putm-acs-agg-final.pdf - Phoenix Group

298

PHOENIX UNIT TRUST MANAGERS MANAGER’S ANNUAL REPORT For the year: 1 February 2021 to 31 January 2022 PUTM Authorised Contractual Scheme (“PUTM ACS Funds” or the “Scheme”)

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of putm-acs-agg-final.pdf - Phoenix Group

PHOENIX UNIT TRUST MANAGERS

MANAGER’S ANNUAL REPORTFor the year: 1 February 2021 to 31 January 2022

PUTM Authorised Contractual Scheme (“PUTM ACS Funds” orthe “Scheme”)

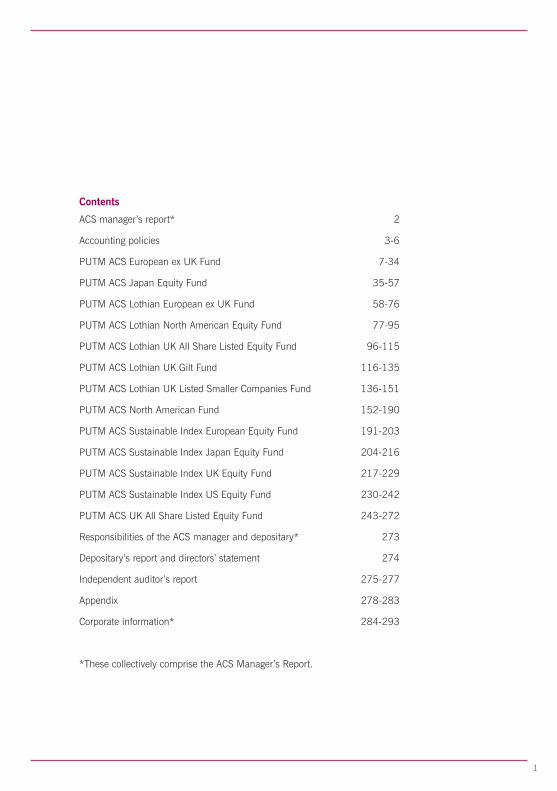

Contents

ACS manager’s report* 2

Accounting policies 3-6

PUTM ACS European ex UK Fund 7-34

PUTM ACS Japan Equity Fund 35-57

PUTM ACS Lothian European ex UK Fund 58-76

PUTM ACS Lothian North American Equity Fund 77-95

PUTM ACS Lothian UK All Share Listed Equity Fund 96-115

PUTM ACS Lothian UK Gilt Fund 116-135

PUTM ACS Lothian UK Listed Smaller Companies Fund 136-151

PUTM ACS North American Fund 152-190

PUTM ACS Sustainable Index European Equity Fund 191-203

PUTM ACS Sustainable Index Japan Equity Fund 204-216

PUTM ACS Sustainable Index UK Equity Fund 217-229

PUTM ACS Sustainable Index US Equity Fund 230-242

PUTM ACS UK All Share Listed Equity Fund 243-272

Responsibilities of the ACS manager and depositary* 273

Depositary’s report and directors’ statement 274

Independent auditor’s report 275-277

Appendix 278-283

Corporate information* 284-293

*These collectively comprise the ACS Manager’s Report.

1

ACS MANAGER’S REPORT

THE SCHEME

PUTM ACS Funds (“the Scheme”) is an Authorised Contractual Scheme. Subsequentreferences to the 'Scheme' relate to PUTM ACS Funds. The Scheme is organised as anumbrella co-ownership scheme comprising separate Sub-funds. Each Sub-fund shall havea segregated portfolio of assets and, accordingly, the assets of a Sub-fund are allocatedexclusively to that Sub-fund and shall not be used or made available to discharge (directlyor indirectly) the liabilities of, or claims against, any other person or body, including anyother Sub-fund and shall not be available for any other purpose.

Unitholders are not liable for the debts of a Sub-fund.

The Scheme is subject to the rules of the FCA as set out in the Collective InvestmentSchemes Sourcebook ("COLL") which form part of the FCA handbook.

The property of the Scheme is entrusted to HSBC Bank Plc as depositary (“theDepositary”).

The object of the Scheme is to invest the scheme property through its Sub-funds, and theobjective of each Sub-fund is for the ACS Manager on behalf of the unitholder's, as co-owners of the relevant Sub-fund's property, to invest that property in transferablesecurities, money market instruments, derivatives and forward transactions, deposits,cash, near cash, units in collective investment schemes and immovable property, inaccordance with the regulations applicable to the Scheme and each Sub-fund with theaim of spreading investment risk and giving the unitholders the results of the managementof that property.

Each Sub-fund has a different investment objective, and in the financial statements youwill find an investment review for each Sub-fund which includes details of the investmentobjectives. As at 31 January 2022 there were 13 active Sub-funds in the PUTM ACSFunds.

AUTHORISED STATUS

The Financial Conduct Authority authorised the PUTM ACS Funds as a UCITS Scheme.

THE FINANCIAL STATEMENTS

We are pleased to present the annual financial statements of the Scheme for the yearended 31 January 2022. As required by the regulations, information for each of the Sub-funds has also been included in these financial statements. On the following pages wereview the performance of each of those Sub-funds during the year. We hope that you findthe review useful and informative.

SUBSEQUENT EVENTS

Please note that the ACS Manager plans to transfer all of the assets out of the PUTM ACSUK All Share Listed Equity Fund into a new PUTM ACS Fund in the last quarter of 2022and has submitted an application to the FCA to wind-up PUTM ACS UK All Share ListedEquity Fund.

2

Accounting Policies

The following accounting policies apply to all Sub-funds, where applicable.

Note 1 Accounting policies

(a) Basis of preparationThe financial statements have been prepared under the historical cost basis, as modified bythe revaluation of investments in accordance with Financial Reporting Standard (FRS 102)and the Statement of Recommended Practice (SORP) for Financial Statements of UKAuthorised Funds issued by The Investment Association (‘IA’) in May 2014, and as amendedin June 2017.The financial statements (with the exception of the PUTM ACS UK All Share Listed EquityFund) have been prepared on a going concern basis. The ACS Manager has made anassessment of the Sub-funds’ ability to continue as a going concern, and is satisfied it has theresources to continue in business for the foreseeable future and is not aware of any materialuncertainties that may cast significant doubt on this assessment. This assessment is made fora period of 12 months from when the financial statements are authorised for issue andconsiders liquidity, declines in global capital markets, known redemption levels, expenseprojections, key service provider’s operational resilience, and the impact of COVID-19.The ACS Manager plans to transfer the assets of PUTM ACS UK All Share Listed Equity Fundinto the new PUTM ACS Fund through in-specie transactions in the last quarter of 2022. TheACS Manager has submitted an application to the FCA to wind up the PUTM ACS UK AllShare Listed Equity Fund and therefore does not consider it to be appropriate to adopt thegoing concern basis of accounting in preparing the financial statements. Accordingly, thefinancial statements for PUTM ACS UK All Share Listed Equity Fund only have been preparedon a break-up basis, all assets are measured at recoverable value and all liabilities atsettlement value. No adjustments were required in these financial statements to reduce assetsto their recoverable value or liabilities to their settlement value. The ACS Manager will bearthe costs relating to any such liabilities arising. Unless otherwise stated all accounting policiesare consistent with those of the prior year.

(b) Valuation of investmentsThe quoted investments of the Sub-funds have been valued at bid dealing prices as at closeof business on 31 January 2022, the last valuation point in the accounting year, inaccordance with the ACS Deed. Investments in collective investment schemes have beenvalued at bid price for dual priced funds or the single price for single priced funds. Wherethese investments are managed by the ACS Manager or an associate of the ACS Manager, theholdings have been valued at the cancellation price for dual priced funds or the single pricefor single priced funds. This price is the last available published price at the year end.Derivatives are valued as at close of business on 31 January 2022, the last valuation point ofthe accounting year. Exchange traded derivatives are priced at fair value, which is deemed tobe the bid price.Over-the-counter derivatives are priced at fair value using valuation models and data sourcedfrom market data providers.

(c) Foreign exchangeTransactions in foreign currencies during the year are translated into Sterling (the functionalcurrency of the Sub-funds), at the rates of exchange ruling on the transaction date. Amountsheld in foreign currencies have been translated at the rate of exchange ruling at close ofbusiness, 31 January 2022, the last valuation point in the accounting year.

3

4

Accounting Policies

Note 1 Accounting policies (continued)

(d) RevenueDividends receivable from equity investments and distributions receivable from collectiveinvestment schemes are credited to revenue when they are first quoted ex-dividend. Interestreceivable on bank deposits is accounted for on a receipts basis and money market funds isaccounted for on an accruals basis. Interest receivable from debt securities is accounted foron an effective interest rate basis. Accrued interest purchased or sold is excluded from thecost of the security and is accounted for as revenue. Any commission arising fromstocklending is recognised on an accruals basis and is disclosed net of fees.Interest received from or paid to the Sub-fund from over-the-counter derivatives designed toprotect income is treated as revenue. Interest received from or paid to the Sub-fund from over-the-counter derivatives designed to protect capital is treated as capital.

(e) Special dividendsSpecial dividends are treated either as revenue or repayments of capital depending on thefacts of each particular case. It is likely that where the receipt of a special dividend results ina significant reduction in the capital value of the holding, then the special dividend should betreated as capital in nature so as to ensure the matching principle is applied to gains andlosses. Otherwise, the special dividend should be treated as revenue.

(f) ExpensesExpenses are accounted for on an accruals basis. Expenses of the Sub-funds are chargedagainst revenue, except for costs associated with the purchase and sale of investments, whichare charged to capital.

(g) Stock dividendsThe ordinary element of stocks received in lieu of cash is recognised as revenue. Any excessin value of shares received over the amount of cash forgone would be treated as capital.

(h) Taxation

As the Scheme is an umbrella co-ownership ACS neither the Scheme or its Sub-funds aresubject to tax on income or capital gains.

On a daily basis unitholders will be advised of their share of the aggregated accrued income,expenses and withholding tax paid. It is the responsibility of the unitholders to maintain arecord of the relevant amounts of income equalisation and to make the appropriateadjustment when completing their tax calculations.

Note 2 Distribution policies

(a) Basis of distributionRevenue produced by the Sub-funds’ investments accumulates during each accountingperiod. If, at the end of each accounting period, revenue exceeds expenses, the net revenue ofthe Sub-fund is available to be accumulated to unitholders.

(b) Unclaimed distributionsDistributions remaining unclaimed after six years are paid into the Sub-funds as part of thecapital property.

(c) Apportionment to multiple unit classesWith the exception of the ACS Manager’s periodic charge, the allocation of revenue andexpenses to each unit class is based upon the proportion of the Sub-funds’ assets attributable

Accounting Policies

5

Note 2 Distribution policies (continued)

(c) Apportionment to multiple unit classes (continued)to each unit class on the day the revenue is earned or the expense is suffered. Consequently,the revenue available to distribute for each unit class will differ.

(d) Special dividendsIt is the policy of the Sub-funds, where applicable, to distribute special dividends which havebeen treated as revenue.

(e) ExpensesIn determining the net revenue available for distribution, FCA fees and charges in relation tosafe custody of investments are ultimately borne by capital.

(f) Stock dividendsIt is the policy of the Sub-funds, where applicable, to distribute the revenue element of stockdividends.

Note 3 Risk management policiesThe risks arising from the Sub-funds’ financial instruments are market price risk, interest raterisk, foreign currency risk, liquidity risk, credit risk and counterparty risk. The ACS Manager'spolicies for managing these risks are summarised below and have been applied throughoutthe year.

(a) Market price risk

Market price risk arises mainly from uncertainty about future prices of financial instrumentsheld. It represents the potential loss the Sub-funds might suffer through holding marketpositions in the face of price movements. The Sub-funds' investment portfolios are exposed tomarket fluctuations which are monitored by the ACS Manager in pursuit of the investmentobjectives and policies. Adherence to investment guidelines and to investment and borrowingpowers set out in the ACS Deed, the Prospectus and in the Collective Investment SchemesSourcebook (“the Sourcebook”) mitigates the risk of excessive exposure to any particular typeof security or issuer.

(b) Interest rate risk

The majority of the Sub-funds' financial assets are equity shares and other investments whichneither pay interest nor have a maturity date.The Lothian UK Gilt Fund's assets are comprised of fixed interest rate securities. There is thereforea risk that the capital value of investments will vary as a result of the market's sentimentregarding future interest rates.Expectations of future rates may result in an increase or decrease in the value of investmentsheld. In general, if interest rates rise the revenue potential of the Sub-fund also rises but the valueof fixed interest rate securities will decline. A decline in interest rates will in general have theopposite effect.Any transactions in fixed interest securities must be used in accordance with the investmentobjective of the Sub-fund and must be deemed by the Investment Manager to be economicallyappropriate. Regular production of portfolio risk reports highlight concentrations of risk, includinginterest rate risk, for the Sub-funds.Interest receivable on bank deposits or payable on bank overdraft positions will be affected byfluctuations in interest rates.

6

Accounting Policies

Note 3 Risk management policies (continued)

(c) Foreign currency risk

On some of the Sub-funds a substantial proportion of the Sub-funds' investment portfolio isinvested in overseas securities and the Balance sheet can be significantly affected by movementsin foreign exchange rates. The Sub-funds may be subject to short term exposure to exchange ratemovements between placing the purchase or sale of securities and agreeing a related currencytransaction albeit usually the two transactions are agreed at the same time.Any such currency transactions must be used in accordance with the investment objective of theSub-funds and must be deemed by the Investment Manager to be economically appropriate.Regular production of portfolio risk reports highlight concentrations of risk, including currencyrisk, for the Sub-funds.

(d) Liquidity risk

The Sub-funds’ assets are comprised mainly of readily realisable securities. If insufficient cash isavailable to finance unitholder redemptions then securities held by the Sub-fund may need to besold. The risk of low market liquidity, through reduced trading volumes, may affect the ability ofthe Sub-funds to trade financial instruments at values previously indicated by financial brokers.From time to time, liquidity may also be affected by stock specific or economic events. Tomanage these risks the ACS Manager performs market research in order to achieve the best pricefor any transactions entered into on behalf of the Sub-funds. All stocks are valued daily but thosestocks identified as being less liquid are reviewed on a regular basis for pricing accuracy.

(e) Counterparty risk

Certain transactions in securities that the Sub-funds enter into expose them to the risk that thecounterparty will not deliver the investment (purchase) or cash (sale) after the Sub-fund hasfulfilled its responsibilities. The Sub-funds only buy and sell investments through brokers whichhave been approved by the ACS Manager as an acceptable counterparty. This list is reviewedannually.

