PT Bank Mandiri (Persero) Tbk

100

0 PT Bank Mandiri (Persero) Tbk Q1 2006 Results Presentation

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of PT Bank Mandiri (Persero) Tbk

0

PT Bank Mandiri (Persero) Tbk

Q1 2006 Results Presentation

97

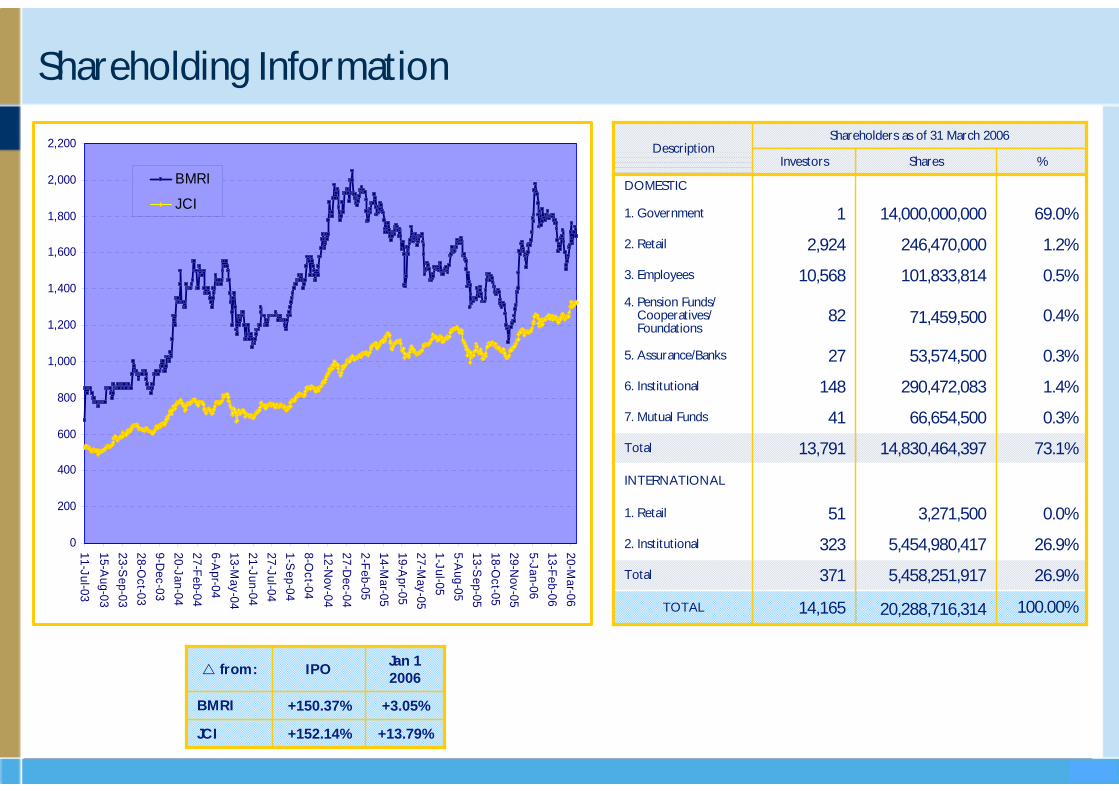

Jan 1 2006

IPOfrom:

+13.79%+152.14%JCI

+3.05%+150.37%BMRI

Shareholding Information

100.00%20,288,716,31414,165TOTAL

26.9%5,458,251,917 371Total

26.9%5,454,980,417 3232. Institutional

0.0%3,271,500 511. Retail

INTERNATIONAL

73.1%14,830,464,39713,791 Total

0.3%66,654,500 41 7. Mutual Funds

1.4%290,472,083 148 6. Institutional

0.3%53,574,500 27 5. Assurance/Banks

0.4%71,459,500 82 4. Pension Funds/

Cooperatives/ Foundations

0.5%101,833,814 10,568 3. Employees

1.2%246,470,000 2,924 2. Retail

69.0%14,000,000,0001 1. Government

DOMESTIC

%SharesInvestors

Shareholders as of 31 March 2006Description

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

11-Jul-0315-A

ug-0323-S

ep-0328-O

ct-039-D

ec-0320-Jan-0427-Feb-046-A

pr-0413-M

ay-0421-Jun-0427-Jul-041-S

ep-048-O

ct-0412-N

ov-0427-D

ec-042-Feb-0514-M

ar-0519-A

pr-0527-M

ay-051-Jul-055-A

ug-0513-S

ep-0518-O

ct-0529-N

ov-055-Jan-0613-Feb-0620-M

ar-06

BMRI

JCI

1

Bank Mandiri Presentation Contents

Results Overview Page #Q1 2006 Summary Financials 2 - 3

Quarterly Asset Mix & Interest Source 4

Quarterly Loan Growth & LDR 5

Business Unit Performance 6

Consumer Loan Portfolio Details 7

Recap Bond Portfolio Summary & Movement 8Quarterly Funding Mix 9

Quarterly Savings Deposits & Funding Rates 10

Quarterly Net Interest Margins and Spread 11 - 12

Quarterly Non-Interest Operating Income 13

Quarterly Overhead Expenses & Detail 14

Quarterly NPL & Cat. 2 Loan Movement 15 - 16

Quarterly Asset Quality 17

Provisioning & Collateral 18

Quarterly Analysis of NPL Downgrades 19

Core Earnings Analysis & Profitability 20

Quarterly Capital Structure 21

Additional Factors 22

Corporate Actions 23 - 26

Service Quality, NPLs & SPV RegulationsService Quality Achievements 27 - 29

Top Debtor Developments 30 - 32

SPV & Regulatory Progress 33 - 37

Results Overview Page #Q1 2006 Summary Financials 2 - 3

Quarterly Asset Mix & Interest Source 4

Quarterly Loan Growth & LDR 5

Business Unit Performance 6

Consumer Loan Portfolio Details 7

Recap Bond Portfolio Summary & Movement 8Quarterly Funding Mix 9

Quarterly Savings Deposits & Funding Rates 10

Quarterly Net Interest Margins and Spread 11 - 12

Quarterly Non-Interest Operating Income 13

Quarterly Overhead Expenses & Detail 14

Quarterly NPL & Cat. 2 Loan Movement 15 - 16

Quarterly Asset Quality 17

Provisioning & Collateral 18

Quarterly Analysis of NPL Downgrades 19

Core Earnings Analysis & Profitability 20

Quarterly Capital Structure 21

Additional Factors 22

Corporate Actions 23 - 26

Service Quality, NPLs & SPV RegulationsService Quality Achievements 27 - 29

Top Debtor Developments 30 - 32

SPV & Regulatory Progress 33 - 37

Financial Summary Page #Summary Balance Sheets & P&L 38 -40

Recap Bond Portfolio Detail 41

Bank Mandiri Credit Ratings 42

Reconciliation to IFRS (FY 2005) 43

Bank Mandiri Strategic Roadmap 44 – 47

Loan Movement & Portfolio DetailBI Regulation PBI no. 7/2/PBI/2005 48

Interest, Provisioning & Collateral 49

Detailed NPL Analysis & Write-Offs 50 - 54

Performing Loan Analysis 55 - 58

Restructured & IBRA Loan Analysis 59 - 61

Loan Portfolio Detail Analysis 62 - 66

Additional InformationConsumer Banking Details 67 - 69

Summary of Principal Subsidiaries 70

Bank Syariah Mandiri Details 71 - 72

Mandiri Sekuritas Details 73

Bank Mandiri at a GlanceNew Directors, Staffing & Network 74 - 79

Q4 2005 Peer Comparisons 80 - 83

Q1 2006 Published Financial Statements 84 - 93

Financial Summary Page #Summary Balance Sheets & P&L 38 -40

Recap Bond Portfolio Detail 41

Bank Mandiri Credit Ratings 42

Reconciliation to IFRS (FY 2005) 43

Bank Mandiri Strategic Roadmap 44 – 47

Loan Movement & Portfolio DetailBI Regulation PBI no. 7/2/PBI/2005 48

Interest, Provisioning & Collateral 49

Detailed NPL Analysis & Write-Offs 50 - 54

Performing Loan Analysis 55 - 58

Restructured & IBRA Loan Analysis 59 - 61

Loan Portfolio Detail Analysis 62 - 66

Additional InformationConsumer Banking Details 67 - 69

Summary of Principal Subsidiaries 70

Bank Syariah Mandiri Details 71 - 72

Mandiri Sekuritas Details 73

Bank Mandiri at a GlanceNew Directors, Staffing & Network 74 - 79

Q4 2005 Peer Comparisons 80 - 83

Q1 2006 Published Financial Statements 84 - 93

2

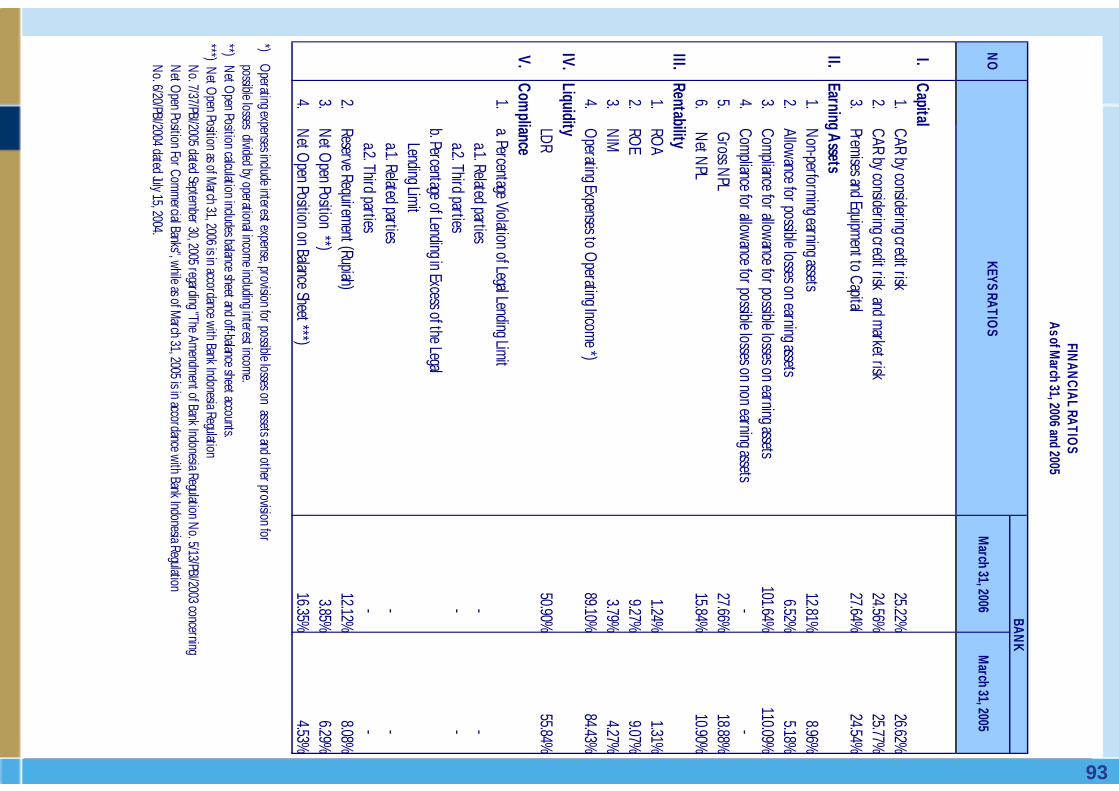

25.2%26.6%23.7%Total CAR(2)

1,150

30

23.2%

18.0%

44.4%

25.3%

51.8%

4.0%

56.6%

2.5%

0.5%

23,215

206,289

263,383

92,056

106,853

FY 2005

(6.4)

(2.5)

(5.8)

15.8

2.2

(1.1)

5.6

YoY Change (%)

1,178

25.14

24.6%

19.5%

46.9%

26.2%

53.0%

3.9%

48.2%

8.7%

1.2%

23,889

198,083

254,885

92,225

105,075

Q1 2006

25,352Total Equity

58.3%LDR

25.8%Total CAR incl. Market Risk

20.5%Tier 1 CAR(2)

51.1%Provisions / NPLs

43.7%Cost to Income(1)

8.3%RoE – after tax (p.a.)

1.3%RoA - before tax (p.a.)

1,259Book Value/Share (Rp)

26EPS (Rp)

17.8%Gross NPL / Total Loans

4.5%NIM (quarterly)

171,016Customer Deposits

249,373Total Assets

93,211Government Bonds

99,650Gross Loans

Q1 2005IDR billion / %

Key Quarterly Balance Sheet Items & Financial Ratios

(1) (G&A and employee expenses) / (Net Interest Income + Other Operating Income), excluding bond gains(2) Bank only – Not including Market Risk

3

Summary P&L Information – Q1 2005 vs. Q1 2006

302.30.6354 0.188 Gain from Increase in Value & Sale of Bonds

(146.2)0.06 0.0(13)Non Operating Income

(19.4)(0.2)(133)(0.3)(165)Other Operating Expenses**

(1.7)1.2787 1.3801 Net Income Before Tax

(6.2)(1.0)(636)(1.1)(678)G & A Expenses

15.1(1.1)(695)(1.0)(604)Personnel Expenses

14.4(1.4)(873)(1.3)(763)Provisions, Net

(1.7)0.8510 0.9519 Net Income After Tax

(4.1)1.2781 1.3814 Profit from Operations

(2.1)0.9554 0.9566 Other Operating Income

(6.8)3.42,210 3.92,370 Net Interest Income

78.5(6.7)(4,297)(4.0)(2,407)Interest Expense

36.210.26,507 7.94,777 Interest Income

(%)% of Av.Assets

Rp (Billions)% of

Av.Assets*Rp (Billions)

YoY ChangeQ1 2006Q1 2005

* % of Average Assets on an annualized basis** primarily premiums paid under the blanket guarantee scheme

4

164.0

172.6

182.9

176.9

173.9

170.3 153.8

153.5

44.6

41.2

43.0

44.5

49.2 42.5

48.3

48.3

50.4

57.0

65.4

60.5

57.3

44.6

39.0

36.1

38.6 54.0

47.1

50.6 55.4

50.2

54.6

60.7

56.6

60.2

51.4

64.5

57.692.2

92.1

92.3

92.5

93.2

93.1

153.8

153.9

155.5

148.8

152.7

94.0

102.3

107.3

122.9

131.4

137.0

105.1

106.9

106.7

104.0

99.5

94.4

42.3

72.6

66.8

68.7

75.9 76.7

82.3

87.0

40.3

30.4

46.6

33.4

18.323.2

25.7

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

Q1 '00

Q2 '00

Q3 '00

Q4 '00

Q1 '01

Q2 '01

Q3 '01

Q4 '01

Q1 '02

Q2 '02

Q3 '02

Q4 '02

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Government Bonds Loans Other Assets

46.2%

46.7%

38.2%40.7%

45.6%47.4%

60.6%

74.1%

68.2% 67.8%63.6%

75.4% 74.7%

74.9%

42.6%

48.0%50.5%

42.3%

34.1%29.9%

22.1%19.3%19.0%18.1%19.0%19.8%

Int. from Bonds Int. from Loans

Total assets grew by 2.2% Y-o-Y – ConsolidatedA

s a % of T

otal Interest Income

Tot

al A

sset

s (R

p tn

)

5

-1.7%

5.6%

QoQ Growth (%)

YoY Growth (%)

44.641.242.343.044.549.242.548.348.350.458.765.468.766.872.675.976.782.387.094.499.5

106.7106.9105.1

104.0

27.5%

36.1%

53.1%

51.8%

26.3% 25.3%28.3%26.5%

35.4%

56.8%

53.7%

42.5%

47.9%

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

Loans (Rp tn)

LDR (%)

22.922.625.6

31.4 33.033.337.7

33.935.1 35.7

1.4 1.6 3.1 3.7 5.1 6.58.5 9.5 10.8 11.511.5

45.142.338.940.6

42.7 41.838.2 39.5

41.5 42.944.0 44.743.140.2

35.3

30.1

36.1

22.2

4.2

11.3

1.5

Q4 '02

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Loan volume was flat or declining across all segments Q-o-Q

Quarterly Loan Data – Consolidated

1.9%85.9%1.82Micro

6.5%14.5%6.40Small

11.7%20.3%11.45Consumer

100.0%5.6%98.07Total

36.0%4.3%35.32Commercial

43.9%0.4%43.07Corporate

% of Portfolio

Loans(Rp tn)

By Segment (Bank only)

Y-O-Y Growth (%)

Quarterly Loan Segment Details – Bank Only

Corporate

Commercial

Consumer

As of March 2006; Non-consolidated numbers* Note: Includes IBRA loan purchases of Rp 5 tr

* SmallMicro

6

18.0%(10.1%)3.8%39.2%24.0%32.1%% of Pre-Prov. Operating Profit***

287(264)(16)601(348)(68)Operating Profit (Incl. Provision)

(33.7%)

(166)

(20)

18

(165)

0

(165)

0

23,844

CRG

(2.0%)

63

(71)

21

113

23

89

1,328

7,670

Small & Micro

7,315111,15423,20458,770Deposits & Borrowings (Avg. Bal.)

106,81311,46623,94524,963Earning Assets (Avg. Bal.)

(139)187207128Interest Margin on Assets

4872722248Other Operating Income

(171)982461546Total Interest Margin

(33)795254419Interest Margin on Liabilities

(22)(611)(90)(68)Other Operating Expenses**

36.7%76.8%(44.4%)(8.7%)% of Operating Profit (Incl. Prov.)

294643392526Pre-Provision Operating Profit

Cons.Corp.Business Unit Performance (Rp bn) Treasury*Comm.

