The Brink of Brexit — Event slideshow | PwC Ireland

135

On the brink of Brexit: the economic consequences for the island of Ireland PwC, 17 October 2019 Presentation Slide Pack Organisers: Thomas Conefrey (Central Bank of Ireland), Katy Hayward (Queens University Belfast/UK in a Changing Europe), Ronan MacNioclais (PwC).

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Brink of Brexit — Event slideshow | PwC Ireland

On the brink of Brexit: the economic consequences for the island of Ireland

PwC, 17 October 2019

Presentation Slide Pack

Organisers: Thomas Conefrey (Central Bank of Ireland), Katy Hayward (Queens University Belfast/UK in a Changing Europe), Ronan MacNioclais (PwC).

Brexit in historical perspective

Kevin Hjortshøj O’Rourke

NYUAD

What the book does

• To understand Brexit and the negotiations that follow, you need to understand– Three histories (UK, EU and Ireland), how they

have shaped attitudes and economies, and how they are interacting today

– The logic of free trade areas vs customs unions vssingle markets

• A lot of what we have lived through during the course of the last three years follows fairly logically from the above

The EU has a history

“We must ensure that our commemoration [of the First World War] does not give any support to the myth that European integration was the result of the two World Wars”

(memo to David Cameron)

Why is the EU supranational?

• “The profound pooling of sovereignty that is a crucial feature of the European Union permits unprecedentedly deep cooperation, which brings benefits. But it also means that when countries are in the minority they must sometimes accept decisions they do not want…So the British electorate made a choice. They chose the power of domestic democratic control over pooling that control” (Theresa May, September 2017)

Maurice Faure, 5 July 1957

• You see, my dear friends, we still maintain the fiction that there are four Great Powers in the world. Well, there are not four Great Powers, there are only two: America and Russia. There will be a third at the end of the century: China. And it is up to you as to whether or not there will be a fourth: Europe

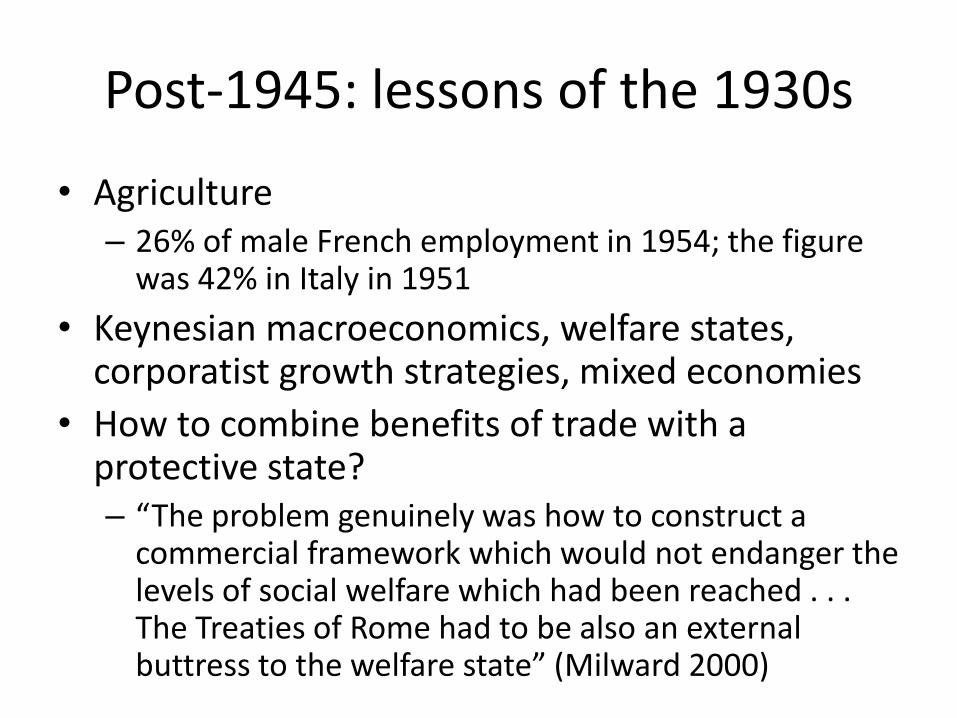

Post-1945: lessons of the 1930s

• Agriculture – 26% of male French employment in 1954; the figure

was 42% in Italy in 1951

• Keynesian macroeconomics, welfare states, corporatist growth strategies, mixed economies

• How to combine benefits of trade with a protective state?– “The problem genuinely was how to construct a

commercial framework which would not endanger the levels of social welfare which had been reached . . . The Treaties of Rome had to be also an external buttress to the welfare state” (Milward 2000)

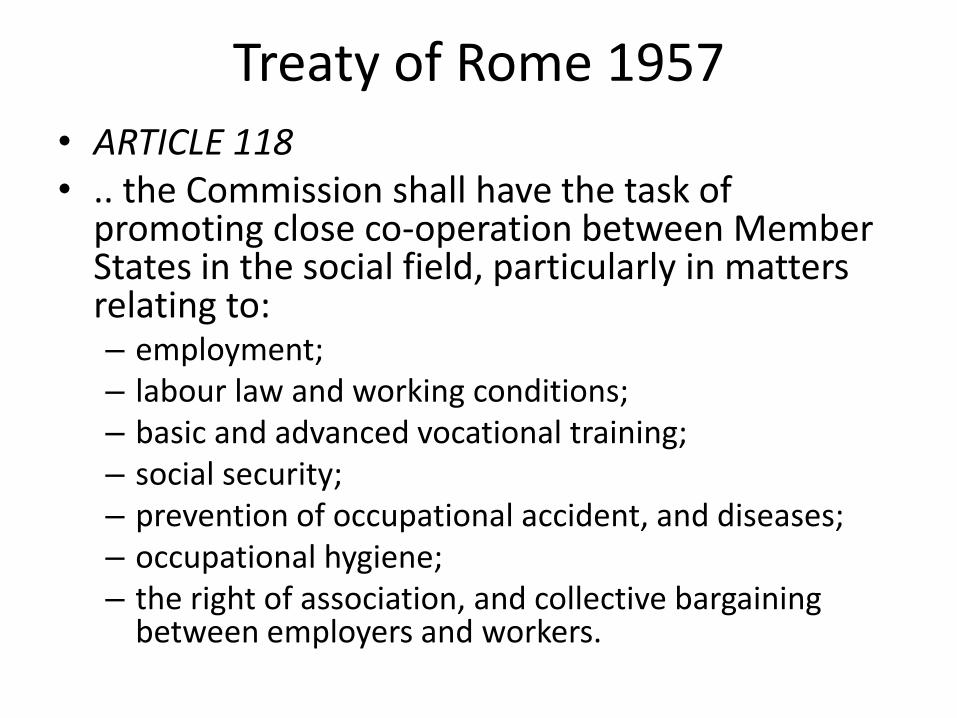

Treaty of Rome 1957

• ARTICLE 118 • .. the Commission shall have the task of

promoting close co-operation between Member States in the social field, particularly in matters relating to: – employment; – labour law and working conditions; – basic and advanced vocational training; – social security; – prevention of occupational accident, and diseases;– occupational hygiene; – the right of association, and collective bargaining

between employers and workers.

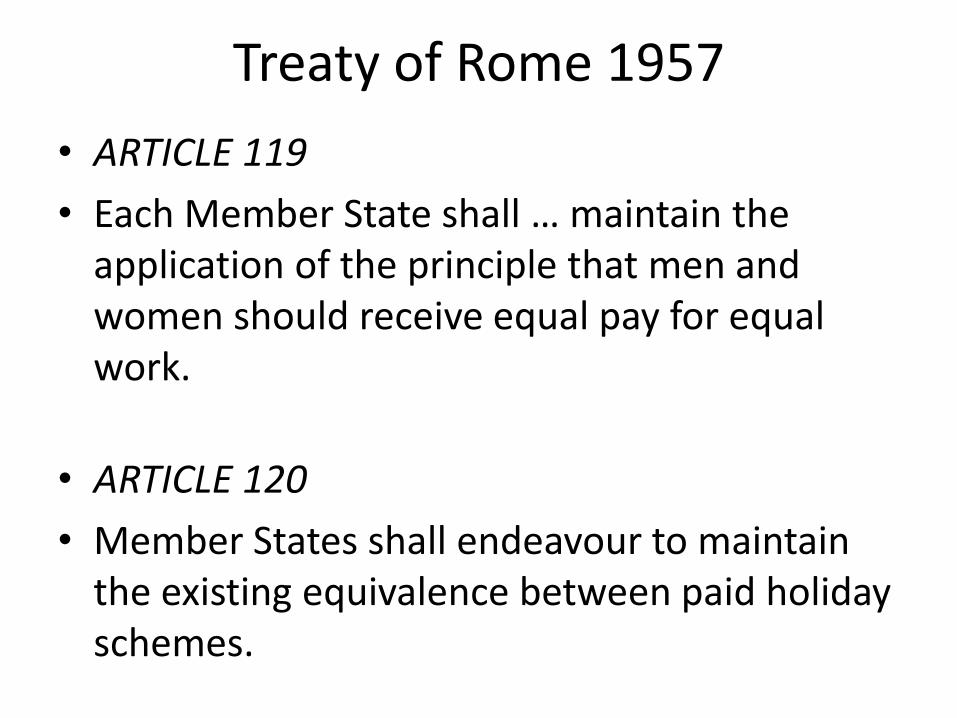

Treaty of Rome 1957

• ARTICLE 119

• Each Member State shall … maintain the application of the principle that men and women should receive equal pay for equal work.

• ARTICLE 120

• Member States shall endeavour to maintain the existing equivalence between paid holiday schemes.

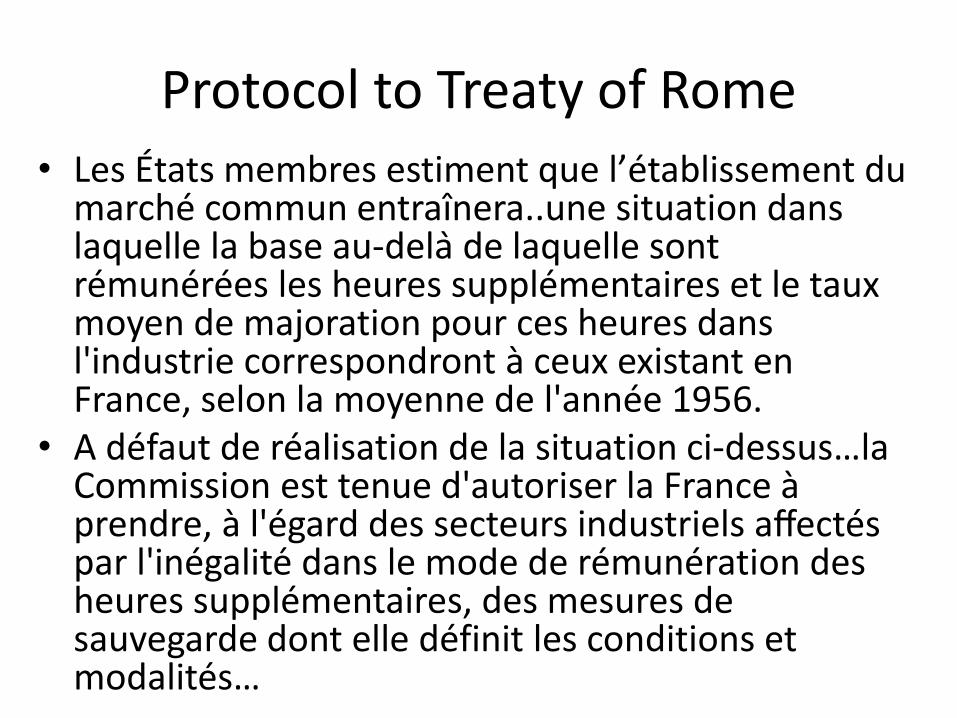

Protocol to Treaty of Rome

• Les Etats membres estiment que l’etablissement du marche commun entrainera..une situation dans laquelle la base au-dela de laquelle sont remunerees les heures supplementaires et le taux moyen de majoration pour ces heures dans l'industrie correspondront a ceux existant en France, selon la moyenne de l'annee 1956.

• A defaut de realisation de la situation ci-dessus…la Commission est tenue d'autoriser la France aprendre, a l'egard des secteurs industriels affectespar l'inegalite dans le mode de remuneration des heures supplementaires, des mesures de sauvegarde dont elle definit les conditions et modalites…

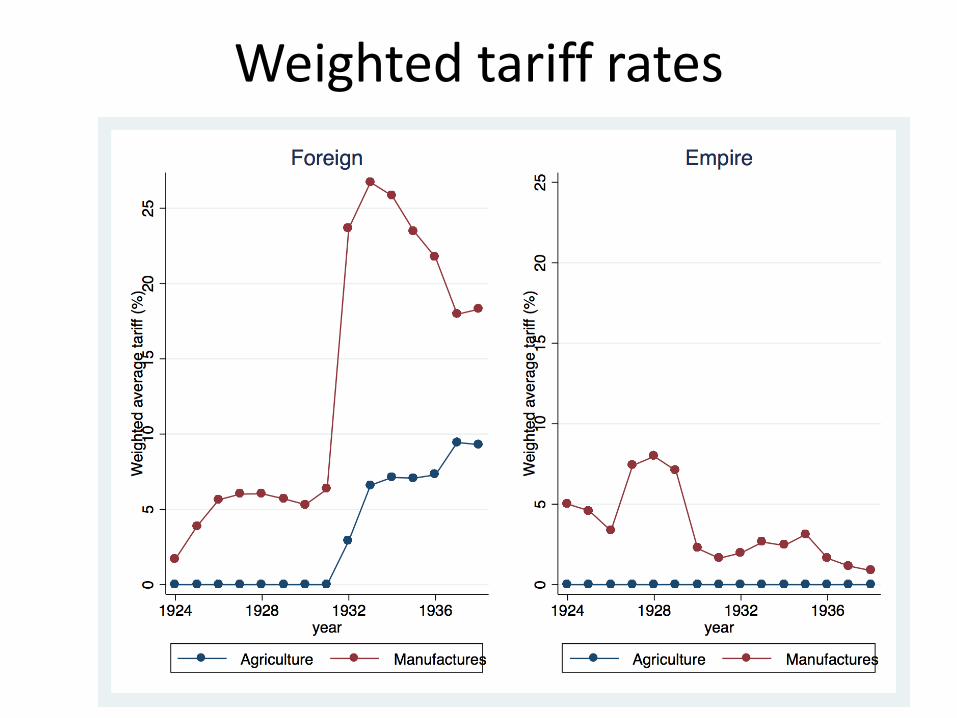

Weighted tariff rates

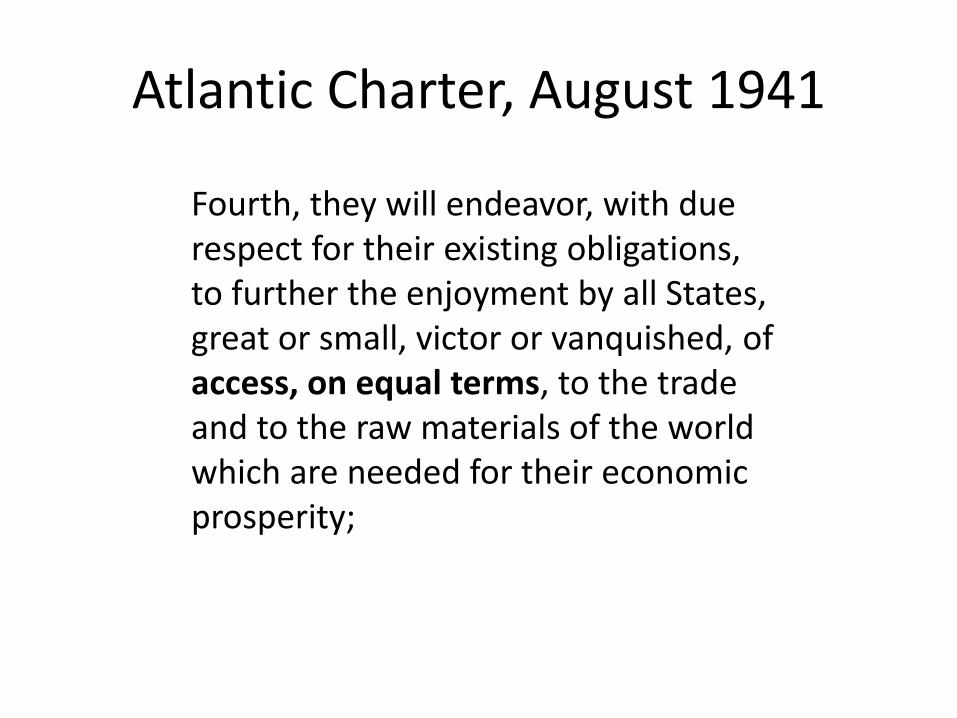

Atlantic Charter, August 1941

Fourth, they will endeavor, with due respect for their existing obligations, to further the enjoyment by all States, great or small, victor or vanquished, of access, on equal terms, to the trade and to the raw materials of the world which are needed for their economic prosperity;

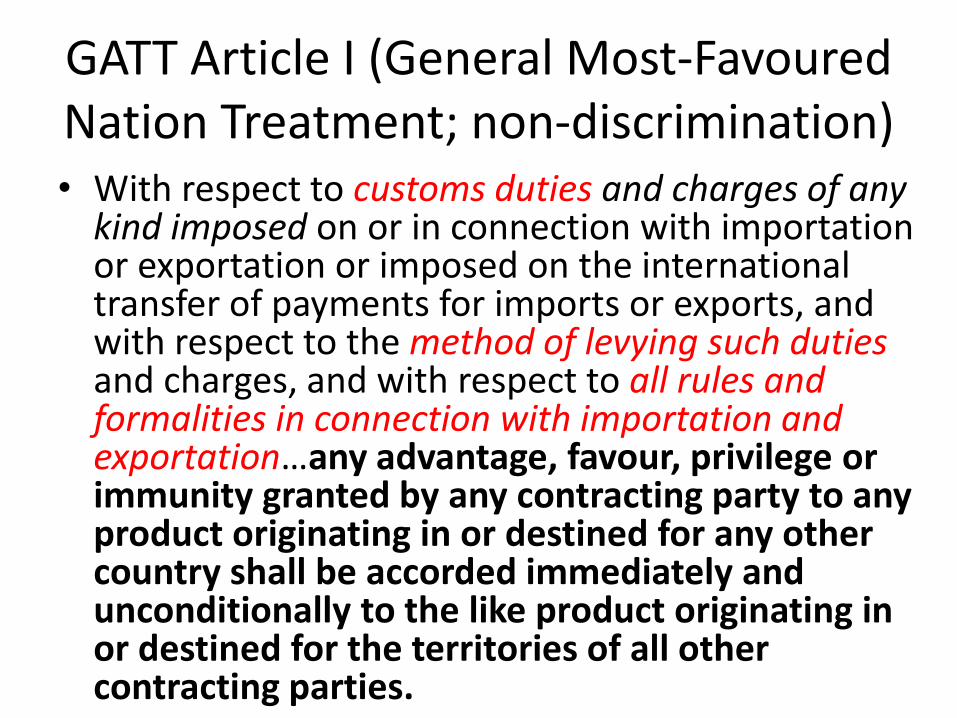

GATT Article I (General Most-Favoured Nation Treatment; non-discrimination) • With respect to customs duties and charges of any

kind imposed on or in connection with importation or exportation or imposed on the international transfer of payments for imports or exports, and with respect to the method of levying such duties and charges, and with respect to all rules and formalities in connection with importation and exportation…any advantage, favour, privilege or immunity granted by any contracting party to any product originating in or destined for any other country shall be accorded immediately and unconditionally to the like product originating in or destined for the territories of all other contracting parties.

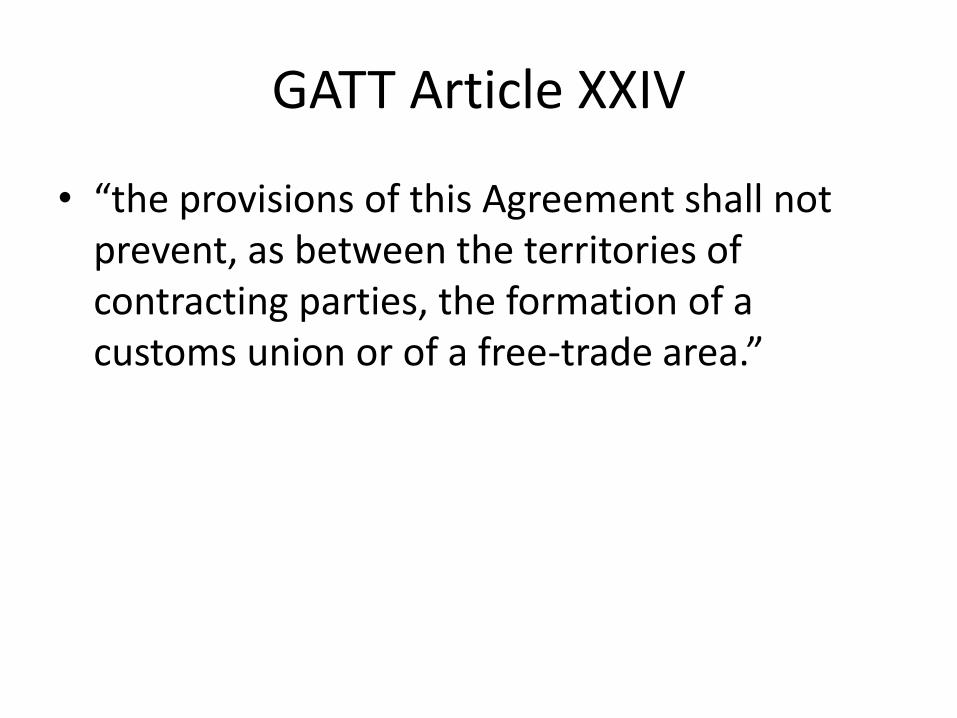

GATT Article XXIV

• “the provisions of this Agreement shall not prevent, as between the territories of contracting parties, the formation of a customs union or of a free-trade area.”

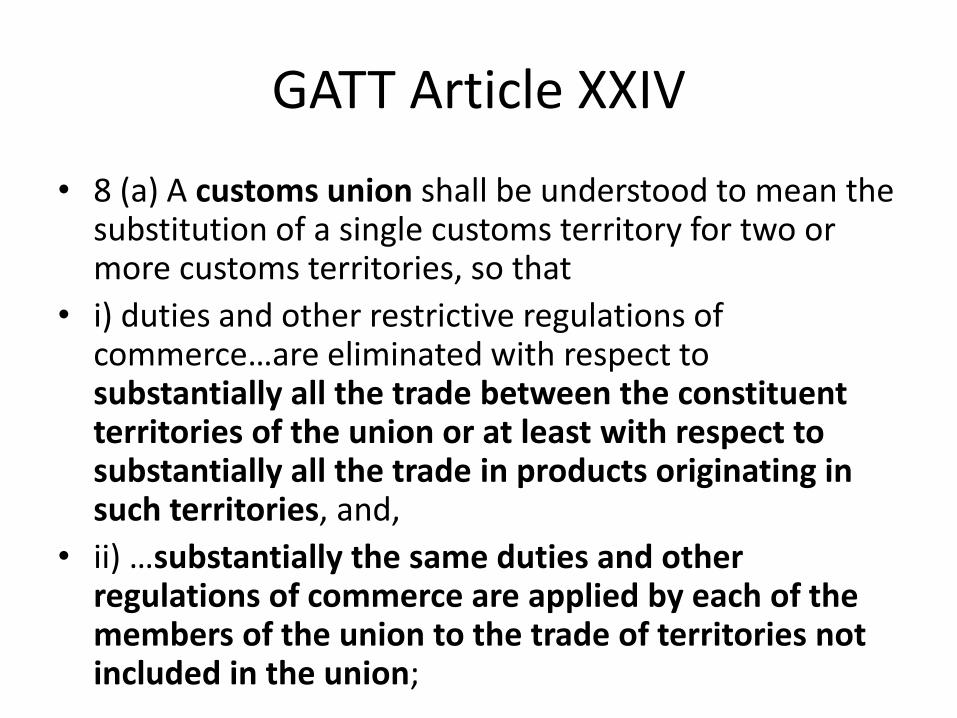

GATT Article XXIV

• 8 (a) A customs union shall be understood to mean the substitution of a single customs territory for two or more customs territories, so that

• i) duties and other restrictive regulations of commerce…are eliminated with respect to substantially all the trade between the constituent territories of the union or at least with respect to substantially all the trade in products originating in such territories, and,

• ii) …substantially the same duties and other regulations of commerce are applied by each of the members of the union to the trade of territories not included in the union;

GATT Article XXIV

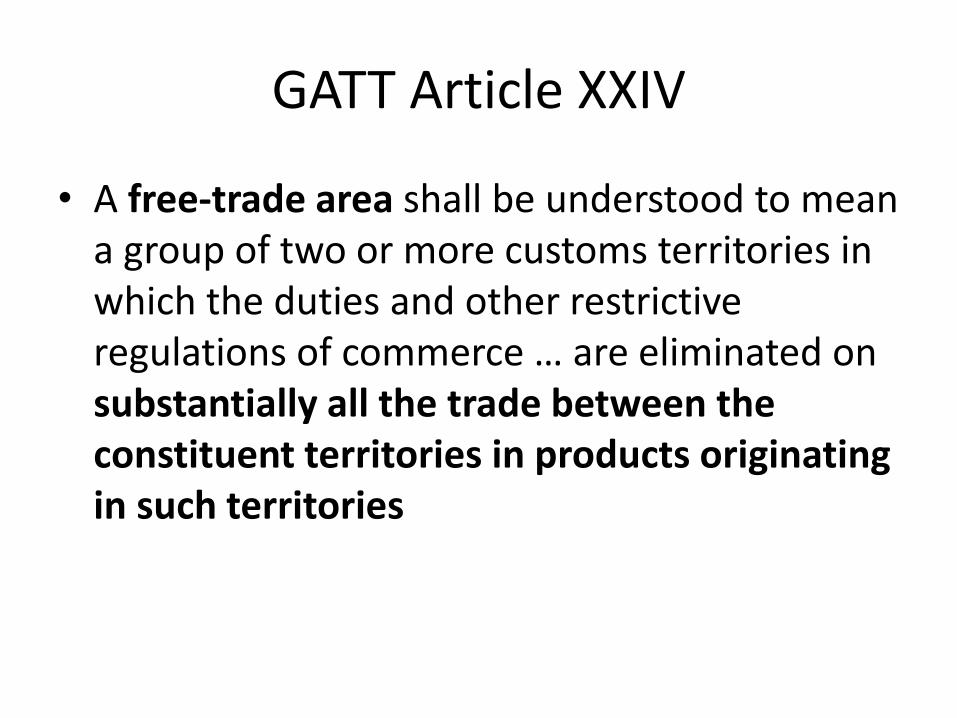

• A free-trade area shall be understood to mean a group of two or more customs territories in which the duties and other restrictive regulations of commerce … are eliminated on substantially all the trade between the constituent territories in products originating in such territories

EU history shaped EU attitudes during the negotiations

• The Single Market represents a complex diplomatic bargain and there were only 12 members in those days..

