South Asian Journal of Marketing & Management Research

13

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X South Asian Academic Research Journals http://www.saarj.com 215 Published by: South Asian Academic Research Journals SAJMMR: South Asian Journal of Marketing & Management Research CONSUMERS’ GRIEVANCE REDRESSAL SYSTEM IN THE INDIAN LIFE INSURANCE INDUSTRY - AN ANALYSIS DR.M.SYED IBRAHIM*; SHAKEEL-UL-REHMAN** *Assistant Professor and Research Supervisor, Post-Graduate Department of Commerce, Govt. Arts College (Autonomous), Salem-636 007, Tamil Nadu, South India. **P.hD Scholar, Sona School of Management, A Unit of Sona College of Technology, Salem-636 005, Tamil Nadu, South India. ABSTRACT Reckoned among the fastest growing industries, the life insurance industry of India has 23 license-holders running their business in this sector. The Life Insurance Corporation of India (LIC), which is the only player in the public sector, contributes over 70% to the business. The remaining area is covered by the 22 private sector companies. Life Insurance Corporation of India (LIC) was established on 1 st September, 1959, with the objective of spreading life insurance much more widely and in particularly to the rural areas with a view to reach all insurable persons in the country, providing them adequate financial cover at a reasonable cost. LIC continues to be the dominant life insurer even in the liberalized scenario of Indian insurance and is moving fast on a new growth trajectory surpassing its own past records. The study would provide some insights into the areas, specifically consumer protection and the awareness with reference to the grievances settlement operations of the Life Insurance Industry in India. The study is diagnostic and exploratory in nature and makes use of secondary data. The study finds and concludes that the Life Insurance Industry have significantly improved their performance with regard to redress the grievances of the insurance customers (policyholders). KEYWORDS: Life Insurance Corporation, Grievance Cell, Policyholders and The Insurance Regulatory and Development Authority ( IDRA). ______________________________________________________________________________

Transcript of South Asian Journal of Marketing & Management Research

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

215

Published by: South As ian Academic Research Journals

SAJMMR:

S o u t h A s i a n J o u r n a l o f

M a r k e t i n g & M a n a g e m e n t

R e s e a r c h

CONSUMERS’ GRIEVANCE REDRESSAL SYSTEM IN THE INDIAN

LIFE INSURANCE INDUSTRY - AN ANALYSIS

DR.M.SYED IBRAHIM*; SHAKEEL-UL-REHMAN**

*Assistant Professor and Research Supervisor,

Post-Graduate Department of Commerce, Govt. Arts College (Autonomous),

Salem-636 007, Tamil Nadu, South India.

**P.hD Scholar,

Sona School of Management, A Unit of Sona College of Technology,

Salem-636 005, Tamil Nadu, South India.

ABSTRACT

Reckoned among the fastest growing industries, the life insurance industry of India has 23

license-holders running their business in this sector. The Life Insurance Corporation of India

(LIC), which is the only player in the public sector, contributes over 70% to the business. The

remaining area is covered by the 22 private sector companies. Life Insurance Corporation of

India (LIC) was established on 1st September, 1959, with the objective of spreading life

insurance much more widely and in particularly to the rural areas with a view to reach all

insurable persons in the country, providing them adequate financial cover at a reasonable cost.

LIC continues to be the dominant life insurer even in the liberalized scenario of Indian insurance

and is moving fast on a new growth trajectory surpassing its own past records. The study would

provide some insights into the areas, specifically consumer protection and the awareness with

reference to the grievances settlement operations of the Life Insurance Industry in India. The

study is diagnostic and exploratory in nature and makes use of secondary data. The study finds

and concludes that the Life Insurance Industry have significantly improved their performance

with regard to redress the grievances of the insurance customers (policyholders).

KEYWORDS: Life Insurance Corporation, Grievance Cell, Policyholders and

The Insurance Regulatory and Development Authority ( IDRA).

______________________________________________________________________________

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

216

I. INTRODUCTION

Financial institutions are the tools to mobilize savings and encourage investments by directing

them to the productive channels and occupy a key position in the modern global economy.

Financial institutions are of two types in general, namely Depository Institutions (e.g., Banks)

and Non-Depository Institutions (e.g., Insurance Companies) and both serve financial markets.

After banking, insurance is the most important segment of the financial sector, capable of

providing huge amounts of funds for the economic development of the country. The

contemporary era is marked as the era of consumers. No country can knowingly or unknowingly

disregard the interest of the consumers. This can be argued on the basis of fast enactment of

consumer protection laws in almost all part of the world. Apart from the consumer protection

laws in developed world, it could find the accelerated rate of lawmaking for consumers in

developing countries like Thailand1, Sri Lanka, Korea, Mongolia, Philippines, Mauritius , China,

Taiwan, Nepal, Indonesia, Malaysia and other countries. India is not an exception to this rule.

