Today's top research idea Market snapshot Bosch: Outlook improves ...

28

1 April 2021 Investors are advised to refer through important disclosures made at the last page of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital. Research Team ([email protected]) Equities - India Close Chg .% CYTD.% Sensex 49,509 -1.3 3.7 Nifty-50 14,691 -1.0 5.1 Nifty-M 100 23,693 0.4 13.7 Equities-Global Close Chg .% CYTD.% S&P 500 3,973 0.4 5.8 Nasdaq 13,247 1.5 2.8 FTSE 100 6,714 -0.9 3.9 DAX 15,008 0.0 9.4 Hang Seng 10,972 -0.4 2.2 Nikkei 225 29,179 -0.9 6.3 Commodities Close Chg .% CYTD.% Brent (US$/Bbl) 62 -1.5 22.0 Gold ($/OZ) 1,708 1.3 -10.0 Cu (US$/MT) 8,788 0.2 13.4 Almn (US$/MT) 2,188 -0.8 10.8 Currency Close Chg .% CYTD.% USD/INR 73.1 -0.4 0.1 USD/EUR 1.2 0.1 -4.0 USD/JPY 110.7 0.3 7.2 YIELD (%) Close 1MChg CYTD chg 10 Yrs G-Sec 6.2 0.02 0.3 10 Yrs AAA Corp 7.2 0.04 0.6 Flows (USD b) 31-Mar MTD CY21 FIIs -0.23 2.40 7.62 DIIs 0.28 0.42 -3.75 Volumes (INRb) 31-Mar MTD* YTD* Cash 603 717 792 F&O 35,377 44,383 41,170 Note: *Average Today’s top research idea Market snapshot Chart of the Day: Bosch (Outlook improves, to reach FY19 revenue levels in FY22) Bosch: Outlook improves, to reach FY19 revenue levels in FY22 ❖ Demand outlook has improved from initial expectations as the recovery has been better. It expects FY22 revenue to be similar to FY19 levels. Depending on the level of economic activity (high case assumes 11% GDP growth in CY21 and 8.5% in a low case), it expects growth in CY21 as follows: a) PVs 25%/35% (low/high case), b) M&HCV: 87%/106%, c) LCVs: 46%/54%, d) Tractors: 2%/19%, e) 2Ws: 21%/27% and f) 3Ws: 9%/25%. It forecasts M&HCV volumes to reach near previous peak levels in FY23, with volumes crossing ~400k units (v/s FY19 peak of ~444k units). ❖ BOS expects electrification to start with 2Ws/3Ws and has relevant solutions for e-2Ws, e-3Ws, and e-LCVs. For M&HCVs, it expects fuel cells to be relevant solution and is globally strong in this technology. ❖ Supply chain challenges more widespread beyond semi-conductors: The semi-conductor issue is impacting the EU, US, China, and Japan more than India. While the semi-conductor issue is well known, supply chains are under pressure globally due to a shortage of steel, plastics, rare earths, etc. Cos/Sector Key Highlights Strategy A stellar end to the fiscal Bosch The Corner Office: Outlook improves, to reach FY19 revenue levels in FY22 EcoScope What is India’s corporate profitability and what are its determinants? Key highlights – central government finances in Feb’21 Current account moves back into deficit in 3QFY21 Financials Retail credit growth improves to 9.6% YoY; forms ~29% of total loans ECLG scheme extended for another three months Oil & Gas Revision in domestic gas price for 1HFY22 Metals Regional HRC prices rise on tightening demand-supply Trend in sales Source: Company, MOFSL Segment mix Source: Company, MOFSL 120.9 97.0 104.4 116.9 120.9 98.4 94.6 119.4 10.4 0.3 7.6 12.0 3.4 -18.6 -3.9 26.3 FY15 (15m) FY16 FY17 FY18 FY19 FY20 FY21E FY22E Net Sales (INR b) Growth (%) 39 46 48 47 47 46 50 52 26 26 27 28 27 23 18 20 12 3 - - - - - - 8 8 8 8 9 11 11 9 15 17 17 17 16 20 21 19 FY15 (15m) FY16 FY17 FY18 FY19 FY20 FY21E FY22E Fuel Injection Equipment Injectors & Nozzles Starters & Generators Power tools Others Research covered ASIAMONEY Brokers Poll 2020 (India)

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Today's top research idea Market snapshot Bosch: Outlook improves ...

1 April 2021

Investors are advised to refer through important disclosures made at the last page of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Research Team ([email protected])

Equities - India Close Chg .% CYTD.%

Sensex 49,509 -1.3 3.7

Nifty-50 14,691 -1.0 5.1

Nifty-M 100 23,693 0.4 13.7

Equities-Global Close Chg .% CYTD.%

S&P 500 3,973 0.4 5.8

Nasdaq 13,247 1.5 2.8

FTSE 100 6,714 -0.9 3.9

DAX 15,008 0.0 9.4

Hang Seng 10,972 -0.4 2.2

Nikkei 225 29,179 -0.9 6.3

Commodities Close Chg .% CYTD.%

Brent (US$/Bbl) 62 -1.5 22.0

Gold ($/OZ) 1,708 1.3 -10.0

Cu (US$/MT) 8,788 0.2 13.4

Almn (US$/MT) 2,188 -0.8 10.8

Currency Close Chg .% CYTD.%

USD/INR 73.1 -0.4 0.1

USD/EUR 1.2 0.1 -4.0

USD/JPY 110.7 0.3 7.2

YIELD (%) Close 1MChg CYTD chg

10 Yrs G-Sec 6.2 0.02 0.3

10 Yrs AAA Corp 7.2 0.04 0.6

Flows (USD b) 31-Mar MTD CY21

FIIs -0.23 2.40 7.62

DIIs 0.28 0.42 -3.75

Volumes (INRb) 31-Mar MTD* YTD*

Cash 603 717 792

F&O 35,377 44,383 41,170

Note: *Average

Today’s top research idea

Market snapshot

Chart of the Day: Bosch (Outlook improves, to reach FY19 revenue levels in FY22)

Bosch: Outlook improves, to reach FY19 revenue levels in FY22 ❖ Demand outlook has improved from initial expectations as the recovery has

been better. It expects FY22 revenue to be similar to FY19 levels. Depending

on the level of economic activity (high case assumes 11% GDP growth in CY21

and 8.5% in a low case), it expects growth in CY21 as follows: a) PVs 25%/35%

(low/high case), b) M&HCV: 87%/106%, c) LCVs: 46%/54%, d) Tractors:

2%/19%, e) 2Ws: 21%/27% and f) 3Ws: 9%/25%. It forecasts M&HCV volumes

to reach near previous peak levels in FY23, with volumes crossing ~400k units

(v/s FY19 peak of ~444k units).

❖ BOS expects electrification to start with 2Ws/3Ws and has relevant solutions

for e-2Ws, e-3Ws, and e-LCVs. For M&HCVs, it expects fuel cells to be relevant

solution and is globally strong in this technology.

❖ Supply chain challenges more widespread beyond semi-conductors: The

semi-conductor issue is impacting the EU, US, China, and Japan more than

India. While the semi-conductor issue is well known, supply chains are under

pressure globally due to a shortage of steel, plastics, rare earths, etc.

Cos/Sector Key Highlights

Strategy A stellar end to the fiscal

Bosch The Corner Office: Outlook improves, to reach FY19 revenue levels in FY22

EcoScope

What is India’s corporate profitability and what are its determinants?

Key highlights – central government finances in Feb’21

Current account moves back into deficit in 3QFY21

Financials Retail credit growth improves to 9.6% YoY; forms ~29% of total loans

ECLG scheme extended for another three months

Oil & Gas Revision in domestic gas price for 1HFY22

Metals Regional HRC prices rise on tightening demand-supply

Trend in sales

Source: Company, MOFSL

Segment mix

Source: Company, MOFSL

12

0.9

97

.0

10

4.4

11

6.9

12

0.9

98

.4

94

.6

11

9.4

10.4

0.37.6

12.0

3.4

-18.6

-3.9

26.3

FY15(15m)

FY16 FY17 FY18 FY19 FY20 FY21E FY22E

Net Sales (INR b) Growth (%)

39 46 48 47 47 46 50 52

26 26 27 28 27 23

18 20

12 3 - - - - - -8 8 8 8 9 11

11 9

15 17 17 17 16 20 21 19

FY15(15m)

FY16 FY17 FY18 FY19 FY20 FY21E FY22E

Fuel Injection Equipment Injectors & NozzlesStarters & Generators Power toolsOthers

Research covered

ASIAMONEY Brokers Poll 2020 (India)

1 April 2021 2

Core sector contracts 4.6 per cent in February; highest in six months The core sector index, which measures output of eight infrastructure industries declined by 4.6% in February 2021 compared to February last year. This is a sharp dip and a reversal of sorts of the marginal uptake seen in the preceding months with growth of 0.9% in January…

Four PSU banks to get ₹14,500 cr via zero coupon bonds The central government will infuse ₹14,500 crore capital in Central Bank of India, Indian Overseas Bank, Bank of India, and UCO Bank through non-interest bearing bonds, after a similar infusion of ₹5,500 crore in Punjab and Sind Bank in December…

Non-food bank credit offtake slows to 6.5% in February Bank credit offtake in the non-food sector slowed to 6.5 per in February 2021 on an annual basis, mainly on account of the impact of the coronavirus pandemic. Also, the slowdown in growth of personal loans continued as it decelerated to 9.6 per cent in February 2021 from 17 per cent a year ago, said the RBI's data on sectoral deployment of bank credit collected…

Government mops up Rs 32,835 crore from disinvestment in FY21, exceeds RE target The government has mopped up Rs 32,835 crore from CPSE share sale and buybacks, thus exceeding the disinvestment target set in the revised estimates (RE) for current fiscal. The realisation is, however, lower than the record Rs 2.10 lakh crore originally budgeted. In the RE, the target was scaled down…

Cost of domestic LPG cylinder reduced by Rs 10 Prices of cooking gas have been cut by Rs 10 per cylinder following a drop in international rates, Indian Oil Corporation said in a statement. This is the first reduction in prices that have risen by Rs 225 since November. A refill will now cost Rs 809 per cylinder in Delhi…

Piramal Pharma to acquire 100 pc stake in Hemmo Pharma for Rs 775 cr Piramal Pharma Ltd, a subsidiary of the company, has entered into an agreement to acquire a 100 per cent stake in Hemmo Pharmaceuticals for an upfront consideration of Rs 775 crore and earn-outs linked to the achievement of milestones, Piramal Enterprises…

PPF hits 46 year low of 6.4% as govt cuts interest rates of small savings schemes As per a finance ministry circular, dated March 31, 2021, interest rates on small savings schemes have been cut by massively between 40 -110 basis points (100 basis points/bps = 1%) for the first quarter of the financial year 2021-22. The PPF interest rate below 7% would be…

Kindly click on textbox for the detailed news link

In the news today

2

5

6 7

4

1

3

1 April 2021 3

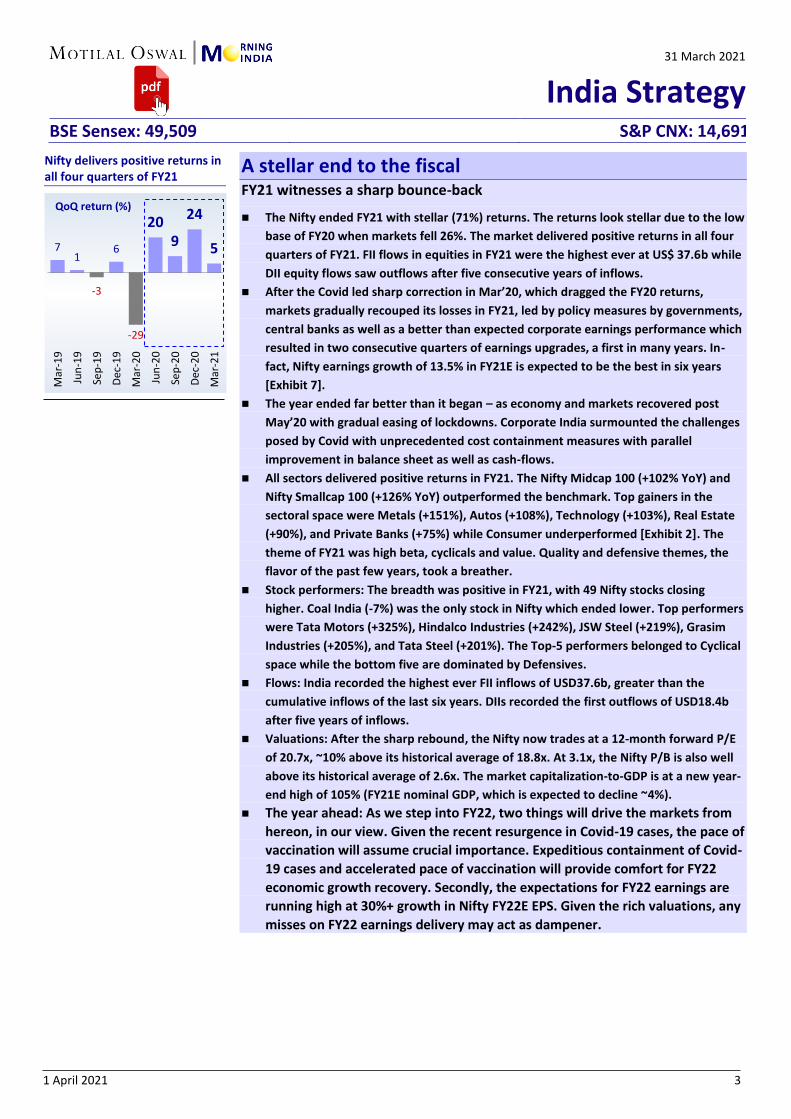

A stellar end to the fiscal FY21 witnesses a sharp bounce-back

◼ The Nifty ended FY21 with stellar (71%) returns. The returns look stellar due to the low

base of FY20 when markets fell 26%. The market delivered positive returns in all four

quarters of FY21. FII flows in equities in FY21 were the highest ever at US$ 37.6b while

DII equity flows saw outflows after five consecutive years of inflows.