– UK can’t be allowed to unravel that bargain

• Need to retain control of Single Market rules

– UK can’t be allowed to influence EU regulations from the outside; it can’t influence the way the EU applies those regulations (e.g. at borders)

EU concerns regarding Northern Irish border

• Here we are talking very practically about –imagine – an import of shrimps from an Asian country where they treat shrimps with antibiotics, which are prohibited in the EU because they can lead to blindness. Now this shipment arrives in Liverpool and is destined for the market in Northern Ireland and also the EU27. At what moment and how do we check that there are no residues of prohibited antibiotics? . . .

EU concerns regarding Northern Irish border

• The second example is bicycles imported from China on which the EU levies anti-dumping duties. Maybe the UK in the future decides not to have such anti-dumping duties because you want to have your own system on this, so how can we ensure that bicycles, arriving in Liverpool again or somewhere else, do not end up undermining the anti- dumping duties that the EU is levying? How can we avoid that this becomes an entry point into the single market?

EU concerns regarding Northern Irish border

• The third issue – and a very important one – is VAT. How can we ensure that VAT is levied correctly? That is a major source of revenue for all our member states and is also a major source of fraud in the EU but also in the UK.

• Therefore, we will need to have a system where we can protect the integrity of the single market and the customs union, in a situation where we do not have a hard border between Ireland and Northern Ireland. It is on these very precise and concrete issues that we need to find a solution.

EU suspicions

• UK supply chains versus “taking back control”

• June 2017: “the EU will feel obliged to guaran-tee a softer border with Ireland, and that the Republic is the European Union negotiator’s Achilles Heel” (DUP)

• July 2017: David Davis on Ireland as a “test border”

• November 2017: Johnson links Irish border to Dover-Calais

EU history shaped EU attitudes during the negotiations

• Level playing field was always crucial and remains so

• Johnson’s stated wish to get rid of the (already weak) LPF conditions of the previous deal makes a free trade agreement unlikely

• Reduces opportunity cost of sticking to backstop demands

– (but obviously not good news)

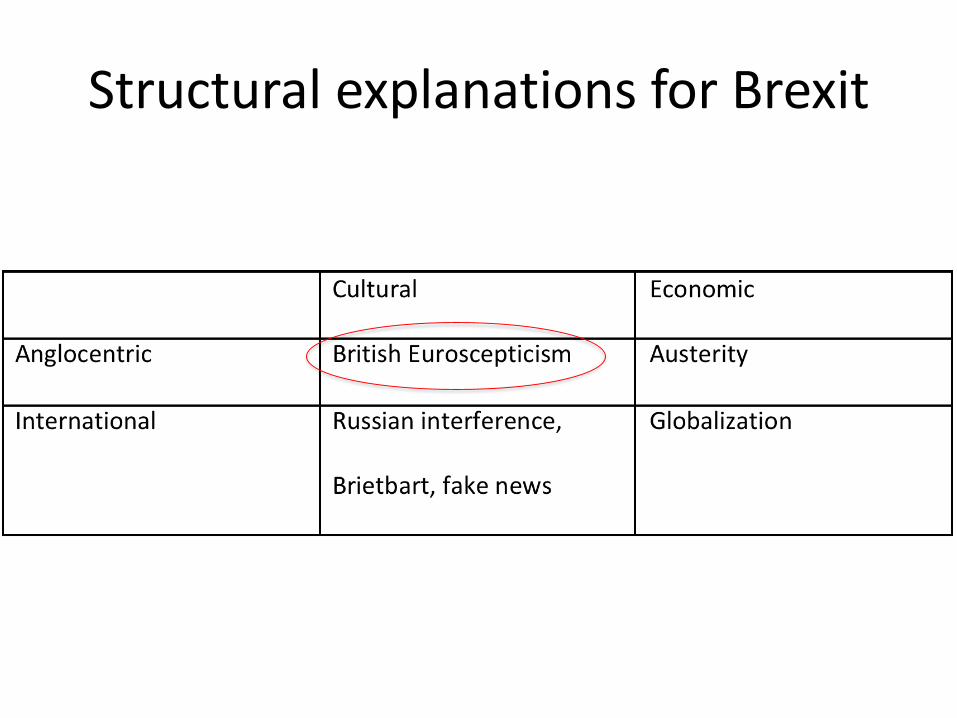

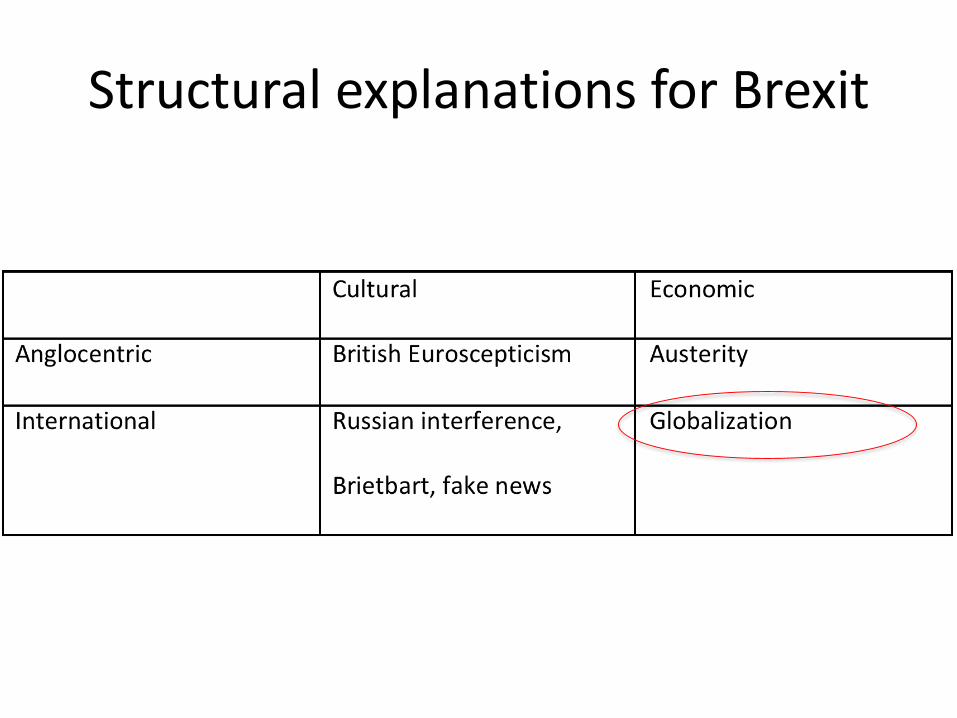

Structural explanations for Brexit

Structural explanations for Brexit

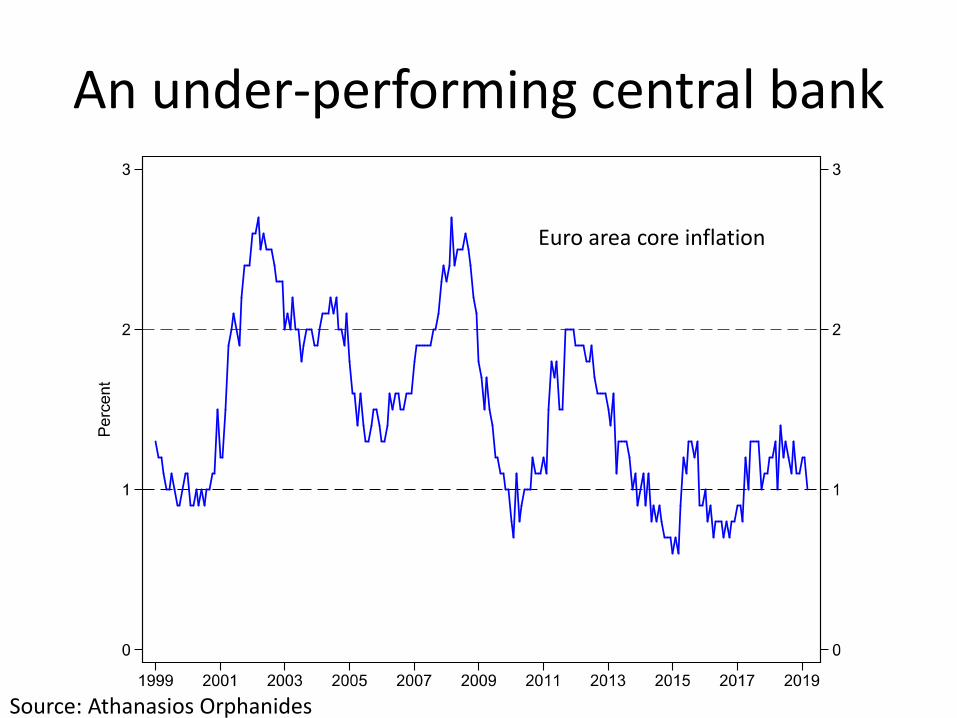

An under-performing central bank

Euro area core inflation

Source: Athanasios Orphanides

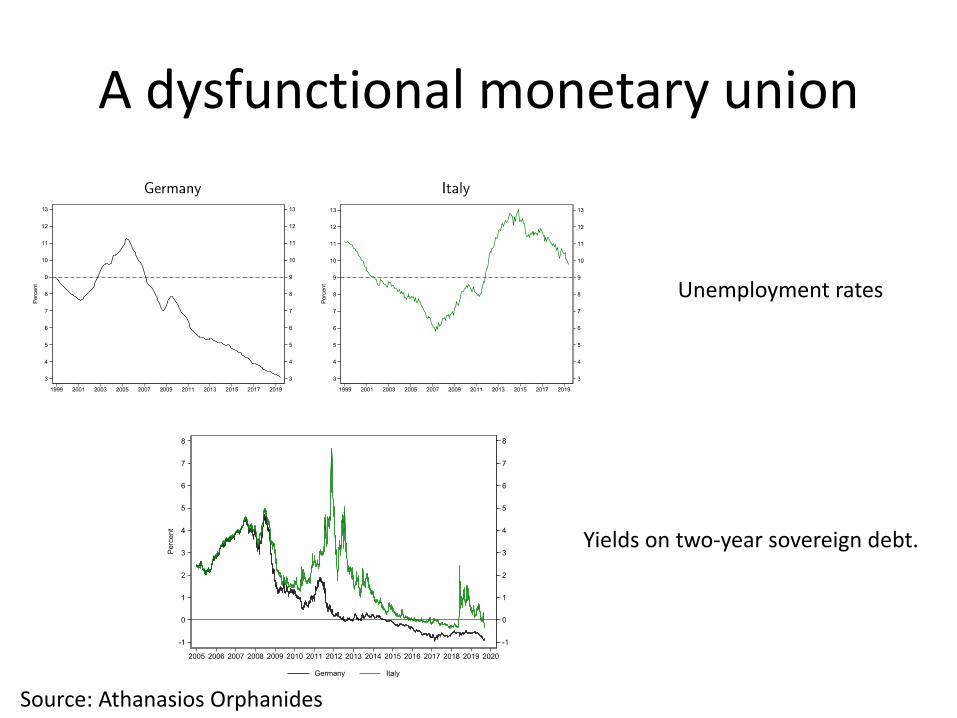

A dysfunctional monetary union

Unemployment rates

Yields on two-year sovereign debt.

Source: Athanasios Orphanides

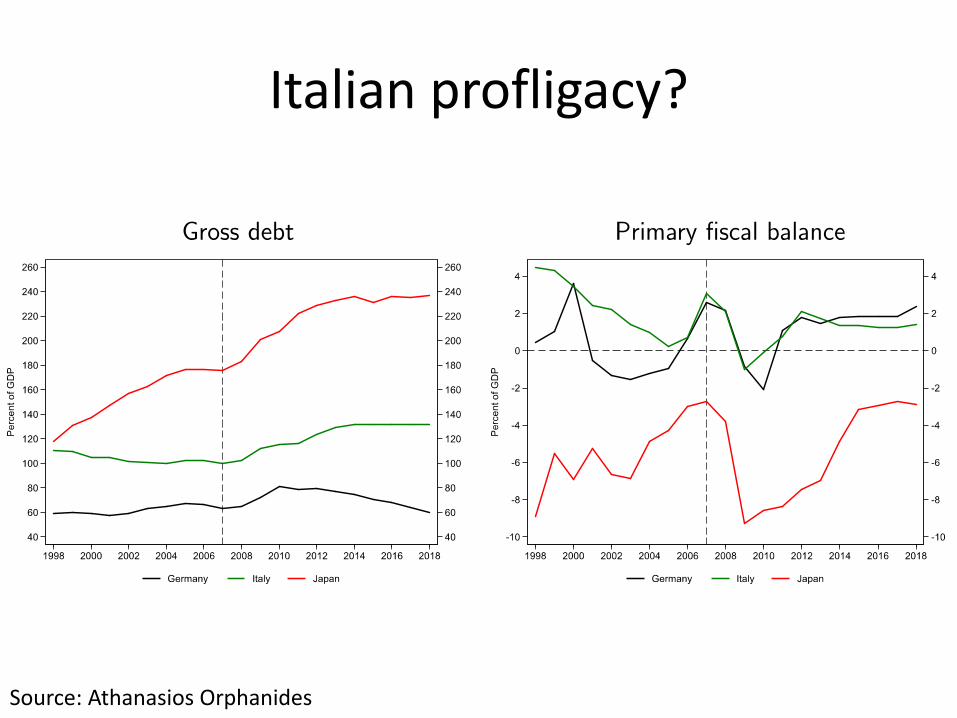

Italian profligacy?

Source: Athanasios Orphanides

Maintaining support for the EU and globalization

• Going back to the spirit of the 1950s: what is required to maintain political support for openness?

• What policies are in Ireland’s long run interest?

– Taxation

– EMU

– Strategic cooperation

The Impact of a Disorderly Brexit on the Irish Economy

Thomas Conefrey

On the Brink of Brexit, PwC, 17 October 2019

32

Overview

1. The impact of Brexit so far:

UK economic performance

Ireland

2. Modelling the effect of Brexit on the Irish economy.

3. Sector and region-specific problems.

4. Conclusion.

33

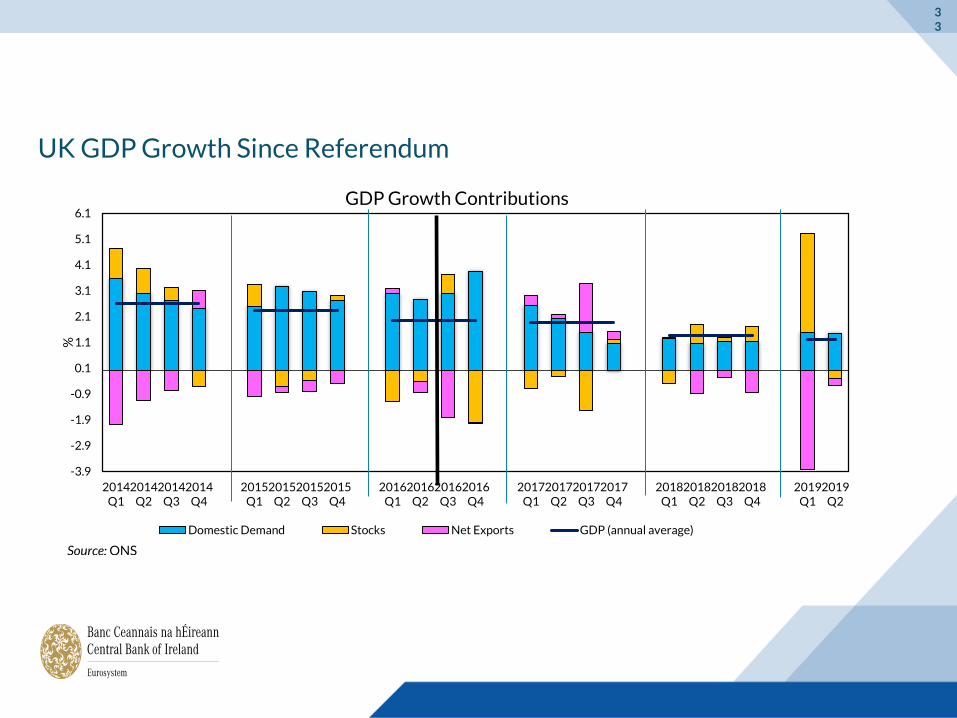

UK GDP Growth Since Referendum

-3.9

-2.9

-1.9

-0.9

0.1

1.1

2.1

3.1

4.1

5.1

6.1

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

2018Q4

2019Q1

2019Q2

%

GDP Growth Contributions

Domestic Demand Stocks Net Exports GDP (annual average)

Source: ONS

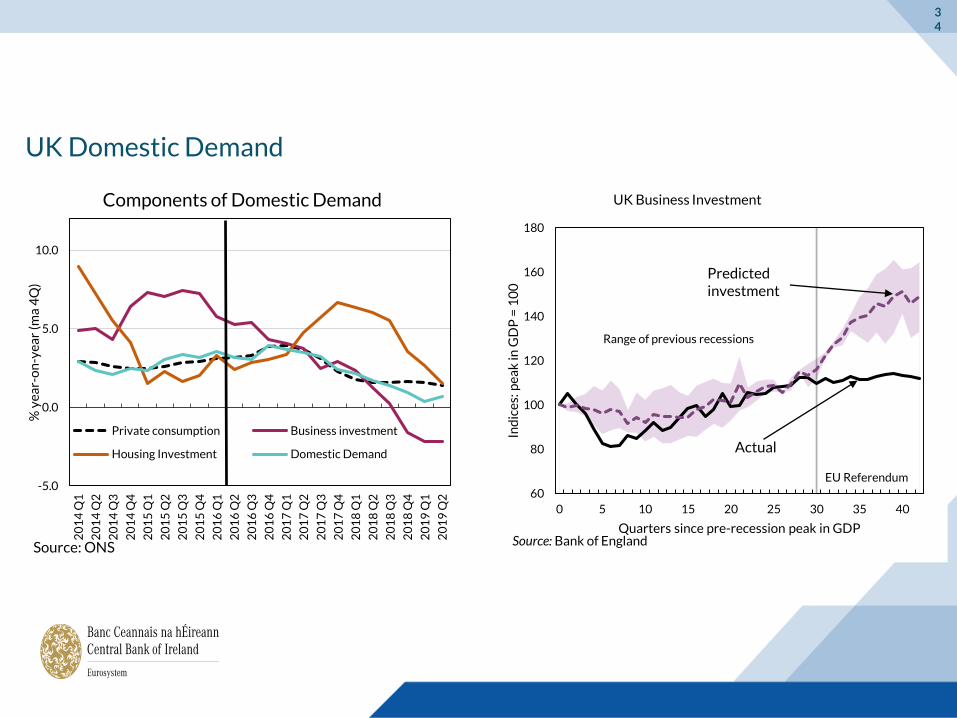

34

UK Domestic Demand

60

80

100

120

140

160

180

0 5 10 15 20 25 30 35 40In

dic

es:

pe

ak

in G

DP

= 1

00

Quarters since pre-recession peak in GDP

Range of previous recessions

EU Referendum

Source: Bank of England

Actual

Predicted investment

-5.0

0.0

5.0

10.0

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

19

Q1

20

19

Q2

% y

ea

r-o

n-y

ea

r (m

a 4

Q)

Components of Domestic Demand

Private consumption Business investment

Housing Investment Domestic Demand

Source: ONS

UK Business Investment

35

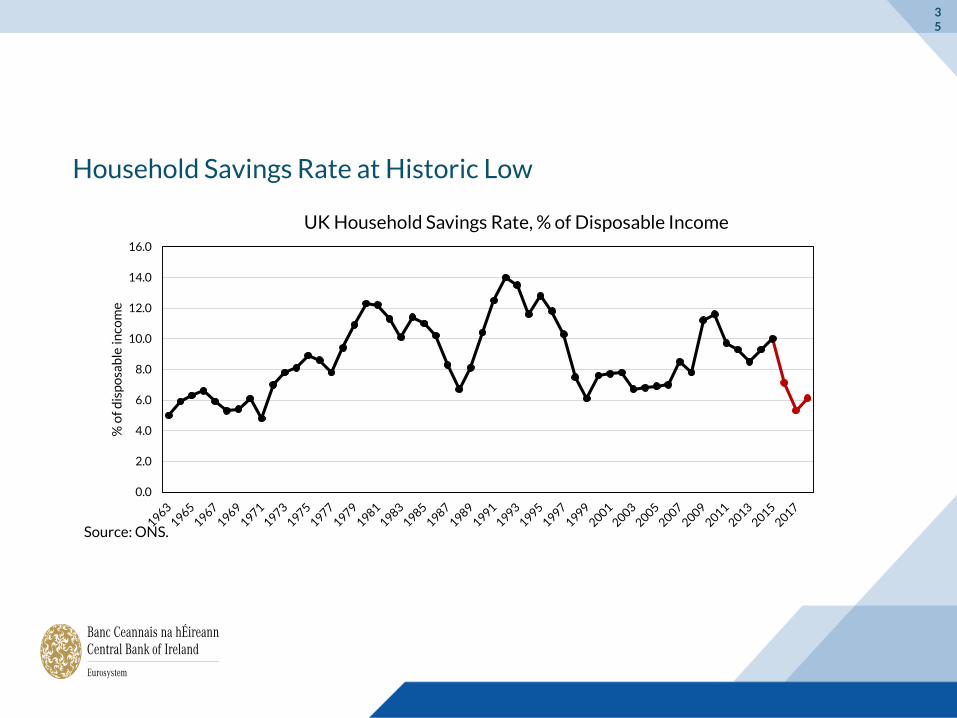

Household Savings Rate at Historic Low

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

% o

f d

isp

osa

ble

inco

me

UK Household Savings Rate, % of Disposable Income

Source: ONS.

36

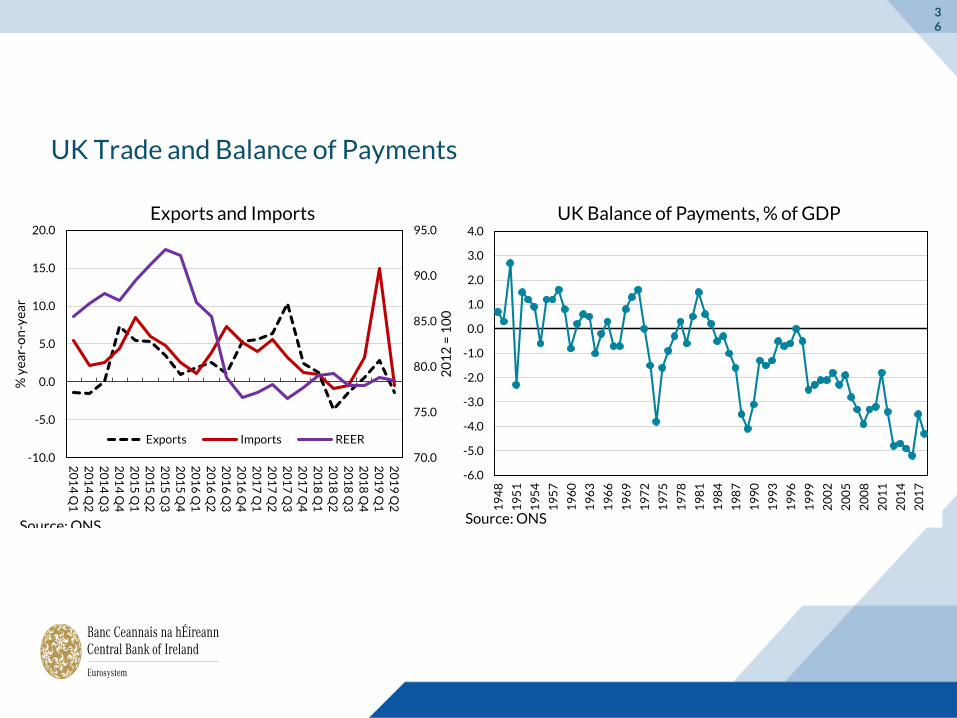

UK Trade and Balance of Payments

70.0

75.0

80.0

85.0

90.0

95.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

19

Q1

20

19

Q2

20

12

= 1

00

% y

ea

r-o

n-y

ea

r

Exports and Imports

Exports Imports REER

Source: ONS

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

19

48

19

51

19

54

19

57

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

20

17

UK Balance of Payments, % of GDP

Source: ONS

37

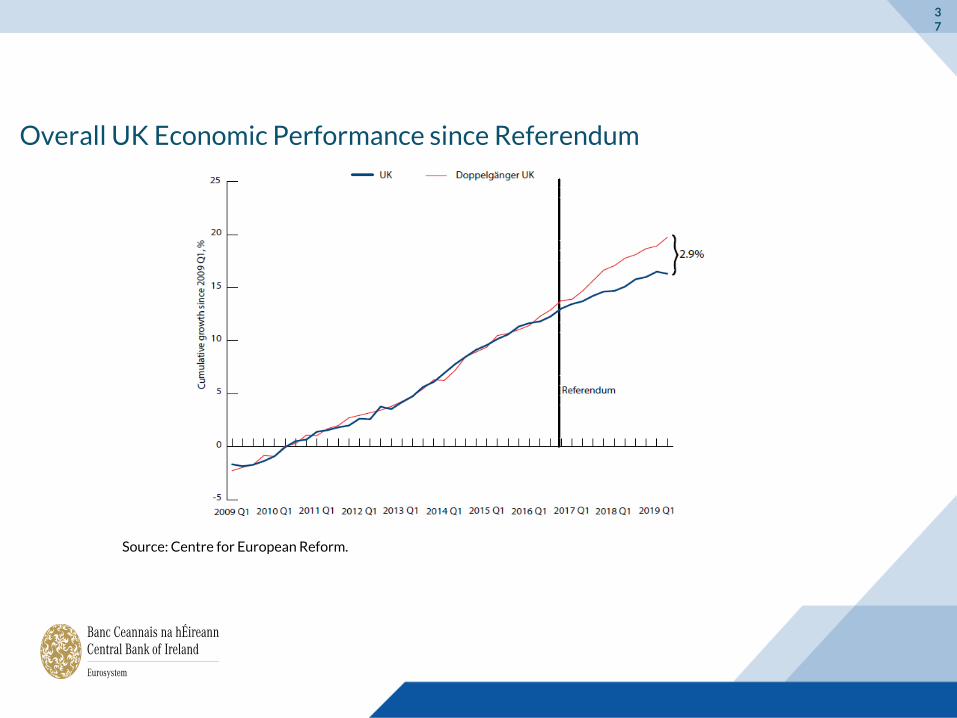

Overall UK Economic Performance since Referendum

Source: Centre for European Reform.

