Multinational Corporations, International Unionism, and NGOs

Doc. INFRASTRUCTURE.ZZ

THE ROLE OF TRANSNATIONAL

CORPORATIONS IN INFRASTRUCTURE IN

DEVELOPING COUNTRIES

BACKGROUND PAPER AND LITERATURE REVIEW

Prepared for UNCTAD1

Zbigniew Zimny

Geneva, October 2007

1 The paper has served as a background study for World Investment Report 2008. Transnational

Corporations and the Infrastructure Challenge (New York and Geneva: United Nations, 2008).

2

Table of contents

Introduction

I. FORMS OF TNC INVOLVEMENT IN INFRASTRUCTURE

A. Private greenfield investment

B. Public-private partnerships

C. Mergers and acquisitions

D. Forms of investment and FDI data

II. TRENDS IN FDI IN INFRASTRUCTURE

A. A shift from public to private provision of infrastructure services

B. Trends in private investment in infrastructure

1. Growth and decline

2. Regions

3. Sectors

4. Forms

C. The role of FDI

D. TNC players and home countries

III. IMPACT

A. What infrastructure TNCs offer to developing countries?

B. Impact in individual infrastructure sectors

1. Telecommunications

2. Electricity

3. Transportation

a. Rail

b. Ports

4. Water

C. Impact by areas

1. Supply and coverage

2. Efficiency

3. Quality of services

4. Fiscal impact

5. Employment

6. Prices

7. Impact on the poor

8. Conclusion

D. The sources of discontent

IV. POLICY ISSUES

A. Policy reforms

B. FDI policy: to what extent countries allow FDI and TNCs in

infrastructure?

C. Policies to benefit and address concerns

D. The role of international agreements

3

Boxes

1. Infrastructure needs of developing countries

Figures

1. PPI in developing and transition economies, 1990-2005

2. Private investment in infrastructure by region, 1990-2005

3. Private investment in infrastructure in developing countries by sector, 1990-2005

4. Forms of private investment in infrastructure in developing countries, 1990-2005

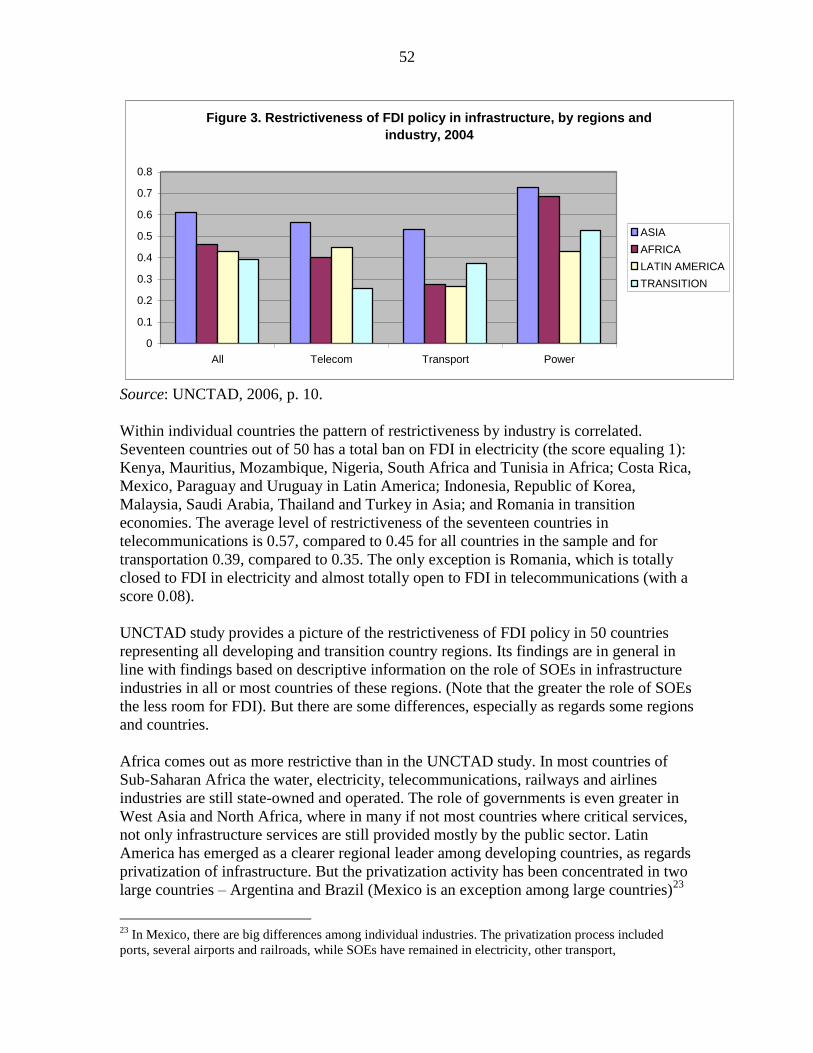

4. Restrictiveness of FDI policy in 50 developing countries in service industries, 2004

5. Restrictiveness of FDI policy in infrastructure by regions and industry, 2004

6. Restrictiveness of FDI policy in infrastructure in developing and transition economies,

2004

Tables

1. The top 10 TNCs in private infrastructure projects in developing countries, 1990-2001

2. The share of FDI in total investment in infrastructure in developing countries

3. Annual growth rate of telecommunications lines in reforming and non-reforming

countries of Latin America

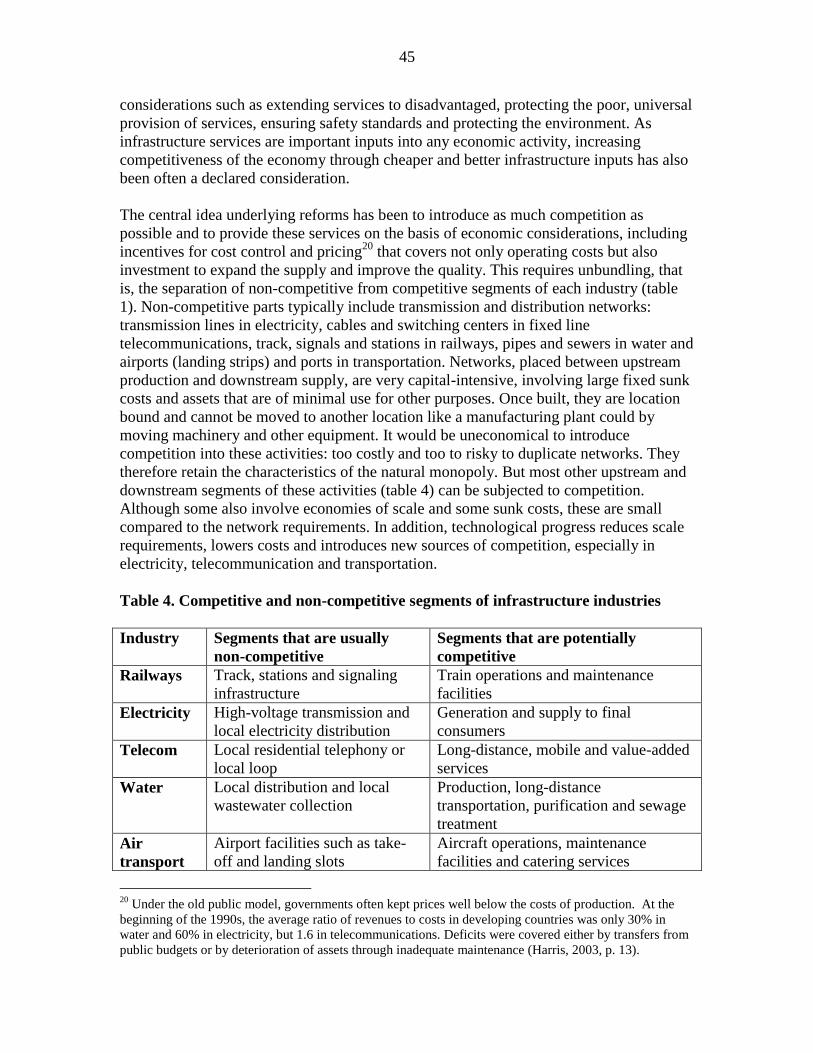

4. Competitive and non-competitive segments of infrastructure industries

REFERENCES

4

Introduction

Physical infrastructure – transportation infrastructure (roads, ports, airports, etc.)

telecommunication, electricity, water, sewage and waste treatment – is a backbone of any

economy. Good infrastructure facilitates economic activities. Bad infrastructure hampers

these activities, making them costly and uncompetitive. Missing infrastructure (e.g.,

roads or power) makes it impossible to undertake production or trade, thus making it

impossible to exploit potential for larger output (e.g., in mining or tourism). Infrastructure

produces also basic services for households and consumers, determining their well-being.

It also determines living standards of high-income consumers. For example, tourism

relies heavily on all components of physical infrastructure. On the other hand, access to

water and electricity is among chief concerns in the fight against poverty. As regards

FDI, the quality and prices of infrastructure have always stood high in rankings of the

determinants of inward FDI. Excellent infrastructure has been credited, among others, for

spectacular success of such countries as Singapore or Ireland in attracting FDI and using

it to promote development. Poor infrastructure reduces potential to attract FDI in many

African countries.

