Tata AIA Life Insurance Smart Health Shield Plan

44

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan (UIN: 110N135V01) 1. Part A Dear XXXXXXXXXX Thank You for choosing Us for Your insurance needs. Tata AIA Life Insurance Company Limited is committed to give You world-class products and professional service. We take great pleasure in presenting Your Policy document. Please check Your personal details and the Policy provisions carefully. Should You have any queries, please contact Your agent or contact Us at the address mentioned below. You can also reach Us via email at [email protected] or call Our helpline number 1860-266-9966 (Local charges apply). Agent/Intermediary Name: XXXXXXXXXXX Agency/Intermediary Code: XXXXXXXXXXX Agent/Intermediary Contact details: XXXXXXXXXXX In order to provide better services, We request You to intimate Us in the event of any change in the address of the Policyholder or the Nominee. If You are not satisfied with the terms & conditions/features of the Policy and benefits stated in the Benefit Illustration, You have the right to return the Policy for cancellation by providing a written notice to Us stating objections/reasons and receive the refund of all Premiums paid without interest after deducting proportionate risk premium, stamp duty and medical examination cost along with applicable taxes, cesses and levies which have been incurred for issuing the Policy. Such notice must be signed by You and received directly by Us within 15 days from the date of receipt of the Policy document by You or person authorized by You. The said period of 15 days shall stand extended to 30 days, if the Policy is sourced through electronic or distance marketing mode, which includes solicitation through any means of communication other than in person. If You notice any error on examination of the Policy, please return the Policy to the Company immediately for correction. At Tata AIA Life Insurance Company Limited, We believe that life inspires Us to think ahead. Our insurance solutions are therefore designed to be a step ahead, thus giving You an advantage to adapt to tomorrow’s changes, starting today. We look forward to a long and cherished relationship with You. For and on behalf of Authorised Signatory Tata AIA Life Insurance Company Limited Tata AIA Life Insurance Company Ltd. (IRDAI Regn. No. 110) CIN: U66010MH2000PLC128403 Registered & Corporate Office Address: 14 Floor, Tower A, Peninsula Business Park, Senapati Bapat Marg, Lower Parel, Mumbai 400013. Tata AIA Life Insurance Smart Heath Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Tata AIA Life Insurance Smart Health Shield Plan

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan (UIN: 110N135V01)

1. Part A Dear XXXXXXXXXX Thank You for choosing Us for Your insurance needs. Tata AIA Life Insurance Company Limited is committed to give You world-class products and professional service. We take great pleasure in presenting Your Policy document. Please check Your personal details and the Policy provisions carefully. Should You have any queries, please contact Your agent or contact Us at the address mentioned below. You can also reach Us via email at [email protected] or call Our helpline number 1860-266-9966 (Local charges apply). Agent/Intermediary Name: XXXXXXXXXXX Agency/Intermediary Code: XXXXXXXXXXX Agent/Intermediary Contact details: XXXXXXXXXXX In order to provide better services, We request You to intimate Us in the event of any change in the address of the Policyholder or the Nominee. If You are not satisfied with the terms & conditions/features of the Policy and benefits stated in the Benefit Illustration, You have the right to return the Policy for cancellation by providing a written notice to Us stating objections/reasons and receive the refund of all Premiums paid without interest after deducting proportionate risk premium, stamp duty and medical examination cost along with applicable taxes, cesses and levies which have been incurred for issuing the Policy. Such notice must be signed by You and received directly by Us within 15 days from the date of receipt of the Policy document by You or person authorized by You. The said period of 15 days shall stand extended to 30 days, if the Policy is sourced through electronic or distance marketing mode, which includes solicitation through any means of communication other than in person. If You notice any error on examination of the Policy, please return the Policy to the Company immediately for correction. At Tata AIA Life Insurance Company Limited, We believe that life inspires Us to think ahead. Our insurance solutions are therefore designed to be a step ahead, thus giving You an advantage to adapt to tomorrow’s changes, starting today. We look forward to a long and cherished relationship with You. For and on behalf of Authorised Signatory Tata AIA Life Insurance Company Limited

Tata AIA Life Insurance Company Ltd. (IRDAI Regn. No. 110) CIN: U66010MH2000PLC128403 Registered

& Corporate Office Address: 14 Floor, Tower A, Peninsula Business Park, Senapati Bapat Marg, Lower Parel, Mumbai 400013.

Tata AIA Life Insurance Smart Heath Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

LIFE INSURED: << >> POLICY NUMBER: << >> PREAMBLE

Tata AIA Life Insurance Company Limited (“the Company”) having received a Proposal Form and other related documents with Declaration thereto and initial Premium from the Policyholder hereby issues Tata AIA Life Insurance Smart Health Shield Plan, a Non-Linked, Non-Participating Individual Health Insurance Plan. The basic insurance plan, coverage, Premium and benefits provided under this Policy, are specified in the Policy Schedule. We agree to pay the benefits under this Policy on the happening of the insured event, while this Policy is in force subject to the terms and conditions stated herein.

This is a system generated document requiring no physical signature

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

POLICY SCHEDULE

Tata AIA Life Insurance Smart Health Shield Plan (UIN: 110N135V01)) Non-Linked, Non-Participating Individual Health Insurance Plan

THIS SCHEDULE MUST BE READ WITH THE POLICY DOCUMENT AND IS PART OF THE LIFE INSURANCE CONTRACT Personal Details

Name of Policyholder : << Title / First Name / Surname >> Address of Policyholder : << Address for communication >> Client ID of Policyholder : << >> Date of Birth of Policyholder : << dd/mm/yyyy>> Age at entry of Policyholder : << >> Gender : << Male / Female / Transgender>>

Name of Life Insured : << Title / First Name / Surname >> Address of Life Insured : Client ID of Life Insured : << >> Date of Birth of Life Insured : << dd/mm/yyyy>> Age at entry of Life Insured : << >> Age Admitted : << Yes / No >> Gender : << Male / Female >>

Policy Details

Policy Number : << >> Date of Commencement of Policy : << dd/mm/yyyy>> Date of Commencement of Risk : << dd/mm/yyyy>> Date of Maturity of Policy : << dd/mm/yyyy>> Premium Due Date (s) : << dd/mm/yyyy>> Policy Term : << years >>

Premium Paying Term : << years >> Mode of Premium Payment : << >> Annualised Premium (Excl. taxes) (Rs.) : << >> Premium (Excl. taxes) (Rs.) : << >> Applicable Taxes, Cesses and Levies (Rs.) : << >> Total Modal Premium (Incl. taxes) (Rs.) : << >>

Base Plan/Rider Name Sum Assured

(Rs.) Total Modal

Premium (Incl. taxes) (Rs.)

Maturity Date Due Date of Last Premium Payment

Policy Term

(Years)

Premium Payment Term

(Years)

Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

<< >> << >> << dd/mm/yyyy>> << dd/mm/yyyy>> << >> << >>

<<Applicable Riders, if any>>

<< >> << >> << dd/mm/yyyy>> << dd/mm/yyyy>> << >> << >>

Benefit Payable/Opted

Health Benefit Option A/Option B/Option C Income Benefit Opted/Not Opted Return of Balance Premium Benefit on Maturity

Opted/Not Opted

Wellness Benefit Opted/Not Opted

Nominee details (under section 39 of the Insurance Act 1938)

Name of the Nominee (s) Relationship with Life Insured Gender Age Nomination % << >> << >> << Male / Female /

Transgender>> << >> << >>

<< >> << >> << Male / Female / Transgender>>

<< >> << >>

Appointee Details (Applicable in case the Nominee is a minor)

Name of the Appointee (s) Relationship with nominee Age << >> << >> << >>

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

2. PART B Tata AIA Life Insurance Smart Health Shield Plan is a Non-Linked, Non-Participating Individual Health Insurance Plan. 2.1. Basic definitions

• “Accident” means a sudden, unforeseen and involuntary event caused by external, visible and violent means.

• “Adventurous Pursuits or Hobbies” include but are not limited to any kind martial arts, racing (other than on foot or swimming); potholing, rock climbing (except on man-made walls), hunting, mountaineering or climbing requiring the use of ropes or guides, any underwater activities involving the use of underwater breathing apparatus including deep sea diving, sky diving, cliff diving, bungee jumping, paragliding, hand gliding and parachuting.

