Reconciling sustainability and discounting in Cost–Benefit Analysis: A methodological proposal

14

METHODS Reconciling sustainability and discounting in Cost–Benefit Analysis: A methodological proposal Carmen Almansa Sáez a, ⁎ , Javier Calatrava Requena b a Departamento de Gestión de Empresas, Universidad Pública de Navarra, Campus de Arrosadía s/n, 31.006 Pamplona, Spain b Departamento de Economía y Sociología Agrarias, Instituto Andaluz de Investigación y Formación Agraria y Pesquera, Alimentaria y de Producción Ecológica (IFAPA), Junta de Andalucía, Camino Purchil s/n, 18.080, Granada, Spain ARTICLE INFO ABSTRACT Article history: Received 1 September 2005 Received in revised form 3 April 2006 Accepted 3 May 2006 Available online 3 July 2006 The incorporation of the intergenerational equity objective has rendered the traditional Cost–Benefit Analysis (CBA) approach obsolete for the evaluation of projects presenting an important number of environmental externalities and for those whose impacts extend throughout a long period of time. Based on the assumption that applying a discount rate rewards current consumption and, therefore, that it is only possible to introduce a certain intergenerational equity in a Cost–Benefit Analysis, in this work we propose an approach to discounting based on a different rationale for tangible and intangible effects. We designed two indicators of environmental profitability: a) the Intergenerational Transfer Amount (ITA), which quantifies in monetary units what the current generation is willing to pass on future generations when an environmental restoration project is carried out, and b) the Critical Environmental Rate (CER), measures the implicit environmental profitability. These concepts were tested through an empirical case study pertaining to the assessment of an Erosion Control Project in the southeast of Spain. The results yield traditional profitability indicators that are higher — and probably closer — to the real values set by the contemporary society. The information provided by the environmental profitability indicators proposed renders more transparency to the quantification of the levels of intergenerational equity applied, thereby facilitating the difficult reconciliation of the CBA technique with the objective of sustainability. © 2006 Elsevier B.V. All rights reserved. Keywords: Intergenerational equity Sustainability Social Discount Rate Environmental discounting Cost–Benefit Analysis 1. Introduction The incorporation of the intergenerational equity objective has turned the traditional Cost–Benefit Analysis (CBA) ap- proach into an obsolete tool for the evaluation of certain types of projects, particularly those exhibiting many environmental externalities and those whose effects extend throughout a long period of time. A series of changes in the CBA is being proposed in the literature, in order to adapt the analytical context to the demand for sustainability, resulting in what is alternatively denominated Extended or Environmental Costs Benefits Analysis (ECBA). From an analytical point of view, changes in the CBA are taking place in a twofold way: Firstly, by developing new tools for the economic valuation of environmental externalities that were traditionally left out of the analysis. Secondly, through an in-depth revision of the theoretical foundations underlying the traditional approaches to discounting, since ECOLOGICAL ECONOMICS 60 (2007) 712 – 725 ⁎ Corresponding author. Tel.: +34 948 169425; fax: +34 948 169404. E-mail address: [email protected] (C.A. Sáez) 0921-8009/$ - see front matter © 2006 Elsevier B.V. All rights reserved. doi:10.1016/j.ecolecon.2006.05.002 available at www.sciencedirect.com www.elsevier.com/locate/ecolecon

-

Upload

juntadeandalucia -

Category

Documents

-

view

1 -

download

0

Transcript of Reconciling sustainability and discounting in Cost–Benefit Analysis: A methodological proposal

E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

ava i l ab l e a t www.sc i enced i r ec t . com

www.e l sev i e r. com/ loca te / eco l econ

METHODS

Reconciling sustainability and discounting in Cost–BenefitAnalysis: A methodological proposal

Carmen Almansa Sáeza,⁎, Javier Calatrava Requenab

aDepartamento de Gestión de Empresas, Universidad Pública de Navarra, Campus de Arrosadía s/n, 31.006 Pamplona, SpainbDepartamento de Economía y Sociología Agrarias, Instituto Andaluz de Investigación y Formación Agraria y Pesquera,Alimentaria y de Producción Ecológica (IFAPA), Junta de Andalucía, Camino Purchil s/n, 18.080, Granada, Spain

A R T I C L E I N F O

⁎ Corresponding author. Tel.: +34 948 169425;E-mail address: carmen.almansa@unavar

0921-8009/$ - see front matter © 2006 Elsevdoi:10.1016/j.ecolecon.2006.05.002

A B S T R A C T

Article history:Received 1 September 2005Received in revised form 3 April 2006Accepted 3 May 2006Available online 3 July 2006

The incorporation of the intergenerational equity objective has rendered the traditionalCost–Benefit Analysis (CBA) approach obsolete for the evaluation of projects presenting animportant number of environmental externalities and for those whose impacts extendthroughout a long period of time.Based on the assumption that applying a discount rate rewards current consumption and,therefore, that it is only possible to introduce a certain intergenerational equity in aCost–BenefitAnalysis, in this work we propose an approach to discounting based on a different rationale fortangible and intangible effects.Wedesigned two indicatorsof environmental profitability: a) theIntergenerational Transfer Amount (ITA), which quantifies inmonetary units what the currentgeneration iswilling to pass on futuregenerationswhenanenvironmental restorationproject iscarried out, and b) the Critical Environmental Rate (CER), measures the implicit environmentalprofitability.These concepts were tested through an empirical case study pertaining to the assessment of anErosion Control Project in the southeast of Spain. The results yield traditional profitabilityindicators that are higher — and probably closer — to the real values set by the contemporarysociety.The informationprovidedby theenvironmentalprofitability indicatorsproposedrendersmore transparency to the quantification of the levels of intergenerational equity applied, therebyfacilitating the difficult reconciliation of the CBA technique with the objective of sustainability.

© 2006 Elsevier B.V. All rights reserved.

Keywords:Intergenerational equitySustainabilitySocial Discount RateEnvironmental discountingCost–Benefit Analysis

1. Introduction

The incorporation of the intergenerational equity objectivehas turned the traditional Cost–Benefit Analysis (CBA) ap-proach into an obsolete tool for the evaluation of certain typesof projects, particularly those exhibiting many environmentalexternalities and those whose effects extend throughout along period of time. A series of changes in the CBA is beingproposed in the literature, in order to adapt the analytical

fax: +34 948 169404.ra.es (C.A. Sáez)

ier B.V. All rights reserve

context to the demand for sustainability, resulting in what isalternatively denominated Extended or Environmental CostsBenefits Analysis (ECBA).

From an analytical point of view, changes in the CBA aretaking place in a twofold way: Firstly, by developing new toolsfor the economic valuation of environmental externalitiesthat were traditionally left out of the analysis. Secondly,through an in-depth revision of the theoretical foundationsunderlying the traditional approaches to discounting, since

d.

713E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

the repercussions of decisions that are presently beingdebated will extend to a distant future (in some cases forcenturies), whereas in the classical CBA we deal with fewdecades at best. Therefore, many authors are stressing theneed for a modification of the Social Discount Rate (SDR) byquestioning the assumptions that are traditionally taken forgranted and applied in its calculation.

The present work begins with some reflections on thediscounting problem drawn from a review of the differentapproaches found in the literature. Subsequently, we propose anumber of methodological approaches and report on theirapplication for the economic valuation of an environmentalimprovement project designed to stop the desertification pro-cesses in an area of south eastern Spain: The WatershedRestorationandControl ErosionProject ofLubrín (Almería, Spain).

1 Some of the main arguments used to justify the use of a positivesocial discount rate, specifically of the so-called social timepreferencerate (STPR), are: a) the argument based on the psychological discountcaused by the individuals' short-sightedness in looking into thefuture, whereby any future satisfaction seems less important thanthat in the present; b) the decreasing social consumption marginalutility argument over time; and c) the uncertainty argument.2 Weuse thisdenomination to refer todiscountingassociatedwith

projects involving important intergenerational repercussions,usually because they have a long term impact on the environment.3 Some of the authors that question the use of ECBA are Sagoff,

1988; Bromley, 1990; Vatn and Bromley, 1994; Munda, 1996; Goulderand Kennedy, 1997; Joubert et al., 1997; Goulder and Kennedy, 1997;Prato, 1999; Neumayer, 1999b; Martínez-Alier and Roca-Jusmet,2000. Researchers that favour the use of ECBA are, among others,Navrud (1992) and Hanemann (1994).

2. Discounting in Cost–Benefit Analysis:background

Discounting has traditionally been a controversial subject. Inthe seventies, after the great oil crisis of 1973 that took place inthe USA, this country and many others faced the need toinvest in research for alternative energy sources. It was at thattime that the subject of discounting began to arouse greatinterest among a small group of researchers, since they weredealing with investments whose benefits were not to takeplace until many years later. Thus in 1977, Resources For theFuture (RFF) made a call for a conference to discuss theadequate discount rate for public investments in energy andother technologies, the seminal ideas of which took form inthewell-known book “Discounting for Time and Risk in EnergyPolicy”, published by Robert C. Lind (1982), which was anoutstanding contribution, and the basis, during the followingfifteen years, of a widespread consensus on the subject ofdiscounting.

