THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT WEAKNESSES IN INTERNAL CONTROL...

17

Indian J.Sci.Res.4 (4):36-53, 2014 ISSN: 0976-2876 (Print) ISSN: 2250-0138(Online) 1Corresponding author THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT WEAKNESSES IN INTERNAL CONTROL AND BUSINESS UNIT PERFORMANCE ARASH DARAEI 1a AND HASSAN RANGRIZ (Ph.D) b a Department of Accounting, Science and Research Branch, Islamic Azad University, Zahedan, Iran. b Faculty Member, faculty of Management, University of Economic Sciences, Tehran, Iran. ABSTRACT Today, modern businesses to implement various activities are essentially established based on IT. The increasing reliance on IT knowledge along with the complexity of IT systems development and nature of its interference and continuous changes have increased the risk of using these systems and it required to implement internal controls to reduce these IT risks. The question is that whether to invest in the quality of control processes will improve the financial performance of the companies or not? and if yes, how will this happen? That we have examined in this study.Due to the increasing importance of the control of IT, designing management process to focus on the control of these processes remains a challenge and there are various aspects to identify and manage risks. Unlike the vast resources available in the field of computer science that investigates the technical aspects of IT security, computer systems, standards and procedures, research to examine the economic aspects of IT controls would have been very few. Data for this study consists of the weaknesses of modern IT and Software deal has been used for other variables through questionnaire. In this study, the regression method was used to predict and the results will be generalized to the community analytically. According to the results of this study can be said that IT weaknesses in the internal control process adversely affect the accounting profits and reduces it. The mentioned weaknesshasadverse and modified effect on relationship between accounting earnings and the market value. KEYWORDS: Internal control, information technology, IT business value, market value Today, modern businesses to implement various activities are essentially established based on IT. The increasing reliance on IT knowledge along with the complexity of IT systems development and nature of its interference and continuous changes have increased the risk of using these systems and it required to implement internal controls to reduce these IT risks. These controls include safety principles management, operation and technique in information system in order to maintain reliability, integrity and availability of information systems (ISO/IEC 2005; ITGI 2005; NIST 2006). In the United States most recent state and federal laws such as HIPPA law in 1996, the Gram Leach Bliley in 2001 and the most important law for firms in the exchange that is Sarbanes Oxley Act or SOX in 2002 have raised issues in the field of IT process control in business activities. Despite the growing importance of IT controls, designing management process to focus on IT control processes remains a challenge and there are various aspects to identify and manage risks (Power, 2009). In this study, we developed the idea based on that any shortcoming in the conduct of these controls causes corporate responsibility of the company and empirically examine the performance indicators of weakness in the internal control process of IT. Unlike the vast resources available in the field of computer science that investigates the technical aspects of computer systems and information technology standards and procedures (Baskerville 1993; Dhillon 1997; Backhouse et al, 2006; Siponen and Livari 2006) So far researchto examine the economic aspects of IT controls have been very few; many of these resources are in relation to the models to determine the optimal amount of capital to be used to protect a set of data(Gordon & Loeb, 2002),provide methods to identify and quantify potential security events and estimate potential losses (Baskerville 1991; Straub &Welke 1998; Wang et al. 2008)or analytical and experimental studies testing economic issues associated with software vulnerabilities such as disclosure of information and patching the software by vendor (customer perspective). The main part of the research in this field has been by reading online resource that is closely related to our paper in response to stock issues in the field of information security, and invasion of privacy (Campbell et al. 2003; Cavusoglu et al. 2004; Acquisti et al, 2006). These studies have tried to estimate economic costs of ineffective security controls indirectly by focusing on a group of defects that are identified as violating the privacy of personal information. These reports were somewhat complicated. Analysis conducted by Cavusogluand others in 2004 presented significant negative reactions in this field and research conducted by Campbell and others in 2003 did not show such results. Research conducted byAcquistiand others in 2006 showed that there was a considerable negative reaction to the news of the day in the field of

Transcript of THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT WEAKNESSES IN INTERNAL CONTROL...

Indian J.Sci.Res.4 (4):36-53, 2014 ISSN: 0976-2876 (Print) ISSN: 2250-0138(Online)

1Corresponding author

THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN

IT WEAKNESSES IN INTERNAL CONTROL AND BUSINESS UNIT PERFORMANCE

ARASH DARAEI1a AND HASSAN RANGRIZ (Ph.D)b

aDepartment of Accounting, Science and Research Branch, Islamic Azad University, Zahedan, Iran.

bFaculty Member, faculty of Management, University of Economic Sciences, Tehran, Iran.

ABSTRACT

Today, modern businesses to implement various activities are essentially established based on IT. The increasing

reliance on IT knowledge along with the complexity of IT systems development and nature of its interference and continuous changes have increased the risk of using these systems and it required to implement internal controls to reduce

these IT risks. The question is that whether to invest in the quality of control processes will improve the financial

performance of the companies or not? and if yes, how will this happen? That we have examined in this study.Due to the

increasing importance of the control of IT, designing management process to focus on the control of these processes remains a challenge and there are various aspects to identify and manage risks. Unlike the vast resources available in the

field of computer science that investigates the technical aspects of IT security, computer systems, standards and

procedures, research to examine the economic aspects of IT controls would have been very few. Data for this study consists

of the weaknesses of modern IT and Software deal has been used for other variables through questionnaire. In this study, the regression method was used to predict and the results will be generalized to the community analytically. According to

the results of this study can be said that IT weaknesses in the internal control process adversely affect the accounting

profits and reduces it. The mentioned weaknesshasadverse and modified effect on relationship between accounting earnings and the market value.

KEYWORDS: Internal control, information technology, IT business value, market value

Today, modern businesses to implement

various activities are essentially established based on

IT. The increasing reliance on IT knowledge along

with the complexity of IT systems development and

nature of its interference and continuous changes

have increased the risk of using these systems and it

required to implement internal controls to reduce

these IT risks. These controls include safety

principles management, operation and technique in

information system in order to maintain reliability,

integrity and availability of information systems

(ISO/IEC 2005; ITGI 2005; NIST 2006). In the

United States most recent state and federal laws such

as HIPPA law in 1996, the Gram Leach Bliley in

2001 and the most important law for firms in the

exchange that is Sarbanes Oxley Act or SOX in 2002

have raised issues in the field of IT process control in

business activities. Despite the growing importance

of IT controls, designing management process to

focus on IT control processes remains a challenge and

there are various aspects to identify and manage risks

(Power, 2009). In this study, we developed the idea

based on that any shortcoming in the conduct of these

controls causes corporate responsibility of the

company and empirically examine the performance

indicators of weakness in the internal control process

of IT. Unlike the vast resources available in the field

of computer science that investigates the technical

aspects of computer systems and information

technology standards and procedures (Baskerville

1993; Dhillon 1997; Backhouse et al, 2006; Siponen

and Livari 2006) So far researchto examine the

economic aspects of IT controls have been very few;

many of these resources are in relation to the models

to determine the optimal amount of capital to be used

to protect a set of data(Gordon & Loeb,

2002),provide methods to identify and quantify

potential security events and estimate potential

losses (Baskerville 1991; Straub &Welke 1998;

Wang et al. 2008)or analytical and experimental

studies testing economic issues associated with

software vulnerabilities such as disclosure of

information and patching the software by vendor

(customer perspective). The main part of the research

in this field has been by reading online resource that

is closely related to our paper in response to stock

issues in the field of information security, and

invasion of privacy (Campbell et al. 2003; Cavusoglu

et al. 2004; Acquisti et al, 2006). These studies have

tried to estimate economic costs of ineffective

security controls indirectly by focusing on a group of

defects that are identified as violating the privacy of

personal information. These reports were somewhat

complicated. Analysis conducted by Cavusogluand

others in 2004 presented significant negative

reactions in this field and research conducted by

Campbell and others in 2003 did not show such

results. Research conducted byAcquistiand others in

2006 showed that there was a considerable negative

reaction to the news of the day in the field of

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

information security in the stock market; However,

they also found that after two days of unusual

feedbacks have been lessened and after five days these

feedbacks disappeared. On the other hand, in all these

studies only focus was to declare the security

issues and there was no reference to the impact of IT

internal control processes on business performance

thus, compared with previous studies this paper

provides direct empirical evidence about the

effectiveness of internal control processes dereliction

of performance in IT companies and we do not focus

on the results of public disclosure. The total number of

recent studies has addressed issues related to weak

internal control processes. Further work has been done

to focus to investigate the determinants of internal

control weaknesses processes of IT (AshbaughSkaife

et al. 2007 , Doyle et al. 2007a) and the potential

impact of weaknesses on quality system

(AshbaughSkaife et al. 2008). In addition to two

studies that have been carried out recently in the capital

costs (Beneish et al. 2008; AshbaughSkaife et al. 2009)

different results have been obtained. Research paper

very similar to the current paper illustrated market

reaction to the disclosure of information in this area

with numerous examples (Hammarsley et al.

