t Y#/Y' 7)

88

t Y#/Y' 7) AN ASSESSMENT OF THE MARKET FOR SWAZI NATION LAND FARMERS SWAZILAND Ronco Consulting Corporation Prepared By: 1629 K Street, N.W. Suite 401 Mohamed Cassam Washington, D.C. 20006 (Agricultural Economist/ Marketing Specialist) Contract No. PDC- 1406- I- 17-1138 -00O

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of t Y#/Y' 7)

t Y#/Y' 7)

AN ASSESSMENT OF THE MARKET FOR SWAZI NATION LAND FARMERS

SWAZILAND

Ronco Consulting Corporation Prepared By: 1629 K Street, N.W. Suite 401 Mohamed Cassam Washington, D.C. 20006 (Agricultural Economist/

Marketing Specialist)

Contract No. PDC- 1406- I-17-1138 -00O

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY .................. 1

II. ALN ASSESSMENT OF THE MARKET FOR VEGETABLES PRODUCED BY SNL FARMERS ..... ................. 6

Present Supply and Demand for Vegetables ... ....... 6

Production........ ....................... 8

Demand ......... ........................ ... 14

The Effect of the Ban ...... ................ ... 18

Future Demand and Supply ..... ............... ... 19

Projected Demand ....... ................... ... 19

Projected Supply ....... ................... ... 20

Conclusion ...... ...................... 28

The Role of Extension ..... ................. .. 28

The Small-Scale Dairying Option ......... .. 29

III. MARKETING ........ ....................... 32

Market Outlets ........ ................... .. 32

Effects of the Ban...... .................. ... 38

Vegetable Sales by Farmers ...... ............. ... 39

The Wholesale Trade ....... ................ .. 41

The Retail Trade....... .................. ... 42

Institutions ........ ..................... ... 44

Pricing ......... ....................... ... 44

Canning and Processing ...... ................ ... 49

The Proposed Wholesale Market .... ............ . 51

Control of Imports and Exports .... ............ ... 53

Controls on Local Marketing .... .............. 54

PAGE

Market Information ...... ................. ... 55

Credi.t....................... . 55

Jummary and Conclusions .... ................... 56

ANNEX . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

1. SIZE OF CURRENT PRODUCTION .... ............. ... 60

62Dryland and Irrigated Farming .... ...............

2. CROP AND LIVESTOCK PRODUCTION.... ............... 65

65Maize......... ........................ ...

66.....................

Citrus ........... ....................... 67

Fruits .......... . . ................. 69

Pineapples ........ ..................... . 70

Oilseeds ......... ...................... .. 71

Tobacco........... ....................... 72

Livestock........ ......................... 73

Other Grains .......

3. THE IFAD MARKETING PROJECT ............ ....... 74

BIBLIOGRAPHY ........ ........................... 80

LIST OF PERSONS MET........ ....................... 82

ABBREVIATIONS

ha hectares

km kilometers

SNL Swazi National Land

TDL Title Deed Land

RDA Rural Development Areas

RSA Republic of South Africa

i

EXCHANGE RATE

US$1.0 " 1.05 Emalengeni (E)

E1.0 = R1.0 1 US$0.95

ii

I. EXECUTIVE SUMMARY

Present Supply and Demand for Vegetables

Vegetable production in Swaziland depends on a very small number

of farmers: only 25 TDL and perhaps up to 400 SNL farmers are

estimated to be full-time commercial horticulturalists. TDL

farmers grow 600 ha. of vegetables, in total, averaging 30 ha.

each, and produced 59% of the total output in 1982. SNL farmers

had 749 ha. in total, and most grew just a hectare. TDL farmers

concentrated mostly on three veg cables: potatoes, tomatoes and

cabbages. On SNL farms, green mealies, tomatoes, cabbages, and

potatoes accounted for 92% of zhe area under vegetables, with

green mealies alone covering 45% of this area.

TDL vegetable farms are concentrated in the central area between

Mbabane and Siphofanei. Of the SNL farms, 35% of the vegetable

area is in the Vuvulane Irrigation Scheme, and 20% in the NRDA,

with the rest scattered throughout the country. Two-thirds of

the SNL vegetable area are in the RDAs, and a third is on pri

vate schemes outside the RDAs.

Four vegetables, potatoes, cabbages, tomatoes and green mealies,

account for 80% of the 1982 national vegetable production esti

mate of about 18,100 tons. A brief description of these four main

vegetables is given below:

-1

* Potatoes: are mainly grown in the lowveld under

irrigation. TDL growers produce 75% of the crop, while

Vuvulane farmers grow much of the rest. Potatoes are

Swaziland's major vegetable export; in 1978, 2,000 tons

were exported, over half the production, all from

TDL. Potatoes can be grown year-round in the middleveld,

and in the winter under irrigation in the lowveld. In

1982, production was 3,580 tons.

" Tomatoes: are the main vegetable, accounting for 36% of

all vegetables produced. With irrigation, they can be

grown year-round in the iiddleveld and in the winter in

the lowvelV. The bulk of the production occurs in July-

November, and Swaziland has a good market in South Africa

in October-November, when the land there under winter

tomatoes is ploughed for cotton. In 1982, production

was 6,500 tons, of which 55% came from TDL farmers and

33% from NRDA. Exports accounted for under 5% of the

production.

" Cabbages: are grown throughout the country, and are in

over-supply between August and December, but short at

other times. Varieties are now available that grow well

in the summer, when humidity increases production risks.

Production in 1982 was estimated at 4,000 tons, with 75%

from TDL and 11% from Vuvulane.

" Green Mealies: are the most popular vegetables among

SNL farmers, since maize is the one crop they are most

-2

familiar with. They are in demand year-round, but in

January-March, when rainfed cobs are available, the

market is in over-supply. Green mealies can be planted

in the lowveld with irrigation from April to September,

and f-om July to December elsewhere. In 1982, produc

tion was 1,500-1,700 tons, with SNL farmers producing

73%; Vuvulane farmers, with 60% of their vegetable.area

under mealies, supplied 27% of all mealies. Most of

the mealies are currently consumed domestically, but in

1978, a year of no drought and relatively more abundant

supplies, 30% of the production was exported.

According to FAO estimates, current demand for vegetables should

be about 35 kgs. per capita, for a total of 20,300 tons. Total

1982 production was 18,000 tons, and the net available after

exports was 16,000 tons. With illicit imports at about 1,000

tons, supply, and thus total consumption, was 17,000 tons, 3,300

tons short of the potential demand. This deficit could have been

covered by imports, but since October, 1980, there has been a ban

on imports of all fruits and vegetables, and thus shortages and

the resultant high prices constrained consumption to the level of

domestic supply.

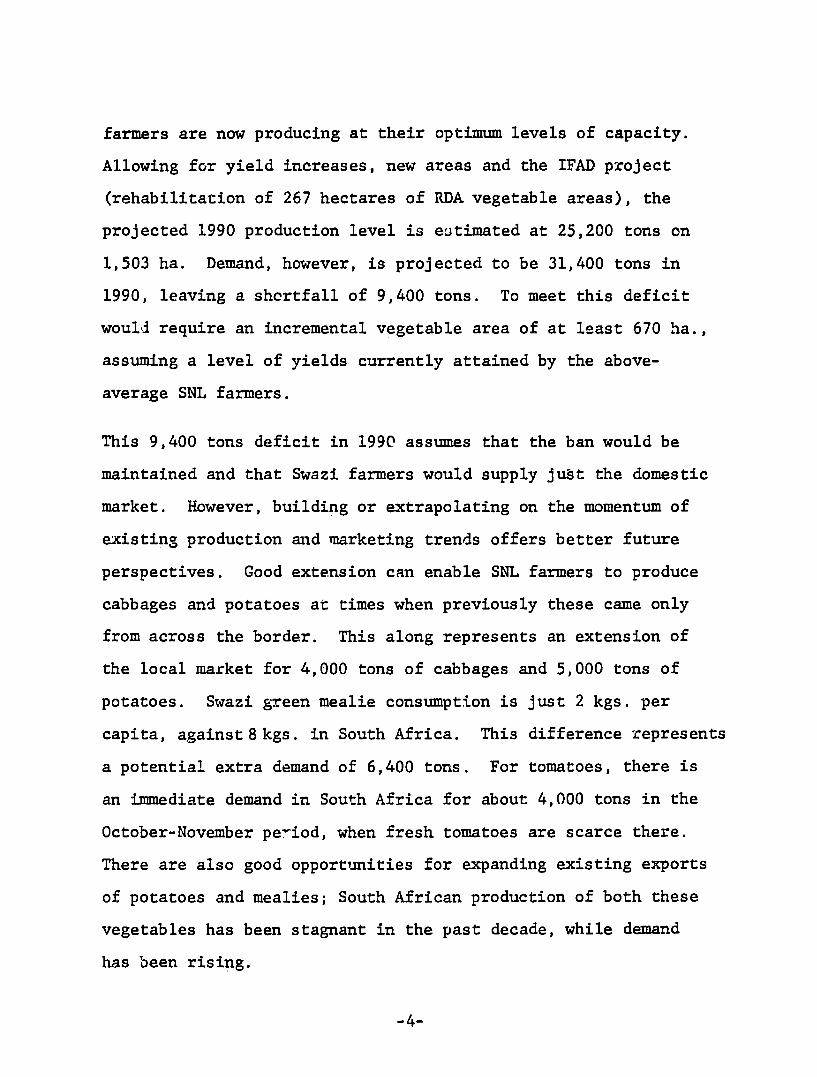

Future Supply and Demand

Production increased 31% from 1978/80 to 1982, as a result of

the incentives (high prices and no competition) flowing out of

the ban. Given the levels of on-farm technology, vegetable

-3

farmers are now producing at their optimum levels of capacity.

