The European "Creative Sector": Definitions and structures of the "Culture & Creative Industries"...

39

The European "Creative Sector": Definitions and structures of the "Culture & Creative Industries" (CCI), with data on economic development Prof. Dr. Andreas Joh. Wiesand, Executive Director, European Institute for Comparative Cultural Research gGmbH (ERICarts) Presentation I at the EUCTP Workshop Development of Trade in Cultural Goods and Services in Hefei, China (26-27 April) Parts of this presentation are based on research of Michael Söndermann, Office for Culture Industries Research, Cologne/Germany (KWF) and President of the German Working Group on Culture Statistics

-

Upload

dresden-international-university -

Category

Documents

-

view

2 -

download

0

Transcript of The European "Creative Sector": Definitions and structures of the "Culture & Creative Industries"...

The European "Creative Sector": Definitions and structures of the "Culture & Creative

Industries" (CCI), with data on economic development

Prof. Dr. Andreas Joh. Wiesand, Executive Director, European Institute for Comparative Cultural Research gGmbH (ERICarts)

Presentation I at the EUCTP WorkshopDevelopment of Trade in Cultural Goods and Services

in Hefei, China (26-27 April)

Parts of this presentation are based on research of Michael Söndermann, Office for Culture Industries Research, Cologne/Germany (KWF) and

President of the German Working Group on Culture Statistics

About the ERICarts InstituteThe European Institute for Comparative Cultural Research (ERICarts), established 1993 and based in Bonn/Germany, is an independent provider of empirical information and analysis to policymakers and other actors in the cultural field and in related policy sectors (e.g. media; education; youth; regional development; economy; security). It relies on a network of experienced partner institutionsand permanent correspondents in over 50 countries; many of them contribute to the Council of Europe /ERICarts "Compendium of Cultural Policies & Trends in Europe" (www.culturalpolicies.net).Recent comparative studies for the European Union include:• "The Contribution of Culture to Local and Regional Economic

Development - Evidence from the Structural Funds" (with CSES);• Mobility of Cultural Professionals (www.mobility-matters.eu); and • "Sharing Diversity" (approaches to intercultural dialogue in Europe –

www.interculturaldialogue.eu).

The Council of Europe/ERICarts "Compendium":

A Pan-European research and monitoring tool

A.J.Wiesand/ERICarts 2012

1. Disputed Definitions

A.J.Wiesand/ERICarts 2012 4

Entering a conceptual playground0(Examples of empirical studies and major debates)

A. PRIVATE SECTOR CONCEPTS:• "Kulturwirtschaft / Culture Economy" (e.g. 5 Reports in NorthRhine-

Westphalia 1991-2007; other German Länder Reports; Switzerland 2003)• "Cultural Industries / Industries Culturelles" (France 2006; Istanbul 2007)• "Cultural Industries Cluster" (Barcelona/Spain 2004)• "Cultural Products and Services Industry" (e.g. EUCLID for EU 2003)• "Show Business" (traditional: USA)B. MIXED NEW ECONOMY (OR UK-) MODELS:

• "Creative Industries" (e.g. UK, 1998-2008; Austria 2000 / 2006; KEA for EU, 2006, 2010)

• "Creative Class" (e.g. Richard Florida 2002; Netherlands 2005)• "Copyright Industries" (e.g. USA 2000, Singapore 2004)• "Knowledge Economy" (e.g. Canada 1997/2005; Finland 2006)C. ALTERNATIVE OR "HYBRID" CONCEPTS:

• "Experience Industry" (Sweden 2003)• "Creative Capital" (Conference Amsterdam 2005; Denmark 2006) • "Cultural Goods" (traditional: UNESCO)• "Creative Sector / Kreativsektor" (e.g. Conference UNESCO @ Univ. of

Austin/USA 2003; ERICarts Report for European Cult. Foundation 2005;• "Cultural & Creative Sector" (Conference Portuguese EU Presidency 2007)

A.J.Wiesand/ERICarts 2012 5

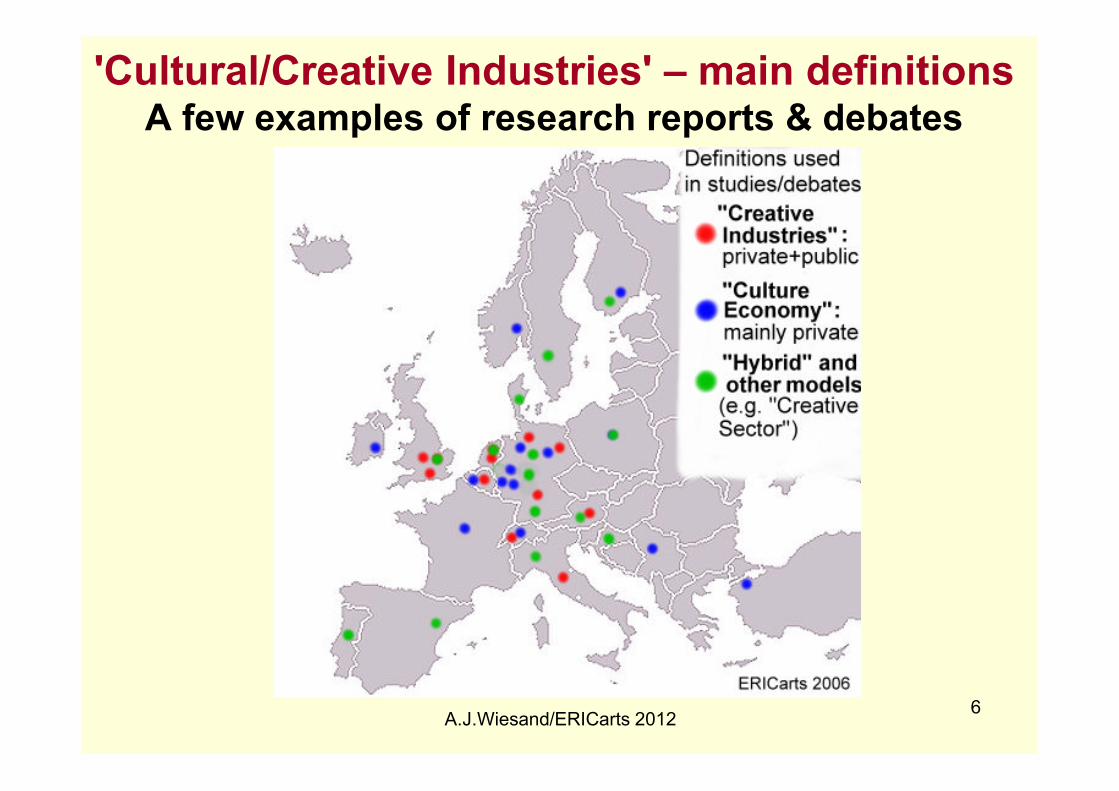

'Cultural/Creative Industries' – main definitionsA few examples of research reports & debates

A.J.Wiesand/ERICarts 20126

CREATIVE ECONOMY incl. COPYRIGHT INDUSTRIES (780 billion € turnover, ~ 8.8-10 million employees)

+R&D

On-line publis-

hing,ICT

CREATIVE INDUSTRIES(490 billion €, ~6.3m employees)

+Software

Computer gamesAdver-tising

Fashion

Definitions can indeed make a difference0Economic output & jobs as seen in older studies

Notes: Figures are estimates from different sources (ARKStat, Howkins, Mercer, Eurostat)Sources: John Howkins 2001; Research Group Creative Industries Zurich; M. Soendermann 2006

CULTURE INDUSTRIES(310 billion €, ~4m empl.)