• “Age” means age as on the last birthday; i.e. the age of the Life Insured in completed years as on Date of Commencement of Policy and is as shown in the Policy Schedule.

• “Annualized Premium” shall be the premium payable in a year chosen by You, excluding the taxes, underwriting extra premiums, discounts, rider premiums, and loading for modal Premium, if any.

• “Balance Premium” is the ‘Total Premiums Paid’ (excluding loading for modal Premiums) towards the respective Benefit Option, less any claim amount already paid out under the respective Benefit Option.

• “Claimant” means the person entitled to receive the Policy benefits and includes the Policyholder, the nominee, the assignee, the legal heir, the legal representative(s) or the holder(s) of succession certificate as the case may be;

• “Congenital Anomaly” means a condition which is present since birth, and which is abnormal with reference to form, structure or position - o Internal Congenital Anomaly: Congenital anomaly which is not in the visible and accessible parts of the body. o External Congenital Anomaly: Congenital anomaly which is in the visible and accessible parts of the body

• “Critical Illness” shall mean and include below - Critical Illness Definition

1) Apallic Syndrome A persistent vegetative state in which patients with severe brain damage (universal necrosis of the brain cortex with the brainstem remaining intact), are in a state of partial arousal rather than true awareness. The Diagnosis must be confirmed by a Specialist Medical Practitioner (Neurologist) acceptable to the Company and condition must be documented for at least 30 days.

2) Aplastic Anaemia: Irreversible persistent bone marrow failure which results in anaemia, neutropenia and thrombocytopenia requiring treatment with at least two (2) of the following: (a) Blood product transfusion; (b) Marrow stimulating agents; (c) Immunosuppressive agents; or (d) Bone marrow transplantation. The Diagnosis of aplastic anaemia must be confirmed by a bone marrow biopsy. Two out of the following three values should be present: • Absolute Neutrophil count of 500 per cubic millimetre or less; • Absolute Reticulocyte count of 20,000 per cubic millimetre or less; and • Platelet count of 20,000 per cubic millimetre or less.

3) Alzheimer's Disease Deterioration or loss of intellectual capacity as confirmed by clinical evaluation and imaging tests, arising from Alzheimer's Disease or irreversible organic disorders, resulting in significant reduction in mental and social functioning requiring the continuous supervision of the Life Assured. This diagnosis must be supported by the clinical confirmation of an appropriate

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Registered Medical practitioner who is also a Consultant Neurologist and supported by the Company’s appointed doctor.

Critical Illness Definition

The following are excluded: • Non-organic disease such as neurosis and psychiatric illnesses; and • Alcohol-related brain damage.

4) Bacterial Meningitis

A definite diagnosis of bacterial meningitis resulting in a persistent neurological deficit documented for at least 3 months following the date of diagnosis. The diagnosis must be confirmed by a Consultant Neurologist and supported by growth of pathogenic bacteria from cerebrospinal fluid culture. For the above definition, the following are not covered:

- Aseptic, viral, parasitic or non-infectious meningitis 5) Benign

Brain Tumor Benign brain tumor is defined as a life threatening, non-cancerous tumor in the brain, cranial nerves or meninges within the skull. The presence of the underlying tumor must be confirmed by imaging studies such as CT scan or MRI. This brain tumor must result in at least one of the following and must be confirmed by the relevant medical specialist: • Permanent Neurological deficit with persisting clinical symptoms for a continuous

period of at least 90 consecutive days or • Undergone surgical resection or radiation therapy to treat the brain tumor The

following conditions are excluded: Cysts, Granulomas, malformations in the arteries or veins of the brain, hematomas, abscesses, pituitary tumors, tumors of skull bones and tumors of the spinal cord.

6) Blindness Total, permanent and irreversible loss of all vision in both eyes as a result of illness or Accident. The Blindness is evidenced by:

- corrected visual acuity being 3/60 or less in both eyes or; - the field of vision being less than 10 degrees in both eyes.

- The diagnosis of blindness must be confirmed and must not be correctable by aids or surgical procedure.

7) Coma of Specified Severity

A state of unconsciousness with no reaction or response to external stimuli or internal needs. This diagnosis must be supported by evidence of all of the following: • No response to external stimuli continuously for at least 96 hours; • Life support measures are necessary to sustain life; and • Permanent neurological deficit which must be assessed at least 30 days after the onset of

the coma. The condition has to be confirmed by a specialist medical practitioner. Coma resulting from alcohol or drug abuse is excluded.

8) Chronic Recurrent Pancreatitis

An unequivocal diagnosis of Chronic Relapsing Pancreatitis, made by a Specialist in gastroenterology and confirmed as a continuing inflammatory disease of the pancreas characterised by irreversible morphological change and typically causing pain and/or permanent impairment of function. The condition must be confirmed by pancreatic function tests and radiographic and imaging evidence. Relapsing Pancreatitis caused directly or indirectly, wholly or partly, by alcohol is excluded.

9) Deafness Total and irreversible loss of hearing in both ears as a result of illness or Accident. This diagnosis must be supported by pure tone audiogram test and certified by an Ear, Nose and Throat (ENT) specialist. Total means “the loss of hearing to the extent that the loss is greater than 90decibels across all frequencies of hearing” in both ears.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

10) Encephalitis Severe inflammation of the brain substance (cerebral hemisphere, brainstem or cerebellum) caused by viral infection and resulting in permanent neurological deficit. This diagnosis must be certified by a consultant neurologist and the permanent neurological deficit must be documented for at least 6 weeks..

11) End Stage Liver Failure

Permanent and irreversible failure of liver function that has resulted in all three of the following: • permanent jaundice; and • ascites; and • hepatic encephalopathy. Liver failure secondary to drug or alcohol abuse is excluded.

12) End Stage Lung Failure

End stage lung disease, causing chronic respiratory failure, as confirmed and evidenced by all of the following:

Critical Illness Definition

- FEV1 test results consistently less than 1 litre measured on 3 occasions 3 months apart; and

- Requiring continuous permanent supplementary oxygen therapy for hypoxemia; and - Arterial blood gas analyses with partial oxygen pressures of 55mmHg or less (PaO2

< 55 mmHg); and - Dyspnea at rest.

13) Fulminant Viral Hepatitis

A definite diagnosis of fulminant viral hepatitis evidenced by all of the following: • Typical serological course of acute viral hepatitis • Development of hepatic encephalopathy • Decrease in liver size • Increase in bilirubin levels • Coagulopathy with an international normalized ratio (INR) greater than 1.5 • Development of liver failure within 7 days of onset of symptoms • No known history of liver disease The diagnosis must be confirmed by a Consultant Gastroenterologist or Hepatologist. For the above definition, the following are not covered: • All other non-viral causes of acute liver failure (including but not limited to paracetamol

or aflatoxin intoxication) • Fulminant viral hepatitis associated with intravenous drug use

14) Kidney Failure Requiring Dialysis

End stage renal disease presenting as chronic irreversible failure of both kidneys to function, as a result of which either regular renal dialysis (hemodialysis or peritoneal dialysis) is instituted or renal transplantation is carried out. Diagnosis has to be confirmed by a specialist medical practitioner.

15) Loss of Speech Total and irrecoverable loss of the ability to speak as a result of injury or disease to the vocal cords. The inability to speak must be established for a continuous period of 12 months. This diagnosis must be supported by medical evidence furnished by an Ear, Nose, and Throat (ENT) specialist. All psychiatric related causes are excluded.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

16) Major Head Trauma

Accidental head injury resulting in permanent Neurological deficit to be assessed no sooner than 3 months from the date of the Accident. This diagnosis must be supported by unequivocal findings on Magnetic Resonance Imaging, Computerized Tomography, or other reliable imaging techniques. The Accident must be caused solely and directly by accidental, violent, external and visible means and independently of all other causes. The Accidental Head injury must result in an inability to perform at least three (3) of the following Activities of Daily Living either with or without the use of mechanical equipment, special devices or other aids and adaptations in use for disabled persons. For the purpose of this benefit, the word “permanent” shall mean beyond the scope of recovery with current medical knowledge and technology. Activities of Daily Living are: i. Washing: The ability to wash in the bath or shower (including getting into and out of the

bath or shower) or wash satisfactorily by other means; ii. Dressing: The ability to put on, take off, secure and unfasten all garments and, as

appropriate, any braces, artificial limbs or other surgical appliances; iii. Transferring: The ability to move from a bed to an upright chair or wheelchair and vice

versa; iv. Mobility: The ability to move indoors from room to room on level surfaces; v. Toileting: The ability to use the lavatory or otherwise manage bowel and bladder

functions so as to maintain a satisfactory level of personal hygiene; vi. Feeding: the ability to feed oneself once food has been prepared and made available.

