Report on Study on power purchase/sale/surrender of power ...

179

Report on Study on power purchase/sale/surrender of power along with drawal/sales under UI and Transmission System Improvement for Punjab State Power Corporation Limited from April 1, 2010 to March 31, 2013. Submitted to Punjab State Electricity Regulatory Commission Prepared by: ABPS Infrastructure Advisory Pvt. Ltd January 2014

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Report on Study on power purchase/sale/surrender of power ...

Report on Study on power purchase/sale/surrender of power along with drawal/sales under UI and Transmission System

Improvement for Punjab State Power Corporation Limited from April 1, 2010 to March 31, 2013.

Submitted to

Punjab State Electricity Regulatory Commission

Prepared by:

ABPS Infrastructure Advisory Pvt. Ltd

January 2014

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page i

Executive Summary

Background

The total capacity available to State of Punjab is 7943 MW with major dependence on the coal fired thermal generating stations and hydel generating stations. The demand supply scenario in Punjab suggests that despite the increase in generation capacity, there have been acute power shortages. The peak demand has been around 11520 MW whereas the peak demand met has been around 9074 MW in FY 2012-13 with peak deficit of around 21%. Similarly, the total energy requirement for the State of Punjab has been around 48 BU whereas energy availability has been around 45 BU in FY 2012-13 with energy shortage of around 5.4%.

PSERC engaged ABPS Infrastructure Advisory Private to carry out a study on power purchase/ sales/ surrender of power along with drawal/sales under Unscheduled Interchange for Punjab State Power Corporation Limited for the period of April 1, 2010 to March 31, 2013.

Based on the analysis of the information collected from the Commission’s office and information available in public domain, the list of additional data and information required for carrying out the study was prepared for obtaining the same from PSPCL and PSTCL. Three rounds of discussions were also held with PSPCL and PSTCL along with Commission officials to discuss in detail the information required and on the information submitted by PSPCL. Based on the information available with the Commission, information received from PSPCL and PSTCL till date and the information available in the public domain, detailed analysis has been carried out on various aspects of the Study for FY 2010-11 to FY 2012-13.

The brief overview of the various aspects pertaining to the power purchase/sale/surrender of power along with drawl/sales under UI and Transmission system improvement for PSTCL as covered in this study along with the key findings and recommendations are summarised in Executive Summary.

Analysis of Sales

The major contribution to energy sales in the State of Punjab is from the Industrial and Agricultural Consumers. During the analysis, it is observed that the methodology adopted for projecting the energy sales for the ensuing year is based on trend analysis i.e., three year CAGR. Prima-facie, this methodology appears to be appropriate, however, variations were observed in the approved annual energy sales and the actual energy sales.

A detailed analysis has been carried out to assess the reasons behind the variations in growth rate considered for projecting category wise actual energy sales and the actual

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page ii

growth rate as compared to actual sales for previous years. It is observed that these variations were occurring because of the non-consideration of the category-wise variations in number of consumers, connected load, specific consumption, load factor and sudden spurt in energy demand due to changed economic and regulatory scenario.

The analysis of category-wise variation indicates that the major variations have been mainly in Large Supply, Railway traction and medium supply categories. The variation in Domestic Category, Large Supply and Agricultural categories substantially affects the total quantum of sales and thus the energy requirement. Further, it is observed that with the implementation of Open Access there has been a sharp variation in the energy sales as the consumers have opted for other sources of power.

The approved and actual sales along with variations for FY 2010-11 to FY 2012-13 is as shown in the table below:

Table : Summary of Approved and Actual Sales for FY 2010-11 to FY 2012-13

SL No Category

FY 2010-11 FY 2011-12 FY 2012-13

Approved Sales (MU)

Actual Sales (MU)

Variation (%)

Approved Sales (MU)

Actual Sales (MU)

Variation (%)

Approved

Sales (MU)

Actual

Sales (MU)

Variation (%)

1 Domestic 7865 8176 3.95% 8854 8818 -0.41% 9642 9285 -3.70%

2 Non residential 2405 2468 2.62% 2623 2682 2.24% 2838 2712 -4.43%

3 Small power 759 841 10.75% 835 884 5.83% 891 876 -1.65%

4 Medium Supply 1541 1768 14.75% 1755 1823 3.85% 1815 1768 -2.57%

5 Large Supply 9093 8522 -6.27% 9607 8996 -6.36% 7856 9475 20.61%

6 Public Lighting 136 131 -3.65% 137 139 1.53% 135 146 8.02%

7 Bulk Supply 496 540 8.78% 539 560 3.88% 552 566 2.48%

8 Railway Traction 138 144 4.39% 181 138 -23.63% 184 135 -26.73%

9 Agricultural Cons. 10305 10150 -1.50% 10843 10256 -5.41% 11003 10779 -2.04%

Total within the State

32738 32749 0.01% 35374 34295 -3.05% 34916 35742 2.37%

Based on these findings, it is recommended that:

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page iii

• The methodology of energy sales projection based on the historical trends i.e., 3 years CAGR appears to be appropriate for categories such as Domestic, Non Residential, Small Power, Public Lighting and Bulk Supply.

• For projecting energy sales, variation in other variables such as number of consumers (Domestic Category), connected load, specific consumption (Domestic Category) and load factor may also be analysed as their growth may depend upon different factors and the quantum of impact is different on these variables to improve the projections of energy sales.

• Any change in policy and Regulations that may impact the energy sales especially in the industrial category may be considered by taking suitable assumptions and incorporating the same. In addition, the impact of pending applications and industrial growth in the State may be considered for more accurate projection of sales.

• The Commission in its Tariff Order for FY 2013-14 has approved the implementation of Time of Day Tariff, the same shall also have a bearing on the consumption pattern and therefore needs to be analysed for projecting the sales.

• The data submitted by PSPCL varied at certain instances. It is suggested that uniformity of the data for submission to the Commission shall be maintained so that errors in actual audited data can be avoided.

Energy Availability from Own Generating Stations

PSPCL has three thermal generating stations namely, Guru Gobind Singh Super Thermal Plant at Ropar, Guru Nanak Dev Thermal Plant at Bathinda, Guru Hargobind Thermal Plant at Lehra Mohabbat. The Hydel Power Plants under PSPCL are Shanan Power house, Ranjit Sagar DAM, UBDC power houses, Mukerian Hydel Project, Anand Pur Sahib Hydel Channel, Mini and Micro Hydro Power Plants.

It is observed that PSPCL projects the net energy availability from own thermal generating stations based on the operational parameters, like Plant Availability, Scheduled Renovation & Modernisation, Plant Load Factor and Auxiliary Consumption. Further, PSPCL projects the hydel generation from own hydel generating stations on the basis of average of the actual hydel generation for last three years barring the immediately preceding year. The Commission for projecting the generation from the PSPCL’s thermal generating stations considers the average of actual availability and generation from the thermal generating

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page iv

stations for the past three years barring the immediately preceding year and Planned Maintenance Schedules and Scheduled R&M. Further, The Commission projects the net hydel generation from the PSPCL’s own hydel generating stations by taking an average of the actual hydel generation for last three years barring the immediately preceding year. The methodology of projected quantum of power generation from PSPCL’s Generating Stations appear to be appropriate, however, variations were observed in the actual energy availability and the energy availability approved by the Commission.

A detailed analysis has been carried out to assess the reasons behind these variations and these variations were occurring on account of the following:

• Variations in actual availability and PLF of the generating stations and due to the variations in the actual and approved Maintenance and R&M schedule.

• Backing down of thermal generating stations due to less power demand in some hours in some months.

During the analysis, it is observed that the actual generation from thermal generating stations for all three years was lower than the generation approved by the Commission. Apart from the variation in planned and actual maintenance schedule, the other reason submitted by PSPCL for reduction in net generation is backing down due to less power demand during some of the hours in some months. Based on the analysis of generation loss due to backing down as shown, it is observed that for all the three years from FY 2010-11 to FY 2012-13, the Generation loss due to backing down as % of net generation for GHTP is higher than GGSSTP while the cost of power of GHTP is less than that of GGSSTP. Based on this it appears that PSPCL has not followed merit order strictly while backing down its own generating stations.