2008).Theresults and events of these studies are

complex, one reason is that revealing disclosure results

do not ever give new entries in the market and

weaknesses in internal control processes in

performance results and other irregularities in a

company is expressed; another reason for the

inconsistent results obtained could also be that this

previous research in general just had weak internal

control processes and differences in the types of

weaknesses in the process of the surveyed companies

have been ignored. Many researches are currently

investigating the relationship between the weakness of

internal control processes of IT and monitoring these

controls (Li et al. 2007), audit fees (Canada et al.

2009), and investment return in this regard (Masli et al.

2009). In this paper, we present a discussion based on

the existence of weaknesses in internal control over IT

processes that is indicative of poor data quality and the

results of a concurrent study shows that forecasts of

revenue in financial statements of companies that have

weakness in the system are less accurate. The

functional results of such weakness have not been

investigated in our research. The question is that

whether to invest in the quality of control processes

will improve the financial performance of the

companies or not? and if yes how this can happen.

In this paper, we first examine corporate

responsibility in the process of creating an IT internal

control and impact ofweaknesses on firm performance

and then the relationship between IT weaknesses in

internal control processes and firm performance will

be evaluated in two areas.One of these issues was a

correlation between internal control processes of IT

quality and impacts ofthese weaknesses on company's

current performance that is measured using return on

assets (ROA). We found that companies with

weakness in these control processes relatively

havelessreturn on assets (ROA) than the companies

that have no such weakness. In the second part of the

analysis, this paper examines the relationship between

quality of control processes and corporate performance

by providing and testing a model in the field ofhow to

engage in risk-related effects on stock prices by

investors.In this case particularly using the framework

provided by Olson in residual income valuation (RIV),

we will examine the effects of direct and indirect

quality control processes on corporate market value. In

this study we found that the quality of the internal

control process of IT does not have a direct impact on

market value, although we found that the quality of

these processes have the opposite and modified effect

on the relationship between financial income and the

market value of the company; In other words, the

empirical results obtained show that the income level

have less use in determining the market value of the

Company's internal control over IT processes and is in

proportion to the view which we have discussed in this

article, based on which the non-implementation of the

internal control process by the techniques of

information technology can indicate poor performance

and low-quality financial reporting. This paper

provides empirical evidence suggesting that the risks

related to information systems are priced by capital

markets and offers information on the quality and

usefulness of IT control processes to investors.

Another result of this study in theory is that the

implementation of internal accounting control

processes using IT is to create competitive advantage

and the focus of this paper is not to recognize the

benefits of these powerful techniques utilizing IT

control causing to be existed, but the risk is more due

to lack of proper implementation of these processes. In

the next section the theoretical framework, the

operation of the internal control weaknesses of IT and

related assumptions have been provided. Our research

model and its associated design are presented in

section 3 of this article. In the fourth section of this

article we will review the data and its analysis. The

fifth section is also devoted to the implementation of

additional tests, during which the modified

relationship (formula) used and also instead of using a

whole range of IT weaknesses in the internal control

process variables,separate variables are used. One of

the strengths of this study is the separation of IT

weaknesses intoeight separated subsets that will follow

more and accurate management of these weaknesses.

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Finally, the sixth section will discuss the results

obtained.

Theoretical Framework, the Importance Of

Performance And Assumptions

Theoretical Framework: IT ICW as a corporate

responsibility

Transformation description in company's

performance mainly focuses on many resources on the

organization's financial policy. Powell and

Arregle(Powell and Arregle 2007) stated that

companies compete on the basis of two main basis one

of which iscompetitionadvantage based on that the

propulsion performance of a company is based on its

high functionality and no imitation and other one is

company errors based on a company's performance

which is affected by errors associated with the

activities, resources and opportunities that companies

confront. Arend (Arend 2004) called these errors as

corporate debt and other researchers (Powell 2001)

called competitive disadvantages due to factors that

reduce the corporate responsibility also some

researchers have labeled these factors as sources

weakness and characterized failure (West and

DeCastro, 2001). As a result, companies even in the

absence of pro-competitive benefits can also act

differently. Corporate responsibility or competitive

errors are not considered mirror image forms of

competitive advantages and are completely

independent of each other so if the competitive

advantage starts from of a company's non-duplication

of functionality and specific resources, competitive

errors are not related only to the absence of such

resources and is defined as the failure to achieve even

minimal success or failure of a company to achieve

strategic factors of relevant industry (Amit and

Schoemaker , 1993) that is primary requirement is each

company (Powel , 2001:877). Corporate debt will

cause damage to the credibility of a company and

through this strikes company and the case is different

with organizational no success (Arend, 2003) and thus

cause effects on firm performance without reference to

competitive advantage. In the research we will check

whether the type of corporate debt as due to weakness

in IT control processes will change company's

performance or not.

By focusing on primary basis of competition

(the basis of competitive advantages), major part of

this work examines the competing values associated

with application of information technology since the

advent of this technology two decades ago up today. A

large part of recent research is related to resource-

based theory of the firm as a basic theoretical

framework. Resource based view (Wernerfelt 1984;

Barney 1991) or RBV is in search of an explanation for

the description of competitive resources.

This theory attributes competitive advantage to

the particular workings of companies, resources,

capabilities and tangible and intangible assets. Based

on the theory of RBV, several papers have discussed

(Eg, Aral & Weill 2007; Bharadwaj 2000, Jeffers et al,

2008; Mata et al, 1995; Melville et al, 2004; Ray et al,

2005; Ravichandran&Lertwongstein 2005; Wade

&Hulland 2004; Wang &Alam, 2007) in the field of

authenticated empirical basis for the concept that IT

technology can create a source of competitive features

of the following at least two methods.

(A) When a company has the resources and

capabilities of valuable, rare and costly IT to be copied,

these processes can create competitive advantages for

companies.

(B) When companies complete these

processes in order to identify potential uses as an

additional process.

However, according to RBV theory a

company to create a competitive advantage shall be

able to follow many organizational requirements and

invest in a variety of resources that are rare and

difficult to copy including IT resources. One can also

say that according to this theory that is based on

expectations of resources based, hardware and

standard software and also advanced technologies of

IT which are available and information technology

increasingly becomes an appropriate agent to produce

(Carr, 2003,Clemons, 1991). This does not mean that

companies should not invest on public resources of

information technology investment on such resources

needed to achieve success in the modern economy and

companies that do not invest enough in technology and

do not manage the risks associated with will be

includedin those companies faced competitive

disadvantages. As organizations increasingly rely on

information technology we conclude that the inability

to achieve internal control processes for their IT will

inevitably cause defects and is considered negative

factor that the company is responsible for making

changes in performance.

Performance Importance of IT ICWs

Integrity and reliability of data generated by

an organization's information systems are critical

issues that are not only to generate acceptable financial

reports but also are necessary for the overall success of

the financial system (Krishnan et al, 2005). Although

weaknesses in financial reporting performed in internal

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

control without IT may be a misrepresentation of

financial events but weaknesses in the internal control

of financial reporting by business IT can also affect

important business functions (such as administrative

processes, archive and protect raw transactional data)

and also effective on the creation of reliable financial

reporting. These differences in how to implement

internal controls monitoring on evaluating companies

is no different but an important point for these

companies in the ranking is the existence of

weaknesses in internal controls which in turn comes

from the implementation of these control processes.

Researchers called Moody (Moody) has stated that

although the weaknesses associated with financial

calculations (weaknesses of type A) through actual

tests are detected by auditors and therefore there is no

concern for the reliability of these reports but

identifying internal weaknesses of each company

(weaknesses of type B) is made more difficult by the

audit because these weaknesses are pervasive, not only

stops its preparation of accurate financial reports but

also can influence on taking control of management

capabilities to the company's performance (Doss &

Jonas, 2004).Although weaknesses of the internal

control process without creating information

technology can be both put in weaknesses group but

PCAOB Standard No. two of institution in particular

expresses that IT controls shall be accomplished in the

company's internal control and should be widely used

to process performance and preparing financial reports

(PCAOB 2004).

