The political economy of prices in China's planned and market economies: competition and control in...

28

Asian Studies Review. ISSN 1035-7823 Volume 24 Number 3 September 2000 © Asian Studies Association of Australia 2000. Published by Blackwell Publishers, 108 Cowley Road, Oxford OX4 1JF, UK and 350 Main Street, Malden, MA 02148, USA. THE POLITICAL ECONOMY OF PRICES IN CHINA’S PLANNED AND MARKET ECONOMIES: COMPETITION AND CONTROL IN THE COAL INDUSTRY TIM WRIGHT 1 Murdoch University The gradual transformation of the Chinese economy from a planned system to one dominated by market forces is reshaping the political economy of China and the Asia-Pacific region. New groups—notably the burgeoning local corporate and private sectors—are emerging as important players, while some of the old power bases such as the heavy industry bureaucracies are in decline (White 1993, 126–28; Findlay and Jiang 1992). Important manifestations of these changes have been the substantial shifts in relative prices over the past twenty years and the major political struggles sur- rounding them. Up to the early 1990s changes in prices were propelled largely by government policies of price reform, which aimed to make prices more closely reflect changing supply and demand. The threat posed by these changes to the interests of powerful groups in society made price reform difficult to implement. Nevertheless, by the mid-1990s most prices came to be determined by the market. This has not ended the contention over relative prices—rather, different interest groups continue to struggle for position and call on the government for support. This paper examines the political and economic issues that have surrounded the attempts to adjust, regulate or deregulate the price of coal, and analyses the interests involved. Coal was substantially underpriced under the planned economy, so its price was a particular focus of contention. Its undervaluation led to serious inefficiencies in resource distribution and technology, and to large deficits for state-owned-enterprise (SOE) coal mines. Coal users, both enterprises and house- holds, however, became accustomed to cheap coal. As the World Bank wrote in 1985: The most obviously distorted of all China’s producer prices are the state- set prices of energy and some raw materials—far below opportunity costs

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of The political economy of prices in China's planned and market economies: competition and control in...

Asian Studies Review. ISSN 1035-7823Volume 24 Number 3 September 2000

© Asian Studies Association of Australia 2000. Published by Blackwell Publishers, 108 Cowley Road,Oxford OX4 1JF, UK and 350 Main Street, Malden, MA 02148, USA.

THE POLITICAL ECONOMY OF PRICES IN CHINA’S PLANNED AND MARKETECONOMIES: COMPETITION AND

CONTROL IN THE COAL INDUSTRY

TIM WRIGHT1

Murdoch University

The gradual transformation of the Chinese economy from a planned system toone dominated by market forces is reshaping the political economy of China andthe Asia-Pacific region. New groups—notably the burgeoning local corporateand private sectors—are emerging as important players, while some of the oldpower bases such as the heavy industry bureaucracies are in decline (White 1993,126–28; Findlay and Jiang 1992).

Important manifestations of these changes have been the substantial shifts inrelative prices over the past twenty years and the major political struggles sur-rounding them. Up to the early 1990s changes in prices were propelled largely bygovernment policies of price reform, which aimed to make prices more closelyreflect changing supply and demand. The threat posed by these changes to theinterests of powerful groups in society made price reform difficult to implement.Nevertheless, by the mid-1990s most prices came to be determined by the market.This has not ended the contention over relative prices—rather, different interestgroups continue to struggle for position and call on the government for support.

This paper examines the political and economic issues that have surroundedthe attempts to adjust, regulate or deregulate the price of coal, and analyses theinterests involved. Coal was substantially underpriced under the planned economy,so its price was a particular focus of contention. Its undervaluation led to seriousinefficiencies in resource distribution and technology, and to large deficits forstate-owned-enterprise (SOE) coal mines. Coal users, both enterprises and house-holds, however, became accustomed to cheap coal. As the World Bank wrote in1985:

The most obviously distorted of all China’s producer prices are the state-set prices of energy and some raw materials—far below opportunity costs

in domestic and world markets. But the sheer magnitude of thesedistortions makes them hard to correct: to introduce the required priceadjustments at one stroke would involve dramatic changes in the financialcircumstances of many enterprises and institutions (World Bank 1985,175).

As a result, a large proportion of coal continued to circulate at a fixed price rightinto the 1990s. From 1993–94, the government basically decontrolled the priceof coal, but this did not solve the problems of the SOE mines, which now facedlow prices because of excess supply, and therefore looked for other ways to main-tain or improve their relative price position.

Price reform, both in the coal industry and more broadly, has not been atechnical matter but rather has inherently involved a political struggle betweencompeting interests. As Susan Shirk wrote,

A transformation of the economic structure involves redistributingauthority and rewards among sectors, bureaucratic agencies and regions. . . The groups who were favored and protected by the old commandeconomy and who feel threatened by changes in the economic systemresist the reforms or fight to retain as much of their original privileges asthey can (Shirk 1992, 59).

It is not easy to document this contention because the Chinese political systemhas tended to delegitimate the expression of sectional interests (Pye 1981, 118;Pye 1995, 45). Although at inner Party gatherings or work conferences officialsare more or less able to speak on behalf of the industry (although less so of thegeographical area) that they represent (Shirk 1993, 98–99), it is still difficult forthem to express such opinions in the public arena. Nevertheless, Vice-PremierTian Jiyun recognised in 1986: “The overall reform of the economic structure is,in a sense, a readjustment of power and interest, in which a large amount of con-tradictions exist” (cited in Shirk 1992, 59). Government organs at all levels, aswell as state and private coal producers, the mining labour force and coal users,have all had an interest in coal prices.

The first section of this paper summarises the process of price reform ingeneral, while the second outlines the development of the coal industry underthe planned economy. The next two sections analyse the dual track price systemof the 1980s and the interests it created and favoured. Three further sectionsdo the same for the deregulated system of the late 1990s. A conclusion askswhat lessons can be drawn for understanding the process of economic changein China.

350 Tim Wright

© Asian Studies Association of Australia 2000.

PRICE REFORM

Price reform has been a key thrust of post-Mao reform (Guo 1992). Two aimshave been paramount. The first has been to adjust resource allocation betweensectors. Broadly, there were three sectors where prices under the planned economyfell furthest behind what would be dictated by supply and demand: agriculturalprocurement prices—the prices paid by the monopsonist state to the farm sectorfor agricultural products; urban food prices—the prices charged by themonopolist state to urban workers for basic foods; and raw materials and energyprices in the industrial sector (Xue 1981, 143–44; Watson and Findlay 1999, 6–7).

Excessively low prices caused a number of problems. The low agriculturalprocurement prices policy, on which low urban food prices were predicated, wasa major factor in China’s poor agricultural performance. In industry, low energyand materials prices acted as disincentives to increase production of those com-modities or to economise on their use. Low administered prices posed particu-larly severe problems for extractive industries, where diminishing returns tend tomean that costs rise over time (Hu 1991, 151), and the state budget had to sub-sidise increasing deficits of loss-making enterprises in the materials sectors.

Addressing these problems has not been merely a matter of technical adjust-ment. The urban population as a whole was a major beneficiary of the cheap foodsupply (Findlay and Jiang 1992, 25–28; Watson and Findlay 1999, 7), and fear ofworker disturbances on the Polish model were an ever-present constraint onincreases in retail food prices (Nolan 1990, 25). In the late 1970s, agriculturalprices were raised in order to increase production and raise rural morale, butfrom 1984 movements in prices were less favourable to the rural sector. Later,attempts to deregulate grain prices in the early 1990s caused unrest among theurban population (Watson and Findlay 1999, 31–32).

In the case of industrial materials, the user industries formed a powerful lobbyopposing price reform (Shirk 1993, 264–65). Their cost structure and technologywere dependent on cheap materials, and they resisted the imposition of marketprices for their inputs. Expressions such as “coal is the food of industry” wereused to emphasise how price rises might affect the whole economy. Any rapidadjustment was therefore difficult (Xue 1981, 153).

The second and related aim of price reform was to encourage efficient resourceallocation at the micro level, by providing management with “rational” pricesignals on which to base decisions. Because of the old system of low materialsprices, but high prices for consumer goods, a manufacturer of, for example, tele-vision sets could hardly fail to be highly profitable, regardless of efficiency, whilean iron ore mine was more or less doomed to loss making (Shirk 1985, 200).There was therefore little incentive in either case to improve efficiency or formaterials producers to increase output.

The Political Economy of Prices in China’s Planned and Market Economies 351

© Asian Studies Association of Australia 2000.

In order to address these problems, during the early 1980s the governmentremoved price controls for some commodities and allowed the market to deter-mine prices. However, for many important products it first attempted a halfwayhouse of a dual price system, whereby commodities circulated at state priceswithin the plan and at market prices for output produced outside the plan, withoften one or more negotiated prices in between.

