SOFR and how it is covered in SAP Treasury - compiricus

49

Boston, June 26, 2020 COMPIRICUS Webinar: „SOFR and how it is covered in SAP Treasury“

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SOFR and how it is covered in SAP Treasury - compiricus

Boston, June 26, 2020

COMPIRICUS Webinar:„SOFR and how it is covered in SAP Treasury“

2

Welcome!

Your Speakers

Jorg Pappertis CEO at COMPIRICUS Inc. and focuses on finance market in combination with SAP Treasury for more than 30 years.

Fabian Geueis Principal Consultant at COMPIRICUS and focuses on financial instrument management with SAP since more than 15 years.

3

Agenda

COMPIRICUS at a Glance

Benchmark Rates and their Impact on Capital Markets

Requirements for and Solutions in SAP Treasury

Questions and Answers

4

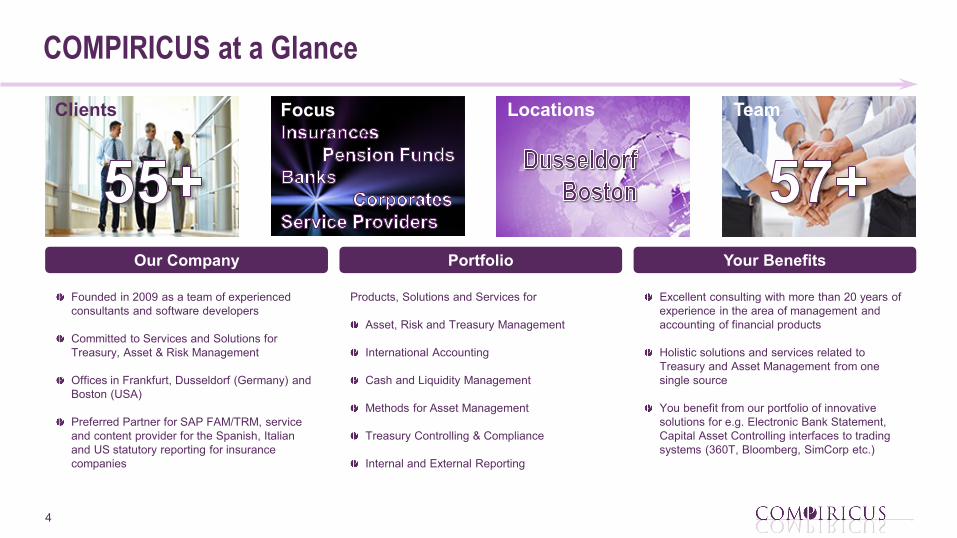

COMPIRICUS at a Glance

Our Company

Founded in 2009 as a team of experienced consultants and software developers

Committed to Services and Solutions for Treasury, Asset & Risk Management

Offices in Frankfurt, Dusseldorf (Germany) and Boston (USA)

Preferred Partner for SAP FAM/TRM, service and content provider for the Spanish, Italian and US statutory reporting for insurance companies

Portfolio

Products, Solutions and Services for

Asset, Risk and Treasury Management

International Accounting

Cash and Liquidity Management

Methods for Asset Management

Treasury Controlling & Compliance

Internal and External Reporting

Your Benefits

Excellent consulting with more than 20 years of experience in the area of management and accounting of financial products

Holistic solutions and services related to Treasury and Asset Management from one single source

You benefit from our portfolio of innovative solutions for e.g. Electronic Bank Statement, Capital Asset Controlling interfaces to trading systems (360T, Bloomberg, SimCorp etc.)

Clients Focus TeamLocations

5

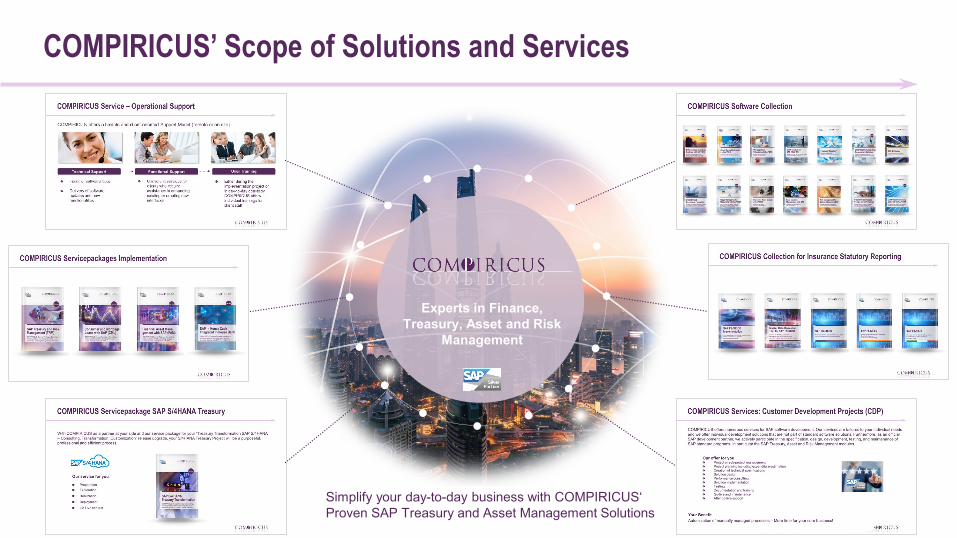

COMPIRICUS’ Scope of Solutions and Services

Experts in Finance, Treasury, Asset and Risk

Management

Simplify your day-to-day business with COMPIRICUS‘Proven SAP Treasury and Asset Management Solutions

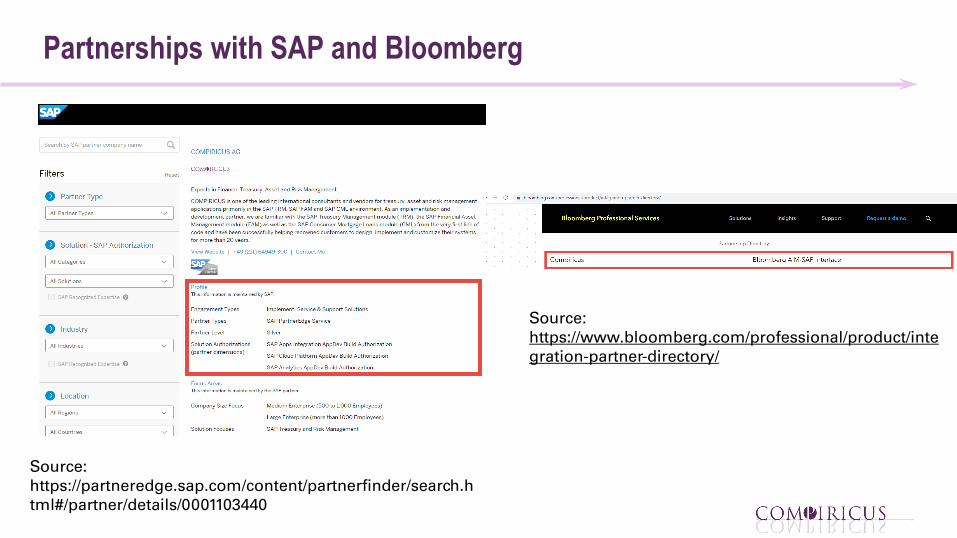

Partnerships with SAP and Bloomberg

Source:https://partneredge.sap.com/content/partnerfinder/search.html#/partner/details/0001103440

Source:https://www.bloomberg.com/professional/product/integration-partner-directory/

7

COMPIRICUS Webinars in 2020

For the second half of the year we have planned a webinar on the “COMPIRICUS Process Cockpit for SAP - a modern SAP UI5 app for the automation of complex financial processes”. Invitation follows.

As a consulting company and software partner specialized in

finance, we would like to support you as usual in all questions concerning the LIBOR-SOFR

Transition. In recent months, we have therefore paid particular attention to the effects of the

benchmark changes on your SAP Treasury (TRM, FAM, CML)

System. Explore in our Webinar, what is important now!

If you have any questions about the above-mentioned topics, please do not hesitate to contact us at any time.At the end of the presentation you will find the contact details.