The Consumer Protection Act, 1986 is one of the examples that are to be treated as a milestone

in the history of socio-economic legislation to protect the interests of the consumers in India. The

legislation to protect and advance the interest of consumers in India was finally materialized after

in-depth study of consumer protection laws operating in other countries and in consultation with

representatives of consumers, trade and industrial segments of India and abroad. In order to

better serve the interests of the consumer and to settle their disputes, consumer council and other

authoritative mechanism are also being established. In an insurance industry, the Consumer

Affairs Department of IRDA handles policyholders’ (insurance consumers) grievances. The

Grievance Cell looks into the complaints from policyholders against life and non-life insurance

companies.

II. STATEMENT OF THE PROBLEM

The Insurance Regulatory and Development Authority (IRDA) has been established to regulate

the business of both the life and non-life insurance in India. While framing the regulations for the

insurers, the Authority keeps in mind the primary objectives of protecting the interests of and

secure fair treatment to policyholders (insurance consumers). Consistent with this, the Authority

has set up Grievances Redressal Cell and tries to ensure speedy redressal of the complaints

received from the policyholders. Policyholders who have complaints against insurers are

required to first approach the Grievance/Customer Complaints Cell of the concerned insurer

(insurance companies).If they do not receive a response of the company, they may approach the

Grievance Cell of the IRDA. Many researchers have attempted to make a contribution in the

field. Among all these researchers, no one has attempted to make the study of appraisal of the

life insurance industry in terms of grievance settlement exclusively. It is against this backdrop

that the present study has been undertaken to fill up this gap.

III. OBJECTIVES OF THE STUDY

The primary objectives of the study are;

(a) To address the consumer awareness with regard to the grievance redressal machinery in the

insurance business;

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

217

(b) To analyze the performance of the LIC in terms of grievance settlement operations;

(c) To analyze the performance of the private sectors’ life insurance business in terms of

grievance settlement operations;

(d) To give suggestion for the improvement of the grievance settlement operations in the Life

insurance Industry in India.

IV. REVIEW OF LITERATURE

A considerable amount of research has been done on the working and performance of insurance

industry in India, by academicians and researchers. The literature obtained by investigators, in

the form of reports of various committees, commissions and working groups established by the

Union Government, the research studies, articles of researchers, insurance officials and news, is

briefly reviewed in this part.

Mathur, N.D (2002) in his study conclude that competition in insurance is one aspect of the past

liberalization scenario, the other aspect would be the public and private sector companies

working together to ensure the healthy growth and development of the sector.

FORTE (Joint Venture between FICCI and ING Insurance) in collaboration with Insurance

Regulatory Development Authority. (2003) has organized a Conference on 'Consumer

Awareness: Insurance Sector' at Federation House, New Delhi discussed IRDA (Protection of

Policyholders' Interests) Regulations, 2002 and the changing consumer awareness / expectations

from the insurance industry, post liberalization, and how far they have been met with by the

industry.

Dr. Narayana Rao, S.B. and Dr. Madhavi, C.(2006) in their study analyzed the performance of

the insurance industry in India and concluded that Government sector should further improve

their product varieties and attract schemes to compete with the private sector and also change

their attitude further towards service to survive in the market.

Vanniyarajan, T. & Balasenthil, R. S. (2008) in their study analyzed the various quality

dimensions in the life insurance market.

Vara Praad & Murali Krishna (2009) in their study attempts to analyze the success of insurance

business depends on the role played by the intermediaries and changed marketing strategies to

suit the customer needs.

Sorab sadri (2009) in his study discussed the social image in a highly competitive market where

even foreign players are steadily entering the domestic scene, people management expertise is

inevitable to sustain the Indian life insurance industry.

Syed Ibrahim, M. (2009) in his study discussed the growth and port-folio of investment of the

Life Insurance Corporation of India.

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

218

Wenyong Tian & Dongmei Li (2011) in their study analyzed the influencing factors of rural

insurance salesman’s sales performance in China by applying the Multiple Ordered and

Classification Logistic Model.

Monica Suri (2011) in her study attempts to analyze the market share of the Quarts insurances

and concludes the insurance sector in India has come to a position of very high potential and

competitiveness in the market.

