UNIT-II - SNS Courseware

49

1 UNIT-II BRANCH ACCOUNTS Meaning: The dictionary meaning of the word ‘branch’ is any subordinate of a business, subsidiary shop, office etc. according to the provision contained in section 29 of the companies Act 1956, it would appear that a branch is any establishment carrying on either the some or substantially the same activity as that carried on by head office of the company. It must also be noted that the concept of a branch means existence of a head office for there can be branch without a head office – principle place of business. Objects of Branch Accounts: The following are the main objects of maintaining branch accounts: (i) Profit or loss of each branch can be found out. (ii) They help in controlling branches. (iii) Actual financial position of the business can be found out on the basis of head office and branch accounting records. (iv) Branch requirement of goods and cash can be estimated. (v) Suggestions for increasing the efficiency of the branch can be sent on the basis of branch Accounts. (vi) They help in complying with the requirements of law because according to Companies Act 1956, maintenance of accounting record of branches by companies is essential. Types of Branches: Form the Accounting point of view, branches may be classified as follows: (i) Dependent Branch (ii) Independent branch 1. Dependent Branch / Branch not keeping full system of accounting/ branches of which accounts are kept in the head office. The term ‘Dependent Branch’ means a branch which does not maintains its own set of books. All records have to be maintained by the head office. When the business policies and the administration of a branch are wholly controlled by the head office, its accounts also are maintained by it. Branch accounts, in such a case, are written up at the head office out of report and returns received from the branch. Some of the significant types of branches that are operated in this manner are described below:

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of UNIT-II - SNS Courseware

1

UNIT-II

BRANCH ACCOUNTS

Meaning:

The dictionary meaning of the word ‘branch’ is any subordinate of a business,

subsidiary shop, office etc. according to the provision contained in section 29 of the

companies Act 1956, it would appear that a branch is any establishment carrying on either the

some or substantially the same activity as that carried on by head office of the company. It

must also be noted that the concept of a branch means existence of a head office for there can

be branch without a head office – principle place of business.

Objects of Branch Accounts:

The following are the main objects of maintaining branch accounts:

(i) Profit or loss of each branch can be found out.

(ii) They help in controlling branches.

(iii) Actual financial position of the business can be found out on the basis of head

office and branch accounting records.

(iv) Branch requirement of goods and cash can be estimated.

(v) Suggestions for increasing the efficiency of the branch can be sent on the basis of

branch Accounts.

(vi) They help in complying with the requirements of law because according to

Companies Act 1956, maintenance of accounting record of branches by companies

is essential.

Types of Branches:

Form the Accounting point of view, branches may be classified as follows:

(i) Dependent Branch

(ii) Independent branch

1. Dependent Branch / Branch not keeping full system of accounting/ branches of which

accounts are kept in the head office.

The term ‘Dependent Branch’ means a branch which does not maintains its own set of

books. All records have to be maintained by the head office. When the business policies and

the administration of a branch are wholly controlled by the head office, its accounts also are

maintained by it. Branch accounts, in such a case, are written up at the head office out of

report and returns received from the branch. Some of the significant types of branches that are

operated in this manner are described below:

2

(a) A branch set up merely for booking orders which are executed by the head office,

such a branch only transmits orders to the head office.

(b) A branch established at a commercial centre for the sale of goods supplied by the head

office and under its direction all collections are made by the H.O and

(c) A branch for the retail sale of goods, supplied by the head office.

Accounting in the case of first two types is simple, only records of expenses incurred

at the branch have to be maintained. But it is not so in the case of the third type. A retail

branch is essentially a sales agency that principally sells goods supplied by the head office for

cash and, if so authorized, also on credit to approved customers.

Accounting in respect of Dependent Branches:

In case of a dependent branch, the head office may keep accounts of the branch

according to any of the following systems:

(i) Debtors systems

(ii) Stock and Debtors system.

(iii) Wholesale branch system

(iv) Final Accounting system

All these systems are now explained one by one in detail.

Debtors system (synthetic method)

This system is adopted in case for branches of small size. Under this system, a branch

account is opened separately for each branch in the books of head office. This account is

nominal account in nature. The opening balance of stock, debtors, patty cash are debited to

the branch account. The cost of goods sent to branches as well as expenses of the branch paid

by the head office like salaries, rent, insurance etc., and closing balance of liabilities if any

are also debited to it. Conversely, the opening balance of liabilities if any, cash remitted by

the branch and cost of goods returned by the branch are credited. At the end of the year. The

values of unsold stock, the total customers balance outstanding and that of petty cash are

brought in to the branch account on the credit side. The branch account reveals profit or loss.

If the branch account shows a credit balance, it is branch profit and if debit balance is shown,

it is branch loss. If branch is allowed to make small purchases of goods locally as well as to

incur expenses, details of such expenditure will be furnished by the branch to the head office.

On the other hand, purchases are made out of cash receipts, it will also be necessary for the

branch to supply to the head office a copy of the cash account. To illustrate the various

entries which are made in the branch account the proforma of a branch is shown below.

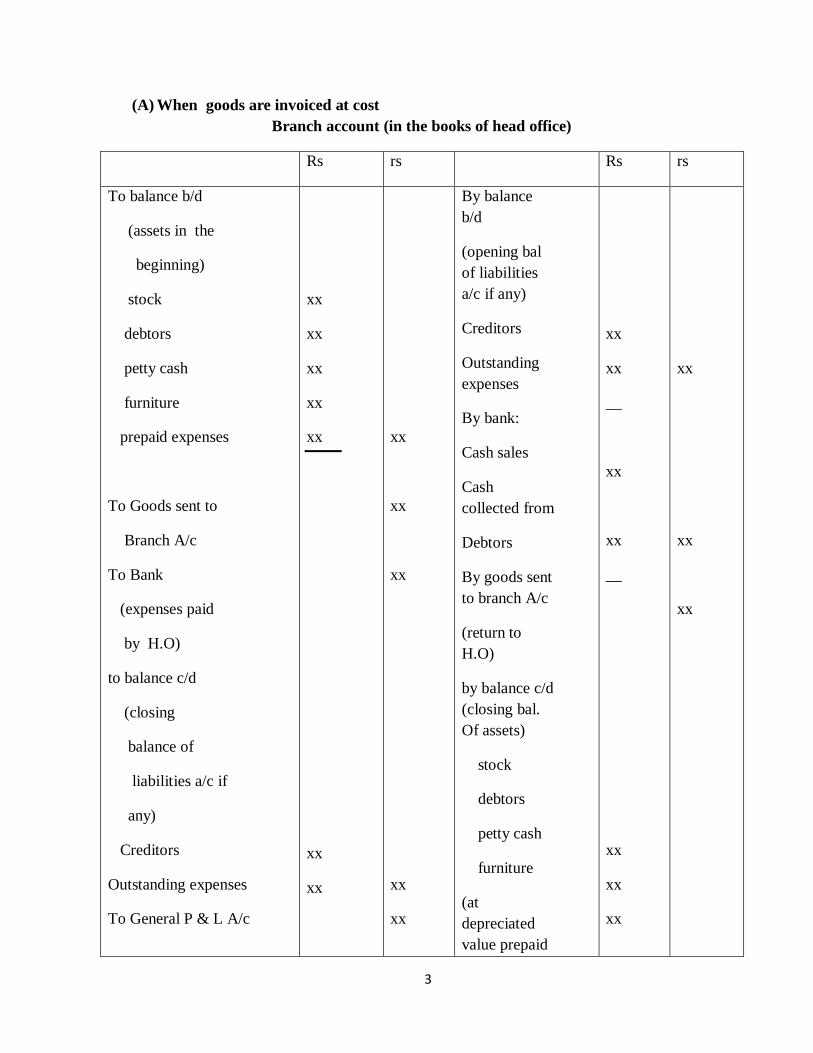

3

(A) When goods are invoiced at cost

Branch account (in the books of head office)

Rs rs Rs rs

To balance b/d

(assets in the

beginning)

stock

debtors

petty cash

furniture

prepaid expenses

To Goods sent to

Branch A/c

To Bank

(expenses paid

by H.O)

to balance c/d

(closing

balance of

liabilities a/c if

any)

Creditors

Outstanding expenses

To General P & L A/c

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

By balance

b/d

(opening bal

of liabilities

a/c if any)

Creditors

Outstanding

expenses

By bank:

Cash sales

Cash

collected from

Debtors

By goods sent

to branch A/c

(return to

H.O)

by balance c/d

(closing bal.

Of assets)

stock

debtors

petty cash

furniture

(at

depreciated

value prepaid

xx

xx

__

xx

xx

__

xx

xx

xx

xx

xx

xx

4

(branch profit) (bal.fig)

*(branch profit) (bal. fig)

exp)

by General

P&L A/c

(branch loss)*

(bal.fig)

xx

xx

__

xx

The following journal entries are passed in the books of head office to record branch

transaction:

(i) When goods are sent to branch

Branch A/c Dr.

To goods sent to branch A/c.

Note : Reverse entry for goods returned to head office.

(ii) When cheque or draft is sent for branch expenses

Branch A/c Dr

To bank A/c

(iii) When cheque or draft id received as remittance from branch:

Bank A/c Dr.

To Branch A/c

For closing balance of assets

Branch Account A/c Dr.

To Branch A/c

(iv) For opening balance of assets

Branch A/c Dr

5

To Branch Asset A/c

(v) For closing balance of liabilities:

Branch A/c Dr

To Branch Asset A/c

For opening balance of liabilities

Branch liabilities A/c Dr

To Branch A/c

(vi) For transferring the balance of goods sent to branch A/c:

Goods sent to branch A/c Dr.

To purchases A/c (trading concern)

To trading A/c (manufacturing concern)

(vii) For branch profit:

Branch A/c Dr.

To General profit and loss A/c

Note: Reverse entry for loss.

II stock and Debtors system (analytical method)

Profit or loss a branch can be found out by preparing branch account which has been

discussed earlier, but there is another method for the same purpose. This method is known as

stock and debtors methods. If it is desired to exercise a more detailed control over the working

of a branch, the accounts of the branch are maintained under what is described as the stock

and debtors methods. In these methods, the head office keeps separate accounts relating to

various types of transactions at the branch instead of one branch account. The following

accounts are kept in the office books relating to a branch under this system.

(i) Branch stock account.

(ii) Branch Debtors account.

