The Use of Derivatives by Investment Managers and Implications for Portfolio Performance and Risk...

29

The Use of Derivatives by Investment Managers and Implications for Portfolio Performance and Risk n KINGSLEY FONG, DAVID R. GALLAGHER AND AARON NG School of Banking and Finance, The University of New South Wales, Australia ABSTRACT This study provides an empirical examination of derivative instruments used by institutional investors. Our analysis provides a unique insight into the role and benefits of derivative securities in active equity portfolio manage- ment. We contribute to the literature by using a database that comprises the periodic portfolio holdings and daily trades of institutional fund managers. The consequence of derivative use is analyzed using a number of performance and risk measures. Overall, we find the use of derivatives have a negligible impact on fund returns, and is primarily attributed to low levels of derivative exposure relative to total fund size. We also evaluate how derivatives are used by considering the trading strategies executed by active investment managers. Specifically, option trading patterns are consistent with the execution of momentum trading strategies. This study also documents that active investment managers prefer not to use options markets to engage in informed trading. I. INTRODUCTION Recent decades have witnessed a dramatic shift in the nature of risk in global financial markets and increased volatility of many asset classes. 1 As investors are continuously exposed to a broad range of dynamic risks, derivatives have become a valuable tool in the risk management practices of institutions. Despite the potential for derivative instruments to effectively manage the risks faced by institutions, public opinion concerning these securities suggests the general public view derivative securities as inherently dangerous (McGough 1995). Anecdotes such as Long-Term Capital Management (LTCM) in the US, Barings Bank in the UK, and the foreign exchange episode occurring at National n The authors gratefully acknowledge the helpful comments and suggestions from an anonymous referee, Bruce Grundy (the Editor), Anthony Asher, and seminar participants at the 2004 Australasian Finance and Banking Conference. 1 Campbell et al. (2001) document the upward trend in idiosyncratic volatility in equity markets. Gross (1997) also notes the increase in the volatility of US bond yields. r International Review of Finance Ltd. 2006. Published by Blackwell Publishing Ltd., 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA. International Review of Finance, 5:1–2, 2005: pp. 1–29

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The Use of Derivatives by Investment Managers and Implications for Portfolio Performance and Risk...

The Use of Derivatives byInvestment Managers andImplications for Portfolio

Performance and Riskn

KINGSLEY FONG, DAVID R. GALLAGHER AND AARON NG

School of Banking and Finance, The University of New South Wales, Australia

ABSTRACT

This study provides an empirical examination of derivative instruments usedby institutional investors. Our analysis provides a unique insight into therole and benefits of derivative securities in active equity portfolio manage-ment. We contribute to the literature by using a database that comprises theperiodic portfolio holdings and daily trades of institutional fund managers.The consequence of derivative use is analyzed using a number ofperformance and risk measures. Overall, we find the use of derivatives havea negligible impact on fund returns, and is primarily attributed to low levelsof derivative exposure relative to total fund size. We also evaluate howderivatives are used by considering the trading strategies executed by activeinvestment managers. Specifically, option trading patterns are consistentwith the execution of momentum trading strategies. This study alsodocuments that active investment managers prefer not to use optionsmarkets to engage in informed trading.

I. INTRODUCTION

Recent decades have witnessed a dramatic shift in the nature of risk in globalfinancial markets and increased volatility of many asset classes.1 As investors arecontinuously exposed to a broad range of dynamic risks, derivatives havebecome a valuable tool in the risk management practices of institutions.

Despite the potential for derivative instruments to effectively manage therisks faced by institutions, public opinion concerning these securities suggeststhe general public view derivative securities as inherently dangerous (McGough1995). Anecdotes such as Long-Term Capital Management (LTCM) in the US,Barings Bank in the UK, and the foreign exchange episode occurring at National

n The authors gratefully acknowledge the helpful comments and suggestions from ananonymous referee, Bruce Grundy (the Editor), Anthony Asher, and seminar participants at the2004 Australasian Finance and Banking Conference.1 Campbell et al. (2001) document the upward trend in idiosyncratic volatility in equity markets.

Gross (1997) also notes the increase in the volatility of US bond yields.

r International Review of Finance Ltd. 2006. Published by Blackwell Publishing Ltd., 9600 Garsington Road,Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

International Review of Finance, 5:1–2, 2005: pp. 1–29

Australia Bank in 2004, highlight the potential hazards of derivative use, andhave attracted the close attention of risk management executives, investors,governments, market regulators, as well as the media.

Regulators attempting to prevent corporate failure associated with deriva-tives usage have relied on mandated disclosure.2 In contrast, regulation ofderivative use in the Australian investment management industry has notrequired quantitative disclosure, but rather design features, implementation ofrisk management policies, and constraints placed on the use of derivatives.3 TheAustralian Prudential Regulation Authority (APRA) prescribes that derivativesmay not be used for speculative purposes, and managed funds cannot holduncovered positions in derivatives. Derivative use must also be conductedwithin the confines of the trust deed.4

Theoretical literature proposes that derivatives provide users with efficiencybenefits in the form of reduced transaction costs and improved risk control(Merton 1995). The extant literature on derivative usage focuses on corporatehedging rather than derivative use within the investment managementindustry.5 There are only a few studies which directly analyze the use ofderivatives by investment managers. Despite these alleged benefits, severalstudies from both the corporate and investment management literature havefound that the risk and return characteristics of derivative users are indeedsimilar to those of non-users. Specifically, Koski and Pontiff (1999) examinemutual fund return distributions of derivative users and non-users, and theyconclude that derivatives do not lead to significant differences in fundperformance or risk. Pinnuck (2004) shows that Australian equity managersutilize options to both increase or decrease exposure to underlying stocks heldin the fund. However, Pinnuck does not attempt to infer the motivation forderivative use by portfolio managers.

The primary contribution of this study is to better understand howderivatives are used by institutional investment managers. We study theexposure and the implicit strategies used by active equity managers inderivative trading.6 The empirical literature has been unable to characterizehow derivatives are used by investment managers.

This study benefits significantly from a unique and confidential dataset ofequity manager transactions and portfolio holdings. Prior studies examining US

2 Accounting regulators have formulated standards which require the disclosure of nominal

contract exposures and fair value of derivative instruments in financial accounting statements.

3 For a detailed discussion of risk management practices in the Australian investment manage-

ment industry, see Brown et al. (2005). The governance mechanism is most well known among

superannuation funds, which are required to maintain a Part B Risk Management Statement

(RMS) outlining their response to how risks are monitored.

4 APRA Circular (No. II.D.7).

5 Although the motivation to use derivatives as a part of a risk management strategy still exists

for investment managers, derivatives also represent a direct alternative to investment in

underlying asset markets.

6 See also Hentschel and Kothari (2001).

International Review of Finance

2 r International Review of Finance Ltd. 2006

funds have typically analyzed the portfolio holdings of investment managersobserved at quarter-end periods, where these data include only equity holdingsand not other instruments such as derivatives (Moskowitz 2000).7 In terms ofthe link between performance and derivatives use, Koski and Pontiff (1999)conduct telephone interviews to determine whether or not mutual funds arepermitted to trade derivatives. However, this binary approach is unable tocapture the size of derivative exposures held by funds. Although the data usedby Pinnuck (2004) include the month-end holdings of options, the sample didnot include data showing holdings of futures contracts. Our study offers asignificant improvement on Pinnuck (2004) given our database contains themonth-end portfolio holdings and daily trades of all securities, includingderivatives, and also investigates derivative use in considerably finer detail.

In evaluating the impact of derivatives on the returns of active equitymanagers, tests are used to measure the differences in the distributions across awide range of fund performance and risk measures (see Koski and Pontiff 1999).Consistent with the literature, we document few observable differences ineither performance or risk between derivative users and non-users. We attributethis result to the low level of derivative exposure relative to the total size of fundportfolios.

We next examine the propensity for active equity managers to transact inoptions on stocks exhibiting momentum by analyzing the proportion of optiontrades on stocks whose future price movements are expected to followmomentum patterns. Investment managers are shown to uniformly avoidtrading options on stocks with relatively poor past returns, whereas some fundsalso trade disproportionately more in options on stocks with relatively strongpast price performance. This provides empirical support that active investmentmanagers indeed use options to capture momentum returns.

Finally, we examine the information content of option trades by activeequity managers and document no abnormal price movements in the under-lying stocks over short-run event windows, both immediately prior andsubsequent to option trades. We interpret these findings as evidence thatinvestment managers do not execute informed trading in options markets.

The remainder of the paper is structured as follows. Section II summarizes therelevant extant literature and formulates the hypotheses that are addressed inthe paper. Section III outlines the empirical methodologies used in testing thehypotheses. Section IV presents the results and provides a discussion of the keyfindings. The final section concludes.

II. HYPOTHESES

Theoretical work suggests investment managers use derivatives to better exploitinformation, manage risk, and reduce transaction costs (Scholes 1981; Silber

7 The portfolio holdings of US institutional investors have been derived from 13F disclosure

forms reported on a quarterly basis to the Securities & Exchange Commission (SEC).

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 3

1985; Stoll and Whaley 1985; Merton 1995). Koski and Pontiff (1999) predictthat on this basis, portfolios whose managers use derivatives, shoulddemonstrate improved performance relative to otherwise comparable portfoliosthat do not use derivatives. Although this prediction may not hold incompetitive market equilibrium, where marginal benefits and costs in tradingacross derivatives and underlying markets are arbitraged away,8 managers whodo not consider derivatives for policy reasons may miss out on opportunities toexploit intermarket disequilibrium.9 One opportunity that derivatives offer is tosell out-of-the-money covered call options at a favorable premium, and at thesame time generate cash flow for distribution. Lastly, managers may not tradederivatives because they focus on stocks with no derivatives. However, there arefew, if any, cheaper and faster alternatives for adjusting equity market exposurethan through trading index futures. In conclusion, the relationship betweenderivatives use and fund performance is an interesting empirical question.Following Koski and Pontiff (1999) we frame the first hypothesis as follows:

H1. The use of derivatives causes significant impacts on the performance andrisk of Australian investment managers.

The momentum strategy outlined by Jegadeesh and Titman (1993) consistsof buying recent past winner stocks and short-selling recent past loser stocks.Fong and Lee (2005), Demir et al. (2004), and Hurn and Pavlov (2003) verify theprofitability of this strategy in the Australian market. In this study, we examinethe extent to which a momentum strategy motivates fund managers to trade inderivative securities.

Previous studies have shown that mutual funds do engage in momentumstrategies in their equity stock holdings.10 Several factors in the Australianinstitutional environment make derivatives potentially more appropriate thanshares in implementing momentum strategies.

First, regulations and investment mandates often prevent fund managersfrom leveraging the portfolio or short-selling securities.11 Interestingly, Fongand Lee (2005) find that the momentum of loser stocks is an importantcontributor to overall momentum returns in Australia. However, the inability toshort-sell loser stocks represents a constraint for fund managers in taking fulladvantage of a momentum strategy. Although it can be argued that under-weighting loser stocks (relative to the benchmark index) is an adequatesubstitute for short-selling, purchasing put options of loser stocks provides anaggressive alternative to create an effective short position under short-sellingconstraints.

