RB-VIGILANCE_Bulletin.pdf - Indian Railway

96

2010

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of RB-VIGILANCE_Bulletin.pdf - Indian Railway

2010

ON THIS EARTH THERE

IS ENOUGH FOR

EVERYONE’S NEED.

BUT NOT FOR THEIR GREED.

ON THIS EARTH THERE

IS ENOUGH FOR

EVERYONE’S NEED.

BUT NOT FOR THEIR GREED.

ABILITY WILL ENABLE A MAN

TO GET TO THE TOP,

BUT IT TAKES CHARACTER

TO KEEP HIM THERE

M.K. GandhiM.K. Gandhi

Hkkjr ljdkjHkkjr ljdkjHkkjr ljdkjHkkjr ljdkjHkkjr ljdkjjsy ea=ky; ¼jsyos cksMZ½jsy ea=ky; ¼jsyos cksMZ½jsy ea=ky; ¼jsyos cksMZ½jsy ea=ky; ¼jsyos cksMZ½jsy ea=ky; ¼jsyos cksMZ½

GOVERNMENT OF INDIAMINISTRY OF RAILWAYS

(RAILWAY BOARD)

lrdZrk cqysfVulrdZrk cqysfVulrdZrk cqysfVulrdZrk cqysfVulrdZrk cqysfVuVIGILANCE BULLETIN

tqykbZ tqykbZ tqykbZ tqykbZ tqykbZ JULY ’2010

FOREWORD

Good governance encompasses accountability, transparencyin public dealings, participatory decision making and adherenceto the rule of law. Corruption undermines the attributes ofgood governance. It leads to sub-optimal allocation of resourcesand reduces efficiency. Pervasive corruption also distorts thepublic perception about rules and procedures.

Vigilance Directorate publishes a Vigilance Bulletin every year.Publication of the Vigilance Bulletin is an attempt to createawareness about the facets of corruption and also to educaterailwaymen about the correct procedures and practices whichneed to be followed during the course of work.

A two days SDGMs/CVOs Workshop was held in May, 2010at CSTM, Mumbai, Central Railway. Some photographs ofthis Workshop have been included in this bulletin. The ZonalRailways had also celebrated Vigilance Awareness Week inNovember ’2009. Photographs of the last Vigilance AwarenesWeek ‘2009 and training course organized for VigilanceInspectors/Intelligence Inspectors in April, 2010 are alsoincluded in the Vigilance Bulletin.

Both Hindi and English editions of the Vigilance Manual,Statistical Compendium of Vigilance Statistics for the year2009, other publications of the Vigilance Directorate, importantRailway Board Vigilance Circulars, activities and functions ofthe Vigilance Department are now in the public domain.These are available on Indian Railways’ website athttp://10.1.10.21/vigilance/ and also at http://www.indianrailways.gov.in/vigilance/Home.htm. This is buta small step in making the working of the Vigilance Departmentmore and more transparent.

However, there is always scope for improvement. Thesuggestions for making the Vigilance Bulletin better are alwayswelcome and may be sent to Adviser (Vigilance), Ministry ofRailways (Railway Board), Rail Bhawan, New Delhi-110 001.

(A.K. Maitra)New Delhi Adviser (Vigilance)July, 2010 Railway Board

om

Rectangle

om

Rectangle

CONTENTS

S.No. Title Page No.

1 Irregularities in execution of contracts 1for replacement of pipe lines and otherassociated works

2 Procurement of materials through Works 3Contract without taking cognizance ofprevailing Stores Contract rates for samematerials

3 Irregularities in construction of a 6Road Over Bridge

4 Irregularities in operation of a labour 11supply works contract

5 Consignees beware – frauds by firm 14

6 Forgery and fraud by firm in 16claiming payment

7 Important cases in mass contact area 18

8 Earning contracts in commercial 20department: some important issues

9 Excess payment to the contractor 24through various on account bills inviolation of contract provisions

10 Illegal bill entry and test check 26performed on material not receivedphysically

11 Irregularities in execution of mechanized 28cleaning contract

S.No. Title Page No.

12 Department-wise break-up of action 37advised by CVC during the periodJanuary, 2009 to December, 2009

13 Work done by Vigilance Organization 39during the year 2009 at a Glance

1

IRREGULARITIES IN EXECUTION OFCONTRACTS FOR REPLACEMENT OF PIPELINES AND OTHER ASSOCIATED WORKS

- R.K. ShekhawatDV(E)-I

During Vigilance investigation in contract cases forreplacement of pipe lines and other associated works, in adivision, following irregularities were detected:

(i) For the item of “supply and fixing of PVC tanks,valves and connections etc.”, excess billing was foundto have been done for Rs. 6.96 Lakhs.

(ii) One of the Contract Agreement was for a value of Rs.1.51 Crores and majority of the work consisted ofsupply and laying pipes. About 35573 m length ofpipes were accepted and billed under this contract. Butwhile passing the pipes by ADEN, other than a blueband (indicating it to be of Medium quality), andembossing of IS-1239 on the pipe, no other check/verification was carried out. In the material passingregister, only diameter and length of pipes received ismentioned without any details about brand name,manufacturer name, IS No. and supporting vouchers/invoices etc.

For checking quality of the GI pipes supplied, 10samples were taken for the GI Pipes supplied underthe contract. On testing, only 2 samples could pass therequirements of IS-1239 with regard to thickness ofpipe and weight of pipe per m length. Thus, out oftotal 35573 m length of pipes accepted and billed,28973 m length of pipes were sub-standard.

2

The results of the vigilance check show that IS numberembossing was wrong/fake. Even if ADEN had goneby this wrong embossing, he should have at leastasked for manufacturer’s internal test reports forpassing such a huge quantity of pipes, which is partof IS certification. In any case, checking the thicknessand weight of pipes is easily possible and should havebeen done for passing such huge quantity of GI pipes.

By converting the accepted rate of GI pipe to per Kgbasis, the financial loss caused due to supply ofsubstandard (underweight) pipe was to the tune of Rs.29.48 Lakhs.

(iii) In another contract agreement, it was found that thesupervisor in-charge of work has not maintained anysite record like field book, site order book, etc. This isin violation of Para 1122 and 1123 of EngineeringCode, as these are crucial records w.r.t. execution andquality of work.

For the above irregularities, suitable DisciplinaryActions are being initiated against the concernedsupervisors and ADEN. The case also reinforces therequirement for carrying out suitable checks on qualityof pipes/other similar items and verifications of testcertificates, rather than merely going by the marking/embossing of IS number on them, which may be fake/forged also.

❈❈❈❈

3

PROCUREMENT OF MATERIALS THROUGHWORKS CONTRACT WITHOUT TAKINGCOGNIZANCE OF PREVAILING STORES

CONTRACT RATES FOR SAME MATERIALS

- R.K. ShekhawatDV(E)-I

During Vigilance Check on few cases of award ofWorks Contracts in a division, it was observed that anumber of signalling items procured through thesecontracts were being procured through StoresContracts also. Comparison of rates accepted for theseitems shows that these items were procured at about215% higher rates as compared to the prevailingaccepted rates in the Stores contracts for the sameitems.