This system emerged on a de facto basis from the late 1970s, with a semi-legalblack market operating alongside the planning system. In 1984, the Ten StateCouncil Regulations for Industry explicitly allowed “prices of goods producedoutside the state quota system to be manipulated within a range of 20 percentabove or below state prices” (Zhongguo jingji nianjian 1985, X21). Such a differ-ential was insufficient to bring supply and demand for various commodities intobalance and, from early the following year, enterprises were allowed to tradeabove-quota output at free market prices (Zhang 1992a, 271).

Price reform and dual-track prices continued to be highly contentious through-out the 1980s and 1990s. Despite the efficiency factors favouring more realisticprices, powerful interests stood in the way of rapid or easy reform. Bureaucraticorgans had an entrenched interest in the old system of administrative direction,rather than one where enterprises responded autonomously to market signals(Findlay and Jiang 1992, 31–32), and they could point to the real problems gen-erated by overheating of the economy and consequent inflation. Inflationaryoutbreaks in 1985, 1989 and 1994 caused unrest among the urban populationand slowed the process of reform (Findlay and Jiang 1992, 27; Watson and Findlay1999, 31). More conservative elements engineered recessions to put an end tothe first two such outbreaks (Fewsmith 1994, 185–94, 225–30).

On the other hand, the dual-track system was very exposed politically toaccusations both among the people and from the World Bank that it was the“economic basis” of corruption (Zhang 1992b, 93, 99). The popular movementagainst corruption in 1989 seriously eroded the legitimacy of the dual price sys-tem across the political spectrum (Kwong 1997, 126, 139).

From the early 1990s, the government began to reunify the price system andderegulate most prices. In addition to the more favourable political environ-ment, inflation during the 1990–91 slow-down was low, making it more difficultfor opponents to criticise reform on those grounds. So, as early as May 1991, thegovernment raised the prices of basic foods to levels closer to their cost, moving,although only temporarily, to a more or less free market in 1993 (Guo 1999, 55;Watson and Findlay 1999, 13–16). In the first three years of the 1990s, basicmaterials such as cement, oil and coal were successively targeted in order to estab-lish “a level playing field” (Li 1991).

Nevertheless, the conflicts of interest surrounding price reform did not dis-appear. Local governments, facing pressure from local consumers or producers,

352 Tim Wright

© Asian Studies Association of Australia 2000.

set prices for a variety of consumer goods and food, and the central governmentmoved to reimpose a level of control over grain (Watson and Findlay 1999,31–33). Even the reformer Zhu Rongji said that decontrol of grain prices did notmean the end of government intervention, and called on local governments tostrengthen management of the grain market (China Central Television 1994).

These countervailing tendencies have not reversed the general trend towardsan expansion of the role of free market prices and a contraction of that of plan-ning. An OECD study states that “price reform in China will remain an exampleof successful transition from a planned economy to a market economy. Priceliberalisation . . . was virtually complete in 1993” (Laffont 1997, 17). Retail salesat state-controlled prices fell from 97 per cent in 1978 to under 30 per cent in1990 and only 6 per cent in 1998; those at market prices rose from 3 to 53 and 93per cent (Nolan 1994, 9; CD 28 September 1998). Low and declining prices in1999 provided an auspicious environment to push further with price reform ofsome key commodities such as cotton, chemical fertilisers, electricity, telecom-munications and water (Xinhua 1999).

COAL MINING DURING THE MAO ERA

Under Mao, the coal mining industry was a pillar of the planned economy.Although the degree of control varied over time, the major mines were coordin-ated by the Ministry of Coal or similar bodies (Lieberthal and Oksenberg 1988,89–94). Coal mining was an integral part of the heavy industry bureaucracy, whichconstituted a powerful pressure group protecting the interests of its constituentindustries (Shirk 1989, 344).

Although price was not a major tool of resource allocation, and most coal wasdistributed directly through the planning institutions, the low price of coal was still an issue. Under Mao, that price was low in comparison with both pre-warrelative prices and world prices. Low prices affected profits and by 1957 half ofChina’s coal mines were operating at a loss. Chinese economists realised that thisdepressed production and argued, when they could, for higher prices in order tostimulate output (Donnithorne 1967, 242, 285, 451–53). In addition, coal prices,like prices in general, made insufficient allowance for regional differences inproduction or transport costs or for differences in quality. This discouragedvalue-added processes like coal washing (Tian and Qiao 1991, 360).

In order to address some of these problems, there were a number of adjust-ments to the price of coal—a 20 per cent increase in 1958, a further 14 per cent(for lump coal) in 1962, and another 10 per cent in 1965. After that there was along period of stability until a 31.8 per cent price rise in 1979. While these adjust-ments eased the immediate problems of coal mines, over the longer term prices

The Political Economy of Prices in China’s Planned and Market Economies 353

© Asian Studies Association of Australia 2000.

rose more slowly than costs: at 2.7 per cent per annum between 1950 and 1983,as against a 2.85 per cent rise in costs. So, whereas prices were 22 per cent greaterthan production costs in 1950, the gap had narrowed to only 16 per cent in 1983(Hu 1991, 145–46).

Because prices played a limited role, the history of coal mining during thisperiod must be analysed in different terms. Growth of output, rather than anyfinancial measure, was the primary target under the planning system and, asshown in Figure 1, the Maoist period saw substantial growth in coal output: from66 million tons in 1952 to 483 million in 1976, at an average rate of 7.1 per cent(though only 4.7 per cent between 1956 and 1976). In the latter year, 274 milliontons came from mines controlled by the central government and 209 millionfrom local mines, of which commune and brigade (now township-and-village-enterprise—TVE) coal mines produced 65 million tons, growing by 24 per centper year between 1967 and 1976 (Zhongguo nengyuan tongji nianjian 1989, 83).Coal use was concentrated heavily in industry, with only 19 per cent devoted tohousehold consumption. The most important users included power generation(17.5 per cent), metallurgical coke (9.7 per cent) and railway transport (4.8 percent) (Zhongguo meitan gongye nianjian 1982, 14).

The key question for policy makers was whether production was expandingsufficiently rapidly to meet the demands of economic growth. Throughout theperiod, coal was by far the most important provider of commercial energy in China,

354 Tim Wright

© Asian Studies Association of Australia 2000.

Sources: Zhongguo tongji nianjian, various years; Zhongguo meitan gongye nianjian, various issues;Zhongguo jingji nianjian, 1998, 184; Zhongguo meitan xinxi wang 2000a; the 1998 and 1999 figures areestimates from incomplete figures.

NOPQRSZ[\]̂_fghijkcd1400

1200

1000

800

600

400

200

0

Mill

ion

tons

TVE and non-state mines

Local SOE mines

Central SOE mines

19491951

19531955

19571959

19611963

19651967

19691971

19731975

19771979

19811983

19851987

19891991

19931995

19971999

Figure 1: Growth of Chinese Coal Output, 1949–1999

even though its share fell from over 95 per cent at the beginning of the period tojust under 70 per cent in the mid-1970s (Zhongguo nengyuan tongji nianjian 1989,81). The growth especially of the energy-intensive industrial sector dependedheavily on supplies of coal.

Low prices, however, impeded the achievement of growth targets, and by the1970s production of primary energy was falling behind the needs of the economyand the coal industry had become a bottleneck (Howe 1978, 109; Tian and Qiao1991, 359). An authoritative study reflecting perceptions on the eve of reformargued that there was a structural imbalance between supply and demand forenergy. In particular, there was a severe shortage of energy for domestic use,especially in rural areas, which remained static in per capita terms during theCultural Revolution (Sun 1981, 277). In industry, energy shortages forced manyfactories to operate at far less than full capacity. While shortages were at firstlimited to a few industrial centres in the east and the north, over the 1970s and1980s the problem became nation-wide (Zhongguo shehui diaocha suo 1990,171). Moreover, the low price of energy offered little incentive for efficiency inuse. China was a profligate user of energy, both because its overall industrialstructure was biased towards heavy energy-intensive industries, and because lowlevels of technology led to wasteful use of energy by industry (Zhongguo shehuidiaocha suo 1990, 177–78).

From the early 1980s, the government identified the energy sector as a seriousbottleneck in relation to its plans for economic growth, and gave it priority in the allocation of investment (Zhongguo jingji nianjian 1981, II, 25). There was,however, no thorough restructuring of prices (Hu 1991, 145).

THE DUAL-TRACK SYSTEM

The complexities involved in changing relative prices for important commoditiesled to the emergence of a dual price system, whereby some coal circulated atmarket prices and other coal was distributed through the planning system at stateprices. The aim was to ensure that at the margin coal producers had sufficientincentive to increase production, and coal users faced more-or-less economiccosts (Diao 1987, 37). In the chronic sellers’ market of the 1980s, it was possibleto develop a market-oriented sector at the margin, while still maintainingprevious levels of distribution under the state plan in order to protect those whohad benefited from cheap coal under the planning system (Byrd 1991, 198–99).However, the new system itself created new interests and contradictions, whichimpeded further progress towards a market economy.

The dual pricing system originated in the late 1970s, long before it becameofficial policy. Thus there was a steady rise in the proportion of coal—mainly that

The Political Economy of Prices in China’s Planned and Market Economies 355

© Asian Studies Association of Australia 2000.

