Spatial competition with endogenous location choices: An application to discount retailing

35

Quant Mark Econ (2009) 7:1–35 DOI 10.1007/s11129-008-9048-6 Spatial competition with endogenous location choices: An application to discount retailing Ting Zhu · Vishal Singh Received: 6 July 2007 / Accepted: 1 December 2008 / Published online: 31 January 2009 © Springer Science + Business Media, LLC 2009 Abstract This paper examines the importance of geographical differentiation in store location decisions of firms in the retail discount industry. Using a novel data set that includes the store locations and accompanying market conditions for all stores belonging to the Wal-Mart, Kmart, and Target chains, we study the factors that influence the entry and location decisions of these firms. The model involves an incomplete information game between the three players where each firm has private information about its own profitability. A key feature of our modeling approach is that it permits asymmetries across firms in the impact of exogenous market characteristics and competitive interaction effects. Variations in the exogenous firm specific characteristics, such as the distances from the market to firms’ headquarters and the nearest distribution centers, serve as exclusion restrictions and provide the source for model identification. Parameter estimates of the payoff functions are used to predict the equilibrium market structure under a variety of market conditions that provide insights into the competitive landscape of the industry. Results show that all firms exert a strong negative impact on competitors when they are in close proximity, but the effect decreases with distance to rivals suggesting The paper is based on Ting Zhu’s thesis at Carnegie Mellon University. T. Zhu (B ) · V. Singh University of Chicago Booth School of Business, 5807 S. Woodlawn Ave., Chicago, IL 60637 USA e-mail: [email protected] T. Zhu · V. Singh Leonard N Stern School of Business, Marketing Department, New York University, New York, NY, USA V. Singh e-mail: [email protected]

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Spatial competition with endogenous location choices: An application to discount retailing

Quant Mark Econ (2009) 7:1–35DOI 10.1007/s11129-008-9048-6

Spatial competition with endogenous location choices:An application to discount retailing

Ting Zhu · Vishal Singh

Received: 6 July 2007 / Accepted: 1 December 2008 / Published online: 31 January 2009© Springer Science + Business Media, LLC 2009

Abstract This paper examines the importance of geographical differentiationin store location decisions of firms in the retail discount industry. Using a noveldata set that includes the store locations and accompanying market conditionsfor all stores belonging to the Wal-Mart, Kmart, and Target chains, we studythe factors that influence the entry and location decisions of these firms. Themodel involves an incomplete information game between the three playerswhere each firm has private information about its own profitability. A keyfeature of our modeling approach is that it permits asymmetries across firmsin the impact of exogenous market characteristics and competitive interactioneffects. Variations in the exogenous firm specific characteristics, such as thedistances from the market to firms’ headquarters and the nearest distributioncenters, serve as exclusion restrictions and provide the source for modelidentification. Parameter estimates of the payoff functions are used to predictthe equilibrium market structure under a variety of market conditions thatprovide insights into the competitive landscape of the industry. Results showthat all firms exert a strong negative impact on competitors when they arein close proximity, but the effect decreases with distance to rivals suggesting

The paper is based on Ting Zhu’s thesis at Carnegie Mellon University.

T. Zhu (B) · V. SinghUniversity of Chicago Booth School of Business,5807 S. Woodlawn Ave., Chicago, IL 60637 USAe-mail: [email protected]

T. Zhu · V. SinghLeonard N Stern School of Business, Marketing Department,New York University, New York, NY, USA

V. Singhe-mail: [email protected]

2 T. Zhu, V. Singh

strong returns to spatial differentiation in this industry. Target stores farewell under competition except when these competitors are in close proximity.Wal-Mart’s supercenter format is found to be the most formidable player asit substantially impacts competitors even at a large distance. We also findsignificant asymmetries across players in their response to market conditionsand competition interactions.

Keywords Entry · Discrete games · Location choice ·Retail competition · Discount stores

JEL Classifications L1 · L2 · L81 · R3

1 Introduction

Firms employ a variety of strategies to differentiate their product offeringsfrom competition. In the retailing sector, these strategies include the breadthand depth of product assortment, price, promotions, merchandise quality,customer service, and so forth. However, as a well known aphorism states, thethree most important decisions in retailing are location, location, and location.Store location decisions are particularly important since, unlike other market-ing mix elements, they are less adjustable in the short-run without incurringsignificant costs. When deciding whether to enter a particular local marketand where to locate within that market, firms consider a variety of factorsincluding demand and cost conditions, logistical issues, and proximity to andsize of their consumer base. In addition, firms must account for the actual andpotential presence of competitors. While favorable market conditions suchas large population base and low cost labor encourage entry, such marketsare also likely to attract competitors. In the long-run, the interaction of thesedifferent factors determines the observed entry patterns by firms.

We study the strategic entry and location choice decisions in the retaildiscount industry. For all practical purposes, the industry involves an oligopolycomprised of three dominant firms: Wal-Mart, Kmart, and Target. We as-semble a novel data set that includes store locations and associated marketconditions for all stores belonging to these three chains and study the factorsthat determine firm’s entry and location choices. Our primary objective inthe paper is to provide insights into the competitive landscape facing thesediscount retailers. In particular, we seek to answer the following questions: (1)How important is geographical differentiation in this industry? (2) Do notabledifferences exist in the types of locations that these firms find attractive? (3)How important are competitive effects across these retailers? (4) How dothese competitive effects vary depending on the identities and formats of thecompeting firms?

Ideally, answers to these questions would involve a model in which weexplicitly consider the demand impact of market characteristics as wellas substitution across retailers. With such information, one could evaluate

Spatial competition with endogenous location choices 3

competitive issues across the firms by evaluating the features of demand. Whileintuitively appealing, this approach is difficult to operationalize since accessto the necessary data at the level required for our analysis is problematic.Instead, we seek to answer these questions indirectly through an analysis of theobserved location choices by these retailers. The basic endeavor in our exerciseis to infer features of the firms’ payoffs and the competitive interactionsbetween firms even when one has no access to price, cost or quantity data. Theintuition behind the approach is to invoke revealed preference arguments: thefact that we observe a certain market structure (no entry, monopoly, duopoly,and oligopoly) reveals something about the underlying economic profits atthose locations. Our approach involves setting the decisions of the firms asan outcome of a game of location choices where distance to rivals servesas a form of product differentiation. The empirical analysis then relates thepredictions of the model to the observed behavior of the three chains. Theanalysis provides insights into a fundamental tension faced by these firms,namely the desire to be in attractive locations while also obtaining insulationfrom competition through spatial differentiation.

To model firm’s entry and location choice decisions, we build on theliterature on static discrete games advanced by Bresnahan and Reiss (1987,1990, 1991a, b) and Berry (1992). This literature endogenizes the competitivestructure in a market by implicitly analyzing the first stage of a two-stage gamein which firms first decide whether or not to enter followed by price or quantitycompetition. Mazzeo (2002a, b) extends this literature by incorporating prod-uct differentiation where a firm’s payoff asymmetrically depends on whether acompetitor is more or less similar to the firm. However, in Mazzeo’s frameworkfirms are restricted to choose from a few possible product “types” as a largerchoice set becomes computationally cumbersome due to the large number ofprofit constraints that need to be satisfied in equilibrium. Seim (2001, 2006)solves this dimensionality problem by allowing firms to possess private infor-mation about their own profitability. Her incomplete information approachcircumvents the need for checking a large number of entry configurations tofind the equilibria and allows for a considerably larger dimensional set ofproduct types than is feasible in games of complete information. In a recentpaper, Jia (2008) analyzes the impact of the discount stores on small retailers.An interesting feature of her model is that she allows for spill over effectswithin the same chain across markets. Nishida (2008) extends Jia’s frameworkto study the strategic store network choices by two chains in Japan. However,both authors do not model spatial differentiation across players. In particular,firms in Jia’s framework choose whether to enter a particular market, while inour model each firm decides entry as well as location such that the competitioneffect varies with the distance within a market.

We follow Seim (2001, 2006) by setting up the model as an incompleteinformation game where players privately observe their own location-specificpotential profits, but observe only the distribution of their rivals’ profitability.A firm’s payoff from entering a market and choosing a particular locationdepends on its expectation of the optimal location choices of its competitors

4 T. Zhu, V. Singh

and exogenous market characteristics. These market conditions include de-mand and cost factors such as population and retail wages. In addition to theobserved variables, all firms’ profits also depend on market components thatare unobserved by the analyst, but are observed by all firms. For example,positive or negative market wide shocks such as the availability of commercialland or the restrictiveness of zoning laws are difficult to measure and quantify,but are likely to play an important role in the entry decisions of all firms.Finally, a firm’s payoff in each location includes a component specific to thatfirm and location which could represent idiosyncratic operational costs ormanagerial talent that are unobserved by both the analyst and other players.