MusicBooks & PressArtsFilmTV & RadioPerforming Arts

Artists & other cultural occupations, designers & architects, some technical & scientific occupations

PUBLIC

BROAD-

CASTING

(75 bill. €)

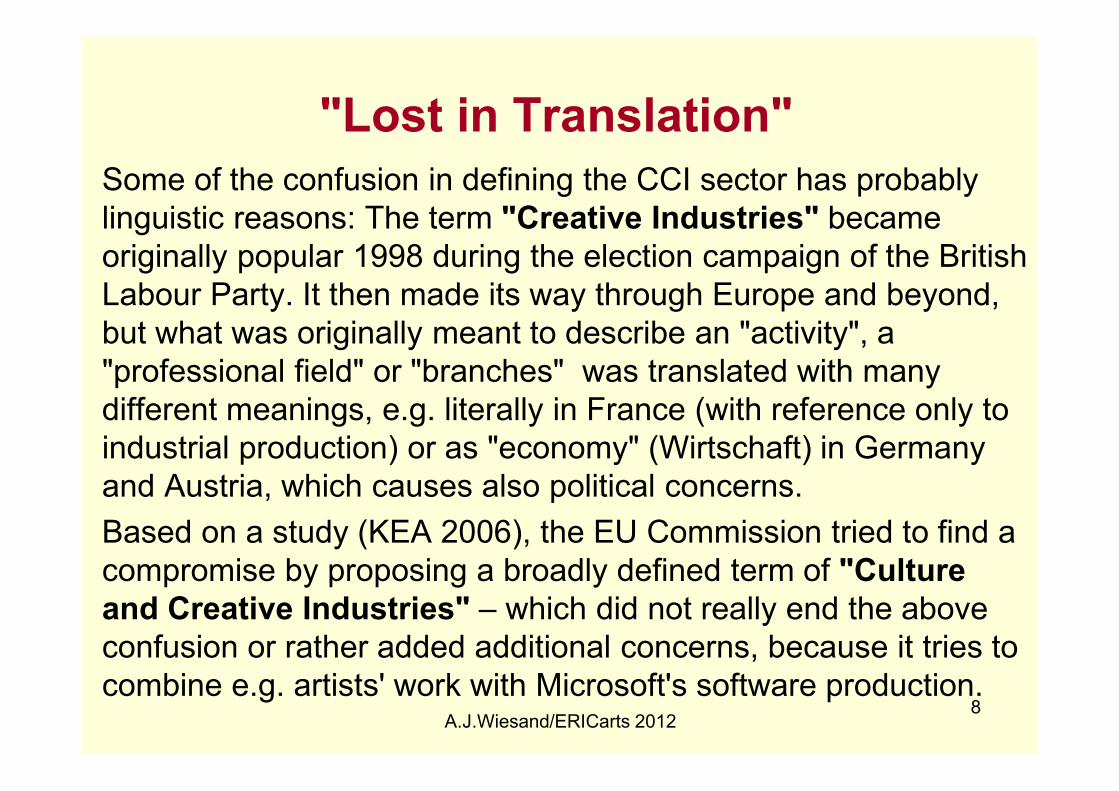

"Lost in Translation"

Some of the confusion in defining the CCI sector has probably linguistic reasons: The term "Creative Industries" became originally popular 1998 during the election campaign of the British Labour Party. It then made its way through Europe and beyond, but what was originally meant to describe an "activity", a "professional field" or "branches" was translated with many different meanings, e.g. literally in France (with reference only to industrial production) or as "economy" (Wirtschaft) in Germany and Austria, which causes also political concerns.

Based on a study (KEA 2006), the EU Commission tried to find a compromise by proposing a broadly defined term of "Culture

and Creative Industries" – which did not really end the above confusion or rather added additional concerns, because it tries to combine e.g. artists' work with Microsoft's software production.

8A.J.Wiesand/ERICarts 2012

Despite all conceptual ambiguity:

Harmonizing classifications is progressingNo. ISIC

Rev. 4

NACE

Rev.2

WZ-

2008

German -

Description

English -

Description

Chinese -

Description

4-digit 4.Digit 5-digit German -Description

English -Description

Chinese -Description

1 5811 58.11 58.11.0 Verlegen von Büchern

Book publishing 書籍出版

2 5812 58.12 58.12.0 Verlegen von Adressbüchern Verzeichnissen

Publishing of directories and mailing lists

名錄和郵寄名單

的出版

3 5813* 58.13 58.13.0 Verlegen von Zeitungen

Publishing of newspapers

報紙出版

4 5813* 58.14 58.14.0 Verlegen von Zeitschriften

Publishing of journals and periodicals

雜誌和期刊出版

5 5819 58.19 58.19.0 Sonstiges Verlagswesen

Other publishing activities

其他出版活動

6 5820* 58.21 58.21.0 Verlegen von Computer-spielen

Publishing of computer games

電腦遊戲發行

7 5820* 58.29 58.29.0 Verlegen von sonst. Software

Other softwarepublishing

其他電腦軟體發

行

Combining UNESCO and EU concepts

A possible, pragmatic solution, that is based on the availability of statistical data, has recently been proposed by Michael Soendermann (KWF):

He tries to harmonize the classification ISIC REV.4

with the EU concept of 'Culture & Creative

Industries', based on the global approach proposed by the UNESCO Framework for Cultural Statistics.

Here are the main elements of that solution:

10A.J.Wiesand/ERICarts 2012

A.

-

( )

-

-

-

B.

-

-

-

C.

-

-

-

D.

-

-

-

-

( )

-

E.

-

-

( )

-

-

( )

F.