8 The authors thank the Editor for providing this equilibrium insight.

9 Exploiting intermarket disequilibrium is similar to exploiting short-term pricing inefficiency in

individual securities through stock picking.

10 See Grinblatt et al. (1995) and Carhart (1997).

11 For instance, the Superannuation Industry (Supervision) Act prohibits superannuation funds to

engage in leveraging and short selling. In addition, the mandates of the sample funds in this

study all prohibit short-selling, leveraging, and writing uncovered call options.

International Review of Finance

4 r International Review of Finance Ltd. 2006

Secondly, the leveraged exposure that options markets provide may be anefficient way for fund managers to establish positive exposure to winner stocks.

Thirdly, implementing a momentum strategy with derivatives can reduceexcessive realization of long-term accumulated capital gains. In comparison, amomentum strategy implemented in the cash market involves retaining onlyrecent past winners and losers in the portfolio, and this represents a relativelyhigh turnover strategy. Managers might be required to sell stocks that areclassified as losers over the past 12 months in using the momentum strategy,but these stocks might have been purchased 5 years ago with an accumulatedcapital gain of 100%. If these stocks are to be repurchased after a few months, itwould be better to use derivatives to implement the strategy and avoidunnecessary realization of capital gains.

We state our second hypothesis as follows:

H2. Active investment managers use options markets to implement momen-tum-based trading strategies.

Investment managers, through their skills in stock selection and markettiming, are theoretically able to generate and trade on their private informationto generate abnormal returns. Option contracts provide leverage, improvedtransaction cost benefits, and are potentially highly desirable instruments forinformed traders. However, there is no study that examines informed trading inindividual stock options. At the aggregate market level, prior studies find onlymixed evidence of informed trading in option markets.12 This study fills a gapin the literature on the role of derivative use in informed trading. We test thefollowing cross-market return implications of information trading by profes-sional traders:

H3. The option trades of active investment managers are associated withabnormal stock price performance.

III. EMPIRICAL METHODOLOGY

A. Data

We study Australian equity funds sourced from the Portfolio AnalyticsDatabase. This unique database, containing month-end portfolio holdingsand daily trading data, was formed on an invitation basis to the largestinvestment managers operating in Australia.13 The sample period for this studyis 1 January 1993 to 31 December 2003. Further details concerning theconstruction and composition of the database can be obtained from Brown etal. (2005), Gallagher and Looi (2006), and Foster et al. (2005). These studies also

12 Easley et al. (1998) show that option volumes lead stock prices, whereas Chakravarty et al.

(2004) provide evidence of price discovery in options markets.

13 The size of investment managers was measured by total funds under management.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 5

show that the sample of funds drawn from the database is not significantlydifferent from the universe of funds in terms of performance.

In addition to the managed fund data, daily stock price data and details ofdividends paid are collected from the SEATS system, sourced from the SecuritiesInstitute Research Centre of Asia-Pacific (SIRCA). The All Ordinaries Accumula-tion Index was used as the market proxy, whereas the Reserve Bank of Australiashort interest rate was used as the risk-free rate.

The initial sample consists of 48 equity funds, across all fund styles (growth,growth-at-a-reasonable price, value, and style neutral). Investment style is self-classified by the fund managers. We sample only actively managed funds thathave the discretion to trade in derivatives. There are no exchange-tradedderivatives listed on shares of companies outside of the largest 100. Thereforewe exclude index funds, enhanced passive funds, and small-cap equity funds.Of the remaining 34 funds, 50% are classed as derivative users. A derivative userwas defined as a fund that had holdings of derivatives at any time during thesample period, and includes index futures contracts and option securities.Funds did not invest in futures contracts over individual stocks. Value fundsaccounted for 11 of the total sample funds, of which three were derivative users.Growth-at-a-reasonable-price (GARP) funds represented nine of the samplefunds, of which five were derivative users.

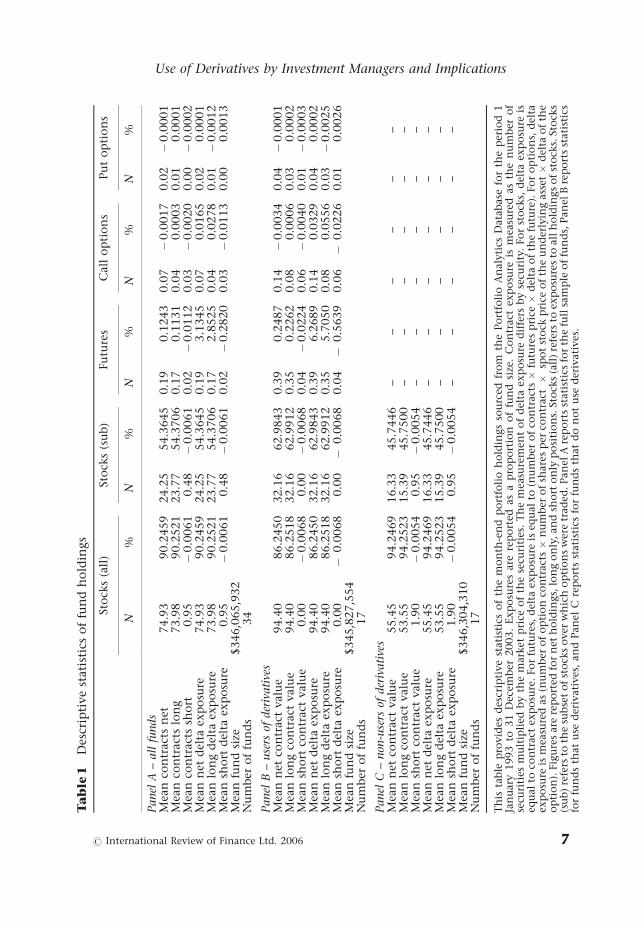

Table 1 reports descriptive statistics of the month-end portfolio holdings bysecurity type across the sample of active equity funds. We convert all derivativecontracts into dollar exposures before computing a fund’s percentage holdings.In computing the mean values we first calculate, for each fund, the meannumber of a particular type of securities held across month ends, and then wetake the mean of these fund-specific values. For instance, in Panel A the lownumber of call options relative to the number of stock holdings shows thatmanagers do not hold diversified portfolios of options. N less than 1 shows thatthere are months in which funds have no option holdings at all.

Panels B and C contrast the holdings of derivatives users and non-users. Table1 shows that although derivative users still hold large exposures to stocks forwhich there are options, the size of exposures to these stocks taken by non-usersare smaller as a proportion of the fund. Derivative users therefore appear toutilize options as either a direct alternative to taking exposures in stock markets,or as a means of further increasing their direct stock holdings exposures. At anygiven time, derivative users hold positions in a small number of differentfutures contracts, suggesting that holdings in futures are confined to singlematurities. This may also imply that as futures holdings are limited to fewmaturities, contracts are rolled-over as they mature. Across the entire sample,funds trade only in Share Price Index futures, and do not trade in individualshare futures. Funds are on average net short in call options when measured atthe market price, providing some evidence that they are writing call options togenerate income.

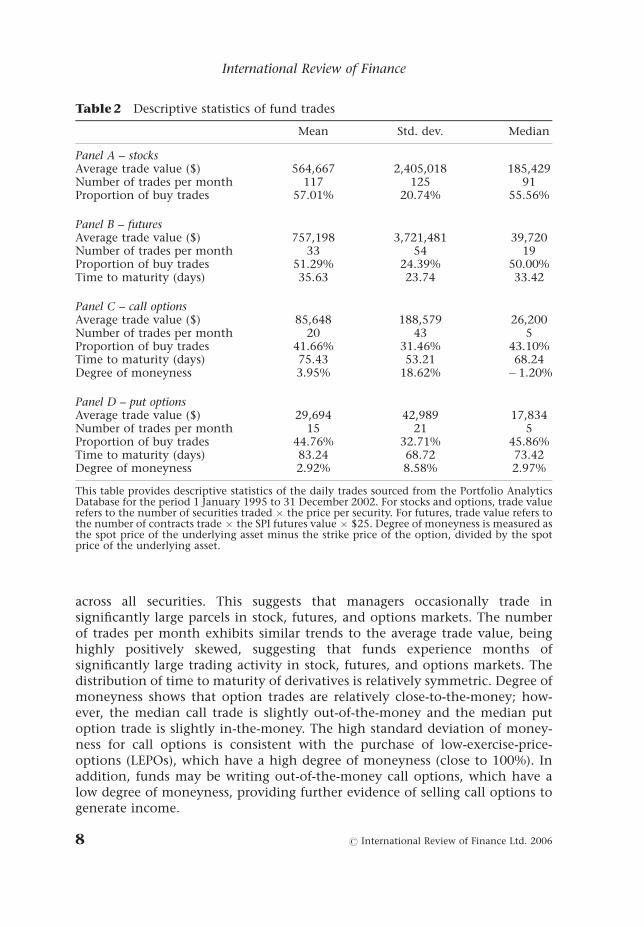

Table 2 reports descriptive statistics of the daily trading data for the samplefunds. The distribution of average trade value is considerably positively skewed