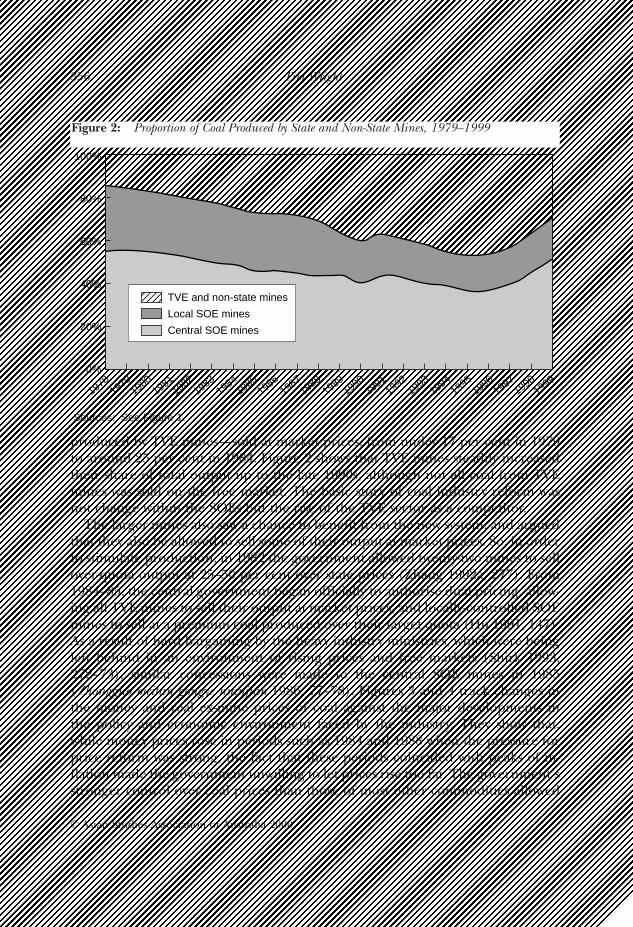

produced by TVE mines—sold at market prices, from under 17 per cent in 1979to around 25 per cent in 1984. Figure 2 shows that TVE mines steadily increasedtheir share of total output up to the late 1990s, although not all coal from TVEmines was sold on the free market. The basic story of coal industry reform wasnot change within the SOEs but the rise of the TVE sector as a competitor.

The larger mines also saw a chance to benefit from the new system, and arguedthat they also be allowed to sell some of their output at market prices. So, in orderto stimulate production, in 1982 the government allowed twenty-two mines to sellover-quota output at 25–50 per cent over state prices (Zhang 1992a, 277). From1984–85, the central government began officially to authorise dual pricing, allow-ing all TVE mines to sell their output at market prices, and locally-controlled SOEmines to sell at a premium coal produced over their target quota (Hu 1991, 147).As a result of hard bargaining by the heavy industry ministries, which were beingleft behind in an environment of rising prices and free markets (Shirk 1993,272–73), similar concessions were made to the central SOE mines in 1985(Zhongguo meitan gongye nianjian 1986, 77–78). Figures 3 and 4 track changes inthe money and real ex-mine prices of coal against the major developments in the policy and economic environment faced by the industry. They show that,while money prices rose in periods such as 1984 and 1988 when the pressure forprice reform was strong, the fact that these periods coincided with peaks of in-flation made the government unwilling to let prices rise too far. The government’sstronger control over coal prices than those of most other commodities allowed

356 Tim Wright

© Asian Studies Association of Australia 2000.

Sources: See Figure 1.

?@ABCDEFKLMNOPQRWXYZ[\]̂cdefghij?@ABCDEFKLMNOPQRWXYZ[\]̂cdefghij?@ABCDEFKLMNOPQRWXYZ[\]̂cdefghij?@ABCDEFKLMNOPQRWXYZ[\]̂cdefghijKLTVE and non-state mines

Local SOE mines

Central SOE mines

19781979

19801981

19821983

19841985

19861987

19881989

19901991

19921993

19941995

19961997

19981999

100%

80%

60%

40%

20%

0%

Figure 2: Proportion of Coal Produced by State and Non-State Mines, 1979–1999

it to limit any rise in the real price of coal. Prices remained far below world levels.Even using the inflated official value of the yuan, in 1987 Chinese prices were lessthan half the US dollar price of Australian coal (Warren 1992, 79).

The dual price system was by no means a total failure (Zhang 1992b, ch. 5). In general, the system reaped most of the gains in allocative efficiency availableto price reform (Wood 1994, 32), and helped the Chinese economy to functionvery successfully for many years (Nolan 1993, 284–92). In coal mining, highermarginal prices stimulated increased production, which grew by 6.3 per centthroughout the 1980s, compared to 4.7 per cent between 1956 and 1976. Thesystem also fostered the growth of TVEs in coal mining and other sectors (Zhang1992b, 96). Moreover, higher prices also promoted technical progress in the useof coal, and energy intensity declined substantially. Whereas around 0.7 kg of coalequivalent was used for each yuan of GDP in 1978, by 1995 this figure had halved

The Political Economy of Prices in China’s Planned and Market Economies 357

© Asian Studies Association of Australia 2000.

Sources: Zhongguo tongji nianjian, various years; Cheng 1998, 1086–87; Pan 1999; Zhongguo meitanxinxi wang 2000b. The estimates for 1998 and 1999 are made using the last two sources.

Notes: The exact nature of these prices is poorly specified in the sources. Both series are for national “Ex-Factory Prices” for the coal industry. According to the Zhongguo tongji nianjian, 1994 “Figures for industrialprice index in this table and below are based on some products produced by key enterprises”. Both seriesappear to include a component both of state-administered prices and of market prices, with the rise inprices in the early 1990s reflecting a growing proportion of coal sold at market rather than administeredprices.

There must be some question over the very sharp price increase for 1990 shown by Cheng 1998: there isno such increase at all either in the Zhongguo tongji nianjian series also illustrated in the chart or in theseries for mixed retail coal prices in the same source.

Cheng 1998EstimateStatistical Yearbook

1984–85:officialapproval ofdual pricesystem

1986 recession

1989: Popularopposition tocorruptionunderminesdualprice system

1993–94:deregulation ofcoal prices

1990–91recession

1997–2000:oversupply incoal market

19781979

19801981

19821983

19841985

19861987

19881989

19901991

19921993

19941995

19961997

19981999

19751976

1977

70

60

50

40

30

20

10

0

–10

Incr

ease

in c

oal p

rices

(%

)

Figure 3: Percentage Increase in Coal Prices in China, 1975–1999

to under 0.35, although some of this decrease was also due to changes in theindustrial structure towards light industry (Smil 1998, 947).

Nevertheless, many of the problems of the old system remained. As the relativeprice of coal fell, especially in relation to production materials, losses by state coalmines increased from 300 million yuan in 1985 to 5.9 billion in 1992 (Li and Zhu1992, 3; Guojia jiwei 1996, 18). According to one source, SOE prices grew so muchmore slowly than costs that the loss per ton of coal grew from 2.48 yuan to 34.49yuan (Tu 1992). By the early 1990s, 86 of the 89 mines under central governmentcontrol were making losses (Zhu 1993, 12).

This problem was exacerbated by the failure of coal-using industries to pay fortheir coal. The “triangular debt” structure plagued the whole state-owned sectorand was particularly serious in coal mining. By the end of 1993 debts incurred bycoal users to coal mines amounted to 19.1 billion yuan, of which 3.8 billion hadbeen accumulated in the previous year (Zhongguo Xinwen She 1994).

In the absence of any working law of bankruptcy, the “soft budget constraint”meant that SOE losses became an increasing burden on the government budget.Subsidies to all SOEs amounted to 45 billion yuan in 1988 and 60 billion in 1989(Zhongguo tongji nianjian 1998, Table 8–5), and those specifically to coal miningenterprises increased from 300 million yuan in 1985 to over 4 billion in 1989 (Hu 1991, 149).

358 Tim Wright

© Asian Studies Association of Australia 2000.

Sources: See Figure 3.

The figures for coal prices are deflated by the general retail price index in Zhongguo tongji nianjian.

240

220

200

180

160

140

120

100

80

Cheng 1998EstimateStatistical Yearbook

1984–85:officialapproval ofdual pricesystem

1986recession

1989: Popularopposition tocorruptionundermines dualprice system

1993–94:deregulation ofcoal prices

1990–91recession

1997–2000:oversupply incoal market

19781979

19801981

19821983

19841985

19861987

19881989

19901991

19921993

19941995

19961997

19981999

Inde

x, 1

978

= 1

00

Figure 4: Index of Real Coal Prices in China, 1978–1999

The level of administered coal prices was still insufficient to encourage invest-ment. This had not mattered as long as investment funds were allocated free bycentral authorities, but when in the reform era they were made available partlyon the basis of profits and at partially realistic rates of interest, it became a majorissue. So, in the short and medium term, output continued to expand becauselarge mines were able to make use of past investments, while the low-cost smallmine sector expanded rapidly. In the longer term, however, the lack of invest-ment in an industry that required a long lead-time provided a poor basis for thecontinuing expansion of production (Tian and Qiao 1991, 362–63; Zhang 1992b,181).