Allowing for yield increases, new areas and the IFAD project

(rehabilitation of 267 hectares of RDA vegetable areas), the

projected 1990 production level is eutimated at 25,200 tons on

1,503 ha. Demand, however, is projected to be 31,400 tons in

1990, leaving a shortfall of 9,400 tons. To meet this deficit

would require an incremental vegetable area of at least 670 ha.,

assuming a level of yields currently attained by the above

average SNL farmers.

This 9,400 tons deficit in 1990 assumes that the ban would be

maintained and that Swazi farmers would supply juWt the domestic

market. However, building or extrapolating on the momentum of

existing production and marketing trends offers better future

perspectives. Good extension can enable SNL farmers to produce

cabbages and potatoes at times when previously these came only

from across the border. This along represents an extension of

the local market for 4,000 tons of cabbages and 5,000 tons of

potatoes. Swazi green mealie consumption is just 2 kgs. per

capita, against8 kgs. in South Africa. This difference represents

a potential extra demand of 6,400 tons. For tomatoes, there is

an immediate demand in South Africa for about 4,000 tons in the

October-November pe-iod, when fresh tomatoes are scarce there.

There are also good opportunities for expanding existing exports

of potatoes and mealies; South African production of both these

vegetables has been stagnant in the past decade, while demand

has been rising.

-4

Building on the momentum of current production and marketing

trends indicates a need for 900-1,000 hectares of additional

Lrrigated vegetable areas, assuming good yield levels. This in

turn presupposes good extension and research, and that the IFAD

narketing project would be implemented.

The small-scale irrigation projects that USAID proposes to

finance would mainly benefit SNL farmers who have limited or no

previous experience in commercial vegetable production or even

irrigated agriculture. They kniow that irrigation provides better

incomes per unit of labor or area of land and their basic inten

tion is to grow cotton in the summer and vegetables in the winter.

For these farmers, the first priority is to teach them the correct

techniques pertaining to irrigation practice, on crops they are

already familiar with. This implies heavy extension, and concen

tration on cotton and basic vegetables, such as green mealies,

tomatoes and cabbages.

-5

II. AN ASSESSMENT OF THE MARKET FOR VEGETABLES PRODUCED BY SNL FARMERS

A. PRESENT SUPPLY AND DEMAND FOR VEGETABLES

Vegetable production in Swaziland depends on a very few

farmers: cnly 25 TDL farmers and perhaps up to 400 SNL farmers

are estimated to be full-time horticulturalists.- TDL farmers

are large-scale producers, averaging 30 ha of vegetables, and

were responsible for 59% of the total output in 1982. Of the

estimated 600 ha that TDL farmers have under vegetables, three

crops dominate: potatoes, tomatoes and cabbages, each occupying

about a quarter of the area under vegetables. Among SNL farmers,

about 45% of the area is under green mealies, followed by toma

toes (21%), cabbages (14%), potatoes (12%), and :thers (8%).

Of the 25 TDL farmers growing vegetables (one in 14 of all

operational TDL farmers), themajority are located in the central

corridor between Mbabane and Siphofaneni, within the watershed

of the Usutu River and its tributaries. Of the 400 SNL vegetable

growers (one in 135 homesteads), 35% of their area is in just one

block, the Vuvulane Irrigation Scheme (VIF), while another 20% of

their area is in the Northern Rural Development Area, in the

Lomati River Valley. The other SNL farmers are scattered through

out the country, most of them in the other RDAs. About a third

of the SNL farmers outside Vuvulane are on private schemes, where

1/ Originally estimated by B. Hanson, Horticulture in Swaziland

1978, pp. 2 & 4, and updated by Market Advisory Unit, MOAC.

-6

farmers, individually or more commonly in cooperatives, have

initiated irrigation, and contribute towards the schemes' costs.

The other two-thirds of SNL vegetable growers are on RDA schemes,

where the water is free. Table 1 gives the estimated 1981 areas

of vegetable producers.

TABLE 1

ESTIMATED AREA UNDER VEGETABLES IN 1982 (Ha)

SNL: 749

RDAs 339 Private Schemes 150 Vuvulane 260

TDL 600

Total 1,349

Source: MOAC Irrigation Section

Swaziland's vegetable growers, as described above, are a

highly specialized group, only a very small percentage of local

farmers actually grow vegetables, and this is true elsewhere in

the world: vegetable growing is an option practiced by the small

minority, often the very best of the farmers. It requires the

highest level of skill, plus considerable capital and business

or marketing acumen. Furthermore, Swaziland's vegetable produ

cers are also concentrated spacially, with half of them in the

Usutu valley, and'important concentrations in the north, at VIF

and Lomati Valley (NRDA).

-7

Production

Concentration is also evident in the range of vegetables

which these farmers produce. No more than four vegetables- cab

bages, potatoes, tomatoes and green mealies- account for 80% of

the area under vegetables and close to 90% c! the total produc

tion. This concentration on such a small number of vegetables

is not unusual in commercial horticulture; in South Africa, for

example, just three crops- potatoes. onions and tomatoes - account

for 80% of the fresh vegetables traded, with potatoes along being

48%Y

Table 2 gives the estimates of vegetable production in 1978

and 1982, broken doqn by type of grower as well as type of vege

table. TDL farmers produced 50% of all vegetables, down from 64%

in 1978. The best increase has come from private farmers on SNL

land, who have almost doubled their share from 4% to 7%. A brief

description of the main vegetables is given below, and their

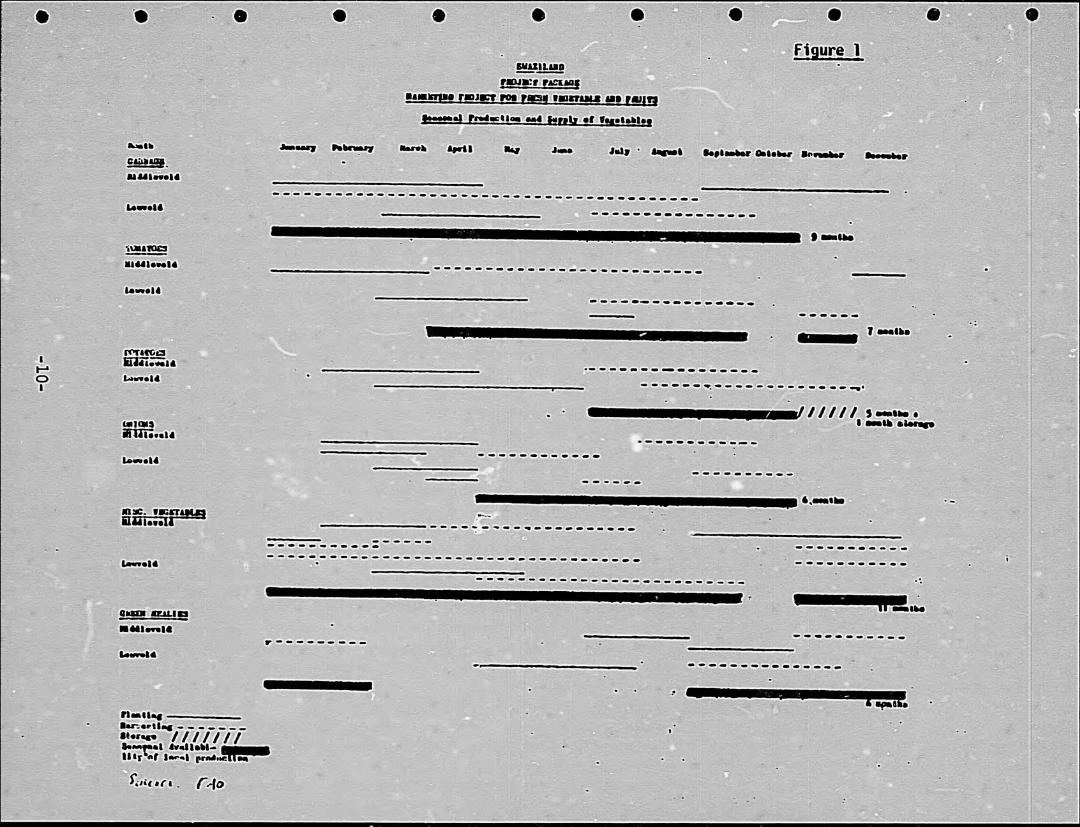

seasonal availability is shown in Figure 1.

Potatoes are mainly grown under irrigation in the lowveld

during the winter months, on land that is used for cotton in the

summer. TDL farmers produce 75% of all potatoes, while Vuvulane

farmers dominate amongst the SNL producers. Potatoes are

available between August and November and local production at

that time is in excess of local demand, leading to large potato

exports to Durban and Johannesburg markets and to the Simba Chip

2/ Crops and Market, Dec. 1982, Vol. 61, issued by Division of

Economic Services, Department of Agriculture, Pretoria.

-8

TABLE 2

Estimated Production of Vegetables 1978 and 1982 (tons)

RDA Private SNL Vuvulane T.D.L. TOTAL

.978 1982 1978 1982 1978 1982 1978 1982 1978 1982

Cabbage 498 554 135 151 385 429 2,680 2,979 3.598 4,000

Tomatoes 1,295 2,135 130 325 240 400 2.860 3.575 4,505 6.500

Potatoes 84 85 80 450 588 735 2,310 2,310 3,062 3,580

Green Maize 440 440 95 95 680 680 455 455 1.670 1,670

Beans 21 34 5 8 - - 100 162 126 200

Onions 240 500 20 200 - - 180 400 440 1,000

Pumpkin 7 14 5 10 - - 100 326 172 350

Carrots 40 120 8 25 - - 75 250 123 400

Beetroot 30 32 8 8 - - 30 30 68 70

Other 6 17 2 6 - - 50 155 58 180

TOTAL 2,641 3,933 488 1,278 1,793 2,244 8,900 10,642 13,822 18,097

SOURCE: Ministry of Agriculture and Cooperatives, Mbabane

~;2~

'~y

~

2' ~

'

-~

* N

" c'~'~ ~i 2 i< ~

~

.~.