IV. HYPOTHESES OF THE STUDY

Hypotheses framed for the study are as follows;

(a) There is no significant difference in grievance settlement operations of the public and

private insurers (H0);

(b) There is significant difference in grievance settlement operations of the public and private

insurers (H1);

V. METHODOLOGY OF THE STUDY

Methodology describes the research route to be followed, the instruments to be used, universe

and sample of the study for the data to be collected, the tools of analysis used and pattern of

deducing conclusions.

SAMPLE SELECTION

For the purpose of the present study, there are 23 insurance companies (life insurers) that have

been included for the present study. (Total private insurance companies is 22 and only one public

sector company-LIC, operating as of 30th

September, 2010)

DATA COLLECTION

The present study is diagnostic and exploratory in nature and makes use of secondary data. The

relevant secondary data has been collected mainly through the data bases of Insurance

Regulatory Development Authority of India (IRDA), Reserve Bank of India (RBI), various

reports and other studies. Various insurance related journals have also been referred to.

PERIOD OF THE STUDY

The study period is recent five years starting from the year 2005-06 to the year 2009-10.

TOOLS USED

In order to analyze the data and draw conclusions on this study, various statistical tools like

Descriptive Statistics and Paired-Samples t-Test have been used through EXCEL and SPSS

Software.

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

219

LIMITATIONS OF THE STUDY

The study, as limitations, is confined only to settlement of complaints of the insurance

consumers (policyholders) in an Indian life insurance industry.

VI. ANALYSIS AND DISCUSSION

REDRESSAL OF GRIEVANCES OF THE INSURANCE CONSUMERS-(PUBLIC

SECTOR)

The main objectives of the consumers protection is to ensure the better protection of consumers

and is intended to provide simple, speedy and inexpensive redressal to the consumers’

grievances. The Grievances Cell of the Authority (IRDA) receives grievances from the

policyholders against insurance companies. Such complaints are forwarded to the companies for

resolution at their end. The insurance companies are required to keep the Grievances Cell of

IRDA informed about the status of respective grievances and whether the complaints have been

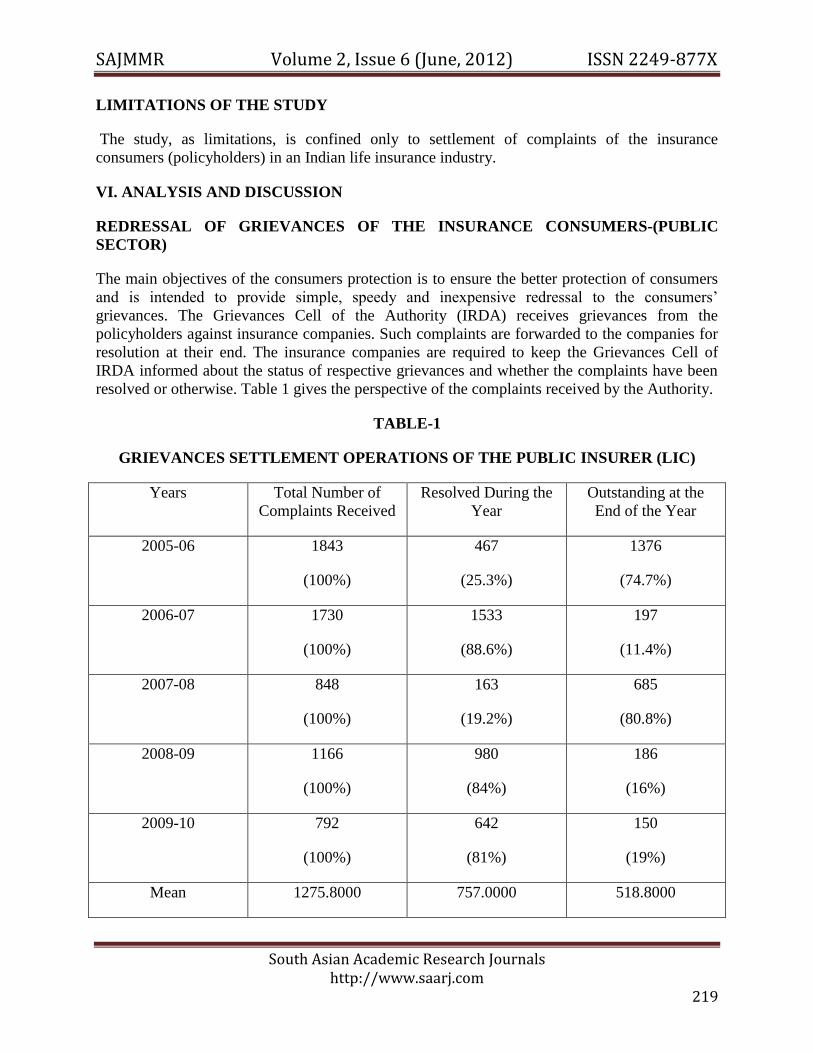

resolved or otherwise. Table 1 gives the perspective of the complaints received by the Authority.

