small enterprise managers attitude towards the application of major element of Accounting system(a...

28

SMALL ENTERPRISE MANAGERS ATTITUDE TOWARDS THE APPLICATION OF MAJOR ELEMENTS OF ACCOUNTING SYSTEM[a case study in debre markos town] RESEARCH PROPOSAL SUBMITTED FOR THE PARTIAL FULFILMENT OF BA DEGREE IN ACCOUNTING AND FINANCE PREPARED BY: SIMENEH ALMAW ADVISOR: ABATE GASHAW[MSC]

Transcript of small enterprise managers attitude towards the application of major element of Accounting system(a...

SMALL ENTERPRISE MANAGERS ATTITUDE TOWARDS THE APPLICATION OF MAJOR ELEMENTS OF ACCOUNTING SYSTEM[a case study in debre markos town]

RESEARCH PROPOSAL SUBMITTED FOR THE PARTIAL FULFILMENT OF BA DEGREE IN ACCOUNTING AND FINANCE

PREPARED BY: SIMENEH ALMAW

ADVISOR: ABATE GASHAW[MSC]

DEBRE MARKOS UNIVERSITYCOLLEGE OF BUSINESS AND ECONOMICSDEPARTMENT OF ACCOUNTING AND FINANCE

FEBRUARY,2007 DEBRE MARKOS,ETHIOPIA Table of contentcontent page

CHAPTER ONE- Introduction

1.1 Background of the study……………………………………………………………………. 21.2 Statement of the problem……………………………………………………………………. 31.3 Objective of the study 1.3.1 General objective………………………………………………………………………….4 1.3.2 Specific objective………………………………………………………………………….41.4 Scope of the study…………………………………………………………………………….. 41.5 Limitation of the study…………………………………………………………………………. 41.6 Significance of the study………………………………………………………………………..51.7 Organization of the paper……………………………………………………………………….5 CHAPTER TWO- Literature review2.1 Introduction……………………………………………………………………………………… 62.2 Accounting cycle……………………………………………………………………………….... 62.3 system of bookkeeping………………………………………………………………………… 72.4 Inventory system……………………………………………………………………………….... 8 2.4.1 Inventory valuation method………………………………………………………………… 82.5 Internal control system………………………………………………………………………… 8

CHAPTER THREE-Research Methods3.1 Research design………………………………………………………………………………… 93.2 participant of the study……………………………………………………………………….... 93.3 Sampling techniques……………………………………………………………………………. 93.4 Sample size……………………………………………………………………………………. 93.5 Data type and source…………………………………………………………………………..93.6 Data collection techniques……………………………………………………………………. 10

2

3.7 Data analysis and Interpretation………………………………………………………………10

CHAPTER FOUR-Time and Budget plan4.1 work schedule…………………………………………………………………………………....114.2 Budget breakdown plan…………………………………………………………………………. 12

Bibliography…………………………………………………………………………………….13

CHAPTER ONE

INTRODUCTION 1.1 Background of the study

An Accounting system consists of the personnel,procedures,technologies and records used by an organization to develop accounting information and to communicate this information to decision makers. Therefore,the basic purpose of Accounting system is to meet the organization’s need for information as efficiently as possible( Janr.williams.et al,2006).

Accounting plays an important role in our economic and social system. sound decisions made by individuals, businesses, governments and other entities are essential for the efficient distribution and use of the nations scarce resource. To make such decisions those groups must have reliable information provided by the accounting system( Warren,1999).

3

Accounting is the process of identifying,measuring and communicating economic information to permit informed judgments and decisions by the users of information.Accounting information is used by every profit seeking business organization that uses economic resources and by non profit seeking organizations.The accounting system used by profit seeking business may be viewed as an informationsystem designed to provide relevant financial information on the resource of business and the effect of the use of these resources( Fass warren,1984). This study will also focus on the different major elements of accounting systems;those are accounting cycle,internal control and inventory valuation.

Accounting cycle is a complete sequence of accounting procedures,used to record ,classify and summarize accounting information in financial reports,that is repeated in the some order during each accounting period( williams et al,2006).it includes

Journaling transaction posting to ledger accounts preparing trial balance making end of period adjustment preparing an adjusted trial balance preparing financial statements Journalizing and posting closing entries and preparing an after closing trial balance

Financial statements are the means of convey to management and to interested outsiders provide concise pictures or profitability and financial position of business. the two widely used financial statements are balance sheet and income statements( hermanson,1989).