COMPIRICUS has developed an application for investment/financing projection to forecast interest income/expense as well as a future investment/debt portfolio under scenario assumptions (market assumptions and portfolio assumptions).

9

Agenda

COMPIRICUS at a Glance

Benchmark Rates and their Impact on Capital Markets

Requirements for and Solutions in SAP Treasury

Questions and Answers

10

Reference Interest Rates and its Manipulation

Why Reference Interest Rates?Reference for transactions with variable interest such assecurities and loans as well derivatives like swaps, caps/floor, options

Current typical reference interest rates?Best known is the LIBOR (London Interbank Offered Rate) as a rate that banks lend short-term money to each otherPublished with several maturities: From Overnight up to 12 months

Manipulation of Reference Interest Rates by participating Banks for several yearsConstruction of “IBOR-Determination” (inter-banking market) leaves room for collusion between the participating banks“LIBOR-Scandal“ (2011): Published LIBOR-Rates were not traded but arranged by participating banks over a period of several years

11

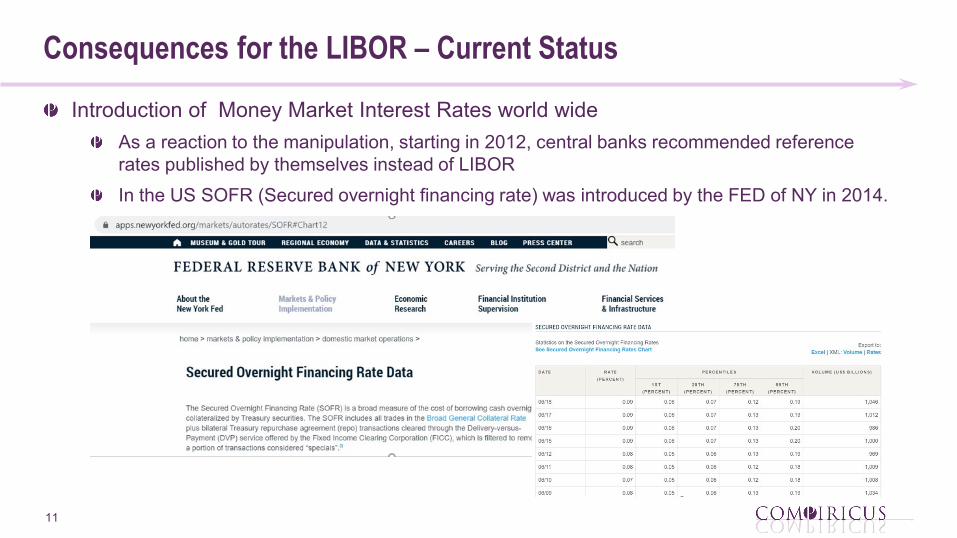

Consequences for the LIBOR – Current Status

Introduction of Money Market Interest Rates world wide As a reaction to the manipulation, starting in 2012, central banks recommended reference rates published by themselves instead of LIBORIn the US SOFR (Secured overnight financing rate) was introduced by the FED of NY in 2014.

12

Consequences for the LIBOR – Current Status

LIBOR will be decommissioned by 2021In 2017 the British Bank Regulation FCA announced support of the LIBOR only until 2021.Since then, national regulating authorities urge market participants to actively convert their financial instruments to the new reference rates.As a result, LIBOR trading volume decreases constantly.

13

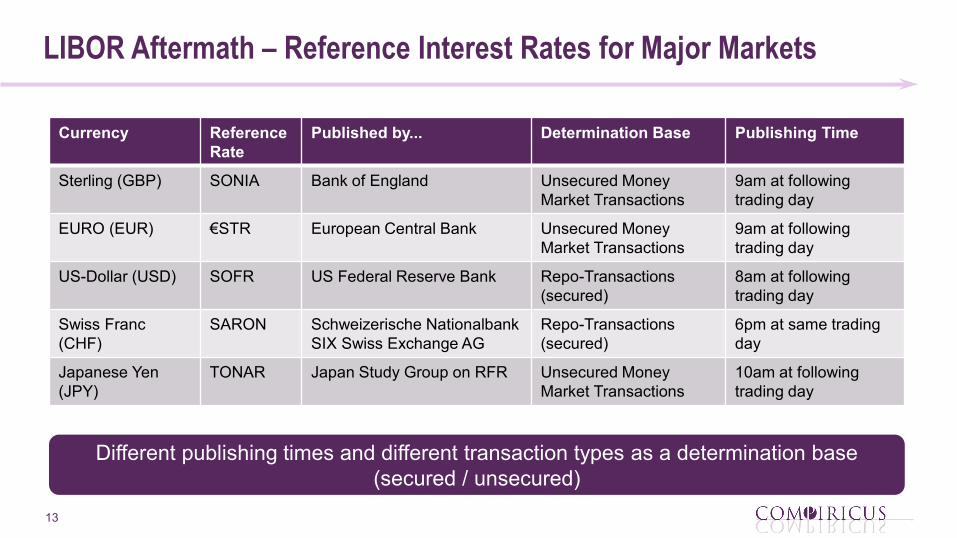

LIBOR Aftermath – Reference Interest Rates for Major Markets

Currency Reference Rate

Published by... Determination Base Publishing Time

Sterling (GBP) SONIA Bank of England Unsecured Money Market Transactions

9am at following trading day

EURO (EUR) €STR European Central Bank Unsecured Money Market Transactions

9am at following trading day

US-Dollar (USD) SOFR US Federal Reserve Bank Repo-Transactions (secured)

8am at following trading day

Swiss Franc (CHF)

SARON Schweizerische NationalbankSIX Swiss Exchange AG

Repo-Transactions (secured)

6pm at same trading day

Japanese Yen (JPY)

TONAR Japan Study Group on RFR Unsecured Money Market Transactions

10am at following trading day

Different publishing times and different transaction types as a determination base (secured / unsecured)

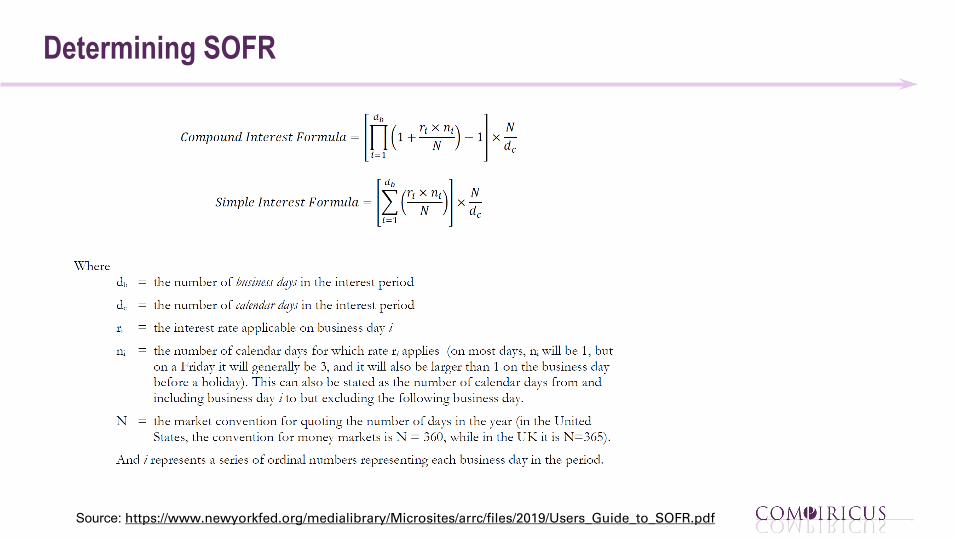

Determining SOFR

Source: https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2019/Users_Guide_to_SOFR.pdf