(f) Derivatives

Derivative transactions may be used by the Sub-funds for the purposes of meeting its investmentobjectives and also for hedging. In doing so the ACS Manager may make use of a variety ofderivative instruments in accordance with the Sourcebook. The use of derivatives for investmentpurposes means that the net asset value of the Sub-funds may at times have high volatility,although derivatives will not be used with the intention of raising the risk profile of the Sub-funds.Where derivatives are used for hedging this will not compromise the risk profile of the Sub-funds.Use of derivatives will not knowingly contravene any relevant investment objective or limits.

The ACS Manager has used exchange traded futures to hedge the Sub-funds' assets againstmarket volatility in the FTSE All Share index and to hedge against assets denominated in foreigncurrency.

Interest rate swaps have been used to hedge the interest rate risk of holding fixed rate bondsduring the period.

The derivative counterparty is shown at the bottom of the Portfolio of investments in each Sub-fund where applicable.

7

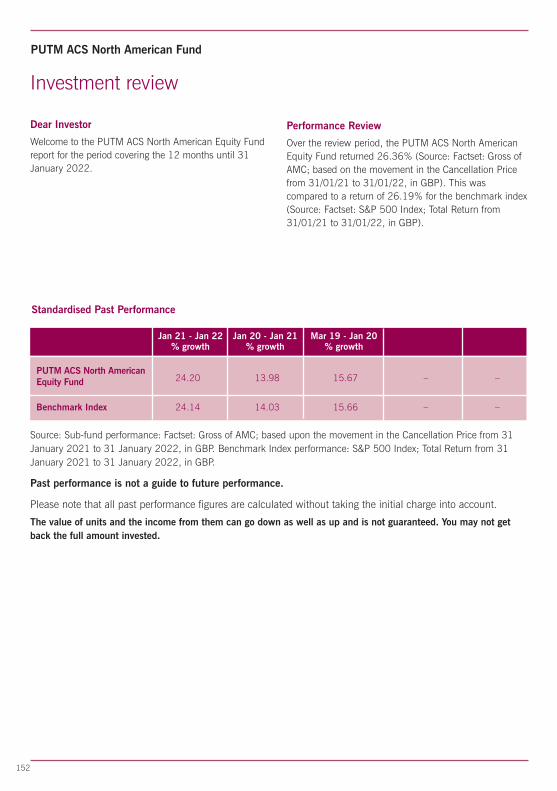

Dear Investor

Welcome to the PUTM ACS European (ex-UK) Fund reportfor the 12 months to 31 January 2022.

Performance Review

Over the review period, the PUTM ACS European (ex-UK)Fund returned 15.84% (Source: Factset, Gross of AMC,GBP, based upon the movement in the Cancellation Pricefrom 31/01/21 to 31/01/22). This was compared to areturn of 13.97% for the benchmark index (Source:Factset, MSCI Europe (ex-UK), Total Return in GBP, from31/01/21 to 31/01/22).

Investment review

Source: Sub-fund performance: Factset, Gross of AMC, in GBP, based upon the movement in the Cancellation Pricefrom 31 January 2021 to 31 January 2022. Benchmark index performance: MSCI Europe (ex- UK), Total Return inGBP, from 31 January 2021 to 31 January 2022.

Past performance is not a guide to future performance.

Please note that all past performance figures are calculated without taking the initial charge into account.

The value of units and the income from them can go down as well as up and is not guaranteed. You maynot get back the full amount invested.

Standardised Past Performance

PUTM ACS European (ex-UK) Fund 15.84 6.75 10.40 – –

Benchmark Index 13.97 7.46 11.48 – –

Jan 21 - Jan22 Jan 20 - Jan21 Mar 19 - Jan 20% growth % growth % growth

PUTM ACS European ex UK Fund

8

PUTM ACS European ex UK Fund

Investment review

Market Review

European shares finished substantially higher over the 12months. Most European indices fell at the beginning of theperiod amid renewed lockdown measures. Nevertheless,the region's equities performed well from February onwards,despite ongoing lockdown measures and rising Covid-19cases. After rising for seven consecutive months, Europeanshares fell again in September, with Germany among theworst performers. Outgoing Chancellor Angela Merkel’sChristian Democratic Union-Christian Social Union bloc lostout to the Social Democratic Party in the federal election,although forming a coalition government is expected to takesome time. Equities fell again sharply at the end of theperiod, as tightening monetary policies and geopoliticaltensions between Russia and Ukraine weighed onsentiment.

September saw Norway’s Norges Bank became the firstmajor developed bank to raise interest rates since the startof the pandemic. Attempting to reassure investors that theEuropean Central Bank (ECB) would not follow suit,President Christine Lagarde said the central bank would nottaper bond market support. However, the ECB hasindicated it would end its Pandemic Emergency PurchaseProgramme in March 2022. Eurozone officials alsoacknowledged that rising inflation may not be as short-livedas predicted, with inflation reaching 5.1% in January.

Sub-fund Review

The investment process underlying the Sub-fund targetssimultaneous exposure to a broad range of factors thatacademic and empirical research has shown deliversuperior returns over the long term. Examples of suchfactors are value, quality and momentum. Combining thesefactors within a multifactor framework then allows the Sub-fund to reap the benefits of diversification, with the aim ofoutperforming throughout the market cycle.

The performance of our proprietary quality factors over theperiod was mixed, with accruals underperforming whileinvestment and profitability outperformed.

The Sub-fund’s composite value strategy (a blend of severalvalue metrics ranging from deep, cyclical measures ofvalue, such as book yield, to value metrics with moredefensive attributes, for example dividend yield and freecash flow yield) outperformed.

Drilling down to a stock level, an overweight position in theDanish shipping company A.P. Moller - Maersk was apositive contributor to performance. The stock rose 79.9%over the 12 months on the back of higher container linerrates due to the ongoing disruption in global supply chains.The stock had a high score based on our trend metrics. TheSub-fund also benefited from an active holding in theFrench bank BNP Paribas. The company performed wellafter it forecast higher revenue for this year and announceda share buyback programme. BNP Paribas has a positivescore according to our measures of sentiment. On thedownside, Airbus was one of the Sub-fund’s top detractorsafter its share price suffered from Omicron-relatedweakness towards the end of the period. Investors wereconcerned about the impact the new Covid-19 variantmight have on the travel sector. Santander and ZurichInsurance also weighed on the Sub-fund’s returns.

Outlook at Year End

Uncertainty around the new variant Omicron andgeopolitical tensions between Russia and Ukraine willcontinue to dominate news flow in the short term.However, many of the risk factors throughout 2021 havemoderated, with global vaccination rates rising and thedirection of Chinese policy becoming clearer. Meanwhile,the removal of central bank support has been priced in, tosome extent. Nevertheless, persistently high inflation andsupply-chain strains may lead to earnings pressure formany businesses.

As the market outlook was completed as of 31st January,there is no mention of the ongoing Ukraine crisis thatbegan at the end of February. Naturally, this woulddramatically affect any future expectations of marketoutlook that would not have been factored in at the time ofwriting.

9

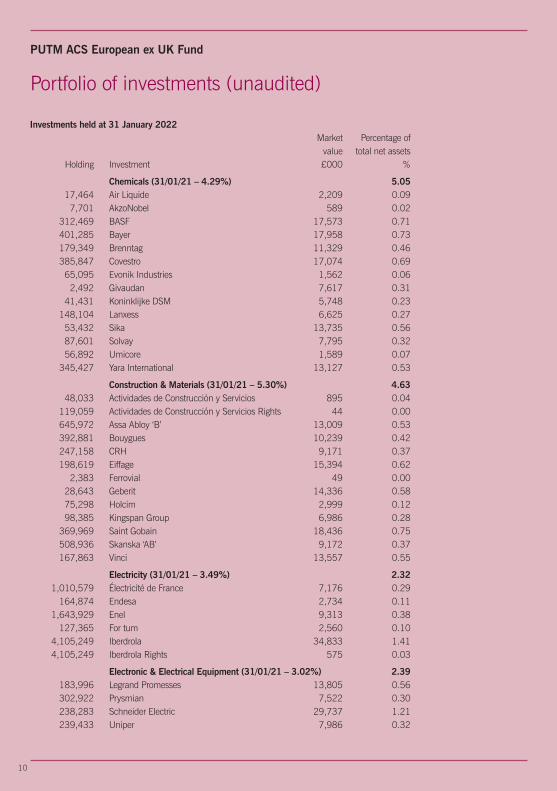

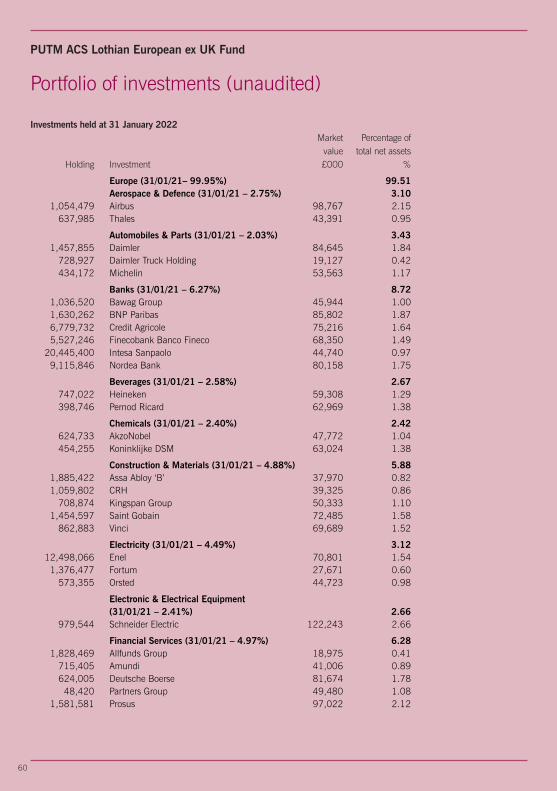

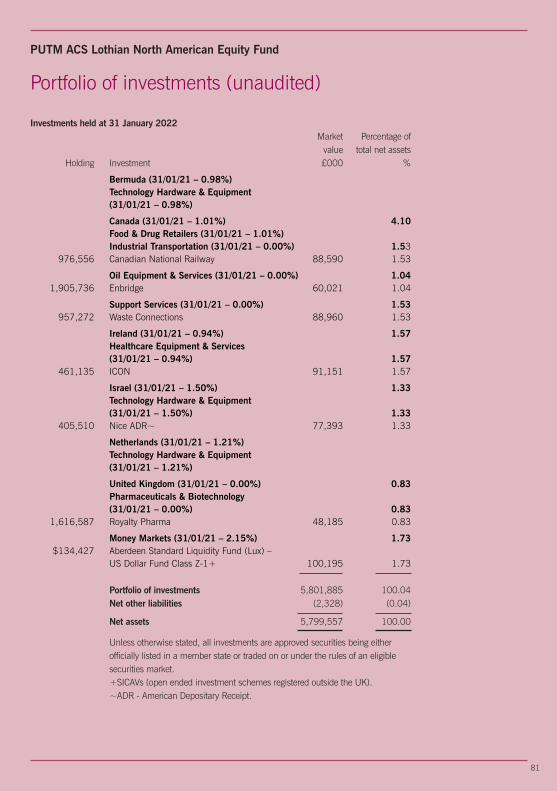

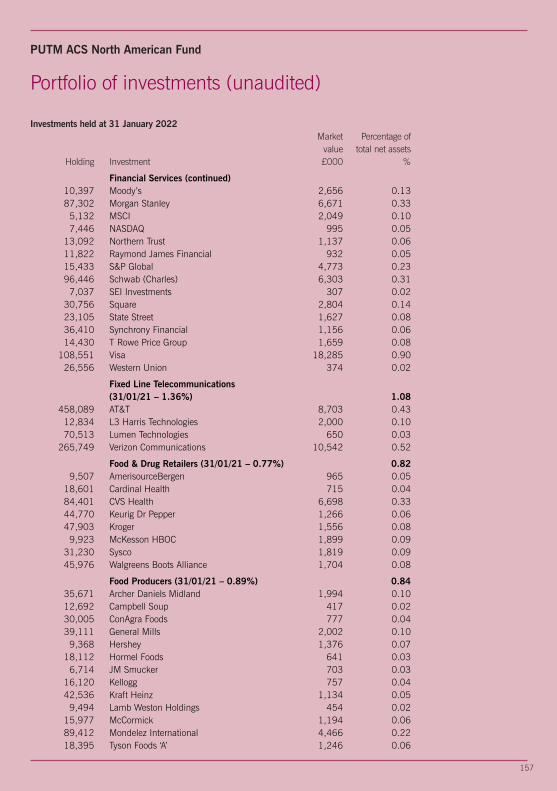

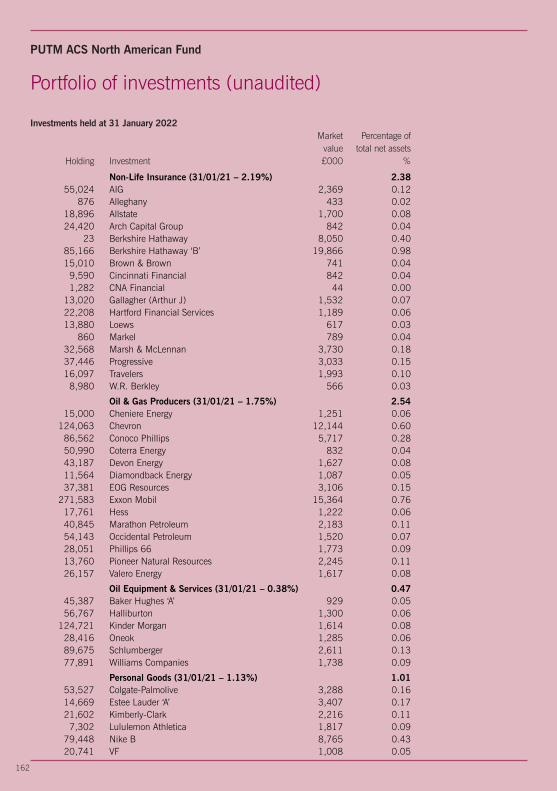

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Europe (31/01/21 – 98.99%) 99.68

Aerospace & Defence (31/01/21 – 1.03%) 0.68 75,504 Airbus 7,072 0.29 20,020 Safran 1,776 0.07 117,420 Thales 7,986 0.32