Costs associated with weakness in the

financial statements may include various

components. First the cost of correcting errors

and losses from the system and unreliable and

unsafe data including cleanup process, removal

claiming in this field, damage to company

reputation and reduce organizational IT systems

to ensure employees. On the other hand, these

certain expenses that are a manifestation of

weakness in internal control processes will

reduce income due to loss of positions and lack

of customers and business partners’ happiness.

With respect to the integrated nature of

economic systems, decision making and current

performance, existence of weakness in internal

control process using information technology

show thatthe organization to reach objectives

related to achieving secure systems and reliable

financial data to support their functional

activity, management decisions and expectations

of customers and suppliers and their trading

partners has failed. In other words, the weakness

in internal control processes lead to weakness in

the company's performance capabilities which

are related to Information Technology and

create competitive disadvantages that have a

negative impact on corporate profitability. This

will form the basis of our first hypothesis:

First hypothesis: Existence of weaknesses in

the internal control of information is inversely related

to the accounting profit.

Existence of such weaknesses as well as

cause effects on the company's current income

willcause also effects on investors and their

expectations about the future prospects of a company.

With respect of the capital markets with high

efficiency, estimating the size and value of a company

should reflect the best assessment of the present value

of the future earnings of the company (Fama, 1970). A

large part of this research is to show the perspective of

capital markets in financial data and accounting firms

(especially income) (Kothari, 2001). Reviewing

current earnings of a company is not necessarily

indicative of future profitability and hence not fully

reflects the value of the firm in the capital market.

Previous research has shown that IT can improve the

future performance of the Company's internal control

processes. For example, this technology can improve

customer service, better quality of services and

products, supporting modernization plans and the

flexibility of the better system in any company.

Previous research has shown that investors have the

ability to identify and pricing such capabilities

(Anderson et al, 2006; Bharadwaj et al, 1999;

Brynjolfsson et al, 2002; Sambamurthy et al, 2003;

Wang &Alam, 2007).

With a similar expression we shall say that

weakness in internal control over IT processes lead to

organizational liabilities (organizational liability) that

reflect a decline in the ability to achieve future value

of the assets of ITincluding IT tools and also

uncertainty about the quality of organizational

processes provided by IT. Existence ofthese

weaknesses has a negative effect on the market value

of a company on capital market and amount of this

effect is to the extent that investors consider their

weaknesses and drawbacks in terms of their estimates.

So we claim that this lack of effect in addition to the

current income of the company (first hypothesis), has

a direct and negative impact on the future value of the

company.

Second hypothesis: the existence of IT

weaknesses in the internal control process is associated

with the market value of a company (ie. a negative

correlation with equity market value of a company).

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Existence of these weaknesses, in addition

to the direct impact on the market value of a company

can also affect the amount of believability of future

profits of a company by investors and hence affect the

market value of a company. Much of this research

suggests that a firm's accounting information

(especially information related to corporate profits), is

in fact awareness information about a company's future

financial condition therefore the market value of a

company is affected by them (Kotahri 2001). Strong

internal controls are keys to build strong and reliable

financial reports (AshbaughSkaife et al, 2008, Doyle et

al. 2007b). To the extent that financial reporting

processes in modern enterprises are performed by

using IT, weaknesses in these processes can Change

attitudes of investors about the reliability and validity

of reported by corporate profits. Reduce the feeling of

confidence increases the risk of reliance on the

information associated with the company's current

earnings to predict future earnings of the company.

This risk will increase the probability that investors

make decisions related to pricing, the company as a

weak and inefficient with respect to these casesboth in

theory and practice (eg, Easley and O'Hara 2004) and

empirical (eg, Francis et al. 2004 , 2005) associated

with participation in the capital market are valued. In

summary, it should be noted weaknesses in internal

accounting control processes using information

technology due to influence market expectations by

creating signs that the company reports are not reliable

or are less validated than before. Therefore, we assume

that dividends and earnings of a company when it has

a weak internal control processes in IT is having less

of an impact on the value (valuation) of the company

(or is less efficient to increase the company's market

value).

The third hypothesis: there are weaknesses in

the internal control of information technology has a

negative impact on the relationship between profits

and market value adjustment of the company

RESEARCH METHODOLOGY

The research method in this research study is

the predictiontype:this type of research is to learn the

relation between variables but it is not after the cause-

effect relationship between variables.Methods of

analyzing data are quantitative or statistical that in this

case research findings are quantifiable. The use of

quantitative statistical method in this project is

performed using inferential statistics: in this type of

analysis results of the study on a small group called the

sample can be generalized to the larger group as

population. Data are quantitative and in case of

usingqualitative data initialize them with 0, 1, or in

other cases, that are converted into quantitative data.

Type of research application in this paper is

fundamental research (basic) (the

Researchclassification based on target): basic research

discovers scientific laws and principles and seeks to

develop knowledge of the principles and scientific

laws. A fundamental study on the applicationmay not

be objective but in the long run it will be the basis for

the development of knowledge and perform other

research. The purpose of this research is to establish a

theory by exploring the principles or general rules and

does not pay attention on much practical application.

The results of such research are often general and

abstract. The purpose of this research is to further

theorizing. Fundamental research is on both empirical

and theoretical issues. In thepresentstudy that is

fundamental-experimental, data and original

informationcollected using observation, interviews

and… and analyzes them by regression statistical

methods and correlation.

Data and Sample Selection

Data collected in this study was based on the

methods and documents to the library, so the library is

used to develop a theoretical investigation of

information needed to test hypotheses based on the

available data on the stock exchange and in part of the

work related to IT in the process of gathering

information about the state of internal control of the

company data were collected using a questionnaire.

The questionnaire contains 45 questions related to IT

controls respectively. The data collected by the New

Deal 3 software is also used. Mentioned software did

not offer directly advertising fee which is one of the

variables used in this study, website of ”research,

development and Islamic studies” have been used in

the internet address of www.rdis.ir to receive PDF files

of financial statements of companies.

The data for this study is collected from the

Stock Exchange and if necessarywill be taken from the

archived audit firms. The survey was performed on 400

companies listed on the Stock Exchange during the ten

year period from 2001 to 2010. This process creates a

sample consisting of 4,000 firm observations of FY.

Research model for this study are the following

assumptions:

H1

H2

H3

Financial

Income

Reported

IT Weaknesses in

the Internal Control

Process

Market

Value

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Std

dev

0.0

44663

0.0

49566

0

134.4

50821

1.9

8E

+13

1.3

83246

0.1

88024

0.3

86953

0.2

18002

1.9

3E

+12

3.2

4E

+11

4.5

0E

+11

11255668373

1.6

2E

+12

0.0

1241

37395929809

0.0

06714

4.5

0E

+11

Ob

serv

ati

on

s w

ith

IT

IC

W (

IT I

CW

= 1

)

Med

ian

0.0

5

0.0

6

1

204.5

7.2

7E

+11

0.0

79942

0.2

11662

0

0

1.5

8E

+11

16866030000

35424000000

0

1.9

2E

+11

0

1813750868

0.0

03222

35424000000

Mea

n

0.0

48529

0.0

59118

1

245.3

52941

5.6

7E

+12

0.3

06491

0.2

50833

0.1

76471

0.0

78424

7.7

6E

+11

98286443167

1.4

8E

+11

1939794118

6.2

1E

+11

0.0

02135

14897141795

0.0

0544

1.4

8E

+11

N

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

2267

Ob

serv

ati

on

s w

ith

no

n-I

T I

CW

(IT

IC

W =

0 )

Std

dev

0.0

90064

0.1

17984

0

119.0

97969

2.8

4E

+13

0.2

68065

0.1

49888

0.3

25813

0

1.0

1E

+13

2.7

2E

+12

3.1

6E

+12

3.2

9E

+11

9.4

8E

+12

0.0

11338

6505250

9899

0.0

03999

0

Med

ian

0.1

3

0.1

8

0

15

6.5

1.5

7E

+12

0.1

58749

0.2

3723

0

0

9.5

4E

+11

1.9

4E

+11

1.4

6E

+11

0

4.8

1E

+11

0

20

84108182

0.0

01339

0

Mea

n

0.1

66

53

8

0.1

98

07

7

0

17

2.3

84

61

5

1.4

2E

+1

3

0.0

99

68

9

0.2

27

57

3

0.1

15

38

5

0

6.1

1E

+1

2

1.5

2E

+1

2

1.8

4E

+1

2

64

61

53

84

61

5

5.3

6E

+1

2

0.0

02

22

4

28

23

86

92

29

7

0.0

03

13

6

0

N

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

17

33

𝑅𝑂

𝐴 𝑡

𝑅𝑂

𝐴 𝑡

−1

IT_

ICW

Ag

e

Sale

s

Gro

wth

Inve

nto

ry/A

sset

s

Au

dit

or_

Ch

an

ge

Pri

orL

oss

MV

E

Net

Div

iden

ds

Ea

rnin

gs

R&

D

Eq

uit

y

R&

D/A

sset

s

Ad

vert

isin

g

Ad

v/A

sset

s

IT_IC

W *

Earn

ing

s

IT_ICW*Earnings

1

Dat

a def

init

ions:

RO

A 𝑡

= N

et I

nco

me 𝑡

/Ass

ets 𝑡

; R

OA

𝑡−

1 =

Net

In

com

e 𝑡−

1/A

sset

s 𝑡−

1; I

T_IC

W =

Info

rmat

ion T

echnolo

gy I

nte

rnal

Contr

ol

Wea

knes

ses;

Age

= T

he

nu

mber

of

month

s th

at c

om

pan

ies

list

ed o

n t

he

Sto

ck E

xch

ange;

Sal

es =

N

et s

ales

; Gro

wth

= N

et s

ales

𝑡 -

Net

sal

es𝑡−

1/N

et s

ales

𝑡−1

; In

ven

tory

/Ass

ets

= i

nven

tory

to a

sset

s ra

tio

; Chan

ge_

Audit

or

= C

han

gin

g a

ud

itors

in c

urr

ent

yea

r; P

riorL

oss

= %

of

yea

rs w

ith l

oss o

ver

las

t 3 y

rs;

MV

E = M

arket

val

uat

ion =

pri

ce ∗

shar

es;

Net

Div

iden

ds

= c

om

mo

n d

ivid

end

s;

Net

Ear

nin

g =

Net

inco

me

from

curr

ent

yea

r; R

&D

= R

esear

ch a

nd d

evel

opm

ent

expen

dit

ure

s; E

quit

y =

Equit

y f

rom

curr

ent

yea

r; R

&D

/Ass

ets

= R

esea

rch a

nd

dev

elopm

ent

expen

dit

ure

s to

ass

ets

rat

io;

Ad

v =

Ad

ver

tisi

ng

ex

pen

se;

Adv/A

sset

s =

Adver

tisi

ng e

xpen

se t

o a

sset

s ra

tio;

IT_IC

W *

Ear

nin

gs

= I

mpac

t of

Info

rmat

ion T

echn

olo

gy I

nte

rnal

Contr

ol

Wea

knes

ses

and n

et i

nco

me,

per

dep

enden

t var

iable

.

Adv/Assets

1

-0.0

22

Advertising

1

0.0

71

.450**

R&D/Assets

1

-0.0

54

0.0

64

-0.0

28

Equity

1

0.0

98

.621**

-0.1

32

0.0

93

R&D

1

0.2

11

.64

6**

-0.0

54

-0.0

95

-0.0

32

Earning

1

0.1

79

.981**

0.0

76

.557**

-0.1

33

0.0

66

NetDividends

1

.941**

0.2

05

.975**

0.0

94

.609**

-0.1

18

-0.0

42

MVE

1

.954**

.941**

.330**

.962**

0.1

68

.551**

-0.1

56

0.0

93

PriorLoss

1

-0.1

07

-0.1

-0.1

08

-0.0

36

-0.1

02

-0.0

49

-0.1

09

-0.2

07

-0.0

79

Auditor_Change

1

0.0

75

-0.1

43

-0.1

38

-0.1

47

-0.0

57

-0.1

44

-0.0

78

-0.1

42

-0.0

46

-0.0

81

Inventory/Assets

1

-0.0

73

-0.1

69

-0.1

76

-0.1

57

-0.1

7

-0.1

32

-0.1

64

-0.0

34

-0.2

15

0.2

17

-0.0

96

Growth

1

-0.1

45

-0.1

04

-0.0

29

-0.0

66

-0.0

41

-0.0

51

-0.0

43

-0.0

56

-0.0

41

-0.0

18

0.0

14

0.0

23

Sales

1

-0.0

41

-.287*

-0.1

54

-0.0

98

.693**

.526**

.622**

.493**

.610**

.274*

.539**

-0.1

61

.493**

**.C

orr

elat

ion

is

sig

nif

ican

t at

th

e 0

.01

lev

el (

2-t

aile

d)

*.C

orr

elat

ion

is

sig

nif

ican

t at

th

e 0

.05

lev

el (

2-t

aile

d)

AGE

1

-.2

96

*

0.1

97

0.1

64

-0.0

23

-0.1

61

-.3

78

**

-.3

33

**

-.3

52

**

-0.1

84

-.3

46

**

0.0

15

-0.1

21

0.2

42

-0.0

07

IT_ICW

1

.27

6*

-0.1

78

0.0

98

0.0

68

0.0

85

0.2

34

-.3

69

**

-.3

69

**

-.3

76

**

-0.1

44

-.3

53

**

-0.0

04

-0.1

3

0.1

99

0.2

14

ROA𝑡−1

1

-.6

31

**

-0.2

33

.52

5*

*

-0.0

91

-0.2

29

-0.0

49

-.3

90

**

.59

3*

*

.49

1*

*

.54

3*

*

.46

4*

*

.49

2*

*

.25

6*

0.1

04

-0.1

57

-0.1

34

ROA𝑡 1

.75

8*

*

-.6

58

**

-.3

86

**

.25

6*

-0.0

57

-0.0

97

0.0

17

-.4

05

**

.42

6*

*

.39

5*

*

.41

3*

*

.26

2*

.37

6*

*

0.1

32

0.0

57

-0.1

67

-0.1

85

𝑅𝑂

𝐴𝑡

𝑅𝑂

𝐴𝑡−

1

IT_

ICW

Ag

e

Sale

s

Gro

wth

Inve

nto

ry/A

sset

s

Au

dit

or_

Ch

an

ge

Pri

orL

oss

MV

E

Net

Div

iden

ds

Ea

rnin

gs

R&

D

Eq

uit

y

R&

D/A

sset

s

Ad

vert

isin

g

Ad

v/A

sset

s

IT_IC

W *

Earn

ing

Panel

B—

Poole

d s

am

ple

co

rrel

ati

on

ta

ble

Ta

ble

1. p

rese

nts

des

cri

pti

ve s

tati

stic

s of

orig

ina

l d

ata

sa

mp

les

an

d t

hei

r c

orr

ela

tio

n t

ab

le

Panel

A—

Des

crip

tive

sta

tist

ics

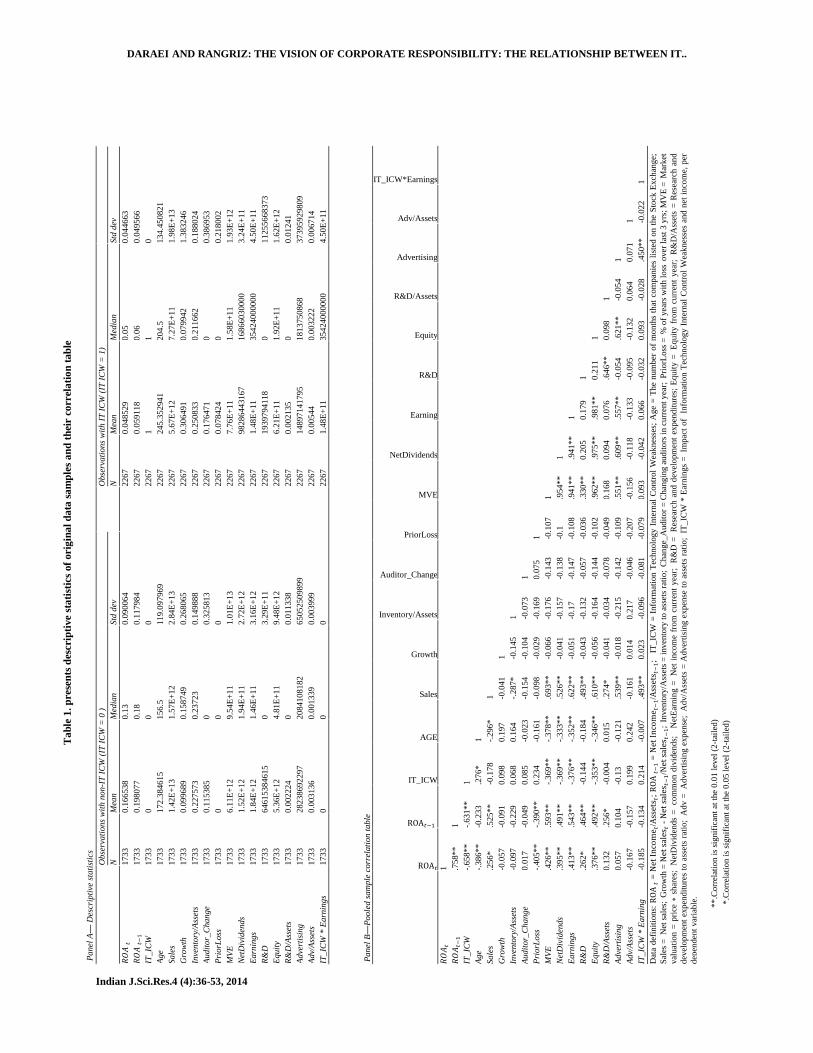

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Experimental Tests In Hypothesis 1, we claimed that the