4

Management needs assurance that accounting information it receives to be accurate and reliable. this accuracy comes from the company’s system of internal control.this study will focus on cash control, purchase control and selling control that likely to be directed and used improperly by employees.

Inventors are asset items held for sale in the ordinary course of business or are goods that will be used or consumed in the production of goods to be sold. the description and measure of inventory requiredcareful intention because the investment in inventory is frequently the largest current asset of merchandise and manufacturing business( Donald.E kieso,1998). Thus, in this study the researcher intends to understand and describe the attitude of small enterprise managers towards the application of those major elements of accountingsystem. 1.2 Statement of the problem

Today it is impossible to manage business operation without accurate and uptodate accounting information. Managers and employees, lenders, suppliers and government agencies are rely on the informationcontained in two financial statements each no more than one page in length. According to Jilly hussey and roger hussey(1999),cost and management accounting, all efficiently managed organization needs to keep some form of accounting system. for big organization like limited companies there are legal requirement that must be adhered. for small enterprises it is important to keep some form of accounting records for taxation and decision making purpose.

5

The researchers personal observation witnessed that most of small enterprise managers handle their business traditionally. they do not have any knowledge of accounting\modern business.all larger or small business have to establish accounting system in order to produce financial statements so as to give precise information for personnel or groups in business and to satisfy external parties. in addition tothis,accounting system provides information to understand better how business has get profit and help to management or organization to plan for future of the business.Hence,in this study the researcher tries to answer the following research questions.

What is the attitude of small business managers towards business events and the accounting treatment?

Does the enterprise managers prepare a crucial financial statements periodically?

What is the attitude of those enterprise managers towards internal control system?

What is the attitude of those enterprise managers towards inventory system?

what is the attitude of small enterprise managers towards double entry bookkeeping system?

why managers apply major elements of accounting system?

1.3 Objectives of the study 1.3.1 General objectiveThe general objective of this study is to evaluate the attitude of small enterprise managers towards the application of major element of accounting system. 1.3.2 Specific objective

1. To assess the attitude of small enterprise managers towards business events and its accounting treatment.

2. To assess whether the enterprise managers prepare crucial financial statements.

3. To assess the attitude of small enterprise managers towards establishing internal control system.

6

4. To assess the attitude of enterprise managers towards inventory system.

5. To assess the attitude of enterprise managers towards doubleentry bookkeeping.

6. To identify the reasons which hinder managers from applyingmajor elements of accounting system.

1.4 scope of the study

This study was very important, if it would conduct over the counter wide.but because of the restriction of time and finance ,it is intended to conduct in debre markos town. moreover, this study focus on small enterprises with employees 6-30 and which has paid up capitalfor, industrial sector from 100,001 up to 1.5 million , and for service sector from 50,001 up to 500,000 excluding high technologicalconsultancy service and other higher technological establishments.

1.5 limitation of the study

The researcher will face the following limitations. The time provided for the study will not enough for the

researcher to collect all necessary information The respondent’s will have heavy work and do not provide the

information on time Some of the respondents will not understand the objective of

the study and think otherwise Some respondents will not give the true information for

their own reason 1.6 Significance of the study

This study will be used for the following significance. It provides important information in accounting system as

having knowledge of accounting system in running business is mostimportant solution for the growth of business.

7

It will give important information on the important accounting system for the profitability of enterprises.

It will identify the reasons why managers apply accounting system.

It may help other researchers who want to conduct a researchon similar topics or area.

1.7 Organization of the paperThis research will be contain five chapters. the first chapter, introduction, the second chapter, literature review, the third chapter, research methods, the fourth chapter, data analysis and interpretation , the fifth chapter ,conclusion and recommendation for the finding of the study.

8

CHAPTER TWO- literature review 2.1 introduction Small business enterprises are a fast growing sector in the worldwide economy .it faces unique problem and it is necessary for them to have effective risk control system. they also provide very important contribution to the development of country in general and surrounding society in particular. The government has recognized the importance of micro and small enterprise development to the overall economic growth of the country and poverty alleviation . it has established micro and small enterprises development agency to coordinate and support this sectors.According to proclamation no/ 33/1998,the agence should be involved indesigning policies and strategies for the development and expansion ofmicro and small enterprises. To this end many developing economy have developed and have been providing credit to poor and small business through micro-financeschemes.in ethiopia several institution have established and have beenoperating towards resolving credit access problem of poor ,particularly those participat in small business activites.