A unique feature of our modeling approach is that we explicitly allow forasymmetries related to the identity of the firms. The previous literature hasassumed that firms are symmetric in terms of their sensitivity to exogenousmarket conditions and in their impact on other competitors. In other words,a firm’s profits are assumed to depend on the total number of other firms inthe market rather than their actual identities beyond simple type differencesas in Mazzeo (2002a, b). In reality, firms care about the actual identities oftheir competitors rather than simply the total number of competitors. Forinstance, entry by firms such as Exxon-Mobil, Microsoft, Home Depot, orCitigroup into a geographical or product market may be viewed by competingfirms as a greater threat to profits than entry by smaller independent firms.1

In the current context of discount stores, such asymmetries may be crucial.For instance, Kmart’s profit may be different when it faces a Wal-Mart ratherthan a Target or when it faces a Wal-Mart supercenter rather than a Wal-Martdiscount store. Similarly, the impact of market demand and cost conditionsmay vary across firms as well as store formats. As such, it is paramount toallow such asymmetries in an analysis of this industry.

Our modeling approach allows for both competitive effects and preferencesover exogenous market conditions to be firm-specific. However, allowing forsuch firm asymmetries is not without cost since it leads to a significantly largernumber of parameters to be estimated. More importantly, it raises questionsabout model identification since, as discussed in Bajari et al. (2005a, b), onewould need exclusion restrictions in firm’s payoff functions. In particular, topin down the form of strategic interaction we would need variables that impacta firm’s profit but not impact its rival’s profits directly. In our application,we compute the distance of each market from firm’s headquarters and thenearest distribution center and use them as exclusion restrictions. Since moststates have only one or two distribution centers that cater to all stores inthe region, we take the location of distribution centers as given and focus oncompetition between firms at the retail outlet level. Given this assumption, theincomplete information model provides a tractable framework for studyingthe complex interactions of optimal site selection in which a trade-off exists

1Kyle (2006) makes similar arguments in the context of entry in pharmaceutical drugs.

Spatial competition with endogenous location choices 5

between proximity to competitors and the desirability of certain locationcharacteristics. The model translates the discrete actions of competitors intosmooth location choice probabilities that represent the likelihood of competi-tor entry into a location rather than actual realizations, thus allowing for alarger set of locations (or product types) than is generally feasible in gamesof complete information. The resulting Bayesian Nash equilibrium (BNE) isderived using a nested fixed-point algorithm which is then embedded in asimulated maximum likelihood procedure to estimate the model parameters.

To implement the model, we assembled an original data set that includesall store locations for the three largest players in the discount store industry:Wal-Mart, Kmart, and Target. The data includes the exact location (latitude/longitude) of all stores in operation as of 2003 across the United States. Wepartition the United States into a series of smaller markets and further divideeach market into smaller neighborhoods. Each store can then be mapped toone of these neighborhood locations. In addition, we collected information onthe location of firm’s headquarters and their distribution centers. As discussedabove, distances from the distribution centers to each market location areused as exclusion restrictions and serve as proxies to capture logistical issuesin firm’s location choice decisions. Finally, we supplement the data withdetailed information collected from the US Census Bureau and the Bureau ofLabor Statistics to capture demand and cost conditions at every geographicallocation.

The results show that population in closer distance bands to a locationcontribute more to profitability than population in distant bands. Interestingly,the parameters for distant population are significantly larger for Wal-Mart,especially for its supercenter format, suggesting that Wal-Mart’s trading areais larger than those of its rivals. All firms are found to prefer markets with lowerretail wages, markets where a larger proportion of families have children andvehicles, and markets that are closer to their respective headquarters. We alsofind significant differences across firms in certain demand characteristics. Forinstance, Target is found to prefer markets with higher income and educationlevels compared with its rivals, which is consistent with the common percep-tions of these stores. Wal-Mart, particularly for its supercenter format, givesmore weight to locations that are closer to its distribution center, reflectingits logistical efficiencies. In terms of competitive interactions, we find thatproximity to competitors is an important determinant of profitability. All firmsare found to exert negative impact on competitors when they are in close prox-imity, but the effect decreases with distance to rivals suggesting strong returnsto spatial differentiation in this industry. Looking at the competitive effectsacross firms, we find significant asymmetries in the competitive interactionparameters. For example, while a nearby Kmart strongly impacts Wal-Mart,the effect is significantly lower than the corresponding impact of a Wal-Mart onKmart’s payoffs. Target stores are found to fare well under competition fromother discount stores except when these competitors are in particularly closeproximity. Wal-Mart’s supercenter format is found to be the most formidableplayer as it substantially impacts competitors even at a large distance.

6 T. Zhu, V. Singh

We use the parameter estimates from the latent payoff functions to predictequilibrium market structures under a variety of market conditions that yield anumber of insights into the competitive structure of the industry. For example,as market population and income vary with all other variables held constant,we find that Wal-Mart is able to operate as a monopolist under a wide rangeof market conditions. Target is able to enter as monopolist in certain extremeconditions, such as a relatively small population and very high income, whichgenerally is not attractive to its rivals. Conversely, Kmart is rarely able to findlocations that are not attractive to at least one other player. Similarly, we findthat when entry involves only discount store formats, multiple firms are ableto enter the market under moderately good demand conditions by choosingdifferent locations within a market. On the other hand, Wal-Mart supercentertends to deter entry by competitors altogether unless a market becomes veryattractive. This effect arises since the supercenter format hurts even thosecompetitors that are located far away implying that the opportunities to mutecompetition through geographical differentiation are limited. However, as amarket becomes more and more attractive, good demand conditions overcomethe competition effect.

The rest of the paper is organized as follows. In the next section, we describeour modeling approach. The data used in the study are described in Section 3.Section 4 outlines the estimation strategy and presents the results. Section 5concludes with a discussion of limitations of the current study and directionsfor future research.

2 Model

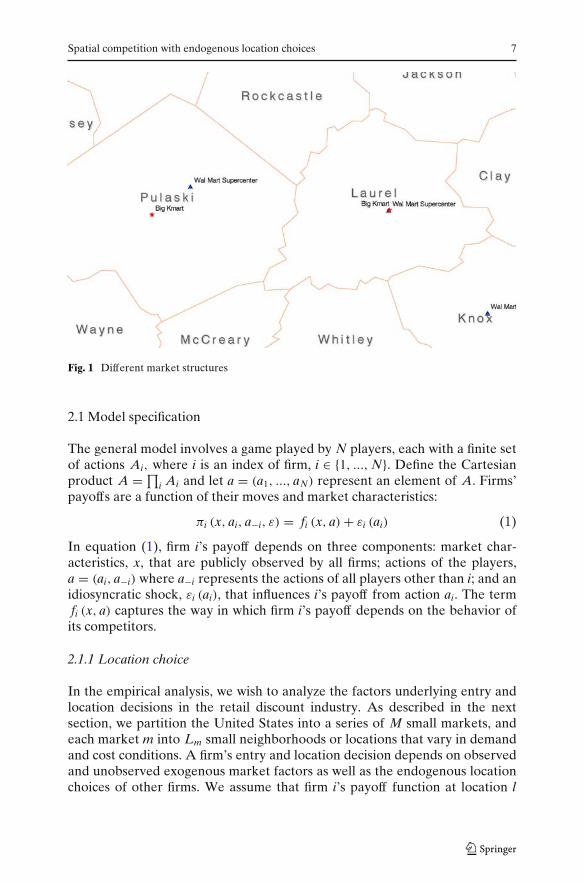

In this section we describe a model of the store location choices of firms in theretail discount industry. The model is structured as an incomplete informationgame following the framework originally developed in Seim (2006). However,as noted above, we allow for competitive effects and preferences overexogenous market conditions to be firm-specific. To illustrate, consider thetwo markets in Fig. 1 each with a Wal-Mart supercenter and Kmart. In the ap-proach of Bresnahan and Reiss (1991a, b) and Berry (1992), both marketswould have the same market structure as their models consider only thetotal number of undifferentiated competitors (besides the non-strategicfixed costs in Berry’s model.) Seim’s framework would categorize these twomarket structures differently due to the presence of geographic differentiation.However, if a Wal-Mart discount store or a Target store replaced the Wal-Martsupercenter, the market structure would not change as Seim (2006) does notconsider identities of the players. In the model presented below, we explicitlyaccount for firm identities and allow for firm-specific effects that are related tocompetitive interactions and the impact of exogenous market characteristics.