weakness in internal control processes of IT has a

negative impact on the earnings of a company. To

investigate this hypothesis a measure of the extent of

the earnings and return on assets (ROA) and we rely

on using two alternative explanatory models that

iswidelyused in the resources and are in the

randomwalk model (Random walk) and the production

function (Production function). The first feature that

we use is consistent with computational studies related

to the time series properties of annual income which

implies income based on random walk (Albrecht et al,

1977; Watts &Leftwich, 197).

𝑹𝑶𝑨𝒊,𝒕= 𝑏0 + 𝑏1𝑅𝑂𝐴𝑖,𝑡−1 + 𝑏2𝐼𝑇_𝐼𝐶𝑊𝑖,𝑡 + 𝑏3𝐴𝑔𝑒𝑖,𝑡 + 𝑏4𝑆𝑎𝑙𝑒𝑠𝑖,𝑡 Equation 1

+𝑏5Growth𝑖,𝑡+𝑏6𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡+ 𝑏7𝐿𝑎𝑟𝑔𝑒 𝐴𝑢𝑑𝑖𝑡𝑜𝑟𝑖,𝑡

+ 𝑏8𝐴𝑢𝑑𝑖𝑡𝑜𝑟_𝐶ℎ𝑎𝑛𝑔𝑒𝑖,𝑡+ 𝑏9𝑃𝑟𝑖𝑜𝑟 𝐿𝑜𝑠𝑠𝑖,𝑡 +𝜀𝑖,𝑡

The second measure used in studies by Lev and

Sougiannis (1996Lev and Sougiannis) and

Rajgopal et al (Rajgopal et al, 2003), have

been modeling as a function of revenue

collection and measurement of tangible and

intangible assets/risk.

𝑹𝑶𝑨𝑖,𝑡 =𝑏0 + 𝑏1𝐴𝑑𝑣𝑒𝑟𝑡𝑖𝑠𝑖𝑛𝑔/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡 + 𝑏2𝑅&𝐷/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡 + 𝑏3𝐼𝑇_𝐼𝐶𝑊𝑖,𝑡Equation 2 Equation 2

+ 𝑏4𝐴𝑔𝑒𝑖,𝑡+ 𝑏5𝑆𝑎𝑙𝑒𝑠𝑖,𝑡 + 𝑏6𝐺𝑟𝑜𝑤𝑡ℎ𝑖,𝑡+ 𝑏7𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡

+ 𝑏8𝐿𝑎𝑟𝑔𝑒 𝐴𝑢𝑑𝑖𝑡𝑜𝑟𝑖,𝑡+ 𝑏9𝐴𝑢𝑑𝑖𝑡𝑜𝑟_𝐶ℎ𝑎𝑛𝑔𝑒𝑖,𝑡 + 𝑏10𝑃𝑟𝑖𝑜𝑟 𝐿𝑜𝑠𝑠𝑖,𝑡 + 𝜀𝑖,𝑡

Many researchers including AshbaughSkaife

et al , 2007; Doyle et al , 2007a; Ge&McVay 2005

found that companies that are novice, smaller, fast

growing, with a more complexity of performance and

the changing structure and have been auditedby large

firms or their auditor has changed have more of these

weaknesses. So, we've been monitoring the following

corporate characteristics:

Age of company, sales rate as a measure of firm size

and growth rate in sales

In this study, variables associated with the

presence of a large audit firm (Large_Auditor),

indicating a change in the auditor (Auditor_Change),

variable loss of financial (Prior_loss) the percentage

of reported financial losses in the last three years have

been marked. In this model, if there is a correlation

between the independent variables, these factors can

cause a deviation of the regression coefficients (linear

optimization).

To test hypotheses 2 and 3, the direct and

indirect impact on the value of IT weaknesses in

internal control processes and corporate credit in the

capital markets is a version of Ohlson's theory (1995

Ohlson) the remaining credit worthiness or RIV

model was used where the value of the firm are now

modeling in the capital market functions of the offices

of the company's financial assets (book value of

assets), current abnormal earnings and revenue

forecasts and other information that led to the creation

and modification of future profitability.

This model is widely used and accepted in

the resources related to capital markets, particularly in

areas such as cross validation to test the validity of

various non-financial components of the brand (Barth

et al, 1998) and disclosure of financial information

(Shevlin, 1996), wireless networks (Amir & Lev,

1996) and the benefits of a credit network sites created

by e-commerce companies (Rajgopal et al, 2003) there

are many implementation of RIV model. Our research

methods course offered by Rajgopaland others to

examine the factors modulating the response to income

or other relationship between income and market

valuehas been used. According to these measures, the

company's reputation can be considered as a linear

function of the value of the assets registered in

financial books and current profits and used the

following credit models:

𝑴𝑽𝑬𝒊,𝒕 = 𝑏0+ 𝑏1𝐸𝑞𝑢𝑖𝑡𝑦𝑖,𝑡 + 𝑏2𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑡

+𝑏3𝑁𝑒𝑡𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠𝑖,𝑡+𝑏4𝐴𝑑𝑣𝑒𝑟𝑡𝑖𝑠𝑖𝑛𝑔𝑖,𝑡

+ 𝑏5𝑅&𝐷𝑖,𝑡 + 𝑏6𝐼𝑇 𝐼𝐶𝑊𝑖,𝑡 + 𝑏7𝐴𝑔𝑒𝑖,𝑡

+ 𝑏8𝑆𝑎𝑙𝑒𝑠𝑖,𝑡 + 𝑏9𝐺𝑟𝑜𝑤𝑡ℎ𝑖,𝑡

+𝑏10𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡

+𝑏11𝐿𝑎𝑟𝑔𝑒 𝐴𝑢𝑑𝑖𝑡𝑜𝑟𝑖,𝑡

+ 𝑏12𝐴𝑢𝑑𝑖𝑡𝑜𝑟_𝐶ℎ𝑎𝑛𝑔𝑒𝑖,𝑡

+ 𝑏13𝑃𝑟𝑖𝑜𝑟 𝐿𝑜𝑠𝑠𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 3

MVEi: value of the company's market capitalization at

the end of the fiscal year for firm i in year Equityi t:

Total equity at the end of financial year Eariningsi: net

income and NetDividensi, t: Net dividends paid

ordinary shares at the end of the fiscal year. Our

advertising and research and development expenses in

fiscal balances that have not come we

investigateintangible costs.

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Hypothesis 3 stated that there are weaknesses

in the internal control processes of IT which has a

negative impact on the relationship between corporate

profits and the value of the capital market. To test this

hypothesis we involve confrontation between revenues

and IT ICW in our model. This expression allows us to

reflect these shortcomings of the relationship between

income and the value of our company. Our hypothesis

is that factors affecting this relationship is negative,

indicating a role in determining the market value of the

discounted earnings weakness in internal control over

IT processes.

