/22 = 85454

XISS-Marketing/case study/Finance-1 Page 18

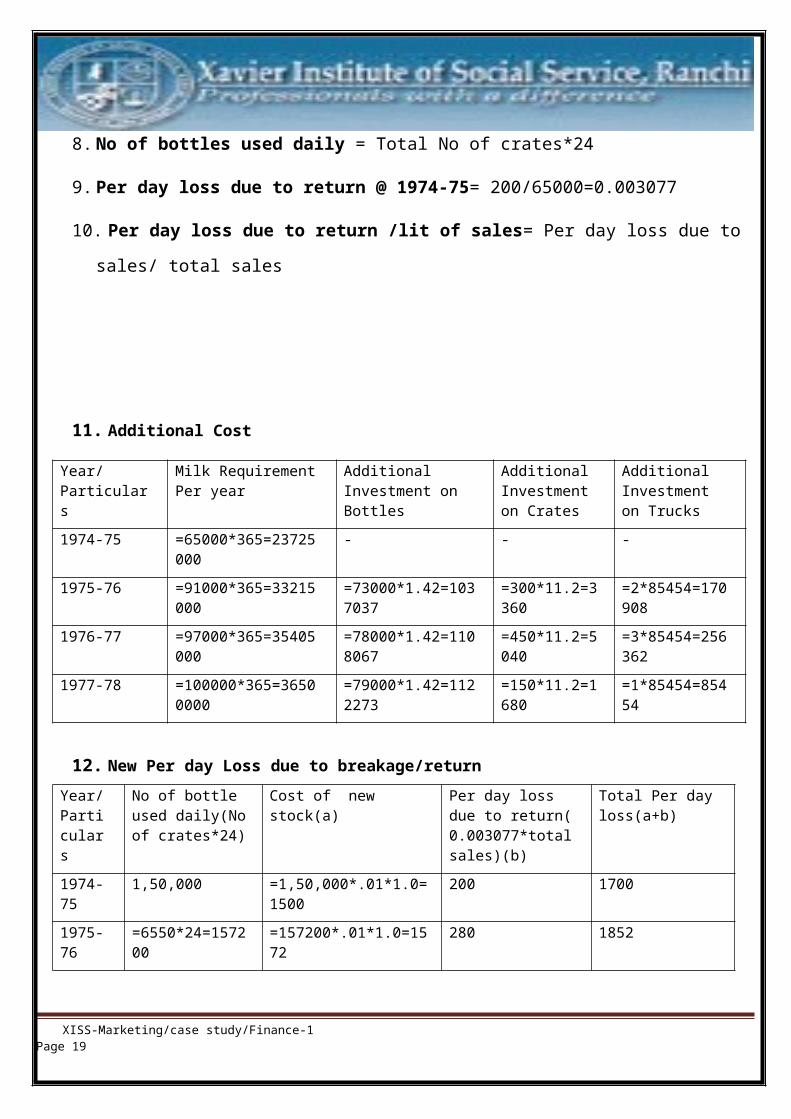

8. No of bottles used daily = Total No of crates*24

9. Per day loss due to return @ 1974-75= 200/65000=0.003077

10. Per day loss due to return /lit of sales= Per day loss due to

sales/ total sales

11. Additional Cost

Year/Particulars

Milk RequirementPer year

Additional Investment on Bottles

Additional Investment on Crates

Additional Investment on Trucks

1974-75 =65000*365=23725000

- - -

1975-76 =91000*365=33215000

=73000*1.42=1037037

=300*11.2=3360

=2*85454=170908

1976-77 =97000*365=35405000

=78000*1.42=1108067

=450*11.2=5040

=3*85454=256362

1977-78 =100000*365=36500000

=79000*1.42=1122273

=150*11.2=1680

=1*85454=85454

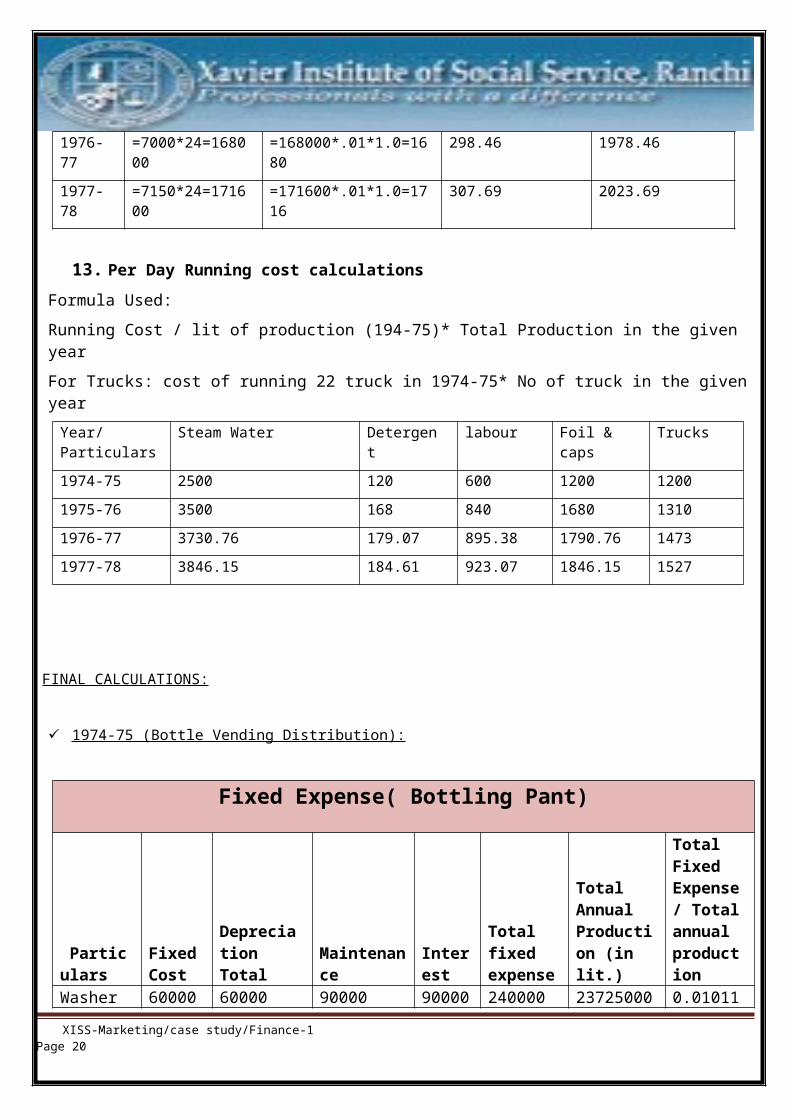

12. New Per day Loss due to breakage/returnYear/Particulars

No of bottle used daily(Noof crates*24)

Cost of new stock(a)

Per day loss due to return(0.003077*totalsales)(b)

Total Per day loss(a+b)

1974-75

1,50,000 =1,50,000*.01*1.0=1500

200 1700

1975-76

=6550*24=157200

=157200*.01*1.0=1572

280 1852

XISS-Marketing/case study/Finance-1 Page 19

1976-77

=7000*24=168000

=168000*.01*1.0=1680

298.46 1978.46

1977-78

=7150*24=171600

=171600*.01*1.0=1716

307.69 2023.69

13. Per Day Running cost calculationsFormula Used:Running Cost / lit of production (194-75)* Total Production in the given yearFor Trucks: cost of running 22 truck in 1974-75* No of truck in the givenyearYear/Particulars

Steam Water Detergent

labour Foil & caps

Trucks

1974-75 2500 120 600 1200 12001975-76 3500 168 840 1680 13101976-77 3730.76 179.07 895.38 1790.76 14731977-78 3846.15 184.61 923.07 1846.15 1527

FINAL CALCULATIONS:

1974-75 (Bottle Vending Distribution):

Fixed Expense( Bottling Pant)

Particulars

FixedCost

Depreciation Total

Maintenance

Interest

Total fixed expense

Total Annual Production (in lit.)

