SUPPORTING TRUSTED DATA EXCHANGES IN COOPERATIVE INFORMATION SYSTEMS

Upload

khangminh22Category

view

4download

0

Vol. 15 No. 10 • October 2012 The Newspaper of the New York State Society of Certified Public Accountants www.trustedprofessional.com

Trusted Professionalhe

President’s Commentary .....2Newsmaker .........................3Industry ..............................7Tech..................................12

Chapter News....................24 FAE Listings ......................27Classifieds ........................30NYSSCPA

n e w y o r k s t a t e s o c i e t y o f

c e r t i fi e d p u b l i c a c c o u n t a n t s

www.nysscpa.org

AdirondackManhattan/BronxMid Hudson

NassauRocklandSyracuse

CHAPTERS INSIDE:

See Breakfast Briefing, on page 4See Fiduciary, on page 4

BY CHRIS GAETANOTrusted Professional Staff

Though the Patient Protection and Affordable Care Act(PPACA) was signed into law in 2010, many of its moresweeping effects have yet to be implemented and,indeed, legal challenges made it uncertain whether

major parts of the act would be implemented at all. TheSupreme Court upheld the constitutionality of the reform act,for the most part, in June; however, GOP presidential candi-date Mitt Romney has promised to repeal the law if he is votedinto office. Whatever the outcome, the PPACA is leading tobig changes in many areas of the economy.

To assess how some of these changes may play out, theNYSSCPA convened a panel of experts during a Sept. 5 break-fast briefing entitled, “SCOTUS Approved: The AffordableCare Act―What It Means for Your Clients and Business.” Thepanel was moderated by Trudy Lieberman, contributing editorto the Columbia Journalism Review, and included NYSSCPAPast President and tax planning specialist David A. Lifson;Shawn J. Nowicki, director of health policy at the NortheastBusiness Group on Health; Les Funtleyder, president ofPoliwogg’s Investment Advisory Division; and Charles W. F.Bell, programs director for the Consumers Union, which pub-lishes Consumer Reports magazine.

One of the changes that will come with the implementa-tion of the health care law will be the introduction of a num-ber of new tax provisions, such as the increased Medicaretax on high earners. Among the first of new levies to be intro-duced, it will take effect Jan. 1, 2013, with single peoplemaking more than $200,000 and married couples makingmore than $250,000 seeing a .9 percent tax increase on theirwages, according to Nowicki.

However, not all of the act’s tax provisions occur in thefuture. Bell noted that the small business tax credits thatcame with the bill are available right now: Employers withunder 25 full-time employees with average annual wages of$50,000—not counting the wages of the owner or their fam-ily—can qualify for a credit of up to 35 percent, providedthat the employer pays at least 50 percent of his workers’premiums, Bell said. He brought up the case of a bagel shopowner from Utica, who utilized the act’s 35 percent tax cred-it to increase the contribution to his employees’ premiumsfrom 50 percent to 65 percent, as an example of the type ofsmall business that could benefit from this credit. However,while 81 percent of small businesses in New York state areeligible for the credit, fewer than expected have claimed it,mainly because they simply don’t know about it, he added.

Reflecting on the numerous tax provisions that will comewith the act, Lifson wondered whether the IRS, which has beencharged with overseeing many parts of the law’s implementa-tion, has the capacity to handle the responsibility. He said thatthe service’s staff has been working for two years on writingthe numerous regulations connected with the act, which takestime away from tasks such as answering matching notices.

For example, the IRS will also need to administer the newpremium tax credit in 2014, which facilitates the purchase of

Experts talkhealth reform atbreakfast briefing

NYSSCPA warnsagainst changing definition of ‘fiduciary’

Society weighs in on 3AICPA exposure drafts

NYSSCPA Past President David A. Lifson, left, addresses fellow panelists at the Society’s Sept. 5 breakfast briefing.

BY CHRIS GAETANOTrusted Professional Staff

T he NYSSCPA is urging Sen. Kirsten Gillibrand (D-N.Y.) to cosponsor a bill that would protect CPAsfrom being considered fiduciaries, that is, as someoneresponsible for the administration of property owned

by others, under the Employee Retirement Income SecurityAct (ERISA). The Society made its appeal in a letteraddressed to the senator on Aug. 16.

The bill, S.1232, was written in response to a proposedrule change from the Department of Labor (DOL) in 2010that would expand the definition of fiduciary to mean onewho provides investment advice to pension plans for a fee orother compensation. The DOL proposal is intended to pro-tect plans, participants and beneficiaries from conflicts ofinterest, according to a press release issued at the time. Thedepartment has argued that the current rules inappropriatelylimit its ability to do so.

The Society’s letter, however, warned that this might holdnegative consequences for CPAs because their valuationactivities in service of employee stock ownership planswould cause them to fall under the definition of a fiduciary,which would lead to a shift in the fundamental nature oftheir activities with such plans.

“CPAs would be required to abandon the current purposeof their appraisal–attempting to find the most likely fair mar-

BY CHRIS GAETANOTrusted Professional Staff

T he NYSSCPA expressed its general support for a seriesof AICPA proposals regarding audit data, the simplifica-tion and clarification of compilation and review stan-dards, and the association’s ethics standards, in three

comment letters published in August and September.The letter regarding ethics standards, which was drafted

by the Society’s Professional Ethics Committee, was inresponse to the AICPA exposure draft Proposed Revised andNew Interpretations and Proposed Deletion of EthicsRulings, which was released in June. The draft is intended to address a perceived inconsistency within Interpretation101-3, regarding the independence of the CPA.

Specifically, the AICPA is proposing to add a provision toits ethics rules that would emphasize how providing multiplenon-attest services to a client could increase the significance ofthreats to independence, even if each individual service doesnot, itself, impair independence. The NYSSCPA, in its com-ment letter, expressed support for this addition, agreeing thatthe cumulative effect of providing multiple non-attest servicescan be problematic with regards to independence if there arenot multiple safeguards to eliminate or reduce such a threat.

For example, the letter said, if a CPA provides multiple non-attest services to an attest client, it could be construed that theattest client has a dependency on the CPA. Conversely, basedon the aggregation of non-attest fees, a CPA may lose or maybe perceived to lose his or her objectivity.

“If the practitioner provides too many permissible nonattestservices, the cumulative effect may cross the line in the eyes of

See AICPA, on page 4

Society leaders met in Albany duringSeptember for the NYSSCPA’s firstannual Governance Forum. As afocused event attending to the busi-

ness of running the Society, the GovernanceForum brought together members of our Boardof Directors, FAE trustees, chapter president-elects and Political Action Committee trustees.By consolidating these important face-to-facemeetings into two days, we were able toachieve significant cost savings and also createa streamlined and efficient program, allowingattendees to exchange ideas and build a rap-port with one another through networkingopportunities and targeted work sessions.

Attendees were armed with information onupcoming legislative issues the Society will beaddressing, and resources to bring back tomembers at home. Incoming chapter presi-dents-elect received tips on chapter businessfrom NYSSCPA President-elect J. MichaelKirkland; learned how to run a chapter boardfrom past chapter presidents Greg Altman andBarbara Marino; and picked up some lessonson leadership from Marilyn Pendergast, a

past president of theNYSSCPA.

The forum also fea-tured an enhanced focuson the importance of the NYSSCPA’s PoliticalAction Committee, whichallows the collective voiceof the NYSSCPA to beheard in Albany. (Formore information on thePAC, talk to your chaptertrustee, listed on the nyss-cpa.org website under theGovernment Affairs tab.)Of particular value wasthe opportunity to con-nect the dots on how sup-porting our PAC speaks toleaders in Albany, not only with respect toannual donations but—more importantly—in regard to overall constituency representa-tion. To that end, we had an opportunity tocollect funds for the PAC. I would like tothank all who contributed and ask that all

Society leaders considermaking such a contribution.

The forum was also atime for the Board ofDirectors to take criticalvotes that moved importantSociety issues forward,including adoption of formalresolutions accepting thecombined audited financialstatements for the fiscal yearending May 31, 2012. In itsindependent auditors report,the NYSSCPA’s auditor,Friedman LLP, stated thatthe combined financialstatements were, in all mate-rial respects, fairly present-ed. The board also approved

a new government relations plan and author-ized Executive Director Joanne S. Barry tonegotiate lease transactions on behalf of theboard, in order to facilitate the organiza-tion’s relocation in August 2013; you will bereading more about these critical votes in the

next issue of The Trusted Professional.Following an open Board meeting, membersobserved proceedings and were able to takeadvantage of the opportunity to share ques-tions and concerns they had, although com-munications with Society leadership canoccur at any time through your chapter andcommittee leaders, or me. My email addressis listed below.

