Environmental Legislation - ICSI

156

Environmental Legislation - The Role of CS in Practice and Employment VOL 51 | NO. : 06 | Pg. 1-156 | June 2021 | `100/- (Single Copy) ISSN 0972-1983 THE JOURNAL FOR GOVERNANCE PROFESSIONALS

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Environmental Legislation - ICSI

Environmental Legislation - The Role of CS in Practice and Employment

VOL 51 | NO. : 06 | Pg. 1-156 | June 2021 | `100/- (Single Copy)ISSN 0972-1983

THE JOURNAL FOR GOVERNANCE PROFESSIONALS

Annual Subscription

The Council Contents

Mode of Citation: CSJ (2021)(06/--- (Page No.)

‘Chartered Secretary’ is generally published in the first week of every month. n Non-receipt of any issue should be notified within that month. n Articles on subjects of interest to company secretaries are welcome. n Views expressed by contributors are their own and the Institute does not accept any responsibility. n The Institute is not in any way responsible for the result of any action taken on the basis of the advertisements published in the journal. n All rights reserved. n No part of the journal may be reproduced or copied in any form by any means without the written permission of the Institute. n The write ups of this issue are also available on the website of the Institute.

Printed & Published byThe Institute of Company Secretaries of India‘ICSI House’, 22, Institutional Area, Lodi Road, New Delhi - 110 003. Phones : 41504444, 45341000, Grams : ’COMPSEC’ Fax : 91-11-24626727 E-Mail : [email protected] Weblink : http://support.icsi.eduWebsite : http://www.icsi.edu

Editor : Ashok Kumar Dixit

Vol. : LI n No.06 n Pg 1-156 n JUNE-2021

QR Code/Weblink of Chartered Secretary Journalhttps://www.icsi.edu/JournalsBulletins/CharteredSecretary.aspx

Printed at SAP PRINT SOLUTIONS PVT. LTD.Plot No. 3 & 30, Sector II, The Vasai Taluka Industrial Co-op. Estate Ltd., Gauraipada, Vasai (E), Dist. Palghar - 401 208www.sapprints.com

�

President

Nagendra D. Rao

Vice President

Devendra V. Deshpande

Members (in alphabetical order)

Dr. Ahalada Rao Vummenthala

Anil Gupta (Govt. Nominee)

Ashish Garg

Balasubramanian Narasimhan

Chetan Babaldas Patel

Deepak Kumar Khaitan

Gyaneshwar Kumar Singh (Govt. Nominee)

Hitender Mehta

Dr. (Ms.) Madhu Vij (Govt. Nominee)

Manish Gupta

Manoj Pandey (Govt. Nominee)

Niraj Preet Singh Chawla

Praveen Soni

Ramasubramaniam C.

Ranjeet Pandey

S Santhanakrishnan (Govt. Nominee)

Vineet K. Chaudhary

Secretary

Asish Mohan

Chairman

N. P. S. Chawla

Members (in alphabetical order)

Dr. Ahalada Rao Vummenthala

Amit Kaushal

Anil Gupta

Ms. Aastha Gupta

Chetan Nayak k

Dr. D. K. Jain

G. R. Bhatia

H. M. Dattatri

Dr. (Ms.) Madhu Vij

Manoj Bisht

Puneet Handa

Vasudev Rao Devki

Vivek Hegde

Editor & Publisher

Ashok Kumar Dixit

Legal Correspondent

T. K. A. Padmanabhan

Editorial Advisory Panel06

®ISSN 0972-1983

[ Registered under Trade Marks Act, 1999 ]

Environmental Legislation - The Role of CS in Practice and Employment

VOL 51 | NO. : 06 | Pg. 1-156 | June 2021 | `100/- (Single Copy)ISSN 0972-1983

THE JOURNAL FOR GOVERNANCE PROFESSIONALS

PAGE 04 – FROM THE PRESIDENT

PAGE 23 – ARTICLES

PAGE 107 - LEGAL WORLDPAGE 117 – FROM THE GOVERNMENTPAGE 129 – NEWS FROM THE INSTITUTEPAGE 145 – MISCELLANEOUS CORNERPAGE 146 – GST CORNER

PAGE 151 – ETHICS IN PROFESSION

PAGE 152 – CG CORNER

PAGE 153 – START UP INDIA

JUNE 2021 | 3 CHARTERED SECRETARY

FRO

M T

HE

PR

ES

IDE

NT

Dear Professional Colleagues,

W hile ech time we ponder over the ongoing situations, where on one hand our mind are bogged and boggled by the impact the pandemic has had on our lives and

on those we call our brethren, our hearts are filled with greater hope, gratitude and prayers towards the Lord Almighty seeking calmness, peace and tranquility. It is at this juncture that it seems apt to reconnect with the ancient scriptures for wisdom and strengthening of our belief in the fact that no matter what the circumstances, the good shall always prevail.

One such ancient scripture which holds popularity amongst the masses and especially amongst us professionals is the Shrimad Bhagavad Gita, the discourse of knowledge and wisdom from Lord Shri Krishna to Arjuna in the battlefield of Mahabharata. Given the fact that the words of this Scripture come to befit any and every scenario, it only seems apt to revisit the pages so as to understand our connections with the nature and the significance of building them.

It is in the tenth Chapter that deals with Vibhūti Yog or Yog through appreciating the infinite opulence of God that Arjun seeks knowledge as to how should one find oneness with the Supreme Lord. Although the reply is spread out over many verses, the crux of the same lies in the fact that the Lord himself claims to reside in the sun and the moon, the trees and the mountains, the animals and the birds, the air and the water bodies.

Ah_mË_m JwSm>Ho$e gd©^yVme`pñWV: &Ah_m[Xü _Ü`§ M ^yVmZm_ÝV Ed M &&20&&

(O Arjun, I am seated in the heart of all living entities. I am the beginning, middle, and end of all beings.)

ENVIRONMENT LEGISLATIONS: HEIGHTENING ROLE OF GOVERNANCE PROFESSIONALS

_mVm ^y[_: nwÌmoh§ n¥[Wì`m:&Z_mo _mVm n¥[Wì`¡ Z_mo _mVm n¥[Wì`¡&&

(The Earth is my mother and I am her child. Salutations to mother earth. Salutations to mother earth)

Hailing from the land of vedas, hailing from the nation where touching of mother earth in reverence, along with the above salutations from the AtharvaVeda mark the beginning of our normal days, the pedestal at which we place the nature and environment.

The celebration of the World Environment Day on the 5th of June, although maybe a reiteration of the commitment of environmental protection, the world over; yet for us in the heart of this nation, the day marks the celebration of seeking God and godliness in everything surrounding us. Although the environmental legislations have been put in place for the past so many decades, it is these times which while seeming wanton have accorded us the opportunity to pursue good governance not only in other areas of legislation but in this arena as well and not to mention, with greater diligence.

dºw$_h©ñ`eofoU [Xì`m ømË_[d^yV`:&`m[^[d©^y[V[^cmo©H$m[Z_m§ñËd§ ì`mß` [Vð[g&& 16&&

H$W§ [dÚm_h§ `moqJñËdm§ gXm n[a[MÝV`Z²&Ho$fw Ho$fw M ^mdofw [MÝË`mo@[g ^JdÝ_`m &&17&&

[dñVaoUmË_Zmo `moJ§ [d^yqV M OZmX©Z &^y`: H$W` V¥[á[h© ûm¥ÊdVmo ZmpñV _o@_¥V_² &&18&&

(Dear Lord Krishna ! Please describe to me your divine opulences, by which you pervade all the worlds and reside in them. O Supreme Master of Yog, how may I know you and think of you. And while meditating, in what forms can I think of you, O Supreme Divine Personality? Tell me again in detail your divine glories and manifestations, O Janardan. I can

never tire of hearing your nectar.)

4 | JUNE 2021 CHARTERED SECRETARY

FRO

M T

HE

PRE

SID

EN

T

Yours Sincerely

CS Nagendra D. RaoPresident, ICSI

Amongst all these expectations, are entrenched the roles of professionals hailing from various backgrounds in their varied capacities as regards a large base of multifarious stakeholders. As Governance Professionals, while a part of our profile pertains to the efficient and diligent compliance with the laws, the other part involves playing a significant and effective role in the decision making at Board levels. Environment legislations are no different, rather in light of the paradigm shift being witnessed at a global level towards environmental sensitization and a more sustainable approach being solicited from corporates globally on this front, as well as the transference in the reporting from financial to non-financial, it is not just the ‘Business Responsibility’ that has increased but the responsibility of professionals too has enhanced by many degrees.

Although the Business Responsibility Reporting or BRR has been a part of reporting culture under SEBI for quite a while, the same is expected to garner greater support from stakeholders, and hence the responsibilities of professionals especially the Company Secretaries being multiplied.

While, as an Institute having always propagated the agenda of constant knowledge upgradation, skill updation and scaling all the opportunities available, if the future was to be foreseen, it would indeed rest upon our shoulders to assist, guide and handhold our corporates towards making not just environment friendly but ecosystem sustainable decisions. For as the old proverb goes, “We do not inherit the earth from our ancestors, we borrow it from our children”.

