![Towards a phonetically grounded diachronic phonology of Basque [Thesis]](https://static.fdokumen.com/doc/165x107/63226867078ed8e56c0a658e/towards-a-phonetically-grounded-diachronic-phonology-of-basque-thesis.jpg)

Towards a phonetically grounded diachronic phonology of Basque [Thesis]

Upload

independentCategory

view

1download

0

1 23

Environmental and ResourceEconomicsThe Official Journal of the EuropeanAssociation of Environmental andResource Economists ISSN 0924-6460 Environ Resource EconDOI 10.1007/s10640-012-9589-8

The Equivalency Principle for Discountingthe Value of Natural Assets: AnApplication to an Investment Project in theBasque Coast

Aline Chiabai, Ibon Galarraga, AnilMarkandya & Unai Pascual

1 23

Your article is protected by copyright and

all rights are held exclusively by Springer

Science+Business Media B.V.. This e-offprint

is for personal use only and shall not be self-

archived in electronic repositories. If you

wish to self-archive your work, please use the

accepted author’s version for posting to your

own website or your institution’s repository.

You may further deposit the accepted author’s

version on a funder’s repository at a funder’s

request, provided it is not made publicly

available until 12 months after publication.

Environ Resource EconDOI 10.1007/s10640-012-9589-8

The Equivalency Principle for Discounting the Valueof Natural Assets: An Application to an InvestmentProject in the Basque Coast

Aline Chiabai · Ibon Galarraga · Anil Markandya ·Unai Pascual

Accepted: 30 July 2012© Springer Science+Business Media B.V. 2012

Abstract Making decisions about optimal investments in green infrastructure necessitatessetting social discount rates. This paper suggests a practical way for determining the discountrate for projects or programmes in which one of the options is to maintain or restore landto an undeveloped state. We propose an “equivalency principle” to derive a simple rule thatsets the discount rate. The rule is based on the premise that the long term value of a piece ofundeveloped land ought to be at least the same as the value of an identical piece of land in thevicinity to which permission has been granted for development. We illustrate this principlewith various case studies and we apply it to a contentious investment project in the BasqueCountry associated with the regeneration of a large scale harbour that involves reclaimingundeveloped land that has important ecological values, including for the conservation of amarine ecosystem.

Keywords Equivalency principle · Land development · Cost-benefit analysis ·Total economic value · Discounting · Basque Country

1 Introduction

The standard discounted utility model from which ‘appropriate’ discount rates are sought isnot new in the economic literature. Scholars such as Arrow (1963, 1965), Arrow et al. (1996),Solow (1974), Sen (1961, 1967), Samuelson (1980), Lind (1982), Dasgupta et al. (1999),Weitzman (2001) and Zeckhauser and Viscusi (2008) among many others have addressed howto reconcile the wellbeing of present and future generations based on a financial investment

A. Chiabai (B) · I. Galarraga · A. Markandya · U. PascualBasque Centre for Climate Change (BC3), Alameda Urquijo 4, 4◦–1a, 48008 Bilbao, Spaine-mail: [email protected]: www.bc3research.org

A. Markandya · U. PascualIKERBASQUE, Basque Foundation for Science, Bilbao, Spain

U. PascualDepartment of Land Economy, University of Cambridge, 19 Silver St., CB39EP Cambridge, UK

123

Author's personal copy

A. Chiabai et al.

model (see also Frederick et al. 2002 for a recent review). While the original justificationof the standard discounted utility model relates to the social opportunity cost of capital,discounting has significant ethical implications regarding intergenerational equity and thesalience of the discounting debate becomes clear when the model is applied to evaluate pol-icies regarding major environmental issues, such as climate change and biodiversity loss(Gowdy et al. 2010; Graaff 1987); issues that in terms of policy making are fraught with ourcurrent lack of scientific knowledge and hence high levels of uncertainty (Bromley 2007).As Weitzman (2007, 705) notes “it is not an exaggeration to say that the biggest uncertaintyof all in the economics of climate change is the uncertainty about which interest rate to usefor discounting”. A prime example of the importance of discounting climate change impactsis attested by the celebrated but equally contentious debate about the ‘proper’ social discountrate used in the Stern Review (Stern 2007). The Stern review supports the use of a pure timepreference rate close to zero on the grounds that future generations might face the risk ofextinction. This line of reasoning has triggered the reaction of scholars such as Nordhaus(2007), who argues in favour of using relatively higher discount rates. Tol and Yohe (2006,2009) also suggest that Stern might be right but for the wrong reasons and that the use of lowdiscount rates if the time horizon is extended can increase the present value of damages verysubstantially.

The Ramsey rule for discounting is generally used to determine the social discount rate.This is based on the rate of pure time preference, the curvature of the inter-temporal utilityfunction (i.e., elasticity of the marginal utility of consumption) and the growth of per capitaconsumption. So far there is no consensus on the parameters associated with these three com-ponents of the utility discount rate. (Frederick et al., 2002, 394) argue that empirical studiesof discount rates offer no guidance as to which one should be used, and that economistsshould continue “to import insights from psychology, by relinquishing the assumption thatthe key to understanding inter-temporal choices is finding the right discount rate (or even theright discount function)”. When looking into the different components of the Ramsey equa-tion, Gowdy et al. (2010) point out that, despite the large literature that exists arguing for avariety of values for the pure time preference component, there is no econometric method yetavailable to determine it. While Ramsey himself (in Gowdy et al. 2010) defends a zero puretime preference, others such as Nordhaus (2007) support the use of the market rate of interestto reveal individuals’ time preference. Sen (1961) has consistently argued against setting asocial discount rate equal to the market rate of return affirming that individual preferencesare interconnected. But even if the market rate is chosen it is not clear which one it shouldbe. As for the elasticity of marginal (social) utility of consumption, both Nordhaus (1994)and Stern (2007) defend to make it equal to unity. Although, as Cole (2008) and Weitzman(2009) argue, this parameter is largely a normative one that, besides incorporating risk aver-sion, necessitates setting a moral ground about intra-temporal inequality of income amongindividuals and about the evolution of income inequality over time. The Stern Review usesa near to zero rate of pure time preference (0.1) and given a unit marginal social utility ofconsumption, the key to set the discount rate is the growth rate of per capita consumptionwhich the review sets around 1.3 %, rendering a social discount rate of 1.4 %, lower thanmost previous economic studies on climate change (Dietz 2008).

