THE DIGITAL SPACE - Tata Mutual Fund

34

INDIA IS INVESTING IN THE DIGITAL SPACE ARE YOU READY TO INVEST? Khud Pe Vishwaas Hai Sabse Badi Investment This product is suitable for investors who are seeking*: • Long Term Capital Growth. • An exchange traded fund that aims to provide returns that corresponds to the returns provided by Nifty India Digital Index, subject to tracking error. *Investors should consult their financial advisors if in doubt about whether the product is suitable for them Scheme Risk-O-Meter Risk-O-Meter of Nifty India Digital Index Mutual Fund investments are subject to market risks, read all scheme related documents carefully. NFO Opens: 14 th March 2022 | NFO Closes: 25 th March 2022

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of THE DIGITAL SPACE - Tata Mutual Fund

INDIA IS INVESTING IN

THE DIGITAL SPACEARE YOU READY TO INVEST?

Khud Pe Vishwaas Hai Sabse Badi Investment

This product is suitable for investors who are seeking*:

• Long Term Capital Growth.• An exchange traded fund that aims to provide

returns that corresponds to the returns provided by Nifty India Digital Index, subject to tracking error.

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them

Scheme Risk-O-Meter Risk-O-Meter of Nifty India Digital Index

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

NFO Opens: 14th March 2022 | NFO Closes: 25th March 2022

Companies with theworld’s largest market capitalisation

2005 → 2022

1/8 Tech company →6/8 Tech companies

Source: Statista & companiesmarketcap.com (15th Feb 2022)