Total Fixed Expense/ Totalannual production

Washer 60000 60000 90000 90000 240000 23725000 0.01011 XISS-Marketing/case study/Finance-1 Page 20

, filler etc 0 6Crates 70000 7000 10500 10500 28000 23725000 0.00118

Bottles175000 17500 26250 26250 70000 23725000 0.00295

Trucks1880000 188000 282000

282000 752000 23725000

0.031697

Milk Cabins

230000 23000 34500 34500 92000 23725000

0.003878

Total cost (1974-75)

2955000 295500 443250

443250 1182000

0.049821

1975-76

Bottle Vending Distribution:

Fixed Expense( Bottling Pant)

Particula Fixed Depreciat Maintenan Interes Total Total Annual Total

XISS-Marketing/case study/Finance-1 Page 21

Running Expense (Bottling Plant )

ParticularsPer Day Running cost

Annual Running Cost

Running cost/ Lit.of sales

steam water 2500 912500 0.0384615detergent 120 43800 0.0018462labour 600 219000 0.0092308foil and caps 1200 438000 0.0184615trucks 1200 438000 0.0184615losses 1700 620500 0.0261538Total annual Running cost/Total annualProd. 0.1126154

Total Expense (Bottling Plant)

Total Annual Expense/Lit of milk production (a)

RS/lit.

Fixed Cost + Running Cost 0.1624362

Avg. annual sale of milk in a booth (b)

Lit. =278*365 101470

Total CP on a booths (c ) Rs. a*b 16482.406Total CP on 35 Booths (d) Rs. C*35 576884.22Total Annual Commission Paid to 35 booths (e) Rs. =35*b*.02 71029Total Annual Net cost price on 35 Booths Rs. d+e 647913.22 In lakh 6.4791322

rs Cost ion (a) ce (b) t (c )fixed expense

Production (in ltr)

Fixed Expense/ Unit lit of Milk sold

Washer , filler etc 540000 54000 81000 81000 216000 33215000 0.006503Crates 66360 6636 9954 9954 26544 33215000 0.000799

Bottles 1194537 119453.7 179180.6179180.6

477814.8 33215000 0.014386

Trucks 1862909 186290.9 279436.4279436.4

745163.6 33215000 0.022435

Milk Cabins 207000 20700 31050 31050 82800 33215000 0.002493Total cost(1974-75) 3870806 387080.6 580620.9

580620.9 1548322 0.046615

Total Expense (Bottling Plant)

Total Annual Expense/Lit of Milk (a)

Rs./lit

Fixed cost+ RunningCost 0.1493624

Avg. annual sale of a booth (b)

Lit. =(91000/246)*365 135020.33

Total CP on a booth Rs a * b 20166.961Total CP on 35 booths (c ) Rs. 705843.63Total Annual Commission Paid to 35 booth (d ) Rs.

=35*.02*(91000/246)*365 94514.228

Total Annual Net cost price on 35 booth Rs. c + d 800357.86 In lakh. 8.0035786

BULK VENDING DISTRIBUTION:

Fixed Cost

Particulars Investment

Depreciation

Interest

Maintenance

Total Fixed Expense

Total Fixed Expense

Total fixed expense

XISS-Marketing/case study/Finance-1 Page 22

Running Expense (Bottling Plant )

ParticularsPer Day Running cost

Annual Running Cost

Running cost/ Lit of sales

steam water 3500 1277500 0.0384615detergent 168 61320 0.0018462labour 840 306600 0.0092308foil and caps 1680 613200 0.0184615trucks 1310 478150 0.0143956losses 1852 675980 0.0203516Total annual Running cost/Total annualProd. 0.1027473

