Spending on Social Events through Microfinance- Evidence from an impact evaluation programme...

47

Spending on Social Events through Microfinance- Evidence from an impact evaluation programme conducted in Hyderabad, India Pochampally Gargi Rao Candidate No: 122783 Submitted in partial fulfilment of the requirements for the degree of MSc in Development Economics BMEc – School of Business, Management and Economics University of Sussex 6 November 2014

Transcript of Spending on Social Events through Microfinance- Evidence from an impact evaluation programme...

Spending on Social Events

through Microfinance-

Evidence from an impact

evaluation programme conducted

in

Hyderabad, India

Pochampally Gargi Rao

Candidate No: 122783

Submitted in partial fulfilment of the requirements for the degree of

MSc in Development Economics

BMEc – School of Business, Management and Economics

University of Sussex

6 November 2014

Candidate Number: 122783

i

Acknowledgments

I am pleased to submit my dissertation as part fulfillment of the requirements to

complete my MSc in Development Economics. I owe a lot to all those who helped me

in completion of this task within the given time. I would be failing in my duty if I do

not thank my supervisor Dr. Pedro Rosa Dias without whose valid suggestions and

guidance this could have not been completed.

I thank my course coordinator Mr. Alan Winters who helped me in successfully

completing my degree with an internship variant and was kind enough to give me an

extension to submit my thesis.

I owe a lot to my parents who have given me a great support and strength during my

stay in Brighton. Equally important is my uncle, Dr. PSM Rao whom I cannot afford to

miss. Discussions with him on microfinance systems in Hyderabad were always a

pleasure and showed me a path to take up this research topic.

Last but not the least, I thank the staff of School of Business, Management, and

Economics; the library staff who always helped me whenever I wanted.

I again take the opportunity to thank all those who have been helpful in completing

this work. If I missed anyone, I may be pardoned since it is not deliberate.

Candidate Number: 122783

ii

Contents Acknowledgments ........................................................................................................... i

Contents .......................................................................................................................... ii

List of tables and figures .............................................................................................. iii

Abbreviations ................................................................................................................ iv

Abstract........................................................................................................................... v

1. Introduction ......................................................................................................... 1

2. Background of Microfinance ............................................................................... 4

2.1 Microfinance in Andhra Pradesh ................................................................... 6

2.2 Social pressure and need for credit ................................................................ 8

3. Literature Review .............................................................................................. 12

3.1 Health and Microfinance ............................................................................. 13

3.2 Education and Microfinance ........................................................................ 16

3.3 Social traditions and expenditure ................................................................ 18

4. Data.................................................................................................................... 22

4.1 Background on the Microfinance Policy.....................................................22

4.2 Structure of the Randomised Control Trial.................................................23

4.3 Results of Duflo et al...................................................................................24

4.4 Descriptive Statistics...................................................................................25

5. Methods ............................................................................................................. 27

6. Results ............................................................................................................... 29

6.1 Quantile Regressions ................................................................................... 33

7. Conclusions ....................................................................................................... 36

8. References ......................................................................................................... 38

Candidate Number: 122783

iii

List of tables and figures

List of figures

Figure 1: Growth in Private sector MFIs in AP ............................................................. 7

Figure 2: Social pressure on borrowing from MFIs and moneylenders for social

expenditure ..................................................................................................................... 9

Figure 3: Quantile graphs for social expenditures ........................................................ 34

List of Charts

Chart 1: Unadjusted treated-control difference for social expenditures ....................... 26

Chart 2: Adjusted treated-control difference for social expenditures .......................... 26

List of tables

Table 1: Description of variables ................................................................................. 28

Table 2: Treatment coefficients in regression models for social, health and education

expenditures .................................................................................................................. 29

Table 3: Treatment coefficients in regression models for social, health and education

expenditures .................................................................................................................. 31

Table 4: Treatment coefficients in regression models for social expenditures ............ 32

Candidate Number: 122783

iv

Abbreviations

AP Andhra Pradesh

ITT Intent-to-treat

LFP Low Fee Private Schools

MFI Microfinance Institutions

NABARD National Bank for Agriculture and Rural Development

NGOs Non-Governmental Organisations

OLS Ordinary Least Square

SEWA Self Employment Women Association

SHG Self-help group

RCT Randomized Control Trials Randomised Control Trials

RRB Regional Rural Banks

Candidate Number: 122783

v

Abstract Microcredit is a tool to reduce poverty. It is documented that microfinance

leads to improvements in health, education, improving businesses and

standard of living of the poor. This research tries to look at a possible second

channel of microfinance linked to social expenditures. These comprise

festivals, other ceremonies, weddings and funerals. This dissertation

estimates the effect of microfinance on household social expenditure by re

examining data from a randomised control trial, previously used to evaluate

the impact of a well-known microfinance intervention: the provision of

microcredit to poor in Hyderabad by Spandana, a leading Microfinance

institution (MFI) in India. Recent literature suggests that this social

expenditure can be largely ‘unwanted’ and caused by social pressure; it has

also been shown that it can make poor households poorer. This dissertation

finds large and statistically significant effects of microcredit on social

expenditures; in some cases microcredit indices an increase in these

expenditures that is larger than its effect on education and healthcare.

Candidate Number: 122783

1

1. Introduction

Microfinance has both economic and social impacts on poor households. These

economic and social impacts come in the form of affecting the expenditure pattern

of the poor households. Poor households are in need of financial assistance to have

better economic standards of living. Hence, microfinance has emerged as a helping

hand not only for the needy but also for economists and anthropologists to suggest

models to deal with poverty. Microcredit has generated considerable enthusiasm

and hope for poverty alleviation at a faster pace, culminating in the Nobel Prize for

Peace, awarded in 2006 to Mohammed Yunus and the Grameen Bank for their

contribution to the reduction in world poverty.

A strong link between access to credit and poverty persists in economic literature.

Microfinance; giving credit in small quantities to poor households; is now a tool to

deal with poverty and is considered as a poverty reduction strategy to target the

inaccessible and provide them with loans to enable them generate sustainable

livelihoods. The character of Microfinance has thus come up with a promising hand in

enabling policymakers to rethink about banking for the poor. There is another side of

the argument, which talks about being in poverty leads to inaccessibility to loans.

Therefore, a causal link between access to credit and poverty cannot go unnoticed.

According to Armendariz1, “one of the notable aspects of these microfinance

approaches is that improvements are possible even when lenders do not actually

acquire more information. Instead, the contracts harness local information and give

borrowers incentives to use their own information on their peers to the advantage of

the bank. It is not that the older analyses of information problems were incorrect, it

is just that they failed to consider new ideas to circumvent information

problems.”The microfinance revolution started with the recognition that poor people

1Beatriz Armendáriz de Aghion and Jonathan Morduch –“The Economics of Microfinance”; The MIT

Press Cambridge, Massachusetts, London, England.

Candidate Number: 122783

2

needed access to loans and that they could use these funds productively. It has also

changed the perception that poor people are not credit worthy. However, these

programmes do not intend to divert the credit to un-viable and avoidable

extravagant expenditure like expenditure on social events, and customary practices.

Economists have looked into the direct link between microfinance and better

economic outcomes such as improvement in health care services, better schooling,

setting up new businesses, etc. The literature highlights that there is a positive link

between microfinance and these economic aspects when it comes to poor

households who are in need of money. Such as Dunford (2001)2 studies the

integration of microfinance with promotion of family planning/birth control and

combating HIV/AIDS; Pronyk et al. (2006)3 found that microfinance is associated with

reduced risk of physical or sexual abuse; Barnes et al (2001)4 looked at significant

increase in paying the school fees for households who were treated with

microfinance; Khandker (2001)5 found out that by providing small loans to poor

households led to fall in dropout rates for children in the treatment group, etc. But

there are leakages as well to this concept and positive link can be questioned.

As poor individuals get more money due to microfinance, they tend to spend it for

their immediate economic and social needs to enhance their standard of living and

improve their social image. Hence, there could be a plausible ‘social link’ through

microfinance. Thus this research paper tries to see whether there is a link between

microfinance and social expenditures.

