THE FIRM AND THE FINANCIAL MANAGER

40

Chapter 1: THE FIRM AND THE FINANCIAL MANAGER Organizing a Business Sole Proprietorship - is the simplest business form under which one can operate a business. It does not have a separate legal entity. It simply refers to a person who owns the business and is personally responsible for its debts. - is an individual entity that is separate and distinct from the owner. Partnerships - is form by two or more persons binding themselves to contribute money, property or industry to a common fund, with the intention of dividing the profits among themselves. - The partnership is an individual entity that is separate and distinct from each of the partners. 1 | Page

Transcript of THE FIRM AND THE FINANCIAL MANAGER

Chapter 1:

THE FIRM AND THE FINANCIAL MANAGER

Organizing a Business

Sole Proprietorship

- is the simplest business form under which one can

operate a business. It does not have a separate legal

entity. It simply refers to a person who owns the

business and is personally responsible for its debts.

- is an individual entity that is separate and distinct

from the owner.

Partnerships

- is form by two or more persons binding themselves to

contribute money, property or industry to a common

fund, with the intention of dividing the profits among

themselves.

- The partnership is an individual entity that is

separate and distinct from each of the partners.

1 | P a g e

- Two or more persons may also form a partnership for the

exercise of profession.

- Partnership Agreement set out how management decisions are

to be made and the proportion of the profits that each

partner is entitled to.

Corporation

is an artificial being created by operation of law,

having the right of succession and the powers,

attributes and properties expressly authorized by law

or incident to its existence.

Articles of incorporation set out the purpose of the business

and how it is to be financed, managed and governed.

Corporations have limited liability - corporate

creditors have claims against corporate assets only

which means that the owners are not personally

responsible for the corporation’s debt.

Separation of ownership and management is one distinctive

feature of corporations.

2 | P a g e

Characteristics of business organizations

Who owns the business?

Are managers andowner(s) separate?

What is the owner’sliability?

Are the owner andbusiness taxed separately?

Main Role of a Financial Manager

Financial activities of a firm is one of the most important

and complex activities of a firm. Therefore in order to take

care of these activities a financial manager performs all

the requisite financial activities.

REAL ASSETS are assets used to produce goods and

services.

FINANCIAL ASSETS - Claims to the income generated by

3 | P a g e

Themanager Partners

Shareholders

No No Usually

Unlimited Unlimited Limited

No No Yes

real assets. Also called securities.

A financial manger is a person who takes care of all the

important financial functions of an organization. The person

in charge should maintain a farsightedness in order to

ensure that the funds are utilized in the most efficient

manner. His actions directly affect the Profitability,

growth and goodwill of the firm.

a. Capital Budgeting Decision is the planning process used to

determine whether an organization's long term

investments such as new machinery, replacement

machinery, new plants, new products, and research

development projects are worth the funding of cash

through the firm's capitalization structure (debt,

equity or retained earnings). It is the process of

allocating resources for major capital, or

investment, expenditures.

4 | P a g e

Chief Financial Officer (CFO)

Responsible for:Financial Policy

Corporate Planning

TreasurerResponsible for:Cash ManagementRaising Capital

Banking Relationship

ControllerResponsible for:Preparation of

Financial StatementsAccounting-Taxes

b. Financial Decision is concerning the liabilities and

stockholders' equity side of the firm's balance

sheet, such as a decision to issue bonds.

Who is The Financial Manager?

Financial Manager refers to anyone responsible for a

significant corporate investment or financing decision. They

hold the most important ingredient of a company in the palm of

their hands, management of cash flow of a company. Since

financial managers can be found in almost every organization,

it is important to understand their role in an organization.

Financial manager faces two basic problems.

5 | P a g e

TreasurerResponsible for:Cash ManagementRaising Capital

Banking Relationship

ControllerResponsible for:Preparation of

Financial StatementsAccounting-Taxes

Goals of Corporation

Maximize Profit - A company's most important goal is to make

money and keep it. Profit-margin ratios are one way to

measure how much money a company squeezes from its total

revenue or total sales.