LAUNCH OF MCA21 V3: A MUCH MORE ROBUST INTERFACE Where on one hand the deliberation has been on strengthening our roots as mankind, it is indeed imperative that the road ahead is chalked and paved in sync with our growing needs. This statement although would be equally validated in all spheres of human activity, yet would be of much greater significance as and where governance and even so good governance is concerned. Over the past decade or so, an understanding that has dawned upon all of us commonly is that good governance and ease of doing business are two sides of the same coin. Even further, what binds the two together is the strength, dynamism and flexibility of technology. Some of the most important parameters which build up a nation’s position on the Ease of Doing Business Index find their very foundation relayed in the foothills of technology. And it is with this very intent that the Ministry of Corporate Affairs had conceived the thought, idea and ideology of revamping and refurbishing the very first medium of interaction between the Regulatory Authority and its various stakeholders, i.e., the MCA21 web portal. It gives me immense pleasure to share that in the Phase-I, the upgraded version of MCA website, was launched at the hands of Shri Anurag Singh Thakur, Hon’ble Minister of State for Finance and Corporate Affairs in the presence of Shri Rajesh Verma, Secretary, MCA and Shri Manoj Pandey, Joint Secretary, MCA and CCM (Govt. Nominee), ICSI at a Webinar organized by the ICSI. Congratulating the Ministry and all the Officers on this wondrous measure undertaken towards the fulfillment of our national agenda of promoting ease of doing business, I am sure that the same shall indeed be of great assistance and support to our professional fraternity in dispensing with their duties, roles and responsibilities.

APPROVAL OF UNION CABINET TO ICSI MOUs: EXPANDING BOUNDARIES For an Institute with a vision to be a global leader in promoting good corporate governance the need to have relations perfected with

international governance institutions and entities gains supremacy prima facie. In view of the same and in achievement of our very vision, the Institute of Company Secretaries of India has signed various Memorandum of Understanding (MoUs) with International Associations with similar objectives.

It is indeed a moment of great delight to share that the Union Cabinet, chaired by the Hon’ble Prime Minister, Shri Narendra Modi, has granted post facto approval to the Memorandum of Understandings (MoUs) entered into by the Institute of Company Secretaries of India (ICSI) with The Institute of Chartered Secretaries and Administrators (ICSA), UK and The Chartered Institute for Securities & Investment (CISI), UK. On behalf of all the Company Secretaries, both in India and abroad I would like to convey our sincere thanks to Ministry of Corporate Affairs for providing all the support and gratitude to the Government of India for granting approval for such associations.

CAPACITY BUILDING INITIATIVES: MARCHING AHEAD IN TOGETHERNESS A professional institution such as ours is only as good as its Brand Ambassadors, i.e., its members and students. For us, each one of the 65,000 members and 3,00,000 students spread across the entire nation are unequivocally significant. Just as the Mother Earth, the nature, the environment surrounding is witnessed to be in ever so giving stance and posture, the Institute while aligning its initiatives with the same thought has endeavored to alight the path of its stakeholders. Their growth, both personal and professional is a noteworthy aspect for us to undertake initiatives in that direction. And while we have been organizing webinars for both these stakeholders on various topics of professional and academic interest as well as personal health and wellness, the agenda has been to strive for more.

It is with this intent that the Institute has been continuing its Bi-weekly Academic interaction between students and Expert Faculties and its own Academic Officers which has been garnering much appreciation. Besides, to further the academic interests and knowledge pursuits of our members, the Institute is intending to re-launch its Webinar Series on Companies Act and SEBI Regulations under the umbrella of EEE 2.0 or the Enable, Evaluate and Excel – Webinar Series.

Getting back to the point from where we started; Andy Goldsworthy said and I quote, “We often forget that we are nature. Nature is not something separate from us. So when we say that we have lost our connection to nature, we have lost our connection to ourselves.” That said, the ongoing times while moving towards hope and positivity and to fresh beginnings once again seek the forging of stronger connections and deeper ties both with the outside nature and with our own selves on the inside. A self-introspection is what shall provide as a clearer insight into our strengths and weaknesses and the ways in which they can help us in realization of our professional goals with ease and grace.

To put in finality, the idea and intent is to keep the growth in process and our journeys ahead in motion. As true professionals at the very core, it shall require not just individual but our combined effort to come out on the other side of the pandemic, not just undaunted but completely future ready; and hence our thought,

Together we can. Together we will.

With warm regards,

JUNE 2021 | 5 CHARTERED SECRETARY

REC

ENT

INIT

IATI

VES

TA

KEN

BY

ICSI INITIATIVES UNDERTAKEN DURING THE

MONTH OF MAY, 2021INITIATIVES FOR MEMBERSUNION CABINET APPROVES MoUs ENTERED WITH ICSA, UK AND CISI, UK

The Union Cabinet, chaired by the Hon’ble Prime Minister, Shri Narendra Modi, has granted post facto approval to the Memorandum of Understandings (MoUs) entered into by the ICSI with The Institute of Chartered Secretaries and Administrators (ICSA), UK and The Chartered Institute for Securities & Investment (CISI), UK. ICSI had signed a MoU with the Chartered Governance Institute (CGI) (formerly known as ICSA) UK, in 1998, to provide reciprocal exemptions to subjects as well as training requirements to each other’s members. The MoU was supplemented in 2018 and has been extended to CGI divisions in Australia, Canada, Hong Kong/China, Malaysia, New Zealand, Singapore, Zimbabwe, Southern Africa and UK. The MOU with the CISI [erstwhile Securities & Investment Institute (SII)] was signed in the year 2008 making ICSI members directly eligible for the CISI membership which provides them with a better access and opportunity in the international capital and financial markets. The MoUs will nurture and sustain the two-way flow of knowledge and professional potential. Along with providing a range of collaborative activities, the MoUs augment ICSI’s international footprint and accentuate its efforts in providing its stakeholders with opportunities sans boundaries. The details of the MoUs are available at https://www.icsi.edu/international-perspective/

ICSI SPECIAL COVID-19 ASSISTANCE CORPUS ICSI Special Covid-19 Assistance Corpus was launched with a dedicated Corpus Fund of Rs.10,00,00,000/- (Rupees Ten Crore only) for providing a one-time financial assistance of maximum Rs. 5,00,000/- to the dependent (s) / legal heir(s) of a member of ICSI, in case of his/her unfortunate demise during the period from 1st April, 2020 to 31st March, 2022 on account of Covid infection and medical complications arising therefrom.

The Scheme is applicable for current members (as on the date of demise) who were not life members of CSBF and for those life members of CSBF who had completed 60 years of age on the date of demise. In case of life members of CSBF who had completed 60 years of age on the date of demise, the claim shall be limited to Rs. 2 lakh (the balance amount of Rs. 3 lakh could be claimed from CSBF).

REVISED LIMITS OF CSBF

Medical reimbursement limits under CSBF for those affected by Covid-19 have been enhanced w.e.f. 1st May, 2021. Members and / or their declared dependents who have tested COVID positive and have incurred expenses related to treatment for COVID in hospital (private/government/military) or under home quarantine/isolation shall be eligible for reimbursement as under:

� For life members of CSBF - Limit enhanced from Rs. 75,000/- to Rs. 1,50,000/- for self and declared dependents.

� For life members of CSBF who have not completed 3 years of subscription – Limit enhanced from Rs. 50,000/- to Rs. 1,00,000/- for self and declared dependents.

� For Company Secretaries who are non-members of CSBF - Limit enhanced from Rs. 50,000/- to Rs.1,00,000/- for self only.

As per existing Bye Laws of CSBF, the annual income criteria for deserving cases (i.e. annual income upto Rs. 7.5 lakh during the previous Financial Year) will remain the same.

Members who have not yet become the member of CSBF are requested to become a life member by remitting a one-time subscription of Rs. 10,000/- through Institute’s portal (http://www.icsi.edu) with ‘Form-A’ duly filled in and signed available at the link: https://www.icsi.edu/csbf/home. Contribution to the CSBF can be made through http://www.icsi.in/ICSIDonation/ as contribution to CSBF qualifies for deduction under Section 80G of the Income Tax Act, 1961.

GROUP INSURANCE POLICY A customized Group Insurance Policy for hospitalization due to Covid-19 (Digit Illness Group Insurance Cover) was launched in association with Go Digit General Insurance Ltd. w.e.f. 15th May, 2021 for ICSI members, students, employees and their families. Cover duration - one year with 30/60 days pre/post hospitalization periods. Age group covered - 18-55 years. The policy could be purchased till 30 days from the launch date.

MANDATORY CPE CREDITS FOR THE YEAR 2020-21 – COMPLETE WAIVERConsidering the difficulties posed by the pandemic and in order to facilitate the members in fulfilling the mandatory requirement of CPE Credits for the year commencing 1st April, 2020 to 31st March, 2021, the Council of the Institute had extended the last date for obtaining the mandatory CPE credits by the members till June 30, 2021. Furthermore, in view of the ongoing circumstances and situations, the Central Council at its 276th (Special) Meeting held on 5th May, 2021 has decided to grant complete waiver of the shortfall in the CPE Credit Hours (both structured & unstructured) for the Financial Year 2020-21.

