THE JOURNAL FOR GOVERNANCE PROFESSIONALS - ICSI

156

VOL 51 | NO. : 02 | Pg. 156 | February 2021 | `100/- (Single Copy) ISSN 0972-1983 THE JOURNAL FOR GOVERNANCE PROFESSIONALS BUDGET 2021 SHRI AMIT SHAH, HON’BLE UNION MINISTER OF HOME AFFAIRS, GOVT. OF INDIA CS NAGENDRA D. RAO PRESIDENT, ICSI CS DEVENDRA V. DESHPANDE VICE PRESIDENT, ICSI

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of THE JOURNAL FOR GOVERNANCE PROFESSIONALS - ICSI

VOL 51 | NO. : 02 | Pg. 156 | February 2021 | `100/- (Single Copy)ISSN 0972-1983

THE JOURNAL FOR GOVERNANCE PROFESSIONALS

BUDGET 2021 SHRI AMIT SHAH, HON’BLE UNION MINISTER OF HOME AFFAIRS, GOVT. OF INDIA

CS NAGENDRA D. RAOPRESIDENT, ICSI

CS DEVENDRA V. DESHPANDEVICE PRESIDENT, ICSI

Annual Subscription

The Council Contents

Mode of Citation: CSJ (2021)(02/--- (Page No.)

‘Chartered Secretary’ is generally published in the first week of every month. n Non-receipt of any issue should be notified within that month. n Articles on subjects of interest to company secretaries are welcome. n Views expressed by contributors are their own and the Institute does not accept any responsibility. n The Institute is not in any way responsible for the result of any action taken on the basis of the advertisements published in the journal. n All rights reserved. n No part of the journal may be reproduced or copied in any form by any means without the written permission of the Institute. n The write ups of this issue are also available on the website of the Institute.

Printed & Published byThe Institute of Company Secretaries of India‘ICSI House’, 22, Institutional Area, Lodi Road, New Delhi - 110 003. Phones : 41504444, 45341000, Grams : ’COMPSEC’ Fax : 91-11-24626727 E-Mail : [email protected] Weblink : http://support.icsi.eduWebsite : http://www.icsi.edu

Editor : Ashok Kumar Dixit

Vol. : LI n No.02 n Pg 1-156 n February-2021

QR Code/Weblink of Chartered Secretary Journalhttps://www.icsi.edu/JournalsBulletins/CharteredSecretary.aspx

CHARTERED SECRETARY[ Registered under Trade Marks Act, 1999 ]

®ISSN 0972-1983

Printed at SAP PRINT SOLUTIONS PVT. LTD.Plot No. 3 & 30, Sector II, The Vasai Taluka Industrial Co-op. Estate Ltd., Gauraipada, Vasai (E), Dist. Palghar - 401 208www.sapprints.com

�

President

Nagendra D. Rao

Vice President

Devendra V. Deshpande

Members (in alphabetical order)

Dr. Ahalada Rao Vummenthala

Anil Gupta (Govt. Nominee)

Ashish Garg

Balasubramanian Narasimhan

Chetan Babaldas Patel

Deepak Kumar Khaitan

Gyaneshwar Kumar Singh (Govt. Nominee)

Hitender Mehta

Dr. (Ms.) Madhu Vij (Govt. Nominee)

Manish Gupta

Manoj Pandey (Govt. Nominee)

Niraj Preet Singh Chawla

Praveen Soni

Ramasubramaniam C.

Ranjeet Pandey

S Santhanakrishnan (Govt. Nominee)

Vineet K. Chaudhary

Secretary

Asish Mohan

Chairman

Niraj Preet Singh Chawla

Members (in alphabetical order)

Dr. Ahalada Rao Vummenthala

Amit Kaushal

Anil Gupta

Ms. Aastha Gupta

Chetan Nayak k

Dr. D. K. Jain

G. R. Bhatia

H. M. Dattatri

Dr. (Ms.) Madhu Vij

Manoj Bisht

Puneet Handa

Vasudev Rao Devki

Vivek Hegde

Editor & Publisher

Ashok Kumar Dixit

Legal Correspondent

T. K. A. Padmanabhan

Editorial Advisory Board02

From the President 10Union Budget - 2021-22 28Articles 55Legal World 117From the Government 127News from the Institute 141Ethics in Profession 149CG Corner 151

FEBRUARY 2021 | 3 CHARTERED SECRETARY

CHARTERED SECRETARY GREETS AND CONGRATULATES

CS NAGENDRA D. RAO AND CS DEVENDRA V. DESHPANDE ON THEIR ELECTION AS PRESIDENT AND VICE PRESIDENT RESPECTIVELY OF THE INSTITUTE FOR THE YEAR 2021-22

CS Devendra V. Deshpande, Vice President, The ICSI

A Fellow Member of the ICSI and a Post Graduate in Commerce from Pune University, CS Devendra V Deshpande was elected to the Central Council of the ICSI for the term 2019 -

2022. He was the Chairman of ICSI Centre for Corporate Governance, Research and Training (CCGRT), Mumbai and ICSI Centre of Excellence (CoE), Hyderabad in the 2020. He is a Nominee Director at ICSI IIP.

CS Deshpande also headed the Information Technology Committee of the ICSI for the year 2019. He was member of various committees Constituted by ICSI including Executive Committee,

Corporate Laws and Governance Committee, Training & Educational Facilities Committee, Placement Committee, PMQ Course Committee, Election Reforms Committee and International Affairs Committee for the year 2019.

He has been actively associated with the Institute since 2004. Elected to the WIRC of lCSI, for the term 2015 – 18, he served as Chairman of Pune Chapter of WIRC of ICSI in the year 2013 and was an active Managing Committee member for the period from 2007 - 2014. CS Devendra V Deshpande has been a practicing Company Secretary since 2004 and specialises in the field of Corporate Laws, Foreign Exchange Laws, Audits under Company Law and Allied Laws, Secretarial Audit and Corporate Restructuring.

CS Nagendra D. Rao, President, The ICSI

A Fellow Member of The ICSI, CS Nagendra D. Rao is a Law Graduate from University of Mumbai and has a Bachelor’s Degree in Commerce. He is a Designated Partner and

Founder of CS Nagendra D. Rao and Associates, LLP, a firm of Practising Company Secretaries in Bengaluru. He was elected to the Central Council of the ICSI for the term 2019-2022 and served as Vice-President of The ICSI for the year 2020 before being elected as President for 2021. With over 15 years of experience in Corporate Sector he specializes in Corporate and Securities Laws, Capital Markets Transactions, Business Planning, Mergers & Acquisitions,

Financial Restructuring, Strategic Investment, Funds Planning & Arrangement.

He has been associated with the ICSI for several years now. He was elected to the Southern India Regional Council for two terms viz., 2011-2014 & 2015-2018 and has served as Chairman for the year 2015. Prior to that he was elected to the Managing Committee of the Bengaluru Chapter of the ICSI for the period 2007-2010 and was elevated as Chairman during the year 2009.

CS Nagendra D. Rao was a member of the Central Taxes, Corporate Laws & GST Committee of the Federation of Karnataka Chambers of Commerce & Industry for the year 2018-19. He was a member of the Corporate Affairs and Taxation Committee of the Bangalore Chamber of Industry & Commerce during the period 2000 – 2004. In recognition for his outstanding service rendered in the field of education CS Nagendra D. Rao was conferred the title “VIDYA VIKAS” by Dr. D.G. Shetty Educational Society (R), Dharwad, Karnataka.

4 | FEBRUARY 2021 CHARTERED SECRETARY

IMA

GE

SElection of ICSI President and Vice President

for the year 2021-22

FEBRUARY 2021 | 5 CHARTERED SECRETARY

IMA

GE

S ICSI delegation led by CS Nagendra D. Rao, the newly elected President met Shri Amit Shah, Hon’ble Union Minister of Home Affairs, Govt. of India.

ICSI Delegation led by CS Nagendra D. Rao, the newly elected President met officials of Ministry of Corporate Affairs, Govt. of India

Meeting with Shri Rajesh Verma, Secretary, MCA

Meeting with Shri Gyaneshwar Kumar Singh, Joint Secretary, MCA Meeting with Shri K.V.R. Murty, Joint Secretary, MCA

Meeting with Shri Manoj Pandey, Joint Secretary, MCA

6 | FEBRUARY 2021 CHARTERED SECRETARY

IMA

GE

S

1 2

3

61. ICSI President, CS Nagendra D. Rao and Vice President, CS Devendra V. Deshpande met Dr. T. V. Somanathan, Secretary, Department of

Expenditure, Ministry of Finance and deliberated upon role of Company Secretaries professionals as regards the recently rolled out Union Budget 2021-22

2. ICSI delegation led by CS Ashish Garg, Immediate Past President Felicitated Smt. Sumitra Mahajan (Ex Speaker, Lok Sabha) on conferring Padma Bhushan Award.

3. Group photo of CS Nagendra D. Rao, the newly elected President with Council Members and ICSI Officials.4. Group photo of CS Nagendra D. Rao, the newly elected President, CS Devendra V. Deshpande, Council Members and ICSI Official Smt. Sarah

Arokiaswamy.5. CS Nagendra D. Rao addressing at Bengaluru Chapter of ICSI.6. Group photo of ICSI Bengaluru Chapter Members with ICSI President, CS Nagendra D. Rao.