Minimize cost- Companies use cost controls to manage and/or

reduce their business expenses. By identifying and

evaluating all of the business's expenses, management can

determine whether those costs are reasonable and affordable.

The cost-control process seeks to manage expenses ranging

6 | P a g e

from phone, internet and utility bills to employee payroll

and outside professional services.

Shareholders want managers to maximize market value-

Companies are always looking to expand their share of the

market, in addition to trying to grow the size of the total

market by appealing to larger demographics, lowering prices

or through advertising. Market share increases can allow a

company to achieve greater scale in its operations and

improve profitability.

Chapter 2:

THE FINANCIAL ENVIRONMENT

A financial environment is a part of an economy with the

major players being firms, investors, and markets. Essentially,

7 | P a g e

this sector can represent a large part of a well-developed

economy as individuals who retain private property have the

ability to grow their capital. Firms are any business that offers

goods or services to consumers. Investors are individuals or

businesses that place capital into businesses for financial

returns. Markets represent the financial environment that makes

this all possible.

FINANCIAL MARKETS

Stock Market

Financial Market is a market in which people and entities

can trade financial securities, commodities, and other fungible

items of value at low transaction costs and at prices that

reflect supply and demand. Securities include stocks and bonds,

and commodities include precious metals or agricultural goods.

Primary Market is the part of the capital market that deals

with issuing of new securities. Companies, governments or public

8 | P a g e

sector institutions can obtain funds through the sale of a new

stock or bond issues through primary market.

Secondary Market is a market where investors purchase

securities or assets from other investors, rather than from

issuing companies themselves.

Other Financial Market

Fixed-income market is market for debt securities.

Capital Market is a part of a financial system concerned with

raising capital by dealing in shares, bonds, and other long-term

investments.

Money Market is the trade in short-term loans between banks

and other financial institutions.

Financial Intermediaries

It is an entity which acts as a middleman between two

parties in a financial transaction. While a commercial bank is a

typical financial intermediary, this category also includes other

9 | P a g e

financial institutions such as investment banks, insurance

companies, broker-dealers, mutual funds and pension funds.

Financial intermediaries offer a number of benefits to the

average consumer including safety, liquidity and economies of

scale.

A financial intermediary is an organization that raises money

from investors and provides financing for individuals, companies,

and other organizations. For corporations, intermediaries are

important sources of financing. Intermediaries are a stop on the

road between savings and real investment.

Mutual funds raise money by selling shares to investors. The

investors’ money is pooled and invested in a portfolio of

securities. Investors can buy or sell shares in mutual funds as

they please, and initial investments are often $3,000 or less.

Mutual funds offer investors low-cost diversification and

professional management. For most investors, it’s more efficient

to buy a mutual fund than to assemble a diversified portfolio of

stocks and bonds.

10 | P a g e

Issue debt (borrower)

There are other ways of pooling and investing savings and

one is the pension plan. The most common type of plan is the

defined-contribution plan. In this case, a percentage of the

employee’s monthly paycheck is contributed to a pension fund.

Contributions from all participating employees are pooled and

invested in securities or mutual funds. The balance in the plan

can be used to finance living expenses after retirement. Pension

funds are designed for long-run investment. They provide

professional management and diversification. They also have an

important tax advantage: Contributions are tax-deductible, and

investment returns inside the plan are not taxed until cash is

finally withdrawn.

Financial Institutions

An establishment that focuses on dealing with financial

transactions, such as investments, loans and deposits.

11 | P a g e

COMPANY INVESTORS

Invest 2.5M

Conventionally, financial institutions are composed of

organizations such as banks, trust companies, insurance companies

and investment dealers. Almost everyone has deal with a financial

institution on a regular basis. This includes the financial

institution (such as a bank, credit union, finance company,

insurance company, stock exchange, and brokerage.