The following are excluded: Spinal cord injury

17) Major Organ (less heart)/ Bone Marrow Transplant

The actual undergoing of a transplant of: • One of the following human organs: lung, liver, kidney, pancreas, that resulted from

irreversible end stage failure of the relevant organ, or • Human bone marrow using haematopoietic stem cells The undergoing of a transplant has to be confirmed by a specialist medical practitioner.

Critical Illness Definition

The following are excluded: • Other stem-cell transplants • Where only Islets of Langerhans are transplanted

18) Medullary Cystic Kidney Disease

Medullary Cystic Disease is a disease where the following criteria are met: • The presence in the kidney of multiple cysts in the renal medulla accompanied by the

presence of tubular atrophy and interstitial fibrosis; • Clinical manifestations of anaemia, polyuria and progressive deterioration in kidney

function; and • The diagnosis of medullary cystic disease is confirmed by renal biopsy. • Isolated or benign kidney cysts are specifically excluded from this benefit.

19) Motor Neuron Disease with Permanent Symptoms

Motor neuron disease diagnosed by a Specialist Medical Practitioner as spinal muscular atrophy, progressive bulbar palsy, amyotrophic lateral sclerosis or primary lateral sclerosis. There must be progressive degeneration of corticospinal tracts and anterior horn cells or bulbar efferent neurons. There must be current significant and permanent functional neurological impairment with objective evidence of motor dysfunction that has persisted for a continuous period of at least 3 months.

20) Multiple Sclerosis with Persisting Symptoms

The unequivocal diagnosis of Definite Multiple Sclerosis confirmed and evidenced by all of the following: • investigations including typical MRI findings which unequivocally confirm the

diagnosis to be multiple sclerosis and • there must be current clinical impairment of motor or sensory function, which must have

persisted for a continuous period of at least 6 months. Other causes of neurological damage such as SLE are excluded.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

21) Muscular Dystrophy

Muscular Dystrophy is a disease of the muscle causing progressive and permanent weakening of certain muscle groups. The diagnosis of muscular dystrophy must be made by a consultant neurologist, and confirmed with the appropriate laboratory, biochemical, histological, and electromyographic evidence. The disease must result in the permanent inability of the insured to perform (whether aided or unaided) at least three (3) of the six (6) “Activities of Daily Living”. Activities of Daily Living are defined as: • Washing - The ability to wash in the bath or shower (including getting into and out of the

bath or shower) or wash satisfactorily by other means; • Dressing - The ability to put on, take off, secure and unfasten all garments and, as

appropriate, any braces, artificial limbs or other surgical appliances; • Transferring: The ability to move from a bed to an upright chair or wheelchair and vice

versa; • Toileting: The ability to use the lavatory or otherwise manage bowel and bladder

functions so as to maintain a satisfactory level of personal hygiene; • Feeding: The ability to feed oneself once food has been prepared and made available

Mobility: The ability to move indoors from room to room on level surfaces. 22) Parkinson's

Disease Unequivocal Diagnosis of Parkinson’s disease by a Registered Medical Practitioner who is a neurologist where the condition: • cannot be controlled with medication; and • shows signs of progressive impairment; and • Activities of Daily Living assessment confirms the inability of the Member to perform at

least 3 of the Activities of Daily Living as defined below, either with or without the use of mechanical equipment, special devices or other aids or adaptations in use for disabled persons, for a continuous period of six months: i. Washing: The ability to wash in the bath or shower (including getting into and out

of the bath or shower) or wash satisfactorily by other means; ii. Dressing: The ability to put on, take off, secure and unfasten all garments and, as

appropriate, any braces, artificial limbs or other surgical appliances; iii. Transferring: The ability to move from a bed to an upright chair or wheelchair and

vice versa; iv. Mobility: The ability to move indoors from room to room on level surfaces;

Critical Illness Definition

v. Toileting: The ability to use the lavatory or otherwise manage bowel and bladder functions so as to maintain a satisfactory level of personal hygiene;

vi. Feeding: The ability to feed oneself once food has been prepared and made available.

vii. Only idiopathic Parkinson’s Disease is covered. Drug-induced or toxic causes of Parkinson’s Disease are excluded.

23) Permanent Paralysis of Limbs

Total and irreversible loss of use of two or more limbs as a result of injury or disease of the brain or spinal cord. A specialist medical practitioner must be of the opinion that the paralysis will be permanent with no hope of recovery and must be present for more than 3 months.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

24) Progressive Scleroderma

A systemic collagen-vascular disease causing progressive diffuse fibrosis in the skin, blood vessels and visceral organs. This diagnosis must be unequivocally supported by biopsy and serological evidence and the disorder must have reached systemic proportions to involve the heart, lungs or kidneys. The systemic involvement should be evidenced by any two of the following findings - • Lung fibrosis with a diffusing capacity (DCO) of less than 70% of predicted • Pulmonary hypertension with a mean pulmonary artery pressure of more than 25 mmHg

at rest measured by right heart catheterization • Chronic kidney disease with a GFR of less than 60 ml/min (MDRD-formula) • Echocardiographic findings suggestive of Grade III and above left ventricular diastolic

dysfunction The diagnosis must be confirmed by a Consultant Rheumatologist or Nephrologist. The following conditions are excluded: • Localised scleroderma (linear scleroderma or morphea); • Eosinophilic fascitis; and • CREST syndrome

25) Severe Rheumatoid Arthritis

Unequivocal Diagnosis of systemic immune disorder of rheumatoid arthritis where all of the following criteria are met: (a) Diagnostic criteria of the American College of Rheumatology for Rheumatoid Arthritis; (b) Permanent inability to perform at least three (3) of the six (6) Activities of Daily Living; The Activities of Daily Living are:

i. Washing: The ability to wash in the bath or shower (including getting into and out of the bath or shower) or wash satisfactorily by other means; ii. Dressing: The ability to put on, take off, secure and unfasten all garments and, as appropriate, any braces, artificial limbs or other surgical appliances; iii. Transferring: The ability to move from a bed to an upright chair or wheelchair and vice versa; iv. Mobility: The ability to move indoors from room to room on level surfaces; v. Toileting: The ability to use the lavatory or otherwise manage bowel and bladder

functions so as to maintain a satisfactory level of personal hygiene; vi. Feeding: The ability to feed oneself once food has been prepared and made available. (c) Widespread joint destruction and major clinical deformity of three (3) or more of the following joint areas: hands, wrists, elbows, knees, hips, ankle, cervical spine or feet; and (d) The foregoing conditions have been present for at least six (6) months. For the above definition, the following are not covered: Reactive arthritis, psoriatic arthritis and activated osteoarthritis

26) Systemic Lupus Erythematosus

(SLE) with Renal Involvement

Multi-system, autoimmune disorder characterized by the development of auto-antibodies, directed against various self-antigens. For purposes of the definition of “Critical Illness”, SLE is restricted to only those forms of systemic lupus erythematosus, which involve the kidneys and are characterized as Class III, Class IV, Class V or Class VI lupus nephritis under the Abbreviated International Society of Nephrology/Renal Pathology Society (ISN/RPS) classification of lupus nephritis (2003) below based on renal biopsy. Other forms such as discoid lupus, and those forms with only hematological and joint involvement are specifically excluded. Abbreviated ISN/RPS classification of lupus nephritis (2003): Class I - Minimal mesangial lupus nephritis Class II - Mesangial proliferative lupus nephritis Class III - Focal lupus nephritis Class IV - Diffuse segmental (IV-S) or global (IV-G) lupus nephritis

Critical Illness Definition

Class V - Membranous lupus nephritis Class VI - Advanced sclerosing lupus nephritis The final diagnosis must be confirmed by a certified doctor specialising in Rheumatology and Immunology.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

27) Third Degree Burns

There must be third-degree burns with scarring that cover at least 20% of the body’s surface area. The diagnosis must confirm the total area involved using standardized, clinically accepted, body surface area charts covering 20% of the body surface area.