ICSI UDIN AMNESTY SCHEME, 2021 – EXTENDED The Institute considering the challenges being faced due to global pandemic COVID-19 and taking into account the genuine cases where default has happened, and the defaulting PCS are willing to rectify the default and disclose the details and hence a UDIN Amnesty Scheme be released wherein a PCS may:

6 | JUNE 2021 CHARTERED SECRETARY

REC

ENT IN

ITIATIVES TA

KEN

BY IC

SI� Generate UDINs missed earlier,� Modify UDIN details recorded at the time of generation,� Complete online process through STP Mode, � Revoke the UDINs not used,

while having immunity from disciplinary proceeding and without fees.

The window was initially kept open from 20th April, 2021 upto 15th May, 2021. Keeping in view the persisting pandemic situation in the country, the ICSI UDIN Amnesty Scheme - 2021 has been extended till 15th June, 2021.

ICSI eCSIN AMNESTY SCHEME, 2021 – EXTENDEDDue to the widespread of COVID-19 pandemic and the lockdowns imposed, there have been genuine cases where default has happened and the defaulting members are willing to rectify the default and disclose the details. In view of the same, the eCSin Amnesty Scheme-2021 has been put in place wherein members may:� Generate the eCSin, if not yet generated;� Rectify the eCSin details recorded at the time of generation

for appointment;� Update information in the eCSin generated ;� Revoke eCSin if employment already ceased;The members applying under ICSI eCSin Amnesty Scheme, 2021 shall be granted immunity from the applicability of the provisions of the eCSin Guidelines in respect of the eCSin for which request under this Amnesty Scheme has been made and disciplinary proceedings shall not be initiated or entertained in this respect. The Scheme was made effective from April 20, 2021 to May 15, 2021. However, in view of the ongoing situation, the ICSI eCSin Amnesty Scheme - 2021 has been extended till 15th June, 2021.

FORMATION AND RENEWAL OF STUDY CIRCLESICSI has been creating knowledge upgradation avenues for members by promoting formation of Study Circles across the country.� A new Study Circle namely “B.T. Road Study Circle of the

ICSI” was formed under EIRC for the financial year 2021-22. � Further, renewal of the “New Udaan Bhawan Study Circle

of ICSI” under NIRC has been approved for the financial year 2021-22.

REPRESENTATIONS SUBMITTED During the month, following representations were submitted to various Regulatory Authorities:� Request to include Company Secretary in Practice under

Regulation 45(3) of the SEBI (LODR) Regulations, 2015 submitted to the SEBI on May 13, 2021.

� Request to relax the time gap between two board / Audit Committee meetings of listed entities owing to the Second Wave of CoVID-19 pandemic submitted to the SEBI on May 17, 2021.

� Request for relaxation in levy of additional fees in filing of certain forms under the Companies Act, 2013 & LLP Act, 2008 on May 19, 2021.

WEBINARS CONDUCTEDDuring the month, the following Webinars were conducted with the intent of knowledge enhancement and upgradation of our members:� Associate Partner in the webinar organised by the PHD

Chamber of Commerce and Industry on the theme “Indirect Tax Relief Measures in view of Covid Pandemic” on Thursday, May 13, 2021.

� Webinar on the theme COVID-19 Mental Health and Wellness during the pandemic held on Friday, May 14, 2021.

� Webinar on launch of New Version (V3) of the website of Ministry of Corporate Affairs in the presence of senior officers of MCA on May 24, 2021.

� Supporting Partner in the webinar organized by ASSOCHAM Southern Region on the theme “Recent Decisions of the Supreme Court/Tribunals and Appellate Tribunal and Pre-packaged Insolvency Resolution Process under IBC for MSMEs” on Saturday, May 29, 2021. President, ICSI was the eminent speaker in the webinar.

CRASH COURSES LAUNCHEDICSI continuously endeavors to ensure that its members’ knowledge stay up to date with changing times. The pace of change is probably faster than it’s ever been and this is a feature of the new normal that we live and work in. Keeping this motive, the ICSI has come up with two Crash Courses, on the topics such as Related Party Transactions & Business Responsibility Reporting (Batch-2). More than 260 candidates have registered so far cumulatively in both the crash courses.

ONLINE TRAINING PROGRAMME FOR EMPANELMENT OF PEER REVIEWERSOnline training programme for empanelment of Peer Reviewers was organised on Saturday, the 8th May, 2021. Around 110 members participated in the training programme. The participants will be empanelled as Peer Reviewer subject to the fulfilment of criteria mentioned in the Guidelines for Peer Review of Attestation and Audit Services by Company Secretaries in Practice.

ICSI SOCIAL CONNECTIn these critical times with surge in COVID pandemic, several humanitarian initiatives were taken. Members were sensitised about registering themselves on ICSI Social Connect portal for plasma donation. Members were urged to inform how they may be of help to others in need for arranging hospital treatment, oxygen, medicines, vaccine, medical equipment, food, COVID/medical insurance, isolation centres, plasma, etc. Information shared by the members have been hosted on Institute’s website as ICSI COVID Heroes.

Members were sensitised about the benefits of becoming a life member of CSBF where COVID related medical expenses are also reimbursable in addition to other benefits.

JUNE 2021 | 7 CHARTERED SECRETARY

REC

ENT

INIT

IATI

VES

TA

KEN

BY

ICSI ICSI INSTITUTE OF INSOLVENCY

PROFESSIONALS� Pre-Registration Educational Course

Pursuant to Regulation 5(b) of the IBBI (Insolvency Professionals) Regulations, 2016, individuals are eligible to register themselves as Insolvency Professionals (IP) only after undergoing through the mandatory 50 hours Pre Registration Educational Course from an Insolvency Professional Agency after his/her enrolment as a Professional Member.ICSI IIP jointly with the other three Insolvency Professional Agencies conducted Pre-Registration Educational Course online from 26th April, 2021 to 2nd May, 2021.

� Workshops organized

® Workshop on ‘Analysis of Supreme Court Judgements w.r.t. IBC’ on 8th May, 2021.

® Workshop on ‘Immunities accessible for Insolvency Professionals under IBC’ on 15th May, 2021.

® Workshop on ‘Valuation under IBC’ on 22nd May, 2021.

® Workshop on ‘Asset Reconstruction Companies w.r.t IBC: Need of the hour’ on 29th May, 2021.

INITIATIVES FOR STUDENTSTEMPORARY RELAXATION FOR COMPLYING WITH PRE-EXAM TEST & ONE DAY ORIENTATION PROGRAMME- JUNE, 2021 SESSIONThe Institute has given temporary relaxation to the students to comply with Pre-Exam Test & One day Orientation Programme to enable them to enroll for June, 2021 Session by 25th March, 2021 (without late fees) and 9th April, 2021 (with late fees) without checking the status of compliance with the aforesaid requirements. Such relaxation is being allowed subject to the condition that the students shall comply with the requirement of Pre-Exam Test & One day Orientation Programme by 16:00 Hours, 31st July, 2021.

BI-WEEKLY PHONE IN / VIDEO INTERACTIVE SESSIONS FOR STUDENTS OF ICSIThe Institute of Company Secretaries of India has created a unique platform to deliberate upon crucial aspects of modules and subjects and clarify academic queries of students in a streamline manner by Academic Officers and Expert Faculties. The details of the sessions conducted during the month of May, 2021 are as under:

Session Date Subject9th 4th May, 2021 Banking Laws and Practice

10th 6th May, 2021 Securities Laws and Capital Markets

11th 11th May, 2021 Insolvency Law and Practice12th 13th May, 2021 Secretarial Audit, Compliance

Management & Due Diligence13th 18th May, 2021 Multidisciplinary Case Studies14th 20th May, 2021 Advanced Tax Laws

15th 26th May, 2021 Jurisprudence, Interpretation & General Laws

16th 27th May, 2021 Intellectual Property Rights - Laws and Practice

The video recordings of the sessions are available on the Academic Portal of the Institute under video lectures https://www.icsi.edu/bi_weekly_sessions_for_students/?edit_off=true

4TH ICSI SAMADHAN DIWAS HELD ON 12TH MAY, 2021The Samadhan Diwas is an initiative by the ICSI towards on-the-spot solution of the grievances of the trainees and trainers.The ICSI had successfully organized the Fourth Samadhan Diwas on Wednesday, 12th May 2021. The focus area of this Samadhan Diwas was TCC (Training Completion Certificate). In the Samadhan Diwas students got opportunity to present their case to the Director (Training & Placement), ICSI along with other officials of the Directorate of Training. More than 40 students had attended and got the solutions on the spot.

RE-OPENING OF ONLINE WINDOW FOR SUBMISSION OF CS EXAMINATION FORM FOR JUNE 2021 EXAM SESSION (NOW POSTPONED AND FRESH DATES ARE YET TO BE ANNOUNCED)

In view to facilitate the students who could not submit the exam form and are desirous of appearing in June 2021 exam session, an online window for the submission of exam form for June 2021 session for Foundation/Executive /Professional Programme examinations was re- opened from 15th May, 2021 to 22nd May, 2021.