2. There are many components of extra expenditures forgetting the supply through works contracts ascompared to rates accepted in Stores ContractPurchase Orders. These are mainly excise duty (notincluded in basic rates of stores contracts, to be paidby consignee), non-issue of Form-D (entailing paymentof sales tax in works contract), inspection charges(paid by consignee in Stores Contracts), freight to depotand transportation charge from depot to site (paid byconsignee in Stores Contracts, Works Contract tax(depending on State where work is being carried out),scales/magnitude of supply (which is normally morein stores contracts leading to some reduction in rates),contractors’ profit on supply portion and paymentsgetting locked up for a longer period in the form ofretention of security deposit etc. in works contracts. Allthese add-ons combined constituted about 30-40% inthe case investigated. But in the cases investigated, thedifference was about 215% etc. Thus, higher cost has

4

been incurred due to adoption of works contractsmode for supply of these items.

3. It was also observed that procurement of the saiditems through works contracts was being followed inmany other units, at that point of time and the ratesawarded in the cases investigated were in line withprevailing accepted rates of Works contracts. The issuehas to be looked onto in overall perspective,considering the feasibility and relative merits ofprocuring these items through stores contracts orworks contracts, keeping in mind both the needs ofthe project and cost implications involved. This was tobe done by the Tender Committee, but the TCs inthese cases could not examine the relative merits ordemerits of procuring the said items through workscontracts, in absence of the fact about these items beingprocured through stores contracts also not beingbrought on record.

4. The Convenor Member of the TC, who was thetechnical branch officer also, was not unaware of thefact that these items are being procured through storescontracts. Many Purchase Orders for Stores Contractswere issued in the same division before finalisation ofthe tender cases investigated. But his fact not beingbrought to the notice of the notice of TenderCommittee, resulted into the TC not being able toobjectively analyse the overall rate reasonability, dulyexamining the alternative of procuring these itemsthrough Stores Contract.

5. The indents for all the materials procured throughStores Contract, were vetted by finance and copies ofPOs were also marked to Finance. Thus by a little bitinvolved approach, the Finance member of the TC,was in a position to know the fact about the storescontracts for these items and rates thereof.

5

6. Suitable Disciplinary/Administrative is being takenagainst the Convenor/Finance member of the TenderCommittees. The case also brings out the point that incase of procurement of some items through WorksContracts, the prevailing Stores Contract rates for thesame items, if available, also need to be takencognizance of; of course duly adding all extraapplicable add-ons to bring Stores Contract rates atpar with Works Contract rates and taking into accountthe requirements of Work/Project.

❈❈❈❈

6

IRREGULARITIES IN CONSTRUCTION OFA ROAD OVER BRIDGE

- R.K. ShekhawatDV(E)-I

In one of the Zonal Railways, a single span Road OverBridge (ROB) was constructed in lieu of existing LevelCrossing and the work of span over Railway Track wasexecuted by Railway. The substructure was RCC piles withpile cap/piers over it and the superstructure was PSC Boxgirder. Within 9 months of opening of bridge, heavy spallingof concrete, exposing the reinforcement, was observed onthe underside of the deck slab of PSC girder. Due to this,heavy traffic has been stopped over ROB. Technicalassistance was taken from RDSO for ascertaining cause offailure. The consultancy from IIT/Kanpur was also takento ascertain cause of failure and to formulate rehabilitationplan. Technical/vigilance investigation in this case, broughtout following serious irregularities:

(i) Poor Quality of concrete in deck slab

The deck slab was of M-45 Grade concrete, as percontract agreement, which means having a compressivestrength of 45 MPa. The quality of concrete was foundbad in visual inspection, showing severe spalling on thebottom inside surface of deck slab.

In the rebound hammer tests done on deck slab byRDSO, at 8 out of 17 locations, the compressivestrength of concrete was reported to be less than 45MPa. The strength varied from 20.60 MPa to 68.90MPa and such a large variation in strengths showsinconsistency in compressive strength of concrete,which is an indication of poor quality control.

7

In the rebound hammer tests done by IIT/Kanpur, at74 locations, the compressive strength value in deckslab was reported as low as 10.0 MPa. The coefficientof variation (COV) for compressive strength was 37.6%for deck slabs and such a large value of COV is anindication of non-uniformity of concrete, making itsquality a suspect.

The Ultrasonic Pulse Velocity (UPV) tests conducted byIIT/Kanpur, has shown the concrete in the deck slabto be of questionable quality.

Profometer tests, conducted by RDSO, gave theconcrete cover of 36.05 to 56.20mm, against thespecified value of 50mm. This shows that no controlwas kept on concrete cover.

Windsor Probe tests by RDSO at 2 locations gavecompressive strength as 29 MPa and 40.58 MPa,against minimum stipulated value of 45 MPa.

Testing of concrete cores, taken from the deck slab byRDSO and tested at NTH/Ghaziabad, gave compressivestrength values of 22.9, 21.3, 27.7 and 23.9 MPa only.Similarly, testing of concrete cores, taken and tested atIIT/Kanpur, gave average compressive strength valuesof 35.6 MPa for soffit, 20.2 MPa for Web and 13.8MPa for deck slab. The cores from deck slab werehaving large voids and showing signs ofhoneycombing.

8

The facts above establish that the concrete, especiallyin deck slab, was of sub-standard strength and quality.This has affected load carrying capacity as well as longterm durability of the structure.

(ii) Concrete mix design not done

Concrete mix design was done only for RCC piles andit was not done for pile caps, piers, PSC box girder,end cantilevers, railing beams, anti-crash railings andwearing coat.

For PSC box girders (Grade M-45), mix design of someother site, about 150 Kms away for M-60 Gradeconcrete, was used. Changing grade of concrete willhave a design implication in PSC structures and thus,it cannot be done without design check. Moreover, themix design was copied without any consideration/comparison of necessary inputs for mix design i.e.type/properties of input materials (cement, fineaggregate and coarse aggregate), use of admixtures etc.

In fact, the mix design was for different brand ofcement but during execution of work other brands ofcements have also been used.

What is more surprising is that even by using M-60Grade concrete for PSC girder, the strengths actuallytested, after failure, were not even meeting therequirement of M-45 Grade concrete also. Thisindicates that probably no proper mix design wasfollowed.

9

Not adopting proper mix design was not only violationof contract agreement provision, contractor got benefitof not spending money for mix design/testing byprofessional agency. This also entailed unnecessary useand payment for extra quantity of cement

(iii) Testing not done for the materials used

For Cement, Manufacturer’s Test Certificate (MTC) wasto be kept on record and testing was also to be donefor each batch. But challans and MTCs for all batchesused were not kept on record. Cement was got testedfrom the laboratory only for three batches.

Approval for source of aggregates was not taken.Aggregates were not tested regularly (once a month)for water absorption, potential alkali reaction, chloridecontent, sulphate content and shrinkage characteristics.No record of slump has been maintained at site. Allthese were in violation of contract agreementprovisions.

