Toward a Wider Analysis of Market Definition: Theory and Evidence from the Turkish...

21

Tamer Çetin is a visiting lecturer at the Northeastern University, Boston. He is grateful to Christopher Brown and two anonymous referees for their valuable comments. This research was supported in the scope of Project No. 2016-02-01- KAP01 by the Division of Research of Yildiz Technical University (Turkey), when Çetin was an associate professor at that university. The earlier versions of this article were presented at the XVII April International Academic Conference on Economic and Social Development, held at the Higher School of Economics in Moscow (Russia) in 2016 and at the Fourth European Academic Research Conference on Global Business, Economics, Finance and Banking (EAR16 Swiss Conference) in Zurich (Switzerland) the same year. The author is grateful to the participants for their valuable comments. The responsibility for any errors remains with the author. 1137 ©2017, Journal of Economic Issues / Association for Evolutionary Economics JOURNAL OF ECONOMIC ISSUES Vol. LI No. 4 December 2017 DOI 10.1080/00213624.2017.1391597 Toward a Wider Analysis of Market Definition: Theory and Evidence from the Turkish Telecommunications Industry Tamer Çetin Abstract: This article develops a novel approach to the analysis of market definition. The article empirically investigates the main components of market definition, such as market power, substitution, and the simultaneous interaction between the demand and its determinants for the fixed and mobile voice services. To this end, I employ the multivariate Johansen cointegration methodology and analyze the Turkish voice telecommunications industry. While the VECM analysis confirms the presence of a simultaneous long-term causality relationship among the variables, the Johansen normalization results reveal demand elasticities that enable the analysis of market power and fixed-to-mobile substitution. My findings suggest that the fixed and mobile voice services, which are traditionally viewed as separate markets, can be defined as products that compete in the single market. Keywords: cointegration methodology, (de)regulation, fixed-mobile substitution, market definition, market power JEL Classification Codes: C32, L43, L51, L96, K21 Market definition has long been a very controversial field in antitrust cases (Baker 2007; Kaplow 2014; Massey 2000; Tardiff and Weisman 2009; Werden 2014). Even though different approaches to market definition have been presented so far, consensus has not been achieved on which approach is the best to define a market. The aim of market definition is to understand market power and its anticompetitive effects. Thus, the Lerner index, the market shares of firms, and market concentration have been used as traditional tools to measure market power. However, these approaches suffer from some shortcomings when used to analyze market definition

-

Upload

uni-hamburg -

Category

Documents

-

view

0 -

download

0

Transcript of Toward a Wider Analysis of Market Definition: Theory and Evidence from the Turkish...

Tamer Çetin is a visiting lecturer at the Northeastern University, Boston. He is grateful to Christopher Brown and two

anonymous referees for their valuable comments. This research was supported in the scope of Project No. 2016-02-01-

KAP01 by the Division of Research of Yildiz Technical University (Turkey), when Çetin was an associate professor at

that university. The earlier versions of this article were presented at the XVII April International Academic Conference

on Economic and Social Development, held at the Higher School of Economics in Moscow (Russia) in 2016 and at the

Fourth European Academic Research Conference on Global Business, Economics, Finance and Banking (EAR16 Swiss

Conference) in Zurich (Switzerland) the same year. The author is grateful to the participants for their valuable

comments. The responsibility for any errors remains with the author.

1137

©2017, Journal of Economic Issues / Association for Evolutionary Economics

JOURNAL OF ECONOMIC ISSUES Vol. LI No. 4 December 2017 DOI 10.1080/00213624.2017.1391597

Toward a Wider Analysis of Market Definition: Theory and Evidence from the Turkish Telecommunications Industry

Tamer Çetin

Abstract: This article develops a novel approach to the analysis of market definition. The article empirically investigates the main components of market definition, such as market power, substitution, and the simultaneous interaction between the demand and its determinants for the fixed and mobile voice services. To this end, I employ the multivariate Johansen cointegration methodology and analyze the Turkish voice telecommunications industry. While the VECM analysis confirms the presence of a simultaneous long-term causality relationship among the variables, the Johansen normalization results reveal demand elasticities that enable the analysis of market power and fixed-to-mobile substitution. My findings suggest that the fixed and mobile voice services, which are traditionally viewed as separate markets, can be defined as products that compete in the single market.

Keywords: cointegration methodology, (de)regulation, fixed-mobile substitution, market definition, market power

JEL Classification Codes: C32, L43, L51, L96, K21

Market definition has long been a very controversial field in antitrust cases (Baker

2007; Kaplow 2014; Massey 2000; Tardiff and Weisman 2009; Werden 2014). Even

though different approaches to market definition have been presented so far,

consensus has not been achieved on which approach is the best to define a market.

The aim of market definition is to understand market power and its anticompetitive

effects. Thus, the Lerner index, the market shares of firms, and market concentration

have been used as traditional tools to measure market power. However, these

approaches suffer from some shortcomings when used to analyze market definition

1138

Tamer Çetin

(Carlton 2007). Instead, the own-price elasticity of demand is employed in

determining market power. But, the demand elasticity is also not sufficient to define

the relevant market. In particular, in the industries in which firms have high market

shares, even if the own-price elasticity of demand is high, one has to find a good

substitute for the analyzed product/service to define market. To do this, one has to

estimate the cross-price elasticity of demand. Although the cross-price elasticity of

demand is rather useful in market definition, it is also not sufficient to define the

relevant market (Kaplow 2014). When the cross-elasticity of demand fails to address

the question, some researchers use the income elasticity of demand (Vogelsang 2010;

Ward and Woroch 2010). Consequently, researchers and regulators have used new

and different approaches to define markets.

My purpose in this article is to bring together these approaches and to introduce

a wider analysis of market definition. I empirically investigate the Turkish fixed and

mobile voice markets. The aim is to show how to define a market through the

approach I introduce here. In that sense, my argument differs from the previous

literature in three ways. First, following a simultaneous cointegration methodology

developed by Søren Johansen (1992, 1995), my approach enables defining a market

by simultaneously and empirically investigating both the main components of market

definition, such as market power and substitution, and the long-term relationship

between the demand for fixed voice service and market developments driven by

technological change, such as the changes in the own price of fixed voice services, the

price of substitute services, and the effect of income. This is particularly important in

telecommunications. Because technology in the telecommunications industry has

dramatically changed over time, market structures, prices, and the dynamics of

demand also (and simultaneously) have adjusted to this technological change (Miller

1996, 2001; Spulber and Yoo 2009). As Ingo Vogelsang (2010) points out, in order to

better understand these dynamics and to reach a more realistic and plausible analysis

of market definition, regulators have to simultaneously assess those dynamic

developments in the fixed and mobile markets. I argue that the estimation of price

and income elasticities is necessary for market definition, but not sufficient. For a more

realistic and reliable market definition, one should estimate the long-term causality

relationship between the demand for fixed telephony service and market

developments driven by technological change and the main components of market

definition, such as market power and fixed-to-mobile substitution (FMS). In this

sense, my methodology, which includes a novel empirical perspective to the previous

literature, introduces a more contemporary and wider approach to the analysis of

market definition.

Second, I focus on the voice market of Turkey as an emerging market. The

Turkish experience presents a unique case for the analysis of market definition

because the incumbent fixed operator in the Turkish voice market was privatized in

2005, and thus the transition to competition has been performed relatively recently.

Taking into account only the market share of fixed operator in market definition,

regulators have not defined the fixed and mobile voice markets as the single market,

even though market developments suggest a clear substitution relationship between

fixed and mobile voice services (Oguz and Benli 2015). Because such developments in

Toward a Wider Analysis of Market Definition

1139

the telecommunications industries have recently occurred, regulators have been

having difficulties in understanding the meaning of these developments in terms of

market definition. In that sense, the case of Turkey presents a unique opportunity to

understand the dynamic processes of market definition and to introduce new

evidence from an emerging industry into the literature.

