SAGE PUBLICATIONS Los Angeles Communicating in China's Lower Tier Markets

24

Journal of Creative Communications 3:2 (2008): 185–208 SAGE PUBLICATIONS Los Angeles London New Delhi Singapore DOI: 10.1177/097325860800300204 Communicating in China’s Lower Tier Markets KUNAL SINHA In the last decade, much attention has been devoted in marketing literature to the rapid growth in the megalopolises of Shanghai, Beijing, Guangzhou and Chongqing. But lower tier cities in China pose a challenge for most marketers and communicators. Even as we risk the temptation of extrapolating China’s breakneck rise and development to all parts, we tend to ignore the cultural diversity in a land that speaks in ten dialects and is home to significant minority populations whose identities remain strong outside the big city. From the creative standpoint, taking into account the cultural diversity is extremely valuable. The Real China Revealed study, on which this article is based, was an exploration into the ‘other half’. It is the half that promises huge growth in the near future, as markets in the upper tiers are saturated and get very competitive. In 2006, two of WPP Group plc’s agencies, Ogilvy & Mather and Mindshare collaborated to plan, execute, analyze and draw learnings for creative communications from this far-reaching study. Why will the Lower Tier be so Important? Until recently, China’s wealth was concentrated in the big cities along the east coast. Fifty- one per cent of the population that resides here, accounts for 64 per cent of the nation’s GDP (National Bureau of Statistics , China 2005: 339). But the central leadership’s ‘Go West’ drive has already put the infrastructure in place, on which will ride consumer demand. Already, two-thirds of all retail sales in China come from outside the 24 largest cities (Access Asia Limited 2005). Most marketers have traditionally chosen to target the affluent consumer. Many of them are currently in the big cities, but not for much longer. The proportion of affluent households (those earning more than 80,000 yuan per annum) in the top eight cities is expected to decline sharply by 2012, from the current 70 per cent to only 11 per cent, while their number will increase by more than four times in the smaller cities (Asian Demographics Limited 2003).

Transcript of SAGE PUBLICATIONS Los Angeles Communicating in China's Lower Tier Markets

Journal of Creative Communications 3:2 (2008): 185–208SAGE PUBLICATIONS Los Angeles London New Delhi SingaporeDOI: 10.1177/097325860800300204

Communicating in China’s Lower Tier Markets

KUNAL SINHA

In the last decade, much attention has been devoted in marketing literature to the rapid growth in the megalopolises of Shanghai, Beijing, Guangzhou and Chongqing. But lower tier cities in China pose a challenge for most marketers and communicators. Even as we risk the temptation of extrapolating China’s breakneck rise and development to all parts, we tend to ignore the cultural diversity in a land that speaks in ten dialects and is home to signifi cant minority populations whose identities remain strong outside the big city. From the creative standpoint, taking into account the cultural diversity is extremely valuable.

The Real China Revealed study, on which this article is based, was an exploration into the ‘other half ’. It is the half that promises huge growth in the near future, as markets in the upper tiers are saturated and get very competitive. In 2006, two of WPP Group plc’s agencies, Ogilvy & Mather and Mindshare collaborated to plan, execute, analyze and draw learnings for creative communications from this far-reaching study.

Why will the Lower Tier be so Important?

Until recently, China’s wealth was concentrated in the big cities along the east coast. Fifty-one per cent of the population that resides here, accounts for 64 per cent of the nation’s GDP

(National Bureau of Statistics , China 2005: 339). But the central leadership’s ‘Go West’ drive has already put the infrastructure in place, on which will ride consumer demand. Already, two-thirds of all retail sales in China come from outside the 24 largest cities (Access Asia Limited 2005).

Most marketers have traditionally chosen to target the affl uent consumer. Many of them are currently in the big cities, but not for much longer. The proportion of affl uent households (those earning more than 80,000 yuan per annum) in the top eight cities is expected to decline sharply by 2012, from the current 70 per cent to only 11 per cent, while their number will increase by more than four times in the smaller cities (Asian Demographics Limited 2003).

186 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

There is a great opportunity to ride on the aspirations, prosperity and creative ability of those living in the lower tier.

As recently as two years ago, retail in the lower tier operated almost solely through mom-and-pop stores that lacked sophisticated sales, merchandizing and logistics capabilities. To rectify this, in early 2005, the Chinese government launched the Project of Rural Retailing Development to overhaul the entire retail and distribution system.

The strong sense of community in the lower tier provides marketers and communicators with an opportunity. We may not have to convince the individual customer to buy our brand. Rather, we can target communities that share certain characteristics, or opinion formers and gatekeepers in the community.

Research Objectives

There were three parts to the study:

We wanted to understand what drives people to make choices in their lives and adopt new ideas and brands;

We audited brand and communication presence at different types of retail formats spanning hypermarkets to neighbourhood mom-and-pop stores, and conducted shopper intercept interviews to get a real sense of the choices made during that shopping trip, including impulse buys.

We photographed families and their favourite possessions, shopping environments and in-store and near-store communications to paint a vivid picture of the consumer and the retail environment for us.

Scope and Methodology

We chose to study the second tier, comprising 17 provincial capitals, 50 prefecture-level cities, and 15 other cities with population between 500,000 and two million, and the third tier, which is made up of 200 county-level towns. We visited almost 3,500 homes and 300 retail stores and interviewed 4,000 people in 22 cities. Ten of those cities were from Tier Three, seven from Tier Two, and we added fi ve from Tier One so that we could have a point of comparison.