PROVISIONAL REGISTRATION IN EXECUTIVE PROGRAMME FOR CSEET PASSED CANDIDATES

ln view of the difficulties faced by the students who have already passed CSEET and awaiting the results of 10+2 examination, it has been decided to allow such students to seek provisional registration to the Executive Programme subject to the submission of proof of passing 10+2(12th) examination within six months from the date of such provisional registration to the Executive Programme.

COMPANY SECRETARY EXECUTIVE ENTRANCE TEST (CSEET)To test the aptitude of the candidates required for the profession of Company Secretaries, Company Secretary Executive Entrance Test (CSEET) has been introduced as the qualifying test for registration to Executive Programme through the Company Secretaries (Amendment) Regulations, 2020. Various initiatives were taken for the CSEET students:� CSEET conducted on 8th May, 2021 through remote

proctored mode

On account of Covid-19 Pandemic restrictions and undertaking necessary precautions, the Institute successfully conducted the May CSEET on 8th and 10th May 2021 respectively through REMOTE Proctored mode instead of conducting the same from Test Centers. Candidates were allowed to appear for the test through their own laptop/ desktop from home/ such other convenient place.

8 | JUNE 2021 CHARTERED SECRETARY

REC

ENT IN

ITIATIVES TA

KEN

BY IC

SI� Facility to opt out and carry forward of CSEET fees for

candidates of May session

In view of continuing health crisis in the country due to spread of Covid-19 Pandemic, the Institute decided to give the facility to the CSEET candidates to opt out from CSEET held on 8th May 2021 to CSEET to be held in July 2021 and granting them benefit of carrying forward the credit of CSEET fee paid for the May 2021 Session to July, 2021 Session.� CSEET(July session) will be held on 10th July, 2021 July 2021 Session of CSEET will be held on 10th July, 2021 through remote proctored mode. Students can register upto 15th June, 2021 for CSEET which is the next cut-off date of CSEET registration. Registration can be done at https://smash.icsi.in/Scripts/CSEET/Instructions_CSEET.aspx� Commencement of online CSEET classes

Most of the Regional/Chapter Offices have commenced classes for the students appearing in CSEET to be held in July 2021. Interested students can click at the link to contact Regional/Chapter offices: https://www.icsi.edu/media/webmodules/websiteClassroom.pdf� Mock tests for Candidates appeared in May CSEET.

The Institute conducted three mock tests for the candidates who appeared in May 2021 session of CSEET. The Mock tests which conducted on 4th, 5th and 6th May 2021 respectively.

COMMENCEMENT OF CRASH COURSE/REVISION CLASSES Regional/Chapter Offices of the Institute are conducting Crash Course/Revision Classes for the students of Foundation/Executive/Professional Programme appearing in June 2021 exam. Interested students can contact the nearest Region/Chapter to join the classes. Details of Regional/Chapter offices are available at https://www.icsi.edu/media/webmodules/websiteClassroom.pdf

ONLINE DOUBT CLEARING CLASSES Online doubt clearing classes are being conducted for the students appearing in June 2021 exam for all stages, all subjects and students of both new and old syllabus. The online classes are being conducted in particular for the students appearing in June 2021 examination; however other students of the Institute can also join the classes. The classes are being taken by renowned and distinguished faculties with enriched teaching experience. The students can submit their queries through Google link which will be sent to them after registration. They can also interact live with the faculties through the chat box during the classes. Students are required to register at the following link to attend the classes https://tinyurl.com/uz7j7jf

CLARIFICATION REGARDING ELIGIBILITY OF STUDENTS WHOSE REGISTRATION HAS LAPSED /WILL LAPSE, FOR JUNE 2021 SESSION OF EXAMINATION (NOW POSTPONED & FRESH DATE YET TO BE ANNOUNCED)

Due to Postponement of June 2021 session of examination, it is clarified that students whose registration at the time of submitting their enrolment request for June 2021 Session

of Examination were valid, they all will be treated eligible to appear in the CS June 2021 Examination without seeking De-novo Registration, irrespective of the dates when the said examinations are actually being conducted. The said facility is only for appearing in June 2021 Examination.

STUDENT COMPANY SECRETARY, CS FOUNDATION E-BULLETIN AND CSEET E-BULLETIN

The Student Company Secretary e-journal for Executive/ Professional programme students of ICSI, CS Foundation course e-journal for Foundation programme students of ICSI and CSEET e-bulletin covering the latest update on the subject on the CSEET have been released for the month of May, 2021. The journals are available on the Academic corner of the Institute’s website at the link: https://www.icsi.edu/e-journals/

RECORDING OF VIDEO LECTURES ICSI is recording video lectures of eminent faculties for the students of ICSI which help them to prepare for the examination. Students of the Institute can access recorded videos available on the E-learning platform by logging in to https://elearning.icsi.in

Login credentials are sent to all registered students at email. After successful login, go to “My courses” or “My Communities” section, where you will find the recorded videos and other contents.

IMPORTANT LINKS FOR STUDENTS To facilitate and update the students, a list of important links at the website of the Institute has been compiled. Students can go through the links given below to get all important details:

� For Student Services related updates: https://www.icsi.edu/media/webmodules/Student_Services_links.pdf

� For Academic updates: https://www.icsi.edu/media/webmodules/Academic_links.pdf

� For Training related updates: https://www.icsi.edu/media/webmodules/Training_Links.pdf

� Info Capsule- A Daily update for members and students, covering latest amendment on various laws for the benefits of our members and students available at https://www.icsi.edu/infocapsule/

IT RELATED INITIATIVES � The Institute’s Website (www.icsi.edu) has been migrated

to Cloud Services successfully to enable smooth services to ICSI Stakeholders.

� Email System has been migrated to Microsoft O365 Cloud services successfully.

� Procured 4 latest Servers for ICSI Data Centre to strengthen the ICSI IT Infrastructure.

� Procured latest CISCO WebEx meeting suite for cater Webinar/meeting/Virtual class sessions for ICSI stakeholders.

JUNE 2021 | 9 CHARTERED SECRETARY

ICSI Congratulates Ministry of Corporate Affairs on the launch of MCA21 Version 3.0 at the hands of Shri Anurag Singh Thakur,

Hon’ble Minister of State for Finance & Corporate Affairs.

10 | JUNE 2021 CHARTERED SECRETARY

Glimpses of ICSI Webinars

WEBINAR ON“RECENT DECISIONS OF THE SUPREME COURT/TRIBUNALS AND

APPELLATE TRIBUNAL AND PRE-PACKAGED INSOLVENCY RESOLUTION PROCESS UNDER IBC FOR MSMEs” ORGANIZED BY ASSOCHAM ALONG

WITH ICSI ON 29TH MAY, 2021

JUNE 2021 | 11 CHARTERED SECRETARY

Glimpses of ICSI Webinars

WEBINAR ONWEBINAR ON “DIRECTORS’ REMUNERATION” ORGANIZED BY THE ICSI - BENGALURU CHAPTER AND BANGALORE CHAMBER OF INDUSTRY AND

COMMERCE ON 29TH MAY, 2021

WEBINAR ON“GST IMPACT ON SOFTWARE SERVICES AND IPR” ON 29TH MAY, 2021

WEBINAR ON“LAUNCH OF NEW VERSION (V3) OF THE WEBSITE” OF MINISTRY OF

CORPORATE AFFAIRS ON 24TH MAY, 2021

12 | JUNE 2021 CHARTERED SECRETARY

Glimpses of ICSI Webinars

WEBINAR ON “SILVER JUBILEE FOUNDATION DAY CELEBRATION” BY NASHIK

CHAPTER OF WIRC OF ICSI ON 21ST MAY, 2021

WEBINAR ONCELEBRATION OF 22ND FOUNDATION DAY OF ICSI-CCGRT

ON 19th MAY, 2021

WEBINAR ON “POSITIVE THINKING- KEY TO A HEALTHY LIFESTYLE”

ORGANIZED BY NIRC OF ICSI ON 17TH MAY, 2021

Speaker: Sis BK Shivani

JUNE 2021 | 13 CHARTERED SECRETARY

Glimpses of ICSI Webinars

WEBINAR ON“MENTAL HEALTH & WELLNESS DURING THE PANDEMIC”

ON 14TH MAY, 2021

WEBINAR ON“INAUGURAL SESSION OF FIRST ONLINE CLDP” ORGANIZED BY ICSI-

CCGRT ON 10TH MAY, 2021

WEBINAR ON “OPPRESSION AND MISMANAGEMENT (IN-DEPTH ANALYSIS OF THE RECENT

TATA-CYRUS MISTRY JUDGEMENT PASSED BY THE HON’BLE SUPREME COURT OF INDIA AND ITS IMPACT ON COMPANY LAW JURISPRUDENCE”

ORGANIZED BY CHANDIGARH CHAPTER OF NIRC OF ICSI ON 1st MAY, 2021

Speaker: Dr. Vibhuti Sharma, Senior Counsellor

14 | JUNE 2021 CHARTERED SECRETARY

The Samadhan Diwas is an initiative by the ICSI towards on the spot solution of the grievances of the trainees and trainers. The ICSI had successfully organized the Fourth Samadhan Diwas on Wednesday, 12th May 2021. The focus of this Samadhan Diwas was TCC (Training Clearance Certificate). In the Samadhan Diwas, students got opportunity to present their case to the Institute. More than 40 students attended and got the solutions instantly.