Further, it is observed that the total actual power availability from hydel sources has been more than the power projected by PSPCL as well as projected by the Commission for all the three years from FY 2010-11 to FY 2012-13. However it is observed that the gross generation from Shanan HEP has reduced by only around 17% inspite of 50 MW of its capacity being shut down for almost entire year of FY 2012-13 on account of rehabilitation work.

On the basis of the above analysis, to minimise variations and for better management of own generating stations following are the recommendations:

1) The projections for availability and PLF for thermal stations appears to be on a higher side as the actual availability and PLF for the last few years had continuously

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page v

been on the lower side than the values projected by the Commission. It is therefore suggested that the projections for availability and PLF of the State Generating Stations may be made considering the actual generation during last 3 years in addition to planned maintenance schedules. This kind of projection will help in reducing variations in the power purchase quantum from short term sources.

2) It is suggested that PSPCL may be asked to record the instances wherein it has to back down its own generating stations both thermal and hydro generating stations along with the duration for which such backing down was done with appropriate justification with regard to circumstances leading to such backing down of its own generating stations. The Commission may ask PSPCL to furnish daily report for instances wherein the State Generating Stations were backed down with reasons leading to such backing down.

3) The Commission may ask PSPCL to submit the details of Station wise daily generation data from its own generating stations including hydro stations to the Commission on regular basis.

Quantum of Power Procurement from CGS and other sources

The State of Punjab is unique in a way that it is an agricultural State and hence faces the problem of shortfall/gap in demand and supply of electricity, especially during the paddy period (June to October). In order to bridge this demand supply gap and to cater to the electricity demand of its consumers, PSPCL procures power from the various sources other than the state generating stations namely, Central Generating Stations, Energy Banking Arrangements, BBMB and Short term Power Purchase through traders.

PSPCL projects energy availability from the Central Generating Stations on the basis of the average of energy received from these stations for the last 3 years barring the immediately preceding year. In order to estimate the energy entitlement of PSPCL from different Central Generating Stations, the Commission considers the average of the actual energy purchased by PSPCL from these stations for the last three years barring the immediately preceding year. Prima-facie the above methodology appears to be appropriate, however, variations were observed in the actual energy availability and the energy availability approved by the Commission from the Central Generating Stations.

Further, for new generating stations it is observed that the quantum of power purchase projected by PSPCL was in not in accordance with the actual progress of these projects which resulted in variations in power purchase quantum from those approved by the

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page vi

Commission. The delay in commissioning of new generating stations and failure to accurately assess the availability of power from these stations led to increase in short term power purchase and resulted into a financial implication of Rs. 745.62 crore in FY 2010-11, Rs. 229.62 in 2011-12 and Rs. 491.59 crore in FY 2012-13 with the cumulative implication of Rs. 1466.83 crore for FY 2010-11 to FY 2012-13.

The summary of variations in power purchase quantum, total cost of power purchase and average cost of power purchase per unit for FY 2010-11, FY 2011-12 and FY 2012-13 is as shown in the table:

Table: Approved and Actual Power Purchase Cost for FY 2010-11

Source Quantum (MU) Cost (Rs Crore) Avg. Cost (Rs/kWh) Variations

(Avg Cost) Approved Actual Approved Actual Approved Actual NTPC 7787 6795 1648 1770 2.12 2.60 22.64% NHPC 2534 2513 361 531 1.42 2.11 48.59% NPC 845 1269 235 335 2.78 2.64 -5.04% Other Sources 4453 4884 1391 2514 3.12 5.15 65.06% Total 15619 15461 3635 5149 2.33 3.33 42.92%

Table: Approved and Actual Power Purchase Cost for FY 2011-12

Source Quantum (MU) Cost (Rs Crore) Avg. Cost (Rs/kWh) Variations

(Avg Cost) Approved Actual Approved Actual Approved Actual NTPC 7888 6552 2168 2052 2.75 3.13 13.82%

NHPC 2580 2519 455 511 1.76 2.03 15.34%

NPC 800 1446 213 420 2.66 2.91 9.40%

Other Sources 7220 4840 2768 1904 3.83 3.93 2.61%

Total 18488 15357 5603 4888 3.03 3.18 4.95%

Table: Approved and Actual Power Purchase Cost for FY 2012-13

Source Quantum (MU) Cost (Rs Crore) Avg. Cost (Rs/kWh) Variations

(Avg. Cost) Approved Actual Approved Actual Approved Actual NTPC 7899 6332 2558 1883 3.24 2.97 -8.33%

NHPC 2835 2558 631 621 2.22 2.43 9.46%

NPC 794 1499 208 433 2.62 2.89 10.31%

Other Sources 5623 9433 1732 3735 3.08 3.96 28.57%

Total 17151 19821 5128 6673 2.99 3.37 12.71%

It is observed that the actual average rate of power purchase during FY 2010-11 from other sources is Rs. 5.15/kWh which is considerably higher than the Commission approved rate of

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page vii

power purchase of Rs. 3.12/kWh. Further, there was also substantial increase in average power purchase rate of NTPC and NHPC which is due to revision in tariffs by CERC based on Tariff Regulations applicable for FY 2009-10 to FY 2013-14. The reasons for reduction in quantum of power purchase from the Central Generating Stations are elaborated in the Table 22, Table 25 and Table 28. Further, the reason for higher power purchase cost from other sources is due to the reason that the actual power purchase from the New Generating Stations was substantially lower than the projected power purchase from new sources and hence PSPCL has to procure power from other sources.

It is observed that these variations were occurring on account of the following:

• Variations in the generation considered and the actual generation from the central generating station.

• The entitlement of PSPCL in the Central Generating Stations considered for projecting power purchase varies from the actual entitlement of PSPCL in the Central Generating Stations.

• In some of the stations the difference in the power purchase quantum was not completely attributable to the above two reasons.

On the basis of these findings it is suggested that the following additional aspects may also be considered by PSPCL while projecting the energy available from the existing Central Generating Stations:

• Analysis of Actual Generation by the station during the last three years as the energy received by PSPCL during the last 3 years also includes the impact of less scheduling of power by PSPCL at some instances by applying merit order dispatch.

• Details of major outages due to Renovation & Modernisation may be factored while projecting the quantum of energy available from these stations.

• For New Generating stations, it is suggested that before projecting availability of power from new generating stations actual work progress of such projects be factored in.

• Demand fluctuations due to frequent shifting of open access consumers makes it difficult to project power purchase requirement and so it is suggested that the

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page viii

Commission may approve the Two Part Tariff specifying demand charges and energy charges for large industrial consumers so that even when the large industrial consumers are drawing power under Open Access, they will be paying the Demand Charges.

Power Procurement Cost

It is observed during the analysis that the Commission projects the power purchase cost in two parts namely Fixed Charges (FC) and Variable Charges (VC). The Commission projects the fixed charges for power procured from the Central Generating Stations on the basis of the Annual Fixed Charges (AFC) of the Central Generating Stations approved by the CERC and the percentage allocation of PSPCL in these Central Generating Stations. The Commission projects the Variable Charges for power procured from the Central Generating Stations on the basis of the bills of September month of the previous year. Prima-facie, the approach appears to be appropriate; however, variations were observed in the actual FC and VC of the Central Generating Station and FC and VC as approved by the Commission.

Based on analysis, it is recommended that:

• The variable charges of the power purchase from Central Generating Stations may be projected on the basis of the variable cost for last three or six months so as to capture the recent trend. PSPCL may consider the average of three months or six months actual variable charges to average out the impact of adjustments etc.,.

• In case the Petition filed by any of Central Generating Stations is pending with CERC for approval of tariff based on new Regulations, PSPCL while projecting the power purchase cost may consider certain percentage of tariff increase sought by CGS on provisional basis while projecting the power purchase cost to avoid substantial variation in power purchase cost.

