sc/civ. 6 and 7/2018 in the supreme court of sierra leone (civil ...

Upload

khangminh22Category

view

1download

0

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 115408-SL

REPUBLIC OF SIERRA LEONE

PRIORITIES FOR SUSTAINABLE GROWTH AND POVERTY REDUCTION

SYSTEMATIC COUNTRY DIAGNOSTIC (SCD)

February 6, 2018

International Development Association Country Department AFCW1 Africa Region

International Finance Corporation Sub-Saharan Africa Department Multilateral Investment Guarantee Agency

Sub-Saharan African Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

REPUBLIC OF SIERRA LEONE

GOVERNMENT FISCAL YEAR

January 1 – December 31

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of October 31, 2017)

Currency Unit = Sierra Leonean Leones

US$1.00 = 7,645.5

LIST OF ABBREVIATIONS

ABC Agricultural Business Center ACC Anti-Corruption Commission ACE Africa Coast to Europe AD Asset Declaration AfDB African Development Bank AfP Agenda for Prosperity AIDI AfDB’s Infrastructure Development Index AML Anti-money Laundering APC All People’s Congress BSL Bank of Sierra Leone CCKP Climate Change Knowledge Portal CFSVA Comprehensive Food Security and Vulnerability Analysis CFT Combating the Financing of Terrorism CSIRO Commonwealth Scientific and Industrial Research Organization DEO District Education Offices DHS Demographic and Health Survey DTIS Diagnostic Trade Integration Study EIA Environmental Impact Assessment EITI Extractive Industries Transparency Initiative EPA Environmental Protection Act ESIA Environmental and Social Impact Assessment FAO Food and Agriculture Organization FBO Farmer Based Association FDI Foreign Direct Investment FGM Female Genital Mutilation FIU Financial Intelligence Unit GBV Gender-based Violence

ii

GDP Gross Domestic Product GPI Gender Parity Index GST Goods and Services Tax ICT Information and Communication Technology IFPRI International Food Policy Research Institute IMF International Monetary Fund LC Local Council LFS Labor Force Survey MAFFS Ministry of Agriculture, Forestry, and Food Security MIROC Model for Interdisciplinary Research on Climate MCAS Mining Cadaster Administrative System MDAs Ministries, Departments, and Agencies MEST Ministry of Education, Science and Technology MMA Mines and Minerals Act MPR Monetary Policy Rate MWR Ministry of Water Resources NGO Nongovernmental Organization NMA National Minerals Agency NPL Nonperforming Loan NRA National Revenue Authority OTC Over the Counter PCR Primary Completion Rate PEFA Public Expenditure and Financial Accountability PFM Public Financial Management RUF Revolutionary United Front SCD Systematic Country Diagnostic SLIHS Sierra Leone Integrated Household Survey SLPP Sierra Leone People’s Party TDSF Transformational Development Stabilization Fund UNICEF United Nations Children’s Fund WDI World Development Indicators WDR World Development Report

Regional Vice President, IDA Makhtar Diop Vice President, IFC Sergio Pimenta Vice President, MIGA Keiko Honda Country Director, IDA Henry G. R. Kerali Regional Director, IFC Cheikh Oumar Seydi

MFM Poverty Governance Senior Directors Carlos Felipe Jaramillo Carolina Sanchez-Paramo Deborah Wetzel Directors Paloma Anos Casero James Brumby Practice Managers Abebe Adugna Andrew Dabalen George Larbi Task Team Leaders Mamadou Ndione Kristen Himelein Kastelic Deborah Isser

iii

ACKNOWLEDGEMENTS This report was prepared by a team led by Kristen Himelein (Senior Economist/Statistician, GPV07); Deborah Isser (Lead Governance Specialist, GGO19); and Mamadou Ndione (Senior Economist, GMF01), with additional contributions from Elizabeth Foster (Consultant, GPV07); Inder Sud (Consultant); and Cyrus Talati (Senior Economist, OPSPQ). The team gratefully acknowledges the overall guidance of Henry Kerali (Country Director, AFCW1); Parminder Brar (Country Manager for Sierra Leone, AFCW1); Andrew Dabalen (Practice Manager, GPV07); Abebe Adugna (Practice Manager, GFM01); Kathleen Beegle (Program Leader, AFCW1); Errol Graham (Program Leader, AFCW1); and Ivo Imparato (Program Leader, AFCW1). The table below identifies the full list of team members that have provided written comments to the Systematic Country Diagnostic. The peer reviewers were Kevin Carey (Lead Economist, GMF07); Ruth Hill (Senior Economist, GPV01); and Edouard Al Dahdah (Senior Public Sector Specialist, GGOOS).

Table of Input Providers

Global Practice/ Cross Cutting Solutions Area

Input Providers

Agriculture Hardwick Tchale Education Peter Darvas, Andaleeb Jahan Alam, Kaliope Huck-Aziz,

Ibironke Folashade Oyatoye Energy and Extractives Daniele La Porta, Jianping Zhao, Nash Fiifi Eyison Environment and Natural Resources Jingjie Chu Finance and Markets Nicholas Smith, Cari Votava, Michael Corlett Governance Don Mphande, Helene Marie Grandvoinnet Health, Nutrition, and Population Shiyong Wang, Francisca Ayodeji Akala Macroeconomic and Fiscal Management Kemoh Mansaray, Sona Varma, Santiago Herrera, and

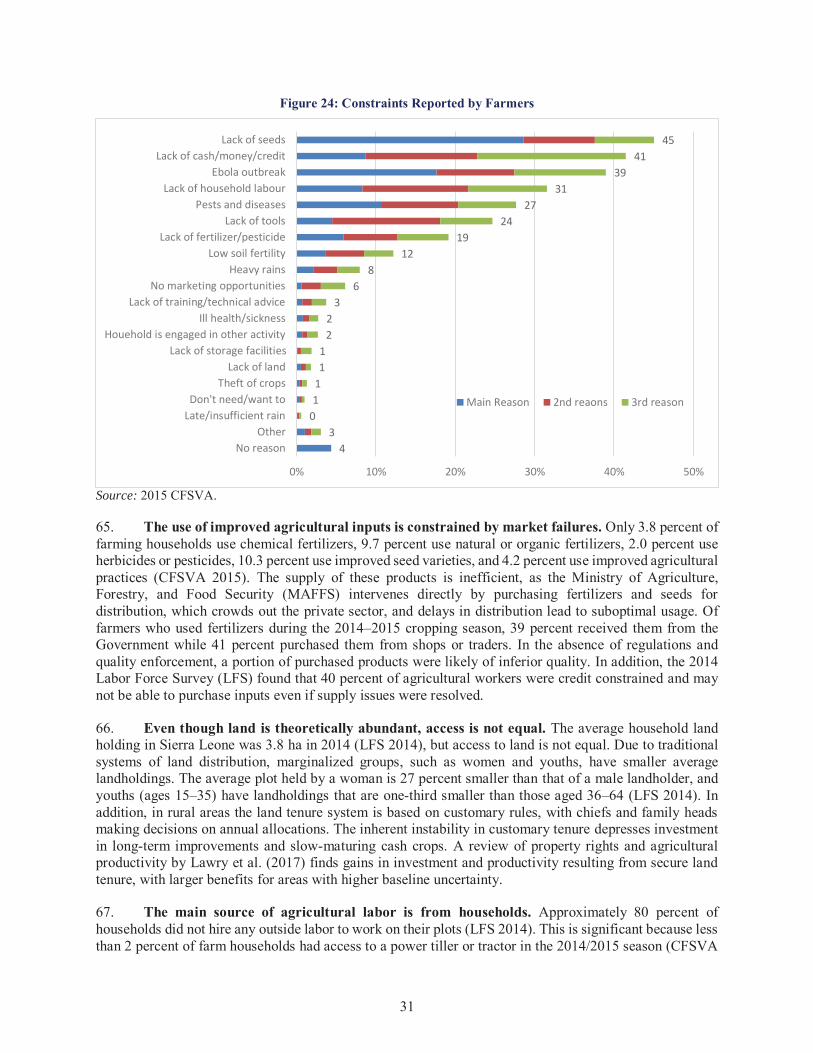

Kevin Carey Poverty Ambar Narayan, Ruth Hill, Elizabeth Foster Social Protection and Labor Stefano Paternostro, Suleiman Namara, Nina Rosas Raffo Trade and Competitiveness Kaliza Karuretwa Transport and ICT Olatunji Ahmed Social, Urban, Rural and Resilience Gregory Wilson Myers, Linus Potts Water Dominick Revell de Waal Fragility, Conflict, and Violence Luigi Giovine, Vishal Ashvin Patel, Neelam Nizar Verjee Public-Private Partnerships Climate Zhihong Zhang Gender Daniel Kirkwood, Niklas Buehren Jobs IFC Frank Ajilore, Giima Mabel Lavaly

iv

TABLE OF CONTENTS

Executive Summary ...................................................................................................................................vii

