The origins and early diffusion of “shareholder value” in the United States

22

The origins and early diffusion of “shareholder value” in the United States Johan Heilbron & Jochem Verheul & Sander Quak Published online: 12 October 2013 # Springer Science+Business Media Dordrecht 2013 Abstract The shareholder value conception of the firm and its consequences for the functioning of corporations have been studied from a variety of disciplinary and theoretical perspectives. In this article we examine in more detail than has been done sofar the origins and early adoption of this particular conception. By investigating public business sources from the perspective of field theory, we argue that the rise and early diffusion of “shareholder value” are best understood as a function of the changing power relations in the economic field during the first half of the 1980s. The deep economic recession at the end of the 1970s and early 1980s led to a crisis in the prevailing management beliefs, offering newcomers the opportunity to promote alternative business strategies, among which the shareholder value conception be- came dominant. The sources studied indicate that the spokespersons of the new business conception were initially wealthy outsiders, corporate “raiders,” who used the economic crisis to oppose management and acquire shares in undervalued firms with the threat of restructuring and selling parts of them in the name of shareholders’ interests. Although these hostile take-overs, or threats of take-overs, were widely contested, the Reagan administration blocked regulation and stimulated the take-over market. The rivalry between “raiders” and public pension funds over the profits of these takeovers led to the founding the Council of Institutional Investors (1985), Theor Soc (2014) 43:1–22 DOI 10.1007/s11186-013-9205-0 J. Heilbron Centre européen de sociologie et de science politique de la Sorbonne (CESSP-CNRS-EHESS) & Erasmus University Rotterdam, Rotterdam, The Netherlands J. Heilbron (*) Erasmus Center for Economic Sociology, Erasmus University Rotterdam, Room M 6-31, P.O. Box 1738, 3000 DR Rotterdam, The Netherlands e-mail: [email protected] J. Verheul : S. Quak Erasmus University Rotterdam, Rotterdam, The Netherlands J. Verheul e-mail: [email protected] S. Quak e-mail: [email protected]

Transcript of The origins and early diffusion of “shareholder value” in the United States

The origins and early diffusion of “shareholder value”in the United States

Johan Heilbron & Jochem Verheul & Sander Quak

Published online: 12 October 2013# Springer Science+Business Media Dordrecht 2013

Abstract The shareholder value conception of the firm and its consequences for thefunctioning of corporations have been studied from a variety of disciplinary andtheoretical perspectives. In this article we examine in more detail than has been donesofar the origins and early adoption of this particular conception. By investigatingpublic business sources from the perspective of field theory, we argue that the rise andearly diffusion of “shareholder value” are best understood as a function of thechanging power relations in the economic field during the first half of the 1980s.The deep economic recession at the end of the 1970s and early 1980s led to a crisis inthe prevailing management beliefs, offering newcomers the opportunity to promotealternative business strategies, among which the shareholder value conception be-came dominant. The sources studied indicate that the spokespersons of the newbusiness conception were initially wealthy outsiders, corporate “raiders,” who usedthe economic crisis to oppose management and acquire shares in undervalued firmswith the threat of restructuring and selling parts of them in the name of shareholders’interests. Although these hostile take-overs, or threats of take-overs, were widelycontested, the Reagan administration blocked regulation and stimulated the take-overmarket. The rivalry between “raiders” and public pension funds over the profits ofthese takeovers led to the founding the Council of Institutional Investors (1985),

Theor Soc (2014) 43:1–22DOI 10.1007/s11186-013-9205-0

J. HeilbronCentre européen de sociologie et de science politique de la Sorbonne (CESSP-CNRS-EHESS) &Erasmus University Rotterdam, Rotterdam, The Netherlands

J. Heilbron (*)Erasmus Center for Economic Sociology, Erasmus University Rotterdam, Room M 6-31,P.O. Box 1738, 3000 DR Rotterdam, The Netherlandse-mail: [email protected]

J. Verheul : S. QuakErasmus University Rotterdam, Rotterdam, The Netherlands

J. Verheule-mail: [email protected]

S. Quake-mail: [email protected]

which adopted the shareholder value doctrine inaugurating the organized activism ofpublic pension funds with regard to the management of firms. It was thus in alllikelihood the competition and conflict among different groups of shareholders,primarily corporate raiders and pension funds, that triggered the shift in the balanceof power between managers and shareholders. Since managers found profitable waysto adapt to the new balance of power, the shareholder value ideology spread rapidlythrough the economic field, becoming the dominant business model of North Americanfirms in the second half of the 1980s.

Keywords Shareholder value .Corporate raiders . Institutional investors . Field theory.

Economic sociology

The large corporations that have dominated Western economies since the secondindustrial revolution have been managed in a variety of ways. Their chief executivesallied themselves to specialists whose expertise corresponded to the dominant businessconception. Production and organisation specialists (engineers, military personnel) wereinitially the predominant group, later followed by marketing specialists and, then,increasingly by financial experts (Fligstein 1990, 2001). The last two decades of thetwentieth century saw another transformation, one in which companies tended to bemanaged in the name of relative outsiders, who are not directly involved in companyaffairs, who do not bear any responsibility for the daily functioning of the company, andwho often have only limited knowledge of market conditions and business opportuni-ties: shareholders. How did it become possible that companies’ performance was judgedon the basis of their quarterly increase of shareholder value, and that other businessobjectives (sales growth, innovative capacity, sustainability, increase of market share)became subordinate to that particular aim? Although an extensive literature exists on thenewly acquired power of shareholders and the doctrine of shareholder value, some keyquestions about this far-reaching transformation of corporate strategy have remainedunanswered.

It is by now well documented that the idea of “shareholder value” emerged in theUnited States as a response to the economic crisis of the late 1970s and early 1980s.Due to increased competition from Japanese companies, two oil crises (1973, 1979),and a stagnating economy accompanied by high inflation (“stagflation”), Americancompanies experienced severe economic and financial difficulties (Fligstein 2001,2005). The market value of these large, diversified firms was often below thecombined value of their assets, and after decades of growth many of them hadbecome so large that they had difficulty in adapting to changing circumstances(Fligstein 2001; Lazonick and O’Sullivan 2000).

Following Neil Fligstein’s analysis, the economic crisis caused a breakdown in theprevailing conception of how firms should be managed provoking the outbreak of astruggle about a new business strategy (Fligstein 1990). Fligstein has called thedominant orientation that came out of this struggle the “shareholder value conceptionof control.” Because companies operate under uncertainty and seek stable relations ofexchange, they need a strategic orientation to position themselves vis-à-vis theircompetitors and their internal conflicts. This strategic orientation is for Fligstein aconception of control, because its primary function is to manage the conflictual and

2 Theor Soc (2014) 43:1–22

potentially disruptive relationships between and within companies. During the 1980s,maximizing shareholder value became the new conception of control.

Somewhat analogous to Fligstein, other authors have described the new businessstrategy as a form of corporate governance aimed at splitting up and trading businessunits with the sole purpose of creating short-term shareholder value. Instead of thepreviously dominant business strategy, which focused on company growth and reserv-ing and reinvesting profits—the “retain and reinvest” strategy—serving the immediateshareholder interest became key in the 1980s (Lazonick and O’Sullivan 2000). Thischange in corporate strategy formed the core of the more general transition from“managerial capitalism” to “investor capitalism” (Useem 1996), which can be charac-terized as a historically new form of finance capitalism (Davis 2009; Heilbron 2005).