Short Term Power Purchase

As stated earlier, PSPCL procures power from various sources including the short term power purchase through traders which generally results into huge financial implications. It is observed that in order to avail short term power purchase, PSPCL follows the Competitive Bidding Mechanism wherein first of all, PSPCL makes an estimation of the shortfall in demand and supply of electricity after considering availability from all the other sources. Afterwards, PSPCL generally projects that 80% of this shortfall to be procured under the short term power purchase route and with this submits its application to the Short Term Power Purchase Committee (STPP) which approves a certain amount of power to be procured under the said route of short term power purchase. The Competitive Bidding

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page ix

Process is then carried out to procure the approved quantum of power under short term purchase.

The bid evaluation reports submitted by PSPCL for procurement of power on short term basis were analysed and it is observed that on an average 20-30 bids were received for every month (June to October) for short term power purchase in each of the three Financial Years, i.e. FY 2010-11, 2011-12 and FY 2012-13. Based on the analysis, it is observed that PSPCL has made short term power purchase Agreements with the Bidders providing power at the lowest rates at the Punjab Periphery. After detailed analysis of the tender specifications, bid evaluation reports and agreements signed by PSPCL, it appears that Competitive bidding process has been adopted for procuring power on short term basis.

In FY 2010-11, PSPCL in its application to the Short Term Power Purchase Committee had projected the ratio of power procured through short term agreements to the power procured under spot purchase including UI overdrawal as 60:40 whereas the ratio of actual power procured under short term agreements to the spot purchase including net UI overdrawal works out to around 73:27.

In FY 2011-12, PSPCL in its application to the Short Term Power Purchase Committee had projected the ratio of power procured through short term agreements to the power procured under spot purchase including UI overdrawal as 80:20 whereas the ratio of actual power procured under short term agreements to the spot purchase including net UI overdrawal works out to around 96:4.

In FY 2012-13, PSPCL in its application to the Short Term Power Purchase Committee had projected the ratio of power procured through short term agreements to the power procured under spot purchase as 80:20 whereas the ratio of actual power procured under short term agreements to the spot purchase including net UI overdrawal works out to around 67:33.

Further, it is observed that the need to procure power under the short term purchase route arose because the power purchase from the New Generating Stations as projected by PSPCL for various years was not achieved in actual and the actual power purchase from the New Generating Stations was substantially lower.

Based on these findings, it is recommended that:

• PSPCL may consider the availability of power from the New Generating Stations on the basis of the actual current status of the project as well as the realistic date of Commercial Operation rather than considering the Scheduled date of Commercial Operation. It is suggested that PSPCL may directly ask the Generators about the likely Commercial Operation Date for new Generating stations and the same can be further cross-checked with the information available with CEA on progress of new

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page x

projects. This will allow PSPCL to plan for purchase of deficit power which if known before hand can be better planned through other sources.

• The Commission may ask PSPCL to prepare monthly sales plan based on historical monthly sales and the annual sales approved by the Commission and on this basis shall prepare monthly power purchase plan including short term power purchase and banking. The Commission may also ask PSPCL to submit the monthly budget for procurement of power based on its power procurement plan. The Commission may ask PSPCL to adhere to this plan and in case of any variation observed which could lead to increase in the budget; the same to be informed to the Commission with appropriate justification and actions to be taken so that the impact is absorbed in the next monthly budgets.

• The Commission may specify the limit on additional procurement of power in terms of both quantum and cost and in case either of the factors is likely to increase beyond the limit, PSPCL may be asked to obtain prior approval of the Commission.

Costly Power Procurement

PSPCL has been sourcing expensive power from RLNG and liquid fuel based stations for all the years i.e. FY 2010-11 to FY 2012-13, whose average variable cost exceeded Rs. 8.00/kWh. It is observed that the State of Punjab has been continuously reeling under acute power deficit scenario and hence it has been procuring this power.

It is observed that at times PSPCL is required to purchase such power on directions of the load despatch center; however option of procurement of cheaper power through power exchanges may be explored.

UI Transactions

The UI transactions and its financial implication have been analyzed considering the data provided by PSPCL and obtained from various sources like NRPC and NRLDC. PSPCL has incurred the following additional cost in FY 2010-11 to FY 2012-13 in the form of Additional UI charges and interest charges on UI amount owing to its failure to adhere to grid discipline:

Table: Financial Implication due to UI Transaction

Financial Implication due to UI Transactions (Rs. Crore) Parameter FY 2010-11 FY 2011-12 FY 2012-13

UI Charges 507.54 -48.98 284.09

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page xi

Financial Implication due to UI Transactions (Rs. Crore) Parameter FY 2010-11 FY 2011-12 FY 2012-13

Payable/Receivable (+/-) Additional UI Payable 63.51 23.56 23.63 Interest Charges due to Delay in Payment

24.09 15.85 20.27

It is observed that PSPCL had to pay Rs. 507.54 crore for FY 2010-11 and Rs. 284.09 crore for FY 2012-13 on account of UI whereas it received UI of Rs. 48.98 crore in FY 2011-12. Thus the overall financial impact on account of UI is Rs. 742.65 crore for FY 2010-11 to FY 2012-13.

On the basis of the findings it is recommended that for days wherein additional UI is paid by PSPCL, the same to be documented with appropriate justification with circumstances leading to such over-drawal. Based on the detailed analysis, it is observed that during the months of February 2011, January, 2012 and February 2013 although the net UI quantum was negative but PSPCL had paid amounts of Rs. 481.72 lakh, Rs. 478.82 lakh and Rs. 231.66 lakh respectively during these months. The same indicates that substantial improvement in power procurement planning is required. PSPCL may be asked to take adequate steps to avoid such instances in future.

Drawal/Surrender of Power under UI Mechanism

The drawal/surrender of power is analyzed on a sample basis and the months of April and September of each year are considered based on the energy sales, load shedding and UI charges paid. The injection schedule, implemented schedule and drawal schedules obtained from NRPC and NRLDC is used to analyze the same.

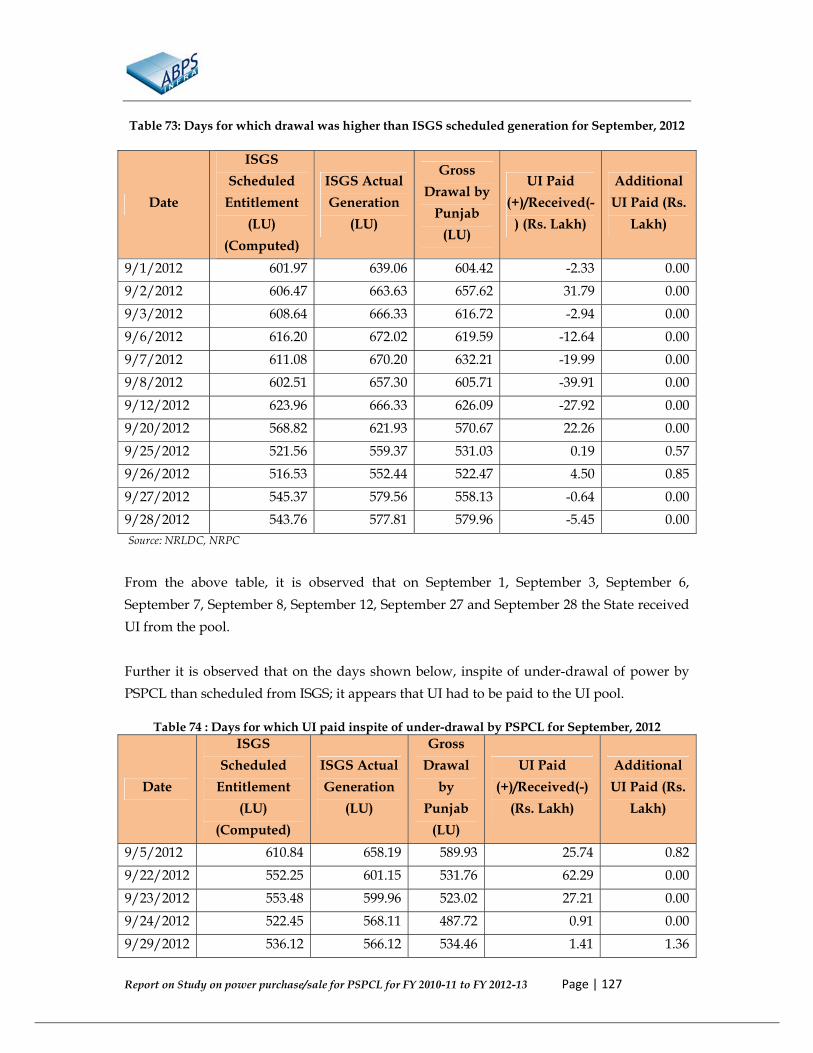

Most of the days in the months considered for the study namely May 2010, September 2010, April 2011, September 2011, April 2012 and September 2012 shows a deviation in the actual drawal from the actual generation. Hence it appears PSPCL has drawn less power.