The chosen centres were:

Tier One: Beijing, Shanghai, Xi’an, Jinan, WuhanTier Two: Mudanjiang, Lanzhou, Taiyuan, Shijiazhuang, Yichang, Nanning, MaomingTier Three: Taian, Hailin, Xianyang, Linxia, Linfen, Zhangjiahou, Xinyi (Jiangsu province),

Cenxi, Xinyi (Guangdong province), Dangyang

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 187

We made sure that no region was left out, barring the far west, which is sparsely inhabited. Respondents were equally represented among the three income classes—high, middle and low; our retail study spanned hypermarkets, supermarkets and neighbourhood mom-and-pop stores.

The research was conducted through quantitative questionnaires for most part. We chose fi ve locations in Tier Two and Three towns to visit families and have free-fl owing conversations about their lives, aspirations, consumption and the problems they faced. In these towns, we observed the shopping environment and shoppers in local marketplaces. All living and shopping environments were photographed.

The study covered 25 product and service categories—ranging from automobiles to in-surance and banking to soft drinks, in addition to the data about consumers, their shopping and media habits and drivers for choice, as outlined in this article.

PART ONE: CONSUMER ATTITUDES

Attitudes towards Family

The small-town family does not always mean father-mother-little emperor/empress, but three generations living together under one roof, with some relatives thrown in for good measure. It is the interdependence on members of the extended family that characterizes the strong bonds between the generations.

We begin by pointing out a paradox between what people think and what they do (Figure 1).

Figure 1Relative Importance of Family over Career

188 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

When more people in Tier One cities say that they believe their families are more important than their careers, they are merely trying to alleviate their guilt of giving their careers preference in their lives. They make explicit efforts to assert that they care about their families.

Lower tier families consider their family ties more important and care about family values instinctively. Said Wen Huang in Nanning, ‘I come from a large family and am the eldest. All my husband’s brothers and sisters are peasants living in the countryside. I have to bear my parents’ medical expenses, and his nephew lives with us so that he can get a good education, which he would not in the village where he comes from.’ Almost in agreement, Wu Qian in Cenxi said, ‘If we didn’t help our own siblings, then who else would we help? We once gave money to my husband’s younger brother to build a house.’

The interdependence is remarkable, because in many ways, fi nancial assets are pooled by extended families, and expenditure incurred not only on the immediate family but the extended one. Pointing out to the desktop computer in his home, Qian Jinghong in Nanning explained, ‘This computer was bought by my relative. All my relatives and friends are very good towards my son.’ Nao Bai Jin, a brand of health supplement, has built its franchise in an overcrowded market, simply by focusing on gifting to the elderly.

Families in small towns are family-oriented in more ways than one. We found that they do not have to make the effort of eating together, as much as those in the bigger cities. They do so anyway (Figure 2).

Figure 2Making the Effort of Eating Together

Attitudes towards Life

It is the reward of pursuing that golden dream that makes residents of Tier One cities more satisfi ed. Life in many ways is better for them as a result of their higher economic status; the opportunities for them and their children, greater (Figure 3).

More than half the respondents in the lower tier felt dissatisfi ed with their lives and their family’s living standards. Some of this feeling is the result of their exposure to life in the big city, through the tales that they hear from their relatives and friends who have prospered there

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 189

and through occasional travel. ‘Shanghai left a very good impression on me. People there look so well educated. Men were riding bicycles, and yet they wore ties!’, observed Li Lin, a resident of Cenxi in Guangxi province. Hai Ming from Yichang said, ‘The big city has many more opportunities for earning and spending. When our daughter fi nishes high school, we will send her either to Tsinghua University or to Fudan University. It will be more expensive, but she will do well there.’ Sun Xiaoyu in Linxia expressed her unhappiness: ‘I’ll send my daughter to the East or the South, at least to Lanzhou. She can’t even speak good Mandarin—she speaks the Linxia dialect. Linxia people are not as civilized as those in Lanzhou. I don’t want her to live in this less-civilized town.’

Chen Yuanyuan and his family tried to move to Nanjing from Lanzhou in Gansu province: ‘We moved to Nanjing to fi nd a better job. But my husband couldn’t get a hukou (residence permit) for Nanjing, so we had to go back after six months’, his wife told us. His daughter added, ‘Kids in Nanjing are smarter than those in Lanzhou. When I was in Nanjing in that half year, I found my classmates so smart that they could invent games themselves.’

By making brands more relevant to their lives and through more empathetic communication, such as using celebrities that are not very distant, or pegging the level of aspiration at a realistic level, we have the opportunity of turning that feeling of inadequacy around.

Attitudes towards Risk

Signifi cantly, the attitude towards risk-taking was almost the same across the tiers. While the majority still believed in staying with convention, there were many who were taking social risks (Figure 4). Young women in Nanjing, for example, were getting nude portfolios shot in the hope of instant stardom. Lao Wang, who was a triathlon champion from Gansu, no longer had his job with the state-owned enterprise. He said, ‘When my daughter said she wanted to quit school and learn dancing and become a model, I did not stop her. She must try something different to be successful.’

Figure 3Satisfaction with Life

190 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

But then there were those who are embracing economic risk, even as the majority continues to save amidst rising real-estate education, and medical costs. The change was marginally higher in Tier One cities, where the continuous availability of jobs makes residents confi dent to take on debt. A junior executive in Guanzhou bragged, ‘I know I will get a raise this year. I will then pay off all my credit card bills.’