Tech

Oil/Energy

Finance

Physical Distribution

Conglomerate

Health

The Rise OfDigital Businesses

Apple

Microsoft

Saudi Aramco

Alphabet

Amazon

Tesla

Berkshire Hathaway

NVIDIA

General Electric

Exxon Mobil

MicrosoftCitigroup

BPWal-Mart

Royal Dutch ShellJohnson & Johnson

382

381263234221212211

200

2005

2,819

2,252

1,986

1,805

1,592

936

660

2022

705

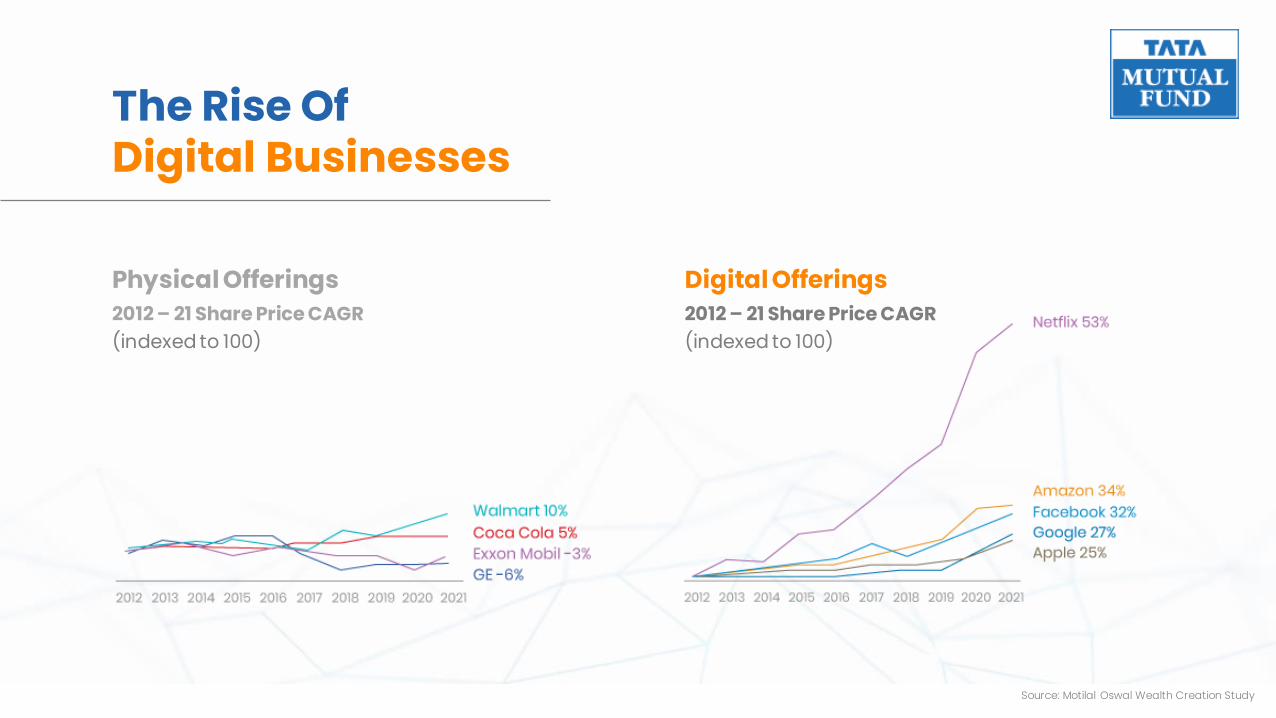

The Rise OfDigital Businesses

Source: Motilal Oswal Wealth Creation Study

Physical Offerings2012 – 21 Share Price CAGR(indexed to 100)

Digital Offerings2012 – 21 Share Price CAGR(indexed to 100)

How Are Digital Businesses Different

Source: Motilal Oswal Wealth Creation Study

Attribute Physical Business Digital Business

Asset Ownership

Replication of offering

Delivery

Network effects

Winner-takes-all/most

Owns tangible assets

High friction: Requires time, physical and financial resources

Time and Money to reach end user

Nil

Due to geographical limitation, there may be many large players

Generates intangible assetsScalability of opportunity

Frictionless: Low marginal costs

Reaches end user at negligible additional costs

Addition of every new buyer(s), attracts more sellers to register on the market place, in turn, leading to more buyers

No limitation on reach, a single business can capture most of the market

Digital BusinessesSubstitutes And Complements

Digital Businesses are displacingsome traditional businesses

Digital Businesses are supportingsome traditional businesses

Growth of online food services in IndiaDegrowth of Traditional TV and Cinema as OTTs gain share

Source: Redseer (Estimated for 2025)Source: eMarketer (Estimated for 2024)

Segment CAGR % 2020-2024Cinema

Traditional TV andHome Video

Books

Music, radio and podcast

Video Games and Esports

OTT Video

Total growth/de-growth(in $ Billion)

CAGR

2016

2017

2018

2019

2020

2025

Covid Impact

+ 148%

-32%

+35%

Unlocking The Potential Of TechnologyDigital India

343

749

2016 2017 2018 2019 2020

Number of Smartphone users (in Million)

305

748

2016 2017 2018 2019 2020

Number of Internet users(in Million)

18

22,331

FY17 FY18 FY19 FY20 FY21

UPI as a % of total Retail Payments (Volume)

2758

13462

2016 2017 2018 2019 2020

Average data consumption per user per month(in MB)

Source: Statista, NPCI

Macro Drivers In PlacePushing Digital Adoption

268.97

226.8

75.57

19.35 11.78 11.17 10.93.24 4.86 13.63

49.29

91.25

117.89

141.11

0

20

40

60

80

100

120

140

160

0

50

100

150

200

250

300

Dat

a Us

age

Dat

a C

ost

Data Cost to Subscriber per GB (in Rs.) Data Usage per Data Subscriber in GB

Internet subscribers

225%(2014-2020)

Wireless Teledensity

24.06%(2014-2020)

Data Usage

4500%(2014-2020)

Data Tariffs

2400%(2014-2020)

Source: TRAI

DIGITAL INDIALOGISTICS

COMMERCE

HEALTHCARE

EDUCATION

E-COMMERCE

Q-COMMERCE

HEALTH TECH

FOOD TECH

FINTECH

ED TECH

FINANCE

DIGITAL ENABLERS

DIGITAL CHANGE AGENTS

IT SERVICES

CLOUD TRANSFORMATION

AUTOMATION

ROBOTICS

IOT

DIGITAL INDIA

DIGITAL ENABLERS

DIGITAL CHANGE AGENTS

Refer to slide 30 for entire portfolio of Nifty India Digital Index. Naukri.com and Jeevansathi.com are offerings of Info Edge

Digital disruptions across sectors

Fintech

Healthtech

Edtech

E-Commerce

Q-Commerce

Food Tech

• Post the pandemic, technology adoption has increased

• Going Digital is helping sectors optimize cost

and drive revenues

• The impact of Digitisation is resulting in transformation across sectors

Digital Change Agents

Note: The sector(s)/stock(s)/issuer(s) mentioned in this document do not constitute any research report/recommendation of the same. Tata Nifty India Digital Exchange Traded Fund will replicate/ track constituents of Nifty India Digital Index.