TABLE-1

GRIEVANCES SETTLEMENT OPERATIONS OF THE PUBLIC INSURER (LIC)

Years Total Number of

Complaints Received

Resolved During the

Year

Outstanding at the

End of the Year

2005-06 1843

(100%)

467

(25.3%)

1376

(74.7%)

2006-07 1730

(100%)

1533

(88.6%)

197

(11.4%)

2007-08 848

(100%)

163

(19.2%)

685

(80.8%)

2008-09 1166

(100%)

980

(84%)

186

(16%)

2009-10 792

(100%)

642

(81%)

150

(19%)

Mean 1275.8000 757.0000 518.8000

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

220

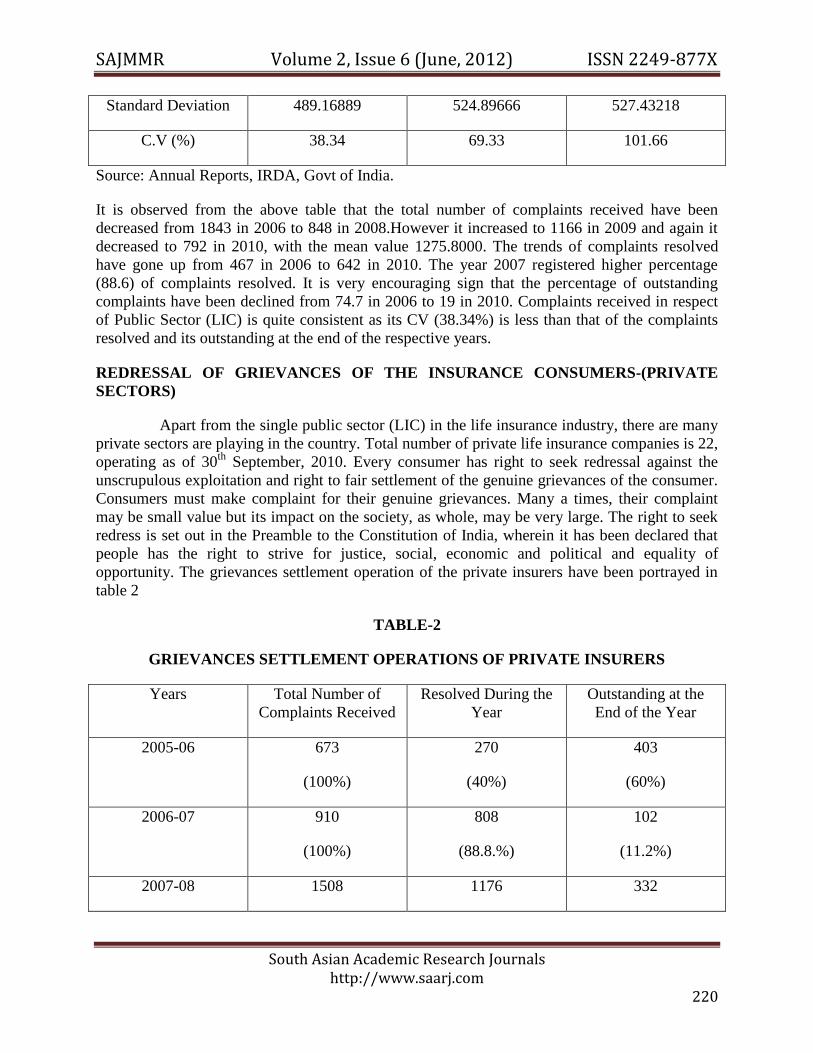

Standard Deviation 489.16889 524.89666 527.43218

C.V (%) 38.34 69.33 101.66

Source: Annual Reports, IRDA, Govt of India.

It is observed from the above table that the total number of complaints received have been

decreased from 1843 in 2006 to 848 in 2008.However it increased to 1166 in 2009 and again it

decreased to 792 in 2010, with the mean value 1275.8000. The trends of complaints resolved

have gone up from 467 in 2006 to 642 in 2010. The year 2007 registered higher percentage

(88.6) of complaints resolved. It is very encouraging sign that the percentage of outstanding

complaints have been declined from 74.7 in 2006 to 19 in 2010. Complaints received in respect

of Public Sector (LIC) is quite consistent as its CV (38.34%) is less than that of the complaints

resolved and its outstanding at the end of the respective years.