Various interpretations

Although this development has been interpreted and appreciated in radically differentways, its main characteristics are fairly generally agreed upon: the power over largecorporations shifted partly from management to shareholders, diversified conglom-erates gave way to more focused firms, and finance and financial markets becamemore central in the functioning of American businesses. Although many aspects ofthis transformation have been extensively researched and discussed, the origins andearly diffusion of the shareholder value conception have remained unclear. Theexisting literature offers suggestions as to how the rise and dominance of shareholdervalue occurred, but these interpretations diverge and none of them has been convincinglyempirically tested.

Beyond the idea that the doctrine of shareholder value was primarily carried bycorporate outsiders, there is not much consensus about the groups that initiated theshareholder revolt and how their actions contributed to a reconfiguration of theeconomic field in the United States. According to Neil Fligstein, financial outsiders,such as institutional investors, investment banks, and pension funds, were the first toadvocate actively for more influence for shareholders (Fligstein 2001). Besidesinstitutional investors, Frank Dobbin, Dirk Zorn and others have added financialanalysts and hostile take-over firms to the protagonists of the new conception(Dobbin and Zorn 2005, Zorn et al. 2005). Among these outsider groups, severalauthors have argued that institutional investors were the driving force (Useem 1996;Zorn 2004). Since then pension funds and other institutional investors had signifi-cantly expanded their resources they gradually gained ascendancy over management.Unlike scattered individual shareholders, they were capable of buying significantportions of shares, which allowed them to impose their views on management,especially since they organized themselves from the mid-1980s onwards (Davis andThompson 1994). Beside organized investors some authors have claimed that“corporate raiders,”who acquired stock and reorganized companies without the consentof management, played a significant role as well (Kochan and Useem 1992);others do not consider “raiders” an additional, but rather the primary factor (Lipton andRosenblum 1991).

Aside from various groups of financial outsiders, it has also been argued thateconomists were the actual source of the new conception (Lazonick and O’Sullivan

Theor Soc (2014) 43:1–22 3

2000). Financial economists like Jensen and Meckling started arguing that the relation-ship between management and shareholders has to be conceived as one between an“agent” and a “principal.” Management should be viewed as the principal’s agent,because the shareholders are the company’s owners. This “agency-theory,” based uponJensen and Meckling’s 1976 article “The Theory of the Firm,” would have beendiffused, among others through business schools, thus progressively reshaping mana-gerial practice (Dobbin and Jung 2010; Fourcade and Khurana 2013). This view isconsistent with the literature on performativity, according to which economic theoriesand models instead of simply describing or explaining the economy actively shape andformat the functioning of markets (MacKenzie et al. 2007).

Proposing yet another version of the story, Karel Williams argued that the idea ofshareholder value was introduced during the 1980s by consultants. They would haveprovided managers with the concept of “value based management,” a method ofgovernance that analyzes all business activities in terms of shareholder value. Thisway of thinking would have offered management that was under pressure because oflow stock prices a way to defend themselves against criticism from shareholders andto regain their support (Williams 2000, pp. 1–12).

Aside from questions of terminology and interpretation, the existing literature hasleft three empirical questions unanswered. All are related to the process dynamics ofthe transformation and, as such, have theoretical significance as well. First, there is alack of clarity about the chronology. Commonly the late 1970s and the 1980s arementioned in relation to the economic crisis, but without specifying the sequence ofevents and the temporal pattern of change. Specifying the sequential order seems aprerequisite for deciphering the social dynamics of the process. Second, there arediverging views about which actors started to promote the idea that shareholdersshould control companies. Not only are different groups mentioned, but the evolvingrelationships and interactions among them are rarely dealt with, which makes itdifficult to understand fully the social dynamics of the change. Third, it is not clearwhen and by whom the idea of shareholder value was subsequently adopted andthrough which channels the diffusion took place. Here again the transformation canbe understood only when the most important groups of actors are identified and whenis understood how and why the relationships among them shifted. In this article weprovide some clarification of these three questions.

Theoretical framework

From an economic sociological perspective, the behavior of (economic) actors can beunderstood from the way it is “embedded” in the most relevant set of social relations(Granovetter 1985, Swedberg 2003, Convert and Heilbron 2007). This approach is atodds with assumptions in both economic and culturalist understandings. Unlike theassumptions of “undersocialized” micro-economics, firms are not isolated actors thatmaximize their utility independent of their relations to other relevant actors. And incontrast to the “oversocialized” assumptions of cultural approaches, (economic)actors do not solely act on the basis of beliefs, ideas or norms. Economic sociologistsshould instead focus on how (economic) actors are embedded in concrete systems ofsocial relations and how these relations affect their behavior. This premise, which

4 Theor Soc (2014) 43:1–22

Granovetter bases on network analysis, is also found in other relational approaches,especially in the field theories of Pierre Bourdieu and Neil Fligstein (Bourdieu 2005;Fligstein 2001; Fligstein and McAdam 2012). The relational perspective assumes thata company’s interests are not simply given, but instead have to be defined by actorsthat are positioned in a specific, relatively autonomous field that is in a dynamicconstellation of interrelated and competing firms, financiers, and their various allies,forming the core of the economic field.

From this perspective, the first step toward understanding changes in corporatestrategy is to analyze how the structure of relationships in which large corporationsare embedded has evolved. In doing so, Bourdieu focuses on the position actorsoccupy in the field in which they operate, on the volume and composition of thecapital they dispose of, and on their dispositions, that is their inclination to use theseresources in certain, and not in other ways (Bourdieu 2005). Understanding thetransformation of a field implies analyzing how groups of challengers have beenable to intervene in the existing power relations to their advantage, in this case howthe power relations between managerial elites and groups of shareholders shifted infavor of the latter. Fligstein’s version of field theory, which has been informed by neo-institutionalism, puts specific emphasis on business conceptions, which stabilize theeconomic field over longer periods of time, until they lose their role during a crisisand are replaced by a new conception. The shareholder value conception of the firmillustrates that the stuggles in the economic field have an important cultural dimen-sion. As Bourdieu and Fligstein have insisted, economic and financial interests do notautomatically lead to action, they have to be framed in a certain manner in order toacquire legitimacy and lead to the active involvement of specific groups. In particularfor understanding periods of field transformation, insights of social movement theoryare relevant and can be integrated into field theory (Fligstein and McAdam 2012).

Since the economic field is only relatively autonomous, Bourdieu and Fligsteinhave both called attention to the broader field environment, and, like Karl Polanyiearlier, insisted on the crucial role of the state and the political and legal conditionsunder which the economic field functions. For understanding the emergence of theshareholder value conception of the firm the changing political context was immedi-ately relevant, since it was characterized by government policies aimed at tax relieffor corporations, deregulation and market liberalization. After the presidency ofJimmy Carter (1977–1981), who took the first steps in this direction, the Reaganadministration (1981–1989) dismantled protective measures, facilitated the marketfor corporate control, and restricted union power (Fligstein 2001, 2005; Davis andThompson 1994). Under these conditions it became much easier to buy, reorganizeand sell firms, thus contributing directly to the shifting power relations in theeconomic field from corporate executives and their social networks to shareholdersand other market-based groups.

This briefly summarized field approach can be fruitfully used to investigate boththe origins and the diffusion of corporate strategies. A number of general expectationsmight be derived from field theory for this particular case. It is most likely, forexample, that the change was initiated and carried by relative outsiders, and that theiractions provoked a period of crisis and struggle with the ruling elites. It is also quitelikely that such outsiders did not distinguish themselves from the managerial elitemerely in terms of material interests and resources, but also in symbolic or cultural

Theor Soc (2014) 43:1–22 5

terms and in terms of their dispositions. The appearance of challengers and the effectof their actions, furthermore, depend on conditions beyond the economic field proper,and in particular on the role of the state, the juridical apparatus, and the regulators.