Markets for infrastructure services are prone to market failures (because of natural

monopoly element, externalities, very high capital intensity or uncertain returns). Some

are public goods while the provision of others is strongly affected by social

considerations such as universal access to basic services by remote areas and

disadvantaged segments of population. It was, therefore, long thought that the best way to

provide these services is through government controlled or owned companies. Such was,

indeed, the infrastructure paradigm after world war two in developing and developed

countries. Given increasingly disappointing performance of many state-owned

monopolies, during the 1980s and 1990s of the past century, however, an old paradigm,

has been replaced by a new one, that is, the private provision of infrastructure services,

manifested by the deregulation of service markets and massive privatization in developed

and most developing and transition countries.

In privatizing infrastructure, many countries turned to foreign investors for participation

in sales of state-owned enterprises (SOEs) (especially countries in Latin America and

Africa as well as transition countries) or for undertaking greenfield investment (East

Asia). FDI in infrastructure, especially in telecommunication and electricity, surged

during the 1990s, fuelling FDI in general and an increasing role of services in inward FDI

of developing countries. According to the Private Participation in Infrastructure (PPI)

data base of the World Bank, during 1990-2005 developing and transition countries

received $962 billion of investment commitments into some 3360 infrastructure projects

with private participation. TNCs participated in 83-85% of these projects. Private

investment and FDI in infrastructure peaked in the second half of the 1990s (1997-1998),

and have fallen ever since.

The decline was partly due to the fact that many developing countries (including large

ones such as Brazil, Mexico or Argentina) which decided to turn to FDI for the private

provision of infrastructure services completed their privatization programmes. Further

5

FDI in such countries has taken the form of re-investment to expand supply capacity

(such investment is typically much smaller than original huge sale transactions). The

giants of Asia, China and India, have not joint in with privatization programmes,

although they allowed some private participation in the form of greenfield investment and

concessions. Partly, foreign involvement in some infrastructure industries (roads, airports

and airport management, water and waste management) takes the form of non-equity

arrangements (such as concessions, leases or BOT arrangements) that go unrecorded by

FDI statistics.

But there have also been reports on disillusionment and disappointment with many

projects on the part of foreign investors and the governments and the public in developing

countries. Some of high-profile have been cancelled or renegotiated. Around 2000 FIAS

wrote that “nightmare stories abound of investors experiencing lengthy delays or project

cancellations because of political, administrative and legal impediments”.2 In some parts

of the world public opinion has become disappointed with the private provision of

infrastructure services, although there have been, so far, few attempts to revert to the

public provision of these services

So, the situation is as follows. After enthusiasm of the 1990s concerning the participation

of TNCs in infrastructure, reflected in huge FDI and many non-equity agreements, the

period of cooling of and perhaps reflection has followed, and FDI has subsided. Investors

(both TNCs and financiers – large projects are often financed by consortia) have lost

some appetite for this investment. Governments are caught between huge, virtually

unlimited, investment needs, far exceeding the capacity of the public purse, and

disappointment of parts of populations with expensive and often unaffordable (though in

most cases better than before) services.

Thus, the challenge to the WIR is to find out what went well and what went wrong and to

propose realistic policy options. The time perspective – ten years after the infrastructure

FDI peak – should provide enough material for cool and reasonable analysis. There have

been also some new developments and issues which require attention. One is, for

example, the growing public private partnerships (PPPs) legislation. PPPs are seen by

some as a new avenue for infrastructure investment. Another is the emergence of

infrastructure TNCs from developing countries. There is also a growing interest in how to

link better FDI and ODA in infrastructure. And after a period of heavy criticism,

governments, international organizations and TNCs are finally seriously considering how

private provision of infrastructure services can benefit more the poor.

I. FORMS OF TNC INVOLVEMENT IN INFRASTRUCTURE

As in other sectors, FDI is not the only form of TNC participation in host countries’

infrastructure. In fact, in some infrastructure industries it is rather an exception than a

rule. Consequently FDI data do not adequately reflect trends in, and scope of, TNC

2 FIAS (2000). Attracting FDI Into Infrastructure. Why Is It So Difficult?, The IFC and the World Bank,

Washington D.C., p. xvii.

6

operations in the sector. What follows is a discussion of these forms and their incidence

in individual infrastructure industries and developing regions.

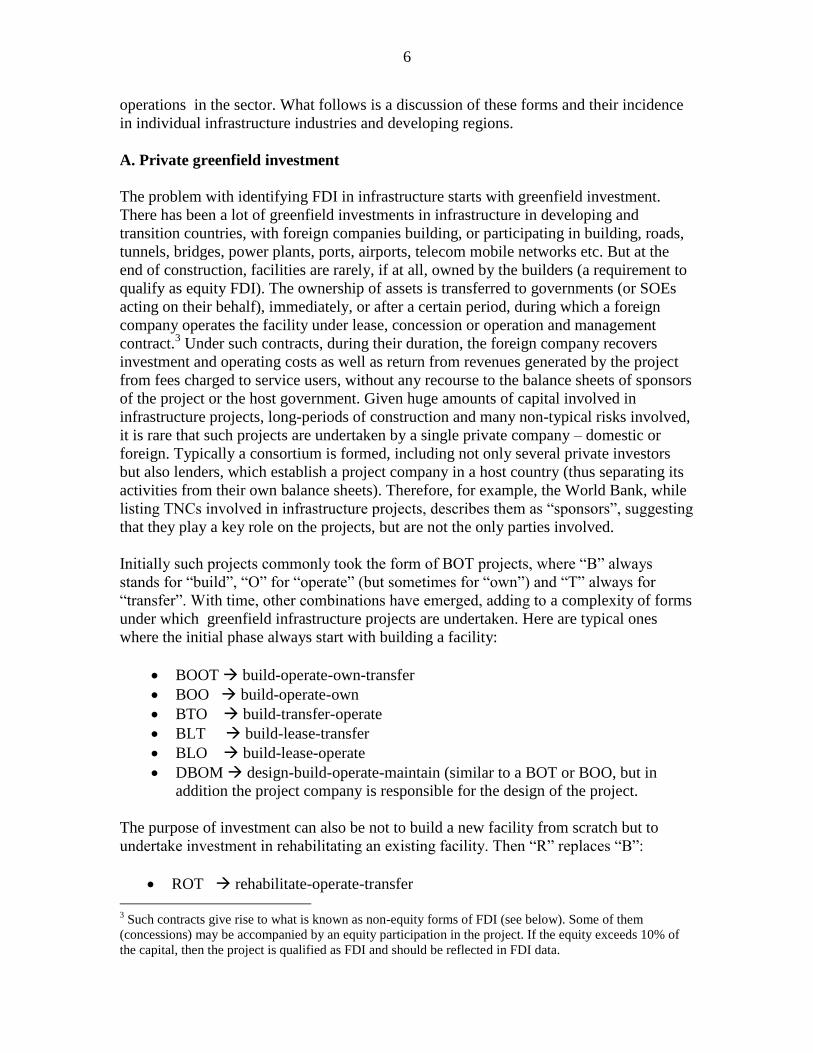

A. Private greenfield investment

The problem with identifying FDI in infrastructure starts with greenfield investment.

There has been a lot of greenfield investments in infrastructure in developing and

transition countries, with foreign companies building, or participating in building, roads,

tunnels, bridges, power plants, ports, airports, telecom mobile networks etc. But at the

end of construction, facilities are rarely, if at all, owned by the builders (a requirement to

qualify as equity FDI). The ownership of assets is transferred to governments (or SOEs

acting on their behalf), immediately, or after a certain period, during which a foreign

company operates the facility under lease, concession or operation and management

contract.3 Under such contracts, during their duration, the foreign company recovers

investment and operating costs as well as return from revenues generated by the project

from fees charged to service users, without any recourse to the balance sheets of sponsors

of the project or the host government. Given huge amounts of capital involved in

infrastructure projects, long-periods of construction and many non-typical risks involved,

it is rare that such projects are undertaken by a single private company – domestic or

foreign. Typically a consortium is formed, including not only several private investors

but also lenders, which establish a project company in a host country (thus separating its

activities from their own balance sheets). Therefore, for example, the World Bank, while

listing TNCs involved in infrastructure projects, describes them as “sponsors”, suggesting

that they play a key role on the projects, but are not the only parties involved.

Initially such projects commonly took the form of BOT projects, where “B” always

stands for “build”, “O” for “operate” (but sometimes for “own”) and “T” always for

“transfer”. With time, other combinations have emerged, adding to a complexity of forms

under which greenfield infrastructure projects are undertaken. Here are typical ones

where the initial phase always start with building a facility:

BOOT build-operate-own-transfer

BOO build-operate-own

BTO build-transfer-operate

BLT build-lease-transfer

BLO build-lease-operate

DBOM design-build-operate-maintain (similar to a BOT or BOO, but in

addition the project company is responsible for the design of the project.

The purpose of investment can also be not to build a new facility from scratch but to

undertake investment in rehabilitating an existing facility. Then “R” replaces “B”:

ROT rehabilitate-operate-transfer

3 Such contracts give rise to what is known as non-equity forms of FDI (see below). Some of them

(concessions) may be accompanied by an equity participation in the project. If the equity exceeds 10% of

the capital, then the project is qualified as FDI and should be reflected in FDI data.

7

ROO rehabilitate-operate-own

ROL rehabilitate-operate-lease

There are also hybrid arrangements such as DOT (develop-operate-transfer) under which,

in addition to BOT arrangement, the company receives development rights to adjoining

property. None of these forms (except for BOO, build-operate-own) is a classic FDI and,

as such, will not be reflected in FDI data.4 Exceptions can be found in mobile telephony,

where projects typically take the form of equity FDI, that is, foreign investor, after having

received a mobile telephony license, establishes a foreign equity affiliate, which builds,

owns and operates a network, as in “classic” FDI.