Introduction.................................................................................................................................................. 1

Chapter 1: Country Context ....................................................................................................................... 3 Geography and Natural Resources ............................................................................................................ 3 The People of Sierra Leone ....................................................................................................................... 3 Governance and Institutions ...................................................................................................................... 4

The Resilience of the Patrimonial Political Settlement ......................................................................... 4 The Challenge of Public Sector Institutions ........................................................................................ 11

Chapter 2: Progress on Shared Prosperity ............................................................................................. 17 National Development Strategy ............................................................................................................... 17 Trends in Poverty ..................................................................................................................................... 17

Chapter 3: Drivers of Growth and Risk to Sustainability ..................................................................... 24 Postwar Drivers of Growth ...................................................................................................................... 24 Risk to Sustainability of Current Economic Growth and Poverty Reduction Patterns ........................... 27

Chapter 4: Future of Shared Prosperity ................................................................................................. 29 Strengthening the Productivity of the Agricultural Base ......................................................................... 29

Opportunities ....................................................................................................................................... 29 Constraints ........................................................................................................................................... 30

Diversifying the Economy and Creating Poverty-Alleviating Jobs......................................................... 33 Constraints ........................................................................................................................................... 36 Opportunities ....................................................................................................................................... 45

Strengthening the Management of Mineral Resources ............................................................................ 50 Increasing Human Capital for New Opportunities .................................................................................. 54

Opportunities ....................................................................................................................................... 55 Constraints ........................................................................................................................................... 56

Chapter 5: Prioritization ........................................................................................................................... 71 Criteria for Selection ................................................................................................................................ 71 Foundational Issues ................................................................................................................................. 72 Mitigating the Impact of Governance Constraints on Development ....................................................... 72 Fiscal Constraints..................................................................................................................................... 73 Possible Policy Interventions ................................................................................................................... 74 Foundational issues .................................................................................................................................. 75

Mitigating Overarching Governance Constraints ................................................................................ 75 Alleviating Fiscal Constraints.............................................................................................................. 76

Specific Priority Areas ............................................................................................................................. 76 Strengthening the Productivity of the Agricultural Base ..................................................................... 76 Diversifying the Economy and Creating Poverty-Alleviating Jobs..................................................... 79 Strengthening the Management of Mineral Resources ........................................................................ 83 Increasing Human Capital for New Opportunities .............................................................................. 85

v

Chapter 6: Risks ........................................................................................................................................ 89 Fragility.................................................................................................................................................... 89 Political Risks .......................................................................................................................................... 90 Environmental Risks ................................................................................................................................ 90

Chapter 7: Knowledge Gaps ..................................................................................................................... 92

Annex 1: Recent World Bank Group Reports and Papers on Sierra Leone ....................................... 94

Annex 2: Recent Reports and Academic Papers from Outside the World Bank Group .................... 98

Annex 3: Government Documents ......................................................................................................... 102

Annex 4: Poverty Headcount and Distribution of the Poor, 2011 ....................................................... 103

LIST OF FIGURES

Figure 1: Evolution of Urbanization in Sierra Leone, 1967 to 2015 ............................................................. 4 Figure 2: 2017 WDR, Conceptual Framework .............................................................................................. 7 Figure 3: Governance Indicators ................................................................................................................. 11 Figure 4: World Governance Indicators ...................................................................................................... 12 Figure 5: Percentage of Respondents Reporting They Paid a Bribe for Access to Service in the Past 12 Months ......................................................................................................................................................... 13 Figure 6: Percentage of Respondents Who Feel that ‘Most’ or ‘All’ People in These Institutions Are Corrupt ......................................................................................................................................................... 13 Figure 7: Poverty Headcount (2003 and 2011) ............................................................................................ 18 Figure 8: Sectoral Contribution to Poverty Reduction (percentage points) ................................................ 19 Figure 9: Imported Rice Prices, International Prices, and the Exchange Rate ............................................ 19 Figure 10: Imputed Poverty at the Subdistrict Level (2015) ....................................................................... 21 Figure 11: Estimated Change in Poverty Since 2011 .................................................................................. 21 Figure 12: Projected Reductions in Poverty, 2011 to 2016 ......................................................................... 22 Figure 13: Mean Per Adult Equivalent Consumption by Decile ................................................................. 23 Figure 14: World Price of Iron Ore (US$ per MT) ..................................................................................... 24 Figure 15: Per Capita GDP Growth (Annual %) ......................................................................................... 26 Figure 16: Per Capita GDP for Selected Countries (US$ Current) ............................................................. 26 Figure 17: Contribution to GDP Growth by Sector ..................................................................................... 26 Figure 18: Decomposition of Agricultural Growth by Land Use and Productivity .................................... 26 Figure 19: Contribution to Economic Growth by Factor Input (average 2001–2014) ................................ 27 Figure 20: Labor Productivity (Value Added Per Worker) Growth by Sector ............................................ 27 Figure 21: GDP per Capita and Value Added per Worker (projection 2016–2030) ................................... 28 Figure 22: Value Added per Worker by Sector (projection 2016–2030) .................................................... 28 Figure 23: Cereal Yield, Average 2010–2014 (kg/ha) ................................................................................ 30 Figure 24: Constraints Reported by Farmers ............................................................................................... 31 Figure 25: Yield under Climate Change of Rain Fed Rice .......................................................................... 33 Figure 26: Relative Share of Renewable and Nonrenewable Resources (average 2001–2016) .................. 34 Figure 27: Relative Share in Renewable Resource Sector (average 2001–2016) ....................................... 34 Figure 28: Labor Market by Type of Employment ..................................................................................... 34

vi

Figure 29: Labor Market Employment by Sector ........................................................................................ 34 Figure 30: Composition of the Service Sector (average 2002–2015).......................................................... 36 Figure 31: Employment in Western Area by Sector (average 2002–2015) ................................................. 36 Figure 32: Evolution of Exports, Revenue, and Expenditure (in % of GDP) ............................................. 37 Figure 33: Evolution of Inflation Rate and Depreciation Rate (year-on-year basis) ................................... 37 Figure 34: Evolution of Credit to Government and Private Sector ............................................................. 37 Figure 35: Evolution of Interest Rates Applied by Commercial Banks ...................................................... 37 Figure 36: Infrastructure Development Index ............................................................................................. 38 Figure 37: Credit to Private Sector in Percentage of GDP (average 2011–2015) ....................................... 43 Figure 38: Most Problematic Factors for Doing Business ........................................................................... 44 Figure 39: Evolution of Rice Balance Sheet (in tons of milled rice)........................................................... 48 Figure 40: Change in Exchange Rate and Evolution of Market Share for Rice Imports ............................ 48 Figure 41: Mining Value Added and Income Paid to Non-residents (% of GDP) ...................................... 51 Figure 42: Potential and Actual Revenue from Mining (% of GDP) .......................................................... 51 Figure 43: Volatility of Selected Macroeconomic Variables, Measured as Standard Deviation Calculated in 2006–2015 ............................................................................................................................................... 53 Figure 44: GDP per Capita and Human Development Index ...................................................................... 55 Figure 45: Gross Primary Enrollment Ratio ................................................................................................ 57 Figure 46: Gross Secondary Enrollment Ratio ............................................................................................ 57 Figure 47: Attendance Gaps ........................................................................................................................ 59 Figure 48: Infant Mortality Rate (per 1,000 live births) .............................................................................. 61 Figure 49: Under-five Mortality Rate (per 1,000 live births) ...................................................................... 61 Figure 50: Life Expectancy at Birth ............................................................................................................ 61 Figure 51: Maternal Morality Ratio (per 100,000 live births) ..................................................................... 61 Figure 52: Health Expenditure, Public and Private, 2014 (% of GDP) ....................................................... 62 Figure 53: Health Spending by Expenditure Category ................................................................................ 63 Figure 54: Evolution of the Dependency Ratio for Selected Countries ...................................................... 64 Figure 55: Probability of Enrollment (by Gender) and Probability of Pregnancy ...................................... 68 Figure 56: Percentage of Women Agreeing that Wife Beating Is Justified for Any of Five Reasons ........ 69 Figure 57: Government Resources (% of GDP) .......................................................................................... 73