Throughout the forum, I was reminded ofwhat can be accomplished in an atmosphereof trust, mutual respect and shared commit-ment to a common cause. I was also remind-ed of why the Society has been able to makesuch tremendous gains over the past fewyears, when a difficult economy has crippledother organizations: because our leaders arededicated to representing our members andthe public we serve.

2 www.trustedprofessional.comOPINIONThe Trusted Professional / October 2012

PRESIDENTGail M. Kinsella, CPA

PRESIDENT-ELECTJ. Michael Kirkland, CPA

SECRETARY/TREASURERScott M. Adair, CPA

VICE PRESIDENTSSherry L. DelleBovi, CPADavid Evangelista, CPASuzanne M. Jensen, CPAAnthony J. Maltese, CPA

EXECUTIVE DIRECTORJoanne S. Barry

DIRECTOR OF COMMUNICATIONS

Colleen Lutolf

EDITORNicole Saunders

STAFF WRITERChris Gaetano

COPY EDITORSGene Cioffi

Christopher Davis

EDITORIAL ASSISTANTAnna Rakovsky

ART DIRECTORLarry E. Matthews

GRAPHIC DESIGN Sara Gold

GRAPHIC DESIGN MANAGERErnesto Darío Lara

Permission to reprint The Trusted Professional articles is grantedwith few exceptions. Written requests indicating title, author, pub-lication date and intended use of the reprint should be made priorto each use by contacting the editor at 3 Park Avenue, New York,NY 10016-5991, 212-719-8321, or [email protected].

Views expressed in articles printed in The TrustedProfessional are the authors’ only and are not to be attributed to the publication, its editors, theNYSSCPA or FAE, or their directors, officers, oremployees, unless expressly so stated. Articles contain information believed by the authors to beaccurate, but the publisher, editors and authors arenot engaged in rendering legal, accounting or otherprofessional services. If specific professional adviceor assistance is required, the services of a competentprofessional should be sought.

T he New York State Society of CPAs and The TrustedProfessional greatly value editorial contributionsfrom our members, readers and those affiliated withthe accounting profession. Additionally, we are

happy to publish pertinent ads and notices. To ensure thateach issue of The Trusted Professional is distributed on atimely basis, we have issued the following deadlines bywhich such materials must be received:

December issue—October 29

January issue—November 26

February issue—December 26

For more information on submitting an article, email [email protected].

To update subscription information, contact MemberServices at 800-633-6320.

The Trusted Professional (USPS 017-482) is published on the 1st of each month, by the New York State Society of Certified Public Accountants, 3 Park Avenue, New York,NY 10016-5991. Copyright © 2012 by the New York State Society of Certified Public Accountants. The NYSSCPA retains the copyright on all material. Subscription Rate:members $15, nonmembers $20. Periodicals postage paid at New York, N.Y., and additional mailing offices. POSTMASTER: Send address changes to The TrustedProfessional, 3 Park Avenue, New York, NY 10016-5991, Attn: Subscription Department.

Trusted Professionalhe

PRESIDENT’S COMMENTARY

Are you an NYSSCPA member interested in writing for The Trusted Professional?

No matter what your practice area, The Trusted Professional might be interested in publishing your work. All published stories

should be between 700 and 1,500 words in length and must follow Associated Press—not academic—style guidelines. Submitted

stories should be geared toward the education and general interests of the readership. Articles written to sell a service or to

promote a business or office will not be considered. Final acceptance of material submitted for publication is at the editor’s

sole discretion. Interested members should email Nicole Saunders at [email protected] for more information.

Interested in Writing for The Trusted Professional?

Gail M. Kinsella

Governance Forum: Leadership in Action

www.trustedprofessional.com 3The Trusted Professional / October 2012

❖

Risk ManagementHow to handle a nonpaying client

Page 11

❖

TechKeeping sensitive documents

out of the wrong hands

Page 12

❖

Career

Positioning yourself for a promotion

Page 13

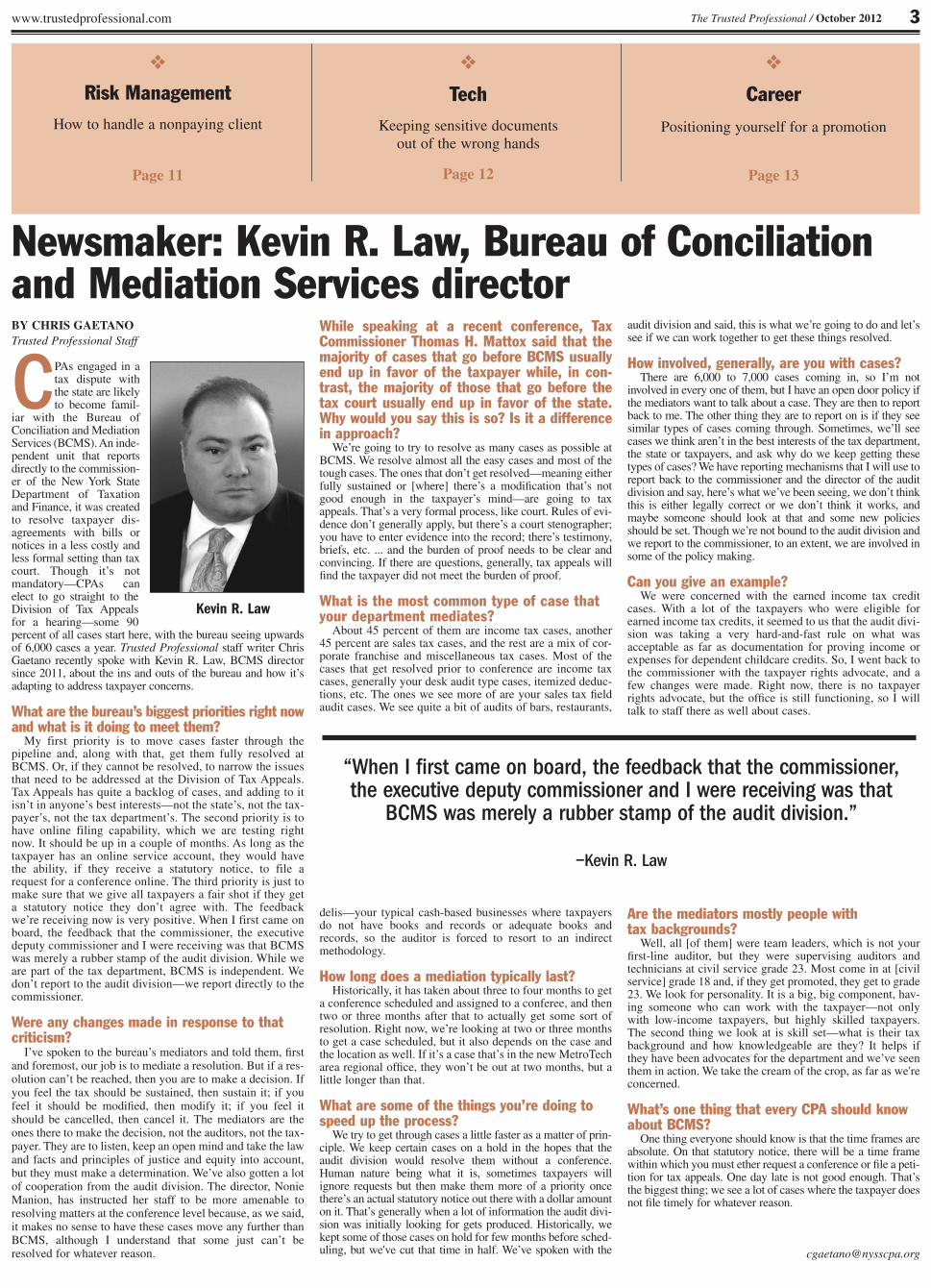

BY CHRIS GAETANOTrusted Professional Staff

CPAs engaged in atax dispute withthe state are likelyto become famil-

iar with the Bureau ofConciliation and MediationServices (BCMS). An inde-pendent unit that reportsdirectly to the commission-er of the New York StateDepartment of Taxationand Finance, it was createdto resolve taxpayer dis-agreements with bills ornotices in a less costly andless formal setting than taxcourt. Though it’s notmandatory—CPAs canelect to go straight to theDivision of Tax Appealsfor a hearing—some 90percent of all cases start here, with the bureau seeing upwardsof 6,000 cases a year. Trusted Professional staff writer ChrisGaetano recently spoke with Kevin R. Law, BCMS directorsince 2011, about the ins and outs of the bureau and how it’sadapting to address taxpayer concerns.

What are the bureau’s biggest priorities right nowand what is it doing to meet them?