On the basis of these findings it is suggested that:

• The reason for improper decision making with regards to power purchase and scheduling was the variation in reading of tele-metered data and SEM data. It is recommended that whenever such variation is observed, the same to be properly documented along with steps taken to improve the tele-metered reading. Such reports to be submitted to the Commission on monthly basis.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page xii

• In order to bring in more transparency in the power purchase procurement, the Commission may ask PSPCL to prepare the following daily and monthly reports and submit the same on regular basis:

o Daily Reports (i) Station wise daily generation data from its own generating stations including

hydro stations. (ii) Final Drawal Schedule (Day ahead scheduling) submitted to NRLDC from

Inter State Generating Stations (ISGS). (iii) Instances wherein State Generating Stations were Backed Down with reasons

leading to such backing down. (iv) Instances wherein low cost Central Generating Stations were Backed Down

(not as per merit Order) with justification along with circumstances leading to backing down.

(v) Quantum and Cost of short term power purchase (vi) Hourly Load shedding along with the reasons for the same.

o Monthly Reports (i) Daily Time block wise UI Injection/Drawl for the previous month including

following details: • Time block wise UI Drawal both in units and Amount • Time block wise UI Injection both in units and Amount • Time block wise Additional UI paid including reasons for same • Time block wise load shedding carried out, if any

(ii) Monthly Power Purchase plan versus actual power purchase done with reasons for variations in quantum and cost.

Energy Banking

PSPCL enters into banking arrangements every year to manage its peak demand during the paddy season when demand is high owing to agricultural load. An analysis of banking arrangements for the period from FY 2010-11 to FY 2012-13 was carried out to study the overall approach of banking, methodology; quantum of energy banked each year and other implications of the arrangement. The practice is beneficial for better management of surplus and deficit power but the same has not be planned judiciously as is evident from the UI charges imposed on PSPCL during the period when energy was being banked. The summary of quantum of energy banked is as follows:

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page xiii

Table: Import/Export of Banked Power

Month FY 2010-11 FY 2011-12 FY 2012-13

Import (MU)

Export (MU)

Import (MU)

Export (MU)

Import (MU)

Export (MU)

April 1.20 187.00 0.00 142.45 10.97 71.72 May 0.00 55.80 14.40 0.00 28.20 0.00 June 256.87 0.00 364.43 2.94 261.78 0.00 July 379.19 0.00 656.69 2.99 458.69 0.00 August 361.93 0.00 643.49 0.00 355.06 0.00 September 231.25 0.00 509.64 0.00 401.67 0.00 October 36.51 12.12 45.67 47.49 15.48 34.23 November 0.00 415.88 0.00 343.02 0.00 260.11 December 0.00 447.93 3.70 328.08 3.46 362.69 January 0.00 493.55 0.00 238.08 0.00 310.72 February 0.00 303.93 0.00 190.53 0.00 232.79 March 0.00 303.93 0.00 114.79 0.00 183.36

It is observed that PSPCL had committed outward banking in months when it actually faced acute shortage of power due to which it had to overdraw from the grid paying UI charges and additional UI charges. The total financial impact on account of mis-management in the banking schedules is estimated to be approximately Rs. 104.07 crore for FY 2010-11 to FY 2012-13.

It is observed that most of the banking agreements are signed at an average of two to three months prior to the date of delivery inspite of which a deficit condition is not anticipated as is evident from the situation in FY 2010-11. During the period, PSPCL had been over-drawing from the grid and resorting to load shedding when simultaneously power was being exported under banking obligations. These types of situations can be avoided through proper planning while entering into banking arrangements.

Further, most of the banking agreements have been signed through intermediary traders, who receive the trading margin of 3 paise/kWh. This trading margin is being paid by both the parties individually and is paid in the instance when the power is consumed by each of them. It is suggested that this can be avoided through direct banking as PSPCL has the requisite expertise to carry out the same.

Financial Implication of Power Purchase

The financial implication of power purchase cost that may have been optimised by proper planning is summarised in table below:

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page xiv

Table: Total Loss incurred by PSPCL due to inefficient planning of power purchase

Particulars

FY 2010-11 FY 2011-12 FY 2012-13

MU

Financial impact

(Rs. Crore)

MU

Financial impact

(Rs. Crore)

MU

Financial impact

(Rs. Crore)

Short Term Power Purchase on account of projecting higher generation from new Generating Stations

2492.79 745.62 2613.20 229.62 4602.92 491.59

Banking of Power 242.80 41.09 233.03 58.57 9.41 4.41 Additional UI - 63.52 - 23.56 - 23.63 Interest on UI - 24.09 - 15.85 - 20.27 Total (Rs. Crore) 874.32 327.60 539.90

Transmission Infrastructure

A detailed analysis of the steps taken by PSPCL and PSTCL to improve inter as well as intra transmission system of the State to relieve network constraints and to provide system strengthening has been carried out. PSTCL has been coordinating with entities like PGCIL/CEA for improvement in inter-state transmission constraints. It appears that the import of power from Western region is constrained due to the overloading of 765 kV Gwalior-Agra line. It appears that the import of power from Eastern region is constrained due to delay in commissioning of Gaya Pooling Station and delay in commencement of construction of Lucknow- Bareilly-Meerut line. Additionally it may not be possible to import more power from Sasan to Punjab (more generating units commissioned at Sasan) as Gwalior-Agra 765 kV line is overloaded. PSTCL has submitted that expedition of work in the augmentation of ICTs at Moga, Ludhiana and Amritsar stations along with addition of new sub-station at Patran will enable to improve the inter-state transfer capacity by 500MW. In the intra-state transmission, capacity addition has been observed more at higher voltages i.e. 400 kV and 220 kV and comparatively less in the lower voltages. Sub-stations addition has also been observed along with augmentation/up-gradation to higher voltages to improve transfer capacity.

The reactive energy charges incurred by PSPCL have been analyzed from data provided by PSPCL and obtained from NRPC. PSPCL has been incurring reactive energy charges during the paddy period i.e. during June to September each year.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

Table of Contents

1 Background and Context ............................................................................................................ 1

1.1 Over view of Punjab Power Sector .................................................................................... 1

1.2 Background of the Study .................................................................................................... 3

1.3 Scope of Work ....................................................................................................................... 4

1.4 Aspects covered in the Study ............................................................................................. 5

1.5 Approach and Methodology for Carrying Out the Study ............................................. 6

1.6 Structure of the Report ........................................................................................................ 9

2 Analysis of Energy Sales ........................................................................................................... 10

2.1 Methodology adopted by PSPCL for Projecting Energy Sales .................................... 10

2.2 Methodology adopted by Commission for Approving Energy Sales ........................ 10

2.3 Analysis of Variation in Actual Energy Sales for FY 2010-11 ...................................... 10

2.4 Analysis of Variation in Actual Energy Sales for FY 2011-12 ...................................... 17

2.5 Analysis of Variation in Energy Sales for FY 2012-13 ................................................... 21

2.6 Summary of Sales Approved and Actual Sales for FY 2010-11, FY 2011-12 and FY 2012-13 ............................................................................................................................................. 25