~,'

* A' v~"~'~

'~

"

~''"

'

jJ f

i S

.I

S

~

*~4~

'*'<'

"'ix"'. I 4

U

I "~

'

I %

U

I I .

.

* A

-U

I 2.

'

'<''6

I~

I' I

'~v'' I

'I

'~

I ,"''~

' ''

'~K

'' ~

*2"' S

~

.m~

m

U

I'

, ,,

I ~ ' aS

I'

''~ I

<

I~~ ,*

'' ~

"

~ 5

' 1

S

V

, ~

*

"'~

"2~~

~'~

<

2s""''

~

" '~

*'*"'"

~

' 1

hf

*1

gil:

I

, ~

, ~

*

-

S

a S

"~

-

'I'-' g.,

I ~

V

*

I S

-:: I I

6' ~

'

I~ "''''

'-'-v'

" ~

'

Ar

* a

52

1 I I

I I

I I

IS

SI

--

* .5 S

-'

I''I ''

''

It5,

Is,62IIIIs

,

I

'-I-'" 4'"

2

I

a ~I

*1

0' "" '2

"'

III -'

2 -" I

b

'2

1 2

a

2' 2

2'2 "

2 ~

'~'2"~

2~'

"~'

* ~

-"' 2K

,,~t

~

24 &

' P

" 1

jil ,I,

t'A--

'~ A

-

)

2 ''

-"' I,'<

~

22I'

'~tI

2 ~

-~

-"

~

I -

''~ I

"

22

22 ''''~

-~

~7""'~"~ '

~0-. '2~

~~

~

4' --

-

' '"'2

-P

t 2A

i~'2~

~"j

4' '"2

'IP"2

~-t"2

2

22

4

'--'

r2,~

-,I. ~

Q"2

-",-~~

~

'~

22~'N

' ~

'i2

~ 1

~ r~-

2 ~ < 1

~

>~

--

p0'<

t'2<

>

.1

-'

---

~ 2 2'""2P

'2~~

'p(222A~

'2'

iAi 2 ' 2 ' 227 'A7 ' 27 '" 2 ',~ 2~

~24" j-

2 ~2"-7

21t

2~

~J~

~3'~ *

~

2 '

2 "Y

'2

2'2

~~,-

42~

p2I2

~, 2 4

~ ''p~

t~

-'-'2 A

--P

'2

~~

''~

~

-

,2 -'~

~

,2'2

,~

4 ~

2~

4~

4' r

'

'(5

--'-t'2

-

'

,2 ~

'~>

'~~

-g~

-,

-,4

''2'j?

~

~'

2''

processing plant in South Africa. Potato production is possible

year-round in the middleveld and under irrigation in the lowveld

during the winter. The cedara variety in particular is very suit

able for small farmers, because of its climatic adaptability and

hardiness, which permits an extended harvesting period. Before

the cholera ban in October, 1980, TDL farmers would be exporting

to contract buyers in the Johannesburg area, while simultaneously

farmers from Eastern Transvaal would truck in their undergrade

potatoes into Swaziland. Potatoes are Swaziland's biggest vegeta

ble export, because the buoyant market in South Africa has

encouraged TDL farmers to specialize in this crop. TDL farmers

export up to 80% of their production, and almost 50% of the total

production is exported. There is also a large potential in Mozam

bique, providing official channels are developed. In 1978, potato

production was estimated at 3,100 tons, and in 1982, 3600 tons.

Tomatoes are one of the most profitable crops. They are

especially suitable for winter production in the lowveld under

irrigation, while middleveld production uneer irrigation is possi

ble year-round, although costs and disease risks are higher in the

summer. Most tomatoes are marketed from July to November, which

means that Swaziland enjoys a particular niche in October-November,

when production ceases in the Transvaal and Natal as the farmers

there clear their tomato fields to prepare for summer cotton. The

tomato cannery in Malelane in the Transvaal is anxious to purchase

3,000 tons of Roma tomatoes in October and November, when Trans

vaal supplies stop. This is quite a large market, given that

-11

the total Swaziland production of tomatoes in all of 1982 was

about 6500 tons, almost a third of all vegetable production. In

Natal, fresh tomatoes are also scarce during October-November,

and traders come from Durban up to the NRDA schemes to buy toma

toes, even the Roma canning varieties, going from farm to farm

in their 10-ton trucks. This is an extremely expensive system

of produce procurement, considering that it involves committing

a truck for a 1200 km round trip, implying a minimum transport

cash outlay of R1000-1200. It is, though, indicative of a very

under-supplied Durban market for that time of the year. Of the

1982 tomato production of 6,500 tons, 55% came from TDL farms

and 33% from NRDA farms. Exports were about 200 tons to Durban

buyers, and 100 tons to Malelane.

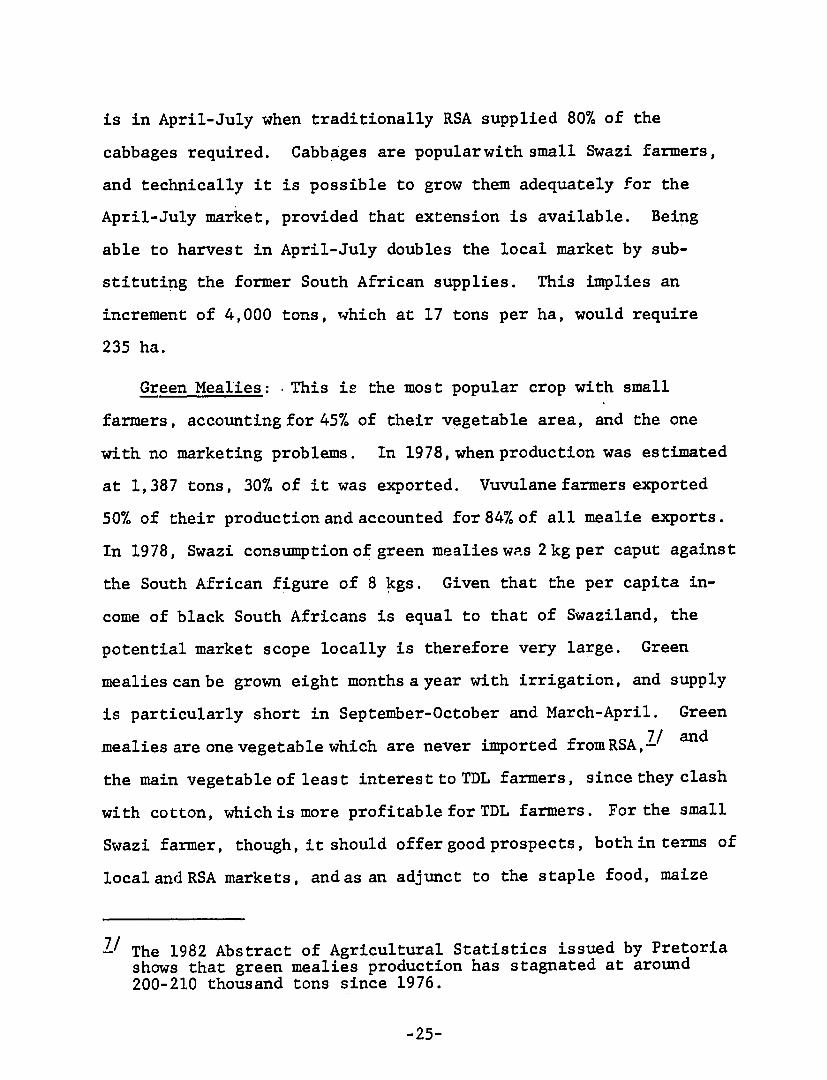

Cabbages from domestic growers are in over-supply between

August and December, when winter cabbages are available. Supply

cannot meet demand in summer, between January and July. Al

though varieties (K-K) are available that can grow in the sum

mer, high humidity and temperatures increase the costs of dis

ease and pest control measure. Production in 1982 was estimated

at 4000 tons, with TDL producing 75% and VIF 11%.

Green Mealies are the most popiular vegetables with SNL

farmers. They are in demand throughout the year, although the

market is saturated from January to March when the rainfed

mealies are available. Green mealies can be planted in -he low

veld with irrigation from April to September, and in the high

-12

and middlevelds from July to December, and be available from July

to February. Green mealies are popular with SNL farmers, since

maize is the one crop they are most familiar with, and its mar

keting is very easy; if there is no market, the mealies can be

ripened for grain. Apparently over half of the green mealies pro

duced are consumed within the rural areas where they are grown,

and compared to the cabbages, potatoes and tomatoes, very little

(15%) enters the central area market. Production in 1978 was

estimated at 1,600-1,700 tons, and about the same in 1982 because

of the drought. SNL farmers produce 73% of all green mealies (re

verse the ratio'for the other major vegetables), with VIF farmers

the most important suppliers, producing 27% of all mealies. In

fact, over 60% of the VIF vegetable area is given to green mealies,

and in the RDAs, the ratio is one-third.

Other vegetables are onions, leeks, green beans, lettuce,

pumpkins, peppers, chillies, Swiss chard (spinach), cucumbers,

beetroots, cauliflower and carrots. In volume terms, onions are

the most important of this group, and 70% are produced and sold

by farmers on SNL. The estimated production of onions in 1978

was 440 tons, and 1,000 tons in 1982. All other vegetables

totalled 550 tons in 1973, and 1,200 tons in 1982, faster than

growth in production of the major vegetables. But all these

vegetables account for only 15% of total local vegetable produc

tion. TDL farmers produce over 60% of these vegetables.