Excludes Overseas* Includes Government Bonds** Includes Allocated Cost*** Balance of pre-provision operating profit attributable to funds transfer pricing on capital not allocated to BU

Business Unit Performance, Q1 2006 (Reviewed)

7

283 411 655199 328540

1,802

1,860

1,902

1,912

1,918

1,932

1,938

1,930

1,906823

815786

934

428494

594

479

510

816

727

653688 888 792

3,250

3,050

2,885

2,591

1,996

1,011

1,52 2

152

4,033

4,131

4,217

4,2233,5672,852

1,058

1,939

1,921

1,493

1,279

1,367

1,354

1,257

1,206

1,270

1,136

0

2,000

4,000

6,000

8,000

10,000

12,000

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Other

Cash Collateral LoansCredit Cards

Payroll Loans

Home Equity LoansMortgages

Consumer lending contracted 0.8% despite Mortgage growth

(10.81%)9.03%Cash Collateral Loans

(6.44%)6.10%Credit Cards

(1.25%)(0.59%)Payroll Loans

(2.38%)13.07%Home Equity Loans

6.56%62.86%Mortgages

Growth (%)

Q-o-QY-o-Y

20.33%

80.91% 9.17%Other

Total Consumer

Loan Type

(0.78%)

*Auto & Motorcycle Loans channeled or executed through finance companies = Rp 3.77 tn in our Commercial Loan Portfolio

Quarterly Consumer Loan Balances by Type Consumer Loan Growth by Type

8

Sales of Rp20 bn from the Recap Bond Portfolio in Q1 ‘06

Portfolio Sales as of March 2006 (Rp bn)

92.261.128.92.2Total

-

88.4

3.9

Total

66.2%31.4%2.4%% of Total

----Hedge Bonds

95.8%59.727.01.6Variable Rate

4.2%1.41.90.6Fixed Rate

% of TotalHTM(Nominal Value)

AFS(Mark to Market#)

Trading(Mark to Market*)

At Fair Value, Mar 2006 (Rp tn)

177.4

176.9 153.5

148.8 123.0

93.1

92.2

92.1

4.0

0.0

32.3

2.51.0

15.8

24.5

0

40

80

120

160

200

1999 2000 2001 2002 2003 2004 2005 Q1 '06

0

5

10

15

20

25

30

35Recap Bonds

Bond Sales

Bond Portfolio Movement (Fair Value) 1999 – Q1 ‘06

Rup

iah

(Tri

llion

s)

(66)

257

2,544

2005

48

5

20

Q1 ‘06

66

1,365

32,334

2004

1,868Realized Profit

Unrealized Profit

Bonds Sold

IDR bn

(52)

24,505

2003

* Mark to Market impacts Profit# Mark to Market impacts Equity

9

15.3

16.6

16.6

18.0

17.6

19.7

19.8

22.1

22.3

24.4

25.1

29.6

28.9

31.9

33.4

40.6

40.5

42.3

44.6

52.0

49.5

47.8

44.2

45.2

41.8

14.3

19.5

23.4

31.1

29.6

29.7

29.2

31.2

27.7

27.2

26.1

24.8

24.8

27.9

30.1

28.8

30.8

30.7

30.9

28.0

27.5

30.8

28.3

30.1

30.2

97.2

92.9

90.3

87.8

100.9

91.5

106.9

107.7

106.1

104.1

100.7

105.1

96.7 66.5

65.0

72.3

79.8

93.2 90.8

17.3 19.1 19.921.5

23.625.9 21.3

23.4 21.5 17.8 20.6 20.6 19.4 18.618.0 17.3

16.5 13.8 12.511.6

11.113.3 16.3

15.715.9

12.314.911.612.311.911.9

10.210.79.1

12.1 11.5

94.0

85.9

80.5

70.3

68.4

63.4

0

20

40

60

80

100

120

140

160

180

200

Q1 '00

Q2 '00

Q3 '00

Q4 '00

Q1 '01

Q2 '01

Q3 '01

Q4 '01

Q1 '02

Q2 '02

Q3 '02

Q4 '02

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Rp Savings Deposits Rp Demand Deposits FX Demand Deposits Rp Time Deposits FX Time Deposits

Q1 fall of 4.0% on Rp Time & Savings, FX Demand accounts

Deposit Analysis – Bank Only

Dep

osits

by

Typ

e (R

p tn

)

54.1%

45.3%

67.2%68.6%66.5%

68.3%

62.6%

48.7%44.6% 46.4%

53.7% 51.7%57.3% 56.2%

61.5%

47.8%

44.2%

51.5%50.9%

26.8%

44.5%

37.0%

33.8%32.1%31.4%32.1%32.9%

22.6%

Retail Deposits (%) Low-Cost Deposits (%)

As a %

of Total D

eposits

10

Savings deposit volume slips 7.5% in Q1

15.316.616.618.017.619.719.822.122.324.425.129.628.931.933.440.540.542.344.652.049.547.844.245.241.8

21.9%

22.7%

27.1%

30.6%

10.3%

16.2%

11.7%11.0%

22.8%

15.6%

16.0%16.8%

17.4%

16.9%13.5%

11.5%11.2% 15.2%

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

Savings Deposits (Rp tn)

As % of Total Deposits

National Share of Savings Deposits (%)

3.7%

6.1%

3.7% 3.4% 3.5%3.3%

6.0% 4.4%4.8%4.3%

9.5%

6.9% 5.3%

10.6%

11.9%11.4%

6.8%8.4%

13.9%

6.4%

17.1%

12.7%11.9%

7.8%

13.1%

8.5%7.4%

17.0%Rp DDRp SavingsRp TD1 Mo. SBIs

Savings Deposit Growth Average Quarterly Deposit Costs (%)