My first priority is to move cases faster through thepipeline and, along with that, get them fully resolved atBCMS. Or, if they cannot be resolved, to narrow the issuesthat need to be addressed at the Division of Tax Appeals.Tax Appeals has quite a backlog of cases, and adding to itisn’t in anyone’s best interests—not the state’s, not the tax-payer’s, not the tax department’s. The second priority is tohave online filing capability, which we are testing rightnow. It should be up in a couple of months. As long as thetaxpayer has an online service account, they would havethe ability, if they receive a statutory notice, to file arequest for a conference online. The third priority is just tomake sure that we give all taxpayers a fair shot if they geta statutory notice they don’t agree with. The feedbackwe’re receiving now is very positive. When I first came onboard, the feedback that the commissioner, the executivedeputy commissioner and I were receiving was that BCMSwas merely a rubber stamp of the audit division. While weare part of the tax department, BCMS is independent. Wedon’t report to the audit division—we report directly to thecommissioner.

Were any changes made in response to thatcriticism?

I’ve spoken to the bureau’s mediators and told them, firstand foremost, our job is to mediate a resolution. But if a res-olution can’t be reached, then you are to make a decision. Ifyou feel the tax should be sustained, then sustain it; if youfeel it should be modified, then modify it; if you feel itshould be cancelled, then cancel it. The mediators are theones there to make the decision, not the auditors, not the tax-payer. They are to listen, keep an open mind and take the lawand facts and principles of justice and equity into account,but they must make a determination. We’ve also gotten a lotof cooperation from the audit division. The director, NonieManion, has instructed her staff to be more amenable toresolving matters at the conference level because, as we said,it makes no sense to have these cases move any further thanBCMS, although I understand that some just can’t beresolved for whatever reason.

While speaking at a recent conference, TaxCommissioner Thomas H. Mattox said that themajority of cases that go before BCMS usuallyend up in favor of the taxpayer while, in con-trast, the majority of those that go before thetax court usually end up in favor of the state.Why would you say this is so? Is it a differencein approach?

We’re going to try to resolve as many cases as possible atBCMS. We resolve almost all the easy cases and most of thetough cases. The ones that don’t get resolved—meaning eitherfully sustained or [where] there’s a modification that’s notgood enough in the taxpayer’s mind—are going to taxappeals. That’s a very formal process, like court. Rules of evi-dence don’t generally apply, but there’s a court stenographer;you have to enter evidence into the record; there’s testimony,briefs, etc. ... and the burden of proof needs to be clear andconvincing. If there are questions, generally, tax appeals willfind the taxpayer did not meet the burden of proof.

What is the most common type of case thatyour department mediates?

About 45 percent of them are income tax cases, another45 percent are sales tax cases, and the rest are a mix of cor-porate franchise and miscellaneous tax cases. Most of thecases that get resolved prior to conference are income taxcases, generally your desk audit type cases, itemized deduc-tions, etc. The ones we see more of are your sales tax fieldaudit cases. We see quite a bit of audits of bars, restaurants,

delis—your typical cash-based businesses where taxpayersdo not have books and records or adequate books andrecords, so the auditor is forced to resort to an indirectmethodology.

How long does a mediation typically last? Historically, it has taken about three to four months to get

a conference scheduled and assigned to a conferee, and thentwo or three months after that to actually get some sort ofresolution. Right now, we’re looking at two or three monthsto get a case scheduled, but it also depends on the case andthe location as well. If it’s a case that’s in the new MetroTecharea regional office, they won’t be out at two months, but alittle longer than that.

What are some of the things you’re doing tospeed up the process?

We try to get through cases a little faster as a matter of prin-ciple. We keep certain cases on a hold in the hopes that theaudit division would resolve them without a conference.Human nature being what it is, sometimes taxpayers willignore requests but then make them more of a priority oncethere’s an actual statutory notice out there with a dollar amounton it. That’s generally when a lot of information the audit divi-sion was initially looking for gets produced. Historically, wekept some of those cases on hold for few months before sched-uling, but we've cut that time in half. We’ve spoken with the

audit division and said, this is what we’re going to do and let’ssee if we can work together to get these things resolved.

How involved, generally, are you with cases? There are 6,000 to 7,000 cases coming in, so I’m not

involved in every one of them, but I have an open door policy ifthe mediators want to talk about a case. They are then to reportback to me. The other thing they are to report on is if they seesimilar types of cases coming through. Sometimes, we’ll seecases we think aren’t in the best interests of the tax department,the state or taxpayers, and ask why do we keep getting thesetypes of cases? We have reporting mechanisms that I will use toreport back to the commissioner and the director of the auditdivision and say, here’s what we’ve been seeing, we don’t thinkthis is either legally correct or we don’t think it works, andmaybe someone should look at that and some new policiesshould be set. Though we’re not bound to the audit division andwe report to the commissioner, to an extent, we are involved insome of the policy making.

Can you give an example? We were concerned with the earned income tax credit

cases. With a lot of the taxpayers who were eligible forearned income tax credits, it seemed to us that the audit divi-sion was taking a very hard-and-fast rule on what wasacceptable as far as documentation for proving income orexpenses for dependent childcare credits. So, I went back tothe commissioner with the taxpayer rights advocate, and afew changes were made. Right now, there is no taxpayerrights advocate, but the office is still functioning, so I willtalk to staff there as well about cases.

Are the mediators mostly people with tax backgrounds?

Well, all [of them] were team leaders, which is not yourfirst-line auditor, but they were supervising auditors andtechnicians at civil service grade 23. Most come in at [civilservice] grade 18 and, if they get promoted, they get to grade23. We look for personality. It is a big, big component, hav-ing someone who can work with the taxpayer—not onlywith low-income taxpayers, but highly skilled taxpayers.The second thing we look at is skill set—what is their taxbackground and how knowledgeable are they? It helps ifthey have been advocates for the department and we’ve seenthem in action. We take the cream of the crop, as far as we'reconcerned.

What’s one thing that every CPA should knowabout BCMS?

One thing everyone should know is that the time frames areabsolute. On that statutory notice, there will be a time framewithin which you must ether request a conference or file a peti-tion for tax appeals. One day late is not good enough. That’sthe biggest thing; we see a lot of cases where the taxpayer doesnot file timely for whatever reason.

Newsmaker: Kevin R. Law, Bureau of Conciliationand Mediation Services director

“When I first came on board, the feedback that the commissioner,the executive deputy commissioner and I were receiving was that

BCMS was merely a rubber stamp of the audit division.”

–Kevin R. Law

Kevin R. Law

plans bought on the health insurance exchangesthat, as part of the act, are to be set up through-out the country starting that same year,Nowicki said. The exchanges are meant to be aone-stop shop for buying health insurance,which allows consumers to make comparisonsbetween plans so as to encourage competitionbetween companies and creates a single riskpool for individual and small group markets.Nowicki pointed out that the exchanges are acenterpiece of health reform, and while theywill initially only be open to small groups—those with 1 to 100 employees—in 2017, larg-er groups will be able to access them as well.

Some states are already working on settingup their exchanges. Connecticut has the mostadvanced exchange in the country so far,Nowicki said, having set it up more than a yearago as an active purchaser that will negotiate toget high-quality and low-cost plans.Connecticut has already hired staff, but stillneeds to do a lot of the policy and businessprocess work before opening next year for itstest launch. New York state established its ownexchange, housed in its Department of Health,

through executive order during the 2012–2013budget cycle after legislation doing so stalled incommittee, though much work is still requiredfor implementation, such as hiring staff, build-ing the information technology infrastructure,and applying for federal exchange certification.New Jersey, Nowicki added, is at a standstill:While the executive branch is studying the proj-ect, legislation that would formally establishthe exchange was vetoed by the governor thispast May.

While one audience member noted that,except for the past year, health care costs haveonly been increasing since the passage of thelaw, Bell said that small businesses may seebenefits in a reduction in administrative costsassociated with maintaining a health care ben-efits package program for their employees.

“This could provide relief of the adminis-trative burden for small businesses withfewer than 10 employees,” he said, addingthat the exchanges could provide “de factoHR services for them.”

Beyond taxes and exchanges, the reform actwill also have an impact on the industry itself,

said Funtleyder. Since the Supreme Courtdecision, he said, there have already been threemajor mergers and acquisitions in the healthcare industry, and this is likely to continue;while it’s not strictly on account of the reformact, he said that it has accelerated the process.Part of this is because, as time goes on, com-panies will need to get bigger. This means thatone of the big winners of this process will beHMOs, he said, noting that someone is goingto have to control costs in the face of far morepatients entering the system. He pointed outthat the losers, on the other hand, will be thephysicians, due to changes in the Medicarereimbursement rates, as well as pharmacies,medical device manufacturers and testing lab-oratories, because the impression people haveis that there is too much costly testing in thesystem right now.

Less clear, he said, are how things willwork out for small businesses, due to thetaxes and penalties that are matched withlower premiums, theoretically, as well as hos-pitals, who will have more patients but willalso be more tightly regulated and controlled.