Spatial competition with endogenous location choices 7

Fig. 1 Different market structures

2.1 Model specification

The general model involves a game played by N players, each with a finite setof actions Ai, where i is an index of firm, i ∈ {1, ..., N}. Define the Cartesianproduct A = ∏

i Ai and let a = (a1, ..., aN) represent an element of A. Firms’payoffs are a function of their moves and market characteristics:

πi (x, ai, a−i, ε) = fi (x, a) + εi (ai) (1)

In equation (1), firm i’s payoff depends on three components: market char-acteristics, x, that are publicly observed by all firms; actions of the players,a = (ai, a−i) where a−i represents the actions of all players other than i; and anidiosyncratic shock, εi (ai), that influences i’s payoff from action ai. The termfi (x, a) captures the way in which firm i’s payoff depends on the behavior ofits competitors.

2.1.1 Location choice

In the empirical analysis, we wish to analyze the factors underlying entry andlocation decisions in the retail discount industry. As described in the nextsection, we partition the United States into a series of M small markets, andeach market m into Lm small neighborhoods or locations that vary in demandand cost conditions. A firm’s entry and location decision depends on observedand unobserved exogenous market factors as well as the endogenous locationchoices of other firms. We assume that firm i’s payoff function at location l

8 T. Zhu, V. Singh

in market m is a linear function of market and location characteristics andcompetition effects:

πiml = ximlβi −∑

i′ �=i

Lm∑

k=1

δii′klai′mk + ξm + εiml (2)

i, i′ = 1, 2, ...N (firms),

m = 1, 2, ...M (markets),

l, k = 1, 2, ..., Lm (locations),

where ximl are the observed exogenous variables that vary across differentlocations and markets. In addition, these exogenous characteristics includefirm-specific variables such as distance to the firm’s headquarters or the nearestdistribution center. The indicator variables am = (aim, a−im)N×Lm

denote firms’location choices such that aiml = 1 when firm i chooses location l and aiml = 0otherwise. The dimension of am is N × Lm, where N is the number of players,and Lm is the number of possible locations in market m.

Besides the observed variables, profits also depend on unobserved factors.Of these, ξm are market characteristics that are unobserved by the analyst,but are observed by all firms.2 We assume that ξm is normally distributed withmean 0 and variance σ 2. For example, market-specific shocks related to theoverall availability of commercial land or the stringency of zoning restrictionsare likely to play an important role in the entry decisions of all firms, but aredifficult to measure and quantify. Finally, εiml are firm-specific unobservablesrepresenting the private information of firm i’s profitability in location l. Thesefactors could include idiosyncratic operational costs or managerial talent thatare unobserved by both the analyst and other players. If firm i does not enterthe market so that aiml = 0 for all l = 1, ..., Lm, we normalize the payoff as

πim0 = εim0. (3)

The unknown parameters are (βi, δii′kl, σ ) where βi represents firm ı́’spreference for various market characteristics and δii′kl reflect the competitiveeffect that player i′ exerts on player i when they respectively operate stores inlocations k and l. As discussed earlier, we allow all the model parameters to befirm-specific. Thus, the model permits different firms (i) to impact competitorsdifferently and (ii) to put different weight on market conditions.3

Since εiml is private information, a firm cannot predict its competitors’responses (a−im) with certainty. Instead, a firm’s actions is based on its

2In principle, the unobserved market characteristics can impact firms differently. In the empiricalapplication we allowed for this possibility by estimating an additional model which allows for theunobserved market factor to vary across firms and found no substantial differences in results.3As discussed below in the context of format choices, it is also possible for the parameters to becontingent on the actions taken by firms.

Spatial competition with endogenous location choices 9

conjectures or expectation of its competitors’ responses. Thus, firm i’s expectedpayoff of choosing location l in market m is

π̂iml = ximlβi −∑

i′ �=i

Lm∑

k=1

δii′kl E (ai′mk) + ξm + εiml (4)

where E (ai′mk) denotes the expectation of firm i′ choosing location k. Firm ichooses the location that maximizes its expected payoff:

aiml ={

1 if π̂iml ≥ π̂imk, ∀ k = 0, 1, ..., Lm

0 otherwise

If firm’s private information εim (aim) is independently and identically distrib-uted across firms and locations with a type 1 extreme value distribution, theequilibrium probability of firm i choosing location l in market m conditionalon its beliefs of other firms’ behavior is given by

Piml =exp

(ximlβi − ∑

i′ �=i

∑Lmk=1 δii′kl Pi′mk + ξm

)

1 + ∑Lml′=1 exp

(ximl′βi − ∑

i′ �=i

∑Lmk=1 δii′kl′ Pi′mk + ξm

) . (5)

The probability of no entry in the market is then Pim0 = 1 − ∑Lml=1 Piml. Other

firms similarly construct their beliefs and choose their best responses based onthe expected payoffs. Since firms are asymmetric in terms of their preferencesof market conditions and competition, each firm may have different probabilityof choosing a given location. Define Pm = (Pim, P−im)(Lm×N) as a vector withLm × N elements that describes the conjectures of each location being chosenby each individual firm. In the ensuing Bayesian Nash equilibrium, firms’choices are consistent with their conjectures yielding a fixed-point mapping

Pm = F (Xm, ξm, Pm; δ, β) (6)

from the probability space of firms’ beliefs to their own strategies. The equilib-rium location conjectures is a vector with Lm × N probabilities resulting fromthe system of Lm × N equations defined in Eq. (5).

2.1.2 Location and format choice

As discussed in the data section below, the players in this industry operate twostore formats: discount stores and supercenters. The supercenter format com-bines the general merchandize aspect of the discount stores with a full-servicegrocery store. The model described above can be extended to allow the firms tochoose a store format. With Lm available locations in a market and a choice ofstore format, the total number of options available to firms are 2Lm + 1,wherethere are Lm possible locations for the discount store format, Lm possiblelocations for a supercenter, and one “no entry” option. To capture differencesin the impact of competition and exogenous characteristics across formats, the

10 T. Zhu, V. Singh

latent payoff of player i with store format f ∈ {Discount store, Supercenter

}

at location l in market m can be reformulated as

πiml f = ximlβi f −∑

f ′

∑

i′ �=i

Lm∑

k=1

δii′k f ′ l f ai′mkf ′ + ξm + εiml f , (7)

where εiml f is known to Wal-Mart but unobserved by other firms. As before,firms choose action that maximizes their expected latent payoff where theynow choose a format in addition to a location. In the current application, sinceKmart and Target have significantly fewer supercenters than discount stores,we restrict the format choice to Wal-Mart.

2.2 Identification

Bajari et al. (2005a, b) discuss identification in models of incomplete infor-mation game. They establish the sufficient conditions for model identificationwhen the unobservables in firms’ payoff functions are distributed i.i.d. acrossactions ai and agent i. In particular, these authors point out the role ofexclusion restrictions as a source of model identification. Suppose that thereis some variable xi that enters the firm i’s payoff but does not enter thepayoff of other firms directly. This exogenous variation in xi can pin downthe form of strategic interaction. For instance, in the current application,distances from the local market to firm i’s nearest distribution center andheadquarter are productivity shocks that only affect firm i’s entry decisionsdirectly but don’t affect other firms’ payoffs. Consider two market A andB that have similar market characteristics except that market A is closer toWal-Mart’s distribution center than B. The probability of Wal-Mart havinga store in market A is likely to be greater due to the logistical efficiency.In addition, suppose we observe fewer Kmart stores in market A, then wecan infer the intensity of competition by comparing the difference of Kmart’sentry decisions in market A and B. The intuition is the difference of Kmart’sdecisions between the two markets is only driven by its expectation on Wal-Mart’s choices rather than any other market characteristics.

2.3 Illustration of asymmetric competition effects

The model presented above is quite flexible in the asymmetries that it allowsin the model parameters. In order to understand how the primitives of themodel affect firms’ choices, we conducted a series of simulations to explorehow the probability of market entry and location choice depends on thestrength of competition among players. For this exercise, we consider asimplified version the model (Eq. (4)) discussed above and assume that thereare two players—firm A and firm B− and two possible locations—location 1and location 2. We further assume that the characteristics of locations xl

is unidimensional and βi = 1 so that firms are not heterogeneous in their

Spatial competition with endogenous location choices 11

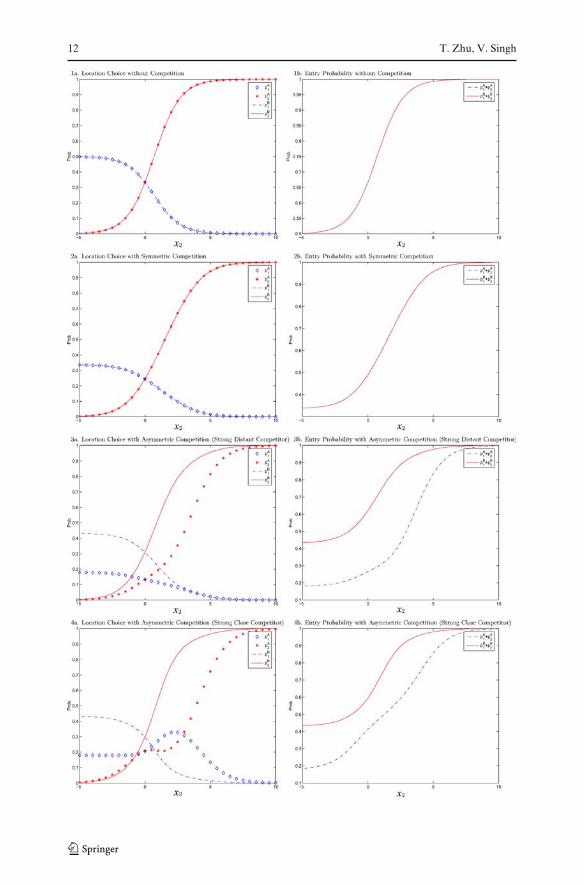

sensitivity to the exogenous variable.4 In the exercise below, we normalizedx1 = 0 for location 1 and change market characteristics of location 2, x2, tostudy how firms’ location choices change as the attractiveness of location 2changes.