◼ After the Covid led sharp correction in Mar’20, which dragged the FY20 returns,

markets gradually recouped its losses in FY21, led by policy measures by governments,

central banks as well as a better than expected corporate earnings performance which

resulted in two consecutive quarters of earnings upgrades, a first in many years. In-

fact, Nifty earnings growth of 13.5% in FY21E is expected to be the best in six years

[Exhibit 7].

◼ The year ended far better than it began – as economy and markets recovered post

May’20 with gradual easing of lockdowns. Corporate India surmounted the challenges

posed by Covid with unprecedented cost containment measures with parallel

improvement in balance sheet as well as cash-flows.

◼ All sectors delivered positive returns in FY21. The Nifty Midcap 100 (+102% YoY) and

Nifty Smallcap 100 (+126% YoY) outperformed the benchmark. Top gainers in the

sectoral space were Metals (+151%), Autos (+108%), Technology (+103%), Real Estate

(+90%), and Private Banks (+75%) while Consumer underperformed [Exhibit 2]. The

theme of FY21 was high beta, cyclicals and value. Quality and defensive themes, the

flavor of the past few years, took a breather.

◼ Stock performers: The breadth was positive in FY21, with 49 Nifty stocks closing

higher. Coal India (-7%) was the only stock in Nifty which ended lower. Top performers

were Tata Motors (+325%), Hindalco Industries (+242%), JSW Steel (+219%), Grasim

Industries (+205%), and Tata Steel (+201%). The Top-5 performers belonged to Cyclical

space while the bottom five are dominated by Defensives.

◼ Flows: India recorded the highest ever FII inflows of USD37.6b, greater than the

cumulative inflows of the last six years. DIIs recorded the first outflows of USD18.4b

after five years of inflows.

◼ Valuations: After the sharp rebound, the Nifty now trades at a 12-month forward P/E

of 20.7x, ~10% above its historical average of 18.8x. At 3.1x, the Nifty P/B is also well

above its historical average of 2.6x. The market capitalization-to-GDP is at a new year-

end high of 105% (FY21E nominal GDP, which is expected to decline ~4%).

◼ The year ahead: As we step into FY22, two things will drive the markets from

hereon, in our view. Given the recent resurgence in Covid-19 cases, the pace of

vaccination will assume crucial importance. Expeditious containment of Covid-

19 cases and accelerated pace of vaccination will provide comfort for FY22

economic growth recovery. Secondly, the expectations for FY22 earnings are

running high at 30%+ growth in Nifty FY22E EPS. Given the rich valuations, any

misses on FY22 earnings delivery may act as dampener.

31 March 2021

India Strategy BSE Sensex: 49,509 S&P CNX: 14,691

Nifty delivers positive returns in all four quarters of FY21

71

-3

6

-29

209

24

5

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

QoQ return (%)

1 April 2021 4

FY21 Nifty returns best in the last 11 years; low base of FY20 coupled with solid earnings drove the returns

Sectoral performance FY21 (%) – Metals, Autos, Technology Outperform while Consumer Underperforms

Best and worst Nifty performers for FY21 (%) – 29 companies outperform the benchmark

244

-48

78

-16

0 -2

15

-3

42

-25

-2-13

81

15

67

1224

-36

74

11

-9

7

1827

-9

19 10 15

-26

71

FY9

2

FY9

3

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

Nifty annual return YoY (%)

CAGR of 13.1%

Four years of negative return in the 2000s cycle

Five years of negative return in the 1990s cycle

Three years of negative return in the FY11-20 cycle

71

102

126

151

108 10390

75 73 7163 63

49

28

Nif

ty-5

0

Mid

cap

10

0

Smal

lcap

10

0

Met

al

Au

to

Tech

no

logy

Rea

l Est

ate

Ban

k P

VT

Infr

a

Hea

lth

care

Oil

& G

as

Ban

k P

SU

Med

ia

Co

nsu

mer

FY21 change (%)

32

52

42

21

92

05

20

11

80

17

91

72

13

21

25

11

71

14

11

11

11

10

79

99

79

38

58

48

38

38

28

17

97

67

57

47

3

71

70

68

67

60

58

53

52

50

45

37

36

35

35

35

27

26

17

12

6 5-7

Tata

Mo

tors

Hin

dal

coJS

W S

teel

Gra

sim

Ind

Tata

Ste

el

Ad

ani P

ort

sM

&M

Ind

usI

nd

Bk

Baj

aj F

in.

HC

L Te

chTa

ta C

on

sum

erIn

fosy

sW

ipro

Baj

aj F

inse

rvU

ltra

Tech

Eich

er M

oto

rsU

PL

Cip

laSB

IA

xis

Ban

kH

ero

Mo

toD

ivi's

Lab

.R

elia

nce

Ind

.B

ajaj

Au

toIC

ICI B

ank

L&T

Tech

Mah

.TC

SH

DFC

Ban

kN

ifty

Sun

Ph

arm

aSh

ree

Cem

ent

Tita

n C

oM

aru

tiH

DFC

Lif

eH

DFC

Asi

an P

ain

tsO

NG

CD

r R

edd

y's

SBI L

ife

Ins

Po

wer

Gri

dB

PC

LK

ota

k M

ah.B

kB

rita

nn

iaIT

CN

TPC

Bh

arti

Air

tel

IOC

HU

LN

est

leC

oal

Ind

ia

1 April 2021 5

Outlook improves, to reach FY19 revenue levels in FY22 EVs: Good presence in 2Ws/PVs | PLI opportunity attractive, but awaits clarity

We hosted the senior management of Bosch. Our meeting with Mr. Soumitra Bhattachrya,

MD, Bosch, and Regional President, Bosch Group India, included discussions on the business,

its preparedness for technological disruptions, and the PLI opportunity.

◼ Demand recovery better than originally estimated: The outlook has improved from

initial expectations as the recovery has been better. It expects FY22 revenue to be

similar to FY19 levels. Depending on the level of economic activity (high case

assumes 11% GDP growth in CY21 and 8.5% in a low case), it expects growth in CY21

as follows: a) PVs 25%/35% (low/high case), b) M&HCV: 87%/106%, c) LCVs:

46%/54%, d) Tractors: 2%/19%, e) 2Ws: 21%/27% and f) 3Ws: 9%/25%. It forecasts

M&HCV volumes to reach near previous peak levels in FY23, with volumes crossing

~400k units (v/s FY19 peak of ~444k units).

◼ EVs – BOS supplies to relevant 2Ws, PVs models: BOS expects electrification to

start with 2Ws/3Ws and has relevant solutions for e-2Ws, e-3Ws, and e-LCVs. It is

already supplying to: a) Bajaj Chetak (drive, battery, ECU, connectivity box, and

App/Cloud services), b) TVS iQube (ECU and in-hub drive system), and c) Tata

Nexon. For M&HCVs, it expects fuel cells to be relevant solution and is globally

strong in this technology. For EVs, the parent had a total upfront investment of

EUR5b and invested EUR700m in CY21. It has won 90 projects and orders worth

EUR7.5b.

◼ PLI scheme seems attractive, but details awaited: Of the four PLI schemes for Auto,

BOS would benefit from three of them (excluding the OEM scheme). The group, it

indicated, can claim up to USD1b under this scheme. It will work on these schemes

once the final details are out.

◼ Other takeaways

➢ Supply chain challenges more widespread beyond semi-conductors: The semi-

conductor issue is impacting the EU, US, China, and Japan more than India.

While the semi-conductor issue is well known, supply chains are under pressure

globally due to a shortage of steel, plastics, rare earths, etc.

➢ 100% subsidiary to offer manufacturing as a service: Its 100% subsidiary,

Robert Bosch India Manufacturing, would offer manufacturing as a service in

the Automotive segment for both external customers as well as group

companies.

➢ Margin to see steady improvement based on mix improvement/content increase, restructuring/reskilling,

and cost controls.

➢ BS-VI confirmatory factors are ahead of regulatory norms, with 9%/70% of projects confirming to the factor

of 2.1/1.43.

➢ Its smart campus (75 acres) in the heart of Bengaluru will be operational in Jun’22, its 100th year in India. It

has invested INR8b on this smart campus and would house the second highest number of Bosch employees

in the world.

31 March 2021

CornerOffice

the

Interaction with the CEO

Bosch Limited

Mr. Soumitra Bhattacharya,

MD, Bosch, and Regional President, Bosch Group

in India

Mr. Bhattacharya has been

associated with the Bosch

Group for more than 24

years. A Chartered

Accountant by profession,

over the years he has

handled varied roles across

the group in India and

overseas. He was the CFO of

Bosch India from CY11 till

CY18. In CY16, he took over

as CEO. Prior to joining

Bosch, he worked at the

Tata group where he was

the founding member of the

Tanishq brand for Titan

Company. He also worked

at INDAL, the core

aluminum business of the

ALCAN group, and was a

founding member of its

electronics business

1 April 2021 6

◼ Valuation and view: The transition to BS-VI led to further market share loss in CVs as well as a continuous

decline in its stronghold PV diesel, although the 2W segment has opened up for BOS (one of the 3-4 players in

2W EFI). Valuations have corrected in line with muted earnings over the last four years, dilution in its

competitive positioning, as well as on concerns due to EVs. While it is too early to assess the competitive

landscape in EVs, BOS is very well-prepared to leverage electrification in 2Ws. We expect it to outperform

underlying industry volumes, barring the substantial divergence in segmental trends, driven by an increase in

content under BS-VI as well as additional revenue from 2W EFI. The stock trades ~29.3x/25.4x FY22E/FY23E EPS.

The stock price largely reflects all the negatives, but a re-rating catalyst may emerge in 2-3 quarters. We

maintain Neutral with a TP of ~INR15,550/share (~28x Mar’23E EPS at a 20% discount to its 10-year LPA of 35x).

P/E and P/B band

Source: MOFSL

Source: MOFSL

30.536.5

54.2

18.7

45.8

27.3

10.0

22.0

34.0

46.0

58.0

Mar

-11

Jun

-12

Sep

-13

Dec

-14

Mar

-16

Jun

-17

Sep

-18

Dec

-19

Mar

-21

P/E (x) Avg (x) Max (x)

Min (x) +1SD -1SD

4.05.5

8.7

2.9

6.9

4.1

2.0

4.0

6.0

8.0

10.0

Mar

-11

Jun

-12

Sep

-13

Dec

-14

Mar

-16

Jun

-17

Sep

-18

Dec

-19

Mar

-21

P/B (x) Avg (x) Max (x)

Min (x) +1SD -1SD

1 April 2021 7

31 March 2021

ECOSCOPE The Economy Observer

What is India’s corporate profitability... …and what are its determinants?

