the integration of corporate social - RMIT Research Repository

493

THE INTEGRATION OF CORPORATE SOCIAL RESPONSIBILITY INTO BUSINESS STRATEGY AND ITS IMPACT ON COMPANY PERFORMANCE: AN INVESTIGATION OF THE INDONESIAN MANUFACTURING INDUSTRY A thesis submitted in fulfilment of the requirements for the degree of Doctor of Philosophy Esti Dwi Rinawiyanti Master of Business Administration, University of Nuertingen-Geislingen, Nuertingen, Germany Bachelor of Industrial Engineering, Institute of Technology Sepuluh Nopember, Surabaya, Indonesia School of Management College of Business and Law RMIT University June 2021

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of the integration of corporate social - RMIT Research Repository

THE INTEGRATION OF CORPORATE SOCIAL

RESPONSIBILITY INTO BUSINESS STRATEGY AND ITS

IMPACT ON COMPANY PERFORMANCE:

AN INVESTIGATION OF THE INDONESIAN

MANUFACTURING INDUSTRY

A thesis submitted in fulfilment of the requirements for the degree of

Doctor of Philosophy

Esti Dwi Rinawiyanti

Master of Business Administration, University of Nuertingen-Geislingen,

Nuertingen, Germany

Bachelor of Industrial Engineering, Institute of Technology Sepuluh Nopember,

Surabaya, Indonesia

School of Management

College of Business and Law

RMIT University

June 2021

i

DECLARATION

I certify that except where due acknowledgement has been made, the work is that of the author

alone; the work has not been submitted previously, in whole or in part, to qualify for any other

academic award; the content of the thesis is the result of work which has been carried out since

the official commencement date of the approved research program; any editorial work, paid or

unpaid, carried out by a third party is acknowledged; and, ethics procedures and guidelines

have been followed.

Esti Dwi Rinawiyanti

2 June 2021

ii

DEDICATION

This thesis is dedicated to:

My beloved parents,

Erudhito Sudjono (deceased)

Astiti Wardojo

AND

My loving husband,

Sahrum Beru

AND

My lovely children,

Syafero Neumarzello Beru

Rieny Gracierra Beru

iii

ACKNOWLEDGEMENTS

Praise God for all His blessings that have made my endeavor fruitful. I thank Him for giving

me patience, strength, and endurance throughout my PhD journey. The journey of working on

this thesis has been one of the most challenging but rewarding experiences of my life. By His

grace, I can finish this thesis well.

This thesis would not have the soul it has without valuable academic and moral support and

trust in me as a researcher, given by scholars, family, and friends. I am wholeheartedly thankful

to my main supervisor, Dr Xueli (Charlie) Huang, for his patience, supportive feedback,

valuable guidance, and inspiration. My heartfelt thanks go to Prof Sharif As-Saber, my

associate supervisor, for his concern, insightful comments, and encouragement. I regard both

of them not only as research supervisors, but also as mentors in the development of academic

skills needed to be a successful scholar and in improving my publication writing skills. They

comforted and strengthened me to keep on getting up and moving again when I fell and gave

up hope. I feel incredibly lucky and proud to be a student of them.

My sincere appreciation goes to Indonesia Endowment Fund for Education (LPDP) in

collaboration with Directorate General of Higher Education (DIKTI), who gave me the

opportunity to undertake my study with full financial support. I am so grateful that I was chosen

as one of the awardees of the Indonesian Lecturer Excellence Scholarships (BUDI).

I also thank the University of Surabaya for allowing me to further study and providing

support for my studies. Special thanks to the academic and administrative staff at the School

of Management, RMIT University and at the Study Program of Industrial Engineering as well

as at the Faculty of Engineering, University of Surabaya, for being supportive, helpful, and

pleasant. This thesis is also dedicated to my friends and PhD colleagues in RMIT University

whose names I cannot mention one by one. I would like to thank them for our friendship and

unforgettable wonderful times that we cherished together.

iv

Besides, I am grateful for my Indonesian friends and community in Melbourne. I thank them

for their help, gathering and prayer that made my life here colourful and joyful. Because of

them, I felt at home during my stay in Melbourne.

I am very grateful for the support provided by Sahrum, my husband. His immense love, care

and patience during this journey have enabled me to complete this thesis. I thank him for always

being with me physically and emotionally to share all the ups and downs. My deepest thanks

go to my lovely children, Syafero and Riri, who always comforted me and excited me.

Last but not least, to my dear parents, thank you for allowing me to go far for such a long

time to pursue my dreams. I am also deeply indebted to my brothers and sisters, for their

support, assistance, and understanding while I was away.

v

TABLE OF CONTENTS

DECLARATION....................................................................................................................... i

DEDICATION.......................................................................................................................... ii

ACKNOWLEDGEMENTS .................................................................................................. iii

TABLE OF CONTENTS ........................................................................................................ v

LIST OF TABLES .................................................................................................................. xi

LIST OF FIGURES ................................................................................................................ vi

LIST OF APPENDICES ....................................................................................................... vii

LIST OF ACRONYMS .......................................................................................................... xi

ABSTRACT .............................................................................................................................. 1

CHAPTER 1: INTRODUCTION ........................................................................................... 4

1.1 Research Background ...................................................................................................... 4

1.2 An Overview of CSR Practices in Indonesia .................................................................. 8

1.3 Research Questions and Research Objectives ............................................................... 10

1.4 Research Contributions and Implications ..................................................................... 11

1.5 Overview of Research Methodology ............................................................................ 13

1.6 Structure of Thesis ........................................................................................................ 15

1.7 Summary of Chapter 1 .................................................................................................. 17

CHAPTER 2: LITERATURE REVIEW ............................................................................ 19

2.1 Non-Market Strategies .................................................................................................. 19

2.2 Corporate Social Responsibility .................................................................................... 22

2.2.1 CSR Definitions .................................................................................................. 23

2.2.2 CSR Dimensions ................................................................................................. 26

2.2.3 CSR Strategies .................................................................................................... 27

2.2.4 Different Theories in CSR Studies ...................................................................... 30

vi

2.3. Business Strategy ......................................................................................................... 33

2.3.1 Porter’s Generic Strategy .................................................................................... 34

2.3.2 Business Strategy and Company Performance ................................................... 35

2.4. The Integration of CSR into Business Strategy ........................................................... 40

2.4.1 Findings from Prior Studies ................................................................................ 41

2.4.2 Dimensions of the Integration of CSR and Business Strategy ............................ 52

2.5 Company Performance .................................................................................................. 61

2.5.1 Financial Performance ........................................................................................ 61

2.5.2 Non-Financial Performance ................................................................................ 63

2.6 Research Gaps ............................................................................................................... 67

2.7 Indonesia as a Context for the Research ....................................................................... 69

2.7.1 An Overview of Indonesia .................................................................................. 69

2.7.2 The Indonesian Manufacturing Industry ............................................................. 72

2.7.3 CSR Implementation in Indonesia ...................................................................... 75

2.7.4 CSR Studies in the Indonesian Manufacturing Industry ..................................... 81

2.8 Summary of Chapter 2 .................................................................................................. 82

CHAPTER 3: RESEARCH FRAMEWORK ...................................................................... 83

3.1 Theoretical Framework ................................................................................................. 83