The focus of the simulation exercise is to investigate how competitionbetween firms influences their decisions and how firms’ locations choices differwhen they have different competitive positions in the market (i.e., strongplayers vs. weak players). Define the competition parameters δi

lk as the impacton firm i if it chooses location l and the competitor chooses location k. Weconsider four cases that involve different competitive interactions.5 In Case 1,there is no competition between players. In Case 2, firms are symmetric intheir competition effects. Further, the competition effect is stronger whenplayers are in the same location implying returns to differentiation. This case issimilar to the model considered in Seim (2006). The next two cases incorporateasymmetry in terms of competition where Firm B is a stronger player in themarket as it exerts a larger negative impact on Firm A. The difference betweenthe two scenarios is that in Case 3, Firm B can significantly impact A even at adistance whereas spatial differentiation can shield A from B in Case 4.

Parametersx1 = 0, βA = βB = 1

Case 1 δill = 0, δi

lk = 0

Case 2 δill = −2, δi

lk = −1

Case 3 δAll = −3.5, δA

lk = −2, δBll = −1.5, δB

lk = 0

Case 4 δAll = −3.5, δA

lk = 0, δBll = −1.5, δB

lk = 0

i = A, B, l, k = 1, 2 and l �= k

In Fig. 2, we plot the probability of location choice and market entryas the attractiveness of location 2 varies. The left panel depicts the choiceprobabilities of each firm with respect to the two locations. The diamond lineand the star line represent the probability that firm A chooses location 1 andlocation 2, respectively. The probability of location 1 and 2 being chosen byfirm B are plotted as dashed lines and dotted lines, respectively. The rightpanels summarize the overall probability of entry for two firms with the dashedline representing firm A’s entry probability and dotted lines firm B’s.

Case 1: With no competition between firms, the model degenerates to astandard single agent model, and both firms act identically. Thechoice probabilities and entry probabilities are monotonic functionsof location 2’s attractiveness.

4The marketwide random component is ignored as it does not provide any additional insight intothe importance of asymmetric effects.5The scenarios and parameter values are partly motivated by our empirical results.

12 T. Zhu, V. Singh

Spatial competition with endogenous location choices 13

�Fig. 2 Competition effects

Case 2: When firms are symmetric and the strength of competition decreaseswith distance, both firms have the same probability of choosingeach of the two locations. The choice probability of location 2 isagain a monotonic function of its attractiveness as is the overallprobability of entry. However, if we contrast this case to Case 1,we observe that entry probabilities and the probability of choosinga more attractive location are lower in this case where competitiveeffects exist. This observation indicates that each player makes atrade-off between the attractiveness of location and the intensifiedcompetition. Competition makes the “good” locations less attractivedue to concerns about entry by rivals.

Case 3: When firm B is a stronger player and can impact firm A significantlyat different distances, firm A is much less likely to enter the marketrelative to firm B and is correspondingly less likely to enter either ofthe two individual locations. In this scenario, firm B deters firm Afrom entering at all unless location 2 becomes sufficiently attractiveat which point A’s desire to avail itself to the attractive locationovercomes its wariness about competing with B.

Case 4: When firm B is a stronger player, but competitive effects are local,the choice patterns over the two locations differ dramatically acrossthe two firms. The stronger player (firm B) continues to be moreinclined to choose location 2 as location 2 becomes more attractive.The behavior of the weaker player (firm A) is more interesting.Unlike in all other cases, its choice probability of location 1 is notmonotonically decreasing in the attractiveness of location 2. Thebell-shaped function reveals that the weak firm will sacrifice a goodlocation in order to avoid competition when location 2 is moderatelyattractive. In this situation, firm A believes that firm B is sufficientlylikely to enter the relatively attractive location 2 that A is willingto enter the less attractive location in order to insulate itself fromcompetition with B. However, as location 2 becomes more attractive,the attractive market conditions eventually dominate the desire todifferentiate implying that firm A will also be more likely to choosethe good location. Comparing cases 3 and 4, location differentiationwill be more attractive when the relative competitive position changeswith distance. In case 3, firm A cannot shield itself from competitionby differentiation and thus is unlikely to enter at all for moderatelyattractive markets. This case would thus be associated with a domi-nant firm monopoly in moderately attractive markets and agglomer-ation to good locations in very attractive markets. Conversely, case 4would be more likely to yield a spatially differentiated duopoly inmoderately attractive markets with agglomeration again occurringwhen one location becomes sufficiently attractive.

14 T. Zhu, V. Singh

These simulations indicate the potential impact of asymmetries in com-petitive effects across locations as well as heterogeneity across firms. Addi-tionally, they indicate the way in which the parameters capturing the effectof spatial differentiation in the payoff functions are empirically identifiedfrom firms’location choice patterns. As market characteristics vary, differentscenarios will yield different entry patterns. Intuitively, the empirical analysiswill then attempt to identify the relevant “case” and associated parametervalues that make observed entry patterns as close as possible to those predictedby the model.

3 Data description

We apply the model to the discount store industry. Discount stores originatedin the late 1950s to offer general merchandise items at a substantial discountrelative to conventional department stores. For the most part, the industryis currently an oligopoly with three dominant firms: Wal-Mart, Kmart, andTarget. Interestingly, all three chains started in 1962 with Wal-Mart opening itsfirst store in Rogers, Arkansas, Kmart in Garden City, Michigan, and Targetin Roseville, Minnesota. Over the past few decades, these firms have obtaineddominant positions in the retail world while expanding their operations bothdomestically and internationally. They have also experimented with severalother retail formats, most prominently the supercenter which combines a full-service grocery store and a general merchandise outlet.

Besides physical store locations considered in this study, the firms havealso looked to differentiate themselves in other dimensions. For instance, withits EDLP strategy and the “Always Low Prices, Always” slogan, Wal-Marthas tried to establish itself as the low price leader in the industry. It hasalso emphasized the supercenter format more than Target and Kmart withapproximately half of its 3,000 stores selling grocery products. Similarly, Targethas looked to place itself in a niche as an “upscale” discounter with higher-end products. It has partnered with several designers to offer contemporarymerchandise, runs its own Target Guest credit card, and heavily promotes itsnationwide bridal and baby shower gift registries. Target’s panache is reflectedin the pop-culture use of a French-influenced pronunciation for its name(Tar-jay).6

We assemble a novel dataset that includes locations (street addresses andzip codes) of all stores in operation as of 2003 for Wal-Mart, Kmart, andTarget. In addition, we observe store format information, discount store versus

6For a detailed background on these firms, interested readers are referred to Zhu et al. (2008)and three recent books on each firm: The Wal-Mart Decade: How a New Generation of LeadersTurned Sam Walton’s Legacy into the World’s #1 Company (Robert Slater) Portfolio Hardcover(2003); On Target: How the World’s Hottest Retailer Hit a Bullseye ( Laura Rowley) Wiley (2003);Kmart’s Ten Deadly Sins: How Incompetence Tainted an American Icon, (Marcia Layton Turner)John Wiley & Sons (July 18, 2003).

Spatial competition with endogenous location choices 15

Table 1 Number ofstores in US

Store names Number of stores

Kmart discount store 1425Super Kmart center 59Target discount store 1133SuperTarget center 127Wal Mart store 1490Wal Mart supercenter 1442

supercenter. The total number of stores belonging to each chain is presentedin Table 1. We do not consider Sam’s Club as its main competitors are othermembership clubs such as Costco and BJ’s. Wal-Mart is the largest playerwith almost 3000 total stores and, as mentioned above, has stores equally splitbetween the two store formats. By contrast, Kmart and Target are relativelyminor players in the supercenter format. In Table 2, we show the distributionof stores for these three chains across the country. Not surprisingly, the highestnumber of stores are found in the two largest states, California and Texas. Thethree chains have the highest share (in terms of number of stores) in their statesof origin: Kmart in Michigan, Wal-Mart in Arkansas, and Target in Minnesota.The chains also tend to have a disproportionate share of stores in the statesneighboring their headquarters.

