Quasi-Robust Multiagent Contracts

25

Quasi-Robust Multiagent Contracts Anil Arya The Ohio State University Joel Demski University of Florida Jonathan Glover Carnegie Mellon University Pierre Jinghong Liang Carnegie Mellon University July 2005 (First Draft: December 2002)

Transcript of Quasi-Robust Multiagent Contracts

Quasi-Robust Multiagent Contracts

Anil AryaThe Ohio State University

Joel DemskiUniversity of Florida

Jonathan GloverCarnegie Mellon University

Pierre Jinghong LiangCarnegie Mellon University

July 2005(First Draft: December 2002)

Abstract

A criticism of mechanism design theory is that the optimal mechanism designed for

one environment can produce drastically different actions, outcomes, and payoffs in a

second, even slightly different, environment. In this sense, the theoretically optimal

mechanisms usually studied are not "robust." In order to study robust mechanisms while

maintaining an optimal contracting approach, we study a multiagent model in which the

contract must be designed before the environment is as well understood as is usually

assumed. The particular model is of an auction setting. Our main result is that if the prior

about the correlation in the agents' environments is diffuse enough, the optimal Bayesian-

Nash auction is a simple dominant strategy auction (a modified second-price auction) that

completely ignores the correlation in the agents' environments.

Why are [theoretical] mechanisms … typically not used in practice …Arguably, the answer has something to do with their lack of robustness.That is, intricate mechanisms may perform poorly in the "imperfect" worldof reality--either because (i) there are flaws in the agents' reasoning; orbecause (ii) mistakes are made in the specification of the agents' preferences,knowledge, or situation (Moore, 1992).

1. Introduction

A criticism of mechanism design theory, eloquently expressed by John Moore

above, is that the optimal mechanism designed for one environment can produce drastically

different actions, outcomes, and payoffs in a second, even slightly different, environment.

The theoretically optimal mechanisms are in this sense not "robust" and seem to be more

complicated than those we observe in practice. It seems robustness is an essential

requirement for well-functioning real-world mechanisms.

In order to study robust mechanisms while maintaining an optimal contracting

approach, we study a multiagent model in which the contract must be designed before the

environment is as well understood as is usually assumed. The principal designs the contract

to maximize her expected payoff, taking expectations over the variety of possible

environments that could subsequently emerge. We assume the contract cannot later be fine-

tuned. It is either impossible or prohibitively costly to design a different contract for each

environment.

The particular setting we study is an auction model which, other than the early

design assumption, is a special case of the model of Cremer and McLean (1988). Of

course, the model applies also to multiagent procurement as in Laffont and Tirole (1993,

Chapter 7), since procurement can be viewed as the negative of an auction setting. (Change

the sign of the values and transfers.)

In Cremer-McLean, the auctioneer can extract the full surplus if the agents are risk

neutral and have beliefs that satisfy a spanning condition, but their optimal auction seems

particularly plagued by the robustness criticism as they themselves observe:

2

In "nearly all" auctions, the seller should be able to extract the full surplus,which implies that asymmetry of information between buyers and sellersshould be of no practical importance. Economic intuition and informalevidence (we know of no way to test such a proposition) suggest this resultis counterfactual ... Costly information gathering, not explicitly modeled inauction problems, may result in less profitable but vastly simpler auctionsbeing used in practice (Cremer and McLean, 1988, p. 1254).

Correlation is a key variable in Cremer-McLean. In particular, the transfers from the

agents go to negative and positive infinity as the correlation becomes arbitrarily small. This

is the feature of the environment we focus on. Our auction is designed at a time the

principal and the agents have only imperfect information about the correlation in the agents’

environments.

As alluded to earlier, to make the early auction design assumption meaningful, we

assume the auction will not later be fine-tuned to the correlation once the principal and the

agents observe what the actual correlation is. The auction is restricted to be a function of

simple bids (bidders report their values) and not reports on the correlation. In other words,

the initial design is of an auction instead of a menu of auctions.

As in Cremer-McLean, we assume the bidders are Bayesian-Nash as a behavioral

principle. One difference between our results and theirs is that the uncertainty about the

correlation makes the characterization unique in our model. The Cremer-McLean model

has enough degrees of freedom (because of the known correlation, the agents' risk

neutrality, and the agents' beliefs satisfying the spanning condition) that any optimal

Bayesian-Nash auction can be equivalently characterized as one that satisfies dominant

strategy incentive constraints.1

Our main result is that if the prior about the correlation in the bidders’ environments

is diffuse enough, the optimal Bayesian-Nash auction is a simple dominant strategy auction

1 Mookherjee and Reichelstein (1992) also study settings in which Bayesian-Nash incentive constraintscan be replaced by dominant strategy incentive constraints. Key assumptions are risk-neutrality,uncorrelated types, and the single crossing property. Mookherjee and Reichelstein's model can bethought of as studying settings in which second-best outcomes are to be implemented, while the first-best is implemented in Cremer-McLean.

3

that completely ignores the correlation in the bidders’ environments. This is in contrast to

the Cremer-McLean optimal auction, which although it can be characterized as a dominant

strategy auction, is highly fine-tuned to the correlation in the agents' environments. Our

optimal auction (with a diffuse enough prior) is a "modified second-price auction." The

transfers are bounded and even satisfy ex-post individual rationality.

If instead the prior about the correlation is concentrated enough, our optimal auction

is fine-tuned to the lowest possible correlation level. In this case, the optimal auction is

identical to an optimal auction in Cremer-McLean, with the lower bound on the correlation

in our model playing the role of the known correlation in Cremer-McLean. The difference

is that our optimal auction (for the concentrated prior case) cannot be characterized as one

that provides dominant strategy incentives.

We model the common prior on the correlation as a uniform distribution between

some (positive) lower bound and one. This simplifies the analysis and, in particular, allows

us to confine attention to truth-telling mechanisms. (The Revelation Principle does not

apply to our setting.) We show by means of a numerical example that it can sometimes be

optimal to motivate lying for other probability distributions, but the form of the optimal

auction remains the same as those we just described. Nevertheless, a limitation of our

analysis is the specificity of the model we employ and, in particular, the narrow way in

which we model robustness. In this sense, our paper studies quasi-robust mechanisms.

There is a developing literature in economics on robust implementation, with

Bergemann and Morris (2005a) as an important paper. They study a general

implementation model and derive a robust monotonicity condition that is necessary for

implementation in large type spaces. Bergemann and Morris (2005b) study ex post

implementation--they confine attention to Bayesian-Nash equilibria of games of incomplete

information that are also Nash equilibria if the agents' information were instead complete

(the agents' knew each other's types). These approaches are related to ours in their focus on

robustness but quite different in the type of models and results presented. Our paper

4

studies a particular problem--auction design--which enables us to characterize optimal

mechanisms. We comment on the literature on auctions later in the paper.