In addition to above, the pending matters of the students’ in the following areas were also heard and resolved .

1. Issues relating to Switchover from Old training to New Training Structure

2. Pending registration in Classroom EDP, e-EDP, e-MSOP

3. Instant issue of sponsorship letters for Practical Training

4. Exemption related matters in Practical Training

5. Resolving the issues of Training Completion Certificate

The students appreciated the efforts of the institute for creating a platform for direct interaction with the ICSI officials to solve their matter on the spot.

Team ICSI

ICSI Conducted 4th Samadhan Diwas on Wednesday, 12th May 2021

JUNE 2021 | 15 CHARTERED SECRETARY

Call for Articles for publication in Chartered Secretary Journal – August 2021

Call for Articles

Unearthing Corporate Frauds – The ever-increasing role and scope for Governance Professional

Any and every law, rule and regulation have always been put in place to regulate a certain area and arena of human life and activity. The Companies Act, 1956 followed by the Companies Act, 2013 along with their Rules have governed and regulated the corporate arena creating a sense of security for all the stakeholders. It was for the reiteration of this very intent that the roles and responsibilities of various professionals had been adequately outlined and defined. However, with expanding territorial boundaries and usage of technology and other new techniques to give effect to crimes, corporate scandals have still been haunting the corporate world. What is more significant is the fact that these frauds while requiring the government to pass effective laws have increased the responsibility of auditors. Not only companies but the statutory auditors as well as governance professionals have been bound by the laws including the corporate governance guidelines and procedures, so that chances of fraudulent activities can be reduced.Given the ever-increasing role of Governance Professionals, we are pleased to inform that the August 2021 issue of Chartered Secretary Journal will be devoted to the theme “Unearthing Corporate Frauds- The ever-increasing role and scope for Governance Professional” covering inter alia the following aspects:• Analysis of the major areas of frauds.• To examine role of top management in fraudulent practices.• Analysis of the efficacy of various laws and rules passed for enhanced corporate governance.• Role and importance of financial statements in investment decision making.• Corporate Governance Policies.• Legislative Framework of Corporate Governance in India.And many more…Members and other readers desirous of contributing articles may send the same latest by Monday, July 19, 2021 at [email protected] for considering in the August 2021 issue of Chartered Secretary.The length of the article should ordinarily be between 2,500 - 4,000 words. However, a longer article can also be considered if the topic of discussion so demands. The articles should be forwarded in MS Word format. All the articles are subject to plagiarism check and will be blind screened. Direct reproduction or copying from other sources is to be strictly avoided. Proper references are to be given in the article either as a footnote or at the end. The rights for selection/rejection of the article will vest with the institute without assigning any reason.We look forward to your co-operation in making this initiative of the Institute a success.

Regards, Team ICSI

16 | JUNE 2021 CHARTERED SECRETARY

Articles in Chartered Secretary

Guidelines for Authors1. Articles on subjects of interest to the profession of company secretaries are published in the Journal.2. The article must be original contribution of the author.3. The article must be an exclusive contribution for the Journal.4. The article must not have been published elsewhere, and must not have been or must not be sent

elsewhere for publication, in the same or substantially the same form.5. The article should ordinarily have 2500 to 4000 words. A longer article may be considered if the subject so

warrants.6. The article must carry the name(s) of the author(s) on the title page only and nowhere else.7. The articles go through blind review and are assessed on the parameters such as (a) relevance and

usefulness of the article (from the point of view of company secretaries), (b) organization of the article (structuring, sequencing, construction, flow, etc.), (c) depth of the discussion, (d) persuasive strength of the article (idea/ argument/articulation), (e) does the article say something new and is it thought provoking, and (f) adequacy of reference, source acknowledgement and bibliography, etc.

8. The copyright of the articles, if published in the Journal, shall vest with the Institute.9. The Institute/the Editor of the Journal has the sole discretion to accept/reject an article for publication in

the Journal or to publish it with modification and editing, as it considers appropriate.10. The article shall be accompanied by a summary in 150 words and mailed to [email protected]. The article shall be accompanied by a ‘Declaration-cum-Undertaking’ from the author(s) as under:

Declaration-cum-Undertaking

1. I, Shri/Ms./Dr./Professor........................... declare that I have read and understood the Guidelines for Authors.2. I affirm that:

a. the article titled”............” is my original contribution and no portion of it has been adopted from any other source;

b. this article is an exclusive contribution for Chartered Secretary and has not been/nor would be sent elsewhere for publication; and

c. the copyright in respect of this article, if published in Chartered Secretary, shall vest with the Institute.d. the views expressed in this article are not necessarily those of the Institute or the Editor of the

Journal.3. I undertake that I:

a. comply with the guidelines for authors,b. shall abide by the decision of the Institute, i.e., whether this article will be published and/or will be

published with modification/editing.c. shall be liable for any breach of this ‘Declaration-cum-Undertaking’.

Signature

40 OCTOBER 2019 I CHARTERED SECRETARY

Articles in Chartered Secretary

Guidelines for Authors1. Articles on subjects of interest to the profession of company secretaries are published in the Journal.2. The article must be original contribution of the author.3. The article must be an exclusive contribution for the Journal.4. The article must not have been published elsewhere, and must not have been or must not be sent

elsewhere for publication, in the same or substantially the same form.5. The article should ordinarily have 2500 to 4000 words. A longer article may be considered if the subject so

warrants.6. The article must carry the name(s) of the author(s) on the title page only and nowhere else.7. The articles go through blind review and are assessed on the parameters such as (a) relevance and

usefulness of the article (from the point of view of company secretaries), (b) organization of the article (structuring, sequencing, construction, flow, etc.), (c) depth of the discussion, (d) persuasive strength of the article (idea/ argument/articulation), (e) does the article say something new and is it thought provoking, and (f) adequacy of reference, source acknowledgement and bibliography, etc.

8. The copyright of the articles, if published in the Journal, shall vest with the Institute.9. The Institute/the Editor of the Journal has the sole discretion to accept/reject an article for publication in

the Journal or to publish it with modification and editing, as it considers appropriate.10. The article shall be accompanied by a summary in 150 words and mailed to [email protected]. The article shall be accompanied by a ‘Declaration-cum-Undertaking’ from the author(s) as under:

Declaration-cum-Undertaking

1. I, Shri/Ms./Dr./Professor........................... declare that I have read and understood the Guidelines for Authors.2. I affirm that:

a. the article titled”............” is my original contribution and no portion of it has been adopted from any other source;

b. this article is an exclusive contribution for Chartered Secretary and has not been/nor would be sent elsewhere for publication; and

c. the copyright in respect of this article, if published in Chartered Secretary, shall vest with the Institute.d. the views expressed in this article are not necessarily those of the Institute or the Editor of the

Journal.3. I undertake that I:

a. comply with the guidelines for authors,b. shall abide by the decision of the Institute, i.e., whether this article will be published and/or will be

published with modification/editing.c. shall be liable for any breach of this ‘Declaration-cum-Undertaking’.

Signature

40 OCTOBER 2019 I CHARTERED SECRETARY

JUNE 2021 | 17 CHARTERED SECRETARY

AT

A G

LAN

CE

Company Secretaries are our New Eco-WarriorsMrs. Almitra H. Patel

T his article highlights the many areas where a CS can shape company policies. Many eco-friendly moves unexpectedly end up saving costs and improving profits

as well as the environment. Six sustainability targets are described: becoming water-neutral by capturing and storing rainwater and surface runoff equal to the firm’s annual freshwater consumption, plus use of recycled wastewater. It describes ways towards net-zero energy consumption by reduced use of electricity and fossil fuels, plus funding of adequate renewable-energy capex and opex. Minimise use of materials and generation of waste and pollution. Most importantly, it addresses the mandatory requirement of EPR, Extended Producer Responsibility, and ways to comply with the various Rules on this.

SEBI and Sustainability Reporting in India - Embracing the FuturePradeep Ramakrishnan & Surabhi Gupta & Ishita Sharma

A sustainability report is used to communicate company’s performance on indicators based on relevant environmental, social and governance issues. Non-

financial, sustainability reporting provides an opportunity to businesses to communicate in an open and transparent way with stakeholders. SEBI was one of the early adopters of sustainability reporting for listed entities amongst global peers. The filing of the Business Responsibility Report (BRR) containing ESG (Environment, Social and Governance) disclosures was first introduced for the top 100 listed entities (by market capitalization) in 2012. The same has now been revamped considerably by SEBI in line with the NGRBCs. The new format is called the Business Responsibility and Sustainability Report (BRSR) and marks a significant improvement in the way in which Corporate India looks at sustainability reporting. This article provides a snapshot of the major changes envisaged by the BRSR.