2 Christopher, Dunford. “Sustainable Integration of Microfinance and Education in Child Survival, Reproductive Health, and

HIV/AIDS Prevention for the Poorest Entrepreneurs” Journal of Microfinance, Volume 3 Number 2

3 Pronyk PM, Hargreaves JR, Kim JC, Morison LA, Phetla G, Watts C et al. Effect of a structural intervention for the prevention

of intimate-partner violence and HIV in rural South Africa: a cluster randomised trial. Lancet 2006;368:1973–83.

doi:10.1016/S0140-6736(06)69744-4 PMID:17141704

4 Barnes, C., Keogh, E., & Nemarundwe, N. (2001b). Microfinance program clients and impact: An assessment of Zambuko

Trust Zimbabwe. Washington, DC: Assessing the Impact of Microenterprise Services (AIMS).

5 Khandker, S. (2001). Does micro-finance really benefit the poor? Evidence from Bangladesh. Paper delivered at the Asia and

Pacific Forum on Poverty: Reforming Policies and Institutions for Poverty Reduction, 5–9 February.

Candidate Number: 122783

3

The growing concern is that households now spend more on social events and social

occasions than on economic and sustenance activities. Due to social pressure from

the society they live in, in the form of fear of social exclusion, stigmatisation, ridicule,

peer pressure, the poor households struggle to acquire social recognition and status

in society. To live up to these expectations and due to pressure from social

surroundings and circumstances, households take loans from institutions and

individuals. Overall, social spending could lead to negative externalities and welfare

loss, especially for poor households. Some documented to this effect is available in

the literature. Splendid funerals (The Economist, 2007; Mango et al., 2009), roaring

bride‐prices and dowries (Rao, 1993; Dekker and Hoogeveen, 2002), inflating social

spending (Brown et al., 2011), lavish ceremony expenditure squeezing out nutritional

outcomes (Chen and Zhang, 2012), and lavish festivals (Banerjee and Duflo, 2007).

This raises an important topic about social pressures governing the expenditure

pattern of poor income households. Thus, I try to formulate my hypothesis by looking

at how microfinance and social expenditures are linked.

This research is a re-search (Searching again) into the data based on secondary

datasets produced for Spandana, hence results are subject to the data published by

Spandana way back in 2010. Further, this study tries to replicate the study performed

by Banerjee and Duflo (2009) but looking at social pressure impacts on expenditure

of low-income households. Hence, this research thesis takes up a randomised control

trial that was conducted by Banerjee and Duflo (2009) to access the impact of

microfinance on various economic outcomes. The study uses the data collected from

household surveys of various households living in the slums of Hyderabad.

From the available literature, we can predict that microfinance has a positive effect

on social expenditure. The indicative results suggest that there might be a positive

effect on festival spending and wedding spending as a percentage of health and

education expenditures. In order to test the hypothesis, the research is divided into

seven sections. Section one, deals with the introduction of the research, which traces

the evidences of formulating the hypothesis; section two provides brief on

Candidate Number: 122783

4

microfinance and its origins, looks at evidence of microfinance structure in

Hyderabad and the need of microfinance for social spending. Section three looks at

the evidence from past literature on social spending, health and education. Section

four looks at the collection of data including the microfinance policy adopted

structure of the RCT, and descriptive statistics. Section five looks at regression

strategy implemented to support the hypothesis. Section six analyses the results,

including quantile regressions. Finally, the paper is concluded in the seventh section.

The usage of graphs, tables and charts are seen wherever relevant. Simple

percentages are used to analyse the data and to support conclusions, and to give a

reader the basic facts and ground realities.

2. Background of Microfinance Microfinance is a developing concept that has mushroomed from the ideas of

Muhammad Yunus of supplying small loans to poor households. He argued that one

day these small loans would generate income and the poor clients would be able to

repay the loans. Now, this idea of providing small loans to poor households has

brought in structural changes in economies and the way to fight back poverty. As

Armendariz puts it, ‘Muhammad Yunus is recognized as a visionary in a movement

that has spread globally, claiming over 65 million customers at the end of 2002.’6

Otero (1998) defines “Microfinance as the provision of financial services to low-

income poor and very poor self-employed people”. It focuses on providing financial

services such as short-term loans, savings and insurance products to poor

households, who lack access to credit. The importance of Microfinance was

reinforced with the launch of the Microcredit Summit in 1997, where the aim to

reach 175 million poor households with credit, and other financial services by the

end of 2015 was discussed. With the acceleration of participations of various

international organizations and Non Governmental organizations, recently led the

UN to recognise 2005 as the International Year of Microcredit.

6Beatriz Armendáriz de Aghion and Jonathan Morduch –“The Economics of Microfinance”; The MIT Press Cambridge, Massachusetts, London, England .

Candidate Number: 122783

5

In fact, institutionalisation for microfinance through public sector banking began way

back in 1975 in India with the establishment of Regional Rural Banks (RRBs) or

Grameen Banks, and regulating them with a Regional Rural Bank Act 1976. Through

this act, the financial needs of farmers with smallholdings, (up to a maximum of five

acres of land); agricultural labourers, rural artisans, small businesspersons in rural

areas, rural women, vegetable vendors etc. were supported with institutional credit.

These banks served a cluster of 10 to 15 villages and they were made accessible for

users. They have transformed rural economic scenario altogether. The main

philosophy behind the establishment of those banks by the Government was to

reduce rural indebtedness, and take out the farmers and others with small means

out of the clutches of rural unregulated/traditional moneylenders (Rao, P. Madhava,

Vishalandhra, 1989). Major public sector banks have sponsored these RRB, and by

1990 almost all the villages in India were served by these banks. Coming to urban

areas like Hyderabad, it was urban cooperative banks, and regulated private money

lenders extended credit to the people with small means for business purposes.

The awareness about the need for microfinance lies with the policymakers who have

tried to work their way out to develop exiting credit institutions to work on poverty

reduction by providing credit to the poor households for whom the credit was

inaccessible, but with disappointing results. In that sense, Microfinance has come up

with a promising hand in enabling policymakers to rethink about banking for the

poor. According to Armendariz7, the existence of microfinance institutions is a

solution to existing problems of adverse selection and moral hazard in financial

sectors. In her words, “one of the notable aspects of these microfinance approaches

is that improvements are possible even when lenders do not actually acquire more

information. Instead, the contracts harness local information and give borrowers

incentives to use their own information on their peers to the advantage of the bank.

It is not that the older analyses of information problems were incorrect, it is just that

they failed to consider new ideas to circumvent information problems.”

7Beatriz Armendáriz de Aghion and Jonathan Morduch –“The Economics of Microfinance”; The MIT

Press Cambridge, Massachusetts, London, England.

Candidate Number: 122783

6

In a related argument, interest rates to play a vital role in augmenting the growth of

Micro Finance Institutions. They rose as high as is needed to fully cover operating

costs, and profits to the promoters otherwise programs could not be financially

sustainable. This is the Microfinance institution’s (MFI) viewpoint of financing itself

to help the needy. Armendariz says “this has been a hard-fought argument, and we

agree that prudently raising interest rates can be a key to microfinance success”8.

Thus, the challenge for microfinance is to couple smart interest rate policies with

new ways of doing business to ensure good incentives for its clients. The MFIs set up

after 2000 saw themselves less in developmental mould and more as businesses in

the financial services space. This overriding shift brought about changes in

institutions’ legal forms, capital structures, sources of funds, growth strategies and

strategic alliances. We will now look at the growth of microfinance in Andhra

Pradesh, the place we are interested in. This research takes up the data collected

from slums of Hyderabad, Andhra Pradesh.

