The Interlinking of Rivers Project in India and International Water Law: An Overview

Upload

independentCategory

view

1download

0

THE QUICK SERVICE RESTAURANT

INDUSTRY OF INDIA

COMPILED BY-

NACHIKET BHALE 10

SHRUTHY NAIR 33

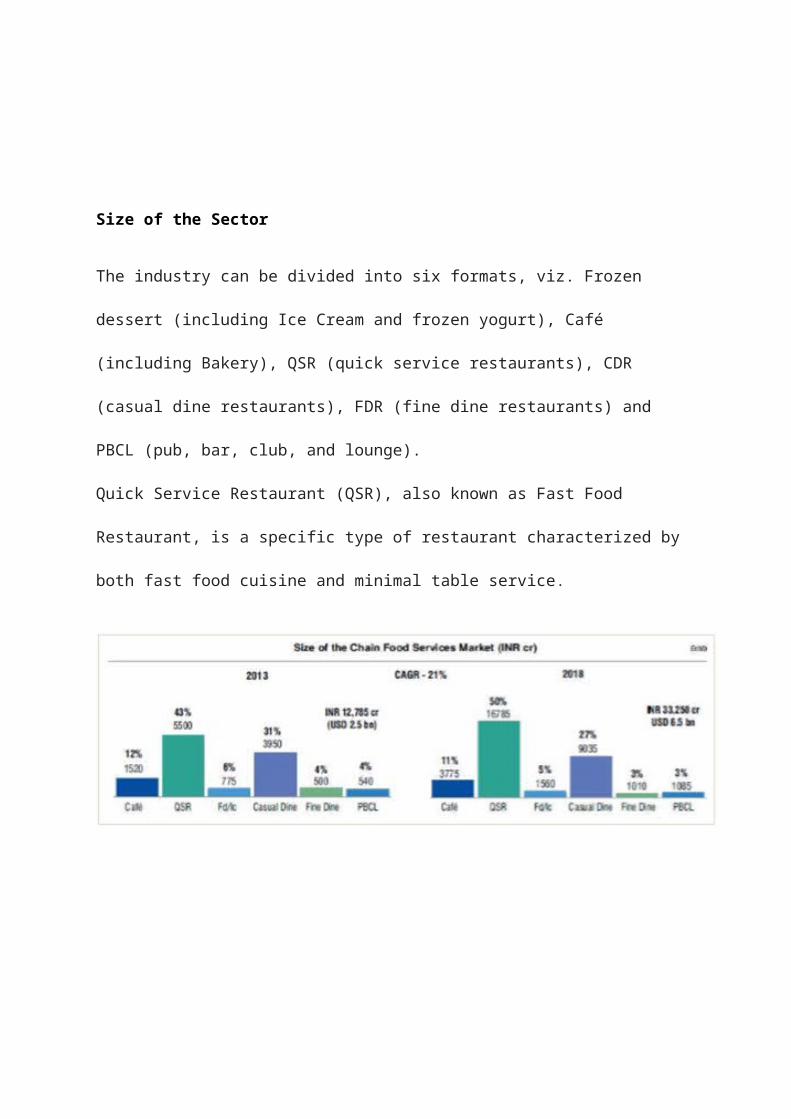

Size of the Sector

The industry can be divided into six formats, viz. Frozen

dessert (including Ice Cream and frozen yogurt), Café

(including Bakery), QSR (quick service restaurants), CDR

(casual dine restaurants), FDR (fine dine restaurants) and

PBCL (pub, bar, club, and lounge).

Quick Service Restaurant (QSR), also known as Fast Food

Restaurant, is a specific type of restaurant characterized by

both fast food cuisine and minimal table service.