For Admixture, Manufacturer’s Test Certificate (MTC)was to be kept on record but no MTC was not kepton record. There are no records as to what admixturewas used and in what dosages.

For reinforcement steel, Manufacturer’s Test Certificate(MTC) was to be kept on record and testing was alsoto be done for each batch. But no MTC was kept onrecord and steel was got tested from the laboratoryonly three times. Moreover, against the contract

10

agreement provision for use of steel procured frommain producer/their authorized dealer only,confirming to latest relevant IS specification, no recordswere maintained to ensure compliance of this provisionof contract.

Thus, there was no control on use of the inputmaterials, and their properties. Various testing chargeswere also saved for the contractor, which gave thebenefit to the contractor.

(iv) Testing facilities not available at site

As per contract condition, testing facilities were to beprovided in the site lab, to be set up by the contractor.But site lab was not set up by the contractor. Thus notonly compromise was made with quality but unduebenefit was passed to the contractor.

(v) Non-maintenance of Site Records

Very crucial site records related with pre-stressingoperations, concreting operations, calibration of tools/equipments etc. were not maintained. Daily ProgressRegister & Material passing registers were notmaintained.

(vi) Fake payments for load testing of PSC girder

Based on available evidences, it was observed that noload testing was carried out on PSC girder, butpayment for load testing of PSC girder was made tocontractor. This has not only compromised with qualitybut has passed on undue benefit to the contractordeliberately.

For the above irregularities, suitable disciplinary actions havebeen recommended against the concerned officials.

❈❈❈❈

11

IRREGULARITIES IN OPERATION OFA LABOUR SUPPLY WORKS CONTRACT

- R.K. ShekhawatDV(E)-I

A Works Contract was awarded by one of the loco shedsin a division for “maintenance and upkeep of officepremises as well locos”, at the said loco shed as well 5 othertrip shed spread over the division. This was predominantlya labour works contract. For each location of the work,minimum number of labour to be employed was specifiedin the contract agreement. Being a labour work contract,the deployment of labour on daily basis was required to bewatched and documented for the purpose of the payment.

2. In a vigilance check of this work, followingirregularities were detected:

(i) As per contract agreement, the daily attendancesheet was to be maintained by the concerned tripshed SSE, the presentee statement was to besubmitted with monthly bills and a specifiedpenalty to be imposed for any shortfall of labour.

But in the check it was found that at some tripsheds, the attendance of staff deputed by thecontractor was not recorded on register, it wasrecorded in individual muster card which waskept with the contract labour themselves. Atsome trip shed, the daily attendance register wasnot countersigned by Railway representative. Atsome trip shed, no attendance record wasavailable for some of the periods.

12

As per monthly attendance sheet submitted toloco shed, recoveries were to be made for shortsupply of minimum stipulated labour. But norecoveries were made in the bills prepared andpassed by Loco Shed. Based on vigilance checkonly, recoveries were made later on.

(ii) As per contract agreement conditions, theContractor was required to issue Identity Cardsto his staff, duly giving a list of staff to beemployed at each work location. Contractor wasalso required to submit Police Verification reportand Medical Certificate of all the staff employedby him.

But in the check it was found that the contractorhas not submitted any list of staff, work locationwise. At only 2-3 locations, the contractor staffwas found with ID card but this was also notas per contract agreement condition. No PoliceVerification Certificate and Medical Certificate offitness were submitted by contractor, for any ofthe labour employed by him, at any of the loco/trip shed. All these facts can create security riskwithin the loco/trip shed premises.

(iii) As per contract agreement conditions, jointrecord was required to be kept of all maintenanceworks carried out by contractor on daily basis.

But in the check it was found that no such jointrecord of the work carried out, on daily basis,was maintained at any of the trip sheds. Inabsence of this, no verification/cross checking ofthe work executed is possible, at a later date

13

(iv) The officials of the trip shed were only sending theattendance sheets (that too not countersigned by theRailway representative) and work executioncertificate to the Loco Shed. Recording ofmeasurements in the MB, test checks ofmeasurements, bill preparation, technical check ofbill and bill passing was all done by the Loco Shedofficials.

With the work being carried out at 5 trip shed also,the concerned SSEs of the trip sheds should haverecorded the record measurements in the MB(because MB recording by the concerned SSE and testcheck by the concerned field officer, and not byanybody else, is necessarily required in workscontract bills, to ensure certification of compliancewith C. A. conditions) and these should have beentest checked by the officers of trip sheds). Based onthese record measurements, the loco shed officialscould have made the combined bill. But in this case,based on insufficient/incomplete papers from tripsheds, loco shed officials recorded the combinedmeasurements, without ensuring compliance of C.A. conditions at all Trip sheds. The test checks for themeasurements were also certified as a whole, by theloco shed officer, whereas he has not carried out anytest checks at Trip sheds.

(v) Other than one Trip shed, the SSEs at other 4 tripsheds did not even have the copy of Letter ofAcceptance (LOA) and/or Contract Agreement(CA) with them.

3. For the aforesaid irregularities, suitable disciplinaryactions have been initiated against the concernedofficials. The case also brings out the need for ensuringstrict compliance of contract agreement conditions insuch predominantly labour supply contracts.

❈❈❈❈

14

CONSIGNEES BEWARE – FRAUDS BY FIRM!

- N.K. Sharma,JDV(S)

A complaint was received from an officer of indentingdepartment in which it was alleged that the firm suppliedonly part quantity of material against a supply order underDGS&D R/C but debit for the entire supply order quantitywas raised by DGS&D.

Investigation revealed that out of the total quantity of 135nos., the firm supplied 60 nos. in the first lot along withinspection note. During a joint check conducted by vigilanceand consignee, inspection facsimile could not be found onthe supplied items due to negligence or probable collusionof the receiving official. The acknowledgment given by himallowed the firm to raise the bill for payment. As per themodus operandi of the firm and the colluding inspectingofficial, the serial numbers of the equipment were mentionedin the delivery challan but not on the inspection note.

Investigation also brought out that the firm raised the firstbill prior to supply of first lot. The second bill was alsoraised prior to supply and for quantity, which exceeded thesupplied quantity of 19 nos. and the third bill was raisedwithout any supply. The receiving official whileacknowledging receipt of the second lot failed to put anyqualifying remarks regarding non receipt of inspection note.As already mentioned, the third lot was not received at all.Payments against these bills to the firm were made byController of Accounts, Department of Supply. In terms ofthe RC , 90% payment is to be released against proof ofinspection and provisional receipt certificate of stores byconsignee for having received the material.

15

Collusion of the inspecting official of DGS&D’s (QA)/ DQAis apparent because he failed to indicate the serial numbersof the inspected stores in the inspection note covering thesupply of first lot of 60 nos., in departure from earlierpractice. Besides this irregularity, inspected stores bear asticker indicating the name of some other supplier than thefirm on whom the order was placed.