Since small enterprises has great role to the economy of agiven country, it matter to economic whether they are work well or not. However, without the support of microfinance institutions, small business may not work by themselves due to capital constraint. if a given enterprise work well in addition to help of microfinance institution, it is also assumed to be accounting system of the business well,which is the subject area of this study.

9

The main constraint of micro and small business includes;lack of,finance,business information,skill and management expertise, access to appropriate technology,adequate infrastructure and in some instance discriminatory regulatory practices( ministry of trade and industry,1997).

2.2 Accounting cycle

In a well designed accounting system , all accounting process are undertaken in a form of a cycle known as accounting cycle An accounting cycle is a complete sequence of accounting procedures within an accounting system of an enterprises that are repeated in the same order during each accounting period( Fess warren,1984).it outlines the various accounting process that are undertaken by the accountant so as to process transaction data throughthe book of accounts such as journals, cash books,ledger to summarize and draw up financial statements and reports on the

enterprises performance continuously and at year end. an accounting cycle for a typical business organization consists of the following key procedures

Record daily transaction data in source documents;this is apiece of paper or document that initiates a transaction and reports its occurrence.

Analyses and records day by day and in chronological order the daily source document transactions in the journal.

Classify and post the journal transaction data to the ledger.

10

Balance,foot and rule the ledger accounts to ascertain the balance in such accounts.

Prepare a trial balance to summarise and list balance in theledger account to test their arithmetic accuracy.

Prepare a worksheet as a tool used to sort out, update and organize trial balance information needed at the end of the period to summarize and report on the performance of the entity in the form of financial statements.

correct,adjust and update the trial balance information in the worksheet to ensure that all the transaction data and other accounting information that ought to be recorded in the accounts in the ledger have in fact been recorded and that errors committed in the processing of accounting information in the source documents, ledger and trial balances are corrected.

Prepare financial statements in the form of income statement,balance sheet,owners equity statement and statement of cash flow.the two most widely used are income statement and balance sheet.

2.3 system of bookkeeping

2.3.1 Double entry bookkeeping

Double entry bookkeeping is the most efficient and effective method for recording financial transaction in a way which allows the easy preparation of financial statements. in a double entry bookkeeping system every transaction is recorded twice. this reflects the dual nature of transactions and provides an arithmetical check advantage of double entry bookkeeping

Presents a complete picture of the initiation and occurrenceof each and every transaction.

It gives operation support for the accounting equation framework that is the total economic resources of the business(its asset) must always be equal to the source of funds which were used to acquire the resource.

It makes easy to logically follow the movement of funds in the course of trading.

11

It gives a double check on each transactions recorded in theaccounts as equal debit and credit entries are made for every transaction.

It provides a reliable way for the basic requirements expected from accounting records

It permits the orderly classification and summarization of transactions and preparation of financial statements from them.

2.3.2 Single entry systemAn incomplete double entry system can be termed as a single entry system. which is a system of bookkeeping in which as a rule only records of cash and personal accounts are maintained.

2.4 Inventory system

There are two alternative approaches or systems as to determination ofinventory,those are perpetual and periodic inventory system. under periodic system, no attempt is made to record the cost of inventories as sold until at the end of the period. On the other hand ,perpetual inventory system uses accounting record that continuous discloses inventory of each type of commodity at least once a year. the records are then compared with actual quantities on hand and any difference are corrected.

2.4.1 Inventory valuation method.

The price of many kind of merchandise are subject to frequent changes when identical lots of merchandises are purchased at various duties. during the year each lot may be acquired at different cost price. There are several assumption of inventory valuation methods, each assumption mades as to cost of units in ending inventory leads todifferent methods of pricing inventory and to different amounts in financial statement.those four acceptable assumption are, specific identification,average cost,FIFO and LIFO methods(Robert.Anthony,2006).