(iii) Branch Expenses account

(iv) Branch Adjustment account (required only when the goods are sent at invoice

price)

(v) Branch Profit and Loss account

(vi) Goods sent to the Branch account

A brief description of each of these accounts is given below:

6

(i) Branch stock account:

This account deals with all goods received, returned and sold by the branch.

The account helps the office in maintaining an effective control over the branch stock. It is

debited with (a) opening stock (b) good sent to branch (c) goods spoiled and goods lost like

loss in weight, pilferage, loss in transit (d) goods returned to head office by branch (e) closing

stock. It given information about shortage or surplus of stock of stock and the closing stock at

the branch.

(ii) Branch Debtors Account

This account is prepared to record all the transactions relating to branch debtors and

ascertain either the closing balance of debtors or credit sales.

(iii) Branch Expenses Account:

This account is prepared to disclose branch expenses, losses on account of discount on

debtors, allowances, bad debts and other charges etc., incurred at the branch. All expenses

incurred by branch are recorded in the debit side of this account and balance of this account is

transferred to branch profit and loss account.

(iv)Branch adjustment account

When the goods are sent to branch at cost price, this account need not be prepared.

Instead when the goods are supplied to branch at invoice price, it must be prepared to

ascertain gross profit made by the branch. This account is debited with (a) closing stock

reserve (b) profit element of stock shortages, defectives, loss on transit and pilferage and (c)

value of loss in weight (full amount). It is credited with (d) stock reserve on the opening

stock (e) loading on goods sent to branch and (f) the profit element of stock surplus. Business

of this account indicates gross profit or gross loss which is transferred to branch profit and

loss account.

(v) Branch profit and loss account:

This account is prepared to ascertain the net profit made by the branch. It is debited

with (a)the balance of branch expenses account (b) cost of goods lost due to shortage or

defectives, loss in transit, and pilferage. It is credited with (a)gross profit as shown in branch

adjustment account (b) cost of surplus if any revealed by the branch stock account and (c)

amount recoverable from insurance company for any losses of stock. Balance of this account

indicates net profit or net loss which is transferred to General profit and loss Account.

7

(iv) Goods sent to Branch Account:

This account is prepared to find out the net value of goods sent to the branch. Goods

sent to branch and goods returned by the branch and loading included in them if any are

recorded in thid account. Balance of this account is transferred to either purchase account or

trading account depending on whether the firm is trading concern or a manufacturing concern

respectively.

JOURNAL ENTRIES

The following journal entries are required for various types of transactions under

this method.

(i) When goods are sent to branch.

Branch stock A/c Dr.

To goods sent to branch A/c

Note :

Reverse entry will be passed for goods returned by branch to head office.

(ii) When sales are made by the branch

(a) For cash sales

Cash A/c Dr.

To branch stock A/c

(b) For credit sales

Branch debtors A/c Dr.

To branch stock A/c

Note ;

Reverse entry will be passed for goods returned by customers

(iii) When cash is received from debtors

Cash A/c Dr.

To branch stock A/c

(iv) For discount allowed allowances and bad debts.

Branch expenses A/c Dr.

8

To branch debtors a/c

(v) For branch expenses paid in cash

Branch expenses A/c Dr.

To cash / bank a/c

(vi) For closing branch expenses account

Branch P & L A/c Dr.

To branch expenses A/c

The following additional adjustment entries are to be passed when the goods are sent

at invoice price.

(vii) For the difference between the invoice price and cost price of the opening stock.

Stock reserve A/c Dr.

To branch adjustment A/c

(viii) For the difference between the invoice price and cost price of the closing stock.

Branch adjustment A/c Dr.

To stock reserve A/c

(ix) For the different between selling price and cost of the goods sent to branch less

returns:

Goods sent to branch A/c Dr.

To branch adjustment A/c

(x) For insurance claim received

Insurance claim A/c Dr.

To branch P & L A/c

(xi) For any shortage in the branch stock account

(a) loading on such shortage

Branch adjustment A/c Dr.

To branch stock A/c

(b ) cost of such shortage

Branch profit and loss A/c Dr.

To branch stock A/c

9

(xii) For any surplus in the branch stock account

(a) Loading on such surplus

Branch stock A/c Dr.

To branch adjustment A/c

(b) Cost of such surplus

Branch stock A/c Dr

To branch profit and loss A/c

(xiii) For gross profit made by the branch:

Branch adjustment A/c Dr.

To branch P & L A/c

Note: Reverse entry for gross loss

(xiv) For net profit disclosed by branch P & L A/c

Branch P & L A/c Dr.

To General P & L A/c

Note : Reverse entry for net loss

(xv) For closing goods sent to branch A/c

Goods sent to branch a/c Dr.

To purchases or trading a/c

III Wholesale Branch System

(Goods invoiced at wholesale price to retail branches)

Manufacturers may sell goods to the consumers either through the wholesale and

approved stockiest or though their branches. In order to know whether self – retailing through

branch is more profitable than wholesaling it is necessary to make distinction between profit

due to wholesale and profit due to retail business of the branch. Wholesale price is always less

than retail price. Let us assume that the cost price is Rs.100, wholesale price is Rs.115 and

retail price is Rs.125. in this case, branch has made a profit of Rs. 25 i.e., 125-100: but the fact

is that real profit of the branch is only Rs.10 i.e 125 -115, because by selling to wholesalers

Rs.15 profit would have been made by head office contribution of branch is only Rs.10. hence

when head office wants to know retail profit of the branch, it charges the branch with

wholesale price.

(i) The value of opening stock at the branch and

10

(ii) Price of goods sent during the year at wholesale price it is credited with:

(iii) Sales effected at the branch:

(iv) Closing stock of goods valued at wholesale price.

(Iv) Final Accounts System:

The head office can also ascertain in the profit or loss of a dependent branch by

preparing branch trading and profit and loss account at cost. In such cases, the head office

may also maintain a branch account. The branch account so prepared is personal account in

nature as different from the branch account prepared by head office in case of debtors system

which is of the particular period represents the net assets at the branch.

INDEPENDENT BRANCHES

(where the branch trades independently of the head office)

or

(Branch keeping full system of accounting)

Independent branch means a branch which maintains its own set of books and has

freedom to operate independently. If a branch is big and carries on manufacturing operations

also, it is allowed to operate freely within the frame work of head office policies. Therefore

for all practical purpose, the branch acts as an independent unit. The branch receives goods

from head office and also purchases from outside. The branch manager is not required to

remit the daily cash receipts, as he would require some working capital to pay for his

purchases and also to defray local expenses. Remittance are made by the branch in round

sums as and when convenient, i.e., cash may be sent to head office if there is a surplus or if

the office is in need of funds. Similarly, the branch is supplied with funds for the purpose of

carrying on business.

Incorporation of branch Trial Balance in Head office Books

For the benefit of the shareholders and the outsides, the consolidated final accounts of

the head office and its branch have to be prepared. The process by which the consolidated

balance sheet will be prepared is known as incorporation of branch trial balance. In other

words, the branch sends its trial balance (together with its trading and profit & loss A/c and

balance sheet, if these are prepared by the branch) to the head office for incorporation in head

office books. On receipt of the trial balance form the branch at the time of balancing, the head

office will incorporate the figures there of at the time of balancing, the head office will

incorporate the figures there of in its own books by means of the following entries, in order to

ascertain the separate trading result of each branch as also the combined result of the business

as a whole.

11

(i) For debit side items of trading A/c (total of opening stock, net purchases and

direct expense)

Branch Trading A/c Dr.

To branch A/c

(ii) For credit side items of trading A/c (total of net sales and closing stock)

Branch A/c Dr.

To branch Trading A/c

(iii) For transfer of gross profit or gross loss

(a) For Gross profit

Branch Trading A/c Dr.

To branch P & L A/c

(b) For gross loss

Branch P & L A/c Dr.

To branch Trading A/c

(iv) For various expenses and losses (i.e, salaries, rent depreciation and discount

allowed etc.) which appear on the debit side of P & L A/c.

Branch P & L A/c Dr.

To branch A/c

(v) For various incomes and gains (e.g. discount earned) which appear on the credit

side of P & L A/c.

Branch A/c Dr.

To Branch P & L A/c

(vi) For transfer of net profit or net loss:

(a) For net Profit

Branch P & L A/c Dr.

To General P & L A/c

(b) For net loss

General P & L A/c Dr.

To branch P & L A/c

12

(vii) For total of various branch assets (i.e branch debtors, branch stock, cash in hand at

branch, cash in transit etc. )

Branch Assets A/c Dr.

To branch A/c.

(viii) For total of various branch liabilities (i.e., branch creditors baranch Expenses

outstanding etc.)

Branch a/c Dr.

To branch liabilities A/c .

Branch Account

(a) When goods are sent to branch at cost price

Illustration 1

LOYAL shone company opened a branch at Madras on 1.1.2002. From the following

particulars, prepare the Madras Branch Acoount for the year 2002 and 2003.

2002 2003

Goods sent to Madras Branch

Cash sent to Branch for

Rent

Salaries

Other expenses

Cash received from the branch

Stock on 31st December

Petty cash in hand on 31st December

15,000

1,800

3,000

1,200

24,000

2,300

40

45,000

1,800

5,000

1,600

60,000

5,800

30

Solution;

Madras Branch A/c for 2002

Rs. Rs.

Jan. 1 To Balance b/d

To Goods sent to Branch

To Bank :

Rent : 1,800

Salaries : 3,000

Other expenses : 1,200

Nil

15,000

6,000

By Bank

By balance c/d

Stock

Petty cash

24,000

2,300

40

13

_______

To General P & LA/c (Profit)

5,340

26,340

26,340

Madras Branch A/c for 2003

Rs Rs

Jan 1 To Balance b/d

Stock 2,300

Petty cash 40

To Goods sent to branch

To Bank

Rent : 1,800

Salaries : 5,000

Other expenses : 1,600

________

To General P & L a/c

2,340

45,000

8,400

10,090

65,830

By Bank

By balance c/d

Stock

Petty cash

60,000

5,800

30

65,830

Illustration 2

From the following particulars prepare a branch account showing the profit or

loss at the branch.

Rs.

Opening stock at the branch

Goods sent to the branch

Sales

Salaries

Other expenses

15,000

45,000

60,000

5,000

2,000

Closing stock could not be ascertained but it is know that the branch usually sells at

cost plus 20%. The branch manager is entitled to a commission of 5% on the profit

of the branch before charging such commission.