The full impact of the health care reformlaw remains to be seen, Lifson said.

“Things could change,” Lifson said.“There are some things in this law that couldlead to negotiation at a later date.”

“In the meantime, CPAs and advisers willneed to create links with subject matterexperts to navigate this responsibility,” hesaid, in much the same way as a practitionermight reach out to a LIFO (last-in, first-out)expert if she takes on an auto dealer as aclient. Bell agreed, saying that people needto get the word out about programs like thesmall business tax credit, which, he added,not enough people know about.

Lifson encouraged anyone who wants acomprehensive summary of the PPACA’s tax provisions to log onto the IRS’sAffordable Care Act Tax Provisions page atwww.irs.gov/uac/Affordable-Care-Act-Tax-Provisions.

Breakfast Briefing

4 www.trustedprofessional.comFROM THE COVEROctober 2012 / The Trusted Professional

FiduciaryContinued from page 1

Continued from page 1

ket value—and adopt a new purpose—deter-mining the value that most favors the benefi-ciaries of the plan,” NYSSCPA PresidentGail Kinsella said in the letter.

This, in turn, would contradict the AICPA’sCode of Professional Conduct, as well as theNYSSCPA’s, which requires that a CPA be“impartial, intellectually honest, disinterestedand free from conflicts of interest.”

The NYSSCPA has plans to eventuallyadopt the AICPA’s code of conduct, howev-er; currently, the NYSSCPA’s code has veryfew differences from that of the AICPA.

The two-page S.1232 bill, which was intro-duced in June 2011, would exclude from theexpanded definition of fiduciary anyone whoprovides appraisal or fairness opinions withrespect to qualifying employer securities includ-ed in an employee stock ownership plan. In itsletter, the NYSSCPA said that the DOL shouldalso require plans to hire only qualified valua-tion analysts with requisite training and creden-tials, as well as mandate the use of professionalstandards, which would be more cost-effective.

The bill is currently being considered bythe Senate Committee on Health, Education,Labor and Pensions.

a reasonable person,” said Sal Collemi, a mem-ber of the Professional Ethics Committee andone of the letter’s principal authors. “We hopeto give our practitioners as much consistency,clarity and guidance as possible by providingexamples within the Code.”

The AICPA also proposed in this expo-sure draft that financial statement prepara-tion and cash-to-accrual conversions per-formed by an AICPA member for a client beconsidered non-attest services, regardless ofwhether the services are performed as part ofan audit. The NYSSCPA agreed with thispoint in its comment letter.

In response to potential impediments toauditor independence posed by management,the AICPA proposal suggests that membersevaluate the significance of management par-ticipation threat created by performing separateevaluations of a client’s internal control system,and examine how ongoing monitoring proce-dures that are management’s responsibilitycould impair independence, an idea that, again,the NYSSCPA supported.

Requesting additional guidanceThough the NYSSCPA expressed its gen-

eral support for another of the AICPA’s pro-posed standards, Association WithUnaudited Financial Statements andCompilation of Financial Statements, it alsosuggested the AICPA clarify some areas thatseemed insufficient or unclear. The exposuredraft—released to the public June 29, andmeant to bring clarity and simplification toaccounting and review standards by makingthem easier to read, understand and apply—does not include specific application guid-ance with respect to governmental entitiesand smaller, less complex entities.

The changes the AICPA has proposed inthe draft include a clarification that financialstatement preparation is a non-attest service;clarification that a CPA should exercise aprofessional judgment in the performance ofa compilation engagement; a requirementthat the engagement letter be signed by boththe CPA or CPA’s firm and management orthose charged with governance; a stipulationthat the CPA consider the effects of addi-tional or revised information on the financial

statements, including whether they are mate-rially misstated; and a requirement thatheadings throughout the compilation reportclearly distinguish report sections.

The draft also proposes requiring CPAs toinclude other-matter paragraphs in their compi-lation reports on financial statements that referto required supplementary information whenthey have unresolved doubts about whether therequired supplementary information is present-ed in accordance with prescribed guidelines orhas departed from prescribed guidelines entire-ly, as well as when some or all of that informa-tion is omitted or has been uncompiled, unre-viewed or unaudited. Required supplementaryinformation is defined in the proposal as infor-mation that a designated accounting standardsetter requires to accompany an entity’s basicfinancial statements.

The AICPA also suggests that entities indi-cate a financial statement was not compiled,reviewed or audited by noting this on each pageof the financial statement, or attaching a reportto unaudited financial statements explicitly say-ing so. The NYSSCPA, in a comment letter pre-pared by the Accounting and Review ServicesCommittee, said that the understanding betweenthe accountant and client in the area of uncom-piled financial statements needs to be docu-mented, but recommended that additionalrequirements to obtain an engagement letterdesigned for the type of engagement be added.

“The engagement letter, if required,should include a client’s acknowledgementthat an accountant will not report on thefinancial statements and a disclaimer on thereport to be issued,” the Society wrote.

The NYSSCPA also suggested that thefinal proposal include additional guidance toclarify the difference between “materialinconsistencies” and “material misstate-ments” on financial statements, saying thatwhile people understand the origin of theseconcepts, there needs to be further elabora-tion to distinguish one from the other.

The Society also asked for additionalguidance regarding the draft’s directives forCPAs who believe a financial statement maybe materially misstated. Existing literature,specifically paragraph 13 of AR section 80,says that in circumstances where the CPA

believes that the financial statements may bematerially misstated, he or she should obtainadditional or revised information. However,when taken with the draft, which would alsorequire that those CPAs obtain additional orrevised information and then consider itseffects, “it gives the impression of a loopprocess,” the Society said. “We do not feelparagraphs A18 and A19 are providing anyproper guidance or explanations. Additionalguidance is needed on the purpose to be con-veyed or a re-writing that will convey moreclearly the message of the standard-setter.”

In addition, the proposal says that account-ants should possess or obtain an understandingof the industry in which the reviewed entityoperates, which includes knowing the account-ing principles and practices generally used inthat industry. The comment letter suggested astronger wording, changing “should” to “must,”but also noted that this seems self-evident, as itis unclear how a practitioner would be able towork effectively without one.

Audit data standardsMeanwhile, the NYSSCPA’s Technology

Assurance Committee had a number of sugges-tions for an AICPA exposure draft on audit datastandards. The proposed standard, released tothe public on July 18, is the first that the AICPAhas drafted concerning the use of informationtechnology during the course of an audit.

The proposed standard itself covers anumber of technical areas, such as the for-mat in which such data is compiled (eitherXBRL GL or flat file format), user informa-tion within the data (every systems usershould have a full name, title, and role, ifavailable, within the system), and what testsshould be performed on extracted data,among many other points. The NYSSCPAapplauded the AICPA for turning its atten-tion to audit data standards, in a commentletter published on Sept. 5.

“The advances in technology in auditing cre-ated a growing need for this Audit DataStandard. So the AICPA’s response—by way ofthis exposure draft—is both timely and rele-vant,” said Yigal Rechtman, a member ofNYSSCPA’s Technology Assurance Commi-ttee and the letter’s principal author.

AICPA Continued from page 1

However, the letter also noted that there areseveral areas where the standard could beimproved. For example, audit data should notcontain the breadth of internal user informationadvocated by the proposed standard, as it couldleave people open to risks of identity theft.Conversely, the Society suggested that the stan-dards include a type of record that identifies afile as associated with integrated testing facili-ties, a method of continuous auditing. The let-ter also said there should be a field to contain aserial number of the journal entry and a date-posted field.

BY CHRIS GAETANOTrusted Professional Staff

Just in time for the final deadline of taxseason, the IRS has unveiled the latestincarnation of its website, IRS.gov,with features the agency said had been

designed to better reflect how people typi-cally use the site, as well as deliver servicesat a faster pace.

The changes are part of an estimated$320 million the IRS intends to spend on itswebsite over the next decade. According to aU.S. Government Accountability Office(GAO) report released last December enti-tled, “2011 Tax Filing: Processing Gains,but Taxpayer Assistance Could Be Enhancedby More Self-Service Tools,” use of IRS.govhas grown significantly over the past fewyears: The site recorded 250 million visits in2011, vs. 168 million visits in 2007. Yet, thenumber of searches tripled in that time, from106 million to 312 million, in part becausetaxpayers had such difficulty locating infor-mation, the report said. Having an easilysearchable website is important for the IRSbecause it reduces the number of phone callsthe agency receives, the report added.

As part of the new rollout, the site fea-tures a rearranged menu that provides easieraccess to what analyses have determined arethe most used features—information about

filing, payments, refunds, credits and vari-ous forms. It will also offer a variety ofonline tools to help people interact with theIRS. The lineup of those tools, according toan IRS press release, will regularly changein order to coincide with filing and registra-tion due dates, as well as new programs andsystem enhancements.

