THE CASE OF OFFICE DEVELOPMENT IN TORONTO

273

THE CONDITIONS FOR CAPITAL INVESTMENT IN THE REAL ESTATE SECTOR: THE CASE OF OFFICE DEVELOPMENT IN TORONTO lgal Chamey A thesis subrnitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of Geography University of Toronto O Copyright by lgal Chamey 2000

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of THE CASE OF OFFICE DEVELOPMENT IN TORONTO

THE CONDITIONS FOR CAPITAL INVESTMENT IN

THE REAL ESTATE SECTOR:

THE CASE OF OFFICE DEVELOPMENT IN TORONTO

lgal Chamey

A thesis subrnitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of Geography

University of Toronto

O Copyright by lgal Chamey 2000

National Library 1+1 of Canada Bibiiotheque nationale du Canada

Acquisitions and Acquisitions et Bi bliograp hic Services services bibliographiques

395 Wellington Street 395, Ne W m Onawa ON K I A ôN4 OcrawaON K 1 A W Canada canada

The author has granted a non- exclusive licence aliowing the National Lïbrary of Canada to reproduce, loan, distribute or seU copies of this thesis in microform, paper or electronic formats.

n ie author retains ownership of the copyright in this thesis. Neither the thesis nor substantial extracts from it may be printed or otherwise reproduced without the author's permission.

L'auteur a accordé une licence non exclusive permettant a la Bibliothèque nationale du Canada de reproduire, prêter, distribuer ou vendre des copies de cette thèse sous la forme de microfiche/nlm, de reproduction sur papier ou sur format électronique.

L'auteur conserve la propriété du droit d'auteur qui protège cette thèse. Ni la thèse ni des extraits substantiels de celle-ci ne doivent être imprimés ou autrement reproduits sans son autorisation.

A b s t r a c t

THE CONDITIONS FOR CAPITAL INVESTMENT IN

THE REAL ESTATE SECTOR:

THE CASE OF OFFICE DEVELOPMENT IN TORONTO

Doctor of Philosophy 2000

lgal Chamey

Graduate Department of Geography University of Toronto

This study presens an examination of office development in Canada and speclically in the Toronto

metropolitan region in the post-WWII era. The major purpose of this inquiiy is to document and analyze

the spatial patterns of office development produced by real estate devetopers in conjunction with

financial agents. The changing real estate sector in Canada during the last f i i yean provides the

backdrop for this research.

The major argument put forward emphasizes spatial limits that shape the geographic scope of office

development. The heterogeneity of space prompts the production and maintenance of distinctive

surfaces over which office development takes place. The idea of capital switching between circuits of

accumulation is expanded to include switching practices within the real estate sector. This notion is

introduced throug h the concept of 'three dimensions of capital switching'.

In the office development process, one of the major agents is the real estate developer. Developers

perforrn two basic spatial tasks: they 'lock' capital into specific places by engaging in the development

of office buildings, and they either continue to operate in customary locations or switch their operational

preferences between different places. W i i respect to spatial fields of operations, a distinction between

two spatial scales is made.

Uneven conditions experienced by different cities are a major stimulus for variable spatial practices

experienced by developers. Wi i in the Canadian urban system, large developers prefer to invest in

specific top-tier cities, particubrly Toronto and Calgary and to a lesser extent in Montreal and

Vancouver. The preferences of developers indicate that office development is spatially selective and

based on specific regional and local conditions.

At the intra-metropolitan level, uneven conditions resut in a distinct spatial division of labour among the

developers of office buildings. Office development in the Toronto area illustrates the ability of

developers to pursue development in paiücular settings. Their practices result from compatibility with

particular environments and with specific societal arrangements. This in tum produces and reproduces

territories that are conceptualized as office development districts.

iii

Acknowledgements

In sober-mined retrospect, when I arrived in Toronto in August 1996,l did not fully realize the scale and

scope of punuing the Ph.D. quest. In punuing this enonous task, I was very fortunate to have

tremendous help and constant caring and nourishing without which t could not have managed. I was

fortunate to have an outstanding supewisor and a very supportive committee that enabled me to

complete this project in four-years. I was also able to take full advantage of the excellent living

environrnent and educational facilities in the City of Toronto, and the resources of the University of

Toronto.

I am deeply grateful to my Ph.D. supervisor. Professor Gunter Gad, for his support.

professional guidance, and his generous nature. His caring and mindful attendance were essential for

the completion of this project. Gunter has been professional anchor and friend throughout my Ph.0.

program and I feel fortunate to have been able to work with him.

I would also like to thank my PhD. committee memben, Professor Lany Boume, Professor

Robert Lewis and Professor Susan Ruddick, for their interest, suggestims, and constructive

cornments. Their input and support are deeply appreciated. Professor Ted Relph provided direction in

the earlier stages on this dissedation for which I am grateful. I owe particular thanks to Professor Anne

Haila of the University of Helsinki for acting as extemal examiner, and for her very strong interest in my

research. Also, I have thanks to Professor Pierre Filion of the University of Waterloo for agreeing to be

on the final examination committee.

I would like to thank the Department of Geography at the University of Toronto that hosted me

for four years and provided me with scholarships and teaching opportunities. Also, I am thankful for the

staff that rnake this department such a pleasant place to study in. In particular, I am grateful to

Marianne Ishibashi and Donna Jeynes for their willingness to help and their good spirit.

I would like to thank the people who agreed to be interviewed for this research and shared with

me their thoughts and ideas, and to Mark Knowles and Dean April of Royal LePage Commercial Inc.

for their assistance in the process of data collection.

Finally, I would like to thank Professor Amiram Gonen of the Department of Geography at the

Hebrew University of Jerusalem who encouraged me to widen my horizons and pursue a Ph.D.

program abroad, and for his ongoing interest in the progress of my research. Professor Bryan Massam

of York University provided me with moral support in rny first two years in Toronto. Most of all, I would

like to thank my family for al1 of the support they have provided over the years.

Table of Contents

Abst ract

Acknowledgements

Table of Contents

List of Tables

List of Figures

INTRODUCTION

THEORlZlNG OFFICE DEVELOPMENT

Principal Approaches 1 .l. 1 Neo-classical approaches 1 .1.2 Political economy approaches 1 .1.3 Institutional approaches

Components of the Real Estate Development Process 1.2.1 Building cycles and their spatial aspects 1 -2.2 Financial institutions and real estate development 1 -2.3 The state and real estate development 1.2.4 Real estate developers

Steps Toward a Theory of Office Development 1 -3.1 The intrinsic dynamic of real estate capital 1.3.2 The 'three dimensions of capital switching' 1.3.3 Reciprocal relations: Real estate and other capitals

A Provisional Framework

xiii

2 RESEARCHING OFFICE DEVELOPMENT IN TORONTO: CONTEXT, APPROACH, METHODS, AND DATA

Context: The Conditions for Office Development in Toronto 2.1 .1 Population and employment growth 2.1.2 Municipal organization 2.1.3 The planning system 2.1.4 Taxation 2.1.5 General development issues 2.1.6 Office users in the Census Metropolitan Area 2.1.7 The scope for office development

The Research Process and the Use of Realist Method

Data of lnterest and Data Collection 2.3.1 Extensive data 2.3.2 Intensive research

THE CHANGING CANADIAN REAL ESTATE SECTOR

The Trajectory of Commercial Real Estate Companies in Canada 3.1 -1 Office development in the first half of the twentieth

century 3.1.2 The formative era of modem developers:

Entrepreneurial skills and 'extemal' capital 3.1.3 The golden era of office development: Expansion and

the establishment of real estate powerhouses 3.1.4 The institutionalization of the real estate sector and

the emergence of new entrepreneurs

Canadian-Based Real Estate Companies and Office Development in the United States

Office Development and Foreign lnveston in Canada

ldentifying Primary Office Developers and Owners in the Toronto Area

Unpacking Real Estate Developers

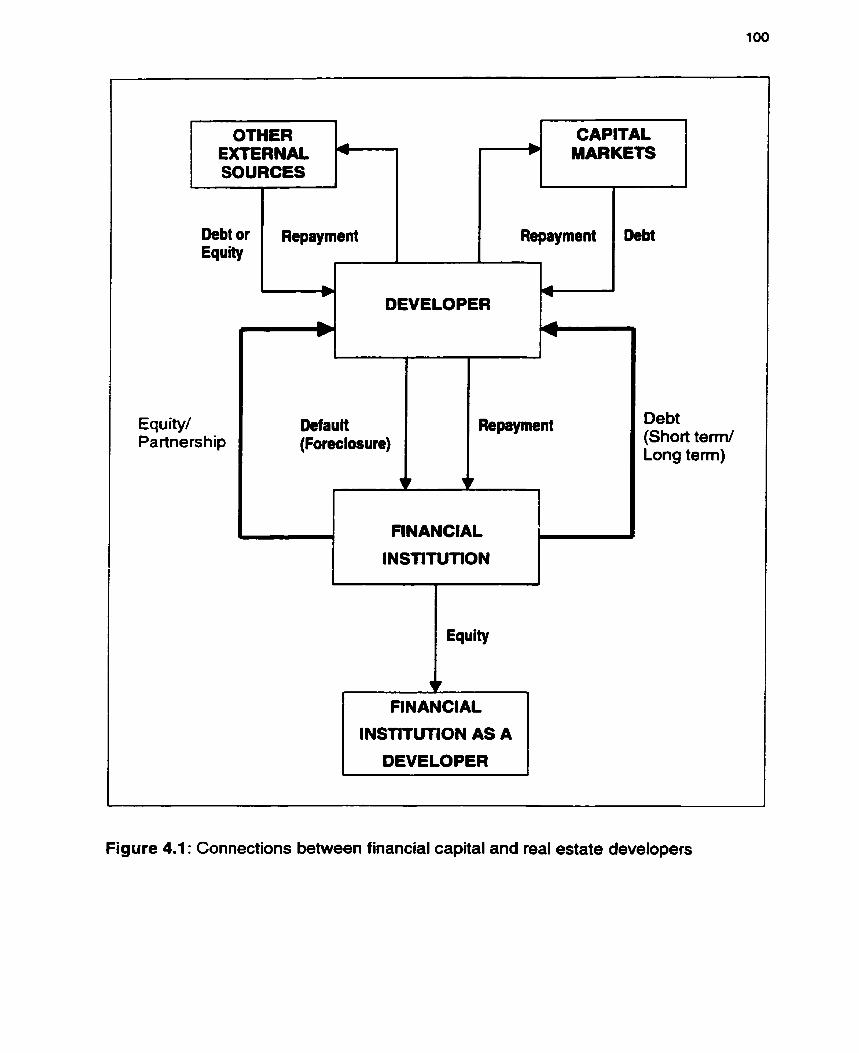

4 FlNANClNG OFFICE DEVELOPMENT AND THE ROLE OF FIN ANCIAL INSTlTUllONS 99

The Configuration of the Canadian Financial System and the Financial Arrangements in the Real Estate Sector 101

Sources of Financing Office Development: The Developer's Perspective 1 06 4.2.1 Olympia & York: Social networks, ingenuity and the

provision of financing 1 08 4.2.2 Corporate sire and real estate financing 110

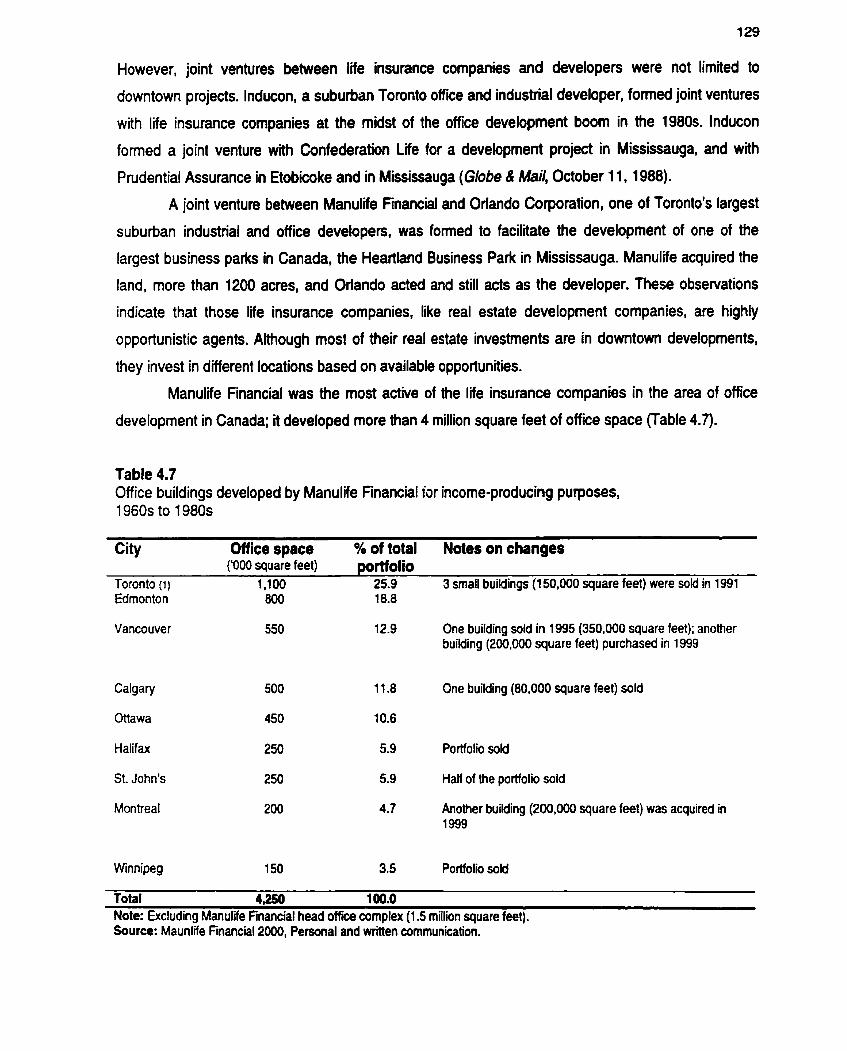

Financial lnstitutions as Investors in Office Buildings and as Developers 112 4.3.1 Banks and office development 114 4.3.2 Life insurance companies and office development 118

The Spatial Practices of Office Development and Ownership by Financial Institutions 122 4.4.1 Banks 123 4.4.2 Life insurance companies 126