In Nanjing, Zhu Zhiwei’s parents made the down payment for a small apartment and com-pelled him to pay the monthly instalments when they saw their son, only in his fi rst year at work, spending most of his money partying with his friends. Such recklessness with money is not welcome — saving is a good habit that lower-tier residents believe must be inculcated and preserved. Wu Qian in Cenxi seemed to encapsulate the sentiment well when he said, ‘We usually don’t go in for bank loans. We borrow money from relatives and friends.’ The re-payment is almost always without any interest, and it serves to cement the obligatory sense of relationship, guanxi.

Attitudes towards Ambition

Risk and ambition go together, and the difference between the tiers was quite similar (Figure 5).

Figure 5Degrees of Ambition

When Dudu, a young cellist in Lanzhou mentioned that she wanted to emulate Yo Yo Ma—the famous cellist, she was merely echoing the feeling of a million other youngsters across China

Figure 4Attitudes towards Risk

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 191

who are learning to play string instruments. The creative fi elds offer a huge opportunity, and many believe that they can catapult their way to fame and fortune in the new China, where the winners of TV talent shows like ‘Supergirl’ come from smaller cities like Chengdu. Having a role model with Chinese origins, such as Olympic gold-medalist hurdler Liu Xiang, certainly helps fi re up the ambitions of lower-tier youth.

Many young Chinese want to gain experience working for organizations in the early part of their careers, then quickly strike out on their own. This is a feeling that cuts across big cities and small towns; it is only the kind of business that’s different. If the big city residents wanted to start a software company or a fashion boutique, then Sun Xiaosu from Linxia revealed, ‘My husband is planning to invest in the mining business and I’m thinking of opening a kindergarten. It can get us big money.’

For older people, their ambitions were a bit modest—more in terms of being able to provide a comfortable life for themselves and their family. ‘Our plan is to have a new apartment. We want to move to a “high-class area” like Pudong in Shanghai, which is for rich people,’ said Wei Yuemei in Nanning. How would they realize their dream? Once again, through guanxi. ‘We have friends in the construction business, they would give us a discount,’ she says confi dently. Then there are some whose ambitions are more rooted—they are looking for business opportunity within the local culture. Li Lin in Cenxi said: ‘My dream is to open a Chinese-character tea house. Tea culture has thousands of years of history behind it. I think the ambience of a tea house will be great for people to socialize.’

Attitudes towards Fashion

Interestingly, the craving to keep up-to-date with fashion was somewhat higher in Tier Three towns (Figure 6). It challenged our belief that it was big city folks who are the most fashion conscious. The small-town consumer was, however, fashionable through subversion. She had huge access to beauty and fashion, even if it was not always branded. She gets a pedicure for one yuan, a haircut for fi ve. Miao Miao from Cenxi quipped, ‘Why should I spend 200 yuan

Figure 6Attitudes towards Fashion

192 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

on a pair of branded jeans, even if it is a Metersbonwe, when I can pick up fi ve stylish pairs from the local wholesale market for that price? In any case, the jeans I buy this winter will be out of style next year.’ She must rummage through the boxes in that market, but she certainly creates greater variety in her wardrobe.

Attitudes towards Novelty

Novelty is a big draw. All across China, consumers are embracing change; the craving for new ideas and goods, be they functional or aesthetic, is only marginally lesser in the lower tier. While 59.1 per cent of the respondents agreed with the statement, ‘I enjoy trying new things’ in Tier One cities, the fi gure decreased only slightly to 54.6 per cent in Tier Two and 53.6 per cent in Tier Three. The spas may not be as luxurious as the Dragonfl y in the big city, but they are just as popular. The Gameboys may be locally manufactured, but when a kid gets one, all his friends are curious to play with it and want one. ‘We fi nd out about the latest model from the magazines, and ask the local shop owner when he’s going to get it,’ said a teenager in Hailin. All this points towards an appetite for creativity.

Television and the internet are popular in the small towns quite simply because the fare that they offer is always new and interesting. While there is a wave of self-expression in the digital space that is not confi ned to the big city, TV now offers the opportunity for interaction and stardom. If ‘Supergirl’ was popular one year, then it was the turn of ‘My Hero’, ‘The Winner’ (a business / entrepreneurship programme), and ‘Happy Base Camp’(a series loosely based on the American reality show ‘Survivor’) after that.

Key Implications: Part One

So what do these attitudes tell us? They tell us that there are some universal themes, particularly those around family values, ambition, risk and fashion/ status, which can work for brands and communications across the tiers. The level of risk, ambition and status, must however, be calibrated. If the young boy in Nanning wants to be like Liu Xiang, the 100 metres hurdles champion, then the one in Guangzhou wants to be like Kobe Bryant. For the college girl in Linxia, just getting to Shanghai, working as an offi ce lady and living alone is perceived as risky. But for the deskbound offi ce assistant in Beijing, risk means a trek alone in the Himalayas. In the new China driven by a desire to succeed, stories about confi dent achievers would counter the risk-aversion of the majority and are quite likely to strike a chord.

As brands penetrate the lower tiers, we must be careful not to pass on ‘me-too’ brands or products that are stripped down to reduce cost. Consumers are looking for novelty, creativity

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 193

and differentiation even here, and tired clichés will not work. Since the lower tier marketplace has relatively fewer options than in the big cities, early movers will be at an advantage. Just as in the big city, we will need to innovate.