14

Solution

Working Note:

Computation closing stock

Rs.

Opening stock

Add: Goods sent to Branch

Less: Cost of goods Sold

[sales * 100/120=

[60,000*100/120]]

15,000

45,000

60,000

50,000

10,000

In the books of Head office

Branch A/c

Rs Rs

To opening stock

To goods sent to branch

To bank (salaries)

Other expenses

To Manager’s commission

[3,000*5%]

To Net profit – transferred to

General P & L A/c

15,000

45,000

5,000

2,000

150

2,850

70,000

By Branch Cash (sales)

By closing stock

60,000

10,000

70,000

15

Illustration 3

A head office invoices goods to its branch at cost price. The balance is

permitted to incur petty expenses and maintain petty cash balance of Rs. 1,000

on the imprest system. It is also permitted to buy furniture of the value of

Rs.2,000.

Stock 1.1.93

Debtors “

Petty cash “

Creditors ‘

Rent upto 31.3.93

Goods sent to branch

Credit sales

Cash sales

Cash received from debtors

Allowances

Discount

Bad debt

Cash purchase by the branch

Payments to creditors

Closing balance of creditors A/c

Rent for on year

Salaries

Insurance paid upto 31.3.94

Furniture

Petty expenses

Stock on 31.12.93

Rs.

41,000

12,500

1,000

10,000

250

75,000

40,000

75,000

45,000

50

100

150

12,500

45,000

27,500

1,200

6,000

750

2,000

1,00,000

Prepare branch A/c in the Books of Head Office.

16

1993 Rs. 1993 Rs.

Jn 1 To bal b/d

Stock

Debtors

Petty cash

Creditors

Rent prepaid

To Goods sent to

Branch

To Bank

Rent 1,200

Salaries 6,000

Insurance 750

To Petty expenses

41,000

12,500

1,000

10,000

250

75,000

7,950

250

1,80,937.50

Jan1 By Balance b/d

Creditors

By Bank

Cash remitted to

H.O

By Balance c/d

Stock

Debtors

Petty cash

Furniture

Rent prepaid

[1200*3/12]

Insurance prepaid

[750*3/12]

10,000

60,250

1,00,000

7,200

1,000

2,000

300

187.50

1,80,937.50

Working Note:

Branch Debtors A/c

Rs Rs

To balance b/d 12,500

40,000

52,500

Branch cash

By Allowances

By Discount

By Bad debt

By balance c/d (bal. fig)

45,000

50

100

150

7,200

52,500

Branch Cash A/c

Rs Rs

To Sales (cash)

To debtors

12,500

40,000

1,20,000

By branch petty cash

By purchases

By creditors

By furniture

By Remittance to H.O

(bal.fig)

250

12,500

45,000

2,000

60,250

1,20,000

17

Branch petty cash A/c

Rs Rs

To balance b/d

To branch cash (bal.fig)

1,000

250

1,250

By Expenses

By Balance c/d

250

1,000

1,250

Illustration 4

A Madras head office has a branch at Salem to which goods ae invoiced at cost plus20%.

From the following particulars, prepare branch A/c in the head office books;

Rs.

Goods sent to branch

Total sales

Cash sales

Cash received from branch debtors

Branch debtors on 1.1.96

Branch stock on 1.1.96

Branch stock on 31-12.96

2,11,872

2,06,400

1,10,400

88,000

24,000

7,680

13,440

solution :

Salem Branch A/c for the year ended 31.12.96

Rs Rs

To balance b/d

Stock

Debtors

To Goods sent to branch

To stock reserve

[13,440*20/120]

To profit –transferred to

general P&L a/c

7,680

24,000

2,11,872

2,240

34,640

2,80,432

By Bank

Cash sales 1,10,400

Cash received 88,000

________

By stock reserve

[7,680*20/120]

By Goods sent to branch

Loading

[2,11,872 *20/120]

By balance c/d

Stock

Debtors

1,98,400

1,280

35,312

13,440

32,000

2,80,432

18

working Note :

calculating of closing debtors

Branch Debtors A/c

Rs Rs

To balance b/d

To sales – credit

24,000

96,000

1,20,000

By Branch cash

By balance c/d (bal.fig)

88,000

32,000

1,20,000

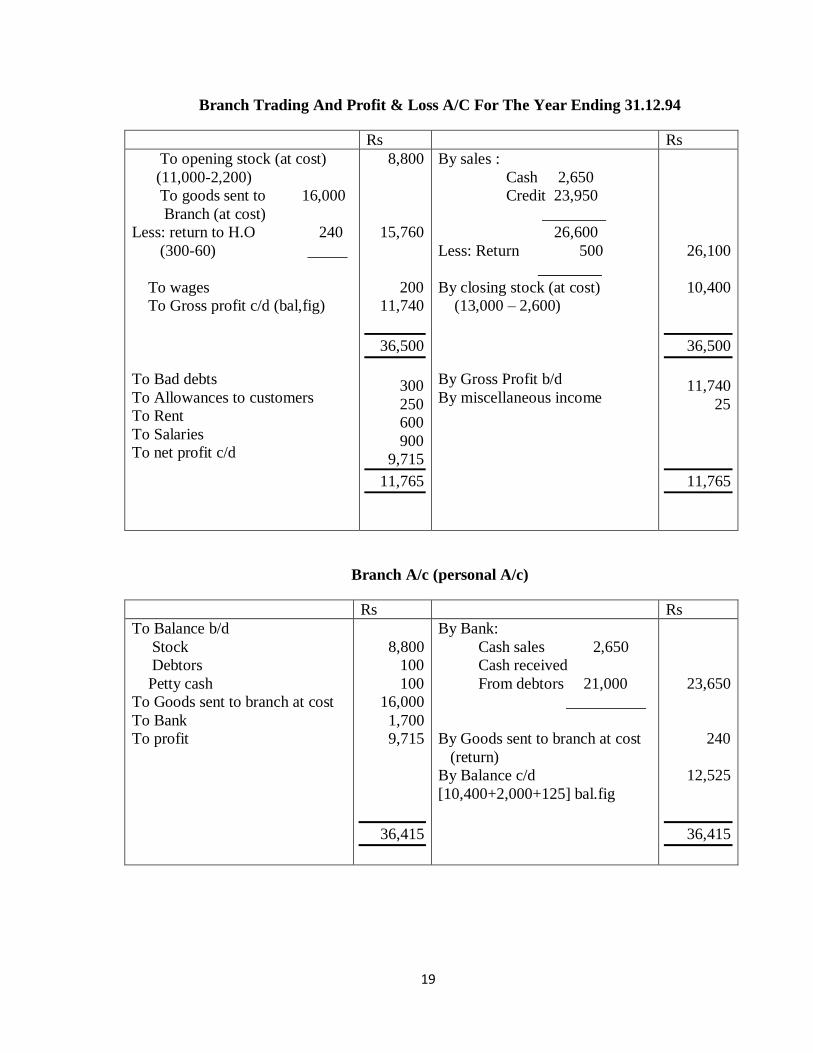

Illustration 5

A madras merchant has a branch at pudukkottai to which goods are sent at cost plus 25%.

The branch keeps its own sales ledger and remits all cash received to the head office every day.

All expenses are paid from the head office. The transactions for the branch were as follows:

Rs.

Stock 1.1.94 at I.P

Debtors 1.1.94

Petty cash 1.1.94

Cash sales

Credit sales

Goods sent to branch at I.P

Goods returned to head office

Bad debts

Allowances to customers

Return inwards

Cheques sent to branch:

Rent

Wages

Salary

Stock 31.12.94 at I.P

Debtors 31.12.94 at I.P

Petty cash31.12.94

(including miscellaneous income Rs. 25 not remitted)

Collection from debtors

11,000

100

100

2,650

23,950

20,000

300

300

250

500

600

200

900

13,000.

2,000

125

21,000

Solution:

19

Branch Trading And Profit & Loss A/C For The Year Ending 31.12.94

Rs Rs

To opening stock (at cost)

(11,000-2,200)

To goods sent to 16,000

Branch (at cost)

Less: return to H.O 240

(300-60) _____

To wages

To Gross profit c/d (bal,fig)

To Bad debts

To Allowances to customers

To Rent

To Salaries

To net profit c/d

8,800

15,760

200

11,740

36,500

300

250

600

900

9,715

11,765

By sales :

Cash 2,650

Credit 23,950

________

26,600

Less: Return 500

________

By closing stock (at cost)

(13,000 – 2,600)

By Gross Profit b/d

By miscellaneous income

26,100

10,400

36,500

11,740

25

11,765

Branch A/c (personal A/c)

Rs Rs

To Balance b/d

Stock

Debtors

Petty cash

To Goods sent to branch at cost

To Bank

To profit

8,800

100

100

16,000

1,700

9,715

36,415

By Bank:

Cash sales 2,650

Cash received

From debtors 21,000

__________

By Goods sent to branch at cost

(return)

By Balance c/d

[10,400+2,000+125] bal.fig

23,650

240

12,525

36,415

20

WHOLESALE BRANCH SYSTEM

Illustration 1

A head office sends goods to its branch at 20% less the list price. Goods are sold to

customers at cost plus 100%. From the following particulars ascertain the profit made at the

head office and the branch on wholesale basis.

Head office

Rs.

Branch

Rs

Purchases

Goods sent to branch (invoice price)

Sales

2,00,000

80,000

1,70,000

-

-

80 ,000

solution :

Trading and Profit & Loss A/c

H.O

Rs.

Branch

Rs.

H.O

Rs.

Branch

Rs.

To purchases

To Goods received

From H.O

To Gross profit c/d

To stock Reserve

(closing stock)

[16,000×60/160]

To Net profit c/d

2,00,000

-

1,15,000

3,15,000

6,000

1,09,000

1,15,000

-

80,000

16,000

96,000

-

16,000

16,000

By sales

By Goods sent to

branch

By closing stock

By Gross profit b/d

1,70,000

80,000

65,000

3,15,000

1,15,000

1,15,000

80,000

16,000

96,000

16,000

16,000

Working Note:

Calculated of closing stock

Value of closing stock at H.O Rs. Rs.