International Review of Finance

6 r International Review of Finance Ltd. 2006

Ta

ble

1D

escr

ipti

ve

stati

stic

so

ffu

nd

ho

ldin

gs

Sto

cks

(all

)St

ock

s(s

ub

)Fu

ture

sC

all

op

tio

ns

Pu

to

pti

on

s

N%

N%

N%

N%

N%

Panel

A–

all

funds

Mea

nco

ntr

act

sn

et74.9

390.2

459

24.2

554.3

645

0.1

90.1

243

0.0

7�

0.0

017

0.0

2�

0.0

001

Mea

nco

ntr

act

slo

ng

73.9

890.2

521

23.7

754.3

706

0.1

70.1

131

0.0

40.0

003

0.0

10.0

001

Mea

nco

ntr

act

ssh

ort

0.9

5�

0.0

061

0.4

8�

0.0

061

0.0

2�

0.0

112

0.0

3�

0.0

020

0.0

0�

0.0

002

Mea

nn

etd

elta

exp

osu

re74.9

390.2

459

24.2

554.3

645

0.1

93.1

345

0.0

70.0

165

0.0

20.0

001

Mea

nlo

ng

del

taex

po

sure

73.9

890.2

521

23.7

754.3

706

0.1

72.8

525

0.0

40.0

278

0.0

1�

0.0

012

Mea

nsh

ort

del

taex

po

sure

0.9

5�

0.0

061

0.4

8�

0.0

061

0.0

2�

0.2

820

0.0

3�

0.0

113

0.0

00.0

013

Mea

nfu

nd

size

$346,0

65,9

32

Nu

mb

ero

ffu

nd

s34

Panel

B–

use

rsof

der

ivati

ves

Mea

nn

etco

ntr

act

valu

e94.4

086.2

450

32.1

662.9

843

0.3

90.2

487

0.1

4�

0.0

034

0.0

4�

0.0

001

Mea

nlo

ng

con

tract

valu

e94.4

086.2

518

32.1

662.9

912

0.3

50.2

262

0.0

80.0

006

0.0

30.0

002

Mea

nsh

ort

con

tract

valu

e0.0

0�

0.0

068

0.0

0�

0.0

068

0.0

4�

0.0

224

0.0

6�

0.0

040

0.0

1�

0.0

003

Mea

nn

etd

elta

exp

osu

re94.4

086.2

450

32.1

662.9

843

0.3

96.2

689

0.1

40.0

329

0.0

40.0

002

Mea

nlo

ng

del

taex

po

sure

94.4

086.2

518

32.1

662.9

912

0.3

55.7

050

0.0

80.0

556

0.0

3�

0.0

025

Mea

nsh

ort

del

taex

po

sure

0.0

0�

0.0

068

0.0

0�

0.0

068

0.0

4�

0.5

639

0.0

6�

0.0

226

0.0

10.0

026

Mea

nfu

nd

size

$345,8

27,5

54

Nu

mb

ero

ffu

nd

s17

Panel

C–

non

-use

rsof

der

ivati

ves

Mea

nn

etco

ntr

act

valu

e55.4

594.2

469

16.3

345.7

446

––

––

––

Mea

nlo

ng

con

tract

valu

e53.5

594.2

523

15.3

945.7

500

––

––

––

Mea

nsh

ort

con

tract

valu

e1.9

0�

0.0

054

0.9

5�

0.0

054

––

––

––

Mea

nn

etd

elta

exp

osu

re55.4

594.2

469

16.3

345.7

446

––

––

––

Mea

nlo

ng

del

taex

po

sure

53.5

594.2

523

15.3

945.7

500

––

––

––

Mea

nsh

ort

del

taex

po

sure

1.9

0�

0.0

054

0.9

5�

0.0

054

––

––

––

Mea

nfu

nd

size

$346,3

04,3

10

Nu

mb

ero

ffu

nd

s17

Th

ista

ble

pro

vid

esd

escr

ipti

ve

stati

stic

so

fth

em

on

th-e

nd

po

rtfo

lio

ho

ldin

gs

sou

rced

fro

mth

ePo

rtfo

lio

An

aly

tics

Data

base

for

the

per

iod

1Ja

nu

ary

1993

to31

Dec

emb

er2003.

Exp

osu

res

are

rep

ort

edas

ap

rop

ort

ion

of

fun

dsi

ze.

Co

ntr

act

exp

osu

reis

mea

sure

das

the

nu

mb

ero

fse

curi

ties

mu

ltip

lied

by

the

mar

ket

pri

ceo

fth

ese

curi

ties

.T

he

mea

sure

men

to

fd

elta

exp

osu

red

iffe

rsb

yse

curi

ty.

Fo

rst

ock

s,d

elta

exp

osu

reis

equ

al

toco

ntr

act

exp

osu

re.

Fo

rfu

ture

s,d

elta

exp

osu

reis

equ

al

to(n

um

ber

of

con

trac

ts�

futu

res

pri

ce�

del

tao

fth

efu

ture

).Fo

ro

pti

on

s,d

elta

exp

osu

reis

mea

sure

das

(nu

mb

ero

fo

pti

on

con

trac

ts�

nu

mb

ero

fsh

are

sp

erco

ntr

act�

spo

tst

ock

pri

ceo

fth

eu

nd

erly

ing

ass

et�

del

tao

fth

eo

pti

on

).Fig

ure

sare

rep

ort

edfo

rn

eth

old

ings,

lon

go

nly

,an

dsh

ort

on

lyp

osi

tio

ns.

Sto

cks

(all

)re

fers

toex

po

sure

sto

all

ho

ldin

gs

of

sto

cks.

Sto

cks

(su

b)

refe

rsto

the

sub

set

of

sto

cks

over

wh

ich

op

tio

ns

wer

etr

ad

ed.Pan

elA

rep

ort

sst

ati

stic

sfo

rth

efu

llsa

mp

leo

ffu

nd

s,Pan

elB

rep

ort

sst

ati

stic

sfo

rfu

nd

sth

at

use

der

ivati

ves

,an

dPan

elC

rep

ort

sst

ati

stic

sfo

rfu

nd

sth

at

do

no

tu

sed

eriv

ati

ves

.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 7

across all securities. This suggests that managers occasionally trade insignificantly large parcels in stock, futures, and options markets. The numberof trades per month exhibits similar trends to the average trade value, beinghighly positively skewed, suggesting that funds experience months ofsignificantly large trading activity in stock, futures, and options markets. Thedistribution of time to maturity of derivatives is relatively symmetric. Degree ofmoneyness shows that option trades are relatively close-to-the-money; how-ever, the median call trade is slightly out-of-the-money and the median putoption trade is slightly in-the-money. The high standard deviation of money-ness for call options is consistent with the purchase of low-exercise-price-options (LEPOs), which have a high degree of moneyness (close to 100%). Inaddition, funds may be writing out-of-the-money call options, which have alow degree of moneyness, providing further evidence of selling call options togenerate income.

Table 2 Descriptive statistics of fund trades

Mean Std. dev. Median

Panel A – stocksAverage trade value ($) 564,667 2,405,018 185,429Number of trades per month 117 125 91Proportion of buy trades 57.01% 20.74% 55.56%

Panel B – futuresAverage trade value ($) 757,198 3,721,481 39,720Number of trades per month 33 54 19Proportion of buy trades 51.29% 24.39% 50.00%Time to maturity (days) 35.63 23.74 33.42

Panel C – call optionsAverage trade value ($) 85,648 188,579 26,200Number of trades per month 20 43 5Proportion of buy trades 41.66% 31.46% 43.10%Time to maturity (days) 75.43 53.21 68.24Degree of moneyness 3.95% 18.62% �1.20%

Panel D – put optionsAverage trade value ($) 29,694 42,989 17,834Number of trades per month 15 21 5Proportion of buy trades 44.76% 32.71% 45.86%Time to maturity (days) 83.24 68.72 73.42Degree of moneyness 2.92% 8.58% 2.97%

This table provides descriptive statistics of the daily trades sourced from the Portfolio AnalyticsDatabase for the period 1 January 1995 to 31 December 2002. For stocks and options, trade valuerefers to the number of securities traded � the price per security. For futures, trade value refers tothe number of contracts trade � the SPI futures value � $25. Degree of moneyness is measured asthe spot price of the underlying asset minus the strike price of the option, divided by the spotprice of the underlying asset.

International Review of Finance

8 r International Review of Finance Ltd. 2006

B. Research design

i. Distributional moments and risk metricsWe use a broad range of risk measures to capture distinct elements of risk. Thesemetrics include the variables examined by Koski and Pontiff (1999) andadditional variables as proposed by other studies.

Distributional parameters characterize the performance and risk of a fundrelative to the fund’s mean return. The first four moments of the fund returndistribution are examined.

Market model parameters are used as measurements of fund performanceand risk relative to market factors. The a and b of each fund are derived from asingle factor model, and idiosyncratic risk calculated as the standard deviationof the residuals.14 In addition, a market timing variable is included to capturethe ability of managers to utilize portfolio insurance to protect the portfolioagainst adverse market conditions.

Sortino (2001) stresses the importance of considering the risk of falling belowa ‘minimal acceptable return’ (MAR). A downside risk metric is included tocapture both the likelihood and magnitude of underperforming the relevantbenchmark return.15

ii. Classifying momentum tradesIn order to analyze the proportions of trades that follow momentum patterns,each trade must be classified as a momentum or non-momentum trade.Jegadeesh and Titman (1993) show that stocks exhibit persistent returns basedon past 3–12-month performance. Carhart (1997) shows that the persistence ofmutual fund performance is attributable to the 12-month momentum effect.This study defines momentum based on past 12-month performance. Recentstudies, such as Badrinath and Wahal (2002), continue to use momentumwindows ranging from 3 to 12 months. Demir et al. (2004) find significantmomentum effects in Australian equities over both short-term (1 week to 1month) horizon, and intermediate-term (3–12 month) horizon. Therefore, the12-month momentum effect should provide trading opportunities to invest-ment managers, where it may be appropriate to transact in options markets.

To derive momentum rankings, the constituents of the All Ordinaries Indexare taken at each month-end of the sample period. Taking these constituents ateach month-end captures the entry of new firms into the market, and removes

14 The single-factor model is estimated from the equation rt � rf,t 5 a 1 b(rMkt,t � rf,t) 1 et, where

rt is the return for month t, rf,t is the risk-free rate at the end of month t, and rMkt,t is the ex-post

return on the market during month t. A continuously compounded RBA cash rate is used to

proxy for the risk-free rate, and the logarithmic change in the All Ordinaries Index used as a

proxy for the market return.

15 Downside risk is defined by the equationPMAR�1 ðRt � MARtÞ2Pr

h i1=2, where Rt is the return of

the fund during month t, MARt is the minimal acceptable return for month t, and Pr is the

probability associated with observing that level of return. The MAR for each month is set at the

return on the All Ordinaries Accumulation Index.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 9

firms as they are delisted from the ASX. The 12-month buy-and-hold return iscalculated for each stock at each month-end date, which is then used as thebasis of ranking.

Two alternative classifications of momentum are defined. Jegadeesh andTitman (1993) construct a zero-cost trading strategy to profit from themomentum effect, which involves buying a portfolio of stocks consisting ofthe top decile firms based on past performance, and selling a portfolio of stocksconsisting of the bottom decile of firms. Therefore, stocks in the ‘loser’ portfolioare firstly defined as firms in the bottom decile of the performance ranking,whereas stocks in the ‘winner’ portfolio are defined as firms in the top decile ofthe performance ranking. As an alternative measure, the ‘loser’ portfolio is alsodefined as the bottom quintile of firms, and the ‘winner’ portfolio defined as thetop quintile of firms.

Individual options trades are then classified as either loser momentumtrades, winner momentum trades, or non-momentum trades. Loser momentumtrades are options on any underlying stock that fell within the loser portfolio asat the previous month-end date. Similarly, winner momentum trades are optiontrades on any underlying stock that fell within the winner portfolio as at theprevious month-end date. Non-momentum trades are all remaining trades thatwere not considered winner or loser trades.

The momentum strategy proposed by Jegadeesh and Titman (1993) profitsfrom upside exposure to the winner portfolio, and downside exposure to theloser portfolio. Options provide linear price exposure to either upside ordownside price movements. Furthermore, options may be both written orbought, providing opposite price exposures. Therefore, the sample of optiontransactions are separated by both call option and put option trades, and by buytrades and sell trades. This yields a total of four trade types. In addition to this,two trade types are defined in order to capture similar exposures gained bydifferent trade types:

1. delta increasing trades are transactions that profit from upside pricechanges in the underlying stock, and consist of call option buy tradesand put option sell trades; and

2. delta decreasing trades are transactions that profit from downside pricechanges in the underlying stock, and consist of call option sell tradesand put option buy trades.