Alternative Energy (31/01/21 – 0.34%) 0.05 85,152 Gamesa 1,359 0.05

Automobiles & Parts (31/01/21 – 3.64%) 3.29 111,747 BMW 8,644 0.35 606,931 Daimler 35,239 1.43 245,158 Daimler Truck Holding 6,433 0.26 3,538 Faurecia 114 0.00 71,238 Michelin 8,788 0.35 53,006 Porsche Preference 3,627 0.15 587,194 Stellantis 8,321 0.34 9,057 Stellantis 128 0.01 64,342 Volkswagen Preference 9,792 0.40

Banks (31/01/21 – 5.96%) 7.18 4,919,640 Banco Bilbao Vizcaya Argentaria 23,151 0.94 3,834,978 Banco Santander 9,916 0.40 538,408 BNP Paribas 28,337 1.15 1,186,831 CaixaBank 2,822 0.12 1,052,820 Credit Agricole 11,680 0.47 399,396 Deutsche Bank 4,086 0.17 146,272 DNB 2,575 0.10 1,278,532 ING Groep 13,952 0.57 10,508,693 Intesa Sanpaolo 22,996 0.93 11,252 Julius Baer Group 541 0.02 93,210 KBC Group 5,991 0.24 1,541,468 Mediobanca 13,021 0.53 1,799,612 Nordea Bank 15,833 0.64 261,755 Raiffeisen Bank International 5,428 0.22 244,270 Skandinaviska Enskilda Banken ‘A’ 2,329 0.10 521 Skandinaviska Enskilda Banken ‘C’ 5 0.00 525,940 Société Générale 14,357 0.58

Beverages (31/01/21 – 1.38%) 2.11 202,421 Anheuser-Busch InBev 9,424 0.38 211,410 Carlsberg ‘B’ 25,509 1.03 163,047 Coca-Cola European Partners 6,938 0.28 68,011 Heineken 5,400 0.22 67,693 JDE Peets 1,503 0.06 21,193 Pernod Ricard 3,347 0.14

PUTM ACS European ex UK Fund

10

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Chemicals (31/01/21 – 4.29%) 5.05 17,464 Air Liquide 2,209 0.09 7,701 AkzoNobel 589 0.02 312,469 BASF 17,573 0.71 401,285 Bayer 17,958 0.73 179,349 Brenntag 11,329 0.46 385,847 Covestro 17,074 0.69 65,095 Evonik Industries 1,562 0.06 2,492 Givaudan 7,617 0.31 41,431 Koninklijke DSM 5,748 0.23 148,104 Lanxess 6,625 0.27 53,432 Sika 13,735 0.56 87,601 Solvay 7,795 0.32 56,892 Umicore 1,589 0.07 345,427 Yara International 13,127 0.53

Construction & Materials (31/01/21 – 5.30%) 4.63 48,033 Actividades de Construcción y Servicios 895 0.04 119,059 Actividades de Construcción y Servicios Rights 44 0.00 645,972 Assa Abloy ‘B’ 13,009 0.53 392,881 Bouygues 10,239 0.42 247,158 CRH 9,171 0.37 198,619 Eiffage 15,394 0.62 2,383 Ferrovial 49 0.00 28,643 Geberit 14,336 0.58 75,298 Holcim 2,999 0.12 98,385 Kingspan Group 6,986 0.28 369,969 Saint Gobain 18,436 0.75 508,936 Skanska ‘AB’ 9,172 0.37 167,863 Vinci 13,557 0.55

Electricity (31/01/21 – 3.49%) 2.32 1,010,579 Électricité de France 7,176 0.29 164,874 Endesa 2,734 0.11 1,643,929 Enel 9,313 0.38 127,365 For tum 2,560 0.10 4,105,249 Iberdrola 34,833 1.41 4,105,249 Iberdrola Rights 575 0.03

Electronic & Electrical Equipment (31/01/21 – 3.02%) 2.39 183,996 Legrand Promesses 13,805 0.56 302,922 Prysmian 7,522 0.30 238,283 Schneider Electric 29,737 1.21 239,433 Uniper 7,986 0.32

PUTM ACS European ex UK Fund

11

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Financial Services (31/01/21 – 4.64%) 4.85 159,415 Amundi 9,137 0.37 114,321 EQT 3,286 0.13 470,609 Hexagon B 4,673 0.19 33,042 Industrivärden ‘C’ 758 0.03 1,426,468 Investor B 22,855 0.93 307,650 Kinnevik 6,758 0.28 29,575 Partners Group 30,223 1.22 155,165 Prosus 9,519 0.39 8,540 Sofina 2,515 0.10 2,174,579 UBS 29,769 1.21

Fixed Line Telecommunications (31/01/21 – 1.02%) 0.82 15,530 Elisa 675 0.03 1,837,245 Koninklijke 4,493 0.18 949,541 Orange 8,264 0.33 158,014 Proximus 2,392 0.10 10,742 Swisscom 4,542 0.18

Food & Drug Retailers (31/01/21 – 2.05%) 1.89 392,124 Carrefour 5,542 0.22 40,232 Colruyt 1,213 0.05 38,979 ICA Gruppen 1,665 0.07 329,841 Jeronimo Martins 5,873 0.24 225,292 Kesko ‘B’ 5,256 0.21 1,130,760 Koninklijke Ahold Delhaiz 27,163 1.10

Food Producers (31/01/21 – 4.54%) 4.57 1,080 Barry Callebaut 1,835 0.07 340,248 Danone 15,704 0.64 247 Lindt & Spruengli 2,118 0.09 54,285 Marine Harvest 985 0.04 958,074 Nestle ‘R’ 91,333 3.70 89,377 Orkla 634 0.03

Forestry & Paper (31/01/21 – 0.00%) 0.06 111,998 SCA ‘B’ 1,439 0.06

Gas, Water & Multiutilities (31/01/21 – 2.26%) 2.62 550,059 E.On 5,616 0.23 279,312 Enagás 4,480 0.18 1,930,460 Engie 21,862 0.89 145,770 Naturgy Energy 3,426 0.14 1,178,916 Red Electrica Corporation 17,642 0.71 787,748 Snam 3,265 0.13 52,740 Suez Environnement 874 0.03 282,761 Veolia Environnement 7,544 0.31

PUTM ACS European ex UK Fund

12

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

General Industrials (31/01/21 – 1.38%) 1.83 7,656 Knorr-Bremse 572 0.02 343,964 Siemens 40,057 1.62 118,976 Smurfit Kappa 4,626 0.19

General Retailers (31/01/21 – 2.20%) 1.97 1,199,137 Inditex 26,791 1.09 39,621 Kering 21,727 0.88

Healthcare Equipment & Services (31/01/21 – 3.76%) 3.61 40,094 Carl Zeiss Meditec 4,745 0.19 31,376 Coloplast ‘B’ 3,379 0.14 60,696 Essilor International 8,455 0.34 89,293 Eurofins Scientific 6,619 0.27 596,149 Fresenius 18,158 0.74 117,962 Fresenius Medical Care 5,902 0.24 127,828 Getinge ‘B’ 3,697 0.15 535,918 Koninklijke Philips 13,158 0.53 44,619 Qiagen 1,628 0.07 56,507 Sonova ‘N’ 14,792 0.60 6,951 Straumann Holdings 8,433 0.34

Household Goods (31/01/21 – 0.35%) 0.85 158,126 Electrolux AB 2,426 0.10 156,644 Henkel Preference 9,468 0.38 780,005 Husqvarna ‘B’ 8,032 0.33 8,719 SEB 977 0.04

Industrial Engineering (31/01/21 – 3.52%) 2.61 322,420 ABB 8,185 0.33 121,975 Alfa Laval 3,037 0.12 213,638 Alstom 5,114 0.21 286,717 Atlas Copco ‘A’ 12,441 0.50 147,327 CNH Industrial 1,641 0.07 113,636 Epiroc A 1,793 0.07 162,528 GEA Group 5,664 0.23 47,515 Kone ‘B’ 2,272 0.09 11,490 Sartorius Preference 4,564 0.19 40,386 Schindler participation certificates 7,439 0.30 295,326 Vestas Wind Systems 5,855 0.24 240,065 Volvo ‘B’ 3,996 0.16 264,315 Wartsila 2,390 0.10

Industrial Metals (31/01/21 – 0.32%) 0.21 454,943 Norsk Hydro 2,585 0.10 108,633 Voestalpine 2,681 0.11

PUTM ACS European ex UK Fund

13

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Industrial Transportation (31/01/21 – 2.45%) 3.89 7,698 A.P. Møller - Maersk A/S 20,496 0.83 884,861 Bolloré 3,519 0.14 701,447 Deutsche Post 30,881 1.25 153,843 DSV 23,150 0.94 86,138 Kuehne & Nagel International 17,950 0.73

Life Insurance (31/01/21 – 1.53%) 1.94 387,619 Aegon 1,617 0.07 134,199 Ageas 4,774 0.19 66,529 CNP Assurances 1,212 0.05 483,910 NN Group 20,042 0.81 1,078,307 Poste Italiane 10,676 0.43 20,209 Swiss Life Rentenanstalt 9,578 0.39

Media (31/01/21 – 1.50%) 1.33 276,151 Publicis Groupe 13,775 0.56 123,788 Universal Music Group 2,256 0.09 914,980 Vivendi 8,864 0.36 103,549 Wolters Kluwer Certificates 7,807 0.32

Mining (31/01/21 – 0.21%) 0.46 383,034 Boliden 11,415 0.46

Mobile Telecommunications (31/01/21 – 0.66%) 0.52 548,498 Deutsche Telekom 7,605 0.31 1,447,604 Telefónica Deutschland 3,071 0.13 28,857 Telenor 354 0.01 609,188 TeliaSonera 1,777 0.07

Non Equity Invest Instruments (31/01/21 – 0.20%) 0.00 Non-Life Insurance (31/01/21 – 3.26%) 2.50 202,196 Allianz 38,189 1.55 416,605 AXA 9,717 0.39 341,628 Gjensidige Forsikring 6,186 0.25 1,633 Muenchener Rueckver 380 0.02 50,625 Sampo Oyj 1,856 0.08 144,076 Tryg 2,539 0.10 7,846 Zurich Insurance Group 2,767 0.11

Oil & Gas Producers (31/01/21 – 2.57%) 2.51 126,290 OMV 5,690 0.23 723,915 Repsol 6,795 0.28 1,178,616 TotalEnergies 49,446 2.00

Personal Goods (31/01/21 – 6.42%) 8.09 136,288 Adidas 27,449 1.11 24,663 Beiersdorf 1,812 0.07

PUTM ACS European ex UK Fund

14

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Personal Goods (continued) 165,565 CIE Financiere Richemont ‘A’ 17,615 0.71 469,855 Essity ‘B’ 9,815 0.40 1,924 Hermes International 2,112 0.09 112,879 L’Oreal 35,533 1.44 138,048 LVMH 83,256 3.38 146,256 Moncler 6,885 0.28 70,373 Pandora 5,650 0.23 106,630 Puma 8,362 0.34

4,702 The Swatch Group ‘B’ 1,010 0.04

Pharmaceuticals & Biotechnology (31/01/21 – 10.98%) 11.36 45,424 BioMérieux 3,945 0.16 36,369 Genmab 9,083 0.37 49,578 Ipsen Promesses 3,572 0.14 48,279 Merck KGaA 7,838 0.32 784,514 Novartis ‘R’ 50,319 2.04 722,692 Novo Nordisk ‘B’ 53,409 2.17 20,717 Novozymes 1,056 0.04 258,535 Orion Oyj 7,794 0.32 28,795 Recordati 1,192 0.05 365,464 Roche Holding 104,404 4.23 418,775 Sanofi 32,450 1.31 20,871 Vifor Pharma 2,734 0.11 73,036 William Demant Holding 2,392 0.10

Real Estate & Investment Services (31/01/21 – 1.05%) 1.00 877,750 Aroundtown 4,019 0.16 16,051 Fastighets Balder ‘B’ 786 0.03 121,473 LEG Immobilien 11,931 0.49 56,272 Swiss Prime Site 4,111 0.17 89,025 Vonovia 3,724 0.15

Real Estate Investment Trusts (31/01/21 – 0.37%) 0.24 300,764 Klépierre 5,893 0.24

Software & Computer Services (31/01/21 – 3.95%) 3.51 138,976 Bechtle 6,117 0.25 102,501 Capgemini 16,910 0.68 175,247 Dassault Systems 6,215 0.25 139,475 Embracer Group ‘AB’ 1,021 0.04 486,798 SAP 44,660 1.81 3,510 Teleperformance 977 0.04 39,754 Temenos Group 3,501 0.14 85,808 United Internet 2,480 0.10 135,262 Worldline 4,821 0.20

PUTM ACS European ex UK Fund

15

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Support Services (31/01/21 – 0.35%) 0.40 19,394 Adecco 680 0.03 152,949 Randstad 7,338 0.30 188,366 Securitas ‘B’ 1,691 0.07

Technology Hardware & Equipment (31/01/21 – 5.58%) 6.73 6,072 ASM International 1,532 0.06 186,564 ASML Holding 92,438 3.75 1,890,192 Ericsson ‘B’ 17,346 0.70 750,908 Infineon Technologies 22,603 0.92 3,478,170 Nokia 15,260 0.62 485,432 ST Microelectronics 16,725 0.68

Tobacco (31/01/21 – 0.46%) Travel & Leisure (31/01/21 – 0.00%) 0.04 8,592 Flutter Entertainment 964 0.04

Money Markets (31/01/21 – 2.99%) 1.58 €47,273 Aberdeen Standard Liquidity Fund (Lux) – Euro Fund Class Z-3+ 38,964 1.58

Futures (31/01/21 – (0.03%)) (0.01) 1,204 EUX Euro Stoxx 50 March 2022 (230) (0.01)

Portfolio of investments^ 2,458,653 99.68 Net other assets 7,907 0.32

Net assets 2,466,560 100.00

Unless otherwise stated, all investments are approved securities being eitherofficially listed in a member state or traded on or under the rules of an eligiblesecurities market.

The counterparty for the Futures is Merrill Lynch International.

^ Includes investment liabilities.

+SICAVs (open ended investment schemes registered outside the UK).