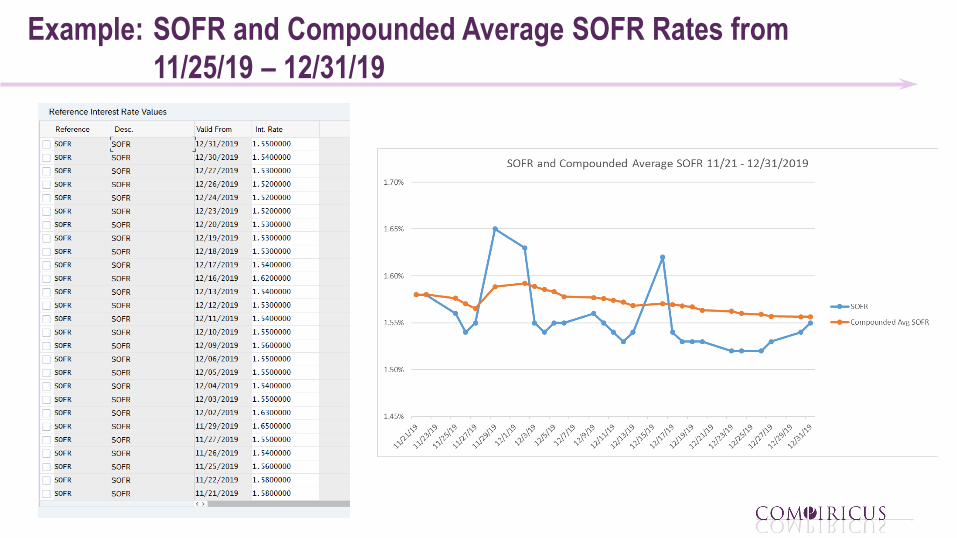

Example: SOFR and Compounded Average SOFR Rates from 11/25/19 – 12/31/19

16

Explaining SOFR Parameters

Source:https://www.newyorkfed.org/medialibrary/microsites/arrc/files/2019/How_to_Use_SOFR.pdf

Parameters to determine interest payments“In Advance“ versus “In Arrears“ Compounding vs. Average CompoundingLookback PeriodLockout PeriodPayment DelaySpreads

included in compounding or added laterARRC recommends not to compound the spread

17

Impacts of the Reference Interest Rate Reform - Overview

Conversion of Financial

Transactions

Model Calculations

Interest Conditions and Cash Flow

Calculation

Determination of Yield Curves and NPV Calculation

Impact on Accounting

18

Agenda

COMPIRICUS at a Glance

Benchmark Rates and their Impact on Capital Markets

Requirements for and Solutions in SAP Treasury

Questions and Answers

19

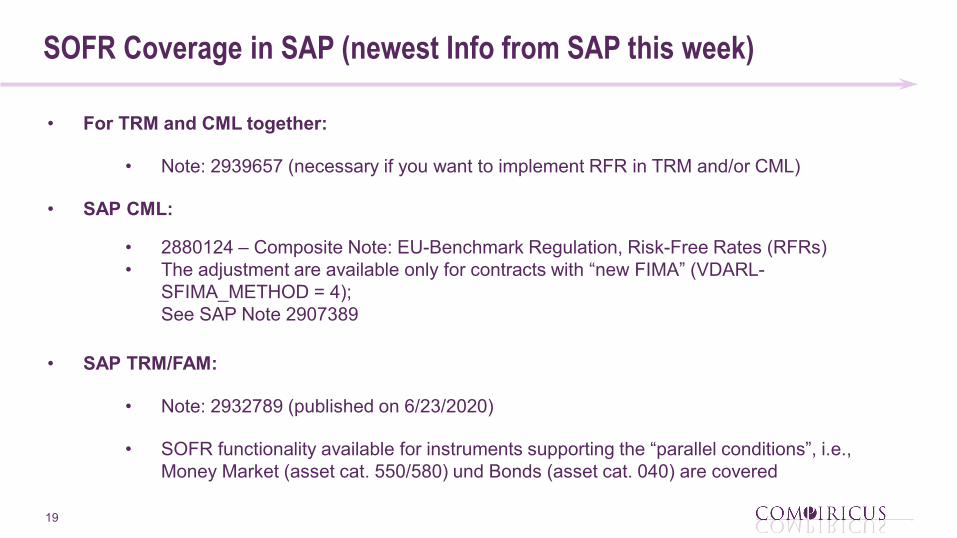

SOFR Coverage in SAP (newest Info from SAP this week)

• For TRM and CML together:

• Note: 2939657 (necessary if you want to implement RFR in TRM and/or CML)

• SAP CML:

• 2880124 – Composite Note: EU-Benchmark Regulation, Risk-Free Rates (RFRs)• The adjustment are available only for contracts with “new FIMA” (VDARL-

SFIMA_METHOD = 4);See SAP Note 2907389

• SAP TRM/FAM:

• Note: 2932789 (published on 6/23/2020)

• SOFR functionality available for instruments supporting the “parallel conditions”, i.e., Money Market (asset cat. 550/580) und Bonds (asset cat. 040) are covered

20

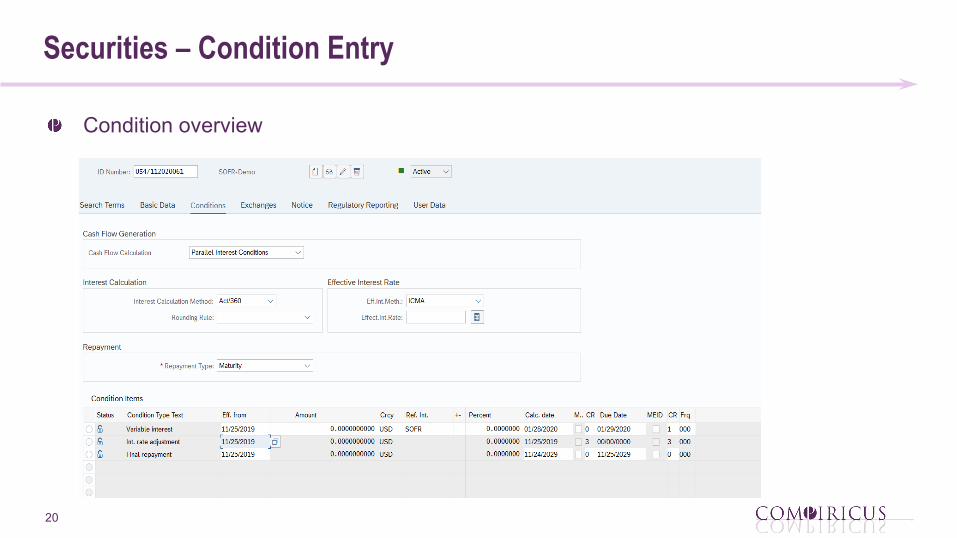

Securities – Condition Entry

Condition overview

21

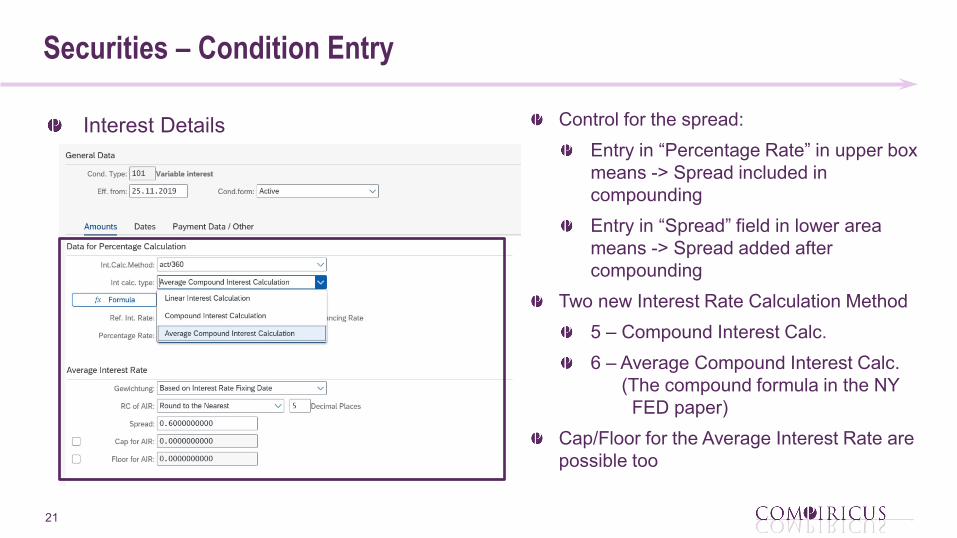

Securities – Condition Entry

Interest Details Control for the spread:Entry in “Percentage Rate” in upper box means -> Spread included in compoundingEntry in “Spread” field in lower area means -> Spread added after compounding

Two new Interest Rate Calculation Method5 – Compound Interest Calc.6 – Average Compound Interest Calc.