4 5

FEBRUARY 2021 | 7 CHARTERED SECRETARY

IMA

GE

S

9

7. CS Nagendra D. Rao, the newly elected President, ICSI addressing at Kolhapur Chapter of ICSI on 1st February, 2021.8. Felicitation of CS Nagendra D. Rao, the newly elected President, ICSI and CS Devendra V. Deshpande, the newly elected Vice President, ICSI at Kolhapur

Chapter of ICSI.9. ICSI President, CS Nagendra D. Rao addressing during 72nd Republic day celebration at ICSI House, Lodi Road. 10. 72nd Republic day celebration at NIRC of ICSI. Group photograph of CS Nagendra D. Rao, the newly elected President, CS Devendra V. Deshpande, Council

Member and ICSI Officials. 11. CS Balasubramanian N met Dr. K. Thirumalai muthu, Regional Director (Southern Region), Ministry of Corporate Affairs.12. CS Balasubramanian N met Shri K.G. Joseph Jackson, Registrar of Companies, Tamil Nadu, Andaman & Nicobar Islands.13. Felicitation Ceremony of newly elected President & Vice-President of ICSI organized by Belagavi Chapter of SIRC of ICSI on 31st January, 2021.

11 12

7 8

9 10

13

8 | FEBRUARY 2021 CHARTERED SECRETARY

Glimpses of ICSI Webinars

WEBINAR ONWEBINAR ON UNION BUDGET 2021-22 ON 2ND FEBRUARY, 2021

WEBINAR ONWEBINAR ON IMPLEMENTATION OF NEW TRAINING STRUCTURE

UNDER CS (AMENDMENT) REGULATIONS, 2020 ON 3RD FEBRUARY, 2021

Addressed by:Dr. Girish Ahuja, Eminent Tax Expert & Past Central Council Member, ICSI

CS Bimal Kumar Jain, Eminent Tax Expert

Addressed by:CS Nagendra D. Rao, President, ICSI, CS Devendra V. Deshpande, Vice-President, ICSI

FEBRUARY 2021 | 9 CHARTERED SECRETARY

FRO

M T

HE

PR

ES

IDE

NT

The Institute of Company Secretaries of India with its legacy of more than five decades, is an Institution which has not

only upheld the masthead of good governance but has been a proud partner and a key player in the journey of nation building. Akin to all other academic institutions, the core task is to embed the knowledge, skill and talent and create fine professionals; what makes it stand out is the uniqueness in the part played by our members in the Indian Corporate Arena.

Being elected as the President of my Alma Mater, to me is not just a reposing faith by my fellow Council Colleagues but a responsibility bestowed on me by all the members, students and all the stakeholders of the Institute. While I assure you that I will keep the best interests of all of you in sight in my decisions, I believe that the achievement of the vision and mission of this Institution has always counted on the support of each one of you. And it is for this journey of marching ahead to achieve our shared goals that I seek the blessings of Lord Ganesha in the shloka above.

UNION BUDGET 2020-21: MAKING AN ATMANIRBHAR BHARAT Charles Darwin said and I quote, “It is the long history of humankind that those who learned to collaborate and improvise most effectively have prevailed.” While it was a first-of-its-kind measure in 2020 to have rolled out a package of Rs. 20 lakh crore with the sole intent of enhancing the economic resilience of the country. The Union Budget presented on 1st February 2021 by Smt. Nirmala Sitharaman, Hon’ble Minister of Finance and Corporate Affairs, touches

upon every facet and aspect of the Indian economy and its stakeholders with unprecedented proposed outlay with specific focus on Infrastructure Development re-iterate the commitment for making a self-reliant Bharat.

The Institute is bringing out a dedicated publication titled ‘Union Budget 2021-22’ comprising views from Industry Experts and learned professionals so as to share detailed insights with all the stakeholders. This edition of Chartered Secretary, too, has been dedicated as a special edition with focus on the Union Budget for FY 2021-22.

EXCELLENCE AND HIGHEST STANDARDS OF ETHICAL CONDUCT: THE MAKINGS OF A TRUE PROFESSIONAL With focus on the new age of digital transformation, promotion of ease of doing business, enhance user experience and strengthen enforcement, the Hon’ble Finance Minister in her Budget speech proposed to revamp the Ministry of Corporate Affairs (MCA) portal using data analytics, artificial intelligence, and machine learning to make regulatory filings much more convenient for corporates and professionals. The developments what we are looking at is a futuristic AI-based in MCA-21 when version 3.0 of the portal is rolled out.

In the wake of the developments of the likes of e-adjudication and online compliance monitoring; the roles, responsibilities and expectations of all stakeholders are being redefined, more than ever. All these would call for a heightened level of awakening on the part of our members to constantly strive towards excellence with a rejuvenated

Dear Professional Colleagues,

AJOmZZ nÙmHª$ JOmZZ§ Ah[Z©e_² &AZoH$X§V§ ^º$mZm§ EH$XÝV§ Cnmñ_ho &&

(As the rays from the lotus-face of Devi Parvati is always on her beloved son, similarly, the grace of Lord Sri Ganesha is always on his Devotees; granting their many prayers;

the Devotees who worship him with deep devotion.)

10 | FEBRUARY 2021 CHARTERED SECRETARY

FRO

M T

HE

PRE

SID

EN

Tsense of zeal and vigour and move beyond the confines of our contemporary set of activities.

Friends, while I might have shared this earlier, but to me, the role of professionals is obviously very important in all situations and particularly so when the economy is on the cusp of faster growth trajectory given the significance of further strengthening of good corporate governance. Being a professional body of high repute, highest standards of ethical conduct, the expectation by all the stakeholders is natural. It is for these reasons that all of us need to ensure adherence to not just sound corporate governance practices by the corporates but self-governance as well.

MEETINGS WITH DIGNITARIESAfter becoming the President, the first priority is to receive blessings of those who have been pillars of support and who continue to be the guiding light in all our initiatives and endeavours.

I feel extremely happy that my journey has begun with the blessings of Shri. Amit Shah ji, Hon’ble Minister of Home Affairs, Government of India and also with various senior Officials and members of the Ministry of Corporate Affairs. Numerous meetings have been held with Senior officials and Members of the Ministry of Corporate Affairs, on various occasions, but the meetings with Shri Rajesh Verma, Secretary, MCA; Shri Manoj Pandey, Shri Gyaneshwar Kumar Singh, Shri K.V.R. Murty, Joint Secretaries, Ministry of Corporate Affairs were a reinstatement of their continued support and that of their expectations from the Institute as well as the profession in future too. It was indeed a great honour to have met Dr. T. V. Somanathan, Secretary, Department of Expenditure, Ministry of Finance and deliberate upon the role of professionals in the recently rolled out Union Budget 2021-22.

The Institute of Company Secretaries of India has always taken pride in the fact that it has stood tall in meeting the expectations of the Regulatory Authorities, taking forward their objectives and rendering them successful. The role played by our Institute is very much appreciated by the Regulatory Authorities.

NEW TRAINING STRUCTURE: NEW LEARNINGS, NEW BEGINNINGS Given the pandemic in the past year and the lockdown, the Institute had granted temporary relaxation to the students on the applicability of Regulation 46BA and 46BB of the Company Secretaries (Amendment) Regulations, 2020 for a period of six months i.e., upto 2nd February, 2021. Accordingly, with effect from 3rd February, 2021, the new training structure shall be applicable. As per the new training structure, students shall be required to complete Executive Development Programme (EDP) of one month after passing Executive Programme; Practical Training for 21 months after completion of EDP and undertake a Corporate Leadership Development Programme (CLDP) for minimum period of 30 days but not exceeding 60 days after passing the Professional Programme.

I am absolutely sure that these new Trainings shall not only hone the soft skills of the next gen professionals but enhance

their capabilities rendering them well equipped to serve both the profession, the corporates and the entire nation.

WAY FORWARD: FUTURE AND BEYOND…The new Training Structure is just the first of the many firsts to follow; I hope and believe that the journey and road ahead shall mark the ushering in a new era of governance in all spheres for our professionals.

Our Vision is to be a global leader in promoting good corporate governance and Mission is to develop high calibre professionals facilitating good corporate governance. It is imperative that all of us indulge and engage in continued Action, striving fervently towards achievement of these aims. The Institute intends to achieve its Vision and Mission by undertaking following initiatives

Gaining recognitions under varied laws of the land,

Creating opportunities of knowledge upgradation and Upskilling by way of Webinars, Seminars, Courses and other Programmes,

holistic development of our students as future Governance Professionals and

building the brand ICSI which resonates with the word governance on the global platform.

As they saying goes, “No one can whistle a symphony. It takes a whole orchestra to play it”. I indeed feel extremely gratuitous towards all the Past Presidents, Secretaries, Council Members and members of Team ICSI and all our well-wishers for having strengthened the foundation of this great organisation. The combined efforts have contributed for the high reputation of the ICSI, which is looked upon with great admiration. While feeling extremely humbled and honoured, I look forward to your continued support in all our future endeavours to be undertaken for the betterment of the Institute and the profession.

Seeking blessing for a fulfilling journey ahead, I would conclude with the following shloka:

› gh ZmddVw &gh Zm¡ ^wZºw$ &

gh dr`ª H$admdh¡ &VoO[ñd ZmdYrV_ñVw _m [d[Ûfmdh¡ &

Together may we move.Together may we relish.

Together may we perform with vigour.May what has been studied by us be filled with brilliance.

Together we can. Together we will.

With kind regards,

Yours Sincerely

CS Nagendra D. RaoPresident, ICSI

FEBRUARY 2021 | 11 CHARTERED SECRETARY

REC

ENT

INIT

IATI

VES

TA

KEN

BY

ICSI INITIATIVES UNDERTAKEN DURING

THE MONTH OF JANUARY, 2021INITIATIVES FOR MEMBERSMEETINGS WITH DIGNITARIESDuring the month of January, 2021, meetings were held with:

Dr. Harsh Vardhan, Hon’ble Union Minister for Health and Family Welfare

Prof. (Dr.) D. P. Singh, Chairman, University Grants Commission

Shri Rajesh Verma, Secretary, Ministry of Corporate Affairs

Shri Manoj Pandey, Joint Secretary, Ministry of Corporate Affairs

Shri K.V.R. Murty, Joint Secretary, Ministry of Corporate Affairs

Shri Gyaneshwar Kumar Singh, Joint Secretary, Ministry of Corporate Affairs

Shri B. Srikumar, Joint Director, Ministry of Corporate Affairs

REPRESENTATIONS SUBMITTED DURING JANUARY, 2021During the month of January, 2021, the following suggestions, views and representations were submitted to various Regulatory Authorities:

Suggestions of ICSI on the Occupational Safety, Health and Working Conditions Code (Central) Rules, 2020 submitted to the Ministry of Labour & Employment on January 3, 2021.