The total number of option transactions for each trade type in the loser,winner, and non-momentum categories are calculated for each fund over theentire sample period. These totals form the basis of the tests of proportions. Foreach fund, the distribution of trades over the three categories is comparedagainst the expected number of trades in each category using a w2 goodness-of-fit test.

For the goodness-of-fit tests over decile-based momentum trades, theexpected number of trades in winner and loser categories are each equalto 10% of the total number of option trades, whereas the expected number of

International Review of Finance

10 r International Review of Finance Ltd. 2006

non-momentum trades is equal to 80% of total option trades. Similarly for thegoodness-of-fit tests over quintile-based momentum trades, the expectednumber of trades in winner and loser categories are each equal to 20% of thetotal number of option trades, whereas the expected number of non-momentum trades is equal to 60% of total option trades.

Tests of the nominal number of trades will not incorporate relativedifferences in trade size, and the level of exposure generated by each trade.For this reason, a measure of the value-weighted number of trades is introduced.This variable is calculated for each trade category as

Value � Weighted number of tradesi

¼ Total number of tradesi �Total exposure of tradesiPki¼1 Total exposure of tradesi

ð1Þ

The exposure of each trade is calculated as the equivalent ordinary shareexposure (see the Appendix). The w2 goodness-of-fit tests are then conducted, asdescribed, over the value-weighted number of trades.16

iii. Event study of option tradesThe literature approaches the use of options for informed trading at a marketlevel by comparing aggregate variables such as prices and volumes betweenstock and option markets. Much of this literature has utilized high-frequencyintraday data to establish lead/lag relationships between option and stockmarkets, finding mixed support for informed trading using options. Easley et al.(1998) show that price changes in stock markets lead option volumes with a lagof 20–30 min, whereas option volumes affect stock price changes more rapidly.Jarnecic (1999) shows that stock volumes on the ASX lead option volumes onthe ASX options market. Cairney and Swisher (2004) represent one of fewstudies which analyze informed trading in options markets on a lower-frequency basis, showing abnormal volume in Chicago Board OptionsExchange (CBOE) options for three days before earnings announcements.Importantly, prior studies have found evidence that mutual funds possessprivate information (Daniel et al. 1997; Wermers 2000). Therefore, this studyprovides an evaluation of the decision to disseminate private information inoptions markets as opposed to stock markets.

The information content of investment manager option trades is assessed byexamining the behavior of the share price of the underlying stock both beforeand after option transactions are executed. An event study methodology is used

16 In order to ensure that the w2 distribution adequately approximates the discrete sampling

distribution, the goodness-of-fit tests must conform to the rule of five. As a consequence, funds

with an insufficient number of trades were excluded from these tests (less than 50 trades for

decile-based tests, and less than 25 for quintile-based tests). Across all option trade types, eight

to nine funds were excluded from the decile-based tests, and between three and eight funds

were excluded from the quintile-based tests.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 11

to measure the significance of share price movements around an option tradeby an active investment manager.

Standard event study methodologies typically pool abnormal returns acrossall observed events, and test the hypothesis that the mean abnormal return isequal to zero (Kritzman 1994). This approach is inappropriate in this study forseveral reasons. Firstly, there are many factors influencing the decision byinvestment managers in choosing to transact in options markets, such asequitizing fund flows, attempting to add value through hedging, or byimplementing trading strategies based on public information.17 Thus, not alloption trades will be motivated by acting upon private information. Poolingoption trades will create significant noise in the event study model by includingtrades initiated for different motivations, and may distort the underlying shareprice impacts of option trades. Secondly, since options are short-term tradinginstruments, investment managers are likely to implement further trades toreverse initial trading positions. The timing of this reversal trade will beinfluenced by factors other than information motives, such as managing theloss of time value of the option exposure. This effect also prevents a pooledanalysis of investment manager option trades.

To implement the event study, abnormal returns are calculated from 10 daysbefore the option trade, to 10 days subsequent to the option transaction. Foreach event date, we estimate the standard deviation of returns as the squareroot of the sample variance of returns from t�100 to t�11, where t is the day ofthe option trade.

IV. RESULTS

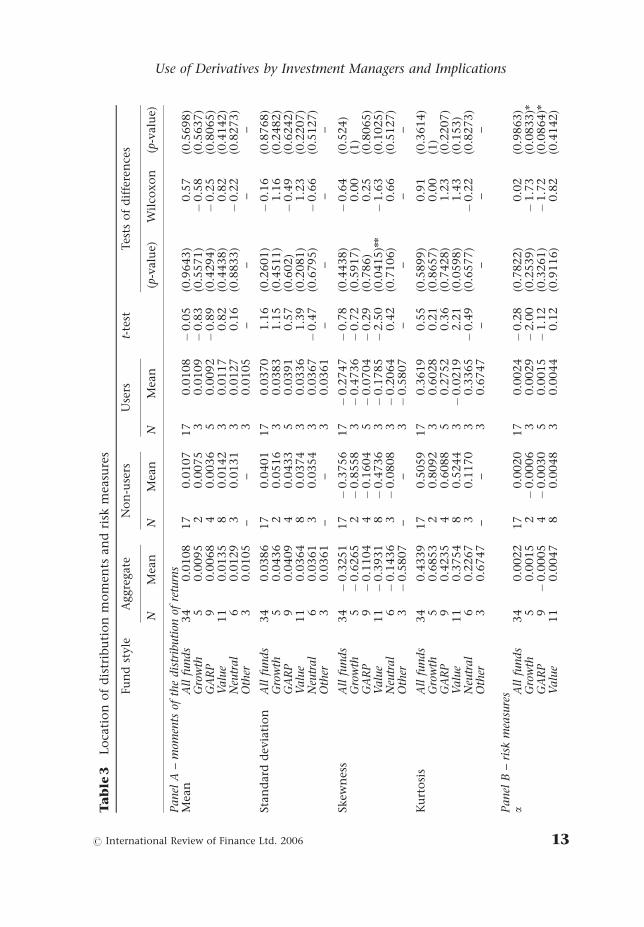

A. Distributional moments and risk measures

Table 3 presents the results for the difference in cross-sectional mean tests forthe distributional moments and risk measures. Panel A shows active equityfunds yield positive mean returns that are negatively skewed and leptokurtic.This is consistent with previous studies that have found similar non-normalityin the return distributions of equities and fixed income funds in Australian andinternational markets (Bird and Gallagher 2002). Across the entire sample offunds, derivative users do not display significantly higher mean returns, norsignificantly lower standard deviation, skewness and kurtosis. This observationholds across subsets of funds as well.

Panel B shows that on average, funds display positive a’s. Growth and GARPfunds that did not use derivatives are the only group to derive negative a’s.There is weak evidence indicating a difference in the mean a between derivativeusers and non-users for growth and GARP-style funds, with the Wilcoxon

17 Trading on the basis of public information will not result in any abnormal share price reaction

in the underlying stock. An example of a trading strategy based on public information is the

momentum strategy, where the trading decisions are formed solely on historical performance.

International Review of Finance

12 r International Review of Finance Ltd. 2006

Ta

ble

3Lo

cati

on

of

dis

trib

uti

on

mo

men

tsan

dri

skm

easu

res

Fu

nd

style

Aggre

gate

No

n-u

sers

Use

rst-

test

Tes

tso

fd

iffe

ren

ces

NM

ean

NM

ean

NM

ean

(p-v

alu

e)W

ilco

xo

n(p

-valu

e)

Panel

A–

mom

ents

ofth

edis

trib

uti

onof

retu

rns

Mea

nA

llfu

nds

34

0.0

108

17

0.0

107

17

0.0

108

�0.0

5(0

.9643)

0.5

7(0

.5698)

Gro

wth

50.0

095

20.0

075

30.0

109

�0.8

3(0

.5571)

�0.5

8(0

.5637)

GA

RP

90.0

068

40.0

036

50.0

092

�0.8

9(0

.4294)

�0.2

5(0

.8065)

Valu

e11

0.0

135

80.0

142

30.0

117

0.8

2(0

.4438)

0.8

2(0

.4142)

Neu

tral

60.0

129

30.0

131

30.0

127

0.1

6(0

.8833)

�0.2

2(0

.8273)

Oth

er3

0.0

105

––

30.0

105

––

––

Stan

dard

dev

iati

on

All

funds

34

0.0

386

17

0.0

401

17

0.0

370

1.1

6(0

.2601)

�0.1

6(0

.8768)

Gro

wth

50.0

436

20.0

516

30.0

383

1.1

5(0

.4511)

1.1

6(0

.2482)

GA

RP

90.0

409

40.0

433

50.0

391

0.5

7(0

.602)

�0.4

9(0

.6242)

Valu

e11

0.0

364

80.0

374

30.0

336

1.3

9(0

.2081)

1.2

3(0

.2207)

Neu

tral

60.0

361

30.0

354

30.0

367

�0.4

7(0

.6795)

�0.6

6(0

.5127)

Oth

er3

0.0

361

––

30.0

361

––

––

Skew

nes

sA

llfu

nds

34

�0.3

251

17

�0.3

756

17

�0.2

747

�0.7

8(0

.4438)

�0.6

4(0

.524)

Gro

wth

5�

0.6

265

2�

0.8

558

3�

0.4

736

�0.7

2(0

.5917)

0.0

0(1

)G

AR

P9

�0.1

104

4�

0.1

604

5�

0.0

704

�0.2

9(0

.786)

0.2

5(0

.8065)

Valu

e11

�0.3

931

8�

0.4

736

3�

0.1

785

�2.5

0(0

.0415)n

n�

1.6

3(0

.1025)

Neu

tral

6�

0.1

436

3�

0.0

808

3�

0.2

064

0.4

2(0

.7106)

0.6

6(0

.5127)

Oth

er3

�0.5

807

––

3�

0.5

807

––

––

Ku

rto

sis

All

funds

34

0.4

339

17

0.5

059

17

0.3

619

0.5

5(0

.5899)

0.9

1(0

.3614)

Gro

wth

50.6

853

20.8

092

30.6

028

0.2

1(0

.8657)

0.0

0(1

)G

AR

P9

0.4

235

40.6

088

50.2

752

0.3

6(0

.7428)

1.2

3(0

.2207)

Valu

e11

0.3

754

80.5

244

3�

0.0

219

2.2

1(0

.0598)

1.4

3(0

.153)

Neu

tral

60.2

267

30.1

170

30.3

365

�0.4

9(0

.6577)

�0.2

2(0

.8273)

Oth

er3

0.6

747

––

30.6

747

––

––

Panel

B–

risk

mea

sure

sa

All

funds

34

0.0

022

17

0.0

020

17

0.0

024

�0.2

8(0

.7822)

0.0

2(0

.9863)

Gro

wth

50.0

015

2�

0.0

006

30.0

029

�2.0

0(0

.2539)

�1.7

3(0

.0833)n

GA

RP

9�

0.0

005

4�

0.0

030

50.0

015

�1.1

2(0

.3261)