Our main objective in this paper is to analyze the factors underlying theentry and location choices of these firms and to infer competitive interactionparameters based on their revealed preferences. For the purpose, we need topartition the United States into small markets and each market into smallerneighborhoods. While various market definitions are possible, a practical con-sideration is the availability of data that capture demand and cost conditionsat each location. Our approach relies on census-delineated lines to define theindividual markets as well as the locations within markets. In particular, weuse counties as our definition of markets and census tracts within counties aslocations.7 Census tracts are small, relatively permanent geographic entitieswithin counties (or the statistical equivalents of counties) delineated by acommittee of local data users and tend to be fairly homogeneous with respectto population characteristics, economic status, and living conditions. In theempirical estimation, neighboring locations will be defined to be all locationswithin a given distance range which we specify below.

In Table 3, we present the competitive configurations across US countiesalong with some characteristics of those markets. The letters W, K, and Trepresent the presence of Wal-Mart, Kmart, and Target firms in the marketwhere, for the sake of brevity, we have omitted information associated with

7For very large urban counties (for example LA county), we use the first three digits of thetract number to create sub-markets. The complete census tract ID is defined as follows: SS-CCC-TTTTTT, where the first two digits “SS” represents State FIPS code, the next three digits “CCC”represents County FIPS Code, and the last six digits “TTTTTT” is the census tract number. Thisdefinition defines a market as the tracts within a county with the same first three digits in theirtract numbers and all six digit codes as locations.

16 T. Zhu, V. Singh

Table 2 Number of stores across states

State Kmart Target Wal-Mart Total

AK 5 0 9 14AL 29 10 87 126AR 6 4 86 96AZ 23 37 43 103CA 130 186 142 458CO 23 31 53 107CT 9 11 32 52DE 6 2 8 16FL 113 79 194 386GA 40 40 105 185HI 7 0 6 13IA 25 22 53 100ID 8 5 16 29IL 70 64 116 250IN 45 37 87 169KS 13 14 55 82KY 31 12 79 122LA 12 10 82 104MA 20 20 43 83MD 24 24 39 87ME 6 1 22 29MI 93 52 68 213MN 33 66 57 156MO 29 26 114 169MS 9 2 66 77MT 10 7 11 28NC 47 32 101 180ND 7 4 8 19NE 8 11 22 41NH 9 5 26 40NJ 43 29 35 107NM 15 8 26 49NV 11 14 20 45NY 62 37 78 177OH 90 44 105 239OK 10 10 94 114OR 14 16 28 58PA 106 31 104 241RI 1 2 8 11SC 29 15 60 104SD 10 4 10 24TN 39 23 96 158TX 20 110 310 440UT 18 9 27 54VA 46 31 77 154VT 3 0 4 7WA 21 29 35 85WI 39 29 71 139WV 17 3 29 49WY 9 2 10 21All 1493 1260 3057 5810a

aThe number of stores is larger than Table 1 because some neighborhood stores are included inTable 2

Spatial competition with endogenous location choices 17

Table 3 Marketconfigurations definedby county

Market structure CountyN Population Income

(0,0,0) 1356 15,029 31,260(W,0,0) 913 36,507 33,630(0,K,0) 70 93,493 38,582(0,0,T) 9 341,596 46,940(W,K,0) 339 78,374 36,657(W,0,T) 106 249,937 45,213(0,K,T) 17 395,953 44,314(W,K,T) 410 395,574 43,836

store format. For instance, (0,0,0) represents markets with no firms; (W,0,0)are Wal-Mart monopoly counties; (W,K,0) are duopoly counties of Wal-Martand Kmart, and so on. A few patterns are apparent from the numberspresented in Table 3. First, markets with no firms have significantly smallerpopulations compared to markets with at least one firm. Second, Wal-Martoperates as a monopolist in a larger number of counties than its rivals. Asthe associated market populations suggest, this reflects its ability to operate insmaller markets. Third, Target stores generally operate in markets with largerpopulation and significantly higher incomes compared to Wal-Mart and Kmartwhich is consistent with the anecdotal evidence discussed above. Finally, thepopulation numbers generally indicate that larger markets are required foradditional entry.

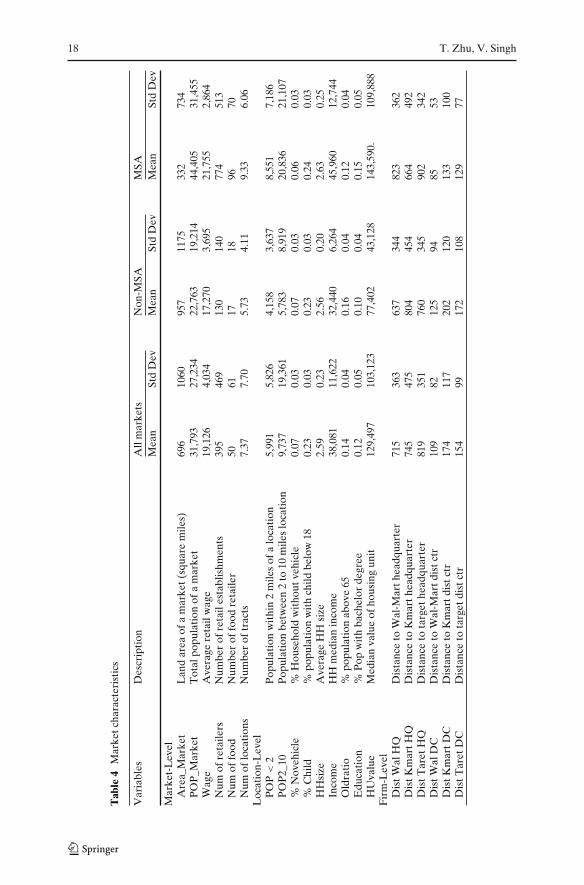

Table 4 lists the full set of variables used in the estimation where we separatethe variables that are observed at the market, location, and firm level. Wealso present the overall averages and means by MSA and rural Non-MSAmarkets. The average market size in our data is approximately 700 squaremiles although the rural markets tend to be larger in size than MSA markets.In terms of population we find the opposite as MSA markets have double thenumber of people reflecting that the urban areas are quite densely populatedcompared to rural markets. We can also see that MSA markets tend to havehigher retail wages and more retail establishments. The next row shows thenumber of census tracts within a market. The average number of locations ina market ranges from approximately six in the rural markets to over nine inMSA markets.

The next panel of the table describes the location-specific variables. Thefirst two rows are the populations within a two and a two-to-ten mile radiusof the location. We find a similar pattern to the market-level characteristics asMSA markets have significantly larger population numbers than the non-MSAmarkets. The next three variables %Novehicle, %Child, and HHsize are thepercent of population with no vehicles, percent of population with children inthe family, and household size respectively. These three variables do not differsubstantially across MSA and rural markets. However, MSA locations do tendto have higher levels of income and house values as well as a higher proportionof younger and educated population.

18 T. Zhu, V. Singh

Tab

le4

Mar

ketc

hara

cter

isti

cs

Var

iabl

esD

escr

ipti

onA

llm

arke

tsN

on-M

SAM

SAM

ean

Std

Dev

Mea

nSt

dD

evM

ean

Std

Dev

Mar

ket-

Lev

elA

rea_

Mar

ket

Lan

dar

eaof

am

arke

t(sq

uare

mile

s)69

610

6095

711

7533

273

4P

OP

_Mar

ket

Tot

alpo

pula

tion

ofa

mar

ket

31,7

9327

,234

22,7

6319

,214

44,4

0531

,455

Wag

eA

vera

gere

tail

wag

e19

,126

4,03

417

,270

3,69

521

,755

2,86

4N

umof

reta

ilers

Num

ber

ofre

tail

esta

blis

hmen

ts39

546

913

014

077

451

3N

umof

food

Num

ber

offo

odre

taile

r50

6117

1896

70N

umof

loca

tion

sN

umbe

rof

trac

ts7.

377.

705.

734.

119.

336.

06L

ocat

ion-

Lev

elP

OP

<2

Pop

ulat

ion

wit

hin

2m

iles

ofa

loca

tion

5,99

15,

826

4,15

83,

637

8,55

17,

186

PO

P2_

10P

opul

atio

nbe

twee

n2

to10

mile

slo

cati

on9,

737

19,3

615,

783

8,91

920

,836

21,1

07%

Nov

ehic

le%

Hou

seho

ldw

itho

utve

hicl

e0.

070.

030.

070.

030.

060.