Indian E-commerce Is Booming

49

36

2112

6855.5 50.5

26

Access to Internet Smartphone Users Online ServicesUsers

Online Shoppers

Online Consumers(% of total population)

2020 2025P

Drivers for Growth:

• Large Young Population

• Increasing Urbanisation

• Digitisation Trends

• Access to Internet

• Online Shoppers

• Smartphone Users

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Source: Redseer Estimates, Averages of range. Numbers for 2025 are estimated

Growth Of OnlineBeauty & Personal Care

Online BPC retail platforms are resolving

industry challenges with the help of

• Superior technology

• Efficient supply chain

• Quality control

• Wide selection of products and brands14 70 912

68

0

5

10

0

50

100

2016 2019 2020

India Online Beauty and Personal Care Market

Market Size (Rs Billion) % of overal Market

6

3017.5

0

20

40

India China US

Online Beauty and Personal Care Market

% of overal MarketSource: Redseer Estimates

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Growth Of Fashion Segment Led By Younger Population

• Online shopper base in Tier 2+ cities

• Digital maturity of young consumers

• Strong emergence of digital-first brands

• Adoption of e-commerce by premium brands

• Convenience of online shopping

• Hassle-free returns

16 436 4504 8

12

0

5

10

15

0

200

400

600

2016 2019 2020

India Fashion Market

Market Size (Rs Billion) % of overal Market

8

37.5 32.5

0

20

40

India China US

Online Fashion Market

% of overal MarketSource: Redseer Estimates

The rapid growth is led by

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Quick-CommerceBooming

Online Quick Commerce Market GMV and Forecast

• Micro-warehouses close to the

point of delivery

• Restrict stock to focussed high-

demand items

• Existing online commerce use

their established delivery

mechanisms

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Source: Redseer Estimates

Quick Commerce CAGR % (2021-25E)

CY2020 CY2021

+133%

+105%

+92%

+80%~ 0.1 Bn ~ 0.3 Bn

~ 5.3 Bn

~ 1.5 Bn

~0.8 Bn

~3.1 BnConservative

Scenario

Base Case

Aggressive Case

CY2025E2.6% 6.7% 10 to 17.5%

X%

Quick commerce: Delivery of ordered products in less than an hour

Drivers:

Growth Of Food Segment

Growth will be driven by • Changing consumer

behaviour• Reduced dependence on

home-cooked food/kitchen set-up

• Increasing participation of women in the workforce

• Increasing consumer disposable income and

spending• Higher adoption among the

smaller cities

9

5036

0

20

40

60

India China US

Online Food Delivery/Access to Internet

1058 54

0

100

India China US

Comparison of India, US and China Markets

Restaurant Food/Food Consumption

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Source: Redseer Estimates, 2019

Cloud Kitchen: a commercial kitchen for the purpose of preparing food for delivery or takeout only

Drivers:• Allow restaurants to deliver

straight to customers• Operate in a fraction of

traditional restaurant space• Analytics to understand

customer preferences and buying patterns

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Emerging Cloud KitchenGMV : Share Of Online Food Delivery Market In India To GlobalThe market growth rate in India is 15% in comparison to global 9.01%

ORDER NOW

Numbers for 2022 and 2023 are estimated

86.1 97.4 108.2 117.9 126.3 132.6

6.27.7

9.210.5

11.6 12.5

0

20

40

60

80

100

120

140

160

2018 2019 2020 2021 2022 2023

Global ($Bn) India ($Bn)