Low state prices also still offered insufficient incentive for efficient utilisationof coal. As a result, despite the progress in lowering energy intensity, industrialboilers used much more coal than was necessary with existing technology; similarly,building insulation was a low priority when coal for heating was cheaply available(Albouy 1991, 9–10). One authoritative estimate had it that if coal reached arational price level the return on energy economising investment would rise to50 per cent above the current normal return (Tian and Qiao 1991, 363).

In addition to the problems left over from the planned economy, the dual price system engendered its own contradictions. It created large rents, althoughthese were in fact probably less under the dual price system than under planning,because the increase in output generated by the system reduced the gap betweenthe planned and the (black) market price (Liew 1997, 68–77). Speculation andcorruption in the form of private appropriation of state assets was too temptingfor the good of the system, because of the profits available by selling on the openmarket coal acquired within the plan (Hu 1991, 147; Zhang 1992a, 276).

Enterprises as well as individuals struggled to appropriate the rents available. Itwas obviously in their interests to maximise the proportion of their output sold atthe much higher market prices and to minimise that which circulated within theplan. This directed an uneconomic amount of energy into negotiating the enter-prise’s obligations under the plan (a common feature of the reform economy,although also of the planned economy) in order to maximise its returns (Ellman1989, 45–46; Fan 1994, 143). In Shanxi, the state purchasing price was around 80yuan while the price in local cities was 130 and in Shanghai 260 yuan, so thatanyone who could manage to sell their coal outside the plan or outside the pro-vince did so (Parker 1995). In addition, the structure of prices, whereby the freemarket price was far above the marginal cost, and the state price far below, mightactually have provided too strong an incentive to increase short-term output,encouraging enterprises to mine their resources at maximum rates without con-cern for long-term conservation or environmental factors. Thus, the plannedoutput of the Xuzhou Mining Bureau in 1989 was less than 10 million tons, butactual output was over 12 million (Hu 1991, 148).

The Political Economy of Prices in China’s Planned and Market Economies 359

© Asian Studies Association of Australia 2000.

Nor did the system function very well in promoting a transition to marketprices. For consumer goods as a whole, the gap between free market and stateprices declined from 80 per cent in 1975 to 48 per cent in 1980, 28 per cent in1985 and only 5 per cent by 1991 (World Bank 1994, 33–34). While state pricesfor coal remained relatively static in the late 1980s before rising sharply in 1990–91, free market prices more than doubled between 1986 and 1989, in coastal areassometimes rising to more than the international price (Warren 1992, 85–86).Thus the gap between planned and market coal prices increased from 45 percent in 1986 to a peak of 168 per cent in 1989, before declining to 70 per centover in 1991.

INTEREST GROUPS AND THE REFORM OF COAL PRICES

It was, however, difficult to mobilise the political will to implement reform, asmost of those involved benefited from the existing system and feared a change.Some SOE managers looked to price reform as a possible panacea for their prob-lems (ZMB 8 October 1994, 1), and the big coal mining combines, on the face ofit, stood to gain from an increase in coal prices that would make their operationseconomically viable. Nevertheless, incentives for managers to support reformwere weakened by the fact that the SOEs were not fully independent accountingunits solely responsible for their own profits and losses (Guojia jiwei 1996, 18).The pressure they were facing was thus much less than in a fully capitalist eco-nomy. Indeed, many managers believed that the state would never let such a basicindustry sink, and just sat and waited for more subsidies (ZMB 12 May 1994, 3).Price reform would inevitably be accompanied by a reduction in these subsidiesand a harder budget constraint. Politically, the major SOEs had long been pillarsof the planned economy, and the head of a huge combine like Kailuan in Hebeior Datong in Shanxi could expect a place at the table when major decisions weremade (Shirk 1993, 108–09). Whether managers in such positions would relish thegreater risks of involvement in the market might be questioned. Old bureaucratichabits of thought died hard, and advocates of reform saw one of its main aims asbreaking the old model of the planned economy and changing those old habitsof thought (Huang 1994, 52).

Resistance from the state enterprises was a major constraint. A recent OECDstudy writes of “strong political constraints protecting the public enterprises” inthe course of price reform (Laffont 1997, 22). Moreover, public enterprises weresupported by the old economic ministries, which in the transitional periodbecame no more than the representatives of their constituent enterprises, leavingany mediation function in the general interest to higher level bodies such as theState Planning Commission (SPC) (Chen 1996, 23).

360 Tim Wright

© Asian Studies Association of Australia 2000.

Nor were the workers likely to support reform. Again, some aspects of reformoffered benefits for them. Wages in coal mines were low, a problem that might beaddressed by higher prices (Hu 1991, 149). Moreover, the financial difficulties ofthe SOEs had resulted in many being unable to pay wages; by the end of 1993, 70mining bureaux owed 2.5 million workers 1.6 billion yuan in wages (Liu Huaxin1994, 4).

Nevertheless, price reform could be expected to be accompanied by a broadermarket-oriented package of enterprise reform, a major part of which was thelaying off of large numbers of workers (Guojia jiwei 1996, 18), and in fact 870,000workers were laid off between 1993 and 1998 (CD 4 May 1998). Moreover, theenterprises began to withdraw from the many subsidiary services that contributedto the social wage of their workers and indeed kept many of them employed. Asthe government pointed out, labour welfare payments at 4.8 billion yuan weremore than two and a half times the net losses posted by the mines (Pu 1995, 6).The huge Datong Coal Mining Bureau ran 82 schools with 90,000 students; itsupported 35,000 retired workers, and in all spent over 700 million yuan onwelfare and services (Liu Jingze 1994, 7). These services would now be com-moditised, and one mine manager suggested that a prerequisite for successfulreform was “smashing the idea that state workers should be looked after by theenterprise from birth to death” (Li 1995, 9). Higher prices for coal would notnecessarily translate into higher or more secure incomes for workers. Thus, thoserepresenting the workers as well as those in management with a commitment tothe old system could see benefits in the system of administered prices.

Price reform was not expected to increase market prices. To a considerable ex-tent, the overall market was distorted by the fact that a relatively high proportionof coal was still allocated through the plan. Because many large producers andusers operated through the plan, the market was smaller than it would otherwisehave been and thus more vulnerable to temporary fluctuations (Warren 1992,88). By the same token, of course, the large profits available in these marketscreated an interest in maintaining the system. This meant that even the market-oriented TVE mine sector had little incentive to support reform. Even if they hadwanted to, they did not have the political clout that the SOEs, supported by amajor industrial ministry, had; rather they were scattered and vulnerable, eco-nomically to credit squeezes, and politically to any change in policy.

Those coal-using industries that were allocated supplies of cheap state coalwere even less likely to support price reform, given that they expected to be themain initial losers (Zhu 1993, 12; Lu 1992, 45; Lieberthal and Oksenberg 1988, 93).Geographically, coal production tended to be concentrated inland, and coal usein the coastal areas that had provided much of the broader impetus for economicreform (Shirk 1993, 264–65). Increasing coal prices would thus benefit theinterior at the expense of the coast, except in cases such as Guangdong, which

The Political Economy of Prices in China’s Planned and Market Economies 361

© Asian Studies Association of Australia 2000.

already acquired much of its coal through the market (Economist 1994b). Somecoal-using industries themselves faced state-determined prices for their products,and therefore could not pass on increased prices for one of their major inputs.On the other hand, coal users mainly dependent on the market welcomed theopportunity for more reliable supplies that was offered by a more open market(Lu 1992, 45).

Reluctance by users to pay higher prices was shown by the complaints of theelectric power industry, which argued even before deregulation that the risingcost of fuel was increasing costs while prices were controlled, so that profit rateswere squeezed (Zhongguo jingji nianjian 1993, 166). Between 1978 and 1987 theaverage price paid for coal by the power industry rose by over 150 per cent. Asthere were much smaller rises in electricity rates, the power utilities had to try toabsorb increased costs by seeking technological solutions (which was, of course,one of the objectives of reform) (Johnson 1992, 1087).

At first glance, the state’s fiscal organs would appear to be major beneficiariesof any freeing of coal prices, given the massive subsidies that had to be paid tokeep coal mines afloat in the 1980s and 1990s (Xiao 1994, 62). The state had toallocate one billion yuan in 1994 solely for the purpose of allowing mining com-panies to pay their wage bills (ZMB 18 April 1995, 1). On the other hand, thesesubsidies were to some extent balanced by remittances of profits from coal-usingindustries. Increasing the price of coal to an economic level would reduce profitsin those industries, and thus reduce government income as well as expenditure.

THE DEREGULATION OF COAL PRICES

At the beginning of the 1990s, after the legitimacy of the dual price system hadbeen undermined by its being targeted as a cause of corruption, opinion washardening in favour of a reunification of the price of coal. While some stillfavoured a reunification at a state-determined price, because of the central roleplayed by coal in both industry and the people’s livelihood (Hu 1991, 148), thelogic of the system, as well as external advice from the World Bank (Albouy 1994,13), was increasingly in the direction of use of market prices. In 1992, the newlyre-established Ministry of Coal was given the job of reforming the industry andwiping out the deficits. It immediately introduced a 20 per cent increase in theprice of state-allocated coal, looking to more general price deregulation in thenear future (Economist 1994a).