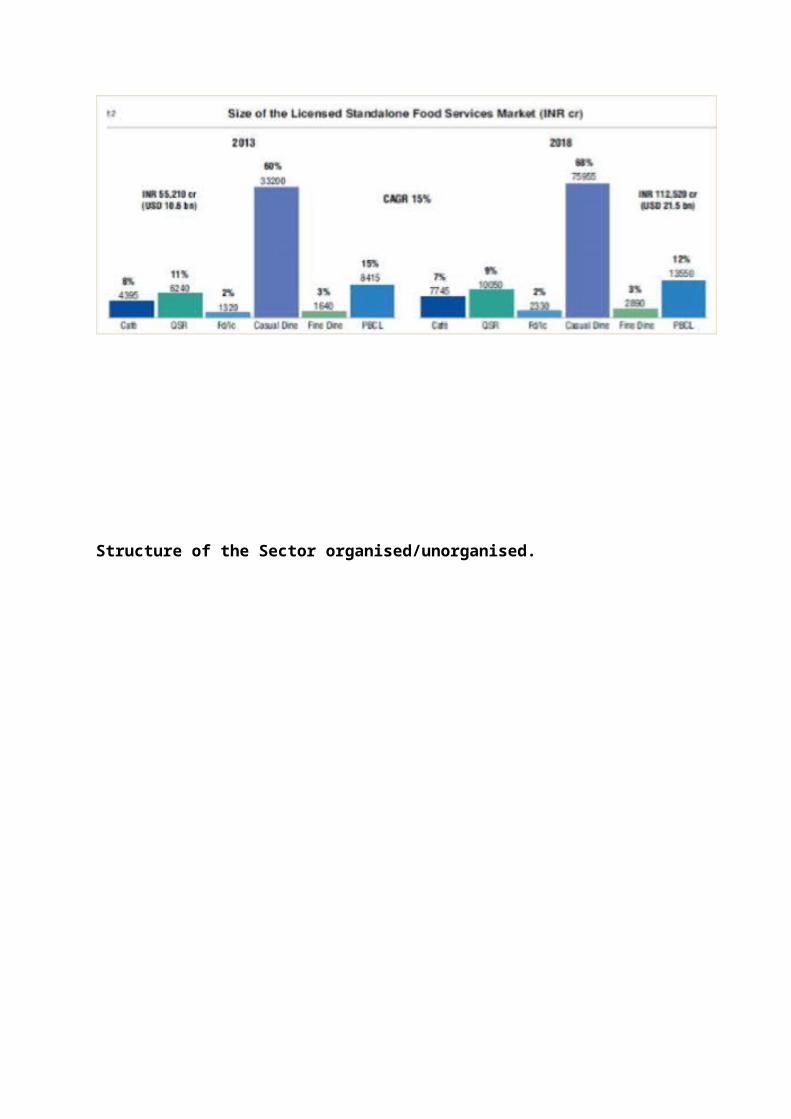

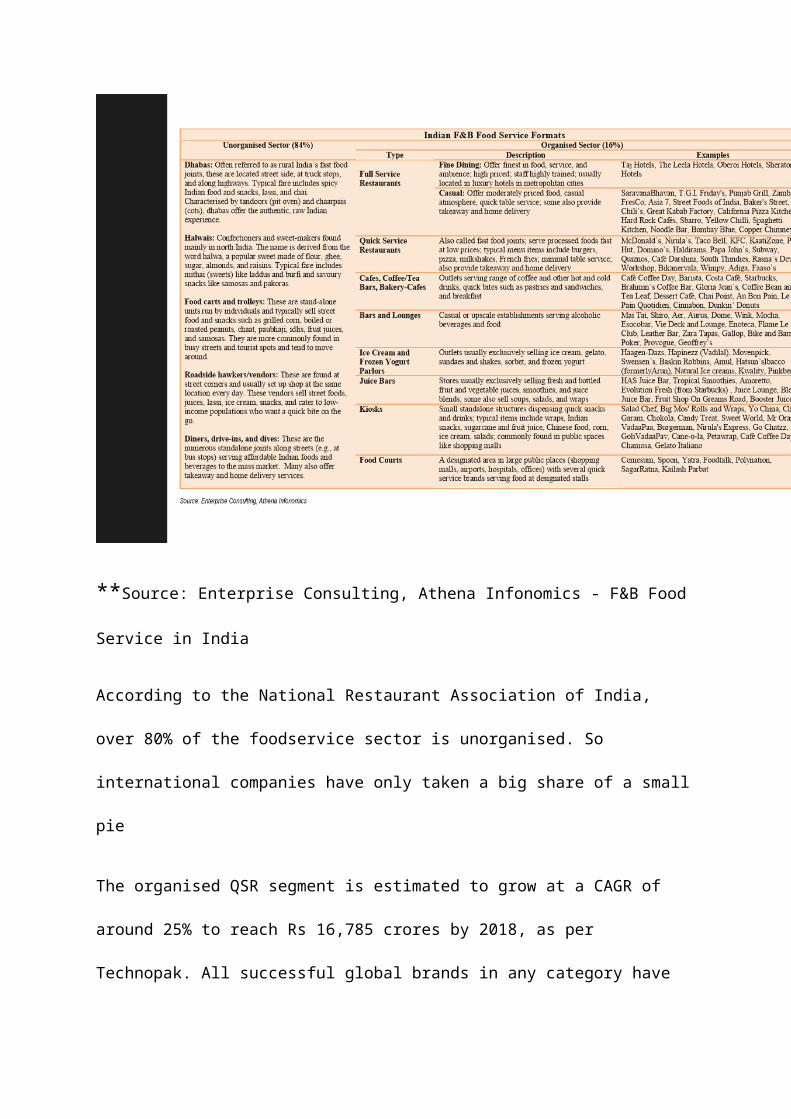

Structure of the Sector organised/unorganised.

**Source: Enterprise Consulting, Athena Infonomics - F&B Food

Service in India

According to the National Restaurant Association of India,

over 80% of the foodservice sector is unorganised. So

international companies have only taken a big share of a small

pie

The organised QSR segment is estimated to grow at a CAGR of

around 25% to reach Rs 16,785 crores by 2018, as per

Technopak. All successful global brands in any category have

localised, more so in food; even if it means rejigging the

entire portfolio or doing things which are counter-intuitive.

The quintessential nonvegetarian KFC (Kentucky Fried Chicken)

opted to launch vegetarian offerings in India. Their outlets

even run a campaign to bring home the fact that the oil and

utensils used for vegetarian cooking are kept separate. It has

helped the brand broaden its relevance and find newer

consumers, says Dhruv Kaul, director - marketing, KFC India.

In addition the brand launched it's WOW menu at price points

of Rs 25 onwards and the RiceBowlz to cater to the lunch

segment, both hitherto untapped. With over 6.9 million fans,

the brand is amongst the top on social media, and among the

top 5 most socially devoted brands in the category.

Changing lifestyles, a younger workforce with higher

disposable incomes and better standards of living have added

muscle to the growth of QSRs. Says marketing consultant Harish

Bijoor, "The QSR brand is an eclectic mix — it is young,

global, quick, and caters to the impatient generation with

panache, and the mix works."