03%

Chi

ld%

popu

lati

onw

ith

child

belo

w18

0.23

0.03

0.23

0.03

0.24

0.03

HH

size

Ave

rage

HH

size

2.59

0.23

2.56

0.20

2.63

0.25

Inco

me

HH

med

ian

inco

me

38,0

8111

,622

32,4

406,

264

45,9

6012

,744

Old

rati

o%

popu

lati

onab

ove

650.

140.

040.

160.

040.

120.

04E

duca

tion

%P

opw

ith

bach

elor

degr

ee0.

120.

050.

100.

040.

150.

05H

Uva

lue

Med

ian

valu

eof

hous

ing

unit

129,

497

103,

123

77,4

0243

,128

143,

590.

109,

888

Fir

m-L

evel

Dis

tWal

HQ

Dis

tanc

eto

Wal

-Mar

thea

dqua

rter

715

363

637

344

823

362

Dis

tKm

artH

QD

ista

nce

toK

mar

thea

dqua

rter

745

475

804

454

664

492

Dis

tTar

etH

QD

ista

nce

tota

rget

head

quar

ter

819

351

760

345

902

342

Dis

tWal

DC

Dis

tanc

eto

Wal

-Mar

tdis

tctr

109

8212

594

8553

Dis

tKm

artD

CD

ista

nce

toK

mar

tdis

tctr

174

117

202

120

133

100

Dis

tTar

etD

CD

ista

nce

tota

rget

dist

ctr

154

9917

210

812

977

Spatial competition with endogenous location choices 19

The last set of variables are firm-level variables that are specific to eachlocation. In particular, the data include distances from locations to the head-quarters and distribution centers of firms. These variables were created toproxy for logistical issues in a firm’s location decisions and, as we shall seebelow, tend to be quite important.

4 Empirical application

4.1 Estimation issues

The model described in (4) is very flexible as it allows for competition effectsto be asymmetric across firms and for the intensity of competition to dependon proximity. However, the general model has a large number of competitiveparameters (the δ’s) to be estimated. Without any constraints the number ofcompetitive interaction parameters is Lm × Lm × N × (N − 1) which growsquickly even with a small number of players and locations. For instance, withthree players and ten locations, the number of competition parameters is 600.Clearly, some restrictions on the number of parameters are required. To dealwith this difficulty, we create discrete distance bands and assume that thecompetitive intensity between players is the same as long as they are within thesame band.8 In the estimation, we categorize the distance between locationsinto three bands: less than 2 miles, 2 to 10 miles, and more than 10 miles.Note that this approach implies that if δii′0 is the competitive impact of firmi at location k1 that is within 2 miles from location l chosen by player i′,then the competitive effect is still δii′0 were firm i to choose another locationk2 that is also within 2 miles of l. In other words, in this framework theintensity of competition is determined by the distance between locations andnot the identities of those locations. The advantage of the approach is thatthe number of parameters reduces significantly. For instance, using the threedistance bands described above, the total number of parameters is reduced to3 × 3 × 2 = 18.

The model can be summarized as follows:

πiml = ximlβi −∑

i′ �=i

B−1∑

b=0

Lm∑

k=1

δii′b ai′mk1 (k ∈ bl) + ξm + εiml (8)

8We assume that firms are located at the centroid of the location, i.e., census tract. We calculate thedistance between locations using the Haversine Formula. Based on latitude-longitude coordinatedata, the distance between two points, a and b , is given by

da,b =2R arcsin

[

min

{((sin (0.5 (latb −lata)))2+cos (lata) cos (latb ) (sin (0.5 (lonb −lona)))

2)0.5

, 1

}]

where R = 3961 miles denotes the radius of the earth.

20 T. Zhu, V. Singh

where B is the total number of bands and 1 (k ∈ bl) is an indicator functionwith

1 (k ∈ bl) ={

1 if db ≤ dlk < db+1

0 otherwise, (9)

where db and db+1 denote cut-offs that define a distance band. In other words,1 (k ∈ bl) = 1 whenever location k is in distance band b relative to location l.

The parameters to be estimated are θ = {β, δ, σ } where β captures firms’preferences over the exogenous market conditions, δ reflects competitiveeffects across firms and locations, and σ measures the importance of themarket level random component. To estimate the model, we nest the fixedpoint algorithm in (5) into a maximum likelihood routine. For a given set ofvalues of the parameters and the market, location, and firm specific exogenousvariables, the system of equations in (5) is solved numerically for its fixedpoint for each market. The fixed point is a vector with

∑i Lim elements which

represent the probability of each location being chosen by each firm. Giventhose probabilities, P (ym) = ∏

i P (yim) is the probability of the equilibriumrealization that is consistent with the observed market outcome. The likelihoodfunction is given by

L (y, X, ξ ; θ) =M∏

m=1

P(ym|Xm, ξm; β, δ

). (10)

The unconditional likelihood then involves integrating over the distributionG (.) of the unobserved market component ξm, where ξm is assumed normallydistributed with variance σ in our application.

L (y, X; θ) =M∏

m=1

∫

P(ym|Xm, ξm; β, δ

)dG

(ξm|σ )

, (11)

where ym = (yWm, yKm, yTm) are observed actions taken by Wal-Mart, Kmartand Target.

Computationally, the model is quite complicated. To simplify the estima-tion, we employ a simulated maximum likelihood routine as follows.9 Given aset of parameter values and a vector of simulated draws with standard normaldistribution ς = (

ς1, ς2, ..., ς R)

for the unobserved market characteristic, webegin with an initial guess of the choice probability for each firm P0

m ∈[0, 1]

∑i Lim in each market. We then calculate each firm’s expected payoff for

each location conditional on its beliefs about its competitors’ location choiceprobability P0

−im. For each random draw ς r, we solve the fixed point problem(5) by successive approximation to obtain the Bayesian Nash equilibrium

9One problem of the likelihood approach is that there might be multiple equilibria in the incom-plete information game. Although we solved for the fixed point by using different starting values,uniqueness of the solution is not guaranteed. However, as long as the strength of competitioneffect is moderate, the equilibrium can be solved uniquely. We show analytical and simulationresults in the Appendix.

Spatial competition with endogenous location choices 21

probabilities Prm. We then repeat the procedure R times to find the Bayesian

Nash equilibrium for each random draw. The predicted probability of theobserved outcome is approximated by

∫

P(ym|Xm, ξm; β, δ

)dG

(ξm|σ ) = 1

R

R∑

r=1

Prm (ym) . (12)

We then use the simulated probabilities in a log-likelihood function:

θ̂ = arg maxθ

LL (y, X; θ) =M∑

m=1

ln

[1

R

R∑

r=1

Prm (ym)

]

. (13)

4.2 Results

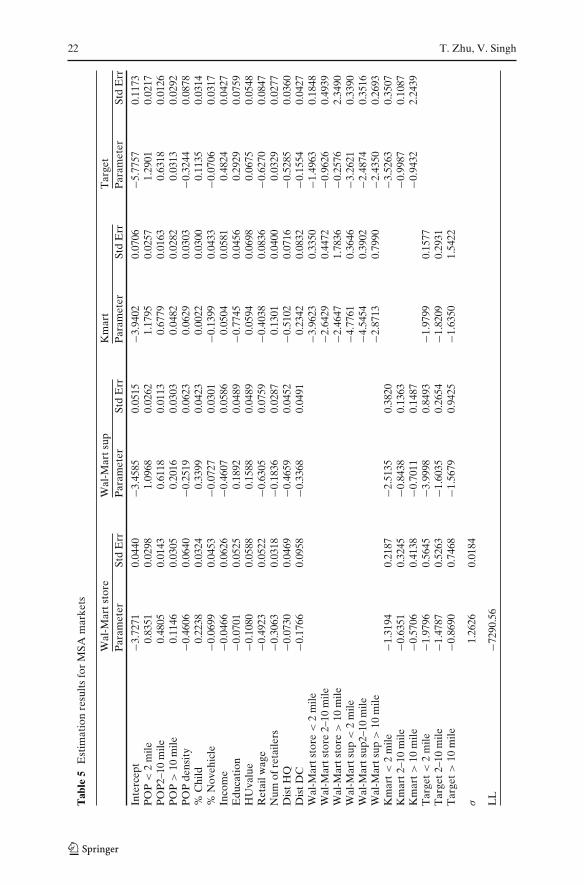

We include a variety of variables that capture demand, cost, and logisticalfactors that could be important in a firm’s location decision. Since these factorsmight operate differently in large MSA markets compared to rural areas, wedivide the sample into MSA and non-MSA markets and estimate separatemodels for each.10 We also allow Wal-Mart to choose between its discountstore and supercenter formats. As noted in the data section above, the othertwo players mainly operate discount stores so we ignore the format choicedecisions for these players.