Third, I estimate two different models — including two different data — in order

to reach more realistic and reliable results. While the first model includes the analysis

of market definition through data for the traffic volume and call price per minute, the

second one analyzes market definition by data for the number of subscriptions and

average revenue per user (ARPU). Because the results of the two models are similar,

my findings suggest strong, fresh evidence concerning market power, substitution, and

the long-term relationship of technological development to the telecommunications

industry. Also, I analyze the effect of these findings on the regulatory process, and

thus make an important contribution to the literature of market definition.

Accordingly, I organize the article as follows. In section two, I include a general

statement of the fixed and mobile voice markets within the Turkish

telecommunications industry. In section three, I introduce a detailed discussion of

market definition. In section four, I empirically analyze market definition in the

Turkish voice market and discuss the findings in terms of the regulatory process.

A General Overview of the Turkish Voice Telecommunications Industry

In Turkey, the mobile voice market was opened to competition with the entrance of

mobile telephony operators, Turkcell and Telsim (currently Vodafone), into the

industry in 1994. In the same year, Turk Telecom (TT) was established as a state-

owned fixed telephony operator. Although the government tried to privatize TT

throughout the 1990s, some legal problems and judicial resistance in the process of

privatization impeded the privatization of TT.1 While the block sale of 55 percent of

TT was carried out in 2005, 15 percent of its remaining share was privatized through

offering to the public in 20082 (Bagdadioglu and Cetinkaya 2010). Currently, 30

percent of the shares of TT are under state ownership and TT as a private monopoly

dominates the fixed-line telephony market (Çetin 2014).

In the process of regulatory reform in the Turkish telecommunications industry,

the institutional structure of industry also has changed extensively. The

Telecommunications Authority (ICTA n.d.) as an independent regulator was

established in 2000. Law No. 5369, enacted in 2005, redefined the universal services

in telecommunications in parallel with the EU Directive of 2002 (Directive 2002/22/

EC) (Oguz 2013). The Electronic Communications Law (ECL), Law No. 5809,

enacted in 2008, restricted the regulatory power of the Ministry of Transport in the

1 See Tamer Çetin (2010, 2014) for more detailed discussion about the institutional problems of privatization in Turkey in the 1990s.

2 Following privatizations in 2005 and 2008 by a Cabinet Decision in January 2013, the government vowed to privatize 6.68 percent of the remaining share of TT through offerings to public by the end of 2013. This privatization, however, has not yet materialized.

1140

Tamer Çetin

industry and gave all the regulatory discretion to the ICTA in order to protect

competition, to undertake market analyses for market definition, to determine

operators with significant monopoly power (SMP), to regulate operators with the

SMP, and to approve tariffs and prices if necessary (Atiyas 2011).

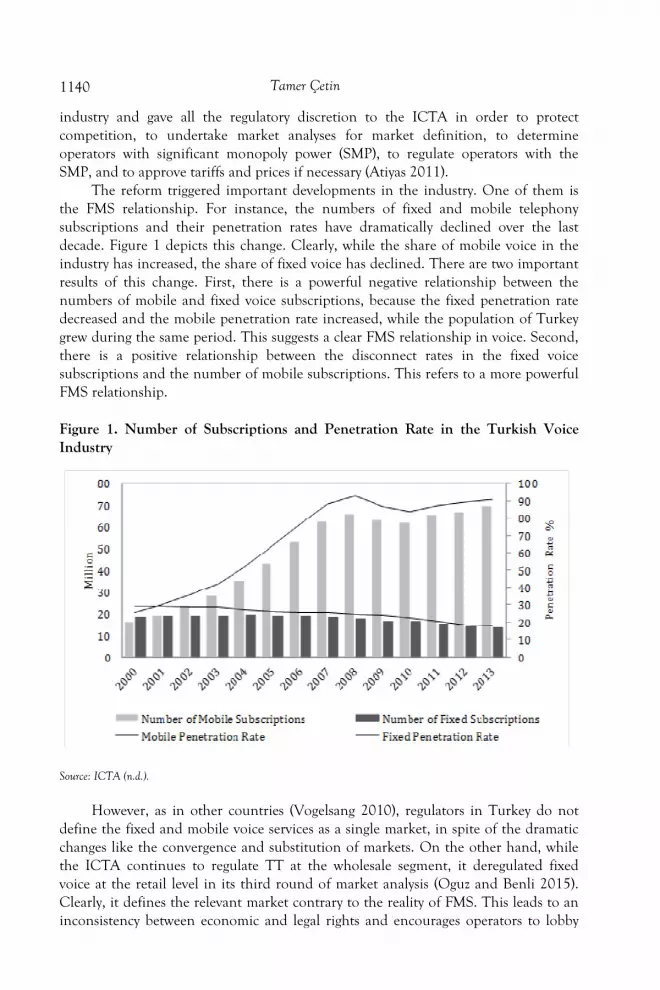

The reform triggered important developments in the industry. One of them is

the FMS relationship. For instance, the numbers of fixed and mobile telephony

subscriptions and their penetration rates have dramatically declined over the last

decade. Figure 1 depicts this change. Clearly, while the share of mobile voice in the

industry has increased, the share of fixed voice has declined. There are two important

results of this change. First, there is a powerful negative relationship between the

numbers of mobile and fixed voice subscriptions, because the fixed penetration rate

decreased and the mobile penetration rate increased, while the population of Turkey

grew during the same period. This suggests a clear FMS relationship in voice. Second,

there is a positive relationship between the disconnect rates in the fixed voice

subscriptions and the number of mobile subscriptions. This refers to a more powerful

FMS relationship.

Figure 1. Number of Subscriptions and Penetration Rate in the Turkish Voice

Industry

Source: ICTA (n.d.).

However, as in other countries (Vogelsang 2010), regulators in Turkey do not

define the fixed and mobile voice services as a single market, in spite of the dramatic

changes like the convergence and substitution of markets. On the other hand, while

the ICTA continues to regulate TT at the wholesale segment, it deregulated fixed

voice at the retail level in its third round of market analysis (Oguz and Benli 2015).

Clearly, it defines the relevant market contrary to the reality of FMS. This leads to an

inconsistency between economic and legal rights and encourages operators to lobby

Toward a Wider Analysis of Market Definition

1141

for wealth transfers. Unfortunately, this approach is common throughout the world.

Because this analysis of market definition neglects the most important components of

market definition and the regulatory decisions are not consistent with market

developments, the current approach to market definition in Turkey (and many other

countries) is not sufficient to define markets in parallel with market developments. I

argue that the analysis of market definition would extensively change and the

individual fixed operator would be deregulated if regulators define the candidate

market as per the methodology I analyze in the next section.