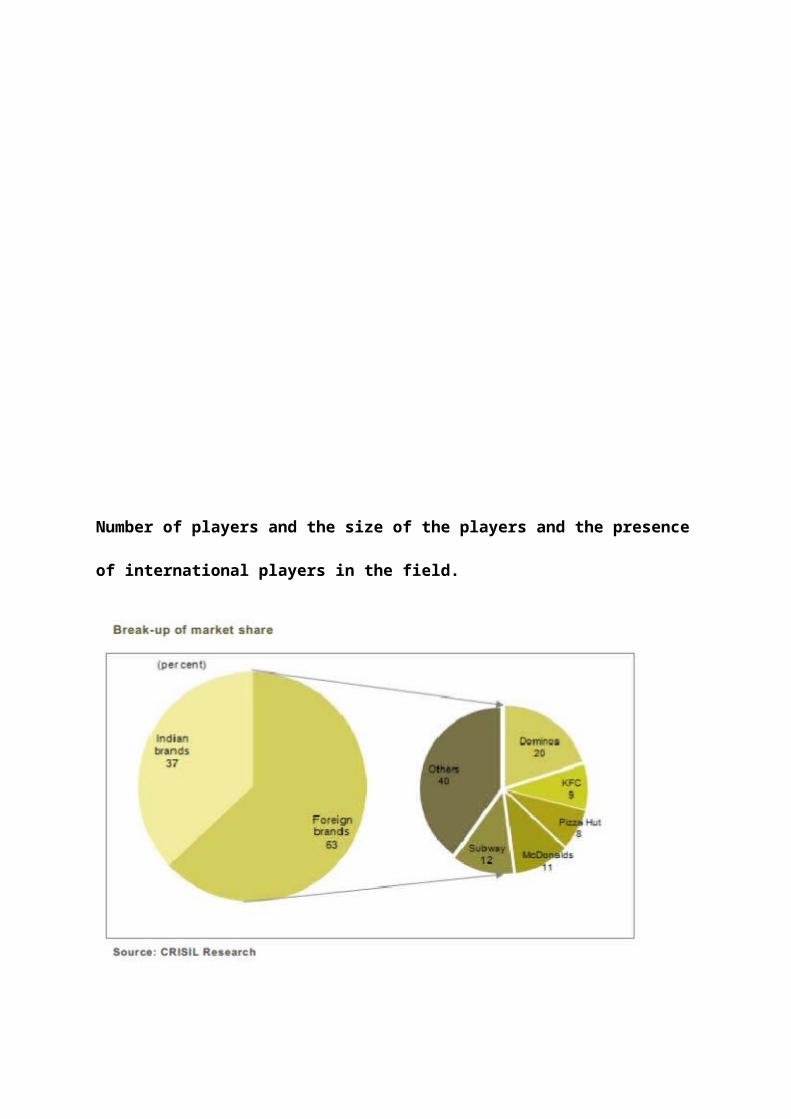

Number of players and the size of the players and the presence

of international players in the field.

According to Crisil, foreign brands have grabbed 63% share of

the India QSR market since McDonald’s opened its first Indian

outlet in 1996. Within the foreign segment, Domino’s Pizza

dominates with a 20% share, followed by Subway (12%),

McDonald’s (11%), Kentucky Fried Chicken (9%) and Pizza Hut

(8%).

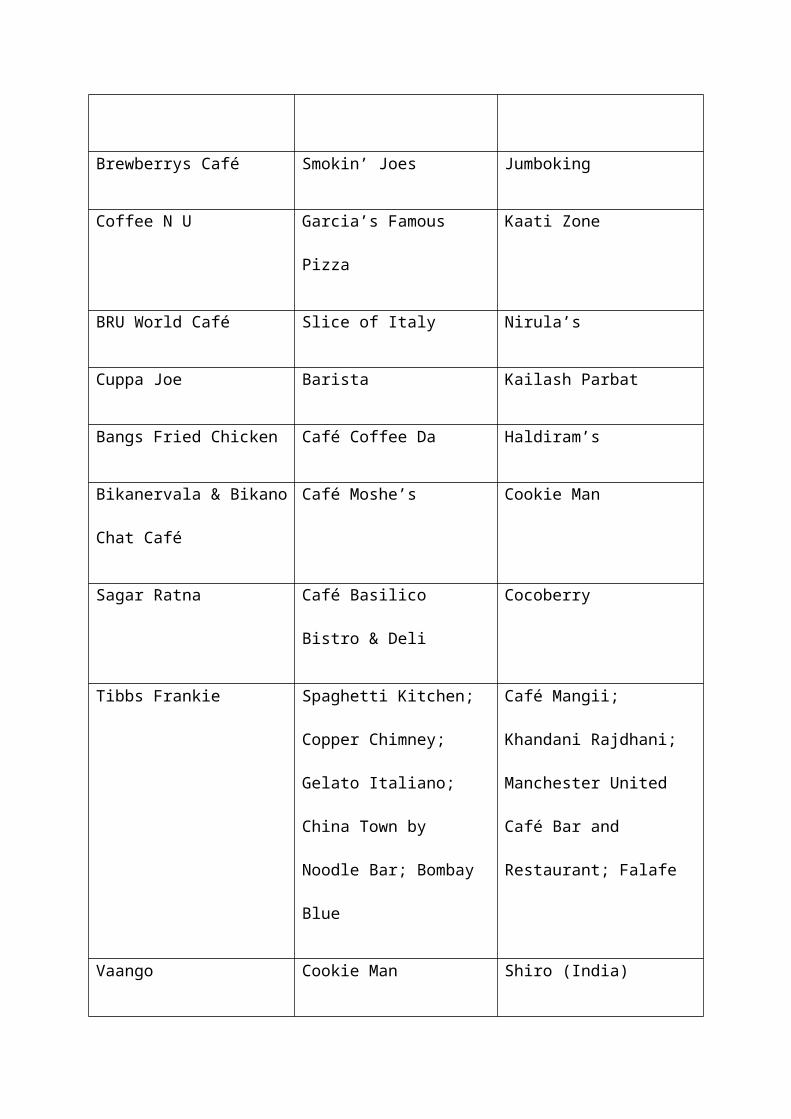

Indian Players

Javagreen Coffee World, Cream

& Fudge Ice Cream,

Pizza Corner, The

Donut Baker

Kent’s Fast Food

Café Mocha US Pizza Dosa Plaza

Brewberrys Café Smokin’ Joes Jumboking

Coffee N U Garcia’s Famous

Pizza

Kaati Zone

BRU World Café Slice of Italy Nirula’s

Cuppa Joe Barista Kailash Parbat

Bangs Fried Chicken Café Coffee Da Haldiram’s

Bikanervala & Bikano

Chat Café

Café Moshe’s Cookie Man

Sagar Ratna Café Basilico

Bistro & Deli

Cocoberry

Tibbs Frankie Spaghetti Kitchen;

Copper Chimney;

Gelato Italiano;

China Town by

Noodle Bar; Bombay

Blue

Café Mangii;

Khandani Rajdhani;

Manchester United

Café Bar and

Restaurant; Falafe

Vaango Cookie Man Shiro (India)