LIST OF BOXES

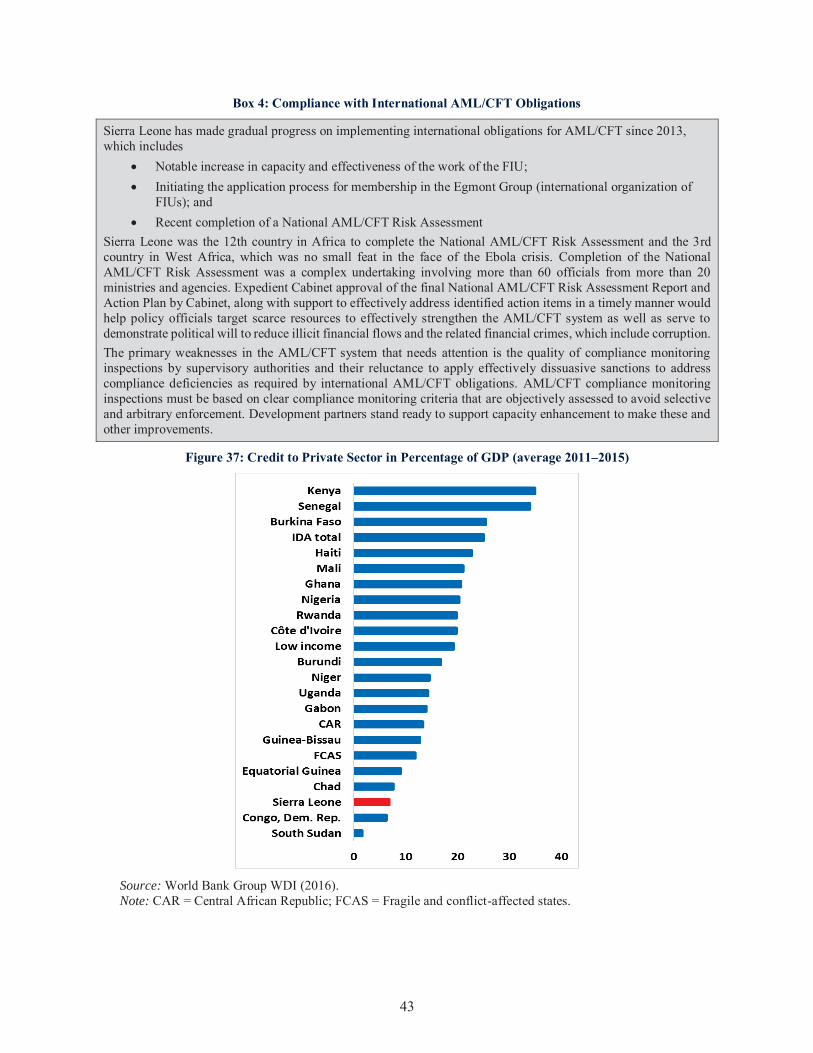

Box 1: Key Concepts from the 2017 WDR, Governance and the Law ......................................................... 7 Box 2: The Demographics of Democracy ..................................................................................................... 8 Box 3: Ebola in Sierra Leone ....................................................................................................................... 16 Box 4: Compliance with International AML/CFT Obligations ................................................................... 43 Box 5: Illegal, Unreported, and Unregulated Fishing Activities in Sierra Leone ....................................... 49

LIST OF TABLES

Table 1: Summary of Fiscal Regime in Sierra Leone .................................................................................. 52 Table 2: Summary of Key Policy Interventions by Thematic Area ............................................................ 74

vii

EXECUTIVE SUMMARY

1. The objective of this Systematic Country Diagnostic (SCD) is to describe the current development challenges facing Sierra Leone and offer a set of priority areas of intervention to accelerate growth and help achieve the World Bank Group twin goals of reducing extreme poverty and boosting shared prosperity. In the 15 years since the end of the civil war in 2002, there has been notable progress. The return to peace and stability and the ample availability of fertile land facilitated recovery and growth in agriculture. Urban areas have become local trading and commercial centers, and the capital of Freetown has seen many sources of new wealth and development. Poverty significantly declined from 66 percent in 2003 to 53 percent in 2011, and access to basic services improved, particularly in education and health. The Government has also been successful in attracting large-scale foreign investment in mining and agriculture, though the overall contribution of these sectors to fiscal revenue and job creation has remained limited. Despite this progress, Sierra Leone’s economic system remains vulnerable, with large imbalances in the distribution of resources, political power, and knowledge. This SCD looks beyond the standard growth and poverty reduction narratives and takes a holistic approach to identify the underlying causes of previous poor growth performances, drawing on both the history of Sierra Leone in the post-colonial period and the conceptual framework developed in the 2017 World Development Report (WDR): Governance and the Law. The result is a proposed set of priority areas to promote sustainable and inclusive growth that synthesize the latest evidence, economic theory, and the current political realities in Sierra Leone.

2. The SCD is an evidence driven exercise that draws together diverse findings into a comprehensive country diagnostic. As part of the process, the SCD team undertook a comprehensive data and literature review covering both quantitative and qualitative evidence (see annexes 1 through 3.) Where gaps were identified, the SCD team attempted to add to the evidence base through new analysis on primary data or by drawing lessons from comparable countries. The SCD process also involved stakeholder consultations with government, civil society, private sector, and citizens of Sierra Leone to incorporate their perspectives. Throughout the process, the SCD team worked closely with World Bank Group sector experts to understand better complex relationships within or between sectors. Those areas in which the team still found the evidence base incomplete have been identified as priority areas for future research and are discussed in the Knowledge Gaps section.

3. The SCD argues that, without taking into account the two main foundational constraints—governance and fiscal space, it is unlikely that the proposed technical solutions will make a substantial impact on the twin goals. Many of the technical solutions that are proposed in this document have been tried in multiple variations over the last 60 years by government, donor partners, and other stakeholders, but the results have been meager. Despite favorable geography and abundant resources, and after hundreds of millions of dollars in soft loans and grants, smart consultants, sound technical approaches, Sierra Leone continues to have development outcomes that rate among the worst in the world. This SCD argues that unless governance constraints are understood and mitigated this situation is unlikely to change very much. It further takes into account severe fiscal constraints in proposing ways to alleviate this while also avoiding reforms that require substantial financial outlays. If the two foundational issues are appropriately addressed, the priority technical interventions proposed here have the potential to unlock growth, reduce poverty, and improve the lives of the Sierra Leonean population.

Sierra Leone’s main assets are abundant resources and a young and dynamic population.

4. Sierra Leone has a highly advantageous geography and abundant renewable and nonrenewable natural resources. The country possesses significant renewable natural resource endowments in land, forests, and fisheries. Almost 75 percent of the total land area is arable, and rainfall and sunlight are abundant. The country’s rainfall, soil, sunlight, and river basins endow the country with

viii

land of high natural fertility, considered suitable for a wide variety of food and cash crops with potentially high crop yields. With more than 400 km of coastline, Sierra Leone has abundant and varied fish resources. The country is also well-endowed with mineral resources. There are extensive alluvial and kimberlitic diamonds, bauxite, rutile, and gold deposits, as well as large quantities of iron ore.