-13

Table 3 gives the areas and quantities of vegetables pro

duced in 1980. The total area given, 1144, was under-estimated

by 150 ha; it should have been 1294 ha. By 1982, the total area

had increased by 4%, 55 ha, all on SNL, but production had risen

31% from 13,822 tons to 18,097 tons. This increase is attributed

to greater intensity of production by all vegetable farmers in

response to the ban on imports imposed in October 1980. This ban

was imposed on imports of all fresh vegetables and fruit coming

from South Africa, and was precipitated by an outbreak of chol

era in the Transvaal. It pushed up local prices by more than

150% in the first six months of operation, and created the in

centives for farmers to increase production through greater ef

fort and input use.

Demand

Table 4 gives the breakdown of per caput consumption of the

principal vegetables as calculated by the FAO for 1979/80. Per

capita consumption of all vegetables was 33.3 kgs, with the four

main vegetables accounting for 29.5 kgs, 88% of the consumption.

Of the total consumption of 18,377 tons, no less than 8,598 tons

or 47%, was imported produce, down from 1978, when 57% of all

consumption was on imports.

- 14

TABLE 3

SWAZILAND

MARKETING PROJECT PACKAGE

PROJECT FOR FRESH VEGETABLES AND FRUITS

1980 Estimated Area and Production of Vegetables

Cabbage

Tomatoes

Area X47

55

99

RDA/SNL % ProductionY

(Lons)

17 633

31 1,405

Area (ha)

19

16

VIF % Production

(tons)

8.6 385

7.2 240

Area (ha)

134

143

TDL

% Production (tons)

22 2.680

24 2,860

Area (ha)

208

257.4

TOTAL

%

18

23

Production (tons)

3.598

4.505

Potatoes

Green Mealies

Others

15

107

45

5

33

14

164

535

392

49

136

-.

22.2

62.0

-

588

680

154

91

81

26

15

13

2,310

455

595

218

334

126

19

29

11

3,062

1,670

987

i-A In

TOTAL

SOURCE:

321 100.0 3,129 220

Horticulture in Swaziland - Hansen (1978)

100.0 1,793 603 100.0 8.900 1.144 100.0 13.822

RDA SHL VIF TDL

= Rural Development Area - Swazi Nation Land - Vuvulane Irrigatcd Farms - Title Deed Land

I/Reported Estimated Actual Production

TABLE 4

ESTIMATED PER CAPITA CONSUMPTION OF MAIN VEGETABLES 1979/80

Cabbages Potatoes Tomatoes Onions Green Others Total Maize

Total .......................... Tons ...........................

Production 3,598 3,062 4,505 440 1,670 547 13,822

Exports 456 1,971 1,199 - 417 - 4,043

Domestic Consumption from lo'al supply 3,142 1,091 3,306 440 1,253 547 9,779

Imports 927 3,883 2,496 1,292 - - 8,598

Total Supply 4,069 4,974 5,802 1,732 1,253 547 18,377

Average Per capitE consumption (kg) 7.4 9.0 10.5 1.1 2.3 1.0 33.3

SOURCE: Swaziland Project Package Preparation Mission FAO Investment Center, Rome, Jan. 16, 1980 Annex 2 p. 13.

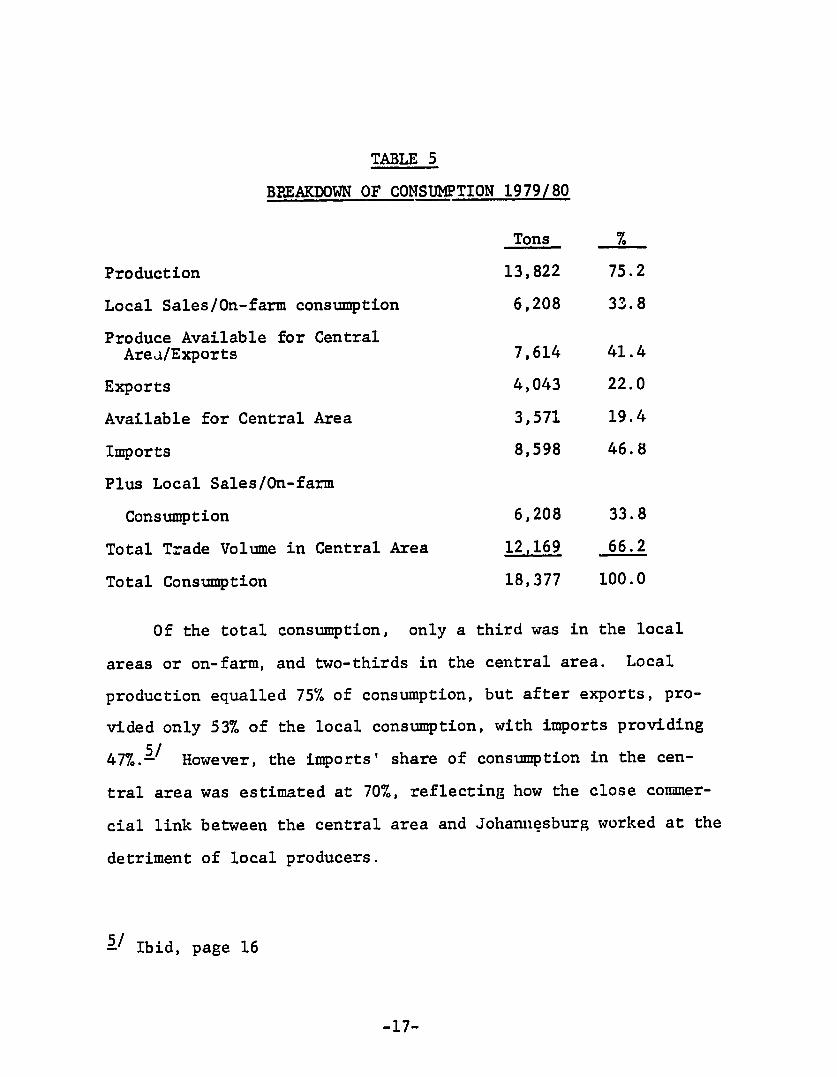

Table 5 gives the breakdown in 1979/80 consumption between

the local, central area, exports and imports, as calculated by

FAO.3/

3/ Project Package Preparation Report. Annex 2, page 16.

-16

TABLE 5

BEEAKDOWN OF CONSUMPTION 1979/80

Tons %

Production 13,822 75.2

Local Sales/On-farm consumption 6,208 33.8

Produce Available for Central Area/Exports 7,614 41.4

Exports 4,043 22.0

Available for Central Area 3,571 19.4

Imports 8,598 46.8

Plus Local Sales/On-farm

Consumption 6,208 33.8

Total Trade Volume in Central Area 12,169 66.2

Total Consumption 18,377 100.0

Of the total consumption, only a third was in the local

areas or on-farm, and two-thirds in the central area. Local

production equalled 75% of consumption, but after exports, pro

vided only 53% of the local consumption, with imports providing

47%.A-/ However, the imports' share of consumption in the cen

tral area was estimated at 70%, reflecting how the close commer

cial link between the central area and Johannesburg worked at the

detriment of local producers.

Ibid, page 16

-17

The Effect of the Ban

The ban in October 1980 shut-out imports, but there is an

illicit flow, estimated at about 1,000 tens. Although produc

tion has increased, shortages and high prices cut consumption in

1981 and 1982 to levels below those of 1979/80. Table 6 gives

the estimates for 1980, 1981 and 1982, as prepared by the

Marketing Advisor to the Ministry of Agriculture and Cooperative

(figures rounded).

TABLE 6

ESTIMATED COMPOSITION OF VEGETABLE SUPPLY 1979 - 1983

1979/80 1982 1983x

Total Production, tons 13,800 18,100 18,000

Export,, 4,000 2,100 2,000

Domestic Consumption from local supply 9,800 16,000 16,000

Imports 8,600 1,000 1,000

TOTAL CONSUMPTION 18,400 17,000 17,000

x = projected

The ban created the incentives for expanding local produc

tion, which in two years increased 31%, from 13,800 tons in

1979/80 to 18,100 tons in 1982. As already mentioned,

most of this increase came from greater intensity of production

and thus higher yields, rather than from expanded area. Local

production now accounts-for 94% of fresh vegetable consumption

and this is about as high as is possible. Swazi consumers are

restricted to a very narrow range of vegetables produced by

-18

local farmers, and only during the season. In the off-season,

they just do without, or increasingly substitute processed or

frozen vegetables imported from South Africa for the previously

fresh produce, also-imported from South Africa. The ban has

benefited local growers and South African processors and freezers,

while penalizing local consumers and South African farmers who

previously supplied the fresh vegetables.

B. FUTURE DEMAND AND SUPPLY

Projected Demand

Table 7 gives the 1979-85 demand projection made by FAO. It

assumed consumption would rise 28% over the period, from 18,377

tons to 23,450 tons, based on annual rates of growth in population

and per capita income of 2.8% and 3% respectively.

TABLE 7

ESTIMATED CURRENT AND PROJECTED VEGETABLE DEMAND 1981-85

Vegetable 1979/80 1981 1982 1983 1984 1985

Cabbages 4,069 4,272 4,486 4,710 4,946 5,192 Potatoes 4,974 5,223 5,484 5,758 6,046 6,347 Tomatoes 4,082 6,092 6,397 6,716 7,052 7,403 Onions 1,732 1,819 1,910 2,005 2,105 2,210 Other Vegetables 547 573 603 633 665 698

Green Maize 1,263 1,316 1,381 1,450 1,523 1,599

Total 18,377 19,295 20,261 21,272 22,337 23,450

Population 550,000 566,000 582,000 598,000 615,000 632,000

Per Capita Consumption (kg/year) 33.3 34.0 34.9 35.6 36.3 37.0

SOURCE: Swaziland Project Package Preparation Mission FAO Investment Center, Rome, January 16, 1980 - Annex 2, page 14.