-

-

-

-

-

-

11

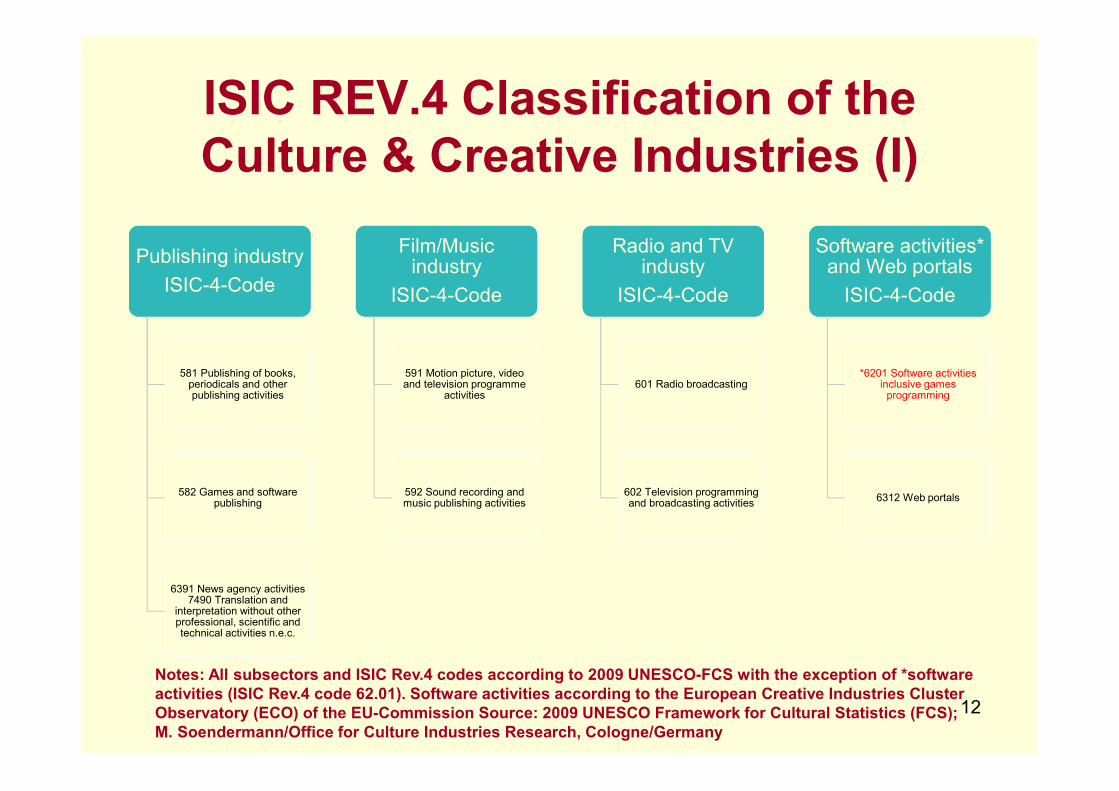

ISIC REV.4 Classification of the

Culture & Creative Industries (I)

Publishing industry

ISIC-4-Code

Publishing industry

ISIC-4-Code

581 Publishing of books, periodicals and other publishing activities

582 Games and software publishing

6391 News agency activities 7490 Translation and

interpretation without other professional, scientific and technical activities n.e.c.

Film/Music industry

ISIC-4-Code

Film/Music industry

ISIC-4-Code

591 Motion picture, video and television programme

activities

592 Sound recording and music publishing activities

Radio and TV industy

ISIC-4-Code

Radio and TV industy

ISIC-4-Code

601 Radio broadcasting

602 Television programming and broadcasting activities

Software activities* and Web portals

ISIC-4-Code

Software activities* and Web portals

ISIC-4-Code

*6201 Software activities inclusive games

programming

6312 Web portals

12

Notes: All subsectors and ISIC Rev.4 codes according to 2009 UNESCO-FCS with the exception of *software

activities (ISIC Rev.4 code 62.01). Software activities according to the European Creative Industries Cluster

Observatory (ECO) of the EU-Commission Source: 2009 UNESCO Framework for Cultural Statistics (FCS);

M. Soendermann/Office for Culture Industries Research, Cologne/Germany

ISIC REV.4 Classification of the

Culture & Creative Industries (II)

Architectural activities

ISIC-4-Code

Architectural activities

ISIC-4-Code

Part of 7110 Architectural

activities

(without engineering activities and related

technical consultancy)

Advertising andDesign industry

ISIC-4-Code

Advertising andDesign industry

ISIC-4-Code

731 Advertising

741 Specialized design activities

742 Photographic activities

Creative and cultural activities

ISIC-4-Code

Creative and cultural activities

ISIC-4-Code

900 Creative, arts and entertainment

activities

910 Libraries, archives, museums and other cultural

activities

Retail sales and arts and craft

ISIC-4-Code

Retail sales and arts and craft

ISIC-4-Code

476 Retail sale of cultural and

recreation goods in specialized stores

3211 Manufacture of jewellery and related

articles

322 Manufacture of musical instruments

13

Notes: All subsectors and ISIC Rev.4 codes according to 2009 UNESCO-FCS

Source: 2009 UNESCO Framework for Cultural Statistics (FCS); M. Soendermann/Office for Culture

Industries Research, Cologne/Germany

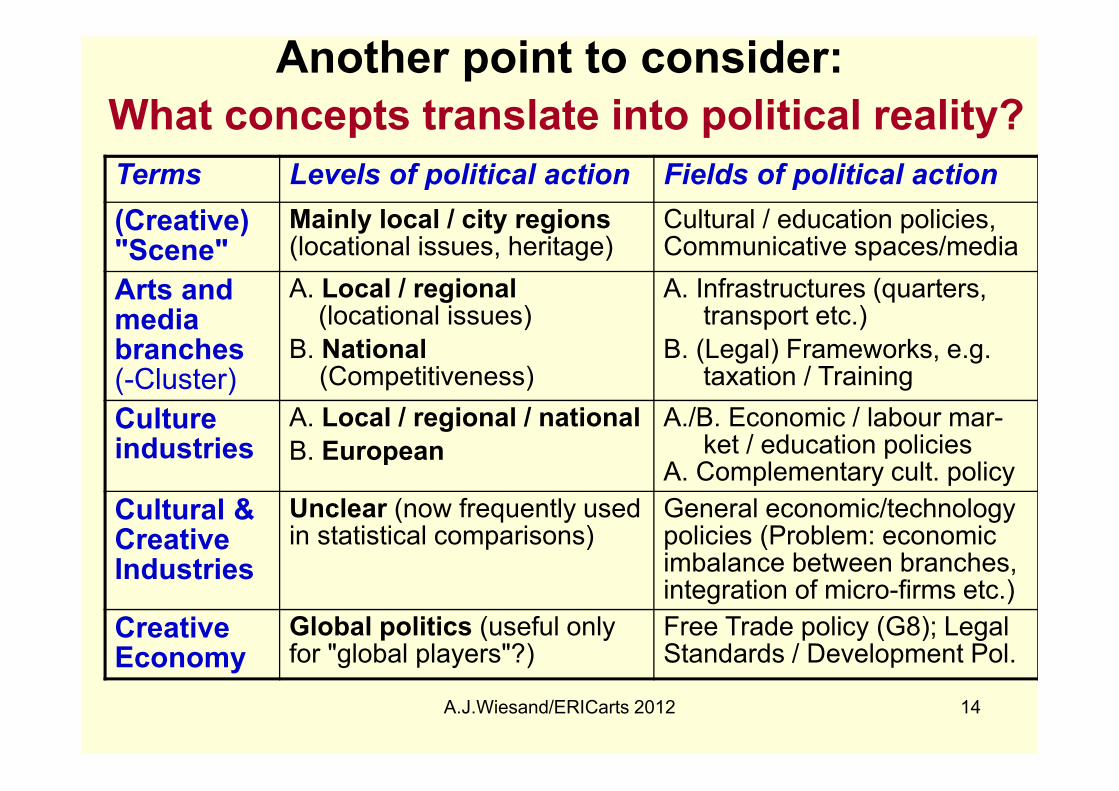

Another point to consider:

What concepts translate into political reality?