Purchases

Less: cost of goods sold

[1,70,00/2 × 100]

Less: cost Goods sent to Branch

[80,000/160 × 100]

85,000

50,000

2,00,000

1.35,000

21

Closing stock

Value of closing stock at Branch

Goods received from H.O

Less: cost of good sold

[80,000/200 ×160]

Closing stock

65,000

80,000

64,000

16,000

Note;

H.O cost price Whole sale Rate I,e. Rate at ehich list price 200(100+100)

Goods supplied to branch

160(200-200 ×20%)

STOCK AND DEBTOR SYSTEM

(A) When Goods are sent at cost price

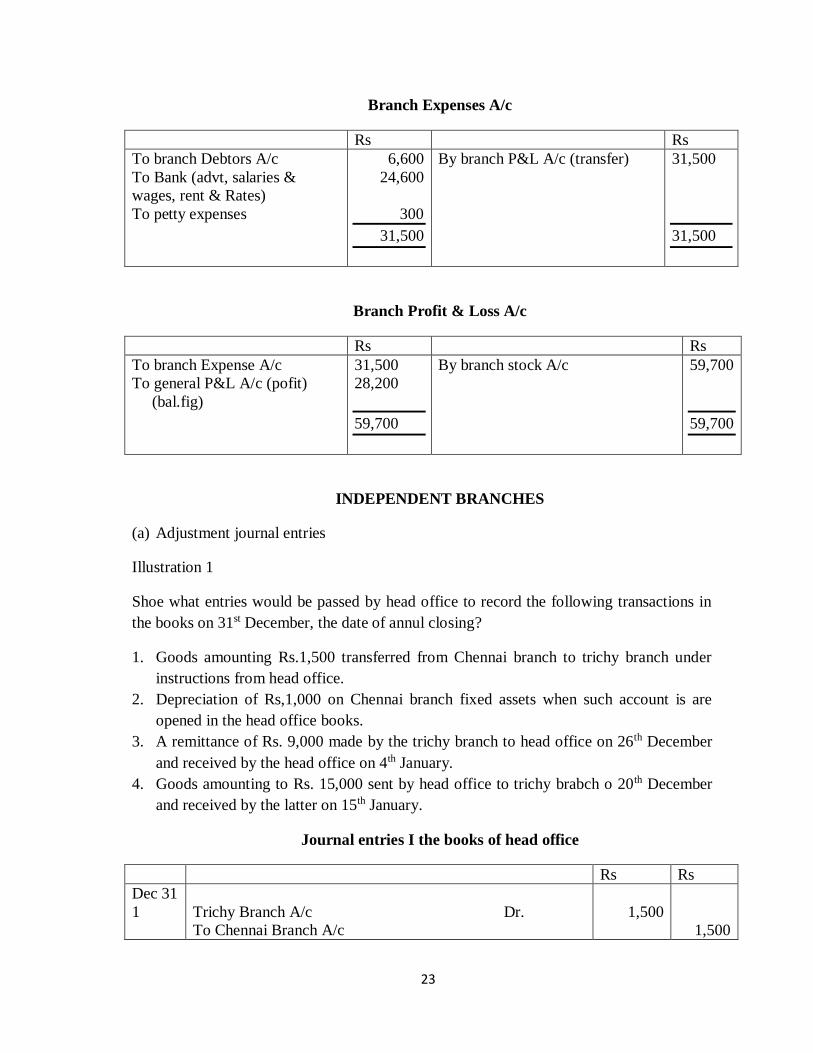

Illustration 1

The calculate commercial company invoiced goods to its Jamshedpur branch at cost. The hed

office paid all the branch expenses from its bank except petty cash expenses. Which were paid

by the branch. From the following details relating to the Branch, prepare.

1. Branch stock A/c

2. Branch Debtors a/c

3. Branch Expenses A/c

4. Branch P & L A/c

22

Rs

Stock

Debtors

Petty cash

Goods sent to branch

Goods returned to head office

Cash sales

Advertisement

Cash received from debtors

Stock (closing)

Allowances to customers

Discount to customers

Bad debts

Goods returned by customers to branch

Salaries & wages

Rent & rates

Debtors ( closing )

Petty cash (closing)

Credit sales

21,000

37,800

600

78,000

3,000

52,500

2,400

85,500

19,500

600

4,200

1,800

1,500

18,600

3,600

29,400

300

85,200

Solution :

Branch stock A/c

Rs Rs

To balance b/d

To Goods sent to branch

To branch Debtors

To branch profit & Loss A/c

21,000

78,000

1,500

59,700

1,60,200

By cash

By Goods sent to branch

By branch Debtors

By Balance c/d

52,500

3,000

85,200

19,500

1,60,200

Branch Debtors A/c

Rs Rs

To balance b/d

To branch stock A/c

37,800

85,200

1,23,000

By cash

By branch Expenses

[bad, allowances, discount]

By branch stock (return)

By balance c/d

85,500

6,600

1,500

29,400

1,23,000

23

Branch Expenses A/c

Rs Rs

To branch Debtors A/c

To Bank (advt, salaries &

wages, rent & Rates)

To petty expenses

6,600

24,600

300

31,500

By branch P&L A/c (transfer) 31,500

31,500

Branch Profit & Loss A/c

Rs Rs

To branch Expense A/c

To general P&L A/c (pofit)

(bal.fig)

31,500

28,200

59,700

By branch stock A/c 59,700

59,700

INDEPENDENT BRANCHES

(a) Adjustment journal entries

Illustration 1

Shoe what entries would be passed by head office to record the following transactions in

the books on 31st December, the date of annul closing?

1. Goods amounting Rs.1,500 transferred from Chennai branch to trichy branch under

instructions from head office.

2. Depreciation of Rs,1,000 on Chennai branch fixed assets when such account is are

opened in the head office books.

3. A remittance of Rs. 9,000 made by the trichy branch to head office on 26th December

and received by the head office on 4th January.

4. Goods amounting to Rs. 15,000 sent by head office to trichy brabch o 20th December

and received by the latter on 15th January.

Journal entries I the books of head office

Rs Rs

Dec 31

1

Trichy Branch A/c Dr.

To Chennai Branch A/c

1,500

1,500

24

2

3

4

[Being goods transferred from Chennai branch to trichy

branch as per instructions]

Chennai Branch A/c Dr.

To Chennai branch fixed asset A/c

[Being depreciation written off on Chennai branch fixed

assets]

The head office will not pass any entry until intimation is

received. When information about it is received the

following entry is passed.

Cash in transit A/c Dr.

To Trichy branch A/c

Goods in transit A/c

To Trichy Branch A/c

[being the entry to adjust the goods sent to Trichy branch on

20th dec. but not received by the branch till 31st dec.]

1,000

9,000

15,000

1,000

9,000

15,000

(b) Independent of Branches Trial Balance

Illustration 2

Rs Rs

Cash in hand

Opening stock

Debtors

Goods from head office

Furniture

Purchases

Wages

Salaries

Trade expenses

9,000

18,000

30,000

1,20,000

6,000

1,80,000

9,000

12,000

6,000

Head office A/c

Sales

creditors

90,000

2,70,000

30,000

3,90,000 3,90,000

Closing stock Rs. 90,000. Pass the necessary journal entries to incorporate branch

trial balance in head office books and also branch trading A/c and P&L A/c and branch A/c

in head office books.

Solution :

In the books of head office

25

Journal Entries

Rs. Rs.

Madras branch Trading A/c Dr

To Madras Branch A/c

[Being incorporation of opening stock, purchases, goods

from H.O and wages]

Madras branch A/c Dr

To Madras branch Trading A/c

[Being incorporation of sales and closing stock]

Madras branch Trading A/c Dr

To Madras Branch P & LA/c

[Being transfer of gross profit]

Madras Branch P & LA/c Dr.

To Madras Branch A/c

[Being incorporation of salaries & trade expenses]

Madras Branch P & LA/c Dr.

To General P & L A/c

[Being transfer of net profit ]

Madras branch Furniture A/c Dr

Madras branch Debtors A/c Dr

Madras branch Cash A/c Dr

Madras branch Stock A/c Dr

To Madras branch A/c

[Being incorporation of various assets from branch trial

balance]

Madras branch A/c Dr

To Madras Branch A/c

[Being incorporation of creditors from branch Trial

balance]

3,27,000

3,60,000

33,000

18,000

15,000

6,000

30,000

9,000

90,000

30,000

3,27,000

3,60,000

33,000

18,000

15,000

1,35,000

30,000

26

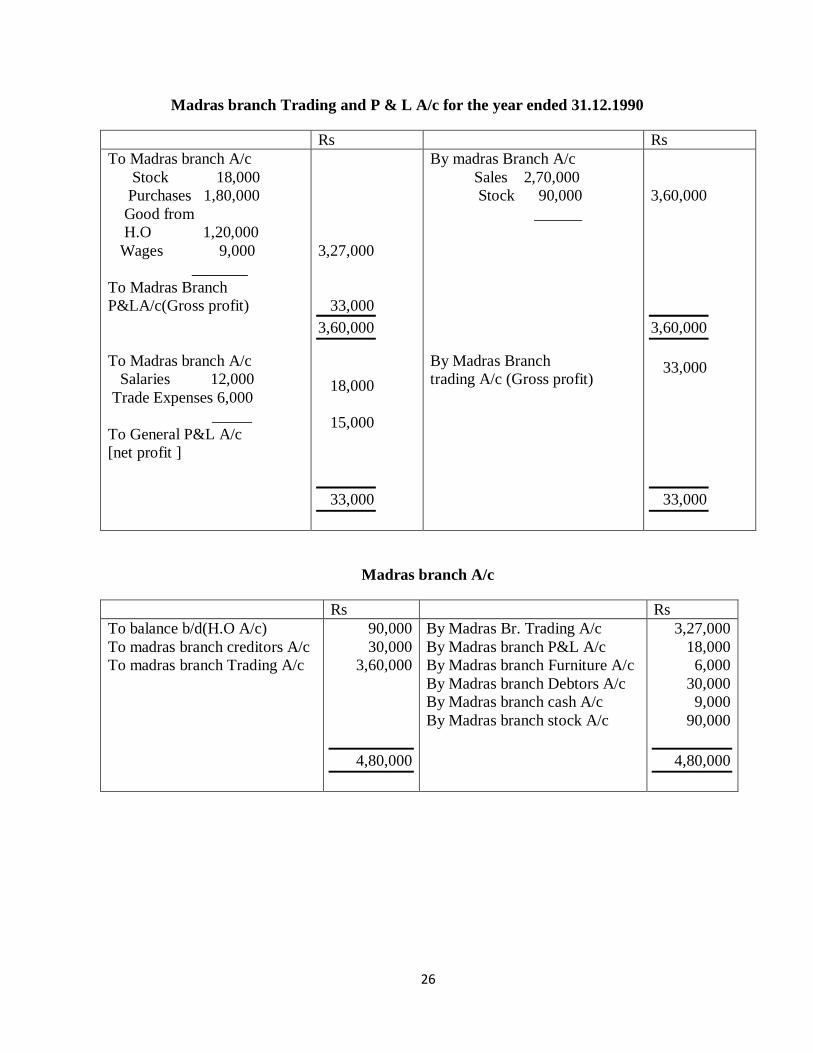

Madras branch Trading and P & L A/c for the year ended 31.12.1990

Rs Rs

To Madras branch A/c

Stock 18,000

Purchases 1,80,000

Good from

H.O 1,20,000

Wages 9,000

_______

To Madras Branch

P&LA/c(Gross profit)