Source: Cloud Kitchen India Market Opportunity Report 2019

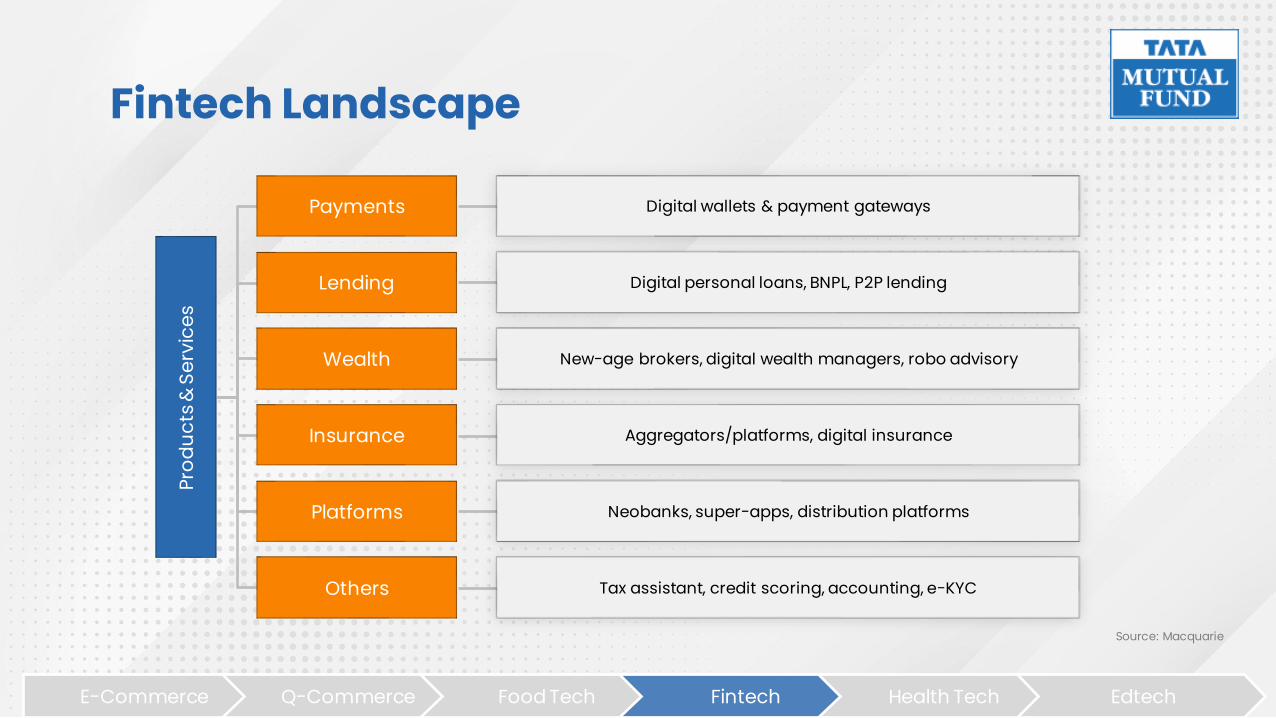

Fintech LandscapePr

oduc

ts &

Ser

vice

sPayments Digital wallets & payment gateways

Lending Digital personal loans, BNPL, P2P lending

Wealth New-age brokers, digital wealth managers, robo advisory

Insurance Aggregators/platforms, digital insurance

Platforms Neobanks, super-apps, distribution platforms

Others Tax assistant, credit scoring, accounting, e-KYC

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Source: Macquarie

The Backbone Of Payments: UPI

UPI has shaken up the business case for standalone payments model

• Payments via UPI are instantaneous, hassle-free and completely free

• Digital wallets which charge Merchant Discount Rate for payments continue to lose relevance

• Many digital wallets now provide an option to pay for services via UPI

Share of UPI in retail payments has been continuously rising

0%

2%4%

6%8%

10%

12%

14%16%

2%6%

22%

36%

0%

10%

20%

30%

40%

50%

60%

70%

50%

59%

UPI as a % of total Retail Payments (Volume)

UPI as a % of total Retail Payments (Value, RHS)

FY17 FY18 FY19 FY20 FY21 FY22 till Jul’21Source: Macquarie

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Fintech’s Monetising ‘Customer + Merchant’Ecosystems

Fintech payment platforms have built a large customer base

125 125 114

6039 24 24 12 7 6 2 2 1

Phon

ePe

Goo

gleP

ay

Payt

m

HDFC

Ban

k

ICIC

I Ban

k

Axis

Ban

k

BAF

- EM

I car

ds

SBIC

ARD

Sim

pl

Zest

Mon

ey

Kraz

ybee

Lazy

pay

Mob

ikw

ik Z

ip

No. of active customers (mn)

Payment Platforms as acquisition tools

Sizable consumer and merchant ecosystems

Ways to monetise• Digital Lending – Consumer lending / Buy Now

Pay Later, merchant lending, digital banking• Cross-selling other products - Super-apps

Fintech platforms have been successful in onboarding merchants at scale

21 20

7 5 5 1 0.10

5

10

15

20

25

Paytm PhonePe BharatPe Razorpay NormalPOS

Mswipe Pinelabs

Source: Macquarie

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

▪ Buying Behaviour ▪ Cash Flow ▪ Bill Payments ▪ Credit History ▪ Savings Patterns