28) Stroke resulting into permanent symptoms

Any cerebrovascular incident producing permanent neurological sequelae. This includes infarction of brain tissue, thrombosis in an intracranial vessel, haemorrhage and embolisation from an extra cranial source. Diagnosis has to be confirmed by a specialist medical practitioner and evidenced by typical clinical symptoms as well as typical findings in CT Scan or MRI of the brain. Evidence of permanent neurological deficit lasting for at least 3 months has to be produced. The following are excluded: • Transient ischemic attacks (TIA) • Traumatic injury of the brain • Vascular disease affecting only the eye or optic nerve or vestibular functions.

29) Necrotising Fasciitis A definite diagnosis of Necrotising fasciitis evidenced by all of the following: - Progressive, rapidly spreading bacterial infection located in the deep fascia, with

secondary necrosis of the subcutaneous tissues of the limbs or trunk - Fever and rapid increase in C-reactive protein (CRP) levels - Surgical resection of all necrotic tissue

Fournier’s gangrene is covered under this definition. The diagnosis must be confirmed by a Consultant Surgeon and evidenced by microbiological or histological findings. For the above definition, the following are not covered:

- Gas gangrene - Gangrene caused by diabetes, neuropathy or vascular diseases

• “Date of Inception/Commencement of Policy” is the date when We issue the Policy and is mentioned on the Policy Schedule.

• “Date of Commencement of Risk” means the date as specified in the Policy Schedule.

• “Diagnosis” means the definitive diagnosis made by a Medical Practitioner during the Policy Term, based upon radiological, clinical, and histological or laboratory evidence acceptable to Us provided the same is acceptable and concurred by Our appointed Medical Practitioner. In the event of any doubt regarding the appropriateness or correctness of the Diagnosis, We will have the right to call for the Life Insured’s examination and/or the evidence used in arriving at such Diagnosis, by a Medical Practitioner or an independent expert selected by Us. The opinion of such an expert as to such Diagnosis shall be binding on both You and Us.

• “Early Stage Cancer” shall mean first Diagnosis of Cancer, which satisfies at least one of the below conditions – o Any malignant tumor of the thyroid, positively diagnosed with histological confirmation and characterised by the uncontrolled growth of malignant cells and invasion of tissue, which is histologically classified as T1N0M0 according to the TNM classification system, or another equivalent classification

o Prostate tumor should be histologically described as TNM Classification T1a or T1b or T1c are of another equivalent classification.

o Chronic lymphocytic leukaemia classified as RAI Stage I or II;.

o Hodgkin’s lymphoma Stage I by the Cotswold’s classification staging system.

o All tumors of the urinary bladder histologically classified as T1N0M0 (TNM Classification)

The Diagnosis must be based on histopathological features and confirmed by a Pathologist. Pre-malignant

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 11 of 44

lesions and conditions, unless listed above, are excluded.

• “Extra Premium” means an additional amount charged by Us, as per Our Underwriting Policy, which is determined on the basis of disclosures made by You in the Proposal Form or any other information received by Us including medical examination report of the Life Insured.

• “Grace Period” means a period of 15 (Fifteen) days from the due date of the unpaid Premium for monthly Premium payment mode and 30 (Thirty) days from the due date of unpaid Premium for all other Premium payment mode.

• “Illness” means a sickness or a disease or pathological condition leading to the impairment of normal physiological function and requires medical treatment.

(a) Acute condition - Acute condition is a disease, illness or injury that is likely to respond quickly to treatment which aims to return the person to his or her state of health immediately before suffering the disease/ illness/ injury which leads to full recovery.

(b) Chronic condition - A chronic condition is defined as a disease, illness, or injury that has one or more of the following characteristics: 1. it needs ongoing or long-term monitoring through consultations, examinations, check-ups, and /or

tests. 2. it needs ongoing or long-term control or relief of symptoms. 3. it requires rehabilitation for the patient or for the patient to be specially trained to cope with it. 4. it continues indefinitely. 5. it recurs or is likely to recur.

• “Injury” means accidental physical bodily harm excluding illness or disease solely and directly caused by external, violent and visible and evident means which is verified and certified by a Medical Practitioner.

• “Insured Amount” is the amount payable under each Benefit Option/coverage and shall be the highest of: o 11 times the Annualised Premium determined for the Benefit Option/coverage. o 105% of

Total Premiums Paid (excluding loading for modal Premiums) up to the date of occurrence of underlying insured event.

o Sum Assured selected for the Benefit Option. • “Lapsed Policy” means a Policy which has not acquired the Surrender Value and where the due Premium has

not been received till the expiry of the Grace Period. • “Life Insured” means the person whose life is insured or assured under the Policy and is shown in the Policy

Schedule.

• “IRDAI” means the Insurance Regulatory and Development Authority of India.

• “Major Cancer Condition” shall be- o Cancer of Specified Severity - A malignant tumor characterized by the uncontrolled growth and spread of malignant cells with invasion and destruction of normal tissues. This diagnosis must be supported by histological evidence of malignancy. The term cancer includes leukemia, lymphoma and sarcoma. The following are excluded –

i. All tumors which are histologically described as carcinoma in situ, benign, pre-malignant, borderline malignant, low malignant potential, neoplasm of unknown behavior, or noninvasive, including but not limited to: Carcinoma in situ of breasts, Cervical dysplasia CIN-1, CIN -2 and CIN-3.

ii. Any non-melanoma skin carcinoma unless there is evidence of metastases to lymph nodes or beyond;

iii. Malignant melanoma that has not caused invasion beyond the epidermis; iv. All tumors of the prostate unless histologically classified as having a Gleason score greater

than 6 or having progressed to at least clinical TNM classification T2N0M0 v. All Thyroid cancers histologically classified as T1N0M0 (TNM Classification) or below; vi.

Chronic lymphocytic leukemia less than RAI stage 3 vii. Non-invasive papillary cancer of the bladder histologically described as TaN0M0 or of a lesser

classification, viii. All Gastro-Intestinal Stromal Tumors histologically classified as T1N0M0 (TNM

Classification) or below and with mitotic count of less than or equal to 5/50 HPFs;

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 12 of 44

• “Major Cardiac Condition” shall be any of the below defined conditions –

Major Cardiac Conditions

Definition

1) Myocardial Infarction (First Heart Attack of specified severity)

The first occurrence of heart attack or myocardial infarction, which means the death of a portion of the heart muscle as a result of inadequate blood supply to the relevant area. The diagnosis for Myocardial Infarction should be evidenced by all of the following criteria:

i. A history of typical clinical symptoms consistent with the diagnosis of acute myocardial infarction (For e.g. typical chest pain)

ii. New characteristic electrocardiogram changes iii. Elevation of infarction specific enzymes, Troponins or other specific biochemical markers.

The following are excluded: i. Other acute Coronary Syndromes ii. Any type of angina pectoris i. A rise in cardiac biomarkers or Troponin T or I in absence of overt ischemic heart disease OR

following an intra-arterial cardiac procedure. 2) Open Chest CABG (Coronary Artery Bypass Graft)

The actual undergoing of heart surgery to correct blockage or narrowing in one or more coronary artery(s), by coronary artery bypass grafting done via a sternotomy (cutting through the breast bone) or minimally invasive keyhole coronary artery bypass procedures. The diagnosis must be supported by a coronary angiography and the realization of surgery has to be confirmed by a cardiologist. The following are excluded: - Angioplasty and/or any other intra-arterial procedures

3) Open Heart Replacement or Repair of Heart Valves

The actual undergoing of open-heart valve surgery is to replace or repair one or more heart valves, as a consequence of defects in, abnormalities of, or disease affected cardiac valve(s). The diagnosis of the valve abnormality must be supported by an echocardiography and the realization of surgery has to be confirmed by a specialist medical practitioner. Catheter based techniques including but not limited to, balloon valvotomy/valvuloplasty are excluded.

4) Major surgery of Aorta

The actual undergoing of major surgery to repair or correct an aneurysm, narrowing, obstruction or dissection of the aorta through surgical opening of the chest or abdomen. For the purpose of this definition, aorta shall mean the thoracic and abdominal aorta but not its branches (including aortofemoral or aortoiliac bypass grafts). The surgery must be determined to be medically necessary by a Consultant Cardiologist / Surgeon and supported by imaging findings. The following are excluded: • Surgery performed using only minimally invasive or intra-arterial techniques. Claim arising due to Internal Congenital Anomalies within 4 years from the date of commencement of cover or revival of coverage, whichever occurs later.