Envisioning Company Secretaries as Champions of Environment ProtectionUsha Ganapathy Subramanian

D ecades of industrialization with indiscriminate use of fossil fuels and unsustainable lifestyle have led to climate change and environmental degradation. With

rising temperature and environmental disasters serving as a wake-up call, governments the world over have enacted legislations to take control of the situation. Various international organizations and think-tanks have been

discussing on measures to counter climate change and have been encouraging environmental, social and governance (ESG) initiatives by corporates. In India too, we have a plethora of environmental laws to rein in environmental degradation and to promote sustainable development. Major requirements include obtaining consent from State Pollution Control Board for emission of pollutants in air or water, providing information on actual or apprehended discharge beyond standard emission levels, getting environmental clearance for certain projects, and making disclosures in respect of compliance with terms of such approvals. Supporting provisions in corporate and securities laws also mandate compliance with environmental laws. Under the Companies Act, 2013, directors have the duty to ensure compliance with all applicable laws and Company Secretaries should facilitate such compliance. Various disclosure requirements are also designed to nudge the companies to migrate to sustainable ways of doing business. The Ministry of Corporate Affairs has issued National Guidelines on Responsible Business Conduct to provide impetus to corporates to take ESG initiatives. Company Secretaries have the opportunity in bringing about this transformation by ensuring compliance with environmental laws as well as by guiding the boards in adopting environment-friendly policies and processes.

Evolution of Environment Protection Laws in India and Challenges AheadHema Gaitonde

T he foundation of environment governance on a global scale was laid at the United Nations (UN) Conference held in the year 1972 in Stockholm. Further, the UN

Sustainable Development Goals (SDGs) 2030 adopted in the UN Summit 2015, created a vision for all the nations of the world to work towards a safe ecosystem. This article is basically about manner in which the environment law evolved in India, over the years, under the impact of the various international agreements/protocols and standards. In spite of several environmental legislations and government incentives, India today is being ranked very low on the environment protection index in the world. Besides strict implementation of law, a basic behavioral change is required. The people of India and the business entities operating here, need to be totally committed to the cause of creating a safe, sustainable and resilient environment. We have to proceed by applying the ethos of” Vasudhaiva Kutumbakam” meaning the entire ecosystem is my family and I am responsible for its protection.

Rio Conference- A Milestone in Environmental ProtectionAnil Kumar Dubey

R io Conference or Earth Summit, a major International Conference, puts the environmental protection on the centre stage of the of the international diplomacy and

P - 23Articles

Part - I Articles

24

27

34

39

45

18 | JUNE 2021 CHARTERED SECRETARY

AT

A G

LAN

CE

discourse. This conference has produced many tangible outcomes in the form of Rio Declaration, Convention on Biological Diversity, Forest Principles and United Nation Framework Convention on Climate Change (UNFCCC). This summit has led the evolution many important environmental principles like Common but Differentiated Responsibilities (CBDR), Polluter Pays Principle, Precautionary Principle etc. Indian Judiciary has taken the lead in implementing the principles of the Rio Conference in the development of the environmental jurisprudence at the domestic level. Journey from Millennium Development Goals (MDGs) of 2000 to the Sustainable Development Goals (SDGs) of 2015. The Rio +20 outcome also contained other measures for implementing sustainable development, including mandates for future programmes of work in development financing, small island developing states and more.

Environment Protection, Regulatory Framework and Role of Company SecretariesVasumathy Vasudevan

W orld Environment Day is celebrated on June 5 every year. On this occasion, it is important to highlight the compliance of Environmental Laws and understanding

of its Regulatory Framework. Environmental Law covers the entire ambit of the Environmental Protection Act, Water Act and Air Act. This Article is an attempt to throw light on the regulatory framework and the role of the Company Secretary in compliance of various laws, regulations governing Environment Protection, proper maintenance of factories surrounding, timely submission of the Returns under the said acts and rules framed there under and timely intimation to the department about any incident or accident occurred in factories.

Landmark Judgements of National Green Tribunal (NGT): Strengthening the Environmental Protection Regime in the CountryPradeep Kumar Ray

T he National Green Tribunal Act, 2010 enables the creation of a National Green Tribunal (NGT) for the effective and expeditious disposal of cases relating to

environmental protection, conservation of forests and other natural resources including enforcement of any legal right relating to environment and giving relief and compensation for damages to persons and property in line with the provision of protection of life and personal liberty under Article 21 of Part III of India’s constitution. Accordingly, NGT was formed in 2010 as a dedicated jurisdiction in environmental matters to provide speedy environmental justice and help reduce the burden of litigation in the higher courts. Since its inception,

it has been strengthening the environmental protection regime in the Country. In this article, the authors critically analyse all relevant aspects, year wise landmark judgements and five topmost judgements that created history in an effort to discern the trends in environmental jurisprudence in India.

Environmental Regulation - Awareness and ActionGeetika Garella

T he Earth needs to be protected if the ecology and economy are to prosper. Environmental Protection is extremely significant in today’s age of climate change

and in the wake of the Covid-19 pandemic, it is a substantial starting point to initiate the process of getting the economy back on track by ensuring complete adherence to the environmental laws. Environmental legislation and resulting environmental agreements have grown internationally to address the danger of global climate change thus placing a heavier burden on nations with respect to environment protection. Environmental Regulation in India has been a combination of statutes, common law, treaties, conventions, regulations, and policies pertaining to various aspects of the Environment. The Company Secretary is the transformative solutions provider who can handhold communities, corporations, individuals, and governments to recognise the environment regulation and take the appropriate actions for the fulfilment of the same.

Part -II

POSH AT WORKPLACE – Its Impact and Influence in CorporatesKrish Narayanan

T he Government of India passed a legislation considering the need and importance to prevent the women from sexual harassment at workplace

called as PoSH Act, 2013. The ILO and CEDAW have come out with certain principles on upholding the right of women and empowerment precedent to this law. The Honourable Supreme Court of India tested the validity of the provisions of IPC under different cases, directed the union of India to pass a separate legislation under vishaka guidelines. The object of Prevention, Prohibition, and redressal mechanism on sexual harassment at workplace considered as an outcome of good governance. This act defines, workplace, aggrieved women, sexual harassment, and penalties to ensure safety and quality environment. It laid emphasis on employer for constitution of committees to receive complaints, conduct enquiry and action taken by the authorities concerned. The employer has to preserve modesty, dignity and self-respect of women in all strides of the organization.

50

55

65

61

JUNE 2021 | 19 CHARTERED SECRETARY

AT

A G

LAN

CE Evolution and Impact of the

Prevention of Sexual Harassment at Workplace (POSH) Act, 2013Sumit Kochar & Shivam Gera & Akanksha Dave

M illions of employees are entering the workforce today due to greater access to education and jobs. Unfortunately, some suffer through sexual harassment

at work. As a result, we must fight to eliminate workplace sexual harassment since employees have the right to work in a secure and safe atmosphere. Much of the harassment that employees face at work isn’t “Sexual” in content or design. This article tries to highlight the measures that tend to spontaneously increase in sexual harassment cases from different time perspectives. The Hon’ble Supreme Court recognised and dealt with the practise of all forms of sexual harassment at work for the first time in the case of Vishaka Judgement and set up various guidelines for formation of a separate Complaints Committee for redressal, penalties and false and frivolous complains in every company under POSH Act. Further, we have highlighted the impact of POSH Act on the corporate through the pros and cons of the POSH Act. Despite the fact that the POSH Act has been in place since 2013, there is still a dearth of information about the consequences of sexual assault and how to respond to it. The POSH Act’s proper implementation involves not only the creation of an environment in which women may openly express their problems and get justice, but also the refinement of males against workplace harassment of women.

POSH at Workplace – Its Impact and Influence in CorporatesNachiket Sohani

T he Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 came into effect in the year 2013. It aims

to provide protection against sexual harassment of women at workplace and to prevent and redress the complaints of sexual harassment and for any incidental matters. It also changed the perspective of society towards the working women resulting in criminalization of certain offences towards the women. The Act also requires every organization to formulate a policy on prevention of sexual harassment at workplace against women and to constitute committee to address the instances of workplace sexual harassment against women. The Companies Act, 2013 also requires certain disclosures under the Act. Internationally, the United Nations General Assembly also recognizes workplace sexual harassment of women as a serious offence by observing June 19 of each year as the International Day for the Elimination of Sexual Violence in Conflict.