The Spatial Limitations of Real Estate Capital 130

Financing and Financial Institutions: Concluding Remarks 1 33

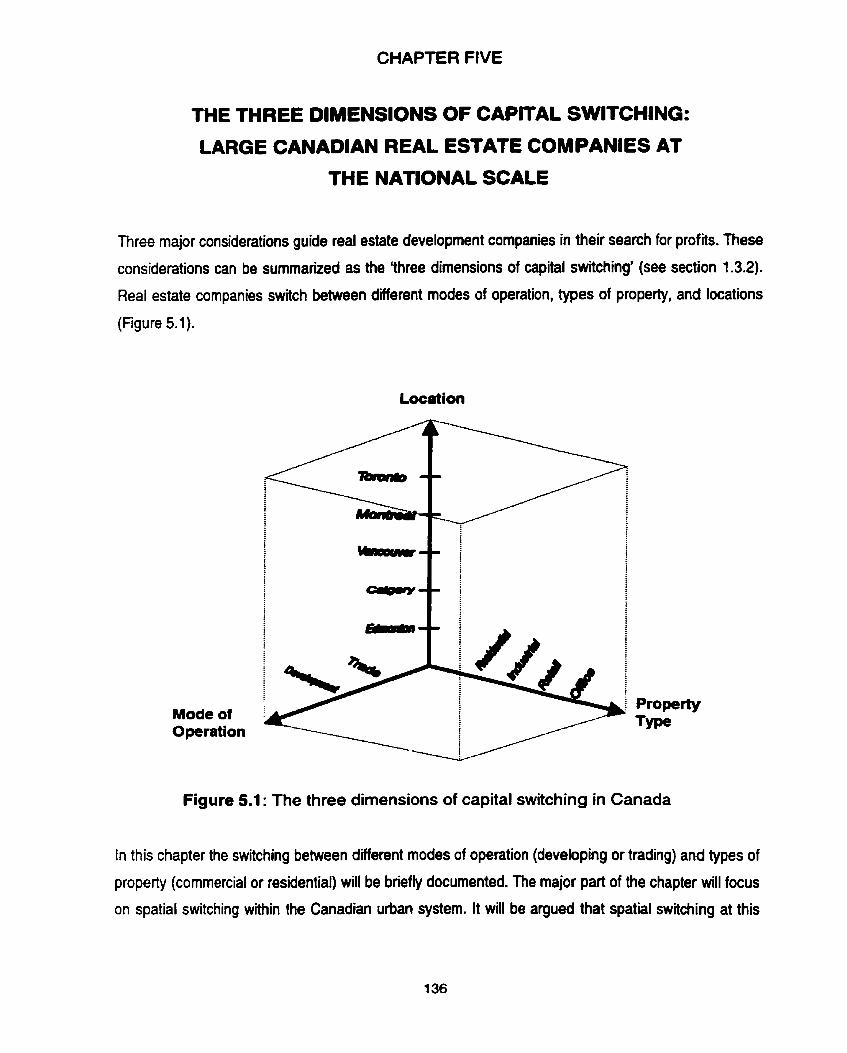

THE THREE DIMENSIONS OF CAPITAL SWITCHING: LARGE CANADIAN REAL ESTATE COMPANIES AT THE NATIONAL SCALE 136

Switching Between Modes of Operation 138

Switching Between Property Types 140

Switching Between Locations at the National Scale 144 5.3.1 The geography of office building cycles in Canada 145 5.3.2 Office building cycles in Toronto and Calgary 150

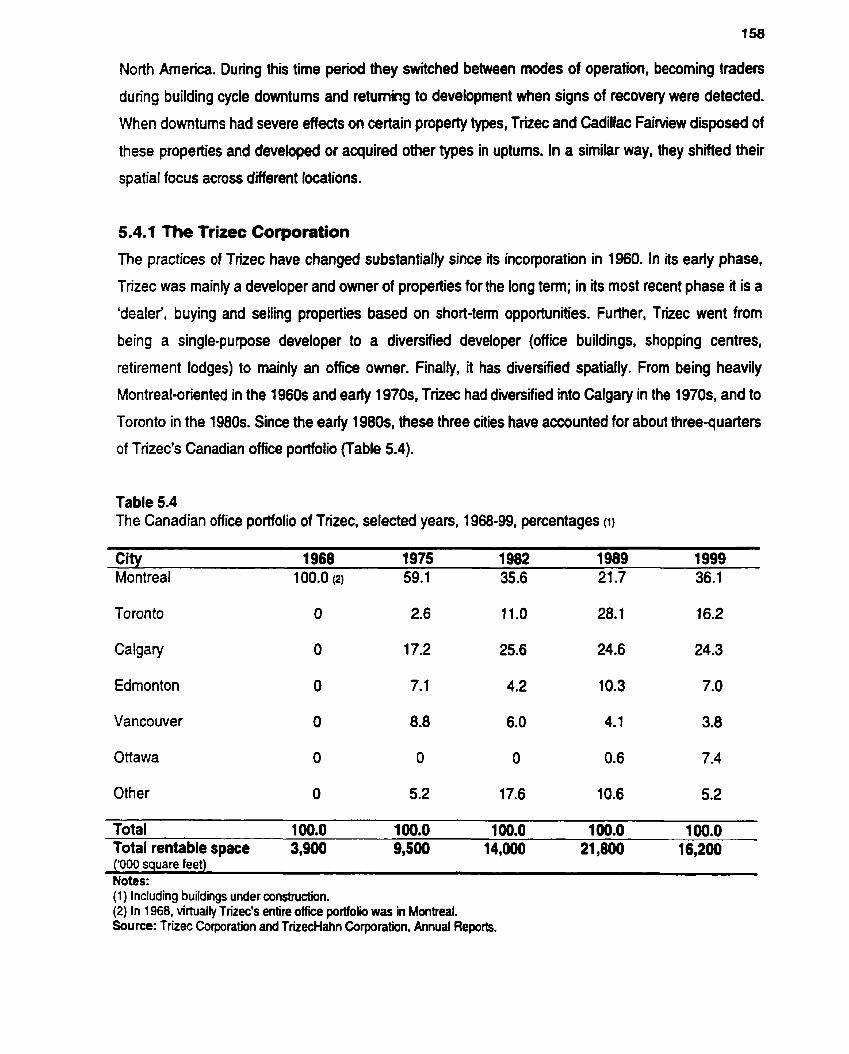

Three Dimensions of Capital Switching and Building Cycles: Two Case Studies 5.4.1 The Trizec Corporation 5.4.2 Cadillac Fairview Corporation

Capital Switching and Real Estate Companies

FROM KING AND BAY TO MEADOWVALE: TORONTO'S OFFICE BUILDINGS AND OFFICE D

Preliminaries: Office Building lnventory and Spatial Frame of Reference

Toronto's Office Stock: A Synopsis

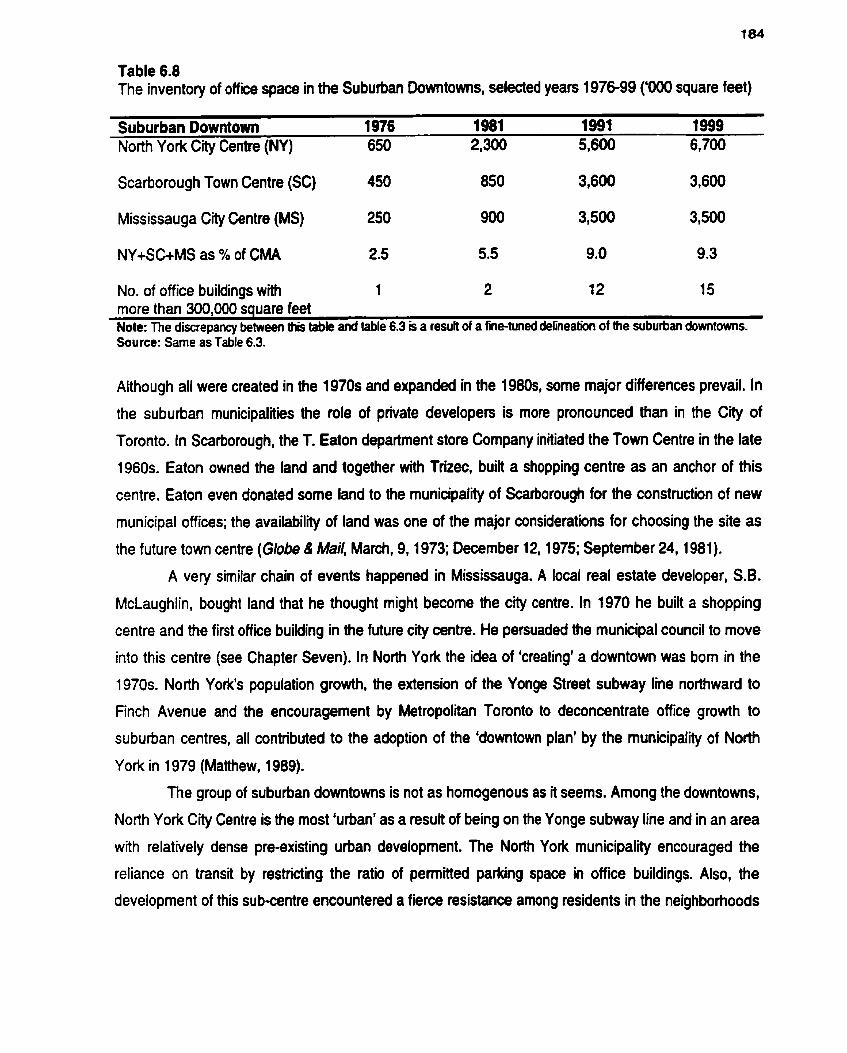

Office Districts in Toronto 6.3.1 The Financial District 6.3.2 Downtown and Midtown 6.3.3 Suburban Downtowns 6.3.4 Office Parks

Sequential Cycles of lnvestment within the Metropolitan Realm

The Changing Character of Toronto's Office Stock

THE SPATIAL PRACTICES OF OFFICE DEVELOPMENT COMPANIES AND OFFICE DEVELOPMENT DISTRICTS IN TORONTO

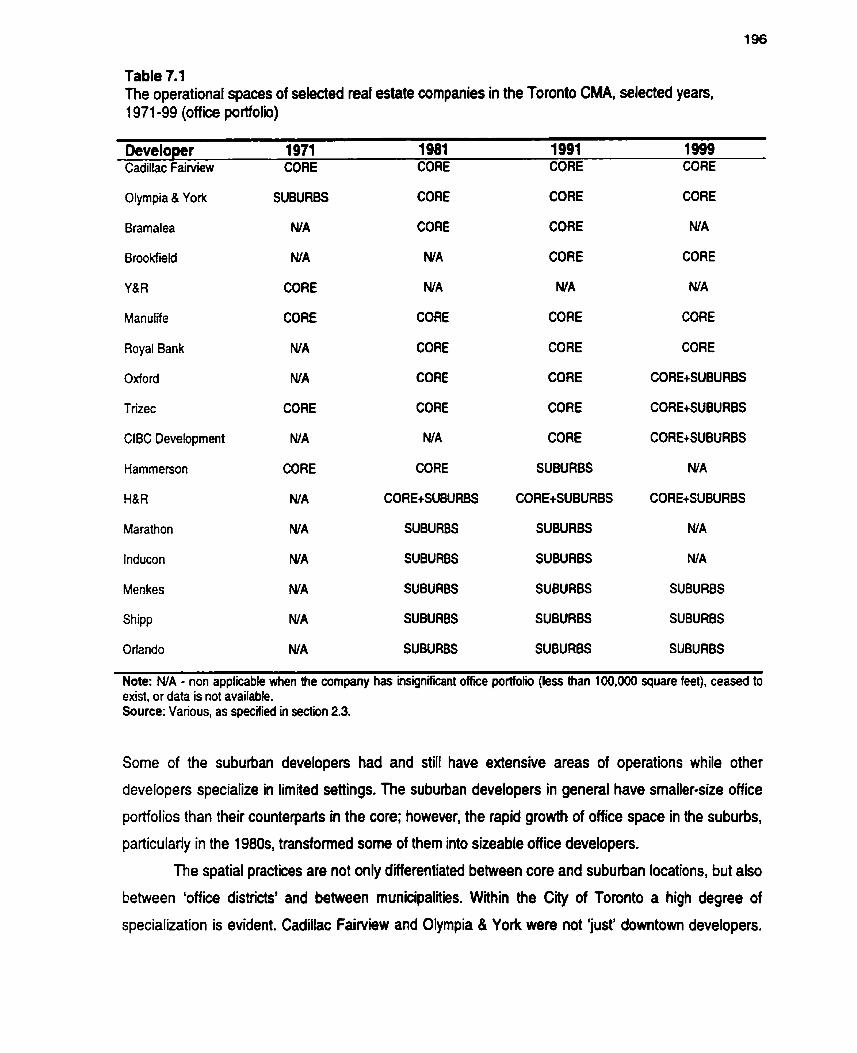

Spatial Selectivity among Real Estate Companies in Toronto 7.1 .1 Cadillac Fairview Corporation 7.1.2 lnducon Development Corporation

Office Development Districts

7.3 Area-Specific Case Studies of Office Development Districts 205 7.3.1 City of Toronto 206 7.3.2 North York 21 3 7.3.3 Mississauga 217

7.4 Uneven Surfaces of Office Development 225

CONCLUSIONS: SPATIAL F1X AND SPATIAL SWlf CHlNG OF REAL ESTATE CAPITAL

List of References

List of Interviews

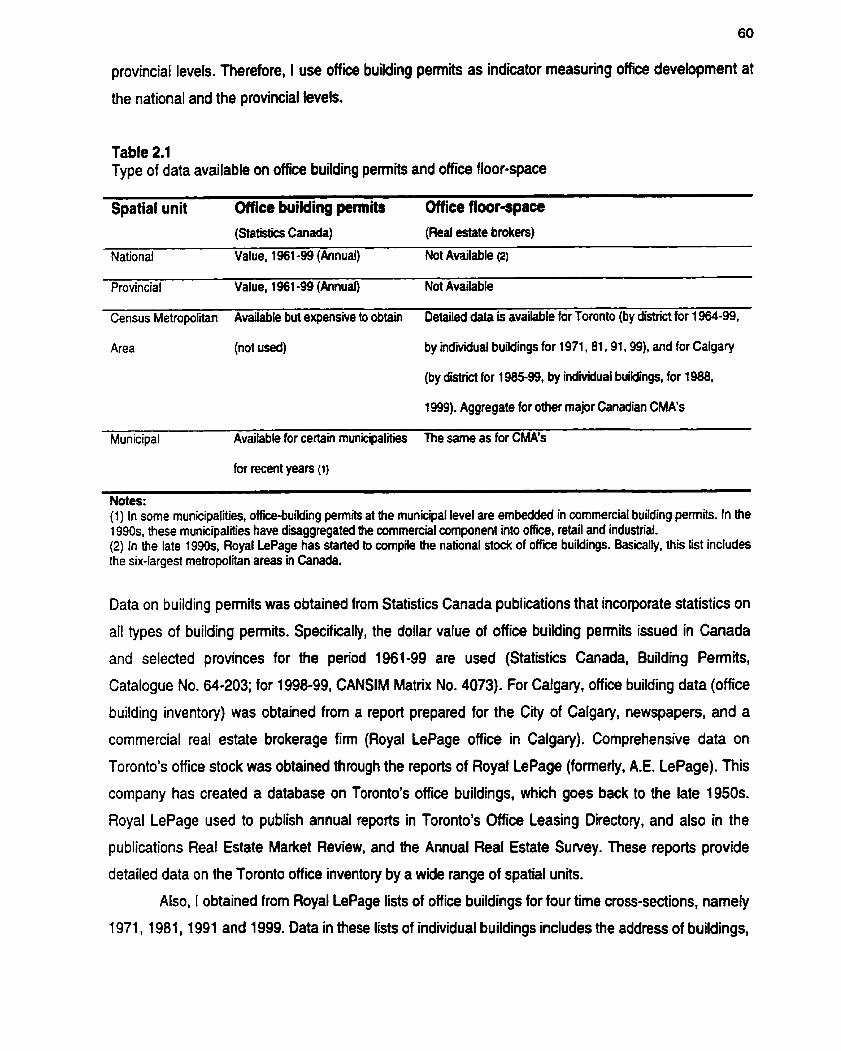

Table

Type of data available on office building permits and office floor-space

List of interviews

Major themes and questions in interviews

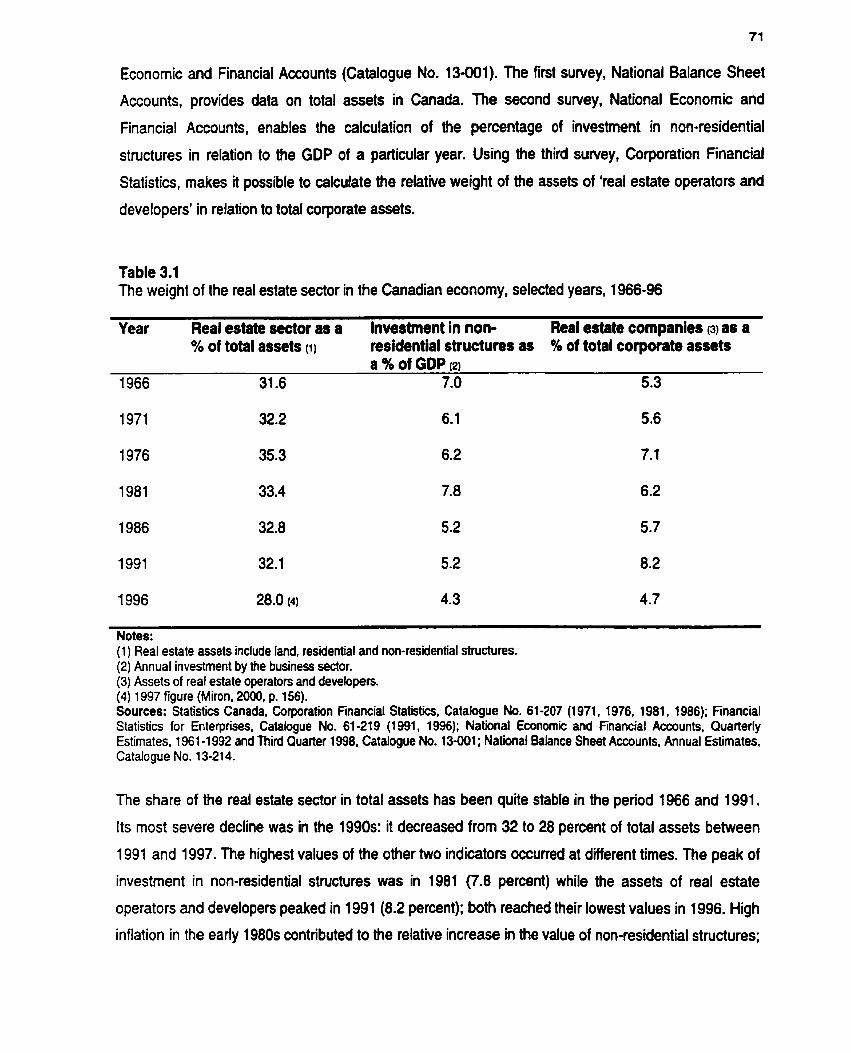

The weight of the real estate sector in the Canadian econorny, selected years, 1 966-96