PUTM ACS European ex UK Fund

16

PUTM ACS European ex UK Fund

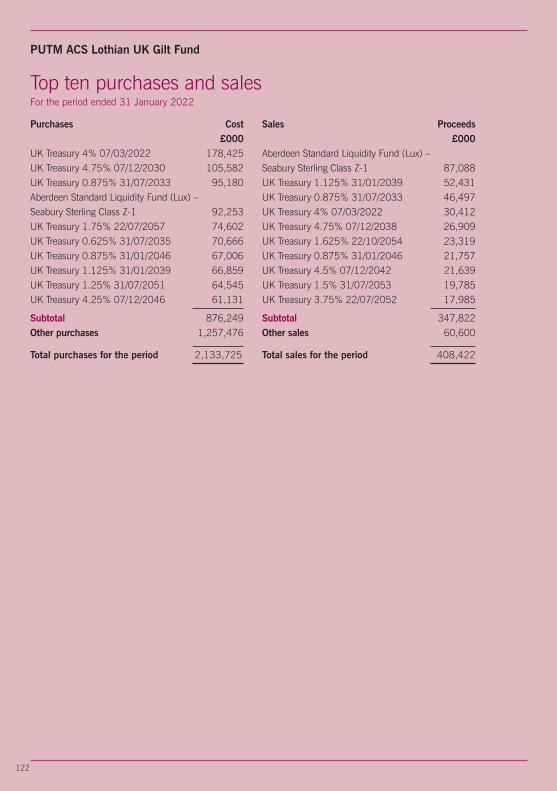

Top ten purchases and salesFor the year ended 31 January 2022

Purchases Cost£000

Aberdeen Standard Liquidity Fund (Lux) –Euro Fund Class Z-3 188,669Roche Holding 70,208ASML Holding 61,655Nestle ‘R’ 55,275LVMH 46,729TotalEnergies 45,896L’Oreal 36,951Novo Nordisk ‘B’ 35,290Siemens 33,535SAP 31,107

Subtotal 605,315Other purchases 1,713,952

Total purchases for the year 2,319,267

Sales Proceeds£000

Aberdeen Standard Liquidity Fund (Lux) –Euro Fund Class Z-3 179,381Vonovia 20,791BNP Paribas 19,646TotalEnergies 19,426Nestle ‘R’ 19,030Logitech ‘R’ 16,303Intesa Sanpaolo 15,112Hermes International 13,312L’Oreal 12,902Essilor International 11,881

Subtotal 327,784Other sales 728,027

Total sales for the year 1,055,811

17

PUTM ACS European ex UK Fund

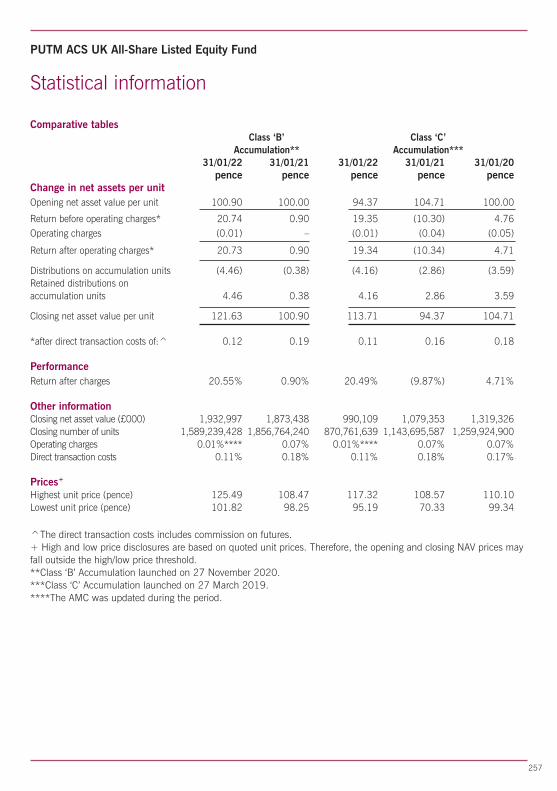

Statistical information

Comparative tables Class ‘B’ Class ‘C’ Accumulation** Accumulation*** 31/01/22 31/01/21 31/01/22 31/01/21 31/01/20 pence pence pence pence penceChange in net assets per unitOpening net asset value per unit 99.45 100.00 117.27 110.29 100.00

Return before operating charges* 15.31 (0.53) 17.90 7.09 10.39Operating charges (0.07) (0.02) (0.10) (0.11) (0.10)

Return after operating charges* 15.24 (0.55) 17.80 6.98 10.29

Distributions on accumulation units (2.51) (0.19) (2.81) (2.18) (2.63)Retained distributions onaccumulation units 2.51 0.19 2.81 2.18 2.63

Closing net asset value per unit 114.69 99.45 135.07 117.27 110.29

*after direct transaction costs of:^ 0.06 0.05 0.07 0.05 0.04

PerformanceReturn after charges 15.32% (0.55%) 15.18% 6.33% 10.29%

Other informationClosing net asset value (£000) 701,329 33,302 277,004 159,660 172,567Closing number of units 611,492,402 33,485,372 205,079,222 136,142,138 156,472,423Operating charges 0.02%**** 0.09% 0.02%**** 0.10% 0.11%Direct transaction costs 0.05% 0.05% 0.05% 0.05% 0.04%

Prices+

Highest unit price (pence) 123.36 105.24 145.29 124.08 115.65Lowest unit price (pence) 99.97 99.45 117.84 83.48 100.00

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.**Class ‘B’ Accumulation launched on 27 November 2020.***Class ‘C’ Accumulation launched on 27 March 2019.****The AMC was updated during the year.

18

Statistical information

Comparative tables Class ‘D’ Class ‘H’ Accumulation** Accumulation*** 31/01/22 31/01/21 31/01/20 31/01/22 pence pence pence penceChange in net assets per unitOpening net asset value per unit 117.36 110.33 100.00 100.00

Return before operating charges* 17.93 7.14 10.43 0.27Operating charges (0.10) (0.11) (0.10) (0.50)

Return after operating charges* 17.83 7.03 10.33 (0.23)

Distributions on accumulation units (2.82) (2.22) (2.67) –Retained distributions onaccumulation units 2.82 2.22 2.67 –

Closing net asset value per unit 135.19 117.36 110.33 99.77

*after direct transaction costs of:^ 0.07 0.05 0.04 0.05

PerformanceReturn after charges 15.19% 6.37% 10.33% (0.23%)

Other informationClosing net asset value (£000) 1,405,958 882,206 910,988 9,864Closing number of units 1,040,009,023 751,688,098 825,719,542 9,886,946Operating charges 0.02%**** 0.10% 0.11% 1.52%Direct transaction costs 0.05% 0.05% 0.04% 0.05%

Prices+

Highest unit price (pence) 145.41 124.17 115.69 107.66Lowest unit price (pence) 117.94 83.52 100.00 97.55

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.**Class ‘D’ Accumulation class launched on 27 March 2019.***Class ‘H’ Accumulation class launched on 8 October 2021, hence there are no comparatives.****The AMC was updated during the year.

PUTM ACS European ex UK Fund

19

Statistical information

Comparative tables Class ‘I’ Class ‘X’ Accumulation** Accumulation*** 31/01/22 31/01/22 31/01/21 pence pence penceChange in net assets per unitOpening net asset value per unit 100.00 136.35 100.00

Return before operating charges* 0.28 20.74 36.46Operating charges (0.50) (0.13) (0.11)

Return after operating charges* (0.22) 20.61 36.35

Distributions on accumulation units – (3.15) (2.35)Retained distributions onaccumulation units – 3.15 2.35

Closing net asset value per unit 99.78 156.96 136.35

*after direct transaction costs of:^ 0.05 0.07 0.06

PerformanceReturn after charges (0.22%) 15.12% 36.35%

Other informationClosing net asset value (£000) 72,327 78 341Closing number of units 72,487,185 50,000 250,000Operating charges 1.52% 0.02%**** 0.10%Direct transaction costs 0.05% 0.05% 0.05%

Prices+

Highest unit price (pence) 107.66 168.85 144.30Lowest unit price (pence) 97.56 136.98 97.08

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.**Class ‘I’ Accumulation class launched on 8 October 2021, hence there are no comparatives.***Class ‘X’ Accumulation class launched on 14 March 2020.****The AMC was updated during the year.

PUTM ACS European ex UK Fund

20

PUTM ACS European ex UK Fund

Statistical information

Investment objective

The Sub-fund aims to provide a total return (a combination of capital growth andincome) by outperforming the MSCI Europe ex UK Index (the ‘Index’) before fees by0.5% to 1% per annum over any given 3 year period.

Investment policyThe Sub-fund aims to achieve its objective primarily by investing over 70% of theportfolio in equities or equity related securities of European excluding United Kingdomcompanies that are constituents of the MSCI Europe ex UK Index. The Sub-fund mayinvest up to 5% in European ex UK companies listed outside of the Index.

Equity related securities will include convertible stocks, stock exchange listedwarrants, depository receipts, and any other such investments which entitle the holderto subscribe for or convert into the equity of the company and/or where the share priceperformance is, in the opinion of the Investment Manager, influenced significantly bythe stock market performance of the company's ordinary shares. The Sub-fund mayalso invest in other transferable securities, moneymarket instruments, deposits, cashand near cash and other collective investment schemes.

Derivatives will be used for efficient portfolio management only.

Investment strategyAlthough over 70% is invested in components of the index. The Sub-fund is activelymanaged and the Investment Manager has discretion to select its investments. TheSub-fund does not concentrate on any particular sector.

Revenue distribution and pricingUnits of the Sub-fund are available as either Class ‘B’ Accumulation, ‘C’ Accumulation,‘D’ Accumulation, ‘H’ Accumulation,‘'I’ Accumulation or ‘X’ Accumulation units (whererevenue is reinvested to enhance the unit price). There will be two potentialdistributions in each accounting year: an interim distribution as at 31 July and a finaldistribution as at 31 January.

At each distribution the net revenue after deduction of expenses, from the investmentsof the Sub-fund, is apportioned amongst the unitholders. Unitholders receive a taxvoucher giving details of the distribution and the ACS Manager’s Report no later thantwo months after these dates.

21

Statistical information

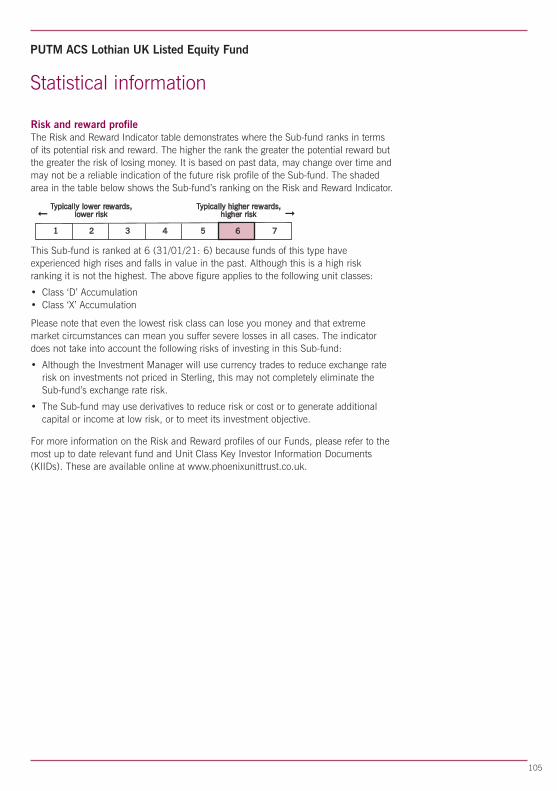

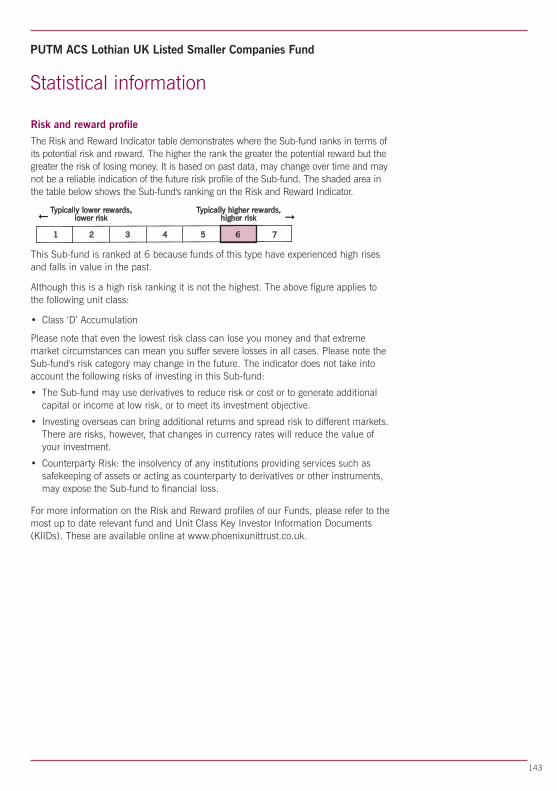

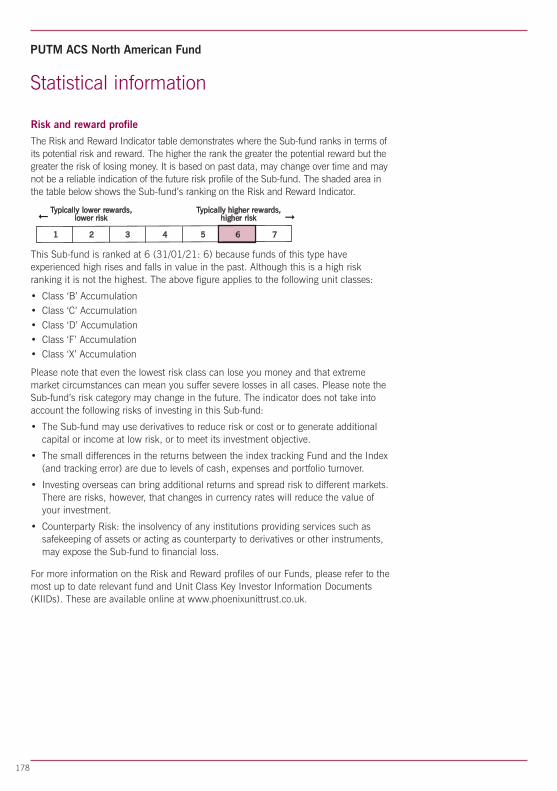

Risk and reward profileThe Risk and Reward Indicator table demonstrates where the Sub-fund ranks in termsof its potential risk and reward. The higher the rank the greater the potential reward butthe greater the risk of losing money. It is based on past data, may change over time andmay not be a reliable indication of the future risk profile of the Sub-fund. The shadedarea in the table below shows the Sub-fund’s ranking on the Risk and Reward Indicator.