In 1993, the government went further and decontrolled prices in elevenprovinces and regions (ZMB 8 October 1994, 1; Zhongguo wujia nianjian 1994,37). As part of a plan to overcome the industry’s losses in three years (Jingji ribao2 May 1993, 3; Guo and Wan 1993, 1–2), the Ministry announced that, from 1994,

362 Tim Wright

© Asian Studies Association of Australia 2000.

most coal would be sold on the open market, and soon thereafter the price of allcoal would be freed (Xinhua 1994). Thus, from July 1994, most of the SOE as wellas the TVE mines sold their coal at prices determined by the market (Guojia jiwei1996, 18; ZMB 12 February 1998, 1).

Remnants of control survived, however, even though there was less of a retreatfrom the principle of market prices than in the case of grain (Watson and Findlay1999, 32). The government still saw itself as having a guiding role. A SPC orderin 1994 said that, while prices should be determined by supply and demand, theyshould not rise too rapidly (up to around 4 per cent was permitted) so that down-stream users were not affected too seriously. Nor were coal users allowed to raisetheir own prices in order to recover the increased costs. Coal sold for householduse was also controlled in accordance with the State Council policy on prices fordaily necessities (Guojia jiwei 1994).

Electricity generation was one of the most sensitive areas. As the SPC realised,deregulating coal but not electricity prices would harm the interests of the powerindustry; deregulation of both would increase the burden on the final consumers(Chen 1996, 26). As a result, the SPC decided in 1996 to introduce an indicativeprice for coal supplied to the power industry (Hou 1995, 46–47; Zhongguo wujianianjian 1996, 30; Zhongguo wujia nianjian 1997, 27, 128–29; Chen 1996, 23).Because of oversupply and competition, however, coal producers could not achievethe indicative prices posted by the government, and in 1998 power plants notonly refused to meet the 5 yuan increase in the indicative price but actuallydemanded price cuts. So, in the middle of that year, a survey of four major coalmines revealed that some sold coal to power plants at market prices, and othersat controlled prices (ZMB 7 May 1998, 1; 25 June 1998, 4).

In addition, intervention by provincial and local governments continued.Indeed, the SPC called for local price authorities to strengthen their supervisionof coal prices (Guojia jiwei 1994). The Yunnan provincial government set a hardand fast mandatory price for coal supplied to the power or fertiliser industriesand an indicative price elsewhere (ZWB 11 June 1995, 2). On a national level, theSPC believed that Shanxi, by far the largest producer of coal entering the nationalmarket, manipulated prices to its own benefit (Chen 1996, 24).

THE COAL MARKET AFTER 1994

In general, from 1994 prices were mainly determined by conditions in the energymarket. These conditions were in fact undergoing a fundamental transformation,from an overall shortage of energy in the 1980s to an adequate or even excesssupply at existing levels of demand in the late 1990s (ZMB 1 October 1998, 1). Asearly as late 1989 a rise in stocks of coal to around 17 per cent of total supply

The Political Economy of Prices in China’s Planned and Market Economies 363

© Asian Studies Association of Australia 2000.

suggested a buyers’ market (14 per cent would indicate a rough balance in themarket) (Hou 1995, 57; Meitan bu 1995, 4). Even in 1993, when rapid economicgrowth created feverish demand for other industrial materials, the coal marketremained, on the whole, in balance (ZWB 11 March 1994, 1), and stocks relativelyhigh, although transport problems limited the utility of stocks at the mine(American Embassy 1994). From 1997, it became clear that there really was a glutof coal, and stocks rose sharply to record levels—200 million tons at the end of1998, and only a little lower in mid-1999 (Harding 1999).

There were a number of causes of the reversal of the earlier chronic shortageof coal. Supplies had increased strongly since the 1980s partly as the result ofprice reform, with TVE production in particular reaching record levels in 1996.One article concluded that the TVE mines would be able to meet any conceivableincrease in demand (Meitan bu 1995, 5). Coal from TVE mines was up to 50 yuancheaper than that from SOEs, forcing the latter either to cut their prices or towithdraw from the market (Pan 1999). Moreover, transport improvements, withthe construction of new rail lines from Datong to Qinhuangdao and Beijing toKowloon, as well as the upgrading of China’s port facilities and the reduction ofgovernment interference, went a long way towards removing the north-southtransport bottleneck (ZMB 15 January 1998, 3).

On the demand side, the decline in energy intensity continued into the late1990s, and energy consumption fell for twenty-four consecutive months in 1998–99. As a result, despite strong economic growth during the early and mid 1990s,demand for coal was static or even falling, certainly not able to absorb the growthin output in 1995–97. When the overall growth rate slowed, as the economy wounddown from its overheating in the mid 1990s and as China felt the impact of theAsian financial crisis, demand fell further behind, and by 1998–99, as coal use fell by 200 million tons, there was major concern over a glut of coal (Zhongguomeitan xinxi wang 2000b). Forecasts differed as to how long this situation wouldcontinue: in 1998 a study predicted an excess supply of coal to 2010 (Li 1998,115), but even at the end of the 1990s some foresaw a bright future for theindustry as the economy grew (ZMB 22 January 1998, 3).

In such a situation prices were relatively weak, lessening any inflationary effectsof reform, but reducing the benefits to the SOE mines. The initial response ofthe SOEs to price deregulation had been to raise their prices substantially. Forexample, China’s largest mine, Datong in Shanxi, raised its price from 90 to 135yuan overnight after the freeing of prices (ZWB 11 March 1994, 1). Figures 3 and4 show that both money and real prices of coal rose sharply in the early 1990s, asthe proportion of coal sold at market rather than at state prices increased rapidly.Market prices, however, were not strong and, even as early as 1994, this weaknesslimited the SOEs’ room to manoeuvre in terms of increasing their revenues(Xinhua 1994). As long as the economy remained strong, the gains from price

364 Tim Wright

© Asian Studies Association of Australia 2000.

reform continued to flow through. But even in 1997, less aggregated indicatorssuggested that prices were slipping, for instance by about 10 per cent in Shanghai(ZMB 15 January 1998, 3). The next year saw a growing price war in the coaltrade, not only between the SOE and the TVE mines, but also between regionswith, for example, Shanxi coal forcing down prices in Liaoning, another majorcoal-producing centre (ZMB 7 May 1998, 1). From 1998, real prices declined asthe money price of coal fell further than did the general price level. The declineaccelerated and reached around 10 per cent in 1999 (Zhongguo meitan xinxiwang 2000b). Some important types of coal, for example Datong coal, fell evenmore sharply, particularly in areas such as East China (Pan 1999).

RESPONSES TO DEREGULATION AND DEFLATION

The main interest groups analysed in previous sections faced a new series ofchallenges with the transition to market prices. The leadership’s goals were toensure adequate supplies of coal to fuel China’s economic growth while main-taining price and economic stability. The first goal was broadly achieved, withsupply more than sufficient to meet demand in the late 1990s, but quality differ-entiation still remained a concern, and the incentives, for example, for ruralmines to establish coal-washing facilities were weak (Lim 1997). Customers were,however, becoming much more discriminating, and the old days when any typeof coal would do were long past (ZWB 11 November 1994, 1).

The leadership’s second aim was to maintain price stability—which meantcombating inflation in 1993–96 and deflation from 1997. Shortages and sharplyrising prices were a major factor behind the roll-back of the 1993 reform in thegrain market (Watson and Findlay 1999, 31; Guo 1999, 59), and, as late as 1995 astudy identified government anti-inflation policies as one reason not to expectmajor rises in the coal price:

Coal is a major material that affects the national economy and people’slivelihood and changes in its price can lead to the effect of “pulling onehair and affecting the whole body”. If the price of coal rises too much,beyond a certain level, on the one hand it will influence the state’s macro-economic regulation target of strictly controlling prices. On the otherhand, because it is beyond the capacity of users to absorb, it might lead toa series of problems that affect social order and unity, so that the statewould have to interfere and adopt control measures (Chen 1995, 42–43).

In the end, however, despite a steep rise in the average price of coal as prices wereunified, market conditions limited the upward movement. Even with a booming

The Political Economy of Prices in China’s Planned and Market Economies 365

© Asian Studies Association of Australia 2000.

economy and price deregulation, coal did not become a major bottleneck orsource of inflation.

Deflation replaced inflation as the main concern for the government from1997, because of the general oversupply in the market. Prices started to fall acrossthe board from October 1997, but those of the means of production had beenfalling from around a year earlier (CD 7 May 1999, although this is not entirelyconsistent with the statistics used in Figures 3 and 4). This was basically the resultof overcapacity installed during the apparent boom in 1992–94, when sharp risesin the prices of many materials encouraged over-investment (Hu 1999). Thegovernment was worried about the fall in coal prices as part of a generaldeflationary situation, as the trigger for renewed losses by the SOEs and as adisincentive to economise on the use of coal (ZMB 21 May 1998, 1).