5. The country’s population is young, diverse, urbanizing, and rapidly growing. According to the 2015 census, the population of Sierra Leone is approximately 7.1 million, with 45.8 percent of the population under the age of 15, and 74.8 percent below the age of 35. The share of the population living in urban areas almost doubled from 21 percent in 1967 to almost 40 percent in 2015, with a high concentration in the capital Freetown, which has grown to a population of more than 1 million. Sierra Leone has a diverse population for its size. There are 16 ethnic groups in the country, though two-thirds of the population belongs to the two main ethnic groups: the Temné, which comprise about 35 percent of the population, live in the north; and the Mendé, with 31 percent population share, live in the south and east.

Contemporary governance and institutions reflect path dependencies and a persistent logic of neopatrimonialism.

6. Despite the shocks of independence, authoritarianism, and civil war (1991–2002), there is marked continuity in the political settlement that underlies the nature of governance and institutions and their ability to deliver development outcomes. British control of the Sierra Leone Colony relied on a system of indirect rule that manipulated customary governance structures to promote paramount chiefs charged with maintaining social order, collecting taxes, and allocating land and resources, to facilitate the extractive colonial regime. Independent Sierra Leone inherited an overly centralized, bureaucratically weak state and mass rural poverty. The preservation of the ‘traditional’ authority structure was a form of elite bargain that helped extend the reach and authority of the state to the interior through patrimonial relations. With a weak central state, paramount chiefs were able to accumulate considerable power as political brokers, which they used to grant their supporters access to residence and land use. Both main political parties—the Sierra Leone People’s Party (SLPP) and the All People’s Congress (APC)—have cultivated a mutually beneficial patronage system with local elites, with the SLPP dominating in the largely ethnic Mendé southern and eastern regions, and the APC dominating in the Temné/Limba majority north and west. This patronage and identity-based party system enables politicians to rely on a comfortable base of popular support, undermining the potential effect of electoral competition and collective action.. At the same time, strategies to appease a young and underemployed urban population call for short-term clientelism in the form of suboptimal—and unsustainable—subsidies. This basic logic survived the period of APC authoritarian rule, economic collapse, and the ensuing civil war.

7. The reestablishment of democracy and maintenance of a stable peace since 2002 is a remarkable achievement. While there are important signs of institutional development, incentives to govern and establish a social contract based on a long-term commitment to the public good have yet to emerge. Decentralization, launched in 2004 as a flagship initiative to shift key policy arenas away from the sharp ethnic divide of national politics and to correct the severe pre-war power imbalances and regional inequalities, has fallen short of critical aims. Elected Local Councils (LCs) have been established, but their ability to deliver decentralized services is compromised by incomplete reform efforts, their politicization, and the continued power of paramount chiefs and other local elites. Strengthening accountability for public resource management and building the foundations for an effective public administration have made some inroads, but are frequently met with resistance. Sierra Leone ranks well below the regional average on indicators of government effectiveness, regulatory quality, rule of law and control of corruption (WGI 2016). Sierra Leone ranks 130 out of 137 economies on the Global Competitiveness Index 2017.Modernization of legislative frameworks for mining, procurement, and anti-corruption has progressed, but implementation lags far behind. (Global Integrity, Africa Integrity Indicators 2017). The power asymmetries that account for continuing inability of the state credibly to commit to needed land and

ix

fiscal reforms, and to induce the coordination and cooperation needed effectively to deliver on its promised free maternal health care initiative is perhaps best evidenced by the appalling outcomes in these sectors.

Poverty has decreased in Sierra Leone in the postwar period.

8. The most recent household survey, the 2011 Sierra Leone Integrated Household Survey (SLIHS), estimated the incidence of poverty to be 53.8 percent. This represents a 12.6 percentage point decrease from 66.4 percent in 2003, the first statistic available following the end of the civil war. However, the number of poor remained nearly constant, at around 3.3 million, over this period due to high population growth. Despite a decrease from 79 percent in 2003 to 66 percent in 2011, poverty in Sierra Leone remains disproportionately rural, with more than three-quarters of the poor living in rural areas in 2011. The decline in rural poverty was mainly driven by gains made by agricultural households, though a small percentage of nonagricultural rural households experienced greater poverty reduction. The largest changes in poverty headcount occurred in urban areas outside of the capital Freetown, where rates declined from 70.9 percent in 2003 to 39.9 percent in 2011. Half of the overall decline (6.5 of the 12.6 percentage points) was recorded in ‘other urban’ areas, excluding Freetown. These areas contributed almost the same to the overall national poverty reduction as rural areas, although they had only one-third of the population. Freetown was the only area to experience a significant increase in poverty between 2003 and 2011, from 14 to 21 percent, but poverty rates remain well below the rest of the country. The increase in poverty in Freetown is believed to have been mainly driven by three factors: in-migration, the slow creation of well-paid jobs, and inflation.

9. Economic growth between 2003 and 2011 was pro-poor, but higher growth or higher pass-through of growth to poverty reduction are needed to meet future poverty reduction targets. As evidenced by a comparison of annualized growth rates for per capita expenditure adjusted for purchasing power parity, the growth rate was the highest for the poorest decile of the distribution and steadily declined toward the wealthiest decile. Overall inequality fell between 2003 and 2011 with the Gini coefficient declining from 0.39 to 0.32 over the period. The overall decrease in inequality can largely be attributed to the measured fall in prosperity in Freetown and by rural areas catching up with urban areas. Despite this, higher growth rates or higher pass-through of growth to poverty reduction are required to meet the Government’s national development targets. Starting from a baseline of 2011, poverty would have to be reduced at a rate of 14 percent per year to achieve the target of 3 percent in 2030. At the current predicted levels of the pass-through of gross domestic product (GDP) growth to poverty reduction, this would require growth of almost 15 percent per year, which is well above the current forecasts of 5–6 percent for the next several years. Therefore, to meet its poverty reduction objectives, Sierra Leone must accelerate growth and continue to ensure that growth benefits the poor.

There was steady growth in the postwar period until 2014, after which there was a severe contraction due to the collapse of iron ore production and the impact of Ebola on Sierra Leone.

10. Sierra Leone experienced a steady increase in income per capita from 2001 to 2014, its longest period since independence in 1961. Per capita GDP went from stagnating in the period from independence to the civil war and contracting 3.4 percent on average per year between 1991 and 2001 (civil war) to increasing 5.9 percent on average per year from 2002 to 2014 (post-civil war period). Economic growth was driven mainly by agriculture. Between 2001 and 2014, agriculture (including livestock, forestry, and fisheries) grew by an average of 8 percent per year, contributing almost 50 percent to the total increase in real GDP over this period. According to Food and Agriculture Organization (FAO) data, crop production increased by an average of 12.5 percent per year during the period, driven mainly by an increase in land use and, to a lesser extent, improvement in yield per hectare. Industry was the second largest contributor to growth, driven mainly by two large-scale iron ore mining projects that began production in 2011. Services increased by 5.8 percent per year during this period.

x

11. Sierra Leone’s period of steady growth ended in 2015, as the country was severely affected by the twin shocks of the Ebola outbreak and the downturn in international iron ore prices. The economy contracted by more than 20 percent due to the spread of the Ebola epidemic and after both iron ore mining operations ceased production due to low international prices. Iron production declined by 84 percent in 2014 and growth in the rest of the economy slowed to near zero, with the services sector being particularly hard-hit. Growth resumed in 2016 following the end of the Ebola outbreak and the return to operation of the largest iron ore mine.

There are four pathways and two foundational areas by which Sierra Leone can accelerate growth and reduce poverty. The four pathways are: (a) strengthening the productivity of the agricultural base; (b) diversifying the economy and creating poverty-alleviating jobs; (c) strengthening the management of mineral resources; and (d) increasing human capital for new opportunities. The two foundational areas are: (i) mitigating overarching governance constraints; and (ii) alleviating fiscal constraints. The pathways and foundational areas should be seen as a whole and not as stand-alone separated parts. There are several linkages between them that reflect the existing complementarities.