An Analysis of Market Definition

The main rationale of defining a market is to ensure a basis for inferring market

power.3 The aim is to understand anticompetitive components in the analyzed market

and thus to take measures to preclude the negative effects of those components on

competition, if necessary4 (Baker 2007; Kaplow 2010). That is, the process of market

definition consists of two important parts: (i) the analysis of market definition and (ii)

the effect of this analysis on regulation. Taking into consideration these feature of

market definition,5 I accept that the analysis of market definition has three main

components: (i) the long-term dynamic interaction between the demand for fixed

voice services and its determinants driven by technological change, (ii) the

hypothetical monopolist test (HMT), and (iii) the FMS relationship. However, the

previous literature on market definition has only focused on the last two of these

components and neglected the first one (Baker 2007; Barth and Heimeshoff 2014;

Briglauer, Schwarz and Zulehner 2011; Cardona et al. 2009; Karacuka, Haucap and

Heimeshoff 2011; Rhee and Park 2011; Sidak, Crandall and Singer 2002; Vogelsang

2010). In fact, the first component is more important than the others, because the

3 In particular, antitrust cases in the US have turned to the question of market definition after the

DuPont Cellophane Case in 1956 (United States v. E.I. du Pont de Nemours & Co., 353 US 586). Even though

the U.S. Supreme Court first accepted cross-price elasticities of demand to define a market in Times-Picayune

in 1952 (Times-Picayune Publishing Co. v. United States, 345 US 594), this approach was only confirmed with

the DuPont case in terms of revealing market power and defining the relevant market (Massey 2000). 4 Of course, market definition is also important in order to understand the anticompetitive effects of

mergers. However, in this article, (following Barth and Heimeshoff 2014; Briglauer, Schwarz and Zulehner 2011; Cardona et al. 2009; Rhee and Park 2011; Vogelsang 2010), I focus on market definition in terms of market power and fixed to mobile substitution, but not mergers because the point of the market definition process is market power (Kaplow 2010).

5 The definition of a relevant market consists of the definition of relevant product and geographic markets. For that reason, regulators apply the process of market definition twice. They first analyze market definition for a product market and then they define the candidate market geographically (Coate and Fischer 2008). However, I only focus on a demand-based market definition for the product market because my aim is to introduce a wider approach to the analysis of market definition by bringing together the most important components of market delineation, as mentioned in this article’s introduction above. By using these components, I only include the analysis of product market and ignore the definition of geographic market. Of course, this approach can also be used to define a relevant geographic market if data is available. As a matter of fact, “geographic markets are defined using the same process as that used to define product markets,” as clearly stated in the Competition Law Guideline of the Office of Fair Trading of the UK and the Market Analysis Guideline of Information and Communication Technologies Authority in Turkey.

1142

Tamer Çetin

main motivation in the analysis of market definition in the telecommunications

industry is to understand the effect of technological and dynamic change on demand

relationships. When technological developments in the mobile markets drive down

the price of mobile products, and thus the mobile services become more accessible for

all users, consumers in the fixed voice market simultaneously prefer the mobile voice

products to the traditional fixed telephone services (Miller 1996, 2001; Spulber and

Yoo 2009; Vogelsang 2010). For that reason, I have to include the effect of these

dynamic and simultaneous developments on the components of market definition

into the analysis of market definition.

Conversely, in the traditional analysis of market definition, regulators and

researchers have generally relied on the observation of changes in prices, penetration

rates, the number of subscription, the revenue of firms, market shares, and market

concentration. In other words, they have neglected the dynamic and simultaneous

effect of technological change on market developments, market definition, and

regulation. According to the traditional approach, the FMS is based on the

observation that the number of fixed subscriptions decreases, while the number of

mobile subscriptions increases in parallel with developments in mobile technologies.

It is accepted that such interaction between the mobile and fixed use rates is a clear

indicator of the FMS (Vogelsang 2010). This approach is flawed because it does not

include the analysis of simultaneous interaction between demand and market

developments that are critical for market definition. Instead of the separate

observation of each indicator, it is necessary to simultaneously analyze the dynamic

interaction among those variables to better understand the real effect of market

developments on market definition and regulation. It has to be clear whether there is

a simultaneous long-term relationship between the demand for fixed telephony and

its determinants because the interaction among these variables is a dynamic

relationship, which also occurs in the long term.

An important component of market definition has become the measure of

market power since the DuPont Cellophane Case of 1956. In contrast to the

traditional approaches, such as the Lerner index6 and market share,7 the best

6 In the traditional microeconomics literature, market power is usually measured by the Lerner

index. The Lerner index is measured by L=(P-MC)/P. In this equation, P is price and MC is marginal cost. If

P=MC, then L=0 and there is no market power. If P >MC, then L>0 and this means market power. This approach is not available to directly define the relevant market through market power because it only

reflects P and MC. In the analysis of market definition, measuring MC is rather difficult, even though prices are straightforward.

7 In particular, in the cases where there is a strong substitution relationship, even if the market share of an incumbent operator is 100 percent, market share cannot be meaningful in terms of market definition (Baker 2007; Kaplow 2010). For example, in the telecommunications industries in which competition is fierce, even if an operator in the traditional fixed-voice market has 100 percent market share, the pressure of competition stemming from substitute products/services can force the fixed operator to hold prices close to marginal cost in its own market. The presence of a substitute product can impede the profitability of a price increase for the incumbent operator in the traditional telecommunications services. That is, because high market share does not necessary mean more market power, market share is not strongly the probative of market power or anticompetitive effect. If market share is not evidence for market power, then market definition is least useful (Baker 2007). For that reason, market share alone is also not the available tool to define a relevant market.

Toward a Wider Analysis of Market Definition

1143

approach used to measure market power is the HMT. The HMT has been intensively

employed in the analysis of market definition in telecommunications by regulators,

courts, and international competition regimes over the last three decades (Baker

2007; Coate and Fischer 2008). The HMT presents an analytical approach to estimate

the profitability of a hypothetical increase in price, and thus to define the relevant

market. A hypothetical price increase refers to a small, but significant, non-transitory

price increase (SSNIP).8 Accordingly, if a 5.0 percent price increase by the

hypothetical monopolist in the relevant market is profitable, it is accepted that this

firm has the market power to raise price. Or, if the price increase leads to a loss in

sales of the hypothetical monopolist and thus it is not profitable, best substitutes are

included in the analysis of market definition and the process is repeated in certain

intervals (Coate and Fischer 2008).

In order to determine market power, one has to measure the own-price elasticity

of demand for fixed voice services. The own-price elasticity will reveal what would

happen when the hypothetical monopolist imposes a SSNIP on the current price of

relevant product (Coate and Fischer 2008). If the price increase is unprofitable, then

the second step is to define the substitute product. If there is a good substitute of the

hypothetical product, then the own-price elasticity will be high. Conversely, if there is

no substitute, then the own-price elasticity will be close to zero. In that case, whereas

the high own-price elasticity refers to a low market power, market power will be higher

when the own-price elasticity of demand is low. In short, instead of the traditional

approaches, the own-price elasticity of demand is the best tool to measure market

power and to define a market through this market power (Kaplow 2010).

The last important component of market definition is the analysis of the FMS

relationship. The cross elasticity of demand is the best tool to measure the FMS.

While the own-price elasticity explains the market power of fixed operator as the

hypothetical monopolist, the cross-elasticity of demand reveals the best substitute for

the traditional fixed products. Such analysis determines the scope of the relevant

market. For instance, if consumers use substitute products or services, these products

can compete within the same market, and thus the markets including those products

can be defined as a single market. Products or services that are traditionally in

different markets can be classified as products that compete in the same market

(Coate and Fischer 2008). For these reasons, in order to define a market, it is

necessary to use an empirical methodology that allows for investigating the

simultaneous long-term relationship among the related variables at issue, the HMT,

and the FMS relationship.

Empirical Methodology

In this section, I construct some hypotheses to clarify my approach and then specify

equation(s) to empirically test these hypotheses. Accordingly, my first hypothesis is:

8 For that reason, the HTP and the SSNIP can be used in the same meaning.

1144

Tamer Çetin

H1: There is a simultaneous long-term relationship running from the prices of mobile and

fixed telephony services and national income to the demand for fixed voice.