Terms Levels of political action Fields of political action

(Creative) "Scene"

Mainly local / city regions (locational issues, heritage)

Cultural / education policies, Communicative spaces/media

Arts and media branches(-Cluster)

A. Local / regional (locational issues)

B. National(Competitiveness)

A. Infrastructures (quarters, transport etc.)

B. (Legal) Frameworks, e.g. taxation / Training

Culture industries

A. Local / regional / national

B. European

A./B. Economic / labour mar-ket / education policies

A. Complementary cult. policy

Cultural & Creative Industries

Unclear (now frequently used in statistical comparisons)

General economic/technology policies (Problem: economic imbalance between branches, integration of micro-firms etc.)

Creative Economy

Global politics (useful only for "global players"?)

Free Trade policy (G8); Legal Standards / Development Pol.

A.J.Wiesand/ERICarts 2012 14

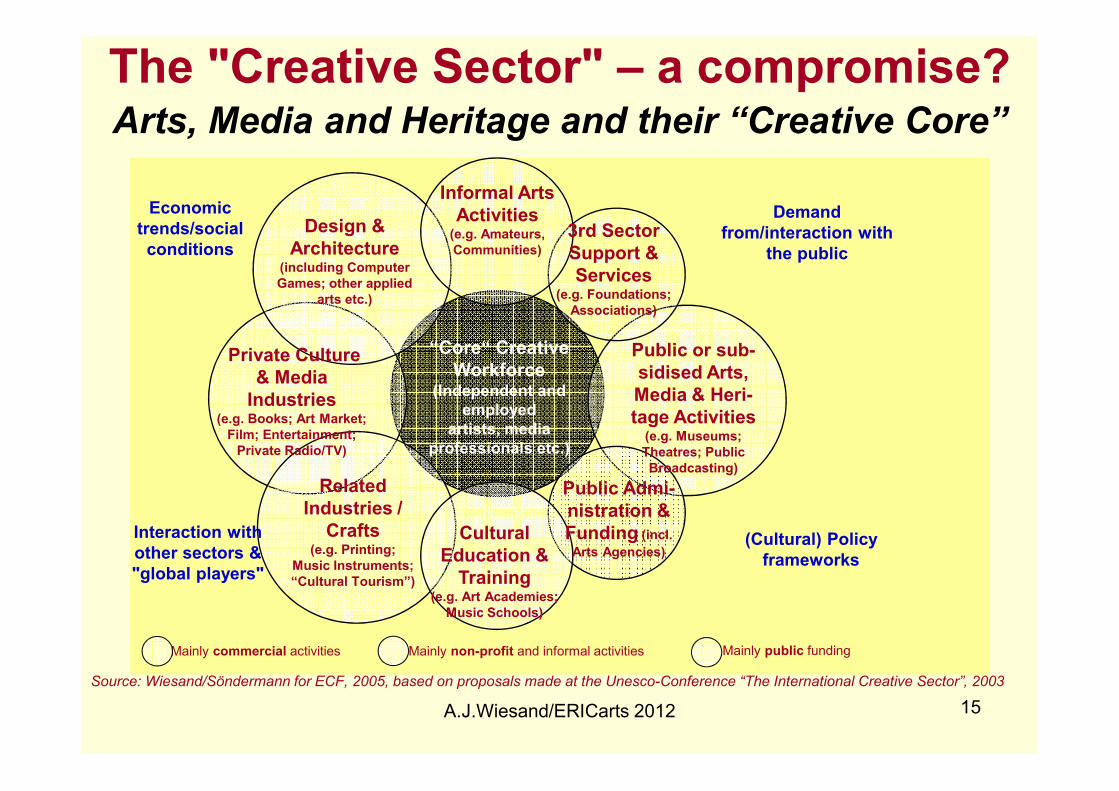

The "Creative Sector" – a compromise?Arts, Media and Heritage and their “Creative Core”

A.J.Wiesand/ERICarts 2012 15

“Core“ Creative

Workforce(Independent and

employed

artists, media

professionals etc.)

Public or sub-

sidised Arts,

Media & Heri-

tage Activities (e.g. Museums;

Theatres; Public

Broadcasting)

Private Culture

& Media

Industries(e.g. Books; Art Market;

Film; Entertainment;

Private Radio/TV)

Public Admi-

nistration &

Funding (incl.

Arts Agencies)

Related

Industries /

Crafts(e.g. Printing;

Music Instruments;

“Cultural Tourism”)

3rd Sector

Support &

Services(e.g. Foundations;

Associations)

Design &

Architecture(including Computer

Games; other applied

arts etc.)

Cultural

Education &

Training(e.g. Art Academies;

Music Schools)

Informal Arts

Activities(e.g. Amateurs,

Communities)

Mainly commercial activities Mainly non-profit and informal activities Mainly public funding

Source: Wiesand/Söndermann for ECF, 2005, based on proposals made at the Unesco-Conference “The International Creative Sector”, 2003

Demand

from/interaction with

the public

(Cultural) Policy

frameworks

Interaction with

other sectors &

"global players"

Economic

trends/social

conditions

16

Results of different studies in the EU:• In a number of EU Member States and candidate countries, the

economic strength of the Creative Sector relies, first of all, on a successful "consumer culture" and its professional or industrial basis (cinema; design; music; the book market; games; etc.);

• In other countries, public infrastructures contribute markedly to this wealth (e.g. the well-developed library systems in the Nordic region that reach out into the smallest towns, or the large public theatre and opera infrastructure in Germany);

• As well, public broadcasting – generally with a "cultural" mission –is often on an equal level with commercial providers;

• Artists are frequently experimental drivers of innovation and new technological developments (hard- and software);

• In some Member and Candidate States, e.g. Cyprus, France, Greece, Italy, Poland or Turkey, the tangible/built cultural heritageis a major economic factor through its incentives for tourism and its importance for the labour market;

• In addition, the Creative Sector contributes markedly to the quality of life in urban and rural areas, fosters social cohesion or helps to regenerate economically degraded regions.

2. Some Statistics

(with ambivalent results!)

A.J.Wiesand/ERICarts 2012 17

Subsectors of the European Culture &

Creative Industries, Value Added 2009

18

Book & press publishing

inclusive games publishing; 58 bn; 21%

Film industry/ Music industry;

20 bn; 7%

Radio/TV;27 bn; 10%Software**

activities incl. webportals,

games software; 64 bn;

23%

Architectural activites;

22 bn; 8%

Advertising/Design industry;

46 bn; 17%

Retail sale of cultural goods;

18 bn; 6%

Creative activities etc.;

22 bn; 8%

277* bn EUR;

100%

Notes:. *No data available for Czech Republic, Ireland, Greece and Malta**Not part of the UNESCO-FCS definition Source: Structural business statistics,Eurostat; M. Soendermann / Office for Culture Industries Research, Cologne/Germany