each vending m/c

on each unit/Litof sales

on pilotper lit of sales

Each Vending M/c(1000 lit capacity) 100000 10000 15000 15000 40000

0.0012043

0.0120428

Each Tanker(9000 lit capacity) 225000 22500 33750 33750 90000

0.0027096

0.0027096

Total 1300000.0039139

0.0147524

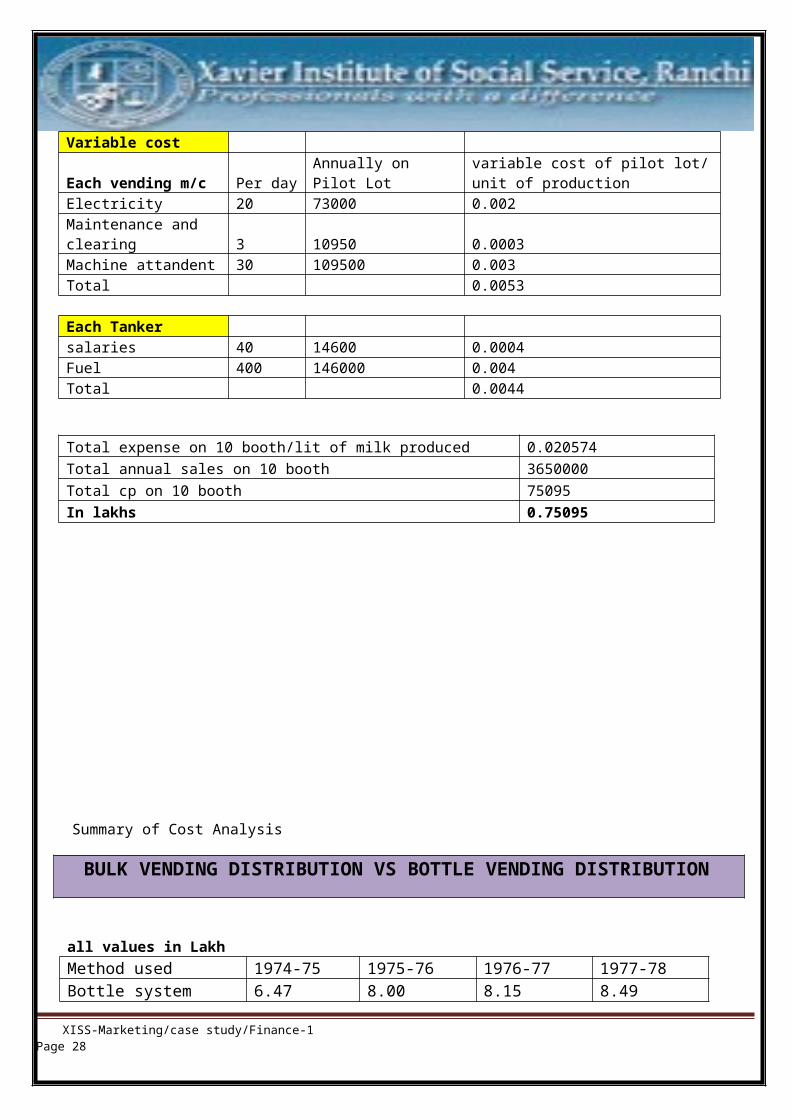

Variable Cost

Each vending m/cper day (a)

Total expense annually (a*365*10)

Total expense/lit of sales

Electricity 20 73000 0.0021978Maintenance and clearing 3 10950 0.0003297Machine attendant 30 109500 0.0032967Total 193450 0.0058242Each Tanker

salaries 40 14600 0.0004396Fuel 400 146000 0.0043956Total variable cost of 1 tanker per lit of milk produced 0.0048352

Total Expense

Total expense on 10 booth/lit of milk produced (Total Fixed Cost+ Total Variable Cost) 0.0254117Total annual sales on 10 booth (10*365*1000) 3650000Total cp on 10 booth 92752.747In lakhs 0.9275275