To Madras branch A/c

Salaries 12,000

Trade Expenses 6,000

_____

To General P&L A/c

[net profit ]

3,27,000

33,000

3,60,000

18,000

15,000

33,000

By madras Branch A/c

Sales 2,70,000

Stock 90,000

______

By Madras Branch

trading A/c (Gross profit)

3,60,000

3,60,000

33,000

33,000

Madras branch A/c

Rs Rs

To balance b/d(H.O A/c)

To madras branch creditors A/c

To madras branch Trading A/c

90,000

30,000

3,60,000

4,80,000

By Madras Br. Trading A/c

By Madras branch P&L A/c

By Madras branch Furniture A/c

By Madras branch Debtors A/c

By Madras branch cash A/c

By Madras branch stock A/c

3,27,000

18,000

6,000

30,000

9,000

90,000

4,80,000

27

Illustration 3

The head office of a business and its branch keep their own books and cash

prepares it own profit & loss A/c. the following ar the balance appearing on the two sets of

the books as on 31st Dec. 1994 after ascertainment of profit and after making all

adjustment except those referred to below:

Dr.

Rs.

Cr.

Rs.

Dr.

Rs.

Dr.

Rs.

Capital

Fixedassets

Stock

Debtors &

Creditors

Cash profit

& Loss

Branch A/c

Head office

A/c

-

36,000

34,200

7,820

10,740

-

29,860

-

1,18,620

1,00,000

-

-

3,960

-

14,660

-

---

1,18,620

-

16,000

10,740

4,840

1,420

-

-

--

33,000

--

-

-

1,920

-

3,060

-

28,020

33,000

Set out the balance sheet of the business as on 31st December 1994 and the journal entries

necessary to record adjustments dealing with the following:

1. On 31st December, the branch had sent a cheque for Rs. 1,000 to the head office, not

received by them nor credited to the branch till next month.

2. Goods valued at Rs.440 had been forwarded by the head office to the branch and invoiced

on 30th December, 1994 but were not received by the branch nor dealt with in their books

till next month.

3. It was agreed that the branch should be charged with Rs.300 for administrative service,

rendered by the head office during the year.

4. Stock stolen in transit from he head office to the branch and charged to the branch by the

head office but not credited to the head office in the branch books as the branch manager

declined to admit any liability Rs,400.

5. Depreciation of branch assets, of which accounts are maintained by the head office, not

provided for Rs.250

6. The balance of profit shown by the branch is to transferred to the head office books.

28

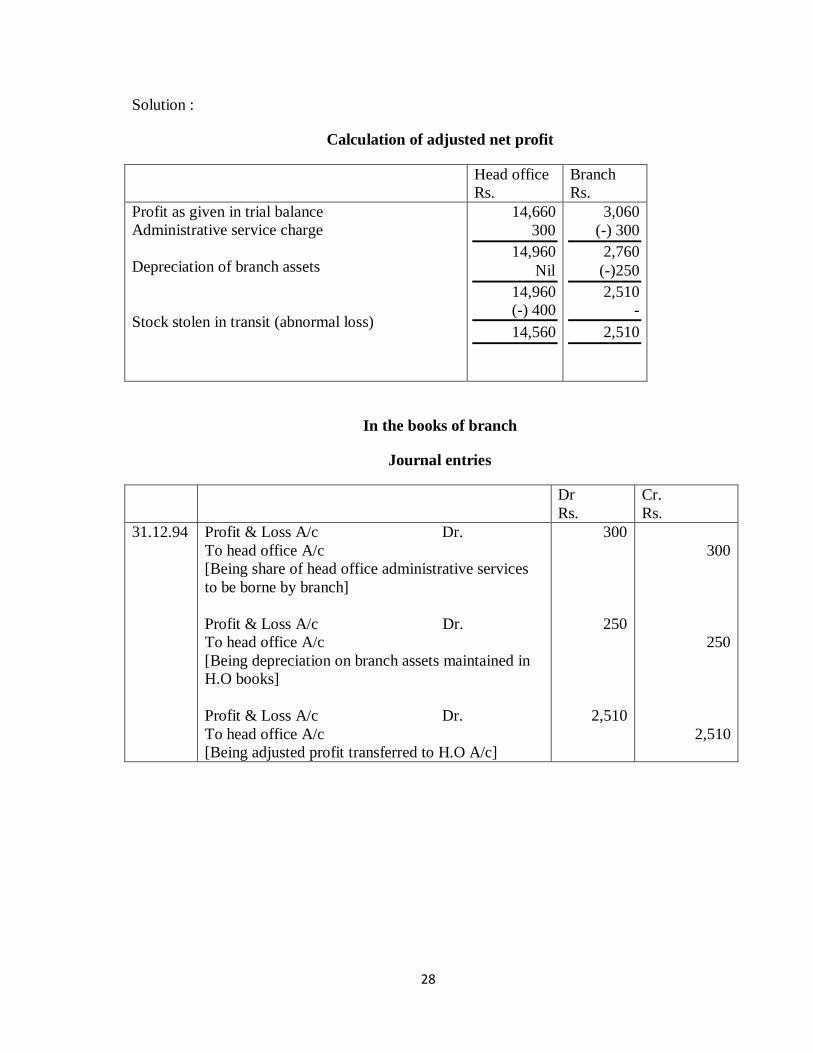

Solution :

Calculation of adjusted net profit

Head office

Rs.

Branch

Rs.

Profit as given in trial balance

Administrative service charge

Depreciation of branch assets

Stock stolen in transit (abnormal loss)

14,660

300

14,960

Nil

14,960

(-) 400

14,560

3,060

(-) 300

2,760

(-)250

2,510

-

2,510

In the books of branch

Journal entries

Dr

Rs.

Cr.

Rs.

31.12.94 Profit & Loss A/c Dr.

To head office A/c

[Being share of head office administrative services

to be borne by branch]

Profit & Loss A/c Dr.

To head office A/c

[Being depreciation on branch assets maintained in

H.O books]

Profit & Loss A/c Dr.

To head office A/c

[Being adjusted profit transferred to H.O A/c]

300

250

2,510

300

250

2,510

29

HIRE PURCASES AND INSTALMENT PURCHASES SYSTEM

Hire purchases and installment system are responsible for bringing high valuable good like

cas, television into the reach of middle class and lower class people. These systems have

revolutionized the world of commerce.

Hire purchase system:

Definition:

Accounting to the Hire purchase Act 1972 section 2 (c)”Hire purchase is an agreement

under which goods are let on hire and under which hirer has an option to purchase them in

accordance with the terms of the terms and includes an agreement under which

(i) Possession of goods is delivered by the owner thereof to a person on condition that such

person pays the agreed amount in periodical installments.

(ii) The property in the goods is to pass to such person on the payment of the last of such

installments.

(iii) Such person has a right to terminate the agreement at any time before the property so

passes”

As per section 4 of the Hire purchases Act 1972, every hire purchases agreement state:

(a) The hire purchases price of the goods to which the agreement relates.

(b) The cash price of the goods, that is to say, the price at which the goods may be purchased

by the hirer for cash.

(c) The date on which the agreement shall be deemed to have commenced.

(d) The number of installments by which the hire purchases price is to be paid, the amount of

each of those installments and the date or the mode of determining the date, upon which it is

payable and the person to whom and the place where it is payable.

(e) The goods to which the agreement relates, the manner sufficient to identify them.

Important terms in the hire purchases system

1. Cash price :

This is the retail price of the articles at which they can be puraches immediately for cash.

2.Hire purchases price:

This is the total amount payable by the buyer, in agreed instalments for the goods

purchased. This price includes cash price and interest.

3. Interest:

This is the additional amount apart from the cash price payable by the buyer as

compensation for postponed payments.

30

4. Hire or Installment:

This is the amount payable by the buyer periodically. The installments may be equal or

different, depending on agreement.

5. Down payment:

This is the advance payable by the buyer while signing the hire purchases

agreement. It is also a part of the hire purchase price.

6. Hirer:

The buyer of the goods on hire purchase basis.

7. Hire vendor or owner:

The seller of the goods on hire purchase basis.

Main features of Hire purchase system.

1. The hirer or buyer gets possession of the goods on signing the hire purchase

agreement and he has right to use them.

2. The ownership of the goods continues to be with the seller or hire vendor. The buyer

gets ownership of the goods on payment of the last installment.

3. The hirer has the duty to keep the good in good condition and take reasonable

precautions for their safety till the last installment is paid.

4. Each installment is treated as hire charges.

5. The hirer has the option to return the goods before the last installment is paid.

Installment purchases system or deferred installment system:

In installment purchases system also, an agreement is entered into by the seller

and buyer. An advance or down payment is paid and possession as well as ownership in

the goods is transferred to the buyer. The buyer agrees to pay the balance of amount due

in a specified number of installment along with agreed rate of interest. If buyer fails to

pay any installment, the seller cannot repossess the goods. He can sue the buyer in a

court for recovery of the dues.

31

Distinction between Hire purchases and Installment system

Basis Hire purchases

system

Installment

system

Nature of

agreement

Transfer of

ownership

Right of loss

Right of sale

Instalment

It is an agreement

of hiring with

option to buy.