SBITD

SDDD

2.7% 2.4%

0.8% 0.5%1.4%

4.4%

2.6%1.7%

1.1%1.9%

2.7%2.1%

4.3%4.0%Q

1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

FX DDFX TD FX TD

FX DD

11

Margins expand slightly on rising bond yields

All figures - Bank Only

2.6%

2.5%

3.0%

2.4%

2.5%

3.0%

3.0%

3.9% 2.9%

2.9%

3.4%

2.8%

3.0%

3.3%

3.3%

3.7%

4.7%

4.5%

4.0%

4.3%

4.3%

3.6%

3.8%

3.6%

3.8%

0.8% 0.8%

1.8%

2.2%

1.1%

1.5%

1.7%

2.2%

2.1%

2.0%

2.5%

2.2%

2.2%

2.5%

3.2% 3.2% 4.2% 4.2%

3.8%

4.1%

4.1%

3.4%

3.7%

3.4%

3.6%

Q1 '00

Q2 '00

Q3 '00

Q4 '00

Q1 '01

Q2 '01

Q3 '01

Q4 '01

Q1 '02

Q2 '02

Q3 '02

Q4 '02

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Spread

NIM

11.3%10.9%

11.9%

13.0%12.3%

12.6%12.8%13.0%

13.9%13.6%13.5%13.0%

11.8%11.5%

10.4%

9.5% 9.3%8.8% 8.7%

8.2%

9.4%

10.7%11.3%

10.5%10.1%10.1%

10.8%11.2%11.1%11.1%10.8%

11.8%11.6%11.0%10.8%

9.6%9.1%

7.2%

6.3%5.7%

7.8%

8.9%8.4%

7.3%

4.8%4.6%4.8%4.6%4.6%

5.1%

Yield on Assets

Cost of Funds

12

Quarterly Margin Analysis by Currency

Quarterly Rupiah Margins Quarterly Foreign Currency Margins

1.4%1.2%

1.6%2.4%2.5%

2.4%2.1%2.5%

3.9%4.0%3.5%4.1%3.6%4.1%

3.0%2.5%1.9%

3.7%4.1%

2.1%

2.6%

2.4%

3.5%4.5%

1.4%

13.0%

15.9%

14.1%

18.3%18.9%

11.9%

12.4%

8.2%

10.2%

14.0%

17.6%

12.5%12.7%

7.4%

8.5%

13.1%

17.6%

14.0%

8.3%

5.4%7.3%

11.7%

14.4%

11.1%

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

Avg SpreadAvg Loan YieldAvg Bond YieldAvg 1-Mo. SBIAvg COF

0.5%1.6%

0.4%-0.5%

0.8%

1.0%1.6%2.9%

3.4%2.5%1.3%0.1%

-0.2%-0.8%

0.8%

2.2%1.4%

0.6%

0.2%

-2.9%

3.0%2.9%

3.0%1.4%3.1%

4.2%

7.3%6.5%

11.8%

5.7%

5.6%

7.6%

3.5%4.6%5.1%

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

Avg SpreadAvg Loan YieldAvg Bond YieldAvg USD 1Mo SIBORAvg COF

13

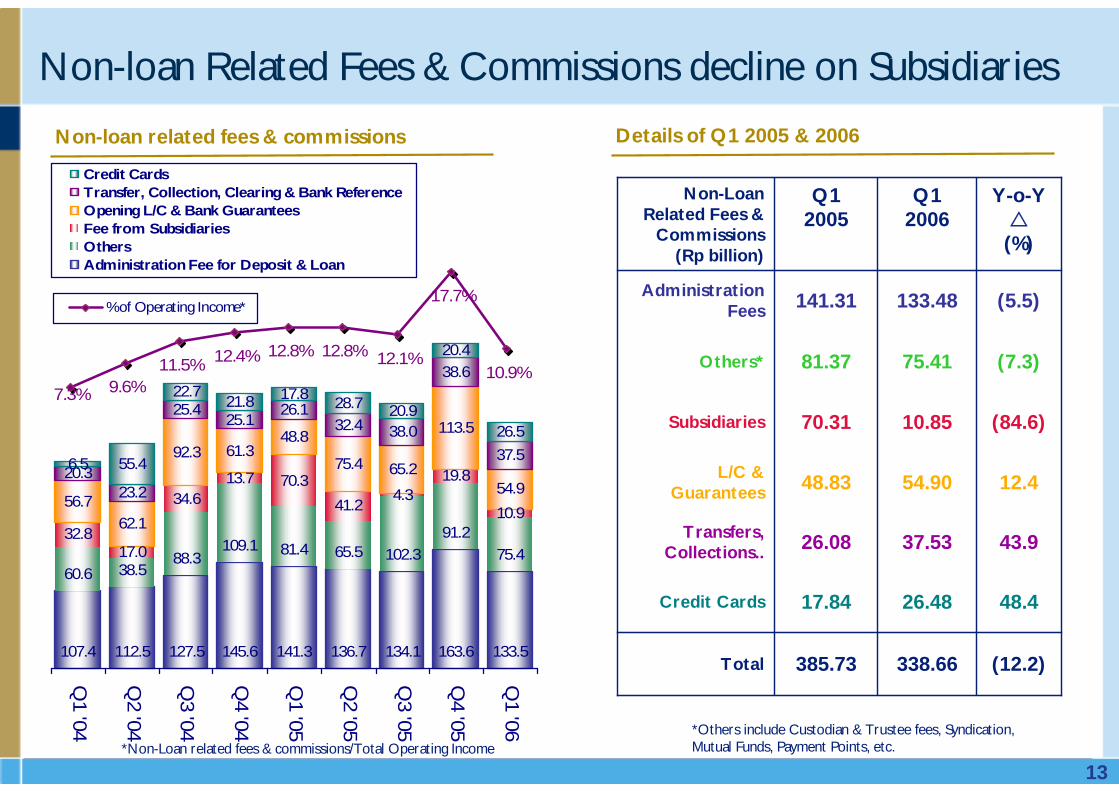

Details of Q1 2005 & 2006

107.4 145.6 141.3 136.7 134.1 163.6 133.5

60.6 38.588.3

109.1 81.4 65.5 102.391.2

75.432.8

17.0

34.613.7 70.3

41.24.3

19.8

10.956.7

62.1

92.3 61.348.8

75.4 65.2

113.5

54.920.3

23.2

25.425.1

26.132.4 38.0

38.6

37.56.5 55.4

22.721.8 17.8

28.7 20.9

20.4

26.5

112.5 127.5

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

Credit CardsTransfer, Collection, Clearing & Bank ReferenceOpening L/C & Bank GuaranteesFee from SubsidiariesOthersAdministration Fee for Deposit & Loan

7.3% 9.6%11.5% 12.4% 12.8% 12.8% 12.1%

17.7%

10.9%

% of Operating Income*

Non-loan Related Fees & Commissions decline on Subsidiaries

Non-loan related fees & commissions

*Non-Loan related fees & commissions/Total Operating Income*Others include Custodian & Trustee fees, Syndication, Mutual Funds, Payment Points, etc.

(12.2)338.66385.73Total

48.426.4817.84Credit Cards

43.937.5326.08Transfers, Collections..

12.454.9048.83L/C & Guarantees

(84.6)10.8570.31Subsidiaries

(7.3)75.4181.37Others*

(5.5)133.48141.31Administration Fees

Y-o-Y

(%)

Q12006

Q12005

Non-Loan Related Fees &

Commissions(Rp billion)

14

379276359336314428270753365500472775388460618749521670763

1,034678793767842

370 325

299298 406

322389475 408495

419377

527555

597723

604677667

1,241637

695

211

327

649

957

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

G&A Expenses (Rp bn) Personnel Expenses (Rp bn)

Cost to Income Ratio returns to below 50% in Q1

48.2%

83.3%

33.7%

43.7%38.9%

36.9%33.8%

37.1%

57.6%

45.4%

31.1%

39.9%42.8%

40.4%

CIR* (%)

Annual Avg CIR (%)

*Excluding Bond gains

15.7%268,354 231,956 Base Salary

14.1%303,387 265,803 Other Allowances

(6.0%)637,037 677,546 Total G & A Expenses

32.4%41,592 31,403 Employee Related

(32.2%)52,140 76,850 Professional Services

1.4%63,355 62,467 Transportation & Traveling

16.5%76,744 65,849 Subsidiaries

103,035

201,310

136,632

604,086

24,821

63,267

18,239

Q1‘05

(58.2%)43,078 Promotion & Sponsorship

(15.6%)169,839 IT & Telecommunication

G & A Expenses

15.1%695,295 Total Personnel Expenses

7.3%26,627 Training

46.6%26,741 Post Employment Benefits

Personnel Expenses

Change (Y-o-Y)

Q1 ‘06

39.3%190,289 Occupancy Related

70,186 10.9%Subsidiaries

Breakdown of Q1 2005 & 2006 Operating ExpensesQuarterly Consolidated Operating Expenses & CIR

15

1,245321

1,7878173,574

70,944

Beg.Balance

U/G fromNPL

D/G toNPL

NetDisburse.

FX Impact EndBalance

Q1 2006 Loan Movement, PL & NPL

Performing Loan Movements (Rp bn) - Bank Only Non-Performing Loan Movements (Rp bn) – Bank Only

27,1268126,752 1,787 120

22834

1,190

Beg.Balance

U/G to PL D/G fromPL

Disburse. CollectionsWrite-OffsFX Impact EndBalance

16

Q1 2006 Movement in Category 1 and 2 Loans

60,662889

20126

257

1,4092,295 58,857

Beg. Bal. D/G to 2 U/G from2

D/G toNPL

U/G fromNPL

NetDisburse.

FX Impact End Bal.

Category 1 Loan Movements (Rp bn) – Bank Only Category 2 Loan Movements (Rp bn) – Bank Only

356

120551,530

1,4092,29512,91212,087

Beg. Bal. Cat. 1 D/G U/G to 1 D/G to NPL NPL U/G NetDisburse.

FX Impact End Bal.

17

NPL Movement - Consolidated

14.1%12.5% 9.4%

9.1%9.0% 6.6%

7.3%7.3%

25.3%26.2%

7.2%8.2%8.4%

23.4%24.6%

9.7% 7.3%

8.6%

7.1%17.8%

9.5% 10.3%15.4%13.7%15.3%15.0%

46.9%

44.4%

139.1%

128.8%

128.4%

190.4%

129.5%

100.2%

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

Gross NPL Ratio Net NPL RatioProv/NPL Prov/NPL incl. Coll.

Provisioning coverage reflects BI requirements

Category 2 Loans – Bank Only

14,81715,48911,93212,65511,02913,37811,37116,20217,43215,58515,34510,983106219,9129,8528,334

12,35214,39416,42312,91212,086

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '03

Q3 '03

Q1 '04

Q3 '04

Q1 '05

Q3 '05

Q1 '06

2 - Special Mention Loans (Rp Bn)

12.3%9.4%

15.0%

24.8%26.2%

0%

10%

20%

30%

40%

50%

Cat 2 %

18

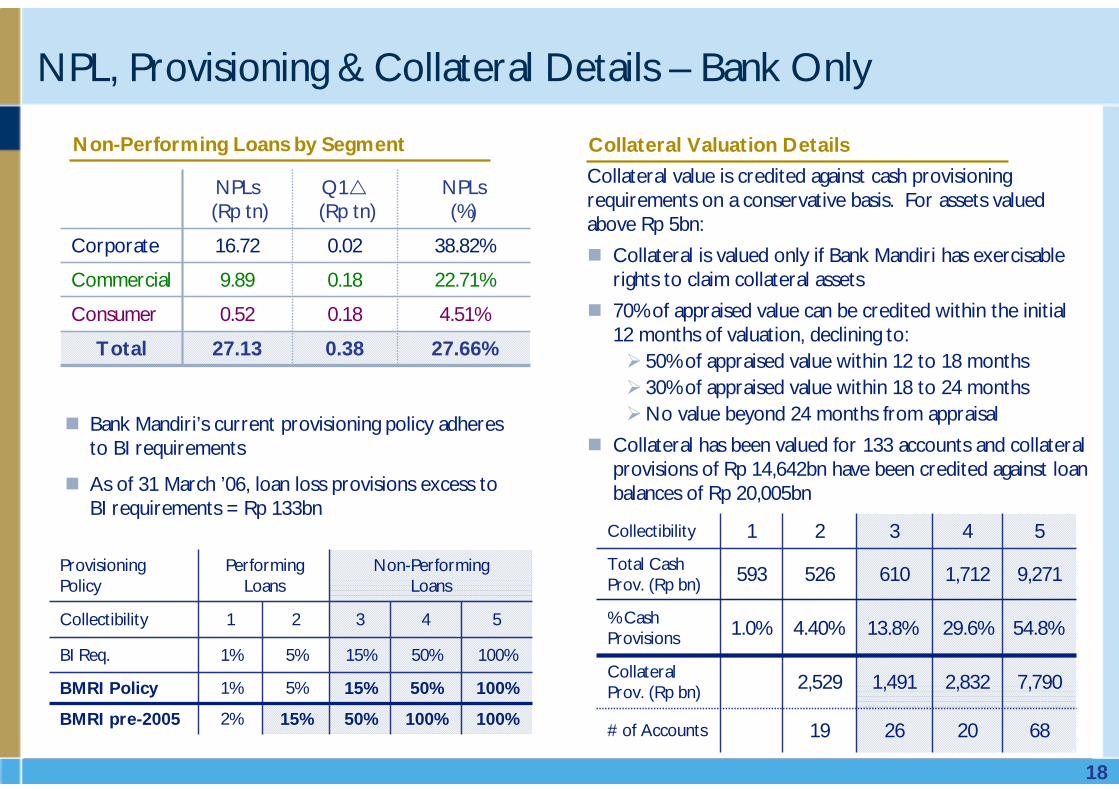

NPL, Provisioning & Collateral Details – Bank Only

27.13

0.52

9.89

16.72

NPLs(Rp tn)

4.51%0.18Consumer

38.82%0.02Corporate

NPLs(%)

Q1(Rp tn)

22.71%0.18Commercial

0.38Total 27.66%

100%50%15%5%1%BMRI Policy

100%

54321Collectibility

Non-PerformingLoans

PerformingLoans

50%

15%

15%

5%

100%2%BMRI pre-2005

100%50%1%BI Req.