However, it is important to note that future income growth can depend on the depreciationof the current natural capital stock. Setting positive discount rates based on positive incomegrowth projections can undermine current natural capital, which in turn would question thereliability of such growth projections in the first place, thus creating the so-called ‘optimist’sparadox’ (Martinez-Alier 1995). Similarly, Dasgupta and Maler (2000) also point out that theprojection on the rate of economic growth is the rate of return of all forms of capital and thus

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

it can be associated with the growth rate of total factor productivity (TFP) of an economy. Ifone accounts for the draw-down of natural capital, TFP can be negative. It is thus plausible tocome up with negative discount rates based on the Ramsey equation. As Gowdy et al. (2010,267) point out, under reasonable assumptions about the pure time preference and the elas-ticity of consumption, “a negative TFP implies that the present generation should consumeless in order to invest more in the well-being of future generations”. According to Weitzman(2007), negative discount rates are possible when assessing the costs of climate change dueto the high expected costs to future generations (albeit at low probability). Dasgupta (2008)argues that discount rates should be set based not only on economic forecasts, but also onsociety′s conception of distributive justice “concerning the allocation of goods and servicesacross personal identities, time and events”. He points out that an optimum policy may wellnot exist. He also argues in favour of using rather low discount rates on the basis of theexpected future income inequalities.

Amidst this debate on discounting, the idea of using ‘low’ social discount rates for naturalresource management has long been defended on various grounds and modelling exercises.In the realm of policies with an impact on environmental goods and services, there continuesto be a thriving debate on whether dual discounting should be used, i.e., whether differentdiscount rates ought to be applied depending whether the policies to be evaluated have animpact on the environment or not.

Fisher and Krutilla (1975, 1985) introduce the idea of a time invariant “environmental”discount rate which is lower than the market rate because it includes a projection of futurewillingness to pay for environmental goods as they become scarcer and/or as incomes grow.Their model points towards a lower discount rate for environmental goods than for othergoods to which the social rate of discount would apply. This hinges on the assumption thatthe proportion of income spent on the environmental goods is expected to grow and that theenvironment is considered a luxury good. Other authors such as Weikard and Xhu (2005,876), argue that dual discounting can serve as “pragmatic device” but should only be usedwhen goods and environmental assets are not substitutable or when future prices for environ-mental assets are not available. They show that when goods and assets are not substitutable,policy makers only worry about the rate of the environmental asset. Therefore this cannot benamed “true” dual rate discounting.

Chichilnisky (1996) introduces two axioms for sustainable development which, in combi-nation, require that neither the present nor the future should play a dictatorial role in society’schoices over time. The implications of her approach to discounting is that the future wouldbe discounted in a conventional manner only in the “near future”, but after a point—theso-called ‘switching date’—the remaining effects would not be discounted at all (i.e. a zerorate should prevail). Li and Lofgren (2000) consider the case of two individuals, identicalin all respects except for their personal rate of time preference. In their model the overallsocietal objective is to maximize a weighted sum of utility for both individuals which resultsin a similar outcome to that of Weitzman’s discounting approach, i.e., the individual withlower discount rate is given the dominant weight as time goes by and the collective discountrate declines over time.

In the context of climate change policies, Summers and Zeckhauser (2008), based on psy-chological principles, suggest four dimensions for climate change policies and defend usingpositive but low discount rates. Cropper and Laibson (1999) support the use of declining(hyperbolic) discounting. Gollier (2008) argues for a systematically declining discount ratejustified on the basis of future shocks on economic growth, going from ranges close to 4 %for 100 years periods to 1–3.5 % ranges for 1,000 year periods. Beltratti et al.’s (1998) greengolden rule for renewable resources state that a near market interest rate should be used in

123

Author's personal copy

A. Chiabai et al.

the present and a rate that asymptotically approaches zero in the distant future. Similarly,Weitzman (2001) advocates for gamma discounting (declining from about 4 % towards 0 %).More recently, Gollier and Weitzman (2010) also recommend that discount rates declineover time towards the lowest possible value.1 While this is an approach that is intuitivelyappealing, the problem of time inconsistency in hyperbolic discounting is a thorny one (Heal1998; Guo 2004).

Given the multiple perspectives on discounting in the context of decisions which have anenvironmental impact, in this paper we make a practical proposal that helps to determine thediscount rate for projects or programmes in which one of the options is to maintain or restoreundeveloped land which is either in or close to its natural state. We illustrate this in the contextof a special case regarding the valuation and management of coastal and marine ecosystemsin the Basque Country where a contentious project to build a large seaport infrastructureinvolves reclaiming undeveloped (natural) land that has significant ecological value. Thiscase study is ideal since, as in the case of other examples that affect marine ecosystems incoastal areas, the financial viability of such projects hinges to a large extent on which discountrate is applied. While some governments offer quite precise advice about discounting, theissue is still controversial and consensus does not exist.2 We recommend an ethically simpleand intuitive approach regarding the choice of the social discount rate when designing andevaluating land conservation options with an impact on marine or terrestrial ecosystems.The rule is based on the idea that any policy maker should try to value equivalently andconsistently a track of land that is in its undeveloped (natural) state and another one whichhas been designated as appropriate for development (namely with the permission to build onit, e.g., for residential or industrial use). This in turn reflects the fact that the long term valueof preserving undeveloped land is at least equivalent to the value of similar land (locatedin the same area) with permission to build up, and improvements to the former should beevaluated using a discount rate that has been determined on the basis of such an “equivalencyprinciple”. This assumption implies giving the same value to both types of land, which in turnassumes that future generations would assign them equal utility and equal economic value.This statement has the advantage of avoiding making other uncertain assumptions about theexpected welfare or growth rate of consumption of future generations, and the magnitude ofthe projected uncertain impacts for example due to climate change (which might turn to bewrong in future realities).

The paper proceeds as follows. Section 2 presents the theoretical formulation of the pro-posed equivalency principle, its basic assumptions and implications for dual discounting.Section 3 illustrates the application of the principle in some selected study areas in theBasque Country and United Kingdom, for land-related assets that can have an impact onmarine or terrestrial ecosystems. Section 4 discusses the implication of using the proposedequivalency rule to a contentious investment project with potential significant economic

1 There is a problem with declining discount rates, namely the possibility of time inconsistency. ‘Time incon-sistency’ refers to the situation where plans made at one point in time are contradicted by later behaviour. Forexample, as Guo (2004) notes, “if a government decides to use high discount rates for the near future but lowerones for the far future, the immediate large spending will be easily justified. However, when later governmentsreview the policy, they may conclude that this earlier policy was not optimal and decide to increase the discountrate again, which will lead to higher consumption than planned.”2 The biggest attempt has been made by the UK Treasury in its Green Book 2003, where the recommendedsocial discount rates are declining with time. The current recommendation is to use rates of 5 % for periods ofzero to 30 years, declining to 1 % for periods of over 300 years. Similarly, France decided in 2004 to replaceits constant discount rate of 8 % to 4 % discount rate for maturities below 30 years, and a discount rate thatdecreases to 2 % for larger maturities. There is not, however, an EU-wide recommendation, or one that appliesto other developed and developing countries.