Cream Center Tikka Town 3H Kitchen

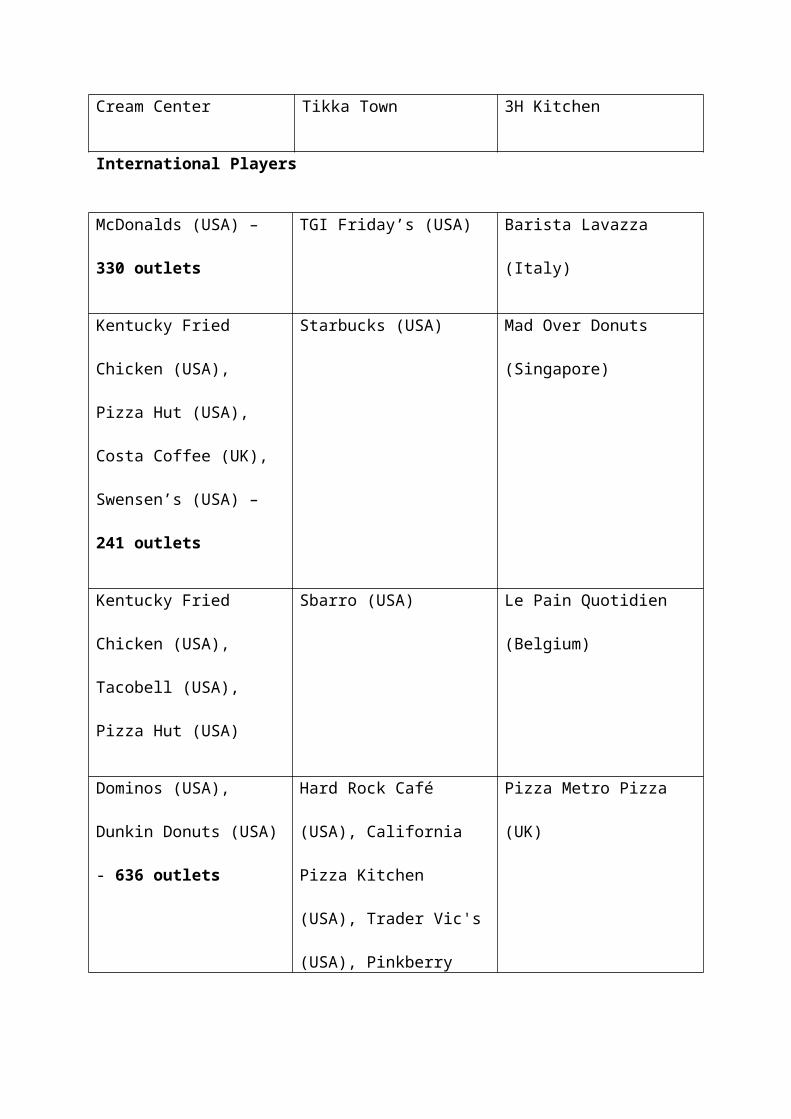

International Players

McDonalds (USA) –

330 outlets

TGI Friday’s (USA) Barista Lavazza

(Italy)

Kentucky Fried

Chicken (USA),

Pizza Hut (USA),

Costa Coffee (UK),

Swensen’s (USA) –

241 outlets

Starbucks (USA) Mad Over Donuts

(Singapore)

Kentucky Fried

Chicken (USA),

Tacobell (USA),

Pizza Hut (USA)

Sbarro (USA) Le Pain Quotidien

(Belgium)

Dominos (USA),

Dunkin Donuts (USA)

- 636 outlets

Hard Rock Café

(USA), California

Pizza Kitchen

(USA), Trader Vic's

(USA), Pinkberry

Pizza Metro Pizza

(UK)

(USA

Papa John’s (USA),

Chili's (USA) -

30 outlets

The Coffee Bean &

Tea Leaf (USA)

Costa Coffee (UK)

Subway (USA) - 390

outlets

Baskin Robbins

(USA)

Breadtalk

(Singapore)

Quiznos (USA) Gloria Jean’s

(Australia)

Japengo Café (UAE)

Yogurberry (USA) Café Pascucci

(Italy)

Eagle Boys Pizza

(Australia)

Ci Gusta! (Italy) Lemp Brewpub &

Kitchen (USA)

Smoothie Factory

(USA)

Wetzel’s Pretzels

(USA)

Manhattan Pizza and

Luv’nberry Frozen

Yogurt (USA)

Patchi (Lebanese)

Cinnabon (USA) Marrybrown

(Malaysia

Chocolateria San

Churro (Australia)

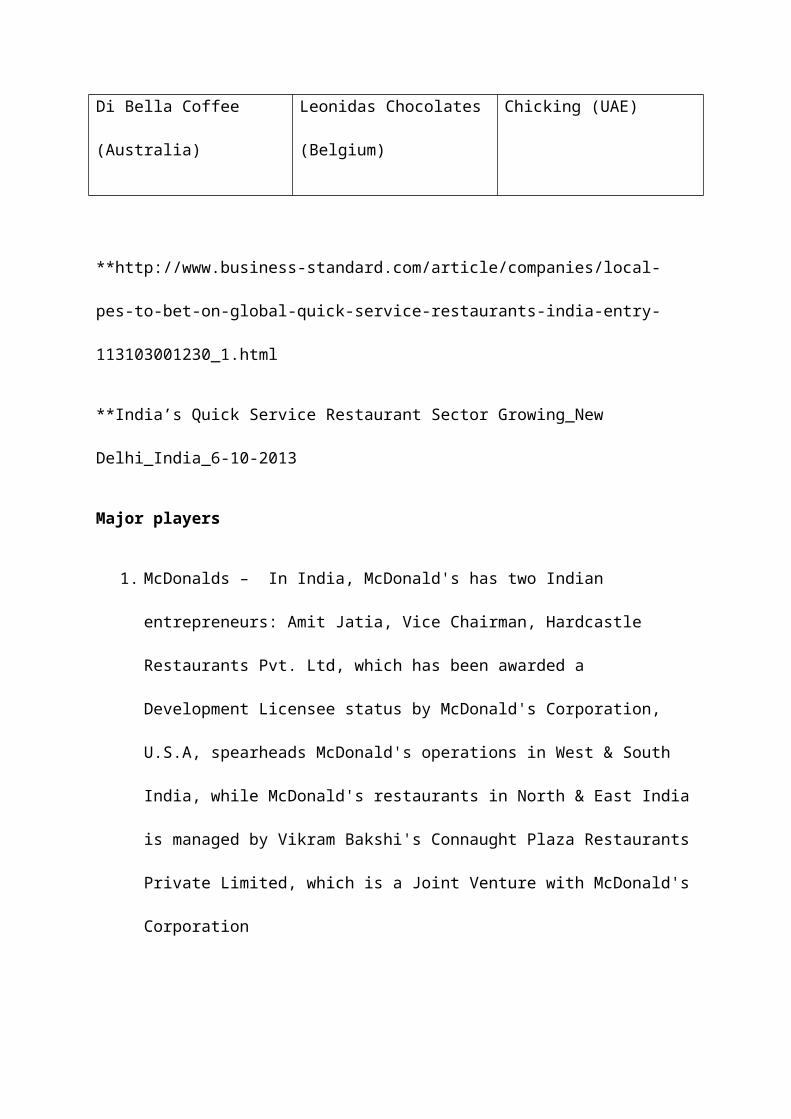

Di Bella Coffee

(Australia)