Request to authorize PCS for certification of maintenance of hundred percent asset cover under Regulation 56(1)(d) of the SEBI (LODR) Regulations, 2015 submitted to Chairman, SEBI on January 5, 2021.

Request for recognition to Company Secretary in Practice under the Rajasthan Investment Promotion Scheme – 2019 submitted to Principal Secretary (Finance), Government of Rajasthan on January 11, 2021.

Request for further relief under various Schemes submitted to the MCA on January 11, 2021.

Suggestions of ICSI on the Report of the Internal Working Group (IWG) of RBI to review extant ownership guidelines and corporate structure for Indian private sector banks submitted to RBI on January 15, 2021.

Request for extension in timelines for annual filing of E-forms submitted to the MCA on January 21, 2021.

Request for extension in timelines for filings by LLPs submitted to the MCA on January 22, 2021

Request to authorize PCS for certification under Regulation 13 of the SEBI (Share Based Employee

Benefits) Regulations, 2014 submitted to SEBI on January 25, 2021.

Recognition of Company Secretary (CS) Qualification equivalent to Post Graduate Degree for appointment of Assistant Professor in Universities and Colleges to University Grants Commission.

HONORARY FELLOW MEMBERSHIPS CONFERREDDuring the Award Ceremony of the 20th ICSI National Awards for Excellence in Corporate Governance, 2020 held on 13th January, 2021, honorary degree of the ICSI was conferred upon Shri Kumar Mangalam Birla, Chairman, Aditya Birla Group.

20TH ICSI NATIONAL AWARDS FOR EXCELLENCE IN CORPORATE GOVERNANCE, 2020The Award Ceremony of the 20th ICSI National Awards for Excellence in Corporate Governance, 2020 was held at Radisson Blu, Noida on 13th January, 2021 in recognition of the impeccable performances by Corporates and Professionals in the Corporate Governance arena.

Shri Piyush Goyal, Hon’ble Union Minister for Railways, Commerce & Industry, Consumer Affairs and Food & Public Distribution, graced the occasion as the Chief Guest while Hon’ble Mr. Justice A.K. Sikri Former Judge, Supreme Court of India and International Judge, Singapore International Commercial Court, was the Chairman of the Jury for the Awards.

The ICSI Lifetime Achievement Award for translating Excellence in Corporate Governance into reality was conferred on Dr. Cyrus S. Poonawalla, Chairman, Poonawalla Group.

The 20th ICSI National Award for Excellence in Corporate Governance for Best Governed Large Medium and Emerging Company in Listed and Unlisted Category, was presented to the following Companies:

ITC Limited (Listed Company: Large Category) TATA Metaliks Limited (Listed Company: Medium

Category) Vaibhav Global Limited (Listed Company: Emerging

Category) Numaligarh Refinery Limited (Unlisted Company: Large

Category) Talwandi Sabo Power Limited (Unlisted Company:

Medium Category) Arohan Financial Services Limited (Unlisted Company:

Emerging Category)To acknowledge the commitment of business houses in integrating social and environmental concerns with their

12 | FEBRUARY 2021 CHARTERED SECRETARY

REC

ENT IN

ITIATIVES TA

KEN

BY IC

SIbusiness operations, the Institute presented the 5th ICSI CSR Excellence Awards to: Reliance Industries Limited (Large Category) Natco Pharma Limited (Medium Category) Minda Industries Limited (Emerging Category)

Aimed at recognising the importance of the Secretarial Audit Report, ICSI instituted Best Secretarial Audit Report Award last year. This year the award was presented to CS Makarand Joshi, for Secretarial Audit Report of Mahindra Logistics Limited.

21ST NATIONAL CONFERENCE OF PRACTISING COMPANY SECRETARIESThe ICSI organised the 21stNational Conference of Practising Company Secretaries on 15-16 January, 2021 at Udaipur, Rajasthan on the theme ‘Achieving Excellence through Digital Transformation’. Shri Arjun Ram Meghwal, Hon’ble Minister of State for Parliamentary Affairs and Heavy Industries &Public Enterprises, presided over as the Chief Guest. The Institute also signed a Memorandum of Understanding with IIM-Bodhgaya on the occasion under the ICSI Academic Collaboration with Dr. Vinita S. Sahay, Director, IIM-Bodhgaya in the benign presence of Hon’ble Minister.

ICSI CONVOCATIONICSI organised its first hybrid Convocation (in physical mode as well as in e-mode) on 18th January, 2021, for awarding certificates to around 3400 Associate Members and 350 Fellow Members of the Institute, for the year 2020. In physical mode the Convocation was held at the four regional centres at Chennai, Delhi NCR, Kolkata and Mumbai for the eligible members who have opted for any of them and also at Hyderabad for a small group of members hailing from the city.

The inaugural event took place at Hotel ITC Kohenur, Knowledge City, Madhapur, Hyderabad in the benign presence of the Chief Guest, His Excellency Shri M. Venkaiah Naidu, Hon’ble Vice President of India. Hon’ble Minister for Home, Prisons and Fire Services, Government of Telangana, Shri Mohammed Mahmood Ali was also present as the Guest of Honour on the occasion. The inaugural event from 10.30 AM to 11.30 AM was common for all centres who joined the ceremony virtually. This was immediately followed by the regional Convocations. After the members received their certificates at Hyderabad, e-convocation commenced for participants who have confirmed for the same.

The inaugural event was live streamed on ICSI social media platforms such as Facebook, You Tube and Twitter. The speech of Hon’ble Vice President of India was also live telecast on Rajya Sabha TV.

CELEBRATION OF 72ND REPUBLIC DAYRepublic Day holds great significance to all of us, as it is the occasion when we honour the day on which the Constitution of India came into effect while replacing the Government of India Act, 1935. To rejoice the glory of India, the Institute celebrated 72nd Republic Day on January 26, 2021 through the flag hosting at the Head Quarters, Regional Offices and Chapters Pan India.

MANDATORY CPE CREDITS FOR THE YEAR 2020-21Continuous Professional Education (CPE) is important for further capacity building and constant upskilling of the members by keeping them abreast with latest developments in profession, widening their knowledge base and improving their skills to maintain the cutting edge by providing training and expertise in critical areas of professional interest.

Accordingly, the Council of the Institute issued the ICSI (Continuous Professional Education) Guidelines, 2019 which came into effect from 1st April 2020. Under the present Guidelines, every member is required to obtain the CPE Credits as under:

Member’s age CPE Credits in a year (1stApril – 31stMarch)

Employment PracticeBelow 60 years 20 20Above 60 years (If member is in gainful employment/ holding CoP)

10 10

The maximum number of CPE Credits that may be obtained by a member through web-based learning activities such as webinars is capped at 8 in a year with the overall limit of 12 CPE Credits under unstructured category.

No set-off of excess CPE Credits obtained under unstructured category is permitted against the CPE Credits to be obtained under structured category. Neither is any carry forward of the excess CPE Credits allowed under the Guidelines.

It may be noted that the PCH requirement for the FY 2020-2021 has to be completed latest by 31.03.2021. Members who have not completed the stipulated hours may complete the said date. The said Guidelines are available at https://www.icsi.edu/media/webmodules/CPE-Gls.pdf

Kindly ensure that the mandatory credit hours are obtained by you before the completion of the block year i.e. 31st March, 2021 as the same will be linked with the payment of annual membership/COP fee for the FY 2021-22.

REVISED GUIDANCE NOTE ON MEETINGS OF THE BOARD OF DIRECTORS AND GENERAL MEETINGSTo facilitate the compliance of Secretarial Standard on Meetings of the Board of Directors (SS-1) and Secretarial Standard on General Meetings (SS-2), the ICSI had issued Guidance Notes on Meetings of the Board of Directors and General Meetings.

To align these Guidance Note with the legal amendments brought in by the Companies (Amendment) Act, 2017 and to specify the relaxations given by MCA due to COVID-19, these have been revised by the ICSI on the basis of the relevant provisions of the Act and the rules, circulars, clarifications etc. issued by the MCA until 31st December, 2020.These Guidance Notes elucidates the basis for setting the particular Standard, explains the procedural & practical aspects thereof

FEBRUARY 2021 | 13 CHARTERED SECRETARY

REC

ENT

INIT

IATI

VES

TA

KEN

BY

ICSI and gives illustrative examples. The responses to various

issues/queries raised by the stakeholders have also been integrated.

The Revised Guidance Notes on Meetings of the Board of Directors and General Meetings were released at the 21st National Conference of Practicing Company Secretaries on 15thJanuary, 2021at Udaipur and made available on the website of ICSI for reference of all the stakeholders.

LAUNCH OF ICSI CERTIFICATE COURSESDuring the month January, 2021, ICSI launched / started registration for the following Certificate Courses:

Certificate Course on Insolvency and Bankruptcy code Certificate Course on Intellectual Property RightsCertificate Courses on Securities Law Certificate Course on Corporate Restructuring Certificate Course for POSH (second batch)Certificate Course on Commercial Contract Management

(second batch)Certificate Course on Independent Director (second

batch)Certificate Course on FEMA (second batch)Certificate Course on Forensic Audit (fourth batch)Certificate Course on Certified CSR Professionals (fifth

batch)Certificate Course on GST (sixth batch) The Institute is getting overwhelming response for the courses and the registration for the above mentioned has been extended till 28th February, 2021. Candidates registered for the above courses will be granted 15 structured CPE credit on completion.