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

and environmental/marine impacts in the Basque Country. Finally, Section 5 offers someconcluding remarks.

2 Implications of the equivalency principle for dual discounting

For heuristic purposes, let us assume the following situation. In time period zero (t = 0) thereare two tracks of land of identical size, named N and U , both with identical environmentaland site-characteristic attributes such as location, slope, type of ecosystem, orientation, prox-imity to infrastructures. In this case the value of N and U would be equal, and it could berepresented by a price PN and PU if a land market exists, i.e., PN = PU . Now let us assumethat in time period one (t = 1) an administrative procedure is granted so that track U nowhas the right to be built upon. U becomes a land with the potential to be developed while Nstays natural (undeveloped land). That is, U is granted the possibility to have industrial orresidential construction. This will automatically and significantly increase the market priceof U . Thus, PN < PU .

This situation is relatively common in most countries where local and regional adminis-trations have the responsibility of land use planning and granting building permits. WhenPN < PU , decisions on the appropriateness of investment projects with environmentalimpacts versus protection of the natural asset will be heavily influenced by the higher valueattached to U . Furthermore, if the project entails long-term environmental impacts, the choiceof the discount rate will be crucial, symbolising the importance attached to the welfare offuture generations.

If both tracks of land remain under the same use in the future, the value for future gener-ations of both N and U would be equal. If instead they stay in the long run as in t = 1, themarket interest rate will play a role for the calculation of the present value of U . But it is notso clear which is the discount rate that should be applied to assess N (undeveloped land) asthe market is unlikely to internalize its environmental values.

In such circumstance, we argue that the discount rate to be used for N is the one resultingfrom assuming the same present value for both N and U . This is the equivalency principle.The value of U is PU , i.e., the price per hectare observed in the market for residential and/orindustrial use. For N , which has environmental values not traded in the market, the valueof the land is usually calculated using non-market valuation methods and estimated as thepresent value PVN per hectare. The flow of benefits for N should be represented by the totaleconomic value (TEV), including both use and non-use values taken from stated or revealedpreference approaches. Using the conventional discounting formula for the present value,the equivalency principle can be expressed as follows:

PVN =T∑

t=1

(VN )t(1 + i∗N

)t = PU (1)

Where PVN is the present value per hectare of undeveloped land, i.e. the discounted valueof the flow of benefits t, (VN )t represents the benefits in year t (TEV), expressed in termsof annual value per hectare (flow) of N , and i∗N is the discount rate for undeveloped land.However, as land generates benefits in perpetuity, the appropriate discounting formula forinfinite time scale should be used (Mills and Hamilton 1994):

PVN = VN

i∗N= PU (2)

123

Author's personal copy

A. Chiabai et al.

The above formulation assumes that the benefits are constant over time. Nevertheless flowscan be expected to increase over time in real terms as a result of growing real incomes andincreasing scarcity of services from natural capital (Krutilla 1967). Furthermore, educationalimprovement in the future might lead to a higher appreciation of the use of natural land(Barker 2006). In this case, the present value of N for a finite time scale would be:

PVN =T∑

t=1

VN (1 + g)t

(1 + i∗N

)t ≈T∑

t=1

VN

(1 + i∗N − g)t(3)

Where g stands for the growth rate or appreciation of the benefits of undeveloped land overtime. Consequently, Eq. (1) for a perpetuity becomes:

PVN = VN

(i∗N − g)= PU (4)

The calculation of i∗N (the discount rate at which the present value of undeveloped landequals the price of land for residential or industrial use), using the conventional discountformula (Eq. 1), relies on numerical or graphical methods based on the same conceptualframework of the Internal Rate of Return, IRR (Hartman and Schafrick 2004). The IRRis the discounted cash flow rate of return generally used in investment appraisals. It is theannualized compounded rate at which the net present value of all cash flows equal to zero.

If T = 1, Eq. 1 simplifies to:

PVN =2∑

1

(VN )t

(1 + i∗N )1 = VN + VN

(1 + i∗N )1 = PU (1’)

and solving for i∗N2VN − PU

PU − VN= i∗N (1”)

For any number of time periods T , the sequence of discounted flow values of N is a poly-nomial function with T degrees, so that finding i∗N that equates PU to PVN requires us tofind the roots of the polynomial. Different methods can be used for this purpose, such asthe linear interpolation using trials and error methods or the Newton–Raphson method. Thefirst is simpler but allows only an approximation of the discount rate, while the second usesalgorithms to find successively improved approximations to the roots of the function (Tjalling1995).

Similarly, Eq. 2 and 4 for the perpetuity can be used to solve for i∗N . With constant flowsof benefits over time:

i∗N = VN

PU(2’)

With increasing flows of benefits over time:

i∗N = VN

PU+ g (4’)

The application of the equivalency principle is theoretically valid under two basic assump-tions. The first requires that past decision making on development versus protection of naturalassets was socially optimal in the “administrative unit”3 of reference having the responsibility

3 In the reminder of the paper we use the term “administrative unit” defined as the public administrationhaving the responsibility for land use planning and for granting building permits in a specified area.

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

for land-use planning and for granting building permits, so that the marginal present value ofthe preserved undeveloped land is equal to the marginal present value of the adjacent devel-oped land. The second is that future generations are affected in the long run by the decisiontaken on the land (Weitzman 1998).