3.1.1 Strategy and Company Performance ................................................................... 83

3.1.2 Theoretical Underpinnings .................................................................................. 84

3.2 The Theoretical Framework of the Integration of CSR into Business strategy ............ 86

3.2.1 CSR Dimensions and Strategies.......................................................................... 87

3.2.2 Business Strategy Applied in This Thesis ........................................................... 88

3.2.3 The Integration of CSR into Business Strategy .................................................. 88

3.2.4 Essential Aspects of Company Performance ...................................................... 95

vii

3.3 Research Hypotheses .................................................................................................... 99

3.3.1 The Relationship between CSR Integration and Company Performance ........... 99

3.3.2 Mediating Effects in the Relationship between CSR Integration and Financial

Performance ............................................................................................................... 101

3.3.3 Moderating Effects in the Relationship between CSR Integration and Company

Performance ............................................................................................................... 104

3.4 Summary of Chapter 3 ............................................................................................... 108

CHAPTER 4: RESEARCH METHODOLOGY .............................................................. 109

4.1 Research Approach ..................................................................................................... 109

4.2 Research Paradigm ...................................................................................................... 110

4.3 Research Design .......................................................................................................... 111

4.4 Questionnaire Development ........................................................................................ 113

4.4.1 The Development of the Measurements and Their Scales ................................ 117

4.4.2 Pilot Study ......................................................................................................... 127

4.5 Sampling Process ........................................................................................................ 128

4.5.1 Population and Sample ...................................................................................... 128

4.5.2 Sampling Frame ................................................................................................ 129

4.5.3 Sample Size ....................................................................................................... 130

4.5.4 Sampling Technique.......................................................................................... 131

4.6 Data Collection ............................................................................................................ 131

4.6.1 Data Collection Methods .................................................................................. 131

4.6.2 Results of Data Collection ................................................................................ 135

4.7 Data Analysis Procedures ........................................................................................... 137

4.7.1 Data Coding ...................................................................................................... 137

4.7.2 Data Screening .................................................................................................. 138

viii

4.8 The Respondents’ Profiles and Characteristics ........................................................... 144

4.9 Partial Least Square with Structural Equation Modelling ........................................... 149

4.9.1 Model Specification .......................................................................................... 151

4.9.2 Reflective and Formative Constructs Specification .......................................... 152

4.9.3 Hierarchical Component Model ........................................................................ 153

4.9.4 Model Assessment ............................................................................................ 157

4.9.5 Mediating Effect................................................................................................ 167

4.9.6 Moderating Effect ............................................................................................. 170

4.10 Ethical Considerations .............................................................................................. 174

4.11 Summary of Chapter 4 .............................................................................................. 175

CHAPTER 5: STRATEGIC INTEGRATION-FINDINGS AND DISCUSSION ......... 176

5.1 Descriptive Statistical Analysis in Strategic Integration ............................................. 176

5.2 Model Specification of Strategic Integration .............................................................. 178

5.3 Model Assessment for Strategic Integration ............................................................... 179

5.3.1 Assessment of the Measurement Model in Strategic Integration ..................... 179

5.3.2 Assessment of the Structural Model in Strategic Integration............................ 185

5.4 Discussion of Strategic Integration ............................................................................. 197

5.4.1 Discussion of Strategic Integration and Company Performance ...................... 197

5.4.2 Discussion of Mediating Effect in Strategic Integration ................................... 202

5.5 The Moderating Effect in Strategic Integration .......................................................... 207

5.5.1 MGA Business Strategy in Strategic Integration .............................................. 208

5.5.2 MGA CSR Strategy in Strategic Integration ..................................................... 219

5.5.3 MGA Company Size in Strategic Integration ................................................... 233

5.5.4 MGA Industry Type in Strategic Integration .................................................... 237

5.5.5 Discussion of Moderating Effect in Strategic Integration................................. 243

ix

5.5.6 Results of all Tested Hypotheses in Strategic Integration ................................ 252

5.6 Summary of Chapter 5 ................................................................................................ 253

CHAPTER 6: FUNCTIONAL INTEGRATION AND COMBINED CSR

INTEGRATION-FINDINGS AND DISCUSSION ........................................................... 255

I. Functional Integration .................................................................................................... 255

6.1 Desriptive Statistical Analysis in Functional Integration ............................................ 255

6.2 Model Specification of Functional Integration ........................................................... 256

6.3 Model Assessment of Functional Integration ............................................................. 257

6.3.1 Assessment of the Outer Measurement Model in Functional Integration......... 257

6.3.2 Assessment of the Structural Model in Functional Integration ......................... 263

6.4 Discussion of Functional Integration .......................................................................... 270

6.4.1 Discussion of Functional Integration and Company Performance ................... 270

6.4.2 Discussion of Mediating Effects in Functional Integration .............................. 275

6.5 Multi-group Analysis in Functional Integration ......................................................... 279

6.5.1 MGA Business Strategy in Functional Integration ........................................... 279

6.5.2 MGA CSR Strategy in Functional Integration .................................................. 283

6.5.3 MGA Company Size in Functional Integration ................................................ 289

6.5.4 MGA Industry Type in Functional Integration ................................................. 292

6.5.5 Discussion of Multi-Group Analysis in Functional Integration ........................ 295

6.6 Results for all Tested Hypotheses in Functional integration ............................... 303

6.7 Conclusion of Functional Integration .......................................................................... 305

II. The Combined CSR Integration .................................................................................... 306

6.8 Model Assessment in The Combined CSR Integration .............................................. 306

6.8.1 Assessment of the Measurement Model in The Combined CSR Integration ... 307

6.8.2 Assessment of the Structural Model in The Combined CSR Integration ......... 312

x

6.9 Model Comparison ..................................................................................................... 316

6.10 Discussion of The Combined CSR Integration ......................................................... 319

6.11 Conclusion of Combined CSR Integration ............................................................... 320

6.12 Summary of Chapter 6 ............................................................................................... 321

CHAPTER 7: CONCLUSIONS AND IMPLICATIONS ................................................ 323

7.1 Introduction ................................................................................................................. 323

7.2 Thesis Summary .......................................................................................................... 325

7.3 Conclusions ................................................................................................................. 331

7.4 Theoretical Contributions ............................................................................................ 337

7.5 Methodological Contributions .................................................................................... 338

7.6 Managerial Implications .............................................................................................. 340

7.7 Research Limitations and Directions for Future Research ......................................... 344

7.8 Summary of Chapter 7 ................................................................................................ 345

REFERENCES ..................................................................................................................... 347

APPENDICES ...................................................................................................................... 385

xi

LIST OF TABLES

Table 2.1: Results of Previous Studies of Porter’s Generic Strategies .................................... 40

Table 2.2: Prior Studies of CSR Integration ............................................................................ 48

Table 2.3: CSR Impacts on Company Performance ................................................................ 67

Table 2.4: Indonesian Manufacturing Snapshot ...................................................................... 73