ICSI SIGNATURE AWARD SCHEMEThe Institute launched the ICSI Signature Award Scheme under which top rank holders in B.Com. Final Examinations in reputed universities and also specialised programmes/ papers of IITs / IIMs are awarded a Gold Medal and a Certificate. During the month, MOUs were signed with:

Sl. No

State University / College /Institute

Date of MoU

1. Telangana Maulana Azad National Urdu University

12.01.2021

2. Bihar IIM Bodh Gaya 14.01.20213. Jammu & Kashmir Govt of Jammu &

Kashmir Higher Education Dept.

18.01.2021

ICSI ACADEMIC COLLABORATIONS WITH UNIVERSITIES AND ACADEMIC INSTITUTIONS ICSI “Academic Collaborations with Universities and Academic Institutions” initiative is aimed to establish a connect

between ICSI and various Universities and institutions of national repute, through a memorandum of understanding (MoU) covering a number of schemes under one umbrella towards learning and development of students, academicians and professionals.

MoUs were signed with the following universities and academic Institutions during the month of January, 2021 under the Academic Collaborations with Universities and Academic Institutions initiative of ICSI:

Maulana Azad National Urdu University, Hyderabad on 12th January 2021

IIM, Bodhgaya, Bihar on 15th January 2021 Dept. of Higher Education, J & K, Jammu & Kashmir on

18.01.2021

ICSI STUDY CENTRE SCHEMEA Memorandum of Understanding was signed by ICSI with Goswami Tulsidas Govt. P G College, Karwi, Chitrakoot on 9th January,.2021 under ICSI Study Centre scheme.

ICSI INSTITUTE OF INSOLVENCY PROFESSIONALS

LIT UP (Limited Insolvency Examination Training)

Pursuant to the IBBI (Insolvency Professionals) Regulations, 2016, an individual is eligible for registration as an Insolvency Professional only after passing Limited Insolvency Examination conducted by IBBI. In view of the same, ICSI IIP organized three days intensive training program for preparation of Limited Insolvency Examination from 22nd January, 2021 to 24th January, 2021. The entire syllabus as prescribed by IBBI for Limited Insolvency Examination was covered by eminent professionals and the program was very well appreciated by all the participants.

Pre-Registration Educational Course

Pursuant to the IBBI (Insolvency Professionals) Regulations, 2016, individuals are eligible to register themselves as Insolvency Professionals (IP) only after undergoing through the mandatory 50 hours Pre Registration Educational Course from an Insolvency Professional Agency after his/her enrolment as a Professional Member. ICSI IIP jointly with the other three Insolvency Professional Agencies conducted Pre-Registration Educational Course online from 18th January, 2021 to 24th January, 2021.

Workshop

7 hours workshop conducted on ‘Practical Aspects of Mergers and Acquisitions in India for IPs’” on 16th January, 2021. It was attended by approximately hundred Professionals.

Roundtable on ‘ILC (sub-committee) report on Pre-packaged Insolvency Resolution Process’

ICSI IIP organized a Roundtable on ‘ILC (sub-committee) report on Pre-packaged Insolvency Resolution Process’ on 18th January, 2021. The round table discussion was attended by 176 participants.

14 | FEBRUARY 2021 CHARTERED SECRETARY

REC

ENT IN

ITIATIVES TA

KEN

BY IC

SIINITIATIVES FOR STUDENTS

YUVOTSAV 2021: 21ST NATIONAL CONFERENCE OF STUDENT COMPANY SECRETARIES

The 21st National Conference of Student Company Secretaries was held at Hyderabad on 12th January, 2020 to mark the 158th Birth Anniversary of Swami Vivekananda in the presence of Tamilisai Soundararajan, Hon’ble Governor of Telangana and Shri G. Kishan Reddy, Hon’ble Minister of State for Home Affairs. ICSI Students participated through both physical and virtual mode.

FINAL ROUND OF ALL INDIA COMPANY LAW QUIZ 2020 HELD ON 11TH JANUARY 2021

All India Company Law Quiz 2020 was organized for the existing students of ICSI to enhance their visibility, level of knowledge and understanding in Company Law & allied areas and to generate interest among the students for in-depth study of the subject including greater conceptual clarity.

Final round of All India Company Law Quiz 2020 was held on 11th January, 2021 in hybrid mode. To create awareness of the profession amongst the other students who aspire to join CS Profession, play along round was also organised simultaneously during the Competition.

48 Finalists (16 Finalists for each Stage) participated in the final round. The winners of Final Round of the Quiz were given three cash awards and commendation certificates under each of the segments, i.e., CS Foundation, Executive, and Professional Programme.

ONLINE QUIZ ON CURRENT AFFAIRS AND GENERAL KNOWLEDGE

The Institute, through a novel initiative, for creating awareness about the profession has is organizing Online Quiz on Current Affairs & General Knowledge. There is no participation fee and the students can register in two different categories:

Category 1 - students pursuing 11&12 class of any stream

Category 2 - Students passed 12th/pursuing Graduation/Post Graduation, in any stream

The final round was held on 10th December, 2020 and the winners in each Category were rewarded with cash prizes.

Apart from the 1st, 2nd and 3rd prize worth Rs. 50000, Rs. 25000 and Rs.10000 respectively, special appreciation award of Rs. 5000/- and also 10 consolation prizes of Rs. 1000 each in both categories will be given. The first prize winners in both categories were awarded at the Award Ceremony of the 20th ICSI National Awards for Excellence in Corporate Governance held on 13th January, 2021.

COMPANY SECRETARY EXECUTIVE ENTRANCE TEST (CSEET) To test the aptitude of the candidates required for the profession of Company Secretaries, Company Secretary Executive Entrance Test (CSEET) has been introduced as the qualifying test for registration to Executive Programme through the Company Secretaries (Amendment) Regulations, 2020. Various initiatives were taken for the CSEET students:3rd CSEET held on 9th January, 2021

CSEET(May session) will be held on 8th May 2021 May 2021 Session of CSEET will be held on 8th May 2021 through remote proctored mode. Students can register upto 15th April, 2021 for CSEET which is the next cut-off date of CSEET registration. Registration can be done at https://smash.icsi.in/Scripts/CSEET/Instructions_CSEET.aspx Webinar on “Technical session on how to appear in

CSEET through remote proctored mode”

A Webinar on “Technical session on how to appear in CSEET through remote proctored mode” was held on 5th January, 2021 for the students who appeared in CSEET held in January 2021.Webinar helped students immensely in clearing their doubts with respect to technical aspects of CSEET.Commencement of online CSEET classes Most of the Regional/Chapter Offices have commenced classes for the students appearing in CSEET to be held in May 2021. Interested students can click at the link to contact Regional/Chapter offices: https://www.icsi.edu/media/webmodules/websiteClassroom.pdfDeclaration of result of Foundation and CSEET on 18th

January 2021.

The result of Foundation and CSEET was declared on 18th January 2021 and the results have been made available at the website of the Institute.

COMMENCEMENT OF ONLINE CLASSES OF CSEET/ FOUNDATION/ EXECUTIVE/ PROFESSIONAL PROGRAMME FOR JUNE 2021 SESSION OF EXAMINATION BY REGIONAL /CHAPTER OFFICESRegional/Chapter Offices of the Institute are conducting online classes for the students of CSEET/ Foundation/Executive/Professional Programme appearing in June 2021 exam. Interested students can contact the nearest Region/Chapter to join the classes. Details of Regional/Chapter offices are available at https://www.icsi.edu/media/webmodules/websiteClassroom.pdf

STUDENT COMPANY SECRETARY, CS FOUNDATION E-BULLETIN AND CSEET E-BULLETINThe Student Company Secretary e-journal for Executive/ Professional programme students of ICSI, CS Foundation course e-journal for Foundation programme students of ICSI and CSEET e-bulletin covering the latest update on the subject on the CSEET have been released for the month of January, 2021. The journals are available on the Academic corner of the Institute’s website at the link: https://www.icsi.edu/e-journals/

FEBRUARY 2021 | 15 CHARTERED SECRETARY

72ND REPUBLIC DAY PAN INDIA CELEBRATIONS HELD ON 26TH JANUARY 2021

16 | FEBRUARY 2021 CHARTERED SECRETARY

FEBRUARY 2021 | 17 CHARTERED SECRETARY

18 | FEBRUARY 2021 CHARTERED SECRETARY

Call for Articles

The term ‘good governance’ is frequently used in all walks of life. Good governance is expected to be participatory, transparent, accountable, effective, equitable and promotes rule of law. Good governance is always linked to Business ethics. International organisations always give paramount importance to good governance. Almost all major development institutions today say that promoting good governance is an important part of their agenda. In a well-cited quote, former UN Secretary-General Kofi Annan noted that “good governance is perhaps the single most important factor in eradicating poverty and promoting development”.

Different schools define governance is different ways. Governance experts are habituated to routinely focus on different types of governance viz. global governance, corporate governance, IT governance, participatory governance and so on, which may tend to be related only peripherally to the good governance agenda vis-à-vis deals with truly ideal governance framework from a country or globe. Considering the different facets, global outlook and its relevance from all spheres, ICSI is happy to invite articles on various facets of Governance which includes : Strategy and Governance – Two sides of the same coin;Global and International Governance;Corporate Governance;Parliament, Participatory and Democratic Governance;IT Governance;Integrated Governance;Governance- Sustainability and Inclusive growth;Minimum Government – Maximum Governance;Lessons of governance from the ancient era; and many more….As a part of Women’s Day Celebrations, we also invite research articles from authors on Women leadership, Women empowerment, Women on Board and other related topics.

Members and other readers desirous of contributing articles on the above said themes may send the same latest by Monday February 22, 2021 at [email protected] for considering in the March 2021 issue of Chartered Secretary. Minimum length of the article should be 2500 words.We look forward to your co-operation in making this initiative of the Institute a success.