In terms of the relevant rate contract, the consigneementioned in the Inspection Note should sign and put hisofficial rubber stamp on the Advance Payment Copy of theInspection Note. Alternatively, it should be signed by anofficial authorised by the consignee in that behalf and insuch cases , the signing official should indicate hisdesignation and the official on whose behalf he is signingand should affix his official rubber stamp. In the instantcase, no rubber stamp of consignee was available on theAdvance Payment Copy of the Inspection Note. Yet 90%payment was released. Thus, supplier was paid withoutsupply. CVO, DGS&D has been requested to take actionagainst the concerned officials.

❈❈❈❈

16

FORGERY AND FRAUD BYFIRM IN CLAIMING PAYMENT

- N.K. Sharma,JDV(S)

During a preventive check conducted by a zonal railwayat a Stores Depot, photocopier paper supplied by a firm wasjointly sampled and got tested from Central Pulp & ResearchInstitute. It was found t hat the sample did not conformto the specifications laid down in RC of DGS&D. It wasdetected during the check that material was deliveredthrough Road Transport but supplier had submitted onlyconsignee copy of inspection certificate.

The said firm, approached the Office of Chief Controller ofAccounts, Department of Commerce and Industries, NewDelhi and took payment by forging the signature ofDy.CMM on accounts copy of inspection certificate as wellas on balance payment copy by using forged seal of thedepot officer.

In the Pay and Accounts department, nobody paidattention to the discrepancy/ contents of the forged sealindicating the signatures of depot officer as Dy. ChiefMaterial Manager in Hindi and Assistant Material Managerin English.

All the Zonal Railways have been alerted about fraudulentaction of the firm to safeguard Railway’s interest.

The matter was taken up with CVO/ DGS&D for fixingresponsibility on the officials concerned, who inspected andpassed inferior quality material and released payment basedon forged signatures of consignee on accounts copy of theinspection concerned as well as on the balance payment

17

copy. He has sought clarification whether the prescribedprocedure as laid down under DGS&D’s circular No.10dated 14.5.2004 regarding rejection of supply order placedunder DGS&D (R/C) has been followed in this case. If not,he has advised to exercise consignee’s request of rejectionof stores as per provision contained in the aforesaid circularbefore seeking further action in the matter.

The Chief Controller of Accounts, Department of Commerce(Supply Division), New Delhi has clarified, inter-alia, thatmany of the letters/ correspondence regarding recoveries tobe made from this firm had been found signed by theAssistant Material Manager for Deputy Chief MaterialManager, leading to confusion in this case. However,recoverable amount has been noted for recovery. He hasalso advised that indenter/ consignee may be asked toobtain confirmation from the paying authority whether thedebit claimed raised by CCA(S) against the said paymentin this case had been passed and no debit note was issuedto RBI reversing the payment.

The matter is being pursued with the Zonal Vigilance.

❈❈❈❈

18

IMPORTANT CASES IN MASS CONTACT AREA

- Samir ShankarJDV(T)II

● A case of fake EFT books being circulated by the ticketchecking base in-charge to the TTEs was detected. Theoriginal EFT books were kept by the concerned officialfor misuse and duplicate EFT books having the samenumbers were got printed and supplied to theworking staff who issued them treating these asgenuine EFTs. The concerned official is being taken upunder major penalty D&AR action.

● In a station the booking staff misappropriated hugeamount of railway revenue by manipulating the DTCof newly installed UTS cum PRS system. The bookingclerk deliberately split the shift hours into two partsand took out the DTC for the later half of the shiftand misappropriated the revenue of the first half ofthe shift. The booking supervisor the CMI and the TIAfailed to detect this fraud. All concerned are beingtaken up under DAR. It has also highlighted the needfor ensuring regular and meaningful inspections at thesupervisors levels

● A case of short remittance by the booking staff hasbeen detected in which the earnings of halt stationswere not being remitted timely. The stations earningswere also not been remitted timely. It is also detectedthat the amount being shown as remitted through CRnote were not actually received at cash office. The caseis under investigation.

● A case of impersonation on a lost metal pass wasdetected when a passengers claiming to be a Railway

19

Board officer was found travelling in Duranto express.The passenger produced a metal pass along withauthority to travel in first AC on demand by the TTEbut they were having different numbers. The messagewas received in Railway Board vigilance and oninquiry it was revealed that these passes were reportedlost. The impersonating person was apprehended andhanded over GRP/NDLS

● A case of issue of invalid ticket by the e-ticket agentof IRCTC was detected. Information was received inrailway board vigilance that a group of passengerswere travelling in coromondal express on fake e-tickets.The zonal Railway vigilance was advised to conducteda check in a train in which a groups of marriage partywas travelling on four different PNR issued by an e-ticket agency in which only one PNR was appearingin the chart. The other PNRs were found to be invalidand never generated. The passengers claimed that theyhad bought these tickets from the agency. Thepassengers were regularized and the matter wasreported to IRCTC for appropriate action.

● In a check conducted on booking of party coaches, itwas detected that the parties were not submittingfolder the containing the details of actual detention ofthe coaches at en -route stations after completion ofthe trip. In many case it was detected the detentioncharges turned out to be much more than the securitydeposits of the party. The balance amount remainedunrealized. A special drive was also launched in thisregard which revealed that this situation was alsoprevailing in many railway. A system improvement hasbeen suggested to increased the amount of securitydeposit to discourage such practices.

❈❈❈❈

SDGMs/CVOs Workshop was held at Mumbai on 13th and 14th May, 2010

Shri R. Vatash, SDGM/Central Railway welcoming Shri A.K. Maitra, Adviser (Vigilance) in SDGMs Conference