While technological development drives down the price of mobile products, and

thus facilitates access to mobile services, the demand for fixed telephony service

simultaneously declines even if the income of consumers increases. This means that

there is a long-term causality relationship among the price of mobile voice service,

income, the price of fixed telephony, and the demand for fixed telephony service. My

goal is to simultaneously investigate this long-term relationship among the variables

instead of the separate observation of each variable as in the previous literature on

market definition. Thus, I include the effect driven by technological development into

the analysis of market definition and introduce a more contemporary approach to

defining a market in the telecommunications industries. My next three hypotheses

are:

H2: The own-price elasticity of demand for fixed telephony should be higher than 1 or

close to 1 because the price increase has not to be profitable in the HMT.

H3: The cross-elasticity of demand should be positive to show the presence of the FMS.

H4: I expect a positive relationship between the demand for fixed voice and income.

In order to empirically test these hypotheses, I employ the Johansen

cointegration methodology because it allows for simultaneously testing the long-term

relationships among the aforementioned variables (Bremnes, Gjerde and Sattem

2001; Johansen 1992, 1995). Also, this methodology allows for estimating the own-

price, cross-price, and income elasticities of demand for fixed services using the

variables under the assumptions of my model. Accordingly, I analyze the long-term

relationship among the variables, the HMT, and the FMS under the four hypotheses

above. While the own-price elasticity enables the analysis of the market power of fixed

operator, the cross-elasticity of demand reveals the FMS relationship. Lastly, if there is

a cointegration relationship among the variables, one can infer that there is a long-

term causality relationship running from the prices of fixed and mobile voice services

and income as independent variables to the demand for fixed telephony as the

dependent variable.

Model Specification

My model specifies the log of the demand for fixed voice services as a function of

the log of the own price of fixed voice, the price of mobile voice as the best substitute,

and income. Thus, I estimate:

lnDFixt = β0 + β1lnPfix + β2lnPmobile + β3lnYt + εt (1)

In equation (1), DFixt is the demand for fixed voice services in the country in period t,

Pfix is the price of fixed voice in period t, Yt is income in the country in period t, and εt

Toward a Wider Analysis of Market Definition

1145

is the error term. In this equation, parameters β0, β1, β2, and β3 are estimated as long-

term elasticities because the variables are used in logarithmic form.

Because my goals is to estimate the long-term relationships among those

variables through two different data, I rewrite equation (1) as follows:

Dqtfixcall = ft (pt

fixppm, ptmobppm, yt

tipi) (2)

Dqtfixsubnum = ft (pt

ARPUfix, ptARPUmob, yt

tipi) (3)

The variables in equations (2) and (3) are as follows:

Dqtfixcall: the log of fixed calls (minutes)

Dqtfixsubnum: the log of fixed subscription numbers

ptfixppm: the log of the price per minute for fixed calls,

ptmobppm: the log of the price per minute for mobile calls

ptARPUfix: the log of ARPU for fixed voice

ptARPUmob: the log of ARPU for mobile voice

yttipi: the log of the adjusted and seasonal total production index (TIPI)

I estimate two different models. In these equations, the demand for fixed voice

is proxied by calls from the fixed operator and the number of fixed subscriptions,

respectively. Accordingly, while Dqtfixcall is the function of pt

fixppm, ptmobppm, and yt

tipi,

Dqtfixsubnum is the function of pt

ARPUfix, ptARPUmob, and yt

tipi. By empirically investigating these

equations, I aim to:

• reveal whether there is a long-term causality relationship among the variables in

order to test H1;

• estimate the own-price elasticity of demand through the relationship between

Dqtfixcall and pt

fixppm or Dqtfixsubnum and pt

ARPUfix. Thus, I will figure out whether the

fixed operator as a hypothetical monopolist has monopoly or market power

through the HMT in H2;

• estimate the cross-elasticity of demand through the relationship between Dqtfixcall

and ptmobppm or Dqt

fixsubnum and ptARPUmob. Thus, I will reveal the presence of the FMS

in H3;

• understand the relationship in H4 through the income elasticity of demand.

The relationship between Dqtfixcall or Dqt

fixsubnum and yttipi will determine income

elasticity.

In the context of this background, I can derive equations to estimate the

following:

lnDqtfixcall = β0 + β1lnpt

fixppm + β2lnptmobppm + β3lnyt

tipi + εt (4)

1146

Tamer Çetin

In equation (4), Dqtfixcall is the total call quantity (million minutes) from fixed operator

in the country in year t, ptmobppm is the price of fixed call per minute in year t, pt

mobppm is

the price of mobile call per minute, yttipi is the seasonally adjusted total production

index, and εt is the error term. In the same equation, the demand for fixed voice is

proxied by the log of the quantity of total fixed calls, and thus the log of fixed calls is

specified as a function of the log of fixed and mobile-call prices per minute and TIPI

that proxies income:

lnDqtfixsubnum = β0 + β1lnpt

ARPUfix + β2lnptARPUmob + β3lnyt

tipi + εt (5)

In equation (5), Dqtfixsubnum is the number of subscriptions for fixed voice in the country

in year t, ptARPUfix is ARPU for fixed voice in year t, pt

ARPUmob is ARPU for mobile voice,

yttipi is the seasonally adjusted total production index, and εt is the error term. In the

same equation, the number of fixed subscriptions represents the demand for fixed

voice and the log of the number of subscriptions is specified as a function of the log

of ARPU for fixed and mobile voice and TIPI. Accordingly, equations (4) and (5)

enable the definition of the Turkish voice market by the estimation of the long-term

relationships among the variables.

Data

Because my empirical analysis includes the estimation of aggregate demand

functions in the Turkish voice market, I use the national-level quarterly-data, but not

the firm-level data. Data cover the period between 2003Q1 and 2015Q3 for all the

variables in both subscription and call analysis.9 The variables for the call analysis in

Model 1 are fixed calls (minutes), the price per minute for fixed calls, and the price

per minute for mobile calls. Also, I use the adjusted and seasonal total production

index (TIPI), which is highly correlated with GDP to control for changes in income.

These variables represent fixcall, fixcallprice, mobcallprice, and income in Model 1.

9 Undoubtedly, the Johansen’s methodology I use here is the best if the sample size is about 100 observations or more, as C.P. Hargreaves (1994) expresses. However, this is not necessary for the Johansen cointegration approach because the residuals are not autocorrelated for only the sample sizes with 100 observations in Hargreaves’s own study. In this article, the residuals are not highly autocorrelated for both models, as I express below. Also, there is no consensus about the number of observations in the cointegration analysis. Some studies clearly suggest that the power of the cointegration analysis depends on the frequency of the data rather than the number of observations (Perron 1989; Shiller and Perron 1985;). As G.S. Maddala and In-Moo Kim (2004) discuss in detail, unit root test based on quarterly data are more powerful than those based on the corresponding yearly data. As a matter of fact, Johansen himself run his own cointegration analyses with 55, 61, and 67 observations by using quarterly data (Johansen and Juselius 1990, 1992). Also, it is possible to find some other studies using the cointegration methodology with 55 observations (Godbout and van Norden 1997; Kama 1992). On the other hand, my goal here is to introduce a new approach to market definition rather than estimating demand through the most suitable econometric technique, and there is no larger data in Turkey. Most importantly, because the residuals are not highly autocorrelated in this article, the models are valid and the results are reliable. For these reasons, I employ the Johansen cointegration technique with 51 observations for Models 1 and 2, even though these observation numbers are relatively less than an ideal dataset.

Toward a Wider Analysis of Market Definition

1147

The variables for the subscription analysis in Model 2 are the number of fixed

subscriptions, ARPU for fixed voice, ARPU for mobile voice, and TIPI. These

variables represent fixsubnum, ARPUfix, ARPUmob, and income in Model 2.