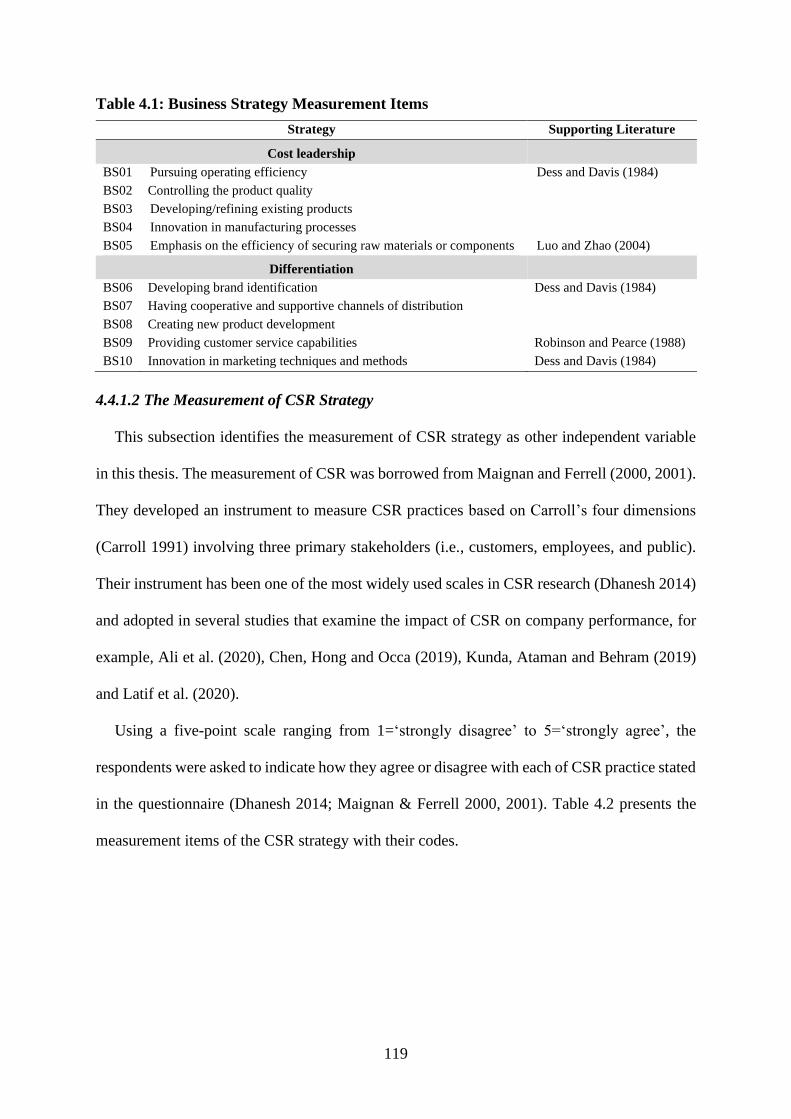

Table 4.1: Business Strategy Measurement Items ................................................................. 119

Table 4.2: CSR Strategy Measurement Items ........................................................................ 120

Table 4.3: Strategic Integration Measurement Items ............................................................. 121

Table 4.4: Functional Integration Measurement Items .......................................................... 122

Table 4.5: Company Performance Measurement Items ......................................................... 125

Table 4.6: Period of Data Collection ..................................................................................... 135

Table 4.7: Results of Data Collection .................................................................................... 137

Table 4.8: Skewness and Kurtosis ......................................................................................... 141

Table 4.9: Respondents’ Profiles ........................................................................................... 144

Table 4.10: Profiles of the Respondents’ Companies ............................................................ 147

Table 4.11: Construct Operationalisation in Strategic and Functional Integration ............... 155

Table 5.1: Reflective Construct Assessments of Model 1 ..................................................... 182

Table 5.2: Fornell-Larcker Testing of Model 1 ..................................................................... 183

Table 5.3: HTMT Values of Model 1 .................................................................................... 184

Table 5.4: Collinearity Test of Formative Measures of Model 1 .......................................... 185

Table 5.5: Indicator Validity of Formative Measurements in Model 1 ................................. 185

Table 5.6: Outer VIF Values of Model 1 ............................................................................... 186

Table 5.7: Inner VIF Values of Model 1................................................................................ 186

Table 5.8: Direct Effects of Model 1 ..................................................................................... 188

Table 5.9: Specific Indirect Effects of Model 1 ..................................................................... 189

ii

Table 5.10: Direct Effects, Indirect Effects and Total Effects of Model 1 ............................ 190

Table 5.11: VAF of Mediation Effect of Model 1 ................................................................. 192

Table 5.12: R2 and Q2 values of Model 1 .............................................................................. 193

Table 5.13: f2 Values of Model 1 ........................................................................................... 195

Table 5.14: q2 Values of Model 1 .......................................................................................... 196

Table 5.15: Factor and Items of Business Strategy ................................................................ 210

Table 5.16: K-means Business Strategy with Three Clusters ................................................ 212

Table 5.17: Respondents Characteristics in Each Cluster of Business Strategy.................... 214

Table 5.18: Step 2 MICOM of Business Strategy in Strategic Integration ........................... 216

Table 5.19: Step 3 MICOM of Business Strategy in Strategic Integration ........................... 216

Table 5.20: Permutation Test of Business Strategy in Strategic Integration ......................... 217

Table 5.21: PLS-MGA Results of Business Strategy in Strategic Integration ...................... 218

Table 5.22: Multi-group Results of Business Strategy in Strategic Integration .................... 218

Table 5.23: Parametric and Welch-Satterthwaite Tests of Business Strategy in Strategic

Integration .............................................................................................................................. 219

Table 5.24: PLS Multi-group Results of Business Strategy in Strategic Integration ............ 219

Table 5.25: Factor and Items of CSR Strategy ...................................................................... 221

Table 5.26: K-means CSR Strategy with Three Clusters ...................................................... 223

Table 5.27: Respondents Characteristics in Each Cluster of CSR Strategy .......................... 225

Table 5.28: PLS-MGA Proactive and Reactive in Strategic Integration ............................... 228

Table 5.29: PLS Multi-group Results of Proactive and Reactive in Strategic Integration .... 229

Table 5.30: MGA Proactive and Accommodative in Strategic Integration ........................... 230

Table 5.31: PLS-MGA Accommodative and Reactive in Strategic Integration .................... 232

Table 5.32: PLS Multi-group Results of Proactive and Reactive in Strategic Integration .... 232

Table 5.33: MGA Results of CSR Strategy in Strategic Integration ..................................... 233

iii

Table 5.34: Comparison of CSR Strategy in Strategic Integration ........................................ 234

Table 5.35: PLS-MGA Company Size in Strategic Integration ............................................ 236

Table 5.36: MGA Results of Company Size in Strategic Integration .................................... 236

Table 5.37: PLS Multi-group Results of Company Size in Strategic Integration ................. 237

Table 5.38: Industry Type Categories .................................................................................... 239

Table 5.39: Respondents Characteristics in Each Category of Industry Type ...................... 240

Table 5.40: PLS-MGA Industry Type in Strategic Integration ............................................. 242

Table 5.41: MGA Results of Industry Type in Strategic Integration .................................... 242

Table 5.42: PLS Multi-group Results of Industry Type in Strategic Integration .................. 243

Table 5.43: Final Results of Hypothesis in Strategic Integration .......................................... 253

Table 6.1: Reflective Construct Assessments of Model 2 ..................................................... 259

Table 6.2: Fornell-Larcker Testing of Model 2 ..................................................................... 261

Table 6.3: HTMT Values of Model 2 .................................................................................... 262

Table 6.4: Collinearity Test of Formative Measures of Model 2 .......................................... 262

Table 6.5: Indicator Validity of Formative Measurements of Model 2 ................................. 263