(The compound formula in the NY FED paper)

Cap/Floor for the Average Interest Rate are possible too

22

Securities – Condition Entry

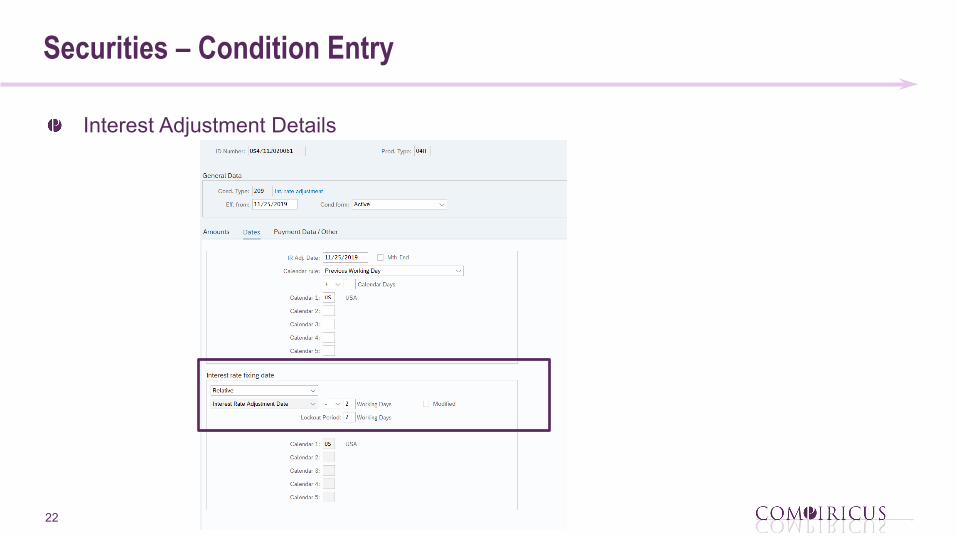

Interest Adjustment Details

23

Securities – Cash Flow Overview (TPM40)