Typically lower rewards, Typically higher rewards,lower risk higher risk fi

1 2 3 4 5 6 7

This Sub-fund is ranked at 6 (31/01/21: 6) because funds of this type haveexperienced high rises and falls in value in the past. Although this is a high riskranking it is not the highest. The above figure applies to the following unit classes:

• Class ‘B’ Accumulation

• Class ‘C’ Accumulation

• Class 'D' Accumulation

• Class ‘H’ Accumulation

• Class ‘I’ Accumulation

• Class ‘X’ Accumulation

Please note that even the lowest risk class can lose you money and that extrememarket circumstances can mean you suffer severe losses in all cases. Please note theSub-fund’s risk category may change in the future. The indicator does not take intoaccount the following risks of investing in this Sub-fund:

• The Sub-fund may use derivatives to reduce risk or cost or to generate additionalcapital or income at low risk, or to meet its investment objective.

• Investing overseas can bring additional returns and spread risk to different markets.There are risks, however, that changes in currency rates will reduce the value ofyour investment.

• Emerging markets or less developed countries may face more political, economic orstructural challenges than developed countries. This means that your money is atgreater risk.

• Counterparty Risk: the insolvency of any institutions providing services such assafekeeping of assets or acting as counterparty to derivatives or other instruments,may expose the Sub-fund to financial loss.

For more information on the Risk and Reward profiles of our Funds, please refer to themost up to date relevant fund and Unit Class Key Investor Information Documents(KIIDs). These are available online at www.phoenixunittrust.co.uk.

fi

PUTM ACS European ex UK Fund

22

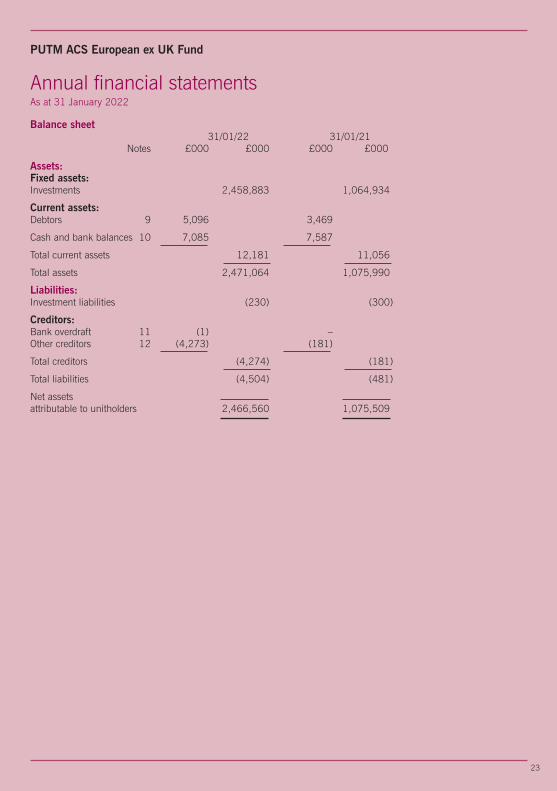

PUTM ACS European ex UK Fund

Annual financial statementsFor the year ended 31 January 2022

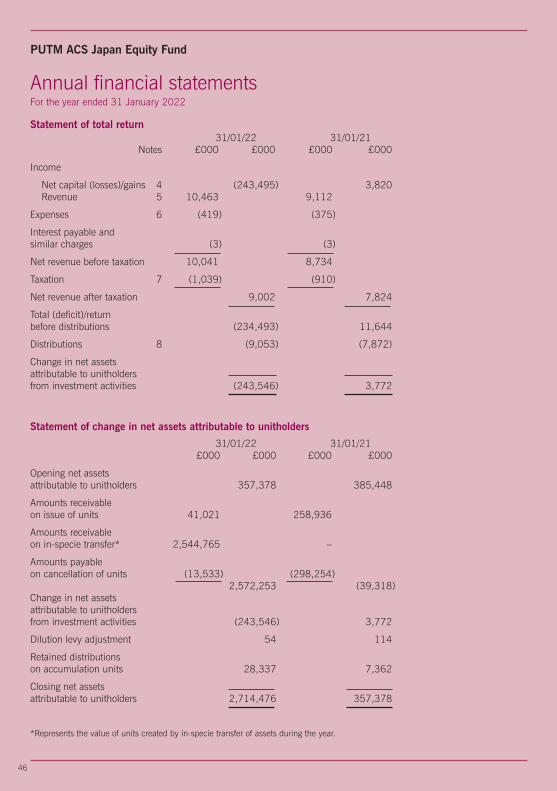

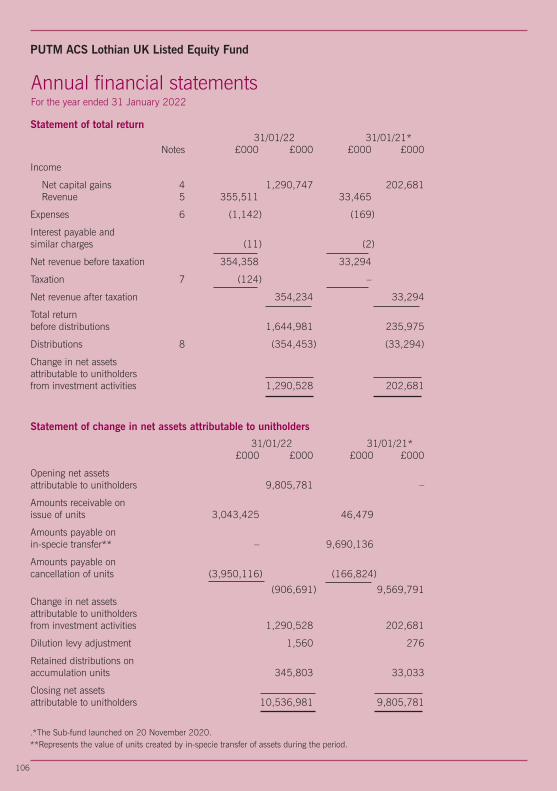

Statement of total return 31/01/22 31/01/21 Notes £000 £000 £000 £000

Income

Net capital gains 4 135,146 36,514 Revenue 5 34,031 23,934

Expenses 6 (1,508) (1,017)

Interest payable andsimilar charges (46) (70)

Net revenue before taxation 32,477 22,847

Taxation 7 (4,229) (2,005)

Net revenue after taxation 28,248 20,842

Total returnbefore distributions 163,394 57,356

Distributions 8 (28,435) (20,947)

Change in net assetsattributable to unitholdersfrom investment activities 134,959 36,409

Statement of change in net assets attributable to unitholders

31/01/22 31/01/21 £000 £000 £000 £000

Opening net assetsattributable to unitholders 1,075,509 1,083,555

Amounts receivableon issue of units 38,196 751,602

Amounts receivableon in-specie transfer* 1,405,597 –

Amounts payableon cancellation of units (218,041) (816,066) 1,225,752 (64,464)Change in net assetsattributable to unitholdersfrom investment activities 134,959 36,409

Dilution levy adjustment 139 122

Retained distributionson accumulation units 30,201 19,887

Closing net assetsattributable to unitholders 2,466,560 1,075,509

*Represents the value of units created by in-specie transfer of assets during the year.

23

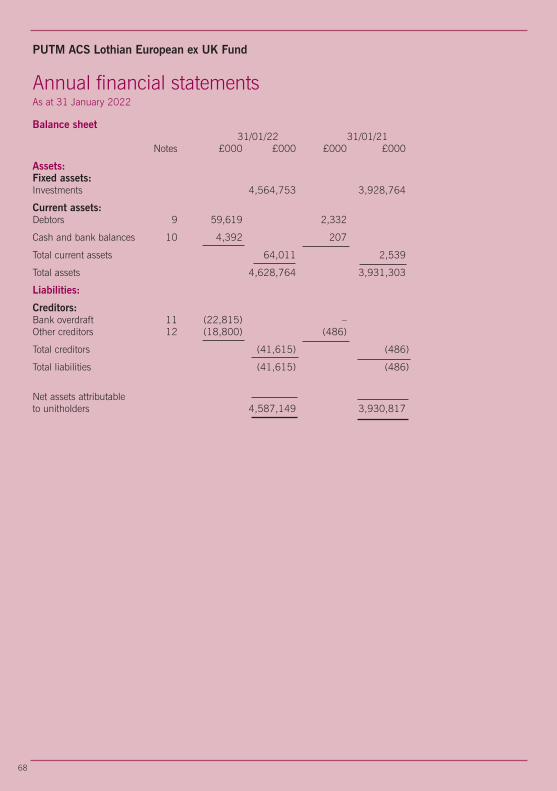

Balance sheet 31/01/22 31/01/21 Notes £000 £000 £000 £000

Assets:Fixed assets:Investments 2,458,883 1,064,934

Current assets:Debtors 9 5,096 3,469

Cash and bank balances 10 7,085 7,587

Total current assets 12,181 11,056

Total assets 2,471,064 1,075,990

Liabilities:Investment liabilities (230) (300)

Creditors:Bank overdraft 11 (1) – Other creditors 12 (4,273) (181)

Total creditors (4,274) (181)

Total liabilities (4,504) (481)

Net assetsattributable to unitholders 2,466,560 1,075,509

Annual financial statementsAs at 31 January 2022

PUTM ACS European ex UK Fund

24

PUTM ACS European ex UK Fund

Notes to the financial statements

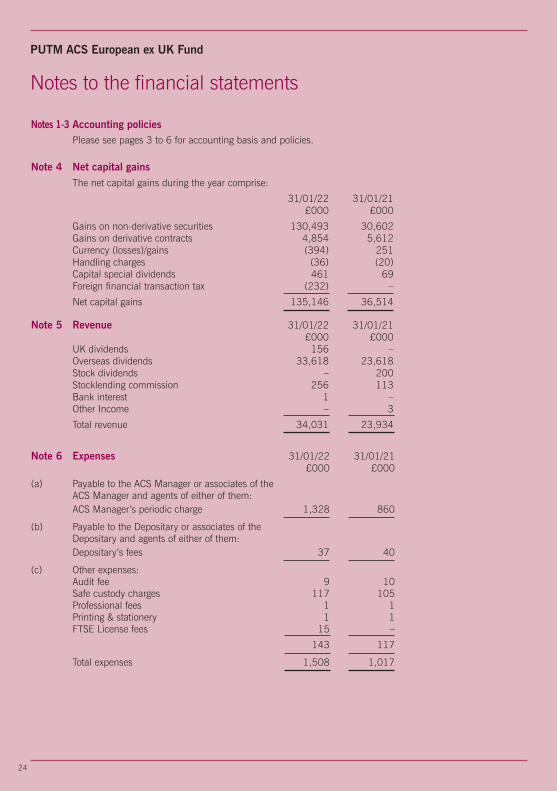

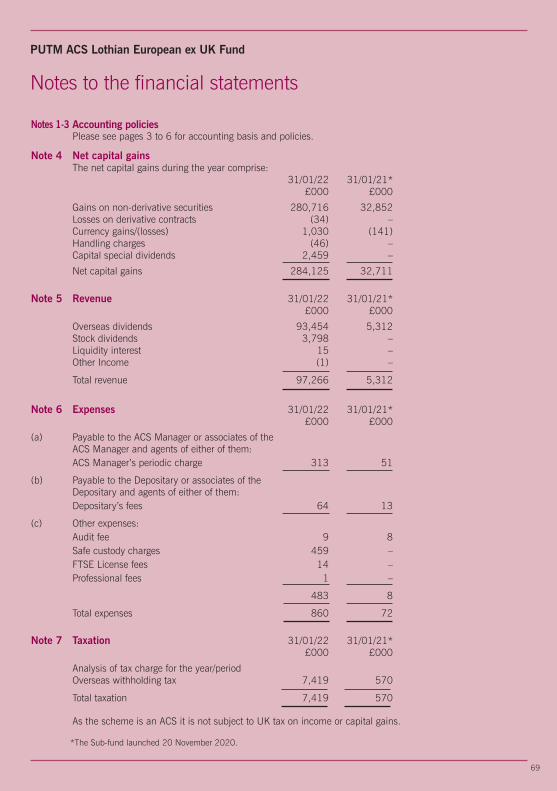

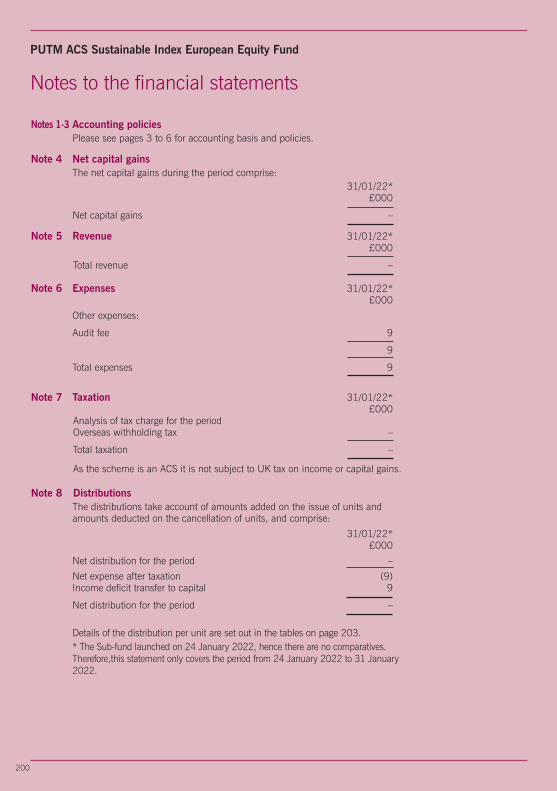

Notes 1-3 Accounting policiesPlease see pages 3 to 6 for accounting basis and policies.

Note 4 Net capital gainsThe net capital gains during the year comprise:

31/01/22 31/01/21 £000 £000

Gains on non-derivative securities 130,493 30,602Gains on derivative contracts 4,854 5,612Currency (losses)/gains (394) 251Handling charges (36) (20)Capital special dividends 461 69Foreign financial transaction tax (232) –

Net capital gains 135,146 36,514

Note 5 Revenue 31/01/22 31/01/21 £000 £000

UK dividends 156 –Overseas dividends 33,618 23,618Stock dividends – 200Stocklending commission 256 113Bank interest 1 –Other Income – 3

Total revenue 34,031 23,934

Note 6 Expenses 31/01/22 31/01/21 £000 £000

(a) Payable to the ACS Manager or associates of theACS Manager and agents of either of them:

ACS Manager’s periodic charge 1,328 860

(b) Payable to the Depositary or associates of theDepositary and agents of either of them:

Depositary’s fees 37 40

(c) Other expenses: Audit fee 9 10

Safe custody charges 117 105Professional fees 1 1Printing & stationery 1 1

FTSE License fees 15 –

143 117

Total expenses 1,508 1,017

25

Notes to the financial statements

Note 7 Taxation 31/01/22 31/01/21 £000 £000(a) Analysis of tax charge for the year

Overseas withholding tax 4,229 2,005

Total taxation 4,229 2,005

As the scheme is an ACS it is not subject to UK tax on income or capital gains.