Functions of Financial Markets and Intermediaries

Transporting Cash across Time

Individuals need to transport expenditures in time. If you

have money now that you wish to save for a rainy day, you

can (for example) put the money in a savings account at a

bank and withdraw it with interest later. If you don’t have

money today, say to buy a car, you can borrow money from the

bank and pay off the loan later. Modern finance provides a

kind of time machine. Lenders transport money forward in

time; borrowers transport it back.

Liquidity

12 | P a g e

The degree to which an asset or security can be bought or

sold in the market without affecting the asset's price.

Liquidity is characterized by a high level of trading

activity. Assets that can be easily bought or sold are known

as liquid assets.

The Payment Mechanism

Think how inconvenient life would be if you had to pay for

every purchase in cash or if Boeing had to ship truckloads

of hundred-dollar bills around the country to pay its

suppliers. Checking accounts, credit cards, and electronic

transfers allow individuals and firms to send and receive

payments quickly and safely over long distances.

Reducing Risk

The chance that an investment's actual return will be

different than expected. Risk includes the possibility of

losing some or all of the original investment. Different

versions of risk are usually measured by calculating the

13 | P a g e

standard deviation of the historical returns or average

returns of a specific investment.

Provide information

In well-functioning financial markets, you can see what

securities and commodities are worth, and you can see—or at

least estimate—the rates of return that investors can expect

on their savings. The information provided by financial

markets is often essential to a financial manager’s job.

Here are three examples of how this information can be used.

Chapter 3

ACCOUNTING and FINANCE

A financial statement (or financial report) is a formal record of

the financial activities of a business, person, or other entity.

14 | P a g e

It is a summary report that shows how a firm has used the

funds entrusted to it by its stockholders (shareholders) and

lenders, and what is its current financial position. The three

basic financial statements are the (1) balance sheet, which shows

firm's assets, liabilities, and net worth on a stated date; (2)

income statement (also called profit & loss account), which shows

how the net income of the firm is arrived at over a stated

period, and (3) cash flow statement, which shows the inflows and

outflows of cash caused by the firm's activities during a stated

period.

Types of Financial Statements

- Balance Sheet or Statement of Financial Position

- Income Statement or Statement of Financial Performance

- Statement of Cash Flow

- Statement of Changes in Shareholder’s Equity

- Statement of Comprehensive Income

- Notes and Supporting details

15 | P a g e

BALANCE SHEET OR FINANCIAL POSITION

- An accountant’s snapshot of the firm’s accounting value

on a particular date, as though the firm stood

momentary still.

- States what the firm owns and how it is financed.

- A summary of a management's performance as reflected in

the profitability (or lack of it) of an organization

over a certain period. It itemizes the revenues and

expenses of past that led to the current profit or

loss, and indicates what may be done to improve the

results.

Assets = Liabilities + Stockholders’ equity

Sections of the balance sheet:

Assets - resources of the firm that are expected to increase

or cause future cash flows (everything the firm owns)

Liabilities - obligations of the firm to outsiders or claims

against its assets by outsiders (debts of the firm)

16 | P a g e

Owners’ Equity - the residual interest in, or remaining

claims against, the firm’s assets after deducting

liabilities (rights of the owners)

INCOME STATEMENT

- Measures performance over a specific period of time,

say, a year.

- It is composed of the following two elements:

Income: What the business has earned over a period

(e.g. sales revenue, dividend income, etc)

Expense:The cost incurred by the business over a

period (e.g. salaries and wages, depreciation

rental charges, etc)

The accounting definition of income is:

Revenue – Expenses = Income

STATEMENT OF CASH FLOWS

17 | P a g e

- One of the quarterly financial reports any publicly

traded company is required to disclose to the SEC and

the public. The document provides aggregate data

regarding all cash inflows a company receives from both

its ongoing operations and external investment sources,

as well as all cash outflows that pay for business

activities and investments during a given quarter.