2.1 Microfinance in Andhra Pradesh Microfinance is not a new concept when it comes to India. It had its roots from the

cooperative moment in India, Self Employed Women Association (SEWA) Gujarat

Model of savings of 1974, and the Government of India’s Flagship Banking for the

poor approaches of 1975 to establish Grameen Banks. These Grameen banks were

established to provide small loans to farmers for agriculture purposes and for small

businesses. This approach was later given a legal status through a Regional Rural

Bank Act 1976. The microfinance movement was initiated by Government of India,

and later by National Bank for Agriculture and Rural Bank Development (NABARD) in

collaboration with Banks and Non-Governmental Organizations (NGOs) for unbanked

population known as Self-help groups (SHGs) - bank linkage program in 1992. Thus,

the microfinance concept started to grow with Government endeavours to engage

itself in financing the poor, and later with the involvement of private sector by

8Beatriz Armendáriz de Aghion and Jonathan Morduch –“The Economics of Microfinance”; The MIT

Press Cambridge, Massachusetts, London, England.

Candidate Number: 122783

7

setting up Microfinance Institutions (MFIs). From there on microfinance activities

were being implemented by two channels MFI model and SHG bank linkage model.

The Micro Finance sector with private sector participation witnessed growth from

2006 to 2010.

Coming to Andhra Pradesh (AP), there has been a large amount of lending through

MFIs in gross terms until the government of AP decided to regulate their functioning

in 2010, which led to drastic fall in microfinance history. As Taylor (2011, p. 3)

explains, within the expansion of microfinance in the late 1990s: “Andhra Pradesh

became a magnet for microfinance start-ups and witnessed a proliferation of loans

from private MFIs. [. . .] The ability of MFIs to scale up their operations in Andhra

Pradesh rests in part upon the institutional infrastructure and culture of formal credit

put in place through the social and development banking schemes of the 1970s and

1980s, alongside the expansion of the self-help group (SHG) model under the auspices

of the state in the 1990s and 2000s”.

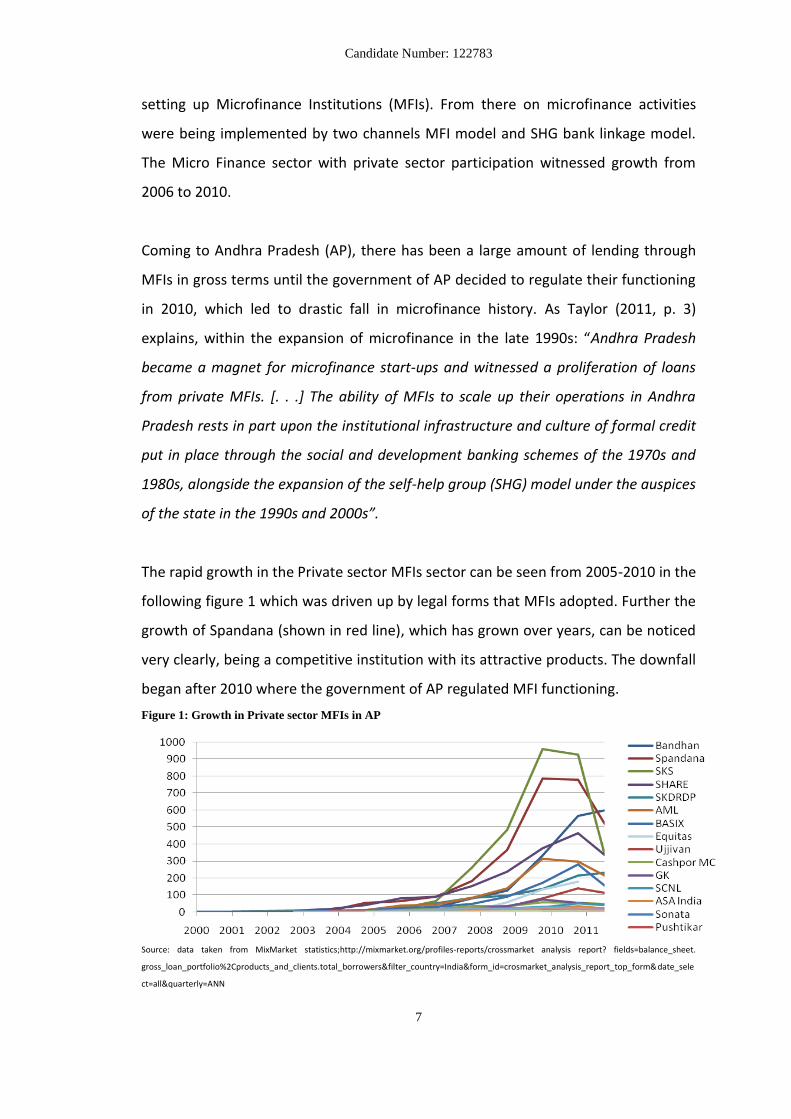

The rapid growth in the Private sector MFIs sector can be seen from 2005-2010 in the

following figure 1 which was driven up by legal forms that MFIs adopted. Further the

growth of Spandana (shown in red line), which has grown over years, can be noticed

very clearly, being a competitive institution with its attractive products. The downfall

began after 2010 where the government of AP regulated MFI functioning.

Figure 1: Growth in Private sector MFIs in AP

Source: data taken from MixMarket statistics;http://mixmarket.org/profiles-reports/crossmarket analysis report? fields=balance_sheet.

gross_loan_portfolio%2Cproducts_and_clients.total_borrowers&filter_country=India&form_id=crosmarket_analysis_report_top_form&date_sele

ct=all&quarterly=ANN

Candidate Number: 122783

8

The AP government required the MFIs operating in the state to get registered with

local district authorities who forced the MFIs to put on hold their collections and

disbursements. Overall, this led to a crisis in the microfinance sector as it faced with

funding constraints due to regulatory uncertainty.

Having briefly looked at the trend of microfinance in AP, we now look at the need for

microfinance. This will be analysed by looking at social pressure as a need for

microcredit so as to spend more on social occasions and events. The next section

tries to find an answer to why poor households spend on social occasions and the

reasons for it being bad.

2.2 Social pressure and need for credit Many poor households come from closely-knit community. Hence, they are highly

integrated into the society in every aspect including social expenditure. It is highly

documented that a significant amount of their income goes into social spending such

as spending on lavish festivals, extravagant wedding ceremonies and funerals

accompanied by higher spending on gifts (Chen 2012). In recent years, economists

have increasingly interested to look at the connection between consumption and

social experience, especially in connection with consumption of global commodities

(Friedman, 1994; Miller 1987).

Access to credit and reason to get credit from Microfinance institutions (MFIs)

among poor households is governed by social pressure. In the following diagram

(figure 2), we look at five different dimensions that define social pressure, which

causes households to spend on social occasions at the cost of health and education.

The first reason, which is very common to think of, is that of Social Status. This is

because higher social status is associated with higher rewards in near future. Taking

the case of Chinese rural areas, according to an experiment conducted by Chen

(2012), “Gift giving may also signal wealth and social status. If a higher social status

is associated with greater rewards, such as a higher likelihood of marriage for

Candidate Number: 122783

9

offspring, than concerns for status may intensify gift-giving competition.” To this V.

Rao, explains the paradox between rational and non-rational behaviour of

households in consumption expenditure. This is because money spent on

celebrations, festivals, funerals, weddings and other ceremonies is after all the

money that was not spent on health, education and other production inputs.

Another aspect explaining social pressure is that of customs and traditions. It is a

well-known fact that poor households are excluded from society. In order to acquire

a social recognition, getting included in their social group, they tend to spend more

on festivals, traditions, customary rituals, and feasts. Turner (1982), for instance,

describes festivals as "generally connected with expectable culturally shared events."

He suggests that when a social group celebrates a particular event, it “celebrates

itself” by “manifesting in symbolic form what it conceives to be its essential life."

Thus, festivals may serve to build social cohesion by reinforcing ties within a

community. Public rituals identify and shape individual preferences. To this V. Rao,

takes the case of households in South India and looks at their expenditure pattern on

festivals and ceremonies. He concludes that for the maintenance of status and rank,

households tend to acquire greater assets such as wealth, a prestigious job, or

acquisition of rich husband or son-in-law is desired. And these are some of the

preconditions to the acquisition of greater public respect and regard.