In the desire to play along with people’s ambitions, we must remain careful not to always paint a rosy picture of life in the big city and push up the feeling of inadequacy among those in the small towns. Rather, brands and communication must fi nd ways of making them feel good about their condition, or enhance their lives, within the social and economic circumstances—for example, by emphasizing family values. Besides, fame and popularity are far easier to achieve in a small town than in the big city.

PART TWO: BRANDS, COMMUNICATION & SHOPPING BEHAVIOUR

Brands and Advertising

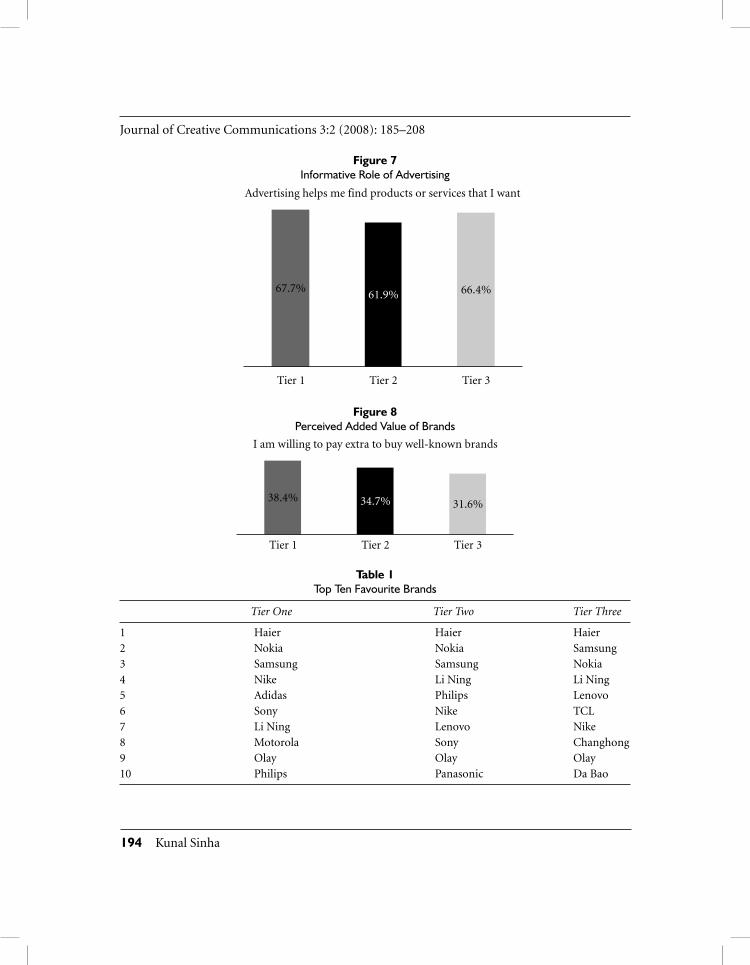

Most lower-tier consumers viewed advertising as a source of knowledge. It is this perceived role that sometimes makes us cram the advertising with a lot of information—fuelled by companies who believe that more is better, even in 30 seconds. ‘Sometimes I am confused by how a fi ve yuan product can have so much!’, admitted Hwang Jun in Linxia. On the other hand, brand power is only beginning to set in, especially in the small towns. The majority is still not willing to pay more for well-known brands—as many as 68.4 per cent of the respondents in Tier Three cities said so. Lack of availability of well-known brands is another factor. ‘There are no good brands available in Cenxi. When we want to buy something good, we go to Lanzhou,’ lamented Sun Xiaoyu. We saw evidence of this not just in apparel purchase, as illustrated earlier, but also in some fast-moving consumer good categories (Figure 7).

The big challenge that we face collectively is to enable consumers to fi nd value in brands, especially as some of the quality assurance comes out of buying from a supermarket or the neighbourhood mom-and-pop store (Figure 8). It is by making emotional and cultural con-nections that we will be able to add value.

Foreign Brands

The openness to adopt foreign brands was quite low in the Tier Three towns. There was a general belief (as well as experience, while shopping) that foreign brands are more expensive.

As one went down from Tier One to Tier Three, the number of MNC brands in the top ten favourites list was cut by half, from eight to four (Table 1). Haier, the consumer durable

194 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

Figure 7Informative Role of Advertising

Figure 8Perceived Added Value of Brands

Table 1Top Ten Favourite Brands

Tier One Tier Two Tier Three

1 Haier Haier Haier2 Nokia Nokia Samsung3 Samsung Samsung Nokia4 Nike Li Ning Li Ning5 Adidas Philips Lenovo6 Sony Nike TCL7 Li Ning Lenovo Nike8 Motorola Sony Changhong9 Olay Olay Olay10 Philips Panasonic Da Bao

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 195

manufacturer, remained the favourite brand for most people across all tiers. Nokia, Samsung, Nike and Olay did well among the multinational brands. What makes the above list interesting is the complete absence of service brands. Google may be at the top of the BrandZ (a survey of the most valuable brands list worldwide done by Millward Brown Optimor, a WPP company) but consumers across China are still looking for tangibility when they are evaluating their brands.