In addition, the revamped site includessocial media functionality, which will allowthe IRS to share the latest information on taxchanges, initiatives, products and services,and will feature YouTube videos, Twitterupdates and podcasts. It also has non-English support on each of its pages forspeakers of Spanish, Chinese, Korean,Vietnamese and Russian.

The GAO report criticized the IRS’sonline strategy for not allowing taxpayers to

access account information, but that compo-nent remains unchanged with the redesign.

Several Society members said they wereexcited by the ease in navigation that therevamped website offers, including DavidSands, a member of the Tax DivisionOversight Committee. Sands said he’dthought that that the older version had been“a little behind the times,” as it didn’t pro-vide as many options on a page and requireda number of clicks to get through.

“I like that it brings you a lot more quicklyto the area you’re looking for … so that youdon’t have to drill down as much, and that itgets to the most frequent issues that needanswers,” he added.

Still, Jeffrey Gold, chair of the NewYork, Multistate and Local TaxationCommittee, pointed out that the transition

hasn’t been completely seamless, notingthat, as of press time, some links, such as“Pros,” go to different pages depending onwhether one clicks the screen or uses thedrop-down menu. He also noted that thesearch function is still difficult to navigateand not very intuitive. The IRS has said thatthe site’s search capabilities will evolve asit is used more, and the agency identifiescontent to tag and deliver in search results.

Gold also advised that people update theirbookmarks to correspond to the new site, asthe transition to the website might causethem to be out-of-date.

IRS unveils a more user-friendly website

www.trustedprofessional.com 5TAXATION The Trusted Professional / October 2012

DO YOU CONSIDER THE NEW IRS SITE TO BE AN IMPROVEMENT?

Tweet us about it, @nysscpa.

JOIN THE CONVERSATION.

FAE 2012 Conferences

FAEf o u n d a t i o n f o r a c c o u n t i n g

e d u c a t i o n

For More Information and to Register for This Conference: Visit www.nysscpa.org/nytax or call 800-537-3635.To Register for the Live Video Webcast: Visit www.nysscpa.org/e-cpe or call 877-880-1335.FAE

YEARS 1972-2012

Your Partner in Educational Excellence

40

New York State Taxation Conference

■ Tax Preparer Responsibility■ New York State Residency Audit Guidelines■ Business and Sales Tax Nexus■ Combined/Unitary Reporting

Wednesday, December 5, 2012Doubletree by Hilton Metropolitan Hotel569 Lexington Avenue, at 51st StreetNew York, NY 100228:00 a.m.–5:00 p.m.

Stay on top of the latest tax preparation and planning developments to best serve your clients or company

This is an FAE Paperless Event. Visit www.nysscpa.org for more information.

HOT TOPICS

■ Thomas H. Mattox, Commissioner, New York State Department of Taxation and Finance

FEATURING:REGISTRATION DETAILS:

Course Code: 25612311 (In-Person)CPE Credit Hours: 8

Field of Study: TaxationIn-Person Member Fee: $385

Nonmember Fee: $510

CAN’T ATTEND THE EVENT IN PERSON? Experience the same great speakers and topics directly from your computer.

Course Code: 35612311 (Live Video Webcast) CPE Credit Hours: 8

Field of Study: TaxationLive Webcast Member Fee: $285

Nonmember Fee: $410

BY RICHARD J. KORETOTrusted Professional Correspondent

T he New York State Department ofTaxation and Finance (NYSDTF)recently announced three proposalsand two adoptions on a wide range of

tax issues, including fuel use tax regulations,real property tax administration, franchisetaxes and hotel use. For the proposals, thedepartment is inviting commentary frominterested parties through October; sum-maries of the proposals as well as instruc-tions for commenting by email or by printedletter are available at www.tax.ny.gov/rulemaker.

The end of the one-week ruleIn this proposal, the state is suggesting the

elimination of a one-week stay test that wasused as one of the factors to determinewhether the rental of a bungalow or similarliving unit was subject to sales tax, accord-ing to a description on the NYSDTF’s site.As the department’s summary says, previ-ously, a one-week test was used to determinewhether the rental of a bungalow or similarliving unit was essentially a “hotel occu-pancy” and, thus, subject to sales tax, or wasto be considered the rental of real property,which is not subject to sales tax.

Earlier, a Division of Tax Appeals admin-istrative law judge had struck down this test,

and the department decided not to fight it butto incorporate the change into state tax law.(Visit our website, www.nysscpa.org/trustedprof, for more on this ruling.) This proposalis open for comments, but the summarynotes that objections are not expected“because it merely repeals a regulatory pro-vision that is no longer applicable to anyperson. …”

Leo Parmegiani, a member of theHospitality Industry Committee, said thatthe ruling and regulation had to do with theline drawn between a rental space and ahotel space, which was why there had beena cutoff when it came to differentiatingbetween the two. While he wasn’t certainwhat the effects of the proposal would be, hesaid that it would ease one more administra-tive burden on the hotel industry.

“It’s a policy to administer. … The stateforces you to collect it until that time framepasses, then it becomes a credit,” he said.

The NYSDTF is also using this opportu-nity to make the regulatory language morepolitically correct: References to hotel“maid services” are being changed to thegender-neutral “housekeeping services.”

Real property: new administrativechanges adopted

According to the NYSDTF’s summary,Part W of Chapter 56 of the Laws of 2010transferred various responsibilities relating

to real property tax administration from theNew York State Board of Real PropertyServices and the Office of Real Property TaxServices to the Commissioner of Taxationand Finance. Therefore, certain rules had tobe renumbered, obsolete references had tobe corrected and various other technicalchanges had to be made, according to thesummary.

Among the terms included in definitionchanges are “arm’s length transfer,” whichhas been changed to conform to currentforms and procedures, according to the sum-mary, as well as “certified counties” and“certified school districts.”

Franchise taxes: a technical mixThese proposed changes are a hodge-

podge of alterations. Some are mere coderenumberings with relatively minor techni-cal changes, but a few could be more signif-icant. The NYSDTF is proposing—

• to amend section 3-2.2 of the regula-tions to eliminate language relating to for-eign sales corporations (FSCs) because thecorresponding Internal Revenue Code provi-sions relating to FSCs have been repealed;

• to delete language which provides thata foreign corporation not subject to tax willnot be required to be included in a combinedreport unless inclusion is necessary to prop-erly reflect the tax liability of one or moretaxpayers in the group because of various

reasons, outlined in the regulations (anexample is given); and

• to add new language providing thatwhere a corporation’s taxable year differsfrom that of the taxpayer parent, the applica-ble taxable year to be included in the com-bined report is the taxable year that endswithin the taxable year of the taxpayer parent.

Fuel tax: adopted and proposedThese final and proposed changes relate

to the sales tax component and the compos-ite rate-per-gallon of the fuel use tax onmotor fuel and diesel motor fuel for the thirdquarter of 2012, as well as possible rates forthe fourth quarter.

The NYSDTF is keeping it simple: Theadopted rules for the third quarter show thatthere are no rate changes from the secondquarter, and the proposed rules for the fourthquarter show that the department is not plan-ning on changing them going forward either.However, anyone who disagrees with thelack of changes in the fourth quarter is wel-come to comment.

Hotels, property and fuel: new rules at the NYSDTF

6 www.trustedprofessional.comTAXATIONOctober 2012 / The Trusted Professional

FAE 2012 Conferences

FAEf o u n d a t i o n f o r a c c o u n t i n g

e d u c a t i o n

For More Information and to Register for This Conference: Visit www.nysscpa.org/banking or call 800-537-3635.FAE

YEARS 1972-2012

Your Partner in Educational Excellence

40

Banking Conference How major developments in accounting, auditing, andtax will impact banks and financial institutions

KEYNOTE ADDRESS: Benjamin M. Lawsky, Superintendent, NewYork State Department of Financial Services. Mr. Lawsky will sharehis unique perspective on recent updates in the banking environ-ment and will provide a look toward next year.

This is an FAE Paperless Event. Visit www.nysscpa.org for more information.

CONFERENCE INFORMATION

■ CFO/Presidents’ Panel: current concerns about future business■ Expert Panel on enterprise risk management■ Federal and state tax developments impacting the financial services industry■ And Much More!