Condition overview

24

Money Market (Borrowing) – Conditions

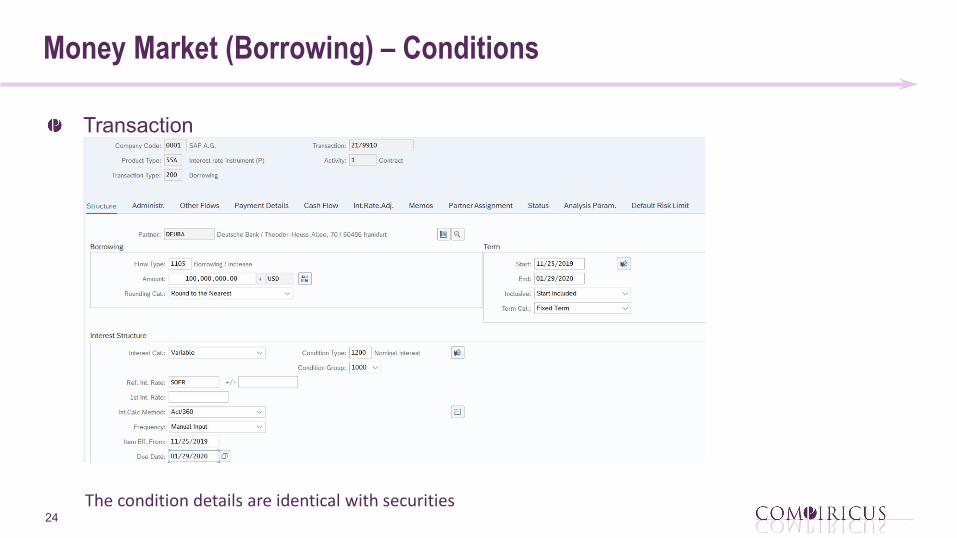

Transaction

The condition details are identical with securities

25

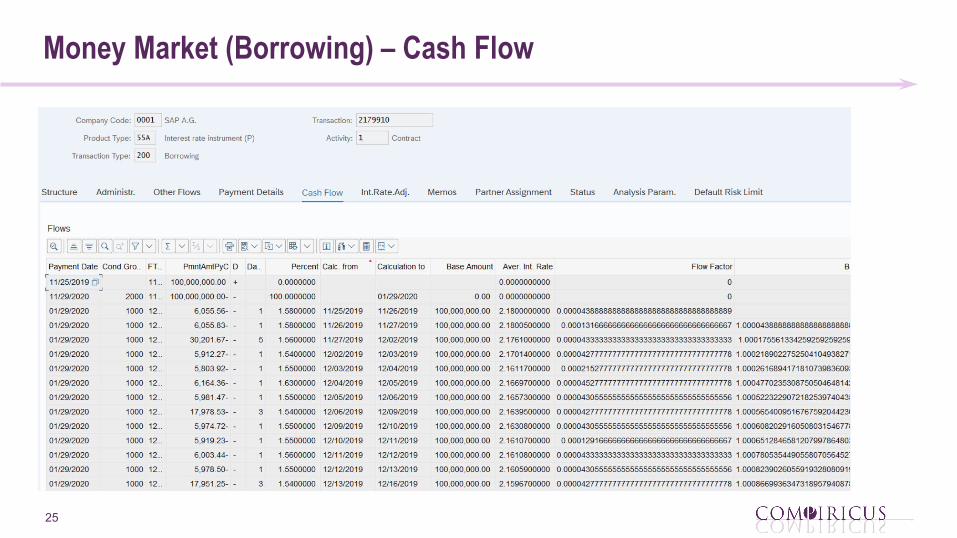

Money Market (Borrowing) – Cash Flow

26

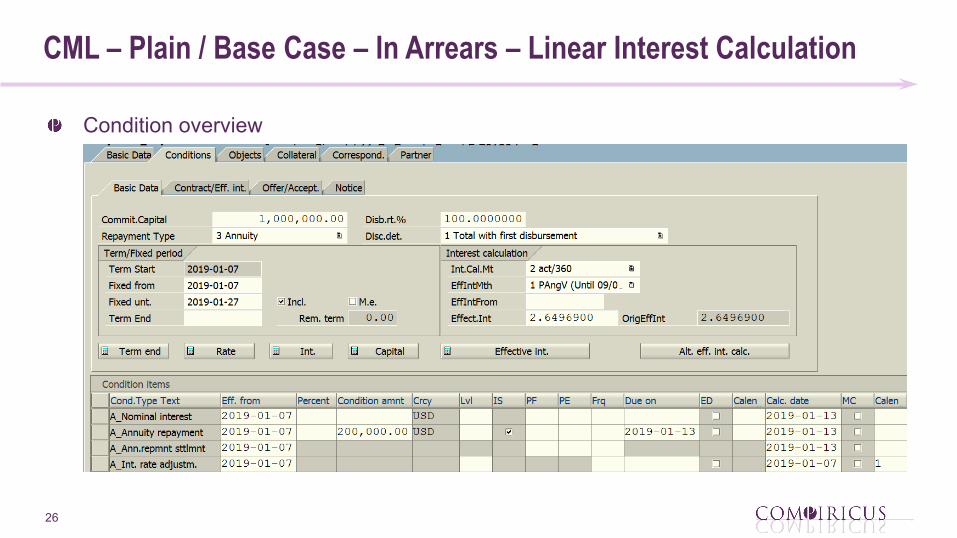

CML – Plain / Base Case – In Arrears – Linear Interest Calculation

Condition overview

27

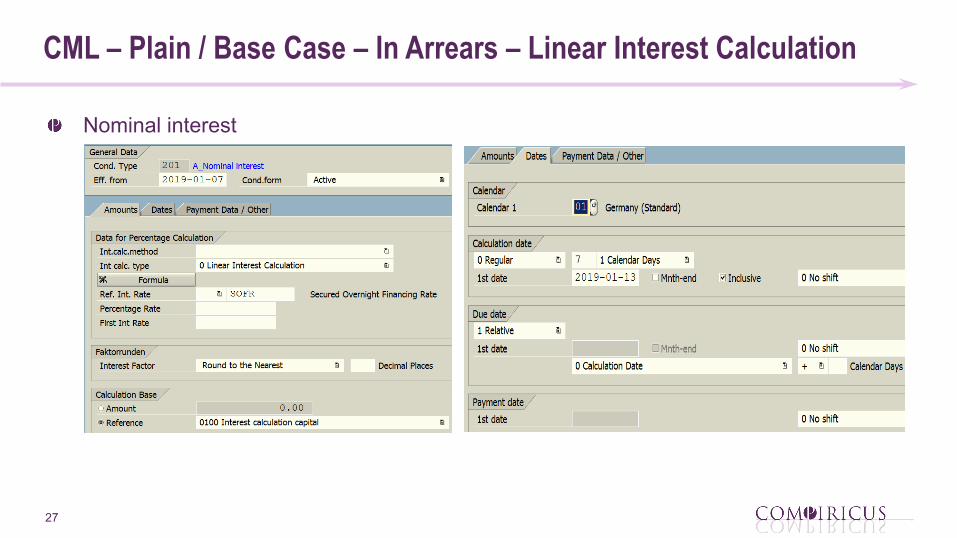

CML – Plain / Base Case – In Arrears – Linear Interest Calculation

Nominal interest

28

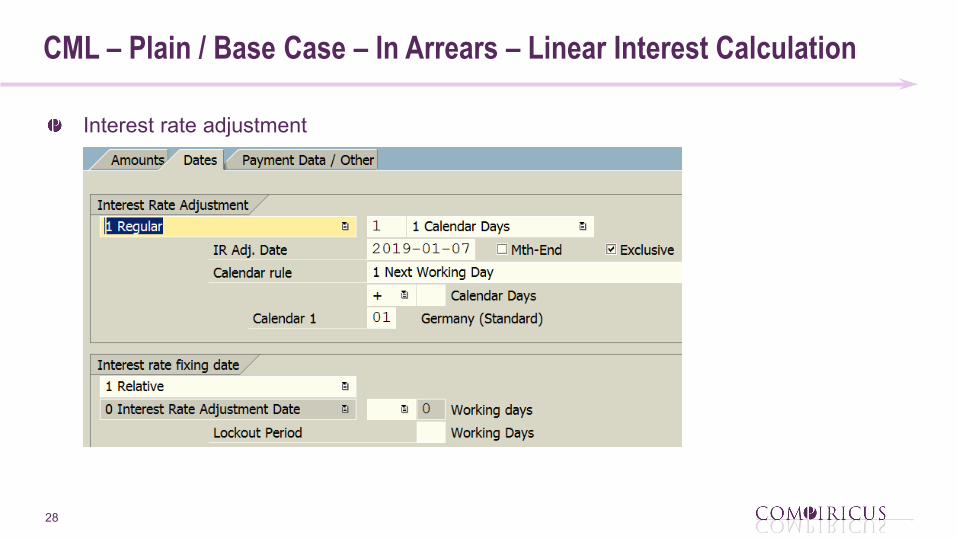

CML – Plain / Base Case – In Arrears – Linear Interest Calculation

Interest rate adjustment

29

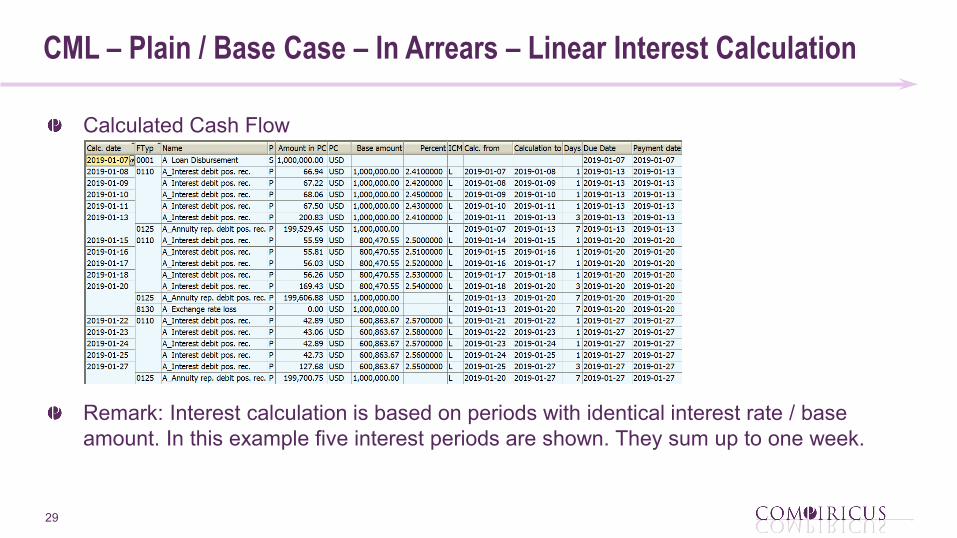

CML – Plain / Base Case – In Arrears – Linear Interest Calculation

Calculated Cash Flow

Remark: Interest calculation is based on periods with identical interest rate / base amount. In this example five interest periods are shown. They sum up to one week.

30

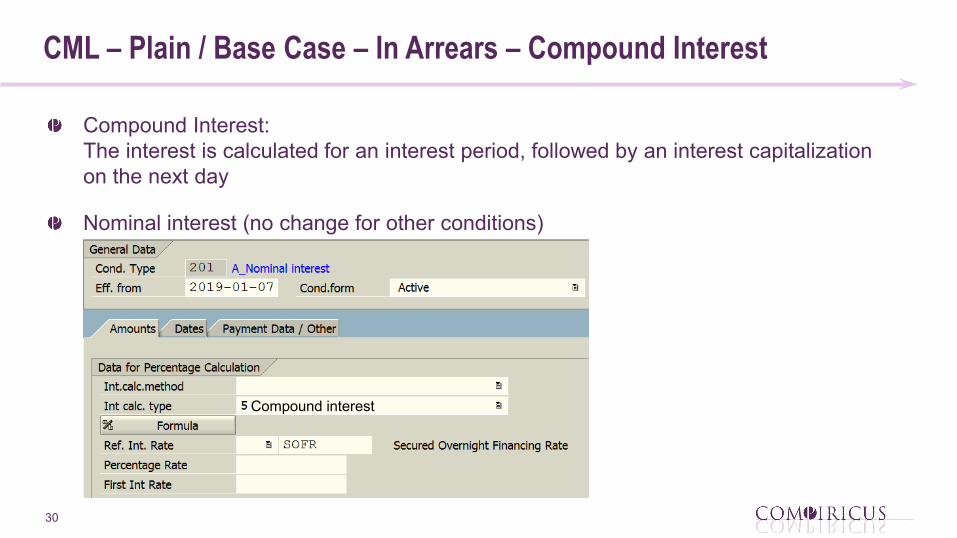

CML – Plain / Base Case – In Arrears – Compound Interest

Compound Interest:The interest is calculated for an interest period, followed by an interest capitalization on the next day

Nominal interest (no change for other conditions)