◼ When anyone talks about India’s corporate profitability, we tend to narrow down our analysis to the listed

sector comprising of about 6,500 companies. Corporate profitability in India, in this narrow sense, peaked out

at 6.3% of GDP in FY08 and has fallen to a 27-year low of 1.5% of GDP in FY20. During the same period,

corporate profitability in the US moved to 9% from 8% of GDP. The same for the UK rose slightly to 9.1% from

8.6% of GDP. In short, while corporate profitability in India fell in the 2010s decade, it rose to a record high in

the US and was stable in the UK.

◼ This wide gap between India and the Western world in terms of corporate profitability is highly misleading

because it’s like comparing apples with oranges. While the US and the UK are organized/formal economies,

India has a very large unlisted/unorganized sector. According to the Ministry of Corporate Affairs (MCA), only

~0.5% of registered companies in India (6,741 out of 1.33m) are listed and less than half of them are actively

traded. From an economic perspective, the large set of unlisted companies plays a very crucial role. In this

note, we provide a long-term series on India’s corporate profitability, including unlisted companies. Since our

estimates are based on a macroeconomic identity, we discuss in detail about the key determinants of

corporate profitability in a nation.

◼ Using the macroeconomic identity, which we call the ‘Theory of Everything’, our estimates suggest that India’s

corporate profitability (listed + unlisted) moved up from a paltry 5% of GDP in the late 1990s and early 2000s

to its peak of 12.4% of GDP in FY08 and has been in a narrow range (8.5% to 9.5% of GDP) between FY09 and

FY18. It fell to a 15-year low of 7.9% of GDP in FY19, before recovering to 8.9% of GDP in FY20 (subject to

revisions). India’s corporate profitability in recent years was comparable to that of the US and the UK.

However, there are two highlights: a) corporate profitability in India has weakened compared to pre-CY08

levels, while it has increased in the US and the UK, and b) the share of unlisted companies in India’s corporate

profitability has risen to about 70% in recent years from less than half in the 2000s decade.

◼ We also analyze the only available data set on domestic private limited (unlisted) companies by the Reserve

Bank of India (RBI) to get more confidence on these findings. According to RBI data, the profitability of private

limited companies has increased at an average 21% during the past seven years (FY13-19) vis-à-vis an average

growth of just 3% for listed companies. The rising share of unlisted companies in India’s corporate profitability

is thus confirmed by RBI’s data set.

◼ Corporate profitability in an economy is dependent on the corporate sector and behavior of households,

government, and the external sector. Corporate profitability is positively correlated with total investments

and fiscal deficit in a country, while it is inversely correlated with household savings and current account

deficit (CAD) in an economy. In other words, greater the investments/fiscal deficit and lower the household

savings/CAD, the higher is corporate profitability.

◼ Based on these key drivers, the trends in India’s corporate profitability can be broadly divided into five phases

in the past three decades. The rapid surge in profitability between FY03 and FY08 was entirely driven by

higher investments, while the decline in the immediate period post-GFC (FY09-13) was led by higher

household savings and wider CAD. Recently, corporate profitability has been stable, as lower investments

were almost entirely offset by lower household savings.

◼ It will not be advisable to extrapolate trends of listed companies to the entire corporate sector, and thus, the

economy. While listed companies have seen a rise in profitability in 2HCY20, unlisted companies are likely to

have suffered more due to COVID-19. Also, we must appreciate the inter-linkages between different sectors

and its impact on corporate profitability.

1 April 2021 8

31 March 2021

ECOSCOPE The Economy Observer

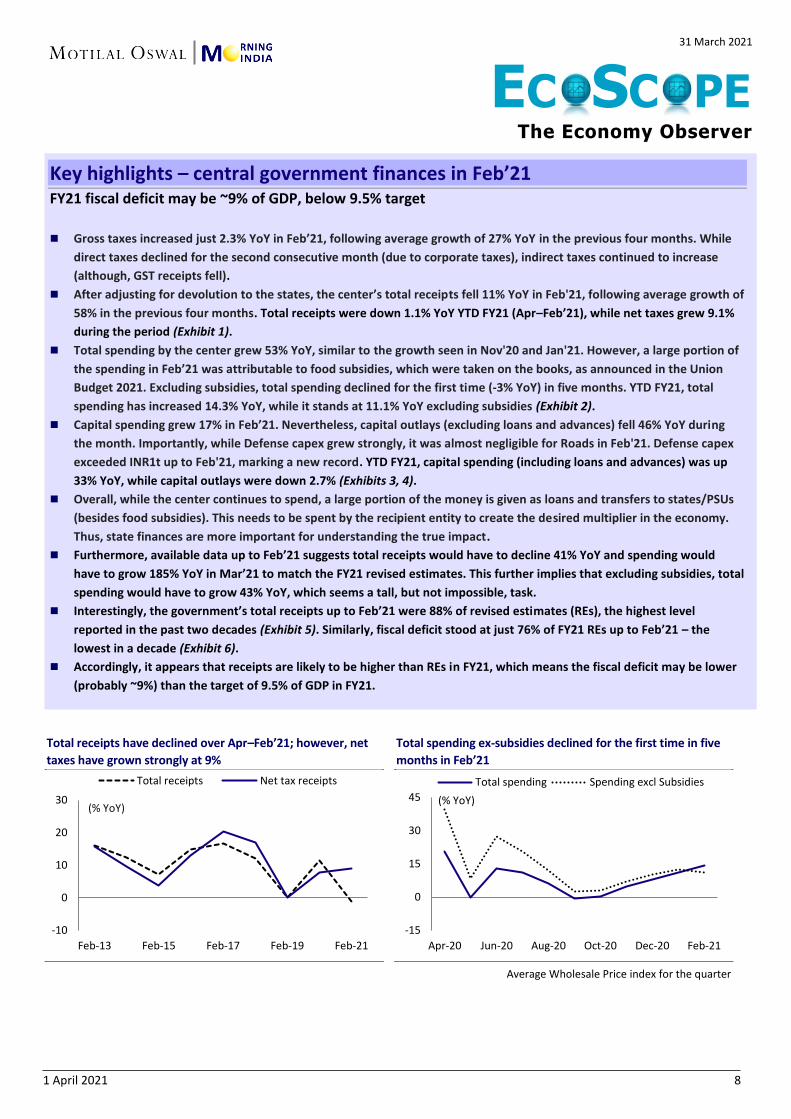

Key highlights – central government finances in Feb’21 FY21 fiscal deficit may be ~9% of GDP, below 9.5% target

◼ Gross taxes increased just 2.3% YoY in Feb’21, following average growth of 27% YoY in the previous four months. While

direct taxes declined for the second consecutive month (due to corporate taxes), indirect taxes continued to increase

(although, GST receipts fell).

◼ After adjusting for devolution to the states, the center’s total receipts fell 11% YoY in Feb'21, following average growth of

58% in the previous four months. Total receipts were down 1.1% YoY YTD FY21 (Apr–Feb’21), while net taxes grew 9.1%

during the period (Exhibit 1).

◼ Total spending by the center grew 53% YoY, similar to the growth seen in Nov'20 and Jan'21. However, a large portion of

the spending in Feb’21 was attributable to food subsidies, which were taken on the books, as announced in the Union

Budget 2021. Excluding subsidies, total spending declined for the first time (-3% YoY) in five months. YTD FY21, total

spending has increased 14.3% YoY, while it stands at 11.1% YoY excluding subsidies (Exhibit 2).

◼ Capital spending grew 17% in Feb’21. Nevertheless, capital outlays (excluding loans and advances) fell 46% YoY during

the month. Importantly, while Defense capex grew strongly, it was almost negligible for Roads in Feb'21. Defense capex

exceeded INR1t up to Feb'21, marking a new record. YTD FY21, capital spending (including loans and advances) was up

33% YoY, while capital outlays were down 2.7% (Exhibits 3, 4).

◼ Overall, while the center continues to spend, a large portion of the money is given as loans and transfers to states/PSUs

(besides food subsidies). This needs to be spent by the recipient entity to create the desired multiplier in the economy.

Thus, state finances are more important for understanding the true impact.

◼ Furthermore, available data up to Feb’21 suggests total receipts would have to decline 41% YoY and spending would

have to grow 185% YoY in Mar’21 to match the FY21 revised estimates. This further implies that excluding subsidies, total

spending would have to grow 43% YoY, which seems a tall, but not impossible, task.

◼ Interestingly, the government’s total receipts up to Feb’21 were 88% of revised estimates (REs), the highest level

reported in the past two decades (Exhibit 5). Similarly, fiscal deficit stood at just 76% of FY21 REs up to Feb’21 – the

lowest in a decade (Exhibit 6).

◼ Accordingly, it appears that receipts are likely to be higher than REs in FY21, which means the fiscal deficit may be lower

(probably ~9%) than the target of 9.5% of GDP in FY21.

Total receipts have declined over Apr–Feb’21; however, net

taxes have grown strongly at 9%

Total spending ex-subsidies declined for the first time in five

months in Feb’21

Average Wholesale Price index for the quarter

-10

0

10

20

30

Feb-13 Feb-15 Feb-17 Feb-19 Feb-21

Total receipts Net tax receipts

(% YoY)

-15

0

15

30

45

Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 Feb-21

Total spending Spending excl Subsidies

(% YoY)

1 April 2021 9

Capital spending has increased sharply, primarily due to

‘loans & advances’…

…as capital outlays in FY21 are weak v/s previous years

Average Wholesale Price index for the quarter

Total receipts in YTD FY21 as % of REs are the highest since

FY01…

…while fiscal deficit in YTD FY21 (as % of REs) is the lowest in

a decade

Average Wholesale Price index for the quarter

-40

-14

12

38

64

Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 Feb-21

Capital spending Capital outlays

(% YoY)

-40

-10

20

50

80

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Capital Outlays YTD (% YoY)

FY19 FY20 FY21

0

30

60

90

120

FY01 FY03 FY05 FY07 FY09 FY11 FY13 FY15 FY17 FY19 FY21

Total receipts(% of REs)

-10

30

70

110

150

FY01 FY03 FY05 FY07 FY09 FY11 FY13 FY15 FY17 FY19 FY21

Fiscal deficit(% of REs)

1 April 2021 10

Current account moves back into deficit in 3QFY21

Expect CAD to widen in subsequent quarters

◼ India’s current account balance moved to a deficit of USD1.7b (or 0.2% of GDP) in 3QFY21, against an average surplus of

USD17b (3% of GDP) in 1HFY21. CAD was marginally better than the market consensus of USD2.4b (or 0.3% of GDP).

Merchandise deficit stood at 4.7% of GDP in 3QFY21, vis-à-vis 2.2% of GDP in 1HFY21, while the surplus on the invisibles

(services + income) account was at a 10-quarter low of 4.4% of GDP.

◼ Net foreign capital inflows in India amounted to USD33.5b, the highest ever in absolute terms; however, they stood at

4.5% of GDP, the highest in the past six years, but less than half the peak inflows of 11.7% of GDP reported in 2QFY08.

Foreign direct investment (FDI) inflows stood at USD17b, followed by an all-time high of USD25b in 2QFY21. Foreign

portfolio investment (FPIs) inflows came in at USD21.2b – the highest in absolute terms.

◼ As foreign capital inflows outpaced CAD, India added more than USD30b in foreign exchange reserves (FXR) for the

second consecutive quarter in 3QFY21.

◼ With a marginal uptick in investments to 29.5% of GDP and small CAD in 3QFY21, gross domestic savings (GDS) stood at

29.3% of GDP last quarter. For the three quarters in FY21, however, gross domestic savings (GDS) stood at 28.8% of GDP,

lower than 29.6% of GDP in the corresponding period in FY20.

◼ Current account posts deficit after three successive surpluses in 3QFY21:

India’s current account balance moved to a deficit of USD1.7b (or 0.2% of GDP),

after reporting an average surplus of USD17b (or 3% of GDP) in 1HFY21 (Exhibit

1). It was marginally lower than the market consensus of a deficit of USD2.4b (or

0.3% of GDP). This implies India’s current account surplus was 1.7% of GDP in

9MFY21.