OTHER HOT TOPICS INCLUDE:

Course Code: 25538311 (In-Person) 35538311 (Live Video Webcast)CPE Credit: 8 hours (6 Specialized Knowledge and Applications, 1 Auditing, 1 Taxation)

NYSSCPA Member Fee (by October 17)$305 (In-Person); $205 (Live Video Webcast)

Non-Member Fee: (by October 17)$430 (In-Person)$330 (Live-Video Webcast)

NYSSCPA Member Fee (after October 17): $335 (In-Person); $235 (Live Video Webcast)

Nonmember Fee:(after October 17): $460 (In-Person)$360 (Live Video Webcast)

Early Bird Discount - Save $30

Wednesday, November 14, 2012FAE Conference Center3 Park Avenue, at 34th Street 19th FloorNew York, NY 10016

BY CHRIS GAETANOTrusted Professional Staff

A pair of releases from the PublicCompany Accounting OversightBoard (PCAOB)—one a discussionpaper aimed at audit committees,

the other a standard aimed at auditors—looks to improve the quality of communica-tions between the two on both sides of theconversation.

The publications, “Information for AuditCommittees About the PCAOB InspectionProcess,” and the PCAOB’s AuditingStandard 16, Communications with AuditCommittees, were put out in August. Theformer presents audit committee memberswith a primer on topics and issues theymight wish to raise with auditors, while thelatter creates new rules for what auditorsmust communicate to audit committees.

“Communications between the auditorand the audit committee allow the auditcommittee to be well-informed aboutaccounting and disclosure matters, includingthe auditor’s evaluation of matters that aresignificant to the financial statements,” saidPCAOB board member Jeanette M. Franzelin a statement of support for the new stan-dard. “An informed and engaged audit com-mittee will be better equipped to execute itsoversight responsibilities.”

The Society voiced its own thoughts on thematter when the standard was first proposed.In a comment letter published on Feb. 28,2012 and drafted by members of the AuditingStandards, Stock Brokerage and SEC PracticeCommittee, it voiced overall support for theproposal, noting that “audit committees fulfillan important role in enhancing audit qualityand that this standard appropriately recog-nizes their contributions in this regard.”

On the auditor side, the new standard isthe result of years of deliberation and out-reach; it was first proposed in 2010 and thenreproposed in 2011. It defines what an auditcommittee actually is―a committee orequivalent body established by a company’sboard to oversee the accounting and finan-cial reporting process―and expands thenumber of points that an auditor is requiredto go over with that committee.

For example, under AU sec. 310, the audi-tor is required to establish an understandingwith the client regarding the services to beperformed. But under the new standard, theauditor must establish an understanding ofthe terms of the audit engagement itself withthe committee, and record them in anengagement letter.

The new standard also expands therequired communications outlined in AUsec. 380 by requiring the auditor to talk withthe committee about the company’s account-ing policies and practices, the quality of thecompany’s financial reporting, informationrelated to significant unusual transactionsand the business rationale behind them, andany identified concerns about significantaccounting or auditing matters that arisewhen management consults with anotheraccountant.

In addition, auditors are required to com-municate, among other things, an overviewof the overall audit strategy, informationabout the nature and extent of the special-ized skill needed in the audit, difficult or

contentious matters and other matters thatthe auditor deemed to be significant to theoversight of the financial reporting process.

Anthony S. Chan, past chair of the SECPractice Committee who also sits on itsPCAOB subcommittee, said the new stan-dard doesn’t represent a radical departurefrom what auditors have typically done inthe past. As a practical matter, he said, mostauditors already include such communica-tions in their quarterly discussions and com-munications with audit committees.

“For most auditors, it should not be a bigchange, as such communications have beenconducted informally and orally during thequarterly discussion with the audit commit-tee,” he said. “It has [just] been formalizedand will be evidenced in writing.”

Steven Kreit, who is also on the commit-tee and serves as an audit partner in his firm,made a similar assessment, noting that whatthe standard does is require that which hadbeen previously offered by auditors on a vol-untary basis. However, he said it will still behelpful, particularly for new audit commit-tee members who may not be as experiencedin interacting with auditors as some of theirmore seasoned colleagues.

“It [will] spur important conversationsbetween audit committees, the board and audi-tors,” he said. “That’s a positive [that] I don’tthink adds a significant burden to anyone. Soit’s a lot of good without a lot of bad.”

The exception, he said, is the requirementthat auditors discuss significant and unusualtransactions and the business rationalebehind them, which, he said, strays fromwhat the auditor’s role generally is. It is thecompany that determines the businessrationale, not the auditor, he pointed out.

“The auditor can certainly relay to theaudit committee what management has toldthem, but … there’s not really a lot there thatthe auditors can add insight into becausewe’re not part of the decision-makingprocess,” Kreit said. “So, that might be onearea where the PCAOB is asking auditors togo beyond the scope of what they had [done]in the past.”

Empowering audit committeesOn the audit committee side,

“Information for Audit Committees Aboutthe PCAOB Inspection Process” was intend-ed to be a primer for audit committee mem-bers on communicating with auditors, par-ticularly about the PCAOB inspectionprocess and their audit firms’ performancewithin it.

The document explains the nature of thePCAOB inspection process, including how itis performed and what the report on theinspection includes, and suggests possiblequestions that audit committee members canask the auditor about it. For example, it saysthat audit committee members can askwhether the PCAOB identified deficienciesin the audit process, whether the firm agreedwith the PCAOB’s findings, and if not, whyand what topics are included in the Part IIfindings.

The purpose of the document, PCAOBChair James R. Doty said in a press callwhen it was released, is to empower auditcommittee members, who have told thePCAOB that they desire more substantiveand complete discussion with their auditors,

but that because some information about theinspection findings are not made public,there can sometimes be confusion over whatcan and can’t be asked.

“This is a little different [from AuditingStandard 16 in that] this doesn’t require any-one to do anything; this is simply an infor-mation device which audit committee mem-bers may or may not think they need to takeadvantage of,” Doty said.

David M. Rubenstein, a member of theChief Financial Officers Committee, notedthat even though audit committees musthave at least one financial expert, not allfinancial experts have the same level ofknowledge. For example, he said, somemight do a lot of work in the tax area butmay not have as much experience withfinancial reporting, while others may havebeen retired for a while and aren’t up-to-dateon the latest rules and regulations. However,

Rubenstein added that there has been muchmore education of audit committees takingplace, and the release’s information regardingwhat audit committee members can discusswith their auditors is part of this overall effort.

“I think everyone’s trying to do the samething: They’re trying to get it right andthey’re trying to get the financial reportingand underlying systems of control in place,and better and better,” he said.

The new standard and related amend-ments, if approved by the Securities andExchange Commission, will be effective forpublic company audits of fiscal periodsbeginning after Dec. 15, 2012.

PCAOB looks to improve relations between audit committees and auditors

www.trustedprofessional.com 7INDUSTRY The Trusted Professional / October 2012

Upcoming Industry Committee Meetings

Banking Thurs., Oct. 11

Chief Financial Officers Wed., Oct. 31

Construction Contractors Thurs., Oct. 25

Entertainment, Arts and Sports Wed., Oct. 17

Fashion and Furnishings Tues., Oct. 23

Hospitality Industry Tues., Oct. 30

Internal Audit Tues., Oct. 2

Investment Companies Thurs., Oct. 25

Private Equity and Venture Capital Mon., Oct. 22

Real Estate Wed., Oct. 3

Small Business Outreach Wed., Oct. 17

Stock Brokerage Tues., Oct. 16

This is a partial listing, which is subject to change. For a complete and updatedlisting of meetings, visit www.nysscpa.org, click on “About Us,” and choose

“Committees” from the drop-down menu.

Interested in joining a committee? Fill out an application online or contactNereida Gomez, Manager, Committees and Administrative Services,

at 212-719-8358 or [email protected], to find out more information.

Upcoming Industry Conferences

Restaurant & Hospitality Breakfast Thurs., Oct. 4

CFOs, Controllers, and Financial Executives Wed., Oct. 10

Private Equity and Venture Capital Thurs., Oct. 25

Real Estate Wed., Oct. 31

BY CHRIS GAETANOTrusted Professional Staff

T hough the party was nice while it lasted,the days of 100 percent bonus deprecia-tion are over, and construction compa-nies need to know which expenditures

must now be capitalized during the course of business, according to Anthony F.Dannible, a speaker at the FAE’s ConstructionContractors Accounting, Consulting, andTaxation Conference held Aug. 9.

As a temporary measure to help spur eco-nomic activity, the government raised thebonus depreciation allowance from 50 percentto a full 100 percent, under the Tax Relief,Unemployment Insurance Reauthorization,and Job Creation Act of 2010. But when thatmeasure expired at the end of 2011, theallowance was cut back in half, “meaningmore work must now be done to capitalize anddepreciate,” said Dannible, a member of theClosely Held and S Corporations Committee.

“We’ve sort of been lulled asleep with the100 percent bonus depreciation. … Much ofthe new equipment [companies] got, [they]expensed, but now we’re in 2012 and it’s 50 percent this year,” he said.

What’s more, depreciation and capitaliza-tion rules are currently being governedunder a set of temporary IRS regulations thatwill expire in early 2014 but are significant

for the time being because they “change a lotof the [previous] concepts we’ve dealt with,”he added.