XISS-Marketing/case study/Finance-1 Page 23

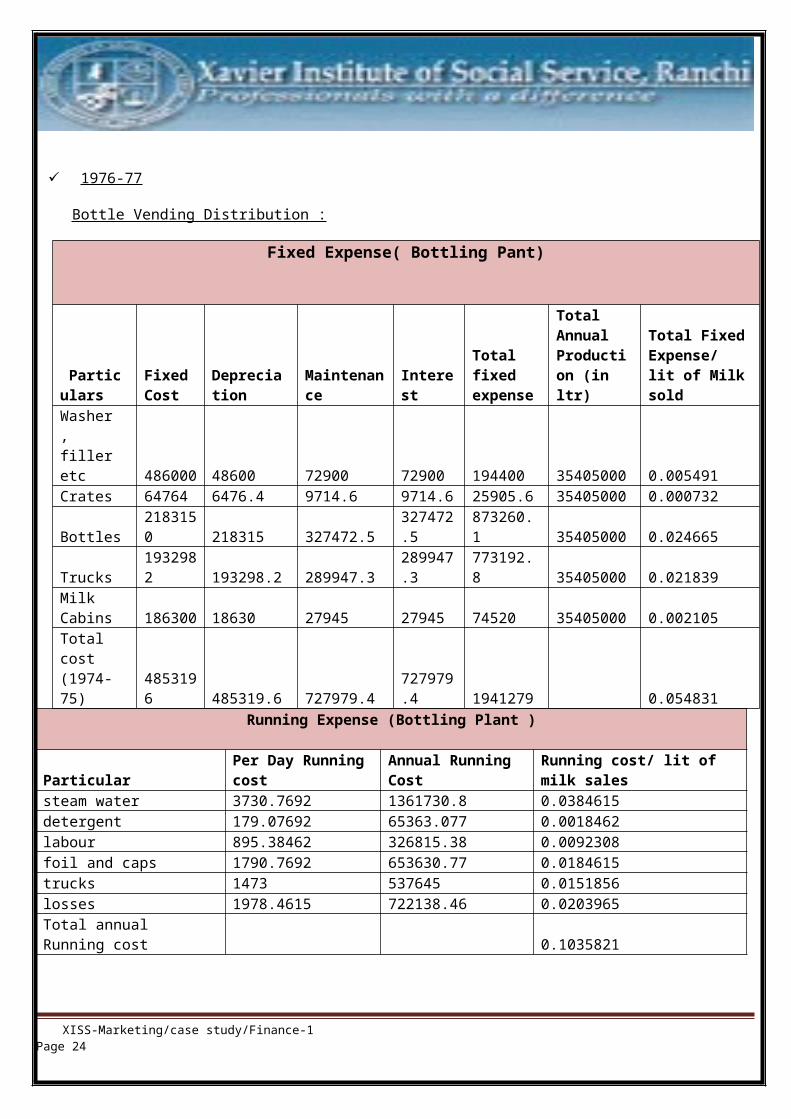

1976-77

Bottle Vending Distribution :

Fixed Expense( Bottling Pant)

Particulars

Fixed Cost

Depreciation

Maintenance

Interest

Total fixed expense

Total Annual Production (in ltr)

Total FixedExpense/ lit of Milksold

Washer , filler etc 486000 48600 72900 72900 194400 35405000 0.005491Crates 64764 6476.4 9714.6 9714.6 25905.6 35405000 0.000732

Bottles2183150 218315 327472.5

327472.5

873260.1 35405000 0.024665

Trucks1932982 193298.2 289947.3

289947.3

773192.8 35405000 0.021839

Milk Cabins 186300 18630 27945 27945 74520 35405000 0.002105Total cost (1974-75)

4853196 485319.6 727979.4

727979.4 1941279 0.054831

Running Expense (Bottling Plant )

ParticularPer Day Running cost

Annual Running Cost

Running cost/ lit of milk sales

steam water 3730.7692 1361730.8 0.0384615detergent 179.07692 65363.077 0.0018462labour 895.38462 326815.38 0.0092308foil and caps 1790.7692 653630.77 0.0184615trucks 1473 537645 0.0151856losses 1978.4615 722138.46 0.0203965Total annual Running cost 0.1035821

XISS-Marketing/case study/Finance-1 Page 24

Total Expense (Bottling Plant)

Total Annual Expense/Lit of Milk Production

Rs/Lit 0.1584127

Avg. annual sale of a booth Lit 130645.76Total Annual CP in a booth Rs. 20695.948Total CP on 35 booth Rs. 724358.19Total Annual Commission Paid on 35 booth Rs. 91452.03Total Annual Net cost price on 10 booth Rs. 815810.22