A.J.Wiesand/ERICarts 2012 19

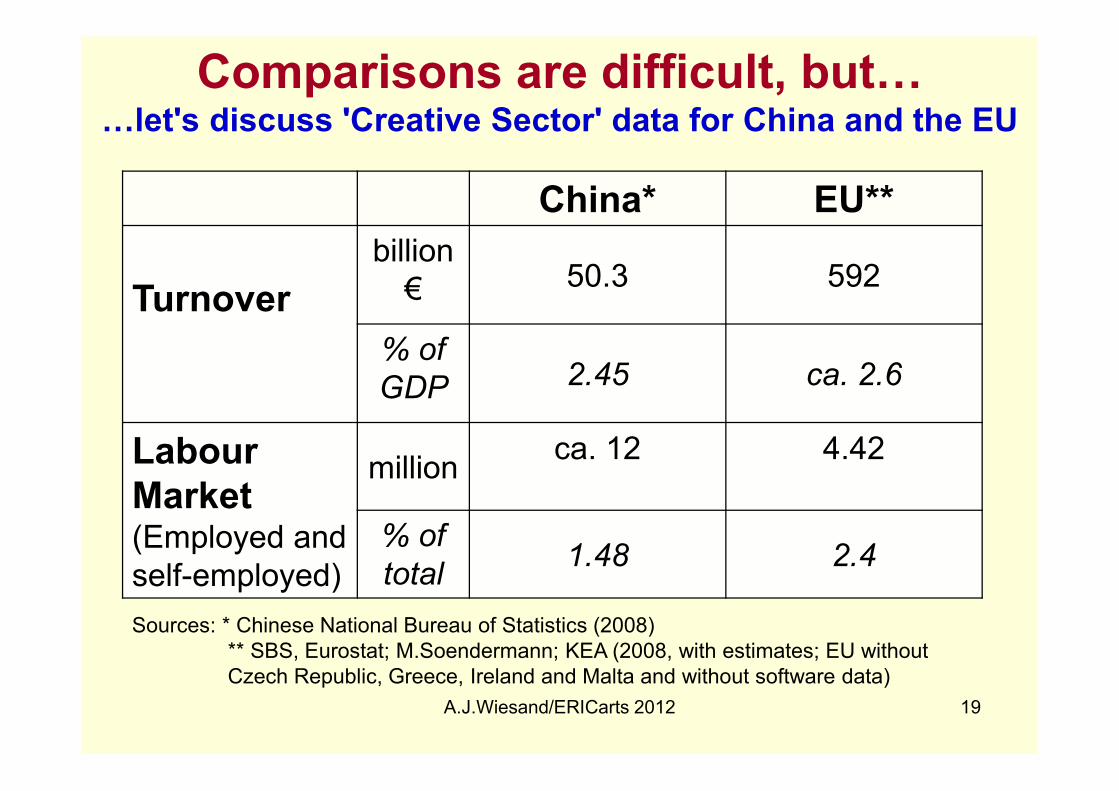

Comparisons are difficult, but00let's discuss 'Creative Sector' data for China and the EU

China* EU**

Turnover

billion € 50.3 592

% of GDP 2.45 ca. 2.6

Labour

Market(Employed and self-employed)

millionca. 12 4.42

% of total

1.48 2.4

Sources: * Chinese National Bureau of Statistics (2008)** SBS, Eurostat; M.Soendermann; KEA (2008, with estimates; EU without Czech Republic, Greece, Ireland and Malta and without software data)

The Top 10 Countries in the European

Culture & Creative Industries, 2009

20

6,4278

7,0146

7,2136

9,6109

19,2461

21,8561

27,1198

43,4344

51,3282

62,2986

,00 20,00 40,00 60,00 80,00

Belgium

Poland

Denmark

Sweden

Netherlands

Spain

Italy

France

United Kingdom

Germany

Value added in billion EUR

Value added in absolute terms

Notes:

All figures

preliminary or

estimates

Source:

Structural business

statistics, Eurostat;

M. Soendermann /

Office for Culture

Industries

Research,

Cologne/Germany

The Top 10 Countries in the European

Culture & Creative Industries, 2009

21

02%

02%

02%

02%

03%

03%

03%

03%

03%

03%

00% 01% 02% 03% 04%

Spain

Austria

Poland

France

Germany

Finland

Denmark

United Kingdom

Sweden

Netherlands

Share of the culture and creative industries of GDP in %

Value added in relative terms

Notes:

All figures

preliminary or

estimates

Source:

Structural business

statistics, Eurostat;

M. Soendermann /

Office for Culture

Industries

Research,

Cologne/Germany

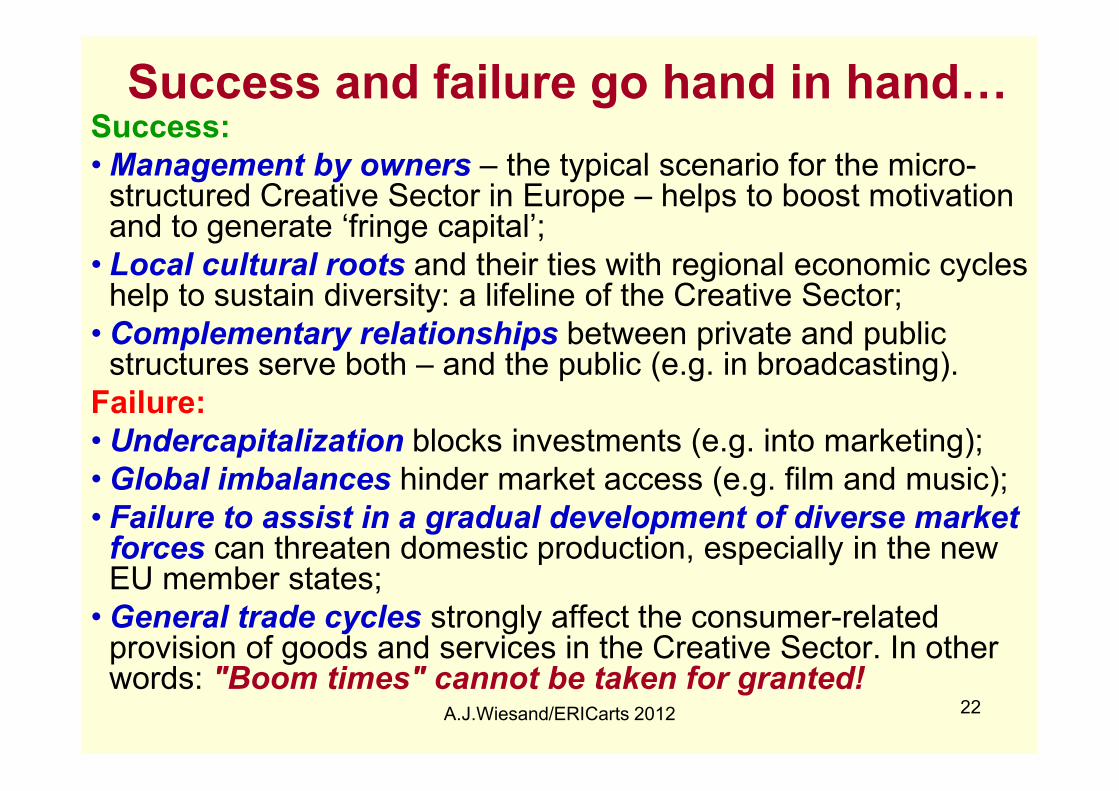

Success and failure go hand in hand0Success:

• Management by owners – the typical scenario for the micro-structured Creative Sector in Europe – helps to boost motivation and to generate ‘fringe capital’;

• Local cultural roots and their ties with regional economic cycles help to sustain diversity: a lifeline of the Creative Sector;

• Complementary relationships between private and public structures serve both – and the public (e.g. in broadcasting).