Figure 2: Social pressure on borrowing from MFIs and moneylenders for social expenditure

Candidate Number: 122783

10

Going further, more recent development shows peer pressure as a motive behind

high social expenditure. This was well laid out by Chen (2012), who looked at the

increased expenditure on expensive gifts among poor households in rural China. In

his words “Peer effects can generate both positive and negative externality. On the

positive side, peer pressure may facilitate technology adoption and social learning

(Benabou, 1993; Hoxby 2000; Glaeser and Scheinkman 2001; Conley and Udry 2010).

However, peer pressure can also induce socially undesirable behaviour, such as

juvenile delinquency (Haynie 2001). It is therefore likely that one’s gift-giving

behaviour is influenced by peers as well.”

Studies have shown that there have been increases in social demands, which mount

for status in society. A study from Ethiopia, that looked at the village poultry

consumption and marketing in relation to gender, socio-cultural events and market

access, shows that vital consumption has reduced. Religious festivals and traditions

periodically shift the local demand towards unwanted products rather than

productive inputs.

Moving on, poor households tend to live in the present rather than saving for the

future. This is because they are tied with social commitments. Dupas and Robinson

(2011), closely looked at the spending and savings pattern of households in Kenya;

where they estimated the bundle with social commitment and credit to have the

largest effect on naive present-based individuals. Another form of commitment

arises from households being risk averse. Even though, money is fungible,

households tend to spend it on ‘unwanted expenditures’ just to treat them with

luxury. The terminology used ‘unwanted’ expenditure was well versed by Banerjee

and Mullainathan (2010).

Taking up the argument of Banerjee and Mullainathan (2010) further, there have

been studies that looked at why social expenditure was ‘unwanted’. They propose

that the sophisticatedly tempted poor will not save money that they know will be

wasted in the future. They explore the idea “that the fraction of the marginal dollar

Candidate Number: 122783

11

that is spent on temptation goods decreases with overall consumption,”9 where

temptation goods are goods in a multi-period/multi-self-model that only generate

utility for the self of the period when they are consumed.

To add to this, a study conducted by Mango, et al (2009) identifies the reason behind

poor people falling into poverty trap through increased social expenditure, in a study

conducted in Kenya. He suggests that heavy funeral expenditures is one of the

reasons why poor households fall into deep poverty. He described, “A third set of

descent-inducing factors are related to social and cultural practices, which also vary

considerably among the five livelihood zones. Social and cultural factors, giving rise to

uneconomic land subdivision, were of primary importance in Zones 1 and 3, while

heavy funeral expenses are implicated in Zones 1 and 2.”

As our hypothesis looks at the effect of microfinance on social expenditures at cost of

education and health, a recent study by Chen (2010) looked at the increased

ceremony spending at the expense of food consumption among poor households in

China. They found that “because poor often lack the necessary of resources, they are

forced to cut back on basic consumption, like food, in order to afford a gift to attend

the social festivals”. In addition, they found significant results on children health care,

due to less nutrition as a result of gift-giving. To this, he concludes, “the toll of

participating in social events is heavy for the poor- doubling the number of prenatal

exposures to social ceremonies in a village would lower the height-for-age z score of

children”.

Overall, the economic principle behind the expenditure depends on the flow of

income of the poorest households. The main argument here is that households, who

are now had more money in their hand came as a microcredit, tend to choose their

own consumption pattern. Some of this amount goes into expenditure on health,

education, productive assets; and some of the income flows into expenditure on

9 Banerjee, A. Mullainathan, S. “The shape of Temptation: Implications for the economics lives of the

poor”. CEPR Discussion Papers 7828, C.E.P.R. Discussion papers. 2010

Candidate Number: 122783

12

social occasions such as festivals, funerals, weddings, gifts, and other ceremonies. In

economic terms, this is called a leakage. The recent literature highlights some

evidence on these leakages and how spending pattern of poor households has

changed with regards to social reasons. We have identified some of the prominent

social reasons (discussed above), and now we move to analyse the empirical

literature showing evidence that social expenditure has increased.

3. Literature Review Microfinance Institutions (MFIs) are often seen by the aid practitioners as

transparently effective means of improving the position of the poor. There is an

abundance of literature available today on microfinance. Literature reveals many

impact evaluation studies that look at the success of microfinance institutions in

helping and aiding the poor for better economic outcomes. Most of these studies

have been conducted in developing countries. Also, little is known about the

effectiveness of targeting the ‘core poor’- which is a major flaw in Spandana’s

intervention. However, keeping in view the wider area of microfinance knowledge

and limited area of my research, I would focus here on some selected works that are

relevant to our study. Moreover, it is the general perception and belief that social

responsibilities, cultural rituals, traditions, customs, festivals, etc. play a dominant

role in the lives of many who are in financial needs. These events, even decide the

quantum of credit requirements, and expenditure patterns of borrowers from MFIs.

The paper that throws light on microfinance is by Banerjee and Duflo (2009)10 which

looks at randomized control trial of microfinance implemented in Hyderabad, India.

The details on the randomized control trial will be taken up in the Data and Analysis

section. Banerjee and Duflo (2009) in their paper look at the impact of microfinance

on various issues such as expenditure on health, education, setting up new

businesses, women's participation, etc. The program in Hyderabad does not mandate

microloans to be spent on businesses; moreover, the spending pattern of the

10

Banerjee, Abhijit V., Esther Duflo, Rachel Glennerster, and Cynthia Kinnan. 2010. “The Miracle of Microfinance? Evidence

from a Randomized Evaluation.” Cambridge, Mass.: J-PAL and MIT, June.

Candidate Number: 122783

13

households is not monitored by the MFI. Although, the conventional motivation for

the household to take up the loans were to start a business, but this was not

mentioned specifically when the experiment was conducted, hence it’s a form of a

randomized control trial. Briefly, this paper showed that microfinance did help the

poor households to overcome the shocks of health and improve school facilities, but

it did not lead to support a greater increase in expenditure for health care or better

health outcomes for children neither there were any scarring effects on education as

a whole.

In parts, I would like to evaluate the existing literature on microfinance and its impact

on health, education and social traditions in light of how much households spend

when microloans are being provided.

3.1 Health and Microfinance At the global level, strengthening health systems and giving priorities to health

indicators is one of the tools to achieve poverty reduction. Many MFIs are now

inclined towards achieving better health outcomes and reduce poverty. Numerous

impact evaluation studies support the effectiveness of microfinance and its impact

on poverty. Research funded by The World Bank examined the impact of three

microfinance institutions in Bangladesh over a seven-year period and found dramatic

decreases in overall poverty, with the highest impact on those families in extreme

poverty.11 To this Leatherman and Dunford (2010)12 say that “However, microfinance

is not a silver bullet; legitimate issues exist, such as the ability to address the needs of

extremely poor people, the level of debt burden for individuals, and the uneven

performance of microfinance institutions worldwide.”

11Khandker SR. Micro-finance and poverty: evidence using panel data from Bangladesh. World Bank Econ Rev 2005;19:263–86.

doi:10.1093/wber/lhi008

12 Sheila Leatherman & Christopher Dunford. “Linking Health to Microfinance to reduce Poverty.” Bull World Health Organ

2010;88:470–471 | doi:10.2471/BLT.09.071464

Candidate Number: 122783

14

A small but growing number of studies show that the MFIs are capable of

contributing to health improvement. Dunford (2001)13 in his paper looks at the

integration of microfinance with promotion of family planning/birth control and

combating HIV/AIDS in Bolivia and Uganda. They show that there has been positive

impact on health situation by creating awareness about HIV/AIDS. Pronyk et al.

(2006)14 found that microfinance is associated with reduced risk of physical or sexual

abuse in South Arica. In Ghana, de la Cruz15 et al found that microfinance institutions

could effectively contribute to community and national malaria initiatives by

increasing knowledge, leading to increased ownership of bed-nets used by

vulnerable members of the households. Another study by Gertler et al (2009)16, show

that there is a positive correlation between household’s consumption and measure

of health in Indonesia.

Recently, MFIs in India have integrated their services into achieving better healthcare

for the poor households. Some run health camps by educating their clients about the

basic health needs and management of diseases such as malaria, dengue and

HIV/AIDS. According to Metcalfe, et al (2012)17, MFIs have achieved significant

impacts in areas such as neonatal and maternal mortality and infant and child

feeding. Dunford and Metcalfe (2011)18 look at the low marginal costs of MFIs as an

indicator for them to participate and engage themselves in providing better

healthcare systems.