�1.7

2(0

.0864)n

Valu

e11

0.0

047

80.0

048

30.0

044

0.1

2(0

.9116)

0.8

2(0

.4142)

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 13

Fu

nd

style

Aggre

gate

No

n-u

sers

Use

rst-

test

Tes

tso

fd

iffe

ren

ces

NM

ean

NM

ean

NM

ean

(p-v

alu

e)W

ilco

xo

n(p

-valu

e)

Neu

tral

60.0

027

30.0

030

30.0

024

0.4

6(0

.6684)

0.6

6(0

.5127)

Oth

er3

0.0

015

––

30.0

015

––

––

bA

llfu

nds

34

0.9

208

17

0.9

044

17

0.9

371

�0.8

5(0

.3991)

�1.0

5(0

.2935)

Gro

wth

50.9

181

20.8

695

30.9

505

�0.5

3(0

.68)

�0.5

8(0

.5637)

GA

RP

90.9

444

40.9

594

50.9

324

0.3

1(0

.7709)

0.0

0(1

)V

alu

e11

0.8

607

80.8

620

30.8

573

0.0

5(0

.9621)

�0.4

1(0

.6831)

Neu

tral

60.9

698

30.9

676

30.9

721

�0.1

3(0

.9053)

�0.2

2(0

.8273)

Oth

er3

0.9

762

––

30.9

762

––

––

Idio

syn

crati

cri

skA

llfu

nds

34

0.0

159

17

0.0

179

17

0.0

139

1.0

5(0

.3019)

0.9

1(0

.3614)

Gro

wth

50.0

226

20.0

349

30.0

144

0.7

8(0

.5773)

0.0

0(1

)G

AR

P9

0.0

184

40.0

185

50.0

184

0.0

1(0

.9953)

�0.2

5(0

.8065)

Valu

e11

0.0

157

80.0

167

30.0

131

0.7

2(0

.5249)

1.0

2(0

.3074)

Neu

tral

60.0

103

30.0

091

30.0

115

�1.0

7(0

.3874)

�0.6

6(0

.5127)

Oth

er3

0.0

090

––

30.0

090

––

––

Tim

ingb

All

funds

34

�0.0

505

17

�0.0

519

17

�0.0

491

�0.0

2(0

.9828)

�0.3

3(0

.7435)

Gro

wth

5�

0.2

037

2�

0.4

359

3�

0.0

488

�0.8

7(0

.5433)

0.0

0(1

)G

AR

P9

0.1

624

40.3

814

5�

0.0

128

0.9

1(0

.4244)

0.4

9(0

.6242)

Valu

e11

�0.1

486

8�

0.1

835

3�

0.0

558

�1.5

3(0

.1616)

�0.8

2(0

.4142)

Neu

tral

60.0

162

3�

0.0

229

30.0

553

�1.7

6(0

.1562)

�1.5

3(0

.1266)

Oth

er3

�0.2

077

––

3�

0.2

077

––

––

Do

wn

sid

eri

skA

llfu

nds

34

0.0

108

17

0.0

126

17

0.0

090

1.1

9(0

.2439)

1.4

0(0

.163)

Gro

wth

50.0

149

20.0

241

30.0

088

0.8

1(0

.5659)

0.0

0(1

)G

AR

P9

0.0

141

40.0

153

50.0

131

0.2

8(0

.7873)

0.0

0(1

)V

alu

e11

0.0

100

80.0

108

30.0

080

0.7

9(0

.489)

1.0

2(0

.3074)

Neu

tral

60.0

063

30.0

060

30.0

067

�0.3

4(0

.7543)

�0.2

2(0

.8273)

Oth

er3

0.0

057

––

30.0

057

––

––

Th

ista

ble

rep

ort

sth

em

ean

of

dis

trib

uti

on

al

mo

men

tsan

dri

skm

easu

res

of

fun

dre

turn

s.Pan

elA

rep

ort

sth

em

ean

,st

an

dard

dev

iati

on

,sk

ewn

ess,

an

dku

rto

sis

for

the

full

sam

ple

of

fun

ds,

then

sep

arate

db

yd

eriv

ati

ve

use

rsan

dn

on

-use

rs.Pan

elB

rep

ort

sth

ea,

b,id

iosy

ncr

ati

cri

sk,

tim

ingb,

an

dd

ow

nsi

de

risk

of

fun

dre

turn

s.Tes

tso

fd

iffe

ren

ces

test

sth

en

ull

hyp

oth

esis

that

the

mea

nes

tim

ate

sare

equ

alfo

rn

on

-use

rsan

du

sers

of

der

ivat

ives

.T

he

t-te

stis

ap

ara

met

ric

test

,w

her

eas

the

Wil

coxo

nra

nk

sum

test

isa

no

n-p

ara

met

ric

test

.

Ta

ble

3(C

onti

nued

)

International Review of Finance

14 r International Review of Finance Ltd. 2006

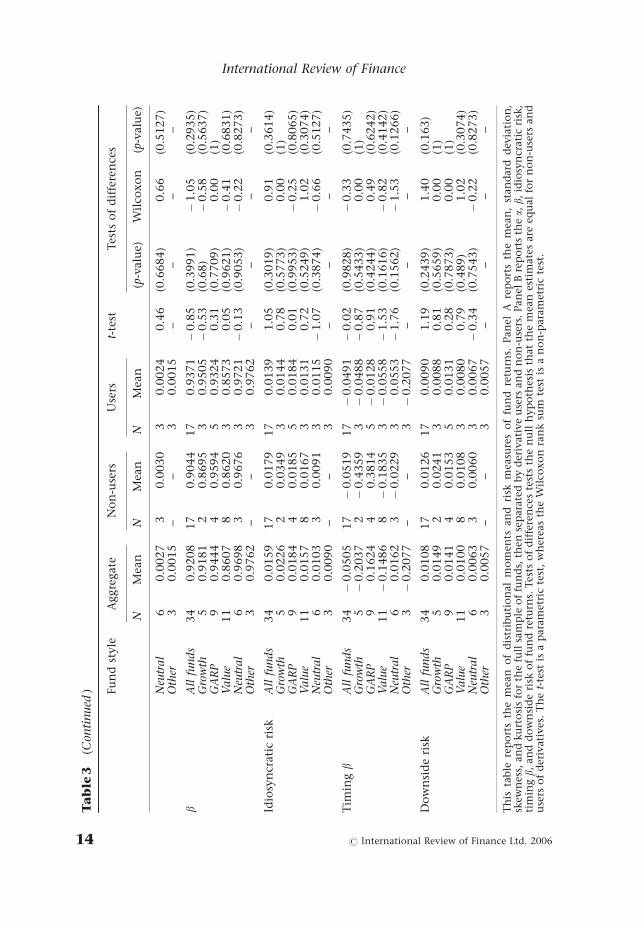

rank-sum test significant at the 10% level. Panel B also shows that there is nosignificant difference in other risk measures across derivative users and non-users.

Although the size of derivative exposures is small as a proportion of the totalportfolio, intra-month variation in derivative positions can potentially cause asignificant difference in portfolio risk and return between derivatives users andnon-users.18 The results in Table 3 show no systematic difference in the meansof distributional moments and risk measures between derivative users and non-users. This observation is consistent with the findings of Koski and Pontiff(1999).

B. Analyzing the proportions of option trades

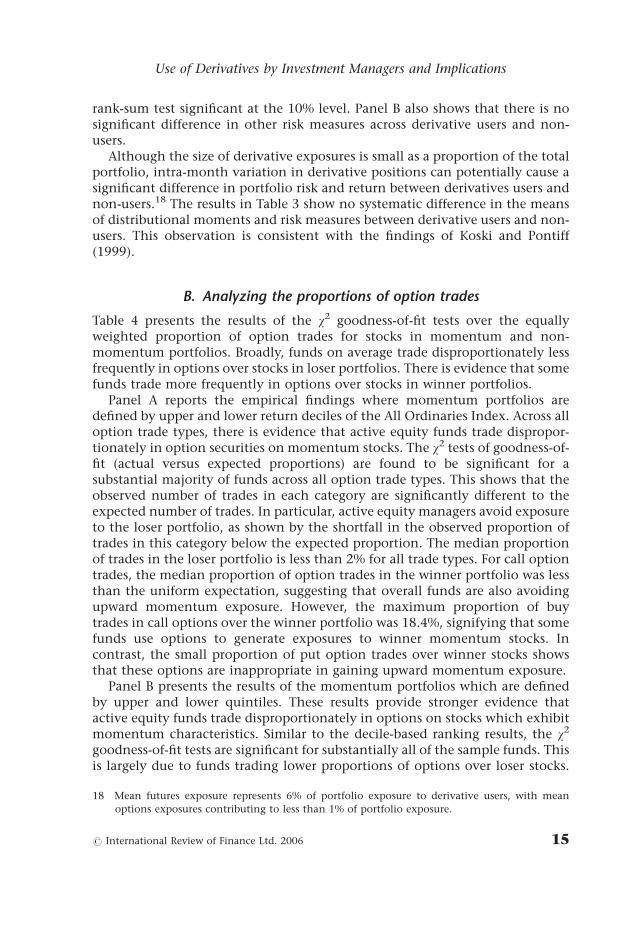

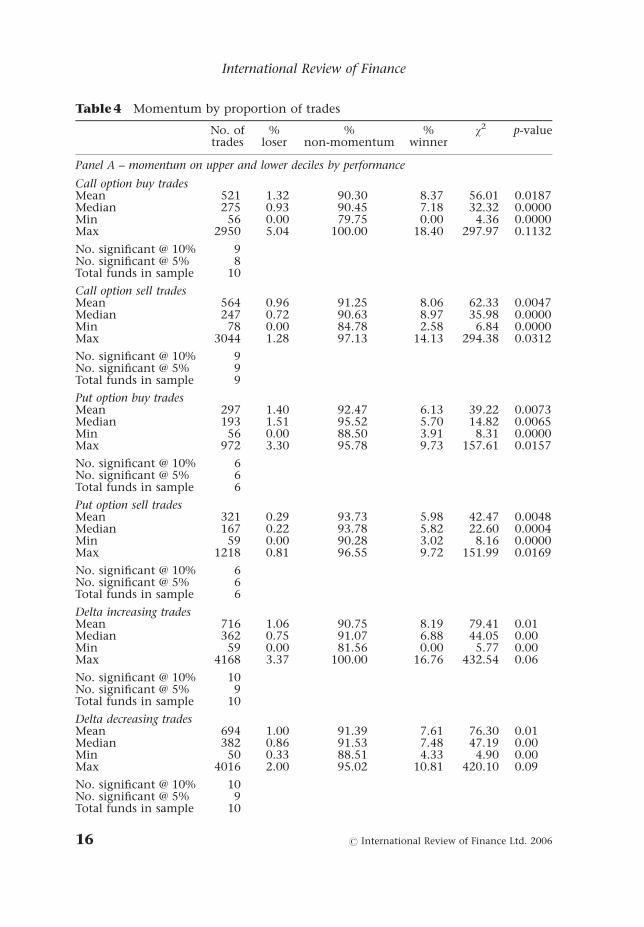

Table 4 presents the results of the w2 goodness-of-fit tests over the equallyweighted proportion of option trades for stocks in momentum and non-momentum portfolios. Broadly, funds on average trade disproportionately lessfrequently in options over stocks in loser portfolios. There is evidence that somefunds trade more frequently in options over stocks in winner portfolios.