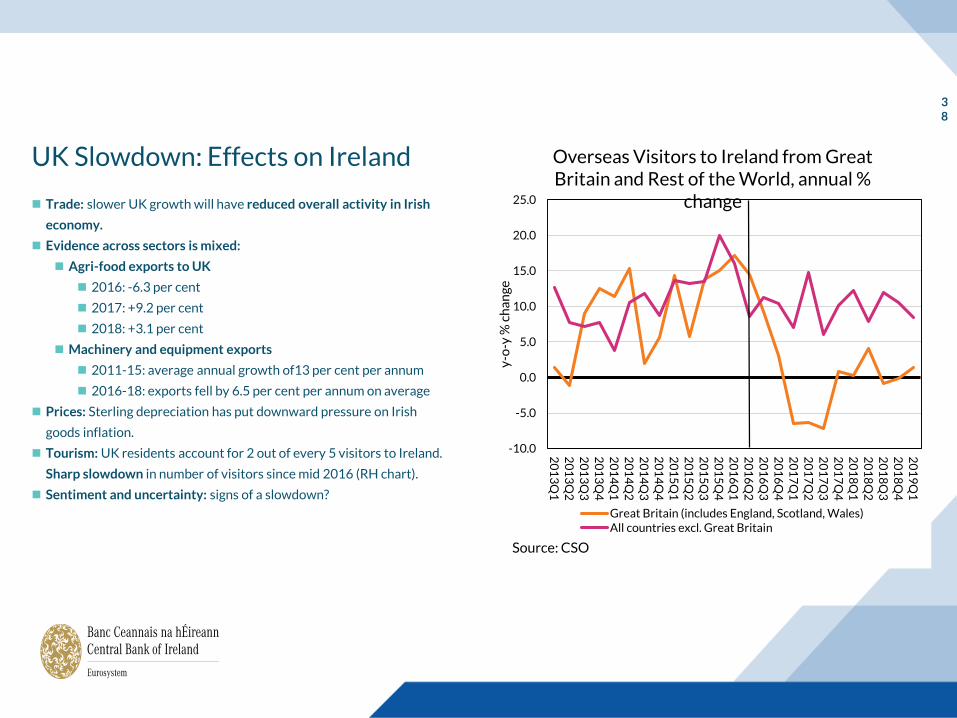

UK Slowdown: Effects on Ireland

Trade: slower UK growth will have reduced overall activity in Irish

economy.

Evidence across sectors is mixed:

Agri-food exports to UK

2016: -6.3 per cent

2017: +9.2 per cent

2018: +3.1 per cent

Machinery and equipment exports

2011-15: average annual growth of13 per cent per annum

2016-18: exports fell by 6.5 per cent per annum on average

Prices: Sterling depreciation has put downward pressure on Irish

goods inflation.

Tourism: UK residents account for 2 out of every 5 visitors to Ireland.

Sharp slowdown in number of visitors since mid 2016 (RH chart).

Sentiment and uncertainty: signs of a slowdown?

38

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

19

Q1

y-o

-y %

ch

an

ge

Overseas Visitors to Ireland from Great Britain and Rest of the World, annual %

change

Great Britain (includes England, Scotland, Wales)All countries excl. Great Britain

Source: CSO

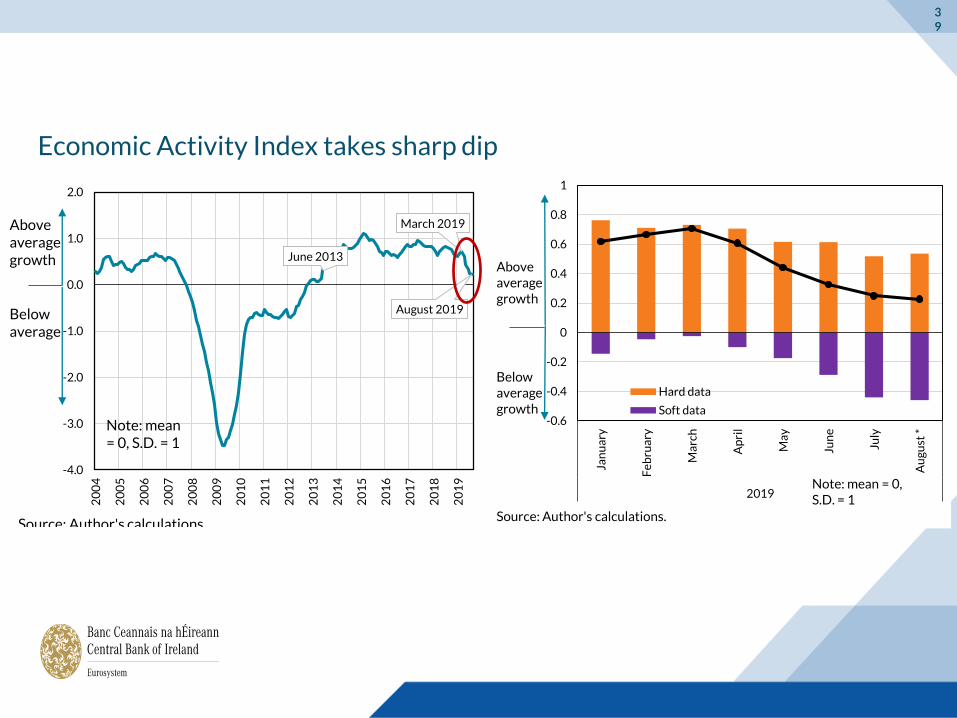

Economic Activity Index takes sharp dip

39

June 2013

March 2019

August 2019

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Below average

Above average growth

Note: mean = 0, S.D. = 1

Source: Author's calculations.

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Jan

ua

ry

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Jun

e

July

Au

gu

st *

2019

Hard data

Soft data

Below average growth

Above average growth

Source: Author's calculations.

Note: mean = 0, S.D. = 1

40

Brexit - Modelling the Unknown

The UK is the first country to leave the EU. The consequences of that exit are therefore largely unknown.

“Soft” or “hard” ?: a wide range of Brexit outcomes (still) possible.

Can the model capture the complexity of the change?

Does Brexit cause a structural shift that alters basic relationships embedded within the model?

How quickly will trade fall in a no-deal Brexit?

What will be the scale of the logistical and supply chain disruption?

How will financial markets react?

Nevertheless, quantitative estimates are needed to inform debate and assist policymakers.

Examples of Brexit modelling work carried out in CBI using COSMO:

May 2018 (NIESR Economic Review): impact of an orderly WTO Brexit.

October 2018 (Central Bank Quarterly Bulletin, Box A) : preliminary assessment of impact of UK Government Brexit White Paper (Chequers).

January 2019 (Central Bank Quarterly Bulletin, Box B) : Impact of a disorderly Brexit.

Builds on other similar work for Ireland by Department of Finance, ESRI and others.

41

Approach

1. Model effect of Brexit on UK economy and broader external environment using NiGEM.

2. Use NiGEM outputs as inputs into model of Irish economy (CBI-COSMO).

3. Consider additional shocks important in a disorderly UK exit.

4. Simulate the full scenario.

42

Transmission Channels and Assumptions (1)

1. Reductions in trade

Tariff and non-tariff barriers reduce UK-EU trade. Estimated 40-50 per cent reduction in goods

trade, 35 per cent in services.

2. Foreign Direct Investment

Free movement of capital encourages cross-border investment.

Reduction in trade reduces FDI.

3. Migration

Barriers to free movement of labour may be introduced.

UK may become less attractive destination for migrants.

4. Productivity

Immediate: rebalancing of economy towards less productive sectors as trade falls.

Long run: lower trade, FDI and migration could reduce productivity. Source: NIESR.

43

Other channels:

5. Financial Markets: Potentially large depreciation of sterling. Impact on borrowing costs, equity and

bond prices.

6. Sentiment and Uncertainty: Consumer spending and investment would be negatively affected by fall in

sentiment and adjustment to weaker future growth and incomes.

7. Importing and exporting: around 25 per cent of Irish goods imports come from UK. Disruption to supply

chains with implications for production, distribution and retailing. Added importance due to landbridge.

8. FDI: potential increase in Irish FDI. Magnitude of effect is uncertain. Size of FDI efffect based on Lawless

and Morgenroth (2016).

Calibrate these shocks based on a synthesis of the available literature. Some judgement is also required.

Transmission Channels and Assumptions (2)

44

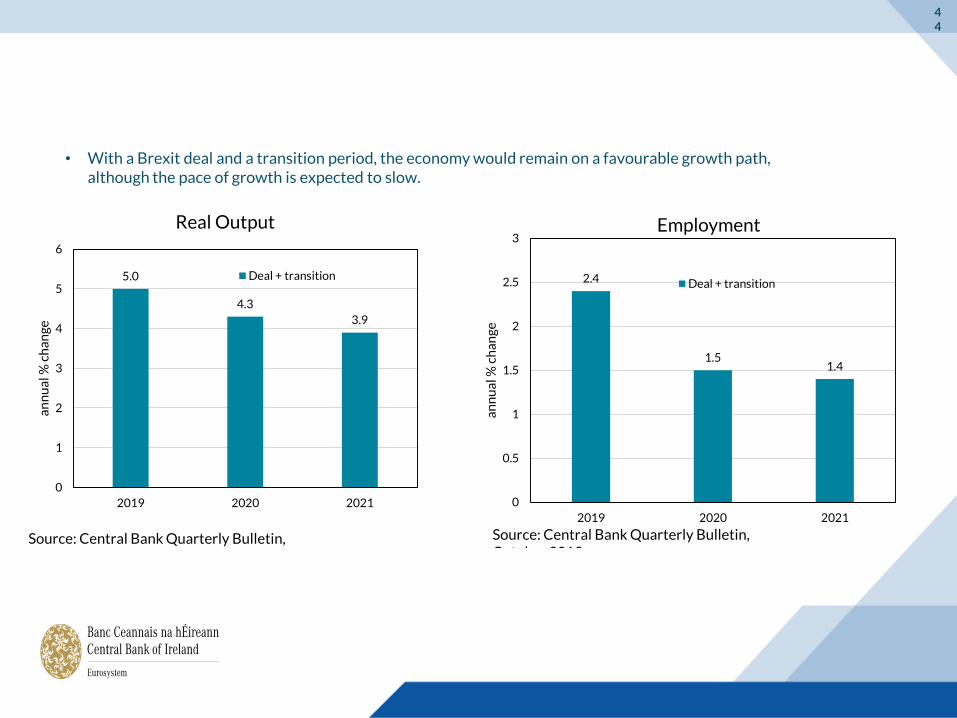

• With a Brexit deal and a transition period, the economy would remain on a favourable growth path, although the pace of growth is expected to slow.

5.0

4.3

3.9

0

1

2

3

4

5

6

2019 2020 2021

an

nu

al %

ch

an

ge

Real Output

Deal + transition

Source: Central Bank Quarterly Bulletin,

2.4

1.51.4

0

0.5

1

1.5

2

2.5

3

2019 2020 2021

an

nu

al %

ch

an

ge

Employment

Deal + transition

Source: Central Bank Quarterly Bulletin, October 2019.

45

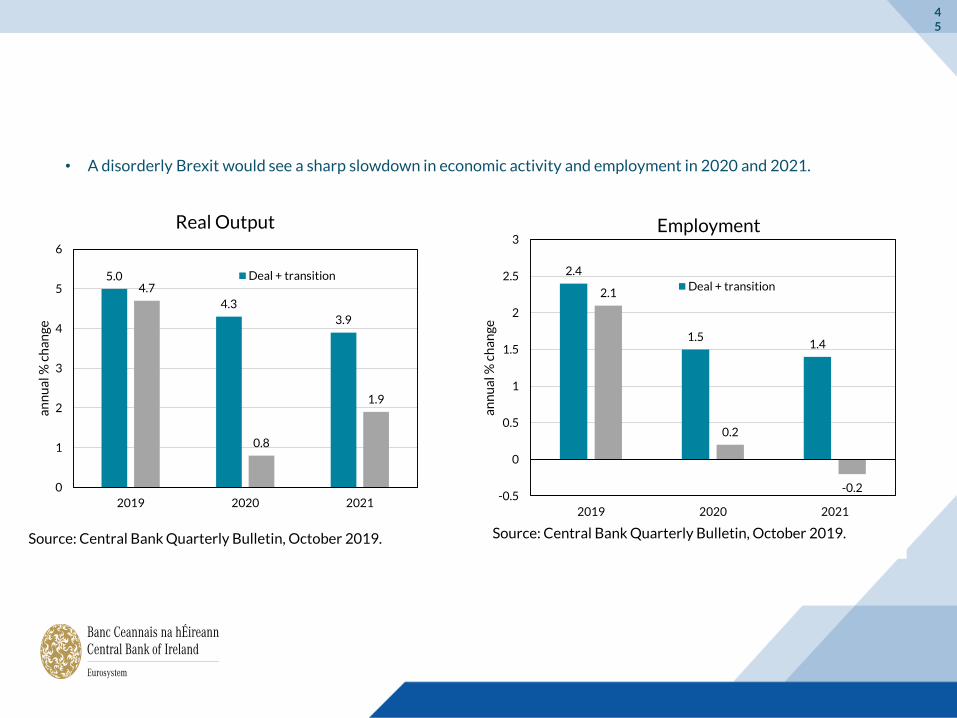

5.0

4.3

3.9

4.7

0.8

1.9

0

1

2

3

4

5

6

2019 2020 2021

an

nu

al %

ch

an

ge

Real Output

Deal + transition

Source: Central Bank Quarterly Bulletin, October 2019.

2.4

1.51.4

2.1

0.2

-0.2-0.5

0

0.5

1

1.5

2

2.5

3

2019 2020 2021

an

nu

al %

ch

an

ge

Employment

Deal + transition

Source: Central Bank Quarterly Bulletin, October 2019.

• A disorderly Brexit would see a sharp slowdown in economic activity and employment in 2020 and 2021.

46

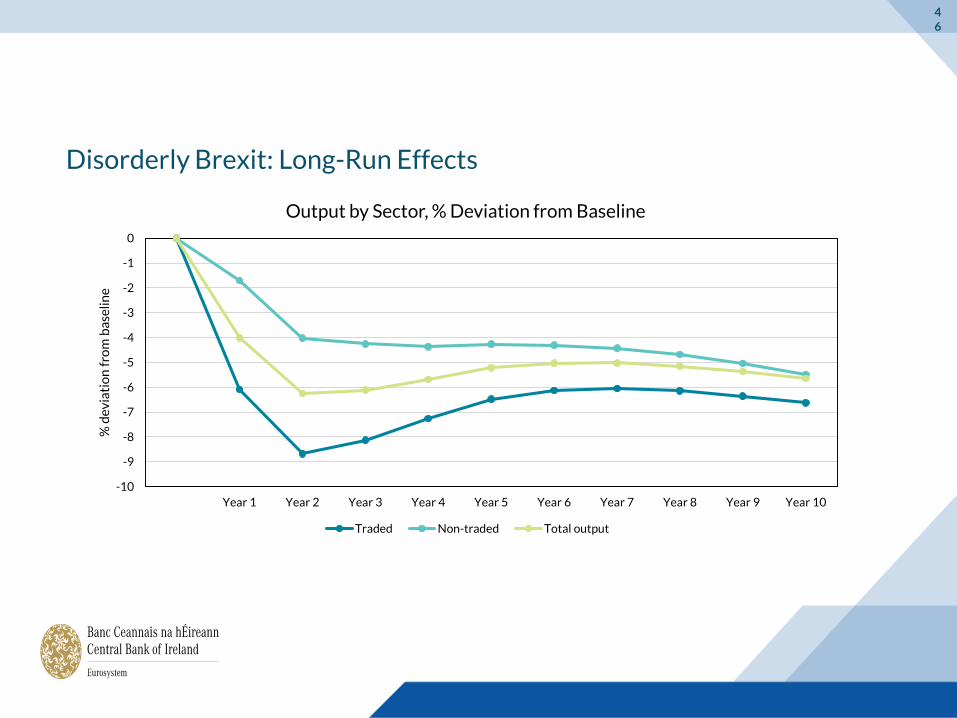

Disorderly Brexit: Long-Run Effects

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

% d

ev

iati

on

fro

m b

ase

lin

e

Output by Sector, % Deviation from Baseline

Traded Non-traded Total output

47

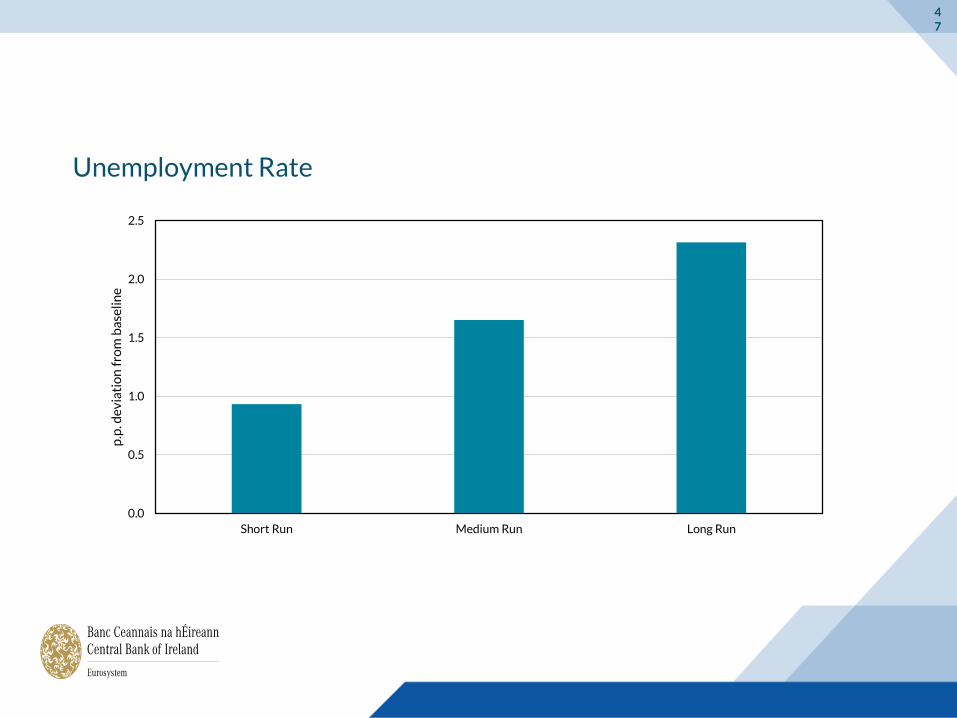

Unemployment Rate

0.0

0.5

1.0

1.5

2.0

2.5

Short Run Medium Run Long Run

p.p

. de

via

tio

n f

rom

ba

seli

ne

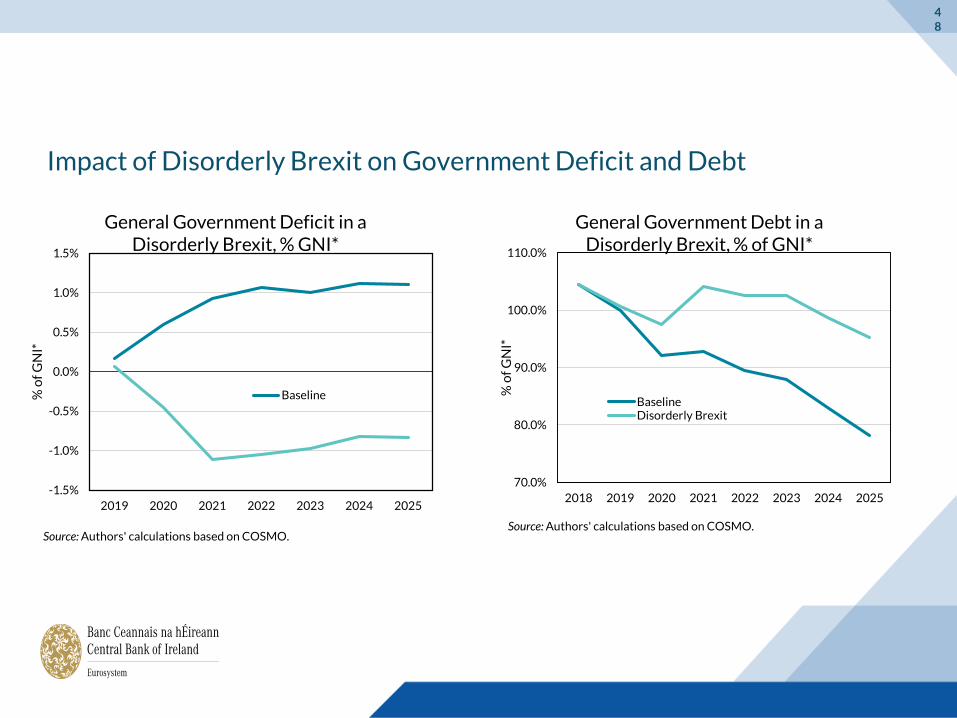

Impact of Disorderly Brexit on Government Deficit and Debt

48

70.0%

80.0%

90.0%

100.0%

110.0%

2018 2019 2020 2021 2022 2023 2024 2025%

of

GN

I*

General Government Debt in a Disorderly Brexit, % of GNI*

BaselineDisorderly Brexit

Source: Authors' calculations based on COSMO.

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2019 2020 2021 2022 2023 2024 2025

% o

f G

NI*

General Government Deficit in a Disorderly Brexit, % GNI*

Baseline

Source: Authors' calculations based on COSMO.

49

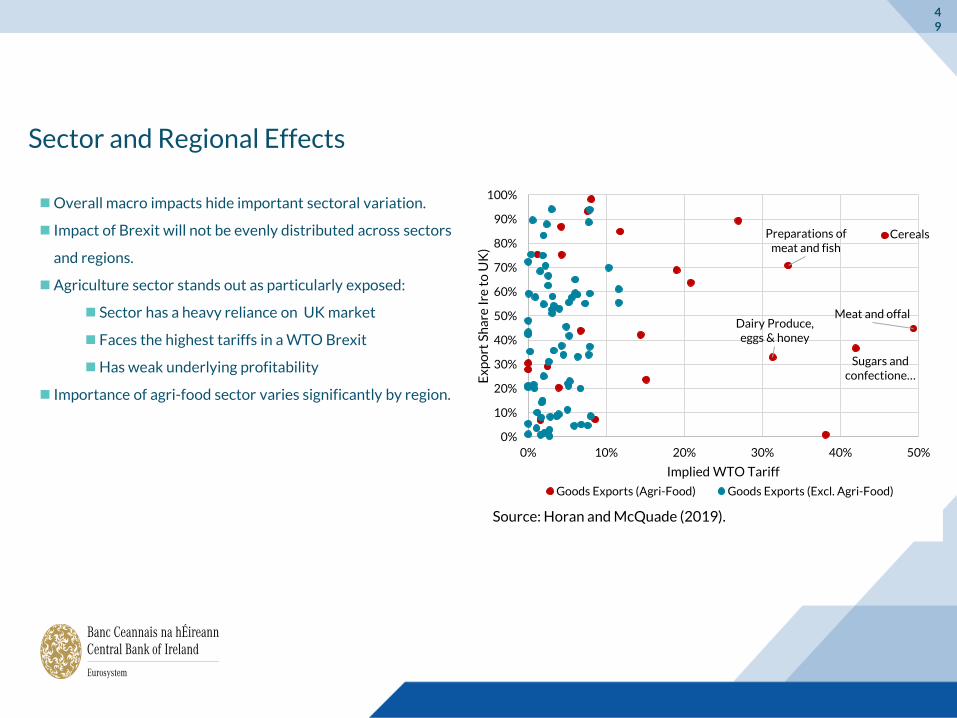

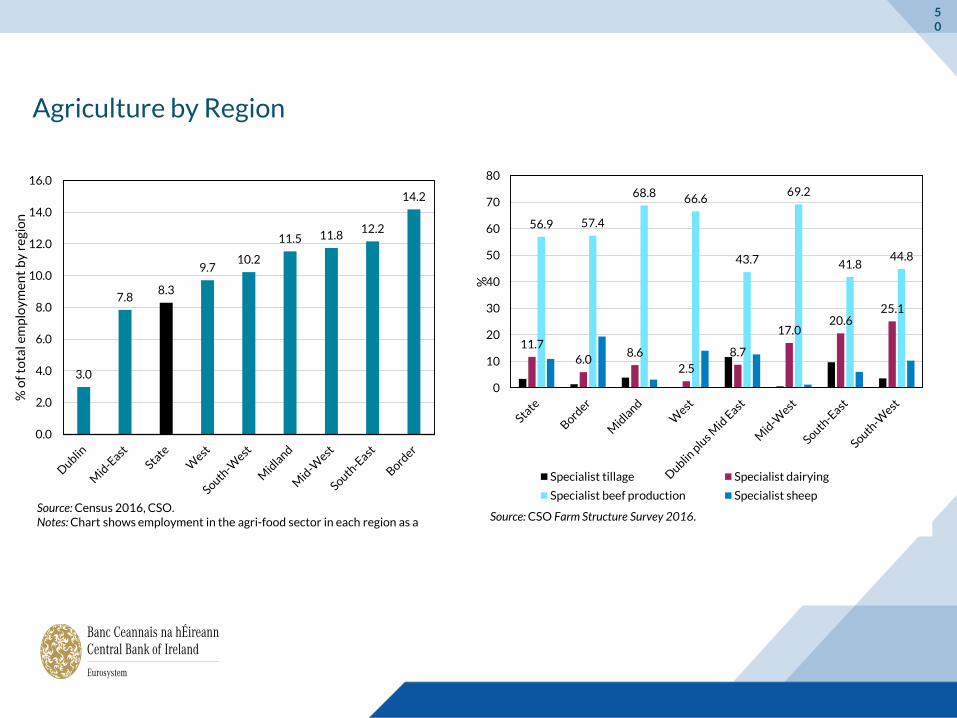

Sector and Regional Effects

Overall macro impacts hide important sectoral variation.