Table 6.6: Outer VIF values of Model 2 ................................................................................ 264

Table 6.7: Inner VIF values of Model 2 ................................................................................ 264

Table 6.8: Direct Effects of Model 2 ..................................................................................... 265

Table 6.9: Specific Indirect Effects of Model 2 ..................................................................... 266

Table 6.10: Direct Effects, Indirect Effects and Total Effects of Model 2 ............................ 267

Table 6.11: VAF for Mediation Effect of Model 2 ................................................................ 268

Table 6.12: R2 and Q2 values of Model 2 .............................................................................. 268

Table 6.13: f2 Values of Model 2 ........................................................................................... 269

Table 6.14: q2 Values of Model 2 .......................................................................................... 270

Table 6.15: PLS-MGA Business Strategy in Functional Integration .................................... 281

iv

Table 6.16: Multi-group Results Business Strategy in Functional Integration ...................... 282

Table 6.17: PLS Business Strategy in Functional Integration across Methods ..................... 282

Table 6.18: PLS-MGA Proactive and Reactive in Functional Integration ............................ 284

Table 6.19: PLS Proactive and Reactive in Functional Integration across Methods ............. 285

Table 6.20: PLS-MGA Proactive and Accommodative in Functional Integration ................ 286

Table 6.21: PLS Proactive and Accommodative in Functional Integration across Methods 287

Table 6.22: PLS-MGA Accommodative and Reactive in Functional Integration ................. 288

Table 6.23: MGA Results CSR Strategy in Functional Integration....................................... 289

Table 6.24: Comparison of CSR Strategy in Functional Integration ..................................... 289

Table 6.25: PLS-MGA Company Size in Functional Integration.......................................... 291

Table 6.26: MGA Results Company Size in Functional Integration ..................................... 291

Table 6.27: PLS Company Size in Functional Integration across Methods .......................... 292

Table 6.28: PLS-MGA Industry Type in Functional Integration .......................................... 294

Table 6.29: MGA Results Industry Type in Functional Integration ...................................... 294

Table 6.30: PLS Industry Type in Functional Integration across Methods ........................... 295

Table 6.31: Final Results of Hypothesis in Functional integration ....................................... 304

Table 6.32: Reflective construct assessments of Model 3 ..................................................... 308

Table 6.33: Fornell-Larcker Testing of Model 3 ................................................................... 311

Table 6.34: HTMT Values of Model 3 .................................................................................. 312

Table 6.35: Direct Effects of Model 3 ................................................................................... 314

Table 6.36: R2 and Q2 values of Model 3 .............................................................................. 315

Table 6.37: f2 Values of Model 3 ........................................................................................... 315

Table 6.38: q2 Values of Model 3 .......................................................................................... 316

Table 6.39: Direct Effects and Total Effect Comparison across Three Models .................... 317

Table 6.40: Specific Indirect Effects Comparison across Three Models ............................... 318

v

Table 6.41: MGA Results Model 1 and Model 2................................................................... 319

Table 7.1: Final Results of Hypothesis of CSR Integrtation ................................................. 329

Table 7.2: Summary of Hypotheses Verification .................................................................. 331

vi

LIST OF FIGURES

Figure 1.1 Thesis Outline ......................................................................................................... 16

Figure 2.1 The Biggest Economies in the World ..................................................................... 70

Figure 2.2 Indonesia’s Vision 2025 ......................................................................................... 71

Figure 3.1: The Conceptual Framework for the Integration of CSR into Business Strategy and

Its Impact on Company Performance ...................................................................................... 86

Figure 3.2: The Theoretical Framework for the Integration of CSR into Business Strategy with

the Hypotheses ....................................................................................................................... 108

Figure 4.1: Research Approach of This Thesis ...................................................................... 113

Figure 4.3: Main Products of Respondents’ Companies ....................................................... 148

Figure 4.4: The Four Types of Hierarchical Component Models .......................................... 154

Figure 4.5: A Conceptual Model of CSR Integration into Business Strategy ....................... 157

Figure 4.6: Repeated-Indicator Approach for Type II HCM ................................................. 159

Figure 4.7: (A) Illustration of a direct effect. X affects Y; (B) Illustration of a mediation design.

X is hypothesized to exert an indirect effect on Y through M. .............................................. 168

Figure 5.1: Model of Strategic Integration and Company Performance (Model 1) ............... 179

Figure 5.2: Results of PLS Algorithm of Model 1................................................................. 180

Figure 6.1: Model of Functional Integration and Company Performance (Model 2) ............ 257

Figure 6.2: Results of PLS Algorithm of Model 2................................................................. 258

Figure 6.3: Model of CSR Integration and Company Performance (Model 3) ..................... 307

Figure 6.4: Results of PLS Algorithm of Model 3................................................................. 313

vii

LIST OF APPENDICES

Appendix A.1: Concept Definition and Concept Measurement Used in This Thesis ........... 385

Appendix A.2: Questionnaire - English Version ................................................................... 390

Appendix A.3: Questionnaire – Indonesia Version ............................................................... 395

Appendix A.4: Mann-Whitney Test of Business Strategy..................................................... 400

Appendix A.5: Kruskal-Wallis Test of Strategic Integration ................................................ 401

Appendix A.6: Normality Test of Business Strategy ............................................................. 402

Appendix A.7: Skewness and Kurtosis for All Items ............................................................ 403

Appendix A.8: Kruskall-Wallis Test of Company Performance ........................................... 404

Appendix A.9: Mann-Whitney Test of Strategic Integration ................................................ 405

Appendix A.10: Mann-Whitney Test of Company Performance .......................................... 406

Appendix A.11: Ethics Approval ........................................................................................... 407

Appendix A.12: PCA Constructs of Strategic Integration ..................................................... 408

Appendix A.13: PCA Constructs of Functional Integration .................................................. 409

Appendix A.14: PCA Constructs of Company Performance ................................................ 410

Appendix B.1: Descriptive Analysis of Business Strategy .................................................... 411

Appendix B.2: Descriptive Analysis of CSR Strategy .......................................................... 412

Appendix B.3: Descriptive Analysis of Strategic Integration ............................................... 413

Appendix B.4: Descriptive Analysis of Company Performance ........................................... 414

Appendix B.5: Outer Model Loadings and Cross Loadings of Model 1 ............................... 415

Appendix B.6: Varimax-Rotated Common Factor Matrix of Business Strategy .................. 416

Appendix B.7: Collinearity of Business Strategy .................................................................. 417

Appendix B.8: Notification from SmartPLS about Small Sample Size ................................ 418

Appendix B.9: Varimax-Rotated Common Factor Matrix of CSR Strategy ......................... 419

Appendix B.10: Collinearity of CSR Strategy ....................................................................... 420

viii

Appendix B.11: Step 2 MICOM Proactive and Reactive of Strategic Integration ................ 421

Appendix B.12: Step 3 MICOM Proactive and Reactive of Strategic Integration ................ 422

Appendix B.13: Permutation Test Proactive versus Reactive of Strategic Integration ......... 423

Appendix B.14: Parametric and Welch-Satterthwaite Tests Proactive and Reactive of Strategic

Integration .............................................................................................................................. 424

Appendix B.15: Step 2 MICOM Proactive and Accommodative of Strategic Integration ... 425

Appendix B.16: Step 3 MICOM Proactive and Accommodative of Strategic Integration ... 426