Strengthening the Productivity of the Agricultural Base

12. Agriculture is the main source of livelihood in Sierra Leone, particularly for the poor, and therefore improving agricultural outcomes for food security and rural income generation is at the core of poverty alleviation. Agriculture also employs more than half of the country’s formal and informal workforce and accounts for about half of GDP. The recent Diagnostic Trade Integration Study highlighted a competitive advantage for import substitution of rice and palm oil production if productivity could be increased, as well as potential expansion of processed cassava cash crop production for export markets. Therefore, increasing the productivity of the agricultural sector provides direct channels for both economic growth and poverty reduction.

13. Productivity is constrained by failures in input markets. Yields are well below their productive frontier for the climatic conditions and soil fertility due to low uptake of modern seeds, chemical and organic fertilizers, and mechanization. The cause of low uptake is a combination of ineffective and inefficient intervention by the Government in input markets, a lack of access to credit, and nonexistent insurance markets to lower risk. This leads to increases in the overall costs of production, reduced farmer margins on sales, and insufficient production to meet both household consumption and commercialization objectives. The traditional system of land tenure is also unequal, with women, youth, and migrants from outside the community less able to access land, and perceived to reduce tenure security, impeding long-term investment.

14. Output markets are not sufficient to promote sales and rural income. Less than 40 percent of rice-growing households sold any of their crop during the 2014/2015 agricultural season. Sales are constrained by poor storage, a lack of rural roads linking rural areas to Freetown and other urban centers, and insufficient processing facilities. Farmers also face competition from inexpensive imported food, particularly during boom periods in the mining sector when the appreciation of the Leone makes imports comparatively less expensive. Even when the exchange rate is not an issue, tariff waivers for rice—put in place during the 2008 food crisis—keep imported prices artificially low, further damaging competitiveness of local agriculture produce.

Diversifying the Economy and Creating Poverty-alleviating Jobs

15. To boost shared prosperity, Sierra Leone must create poverty-alleviating nonfarm jobs outside the mineral sector, especially for youth and women. Each year, more than a hundred thousand people move from rural to urban areas in search of employment and better living conditions. In the absence

xi

of well-paid formal manufacturing and services jobs, almost nine in ten of these Sierra Leoneans end up in the highly vulnerable informal sector. Employment growth in the formal sector is slowed by a myriad of constraints in doing business, including high macroeconomic volatility, low access to electricity, high transportation and communication costs, competition from imports and state-owned enterprises, lack of access to credit, and an unfavorable regulatory environment, while productivity is extremely low in the informal sector.

16. Decisions made by private enterprises are influenced by several macroeconomic variables, such as the aggregated demand, the inflation rate, the exchange rate, tax rates, and the interest rate. As the single largest purchaser of goods and services, the state is a vital source of business for companies in Sierra Leone. However, because of the uncertain contribution of the mining sector to government revenue, public expenditures have been traditionally volatile, making market projections and investment planning at the level of the firm very difficult. In addition to the high volatility of aggregate demand, the exchange rate policy makes it more difficult for local firms to compete with imports.

17. Sierra Leone’s infrastructure deficit in energy, transport, and information and communication technology (ICT) impedes private sector investment by increasing costs and preventing links between internal and external markets. According to the African Development Bank (AfDB), the country’s infrastructure compares poorly to the rest of Sub-Saharan Africa, and it was ranked 46 out of 54 countries on the AfDB’s Infrastructure Development Index (AIDI) in 2016. Access to electricity is currently only about 10 percent of the total population, of which 95 percent is located in Freetown. The transport system consists of an estimated 11,311 km of roads, with only 1,325 km of paved roads, representing 11.5 percent of the total road network. Mobile phone use is rapidly growing in Sierra Leone, increasing from 34.8 mobile cellular subscriptions per 100 people in 2010 to 89.5 per 100 in 2015. The 2015 Comprehensive Food Security and Vulnerability Analysis (CFSVA) estimated that 56 percent of households had at least one mobile phone, an increase from 39 percent of households as recorded by the 2011 SLIHS.

18. Access to capital appears to be a binding constraint to the entry of new entrepreneurs as well as for existing businesses. Only 15 percent of the adult population has an account with a formal institution, which is lower than the average of 24 percent in Sub-Saharan Africa and low-income countries while only 6 percent of the adult population has received a loan from a formal institution, which is in line with the regional average but lower than the 11 percent average for low-income countries.

19. Sierra Leone lacks adequate and relevant labor policy and legislation, and there are no comprehensive regulations for labor market operations in the country. Many of the important laws regulating the labor market in Sierra Leone date back to 1960, a year before independence, and need to be modernized to provide greater flexibility. These include the Employers and Employed Ordinance and the Trade Unions Ordinance.

Strengthening the Management of Mineral Resources

20. Despite employing only 1.5 percent of the workforce, the mining sector plays an important role in Sierra Leone’s economy. From 2012 and 2014, the extractive industry boomed in Sierra Leone to represent 14 percent of GDP on average per year, up from 3.7 percent in 2009–2011, and accounts for 70 of merchandize exports, up from 38 percent in 2009–2011. These performances were mainly driven by the starting of operation in two large-scale iron ore companies attracted by the high level of iron ore prices and the reform of the mining sector. Sierra Leone modernized the legislative framework for the mining sector, which improved the overall governance in the sector.

xii

21. However, the boom did not translate into commensurate welfare improvement of Sierra Leone citizens. Not only the share of the mining sector remained low in total employment (1.5 percent), but the Government revenue mobilized from the extractive industry remained well below potential. If Sierra Leone’s fiscal regime for the mining sector was fully implemented, revenue collected between 2012 and 2014 would have reached 11.8 percent of GDP, more than triple the actual revenue collected in the period (3.7 percent of GDP). This could have financed better growth, higher social spending and built stronger resilience. For example, higher revenue from mining could have increased public expenditures on education and health by more than 40 percent. Most of the counter-performance reflects the weakness remaining in the legal and regulatory framework. The 2009 Mines and Minerals Act (MMA) and 2011 Petroleum Act are rife with inconsistencies, leaving the Government and license holders to rely on highly interpretive and often personalized agreements on operating terms. In such a weak governance environment, this leaves the door wide open to corruption.

22. In addition, the recent evolution of the mining sector has increased the volatility of the economy. Sierra Leone is one of the most volatile economies in the world. Between 2013 and 2015, GDP growth fluctuated from −21.1 percent to +20.7 percent, inflation rate ranged from −35 percent to +22 percent, and exchange rate depreciation varied from −0.2 percent to +17.5 percent, while Government current expenditure ranged from 10 percent to 21 percent of GDP. These ranges are much wider in Sierra Leone than in Liberia or Guinea (the two neighboring countries impacted by the twin shocks).

Increasing Human Capital for New Opportunities

23. To create the conditions for economic growth and poverty reduction, Sierra Leone must invest in its people, particularly the poor. Improving human capital, however, will require a dramatic increase in the quality of public services. Better public service delivery has impacts on poverty and income in the short, medium, and long term. In the short term, better public service provision will free up household resources previously used to purchase these services in the private sector, allowing for increased consumption or for productive investments. This alone can improve outcomes, as lack of funding or capital was identified as the main reason for not sending children, particularly girls, to school and a key reason for not starting or expanding businesses and farming activities. In the medium term, an increase in human capital resources on the national level will improve the business climate, boosting the output of private sector activities and the attractiveness of Sierra Leone for future investment. Improved health also reduces days lost to illness, increasing the supply of labor for agriculture or informal nonfarm enterprises. Better services in rural areas can also reduce migration to urban areas that are already under pressure to provide basic services and jobs. In the long term, a healthy and educated population will constitute an attractive workforce for new foreign direct investment (FDI) in the manufacturing and service industries or increased domestic entrepreneurial activities. In parallel to the development of the public sector, there is also scope for more effective Government engagement with non-state actors who are providing primary health and basic education services, with the Government potentially playing a catalyzing role in coordinating across stakeholders in health and education as well as leading policy and standards.