Call for articles for publication in Chartered Secretary – March 2021

FEBRUARY 2021 | 19 CHARTERED SECRETARY

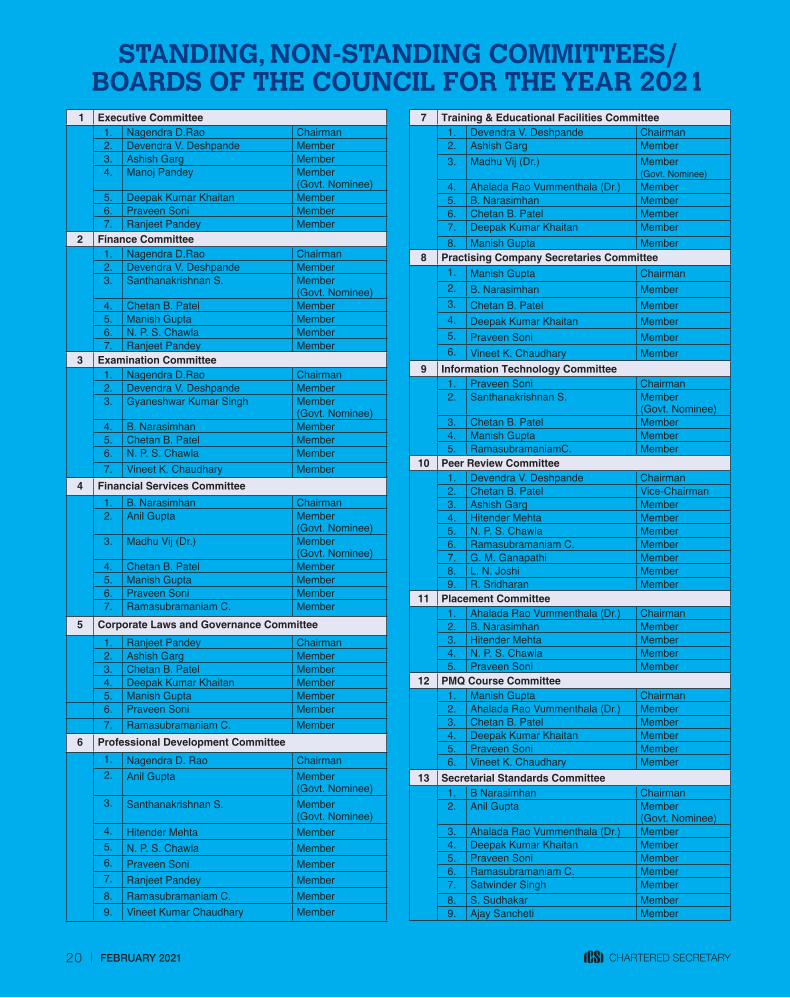

STANDING, NON-STANDING COMMITTEES/ BOARDS OF THE COUNCIL FOR THE YEAR 2021

1 Executive Committee1. Nagendra D.Rao Chairman2. Devendra V. Deshpande Member3. Ashish Garg Member4. Manoj Pandey Member

(Govt. Nominee)5. Deepak Kumar Khaitan Member6. Praveen Soni Member7. Ranjeet Pandey Member

2 Finance Committee1. Nagendra D.Rao Chairman2. Devendra V. Deshpande Member3. Santhanakrishnan S. Member

(Govt. Nominee)4. Chetan B. Patel Member 5. Manish Gupta Member6. N. P. S. Chawla Member7. Ranjeet Pandey Member

3 Examination Committee1. Nagendra D.Rao Chairman2. Devendra V. Deshpande Member3. Gyaneshwar Kumar Singh Member

(Govt. Nominee)4. B. Narasimhan Member 5. Chetan B. Patel Member6. N. P. S. Chawla Member7. Vineet K. Chaudhary Member

4 Financial Services Committee1. B. Narasimhan Chairman2. Anil Gupta Member

(Govt. Nominee)3. Madhu Vij (Dr.) Member

(Govt. Nominee)4. Chetan B. Patel Member5. Manish Gupta Member6. Praveen Soni Member7. Ramasubramaniam C. Member

5 Corporate Laws and Governance Committee

1. Ranjeet Pandey Chairman2. Ashish Garg Member3. Chetan B. Patel Member4. Deepak Kumar Khaitan Member5. Manish Gupta Member6. Praveen Soni Member7. Ramasubramaniam C. Member

6 Professional Development Committee1. Nagendra D. Rao Chairman2. Anil Gupta Member

(Govt. Nominee)3. Santhanakrishnan S. Member

(Govt. Nominee)4. Hitender Mehta Member5. N. P. S. Chawla Member6. Praveen Soni Member7. Ranjeet Pandey Member8. Ramasubramaniam C. Member9. Vineet Kumar Chaudhary Member

7 Training & Educational Facilities Committee1. Devendra V. Deshpande Chairman2. Ashish Garg Member 3. Madhu Vij (Dr.) Member

(Govt. Nominee)4. Ahalada Rao Vummenthala (Dr.) Member5. B. Narasimhan Member6. Chetan B. Patel Member7. Deepak Kumar Khaitan Member8. Manish Gupta Member

8 Practising Company Secretaries Committee1. Manish Gupta Chairman2. B. Narasimhan Member3. Chetan B. Patel Member4. Deepak Kumar Khaitan Member5. Praveen Soni Member6. Vineet K. Chaudhary Member

9 Information Technology Committee1. Praveen Soni Chairman2. Santhanakrishnan S. Member

(Govt. Nominee)3. Chetan B. Patel Member4. Manish Gupta Member5. RamasubramaniamC. Member

10 Peer Review Committee1. Devendra V. Deshpande Chairman2. Chetan B. Patel Vice-Chairman3. Ashish Garg Member4. Hitender Mehta Member5. N. P. S. Chawla Member6. Ramasubramaniam C. Member7. G. M. Ganapathi Member8. L. N. Joshi Member9. R. Sridharan Member

11 Placement Committee1. Ahalada Rao Vummenthala (Dr.) Chairman2. B. Narasimhan Member3. Hitender Mehta Member4. N. P. S. Chawla Member5. Praveen Soni Member

12 PMQ Course Committee1. Manish Gupta Chairman2. Ahalada Rao Vummenthala (Dr.) Member3. Chetan B. Patel Member4. Deepak Kumar Khaitan Member5. Praveen Soni Member6. Vineet K. Chaudhary Member

13 Secretarial Standards Committee1. B Narasimhan Chairman2. Anil Gupta Member

(Govt. Nominee)3. Ahalada Rao Vummenthala (Dr.) Member 4. Deepak Kumar Khaitan Member5. Praveen Soni Member6. Ramasubramaniam C. Member7. Satwinder Singh Member8. S. Sudhakar Member 9. Ajay Sancheti Member

20 | FEBRUARY 2021 CHARTERED SECRETARY

14 Expert Advisory Committee1. Hitender Mehta Chairman2. Anil Gupta Member

(Govt. Nominee)3. Madhu Vij (Dr.) Member

(Govt. Nominee)4. Ahalada Rao Vummenthala (Dr.) Member 5. N. P. S. Chawla Member6. K. Sethuraman Member7. Raj Kumar Agarwal Member

15 Editorial Advisory Panel1. N. P. S. Chawla Chairman2. Anil Gupta Member

(Govt. Nominee)3. Madhu Vij (Dr.) Member

(Govt. Nominee)4. Ahalada Rao Vummenthala (Dr.) Member5. Amit Kaushal Member6. Astha Gupta (Ms.) Member7. Chetan Nayak K. Member8. D. K. Jain (Dr.) Member9. G. R. Bhatia Member

10. H. M. Dattatri Member11. Manoj Bisht Member12. Puneet Handa Member13. Vasudev Rao Devki Member14. Vivek Hegde Member

16 ICSI-CCGRT & COEs Management Committee1. Chetan B. Patel Chairman2. B. Narasimhan Member 3. Manish Gupta Member4. Praveen Soni Member5. Ramasubramaniam C. Member6. Veerash M J Member7. Pradeep Kulkarni Member

17 Election Reforms & Chapter Guidelines Committee1. Ranjeet Pandey Chairman2. Santhanakrishnan S. Member

(Govt. Nominee)3. Chetan B. Patel Member4. Deepak Kumar Khaitan Member5. Manish Gupta Member6. N. P. S. Chawla Member 7. Praveen Soni Member8. Ramasubramaniam C. Member

18 Quality Review Board1. Nishi Singh (Ms.) Chairperson2. Devendra Kumar Member3. Ritika Bhatia (Ms.) Member4. Manish Gupta Member5. Pramod Kumar Rai Member

19 International Affairs Committee1. Ashish Garg Chairman2. B. Narasimhan Member 3. Hitender Mehta Member4. N. P. S. Chawla Member5. Ranjeet Pandey Member

20 Auditing Standards Committee1. Vineet K. Chaudhary Chairman2. Hitender Mehta Vice-Chairman3. Ahalada Rao Vummenthala (Dr.) Member4. Ramasubramaniam C. Member 5. G. V. Srinivasa Murthy Member6. Rajeev Bhambri Member

21 Disciplinary Committee*1. Nagendra D. Rao Presiding Officer2. Meenakshi Datta Ghosh (Ms.) Member

(Govt. Nominee)3. Nalin Kohli Member

(Govt. Nominee)4. B. Narasimhan Member5. Ranjeet Pandey Member

22 Board of Discipline*1. Deepak Kumar Khaitan Presiding Officer2. Manish Gupta Member3. Asish Mohan Member

23 Expert Group on Secretarial Standards1. Satwinder Singh Chairman 2. S. Sudhakar Vice-Chairman3. Awanish Dwivedi Member4. Narayan Shankar Member 5. R Kalidas Member 6. B. Renganathan Member7. D. C. Jain Member8. Deepak Sharma Member9. Dwarakanath C. Member

10. Jayan K. Member11. Makarand Joshi Member12. Morur Elayappan Vadivel Selvamm Member13. Rajveer Singh Member14. Sanjeev Grover Member15. S. C. Sharada (Ms.) Member16. S. C. Vasudeva Member17. Tridib Barat Member18. V. Karthick Member

24 Research Committee1. Ramasubramaniam C. Chairman2. Ahalada Rao Vummenthala (Dr.) Member3. Hitender Mehta Member4. N. P. S. Chawla Member5. Avnish Mahta Member6. Gaurav Gunjan Member

* Till the constitution of new Committee.