Impact of Brexit will not be evenly distributed across sectors

and regions.

Agriculture sector stands out as particularly exposed:

Sector has a heavy reliance on UK market

Faces the highest tariffs in a WTO Brexit

Has weak underlying profitability

Importance of agri-food sector varies significantly by region.

Meat and offalDairy Produce, eggs & honey

CerealsPreparations of meat and fish

Sugars and confectione…

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50%

Ex

po

rt S

ha

re I

re t

o U

K)

Implied WTO Tariff

Goods Exports (Agri-Food) Goods Exports (Excl. Agri-Food)

Source: Horan and McQuade (2019).

50

Agriculture by Region

3.0

7.88.3

9.710.2

11.5 11.812.2

14.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

% o

f to

tal e

mp

loy

me

nt

by

re

gio

n

Source: Census 2016, CSO.Notes: Chart shows employment in the agri-food sector in each region as a

11.7

6.08.6

2.5

8.7

17.020.6

25.1

56.9 57.4

68.8 66.6

43.7

69.2

41.844.8

0

10

20

30

40

50

60

70

80

%Specialist tillage Specialist dairying

Specialist beef production Specialist sheep

Source: CSO Farm Structure Survey 2016.

51

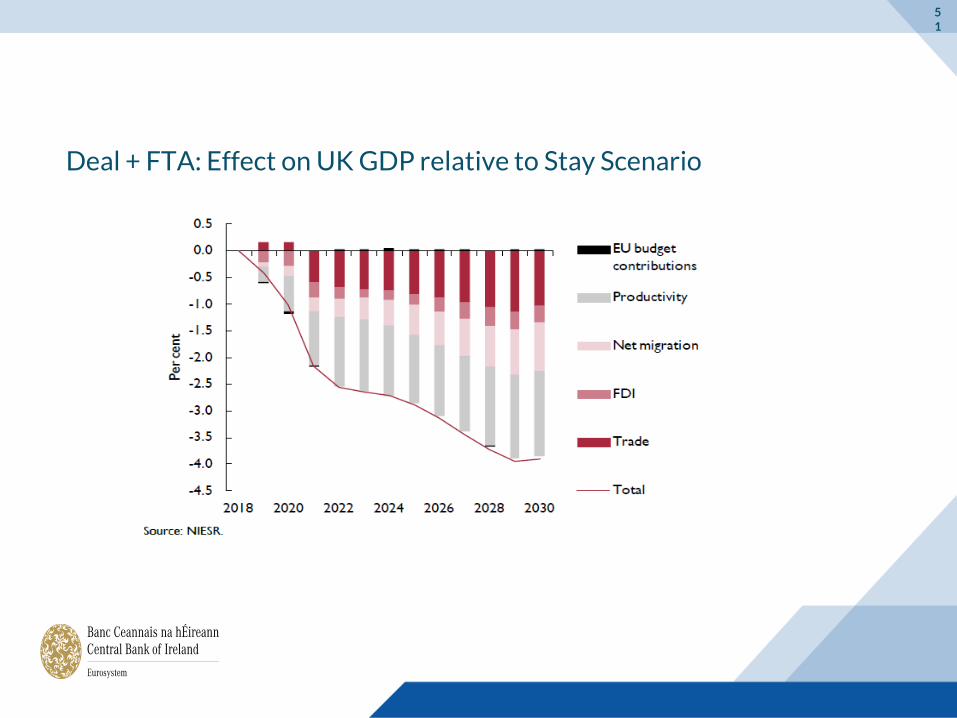

Deal + FTA: Effect on UK GDP relative to Stay Scenario

52

Summary

Evidence that UK economy has slowed since June 2016 referendum.

Reduced UK demand for Irish exports will have lowered overall Irish growth with evidence of more pronounced

effects in some sectors.

Modelling the effect of a disorderly Brexit is an inherently uncertain exercise.

Based on assumptions grounded in the academic literature, we find a significant long-run negative effect on Irish

output, with the output loss front-loaded in a disorderly Brexit.

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublicationswww.esri.ie

Brexit and Cross-Border Trade

DATE17th October 2019

VENUEOn the brink of Brexit: economic consequences for the island of Ireland

AUTHORMartina Lawless

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

Outline

Levels of economic integration

Potential impact on Ireland of “no-deal”

outcome

Cross-border trade and integration

Current state of play

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

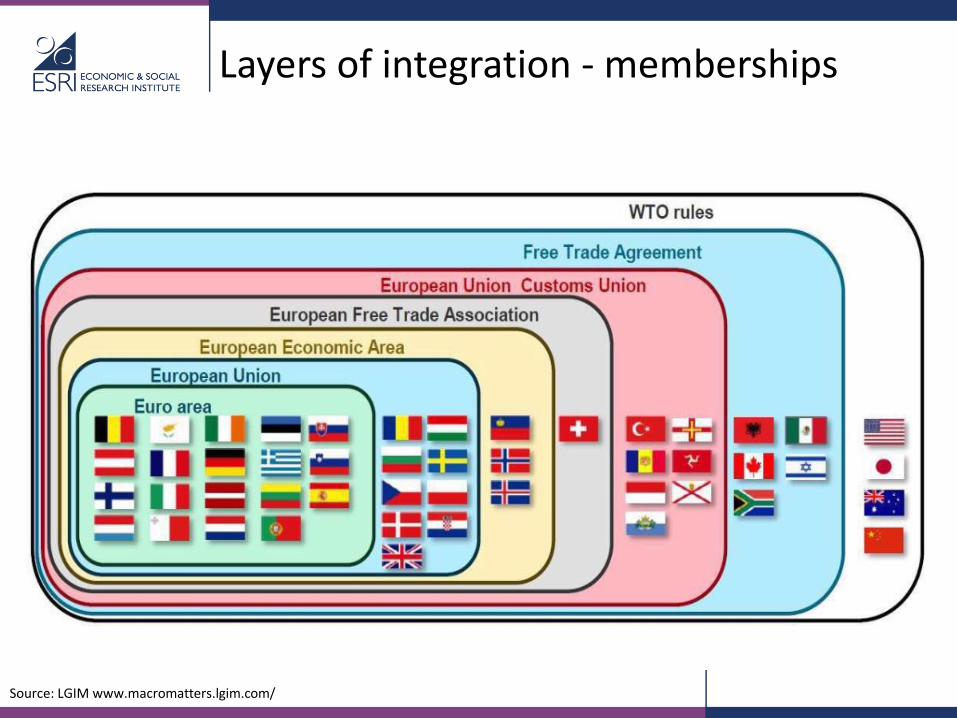

Layers of integration - memberships

Source: LGIM www.macromatters.lgim.com/

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

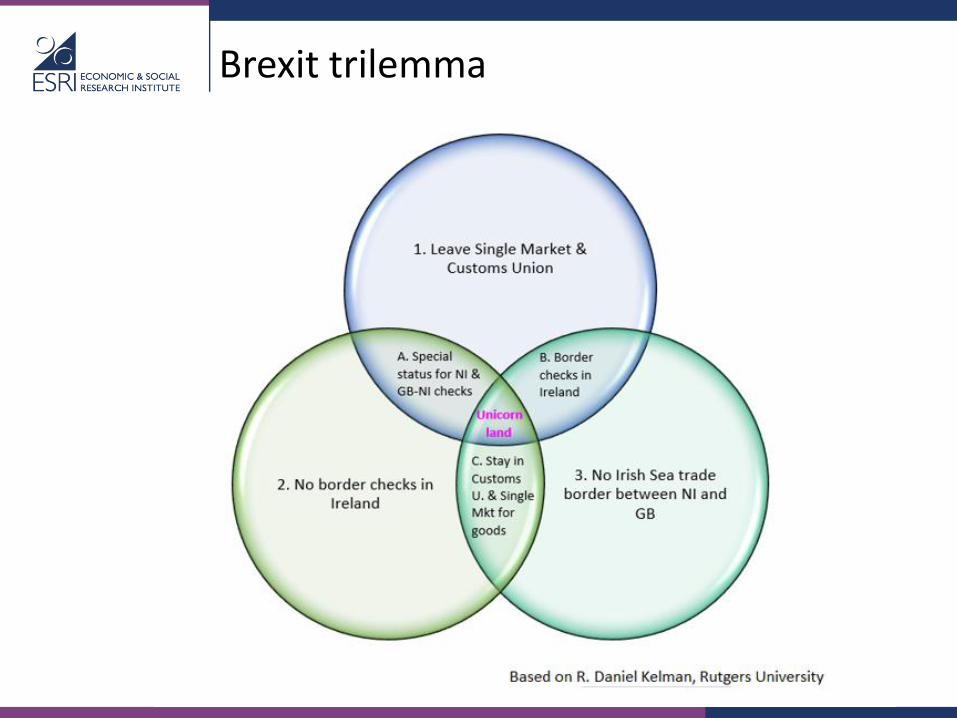

Brexit trilemma

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

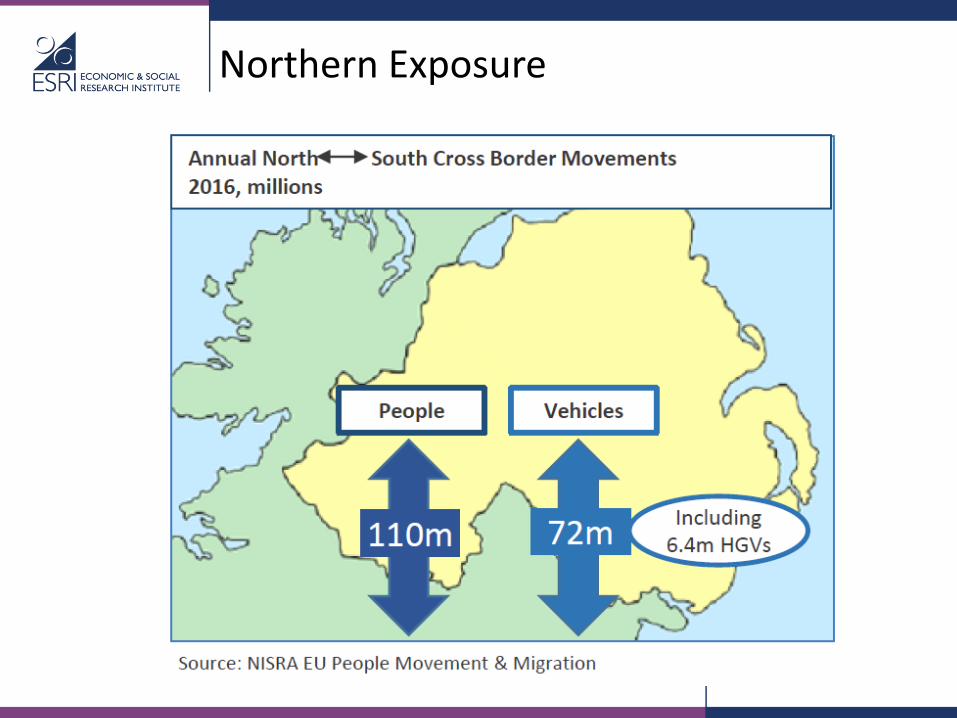

Northern Exposure

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

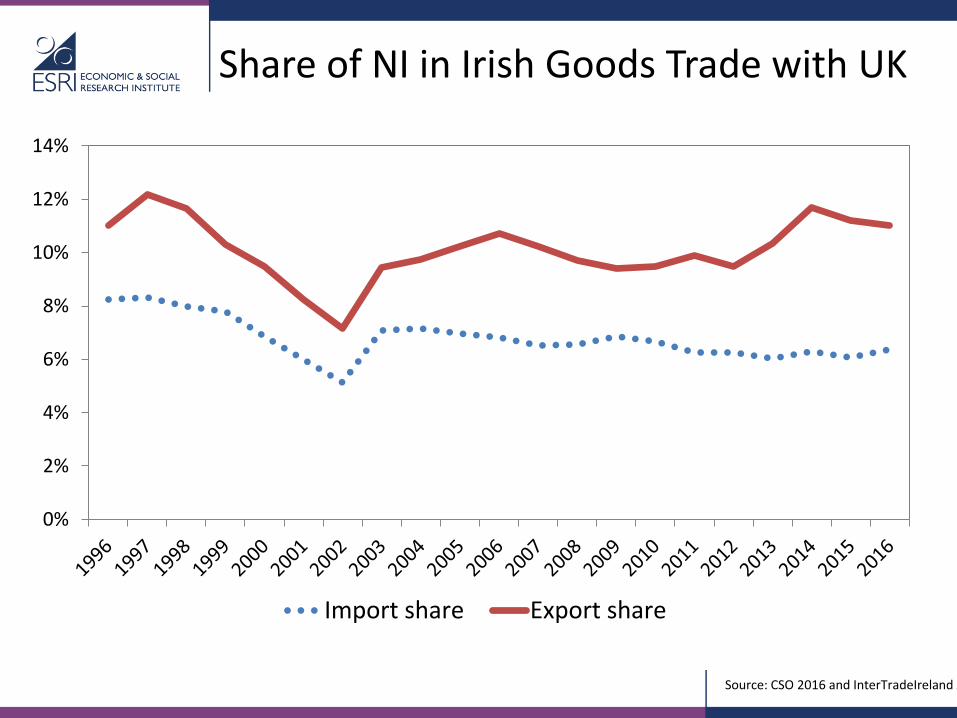

Share of NI in Irish Goods Trade with UK

0%

2%

4%

6%

8%

10%

12%

14%

Import share Export share

Source: CSO 2016 and InterTradeIreland 2018

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

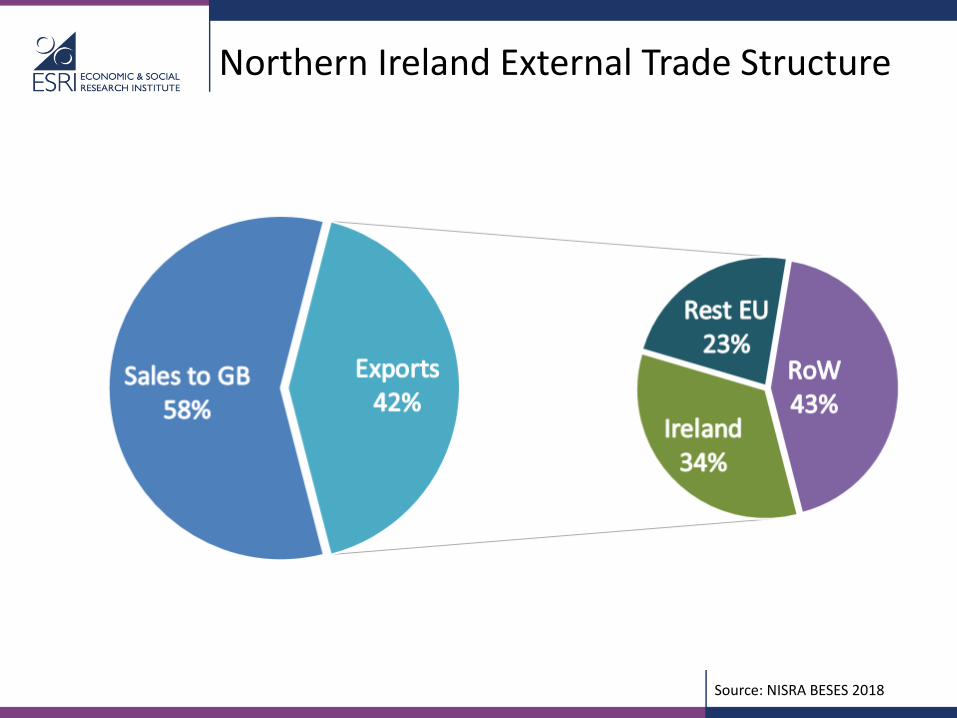

Northern Ireland External Trade Structure

Source: NISRA BESES 2018

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

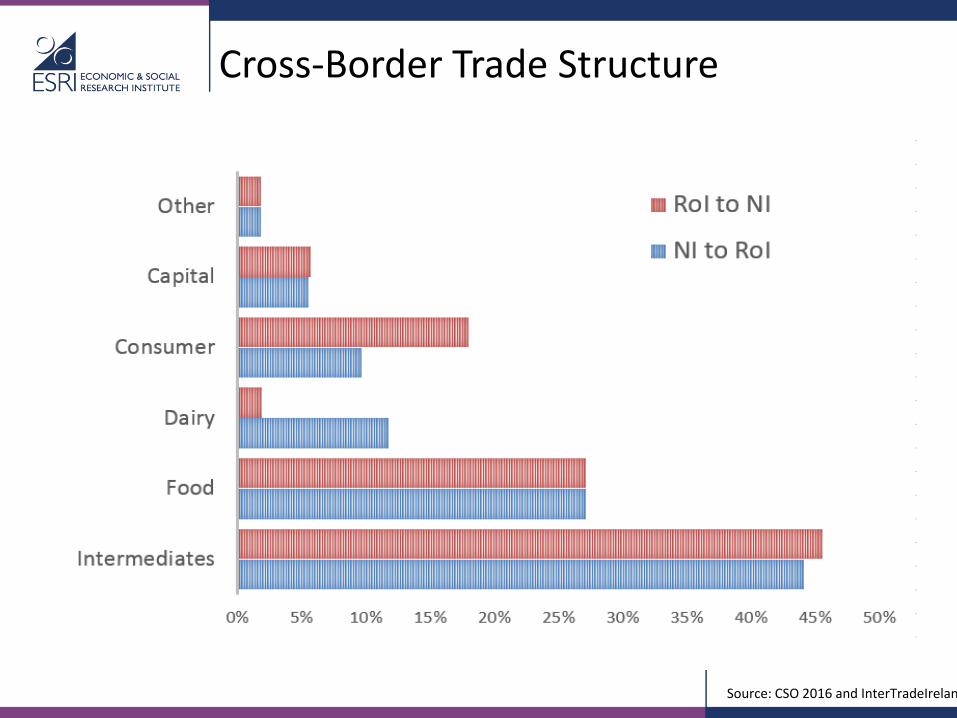

Cross-Border Trade Structure

Source: CSO 2016 and InterTradeIreland

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

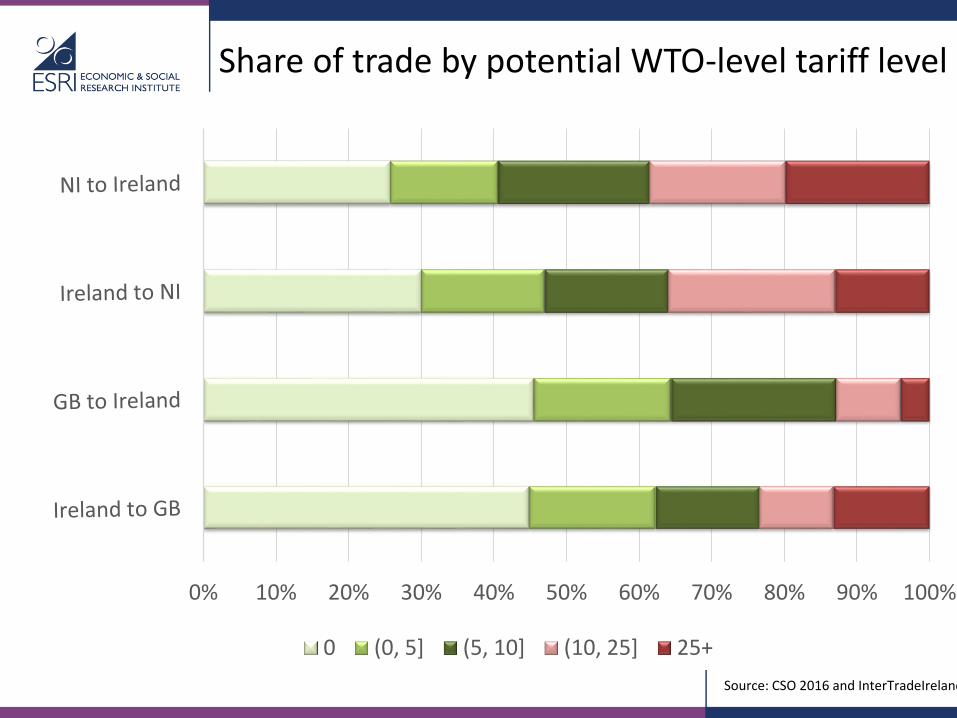

Share of trade by potential WTO-level tariff level

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

0 (0, 5] (5, 10] (10, 25] 25+

Source: CSO 2016 and InterTradeIreland 2018

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

Who Exports? (NI firms)

Source: CSO 2016 and InterTradeIreland 2018

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

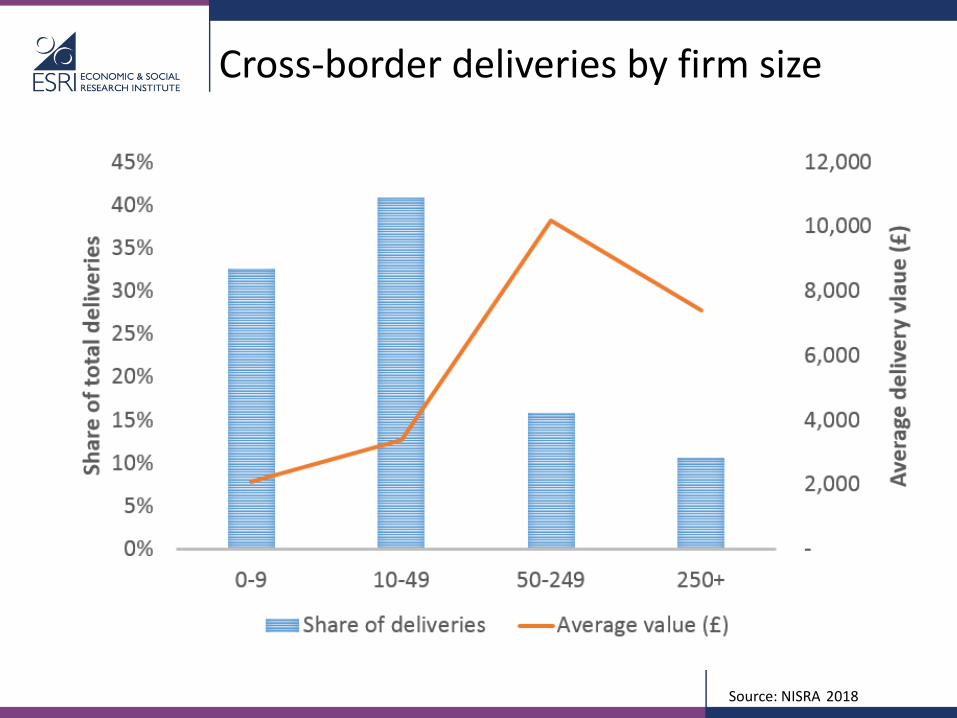

Cross-border deliveries by firm size

Source: NISRA 2018

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

Technological solution?

Source: Deirdre Heenan via Twitter

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

Promise of world trade deals?

• For UK as a whole:

• Unlikely to replace levels of trade in integrated EU market.

• Distance still matters to trade.

• Trade-offs part of any international deal – across sectors, standards, migration(?).

• Financial services and car industry most likely to be prioritised.

• For Northern Ireland:

• If trade-offs above mean opening UK up to world food imports, would pose major competitive challenges for NI.

• Services exports not (currently) a major feature of economy.

• Any deal involving changes in food standards very problematic for cross-border flows – technology unlikely to help if standards diverge.

www.esri.ie @ESRIDublin #ESRIevents #ESRIpublications

Impact summary

Cross-border trade between Northern Ireland and Ireland more like local trade than international export activity

Almost all exporting firms in Northern Ireland include Ireland as one of their destination markets.

Over 80% of the smallest firm size group that export from Northern Ireland have all of their export sales in Ireland.

High degree of cross-border integration through supply chains.

High frequency of deliveries and low value per delivery for NI traders across the border.

Impacts of any changes in the cost of trading post-Brexit liable to be felt most particularly by very small firms trading across the border.