12

2.5 Internal control system

Internal control system is designed by the organization for the purpose of

1. protecting its resources against waste and frauds.2. securing compliance with management policies.3. Ensuring the accuracy and reliability of accounting and

operating data.The system of internal control includes all policies and procedures that enable an organization to operate in accordance with management plans and policies(Edmonds/olds/mcnair/tsay,2010). Internal controls categorised into two categories. thoseare;accounting controls and administrative controls.accounting controls are measures that relate directly to the protection of assetsor to the reliability of accounting information. administrative controls are policies designed to increase operational efficiency. they have no direct brought upon reliability of accounting records.however,sounds administrative controls may have vital role in successful operation of the business(Robert Meigs,1990).

CHAPTER THREERESEARCH METHODS 3.1 Research design

This descriptive type of research will follow qualitative data collection methods by using questionnaires and structured and unstructured interviews. this interview will have the aim of solving(making clear) difficult questionnaires and to surveying the attitude of enterprise managers. 3.2 participant of the studyThe managers or owners of the enterprise will be the human participantof the study. 3.3 Sampling techniques

13

This research will be conducted by using stratified simple random sampling techniques .Because,the the target population (participant) of the study is most populous and they manage enterprises engaged in different or heterogeneous business activity such as manufacturing,construction,urban agriculture,service and trade.so as to obtain the most representative sample the researcher will use stratified simple random samplig techniqu by makeing strata based on their business activity so that each business group will be represent. 3.4 Sample size

From the total population of ‘82 ‘enterprises(debre markos town micro and small enterprise agence total data summary slip, code 004), the researcher will select a sample of’ 46 ‘ enterprises by 90% level of confidence,by using the formula below;

n=N/1+N(e)2 when: n = sample size N = total population e = significance level(1-level of confidence)among those sampled enterprise 23 will be from manufacturing,5 will befrom construction,13 will be from service,2 will be from urban agriculture and 3 will be from trade based on their proportion. 3.5 Data type and source The most important data used for this study will be primary data that will be collected from managers or owners of the enterprises.there will be no secondary data that used to measure the attitude. 3.6 Data collection techniquesThe data will be collected by using primary data collection techniquessuch as questionnaires and interviews(both structured and unstructured).

14

3.7 Data analysis and interpretation

After the collection of available data ,from debre markos town small enterprise managers about their attitude towards the applicationof major element of accounting systems, the the researcher will analysis by using table,percentage and also simple descriptive statistics. Interpretation will be made on unbiased manner and it will focus on quantitative and qualitative results.the quantitative results will be presented in tabulation form.