B. Public-private partnerships

Then there is a question, what are public-private-partnerships (PPPs), an increasingly

popular form of investing in infrastructure, and how do they relate to grienfield

investment and cross-border M&As. PPPs can be any of the above arrangements (and, in

addition, a joint venture), if the host government participates in financing the project,

typically in exchange for equity (proportional to capital contribution), to support

commercial viability of the project.

There are several explanations of the recent resurgence of PPPs,5 but a plausible one is as

follows. Initially private projects in infrastructure were based on the belief, that it is

possible to provide infrastructure services at no cost to the public. But many projects ran

into problems and were either canceled or required difficult renegotiations. The East

Asian and Argentinean financial crises undermined economic viability of many

infrastructure projects and revealed their high-risk nature. As a result, private investment

in infrastructure fell drastically during the late 1990s and at the beginning of 21st century,

as investors and lenders were put off by the risks involved and unaccounted for in the

original contracts. On the other hand it turned out that in successful private projects in

developed countries (and most likely in developing ones) in the early 1990s the cost of

private provision of services was often much higher “than could have been achieved

under the standard model of public procurement” (http:/en.wikipedia.org/wiki/Public-

private_partnership; and FIAS, 2000). In addition, private investors received a rate of

4 They should find their way to other items of the balance of payments such international loans, trade in

services (construction or engineering services) or transactions related to labour movement (if foreign

workers were involved in construction). 5 Authors of studies and papers on PPPs take it for granted that there has been a recent growing interest in

PPPs and, as a result the number of PPPs has grown, but, surprisingly, none of the papers on PPPs reviewed

for this study has provided evidence for this growth. Hodge and Greve state that “PPPs are enjoying a

global resurgence in popularity” (2007, p. 545). The IMF study describes the situation as follows: “It was

at this time [late 1990s] that PPPs began to emerge significantly as a means of obtaining private sector

capital and management expertise for infrastructure investment, both to carry on where privatization had

left off and as an alternative where there had been obstacles to privatization. After a modest start, a wave of

PPPs is now beginning to sweep the world” (IMF, 2004, p. 4). A UN ECE expert on PPPs G. Hamilton

refers to “thousands of PPPs transactions completed” but does not give any details (Hamilton, 2007). My

explanation is, as argued in the text, that PPPs are, in spite of some claims to the contrary, nothing else than

versions of the forms of PPI with some participation of the public sector. Another IMF study uses PPI data

as a proxy for PPPs (Hammami et.al., 2006, pp. 11-12).

8

return that was higher that government’s bond rate. So, one can say that PPPs have

emerged in reaction to failures of infrastructure projects in developing countries and their

successes (excessive profitability) in developed ones.

Initially, most PPPs were negotiated individually, as one off-deals. But after a number of

studies in Australia and the United Kingdom concluded that private schemes were often

inferior to public procurement (see, for example, EPAC, 1995, a and b), based on

competitive tender, countries started introducing PPP legislation to provide a framework

for financing, risk sharing, mutual responsibilities and, more importantly, for introducing

a systematic framework for assessment procedures. While the initial approach aimed at

avoiding public expenses, a new one involved an appropriate allocation of risks so that

governments could obtain “value for money”. So the idea of purely private financing of

infrastructure projects has given way to the recognition that that public money should be

involved, in exchange, however, for a redefined sharing of risks and responsibilities. The

1992 Private Finance Initiative of the United Kingdom was the first systematic

programme aimed at facilitating PPPs under the new approach. Australia and many other

countries, including developing ones, have followed, introducing legislation guiding

PPPs. As it is easier to say than to implement the rule that governments should seek

“value for money” in PPPs, the debate on how to do it continues (Hodge and Greve,

2007; Spackman, 2002; and Monbiot, 2000). But PPP legislation is spreading to an

increasing number of both developed and developing countries.

C. Mergers and acquisitions (M&As)

M&As as a form of FDI in infrastructure result, as in other sectors, from the sale of state-

owned or private assets to foreign investors. In developing and transition economies,

before they embarked on the path towards the private provision of infrastructure services,

these services were typically provided by SOEs. Therefore this type of FDI initially

involved almost exclusively the sale of SOEs to foreign investors, of course in countries,

which decided to allow FDI in privatizations. Although listed under “M&As”, such

transactions have been acquisitions. They are often called, in an alternative to

“privatizations”, “divestitures”. Infrastructure-related cross-border M&As were the

driving force of FDI in general in a number of countries, when they implemented mass

privatization programmes. Notable examples include Brazil and Argentina as well as a

number of transition economies (UNCTAD, 2004).

A number of SOEs had been privatized to domestic investors, which after some time of

(often successful) operations were purchased by foreign investors. A case of a Chilean

power company, Enersis, is illustrative in this respect. Having emerged from

privatizations, during the 1990s it became a leading regional TNC, acquiring assets in

Argentina, Brazil, Colombia in Peru. In 1997, Enersis sold some 30% of its equity to a

Spanish TNC, Endesa, which, by acquiring further 32% in 1999, took over control and

management of Enersis (ECLAC, 2006, pp. 144-145). With more and more private

companies – domestic and foreign – operating in infrastructure of developing and

transition economies, cross-border M&As more often take the form of acquisitions of

private companies, while privatization-related M&As have subsided.

9

D. Forms of investment and FDI data

To summarize, private participation in infrastructure, including that by TNCs, can take

various forms, which, in the case of TNCs involvement can lead to either equity and non-

equity forms of FDI, or both. For conceptual clarity and statistical purposes (for example,

in the World Bank’s data base on Private Participation in Infrastructure, PPI, World

Bank, 2003) four principal forms of private involvement are typically distinguished:

Management and lease contracts. For the duration of a contract a TNC manages

an SOE, which is owned by the government. The public sector takes investment

decisions and assumes financial responsibilities.

Concessions. A TNC manages an SOE. The difference from the management

contract is that the TNC contributes also capital and thus assumes an investment

risk during the contract.

Greenfield projects. A TNC or a public-TNC joint venture builds and operates

an infrastructure facility during the duration of the contract. But as it is clear from

the earlier discussion of BOT agreements, the final phase of the contract may

involve the return of the facility to the public sector, ownership of the facility by

the TNC or operation of the facility under a non-equity form such as a

management or lease contract.

Privatizations/divestitures. A TNC buys an equity stake or the entire equity in a

SOE and, as a result, owns or controls it (in line with FDI definitions a stake of

10% qualifies as a controlling stake).

FDI data include only projects with at least 10% of foreign equity. So called non-

equity forms, giving a TNC control of a foreign affiliate on the basis of an agreement

without an equity stake are not recorded in FDI data. But they are commonly called

non-equity FDI, because the control is strong enough to manage the affiliate. In

addition, except for capital,6 various components of the FDI package, such as

technology, knowledge and better management are typically transferred to the host

country.

Of the four forms listed above, only the case of privatizations is straightforward as

regards FDI. The acquisition of equity by foreign investors is normally reported in

FDI flows and stocks. Management and lease contracts, not involving equity, are not

included in FDI data. The situation with concessions is unclear. They might meet FDI

criteria, if a TNC provides an equity above 10%. In addition, debt financing by the

parent should be added to FDI flows. But since concessions are limited in time, it is

uncertain if they meet the criterion of “the long-term interest and commitment” by the

parent company.

The situation with greenfield investment is unclear, too. A TNC contributes capital

for the construction of the facility, but the project goes through several phases and it

6 Even though under non-equity forms a TNC does not contribute capital directly, a contract with a TNC

may greatly facilitate obtaining financing from foreign sources.

10

may end up being owned (and operated) by the public sector, a TNC or owned by the

public sector and operated by the TNC under a contract involving or not involving

equity. Wherever the TNC provided enough equity this should qualify as an FDI

project. Debt, if it is provided by the (foreign) equity investor, should also qualify as

FDI. Typically in BOT-type projects and concessions equity tends to be significantly

smaller than debt flows. But on the other hand TNC sponsors of the project tend to

rely on commercial lenders for debt financing (FIAS, 2000, p. 149). In general

information on the financing of such transactions is difficult to obtain.

Further complications arise, because the boundaries between the four categories are

not always clear, and some projects have features of more than one category (World

Bank, 2003, p. 7; in the World Bank PPI data base, which will be used later on,

projects are included in the category which better reflects the risk borne by private

investor).

II. TRENDS IN FDI IN INFRASTRUCTURE

A. A shift from public to private provision of infrastructure services

Until the early 1990s, most developing countries and all transition economies relied on

state-owned enterprises (SOEs) for the provision of infrastructure services. In the 1980s a

few developing countries started liberalizing and privatizing infrastructure (for example,

Chile). In the 1990s, this trend gained strength and turned into a wave, which included

well over 100 of developing countries.