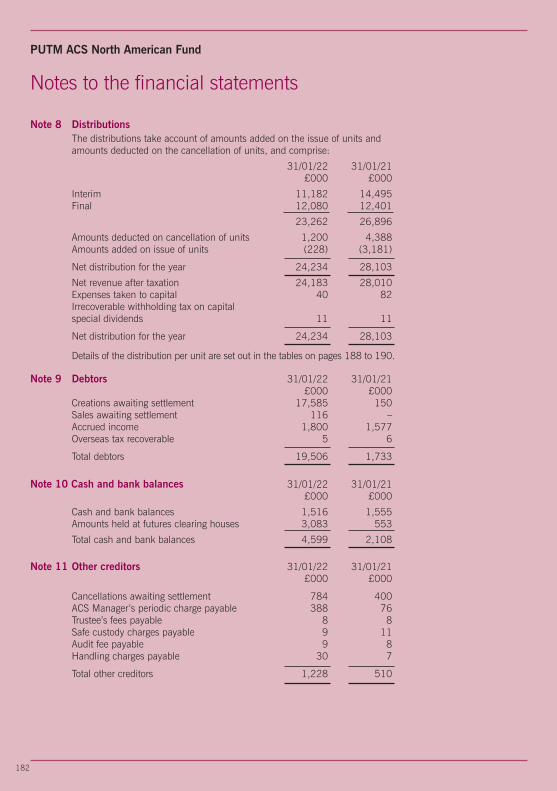

Note 8 DistributionsThe distributions take account of amounts added on the issue of units and amountsdeducted on the cancellation of units, and comprise:

31/01/22 31/01/21 £000 £000

Interim 19,213 14,742 Final 10,988 5,145

30,201 19,887

Amounts deducted on cancellation of units 936 2,201 Amounts added on issue of units (2,702) (1,141)

Net distribution for the year 28,435 20,947

Net revenue after taxation 28,248 20,842 Expenses taken to capital 117 105 Foreign Financial Transaction Tax charged in capital (76) – Income deficit transfer to capital 127 – Withholding tax on capital special dividend 19 –

Net distribution for the year 28,435 20,947

Details of the distribution per unit are set out in the tables on pages 32 to 34.

Note 9 Debtors 31/01/22 31/01/21 £000 £000

Creations awaiting settlement 80 –Accrued income 245 32Overseas tax recoverable 4,771 3,437

Total debtors 5,096 3,469

Note 10 Cash and bank balances 31/01/22 31/01/21 £000 £000

Cash and bank balances 733 1,722Amounts held at futures clearing houses 6,352 5,865

Total cash and bank balances 7,085 7,587

Note 11 Bank overdraft 31/01/22 31/01/21 £000 £000

Bank overdraft 1 –

Total bank overdraft 1 –

PUTM ACS European ex UK Fund

26

PUTM ACS European ex UK Fund

Notes to the financial statements

Note 12 Other creditors 31/01/22 31/01/21 £000 £000

Cancellations awaiting settlement 3,226 75ACS Manager’s periodic charge payable 803 75Trustee’s fees payable 9 7Safe custody charges payable 24 16Audit fee payable 9 8Foreign financial transaction tax payable 200 –Handling charges payable 2 –

Total other creditors 4,273 181

Note 13 Reconciliation of units Class ‘B’ Class ‘C’ Class ‘D’ Class ‘H’* Class ‘I’* Class ‘X’ Accumulation Accumulation Accumulation Accumulation Accumulation Accumulation

Opening units issuedat 01/02/21 33,485,372 136,142,138 751,688,098 – – 250,000Unit movements in year:Units issued 21,477,029 8,979,125 882,482 – 31,140 –-Units cancelled (43,433,572) (27,251,410) (97,261,450) (242,178) (1,487,357) (200,000)In-specie transactions 599,963,573 87,209,369 384,699,893 10,129,124 73,943,402 –

Closing units at 31/01/22 611,492,402 205,079,222 1,040,009,023 9,886,946 72,487,185 50,000

*Class ‘H’ Accumulation and ‘I’ Accumulation launched on 8 October 2021.

Note 14 Contingencies and commitmentsAt 31 January 2022 the Sub-fund had no outstanding calls on partly paid shares, no potential underwritingcommitments or any other contingent liabilities (31/01/21: £nil).

Note 15 StocklendingThe total value of securities on loan at the Balance sheet date was £1,136,994 (31/01/21: £276,493).Collateral was held in the following form:

31/01/22 31/01/21 £000 £000

UK Equities 1,284 323

1,284 323

The gross earnings and fees paid for the year were £312,539 (31/01/21: £137,538) and £56,257(31/01/21: £24,757) respectively.The gross earnings were split by the lending agent as follows:– 82% to the Lender (PUTM ACS European ex UK Fund)– 8% to the ACS Manager (Phoenix Unit Trust Managers Limited)– 10% retained by the Lending Agent (eSec)

The counterparties for the securities on loan are shown in the appendix on page 278.

27

Note 16 Unitholders’ fundsThere are six unit classes in issue within the Sub-fund. These are Class ‘B’ Accumulation, Class ‘C’Accumulation, Class ‘D’ Accumulation, Class ‘H’ Accumulation, Class ‘I’ Accumulation and Class ‘X’Accumulation. The ACS Manager’s periodic charge in respect of Class ‘B’, Class ‘C’, Class ‘D’, Class ‘X’ ,Class 'H' and Class 'I' is expressed as an annual percentage of the value of the property of the Sub-fundattributable to each unit class and is currently 0.005% in respect of Class ‘B’units, Class ‘C’ units, Class ‘D’units and Class ‘X’ units and 1.505% in respect of Class 'H' units and Class 'I' units.

Consequently, the level of net revenue attributable to each unit class will differ. Should it be necessary towind-up the Sub-fund, each unit class will have the same rights as regards to the distribution of the propertyof the Sub-fund.

Note 17 Related party transactionsThe ACS Manager is a related party to the Sub-fund by virtue of its controlling influence.

The ACS Manager is part of the Phoenix Group. Phoenix Life Limited which is also part of the PhoenixGroup, is a material unitholder in the Sub-fund and therefore a related party, holding the following percentageof the units at the year end.

Class ‘B’ Class ‘C’ Class ‘D’ Class ‘H’* Class ‘I’* Class ‘X’

% % % % % %

As at 31 January 2022: 100.00 100.00 100.00 100.00 100.00 100.00

As at 31 January 2021: 100.00 100.00 100.00 n/a n/a 100.00

*Class ‘H’ Accumulation and ‘I’ Accumulation launched on 8 October 2021, hence there are nocomparatives.

ACS Manager’s periodic charge paid to the ACS Manager, Phoenix Unit Trust Managers Limited, or itsassociates, is shown in Note 6(a) and details of the units issued and cancelled by the ACS Manager areshown in the Statement of change in net assets attributable to unitholders and Note 8.

Any balances due to/from the ACS Manager or its associates at 31 January 2022 in respect of thesetransactions are shown in Notes 9 and 12.

Note 18 Financial instrumentsIn accordance with the investment objective, the Sub-fund holds certain financial instruments. Thesecomprise:• securities held in accordance with the investment objective and policies;• derivative transactions which the Sub-fund may also enter into, the purpose of which is to manage the

currency and market risks arising from the Sub-fund’s investment activities; and• cash and short term debtors and creditors arising directly from operations.

Counterparty exposureThe economic exposure of future derivative contracts is equal to the market value. The value of exposure andthe related counterparty are disclosed in the Portfolio of investments.

Notes to the financial statements

PUTM ACS European ex UK Fund

28

PUTM ACS European ex UK Fund

Notes to the financial statements

Note 18 Financial instruments (continued)Currency exposureAn analysis of the monetary assets and liabilities at the year end is shown below:

Net currency assets Net currency assets 31/01/22 31/01/21

Currency Monetary Non- Total Monetary Non- Total exposure monetary exposure exposure monetary exposure exposure exposure £000 £000 £000 £000 £000 £000

Danish Krone 225 152,521 152,746 124 55,828 55,952 Euro 9,772 1,659,129 1,668,901 8,918 701,600 710,518 Norwegian Krone 8 26,446 26,454 42 13,753 13,795 Sterling (4,170) - (4,170) 407 - 407 Swedish Krona - 161,056 161,056 - 89,407 89,407 Swiss Franc 2,049 452,563 454,612 1,326 202,722 204,048 US Dollar 23 6,938 6,961 58 1,324 1,382

7,907 2,458,653 2,466,560 10,875 1,064,634 1,075,509

Income received in other currencies is converted to Sterling on or near the date ofreceipt. The Sub-fund does not hedge or otherwise seek to avoid, movement risk onaccrued income.

Interest profileAt the year end date, 1.87% (31/01/21: 3.70%) of the Sub-fund’s net assets byvalue were interest bearing.

Interest rates earned/paid on deposits are earned/paid at a rate linked to SONIA(Sterling Overnight Index Average) or international equivalent. Interest was alsoearned on the investments in the the Aberdeen Standard Liquidity Fund.

Sensitivity analysisInterest rate risk sensitivityAs the majority of the Sub-fund’s financial assets are non-interest bearing, theSub-fund is only subject to limited exposure to fair value interest rate risk due tofluctuations in levels of market interest rates and therefore, no sensitivity analysishas been provided.

Foreign currency risk sensitivityA five percent increase in the value of the Sub-fund’s foreign currency exposurewould have the effect of increasing the return and net assets by £123,536,493(31/01/21: £53,755,100). A five percent decrease would have an equal andopposite effect.

Price risk sensitivityA five percent increase in the value of the Sub-fund’s portfolio would have theeffect of increasing the return and net assets by £122,932,664 (31/01/21:£53,775,450). A five percent decrease would have an equal and oppositeeffect.

29

Notes to the financial statements

Note 19 Fair value of investmentsThe fair value of the Sub-fund’s investments has been determined using the hierarchy below.

This complies with the ‘Amendments to FRS 102 – Fair value hierarchy disclosures’ issuedby the Financial Reporting Council in March 2016.

Level 1 The unadjusted quoted price in an active market for identical assets orliabilities that the entity can access at the measurement date.

Level 2 Inputs other than quoted prices included within Level 1 that areobservable (i.e. developed using market data) for the asset or liability,either directly or indirectly.

Level 3 Inputs are unobservable (i.e. for which market data is unavailable) for theasset or liability.

For the year ended 31/01/22Level 1 2 3 Total

Investment assets £000 £000 £000 £000Equities 2,419,919 – – 2,419,919Money markets 38,964 – – 38,964

2,458,883 – – 2,458,883

Investment liabilities £000 £000 £000 £000Derivatives (230) – – (230)

(230) – – (230)

For the year ended 31/01/21Level 1 2 3 Total

Investment assets £000 £000 £000 £000Equities 1,032,777 – – 1,032,777Money markets 32,157 – – 32,157

1,064,934 – – 1,064,934

Investment liabilities £000 £000 £000 £000Derivatives (300) – – (300)

(300) – – (300)

PUTM ACS European ex UK Fund

30

PUTM ACS European ex UK Fund

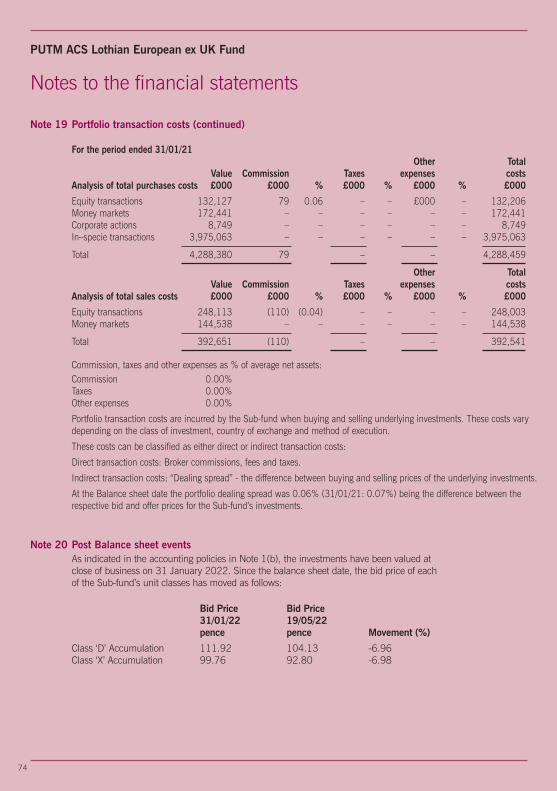

Note 20 Portfolio transaction costs

For the year ended 31/01/22Other Total

Value Commission Taxes expenses costsAnalysis of total purchases costs £000 £000 % £000 % £000 % £000

Equity transactions 728,402 7 – 693 0.01 75 – 729,177Money markets 188,669 – – – – – – 188,669Corporate actions 3,977 – – – – – – 3,977In-specie transactions 1,397,444 – – – – – – 1,397,444

Total 2,318,492 7 693 75 2,319,267

Other TotalValue Commission Taxes expenses costs

Analysis of total sales costs £000 £000 % £000 % £000 % £000

Equity transactions 876,178 (10) – – – – – 876,168Money markets 179,381 – – –- – – – 179,381Corporate actions 262 – – – – – – 262

Total 1,055,821 (10) – – 1,055,811

The Sub-fund has paid £19,936 as commission on purchases and sales of derivatives transactions for the yearended 31/01/22.

Commission, taxes and other expenses as % of average net assets:Commission 0.00%Taxes 0.04%Other expenses 0.01%

For the year ended 31/01/21Other Total

Value Commission Taxes expenses costsAnalysis of total purchases costs £000 £000 % £000 % £000 % £000

Equity transactions 589,430 8 – 453 0.08 2 – 589,893Money markets 96,844 – – – – – – 96,844Corporate actions 475 – – – – – – 475

Total 686,749 8 453 2 687,212

Other TotalValue Commission Taxes expenses costs

Analysis of total sales costs £000 £000 % £000 % £000 % £000

Equity transactions 646,640 (9) – – – (1) – 646,630Money markets 86,658 – – – – – – 86,658Corporate actions 87 – – – – – – 87

Total 733,385 (9) – (1) 733,375

The Sub-fund has paid £14,569 as commission on purchases and sales of derivatives transactions for the yearended 31/01/21.