Panel A reports the empirical findings where momentum portfolios aredefined by upper and lower return deciles of the All Ordinaries Index. Across alloption trade types, there is evidence that active equity funds trade dispropor-tionately in option securities on momentum stocks. The w2 tests of goodness-of-fit (actual versus expected proportions) are found to be significant for asubstantial majority of funds across all option trade types. This shows that theobserved number of trades in each category are significantly different to theexpected number of trades. In particular, active equity managers avoid exposureto the loser portfolio, as shown by the shortfall in the observed proportion oftrades in this category below the expected proportion. The median proportionof trades in the loser portfolio is less than 2% for all trade types. For call optiontrades, the median proportion of option trades in the winner portfolio was lessthan the uniform expectation, suggesting that overall funds are also avoidingupward momentum exposure. However, the maximum proportion of buytrades in call options over the winner portfolio was 18.4%, signifying that somefunds use options to generate exposures to winner momentum stocks. Incontrast, the small proportion of put option trades over winner stocks showsthat these options are inappropriate in gaining upward momentum exposure.

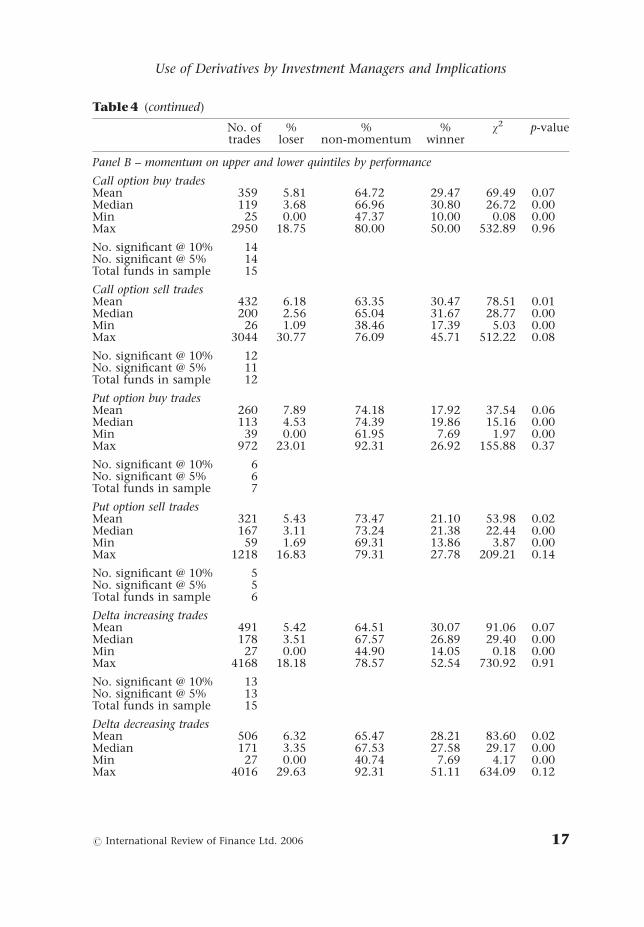

Panel B presents the results of the momentum portfolios which are definedby upper and lower quintiles. These results provide stronger evidence thatactive equity funds trade disproportionately in options on stocks which exhibitmomentum characteristics. Similar to the decile-based ranking results, the w2

goodness-of-fit tests are significant for substantially all of the sample funds. Thisis largely due to funds trading lower proportions of options over loser stocks.

18 Mean futures exposure represents 6% of portfolio exposure to derivative users, with mean

options exposures contributing to less than 1% of portfolio exposure.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 15

Table 4 Momentum by proportion of trades

No. oftrades

%loser

%non-momentum

%winner

w2 p-value

Panel A – momentum on upper and lower deciles by performance

Call option buy tradesMean 521 1.32 90.30 8.37 56.01 0.0187Median 275 0.93 90.45 7.18 32.32 0.0000Min 56 0.00 79.75 0.00 4.36 0.0000Max 2950 5.04 100.00 18.40 297.97 0.1132

No. significant @ 10% 9No. significant @ 5% 8Total funds in sample 10

Call option sell tradesMean 564 0.96 91.25 8.06 62.33 0.0047Median 247 0.72 90.63 8.97 35.98 0.0000Min 78 0.00 84.78 2.58 6.84 0.0000Max 3044 1.28 97.13 14.13 294.38 0.0312

No. significant @ 10% 9No. significant @ 5% 9Total funds in sample 9

Put option buy tradesMean 297 1.40 92.47 6.13 39.22 0.0073Median 193 1.51 95.52 5.70 14.82 0.0065Min 56 0.00 88.50 3.91 8.31 0.0000Max 972 3.30 95.78 9.73 157.61 0.0157

No. significant @ 10% 6No. significant @ 5% 6Total funds in sample 6

Put option sell tradesMean 321 0.29 93.73 5.98 42.47 0.0048Median 167 0.22 93.78 5.82 22.60 0.0004Min 59 0.00 90.28 3.02 8.16 0.0000Max 1218 0.81 96.55 9.72 151.99 0.0169

No. significant @ 10% 6No. significant @ 5% 6Total funds in sample 6

Delta increasing tradesMean 716 1.06 90.75 8.19 79.41 0.01Median 362 0.75 91.07 6.88 44.05 0.00Min 59 0.00 81.56 0.00 5.77 0.00Max 4168 3.37 100.00 16.76 432.54 0.06

No. significant @ 10% 10No. significant @ 5% 9Total funds in sample 10

Delta decreasing tradesMean 694 1.00 91.39 7.61 76.30 0.01Median 382 0.86 91.53 7.48 47.19 0.00Min 50 0.33 88.51 4.33 4.90 0.00Max 4016 2.00 95.02 10.81 420.10 0.09

No. significant @ 10% 10No. significant @ 5% 9Total funds in sample 10

International Review of Finance

16 r International Review of Finance Ltd. 2006

Table 4 (continued)

No. oftrades

%loser

%non-momentum

%winner

w2 p-value

Panel B – momentum on upper and lower quintiles by performance

Call option buy tradesMean 359 5.81 64.72 29.47 69.49 0.07Median 119 3.68 66.96 30.80 26.72 0.00Min 25 0.00 47.37 10.00 0.08 0.00Max 2950 18.75 80.00 50.00 532.89 0.96

No. significant @ 10% 14No. significant @ 5% 14Total funds in sample 15

Call option sell tradesMean 432 6.18 63.35 30.47 78.51 0.01Median 200 2.56 65.04 31.67 28.77 0.00Min 26 1.09 38.46 17.39 5.03 0.00Max 3044 30.77 76.09 45.71 512.22 0.08

No. significant @ 10% 12No. significant @ 5% 11Total funds in sample 12

Put option buy tradesMean 260 7.89 74.18 17.92 37.54 0.06Median 113 4.53 74.39 19.86 15.16 0.00Min 39 0.00 61.95 7.69 1.97 0.00Max 972 23.01 92.31 26.92 155.88 0.37

No. significant @ 10% 6No. significant @ 5% 6Total funds in sample 7

Put option sell tradesMean 321 5.43 73.47 21.10 53.98 0.02Median 167 3.11 73.24 21.38 22.44 0.00Min 59 1.69 69.31 13.86 3.87 0.00Max 1218 16.83 79.31 27.78 209.21 0.14

No. significant @ 10% 5No. significant @ 5% 5Total funds in sample 6

Delta increasing tradesMean 491 5.42 64.51 30.07 91.06 0.07Median 178 3.51 67.57 26.89 29.40 0.00Min 27 0.00 44.90 14.05 0.18 0.00Max 4168 18.18 78.57 52.54 730.92 0.91

No. significant @ 10% 13No. significant @ 5% 13Total funds in sample 15

Delta decreasing tradesMean 506 6.32 65.47 28.21 83.60 0.02Median 171 3.35 67.53 27.58 29.17 0.00Min 27 0.00 40.74 7.69 4.17 0.00Max 4016 29.63 92.31 51.11 634.09 0.12

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 17

In contrast to the decile-based results, the majority of funds trade disproportio-nately in call options over winner stocks, representing around 30% of themedian fund’s trades. Furthermore, at the maximum, funds place close to halfof their call option trades over stocks in the winner portfolio. The samephenomenon is less acute in put option securities, where the medianproportion of fund trades is close to the expected 20%, and the maximumproportion is not substantially greater (at around 27%).