However, by the mid-nineties, the apparent consensus ondiscounting starts to evaporate. In 1995, a report appears onthe economic and social consequences of the climatic changeand the policies to pursue (IPCC, 1995), in which one chapter isdedicated to subjects related to discounting and intergenera-tional equity (Arrow et al., 1996). Although there are frequentreferences to Lind's book (and to others), a general agreementon discounting is no longer envisioned and the differentapproaches to discounting could justify discount rates withina wide range of possibilities.

Under these circumstances, RFF once again organised anencounter in 1996. Climatic change was the example thatmotivated the discussion, although the conclusions in relationto discounting were meant to be generalised to all decision-making processes of intergenerational nature. Some of thequestions openly put forward on that occasion that are centralto the current debate and upon which we will focus ourattention are the following: (1st) Should projects whose effectsspread over hundreds of years be dealt simply as “extendedversions” of projects whosemain effects do not last more than30 or 40 years? (2nd) If the answer to the previous question isyes, what is the appropriate discount rate to be applied? and,(3rd) If projectswith significant intergenerational effects are tobe valued in a different way, how should it be done?

3. Assessing discounting approaches

Many are the ethical, philosophical and economic arguments infavour of discounting future costs and benefits1 (Pearce andTurner, 1990; Broome, 1992; Lind, 1982); however, for someauthors, (see, for instance, Pearce and Turner, 1990) the use of apositive Social Discount Rate is incompatible with the intergen-erational equity objective. The present debate on discountingenvironmental benefits and costs is centred on the inconsistencyof discounting with the philosophy of sustainability. In otherwords, discounting is paramount to undervaluing the future,which means that future generations' preferences count lessthan our own present ones. As we shall see further down, anydiscussion on discounting will be closely related to the discus-sions on the various theoretical conceptions of sustainability.

The conclusions drawn from the previouslymentioned RFF1996 conference, which have been gathered by Portney andWeyant (1999), evidence once again the differences in opinionin relation to discounting in the scientific community and thevarious ethical positions held. The authorsmake two clear-cutcase distinctions in the subject under debate: short to mid-term projects (40 years and under) and projects of a lengthiertime span. One issue all the authors in the book agree on, withone exception, is that of considering it appropriate — evenessential — to discount future benefits and costs with somepositive discounting. Regarding the short to mid-term timespan (40 years and under), most authors believe that failing todiscount future benefits and costswouldbedamaging to futuregenerations, and that the appropriate discount rate in this caseis the capital's opportunity cost. Other experts, albeit aminority, are in favour of lower discount rates in this casealso. It is in regard to longer time spans than these that theauthors most clearly disagree.

Generally speaking, in the environmental discounting2

literature, where projects carrying an intergenerational im-pact receive special attention, the different authors tend tofavour one of the following options:

• To question the appropriateness of the Economic WelfareTheory, and consequently of the CBA technique, as the rightapproach in the decisionmaking process when dealing withclimate change policies, and in general with other problemsbearing significant intergenerational consequences.3

714 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

• To consider unnecessary and/or inappropriate any reduc-tion of the traditional Social Discount Rate (SDR) due tointergenerational equity issues.

• To favour the need to use discount rates (either constant orvariable in time), within the interval (0, SDR).

• To retain the conventional discount rate but increasing thevalue of the environmental good with time, as suggested byKrutilla and Fisher (1975).

• To design different mechanisms to take future generationsinto account in theanalysis (IntergenerationalCBAApproach).

Particularly, the most representative stances on applyingdiscounting through the ECBA technique, and beginning withthe most extreme positions of the interval (0, SDR), areembodied in the following opinions:

a)The only valid discount rate is zero, since it is the only rate thatis in accordwith a fully intergenerational equity scenario. This isan extreme position, defended by a very small minority, andwhich more readily represents — in some cases — a criticalposition against the CBA approach in the decision makingprocess in projects with intergenerational repercussions ratherthan a discount rate proposal.

For instance, Ciriacy-Wantrup (1942) has suggested applying azero discount rate or even a negative rate for certain socialpurposes such as public health, defence, or education. Harrod(1948) have taken the argument that “a zero discount rate wouldensure intergenerational equity by preventing the present gen-erations from ignoring the long-term environmental” and onestep further by arguing that discounting is ethically indefensibleand is, indeed, a “polite expression for rapacity”. More recently,Shue (1999) investigates the rights of future generations inresource and environmental policy (both property rights and thefundamental and non-marketable right of physical security)arguing that such rights should not be attenuated by discounting,let alone by application of a net present-value criterion.

b) The social time preference rate (STPR)4 is the appropriate andnecessary rate to evaluate intertemporal efficiency (among genera-

4 In practice, the STPR formula works as follows (Ramseyequation (Ramsey, 1928), referred in Pearce and Turner, 1990):STPR ¼ ceþ pwherecthe real per capita consumption rate;e=theelasticity of the consumption function's marginal utility; an-d p=the type of interest of pure time preference.While componentp reflects impatience, parameter e reflects the utility we believe isderived from the additional consumption units and, for the sake ofanalytical convenience, this relationship is expressed as anelasticity, that is, the change in marginal utility that arises arisefrom a change in marginal consumption. The component ce,hence, represents the idea that, since it is likely that futuresocieties will be richer, we allot a smaller weight to their earnings,and should therefore discount those future earnings. This is whatis called the decreasing consumption marginal utility principle. It is astraightforward principle, that, translated, amounts to the follow-ing: the more we have of something, the lower the increase insatisfactionwe derive from the addition of another unit of the samething. Generally speaking, the better offwe find ourselves, the lowerthe increase in satisfaction we get out of improving a little more.Thus, according to this logic, if in fifty years, judgingby thehistoricalevidence in this respect, people will be better off in terms ofwelfare,the damage that they will be caused when depriving them ofsomething will be smaller than the damage that will be caused tothose that are alive today, who are worse off, and havemore urgentneeds to meet.

tions). Lesser et al. (1997), among others, sustain that aninvestment project (or group of these) complies with the ruleof intergenerational equity, if present generations can improvetheirwelfare— in termsof consumption—without diminishingthe welfare of future generations. Conversely, we will be unfairwith regard to future generations ifwe leave themworseoff thanwe could. At the foundation of this line of reasoning lies the ideathat, in practice, a positive discount rate is associated withcapital accumulation and to technological change, which willallow future generations to be better off.

In our opinion, this reasoning could only be true if a perfectsubstitution capability existed between natural capital andother types of capital, which no doubt is very debatable,especially when we consider that decisions affecting theenvironment are often associated with irreversible changes.In other words, underlying these authors' reasoning is theconcept of weak sustainability, also called “neoclassical”sustainability, a concept that has been heavily criticised, aswe will comment on further down. Furthermore, assumingthat one accepts the argument that the “consumption” ofnatural goods has placed the present generation in a positionthat is better off than that of past generations, we cannotapply this same reasoning to future generations. Naturalcapital can be considered replaceable to a certain extent byanother kind of capital so long as humanity doesn't reach acertain “critical natural capital” level (Faucheux and O'Connor,1998),5 in which damage to the environment cannot be com-pensated for by any amount of alternative good(s).

In this sense, Solow (1991) offers a short definition forsustainability in the neoclassical sense. He affirms that ourobligation towards future generations is to behave in such away that they will have the option or the capacity of living aswell as we do. According to Solow, sustainability does notentail any specific objective; what we transmit to posterity is ageneral capability to live as well as we do. This definitionassumes perfect intersubstitution: monetary capital, labourand natural resources are interchangeable elements of capital.

However, this concept of sustainability has been the objectof severe criticism. As Carpenter (1997) affirms, calling it weakis the most optimistic thing that can be said about it. In ouropinion, and in agreement with such authors as SimónFernández (1995), the “flaw” in the weak sustainability pointof view is that it allows for compensation among the differentkinds of capital. Changes associated with the environmentfrequently entail irreversibility, and this is the extreme form ofincapability of substitution. Moreover, once an irreversibleevent has taken place it is suffered by the next generation andby all following generations.

c) Reductions in discount rates in favour of the environment areunnecessary if we operate with a strict no-decrease restriction on theendowment of natural capital. This is the position held by authors(seePearceandTurner, 1990; Pearceetal., 1990;Barbieretal., 1990)who believe that adjusting the STPR after the environmentalexternalities have been included is wrong as it involves a double

5 Faucheux and O'Connor (1998) describe critical natural capitalas a set of environmental resources which (at the prescribedgeographical scale) performs important environmental functionsand from which no substitute in terms of manufactured, humanor other natural capital exist.

715E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

accountancy. Acknowledging the shortcomings of the weaksustainability concept, Pearce and Turner (1990) try to make thestrong or strict sustainability concept compatible with thedecision evaluating process, by imposing the constraint that, nomatter what the benefits and costs associated with the decisionmay be, the environmental capital stock must remain constant.For example, in order to back acertainproject, thebenefits shouldbe greater than the costs, but there must also be a provisorequiring any environmental damage caused by this project to becompensated through restoration and rehabilitation.