3 Illustrating the equivalency principle

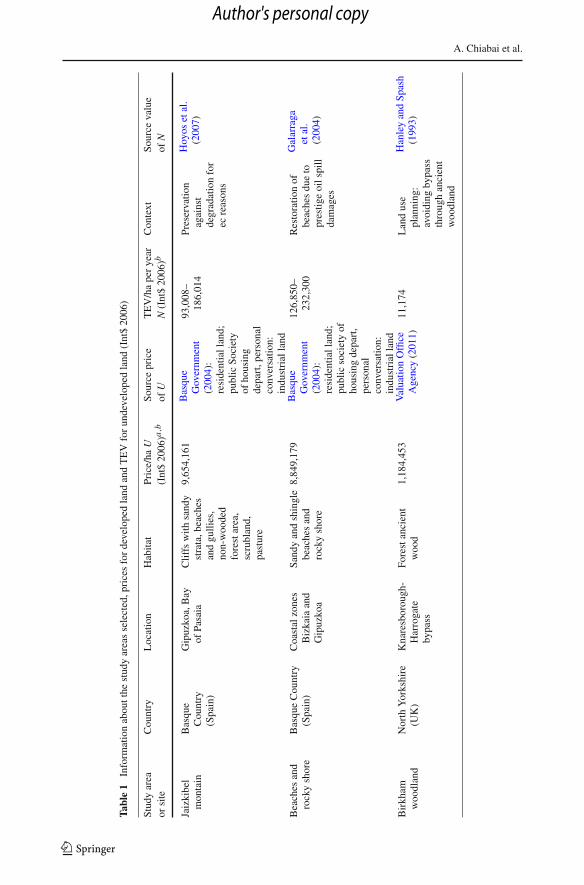

In order to illustrate the application of the equivalency rule we have identified a number ofstudy areas located in administrative units in the Basque Country and the United Kingdomwhich appear to be characterized by a fairly balanced allocation of developed and undevel-oped land tracks. We are thus assuming that in these units the allocation between developedand undeveloped land was deemed socially optimal. The study areas have been selected basedalso on the availability of valuation studies in the literature providing explicit and detailedinformation about TEV for different types of undeveloped land which could be affected bythe realization of an investment project for industrial or residential purposes. The selectedvaluation studies refer to a context of preservation of terrestrial or marine ecosystems. Thevalue of N (undeveloped land) for each study area is recorded based on its TEV and isreported as an annual flow value per hectare for a specific point in time. Since, due to eco-nomic growth or associated scarcity of the selected habitats, people in the future might bewilling to pay more for the benefits of preserving those habitats, an exogenous growth rateof the TEV based on the expected growth of real per capita income has been calculated foreach of the case studies.

We use the equivalency principle to calculate the implicit discount rate that might appliedfor the optimal management of undeveloped land under two assumptions: (a) that future flowvalues are equal to the present ones and (b) future flow values grow at the rate of expectedgrowth of real per capita income (on the basis of A2 and B2 IPCC scenarios).

As regards the price of U (land for residential or industrial use), this is calculated, forillustrative purposes, using the average price observed in the market for residential/industrialland located within the administrative unit where the selected study area is placed. However,the choice of the type of developed land (residential versus industrial or other) will dependon the investment project that is expected to be realized and on the adjacent areas that willbe affected (residential or industrial or both). If the project is about the industrial develop-ment of an area or entails conversion of undeveloped land for industrial purposes only, oneshould use the price of industrial land. By contrast, if the project entails the conversion forboth industrial and residential purposes, then an average of both land prices would be moreappropriate. Prices of U are reported per hectare.

For each study area, we proceed by estimating the discount rate i∗N that would result fromthe application of the suggested equivalency rule in the case of a perpetual income flowsituation, using Eq. 2’ (constant flows of benefits) and Eq. 4’ (increasing flows of benefitsunder scenarios B2 and A2 IPCC). We first provide a reliable range of discount rates thatcould be applied in the selected study areas if an investment project (for industrial and resi-dential purposes) associated with long-term environmental impacts were realised. Secondly,we examine the conditions for applying the estimated discount rates in other contexts.

Table 1 presents some basic information about the selected study areas, their location, typeof habitat, prices per hectare of developed land, total economic values (TEV) of undevelopedland, as well as data sources and contexts of the valuation studies. Prices and TEV infor-mation are converted into international dollars of year 2006 using the implied purchasingpower parity (PPP) conversion rate and the average consumer prices. Among the study areas

123

Author's personal copy

A. Chiabai et al.

Tabl

e1

Info

rmat

ion

abou

tthe

stud

yar

eas

sele

cted

,pri

ces

for

deve

lope

dla

ndan

dT

EV

for

unde

velo

ped

land

(Int

$20

06)

Stud

yar

eaC

ount

ryL

ocat

ion

Hab

itat

Pric

e/ha

USo

urce

pric

eT

EV

/ha

per

year

Con

text

Sour

ceva

lue

orsi

te(I

nt$

2006

)a,b

ofU

N(I

nt$

2006

)bof

N

Jaiz

kibe

lm

onta

inB

asqu

eC

ount

ry(S

pain

)

Gip

uzko

a,B

ayof

Pasa

iaC

liffs

with

sand

yst

rata

,bea

ches

and

gulli

es,

non-

woo

ded

fore

star

ea,

scru

blan

d,pa

stur

e

9,65

4,16

1B

asqu

eG

over

nmen

t(2

004)

:re

side

ntia

llan

d;pu

blic

Soci

ety

ofho

usin

gde

part

,per

sona

lco

nver

satio

n:in

dust

rial

land

93,0

08–

186,

014

Pres

erva

tion

agai

nst

degr

adat

ion

for

ecre

ason

s

Hoy

oset

al.

(200

7)

Bea

ches

and

rock

ysh

ore

Bas

que

Cou

ntry

(Spa

in)

Coa

stal

zone

sB

izka

iaan

dG

ipuz

koa

Sand

yan

dsh

ingl

ebe

ache

san

dro

cky

shor

e

8,84

9,17

9B

asqu

eG

over

nmen

t(2

004)

:re

side

ntia

llan

d;pu

blic

soci

ety

ofho

usin

gde

part

,pe

rson

alco

nver

satio

n:in

dust

rial

land

126,

850–

232,

300

Res

tora

tion

ofbe

ache

sdu

eto

pres

tige

oils

pill

dam

ages

Gal

arra

gaet

al.