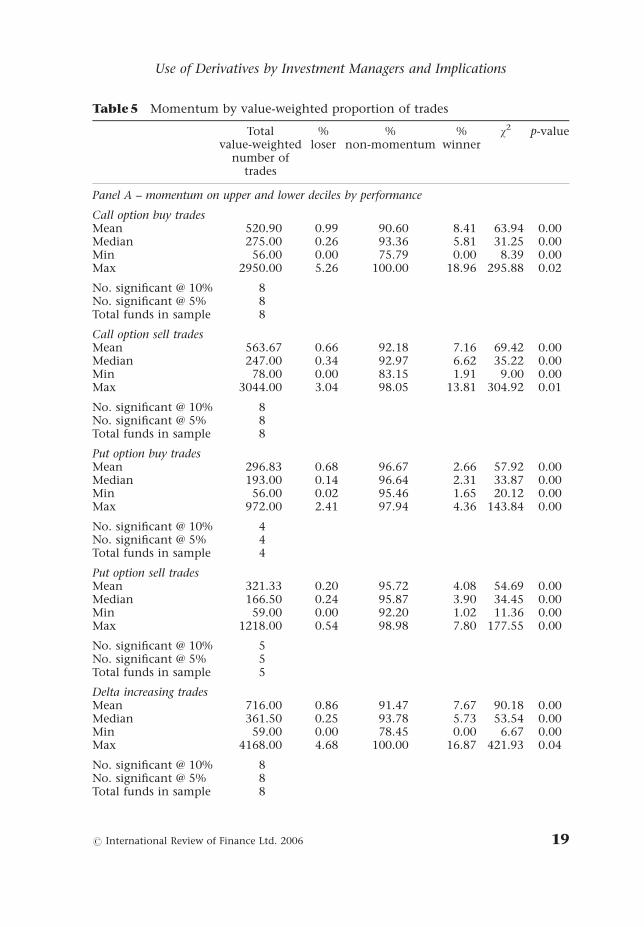

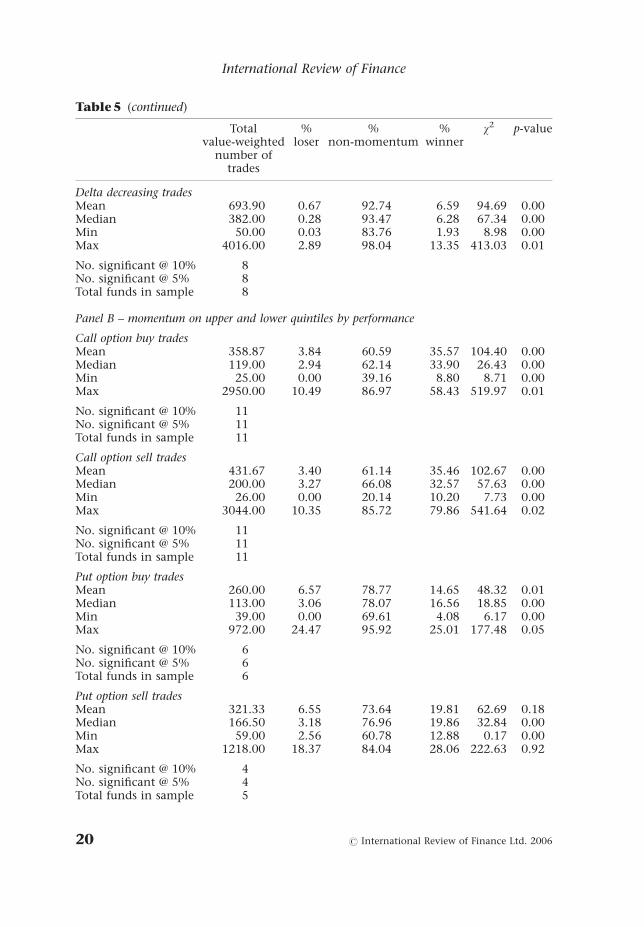

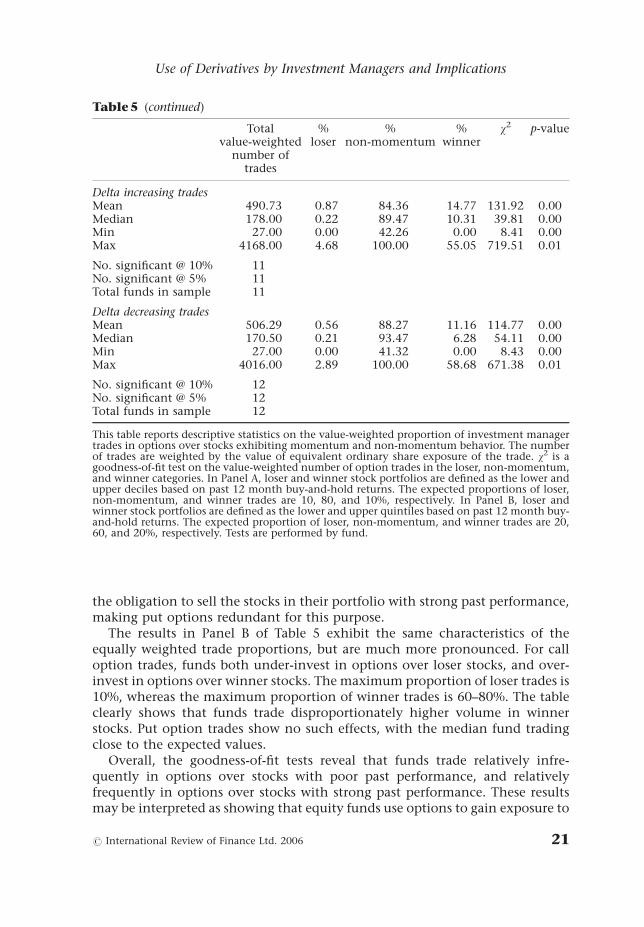

Table 5 reports the results of the w2 goodness-of-fit tests over the value-weighted number of option trades for stocks in momentum and non-momentum portfolios. These tests incorporate the relative size of each optiontrade, measuring the value of each transaction as the equivalent ordinary shareexposure. These results confirm the findings of the equally weightedmomentum tests in Table 4. Substantially all equity funds trade disproportio-nately around these momentum categories.

Panel A of Table 5 shows that the value of option trades over stocks in loserportfolios is substantially lower than expected, and to an even greater degreethan for the results of the equally weighted proportions. Some funds are shownto completely avoid portfolio exposures to loser stocks, as shown by the 0%minimum proportions across call option trades, and for put option sell trades.The median value-weighted proportion of trades over winner stocks is lowerthan the equally weighted proportion, providing further evidence that fundsare, on average, also avoiding options exposure to winner stocks. Further, thereis evidence that some funds acquire exposure to the winner portfolio usingoption securities, with the maximum proportion of trades over winner stocksexceeding the expected value of 10%. Funds unanimously trade disproportio-nately less in put options over winner stocks. This is consistent with thefindings of Pinnuck (2004), which show that funds prefer to hold stocks that arepast winners. Therefore, investment managers would not require the right or

Table 4 (continued)

No. oftrades

%loser

%non-momentum

%winner

w2 p-value

No. significant @ 10% 12No. significant @ 5% 12Total funds in sample 14

This table reports descriptive statistics on the proportion of trades in options over stocksexhibiting momentum and non-momentum behavior. w2 is a goodness-of-fit test on the numberof option trades in the loser, non-momentum, and winner categories. In Panel A, loser andwinner stock portfolios are defined as the lower and upper deciles based on past 12-month buy-and-hold returns. The expected proportions of loser, non-momentum, and winner trades are 10,80, and 10%, respectively. In Panel B, loser and winner stock portfolios are defined as the lowerand upper quintiles based on past 12-month buy-and-hold returns. The expected proportion ofloser, non-momentum, and winner trades are 20, 60, and 20%, respectively. Tests are performedby fund.

International Review of Finance

18 r International Review of Finance Ltd. 2006

Table 5 Momentum by value-weighted proportion of trades

Totalvalue-weighted

number oftrades

%loser

%non-momentum

%winner

w2 p-value

Panel A – momentum on upper and lower deciles by performance

Call option buy tradesMean 520.90 0.99 90.60 8.41 63.94 0.00Median 275.00 0.26 93.36 5.81 31.25 0.00Min 56.00 0.00 75.79 0.00 8.39 0.00Max 2950.00 5.26 100.00 18.96 295.88 0.02

No. significant @ 10% 8No. significant @ 5% 8Total funds in sample 8

Call option sell tradesMean 563.67 0.66 92.18 7.16 69.42 0.00Median 247.00 0.34 92.97 6.62 35.22 0.00Min 78.00 0.00 83.15 1.91 9.00 0.00Max 3044.00 3.04 98.05 13.81 304.92 0.01

No. significant @ 10% 8No. significant @ 5% 8Total funds in sample 8

Put option buy tradesMean 296.83 0.68 96.67 2.66 57.92 0.00Median 193.00 0.14 96.64 2.31 33.87 0.00Min 56.00 0.02 95.46 1.65 20.12 0.00Max 972.00 2.41 97.94 4.36 143.84 0.00

No. significant @ 10% 4No. significant @ 5% 4Total funds in sample 4

Put option sell tradesMean 321.33 0.20 95.72 4.08 54.69 0.00Median 166.50 0.24 95.87 3.90 34.45 0.00Min 59.00 0.00 92.20 1.02 11.36 0.00Max 1218.00 0.54 98.98 7.80 177.55 0.00

No. significant @ 10% 5No. significant @ 5% 5Total funds in sample 5

Delta increasing tradesMean 716.00 0.86 91.47 7.67 90.18 0.00Median 361.50 0.25 93.78 5.73 53.54 0.00Min 59.00 0.00 78.45 0.00 6.67 0.00Max 4168.00 4.68 100.00 16.87 421.93 0.04

No. significant @ 10% 8No. significant @ 5% 8Total funds in sample 8

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 19

Table 5 (continued)

Totalvalue-weighted

number oftrades

%loser

%non-momentum

%winner

w2 p-value

Delta decreasing tradesMean 693.90 0.67 92.74 6.59 94.69 0.00Median 382.00 0.28 93.47 6.28 67.34 0.00Min 50.00 0.03 83.76 1.93 8.98 0.00Max 4016.00 2.89 98.04 13.35 413.03 0.01

No. significant @ 10% 8No. significant @ 5% 8Total funds in sample 8

Panel B – momentum on upper and lower quintiles by performance

Call option buy tradesMean 358.87 3.84 60.59 35.57 104.40 0.00Median 119.00 2.94 62.14 33.90 26.43 0.00Min 25.00 0.00 39.16 8.80 8.71 0.00Max 2950.00 10.49 86.97 58.43 519.97 0.01

No. significant @ 10% 11No. significant @ 5% 11Total funds in sample 11

Call option sell tradesMean 431.67 3.40 61.14 35.46 102.67 0.00Median 200.00 3.27 66.08 32.57 57.63 0.00Min 26.00 0.00 20.14 10.20 7.73 0.00Max 3044.00 10.35 85.72 79.86 541.64 0.02

No. significant @ 10% 11No. significant @ 5% 11Total funds in sample 11

Put option buy tradesMean 260.00 6.57 78.77 14.65 48.32 0.01Median 113.00 3.06 78.07 16.56 18.85 0.00Min 39.00 0.00 69.61 4.08 6.17 0.00Max 972.00 24.47 95.92 25.01 177.48 0.05

No. significant @ 10% 6No. significant @ 5% 6Total funds in sample 6

Put option sell tradesMean 321.33 6.55 73.64 19.81 62.69 0.18Median 166.50 3.18 76.96 19.86 32.84 0.00Min 59.00 2.56 60.78 12.88 0.17 0.00Max 1218.00 18.37 84.04 28.06 222.63 0.92

No. significant @ 10% 4No. significant @ 5% 4Total funds in sample 5

International Review of Finance

20 r International Review of Finance Ltd. 2006

the obligation to sell the stocks in their portfolio with strong past performance,making put options redundant for this purpose.

The results in Panel B of Table 5 exhibit the same characteristics of theequally weighted trade proportions, but are much more pronounced. For calloption trades, funds both under-invest in options over loser stocks, and over-invest in options over winner stocks. The maximum proportion of loser trades is10%, whereas the maximum proportion of winner trades is 60–80%. The tableclearly shows that funds trade disproportionately higher volume in winnerstocks. Put option trades show no such effects, with the median fund tradingclose to the expected values.