In lakh 8.1581022

Bulk vending distribution system

Particulars

Fixed Cost

Depreciation

Interest

Maintenance

TotalFixedExpense each vending m/c

Total Fixed Expenseon eachunit/Lit of production

Total fixed expenseon pilot per litof annual production

Each Vending M/c (1000 lit capacity) 90000 9000 13500 13500 36000

0.0010168

0.0101681

Each Tanker (9000li capacity)

202500 20250 30375 30375 81000

0.0022878

0.0022878

Total117000

0.0033046

0.0124559

Variable cost

Each vending m/c Per day

Annually on PilotLot Variable cost of pilot lot/

unit of productionElectricity 20 73000 0.0020619Maintenance and clearing 3 10950 0.0003093Machine attandent 30 109500 0.0030928

XISS-Marketing/case study/Finance-1 Page 25

Total 0.0054639Each Tanker salaries 40 14600 0.0004124Fuel 400 146000 0.0041237Total 0.0045361

Total Expense

Total expense on 10 booth/lit of milk produced 0.0224559Total annual sales on 10 booth 3650000Total cp on 10 booth 81963.918In lakhs 0.8196392

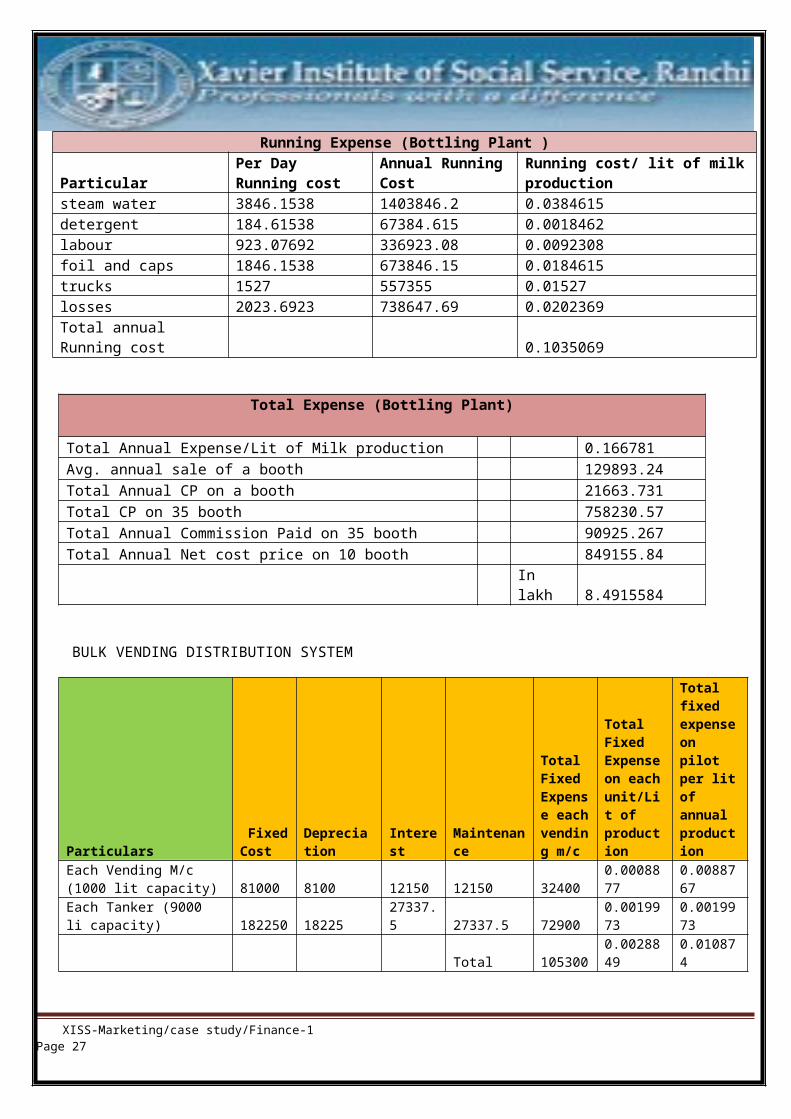

1977-78 Bottle vending distribution system

Fixed Expense( Bottling Pant)