Many of the big changes affect what maybe counted as a unit of property, with individ-ual components of a structure now consideredwhole units in and of themselves, Danniblesaid. For example, while just a few years ago,

an entire building and everything within itwould collectively count as a single unit ofproperty—making things like construction,renovation and repair easier to expense—under the temporary regulations, a building’splumbing; heating, ventilation and air condi-tioning system; electric wiring; security sys-tem and gas distribution would all be brokenout as separate units of property.

Under the temporary regulations, ifexpenditures related to each of those indi-vidual units of property pass what Danniblereferred to as the “BAR” or “betterment,

adaptation, restoration” test, they willprobably need to be capitalized.

The betterment criteria, Dannible said,essentially asks whether an improvement thathas been made to the property results in amaterial addition. “Does it enlarge? Does itexpand? Does it extend that particular proper-ty? If that’s the case, you have a betterment,”

he said. However, construction could alsocreate an improvement in areas such ascapacity, production or efficiency at a plant,which can also count as a betterment.

Under the adaptation test, the questionposed would be: Does it adapt a particularbuilding or equipment to a new or differentuse? And for the final test, restoration, theIRS will want to know if the work returnsthe unit to its operating efficiency, if it con-stitutes a major component or substantialunit of property, and if it returns the buildingto a like-new condition after its class life.

For example, Dannible said, imagine thatyou’re putting a new roof onto a building.That would appear to be a betterment, mean-ing that it would have to be capitalized. Ifinstead of a new roof, a significant portion ofthe old roof was repaired, it would still beconsidered a materially significant better-ment and would be capitalized. However, if

an insignificant portion of the roof wererepaired, he said, the company could writeoff the expense.

“When you look at your particular addi-tions and look at the BAR test—the better-ment, the adaptation, the restoration—twokey words are ‘material’ and ‘significant,’so there’s an awful lot of subjectivity ingetting you to take some of those deduc-tions,” he said.

Temporary regulations change thinking on capitalizing expenses

8 www.trustedprofessional.comINDUSTRYOctober 2012 / The Trusted Professional

“We’ve sort of been lulled asleep with the 100 percent bonus depreciation.… Much of the new equipment [companies] got, [they] expensed, but now

we’re in 2012 and it’s 50 percent this year.”

— Anthony F. Dannible, Closely Held and S Corporations Committee member

FAE 2012 Conferences

FAEf o u n d a t i o n f o r a c c o u n t i n g

e d u c a t i o n

For More Information and to Register for This Conference: Visit www.nysscpa.org/auditing or call 800-537-3635.To Register for the Live Video Webcast: Visit www.nysscpa.org/e-cpe or call 877-880-1335.FAE

YEARS 1972-2012

Your Partner in Educational Excellence

40

Auditing Conference

■ Comprehensive updates from professionals involved in standards setting and in the comment and implementation processes

■ Emphasis on audits of smaller, less complex entities■ Practitioner insights into contentious issues

Thursday, November 8, 2012FAE Conference Center 3 Park Avenue, at 34th Street19th FloorNew York, NY 100168:30 a.m.–4:50 p.m.

Find practical guidance on significant developments—including the rollout of auditing (clarity) standards

This is an FAE Paperless Event. Visit www.nysscpa.org for more information.

DON’T MISS OUT ON THESE ESSENTIAL TOPICS:

■ Martin F. Baumann, CPA, MBA, Chief Auditor and Director of Professional Standards, PCAOB■ Cynthia M. Fornelli, Executive Director, Center for Audit Quality

FEATURED SPEAKERS INCLUDE:

REGISTRATION DETAILSCourse Code: 25135311 (In-Person)35135311 (Live Video Webcast)CPE Credit Hours: 8Field of Study: Auditing

NYSSCPA Member Fee: $335 (In-Person);$235 (Live Video Webcast)Nonmember Fee: $460 (In-Person);$360 (Live Video Webcast)

BY CHRIS GAETANOTrusted Professional Staff

T hough New York State MedicaidDirector Jason Helgerson has alreadymade significant changes to the state’spublic health system, netting billions

in cost savings for the program during the last budget cycle, he’s not done by a longshot, he said in a speech at the NYSSCPA’sHealthcare Conference Sept. 13.

Helgerson, who delivered the confer-ence’s keynote address, said that New York’spublic health system faces considerablechallenges―the state is the largest purchas-er of medical services in the country, andMedicaid makes up one-third of its budget.

While he acknowledged that Medicaid hasoften been a “political football,” he said thatthe problems it faces in the state have madeAlbany eager to work with him to improve thesystem. Moreover, the Affordable Care Act,upheld by the Supreme Court this past sum-mer, has sparked an overall national climate ofreexamining health care.

Still, changing the system has never been,nor will it be, easy, he noted. “We not onlyhave the largest program in the country butone of the most complex, so it’s not some-thing you can turn on a dime,” he said.

According to Helgerson, state-levelreforms will come in three phases. Phase one,finding $2.3 billion in savings in the overallprogram budget, has already been completedand was approved as part of the most recentbudget. That gives the program some breath-ing room to begin working on more substan-tive and sustainable reforms for the long term,he said. Phase two is built around a five-yearplan that will focus on improving care, lower-ing costs and improving health.

A central part of this phase will be shift-ing the Medicaid program from a fee-for-service model to managed care, a “major seachange” that is intended to realign incentivesto encourage cost savings among health careproviders. The current fee-for-service modelincentivizes a mentality of “the more I do,the more I get paid,” whereas a managedcare model makes providers ask, “how can Ido shared savings around better populationmanagement,” he said. Because this repre-sents a major change not only in the struc-ture of the program but of the mindset and

culture that comes with it, Helgerson saidthat “it cannot happen overnight,” and thestate will need additional resources to helpfacilitate the transition among providers.

The switch to a managed care paradigmwill essentially mean that the state Medicaidprogram will operate similarly to privatehealth plans and, similar to what states likeArizona have already done, offer a variety ofprepaid health care plans.

Annmarie Covone, a conference speakerwho gave a presentation on the future oflong-term care, said that the state has

already been talking a lot about managedcare with providers, noting that it “is reallythe buzzword now in long-term care.”

“The environment is changing [and]reimbursement will change as time goeson,” she added.

Managed care, she explained, deals withwhat she called “capitation,” which is a fixedmonthly payment to a managed care organi-zation for each member enrolled in thehealth plan. This means that “we don’t lookat days and rates; we look at per member permonth,” she said. Within this capitated pay-ment structure, the provider must administerall medical services for each individual,whether it be nursing or hospital care or X-ray labs, or even support services like trans-portation and nursing homes―all with theallotment given by the state each month.

This, she said, shifts risks from the payer,as it is under a fee-for-service model, to theplan, as it is under the managed care model.She said that the focus of long-term care isthe member health status over the long term,which means oversight of chronic condi-

tions, and providers will have to activelymanage that patient’s care or else their riskwill increase. This is contrasted with fee-for-service, which has episodic payments.

This active management of patient health isa major component of the overall reforms thatHelgerson is seeking. He noted that a minori-ty of patients, often with chronic illnesses,account for the majority of health care costs.This means that by actively managing the“most complex” patients, care can beimproved, while significant cost savings forthe rest can be made. Active management,though, will come with providers coming

together to focus on a single patient. Ratherthan having a number of medical profession-als whose only interactions with each otherare through making referrals, the new modelwill require them to actively work together.

“We really want health care to be a teamsport in New York. We want to integratedelivery and have providers working togeth-er,” he said. “We can no longer afford to havea system where providers sit in silos and notcommunicate or work together because whenwe do that, we are not serving the needs ofthese complex patients and incurring costsbeyond what we can afford.”

Working in harmonyTo enable such coordination, Helgerson

said that the state is going to encourage theuse of a network of providers he called“health homes,” though he noted that theterm is used loosely because it also includesa wide array of organizations such as com-munity health organizations and local gov-ernments that come together and coordinatecare. This network, he said, will be held

accountable for managing the needs ofMedicaid’s highest cost patients. To give anidea of what kinds of costs are involved, hesaid that the 100 most expensive Medicaidpatients cost about $54 million—roughly ahalf million dollars per person.

“If we can find some way to get theseindividuals moving in the right direction forthe basic services we pay for, we canimprove the qualities of their lives and lowercosts,” he said.

In order to incentivize health homes tofocus on these patients, he said that each ofthese organizations will not only be paid carepayments, but if they are successful in lower-ing the costs of these individuals, they will beable to share in the savings generated.

“It’s a change in philosophy in how to payfor health care [that is] much more focusedon outcomes than inputs, and we think thishas merit for us moving forward,” he said.