As institutions with a stake in the old system, SOE mines had been ambivalentabout price reform from the start, and some at least supported continuedregulation. A member of staff of the Datong Coal Mining Bureau, China’s largest,called for the “comprehensive use of economic, legal and administrative methodsto strengthen [government] management of the post-decontrol coal price”, anddrew a sharp distinction between a market economy and a laissez-faire economy(Liu Jingze 1994, 7). After the implementation of price reform, commentatorssuggested that the state mines had been “pushed into” reform, and that many,instead of embracing market ideas, just took a very passive attitude and waited fordevelopments (ZMB 12 May 1994, 3; 12 January 1995, 2). Many enterprises werestill looking for government help—such as protection or tax holidays—and ad-ministrative measures to get them out of their difficulties, rather than embracinginnovation and cost-cutting in the market (ZWB 28 March 1994, 1). The managerof the Xuzhou coal mine said that while SOEs benefited from price deregulationthey also faced higher risks and at the same time lost government subsidies. Thismeant that when prices fell in 1997, the mine made large losses (ZMB 12 February1998, 1).

Nevertheless, for a short time price reform did reduce the massive SOE losses,partly through a reduction in their output, as prices received were less thanproduction costs. Subsidies to SOEs in general declined from their level in thelate 1980s to 30 billion yuan by 1995, before rising a little to 37 billion in 1997(Zhongguo tongji nianjian 1998, Table 8–5). Despite government warnings thatprice reform might actually worsen the situation of the SOE coal mines (ZMB13 January 1994, 1), higher real prices of coal reduced SOE losses from 6 billionyuan in 1991 to 2 billion in 1994, 1 billion in 1995, and 400 million in 1996(Zheng 1996, 23; Xinhua 1996; Economist 1997). A profit was registered for thefirst time in many years in 1997 (Reuters 1997). On the level of individual mines,the Kailuan mine in Hebei attributed its move back into the black in 1995 partlyto the removal of the ceiling on prices (South China Morning Post 1996).

366 Tim Wright

© Asian Studies Association of Australia 2000.

Deflation from 1997 plunged the SOE mines back into losses. The situation wasalready deteriorating in the latter part of 1997 and losses mounted through 1998.Thus 79 of the 94 central SOE mines made losses totalling 3.7 billion yuan in1998 and 2.28 billion in the first five months of 1999 alone (CD 29 June 1999).Mining companies also failed to pay wages: in mid-1998, 52 SOE mines owedtheir workers over 3 billion yuan (ZMB 23 July 1998, 3).

Previous state subsidies to balance these losses were also brought into question.Control over the major SOE mines was devolved from the centre to the provincesin mid-1998, and the mines felt like “abandoned children meeting a new step-mother”. They found that the provincial governments were unable to continuesubsidies and asked instead for protection of their internal markets, althoughcritics said that this would only accentuate their “dependent mentality” (ZMB 29October 1998, 1).

The weak market also undermined attempts by SOE mines to call in theirunpaid bills. In 1995, the Ministry introduced a policy known as the “three-noes”to try to solve the problem—that is, no supply of coal to enterprise users who donot pay, if no bank draft is available, or if customers fail to pay their debts(Zhongguo Xinwen She 1995). This policy did reduce stocks held by users anddistributors and thus tightened the market for coal and increased prices (ZWB21 June 1995, 2). It reduced the gross amounts owed to SOE mines from 29 to21 billion yuan between 1994 and 1995 (Zhongguo jingji nianjian 1996, 180), but itseffect was limited in isolation, without broader measures to tackle the “triangulardebt” problem (ZWB 6 April 1995, 2). After the coal industry went into depressionfrom 1997, mines were in too weak a position to demand payment (ZMB 7 May 1998,1). Unpaid bills increased rapidly, from 29 billion in early 1998, to 36 billion laterin the year and 38.5 billion in early 1999 (ZMB 9 January 1999, 2; Kyodo 1999).

ATTEMPTS TO CONTROL COAL PRICES UNDER MARKETCONDITIONS

There were no easy answers to the low price of coal and the consequent losses by SOE mines. The situation reflected that of the 1930s, when supply likewiseexceeded demand, leading to weak prices and losses by coal mining enterprises.In response, there were proposals to establish a coal cartel to regulate sales andprotect existing producers. However, coal resources were relatively easily acces-sible in many areas of the country, so the cartel had limited chances of success,although war broke out before its fate was clearly decided (Wright 1985).

Attempts to raise prices by controlling output in the 1990s had little chance ofsuccess for similar reasons (ZMB 8 October 1998, 1). Moreover, in the 1990s thelevel of concentration in the industry was extremely low, with the largest four

The Political Economy of Prices in China’s Planned and Market Economies 367

© Asian Studies Association of Australia 2000.

producers accounting for under 10 per cent of total output—far less than inother major coal-producing countries (Pan 1997, 31–32). No one producer couldinfluence the price, and enterprises were all price-takers. Moreover, barriers toentry were low, and barriers to exit high (Wu 1999, 19). Indeed, when in late1998 the government called for self-regulation of prices for twenty-one industriesin an attempt to ward off deflation, coal was excluded because of its highly frag-mented structure of production (ZMB 8 October 1998, 1). There were strongincentives for individual enterprises to break ranks, and official sources com-plained that “some units” could not see the larger picture but just catered to theirown selfish interests, and used output restrictions to take over others’ markets(ZMB 1 January 1998, 1). Different regions also had different interests, and “localprotectionism” undermined the effectiveness of efforts to control output andprices (ZMB 22 January 1998, 3).

The formation of conglomerates offered one solution to the excessive frag-mentation of the industry, and indeed had been tried in the 1960s and 1980s(Pan 1997, 34). At the January 1999 Coal Conference, the head of the CoalIndustry Bureau (successor of the Ministry of Coal) called for the formation ofenterprise groups based on large or very large SOEs, which would “change thefragmented structure of the coal industry and strengthen its overall competitive-ness” (ZMB 9 January 1999, 2)—and (although this was not stated openly) makeit easier to impose oligopolistic price controls. Conglomerates could be based onreliance on a particular railway line or collection point, or be vertically integrated,involving power plants or transport facilities as well as mines (Shi 1999, 33). Theycould be formed by direct purchase, share purchase, amalgamation and leasing,as well as by administrative action (Wu 1997, 79–80). Such a process has only justbegun, and the first major group, Shenhua in Shaanxi and Inner Mongolia, wasestablished in 1995, with a target output of 100 million tons and responsibility for power stations, railways, ports and fleets as well as mines (Xinhua 1995). Theprocess of forming conglomerates has, however, not yet gone nearly far enoughto have a real effect on prices.

Coal interests argued that the industry itself needed to work together to resistconcerted attempts by users to force down prices (ZMB 19 February 1998, 1) andto try to force customers to pay their debts, as when nine coal companies jointlyconfronted the Shanghai Coke Company (ZMB 3 November 1998, 1). Someproposed to do this at a national level, while others focused on the locality orregion; an article in China Coal News argued that provincial level associations werethe most practical (ZMB 10 December 1998, 1). There had been for a number ofyears associations for coal sales in north and in east China (ZMB 14 May 1998, 1).In addition, an association of mines in Shanxi, Shaanxi and Inner Mongolia was formed in 1998 to control output and sales, thus keeping prices up, and toinitiate joint action to recover debts (ZMB 10 December 1998, 1).

368 Tim Wright

© Asian Studies Association of Australia 2000.

A still fragmented industry, however, looked to direct government interventionto control prices. In April 1999, the Coal Industry Bureau announced that “Dump-ing coal at low prices will be resolutely prevented, and sector self-discipline willbe implemented to maintain normal competitive order in the market” (Zhao1999). At the provincial level, the authorities in Shanxi moved in April 1998 to“strengthen the management” of coal prices and ensure producers received theposted rise in the price of coal sold to power plants (ZMB 9 April 1998, 3). TheGuizhou provincial government acted to enforce uniform prices for both TVEand SOE mines to supply coal to the electricity industry (ZMB 24 September1998, 1).

Governments at various levels also became involved in attempts to maintainprices indirectly through cutting production. Much of the initiative occurred asusual at the provincial level: the efforts of the Fujian government to control themarket by measures such as fining mines for excess production were criticised in1995, but began a year later to be seen as a model for the rest of the country(ZMB 22 January 1998, 3). Most importantly, the Shanxi government launched aseries of initiatives which reduced coal stocks from 50 to 30 million tons (ZMB22 January 1998, 3), and later established a coal sales office to regulate sales ofall coal mined in the province. The aim was to present a united front to users andto regulate prices. Companies breaking price discipline would face economicsanctions (ZMB 8 October 1998). Inter-provincial policies for output controlwere also canvassed at a 1997 meeting called by the Shanxi authorities with Hebei,Shaanxi, Inner Mongolia and Ningxia (ZMB 22 January 1998, 3).