A common reason for this shift was an increasing dissatisfaction with the quality and

insufficient supply of infrastructure services. But disappointment had many roots. In

some countries (notably of Latin America and Africa), SOEs were badly managed and, as

state monopolies, had no incentives and funds for investment and improvement.7 Subject

to political interference, they were depleted of funds by always hungry governments,

which on the other hand subsidized services and were hostile to increasing prices to

reflect inflated costs of inefficient operations. In addition, SOEs were treated as

reservoirs of employment for politically connected. The debt crisis in the 1980s imposed

very tight budgetary constraints in these countries, excluding any possibility of large

public financing of infrastructure investment. In other countries, mostly Asian ones,

SOEs, at least in some countries, were not doing badly and governments were not

indebted. But rapid economic growth led also to a rapidly growing demand for all types

of infrastructure services, which, to satisfy the demand, required amounts of investment

beyond the means of both SOEs and governments. So in the late 1980s and early 1990s,

some 1-1.2 billion people in developing countries had no access to electricity, clean water

and adequate sanitation (World Bank, 1994, p. 1). Telecommunication in a world relying

increasingly on IT technologies was in many countries a costly (but often unreliable)

luxury. The cost of losses caused by inefficient operations of roads, railways, power and

water systems was estimated by the World Bank at $55 billion a year in the early 1990s,

or “an equivalent to 1% of the GDP of all developing countries, a quarter of their annual

7 See, for example, Panayotou (????, pp. 49-51), Kessides (2004, pp. 34-35) and Nellis (2006, pp. 5-6).

11

investment in infrastructure, and twice the annual development finance for infrastructure

in the developing world” (ibid., p. 11).

The shift towards the private provision of infrastructure has spread to former centrally

planned economies, when they started the transition towards market economy in the early

1990s. Infrastructure industries have been, however, included to a various extent in this

undertaking. Privatization has been common in telecommunications and electricity and

less common in other industries, especially in water and sanitation. Countries of Central

and Eastern Europe, which became members of the European Union in 2004, have been

obliged to implement the rules of the internal markets, which emphasized deregulation of

infrastructure industries, while leaving decisions concerning ownership matters to

individual countries.

Whatever the reasons for this shift, it was so strong that during the 1990s hundreds of

billions of private dollars were invested and, at the beginning of the 21st century, almost

all developing countries and transition economies had some private operations in

infrastructure, a huge change from the 1980 when most or almost all of them relied on the

public provision. FIAS estimates, that, among private investors, during 1990-1998, when

most of the private investment took place (71% out of almost 1 trillion dollars committed

during 1990-2005), foreign investors were involved in 83% of private projects or projects

with private participation, measured by both their number and value, in developing and

transition economies (FIAS, 2000, p. vii). During 1998-2003, the involvement of foreign

investors has further increased, to 86% of the projects measured by investment value

(Ettinger et. al, 2005, p. 15). Therefore, it is justified, in the following overview of the

investment trends to begin with a review based on the World Bank’s data base on the

private participation in infrastructure (PPI), even though in its aggregated data part the

data base does not distinguish projects with and without foreign involvement.8 But

knowing that well over 80% of the projects came with foreign involvement, the data base

reflects also well trends in TNC participation in equity and non-equity forms. On the

other hand, as it is widely known, FDI data are very imperfect and, using only these data

it would be impossible to get a picture of investment in infrastructure by regions of

developing countries, by infrastructure sectors and by forms of investment, not saying

about region/sector/forms composition. Nevertheless, available FDI/TNC data will be

used at the end of this chapter. In between, we will also review trends in FDI in

infrastructure, based on FIAS estimates for 1990-1998. They are closely correlated with

overall trends, because, as mentioned earlier, foreign investors participated in 84% of all

projects during 1990-2003.

B. Trends in private investment in infrastructure

1. Growth and decline

8 Information on foreign participants of the projects (including their financial contribution and forms of

investment) is included in the part of the data base providing descriptive profiles of individual projects.

But the data base does not distill this information and although it is publicly available, it would be very

cumbersome to do so, as by 2007 the base included 3,413 profiles. FIAS made an estimate of FDI

participation for the period 1990-1998, retrieving necessary information from 542 projects and then

extrapolating it to 1,707 projects, which took place during this period (FIAS, 2000, pp. 147-153). See

below the discussion of FDI trends, based on FIAS data.

12

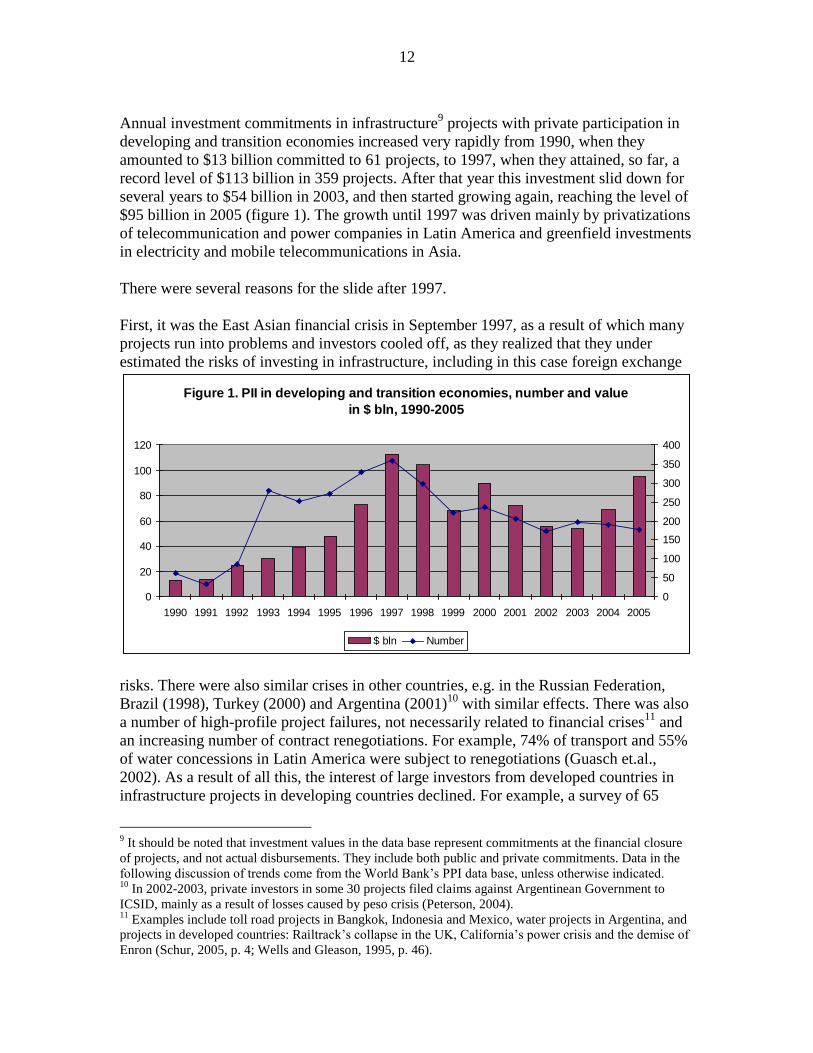

Annual investment commitments in infrastructure9 projects with private participation in

developing and transition economies increased very rapidly from 1990, when they

amounted to $13 billion committed to 61 projects, to 1997, when they attained, so far, a

record level of $113 billion in 359 projects. After that year this investment slid down for

several years to $54 billion in 2003, and then started growing again, reaching the level of

$95 billion in 2005 (figure 1). The growth until 1997 was driven mainly by privatizations

of telecommunication and power companies in Latin America and greenfield investments

in electricity and mobile telecommunications in Asia.

There were several reasons for the slide after 1997.

First, it was the East Asian financial crisis in September 1997, as a result of which many

projects run into problems and investors cooled off, as they realized that they under

estimated the risks of investing in infrastructure, including in this case foreign exchange

Figure 1. PII in developing and transition economies, number and value

in $ bln, 1990-2005

0

20

40

60

80

100

120

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

0

50

100

150

200

250

300

350

400

$ bln Number

risks. There were also similar crises in other countries, e.g. in the Russian Federation,

Brazil (1998), Turkey (2000) and Argentina (2001)10

with similar effects. There was also

a number of high-profile project failures, not necessarily related to financial crises11

and

an increasing number of contract renegotiations. For example, 74% of transport and 55%

of water concessions in Latin America were subject to renegotiations (Guasch et.al.,

2002). As a result of all this, the interest of large investors from developed countries in

infrastructure projects in developing countries declined. For example, a survey of 65

9 It should be noted that investment values in the data base represent commitments at the financial closure

of projects, and not actual disbursements. They include both public and private commitments. Data in the

following discussion of trends come from the World Bank’s PPI data base, unless otherwise indicated. 10

In 2002-2003, private investors in some 30 projects filed claims against Argentinean Government to

ICSID, mainly as a result of losses caused by peso crisis (Peterson, 2004). 11

Examples include toll road projects in Bangkok, Indonesia and Mexico, water projects in Argentina, and

projects in developed countries: Railtrack’s collapse in the UK, California’s power crisis and the demise of

Enron (Schur, 2005, p. 4; Wells and Gleason, 1995, p. 46).

13

foreign investors in the electricity sector, published in 2003, revealed that 52% of them

were either less interested in, or retreating from, projects in developing countries, while

only 6% responded that they were more interested (Lamech and Saeed, 2003). There has

also been an increase in popular discontent throughout developing world with the private

provision of infrastructure services, including violent incidents and street riots in some

cases (Kikeri and Kolo, 2005, p. 22-24).

Secondly, big infrastructure privatizations in Latin America and Central and Eastern

Europe came to an end. There was not much more to sell to fuel further increases in

investment and significant new countries did not join the club of “privatizers”. Most

notably, Brazil’s privatization programme, the biggest in the world, was largely

completed by 1998, which was a peak year in Brazil (UNCTAD, 2005, p.12). In 1998

Brazil privatized its largest telecommunications company, the Telebras, and several

power distribution firms. These transactions accounted for 46% of developing country

private infrastructure investment in that year, and prevented it from a deeper decline.