Provisioning Policy

Collateral Valuation DetailsNon-Performing Loans by Segment

Bank Mandiri’s current provisioning policy adheres to BI requirements

As of 31 March ’06, loan loss provisions excess to BI requirements = Rp 133bn

Collateral value is credited against cash provisioning requirements on a conservative basis. For assets valued above Rp 5bn:

Collateral is valued only if Bank Mandiri has exercisable rights to claim collateral assets

70% of appraised value can be credited within the initial 12 months of valuation, declining to:

50% of appraised value within 12 to 18 months30% of appraised value within 18 to 24 monthsNo value beyond 24 months from appraisal

Collateral has been valued for 133 accounts and collateral provisions of Rp 14,642bn have been credited against loan balances of Rp 20,005bn

9,2711,712 610 526 593 Total Cash Prov. (Rp bn)

54321Collectibility

68

54.8%29.6%13.8%4.40%1.0%% Cash Provisions

26

1,491

19

2,529

20# of Accounts

7,790 2,832 Collateral Prov. (Rp bn)

19

4.5%

3.6%

5.1%

1.2%

4.8%

2.9%

Q4 2005

Q1 2006 Details

84,767.6

1,972.6

59,005.7

902.8

4,123.9

18,762.7

Q1 ‘06 Balance (Rp

bn)

Q3 2005

Q1 2006

UG toPL

DG to NPL

Q2 2005

Loan Background

1.8%

0.2%

2.3%

0.2%

0.3%

0.8%

Total Corporate, Commercial & Small Business Loans

Net Upgrades/Downgrades#

2.0%

0.4%

1.4%

0.1%

0.5%

4.5%

8.0%

1.8%

8.2%

0.1%

3.4%

10.0%

0.1%

0.3%

0.1%

0.1%

-

0.1%

1.8%

0.4%

2.3%

0.2%

0.3%

0.9%

Total

Overseas

Post-Merger

Pre-Merger

IBRA

Restructured

Quarterly Analysis of Upgrades and Downgrades*

* Excluding Micro & Consumer Banking# % downgrades and upgrades are quarterly figures

Note: For a breakdown of Corporate and Commercial loans, please refer to the detail slide in the appendix.

20

1,483

3,357

4,145

3,514

4,787

5,492

2,650

1,196

260

114

402

103

2,021

2,072

1,651

74

1,454

354

367

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2000 2001 2002 2003 2004 2005 Q1 '06

Gain on Sale/Value of Securities

FX Gain

Core Earnings

Pre

-Pro

visi

on

Ope

rati

ng P

rofit

IDR bn

Q1 2006 core earnings decline 19.4% from Q1 2005

472 308

1,1681,549 1,744

519 510290

1,300

602

690

1,329

97

9671,017

1,528

1,408

668

(410)

645799

819

775

(623)

829

2000 2001 2002 2003 2004 2005 2006

Q1 PAT Q2 PAT Q3 PAT Q4 PAT

8.1%

21.5%23.6%

8.7%

22.8%

26.2%

2.5%

RoE - After Tax(Annualized)

Core Earnings Profit After Tax & ROE

21

44.0

42.3

42.6

59.2 51.3

51.6

58.1

61.0

56.1

64.3

72.5

77.8

79.5

89.5

91.9

94.2

96.2

102.3

108.9

114.1

115.9

117.5

115.9

110.7

15.5

14.6

15.1

15.4

17.8

16.8

18.4

17.0

20.7

24.4

25.0

25.5

28.1

26.5

27.2

27.5

30.4

27.5

27.8

27.4

27.9

13.3

13.3

9.7Q

2 '00

Q3 '00

Q4 '00

Q1 '01

Q2 '01

Q3 '01

Q4 '01

Q1 '02

Q2 '02

Q3 '02

Q4 '02

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Q3 '05

Q4 '05

Q1 '06

RWA (Rp tn) Total Capital (Rp tn)

26.1%

31.3%

26.4%27.5%

25.3% 25.2%

23.7%

23.7%

28.5%29.8%

23.4%

27.7%

30.7%

CAR

BI Min Req

High CAR maintained at 25.2%

22

Additional Factors

Written-off Loans

Written-off Loans

Aggregate of IDR 22.93 tn (US$ 2.53 bn) in written-off loans as of end-March 2006, with significant recoveries on-going:

2001: IDR 2.0 tn2002: IDR 1.1 tn2003: IDR 1.2 tn2004: IDR 1.08 tn2005: IDR 0.818 tn (US$ 83.2 mn)Q1 ’06: IDR 0.204 tn (US$ 22.5 mn)

Loan Collateral

Undervalued

Loan Collateral

Undervalued

Collateral values included for provisioning purposes on only 133 accounts. This will rise as current valuations are completed

23

Corporate Actions

DividendPaymentDividendPayment

Dividend Payment of Rp14.853 per share

Schedule :

a. Cum Date : June 14, 2006

b. Ex Date : June 15, 2006

c. Payment Date : June 30, 2006

Total Dividend payments for 2005 = Rp301,684,655,575.70

24

Annual General Meeting Results

1. Approved Annual Report of the Company for the Financial Year Ending on 31 Dec ’05 and ratified Consolidated Financial Report of the Company for the Financial Year Ending on 31 Dec ’05.

2. Approved Annual Report of the Partnership and Environment Construction Program for the Financial Year Ending on 31 Dec ’05.

3. Gave full release and discharge (volledig acquit et de charge) to the Board of Directors and Board of Commissioners for their management and supervision during the Financial Year Ending 31 Dec ’05.

1. Approved and determined the use of the net profit of the company for the Financial Year of 2005, in amount of Rp603,369,311,151.39.

1. To appoint the Public Accountant Office Purwantono, Sarwoko & Sandjaya – Ernst & Young as the Public Accountant Office to audit the Consolidated Financial Report of the Company for the Financial Year Ending 31 Dec ’06.

2. To Appoint the Financial and Development Supervisory Board of the Province of DKI Jakarta II (BPKP Provinsi DKI Jakarta II) to audit the Annual Report of Partnership and Environment Construction Program for the Financial Year Ending on 31 Dec ’06.

Agenda 1Agenda 1

Agenda 2Agenda 2

Agenda 3Agenda 3

25

1. Approved that Salary of the members of The Board of Directors and the members of the Board of Commissioners shall not increase, therefore the amount of such salary and honorarium remains the same as the amount of salary and honorarium as determined in the Annual General Meeting of shareholders held on 16 May ’05.

2. Approved that Facilities and Benefits of the members of the Board of Directors and the members of the Board of Commissioners is determined pursuant to the resolution of the Annual General Meeting of Shareholders held on 14 Jun ’02 and Letter of The Ministry of The State-owned Enterprise No. S-412/MBU/2004, dated 10 August ’04.

3. Approved that Post-service benefits of the members of the Board of Directors and the members of Board of Commissioners is determined pursuant to the resolution of the General Meeting of Shareholders held on 22 Jan ’03.

1. Approved to grant options for phase-III amounting to 309,416,215 options or 1.55% of the fully issued and paid-up capital at the time of IPO, to buy the Company’s new Series B shares which will be issued, in which every 1 (one) option gives right to the holder to buy 1 (one) Company’s new Series B shares.

2. Determined the price and the implementation guidelines of MSOP phase-III shall follow the Decision of the Board of Directors of Jakarta Stock Exchange No. Kep-305/BEJ/07/2004, dated on 19 Jul ’04, particularly Rule No.1-A.

Annual General Meeting ResultsAgenda 4Agenda 4

Agenda 5Agenda 5

26

3. Approved that to grant authority to the Board of Commissioners to:a. Increase the issued and paid-up capital of the Company, which followed by the amendment of

article 4 paragraph 2 and paragraph 3 of the Company’s Articles of Association in case there is an execution of the option by purchasing the Company’s new Series B shares.

b. Determine the implementation and supervision policy of MSOP phase-III, including to determine the option receiver, and to report it to the next General Meeting of Shareholders.