Since this provision would be very strict and hardly ope-rative, these authors recommend considering a whole series ofdecisions on development projects and imposing on them thestrong sustainability condition in the following way: the totalsum of the environmental damage caused by an entire se-quence of projects can be counteracted by separate projectswithin the set of “decisions to be made”. These corrective, or“shadow”, projects would be an attempt to compensate for thereduction in natural capital stock through the creation anddeliberate increase of this stock. Shadow projects would not berequired to pass any kind of test relating the costs with thebenefits, since their justification would lie in their compliancewith the requirement of this type of sustainability. Thephilosophy of strong sustainability underlying this position isnot free from objections and criticism either. Rather than in itstheoretical conceptualisation, the problem lies in the difficultyin making it operational.6

The point is that a CBA approach to the decision makingprocess is only compatible, at best, with a philosophy of weaksustainability, which leads us to acknowledge a number offundamental problems of the Cost–Benefit Analysis when itincorporates the economic valuation of environmental exter-nalities: i) the very analytic design of this technique assumesthat all goods are commensurable, ii) that, nomatter howheavythe loss of any good may be, the losers, in theory, would bewilling to accept a certain level of compensation, and that is not

6 Pearce et al. (1990) and Turner (1993) define strict sustain-ability as the need to maintain natural capital stock constant,affirming that a constant or growing stock of natural resourcesallows us to attain higher degrees of intergenerational equitywhen the sustenance of the poor is associated with theecosystems' productivity levels. As Simón Fernández (1995)pointed out, in Pearce and Turner (1990) and in Pearce et al.(1990), the authors discuss this last question without giving asatisfactory answer: that either the physical amount of stock, thetotal economic value of the stock, the price of the naturalresources or the flow value of the resources should remainconstant are all marked as options, without opting for any one ofthem as indicator of natural capital constancy. In order to makestrict sustainability operative, they make a distinction betweenrenewable and non-renewable resources. They believe renewableresources can be maintained over time if the rate of their usagedoes not surpass the rate of their reproduction. In this way, thoserenewable resources would be available for future use. But if thisis the rule to follow, a problem arises as far as the non-renewableresources are concerned: their stock cannot be maintainedconstant unless they are not consumed. These authors' positionin this question is as follows: decreases in the resources' stock areto be compensated for by increases in renewable resources. Thatis, they assume substitution capability between renewable andnon-renewable resources. However, they do not make clear whatimplications this assumption may bear.

necessarily so at anygivenmoment, and it is even less truewhendealing with different time brackets. Neumayer (1999a) arguesthat CBA would only be consistent with “weak sustainability” ifthe (hypothetical) compensation in which the analysis is basedwas effective and not just hypothetical, at least in the case ofprojects with costs in the future. Thus, the “weak sustainabilitycriterion” denies the compensation criteria in the intergenera-tional context. Attempts to make this tool compatible with thestrong sustainability concept are also debatable, aswehave seenearlier.We agreewith Neumayer (1999b) that “discounting is notthe issue but substitutability is” since sustainability is not amatter of efficiency but of intergenerational ethics.7

This implies accepting the limitation of ECBA as a “mono-criterion” decision approach. We still consider CBA a usefulvaluation tool but we believe that it should be applied in abroader context jointly with other criteria, though this wouldnot be, strictly speaking, a multi-criterion approach.

Recent studies such as those of Brouwer and Van Ek (2004)andGulli (2006) illustrate thepractical relevance of this tool and,in fact, ECBA is being applied by Public Administrations, albeitits implementation in practice is not always clear-cut. Forinstance, the new European regulations that pertain to theapplication of Structural and Cohesion Funds, among others,explicitly require a Cost–Benefit Analysis for investmentprojects with budgets surpassing a given threshold. The CBAevaluation guide8 explicitly supports themonetary valuation ofincrements of environmental quality. Social Discount Ratesaround 5% are recommended, although projects with lowerInternal Return Rate (IRR) are not automatically discarded. Thisimplicitly acknowledges that the traditional profitability returncriteria are not sufficient for the scope of application of ECBA.This is thus the practical standpoint of the work here reported.

d) After outlining and briefly discussing the extremepositions of the interval (0, SDR), a group of opinions thatshare a common preference for coherence and which defendthe need to use discount rates located within this interval, which canbe constant or variable in time, are presented next. Within thisgroup three main orientations (albeit not clearly separable inpractice) are considered.

d.1) Constant reduced discount ratesMany authors defend the reduction in discount rates due to

environmental considerations, established in a conventionalmanner, as a type of rational adjustment in the conventionaldiscount rates. Thus, due to thedifficulty of findinga convincing

7 Therefore, decisions that affect problems as important andirreversible as global warming, require approaches solidly basedon a post-normal epistemological concept that rely on democra-tisation of knowledge (Funtowicz and Ravetz, 1994; Martínez-Alieret al., 1998). Such democratisation of discourse arises from thenature of the problems at hand, from their urgency, theirinterdisciplinarity, their uncertainty, and their irreversibility.Post-normal science proponents advocate a combination ofinstitutional analysis and iterative public dialogue using multi-criteria decision analysis as a tool to understand the structure ofconflict and potential for conflict resolution (O'Conner et al., 1996;Munda, 2000) and facilitating public understanding of thedecision problems at hand (Munda, 1995; De Marchi et al., 2000;Strassert and Prato, 2002).8 European Commission (2002): Guide to cost-benefit analysis

of investment projects. Available on line: http://ec.europa.eu/regional_policy/sources/docgener/guides/cost/guide02_en.pdf.

716 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

discount rate to apply in practice, they request a pronounce-ment from the public administrations regarding the rate thatshould be applied in public capital endowment projects (Horta,1998; European Commission, 1998; Rabl, 1996).

There are, however, a number of authors that opposethis proposition: Lind (1997) questions whether a lowerdiscount rate guarantees intergenerational equity; others,such as Neumayer (1999b), warn that the demand for alower discount rate may divert the debate from its centralquestion of rightly placing it within the political decision-making process; Padilla (2001) claims that modifyingarbitrarily discounting entails ignoring the preferencesbetween present and future consumption, which may resultin accepting projects with low social profitability; and, forPhilibert (1999), most of the arguments made in favour ofconstant, low discount rates for the sake of future genera-tions are weak.

Also Pearce and Turner (1990) have argued that the idea ofreducing discount rates due to environmental constraints israther problematic, since there is no unique relationshipbetweendiscount rates andenvironmental degradation. Accord-ing to these authors, allowing the discount rate to determine thelevel of investment will have negatively influence, through theconsequent depressing effect on the investment, the generalpace of development. However, we believe that, as referred byO'Neill (1993), a rational planning of the future cannot be basedon the application of discount rates that govern all activities,project and resources. For example, it is common practice toapplyaparticularly lowrate to forestryprojects.As rightly arguedby Martínez-Alier and Roca-Jusmet (2000), and O'Neill (1993),these “ad hoc adjustments are not irrational but are rather arational variant within an irrational procedure”.

d.2) Obtaining the discount rate empiricallyOne can find in the literature some attempts to obtain

empirically the discount rate that would be necessary to applytowards the welfare of future generations. Several routes arefollowed. One of them consists in assessing the presentgeneration's opinion in this respect. In other words: to ascertainwhat is the value attached to a change thatwill take place in thefuture (Luckert and Admowicz, 1993; Cropper et al., 1992;Benzion et al., 1989; Poper and Perry, 1989; among others).

Frederick et al. (2002) reviews 34 studies that aimed atobtaining empirically discount rate values, but the timehorizons considered in those studies are clearly insufficientto allow drawing conclusions at intergenerational scale.9 Theuse of time ranges of a few years or even months logicallyentails inferring very high discount rates. Indeed, in thosestudies, the shorter the time range applied in the experiment,the higher is the discount rate obtained. This highlights theneed both for research studies more focused on the kind ofresource to be valued and with coherent time range, and forgathering empirical evidence for Declining Discount Rate(DDR) approaches, which we address below.

d.3) Discount rates variable in time

9 The study by Johanneson and Johanneson (1997) — the onlyone that encompasses a multigenerational timeframe — extendsthe temporal horizon to 57 years and yields a yearly discount ratebetween 0% and 3%.

This idea of a variable discount rate is gaining support froma growing number of studies in which individual discountrates can be inferred or observed in the present marketbehaviour (Hausman, 1979) or in response to hypotheticalissues connected to people's attitude toward risk (Horowitz,1991), savings behaviours (Thaler, 1981), or found in life savinggovernment agency programs (Cropper et al., 1994). Weitzman(1994) provides a theoretical foundation for the low anddeclining discount rates in long-term CBA; and Azar andSterner (1996), in which discounting in relation to the Earth'sover-warming effect is analysed, believe that the discountrates used in the economic models of climatic change shouldbe lower than those traditionally used, and that constantdiscount rates in time are unreasonable; instead, the discountrate should decrease over time.

Henderson and Bateman (1995), following the works ofCropper et al. (1992), obtain for the discounting on human livesa form of the hyperbolic discount curve that is different fromthe curve generated by the classical discounting (exponential),and which they consider more realistic for projects withintergenerational implications.

In the same vein, more and more authors defend applyingvariable discount rates in time following a decreasinghyperbolic function (Loewenstein and Prelec, 1992; Sterner,1994; Henderson and Bateman, 1995; Azqueta, 1996; Fredericket al., 2002; among others).

Decreasing functions other than the hyperbolic have beenstudied, such as those proposed by Weitzman (2001), whoconcludes that the underlying distribution of discount ratesfollows a Gamma distribution in a context of uncertaintiesabout future economic conditions. Newell and Pizer (2003)tried to operationalize Weitzman's (2001) work, whereas thework of Groom et al. (2004) builds further upon this idea.