Nationally, the leadership saw the control of output as the key to restoring theindustry to economic health (ZMB 19 September 1998). From 1997, it intro-duced the “double control” (of output and stocks) policy, which did reduce TVEoutput (ZMB 1 January 1998, 2). The declining market required more, however,and all mines agreed to a close-down during the 1998 Spring Festival holiday(ZMB 22 January 1998, 1; 26 February 1998, 4). Even this was not enough, andfrom mid-1998 the government launched a massive campaign to close down 25,800TVE mines, which was explicitly aimed at cutting their output by 250 million tons(ZMB 12 November 1998, 1). The year 1999 saw 31,000 TVE mines closed, a 15 per cent reduction in total coal output and a target of 870 million tons for2000 (as against a 1996 output of 1.4 billion tons) (Zhongguo meitan xinxi wang2000a; 2000b). Critics, however, argued that such administrative measures couldonly have a temporary effect and reflected an incomplete transition towards themarket; attempts to interfere with the market were doomed to failure (ZMB23 April 1998, 3).

The powerful user lobby, which had done better than expected out of pricereform, regarded such measures with caution. Originally, users had been appre-hensive about deregulation, which the electric power industry, the largest user of

The Political Economy of Prices in China’s Planned and Market Economies 369

© Asian Studies Association of Australia 2000.

coal, had long opposed. Thus, a pilot decontrol project in Shandong in 1992 ledto an increase in costs to the electricity industry (Sun 1993, 28), and later powerinterests argued, “If the price of coal rises and electricity prices are not allowedto rise with them, who will be able to guarantee electricity generation?” (ZWB11 March 1994, 1). Deregulation of coal prices was followed by a series of disputesbetween coal suppliers and power plants—especially between producers in Shanxiand the Beijing-Tianjin power grid—involving suppliers cutting off coal deliveriesand power plants failing to deliver electricity. The living quarters at Datongsuffered their first electricity black-out two days after the mine had raised its coalprices (ZWB 11 March 1994, 1)! The respective ministries weighed in on the sideof their constituent enterprises. Other industries were also hit: Shandong chem-ical fertiliser plants went from profit to loss during the 1992 experiment (Sun1993, 28). When, however, various levels of government responded by imposingcontrols on the price of coal supplied for power generation, mining companies,as elementary theory would predict, were unwilling to supply coal, at least untilthe market conditions turned clearly against them (ZMB 22 January 1998, 3).

When the market situation changed, coal users made full use of their powerand, for example, forced producers to absorb the increases in costs generated bytransport reform (Pan 1999). Electric power plants did not hesitate to switchsuppliers in search of cheaper inputs (ZMB 27 August 1998, 1), although coalproducers complained that they had to buy expensive electricity to producecheap coal for the electricity producers (ZMB 24 September 1998, 1). Users alsoresisted any attempts to increase coal prices artificially: Guizhou steel producerscomplained that they “could not bear” the increased costs imposed by the attemptsto control prices (ZMB 24 September 1998, 1). In fact, coal interests bemoanedthe fact that the producers’ cartels were too weak to challenge the user cartels(ZMB 22 January 1998, 1).

CONCLUSION

The case of coal illustrates well the complexity of economic change in China, notso much in a technical sense, but more in that each stage of the process createdkey interest groups with a stake in its continuation. The rents created by the dualprice system acted as incentives for both existing and new economic players toresist further change. Many western economists therefore advocated the “big bang”approach—an immediate or very rapid decontrol of prices and privatisation ofindustrial enterprises. This advice was listened to in Eastern Europe, where manygovernments instituted such a rapid transition. At least from the perspective of2000, however, it is difficult to say that these policies have been a success (see alsoChang and Nolan 1995).

370 Tim Wright

© Asian Studies Association of Australia 2000.

Rather, the recent history of the coal industry illustrates the very considerablesuccess of the Chinese government in gradually moving towards a marketeconomy with “rational” prices, while not undermining the continuity and on-going viability of the economy. Of course, incrementalism was not simply a matterof conscious policy choice, but also reflected the nature of the decision-makingprocess in the Communist political system (Shirk 1992). This success dependedon the fact that in this sector, as in others, economic reform for a long timeconsisted primarily, although not exclusively, of the emergence of a semi-privatemarket-oriented system alongside the old state enterprises operating underplanning.

The introduction of market prices by no means meant “the end of history”.Market conditions meant that prices ended up far lower than had been expectedor than were necessary to make the SOE mines economically viable. As reformbegan to impinge on the SOEs themselves, they started to mobilise political sup-port against their TVE competitors. More broadly, the sector began to face prob-lems similar to those faced by coal industries elsewhere in times of depressionand oversupply. Likewise, the solutions—regulation of output and prices both bythe state and by the industry—were similar to those attempted, with very limitedsuccess, by the Chinese coal industry before the war and by other coal industriesin capitalist economies.

NOTES

1This research was undertaken with the aid of a grant from the Asia Research Centre on SocialEconomic and Political Change at Murdoch University, which published earlier results as‘Price Reform in the Chinese Coal Industry’, Working Paper No. 66, August 1996. I would liketo thank the following people: Zhu Xiaoyang, Him Chung and the Universities Service Centrefor their help in collecting materials; Dr Chris Bramall, Ching Sun and Andrew Gosling forproviding crucial information at the final stage; and the participants in the Asia ResearchCentre seminar and two anonymous referees for Asian Studies Review for useful comments andsuggestions.

REFERENCES

Albouy, Yves. 1991. Coal pricing in China: Issues and reform strategy. World Bank Discussion Papers:China and Mongolia Department Series, no. 138. Washington, DC: The World Bank.

American Embassy, Beijing. 1994. China—coal industry news. Telegraphic report, 28 February.National Trade Data Bank Market Reports. Online: LN (3 October 1995).

Byrd, William A. 1991. The market mechanism and economic reforms in China. Armonk, NY: M. E. Sharpe.

The Political Economy of Prices in China’s Planned and Market Economies 371

© Asian Studies Association of Australia 2000.

CD: China Daily. 1998. Beijing: Zhongguo ribao; Online: http://www.chinadaily.com.cn/1999.

Chang, Ha-Joon and Peter Nolan. 1995. The transformation of Communist economies: Against themainstream. Houndmills: Macmillan Press.

Chen Shutong. 1996. Woguo nengyuan jiage zhong de longduan xianxiang fenxi ji duiceyanjiu. Zhongguo nengyuan, no. 3, March: 22–28.

Chen Xiuzhi. 1995. Jinnian woguo meitan shichang zhuangkuang ji jiben zoushi. Zhongguowuzi jingji, no. 4, April: 41–43.

Cheng Zhiping. 1998. Zhongguo wujia wushi nian (1949–1998). Beijing: Zhongguo wujiachubanshe.

China Central Television. 1994. Zhu Rongji in Tianjin speaks on grain market regulation. 1100gmt, 5 April. In SWB, FE/1979. 23 April: G/3.

Diao Xinshen. 1987. The role of the two-tier price system. In Reform in China: Challenges andchoices, ed. Bruce L. Reynolds: 35–46. Armonk, NY: M. E. Sharpe.

Donnithorne, Audrey. 1967. China’s economic system. London: C. Hurst & Co.

Economist Intelligence Unit. 1994a. Coal: A sector in decay. Business China, 10 January. Online:LN (3 October 1995).

Economist Intelligence Unit. 1994b. Coal prices: Hot stuff. Business China, 10 January. Online:LN (3 October 1995).

Economist Intelligence Unit. 1997. China: Industry—coal sector moves back into black.Business China, 5 September. Online: RBB (4 October 1999).

Ellman, Michael. 1989. Socialist planning, 2nd edition. Cambridge: Cambridge UniversityPress.

Fewsmith, Joseph. 1994. Dilemmas of reform in China: Political conflict and economic debate. Armonk,NY: M. E. Sharpe.

Findlay, Christopher and Jiang Shu. 1992. Interest group conflicts in a reforming economy. In Economic reform and social change in China, ed. Andrew Watson: 17–38. London: Routledge.

Guo, Jiann-Jong. 1992. Price reform in China, 1979–86. Houndmills: Macmillan Press.

Guo Shutian. 1999. The relationship between grain prices and inflation. In Food security andeconomic reform: The challenges facing China’s grain marketing system, ed. Christopher Findlay andAndrew Watson: 54–61. Houndmills: Macmillan.

Guojia jiwei. 1994. Guojia jiwei fachu guanyu meitan jiage youguan wenti de tongzhi. Zhongguowujia, no. 9, September: 22.

Guojia jiwei jiage guanli si nengyuan yuancailiao chu. 1996. Meitan jiage gaige huigu yuqianzhan. Jiage lilun yu shijian, no. 10, October: 17–20.

Guo Quan and Wan Guixian. 1993. Shilun meitan gongye fazhan xin shiqi. Zhongguo nengyuan,no. 7, July: 1–2.

Harding, James. 1999. Closing down sale. The Financial Times, 23 September. Online: LN (28 October 1999).