Leonidas Chocolates

(Belgium)

Chicking (UAE)

**http://www.business-standard.com/article/companies/local-

pes-to-bet-on-global-quick-service-restaurants-india-entry-

113103001230_1.html

**India’s Quick Service Restaurant Sector Growing_New

Delhi_India_6-10-2013

Major players

1. McDonalds – In India, McDonald's has two Indian

entrepreneurs: Amit Jatia, Vice Chairman, Hardcastle

Restaurants Pvt. Ltd, which has been awarded a

Development Licensee status by McDonald's Corporation,

U.S.A, spearheads McDonald's operations in West & South

India, while McDonald's restaurants in North & East India

is managed by Vikram Bakshi's Connaught Plaza Restaurants

Private Limited, which is a Joint Venture with McDonald's

Corporation

2. KFC - Yum brands Inc. owns and operates KFC. KFC is the

world's most popular chicken restaurant chain. Kfc

presently has 223 restaurants across 35 cities and will

have 500 restaurants across 75 cities by 2015. It mainly

expanded within the metros, but also in cities like

Durgapur, Calicut, Kochi and other tier-two towns.

Recently, in a bid to increase its consumer base KFC has

introduced products at low rates in its new Streetwise

range, starting from Rs. 25/-. In response to their new

campaign and menu, their share with teens grew by 20%.

3. Pizza hut - Pizza Hut is one of the flagship brands of

Yum! Brands, Inc. Pizza Hut is the world’s largest pizza

chain with over 12,500 restaurants across 91 countries.

In India, Pizza Hut has 140 restaurants across 34 cities,

including Delhi, Mumbai, Bangalore, Chennai, Kolkata,

Hyderabad, Pune, and Chandigarh amongst others. Yum! is

in the process of opening Pizza Hut restaurants at many

more locations to service a larger customer base across

the country

4. Dominos - Jubilant Food Works Limited (the Company) is a

Jubilant Bhartia Group Company, The Company was

incorporated in 1995 and initiated operations in 1996.

The Company & its subsidiary operates Domino's Pizza

brand with the exclusive rights for India. The Company is

India's largest and fastest growing food service company,

with a network of 500+ Domino's Pizza stores.

Method of retailing within the sector

Company owned:

Majority of the stores will be company-owned while the

remaining will be franchisee-run. Deval says the Indian QSR

market is estimated to grow to $29 billion by 2018.

Franchise outlets

On the strategic front, it has been found that the franchising

concept in India is continuously rising, with the increase in

the number of international players opening more franchise

outlets in India. The increasing revenue figures from

franchise outlets encourage the players to opt for the

concept.

As a result, many international fast food giants are opening

up their franchise outlets in India to grab the huge untapped

potential in a fast emerging market. In a recent development,

Nando, South Africa-based Afro-Portuguese, global restaurant

chain is starting up around 35 outlets by 2013 in various

parts of India through the franchise route. The company

expects to expand enormously in the northern parts of India.

**Indian Fast Food Industry -pdf

Supply chain:

An efficient supply chain will help provide standard product

quality to customers across stores, but supply fragmentation

in India is significant, creating quality issues at the ‘back-

end’. Limited modern storage and transportation infrastructure

adds to the problem, which is even more pronounced in

perishable products. Also the supply chain is much more

complex. As such, capital investments in the upstream and

midstream processing parts of the supply chain are critical,

especially since food production, processing and preparation

on a large scale are just beginning in India.

QSR players prefer to have multiple supplier options to

diversify the risk and help in price negotiations. In segments

such as poultry, cheese and French fries there are only a few

processors currently, but QSRs may look at either developing

small players as vendor partners or even consider backward

integration into the business.

There is an emergence of logistics providers and Contract

Cultivation such as Companies signing contracts with farmers

to grow a specific crop and guaranteeing to buy the produce at

an agreed price has emerged as a preferred way for big global

and domestic F&B brands to source agricultural produce.

It is crucial to employ the right sourcing strategies in a

market like India. A well planned supply chain requires strong

domain knowledge as well as a localised approach and is a

major contributor to running an efficient, successful Indian

QSR operation.

Internet retailing

Domino's, with its network of over 700 outlets across nearly

150 cities, apportions 15%-20% of it's investments online. The

brand has over 1.5 million downloads of the mobile ordering

app, over 6.2 million fans on Facebook, making it one of the

top brand fan pages across the country and more than 30,000

followers on Twitter. Shares Harneet Singh Rajpal, VP -

marketing, Domino's Pizza, "Our online ordering platform has

shown great promise for future and also given us the first

movers advantage." The average OLO (online order) contribution

to delivery sales in around 18%-20%. A host of new products

launched last year like spicy baked chicken, Lebanese rolls

and calzone pockets, fresh pan pizza as well as high decibel

marketing campaigns have kept the counters busy.

Role of Apps and Web-based Ordering

With the growth in computer literacy and access to smartphones

and the Internet, the home delivery business is all set to

grow. Domino’s Pizza is leading this change from the front; of

its total reported revenue of ~INR 385 crore in third-quarter

2013, about 50% came from the delivery business. Again, ~14%

of the total delivery sales (~INR 27 crore) were made through

online channels, through both mobile apps and online ordering.

Although the mobile app business, started in 2012, only

contributes about 10% of the online business (which started in

2011), Domino’s Pizza expects this to double within a year.

About a million apps have already been downloaded, as per the

company’s claims. This is line with the experience of other

retailers, who are realizing the potential of the e-tailing

opportunity in India against the brick-and mortar format.