After 1998, Brazil’s share fell, but was still significant (20%). Overall, between 1997 and

2001, privatization-related investment declined by 80%, while those related to expansion

by only 40% (World Bank, 2003, p. 13).

Thirdly, as regards other types of projects, that are not privatization-related projects,

opportunities also diminished. Much of investment prior to 1998 took place in more

developed middle-income countries. Opportunities, which remained thereafter tended to

be in more risky and politically sensitive countries and sectors, such as roads and water

(Schur, 2005, p. 2).

Fourthly, one should not forget an economic downturn of 2001-2003 in developed

countries, which resulted in a drastic reduction of their outward FDI. TNCs, as all firms,

typically invest much less, including abroad, during recession than before or after it. As

they dominate investment in infrastructure in developing countries, as indicated above,

the downturn must also have affected this investment. As in 2004 and 2005 FDI started

rising again, so did private infrastructure investment in developing countries.

How to assess the rise and decline in private infrastructure investment? Is it a demise

after the initial euphoria of the 1990s or was it mostly caused by cyclical factors? Initially

the fall caused concern. Infrastructure needs of developing countries have continued to be

vast (box 1) and the problems many projects encountered and withdrawal or more

cautious attitudes of many large investors were indeed often interpreted as a demise.

Investors did not properly assess risks and many developing country governments did not

really understand what meant to hand over the provision of infrastructure services to the

market or, even worse, to a private monopoly. Privatization was portrayed in

oversimplified terms, oversold and consequently raised unrealistic expectations.

Disappointment was great, when delivery did not meet promises (Kessides, 2005). In

2000, FIAS published a study under a symptomatic title: why is it so difficult to attract

FDI into infrastructure? Earlier, when private investment in infrastructure started

booming Louis Wells published an article warning foreign investors about many risks

associated with this investment, saying “the theory starts with a simple principle: most

14

countries would strongly prefer local ownership to foreign ownership” (Wells and

Gleason, 1995, str. 47). This type of investment is considered very risky, prone to

“obsolescence bargaining” and from time to time such and other concerns are expressed

in the literature (see for example, Ramamurti and Doh, 2004).

Box 1. Infrastructure needs of developing countries

It is easier to say that infrastructure needs of developing countries are vast than to put realistic investment

figures on these needs. Everybody agrees that infrastructure financing needs in developing countries are

considerable or vast, “but no one really knows how much is needed” (Estache, 2004, p. 6). Yet estimating

investment needs, even very broadly, is important for this study, given many question marks and doubts

surrounding the experience with the private participation, including foreign participation, in the provision

of infrastructure services. If needs exceed the financing capacity of the public sector, they will remain

unsatisfied or the private sector has to continue investing in infrastructure. If private investors in

developing countries will not be able to finance the balance (as has been the case so far in many developing

countries), foreign investors would have to continue investing in infrastructure to fill the gap.

Economics is about satisfying unlimited people’s needs with scarce resources. So when we talk about

infrastructure needs, we have to make assumptions, what needs do we have in mind. (We would also have

to decide whether these needs will be satisfied through the market mechanism or otherwise).

Needs for water and sanitation have been estimated within the Millennium Development Goals (MDG),

considering access to safe water a fundamental human need and a basic human right (UNDP, 2006, p. 78).

At present, some one billion people in the world do not have access to clean water and 2.6 billion do not

have access to proper sanitation. Nearly 2 million children die every year of illnesses related to unclean

water and poor sanitation. MDG has thus set a modest goal of ensuring, by 2015, access to water for 900

million people and to sanitation for 1.3 billion (ibid., p. 55). Satisfying these needs with basic technologies

available today would require $10 billion of additional financing annually. (Current spending on water and

sanitation in developing countries is estimated at $14-16 billion annually without waste-water treatment).

“Providing a higher level of service while maintaining provision at current levels to people who are already

supplied would add another $15-20 billion a year. Much larger sums would be involved if the target

included costs for collecting and treating household water” (ibid., p. 58).

These are relatively precise estimates. There are many “back of the envelope” estimates for different

sectors, but there is not yet credible assessment of global infrastructure needs from a single source.

International organizations (WHO, ITU, IEA) provide estimates of financing needs in their areas of

responsibility, but these estimates are typically questioned by specialists. For example, WHO estimates for

water, $50 per year (much higher than MDG goals for water and sanitation) have been criticized by the

academic community for unrealistic assumptions: access rates unadjusted for differences in quality

(Estache, 2004, p. 6).

But estimates are needed to inform national debates on resource allocations and both the World Bank and

the United Nations have been working on this, producing some overall preliminary estimates. A UN team

led by J. Sachs has produced infrastructure investment, operations and maintenance needs for Sub-Saharan

Africa. They amount to 12 cents per person, per day (or $44 a year) in the region where more than half of

the population lives on less than $1 per day (ibid.).

The World Bank has produced detailed estimates of infrastructure investment needs for developing

countries (by regions, sectors and income groups) for 2005-2010, based on the investment12

necessary to

satisfy consumer and producer demand based on predicted GDP growth (Fay and Yepes, 2003, p. 1). The

12

Investment includes resources for maintenance (the minimum expenditure needed to maintain the

integrity of infrastructure systems) and investment needed to satisfy new demand. The study covers most

infrastructure industries except for ports, airports and canals.

15

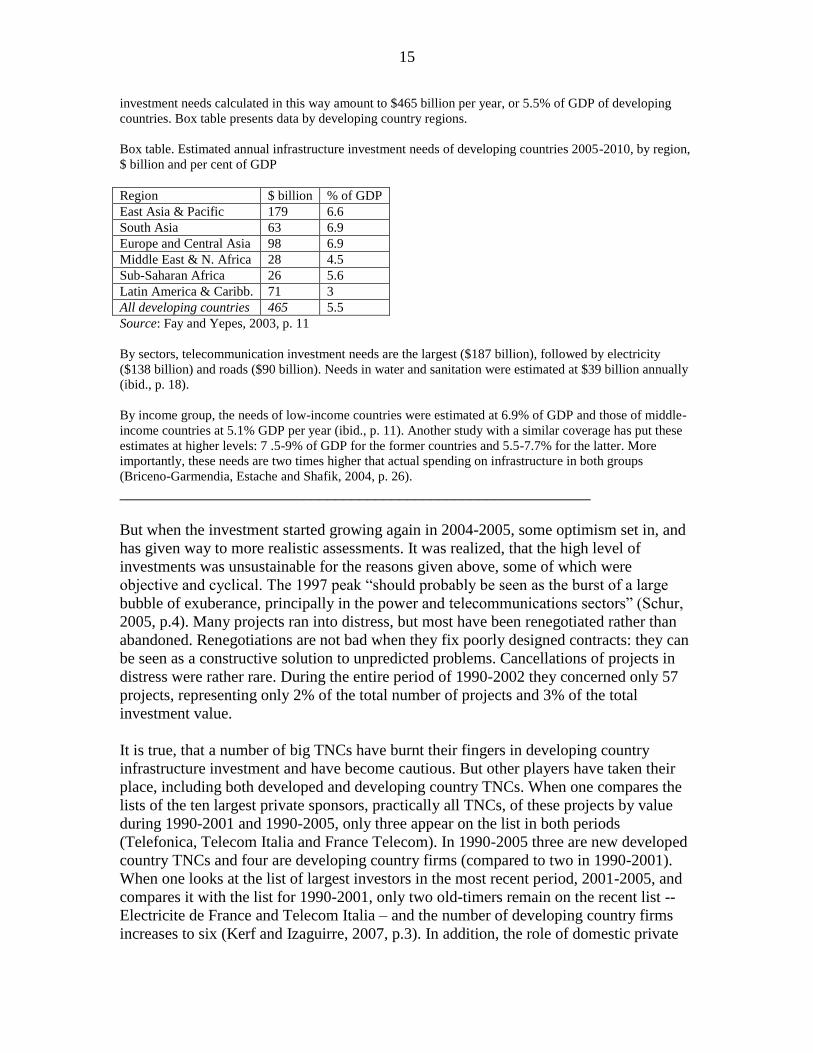

investment needs calculated in this way amount to $465 billion per year, or 5.5% of GDP of developing

countries. Box table presents data by developing country regions.

Box table. Estimated annual infrastructure investment needs of developing countries 2005-2010, by region,

$ billion and per cent of GDP

Region $ billion % of GDP

East Asia & Pacific 179 6.6

South Asia 63 6.9

Europe and Central Asia 98 6.9

Middle East & N. Africa 28 4.5

Sub-Saharan Africa 26 5.6

Latin America & Caribb. 71 3

All developing countries 465 5.5

Source: Fay and Yepes, 2003, p. 11

By sectors, telecommunication investment needs are the largest ($187 billion), followed by electricity

($138 billion) and roads ($90 billion). Needs in water and sanitation were estimated at $39 billion annually

(ibid., p. 18).

By income group, the needs of low-income countries were estimated at 6.9% of GDP and those of middle-

income countries at 5.1% GDP per year (ibid., p. 11). Another study with a similar coverage has put these

estimates at higher levels: 7 .5-9% of GDP for the former countries and 5.5-7.7% for the latter. More

importantly, these needs are two times higher that actual spending on infrastructure in both groups

(Briceno-Garmendia, Estache and Shafik, 2004, p. 26). ___________________________________________________________

But when the investment started growing again in 2004-2005, some optimism set in, and

has given way to more realistic assessments. It was realized, that the high level of

investments was unsustainable for the reasons given above, some of which were

objective and cyclical. The 1997 peak “should probably be seen as the burst of a large

bubble of exuberance, principally in the power and telecommunications sectors” (Schur,

2005, p.4). Many projects ran into distress, but most have been renegotiated rather than

abandoned. Renegotiations are not bad when they fix poorly designed contracts: they can

be seen as a constructive solution to unpredicted problems. Cancellations of projects in

distress were rather rare. During the entire period of 1990-2002 they concerned only 57

projects, representing only 2% of the total number of projects and 3% of the total

investment value.