24. In the education sector, there are issues of both access and quality. One in three Sierra Leonean children is out of school, and gaps in access remain for those in rural areas and for girls at higher levels. Access is not the only issue; quality and relevance of instruction are lacking. Scores on international tests show very low levels of achievement, even when compared to regional neighbors and countries with comparable income levels. A recent higher education study concluded that links between higher education institutions and employers were weak and often ad hoc. Private sector stakeholders have difficulties in finding ‘employable’ graduates, and there is an acute shortage of technicians, such as auto repair mechanics and welders; health professionals, including doctors, nurses, birth attendants, and other health workers; science and math teachers; and those with skills in applied sciences, technology, and engineering.

xiii

25. Health outcomes are among the worst in the world despite high levels of private spending. Sierra Leone has the lowest life expectancy at birth in the world (at 50 years) and the worst maternal and child mortality rates in the world, with one death for every 100 births. Poor health affects economic growth as well as the ability of households to increase their incomes. Insufficient access to contraception, along with lower levels of female education, job opportunities, and empowerment, results in high fertility, which leads to a vicious cycle, as it strains public service delivery, constrains women’s time and empowerment, and limits the resources available to invest in individual children. Labor lost to poor health lowers farm productivity, particularly in labor-intensive agricultural activities, and poor access to health has been identified as one of the major reasons for the high prevalence of food and nutrition insecurity in Sierra Leone. Health shocks also limit households’ ability to save and invest, including in income-generating assets. In addition, Sierra Leone has extremely high out-of-pocket expenditures. This burden falls disproportionately on the poor, as out-of-pocket health payments are regressive and the poor are more likely to forgo health care.

26. Progress in the water and sanitation sectors has been mixed. Access to improved water increased nationally in the postwar period but has seen a decline in urban areas in recent years. Access to improved sanitation in Sierra Leone has been constant, at 13 percent of the population in the postwar period (UNICEF and WHO 2015), which is low compared to other countries in the region; open defecation is prevalent in the country, particularly in rural areas and fecal sludge disposal remains a major issue, particularly in Freetown. Poor sanitation, combined with food insecurity; inadequate caregiving resources at the maternal, household, and community levels; and limited access to health services leads to high levels of malnutrition and stunting among Sierra Leonean children. The consequences of stunting in young children include delayed schooling, poor educational performance, and less years of completed education, which increases the chances of them having low incomes and becoming trapped in poverty later in life.

Prioritization

The SCD identifies two foundational areas and nine sectoral priority areas for Sierra Leone to accelerate growth, and support poverty reduction and shared prosperity.

27. In selecting a set of strategic priorities, the SCD uses four main considerations. The first assesses the level of each potential intervention’s expected impact on the twin goals of eliminating extreme poverty and promoting shared prosperity. The second assesses the potential impact of each intervention on medium- to long-term growth acceleration. The third assesses complementarity, that is, the degree to which progress on a given objective will positively influence other objectives. The fourth evaluates the feasibility of specific priorities in terms of the possibility that the political, financial, and social constraints could be sufficiently addressed. In line with the 2017 WDR, this consideration takes into account the potential for the policy arena to be reshaped through the levers of contestability; elite incentives; and the ideas, preferences, and beliefs of participants in the policy arena. It also takes account of how, over time, policy outcomes might alter the underlying distribution of power to allow for a broader range of policy options in future.

Foundational Areas

28. The SCD argues that progress on the pathways to development must take into account two foundational issues: governance and fiscal space. The former must be understood as a long-term condition, rather than as a time-bound constraint. The shift from extractive to inclusive institutions (Acemoglu and Robinson, 2012) will take place over time in response to a variety of endogenous and exogenous shocks. In the meantime, the challenge is to identify opportunities to promote outcomes that in turn can reshape a developmental link between demand and incentives of those in power. The constraint of fiscal space manifests in a time-bound way, given the dependence of the country on natural resource

xiv

revenues, but is the result of underlying fiscal and economic policy failures. The SCD highlights key dimensions of and priority interventions to mitigate these constraints, while they are also carried through in the analysis of the specific sectoral priorities.

Mitigating Overarching Governance Constraints

29. The perverse incentives and poor equilibrium in governance are a major determinant of policy effectiveness. These incentives are the product of historical path dependencies that have been self-reinforcing, creating a logic of centralist, patrimonial methods of exercising power and managing relations between state and society. As documented by several scholars, these conditions disincentivize the need to invest in a capable bureaucracy and the provision of public services and corruption is entrenched as part of the rent distribution that keeps the political settlement intact.1 Mitigating governance constraints will require efforts to institutionalize rule-based mechanisms while enhancing the endogenous demand for a more inclusive social contract. Tackling public sector reform directly requires an adaptive, incremental, and opportunity-driven approach. Over time, progress on these technical areas may serve to shift incentives and promote accountability, and while this may elicit resistance, sustained incremental efforts on select reform priorities will pay off.

Priority 1: Strengthen accountability and contestability in key sectors. Elite capture and corruption happens at all levels and can be reduced by increasing the risk of exposure and strengthening accountability in institutions. Some forms of corruption are ‘transactional’ in nature—in other words, they are inherent to the political settlement. Others are ‘predatory’, or opportunistic in nature, making efforts to mitigate them more feasible. On the latter, it is important to improve the collection of information, the capacity to analyze it, and share results in the public domain. Also critical is the creation of spaces for participation, deliberation, and contestation in ways that can level the playing field and counter power asymmetries. Sierra Leone has already experimented with social accountability and legal and paralegal services on a relatively small scale and has developed a few important entry points for scaling up and institutionalizing these services, through the Legal Aid Act and the National Land Policy, for example. Targeted investments to enable citizen collective action and increase transparency and accountability could serve to change incentives in ways that improve results and equity in agriculture input markets, health service delivery, and land acquisition processes.

Priority 2: Incentivize functional solutions to improve public administration and effective local governance. While initial expectations of LCs have been dampened by a series of policy decisions, the incomplete transfer of authority and resources, and the re-institutionalization of the chieftaincy, local governance remains an important site for increasing accountability and service provision to citizens. Incremental reforms to increase the effectiveness of LCs by deepening administrative and fiscal decentralization should be complemented by efforts functionally to improve coordination between LCs and chieftaincy and accountability of local officials for the provision of public goods. Building on promising evidence that increasing voter information can break down traditional partisan voting patterns, efforts to increase accountability to citizens can not only improve the provision of public goods but could also begin to reshape the social contract. Engaging in these

1 See for example, Van de Walle, Nicolas (2005). Democratic Reform in Africa. United States: Lynne Rienner Publishers. Regarding Sierra Leone in particular, see Robinson, James A. 2008. Governance and Political Economy Constraints to World Bank CAS Priorities in Sierra Leone. Washington, DC: World Bank.

xv

generative dynamics at the local level may yield results more immediately than pushing formal reforms from the top down.

Alleviating Fiscal Constraints

30. Sierra Leone’s Government faces huge fiscal constraints. Fiscal space is narrow because of: (a) the low level of tax revenue (below 12 percent of GDP in 2016, mining royalties included) extracted from a narrow tax base, as agriculture and mining, the two biggest sectors of the economy, are not appropriately taxed, and widespread exemptions further limit the tax base; (b) the declining level of aid as a share of GDP (from 5.2 percent in 2015 to 2.5 percent in 2016), as donors perceive the country as suffering from weak governance and widespread corruption; (c) the small domestic banking and financial sector, which limits domestic borrowing; and (d) the high level of nondiscretionary spending, which absorbs almost all domestic revenue (for example, 60 percent of all tax revenues goes to salaries). Alleviating fiscal constraints is critical for the improvement of the country’s macroeconomic framework, and has been identified as one of the constraints to economic diversification and poverty-alleviating job creation (Pathway 2).