Commission, taxes and other expenses as % of average net assets:Commission 0.00%Taxes 0.05%Other expenses 0.00%

Notes to the financial statements

31

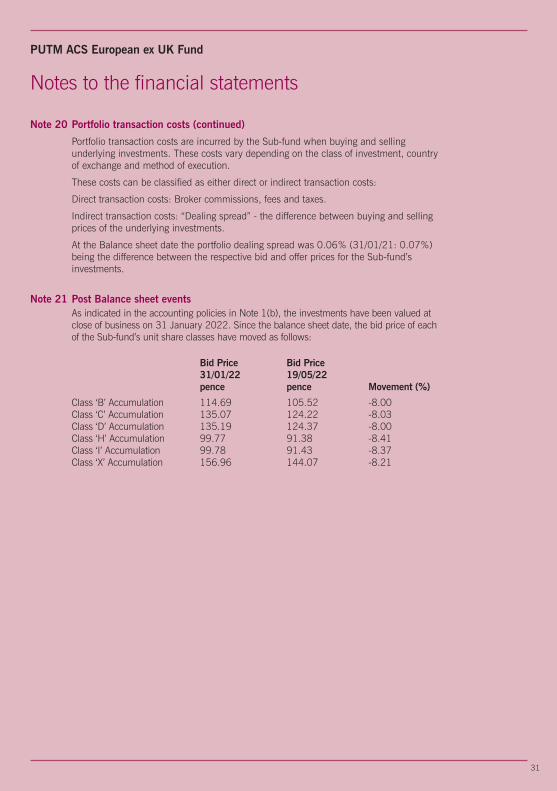

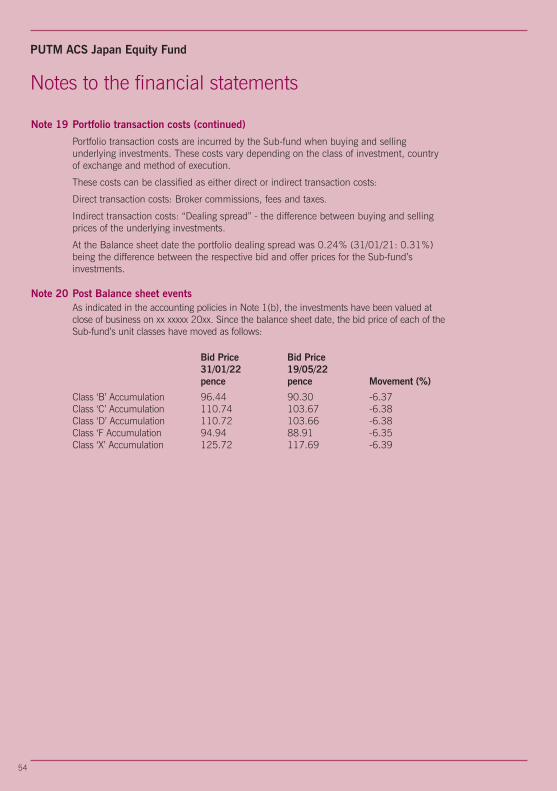

Note 20 Portfolio transaction costs (continued)

Portfolio transaction costs are incurred by the Sub-fund when buying and sellingunderlying investments. These costs vary depending on the class of investment, countryof exchange and method of execution.

These costs can be classified as either direct or indirect transaction costs:

Direct transaction costs: Broker commissions, fees and taxes.

Indirect transaction costs: “Dealing spread” - the difference between buying and sellingprices of the underlying investments.

At the Balance sheet date the portfolio dealing spread was 0.06% (31/01/21: 0.07%)being the difference between the respective bid and offer prices for the Sub-fund’sinvestments.

Notes to the financial statements

PUTM ACS European ex UK Fund

Note 21 Post Balance sheet eventsAs indicated in the accounting policies in Note 1(b), the investments have been valued atclose of business on 31 January 2022. Since the balance sheet date, the bid price of eachof the Sub-fund’s unit share classes have moved as follows:

Bid Price Bid Price 31/01/22 19/05/22

pence pence Movement (%)

Class ‘B’ Accumulation 114.69 105.52 -8.00Class ‘C’ Accumulation 135.07 124.22 -8.03Class ‘D’ Accumulation 135.19 124.37 -8.00Class ‘H’ Accumulation 99.77 91.38 -8.41Class ‘I’ Accumulation 99.78 91.43 -8.37Class ‘X’ Accumulation 156.96 144.07 -8.21

32

PUTM ACS European ex UK Fund

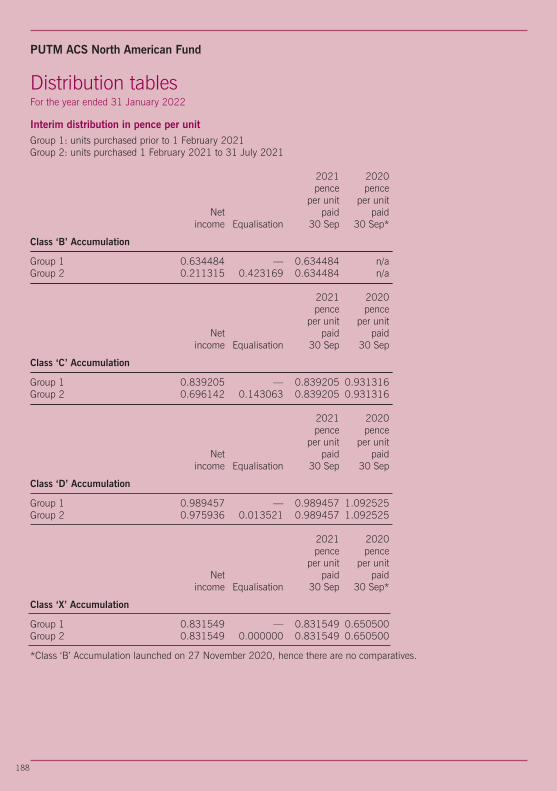

Interim distribution in pence per unitGroup 1: units purchased prior to 1 February 2021Group 2: units purchased 1 February 2021 to 31 July 2021 2021 2020 pence pence per unit per unit Net paid paid income Equalisation 30 Sep 30 Sep*

Class ‘B’ Accumulation

Group 1 1.897488 — 1.897488 n/aGroup 2 0.318815 1.578673 1.897488 n/a

2021 2020 pence pence per unit per unit Net paid paid income Equalisation 30 Sep 30 Sep

Class ‘C’ Accumulation

Group 1 2.213934 — 2.213934 1.621162Group 2 1.168133 1.045801 2.213934 1.621162

2021 2020 pence pence per unit per unit Net paid paid income Equalisation 30 Sep 30 Sep

Class ‘D’ Accumulation

Group 1 2.244345 — 2.244345 1.647188 Group 2 1.710504 0.533841 2.244345 1.647188

2021 2020 pence pence per unit per unit Net paid paid income Equalisation 30 Sep 30 Sep

Class ‘X’ Accumulation

Group 1 2.373533 — 2.373533 1.700340 Group 2 2.373533 0.000000 2.373533 1.700340

* The Class ‘B’ Accumulation launched on 27 November 2020, hence there are nocomparatives.

Distribution tablesFor the year ended 31 January 2022

33

Final distribution in pence per unitGroup 1: units purchased prior to 1 August 2021Group 2: units purchased 1 August 2021 to 31 January 2022 2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar

Class ‘B’ Accumulation

Group 1 0.609258 — 0.609258 0.190516Group 2 0.360658 0.248600 0.609258 0.190516

2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar

Class ‘C’ Accumulation

Group 1 0.596482 — 0.596482 0.558099 Group 2 0.349851 0.246631 0.596482 0.558099

2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar

Class ‘D’ Accumulation

Group 1 0.580653 — 0.580653 0.574613 Group 2 0.383049 0.197604 0.580653 0.574613

2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar*

Class ‘H’ Accumulation

Group 1 0.000000 — 0.000000 n/a Group 2 0.000000 0.000000 0.000000 n/a

*Class ‘H’ Accumulation launched on 8 October 2021, hence there are no comparatives.

Distribution tablesFor the year ended 31 January 2022

PUTM ACS European ex UK Fund

34

PUTM ACS European ex UK Fund

Final distribution in pence per unitGroup 1: units purchased prior to 1 August 2021Group 2: units purchased 1 August 2021 to 31 January 2022 2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar*

Class ‘I’ Accumulation

Group 1 0.000000 — 0.000000 n/aGroup 2 0.000000 0.000000 0.000000 n/a

2022 2021 pence pence per unit per unit Net payable paid income Equalisation 31 Mar 31 Mar

Class ‘X’ Accumulation

Group 1 0.779660 — 0.779660 0.650976Group 2 0.779660 0.000000 0.779660 0.650976

*Class ‘I’ Accumulation launched on 8 October 2021, hence there are no comparatives.

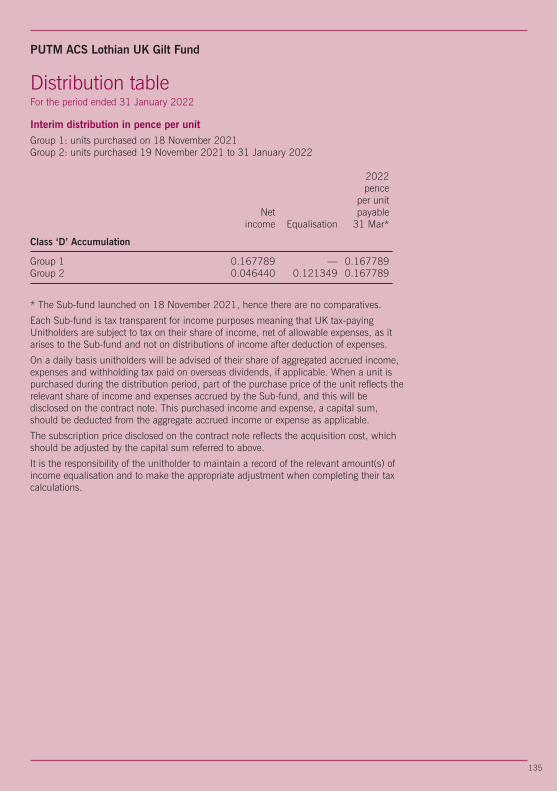

Each Sub-fund is tax transparent for income purposes meaning that UK tax-payingunitholders are subject to tax on their share of income, net of allowable expenses, asit arises to the Sub-fund and not on distributions of income after deduction of expenses.

On a daily basis unitholders will be advised of their share of aggregated accrued income,expenses and withholding tax paid on overseas dividends, if applicable. When a unit ispurchased during the distribution period, part of the purchase price of the unit reflectsthe relevant share of income and expenses accrued by the Sub-fund, and this will bedisclosed on the contract note. This purchased income and expense, a capital sum,should be deducted from the aggregate accrued income or expense as applicable.

The subscription price disclosed on the contract note reflects the acquisition cost, whichshould be adjusted by the capital sum referred to above.

It is the responsibility of the unitholder to maintain a record of the relevant amount(s) ofincome equalisation and to make the appropriate adjustment when completing their taxcalculations.

Distribution tablesFor the year ended 31 January 2022

35

PUTM ACS Japan Equity Fund

Dear Investor

Welcome to the PUTM ACS Japan Equity Fund report forthe 12 months to 31 January 2022.

Performance Review

Over the review period, the PUTM ACS Japan EquityFund returned -2.16% (Source: FactSet, Gross of AMC,in GBP, based on the movement in the Cancellation Pricefrom 31/01/21 to 31/01/22). This was compared with areturn of 0.14% for the benchmark index (Source:FactSet, MSCI Japan, Total Return, GBP from 31/01/21to 31/01/22).

Investment review

Source: Sub-fund performance: FactSet, Gross of AMC, GBP, based on the movement in the Cancellation Price from 31January 2021 to 31 January 2022. Benchmark Index performance: MSCI Japan, Total Return in GBP, from 31January 2021 to 31 January 2022.

Past performance is not a guide to future performance.

Please note that all past performance figures are calculated without taking the initial charge into account.

The value of units and the income from them can go down as well as up and is not guaranteed. You maynot get back the full amount invested.

Standardised Past Performance

PUTM ACS Japan Equity Fund -2.16 4.92 9.76 – –

Benchmark Index 0.14 10.71 10.50 – –

Jan 21 - Jan 22 Jan 20 - Jan 21 Mar 19 - Jan 20% growth % growth % growth

36

PUTM ACS Japan Equity Fund

Investment review

Market Review

Japanese equities were flat over the 12-month period.While the coronavirus pandemic continued to dominatesentiment at the beginning of the period, stimulusmeasures announced in early 2020 helped support localequity markets.

Early in the period, markets benefited from positive investorsentiment arising from vaccine breakthroughs and positiveeconomic data. However, a rise in infection numbersdampened stock returns somewhat. The governmentdeclared an emergency lockdown in Tokyo and othereconomic hubs in July. Meanwhile, fears of risinginfections, the slow vaccination programme and Tokyoentering its third emergency lockdown weighed on markets.However, Japan was one of the strongest major developedmarkets in August and September, as investors reactedpositively to the change in the political landscape and animproving Covid-19 picture.

Prime Minister Yoshihide Suga’s approval rating sunk to arecord low due to the government's handling of Covid-19,and the decision to go ahead with staging the Olympicsduring a global pandemic. He has since been replaced byFumio Kishida as leader of the ruling Liberal DemocraticParty, and, against expectations, the party comfortablyretained power in the general election at the end of October.Kishida's ascent to power was initially welcomed byinvestors due to expectations of an additional economicstimulus. Sentiment soon turned, however. Investorsbecame concerned that the new prime minister would raisetaxes on financial income, primarily for the wealthy.

In November, Prime Minister Kishida released details of astimulus package of almost ¥56 trillion. The measuresincluded direct payments to families with children andsupport for businesses. There are also plans to supportconsumers who have been hit by high energy prices.

In common with global stock markets, Japanese equitiessold off abruptly in January, with the technology-focusedMothers market especially weak. Unlike the US FederalReserve, however, the Bank of Japan is not under pressureto raise interest rates. Japanese inflation remains relativelysubdued despite higher energy costs.

Sub-fund Review

The Sub-Fund’s mandate was changed during the periodfrom an enhanced index strategy to an active approach.The new strategy was implemented at the end of October2021.