2.7 Recommendations for Projecting Sales and Energy Requirement .............................. 27

3 Analysis of Quantum of Generation from PSPCL Own Generating Stations including analysis of Planned and Actual Outages ........................................................................................ 29

3.1 Methodology adopted by PSPCL for Assessment of Power Available from Own Generating Stations: ....................................................................................................................... 29

3.2 Methodology adopted by the Commission for Assessment of Power Available from Own Generating Stations: ............................................................................................................. 29

3.3 Analysis of Variation in Actual Generation for Thermal Generating Stations for FY 2010-11 ............................................................................................................................................. 30

3.4 Variation in Planned and Actual Maintenance Schedules ........................................... 31

3.5 Analysis of Variation in Actual Generation for Thermal Stations for FY 2011-12 .... 34

3.6 Variation in Planned and Actual Maintenance Schedules for FY 2011-12 ................. 35

3.7 Analysis of Generation for Hydel Stations for FY 2011-12 ........................................... 36

3.8 Analysis of Variation in Actual Generation for Thermal Stations for FY 2012-13 .... 37

3.9 Variation in Planned and Actual Maintenance Schedules for FY 2012-13 ................. 38

3.10 Analysis of Generation for Hydel Stations for FY 2012-13 ........................................... 40

3.11 Recommendations with respect to PSPCL’s Own Generation .................................... 42

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

4 Analysis of Power Purchase ..................................................................................................... 43

4.1 Analysis of variation in Power Purchase Quantum ...................................................... 43

4.2 Power Purchase Cost ......................................................................................................... 74

4.3 PSERC (Power Purchase and Procurement Process of Licensee) Regulations, 2012 92

4.4 Recommendations : ............................................................................................................ 94

5 Analysis of Banking Agreements, UI (Sale/Purchase), Surrender of Power and Transmission System Improvement .............................................................................................. 102

5.1 Procurement of Costly Power ........................................................................................ 102

5.2 UI (Sale/Purchase) and Additional UI: ........................................................................ 106

5.3 Drawal /Surrender of Power under UI Mechanism ................................................... 112

5.4 Energy Banking Arrangement by PSPCL ..................................................................... 128

5.5 Reactive Energy Charges ................................................................................................ 135

5.6 Transmission Infrastructure ........................................................................................... 136

5.7 Recommendations ............................................................................................................ 150

6 Summary of Recommendations ............................................................................................. 152

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

List of Figures

Figure 1: Source Wise Installed Capacity for Punjab ...................................................................... 1 Figure 2: Peak Demand vs. Peak Met for Punjab ............................................................................ 2 Figure 3: Energy Requirement and Availability .............................................................................. 3

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

List of Tables Table 1: Source-Wise Available Capacity (MW) including allocated Shares in Joint and Central Sector Utilities as on March 31, 2013 ................................................................................... 1 Table 2: Computation of Net Energy Sales as submitted by PSPCL .......................................... 11 Table 3: Analysis of Sales for FY 2010-11 ........................................................................................ 12 Table 4: Variation in Number of Consumers, Connected Load, Specific Consumption/Load Factor and Sales for FY 2010-11 vis-à-vis FY 2009-10 .................................................................... 13 Table 5: Analysis of Sales for FY 2011-12 ........................................................................................ 17 Table 6: Variation in Number of Consumers, Connected Load, Specific Consumption/Load Factor and Sales for FY 2011-12 vis-à-vis FY 2010-11 .................................................................... 18 Table 7: Analysis of Sales for FY 2012-13 ........................................................................................ 22 Table 8: Variation in Number of Consumers, Connected Load, Specific Consumption/Load Factor and Sales for FY 2012-13 vis-à-vis FY 2011-12 .................................................................... 23 Table 9: Summary of Approved and Actual Sales for FY 2010-11 to FY 2012-13 ...................... 26 Table 10: Variation in Actual vis-à-vis Commission Approved Net Generation (MU) for Thermal Generating Stations for FY 2010-11.................................................................................. 30 Table 11: Planned Vs Actual Maintenance Schedules for FY 2010-11 ........................................ 31 Table 12: Generation Loss due to backing down for FY 2010-11 (MU) ...................................... 32 Table 13: Hydel Generation for FY 2010-11 .................................................................................... 33 Table 14: Variation in Actual vis-à-vis Commission Approved Net Generation (MU) for Thermal Generating Stations for FY 2011-12.................................................................................. 34 Table 15: Planned Vs Actual Maintenance Schedules for FY 2011-12 ........................................ 35 Table 16: Generation Loss due to backing down for FY 2011-12 ................................................ 36 Table 17: Hydel Generation for FY 2011-12 .................................................................................... 36 Table 18: Variation in Actual vis-à-vis Commission Approved Net Generation (MU) for Thermal Generating Stations for FY 2012-13.................................................................................. 37 Table 19: Planned Vs Actual Maintenance Schedules for FY 2012-13 ........................................ 39 Table 20: Generation Loss due to backing down for FY 2012-13 ................................................ 40 Table 21: Hydel Generation for FY 2012-13 .................................................................................... 41 Table 22: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum from Central Generating Stations for FY 2010-11 .......................................................................... 44 Table 23: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for New Generating Stations for FY 2010-11 ........................................................................................ 51 Table 24: Break up of Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for Central Generating Stations for FY 2010-11 ........................................................... 52 Table 25: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for Central Generating Stations for FY 2011-12 ................................................................................... 53 Table 26: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for New Generating Stations for FY 2011-12 ........................................................................................ 61

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

Table 27: Break up of Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for Central Generating Stations for FY 2011-12 ........................................................... 62 Table 28: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for Central Generating Stations for FY 2012-13 ................................................................................... 63 Table 29: Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for New Generating Stations for FY 2012-13 ........................................................................................ 69 Table 30: Break up of Variation in Actual vis-à-vis Commission Approved Power Purchase Quantum for Central Generating Stations for FY 2012-13 ........................................................... 73 Table 31: Analysis for variation in actual AFC vis-à-vis Commission Approved AFC ........... 75 Table 32: Variation in Actual vis-à-vis Commission Approved Variable Cost for Central Generating Stations ............................................................................................................................ 80 Table 33: Variation in Actual vis-à-vis Commission Approved Power Purchase Cost for NPC .............................................................................................................................................................. 81 Table 34: Analysis of Short Term Power Procurement ................................................................. 85 Table 35: Variation in Actual vis-a-vis Commission Approved Transmission Charges to PGCIL .................................................................................................................................................. 86 Table 36: Summary of Variation in Power Purchase for FY 2010-11 .......................................... 87 Table 37: Summary of Variation in Power Purchase for FY 2011-12 .......................................... 87 Table 38: Summary of Variation in Power Purchase for FY 2012-13 .......................................... 87 Table 39: Total Financial Impact of Variation in Power Purchase Cost including PGCIL Charges ................................................................................................................................................ 88 Table 40: Actual Power Purchase vis-à-vis Commission Approved from New Generating Stations ................................................................................................................................................ 88 Table 41: Financial Implication on account of short term power purchase for FY 2010-11 ..... 89 Table 42: Financial Implication on account of short term power purchase for FY 2011-12 ..... 90 Table 43: Financial Implication on account of short term power purchase for FY 2012-13 ..... 91 Table 44: Demand Charges for other States ................................................................................... 99 Table 45: Power Procurement for FY 2010-11 from RLNG/Liquid fired Stations .................. 102 Table 46: Demand Supply Scenario in FY 2010-11 ...................................................................... 102 Table 47: Power Procurement for FY 2011-12 from RLNG/Liquid fired Stations .................. 103 Table 48: Demand Supply Scenario in FY 2011-12 ...................................................................... 104 Table 49: Power Procurement for FY 2012-13 from RLNG/Liquid fired Stations .................. 105 Table 50: Demand Supply Scenario in FY 2012-13 ...................................................................... 105 Table 51: Net UI drawal/surrender .............................................................................................. 106 Table 52: Additional UI paid by PSPCL in FY 2010-11 ............................................................... 108 Table 53: Additional UI paid by PSPCL in FY 2011-12 ............................................................... 109 Table 54: Additional UI paid by PSPCL in FY 2012-13 ............................................................... 109 Table 55: Interest Charges on un-paid UI amount ...................................................................... 111 Table 56: Monthly Energy Sales as submitted by PSPCL (MU) ................................................ 112 Table 57: Load Shedding carried out by PSPCL (MW) ............................................................... 112 Table 58: Injection and Drawl from ISGS for May 2010 ............................................................. 114 Table 59: Injection and Drawl from ISGS for September 2010 ................................................... 115