Delivery-focused Websites

While Domino’s Pizza has gone ahead with its own website and

app, other operators are also tapping the food delivery

market. Many players have joined hands with specialized

delivery portals like FoodPanda, Tastykhana, JustEat, etc. as

a means of testing waters. These businesses work on a

commission-based model. The advantage to the consumer is that

he can access multiple restaurants through a single

website/mobile number, and that these companies often

negotiate exclusive offers in terms of value from the

restaurants.

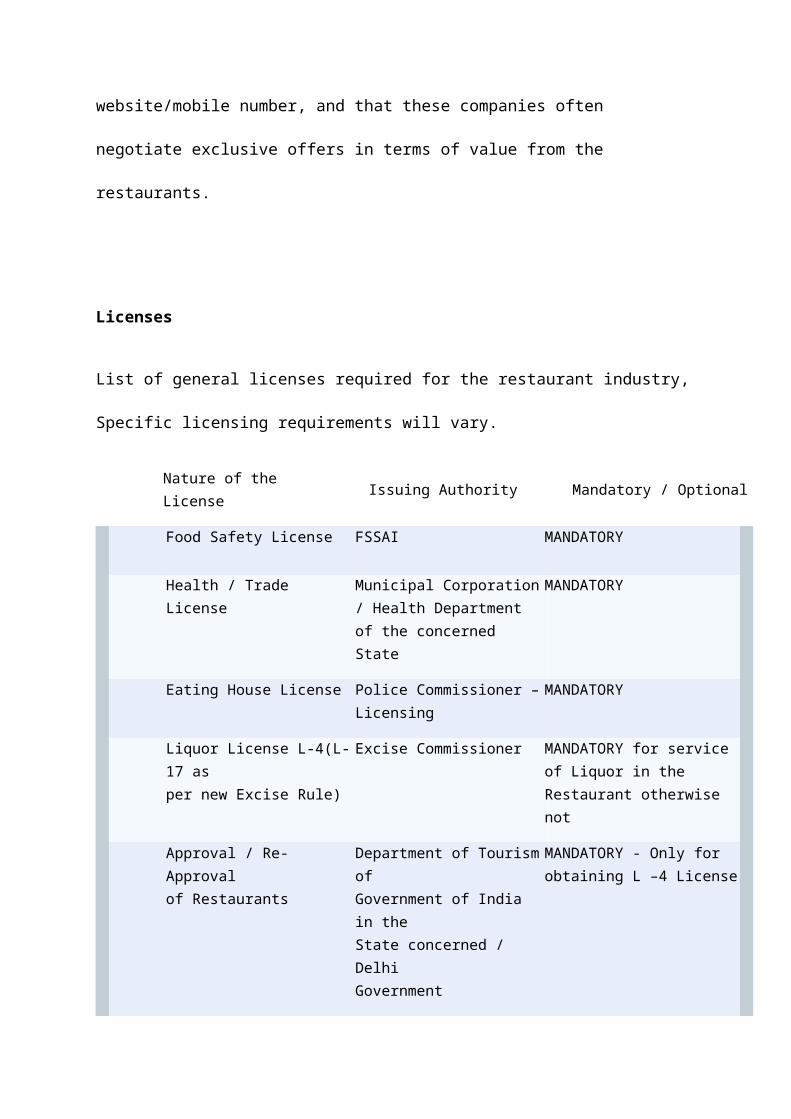

Licenses

List of general licenses required for the restaurant industry,

Specific licensing requirements will vary.

Nature of the License Issuing Authority Mandatory / Optional

Food Safety License FSSAI MANDATORY

Health / Trade License

Municipal Corporation/ Health Department of the concerned State

MANDATORY

Eating House License Police Commissioner –Licensing

MANDATORY

Liquor License L-4(L-17 as per new Excise Rule)

Excise Commissioner MANDATORY for service of Liquor in the Restaurant otherwise not

Approval / Re-Approvalof Restaurants

Department of TourismofGovernment of India in theState concerned / DelhiGovernment

MANDATORY - Only forobtaining L –4 License

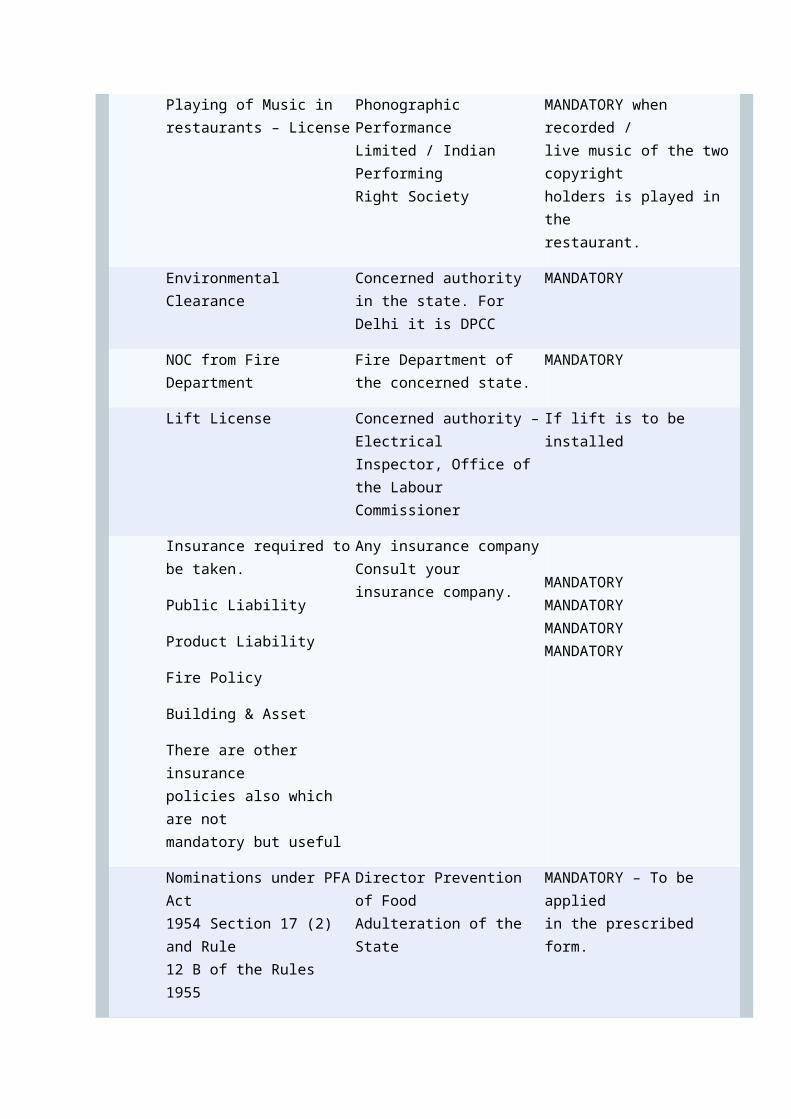

Playing of Music inrestaurants – License

Phonographic PerformanceLimited / Indian Performing Right Society

MANDATORY when recorded /live music of the two copyrightholders is played in therestaurant.