The largest (publicly held) Canadian-based owners of real estate assets, selected years, 1971 -99

A profile of the largest Canadian-based reai estate companies in their initial phases

The largest real estate investment trusts in Canada, 1999

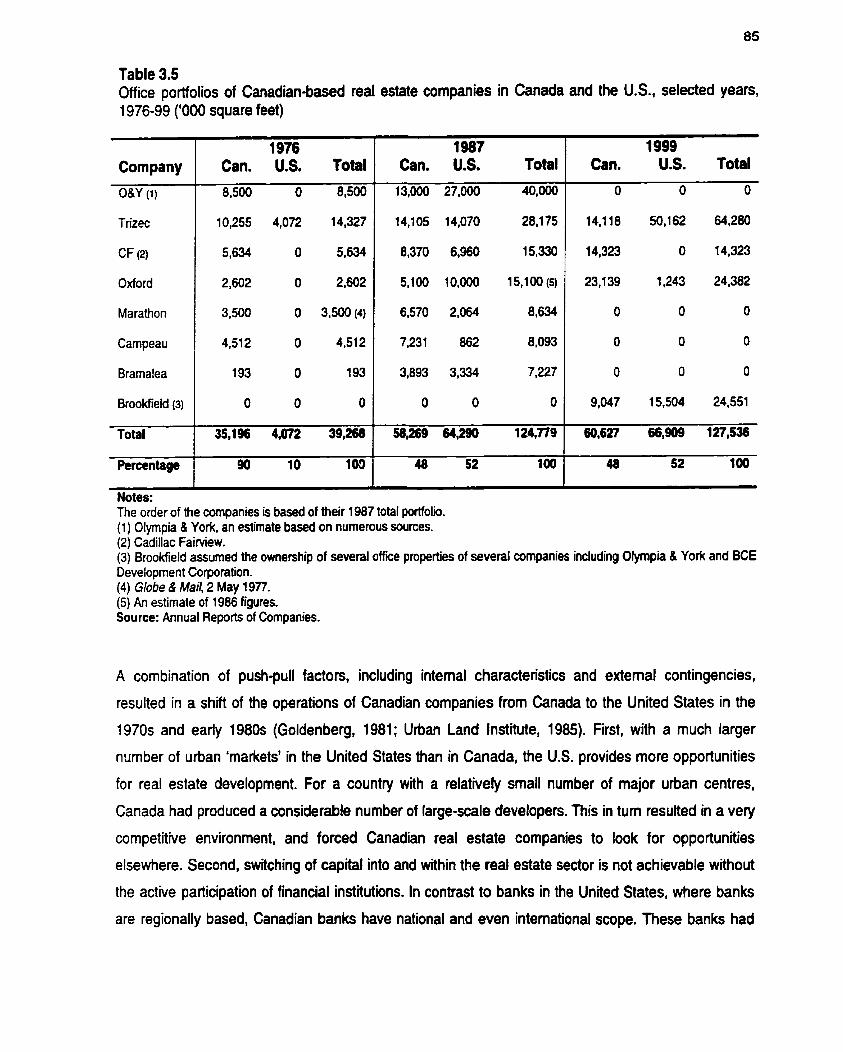

Office portfolios of Canadian-based real estate companies in Canada and the U.S., selected yean, 1976-99

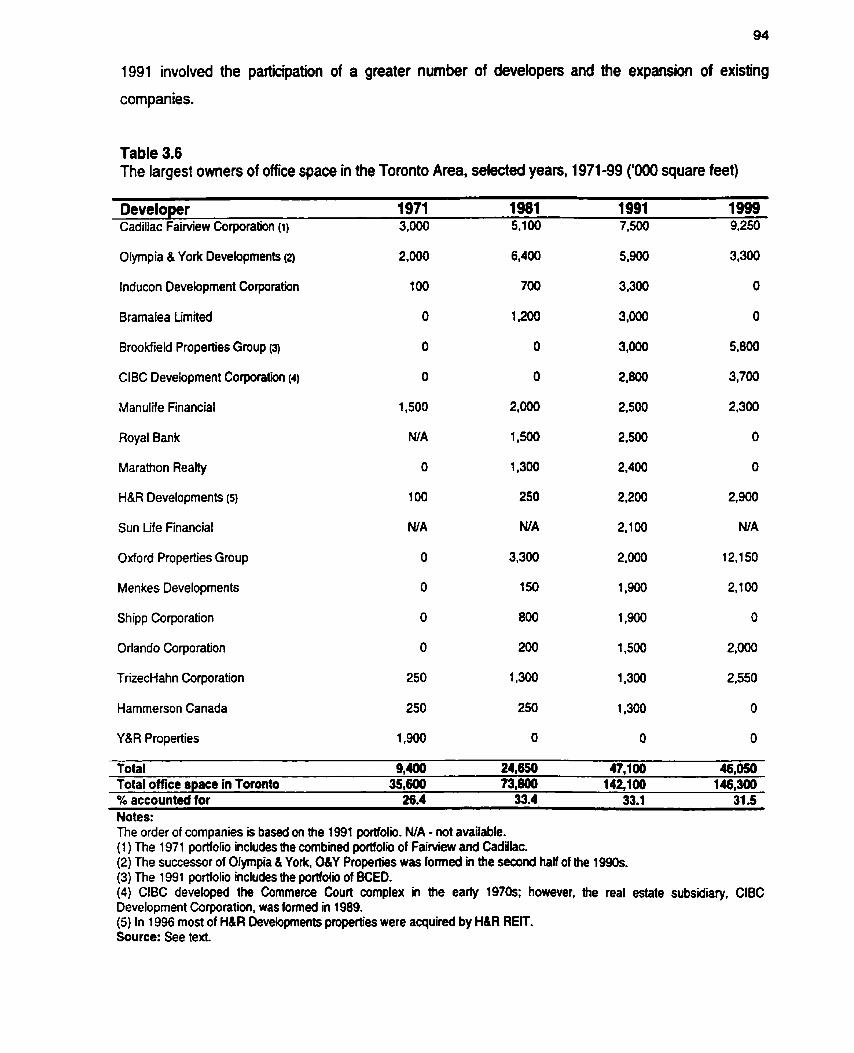

The largest owners of office space in the Toronto area, selected years, 1971 -99

Debt-to-equity ratio, al1 industries and real estate, selected years, 1971 -96

Banks involvement in the development and ownership of their head offices in Toronto

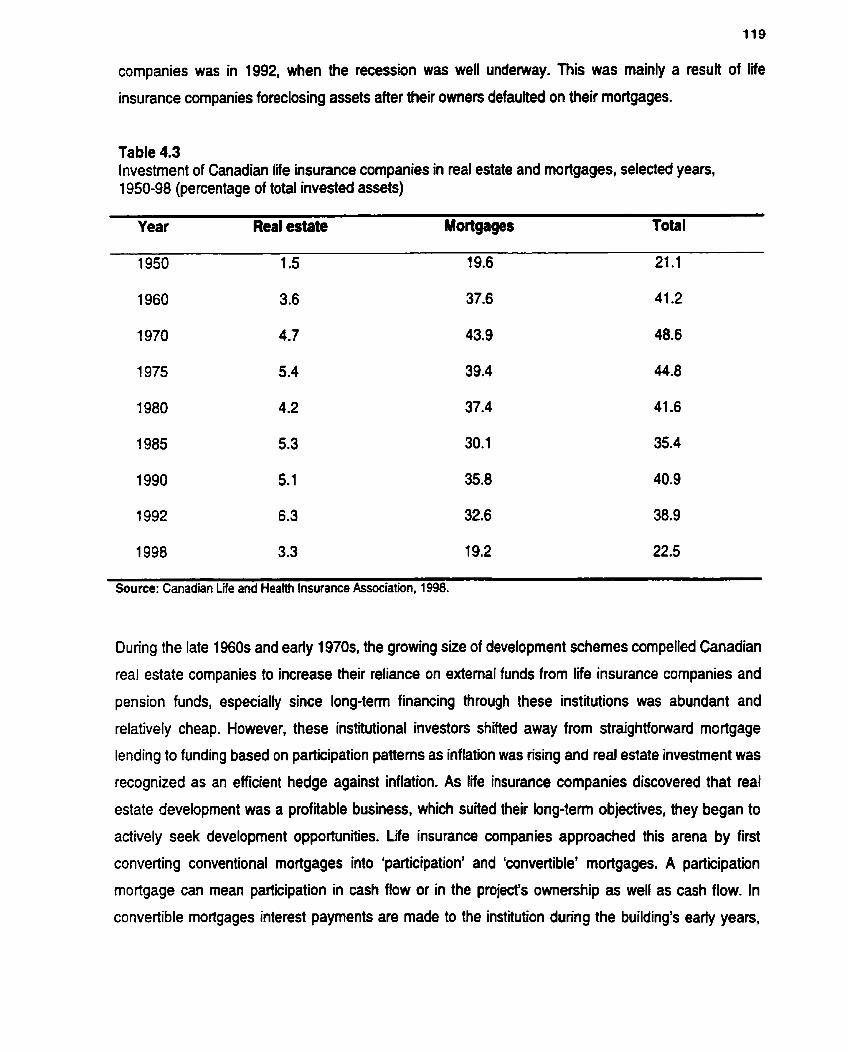

lnvestment of Canadian life insurance companies in real estate and mortgages, selected years, 1950-98

Bank of Nova Scotia and office developrnent joint ventures

ClBC Development Corporation and Royal Bank's owned office portfolio, 1 998, 1 999

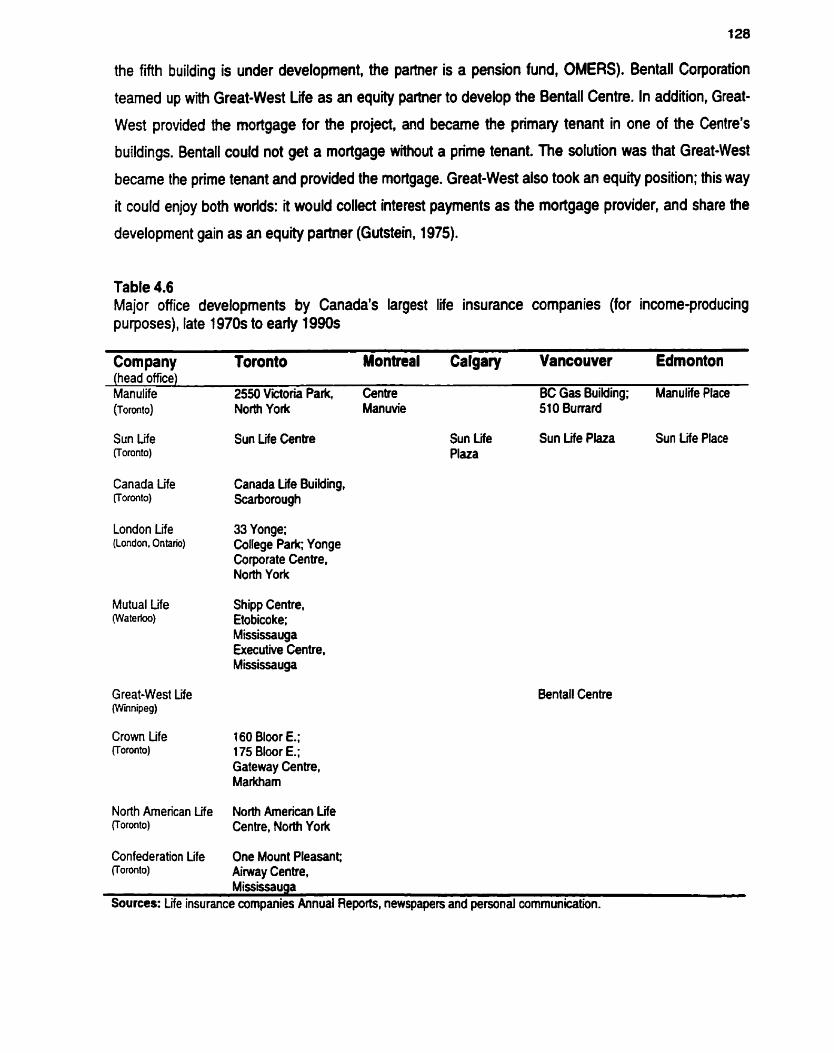

Major developments by Canada's largest life insurance companies (for income-producing purposes), late 1970s to early 1990s