- Reports the sources and uses of cash by operating activities,

investing activities, financing activities, and certain supplemental

information for the period specified in the heading of

the statement. The statement of cash flows is also

known as the cash flow statement.

Classification of Cash flow Activities

1. Operating Activities – key indicator of the extent to

which the operations of the enterprise have

generated sufficient cash flows to repay loans,

maintain the operating capability of enterprise, pay

18 | P a g e

dividends and make new investments without recourse

to external sources of financing.

2. Investing Activities –cash flow which extent to which the

expenditures have been made for resources intended

to generate future income and cash flow. It includes

acquiring and selling, or otherwise disposing of (a)

securities that are not cash equivalents and (b)

productive assets that are expected to benefit the

firm for long term periods of time; and lending

money and collecting on loans.

3. Financing Activities is important in predicting claims on

future cash flows by providers of capital to the

enterprise. It include borrowing from creditors and

repaying the principal; and obtaining resources from

owners and providing them with a return on the

investment.

STATEMENT OF CHANGES IN SHAREHOLDER’S EQUITY

19 | P a g e

- Often referred to as Statement of Retained Earnings in

U.S. GAAP, details the change in owners' equity over an

accounting period by presenting the movement in

reserves comprising the shareholders' equity.

- Statement of changes in equity helps users of financial

statement to identify the factors that cause a change

in the owners' equity over the accounting periods.

Whereas movement in shareholder reserves can be

observed from the balance sheet, statement of changes

in equity discloses significant information about

equity reserves that is not presented separately

elsewhere in the financial statements which may be

useful in understanding the nature of change in equity

reserves

STATEMENT OF COMPREHENSIVE INCOME

- is the change in equity (net assets) of a business

enterprise during a period from transactions and other

events and circumstances from non-owner sources.

20 | P a g e

- It illustrates the financial performance and results of

operations of a particular company or entity for a

period of time.

NOTES and SUPPORTING DETAILS

Additional information provided in a company's financial

statements. Footnotes to the financial statements report the

details and additional information that are left out of the main

reporting documents, such as the balance sheet and income

statement. This is done mainly for the sake of clarity because

these notes can be quite long, and if they were included, they

would cloud the data reported in the financial statements.

THE MARKET VALUE VERSUS BOOK VALUE

Book Value literally means the value of the business

according to its "books" or financial statements. In this case,

book value is calculated from the balance sheet, and it is the

21 | P a g e

difference between a company's total assets and total

liabilities.

Market Value is the value of a company according to the stock

market. Market value is calculated by multiplying a company's

shares outstanding by its current market price.

There are three basic generalizations about the relationships

between book value and market value:

Book Value Greater Than Market Value: The financial market

values the company for less than its stated value or net

worth. When this is the case, it's usually because the market

has lost confidence in the ability of the company's assets to

generate future profits and cash flows.

Market Value Greater Than Book Value: The market assigns a

higher value to the company due to the earnings power of the

company's assets.

Book Value Equals Market Value: The market sees no compelling

reason to believe the company's assets are better or worse

than what is stated on the balance sheet.

22 | P a g e

Chapter 4:

The Time Value of Money

Time Value of Money (TVM) is an important concept in financial

management. It can be used to compare investment alternatives and

to solve problems involving loans, mortgages, leases, savings,

and annuties.

Future Values

Future Value - Amount to which an investment will grow after

earning interest.

Compound Interest - Interest earned on interest.

Simple Interest - Interest earned only on the original

investment.

23 | P a g e

Example - Simple Interest

Interest earned at a rate of 6% for five years on a

principal balance of $100.

Interest Earned Per Year = 100 x0 .06 = $ 6

Present Values

Present Value

- Value today of a future cash flow.

Discount Factor

- Present value of a $1 future payment.

Discount Rate

- Interest rate used to compute present values

of future cash flows.