Existing approaches to robustness in the accounting literature include Reichelstein

(1997) and Dutta and Reichelstein (2002), who study the design of optimal performance

measures in investment settings. They use robustness as a way to choose between multiple

optimal performance measures. In contrast, we build robustness into the objective function

of the principal by assuming the contract has to be designed at an earlier point than is

typically assumed.2

The remainder of the paper is organized into four sections. Section 2 presents the

model and Section 3 the results. Section 4 discusses related research on auctions. Section

5 concludes the paper.

2. Model

A risk-neutral seller has one unit of a good that must be sold to one of two risk-

neutral bidders. The seller does not value the object, so her expected utility is just the

expected transfers received from the bidders. Bidder i, i = 1,2, values the object being sold

at Vi, and his expected utility is the probability of winning the auction times Vi less his

expected transfer to the seller. Bidder i's value for the object takes on one of two values VL

or VH, 0 ≤ VL < VH, and this value is privately known to bidder i.

It is common knowledge that Vi is equally likely to be VL or VH. (We relax this

assumption in Appendix B.) The parameter of interest is the probability p that Vj = Vk

given Vi = Vk. That is, p is the conditional probability the bidders' values match.3 p is

2 In recent work, Glover (2004) and Glover, Ijiri, Levine, and Liang (2005) explore contracting issuesrelated to the quality of information in single-agent models of moral hazard. Their formulations arerelated to ours in that they assume the contract designer knows less than is usually assumed at the timethe optimal contract is designed. They derive conditions under which informative signals are ignoredbecause of their poor quality. The optimal contract favors large probability events and events for whichthe agent's marginal productivity is large.

3 The correlation in the bidders' valuations is p2 - (1-p)2.

5

common knowledge among the bidders and the seller at the time the bidders agree to

participate in the auction, but the auction is designed at an earlier time.

Before p is known, the seller designs a single auction to handle the variety of

different possible correlations, knowing only that p is uniformly distribted on the interval

[p_,1], p_ > 1/2.4 The same auction is to be used for each correlation (pair of bidders that

might be faced). This can be thought of as a seller who will conduct many sales, each with a

different set of bidders, using the same auction mechanism. Designing an auction for each

situation (either by waiting until the situation arises or by designing a complex menu of

auctions) is prohibitively costly.

The auction mechanism consists of a rule that specifies the transfers the bidders

make to the seller and the probability each bidder is awarded the object. The rule can be

conditioned on the bidders' reports of their respective valuations. Denote bidder i's report

by V^ i, V^ i ∈ {VL,VH}. Given reports V^ i and V^ j, the transfer required from bidder i is

ti(V^ i,V^ j), and the probability bidder i wins the object is Wi(V^ i,V^ j). We make the trivial

observation the auction could be to procure rather than sell an object. Positive transfers

become negative ones and vice versa.

Although the generic auction has to be designed before the correlation in the bidders'

environments is known, by the time a specific application arises, the correlation is common

knowledge. Hence, bidders can condition their reports on their values as well as their

conditional beliefs, captured by the variable p. When bidder i observes Vk and his beliefs are

p, his reporting strategy is denoted by V^ i(Vk,p).

4 Stefan Reichelstein suggested an alternative view to one of us at a conference. Before the correlation isknown, the auctioneer designs a variety of auctions, with the constraint that each auction must workfor all possible environments. Once the correlation is known, the seller chooses which of theseauctions to use. If attention is confined to truth-telling mechanisms (which is not without loss ofgenerality in our setting), Stefan's formulation and ours produce the same result in this model. If lyingmechanisms are admitted here, we are back to being able to achieve the first-best by designing oneauction for each value of p. We think it would be interesting to explore this alternative (but similar)formulation of the question in a more general model in future research.

6

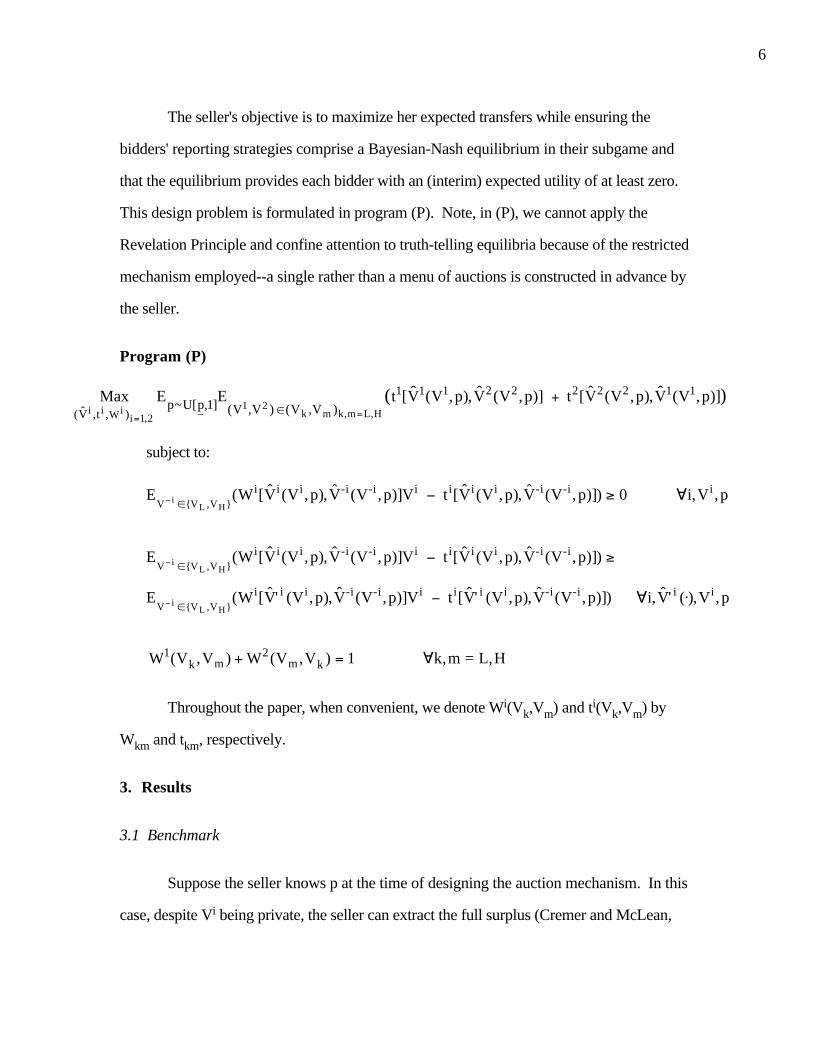

The seller's objective is to maximize her expected transfers while ensuring the

bidders' reporting strategies comprise a Bayesian-Nash equilibrium in their subgame and

that the equilibrium provides each bidder with an (interim) expected utility of at least zero.