In the period from 31 October 2021 to 31 January 2022,the top performing holding was the semiconductorequipment maker Tokyo Electron, whose recent results havesurprised on the upside. Profits significantly exceededmarket expectations and the company raised its guidance.The company expects strong demand from data centresand 5G. Automotive components maker Denso gained afterToyota upwardly revised its 2030 sales target for electricvehicles. Elsewhere, the electronics conglomerate Sonyadvanced, as its September-quarter results beat investorforecasts. Results were positive across business segments,and the company also revised up its full-year guidance.

On the downside, the brewer Asahi Group fell, asmanagement cautioned that rising raw material costs coulddelay achieving financial targets until next fiscal year.Musical instrument maker Yamaha detracted fromperformance as recent results were below consensus andthe company cut its full-year guidance substantially, due todifficulties securing supplies of semiconductors and logisticsdisruptions. West Japan Railway also lagged on concernsover the new Omicron variant.

Outlook at Year End

Japanese corporates have recovered as the global economyhas picked up. However, inflationary pressures are startingto impact profitability. While some companies are passinghigher prices on to their end customers, these actions comewith a lag. Meanwhile, the low number of Covid-19 casesin Japan should bolster a return to some normalcy after atough year. Companies with strong business models andmanagement teams have coped and even thrived in the lasttwo years. Alongside structural improvements ingovernance in Japan, we remain resolute in our belief thatthese companies will do well. Weighing the risk-reward inthe market, we believe valuations remain attractive forthese companies for the medium term.

As the market outlook was completed as of 31st January,there is no mention of the ongoing Ukraine crisis thatbegan at the end of February. Naturally, this woulddramatically affect any future expectations of marketoutlook that would not have been factored in at the time ofwriting.

37

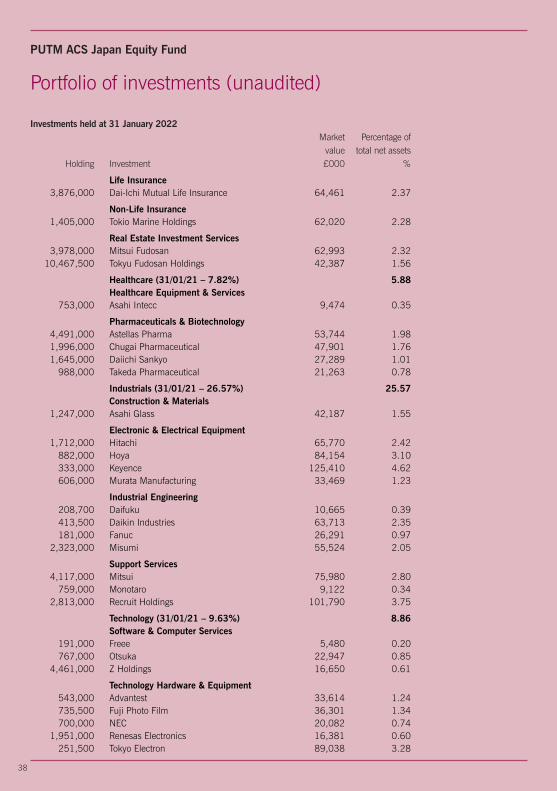

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Basic Materials (31/01/21 – 4.17%) 5.48 Chemicals 821,900 Kansai Paint 12,611 0.46 5,152,000 Mitsubishi Chemical 29,814 1.10 2,240,000 Nippon Paint 13,171 0.49 607,400 Shin-Etsu Chemical 74,790 2.76 1,241,500 Taiyo Nippon Sanso 18,166 0.67

Consumer Goods (31/01/21 – 20.63%) 22.22 Automobiles & Parts 1,174,000 Denso 64,498 2.38 2,728,000 Honda Motor 59,169 2.18 11,567,000 Toyota Motor 167,978 6.19 Beverages 1,404,000 Asahi Breweries 42,386 1.56

Household Goods 735,000 Makita 20,211 0.74

Leisure Goods 64,000 Nintendo 23,250 0.86 1,936,500 Sony 159,275 5.87 666,500 Yamaha 22,333 0.82

Personal Goods 798,100 Kao 29,592 1.09 382,500 Shiseido 14,254 0.53

Consumer Services (31/01/21 – 9.02%) 9.04 Food & Drug Retailers 702,000 Welcia Holdings 14,054 0.52

General Retailers 255,000 Nitori Holdings 27,052 1.00 2,346,000 Seven & I Holdings 84,831 3.13

Media 390,900 So-Net M3 10,994 0.41

Travel & Leisure 357,500 Oriental Land 45,962 1.69 2,012,000 West Japan Railway 62,289 2.29

Financials (31/01/21 – 10.81%) 15.31 Banks 20,548,000 Mitsubishi UFJ Financial Group 91,860 3.38 2,710,000 Sumitomo Mitsui Financial 72,101 2.66

Financial Services 347,200 Century Tokyo Leasing 12,622 0.46 655,500 Nihon M&A Center 7,569 0.28

PUTM ACS Japan Equity Fund

38

PUTM ACS Japan Equity Fund

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Life Insurance 3,876,000 Dai-Ichi Mutual Life Insurance 64,461 2.37

Non-Life Insurance 1,405,000 Tokio Marine Holdings 62,020 2.28

Real Estate Investment Services 3,978,000 Mitsui Fudosan 62,993 2.32 10,467,500 Tokyu Fudosan Holdings 42,387 1.56

Healthcare (31/01/21 – 7.82%) 5.88 Healthcare Equipment & Services 753,000 Asahi Intecc 9,474 0.35

Pharmaceuticals & Biotechnology 4,491,000 Astellas Pharma 53,744 1.98 1,996,000 Chugai Pharmaceutical 47,901 1.76 1,645,000 Daiichi Sankyo 27,289 1.01 988,000 Takeda Pharmaceutical 21,263 0.78

Industrials (31/01/21 – 26.57%) 25.57 Construction & Materials 1,247,000 Asahi Glass 42,187 1.55

Electronic & Electrical Equipment 1,712,000 Hitachi 65,770 2.42 882,000 Hoya 84,154 3.10 333,000 Keyence 125,410 4.62 606,000 Murata Manufacturing 33,469 1.23

Industrial Engineering 208,700 Daifuku 10,665 0.39 413,500 Daikin Industries 63,713 2.35 181,000 Fanuc 26,291 0.97 2,323,000 Misumi 55,524 2.05

Support Services 4,117,000 Mitsui 75,980 2.80 759,000 Monotaro 9,122 0.34 2,813,000 Recruit Holdings 101,790 3.75

Technology (31/01/21 – 9.63%) 8.86 Software & Computer Services 191,000 Freee 5,480 0.20 767,000 Otsuka 22,947 0.85 4,461,000 Z Holdings 16,650 0.61

Technology Hardware & Equipment 543,000 Advantest 33,614 1.24 735,500 Fuji Photo Film 36,301 1.34 700,000 NEC 20,082 0.74 1,951,000 Renesas Electronics 16,381 0.60 251,500 Tokyo Electron 89,038 3.28

39

Portfolio of investments (unaudited)

Investments held at 31 January 2022 Market Percentage of value total net assets Holding Investment £000 %

Telecommunications (31/01/21 – 7.19%) 6.59 Fixed Line Telecommunications 3,819,000 Nippon Telegraph & Telephone 80,707 2.97

Mobile Telecommunications 3,319,000 KDDI 78,235 2.88 618,500 Softbank 20,044 0.74

Utilities (31/01/21 – 0.14%) 0.00

Futures (31/01/21 – 0.08%) 0.00

Portfolio of investments 2,685,918 98.95 Net other assets 28,558 1.05

Net assets 2,714,476 100.00

Unless otherwise stated, all investments are approved securities being eitherofficially listed in a member state or traded on or under the rules of an eligiblesecurities market.

PUTM ACS Japan Equity Fund

40

PUTM ACS Japan Equity Fund

Top ten purchases and salesFor the year ended 31 January 2022

Purchases Cost£000

Sony 169,957Keyence 147,823Toyota Motor 145,632Recruit Holdings 129,445Hoya 104,026Mitsubishi UFJ Financial Group 90,589Tokyo Electron 90,550Dai-Ichi Mutual Life Insurance 81,040Shin-Etsu Chemical 76,164Asahi Breweries 75,735

Subtotal 1,110,961Other purchases 2,021,625

Total purchases for the year 3,132,586

Sales Proceeds£000

Asahi Breweries 31,760Dai-Ichi Mutual Life Insurance 21,865Softbank 20,665Makita 13,584NEC 13,428Nabtesco 12,828Renesas Electronics 12,677Yamaha 9,724So-Net M3 8,176Shiseido 8,051

Subtotal 152,758Other sales 393,095

Total sales for the year 545,853

41

PUTM ACS Japan Equity Fund

Statistical information

Comparative tables Class ‘B’ Class ‘C’ Accumulation** Accumulation*** 31/01/22 31/01/21 31/01/22 31/01/21 31/01/20 pence pence pence pence penceChange in net assets per unitOpening net asset value per unit 98.74 100.00 113.43 108.54 100.00

Return before operating charges* (2.22) (1.24) (2.59) 5.01 8.65Operating charges (0.08) (0.02) (0.10) (0.12) (0.11)

Return after operating charges* (2.30) (1.26) (2.69) 4.89 8.54

Distributions on accumulation units (1.93) (0.13) (2.21) (2.32) (1.38)Retained distributions onaccumulation units 1.93 0.13 2.21 2.32 1.38

Closing net asset value per unit 96.44 98.74 110.74 113.43 108.54

*after direct transaction costs of:^ 0.02 0.01 0.03 0.01 0.00

PerformanceReturn after charges (2.33%) (1.26%) (2.37%) 4.51% 8.54%

Other informationClosing net asset value (£000) 14,405 10,475 48,555 50,815 60,675Closing number of units 14,936,790 10,608,464 43,847,654 44,799,202 55,899,799Operating charges 0.02%**** 0.11% 0.02%**** 0.11% 0.12%Direct transaction costs 0.02% 0.01% 0.02% 0.01% 0.00%

Prices+

Highest unit price (pence) 111.70 104.07 128.26 119.50 111.90Lowest unit price (pence) 93.31 98.56 107.14 87.88 98.30

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.** Class ‘B’ Accumulation launched on 27 November 2020.***Class ‘C’ Accumulation launched on 27 March 2019.****The AMC was updated during the year.

42

Statistical information

Comparative tables Class ‘D’ Class ‘F’ Accumulation** Accumulation*** 31/01/22 31/01/21 31/01/20 31/01/22 pence pence pence penceChange in net assets per unitOpening net asset value per unit 113.42 108.54 100.00 100.00

Return before operating charges* (2.64) 5.00 8.65 (5.05)Operating charges (0.06) (0.12) (0.11) (0.01)

Return after operating charges* (2.70) 4.88 8.54 (5.06)

Distributions on accumulation units (2.19) (2.32) (1.37) (0.09)Retained distributions onaccumulation units 2.19 2.32 1.37 0.09

Closing net asset value per unit 110.72 113.42 108.54 94.94

*after direct transaction costs of:^ 0.03 0.01 0.00 0.02

PerformanceReturn after charges (2.38%) 4.50% 8.54% (5.06%)

Other informationClosing net asset value (£000) 2,616,231 295,766 324,773 35,222Closing number of units 2,362,915,134 260,763,744 299,218,230 37,098,184Operating charges 0.02%**** 0.11% 0.12% 0.02%Direct transaction costs 0.02% 0.01% 0.00% 0.02%

Prices+

Highest unit price (pence) 128.26 119.50 111.90 105.39Lowest unit price (pence) 107.12 87.88 98.30 91.86

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.**Class ‘D’ Accumulation launched on 27 March 2019.*** Class ‘F’ Accumulation class launched on 22 October 2021, hence there are no comparatives.****The AMC was updated during the year.

PUTM ACS Japan Equity Fund

43

PUTM ACS Japan Equity Fund

Statistical information

Comparative tables Class ‘X’ Accumulation** 31/01/22 31/01/21 pence pence Change in net assets per unitOpening net asset value per unit 128.69 100.00

Return before operating charges* (2.84) 28.81Operating charges (0.13) (0.12)

Return after operating charges* (2.97) 28.69

Distributions on accumulation units (2.54) (2.56)Retained distributions onaccumulation units 2.54 2.56

Closing net asset value per unit 125.72 128.69

*after direct transaction costs of:^ 0.03 0.01

PerformanceReturn after charges (2.31%) 28.69%

Other informationClosing net asset value (£000) 63 322Closing number of units 50,000 250,000Operating charges 0.03%*** 0.11% Direct transaction costs 0.02% 0.01%

Prices+

Highest unit price (pence) 145.63 135.63Lowest unit price (pence) 121.63 99.77

^The direct transaction costs includes commission on futures.+ High and low price disclosures are based on quoted unit prices. Therefore, the opening and closing NAV pricesmay fall outside the high/low price threshold.** Class ‘X’ Accumulation launched on 14 March 2020.***The AMC was updated during the year.

44

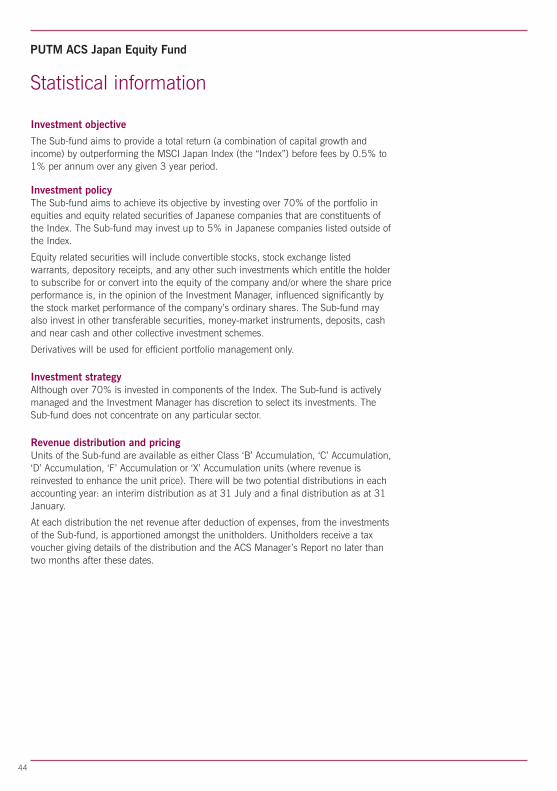

PUTM ACS Japan Equity Fund

Statistical information

Investment objective

The Sub-fund aims to provide a total return (a combination of capital growth andincome) by outperforming the MSCI Japan Index (the “Index”) before fees by 0.5% to1% per annum over any given 3 year period.