It is true, that a number of big TNCs have burnt their fingers in developing country

infrastructure investment and have become cautious. But other players have taken their

place, including both developed and developing country TNCs. When one compares the

lists of the ten largest private sponsors, practically all TNCs, of these projects by value

during 1990-2001 and 1990-2005, only three appear on the list in both periods

(Telefonica, Telecom Italia and France Telecom). In 1990-2005 three are new developed

country TNCs and four are developing country firms (compared to two in 1990-2001).

When one looks at the list of largest investors in the most recent period, 2001-2005, and

compares it with the list for 1990-2001, only two old-timers remain on the recent list --

Electricite de France and Telecom Italia – and the number of developing country firms

increases to six (Kerf and Izaguirre, 2007, p.3). In addition, the role of domestic private

16

investors from developing countries, often former minority partners in projects with

TNCs, has also increased during 2001-2005 (Schur, von Klaudy and Dellacha, 2006, pp.

1-3).

But more importantly, both firms and governments have learnt from past mistakes and

recently designed and renegotiated contracts are more realistic than before. As mentioned

in the previous chapter, there is more emphasis on improved risk mitigation and more

realistic risk sharing between private and public partners. Private investors are no longer

ready to take excessive risks, in particular financing and payment risks. On the other hand

governments realize that it is very difficult to develop infrastructure expecting that user

charges will cover all the costs and increasingly recognize the need to complement

revenues with public funds. Hence the growing popularity of PPPs, discussed in the

previous chapter.

* * *

There were no exceptions from the decline after 1997 or 1998, as regards regions and

sectors (figures 2 and 3), but in some regions investment quickly recovered, while in

others it remained at much lower levels than in the peak years of the boom.

Latin America and East Asia, which accounted for most of the boom and the highest

shares in the first half of the 1990s, experienced most of the decline. In Sub-Saharan

Africa and Europe and Central Asia the decline was relatively modest and investment

levels quickly recovered: in the former region in 2001 and in the latter in 2000,

fluctuating, however in the following years. By 2005 the value of private investment

commitments in Sub-Saharan Africa was two times higher ($6 billion) and in Europe and

Central Asia 2.4 times higher than in 1997. Private investment recovered also

significantly in South Asia (2.2 times higher) and to a much smaller degree in West Asia

and North Africa (by 40%). In 2005, in LAC countries and East Asia it was at much

lower levels than in peak years of the boom, respectively, at 37% and 28%. Consequently

the latest regional picture differs from that of the 1990s. In 2004-2005, the largest

investment took place in the transition economies ($50 billion), followed by LAC ($38

billion) and East Asia ($27 billion), with other regions not that far behind as during the

first half of the 1990s: South Asia ($25 billion), West Asia and North Africa ($15) and

Sub-Saharan Africa ($10 billion).

The decline affected also all sectors, including both telecommunications and electricity,

which experienced initially the fastest growth and accounted for the dominant share of

this investment. Decreases were largest in water and electricity and much smaller in the

other two sectors. By 2005, investment recovered only in telecommunications, compared

to a peak year ($60 billion vs. $ 51 billion) and nearly recovered in transportation ($16

billion compared to $18 billion). In electricity it amounted to $17 billion, or 38% of the

1997 level and in water to $1.6 billion, or only 15% of investments in 1997 (figure 3).

17

Figure 2. Private investment in infrastructure by region, 1990-2005, $ mln

0

10000

20000

30000

40000

50000

60000

70000

80000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

East Asia&P.

South Asia

West Asia & NA

S-S Africa

LA & Car.

Europe&CA

Figure 3. Private investment in infrastructure in developing countries,

by sector, $ mln, 1990-2005

0

10000

20000

30000

40000

50000

60000

70000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Energy

Telecom

Transport

Water

What follows is an overview of trends during 1990-2005 from three different angles:

developing country regions, sectors and forms of investment.

2. Regions

18

Among developing regions Latin America received by far the largest amounts of

investment in infrastructure during 1990-2005: 42% of the developing country total.

Telecommunications was by far the largest sector, followed by electricity. This pattern is

characteristic for all regions. But Latin America received also significant investments in

transportation and water and sewage in distinction from other regions, where private

investments in these two sectors were low or non-existent. Privatizations and concessions

of the existing assets were the dominant form of investment, accounting for three quarters

of it during 1990-2001. In most countries of the region, opening to private investment has

been part of broader sectoral reforms, including the introduction of competition, the

establishment of regulatory agencies and tariff adjustments aimed at generating resources

to improve the coverage and quality of services. As Latin America was the first region to

allow private investment and implement reforms, initially (during 1990-1992), it

accounted for almost three quarters of developing country total. When the sales of large

SOEs were completed and other countries allowed private investment, the share of Latin

America fell to one quarter in 2003-2005.

East Asia turned to private investment mainly because of the strain on its infrastructure

caused by the rapid economic growth. Therefore letting private investment in the

countries of the region was not, in distinction from Latin America, part of broader

reforms, but rather a measure to increase the supply of services, by complementing public

sector investment. Still, the sub-region received enough investment to be behind Latin

America as a second most important destination of this investment, accounting for 23%

of it during 1990-2005. Privatizations were rather rare, and greenfield projects attracted

over 60% of this investment (during 1990-2001). The share of East Asian countries

increased from 23% in 1990-1992 to 34% in 1996-1997 and fell as a result of the 1997

financial crisis to 10% in 1998, to recover to 23% in 2003-2005. In distinction from all

other regions, where telecommunications was the leading sector, energy attracted the

largest amounts of investment in East Asia. Similarly to Latin America, East Asia also

attracted sizeable investments to transport and water sectors.

In both regions investments never recovered from the fall after the record levels attained

in 1997-1998. In East Asia they were in 2005 only at 39% of the 1997 level and in Latin

America at 28% of the 1998 level. In other regions and sub-regions investments also fell

after 1997, but they recovered: in South Asia and West Asia and North Africa by 2003

and in Sub-Saharan Africa and CEE and Central Asia by 2000-2001. Consequently in

2003-2005 annual flows of investment were more evenly distributed among developing

country regions than in the early 1990s.

CEE and Central Asia was the third region by the size of investment with a share of

19% during 1990-2005. In most countries of the European sub-region, as in Latin

America, private investment was part of broader reforms aimed at reducing the role of the

state and putting infrastructure operations on a more commercial footing. Countries,

which became members of the European Union in 2004, had to comply with the

accession requirements. Privatizations and concessions of existing assets accounted for

55% of investments in the entire region. Apart from telecom (the largest investment

19

sector) and energy, the region received also fair amounts of investments in transport and

water.

Investments in, and shares of, other sub-regions were much smaller than in the above

regions. The shares for the entire period of 1990-2005 were 7% for South Asia, 5% for

Sub-Saharan Africa and 4% for West Asia and North Africa. South Asia and West

Asia and North Africa followed a similar approach to that in East Asia: they invited

private investment to an un-reformed infrastructure system. Thus, SOEs remained largely

in place, and private investment took mainly the form of greenfield investment, which

accounted for 90% of the total in the former region and 50% in the latter. In both regions

telecommunications was the largest sector for private investment, followed by electricity.

In South Asia there was no private investment in water and sewage and in West Asia and

North Africa it began to take place on a visible scale only in 2004-2005.

In Sub-Saharan Africa telecommunications dominated investment to a greater extent than

in other regions, accounting for 70% of the total during 1990-2005. Telecom investment

took both the form of privatizations and greenfield investment in mobile telephony. There

was also some investment in energy and transport and no investment in water and

sewage.

Although, as mentioned earlier, private participation in infrastructure has spread to

almost all developing and transition economies, as with other types of investment, and

notably with FDI, 10 countries have dominated private infrastructure investment. They

were three large Latin American countries (Brazil, Mexico and Argentina leading the list

by the value of projects) and the balance Asian economies: China, Malaysia, the Republic

of Korea, the Philippines, Indonesia, India and Thailand, in that order. Top ten accounted

during 1990-2001 for 47% of the projects and 68% of the value of investment (World

Bank, 2003, p. 20). By 2005 the Republic of Korea and Thailand were replaced on the list

by the value of investment by the Russian Federation and Turkey. China advanced to the

third position before Mexico (World Bank PPI data base). The share of top ten in the

number of projects increased to 60% but decreased by value to 64%.

But when this investment is related to the size of the population or the economy a

different ranking emerges for 1990-2001. Hungary, Panama, Chile, Estonia and Belize

lead the list of top ten, based on the value of investment per head of population, while

Bolivia, Panama, the Lao People’s Democratic Republic and Cape Verde are top

countries as regards the share of private infrastructure investment in GDP. Argentina and

Malaysia are on the three lists (ibid., pp. 20-21).