5) Heart transplant The actual undergoing of a transplant of human heart that resulted from irreversible end stage heart failure. The undergoing of a heart transplant has to be confirmed by a specialist medical practitioner.

6) Cardiomyopathy

An impaired function of the heart muscle, unequivocally diagnosed as Cardiomyopathy by a Registered Medical Practitioner who is a cardiologist, and which results in permanent physical impairment to the degree of New York Heart Association Classification Class III or Class IV, or its equivalent, for at least six (6) months based on the following classification criteria: • Class III - Marked functional limitation. Affected patients are comfortable at rest but performing

activities involving less than ordinary exertion will lead to symptoms of congestive cardiac failure • Class IV - Inability to carry out any activity without discomfort. Symptoms of congestive cardiac

failure are present even at rest. With any increase in physical activity, discomfort will be experienced and Echocardiography findings confirming presence of cardiomyopathy and Left Ventricular Ejection Fraction (LVEF %) of 40% or less.

The following are excluded: Cardiomyopathy directly related to alcohol or drug abuse.

• “Maturity Date” means the date specified in the Policy Schedule on which the Policy Term expires.

• “Medical Advice” means any consultation or advice from a Medical Practitioner including the issuance of any prescription or follow-up prescription.

• “Medical Practitioner” means a person who holds valid registration from the medical council of any state of India and is thereby entitled to practice medicine within its jurisdiction; and is acting within the scope and

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 13 of 44

jurisdiction of his license; provided such Medical Practitioner is not the Life Insured or You or their spouse or lineal relative or a Medical Practitioner employed by You/Life Insured;

• “Medically Necessary Treatment” means any treatment, tests, medication, or stay in hospital or part of a stay in hospital which - o is required for the medical management of the illness or injury suffered by the insured; o must not exceed the level of care necessary to provide safe, adequate and appropriate medical care in scope, duration, or intensity;

o must have been prescribed by a medical practitioner; o must conform to the professional standards widely accepted in international medical practice or by

the medical community in India. • “Minor Cancer Condition” shall be any of the below defined conditions – o Early stage Cancers

• Any malignant tumor of the thyroid, positively diagnosed with histological confirmation and characterised by the uncontrolled growth of malignant cells and invasion of tissue, which is histologically classified as T1N0M0 according to the TNM classification system, or another equivalent classification

• Prostate tumor should be histologically described as TNM Classification T1a or T1b or T1c are of another equivalent classification.

• Chronic lymphocytic leukaemia classified as RAI Stage I or II;.

• Hodgkin’s lymphoma Stage I by the Cotswold’s classification staging system. • All tumors of the urinary bladder histologically classified as T1N0M0 (TNM Classification) The Diagnosis

must be based on histopathological features and confirmed by a Pathologist. Premalignant lesions and conditions, unless listed above, are excluded

o Carcinoma-in-Situ

a) Carcinoma in situ (CIS) means the focal autonomous new growth of carcinomatous cells confined to the cells in which it originated and has not yet resulted in the invasion and/or destruction of surrounding tissues. 'Invasion' means an infiltration and/or active destruction of normal tissue beyond the basement membrane.

b) The diagnosis of the Carcinoma in situ must always be supported by a histopathological

report. c) Furthermore, the diagnosis of Carcinoma in situ must always be positively diagnosed upon

the basis of a microscopic examination of the fixed tissue, supported by a biopsy result. Clinical diagnosis does not meet this standard.

d) In the case of the cervix uteri, Pap smear alone is not acceptable and should be accompanied

with cone biopsy or colposcopy with the cervical biopsy report clearly indicating presence of CIS.

e) Clinical diagnosis or Cervical Intraepithelial Neoplasia (CIN) classification which reports

CIN I, and CIN II (where there is severe dysplasia without carcinoma in situ) does not meet the required definition and are specifically excluded.

f) All CIS of the skin and prostrate are specifically excluded. g) This coverage is available to the first occurrence of CIS of same organ. Multiple claims from

same organ will not be admissible. For the conditions Early Stage Cancer and Carcinoma in Situ, multiple Minor category claims on the same organ and/or histological types will not be admissible where in organs in a pair are considered as the same organ.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 14 of 44

• “Minor Cardiac Condition” shall be a condition as per any of the below definitions –

Minor Cardiac Conditions

Definition

1) Angioplasty Coronary Angioplasty is defined as percutaneous coronary intervention by way of balloon angioplasty with or without stenting for treatment of the narrowing or blockage of minimum 50 % of one or more major coronary arteries. The intervention must be determined to be medically necessary by a cardiologist and supported by a coronary angiogram (CAG). Coronary arteries herein refer to left main stem, left anterior descending, circumflex and right coronary artery. Diagnostic angiography or investigation procedures without angioplasty/stent insertion are excluded.

2) Balloon Valvotomy or Valvuloplasty

The actual undergoing of percutaneous intravascular Valvotomy or percutaneous intravascular Valvuloplasty not involving the deployment of any device or prosthesis necessitated by damage of the heart valve as confirmed by a specialist in the relevant field and established by a cardiac echocardiogram or any other appropriate diagnostic test that is available. The following are excluded: • All other surgical corrective methods will be excluded from this benefit. Claim arising due to Internal Congenital Anomalies within 4 years from the date of commencement of cover or revival of coverage, whichever occurs later.

3) Carotid Artery Surgery

The actual undergoing of surgery to the Carotid Artery to treat carotid artery stenosis of fifty percent (50%) and above, as proven by angiographic evidence, of one (1) or more carotid arteries. Both criteria (a) and (b) below must be met: (a) Either: • Actual undergoing of endarterectomy to alleviate the symptoms; or • Actual undergoing of an endovascular intervention such as angioplasty and/or stenting or

atherectomy to alleviate the symptoms; and (b) The Diagnosis and medical necessity of the treatment must be confirmed by a Registered Medical Practitioner who is a specialist in the relevant field.

4) Implantable Cardioverter Defibrillator

Actual undergoing of insertion of an implantable cardiac defibrillator to correct serious cardiac arrhythmia which cannot be treated via other methods or the insertion of permanent cardiac defibrillator to correct sudden loss of heart function with cessation of blood circulation around the body resulting in unconsciousness Insertion of Cardiac Defibrillator means surgical implantation of either Implantable Cardioverter Defibrillator (ICD), or Cardiac Resynchronization Therapy with Defibrillator (CRT-D). The insertion of a permanent Cardioverter-Defibrillator (ICD) must be certified to be absolutely necessary by a specialist in the relevant field. Cardiac arrest secondary to alcohol or drug misuse will be excluded.

5) Implantation of Pacemaker of Heart

Actual undergoing of Insertion of a permanent cardiac pacemaker to correct serious cardiac arrhythmia which cannot be treated via other means. The insertion of the cardiac pacemaker must be certified to be medically necessary by a Cardiologist. Cardiac arrhythmias to be evidenced by 24 Holter monitoring report or any such other established diagnostic reports. The insertion of any other type of temporary cardiac pacemaker is specifically excluded. Cardiac arrest secondary to alcohol or drug misuse will be excluded.

6) Infective Endocarditis

Inflammation of the inner lining of the heart caused by infectious organisms, where all of the following criteria are met: - Positive result of the blood culture proving presence of the infectious organism(s) - Presence of at least moderate heart valve incompetence (meaning regurgitate fraction of twenty percent (20%) or above) or moderate heart valve stenosis (resulting in heart valve area of thirty percent (30%) or less of normal value) attributable to Infective Endocarditis; and - The diagnosis of Infective Endocarditis and the severity of valvular impairment are confirmed by a consultant cardiologist.

Minor Cardiac Conditions

Definition

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 15 of 44

7) Minimally Invasive Surgery of Aorta

The actual undergoing of minimally invasive surgical repair (i.e. via percutaneous intra-arterial route) of a diseased portion of an aorta to repair or correct an aneurysm, narrowing, obstruction or dissection of the aorta with a graft. For the purpose of this definition, aorta shall mean the thoracic and abdominal aorta but not its branches. The following are excluded:

- Claim arising due to Internal Congenital Anomalies within 4 years from the date of commencement of cover or revival of coverage, whichever occurs later.

8) Pericardiectomy The undergoing of a pericardectomy performed by open heart surgery or keyhole techniques as a result of pericardial disease. The surgical procedures must be certified to be medically necessary by a consultant cardiologist. The following are excluded: Other procedures on the pericardium including pericardial biopsies, inand pericardial drainage procedures by needle aspiration are excluded.