Failure:

• Undercapitalization blocks investments (e.g. into marketing);• Global imbalances hinder market access (e.g. film and music);• Failure to assist in a gradual development of diverse market

forces can threaten domestic production, especially in the new EU member states;

• General trade cycles strongly affect the consumer-related provision of goods and services in the Creative Sector. In other words: "Boom times" cannot be taken for granted!

A.J.Wiesand/ERICarts 2012 22

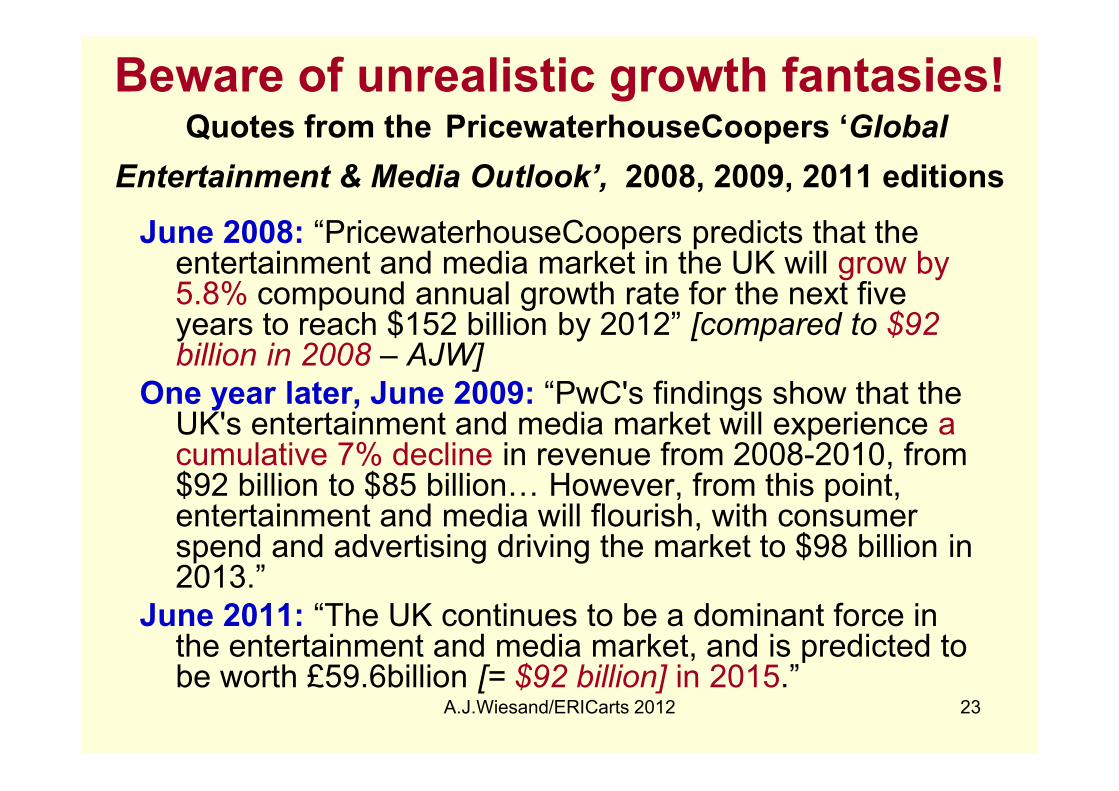

Beware of unrealistic growth fantasies!Quotes from the PricewaterhouseCoopers ‘Global

Entertainment & Media Outlook’, 2008, 2009, 2011 editions

June 2008: “PricewaterhouseCoopers predicts that the entertainment and media market in the UK will grow by 5.8% compound annual growth rate for the next five years to reach $152 billion by 2012” [compared to $92 billion in 2008 – AJW]

One year later, June 2009: “PwC's findings show that the UK's entertainment and media market will experience a cumulative 7% decline in revenue from 2008-2010, from $92 billion to $85 billionV However, from this point, entertainment and media will flourish, with consumer spend and advertising driving the market to $98 billion in 2013.”

June 2011: “The UK continues to be a dominant force in the entertainment and media market, and is predicted to be worth £59.6billion [= $92 billion] in 2015.”

A.J.Wiesand/ERICarts 2012 23

We should have known: CI setbacks in a crisis2003-2006 growth of turnover / No. of companies / employees in French

culture industries (in comparison with the general economy, in %)

A.J.Wiesand/ERICarts 2012 24

Volatility + 2009 crisis: CCI trends in the EUA. Subsectors with strong dynamics 2005-11

100

95

101

107104 105

112

100 99103

107100

104

111113

109 109

123

70

80

90

100

110

120

130

2005 2006 2007 2008 2009 2010 2011

film industry/musicindustry

advertising/research etc.

designindustry/foto/translation etc.

Turnover index, 2005 = 100 (provisional estimates)

Notes: definition of film and music industry motion picture, video and TV programme production, sound recording and

music publishing (ISIC rev.4 code: 59), definition of advertising and market research (ISIC rev.4 code: 73); definition of

design and photographic activities, translation and other professional, scientific and technical activities n.e.c. (ISIC

rev.4 code: 74)

Source: Short-term business statistics, Eurostat; M. Soendermann/Office for Culture Industries Research, Germany

B. Subsectors with low dynamics 2005-11

26

100104

107 108

102 101 101

100103

107 109

102 103 104

70

80

90

100

110

120

130

2005 2006 2007 2008 2009 2010 2011

publishingindustry

radio/tvindustry

Notes: definition of publishing industry comprises books, press, other publishing, games and software publishing

(ISIC rev.4 code: 58), radio/TV activities (ISIC rev.4 code: 60)

Source: Short-term business statistics, Eurostat; M. Soendermann/Office for Culture Industries Research, Germany

Turnover index, 2005 = 100 (provisional estimates)

C. Subsectors with negative dynamics

2005-11

27

Notes: definition manufacture of jewels, bijouterie and related (ISIC rev.4 code: 321), manufacture of musical

instruments (ISIC rev.4 code: 322)

Source: Short-term business statistics, Eurostat; M. Soendermann/Office for Culture Industries Research, Germany

104,62098,330

82,640

69,240

80,53083,650

95,89096,480

94,870

85,73085,010

90,790

60,0

70,0

80,0

90,0

100,0

110,0

120,0

130,0

2005 2006 2007 2008 2009 2010 2011

Italy - Manufacture ofjewellery, bijouterie andrelated articles

Germany - Manufactureof musical instruments

Turnover index, 2005 = 100 (provisional estimates)

Structural conditions to be considered:1. Micro-business structures dominate

2. Work conditions often precarious

ad 1: % of micro-businesses in publishing (Eurostat 2011)

28

ad 2: More short-term employment

for less money? The fate of freelances in France(Source: Caisse de congés spectacles/Cesta/Deps 2010)