-19

The demand projections for 1982, 1982 and 1983 exceeded the

actual estimated consumption. In 1981, demand was cut by the

ban on imports, and in 1982 and 1983, although local production

has increased substantially, supplies are still below demand. In

1982, the market was under-supplied by over 3,000 tons, with

supplies at 17,000 tons (Table 6) against a demand, in the absence

of a ban, of 20,261 tons. Projecting the FAO series at 6%

p.a. to 1990 gives a total demand of about 31,400 tons, 75%

above the 1983 production forecast of 18,000 tons. It should be

noted from Table 7 that in 1985, the four main vegetables would

account for 20,541 tons, 38% of the total projected consumption

of vegetables, the same ratio as in 1979/80.

Projected Supply

Table 8 gives the projected production of vegetables for 1979

85, made by FAO. For 1982, the projection was 15,020 tons against

the actual estimate of 18,100 tons, while for 1983, the projection

was 16,441 tons, against the most recent projection of 18,000

tons. The FAO projections for 1982 and 1983 were exceeded in

actuality because the ban created incentives for local producers

to intensify production.

-20

TABLE 8

ESTIMATED PRESENT AND FUTURE ANNUAL PRODUCTION OF VEGETABLES BY TYPE

Pre-Project ..... ..... Project Year ...... 0 1 2 3 4 5

1979/80 1981 1982 1983 1984 1985

Tomatoes 4,505 4,620 5,096 5,761 8,393 10,150 Cabbages 3,589 2,556 2,664 3,033 4,113 4,518 Potatoes 3,062 3,762 3,810 3,894 4,992 5,172 Onions 440 858 906 1,050 1,728 2,112 Green Maize 1,670 1,206 1,206 1,152 1,212 1,343 Miscellaneous 547 _1,331 1,338 1,551 1,793 1,969

Total 13,822 14,333 15,020 16,441 22,231 25,264

SOURCE: FAO Project Package Preparation Mission., January 16, 1980, Annex 2.

These projections were based on an increase in the total vege

table area of about 700 ha by 1985. They also include production

expected from the IFAD project, which will rehabilitate 267 ha of

vegetable areas in six RDAs, for an incremental production of 2,780

tons by 1987/88,- / given the necessary extension and other institu

tional support. The FAO projection is reproduced in Table 9,

together with the more recent estimate from the Ministry of Agri

culture's Irrigation Section.

./Appraisal Report. Smallholder Credit and Marketing Project,

Swaziland, ADB/IFAD Joint Program, September 1982, pp 19 and 38.

-21

TABLE 9

PROJECTED AND ACTUAL AREA UNDER VEGETABLES (HA)

1982 1985 Forecast

FAO1ProJected Actual MOAC2

RDAs 251 339 701 339

Umtilane 20 0 274 0

Private Schemes 50 150 80 210

Vuvulane 260 260 260 260

TDL 600 600 600 694

TOTAL 1,181 1,349 1,815 1,503

i/Projection of FAO mission, 1980.

!/Projection of MOAC's Irrigation Section, assuming no further external assistance.

The FAO's projection was made on the 1981 base estimate of

1,116 ha, and underestimated the then-extent of RDA and private

schemes by about 150 ha, while including 20 ha at Umtilane which

did not materialize. With these 1982 modifications, the FAO 1982

projection should read 1,311 ha, instead of 1,181 ha, close to the

actual 1,349 ha, and the 1985 target would be reduced by 312 ha,

for an increase of 150 ha from 1,349 ha to 1,503 ha. Thus the

original projection of 1,815 ha will not be achieved, since there

are no funds for further expansion in the RDAs, and because the

Umtilane scheme has been dropped.

Thus the FAO projections of total domestic production for

1982 and 1983 were within 85-95% of the most recent estimates.

Although the base area was underestimated by 150 ha, or 13%, the

increase in yields in the past two years more than made up for

-22

this underestimation. However, for 1982-85, the FAO projection

of increased production was based on an assumption that by 1985,

the area of irrigated vegetables would total 1,815 ha; it is now

estimated that the increase in 1983 and 1984 would be only 154

ha, for a 1981 total of 1,503 ha, a shortfall of 312 ha on the

FAO projection. Also, experts now consider that the country's

vegetable growing capacity is generating at full capacity, given

the existing levels of on-farm technology. Without additional

areas coming into irrigation, production can only increase by

improvements in yields, at best 4% per year. The 1983 production

estimate is 18,000 tons, and for 1984, assuming normal rains, the

projection is 20,000 tons. With no increase in area, and produc

tion augmented by 4% per year through yield improvements, total

vegetable output would reach 25,200 tons in 1990.

Taking the 1984 production projection of 20,000 tons and

assuming exports are maintained at the 1982-83 level of 2,000

tons, the amount available for the local markets is 18,000 tons.

However, demand for 1984 is estimated at 22,331 tons, and if the

import ban is maintained, the shortfall will be 4,337 tons. For

1990, the projected production is 25,200 tons, and if exports

regain the 1980/82 average of 3,200 tons, the local supply will be

22,000 tons, against a demand of 31,400 tons, leaving a short

fall of 9,400 tons, if there are no imports.

This 9,400 ton shortfall indicates that there is a need to

increase the area under vegetables. Taking the 1985 FAO break

down of the major vegetables (Table 8) in total demand, and

-23

applying the full development yields used in the FAO Preparation

Mission report, gives the following areas required to meet the

9,400 ton deficit:

TABLE 10

AREA REQUIRED TO PRODUCE 9,400 TONS

Vegetable % Demand!/ Tons Yield=/ Area

Cabbage 22 2,068 17 122 Potatoes 27 2,538 15 169 Tomatoes 32 3,008 18 167 Green Maize 7 658 5 132 Onions 8 752 18 42 Other 4 376 10 38

TOTAL 100 9,400 670

1/ Table 8

2/ Project Package Preparation Mission. Annex 2, Table 4. Yield in tons per hectare at full development on SNL farms. These levels are considered rather optimistic.

To meet the 1990 demand for the major vegetables requires

about 670 ha of additional irrigated land, if one looks at the

market strictly from the input substitution bias, and assumes

that the present ban will continue, despite the Customs Union

rules. Another more realistic perspective is to look at what the

Swazi vegetable producers have been doing, and to expand thereon.

Taking each of the four major vegetables, the following conclu

sions can be made:

Cabbages: Before the ban, 83% of the cabbages were consumed

locally, and 13% exported, with all the latter coming from TDL

farms. Cabbages are available nine months a year, but the peak

supply is in August-November. However, half the overall market

-24

is in April-July when traditionally RSA supplied 80% of the

cabbages required. Cabbages are popularwith small Swazi farmers,

and technically it is possible to grow them adequately for the

April-July market, provided that extension is available. Being

able to harvest in April-July doubles the local market by sub

stituting the former South African supplies. This implies an

increment of 4,000 tons, which at 17 tons per ha, would require

235 ha.

Green Mealies: This is the most popular crop with small

farmers, accounting for 45% of their vegetable area, and the one

with no marketing problems. In 1978, when production was estimated

at 1,387 tons, 30% of it was exported. Vuvulane farmers exported

50% of their production and accounted for 84% of all mealie exports.

In 1978, Swazi consumption of green mealies was 2kg per caput against

the South African figure of 8 kgs. Given that the per capita in

come of black South Africans is equal to that of Swaziland, the

potential market scope locally is therefore very large. Green

mealies can be grown eight months a year with irrigation, and supply

is particularly short in September-October and March-April. Green

andmealies are one vegetable which are never imported from RSA,

1

the main vegetable of least interest to TDL farmers, since they clash

with cotton, which is more profitable for TDL farmers. For the small

Swazi farmer, though, it should offer good prospects, both in terms of

local and RSA markets, and as an adjunct to the staple food, maize

The 1982 Abstract of Agricultural Statistics issued by Pretoria shows that green mealies production has stagnated at around 200-210 thousand tons since 1976.

-25

flour. A doubling of production would imply an increment of 1,670

tons on the 1982 production level, which at five tons per ha,

would require an additional 334 ha.

Tomatoes can be grown seven months a year, but the peak

production is August-December. In October-November, Swaziland

has a particular niche in the South African market, when tomatoes

of both the canning and round varieties are very short. The

reason for this is that South African farmers like to get their

tomato fields clear by October in preparation for planting summer

cotton. In 1978, 1,200 tons, 27% of the production, was exported,

with supplies coming equally from TDL and SNL farmers. There is

a market for 3,000 tons in October-November at the Malelane Can

nery, and at least another 1,000 tons to the Durban fresh market;

this 4,000 tons is equal to 62% of the 1982 crop. Local consump

tion of domestic production can be increased if farmers could

produce earlier, for marketing in May-July. The key requirements

are extension and research, to help farmers grow earlier, and

introduce varieties that withstand bacterial wilt, a major prob

lem during heat waves, in October-November. An increase of 4,000

tons, at 18 tons per ha, would require an additional 222 ha.

Potatoes: This crop is Swaziland's major vegetable export.

In 1978, 2,000 tons of potatoes were exported, representing 50%

of all vegetable exports. TDL farmers provided nearly all these

potatoes, and in fact 81% of their potato sales were to RSA.