Compound interest

31

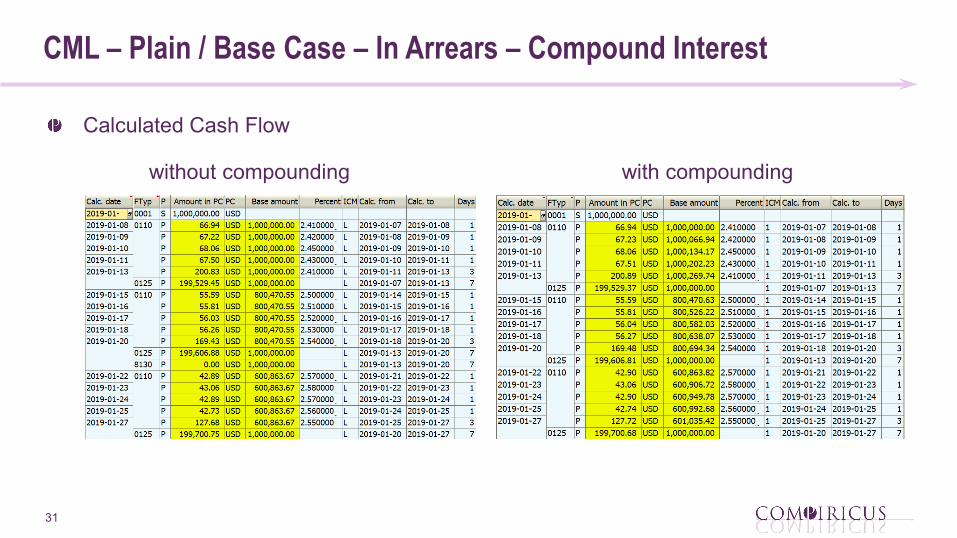

CML – Plain / Base Case – In Arrears – Compound Interest

Calculated Cash Flow

without compounding with compounding

32

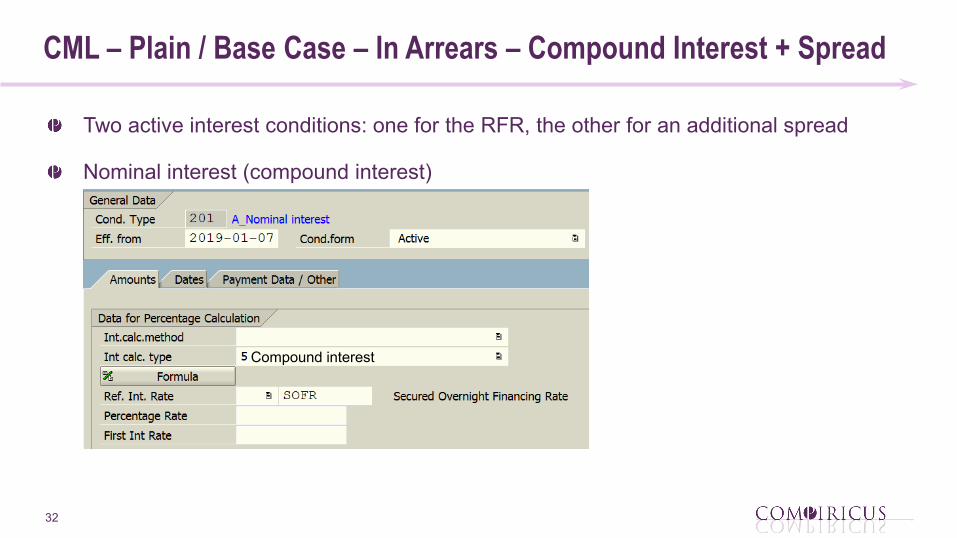

CML – Plain / Base Case – In Arrears – Compound Interest + Spread

Two active interest conditions: one for the RFR, the other for an additional spread

Nominal interest (compound interest)

Compound interest

33

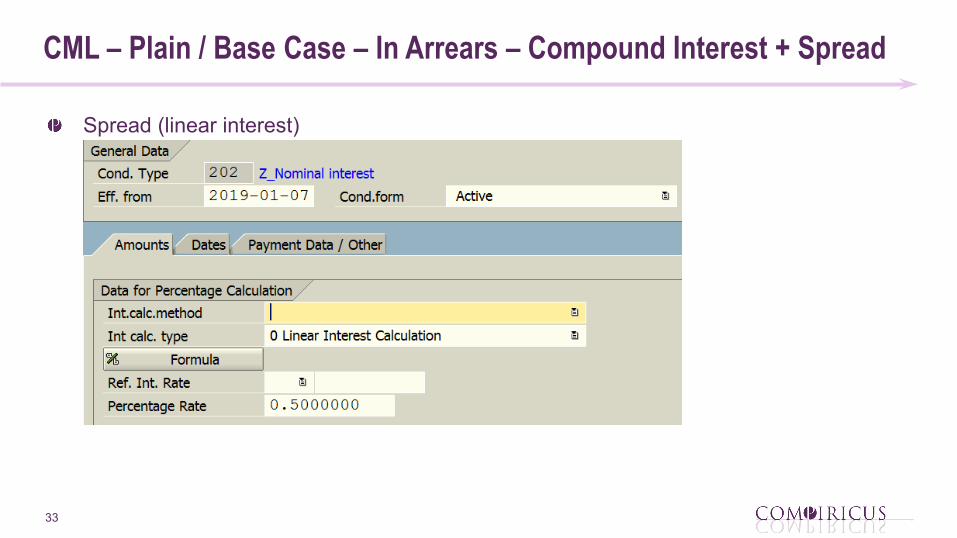

CML – Plain / Base Case – In Arrears – Compound Interest + Spread

Spread (linear interest)

34

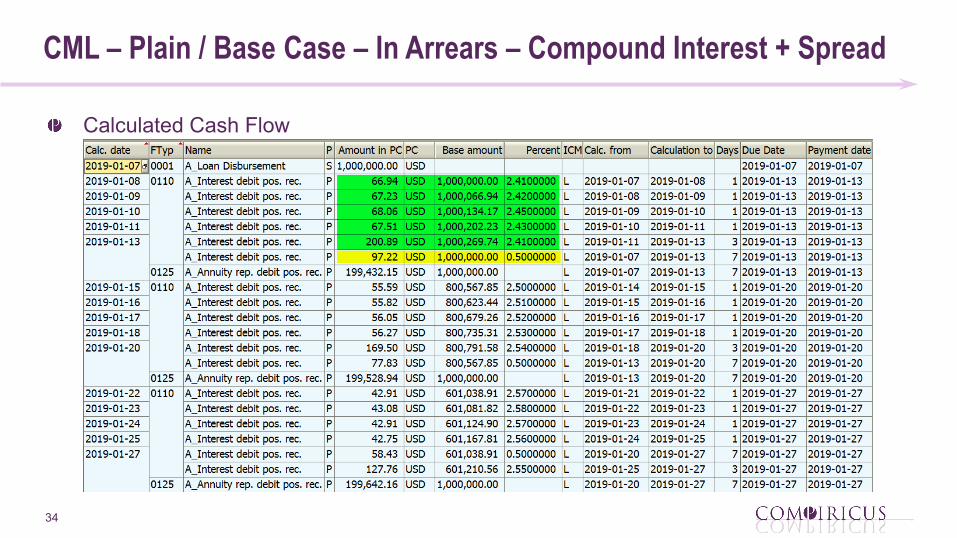

CML – Plain / Base Case – In Arrears – Compound Interest + Spread

Calculated Cash Flow

35

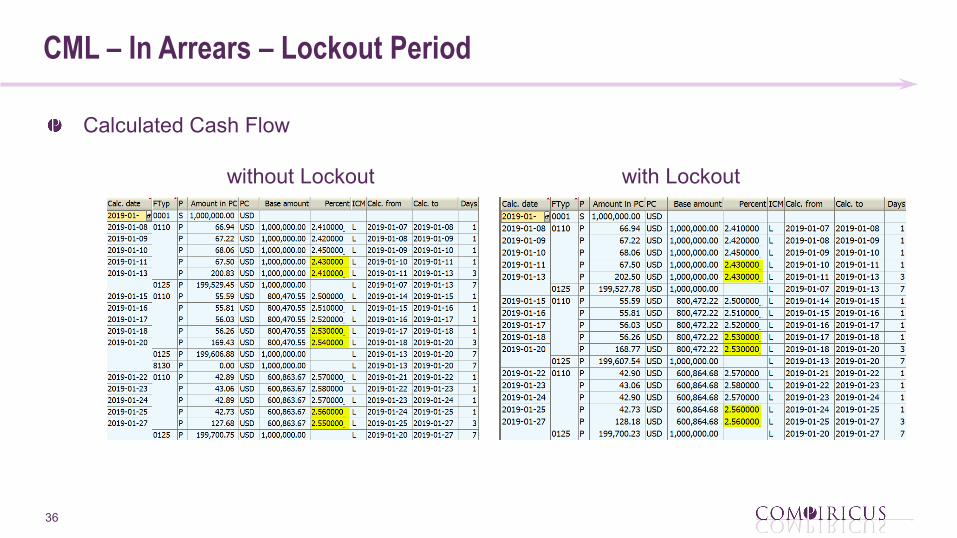

CML – In Arrears – Lockout Period

Lockout working days are set relative to the period end in the interest rate adjustment condition; in this example 1 working day