In Table 5, we report the parameter estimates for MSA markets. We willfocus on those estimates since similar results obtain for non-MSA marketsas displayed in Table 6. Not surprisingly, we find that closer populationcontributes more to profitability that more distant population as reflectedin the lower value of the coefficients for population in more distant bands.However, the parameters for distant population are significantly larger forWal-Mart, particularly for its supercenter format. This finding suggests thatthe trading area for Wal-Mart is larger than that of its rivals. The estimatedeffect of population density is negative for all players except Kmart. While thismay seem counterintuitive, note that population density is measured at thespecific location cell level, while the population measures include populationsfrom the immediate as well as neighboring locations that fall within therespective distance band. Since the discount stores tend be large in size, it is notnecessarily surprising that population density in the immediate location is low.In addition, a location with high population density may have high real estatecosts implying that the chains would prefer locations with lower immediatepopulation density, but higher overall surrounding population.

10A concern in our modeling framework is potential cannibalization across markets since eachmarket is treated independently. This is less likely to be an issue in the non-MSA markets wherethe distance between the adjacent stores is quite large. Note however that the travel time in MSAmarkets is likely to larger potentially mitigating cannibalization. Jia (2008) makes contribution tothe literature by incorporating the “spill over” effects across market within a firm. However theimplicit assumption in her approach is the externality between two close-by stores within the samechain is positive.

22 T. Zhu, V. Singh

Tab

le5

Est

imat

ion

resu

lts

for

MSA

mar

kets

Wal

-Mar

tsto

reW

al-M

arts

upK

mar

tT

arge

tP

aram

eter

Std

Err

Par

amet

erSt

dE

rrP

aram

eter

Std

Err

Par

amet

erSt

dE

rr

Inte

rcep

t−3

.727

10.

0440

−3.4

585

0.05

15−3

.940

20.

0706

−5.7

757

0.11

73P

OP

<2

mile

0.83

510.

0298

1.09

680.

0262

1.17

950.

0257

1.29

010.

0217

PO

P2–

10m

ile0.

4805

0.01

430.

6118

0.01

130.

6779

0.01

630.

6318

0.01

26P

OP

>10

mile

0.11

460.

0305

0.20

160.

0303

0.04

820.

0282

0.03

130.

0292

PO

Pde

nsit

y−0

.460

60.

0640

−0.2

519

0.06

230.

0629

0.03

03−0

.324

40.

0878

%C

hild

0.22

380.

0324

0.33

990.

0423

0.00

220.

0300

0.11

350.

0314

%N

oveh

icle

−0.0

699

0.04

53−0

.072

70.

0301

−0.1

399

0.04

33−0

.070

60.

0317

Inco

me

−0.0

466

0.06

26−0

.460

70.

0586

0.05

040.

0581

0.48

240.

0427

Edu

cati

on−0

.070

10.

0525

0.18

920.

0489

−0.7

745

0.04

560.

2929

0.07

59H

Uva

lue

−0.1

080

0.05

880.

1588

0.04

890.

0594

0.06

980.

0675

0.05

48R

etai

lwag

e−0

.492

30.

0522

−0.6

305

0.07

59−0

.403

80.

0836

−0.6

270

0.08

47N

umof

reta

ilers

−0.3

063

0.03

18−0

.183

60.

0287

0.13

010.

0400

0.03

290.

0277

Dis

tHQ

−0.0

730

0.04

69−0

.465

90.

0452

−0.5

102

0.07

16−0

.528

50.

0360

Dis

tDC

−0.1

766

0.09

58−0

.336

80.

0491

0.23

420.

0832

−0.1

554

0.04

27W

al-M

arts

tore

<2

mile

−3.9

623

0.33

50−1

.496

30.

1848

Wal

-Mar

tsto

re2–

10m

ile−2

.642

90.

4472

−0.9

626

0.49

39W

al-M

arts

tore

>10

mile

−2.4

647

1.78

36−0

.257

62.

3490

Wal

-Mar

tsup

<2

mile

−4.7

761

0.36

46−3

.262

10.

3390

Wal

-Mar

tsup

2–10

mile

−4.5

454

0.39

02−2

.487

40.

3516

Wal

-Mar

tsup

>10

mile

−2.8

713

0.79

90−2

.435

00.

2693

Km

art<

2m

ile−1

.319

40.

2187

−2.5

135

0.38

20−3

.526

30.

3507

Km

art2

–10

mile

−0.6

351

0.32

45−0

.843

80.

1363

−0.9

987

0.10

87K

mar

t>10

mile

−0.5

706

0.41

38−0

.701

10.

1487

−0.9

432

2.24

39T

arge

t<2

mile

−1.9

796

0.56

45−3

.999

80.

8493

−1.9

799

0.15

77T

arge

t2–1

0m

ile−1

.478

70.

5263

−1.6

035

0.26

54−1

.820

90.

2931

Tar

get>

10m

ile−0

.869

00.

7468

−1.5

679

0.94

25−1

.635

01.

5422

σ1.

2626

0.01

84

LL

−729

0.56

Spatial competition with endogenous location choices 23

Tab

le6

Est

imat

ion

resu

lts

for

non-

MSA

mar

kets

Wal

-Mar

tsto

reW

al-M

arts

upK

mar

tT

arge

tP

aram

eter

Std

Err

Par

amet

erSt

dE

rrP

aram

eter

Std

Err

Par

amet

erSt

dE

rr

Inte

rcep

t−3

.297

70.

2169

−3.4

794

0.16

11−3

.592

80.

2495

−6.4

059

0.43

48P

OP

<2

mile

2.14

010.

1202

1.02

890.

1284

1.67

240.

1833

2.10

040.

1759

PO

P2–

10m

ile0.

8925

0.08

110.

5954

0.08

560.

9375

0.08

640.

8084

0.17

29P

OP

>10

mile

0.04

850.

0967

0.20

690.

1021

0.04

210.

1107

0.07

360.

2234

PO

PD

ensi

ty−0

.348

50.

0937

−0.2

903

0.08

95−0

.172

50.

0998

−0.8

512

0.25

91%

Chi

ld0.

1469

0.09

980.

2552

0.10

040.

4373

0.11

780.

3662

0.25

88%

Nov

ehic

le−0

.221

60.

1070

−0.1

036

0.11

49−0

.275

50.

1515

0.04

130.

4817

Inco

me

0.30

440.

2321

−0.3

087

0.22

91−0

.566

70.

2706

0.80

650.

5457

Edu

cati

on0.

3539

0.14

22−0

.027

70.

1546

0.51

900.

1523

0.67

730.

2823

HU

valu

e−0

.057

60.

1001

0.13

320.

0595

0.22

310.

0724

−0.0

243

0.19

07R

etai

lwag

e0.

6232

0.13

62−0

.642

80.

1491

0.46

380.

1535

0.26

340.

3613

Num

ofre

taile

rs0.

1995

0.27

29−0

.239

80.

2205

1.74

930.

3029

2.40

260.

7522

Dis

tHQ

−0.4

644

0.09

49−0

.468

20.

1036

−0.6

043

0.10

61−0

.919

90.

2128

Dis

tDC

−0.3

610

0.10

33−0

.353

50.

1156

−0.0

306

0.06

68−0

.174

50.

2273

Wal

-Mar

tsto

re<

2m

ile−3

.395

71.

0625

−0.8

024

1.72

54W

al-M

arts

tore

2–10

mile

−2.9

987

0.95

24−0

.545

41.

9186

Wal

-Mar

tsto

re>

10m

ile−1

.966

91.

2111

−0.0

583

3.85

55W

al-M

arts

up<

2m

ile−4

.595

50.

9996

−3.6

291

2.23

09W

al-M

arts

up2–

10m

ile−3

.309

00.

9154

−2.7

650

0.96

55W

al-M

arts

up>

10m

ile−2

.950

01.

5134

−2.5

663

2.54

04K

mar

t<2

mile

−1.7

034

0.50

70−2

.508

10.

2337

−1.4

193

2.66

51K

mar

t2–1

0m

ile−1

.357

80.

7639

−1.6

668

0.63

62−1

.340

21.

2559

Km

art>

10m

ile−0

.459

71.

6763

−1.2

101

1.75

19−1

.019

44.

0983

Tar

get<

2m

ile−3

.510

51.

0283

−2.9

020

0.74

82−2

.250

71.

0300

Tar

get2

–10

mile

−2.6

986

1.16

95−1

.724

41.

0328

−1.8

001

0.67

65T

arge

t>10

mile

−0.9

601

1.75

60−1

.641

31.

6655

−0.7

464

1.52

87

σ1.