Example:

24 | P a g e

PV F V r t 1

1( )PV= Future Value after t periods(1+r)t

You just bought a new computer for $3,000. The payment terms are 2 years

same as cash. If you can earn 8% on your money, how much money should you set

aside today in order to make the payment when due in two years?

The PV formula has many applications. Given any variables

in the equation, you can solve for the remaining variable.

PV of Multiple Cash Flows

Your auto dealer gives you the choice to pay $15,500 cash now, or make three

payments: $8,000 now and $4,000 at the end of the following two years. If your cost of

money is 8%, which do you prefer?

PVs can be added together to evaluate multiple cash flows.

25 | P a g e

PV= 3000(1.08 )2

=$2,572

Immediate payment 8,000.00PV1=

4,000(1+.08)1

=3,703.70

PV2=4,000

(1+.08)2=3,429.36

Total PV = $15,133.06

PV=C1

(1+r )1+

C2

(1+r)2+....

Perpetuities & Annuities

Perpetuity- A stream of level cash payments that never

end.

Annuity- Equally spaced level stream of cash flows for a

limited period of time.

PV of Perpetuity Formula

C = cash payment r = interest rate

Example:

In order to create an endowment, which pays $100,000 per year, forever, how much

money must be set aside today in the rate of interest is 10%?

If the first perpetuity payment will not be received until three years from today, how

much money needs to be set aside today?

26 | P a g e

PV=Cr

PV=100 ,000.10 =$1,000,000

PV of Annuity Formula

C = cash payment

r = interest rate

t = Number of years cash payment is received

PV Annuity Factor (PVAF)

- The present value of $1 a year for each of t

years.

Inflation

- Rate at which prices as a whole are increasing.

Nominal Interest Rate

- Rate at which money invested grows. 27 | P a g e

PV=1,000,000(1+.10 )3

=$751,315

PV=C [ 1r− 1r(1+r )t ]

PVAF=[ 1r− 1r (1+r )t ]

Real Interest Rate

- Rate at which the purchasing power of an

investment increases.

Example

If the interest rate on one year govt. bonds is 5.0% and the inflation rate is 2.2%,

what is the real interest rate?

Effective Annual Interest Rate

- Interest rate that is annualized using compound

interest.

Annual Percentage Rate

28 | P a g e

1+real interest rate= 1+nominal interest rate1+inflation rate

Real int. rate≈nominal int. rate-inflation rate

- Interest rate that is annualized using simple

interest.

Chapter 5:

Bond Valuation

Valuation Fundamentals

A bond is an IOU issued by a corporation, government, or

governmental agency to cover money the bondholder has lent. If

you own stock in a company, you are a part owner of the company.

29 | P a g e

Valuation

As a bondholder, you are a creditor.Although less exciting than

stocks, bonds play a critical role in our economy and an

important role in every well-balanced portfolio.

Returns from bonds are generally lower than stocks; however,

they're a much safer investment. Bonds' safety and stability act

as a counter to the fluctuations common to stocks.

Most investors should have a mix of stocks and bonds in their

portfolio. The more risk you are able and willing to take the

higher percentage of stocks in your portfolio. The more

conservative investor will want a higher percentage of bonds.

Look at my article on the basics of asset allocation.

Bonds are debt instruments used by business and governmentto raise large sums of money

Most bonds share certain basic characteristics.

First, a bond promises to pay investors a fixed amountof interest, called the bond’s coupon.

Second, bonds typically have a limited life, ormaturity.

Third, a bond’s coupon rate equals the bond’s annualcoupon payment divided by its par value.

30 | P a g e

Fourth, a bond’s coupon yield equals the coupon paymentdivided by the bond’s current market price.

Corporations issue bonds as a way to borrow large sums of money.

Companies have two basic ways to raise money for expansion,

acquisitions, or other uses. They can issue stock or borrow the

money.Corporate bonds usually come in 1,000 denominations and

have maturities ranging up to 40 years, but are usually shorter.