But such “predictions” remain rather general and run the risk of using theempirical material merely as an illustration of theoretical propositions. Instead offollowing a deductive procedure, a field perspective is more properly used heuristi-cally and to explore the empirical material by focusing on the structure and strategiesof interrelated groups and on the power relations between them. Bourdieu neveradopted a hypothetical-deductive style, in Fligstein’s work it is not predominant, andaccording to some field theory is, in fact, “diametrically opposed” to the hypothetico-deductive model (Martin 2011, p. 282). Without lapsing into the opposite, inductiviststyle, field theory is most fruitfully used as a framework that provides a generalrelational perspective on the object of study as well as a number of explanatoryconcepts that can account for both stability and change in relatively autonomous,social universes, with specific stakes.

Research strategy

Following such a more exploratory research strategy, we first try to specify when andamong which groups the notion of “shareholder value” arose. Then we consider howthis new conception spread and in particular show how the diffusion was affected byconflict and competition within the group of shareholders. Contrary to a widespreadassumption, shareholders do not form a homogeneous or unified group: their positionwithin the economic field differed, as did their resources, dispositions, and relation-ships to managerial elites. The diffusion of the shareholder value conception was aconflictual process as well, depending on changing power relations within theeconomic field, which were in turn conditioned by changes in the political field,and in particular by the politics of deregulation, which reshaped the economic fieldduring the 1980s. In the last section of this article, we come back to the theoreticalquestions and try to formulate some implications of the case study presented.

To explore the origins and spread of shareholder value we followed an indirectmethod of inquiry. In the absence of having direct access to key players, we analyzedpublications in prominent business media. This method and the selected sourcesobviously have serious limitations. Much of what is relevant to such issues is notproperly covered in public media. But the limitations of public sources apply tocertain topics more than to others, and to certain actors more than others. With regardto the question of “shareholder value,” it may be assumed that it has been discussed inpublic media to a significant degree, because it dealt with the strategic issue ofwhether or not firms should change their way of doing business. Such a topic can,in principle, be legitimately researched by using public sources, although the validityof the results of such an analysis depends on evidence from other sources. The degreeof public exposure, furthermore, varies considerably for different actors. While someactors consistenly avoid public exposure, others actively seek it. Investment bankers,for instance, operate under great discretion (cf. Eccles and Crane 1988). Othersgroups, such as “corporate raiders,” had an interest in a public stir and often usedthe media for opposing management and promoting their view. Because of thedivergent meanings of public reporting for the various parties involved, public reports

6 Theor Soc (2014) 43:1–22

cannot be assumed to have adequately represented what occurred, and they have to betreated with caution and a sociological sense for the differential public strategiesemployed by the actors.

To overcome somewhat the limitations of public sources, we chose a primarysource that is considered to be fairly reliable for developments in corporate America,the Wall Street Journal. Information derived from this source was supplemented bydata obtained from more specialized media. Obviously these choices do not takeaway the aforementioned limitations. Only further research can determine to whatextent media coverage from the chosen sources can be said to have been more or lessaccurate or whether it should be complemented and corrected by other sources.

As the leading US business newspaper, the Wall Street Journal is the main sourceof our analysis. We used its historical archive, which dates back to 1889 and isavailable via Proquest. 1 Certain articles in this newspaper lead us to consult otherpublic media as well. All issues of the Institutional Investor from 1975 to 1986 wereconsulted in order to have an indication about the responses and views of institutionalinvestors. The role of business scholars was explored through the Harvard BusinessReview (using the archives of EBSCO host). 2 And for inquiring into the possible roleof economists and “agency,” theory, we consulted the Journal of Financial Economics(available via Science Direct).3

First, we determined how the frequency of the articles in which the notion of‘shareholder value’ occurred evolved. Then, we examined the content of the articlesin which the expression appeared, identifying both the main actor and the context ofeach occurence. For each article, one actor and one context were distinguished,because it became apparent that one actor and one context were dominant in nearlyall cases. The number of articles that displayed multiple contexts was so small that itcould be neglected. Because it was not clear in advance that the idea of “shareholdervalue” was covered by a single term, we studied a number of combinations of theterms “share,” “stock,” “holder,” and “value.” We soon discovered that “shareholdervalue”was indeed the generic term, whichwe have therefore used throughout the article.

Shareholder value in the United States

Although “shareholder value”may seem a conception that is as old as capitalist firms,the expression appears to be fairly recent. The term was not mentioned in the WallStreet Journal before 1965; terms with a similar meaning did not occur either. From1965 to 1979, only eight articles mention shareholder value. The frequency started toincrease from 1980 onwards, slowly at first, rapidly from 1983 until a first peak wasreached in 1988. From then on the frequency fluctuated (see Fig. 1). The fluctuationsseem to be related to the economic conjuncture and especially to the movement of the

1 ProQuest LCC is an online distributor of written sources and videos. ProQuest provides archives to(among others) newspapers, journals and microfilms to universities, schools, libraries and governmentagencies around the globe.2 Ebscohost Publishing is an online distributor of written sources such as (scientific) journals, books andreports. Ebscohost services universities, schools, libraries and governments agencies around the globe.3 ScienceDirect is an online distributor of published scientific articles, primarily from the natural sciencesbut also a selection of the social sciences.

Theor Soc (2014) 43:1–22 7

stock market. The frequency dropped during the economic downturn in the beginningof the 1990s, and rapidly increased during the bull market of the second half of the1990s. When the “dotcom bubble” burst in the early 2000s, the frequency drasticallydecreased, after which, when the stock market recovered, it slowly increased again.

During the period in which the expression “shareholder value” made its firstappearance, the term was used not by shareholders or their representatives but, rather,primarily by executives (see Table 1). This applies to six of the eight articles in

Fig. 1 Frequency of the term “shareholder value”’ in the Wall Street Journal (1965–2007)

Table 1 Frequency ‘shareholder value’ in the Wall Street Journal (1965–1979)

Year Actor and context Frequency

Executive board Investment fund Shareholder

1965 Company results – – 1

1967 Hostile takeover – – 1

1969 Appeal to investors – – 1

1970 – Appeal to investors – 1

1972 – – Reward executive board 1

1975 Appeal to investors – – 1

1976 Restructuring – – 1

1977 Appeal to investors – – 1

Total 8 1 1 8

8 Theor Soc (2014) 43:1–22

question. In these articles, half of which were ads, corporate executives promisedattractive dividends to new investors.

The first article in which the notion of shareholder value appeared is a report from1965 about the company Allied Chemical, according to which the chairman of theboard announced a higher dividend, because the company results were excellent andthe prospects favorable (WSJ, 29-01-1965). The first ad with the notion of share-holder value is from 1969 and concerned the initial public offering (IPO) of Masco.This company was headed by Richard Manoogian, son of the founder AlexManoogian, and the IPO was accompanied by a clear mission statement: “It’s Masco’sphilosophy to provide greater returns to its shareholders” (WSJ, 5-5-1969). A secondad appeared in 1975 and was signed by the chairman of Bendix: W.M. Blumenthal. Inthis ad Blumenthal states that creating shareholder value is more important than thecompany’s growth: “Bendix’ growth in recent years has been directed not primarilyto volume, but more specifically to what we call shareholder value.” Blumenthaldescribed shareholder value as the potential growth of revenues and profits:“Shareholder value means … the ability to grow in sales and earnings” (WSJ, 22-5-1975). This description seems to be a combination of the traditional pursuit of growth inearnings and profits and a new conception in which shareholder value tends to prevailover other business objectives. Other publications, however, indicate that Blumenthal,who two years later became Secretary of the Treasury in the Carter administration, wasby no means an advocate of the strategy that was later referred to as shareholder value(Blumenthal 1976).