36

CML – In Arrears – Lockout Period

Calculated Cash Flow

without Lockout with Lockout

37

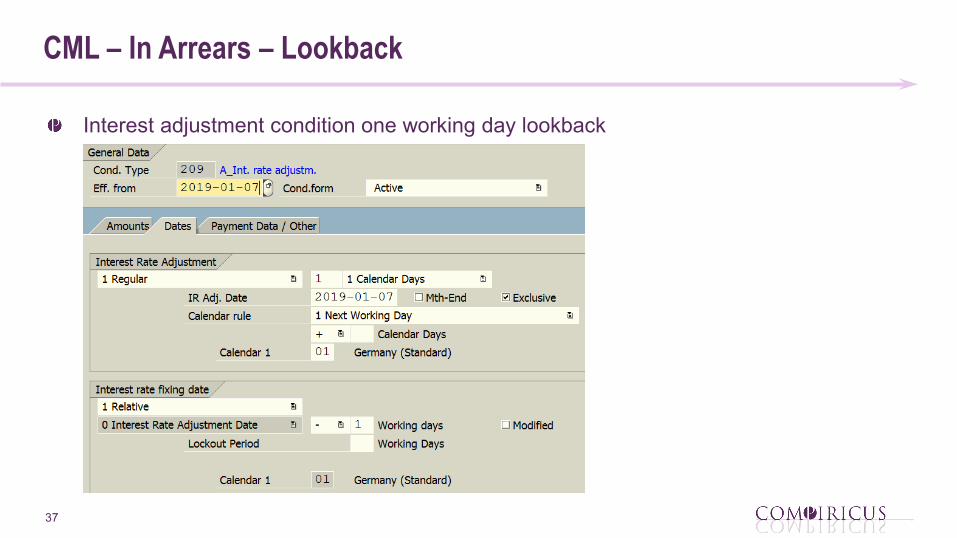

CML – In Arrears – Lookback

Interest adjustment condition one working day lookback

38

CML – In Arrears – Lookback

Calculated Cash Flow

without Lookback with Lookback

39

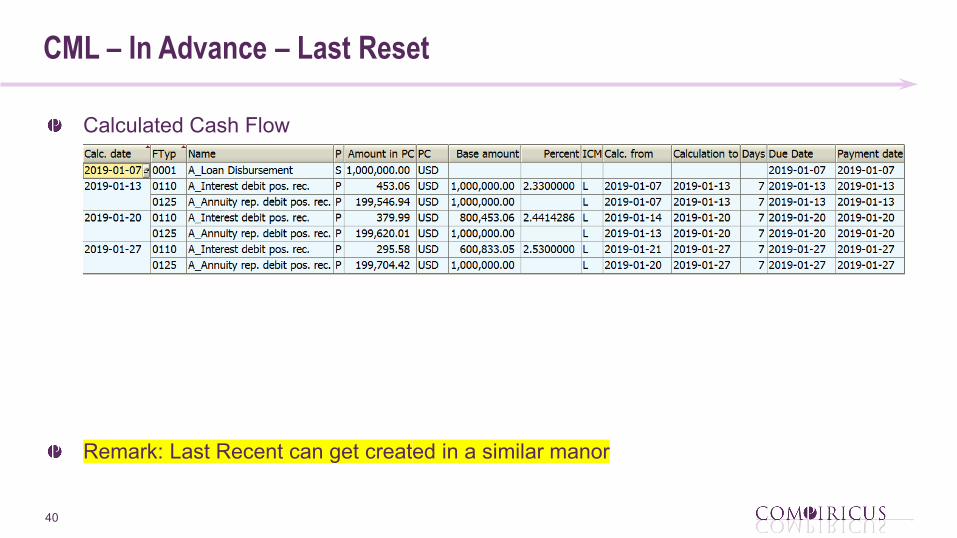

CML – In Advance – Last Reset

Assumption: average reference interest rate, e.g. SOFR 7-day average, is supplied by market data provider. A calculation within SAP is not required anymore

Interest rate adjustment condition

In Arrears In Advance

40

CML – In Advance – Last Reset

Calculated Cash Flow

Remark: Last Recent can get created in a similar manor

41

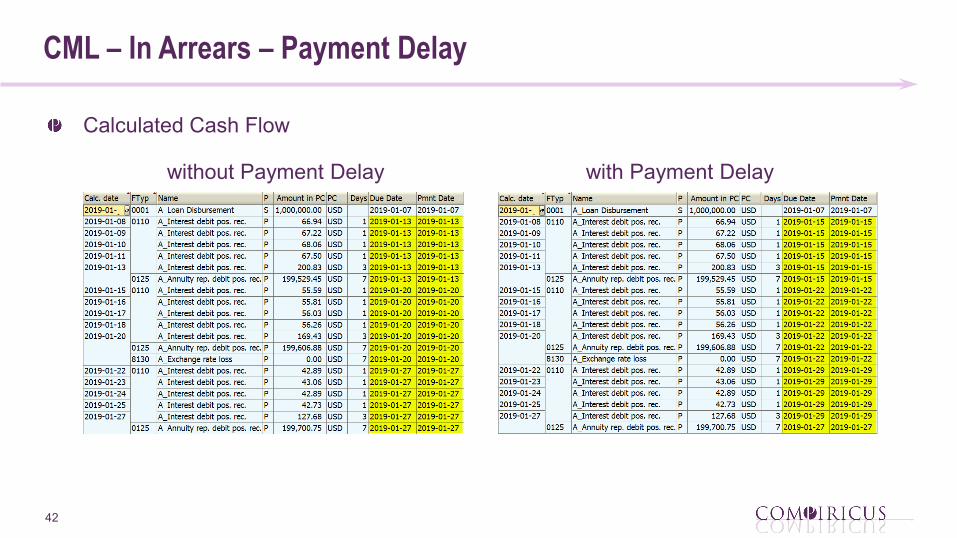

CML – In Arrears – Payment Delay

Nominal interest (linear interest calculation) and annuity repayment with payment delay of two days

42

CML – In Arrears – Payment Delay

Calculated Cash Flow

without Payment Delay with Payment Delay

43

Agenda

COMPIRICUS at a Glance

Benchmark Rates and their Impact on Capital Markets

Requirements for and Solutions in SAP Treasury

Questions and Answers

44

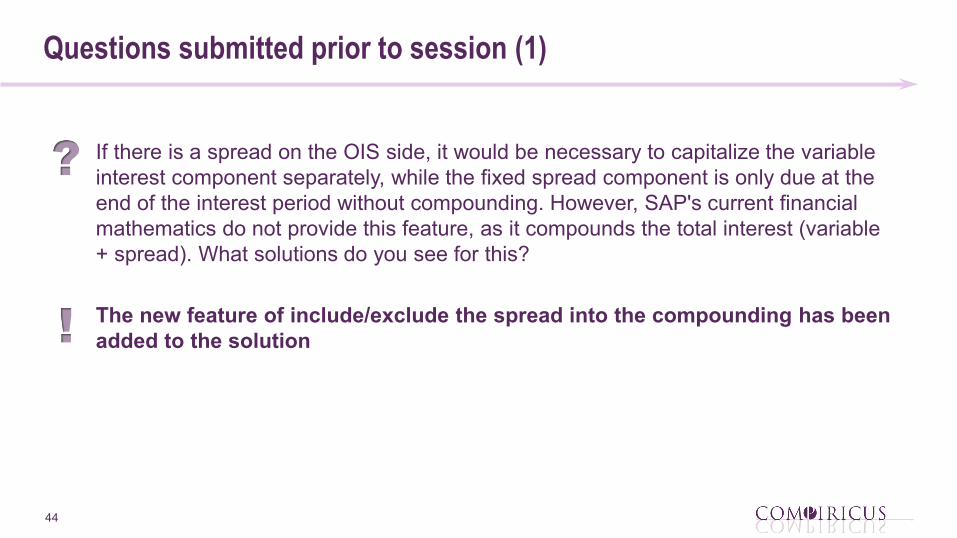

Questions submitted prior to session (1)

If there is a spread on the OIS side, it would be necessary to capitalize the variable interest component separately, while the fixed spread component is only due at the end of the interest period without compounding. However, SAP's current financial mathematics do not provide this feature, as it compounds the total interest (variable + spread). What solutions do you see for this?