Appendix B.17: Permutation Test Proactive and Accommodative of Strategic Integration . 427

Appendix B.18: Parametric and Welch-Satterthwaite Tests Proactive and Accommodative of

Strategic Integration ............................................................................................................... 428

Appendix B.19: Step 2 MICOM Accommodative and Reactive of Strategic Integration..... 429

Appendix B.20: Step 3 MICOM Accommodative and Reactive of Strategic Integration..... 430

Appendix B.21: Permutation Test Accommodative and Reactive of Strategic Integration .. 431

Appendix B.22: Parametric and Welch-Satterthwaite Tests Accommodative and Reactive of

Strategic Integration ............................................................................................................... 432

Appendix B.23: Step 2 MICOM Company Size of Strategic Integration ............................. 433

Appendix B.24: Step 3 MICOM Company Size of Strategic Integration ............................. 434

Appendix B.25: Permutation Test Company Size of Strategic Integration ........................... 435

Appendix B.26: Parametric and Welch-Satterthwaite Tests Company Size of Strategic

Integration .............................................................................................................................. 436

Appendix B.27: Step 2 MICOM Industry Type of Strategic Integration .............................. 437

Appendix B.28: Step 3 MICOM Industry Type of Strategic Integration .............................. 438

Appendix B.29: Permutation Test Industry Type of Strategic Integration ............................ 439

Appendix B.30: Parametric and Welch-Satterthwaite Tests Industry Type of Strategic

Integration .............................................................................................................................. 440

ix

Appendix C.1: Descriptive Analysis of Functional Integration............................................. 441

Appendix C.2: Outer Model Loadings and Cross Loadings of Model 2 ............................... 442

Appendix C.3: Step 2 MICOM Business Strategy of Functional Integration ....................... 443

Appendix C.4: Step 3 MICOM Business Strategy of Functional Integration ....................... 444

Appendix C.5: Permutation Test Business Strategy of Functional Integration ..................... 445

Appendix C.6: Parametric and Welch-Satterthwaite Tests Business Strategy of Functional

Integration .............................................................................................................................. 446

Appendix C.7: Step 2 MICOM Proactive and Reactive of Functional Integration ............... 447

Appendix C.8: Step 3 MICOM Proactive and Reactive of Functional Integration ............... 448

Appendix C.9: Permutation Test Proactive and Reactive of Functional Integration ............. 449

Appendix C.10: Parametric and Welch-Satterthwaite Tests Proactive and Reactive of

Functional Integration ............................................................................................................ 450

Appendix C.11: Step 2 MICOM Proactive and Accommodative of Functional Integration. 451

Appendix C.12: Step 3 MICOM Proactive and Accommodative of Functional Integration. 452

Appendix C.13: Permutation Test Proactive and Accommodative of Functional Integration

................................................................................................................................................ 453

Appendix C.14: Parametric and Welch-Satterthwaite Tests Proactive and Accommodative of

Functional Integration ............................................................................................................ 454

Appendix C.15: Step 2 MICOM Accommodative and Reactive of Functional Integration .. 455

Appendix C.16: Step 3 MICOM Accommodative and Reactive of Functional Integration .. 456

Appendix C.17: Permutation Test Accommodative and Reactive of Functional Integration 457

Appendix C.18: Parametric and Welch-Satterthwaite Tests Accommodative and Reactive of

Functional Integration ............................................................................................................ 458

Appendix C.19: Step 2 MICOM Company Size of Functional Integration .......................... 459

Appendix C.20: Step 3 MICOM Company Size of Functional Integration .......................... 460

x

Appendix C.21: Permutation Test Company Size of Functional Integration ........................ 461

Appendix C.22: Parametric and Welch-Satterthwaite Tests Company Size of Functional

Integration .............................................................................................................................. 462

Appendix C.23: Step 2 MICOM Industry Type of Functional Integration ........................... 463

Appendix C.24: Step 3 MICOM Industry Type of Functional Integration ........................... 464

Appendix C.25: Permutation Test Industry Type of Functional Integration ......................... 465

Appendix C.26: Parametric and Welch-Satterthwaite Tests Industry Type of Functional

Integration .............................................................................................................................. 466

Appendix D: Thesis Related Publications…………………………………………………..467

xi

LIST OF ACRONYMS

AVE Average Variance Extracted

BPS Biro Pusat Statistik (Central Bureau of Statistics)

CCP Company Customer Performance

CEO Chief Executive Officer

CEP Company Employee Performance

CFA Confirmatory Factor Analysis

CFP Company Financial Performance

CIVETS Colombia, Indonesia, Vietnam, Egypt, Turkey and South Africa

COP Company Operational Performance

CP Company Performance

CR Composite Reliability

CSP Company Social Performance

CSR Corporate Social Responsibility

EFA Exploratory Factor Analysis

ESI Environmentally Sensitive Industries

GDP Gross Domestic Product

GRI Global Reporting Initiative

HCM Hierarchical Component Model

HOC Higher-Order Component

HTMT Heterotrait-Monotrait Ratio of Correlations

IDR Indonesian Rupiah

IDX Indonesian Stock Exchange

ISIC Indonesian Standard Industrial Classification

ISO International Organisation for Standardisation

xii

ISRA Indonesian Sustainability Reporting Award

JIEP Jakarta Industrial Estate Pulogadung

LOC Lower-Order Component

KIW Kawasan Industri Wijayakusuma

KMO Kaiser-Meyer-Olkin Measure

MCAR Missing Completely At Random

MGA Multi-Group Analysis

MICOM Measurement Invariance of Composite Models

MP3EI Master Plan Acceleration and Expansion of Indonesia Economic Growth

NCF Net Cash Flow

NGO Non-Governmental Organisation

NMS Non-Market Strategy

PCA Principal Component Analysis

PKM Persuasion Knowledge Model

PLS Partial Least Squares

PLS-SEM Partial Least Squares-Structural Equation Modelling

R2 Coefficient of Determination

RBV Resource Based View

RDT Resource Dependency Theory

ROA Return On Assets

ROE Return On Equity

ROI Return On Investment

ROS Return On Sales

SDG Sustainable Development Goals

SEM Structural Equation Modelling

xiii

SME Small Medium Enterprises

SOE State-Owned Enterprise

SPSS Statistical Package for the Social Sciences

SRA Sustainability Reporting Awards

SRMR Standardized Root Mean Square Residual Value

TOL Tolerance

UNIDO United Nations Industrial Development Organisation

USD United States Dollar

UU Undang-Undang

VAF Variance Accounted For

VIF Variance of Inflation Factor

1

ABSTRACT

Although the extant literature pays considerable attention to whether corporate social

responsibility (CSR) should be integrated with business strategies to gain benefits, research on

how CSR and business strategies could be successfully integrated is scant. This thesis aims to

investigate how CSR and business strategies are integrated, strategically and functionally, and

to examine the impact of such integration on company performance. In addition to direct effect

analyses, this thesis also assesses the mediating effect of company social performance (CSP)

on the relationship between CSR and company financial performance (CFP) and analyses the

moderating effect of business and CSR strategies, company size, and industry type in this

relationship.