Office buildings developed by Manulife Financial for income-producing purposes, 1960s ta 1980s

x

Paae

60

66

67

71

73

76

83

85

94

1 O?

115

119

1 24

1 25

128

129

Table

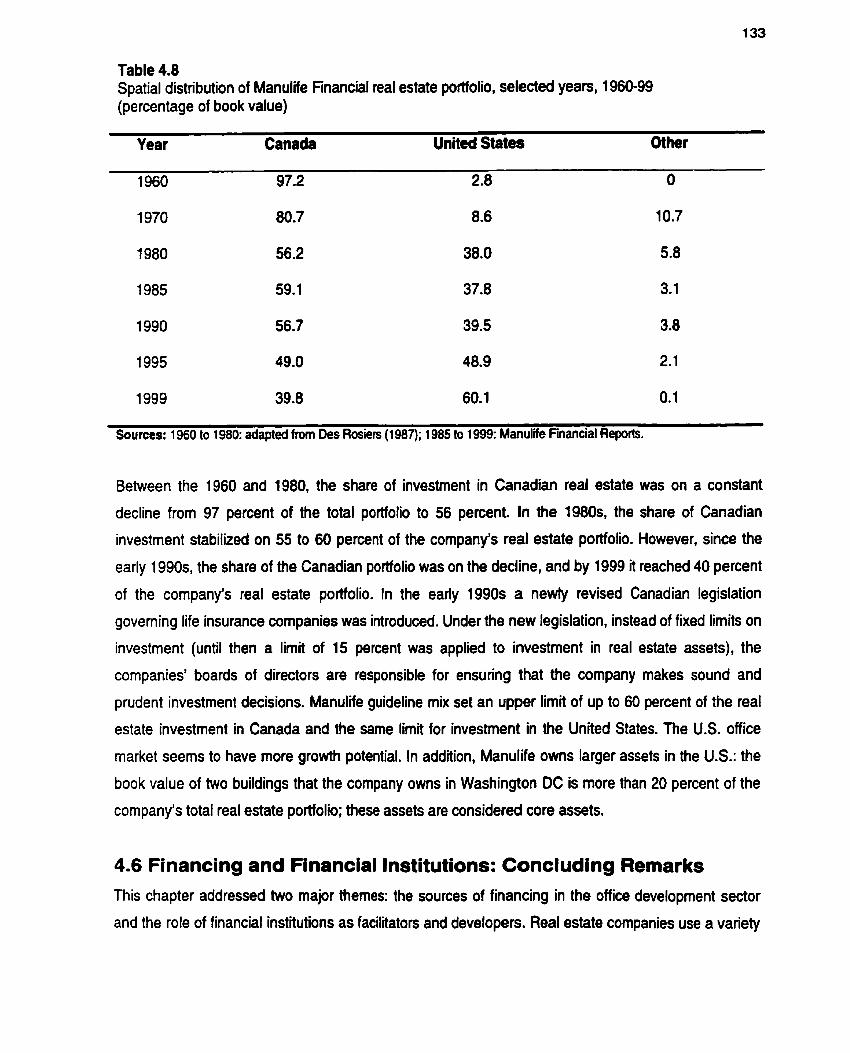

Spatial distribution of Manulife Financial real estate portfolio, selected years, 1960-99

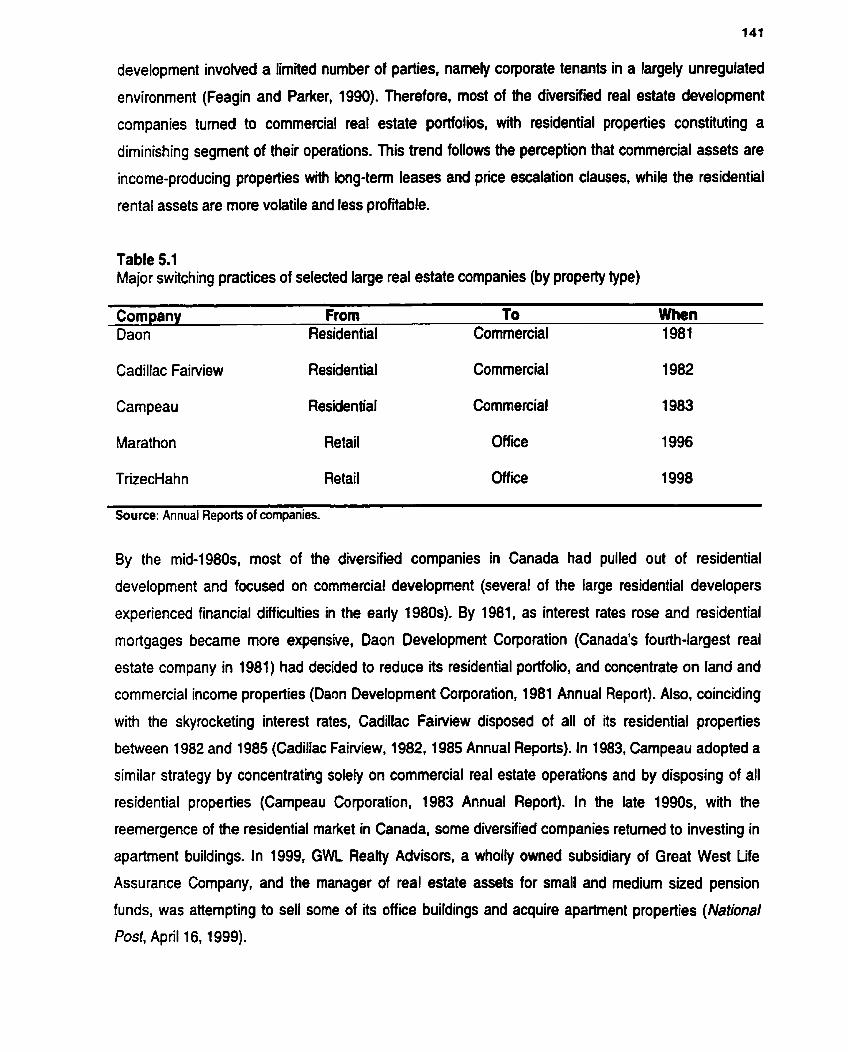

Major switching practices of selected large real estate companies (by property type)

The largest owners of office space by the location of their Canadian office portfolio, selected years, 1975-99

The growth of office space in Toronto and Calgary, selected years, 1978-99

The Canadian office portfolio of Trizec, selected years, 1968-99

The Canadian office portfolio of Cadillac Fairview, selected years, 1 968-99

A typology of office districts in the Toronto CMA

The growth of office space inventory in the Toronto CMA. selected years, 1954-99

Additions of new office space in the Toronto CMA, selected yean, 1954-99

Average size of newly constructed office buildings in the Toronto CMA, 1 954-99

Average densities of office buildings in Metropolitan Toronto, 1991

Physical characteristics of office buildings in selected districts in the Toronto CMA, 1999 179

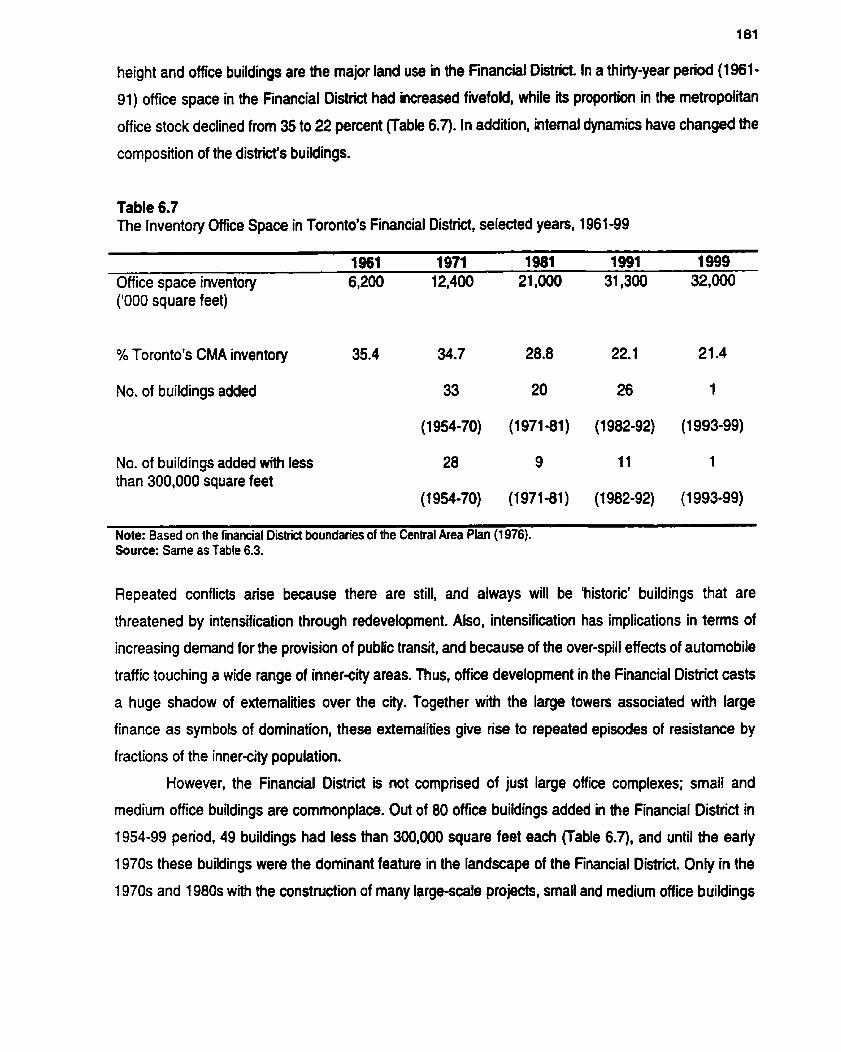

The inventory of office space in Toronto's Financial District, selected yean, 1961 -99 181

The inventory of office space in the Suburban Downtowns, selected years, 1976-99 1 84

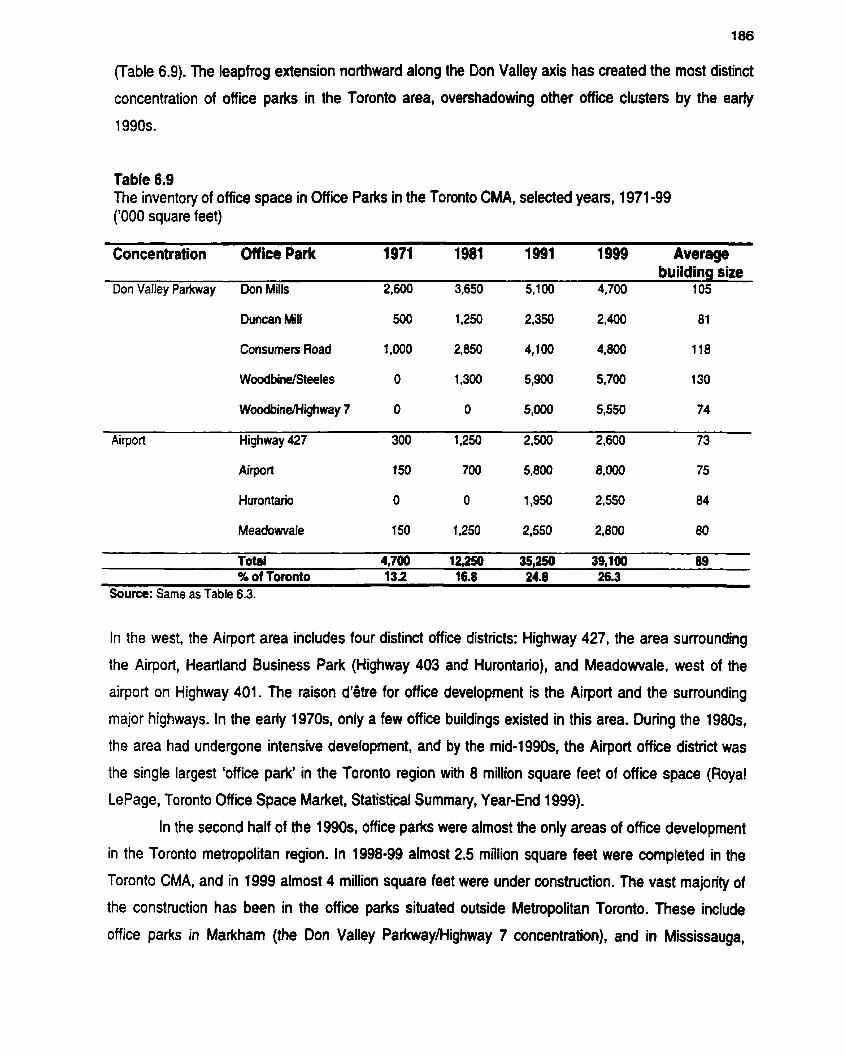

The inventory of office space in Office Parks in the Toronto CMA, selected years, 1 971 -99 186

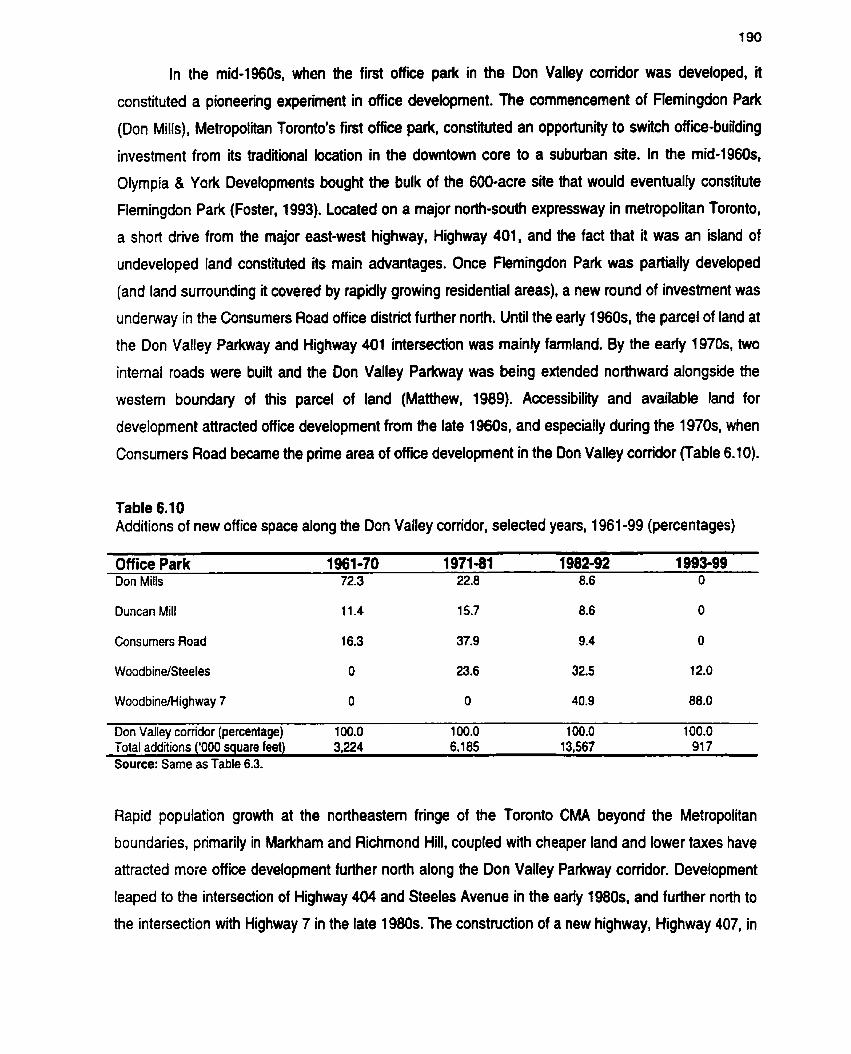

Additions of new office space along the Don Valley corridor, selected years, 1 961 -99 190