The remaining four articles refer to shareholder value in a different context. In twoof them the concept of shareholder value is related to changes within a company. Anacquisition, which is reported about in 1967, was partially defined in terms ofshareholder value. Kaiser Industries, a family business, was broken up intothree parts in 1976 and the parent company was liquidated. At the pressconference after the shareholders’ meeting, Edgar F. Kaiser, member of thesupervisory board and son of the founding father, stated: “The only reason for theliquidation is to enhance the financial position of the company’s shareholders”(WSJ, 6-5-1976).

The early uses of the term indicate that the expression “shareholder value” wasrarely used before 1980. All articles in which it occurred are texts in which manage-ment directly addresses shareholders and the expression “shareholder value” isintended to appeal to their interests, since they are asked to invest in the companyor support the management with regard to specific plans. There is no indication thatthe term referred to a specific conception of the company’s strategy or to a theoret-ically based idea of corporate governance or control, such as Jensen and Meckling’stheory of the firm. The Wall Street Journal, furthermore, did not refer to “agencytheory” or “theory of the firm” until 1987; nor was there any reference to Jensen or toMeckling in the newspaper prior to that year. The Wall Street Journal then does notoffer support for the hypothesis that agency theory played an important role in the riseor early diffusion of shareholder value.

The way Jensen and Meckling’s article was received in the academic journal inwhich it was originally published, the Journal of Financial Economics, seems toindicate that even in circles of financial economists, agency theory had a relativelymarginal position for quite a while. It was increasingly cited only from 1987 onwards,

Theor Soc (2014) 43:1–22 9

especially during the years 1987–1991.4 This citation pattern suggests that agencytheory started to play an important role only after shareholder value had obtained asignificant role in the economic field itself. Agency theory thus seems to haveprovided academic legitimacy after the fact, rather than exemplfying a form ofperformativity.

Redefining shareholder value (1980–1982)

During the years 1980–1982 the attention for shareholder value in the Wall StreetJournal increased (see Table 2), and both the meaning and the context of theexpression changed. Shareholder value was no longer defined in terms of dividend,but, instead, in terms of actual or potential market value of the company. This changetook place in the context of “hostile takeovers,” which put management underpressure, while shareholders were becoming more actively and prominently involvedin business affairs. During these 3 years the new meaning became more dominant aswell. The first article in 1980 is revealing in this respect. It discussed a book calledFinancial Strategy (1979), written by the business scholar William E. Fruhan Jr., whowas affiliated with Harvard Business School. Fruhan was alledgedly one of the first tofocus on the business aspects of shareholder value (WSJ, 8-3-1980). His studydiscusses how shareholder value can be established in terms of market value andcash flow, and how these can be increased by the executive board. The book onlycasually refers to Jensen and Meckling’s (1976) article, “The theory of the firm.”With three other articles, it is catagorized as one of the “most recent advances in thetheory of the capital structure.” Fruhan, in other words, regarded the article about the“theory of the firm” as being relevant to issues of corporate finance, and not primarilybecause it developed the idea of “agency” and its implications for redefining howfirms should be managed.

In the articles that followed, shareholder value obtained a different meaning. Thethird article from 1980 discussed a company called Bendix. The firm sold parts of theenterprise that were not profitable enough and that didn’t fit with its “core business.”

4 Number of citations of ´The Theory of the Firm´ (1976) in the Journal of Financial Economics (1976–1986)excluding self-citations:

Jaar

1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986

N = - - 2 - - - - 3 - 3 1

Number of citations of ´The Theory of the Firm´ (1976) in the Journal of Financial Economics (1987–1996)

without self-citations:

Jaar

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996

N = 9 14 11 10 3 4 2 7 6 6

10 Theor Soc (2014) 43:1–22

After selling these parts, the company’s chairman, William M. Agee, wanted toacquire other companies in order to increase the firm’s shareholder value (WSJ, 23-9-1980). In an article from 1981, a pension fund, the Quebec provincial government’spension fund, has a leading role for the first time. In this case the executive managementwas no longer the main actor in the story and the context was that of a hostile takeover.The Canadian pension fund was planning to form a consortium for the hostile takeoverof Noranda. The consortium’s objective was to force Noranda to change its strategy andmake shareholder value its central goal (WSJ, 24-6-1981).

In 1982 Louis J. Brindisi Jr. of consulting firm Booz, Allen & Hamilton publishedan interesting article. Brindisi, an expert in remuneration policy, argued that it is notappropriate for managers to receive large pay increases when the value created forshareholders had been limited: ‘High earnings won’t help shareholders.” Accordingto the author, shareholders own the company and management must therefore act inline with their interests (WSJ, 14-6-1982).

It is quite telling that although the meaning of the notion of shareholder value waschanging, management continued to be the primary actor of the news coverage. Withone exception all articles during these years (1980–82) discuss takeovers, nearly allhostile takeovers, but it is not the take-over firm that is central in the reports. Perhapsfollowing a convention from the era of managerial capitalism, management remainsat the center of the journalistic attention.

The breakthrough of shareholder value (1983–1986)

In the years from 1983 through 1986 the use of the term shareholder value increasedrapidly. The context in which the term appeared is again most frequently that ofhostile take-overs, immediately followed by related issues of restructuring andcorporate strategy. The uses of the notion of shareholder value thus seem clearlyrelated to a struggle over the reorientation of corporate strategy. In addition tomanagement, corporate raisers now appear as the second most important actor, wellbefore other groups. The structuring principle of the debate over shareholder valuethus appears to be the opposition between managers and raiders. Because of the

Table 2 Frequency of “shareholder value” in the Wall Street Journal (1980–1982)

Year Actor and context

Management Publicpension fund

Businessscholar

USSenate

Consultant Frequency

1980 - hostile takeover (2) - Opinion piece 3

1981 - non-hostiletakeover

- hostile takeover 2

1982 - hostile takeover (2) - reward executiveboard (2)

- corporate strategy

5

total 5 1 1 1 3 10

Theor Soc (2014) 43:1–22 11

widening range of actors, however, it is no longer possible to provide a combinedactor/context overview, so we provide separate tables for the context and the actors(Table 3 and 4).