The Impact of Brexit on the Agri-Food Sector, North and South

Kevin Hanrahan and Trevor DonnellanTeagasc

On the brink of Brexit: the economic consequences for the island of Ireland

Dublin, October 17 2019

Overview

• Agri-Food on the Island of Ireland

– Similarities and differences

• Why Brexit matters (more) to agri-food

• Analysis of Brexit impacts on Irish agri-food

• Work to do

Agriculture on the island of Ireland

• Agri-food North and South dominated by ruminant grassland agricultural production systems and processing of the resultant meat and milk output

• Both agri-food economies overwhelmingly export dependent

• Agri-food stories of Ireland (North & South) can largely be told through the stories of beef & dairy

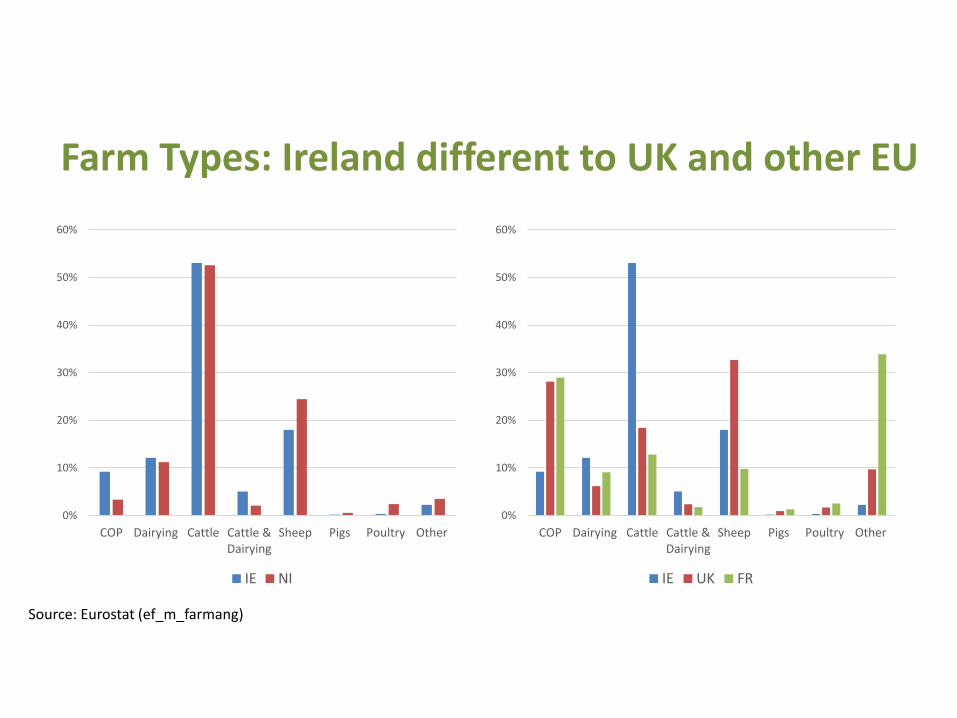

Farm Types: Ireland different to UK and other EU

0%

10%

20%

30%

40%

50%

60%

COP Dairying Cattle Cattle &Dairying

Sheep Pigs Poultry Other

IE NI

0%

10%

20%

30%

40%

50%

60%

COP Dairying Cattle Cattle &Dairying

Sheep Pigs Poultry Other

IE UK FR

Source: Eurostat (ef_m_farmang)

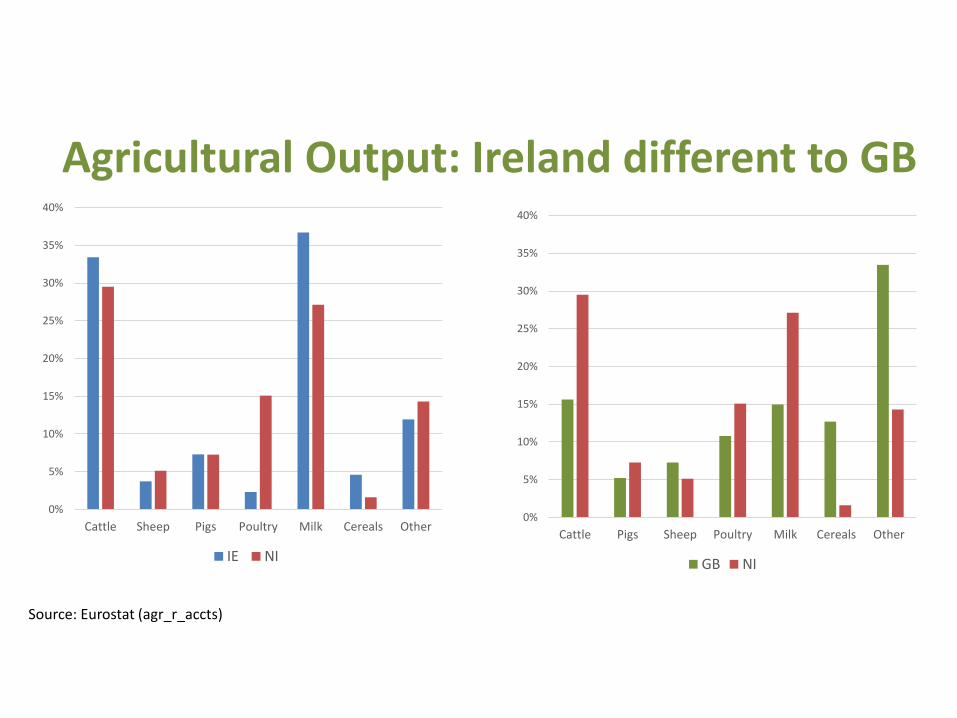

Agricultural Output: Ireland different to GB

0%

5%

10%

15%

20%

25%

30%

35%

40%

Cattle Pigs Sheep Poultry Milk Cereals Other

GB NI

0%

5%

10%

15%

20%

25%

30%

35%

40%

Cattle Sheep Pigs Poultry Milk Cereals Other

IE NI

Source: Eurostat (agr_r_accts)

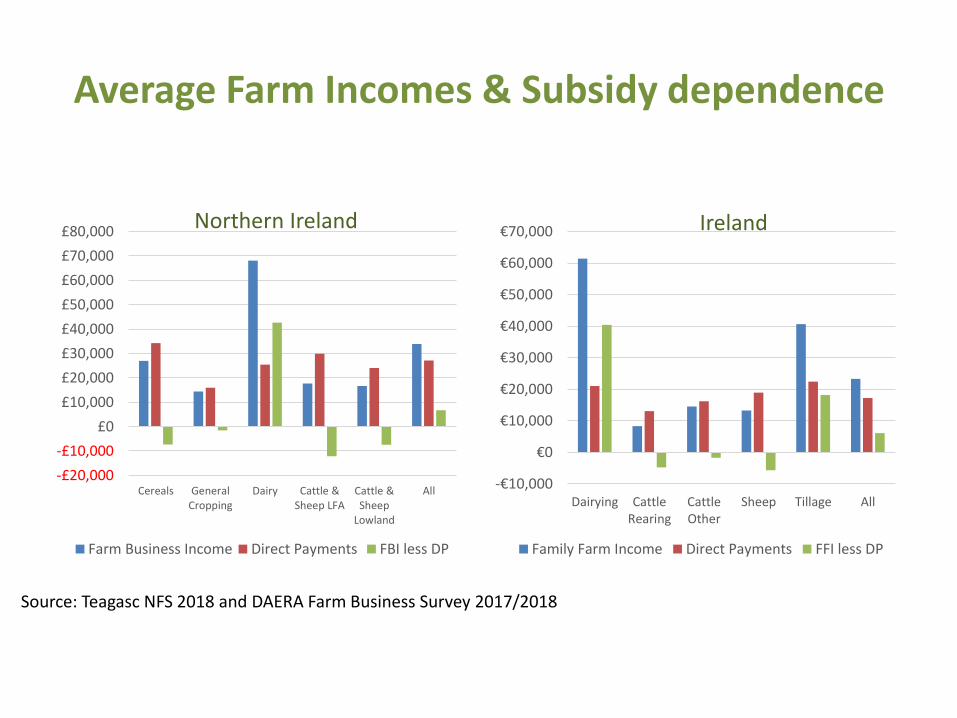

Average Farm Incomes & Subsidy dependence

-£20,000

-£10,000

£0

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

Cereals GeneralCropping

Dairy Cattle &Sheep LFA

Cattle &Sheep

Lowland

All

Farm Business Income Direct Payments FBI less DP

-€10,000

€0

€10,000

€20,000

€30,000

€40,000

€50,000

€60,000

€70,000

Dairying CattleRearing

CattleOther

Sheep Tillage All

Family Farm Income Direct Payments FFI less DP

Source: Teagasc NFS 2018 and DAERA Farm Business Survey 2017/2018

Northern Ireland Ireland

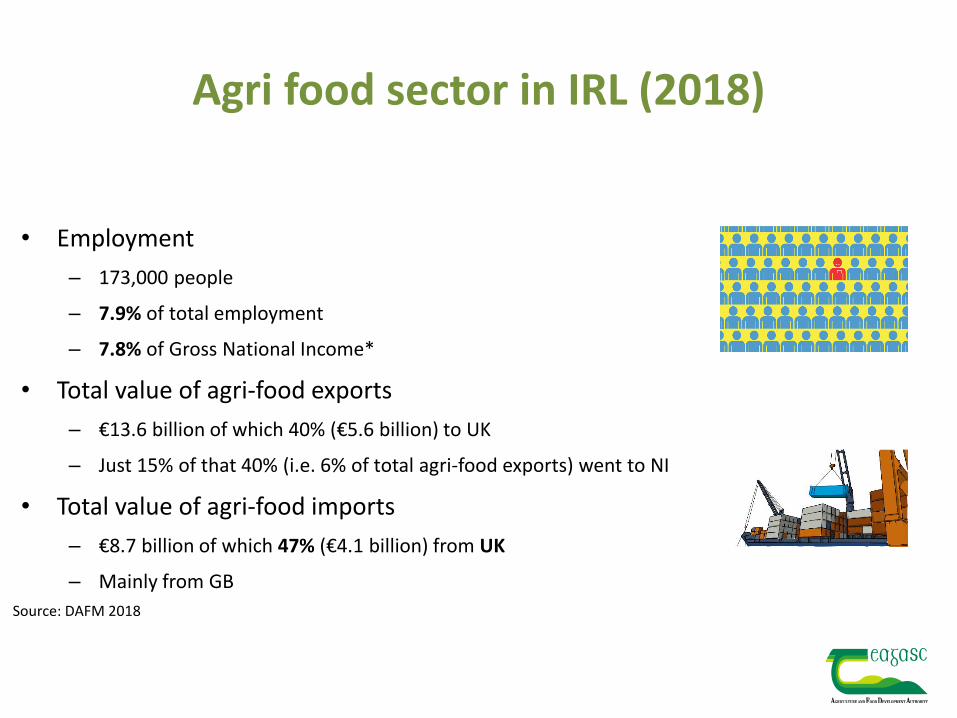

Agri food sector in IRL (2018)

• Employment

– 173,000 people

– 7.9% of total employment

– 7.8% of Gross National Income*

• Total value of agri-food exports

– €13.6 billion of which 40% (€5.6 billion) to UK

– Just 15% of that 40% (i.e. 6% of total agri-food exports) went to NI

• Total value of agri-food imports

– €8.7 billion of which 47% (€4.1 billion) from UK

– Mainly from GB

Source: DAFM 2018

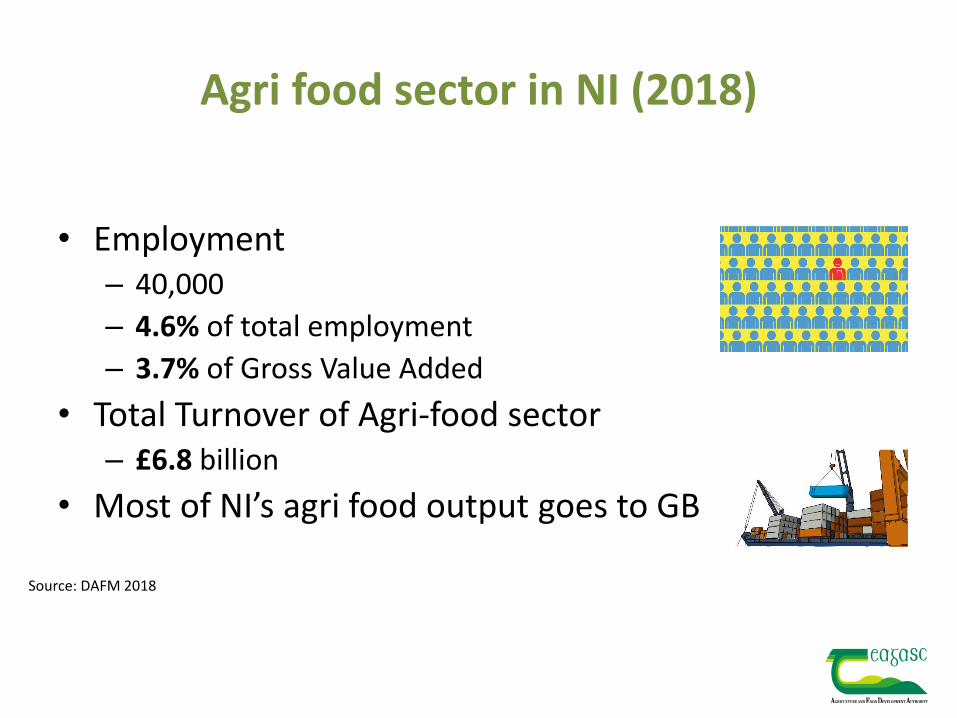

Agri food sector in NI (2018)

• Employment – 40,000

– 4.6% of total employment

– 3.7% of Gross Value Added

• Total Turnover of Agri-food sector– £6.8 billion

• Most of NI’s agri food output goes to GB

Source: DAFM 2018

Agri-food Trade Flows

• East-West agri-food trade flows dominate North-South trade flows

– Gravity matters

• But there are some critical North-South trade flows that are particularly important for NI Ag.

Flow of Trade between IE and NI

• All Island animal health strategy (covering IE and NI)– Treated as a single zone for animal health– EU SPS regulatory alignment

• Agri food trade between IE and NI– Live animals– Finished good and intermediate goods (for further processing)– Trade flows of food products are not so important

• Agri food trade between IE and GB– Large flows in agricultural goods from IE to GB– Large flows in processed food/drink from GB to Ireland

• and onto Northern Ireland

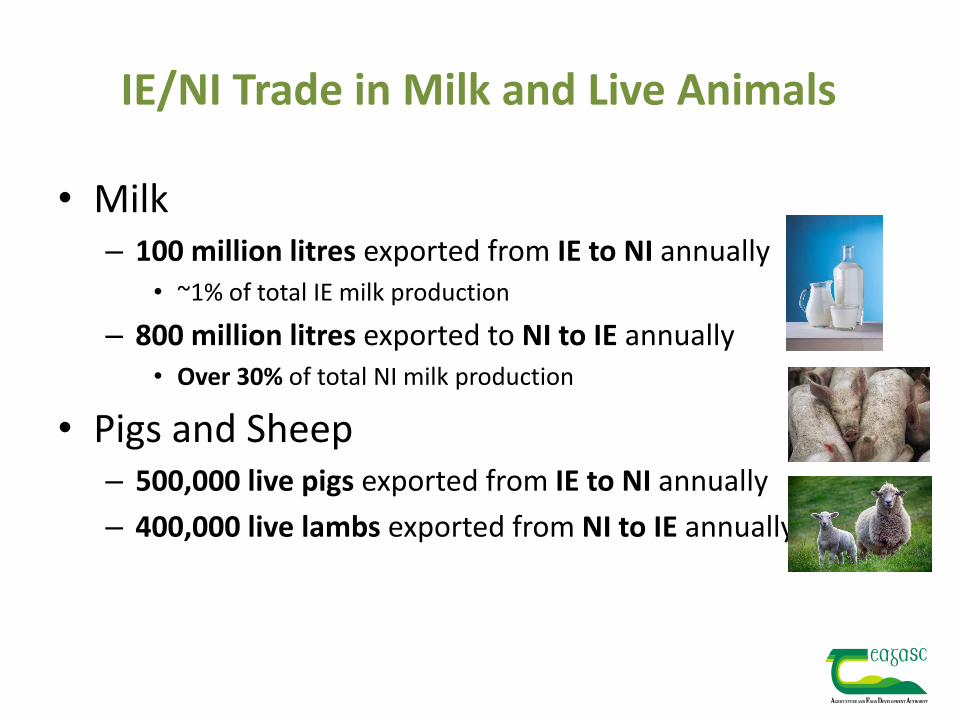

IE/NI Trade in Milk and Live Animals

• Milk– 100 million litres exported from IE to NI annually

• ~1% of total IE milk production

– 800 million litres exported to NI to IE annually• Over 30% of total NI milk production

• Pigs and Sheep– 500,000 live pigs exported from IE to NI annually

– 400,000 live lambs exported from NI to IE annually

Why Brexit Matters to Agri-Food

• Brexit (at least in part) is about changes in trade policy

• Tariffs and non-tariff barriers (NTB) to trade much more important in agri-food than for many other areas of merchandise trade

• Integration of IE and UK (NI) economies means that market price impacts of Brexit likely to be very large

• UK is a large net contributor to the EU budget. – Most of the “juste retour” Ireland gets from the EU budget is via CAP

– UK Brexit “dividend” from lower agricultural income support?

Brexit and Agriculture

• Channels through which Brexit affects Irish/Northern Irish agriculture– Immediate impact via exchange rate

– Tariff & non-tariff barriers to trade

– For IE via impact of Brexit on EU budget and CAP

– For NI via impact of future UK (Devolved?) Ag policy

What does Brexit Mean for Ag ?

• We obviously still don’t know what Brexit means for the magnitude of tariffs and NTB

• We know the No Deal EU trade policy

– The UK is a third country and WTO rules apply

• We think we know the UK trade policy

– The announced “temporary” No Deal tariff schedule

• We don’t know the shape of future UK or devolved NI agricultural policy

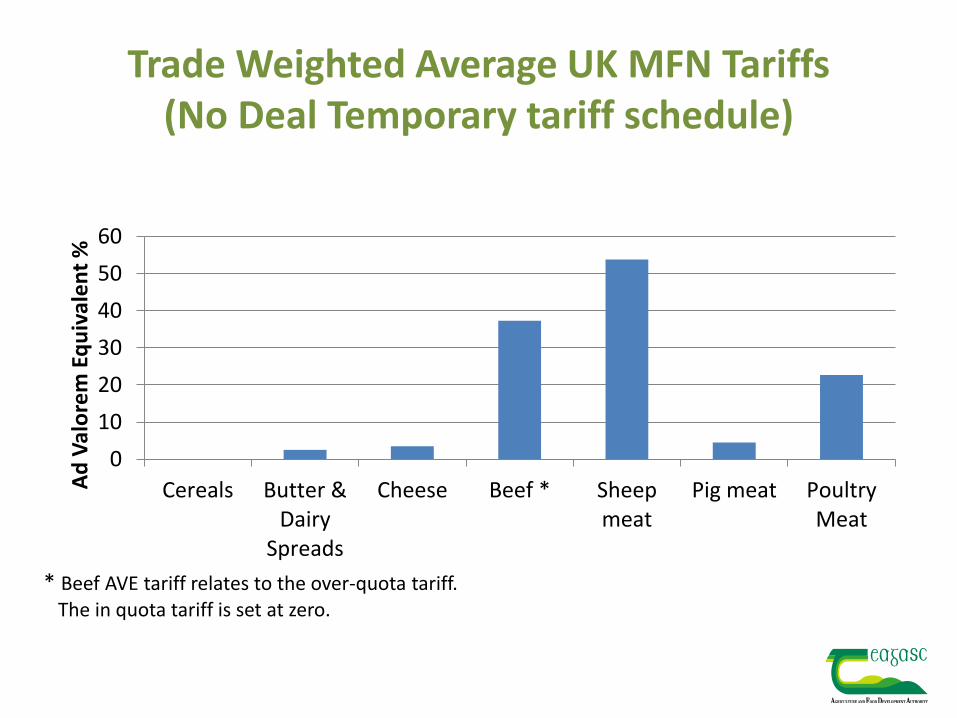

UK No Deal Trade Policy

• UK No Deal tariff schedule (March and October 2019)• Many tariffs set to zero

– so Brexit “delivers” lower prices for UK consumers

• But UK government would apply some tariffs– To protect UK producers– Retain something to “trade” in a future trade negotiation with EU

and/or other third countries

• UK also plans to use Tariff Rate Quota (TRQ)– a TRQ allows in a limited volume of imports at low or no tariff– To be used to manage UK imports of beef & poultry

Trade Weighted Average UK MFN Tariffs(No Deal Temporary tariff schedule)

0

10

20

30

40

50

60

Cereals Butter &Dairy

Spreads

Cheese Beef * Sheepmeat

Pig meat PoultryMeat

Ad

Val

ore

m E

qu

ival

en

t %

* Beef AVE tariff relates to the over-quota tariff.The in quota tariff is set at zero.

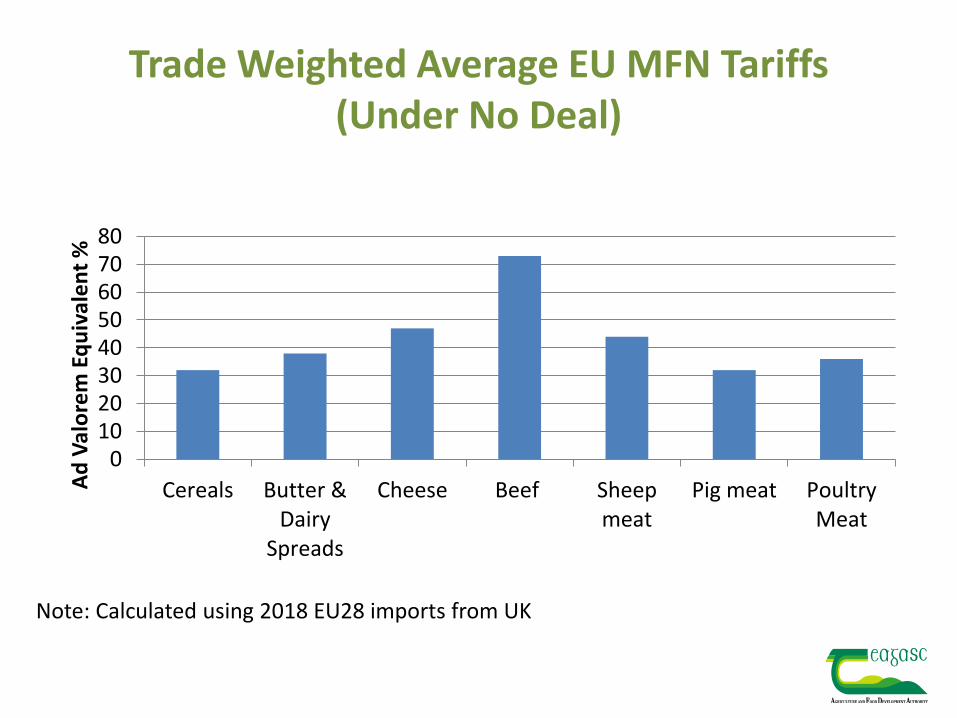

EU No Deal Trade Policy

• MFN tariffs as per EU schedule at WTO – These tariffs are very high

• Regulatory barriers & customs procedures to protect SM integrity will represent an important NTB– Entry of animal and food products only via BIP

– Requirements for physical inspections on entry to EU

– Licensing/inspection premises in the UK that wish to export to the EU

– Rules governing what is an “EU” product & RoOs

Trade Weighted Average EU MFN Tariffs(Under No Deal)

01020304050607080

Cereals Butter &Dairy

Spreads

Cheese Beef Sheepmeat

Pig meat PoultryMeat

Ad

Val

ore

m E

qu

ival

en

t %

Note: Calculated using 2018 EU28 imports from UK

Irish and Northern Irish Agri-Food & Brexit

• Greatest negative economic impact on sectors where

– Large share of output is exported to the UK (EU)

– That have high levels of tariff protection currently (preferential access) and are not internationally competitive

– High level of income dependence on direct payments

– Where existing margins from production are small

Ireland: Beef

• Most exposed Irish agri-food sector is beef

– Very high dependence on exports to UK

– Large loss in preferential access with No Deal

– Lack of competitiveness at world market prices

– High dependence of farm incomes on CAP direct income support payments

– Chronic low levels of profitability => little or no ability to absorb lower margins at either farm or processing stage

Northern Ireland: Dairy

• Under a No Deal Brexit Northern Irish ag sector most exposed is dairy– Very high dependence on exports of milk for

processing/consumption in Ireland

– Both tariff and non-tariff barriers to trade will apply in event of a no deal and will effectively halt this trade

– No feasible processing capacity for the 800 m litres of NI milk (currently shipped south) within the UK

Northern Ireland: Beef

• Sector v. “export” dependent but market is mostly in GB• Any Brexit opportunities (import substitution) will

depend on degree to which UK No deal trade policy leads/doesn’t lead to lower UK beef prices

• Dependence on CAP direct payments means sector very vulnerable to changes in UK Ag. Policy

• Very low profit levels at farm and processor levels mean sector is unlikely to be able to withstand negative market or policy impacts of Brexit

Ireland: Dairy

• Less exposed to UK Market than beef

– Some segments have higher exposure (cheddar)

• UK No Deal Tariffs on dairy are relatively low

• Irish dairy exports competitive at world market prices

– => Loss of preferential market access doesn’t necessarily mean loss of UK market share

• Low dependence on CAP direct income support payments

• Profitable business at farm and processor levels => even with Brexit Irish milk production likely to continue to grow

What impact will tariffs & NTB have on trade?

• Demand curves slope down Tariffs and NTB will reduce trade – Key uncertainty surrounding magnitude of trade elasticities

• With tariffs of >50% applying to some agri trade flows leads to dramatic impacts on trade

• What happens to prices, production and use ?