𝑴𝑽𝑬𝒊,𝒕 = 𝑏0+ 𝑏1𝐸𝑞𝑢𝑖𝑡𝑦𝑖,𝑡 + 𝑏2𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑡 + 𝑏3𝑁𝑒𝑡𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠𝑖,𝑡 + 𝑏4𝐴𝑑𝑣𝑒𝑟𝑡𝑖𝑠𝑖𝑛𝑔𝑖,𝑡 Equation 4

+ 𝑏5𝑅&𝐷𝑖,𝑡 +𝑏6(𝐼𝑇 𝐼𝐶𝑊𝑖,𝑡 × 𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑡) +𝑏7𝐴𝑔𝑒𝑖,𝑡 + 𝑏9𝑆𝑎𝑙𝑒𝑠𝑖,𝑡

+ 𝑏8𝐺𝑟𝑜𝑤𝑡ℎ𝑖,𝑡 + 𝑏9𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦/𝐴𝑠𝑠𝑒𝑡𝑠𝑖,𝑡 + 𝑏10𝐿𝑎𝑟𝑔𝑒 𝐴𝑢𝑑𝑖𝑡𝑜𝑟𝑖,𝑡

+ 𝑏11𝐴𝑢𝑑𝑖𝑡𝑜𝑟_𝐶ℎ𝑎𝑛𝑔𝑒𝑖,𝑡 + 𝑏12𝑃𝑟𝑖𝑜𝑟 𝐿𝑜𝑠𝑠𝑖,𝑡 + 𝜀𝑖,𝑡

Conclusions Analytical results for the relationship

between IT ICW and asset returns are indicated in

Table 2. This table represents the regression results for

the random walk models and production function. IT

ICW ratio in this case is negative and is significant of

both models. Therefore, H1 is a well proven.

Table 2. Regression results for the ROA models.

Random walk Productionfunction

Standardized

Coefficients

sig Tolerance Standardized

Coefficients

sig Tolerance

ROA 𝑡−1 .605 .000 .854

IT_ICW -.199 .045 .927 -.488 .000 .897

Age -.292 .071 .772 -.293 .106 .758

Sales -.180 .064 .897 .005 .965 .720

Growth .073 .347 .903 .048 .606 .906

Inventory/Assets .035 .672 .792 -.042 .667 .815

Auditor_Change .053 .489 .928 .088 .339 .932

PriorLoss -.183 .040 .718 -.358 .001 .798

Adv/Assets -.068 .480 .839

R&D/Assets .127 .176 .903

N 0444 0444

Adjusted 𝑅2 .724 .612

Table notes: (all tests are two tailed).

Standardized regression coefficients are shown in

these cases. We will use the regression standard errors

clustered. Residual values for all models are consistent

with the assumptions of the statistical distribution.

Multi-co-linearity between the independent variables

as shown by the tolerance amounts is consistently low.

The re-evaluation of equations, regression after

removing the unrelated segments gives the same

results. According to the significant amounts in the

table above, the modified model of random walk and

the modified model of production functionin relations

5 and 6 are displayed:

𝑹𝑶𝑨𝒊,𝒕 = 𝑏0 + 𝑏1𝑅𝑂𝐴𝑖,𝑡−1 + 𝑏2𝐼𝑇_𝐼𝐶𝑊𝑖,𝑡 + 𝑏3𝑃𝑟𝑖𝑜𝑟𝐿𝑜𝑠𝑠𝑖,𝑡+ 𝜀𝑖,𝑡 Equation 5

𝑹𝑶𝑨𝑖,𝑡 = 𝑏0 +𝑏1IT_ICW𝑖,𝑡+𝑏2Prior Loss𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 6

Data Definition: ROAt 1: last year return on assets =

net profit in the previous year divided by prior year

assets, IT ICW: indicates weaknesses in internal

control usingof IT and when such weaknesses in

corporate reported equals to 1 and otherwise is 0, R &

D/Assets: assets/expenditure on R & D,

Advertising/Assets: assets/costs, advertising, Age:

number of months in the Stock Market listed

companies Sales: Net sales , Growth: subtracting net

sales from the prior year's net sales divided by net sales

prior, Inventory/Assets: Ratio inventory of assets,

(Large Auditor): In case of large audit firms (trustee

stock), this amount is equal to 1, otherwise 0, Auditor

Change: If the auditing company in the years to change

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

this value is 1, otherwise is 0, prior Loss: percentage of

years of financial losses in the past three

years. According to the regression results, we found

that the coefficient of IT ICW in both models have

statistical meaning.We also found out that financial

losses variable (prior Loss) has a negative effect which

was statistically significant in both models. In table 3

results of regression estimates obtained from equations

3 and 4 is observed which are used to examine the

relationship between market value and IT_ICW.

Table 3. Regression results for the Ohlson/RIV valuation models.

Base model Interaction model

Standardized

Coefficients

sig Tolerance Standardized

Coefficients

sig Tolerance

Equity .523 .017 .665 .101 .706 .846

Earnings .326 .035 .601 -.117 .487 .715

NetDividends .697 .000 .829 .957 .000 .818

Advertising -.204 .000 .754 .228 .000 .975

R&D -.046 .168 .525 -.014 .675 .663

IT_ICW -.020 .443 .719

AGE -.007 .791 .735 -.002 .926 .731

Sales .340 .000 .641 .275 .000 .772

Growth -.012 .608 .900 -.018 .418 .889

Inventory/Assets .012 .622 .801 .010 .651 .801

Auditor_Change .003 .891 .927 .006 .793 .925

PriorLoss -.005 .845 .833 .004 .867 .814

IT_ICW Earnings -.106 .407 .892

N 0444 0444

Adjusted 𝑅2 .978 .981

Table notes: (all tests are two tailed).

Here like previous table standardized

regression coefficients. Residual values for all models

are consistent with the assumptions of the statistical

distribution. Coefficients of the independent variables

multi-co-linearity is consistently low. Due to the high

value of the variable sig IT_ICW (fifth column from

the right) we conclude that these variables have not a

significant relationship with the market value of the

company. Thus, the second hypothesis is rejected.

Similarly with examining the value of the sig variable

IT_ICW earnings (second column from the right) there

is a negative relationship between this variable and the

market value of the company-reduce the impact on the

market value of the benefit in the shadow of internal

control weaknesses of IT. This relationship has proved

our third hypothesis and this hypothesis is strongly

confirmed. In order to work with a heterogeneous

distribution and effects of scale, statistics t (t statistics)

are all based on the heterogeneous distribution of

standard errors by White (white 1980). We have tests

based on standard errors clustered. Of course, the

standard error of the test results on the primary

variables is small and therefore we present our results

using White standard errors. Our inference when

method is based on the separate sections of Cook

(Cook) is apart and re-do the regression analyzes,

remain unchanged. We also repeated our analysis

using alternative version that uses revenues from other

billing information (such as research and development

expenses and advertising costs), and have received

similar results. According to the significant amounts in

the above table, both RIV models in the form of

improved relations between 7 and 8 are displayed:

𝑴𝑽𝑬𝒊,𝒕 = 𝑏0𝐸𝑞𝑢𝑖𝑡𝑦𝑖,𝑡 + 𝑏1𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑡 + 𝑏2𝑁𝑒𝑡𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠𝑖,𝑡 + 𝑏3𝐴𝑑𝑣𝑒𝑟𝑡𝑖𝑠𝑖𝑛𝑔𝑖,𝑡 +𝑏4𝑆𝑎𝑙𝑒𝑠𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 7

𝑴𝑽𝑬𝒊,𝒕 = 𝑏0𝑁𝑒𝑡𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠𝑖,𝑡 + 𝑏1𝐴𝑑𝑣𝑒𝑟𝑡𝑖𝑠𝑖𝑛𝑔𝑖,𝑡 + 𝑏2 (𝐼𝑇_𝐼𝐶𝑊 × 𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑡) + 𝑏3𝑆𝑎𝑙𝑒𝑠𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 8

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Data Definition: Equity: Equity, Earnings: Net

Income, NetDividends: Net profit sharing,

Advertising: Advertising costs, R & D: Research and

development costs, IT_ICW: internal control weakness

is the use of IT When such weaknesses are reported in

the company equal to 1 and otherwise is 0, AGE: The

number of months the company has been included in

the list of securities markets Sales: Net sales, Growth:

subtracting net sales from the prior year's net sales

divided by net sales exp, Inventory / Assets: Ratio

inventory assets, Change_Auditor: If the auditing

company in the years to change this value to 1 and

otherwise is equal to 0, PriorLoss: percentage years of

financial losses in the last three years. IT_ICW

Earning: IT weaknesses in the internal control and

profit impact on the dependent variable. As the above

table IT_ICW variable is not significant at the 95%

level, (sig> 5%) with the use of IT internal controls

therefore has no direct relationship with the market

value (sixth column from right), Thus, the second

hypothesis is not confirmed. Also observed that the

coefficient of the variable IT_ICW Earning negative

(fourth column from left ) and this variable is

significant at the 95% level (sig <5%). Thus, the third

hypothesis is confirmed, this means the relationship

between revenues declined as a determinant of firm

value in the capital market weakness of IT. As a third

hypothesis mentioned the evidence suggests that

IT_ICW is a negative and significant factor between

income and the market value.