2. Sectors

Telecommunications was by far the largest sector for private investment in developing

countries, accounting for nearly half of the total during 1990-2005. It was also the only

sector where investment levels in 2005 exceeded the levels attained in the peak year of

20

1998, while in three other sectors, and particularly in energy and water, they remained

after 1997 at much lower annual levels than in the peak year. In all developing regions

investment was driven by greenfield investment in the mobile telephony. In Latin

America and CEE, in addition, it has also been fuelled by privatizations of state-owned

operators of fixed-line services. Technological changes in the sector have stimulated

private investment by reducing the costs of entry and spurring competition by rapid

advances of the mobile telephony: both led to major changes in the market structure.

During the entire period (1990-2005) 41% of this investment went to Latin America, 27%

to CEE and Central Asia and 14% to East Asia.

Energy, including in the World Bank PPI data base electricity and the transmission and

distribution of natural gas, attracted during 1990-2005 31% of the total investment, with

most of this share accounted for by electricity. Private investment in electricity was

facilitated by new technologies, which reduced the minimum size of efficient power

plants. Half of electricity investments took place during 1993-1998, fuelled by the boom

in greenfield projects in Asia, based on BOO and BOT contracts, and by privatizations in

Latin America and CEE. The share of electricity in total investment fell from 41% in the

1997 peak year to 18% in 2005 on the account of falling investment levels. During the

entire period (1990-2005) 41% of this investment went to Latin America, 29% to East

Asia and 13% to CEE and Central Asia.

In transport and water and sewage private investment was much smaller than in two

other sectors. There has not been much technological change in these sectors, political

and popular opposition to reforms has been much stronger than in other sectors and sub-

national governments have often played major roles. Investments in transport, which

accounted for 15% of the total during 1990-2005, focused on toll roads, which have also

received much of the public investment. In countries which decided to go for private

investment, this investment took both the form of transferring the existing assets through

concessions and building toll roads through greenfield projects. In water, almost all

private investments occurred in East Asia, Latin America and CEE and Central Asia and

took the form of concessioning of existing utilities to private investors. There was also

some small investment activity in expanding new capacity for water treatment, based on

BOO and BOT contracts. During the entire period (1990-2005) 47% of transport

investment went to Latin America, 36% to East Asia and 10% to CEE and Central Asia.

In the case of water investment the shares of these regions were much higher because of

very small or no investment in water in other regions. East Asia took the lead with 47%

share, Latin America was second (41%), followed by CEE and Central Asia (8%).

3. Forms

Greenfield projects were the most common form of private investment in infrastructure

in developing countries, accounting for the value share of 47% during the period of 1990-

2005 (figure 4). They reached the peak of $40 billion in 1997, fell, recovered in 2001 and

increased to $53 billion in 2005. This investment was driven mainly by projects in

electricity and mobile telecommunications and among regions by projects on East Asia,

which accounted for 31% of the total.

21

Privatizations followed, accounting for the share only slightly slower than that held by

greenfield projects, 39% (figure 4). Privatization-related investment took place mainly in

telecommunications and electricity in Latina America. After reaching a peak of $48

billion in 1998, investments fell (to a low of $15 billion in 2003) and never recovered,

amounting to $32 billion in 2005. As mentioned earlier, privatizations transactions of

developing countries in 1997-1998 were significantly increased by huge privatizations in

one country – Brazil. Leaving Brazil out, there would be no decrease after 1997-1998,

but rather annual fluctuations at quite elevated level.

In distinction from greenfield investment, the potential for investments related to

privatizations is limited by the pool of countries, which decided to engage in

privatizations in a given period and, within these countries, by the pool of state-owned

companies to be sold to private investors. Once major companies are sold, it is all natural

that potential for further investment is reduced. (But, of course, new private owners can

invest in expanding capacity, which is indeed the case in most privatized companies).

This is what has happened, when countries in Latin America and CEE completed major

privatizations in electricity and telecommunications. In addition, privatizations, which

take the form of sales of assets, do not take place in all infrastructure sectors. As regards

greenfield investments, given the vast number of developing countries and their

infrastructure needs far from being satisfied, the potential for new building projects is

virtually unlimited. So when these projects fall, it may be worrying, unless the gap is

filled by the public investment, which typically is not the case.

Figure 4. Forms of private investment in infrastructure in developing

countries, %, 1990-2005

39%

47%

14%0%

Privatizations

Greenfield

Concessions

Mngmnt. & leases

Concessions were used mainly in transport and water and sewerage and, to some extent,

in electricity. The leading regions, which have granted concessions have been Latin

America and East Asia. Concessions can be alternatives to privatizations of existing

assets. As mentioned above, greenfield projects can be turned into concessions after the

construction of a utility is completed. It seems that, the former dominated concessions,

which peaked in 1997, when large concessions in a number of countries were granted,

22

such as concessions for the electricity and water utility in Casablanca (Morocco), for the

water utility in Manila (Philippines) and for transport in Brazil (World Bank, 2003, p. 5).

Management and lease contracts were used in sectors, which were not reformed, and

countries wished only to improve management, without private investors assuming

investment risks. They were not too many, only around 100 during 1990-2001. Water and

sewerage sector had 41 projects and transportation 44. Among regions, CEE and Central

Asia granted 30 concessions and Sub-Saharan Africa 25.

C. The role of FDI

As was mentioned earlier, foreign investors were involved during 1990-2005 in over 83%

of private projects in infrastructure, measured by the number of projects or total

investment value, in developing and transition economies. “The primary engine behind

this rapid expansion [of private infrastructure investment] during the 1990s clearly has

been foreign direct investment” (FIAS, 2000, p. 8). Therefore, one can be confident, that

the preceding analysis, although dealing with all private projects, reflects quite correctly

FDI trends, although there are some differences related to the use of non-equity form in

some sectors and regions. The following overview of trends in FDI for 1990-1998 is

based on FIAS estimates.

The average 83% share of FDI in all private infrastructure investment in all developing

countries during 1990-1998 masks sectoral differences, but these differences are not big.

In all sectors and transport subsectors, except for two – roads and seaports – these shares

are higher than 86%, with the highest shares in airports (100%), water (98%) and

telecommunications (98%). Very high shares of FDI reflect the lack of not only capital

but also local expertise to undertake such projects. Where the local expertise existed, as

in road construction, governments tended to rely on domestic investors, often excluding

foreign participation. Therefore the share of FDI in roads was the lowest, 37%. In

seaports it was much higher, 62% (ibid., p. 9).

As with all projects, FDI related projects and associated FDI inflows grew very fast from

1990 to 1997, from $2 billion to $36 billion per year, and fell after the East Asian crisis to

$33 billion in 1998. Only Latin America escaped this contraction, owing to large FDI-

related privatizations in Brazil. Excluding Latin America, flows inflows dropped by

44%. Overall, private infrastructure projects attracted estimated $138 billion of FDI

inflows into developing and transition economies during 1990-1998, representing the

share of over 17% in total FDI inflows into these economies.

In terms of FDI inflows, telecommunications and electricity accounted for 95% of the

total. In terms of the number of transactions, however, transportation and water

represented 1/3rd

of all projects, reflecting differences in the size of projects among

sectors. As water and transportation projects are based mainly on concessions and BOT-

type of projects, while privatizations and greenfield investment dominate in electricity

and telecommunications, similar differences occurred, as regards forms of investment.

Thus privatizations (most popular in telecom and electricity) generated 2/3rd

of FDI

23

inflows, but accounted for only 22% of the total number of transactions. On the other

hand BOTs and concessions were responsible for 30% of inflows, while accounting for

three quarters of the number of transactions (ibid., p.12).

As with all projects, Latin America attracted the largest share of FDI inflows among

developing countries, 57%, with 85% of these inflows generated by prvatizations. But by

the number of FDI-related projects, the composition was more balanced: ¼ were

privatizations, 42% concessions and 30% greenfield investments. East and South Asia

received each $18-19 billion of infrastructure-related FDI inflows during 1990-1998.

Almost all of these inflows came through BOT-type contracts. CEE and Central Asia as

well as Sub-Saharan Africa attracted FDI inflows mainly to privatizations.

D. TNC players and home countries

The top ten TNCs involved in infrastructure projects (that is in projects in which they

hold at least 15% of equity, and ranked by the total value of these projects) in developing

and transition economies accounted for 12% of the projects during 1999-2001 but for

nearly 30% of the investment value. Five TNCs originate from the European Union and

only two from the United States. Five of them, in line with the dominant role of the

sector, were telecommunication TNCs, three TNCs in electricity, one TNC in the water

industry and one a multisector TNC (table 1). The investment of three of them

(Telefonica, Carso Global Telecom and Andrade Gutierrez) was located entirely in Latin

America. Telecom Italia also “specialized” in Latin America, with some projects in the

CEE, while Deutsche Telekom in the CEE, with some projects in East Asia. The

investment of remaining top ten was spread among a couple of regions, but only three

TNCs had a presence in all regions (AES Corporation, Enron Corporation and SUEZ).

Home country data, that is data concerning all TNCs, estimated by FIAS for the period

1990-1998 (FIAS, 2000, pp. 14-15), when most of the considered investment took place,

reveal a picture in some respects similar and in others different from that, based on the

top ten TNCs. The United States, which has only two TNCs on the list of top ten is by far

the largest home country, accounting for 30% of the total of home countries responsible

for infrastructure-related FDI flows. Spain is next with the share of 15%, followed by

Germany and France (7% each), Italy (7%) and the UK (2.5%). TNCs from developing

countries account for 8% of infrastructure FDI in other developing countries.