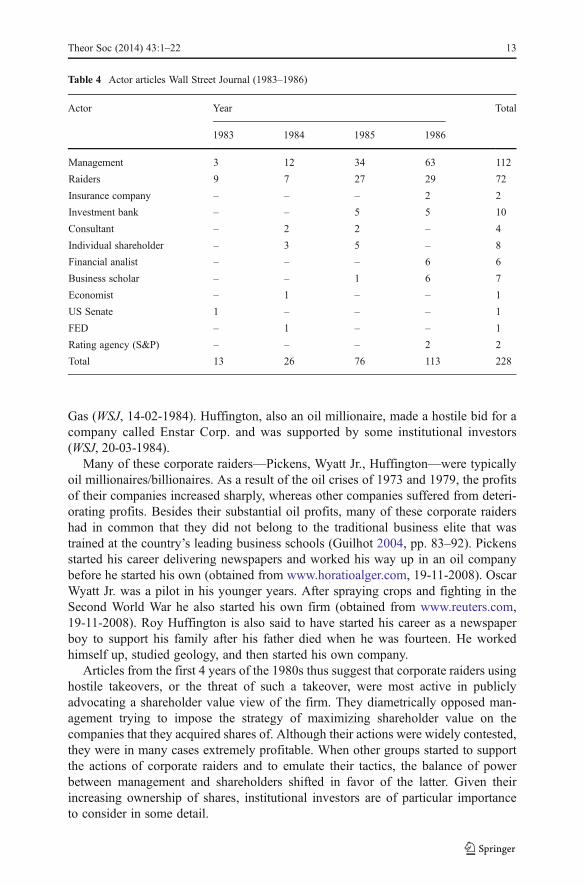

In 1983, thirteen articles refer to shareholder value, eight of which discuss thebattle between Gulf Oil and the “corporate raider” Thomas Boone Pickens. Pickensused his own oil company, Mesa, to form a consortium that was planning to acquireGulf Oil, because its management did not create sufficient value for its shareholders(WSJ, 9-11-1983). The consortium acquired shares of Gulf Oil and placed ads in theWall Street Journal to convoke other shareholders to vote in favor of their plan toestablish a “royalty trust.” Such a construction was used to “strip” a company from itspossessions. Alledgedly Pickens had only one goal: “We are dedicated to the goal ofenhancing shareholder value and oppose any action contrary to that goal.” He castdoubt on the commitment of the management by stating that his consortium ownedmore than 55 times the number of shares management owned: “Ask yourself whichgroup is more interested in maximizing the value of Gulf stock” (WSJ, 21-11-1983).Ultimately, the consortium lost the battle for Gulf Oil, but it remained belligerent:‘We are fully dedicated to maximizing shareholder values. That was our goal in thebeginning. We will be here when the job is finished.’ (WSJ, 14-12-1983).

Pickens’s role in this struggle is a good example. Together with other “corporateraiders,” such as Asher B. Edelman, Oscar Wyatt Jr., David H. Murdoch, Roy M.Huffington, and Carl Ichan, he played a key role in the breakthrough of the concep-tion of shareholder value. They formed a vanguard of people who were most activeand publicly spoke out on behalf of the new concept. In 1983, Edelman, who was theinspiration for the character Gordon Gekko in the movieWall Street (1987), formed aconsortium to take over a company called Canal Randolph. He claimed that this firmwas poorly managed in terms of shareholder value (WSJ, 29-03-1983). Wyatt, an oilmillionaire, was discussed in an article when attempting to acquire Houston Natural

Table 3 Context articles Wall Street Journal (1983–1986)

Context Year Total

1983 1984 1985 1986

Hostile takeover 5 8 27 39 79

Non-hostile takeover – 2 1 4 7

Restructuring – – 13 31 44

Merger – 1 1 1 3

Corporate strategy 2 4 6 11 23

Company results – 1 2 1 4

Share buyback program – 1 1 4 6

Reward of established management – – 1 – 1

Stock price – 1 – – 1

Appeal to investers 6 6 24 14 50

Opinion piece – 1 1 8 10

Total 13 26 76 113 228

12 Theor Soc (2014) 43:1–22

Gas (WSJ, 14-02-1984). Huffington, also an oil millionaire, made a hostile bid for acompany called Enstar Corp. and was supported by some institutional investors(WSJ, 20-03-1984).

Many of these corporate raiders—Pickens, Wyatt Jr., Huffington—were typicallyoil millionaires/billionaires. As a result of the oil crises of 1973 and 1979, the profitsof their companies increased sharply, whereas other companies suffered from deteri-orating profits. Besides their substantial oil profits, many of these corporate raidershad in common that they did not belong to the traditional business elite that wastrained at the country’s leading business schools (Guilhot 2004, pp. 83–92). Pickensstarted his career delivering newspapers and worked his way up in an oil companybefore he started his own (obtained from www.horatioalger.com, 19-11-2008). OscarWyatt Jr. was a pilot in his younger years. After spraying crops and fighting in theSecond World War he also started his own firm (obtained from www.reuters.com,19-11-2008). Roy Huffington is also said to have started his career as a newspaperboy to support his family after his father died when he was fourteen. He workedhimself up, studied geology, and then started his own company.

Articles from the first 4 years of the 1980s thus suggest that corporate raiders usinghostile takeovers, or the threat of such a takeover, were most active in publiclyadvocating a shareholder value view of the firm. They diametrically opposed man-agement trying to impose the strategy of maximizing shareholder value on thecompanies that they acquired shares of. Although their actions were widely contested,they were in many cases extremely profitable. When other groups started to supportthe actions of corporate raiders and to emulate their tactics, the balance of powerbetween management and shareholders shifted in favor of the latter. Given theirincreasing ownership of shares, institutional investors are of particular importanceto consider in some detail.

Table 4 Actor articles Wall Street Journal (1983–1986)

Actor Year Total

1983 1984 1985 1986

Management 3 12 34 63 112

Raiders 9 7 27 29 72

Insurance company – – – 2 2

Investment bank – – 5 5 10

Consultant – 2 2 – 4

Individual shareholder – 3 5 – 8

Financial analist – – – 6 6

Business scholar – – 1 6 7

Economist – 1 – – 1

US Senate 1 – – – 1

FED – 1 – – 1

Rating agency (S&P) – – – 2 2

Total 13 26 76 113 228

Theor Soc (2014) 43:1–22 13

The involvement of institutional investors

During the first years of the 1980s, institutional investors were hardly ever mentionedin the Wall Street Journal in relation to the shareholder value movement. Initiallytheir approach was indeed quite different from that of corporate raiders. Institutionalinvestors were accustomed to refrain from directly interfering in corporate affairs. Ifthey did not agree with management policies, they would vote “with their feet” andsell their shares instead of pressuring management. That is in all likelihood the reasonwhy pension funds and mutual funds are hardly ever mentioned as the primary actorin the newspaper articles (cf. Table 4). It was only after the hostile takeover attemptsof raiders had proved to be very lucrative, and the Reagan administration and theregulators refused to ban or regulate these practices, that public pension funds beganto adopt a more active stance towards management in favor of shareholders.

In the 1970s, the Institutional Investor, the leading magazine for institutionalinvestors, primarily contained practical advice, success stories on well performingcompanies and investment funds, and “ratings” of CEOs and business analysts.Changes in government policy and regulation were also closely followed and suc-cinctly summarized for the readership of professional investors. During the late 1970sand early 1980s the magazine changed and shifted from practical advice to a morestrategic approach. The second oil crisis (1979) seems to have triggered this shift.According to the magazine the new oil crisis had resulted in an “acquisition crisis”:“Target companies, raiders—and the financial companies caught in-between—havebeen thrust into an expanded and fiery arena filled with hazards and conflicts unheardof only a few years ago”’ (Institutional Investor, June 1979, p. 31). Although themagazine occasionally quoted favorable views on hostile takeovers, it remained veryreticent to endorse these tactics. Detecting “target companies” for possible acquisi-tions was explicitely not regarded to be a task of institutional investors (II, June 1981,pp. 47–51). The Institutional Investor, furthermore, did not pay any attention either toJensen and Meckling’s agency theory in the period 1975–1985.

The first significant change in this respect was related to the changing politicalconditions after the presidential election of Ronald Reagan. It was expected that thepolicy of the Reagan administration would have a strong positive effect on the equitymarkets, and the newly appointed chairman of the Securities and ExchangeCommission (SEC), John Shad, who supervised the financial markets, was widelypraised in the journal. Shad was a former investment banker who had worked in thefinancial sector for 30 years and wished to change existing regulation in favor ofinvestors (II, April 1982, pp. 58–69). Although hostile takeovers were highly contro-versial, both within and outside corporate America, the SEC opposed all proposals formore regulation. Because all stringent regulation was expected to be blocked by apresidential veto, not a single one of the many proposals for such regulation was adoptedby Congress (Bruck 1988, p. 260).