Accordingly, as the quantity of demand in the models, I use the number of fixed

subscriptions in the subscription analysis and traffic volume in the call analysis. As

prices, I use ARPU and price per minute for mobile and fixed calls. For real prices, all

price data are deflated by the communication price index (CPI) in Turkey.

Data for the period between 2008Q1 and 2015Q3 for the number of fixed

subscriptions and ARPU in the subscription analysis are obtained from the market

analysis data of the ICTA.10 I use annual data for the remaining period of

subscription data and interpolate annual data to the quarterly data through Michael

Baxter’s (1998) 11 method. Data for the fixed and mobile call price are from TUIK.

The call traffic data as quantity in the call analysis for the period between 2003Q1

and 2011Q3 are from the Telecom Market Matrix Data of Analysis Mason and UDH

(2011). The call traffic data for the period between 2011Q4 and 2015Q3 are from the

ICTA. In order to control for changes in income, I use seasonally and calendar

adjusted TIPI that is highly correlated with GDP. Data for TIPI and CPI are from the

Turkish Statistical Institute (TUIK).

Cointegration Analysis and Estimation Results

I employ the Johansen cointegration methodology with a conditional vector

error correction model (VECM), including k lags in the estimation of the models.

First of all, in the analysis of time series, I cannot empirically investigate the presence

of long-term causalities among the variables through the OLS regression methodology.

For instance, if one time series is cointegrated with the other, the familiar regression

approaches cannot estimate this relationship. Also, if some variables are not

stationary, the analysis of those variables through the OLS regression methodology

can produce spurious results. It is possible to estimate demand elasticities to

understand the presence of market power and substitution relationship through the

OLS regressions, but not the long-term equilibrium relationships among the variables.

Clearly, the OLS regression analysis is not sufficient for a wider analysis of market

definition. Conversely, cointegration methodology allows for investigating both the

presence of long-term relationships among the variables and the sensitiveness of these

relationships through the estimation of elasticities simultaneously. That is, by using

the cointegration approach, I can provide a concurrent statistical evidence for both

the estimation of long-term relationship among the variables and the analysis of

demand elasticities. In other words, using the Johansen cointegration methodology, I

10 For the market analysis data of ICTA, see www.btk.gov.tr/tr-TR/Sayfalar/Pazar-Verileri. 11 The Baxter model is commonly used to quadratically interpolate annual data to quarterly data

because of the problem of missing data. For instance, the UK’s Office for National Statistics officially employs the Baxter model to interpolate missing data. In general, existing academic studies linearly interpolate missing data. However, series do not show a linear trend over time. In this sense, quadratic interpolation ensures the obtaining of more accurate results by converting annual data to quarterly values.

1148

Tamer Çetin

can test the hypotheses H1, H2, H3, and H4 and thus reveal the long-term

relationships that are crucial for the analysis of market definition. Under this

framework, I estimate the existence of long-term relationships by the results of VECM

analysis reported in Table 3 and Table 7 and elasticities through the Johansen

normalization results reported in Table 4 and Table 8. It is clear that the estimation

methodology I present here is more suitable than the previous approaches used in the

analysis of market definition. Accordingly, the VECM model, which was proposed by

Johansen (1995), can be written as:

λt =∑ki=1Θiλt–i + ψλt–k + χϕt + εt (6)

In equation (6), λt is the vector of endogenous variables, ϕt is the vector of

exogenous variables, and Θi and χ are the coefficient matrices of endogenous and

exogenous variables, respectively. Θi and ψ represent the short and long-run

relationships, while k is the lag length. The term εt refers to the independent residuals.

The (5×5) matrix ψ can be converted to αβ. In that case, α represents the coefficients

defining the speed of adjustment of λt toward the long-run equilibrium, while β is the

cointegrating vector and represents the long-term relationship among the variables.

The Johansen (1995) procedure tests the rank r≤5 of matrix ψ. If r=0, there is no

cointegration. Also, a reduced rank r means that there are r possible stationary linear

combinations. Using this estimation methodology, I test the long-term relationships

in equation (4) and equation (5). The VECM and the Johansen normalization results

will allow for interpreting the findings in the context of the analysis of market

definition.

Before the cointegration analysis, I perform pre-estimation tests to determine the

appropriate lag length of the system, to understand the autocorrelation structure of

residuals, and to reveal whether variables are stationary (Bremnes, Gjerde and Sattem

2001). In the Johansen cointegration test, variables must be non-stationary at level.

Accordingly, if variables are non-stationary at level, when all variables are converted

into the first difference, they will be stationary — meaning, they are integrated of the

same order. In order to test whether time series for variables are stationary or not, I

employ the augmented Dickey-Fuller (ADF) test.12 Accordingly, because the t statistics

absolute values are less than 5.0 percent critical values for both Model 1 and Model 2,

the null hypothesis is accepted and the alternative is rejected. All variables have unit

root and are non-stationary at level. Coefficient values for variables are negative and

there is no autocorrelation problem. Because tests are valid, I accept the models and

run the Johansen cointegration analysis.

12 In the VECM analysis, the estimate of structural or policy changes is best for testing the (non)stationary properties of the series in the presence of possible structural breaks. For that reason, I tested the effect of any structural or policy changes, such as the privatization and liberalization of THY in 2005 as exogenous and endogenous structural breaks through Lee-Strazicich LM unit root tests in my preliminary VECM analysis, although the model did not estimate these changes in 2005 as structural breaks. The variables do not include structural breaks, even though they are non-stationary in their levels. For that reason, I used the ADF test in the current version of the article for unit root tests.

Toward a Wider Analysis of Market Definition

1149

Model 1: The Call Analysis

First, I estimate equation (4) as Model 1 through the call data. Table 1 reports

the summary statistics of the variables included in Model 1. I follow Akaiki-

information-criteria (AIC) procedure as the lag selection criteria for Model 1.

According to the results of lag selection criteria, I use two lags for the lag selection in

the Johansen cointegration test and the VECM, because the AIC procedure suggests

that the optimal lag length is two. In other words, I select two lags in all the system-

equation models for Model 1. In order to test the null hypothesis that there are no

cointegrating vectors (r=0) against the alternative that there is at least one

cointegrating vector (r≤1), I employ the Johansen cointegration procedure (Johansen

1995). The Johansen test estimates the number of cointegrating vectors by performing

a sequence of trace tests at a given significance level. If there are no cointegrating

vectors, I will reject the null hypothesis (r=0) and accept the alternative (r≤1), meaning

that there is at least one cointegrating vector. Also, following Johansen (1992), I apply

Sastry Pantula’s (1989) principle13 in the selection of trends, including a comparison

of the maximal Eigenvalue test statistics to its critical value. My results confirm that

constant tests in the selection of trend are more available for both Model 1 and

Model 2.

Table 1. Summary Statistics for Model 1

Note: All variables in natural logarithms.

Table 2 reports the rank analysis of multivariate cointegration system for Model

1, including the results from both trace statistics (λtrace) and maximal Eigenvalue statistics

(λmax). I reject the null hypothesis for r=0 in all the models because trace and max

statistics values for r=0 (75.26) and r=0 (53.54) are higher than the critical values

(47.21) and (27.07) at 5.0-percent significance level. On the other hand, I accept the

null hypothesis for r=1 in trace statistics and r≤1 in maximal Eigenvalue statistics

because trace and max statistics values for r=1 (21.71) and r≤1 (13.19) are less than

critical values (29.68) and (20.97) at 5.0-percent significance level. The results confirm

the presence of one cointegrating vector in Model 1. It means that there is a long-term

relationship among the variables in Model 1. I can run the VECM test.

13 I use the Pantula principle for simplicity to simultaneously determine the cointegration rank and the deterministic components of a cointegration model. However, other procedures can be used to test the same process.