◼ Merchandise deficit drives CAD in 3QFY21: Merchandise trade deficit stood at

4.7% of GDP in 3QFY21, vis-à-vis 2.2% of GDP in 1HFY21 (Exhibit 2). The higher

merchandise deficit was primarily attributable to much slower decline in

imports (-4.7% YoY in 3Q vis-à-vis -24.4% in 2Q), while the fall in merchandise

exports (at 4.9% YoY) was similar to that in 2QFY21 (-5.5% YoY). Notably,

although the deficit on petroleum products widened last quarter, the expansion

in merchandise trade deficit was broad-based. The surplus on the invisibles

(services + income) account was also at a 10-quarter low of 4.4% of GDP – as

exports of invisibles fell 1.6% YoY, while imports declined just 1.5% in 3QFY21.

Excluding petroleum products, India had a current account surplus of 2% of

GDP, lower than in the past four quarters, but higher than in the pre-COVID era.

◼ Capital inflows increase substantially in 3QFY21: Net foreign capital inflows in

India amounted to USD33.5b, the highest ever in absolute terms. However, they

stood at 4.5% of GDP, the highest in the past six years, but less than half the

peak inflows of 11.7% of GDP reported in 2QFY08. FDI inflows stood at USD17b,

followed by an all-time high of USD25b in 2QFY21. FPIs inflows came in at

USD21.2b – the highest in absolute terms. Again, as a percentage of GDP, FPI

inflows were 2.9% in 3QFY21 – lower than ~4% of GDP in FY08 and the peak of

5% of GDP in 2QFY11. As foreign capital inflows outpaced CAD, India added

more than USD30b in FXR for the second consecutive quarter in 3QFY21 (Exhibit

3).

31 March 2021

ECOSCOPE The Economy Observer

1 April 2021 11

◼ Savings up in 3QFY21, but lower in 9MFY21: With a marginal uptick in

investments to 29.5% of GDP and small CAD in 3QFY21, GDS stood at 29.3% of

GDP last quarter. For the three quarters in FY21, however, GDS was 28.8% of

GDP, lower than 29.6% of GDP in the corresponding period in FY20 (Exhibit 4).

◼ Except CAD to continue to widen in subsequent quarters: With oil prices

exceeding USD60/barrel in 4QFY21 and the general widening of merchandise

trade deficit, India’s CAD is very likely to widen to ~1% of GDP in 4QFY21. This

implies India could post a surplus of about 0.9% of GDP for the full-year FY21 –

which could deteriorate to deficit of 0.8% of GDP in FY22.

India’s current account back in deficit for the first time in four

quarters in 3QFY21…

…due to sharp deterioration in merchandise trade deficit and

10-quarter low surplus in invisibles

Source: RBI, MOFSL

Strong capital inflows with small CAD result in accretion of

>USD30b in FXR in 3QFY21

* (-) Implies accretion to reserves, (+) implies withdrawal (reduction)

With marginal uptick in investments and small CAD, GDS up in

3QFY21

# Implied savings; Does not include ‘errors & omissions’

(6)

(3)

0

3

6

3QFY15 3QFY16 3QFY17 3QFY18 3QFY19 3QFY20 3QFY21

CAB CAB ex fuel products(% of GDP)

-4.7

3.2

1.2

(8)

(4)

0

4

8

3QFY18 1QFY19 3QFY19 1QFY20 3QFY20 1QFY21 3QFY21

Goods Services Income

(% of GDP)

(40,000)

(20,000)

0

20,000

40,000

Q3 FY16 Q3 FY17 Q3 FY18 Q3 FY19 Q3 FY20 Q3 FY21

Forex reserves* CAB Capital A/c

(USD mn)

-6

-3

0

3

6

20

24

28

32

36

3QFY17 3QFY18 3QFY19 3QFY20 3QFY21

CAB (RHS) Savings# Investments

(% of GDP) (% of GDP)

1 April 2021 12

Retail credit growth improves to 9.6% YoY; forms ~29% of total loans

Retail loans comprise 78% of incremental credit over FY21YTD

◼ Systemic loan growth stood at 6.5% YoY for the fortnight-ended 12th Mar’21. The

outstanding credit base has now reached INR108t. Retail credit growth improved to

9.6% YoY (v/s 9.1% YoY in Jan’21), with retail loans comprising ~78% of incremental

credit over FY21YTD. Among the retail segments, housing loans grew 8.4% YoY (7.7%

in Jan’21) and vehicle loans rose 8.3% YoY (7.1% in Jan’21). Credit cards grew 4.8% YoY

(flattish on a month-on-month basis).

◼ Industry growth remained flattish, while growth in the Services segment improved to

~9.3% YoY. Agri growth also picked up at 10.2% YoY.

◼ Systemic loan growth is showing signs of revival, aided by rising consumer demand, with

disbursements across various retail products – such as 2W, home, auto, LAP, and gold

loans – surpassing pre-COVID levels. Banks, however, remain cautious about growing the

unsecured book. Even growth in the Corporate segment is recovering, with the focus on

lending to high-rated corporates, primarily for working capital needs.

◼ We expect the 1HFY22E capex cycle to be supported by PSU entities, while private

sector capex would revive from 2HFY22E. Thus, we expect banking system credit to

grow ~6.8%/11% YoY over FY21E/FY22E, with private banks expected to grow higher

at ~15% YoY.

Retail growth improves to 9.6% YoY in Feb’21, led by home/auto loans Retail credit growth improved to 9.6% YoY in Feb’21 (v/s 9.1% YoY in Jan’21), with

growth in home loans improving to 8.4% YoY (v/s 7.7% YoY in Jan’21). Vehicle loan

growth also improved at 8.3% YoY (v/s 7.1% YoY in Jan’21), while credit card growth

moderated slightly to 4.8% YoY. On a monthly basis, retail loans grew 1.8% MoM –

within which home/vehicle loans grew 1.6%/1.5% MoM, while credit card growth

stood flattish. Overall, the share of retail in total systemic credit stood at 29.2%

(v/s 20% four years ago) and comprises ~78% of incremental credit over FY21YTD.

Banks have indicated that growth in segments such as Tractors, 2Ws, Auto Loans,

Gold Loans, and Affordable Housing has surpassed pre-COVID levels; recovery is

seen in the Corporate segment as well.

Industry growth muted; expect capex demand to pick up over FY22E ◼ Large-scale industries posted decline of 1.5% YoY. However, medium-scale

industries grew robustly at 21% YoY, while the trend in micro/small businesses

was muted at 1.5% YoY.

◼ Furthermore, growth in the Services/Agri sector improved to 9.3%/10.2% YoY.

Among sectors, Commercial Real Estate grew 1.6% YoY and Transport Operators

grew 4.6% YoY. NBFC, however, grew strongly at 27% YoY.

◼ Given the government’s focus on improving expenditure, we expect capex demand

to pick up – the 1HFY22E capex cycle is likely to be supported by various PSU

companies and a revival is expected in private sector capex from 2HFY22.

System deposit growth trends robust at 12.1% YoY; CD ratio stands at ~72% Deposit growth for the fortnight stood at 12.1% YoY. The outstanding deposit base

reached INR149.6t. Most banks are focusing on garnering deposits (particularly

CASA and retail TD) to ramp up their liability franchises and reduce dependence on

bulk deposits. The systemic CD ratio stood at ~72% (v/s ~76% in Mar’20).

Sector Update | 31 March 2021

Financials

Systemic loan growth at 6.5%

YoY; deposit growth at 12.1%

YoY as of 12th Mar’21

Source: RBI, MOFSL Retail growth improves to 9.6%

YoY (v/s 9.1% in Jan’21)

Source: RBI, MOFSL

6.5%

12.1%

0%

6%

12%

18%

24%

Mar

-15

Jul-

15

No

v-1

5M

ar-1

6Ju

l-1

6N

ov-

16

Mar

-17

Jul-

17

No

v-1

7M

ar-1

8Ju

l-1

8N

ov-

18

Mar

-19

Jul-

19

No

v-1

9M

ar-2

0Ju

l-2

0N

ov-

20

Mar

-21

Loan growth (%)

Deposit growth (%)

9.6%

5%

10%

15%

20%

25%

Feb

-17

May

-17

Au

g-1

7N

ov-

17

Feb

-18

May

-18

Au

g-1

8N

ov-

18

Feb

-19

May

-19

Au

g-1

9N

ov-

19

Feb

-20

May

-20

Au

g-2

0N

ov-

20

Feb

-21

Retail growth yoy (%)

1 April 2021 13

Monetary easing drives reduction in lending rates; NIMs to exhibit

stable/improving trends Continued monetary easing has resulted in lending rates plunging to all-time lows.

Deposit rates for most large banks have bottomed out, and cost of funds is likely to

remain largely stable given the excess liquidity in the system. Thus, we believe the

gradual deployment of excess liquidity and an uptick in loan growth would result in

the gradual normalization of spreads as well as support margins. Large banks with

strong liability franchises would continue to gain incremental market share, in our

view, and are better placed to tackle margin pressure. Therefore, we expect margins

to exhibit a stable/improving trend going ahead.

Maintain preference for ICICIBC, HDFCB, and SBIN

The balance sheets of large private banks are better placed v/s mid-sized peers

given their a) strong capital position, b) huge liquidity, c) cost of funds advantage,

and d) higher provision coverage in the stressed portfolio. Hence, large banks are

well-placed to gain incremental market share. We prefer the large private banks

(ICICIBC, HDFCB, and AXSB) over the mid-sized ones. Among the PSBs, SBIN would

continue to report steady credit growth and gain further market share.

Systemic loan growth at 6.5% YoY; deposit growth at 12.1% YoY as of 12th Mar’21

Source: RBI, MOFSL

System credit growth across segments

Source: RBI, MOFSL

6.5%

12.1%

0%

6%

12%

18%

24%

Mar

-15

Jul-

15

No

v-1

5

Mar

-16

Jul-

16

No

v-1

6

Mar

-17

Jul-

17

No

v-1

7

Mar

-18

Jul-

18

No

v-1

8

Mar

-19

Jul-

19

No

v-1

9

Mar

-20

Jul-

20

No

v-2

0

Mar

-21

Loan growth (%) Deposit growth (%)

-10%

0%

10%

20%

30%

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

Dec

-17

Feb

-18

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

Dec

-18

Feb

-19

Ap

r-1

9

Jun

-19

Au

g-1

9

Oct

-19

Dec

-19

Feb

-20

Ap

r-2

0

Jun

-20

Au

g-2

0

Oct

-20

Dec

-20

Feb

-21

Non-food Cr Agri Industry Services Retail

Industrial credit declined 0.2% YoY, while Agri

loans grew 10.2% YoY in Feb’21

Retail growth improved to 9.6% YoY in Feb’21

1 April 2021 14

ECLG scheme extended for another three months Scope widened to cover most affected sectors with additional credit support

◼ With the rise in COVID-19 cases again and continuing adverse impact of the

pandemic in certain segments of the economy, the government has once again

extended the Emergency Credit Line Guarantee Scheme (ECLGS) of INR3t for

another three months till 30th Jun’21. The last date for disbursement under the

scheme has been extended till 30th Sep’21.

◼ It has also widened scope of the credit guarantee scheme with the introduction of

ECLGS 3.0 to cover business enterprises in Hospitality, Travel and Tourism, Leisure,

and Sporting sectors with loans not exceeding INR5b as on 29th Feb’20. The scheme

would only consider loans less than 60 days overdue as on 29th Feb’20.

◼ As Hospitality, Travel and Tourism, Leisure, and Sporting are the most affected

sectors by the COVID-19 pandemic and would take longer to revive, the

government has further relaxed ECLGS guidelines with additional credit support of

up to 40% of outstanding loans and increased the loan tenor to six years. As per

earlier guidelines, the maximum additional disbursement is up to 20%, with the

maximum loan tenure of four years in ECLGS 1.0 and five years in ECLGS 2.0.

◼ SME growth for Banks over the last two quarters has been aided by

disbursements under the ECLGS scheme. Total loans sanctioned under this

scheme stands ~INR2.5t (including ECLGS 1.0 and 2.0), while ~INR1.81t has been

disbursed as per the last disclosure by the National Credit Guarantee Trustee

Company as on 28th Feb’21. This implies that ~43% of incremental growth in

systemic credit base has been aided by disbursement under this scheme.

◼ The extension of this scheme and further widening of the scope for impacted

sectors would be positive for all lenders. Select banks like CUBK will benefit the

most owing to relatively higher exposure to these stressed sectors, with 8-10%

exposure to the Hotels and Tourism sector, while it has earlier guided for higher

restructuring up to 6% of loans.