Ownership is

transferred on

payment of final

instlments.

The hirer is not

responsible for

any loss of the

goods if he has

taken reasonable

precautions.

The hire cannot

sell the goods till

he gets ownership.

Each instalments

include hire

charge and part

payments of the

cash price

It is an

agreements of

sales.

Ownership is

transferred on

signing of the

agreement.

The buyer is

responsible for

loss of goods

because he is the

owner.

The buyer has

the right to sell

the goods even

before

instalments are

paid.

Each instalment

includes interest

and part

payment of cash

price.

Calculation of interest

The hire purchase price is always greater than the cash price. It includes cost payable over and

above the price of the goods to compensate the seller sacrifice he has made by agreeing to receive the

price by instalments and risk that he there by undertakes. Interest is the charge for the facility to pay

price for the goods by instalments after they have been delivered. The rate of is generally higher than

that is payable in respect of an advance or a loan it

32

also includes higher than that is payable in respect of an advance or a loan it also includes a charge

to cover the risk that the hirer may fail to pay any instalments and in such an event, the goods may

have to be taken back possession in whatever condition they are at that time.

Interest included in each instalment can be ascertained by making necessary calculations

under the following circumstances:

(i) When the rate of interest, the cash price and the instalments are given

(ii) When the rate of interest is not given

(iii) When the total cash price is not given.

(iv) When the instalment price is not given.

(v) When cash price is calculated by annuity method.

(i)When the rate of interest, the cash price and the instalments are given:

Under this method, the interest is to be calculated on the outstanding balance of the cash

price at the stipulated rate. When interest component is deducted from instalment, the balance

represents the amount paid in reduction of cash price. This amount is deducted from the cash price

to facilitate the calculation of interest for the next period.

(ii)When total cash price and instalment are given but rate of interest is not given:

when the rate of interest is not given, the interest included in each instalment will be

calculated on the basis of the hire purchases price outstanding in the beginning of each year. The

following is the process of ascertaining interest included in various instalments.

Method 1: When the amount and period of instalments are not uniform [Product method]

Hire purchases price - cash price = Total Interest.

Hire purchases price – first instalment = first balance..

First balance – second instalment = second balance.

Second balance - third instalment = Third balance.

Same method can be used for further instalments.

(i) Hire purchase price × period first instalment. = A

(ii) first balance period × of second instalment. = B

(iii) second balance × period of third instalment =C

(iv) third balance × period of fourth instalment = D

A,B,C and D have to be totaled and interest included in each instalment is found as

follows:

33

Interest included in I instalment : total interest × _______A____

A+B+C+D

B

Interest included in II instalment : total interest × ___________

A+B+C+D

C

Interest included in III instalment : total interest × _________

A+B+C+D

D

Interest included in IV installment: total interest × ___________

A+B+C+D

Method 2: When the amount and period of installments are uniform

Hire purchases price - cash price = total interest.

Assuming total interest is Rs.800 and numbers of installments are four, interest

included in each installment is calculated in the following manner:

installments No. Of

outstanding

installments

Ratio

of

interest

Interest

1st

installments

2st

installments

3st

installments

4st

installments

4

3

2

1

10

4/10

3/10

2/10

1/10

800×4/10

Rs. 320

800×3/10

Rs. 240.

800×2/10

Rs. 160

800×1/10

Rs.80

34

(iii)When rate of interest and installments are given but total cash prices is not given.

When the amount of each installment which includes interest is given and rate of interest is

also given, cash price is found out in the following manner:

Rate of interest

(a) First of last installment × __________________

100 + Rate of interest

= Interest included in the last instalment.

(iv) When rate of interest ad total cash price are given but the instalment price is not given.

In this method is also, the interest is to be calculated on the outstanding balance of the ash

price at the stipulated rate. Then cash price paid is deducted from the total cash price and interest is

calculated for the next period falling between the dates of payment of first instalment and second

instalment. This process is repeated till the payment of last instalment. The instalment price is

calculated by adding interest with cash price of each instalment.

(v)calculation of cash price by Annuity method:

when in place of cash price, hire purchase price and annuity rate are given, the annuity factor

given and adding down payment to the product. Then interest is calculated.

Default and Repossession

Repossession

The hire vendor has the right away the goods sold on hire purchase in the event of default

made by the hire purchaser. As per hire purchases Act 1972 goods of small value ot even goods of

higher value when only certain number of instalments are paid, can be repossessed without court’s

permission. A court order is needed to repossess good on which larger number of instalments than

specified are paid.

Types of repossession

(a) complete Repossession :

The hire vendor may take away all the goods on which there is default of instalment.

(b)partial Repossession:

The hire vendor may take away only a portion of the goods on which there is default of

instilments.

Accounting treatment varies in the books of both the hire vendor and hire purchaser for

each of the types of repossession.

(a)Complete repossession of goods:

35

When complete repossession of goods takes place, the ledger account in the books of hire

purchaser and hire vendor are fully closed as far as the hire purchases transaction is concerned.

Books of Hire vendor

1. on the date of default of instalment, entry for interest is passed. The hire purchaser’s account is

closed. Any balance is transferred to repossessed goods account.

2.Hire vendor’s account is to be closed and any balance is transferred to the asset account.

(b)Partial repossession

The hire purchaser might have depreciated the asset as per his assessment of he rate of

depreciation. The hire vendor revalues the hirer who may agree to make some payment in future.

Books of Hire vendor

1. entry for interest upto the date of default is passed.

2. repossessed goods as per hire vendor’s valuation are credited to hire purchaser’s

account and debited to ‘Repossessed good A/c.

3. the hire purchasers account is balanced and balance is carried down.

4. Repossessed goods may be repaired and sold later on.

Books of Hire purchaser:

1. Entries for interest and depreciation on the asset are passed upto date.

2. Hire vendor’s A/c is debited and asset A/c is credited with the value of asset taken away as

per hire vendor’s valuation.

3. The asset account is balanced. Any balance is loss due to repossession and is transferred to

profit and Loss Account.

2. Accounting treatment for goods of small sales value

(hire purchases trading account)

When numerous sales of small value are made in addition to normal sales, the hire vendor

follows an alternative method of recording transactions. This method, known as ‘ stock method’,

avoid the maintenance of a separate account for each individual customer and also the tedious

method of calculating interest in each case.

(i) Stock of goods with customers:

This is also termed as Hire purchase stock. Stock with the customer, instalmetns not yet due,

or amount of instalments unpaid and not due. These are the total amount of those instalments in

respect to goods sold on hire purchases which are to be received in the next accounting period.

36

(ii)Purchases (Goods sold during the year)

The term “Purchase” is used when the business is run independently. But if the business is

run as a department, the information relating rlating to purchase made by the department is given

under the term ‘Goods sold during the year.

(iii)Cash Received

It refers to the total amount received from the customers during the accounting year in the

form of down payment and amount of instalments. It is shown on the credit side of hire purchase

trading account.

(iv)Total instalments due but unpaid

It refers to the total sum of instalments which have become due during the accounting year

but has not been paid by the customers. This is also termed as ‘Hire purchase Debtors’ ‘Instalment

due’, ‘ customers paying’.

(v)Stock

It is shown on the debit side of hire purchase trading account, but when business is run as a

department , this information is not required.

Methods of computation of profit

The profit made by the vendor on hire-purchase transactions in case of goods of small value,

can be calculated by any one of the following methods:

(i)Debtors method (ii)Stock and Debtors method

(i)Debtors method

Under this method, the profit or loss made on goods sold on hire purchase can be found out

by preparing hire purchase hire purchase trading account. The specimen ruling of the hire purchase

trading account is as under:

37

Hire purchase trading account

To stock at shop (opening)

To stock out with customers

(at cost)

To Instalmetn due but unpaid

(opening)

To purchases or cost of goods

sold during the year

To profit (bal.fig)

xxx

xxx

xxxx

xxx

xxx

xxx

By cash received from

customers

By Goods repossessed

By instalment due and

unpaid (closing)

By stock out with

customers(at cost )

By stock at shop (closing)

By Loss (bal.fig)

xxx

xxx

xxxx

xxx

xxx

xxx

Note:

1. If stock out with customers is given at hire purchase price in the question, then either stock

reserve equal to the excess of hire purchase price over cost price should be shown on cresit side

(from opening stock) and debit side (for closing stock) or it should be reduced to cost price.

2. Stock at shop should not be shown in hire purchase trading account when business is run as a

department.

(ii)Stock and Debtors method:

The profit made on hire pur5chase transaction can also be calculated according to stock and

debtors systems. Under this method, the following ledger accounts are to be opened.

1. Hire purchase stock account

2. stock at shop account

3. hire purchases debtors account.

4. goods on hire purchase account

5. hire purchase adjustment account

The following journal entries are to be passed if this method is followed.

(i) When goods are purchases for shop stock :

Stock at shop A/c Dr.(cost price)

38

To purchases A/c

(ii) When goods are sold on hire purchases

Hire purchases stock A/c Dr. (at sale price)

To goods sold on H.P A/c

(iii) For total instalments which become due

Hire purchases debtors A/c Dr.

To hire purchase stock A/c

(iv) When cash is received from debtors

Cash account Dr.

To Hire purchases debtors A/c

(v) For transfer of goods sold on H.P

Goods sold on H.P A/c

To H.P adjustment A/c

To Trading account

(vi) When goods are repossessed on default and loss is transferred to H.P

adjustment A/c

Goods repossessed A/c Dr(for realizable value)

H.P adjustment A/c Dr.(loss)

To Hire purchases debtors A/c (installment due and not received in cash)

To hire purchases stock A/c (for installment not yet due)

To H.P adjustment A/c (profit on repossession)

(vii) For loading in opening stock with customers

Stock reserve A/c Dr.

To H.P adjustment A/c

(viii) For loading in closing stock with customers

H.P adjustment A/c Dr

To Stock reserve A/c

(ix) For loading in goods sold (sent) on hire purchase

Goods sold on H.P A/c Dr

To H.P adjustment A/c

(x) For transfer of profit on hire purchase

39

H.P adjustment A/c Dr

To profit and loss A/c

In case of loss, the entry will be reversed.