Environmental Clearance

Concerned authority in the state. For Delhi it is DPCC

MANDATORY

NOC from Fire Department

Fire Department of the concerned state.

MANDATORY

Lift License Concerned authority –ElectricalInspector, Office of the LabourCommissioner

If lift is to be installed

Insurance required tobe taken.

Public Liability

Product Liability

Fire Policy

Building & Asset

There are other insurancepolicies also which are notmandatory but useful

Any insurance companyConsult your insurance company.

MANDATORYMANDATORYMANDATORYMANDATORY

Nominations under PFAAct1954 Section 17 (2) and Rule12 B of the Rules 1955

Director Prevention of FoodAdulteration of the State

MANDATORY – To be appliedin the prescribed form.

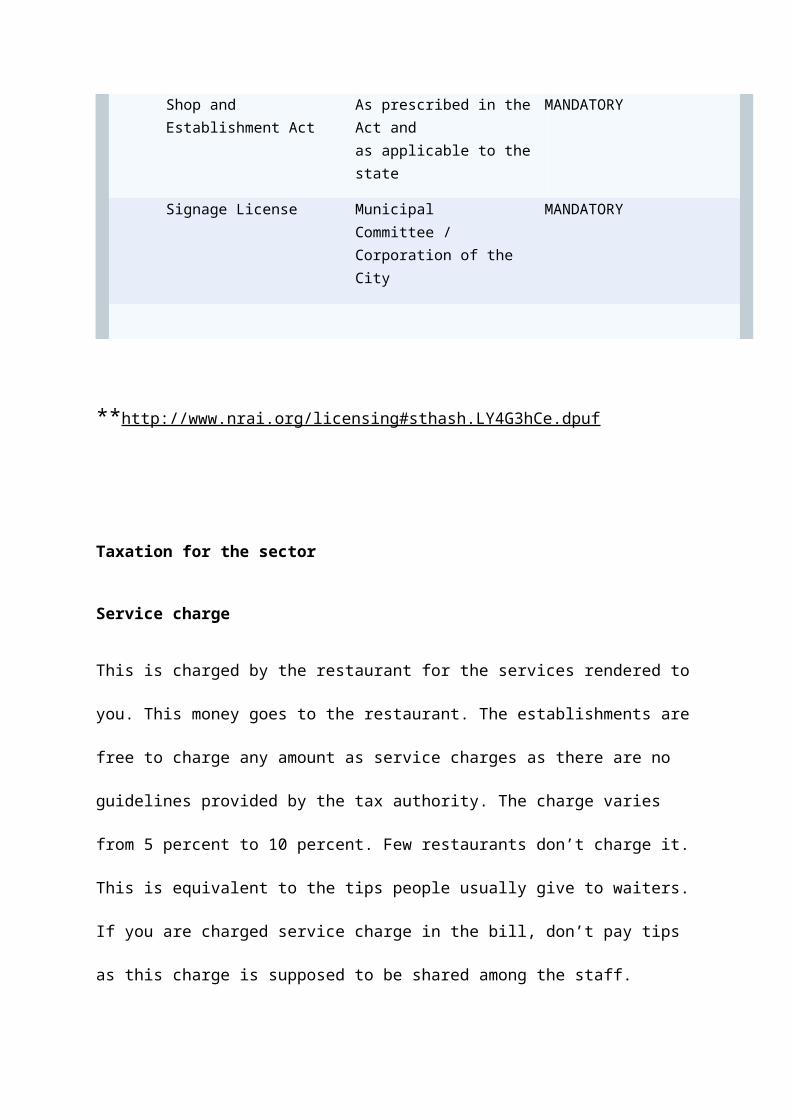

Shop and Establishment Act

As prescribed in the Act andas applicable to the state

MANDATORY

Signage License Municipal Committee / Corporation of the City

MANDATORY

**http://www.nrai.org/licensing#sthash.LY4G3hCe.dpuf

Taxation for the sector

Service charge

This is charged by the restaurant for the services rendered to

you. This money goes to the restaurant. The establishments are

free to charge any amount as service charges as there are no

guidelines provided by the tax authority. The charge varies

from 5 percent to 10 percent. Few restaurants don’t charge it.

This is equivalent to the tips people usually give to waiters.

If you are charged service charge in the bill, don’t pay tips

as this charge is supposed to be shared among the staff.

Most of us don’t bother about it even when we feel the charges

are higher. One reason is that we don’t think anything can be

done about it. Secondly, we don’t want to spoil our evening

because of this and argue with restaurant manager. However,

the ground rule is that if the menu mentions service charges,

you have to pay. If it doesn’t, you can question it.

Service tax

Many people confuse service tax with service charges. Service

tax is the tax levied by the Government on the services

rendered by restaurants. Service tax is same in all states. It

is 12.36 percent on the 40 percent of the bill. The bill

includes your food and drink and the service charge. The

restaurant must be air-conditioned for the service tax. The

problem here is that most of the customers are taxed at the

full bill and not on the 40 percent of the bill as directed.

To make things simple, service tax should be 40 percent *

12.36 percent = 4.94 percent on the total bill. Hence whenever

you see service tax on the total bill exceeding about 5

percent, you can question it.

VAT (Value Added Tax)

There is another tax called VAT (value added tax) that is

state specific. The rates can be as low as 5 percent and as

high as 20 percent depending upon the states. Moreover, VAT

for food items and drink are different. Many restaurants might

club food items and drink and charge a flat rate on the total

bill. In such cases, it is good to ask for separate bills for

food and drinks. This should clearly show the different VAT

for both the items.