Local sales were only about 930 tons, and the supply

-26

evenly split between TDL and SNL producers. Hansen estimated that

in 1978, domestic demand was 5,000 tons, with 83% of the supply met

by imports. Swazi farmers conld supply much of this demand with

cedara varieties from the lowveld from July to November, and from

the middleveld from November to February. SNL producers can also

follow TDL farmers and concentrate on exporting to RSA. In 1982,

exports were estimated at 1,000 tons, as local prices were higher

than in South Africa. In future, extra supplies destined for ex

port would make hardly a dent in the total South African produc

tion of 700,000 tons. South African demand, especially for

processed potatoes, is rising, while water shortages there have

already limited any increase in winter potato hectarages. Future

RSA production increases than will have to come from increases in

yields and imports. / For SNL farmers, problems with this market

are quality (processors are particular about grades) and timing,

both of which require good extension. Another important factor is

transport, and farmers will need to work together to get both the

harvest and trucking coordinated. An increase in production of

3,000 tons, with 2,000 tons for RSA and 1,000 tons sold locally,

would requirean additional area of 200 ha, at a yield of 15 tons

per ha.

From the above, it can be seen that to maintain and enhance

the ongoing momentum for just the four main vegetables requires an

additional area of 991 ha to produce 12,670 tons of fresh vegetables

8/ South African production has fluctuated between 684 and 762

thousand tons in 1975-01 with no trend discernible. Johannesburg buyers say that, provided the quality standards are met, they would buy any incremental production from Swaziland.

-27

for both the local and South African -market. This area could

be brought into production over the next five years, and the

production to build up to 12,570 tons would take three to five

years more, as farmers require this tue to develop skills that

would enable them to attain the optimal yield levels, given the

necessary extension.

Conclusion

To summarize, there is a requirement of 600-700 ha of

additional irrigated vegetable land to meet the demand for the

major vegetables in 1990, as projected by FAO. From the per3pec

tive of maintaining ongoing trends in production, with the output

going to both domestic markets and to South Africa, 900-1,000 ha

would be required in the next five years, just for growing the

four main vegetables. To include the other vegetables, another

20% more land, 180-200 ha, would be required. The area increases

even more if one assumes that SNL farmers are mostly interested

in green mealies, since these account for 45% of their vegetable

lands. To achieve 8 kg per capita, a level of consumption pre

vailing in South Africa, where it is consumed mainly by blacks,

would require a production of 5,600 tons. At five tons per ha,

this implies an irrigated area of 1,120 ha.

The Role of Extension

The type of farmer who may be expected to benefit from a

small-scale irrigation scheme backed by USAID will need the right

kind of extension if he/she is to succeed in the long run. These

-28

potential beneficiaries are the same people who have come to the

MOAC's Irrigation Section for help in vegetable growing because

of the high profits in the past two years consequent to the import

ban. Only a few of them may currently be growing vegetables,

and, in common with SNL farmers, with the exception of perhaps

a dozen or two, they have very poor techniques of growing vegeta

bles. Lack of technology, despite their keenness and commitment

to hard work, increases costs, reduces yields and unnecessarily

frustrates endeavour. These farmers require persistent and good

quality extension to ensure that yields and profits are attained,

so that the heavy investment, in both irrigation facilities and

effort, is not wasted. Farmers, even the wealthiest TDL growers,

need continuous advice on financing of operations, irrigation

techniques, pests and diseases, fertilization, optimum planting

and cultivating techniques, etc. It is urged that any irrigation

project that USAID backs include a generous funding for extension,

and that this extension concentrate on teaching farmers to improve

yields on the crops they are currently growing.

The Small-Scale Dairying Option

If irrigation is available, vegetable production is not the

only, or the most profitable, option. In Swaziland, small-scale

dairying, based on irrigated pastures, should be considered a

viable option. Swazis, being a pastoral people, have a high

demand for milk, particularly fermented milk known as emasi.

-29

Fresh milk in the rural areas fetches 50-60 cents per liter, which

is about the highest free-market price for fresh milk in Africa.

This price makes milk production very profitable, particularly if

the feed is mostly home-grown pastures.

There are presently a small number of RDA village dairy units,

backed by the Dairy Board. The Board sells farmers cull cows,

from its herd of Canadian Holsteins, for E600. Farmers have to

put down pastures, fencing and a shed, for about E50 for two ha

and two cows. However, none of these farmers have been helped

with irrigation, so the basic forage in the dry season is hay

supplemented by purchased feeds costing 32 cents per kg. This

is an unnecessarily expensive method of feeding when irrigation

is available. Even so, farmers report yields of 2,000 liters per

lactation on average, implying a gross return of El,000-El,200

per cow. Two hectares of irrigated lucerne could support two

milkers and one follower, with very little cost for purchased

feed.

The investment costs for three cows would be E1,800, and

for two ha pastures, fencing, cowshed and equipment, about E1,000.

This E2,800 would be on top of the investment in irrigation,

about E3,000 per ha, which would be common for both dairy and

vegetables. It is higher than the working capital needed for

vegetables, E700-El,200 per ha depending on the crop, but it is

long-term, giving daily cash for a little labor. The gross

income at 50 cents per liter and 4,000 liters per year minimum

-30

would be E2,000. Operating costs annually would be E500 for

irrigation,-1 plus about E120 per cow, for feed and veterinary

services, for a total of E860, giving a net of E1,140 per year.

The market for milk would initially be local, for emasi, and

given a reasonable local population, there would be no need to

have a Dairy Board pick-up, which would paya lower price, 35-40

cents per liter.

The existing daizcy units are extremely popular, but

constrained by shortage of cows from the Dairy Board. Their popu

larity must be seen in the light of regular income, no marketing

problems, and a pastoral people's basic affinity for cows and the

milk they produce. Pure Holsteins are not suitable for the hardy

environment of a small farmer; a Holstein-Sahiwal cross, availa

ble from Zimbabwe, would be better. Alternatively, A Jersey-

Nguni cross could be tried.

9/Appraisal Report, Annex 15.

-31

III. MARKETING

Market Outlets

In Table 5 (page 9) there is a break down of consumption in

1979/80, the year preceding the ban. The shares of the various

markets of domestic production were as follows:

Tons %

Local Sales/On-farm Consumption 6,208 44.9 Exports 4,043 29.1 Sales to Central Area 3,571 25.8

Total Production 13,822 100.0

Local sales outside the central area and on-farm consumption

accounted for 44.9%, or the major share of domestic production.

The major markets outoide the central area are the mines, pulp

mills, sugar and citrus estates. Exports were the next most

important, taking 29.1% of local production, while the central

area took only 25.8% of local produce. The central area, that

is the Mbabane-Manzini corridor, is, however, the major market

in Swaziland, since it has 85% of the urban population. It

accounted for two-thirds the national consumption of vegetables

in 1979/80 and 80% of the consumption of imported produce, i.e.,

54% of total consumption.

In 1978, two thirds of the local production of the four main

vegetables was consumed in Swaziland, and one-third exported,

as shown in Table 11.

-32

TABLE 11

Market Outlets for Vegetables Produced on TDL, Vuvulane, NRDA, SRDA - 1978

(tons)

Local Export Central Sales (RSA) Area Total %

Potatoes 490 2,081 473 2,898 24.3

Cabbages 1,467 456 1,473 3,396 28.4

Tomatoes 1,724 1,199 1,344 4,267 35.7

Green Maize 753 417 217 1,387 11.6

Total 4,434 4,153 3,471 11,948

Percentage 37.1 33.9 29.0

Source: Sterkenburg, et al. (1978), the Production and Marketing of Vegetables in Swaziland.

Table 12 gives the break down of sales, by product and producer,

to the central area. TDL farmers supplied 68% of the main vege

tables, followed by those in Vuvulane with 21%. Cabbages were

the main vegetable, 42% of the sales, followed by tomatoes with

39%.

TABLE 12

Estimated Vegetable Sales to the Central Area (1978)

(tons)

Green Potatoes Cabbage Tomatoes Maize Total

Title Deed Farmers 208 1,126 1,001 23 2,358

Vuvulane 229 270 79 156 734

NRDA - 52 259 17 328

SRDA and MRDA - 25 5 21 52

Total 437 1,473 1,344 217 3,471

-33

Table 13 gives the break down of local sales outside the central

area. TDL farmers were again the dominant suppliers, with 67% of

the supplies, followed by the Vuvulane and NRDA farmers, each

supplying about 15%. Tomatoes were the main vegetable, 39% of the

sales, followed by cabbages, with 33%, and the green maize at 17%

TABLE 13

Estimated Local Sales of Vegetables (Not to Central Area) (1978)

(tons)

Green Potatoes Cabbage Tomatoes Maize Total

Title Deed Farmers 231 1,099 1,258 368 2,956

Vuvulane 259 115 113 170 657

NRDA - 140 315 193 648

SRDA and MRDA - 113 38 22 173

Total 490 1,467 1,724 753 4,434

Table 14 gives the break down for exports. TDL farmers provided

72% of the exports, with the Vuvulane and NRDA farmers sharing

the balance equally. Potatoes were the most important vegetable

exported, with half the sales, and 95% of these came from TDL.

Tomatoes were next, with 29%, supplied equally by TDL and SNL

producers. Of the latter, NRDA farmers provided 90%.

TABLE 14

Estimated Exports of Vegetables to South Africa (1978)

(tons)

Green Potatoes Cabbages Tomatoes Maize Total

Title Deed Farms 1,981 456 600 64 2,991

Vuvulane 100 - 48 353 501

NRDA - - 551 - 551

Total 2,081 456 1,199 417 4,153

Source: Sterkenburg, et al., (1978) - The Production and Marketing of Vegetables in Swaziland.

-34

TDL farmers clearly dominated, and still do, the sale of produce

internally and to South Africa. They have the linkages to the

central area, and about a third sell much of their produce through

their own retail stalls. They also know the big buyers in Johannes

burg, whom they supply on contract. They are able to organize

transport on a large scile, and ship to the requirements of such

major buyers as the mines and Simba Chips, the potato processor.