Particulars

FixedCost

depreciation Total

maintenance

interest

Total fixed expense

Total Annual Production(in ltr)

Total Fixed Expense/ Unit lit of Milk production

Washer , filler etc

437400 43740 65610 65610 174960 36500000 0.004793

Crates 59968 5996.8 8995.2 8995.2 23987.2 36500000 0.000657

Bottles3283588 328358.8 492538.2

492538.2 1313435 36500000 0.035985

Trucks1825138 182513.8 273770.7

273770.7 730055.2 36500000 0.020002

Milk Cabins

167670 16767 25150.5

25150.5 67068 36500000 0.001837

Total cost (1974-75)

5773764 577376.4 866064.6

866064.6 2309506 0.063274

XISS-Marketing/case study/Finance-1 Page 26

Running Expense (Bottling Plant )

ParticularPer Day Running cost

Annual RunningCost

Running cost/ lit of milkproduction

steam water 3846.1538 1403846.2 0.0384615detergent 184.61538 67384.615 0.0018462labour 923.07692 336923.08 0.0092308foil and caps 1846.1538 673846.15 0.0184615trucks 1527 557355 0.01527losses 2023.6923 738647.69 0.0202369Total annual Running cost 0.1035069

Total Expense (Bottling Plant)

Total Annual Expense/Lit of Milk production 0.166781Avg. annual sale of a booth 129893.24Total Annual CP on a booth 21663.731Total CP on 35 booth 758230.57Total Annual Commission Paid on 35 booth 90925.267Total Annual Net cost price on 10 booth 849155.84

In lakh 8.4915584

BULK VENDING DISTRIBUTION SYSTEM

Particulars FixedCost

Depreciation

Interest

Maintenance

Total Fixed Expense eachvending m/c

Total Fixed Expenseon eachunit/Lit of production

Total fixed expenseon pilot per litof annual production

Each Vending M/c (1000 lit capacity) 81000 8100 12150 12150 32400

0.0008877

0.0088767

Each Tanker (9000 li capacity) 182250 18225

27337.5 27337.5 72900

0.0019973

0.0019973

Total 1053000.0028849

0.010874

XISS-Marketing/case study/Finance-1 Page 27

Variable cost

Each vending m/c Per dayAnnually on Pilot Lot

variable cost of pilot lot/unit of production

Electricity 20 73000 0.002Maintenance and clearing 3 10950 0.0003Machine attandent 30 109500 0.003Total 0.0053

Each Tanker salaries 40 14600 0.0004Fuel 400 146000 0.004Total 0.0044

Total expense on 10 booth/lit of milk produced 0.020574Total annual sales on 10 booth 3650000Total cp on 10 booth 75095In lakhs 0.75095

Summary of Cost Analysis

BULK VENDING DISTRIBUTION VS BOTTLE VENDING DISTRIBUTION

all values in LakhMethod used 1974-75 1975-76 1976-77 1977-78Bottle system 6.47 8.00 8.15 8.49