This design problem is formulated in program (P). Note, in (P), we cannot apply the

Revelation Principle and confine attention to truth-telling equilibria because of the restricted

mechanism employed--a single rather than a menu of auctions is constructed in advance by

the seller.

Program (P)

Max(V̂i ,t i ,Wi )i=1,2

Ep~U[p,1]

E(V1,V2 ) ∈ (Vk ,Vm )k,m=L,H

(t1[V̂1(V1,p),V̂2(V2,p)] + t2[V̂2(V2,p),V̂1(V1,p)])

subject to:

EV− i

∈ {VL ,VH}(Wi[V̂i (Vi,p),V̂-i (V-i , p)]Vi − ti[V̂i (Vi,p),V̂-i (V-i , p)]) ≥ 0 ∀i,Vi,p

E

V− i ∈ {VL ,VH}

(Wi[V̂i (Vi,p),V̂-i (V-i , p)]Vi − ti[V̂i (Vi,p),V̂-i (V-i , p)]) ≥

EV− i

∈ {VL ,VH}(Wi[V̂' i (Vi,p),V̂-i (V-i , p)]Vi − ti[V̂' i (Vi,p),V̂-i (V-i , p)]) ∀i, V̂' i (⋅),Vi,p

W1(Vk,Vm ) + W2(Vm,Vk ) = 1 ∀k,m = L,H

Throughout the paper, when convenient, we denote Wi(Vk,Vm) and ti(Vk,Vm) by

Wkm and tkm, respectively.

3. Results

3.1 Benchmark

Suppose the seller knows p at the time of designing the auction mechanism. In this

case, despite Vi being private, the seller can extract the full surplus (Cremer and McLean,

7

1988). An auction that accomplishes this is presented in Proposition 1. Since the

proposition is a special case of Cremer and McLean, a formal proof is omitted.

Proposition 1. If the seller knows p at the time of designing the auction, an optimal

auction is:

(V^i,V^j) (VL,VL) (VL,VH) (VH,VL) (VH,VH)

Wi 1/2 0 1 1/2

ti VH2 -

p2(VH - VL)2(2p - 1)

p(1 - p)(VH - VL)2(2p - 1) -

p2(VH - VL)2(2p - 1)

p(1 - p)(VH - VL)2(2p - 1) +

VH2

Under Proposition 1's auction, the object is awarded to the highest bidder with ties

being resolved by giving each bidder an equal chance of winning.5 The transfers have been

characterized so that truthful bidding is not only a Bayesian-Nash equilibrium but also a

dominant strategy equilibrium. Moreover, under truthful bidding, both the VL-type and the

VH-type bidders earn zero rents. (When the seller knows p, confining attention to truth-

telling equilibrium is without loss of generality since the Revelation Principle applies.)

Proposition 1's auction has the feature that each bidder has to make a transfer even

when he is not awarded the object. Further, even when a bidder is awarded the object, his

transfer can exceed his value. That is, the transfers do not satisfy ex post individual

rationality.

Finally, as the correlation in the bidders' environments approaches zero, the transfers

for a bidder become arbitrarily large when the other bidder reports a high value and

arbitrarily small when the other bidder reports a low value. These observations are

summarized in Corollary 1.

5 Other than this randomization to deal with ties, we limit attention to pure strategy equilibria.

8

Corollary 1. If p is known at the time of auction design:

(i) The optimal Bayesian-Nash auction can be characterized so as to also satisfy

dominant strategy incentive constraints.

(ii) The bidders earn no rents under the truth-telling equilibrium.

(iii) The transfers do not satisfy ex-post individual rationality.

(iv) As p → 1/2, tkL → negative infinity and tkH → positive infinity.

3.2 Quasi-Robust Auctions

In this subsection, we characterize the optimal Bayesian-Nash auction under our

original assumption that only p_ is known at the time the auction is designed. The

solution to program (P) is presented in Proposition 2. The proof is provided in

Appendix A.

Proposition 2. If at the time of designing the auction, the seller does not know p but

knows instead p is uniformly distributed on [p_,1], the optimal auction is:

(V^i,V^j) (VL,VL) (VL,VH) (VH,VL) (VH,VH)

Wi 1/2 0 1 1/2

If 2/3 < p_ ≤ 1 (BN Auction)

ti VH2

- p_

2(VH - VL)2(2p_ - 1)

p_(1 - p_)(VH - VL)2(2p_ - 1)

VHVH2

9

If 1/2 < p_ ≤ 2/3 (DS Auction)

ti VL2

0 VL2 +

VH2

VH2

Under the above auctions, truth-telling by the bidders is an equilibrium in their

subgame, i.e., V^ i(Vk,p) = Vk for all p. As we show in Subsection 3.3, uniformly distributed

seller beliefs at the time of auction design are important in ensuring a truth-inducing auction

is optimal.

The intuition behind the construction of the optimal auction is as follows. The linear

structure of the model (including the beliefs about p) implies the solution is one of two

"extreme" corner points. The points are extreme in the sense that rents for one bidder type

are reduced to 0. Determining optimality requires comparing the two corner points or,

equivalently, ranking the expected rents under the two auctions.

Consider the auction that eliminates rents for the VL-type bidder. That is, the

individual rationality constraints bind for the VL bidder no matter what p is realized. For

this to be true, the auction must set tLL = VL/2 and tLH = 0.

The pressing incentive compatibility (truth-telling) constraints are for the VH-type

bidder. Solving the two incentive compatibility constraints for the VH-type bidder

(corresponding to p = p_ and p = 1) as equalities yields tHL = VL/2 + VH/2 and tHH = VH/2.

(The constraints for all other p are dominated by these two values of p.) By reporting VH, a

bidder increases the probability of winning but the transfers increase as well. In fact,

transfers increase at a rate that provide the bidder with dominant strategy incentives to report

truthfully. This is the second auction presented in Proposition 2, labeled as the DS auction.

It is not only a dominant strategy auction but also satisfies ex post individual rationality--the

bidders do not have incentives to walk away without paying, since they are never asked to

pay more than the value of what they receive.