13 Christopher, Dunford. “Sustainable Integration of Microfinance and Education in Child Survival, Reproductive Health, and

HIV/AIDS Prevention for the Poorest Entrepreneurs” Journal of Microfinance, Volume 3 Number 2

14 Pronyk PM, Hargreaves JR, Kim JC, Morison LA, Phetla G, Watts C et al. Effect of a structural intervention for the prevention

of intimate-partner violence and HIV in rural South Africa: a cluster randomised trial. Lancet 2006;368:1973–83.

doi:10.1016/S0140-6736(06)69744-4 PMID:17141704

15 De La Cruz N1, Crookston B, Gray B, Alder S, Dearden K. “Microfinance against malaria: impact of Freedom from Hunger's

malaria education when delivered by rural banks in Ghana.” Trans R Soc Trop Med Hyg. 2009 Dec;103(12):1229-36. doi:

10.1016/j.trstmh.2009.03.018. Epub 2009 Apr 23.

16 Gertler, P., Levine, D. I. and Moretti, E. (2009), Do microfinance programs help families insure consumption against illness?.

Health Econ., 18: 257–273. doi: 10.1002/hec.1372

17 “Integrated Health and Microfinance in India: Harnessing the Strengths of Two Sectors toImprove Health and Alleviate

Poverty”State of the Field of Integrated Health and Microfinance in India, 2012.

18 Metcalfe, M., S.Leatherman with C. Dunford, B. Gray, M. Gash, M. Reinsch and C. Chandler. 2010.”Health and

microfinance:leveraging the strengths of two sectors to alleviate Poverty”. Freedom from Hunger Research

Paper No.9, p. 27.

Candidate Number: 122783

15

There is the other side of the story as well. Considering the Indian health situation,

there could have been a strong linkage between the Micro finance and health care.

Healthcare providers need to look at the importance of social intermediary role

those MFIs play in local communities. However, the literature does not throw much

light on this aspect. Other impact studies show that there is no relationship between

microfinance and health. For instance, the study by Desai and Tarozzi (2013)19 looked

at the effect of family planning services and microcredit in Ethiopia. They conducted

baseline and follow up surveys of cross-section of households. They found that none

of the interventions significantly increased contraceptive use or the intent to use

family planning methods over the control group. In 2004, Dohn et al20, implemented

and evaluated a 13-month health promotion programme targeting childhood illness

and women’s health in the Dominican Republic. They failed to show that microcredit

led to increase in health outcomes in all the 11 indicators that they identified. In

similar lines, Smith21 in his 2002 study about comparison of conventional banking

systems to that of health bank model combining microfinance and health education

services in urban slums of Ecuador did not lead to overall lower diarrhoea

probability.

The recent literature fails to identify the reasons behind low health spending by poor

households. The money, which they get in the form of small loans, is running out into

expenditures governed by social traditions and customs. Taking the example of India,

which is a wide economy mixed with high social values, customs and traditions.

According to Vijendra Rao (World Bank), poor households tend to spend heaps of

money on celebrations to acquire social status and recognition in the society. He

19

Alessandro Tarozzi & Jaikishan Desai & Kristin Johnson, 2013. "On the impact of microcredit: Evidence from a randomized

intervention in rural Ethiopia," Economics Working Papers 1407, Department of Economics and Business, Universitat Pompeu

Fabra.

20 Dohn AL, Chávez A, Dohn MN, Saturria L, Pimentel C. Changes in health indicators related to health promotion and

microcredit programs in the Dominican Republic. Revista Panamericana de Salud Pública. 2004;15(3):185- 93.

21 Smith, Stephen C., 2002, Village banking and maternal and child health: Evidence from Ecuador and Honduras, World

Development 30, 707-723.

Candidate Number: 122783

16

argues that ‘publicly observable celebrations have two functions -- they provide a

space for maintaining social reputations and webs of obligation, and serve as arenas

for status-enhancing competitions’22. Further, the link between health and spending

governed by social customs is not dealt in existing literature. Hence, this research

paper tries to see whether there is a correlation between the microfinance and social

spending, given the data from Spandana.

3.2 Education and Microfinance According to Littlefield et al (2003) one of the first things poor people all over the

world do with new income from microenterprise is to invest in their children's

education. There is an abundance of literature, which focuses on the positive link

between microfinance and attainment of education qualifications among the poorest

households. Most of the recent literature focuses on whether or not microfinance

led to a sizeable impact on education via literacy rates, number of years of schooling,

school dropout rates, etc. In addition, the literature fails to identify any solid

conclusion about the correlation between microfinance and education being

positive.

One such impact evaluation looks at a microfinance program in Uganda that showed

that client households tend to spend more on schooling and education than non-

client households do. Barnes et al (2001)23 in their words, concludes, “Clients have

also been significantly more likely than non-clients pay school charges for a non-

household member.” On similar lines, Khandker (2001)24 found out that by providing

small loans to poor households led to fall in dropout rates for children in the

treatment group as compared to non- treated households. Further, their study found

out that children stayed for a longer period at schools when their families received

loans from microfinance institutions. The Indian example of the Self Employed

22

Poverty and Public Celebrations in Rural India, Vijendra Rao, Development research group, World Bank

23 Barnes, C., Keogh, E., & Nemarundwe, N. (2001b). Microfinance program clients and impact: An assessment of Zambuko

Trust Zimbabwe. Washington, DC: Assessing the Impact of Microenterprise Services (AIMS).

24 Khandker, S. (2001). Does micro-finance really benefit the poor? Evidence from Bangladesh. Paper delivered at the Asia and

Pacific Forum on Poverty: Reforming Policies and Institutions for Poverty Reduction, 5–9 February.

Candidate Number: 122783

17

Women’s Association (SEWA) Bank led to positive improvement in enrolment of boys

in primary and secondary schooling in Ahmadabad. Over the period from 1997 to

1999, borrowing from the SEWA Bank had a positive impact on boys' secondary-

school enrolment rates, which rose to 70 percent.

Holvoet (2004)25 in his study looks at the specific effects of microfinance on

childhood education. They look at South India and gather data on literacy rates; and

how credit enters the household and who bring in the credit. The results were mixed.

It did not matter who brought the credit in when it came in the case of direct bank-

borrower credit delivery. However, the cases where women got credit from women's

associations, the money spent on childhood education somewhat increased in favour

of Girls’ education but left the boys’ education outcomes largely unchanged. He did

not find out any causal link or correlation between micro loans and spending on

children’s education. In addition, he found out that gender of individual bank loan

clients had no impact on their children’s education. Hence, there is ambiguity with

the data in the literature about linkages between education and microfinance.

Adding to this ambiguity, credit constraints often lead to negative impact on

education in the context of poor households. For instance, Todd and Ralph (2007)26

looked at credit constraints and low incomes are the two reasons for the high

number of school dropout rates. They took up panel data estimation to validate their

results, and concluded that while credit constraints likely to play an important role in

the dropout decisions of some students, the large majority of attrition of students

from low-income families should be primarily attributed to reasons other than credit

constraints.

25 Nathalie, Holvoet. “Impact of Microfinance Programs on Children’s Education. Do the gender of the borrower and the delivery

model matter?” Journal of Microfinance, Volume6 Number2.

26 Todd R. Stinebrickner Ralph Stinebrickner. “The effect of credit constraints on the college drop-out decision: A Direct

approach using a panel study” NEBR working paper 13340. NATIONAL BUREAU OF ECONOMIC RESEARCH, 1050

Massachusetts Avenue Cambridge, MA 02138. August 2007

Candidate Number: 122783

18

Apart from credit constraints, literature exists in the quality of education, where

individuals face the choice between private schooling and public schooling.