Municipal governments also issue bonds, which they often use to

build roads or perform other infrastructure projects.

BOND MARKETS

1. Issuing Market (Primary market): The period starts from

issuer's planning stage to passes a series of procedures and

finally until bond is handed to subscribers.

2. Trading Market (Secondary Market): The market for investors to

trade bonds or for bondholders to sell bonds for cash. Recently,

bond tradingmainly deals in the OTC market, only a few bond

trading prosecutes onthe main market. In order to make bond

31 | P a g e

trading more smoothly and safely, GTSM sets up all kinds of

regulations to standardize the market.

TYPES OF BONDS

GovernmentBonds

In general, fixed-income securities are classified according to

the length of time before maturity. These are the three main

categories:

Bills - debt securities maturing in less than one year.

Notes - debt securities maturing in one to 10 years.

Bonds - debt securities maturing in more than 10 years.

Municipal Bonds

Municipal bonds, known as "munis", are the next progression in

terms of risk. Cities don't go bankrupt that often, but it can

happen. The major advantage to munis is that the returns are free

from federal tax. Furthermore, local governments will sometimes

make their debt non-taxable for residents, thus making some

municipal bonds completely tax free. Because of these tax

32 | P a g e

savings, the yield on a muni is usually lower than that of a

taxable bond. Depending on your personal situation, a muni can be

a great investment on an after-tax basis.

Corporate ]Bonds

A company can issue bonds just as it can issue stock. Large

corporations have a lot of flexibility as to how much debt they

can issue: the limit is whatever the market will bear. Generally,

a short-term corporate bond is less than five years; intermediate

is five to 12 years, and long term is over 12 years.

Corporate bonds are characterized by higher yields because there

is a higher risk of a company defaulting than a government. The

upside is that they can also be the most rewarding fixed-income

investments because of the risk the investor must take on. The

company's credit quality is very important: the higher the

quality, the lower the interest rate the investor receives.

Convertible Bonds

33 | P a g e

Other variations on corporate bonds include convertible bonds,

which the holder can convert into stock, and callable bonds,

which allow the company to redeem an issue prior to maturity.

Zero-Coupon bonds

This is a type of bond that makes no coupon payments but instead

is issued at a considerable discount to par value. For example,

let's say a zero-coupon bond with a $1,000 par value and 10 years

to maturity is trading at $600; you'd be paying $600 today for a

bond that will be worth $1,000 in 10 years.