Variables Obs. Mean Std. dev. Min. Max.

Fixcall 51 22.67146 0.5564991 21.67878 23.66481 Fixcallprice 51 1.374712 1.685378 –0.2005515 4.801853

Mobcallprice 51 1.610119 1.260683 –1.243349 3.186996

Income 51 4.973313 0.1393245 4.68481 5.188655

1150

Tamer Çetin

Table 2. Johansen Tests for Co-Integration for Model 1

Note: *Indicates level of statistical significance.

Table 3 reports the results of the VECM test for Model 1. The results show the

short and long-term causality relationships among the variables.14 The model is valid

because the value of the error-correction term for Fixcall is negative (–0.25). Also, this

finding is significant at 1.0-percent significance level because the value of p>|z| is

(0.00). The results are statistically and economically significant and affirm the

presence of cointegration among the variables. Accordingly, the VECM analysis

suggests that there is a long-term causality relationship running from the determinants

of demand, such as the prices of fixed and mobile voice services and the income of

consumers to the demand for fixed telephony service. This result empirically confirms

H1 because the long-term relationship among the variables as per the results of the

VECM is as expected. Note that this finding reveals the presence of this simultaneous

long-term relationship without the need for the separate observation of those market

indicators.

Table 3. Summary Results from the VECM Estimations for Model 1

Notes: Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1.

Null hypothesis Alternative hypothesis 95% critical values

λtrace rank tests Eigenvalue λtrace rank values

H0 : r = 0 H1 : r = 1 75.2670 47.21 H0 : r = 1 H1 : r = 2 0.69577 21.7189* 29.68

H0 : r = 2 H1 : r = 3 0.25418 8.5218 15.41

H0 : r = 3 H1 : r = 4 0.16804 0.2430 3.76

λmax rank tests Eigenvalue λmax rank value

H0 : r = 0 H1 : r > 0 53.5481 27.07 H0 : r ≤ 1 H1 : r > 1 0.69577 13.1970* 20.97

H0 : r ≤ 2 H1 : r > 2 0.25418 8.2788 14.07

H0 : r ≤ 3 H1 : r > 3 0.16804 0.2430 3.76

Coef. z P >|z| 95% conf. Interval R2 Constant

Fixcall –0.252*** –4.16 0.000 –0.371 –0.133 0.869 –0.092

(0.060)

Fixcallprice –1.449 –0.66 0.509 –5.753 2.855 0.345 0.086 (2.196)

Mobcallprice –0.302 –0.24 0.808 –2.739 2.135 0.619 0.336 (1.245)

Income 0.012 0.21 0.836 –0.103 0.128 0.418 –0.017

(0.059)

14 Because I focus on the long-term relationship in this article, I do not analyze the results showing the short-term causality relationships among the variables.

Toward a Wider Analysis of Market Definition

1151

I estimate the demand elasticities for fixed voice services by means of the

Johansen normalization test results. Table 4 reports these results for Model 1. The

results regarding the own-price, cross-price, and income elasticities are statistically

significant at 10, 5.0, and 1.0-percent significance levels. Also, the signs are as

expected economically. While the own-price elasticity (–0.60) suggests that the fixed

operator has market power in the fixed telephony industry, the cross-price elasticity

(1.87) confirms the presence of a strong FMS relationship. Lastly, the income

elasticity of demand (1.99) suggests that the demand for fixed voice services in Turkey

is strongly sensitive to income. The results from the call analysis are compatible with

my hypotheses H1, H2, H3, and H4.15 The results from the call analysis suggest that

the fixed and mobile voice markets in Turkey can be defined as a single market

because the findings confirm the presence of cointegration among the variables and a

strong FMS relationship.

Table 4. Johansen Normalization Test Results for Model 1

Notes: Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1.

Model 2: The Subscription Analysis

In this analysis, I estimate equation (5) as Model 2 through subscription data.

Table 5 reports the summary statistics of the variables in equation (5) for Model 2. I

follow the AIC procedure as the lag selection criteria for Model 2. The results suggest

that the optimal lag length is one. Accordingly, I use one lag in the lag selection for all

the system-equation models for Model 2. I run the Johansen test of cointegration and

the VECM analysis. I also use the Johansen procedure for cointegration tests. Table 6

reports the results of trace and max statistics for Model 2. While the null hypothesis

15 I checked whether the model has autocorrelation by diagnostic checking. According to the Lagrange-multiplier test, there is no autocorrelation problem in the model. Because the probability values (0.91 and 0.32) are bigger than 5.0 percent, the null hypothesis is accepted. There is no autocorrelation at lag order. Also, I tested whether the residuals are normally distributed or not. According to the Jarque-Bera statistics, because the probability values for all variables are bigger than 10 percent, the residuals are normally distributed. The Jarque-Bera statistics suggests the evidence of normality for all variables. The model is acceptable.

Beta Coef. z P > |z| 95% conf. Interval

Fixcall 1

Fixcallprice –0.60** –2.20 0.028 –0.114 –0.006

(0.027)

Mobcallprice 1.871*** 4.77 0.000 0.631 0.125

(0.018)

Income 1.996*** 22.84 0.000 3.653 4.339

(0.174)

Cons. –42.316

1152

Tamer Çetin

for r=0 is rejected as per both the trace and the max statistics values, r=1 for λtrace and

r≤1 for λmax is accepted. As Table 6 shows, the values of both trace (63.65) and max

(39.62) test statistics for r=0 are larger than critical values (47.21) and (27.07) at 5.0-

percent significance level. On the other hand, the values of trace (27.86) and max

(15.25) statistics are less than the critical values (24.03) and (13.60) at 5.0-percent

significance level. Accordingly, the trace and max tests both confirm the presence of

one cointegrating vector in the system. Clearly, there is also a long-term relationship

among the variables in Model 2. I can run the VECM test.

Table 5. Summary Statistics for Model 2

Notes: All variables in natural logarithms.

Table 6. Johansen Tests for Co-Integration for Model 2

Note: *Indicates level of statistical significance.

Table 7 reports the VECM results for Model 2. The value of error correction

term for fixsubnum (–0.01) affirms the existence of a long-term causality from the

independent variables to the dependent variable. Because the probability value of

p>|z| is 0.06, the result is statistically significant. As in the VECM analysis for Model

1, the VECM results from Model 2 also confirm the presence of a long-term causality

relationship among the variables in this model. Clearly, by using this estimation

methodology, I can analyze the relationship in H1 without the need for separate

observation of those market indicators as in the previous literature.

Table 8, which includes the Johansen normalization restriction results, reports

coefficients representing the sensitivity of long-term relationships among the variables

Variables Obs. Mean Std. dev. Min. Max.