• Using PE models of Irish and Northern Irish/UK agricultural economies to assess impact of Brexit “scenarios”

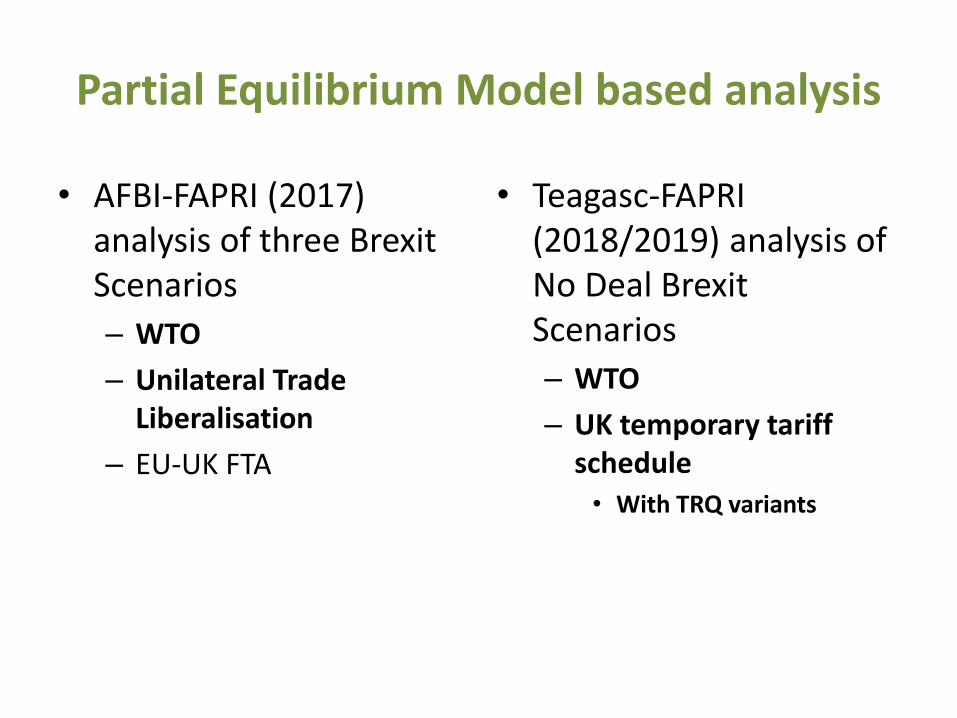

Partial Equilibrium Model based analysis

• AFBI-FAPRI (2017) analysis of three Brexit Scenarios

– WTO

– Unilateral Trade Liberalisation

– EU-UK FTA

• Teagasc-FAPRI (2018/2019) analysis of No Deal Brexit Scenarios

– WTO

– UK temporary tariff schedule• With TRQ variants

AFBI analysis

• AFBI analysis predates the UK No Deal Trade policy announcement

• Highlights the trade offs between an explicitly protectionist UK trade policy and a very liberal trade policy stance– The more “liberal” the UK trade policy stance the

larger the negative impact on N. Irish agriculture

• Management of UK beef imports via TRQ and a solution to the problem of what to do with NI milk production will be critical to mitigating the negative impact of Brexit on N. Irish agriculture

Teagasc Analysis

• Analysis for Government of impact of WTO Scenario and announced UK No Deal trade policy – Assumes its persists over the medium term under a No Deal

Brexit

• Large negative price impact on Irish beef prices of almost 20% versus Baseline if Ireland fails to retain partialpreferential market access offered by UK TRQ

• Negative price impacts for all sectors except Lamb – Due to exclusion of UK lamb from EU markets

• Overall Irish Agricultural Sector Output projected to decline by over €700m per annum and Operating Surplus (Ag Sector Income) declines by over €500m by 2026

Work to do

• Analysis has focused on impact of tariff barriers • Questions about impact of NTB will arise in the

event of a future EU-UK FTA• Clarity on actual trade rules will allow for

scenario analysis grounded in some political facts – That will be novel !!

• Analysis of the impact of Brexit on the structure of the Irish and Northern Irish farm sectors will be needed– Brexit likely to accelerate structural change processes

Brexit: Workers at Risk and Policy Responses to Maintain Employment

PA U L M A C F LY N N

N E R I ( N E V I N E C O N O M I C R E S E A R C H I N S T I T U T E )

B E L FA S T

PA U L . M A C F LY N N @ N E R I N S T I T U T E . N E T

W W W. N E R I N S T I T U T E . N E T

On the brink of Brexit

17 October 2017

ContextoUnemployment in NI - historic low of 2.8% (May – Jul ’19).

oTotal no. of jobs >900k (Q2 2019)

oEconomic Inactivity still higher than UK, almost same as ROI.

oSeems like an odd time to be designing gov programmes to deal with significant increase in unemployment.

oAdvantages:o Time – not exogenous shock, conscious policy decision.

o Impact – some idea of where will be hit

oDisadvantages:o Limits to help – compensation for tariffs cannot be direct.

o Unlike cyclical downturn, hard to see natural recovery.

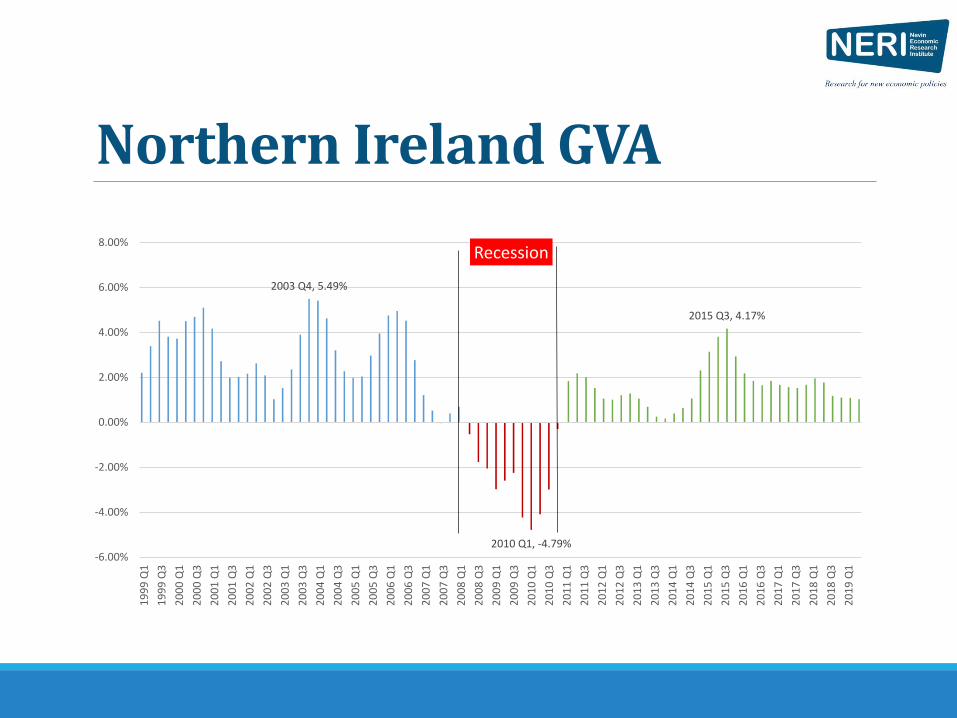

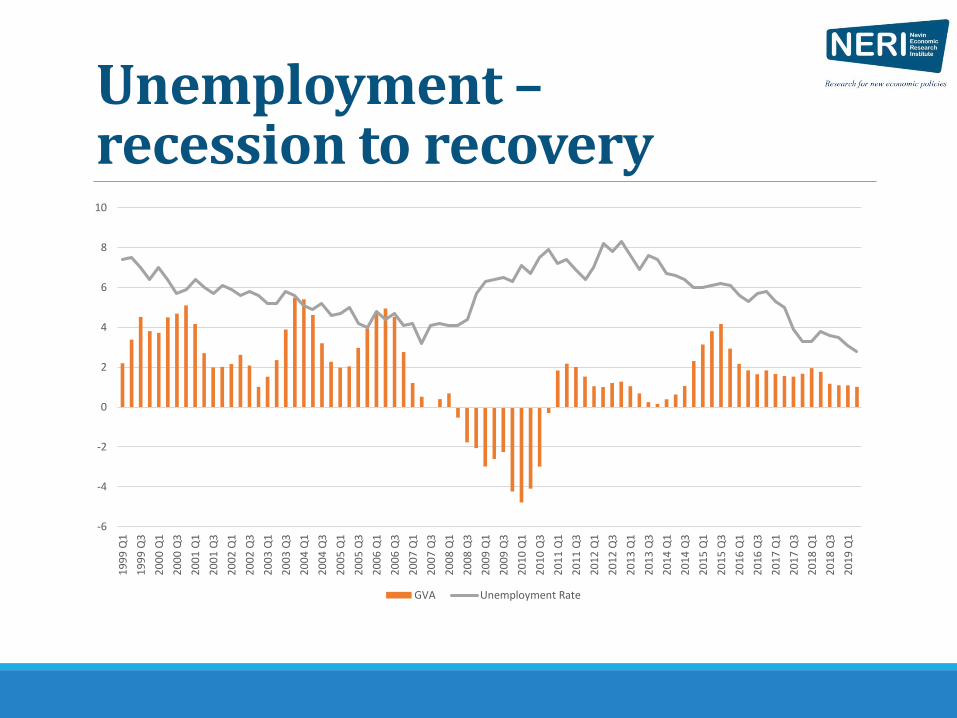

Northern Ireland GVA

2003 Q4, 5.49%

2010 Q1, -4.79%

2015 Q3, 4.17%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

19

99

Q1

19

99

Q3

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

20

18

Q1

20

18

Q3

20

19

Q1

Recession

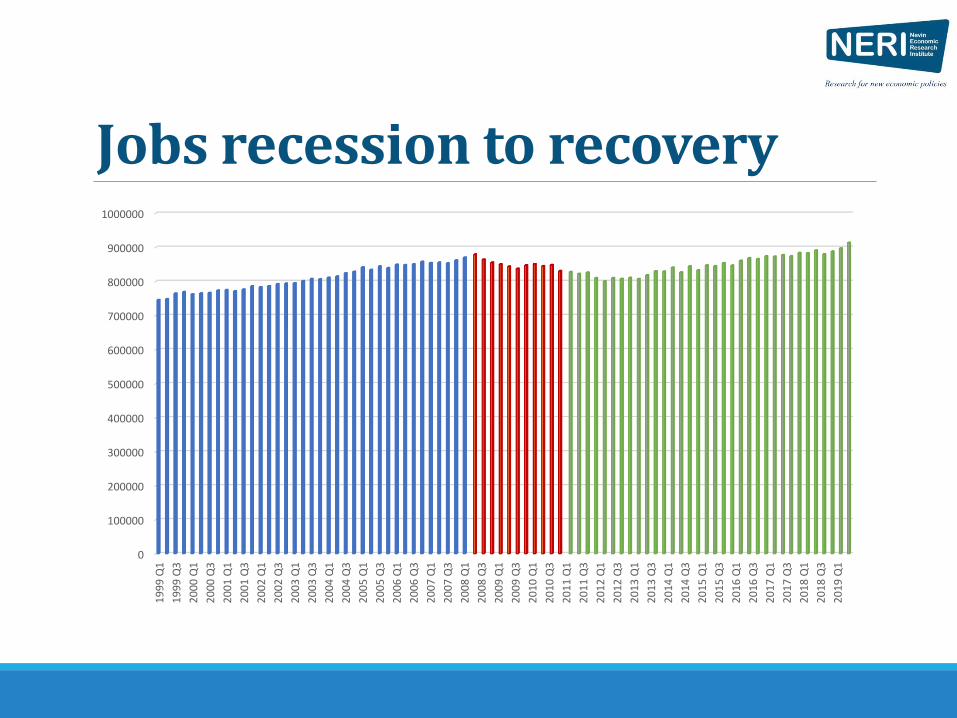

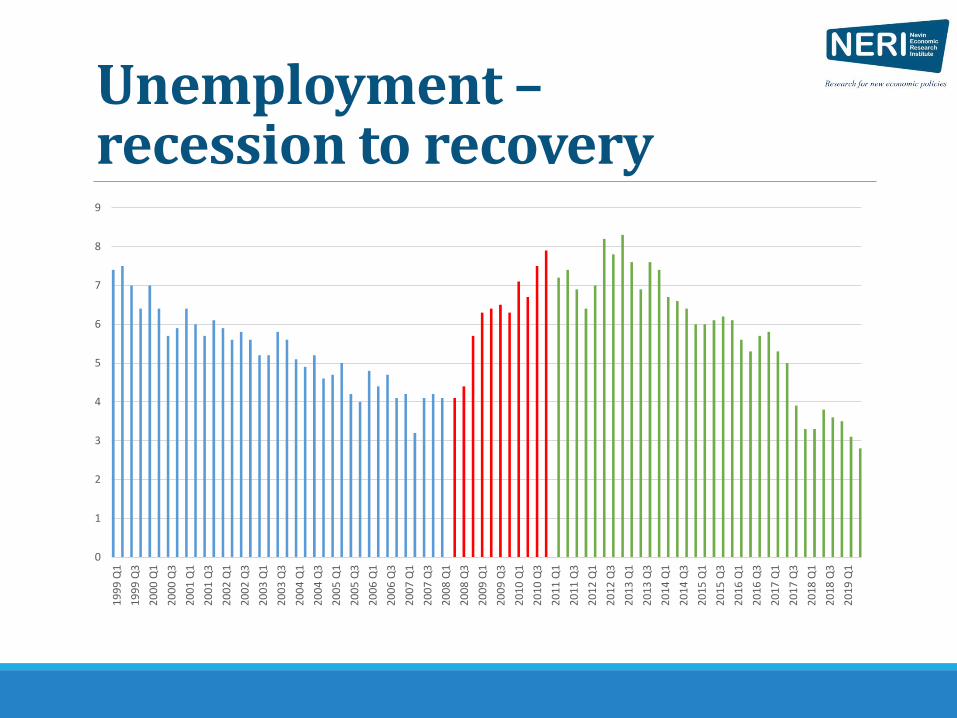

ContextoFinancial crash in NI, similar experience to ROI but more benign on jobs/unemployment.

oUnemployment rate increases from 3.2 in Q2 2017 to 8.3 in Q4 2012

oTotal number of jobs falls by 78,000 between Q2 2008 and Q4 2012

Jobs recession to recovery

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

19

99

Q1

19

99

Q3

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

20

18

Q1

20

18

Q3

20

19

Q1

Unemployment –recession to recovery

0

1

2

3

4

5

6

7

8

9

19

99

Q1

19

99

Q3

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

20

18

Q1

20

18

Q3

20

19

Q1

Unemployment –recession to recovery

-6

-4

-2

0

2

4

6

8

10

19

99

Q1

19

99

Q3

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

20

18

Q1

20

18

Q3

20

19

Q1

GVA Unemployment Rate

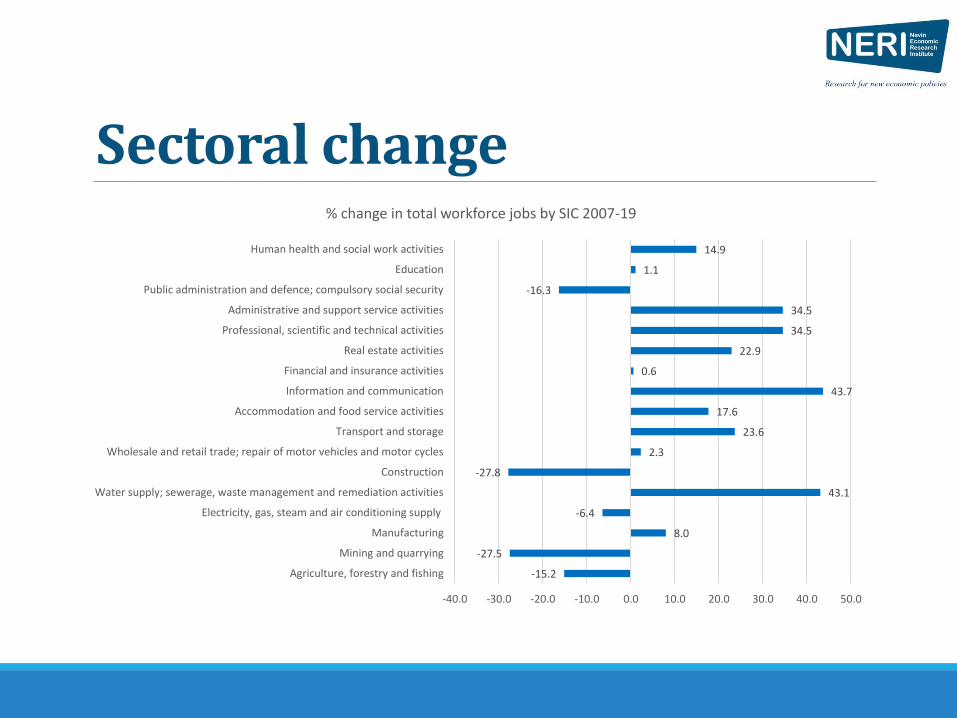

Sectoral change

-15.2

-27.5

8.0

-6.4

43.1

-27.8

2.3

23.6

17.6

43.7

0.6

22.9

34.5

34.5

-16.3

1.1

14.9

-40.0 -30.0 -20.0 -10.0 0.0 10.0 20.0 30.0 40.0 50.0

Agriculture, forestry and fishing

Mining and quarrying

Manufacturing

Electricity, gas, steam and air conditioning supply

Water supply; sewerage, waste management and remediation activities

Construction

Wholesale and retail trade; repair of motor vehicles and motor cycles

Transport and storage

Accommodation and food service activities

Information and communication

Financial and insurance activities

Real estate activities

Professional, scientific and technical activities

Administrative and support service activities

Public administration and defence; compulsory social security

Education

Human health and social work activities

% change in total workforce jobs by SIC 2007-19

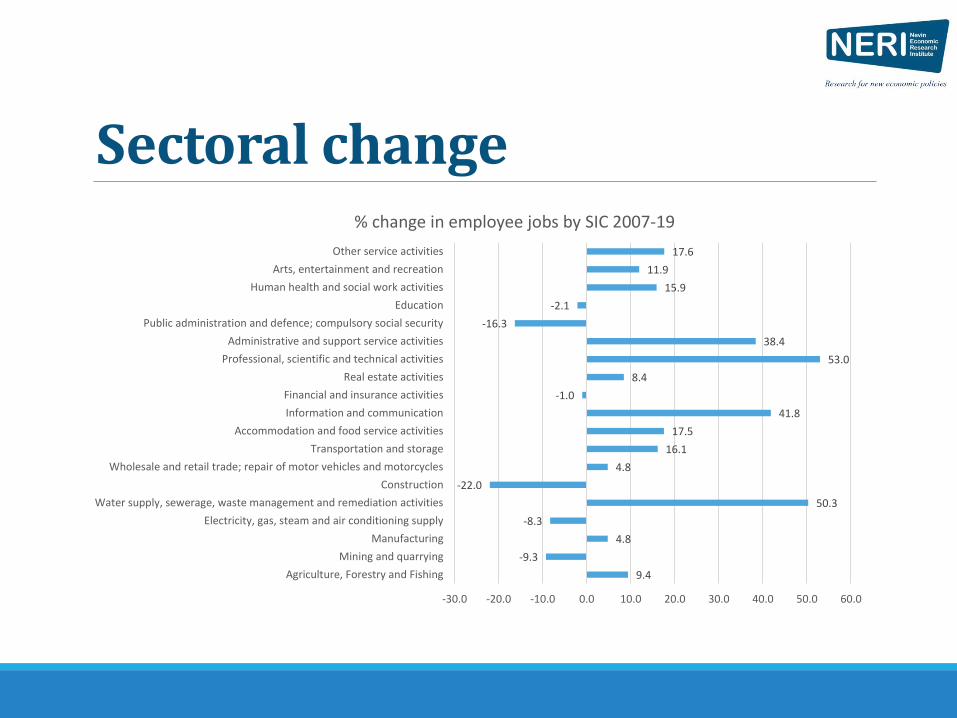

Sectoral change

9.4

-9.3

4.8

-8.3

50.3

-22.0

4.8

16.1

17.5

41.8

-1.0

8.4

53.0

38.4

-16.3

-2.1

15.9

11.9

17.6

-30.0 -20.0 -10.0 0.0 10.0 20.0 30.0 40.0 50.0 60.0

Agriculture, Forestry and Fishing

Mining and quarrying

Manufacturing

Electricity, gas, steam and air conditioning supply

Water supply, sewerage, waste management and remediation activities

Construction

Wholesale and retail trade; repair of motor vehicles and motorcycles

Transportation and storage

Accommodation and food service activities

Information and communication

Financial and insurance activities

Real estate activities

Professional, scientific and technical activities

Administrative and support service activities

Public administration and defence; compulsory social security

Education

Human health and social work activities

Arts, entertainment and recreation

Other service activities

% change in employee jobs by SIC 2007-19

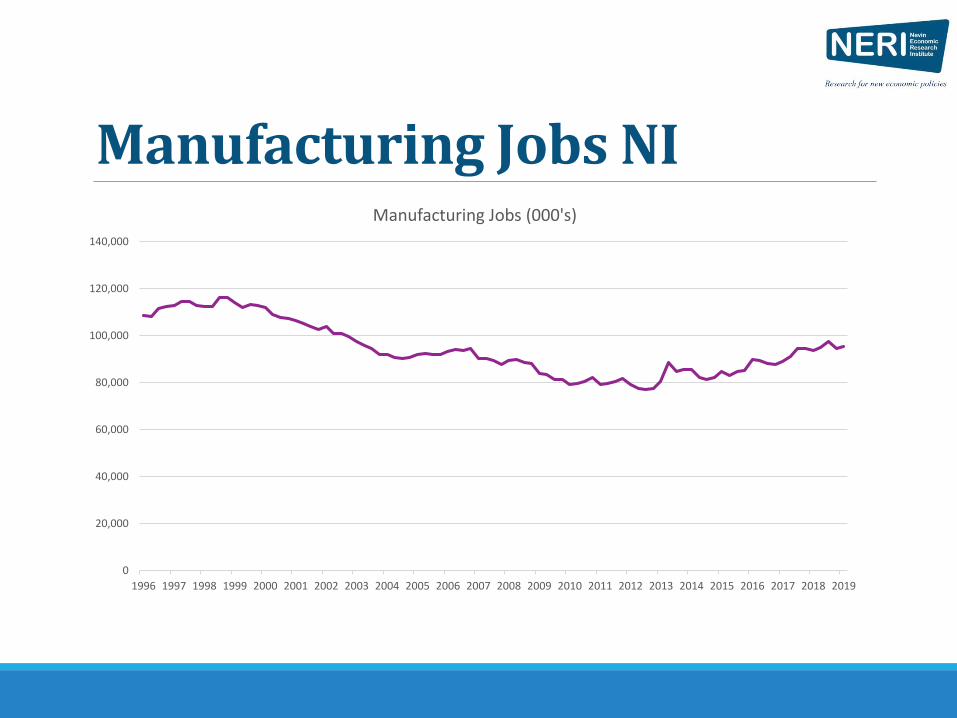

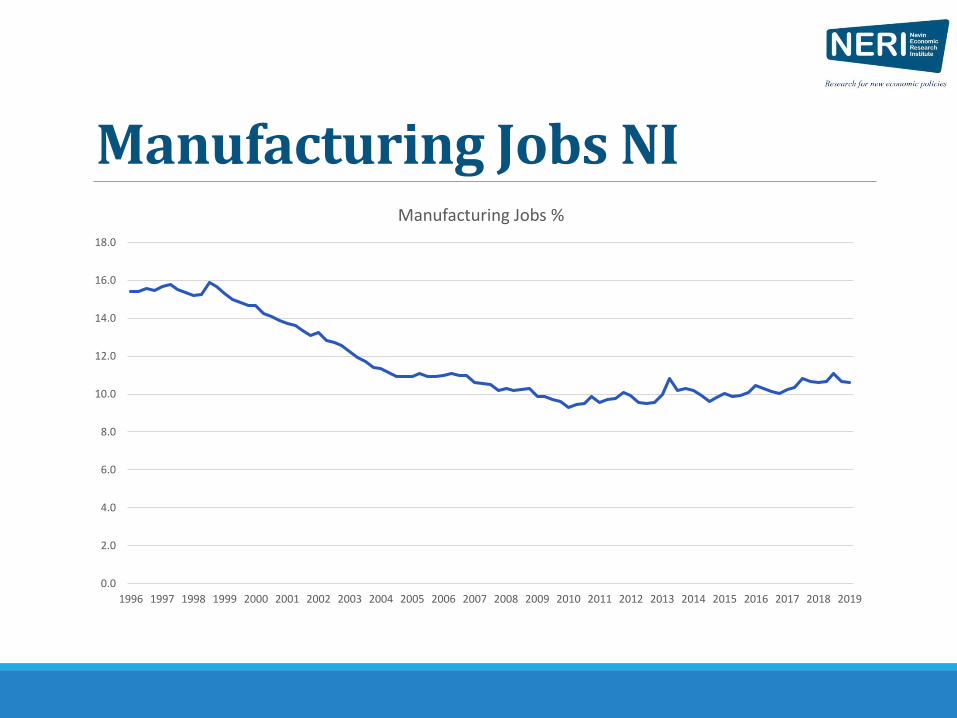

Manufacturing Jobs NI

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Manufacturing Jobs (000's)