Additional Tests

The difference with theprevious studies is

that first modified formula used in the previous

paragraphs, second instead of using a general variable

of IT_ICW, IT eight variables weaknesses used to

show separate effects of IT weaknesses in the cases

studied. This study is also included only propositions

that are proved in the previous paragraphs.

Thus the modified model of random walk

(Equation 5) and the modified version of the

production function (Equation 6),by poor placement of

the variableinstead of the eight IT IT_ICW,

respectively are as follows:

𝑹𝑶𝑨𝒊,𝒕 =𝑏0+𝑏1𝑅𝑂𝐴𝑖,𝑡−1 + 𝑏2𝐴𝑐𝑐&𝑒𝑡𝑐_𝐼𝐶𝑊𝑖,𝑡 + 𝑏3𝑁𝑒𝑡&𝐼𝑛𝑡𝑒𝑟𝑛𝑒𝑡_𝐼𝐶𝑊𝑖,𝑡

+𝑏4𝐵𝑎𝑐𝑘𝑈𝑝_𝐼𝐶𝑊𝑖,𝑡 + 𝑏5 𝐴𝑐𝑐𝑒𝑠𝑠_𝐼𝐶𝑊𝑖,𝑡 + 𝑏6 𝑂𝑆_𝐼𝐶𝑊𝑖,𝑡 + 𝑏7𝑆𝑜𝑓𝑡_𝐼𝐶𝑊𝑖,𝑡 + 𝑏8𝐷𝑜𝑐_𝐼𝐶𝑊𝑖,𝑡 + 𝑏9 𝐻𝑎𝑟𝑑_𝐼𝐶𝑊𝑖,𝑡 + 𝑏10 𝑃𝑟𝑖𝑜𝑟𝐿𝑜𝑠𝑠𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 9

𝑹𝑶𝑨𝑖,𝑡 = 𝑏0 + 𝑏1 𝐴𝑐𝑐&𝑒𝑡𝑐_𝐼𝐶𝑊𝑖,𝑡 + 𝑏2 𝑁𝑒𝑡&𝐼𝑛𝑡𝑒𝑟𝑛𝑒𝑡_𝐼𝐶𝑊𝑖,𝑡

+𝑏3 𝐵𝑎𝑐𝑘𝑈𝑝_𝐼𝐶𝑊𝑖,𝑡 + 𝑏4 𝐴𝑐𝑐𝑒𝑠𝑠_𝐼𝐶𝑊𝑖,𝑡 + 𝑏5 𝑂𝑆_𝐼𝐶𝑊𝑖,𝑡 + 𝑏6𝑆𝑜𝑓𝑡_𝐼𝐶𝑊𝑖,𝑡 + 𝑏7 𝐷𝑜𝑐_𝐼𝐶𝑊𝑖,𝑡 + 𝑏8 𝐻𝑎𝑟𝑑_𝐼𝐶𝑊𝑖,𝑡 + 𝑏9 𝑃𝑟𝑖𝑜𝑟𝐿𝑜𝑠𝑠𝑖,𝑡 + 𝜀𝑖,𝑡 Equation 10

Table 4. Regression results for the ROA model with octet variables of IT_ICW

Random walk Productionfunction

Standardized Coefficients

sig Tolerance Standardized Coefficients

sig Tolerance

ROA 𝑡−1 .713 .000 .699

Acc&etc_ICW .138 .299 .751 .086 .592 .720

Net&Internet_ICW -.049 .004 .868 -.122 .012 .785

BackUp_ICW -.007 .955 .632 -.057 .701 .892

Access_ICW -.083 .501 .841 .002 .988 .701

OS_ICW -.014 .914 .491 -.058 .712 .891

Soft_ICW -.057 .700 .77 .000 .999 .528

Doc_ICW -.547 .043 .693 -.477 .013 .822

Hard_ICW -.781 .012 .883 -.066 .021 .751

PriorLoss -.086 .049 .703 -.276 .046 .909

N 0444 0444

Adjusted 𝑅2 .608 .642

Table notes: (all tests are two tailed).

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

In this analysis standardized regression

coefficients were used. As can be seen, there are three

categories of weaknesses, including weaknesses in

existing IT and network, weaknesses and deficiencies

in the documentation and security-related hardware, in

both models random walk and production function

models were significant and show adversely in the

dependent variable. The two models imply higher

tolerance achieved strong results. Acc&etc_ICW =

accounting &etc_ICW: Weaknesses in accounting

software and other related software, Net

&Internet_ICW: lack of networking and the Internet,

BackUp_ICW: weakness relating to the operation of

the backup files needed, Access_ICW: weaknesses

related to access , OS_ICW: weakness of the whole

system , Soft_ICW: the weak security-related software

, Doc_ICW: lack of documentation related to computer

systems, Hard_ICW: the weak security-related

hardware , PriorLoss: Percentage years of financial

losses in the past three years.

These eight variables were discriminant IT

weaknesses in the internal control process which will

be discussed in detail in Appendix A of this article.

Because of the lack IT_ICW variable in

relation to the revised second hypothesis (Equation 7),

this equation was eliminated from an additional test so

we refer to see equation 8 that its modified equation

with respect to the variable instead of letting IT

IT_ICW eight variables is as follows:

𝐌𝐕𝐄𝐢,𝐭 = b1 NetDividendsi,t + b2 Advertisingi,t + b3 (Acc&etc_ICWi,t × Earningsi,t)

+ b4 (Net&Internet_ICWi,t × Earningsi,t) + b5 (BackUp_ICWi,t × Earningsi,t)

+ b6 (Access_ICWi,t × Earningsi,t) + b7 (OS_ICWi,t × Earningsi,t)

+ b8 (Soft_ICWi,t × Earningsi,t) + b9 (Doc_ICWi,t × Earningsi,t)

+ b10 (Hard_ICWi,t × Earningsi,t) + b11 Salesi,t + εi,t Equation 11

Table 5. Regression results for the Ohlson/RIV valuation Interaction model with octet variables of IT_ICW

Interaction model

Standardized Coefficients

sig Tolerance

NetDividends .831 .000 .611

Advertising .105 .010 .830

Acc&𝑒𝑡𝑐_𝐼𝐶𝑊 × 𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠 -.014 .032 .988

Net&𝐼𝑛𝑡𝑒𝑟𝑛𝑒𝑡_𝐼𝐶𝑊× 𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠

-.198 .007 .752

BackUp_ICW × Earnings -.083 .081 .819

Access_ICW × Earnings -.038 .126 .424

OS_ICW × Earnings -.279 .000 .836

Soft_ICW × Earnings -.382 .000 .957

Doc_ICW × Earnings -.199 .014 .791

Hard_ICW × Earnings -.286 .045 .901

Sales .191 .000 .765

N 0444

Adjusted 𝑅2 .994

Table notes: (all tests are two tailed).

In this analysis standardized regression

coefficients were used. As can be seen six categories

from the weakness of IT with business units to reduce

their impact on the market value of the company's

profits will have the statistic meaning (third column

right) including: Weak impact on bookkeeping and

income variables (Acc&etc_ICWEarnings), the effect

of weakening the network-the internet and the

dependent variable of interest (Net

&Internet_ICWEarnings), the effect of weakening the

whole system and profit on the dependent variable

(OS_ICWEarnings), The impact of software security

weaknesses and interest on the dependent variable

(Soft_ICW Earnings), documenting the impact of the

weaknesses of computer systems and the dependent

variable of interest (Doc_ICWEarnings), hardware

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

security weaknesses and profit impact on the

dependent variable (Hard_ICW Earnings). Except in

the combination of variable,accessweaknesses and

profitthat have much lower tolerances than other

variables, other tolerance values with high accuracy

digit confirmed regression results. Data definition:

NetDividends: Net dividend , Adv: advertising costs ,

Acc&etc_ICWEarnings: lack of effect on the

dependent variable bookkeeping and Income , Net

&Internet_ICWEarnings: the impact of weakness

Network - the Internet and the dependent variable of

interest, BackUp_ICWEarnings: the impact of backup

operations and earnings weakness on the dependent

variable, Access_ICWEarnings: weak effects on

access and benefit -related variables,

OS_ICWEarnings: the impact of weakness in the

whole operating system and profit on the dependent

variable, Soft_ICW Earnings: the impact of software

security weaknesses and interest on the dependent

variable, Doc_ICWEarnings: the impact of poor

documentation of computer systems and the dependent

variable of interest, Hard_ICWEarnings: hardware

security weaknesses and profit impact on the

dependent variable.