Fixsubnum 51 16.60823 0.1536067 16.2751 16.76652 ARPUfix 51 3.03325 0.1162185 2. 87983 3.268846

ARPUmob 51 2.772509 0.1020877 2.603709 2.970811

Income 51 4.973313 0.1393245 4.68481 5.188655

Null hypothesis Alternative hypothesis 95% critical values

λtrace rank tests Eigenvalue λtrace rank values

H0 : r = 0 H1 : r = 1 63.6582 47.21

H0 : r = 1 H1 : r = 2 0.57745 24.0312* 29.68

H0 : r = 2 H1 : r = 3 0.25600 10.4282 15.41

H0 : r = 3 H1 : r = 4 0.15553 2.6521 3.76

λmax rank tests Eigenvalue λmax rank value

H0 : r = 0 H1 : r > 0 39.6270 27.07

H0 : r ≤ 1 H1 : r > 1 0.57745 13.6029* 20.97

H0 : r ≤ 2 H1 : r > 2 0. 25600 7.7762 14.07

H0 : r ≤ 3 H1 : r > 3 0.15553 2.6521 3.76

Toward a Wider Analysis of Market Definition

1153

in the subscription analysis.16 Coefficients are significant at 1.0-percent significance

level for the cross-price and income elasticities and at 10-percent significance level for

the own-price elasticity. The own-price, cross-price, and income elasticities of demand

are –0.85, 1.64, and 1.85 for the subscription analysis, respectively. These findings are

more compatible with hypotheses H1, H2, H3, and H4. The own-price elasticity

suggests that the fixed operator does not have a significant market power because it is

close to one, meaning that a 5.0-percent price increase cannot be profitable. More

importantly, the cross-prices elasticity corroborates this inference since it confirms the

presence of a strong FMS relationship. Overall, the findings suggest that the users of

fixed voice services prefer the mobile voice services, when the fixed operator as the

hypothetical monopolist increases its-own price for fixed services.

Table 7. Summary Results from the VECM Test for Model 2

Notes: Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1.

Table 8. Johansen Normalization Test Results for Model 2

Notes: Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1.

16 I tested whether the model has autocorrelation by diagnostic checking. According to the results of the Lagrange multiplier test, there is no autocorrelation problem in the model. Because the probability values (0.69 and 0.63) are bigger than 5.0 percent, the null hypothesis is accepted — meaning that there is no autocorrelation at lag order and the alternative is rejected. Similarly, I tested to see if residuals are normally distributed through the Jarque-Bera statistics. The results suggest that the residuals for all variables are normally distributed. The model is plausible.

Coef. z P > |z| 95% conf. Interval R2 Constant

Fixsubnum –0.013* –1.88 0.059 –0.028 –0.0005 0.894 –0.006

(0.007)

ARPUfix 0.007* 0.22 0.825 –0.062 0.078 0.432 –0.005 (0.035)

ARPUmob 0.099*** –2.67 0.008 –0.171 –0.026 0.079 –0.007 (0.037)

Income –0.125*** –3.01 0.003 –0.207 –0.043 0.523 0.006

(0.041)

Beta Coef. z P > |z| 95% conf. Interval

Fixsubnum 1

ARPUfix –0.848* –1.83 0.067 –1.755 .059

(0.463)

ARPUmob 1.635*** 4.47 0.000 0.918 2.353

(0.366)

Income 1.845*** 4.28 0.000 1.000 2.691

(0.431) Cons. –27.21

1154

Tamer Çetin

Discussion of the Findings and Policy Suggestions

In this section, I discuss the findings in terms of policy suggestions for market

definition. The results from both models include important findings regarding the

effect of market developments driven by technological change on the demand for

fixed voice services, the HMT, and the FMS. The own-price elasticities in both call

and subscription analyses affirm the presence of a negative relationship between

demand and price in the fixed voice market, as expected. However, the own-price

elasticities suggest that the hypothetical monopolist in the fixed telephony market can

have market power because coefficients are less than one in both models.

Nonetheless, note that the own-price elasticity in Model 2 is close to one. Accordingly,

if one only takes into account the own-price elasticity to define market, then one can

infer that the hypothetical monopolist has monopoly power, and thus the analyzed

industry should be defined as the relevant market. However, it is rather controversial

to define the incumbent firm as monopolist in the voice market by only taking into

account the own-price elasticity if the other findings suggest the reverse. Moreover, as

T.J. Tardiff and D.L. Weisman (2009) claim, whether the magnitude of own-price

elasticity is sufficient to discipline market power would depend on some other

considerations. When prices are high relative to marginal cost (e.g., because of the

need to recover fixed costs) and/or there are high-margin complementary products

that would exacerbate the loss of profits as subscription fell, inelastic demand

elasticity could suggest market power. This means that inelastic demand elasticity

could stem from some other factors, but not only from market power. For that

reason, I have to take into consideration the other findings in the analysis of market

definition as well. When I evaluate all the findings together, I will reach more reliable

and realistic inferences in the analysis of market definition and policy suggestions for

the regulatory process.

Accordingly, in order to understand whether the price increase is profitable and

the incumbent firm has market power, I have to analyze the FMS relationship. In

both models, the cross-price elasticities confirm the presence of a strong FMS

relationship. That is, these two findings together suggest that consumers would

decrease their demands for fixed voice and most probably prefer the alternative

products or services, such as mobile voice to fixed products, when the hypothetical

monopolist increases the price. I can infer that the fixed operator as the hypothetical

monopolist in the Turkish fixed voice market does not have monopoly power, even if

it has a 100 percent market share. Additionally, the fixed and mobile telephony

services in the Turkish telecommunications industry are strongly substitutable. This

suggests that regulators in Turkey should define the fixed and mobile voice markets as

a single market because the fixed and mobile products compete within the same

market. However, this inference is valid for the retail segment of fixed telephony

services because the findings here only confirm that there is sufficient competitive

pressure from mobile to discipline the market power of incumbent fixed operator in

the retail market. Income elasticities also corroborate these market developments.

Because the sensitivity of demand for fixed voice services to income is considerably

high in both models, the high-income elasticities suggest that the high-level income

Toward a Wider Analysis of Market Definition

1155

groups use the fixed voice services in Turkey. This is compatible with market

developments. Even though the technological development makes the mobile

telephony services cheaper, the high-level income groups continue to use the fixed

voice products. Conversely, when the income of traditional fixed phone users

decreases, they prefer to use the mobile voice services which are increasingly becoming

cheaper with technological development.

More importantly, the results from the cointegration analysis corroborate all

these market developments because the Johansen normalization results in both

models are compatible with the presence of cointegration in the VECM analysis.

Clearly, there is a long-term causality relationship running from the independent

variables to the dependent variables. In other words, the findings confirm that the

demand for fixed telephony service simultaneously declines even if the income of

consumers increases, while technological development drives down the price of

mobile products and thus facilitates the access to mobile services. Because this

relationship is driven by the technological development (as I clarified), I can infer that

technological development affects the preferences of fixed users and makes the fixed

and mobile voice services substitutable in the Turkish telecommunications industry.

As a matter of fact, demand elasticities confirm this inference. Clearly, the fixed and

mobile voice services belong to the same market. Regulator can (or should) define the

fixed and mobile voice markets as a single market and deregulate the fixed voice

market.

Conclusion

In this article, I introduced a novel approach to the analysis of market definition in

telecommunications. I employed the multivariate Johansen cointegration

methodology to investigate the long-term relationships among the variables used in

the analysis of the Turkish fixed and mobile voice industries. Because the variables are

simultaneously cointegrated in both models, there is an equilibrium long-term

causality relationship among those variables. This result empirically affirms the

observation that the demand for fixed voice services decreases, whereas the demand

for mobile voice services increases. This means that the approach I developed in this

article enables the simultaneous investigation of this long-term relationship among

the variables instead of the separate observation of each variable as in the previous

literature on market definition. Moreover, using this approach, I can analyze the

HMT and the FMS relationship through the estimation of demand elasticities.

Elasticities confirm that there is a clear and strong long-term substitution relationship

between the fixed and mobile telephony services. Because this analysis was carried out

by a simultaneous empirical methodology instead of the traditional approaches, I

argued that it introduces a more reliable and realistic approach to the analysis of

market definition. Thus, my approach constitutes a wider approach to the analysis of

market definition in telecommunications.