Priority 1: Strengthen Domestic Revenue Mobilization. Getting to and sustaining high investments in human and physical capital is difficult to achieve without an enhanced domestic revenue mobilization. Mobilizing more domestic revenues is the long-term solution to creating fiscal space, and the process has already started in Sierra Leone with the creation of the National Revenue Authority (NRA). However, there are few opportunities that could generate additional revenue in the short to medium term. These include reducing the generous level of tax exemptions and tapping of the existing mineral sector. However, this is unlikely to happen unless the country significantly improves the overall governance of the mining sector, including adopting and enforcing credible legal, administrative, and institutional frameworks through amendments to the mining code. While this may be politically difficult, it is an opportunity to align key incentives to increase domestic revenues in the currently constrained fiscal space.

Priority 2: Improve efficiency of public spending and value for money. Bottlenecks in public financial management (PFM) and procurement lead to inefficient public spending in priority sectors. Greater efficiencies and higher value for money can be achieved through improvements in budgeting (enhanced allocative efficiency), procurement, and financial management, including reporting and oversight. Sierra Leone has built a good legal and regulatory framework that serves as the foundation for PFM. However, the country’s financial management systems continue to operate in an inadequately reliable manner because of weak implementation. A new PFM framework was enacted in 2016 and became effective in January 2017. To better implement the new act, there are several issues that would need to change to render the desired impact. There needs to be considerable institutional change and capacity development across central government and requisite ministries, departments, and agencies (MDAs). On procurement, the Government has decided to implement e-procurement to increase. While resistance to reform can be expected, the approach should be to focus sustained incremental efforts initially on areas that do not directly threaten vested interests and on systematically promoting practical implementation.

Priority Areas

31. The SCD has identified nine priority areas of potential intervention to address the binding constraints to increased economic growth and poverty reduction in Sierra Leone. Many of the suggested interventions have arguably been tried and tested in the past, with disappointing results. The two foundational areas discussed earlier should be considered critical to the success of the technical interventions listed below. The priorities are listed one through nine for presentation purposes, but the order

xvi

does not reflect their relative importance or suggested sequencing. They should be seen as a whole since many are interrelated.

Priority 1: Reforming the role of the Ministry of Agriculture, Forestry, and Food Security (MAFFS) in the provision of agricultural services. To boost productivity and encourage the widespread adoption of modern, high-quality agricultural inputs, a new role should be defined for MAFFS. A main constraint to increased utilization is a state-led delivery system, mainly through MAFFS, that is inefficient, subject to corruption, and crowds out the private sector. A shift to the private sector in input delivery will free up resources to be redirected to quality control of imported inputs, to take the lead on a national campaign of research and development for products better tailored to Sierra Leone, and to expand agricultural extension services.

Priority 2: Improve market opportunities for producers. Expanded use of modern inputs has the potential of lowering production costs, increasing margins and drawing new participants into the market, but further intervention is necessary to realize the full potential. Improving rural incomes requires increased sales and profit for farmers. For import substitution to occur, farmers must be able to process and transport their crops to urban consumers. Processing facilities are limited, and anecdotal evidence suggests that elite capture is rife. In addition, a more extensive network of rural roads is required to reduce transportation costs to Freetown and other regional centers from poorer and more remote rural areas. Beyond decreasing production and marketing costs, higher and more stable prices will increase incomes for sellers. A plan to reduce and eventually remove the tariff waivers for imported rice is key to increasing producer prices and the long-term health of domestic production, but it must be coupled with further investments in domestic production and offsetting social transfers to mitigate the short- and medium-term poverty impacts.

Priority 3: Strengthening macroeconomic stability. The fluctuations in growth, inflation, exchange rate, government spending, and aggregate demand are very high in Sierra Leone and significantly affect the enterprises’ decision making and prevent optimal allocation of resources. Most of this volatility emanates from the mining sector. A stabilization fund is the most common mechanism used by governments and/or central banks in resource-rich countries to insulate the domestic economy from large fluctuation in revenue. The principal motivation is maintaining a steady and predictable path of government expenditure that is commensurate with existing absorption capacity, which fosters macroeconomic stability and sustainability. The Government has taken steps in this direction but it could go further. The new PFM Act (2016) created a Transformational Development Stabilization Fund (TDSF), which now needs to be implemented. Also, the Government should completely eliminate its interventions, particularly in the period of higher influx of mineral revenue, that tend to further appreciate the local currency. In addition, Goods and Services Tax (GST) exemption on electricity was eliminated and import duty, excise tax, and GST on fuel were reinstated after a long period of fixed fuel retail prices that eroded the collected taxes. The Government should now let the retail prices of fuel float to protect the tax base and put the Government fiscal position on a sustainable footing.

Priority 4: Improving access to infrastructure (energy, transport, and ICT) and credit and improving labor market regulations. Diversifying the Sierra Leonean economy and creating poverty-alleviating jobs will require substantial improvement of the country’s business environment. Enterprises face huge constraints when doing business in Sierra Leone, including poor access to electricity, roads, ICT, and credit. Revenue from the mining sector should be invested in priority areas to update the infrastructure platform of the country while deepening financial intermediation could boost access to credit and stimulate private sector growth.

xvii

Priority 5: Promote vertical diversification. Sierra Leone should also tap its potential for vertical diversification by promoting the development of rice and fish value chains. An attractive price policy plays a critical role in developing the rice value chain in Sierra Leone. A first step toward developing the value chain is to provide a good incentive package for private sector involvement both upstream and downstream of the value chain. One element of the incentive package could be the reduction and eventual elimination of the tariff waiver on imported rice (15 percent) to increase the competitiveness of locally produced rice. In addition, the Government should maintain an exchange rate policy that does not harm the agriculture sector by making cheaper imported food compared to locally produced agricultural products. In addition, the Government could reinforce the feeder road network. Farmers have limited access to transportation facilities because of inadequate level of all-weather rural roads to enable easy delivery of produce to processing centers or markets.

Priority 6: Maximize revenue from the mining sector in a sustainable way. Sierra Leone should review its legal and regulatory framework for the mining sector. The revision of the legal and regulatory framework, matched with human and institutional capacity development and practical strategic planning are required for efficient management of the sector and adequate revenue mobilization. In particular, the fiscal regime of the extractive sector should be grouped under one piece of legislation, preferably the tax code. This would clarify the tax rates applied to mining companies and increase the transparency of the fiscal regime. Based on the revised legal framework, Sierra Leone would be able to renegotiate existing mining contracts to reduce tax exemptions.

Priority 7: Manage the volatility from the mining sector. Overall, public expenditures should be rooted in a sound macro-fiscal framework to avoid the deleterious effects of commodity price volatility and to prevent real exchange rate appreciation and non-targeted subsidies or investment spending boom not modulated to the absorptive capacity of the economy. As proposed earlier, a stabilization fund is the most common mechanism to ensure a predictable path of government expenditure that is consistent with existing absorption capacity. The TDSF should be made quickly operational with clear fiscal rules, to make the country ready for saving during the next commodity boom cycle. Sierra Leone should also develop its Public Investment Management Framework so that investment projects will be well prepared and implemented in a transparent and cost-effective manner.