9) Pulmonary Thromboembolism

Acute Pulmonary Thromboembolism: means the blockage of an artery in the lung by a clot or other tissue from another part of the body. The Pulmonary Embolus must be unequivocally diagnosed by a specialist on either a V/Q scan (the isotope investigation which shows the ventilation and perfusion of the lungs), angiography or echocardiography, with evidence of right ventricular dysfunction and requiring medical or surgical treatment on an inpatient basis.

10) Surgery for Cardiac Arrhythmia

Procedures like Maze surgery, RF Ablation therapy or any relevant procedure/surgery deemed absolutely necessary by a cardiologist to treat life threatening arrhythmias. Diagnosis must be evidenced by monitoring through a Holter monitor, event monitor or loop recorder and should be confirmed by a consultant cardiologist. The following are excluded: - Cardio version and any other form of non-surgical treatments - Claim arising due to Internal Congenital Anomalies within 4 years from the date of

commencement of cover or revival of coverage, whichever occurs later. 11) Surgery to Place Ventricular Assist Devices or Total Artificial Hearts

The actual undergoing of open heart surgery to place a Ventricular Assist Device or Total Artificial Heart medically necessitated by severe ventricular dysfunction or severe heart failure, with cardiac echocardiographic evidence of reduced left ventricular ejection fraction of less than 30%. The following are excluded: Ventricular dysfunction or Heart failure directly related to alcohol or drug abuse is excluded.

• “Nominee” means the person named in the Policy Schedule who has been nominated by the Life Assured in accordance with Section 39 of the Insurance Act, 1938 as amended from time to time to receive benefits in respect of this Policy.

• “Policy” means the contract of insurance entered into between You and Us as evidenced by this document, the Proposal Form, the Policy Schedule and any additional information/document(s) provided to Us in respect of the Proposal Form along with any written instructions from You subject to Our acceptance of the same and any endorsement issued by Us.

• “Policy Anniversary” refers to the annual anniversary of the Date of Commencement of Policy. • “Policy Schedule” means the policy schedule and any endorsements attached to and forming part of the Policy

and if any updated Schedule is issued, then, the Schedule latest in time.

• “Policy Term” means the term of the Policy as specified in the Schedule. • “Policy Year” means a period of 12 (Twelve) months commencing from the Date of Commencement of Policy

and every Policy Anniversary thereafter.

• “Premium” means the amount specified in the Policy Schedule, payable by you, by the due dates to secure the benefits under the Policy, excluding applicable tax, cesses or levies, if any.

• “Premium Payment Term” means the term which is equal to Policy Term and as specified in the Schedule, during which the Premium is payable.

• “Proposal Form” means the form filled in and completed by You for the purpose of obtaining insurance coverage under the Policy;

• “Reduced Paid Up Factor” shall be equal to Number of Premiums paid divided by Number of Premiums Payable during the entire Policy Term;

• “Revival Period” means a period of 5 (five) years from the due date of the first unpaid Premium.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 16 of 44

• “Surgery / Surgical Procedure” means manual and/or operative procedure(s) required for treatment of an illness or injury, correction of deformities and defects, diagnosis and cure of diseases, relief from suffering or prolongation of life, performed in a hospital or day care centre by a medical practitioner.

• “Symptom” is a physical or mental feature which is regarded as indicating presence of a disease, particularly such a feature is apparent to an individual and will result in a medical consultation and/or further investigations to confirm the cause.

• “Total Premiums Paid” shall be defined as the sum of all the Premiums paid to date excluding Extra Premium (if any), rider premiums (if any) and taxes, cesses or levies as applicable; In case the Waiver of Premium benefit has triggered, the Premiums waived during this period shall also be considered under the calculation of the Total Premiums Paid to arrive at the Insured Amount.

• “Underwriting Policy” means our then prevailing Underwriting Policy as approved by Our board of directors; • “Waiver of Premium” means waiver of the future Premium/s payable during the Premium Payment Term, if

the Life Insured becomes eligible for Major Condition Payout or Critical Care Payout.

• “We”, “Us”, “Our” or “Company” refers to Tata AIA Life Insurance Company Limited. • “You” or “Your” means the Policyholder of this Policy.

Whenever the context requires, the masculine form shall apply to feminine and singular terms shall include plural.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 17 of 44

3. PART C

3.1. Benefits 3.1.1. Health Benefits On the basis of option chosen by You, at the inception of the Policy, You shall receive following Health Benefit that covers a combination of three health conditions – Cardiac Care, Cancer Care and Critical Care. This product also offers a Waiver of Premium benefit.

3.1.1.1. Option A - Cardiac Care and Cancer Care Benefit

• Minor Condition Payout

Upon Diagnosis of Life Insured with an illness or undergoing of a procedure covered under Minor Cardiac Condition or Minor Cancer Condition during the Policy Term, We shall pay 25% of the Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable, to the Claimant, provided the Policy is in force and the total payout does not exceed the Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable.

• Major Condition Payout

Upon Diagnosis of Life Insured with an illness or undergoing of a procedure covered under Major Cardiac Condition or Major Cancer Condition during the Policy Term, We shall pay an amount equal to Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable, less any payout made under Minor Condition Payout, provided Policy is in force. On the payment of a claim due to a Minor Condition, the Policy shall remain in force for the balance Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable; and multiple claims for Minor Cardiac Condition or Minor Cancer Condition may be preferred until the Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable, is exhausted. For multiple Minor Cardiac Condition or Minor Cancer Condition claims, there needs to be a period of at least 180 days between the date of occurrence of a minor stage condition and date of occurrence of subsequent minor stage condition. However, this requirement of 180 days is not applicable in case of Diagnosis of a Major Cardiac Condition or Major Cancer Condition claim following a minor condition claim. Any particular Minor Cardiac Condition or Minor Cancer Condition can be claimed only once and the benefit shall be payable only upon the first occurrence of any of the conditions covered. Where a Minor Cardiac Condition or Minor Cancer Condition and a Major Cardiac Condition or Major Cancer Condition occur together under the same insured event, We shall pay an amount equal to Insured Amount for Cardiac Care or Insured Amount for Cancer Care, as applicable, less any payout already made under Minor Condition Payout, provided Policy is in force. All coverages under a given condition shall terminate once 100% of the Insured Amount for Cardiac Care or Insured Amount for Cancer Care stands paid out through Minor/Major claim payments or on death, if earlier and no future Premiums towards this condition shall be payable. On the payment of a major claim under Cardiac Care or Cancer Care, all future Premiums under this Benefit Option, if any, shall be waived and the Policy shall stay in force for the other conditions, if any, as per the chosen option. Such Premium waiver will not be applicable in the event of a Minor condition claim.

3.1.1.2. Option B - Critical Care Payout Upon Diagnosis of Life Insured with an illness or undergoing of a procedure covered under Critical Illness during the Policy Term, We shall pay the Insured Amount for Option B, provided the Policy is in force. The coverage under Critical Care shall terminate once the claim for Critical Care is paid or on death, if earlier and no future Premiums towards this condition shall be payable.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 18 of 44

On the incidence of a claim under Critical Illness, all future Premiums (if any) shall be waived and the coverage shall continue for the other conditions, if any, as per the chosen Benefit Option.

3.1.1.3. Option C - Cardiac Care, Cancer Care Benefit and Critical Care Payout You shall be entitled to combined benefit as provided under Option A and Option B.

3.1.2. Optional Benefits On the basis of option chosen by You, at the inception of the Policy, You shall be eligible to receive following Optional Benefit in addition to the Health Benefit:

3.1.2.1. Income Benefit on the diagnosis of a Critical Illness, Minor and Major condition under Cardiac Care or

Cancer Care We shall pay below additional benefit on monthly basis for Option A, B or C as chosen by You, following next monthly anniversary following the date of occurrence of respective condition, for a period of 60 (Sixty) months – a. Minor Cardiac Condition/Minor Cancer Condition - 1% of 25% of the Insured Amount for Cardiac

Care/Insured Amount for Cancer Care as applicable OR b. Major Cardiac Condition/Major Cancer Condition/Critical Care - 1% of (100% of the Insured Amount for

Cardiac Care/Insured Amount for Cancer Care/Insured Amount for Option B, as applicable, less any Minor Cardiac Condition/ Minor Cancer Condition payout already paid).