Paae

133

Table

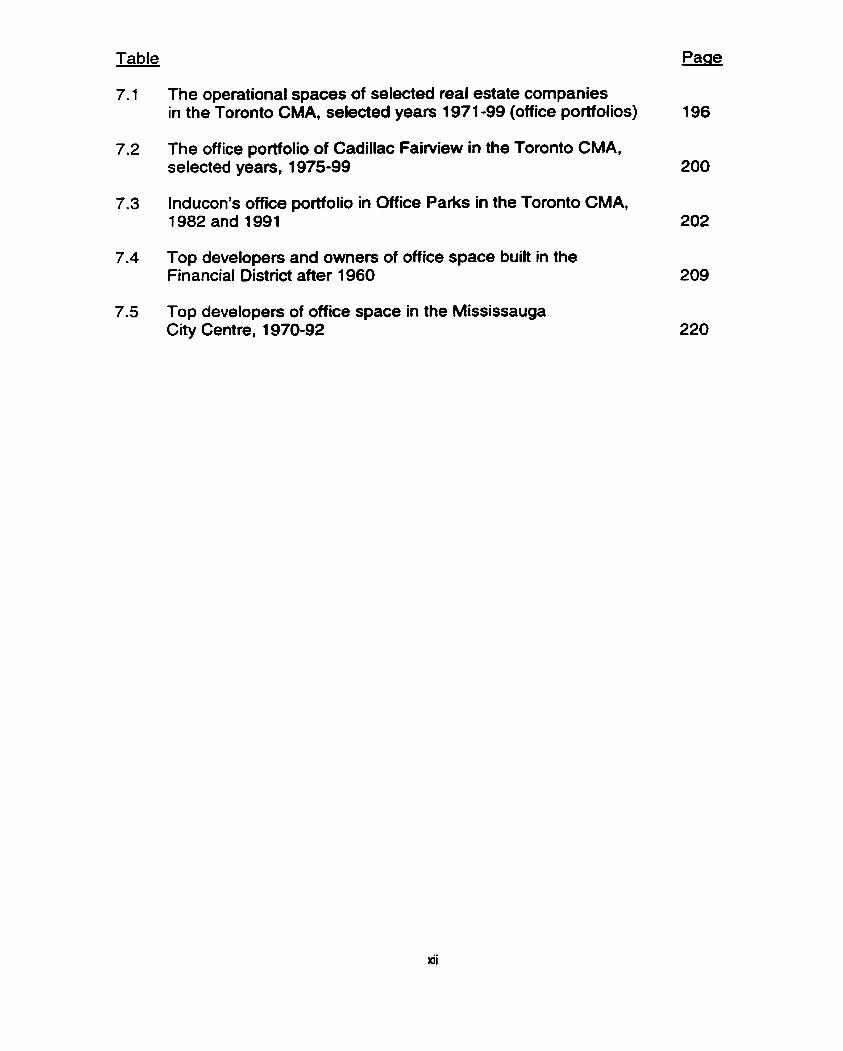

7.1 The operational spaces of selected mal estate companies in the Toronto CMA, selected years 1 97 1 -99 (office portfolios) 196

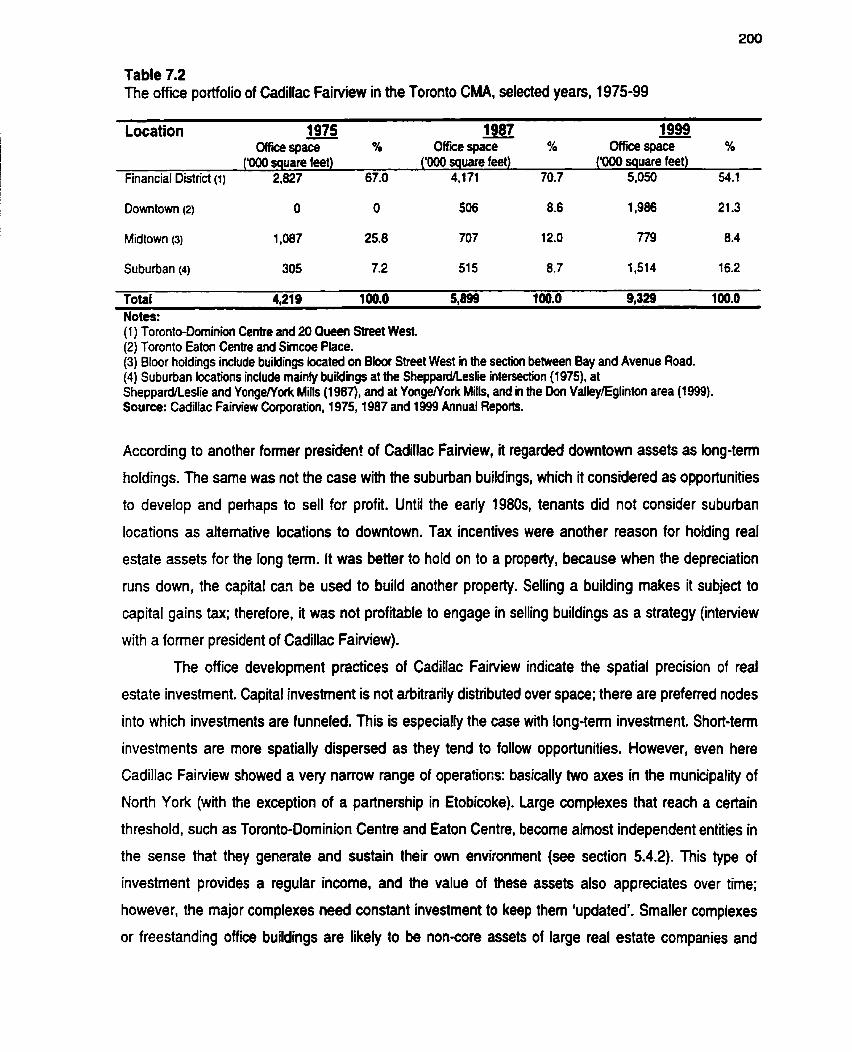

7.2 The office portfolio of Cadillac Fairview in the Toronto CMA, selected years, 1975-99 200

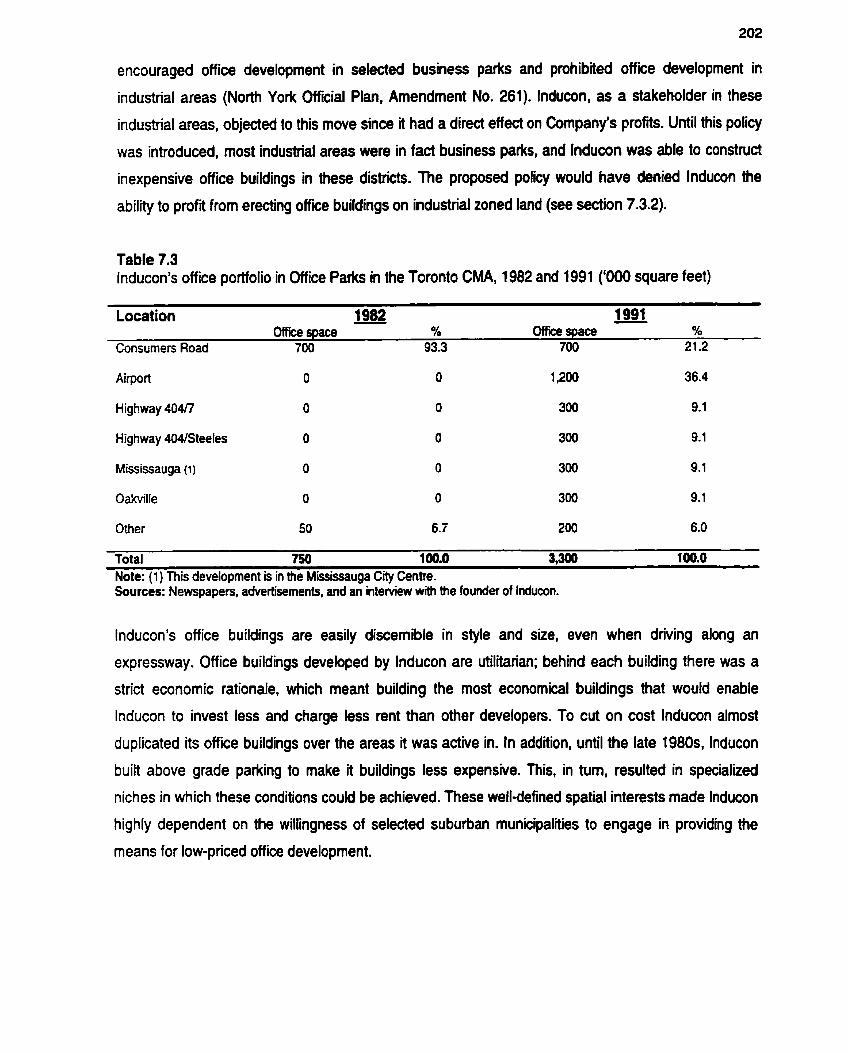

7.3 Inducon's office portfolio in Office Parks in the Toronto CMA, 1 982 and 1991 202

7.4 Top developers and owners of office space built in the Financial District after 1960 209

7.5 Top developers of office space in the Mississauga City Centre, 1 970-92

List of Figures

Paae

Downtown and north-south corridor office devetopers in the Toronto CMA

Suburban office developers in the Toronto CMA

Toronto Census Metropolitan Area

Connections between financial capital and real estate developers

The three dimensions of capital switching in Canada

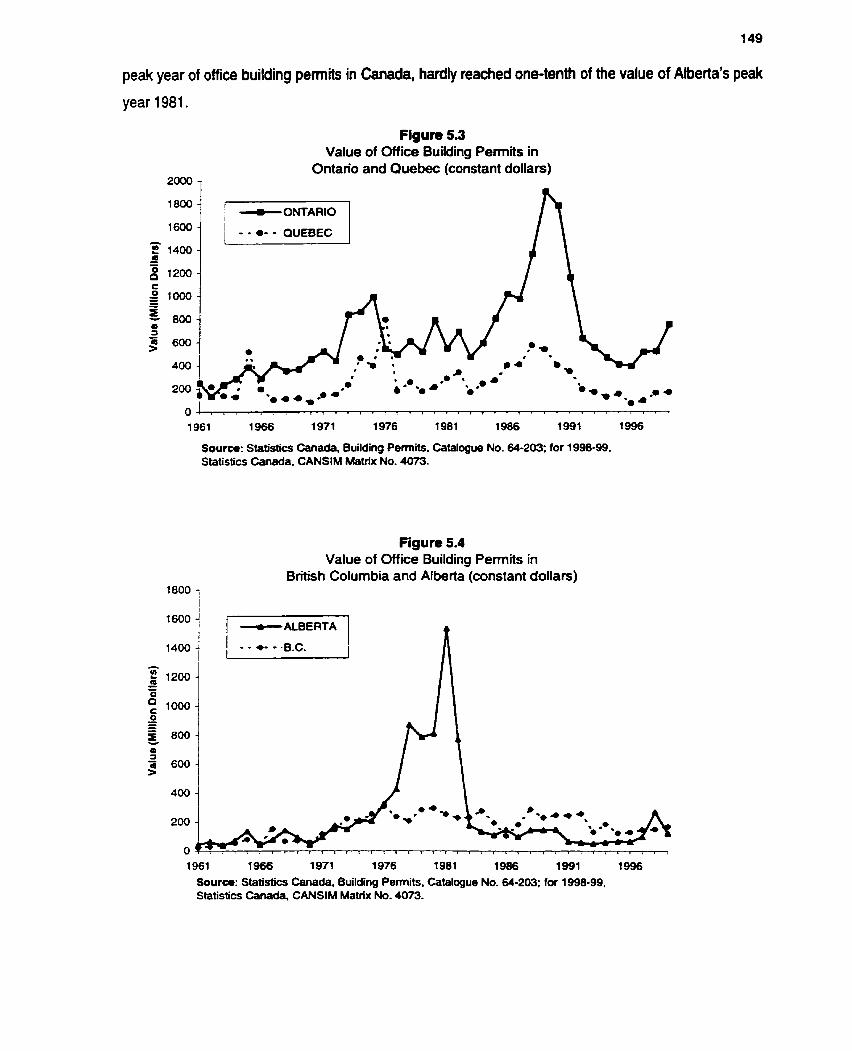

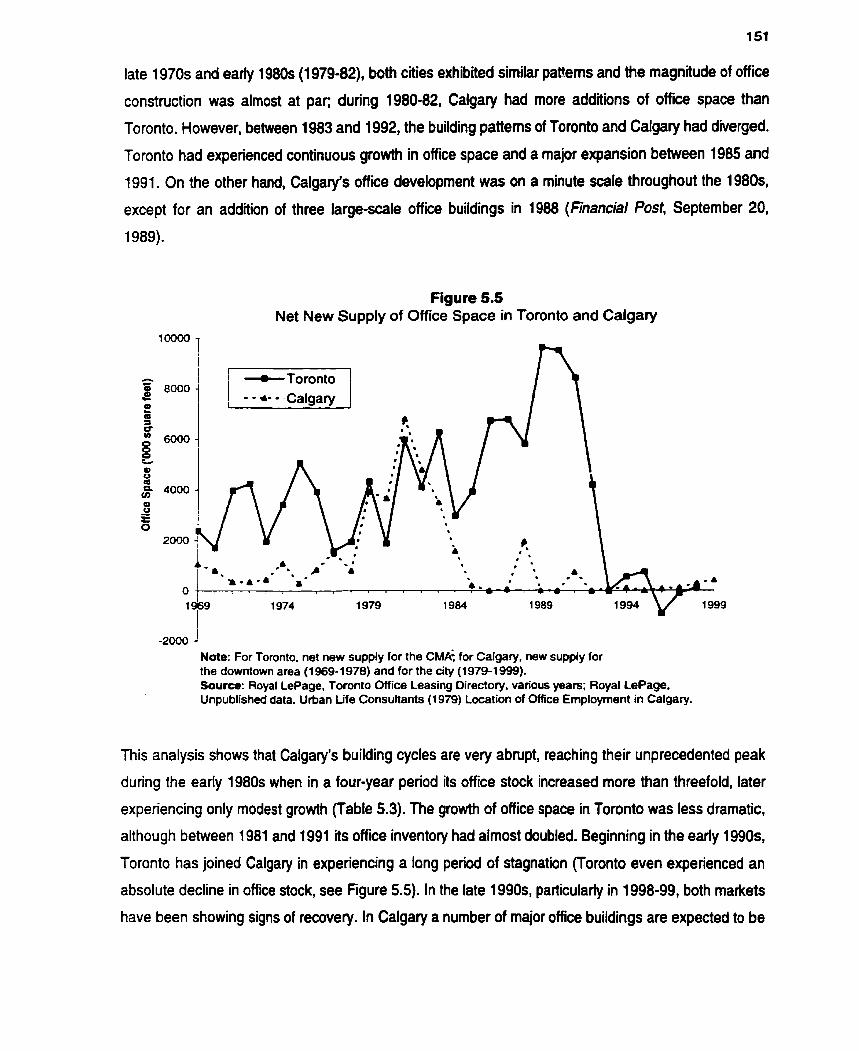

Value of office building pennits in Canada, 1961-99

Value of office building perrnits in Ontario and Quebec, 1961 -99

Value of office building permits in British Columbia and Alberta, 1 961 -99

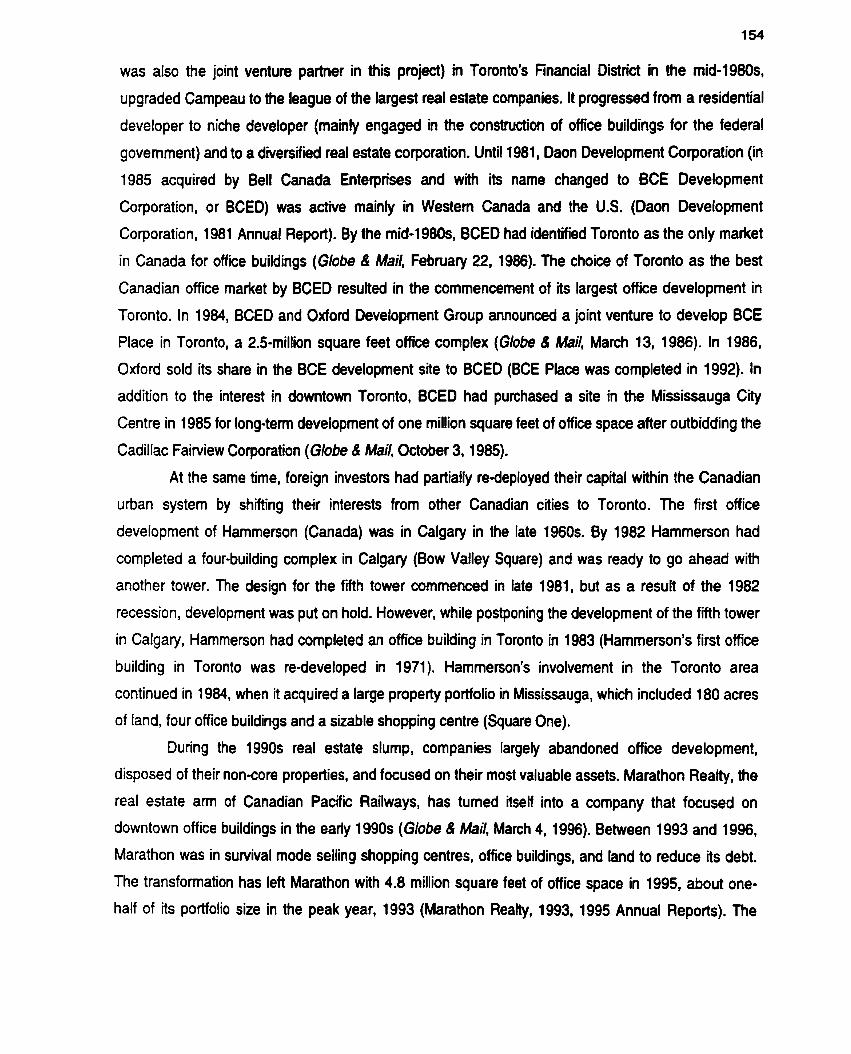

Net New supply of office space in Toronto and Calgary. 1969-99

Major office concentrations in the Toronto Census Metropolitan Area

By the end of the twentieth century, office buildings had become the most prominent structures in many

of the large rnetropolitan areas of the world. Office buildings are part of the iconography of the

metropolis: the Empire State and Chrysler Buildings in New York, the Sean Tower in Chicago, the

Transarnerica Building in S2n Francisco, or the Fint Canadian Place and the Toronto-Dominion Centre

in Toronto. A Toronto-based development company, Olympia 8 York, and its office mega-project,

Canary Wharf in London, England, provided the greatest spectacle of real estate promotion and

subsequent collapse in the M decade of the twentieth century. However, skyscrapen and mega-

projects like Canaiy Wharf are high profile elernents that mask a vast amount of less conspicuous and

rarely publicized office developrnent.