Manufacturing Jobs NI

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Manufacturing Jobs %

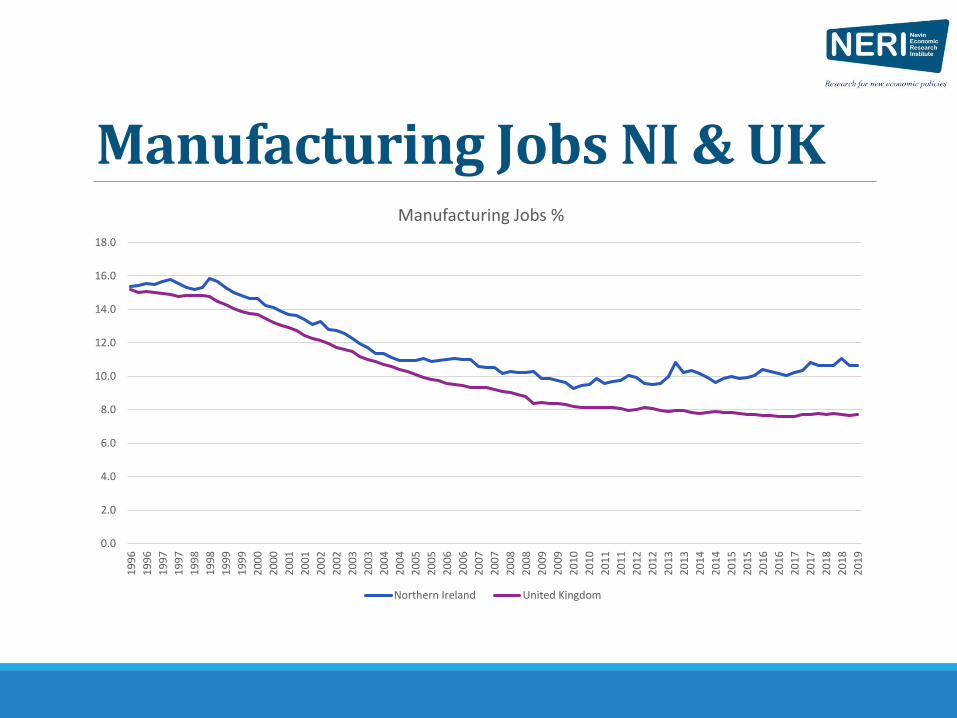

Manufacturing Jobs NI & UK

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

19

96

19

96

19

97

19

97

19

98

19

98

19

99

19

99

20

00

20

00

20

01

20

01

20

02

20

02

20

03

20

03

20

04

20

04

20

05

20

05

20

06

20

06

20

07

20

07

20

08

20

08

20

09

20

09

20

10

20

10

20

11

20

11

20

12

20

12

20

13

20

13

20

14

20

14

20

15

20

15

20

16

20

16

20

17

20

17

20

18

20

18

20

19

Manufacturing Jobs %

Northern Ireland United Kingdom

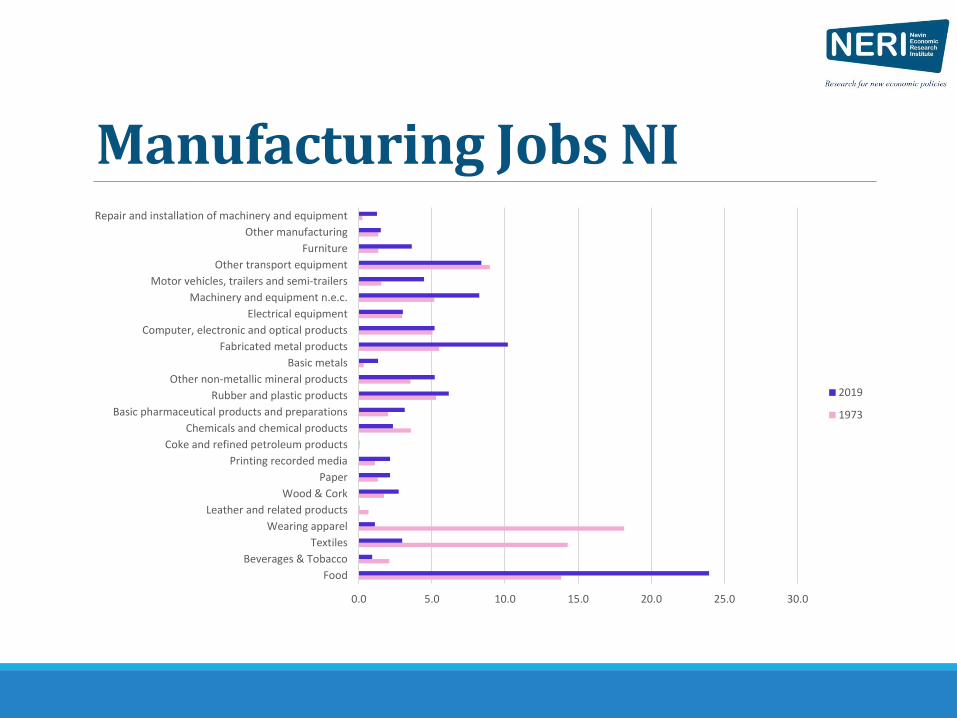

Manufacturing Jobs NI

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Food

Beverages & Tobacco

Textiles

Wearing apparel

Leather and related products

Wood & Cork

Paper

Printing recorded media

Coke and refined petroleum products

Chemicals and chemical products

Basic pharmaceutical products and preparations

Rubber and plastic products

Other non-metallic mineral products

Basic metals

Fabricated metal products

Computer, electronic and optical products

Electrical equipment

Machinery and equipment n.e.c.

Motor vehicles, trailers and semi-trailers

Other transport equipment

Furniture

Other manufacturing

Repair and installation of machinery and equipment

2019

1973

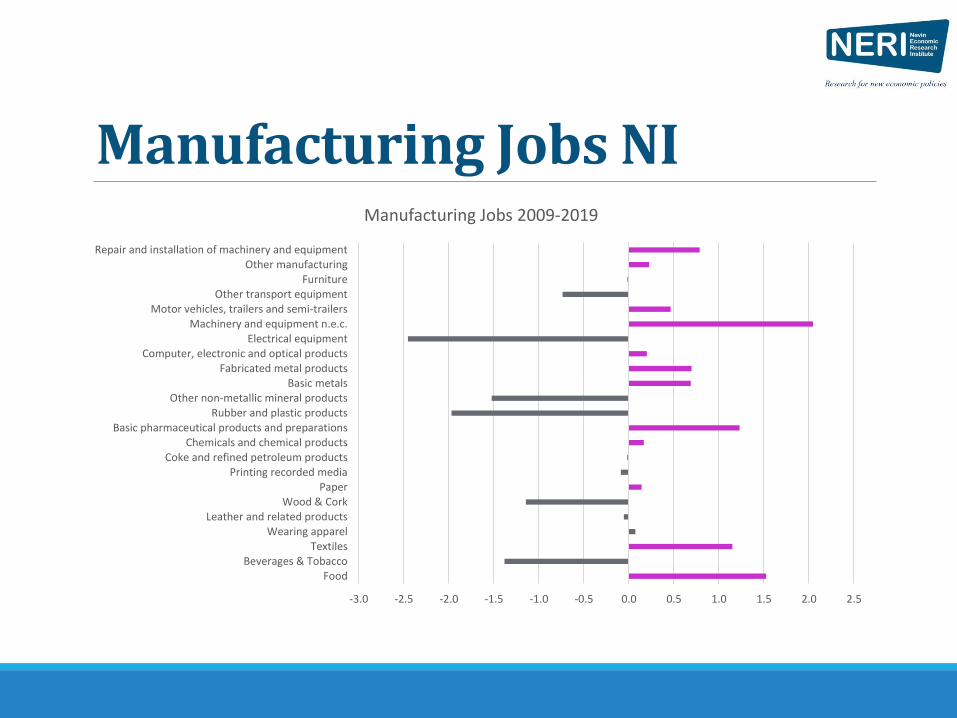

Manufacturing Jobs NI

-3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

FoodBeverages & Tobacco

TextilesWearing apparel

Leather and related productsWood & Cork

PaperPrinting recorded media

Coke and refined petroleum productsChemicals and chemical products

Basic pharmaceutical products and preparationsRubber and plastic products

Other non-metallic mineral productsBasic metals

Fabricated metal productsComputer, electronic and optical products

Electrical equipmentMachinery and equipment n.e.c.

Motor vehicles, trailers and semi-trailersOther transport equipment

FurnitureOther manufacturing

Repair and installation of machinery and equipment

Manufacturing Jobs 2009-2019

Manufacturing Jobs NI

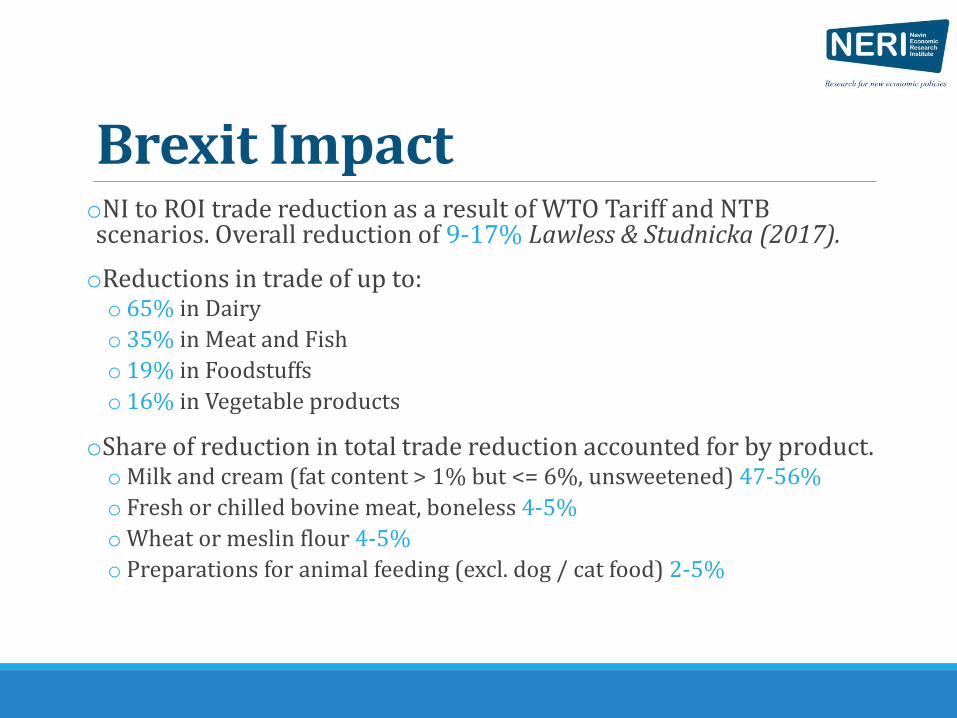

Brexit ImpactoNI to ROI trade reduction as a result of WTO Tariff and NTB scenarios. Overall reduction of 9-17% Lawless & Studnicka (2017).

oReductions in trade of up to:o 65% in Dairy

o 35% in Meat and Fish

o 19% in Foodstuffs

o 16% in Vegetable products

oShare of reduction in total trade reduction accounted for by product. oMilk and cream (fat content > 1% but <= 6%, unsweetened) 47-56%

o Fresh or chilled bovine meat, boneless 4-5%

oWheat or meslin flour 4-5%

o Preparations for animal feeding (excl. dog / cat food) 2-5%

Food Manufacturing Jobs NI

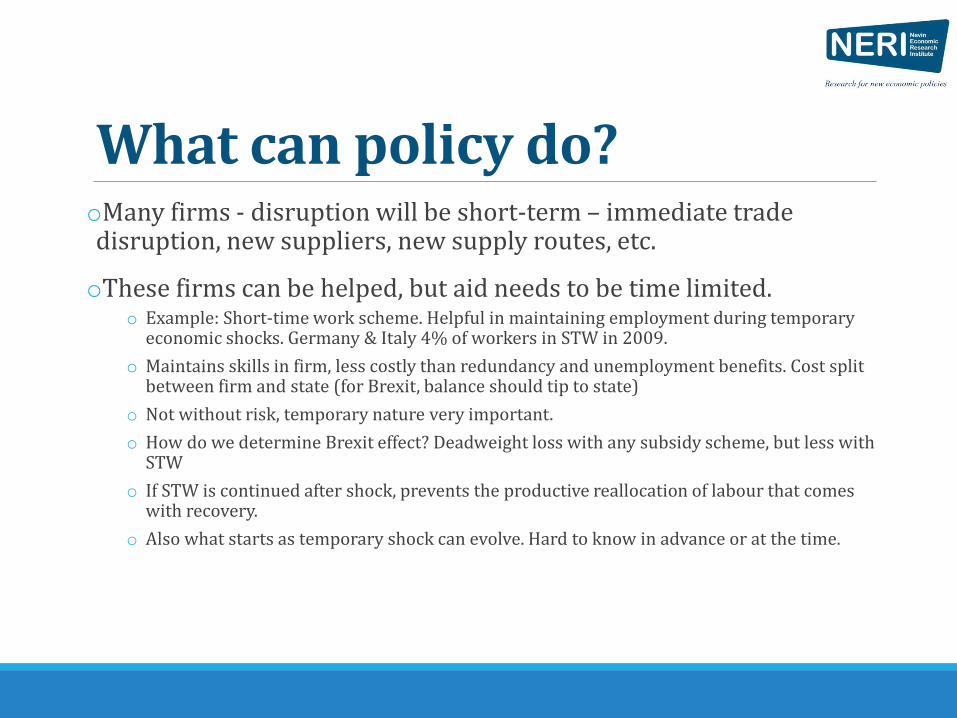

What can policy do?oMany firms - disruption will be short-term – immediate trade disruption, new suppliers, new supply routes, etc.

oThese firms can be helped, but aid needs to be time limited.o Example: Short-time work scheme. Helpful in maintaining employment during temporary

economic shocks. Germany & Italy 4% of workers in STW in 2009.

o Maintains skills in firm, less costly than redundancy and unemployment benefits. Cost split between firm and state (for Brexit, balance should tip to state)

o Not without risk, temporary nature very important.

o How do we determine Brexit effect? Deadweight loss with any subsidy scheme, but less with STW

o If STW is continued after shock, prevents the productive reallocation of labour that comes with recovery.

o Also what starts as temporary shock can evolve. Hard to know in advance or at the time.

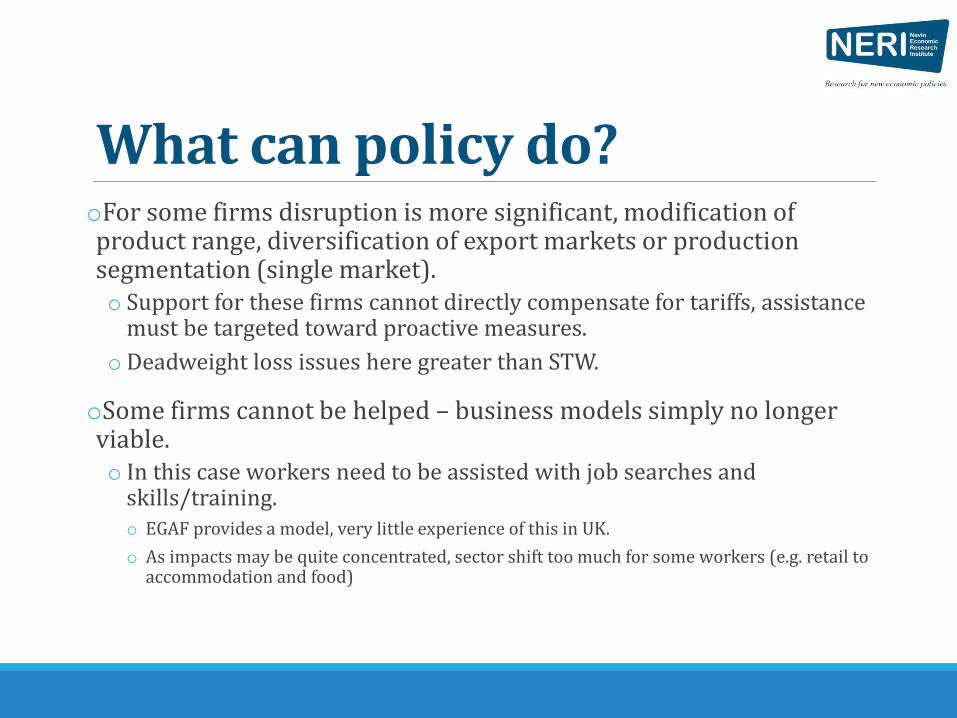

What can policy do?oFor some firms disruption is more significant, modification of product range, diversification of export markets or production segmentation (single market).o Support for these firms cannot directly compensate for tariffs, assistance

must be targeted toward proactive measures.

o Deadweight loss issues here greater than STW.

oSome firms cannot be helped – business models simply no longer viable.o In this case workers need to be assisted with job searches and

skills/training. o EGAF provides a model, very little experience of this in UK.

o As impacts may be quite concentrated, sector shift too much for some workers (e.g. retail to accommodation and food)

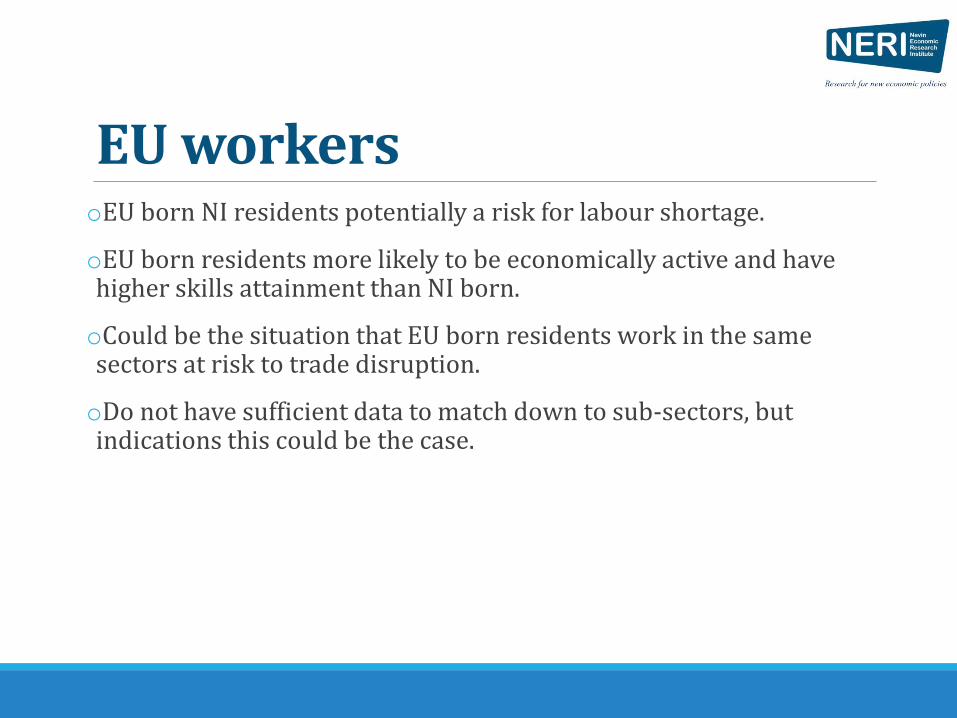

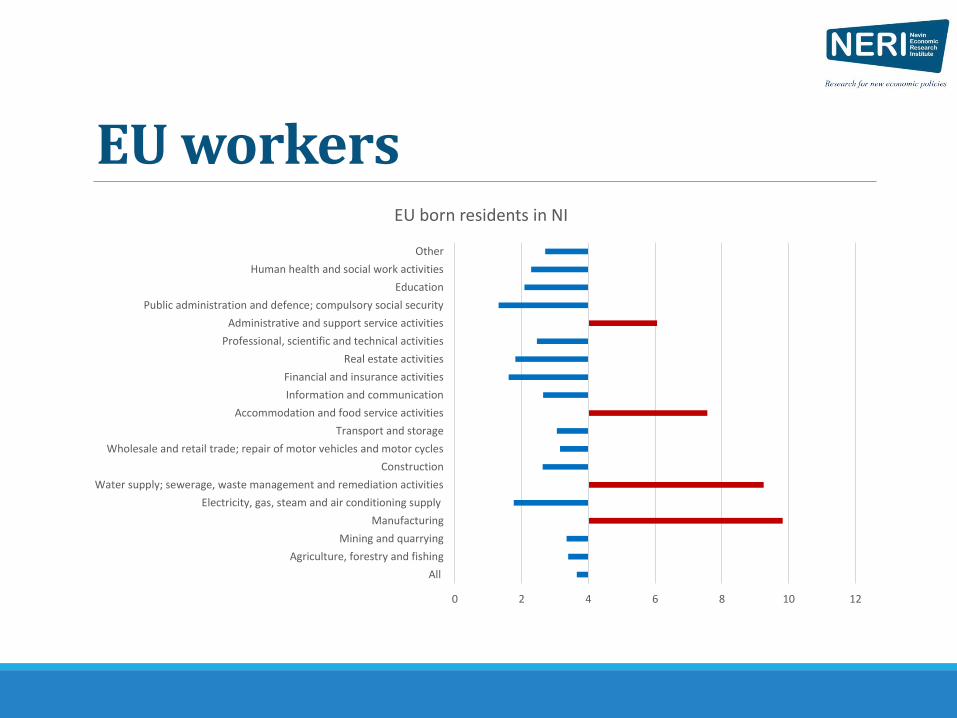

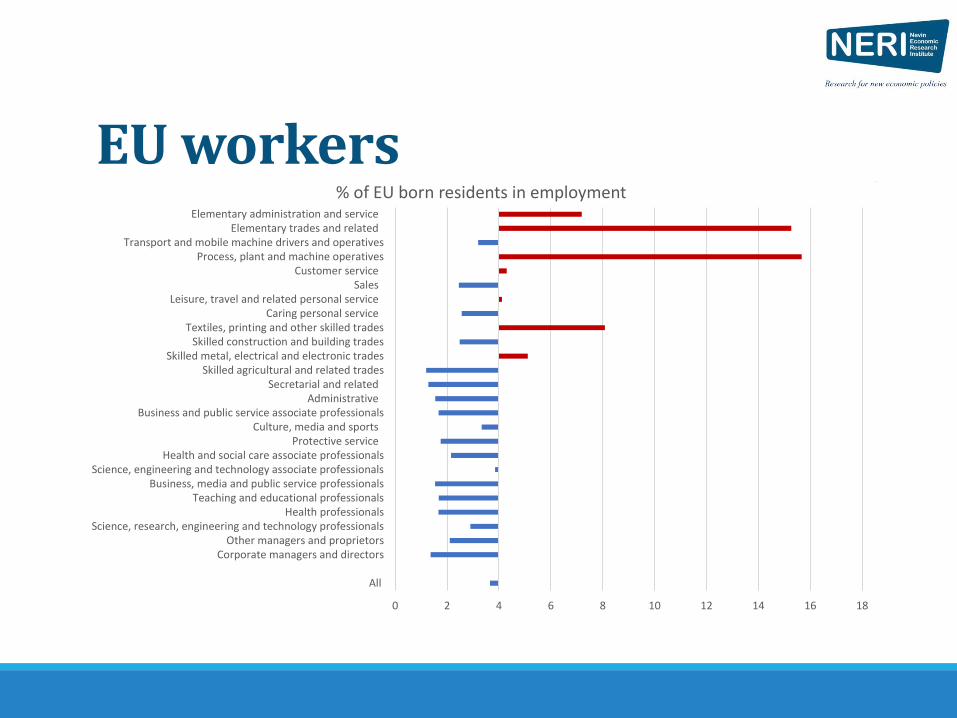

EU workersoEU born NI residents potentially a risk for labour shortage.

oEU born residents more likely to be economically active and have higher skills attainment than NI born.

oCould be the situation that EU born residents work in the same sectors at risk to trade disruption.

oDo not have sufficient data to match down to sub-sectors, but indications this could be the case.

EU workers

0 2 4 6 8 10 12

All

Agriculture, forestry and fishing

Mining and quarrying

Manufacturing

Electricity, gas, steam and air conditioning supply

Water supply; sewerage, waste management and remediation activities

Construction

Wholesale and retail trade; repair of motor vehicles and motor cycles

Transport and storage

Accommodation and food service activities

Information and communication

Financial and insurance activities

Real estate activities

Professional, scientific and technical activities

Administrative and support service activities

Public administration and defence; compulsory social security

Education

Human health and social work activities

Other

EU born residents in NI

EU workers

0 2 4 6 8 10 12 14 16 18

All

Corporate managers and directorsOther managers and proprietors

Science, research, engineering and technology professionalsHealth professionals

Teaching and educational professionalsBusiness, media and public service professionals

Science, engineering and technology associate professionalsHealth and social care associate professionals

Protective serviceCulture, media and sports

Business and public service associate professionalsAdministrative

Secretarial and relatedSkilled agricultural and related trades

Skilled metal, electrical and electronic tradesSkilled construction and building trades

Textiles, printing and other skilled tradesCaring personal service

Leisure, travel and related personal serviceSales

Customer serviceProcess, plant and machine operatives

Transport and mobile machine drivers and operativesElementary trades and related

Elementary administration and service

% of EU born residents in employment

SummaryoSome idea of sectors that will be impacted. Can identify workers.

oNot clear how economy will recover. Preserving existing jobs may not be the answer for all firms.

oImpact of labour shortages also need to be factored in.

oAll of this is avoidable.