10

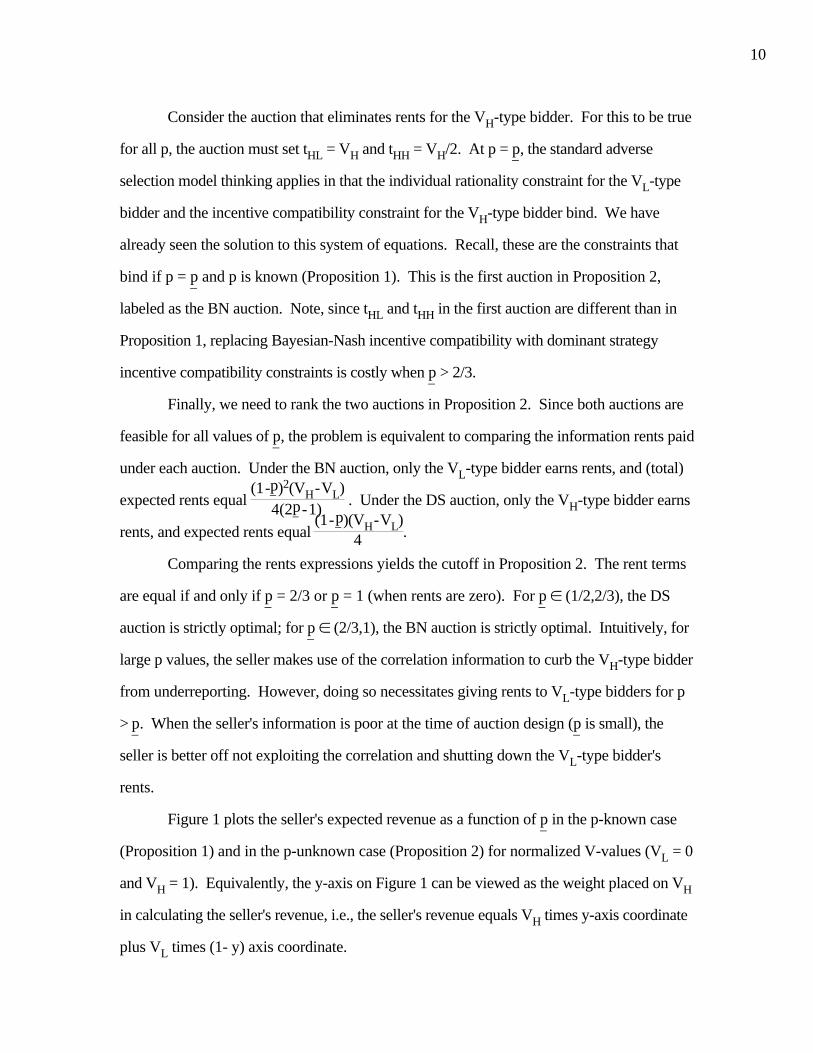

Consider the auction that eliminates rents for the VH-type bidder. For this to be true

for all p, the auction must set tHL = VH and tHH = VH/2. At p = p_, the standard adverse

selection model thinking applies in that the individual rationality constraint for the VL-type

bidder and the incentive compatibility constraint for the VH-type bidder bind. We have

already seen the solution to this system of equations. Recall, these are the constraints that

bind if p = p_ and p is known (Proposition 1). This is the first auction in Proposition 2,

labeled as the BN auction. Note, since tHL and tHH in the first auction are different than in

Proposition 1, replacing Bayesian-Nash incentive compatibility with dominant strategy

incentive compatibility constraints is costly when p_ > 2/3.

Finally, we need to rank the two auctions in Proposition 2. Since both auctions are

feasible for all values of p_, the problem is equivalent to comparing the information rents paid

under each auction. Under the BN auction, only the VL-type bidder earns rents, and (total)

expected rents equal (1

-p_ )2(VH

- VL)

4(2p_ -

1)

. Under the DS auction, only the VH-type bidder earns

rents, and expected rents equal (1

-

p_ )(VH -

VL)

4 .

Comparing the rents expressions yields the cutoff in Proposition 2. The rent terms

are equal if and only if p_ = 2/3 or p_ = 1 (when rents are zero). For p_ ∈ (1/2,2/3), the DS

auction is strictly optimal; for p_ ∈ (2/3,1), the BN auction is strictly optimal. Intuitively, for

large p values, the seller makes use of the correlation information to curb the VH-type bidder

from underreporting. However, doing so necessitates giving rents to VL-type bidders for p

> p_. When the seller's information is poor at the time of auction design (p_ is small), the

seller is better off not exploiting the correlation and shutting down the VL-type bidder's

rents.

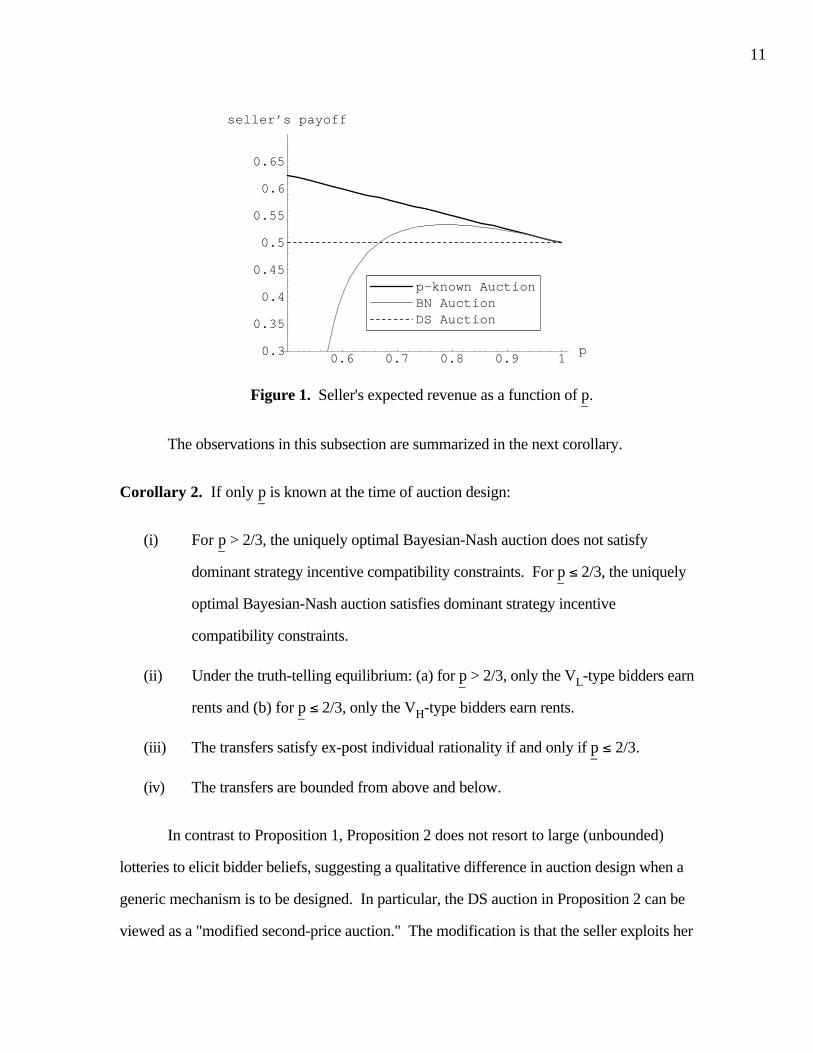

Figure 1 plots the seller's expected revenue as a function of p_ in the p-known case

(Proposition 1) and in the p-unknown case (Proposition 2) for normalized V-values (VL = 0

and VH = 1). Equivalently, the y-axis on Figure 1 can be viewed as the weight placed on VH

in calculating the seller's revenue, i.e., the seller's revenue equals VH times y-axis coordinate

plus VL times (1- y) axis coordinate.