Office development has been uneven in space and time. There have been several cycles of

office development in the twentieth century, bu? in ternis of magnitude, the boom of the 1980s was

unprecedented. In some cities, such as Houston, Texas, more office floor-space was built in this one

decade than in the preceding f i yean. Although the 1980s boom drew a lot of attention to global

cities (Sassen, 1991, 1994) and to office development in cities like London (e.g., Diarnond, 1991;

Zukin, 1 992; Fainstein, 1994; Pryke, 1994a) and New York (Zukin, 1992; Fainstein, 1994), there have

been many other cities where office development was prominent and attracted the attention of

researchers. For instance, the booms in office development in Houston (Feagin, 1987, 1988), Dublin

(MacLaran, 1 993, 1996), Nottingham (Btyson, 1990, 1997), Melbourne (Beny, 1994), or Auckland

(Moricz and Muiphy, 1997) and the research they generated can be rnentioned. However, across

regions and urban systems and within large cities, office devebpment has been uneven.

In order to understand uneven temporal and spatial development of the urban fabric in general,

and office development in paiticular, many researchen have drawn on Harvey's (1982,1985) theory of

capital switching between pnmary and secondary circuits of capital accumulation, and his notion of

capital switching between places (Beauregard, 1991, 1994; Haila, 1991 ; Pryke, 1994a, 1994b).

However, the notion of time scale under investigation is essential in the analysis of the built

environment. Harvey's research on capital accumulation focused on long-terni history; however, other

scholars such as Feagin (1 987) and Beauregard (1 991, 1994) were interested in shorter periods and

as a result conclusions about switching practices are different from these proposed by Harvey.

Harvey's conceptualizations have also implicated finance capital in the process of the

production of the urban fabric, and as suggested by Warf (1994, p. 325) 'Yinance capital is not some

passive actor in the construction of hndscapes, but an adive participant wilh a bgic of its ownn. Some

limited research has punued this avenue as far as offce development is concemed (Feagin, 1987).

Othen have not oniy considered the role of finance capital as an intennediaiy, but also as a direct

participant in office development as financial institutions becarne developers and owners of office

buildings (Des Rosiers, 1 984; MacLaran, 1 986; Lindahl, 1 997). It has also been suggested that the role

of financial institutions as lenden-usen and as ownen-uses might converge, and these institutions

force their locational preferences on office development patterns (Piyke. 1994a. 1994b; LUieri et al..

2000). Another strand of research has argued îhat real estate devebpers have ernerged as large-scale

companies. and become multinational corporations with far-flung projects (Beauregard. 1989; Feagin

and Parker, 1990; Sudjic, 1992; Knox, 1993, Logan, 1993; Olds, 1995; Beauregard and Haila, 1997).

However, the literature on the uneven development of the urban fabric is not as straightforward as this

paragraph may indicate.

The notion advocated by Zukin (1992) and Knox (1993) that real estate developen have global

reach that enables them to engage in development across regions with-in one country and beyond, and

that real estate capital has limitless scope is somewhat extrente and should be questioned. Urban

space is neither flat nor featureless. It has a highly articulated and changeable surface (Harvey, 2000).

Institutions and sets of individuals are grounded in local settings. They respond to these specific

settings and reproduce them, thereby contributing to the pennanently uneven structure of urban space.

Indeed. several authon have argued that office development takes place in very specific historic and

geographic settings as a result of the juxtaposition of specific requirements (Pryke, 1991, 1994a,

1 994b; Beauregard, 1 993; Ball, 1994; Leitner, 1994).

Office developrnent in Canada

The configuration of the real estate development sector in Canada is an outcome of two parallel

processes. At the macro scale, historical shifts in strategies of accumulation have resuhed in a number

of changes. Entrepreneurial developen were the prominent agents of change at the fint phase of the

development of the Canadian commercial real estate sector; largexale development companies

shaped office development in a later stage, and rnost recently, financial institutions became the most

important agents in the real estate sector. In the short nin and in ternis of ongoing process, real estate

companies aiming to grow or to stay afloat have employed capital and spatial switching practices.

There have been several office development cycles at the national level in the last f i i years,

and major urban areas were affected differently by them. Office developen have taken advantage of

these cycles and have produced an extraordinary amount of office space in Canada's largest cities.

Two cities stand out in tems of office development booms: Calgary in the late 1970s, and Toronto in

the 1980s. Toronto is Canada's largest urban area mth by far the largest office floor-space inventoiy

(145 million square feet in 1999 or 40 percent of the national office stock), and Calgary has the third

largest office stock (42 million square feet in 1999). Toronto experienced consistent rates of growth in

office space Mi le Calgary had abrupt cycles of office development. To put the 1980s boom in

perspective: in each post-WWII decade, office fbor-space doubled in Toronto. Between 1981 and

1991, this doubling meant an increase from about 74 to 142 million square feet of floor-space, which is

almost the inventory of Montreal (the city with the second hrgest o f tm inventory, 80 million square feet

in 1999) and about the combined 1999 inventoiy of office space in Vancouver, Edmonton, Halifax and

Winnipeg (68 million square feet). On the other hand. Calgary's history shows an impressive boom in a

very short penod: office space more #an tripled between 1978 and 1982 (from 8 to 28 million square

feet).

Office development within the Toronto metropolitan region has been highly uneven. The towers

of the socalled Financial District are a relatively minor part of a highly articulated landsape of office

buildings and office districts. These districts include several distinct inner city areas, suburban

downtowns, and a variety of office paiks. These districts are diierentiated by the age and size of office

buildings, by development densities, and also by the physical, economic, and social fabric in which

office buildings are embedded. Canadian and especially Toronto-based companies developed almost

al1 of Toronto's office space.

Within the Toronto region, most real estate companies have very specific fields of operation.

Figures 1 and 2 show the different operational spaces of selected development companies in the

Toronto Census Metropolitan Area (CMA, Statistics Canada definition of a metropolitan region).

Cadillac Fairview and Olympia 8 York, two of the largest real estate companies in Canada. operated

mainly in downtown Toronto. Marathon and Bramalea, smaller real estate companies, operated along

Toronto's traditional North-South high-income sector. Other developers, such as Inducon, Menkes,

Orlando, and Shipp, operated only in selected suburban municipalities. The broad picture of office

development in Canada suggests that office development is not only uneven, but also carried out by

agents with highly focused geographic preferences. Developen operate in highly specific locations.

Knowledge of particular places and local opportunities encourage developers to be very selective.

The major issue to be addressed in this study is the relationship between the conditions of

developrnent. and the response to these conditions by specific types of agents who produce the built

environment, especially office buildings and office districts.

Office development in the cities of the Canadian uban system, particulaily within the Toronto Census

Metropolitan Area between 1950 and 2000, is the arena to be investigated. The following paragraphs

outline briefly the major thesis, the approach, the specific research methods used, and the types of

data collected. A final paragraph outlines the organizaton of the thesis.

Thesis

The core of the thesis maintains that office development is spatially uneven, because capital requires

spatial unevenness to create oppominiaes for future aaumulation, and because the practice of

development faces important spatial barriers. F i e components of the thesis contribute to distinct sub-

arguments. Together, they describe the pradice of office development and support the core thesis.

1. Capital switching between primary and secondary circuits of capital accumulation is difficuk to track.

and it may be a phenomenon that is l e u important than some authois suggest. Instead, my focus is on

the real estate sector which has an 'intnnsic dynamic' (Haila. 1991). This intnnsic dynarnic can be

conceptualized as the Yhree dimensions of capital switching' within the real estate sector. This

switching can occur between modes of operation, property types, and locations.

2. The built environment consists of physically discemible structures and the parcels of land they stand

on. These real estate properties are by definition immobile and represent capital investment in concrete

and fixed assets. However, capital is also elusive and nomadic; the 'globalkation hypothesis' with

regard to real estate development relies on this guality (Berry and Huxley, 1992; Olds, 1995). The

development, and the ownenhip, of real estate properties has become increasingly 'delocalized' and

may be detennined by forces beyond the city's boundaries (Savitch, 1995; Beauregard and Haila,

1997; Baum and Liiieri, 1998, 1999). There seems to bel therefore, a paradox or an inherent

contradiction between immobile properties and mobile capital. This contradiction can be reconciled by

scrutinizing the reciprocal relationship between the abstract nature of capital and its concrete

manifestation. On the abstract level, capital is intangible, a restless element of the global financial

markets. Nevertheless, capital invested in real estate assets has to be fixed in definite places, at least

for a limited period of time, thus fumishing capital concemed with office development with a spatial

specificity.

3. Real estate investment, and especially real estate development. is fundamentally a local business.

This 'local dependence' (Cox and Mair, 1988. 1989) means that real estate development has to build

on local knowledge and local conditions. Unifom and perfect knowledge across space is unlikely to be

attained, thus, developen have to decide where they want to put their development efforts. To be well

inforrned and obtain valuable information, developers need to be well connected in their operational

environment. Developers with spatially diverse interests have to familiame thernsehres in the local

arenas in which they invest. This also implies that they negotiate with a variety of local interests,

including specific local govemrnents.

4. Real estate development, including office development, is cyclical. In the case of office development,

cycles are not identical across regions or across the Canadian urban system. Spatial differences in

building cycles encourage soma developen to take advantage of opportunities that are created by

uneven conditions.

5. Finance capital is essential for real estate development, and especially for office developrnent. The

relatively large amounts of rnoney needed, the longevity of office buildings, and the gradua1 strearn of

revenues require that office developen bonow heavily. While flows of money may be flexible in theory,

they tend to be spatially concentrated in practice. Like the developer, the financial institution needs to

know the specific urban conditions in order to assess nsk and avoid undue exposure.

Approach, methods, and data

The approach adopted in this research rests on the political economy perspective. This approach

explains social and economic processes through the investigation of structural conditions, which

include the state and financial institutions as major components in the urban developrnent process. A

political economy approach does not necessarily exclude the juxtaposition of structure and agency.

The acknowledgement of structure and agency is essential in order to explain a process, which is

highly influenced by individuals interpreting structural and local conditions. The theoretical contribution

of this thesis is pnrnarily through ce-conceptualizing and re-interpreting the nexus between structure

and agency in the particular sphere of real estate development.

The realist method as developed by Sayer (1984) is used as a critical tool in this research. This

methodology assigns the agent a critical role in reproducing structure, and it combines necessary and

contingent conditions in expiainhg events. The multiplicity of events, mechanisms, and structures,

provides a useful framework for the anaiysis of real estate and office development.

Office development is not strongly theorized. Harvey provides a general frarnework for the

analysis of the built environment, but in his level of abstraction he under-emphasizes the specific

charaderistics of each part of the buiit environment and the agents that reproduce the structure in

which new rounds of development take place. At the m e time, day-today concepts like 'developer'

are only vaguely defined. One way to analyze real estate development is through 'structures of building

provision' (Ball, 1986). This method of anaiysis suggests that each development is the end result of a

variety of social agents and mediating institutions. To be able to interpret office development as a

particular segment in the buin environment means that exact definitions of the process and the agents

are necessary. Sayer suggests that in a world that is stratified and differentiated, complex relationships

need to be 'unpacked'.

The realist approach emphasizes exact definitions of concepts and wams against the notion of

'chaotic conceptions', in which objects are grouped into categories that have little or no intemal logic or

structural interaction. The idea of using exact definitions is crucial in the realm of office development.

since the dynamic nature of this sector and the fact that in the process of development, a number of

different agents are involved. These agents are ditficuit to categorke, because the functions they

perfonn and the roles they play can be combined in different ways at different times. Hence, to

understand office development, the use of well-defined concepts and the unpacking of everyday ternis

are necessary to provide a sense of clanty.

The term 'real estate developer', commonly used by joumalists, real estate industry

professionals, govemment agencies, and academics, is a 'chaotic concept'. Academic writing

considers the real estate developer as a key agent in the development process, but does not offer a

consistent definition. The developer is sometimes conceived as the catalyst of development. This agent

initiates, coordinates, manages and brings the development from the stage of concept to the point of

completion (Marriott, 1967). Harvey (1985) uses the tenn 'speculativedeveloper, based on the idea

that a developer sells land or makes improvements to land for speculative purposes only. This notion of

the developer also fails to capture the corn plex functions performed by this type of agent.

Within the development process four major types of agents are active: developers, land

owners, financial institutions, and construction companies (Barras, 1979b). These roles can be

embedded in one organization. For example, a developer may be the land owner and the construction

company; a financial institution may assume the role of a lender, land owner, or developer. Pratt (1994)

suggests that the view of the propecty developer as a unitary category is misleading: 'there are a

variety of forms that the 'developet may take. The exact speclication of the developer will depend

upon a whole range of contingent conditions and so cannot be identified a priory' (p. 203).

In this thesis I use the term 'real estate company' to descnbe an organization that engages in

various functions that are related to real estate development and investment, primarily development,

redevelopment, and ownenhip of real estate properties. The terni 'developer' is used when the major

activÏÏ of a real estate company is development. Development is improvement to land either through

the production of new properties or the redevelopment of existing buildings. A major, but not exclusive,

role of real estate companies is to develop real estate assets. However, real estate companies do not

develop office buildings or other structures a l the time, but they also engage in other operations. Real

estate companies may engage in 'ownenhip' and 'trading' of real estate properties, but not necessanly

in developrnent. The term 'real estate sector' is used to situate real estate development within a broad

range of economic activity. It is a faidy loose terni, which coincides with that branch of the economy

designated in the Canadian Standard Industrial Classification as 'Real Estate Developers and

Operaton'. In addition to the traditional real estate mmpanies, financial institutions may assume the

role of developer for a short or long period of time, and may peiform the role as ownea of office

buildings. Since their main role, however, is not real estate development or ownenhip, the term

'financial institution' will be used as a distinct category.