SDGMs/CVOs attending the workshop

SDGMs/CVOs Workshop was held at Mumbai on 13th and 14th May, 2010

Shri A.K. Maitra, Adviser (Vigilance) addressing the Workshop

Shri R.N. Verma, GM/Western Railway addressing the Workshop

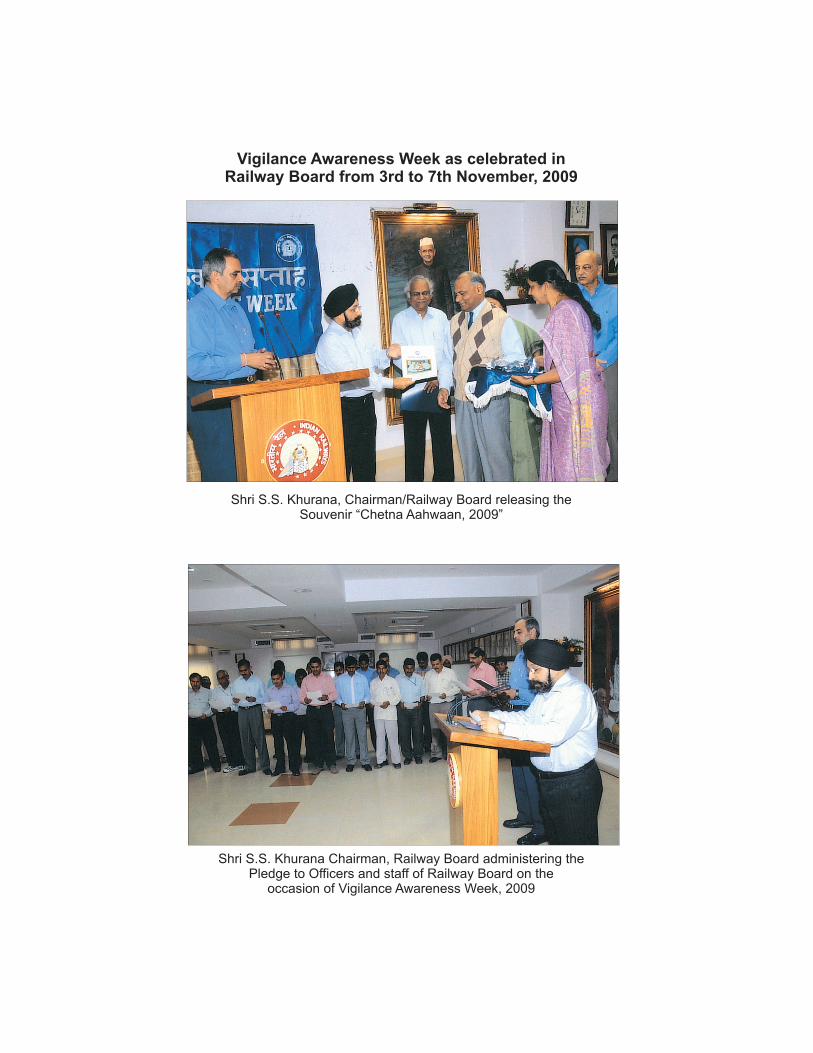

Vigilance Awareness Week as celebrated inRailway Board from 3rd to 7th November, 2009

Shri S.S. Khurana, Chairman/Railway Board releasing theSouvenir “Chetna Aahwaan, 2009”

Shri S.S. Khurana Chairman, Railway Board administering thePledge to Officers and staff of Railway Board on the

occasion of Vigilance Awareness Week, 2009

Vigilance Awareness Week as celebrated inRailway Board from 3rd to 7th November, 2009

Shri A.P. Mishra, Adviser (Vigilance) addressing the gathering on the occasion of Vigilance Awareness Week, 2009

Officers and staff attending the Vigilance Awareness Week, 2009

Training programmes organized at Diesel Simulation Centre, Tughlakabad from

26th April to 30th April, 2010 and 3rd to 7th May, 2010

Shri A.K. Maitra, Adviser (Vigilance), Railway Board giving away thecertificate of training to the participant during valedictory session

Shri Raj Singh, EDV(S), Railway Board giving away the certificate oftraining to the participant during valedictory session

Gro

up p

hoto

gra

ph o

f T

rain

ing C

ours

e for

IIs/

VIs

at D

iese

l Sim

ula

tion C

entr

e, T

ughla

kabad

20

EARNING CONTRACTS IN COMMERCIALDEPARTMENT: SOME IMPORTANT ISSUES

- Samir ShankarJDV(T)II

The earning contract in Commercial department has becomevery common nowadays. These contracts are now awardedon the basis of open tendering. This area is relatively newfor Commercial department as earlier the contracts werebased on licensing system or through auctions. The earningcontracts are typical in nature as they are normally part ofessential passenger amenities and at the same time arebecoming an important source of revenue for Railways. Someof these contracts are: (i) Parking contracts at the stations/circulating areas(ii) Pay & Use contracts(iii) Licensing of SLRs/VPUs(iv) Advertisement contracts at stations/hoardings, walls,

trains(v) STD/PCO booth etc. This area is a developing field in Commercial department.The Railway Board had issued guidelines for revenue andservice licences in Commercial department through theCommercial Circular No.71 of 2001 vide its letter No.2001/TG-I/Comm. Contract dated 31.10.2001. Thereafterguidelines and circulars have been issued from time to time.

In many cases, the parallels are drawn from the instructionsof works contract and stores contract, although the natureof these contracts is intrinsically different from the earningcontracts. The works contracts and the stores contract havewell defined structure. The relationship of Indian Railwayswith contractor follows a meticulous procedure and

21

methodology, which has evolved into a well establishedsystem over the years. There are well laid out schedule ofpowers, methodology and procedures etc. for managementof these contracts. The basic guiding principles oftransparency and equal opportunity in allotment are equallyapplicable in all contracts. The commercial earning contractshave to meet the twin objective of balancing transparencyin allotment and best financial deal for Railways and at thesame time they have to ensure reasonably satisfactory levelof passenger services as most of these contacts are aimedthat providing important passenger amenities. Common Problems observed (i) Before inviting tender for a new contract, feasibility

study not done in view of ground situations andmarket conditions. This leads to unrealistic fixation ofReserve Price or impractical design of the tenderleading to failure of contract.

(ii) Framing of impractical eligibility conditions leading to

failure of tender or post-tender dilution of theseconditions to avoid failure of contract.

(iii) Two packet system of tendering adopted without anydefinite or quantified eligibility conditions or credentialsfor the technical bid leading to disqualification oftenderer on subjective basis.

(iv) Financial solvency guidelines not properly followed.

The bank balance or passbook, one-time transactionsbeing considered as certificate for financial solvency.

(v) Post tender relaxation of conditions such as withrespect to payment terms, security deposits, executionof agreement etc. It has been observed that on manyoccasions, the conditions are relaxed for these

22

contracts in view of impending revenue loss anddisturbance to passenger amenity. But it is clear thatany relaxation allowed in terms of payment conditionsor other requirements ultimately restricts RailwayAdministration further to avoid losses in future.

(vi) Non-finalisation of fresh tender before the end of the

term of present contract leading to extension of presentcontract. Too much time is wasted in processing of caseat various levels and different departments. Thedetermination of Reserve Price is taking a lot of timein view of lack of inter-departmental coordination,finance vetting etc. The registers for licences with duedate of expiry and performance are not usually beingmaintained properly.

Areas which require attention

Eligibility Conditions Normally in works contracts, the eligibility conditions andfinancial credentials are well laid down. But for earningcontracts, these are not very specifically laid down. Forexample, it is seen that in case of Parking Contracts, twopacket system of tendering is adopted, but the credentialscalled for are in many cases in the form of experiencecertificate, financial capability, etc. which are neitherquantified nor elaborated. The guidelines issued by RailwayBoard are general in nature and specific details are to belaid down for each contract. As a result, these are left tothe individual Tender Committee to take subjective decisions. Therefore, it is desirable to lay down uniform guidelines oneligibility conditions keeping in view the following: (i) To select sound, reliable contractors financially and

experience-wise and to keep out unscrupulousparticipants

23

(ii) To protect Railway from default and loss of revenueand to avoid in convenience to passengers in view ofdisturbance of passenger amenities caused due todefault or termination of the contract.

SOP to deal with extraordinary situations As these contracts are related with important passengeramenities which cannot be discontinued immediately, itwould be proper to formulate SOP to deal withextraordinary situations in which powers for extension ofexisting contract may be laid down as in works contract.