Considering India as an example, for households living in the rural areas are unable

to afford the overwhelming costs of seeking good quality education for their

children. A study by Joanna Härmä (2009) looks at the effect of ‘low fee private’ (LFP)

schools to promote education for all, taking the case of Uttar Pradesh in India. They

based their study on a 13‐village survey of 250 households and visits to 26 private

and government schools in rural Uttar Pradesh, India. In particular, the paper

explores the issue of whether private provision is affordable and accessible to poor

rural parents. It finds that LFP school costs are unaffordable for over half of the

sampled children, including the majority of low caste and Muslim families. It also

finds that while LFPs are greatly preferred under current conditions, what parents

actually want is a well‐functioning government school system.

Having discussed the recent literature on education, the question of how traditional

values and customs governing the minds of the poor household’s expenditure

pattern remains a mystery that has to be solved. A poor household living in rural

areas when exposed to small loans tends to spend on social functions to gain

recognition in the society rather than spending on basic needs such as education.

Thus, the available empirical evidence shows that households are spending on social

occasions to develop social capital. By social capital, we mean the internal and social

coherence of society, the norms and the values that govern interactions among

people and institutions in which they are embedded.

3.3 Social traditions and expenditure Nowadays, expenditure of households depends on a variety of issues and specific

when it comes to building social capital. Spending on social events to get recognized

in society; an ambition to attain a high social status is driving the households to

spend their pockets on various cultural programs, marriages, festivals, and other

customary occasions. The growing literature suggests that the financial decision in

the poor household is made mainly on social events, customs, culture, and traditions

Candidate Number: 122783

19

of the individuals who control income in the family. A study by Nazli Kibria (2014)27

looks at the women's garment industry in Bangladesh and their expenditure pattern.

Despite the traditional low economic autonomy of Bangladeshi women, the women's

ability to control their income was varied, and in fact, a substantial number of the

women workers exercised full control over their wages. Socioeconomic background

affected women's income control by shaping both the symbolic meaning of women's

income and the ability of male kin to fulfil their traditional obligations to women.

With the exception of some young unmarried workers, women's employment in the

garment industry had not posed a significant challenge to patriarchal family

relations.28

The literature has shown some plausible insights into social expenditure. For

instance, the study by Cynthia Werner29 looked at consumption pattern in rural

Kazakhstan with regards to changes in wedding feasts. The author points out that

despite economic hardship post-Soviet transition to a market economy, rural Kazakhs

have continued to spend a large amount of their income and resources on feasts and

marriages. She found that exchanging gifts and utilizing imported goods led to the

enhancement of social status and identity among rural Kazakhs. In her own words

she concludes that “The process of further social stratification has intensified the

level of competition in feasting and gift giving among the local elite. And the same

process has generated resentment among poor households who find it more and

more difficult to continue participating in the ritual economy.”

27

Nazli Kibria. “Culture, Social Class, and income control in the lives of women garment workers in Bangladesh” Gender &

Society June 1995 vol. 9 no. 3 289-309

28Nazli Kibria. “Culture, Social Class, and income control in the lives of women garment workers in Bangladesh” Gender &

Society June 1995 vol. 9 no. 3 289-309

29 Cynthia Werner. “Marriage, Markets, and Merchants: Changes in Wedding Feasts and Household Consumption Patterns in

Rural Kazakstan” Culture & Agriculture Vol. 19, Nos. 1/2 Spring/Summer 1997

Candidate Number: 122783

20

A very recent study by Susan Wolcott (2013, The New Handbook of Microfinance)30

looks at the situation of rural credit markets in colonial India and how Indian

cultivators spend on ceremonies, marriages and funerals. She links this leakage at the

expense of increases in agricultural activity and investment. According to her “Indian

cultivators spent a remarkable portion of their income on festivals, marriages and

death ceremonies.” “For all of India, ceremonial expenditures for one year on average

constituted 18 percent of annual crop values.” Further she notes this difference

among poor households who relatively spent more on ceremonies as compared to

agricultural activities; and “for those families, consumption clearly crowed out

investment”. The reason for such high social expenditures is “social caste” and how

different caste demands the needs for ceremonial expenditures. Further the major

implication of her study looked at how poor households took credit for funding

ceremonies rather than investing in their agricultural business.

Some of the recent studies also throw some light on social exclusion as being the

cause for spending on social events. The study by Bittman31 looks at social exclusion

being a multi-dimensional concept explaining the significance of social identity,

culture, agency and power relations. His argument was that households spend on

leisure activities as part of social exclusion. He performed an analysis of the most

recent household expenditure survey that showed consumption of leisure goods and

services was powerfully determined by income. His conclusions looked at how low

income can lead to exclusion from leisure participation.

Another study by Brown, et al (2007) looked at a panel estimation of rural villages in

China on how there has been a sharp increase in socially observable spending. They

suggest that “social spending is either positional in nature (that is motivated by

status concern) or subject to herding behaviour.” They found that the welfare

30

Susan Wolcott. “Microfinance in Colonia India”. Published in “The New Handbook of Microfinance-

A financial market system perspective” 2013.

31 Michael Bittman, 1999.Social Participation and Family Welfare: The Money and Time Costs of Leisure, University of New

South Wales, Social Policy Research Centre.

Candidate Number: 122783

21

implications of spending, in order to ‘keep up with the Joneses” are potentially large,

particularly for poor households.

The dynamics governing the borrowing behaviour of micro credit borrowers show

the trends of growing social capital as a motive to drain expenditure on social

occasions, additionally; social stigma in Indian societies too played an important role.

Poverty reduction among poor households not only means development of health

care services, better educational facilities or setting up a new business, but also to

expand human capabilities by avoiding violence. A recent study in Kerala looked at

the impact of marital violence on the economic outcomes of women in rural

households. Many studies have looked at the correlation between marital violence

and economic prosperity, but often neglected the link though credit constraints. In

achieving social status and sticking to the social norms of the society, households are

pouring money into celebrating festivals and occasions rather than spending on

essential economic needs.

Adding to the above reason of social violence, Chen (2011) looked at the social link,

peer effect, and status concern as being the motivation behind high gift expenditure

in China. He tries to answer the question raised by Banerjee and Duflo (Poor

Economics, 2011) about ‘why do poor people spend more on social occasions such as

marriages, festivals and other ceremonies’. According to his evaluation, he found

that “a 1% increase in peers’ gift spending per occasion leads to a .13-.34% increase

in ones’ own gift per occasion”. Chen (2011) explains that it is easier for poor

household to climb the social ladder while engaging themselves with the rich rather

than insuring themselves against the future risk (risk pooling strategy). “Overall, large

social spending may result in negative externalities and welfare loss, especially for

households living close to subsistence”- but this is subject to Chen’s findings on gift

expenditure as compared to risk-pooling mechanisms.

However, no literature has seriously and strongly looked in to the link between

microfinance and social expenditure (spending on weddings, funerals, festivals, etc.).

Candidate Number: 122783

22

Anthropologists and sociologists did look at the trend on social expenditure, which is

being imposed upon through social pressure, but economists are still in early stages

to find a causal link between access to credit and that credit being used to finance

social occasions. What an economist would think is that it was individuals’ own

satisfaction or behaviour that makes him/her spends on social events, but

sociologists argue that being under pressure poor people focus on social spending

and neglect valuable spending on health outcomes and educational outcomes. The

above papers do provide an insight into growing social expenditure, but this is not

economics. Hence, more research on economic evidences has to be performed to

look at the causal link. Hence, the present paper tries to attempt to fill the gap by

looking at the impact of microfinance on festivals and other social expenditures

varying across households, limiting its conclusions to the dataset designed by

Spandana.

The next section deals with the data and closely looks at the microfinance policy,

structure of the RCT used and descriptive statistics.

4. Data

4.1 Background on the Microfinance Policy

To look at the effect of microfinance on poor household’s, Banerjee and Duflo (2009)

took the help of Spandana to conduct their analysis. They looked at the products and

services being provided by Spandana and laid out their experimental design.

Spandana is believed to be most of the most profitable organizations in the industry

and has been one of the main targets of government activism in Andhra Pradesh.