The recent work of Guo et al. (2006) presents a moreextensive review of the declining discount rate (DDR) ap-proaches.A sensitive analysis presented in this paper concludesthat policies on climate change are more likely to pass a CBAusing DDR schemes. However, not all DDR schemes areadequate and only very few of these (the Weiztman–Gammadiscounting schemeand theuseof a constant STPRof0%)wouldenablepassing aCBA. Schemesbasedonhyperbolic discountingwere dismissed as unrealistic because parameters in thehyperbolic function that are measured empirically imply verylarge initial discount rates, sometimes as high as 30–40%.

Problems with declining discount rates have been ad-dressed by Heal (1998) and Hepburn (2005), who show thatdeclining discount rates result in “time inconsistency” (that is,“if individuals have the opportunity to revise their plans in thefuture, they will deviate from the decisionsmade in the past”).However, we do not consider this argument strong enough todiscourage the growing support for the Declining Discountrates (DDR).

Furthermore, there is a “political” argument in favour ofthe acceptance of time-varying discount rates: in one swoopthis would help to resolve the long standing tension betweenthose who believe the distant future matters and those whowant to continue discounting the future in the traditionalway”, as concluded by Pearce et al. (2003), who, for this reason, predict an increasingly applicability of the method indiscount schemes. In fact, the UK government has already

717E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

recommended it for its public policies (HM Treasury, 2003,“The Green Book: Appraisal and evaluation in CentralGovernment”).

In what follows, we outline two approaches for tackling thebasic conflict between CBA and the long-term environmentalconsequences, which differ from the previous ones in thatthey do not address directly in its discussion the modificationof discount rates:

e) The first approach is that of Fisher and Krutilla (Krutillaand Fisher, 1975; Fisher and Krutilla, 1985; Porter, 1982), whichemploys the traditional Social Discount Rate but increases the value ofthe environmental asset in time. The rationale for this is that asnatural resources become scarcer in time, they becomeincreasinglymore expensive (Tol, 1994; Rabl, 1996; Hasselmannet al., 1997; Hasselmann, 1999, Philibert, 1999). Although thismethodmay bemisinterpreted as if itwould apply two differentdiscount rates, as pinpointed by Padilla (2001), it entails adifferent underlying principle as described below. For instance,Hasselmann (1999) uses a 2% discount rate for mitigation costsand a 0% rate for climate change costs, based on the hypothesisthat a climate catastrophe can be avoided only if it is assumedthat climate damage costs increase significantly in the longterm relative to mitigation costs.

f ) The second approach is that of the use of Intergener-ational CBA, which includes future generations explicitly in theanalysis. Kula (1988) was the first to introduce the idea, andsubsequent works apply an intergenerational weight, whichtakes into account the undeniable observation that indivi-duals do not value equally present and future (Nijkamp andRouwendal, 1988; Bellinger, 1991; among others).

Recently, Padilla (2001) and Padilla and Pascual (2002) haveimproved this approach by developing the concept of “Multi-generational Net Present Value”, which incorporates anintergenerational structure into the model through a methodthat enables to translate the individual level of “altruism” intosocial intergenerational weighing, thereby adding a morerealistic component to the work developed initially.

A number of other proposals with a different methodologybut with the same rationale of including future generationsinto the analysis have been developed. These include that ofFearnside (2002) that proposes an alternative unified indexthat assigns explicit weights to the interests of futuregenerations; and that and Sumaila and Walters (2005), whichincorporate future generations into the discount rates bymeans of an “Intergenerational Discount Factor”.

The use of Intergenerational CBA is a very interestingresearch line for long temporal horizons (centuries), althoughit still encompasses the assignment of weights (which thusentails a degree of subjective judgment) that represent thepreferences of intergenerational altruism of society withregard to future generations.

4. A proposal on environmental discounting

The central idea that we propose for intergenerationaldiscounting is to defend the rationality of applying simulta-neously in the same CBA exercise discount rates for intangible effects(e.g. environmental) that are different than those we use for tangibleones.

We have not found in the literature specific theoreticaldevelopments postulating this approach, nor practical appli-cations thereof, although we did find, as referred above, a fewstudies that use two different discount rates. However, thesestudies (Tol, 1994; Rabl, 1996; Hasselmann et al., 1997;Hasselmann, 1999, Philibert, 1999) are in reality only versionsof the Krutilla–Fisher approach (see (e) above). The onlytheoretical development that we believe to be different isthat of Yang (2003), which we will discuss latter.

Thus, our concept — discussed previously in Almansa andCalatrava (2000, 2002a)— is based on the following reasoning:

1. Since environmental goods are not market goods, individualshave different mindsets and act differently when dealing with“merchandise” that when handling with “environmental goods”.

If we consider that the most coherent Social Discount Ratethat should be applied to market effects is the Social TimePreference Rate (STPR=ce+p), it is only logical to suppose thatthe interest rate of pure time preference (p) will be smaller in thecase of environmental goods, whether it be out of an ethical“imposition” of intergenerational equity (1.a), or simplybecause of empirical evidence that certain studies seem toreveal in this direction (1.b).

(1.a) In fact, governments carry out environmental en-hancement projects that often would not pass the decisionmaking criteria of the conventional CBA, and whose benefitswill be enjoyed by future generations, from which one caninfer a very low discount rate (and therefore, very low interestrate of pure time preference), as the United Kingdom does, byapplying a lower-than-usual discount rate in the case offorestry projects, as a “grant for future generations.”

(1.b) Kopp and Portney (1999) believe that there are noreasons for taking for granted that individuals will be willingto exchange money and the environment with the samelogic. This idea is implicit in Lumeley (1997) commenting onempirical studies that link individual discount rates withpractices carried out in land preservation projects, in whichthere does not seem to be any clear relationship between oneand the other. Gintis (2000) arrives to the same conclusion. Ina study already mentioned above, Luckert and Admowicz(1993), deduce different behaviours when dealing withdiscounting of forests and of holdings securities. Similarly,Taylor et al. (2003) obtained implicit discount rates that weredifferent for forest benefits of distinct nature, namely timberand recreation.

2. It seems logical to think that the hypothesis of the marginaldecline in utility consumption will not hold for environmental goods.

If the environmental benefits or costs take place over a longperiod of time, the term ce of the STPR formula may decreasefor this type of goods, since the hypothesis of the marginalutility consumption decline is not fulfilled. For example, if intwo hundred years people are worse off in terms of “environ-mental welfare”, the damage caused by depriving them of anenvironmental good (a natural space for recreational pur-poses, for example) will not be slighter in any way than thedamage it would cause to those that live today, as it is usuallyclaimed.

The idea that per capita consumption decreases instead ofincreasing with the passage of time has been held by manyauthors (based on the idea that future growth and naturalcapital stockgohand inhand), and it isoneof the central themes

Table 1 – A general proposal of different STPR (Social TimePreference Rate) and EDR (Environmental DiscountingRate) depending on the time span of the project

Time span Discounting

b25 years STPR=ce+pa and EDR=ce+p1

Time span that only affects thepresent generation

p1bp3%bSTPRb5% and 2%bEDRb3%• Reasonable use of the ECBA(Extended Cost–BenefitAnalysis) approach

25–100 years STPR=ce+p and EDR=ce2+p2

Reasonably short time span thataffects our children, grandsonsand great-grandchildren

p2bp and ce2bce3%bSTPRb5% and 1%bEDRb2%• Use of ECBA together withother tools and/or decision-making criteria• Prior strict and/or ecologicalsustainability restriction

100–200 years STPR=ce+p and EDR=ce3+p3

Time span that affects the lessimmediate generations, with areasonable degree of uncertainty

p3bp and ce3bce3%bSTPRb5% and 0%bEDRb1%• Introduce hyperbolic discountrates in the sensitivity analysis• Use of ECBA together withother tools and/or decision-making criteria.• Prior strict and/or ecologicalsustainability restriction.

More than 200 years • Use of hyperbolic discountrates• Adequate ECBA approach?

a See footnote 4.

718 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

in criticising discounting by many ecological economists, whoare accused byothers of creating pessimistic scenarios (seeAzarand Sterner, 1996; Dasgupta et al., 1999; respectively).

This proposal on discounting could be represented asfollows (Eq. (1a)):

NPV ¼Xt¼n

t¼0

Ftð1þ STPRÞt !

þXt¼n

t¼0

N0

ð1þ EDRÞt !

ð1aÞ

where NPV is the Net Present Value, Ft represents the annualnet financial cost or benefit (in general, the shadow price ofthe tangible effects), and N0 the annual environmental cost orbenefit at the current time for the current generation (or, moregenerally, the shadow price of the intangible effects). Thediscount rate is the appropriate STPR (Social Time PreferenceRate) value to account for the financial effects (first term), anda lower Environmental Discount Rate (EDR), for the environ-mental effects (second term).

In what does this proposal differs from that of Krutilla–Fisher?A comparison of Eqs. (1a) and (1b) clearly shows that,

despite of the similarities, our proposal differs significantlyfrom the Krutilla–Fischer (K–F) method in that while K–F usesNt (the value of the environmental good that increases withtime as a result of its decreasing supply) in the numerator andthe same STPR for the environmental and financial term; ourapproach explicitly considers two different discount rates byapplying an EDR to the environmental term, which clearlyentails a different underlying principle.

NPV ¼Xt¼n

t¼0

Ftð1þ STPRÞt !

þXt¼n

t¼0

Nt

ð1þ STPRÞt !

ð1bÞ

NPV ¼Xt¼n

t¼0

Ftð1þ STPRÞt !