A theoretical framework for integration is developed based on a literature review and is

embedded in contingency and stakeholder theories. With a sample of 435 usable responses

from a survey of 1,055 manufacturing companies in Indonesia, this thesis employs Partial Least

Squares with Structural Equation Modelling (PLS-SEM) to analyse the data. Exploratory and

confirmatory factor analyses are conducted, and the hypotheses are verified by examining

direct, indirect, and total effects. The evaluation of measurement models is satisfactorily

achieved. Reflective and formative measures suggest that all constructs are reliable and valid

in the context of this thesis. The assessment of structural models reveals that both strategic and

functional integrations have a significant positive impact on company performance, including

customer, employee, operational and financial performance. More specifically, the empirical

results confirm that strategic and functional integration have an essential effect on customer,

employee, and operational performance, and that these performances can mediate the

relationship between the integrations and financial performance.

The findings also show a positive relationship between strategic and functional integrations.

Integration of CSR at the strategic level has an impact on integration of CSR at the next level,

2

such as at the functional level. Furthermore, the findings presented in this thesis indicate that

business and CSR strategies have a moderating effect on CSR integration. Notably, regarding

business strategy, the results suggest that differentiation strategy has a larger total effect on

customer and financial performance than cost leadership strategy in strategic CSR integration.

However, in functional CSR integration, the findings suggest that differentiation strategy has

a larger total effect than cost leadership strategy, on customer performance only.

With respect to CSR strategy, findings in this thesis highlight that CSR strategy has a

moderating effect on the relationship between CSR integration and company performance.

Proactive and accommodative strategies have a greater total effect on customer and financial

performance than reactive strategy in strategic CSR integration. Conversely, in functional CSR

integration, empirical evidence indicates that reactive strategy has a larger total effect on

employee and financial performance than proactive strategy. In functional integration,

accommodative strategy has a greater total effect on operational performance than proactive

strategy.

In terms of company size, the findings of strategic CSR integration show that large

companies have a greater total effect on customer, employee, operational and financial

performances than small and medium enterprises (SMEs). On the other hand, large companies

have better operational performance than SMEs. These results confirm that company size has

a moderating effect on the relationship between CSR integration and company performance.

Moreover, the results suggest that industry type moderates the relationship between CSR

integration and company performance. In particular, non-environmentally sensitive industries

(non-ESI) have a bigger total effect than ESI in the relationship between strategic CSR

integration and financial performance. In relation to functional CSR integration, findings

indicate that non-ESI groups have a higher total effect in customer and financial performances

than ESI groups.

3

From a theoretical perspective, this research contributes to the body of knowledge by

focusing on CSR integration to understand its impact on company performance. This thesis

contributes to the literature by developing a framework that enables researchers to identify the

different types of benefits provided by CSR integration, and the effect that these benefits have

on the stakeholder-company relationship. This research presents empirical evidence that, in

evaluating the mechanism between CSR integration and company performance, stakeholder

and contingency theories should be taken into account.

From a practical point of view, the findings of this thesis can encourage companies,

particularly Indonesian manufacturing companies, to implement CSR within their company.

Companies should treat primary stakeholders—those who interact with business operations

directly and daily including employees, suppliers, and customers—well, and act on their needs

related to CSR practices. These results could, especially, motivate manufacturing companies

to increase their level of CSR practice. In doing so, they will not conduct CSR merely as a

charity or philanthropy or only to comply with regulations (as many currently practice);

instead, they will strategically and effectively carry out CSR through a range of activities to

achieve superior performance, both socially and financially.

Keywords: CSR integration, company performance, mediating effect, manufacturing sector,

developing countries.

4

CHAPTER 1: INTRODUCTION

This chapter serves as the introduction to the thesis. It begins with a description of the

research background and research questions, and then moves on to the research contributions

and implications. It also contains an overview of research methodology and an explanation of

the thesis' structure as well. There is a summary at the end of this chapter.

1.1 Research Background

The research background for this thesis is discussed in this section. It explains corporate

social responsibility (CSR), CSR integration, and company performance briefly. It also

indicates the research gaps that this thesis will fill.

European Commission (2011) defines CSR as when companies integrate social and

environmental concerns on a voluntary basis into their business practices and relationships with

their stakeholders. This definition implies companies should embrace social, environmental,

ethical human rights and consumer concerns into their business activities and core strategies

when collaborating with their stakeholders. CSR signifies ‘the integration of an enterprise’s

social, environmental, ethical, and philanthropic responsibilities towards society into its

operations, processes and core business strategy in cooperation with relevant stakeholders’

(Rasche, Morsing & Moon 2017, p. 6). These two definitions emphasise the integration of CSR

into business activities and involvement of stakeholders. Because CSR is an organisational

activity that relies on several connections within an organisation’s management and operation

(Valdez-Juárez, Gallardo-Vázquez & Ramos-Escobar 2018), the development of CSR

practices depends on how they are integrated into current business practices (Marín, Rubio &

de Maya 2012; Marques-Mendes & Santos 2016).

Over the past two decades, the concept of CSR has become increasingly popular (Malik

2015). There is growing awareness that business activities create short- and long-term impacts

on society and the environment, as well as economics (Carroll & Shabana 2010). Therefore,

5

CSR has become a concern for all businesses (Martinuzzi & Krumay 2013), as they attempt to

comply and gain advantages from it (Razafindrambinina & Sabran 2014). Managers look for

ways to position their companies to take advantage of the business opportunities created by

CSR, while also trying to find solutions to address environmental and societal problems (Rosen

2001).

Although CSR is a common issue on the agenda of companies, it is not yet a strategic

priority. One reason for this is the lack of understanding of the benefits of CSR for

competitiveness (Porter & Kramer 2006). The relationship between companies’ activities and

their impact on competitive advantage has been extensively examined in recent research (Porter

& Siggelkow 2008), but it remains unclear whether and how CSR can impact company

competitiveness (Carroll & Shabana 2010).

To address this question, previous studies have demonstrated a positive correlation between

CSR and company performance, which leads to improved competitive advantage (Carroll &

Shabana 2010; Orlitzky, Schmidt & Rynes 2003). For example, some research has indicated

that CSR has a positive impact on financial performance (Ameer & Othman 2012; Beck, Frost

& Jones 2018; Sindhu & Arif 2017). Other studies also found that CSR significantly affects

employee performance (Bauman & Skitka 2012; Sprinkle & Maines 2010), customer

performance (García-Madariaga & Rodríguez-Rivera 2017; Park, Kim & Kwon 2017), and

operational performance (Sánchez & Benito-Hernández 2015; Sun & Yu 2015). Many studies

examine the relationship between CSR and company performance and confirm that CSR

provides several benefits to a company’s social and financial performance (Bauman & Skitka

2012; Beck, Frost & Jones 2018; García-Madariaga & Rodríguez-Rivera 2017; Kim, Kim &

Qian 2018; Malik 2015). However, it remains unclear under what mechanism this relationship

can occur.

6

Despite the fact that prior studies have demonstrated that CSR has a positive impact on

company performance, several authors have argued that CSR must be connected and integrated

into business strategy to benefit companies (Dey & Sircar 2012; Ganescu 2012b; Husted &

David 2011). Researchers have emphasised the importance of integration of CSR into business

strategy to enhance companies’ social and financial performance (Carroll & Shabana 2010;

Galbreath 2006; Ganescu 2012b; Hasan et al. 2018; Marín, Rubio & de Maya 2012; Porter &

Kramer 2011). Integration between CSR activities and core business functions is critical to

value creation by CSR and vital to the success of companies (Carroll & Shabana 2010; García-

Madariaga & Rodríguez-Rivera 2017). A common problem with the planning and

implementation of CSR strategies and practices, however, appears to be the lack of alignment

with business strategy (Rangan, Chase & Karim 2012). Many managers agree on a strategic

interest in CSR, but few fully incorporate CSR aspects into their business practices. Integrating

CSR into a business strategy decision is one of the most challenging tasks facing managers

(Carroll & Shabana 2010).