Involvement of mafias/anti-social elements Another disturbing phenomenon is involvement of mafias/anti-social elements in such contracts who do not refrainfrom using any tactics to have their way. It is importantto devise mechanism to discourage such elements inparticipating in such contracts. The earning contracts in Commercial department havebecome the order of the day. It is important that policyguidelines and instructions are consolidated and circulatedfor ready reference. The guidelines on different issues mayalso be formulated at appropriate levels based on theexperiences of these contracts. The efficient and propermanagement of earning contracts is very important for theorganisation.

❈❈❈❈

24

EXCESS PAYMENT TO THE CONTRACTORTHROUGH VARIOUS ON ACCOUNT BILLS IN

VIOLATION OF CONTRACT PROVISIONS

- Ghansham BansalDVE-II

1. A preventive check was conducted in one of theZonal Railways regarding excess payment to the tuneof Rs.37 Lakhs made to the contractor through variouson account bills in some work of supply andcommissioning.

2. More than one Measurement Books were used by thedifferent supervisors for releasing the payments. As percontract conditions, On-Account payments werepermissible on the supply of material as given below:-

i) Up to a certain percentage of material cost to bereleased on receipt of relevant items.

ii) Equal percentage to be released after foundationsof work.

iii) Balance to be released after completion ofstructure.

However there was an overall restriction of 85% onthe payments thus made to the contractor.

3. There was also a provision of ‘Progress Payment’ suchthat the contractor could receive upto 95% paymentagainst the complete supply with the arrangement thatOn-Account payment made already would be set-offprogressively until entire ONA payments are adjusted.

25

4. All the On-Account payments were arranged throughone separate MB in which one JE/Drg used to recordall the measurements based on Material ReceiptCertificate (MRC) issued by the field supervisors.However it was detected that the payments were madeto the contractor for quantities more than the reflectedquantities in the MRCs issued by the field supervisors.

5. Excess payments through some On-Account Bills werecalimed on MRCs against which 95% payments (Max.Admissible payment after completion of work) hadalready been made through earlier On-Account andprogress bills.

6. A total payment of approximately Rs. 37 Lakhs madeto the contractor was detected in this manner. Theproblem could have been easily detected by the dealingofficials while passing the On Account Bills near thecompletion of the work when it was not possible tohave large amounts of pending On Account Bills.

7. Therefore the ‘terms and conditions’ as laid down inthe contract agreement were not followed whilepassing the On-Account Bills. Even upto 100%payments were made through certain On Account Billsagainst supply of some items although there was arestriction of 85% on such payments as per thecontract provisions.

One of the possible reasons for excess payment wasincorporation of certain complicated paymentprovisions in the contract agreement, which aredifficult to comprehend by the supervisors handlingthe case.

As many as eight officials, including one JAG and oneSS, were recommended Major Penalty action includingbanning of business with the firm.

❈❈❈❈

26

ILLEGAL BILL ENTRY AND TEST CHECKPERFORMED ON MATERIAL NOT

RECEIVED PHYSICALLY

- Ghansham BansalDVE-II

1. A preventive check was conducted by Board vigilancein one of the Zonal Railways in connection with thesupply of some electrical material required forreplacement of capacitor bank. In the investigation, itwas found that the material worth approximately Rs49.81 lakhs had been shown as received and enteredin the MB for payment without physically receiving thesame. The test check was also performed by theofficers on this fictitious material.

2. The concerned OS was responsible for checking thecontractor’s bill in a proper manner before processingthe same for the payment, but he failed to do so andprocessed the bill for payment.

3. The concerned supervisors of the work were supposedto record the measurements after complete supply ofthe work as per contract provisions, but they failed todo so and instead recorded false receipt of the saidmaterial in Measurement Book duly certifying that“The material received in the good condition”.

After the vigilance check, the supervisors stated thatthe contractor had approached them and mentionedthat permission from the higher authority has beenobtained, which could not be established. Even if anysuch permission is given the supervisors are notexpected to enter the bill violating the agreementconditions. The agreement conditions clearly stipulated

27

that the payment for supply of materials will be madeonly after receipt of the materials in good condition atcorrect location and all invoices shall be accompaniedby Contractor’s challan duly posted in ledger,Inspection certificate, Manufacturer’s challan, etc.Under normal circumstances all necessary documentsshould be checked and cross-checked before passingbills for payment to contractors.

4. The concerned officer-in-charge was supposed toconduct 20% test checks in the measurement book. Headmitted during clarification that the material was notavailable at site on the date of measurement, but thetest check was certified.

5. It was also detected that the Measurement Book hadbeen handed over to the firm’s representative forexpediting the signature of various official for earlypayment. The MB being the highly sensitive document;should not have been handed over to anyunauthorized persons.

6. The payment of the bill was stopped due to vigilancecheck. But all the supervisors and test checking officialswere recommended for Major Penalty action and thefirm was recommended for banning of business forindulging in unethical trade practices.

❈❈❈❈

28

IRREGULARITIES IN EXECUTION OFMECHANIZED CLEANING CONTRACT

- Vikas PurwarDV(M)

A Preventive Check was conducted at Coaching Complex,of a railway to check various aspects of mechanizedcleaning and disinfection of coaches. During the vigilancecheck, it was observed that the contractor had beenviolating a series of terms and conditions of contractagreement on use of machinery & plant, manpowerdeployment, material/cleaning agents etc. Observationsmade during the course of vigilance check are discussedbelow:

Machinery and Plant (M&P)

1. As per terms and conditions of contract agreement,the contractor will utilize compact and portablecleaning machines covering all safety precautions. Onphysical verification, the machines available at site werein extremely poor condition. The extension boardsused were made of iron sheet instead of non-conducting material. Even the electric cable being usedwas cut at several places and secured with the helpof adhesive tape.

2. As per terms and conditions of contract agreement, forevery pit line, there shall be a set of machines as listedin machine specification. A set of stand-by machinesshall also be provided at site for any breakdown.

Following types of machines using least possible water andelectricity to control expenditure are recommended to beused:

29

(i) Portable type high pressure jet machine(ii) Portable type single disc mini scrubber(iii) Portable type wet and dry vacuum cleaner

At the time of check, 3 HP jet cleaning machines and 1mini scrubber was available at site. These machines werenot being used and were kept secured with lock and chain.At the time of check, key could not be located by therepresentative of the contractor and lock had to be broken.

On checking whether working or not, one jet machine andone scrubber were found in working order, one jet machinefound partially working (creating only low pressure waterjet) and one jet machine out of order.

The above mentioned 4 machines (3 jet machines and 1scrubber) were the only machines available on washing line.No other machine was available even on other washinglines.

No stand-by set of machine was available on washing line.No vacuum cleaner was available on washing line.

Other Machines (Tools & Accessories)

1. High grade insulation power cable – As per termsand conditions of contract agreement, all the machinesused shall have sufficient length of power cable. Thepower cable shall be of class-I insulation and shall beduly protected to avoid leakage of current. During thecheck, the cable being used had joints to increase thelength. Insulation of cable was damaged at severalplaces and protected with adhesive tape.