The causal connections, as suggested by the realist approach, can only be discovered through

intensive research. In the real estate sector in general and in office development in particular extensive

data is limited. This, and the fact that there are very few real estate companies whose major business

is office developrnent, makes the use of intensive research very important. Research presented here

relies heavily on data and information that were obtained through a multi-faceted collection process.

Consequently, this thesis is primarily qualitative research based on insights gained through careful

examination of a multitude of sources including newspapers, trade joumals, official company reports

and company brochures. Information was obtained through semi-structured interviews with prominent

participants in, and observes of, the commercial part of the real estate industry in Canada. Extensive

data on building permits at different spatial scales and a comprehensive office building inventory for the

Toronto Census Metropolitan Area were obtained.

Thesis organization

Chaoter One provides a set of theoretical considerations, synthesizes major components of different

approaches analyzing real estate, and re-conceptualizes office development by focusing on real estate

companies. Three major approaches to real estate development are discussed: neoclassical, political

economy, and institutional. From these approaches, selected components that are considered as

cornentones for understanding off'ke development are chosen. The major part of this chapter consists

of an analysis and synthesis of secondary Merature.

Cha~ter Two outlines the condiions for offm development in Toronto. In order to establish a

Toronto case study of office development, the physical, economic, and politml conditions will be

addressed. stressing the crucial position of municipal organization. This chapter also provides the

methodological framework. Realist methods are explained and related to the study of real estate

development. In the last section of this chapter, the type of data and sources utilized are described in

detail.

Cha~ter Three provides a broad historical account of the modem commercial real estate

development industry in Canada. Focusing primariiy on the publicly heid real estate companies, which

are abo the most spatially divenified companies, this chapter sketches the dynamics of this sector in

Canada. This chapter also establishes a plaîform for the interpretation of the practices of office

developen in the Toronto area by identifying major developen. This identification procedure highlights

the role of local, Toronto-based, companies that have their main field of operation in the Toronto area.

Cha~ter Four addresses the role of finance capital and financial institutions in financing office

development. In this chapter both the perspectives of real estate companies and financial institutions

regarding real estate financing are considered. Financial institutions often undeaake office

development for investment purposes and perform the same functions as real estate companies. This

role, together with their spatial practices in the field of offie development and ownenhip, is a key

cornponent of this chapter. Finally, I present some preliminary observations and thoughts on the role

played by transborder capital flows in real estate development.

Cha~ter Fihm investigates the practices of real estate companies using the conceptuaiization of

'three dimensions of capital switching' within the Canadian urban system. The investigation of the

practices of real estate companies is positioned in the context of building cycles. Office building cycles

at different scales and locations have spatially discrete patterns. I argue that office-building cycles

shape the fields of operation of real estate companies at the scale of the Canadian urban system. The

next two chapten move from the national to the metropolitan scale. The empirical findings of the case

study of the Toronto Census Metropolitan Area are presented in chapten Six and Seven.

Cha~ter Six documents the development of the office building inventory in Toronto in the last

fifty years. Contrary to a common perception based on the high visibility of a limited number of high-rise

office buildings in Toronto's Financial District, the stock of office buildings is far more heterogeneous. It

ranges from a large number of srnall and mid-size buildings to a limited number of large-scale

structures. In ternis of spatial patterns, office buildings are grouped into office districts. These office

districts provide a variety of operational fields for specialized office developen.

Cha~ter Seven articulates the argument of spatial selectN'i of office developen within the

Toronto Census Metropditan Ares. The distinctive spatial operations of developen support the

argument that real estate capital is highly specifc and embedded in particular spaces. The concept of

'office development district' is introduced; these districts sct as the spatial containers for different

developen and at the same time are prduced and reproduced by real estate companies.

CHAPTER ONE

THEORlZlNG OFFICE DEVELOPMENT

It is the purpose of this chapter to extract from the broader literature on real estate development and

from specific writings on office development principal arguments, which help to understand office

development across urbm systems and parkulariy within metropolitan areas.

The structure of this chapter is as follows: first, principal literatures or approaches will be

discussed. The neoclassical, the pollical economy, and the institutional approaches each contribute to

the understanding of office development. There is considerable scope in synthesizing insights from

these three approaches. The second part of this chapter focuses on distinct sub-processes or

components of the real estate development process. These components are building cycles, the

involvement of finance capital, the role of real estate companies, the role of the state, and issues which

are related to the specific settings of real estate development within metropolitan areas. A third part of

this chapter reconceptualizes office development by putting real estate development companies into a

central position.

1.1 Principal Approaches Research on real estate development has relied on quite different approaches. The neoclassical

approach with its focus on the demand-supply aspects of real estate development dominated until

about 1970. Beginning in the late 1960s and the early l9ïOs, another set of approaches emerged and

was employed to analyze real estate development. Scholars, drawing upon the writings of Man,

became interested in the logic of capitalist accumulation as a major factor dominating the production of

real estate properties. The forces of capitalisrn and its monolithic nature were unpacked in the 1980s

by political econorny analyses and institutional approaches. From a thematic point of view, most of the

early research was concemed with housing and less with commercial or office development. Starting in

the 1980s, a growing proportion of research was focused on commercial real estate development,

including retail, industrial, and office development.

1 -1.1 Neo-classical approaches

Researchers relying on neoclassical approaches have studied office development or 'office markets' by

focusing on market forces. Neo-classical approaches used the demand-supply equilibrium concept in

attempts to explain how office markets work (Fisher, 1992; DiPasquale and Wheaton, 1992; Clapp,

1993; 1992; Mills, 1995). Atternpts have been made to explain economk mechanisms, primanly price

adjustments, that shape office markets (Rosen, 1984; Hekmm, 1985; Shilling et al., 1987; Keogh,

1994; Henneberry, 1999). Vacancy rates, for example, reflect the balance between demand and

supply. and demand is detennined by macro-economk conditions, such as business cycles.

Considerable arnount of research has been oriented toward modeling o f f i i building cydes (Barras,

1983.1987.1994; Barras and Ferguson, 1985,1987; Wheaton, 1987; McGough and Tsolacos, 1997).

Another research Stream mthin the neoclassical conceptual framework has been exploring the benefiis

of portfolio diversification based on different propeity types and multiple locations (Hartzell et al., 1987;

Eichhok et al., 1995; Hoesti et A., 1997; Hamelink et al., 2000).

According to the neoclassical perspective. in a market economy, exchange takes place on the

basis of prices determined by the interaction of supply and demand. In the case of real estate, rent is

the price a tenant pays for occupying a paiücular space. The interaction of demand for real estate and

the supply of rental propeflies detemine the level of rentals. Price is detemined by demand. and

supply follows, rather than influences demand (Harvey, 1987). The real estate development pmcess is

therefore demand-driven. Agents engaging in the development process are assumed to act in unison,

collectively providing development at the right time, and reacting automaticalty to the structure of

demand (Boume, 1976). The model implies the existence of a perfect market and the rapid elimination

of any price differences. Both consumers and producen seek to maximire utility and profiiability, and in

doing so they are unhampered by social. legal, or local constraints. However, recenüy some writers of

the neoçlassical school have stressed the role of supply in structuring property markets (D'Arcy and

Keogh, 1997; Nanthakumaran and Watkins, 2000).

As Lichfield and Darin-Drabkin (1980) note, real estate developers operate on a profit-

maximizing basis by considering alternative projects, and selecting among them on the basis of

maximum profiiabiltty per unit of investrnent. Apait from rationality and profa maximization, there are

severa! other assumptions incorporated in the demand-supply model. One such concept. perfect

cornpetition, relies on a simplification of real estate markets by assuming that products are

homogeneous, that there are large numbers of buyers and seilers, and that actors have perfect

information.

However, authon relying on neoclassical frameworks, have increasingly recognized urban

specificity as a major condition shaping supply of and dernand for land and property. As Bakhin et al.

(1988) observe, the property market is very imperfect. In practice, the property market is not one

market but is divided into a number of sub-markets. Property itself is not homogenous and divisible into

small and uniform units, but is instead heterogeneous and comprises different sles, each with their

own characteristics Sites with different characteristics give rise to differential rents (Coakley, 1994;

Rabianski and Cheng, 1997). In the simple case of a monocentric city, an integrated land market

shapes the pattern of land use resulting from the interaction of land prices and location bids by the

different sectors of the economy (Alonso, 1960). This bidding process leads to the emergence of

districts, for exarnple, a financial district, a legal district, or a residential district (Archer and Ling, 1997).

Land prices decrease consistently from the city's centre, because they reflect the value of accessibility

which is maximized in the Central Business District. The land market described by Alonso (1 960) has a

single continuous price gradient because it is integrated. Recently, this spatial integration has been

questioned. The distinction between downtown and suburban districts within the metropolitan area and

the idea of the 'polycentric city' (Ladd and Wheaton, 1991 ; Berry and Kim, 1993) indicate that in fact

the land market is segmented for a variety of reasons. Evidence of multiple price gradients, mostly

unaffected by proximity to downtown suggests that the market is not differentiated with respect to any

single location, but that the market is segmented within the rnetropolitan area (Clapp et al., 1992; Hoch

and Waddell, 1993; Hanink, 1997; Rabianski and Cheng, 1 997).

According to the neoclassical approach, the intensity of real estate development is shaped by

the land value gradient or a series of land value gradients. Transportation lines, which converge at one

location, give rise to what has been referred to as the 'peak land value intersection (PLVI). As a result

of maximum accessibility, land values at the PLV1 are the highest in the city. Demand for space results

in soaring land costs, which reflect the potential value of the land if built upon to the maximum

allowable extent (Ford, 1994). In these locations, the cost of land is the major component in office or

other real estate development. Capital is substituted for land as large amounts of capital are invested in

the erection of more intensive land uses to compensate for high land values (Baume, 1967). In this

case, large-scale office buildings are predominant as a resuH of financial calcu!ations emphasizing

maximum retum on investment (Willis, 1995).

The assumptions regarding a perfectly functioning market have been heavily criticized. Harvey

(1973) argued that land prices in the CBD do not depend on locational advantage, because land

owners want to achieve high rents. Similady, Ball (1985) suggested that large-scale financial

institutions develop office buildings in high-priced locations in the city centre to minimize the risk of

premature obsolescence. The property market is ubiquitous, and there is no formal organized

marketplace, central agency, or instlution, where prices are quoted and publicly witnessed. tnstead of

a large number of buyen and seller's, there are relatively few with sufficient finance to invest; therefore,

financial institutions and property nvesbnent companies dominate the pmperty market. In some cases,

there is no freedom of entry into the real estate market as would be expected under perfect market

conditions (Markusen and Scheffman, 1977; Kostin et al., 1989), and as monopoly or oligopoly power

occur, the geographic division of the market leads to imperfect cornpetition. Another criticism of

neoclassical modek argues that maximizing pmfiiability may not be the prime objective of either the

space user or the real estate developer. Also, changes in income and business conditions and the

difficulties in obtaining up-todate knowledge may prevent the punuit of maximum profits (Momson,

1992). Criticism based on empirical observation about office development indicates that the high cost

of land is not necessarily the reason for large-scale buildings. Feagin (1988) argues that despite the

fact that land costs are only a small fraction of the total development costs, high-rise office buildings

were erected in downtown Houston.

Although it may be generally the case that land values and building densities are strongly

related, the question of how land value surfaces are produced is not adequately addressed by the

neoclassical approaches. Accessibility depends on both the articulation of the publicly produced

transportation system and the spatial patterns of customers or input sources. These spatial pattems

are long-lasting, and their expianations require a form of historical analysis that the subscfibers to the

neoclassical approaches would rather stay away from.

Contrary to the tenets of some of the neoclassical approaches, the supply of buildings is

relatively inelastic, and the changes in the building stock and location are slow due to the durability of

buildings and the small proportion of real property of any type coming ont0 the market at any one time

(D'Arcy and Keogh, 1997). The property market is, therefore, in a constant state of disequilibrium. The

actors who supply the market also do not necessarily respond to demand as assumed in the simple

demand-supply relationship. Various factors, such as taxation, national interest rates, and govemment

policy and subsidies, determine the framework of supply. Real estate developers do not constitute a

homogeneous entity, but rather they make up a group of multiple agents with dÏfferent interests

(Beauregard, 1993; Pratt, 1994). Finally, development often occun speculatively, only remotely related

to actual demand. Development booms may be related to the sharp expansion of money supply, as

was the case in the 1920s (Willis, l995), and more recently in the 1980s (Ball, 1994; Fainstein, 1994).

A recent. and a useful, strand in neoclassical research is the application of portfolio theory. The

use of portfolio theory in real estate analysis has emphasized the position of real estate assets as

distinct financial vehicles that can be switched between products and places (Miles and McCue. 1984;

Coakley, 1994; Hoesli et al., 1997). The reasons for capital switching are emerging opportunities, which

corne about through a change in existing conditions, such as different retums on capital. Different

investment vehicles, different property types, and different locations, possess different rates of retum.

The purpose of this type of analysis is to detenine the optimal resource allocation within a company's

investment portfolio. To combat the perils of unceilainty, diversifikation strategies, including different

property types and different locations, are proposed. In this avenue of research an important topic is

the investigation of the benef i of divenifikation at a number of geographic scales. Corporate Cnancial

interests consider spatial diversifkation as an instrument that is mainly designed to optimize risk-return

relationships (minimizing risk while maximizing retum) of real estate portfolios.

lnveston have sought to divenify according to property type andlor according to geographical

area. The logic of diversification baseci on property type lies in the belief that retums to each type are

determined by different economic 'driven' (retail performance is diiven by consumer expenditure. office

retums by growth of seMce employment. and industrial performance by manufacturing production).

While there are common factors (like GNP growth and interest rates), it is assurned that these different

'divers' do not coincide across different regions, and hence spatial diversification is beneficial.

However, the usefulness of the region as a unit of analysis has been the subject of much debate

(Hoesli et al., 1997; Hamelink et al., 2000). Within portfolio theory, switching strategies between

different property types have been considered as more beneficial than spatial diversification. Spatial

diversification has been more problematic to conceptualize, since it depends on a number of scales

and a multitude of definitions of regions. In general, analyses based on metropolitan statistical areas in

the U.S. suggest that the largest urban areas are the favoured locations for real estate investrnent.

However, the market is segmented: institutional investors prefer to invest in the largest urban areas

while private investors have more dispersed geographical patterns (Shilton and Stanley, 1996; Lindahl,

1 997).

Overall, the principal shorkoming of the neoclassical approach is the absence of the public

sector as a major participant in the real estate developrnent process (although the role of institutionai

structure was addressed by some researches, for example, Bal et al. 1998). Real estate development

is not driven entirely by market forces and an orderly function of real estate markets involves

govemrnent participation. Also, neoclassical approaches emphasize the strong relationship between

building intensity and land values. However, land value surfaces are modulated by accessibility, which

is collectively produced through investment in infrastructure and through the interdependence of many

land uses. There are also many exceptions. For example, high land values predominate in the inner

city. but high-rise buildings do not materialize because of many factors. including social struggle over

the built environment. There are interesting ideas embedded in portfolio theory. Real estate assets are

seen as tradable assets that shift between property types and locations. In later conceptualizations I

will draw strongly on this concept.

1.1.2 Political economy approaches

Harvey's work (1 978, 1982, 1985) on circuits of capital and the role of investment in the production of

the built environment has provided the theoretical framework for a political economy approach, which

focuses on the suppiy of capital as the driving force of real estate development. Harvey's initial

argument suggests that in the long nin, in the absence of profitable investments in the primary

(manufacturing) circuit of capital accumulation, capital will flow into the secondary circuit, where capital

is deployed in the production of the built environment.