The residents of Nanjing shared a special anathema towards Japanese brands, owing to history—the Japanese armed forces had committed unspeakable atrocities on its residents during the Sino-Japanese War. ‘We will never buy anything Japanese, no matter how good the company claims it is, or no matter how well it sells anywhere else in the world,’ said Gu Jin’s mother emphatically. It is a patriotic sentiment that works across China, but especially so in the lower tier.

International entertainment, on the other hand, faces no problems in being adopted. Soap operas from South Korea such as ‘Winter Sonata’ are as popular in smaller towns as they are in the bigger cities. Neither do retail supermarket chains like Carrefour—as they expand with breakneck speed into smaller towns—serving as much as a place for entertainment as one to seek exposure to new brands.

Influences on Purchase Decision

China, across the tiers, remains a price-driven, price-sensitive market. Price remains the overwhelming factor in making choices – both store choices and brand choices. Eighty-eight per cent of respondents said they were infl uenced by price, 70 per cent in Tier One and Three compared prices before making a choice. No small wonder that from hypermarkets to street vendors, they all scream their price out loud. What is interesting is that the brand is the second most important infl uence on purchase decision, with 72 per cent of respondents across the tiers saying they are infl uenced by the brand (Figure 9). So what are the differences between the tiers?

This chart reveals that the shopper’s own experience matters more in Tier One cities, a refl ection of independent and confi dent shopping. Tier Two shoppers are infl uenced by the opinions of others—their social group notably and role models. For Tier Three consumers, the shop owner’s opinion and packaging have an impact on their choices. Small-town residents rely on their long-standing relationships within the community to make choices.

The neighbourhood mom-and-pop store owner also has a special relationship with shoppers, simply because he gives them a credit facility, whereby he keeps track of their purchases and is

Figu

re 9

Fact

ors

Influ

enci

ng B

rand

Cho

ice

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 197

paid at the end of the month. When the migrant worker calls up home to speak to his mother, he enquires about her health, overhearing the conversation.

It is evident that lower-tier consumers look towards others for a ratifi cation of their brand choices. But good packaging is important too, since it provides them reassurance about quality, especially in a marketplace where counterfeits abound.

Little Emperors as Influencers

Children now have signifi cant infl uence on the composition of their mothers’ shopping baskets (Figure 10). They are the source of new information (in a separate study, we found them far more aware about global warming than their parents), eager to adopt new ideas, and in Tier One, are allowed to make their own choices in some product categories, especially food and clothing. Mothers agree: ‘If we allow the kid to choose the snacks, there is little wastage. If they don’t eat it, we tell them—you bought it yourself, now you better fi nish it.’

Figure 10 The Influence of Children

In the lower tier, the degree of autonomy as well as pampering that kids enjoy is relatively lower. ‘My mother taught me to wash my clothes and cook a few dishes. I did the same thing for my son—I want to build his independence,’ opined Li Lin in Cenxi. Parents here like to keep their limited resources within their own control. Lower-tier children are learning to respect their recently acquired wealth. Li Lin continues, ‘When his clothes become small, he never lets me give them away. He says if I were to give him a baby brother, his little brother could wear the same clothes.’ The lower-tier pampering notwithstanding, the majority seeks the opinion of the little emperors, because they are generally aware of and try to keep pace with the rapid changes in their world. As a market, and as communication vehicles, kids are ever important. Parents are making huge investments on the upbringing of their kids—and they do not always have just one kid in the lower tier. ‘We spend 40 per cent of our income on our son every month to make sure he has a good education and is happy,’ the parents of Hua Shen in Linxia told us. It is a mix of pampering, pushing harder and showing off the child’s achievements. Photo studios that document the lives of kids and portray them as angels or

198 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

future TV stars abound in the lower tier. A child’s knowledge is tempered by exposure, and not many kids in the lower tier have access to computers at home yet.

Key Implications: Part Two

It is evident that, if we want to build brands that are differentiated and preferred in the lower tier, we must shift the role of brand communications from providing information and simply repeating the message to creating emotional connections, fi nding fi ts with value systems and by telling stories. A former brand manager credits the success of Procter & Gamble’s brand Olay to shifting their communications to tell more subtle stories. In the future, more creative communications that tease the imagination and entertain will stand out from the huge mass of TV commercials, outdoor and in-store advertising that the consumer is exposed to. It is indeed high time that we stopped underestimating the intelligence of the lower-tier consumer.

As multinational brands move to the lower tier, it may not be necessary to emphasize their origins or use terms like ‘international’. Unlike the big city consumer for whom the pedigree of French wine or German engineering or Italian design is big deal, for the lower-tier consumer such associations immediately create the perception of unaffordability. For them, cultural assimilation might work better.

We will have to fi nd ways of surrounding the lower-tier consumer with favourable word-of-mouth to build their confi dence and ride on their collectivism. This means shop owners and current users of the brand must be motivated to spread the good word and constantly reassure consumers that the choice they have made (or will potentially make) is correct. It may seem to marketers that with the large numbers in the lower tier, this would be an expensive proposition. Not always—simple in-pack / in-store schemes for the consumer, or a leafl et laden with ideas in the carton for the shop owner or hairdresser will do the trick.

If kids play an important role and arguably watch and remember more TV commercials than their parents, we must involve them during the shopping trip by recognizing their presence and power. Especially in the lower tier, through storytelling on the mass media, it may well be possible to nudge their parents to trust them a bit more!