Disbursements across Banks under the ECLG scheme 1.0 and 2.0

As on 3QFY21 Credit under ECLG scheme Disbursements under ECLGS Disbursements under ECLGS

INR b Sanctioned Disbursed FY21 YTD

incremental loans % of

incremental loans SME Loans % of SME loans

KMB* NA 97 (56.5) NA 187 51.9%

FB NA 26 32 80.3% 246 10.6%

HDFCB NA 227 886 25.6% 658 34.5%

AXSB 106 89 113 78.3% 640 13.9%

AUBANK* NA 5 31 17.2% 142 3.7%

IIB 44 29 3 841.0% 158 18.4%

ICICIBC** NA 126 537 23.5% 621 20.3%

BOB NA 80 85 93.8% 853 9.4%

SBIN 260 230 428 53.7% 2,937 7.8%

CUBK 21 19 20 96.0% 127 15.0%

Total system 2,460 1,810 4,276 42.3% 19,100 9.5%

*Please note that for AUBANK we have considered SBL MSME and Agri SME for total SME loans; **For ICICIBC, we have clubbed business

banking and SME loans Source: MOFSL, Company

Sector Update | 31 March 2021

Financials

1 April 2021 15

Bank’s exposure to these sectors (INR b)

Funded (INR b) Hospitality Travel and Tourism Leisure

AXSB 24.2

IIB 17.9 9.4

FB 2.4

DCBB 2.4

SBIN 77.6

System credit 481.0

Note: SBIN exposure in Tourism and Hotels; System credit includes Tourism, Hotels, and Restaurants

Source: RBI, Basel III disclosures, and company presentation

1 April 2021 16

Revision in domestic gas price for 1HFY22 Domestic natural gas price unchanged at USD1.79/mmbtu (GCV) for 1HFY22 (press release) ◼ Unchanged APM gas price bodes well for margins of CGDs, given that the

pressure of an increase in gas cost is past us for at least the two upcoming

quarters. In Feb’21, IGL/MAHGL took a CNG price hike of INR0.7–1.5/kg to

recover higher operational costs. Although, we remain wary of the increase in

commissions demanded by OMCs (to double them to ~INR8/kg). Also, the

country is seeing a second wave of the pandemic, due to which restrictions are

increasing once again. As a result, school buses would remain shut, while

transportation in general would take longer to revive (as offices are re-closed),

thereby affecting the volume uptick in CNG.

◼ Even GAIL is likely to benefit as the company uses domestic gas to produce LPG

– thus aiding better margins in the segment.

Gas price ceiling down to USD3.62/mmbtu (GCV) for 1HFY22, from USD4.06/mmbtu in 2HFY21 (press release) ◼ The announcement would result in lower gas price realization for ONGC and

Oil India.

◼ Even RIL would be impacted as its gas production from the KG Basin would now

be capped at a lower gas price. RIL has already auctioned ~12.5mmscmd of gas

(currently flowing ~5mmscmd) from the basin; it is likely to commission

additional gas (peak potential of ~28mmscmd by FY24) after 3QFY22 (from the

R-cluster and MJ field).

Cutting estimates for ONGC and Oil India ◼ We had built in a 20% rise in gas price from Apr’21. Considering there has been

no change in prices, we cut our FY22/FY23E EPS forecast for ONGC standalone

by 5%/8% and for Oil India by 8%/9%.

◼ As a result, we cut our target price for ONGC to INR125 (from INR135) and for

Oil India to INR155 (from INR170). Reiterate Buy.

◼ We believe Brent would remain in the band of USD50–60/bbl. Our forecasts for

ONGC and Oil India are based on Brent of USD55/bbl for FY22/FY23E. A

sustained higher oil price may call for an upgrade in our estimate / target price.

Domestic gas price (USD/mmbtu) - GCV

Source: MOFSL

4.66

3.82

3.062.50 2.48

2.89 3.063.36

3.693.23

2.391.79 1.79

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

Ap

r-2

1

Domestic gas price (USD/mmbtu) - GCV

Sector Update | 31 March 2021

Oil & Gas

Our Report

1 April 2021 17

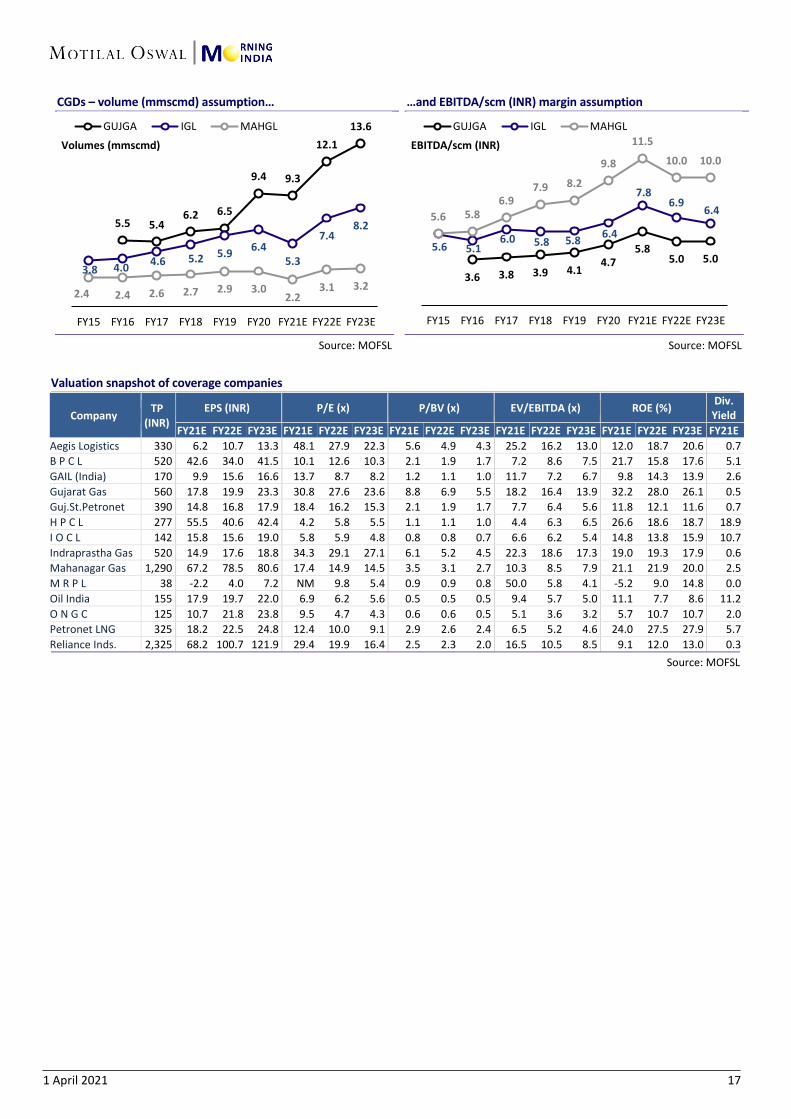

CGDs – volume (mmscmd) assumption…

Source: MOFSL

…and EBITDA/scm (INR) margin assumption

Source: MOFSL

Valuation snapshot of coverage companies

Company TP

(INR)

EPS (INR) P/E (x) P/BV (x) EV/EBITDA (x) ROE (%) Div.

Yield

FY21E FY22E FY23E FY21E FY22E FY23E FY21E FY22E FY23E FY21E FY22E FY23E FY21E FY22E FY23E FY21E

Aegis Logistics 330 6.2 10.7 13.3 48.1 27.9 22.3 5.6 4.9 4.3 25.2 16.2 13.0 12.0 18.7 20.6 0.7

B P C L 520 42.6 34.0 41.5 10.1 12.6 10.3 2.1 1.9 1.7 7.2 8.6 7.5 21.7 15.8 17.6 5.1

GAIL (India) 170 9.9 15.6 16.6 13.7 8.7 8.2 1.2 1.1 1.0 11.7 7.2 6.7 9.8 14.3 13.9 2.6

Gujarat Gas 560 17.8 19.9 23.3 30.8 27.6 23.6 8.8 6.9 5.5 18.2 16.4 13.9 32.2 28.0 26.1 0.5

Guj.St.Petronet 390 14.8 16.8 17.9 18.4 16.2 15.3 2.1 1.9 1.7 7.7 6.4 5.6 11.8 12.1 11.6 0.7

H P C L 277 55.5 40.6 42.4 4.2 5.8 5.5 1.1 1.1 1.0 4.4 6.3 6.5 26.6 18.6 18.7 18.9

I O C L 142 15.8 15.6 19.0 5.8 5.9 4.8 0.8 0.8 0.7 6.6 6.2 5.4 14.8 13.8 15.9 10.7

Indraprastha Gas 520 14.9 17.6 18.8 34.3 29.1 27.1 6.1 5.2 4.5 22.3 18.6 17.3 19.0 19.3 17.9 0.6

Mahanagar Gas 1,290 67.2 78.5 80.6 17.4 14.9 14.5 3.5 3.1 2.7 10.3 8.5 7.9 21.1 21.9 20.0 2.5

M R P L 38 -2.2 4.0 7.2 NM 9.8 5.4 0.9 0.9 0.8 50.0 5.8 4.1 -5.2 9.0 14.8 0.0

Oil India 155 17.9 19.7 22.0 6.9 6.2 5.6 0.5 0.5 0.5 9.4 5.7 5.0 11.1 7.7 8.6 11.2

O N G C 125 10.7 21.8 23.8 9.5 4.7 4.3 0.6 0.6 0.5 5.1 3.6 3.2 5.7 10.7 10.7 2.0

Petronet LNG 325 18.2 22.5 24.8 12.4 10.0 9.1 2.9 2.6 2.4 6.5 5.2 4.6 24.0 27.5 27.9 5.7

Reliance Inds. 2,325 68.2 100.7 121.9 29.4 19.9 16.4 2.5 2.3 2.0 16.5 10.5 8.5 9.1 12.0 13.0 0.3

Source: MOFSL

5.5 5.46.2 6.5

9.4 9.3

12.1

13.6

3.8 4.04.6 5.2 5.9

6.45.3

7.48.2

2.4 2.4 2.6 2.7 2.9 3.02.2

3.1 3.2

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Volumes (mmscmd)

GUJGA IGL MAHGL

3.6 3.8 3.9 4.14.7

5.85.0 5.0

5.6 5.16.0 5.8 5.8

6.4

7.86.9

6.45.6 5.8

6.97.9 8.2

9.8

11.5

10.0 10.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA/scm (INR)

GUJGA IGL MAHGL

1 April 2021 18

Regional HRC prices rise on tightening demand-supply China, Korea FoB export prices rise by 5-7% WoW

◼ The continuing surge in global demand and tightness in supply due to supply-side

issues and productiosn curbs in China has helped regional steel prices inch up

further.

◼ As per Steelmint, regional steel prices have increased 5-7% WoW.

◼ Korea export FOB prices have risen by 5% WoW (10% MoM) to USD838/t (CFR

India - USD875/t). Domestic HRC prices at INR55,500/t are trading at a discount

of INR9,000/t to the landed cost of imports from Korea.

◼ China export FoB prices too increased 7.5% WoW to USD830/t.

◼ We believe domestic HRC prices are likely to see two hikes in India – up to

INR4,000/t now and another INR2,000-3,000/t in Apr’21.