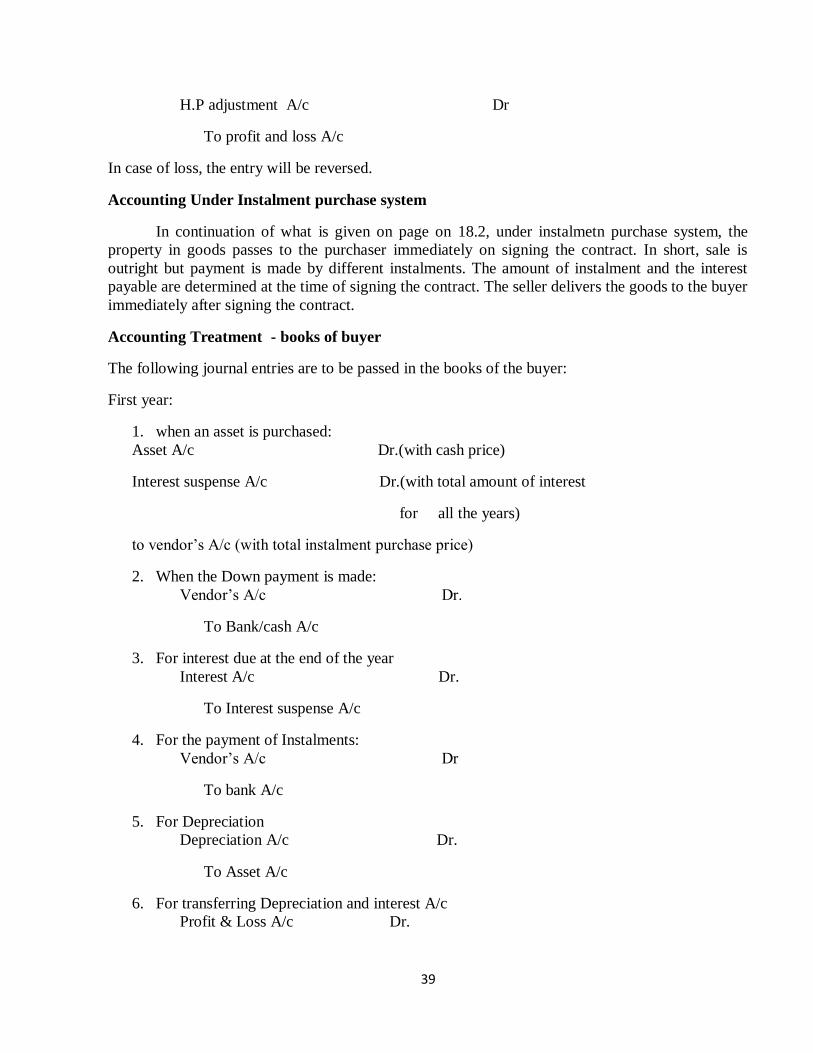

Accounting Under Instalment purchase system

In continuation of what is given on page on 18.2, under instalmetn purchase system, the

property in goods passes to the purchaser immediately on signing the contract. In short, sale is

outright but payment is made by different instalments. The amount of instalment and the interest

payable are determined at the time of signing the contract. The seller delivers the goods to the buyer

immediately after signing the contract.

Accounting Treatment - books of buyer

The following journal entries are to be passed in the books of the buyer:

First year:

1. when an asset is purchased:

Asset A/c Dr.(with cash price)

Interest suspense A/c Dr.(with total amount of interest

for all the years)

to vendor’s A/c (with total instalment purchase price)

2. When the Down payment is made:

Vendor’s A/c Dr.

To Bank/cash A/c

3. For interest due at the end of the year

Interest A/c Dr.

To Interest suspense A/c

4. For the payment of Instalments:

Vendor’s A/c Dr

To bank A/c

5. For Depreciation

Depreciation A/c Dr.

To Asset A/c

6. For transferring Depreciation and interest A/c

Profit & Loss A/c Dr.

40

To Interest A/c

To Depreciation A/c

Note:

Entries (3), (4), (5) and (6) will be repeated in subsequent years.

1. When goods are sold :

Buyer’s A/c Dr. (with total price)

To Sales A/c (with cash price)

To interest suspense A/c (with total interest for all the years)

2. on receipt of down payment

bank A/c Dr.

To buyer’s A/c

3. For interest due on instalments at the end of the year

Interest suspense A/c Dr.

To interest A/c

4. For receipt of the amount of instalment

Bank A/c Dr.

To Buyer’sA/c

5. For transferring interest A/c

Interest A/c Dr.

To profit & Loss A/c

Note :

Entries from (3) to (5) will be repeated in subsequent years.

Illustrations1:

Solution:

Table Showing Calculation of Interest

Particular Total cash

Price

(2)

Rs.

Installment

(3)

Rs.

Interest

Paid

(4)

Rs.

Cash price

Paid

5

(3-4)

Rs.

Cash price

Down payment

14,900

.00

41

1st installment

2nd inst

3rd inst

4,000.

00

10,900.00

3,455.00

7,445.00

3,627.75

3,817.25

3,817.25

4,000

4,000

4,000

4,000

-

545

[10,900

*5%]

372.25

[7,445*

5%]

182.75

[4,000-

3,817.2

5]

4,000.00

3,455.00

3,627.75

3,817.25

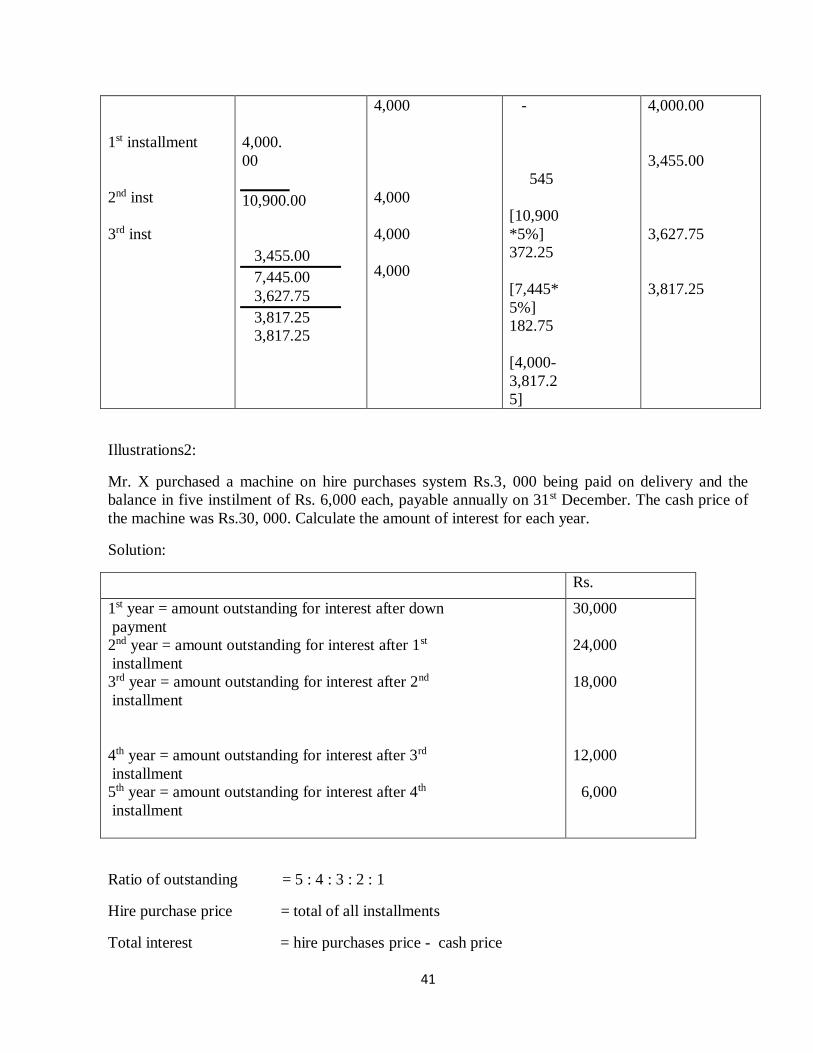

Illustrations2:

Mr. X purchased a machine on hire purchases system Rs.3, 000 being paid on delivery and the

balance in five instilment of Rs. 6,000 each, payable annually on 31st December. The cash price of

the machine was Rs.30, 000. Calculate the amount of interest for each year.

Solution:

Rs.

1st year = amount outstanding for interest after down

payment

2nd year = amount outstanding for interest after 1st

installment

3rd year = amount outstanding for interest after 2nd

installment

4th year = amount outstanding for interest after 3rd

installment

5th year = amount outstanding for interest after 4th

installment

30,000

24,000

18,000

12,000

6,000

Ratio of outstanding = 5 : 4 : 3 : 2 : 1

Hire purchase price = total of all installments

Total interest = hire purchases price - cash price

42

= 33,000-30,000 = 3,000.

Installment outstanding = 30,000:24,000:18,000:12,000:6,000

= 5 : 4 : 3 : 2 : 1

Installments No. Of

outstanding

installments

Ratio of

interest

Interest

Rs.

1st

installment

2nd

installment

3rd

installment

4th

installment

5th

instalment

5

4

3

2

1

5/15

4/15

3/15

2/15

1/15

3,000*5/15

=1,000

3,000*4/15

=800

3,000*3/15

=600

3,000*2/15

=400

3,000*1/15

=200

When cash price is not given

Illustration 3

X purchased a typewritten on hire purchases system. As per terms he is required to pay Rs.800

down. Rs.400 at the end of the first year Rs.300 at the end of the second year and Rs.700 at the end

the third year. Interest is charged at 5% p.a Calculate the total cash price of the typewritten and the

amount of interest payable on cash installment.

Solution:

Each installment paid includes interest for the period. The rate of interest on cash price must be

converted to rate of interest on installment.

We assume the cash price as Rs.100

Interest @ 5% on Rs.100 for one year 5

Installment paid at the end of the year 105

Interest on installment price 5/105 as a ratio.

43

The following table is used to arrive at the cash price of the type writer.

Year

(1)

Installment

(2)

Interest paid

(3)

Cashprice

paid. 4(2-

3)

Rs.