FEBRUARY 2021 | 21 CHARTERED SECRETARY

AT

A G

LAN

CE

P - 27Budget Analysis - 2021-22

Budget 2021-2022: Consolidating the Reforms AgendaM.S. Mani, Sandeep Jaiswal and Meenakshi Krishnamurthy

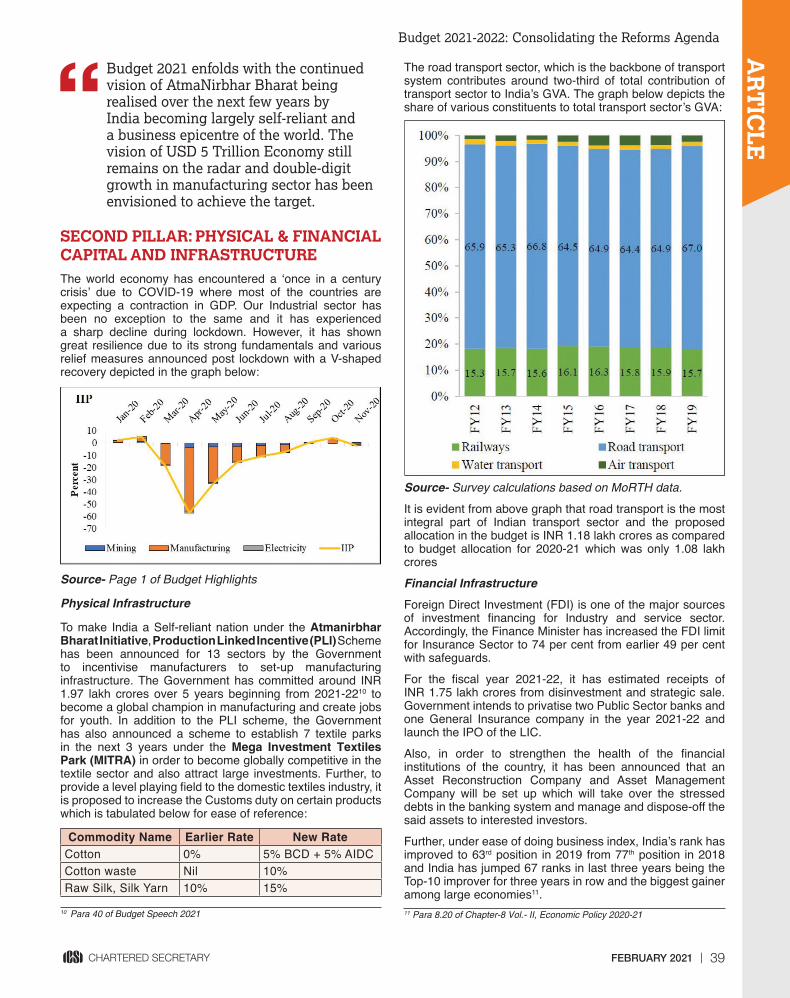

Budget 2021-22 starts with a congratulatory tone for applauding the country for having survived economically

as well as humanely through the once-in-a-century pandemic. The Centre for Economics and Business Research has projected a GDP growth rate of 9% in 2021-22. The pandemic led to the Union Government to present five mini budgets last year to steady the economy and provide a balance between protecting lives and livelihoods. With the ambition still set at becoming a USD 5 Trillion economy in the next few years, the Budget lays down 6 cornerstones with a vision for Atmanirbhar Bharat. These six cornerstones are Health and Wellbeing, Physical & Financial Capital, Infrastructure, Inclusive Development for Aspirational India, Reinvigorating Human Capital, Innovation and R&D and Minimum Government and Maximum Governance. While the earlier economic survey placed emphasis on Thalinomics, the current economic survey identifies the need for a Bare Necessities Index which determines a country’s strength to survive a pandemic. The economic survey and the budget indicate the continued V-shaped recovery of the Indian economy.

Union Budget 2021: A snapshot of key proposed tax amendmentsPramod Achuthan, Meera R. Iyer, Vaibhav Gupta and Divya Khushwani

The Union Budget 2021 presented by the FM on 1 February 2021 has adhered to a ‘no-harm’ strategy in the first paperless

budget The Budget proposals spelling out the government’s plan for economic recovery without worrying about fiscal deficit have been cheered by the markets as well. Budget 2021 focused on providing impetus to 6 specific pillars which are Health and Wellbeing, Capital and Infrastructure, Development for Aspirational India, Reinvigorating Human Capital, Innovation and Research, and Ease of Governance. The article captures the key amendments related to direct tax and indirect tax proposals. On the tax side, one would notice that proposals of the Finance Bill, 2021 are woven around the themes of simplification of tax administration, ease of compliance and reduction in litigation. Some of the noteworthy direct tax proposals include introduction of withholding tax provisions on purchase of goods, dispute resolution mechanism for small taxpayers, clarifications on equalisation levy provisions and allowing tax appeals to take place without in person court appearances. Similarly changes in rates structure in Customs Duty are geared towards promoting domestic manufacturing in sync with the Atmanirbhar Bharat strategy of the Government. Amendments in GST regulations such as self-certified reconciliation statement instead of GST audit, zero-rating benefit to SEZ for authorized operations seek to provide relief to taxpayers and providing clarity.

Budget 2021-22 - A big push towards a $5 Trillion EconomyAnil Gupta

The Union Budget 2021-22 was presented on the back of an unprecedented pandemic shock that hit the Indian economy

and reduced GDP growth by 7.7%. The Finance Minister’s promise of a ‘never-seen-before’ Budget had increased expectations, and after the Budget, the stock markets reacted jubilantly by soaring over 2,300 points. Irrespective of the reaction of the stock markets, there are quite a few positives in the Budget like the push for Ease of Doing Business by increase in the threshold of definition of “Small Company”, setting up of a Dispute Resolution Committee for small taxpayers, addressing various hardships faced by Non-Residents, thrust on implementation of infrastructure projects etc. The article concludes that the Budget has set its priorities right and it has recognised the need to take concrete measures to revive the economic growth engine, which it has done in a spectacular manner.

The Union Budget 2021-22 – A balancing act in the wake of COVID -19Asish Mohan

P resenting the Union Budget 2021-22, the Hon’ble Finance Minister highlighted the six pillars of the Budget

namely Health & Well-being; Physical & financial capital & Infrastructure; Inclusive development for aspirational India; Reinvigorating human capital; Innovation & R&D and Minimum Government and Maximum Governance. For corporate professionals, the proposals for the consolidation of the provisions of Securities and Exchange Board of India Act, 1992, Depositories Act, 1996, Securities Contracts (Regulation) Act, 1956 and Government Securities Act, 2007 into a rationalized single Securities Markets Code is an important highlight. The definition of Small Companies under the Companies Act, 2013 has been proposed to be changed by increasing their thresholds for Paid up capital from “not exceeding Rs. 50 lakh” to “not exceeding Rs. 2 Crore” and turnover from “not exceeding Rs. 2 Crore” to “not exceeding Rs. 20 Crore”. There are also proposals providing incentives for One-Person Company (OPC). The effective booster shots of the budget being a big push for infrastructure sector and thrust for privatisation and with no surprises of higher taxes, the Budget 2021 stands successful in achieving a balanced demand stimulus. The author concludes that overall, it is a budget that ensures that the momentum of economic recovery is sustained with least disruption.

The ambrosia called Mahabharata, the didactic Vidura Neeti and other like beacons His Holiness Shri Eeshapriya Teertha and Dr. Sudheendhra Putty

The Mahabharata is not a mere epic; it is a romance, telling the tale of heroic men and women as also about some

who were divine. It is a whole literature in itself, containing a code of life, a philosophy of social and ethical relations, and

36

28

49

52

56

43

Experts Speak on Union Budget - 2021-22

P - 55Articles

22 | FEBRUARY 2021 CHARTERED SECRETARY

AT

A G

LAN

CE

speculative thought on human problems that is hard to rival. While there is in it that eternal panacea, the Bhagawad Gita, the noblest of scriptures and grandest of sagas, the epic is also home to the sagacious utterances of the right and righteous Vidura. The Vidura Neeti coalesces all that is noble, lofty, wise and congealed wisdom that ought to be essential in today’s world. The conversation, at times, the monologue, encompasses a diaspora of aspects from statecraft to charity and administration to piety. That it is always contemporary is but an ode to the ancient Indian scriptures, its vastness, profundity and timelessness. Together with these pearls of wisdom, this epic and our other scriptures have much to offer and we have much to imbibe from them. That includes the primacy to education which is at the core of a knowledge society and the need for an administrator to be poise personified. Finally, there is the aspect of transition and knowledge diffusion of which the Udupi Krishna Matha is a shining exemplar. This article attempts to assimilate the crème de la crème of the above with a view to guide professionals by drawing on the ancient scriptures and goading India to re-emerge as the thought leader of the world.

SEBI and Green Investing Bonds Green and Blue, let’s give them their duePradeep Ramakrishnan, Richa Agarwal and Pawan Kumar Chowdhary

A green bond is like any other bond where a debt instrument is issued by an entity for raising funds from investors.