Domestic HRC prices trade at a discount of INR9,000/t to the

landed cost of imports

Source: Steelmint, MOFSL

Domestic HRC prices vis-à-vis regional export price trend

Source: Steelmint, MOFSL

64,988

55,500

28,000

38,000

48,000

58,000

68,000

Jan

/17

May

/17

Sep

/17

Jan

/18

May

/18

Sep

/18

Jan

/19

May

/19

Sep

/19

Jan

/20

May

/20

Sep

/20

Jan

/21

Landed cost - Korea Imports Domestic price(INR/t)

300

500

700

900

Jan

/18

Ap

r/1

8

Jul/

18

Oct

/18

Jan

/19

Ap

r/1

9

Jul/

19

Oct

/19

Jan

/20

Ap

r/2

0

Jul/

20

Oct

/20

Jan

/21

Ap

r/2

1

ADD Ref price From China

Domestic price From Korea(USD/t)

Sector Update | 31 March 2021

Metals

1 April 2021 19

\

HPCL: Natural gas a future growth driver; acquisition of Shapoorji shares in-line with that strategy; MK Surana, CMD Company has been expanding its footprint in various product portfolios

Natural gas will be a future growth driver for HPCL

Have been taking efforts to reduce carbon footprint via natural gas

Have 694 gas stations where CNG is being dispensed

HPCL has undertaken expansions in manufacturing and marketing in a few baskets

Refinery segment is getting an uptrend after sluggishness in last few years

Expansion in portfolio will help in de-risking exiting business line

Biocon: Generic formulations are around $70 m; company has a deep pipeline for biosimilars; Siddharth Mittal, MD & CEO Company entered Brazil around a decade back with APIs, insulins and Biosimilar

Trastuzumab

Partnership with Libbis Farmaceutica marks entry of generic formulation in Brazil

Have one oncology molecule in the pipeline for the Brazilian market

Brazil is among the top 10 pharma markets globally

Generic formulations around $70 m

Brazil has huge potential; Brazil, China are among the key markets

Pricing could be under pressure for biosimilars

Insulin Glargine was launched last year by Mylan; market share at around 2%

Seeing many approvals, launches taking place in the biosimilar market of late

Will see an inch up on market share in Insulin Glargine

Have four statins in the US market

Will look at adding more products in the generic portfolio in the coming year

Godrej Properties: Real estate demand steady, focus more on residential space; Mohit Malhotra, MD & CEO Demand has been steady over the last couple of months; seeing strong demand

across all markets

Have done a number of launches in H2 across geographies

Company is launching some projects in Pune; launched plotted development

project in Bengaluru

New round of fund raise was in-line with company strategy; idea is to deploy this

capital in new business opportunities

Navi Mumbai will see a residential project; company has been planning to enter the

Navi Mumbai market for some time

We are not offering any discounts for sales

Demand could be impacted due to reversal of stamp duty cuts from April 1

Difficult to predict when home prices will go up

Focus for the company would be predominantly residential space

In conversation

1 April 2021 20

Amber Enterprise: Commodity price rise will remain a concern for next few months; Jasbir Singh, Chairman & CEO Demand continues to be robust

Commodity price rise will remain a concern for next few months

Will pass on commodity price rise with one-quarter lag

Have not been facing issues related to supply-chain; it’s been smooth

Will outperform industry in FY22; industry seen growing at 20-25%

Have 15 plants, working at an average capacity utilisation of 70-75%

PLI scheme will be supportive to capex plans

Won’t go to market for fund; raised Rs. 400 crore via QIP in September 2020

VA Tech Wabag: Projects worth Rs. 2500 crore to be executed over 24 months; Rajneesh Chopra, Global Head-Biz Development Rs. 2500 crore worth of projects will be executed over 24 months

Internal rate of return is as per expectations of all partners

We will end this year with growth despite the pandemic

Our EBITDA will grow at a better pace than our topline next year

There is now a lot of traction and we will have new tenders in Q1FY22

Allcargo Logistics: Shipping sector will recover fast; container freight rates may rise; Shashi Kiran Shetty Suez Canal blockade impacted 2% of the overall available containers

Now that Ever Given is floating again, 70-80 ships of the 400 waiting will move daily

Suez Canal blockade will have an impact on container shortage

Shipping world will recover fast, don’t see any major challenge

Important cargo moved by air during the time of Suez blockade

Freight rates will go up on the container side; availability of containers is disrupted

in the short term

FY22 likely to be stable for company; gained market share in FY21

Gati turnaround is on its right path

Gati’s debt and contingent liability has been reduced

Liberty Shoes: Retail demand back to 90-95% of pre-COVID; government business strong; Adesh Gupta, CEO Retail demand is back to 90-95% vs last year

Optimistic about demand for the next 2 quarters

Not worried as much about the second wave of COVID-19

Government tenders have been 75% higher than last year

Company’s business amidst CRPF has seen a jump of 100% YoY

95% of the payments have been recovered from the defence ministry

Order from Andhra Pradesh police has Rs. 30 crore outstanding

1 April 2021 21

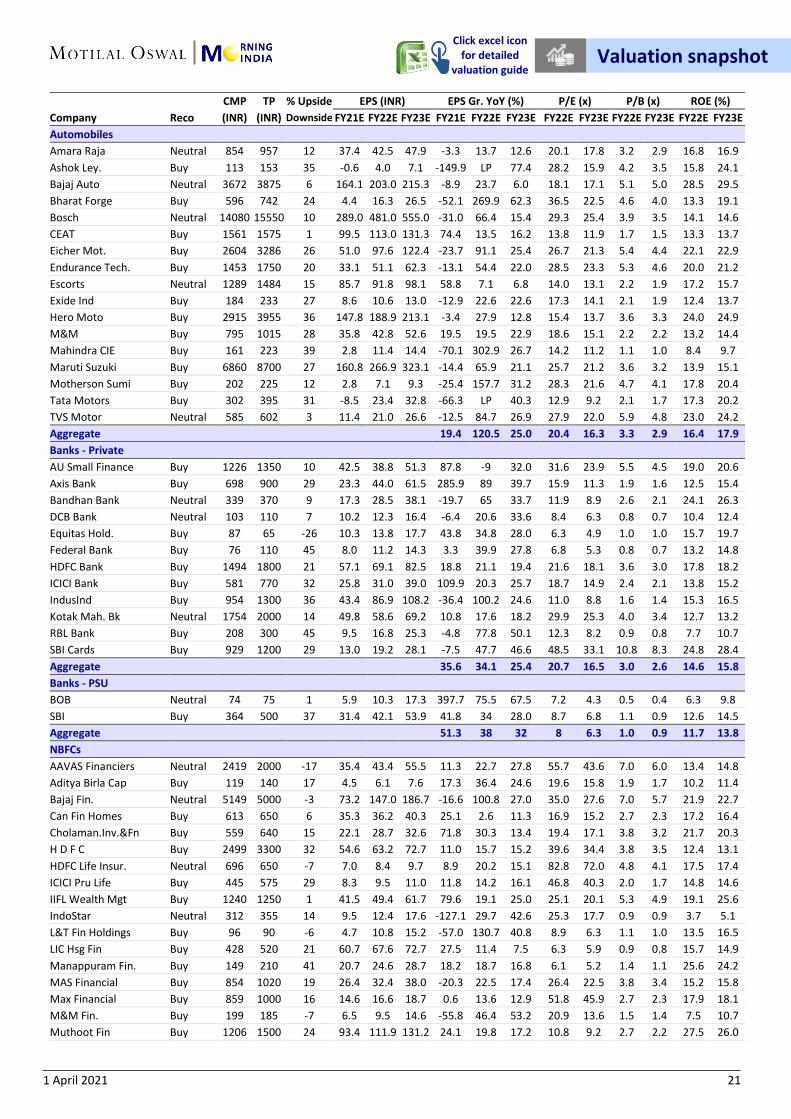

CMP TP % Upside EPS (INR) EPS Gr. YoY (%) P/E (x) P/B (x) ROE (%)

Company Reco (INR) (INR) Downside FY21E FY22E FY23E FY21E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E

Automobiles

Amara Raja Neutral 854 957 12 37.4 42.5 47.9 -3.3 13.7 12.6 20.1 17.8 3.2 2.9 16.8 16.9

Ashok Ley. Buy 113 153 35 -0.6 4.0 7.1 -149.9 LP 77.4 28.2 15.9 4.2 3.5 15.8 24.1

Bajaj Auto Neutral 3672 3875 6 164.1 203.0 215.3 -8.9 23.7 6.0 18.1 17.1 5.1 5.0 28.5 29.5

Bharat Forge Buy 596 742 24 4.4 16.3 26.5 -52.1 269.9 62.3 36.5 22.5 4.6 4.0 13.3 19.1

Bosch Neutral 14080 15550 10 289.0 481.0 555.0 -31.0 66.4 15.4 29.3 25.4 3.9 3.5 14.1 14.6

CEAT Buy 1561 1575 1 99.5 113.0 131.3 74.4 13.5 16.2 13.8 11.9 1.7 1.5 13.3 13.7

Eicher Mot. Buy 2604 3286 26 51.0 97.6 122.4 -23.7 91.1 25.4 26.7 21.3 5.4 4.4 22.1 22.9

Endurance Tech. Buy 1453 1750 20 33.1 51.1 62.3 -13.1 54.4 22.0 28.5 23.3 5.3 4.6 20.0 21.2

Escorts Neutral 1289 1484 15 85.7 91.8 98.1 58.8 7.1 6.8 14.0 13.1 2.2 1.9 17.2 15.7

Exide Ind Buy 184 233 27 8.6 10.6 13.0 -12.9 22.6 22.6 17.3 14.1 2.1 1.9 12.4 13.7

Hero Moto Buy 2915 3955 36 147.8 188.9 213.1 -3.4 27.9 12.8 15.4 13.7 3.6 3.3 24.0 24.9

M&M Buy 795 1015 28 35.8 42.8 52.6 19.5 19.5 22.9 18.6 15.1 2.2 2.2 13.2 14.4

Mahindra CIE Buy 161 223 39 2.8 11.4 14.4 -70.1 302.9 26.7 14.2 11.2 1.1 1.0 8.4 9.7

Maruti Suzuki Buy 6860 8700 27 160.8 266.9 323.1 -14.4 65.9 21.1 25.7 21.2 3.6 3.2 13.9 15.1

Motherson Sumi Buy 202 225 12 2.8 7.1 9.3 -25.4 157.7 31.2 28.3 21.6 4.7 4.1 17.8 20.4

Tata Motors Buy 302 395 31 -8.5 23.4 32.8 -66.3 LP 40.3 12.9 9.2 2.1 1.7 17.3 20.2

TVS Motor Neutral 585 602 3 11.4 21.0 26.6 -12.5 84.7 26.9 27.9 22.0 5.9 4.8 23.0 24.2

Aggregate 19.4 120.5 25.0 20.4 16.3 3.3 2.9 16.4 17.9

Banks - Private

AU Small Finance Buy 1226 1350 10 42.5 38.8 51.3 87.8 -9 32.0 31.6 23.9 5.5 4.5 19.0 20.6

Axis Bank Buy 698 900 29 23.3 44.0 61.5 285.9 89 39.7 15.9 11.3 1.9 1.6 12.5 15.4

Bandhan Bank Neutral 339 370 9 17.3 28.5 38.1 -19.7 65 33.7 11.9 8.9 2.6 2.1 24.1 26.3

DCB Bank Neutral 103 110 7 10.2 12.3 16.4 -6.4 20.6 33.6 8.4 6.3 0.8 0.7 10.4 12.4

Equitas Hold. Buy 87 65 -26 10.3 13.8 17.7 43.8 34.8 28.0 6.3 4.9 1.0 1.0 15.7 19.7

Federal Bank Buy 76 110 45 8.0 11.2 14.3 3.3 39.9 27.8 6.8 5.3 0.8 0.7 13.2 14.8

HDFC Bank Buy 1494 1800 21 57.1 69.1 82.5 18.8 21.1 19.4 21.6 18.1 3.6 3.0 17.8 18.2

ICICI Bank Buy 581 770 32 25.8 31.0 39.0 109.9 20.3 25.7 18.7 14.9 2.4 2.1 13.8 15.2

IndusInd Buy 954 1300 36 43.4 86.9 108.2 -36.4 100.2 24.6 11.0 8.8 1.6 1.4 15.3 16.5

Kotak Mah. Bk Neutral 1754 2000 14 49.8 58.6 69.2 10.8 17.6 18.2 29.9 25.3 4.0 3.4 12.7 13.2

RBL Bank Buy 208 300 45 9.5 16.8 25.3 -4.8 77.8 50.1 12.3 8.2 0.9 0.8 7.7 10.7

SBI Cards Buy 929 1200 29 13.0 19.2 28.1 -7.5 47.7 46.6 48.5 33.1 10.8 8.3 24.8 28.4

Aggregate 35.6 34.1 25.4 20.7 16.5 3.0 2.6 14.6 15.8

Banks - PSU

BOB Neutral 74 75 1 5.9 10.3 17.3 397.7 75.5 67.5 7.2 4.3 0.5 0.4 6.3 9.8

SBI Buy 364 500 37 31.4 42.1 53.9 41.8 34 28.0 8.7 6.8 1.1 0.9 12.6 14.5

Aggregate 51.3 38 32 8 6.3 1.0 0.9 11.7 13.8

NBFCs

AAVAS Financiers Neutral 2419 2000 -17 35.4 43.4 55.5 11.3 22.7 27.8 55.7 43.6 7.0 6.0 13.4 14.8

Aditya Birla Cap Buy 119 140 17 4.5 6.1 7.6 17.3 36.4 24.6 19.6 15.8 1.9 1.7 10.2 11.4