þXt¼n

t¼0

Nt

ð1þ EDRÞt !

ð1cÞ

A combination of both equations as in (1c) (proposed byYang, 2003)would be, in practice, difficult to implement and,importantly, it would result in double accounting, since therationale for the use of EDR already includes the hypothesisof a declining consumption of marginal utility for environ-mental goods.

But what specific value(s) would the EDR take on?. We canhardly give only one answer to this general question, but wehave the following suggestions:

(i) This environmental rate shouldnot be the sameone for alltypes of projects, nor resources, and will depend on the timespan considered. Weitzman (1998) interviewed more than 1700economists, and a group of 15 “experts” on their intergenera-tional discounting preferences, from which were deriveddifferent discount rates for certain time spans that we findquite reasonable, althoughwe obviously need to work harder indefining these discount rates. Thus, Weitzman (1999) proposesthe following discount rates for different time spans: 3–4% (theusual SocialDiscountRate) for timespansof around25years; 2%when they are of 25–75 years; 1%when they are of 75–300 years;

and 0% for more than 300 years. Along the same line goes arecent proposal of the UK Government in its official guidance toMinistries on the appraisal of investments and policies (HMTreasury, 2003), by considering the next time-variant scheme:3.5% for 0–30 years; 3% for 31–75 years; 2.5% for 76–125; 2% for126–200 years; 1.5% for 201 a 300 years); and 1% for over301 years.

(ii) The idea of the hyperbolic discount factor seems to usreasonable in projects with very long time spans (severalcenturies). However, much remains to be done in defining thespecific parameter values for this type of functions.

To summarise, what we seek in discounting, can, in a verygeneral way, be summed up in Table 1.

5. Environmental profitability indicators

As a complement to the previous proposal, and in keeping withthe established approach, two concepts have been tested(Almansa, 2006) that we consider of interest in the CBAapplication:

5.1. Intergenerational Transfer Amount (ITA)

The Intergenerational Transfer Amount (ITA) is a criterion forthe quantification of environmental profitability in absolute

11 As in the previous criterion, for projects with a positive

719E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

terms. It is defined as the difference between the Net PresentValue (NPV) that is obtained using the general STPR for publicinvestments, the NPV (STPR%), and the NPV in which anintergenerational equity adjustment has been carried out onthe discount rate applied to the environmental effects, theNPV (STPR%, EDR%). See Eq. (2) where N represents theenvironmental flow, calculated in year 0.

This indicator relates to what the actual generation passeson to the future generations, as consequence of incorporatinga certain degree of intergenerational equity in the analysis.Therefore, this may be considered as an effort towards thequantification of the degree of sustainability chosen by thecurrent generation. This value, although expressed in mone-tary units, is relevant not somuch in absolute terms but ratheras compared to other investment proposals.

ITA ¼ VPNðSTPR;EDRÞ−VPNðSTPRÞ

¼Xt¼n

t¼0

Ftð1þ STPRÞt

!þXt¼n

t¼0

N0

ð1þ EDRÞt ! !

�Xt¼n

t¼0

Ftð1þ STPRÞt !

þXt¼n

t¼0

N0

ð1þ STPRÞt ! !

¼Xt¼n

t¼0

N0

ð1þ EDRÞt !

−Xt¼n

t¼0

N0

ð1þ STPRÞt ! !

ð2Þ

Logically, this value will be higher or equal to zero, andwhen alternative projects of environmental restoration arecompared, a higher value of ITA will indicate a higherenvironmental profitability of the project.10

5.2. Critical Environmental Rate (CER)

The Critical Environmental Rate (CER) is defined as thediscount rate that, applied to the environmental effects andafter the market effects have been discounted from the usualSTPR, makes the Net Present Value (VPN) equal to zero.

The CER is obtained from Eq. (3), where STPR is a previouslychosen value, Ft the annual financial flow and N0 theenvironmental flow in year 0.

Xt¼n

t¼0

Ftð1þ STPRÞt !

þXt¼n

t¼0

N0

ð1þ CERÞt !

¼ 0 ð3Þ

It is, therefore, a criterion related to the environmentalprofitability of a project in relative terms. In order to interpretit, it is necessary to compare it to the Social EnvironmentalDiscount Rate (SEDR); that is, the environmental discount ratethat adequately represents the level of intergenerationalequity that a society is willing to assume. From this me-thodological perspective, it must be fulfilled that CER (STPR%)NSEDR.

For example, if SEDR and STPR are 1% and 3%, respec-tively, projects with CER (3%)N1% will be profitable from an

10 In the case of projects in which the environmental effects havea negative sign, that is, projects that have a positive financial fluxbut a negative environmental flux (e.g., the activation of a nuclearpower plant where the negative effect would be given by theeffect of radioactive residues), the ITV would be negative as aresult of a sustainability adjustment that assigns more weight tothe environmental damage for the future generations.

environmental point of view (with adjustments for sustain-ability), although they need not to be so from a financialpoint of view (with no adjustments for sustainability), if alsoCER (3%)b3%.

Another way of viewing this criterion is to consider it as anindicator of “environmental profitability that the financialcost produces”.11

6. Applying different discounting approachesto the WREC Project of Almería (Spain)

The Watershed Restoration and Erosion Control Project ofLubrín (De Simón Navarrete, 1993) covers an area of 8.830 hathat experiences “accelerated” or “extremely accelerated”erosion processes in 82% of its territory. There are climaticand orographic conditions which contribute to the desertifi-cation processes, but without doubt, those with the greatestimpact are those of human factors, both historical (defores-tation processes), and the current use of land determined bythe abandonment of farming land, in a typical marginalmountain agricultural zone.

The main corrective actions considered in the project are:a) maintaining farmland but improving the step slopes, b)reforesting 85% of the areas currently covered with degradedMediterranean scrub with indigenous species and regenerat-ing the remaining 15% of Mediterranean scrub, and c) toconstruct specific infrastructures of hydraulic correction.

The project covers a time span of 100 years. Logically, thisperiod was chosen by convention for the analysis, due to thelong maturing period of the species.12 The implementation ofcorrective measures (investment) is planned within the firstsix years (Table 2 summarizes the net financial costs ofimplementation and maintenance of the project). Whereby itis deduced that, whilst the main financial costs are supportedby the present generation, the environmental rewards areonly seen at the medium to long term, thus affecting futuregenerations.

In order to apply the ECBA to the case study (Almansa,2006), the following stages were carried out:

(1) Identification of the positive and negative effects (economic,social and environmental) of the project. Given the multidis-ciplinary nature of the project, numerous experts in variousrelevant areas of the study were consulted. Defining, amongmany other matters, various future scenarios of the zoneboth for the hypothetical case of the project start-up and thatof its non-implementation. In parallel, members of the popu-lation concerned were consulted through qualitative techni-ques (mainly semi-structured interviews), endeavouring to

12 Owing to its intrinsic interest, we did simulations of thedifferent net environmental benefits for a larger time span(500 years) but, as the technical study and financial plan of theproject done by De Simón Navarrete (1993) extends only up to100 years, we did not calculated the Net Present Value.

financial flux but a negative environmental flux, we would rankthe projects also aiming at selecting those with higher CER. In thiscase, a higher CER would be interpreted as a lesser environmentaldamage associated to the financial benefit.

Table 2 – Net Costs of implementing the Lubrín HFRproject (€)

Investment costs

Fictive or previous investment prior to the project(year 0)

166,786.87

Investment year 1 1,680,668.05Investment year 2 1,222,031.90Investment year 3 1,201,681.63Investment year 4 2,416,711.74Investment year 5 2,554,613.97Investment year 6 182,719.70

Maintenance costs

Maintenance and repair ofhydrotechnical infrastructure (year 50)

432,794.53

Maintenance and repair ofhydrotechnical infrastructure (year 100)

433,341.45

Silvicultural treatment (clearing costs) (year 20) 449,915.60Silvicultural treatment (clearing costs) (year 40) 518,492.38Silvicultural treatment (clearing costs) (year 60) 2,880,309.51

Benefits arising from timber sales followingsilvicultural treatments (clearance)

Silvicultural treatment (benefits after clearing)(year 20)

284,192.38

Silvicultural treatment (benefits after clearing)(year 40)

378,923.24

Silvicultural treatment (benefits after clearing)(year 60)

4,090,803.91

720 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

ensure representation of the different groups affected by theproject.