(200

4)

Bir

kham

woo

dlan

dN

orth

Yor

kshi

re(U

K)

Kna

resb

orou

gh-

Har

roga

teby

pass

Fore

stan

cien

tw

ood

1,18

4,45

3V

alua

tion

Offi

ceA

genc

y(2

011)

11,1

74L

and

use

plan

ning

:av

oidi

ngby

pass

thro

ugh

anci

ent

woo

dlan

d

Han

ley

and

Spas

h(1

993)

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

Tabl

e1

cont

inue

d

Stud

yar

eaC

ount

ryL

ocat

ion

Hab

itat

Pric

e/ha

USo

urce

pric

eT

EV

/ha

per

year

Con

text

Sour

ceva

lue

orsi

te(I

nt$

2006

)a,b

ofU

N(I

nt$

2006

)bof

N

Mar

Lod

geE

stat

eSc

otla

nd(U

K)

Scot

tish

Hig

hlan

ds,

Abe

rdee

nshi

re

Nat

ive

anci

ent

Cal

edon

ian

pine

fore

st

1,35

1,87

2V

alua

tion

Offi

ceA

genc

y(2

011)

4,59

9–8,

090

Pres

erva

tion

ofha

bita

tin

the

cont

exto

fla

nd-u

sepl

anni

ng

Cob

bing

and

Slee

(199

4)

Wau

kenw

aeM

oss

and

Red

mos

sSc

otla

nd(U

K)

Sout

hL

an-

arka

shir

eB

ogs,

mar

shes

,w

ater

frin

ged

vege

tatio

n,fe

ns,

hum

idgr

assl

and,

broa

d-le

aved

deci

diou

sw

ood

763,

557

Val

uatio

nO

ffice

Age

ncy

(201

1)

17,6

31Pr

eser

vatio

nag

ains

tde

grad

atio

nfo

rec

reas

ons

Jaco

bs(2

004)

aT

hepr

ice

ofU

isca

lcul

ated

asth

eav

erag

epr

ice

ofin

dust

rial

and

resi

dent

iall

and

regi

ster

edin

the

adm

inis

trat

ive

unit

whe

reth

est

udy

area

islo

cate

d.T

head

min

istr

ativ

eun

itis

refe

rred

asth

epu

blic

adm

inis

trat

ion

havi

ngth

ere

spon

sibi

lity

for

land

use

plan

ning

and

for

grat

ing

build

ing

perm

its.b

Ori

gina

lpri

ces

ofU

and

TE

Vin

form

atio

nar

eco

nver

ted

into

valu

espe

rhe

ctar

ein

orde

rto

appl

yE

q.2’

and

4’,a

ndtr

ansf

orm

edin

toin

tern

atio

nald

olla

rsof

year

2006

usin

gth

eim

plie

dpu

rcha

sing

pow

erpa

rity

(PPP

)co

nver

sion

rate

and

the

aver

age

cons

umer

pric

es

123

Author's personal copy

A. Chiabai et al.

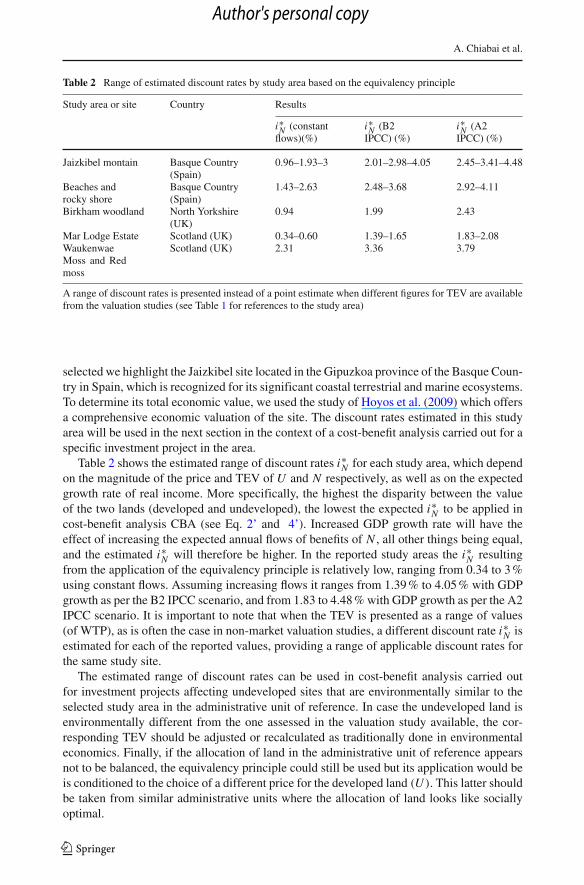

Table 2 Range of estimated discount rates by study area based on the equivalency principle

Study area or site Country Results

i∗N (constantflows)(%)

i∗N (B2IPCC) (%)

i∗N (A2IPCC) (%)

Jaizkibel montain Basque Country(Spain)

0.96–1.93–3 2.01–2.98–4.05 2.45–3.41–4.48

Beaches androcky shore

Basque Country(Spain)

1.43–2.63 2.48–3.68 2.92–4.11

Birkham woodland North Yorkshire(UK)

0.94 1.99 2.43

Mar Lodge Estate Scotland (UK) 0.34–0.60 1.39–1.65 1.83–2.08WaukenwaeMoss and Redmoss

Scotland (UK) 2.31 3.36 3.79

A range of discount rates is presented instead of a point estimate when different figures for TEV are availablefrom the valuation studies (see Table 1 for references to the study area)

selected we highlight the Jaizkibel site located in the Gipuzkoa province of the Basque Coun-try in Spain, which is recognized for its significant coastal terrestrial and marine ecosystems.To determine its total economic value, we used the study of Hoyos et al. (2009) which offersa comprehensive economic valuation of the site. The discount rates estimated in this studyarea will be used in the next section in the context of a cost-benefit analysis carried out for aspecific investment project in the area.

Table 2 shows the estimated range of discount rates i∗N for each study area, which dependon the magnitude of the price and TEV of U and N respectively, as well as on the expectedgrowth rate of real income. More specifically, the highest the disparity between the valueof the two lands (developed and undeveloped), the lowest the expected i∗N to be applied incost-benefit analysis CBA (see Eq. 2’ and 4’). Increased GDP growth rate will have theeffect of increasing the expected annual flows of benefits of N , all other things being equal,and the estimated i∗N will therefore be higher. In the reported study areas the i∗N resultingfrom the application of the equivalency principle is relatively low, ranging from 0.34 to 3 %using constant flows. Assuming increasing flows it ranges from 1.39 % to 4.05 % with GDPgrowth as per the B2 IPCC scenario, and from 1.83 to 4.48 % with GDP growth as per the A2IPCC scenario. It is important to note that when the TEV is presented as a range of values(of WTP), as is often the case in non-market valuation studies, a different discount rate i∗N isestimated for each of the reported values, providing a range of applicable discount rates forthe same study site.

The estimated range of discount rates can be used in cost-benefit analysis carried outfor investment projects affecting undeveloped sites that are environmentally similar to theselected study area in the administrative unit of reference. In case the undeveloped land isenvironmentally different from the one assessed in the valuation study available, the cor-responding TEV should be adjusted or recalculated as traditionally done in environmentaleconomics. Finally, if the allocation of land in the administrative unit of reference appearsnot to be balanced, the equivalency principle could still be used but its application would beis conditioned to the choice of a different price for the developed land (U ). This latter shouldbe taken from similar administrative units where the allocation of land looks like sociallyoptimal.