Age Of Super Apps: Capturing Customer Life Cycles

Super-apps are helping Fintechs get access to:

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Healthcare Segment The eHealth market saw increased

adoption with the onset of Covid

Online consultations, Medicine

Deliveries, Diagnostics helped

individuals seek treatment without

stepping out

The model further solves for-

• Low fill rates of unorganised

pharmacies

• Reduced the need to visit multiple

pharmacies

• Doctors are able to reach a wider

patient base

3289

0

50

100

2018 2020

India eHealthcare Market

Market Size (Rs Billion)

ePharma, 55

eOTC, 35

eDiagnostics, 4eConsultation,

6

India eHealth Market GMV Split

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

Source: Redseer Estimates

EdTech

E-Commerce Q-Commerce Food Tech Fintech Health Tech Edtech

The COVID-19 pandemic compelled parents and educational institutions to implement tech-enabled

learning solutions

EdTech is the most funded sector in the country

Drivers for the sector include:• Gamification

• Hybrid Models offline learning centres complement Online learning

• The National Education Policy 2020 emphasised

the importance of leveraging technology in

Education

Since 2020, India has seen four EdTech start-ups turn into unicorns and one into a decacorn

Source: IBEF

750 1048.3 1465.2 2047.92862.3

4000.7

2020 2021 2022 2023 2024 2025

Indian EdTech Industry (2020-2025) US $Mn

CAGR 39.77%

Indian EdTech Industry : By Category (2020)US $ 750 million 1

923

27

40Language and casual Learninig

Higher Education

Reskilling and online certifications

Test preparations

K-12

Source: IBEF. Numbers for 2022 to 2025 are estimated

What Doesn’t Change?

“I almost never get the question: ‘What’s not going to change in the next 10 years?’

And I submit to you that that second question is actually the more important of the two — because you can build a business strategy around the things that are stable in time … In our retail business, we know that customers want low prices, and I know that’s going to be true 10 years from now. They want fast delivery; they want vast selection.”

-Jeff Bezos

Digital India: Addressing The Stable Wants

Digital disruptions

across sectors

Fintech

Healthtech

EdtechE-Commerce

Q-Commerce

Food Tech

Cloud Kitchens

• Easier access to money• Variety of investment

options

• Access to multiple doctors and medicines

• Convenience

• Anytime-Anywhere learning• Advanced tech to improve

delivery methods

• Reducing cost

• Low Costs• Wide Variety

• Convenience

• Low Costs• Wide Variety• Convenience

growing & established

Digital Change AgentsRe-imagining Automation & New modes of Delivery

Blurring the definition of traditional sectors giving rise to hybrid segments

Digitalisation of the traditional businesses

IT Services/Cloud transformation/SaaS companies

Digital Enablers

DIGITAL INDIA

Investing In Digital India

Cloud Transformation

Automation

Robotics

IoT

EdTech

Health Tech

Food Tech

E-Commerce

Q-Commerce

The Rise Of New Age Digital Companies

The last two years have witnessed increasing spend on Digital Transformation

Companies across businesses, economic activities and various consumption chains are investing in/getting impacted by Digital Transformation

New age companies are re-imagining businesses or the modes of delivery of various goods and services.

These companies are benefiting from availability of risk capital

Due to the pandemic, they have also seen higher penetration and wider acceptance

Companies At The Forefront Of Transformation

The digitisation is still in the early stages. New Age Digital Companies are yet to achieve important milestones

Achieve Scale

Raise Capital

Get listedSuch companies may

increasingly become more prominent to the Economy

and Equity Markets

Play a Greater Role

Growing sales, reducing costs and maintaining customer satisfaction

Companies may go through multiple rounds of raising

capital as they seek to become profitable

The forerunners may look to raise more capital by getting

listed on the Equity Market

Investors can take exposure to companies which are in the forefront of this process through Tata Nifty India Digital Exchange Traded Fund

Digital Universe

• Transforming the traditional businesses by automation

• Re-imagining modes of delivery

• Set to grow strongly over the coming years

• Emergence of new hybrid segments like consumer tech, fintech, edtech, etc.