REDRESSAL OF GRIEVANCES OF THE INSURANCE CONSUMERS-(PRIVATE

SECTORS)

Apart from the single public sector (LIC) in the life insurance industry, there are many

private sectors are playing in the country. Total number of private life insurance companies is 22,

operating as of 30th

September, 2010. Every consumer has right to seek redressal against the

unscrupulous exploitation and right to fair settlement of the genuine grievances of the consumer.

Consumers must make complaint for their genuine grievances. Many a times, their complaint

may be small value but its impact on the society, as whole, may be very large. The right to seek

redress is set out in the Preamble to the Constitution of India, wherein it has been declared that

people has the right to strive for justice, social, economic and political and equality of

opportunity. The grievances settlement operation of the private insurers have been portrayed in

table 2

TABLE-2

GRIEVANCES SETTLEMENT OPERATIONS OF PRIVATE INSURERS

Years Total Number of

Complaints Received

Resolved During the

Year

Outstanding at the

End of the Year

2005-06 673

(100%)

270

(40%)

403

(60%)

2006-07 910

(100%)

808

(88.8.%)

102

(11.2%)

2007-08 1508 1176 332

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

221

(100%) (78%) (22%)

2008-09 1645

(100%)

1373

(83.5%)

272

(16.5%)

2009-10 2115

(100%)

1870

(88.4%)

245

(11.6%)

Mean 1370.2000 1099.4000 270.8000

Standard Deviation 580.32379 601.53288 112.23057

C.V (%) 42.35 54.71 41.44

Source: Annual Reports, IRDA, Govt of India.

In the table 2, it is exhibited that the total number of complaints received has been increased

from 673 in 2006 to 2115 in 2010.The increase over the period of time is 3.14.

During the period under reference the authority has been able to mark a rising trend in its

settlement of grievances from 270 in 2006 to 1870 in 2010. The IRDA has been successful to

manage the outstanding complaints at the end of each year. The outstanding complaints at the

end of the year in respect of Private Sectors is quite consistent as its CV (41.44%) is less than

that of the complaints received and resolved.

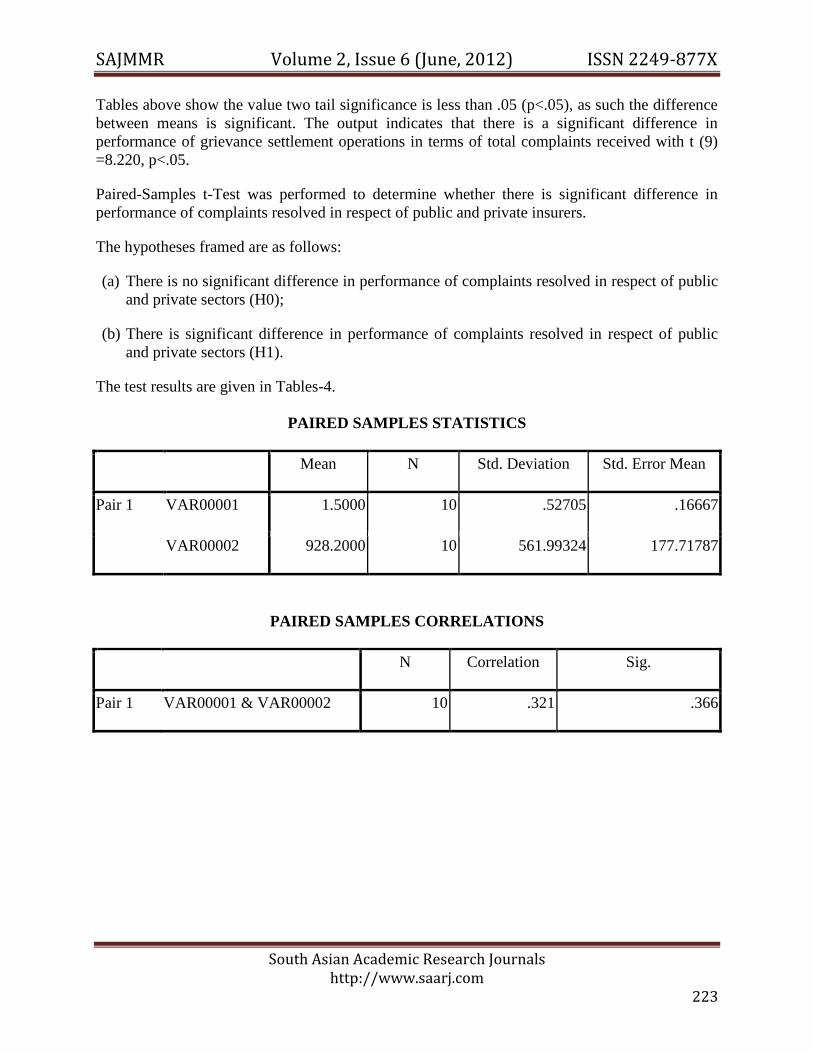

Paired-Samples t-Test was performed to determine whether there is significant difference in

performance of total complaints received in respect of public and private sectors.