11

0.6 0.7 0.8 0.9 1

p0.3

0.35

0.4

0.45

0.5

0.55

0.6

0.65

seller’s payoff

DS AuctionBN Auctionp-known Auction

Figure 1. Seller's expected revenue as a function of p_.

The observations in this subsection are summarized in the next corollary.

Corollary 2. If only p_ is known at the time of auction design:

(i) For p_ > 2/3, the uniquely optimal Bayesian-Nash auction does not satisfy

dominant strategy incentive compatibility constraints. For p_ ≤ 2/3, the uniquely

optimal Bayesian-Nash auction satisfies dominant strategy incentive

compatibility constraints.

(ii) Under the truth-telling equilibrium: (a) for p_ > 2/3, only the VL-type bidders earn

rents and (b) for p_ ≤ 2/3, only the VH-type bidders earn rents.

(iii) The transfers satisfy ex-post individual rationality if and only if p_ ≤ 2/3.

(iv) The transfers are bounded from above and below.

In contrast to Proposition 1, Proposition 2 does not resort to large (unbounded)

lotteries to elicit bidder beliefs, suggesting a qualitative difference in auction design when a

generic mechanism is to be designed. In particular, the DS auction in Proposition 2 can be

viewed as a "modified second-price auction." The modification is that the seller exploits her

12

knowledge of VL and VH. For example, when bidder i reports VH and bidder j reports VL,

bidder i is awarded the object and pays VL/2 for the first 1/2 probability of winning. This is

the second-price aspect: the price of VL/2 comes from bidder j's report. For the second 1/2

probability of winning the object, bidder i pays VH/2. This is the modification relative to a

second-price auction, which exploits the seller's knowledge of the size of VH.

While an essential ingredient of the auctions identified in Cremer and McLean

(1988) is simultaneous reporting, our modified second-price auction can be reformulated as

a sequential auction. Bidder 1 is asked if he is willing to pay VL/2 for 1/2 a chance at

winning the auction. Bidder 2 is asked the same question. Both will say yes (always).

Bidder 1 is then asked if he is willing to pay VH/2 for Bidder 2's 1/2 chance of winning.

Finally, Bidder 2 is asked if he is willing to pay VH/2 for Bidder 1's (first) 1/2 chance of

winning. Truthful bidding is a sequentially dominant strategy. If we subtract any small ε >

0 from the payments, truthful bidding becomes a sequentially strict dominant strategy. This

auction is essentially an English auction with fixed bidding increments. If the seller did not

know the values the bidders' valuations can take on, it seems likely that an auction even

closer to an English auction would emerge as the optimal one.

3.3 Non-uniform distributions can make lying optimal

Under non-uniform seller beliefs, it is no longer the case that the optimal auction

necessarily induces truthful bidding. To see this, consider the following example.

EXAMPLE 1.

VL = 10, VH = 25, p_ = 0.55, and seller beliefs are that p = 0.55 with probability 0.05,

p = 0.85 with probability 0.05, p = 0.86 with probability 0.85, and p = 1 with probability

0.05. (p is now discrete.)

13

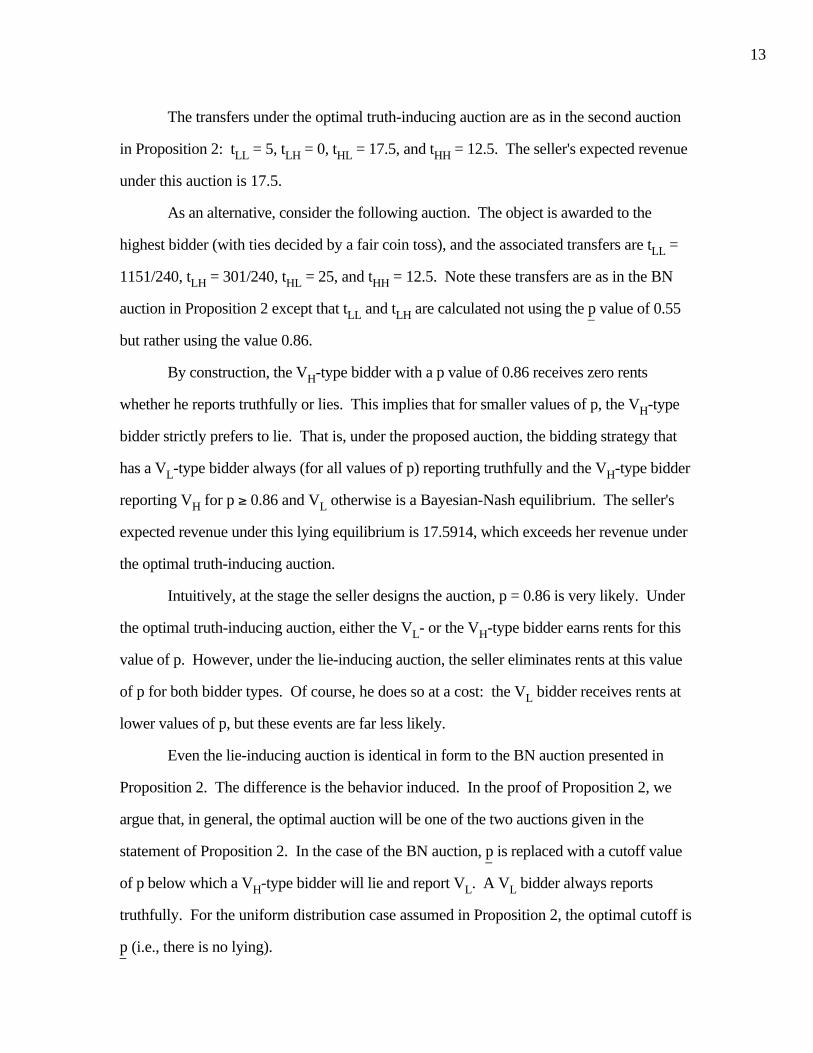

The transfers under the optimal truth-inducing auction are as in the second auction

in Proposition 2: tLL = 5, tLH = 0, tHL = 17.5, and tHH = 12.5. The seller's expected revenue

under this auction is 17.5.

As an alternative, consider the following auction. The object is awarded to the

highest bidder (with ties decided by a fair coin toss), and the associated transfers are tLL =

1151/240, tLH = 301/240, tHL = 25, and tHH = 12.5. Note these transfers are as in the BN

auction in Proposition 2 except that tLL and tLH are calculated not using the p_ value of 0.55

but rather using the value 0.86.