1. To terminate with honor, Johannes Bambang Kendarto as Director of the Company and thank him for his services provided during his post effective as of the closing of this Meeting.

2. To appoint 5 new Directors of the Company , as follows: 1. Sentot A. Sentausa - Director 2. Thomas Arifin - Director 3. Budi G. Sadikin - Director 4. Bambang Setiawan - Director5. Riswinandi - Director

3. To designate Edwin Gerungan, who is the President Commissioner of the Company, as an Independent Commissioner.

4. Approved to grant authority to the Board of Commissioners of the Company to determine the allocation of duty and authority among the Directors of the Company pursuant to the Articles of Association of the Company.

Annual General Meeting ResultsAgenda 5 (cont.)Agenda 5 (cont.)

Agenda 6Agenda 6

27

Comprehensive implementation of Service Excellence Program

A mystery shopping survey by MRI, along with setting up measurement parameters & service level indicators in respective working units at banking industry best practice as well as its rigorous and continuous monitoring Implement scoring tools by SQLO (Service Quality Liaison Officer) of hubs & regional offices to track and monitor branch service quality

On-going training program for Front Liners (Customer Service), Headof hubs & spokesAnnual selection program for The Best Front Liners and The Best BranchParticipation in the National Customer Service Championships

More convenient and efficient Queuing SystemsFreeing up CSOs / CSRs to focus on servicing customersIntroducing Week-end Banking

Measuring Service Quality

Measuring Service Quality

Internalization and

Recognition Program

Internalization and

Recognition Program

Implementing Breakthrough

Projects

Implementing Breakthrough

Projects

28

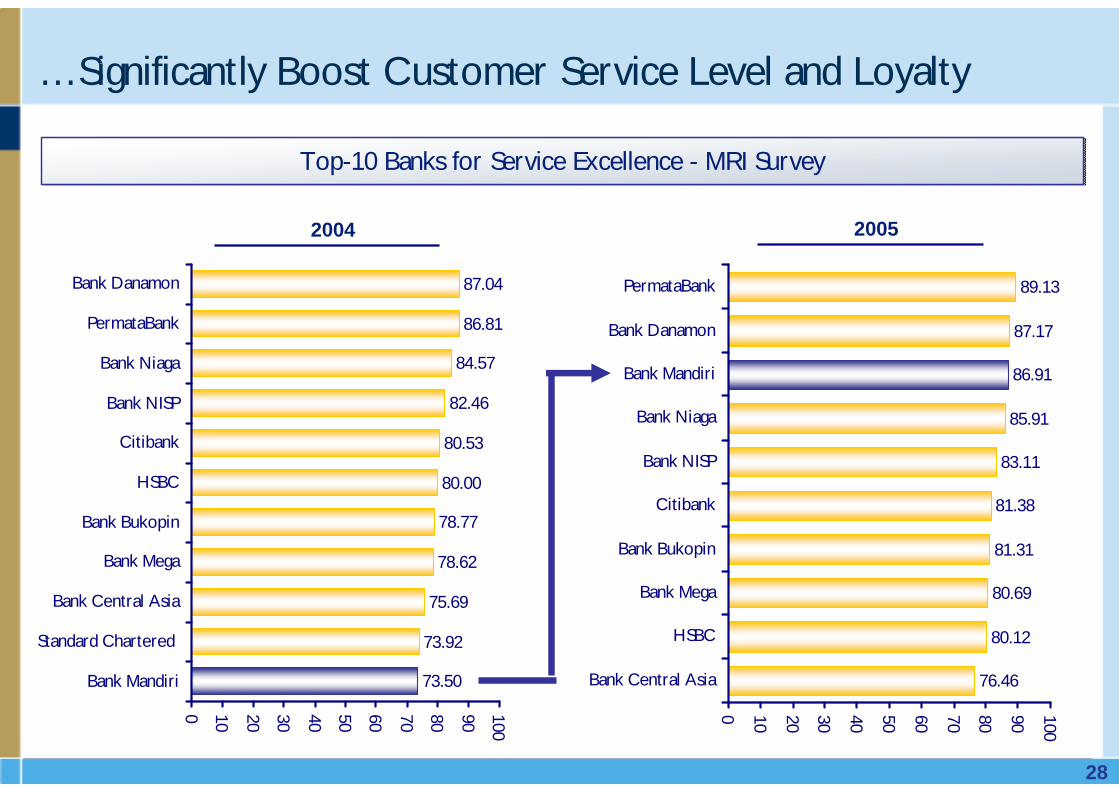

…Significantly Boost Customer Service Level and Loyalty

73.50

73.92

75.69

78.62

78.77

80.00

80.53

82.46

84.57

86.81

87.04

0 10 20 30 40 50 60 70 80 90 100

Bank Mandiri

Standard Chartered

Bank Central Asia

Bank Mega

Bank Bukopin

HSBC

Citibank

Bank NISP

Bank Niaga

PermataBank

Bank Danamon

Top-10 Banks for Service Excellence - MRI SurveyTop-10 Banks for Service Excellence - MRI Survey

76.46

80.12

80.69

81.31

81.38

83.11

85.91

86.91

87.17

89.13

0 10 20 30 40 50 60 70 80 90 100

Bank Central Asia

HSBC

Bank Mega

Bank Bukopin

Citibank

Bank NISP

Bank Niaga

Bank Mandiri

Bank Danamon

PermataBank

2004 2005

29

65.19

68.35

69.66

70.13

70.42

73.74

77.73

78.02

78.12

82.94

0 10 20 30 40 50 60 70 80 90 100

Standard Chartered

Bank Mega

HSBC

Citibank

Bank Bukopin

Bank NISP

Bank Niaga

Bank Mandiri

Bank Danamon

Bank Permata

Customer ServiceCustomer Service Banking HallBanking Hall Phone BankingPhone Banking

Understand product knowledge and communicate well.

Provide product explanation to customers clearly and

sufficiently

Understand product knowledge and communicate well.

Provide product explanation to customers clearly and

sufficiently

Outstanding in several Service Areas

Provide comfort for customers in conducting their transactionsProvide comfort for customers in conducting their transactions

Ability to serve promptly and securely, and provide reliable

peripherals

Ability to serve promptly and securely, and provide reliable

peripherals

96.77

97.42

97.86

98.31

98.65

99.33

99.52

100.00

100.00

100.00

0 10 20 30 40 50 60 70 80 90 100

HSBC

Bank NISP

BII

Bank Central Asia

Bank Permata

Citibank

Bank Mega

Bank Niaga

Bank Mandiri

Bank Danamon

67.13

67.27

70.80

72.35

75.22

76.00

76.56

78.03

78.42

80.43

0 10 20 30 40 50 60 70 80 90 100

Standard Chartered

BII

Bank BNI

Bank Bukopin

Bank Niaga

Bank Mega

Bank Danamon

Bank NISP

Bank Permata

Bank Mandiri

30

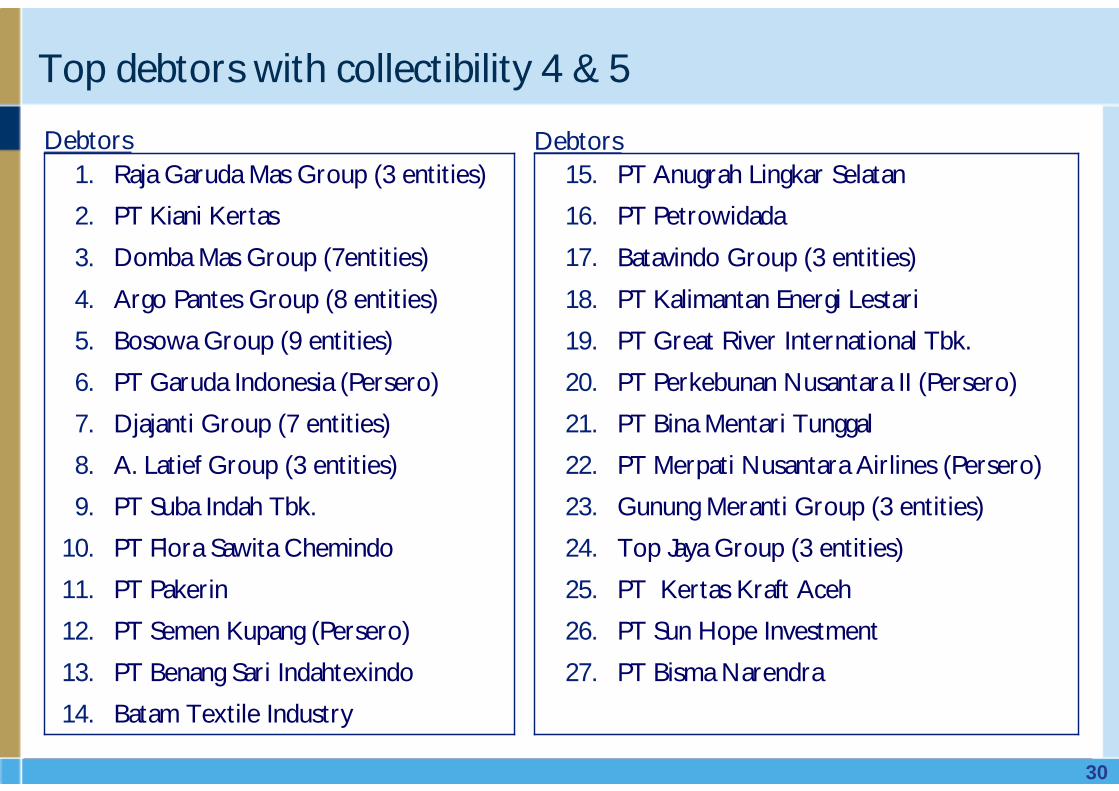

Top debtors with collectibility 4 & 5

Batam Textile Industry14.