2. Floor Mopper – It shall be specially fabricated forRailway coaches to meet the width of coach aisle area.The mop rubber shall be made of special type of

30

sponge material (PVA) so as to absorb and retain atleast one litre of water.

No such mops were available either at work site or inthe Contractor’s Stores. Only wipers having no waterabsorbing capacity were being used.

3. Window glass squeegee– It shall be made of stainlesssteel handle of preferable 10” length with highlydurable rubber blade.

No such squeegees were available with contractoreither at work site or in Contractor’s Stores

4. Special cotton duster for glass. Used/dirty dusterswere available with contractor’s staff. However, nofresh/new dusters were available in Contractor’sStores. Jute cotton duster for washbasin cleaning werefound used at work site

Cleaning Agents

As per Clause on Materials of the Contract Agreement, allthe cleaning agents shall be bio-degradable and environmentfriendly. It will follow all the mandatory International &National Standards. The availability of preferred cleaningagents mentioned in Contract Agreement vis-à-vis availableand used is given in the table below:

S. Description of Preferred Whether Available ActuallyNo cleaning agent Brand/Make being used in being

as per CA as per CA at work site contractor’s used atstores work site

1 . Floor cleaning Spiral Not 6 litre ‘Polli’ Unbrandedagent (Johnson being used brand from so

Diversey) Eco Lab in calledor Sigla sealed “Solvex”Neutral of condition was beingEco Lab used.

31

S. Description of Preferred Whether Available ActuallyNo cleaning agent Brand/Make being used in being

as per CA as per CA at work site contractor’s used atstores work site

2 . Ceramic Task R-1, Not being Not UnbrandedToilet Task R-6 used available blue colourfittings (Johnson cleaningcleaning Diversey) agent beingagents or Sigla used

Neutral ofEco Lab

3 . Glass Task R-3 Not being 15 liters Not beingcleaning (Johnson used (Johnson usedagent Diversey) Diversey)

or OC brand inGlass 3 sealedCleaner of cans ofEco Lab or 5 litreColin capacity

& 2 litre(Task R-3)in anothersealed can.

4 . Laminated Task R-7 Not being Not Nothing beingplastic sheets (Johnson used available used& berth Diversey)rexine cleaner or OC

neutralcleaner ofEco Labor Colin

5 . Painted Spiral Not being Not Nothing beingsurface (Johson used available usedcleaner Diversey)

or Absorbitof EcoLab orColin

6 . Stainless Steel Suma-Inox Not being 4 liters Nothing beingPolish (Johnson used “Sumo-Dip”, used

Diversey) or a cleaningchromol of agent forEco Lab removingor Colin betel stain

32

S. Description of Preferred Whether Available ActuallyNo cleaning agent Brand/Make being used in being

as per CA as per CA at work site contractor’s used atstores work site

7 . Disinfectant Stride Not being Not Nothing(Johson used available beingDiversey) usedorAntibackof EcoLab orColin

8 . Air freshner Task R-5 Not being Not Nothingor used available beingequivalent usedEco Lab

None of the preferred cleaning agents were being used atsite by the contractor. However, some of the brandedcleaning agents although available in contractor’s storeswere in sealed cans. It appears that these are kept just asshow-pieces to be shown/ used in case of inspections bysenior officers but not to be used regularly.

Materials (Workers’ Unform)

As per the Contract Agreement, following items should beprovided to the workmen by the Contractor.

● Overall/ a full bodied apron – minimum 2 pairs per year

● Bright yellow coloured caps - 2 nos. a year

● Hand gloves of orange colour – size depending on palm

size

● Gumboot shoes – 2 pairs per worker per annum

● Goggles for eye protection

● Mask for mouth covering

● Badge

33

None of the contractor’s worker was in uniform. All thecontractor’s staff including the supervisor were in plasticslippers. No badge, mouth mask, goggles etc. were availablewith the contractor’s staff.

Contractor’s Stores – As per the Contract Agreement, thecontractor shall at his own expenses provide shed andstorehouses at such locations and in such numbers asrequired for carrying out the works. At Coaching Depot, thecontractor kept the Stores at three locations. At all the threelocations, the building for housing contractor’s Stores hasbeen provided by Railways and contractor has not built anyshed etc. at his expenditure.

The upkeep of all the three Stores was found very poor andthe material was lying scattered here and there.

Work evaluation (score card) — As per specified terms andconditions of contract, the effectiveness of cleaning is beingevaluated on a scale of 10 depending upon grading ofvarious activities. The contractor is required to strictlyadhere to rating of 9 &10.

Penalty Clauses — The contractor should ensure that theoverall scores should be equal to or more than 90%. If therating is found to be less than 90%, then a penalty asspecified below will be recovered from the bills.

S.No. Overall rating Penalty, if any

1. 90-100% No penalty

2. 80-90% 10% of the accepted rate percoach will be recovered fromthe bills for no. of coaches inthat rake.

34

3. 70-80% 20% of the accepted rate percoach will be recovered fromthe bills for no. of coaches inthat rake.

4. Less than 70% No payment will be allowed forthe no. of coaches in that rake.

Apart from a detailed score card for individual trainsattended on a particular day, a comprehensive score cardindicating train nos., total coaches attended, grading,penalty etc. is being maintained.

From the summarized details of score cards of coachesattended at Coaching Depot for a particular month, it wasseen that majority of coaches had been awarded scoresbetween 70-80% or 80-90%,5.2% of the coaches had evenbeen awarded scores below 70% and about 12.8% coacheshad been awarded scores above 90%, which were therebymeeting the work evaluation criteria laid down.Thesefigures are indicative of the performance of contractualwork i.e. mechanized cleaning of coaches has not been ableto achieve targeted scores of 90-100%. Although it has beenclearly mentioned in the Contract Agreement that overallrating should be more than or equal to 90%. From thescrutiny of records, it was observed that although penaltyhad been regularly imposed on the contractor for the lapse& deficiency in execution of contractual work, there hashardly been any improvement in the performance by thecontractor.

Other Observations:

During the course of vigilance check, in addition to detailsmentioned above, following observations were made:

35

● As per contract conditions, one set each of jet machines,mini scrubber and dry and wet vacuum cleaner shouldbe deployed at each washing line. However, this is notbeing done by the contractor.

● It is a matter of record that contractor was not usingspecified material/ cleaning agents, but no deduction/penalty on this account was getting imposed on thecontractor simply because of the reason that no suchprovision (of penalty) has been incorporated in thisregard in the Contract Agreement.

● The machines available with contractor were in verypoor condition.

● As required vide one of the Clauses of contractagreement, the contractor was not maintainingInspection Register, Site Order Register and Log Book ofevents.

● The contractor had not provided any medical facility atsite. Even the First- Aid box was not available at site.

● As per the terms and condition of contract, contractorhad to give details of total load/consumption per daybut no such details had been provided by the contractor.