(2) Identification and application, from among the differentavailable methods of environmental benefits valuation, the mostsuitable one for the case study, which led us to choose, forvarious reasons, a Contingent Valuation (CV) exercise on theproject as a whole.13 The CV exercise was carried out in summer2000, through personal surveys done by suitably qualified andadvised interviewers. The random sample (stratified by socio-economic profiles) size was a total of 334 individuals. Theinformation package showed, between other information, thecurrent situation of the zone affected by the project and the

13 The reason we did not value the different effects by distinctmethods, as it is generally done, is that since the population involvedis affected simultaneously bymany of these effects, it would not havebeen possible to put into practice correctly a contingent valuationexercise designed to assess only some of the costs and benefits of theproject. Therefore, the Contingent Valuation Method (CVM) wasselected due to its versatility and capacity to capture both use andnon-use values, and to its flexibility to be applied in a wide range ofsituations, non-withstanding the acknowledgement of a number ofethical and technical limitations as extensively described in literature(see Almansa and Calatrava, 2002b and Almansa, 2006, for this casestudy). The application of other methods of expressed preferences,such theChoice Experiment or Conjoint Analysis, which include priceas a variable, was discarded because these methods postulate theinterdependency of variables or, such as here, impacts to be valued,which is clearly not the case in this study.

future situation of the zone in future scenarios within 50 and100 years, if no corrective measures were taken of an environ-mental nature (Fig. 1). A net annual benefit was finally obtainedof around 506,797 €/year.14

(3) Calculation of the project's Economic ProfitabilityIndicators:

The Internal Return Rate (IRR) was 5.23%, which means theproject surpasses the positive net present value (NPVN0) in allcases studied, since the highest discount rate used in thesensitivity analysis was 5%. The different discount approachesapplied were the following:

a) Discount rates recommended by the European Union (5%),and by several experts in the specific Spanish case (3%),following a traditional approach (see Table 3.a).

b) Lower discount rates than the traditional ones, followingthe well-founded lines of reasoning of various authors, inthe 1–3% range (see Table 3.b).

c) Different discount rates for tangible and intangible effects,fol-lowing the methodological approach suggested (seeTable 3.c).

As the respective tables show, the project's NPV variabilityis very large, depending on which discounting approach isused, reaching its lowest value of 303,637 € in the case of theconventional discounting, using a SDR of 5%; and its highestvalue of 22,004,126 € when downward adjustments of thediscount rate were made for the particular case of the netenvironmental benefits (SDR of 5% and EDR of 1%), followingour suggested approach.

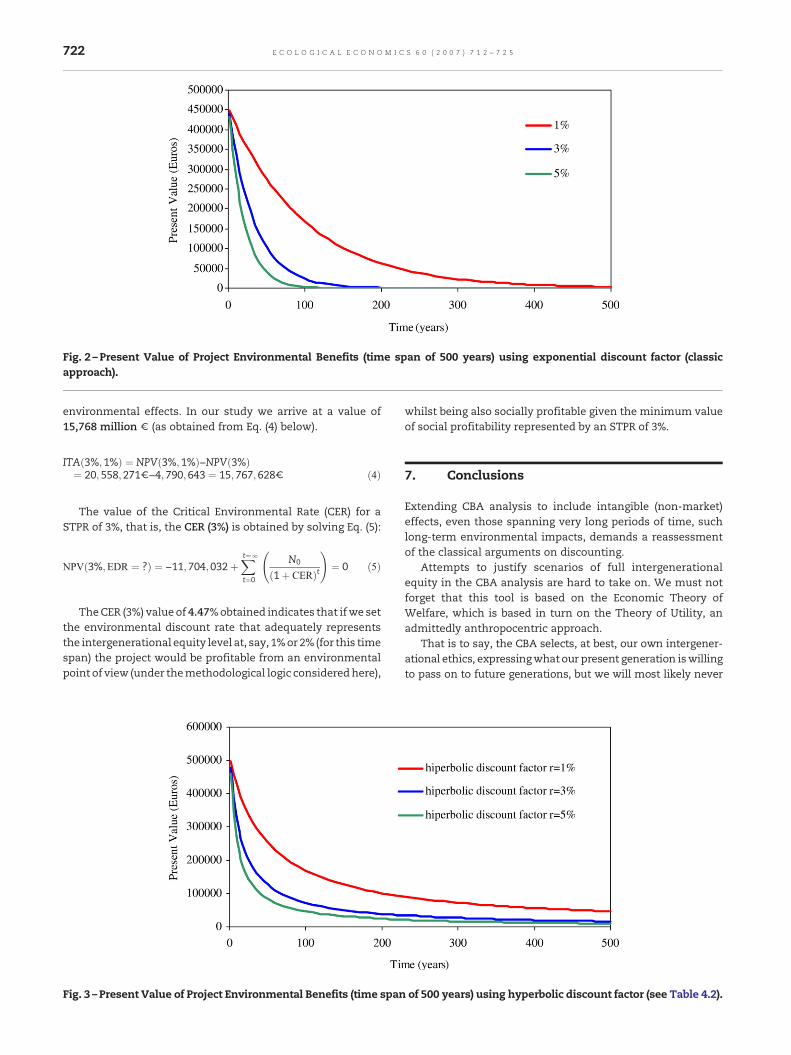

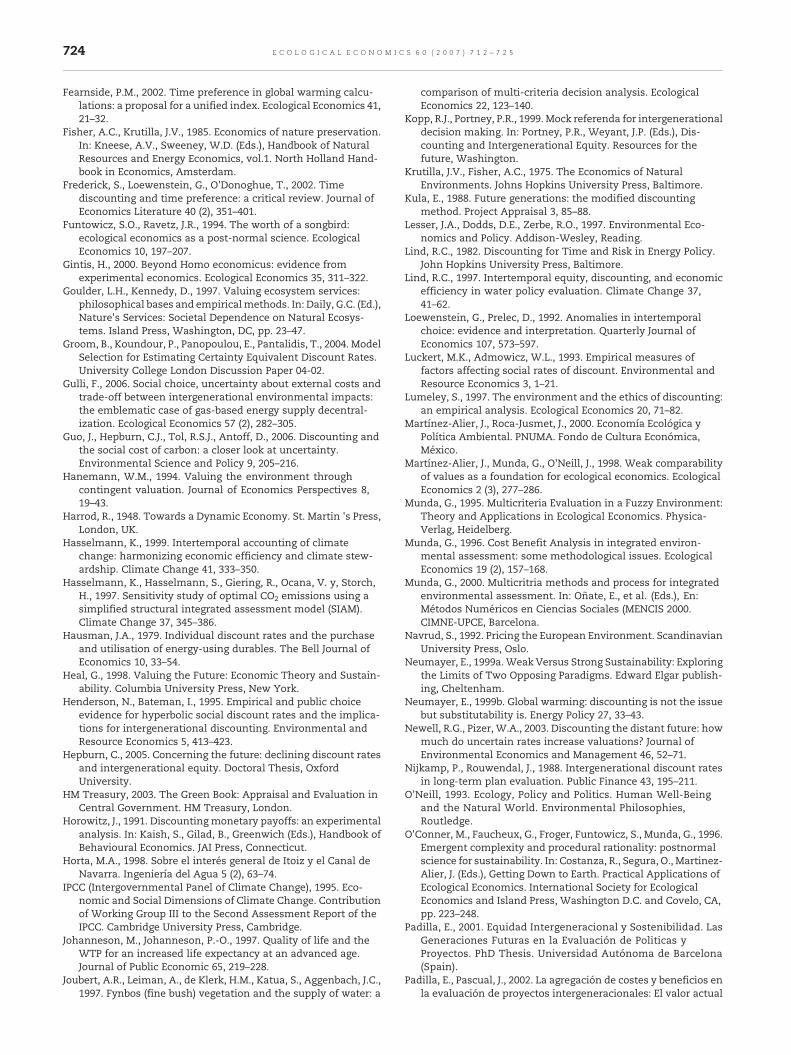

But, what if we consider a time horizon span of the projectin the order of centuries?Whatwill be the yearly present valueat, for example, 200 or 500 years? In the following tables wecalculate and compare the present value of intangible effects(environmental benefits) within 50, 100, 200 and 500 yearsusing an exponential (see Table 4.1 and Fig. 2) and a hyperbolicdiscount factor (see Table 4.2 and Fig. 3).

It can be observed that the maximum values for years 50 and100 correspond to exponential discount factors (EDF) withSDR=1%, while in the case of years 200 and 500 the maximumvalues are represented by hyperbolic discount factors (HDF) withparameters a=b=2r, for r=SDR=1%. This agrees with ourconclusions, as presented in the theoretical section above,regarding the advisability of using hyperbolic discount factors inthe case of very long-term scenarios. This is clear fromFigs. 2 and3, which show how the exponential discounting reduces to zero

14 Value obtained from the average Willingness To Pay (WTP) byresidents and non-residents (return tourists with strong ties to themunicipality) as derived from the equation 1530 Residents⁎€104.04/year/resident]+[4826 Non-residents ⁎€72.03/year/non-resident]=€506,797/year. This is a conservative value since we considered onlythepopulationdirectly involved,althoughthat isnot theonlyone.Thequestion formatwasopen-ended, since itwas themostappropriateasfound fromapre-testingquestionnaire and for specific reasons to thisstudy. The central question of the hypothetical market was, in short:“How much would you be willing to pay, in the form of a sort of“environmental tax”, per year or month (to choose) for the imple-mentationandmaintenanceof theEnvironmentalRestorationProjectin Lubrin?”.

Fig. 1 –Photographs of four future scenarios of the WREC Project of Lubrín.

721E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

thepresentvalueof theenvironmentalbenefit in thecourseof thesecond and third century for discount rates of 3 and 5% (reachingzero in the years 160 and 260, respectively).