PT Bisma Narendra27.PT Benang Sari Indahtexindo13.

PT Sun Hope Investment26.PT Semen Kupang (Persero)12.

PT Kertas Kraft Aceh25.PT Pakerin11.

Top Jaya Group (3 entities)24.PT Flora Sawita Chemindo10.

Gunung Meranti Group (3 entities)23.PT Suba Indah Tbk.9.

PT Merpati Nusantara Airlines (Persero)22.A. Latief Group (3 entities)8.

PT Bina Mentari Tunggal21.Djajanti Group (7 entities)7.

PT Perkebunan Nusantara II (Persero)20.PT Garuda Indonesia (Persero)6.

PT Great River International Tbk.19.Bosowa Group (9 entities)5.

PT Kalimantan Energi Lestari18.Argo Pantes Group (8 entities)4.

Batavindo Group (3 entities)17.Domba Mas Group (7entities)3.

PT Petrowidada16.PT Kiani Kertas2.

PT Anugrah Lingkar Selatan15.Raja Garuda Mas Group (3 entities)1.Debtors Debtors

31

Status of selected large debtors

RGM is required to increase installment amount to improve loan quality and ensure final settlement by June 2010

Awaiting concrete proposal from debtor & Government to improve loan Bank Mandiri holds MCBs of Rp1,018 billion, and is still waiting for formal extension of Government guarantee

Bank Mandiri still open to opportunities to negotiate with potential investors to resolve the outstanding loans

Restructuring of loans to Argo Pantes require debtor to dispose of non-core assets and property of PT. Alfa Goldland Realty (subsidiary) as sources of repayment

Subsidiaries are no longer in operation, so Bank Mandiri will recover loans through collateral sales / asset disposals, and will collect the remainder from the Djajanti Group Owner

Raja GarudaMas

Raja GarudaMas

Kiani KertasKiani Kertas

Argo PantesArgo Pantes

GarudaIndonesiaGaruda

Indonesia

DjajantiGroup

DjajantiGroup

32

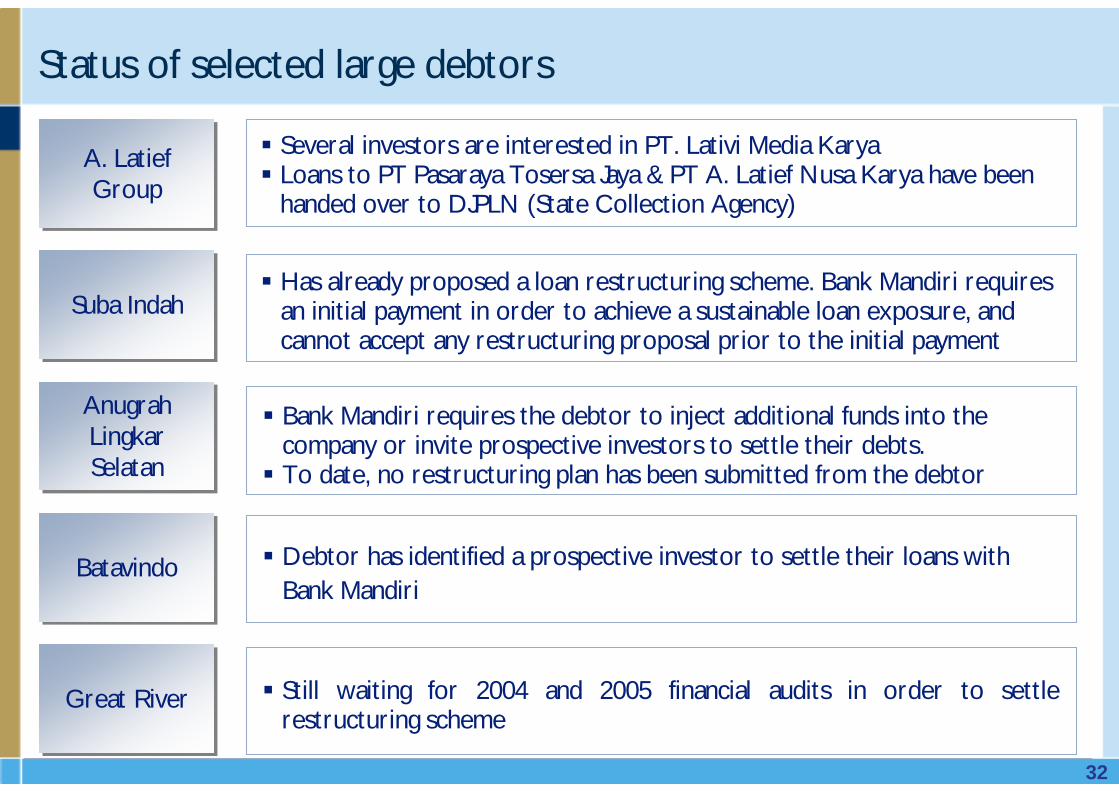

Status of selected large debtors

Several investors are interested in PT. Lativi Media KaryaLoans to PT Pasaraya Tosersa Jaya & PT A. Latief Nusa Karya have been handed over to DJPLN (State Collection Agency)

Has already proposed a loan restructuring scheme. Bank Mandiri requires an initial payment in order to achieve a sustainable loan exposure, and cannot accept any restructuring proposal prior to the initial payment

Bank Mandiri requires the debtor to inject additional funds into the company or invite prospective investors to settle their debts.To date, no restructuring plan has been submitted from the debtor

Debtor has identified a prospective investor to settle their loans with Bank Mandiri

Still waiting for 2004 and 2005 financial audits in order to settle restructuring scheme

A. LatiefGroup

A. LatiefGroup

Suba IndahSuba Indah

AnugrahLingkarSelatan

AnugrahLingkarSelatan

BatavindoBatavindo

Great RiverGreat River

33

Update on regulations to accelerate NPL resolution

Consultations with other stakeholders and regulators are underwayBI strongly supports the issuance of the new regulations, stating that it will help to accelerate the resolution of recently increasing NPLs in the banking systemState auditor (BPK) also says that such regulation can be issued as long as that the process to implement the additional authority is accountable, transparent and done in conjunction with capability development of the state banks

Source: MoF presentations, News search

A Government Regulation (PP) to clarify that State Owned Enterprise’s (SOE) receivables are not state receivables and need not be managed and resolved as suchA Ministry of Finance Regulation clarifying the authority of State Banks to manage receivables, including resolving NPLs, in line with corporate laws and regulations

The Office of the Coordinating Minister of Economy plays an important role in ensuring that all regulations related to the Financial Sector Reform package, including the two regulations mentioned above, will be completed on timeThe two regulations relating to SOE receivables are expected to be completed before the end of June 2006

Ministries of Finance and SOE have publicly stated that the Government is in the process of preparing two regulations to accelerate NPL resolution in State Banks:Ministry of

Finance & Ministry of

SOE

Ministry of Finance & Ministry of

SOE

Bank Indonesia and

Other Key Stakeholders

Bank Indonesia and

Other Key Stakeholders

Other Government

Bodies

Other Government

Bodies

34

New regulations expected to provide flexibility in managing NPLs

Clarification will allow for resolution and management of SOE receivables through mechanisms not available for state receivables

The authority will be implemented through accountable and transparent means and in accordance with good governance principlesThe authority will allow acceleration of NPL resolution through loan disposal or sale in bulk or individuallyIf required, SOEs can provide principal forgiveness to cooperative debtors in settling their obligations in a manner similar to private banks

Initially expect a regulatory framework for establishing an SPV in IndonesiaThe regulation would allow a separation between economic beneficiary and legal ownership of assets Currently there is no clear signal if the regulatory framework is going to be part of the soon to released financial sector package

The regulation is the basis to provide authority to SOE banks to manage NPLs in accordance with corporate laws and regulationsThe regulation is consistent with Law No. 1/ 2004 which defines state receivables as the amount of money owed to the central government

Clarify that SOE

Receivables are not State Receivables

Clarify that SOE

Receivables are not State Receivables

Authority of SOE in

managing and resolving

Receivables

Authority of SOE in

managing and resolving

Receivables

SPV Regulatory Framework

SPV Regulatory Framework

35

Alternatives for NPL resolution with expected new regulations

State Banks can currently provide principal reduction up to Rp 10bn when approved by the Minister of Finance. The new regulations would allow for principal reduction in settlement with existing debtors after consideration of the following aspects

Private banks in Indonesia that have significantly reduced NPLs through such salesDisposal can be done with individual loans or portfolios of loansCriteria need to be defined for eligibility of investors to participate