Because it is critical to have a better understanding of the relationship between CSR

integration and business strategy (Insight 2016), several studies on the integration of CSR into

business strategy have been carried out, either conceptually or empirically. For example, Maon,

Lindgreen and Swaen (2009) integrated top-down and bottom-up processes throughout the

integration process on the basis of the stakeholder theory. They also explained the roles of the

primary and secondary stakeholders and provided specific case studies to support their

interpretation. Notably, they highlighted the importance of integrating CSR into the objectives

and strategies of a company, identifying key stakeholders and their critical problems,

developing an integrated CSR, and engaging employees in implementation, monitoring and

evaluation. Asif et al. (2013) built the framework for integrating CSR into business processes

across all stages of business processes, suggesting top-down and bottom-up approaches to

7

integration. This study implied that CSR integration can be carried out through many activities,

including vertical and horizontal integration. Furthermore, Lindgreen et al. (2011) highlighted

that CSR integration involves cultural change led by top management and other change agents,

who drive CSR values throughout the company. Marques-Mendes and Santos (2016)

developed a more comprehensive framework and explained each stage in detail by providing

indicators and related concepts. Their studies demonstrated how integration can take place

thoroughly, beginning with strategic integration (ideological models), implementation

(procedural models), and then the effect of the integration (consequentialist models).

Nevertheless, there is scant empirical research on the integration of CSR into business

strategy and the resulting impact on organisational performance (Vitolla, Rubino & Garzoni

2017). It remains unclear how CSR and business strategies can be integrated, as well as how

such integration can affect company performance. Furthermore, the integration of CSR is an

important topic, but it is seldom considered in strategic management (Engert, Rauter &

Baumgartner 2016; Kiron et al. 2013). Since most of the relevant literature are prescriptive and

deal with theoretical frameworks and concepts, empirical studies on the integration of corporate

sustainability into strategic management and models that show how CSR can be integrated into

business strategy are needed (Engert, Rauter & Baumgartner 2016; Guadamillas-Gómez,

Donate-Manzanares & Škerlavaj 2010).

This thesis seeks to fill current research gaps by developing and testing a model that

describes CSR integration at the strategic and functional levels. It investigates how CSR and

business strategy are integrated, examines the impact of this integration on organisational

performance and analyses the mechanisms through which CSR integration affects company

performance.

8

1.2 An Overview of CSR Practices in Indonesia

This section describes currect CSR practices and regulations in Indonesia. It also explains

an overview of Indonesia and the impact of CSR rules on the manufacturing industry.

CSR practices are implemented at relatively higher and more intense levels in developed

countries than in developing countries (Bhattacharyya 2010). Most studies on CSR are

concerned with investigating the practices adopted by companies in developed countries (Zhu,

Liu & Lai 2016). CSR is emerging as a distinct area of management studies in developing

countries (Jamali & Karam 2018), and it is essential to identify significant information on the

contribution of CSR and the main factors affecting CSR performance (Blowfield 2007; Branco

& Rodrigues 2006; Crifo, Diaye & Pekovic 2016), including in Indonesia.

Indonesia is not only the world’s fourth most populous nation with more than 267 million

people, but also has the largest economy in Southeast Asia (Worldbank 2020). CSR has become

a major concern in Indonesia over the past two decades (Maris 2014). In particular, the

Indonesian government has released Law No. 40 2007 on Limited Liability Companies (or

Undang-Undang (UU) No. 40 Tahun 2007 tentang Perseroan Terbatas). With this law,

Indonesia is the world's first country to mandate that companies, especially those related to

natural resources, must implement CSR, and report their CSR activities (Maris 2014; Ridho

2018; Rosser & Edwin 2010; Sheehy & Damayanti 2019; Waagstein 2011). In practice,

however, this is problematic as it needs not only a specific definition of CSR, but also an

effective implementation process and tools to evaluate its impact (Waagstein 2011). Hence, the

government needs to develop policy regulation, clearly defining CSR and considering

stakeholders’ perceptions that companies should respond to and implement an appropriate

business practice for their survival. As CSR is a matter of good business practice, companies

should care for their stakeholders across a variety of interactions (Maris 2014).

9

Although there are laws regulating CSR, many Indonesian companies misinterpret it. CSR

is assumed to be a corporate social activity for the community and environment through profit

distribution to philanthropic programs (Radyati 2014). Prior studies show that most Indonesian

companies embrace CSR through charitable practices, corporate philanthropy, and community

development (Ambadar 2017; Joseph et al. 2016; Razafindrambinina & Sabran 2014; Widjaja

2011). Few activities refer to social and environmental concerns (Waagstein 2011), and many

companies enforce CSR through simple and instant activities, such as donations and

fundraising (Maulamin 2017; Ridho 2017).

Because manufacturing companies carry out activities related to natural resources, they have

been affected by this law, while also dealing with a growing number of environmental, labour

and human rights laws at both national and international levels (Bernal-Conesa, de Nieves-

Nieto & Briones-Peñalver 2017). Several studies have investigated CSR implementation in the

Indonesian manufacturing industry. For instance, based on a sample of 53 manufacturing

companies, Hasanudin and Budianto (2013) found that both employee CSR and corporate

reputation have a positive impact on company performance, but environmental CSR has a

negative impact. Purbowati and Mutiarni (2017) assessed the effect of corporate characteristics

on CSR disclosure, using a sample of 50 listed manufacturing companies. They claimed that

company size has a significant impact on CSR disclosure while the company's profile, the size

of the commissioner board, and ownership concentration have no significant impact on the

disclosure of CSR. Furthermore, with survey data from 173 manufacturing companies,

Handayani, Wahyudi and Suharnomo (2017) highlighted the significant influence of CSR on

company performance and emphasised the importance of integrating social and environmental

aspects in CSR implementation.

Even though several studies have examined CSR practices in the context of the Indonesian

manufacturing industry, limited research has comprehensively analysed the relationship

10

between CSR integration and company performance. In particular, the extent to which

manufacturing companies, after 13 years of CSR regulation in Indonesia, improve and enforce

their CSR practices needs to be investigated further.

1.3 Research Questions and Research Objectives

This section begins by determining research questions. It then goes on to research objectives

that this thesis will achieve.

The integration between CSR and business strategy has been discussed in the literature, but

substantial identifiable gaps remain, which lead to this thesis’s key research question (RQ):

what is the extent to which CSR and business strategy are integrated? This main research

question can be divided into several supplementary research questions:

RQ1: To what extent does CSR integrate into business at the strategic and functional levels?

RQ2: To what extent does CSR integration affect company performance?

RQ3: To what extent does social performance mediate the relationship between CSR

integration and financial performance?

RQ4: To what extent do business and CSR strategies moderate the impact of CSR

integration on company performance?

RQ5: To what extent do company size and industry type moderate impact of CSR

integration on company performance?