General Conclusion of The Study

One factor of accounting profit decline is the

existence of weakness in internal control and in their

process; one of the types of internal controls to protect

property, assets and revenues of the entity, is internal

control of IT (Stoel and Muhanna 2011). The first

hypothesis of this study is to reduce accounting

earnings during IT weaknesses during the above

description is not far from the expected. But there is a

question that as an investor willyouchoose a company

to buy shares or invest in it without noticing company

initially reported IT weaknesses? Absolutely not! an

investor is usually looking for finding a company with

an accounting profit and if the intention is to have

control over the entity, the accounting profit is not as

important to him as a result high demand for the

company's shares accounting profits (rather weak

lower IT) will be increased and therefore increases the

company's stock price or market value, so the market

value of a company has no relationship directly with

IT weaknesses in this study 's review of the second

hypothesis, the hypothesis was rejected and the lack of

correlation was proven. With respect to the above

comes to the conclusion that IT Weaknesses despite

having no relation with the market value of the

business unit inversely and significantly reduce the

accounting profit. So we can conclude the weakness

reduces accounting profits and therefore reduces

accounting profits also reduces the demand for the

shares of the company and its business units to reduce

the market value. In conclusion we can say that IT

internal control weaknesses despite not having a

significant positive correlation with the market value

of a company's accounting profit due to the depletion

effect, reduces the stock price of a business unit.

Obviously there is a weakness or lack of weakness in

the internal control process of IT can create

competitive advantages for companies and business

units. According to the material presented to prove the

third hypothesis, there is an inverse relationship

between IT and the weakness of the link between

earnings and the market value of the business unit and

indicates that accounting earnings in the shadow of

internal control weaknesses IT, reduce the company's

market value or at least it will be adjusted.

Appendix A:

Anatomy of the eight variables of IT internal

control weaknesses

Due to the use of IT weaknesses during the

eight variables in this paper, in order to further

understand the results we describe them briefly.

Acc&etc_ICW

This variable indicates the weaknesses

associated with the use of accounting software, office

automation system in use and also how to prepare and

operation of these two cases. The addition of database

development and changes in the enterprises has also

been studied.

Net &Internet_ICW

This variable indicates the weaknesses

associated with the corporate wide area network

(WAN), Internet connections, business unit, business

unit staff how to use the internet and network access

restrictions affect the organizational variables.

BackUp_ICW

This variable indicates the weaknesses

associated with the backup operation of the accounting

records and other necessary information. Issues such

as the time- frequency backup, file storage, file

download time in case of crisis as well as those

authorized to access the files in this section has been

monitored.

Access_ICW

This variable indicates the weaknesses

associated with how to access the various business

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

units of the company including accounting information

and to discuss some issues related to the separation of

incompatible duties.

OS_ICW

This variable represents the weaknesses

associated with the totality of the operation system.

Factors such as the type of used operating system,

operating system version, use or non-use firewall and

anti-virus software installed on the operating system

and general health factors that provide the operating

system on this variable.

Soft_ICW

This variable indicates weakness associated

with security software. Factors such as the control unit

for the prevention and detection of errors in processing,

encryption to prevent incompatible operations by the

same people who have access to information and

assets, and the type and quality of the generated code

(eg, fingerprint, face recognition, passwords, etc) on

the software applications and matches are factors that

control this variable.

Doc_ICW

This variable indicates weaknesses in

computer systems associated with the documentation.

For example, doing documentation of computer

systems, presence or absence of functional systems of

records for each system user's guide or operating

manual for the software used create or not create the

file for software programs that are created within the

company, and ultimately the use of special software for

documentation things that are on the value of this

variable.

Hard_ICW

This variable indicates the weakness of

security related with hardware.Used engines and

electricity generator related factors such as the period

of exposure to the electric motor business unit after the

power failure and the generator circuit to charge the

empty time of motor –generators, using the trans

modulator input current business units, construction of

a computer center in a safe place until it is securely

incurred in place possibility of damage from natural

disasters and finally there is a fire extinguishing tools

in the center are of the effective variables.

All of the above weaknesses if any have the number 1

and otherwise set to 0. Additional note on the last test

multiplies any of the top eight variables in a variable

net profit (Earnings). In this case, there is a definition

for this new variable combination of the following: the

weak and the net effect on the dependent variable.

Appendix B: The variables of the original model

Operational definition Variable

If the company reports weaknesses, it is equal to 1 and otherwise 0 IT Internal Control Material

Weakness (IT_ICW)

IT weaknesses and profit impact on the dependent variable Earnings IT_ICW

Market price per share of stock Market Valuation (MVE)

Total equity at the end of fiscal year Book value of equity (Equity)

Profit or net loss on fiscal year Earnings

Net dividends paid ordinary shares at the end of the fiscal year Net Dividends

Advertising expenses during a fiscal year Advertising expense

(Advertising)

Costs associated with Research and Development Research and development

expense (R&D)

Net income divided by assets Return on Assets (ROA)

Number of months since entering the stock so far Age

Net sales Sales (as a measure of size)

DARAEI AND RANGRIZ: THE VISION OF CORPORATE RESPONSIBILITY: THE RELATIONSHIP BETWEEN IT..

Indian J.Sci.Res.4 (4):36-53, 2014

Net sales minus net sales divided by net sales in the year prior to the

year before Growth

Total assets /aggregate inventory Complexity based on inventory to

assets ratio

If you use a corporate audit (trustee Exchange) 1 otherwise 0 Large_Auditor

Percentage of losses during the past three years Prior_Loss

If the auditors changed from last year it is 1, otherwise 0 Auditor Change

References

Acquisti A, Friedman A, Telang R. Is there a cost

to privacy breaches? An event study. Proceedings

of the twenty seventh international

conference on information systems, Milwaukee,

WI; 2006. p. 1563–80.

Albrecht W, Lookabill L, McKeown J. The time

series properties of annual earnings. J Account

Res 1977;15(2):226–44.

Amir E, Lev B. Value relevance of non financial

information: the wireless communications

industry. J Account Econ 1996;22(1):3–30.

Amit R, Schoemaker P. Strategic assets and

organizational rent. Strategic Management

Journal 1993;14(1):33–46.

Anderson M, Banker R, Ravindran S. Value

implications of investments in information

technology. Manage Sci 2006;52(2):1359–76.

Aral S, Weill P. IT assets, organizational

capabilities, and firm performance. Organ Sci

2007;18(5):763–80.

Arend RJ. Revisiting the logical and research

considerations of competitive advantage.Strateg

Manage J 2003;24(3):279–84.

Arend RJ. The definition of strategic liabilities,

and their impact on performance. J Manage Stud

2004;41(6):1003–27.

AshbaughSkaife H, Collins D, Kinney W,

LaFond R. The effect of SOX internal control

deficiencies and their remediation on accrual

quality. Account Rev 2008;83(1):217–50.

AshbaughSkaife H, Collins D, Kinney W,

LaFond R. The effect of SOX internal control

deficiencies on firm risk and cost of equity. J

Account Res 2009;47(1):1–43.

AshbaughSkaife H, Collins D, KinneyW. The

Discovery and reporting of internal control

material weaknesses prior to SOX mandated

audits. J Account Econ 2007;44(1/2):166–92.

Backhouse J, Hsu CW, Silva L. Circuits of power

in creating de jure standards: shaping an

international information systems security

standard. MIS Quarterly 2006;30(SI):413–38.

Barney JB. Firm resources and sustained

competitive advantage. J Manage 1991;17(1):99–

120.

Barth M, Clement M, Foster G, Kasznik R. Brand

values and capital market valuation. Rev Account

Stud 1998;3(1):41–68.

Baskerville R. Information systems security

design methods: implications for information

systems development. ACM ComputSurv

1993;25(4):375–414.

Baskerville R. Risk analysis: an interpretive

feasibility tool in justifying information systems

security. Eur J InfSyst 1991;1(2):121–30.

Beneish M, Billings M, Hodder L. Internal control

weaknesses and information uncertainty. Account

Rev 2008;83(3):665–703.

Bharadwaj A. A resource based perspective on

information technology capability and firm

performance: an empirical investigation.

MIS Quarterly 2000;24(1):169–96.

Bharadwaj A, Bharadwaj S, Konsynski B.