Vuvulane farmers, who constitute the biggest block of SNL farmers,

specialize in green mealies, and half of this output was exported,

mostly to itinerant traders coming from Durban. Other crops they

are able to sell locally and to the central area. NRDA farmers

specialize in tomatoes, and half their tomato production was

exported to the itinerant traders from Durban and to the Malelane

cannery.

Of the SNL farmers, only a few private farmers, with their own

transport, and possessing business acumen, are able to directly

market their produce in the central market or in South Africa.

The vast majority, lacking both the resources and ability, are

passive participants in the marketing system. They rely entirely

on the traders coming to them at harvest. Before the ban, this

tended to be a haphazard affair, giving rise to incidents of

crops rotting because the trader-producer interests failed to

coincide at the same time.

The SNL farmers suffered because the central area, before the

ban, had better linkages with the South African produce marketing

-35

system than with its own hinterland. This is a reflection of

Swaziland's satellite status within the South African economy,

and although the 1980 ban on fresh produce imports modified it a

bit, this relationship totally holds true for all the other

economic sectors. The central area became dependent on imported

supplies because the buyers in Mbabane and Manzini found it more

convenient to order from Johannesburg brokers, who have the range

of quality vegetables, plus the credit and traIisport arrangements.

They also got supplies delivered to them by vegetable farmers

coming across the border from Eastern Transvaal. These farmers

would bring under-grade vegetables that were not saleable at good

prices to the middle men in Johannesburg and Pretoria wholesale

markets. They could, however, sell to retailers in the Mbabane-

Manzini corridor, where quality standards are not as high. Such

sales were made for cash, and probably escaped income tax. How

ever, they disrupted the market for the local producers, since

the arrival of three or four loads of vegetables from the Trans

vaal in one day would satisfy the immediate needs in the central

area, and dissuade dealers from going to rural areas to pick up

local produce.

Given this scale and operation of the South African sellers and

producers, the small Swazi farmer couldn't compete in the central

area. Central area buyers were so tightly linked to the South

African sources that they had little incentive to develop strong

and permanent linkages with small farmers scattered throughout

the hinterland. The consequent weak linkages in turn became

-36

another set of constraints to production and marketing of more

vegetables by small farmers. The TDL farmers though, because

of their skills, economic and cultural affinities, and scale of

operation, did not suffer so, since they are able to operate the

system, selling locally and to South Africa.

The key weakness in the system for the SNL farmers and the dealers

dependent on them was the lack of a central wholesale market.

Without it, there is no locus for small farmers and traders to

bring in produce; they instead have to hawk their wares to indi

vidual retailers. Lack of a central market also excludes general

transporters, who have a crucial role in vegetable marketing,

from participating in the transporting of local produce. In

Swaziland, there is a flow of goods via general transporters into

the countryside from the central area or even South Africa. How

ever, since the countryside exports bulk commodities such as sugar,

minerals, pulp and timber, by specialized trucks or by rail, these

transporters have no loads to back-haul. A central market would

provide both a destination and a service for these general trans

porters to engage in trucking vegetables into the central area.

They would provide the crucial contract transport service, and

the essential truck capacity, to those actually involved in buy

ing and marketing produce to domestic and South African markets.

-37

Effects of the Ban

The ban definitely forced a rapid strengthening in the linkages

between the central area and the producing centers. With half

the supplies previously imported suddenly shut off, buyers had to

turn quickly to local growers, who responded by increasing produc

tion 31% between 1980 and 1982, and shifting half their expozts

into the local market. The ban, though, was unexpected, and

farmers could not respond by increasing production immediately.

Consequently, prices in the central area shot up 150% between

October 1980 and April 1981. By October 1981, fruit and vegeta

ble prices were 43.8% above the level a year before, against a

16.6% rise in the Index "B" (low income cost of living) prices

series. From October 1981 to July 1982, fruit and vegetable

prices rose another 50%, but then dropped 30% between July 1982

and October 1982, for a twelve months rise of 16.4%, very close

to the overall Index "B" rise of 14.1%. However, from October

1982 to April 1983, the fruit and vegetable price index has risen

26.3%, against the Index "B" rise of .4.8%.

These price trends clearly show that by October 1982, two years

from the imposition of the ban, farmers had been able to increase

production to minimally satisfy the local, but now reduced, fruit

and vegetable demand. Consumers suffered from the ban, particu

larly in the first six months, as well as in April and May of

both 1981 and 1982, when local supplies are seasonally low, and

when traditionally imports from RSA supplied up to 86% of the

central area demand, as opposed to the August-September periods,

-38

when local vegetables supplied 65% of the demand. The 26.3%

increase in fruit and vegetable prices since October 1982 can be

attributed to the prevailing drought, the worst in memory, which

is affecting the whole region. At the Johannesburg wholesale

market, for the period October 1982-February 1983, the increase

in prices has been even worse: 36% for potatoes, 55% for onions,

37% for tomatoes, and these three vegetables account for 80% of

the vegetable index. Except for potatoes and carrots though,

Swaziland retail prices are still higher than those in Johannesbura

or Durban for the first six months of 1983.

Vegetable Sales by Farmers

All TDL farmers assemble their produce in standard packs, after

basic grading, i.e., eliminating the obviously bad items. TDL

farmers who sell to South Africa have to grade according to the

market requirements there. The sales packs in Swaziland for the

most common vegetables are:

cabbage: net bags, 18-25 heads, approx. 25 kg.

tomatoes: 7.5 kg. boxes

green maize: no standard pack

potatoes: 15 kg. pockets

onions: 10 kg. pockets

Except for two or three onion growers, farmers do not store any

vegetables on the farm. Farmers try to space out their harvesting,

within the confines of the market and their labor availability,

and sell without storing.

-39

SNL farmers generally follow the same practices as TDL farmers.

Their major problem, before the ban, was in organizing sales at

harvest. Sales in local areas were easily disposed of, but sales

to the central areas and to South Africa lacked systematic coordi

nation. At NRDA, where tomatoes are the main crop, farmers

generally arranged their transport (just 10 truck loads in 1982)

to the Malelane cannery, at the same time when the Durban traders

would come. The latter offered better prices, and paid cash at

the farm. These Durban traders also went to Vuvulane, where they

bought the green maize. However, since the ban, they have largely

been preempted by the local buyers coming from the central area,

where prices are higher than in Durban, distances shorter, and

alternative supplies of vegetables not available.

Direct selling by farmers to final consumers in the central area

is done oLly by a few TDL farmers. Some of them have set up

roadside retail outlets near their farms, and generate a consider

able proportion of their revenue through these outlets. TDL farmers

also sell directly to institutional buyers, namely hotels and

restaurants. In 1978, institutions purchased a quarter of their

requirements directly from TDL producers; 39% in the case of

restaurants and 20% in the case of hotels. Direct sales by other

farmers do occur, but these sales are within their communities

generally, and generate but a small proportion of their gross

income from vegetables.

-40

The Wholesale Trade

In 1978, the participants in the central area vegetable marketing

system were organized as follows:

Initial Sales Type of Traders No. Per Week (Tons)

1. Full-time Specialist Trader 23 180 2. Part-time Trader 13 .40 3. Specialized Wholesaler 2 13 4. Shops (excluding roadside stalls) 6 7.8 5. Market Traders 73 21

Since 1978, there has been a doubling of the number of traders,

while only one specialized wholesaler and three grocery shops are

still in business.

Prior to the import ban, there were three wholesalers operating

and importing produce into Swaziland. Of these three, two were

operating from Swaziland and the other was of South African ori

gin. Currently, the wholesalers of Mbabane market are relatively

small, and since they can stay at the Mbabane market until 9 a.m.

only, are buying from producers and selling to the market retailers

or to shop owners who buy early in the morning. In addition, a few

growers offer produce on this market, some coming from as far away

as Vuvulane (some 160 km) to offer produce. The market authori

ties in Mbabane recon that about 30 local wholesalers frequent

the market and prior to the ban about six wholesalers came from

the RSA regularly.

At Manzini, wholesalers may remain all day and two wholesalers

offer a range of procude, but mainly concentrating on cabbages,

-41

potatoes, tomatoes and oranges. Each wholesaler has two lorries,

one of which remains at the market whilst the other goes to

collect produce from growers. In addition to these firms, there

are a number of other traders offering a single product, tomatoes

mainly. They remain in the market, in some cases for several days,

until their produce is sold, when they go off for further supplies.

Manzini market also supports a third class of semi-wholesalers who

have stands adjacent to the retail market and who supply the stall

holders there with further supplies as they need them. There is

no long-term storage capacity in either market center.

Currently, two wholesalers resident in Swaziland pursue other

businesses, as they consider wholesaling fruit and vegetables

internally is no longer profitable. The chief reason for this

opinion is the lack of a central point of assembly due to the

fragmented nature of the production process. It was also for

these reasons that one of the wholesalers who, prior to the ban,

was supplying some of the main retail shop outlets in Mbabane and

Manzini, as well as the markets of these two towns and Mahlanya,

bought 90% of his supplies in Johannesburg wholesale market.

Mbabane is 390 km from Johannesburg.

The Retail Trade

The Swaziland Central Statistical Office undertook a survey of

markets in Swaziland. The survey covered all known markets in

Swaziland, these being defined as both those for which licenses

for stalls were issued (e.g., Mbabane, Piggs Peak, Mahlanya) and

-42

those which exist for the selling of produce but for which no

locenses for stalls are issued e.g., Big Bend and Oshoek. Iso

lated roadside stalls, of which a good many exist in the central

Mbabane-Manzini corridor, were excluded. Table 15 below shows

that the total number of stalls in the three central area markets

of Mbabane, Manzini and Mahlanya was 378.