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13

Table 60: Days for which drawal was higher than ISGS scheduled generation for September, 2010 .................................................................................................................................................... 116 Table 61: Days for which UI paid inspite of under-drawal by PSPCL for September, 2010 . 117 Table 62: Injection and Drawl from ISGS for April 2011 ............................................................ 117 Table 63: Days for which drawal was higher than ISGS scheduled generation for April, 2011 ............................................................................................................................................................ 119 Table 64: Injection and Drawl from ISGS for September 2011 ................................................... 120 Table 65: Days on which ISGS Actual Generation deviates from Scheduled Generation for September, 2011 ................................................................................................................................ 121 Table 66: Days for which drawal was higher than ISGS scheduled generation for September, 2011 .................................................................................................................................................... 121 Table 67: Deviation on September 27, 2011 .................................................................................. 122 Table 68: Injection and Drawl from ISGS for April 2012 ............................................................ 122 Table 69: Days for which drawal was higher than ISGS scheduled generation for April, 2012 ............................................................................................................................................................ 124 Table 70: Days for which UI paid inspite of under-drawal by PSPCL for April, 2012........... 124 Table 71: Injection and Drawl from ISGS for September 2012 ................................................... 125 Table 72: Day on which actual gross drawal was higher than ISGS actual generation for September, 2012 ................................................................................................................................ 126 Table 73: Days for which drawal was higher than ISGS scheduled generation for September, 2012 .................................................................................................................................................... 127 Table 74 : Days for which UI paid inspite of under-drawal by PSPCL for September, 2012 127 Table 75 : Energy Banking (FY 2010-11) ........................................................................................ 130 Table 76 : Energy Banking (FY 2011-12) ........................................................................................ 131 Table 77: Energy Banking (FY 2012-13) ......................................................................................... 132 Table 78: Power Banked for Paddy period ................................................................................... 133 Table 79: Energy Banked in MW .................................................................................................... 134 Table 80: Reactive Energy Charges ................................................................................................ 135 Table 81: Installation of capacitors for Reactive energy Compensation ................................... 136 Table 82: Measures to improve inter-state transmission constraints ........................................ 137 Table 83: Transmission Capacity Addition in Ckt. km ............................................................... 138 Table 84: Transmission Capacity Addition in MW ..................................................................... 138 Table 85: Transmission Capacity Addition in MVA (FY 2010-11) ............................................ 139 Table 86: Transmission Capacity Addition in MVA (FY 2011-12) ............................................ 139 Table 87: Transmission Capacity Addition in MVA (FY 2012-13) ............................................ 140 Table 88: Sub-stations Capacity Addition in MVA ..................................................................... 140 Table 89: Improvement Measures in Sub-Stations ...................................................................... 141 Table 90: Improvement Measures in 132kV and 220kV Lines ................................................... 145

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 1

1 Background and Context

1.1 Over view of Punjab Power Sector Available Capacity

The source-wise breakup of total capacity available to the State of Punjab as on March 31, 2013 is as shown below:

Table 1: Source-Wise Available Capacity (MW) including allocated Shares in Joint and Central Sector Utilities as on March 31, 2013

Sector

Thermal

Nuclear Hydro RES

(MNRE) Total

Coal Gas Liquid

Fuel Total

Thermal

State 2620 0 0 2620 0 995 250 3864

Central 1232 0 0 1232 197 1922 0 3351

Private 475 137 0 612 0 116 0 728

Total 4327 137 0 4464 197 3033 250 7943

Source: PSPCL’s Submissions

Source: PSPCL’s Submissions

Figure 1: Source Wise Installed Capacity for Punjab

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 2

As observed from the above figure, the main source of power generation in Punjab has been Coal fired thermal Power Plants and Hydro Power Plants.

Demand Supply Scenario for Punjab

The demand supply scenario in Punjab suggests that despite the increase in generation capacity, there has been acute power shortages and the peak demand has increased from 8672 MW in FY 2007-08 to 11520 MW in FY 2012-13 whereas peak demand met has increased from 7340 MW in FY 2007-08 to 9074 MW in FY 2012-13 with peak deficit of around 21% in FY 2012-13.

Source: PSPCL’s Submission

Figure 2: Peak Demand vs. Peak Met for Punjab The total energy requirement for the State of Punjab has increased from around 43 BU in FY 2007-08 to around 48 BU in 2012-13 whereas energy availability has increased from 39 BU in FY 2007-08 to 45 BU in FY 2012-13 with energy shortage of around 5.4% in FY 2012-13.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 3

Source: PSPCL’s Submission

Figure 3: Energy Requirement and Availability

1.2 Background of the Study Punjab State Power Corporation Ltd. (PSPCL) erstwhile Punjab State Electricity Board (PSEB) submitted Petition for Approval of Aggregate Revenue Requirement (ARR) for FY 2010-11 on November 30, 2009 wherein it proposed a revenue requirement of Rs 19471.84 crore. Out of the total ARR of Rs 19471.84 crore, PSPCL proposed Power Purchase cost of Rs. 5137.61 crore. Subsequently, the Commission issued Tariff Order for FY 2010-11 dated April 23, 2010 in which the Commission approved the aggregate revenue requirement of Rs 13618.02 crore including power purchase cost of Rs 3774.21 crore.

For FY 2011-12, PSPCL submitted Petition for Approval of ARR for FY 2011-12 on December 16, 2010 wherein it proposed an aggregate revenue requirement of Rs 18447.62 crore including power purchase cost of Rs 6349.74 crore. Subsequently, the Commission issued Tariff Order for FY 2011-12 dated May 9, 2011 in which the Commission approved an aggregate revenue requirement of Rs 14925.00 crore including power purchase cost of Rs 5751.26 crore.

For FY 2012-13, PSPCL submitted Petition for Approval of ARR for FY 2012-13 on December 1, 2011 wherein it proposed an aggregate revenue requirement of Rs 19715.46 crore which included power purchase cost of Rs 7207.38 crore. Subsequently, the Commission issued Tariff Order for FY 2012-13 dated July 16, 2012 in which the Commission approved an aggregate revenue requirement of Rs 15967.13 crore including power purchase cost of Rs 5717.04 crore.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 4

PSERC has appointed ABPS Infrastructure Advisory Private Ltd. to carry out a study on power purchase/sales/surrender of power along with drawal/sales under UI for Punjab State Power Corporation Limited for the period of April 1, 2010 to March 31, 2013.

1.3 Scope of Work The scope of work includes analysis of issues related to power purchase and sales for FY 2010-11 to FY 2012-13. Further, the study requires in depth analysis of variations in quantum and cost approved for Power Purchase, Sales vis-à-vis actuals now submitted by PSPCL and suggest improvements in the practices followed by PSPCL with regards to purchase/surrender of power and give recommendations to accurately forecast power purchase quantum and cost and sales associated with the consumers. The study to include the following:

1. Methodology adopted by the Distribution Licensee (PSPCL) with regards to assessment of Demand & Energy Requirement and Availability of Power from all contracted sources and whether it is as per the Regulations laid down in the notified PSERC Determination of Tariff Regulations.

2. Whether Maintenance Schedules of own generating units as finalized by PSPCL with CEA were adhered to and in case of variation, whether reasons were justified.

3. Impact of variation in Power Purchase Cost approved in Tariff Order on the tariff determination for retail supply for the next year.

4. Forecast of energy availability from new generating plants versus actual availability and the financial impact of measures taken by PSPCL to meet the variation forecast and actual availability.