However, what differentiates a Green bond from other bonds is that the proceeds of a Green Bond offering are ‘ear-marked’ for use towards financing ‘green’ projects. SEBI defines that a debt security shall be considered as ‘Green’ if the funds raised through issuance of the debt securities are to be utilised for project(s) and/or asset (s) falling under any of the specified broad categories. It is observed that Municipalities around the world have adopted green bond route to contribute to a climate action and adapt their infrastructure to climate changes. The article also introduces the reader to the concept of blue bond which is a debt instrument issued by governments, development banks or others to raise capital from impact investors to finance marine and ocean-based projects that have positive environmental, economic and climate benefits. SEBI is one of the few regulators in the world to enable the issue of Green bonds prescribing provisions in the SEBI (Issue and Listing of Debt Securities) Regulations, 2008. So far there have been four issues of Green Bonds which have raised Rs. 17120 Million. The article concludes that Green bonds offer a great avenue for investment, more so for investors focused on sustainable investing.

Related Party Transaction – Few suggestions to a practical approach B. Chandra

Related party transactions (RPT’s) are common to any business in any country and are not something unique to

India and it would not be correct to state that such transactions are common to family-owned businesses only. Basically, there are two extremes in related party transactions namely efficient transactions which fulfil underlying economic needs of the company on one hand and transactions which compromise management’s responsibility to shareholders

or a board of director’s monitoring function on the other. The article highlights the key differences in the regulation of the RPT’s under the Companies Act, 2013 and the SEBI (Listing and Disclosure Obligations) Regulations, 2015. SEBI constituted a working group to suggest changes with respect to regulation of RPT’s. To sum up, the article concludes that it is difficult for any regulator to prescribe if such transactions are beneficial or detrimental to the firm’s performance. However, disclosure of RPTs can provide stakeholders with necessary information that can be used by them and the regulators to either discipline firms that engage in RPTs or take precautions against them

Investment in Startups- Stages of investment and challenges for PromotersVivek Sadhale, Vikas Agarwal and Nikita Navindgikar

While the standard market practices in terms of the rights provided to investors may differ in each business, it is

important that the promoters understand the risks associated with the rights they negotiate with the investors. Promoters should remember that while there could be market trends for reasonably acceptable rights and clauses in investment transactions, it ultimately depends on the bargaining power that the promoters have while discussion with investors. Promising businesses and bargaining power can help promoters to take away clauses in their favour and also maintain balance between the rights provided to all categories of investors in their startups.

CS: The Corporate Board’s AnchorArun Balakrishnan

T he Companies Act 2013 had given the status of Key Management Personnel (KMP) to the Company Secretary

(CS) along with the Chief Executive Officer (CEO) and the Chief Financial Officer (CFO). Thus, the importance of the CS in the organisation has been made a part of the statute ever since 2014. Chairperson of the Board depends upon the CS to ensure that the Board’s decision is compliant, and not in violation of the various statutes that govern corporate life in the country. It is the CS who ensures that the minutes contain a fair and correct summary of the proceedings that took place and accurately reflects the decision that has been arrived at. Proper conduct of the Annual General Meeting (AGM) and the occasional Extraordinary General Meeting (EGM) are also the responsibility of the CS and an experienced CS would do a fine balancing act in this regard to keep all interested parties happy. The article concludes that from the perspective of the CS profession, Secretarial Audit becomes an additional parameter for his / her performance appraisal. In this sense, Secretarial Audit could be called a peer review of the work of the whole-time secretary.

Atmanirbhar Bharat-Role of Intellectual Property in FinanceDr. Gouri Gargate

I s there a link between Atmanirbhar Bharat and the Intellectual Property? Is it possible to become Armanirbhar by creating and

exercising intellectual property rights? What are the potential areas in the IP domain that need attention of the professionals in the field of finance and compliance? The author has made an attempt to answer these questions in this article. The article deals with eight types of IPs out of which Patent, copyright, industrial design, trademark, and Trade Secrets are the five most important types. The article highlights the vast potential for the effective utilisation

60

64

72

67

75

FEBRUARY 2021 | 23 CHARTERED SECRETARY

AT

A G

LAN

CE of the IP system in the Indian context through enhanced role for

research organisations and academic organisations. Most of the focus on valuation and taxation concepts in India concentrates on tangible assets while there is huge scope in the areas of IP. The article concludes that If all stakeholders take advantage of IP instrument, there is a possibility that IP can help and contribute in building up trillion-dollar economy, and make India –Atmanirbhar.

Labour reforms agenda–Perspectives of the new labour codesAnupam Malik and Jorawer Singh

T he new labour codes not only extends the protection to those who needed it the most, but also helps in deciding the quantum

of benefits available in much simpler unambiguous terms. The subjective interpretation by officers and middlemen is getting curtailed, ushering in a transparent and collaborative work environment in the organisation, which is further assisted by local level bi-partite dispute resolution mechanisms being promoted under the codes. Simpler, consolidated law no doubt will help is easy understanding, implementation, compliance, reporting and record keeping for compliance professionals. The organisations stuck at 99 “on-role employees” for fear of stringent exit /retrenchment /closure conditions can now add on 200 more people and can test their potential to expand without fear, reaping in benefits of the “economies of scale”. The inclusion of “sales promotion employees”, “interstate migrants”, “gig /unorganised employees” marks a major step towards the “universal social security” for all.

Corporate Governance in India – Concept, Compliance and the way forwardP. Raju Iyer and Rakesh Shankar Ravisankar

E ffective Corporate Governance practices present opportunities to manage risks and add value to business operations thereby

these practices are rightly viewed as a differentiator in promoting sustainable competitive advantage. There is a global consensus about the objective of ‘good’ Corporate Governance - maximizing long-term shareholder value to all stakeholders. Indian belief and practice of “Vasudhaiva Kutumbakam” [Entire Globe is a single Family] has invited multi national corporates from all spheres of the business operations to operate from India and out of India. Further it has to be appreciated that to promote sound corporate governance the management has to adhere to strict compliance standards. An increasing amount of empirical evidence throws into light that good corporate governance contributes to competitiveness and long-term value creation. The article concludes that the way forward should be that Corporate Governance should not only monitor the company’s performance and compliance but also monitor and manage potential conflicts of interests of Board, Management and other stakeholders for which the momentum will come from the market forces and industry best CG practices.

Listed Companies Under CIRP / Liquidation – Remedy for ShareholdersMilind B. Kasodekar and Amar R. Kakaria

S ince 2016, Insolvency and Bankruptcy Code has helped hundreds of ailing companies to revive which has immensely

benefitted various stakeholders ~ Lenders, employees, creditors, suppliers, society, banks, government departments as well as shareholders. Even large corporate houses have been positively exploring this avenue to boost up their growth plans and this process is likely to gain further momentum due to ongoing economic slowdown after COVID-19 outbreak. With multiple success stories across different industries in recent past, there is likely to be an increasing demand for ailing listed companies with proven track record. Needless to mention, with continued listing

status, the chances of revival would be higher and shareholders have better chance of getting an exit opportunity instead of facing complete value erosion of their investments in such companies.

Some important aspects of the Negotiable Instruments ActVadapalli Srinivas

T he Negotiable Instruments Act, 1881 (NI Act) is perhaps among the very important old legislations that have stood the test of

time except for some consequential amendments over more than a century. The only tweaking that became necessary are the ones dealing with penalties in case of dishonour of cheques. The article discusses and analyses some important aspects of the said NI Act in three parts namely Analysis of certain important sections, Analysis of important judgements of Supreme Court and High Court and Analysis of the amendments to the NI Act. While dealing with the amendments, the article concludes that Section 143 A of the NI Act is applicable prospectively, that is, with effect from 01.09.2018 and Section 148 of the NI Act is applicable retrospectively

Competition Law and Health Care Sector: Contemporary PerspectiveDr. Susmitha P. Mallaya

H ealthcare sector has become a highly competitive market where it is difficult to afford the health services including medicines by the

common man in India, especially in the wake of outbreak of COVID-19 pandemic world over, loss of both livelihood and employment opportunities. Though, right to health is recognised as the basic fundamental right by the Supreme Court of India, it has become a challenging task for the States and Central Government to meet the needs of people to protect their health. Unlike the National Health Policies implemented for the citizens in the developed countries, in India, burden of health cost is self-funded by the patients and their families. Hence, they are the primary convalescent of the health system in India. In this regard, the role of Competition Commission of India (CCI) becomes pertinent being a market regulator of sectors including health care. They have come up with a Policy Note which focuses on the idea of making markets work for affordable Health Care. While deciding the cases before them, they have observed that many of the anti-competitive practices are prevailing in the health care sector. Nonetheless, CCI has been using, consistently, advocacy measures as part of its functions to regulate and bring awareness of such practices adopted by the stakeholders in the sector. It has also perceived that information asymmetry in health care sector has significantly restricted the choice of consumers in the health care sector. The issues that arise in this sector are many, it consists of health care professionals, pharmacists, lab technologists, policy frame work of health ministry etc. In March 2020, cease and desist order was issued by CCI against certain pharmaceutical companies for entering into anti-competitive horizontal arrangements with stockist and druggist association. Hence, in the present scenario, there is an enhanced risk of cartelization also in the health care sector with regard to the supply of the essential medicines to their distributors by the pharma companies in the wake of pandemic as well as tie in agreements with hospital network and laboratories which will have an adverse impact on the consumers.