Overall, the goodness-of-fit tests reveal that funds trade relatively infre-quently in options over stocks with poor past performance, and relativelyfrequently in options over stocks with strong past performance. These resultsmay be interpreted as showing that equity funds use options to gain exposure to

Table 5 (continued)

Totalvalue-weighted

number oftrades

%loser

%non-momentum

%winner

w2 p-value

Delta increasing tradesMean 490.73 0.87 84.36 14.77 131.92 0.00Median 178.00 0.22 89.47 10.31 39.81 0.00Min 27.00 0.00 42.26 0.00 8.41 0.00Max 4168.00 4.68 100.00 55.05 719.51 0.01

No. significant @ 10% 11No. significant @ 5% 11Total funds in sample 11

Delta decreasing tradesMean 506.29 0.56 88.27 11.16 114.77 0.00Median 170.50 0.21 93.47 6.28 54.11 0.00Min 27.00 0.00 41.32 0.00 8.43 0.00Max 4016.00 2.89 100.00 58.68 671.38 0.01

No. significant @ 10% 12No. significant @ 5% 12Total funds in sample 12

This table reports descriptive statistics on the value-weighted proportion of investment managertrades in options over stocks exhibiting momentum and non-momentum behavior. The numberof trades are weighted by the value of equivalent ordinary share exposure of the trade. w2 is agoodness-of-fit test on the value-weighted number of option trades in the loser, non-momentum,and winner categories. In Panel A, loser and winner stock portfolios are defined as the lower andupper deciles based on past 12 month buy-and-hold returns. The expected proportions of loser,non-momentum, and winner trades are 10, 80, and 10%, respectively. In Panel B, loser andwinner stock portfolios are defined as the lower and upper quintiles based on past 12 month buy-and-hold returns. The expected proportion of loser, non-momentum, and winner trades are 20,60, and 20%, respectively. Tests are performed by fund.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 21

‘winner’ momentum stocks, and this is consistent with implementing amomentum trading strategy. However, investment manager trading behaviorin options does not show signs of the opposing side of the momentum strategythat prescribes taking short exposure in stocks with poor past performance.That is, the option trades of investment managers are consistent withpurchasing exposure to the winner portfolio, but do not simultaneously sellexposure to the loser portfolio.

Despite the existence of possible alternative explanations, the tests usedclearly identify a systematic trend that the options trades of investmentmanagers are cross-sectionally related to the past performance of the underlyingstock.

C. Event study of option trades

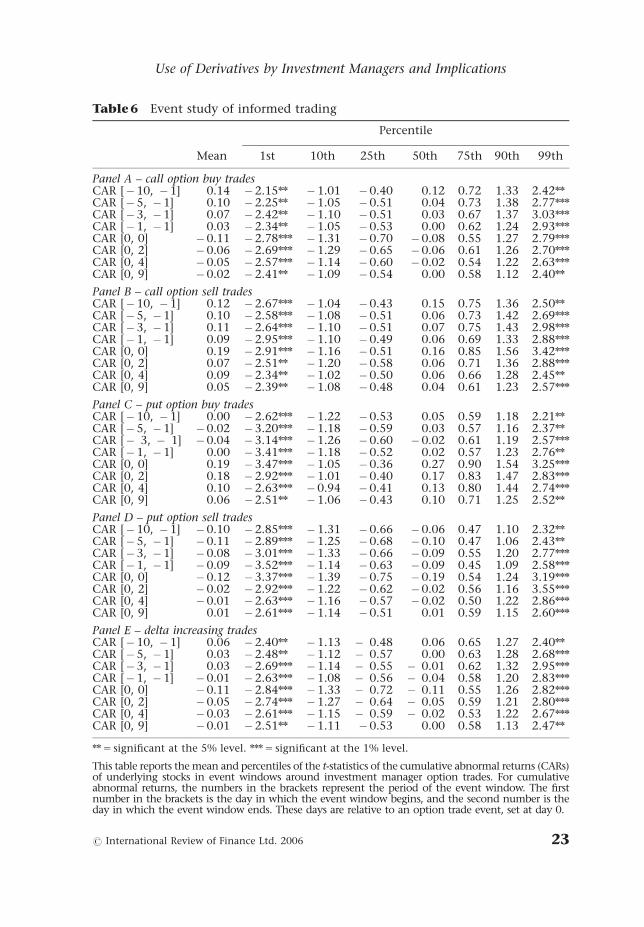

Table 6 presents the results of the event study examining the impact ofinvestment manager option trades on underlying stock returns. These resultsshow that the options trades of investment managers are not associated withabnormal share price reaction in the underlying stock. This suggests that themarket interprets little or no private information content in option trading.

The results shown in Table 6 are the percentiles of the t-statistics for thecumulative abnormal returns (CARs) in the underlying stock calculated for eachoption trade. If investment managers engage in informed trading in optionsmarkets, the information will quickly flow from the option price through to theprice of the underlying stock, driving abnormal stock returns around an optiontransaction. The results in Table 6 do not show such a reaction. To demonstratethat some proportion of option trades contain private information content, it isnecessary to show a significant CAR for a proportion of option tradessubstantially greater than the level of significance. We do not find suchempirical evidence across all option trade types.

At first instance, it appears that this result conflicts with some of the resultsfound in the prior literature (Easley et al. 1998; Chakravarty et al. 2004).Previous studies provide mixed support for the operation of informed trading inoptions markets. Although it should be noted that the issue of whetherinformed trading occurs in options markets is still unresolved, the bulk of thisresearch has been conducted on a market level. To our knowledge, this is thefirst study to investigate informed trading in options markets conductedspecifically by investment managers, and which utilizes a unique dataset ofdaily institutional trading data. Thus, although some degree of informedtrading may be performed using options, the results of this study suggest thatoverall, Australian investment managers do not transact in equity optionsmarkets as a key means of trading on private information.

The sign of CARs provides further insight into the trading behavior ofinvestment managers. For call option buy trades, the mean CARs are steadilydecreasing from 10 days prior until the day of the event. The abnormal shareprice return on the day of the call purchase is the largest negative mean return

International Review of Finance

22 r International Review of Finance Ltd. 2006

Table 6 Event study of informed trading

Percentile

Mean 1st 10th 25th 50th 75th 90th 99th

Panel A – call option buy tradesCAR [�10, �1] 0.14 �2.15nn �1.01 �0.40 0.12 0.72 1.33 2.42nn

CAR [�5, �1] 0.10 �2.25nn �1.05 �0.51 0.04 0.73 1.38 2.77nnn

CAR [�3, �1] 0.07 �2.42nn �1.10 �0.51 0.03 0.67 1.37 3.03nnn

CAR [�1, �1] 0.03 �2.34nn �1.05 �0.53 0.00 0.62 1.24 2.93nnn

CAR [0, 0] �0.11 �2.78nnn �1.31 �0.70 �0.08 0.55 1.27 2.79nnn

CAR [0, 2] �0.06 �2.69nnn �1.29 �0.65 �0.06 0.61 1.26 2.70nnn

CAR [0, 4] �0.05 �2.57nnn �1.14 �0.60 �0.02 0.54 1.22 2.63nnn

CAR [0, 9] �0.02 �2.41nn �1.09 �0.54 0.00 0.58 1.12 2.40nn

Panel B – call option sell tradesCAR [�10, �1] 0.12 �2.67nnn �1.04 �0.43 0.15 0.75 1.36 2.50nn

CAR [�5, �1] 0.10 �2.58nnn �1.08 �0.51 0.06 0.73 1.42 2.69nnn

CAR [�3, �1] 0.11 �2.64nnn �1.10 �0.51 0.07 0.75 1.43 2.98nnn

CAR [�1, �1] 0.09 �2.95nnn �1.10 �0.49 0.06 0.69 1.33 2.88nnn

CAR [0, 0] 0.19 �2.91nnn �1.16 �0.51 0.16 0.85 1.56 3.42nnn

CAR [0, 2] 0.07 �2.51nn �1.20 �0.58 0.06 0.71 1.36 2.88nnn

CAR [0, 4] 0.09 �2.34nn �1.02 �0.50 0.06 0.66 1.28 2.45nn

CAR [0, 9] 0.05 �2.39nn �1.08 �0.48 0.04 0.61 1.23 2.57nnn

Panel C – put option buy tradesCAR [�10, �1] 0.00 �2.62nnn �1.22 �0.53 0.05 0.59 1.18 2.21nn

CAR [�5, �1] �0.02 �3.20nnn �1.18 �0.59 0.03 0.57 1.16 2.37nn

CAR [� 3, � 1] �0.04 �3.14nnn �1.26 �0.60 �0.02 0.61 1.19 2.57nnn

CAR [�1, �1] 0.00 �3.41nnn �1.18 �0.52 0.02 0.57 1.23 2.76nn

CAR [0, 0] 0.19 �3.47nnn �1.05 �0.36 0.27 0.90 1.54 3.25nnn

CAR [0, 2] 0.18 �2.92nnn �1.01 �0.40 0.17 0.83 1.47 2.83nnn

CAR [0, 4] 0.10 �2.63nnn �0.94 �0.41 0.13 0.80 1.44 2.74nnn

CAR [0, 9] 0.06 �2.51nn �1.06 �0.43 0.10 0.71 1.25 2.52nn

Panel D – put option sell tradesCAR [�10, �1] �0.10 �2.85nnn �1.31 �0.66 �0.06 0.47 1.10 2.32nn

CAR [�5, �1] �0.11 �2.89nnn �1.25 �0.68 �0.10 0.47 1.06 2.43nn

CAR [�3, �1] �0.08 �3.01nnn �1.33 �0.66 �0.09 0.55 1.20 2.77nnn

CAR [�1, �1] �0.09 �3.52nnn �1.14 �0.63 �0.09 0.45 1.09 2.58nnn

CAR [0, 0] �0.12 �3.37nnn �1.39 �0.75 �0.19 0.54 1.24 3.19nnn

CAR [0, 2] �0.02 �2.92nnn �1.22 �0.62 �0.02 0.56 1.16 3.55nnn

CAR [0, 4] �0.01 �2.63nnn �1.16 �0.57 �0.02 0.50 1.22 2.86nnn

CAR [0, 9] 0.01 �2.61nnn �1.14 �0.51 0.01 0.59 1.15 2.60nnn

Panel E – delta increasing tradesCAR [�10, �1] 0.06 �2.40nn �1.13 � 0.48 0.06 0.65 1.27 2.40nn

CAR [�5, �1] 0.03 �2.48nn �1.12 � 0.57 0.00 0.63 1.28 2.68nnn

CAR [�3, �1] 0.03 �2.69nnn �1.14 � 0.55 � 0.01 0.62 1.32 2.95nnn

CAR [�1, �1] �0.01 �2.63nnn �1.08 � 0.56 � 0.04 0.58 1.20 2.83nnn

CAR [0, 0] �0.11 �2.84nnn �1.33 � 0.72 � 0.11 0.55 1.26 2.82nnn

CAR [0, 2] �0.05 �2.74nnn �1.27 � 0.64 � 0.05 0.59 1.21 2.80nnn

CAR [0, 4] �0.03 �2.61nnn �1.15 � 0.59 � 0.02 0.53 1.22 2.67nnn

CAR [0, 9] �0.01 �2.51nn �1.11 �0.53 0.00 0.58 1.13 2.47nn

nn 5 significant at the 5% level. nnn 5 significant at the 1% level.

This table reports the mean and percentiles of the t-statistics of the cumulative abnormal returns (CARs)of underlying stocks in event windows around investment manager option trades. For cumulativeabnormal returns, the numbers in the brackets represent the period of the event window. The firstnumber in the brackets is the day in which the event window begins, and the second number is theday in which the event window ends. These days are relative to an option trade event, set at day 0.

Use of Derivatives by Investment Managers and Implications

r International Review of Finance Ltd. 2006 23