5. In depth study of PSPCL’s practice of Banking of Power, defaults made by the entities which were parties to the Banking, financial benefit/loss of swapping power through Banking vis-à-vis short term power purchase through traders or Power Exchange etc.

6. Purchase of costly RLNG and Liquid Fired power from Gas Based stations. Purchase of costly power from Jhajjar Thermal Plant and Pragati Gas Thermal Plant also to be examined.

7. Study of PSPCL’s procedure to draw/surrender of power under UI mechanism, defaults of over-drawal under low frequency conditions and its financial impact.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 5

8. Steps taken by PSTCL and PSPCL to improve the Total Transfer Capacity of the Punjab

State to address the issues of inter-State/intra-State Transmission constraints and low power factor/low voltage of the grid resulting in heavy import of Reactive Power by Punjab during paddy season.

9. Whether transparent open competitive bidding process and negotiations held with bidders for the purchase of power, as per guidelines issued by Govt. of India and Regulations notified by PSERC.

10. Whether PSPCL adhered to the principle of least cost plan/merit order principle while effecting power purchase in case of shortage or surrender of power in case of surplus.

11. Whether power cut was imposed on any category when the power was being surrendered by PSPCL.

12. Merit order dispatch of power from Thermal Plants of PSPCL need to be examined.

13. Methodology adopted by PSPCL to meet the emergency situation of shortage of power due to outage of Central Sector/PSPCL’s generators etc. and its financial impact on cost of power purchase.

14. Recommendations with regards the followings:

• Methodology for accurate assessment of demand and energy requirement to be adopted by PSPCL, so that there is least variation between the assessment and the actuals.

• Methodology for accurate assessment of PSPCL's own generation and long-term and

short-term power purchase by PSPCL, so that power is purchased in most economical manner by PSPCL.

• Probability and the details of replacement of contracts entered by PSPCL for

purchase of power generated using fossil fuels with hydro power.

1.4 Aspects covered in the Study Accordingly, the aspects that are covered in the report are as shown below:

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 6

1.5 Approach and Methodology for Carrying Out the Study

Overall Approach and Methodology

Based on the analysis of the information collected from the Commission’s office and information available in public domain, the list of additional data and information required for carrying out the study was prepared for obtaining the same from PSPCL and PSTCL.

Three rounds of discussions were also held with PSPCL and PSTCL along with Commission officials to discuss in detail the information required and on the information submitted by PSPCL.

Based on the information available with the Commission, information received from PSPCL and PSTCL till date and the information available in the public domain, detailed analysis

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 7

has been carried out on various aspects of the Study for FY 2010-11 to FY 2012-13. The approach adopted for carrying out the analysis of various aspects is discussed below:

Analysis of Sales Projections

This includes analysis of methodology adopted by PSPCL for estimation of category wise sales along with the basis of growth rates considered for FY 2010-11 to FY 2012-13 and methodology adopted by the Commission for approving category-wise sales for FY 2010-11 to FY 2012-13. The growth rates and sales projected by PSPCL and approved by the Commission have been compared with actual sales and actual variation in sales with respect to previous year. The reasons towards the variation in actual category wise sales with respect to the sales approved by the Commission have been analysed.

Analysis of Generation from PSPCL’s Generating Stations

This includes analysis of methodology adopted by PSPCL for estimation of available power from its own generating stations. The variation in quantum of actual generation with the net generation approved by the Commission have been analysed to find out the reason behind such variation including variations in maintenance schedules.

Analysis of Power Purchase Quantum

This includes analysis of methodology adopted by PSPCL for estimation of available power from various contracted sources along with the basis for projecting energy available from these sources including projection from new generating stations. As the actual data is now available, PSPCL projections, Commission approved values and the actual power purchase quantum have been compared to assess the variation in the power purchase. The variation in power purchase have been analysed to find out the reason behind such variation including detailed analysis of actual scheduled generation of Central Generating Stations and steps taken by PSPCL to meet the variation in forecast and actual availability.

Analysis of Power Purchase Cost

This includes analysis of methodology adopted by PSPCL for projecting power purchase cost and methodology adopted by Commission for approving power purchase cost. As the actual data is now available, the Commission approved value has now been compared to actuals to determine the variation in the power purchase cost. The variation is then analysed to find out the reason behind such variation. For assessing the variation in power purchase cost, Orders issued by Central Electricity Regulatory Commission (CERC) for Central Generating Stations are considered. Based on above, the financial impact of variations in power purchase cost on account of variation in approved power purchase cost and actual power purchase cost has been assessed.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 8

Purchase of Costly RLNG and Liquid Fired Power from Gas based Stations

Analysis on power purchase from RLNG and liquid fired power stations has been carried out to assess the quantum of such power purchased, reasons behind such purchase of power and co-relating it with the prevailing demand supply scenario for FY 2010-11 to FY 2012-13.

UI Transactions

Analysis of UI charges along with additional UI charges and interest on non payment of UI charges for PSPCL has been carried out. Apart from the data provided by PSPCL on Additional UI Charges, the data available on NRLDC and NRPC websites have been analysed for this aspect of the study. The data collected and analysed from NRLDC and NRPC website includes:

i. Northern Region allocation orders for FY 2010-11, FY 2011-12 and FY 2012-13 ii. UI Account for FY 2010-11, FY 2011-12 and FY 2012-13

iii. ISGS Injection Schedule iv. State Drawal Schedule v. ISGS and State Implemented Schedules (Form –A, Form –B and Form –C of

Implemented Schedules)

The reasons behind over-drawal has been analysed to understand the circumstances leading to such over-drawal which resulted in payment of UI charges and additional UI charges. Further, analysis has been carried out to see whether PSPCL has surrendered power for a given period and has to overdraw due to surrendering of power or has carried out load shedding.

Banking of Power

The State enters into banking arrangements every year to manage peak demand during the paddy season when demand is high due to agricultural demand. Detailed Analysis of banking of Power in State of Punjab for the period FY 2010-11 to FY 2012-13 was carried out to study the overall approach of banking, its methodology, rationale and month-wise capacity tied up through banking.

Short term Power Purchase

This aspect includes the analysis of the process adopted by PSPCL for entering into short term power purchase contracts and analysis of year-wise short term power purchase. Further, reasons behind procurement of short term power has been analysed and the financial impact arising out of such short term power purchase has been assessed.

Transmission System Capacity

This aspect includes analysis of the steps taken by PSTCL to improve inter as well as intra transmission system of the State to relieve network constraints and to provide system

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 9

strengthening. Further, the steps taken for minimising reactive power import especially during paddy season has been analysed.

1.6 Structure of the Report This report is structured in total 5 Sections as follows:

• This Section (Section 1) “Background and Context” includes overview of Punjab Power Sector, Scope of work for the study and Approach & Methodology adopted for carrying out the study.

• Section 2 “Analysis of Energy Sales” includes the detailed analysis of the variation in the Commission approved vis-a-vis actual sale of energy to different categories of consumers in the State of Punjab.

• Section 3 “Analysis of PSPCL’s Own Generating Stations” includes the detailed analysis of the quantum of power generation from the PSPCL’s own generating stations (Thermal and Hydel) including the analysis of planned and actual maintenance schedules.

• Section 4 “Analysis of Power Purchase” includes the detailed analysis of the quantum and cost of power purchase carried out by PSPCL

• The analysis of Energy Banking Agreements, UI (Sale/Purchase), Surrender of Power and Transmission System Improvements, is carried out in Section 5.

• Section 6 includes the recommendations, categorised on the basis of time frame required for their implementation.

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 10

2 Analysis of Energy Sales

2.1 Methodology adopted by PSPCL for Projecting Energy Sales PSPCL in its Petitions has been projecting the metered energy sales by computing the category-wise Compounded Annual Growth Rate (CAGR) of audited/actual metered energy sales for the last three years barring the immediately preceding year (e.g. CAGR from FY 2005-06 to FY 2008-09 for projecting energy sales of FY 2010-11). PSPCL then applies this 3-year CAGR to the revised estimates of the metered sales for the immediately preceding year for projecting the energy sales for the ensuing year (e.g. 3 year CAGR till FY 2008-09 applied on revised estimates of FY 2009-10 for projecting energy sales of FY 2010-11).