To address these research questions, this thesis investigates how CSR can be integrated into

business at strategic and functional levels. This thesis also aims to examine the impact of

strategic and functional CSR integrations on company performance, particularly in the

Indonesian manufacturing industry. As a result, six specific objectives were established:

▪ Investigate the essential dimensions of CSR integration at the strategic level;

▪ Examine the crucial dimensions of CSR integration at the functional level;

11

▪ Identify the relationship between CSR integration (strategic and functional integrations)

and company performance;

▪ Uncover the mediating effect of customer, employee, and operational performance in the

CSR integration-CFP relationship;

▪ Discover the moderating effect of business and CSR strategies in the CSR integration-

company performance relationship; and

▪ Identify the moderating effect of company size and industry type in the CSR integration-

company performance relationship.

1.4 Research Contributions and Implications

In this section, the contributions of this thesis to current knowledge about CSR are

presented. It also identifies the research implications of this thesis, not only for top managers

but also for policymakers.

From a theoretical perspective, this thesis is one of the first studies to propose a model that

comprehensively examines the relationship between CSR integration and company

performance. Thus, this thesis makes an essential contribution to the existing literature on CSR

integration and the impact of integration on company performance.

First, this thesis develops a conceptual framework by combining CSR integration and its

effect on company performance based on the strategy-context-performance relationship at

strategic and functional levels. Second, this thesis clarifies the relationship between the

proposed variables in the conceptual framework for strategic and functional integration to

demonstrate that the integration of CSR and business strategies has an impact on company

performance. Third, this thesis presents new empirical evidence on the relative impact of

various integration mechanisms on integration by suggesting that social performance can

mediate the impact of CSR integration on financial performance. By incorporating stakeholder

theory, the findings underline that the stakeholder relationship is a key mechanism through

12

which companies can benefit financially from the integration of CSR into their business

strategies. Specifically, this thesis provides new empirical evidence that the stakeholder

relationship should be considered when evaluating the relationship between CSR integration

and financial performance as such a relationship can be mediated by customer, employee and

operational performance. Fourth, this thesis offers new insights into the impact of CSR on

company performance from a contingency perspective. The results of the moderation analysis

show that the impact of CSR integration on company performance is contingent and dependent

on business and CSR strategies, company size and industry type. Finally, this thesis is one of

the first to empirically investigate the performance implications of integrating CSR into

business strategy and reveals new findings on how such integration can substantially improve

company performance.

From a practical perspective, the findings of this thesis have important implications for

executives and managers, particularly those working in manufacturing companies in

developing countries. First, executives and managers can be better motivated to integrate CSR

into their company strategies more strategically and to conduct business operations consistent

with CSR practices. In doing so, CSR should be incorporated from upstream to downstream or

along the value chain, covering all functions within the company and connecting to internal

activities of the company. Second, this thesis provides key findings that instead of undertaking

CSR as mere charity, philanthropy or compliance activities (as many currently practice),

companies integrating CSR with their business strategy can benefit from considerable, positive

impacts on their financial and non-financial performance, which in turn could enhance their

competitive advantage.

In addition, this thesis makes recommendations to decision makers, such as the Indonesian

government. First, they should not only make it mandatory for companies to engage in CSR,

but they should also establish clearer and more extensive guidelines. Companies could then

13

understand to what extent they can implement CSR and the scope of CSR that they can carry

out. Second, the government can communicate regulations and guidelines more frequently and

effectively on their official websites, at association conferences and annual gatherings, and

through awards. In this way, large companies and small and medium enterprises (SMEs) can

recognise the regulations and understand how to comply with them.

1.5 Overview of Research Methodology

This section presents an overview of research methodology applied in this thesis. It starts

with a research paradigm and a research framewok, followed by a research method, a survey,

as well as a data collection. Then, it describes a data analysis that will be conducted in this

thesis and research findings briefly.

This thesis adopts a positivist research paradigm and applies a deductive research design as

it seeks to develop and validate a theoretical model. The theoretical framework is based on

stakeholder and contingency theories. The framework describes the relationship between

strategic and functional integration and company performance, including customer, employee,

operational and financial performance. The theoretical framework contains 47 hypotheses. This

thesis examines several mediating and moderating effects in the relationship between CSR

integration and company performance.

This thesis conducts an explanatory study and uses quantitative research to address the

research questions proposed. It considers three essential dimensions of strategic CSR

integration: (1) aligning CSR with the company’s strategy, (2) gaining support from top

management, and (3) developing effective communication. Functional CSR integration

comprises six critical dimensions: (1) Cost, (2) Innovation, (3) Quality, (4) Supplier, (5)

Customer, and (6) Employee. To comprehensively analyse the impact of CSR integration,

company performance is assessed across four criteria: customer, employee, operational and

financial. The items for integration and company performance are adopted from previous

14

research on strategic management, CSR, and manufacturing. To examine the mediating effect

of the CSR integration-company performance relationship, this thesis uses business and CSR

strategies. Business strategy follows the most widely-used typology from Porter (1980a). The

measurement of CSR is borrowed from Maignan and Ferrell (2000, 2001), based on Carroll’s

four dimensions (Carroll 1979, 1991). In addition, this thesis uses company size and industry

type. Company size uses the number of employees to define small, medium, and large

companies. The criteria for company size follow the classification from Statistic Indonesia or

Badan Pusat Statistik (BPS 2017a). Industry type includes environmentally sensitive industries

(ESI) and non-ESI, and the criteria for industry type were based on the literature review and

prior studies.

To facilitate respondent understanding of the survey, the questionnaire developed was

translated from English to Indonesian using a back-translation method. Pre-tests were

conducted to ensure the survey questions were clear, concise, and specific to the context. Prior

to data collection, the questionnaire was submitted and approved by RMIT University’s Ethics

Committee. Before conducting the survey, a pilot test was undertaken with 30 respondents.

After the pilot test, the main survey with a non-probability purposive sampling method was

officially carried out across five regions in Java, Indonesia: East Java, Central Java,

Yogyakarta, West Java, and Jakarta.

From June to October 2018, the self-completion questionnaires were distributed through

post, e-mail, and personal delivery survey. In total, surveys were sent to 1,055 manufacturing

companies, and 514 surveys were returned. After data screening, 435 usable responses

remained, with a final response rate of 41.23%, which were used for data analysis.

To provide a plausible answer for each research question and research objective (Section

1.3), Statistical Product and Service Solutions (SPSS) 26 and partial least square structural

equation modelling (PLS-SEM) were employed for a series of comprehensive data analyses.

15

Specifically, SmartPLS 3, a professional software of PLS-SEM, was used to determine a model

specification that contained constructs and indicators, and to develop a model. Then, the

evaluation of the model was conducted in two steps: (1) the measurement model and (2) the

structural model. This thesis examined the direct effects, indirect effects, and total effects to

explore direct relationships and mediating effects. In addition, multi-group analysis (MGA)

was performed to assess the mediating effects.

The findings of this thesis demonstrate that structural and functional integrations have an

essential role in achieving better financial and non-financial performance. More specifically,

the findings show that customer, employee, and operational performance can significantly

mediate the impact of CSR integration on financial performance. Notably, the findings suggest

that business and CSR strategies can substantially moderate the effect of CSR integration on

company performance. Also, company size and industry type can significantly affect this

integration’s impact on company performance.

1.6 Structure of Thesis