Their microfinance product is basically a group loan product which was similar to that

of Grameen Banks model. A group is comprised of six to ten women, ageing between

24-45 groups form a “centre”. Women are jointly responsible for the loan of their

group, and of the centre. The first loan is of 10,000 rupees and an interest rate of

12% is charged. It takes fifty weeks for the principal and interest rate to be

reimbursed. If they all reimburse, then they can take up a second loan worth Rs.

Candidate Number: 122783

23

10,000-Rs. 12,000; increasing in the loan amount up to Rs. 20,000. Unlike other MFIs,

Spandana does not require it clients to take up a loan just for starting up a business;

money taken up from Spandana is fungible, and clients are left completely free to

choose the best use of their money, as long as they repay the loan.

The eligibility of taking up a loan is determined by various characteristics. They

should be (a) female, (b) aged 18 to 59, (c) residing in the same area for the last one

year, (d) has valid identification and residential proof, (e) at least 80% of the women

in the group must own their home. Also, these groups are formed by women

themselves and Spandana does not determine loan eligibility based on their

expected productivity of the investment. Further, Spandana is only a lending

organisation and does not directly involve in business training, financial literacy

promotion, etc.

4.2 Structure of the Randomised Control Trial

The data used for this research is from a randomised control trial (RCT) in Hyderabad,

India. The microfinance institution that took up the initiative to survey was

Spandana. Spandana is one of the largest Microfinance Institution (MFI) in India,

which had around 4.2 million loan clients, with an outstanding portfolio of 42 billion

rupees. Spandana took up an evaluation in some areas of Hyderabad city to know the

situation and the impact of microfinance.

Spandana selected 120 areas in Hyderabad as places in which they were interested in

opening up branches, based on those communities having no pre-existing

microfinance presence, and having residents who were desirable potential

borrowers. Banerjee and Duflo (2009) in collaboration with Spandana collected data

from 104 slums in Hyderabad, out of which 52 areas were chosen at random for the

opening of MFI branch immediately, while another 52 served as the comparison

communities. A series of baseline and end line surveys were conducted to look at

various aspects of lending and expenditure pattern of poor households. It conducted

a baseline survey in 2005 by randomly selecting some 20 to 40 households per slum,

leading to 2800 households in total. The baseline survey was used for stratification

Candidate Number: 122783

24

and descriptive analysis, and to collect area-level characteristics that are used for

control group comparisons.

Prior to randomization, Duflo, et al (2009) dropped 16 areas from its sample as those

16 areas consisted of a large number of migrant worker households. They had a rule

to provide loans to only those households that lived at least one year in that

particular community. Spandana then progressively started operating in 52

treatment areas from 2006-07. They also performed a follow up survey in 2008-09 to

look at the expenditure pattern and growth of businesses after 12 months Spandana

began to distribute out loans to the households.

The measured impact is done here through Intention to Treat (ITT) method. By this

we mean that the study conducted by Banerjee and Duflo (2009) was to look at the

impact of microfinance programs exposure to poor households rather than strictly

borrowing from MFI.

4.3 Results of Duflo et al.

Having looked at the structure and design of the RCT, I have taken up this dataset to

look at new variables, which were overlooked by Banerjee and Duflo (2009) in their

study. Duflo et al looked at various outcomes such as loan-take up and use, new

business and business profits, expenditure, education, health, and female

empowerment.

In brief, they found out that nearly 27% of the eligible households in the treatment

area took up loans from Spandana or any other MFI by the time of the end-line

survey. They reported that 30% of Spandana borrowers reported that they used

loans for starting up a new business. Looking at the household use, 15% replied that

they took it to buy durable good and 15% to smooth household consumption.

Coming to the expenditure, they found varying results depending on the pattern of

the different groups. Those with an existing business bought more number of

durable goods for their home and for the businesses. Those most likely to start a new

Candidate Number: 122783

25

business cut back sharply on temptation goods (like tobacco, alcohol, cigarettes, etc.)

and invested more.

Further, they found no significant evidence on education al outcomes and health

outcomes. No evidence was found to suggest that microcredit empowers women as

women in the treated area were no more likely to take household decisions about

spending, investment, savings or education.

Hence, my study takes up this dataset, to look at the increase in social expenditure

compared to expenditures on health and education. I will focus on the link between

microcredit and social expenditure; and look at whether there are any changes to

social expenditure when taken as a percentage of expenditures on health and

education. Further, I will discuss the descriptive statistics of the whole data before

conducting my regression analysis.

4.4 Descriptive Statistics

This section looks at the descriptive statistics differentiated across treated and

control groups both at the baseline and endline levels. The below chart 1 looks at the

differences between treated and control groups among social expenditures as well as

on health and education expenditure at baseline. We find that there is no difference

with respect to spending on health and education among the two groups.

Households tend to spend more on festivals, other ceremonies and funerals when in

treated than in control.

Candidate Number: 122783

26

Chart 1: Unadjusted treated-control difference for social expenditures

Having looked at the unadjusted effects of being in treated area, now I will look at

the adjusted difference referring to endline data. The data is adjusted along with the

regression model used, where area id, household id, number of members in a

household were the control variables. The chart 2 looks at health, education and

social expenditures in relative terms when measured per capita in monthly terms.

The number of observations is different, suggesting that there are missing values.

Clearly, we can see marked difference between the treated and control groups for

various expenditures, when the dataset is unadjusted to any control variables. To

give a clear insight, a t-test of the mean difference has been performed to look at the

significance of this difference between the groups.

Chart 2: Adjusted treated-control difference for social expenditures

0

0.5

1

1.5

2

2.5

3

3.5

Health Education Festivals Funeral Weddingsother ceremonies

Treated

Control

Candidate Number: 122783

27

When looked at relative (taken as a percentage of total expenditure) health and

education expenditures, there was no difference between the two groups.

Households in treated and control groups spend equal amounts when it comes to

health expenditure. From the t-tests, we found no significant results for the mean

difference between the treated and control groups.

Relative festival expenditure in per capita terms, shows only 0.62% difference

between the treated and control areas. The mean difference t-test shows that there

is a highly significant difference in expenditure on festivals when people receive

income in the form of loans from Microfinance Institutions such as Spandana. The

same applies to relative Funeral expenditure, there is no significant difference

between the treated and control groups.

Wedding expenditure and other ceremony expenditures show a remarkable increase

in treated areas rather than control areas. The mean difference was significant at 1%

level of significance. Other ceremony expenditures shot up by nearly 15% in treated

areas as compared to non-treated areas.

Having, looked at the summary statistics, we now run our regressions to see whether

there holds any significant difference between the treated and control areas when it

comes to social expenditure. The next section would evaluate the regression results.

5. Methods In order to look at the difference between treated and control areas, the borrowing

is expected to be higher in treated areas from MFIs as compared to control group.

Hence, the ITT estimates measures the averaging differences in both areas over

customers and non-customers of the MFIs. The formal model32 used is:

.....................................1

Where is the outcome variable for household ‘i’ in area ‘a’; is a dummy

variable which takes a value one if the household is in treatment area (meaning that

32

Banerjee, Abhijit V., Esther Duflo, Rachel Glennerster, and Cynthia Kinnan (2010). “The Miracle of

Microfinance? Evidence from a Randomized Evaluation.” Cambridge, Mass.: J-PAL and MIT, June.

Candidate Number: 122783

28

household has borrowed from MFI) and takes a value zero if the household is in

controlled group (meaning household didn’t borrow from MFI); basically it talks

about the household living in the treated area. Here the MFI is Spandana. The

looks at the control variables, which have to be taken into consideration while

performing the regressions such as area id, household id, household size, etc. The ITT

estimate is given by . The coefficient in percentage points gives the differences in

outcome variable ‘y’ between treatment and control groups.

In this regression model, I take ‘areaid’, ‘age of individuals’, ‘household size’ as the

control variables. I use these controls because the household size which ranges from

having three family members to thirteen family members in one household does

have a direct effect on independent variables such as number of deaths in a family;

thus affecting the spending on funerals. The construction of the independent

variables is described below in the following table 1.