PART THREE: EATING OUT, SHOPPING AND MEDIA HABITS

Eating Out

Tier One cities have signifi cantly more consumers eating at fast food restaurants (such as KFC, Yoshinoya and McDonalds) than Tier Three (Figure 11).

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 199

Families in Tier Three remain conservative with their food habits, even as they eat out at small, local stalls. In a separate ethnographic study among young people in Nanjing, we did not fi nd even one occasion when the subjects under study ate at a Western-style restaurant. ‘Eating fried chicken or a burger is more of a treat for us. We love our dumplings, hotpot and steamed guyi fi sh too much,’ said Gu Qing in Nanjing.

Much of the lower-tier food market is dominated by local food stall and restaurant owners, with food courts and food streets being especially popular. As much as they represent an opportunity for the food service industry, they are also a threat to the overall health profi le of the population. ‘I am not always sure of the quality of food when we eat out. Sometimes it is out of compulsion—my wife is too busy to cook when she is minding our shop, or we eat out when we go shopping. We always drink bottled water or green tea, for example,’ admitted Wang Dongsheng in Lanzhou.

Shopping Frequency, Distance Travelled and Impulse Shopping

Shoppers in Tier One and Two cities made more shopping trips (66 per cent - once a week or more often) than those in Tier Three (52 per cent). This was partly because there were more shops near the residence zone in Tier One and Two, whereas in Tier Three, there were one or two marketplaces where everyone did their shopping.

Interestingly enough, the lower-tier shopper does a bit more impulse shopping than the shopper in Tier One (Table 2). ‘We go shopping about once in a week or ten days. When we do, I keep aside some money so that I can browse and buy something at the spur of the moment,’ said Zhong Wen in Nanning. Tier One shoppers, in their urge to optimize time, stick to their shopping lists, especially while shopping for groceries.

So, what triggers their impulse? By and large, it is discounts (58 per cent say they are lured by them) and free gifts (33 per cent). But once more, there are differences across the tiers. Shelf/shop aisle displays for specifi c brands(like the one shown on the right in Table 2), free gifts and product sampling are more effective in Tier One cities. On the other hand, radio

Figure 11Eating Out

200 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

ads and small countertop displays that use space optimally, work better in the small format stores in Tier Three towns.

The lower tier still retains a neighbourhood marketplace feel, where you fi nd people chatting on the pavements, or lingering in the store to make a phone call using the shopowner’s landline. The advertisements are simple, basic at best—long banners strung across the shop entrance or the supermarket frontage, drawing attention to the stall number, rather than a brand. The malls and supermarkets in the big city, with their escalators and aisles, seem to urge the shopper to move along. Then, we as brand custodians, must fi nd ways to make them stop in their tracks.

Media and Entertainment Habits

Traditional media remain powerful and infl uential in contacting consumers. TV enjoys a penetration of 94 per cent across the tiers. But there are signifi cant variations in the kind of programmes that the residents of the three tiers like to watch (Figure 12).

Across the tiers, national news and TV serials attract the highest viewership—with 41 per cent saying they ‘really like’ the programmes. That apart, residents of each tier have their own preferences, driven by their respective leisure and information needs. Tier One viewers like sports, music, food shows, business, nature and environment programmes. For them, TV is mostly an entertainment medium—something they can unwind with after a hard day’s work. But because they are in the big city in the quest for prosperity, they must also watch business news. Tier Two viewers watch local news, and those in Tier Three watch international news, education and career-oriented programmes. They are looking for information that will help them keep abreast of what’s happening in the world, and fi nd ways to advance in their careers, current and future.

Table 2Impulse Purchases

Factors infl uencing impulse shopping (sample: 460) Total per cent

Discount 58Free gifts 38Music / radio with ads 33Product tasting / sampling 24Standalone displays 14Shelf display for specifi c brands 13TV sets with ads 9

Figu

re 1

2Fa

vour

ite T

V Pr

ogra

mm

es a

cros

s th

e T

iers

202 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

Newspaper and out-of-home media follow TV with an average penetration of 64 per cent and 60 per cent respectively, but it seems that in Tier One, people spend more time out of home, as a result the reach of Out-of-Home media is higher—73 per cent, which is 20 per cent more than its reach in Tier Two and Three towns.

On the fl ip side, magazines are more popular in Tier Three—where 26.3 per cent of the respondents said they had read a magazine the previous day. Undoubtedly, a magazine like Duzhe (Reader) fi nds its loyalists in lower-tier China, and this is also a refl ection of people having more free time. Filled with human–interest stories, devoid of sex and sensationalism, Duzhe is a favourite of all low-income people. It gives them hope in the tough world, and shows them that the human spirit conquers all—a 5.2 million readership for every issue can-not be wrong!

There is a decline of about 10 per cent in regular internet access (‘touched yesterday’) as we go from Tier One to Tier Three, from 46.8 per cent to 37.3 per cent. Many more surfers access the internet from cybercafés in the lower tier. Internet users spend half as much time surfi ng the net during weekends compared with weekdays in Tier One and Two cities, but the drop is relatively lower in Tier Three—a refl ection of the many more formal entertainment and socializing opportunities in the upper tiers.

Even though the pace of life in the lower tier may be slower, residents fi nd ways to fi ll up their time. Be it long games of mahjong in the afternoon, while consuming endless cups of tea, or a game of billiards in the neighbourhood ‘recreation centre’ for two yuan per hour, they create their own opportunities for socializing and entertainment. While it costs fi ve yuan to buy a DVD, local video rental stores rent out the latest DVDs for as low as one yuan in Tier Three towns.