Once it had become clear that the new administration would not take any measureto regulate takeovers and, instead, would block regulation, the Institutional Investorprinted a first article about a corporate raider—Carl Icahn. Although Icahn wasdescribed as a “notorious corporate opportunist” and a “racketeer, who would notgive way for anyone in his search for ‘quick money,’” the same issue quoted aninvestment banker claiming that the strategies of raiders were increasingly recognized

14 Theor Soc (2014) 43:1–22

in corporate America (II, October 1982). One year later, in 1983, an article called“The New Activism at Institutions” stated that institutional investors were increas-ingly taking an activist approach towards management and were more often votingagainst their proposals: “more and more institutional shareholders … are rising up toexert their power” (II, October 1983, p. 177). Corporate raiders are no longercriticized for their brutal and “hostile” approach, but for the fact that their actionswere often solely in their own interest and not in the interest of all shareholders.Raiders such as Icahn and others had the habit of bying 5 or 10 % of the outstandingshares, while threatening to buy more. Management was inclined to buy back theseshares for a considerably higher price. This practice of “greenmailing,” as it wascalled, was widespread between 1979 and 1984. For blocks of stock that wererepurchased companies paid prices that were on average 5 to 50 % higher than themarket price (Kosnik 1987). It was in particular this practice of greenmailing and thetensions it generated among shareholders that provoked institutional investors to takea more active stance themselves (cf. II, January, 1984, pp. 87–88).

By 1984, several articles in the Institutional Investor were explicitely devoted tothe promotion of shareholder value. Corporate raiders were portrayed in a positivemanner as pioneers in influencing management: “Operators like … T. Boone PickensJr. and the Bass family have exploited stockholder discontent masterfully, producingfantastic payoffs in the process” (II, May 1984, p. 186). In the same year, a secondinterview with corporate raider Icahn was published, in which he lashed out at the“‘self-serving” management of American corporations. Icahn believed that institu-tional investors should oppose these practices and stated that the time had come to doso in an organized manner (II, October 1984, p. 11). Six months later the magazineannounced the founding of the Council of Institutional Investors (1985). This council,which twenty-two public pensions funds were members of, stated that it would takeon the enhancement of shareholder value in an organized manner (II, May 1985, pp.107–122). Unlike the far more cautious company pension funds, public pension fundsadvocated an active shareholder value approach. It was a trustee of the CaliforniaPublic Employees’ Retirement System (CalPERS), Jesse Unruh, who initiated thecreation of the council. What triggered his action was a contemporary case of“greenmailing.” In 1984 Texaco had repurchased 10 % of its shares from raiders,the Brass brothers, for $55 per share, while the official share price stood at $35. Sincethe CalPERS was one of the largest shareholders of Texaco, but did not receive thesame offer as the raiders, its trustee contacted other public pension funds to undertakeaction and draft a Shareholder Bill of rights. In this statement the unequal treatment ofshareholders was explicitly rejected within the framework of defining the commoninterests and rights of shareholders (Monks and Minkow 1991).

It seems quite likely that the establishment of the Council of Institutional Investorsand a few contemporary related initiatives tipped the balance of power betweenmanagers and investors in favor of the latter. Corporate raider T. Boone Pickensfounded the United Shareholders Association (1986), which advocated the interestsof individual shareholders from the same view. The U.S.A., as it was characteristi-cally abbreviated, was an association that could be joined by anyone who ownedshares for a total of one hundred US dollars or more. Its goal was to promote theinterests of shareholders and it took a clear stand against poorly performing manage-ment (Tortorello 2004). The organized efforts of shareholders and the activities they

Theor Soc (2014) 43:1–22 15

undertook in the second half of the 1980s and the beginning of the 1990s representedsomething of a social movement that succeeded in organizing and unifying share-holder interests (Davis and Thompson 1994).

Aside from raiders, institutional investors and financial economists, two othergroups have been mentioned with regard to the rise of shareholder value: consultantsand investment bankers. Consultancy firms and investment banks can initiate andoften accompany processes of corporate change, but their role is fundamentallydependent on the primary actors to whom they offer their services. In that sense itis unlikely that they had the same weight as take-over firms or institutional investors.Given their intermediary role, it is most plausible that they worked for both targetedas well as for take-over firms. It is difficult, however, to assess their role in theshareholder movement on the basis of public sources like the Wall Street Journal.Consultants and investment bankers operate discretely and only rarely and selectivelyseek the media, which makes it understandable that consultancy firms and investmentbank appear only relatively late in the coverage of the Wall Street Journal.

Prior to 1984, consultants in the Wall Street Journal were not associated with theidea of shareholder value; in 1984 and 1985 only 4 articles had consultants as theirmain actor. All of these articles were in fact ads from consultancy firms offering theirservices to companies to help them increase their market value. In these ads a highshare price was presented as the best protection against a hostile takeover: “You oweyour shareholders the best defense” (WJS, 01-03-1984). It could be inferred thatconsultants were indeed involved in the spread of shareholder value, but, initially,rather to defend the interests of management by whom they were hired. During theseyears, the “value based management techniques” were also used by management toprotect their own position. Consultants have probably contributed to the spread ofshareholder value, particularly after business schools had adjusted their curricula tothe new trend. Yale’s and Harvard’s business schools, for example, started to offercourses in which the creation of shareholder value during restructuring, mergers, andacquisitions was central. At Harvard Business School, it was Michael Jensen andMichael Porter who took the initiative (WSJ, 12-8-1985). If Harvard Business Reviewcan be considered a valid source for indicating the involvement of consultants, it canbe noted that shareholder value—with the exception of articles in 1955 and1981—appears relatively late as well; it is not mentioned until 1986.5

Investment banks appeared in theWall Street Journal as main actors in relationshipto shareholder value only from 1985 onwards. Given their highly discrete mode ofoperation, it is probably typical that consultants and investment banks appeared in thecoverage of the Wall Street Journal only when the shareholder value view had alreadybecome a legitimate business conception. It is quite plausible that after managementwas forced to meet the demands of activist shareholders, business specialists such asconsultants and investment bankers were hired to develop and implement the new

5 Articles mentioning the term “shareholder value” in the Harvard Business Review

Year

1955 1981 1986 1987 1988 1989 1990

N = 1 1 3 2 1 3 3

16 Theor Soc (2014) 43:1–22

corporate strategy. Yet given the limited significance of public media for understandingthe operations of these groups, other sources would have to be used to properly examinetheir role in the shareholder movement.

Shareholder value as the dominant vision on the firm

From around 1985, the shareholder value conception seems to have acquired apredominant position among the main actors in the economic field. While the notionwas hardly ever mentioned before 1980, it had become widely used. In the beginningof the 1980s the term and the idea associated with it was used primarily by corporateraiders in their battles with management; by the mid-1980s various actors used it.After initial resistance, management by the mid-1980s seems to have accepted thatshareholders were an actor that needed to be taken into account more seriously(Useem 1993). This acceptance seems to have translated into a double strategy. Onthe one hand managers sought to reduce the risk of the increasing power of share-holders. They did so by adopting “poison pills,” a takeover defense that sharplyincreases the costs of a firm for a hostile buyer (Davis 1991), and by introducing“golden parachutes” for themselves in case they were fired after a takeover (Fiss et al.2012). At the same time managers became more cooperative towards shareholdersand their organizations, and in return they negotiated additional compensation pack-ages, which would depend on the creation of shareholder value (share packages,premiums, bonuses, stock options, etc.). The spread of shareholder value as a centralbusiness objective was thus accompanied by a considerable increase in executivecompensation, which partly explains why the new doctrine was relatively quicklyembraced by managerial elites. The spread of shareholder value during the 1980s andthe beginning the 1990s coincides clearly with the rise of executive compensation,which explains a significant part of the rising inequalities in income and wealth(Lazonick 2013).