BREXIT – IMPLICATIONS FOR NORTHERN IRELAND ECONOMY

OCTOBER 2019

2

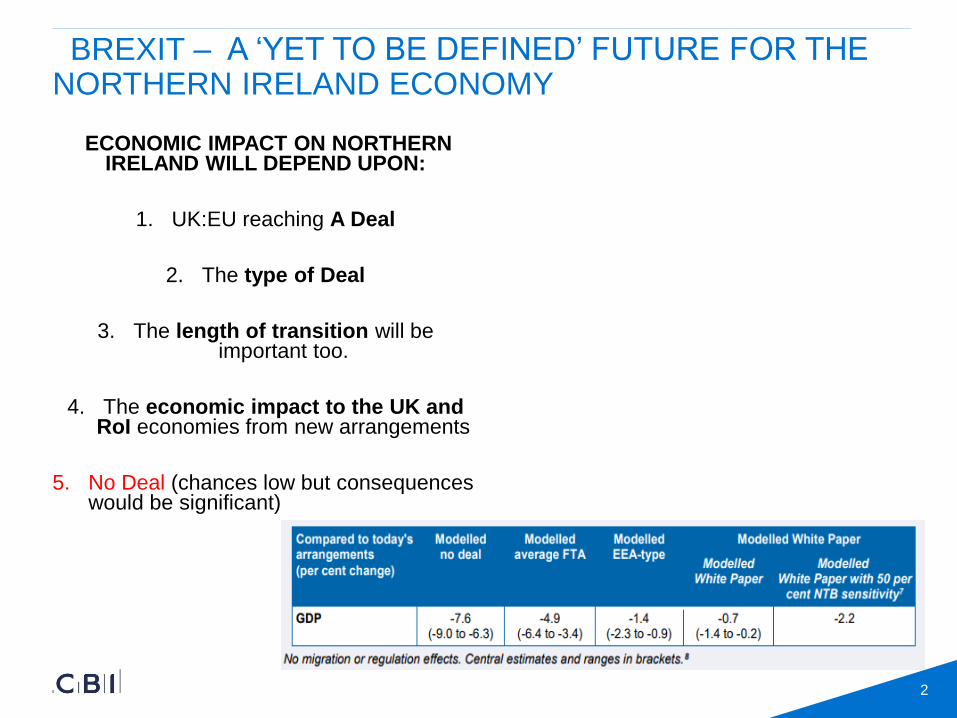

BREXIT – A ‘YET TO BE DEFINED’ FUTURE FOR THE NORTHERN IRELAND ECONOMY

ECONOMIC IMPACT ON NORTHERN IRELAND WILL DEPEND UPON:

1. UK:EU reaching A Deal

2. The type of Deal

3. The length of transition will be important too.

4. The economic impact to the UK and RoI economies from new arrangements

5. No Deal (chances low but consequences would be significant)

3

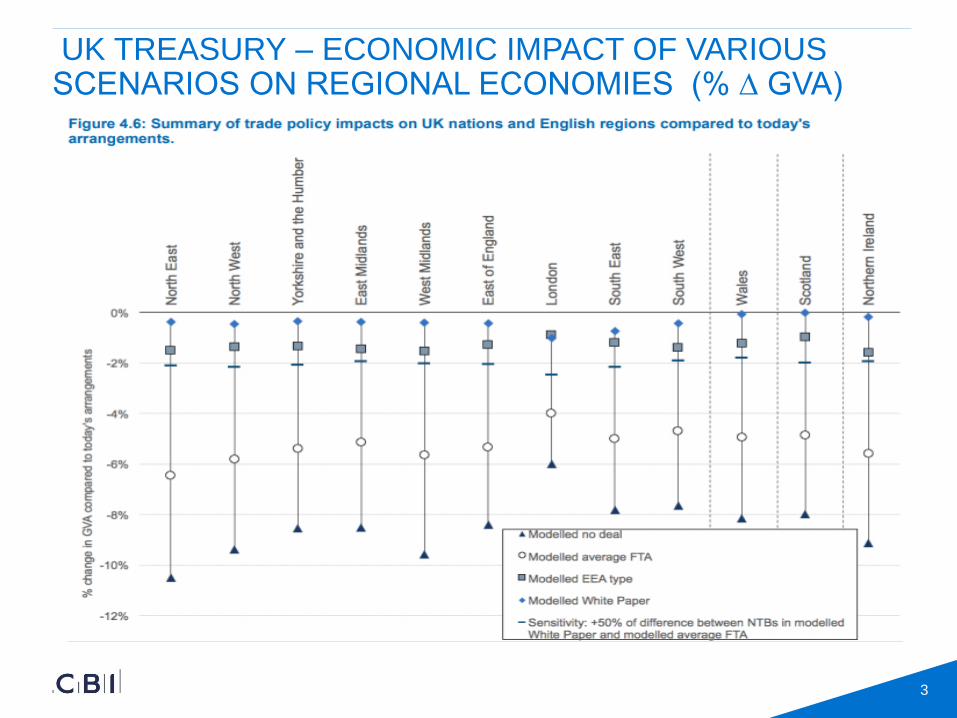

UK TREASURY – ECONOMIC IMPACT OF VARIOUS SCENARIOS ON REGIONAL ECONOMIES (% ∆ GVA)

4

NORTHERN IRELAND ECONOMY – WHY GREATER EXPOSURE TO BREXIT?

- High Integration with EU – particularly agri & food sectors

- Higher proportion of EU FUNDING per capita

- High dependence on RoI trade (goods and services)

- High integration of labour across island

- NI a weaker economy relative to rest of UK

- Significant Skills Gaps (Labour mk)

- Prevalence of Small Firms / lower productivity

- Political stability and cross-border cooperation paid a significant economic “dividend”.

- Fragile Peace Process – connected to Prosperity

5

BREXIT WILL TOUCH EVERY ASPECT OF AN ALREADY WEAK ECONOMY….

INVESTMENT - FDI & Indigenous Investment

BIZ ACTIVITY / PRODUCTIVITY - Allocation of Resources

COMPETITIVENESS - Supply Chains

Cost of Doing Business

(Tariffs and Non-tariff Barriers)

Cost of Imports / Speed

TRADE

THE LABOUR MARKET -

Migration / the Labour Market / Productivity

THE RURAL ECONOMY & EU FUNDING

CROSS-BORDER CO-OPERATION

(Energy Markets / Tourism / Health / Education)

6

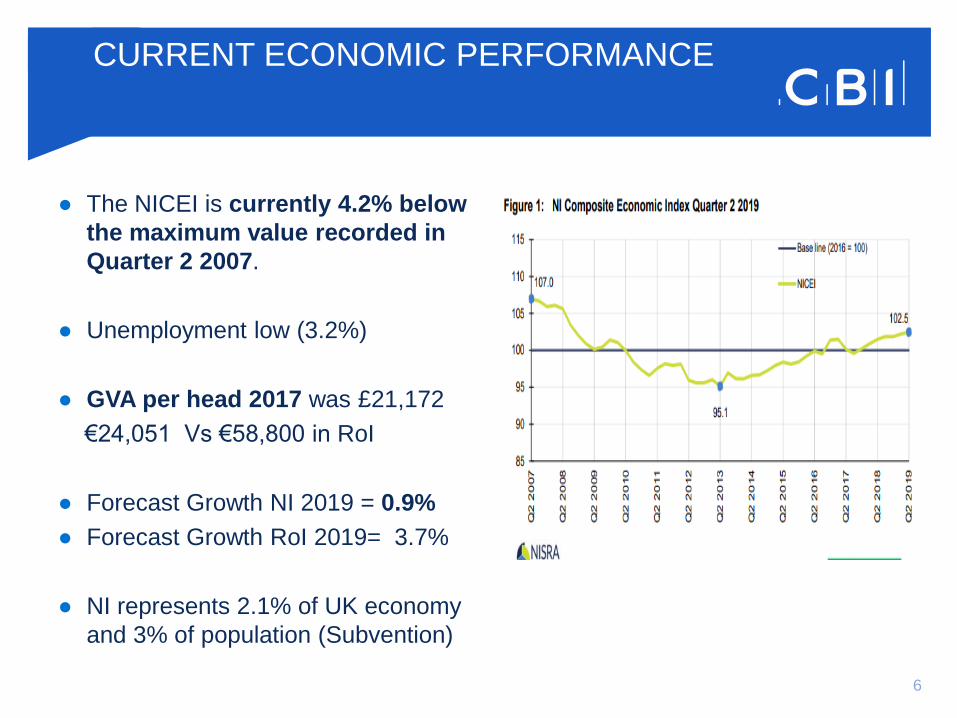

● The NICEI is currently 4.2% below

the maximum value recorded in

Quarter 2 2007.

● Unemployment low (3.2%)

● GVA per head 2017 was £21,172

€24,051 Vs €58,800 in RoI

● Forecast Growth NI 2019 = 0.9%

● Forecast Growth RoI 2019= 3.7%

● NI represents 2.1% of UK economy

and 3% of population (Subvention)

CURRENT ECONOMIC PERFORMANCE

7

-30

-25

-20

-15

-10

-5

0

5

10

15

20

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Business' investment intentions

Business investment, y/y% (right axis)

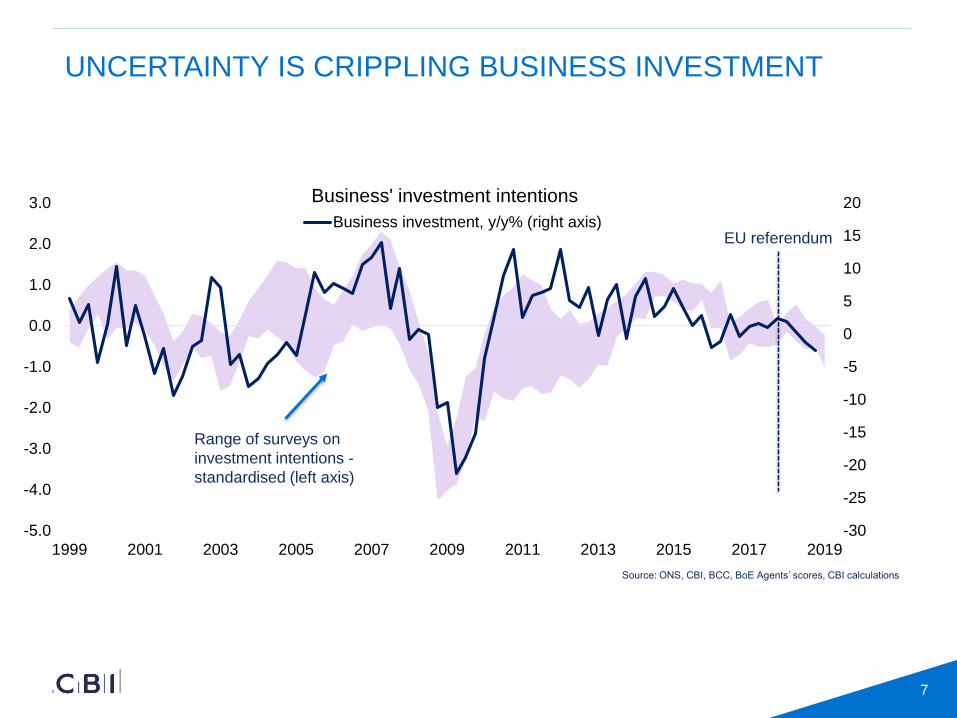

UNCERTAINTY IS CRIPPLING BUSINESS INVESTMENT

Source: ONS, CBI, BCC, BoE Agents’ scores, CBI calculations

EU referendum

Range of surveys on

investment intentions -

standardised (left axis)

8

● PRODUCTIVITY being dragged down because of LOW

INVESTMENT

● Resources SKEWED into – contingency planning & stockpiling

(one company talked of 200 hrs of C-suite time over 12 months)

● Less going into – R&D / Software / Training

● multi-national Investments – on hold

● EU nationals leaving / implications for output / Orders being turned

down

BUSINESS ACTIVITY / PRODUCTIVITY

9

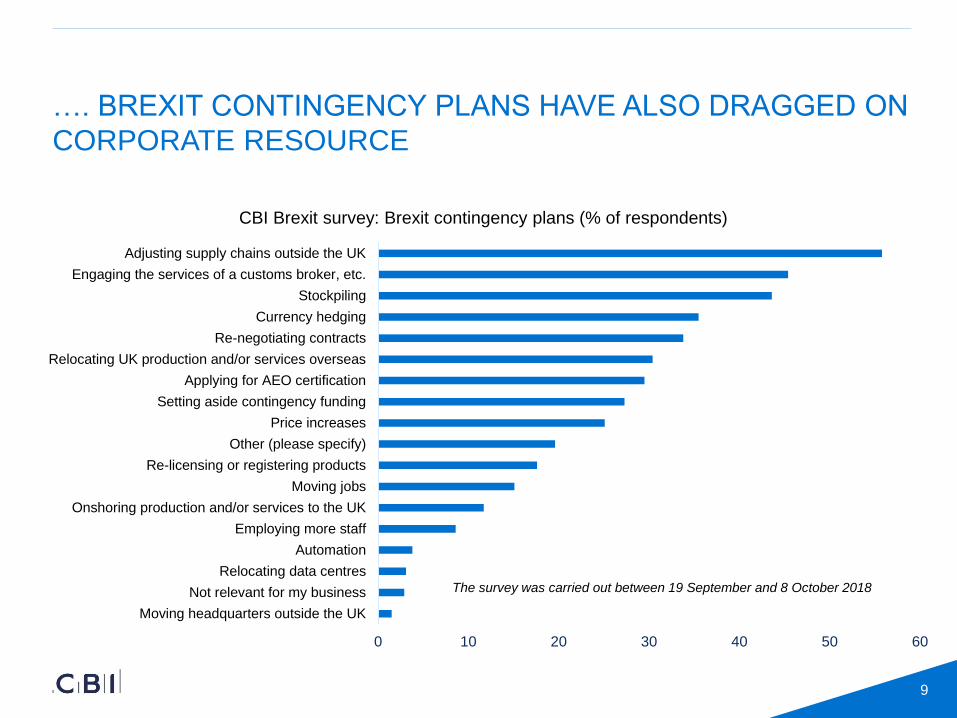

…. BREXIT CONTINGENCY PLANS HAVE ALSO DRAGGED ON

CORPORATE RESOURCE

0 10 20 30 40 50 60

Moving headquarters outside the UK

Not relevant for my business

Relocating data centres

Automation

Employing more staff

Onshoring production and/or services to the UK

Moving jobs

Re-licensing or registering products

Other (please specify)

Price increases

Setting aside contingency funding

Applying for AEO certification

Relocating UK production and/or services overseas

Re-negotiating contracts

Currency hedging

Stockpiling

Engaging the services of a customs broker, etc.

Adjusting supply chains outside the UK

CBI Brexit survey: Brexit contingency plans (% of respondents)

The survey was carried out between 19 September and 8 October 2018

10

Companies in NI facing competitiveness issues around:

I. Rising input costs (with depreciated pound) / forcing price up

II. Some European competitors targeting their customers (need to set up EU /

RoI office)

III. Some European customers have pulled orders for after Oct 31st

IV. Customers requesting that they hold 3+ months inventories (stockpiling)

V. Labour / Immigration policy also having impact on competitiveness

VI. Impact on FDI – unsure of future market access / not waiting for UK

NI’s COMPETITIVENESS

11

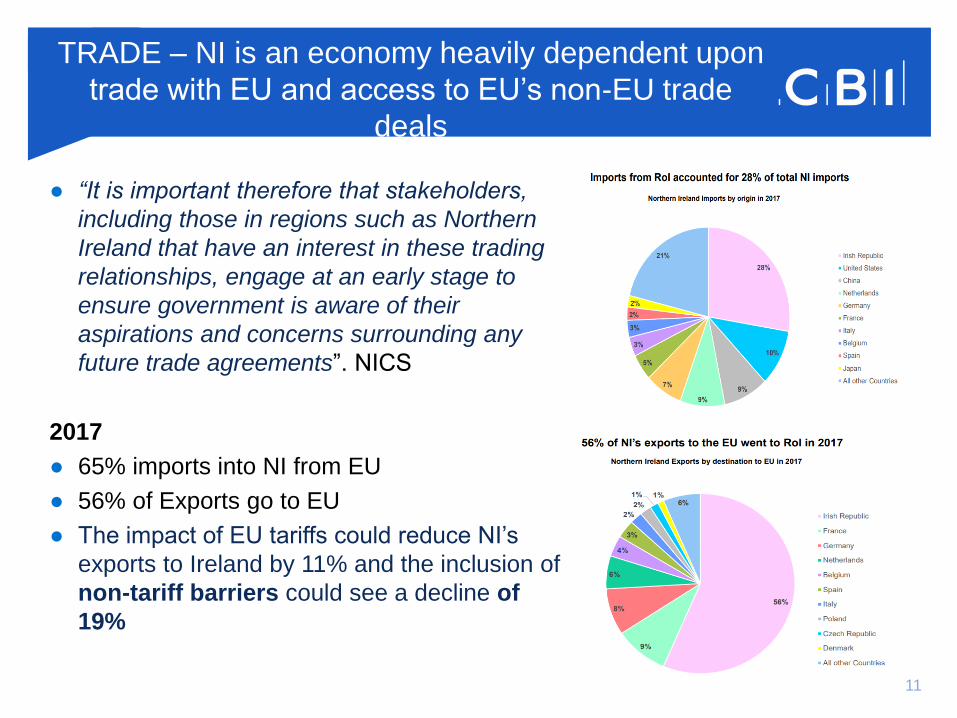

● “It is important therefore that stakeholders,

including those in regions such as Northern

Ireland that have an interest in these trading

relationships, engage at an early stage to

ensure government is aware of their

aspirations and concerns surrounding any

future trade agreements”. NICS

2017

● 65% imports into NI from EU

● 56% of Exports go to EU

● The impact of EU tariffs could reduce NI’s

exports to Ireland by 11% and the inclusion of

non-tariff barriers could see a decline of

19%

TRADE – NI is an economy heavily dependent upon

trade with EU and access to EU’s non-EU trade

deals

12

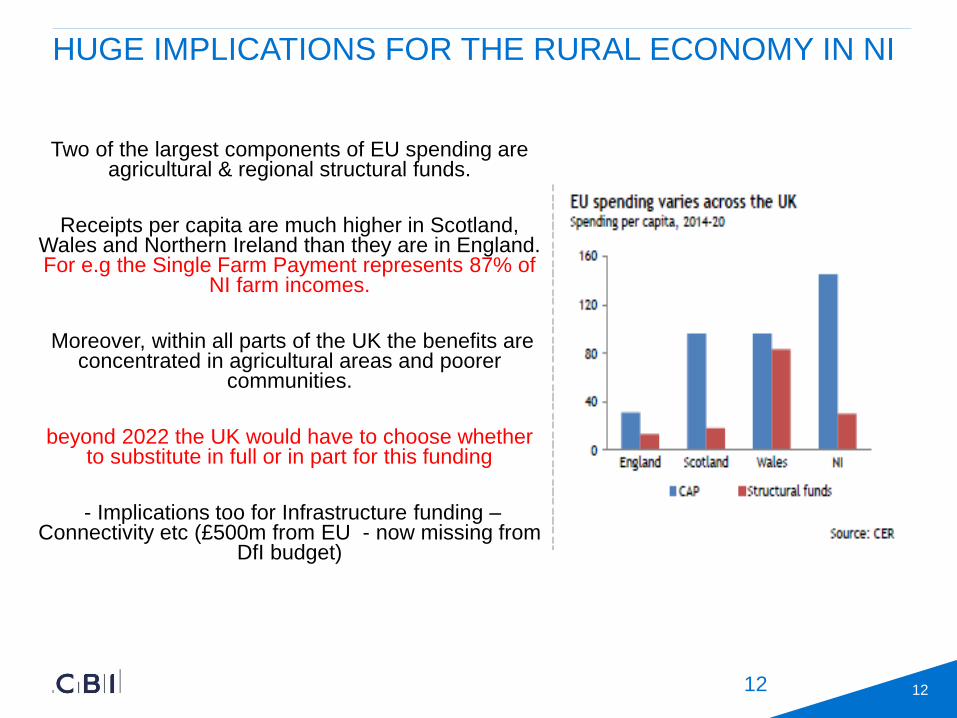

HUGE IMPLICATIONS FOR THE RURAL ECONOMY IN NI

Two of the largest components of EU spending are agricultural & regional structural funds.

Receipts per capita are much higher in Scotland, Wales and Northern Ireland than they are in England. For e.g the Single Farm Payment represents 87% of

NI farm incomes.

Moreover, within all parts of the UK the benefits are concentrated in agricultural areas and poorer

communities.

beyond 2022 the UK would have to choose whether to substitute in full or in part for this funding

- Implications too for Infrastructure funding –Connectivity etc (£500m from EU - now missing from

DfI budget)

12

13

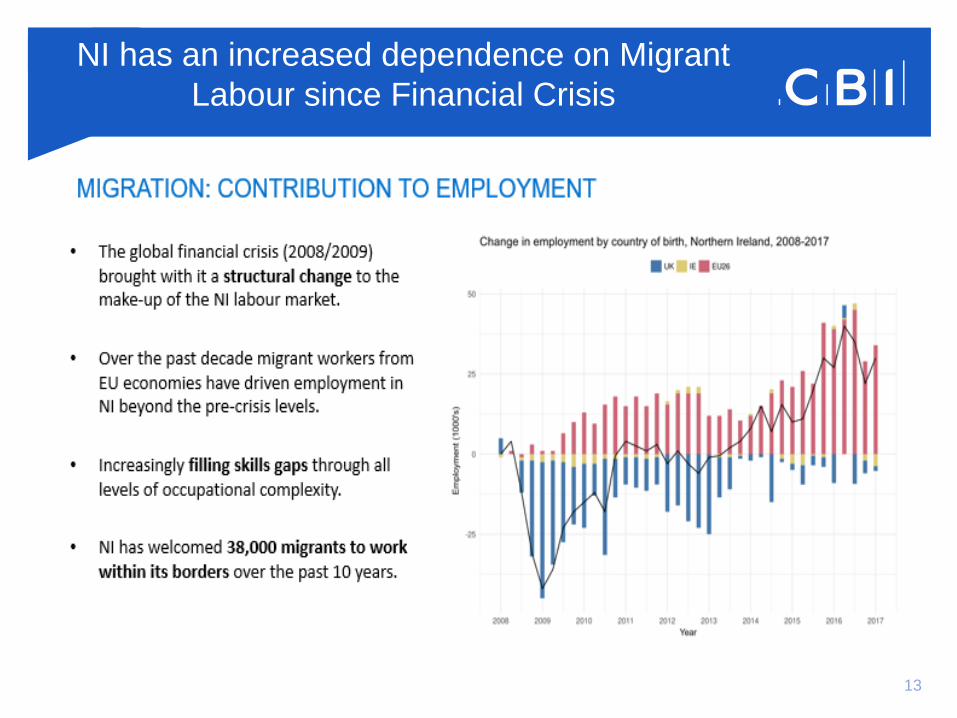

NI has an increased dependence on Migrant

Labour since Financial Crisis

14

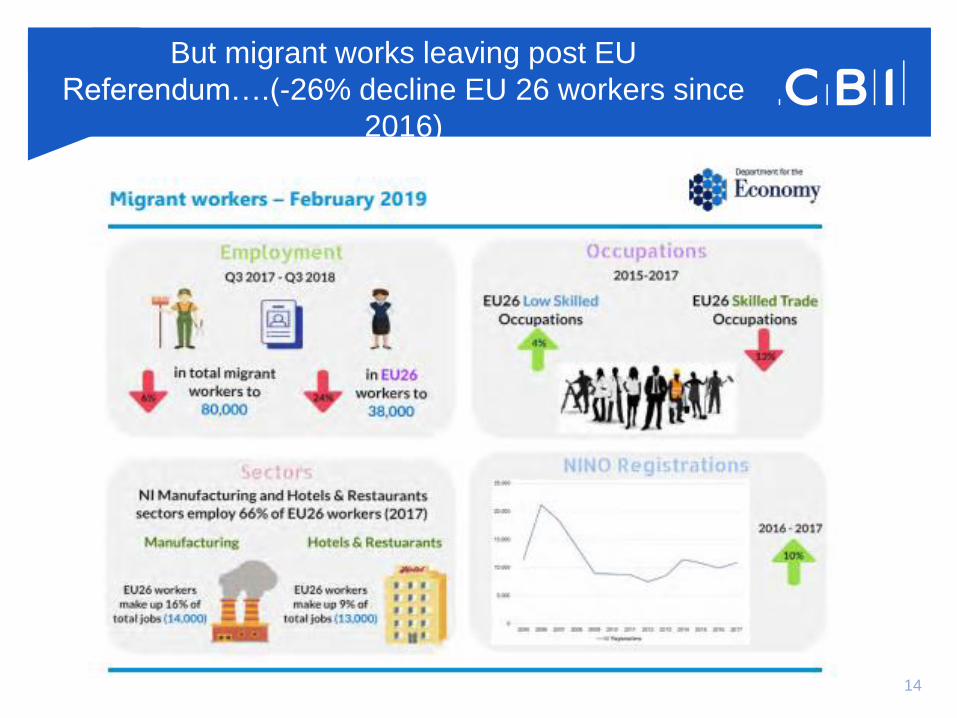

But migrant works leaving post EU

Referendum….(-26% decline EU 26 workers since

2016)

15

● Crashing out of EU without a deal is not a viable option:

● UK would revert to WTO rules

● Tariffs imposed on 90% of our exports to EU market

(Tariffs into EU vary – for agri the ave tariff is 16.4% / textiles 10.5% / 10%

for vehicles and 4.5% on components

● Current proposal on zero UK import tariffs would cripple NI economy

Non-tariff barriers to trade :

● Companies will face the administration burden in terms of paper work trail

(quotas / country of origin w.r.t non-EU intermediate inputs etc)

● Interruption to global supply chains

● Border measures – customs and quotas

● Behind-the-border measures – compliance / regulations / performance

standards etc

WHY “NO DEAL” IS NOT ACCEPTABLE

16

● UK Services currently trade under EU Services Directive

● SERVICES – eg Financial Regulation / Recognition of Professional

Qualifications / Aviation regulation

● For eg, Airlines – UK would no longer be member of Open Skies

● INVESTMENT – rules on international property rights / movement of teams

across borders /

● Data transfer across borders etc

We often forget….this is NOT JUST ABOUT

MOVING GOODS: No deal also has implications

for services, labour, investment

17

● Protects the all-island economy

● Protects the spirit of the Belfast / Good Friday

Agreement

● Ensures no hard infrastructure on NI

● Gives NI ‘unfettered access” to GB market

● Allows NI and RoI to continue with the 142

areas of co-operation currently

● Recognises that NI has unique economic,

geographic and political needs

If we get a deal….

We have only just begun….the discussion on

Services (75% of NI economy will commence)

NI needs a Deal that….

1821/10/2019

NI needs an Executive but in the interim the

business community must speak up

![Community Development as a Way-Out from Crisis. Guidelines from New York City's Experience [Slideshow]](https://static.fdokumen.com/doc/165x107/631b3365d5372c006e03d5e7/community-development-as-a-way-out-from-crisis-guidelines-from-new-york-citys.jpg)