Bond Value = PV of coupons + PV of par

Bond Value = PV annuity + PV of lump sum

Remember, as interest rates increase, the PVs decrease

So, as interest rates increase, bond prices decrease and viceversa

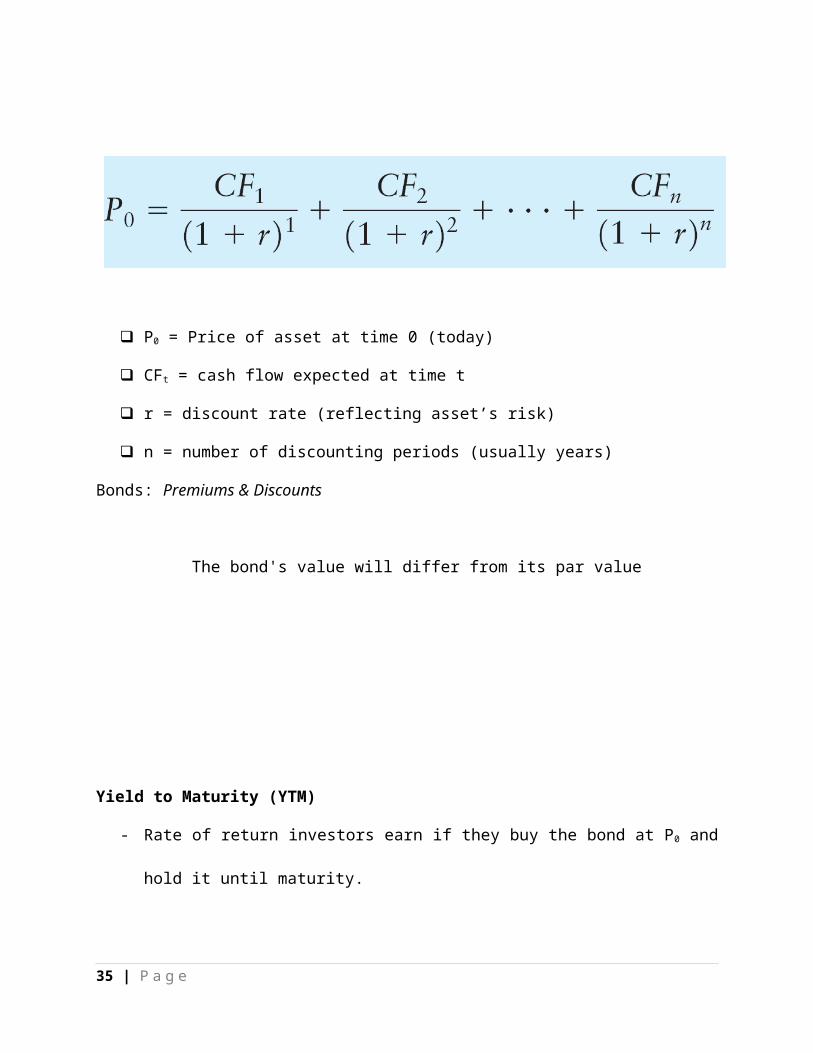

34 | P a g e

P0 = Price of asset at time 0 (today)

CFt = cash flow expected at time t

r = discount rate (reflecting asset’s risk)

n = number of discounting periods (usually years)

Bonds: Premiums & Discounts

The bond's value will differ from its par value

Yield to Maturity (YTM)

- Rate of return investors earn if they buy the bond at P0 and

hold it until maturity.