The Golden Week holidays in May and October have stimulated travel and holidaying habits across the tiers. Three hundred and seventy million households took holidays in 2006, and they went on 1.1 billion trips (China Statistical Yearbook 2006). ‘I spend several thousand yuan in each trip. We don’t buy anything but just taking photos, transport and accommodation costs a lot of money,’ says Wu Qian in Cenxi, without any regrets. On the other hand, Wei Yuemei in Nanning observes, ‘We spend a lot on travel – my husband loves buying things at every travel site.’ Many from the lower tier want the ‘big city’ experience on their holidays, with the Great Wall and Forbidden City among the top attractions, along with West Lake in Hangzhou. Yu Gardens in Shanghai received 4 million visitors in three days during the May holidays in 2007.

Key Implications: Part Three

If lower-tier consumers do not embrace change in their food habits easily, food brands still have the opportunity to stimulate demand by offering traditional cuisine in new and convenient

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 203

formats such as ready to heat, takeaway. Also, ‘new foods’ must localize their menu in creative ways, just as Kentucky Fried Chicken has done so successfully. For food chains, a reassurance about hygiene and food quality standards can provide an added dimension to their service.

Our fi ndings related to shopping behaviour and media consumption provide a direction for channel planning across the tiers. It is local and in-store media that we must use to trigger the shopper’s impulse and enable them to compare, while TV can focus on building the emotional brand values and/or communicating news. Knowing that lower tier residents read magazines, we have the opportunity of using the medium to fulfi ll its traditional informative role. It seems ironic that Duzhe carries very little advertising, while the lifestyle magazines aimed at upper tier consumers are fi lled with ads for, well, lifestyle brands. Maybe it is a fear among marketing / brand managers that advertising in magazines like Duzhe may ‘lower the profi le’ of their brand, but this is clearly an opportunity lost.

We cannot but emphasize the importance of engaging the shop owner/ shop assistant in Tier Two and Three towns—as we know that he/she plays a key role in swinging the choice when the shopper is making comparisons. Local sales representatives would need to identify key infl uencers within communities, motivate them and educate them about the brand. They must also be able to take a promotional message and adapt it to meet local consumers’ desires and motivations. There lies a challenge in designing in-store media based on local preferences and the small shop format in the lower tier. Retail designers, mostly obsessed with creating impressive displays for the hypermarket and fl agship store format, have to gear themselves up to respond to the lower tier’s needs.

Finally, as travel becomes a national obsession, it provides an opportunity for local businesses to use the holiday season to boost their sales, and provide the exposure that travelers from the lower tier seek. At the same time, brands and product categories that are associated with travel and holidaying—cameras, luggage, travel clothes, packaged foods, and travel and fi nancial services have a great opportunity to get their seasonal upward spikes. We believe that a product like ‘travel loans’ would work, simply because it seems a little awkward to borrow money from a friend or relative for a nonessential expenditure like travel (unlike for a child’s education or building a house).

PART D: BRAND PERFORMANCE ACROSS THE TIERS

Fast Moving Consumer Goods (FMCGs)

Our shopping basket analysis showed that multinational brands do well in many FMCG categories; yet some categories seem to be local brand strongholds (Figure 13).

204 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

The multinational company brands that perform well include:

Sprite, Coke and Pepsi in the carbonated soft drink category, with Sprite being a strong Tier Two-Three brand;

Kang Shi Fu Lu Cha and Kang Shi Fu Hong Cha—both brands from Taiwan, in the tea category (Nestle and Suntory, which do well in Tier One, have low penetration in the lower tiers);

Kang Shi Fu and Danone in the biscuits/cookies category (Haochidian does well in Tiers Two and Three)

Dove and Cadbury in the chocolates category; Pantene, Rejoice, Head & Shoulders, Lux and Hazeline in the shampoo category (again,

local brands like Lafang, Houdy and Liangzhuang are strong in Tier Three); Crest and Colgate in the toothpaste category.

At the other end of the spectrum, the strong local brands are:

Nongfu Spring and Wahaha in the bottled water category; Tsingtao and Yan Jing beer;

Figure 13Relative Strength and Weakness of Multinational Companies (MNCs) and Local Brands

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 205

Meng Niu, Yili and Bright dairy milk; Arawana and Lu Hua cooking oil.

In the skincare category, Tjoy, Da Bao, Mini Nurse, Maxam and Olay are the top fi ve brands, with Da Bao and Mini Nurse being strong Tier Two-Three brands. President, Nong Fu and Kang Shi Fu do well across all tiers in the fruit juice category.

Consumer Durables

For most Chinese durable brands, the lower tier consumer is their captive audience. Brands such as Midea, Galanz, Changhong, and Gree fi nd their loyalists here. In Nanning, Qin Jinhong says, ‘We trust Gree. Three out of our four air-conditioners, our refrigerator and washing machine are all from Gree.’ The TV market is completely dominated by Chinese brands – Changhong, Konka, TCL, Hisense and Skyworth (Figure 14).