3rd year

2nd year

1st year

down

payment

700

300

400

800

2,200

________

700×5/105 =33

(300+667)

×5/105=46

(400+254+667)

×5/105 = 46

Nil

142

____________

667

254

337

800

2,058

Interest : 1year Rs.63 : II year Rs.46 iii year Rs. 33

The total cash price : Rs. 2,058

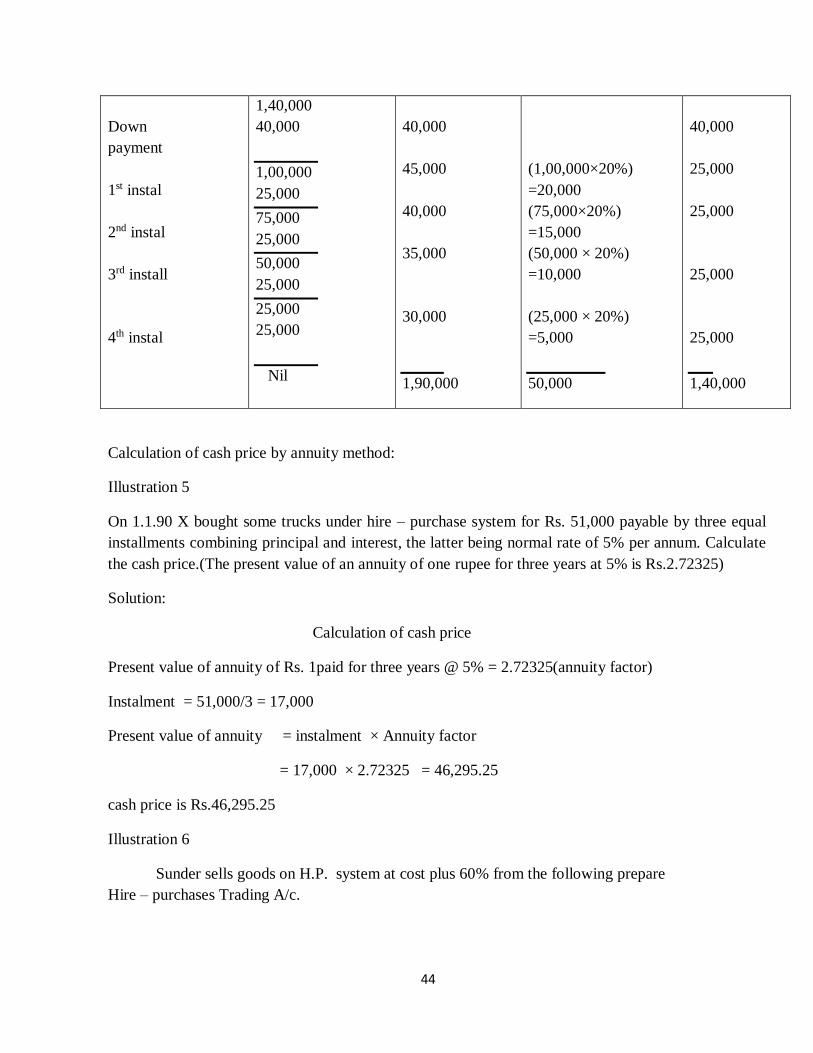

When installments amount are not given but cash price and rate of interest are given:

Illustration 4

X purchases a machine under hire purchases system. According to the terms of the

agreement rs.40, 000 was to be paid on signing of the contract. The balance was to be paid in four

annual installments of Rs.25, 000 each plus interest. The cash price was Rs. 1, 40,000. Interest is

chargeable on outstanding balance at 20% per annum. Calculate interest for each year and the

installment amount.

Solution:

Table showing calculation of interest

Date of payment

(1)

Total cash price

Rs. (2)

Install. Paid

Rs.

(3)=(4+5)

Interest paid rs. (4) Cash price

paid rs.(5)

44

Down

payment

1st instal

2nd instal

3rd install

4th instal

1,40,000

40,000

1,00,000

25,000

75,000

25,000

50,000

25,000

25,000

25,000

Nil

40,000

45,000

40,000

35,000

30,000

1,90,000

(1,00,000×20%)

=20,000

(75,000×20%)

=15,000

(50,000 × 20%)

=10,000

(25,000 × 20%)

=5,000

50,000

40,000

25,000

25,000

25,000

25,000

1,40,000

Calculation of cash price by annuity method:

Illustration 5

On 1.1.90 X bought some trucks under hire – purchase system for Rs. 51,000 payable by three equal

installments combining principal and interest, the latter being normal rate of 5% per annum. Calculate

the cash price.(The present value of an annuity of one rupee for three years at 5% is Rs.2.72325)

Solution:

Calculation of cash price

Present value of annuity of Rs. 1paid for three years @ 5% = 2.72325(annuity factor)

Instalment = 51,000/3 = 17,000

Present value of annuity = instalment × Annuity factor

= 17,000 × 2.72325 = 46,295.25

cash price is Rs.46,295.25

Illustration 6

Sunder sells goods on H.P. system at cost plus 60% from the following prepare

Hire – purchases Trading A/c.

45

Rs

Jan 1 Goods out on H.P system at H.P price

Dec 31 Installments not due and unpaid

Installments due and unpaid

The following transactions book place during the year:

a) goods sole on H.P price

b) cash received from customers at H.P price

c) Goods received back on default valued at

(installment due Rs.4000)

32,000

72,000

4,000

1,60,000

1,12,000

800

Solution :

Rs. Rs.

To Goods out

on H.P (op.

stock)

To Goods sold

during the year

To stock

Reserve

[72,000

×60/100]

To P & L A/c

32,000

1,60,000

27,000

41,800

2,60,800

By cash

By Goods

Repossessed

By instalments due

[closing debtors]

by Stock

Reserve

[32,000 /160×

60]

by instalment not due and

unpaid [closing stock]

By loading on Goods sold

[1,60,000 × 60/160]

1,12,000

800

4,000

12,000

12,000

72,000

60,000

2,60,800

46

Illustration 7

Stock and Debtors Method:

Krishna sells product on H.P. terms, the price being cost plus 33 1/3 %. From the following

particular for the year ended 31.12.95, prepare the necessary account stock on stock – debtors

system to reveal the profit earned.

Rs

1.1.95

31.12.95

Stock out on hie at H.P price

Stock in hand at shop

Instalments due (customers still paying)

Stock out on hie at H.P price

Stock in hand at shop

Instalments due (customers still paying)

Cash received during the year

16,00,000

2,00,000

1,20,000

18,40,000

2,80,000

2,00,000

32,00,000

Solution :

H .P Debtors A/C (Installments due A/c)

Rs rs

To balance b/d

To H.P .stock A/c

1,20,000

32,80,000

34,00,000

By cash

By balance c/d

32,00,000

2,00,000

34,00,000

H.P stock A/c (stock out with customers A/c)

Rs Rs

To balance b/d

To Goods sold on H.P (bal.fig)

16,00,000

35,20,000

51,20,000

By H .P Debtors A/C

By balance c/d

32,80,000

18,40,000

51,20,000

Shop stock A/C

47

Rs Rs

To balance b/d

To purchases (bal.fig)

2,00,000

27,20,000

29,20,000

By H .P Debtors A/C

(cost of goods sold)

[35,20,000 /4× 3]

by balance c/d

26,40,000

2,80,000

29,20,000

H.P Adjustment A/c

Rs Rs

To stock Reserve

[18,40,000×1/4 ]

To P & L A/c

4,60,000

8,20,000

29,20,000

By stock Reserve

[1,60,000 × 1/4]

By H.P stock [35,20,000 ×

1/4]

4,00,000

8,80,000

29,20,000

Stock Reserve A/c

Rs Rs

To H.P Adjustment A/c

To Balance c/d

4,00,000

4,00,000

29,20,000

By Balance b/d

By H.P Adjustments A/c

4,00,000

4,60,000

29,20,000

Illustration: 8

Knight purchases a truck for Rs. 1, 60,000 from S. Waugh on 1.1.93 payment to be

made Rs. 40,000 down and Rs. 46,000 at the end of first year. Rs. 44,000 at the end of second

year and Rs. 42,000at the end of third year. Interest was charged at 5%. Knight depreciates the

truck at 10% per annum on written down value method.

Knight, after having paid down payment and first installment at the end of the first year,

could not pay spending Rs. 4,000 on repairs of the asset, sold it away for Rs.91, 500.

Give journal entries and ledger accounts in the books of both the parties.

48

Calculation of Interest

No .of installment Total cash price

paid Rs.

Inst. paid Interest paid Net Cash

price paid

Rs.

Down

1st inst.

2nd inst.

3rd inst.

1,60,000

40,000

1,20,000

40,000

80,000

40,000

40,000

40,000

Nil

40,000

46,000

44,000

42,000

1,72,000

-

[1,20,000 × 5%] 6000

[80,000 × 5%] 4000

[42,000 -40,000] 2000

____

12,000

40,000

40,000

40,000

40,000

1,60,000

Ledger Account in the books of S. Waugh Knight A/c

Rs Rs

1.1.93

31.12.93

1.1.94

31.12.94

To Hire sales

To interest

To balance b/d

To interest

1,60,000

6,000

1,66,000

80,000

4,000

84,000

1.1.93

31.12.93

31.12.94

By Bank (down

payment)

By Bank (1st )

By balance c/d

By Repossessed

Stock A/c(bal.fig)

(transfer)

40,000

46,000

80,000

1,66,000

84,000

84,000

Repossessed Stock A/c

Rs Rs

31.12.94

31.12.94

To cash A/c

To Knight A/c

To P & L A/C

(bal.fig) (Profit on

sale)

4,000

84,000

3,500

91,500

31.12.94 By Cash 91,500

91,500

49

Ledger A/c’s in the books of Knight Truck A/c

Rs Rs

1.1.93

1.1.94

To Hire vender A/c

To balance b/d

1,60,000

1,60,000

1,44,000

1,44,000

31.12.93

31.12.93

By Depreciation

A/c

By balance c/d

By Depreciation

A/c

By S. Waugh A/c

By P & L A/c

(bal.fig)

16,000

1,44,000

1,60,000

14,400

84,000

45,600

1,44,000

S .Waugh A/c

Rs Rs

1.1.93

31.12.93

31.12.94

To Bank A/c

To Bank A/c (1st)

To balance c/d

To Track A/c

(bal.fig) (transfer)

40,000

40,000

40,000

1,66,000

84,000

84,000

1.1.93

31.12.93

1.1.94

31.12.94

By Truck A/c

By Interest A/c

By balance b/d

By Interest A/c

1,60,000

6,000

1,66,000

80,000

4,000

84,000