29

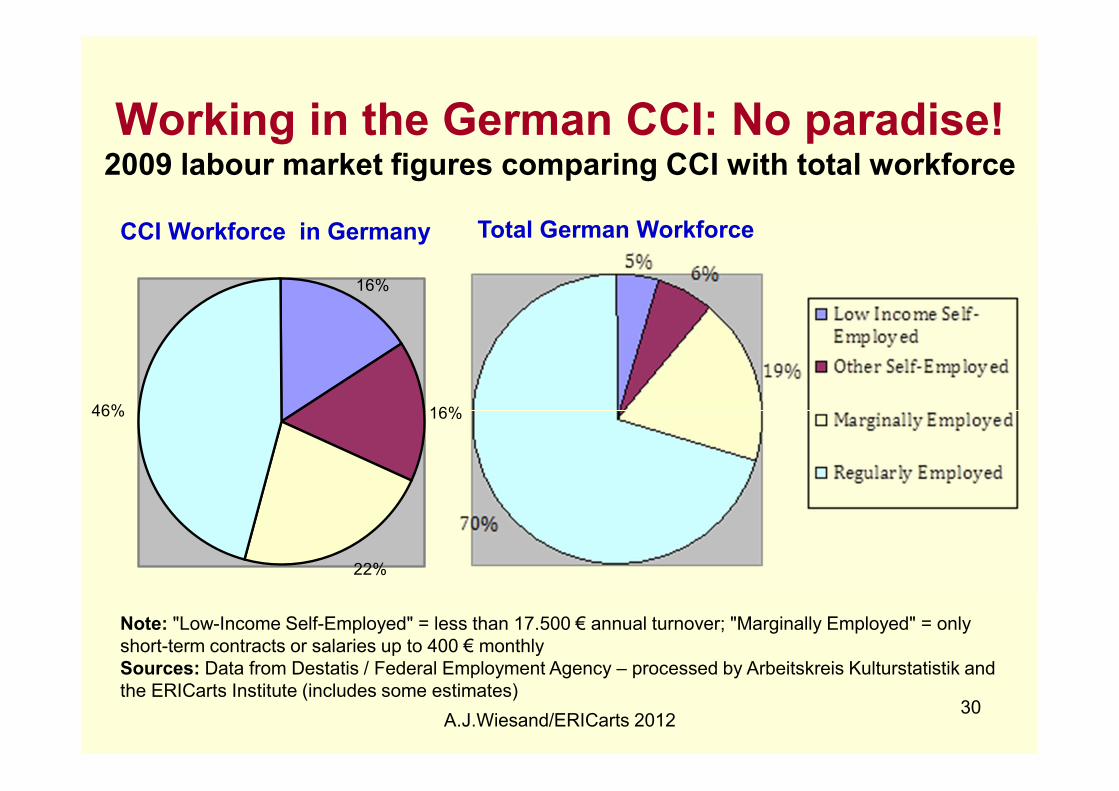

Working in the German CCI: No paradise!2009 labour market figures comparing CCI with total workforce

A.J.Wiesand/ERICarts 201230

Total German Workforce CCI Workforce in Germany

Note: "Low-Income Self-Employed" = less than 17.500 € annual turnover; "Marginally Employed" = only short-term contracts or salaries up to 400 € monthly Sources: Data from Destatis / Federal Employment Agency – processed by Arbeitskreis Kulturstatistik and the ERICarts Institute (includes some estimates)

46%

22%

16%

16%

3. European Policy Aspects

A.J.Wiesand/ERICarts 2012 31

What role of the EU in cultural development?What was missing in the renewed EU 'Lisbon Programme – An Agenda for

Growth and Jobs' (2005) and in the Europe 2020 Strategy has at least been addressed in the 2007 Communication 'A European agenda for culture in a globalizing world' of the EU Commission: The potential strength of the European Creative Sector with inputs from millions of creative individuals, arts initiatives and media companies.

In the words of Polish Vice Minister for Culture, Monika Smolén, culture and creativity "as a foundation for the establishment of a knowledge society and Vone of the most dynamically developing sectors of the economy" can make important contributions to local/regional development and to the goals set in EU Agendas;

On the other hand, only 1.7% of development projects aided by EU Structural Funds address "Culture" and a majority of them focus on the built heritage or related "cultural tourism", thus failing to mobilise the creativity and inspiration offered by e.g. artists and other actors in the Creative Sector.

A.J.Wiesand/ERICarts 2012

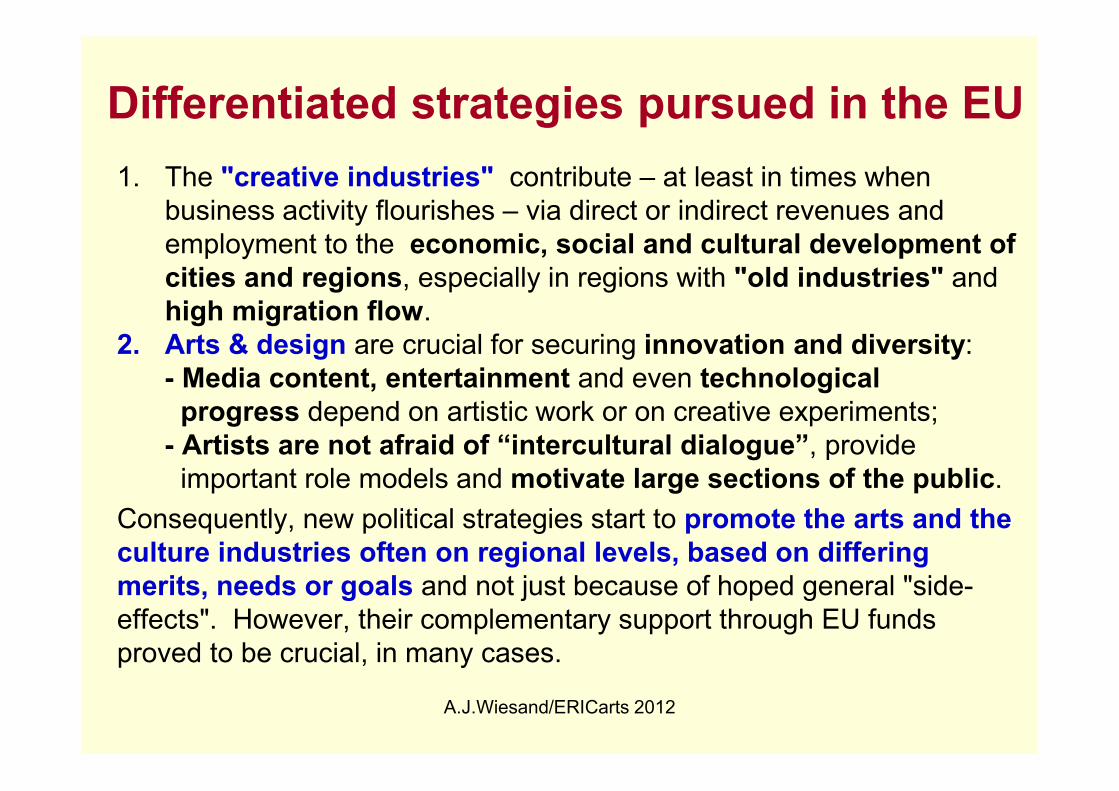

Differentiated strategies pursued in the EU

1. The "creative industries" contribute – at least in times when business activity flourishes – via direct or indirect revenues and employment to the economic, social and cultural development of

cities and regions, especially in regions with "old industries" andhigh migration flow.

2. Arts & design are crucial for securing innovation and diversity: - Media content, entertainment and even technological

progress depend on artistic work or on creative experiments; - Artists are not afraid of “intercultural dialogue”, provide

important role models and motivate large sections of the public.