1052

0.13

45

LL

−524

2.78

24 T. Zhu, V. Singh

The next two variables, %Child and %Novehicle, represent the percentof population with children under the age of 18 and percent of populationwith no vehicles. The parameters for %Child are positive for Wal-Mart andTarget, but are insignificant for Kmart. Thus, both Wal-Mart and Target storesprefer markets where a larger proportion of families have kids. In relativeterms, the impact is larger for Wal-Mart, particularly for its supercenter format.The parameter for %Novehicle is significantly negative for all stores whichis intuitive as these stores are built with large parking lots that are generallyinaccessible without vehicles. The next two demographic variables are medianincome and education measured as the percentage of population with a collegedegree. These two variables reveal some interesting differences across firms.The income parameter is negative for both Wal-Mart formats, insignificant forKmart, and positive for Target. These results suggest that, all else equal, Wal-Mart enters markets with lower incomes while Target stores prefer high in-come areas. In addition, Target stores tend to have a more educated populationbase. These results are consistent with common perceptions of the positioningand target audiences of these stores. For example, as discussed above, Targethas historically attempted to position itself as an upscale discounter that catersto a higher income and more educated clientele than its competitors. Similarly,lower income levels in Wal-Mart locations are consistent with Wal-Mart’severy day low pricing and value positioning.

The next variable HouseValue is the median house value which ideally willcapture the impact of real estate prices. The coefficient is negative for Wal-Mart discount store, positive for its supercenter format, and insignificant forKmart and Target. However, the instability of these results appear to indicatethat residential house value is in fact an inaccurate proxy for commercial landvalue. The coefficients for retail wages are negative and significant indicatingthat all firms strongly prefer markets with lower wages. This is not surprisingsince labor tends to account for a significant proportion of operational costsin retailing. The variable “num of retailers” is the total number of otherretailers and captures the general business density at a location. Note thatthese retail stores are considered to be non-strategic players in our model eventhough some of them may actually compete with the three discount stores. Thecoefficient is negative for the two Wal-Mart stores and positive for Kmart andTarget. This suggests that Wal-Mart tends to prefer stand alone locations whileits competitors are more likely to be surrounded by other businesses.

The last two variables Dist HQ and Dist DC are the distance of differentmarket locations from the headquarters and nearest distribution center of afirm. Unlike all the variables discussed above, these distance measures arefirm-specific. The negative coefficients for distance to headquarters suggeststhat, all else equal, firms prefer markets that are closer to their respectiveheadquarters. This is consistent with the distribution of stores across statesreported in Table 2. Looking at the distance to distribution center, we findthat Wal-Mart, particularly for its supercenter format, prefers locations thatare closer to its distribution center. This is not surprising as Wal-Mart is well

Spatial competition with endogenous location choices 25

known for its efficiency in distribution, and a large part of its success as aretailer has been attributed to these logistical efficiencies.11

Looking at the competitive interaction parameters, some interesting pat-terns emerge. As expected, all parameters are negative indicating that pres-ence of rivals reduce a firm’s profits. However, proximity to competitors isan important determinant of profitability as the competition effect diminisheswith distance. For instance, the point estimates suggest that the impact ofKmart on a Wal-Mart’s discount store is approximately 45% lower when itis located more than ten miles away instead of being located in the immediateneighborhood. This decreasing relationship between distance and competitionis consistent across all firms and formats which suggests strong returns tospatial differentiation in this industry as firms can shield their profits by choos-ing sufficiently different locations. Looking at the competitive effects acrossfirms, we find strong asymmetries in the competitive interaction parameters.For example, looking at Kmart and the two Wal-Mart formats, we find thatwhile Kmart substantially impacts Wal-Mart when it is in close proximity, theeffect is significantly lower than the effect of Wal-Mart on Kmart. Similarly,when Kmart is located beyond ten miles, its effect on Wal-Mart’s discountstore and supercenter are approximately one-fourth of the impact that theWal-Mart stores have on Kmart at a similar distance. Target stores farewell in the face of competition from other discount stores except when thecompetitors are in close proximity. However, the chain appears vulnerable toWal-Mart’s supercenter format. Perhaps most interesting, the impact of Wal-Mart supercenter appears to decline less rapidly with distance when comparedto the effect of any of the other firms. This finding suggests that Wal-Mart’ssupercenter format yields a substantially larger market area relative to otherformats as even competitors which are relatively far from a supercenter are notinsulated from competition with it.

To better interpret the competition effects, one can calculate measures onthe demand reduction in terms of population when a competitor moves intoa location, holding all else constant. For example, moving a new Wal-Martdiscount store within 2 miles of Kmart is equivalent to reduction of 33,600in population for Kmart in the immediate neighborhood. The effect of a newKmart on a Wal-Mart discount store is only 15,800 which is less than half theimpact that Wal-Mart has on Kmart. If a new Wal-Mart supercenter moves in,even in a far away location (beyond 10 miles), it is equivalent to a reductionin population of 24,000 for Kmart and 18,900 for Target. The correspondingnumbers for a Wal-Mart discount store are 20,900 for Kmart and 2,000 forTarget. Thus, Kmart seems vulnerable to both formats of Wal-Mart even infar away locations, while Target fares well when faced with a distant Wal-Mart

11According to an independent study by McKinsey & Co., Wal-Mart’s efficiency gains were thesource of 25% of the entire U.S. economy’s productivity improvement from 1995 to 1999. “CanWal-Mart get any bigger” Time Magazine (Vol. 161, issue 2, 2003).

26 T. Zhu, V. Singh

discount store, but is still affected strongly by a Wal-Mart supercenter. In fact,the impact of Target is stronger on Kmart and Wal-Mart’s discount store whenlocated more than 10 miles away rather than the other way around.

4.3 Varying market conditions and equilibrium outcomes

The model parameters can be used to predict the equilibrium market struc-tures for different sets of market conditions and provide insights on howthese firms shield themselves from competition by spatial differentiation. Forinstance, consider a market with two possible locations that are 10 miles apart,and three potential competitors: Wal-Mart supercenter, Kmart, and Target.Further, suppose the population in location 1 is 30,000 and income is at themean level in the population which is normalized to zero. In addition, allother variables are set at their population mean levels. Figure 3 displays thepredicted market structures as population and income change in location2. Note that the parameter estimates of the latent payoff functions suggestthat the impact of the two variables may work differently for different firms.In particular, while all firms prefer increase in population especially in theimmediate location, Target is the only firm that prefers higher income levels.The darker shade represents choice of location 1, lighter shade the choice oflocation 2 (Red and Blue if viewed in color), and non-shaded areas representsituations where firms stay out of the market. The left panel shows the pre-dicted outcomes without considering competition, while the right panel showsthe equilibrium structures after taking competition into account. Figure 3ashows that when firms do not compete, no entry and monopoly outcomes arerare as all three firms are willing to enter the market with moderate increasesin population and income levels. Figure 3b shows that the region of no-entry and monopoly increase dramatically once we account for competition.Moreover, the occurrence of oligopoly is much less prevalent and only arisesat significantly high population and income levels.

In Fig. 3a to b, we show how the predicted entry and location choices varyby individual firms. Comparing individual firms under competition and no-competition, some interesting patterns emerge. Wal-Mart’s no-entry region,while larger under competition compared to the no-competition case, is rel-atively small compared to its rivals. The impact of competition is highest onKmart as it gives up the majority of the space that it would have occupied ifcompetitive concerns were irrelevant. Looking at Wal-Mart’s location choices,we observe that as the income in location 2 increase above a certain point,Wal-Mart is willing to enter the market by switching to location 1. On the otherhand, both Target and Kmart prefer not to enter the market altogether withmoderate market conditions and choose location 2 as it becomes sufficientlyattractive. These results are primarily driven by Wal-Mart supercenter’s abilityto enter markets with lower population levels, attract population from furtheraway locations, and its ability to impact competitors even when it is locatedfar away. Comparing the monopoly region in Fig. 3b with those of three firmsunder competition (Fig. 3), we can see that majority of the monopoly region

Spatial competition with endogenous location choices 27

is occupied by Wal-Mart with a small region (those with moderate populationand very high income) being Target’s monopoly. Kmart on the other handis rarely able to operate as a monopolist. Of course these predictions wouldchange at different values of the other market variables. For example, Kmartmay have monopoly markets in regions close enough to its headquarters.

Overall, the results show that all firms exert a strong negative impact on itscompetitors when they are in close proximity and that this effect decreases with

Fig. 3 Market structure predictions

28 T. Zhu, V. Singh

Fig. 3 (continued)

distance to rivals. Wal-Mart’s supercenter format is found to be the most formi-dable player as it strongly impacts competitors even from a distant location.Not surprisingly, in our empirical data we observe a large number of monopolymarkets for Wal-Mart supercenter. We also find asymmetries across players interms of exogenous market characteristics. In Table 7, we show the parameterestimates from a model that ignores player identities. With minor differences,this is the model used by Seim (2006) in her application to the video rentalstores. Several similarities exist in the parameter estimates with the full modelpresented above. For instance, payoffs are higher with population closer the

Table 7 Parameter estimates without firm asymmetry

Estimates from separate marketsMSA Non-MSAParameter Std Err Parameter Std Err