Table 3.a – Net Present Value of the Lubrín HFR projectwith the classical discounting approach

Discountrate

Netfinancial

cost

Net environmentalbenefit

Net presentvalue

5% −10,258,177 € 10,561,814 € 303,637 €3% −11,704,032 € 16,494,672 € 4,790,643 €

Table 3.b – Net Present Value of Lubrín HFR project withdiscounting approach “STPR downward adjustment”

Discountrate

Net financialcost

Net environmentalbenefit

Net presentvalue

3% −11,704,032 € 16,494,672 € 4,790,643 €1% −18,474,235 € 32,262,304 € 13,788,068 €

Table 3.c – Net Present Value of the Lubrín HFR projectwith the discounting approach “using different discountrates for tangible and intangible effects”

Discountrate

Net financialcost

Net environmentalbenefit

Net presentvalue

C(5%) andB(3%)

−10,258,177 € 16,494,672 € 6,236,495 €

C(3%) andB(1%)

−11,704,032 € 32,262,304 € 20,558,271 €

C(5%) andB(1%)

−10,258,177 € 32,262,304 € 22,004,126 €

(4) Calculation of the project's Environmental ProfitabilityIndicators:

The Intergenerational Transfer Amount, ITA (3%, 1%)represents the difference between the NPV (3%) and a NPV(3%, 1%) in which an intergenerational equity adjustmentwas made on the discount rate used to account for the

Table 4.1 – Present Value of WREC Project Benefit (506,797€ in year 0) using exponential discount factor(conventional approach of discounting)

Discount rate 50 years 100 years 200 years 500 years

5% 44,220 € 4 € 0 € 0 €3% 115,604 € 27,161 € 1 € 0 €1% 308,153 € 189,230 € 69,272 € 4 €

Table 4.2 – Present Value of WREC Project Benefit (500,787€ in year 0) using hyperbolic discount factor (*)

Discount rate 50 years 100 years 200 years 500 years

FDh, (a=b=2r)r=5%

84,466 € 46,072 € 24,133 € 9,936 €

FDh, (a=b=2r)r=3%

126,699 € 72,400 € 38,864 € 16,348 €

FDh, (a=b=2r)r=1%

253,399 € 168,932 € 101,359 € 46,012 €

(⁎)The discount factors have been calculated according to thefollowing formula, where parameters a and b have been defined asa=b=2r, after Poulos and Whittington (2000).

FDh ¼ 1ð1þ atÞb=a

; a;bN0

Fig. 2 –Present Value of Project Environmental Benefits (time span of 500 years) using exponential discount factor (classicapproach).

722 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

environmental effects. In our study we arrive at a value of15,768 million € (as obtained from Eq. (4) below).

ITAð3%;1%Þ ¼ NPVð3%;1%Þ−NPVð3%Þ¼ 20; 558;271€−4; 790;643 ¼ 15; 767;628€ ð4Þ

The value of the Critical Environmental Rate (CER) for aSTPR of 3%, that is, the CER (3%) is obtained by solving Eq. (5):

NPVð3%;EDR ¼ ?Þ ¼ −11; 704;032þXt¼l

t¼0

N0

ð1þ CERÞt !

¼ 0 ð5Þ

TheCER (3%) value of 4.47%obtained indicates that ifwe setthe environmental discount rate that adequately representsthe intergenerational equity level at, say, 1%or 2% (for this timespan) the project would be profitable from an environmentalpoint of view (under themethodological logic consideredhere),

Fig. 3 –Present Value of Project Environmental Benefits (time span

whilst being also socially profitable given the minimum valueof social profitability represented by an STPR of 3%.

7. Conclusions

Extending CBA analysis to include intangible (non-market)effects, even those spanning very long periods of time, suchlong-term environmental impacts, demands a reassessmentof the classical arguments on discounting.

Attempts to justify scenarios of full intergenerationalequity in the CBA analysis are hard to take on. We must notforget that this tool is based on the Economic Theory ofWelfare, which is based in turn on the Theory of Utility, anadmittedly anthropocentric approach.

That is to say, the CBA selects, at best, our own intergener-ational ethics, expressingwhat our present generation iswillingto pass on to future generations, but we will most likely never

of 500 years) using hyperbolic discount factor (see Table 4.2).

723E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

findaway to reasonably include future generations' preferencesin our formulations.

The controversy about whether or not to adjust the SocialDiscount Rate for intergenerational equity reasons stems fromdifferent concepts of sustainability. This is the reason why thevarious positions are almost impossible to reconcile, thus thebottom line is that the debate does not deal with technical butrather with ethical issues.

If, in spite of the previous limitations, one is still to useCBA, the inclusion of a certain level of intergenerationalequity, as one of the valuation criteria of a project, entails theneed to use lower discount rates. Furthermore, the differentlogics that we adopt in managing goods with and without amarket must be mirrored through the use of differentdiscounting logics.

For all these reasons, we propose the use of the commonSocial Discount Rate for market goods and a lower discountrate (environmental discount rate) for non-market goods, to beused simultaneously in the same CBA exercise.

By quantifying and stating clearly the degree of intergen-erational equity implicit in an environmental project, theindicators of environmental profitability proposed elicits moretransparency, helps in reconciling the CBA technique with theobjective of sustainability and may be useful in public decision-making.

Obviously, our proposal does not claim to solve all theproblems in applying CBA to projects highly irreversible andwith large intergenerational impacts, which should be studiedand previously decided on the basis of criteria external to theanalysis. Neither is this a closed proposition since there arenumber of aspects that were left unaddressed. But we doargue that, as compared to the various options available andrevised here, this proposal, without adding complexity to thecurrent methodologies, does increase rationality and con-tributes to reconcile sustainability and discounting in Cost–Benefit Analysis.

Acknowledgements

Wewould like to thank the collaboration of the Town Hall andresidents of Lubrín. We also thank the Regional Offices of theMinistry of the Environment of Almería (Spain), and the INIA(National Institute of Agricultural Research) of Spain, both forthe its human and material support. We thank the anony-mous reviewers for the valuable suggestions.We acknowledgeas well the FUNCAS foundation (Fundación de las Cajas deAhorros of Spain) and its reviewers for the acceptance andpublication of a preliminary version of this work (N° 231, 2005)in its series of working papers.

R E F E R E N C E S

Almansa, C., 2006. Valoración económica del impacto ambiental en elcontexto del análisis coste-beneficio: aplicación al proyecto derestauración hidrológico forestal de Lubrin (Almeria). PhD Thesis.Universidad Politécnica de Valencia (Spain).

Almansa, C., Calatrava, J., 2000. Ethical and methodological flawsof the inclusion of environmental effects in Cost–Benefit

Analysis: reflections on the hydrologic–forestry restorationproject of the basin of Lubrín (Almería) Spain. 3er InternationalConference of the European Society for Ecological Economics,May 3–6, Vienna.

Almansa, C., Calatrava, J., 2002a. Discounting environmentaleffects in Cost–Benefit Analysis: reflections on various meth-odological alternatives. Xth European Association of Agricul-tural Economists (EAAE) Congress, August 28–31, 2002,Zaragoza, Spain.

Almansa, C., Calatrava, J., 2002b. Do many people really under-stand the hypothetical market of contingent valuation sur-veys? An analysis of the validity of WTP responses. 7rdBiennial Conference of the International Society for EcologicalEconomics, Sousse (Tunisia).

Arrow, K.J., Cline, W.R., Maeler, K.G., Munasinghe, M., Squitieri, R.,Stiglitz, J.E., 1996. Intertemporal equity, discounting andeconomic efficiency. In: Bruce, J.P., Hoesung, L., Haites, E.F.(Eds.), Second Assessment Report of the IPCC. CambridgeUniversity Press, Cambridge.

Azar, C., Sterner, T., 1996. Discounting and distributional con-siderations in the context of global warming. EcologicalEconomics 19, 169–184.

Azqueta, D., 1996. Valoración económica de la calidad ambiental.McGraw Hill, Madrid.

Barbier, E.B., Markandya, A., Pearce, D.W., 1990. Environmentalsustainability and Cost–Benefit Analysis. Environment andPlanning 22, 1259–1266.

Bellinger, W.K., 1991. Multigenerational value: modifying themodified discount method. Project Appraisal 6, 101–108.

Benzion, U., Rapoport, A., Yagil, J., 1989. Discount rates inferredfrom decisions: an experimental study. Management Science35, 270–284.

Bromley, D., 1990. The ideology of efficiency: searching for a theoryof policy analysis. Journal of Environmental and EconomicsManagement 19, 86–107.

Broome, J., 1992. Counting the Cost of Global Warming. WhiteHorse Press, Cambridge.

Brouwer, R., Van Ek, R., 2004. Integrated ecological, economic andsocial impact assessment of alternative flood control policiesin The Netherlands. Ecological Economics 50 (1–2), 1–2.

Carpenter, S., 1997. Desarrollo y Sostenibilidad fuerte. In: Uni-versitat Politècnica de Catalunya (Editors), Tecnología, Desar-rollo Sostenible y Desequilibrios. Icaria, Barcelona.

Ciriacy-Wantrup, S.V., 1942. Private enterprise and conservation.Journal of Farm Economy 24.

Cropper, M.L., Aydede, S.K., Portney, P.R., 1992. Rates of timepreference for saving lives. American Economic Review 82 (2),469–473.

Cropper, M.L., Aydade, S.K., Portner, P.R., 1994. Preferences for live-saving programs: how the public discount time and age.Journal of Risk and Uncertainty 8 (3), 243–246.

Dasgupta, P., Mäler, K.G., Barrett, S., 1999. Intergenerational equity,social discount rates, and global warming. In: Portney, P.R.,Weyant, J.P. (Eds.), Discounting and Intergenerational Equity.Resources for the Future, Washington.

De Marchi, B., Funtowicz, S.O., Lo Cascio, S., Munda, G., 2000.Combining participative and institutional approaches withmulticriteria evaluation: an empirical study for water issues forTroina, Sicily. Ecological Economics 34, 267–282.