Role of Independent Directors – “Bhishma Way or Jatayu Way”Sudhakar Saraswatula

I ndependent Director is given a very significant importance both under the Companies Act, 2013 (CA 2013) and the SEBI

(Listing and Disclosure Obligations) Regulations, 2015 (Listing Regulations). Independent Directors are seen as catalysts of change and have to facilitate the corporates to navigate through the growing complexities and ever-increasing compliances of

79

83

91

95

99

87

24 | FEBRUARY 2021 CHARTERED SECRETARY

AT

A G

LAN

CE

Legal World P-117nLMJ 02: 02: 2021 In our opinion, neither Section 192 IPC

nor Section 199 IPC, incorporate the principle of vicarious liability, and therefore, it was incumbent on the complainant to specifically aver the role of each of the accused in the complaint.[SC]

nLW 09: 02: 2021 The question as to whether the notification dated 24th March 2020 applies to a particular petition that has been filed prior to the said notification or not is also a question to be determined by the Bench of the NCLT and not by the Registrar of the Tribunal.[DEL]

nLW 10: 02: 2021 Further, the mere fact that the Gujarat Act might apply may not be sufficient for the writ courts to entertain the plea of Respondent No. 1 to challenge the ruling of the arbitrator under Section 16 of the Arbitration Act. [SC]

nLW 11: 02: 2021 There being no concluded contract, there could be no question of any breach on the part of the Appellant or of damages or any risk purchase at the cost of the Appellant.[SC]

nLW 12: 02: 2021 In the facts of the present case, the Principal Secretary to the Government of Haryana would be ineligible to be appointed as an arbitrator, since he would have a controlling influence on the Appellant Company being a nodal agency of the State.[SC]

law. Under CA 2013, they have to inter alia perform their duties as director and also comply with the code of conduct as per Schedule IV. . In the case of a listed company, they also have to discharge their obligations and responsibilities as required under the Listing Regulations. The article while deliberating the dilemma and challenges faced by an independent director presented the contrasting approach displayed by Jatayu in the epic Ramayana and Bhishma in the epic Mahabharata, when they faced a similar situation of rescuing a hapless woman. The author concludes with reference to independent directors that when we see some injustice or some problem, and take a decision, we have only two options - either close our eyes to it or do something about it - follow "the Bhishma way" or "the Jatayu way" and whichever way we choose remember there will also be a result - "the Bhishma result" or "the Jatayu result".

Uniform Face Value for Listed Equity Shares –Need of the HourJanak M. Shah

T he Indian equity market is flooded with 5000+ listed companies, each having its own freedom in deciding the face Value of its

equity shares. As a result, in most industries, there are number of companies having different face value of their equity shares. Such a high degree of heterogeneity in face value does not allow investors, a true and fair inter-company comparison by using some of the basic market and financial statistics. Investors expect the market to provide at least basic comfort level in making meaningful comparisons and facilitating thereby in taking right ‘buy-hold-sell’ decisions. This article is an attempt to highlight the urgency for adopting a uniform face value approach.

Anomalies in PIT Regulations intentional or un-intentional!Makarand Joshi

W hile interpreting and applying PIT Regulations, predominantly SEBI relies on purposive interpretation. Many times words

are read in larger context to serve the cause. However there are some occasions where words are not serving the cause and may need amendment in Regulations. This article is dealing with such intentional or un-intentional wording in PIT Regulations!

109

105From The Government P-127n Relaxation on levy of additional fees in filing of e-forms AOC-

4, AOC-4 (CFS), AOC-4 XBRL and AOC-4 Non-XBRL for the financial year ended on 31.03.2020 under the Companies Act, 2013

n Companies(Incorporation) Amendment Rules, 2021 n Commencement Notification dt 22.01.2021n Companies (CSR Policy) Amendment Rules, 2021 n Commencement Notification dt 22.01.2021n Scheme for condonation of delay for companies restored on

the Register of Companies between 01 December 2020 and 31 December 2020. under section 252 of the Companies Act. 2013

n Clarification on spending of CSR funds for Awareness and public outreach on COVID-19 Vaccination programme

n Clarification on holding of AGM through VC other OAVMn Revision of Monthly Cumulative Report (MCR)n Relaxations relating to procedural matters –Issues and Listingn Relaxation from compliance with certain provisions of the SEBI

(Listing Obligations and Disclosure Requirements) Regulations, 2015 due to the COVID -19 pandemic

n Norms for investment and disclosure by Mutual Funds in Exchange Traded Commodity Derivatives (“ETCDs”)

n Revision in Daily Price Limits (DPL) for Commodity Futures Contracts

n Review of Volatility Scan Range (VSR) for Option contracts in Commodity Derivatives Segment

n Amendment to Regulation 20(6) of SEBI (AIF) Regulations, 2012n Monthly Reporting of Portfolio Managersn Transfer of excess contribution made by Stock Exchanges

from Core SGF of one Clearing Corporation to the Core SGF of another Clearing Corporation

n Refund of security deposit

Other Highlights P-147

v NEWS FROM THE INSTITUTE

v MISCELLANEOUS CORNER

v GST CORNER

v ETHICS IN PROFESSION

v CG CORNER v STARTUP INDIA

nLW 13: 02: 2021 This Court has constituted the aforesaid Confidentiality Club keeping in mind the objection, of Xiaomi, to a “two-tier” Confidentiality Club, as sought by Interdigital.[Del]

nLW 14: 02: 2021 The onus was entirely upon the employee to prove that she had worked continuously for 240 days’ in the twelve months preceding the date of her alleged termination, which she failed to discharge.[SC]

nLW 15: 02: 2021 When the Bar Council of India appears to be discharging its regulatory functions, it cannot be said to be an ‘enterprise’ within the meaning of Section 2(h) of the Competition Act.[CCI]

nLW 16: 02: 2021 The Developer cannot compel the apartment buyers to be bound by the one-sided contractual terms contained in the Apartment Buyer‘s Agreement.[SC]

FEBRUARY 2021 | 25 CHARTERED SECRETARY

26 | FEBRUARY 2021 CHARTERED SECRETARY

Budget Analysis 2021-22

FEBRUARY 2021 | 27 CHARTERED SECRETARY

EXPE

RTS

OPI

NIO

NEXPERTS SPEAK ON UNION BUDGET 2021-22

Dream Plan for the Economy

CS Nagendra D. Rao, President, ICSI

›gdo©^dÝVwgw[IZ…&gdo©gÝVw[Zam_`m…&gdo©^Ðm[Uní`ÝVw&_mH$[üËXw…I^m½^doV²&&

May All be Happy, May All be Free from Illness. May All See what is Auspicious, May no one Suffer.

The primary reason as to why the Budget Session of the Parliament is one of the most significant events can be attributed to the fact that it is this very day and the speech of the Hon’ble Minister of Finance shares the Dream Plan for the economy and the vision as to where the goal plans, expectations, initiatives and actions lie as regards the various comprising segments of the Economy.

The six pillars on which the Foundation of the budget for the financial year 2021-22 has been laid are the ones demanding maximum attention in the present times. Health & well-being, Physical & financial capital & infrastructure, Inclusive development for aspirational India, Reinvigorating human capital, Innovation & R&D, and Minimum Government & Maximum Governance; each pillar comes with its own set of needs and yet one which will reap far-reaching and long-term impact.

Amongst others, since Governance forms part of the Budget as one of the six pillars, the same is accompanied by dedicated actions and initiatives, the intended course is heartily welcomed by the Institute of Company Secretaries of India (ICSI).Unveiled by the Hon’ble Finance Minister Smt. Nirmala Sitharaman on 1st February, 2021, the Union Budget 2021 proposes several reforms for the India Inc. including the persuasion of digital transformation in the Regulatory arena building a new MCA-21 3.0 using data analytics, artificial intelligence, and machine learning. With AI based features being inculcated, the times to follow shall witness a much stronger governance framework encasing the Indian

Corporate Sector and a much enhanced role play for the Governance Professionals.

The reforms proposed under the Companies Act, 2013 as well as the Limited Liability Partnership Act, 2008; from amendment in definitions to decriminalization of offences, come across as definitive and resolute attempts to enhance the ease of doing business in the Indian Diaspora.

Moves like no income tax return filing for senior citizens above 75 years, having only pension and interest income, and setting up of faceless dispute resolution committee for individual tax payers, it is indeed applaud-able on the part of the Government that ease is being provided in compliance under the Taxation Laws as well. With the Institute taking pride in being an extended arm of the Regulatory Authorities, the new rules for removal of double taxation for NRIs, and a reduction in the time period of tax assessments among other measures are highly appreciated.

With the Securities Markets forever being in limelight as one of the major representatives of the economic positioning of the nation, the proposition of a ‘one market code’ for rationalizing different security market regulations is a welcome step towards enhancing the advancement in Ease of doing business (EODB) index. Allowing One Person Companies (OPCs) to grow without a restriction on paid up capital and turnover, to convert in any type of company at any time, and alterations in the residency limit would not only simplify the business processes for such companies but also bring much more businesses in the organized sector which again would strengthen the governance scenarios further.

Shifting focus upon the remaining pillars, a boost for the healthcare sector with a significant increase of 137% in the outlay and the decision to spend a major chunk on Covid-19 vaccine development and inoculation is a much needed step.

There is a complete agreement with the thought of the Hon’ble Finance Minister that for achieving a 5-trillion dollar economy, our manufacturing sector has to grow in double digits on a sustained basis and our manufacturing companies need to become an integral part of global supply chains.

If the entire Budget was to be looked at both holistically and categorically, it is indeed quite heartening to witness the efforts made in placing focus on the various sectors, segments and comprising components of the Indian Economy. Furthermore, it would indeed be a greater delight to play our roles both as Governance Professionals and as an Institute in rendering the propositions of the Budget a grand success.

For as we all believe,

Together we can. Together we will.

28 | FEBRUARY 2021 CHARTERED SECRETARY

EXPER

TS OPIN

ION

Anil Sharma, Chartered AccountantPart-time Member of National Financial Reporting Authority, Adjunct Faculty with the Indian Institute of Corporate Affairs., Ex-Independent Director of UCO Bank.

In the Union budget, 2021, Finance Minister Smt Nirmala Sitaraman has made some important proposals to ensure availability of sufficient flow of funds for the economy which is on the recovery path. The important