In response to this change in managerial attitude, raiders also adapted their tactics. In1985, the often discussed corporate raider Pickens stated that his own company Mesawould no longer conduct hostile takeovers. Instead, he would set up an investment fundthat would not act as a takeover machine, but as a management partner: “I have no plansright now other than to be just a general partner” (WSJ, 27-08-1985). The British raiderJames Goldsmith similarly announced that he would cooperate with management toachieve the common goal of enhancing shareholder value: “Sir James is expected toattend his first meeting of the Crown Zellerbach Board in San Francisco tomorrow …and has promised to work together with Crown's board to maximize shareholder valuethrough restructuring Crown” (WSJ, 12-06-1985).

The fact that corporate raiders publicly declared their taking a more cooperativestance probably indicates that the attitude of the executives had changed. Managersincreasingly focused on enhancing shareholder value themselves and hired consul-tants and investment banks to execute the new strategy. In the mid-1980s severalexecutives were quoted in the Wall Street Journal, explaining that they wanted thebest for their shareholders. Chairman J. Hugh Liedtke of Pennzoil, for instance, statedthat he was not busy with “empire building”: “we’re not going to grow at share-holders expense’ (WSJ, 22-11-1985). The change resulted in remarkable financial

Theor Soc (2014) 43:1–22 17

transactions. In 1986, Colt Industries, for instance, decided to pay out $1.5 billion toits shareholders before taking a $1.4 billion loan that was intended for acquisitions inorder to enhance its shareholder value even more (WSJ, 21-06-1981).

The finding that the shareholder conception of the firm seems to have gained aprominent and well established position in the economic field around 1985 corre-sponds to findings of research on proxy statements, regulatory documents, andmarket reactions to stock repurchase plans: by the mid-1980s prevailing beliefs aboutcorporate governance had shifted from a managerial to a shareholder conception ofthe firm (Davis and Thompson 1994; Zajac and Westphal 2004).

Empirical conclusions and theoretical implications

A fairly clear pattern concerning the origins and early spread of shareholder value hasemerged from the Wall Street Journal and the other sources we consulted. After asmall number of incidental occurrences in the 1960s and 1970s, the public use of thenotion quickly increased from 1980 onwards becoming the catch word for a new wayof managing firms. Shareholder value was no longer simply defined in terms ofdividend, as it had been before, but came to be conceived as the actual and potentialmarket value of firms. This change was initiated by corporate raiders, whothreatenend to take over companies that did not generate sufficient value for theirshareholders. In these takeover battles they turned against established management inthe name of enhancing shareholder value, which—they argued—was companies’only legitimate objective.

That the struggle between managerial elites and activist shareholders was settled infavor of the latter in a relatively short timespan can be explained by the swift changein attitude of public pension funds. As a result of the collectivization of shareownership, institutional investors had accumulated more potential power than dis-persed individual investors ever had. The rivalry between raiders and public pensionfunds over the profits of hostile take-overs led to the founding of the Council ofInstitutional Investors (1985), which adopted the shareholder value view of the firmand inaugurated an activist stance with regard to the management of firms. Central tothe social dynamics of the process was the conflict and competition between differentcategories of shareholders, corporate raiders, and public pension funds, which pro-voked the organization of institutional investors, thus shifting the balance of powerbetween managers and shareholders. Since managers found profitable ways to adaptto the new balance balance of power, the shareholder value ideology spread rapidlythrough the economic field, becoming the dominant business model of North Americanfirms in the second half of the 1980s.

Two analytically distinct developments had made these operations possible, onelocated within the economic field itself, the other in the political realm. First, manycorporate raiders had earned their fortunes during the oil crises, when other compa-nies went through a sharp economic downturn that had undervalued their stocks. Asfar as corporate raiders did not only use their own capital, they relied on newinvestment techniques such as the so-called junk bonds, low valued and traditionallyhard to sell corporate bonds. This concentration of financial resources during a deepeconomic crisis enabled a relatively small group of outsiders to gain power over even

18 Theor Soc (2014) 43:1–22

some of the largest corporations. Second, the deregulation of the economy by theReagan administration made hostile takeovers much easier to execute than before andgovernment policies also favored owners of capital in various other ways (Fligstein2005, pp. 126–127). The combination of these two developments shifted the balanceof power in favor of activist investors, which had few ties and loyalties to establishedmanagement and who pursued their interests disregarding those of other groups ofshare and stakeholders.

Although there are good reasons to be cautious about findings based on a limitedsample of public sources, our study has found no indications that other groups mayhave played an equally important role as the corporate raiders. This applies inparticular to financial economists such as Jensen and Meckling who developed theagency theory of the firm. It seems that corporate raiders and their closest allies didnot need agency theory to advocate a shareholder view and justify their financialoperations. According to the sources examined, agency theory does not seem to havegenerated much interest in the beginning, neither in the business world nor in theacademic community. There are some indications that the attention for agency theoryincreased mainly after the shareholder value doctrine had been adopted by institutionalinvestors, which suggests that it has had a legitimizing rather than a performativefunction.

Theoretically, the rise and early spread of shareholder value seems best understoodfrom a field perspective. But the case study we presented raises questions not only offield theory as compared to other theoretical perspectives, but also of issues that areinternal to this approach. Field theory today includes different varieties, ranging frommore culturalist versions that center on the shared understandings of actors in afield to institutionalist accounts in which organizations are the main actors and(de)institutionalization is the central process, to the more structural versions of Bourdieuand Fligstein that we have relied upon in this article (see Fligstein and McAdam 2012;Martin 2011).

Instead of limiting the analysis to either cultural or economic change, or for thatmatter to general features of financialization and neoliberalism,an approach in termsof field dynamics is broad enough to capture the various dimensions of the transfor-mation studied, while at the same time being able to include a plurality of actors.Central to the more structural approach we have followed are the shifting powerrelations between interrelated groups, each of them occupying a particular position inthe economic field and endowed with a set of resources the uses of which areassociated with particular dispositions and strategies. The shareholder value concep-tion of the firm was typically articulated by a group of outsiders, raiders, the actionsof which provoked the involvement of another group: public (but not corporate)pension funds. This involvement of particular groups and the dynamic interactions itproduced under specific political conditions was the predominant characteristic of thereconfiguration of the economc field that took place in the first half of the 1980s.

As our case study suggests, this version of field theory offers distinct analyticaladvantages over other versions and approaches. First, it is better suited to explore andexplain the dynamics of the business world than individualist perspectives, whichignore relatively cohesive groups of actors, and macro approaches, which assumemore or less homogeneous interest groups or classes and abstract from the actualdifferentiation of the economic and financial groups involved. Without inquiring into

Theor Soc (2014) 43:1–22 19

the changing relations among a variety of groups and their specific power basis, fieldtransformations remain unintelligible.

Second, this type of field approach opposes primarily economic as well as culturalaccounts, acknowledging instead the interrelationship of material and symbolicdimensions. Economic interests are not simply given, they need to be defined andinterpreted in certain ways to obtain legitimacy, and these interpretations are part andparcel of the cultural and cognitive frameworks that orient business practices. Culturalunderstandings and frameworks are not disjunct from material interests, neither in theways they are produced nor in the ways they are used.