Table 1: Description of variables

Variable Description of the variable

Treatment Dummy variable taking 0 and 1, for control and treated group

Health_exp_pc Health expenditure per capita (monthly)

Educ_exp_pc Education expenditure per capita (monthly)

Festivals_exp_pc Festival expenditure per capita (monthly)

Funerals_exp_pc Funeral expenditure per capita (monthly)

Ceremony_exp_pc Ceremony expenditure per capita (monthly)

Wedding_exp_pc Weddings expenditure per capita (monthly)

Tot_exp_pc Total expenditure per capita (monthly)

Rel_fest Relative festival expenditure (

Rel_fun Relative funeral expenditure ( )

Rel_cer Relative ceremony expenditure ( )

Rel_wedding Relative wedding expenditure ( )

F Festival spending as percentage of educ and health

Candidate Number: 122783

29

( )

C Ceremony spending as percentage of educ and health

( )

W Wedding spending as percentage of educ and health

( )

Fun Funerals spending as percentage of educ and health

( )

6. Results The effect of the treatment on the dependent variables is shown in table 2. We run

the regressions both in terms of absolute expenditures and in terms of relative

expenditures. The control variables of the regressions were ‘area id’, ‘household size’

and ‘age of the individuals’. The results are subject to a number of observations

when the dataset was clustered by areas into 23 areas.

Table 2: Treatment coefficients in regression models for social, health and education expenditures

Dependant Variable Treatment coefficient

Health expenditure -3.22

Education expenditure 4.45

Festival expenditure -8.14***

Funeral expenditure 43.51

Wedding expenditure 942.1**

Other ceremony expenditure 185.9***

From the above table 2, consistent with Banerjee and Duflo’s findings, we find no

significant impact on health and education expenditure when measured in monthly

terms per capita when the household is being treated by the microfinance program

offered by Spandana. In fact, being in the treated reduces the expenditure on health

Candidate Number: 122783

30

as compared to control group. The difference in the number of observations is due to

missing values and the regressions being controlled for area id.

Coming to social expenditure, the stand out results show that festival expenditure

and ceremony expenditure are highly significant. Hence, being in the treated area

decreases the festival expenditure by 8 rupees per capita as compared to households

who did not receive microfinance from Spandana. Similarly, households in the

treated area, when received more funds spent more on other ceremonies for both

social and individual satisfaction. Thus, they spend approximately 185 rupees per

capita if they were treated with microfinance. The t-values of both these variables

are significant at the one percent level of significance.

As previously noticed that weddings did play a significant role, looking at the

regression, there is a 1% level of significant difference in spending on weddings when

households are treated with microfinance. Overall expenditure on wedding

ceremonies increases by nearly 942 rupees per capita (measured in monthly terms)

when treated as compared to control groups.

In our next table 3, we run the regression on looking at relative expenditures- looking

at social expenditures relative to total expenditure; on the interested variables. The

results for health and education in relative terms remain the same, being

insignificant. As funeral expenditure is mostly considered to be sudden expenditure,

overall it only leads to 4% increase when in treated as compared to control groups.

After controlling for household size and age of the individuals in the household, there

is no significant difference between the two groups. Most prominent and significant

results are that of relative festival expenditure and relative ceremony expenditures.

Both of them are highly significant at the one percent level of significance. The

festival expenditure in relative terms to total expenditure per capita reduces by 0.6%.

Relative ceremony expenditures too are significant showing that households spend

on weddings more lavishly when they are treated with microfinance as compared to

non-treated areas. It increases by nearly 16% per capita. This further explains the

reason being social status and higher social returns in future when there are more

funds in individual’s pocket.

Candidate Number: 122783

31

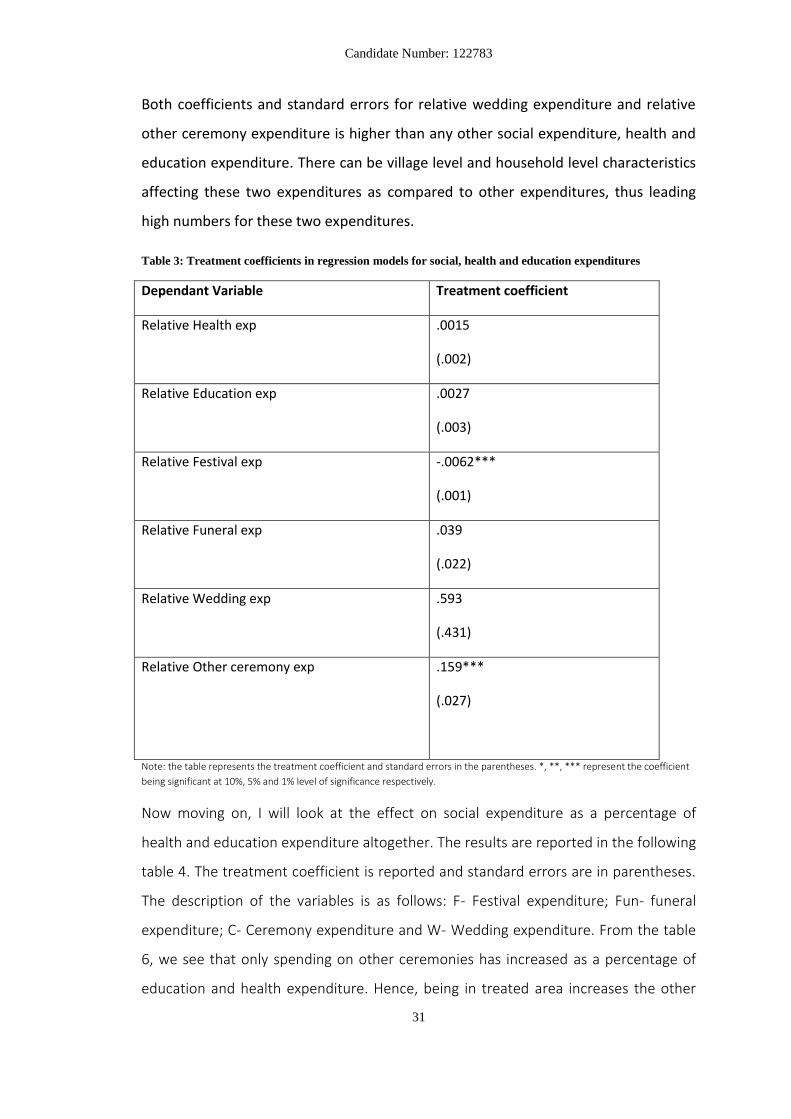

Both coefficients and standard errors for relative wedding expenditure and relative

other ceremony expenditure is higher than any other social expenditure, health and

education expenditure. There can be village level and household level characteristics

affecting these two expenditures as compared to other expenditures, thus leading

high numbers for these two expenditures.

Table 3: Treatment coefficients in regression models for social, health and education expenditures

Dependant Variable Treatment coefficient

Relative Health exp .0015

(.002)

Relative Education exp .0027

(.003)

Relative Festival exp -.0062***

(.001)

Relative Funeral exp .039

(.022)

Relative Wedding exp .593

(.431)

Relative Other ceremony exp .159***

(.027)

Note: the table represents the treatment coefficient and standard errors in the parentheses. *, **, *** represent the coefficient

being significant at 10%, 5% and 1% level of significance respectively.

Now moving on, I will look at the effect on social expenditure as a percentage of

health and education expenditure altogether. The results are reported in the following

table 4. The treatment coefficient is reported and standard errors are in parentheses.

The description of the variables is as follows: F- Festival expenditure; Fun- funeral

expenditure; C- Ceremony expenditure and W- Wedding expenditure. From the table

6, we see that only spending on other ceremonies has increased as a percentage of

education and health expenditure. Hence, being in treated area increases the other

Candidate Number: 122783

32

ceremony expenditure by 1.82 as compared to control groups. The festivals, funerals

and Wedding expenditures do not show any significant increases as percentage of

education and health.

Table 4: Treatment coefficients in regression models for social expenditures

Dependant Variable Treatment coefficient

F .022

(.079)

Fun -.036

(.49)

C 1.82***

(.59)

W 13.44

(7.69)

Note: the table represents the treatment coefficient and standard errors in the parentheses. *, **, *** represent the coefficient