PART-III

Important Learnings from the Judgment of the Hon’ble Supreme Court in Civil no. 440-441 of 2020Vadapalli Srinivas

I n their Judgment, the Hon’ble Apex Court dealt with history of Oppression, Mismanagement and Unfair Prejudice in England and the change of language and

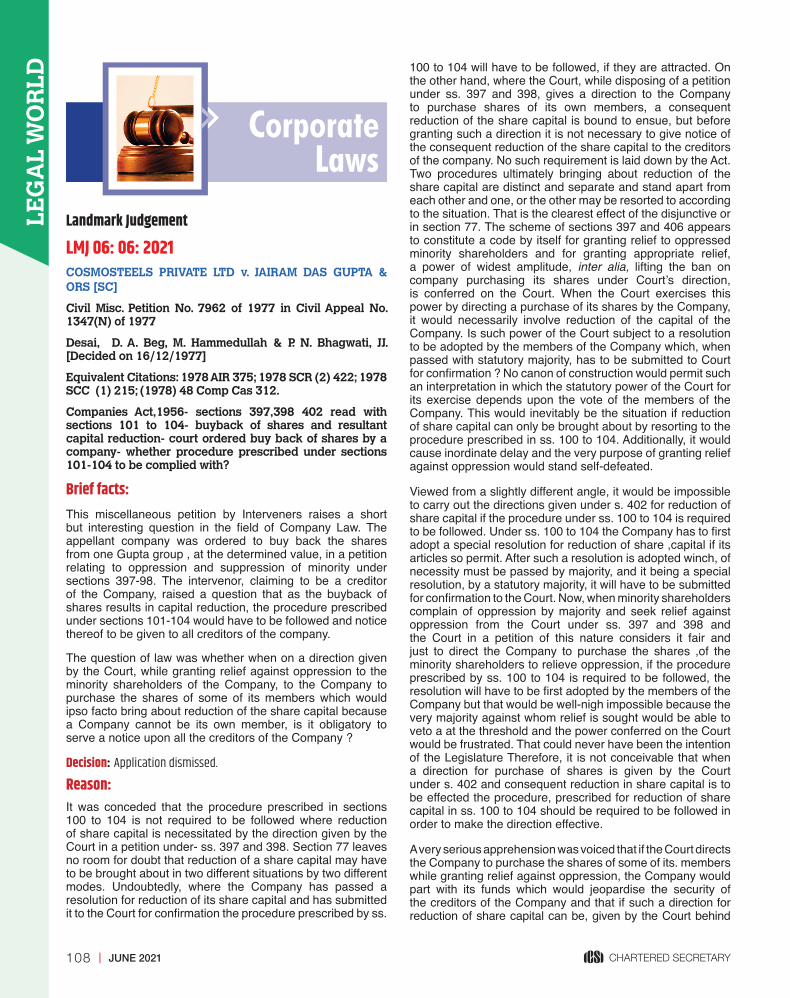

the consequential change of parameters for an enquiry relating to oppression and mismanagement from 1951 to 1956 and from 1956 to 2013 in India. It is observed by the Apex Court that while the conduct of the Company’s affairs in a manner that warrant interference should be “present and continuing” under the 1913 Act and 1956 Act, the conduct could be even “past or present and continuous” under the 2013 Act. It is further observed that under the 2013 Act, conduct prejudicial to any member or prejudicial to public interest or prejudicial to the interest of the company are all added together. It is held that “small shareholders” are different from “minority shareholders” and that the right to claim proportionate representation is available only to “small shareholders” and not to “minority shareholders”. The Judgment is very elaborate, and, in this article, an attempt is made to some of the important observations of the Apex Court.

Risk Management and The Recent Amendments in The SEBI Listing RegulationsSudhakar Saraswatula

R isk is inherent in every business and risk and reward go hand in hand. Risk is omnipresent and all pervasive in any walk of life, more so in the business. The ability of

the managers and their knowledge towards risks play a very critical role in how systematically risks are handled by the organization. The survival of an organization depends upon its ability to anticipate and prepare for the change proactively rather than waiting for the change to happen and then to react to it. The etymology of the word “Risk” may be traced to the Latin word Rescum, which means Risk at Sea. The objective of Risk Management is neither to prevent nor to prohibit from taking any risk but to ensure that the risk is consciously taken with adequate preparation and consciousness with appropriate risk mitigation measures in place before hand.

CSR in context of Bhagavad Gita!Makarand Joshi

S atvik Dana means charities for right cause, right person, and right time with proper process and without any expectation in return. Bhagavad Gita elaborates Satvik,

78

83

86

91

72

20 | JUNE 2021 CHARTERED SECRETARY

AT

A G

LAN

CE

103

Rajas and Tamas charities and destiny arising out of such charities. Recent changes in Section 135 and corresponding rules are actually pushing a corporate to a do a very well thought, well processed CSR without even any remote economic or other benefit in return. There would be corporates which will implement these provisions in true sense and there would be some which will try to somehow meet the letter without adhering to its true intent. If implemented in letter and spirit it will not only help to fulfil the Sustainable Development Goals set by UN but at individual and corporate level also it will forward such person/ entity. This validation we get when we reconcile modern concept of CSR and teachings of Lord Shree Krishna in Bhagavad Gita. This article is trying to throw light on these aspects.

Transfer Pricing and Advance Pricing Agreements in IndiaDr. Rajiv V Shah & Ravisankar G.

T ransfer pricing has become an integral part of international trade today, mainly due the encouragement to international trade and the subsequent spread of

multinational corporations (MNCs). However, this has also led to the possible fear of tax arbitrage, or the transfer of profits to economies having lower tax rates, thus reducing the overall tax liability of the MNC and reducing the tax collection of the country where the profit should have been taxed. To overcome this, many countries have evolved an Advance Pricing Agreement (APA) programme whereby the transfer price of goods and services between related organizations is pre-decided amongst taxpayers and tax authorities, thereby providing all concerned parties with certainty in connection with the transfer price of cross-border transactions between group entities. This article also looks at the growth of the APA programme in India with the number of APA applications filed from 2012-13 to 2018-19 with details of classification, time periods and average processing time per application. It finds that the APA programme can contribute significantly to the reduction of transfer pricing disputes by anticipating and pre-empting them in a mutually agreeable manner.

Moving from Human Resource Management to Human Asset Management: A Key to Competitive AdvantageDr. Manish B. Raval & Dr. Ashish B. Gorvadiya

B y misapprehension, we call it Human Resource Management. In reality, it should be Human Asset Management. Because the people should

be treated like assets not like resources. Out of all the factors of production, human is the only factor which keep other factors in motion. If human is not treated satisfactorily, they may make all the other factors of production useless. If human is treated like resource,

he will be exploited, but if he is treated like an asset, he will be protected. When we see something as an asset our perspective towards it is transformed considerably in a constructive manner. So, the firms should treat its employees as an asset rather than resources. If the organization is managing its employees in excellent manner, it is very much easy for it to gain competitive advantage. If the organization has competitive advantage in terms of its employees, no other firms can beat it.

“The Pre-Pack” - New Insolvency Regime For Micro, Small and Medium Enterprises (MSMEs)Introduced by GovernmentPalak Atul Manek

T he Micro, Small and Medium Enterprises (MSME) sector has emerged as a highly vibrant and dynamic sector of the Indian economy over the last five decades.

It contributes significantly in the economic and social development of the country by fostering entrepreneurship and generating large employment opportunities in our country. But the current COVID-19 pandemic has substantially disrupted the operations of these MSME due to their dependence on the cash economy that is severely hit by the lockdown, the physical non-availability of workers and restrictions in the availability of raw material and transport infrastructure. So, in order to resolve the financial distress in MSMEs, on 4th April,2021, centre has issued an Ordinance to introduce Pre-packaged Insolvency resolution process for corporate entities classified as MSMEs. This law has been introduced to provide an “Efficient Alternative Insolvency Resolution Process”. In this article, The Author has given a brief idea and features of this new insolvency regime introduced by centre to provide quick and value-maximizing outcome for stressed MSMEs.

96

100 Legal World P-107

nLMJ 06: 06: 2021 It is not conceivable that when a direction for purchase of shares is given by the Court under s. 402 and consequent reduction in share capital is to be effected the procedure, prescribed for reduction of share capital in ss. 100 to 104 should be required to be followed in order to make the direction effective.[SC]

nLW 39: 06: 2021 After approval of the Resolution Plan by the Adjudicating Authority, all such claims that are not part of the

JUNE 2021 | 21 CHARTERED SECRETARY

From The Government P-117Other Highlights P-129

v NEWS FROM THE INSTITUTE

v MISCELLANEOUS CORNER

v GST CORNER

v ETHICS IN PROFESSION

v CG CORNER

v STARTUP INDIA

n Clarification on offsetting the excess CSR spent for FY 2019-20

n Clarification on spending of CSR funds for ‘creating health infrastructure for COVID care’, ‘establishment of medical oxygen generation and storage plants’ etc.

n Relaxation on levy of additional fees in filing of certain Forms under the Companies Act, 2013 and LLP Act 2008

n Relaxation of time for filing forms related to creation or modification of charges under the Companies Act, 2013

n Gap between two board meetings under section 173 of the Companies Act, 2013 (CA-13) - Clarification

n Disclosure of the following only w.r.t schemes which are subscribed by the investor:a. risk-o-meter of the scheme and the

benchmark along with the performance disclosure of the scheme vis-à-vis benchmark and

b. Details of the portfolio

n Format of compliance report on Corporate Governance by Listed Entities

n Enhancement of overall limit for overseas investment by Alternative Investment Funds (AIFs)/Venture Capital Funds (VCFs)

n Relaxation from compliance to REITs and InvITs due to the COVID -19 virus pandemic

n Notification under the Bilateral Netting of Qualified Financial Contract Act, 2020

n Procedure for seeking prior approval for change in control of SEBI registered Portfolio Managers

n Business responsibility and sustainability reporting by listed entities

n Relaxation in timelines for compliance with regulatory requirements by Debenture Trustees due to the COVID-19 pandemic