Hanrey's contribution to understanding real estate development has been important in other

respects. Harvey acknowledges the important role of the state in facilitating real estate development.

Both the private sector and the state are part of the capitalist system. The different levels of the state

(federal, intermediate, and local) provide the conditions of the continuous process of real estate

production. At the local level, govemment regulation is needed in order for the speculator-developer to

function (Hatvey, 1985, pp. 68-69).

f i a ~ e y discusses the nature of uneven spatial development of the buift environment at

different spatial scales, impiying that uneven development is an essential condition for capital

circulation in capitalist economies (Harvey, 1985, pp. 19-20, 155-64). In addition, his idea of capital

switching paves the way for the notion of spatial switching. Haivey acknowledges that capital can flow

from one place to another (Harvey, 1985, p. 13). These switching practices, between circuits/sectors

and places are crucial practices of real estate companies as will be demonstrated in later sections.

Other researchen did not substantiate Harvey's argument conceming capital switching between

circuits of capital accumulation. After research on the sources for real estate investment in Houston in

the 1970s and l98Os, Feagin (1 987, 1988) suggests that "financial institutions, both those inside Texas

and those outside, channeled much surplus capital from a variety of sources into Houston real estaten

(1 987, pp. 182-83). Beauregard (1 991, 1994) argues that primary-circuit capital may seek other outlets

than the built environment. However, in spite of the difficuity of establishing a clear link between

industrial and real estate capital in the short nin, Harvey's ideas remain influential in establishing an

office development theory (see section 1.3).

The recognition of the real estate sector as an independent or nearly independent sector of the

econorny, which requires its own analysis, has led to an emerging research agenda within the political

economy approach (Feagin, 1987; Haila, 1991 ; Beauregard, 1994; Fainstein, 1994; Leitner, 1994). In a

preliminary outline. Haila (1 991) argues that the real estate sector has an 'intrinsic dynamic' rather than

being extemally driven by the switching of capital between different circuits of accumulation. This

dynamic shapes investrnent patterns in real estate assets, and is based on the intemal characteristics

of real estate pmperties, narnely tradabiiii, divisibili, and mobili. Real estate assets are tradable;

they are bought and sold in the market. like other types of financial assets (Harvey, 1982). Although

properties cannot be traded in small units in the same way as stocks (Coakley, 1994), they can be

divided into large units because the ownenhip of properties can be shared by a number of

investordpartners. In addition, the real estate sector is segmented into commercial and residential sub-

sectors, and into distinctive property types, such as office, industrial, and retaü (Beauregard, 1994). It is

further segmented spatialty. Some &ers acknowledge that the real estate sector is hrgely a 'local'

business, ahough some components of this sector are beyond the local realm (Logan, 1993; Bryson.

1997). Other theonsts suggest that real estate properties have becorne increasingly 'delocalized',

because some aspects of the real estate sector (architecture, reaf estate ownership) are shaped by

'global' forces (Sassen, 1991 ; Knox, 1993; Savitch, 1995; Beauregard and Haila, 1997). The complex

spatial configuration of real estate investment is further segmented as a resuit of the spatial divergence

of building cycles and the fact that at the level of urban systems different cities experience different

building cycles (Leitner, 1 994).

Within the political economy approach, Marxist authors emphasize issues of land ownership

and rent as core elements in their framework of explaining the production of the built environment

(Harvey, 1 982, 1985; Haila, 1988, 1990, 1991). lnstead of the assumption buik into neoçlassical land

use rnodels, Marxist interpretations suggest th+ possibility of power in the han& of few land owners.

(The existence of several kinds of land owners with distinct interests and modes of behaviour is

recognized by Massey and Catalane, 1978.) In addition, it is suggested that land has a monopolistic

character. Hanrey argued that there are monopoly prîvileges inherent in any fomi of private property in

landn (1 985, p. 102) and Logan and Molotch (1987, p. 23) have wnsidered land markets as 'inherently

monopolistic'. This enables land owners to manipulate or control the land market by charging monopoly

rent.

The major critique of the political economy approach revoives around its high degree of

generaiization and abstraction. More specifically, the relations between the general conception of the

structunng dynamics of the development process and the specific interests and strategies of individual

agents remain to be established. Much more attention needs to be given to the ways individual f i n s

and agents interrelate, and how various economic and political factors. which govern their strategies,

are incorporated into a structure-agency framework (Healey and Barrett, 1990). Also. the impossibility

of documenting some assertions such as flows from the pnrnary to secondary circuit (Feagin, 1987;

Beauregard, 1991; 1994) has attracted criticism (Ball, 1994). Also, there is little research on the role of

transnational flows cf capital in real estate development (Logan, 1993). Regarding the idea of land

rnonopoly, the fact of concentrated ovmenhip in real estate does not automatically mean that a

condition of monopoly is attained; monopoly might only occur in locarued and isolated situations

(Houghton, 1 993; Fainstein. 1 994).

1.1.3 Institutional approaches

Advocates of institutional approaches argue that it is essential to understand the institutionai foms.

relationships, and practices of the real esMe sector. The starting point s the institutional articulation of

the real estate sector and the patterns of netwoiks and relationships between agents. This results in an

institutional rnap of the development industry (Healey. 1992b). As Healey and Banett (1990, p. 93)

argue:

Wuch more attention needs to be given to the way individual fims and agents intenelate in the negotiation of

parkular development projects and how, through these transactions, land and properly 'markets' are constituted

and built environment invesbnent decisians madeg.

Healey (1 992a) and Momson (1 992) have provided expositions on institutional approaches to the reaJ

estate industry. They argue that the focus of institutional approaches is pnmarily on identifying the type

and composition of agents involved in the real estate development process and revealing the interests

and strategies they adopt. The nature of the relationships which occur between acton, their actual

roles, and the relative influence they enjoy in the negotiation of particular projects are analyzed in tum.

Healey (1992a) presents an institutionai modei of the real estate development process that

takes into account the complexw of the events and agencies involved in the process, and the diventty

of forms the process rnay take under different conditions. At the theoretical level 'the critical issue here

is to make the connection with the social relations expressed in the prevailing mode of production,

mode of regulation, and ideology of society within which development is being undertaken" (Healey,

1992a, p. 37).

Various authors have constmcted models about how the actors interact and how the

development process operates. Drewett (1973) presents the simplest model with the focus on the

developer. Arnbrose (1986) suggests a more complex model. There are three sets of agents in

Ambrose's model: the finance industry, the state, and the construction industry. All three sets interact in

the process of creating the built environment (Ambrose, 1986). Apart from depicting the development

process, various researchers have written about the development process in ternis of the stages

developers go through from initiating a scheme to its completion (Drewett, 1973; Cadman and Austin-

Crowe, 1983; Ratcliie and Stubbs. 1996). Many of these stages and issues, such as finance, classes

of developen, or landowners and real estate agents, within the development process have been

elaborated on in depth by other researchen (Cadman and Au&-Crowe, 1983; McNamara, 1985;

Ambrose, 1 986).

These works focus on agents and differ from the neoclassical and Manist approaches in

being concemed with the details of how the davalopment process takes place, rather than makng

generalizations and engaging in abstractions. Agents are not treated as homogeneous entities, but are

clearly differentiated (O'Malley, 1989; Morrison, 1992). Institutional scholan have noted how

developen interact with other intemediaries within the development process. How developers interact

with the state was the focus of several studies undertaken by researchers of the institutional school

(Am brose and Collenutt, 1 975; Lonmer, 1 978; Ambmse, 1 986; Healey, 1 998a). The extensive attention

given to the state is in contrast to the neoclassical literature, which ignores or downplays the role of the

state in the supply-demand model, or the Manist literature, which regards the state as a mediator of

capital flows between the primary and secondary circuits without providing analyses of its exact role.

Institutional analyses have been criticized because they place too much emphasis on the

actors and their interactions. They have also been cnticized for being too descriptive and for not

adequately focusing upon structural factors which govem the behaviour of agents. The descriptive

nature of some of the institutional analyses and the lack of attention to the economic and political

conditions which constrain the actors in question, present major limits to their analytical ability.

Structural factors have to be embedded in institutional analyses, since they affect the provision of real

estate assets (Morrison, 1992).

1.2 Components of the Real Estate Development Process The real estate development process is shaped by various forces, and involves severai types of

agents. Different elements in the approaches discussed in the previous section contnbute to the

knowledge of this process. In this section I merge conceptualizations derived from various approaches.

These concepts are fhen used in an attempt to construct a theory of office development, which will be

presented in section 1.3.

Four major elements are considered as pivotai in the literature on the real estate development

process. (Capital switching was addressed before and will be included later in the conceptualization of

the real estate sector.) These are building cycles, financing arrangements, the role of the state, and the

role of real estate developers. Building cycles are the cumulative reflection of numerous actions that

produce real estate properties. The differentiation of building cycles by property type and location is

addressed, and macroeconomic forces shaping the development process are considered. As is

demonstrated in this section, real estate development cannot proceed without substantial financing that

is outside the realm of the Company that develops a parthlar propeity. As a result, real estate

development depends on the availabiiii of financing. The state, at its various levels, is an essential

part of the development process, since development occun in existing settings that are regulated by

the state. In addition. development is place-specific and developen need to interact with the state level

that is relevant. Finally, the indMduals or organizations that initiate, execute and manage the process

are real estate developers. Their pivotai role as the shapen of the built environment has been

recognized in the literature.

1.2.1 Building cycles and their spatial aspects

Construction activity and investment in the built environment are subject to cyclical patterns known as

building cycles. Building cycles play a major role in neoclassical and in Marxist approaches in

explaining urban development. Kuznets (1 930, 1958) first identified long investment or building cycles

with a period of up to twenty-fie yean, and Hoyt (1933) documented the cyclical pattern of land prices

in Chicago. Harvey's analysis of real estate development in the United States and Britain suggested

that investment in real estate depended on the cyclical nature of the economies of these two countries

(Hawey, 1985).

Building cycles encompass a multitude of components that have to be separated. First,

building cycles are a 'family of property cycles' (Barras, 1994). These cycles Vary in length from long

cycles of 20-ta-30-year periods, to cycles spanning 9 to 10 years, and short cycles of 4 to 5-year

duration (Barras and Ferguson, 1985; Barras, 1994). Second, instead of treating the built environment

as a homogeneous product (Harvey, 1978), real estate products should be differentiated. Within the

real estate sphere each product has a different cycle, which is especially apparent when residential and

commercial development are compared (Ball, 1994; Barras. 1994; Beauregard, 1994; Keogh, 1994).

Within the commercial sector an additional disaggregation is possible, namely between office, retail

and industrial sub-secton. This is required, because different 'drives' propel each sub-sector (for

example, office development is driven by the growth in office-based ernployrnent, Hoesli et al.. 1997).

Building cycles are also shaped by govemment regulation. best exemplified by zoning bylaws.

Govemments tend to enforce restrictive regulations during downtums, and introduce more liberal

regulation during the uptums in building cycles. In an article titled 'The politics of real estate cycles',

Weiss (1991) suggests that govemments intewene in the real estate sector during diierent phases of

the real estate cycles as a resuk of pressure from the large-scale real estate companies. During boom

tirnes, the status quo is prefened, while in downtum periods, the big developers advocate govemment

intervention. Weiss explains the passing of zoning bylaws in Los Angeles and New York in the eariy

twentietb century as the aftermath of a real estate downtum. He also attributes tax policies to buildings

cycles, suggesting, for instance, that the 1981 U.S. tax ad, which offered financial incentives for

developrnent, passed during the depths of a severe recession. Willis (1995) argues that govemment

regulation woiks in tandem with building cycles. Height restrictions on buildings in Chicago in the late

nineteenth and eariy twentieth centuries were shaped by the appropriate phase (boom or slump) in the

building cycle.

Office development has received a great deal of attention in the research on building cycles.

Neoclassical economists attempted to model office-building cycles by examining demand and supply

factors (Barras, 1983; Wheaton, 1987; Downs, 1993). To a large extent, the neoclassical analyses

have failed to discem spatial variations of building cycles by suggesting a synchrony of subnational

building cycles (regional and local) with national cycles as part of the notion of equilibrium (Easterlin,

1968; Gottlieb, 1976). A few studies explored the uneven spatial manifestations of building cycles

(Leitner, 1994; Henneberry, 1999) suggesting, 'the particular cycles in each c w occurred in somewhat

different times and reflected different local conditionsn (Wilfis, 1995, p. 169).

Building cycles are not unifom geographically and have long endurance. The notion that

building cycles should be considered in accordance with the geographic sale under investigation is

increasingly recognized as an essential element in building cycle analysis, since local conditions affect

the outcome of building cycles in different cities (Leitner, 1994). In examining office construction cycles

in downtown areas of major U.S. cities, Leitner (1994) illustrates how local circumstances interact with

wider financial and political trends to produce unique outcomes. Despite the trend toward convergence

in the timing of office construction cycles between different cities, individual cities continue to show

differences in the ways they are affected by and participate in national and international trends.

Changes, such as econornic restruduring, growing demand for office space, the relative attractiveness

of commercial real estate, and govemment regulations have differential effects on urban property

markets. Cities experience different development cycles in t e n s of timing, length and volume, and in

ways that reflect the specific conditions in these localities and their changing position within the larger

urban system (Leitner, 1994).

Henneberry (1999) provides a different interpretation of building cycles. He argues that

property investment has become dislocated from user requirements, and that building cycles are not

shaped by local conditions but rather by the preferences and decisions of major financial investors. In

contrast to the political economy approach advocated by Leitner, he suggests a neotlassical approach

to explain spatial variations of building cycles at the regional level. Based on Keogh's (1 994) analysis,

the propeity market is depicted as a set of three interrelated components: the user market, the

investment market, and the development market. Each is a trading arena where the interaction of

demand and supply determines the price. Changes in use values (rents) or in required rates of retum

on property investment (yields) produce rapid changes in investment (capital) values. Developen who

monitor the market on a regular basis will respond to these changes by increasing or decreasing

development activii. Spatial differentiation is oniy a marginal component in this analysis (Keogh,

1994). According to Hennebeny, the timing of regional office building cycles is determined by the

property price mechanism; in other words, the interplay between rents, yields and capital values. Each

market has its own building stock, vacancy rates, and demand; thus rents minor the local economy.

Rents and yields have locally ernbedded components. As a result, the manifestation of spatial

differences is echoed through the property price mechanism. This argument cancels out the need to

look at specific conditions, since the development is mediated through the property price mechanism.

The explanation of spatial differences on the basis of the price mechanism is insufficient,

because it does not reveal the origin of these cycles and why such differences persist. To explain

building cycles at the regional or the metropolitan level, general economic conditions as well as

conditions specific to the metropolitan areas in question have to be addressed. By combining these

sets of considerations inter-metropolitan variations can be explained.

Building cycles provide a general framework for the analysis of office development The

argument that building cycles Vary across space contributes to the explanation of uneven office

development. Also, spatially diverse building cycles indicate that there is a role for the local arena in

shaping office development. The specific local conditions have to be revealed in order to understand

the uneven investment in office buildings across urban systems and within specific metropolitan areas.

1.2.2 Financial institutions and real estate development

Early Marxiçt writing on urban development has reasoned that real estate development is a 'by-product'

of the capitalist production system (Lamarche, 1976). According to Lamarche, there is a specialized

type of capital, 'property capital', whose sole function is to produce properties in order to increase the

overall efficiency of the capitalist system. This definition puts an emphasis on pmperty as 'servant' to

capital and not as a separate sphere of capital accumulation.

These eariier conceptualizations were supeneded by Harvey's work on conceptualizing the

flows of capital within the capitalist system. According to Harvey's general theory, capital invested in

real estate originates mainly through industrial production. As a result of crises of overaccumulation in