By construction, the VH-type bidder with a p value of 0.86 receives zero rents

whether he reports truthfully or lies. This implies that for smaller values of p, the VH-type

bidder strictly prefers to lie. That is, under the proposed auction, the bidding strategy that

has a VL-type bidder always (for all values of p) reporting truthfully and the VH-type bidder

reporting VH for p ≥ 0.86 and VL otherwise is a Bayesian-Nash equilibrium. The seller's

expected revenue under this lying equilibrium is 17.5914, which exceeds her revenue under

the optimal truth-inducing auction.

Intuitively, at the stage the seller designs the auction, p = 0.86 is very likely. Under

the optimal truth-inducing auction, either the VL- or the VH-type bidder earns rents for this

value of p. However, under the lie-inducing auction, the seller eliminates rents at this value

of p for both bidder types. Of course, he does so at a cost: the VL bidder receives rents at

lower values of p, but these events are far less likely.

Even the lie-inducing auction is identical in form to the BN auction presented in

Proposition 2. The difference is the behavior induced. In the proof of Proposition 2, we

argue that, in general, the optimal auction will be one of the two auctions given in the

statement of Proposition 2. In the case of the BN auction, p_ is replaced with a cutoff value

of p below which a VH-type bidder will lie and report VL. A VL bidder always reports

truthfully. For the uniform distribution case assumed in Proposition 2, the optimal cutoff is

p_ (i.e., there is no lying).

14

4. Related Research on Auctions

The Cremer-McLean result on extracting the full surplus relies on a link between a

bidder's value and his beliefs about the other bidders. In large type spaces, extracting the

full surplus is no longer possible. For example, in Parreiras (2002), type includes not just

the realization of a signal but also the precision of the system that generates the signal.

Independence along the precision dimension of the type forces the seller to leave rents for

the bidders. McLean and Postlewaite (2001) show that bidders with identical beliefs but

different valuations will also earn rents.

Neeman (2003) takes a simple auction (the English auction) as given and examines

its effectiveness (expected price as a percentage of the highest valuation). The paper studies

how the effectiveness of the auction changes with assumptions about the seller's Bayesian

sophistication. Lopomo (1998) also studies the English auction and shows it is optimal

among "simple sequential auctions." In a recent paper, Chung and Ely (2004) study the

foundations for dominant strategy auctions. They emphasize the role of a maxmin objective

function (as in Gilboa and Schmeidler (1989)) in making dominant strategy auctions

optimal.

5. Concluding Remarks

We conclude with some limitations of our analysis. First, we required only that the

desired behavior be an equilibrium, not necessarily the unique equilibrium. When the

seller's information is fairly precise, there is a nontrivial multiple equilibria problem in our

model. The bidders are both better off under the equilibrium that has them always bidding

VL than under the truth-telling equilibrium. When the seller's information is fairly

imprecise, the "modified second-price auction" can easily be modified to produce a unique

equilibrium in strict dominant strategies.

15

Second, we employed a linear programming formulation (including the seller's

beliefs) throughout most of our analysis. Although this formulation made the problem

particularly tractable, it is also limits the generality of our analysis.

Third, although our "modified second-price auction" is robust to different levels of

correlation, this is a narrow focus of robustness. Our auctions are probably better described

as quasi-robust. Nevertheless, we think the broad problem of robustness is an important

problem which has the potential to provide foundational insights as well as to help us better

understand observed institutions. While our model is one of an auction setting, we suspect

similar forces and results (e.g., the optimality of dominant strategy mechanisms, or at least

simpler mechanisms) will show up in other settings.6

6 Demski and Dye's (1999) result that it is always optimal to non-linearize a linear contract in a LEN-style moral hazard setting begs a parallel robustness issue. (LEN stands for linear contracts,exponential utility, and normal and independent noise terms.)

16

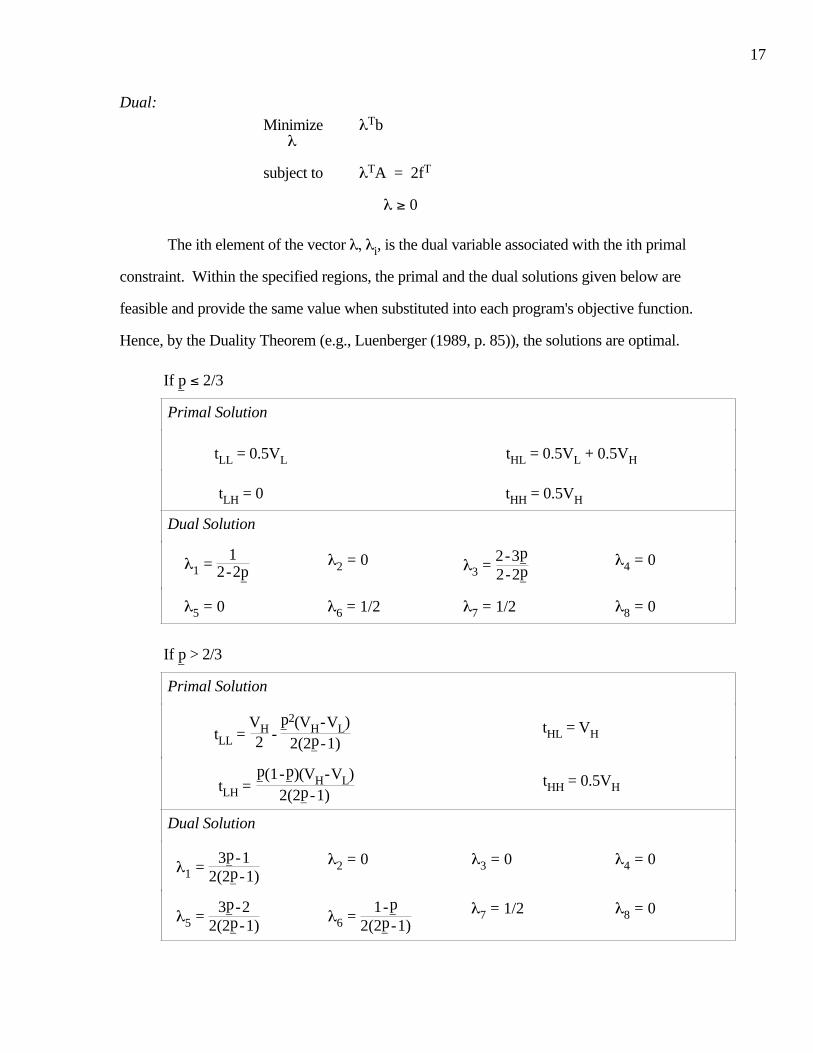

Appendix A

PROOF OF PROPOSITION 2. We first characterize the optimal truth-inducing auction. We

then argue there is no mechanism with a lying equilibrium under which the seller's expected

revenues are higher.

To determine the optimal truth-induction auction, we reformulate (P) in two ways.