In terms of the regulatory process, I can infer that the results support a

deregulation of the fixed voice market. The presence of both the FMS and the long-

term causality relationship confirm that the fixed and mobile operators compete with

1156

Tamer Çetin

each other in the same market. Accordingly, regulators should define the fixed and

mobile markets, which are traditionally separate, as a single market because the fixed

and mobile services or products in these markets belong to the same market. Lastly, in

the analysis of market definition, regulators should use the empirical methodology I

presented in this article instead of the traditional tools as employed in the previous

literature. By allowing a simultaneous analysis of the long-term relationships so crucial

to market definition, my approach generates more reliable and realistic findings

regarding the regulatory process in the analysis of market definition.

References

Atiyas, Izak. “Regulation and Competition in the Turkish Telecommunications Industry.” In The Political

Economy of Regulation in Turkey, edited by Tamer Çetin and Fuat Oguz, pp. 177-191. New York, NY: Springer, 2011.

Bagdadioglu, Necmiddin and Murat Cetinkaya. “Sequencing in Telecommunications Reform: A Review of

the Turkish Case.” Telecommunications Policy 34, 11 (2010): 726-735.

Baker, Jonathan. “Market Definition: An Analytical Overview.” Antitrust Law Journal 74 (2007): 129-173. Barth, Anne-Kathrin and Ulrich Heimeshoff. “What Is the Magnitude of Fixed-Mobile Call Substitution?

Empirical Evidence from 16 European Countries.” Telecommunications Policy 38, 8-9 (2014): 771-782.

Baxter, Michael. Interpolating Annual Data into Monthly or Quarterly Data. Methodological Series No. 6. London, UK: Government Statistical Service, 1998.

Bremnes, Helge, Oystein Gjerde and Frode Sattem. “Linkages Among Interest Rates in the United States,

Germany and Norway.” Scandinavian Journal of Economics 103, 1 (2011): 122-145. Briglauer, Wolfgang, Anton Schwarz and Christine Zulehner. “Is Fixed-Mobile Substitution Strong Enough

to Deregulate Fixed Voice Telephony? Evidence from the Austrian Markets.” Journal of Regulatory

Economics 39, 1 (2011): 50-67. Cardona, Melisande, Anton Schwarz, B. Burcin Yurtoglu and Christine Zulehner. “Demand Estimation

and Market Definition for Broadband Internet Services.” Journal of Regulatory Economics 35, 1 (2009): 70-95.

Carlton, Dennis. “Market Definition: Use and Abuse.” Competition Policy International 3, 1 (2007): 2-27. Coate, Malcolm and Jeffrey Fischer. “Practical Guide to the Hypothetical Monopolist Test for Market

Definition.” Journal of Competition Law & Economics 4, 4 (2008): 1031-1106.

Çetin, Tamer. “The Role of Institutions Over Economic Change in Turkey.” In Understanding the Process of

Economic Change in Turkey: An Institutional Approach, edited by Tamer Çetin and Feridun Yılmaz, pp. 21-40. New York, NY: NOVA Science Publishers, 2010.

———. “Structural and Regulatory Reform in Turkey: Lessons from Public Utilities.” Utilities Policy 31 (December 2014): 94-106.

Hargreaves, C.P. “A Review of Methods of Estimating Cointegrating Relationships.” In Nonstationary Time

Series Analysis and Cointegration, edited by C.P. Hargreaves, pp. 87-131. Oxford, UK: Oxford University Press, 1994.

Johansen, Søren. “Determination of Cointegration Rank in the Presence of a Linear Trend.” Oxford Bulletin

of Economics and Statistics 54, 3 (1992): 383-397.

———. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford, UK: Oxford University Press, 1995.

Johansen, Søren and Katarina Juselius. “Maximum Likelihood Estimation and Inference on Cointegration

— with Applications to the Demand for Money.” Oxford Bulletin of Economics and Statistics 52, 2 (1990): 69-210.

———. “Testing Structural Hypotheses in a Multivariate Cointegration Analysis of the PPP and UIP for UK.”

Journal of Econometrics 53, 1-3 (1992): 211-244.

Kaplow, Louis. “Why (Ever) Define Markets? Harvard Law Review 124, 437 (2010): 437-517.

———. “Market Definition.” In The Oxford Handbook of International Antitrust Economics, vol. 1, edited by R.D. Blair and D.D. Sokol, pp. 345-363. Oxford, UK: Oxford University Press, 2014.

Toward a Wider Analysis of Market Definition

1157

Karacuka, Mehmet, Justus Haucap and Ulrich Heimeshoff. “Competition in Turkish Mobile

Telecommunications Markets: Price Elasticities and Network Substitution.” Telecommunications Policy

35, 2 (2011): 202-210.

Maddala, G.S. and In-Moo Kim. Unit Roots, Cointegration, and Structural Change. Cambridge, UK: Cambridge University Press, 2004.

Massey, Patrick. “Market Definition and Market Power in Competition Analysis: Some Practical Issues.”

Economic and Social Review 31, 4 (2000): 309-328. Miller, Edythe S. “Economic Regulation and New Technology in the Telecommunications Industry.”

Journal of Economic Issues 30, 3 (1996): 719-735. ———. “The Impact of Technological Change on Market Power and Market Failure in

Telecommunications.” Journal of Economic Issues 35, 2 (2001): 385-393.

Ministry of Transportation, Maritime, and Communications (UDH) of Turkey. Statistics for Transportation,

Maritime and Communication in Turkey: 2003–2011. (In Turkish). Turkey’s Ministry of Transportation, Maritime and Communications, 2011.

Oguz, Fuat. “Universal Service in Turkey: Recent Developments and a Critical Assessment.”

Telecommunications Policy 37, 1 (2013): 13-23. Oguz, Fuat and Eerman Benli. “Fixed-Mobile Substitution in the Turkish Telecommunications Market.”

Network Industries Quarterly 13-3 (2015): 19-22.

Pantula, Sastry. “Testing for Unit Roots in Time Series Data.” Econometric Theory 5, 2 (1989): 256-271. Perron, Pierre. “Testing for a Random Walk: A Simulation Experiment of Power When the Sampling

Interval Is Varied.” In Advances in Econometrics and modeling, edited by Baldev Raj, pp. 47-68. New York, NY: Springer, 1989.

Rhee, Hongjai and Minsoo Park. “Fixed-to-Mobile Call Substitution and Telephony Market Definition in

Korea.” Journal of Regulatory Economics 40, 2 (2011): 198-218. Shiller, Robert and Pierre Perron. “Testing the Random Walk Hypothesis: Power versus Frequency of

Observation.” Economics Letters 18 (April 1985): 381-386. Sidak, J. Gregory, Robert Crandall and Hal J. Singer. “The Empirical Case Against Asymmetric Regulation

of Broadband Internet Access.” Berkeley Technology Law Journal 17, 3 (2002): 953-987.

Spulber, Daniel and Christopher Yoo. Networks in Telecommunications: Economics and Law. Cambridge, UK: Cambridge University Press, 2009.

Tardiff, Timothy J. and Dennis L. Weisman “The Dominant Firm Revised.” Journal of Competition Law and

Economics 5, 3 (2009): 517-536.

The Telecommunications Authority (ICTA). Market Analyses. ICTA, n.d. Available at www.btk.gov.tr/kutuphane_ve_veribankasi/pazar_verileri/pazar_verileri.php. Accessed August 21, 2017.

Vogelsang, Ingo. “The Relationship Between Mobile and Fixed Line Communications: A Survey.”

Information, Economics and Policy 22, 1 (2010): 4-17. Ward, Michael and Glenn Woroch. “The Effect of Prices on Fixed and Mobile Telephony Penetration:

Using Price Subsidies as Natural Experiments.” Information, Economics and Policy 22, 1 (2010): 18-32.

Werden, Gregory J. “The Relevant Market: Possible and Productive.” Antitrust Law Journal (April 2014): 1-7.