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

4 Application to an investment project in the Basque Coast

In this section we apply the equivalency principle in the context of a cost-benefit analysis toassess the economic viability of an investment project in the Basque Coast. The construc-tion of a new seaport in the town of Pasaia, in the province of Gipuzkoa has attracted a lotof attention lately in the Basque Country and heated arguments have been made in favourand against the proposal, given that it is planned in a cliff named Jaizkibel with significantenvironmental attributes. This is a zone that was incorporated in the Natura 2000 networkin 2004 and comprises 2,400 hectares of natural land with 15 zones declared of high eco-logical interest. The project is currently being evaluated by the Ministry of the Environment,Rural Affairs and Marine Issues of the Spanish Government within the Environmental ImpactAssessment (EIA) procedure. The total investment (of mainly public resources) requestedfor the implementation of the project ranges from e750 million to e1.2 billion dependingon the alternative chosen.4

The significant environmental value of the Jaizkibel area is documented in terms of bothterrestrial and marine ecosystems, as summarised by Hoyos et al. (2009). The authors makereference to its remarkable landscape, its seabed life, and its autochthonous fauna and flora,with some endemic plants being extremely rare in Europe and in danger of extinction. Thehabitats include cliffs with important geological features, small beaches and gullies formedby the courses of streams, non-wood forest area with scrubland, pasture land and seabedharbours.

In order to decide whether to build the seaport or not, the public authorities need toknow the market benefits which could be generated by the project and compare them withthe environmental damages expected in the area. Hoyos et al. (2007) estimated, using achoice model, the TEV of preserving the Jaizkibel natural area in similar condition asit is today. The study defines three scenarios of preservation, depending on the impactcaused by the construction of the seaport (low, medium and high impact), and providesthe social welfare loss per year (corresponding to the annual, TEV estimated to be respec-tively e172, 110, 000(e2006),e344, 220, 000(e2006), and e535, 520, 000(e2006). Thisinformation is used to calculate the environmental (social) costs of the project.

Information on the total market benefits which could be generated by building the port(namely alternative 45) is taken from the Pasaia Port Authority (2010). The report esti-mates that the investment project would generate positive annual net market benefits ofe542, 686, 980(e2010) in the period 2010–2054, based on various key assumptions suchas incoming and outgoing maritime traffic, new transport lines, as well as industrial andresidential developments in the area. The figure has been estimated applying an input–outputLeontieff model, and falls within the ranges of a similar study carried out by the Bilbao PortAuthority.6 Using this information one can apply a simple cost-benefit analysis and illustratethe implications of the equivalency principle for discounting. For comparability, market ben-efits and environmental costs have been converted into international dollars of the year 2006(using the average consumer prices) (Table 3).

4 The information for this case study has been obtained from the Environmental Sustainability Report(Pasaia Port Authority, Informe de Sostenibilidad Ambiental, 2010) that has been submitted for the EIAprocedure by the Pasaia Port Authority. These documents are available at the official site of the Port Authority.5 The other alternatives are 3,2,1 and 0 which represents not building the port at all.6 The information and values used here reflects the benefits net of the investment costs needed to build the portand the infrastructures. The Bilbao Port Authority report: www.bilbaoport.es/aPBW/web/es/puerto/economia/index.jsp.

123

Author's personal copy

A. Chiabai et al.

Table 3 Annual market benefits and monetised environmental costs (Int$ 2006)

Market benefits per year (Int$ 2006) 641,491,148Environmental costs per year (Int$ 2006)Lower bound 222,364,341Central estimate 444,728,682Upper bound 691,886,305

The market benefits, originally reported in e2010 (Pasaia Port Authority 2010), and the monetised environ-mental costs, originally reported in e2006 (Hoyos et al. 2007), have been converted into Int$ 2006 using theaverage consumer prices

Table 4 Present discounted values of market benefits and environmental costs derived from building theseaport, period 2010–2050 (Int$ 2006; constant TEV flows)

Discount rate applied to market Present value of market benefitsbenefits (%)

11 6,414,128,939

Discount rate applied to Present value of environmental costs %environmental costs (%)

Lower bound Central estimate Upper bound

11 2,223,372,152 4,446,744,303 6,918,019,0274 4,791,693,895 9,583,387,790 14,909,348,1773 na na 17,473,086,2641.93 na 13,550,814,868 na0.96 8,172,036,231 na na

Table 5 Net present value derived from building the seaport, period 2010–2050, based on CBA (Int$ 2006;constant TEV flows and discount rate for market benefits 11 %)

Discount rate applied to Net present valueenvironmental costs (%)

Lower bound Central estimate Upper bound

11 4,190,756,787 1,967,384,635 −503,890,0884 1,622,435,044 −3,169,258,851 −8,495,219,2383 na na −11,058,957,3251.93 na −7,136,685,930 na0.96 −1,757,907,292 na na

Let us assume first that the authority decides to discount the market benefits at a marketrate (for example 11 %) to calculate the present value of expected benefits for the period2010–2054 and uses the same rate for the environmental losses. The resulting present val-ues are reported in Table 4. The construction of the seaport would be justified only in thefirst two scenarios of preservation (lower and medium environmental impact), as the presentvalue of the economic benefits (6.4 billion Int$ 2006) is larger than the present value of theenvironmental cost (2.2 and 4.4 billion Int$ 2006, respectively). In the third scenario (higherenvironmental impact) the construction of the port would produce a negative net present valuedue to the significant higher expected environmental costs. The net present value would be4.2, 1.9 and −0.5 billion (Int$ 2006) for the three scenarios, respectively (Table 5, first row).

In the second example, we use the ranges suggested by Gollier (2008) and apply a 4 %rate for environmental costs, while 11 % is used for the market benefits. In this case, the

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

cost-benefit analysis shows that the construction of the seaport can be justified only underthe first scenario (of low environmental impact) (Table 5, second row).

Let us move now one step further to illustrate the case of choosing the discount ratesresulting from the application of the equivalency principle. In this situation, we would applythree different discount rates to the three scenarios of preservation, namely 0.96, 1.93 and3 % depending on the magnitude of the TEV of the undeveloped land (c.f. Hoyos, 2007),as estimated in Table 2 for the Jaizkibel site (constant flows). The net present value wouldbe negative in all the three scenarios, ranging from a loss of 1.8 to 11 billion (Int$ 2006),meaning that the construction of the port would not be justifiable even in the first scenario oflow environmental impacts (Table 5, last three rows).