First, we replace V^ i(Vk,p) by Vk, i.e., we induce truthful bidding as a Bayesian-Nash

equilibrium. This yields the familiar individual rationality (IR-k) and incentive compatibility

(IC-k) constraints for the k-type bidder. Second, we delete redundant constraints using the

fact that satisfying (IR-k) and (IC-k) constraints for p = p_ and p = 1 ensure the constraints

for other p also hold. The resulting primal and dual are given below.

Primal:

Maximize 2fTt t

subject to At ≤ b

where, in the objective function t, t = (tLL, tLH, tHL, tHH), is the vector of payments and f, f =

(1/4)(1 + p_, 1 - p_, 1 - p_, 1 + p_), is the probability of making each payment.

The constraints make use of matrix A and vector b to list the constraints in the

following order: (IR-L) and (IC-L) for p = p_, (IR-L) and (IC-L) for p = 1, (IR-H) and (IC-

H) for p = p_, and (IR-H) and (IC-H) for p = 1.

A =

p 1 − p 0 0

p 1 − p −p −(1 − p)

1 0 0 0

1 0 −1 0

0 0 1 − p p−(1 − p) −p 1 − p p

0 0 0 1

0 −1 0 1

, and

b = (1/2) (p_VL, -VL, VL, -VL, (2 - p_)VH, VH, VH, VH).

17

Dual:

Minimize λTb λ

subject to λTA = 2fT

λ ≥ 0

The ith element of the vector λ, λi, is the dual variable associated with the ith primal

constraint. Within the specified regions, the primal and the dual solutions given below are

feasible and provide the same value when substituted into each program's objective function.

Hence, by the Duality Theorem (e.g., Luenberger (1989, p. 85)), the solutions are optimal.

If p_ ≤ 2/3

Primal Solution

tLL = 0.5VL tHL = 0.5VL + 0.5VH

tLH = 0 tHH = 0.5VH

Dual Solution

λ1 = 1

2 - 2p_ λ2 = 0 λ3 =

2 - 3p_2 - 2p_

λ4 = 0

λ5 = 0 λ6 = 1/2 λ7 = 1/2 λ8 = 0

If p_ > 2/3

Primal Solution

tLL = VH2 -

p_ 2(VH - VL)2(2p_ - 1)

tHL = VH

tLH = p_ (1 - p_ )(VH - VL)

2(2p_ - 1) tHH = 0.5VH

Dual Solution

λ1 = 3p_ - 1

2(2p_ - 1) λ2 = 0 λ3 = 0 λ4 = 0

λ5 = 3p_ - 2

2(2p_ - 1) λ6 =

1 - p_2(2p_ - 1)

λ7 = 1/2 λ8 = 0

18

We still need to verify there is no mechanism that induces a lying equilibrium under

which the seller receives higher expected revenues. The lying equilibrium of concern takes

the following form. The VL-type bidder reports truthfully for all p ≥ p_. The VH-type bidder

reports VL for p ∈ [p_,p'] and reports truthfully for p ∈ (p',1]. The optimal mechanism that

induces such behavior must make the VH-type bidder indifferent between reporting

truthfully and underreporting when p = p'. This mechanism is simply the first auction in

Proposition 2, with p_ replaced by p' in the transfers.

The (total) information rents under the above lying mechanism can be simplified as:

R' = [1 + 3p'3 - 2p_ + p'(4p_ - 1) - p'2(4p_ + 1)][VH - VL]

4(2p' - 1)(1 - p_ ).

As also mentioned in the text, the information rents under the two feasible truth-

telling auctions in Proposition 2, denoted R1 and R2, are:

R1 = (1

-p_ )2(VH

- VL)

4(2p_ -

1)

and R2 = (1

-

p_ )(VH -

VL)

4 .

For lying to be uniquely optimal it must be the case that R' is less than both R1 and

R2. However, the only p' value, p' ≥ p_, that satisfies R' ≤ R1 and R' ≤ R2 sets p' = p_. That is,

a mechanism that induces lying is never optimal in our setting. The auction in Proposition 2

is revenue maximizing. (Of course, truth-telling is not uniquely optimal: reverse labeling is

not literally the truth but works just fine.)

19

Appendix B

In the text, we assumed Vi is equally likely to be VL or VH, and this (marginal)

distribution is common knowledge. In this appendix, we relax this assumption and show

that auctions similar to those derived in Proposition 2 continue to be optimal.

Let pkm, k,m = L,H, denote the (joint) probability that V1 = Vk and V2 = Vm. The

distribution is symmetric: pLH = pHL and, hence, each is equal to (1/2)(1 - pLL - pHH).

Second, pkk is bounded by p_kk and 1/2, with p_kk > 1/4. At the time the auction is designed,

the priors on pLL and pHH are that each is independently and uniformly distributed on the

interval [p_kk,1/2], with p_kk > 1/4.

Later, when each bidder decides whether or not to accept the auction for a specific

application, bidder i knows Vi = Vk and his belief that Vj = Vk is qk. Our earlier

assumption on pLL and pHH implies that, at the time the auction is designed, the seller knows

qk has a lower bound of q_k and an upper bound of 1, where q_k = 2p_ kk

1 + p_ kk - p_ mm > 1/2.