The Income Benefit is over and above the lump sum benefit in case of Critical Care and Major conditions under Cardiac Care & Cancer Care. Income Benefit option cannot be claimed after death of the Life Insured.

The Policy terminates on the death of the Life Insured and no further benefits shall be payable, except death during the income payout term (if opted). In this case, all the remaining future income payouts shall be paid to the Claimant as due.

3.1.2.2. Return of Balance Premium Benefit on Maturity

We shall pay Balance Premium on Maturity Date.

Any one or combination of two or more optional benefits above may be selected at the Inception of the Policy along with the Health Benefit Option.

3.1.2.3. Wellness Program

This plan offers an Up-front Premium Discount and Premium Discount Flex structure that helps the Life Insured maintain a healthy lifestyle.

Discount on Premium (Provided all due Premiums are paid) Up-front Premium Discount -

We shall give an up-front discount of 10% on your first Policy Year base premium. Premium Discount Flex

o The plan offers an annual Premium Discount Flex based on the Wellness Status of the Life Insured. The Wellness Status shall be driven by objective criterion in line with the Board approved Underwriting Policy.

o The Wellness Status attributed to the Life Insured shall be based on a point based structure and shall be either Bronze, Silver, Gold or Platinum. o A higher Wellness Status translates to a higher level of Premium Discount Flex, i.e. with Bronze being the lowest and Platinum being the highest.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 19 of 44

o The points are allocated through a range of parameters comprising of online assessments, physical activity & health check-up. The same shall be as per objective criteria determined by Us in line with the Board approved Underwriting Policy and subject to review from time to time for any change based on experience. Any change in parameters will be subject to prior approval of the Authority. o The engagement level of the Life Insured shall be monitored during each Policy Year and a Wellness Status of the Life Insured shall be determined accordingly. At the end of each Policy Year, the Wellness Status shall be used to determine the discount on the Premium payable in the following year. The Up-front Premium Discount and Premium Discount Flex shall be taken together to determine the total discount on the Premium payable in the following year. The below table prescribes the discount applicable for each Wellness Status -

Wellness Status at the end of the Policy Year

Premium Discount Flex on Base Premium

Bronze -2% Silver -1% Gold 1%

Platinum 2% In the above table, a negative discount refers to a loading in the Premium

The communication with respect to Wellness Benefit shall be notified to You before the Policy Anniversary on Your registered email id or contact number. For example, the Premium payable in the second Policy Year shall be determined as follows:

Premium in the 2nd Policy Year = (Upfront Premium Discount + Premium Discount Flex earned in the first year) x Base Premium. Hence, if the Wellness Status earned at the end of the 1st Policy Year is Platinum and the applicable upfront discount is 10%, the total discount on the Base Premium shall be 12% in the 2nd Policy Year. Similarly, Premium in the 3rd Policy Year = (Upfront Premium Discount + Premium Discount Flex earned in the first year + Premium Discount Flex earned in the second year) x Base Premium. Hence, in continuation of the above example, if the Wellness Status earned at the end of the 2nd Policy Year is Platinum, the total discount on the Base Premium shall be 14% in the 3rd Policy Year (i.e. 10% upfront discount + 2% Premium Discount Flex earned in the 1st Policy Year + 2% Premium Discount Flex earned in the 2nd Policy Year).

The discounts are on cumulative basis and in any Policy Year, the maximum discount as a percentage of the Premium (excluding modal loading and Extra Premium, if any) in view of both the Up-front Premium Discount and Premium Discount Flex together shall not exceed 30%. For example,

In continuation of the examples given above (assuming 2% Premium Discount Flex is earned in every Policy Year subsequently), the total accumulated Premium Discount Flex earned in the 11th Policy Year, shall be 30%. In the 12th Policy Year, even if the Premium Discount Flex earned is 2% of the total discount on the base Premium shall continue to be 30%.

Further, the Premium payable in any year shall not exceed the base Premium. The Company will have the right to review the base premium rate (on which premium discount is calculated or determined) after 3 (three) years and any modification thereof shall be filed with the Authority for approval. The revised rate shall be applicable to both existing and prospective Policyholders. Objective Criteria: The Wellness Status is driven by an objective criterion where the Life Assured attains the wellness status by accumulation of points. The points are allocated through a range of parameters comprising of online assessments, physical activity & health check-up through our empaneled service providers. The table below gives point distribution structure for determining Wellness status:

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 20 of 44

Status Accumulated Points

Bronze 0 – 9,999

Silver 10,000 – 19,999

Gold 20,000 – 24,999

Platinum 25,000 and above

Points Accumulation Structure: The Life Insured can earn points through a range of parameters as provided below:

Details Limits

Online Assessment 3,900

Health Screening 12,000

Physical activity 15,000

Online Assessment – Annual

Points/Activit y

Activity Max Points

(limit p.a.)

Remarks

Assessments Health Review 1,000 Assessment are available for all Life Insured irrespective of Wellness Status. Points are allocated to all Life Insured who have completed the assessment.

Nutrition Assessment

1,000

Mental Wellbeing 900

Declaration: Smoker / Non-Smoker

1,000

Health Screening – Annual

Details Points for doing the

health screening

Points if the results are within

the clinically accepted range

Remarks

BMI 1,500 1,500 All Life Insured are eligible for Annual Health Screening and points are allocated to Life Assured basis health screenings conducted and also if the results of the test being in line with WHO recommended clinical range

Blood Pressure 1,500 1,500

Cholesterol 1,500 1,500

Glucose 1,500 1,500

Physical Activity – Daily$

Steps / Heart Rate Points per

day Steps: 7,500-9,999 Or, Heart rate: At least 30 mins of physical activity in one exercise session a day at an average heart rate of 60% or more of your age-related maximum heart rate.

50

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 21 of 44

Steps: ≥ 10,000 Or, Heart rate: At least 30 mins of physical activity in one exercise session a day at an average heart rate of 70% or more of your age-related maximum heart rate Or, Heart rate: At least 60 mins of physical activity in one exercise session a day at an average heart rate of 60% or more of your age-related maximum heart rate.

100

$ A maximum of one exercise event is allowed per day to earn points for physical activity. If more than one event is recorded in a single day, the event with the highest number of points will be awarded Each of these parameters have maximum limits to ensure that the Life Assured engages in all the parameters defined above as this will lead to overall improvement of Life Insured’s health. The underlying principle in setting of the objective criteria is to ensure all the Life Assured get equal opportunity for participating in wellness program and all similarly placed Life Assured (basis engagement in wellness activities) derive similar benefits.

The reward point structure, not limited to, status, parameters, points to be allotted to the parameters, sub limits on each parameter, may be subject to change in the future basis experience trends and will be subject to criteria defined in the Board approved Underwriting Policy. Any such change in the reward point structure will be communicated to the Life Assured upfront with a notice of minimum 30 days. Any revision in the Up-front Premium Discount and Premium Discount Flex shall be subject to review and revision based on objective measurable criteria in line with the Board approved Underwriting Policy. Any revision thereof shall be filed with the Authority, and shall apply to prospective policyholders in case of Upfront Premium Discount and shall apply to both existing and prospective policyholders in case of Premium Discount Flex. In case of any change, the same shall be communicated to the Policyholder from time to time. This benefit is offered to You at no additional cost. The benefit shall be applicable in case of an in-force Policy and shall not be available if the Policy is in lapse status. Where the Policy is revived, the benefit shall be available after the date of revival. The objective criteria under this benefit is used solely to ascertain the benefit and shall not be considered as a medical advice or a substitute to a consultation/treatment by a professional medical practitioner.

3.1.3. Health Screening The plan offers an annual health screening which shall not be mandatory, provided all due premiums are paid. The following tests will be performed as part of health screening.

1) Physical Medical Examination to include: Height, Weight, Waist Circumference, Blood pressure, Pulse; 2) Fasting Blood Glucose / Fasting Blood Sugar; 3) HbA1c; and 4) Fasting Lipid Profile (Total Cholesterol, HDL Cholesterol, LDL Cholesterol, Triglycerides).