Resolution Plan shall stand extinguished. [NCLAT]

nLW 40: 06: 2021 The impugned order of the High Court allowing the Respondent No. 1 to operate the account without making good the amount of Rs 32.50 lakhs to be placed in the account of the Corporate Debtor cannot be sustained.[SC]

nLW 41: 06: 2021 It is clear from the reading of the contract that the parties had intended to transfer business from appellant to respondent during the contractual period. This agreement was not meant as a lease or license for the respondent to conduct business. [SC]

nLW 42: 06: 2021 UPPTCL has no power and authority and or jurisdiction to realize labour cess under the Cess Act in respect of the first contract by withholding dues in respect of other contracts and/or invoking a performance guarantee.[SC]

nLW 43: 06: 2021 Sub-section (5) of section 80-IA cannot be pressed into service for reading a limitation of the deduction under sub-section (1) only to ‘business income’.[SC]

nLW 44: 06: 2021 Having examined the allegations and response of GNIDA thereon, for the reasons elaborated in the succeeding paras, the Commission is of the considered opinion that no interference is warranted in the matters.[CCI]

nLW 45: 06: 2021 The Commission is of the view that prima facie a case of contravention of the provisions of Section 3(4) and Section 4 of the Act is made out against Tata Motors, and the matter requires to be investigated. [CCI]

22 | JUNE 2021 CHARTERED SECRETARY

ARTICLES1

n COMPANY SECRETARIES ARE OUR NEW ECO-WARRIORSn SEBI AND SUSTAINABILITY REPORTING IN INDIA - EMBRACING THE FUTUREn ENVISIONING COMPANY SECRETARIES AS CHAMPIONS OF ENVIRONMENT PROTECTIONn EVOLUTION OF ENVIRONMENT PROTECTION LAWS IN INDIA AND CHALLENGES AHEAD n RIO CONFERENCE- A MILESTONE IN ENVIRONMENTAL PROTECTIONn ENVIRONMENT PROTECTION, REGULATORY FRAMEWORK AND ROLE OF COMPANY SECRETARIESn LANDMARK JUDGEMENTS OF NATIONAL GREEN TRIBUNAL (NGT): STRENGTHENING THE ENVIRONMENTAL PROTECTION

REGIME IN THE COUNTRYn ENVIRONMENTAL REGULATION - AWARENESS AND ACTIONn POSH AT WORKPLACE – ITS IMPACT AND INFLUENCE IN CORPORATESn EVOLUTION AND IMPACT OF THE PREVENTION OF SEXUAL HARASSMENT AT WORKPLACE (POSH) ACT, 2013n POSH AT WORKPLACE – ITS IMPACT AND INFLUENCE IN CORPORATESn IMPORTANT LEARNINGS FROM THE JUDGMENT OF THE HON'BLE SUPREME COURT IN CIVIL NO. 440-441 OF 2020

[TATA CONSULTANCY SERVICES LIMITED (APPELLANTS) VERSUS CYRUS INVESTMENTS PVT. LTD AND ORS (RESPONDENTS)]n RISK MANAGEMENT AND THE RECENT AMENDMENTS IN THE SEBI LISTING REGULATIONSn CSR IN CONTEXT OF BHAGAVAD GITA!n TRANSFER PRICING AND ADVANCE PRICING AGREEMENTS IN INDIAn MOVING FROM HUMAN RESOURCE MANAGEMENT TO HUMAN ASSET MANAGEMENT: A KEY TO COMPETITIVE ADVANTAGEn “THE PRE-PACK” - NEW INSOLVENCY REGIME FOR MICRO, SMALL AND MEDIUM ENTERPRISES (MSMEs) INTRODUCED BY

GOVERNMENT

JUNE 2021 | 23 CHARTERED SECRETARY

AR

TIC

LE

INTRODUCTION

C ompany Secretaries are powerful influencers in their organisations. The rising cost of fiscal non-compliance has boardrooms attentively following their advice. This

habit makes boardrooms also listen carefully to CS advice on sustainability issues and environmental compliance also, much of it now mandated by legislation or court rulings. So, a CS is the new Eco-Warrior in many firms.

This article highlights the many areas where a CS can shape company policies. Many eco-friendly moves unexpectedly end up saving costs and improving profits as well as the environment. They also improve company morale, efficiency, productivity and even market value when achievements are communicated well, as Marico does.

How to begin?

Define your objectives and goals in the areas you want to tackle, like use of water, power, fuel, packaging, and reduction in waste, pollution and carbon footprint.

Measure current consumption levels of each of these per crore of sales value or tonnage of product. Benchmark the current levels and monitor progress.

Set Targets for incremental annual reduction in each area. No company begins by knowing exactly how it will achieve the targets, but merely defining a target at the Board level, for reduction or improvement, defines a goal and creates corporate commitment down the line, triggering creativity, kaizen and innovation to achieve it.

Company Secretaries are our New Eco-Warriors

Mrs. Almitra H. Patel, MS MIT USA Member, Supreme Court Committee for SWM. National Expert, Swachh Bharat [email protected]

This article highlights the important role that Company Secretaries can play in moving corporate policies towards sustainability goals. It describes how to define ecofriendly objectives, benchmark targets which are measured per crore of sales, set targets all down the line, reduce the company’s impact on the environment and then effectively communicate the outcomes for enhanced employee and shareholder satisfaction and brand building.

Reduce the use of water, power, fuel, water, packaging. Reducing waste, wastage and pollution yields tangible savings and an immediate addition to profits too.

Communicate the targets, reduction methods and results achieved up to the Board and down through all levels, as well as to shareholders. This builds company morale, team spirit and brand value.

1. BE WATER NEUTRALi. Collect your firms’ data on annual freshwater consumption

of factories or offices. Set small annual reduction targets. This will save money too.

ii. Spend CSR funds to progressively capture annual rainfall equal to your annual consumption, by desilting of local ponds or construction of tiny check-dams to store water all along dry or low-flow streams and tributaries. This helps with drought-proofing as well as flood-control. The excavated silt also improves farm fertility.

iii. Maximize reuse of wastewater from existing or new sewage treatment plants (STPs) and effluent treatment plants (ETPs).

iv. Keep different effluent streams separate for ease and economy of treatment. Handling diluted streams of mixed effluents and sewage is technically difficult and costly.

v. Immediately stop the abhorrent and criminal malpractice of drilling reverse borewells in the ground to pour in pollutants as a way to save treatment costs. This is a moral imperative.

ARTICLES PART - I

24 | JUNE 2021 CHARTERED SECRETARY

AR

TIC

LE2. AIM TO BE CARBON-NEUTRALi. Carbon neutrality is achieved by calculating

a carbon footprint and reducing it to near zero through a combination of efficiency measures in-house and supporting external emission reduction projects.

ii. Reduced power consumption is the easiest way. Instal movement sensors in toilets, conference rooms and wherever lights are not regularly switched off when leaving.

iii. Set air conditioner temperatures at a comfortable 25oC, not cooler. As much as 40% of Mumbai’s power consumption is just for ACs!

iv. Use energy efficient ACs, fans, refrigerators when buying or replacing them, and LED lighting.

v. Minimise CO2 emissions from avoidable air travel and long commuting. Work-from-home has taught us how. Move towards Electric Vehicles whenever the opportunity arises.

vi. Instal rooftop solar if space and sunlight permits, either with or without net-metering.

vii. CSR funds for solar pump sets, off-grid rural power, or a share of a solar farm. Aim to annually generate renewably as much power as you consume annually.

viii. Replace coal with biomass briquettes, fossil fuel with biofuels or ethanol-blended vehicular fuels. Minimise gen-set use. Consciously keeping carbn reduction in everyones consciousness will point to many small options that add up.

ix. When designing new buildings, demand natural lighting, cooling, or heating to build in power-saving features.

x. Encourage a re-look at power usage in manufacturing, transport, and distribution, and while purchasing items requiring power inputs.

3. MINIMIZE USE OF MATERIALSi. Set and monitor targets to consciously reduce the quantity

and weight of packaging.

ii. Set targets for recycled content in what you buy and what you sell, to save virgin material.

iii. Buy products in bulk or refills when possible. Use both sides of paper. Avoid using disposables. Have water-dispensers to refill water-bottles or glasses and avoid creating mountains of PET bottle waste. It all saves pennies too.

iv. Minimise construction remodeling that generates demolition waste. Reuse as much as possible. Publicise and celebrate all big and small improvements and successes.

4. MINIMISE WASTE

i. All post-producer waste saved is pure profit.

ii. Follow and enforce at every location the Solid Waste Mangement Rules 2016 obligation for every individual and firm to keep their biodegradable (Wet) waste free of plastics etc. to enable composting, and hand over all non-biodegradable (Dry) waste free of organics for efficient recycling. Deputy Commissioner Mr. Ramdas Kokare has made four towns almost zero-waste-to-landfill by strict enforcement of this rule. In Kalyan-Dombivli Municipal Corporation (pop 18 lakhs) this strictly segregated waste earns his city royalty on the clean dry waste collection contracted out.

iii. Minimise food waste through starting or supporting food banks for the homeless.

5. MINIMISE POLLUTION

i. Be proactive, in your own interest.