TABLE 15

Number of Stalls and Sellers in Central Area Markets

Covered Stalls Uncovered Stalls

No. No. No. No. Market Stalls Sellers Stalls Sellers

Mbabane 93 130 ....

Manzini 129 129 8 8

Mahlanya 133 133 14 14

Source: Ministry of Agriculture & Cooperatives, Market Advisor

Since that time, other markets have been established in Manzini

and Mbabane as well as at Kwaluseni aid a small market at Malkerns.

There are also plans for further retail markets and roadside

stalls in Manzini and Mbabane in order to satisfy a demonstrated

need which is currently satisfied by illegal streetside retailing.

In total, then, the number of stalls in the central area is some

thing over 500, of which at least 90% are fruit and vegetable

outlets. In addition to the market stalls, there are retail

shops and supermarkets in both Manzini and Mbabane which include

fruit and vegetables Ln their wares and whose turnover in these

commodities must be considerable in some cases. Unfortunately,

no survey data are available on the actual quantities handled.

-43

The main retailers are market women who buy produce brought to

them by producers and hawkers in their pick-ups. These women buy

the produce and repack them in small plastic bags, and by general

agreement, always charge the same price for similar produce.

Institutions

In 1978, there were 52 institutions in the central area, made up

of schools, restaurants, hotels and hospitals. Most important

were the hotels and restaurants, which accounted for over 70% of

the purchases. Half of their purchases were made through whole

salers, and a quarter from producers, mostly TDL potato growers.

Institutions prefer to deal with the wholesalers, who can assemble

the produce in the quantity, quality, and range desired. Before

the ban, the wholesaler preferred to buy from South Africa, but

they now provide some locally grown fresh lettuce, carrots, toma

toes and beans, in competition with a dozen or so TDL farmers who

have developed relations with the restaurants and hotels over the

years. However, in general, because of the high prices, variable

suppiies and limited choice of local vegetables, institutions are

now increasingly dependent on frozen vegetables, all imported

from South Africa.

Pricing

Prior to the ban, local prices were determined by the wholesale

markets in South Africa, particularly Johannesburg. With the ban,

and in the absence of a local wholesale market or a system of

administered prices, the price of vegetables is set by the

-44

retailers in the Mbabane and Manzini markets. This method assures

that retail prices would be set at the highest level. Retail

sellers prefer a higher price and the maximum margin per kg to

lower prices on higher volumes. Retailers can maintain this prac

tice under current conditions, since in the short or even medium

term, with the ban shutting out additional supplies, the volume

traded is fixed, and the retailer's position impregnable.

The situation in 1981, the first year after the ban, is summed up

in the Annual Review of Vegetable Prices and Marketing Trends,

1981, put out by the Marketing Advisory Unit. The overall summary

is quoted below, with the underline added to emphasize the domi

nant role of the retailers in price-fixing.

"In general the same seasonal patterns of supply experience

in 1980 prevailed in 1981, namely that produce was generally

readily available in reasonable quantities from May to

November (winter production) but was in limited or very

short supply from December to April, with March being a

particular lean month.

"Prices followed the availability of supplies, with the

highest prices generally experienced in March and April.

The annual average increase in prices in 1981 over 1980

was 44 percent at the Trader or Wholesale level and 71

percent at the retail level. Onions, cabbages and

tomatoes registered an average annual increase of over

100 percent in 1981 over their 1980 retail levels. At

-45

the wholesale level, only onions registered an increase

of over 100 percent in 1981 over their 1980 price level.

"Average vegetable prices rose sharply in 1981 over 1980

reflecting the often limited availability of produce

especially in the first half of the year, the margins

taken at the retail level have been somewhat exhorbitant

having increased from an average 66 percent in 1980 to

110 percent in 1981. The average wholesale or trader

margin has,, however, registered a downward trend,

dropping from an average 57 percent to 36 percent. It

would appear that the high prices registered at the

retail leval are not finding their way back to the pro

ducer but are retained by the intermediaries. Prices

in the major supermarkets receiving supplies directly

from producers or traders are often considerably below

those found in the town retail fruit and vegetable

markets.

"Local vegetable production has certainly increased in

the wake of the ban on imports due to cholera, but sup

plies are still concentrated in the winter months, with

summer vegetable production, although increasing, still

failing to meet local demand and thereby leading to high

vegetable prices."

-46

In the first half of 1982, the average unweighted retail price

of the main vegetables (tomatoes, potatoes and cabbages) was

EO.70 per kg. The margin breakdown calculated in early 1983 was

as follows:

Retail margin 30c/kg

Traders' margin 6c/kg

Poor Producers' margin 7c/kg (Cost = 27c/kg)

Good Producers' margin 23c/kg (Cost - 4c/kg)

Although the producers' margin is less than 50% of the retail

price, for vegetables this ratio is not out of line, Compared to

other countries, it is in fact rather good. In South Africa, for

example, where the system is more complex and transport costs

greater, the producers receive 27-33% of the retail (consumer)

price. Table 16 gives the average producer and retail prices for

each of the four main vegetables for 1980 (pre-ban), 1981 and

1982, plus the ratio of the producer price to the retail price.

-47

TABLE 16

Average Producer and Retail Prices at Mbabane for Cabbages, Tomatoes, Potatoes and Green Maize

(Cents/kg)

1980 1981 1982

Cabbages: Producer Price 10 13 15 Retail Price 25 53 57 Ratio % 40 25 27

Tomatoes: Producer Price 21 38 50 Retail Price 35 52 81 Ratio % 60 73 62

Potatoes: Producer Price 19 29 30 Retail Price 41 63 62 Ratio 46 46 62

Green Maize: Producer Price 22 45 51 Retail Price 64 85 109 Ratio % 34 53 47

Source: Ministry of Agriculture and Cooperatives, Marketing Advisory Unit. Annual Review of Vegetable Prices and Marketing Trends, 1981-1982.

The producers' share of the final price over the three years varied

according to the vegetable. The share remained constant for toma

toes and potatoes, which together accounted for over 55% of all

sales. However, for cabbages, the producers' share halved after

the ban, to a rather low 22-25%, but for green maize, which is more

storable, the producers' margin went up nearly 50% after the ban,

to half the retail price. The obvious conclusion to draw is that

since the ban, contrary to the general view, most producers have

-48

either held their own or even improved their relative share of

the final price. The winners have been those farmers, mainly

TDL, who are able to market their production directly to the final

consumer. The losers have been the cabbage growers, and of course

the consumers.

Canning and Processing

There is no canning or processing of vegetables in Swaziland, but

growers do depend on processing.plants in South Africa. Prior to

the drought, nearly half of the potato exports accounted for

10-12% of the total vegetable production of Swaziland, was trucked

to the Simba Chip plant in Johannesburg. For tomatoes, the

cannery in Malelane used to be an outlet for growers in Piggs

Peak (NRDA), but at the most it took 452 tons in 1977, about 10%

of total tomato production. In 1982, it took 100 tons, 10% of just

NRDA production.

The Libby cannery at Malkerns is one of the country's major

industries, exporting E18 milliorn worth of canned products in

1982. However, these consisted entirely of pineapples and citrus,

not vegetables. The only major vegetable produced in Swaziland

that can be considered for canning is tomatoes. However, for

the Malkerns factory to have a viable cannery line, it would

require a minimum input of 100 tons per day of good quality

tomatoes for 100 days, i.e., 10,000 tons per year, more than

twice Swaziland's current production, and leaving aside the

issues of transport costs and markets for processed tomatoes. A

-49

similar problem confronts plans to set up a dehydration plant; the

adequate supply and range of quality produce just isn't available

to support a viable plant. NIDC has a proposal to produce 1,500

tons of dehydrafted vegetables per year that would require an in

put of 18,000 tons a year of fresh vegetables, equal to the current

national production of all vegetables. This is supposed to be a

minimum-size plant, but the total supply of vegetables other than

potatoes, tomatoes and green maize, which generally are not de

hydrated, is only 6,000 tons, all of which havea ready fresh market,

where prices are always higher than any processor can pay. Similar

ly for freezing; tomatoes are the only candidate in terms of volume

available in excess of fresh demand, but frozen tomatoes do not exist.

-50

The Proposed Wholesale Market

Institutional buyers and retailers in the central area complain

that there is not one single market center in Swaziland where they

can be sure of buying supplies of the full range of fruits and

vegetables which should be available from regional production

centers. From their point of view, supply services offered by

traders are often uncertain and unreliable, and many found ii.

easier to import from South Africa, when it was permitted.. The

situation would be much improved by the creation of a more effec

tive link between producers and buyers. The proposed project

would establish a central wholesale market to provide the link

between producers and wholesalers/retailers. There is a need for

a central wholesale market where quantities of all types of pro

duce could be brought together to be bought and sold. There is

an allied need for a communications link between the market and

major centers of fruit and vegetable production. A central market

would give producers and traders a central focus of activities,

which would improve efficiency, reduce costs, and attract more

resources into this sector. By contrast, the previous system of

uncoordinated production and marketing, with traders going from

farm to farm on speculation and then hawking their produce along

the Manzini-Mbabane corridor, was extremely inefficient and costly,

and totally uncometitive with the central area-Johannesburg

connection. The ban has provided the one opportunity to create

an organized and formal marketing system that would benefit all

producers.

-51

There is no question that a central wholesale market, with its

market intelligence appendage, is needed for Swaziland. It is a

prerequisite condition for expanding smallholder vegetable produc

tion. Not only will it give the smallholder producei direct

access to the central market, but it will also provide the neces

sary volumes of smallholder potatoes, tomatoes and other produce