The hypotheses framed are as follows:

(a) There is no significant difference in performance of total complaints received in respect of

public and private sectors (H0);

(b) There is significant difference in performance of total complaints received in respect of

public and private sectors (H1);

The test results are given in Tables-3.

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

222

PAIRED SAMPLES STATISTICS

Mean N Std. Deviation Std. Error Mean

Pair 1 VAR00001 1.5000 10 .52705 .16667

VAR00002 1323.0000 10 508.43179 160.78025

PAIRED SAMPLES CORRELATIONS

N Correlation Sig.

Pair 1 VAR00001 & VAR00002 10 .098 .788

PAIRED SAMPLES TEST

Paired Differences

Mean Std. Deviation Std. Error Mean

Pair 1 VAR00001 - VAR00002 -1321.50000 508.38049 160.76403

PAIRED SAMPLES TEST

Paired Differences

95% Confidence Interval of

the Difference

Lower Upper t Df Sig. (2-tailed)

Pair 1 VAR00001 -

VAR00002

-1685.17349 -957.82651 -8.220 9 .000

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

223

Tables above show the value two tail significance is less than .05 (p<.05), as such the difference

between means is significant. The output indicates that there is a significant difference in

performance of grievance settlement operations in terms of total complaints received with t (9)

=8.220, p<.05.

Paired-Samples t-Test was performed to determine whether there is significant difference in

performance of complaints resolved in respect of public and private insurers.

The hypotheses framed are as follows:

(a) There is no significant difference in performance of complaints resolved in respect of public

and private sectors (H0);

(b) There is significant difference in performance of complaints resolved in respect of public

and private sectors (H1).

The test results are given in Tables-4.

PAIRED SAMPLES STATISTICS

Mean N Std. Deviation Std. Error Mean

Pair 1 VAR00001 1.5000 10 .52705 .16667

VAR00002 928.2000 10 561.99324 177.71787

PAIRED SAMPLES CORRELATIONS

N Correlation Sig.