The revised estimates for any financial year is projected by PSPCL by considering the actual energy sales for the first half of the respective year and projecting the energy sales for the second half of that year by considering CAGR for the second half of the last three years.

2.2 Methodology adopted by Commission for Approving Energy Sales The Commission also broadly adopts the similar methodology as adopted by PSPCL for approving the energy sales for any financial year. The Commission first of all determines and approves the revised estimates for the energy sales of immediately preceding year and then applies three year CAGR on this approved revised estimate to arrive at the projections for energy sales for the following year.

2.3 Analysis of Variation in Actual Energy Sales for FY 2010-11

A. Category-wise Sales within State except AP Consumption

PSPCL submitted category wise actual sales for FY 2010-11 as a part of ARR and Tariff Petition for FY 2013-14. Further, as part of this study, PSPCL submitted the month-wise actual sales for each category for FY 2010-11. There is a variation in category-wise actual sales for FY 2010-11 as submitted by PSPCL as a part of ARR and Tariff Petition for FY 2013-14 and month wise actual sales submitted for each category for FY 2010-11. For analysing the variation in actual sales, the actual annual sales for each category as submitted by PSPCL in its ARR and Tariff petition for FY 2013-14, has been considered.

With regards to the variation in category-wise actual annual sales for FY 2010-11 as submitted by PSPCL as a part of ARR and Tariff Petition for FY 2013-14 and month wise actual sales submitted as a part of additional information sought during this study, PSPCL submitted that the annual sales figures also includes the units corresponding to

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 11

energy pilferage, unbilled units and short assessment by CA and in order to compensate the affect of these units, PSPCL proportionately adds these units amongst the annual energy sales for various categories.

PSPCL also submitted computation of total annual energy consumption for FY 2010-11 as shown in the table below:

Table 2: Computation of Net Energy Sales as submitted by PSPCL S. No. Particulars FY 2010-11

(MU) 1 Total Energy Input into the Punjab State 42422 2 Open Access Transaction (Purchased by Punjab Consumers) 2513 3 Net Input Energy into the Punjab State 39909 4(i) Metered Sale of Energy (Except total AP) 22115 (ii) Eq. Units of Energy Pilferage detected by Op. Org. 191 (iii) Eq. Units of Energy Pilferage detected by Enf. Org. 202 (iv) Eq. Units of Energy of Short Assessment by CA 116 (v) Unbilled Units (Figs as received from CAO Revenue) -1 5 Total Metered Sale 4(i+ii+iii+iv+v) 22623 6 (i) Agriculture Consumption (Assessed) 9957 (ii) Agriculture Consumption Metered & AP, SP 160 7 Total Agriculture Consumption 6(i+ii) 10117 8 Total Consumption (5+7) 32740 9 Consumption as %age of net Energy Input (8/3*100) 82 10 T&D losses (3-8) 7169 11 T&D Losses (in % age) (3-8)/3 * 100 18

It may be observed from the above table that the annual metered sale of energy for FY 2010-11 is 22115 MU. However, PSPCL booked around 508 MU on account of pilferage, short assessment by CA and unbilled units. PSPCL has added this 508 MU to the metered sale of energy to arrive at the total metered sale of around 22623 MU for FY 2010-11. However, the total metered sales figures submitted by PSPCL for FY

2010-11 as a part of ARR and Tariff Petition for FY 2013-14 is 22590 MU which is marginally different than the metered sales as submitted by PSPCL in above table while reconciling the total annual sales with monthly sales. These aspects of data mismatch in actual audited figures shall be avoided and uniformity of the data shall be maintained for submission to the Commission.

The summary of growth rates considered by PSPCL for projecting category wise sales for FY 2010-11, category wise sales projected by PSPCL, growth rates considered by the Commission for projecting category wise sales for FY 2010-11 in its Order, category wise

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 12

sales projected by the Commission, actual sales submitted by PSPCL for FY 2010-11 and growth in actual sales of each category with respect to sales for FY 2009-10 is summarised in Table below:

Table 3: Analysis of Sales for FY 2010-11

SL No Category

Actual Sales as

per Petition

(MU) (FY 2009-10)

CAGR considered by PSPCL

for projection

Sales Projected by PSPCL

(MU)

CAGR considered by Commission

Approved Sales

(MU)

Actual Sales as

per Petition

(MU) (FY

2010-11)

Variation in actual sales w.r.t. actual

sales of previous year

(%)

1 2 3 4 5 6 7 8 (8-3)/3 1 Domestic 7310 7.61% 7894 7.74% 7865 8176 11.84% 2 Non residential 2147 10.30% 2355 10.42% 2405 2468 14.97% 3 Small power 775 2.15% 784 2.25% 759 841 8.46% 4 Medium Supply 1619 1.98% 1639 2.10% 1541 1768 9.24%

5 Large Supply 8795 5.39% 9212 5.50% 9093 8522 -3.10%

6 Public Lighting 137 6.12% 157 6.41% 136 131 -4.20%

7 Bulk Supply 499 2.56% 508 2.56% 496 540 8.19%

8 Railway Traction 148 4.32% 155 4.32% 138 144 -2.77%

Total 21429 22704 22433 22590

As it may be observed from the above table, there is marginal variation in CAGR considered by PSPCL for projecting the sales for FY 2010-11 and CAGR considered by the Commission for approving sales for FY 2010-11. However, relatively higher variations can be observed in growth rate in actual sales for FY 2010-11 with respect to actual sales for FY 2009-10 as compared to the growth rates considered by PSPCL for projecting the sales and growth rates considered by the Commission for approving the energy sales for FY 2010-11. The reasons for variation can be attributable to the following reasons:

• Variation in Number of consumers, Connected Load and Specific Consumption or Load Factor

• Sudden spurt in demand due to increased economic activities. • Consumers shifting from Utility to other sources of power (Captive, IPP, Traders and

other bilateral purchase of power)

Report on Study on power purchase/sale for PSPCL for FY 2010-11 to FY 2012-13 Page | 13

To assess the reason for variation, analysis has been carried out with regards to growth in number of consumers, connected load, specific consumption (for Domestic Consumers) and load factor for other categories which is as shown in the table below:

Table 4: Variation in Number of Consumers, Connected Load, Specific Consumption/Load Factor and Sales for FY 2010-11 vis-à-vis FY 2009-10

S. No

Category of Consumer

Variation in No. of

Consumers for FY 2010-11

Variation in Connected Load for FY

2010-11

Variation in Specific

Consumption/Load Factor for FY 2010-

11

Variation in Actual Energy

Sales for FY 2010-11

1 Domestic 6.52% 5.79% 5.00% 11.84%

2 Commercial (NRS) 5.29% 8.19% 6.26% 14.97%

Industrial 3 Small Supply 2.54% -4.69% 13.80% 8.46% 4 Medium Supply 3.72% 4.86% 4.18% 9.24% 5 Large Supply 5.43% 6.10% -8.67% -3.10% Sub-Total 2.93% 4.43% -4.73% -0.51% 6 Street Lighting 10.75% 4.60% -8.41% -4.20% 7 Bulk Supply 0.81% 2.27% 5.79% 8.19% 8 Railway Traction 0.00% 0.00% -2.77% -2.77% *Increase in Specific Consumption of Domestic Consumers for FY 2010-11

PSPCL as well as Commission while projecting sales for FY 2010-11 had considered three year CAGR on the basis of which sales for FY 2010-11 were projected. PSPCL and Commission while projecting the sales has considered past years data which represents a different percentage in increase/decrease in number of consumers or connected load and increase/decrease in specific consumption or load factor for a particular category. Whereas, in actual terms, these parameters have been at variance with the growth based on past years data and therefore has resulted in variations in actual sales vis-à-vis that approved by the Commission.

The analysis of variation in category-wise actual sales in FY 2010-11 with respect to sales for FY 2009-10 and as compared to sales approved by the Commission is discussed in this section.