15

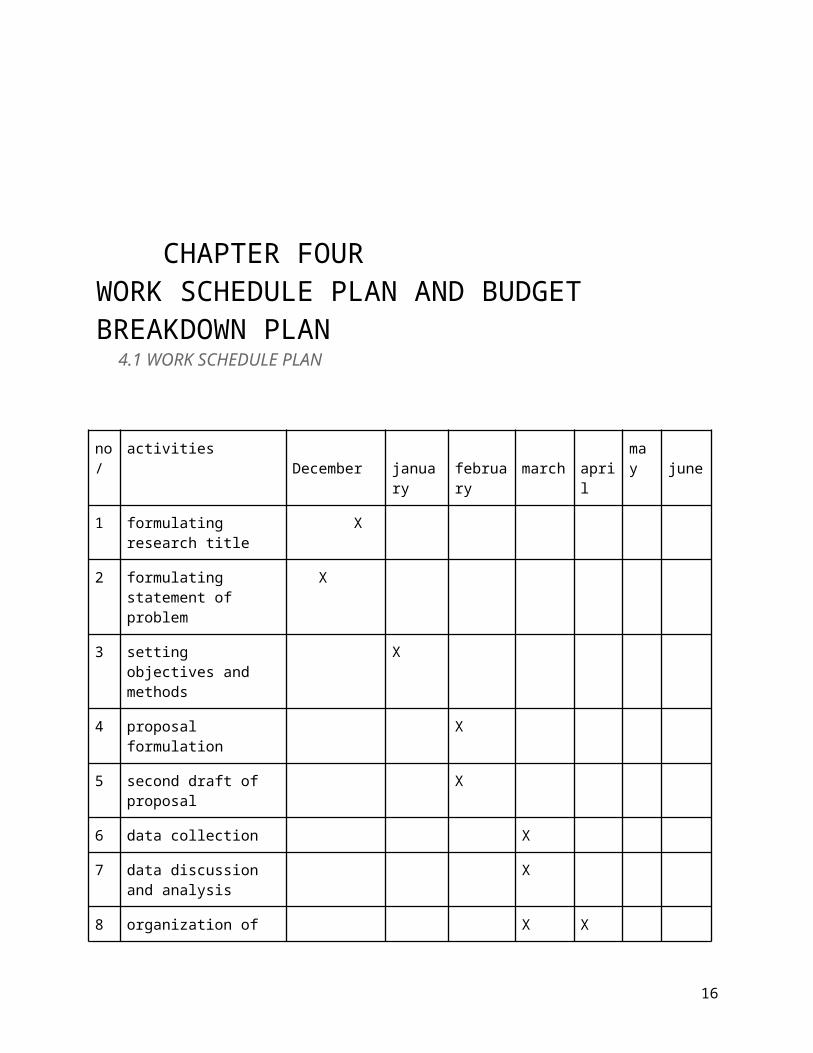

CHAPTER FOURWORK SCHEDULE PLAN AND BUDGET BREAKDOWN PLAN 4.1 WORK SCHEDULE PLAN

no/

activities December

january

february

march

april

may

june

1 formulating research title

X

2 formulating statement of problem

X

3 setting objectives and methods

X

4 proposal formulation

X

5 second draft of proposal

X

6 data collection X

7 data discussion and analysis

X

8 organization of X X

16

research paper

9 conclusion and recommendation

X

10 submission of first draft of the paper

X

11 submission of final research paper

X

12 presentation of the paper

X

17

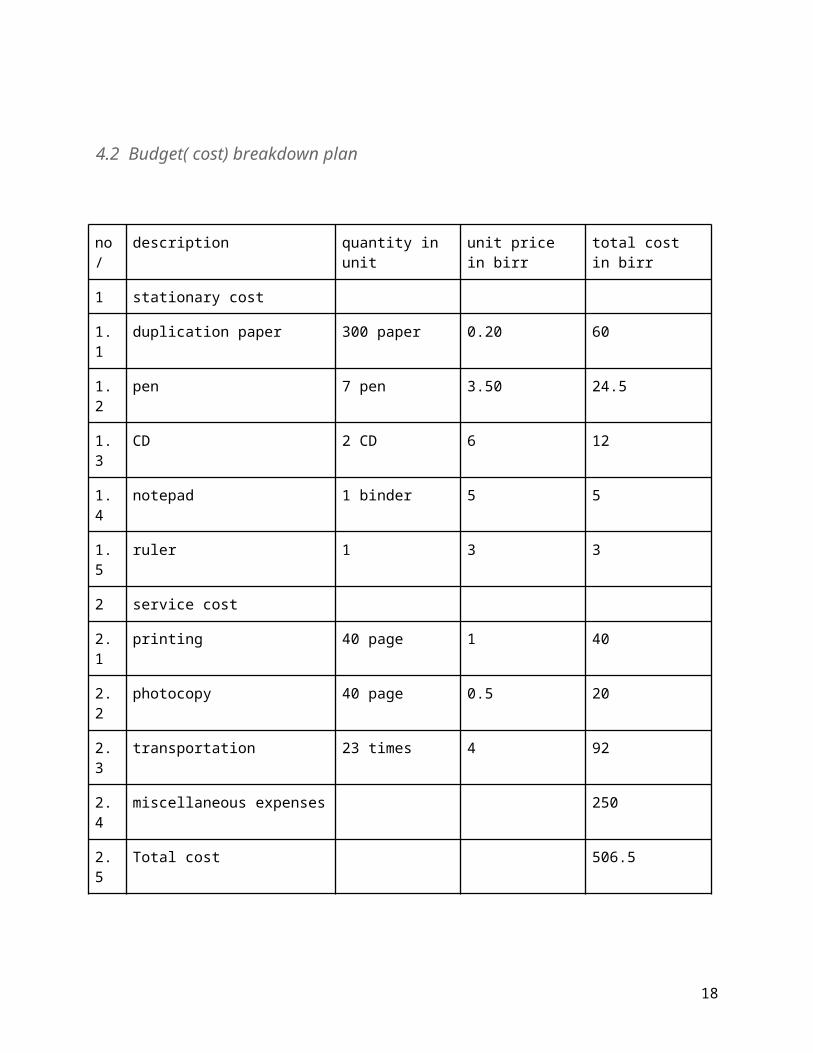

4.2 Budget( cost) breakdown plan

no/

description quantity in unit

unit price in birr

total cost in birr

1 stationary cost

1.1

duplication paper 300 paper 0.20 60

1.2

pen 7 pen 3.50 24.5

1.3

CD 2 CD 6 12

1.4

notepad 1 binder 5 5

1.5

ruler 1 3 3

2 service cost

2.1

printing 40 page 1 40

2.2

photocopy 40 page 0.5 20

2.3

transportation 23 times 4 92