XISS-Marketing/case study/Finance-1 Page 28

Bulk Vending - 0.92 0.81 0.75Difference 6.47 7.080 7.340 7.740

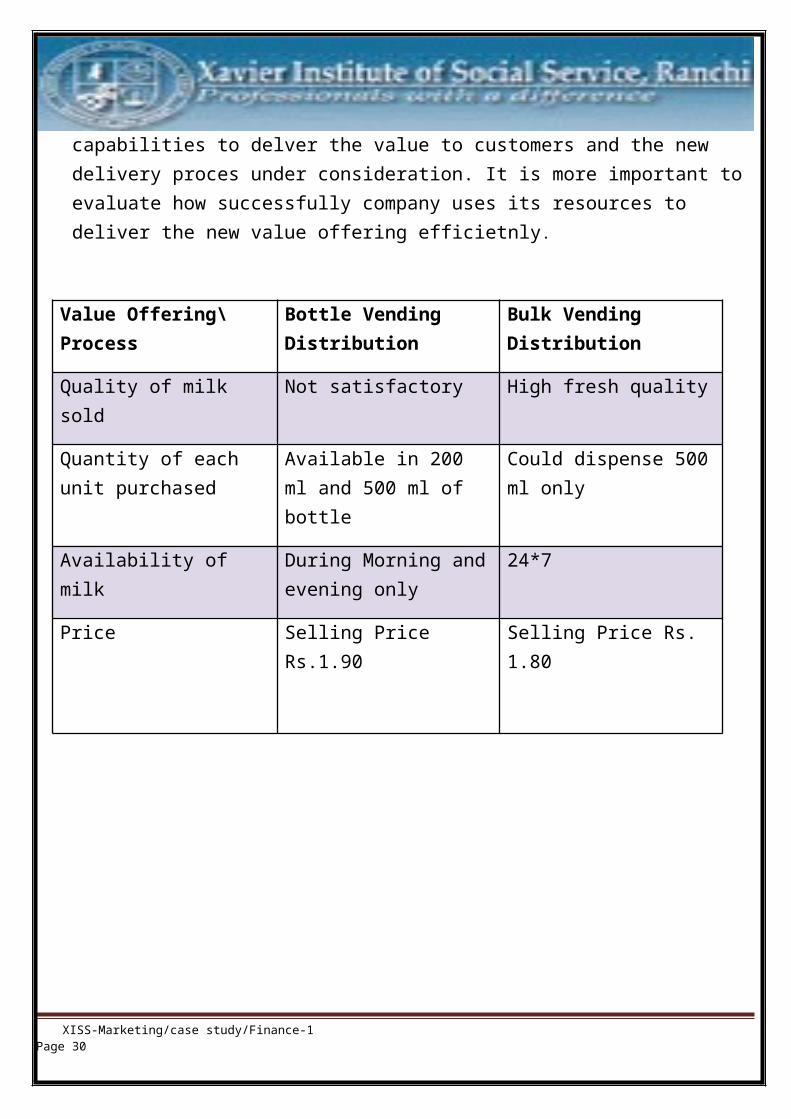

B. VALUE ANALYSIS :

Here we will compare the two different value offrered by the two delivery process. Company exhisting infra and

XISS-Marketing/case study/Finance-1 Page 29

capabilities to delver the value to customers and the new delivery proces under consideration. It is more important to evaluate how successfully company uses its resources to deliver the new value offering efficietnly.

Value Offering\Process

Bottle Vending Distribution

Bulk Vending Distribution

Quality of milk sold

Not satisfactory High fresh quality

Quantity of each unit purchased

Available in 200 ml and 500 ml of bottle

Could dispense 500ml only

Availability of milk

During Morning andevening only

24*7

Price Selling Price Rs.1.90

Selling Price Rs. 1.80

XISS-Marketing/case study/Finance-1 Page 30

Suggestions and RecommendationsThrough cost analysis we have come to the conclusion that Bulk Vending system has advantage over Bottle vending system. In long run it will save lots of fixed and running costs of Unnat Nagar Dairy. Moreover, it will save the fixed investment to be made in coming three years in setting up new bottlingplant and everyday expense of commission on selling the milk though contarctor.Therefore, we recommend that Unnat Nagar Dairy should go with the proposal ofsupplying milk through automatic bulk vending machine.

But under following recommendations:

The automatic Bulk Vending distribution machine should be evenly distributed as per the population of the wards.

Unnat Nagar Dairy should also introduce quality circles to check quality of the milk dispatched.

The dairy should increase the value offering by supplying milk in even smaller quantity than 200 ml.

XISS-Marketing/case study/Finance-1 Page 31

The dairy should not implement the automatic bulk vending system in the high income group region, because that will not offer comfort to these customers who often pay some extra money to get bottle at doorstep.

Dairy should ensure adequate power supply to the automatic bulk vending centre to keep milk in fresh condition.

XISS-Marketing/case study/Finance-1 Page 32