Pair 1 VAR00001 & VAR00002 10 .321 .366

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

224

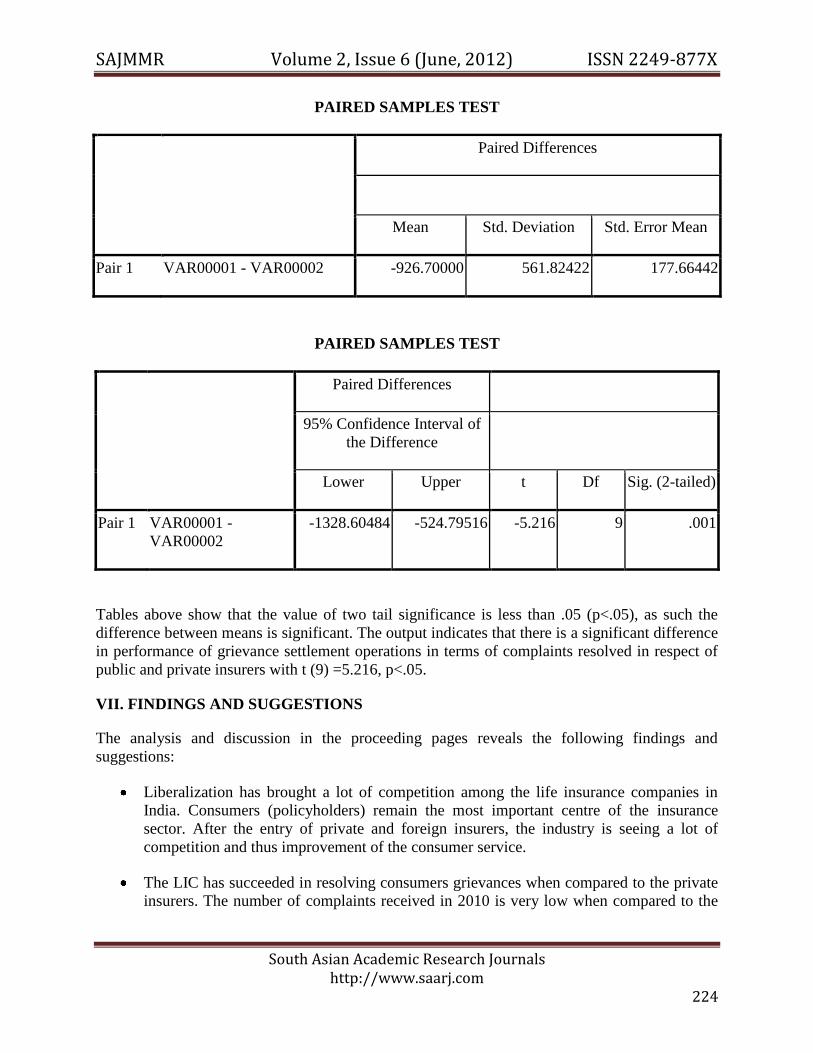

PAIRED SAMPLES TEST

Paired Differences

Mean Std. Deviation Std. Error Mean

Pair 1 VAR00001 - VAR00002 -926.70000 561.82422 177.66442

PAIRED SAMPLES TEST

Paired Differences

95% Confidence Interval of

the Difference

Lower Upper t Df Sig. (2-tailed)

Pair 1 VAR00001 -

VAR00002

-1328.60484 -524.79516 -5.216 9 .001

Tables above show that the value of two tail significance is less than .05 (p<.05), as such the

difference between means is significant. The output indicates that there is a significant difference

in performance of grievance settlement operations in terms of complaints resolved in respect of

public and private insurers with t (9) =5.216, p<.05.

VII. FINDINGS AND SUGGESTIONS

The analysis and discussion in the proceeding pages reveals the following findings and

suggestions:

Liberalization has brought a lot of competition among the life insurance companies in

India. Consumers (policyholders) remain the most important centre of the insurance

sector. After the entry of private and foreign insurers, the industry is seeing a lot of

competition and thus improvement of the consumer service.

The LIC has succeeded in resolving consumers grievances when compared to the private

insurers. The number of complaints received in 2010 is very low when compared to the

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

225

year 2006. The LIC being the only public insurer is quite consistent in receiving the

complaints from the policyholders.

So far as outstanding complaints at the end of the year, private insurers have shown

significant performance. Compared to the complaints received and resolved, private

insurers are quite consistent in terms of outstanding complaints at the end of the year. The

result of the t-test revealed that there is a significant difference in performance of both the

complaints received and resolved in respect of the public and private insurers in the life

insurance industry.

LIC, being the only public player in the country, continues to be the dominant life insurer

even in the liberalized scenario of Indian life insurance industry and is moving fast on a

new growth trajectory surpassing its own past records. Entry of private and foreign

payers in the Indian life insurance industry, Life Insurance Corporation (LIC) of India,

needs to improve its performance in the area of grievances settlement a lot to face the

challenge.

VIII. CONCLUSION

In the early part of 2009, a Seminar on Consumer Protection and Education was conducted by

IRDA at Hyderabad wherein some path breaking decisions were announced. One such decision

was to introduce an integrated grievances software, which will allow IRDA to have access to

complaints across the industry and also enable them to monitor the disposal of grievances. IRDA

has undertaken new initiatives in regard to insurance awareness campaign, consumer education

etc. All insurers were advised to file with IRDA the grievance redressal policy adopted by them.

Redressal policy adopted by different companies was published by IRDA as a separate volume.

These initiatives are making steady progress and are expected to take shape within a reasonable

timeframe. Insurers are also advised to provide details of different grievance channels as well

details of the Insurance Ombudsman, wherever applicable, in the policy document itself. These

will be examined when products are filed with IRDA under the File and Use procedure. The

Authority is also in the process of implementing the Integrated Grievance Management System

(IGMS) through automation of the Grievance Cell for on-line registration of complaints. The

proposed automated system would also enable on-line verification of status and redressal.

Further, under the Corporate Governance guidelines, the Authority has also mandated that

insurers shall have in place the Policyholder Protection Committee.

The IRDA has recently established the Consumer Affairs Department to give a special focus to

and oversee the compliance by insurers of the IRDA Regulations for Protection of Policyholders’

Interests and also to empower consumers by educating them regarding details of the procedures

and mechanisms that are available for grievance redressal. Policyholders must be provided with

inexpensive and speedy mechanisms for complaints disposal and the IRDA (Protection of

Policyholders Interests) Regulations, 2002 require insurance companies to have in place,

effective and speedy grievance redress mechanisms. IRDA has also issued Guidelines for

Grievance Redressal, which will further strengthen the redressal systems insurers already have in

place.