2.4

miscellaneous expenses 250

2.5

Total cost 506.5

18

BIBLIOGRAPHY

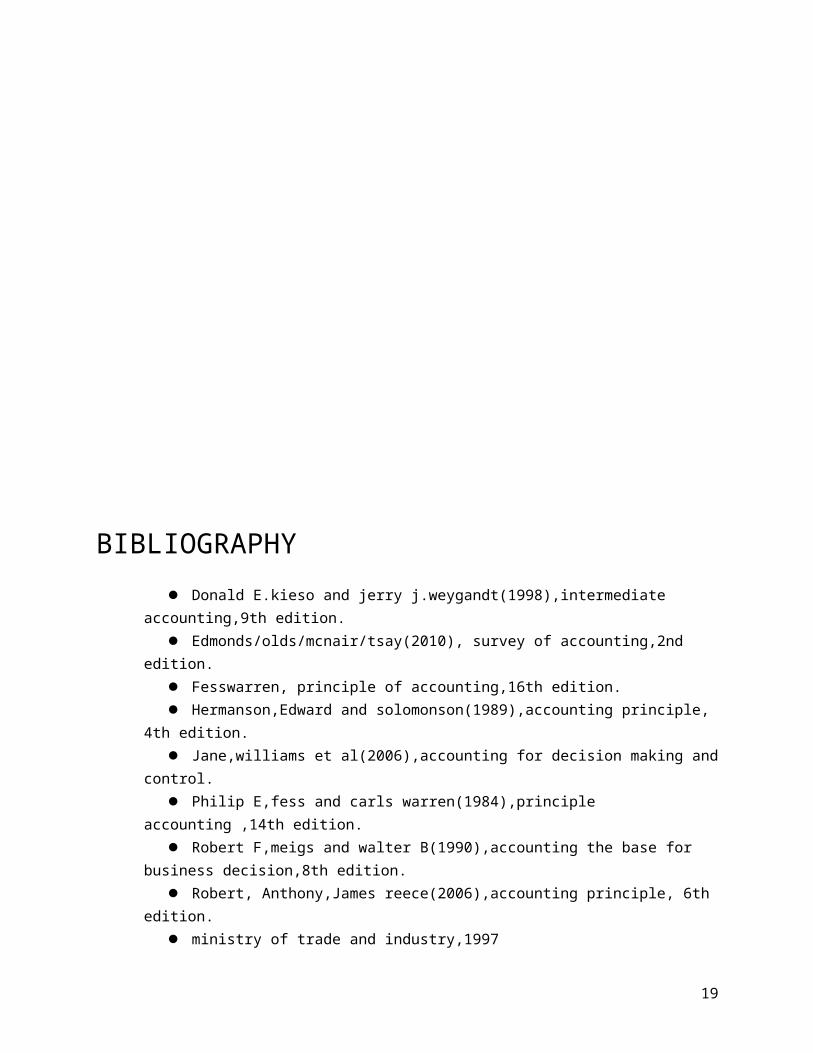

Donald E.kieso and jerry j.weygandt(1998),intermediate accounting,9th edition.

Edmonds/olds/mcnair/tsay(2010), survey of accounting,2nd edition.

Fesswarren, principle of accounting,16th edition. Hermanson,Edward and solomonson(1989),accounting principle,

4th edition. Jane,williams et al(2006),accounting for decision making and

control. Philip E,fess and carls warren(1984),principle

accounting ,14th edition. Robert F,meigs and walter B(1990),accounting the base for

business decision,8th edition. Robert, Anthony,James reece(2006),accounting principle, 6th

edition. ministry of trade and industry,1997

19

Debre markos town administration micro and small enterprises agency total summary data slip,code 004.

website

http:/www.gov.et/ micro and small enterprise development agency.

http:/www.memoireonline.com/accounting system in small enterprise.

20

-7-

21

22

-8-

23

-9-

24

10

25

-11-

26

-12-

27