Priority 8: Improving quality and access to health care. Sierra Leoneans need better access to quality health care, particularly maternal and child health services. Though health outcomes have improved in the postwar period, Sierra Leone still ranks as the worst in the world in maternal mortality, child mortality, and overall life expectancy. The inability of the health system to provide quality health care to the population leads to both poor outcomes and high expenditures on over-the-counter (OTC) drugs and private care. Given the current fiscal constraints, however, investments should focus on improving the efficiency of spending (including reducing staffing absenteeism, reducing corruption, and better coordination within public sector but also with the nonpublic sector providers of health services, such as nongovernmental organizations (NGOs); overall quality improvements (including preventing drug stock outages); and regulation (including quality controls on imported OTC medication). Supporting infrastructure such as rural roads, electricity, reliable mobile networks, and clean water supplies and sanitation are also important components to improving health systems. In addition, improving the systems for disease surveillance, pandemic preparedness, and rapid response would not only protect individual lives but may also bolster investor confidence by decreasing perceived risk.

xviii

Priority 9: Improve quality and access to education. Better schools, better access for marginalized groups, and a more relevant curriculum are the key priorities in the education sector. Learning outcomes indicate that nearly all schools suffer from issues related to quality (not only public schools). As with health, there is a sizable presence of nongovernment schools, and the Government needs to engage with non-state actors to raise and maintain standards. Large gaps between urban and rural areas still exist, as does the gender gap at the secondary and tertiary levels. In addition, technical skills are at the core of improving individuals’ employment outcomes and increasing countries’ productivity and growth, and both the education and vocational training systems should be better aligned with the needs of employers. Interventions that can have maximum impact on quality of learning are improved supervision and accountability mechanisms (including those to reduce teacher absenteeism) and incentives to improve school and teacher performance, updating and realigning the curriculum, enhancing pedagogical skills for teachers, better measurement and dissemination of school and student performance, and strengthening the links to employers for higher education and the technical and vocational education and training (TVET) network.

xix

Objective: Boost inclusive economic growth and poverty reduction

Pathways

Diversifying the economy and

creating poverty-alleviating jobs

• Strengthen macroeconomic stability

• Improve business environment

• Promote vertical diversification

Strengthening the management of

mineral resources

• Maximize revenue from the mining sector in a sustainable way

• Manage the volatility from the mining sector

Increasing human capital for new opportunities

• Improve quality and access to health care

• Improve quality and access to education

Foundational Issue 1: Mitigating the impact of governance constraints

Foundational Issue 2: Alleviating fiscal constraints

Poverty Reduction and Shared Prosperity

Strengthening the productivity of the agricultural base

• Reform the role of the MAFFS in provision of agricultural services

• Improve market opportunities for producers

Constraints

• Instability in macroeconomic climate and poor business environment

• Limited physical infrastructure and human capital

• Lack of efficiency and accountability in public sector

Opportunities

• Highly advantageous geography • Abundant renewable and nonrenewable natural

resources • Young, diverse, and urbanizing population

1

INTRODUCTION

1. The objective of this Systematic Country Diagnostic (SCD) is to describe the current development challenges facing Sierra Leone and offer a set of priority areas of intervention to further the twin goals of reducing extreme poverty and boosting shared prosperity. In the 15 years since the end of the civil war, there has been notable progress. The return to peace and stability and the ample availability of fertile land facilitated recovery and growth in agriculture. Urban areas have become local trading and commercial centers, and the capital of Freetown has seen many sources of new wealth and development. Poverty declined significantly in this period, falling from 67 percent in 2003 to 53 percent in 2011. Access to basic service provision, including education and health, has improved following a substantial injection of donor resources but remains among the poorest in the world. The Government has also been successful in attracting some large-scale foreign investment in mining and agriculture, though less than neighboring Liberia and the overall contribution of these sectors to fiscal revenue and job creation has remained limited. Despite this progress, Sierra Leone’s economic system remains vulnerable, with large imbalances in the distribution of resources, power, and knowledge. As in the first two decades after independence, economic growth in the postwar period continues to be volatile. Output, employment, exports, imports, and government revenue fluctuate with the production and price of minerals, particularly diamonds and iron ore. This has led to a complex relationship between stakeholders and trapped the country in a low growth-poor governance equilibrium. At the same time, poverty rates remain high, with the majority of the population being unable to meet minimum standards of living. Previous diagnostics have focused on technocratic solutions to individual issues or sectors and have been largely unsuccessful in fostering durable growth. This SCD takes a more holistic approach to identify the drivers of previous poor growth performances, drawing on the history of Sierra Leone in the post-colonial period, and proposes a set of priority areas to promote durable and inclusive growth.

2. The SCD relied on the existing literature, new analysis, and diverse consultations to define and refine the priorities for Sierra Leone. The SCD is designed to be an evidence driven exercise that draws together diverse findings into a comprehensive country diagnostic. As part of the process, the team reviewed scores of documents, including survey findings, reports, project documents and journal papers, written by the World Bank, the International Monetary Fund, other bilateral and multilateral donors, think tanks, civil society organizations, non-governmental organizations, and academia, covering both quantitative and qualitative evidence. (See annexes 1 through 3 for a list.) Where gaps were identified, the team attempted to add to the evidence base through new analysis on primary data or by drawing lessons from comparable countries. The SCD process also involved stakeholder consultations with government, civil society, private sector, and citizens of Sierra Leone to incorporate their perspectives. Throughout the process the SCD team worked closely with World Bank sector experts to better understand complex relationships within or between sectors. Those areas in which the team still found the evidence base incomplete have been identified as priority areas for future research and are discussed in the Knowledge Gaps section.

3. Sierra Leone’s state of economic development and prospects for shared prosperity need to be understood as a function of its unique country context. From a technical perspective, traditional constraints on growth and poverty reduction are well-rehearsed and common to other countries in the region of similar income level. As this SCD will highlight, a range of priority reforms can help alleviate those constraints and put the country on a path toward greater diversification and productivity to manage macro-fiscal volatility and improve human development outcomes. Unleashing these reforms, however, will require addressing the overarching constraint of governance—that is, the path dependencies, incentives, and elite power relations that shape the country’s ability to commit to needed reforms and induce the coordination and cooperation needed to carry them out. This SCD applies the framework developed in the 2017 World Development Report (WDR): Governance and the Law to analyze ways that governance constrains progress toward the twin goals, to explain the strong persistence of these constraints, and to identify possible entry

2

points for promoting reform in light of these constraints, to shift to a governance arrangement conducive for achieving the country’s development goals.

3

CHAPTER 1: COUNTRY CONTEXT

4. Sierra Leone’s current economic development and poverty dimensions are shaped by the country’s geography and natural resources, its people and demography, and the interaction of these two with the governance and political institutions that have evolved since independence. This section provides an overview of these three key elements, as they are key to understanding the country’s current development context.

GEOGRAPHY AND NATURAL RESOURCES

5. Sierra Leone has a highly advantageous geography and abundant natural resources. The country is located on the west coast of Africa and is bordered on the north and northeast by the Republic of Guinea, on the east and southeast by the Republic of Liberia, and on the west and southwest by the Atlantic Ocean. It has access to one of the largest and deepest harbors in the world. The country possesses significant renewable natural resource endowments in land, forests, and fisheries. Almost 75 percent of the total land area of about 72,300 km2 is arable. Rainfall is abundant and is highest at the coast, 3,000–5,000 mm per year, and decreases progressively inland to 2,000–2,500 mm at the eastern border. There is an average of 2,187 hours of sunlight per year or an average of 6 hours of sunlight per day. The country contains 12 river basins, including Kolente, Kaba, Rokel, Pampana, Sewa, Moa, and Mano. Internal renewable water resources are estimated at 160 km3 per year, with surface water accounting for 150 km3 per year. Rainfall, soil, sunlight, and river basins endow the country with land of high natural fertility, considered suitable for a wide variety of food and cash crops and high crop yields. With more than 400 km of coastline, Sierra Leone has abundant and varied fish resources and is endowed with diverse species of finfish, shellfish, and wetland resources.

6. The country is also well-endowed with mineral resources. Extensive alluvial and kimberlitic diamond deposits as well as bauxite, rutile, and gold have been found in the east and south of the country. Gold, iron ore, and more recently bauxite have also been discovered and exploited in the north. Known mineral deposits include approximately 14.5 billion MT of iron ore, 4.7 billion MT of magnetite, 108 million MT of bauxite, 867 million MT of rutile, 11.2 million carats of diamonds, and 4.5 million ounces of gold (Sierra Leone National Mineral Agency, February 2017). According to the last Extractive Industries Transparency Initiative (EITI) report (February 2016), Sierra Leone produced 654,000 MT of bauxite in 2013, 3,700 ounces of gold, 10.6 million MT of iron ore, 32,500 MT of ilmenite, 1,22,400 MT of rutile, 158,500 MT of zirconium, and 612,400 carats of diamonds. Though this level of diamond production represents a substantial decline from the estimated 40 million carats that were either exported or smuggled out of Sierra Leone in the three years preceding independence, it remains an important resource, particularly for artisanal mining.

THE PEOPLE OF SIERRA LEONE