This case study illustrates that choosing a ‘wrong’ discount rate can make the traditionalcost-benefit analysis largely biased, suggesting that a project should be promoted while acloser look at the values of natural assets would strongly suggest not undertaking it. Thesenumbers are real numbers from a future project under discussion in the policy arena for thepast few years with a potential severe impact on the marine and coastal ecosystems. Decidingto go ahead with this project is pending on an administrative procedure. Short sighted policymakers could decide to go ahead with a e750 million investment while a more sustainableapproach clearly shows that the port should not be constructed.7 This case study shouldbe seen as an example of many other projects which policy makers tend to support basedon biased discounts. Using the equivalency principle may help reducing wrong decisions,especially for projects affecting environmental assets that are not properly taken into accountor valued. Projects affecting marine ecosystems in coastal areas are certainly among thosewhich could strongly benefit from the use of proposed principle.

5 Concluding remarks

Identifying the appropriate social discount rate is crucial for policy action especially in thecontext of long-term environmental impacts. Two critical arguments should be taken intoaccount in the discussion about the discount rate in regarding intergenerational choices aboutthe environment. The estimation of the discount rate in the standard welfare approach is basedon the assumption that future generation will be richer than ours, according to which “oneshould not be ready to pay one euro to reduce the loss borne by future generations by oneeuro, given that these future generations will be so much wealthier than us” (as mentionedby Gollier 2008, 172). However, in the current situation of economic uncertainty about GDPgrowth it is not straightforward to estimate what future generations’ per capita income willbe. In this context, discount rates cannot be based on the expectations about future economicgrowth alone. Second, if a resource becomes scarcer, its value is expected to raise comparedto the less scarce resources. Some natural ecosystems (such as wetlands, mangroves, coralreefs) can become very rare in the future, and this would increase their value and the priceof the corresponding land. In the most extreme case that human life would be threatened dueto the disappearance of critical natural ecosystems, the value of these ecosystems might seea dramatic escalation, to the point of reaching some critical threshold where the notion ofeconomic value itself would become meaningless. Given that we can reasonably expect ahigher level of scarcity of natural resources in the future, investments to preserve such assetstoday need to take account of that and one way of doing so is to apply a low discount rate

7 At the time of writing this paper the Government of Spain together with some of the political parties in theBasque Country have decided not to support the project, based on the expected environmental impacts.

123

Author's personal copy

A. Chiabai et al.

to such investments. Against this background, we can also plausibly think that low socialdiscount rates could be reflected in higher actual prices of natural lands in the future.

What we propose in this paper simplifies the discussion about which discount rate shouldbe used by policy makers under the current level of uncertainty characterising climate changeimpacts and long-term risks to future generations. While the current “main intellectual bat-tleground is whether we should be using discount rates in the range of 3% or discountingby only a token nonzero amount, such as 0.1%”, as mentioned by Zeckhauser and Viscusi(2008, 99), the results reported in this paper show that the discount rate resulting from theapplication of the equivalency rule depends on the magnitude of the values reported for thegiven land tracks: the larger the disparity between the TEV of undeveloped land and theprice of developed land, the lower the expected discount rate. Based on this rule, we argue infavour of using relatively low discount rates (ranging from 0.34 to 3 % using constant TEVflows) hence supporting policy decisions that are more oriented towards the protection of theenvironment than they actually are. Note that the equivalency principle might prove usefulwhen analysing projects that affect environmental assets that are not adequately taken intoaccount in cost-benefit analysis. This is often the case, among many others, of coastal marineecosystems.

It is also important to note that the application of the equivalency principle is theoreti-cally sound under two basic assumptions. First, past decision making on development versusprotection of natural assets has to be socially optimal in the administrative unit having theresponsibility for land-use planning and granting building permits. Second, the investmentproject on the land has to affect the welfare of future generations through the loss of naturalassets.

Under these circumstances, we argue that the discount rate resulting from the “equivalencyprinciple” can be applied to all natural sites located in the administrative unit of reference,which have similar environmental attributes to the one assessed in the valuation study avail-able. In the case study for the Basque Country, for example, the estimated discount rates(Table 2) can be applied to natural assets other than Jaizkibel, provided that the type of hab-itat is the same. In case the natural site is environmentally different from the one assessedin the valuation study available, the corresponding TEV should be adjusted or recalculated.Finally, if the administrative unit where the natural site is located is characterised by anunbalanced allocation of land, the equivalency principle could be still applied, but the priceof developed land (U ) would need to be taken from similar administrative units where theallocation of land looks like socially optimal.

References

Arrow KJ (1965) Aspects of the theory of risk-bearing. Yrjö Jahnssonin säätiö, HelsinkiArrow KJ (1963) Social choice and individual values, 2nd edn. Wiley, New YorkArrow KJ, Cline WR, Maler KG, Munasinghe M, Squitieri R, Stiglitz J (1996) Intertemporal equity, discount-

ing, and economic efficiency. In: Bruce JP, Lee H, Haites EF (eds) Climate change 1995: economic andsocial dimensions of climate change, contribution of working group III to the second assessment reportof the intergovernmental panel on climate change. Cambridge University Press, Cambridge

Barker K (2006) Barker review of land use planning. Interim report—analysis. Barker review of land useplanning. http://www.barkerreviewofplanning.org.uk

Basque Government (2004) “Estadística de precios del suelo: Encuesta a promotores sobre suelo edificable2003. Dpto. de Vivienda y Asuntos Sociales

Beltratti A, Chichilnisky G, Heal G (1998) Sustainable use of natural resources. In: Chichilnisky G,Heal G, Vercelli A (eds) Sustainability: dynamics and uncertainty, chapter 2.1. Kluwer Academic Pub-lishers, Dordrecht

123

Author's personal copy

The Equivalency Principle for Discounting the Value of Natural Assets

Bromley D (2007) Environmental regulations and the problem of sustainability: moving beyond “market fail-ure”. Ecol Econom 63:676–683

Chichilnisky G (1996) An axiomatic approach to sustainable development. Soc Choice Welfare 13:231–257Cobbing P, Slee B (1994) The application of CVM to a land use controversy in the Scottish Highlands.

Landsc Res 19(1):14–17Cole D (2008) The Stern review and its critics: implications for the theory and practice of benefit-cost analysis.