**http://www.moneycontrol.com/master_your_money/

stocks_news_consumption.php?autono=927376

Major Problems afflicting the sector

Food price inflation is a key factor affecting the consumer

food services market, and is impacted by delayed monsoons, the

economic slowdown, and unfavorable demand-supply conditions.

It keeps fluctuating and averaged 10.33 Percent from 2012

until 2014, reaching an all time high of 14.72 Percent in

November of 2013.

The QSR market has many small and mid-size unorganized

players competing with large chain players. This fragmented

market reflects a number of challenges, including unclear

format segmentation, varied consumer options for eating out,

and the lack of best practices for food services outlets.

Manpower is a big challenge in the food services market,

with an attrition rate of 25-30%.

High real estate and labor costs tend to impact store

profitability.

The industry’s supply chain is fragmented in nature and

marked by the presence of multiple intermediaries. The lack of

appropriate infrastructure, inadequate technologies, and the

non-integration of the food value chain are factors key to the

wastage of nearly 30-40% of prepared food across the supply

chain.

In India, obtaining the requisite licenses, e.g. health

license, food safety license, police license, No Objection

Certificate (or NOC, from the fire department and the state

pollution control board), etc. is a major obstacle hindering

the smooth operation of a restaurant. The process is not

centralized as yet and requires filing applications with

individual stakeholders, which involves a lot of paperwork and

is a time-consuming activity.

The Indian restaurant industry is burdened with multiple

taxes like VAT, excise, and service tax, besides different

state taxes, which add up to 20- 25% of the bill value.

**QSR_Market_in_India

**http://www.tradingeconomics.com/india/food-inflation

Status of the sector in India vis a vis the international

market.

India also offers a wealth of young people, a key market for

fast-food chains. Over 60% of India’s current population is

younger than 30 years old, and are welcoming of international

brands. The fast food industry will benefit from other factors

as well, such as increases in nuclear families, single-person

households and the proportion of women in the workforce; as

well as changing lifestyles and eating patterns.

With markets in the US and Europe offering only slow growth,

and China respectably penetrated by the big international

chains, India offers the next big opportunity. Domino’s Pizza

(US), which recently opened its 600th restaurant in India,

says India is its fastest-growing market and its second-

largest single country operation outside of the US. Of the

500-odd new restaurants it opened in 2012 worldwide, 23% were

in India.

** http://www.eiu.com/industry/article/311021215/india-food-

fast-growth-for-cheap-eats/2013-10-03

Projections on how the sector is likely to grow in the next

five years

Quick Service Restaurants market to grow two-fold in the next

three years. The entry of McDonald's in 1996 marked the

beginning of the QSR concept in India. Many global brands have

followed suit since then, either through company-owned stores

or the franchisee model, or a mix of both. Over the past 5-6

years, many Indian QSR brands have also mushroomed across the

country, serving either foreign cuisine or adapting Indian

cuisine to the fast food service format. This helped the

Indian QSR market to expand rapidly to about Rs 34 billion by

2012-13. CRISIL Research expects this strong growth to

continue over the next three years, as global brands expand

into smaller cities. We expect the QSR market to reach a

turnover of Rs 70 billion by 2015-16, growing at an average

annual rate of about 27 per cent.

Growth to be higher in tier II markets

CRISIL Research has separately analysed per-household spends

on organised fast food or QSRs for the tier I and tier II

markets. (Together these markets account for about 85-90 per

cent of the QSR industry’s 2 CRISIL Opinion revenues).

Interestingly, on an average, a tier I middle class household

spends about Rs 3,700 per annum for eating at QSRs. This

roughly equates to about 12 pizzas per household per annum.

However, the next phase of growth will revolve around tier II

cities. Annual spends on QSRs by middle-class households in

these areas are expected to surge by 150 per cent to Rs 3,750

per annum over the next three years. In comparison, annual

spends in tier I cities are expected to increase by more than

60 per cent to about Rs 6,000 by 2015-16. The quantum jump in

QSR spends in urban areas will be propelled by an increase in

nuclear families and working women, steady growth in incomes,

changing lifestyle and eating patterns, and more importantly,

greater accessibility of QSR outlets.

** http://www.crisil.com/pdf/research/CRISIL

%20Research_Article_QSR_17Sep2013.pdf

In summary, the market represents a vast untapped potential

with eating out becoming a regular form of entertainment for

consumers today. It is also a major contributor to the

exchequer in terms of tax revenues. Therefore, it is important

that the role of the food services market is acknowledged by

the government, and the key concerns of restaurateurs are

addressed in order to catalyze the growth to optimum levels

Five Forces Analysis of the QSR industry

Industria

l Rivalry

Bargaining Power

of Supplier

Bargaining Power

of Buyer

Threat of New

Entraints

Threat of

Substitutes

There are

many

competito

rs;

There are few

suppliers but many

buyers;

Number of buyers

is very high

moderate

amount of

capital

required

Number of

substitutes

are high as

more

competitors

are evolved

Industry

growth

high

Suppliers’ size Customer

switching costs

are low

Retaliation

by existing

companies

no switching

costs for

the

customers to

shift to

other brands

Products

are not

different

iated and

can be

easily

Ability to find

substitute

materials

There are many

substitutes

Legal

barriers

(patents,

copyrights,

etc.)

substitut

ed;

Competito

rs have

more or

less the

dame

product

range

Materials scarcity Price

sensitivity

Brand

reputation

Low

customer

loyalty.

Cost of switching

to alternative

materials is high

There is low

customer

loyalty;

There is low

customer

loyalty;

Products are

nearly

identical;

Industria

l Rivalry

is high

Bargaining Power

of Supplier is

moderate

Bargaining Power

of Buyer is high

Threat of New

Entraints is

very high

Threat of

Substitutes

is very high

Conclusion

Based on the analysis of the above data, the critical success

factors for the Indian Fast Food industry can be listed. The

CSF are those factors which are mandatory for the

profitability of the business.

Critical Success Factors are as follows—

Differentiation

Competing on Low Cost

Branding Location

Turning your supply chain into a cash contributor

Maintaining brand premiums as consumer value perceptions

shift

Improving consumer insight

Copyright © 2022 FDOKUMEN