Figure 14Leading Consumer Durable Brands

A similar trend holds true for washing machines, refrigerators, and air-conditioners, with Haier, Little Swan and Royalstar being the top three washing machine brands, and Haier, Ronshen and Frestech being the top three refrigerator brands. Siemens is the only multinational company brand that features in the top fi ve list for refrigerators. Gree, Midea and Haier

206 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

dominate the air-conditioner market across the three tiers. The DVD (Digital Video Disc) player market features brands that are hardly known outside China – Amoi, BBK, Shinco, Malata and Nintaus. Between them, they have the market more or less carved out, leaving multinational company brands with no room. There is a very strong belief that local DVD players are best equipped to handle the pirated DVDs, and that there is no point in spending more money on a foreign brand, only to fi nd that it does not play many of the DVDs.

The picture for multinational company brands improves dramatically in the mobile phone and digital camera categories. Chinese brands have been unable to keep up with the rapid pace of innovation and have been all but driven out of the market. Sony is the leading brand of digital camera across the tiers, while Kodak does well in Tier Three. Canon, Samsung and Olympus are the other brands that performed well. Similarly, Nokia, Motorola, Samsung and Sony Ericsson are the top performing mobile phone brands, with about 70 per cent of the market shared among them across the tiers, leaving local brands like Lenovo, TCL and onetime market leader Bird well behind.

There are signifi cant differences among the tiers when it comes to the kind of consumer electronics that families intend to buy in the next one year. Most Tier One residents plan to buy new TV sets—it is a market driven by upgrades, as they move from picture tube to plasma and liquid crystal display technology, and from fi lm to digital cameras. More Tier Two residents plan to buy new DVD players, air conditioners and washing machines, whereas Tier Three residents will be buying new mobile phones, computers, digital cameras and refrigerators, mostly for the fi rst time. As lower tier consumers enter these categories, they will look for information on product features and greater functionality at an affordable price—this is one category where comparative communications, especially in-store, would be necessary, as much as providing salespersons with the information that will help consumers make choices. Shoppers will have to be engaged in a two-way dialogue.

Automobiles

While Shanghai Volkswagen is the current market leader in terms of being the highest currently owned car, it faces a challenge in the lower tier in the near future. From a current ownership rate of 21.9 per cent, it falls to 10.9 per cent among those who intend to buy a new car within the next one year. Hyundai takes its place, with 13.6 per cent saying they plan on buying the marque in Tier Three; the same fi gure stands for Honda, and the local brand Qirui (Chery) is being considered by 12.7 per cent. A black Buick may be the sign of infl uence and prosperity in the big city while young couples consider their Chery QQ worthy of being part of their wedding photos!

Journal of Creative Communications 3:2 (2008): 185–208

Communicating in China’s Lower Tier Markets 207

Apparel and Sportswear

The honours are equally divided between multinational company brands Nike and Adidas, and local brands Li Ning, Anta and Double Star in the casual sportswear category. Nike is the leading Tier One brand (34.5 per cent respondents said they own it), followed closely by Li Ning (31.1 per cent). The order fl ips in Tier Two, with Li Ning enjoying a share of 38.3 per cent and Nike 23.9 per cent; in Tier Three, the top two brands are Li Ning and Anta. The pat-tern clearly follows the overall trend that suggests a stronger relationship with local brands as one goes down the tiers.

Key Implications: Part Four

If anything, these brand performance fi gures show that market leadership is but transitory in the China market, and the lower tiers can have a signifi cant impact on changing the fortunes of a brand.

There is no uniform formula that can be applied to the lower tiers—market and commu-nication planning does not work like a scale along which aspirations and ownership/usage can be conveniently calibrated. Lower tier consumers exhibit a native ingenuity in making choices, and are not easily swayed by claimed benefi t or pedigree. They look for proof of performance as much as so-called ‘smart upper tier consumers’ do.

It is absolutely essential, then, for brand owners, to take into account the differences in preferences while deciding to market to the low tier. Consumer durable companies must take into account the different stages of market development and demand across the tiers and design a multi-tier strategy. They must take care not to strip down features too much in order to reduce cost, because buyers—even in smaller towns—are looking for more, not less. It may make sense to offer bundled packages, especially to those who are setting up new homes.

At the same time, to assume that low tier means low price or even cut quality (as we have mentioned before), is to be foolhardy. As the mobile phone, digital camera categories, Korean automobiles and some FMCG companies have shown, lower tier consumers are quite willing to loosen their wallets if they are given the right balance of aspiration and practicality. Chinese brand owners can take heart from the low tier consumer’s sense of pragmatism, but they must protect their turf by boosting the image of their brands and focusing on innovation.

IN CONCLUSION

The opportunity in China’s lower tier markets is there for companies, both local and multi-national, to profi t from. But the easy money in China is history. Corporations will have to fi nd

208 Kunal Sinha

Journal of Creative Communications 3:2 (2008): 185–208

ways to connect with their prospects and existing customers in increasingly creative ways, as they seek novelty in their experiences. Through our study, we have attempted to shed light on those unrecognized towns in China’s hinterland. Now it’s the chance for companies to put this knowledge to use—for communications, and for their brands.

Kunal Sinha is Executive Director (Discovery) at Ogilvy & Mather, Shanghai, People’s Republic of China. E-mail: [email protected]

REFERENCES

Access Asia Limited (2005). China Country Profi le 2005. Shanghai, China.Asian Demographics Limited (2003). Forecast Asia: China. Hong KongChina Statistical Yearbook (2006).National Bureau of Statistics (2005). China Statistical Yearbook No. 24. Page 339. China Statistics Press,

Beijing.