Nat Res J 48:53–90Cropper W, Laibson D (1999) The implications of hyperbolic discounting for project evaluation. In: Portney

P, Weyant J (eds) Discouting and intergenerational equity. Resources for the Future, Washington, DCDasgupta P (2008) Discounting climate change. J Risk Uncertain 37:141–169Dasgupta P, Maler K-G (2000) Net national product, wealth and social well-being. Environ Dev Econom

5:69–93Dasgupta P, Maler K-G, Barrett S (1999) Intergenerational equity, social discount rates, and global warming.

In: Portney PR, Weyant JP (eds) Discounting and intergenerational equity. Resources for the Future,Washington, DC

Dietz S (2008) A long-run target for climate policy: the Stern review and its critics, supporting researchfor the UK committee on climate change’s inaugural report building a low-carbon economy—theUK’s contribution to tackling climate change. http://personal.lse.ac.uk/dietzs/A%20long-run%20target%20for%20climate%20policy%20-%20the%20Stern%20Review%20and%20its%20critics.pdf

Fisher A, Krutilla J (1985) The economics of natural environments. Resources for the Future, Washington,DC

Fisher A, Krutilla J (1975) Resource conservation, environmental preservation, and the rate of discount.Q J Econom 89(3):358–370

Frederick S, Lowenstein G, O’Donoghue T (2002) Time discounting and time preference: a critical review.J Econom Lit 40(2):351–401

Galarraga I, Martín I, Beristain I, Boto A (2004) El método de transferencia de valor (benefit transfer), unasegunda opción para la evaluación de impactos económicos: el caso del Prestige. Ekonomiaz 57:30–45

Gollier C, Weitzman ML (2010) How should the distant future be discounted when discount rates are uncer-tain?. Econom Lett 107:350–353

Gollier C (2008) Discounting with fat-tailed economic growth. J Uncertain 37:171–186Gowdy J, Howardth R, Tisdell C (2010) Discounting, ethics and options for maintaining biodiversity and

ecosystem integrity. In: Kumar P (ed) The economics of ecosystems and biodiversity. Ecological andEconomic Foundations. Edgar Elgar, Northampton

Graaff de V (1987) Social cost. In: Eatwell J, Milgate M, Newman P (eds) The new Palgrave dictionary ofeconomics, vol 4. Macmillan, London, pp 393–395

Guo J (2004) Discounting and the social cost of carbon. Thesis for the Master’s Degree in EnvironmentalChange and Management, University of Oxford

Hanley N, Spash CL (1993) The protection of ancient woodlands. In: Hanley N, Spash CL (eds) Cost-benefitanalysis and the environment. Edward Elgar, Northampton

Hartman JC, Schafrick IC (2004) The relevant internal rate of return. Eng Econom 49(2):139–158Heal GM (1998) Valuing the future: economic theory and sustainability. Columbia University Press,

New YorkHoyos D, Mariel P, Fernández-Macho J (2009) The influence of cultural identity on the WTP to protect natural

resources: some empirical evidence. Ecol Econom 68:2372–2381Hoyos D, Riera P, Fernandez-Macho J, Gallastegui C, García D (2007) Informe final: Valoración económica

del entorno natural del monte Jaizkibel. Instituto de Economía Publica (UPV/EHU9), UniversidadAutónoma de Barcelona (UAB), Barcelona

Jacobs (2004) An economic assessment of the costs and benefits of Natura 2000 sites in Scotland. Final Report.Scottish Executive 2004. Environment Group research report 2004/05

Krutilla JV (1967) Conservation reconsidered. Am Econom Rev 57:777–786Li CZ, Lofgren KG (2000) Renewable resources and economic sustainability: a dynamic analysis with heter-

ogeneous time preferences. J Environ Econom Manag 40:236–250Lind RC (ed) (1982) Discounting for time and risk in energy planning. Johns Hopkins University Press,

BaltimoreMartinez-Alier J (1995) The environment as a luxury good or “too poor to be green”. Ecol Econom 13:1–10Mills ES, Hamilton BW (1994) Urban economics, 5th edn. Harper Collins College Publishers, New YorkNordhaus WD (2007) The Stern review on the economics of climate change. J Econom Lit 45(3):686–702Nordhaus WD (1994) Managing the global commons: the economics of climate change. MIT press,

Cambridge, MA

123

Author's personal copy

A. Chiabai et al.

Pasaia Port Authority (2010) Informe de sostenibilidad ambiental del plan director de infraestructuras delpuerto de Pasaia. http://www.puertopasajes.net/en/index.php?lang=en

Samuelson PA (1980) Economics, 11th edn. McGraw-Hill, New York 747Sen AK (1961) On optimizing the rate of saving. Econom J 71:479–496Sen AK (1967) Isolation, assurance, and the social rate of discount. Q J Econom 81:172–224Solow RM (1974) Intergenerational equity and exhaustible resources. Rev Econom Stud 41(Symposium

Issue):29–45Stern NH (2007) The economics of climate change: the Stern review. Cambridge University Press, Cambridge.

http://www.hm-treasury.gov.uk/sternreview_index.htmSummers L, Zeckhauser R (2008) Policymaking for posterity. J Risk Uncertain 37:115–140Tjalling JY (1995) Historical development of the Newton–Raphson method. SIAM Rev 37(4):531–551Tol RSJ, Yohe G (2009) The stern review: a deconstruction. Energy Policy 37(3):1032–1040Tol R, Yohe G (2006) A review of the Stern review. World Econom 7(4):233–250Valuation Office Agency (2011) Property market report 2011. The annual guide to the property market across

England, Wales and Scotland. Crow copyright 2011. www.voa.gov.uk/dvsWeikard H-P, Xhu X (2005) Discounting and environmental quality: when should dual rates be used?. Econom

Model 22:868–878Weitzman ML (2001) Gamma discounting. Am Econom Rev 91(1):260–271Weitzman ML (2007) The Stern review of the economics of climate change. J Econom Lit 45(3):703–724Weitzman ML (1998) Why the far-distant future should be discounted at its lowest possible rate. J Environ

Econom Manag 36(3):201–208Weitzman ML (2009) On modelling and interpreting the economics of catastrophic climate change. Rev Eco-

nom Stat XCI:1–19Zeckhauser RJ, Viscusi WK (2008) Discounting dilemmas: editors’ introduction. J Risk Uncertain 37:95–106

123

Author's personal copy

Copyright © 2022 FDOKUMEN

![2013 - "Basque Dialects" (in Basque and Proto-Basque [= Mikroglottika 5], edited by M. Martínez-Areta, Peter Lang, 31-87)](https://static.fdokumen.com/doc/165x107/6318db1d65e4a6af370f8b40/2013-basque-dialects-in-basque-and-proto-basque-mikroglottika-5-edited.jpg)