Bajaj Fin. Neutral 5149 5000 -3 73.2 147.0 186.7 -16.6 100.8 27.0 35.0 27.6 7.0 5.7 21.9 22.7

Can Fin Homes Buy 613 650 6 35.3 36.2 40.3 25.1 2.6 11.3 16.9 15.2 2.7 2.3 17.2 16.4

Cholaman.Inv.&Fn Buy 559 640 15 22.1 28.7 32.6 71.8 30.3 13.4 19.4 17.1 3.8 3.2 21.7 20.3

H D F C Buy 2499 3300 32 54.6 63.2 72.7 11.0 15.7 15.2 39.6 34.4 3.8 3.5 12.4 13.1

HDFC Life Insur. Neutral 696 650 -7 7.0 8.4 9.7 8.9 20.2 15.1 82.8 72.0 4.8 4.1 17.5 17.4

ICICI Pru Life Buy 445 575 29 8.3 9.5 11.0 11.8 14.2 16.1 46.8 40.3 2.0 1.7 14.8 14.6

IIFL Wealth Mgt Buy 1240 1250 1 41.5 49.4 61.7 79.6 19.1 25.0 25.1 20.1 5.3 4.9 19.1 25.6

IndoStar Neutral 312 355 14 9.5 12.4 17.6 -127.1 29.7 42.6 25.3 17.7 0.9 0.9 3.7 5.1

L&T Fin Holdings Buy 96 90 -6 4.7 10.8 15.2 -57.0 130.7 40.8 8.9 6.3 1.1 1.0 13.5 16.5

LIC Hsg Fin Buy 428 520 21 60.7 67.6 72.7 27.5 11.4 7.5 6.3 5.9 0.9 0.8 15.7 14.9

Manappuram Fin. Buy 149 210 41 20.7 24.6 28.7 18.2 18.7 16.8 6.1 5.2 1.4 1.1 25.6 24.2

MAS Financial Buy 854 1020 19 26.4 32.4 38.0 -20.3 22.5 17.4 26.4 22.5 3.8 3.4 15.2 15.8

Max Financial Buy 859 1000 16 14.6 16.6 18.7 0.6 13.6 12.9 51.8 45.9 2.7 2.3 17.9 18.1

M&M Fin. Buy 199 185 -7 6.5 9.5 14.6 -55.8 46.4 53.2 20.9 13.6 1.5 1.4 7.5 10.7

Muthoot Fin Buy 1206 1500 24 93.4 111.9 131.2 24.1 19.8 17.2 10.8 9.2 2.7 2.2 27.5 26.0

Valuation snapshot

Click excel icon for detailed

valuation guide

1 April 2021 22

CMP TP % Upside EPS (INR) EPS Gr. YoY (%) P/E (x) P/B (x) ROE (%)

Company Reco (INR) (INR) Downside FY21E FY22E FY23E FY21E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E

Piramal Enterp. Buy 1752 2170 24 119.6 127.2 156.6 -587.6 6.4 23.1 13.8 11.2 1.1 1.0 8.4 9.5

PNB Housing Neutral 375 400 7 63.0 70.5 87.7 64.0 11.9 24.3 5.3 4.3 0.6 0.6 12.8 14.2

Repco Home Fin Buy 337 430 28 49.7 51.3 55.6 10.9 3.2 8.4 6.6 6.1 0.9 0.8 14.4 13.7

SBI Life Insurance Buy 881 1050 19 13.5 19.2 24.2 -5.3 42.2 26.4 46.0 36.4 2.4 2.0 18.0 18.7

Shriram City Union Buy 1363 1400 3 146.0 182.3 224.7 -3.7 24.9 23.2 7.5 6.1 1.0 0.9 13.9 15.1

Shriram Trans. Buy 1422 1575 11 103.7 131.3 149.8 -6.0 26.6 14.1 10.8 9.5 1.4 1.3 14.2 14.3

Aggregate 18.6 31.0 20.1 21.8 18.1 2.9 2.6 13.5 14.4

Capital Goods/Consumer Durables

ABB Buy 1417 1565 10 11.9 20.6 27.1 -28.4 73.7 31.4 68.7 52.3 7.6 6.9 11.1 13.2

Bharat Elec. Buy 125 150 20 6.8 8.6 9.4 -7.2 25.4 9.7 14.6 13.3 2.5 2.2 17.1 16.9

BHEL Sell 49 26 -47 -2.5 1.3 1.9 -41.3 LP 43.5 37.0 25.8 0.6 0.6 1.6 2.3

Blue Star Sell 937 740 -21 9.2 18.0 25.3 -39.8 95.8 40.5 52.0 37.0 10.2 9.2 19.6 24.8

CG Cons. Elec. Buy 394 485 23 8.4 10.6 12.1 19.9 27.1 13.7 37.0 32.6 11.3 9.4 30.5 28.7

Cummins Sell 920 515 -44 19.0 22.5 25.8 -18.2 18.3 14.4 40.8 35.7 5.5 5.3 13.5 14.8

Engineers India Buy 77 85 10 5.6 7.5 7.6 -17.0 32.6 1.2 10.3 10.2 2.1 2.1 19.3 19.1

Havells Neutral 1050 1100 5 16.5 19.6 22.0 40.7 18.8 12.2 53.6 47.8 11.3 9.8 21.2 20.6

K E C Intl. Buy 410 450 10 22.0 26.3 30.0 0.0 19.5 14.2 15.6 13.7 2.7 2.3 17.5 16.9

Larsen & Toubro Buy 1418 1625 15 81.2 66.0 77.7 19.4 -18.7 17.7 21.5 18.3 2.4 2.2 11.4 12.2

Orient Electric Buy 311 350 13 5.3 6.5 7.7 42.8 23.1 18.8 47.8 40.2 13.5 11.5 28.2 28.6

Siemens Neutral 1844 1640 -11 21.3 35.0 36.9 -32.6 64.5 5.5 52.7 50.0 6.3 5.7 11.9 11.4

Thermax Neutral 1346 1100 -18 22.4 33.2 39.6 18.7 48.3 19.1 40.5 34.0 4.5 4.1 11.0 12.0

Voltas Neutral 1002 1170 17 14.3 20.8 24.1 -14.7 45.9 15.9 48.1 41.5 6.5 5.9 13.5 14.1

Whirlpool India Buy 2230 3020 35 27.3 45.5 54.9 -27.4 66.8 20.8 49.1 40.6 8.5 7.2 17.4 17.8

Aggregate -15.6 51.3 16.1 29.5 25.4 3.3 3.1 11.3 12.1

Cement

Ambuja Cem. Neutral 309 275 -11 9.0 8.8 10.4 24.2 -2.1 18.1 35.0 29.6 2.8 2.6 8.4 9.2

ACC Buy 1903 2100 10 78.4 93.0 98.4 8.5 18.6 5.8 20.5 19.3 2.5 2.3 13.1 12.4

Birla Corp. Buy 950 900 -5 71.7 79.6 93.3 9.2 11.1 17.2 11.9 10.2 1.3 1.1 11.0 11.7

Dalmia Bhar. Buy 1587 1495 -6 44.6 45.1 66.7 288.3 1.2 47.7 35.2 23.8 2.5 2.3 7.3 10.0

Grasim Inds. Neutral 1452 1215 -16 82.3 97.4 112.8 -6.8 18.3 15.9 14.9 12.9 2.4 2.3 3.9 5.1

India Cem Neutral 168 160 -4 6.1 5.1 7.2 785.5 -15.7 39.7 32.6 23.4 0.9 0.9 2.8 3.8

J K Cements Buy 2894 2640 -9 81.3 100.6 124.1 30.0 23.7 23.4 28.8 23.3 5.4 4.4 20.3 20.9

JK Lakshmi Ce Buy 433 440 2 25.4 26.1 32.6 12.7 2.7 24.7 16.6 13.3 2.2 1.9 14.3 15.4

Ramco Cem Neutral 1003 805 -20 33.1 32.6 38.7 29.6 -1.5 18.9 30.8 25.9 3.8 3.4 12.9 13.7

Shree Cem Neutral 29475 24300 -18 663.0 702.8 784.7 52.4 6.0 11.6 41.9 37.6 6.1 5.3 15.6 15.1

Ultratech Buy 6737 6650 -1 189.0 225.6 277.8 42.2 19.4 23.2 29.9 24.3 3.7 3.4 13.8 14.9

Aggregate 22.9 13.2 18.8 25.2 21.2 3.2 2.9 12.6 13.6

Consumer

Asian Paints Neutral 2537 2790 10 34.8 40.1 46.4 20.2 15.1 15.9 63.3 54.6 18.8 16.7 31.4 32.4

Britannia Buy 3628 4120 14 82.1 79.4 91.5 40.0 -3.3 15.2 45.7 39.6 18.0 16.5 41.1 43.5

Colgate Buy 1560 1810 16 36.1 40.0 45.3 20.4 10.7 13.3 39.0 34.4 25.6 25.6 65.6 74.3

Dabur Buy 541 640 18 9.9 11.4 13.3 15.0 14.4 17.0 47.6 40.7 11.9 10.6 26.2 27.5

Emami Buy 488 560 15 16.9 17.0 18.7 36.5 0.2 10.1 28.8 26.1 10.2 10.2 35.5 39.0

Godrej Cons. Neutral 729 720 -1 16.8 17.8 20.6 18.7 5.7 15.9 41.0 35.4 8.5 8.2 21.2 23.6

HUL Buy 2431 2690 11 34.1 41.7 48.9 9.3 22.1 17.3 58.3 49.7 11.3 11.3 19.7 22.6

ITC Neutral 219 220 1 10.3 13.1 14.8 -17.0 27.1 12.6 16.7 14.8 4.0 3.8 24.2 26.2

Jyothy Lab Neutral 137 151 10 5.7 5.9 6.2 25.7 3.8 4.9 23.1 22.1 3.9 3.8 17.2 17.6

Marico Buy 412 490 19 8.7 9.8 11.4 6.4 13.1 16.2 42.0 36.1 13.0 12.0 31.5 34.5

Nestle Neutral 17170 17500 2 217.4 253.7 291.8 5.2 16.7 15.0 67.7 58.9 75.8 69.6 116.4 123.4

Page Inds Neutral 30336 28800 -5 303.7 457.3 523.0 -1.3 50.6 14.4 66.3 58.0 37.4 36.2 56.4 62.5

Pidilite Ind. Neutral 1810 1635 -10 22.7 25.5 29.7 -1.6 12.3 16.4 70.9 60.9 14.1 12.2 21.3 21.4

P&G Hygiene Buy 12457 14000 12 180.8 232.9 280.4 32.5 28.8 20.4 53.5 44.4 30.4 26.8 60.3 64.1

Tata Consumer Buy 639 680 6 10.5 13.3 15.5 32.1 26.3 16.5 48.0 41.2 3.8 3.6 8.2 9.1

United Brew Sell 1242 972 -22 7.2 15.3 20.6 -55.8 113.9 34.5 81.1 60.3 8.3 7.7 10.6 13.2

United Spirits Buy 556 725 30 5.7 12.9 17.1 -47.6 126.8 32.5 43.0 32.5 8.0 6.4 18.5 19.7

Valuation snapshot

Click excel icon for detailed

valuation guide

1 April 2021 23

CMP TP % Upside EPS (INR) EPS Gr. YoY (%) P/E (x) P/B (x) ROE (%)

Company Reco (INR) (INR) Downside FY21E FY22E FY23E FY21E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E

Varun Beverages Buy 1006 1145 14 13.7 28.7 38.1 -15.7 109.4 32.8 35.1 26.4 6.8 5.5 21.3 23.0

Aggregate 1.6 21.1 15.4 41.3 35.8 9.7 9.2 23.5 25.7

Healthcare

Alembic Phar Neutral 965 1070 11 59.4 52.4 57.3 35.1 -11.8 9.4 18.4 16.8 3.3 2.9 20.1 19.0

Alkem Lab Buy 2772 3430 24 129.2 137.0 152.9 35.4 6.0 11.6 20.2 18.1 3.8 3.3 20.5 19.6

Ajanta Pharma Buy 1793 2030 13 69.6 78.1 90.5 36.1 12.2 15.9 23.0 19.8 4.4 3.8 20.6 20.4

Aurobindo Buy 882 1100 25 54.5 61.1 68.6 10.9 12.0 12.3 14.4 12.9 2.0 1.8 15.1 14.7