Third, field theory in the more structural sense enables the integration of differenttemporalies, which are an important feature for understanding historical transforma-tions. In this case it allowed articulating a relatively slow, structural socio-economicchange (the rise of institutional investors) with the more punctual revolt of a smallvanguard of outsiders (raiders). It was the revolt of the latter during a period of crisisthat provoked the organized intervention of powerful investors, thus producing thestructural change that until then had remained latent. Although the actual power shiftfrom managers to shareholders happened in a remarkably short period of time, it tookplace within a much longer and more gradual process of change in the relationshipsbetween managers and shareholders (for these issues see Gorski 2013).

Fourth, a field approach to the economy includes, as Bourdieu, Fligstein, and othershave argued, incorporating the broader field environment, in particular that of the stateand law. During the first years of the Reagan administration, the lucrative operations ofcorporate raiders became an example for public pension funds only when it had becomeclear that the government and regulating bodies would not intervene in the take-overmarket but would, on the contrary, consistently favor shareholders’ interests.

References

Blumenthal, W. M. (1976). Ethics, morality and the modern corporate executive. Dividend: The Magazineof the School of Business Administration, 7(3), 4–9.

Bourdieu, P. (2005). The social structures of the economy. Cambridge: Polity Press.Bruck, C. (1988). The predators’ ball. The junk-bond raiders and the man who staked them. New York:

Simon and Schuster.Convert, B., & Heilbron, J. (2007). Where did the new economic sociology come from? Theory and

Society, 36(1), 31–54.Davis, G. (1991). Agents without principles? The spread of the poison pill through the intercorporate

network. Administrative Science Quarterly, 36(4), 583–613.Davis, G. F., & Thompson, T. A. (1994). A social movement perspective on corporate control.

Administrative Science Quarterly, 39, 141–173.Davis, G. (2009). Managed by the markets: how finance reshaped America. New York: Oxford University

Press.Dobbin, F., & Zorn, D. (2005). Corporate malfeasance and the myth of shareholder value. Political Power

and Social Theory, 17, 179–198.Dobbin, F., & Jung, J. (2010). The misapplication of Mr. Michael Jensen. How agency theory brought

down the economy and why it might again. In M. Lounsbury & P. Hirsch (Eds.),Markets on trial: Theeconomic sociology of the U.S. financial crisis. Research in the sociology of organizations. EmeraldGroup Pub, vol 30B (pp. 29–34).

Eccles, R., & Crane, D. B. (1988). Doing deals: investment banks at work. Harvard: Harvard BusinessSchool Press.

20 Theor Soc (2014) 43:1–22

Fiss, P., Kennedy, M. T., & Davis, G. (2012). How golden parachutes unfolded: diffusion and variation of acontroversial practice. Organization Science, 23, 1077–1099.

Fligstein, N. (1990). The transformation of corporate control. Cambridge: Harvard University Press.Fligstein, N. (2001). The architecture of markets: An economic sociology of twentyfirst-century capitalist

societies. Princeton: Princeton University Press.Fligstein, N. (2005). States, markets and economic growth. In V. Nee & R. Swedberg (Eds.), The economic

sociology of capitalism (pp. 119–143). Princeton: Princeton University Press.Fligstein, N., & McAdam, D. (2012). A theory of fields. Oxford: Oxford University Press.Fourcade, M., & Khurana, R. (2013). From social control to financial economics: the linked ecologies of

economics and business in twentieth century America. Theory and Society, 42, 121–159.Fruhan, W. E. (1979). Financial strategy. Homewood: Irwin.Gorski, P. S. (Ed.). (2013). Bourdieu and historical analysis. Durham: Duke University Press.Granovetter, M. (1985). Economic action and social structure: the problem of embeddedness. American

Journal of Sociology, 91(3), 481–510.Guilhot, N. (2004) Financiers, philanthropes. Vocations éthiques er reproduction du capital à Wall Street

depuis 1970, Paris, Raisons d’agir.Heilbron, J. (2005). Taking stock. Toward a historical sociology of financial regimes. Economic Sociology,

7(1), 3–17.Jensen, C., & Meckling, W. (1976). Theory of the firm: managerial behavior, agency costs, and capital

structure. Journal of Financial Economics, 3(4), 305–360.Kochan, T. A., & Useem, M. (1992). Transforming organizations. Oxford: Oxford University Press.Kosnik, R. (1987). Greenmail: a study of board performance in corporate governance. Administrative

Science Quarterly, 32, 163–185.Lazonick, W. (2013). From innovation to financialization: How shareholder value ideology is destroying

the US economy. In M. Wolfson & G. Epstein (Eds.), The handbook of the political economy offinancial crises. Oxford: Oxford University Press. Ch. 24.

Lazonick, W., & O’Sullivan, M. (2000). Maximising shareholder value: a new ideology for corporategovernance. Economy and Society, 29(1), 13–35.

Lipton, M., & Rosenblum, S. A. (1991). A new system of sorporate governance: the quinquennial electionof directors. The University of Chigaco Law Review, 58(1), 187–253.

Martin, J. L. (2011). The explanation of social action. New York: Oxford University Press.MacKenzie, D., Muniesa, F., & Siu, L. (Eds.). (2007). Do economists make markets? On the performativity

of economics. Princeton University Press: Princeton.Monks, R., & Minkow, N. (1991). Power and accountability. New York: HarperCollins.Swedberg, R. (2003). Principles of economic sociology. Princeton: Princeton University Press.Tortorello, N. J. (2004). The rising power of shareholders. Corporate Board, 25, 22–26.Useem, M. (1996). Investor capitalism: how money managers are changing the face of corporate America.

New York: BasicBooks.Useem, M. (1993). Executive defense: shareholder power and corporate reorganization. Cambridge:

Harvard University Press.Williams, K. (2000). From shareholder value to present-day capitalism. Economy and Society,

29(1), 1–12.Zajac, E. J., & Westphal, J. D. (2004). The social construction of market value: institutionalization

and learning perspectives on stock market reactions. American Sociological Review, 69, 433–457.

Zorn, D. M. (2004). Here a chief, there a chief: the rise of the CFO in the American firm. AmericanSociological Review, 69(3), 345–364.

Zorn, D., Dobbin, F., Dierkes, J., & Kwok, M.-S. (2005). Managing investors: how financial marketsreshaped the American firm. In K. Karin Knorr-Cetina & A. Preda (Eds.), The sociology of financialmarkets (pp. 269–289). Oxford: Oxford University Press.

Johan Heilbron is a historical sociologist, member of the Centre Européen de Sociologie et de SciencePolitique de la Sorbonne (CESSP-CNRS-EHESS) in Paris, and affiliated with the Erasmus Center forEconomic Sociology (ECES) in Rotterdam. His work is on the development of the social sciences, thetransformation of economic fields, and transnational exchange and cultural globalization. For moreinformation see: http://cse.ehess.fr/ or http://www.eur.nl/fsw/research/eces/home/.

Theor Soc (2014) 43:1–22 21

Jochem Verheul studied sociology at Erasmus University Rotterdam, where he wrote his masters thesis onthe spread of shareholder value. His interest is in economic and cultural sociology. He is affiliated with theErasmus Center for Economic Sociology (ECES), and is the owner of the consultancy firm It’s a virus.

Sander Quak is a postdoctoral researcher at the Erasmus Center for Economic Sociology (ECES) inRotterdam. He obtained his PhD at the Erasmus University Rotterdam with a study on Transnational Firmsand Their Corporate Labor Policy. Case Studies on Philips and ING in the Netherlands and the UnitedStates, 1980–2010 (2012). He is currently engaged in a research project on the development of thepharmaceutical industry. His research interests lie in the field of economic sociology and include thesociological study of markets, firms, and investors. For more information, see http://www.eur.nl/fsw/research/eces/home/.

22 Theor Soc (2014) 43:1–22