The new feature of include/exclude the spread into the compounding has been added to the solution

?

!

45

Questions submitted prior to session (2)

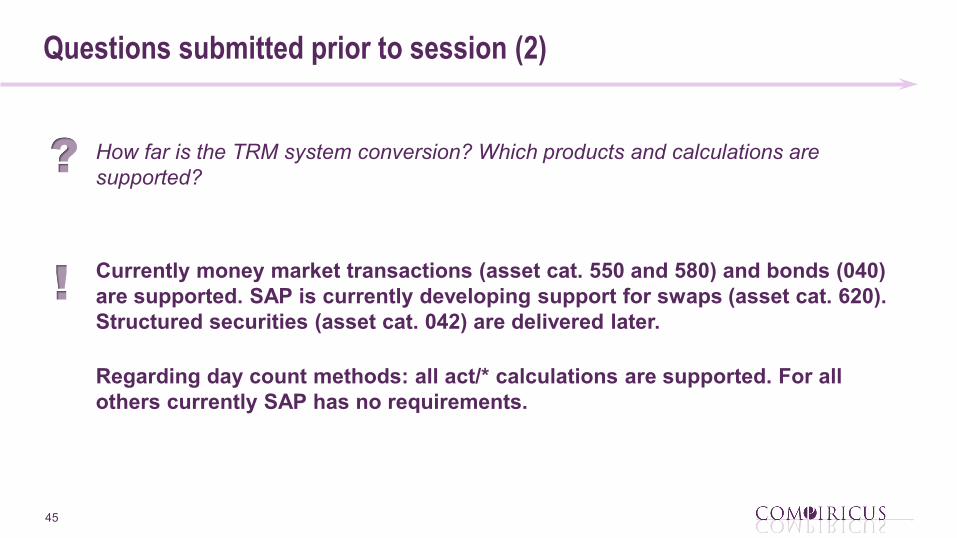

How far is the TRM system conversion? Which products and calculations are supported?

Currently money market transactions (asset cat. 550 and 580) and bonds (040) are supported. SAP is currently developing support for swaps (asset cat. 620). Structured securities (asset cat. 042) are delivered later.

Regarding day count methods: all act/* calculations are supported. For all others currently SAP has no requirements.

?

!

46

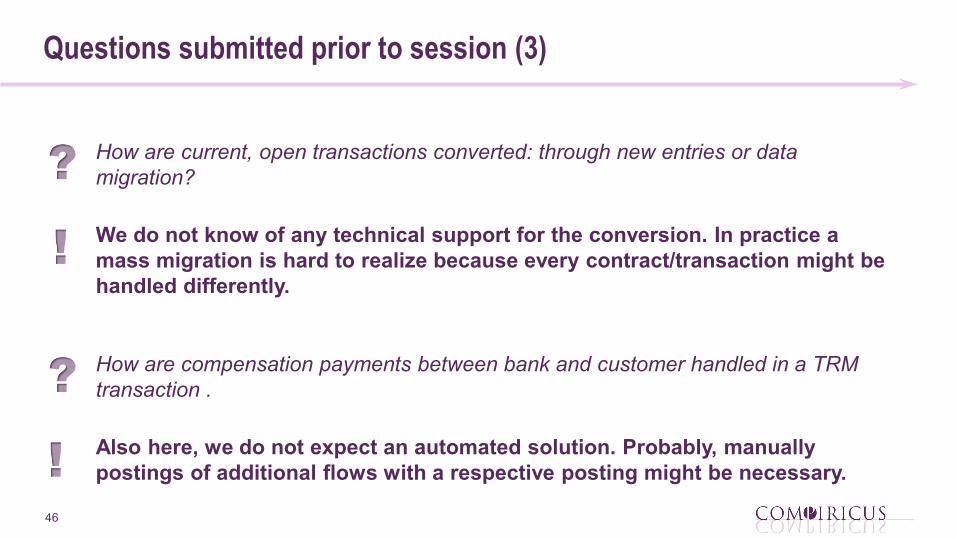

Questions submitted prior to session (3)

How are current, open transactions converted: through new entries or data migration?

We do not know of any technical support for the conversion. In practice a mass migration is hard to realize because every contract/transaction might be handled differently.

How are compensation payments between bank and customer handled in a TRM transaction .

Also here, we do not expect an automated solution. Probably, manually postings of additional flows with a respective posting might be necessary.

?

!

?

!

47

Links

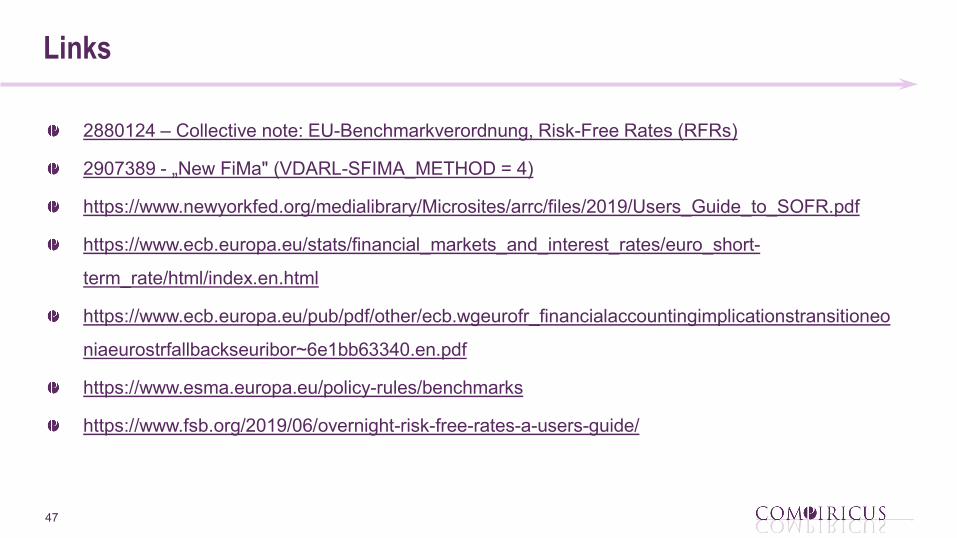

2880124 – Collective note: EU-Benchmarkverordnung, Risk-Free Rates (RFRs)

2907389 - „New FiMa" (VDARL-SFIMA_METHOD = 4)

https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2019/Users_Guide_to_SOFR.pdf

https://www.ecb.europa.eu/stats/financial_markets_and_interest_rates/euro_short-

term_rate/html/index.en.html

https://www.ecb.europa.eu/pub/pdf/other/ecb.wgeurofr_financialaccountingimplicationstransitioneo

niaeurostrfallbackseuribor~6e1bb63340.en.pdf

https://www.esma.europa.eu/policy-rules/benchmarks

https://www.fsb.org/2019/06/overnight-risk-free-rates-a-users-guide/

Don’t hesitate to contact us

Fabian Geue | Principal Consultant

COMPIRICUS AGGraf-Adolf-Platz 6 | 40213 Dusseldorf | Germany

T +49 211 64949-304 | M +49 152 22722304F +49 211 64949-598 | [email protected]

Simplify your day-to-day business with COMPIRICUS’ proven SAP Treasury and Asset Management Solutions

Jorg Pappert | President & CEO

COMPIRICUS INC.Independence Wharf470 Atlantic Avenue, 4th Floor | Boston, MA 02210 | USA

M +1-617-895-7977 | [email protected]

Simplify your day-to-day business with COMPIRICUS’ proven SAP Treasury and Asset Management Solutions

Don’t hesitate to contact us

50