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

226

IX. SCOPE FOR FURTHER RESEARCH

The study can be further extended to investigate the performance in terms of consumer

protection and their welfare and comparison among all the life insurers. Such a study would

enhance the level of understanding for managers, academicians and researchers .This research

paper and its findings may be of considerable use to insurance institutions, policy makers and to

academic researchers in the area of consumer protection and their well-being.

X. REFERENCES

Anuradha et al, 2008, “ European Food Policy: Implications for the Insurance Industry”, Journal

of Insurance & Risk Management, Vol-VI, Issue-12,63-82.

Amuthan, R.2005. “A Study on Insurance Companies Strategies in Private Sector Companies

with special reference to HDFC and ICICI” . Indian Journal of Marketing.

Dr.Chandra Prasad, J. et.al, 2009. “Life Insurance Sector in the Liberalized Environment-The

paradigm shift and player performance”. The Indian Journal of Management, Vol.2, Issue.1, 17-

25.

Ehrlich, I. 1972. “Market Insurance, Self-Insurance and Self-Protection”. Journal of Political

Economy.

Lin-Yhi Chou, 2008. “The Impact of Going Public Strategy on Free Cash Flow:-The case of

Taiwan Life Insurance Industry” , Journal of Insurance & Risk Management, Vol-VI, Issue-12,1-

22.

Mala Srivastaval, 2008, “ An Emprical analysis to study the Impact of switching Costs on

Switching Behaviour in Indian Insurance Seector”, Journal of Insurance & Risk Management,

Vol-VI, Issue-12,47-67.

Mathur, N.D, 2002. “ The Indian Insurance Sector”, Indian Journal of Public enterprises, Vol.17,

No.32, 38-46.

Monika Suri,2011. “Insurance Industry-Issues and Challenges”. International Journal of

Retailing and Marketing,Vol.2, No.1, 68-73.

Narasimhan Committee, 1991.Report of the Committee on the Financial System, Government of

India.

Narayana Rao, S.B. and Madhavi, C. 2006. “Insurance Theory and Practice” Prentice Hall of

india private limited, New Delhi, 2008, 104-115.

Peeyush Prakash & Vinay K. Srivastava. 2003. “Growth and Working of Life Insurance

Corporation (LIC) of India”. Indian Journal of Public Enterprise, Vol. 18, No.34,145-154.

SAJMMR Volume 2, Issue 6 (June, 2012) ISSN 2249-877X

South Asian Academic Research Journals http://www.saarj.com

227

Rachappa Shettewar & Shweta Dixit, 2009. “Life Insurance Agent Profiling: Leading Indicators

to Growth”. Journal of Insurance & Risk Management, Vol.7, Issue.14, 21-30.

Rajendran,R. and Dr. Natarajan, B. 2009, “The Impact of LPG on Life Insurance Corporation of

India (LIC)”. Asia Pacific Journal of Finance and Banking Research, Vol.3, No.3, 41-52.

Saif Siddiqui, 2009, “Indian Life Insurance-An Analysis” . Centre for management studies,

Jamia Millia Islamia (Central University), New Delhi, India, Working Paper Series in SSRS

(Social Science Research Network).

Sangamithra, A & Saravanakumar, T.M. 2009, “ Demand for Healthcare and Moral Hazard in

Insurance Industry”. Journal of Insurance & Risk Management, Vol.7, Issue.14, 43-54.

Saravanan, S, 2004. “ Service Marketing Strategies for the New Millennium in Insurance

Sector”. Indian Journal of Marketing.

Sorab Sadri, 2009. “Insurance Marketing”, SCMS Journal of Indian Management, Vol.6,

No.2,104-115.

Syed Ibrahim, M.2009. “Investment Port-folio of Life Insurance Corporation of India”. Journal

of Insurance and Risk Management, Vol. VII, Issue.14,30-41.

Vanniyarajan, T, and Balasenthil, R.S. 2008, “ Evaluation of Quality Dimensions in Life

Insurance Market:-Customer Segmentation Analysis”, Journal of Insurance & Risk Management,

Vol-VI, Issue-12,23-46.

Vara Prasad, V.V. and Murali Krishna, B. 2009. “Insurance Sector-Strategies for Implementation

and Marketing”, Smart Journal of Business Management Studies, Vol.5, No.2, 9-16.

Wenyong Tian and Dongmei Li, 2011. “ Study on Influencing Factors of Rural Insurance

Salesman’s Sale performance”, International Journal of Business and Management, Vol.6, No.5,

180-189.