Biocon Neutral 409 385 -6 6.0 9.3 12.0 -2.5 54.4 29.2 43.9 34.0 6.1 5.4 14.7 16.9

Cadila Buy 441 550 25 20.0 23.3 24.7 36.1 16.4 6.0 18.9 17.9 2.9 2.6 16.2 15.2

Cipla Neutral 815 900 10 33.6 36.6 41.8 71.1 9.0 14.3 22.3 19.5 3.1 2.7 14.0 13.9

Divis Lab Buy 3630 4530 25 76.4 99.5 129.3 56.2 30.2 29.9 36.5 28.1 8.8 7.0 26.5 27.7

Dr Reddy’s Neutral 4516 5070 12 158.1 180.0 210.6 20.3 13.9 17.0 25.1 21.4 3.7 3.2 15.6 15.9

Gland Pharma Buy 2478 2900 17 57.7 72.6 92.3 15.9 25.7 27.1 34.1 26.9 5.8 4.8 18.5 19.4

Glenmark Neutral 465 540 16 34.3 35.6 40.7 39.4 3.8 14.3 13.1 11.4 1.7 1.5 13.6 13.7

GSK Pharma Neutral 1440 1500 4 29.8 36.0 40.8 5.7 20.7 13.5 40.0 35.3 11.4 10.0 28.6 28.4

Granules India Buy 303 460 52 22.5 26.3 30.3 72.5 17.1 15.1 11.5 10.0 2.7 2.2 26.0 24.2

IPCA Labs Buy 1903 2420 27 95.2 95.5 102.7 85.2 0.3 7.6 19.9 18.5 4.2 3.5 23.3 20.8

Jubilant Pharmova Buy 680 1120 65 58.7 60.3 69.1 -1.9 2.8 14.6 11.3 9.8 2.2 1.8 21.6 20.5

Laurus Labs Buy 362 470 30 18.3 22.5 27.4 282.5 23.4 21.4 16.1 13.2 5.3 4.0 38.7 34.5

Lupin Buy 1021 1180 16 25.3 39.4 45.6 8.6 55.4 15.7 25.9 22.4 3.2 2.9 12.8 13.4

Strides Pharma Buy 845 980 16 25.8 44.1 54.4 70.0 70.9 23.2 19.1 15.5 2.5 2.2 13.6 15.1

Sun Pharma Buy 598 740 24 25.7 26.8 29.9 56.5 4.4 11.6 22.3 20.0 2.7 2.4 12.9 12.9

Torrent Pharma Neutral 2541 2520 -1 73.8 88.5 100.4 31.6 19.9 13.4 28.7 25.3 6.5 5.6 24.6 23.9

Aggregate 38.0 14.0 15.2 23.0 19.9 3.6 3.1 15.6 15.7

Infrastructure

Ashoka Buildcon Buy 102 145 43 13.2 11.2 12.8 -4.6 -15.0 14.6 9.1 7.9 0.9 0.8 10.2 10.7

IRB Infra Neutral 109 122 12 3.9 5.9 9.7 -79.2 51.2 64.0 18.3 11.2 0.6 0.5 3.1 4.9

KNR Constructions Buy 213 265 24 9.1 12.8 16.5 26.0 40.4 28.4 16.6 12.9 2.7 2.3 17.8 19.1

Aggregate 13.9 10.5 1.0 0.9 7.2 8.8

Media

PVR Neutral 1224 1620 32 -89.1 17.1 36.7 -376.7 LP 113.8 71.4 33.4 3.5 3.1 5.0 9.9

Sun TV Buy 470 640 36 38.6 39.8 40.0 10.9 3.1 0.6 11.8 11.7 2.7 2.6 23.9 22.5

Zee Ent. Neutral 203 265 30 7.3 17.1 19.4 32.5 135.2 13.8 11.9 10.4 1.8 1.6 15.9 15.9

Aggregate -21.6 70.0 10.7 13.6 12.3 2.3 2.0 16.6 16.6

Metals

Hindalco Buy 327 390 19 23.1 32.9 36.9 31.9 42.6 12.2 9.9 8.9 1.5 1.3 16.8 16.2

Hind. Zinc Neutral 273 268 -2 18.8 27.2 26.7 16.6 44.7 -1.7 10.0 10.2 3.1 2.8 33.3 29.2

JSPL Buy 344 385 12 54.5 33.8 35.3 -801.9 -38.1 4.7 10.2 9.7 1.0 0.9 10.6 10.0

JSW Steel Buy 468 435 -7 30.7 43.9 40.2 239.7 43.1 -8.6 10.7 11.6 2.1 1.8 21.8 16.7

Nalco Buy 54 59 9 3.4 5.1 5.4 357.1 49.8 5.5 10.6 10.1 1.0 1.0 9.3 9.6

NMDC Buy 135 140 4 20.9 21.8 18.7 36.8 4.2 -14.5 6.2 7.2 1.2 1.1 20.6 16.0

SAIL Buy 79 104 32 14.4 18.5 17.0 ###### 28 -8.6 4.3 4.6 0.6 0.6 15.8 13.0

Tata Steel Neutral 812 708 -13 64.6 85.7 89.0 613.3 33 3.8 9.5 9.1 1.1 1.0 12.7 11.9

Vedanta Neutral 229 182 -20 24.4 24.4 24.1 177.9 0 -0.9 9.4 9.5 1.4 1.3 14.8 14.1

Aggregate 162.8 20.8 -1.9 8.8 9.0 1.4 1.2 15.3 13.7

Oil & Gas

Aegis Logistics Buy 298 330 11 6.2 10.7 13.3 107.7 72.3 25.1 27.9 22.3 4.9 4.3 18.7 20.6

BPCL Buy 428 520 22 42.6 34.0 41.5 67.9 -20.1 22.1 12.6 10.3 1.9 1.7 15.8 17.6

Castrol India Buy 125 170 36 5.9 8.5 8.5 -29.6 44.4 -0.3 14.7 14.8 7.8 7.1 56.2 50.3

GAIL Buy 136 170 25 9.9 15.6 16.6 -39.8 58.0 6.2 8.7 8.2 1.1 1.0 14.3 13.9

Gujarat Gas Buy 550 560 2 17.8 19.9 23.3 2.9 11.8 17.0 27.6 23.6 6.9 5.5 28.0 26.1

Gujarat St. Pet. Buy 273 390 43 14.8 16.8 17.9 -24.5 13.3 6.3 16.2 15.3 1.9 1.7 12.1 11.6

HPCL Neutral 235 277 18 55.5 40.6 42.4 132.1 -26.8 4.5 5.8 5.5 1.1 1.0 18.6 18.7

IOC Buy 92 142 55 15.8 15.6 19.0 53.6 -1.0 21.8 5.9 4.8 0.8 0.7 13.8 15.9

IGL Neutral 511 520 2 14.9 17.6 18.8 -8.2 17.7 7.3 29.1 27.1 5.2 4.5 19.3 17.9

Valuation snapshot

Click excel icon for detailed

valuation guide

1 April 2021 24

CMP TP % Upside EPS (INR) EPS Gr. YoY (%) P/E (x) P/B (x) ROE (%)

Company Reco (INR) (INR) Downside FY21E FY22E FY23E FY21E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E

Mahanagar Gas Buy 1167 1290 11 67.2 78.5 80.6 -16.3 16.8 2.7 14.9 14.5 3.1 2.7 21.9 20.0

MRPL Neutral 39 38 -2 -2.2 4.0 7.2 -85.5 LP 81.2 9.8 5.4 0.9 0.8 9.0 14.8

Oil India Buy 123 155 26 17.9 19.7 22.0 -21.7 10.1 11.7 6.2 5.6 0.5 0.5 7.7 8.6

ONGC Buy 102 125 22 10.7 21.8 23.8 -18.4 103.7 9.2 4.7 4.3 0.6 0.5 10.7 10.7

PLNG Buy 225 325 45 18.2 22.5 24.8 -1.5 23.8 10.3 10.0 9.1 2.6 2.4 27.5 27.9

Reliance Ind. Buy 2003 2325 16 68.2 100.7 121.9 2.5 47.8 21.0 19.9 16.4 2.3 2.0 12.0 13.0

Aggregate 10.0 32.2 16.9 13.8 11.8 1.7 1.5 12.0 12.8

Retail

Avenue Supermarts Neutral 2854 2850 0 17.6 30.5 38.4 -12.4 73.5 25.8 93.5 74.3 12.5 10.7 15.0 16.1

Aditya Birla Fashion Buy 201 230 14 -2.2 -0.1 0.3 1,107.2 Loss LP NM 633.4 23.0 22.2 -1.8 3.6

Jubilant Food. Neutral 2913 2920 0 15.8 38.3 53.1 -30.1 143.1 38.5 76.0 54.9 24.9 19.6 32.8 35.8

Shoppers Stop Neutral 215 220 2 -34.1 -15.4 -15.0 131.8 Loss Loss NM NM -68.3 -11.8 -338.3 141.0

Titan Company Buy 1557 1800 16 9.7 23.0 30.0 -43.0 136.6 30.1 67.6 52.0 17.6 15.5 27.8 31.6

Trent Neutral 752 660 -12 -3.5 4.5 8.0 -218.0 LP 79.8 168.3 93.6 10.3 9.2 6.8 11.1

V-Mart Retail Buy 2768 3500 26 -10.6 25.0 43.4 -139.0 LP 73.8 110.9 63.8 10.3 8.9 9.8 15.0

Westlife Develop Neutral 459 520 13 -6.3 1.6 6.1 ###### LP 274.8 280.5 74.8 14.0 11.8 5.1 17.2

Aggregate -67.7 351.5 37.3 89.3 65.0 13.7 11.9 15.3 18.3

Technology

Cyient Buy 649 660 2 33.2 43.7 47.3 -1.5 31.5 8.3 14.8 13.7 2.3 2.0 16.1 15.6

HCL Tech. Buy 983 1300 32 48.0 56.5 65.0 18.0 17.5 15.1 17.4 15.1 4.1 3.8 24.6 25.9

Infosys Buy 1368 1600 17 46.4 56.9 67.2 19.3 22.6 18.0 24.0 20.4 8.2 7.8 34.8 39.2

L & T Infotech Neutral 4048 3780 -7 107.3 128.2 151.1 23.9 19.5 17.8 31.6 26.8 8.7 7.2 30.6 29.7

L&T Technology Buy 2655 2830 7 64.3 91.0 109.0 -17.0 41.5 19.7 29.2 24.4 7.3 6.1 27.3 27.4

Mindtree Neutral 2085 1930 -7 65.9 75.3 84.1 71.9 14.2 11.7 27.7 24.8 7.4 6.2 29.3 27.2

Mphasis Buy 1783 1950 9 65.1 79.5 91.8 3.1 22.1 15.4 22.4 19.4 4.6 4.1 22.0 22.7

Coforge Neutral 2929 2690 -8 78.9 102.1 116.9 4.4 29.4 14.5 28.7 25.0 5.6 4.8 20.9 20.7

Persistent Sys Buy 1919 1800 -6 56.5 70.0 81.9 26.8 23.9 17.1 27.4 23.4 5.0 4.3 19.4 19.8

TCS Neutral 3178 3175 0 87.9 111.9 127.0 2.0 27.3 13.5 28.4 25.0 13.0 12.2 47.6 50.8

Tech Mah Neutral 991 1095 10 52.6 60.4 68.6 8.8 14.8 13.6 16.4 14.4 3.1 2.7 20.1 20.0

Wipro Neutral 414 450 9 18.5 21.6 23.9 12.5 17.1 10.6 19.2 17.3 4.4 4.4 23.2 25.8

Zensar Tech Neutral 274 265 -3 15.6 17.9 20.3 33.6 14.7 13.4 15.3 13.5 2.3 2.0 16.3 16.3

Aggregate 10.3 22.4 14.6 24.6 21.4 7.6 7.1 31.1 33.3

Telecom

Bharti Airtel Buy 517 720 39 0.8 4.6 8.2 -110.6 483.5 76.2 111.8 63.4 4.3 4.0 3.9 6.5

Indus Towers Neutral 245 245 0 18.2 20.8 20.0 17.6 14.5 -3.8 11.8 12.2 4.1 3.8 35.8 32.1

Vodafone Idea 9 -8.5 -7.3 -6.8 12.2 Loss Loss NM NM -0.7 -0.5 72.8 39.6