All told, the various reforms that the stateis planning to make to its Medicaid programwill save the government about $17 billionover the course of the five years Helgersonestimates it will take to implement them. Thisleads directly into phase three, where the statewill take these savings and reinvest them intothe health care system itself in order toincrease capacity and quality. The money willbe funneled into areas such as increasing pri-mary care services—which Helgerson saidNew York simply does not have enough ofright now—health home development; tech-nological improvements, particularly IT sys-tems; and new care models.

The state will need these improvements ifit is to be able to handle the effects of theAffordable Care Act, which he said will giveinsurance access to roughly 7 million NewYorkers for the very first time. The concernis that the health care workforce is not at alevel to accommodate this increaseddemand, which, he pointed out, is what hap-pened in Massachusetts when they imple-mented a similar plan.

“If we can make the system more effi-cient, we can free up capacity to meet thatdemand,” he said. “There are areas, particu-larly in primary care, where we do not havethat capacity, and we must find a way toexpand that capacity.”

State Medicaid to undergo paradigm shift

www.trustedprofessional.com 9INDUSTRY The Trusted Professional / October 2012

BY CHRIS GAETANOTrusted Professional Staff

In September, the Financial AccountingFoundation (FAF) appointed the first 10members of the new Private CompanyCouncil (PCC), a standards-setting body

for private companies. The roster includesthree members of the NYSSCPA: MarkEllis, a Westchester Chapter member who sitson the Chief Financial Officers Committee;

Nassau Chapter member Neville Grusd, aformer Society vice president; and LawrenceWeinstock, also from the Nassau Chapter.

The council will be chaired by BillyAtkinson, a Texan who previously served aschair of the National Association of StateBoards of Accountancy.

The PCC’s main function will be to deter-mine whether GAAP standards properlyaddress the needs of the users of privatecompany financial statements and, if not, to

craft modifications and exceptions to thesestandards, which will be subject to review bythe Financial Accounting Standards Board(FASB). In addition, it will also serve as theFASB’s main advisory body on mattersrelated to private companies.

“Each of the new Council members hasdemonstrated a strong appreciation for theimportance of independent standard-setting,and unwavering commitment toward greaterclarity and well-informed decision-making

in private company financial accounting andreporting,” said FAF President and CEOTeresa Polley. ”Their diverse backgroundsand perspectives will provide valuableinsights and leadership to the PCC and theFAF.”

Private Company Council boasts three NYSSCPA members

“We can no longer afford to have a system whereproviders sit in silos and not communicate or worktogether because when we do that, we are notserving the needs of these complex patients andincurring costs beyond what we can afford.”

— Jason Helgerson, New York State Medicaid Director

BY CHRIS GAETANOTrusted Professional Staff

Most U.S. retail investors lackbasic financial literacy—andtheir weak grasp of even elemen-tary financial concepts is leaving

them vulnerable to predatory investmentfraud schemes, according to a study by theSecurities and Exchange Commission(SEC).

The SEC was required to conduct thestudy, which was released to the public onAug. 30, as ordered under Section 917 of theDodd-Frank Wall Street Reform andConsumer Protection Act. The research,entitled, “Study Regarding FinancialLiteracy Among Investors,” was intended tonot only assess how financially literate theinvesting public is, but to pinpoint ways inwhich that literacy might be improved so asto create a more informed market.

After undertaking quantitative and quali-tative analyses, soliciting public commentand reviewing existing literature, the SEC’sassessment of how financially literate mostpeople are is a bleak one: Research indicatesthat retail investors often do not understandconcepts such as compound interest andinflation, the difference between a stock anda bond, or how investment costs impactreturns. According to the report, certaindemographics such as women, the elderlyand the poorly educated have “an evengreater lack of investment knowledge thanthe average general population.”

“Low levels of investor literacy have seri-ous implications for the ability of broad seg-ments of the population to retire comfort-ably, particularly in an age dominated bydefined-contribution retirement plans,” thereport said.

Financial professionals who work withthe public share the SEC’s concerns.Catherine Censullo, chair of the PersonalFinancial Planning Committee, said thatwithout the help of a professional, manyinvestors are flying blind in the economic

world and don’t seem able to make the deci-sions necessary to successfully manage aportfolio—if they even know which deci-sions need to be made in the first place.

“Many times, if they do have the advan-tage of some kind of retirement plan, theydon’t necessarily understand the choicesthey have and how to diversify in a portfolioor [what] their risk-taking tolerance is,” shesaid. “And all those things are just very fun-damental things for someone [who is]investing.”

This same dynamic plays out even amongpeople who may be business savvy in otherways, said Joshua DuBrow, chair of theSmall Business Outreach Committee. Themost common financial literacy problemwhen it comes to small businesses, he said,is in properly managing cash flow. Problemsin this area generally occur when peoplewait too long to get a professional—and bythe time they realize they need one, “it’salways, for the most part, too late,” he said.

In terms of investment, DuBrow explainedthat many small business owners have troublebecause of the opaque nature of the variousdocuments that come with it. The SEC, hesaid, gives investors a lot of protections byrequiring myriad disclosures from filers, butthe average investor has no clue what theymean.

The SEC itself makes a note of this intheir report; it said that one change thatcould help investors understand investmentsbetter is to provide them with disclosuresthat are “concise, use plain language andcommon terminology, and incorporate someuse of electronic delivery.” The report alsosuggested that the SEC change the timingsof its disclosures, as the research indicatesthat investors would prefer to receive theinformation either before or at the time theymake a decision on whether to engage afinancial intermediary or purchase an invest-ment product or service.

The report added that changes to how dis-closure content is structured may also be agood way to help investors better understandwhat they are getting into, proposing a two-tiered disclosure framework where one layerwould consist of a concise summary of thedisclosure document, and the other wouldoffer detailed information on fees and serv-ice charges, specific details of all arrange-ments in which the firm receives an eco-nomic benefit, and any other informationneeded to disclose conflicts of interest.

The report also mentioned the importanceof easily accessible and efficiently deliverededucation programs that would be research-based and goal-oriented, emphasizingimportant investor education concepts thatare relevant to target audiences. In particu-lar, the report talked about creating, support-ing or augmenting investor education pro-grams targeted at young investors, lump-sum payout recipients, investment trustees,members of the military, underserved popu-lations and older investors.

The Small Business Outreach Committeeregularly holds financial education work-

shops, with one in particular this year cater-ing to military veterans. DuBrow said thatthese sessions are meant to be an absolutebeginner’s primer, with a special emphasison learning how to ask the right questions.

“What we try to do,” he said, “is educatesmall business owners on the basics … not sothat they learn how to do accounting andfinance in one sitting, but really so they knowthe proper questions and can come away think-ing ‘… I’ve got to reach out to an accountant orattorney or someone else because there’s noway I can do this on my own.’”

SEC: public lacks financial literacy

10 www.trustedprofessional.comINDUSTRYOctober 2012 / The Trusted Professional

Research indicates that retail investors

often do not understandconcepts such as com-

pound interest and inflation, the differencebetween a stock and a

bond, or how investmentcosts impact returns.

Editor’s Note: “War Stories,” drawn fromCamico claims files, illustrate some of thedangers and pitfalls in the accounting pro-fession. All names have been changed.

BY RANDY R. WERNER, CPA, J.D.,LL.M (TAX)

Hope Accounting & Auditing (HAA)had performed financial statementaudits for Pulp Fabrication (PF), alarge paper products manufacturer,

for several years. Though PF had a solid his-tory of paying fees in full and on time, itexperienced cash flow problems as a resultof the recession and began to make partialpayments to HAA instead. This requiredextra patience on the part of HAA collec-tions, which waited until the end of themonth to bill.

During the last audit, PF made a partialpayment after the first month’s billing, andanother partial payment after the secondmonth’s billing. The engagement appearedto be going well, but soon after the secondpartial payment, PF’s largest customer, whoaccounted for nearly half of its revenues,went bankrupt. At this point, PF was nolonger able to pay the audit fees.

PF management did not tell HAA auditorswhat had happened, because it needed a cleanfinancial statement audit in order to qualify formore credit so that it could pay the invoices.When its payments to HAA fell behind sched-ule, PF lied and told HAA collection callersthat the payments were actually scheduled forthe following payment cycle.

HAA continued to perform work for PF,in spite of the company’s delinquentaccount. By the time HAA auditors finallylearned about the bankruptcy of PF’s largestclient, however, and about PF’s inability tosettle its outstanding bill unless it couldqualify for a higher credit limit, HAA’s feeshad accumulated to over $100,000.

HAA considered suing PF, but after con-sulting with legal counsel, realized that PFhad nothing to lose by countersuing for mal-practice, however baseless. Moreover, thelegal fees that would be incurred and thebillable time lost due to litigation would cer-tainly exceed the amount owed to the firm.HAA saw no choice but to accept the loss inrevenue.