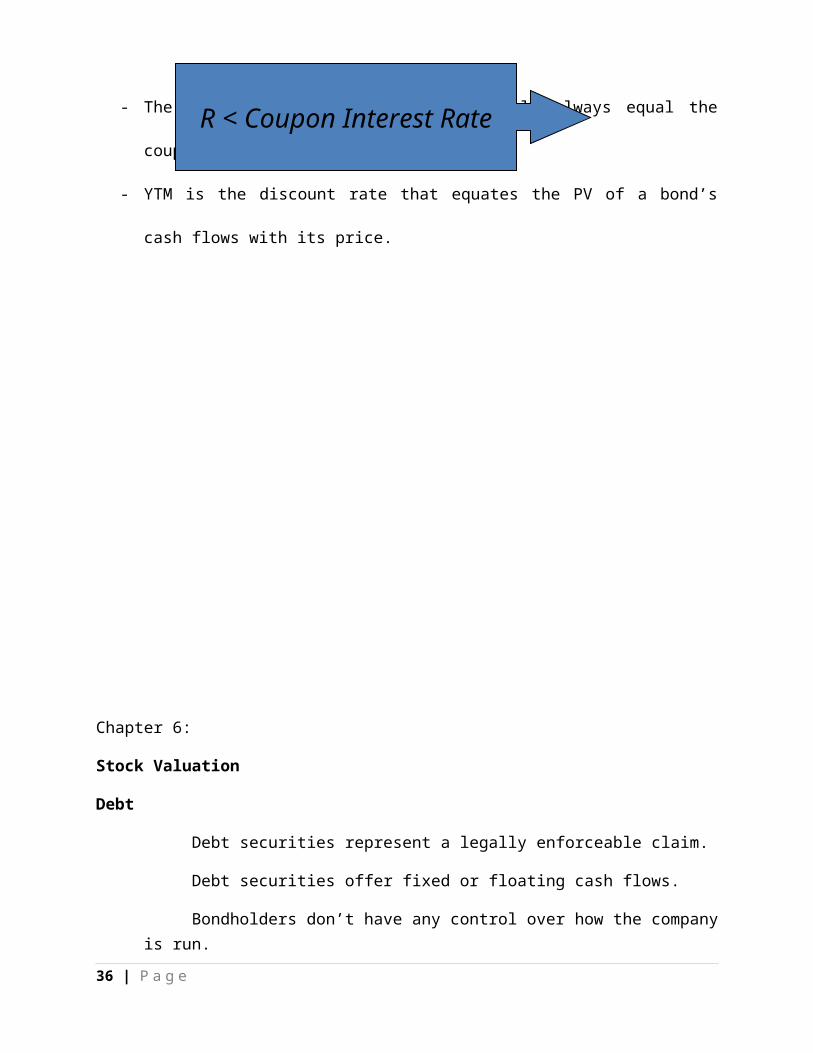

35 | P a g e

- The YTM on a bond selling at par will always equal the

coupon interest rate.

- YTM is the discount rate that equates the PV of a bond’s

cash flows with its price.

Chapter 6:

Stock Valuation

Debt

Debt securities represent a legally enforceable claim.

Debt securities offer fixed or floating cash flows.

Bondholders don’t have any control over how the companyis run.

36 | P a g e

R < Coupon Interest Rate

Equity

Common stockholders are residual claimants

• No claim to earnings or assets until all senior claimsare paid in full

• High risk, but historically also high return

Stockholders have voting rights on important companydecisions.

Debt and equity have substantially different marginal benefits andmarginal costs.

Two Main Types Of Stocks

CommonStock

Common stock is, well, common. When people talk about stocks they

are usually referring to this type. In fact, the majority of

stock is issued is in this form. We basically went over features

of common stock in the last section. Common shares represent

ownership in a company and a claim (dividends) on a portion of

profits. Investors get one vote per share to elect the board

members, who oversee the major decisions made by management. Over

the long term, common stock, by means of capital growth, yields

higher returns than almost every other investment. This higher

37 | P a g e

return comes at a cost since common stocks entail the most risk.

If a company goes bankrupt and liquidates, the common

shareholders will not receive money until the creditors,

bondholders and preferred shareholders are paid.

PreferredStock

Preferred stock represents some degree of ownership in a company

but usually doesn't come with the same voting rights. (This may

vary depending on the company.) With preferred shares, investors

are usually guaranteed a fixed dividend forever. This is

different than common stock, which has variable dividends that

are never guaranteed. Another advantage is that in the event of

liquidation, preferred shareholders are paid off before the

38 | P a g e

Share

s issued and outstandin

g

Number of shares owned by

stockholders

common shareholder (but still after debt holders). Preferred

stock may also be callable, meaning that the company has the

option to purchase the shares from shareholders at anytime for

any reason (usually for a premium).

Preferred stock is a hybrid having some features similar to debtand other features similar to equity.

Claim on assets and cash flow senior to common stock As equity security, dividend payments are not tax

deductible for the corporation. For tax reasons, straight preferred stock held mostly

by corporations.

Valuing Preferred Stock

• Because preferred stock pay a constant dividend, they areeasy to value because the dividends are perpetuity.

• Recall the present value of a perpetuity is:

• Where : D1 is the constant dividend whose first payment is one period from today

Example:

You purchase a preferred stock with a $12 per year dividend. Fora 10% market rate, what is its value?

Book value

39 | P a g e

PV=PMTi =

D1i

Price=PV=D1i =

$120.10

=$120.00

Net assets per share available to common stockholdersafter liabilities are paid in full

Net worth of the firm according to the balance sheet

Liquidation value

Actual net amount per share likely to be realized uponliquidation & payment of liabilities

Net proceeds that could be realized by selling thefirm’s assets and paying off its creditors.

More realistic than book value, but doesn’t considerfirm’s value as a going concern

40 | P a g e