The Indian IT services companies which are ahead in digital and cloud capabilities are enabling:

• Digitalisation of the traditional businesses

• Helping fuel the growth of start-ups through technology solutions

Companies which are in the automation/robotics/IoT space

Digital change agents

Digital Enablers

Based On Nifty India Digital Index

Universe

Stock Selection

Use of AI & MLCapping

With NSE 500 as the universe, Basic industries are defined to cover companies which are focused on digital technology. Eg E-commerce, Digital Entertainment etc

The index selects top 30 companies based on market cap which below to pre defined set of basic industries

The index may use Artificial Intelligence (AI)/Machine Learning (ML) driven tools to identify companies focused on digital technology

Weight of index constituents are capped at the levels below on a quarterly basis:• Sector weights are capped at 50%• Stock weights are capped at 7.50%

Rebalancing & IPOs

• The index rebalances quarterly. • Reconstitution is done semi

annually• IPO inclusion is considered based

post a listing period of 1-3 months

Nifty India Digital IndexConstituents of Nifty India Digital Index as on 11th February 2022

SECURITY NAME WEIGHTAGE

Bharti Airtel Ltd. 8.76

Tata Consultancy Services Ltd. 8.31

Indian Railway Catering And Tourism Corporation Ltd. 8.02

Infosys Ltd. 7.60

Tata Communications Ltd. 7.58

HCL Technologies Ltd. 7.55

Info Edge (India) Ltd. 7.01

Tech Mahindra Ltd. 6.58

Honeywell Automation India Ltd. 5.57

Wipro Ltd. 5.43

Vodafone Idea Ltd. 5.03

Indiamart Intermesh Ltd. 4.46

Sterlite Technologies Ltd. 2.22

Justdial Ltd. 1.97

Larsen & Toubro Infotech Ltd. 1.79

Tata Elxsi Ltd. 1.65

Mindtree Ltd. 1.62

Mphasis Ltd. 1.62

Persistent Systems Ltd. 1.36

Coforge Ltd. 0.88

L&t Technology Services Ltd. 0.80

Tanla Platforms Ltd. 0.76

Oracle Financial Services Software Ltd. 0.56

Birlasoft Ltd. 0.49

Cyient Ltd. 0.48

Happiest Minds Technologies Ltd. 0.44

Affle (India) Ltd. 0.43

Intellect Design Arena Ltd. 0.38

Sonata Software Ltd. 0.37

Firstsource Solutions Ltd. 0.29

Large and Mega IT Services

Companies

Emerging Technologies and Services Companies

New Age Digital Change

Agents: Emerging

Technologies and Services Companies

Core Portfolio

Satellite Portfolio

How Is Tata Nifty India Digital Exchange Traded Fund Different?

Tata Nifty India Digital Exchange Traded Fund

Digital Enablers:Large and

Mega IT Services

Companies

Tata Digital India Fund(An open ended equity scheme investing in

Information Technology Sector)

Fund DetailsScheme Name TATA NIFTY INDIA DIGITAL EXCHANGE TRADED FUND

NFO Date 14th March 2022 to 25th March 2022

Investment Objective

The investment objective of the scheme is to provide returns that corresponds to the total returns of the securities as represented by the Nifty India Digital Index, subject to tracking error.However, there is no assurance or guarantee that the investment objective of the Scheme will be achieved.

Type Of Scheme An Open-Ended Exchange Traded Fund replicating / tracking Nifty India Digital Index

Fund Manager Meeta Shetty

Benchmark Nifty India Digital Index (TRI)

Min. Investment Amount (During NFO) Rs. 5,000/- and in multiple of Re.1/- thereafter

NFO Unit Price On Allotment, value of each unit will be approximately 1/100th of underlying index

Load Structure Entry Load: N.A. Exit Load: NIL

Toll Free Number : 022-62827777 | SMS: TMF to 57575 | www.tatamutualfund.com

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully

This product is suitable for investors who are seeking*:

• Long Term Capital Growth.

• An exchange traded fund that aims to provide returns that correspond to the returns provided by Nifty India Digital Index, subject to tracking error.

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them

33

(Mon to Sat 9:00 am to 5:30 pm)

Fund Benchmark

TATA NIFTY INDIA DIGITAL EXCHANGE TRADED FUND

TATA DIGITAL INDIA FUND

This product is suitable for investors who are seeking*:

• Long Term Capital Appreciation

• Investment in equity/equity related instruments of companies in the Information Technology Sector

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them

Fund Benchmark

Toll Free Number : 022-62827777 | SMS: TMF to 57575 | www.tatamutualfund.com

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully

(Mon to Sat 9:00 am to 5:30 pm)