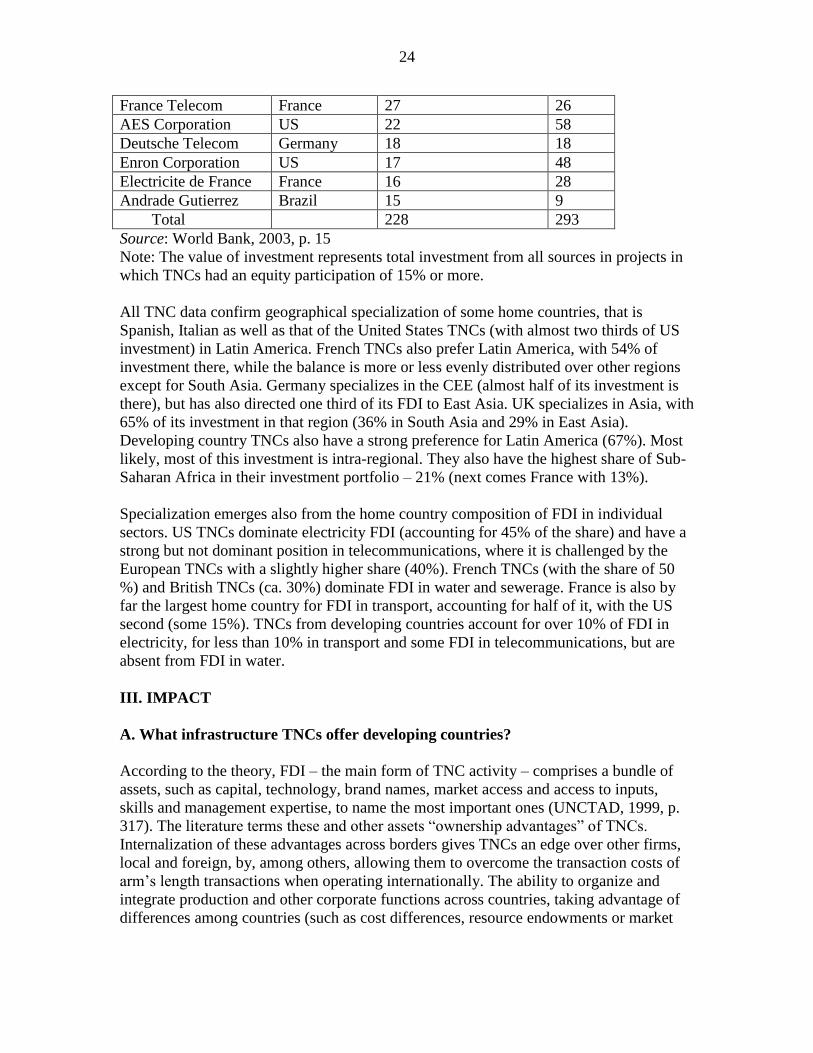

Table 1. The top 10 TNCs in private infrastructure projects in developing countries,

1990-2001 (ranked by total value of investments in which they participated)

TNC Home country Total project investment

2001 $, billions

Number

of

projects

Telefonica Spain 35 12

Carso Global Telecom Mexico 35 5

SUEZ France 33 79

Telecom Italia Italy 31 16

24

France Telecom France 27 26

AES Corporation US 22 58

Deutsche Telecom Germany 18 18

Enron Corporation US 17 48

Electricite de France France 16 28

Andrade Gutierrez Brazil 15 9

Total 228 293

Source: World Bank, 2003, p. 15

Note: The value of investment represents total investment from all sources in projects in

which TNCs had an equity participation of 15% or more.

All TNC data confirm geographical specialization of some home countries, that is

Spanish, Italian as well as that of the United States TNCs (with almost two thirds of US

investment) in Latin America. French TNCs also prefer Latin America, with 54% of

investment there, while the balance is more or less evenly distributed over other regions

except for South Asia. Germany specializes in the CEE (almost half of its investment is

there), but has also directed one third of its FDI to East Asia. UK specializes in Asia, with

65% of its investment in that region (36% in South Asia and 29% in East Asia).

Developing country TNCs also have a strong preference for Latin America (67%). Most

likely, most of this investment is intra-regional. They also have the highest share of Sub-

Saharan Africa in their investment portfolio – 21% (next comes France with 13%).

Specialization emerges also from the home country composition of FDI in individual

sectors. US TNCs dominate electricity FDI (accounting for 45% of the share) and have a

strong but not dominant position in telecommunications, where it is challenged by the

European TNCs with a slightly higher share (40%). French TNCs (with the share of 50

%) and British TNCs (ca. 30%) dominate FDI in water and sewerage. France is also by

far the largest home country for FDI in transport, accounting for half of it, with the US

second (some 15%). TNCs from developing countries account for over 10% of FDI in

electricity, for less than 10% in transport and some FDI in telecommunications, but are

absent from FDI in water.

III. IMPACT

A. What infrastructure TNCs offer developing countries?

According to the theory, FDI – the main form of TNC activity – comprises a bundle of

assets, such as capital, technology, brand names, market access and access to inputs,

skills and management expertise, to name the most important ones (UNCTAD, 1999, p.

317). The literature terms these and other assets “ownership advantages” of TNCs.

Internalization of these advantages across borders gives TNCs an edge over other firms,

local and foreign, by, among others, allowing them to overcome the transaction costs of

arm’s length transactions when operating internationally. The ability to organize and

integrate production and other corporate functions across countries, taking advantage of

differences among countries (such as cost differences, resource endowments or market

25

size and growth) is, itself, a source of additional advantages, termed the advantages of

“multinationality”.

Some of TNC assets are proprietary assets and others are not. Proprietary assets can be

obtained only from firms that create them. Of these assets, the most prized is probably

technology. Proprietary assets can be, theoretically, copied or reproduced by others, if

they have the ability to do so. But the costs can be very high, particularly in developing

countries and where advanced technologies are involved. In addition, TNCs are reluctant

to sell their most valuable assets to unrelated firms that can become competitors or could

leak them to others who have not paid for them. Non-proprietary assets – finance, capital

goods, intermediate inputs and the like – can be obtained from the market, at least in part.

But TNCs can have and, in fact often do have, privileged access to markets for non-

proprietary assets: the may be able to raise capital, or purchase equipment, on better

terms than smaller firms or firms from developing countries. Taken together, these

advantages mean that TNCs can contribute significantly to host developing countries – if

the host country can induce them to transfer these advantages in appropriate forms and

has the capacity to make good use of them.

How does this theory work in infrastructure industries? It does, but given different nature

and economics of infrastructure industries, there are significant differences compared to

other industries, e.g., manufacturing industries.

First, all infrastructure services are not tradable across borders.13

Therefore access to

international markets and contribution to exports, valued very much in manufacturing, do

not matter as a contribution in infrastructure. In addition, this creates dangers when

countries move to the private provision of services. Infrastructure services are natural

monopolies, or at least in part natural monopolies. There is no alternative of competitive

pressure from the imports of services. If privatization transfers natural monopoly from

public to private hands, this also transfers monopoly profits to private firms14

and

deprives the country of many (though not all – the supply and quality of services may still

improve) expected benefits of private provision. Transfer of monopoly to domestic or

foreign firms is, economically, equally damaging. But if private hands are foreign hands,

the backlash is typically stronger than in the case of domestic, public or private,

companies and does not augur well for future privatizations.

Second, infrastructure industries are not, with the exception of telecommunications, high-

tech industries and hard technology is not a strong ownership advantage of TNCs. But

even in telecommunications, technology is not a proprietary asset and can be purchased

in open markets. Leading TNCs, such as Deutsche Telecom, or France Telecom, do

produce technologies, they install in fixed-line or mobile networks. It is rather the ability

13

There are some cases of cross-border trade in electricity and water among neighboring countries (e.g.,

USA-Canada in electricity or Lesotho’s export of water to South Africa), but they are so limited that trade

is practically not a delivery option for infrastructure services. 14

In practice, in many cases, this transfer is illusory, as many SOEs did not make profits before they were

privatized. Even in cases where they were relatively well managed, they operated in systems, where prices

were subsidized, so even if they showed profits, it is difficult to say if they would be able to cover costs in

competitive markets.

26

to know how to use technologies (to, for example, combine the provision of telephony,

internet and media in one service package), marketing know-how and the knowledge of

markets (what will consumers accept) and managerial expertise (including how to assess

risks in private infrastructure markets) which constitute a competitive edge of TNCs. In

the initial phase of privatization, competitive advantages of TNCs vis-à-vis many

developing country public providers were contextual. Both developing and transition

economies did not have firms and investors with the knowledge, how to operate a private

infrastructure entity. So during the transition to market-based delivery, most of these

countries did not have an alternative to turning to TNCs. But with time TNCs may lose

and in fact are losing this advantage, as domestic firms, often minority partners in TNC-

led projects, acquire such knowledge. Witness an increasing role of domestic firms in

infrastructure investment, mentioned earlier.

Third, many projects (though not all) in infrastructure are very large and are characterized

by large economies of scale. They require huge initial capital outlays, while the stream of

revenues to cover the cost of, and return on, capital spreads over many years. Therefore

risks are typically much higher than in, for example, manufacturing projects. There are

also many additional risks that are lower or not existing in other industries, such as

political risks (related to, for example obsolescence bargaining) or regulatory risks. Even

if countries decide to introduce as much competition as possible, in industries relying on

fixed-networks (such as fixed telecommunication lines, electricity distribution or water

pipes), elements of natural monopoly will always remain. They should be managed by a

national regulatory agency, which will determine conditions of access and set prices,

thus, de facto, determining the stream of revenues. For these reasons, although capital

typically is not a proprietary asset of TNCs, in infrastructure projects it practically is.