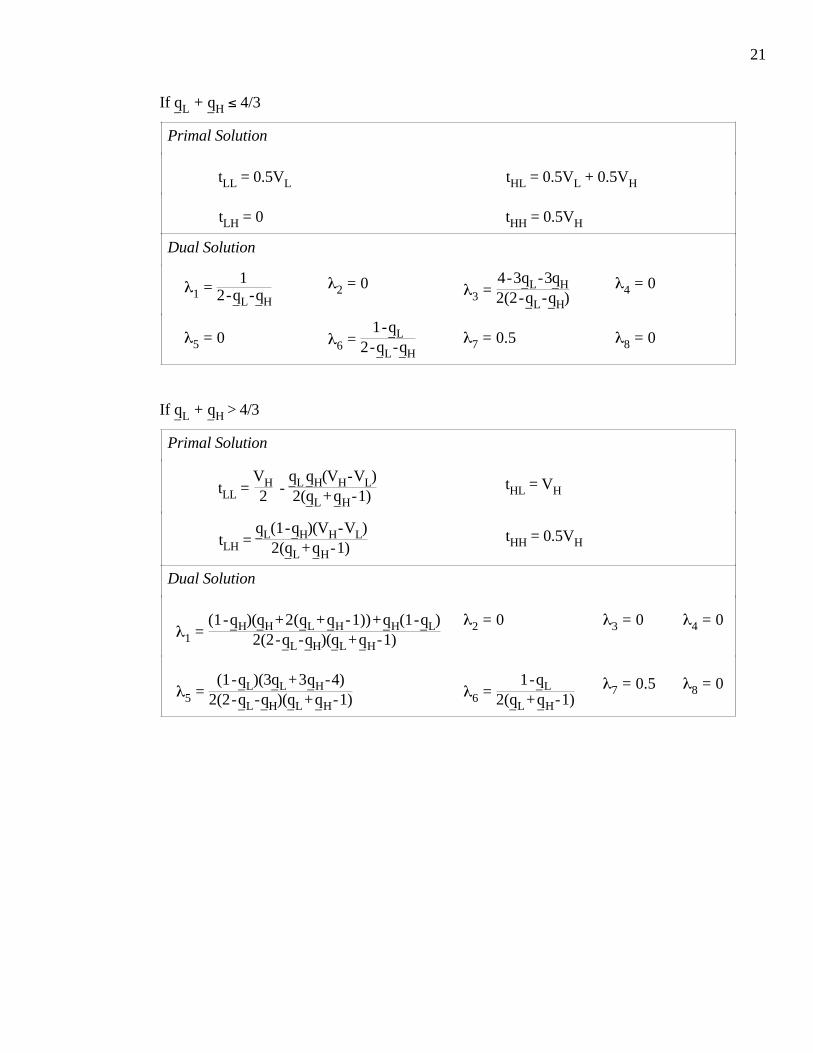

Proposition 3. The optimal auction is:

(V̂i, V̂j) (VL,VL) (VL,VH) (VH,VL) (VH,VH)

Wi 1/2 0 1 1/2

If 4/3 < q_L + q_H ≤ 2 (BN Auction)

tiVH2

- q_L

q_H(VH - VL)

2(q_L + q_H - 1)

q_L(1 - q_H)(VH - VL)

2(q_L + q_H - 1)VH

VH2

If 1 < q_L + q_H ≤ 4/3 (DS Auction)

tiVL2

0VL2

+ VH2

VH2

20

Under the above auctions, truth-telling by the bidders is an equilibrium in their

subgame, but truth-telling was again not assumed. Plugging q_L = q_H = p_ reduces the

auctions (and the cutoff) to those presented in Proposition 2. Thus, not surprisingly,

Corollary 2 (and the intuition from before) continues to apply in this slightly more general

setup.

PROOF OF PROPOSITION 3. The proof follows the same steps as the proof of Proposition

2, with the changes being:

f = (1/4)(1 + p_LL, 1 - p_LL - p_HH, 1 - p_LL - p_HH, 1 + p_HH),

b = (1/2) (q_LVL, -VL, VL, -VL, (2 - q_H)VH, VH, VH, VH) and

A =

qL

1 − qL

0 0

qL

1 − qL

−qL

−(1 − qL

)

1 0 0 0

1 0 −1 0

0 0 1 − qH

qH

−(1 − qH

) −qH

1 − qH

qH

0 0 0 1

0 −1 0 1

.

In this case, the primal and dual solutions are:

21

If q_L + q_H ≤ 4/3

Primal Solution

tLL = 0.5VL tHL = 0.5VL + 0.5VH

tLH = 0 tHH = 0.5VH

Dual Solution

λ1 = 1

2 - q_L - q_H

λ2 = 0 λ3 = 4 - 3q_L - 3q_H2(2 - q_L - q_H)

λ4 = 0

λ5 = 0 λ6 = 1 - q_L

2 - q_L - q_H λ7 = 0.5 λ8 = 0

If q_L + q_H > 4/3

Primal Solution

tLL = VH2 -

q_L q_H(VH - VL)

2(q_L + q_H - 1) tHL = VH

tLH = q_L(1 - q_H)(VH - VL)

2(q_L + q_H - 1) tHH = 0.5VH

Dual Solution

λ1 = (1 - q_H)(q_H + 2(q_L + q_H - 1)) + q_H(1 - q_L)

2(2 - q_L - q_H)(q_L + q_H - 1) λ2 = 0 λ3 = 0 λ4 = 0

λ5 = (1 - q_L)(3q_L + 3q_H - 4)

2(2 - q_L - q_H)(q_L + q_H - 1) λ6 = 1 - q_L

2(q_L + q_H - 1) λ7 = 0.5 λ8 = 0

22

References

BERGEMANN, D., AND S. MORRIS (2005a): "Robust Mechanism Design," Econometrica,

forthcoming.

BERGEMANN, D., AND S. MORRIS (2005b): "Ex post Implementation," Working Paper,

Yale University.

CHUNG, K., AND J. ELY (2004): "Foundations of Dominant Strategy Mechanisms,"

Working Paper, Northwestern University.

CREMER, J., AND R. P. MCLEAN (1988): "Full Extraction of the Surplus in Bayesian and

Dominant Strategy Auctions," Econometrica, 56, 1247-1257.

DEMSKI, J., AND R. DYE (1999): "Risk, Return, and Moral Hazard," Journal of Accounting

Research 37, 27-55.

DUTTA, S., AND S. REICHELSTEIN (2002): "Controlling Investment Decisions:

Depreciation and Capital Charges," Review of Accounting Studies 7, 253-281.

GILBOA, I., AND D. SCHMEIDLER (1989): "Maxmin Expected Utility with a Non-unique

Prior," Journal of Mathematical Economics, 18, 141-153.

GLOVER, J. (2004): "A Discussion of ‘A Model of Auditing Under Bright-Line

Accounting Standards’," Journal of Accounting, Auditing and Finance, 19, 561-564.

GLOVER, J., Y. IJIRI, C. LEVINE AND P. LIANG (2005): "Verifiability, Manipulability, and

Information Asymmetries about Verifiability and Manipulability," Working Paper,

Carnegie Mellon University.

LAFFONT, J-J, AND J. TIROLE. (1993): A Theory of Incentives in Procurement and

Regulation, Cambridge, The MIT Press.

LOPOMO, G. (1998): "The English Auction is Optimal among Simple Sequential Auctions,"

Journal of Economic Theory, 82.

LUENBERGER, D. (1989): Linear and Nonlinear Programming, Reading, Addison Wesley.

23

MCLEAN, R.P., AND A. POSTLEWAITE (2001): "Efficient Auction Mechanisms with

Interdependent Valuations and Multidimensional Signals," Working Paper, Rutgers

University.

MOOKHERJEE, D., AND S. REICHELSTEIN (1992): "Dominant Strategy Implementation of

Bayesian Incentive Compatible Allocation Rules," Journal of Economic Theory, 56,

378-399.

MOORE, J. (1992): "Implementation in environments with complete information," in

Advances in Economic Theory (Sixth World Congress) Vol. 1, edited by J.J. Laffont,

182-282.

NEEMAN, Z. (2003): "The Effectiveness of English Auctions," Games and Economic

Behavior, 43. 214-238.

PARREIRAS, S.O. (2002): "Correlated Information, Mechanism Design and Informational

Rents," Working Paper, University of North Carolina.

REICHELSTEIN, S. (1997): "Investment Decisions and Managerial Performance Evaluation,"

Review of Accounting Studies, 2, 157-180.