Consequently, new political strategies start to promote the arts and the

culture industries often on regional levels, based on differing

merits, needs or goals and not just because of hoped general "side-effects". However, their complementary support through EU funds proved to be crucial, in many cases.

A.J.Wiesand/ERICarts 2012

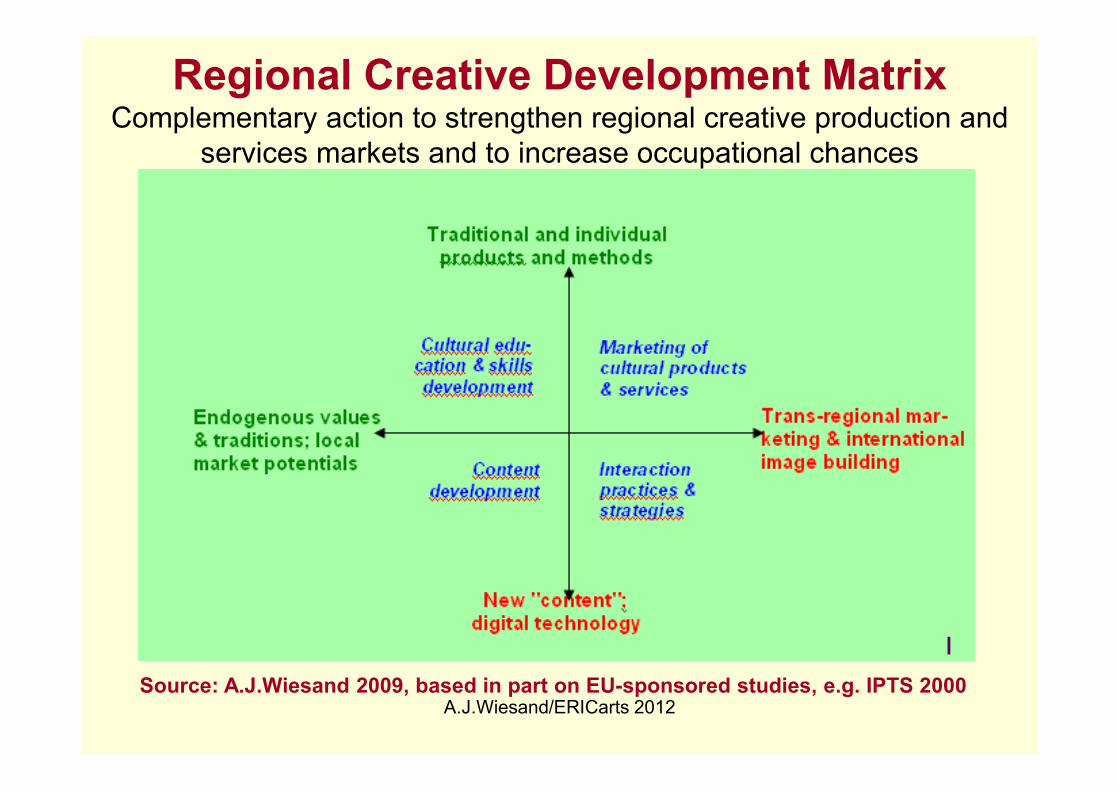

Regional Creative Development MatrixComplementary action to strengthen regional creative production and

services markets and to increase occupational chances

A.J.Wiesand/ERICarts 2012Source: A.J.Wiesand 2009, based in part on EU-sponsored studies, e.g. IPTS 2000

35

Kunstwerk(t) - Art Works (The Netherlands)A project aided by EU Structural funds where Artists worked with 4 target groups: prisoners, illiterate migrant women, youth at risk, people with disabilities. Different methods (theatre performance, choir presentations, etc.) were used to develop skills and competencies of these groups and to promote their integration. The effectiveness of this project has been proven by the University of Amsterdam.

The "Guggenheim-Effect" in Bilbao (Spain)Integrated city developmentin an "old" industrial setting, inspired by an architectural highlight for the arts, the Guggenheim-Museum.

Two examples0

A.J.Wiesand/ERICarts 2012

The EU Audiovisual Media Services DirectiveIn its introduction, the Directive of 10 March 2010 (2010/13/EU) refers specifically to the "cultural" role of audiovisual media services and to "their growing importance for societies, democracy -- in particular by ensuring freedom of information, diversity of opinion and media pluralism." Such concerns and Article 167(4) of the EU Treaty (TFEU), results of the Doha / WTO conferences as well as provisions of the UNESCO Convention on the Protection and Promotion of the Diversity of Cultural Expressions are seen as "justifying the application of specific rules to these services." To this effect, the Directive requires EU countries to coordinate national legislation with each other so that e.g.:• TV programmes and VoD services can be traded freely on the EU market;• TV channels reserve at least half their broadcasting time for films and

programmes made in Europe and 10% to European works created by producers who are independent of broadcasters;

• Cultural diversity and other public-interest objectives are protected;• Children and young people be protected from offensive content; • Parties unfairly criticised in a television broadcast have the right of reply;• AV media respect some basic rules on advertising (incl. human dignity,

restrictions for alcohol, tobacco, etc.) and restrict advertising time.

Some countries have stricter rules0especially as regards AV & music "content quota"

Examples:

• Finland: 15% of TV program by independent producers;

• France: 60% of TV films European productions with 40% original French language content (similar radio) + quota for programme investments (also in Pay-TV);

• Portugal: 60% of music in radio broadcasts to be composed / sung in the Portuguese language;

• Spain: Film quota to foster "cultural identity and diversity".

Outside of the EU:

• Ukraine: 25% of TV/Radio content "national product"Source: CoE/ERICarts: Compendium of Cultural Policies & Trends in Europe, 2012

A.J.Wiesand/ERICarts 2012

EU: New interaction with "Third Countries"Policy makers in (some) member countries, e.g. France, and of the EU have long echoed industries' "concerns that American productions will take the lion’s share of the European market. Although EU countries make more films than the US, 75% of the income of European cinemas comes from American films." (http://europa.eu/pol/av/index_en.htm). The 2005 UNESCO Convention has now partly sensitized them that protection measures against US-Imports should, for the sake of "cultural diversity", not harm trade relations with other "Third Countries".

In this spirit, the new MEDIA Mundus fund was installed with a budget of €15 million over 3 years (2011-13). It funds projects aimed at encouraging mobility and exchanges of European film-makers and their counterparts around the world. According to the Commission, "the idea is to improve access to international markets and to strengthen the distribution of European films in non-European markets and vice versa." A.J.Wiesand/ERICarts 2012

Some Final Conclusions:• Cultural diversity in Europe, including diverse traditions,

passions, languages and infrastructures, forwards openness towards the world. New technologies speed up such processes;

• Empirical studies suggest that many citizens keep pace with

growing diversity: cultural preferences and practices broadened over the last 40 years; regional strengths are now just as much appreciated as international trends and colours;

• This could mean increased chances for Asia, but needs culture-

sensitive promotion & marketing strategies on both sides;

• At the same time, some conditions for creative work need to

gradually converge in Europe and beyond (e.g. basic rights, education, taxes, social protection), so all actors can cooperate and fully benefit from an emerging "World Cultural Space".

Thank you for your attention!A.J.Wiesand/ERICarts 2012