● No monthly progress was submitted by the Contractorto the CDO office. This was also required to be donein terms of contract agreement

To sum up, a no deficiencies have been observed inexecution of contract during the course of Vigilance check.Certain clauses of special terms and conditions of contractwere not being adhered to by the contractor in executionof work.

36

As discussed in preceding paras, a number of deficiencieshave been observed in execution of contract during thecourse of Vigilance check. The agency responsible forexecution of contract has practically executed manualcleaning work instead of mechanized cleaning as the agencyhas not deployed the machines as per terms and conditionsof the tender and some of the machines available in thestore were for show-piece purpose.

In view of serious irregularities found during execution ofthe contract the Zonal Railway was advised from RailwayBoard (Vigilance) to review the contract along with thestringent measures to be taken against the contractor. TheZonal Railway advised that the contract was terminated asthere was neither any response from the firm nor anyimprovement in its functioning. A decision had already beentaken to terminate the contract prematurely even beforevigilance intervention as the firm was not doing coachcleaning work properly.

The Zonal Railway has been advised to identify the officialsfor delayed intimation of sub-standard work and allowingthe work to continue in the field (at the Coaching Depot)for more than 3 years.

❈❈❈❈

37

DEPARTMENT-WISE BREAK-UP OF ACTIONADVISED BY CVC DURING THE PERIOD

JANUARY ’2009 TO DECEMBER ‘2009

Deptt. NGOs JS/SS JAG/SG SAG & TotalAbove

Major/ Misc. Major/ Misc. Major/ Misc. Major/ Misc. Major/ Misc.Minor Minor Minor Minor Minor

T & C 41 19 39 15 25 10 14 6 119 50

Accounts 56 12 28 16 10 7 10 5 104 40

Personnel 51 7 31 10 11 4 2 1 95 22

Civil Engg. 107 13 91 28 37 23 13 5 248 69

Stores 88 12 41 20 27 11 9 5 165 48

Mech. 26 4 7 2 9 5 4 0 46 11

Electrical 37 0 35 6 19 12 6 4 97 22

Medical 11 6 4 3 15 12 3 2 33 23

S&T 28 5 29 9 17 7 2 4 76 25

Security 12 0 5 3 5 0 0 0 22 3

Total 457 78 310 112 175 91 63 32 1005 313

38

ACTION INITIATED AS ADVISED BY CVC DURINGTHE YEAR 2009

Central Vigilance Commission is required to beconsulted for advice in regard to the type of action requiredto be initiated in cases involving Group ‘A’ Officers

GRADE-WISE BREAK UP OF ACTION ADVISED BYCVC DURING THE PERIOD JANUARY ’2009 TODECEMBER ‘2009

Type of action Major Minor Admn. TotalPenalty Penalty Action

Grade SAG &Above 17 46 3 2 95

JAG/SG 60 115 9 1 266

Sr. Scale/ 113 197 112 422Jr. Scale

NGOs 170 287 7 8 535

Total 360 645 313 1318

om

Rectangle

39

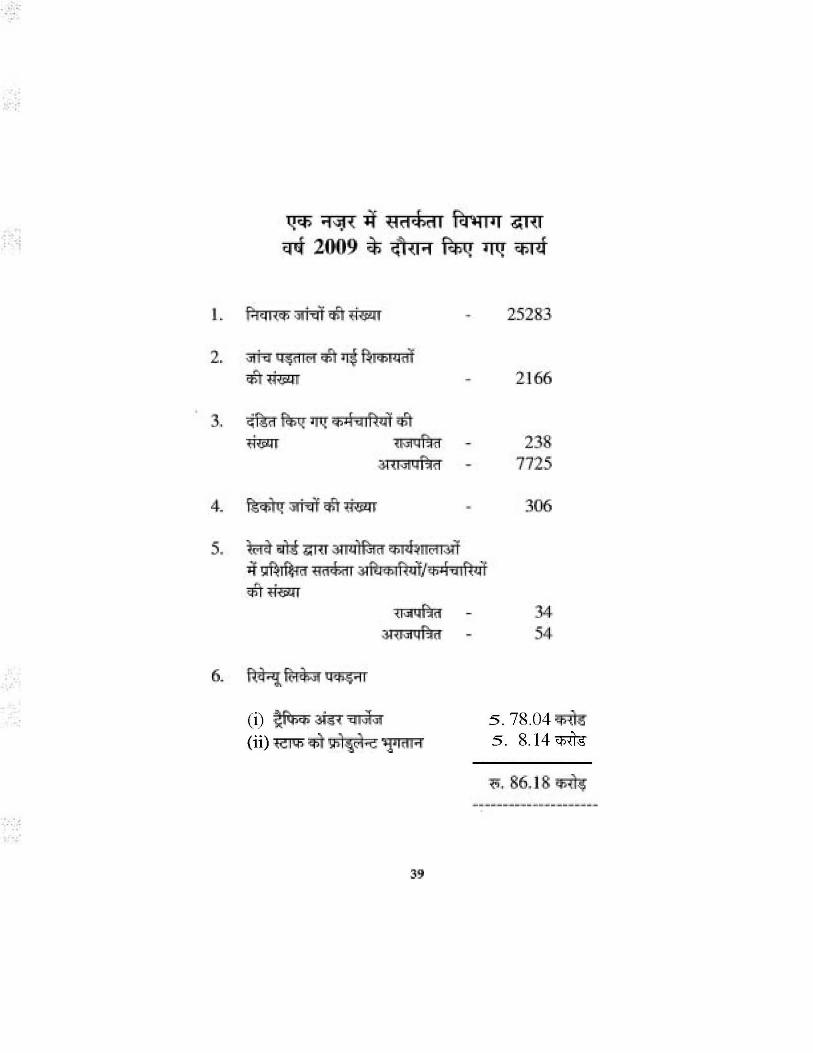

WORK DONE BY VIGILANCE ORGANIZATIONDURING THE YEAR 2009 AT A GLANCE

1. No. of preventive checksdone - 25283

2. No. of complaints investigated - 2166

3. No. of employees punishedGaz. - 238

Non-Gaz. - 7725

4. No. of decoy checksconducted - 306

5. No. of vigilance officers/staff trained in TrainingCourses conducted byRailway Board

Gaz. - 34Non-Gaz. - 54

6. Revenue Leakage Detected

(i) Traffic undercharges - Rs. 78.04 cr.(ii) Fraudulent payment to staff - Rs. 8.14 cr.

————————Total Rs. 86.18 cr.

————————-

“Surely, the law ofProvidence is such that thewealth earned through evil

means is scattered away.The wealth earned through

pious means flourishes;those who earn through

dishonest means aredestroyed.”

- Atharva Veda

Trade without HonestyHappiness without consciencePolitics without PrincipleKnowledge without CultureScience without HumanismIncome without EffortWorship without Sacrifice

HAVE NO MEANINGM.K. Gandhi

Printed by : C. Ravindran, Chief Manager (P&S) Northern Railway Printing Press, Punjabi Bagh, Delhi-110035