Hou Bang’an. 1995. Woguo meitan gongxu pingheng fenxi ji 1995 nian yuce. Zhongguo gongyejingji, no. 4, April: 56–60.

Howe, Christopher. 1978. China’s economy: A basic guide. London: Paul Elek.

372 Tim Wright

© Asian Studies Association of Australia 2000.

Hu Angang. 1999. Hu Angang on deflation. Beijing guanli shijie, 24 June: 10–23. Online: WorldNews Connection, Article Id. FTS19990719001913. FBIS-CHI-1999-0719 (6 September1999).

Hu Changnuan. 1991. Dui woguo meitan jiage de kaocha. Zhongguo shehui kexue, no. 6,November: 145–58.

Huang Xinhai et al. 1994. Xuzhou kuangwu ju meijia fangkai de shijian yu sikao. Meitan jingjiyanjiu, no. 1, January: 52–54, 64.

Jingji ribao. Beijing: Jingji ribao she.

Johnson, Todd M. 1992. China’s power industry, 1980–1990: Price reform and its effect onenergy efficiency. Energy 17, no. 11, November: 1085–92.

Kwong, Julia. 1997. The political economy of corruption in China. Armonk, NY: M. E. Sharpe.

Kyodo News International. 1999. Bankruptcy to be used to slim China’s coal industry, 7 May.Online: LN (2 September 1999).

Laffont, Jean-Jacques with Claudia Senik-Leygonie. 1997. Price controls and the economics ofinstitutions in China. Paris: Development Centre, OECD.

Li Hong. 1991. Government to cut two-tier price system. China Daily, Business Weekly, 14 July.

Li Shubiao. 1998. Woguo nengyuan gongye zhongchangqi qushi yuce yu fenxi. Yuce, no. 2,February: 16–20. In Fuyin baokan ziliao, F3, Gongye jingji, no. 5, May: 113–17.

Li Yucheng. 1995. Shiying shichang jingji xingshi cuojin qiye zouchu kunjing. Meitan jingjiyanjiu, no. 6, June: 9–12.

Lieberthal, Kenneth and Michel Oksenberg. 1988. Policy making in China: Leaders, structures,and processes. Princeton, NJ: Princeton University Press.

Liew, Leong. 1997. The Chinese economy in transition: From plan to market. Cheltenham, UK:Edward Elgar.

Lim, Wendy. 1997. China: Township and private mines resist change. South China Morning Post,5 January. Online: RBB (1 September 1999).

Liu Huaxin. 1994. Meitan gongye muqian mianlin de kunjing yu chulu. Meitan jingji yanjiu, no. 9, September: 4–7.

Liu Jingze. 1994. Jiejue guoyou meitan qiye xiang shichang jingji guoduo wenti de tantao.Meitan jingji yanjiu, no. 8, August: 6–8.

LN: LEXIS-NEXIS. News Library, News Group File, All.

Lu Nan. 1992. Solution to dual pricing of means of production. Chinese Economic Studies 25, no. 4, Summer: 35–47.

Meitan bu zhengce fagui si keti zu. 1995. Jiushi niandai zhong hou qi woguo meitan shichangjiben zoushi ji duice, shang. Meitan jingji yanjiu, no. 4, April: 4–8.

Nolan, Peter. 1990. Introduction. In The Chinese economy and its future: Achievements and problemsof post-Mao reform, ed. Peter Nolan and Dong Fureng: 1–37. Cambridge: Polity Press.

Nolan, Peter. 1993. State and market in the Chinese economy: Essays on controversial issues. Houndmills: Macmillan Press.

Nolan, Peter. 1994. Introduction: The Chinese puzzle. In China’s economic reforms: The costs andbenefits of incrementalism, ed. Qimiao Fan and Peter Nolan: 1–20. Houndmills: Macmillan.

The Political Economy of Prices in China’s Planned and Market Economies 373

© Asian Studies Association of Australia 2000.

Pan Weier. 1997. Meitan qiye chongzu yu jituan fazhan zhanlue. Zhongguo gongye jingji, no. 7,July: 31–35.

Pan Weier. 1999. Dangqian meitan jiage xiadie de da beijing. Online: http://www.coalinfo.ac.cn/chinacoal/9908/5.htm (20 March 2000).

Parker, Jeffrey. 1995. Bottlenecks strangle China’s coal energy growth. The Reuter Asia-PacificBusiness Report, 3 January. Online: LN (3 October 1995).

Pu Hongjiu. 1995. Meitanbu fu buzhang Pu Hongjiu tan guoyou zhongdian meikuang niu kuizeng ying gongzuo. Meitan jingji yanjiu, no. 3, March: 4–7.

Pye, Lucien W. 1981. The dynamics of Chinese politics. Cambridge, MA: Oelgeschlager, Gunn &Hain.

Pye, Lucien W. 1995. Factions and the politics of Guanxi: Paradoxes in Chinese administrativeand political behaviour. The China Journal, no. 34, July: 35–53.

RBB: Reuters Business Briefing.

Reuters News Service. 1997. China coal mines profitable, first time in 13 yrs, 26 DecemberOnline: RBB (1 September 1999).

Shi Zhigui. 1999. Meitan qiye erci chuangye. Zhongguo nengyuan, no. 3, March: 32–33.

Shirk, Susan L. 1985. The politics of industrial reform. In The political economy of reform in post-Mao China, ed. Elizabeth J. Perry and Christine Wong: 195–221. Cambridge, MA: HarvardUniversity Press.

Shirk, Susan L. 1989. The political economy of Chinese industrial reform. In Remaking theeconomic institutions of socialism, ed. Nee and Stark: 328–62.

Shirk, Susan L. 1992. The Chinese political system and the political strategy of economicreform. In Bureaucracy, politics and decision making in post-Mao China, ed. Kenneth G.Lieberthal and David M. Lampton: 59–91. Berkeley and Los Angeles: University ofCalifornia Press.

Shirk, Susan L. 1993. The political logic of economic reform in China. Berkeley and Los Angeles:University of California Press.

Smil, Valcav. 1998. China’s energy and resource uses: Continuity and change. China Quarterly156, December: 935–51.

South China Morning Post. 1996. Miner struggles under weight of huge obligations. 13 June.Online: RBB (4 October 1999).

Sun Shangqing. 1981. Nengyuan jiegou. In Zhongguo jingji jiegou wenti yanjiu, ed. Ma Hong andSun Shangqing: 261–94. Beijing: Renmin chubanshe.

Sun Zhihua. 1993. Shandong meijia fangkai de yingxiang ji duice. Zhongguo wujia, no. 6, June:27–29.

SWB: Summary of World Broadcasts: Far East. 1991–99. British Broadcasting Corporation.

Tian Yuan and Qiao Gang. 1991. Zhongguo jiage gaige yanjiu, 1984–1990. Beijing: Dianzi gongyechubanshe.

Tu Daokun. 1992. Heise guaijuan. Zhongguo shangbao, 1 March.

Warren, Colin J. 1992. Coal pricing in China. In The sectoral foundations of China’s development,ed. Javed Burki and Shahid Yusuf: 79–91. Washington, DC: The World Bank.

374 Tim Wright

© Asian Studies Association of Australia 2000.

Watson, Andrew, and Christopher Findlay. 1999. Food and profit: The political economy andgrain market reform in China. In Food security and economic reform: The challenges facing China’sgrain marketing system, ed. Christopher Findlay and Andrew Watson: 5–38. Houndmills:Macmillan.

White, Gordon. 1993. Riding the tiger: The politics of economic reform in post-Mao China. Stanford:Stanford University Press.

Wood, Adrian. 1994. China’s economic system: A brief description with some suggestions forfurther reform. In China’s economic reforms: The costs and benefits of incrementalism, ed. QimiaoFan and Peter Nolan: 21–45. Houndmills: Macmillan.

World Bank. 1994. China: National market development and regulation. Washington, DC: WorldBank.

World Bank. 1985. China: Long-term development issues and options. Baltimore: Johns HopkinsUniversity Press.

Wright, Tim. 1985. The Nationalist state and the regulation of Chinese industry during theNanjing Decade: Competition and control in coal mining. In Ideal and reality: Social andpolitical change in modern China, 1860–1949, ed. David Pong and Edmund S. K. Fung: 127–52.Lanham: University Press of America.

Wu Yin. 1997. Lun meitan chanye jiegou youhua yu meitan qiye goubing. Meitan jingji yanjiu,no. 10, October: 13–16; no. 11, November: 6–7, 10. In Fuyin baokan ziliao, F3, Gongye jingji,1998, no. 2, February: 75–81.

Wu Yin. 1999. Meitan chanye jingzheng jiegou fenxi. Zhongguo nengyuan, no. 1, January: 17–21.

Xiao Guoan. 1994. Lishun shichang jingji tizhi xia meitan de gongqiu guanxi. Jingji yanjiu,no.10, October: 59–65.

Xinhua News Agency. 1994. Coal output up 5.7 per cent over 1993. 0924 gmt, 12 October. In SWB, FE/2127. 15 October: G/17.