De Simón Navarrete, E., 1993. La restauración hidrológico–forestalen las cuencas hidrográficas de la vertiente mediterránea.Informaciones Técnicas 22/93. Consejería de Agricultura yPesca de la Junta de Andalucía, Sevilla.

European Commission, DGXII, (Joule Programme), 1998. External-ities of Energy, “ExternE” Project, Report on Climate ChangeDamage Assessment.

Faucheux, S., O'Connor, 1998. Valuation for Sustainable Develop-ment, Methods and Policy Indicators. Advances in EcologicalEconomics. Edward Elgar.

724 E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

Fearnside, P.M., 2002. Time preference in global warming calcu-lations: a proposal for a unified index. Ecological Economics 41,21–32.

Fisher, A.C., Krutilla, J.V., 1985. Economics of nature preservation.In: Kneese, A.V., Sweeney, W.D. (Eds.), Handbook of NaturalResources and Energy Economics, vol.1. North Holland Hand-book in Economics, Amsterdam.

Frederick, S., Loewenstein, G., O'Donoghue, T., 2002. Timediscounting and time preference: a critical review. Journal ofEconomics Literature 40 (2), 351–401.

Funtowicz, S.O., Ravetz, J.R., 1994. The worth of a songbird:ecological economics as a post-normal science. EcologicalEconomics 10, 197–207.

Gintis, H., 2000. Beyond Homo economicus: evidence fromexperimental economics. Ecological Economics 35, 311–322.

Goulder, L.H., Kennedy, D., 1997. Valuing ecosystem services:philosophical bases and empiricalmethods. In: Daily, G.C. (Ed.),Nature's Services: Societal Dependence on Natural Ecosys-tems. Island Press, Washington, DC, pp. 23–47.

Groom, B., Koundour, P., Panopoulou, E., Pantalidis, T., 2004. ModelSelection for Estimating Certainty Equivalent Discount Rates.University College London Discussion Paper 04-02.

Gulli, F., 2006. Social choice, uncertainty about external costs andtrade-off between intergenerational environmental impacts:the emblematic case of gas-based energy supply decentral-ization. Ecological Economics 57 (2), 282–305.

Guo, J., Hepburn, C.J., Tol, R.S.J., Antoff, D., 2006. Discounting andthe social cost of carbon: a closer look at uncertainty.Environmental Science and Policy 9, 205–216.

Hanemann, W.M., 1994. Valuing the environment throughcontingent valuation. Journal of Economics Perspectives 8,19–43.

Harrod, R., 1948. Towards a Dynamic Economy. St. Martin 's Press,London, UK.

Hasselmann, K., 1999. Intertemporal accounting of climatechange: harmonizing economic efficiency and climate stew-ardship. Climate Change 41, 333–350.

Hasselmann, K., Hasselmann, S., Giering, R., Ocana, V. y, Storch,H., 1997. Sensitivity study of optimal CO2 emissions using asimplified structural integrated assessment model (SIAM).Climate Change 37, 345–386.

Hausman, J.A., 1979. Individual discount rates and the purchaseand utilisation of energy-using durables. The Bell Journal ofEconomics 10, 33–54.

Heal, G., 1998. Valuing the Future: Economic Theory and Sustain-ability. Columbia University Press, New York.

Henderson, N., Bateman, I., 1995. Empirical and public choiceevidence for hyperbolic social discount rates and the implica-tions for intergenerational discounting. Environmental andResource Economics 5, 413–423.

Hepburn, C., 2005. Concerning the future: declining discount ratesand intergenerational equity. Doctoral Thesis, OxfordUniversity.

HM Treasury, 2003. The Green Book: Appraisal and Evaluation inCentral Government. HM Treasury, London.

Horowitz, J., 1991. Discounting monetary payoffs: an experimentalanalysis. In: Kaish, S., Gilad, B., Greenwich (Eds.), Handbook ofBehavioural Economics. JAI Press, Connecticut.

Horta, M.A., 1998. Sobre el interés general de Itoiz y el Canal deNavarra. Ingeniería del Agua 5 (2), 63–74.

IPCC (Intergovernmental Panel of Climate Change), 1995. Eco-nomic and Social Dimensions of Climate Change. Contributionof Working Group III to the Second Assessment Report of theIPCC. Cambridge University Press, Cambridge.

Johanneson, M., Johanneson, P.-O., 1997. Quality of life and theWTP for an increased life expectancy at an advanced age.Journal of Public Economic 65, 219–228.

Joubert, A.R., Leiman, A., de Klerk, H.M., Katua, S., Aggenbach, J.C.,1997. Fynbos (fine bush) vegetation and the supply of water: a

comparison of multi-criteria decision analysis. EcologicalEconomics 22, 123–140.

Kopp, R.J., Portney, P.R., 1999. Mock referenda for intergenerationaldecision making. In: Portney, P.R., Weyant, J.P. (Eds.), Dis-counting and Intergenerational Equity. Resources for thefuture, Washington.

Krutilla, J.V., Fisher, A.C., 1975. The Economics of NaturalEnvironments. Johns Hopkins University Press, Baltimore.

Kula, E., 1988. Future generations: the modified discountingmethod. Project Appraisal 3, 85–88.

Lesser, J.A., Dodds, D.E., Zerbe, R.O., 1997. Environmental Eco-nomics and Policy. Addison-Wesley, Reading.

Lind, R.C., 1982. Discounting for Time and Risk in Energy Policy.John Hopkins University Press, Baltimore.

Lind, R.C., 1997. Intertemporal equity, discounting, and economicefficiency in water policy evaluation. Climate Change 37,41–62.

Loewenstein, G., Prelec, D., 1992. Anomalies in intertemporalchoice: evidence and interpretation. Quarterly Journal ofEconomics 107, 573–597.

Luckert, M.K., Admowicz, W.L., 1993. Empirical measures offactors affecting social rates of discount. Environmental andResource Economics 3, 1–21.

Lumeley, S., 1997. The environment and the ethics of discounting:an empirical analysis. Ecological Economics 20, 71–82.

Martínez-Alier, J., Roca-Jusmet, J., 2000. Economía Ecológica yPolítica Ambiental. PNUMA. Fondo de Cultura Económica,México.

Martínez-Alier, J., Munda, G., O'Neill, J., 1998. Weak comparabilityof values as a foundation for ecological economics. EcologicalEconomics 2 (3), 277–286.

Munda, G., 1995. Multicriteria Evaluation in a Fuzzy Environment:Theory and Applications in Ecological Economics. Physica-Verlag, Heidelberg.

Munda, G., 1996. Cost Benefit Analysis in integrated environ-mental assessment: some methodological issues. EcologicalEconomics 19 (2), 157–168.

Munda, G., 2000. Multicritria methods and process for integratedenvironmental assessment. In: Oñate, E., et al. (Eds.), En:Métodos Numéricos en Ciencias Sociales (MENCIS 2000.CIMNE-UPCE, Barcelona.

Navrud, S., 1992. Pricing the European Environment. ScandinavianUniversity Press, Oslo.

Neumayer, E., 1999a.Weak Versus Strong Sustainability: Exploringthe Limits of Two Opposing Paradigms. Edward Elgar publish-ing, Cheltenham.

Neumayer, E., 1999b. Global warming: discounting is not the issuebut substitutability is. Energy Policy 27, 33–43.

Newell, R.G., Pizer, W.A., 2003. Discounting the distant future: howmuch do uncertain rates increase valuations? Journal ofEnvironmental Economics and Management 46, 52–71.

Nijkamp, P., Rouwendal, J., 1988. Intergenerational discount ratesin long-term plan evaluation. Public Finance 43, 195–211.

O'Neill, 1993. Ecology, Policy and Politics. Human Well-Beingand the Natural World. Environmental Philosophies,Routledge.

O'Conner, M., Faucheux, G., Froger, Funtowicz, S., Munda, G., 1996.Emergent complexity and procedural rationality: postnormalscience for sustainability. In: Costanza, R., Segura, O., Martinez-Alier, J. (Eds.), Getting Down to Earth. Practical Applications ofEcological Economics. International Society for EcologicalEconomics and Island Press, Washington D.C. and Covelo, CA,pp. 223–248.

Padilla, E., 2001. Equidad Intergeneracional y Sostenibilidad. LasGeneraciones Futuras en la Evaluación de Politicas yProyectos. PhD Thesis. Universidad Autónoma de Barcelona(Spain).

Padilla, E., Pascual, J., 2002. La agregación de costes y beneficios enla evaluación de proyectos intergeneracionales: El valor actual

725E C O L O G I C A L E C O N O M I C S 6 0 ( 2 0 0 7 ) 7 1 2 – 7 2 5

neto multigeneracional. Hacienda Pública Española/Revista deEconomía Pública 163 (4), 9–34.

Pearce, D., Turner, R.K., 1990. Economics of Natural Resources andthe Environment. Harvester Weats Leaf, Hertfordshire.

Pearce, D., Markandya, A., Barbier, E.B., 1990. Blueprint for a GreenEconomy. Earthscan, London.

Pearce, D.W., Groom, B., Hepburn, C., Koundouri, P., 2003. Valuingthe future: recent advances in social discounting. WorldEconomics 4 (2), 121–139.

Philibert, C., 1999. The economics of climate change and thetheory of discounting. Energy Policy 27, 913–929.