The Life Insured will be encouraged to go for health screenings for which points will be allocated on his health check and will be offered once a Policy Year. The points (contributing to the determination of the Wellness Status) will be predefined for this health check and will be awarded to the Life Insured only once a Policy Year. The health screening benefit provided to the Policyholder is fixed benefit and not an indemnity benefit.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 22 of 44

3.1.4. Service Feature Health Management Services: The Life Insured may avail Second Opinion / Personal Medical Case Management / Medical Consultation services from service provider(s) affiliated to/registered with the Tata AIA Life Insurance Co. Ltd. The services are expected to assist the Life Insured to ascertain correct diagnosis of a medical condition and obtain due care for the Life Insured in case of illness. These services are subject to:

- the availability of suitable service provider(s); - primary diagnosis has been done by a registered medical practitioner as may be authorized by a competent

statutory authority; and - the eligibility of the Life Insured as may be determined by Board approved Underwriting Policy.

Note: - This service feature is expected to reduce mortality / morbidity rates and thereby reduce expected claim outgo

for the Company. - Medical Second Opinion / Personal Medical Case Management / Medical Consultation is an optional service

offered at no additional cost to the Life Insured(s). The Life Insured may exercise his/her own discretion to avail the services and to follow the treatment path suggested by the service provider.

- These services shall be directly provided by the service provider(s). - The services can be availed only where the policy is in-force. - All the supporting medical records should be available to avail the service. - We reserve the right to discontinue the service or change the service provider(s) at any time. - The services are being provided by third party service provider(s) and We will not be liable for any liability.

3.1.5. Premium details 3.1.5.1. Payment of Premium

• You can pay Premium at any of Our offices or through our website www.tataaia.com or by any other means, as informed by Us. Any Premium paid by You will be deemed to have been received by Us only after the same has been realized and credited to Our bank account.

• Collection of advance premium shall be allowed within the same financial year for the Premium due in that financial year. However, where the Premium due in one financial year is being collected in advance in earlier financial year, the Company may collect the same for a maximum period of three months in advance of the due date of the Premium.

• The Premium so collected in advance shall only be adjusted on the due date of the Premium. 3.1.5.2. Change of frequency of Premium payment You may change the frequency of Premium payments by written request. Subject to our minimum Premium requirements, Premiums may be paid on monthly, quarterly, half-yearly or annual mode at the Premium rates applicable on the Date of Commencement of Policy. Alteration in the frequency of Premium payment may lead to a change in the Premium. No alterations are permissible under the Policy except change in frequency of Premium payment. The loading on Premium shall be applicable as below:

Mode Modal Loading

Annual Multiply Annual Premium Rate by 1 (i.e. No loading)

Half – Yearly Multiply Annual Premium Rate by 0.51

Quarterly Multiply Annual Premium Rate by 0.26

Monthly Multiply Annual Premium Rate by 0.0883

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 23 of 44

3.1.5.3. Default in Premium Payment After payment of the first Premium, failure to pay a subsequent Premium on or before its due date will constitute a default in Premium payment. 3.1.5.4. Grace period

• The Premium is due and payable by the due date specified in the Schedule. If the Premium is not paid by the due date, You may pay the same during the Grace Period without any interest. The Policy will remain in force during this period.

• During the Grace Period, if the overdue Premium is not paid and if a claim arises, We will pay the benefit after deducting the due Premium (without interest) for the Policy Year.

3.1.6. Payment of benefits

• The benefit under the Policy shall be payable to the Claimant. • Once the benefits under this Policy are paid to a Claimant, the same shall constitute a valid discharge of Our

liability under this Policy. 3.1.7. Change in address of Policyholder or Nominee In order to provide better services, We request you to intimate us in the event of any change in the address of the Policyholder or the Nominee.

Policy Document - Tata AIA Life Insurance Smart Health Shield Plan Non-Linked, Non-Participating Individual Health Insurance Plan

Page 24 of 44

4. PART D 4.1. Free look period If You are not satisfied with the terms & conditions/features of the Policy and benefits stated in the Benefit Illustration, You have the right to return the Policy for cancellation by providing a written notice to Us stating objections/reasons and receive the refund of all Premiums paid without interest after deducting proportionate risk premium, stamp duty and medical examination cost along with applicable taxes, cesses and levies which have been incurred for issuing the Policy. Such notice must be signed by You and received directly by Us within 15 days from the date of receipt of the Policy document by You or person authorized by You. The said period of 15 days shall stand extended to 30 days, if the Policy is sourced through electronic or distance marketing mode, which includes solicitation through any means of communication other than in person. 4.2. Non-forfeiture provisions 4.2.1. Lapsation of Policy

4.2.1.1. Policy with no Return of Balance Premium Benefit If the Premium is not paid within the Grace Period, the Policy will lapse from the due date of first unpaid Premium and no benefits will be payable.

4.2.1.2. Policy with Return of Balance Premium Benefit

If the Premium is not paid within the Grace Period and - • the Policy has not acquired Surrender Value, the Policy will lapse from the due date of first unpaid

Premium and no benefits will be payable. • the Policy has acquired Surrender Value and subsequent Premiums remain unpaid policy will be

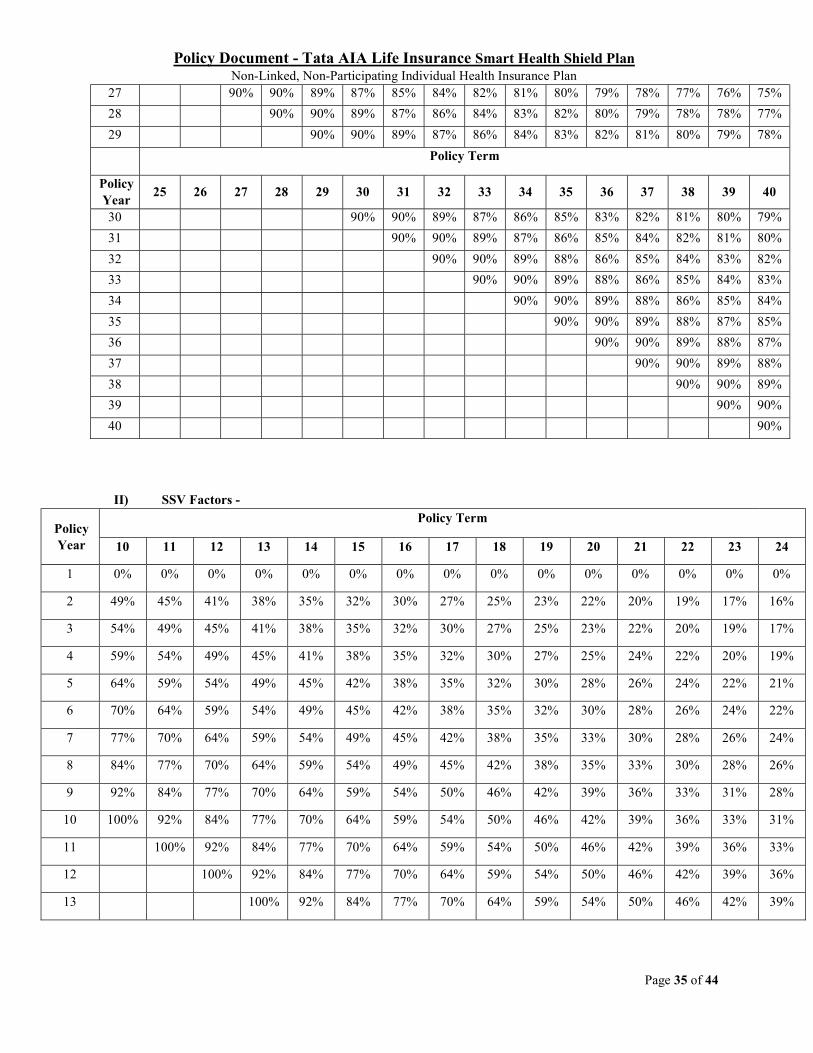

converted into a Reduced Paid-up Policy by default as per Clause 4.2.3. of Part D. 4.2.2. Surrender Benefit: If You have chosen Return of Balance Premium Benefit at the proposal stage, the Policy can be surrendered at any point during the Policy Term, however it shall acquire Surrender Value only if at least 2 (two) full years’ Premium have been paid. The Surrender Value shall be the higher of -

• Guaranteed Surrender Value (GSV) is equal to GSV Factor multiplied by Total Premiums Paid (excluding loading for modal premiums) less claims amount already paid, if any. or

• Special Surrender Value (SSV) is equal to SSV Factor multiplied by Balance Premiums as on date of surrender.

No surrender benefit is payable if the total claims value paid exceeds the Total Premiums Paid by You.