Establishing an off-shore SPV(s) as the new legal owner of the assetsEstablishing a JV Financial Company in Indonesia to manage problem loans/NPLsPotential investors can be invited to be joint owners of the company/entity

Debtors’ cooperation & good intentions. Uncooperative debtors will not be eligibleCash flows both from operations as well other assetsCommercial considerations - settlement of problem loans > other alternatives including restructuring through interest rate reduction or increasing tenor/ postponement of principal payment

The authority to optimally resolve NPLs should include pursuing disposal or sale of loans to third parties, if necessary at below the principal value

The legal framework for establishing SPV in Indonesia is not expected, but it is still possible to establish a company for managing and resolving NPLs by:

Principal Reduction for

Settlement with Debtors

Principal Reduction for

Settlement with Debtors

Loan Disposal Loan Disposal

Establishing off-shore SPV

or JV Financial Company

Establishing off-shore SPV

or JV Financial Company

36

Establishing a “Bad Bank” remains an option

Achieve the target of 5% Net NPL by 2007Bank Mandiri has Rp ~27.1tn on-balance sheet NPLs & Rp 22.9tn off-balance-sheetImplementation of the bad-bank concept could accelerate the resolution and allow management to focus on business/debtors with future prospects

Significant management time is now allocated to manage and resolving NPLs, hindering our ability to grow good business Significant personnel from our credit restructuring unit (22.5%) are now dedicated to managing off-balance sheet problem loansThese resources can be allocated to debtors with better prospects if our off-balance sheet loans can be managed by the bad bank

With the revision, State Banks can dispose of NPLs in the same manner as private banksFor optimal returns, Bank Mandiri would like to retain the economic benefits from future collection from the NPLs

Due to the high level of NPLs both off and on balance sheet, Bank Mandiri needs to pursue options which could quickly:

Resolution of NPLs in bulkResolution of NPLs in bulk

Limited Resources to Manage NPLs

Limited Resources to Manage NPLs

Retaining Upside from

NPL Collections

Retaining Upside from

NPL Collections

37

Internal work in progress to accelerate NPL resolution

In AGM/EGMs, a limit of Rp 5 tn in principal reduction has been approved and is available for written-off loansOur credit restructuring unit will centrally monitor the utilization of these limits

We are revising or developing new policies and procedures to be implemented with the additional authority provided by the new regulationDeveloping eligibility criteria for principal reduction or loan disposalUn-cooperative debtors will not be eligible for principal reduction

Independent parties to conduct legal & commercial review of loan disposalNew and revised policies will need to be reviewed by the commissioners Regulators and supervisor body are to be consulted to ensure policies are in line with good governance as expected by these stakeholders

BOD has proposed a separate Directorate to manage NPLs:A separate unit within Credit Restructuring will focus on disposal and other exit strategies made possible with the new regulationsCMO will explore options to establish a bad-bank with help of advisors

Shareholder Approval for

Principal Reduction

Shareholder Approval for

Principal Reduction

OrganizationOrganization

Policies and Criteria

Policies and Criteria

Review by Independent

Parties

Review by Independent

Parties

38

25.4

79.351.140.6

171.090.6(9.1)17.881.999.762.529.01.7

93.24.18.25.13.7

14.3

2.4

249.4Rp (trillions)

Q1’05

98.30.87.36.5Certificates of BI

55.32.422.220.3Current Account w/BI

36.00.43.32.5Cash

23.9

110.143.844.1

198.192.2

(12.9)27.577.6

105.161.128.92.2

92.23.5

16.30.0

254.9Rp (trillions)

Q1 ‘06

(5.8)2.623.2Shareholders’ Equity

38.912.1112.7Certificate & Time Deposits

(14.2)4.847.2Savings Deposits

8.74.946.4Demand Deposits

15.821.9206.3Total Deposits – Non-Bank

55.53.027.0Non-Performing Loans

5.611.6106.9Loans

44.7(1.4)(12.0)Allowances

(2.3)6.761.1HTM

(0.2)3.228.8AFS

(1.1)10.292.1Government Bonds

1.710.297.9Loans – Net

(5.2)8.679.8Performing Loans

31.10.22.1Trading

(14.1)0.44.0Securities - Net

98.61.816.1Current Accounts & Placements w/Other Banks

(100.0)0.08.3Other Placements w/BI

2.228.1263.4Total Assets

Rp % ChangeUSD (billions)#Rp (trillions)

Y-o-YQ4‘05

Summary Balance Sheet: March & Dec 2005, March 2006

# USD1 = Rp9,065.5

39

Summary Quarterly Balance Sheet: Q2 ‘05 – Q1 ‘06

13.30.87.36.50.15.4Certificates of BI

9.42.422.220.318.815.9Current Accounts w/BI

29.50.43.32.52.62.3Cash

23.2

112.7

47.2

46.4

206.3

97.9

-12.0

27.0

79.8

106.9

61.1

28.8

2.1

92.1

4.0

16.1

8.3

263.4

Rp (tn)

Q4 ‘05

23.9

110.1

43.8

44.1

198.1

92.2

(12.9)

27.5

77.6

105.1

61.1

28.9

2.2

92.2

3.5

16.3

0.0

254.9

Rp (tn)

Q1 ‘06

2.92.623.622.8Shareholders’ Equity

(2.3)12.199.489.2Certificate & Time Deposits

(7.0)4.846.049.5Savings Deposits

(4.9)4.941.144.4Demand Deposits

(4.0)21.9186.4183.2Total Deposits – Non-Bank

1.73.025.025.6Non-Performing Loans

(1.7)11.6106.7104.0Loans

7.6(1.4)(11.9)(10.9)Allowances

0.06.761.161.1HTM

0.43.228.829.0AFS

0.210.292.392.5Government Bonds

(5.8)10.294.793.1Loans – Net

(2.8)8.681.778.5Performing Loans

3.10.22.32.4Trading

(12.2)0.44.23.3Securities - Net

1.51.812.613.4Current Accounts & Placements w/Other Banks

(100.0)0.02.44.1Other Placements w/BI

(3.1)28.1250.3256.8Total Assets

Rp % ChangeUS$ (bn)#Rp (tn)Rp (tn)

Q-o-QQ3 ‘05Q2 ‘05

# USD1 = Rp9,065.5

40

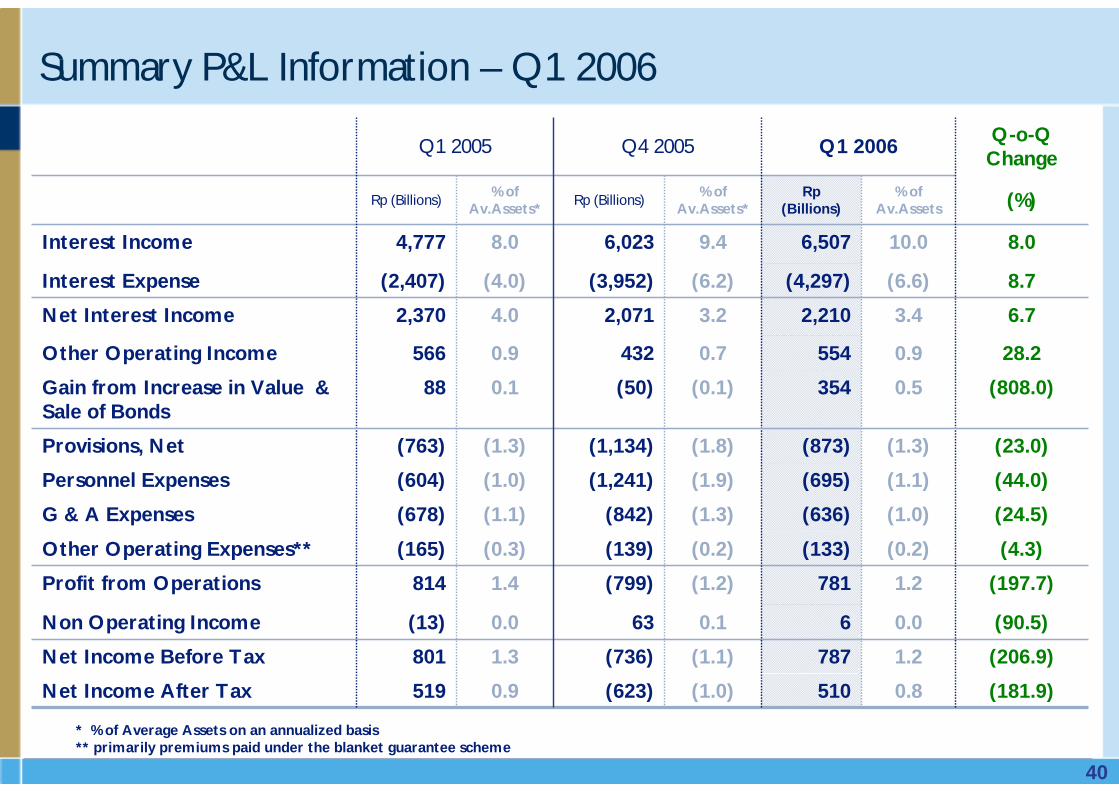

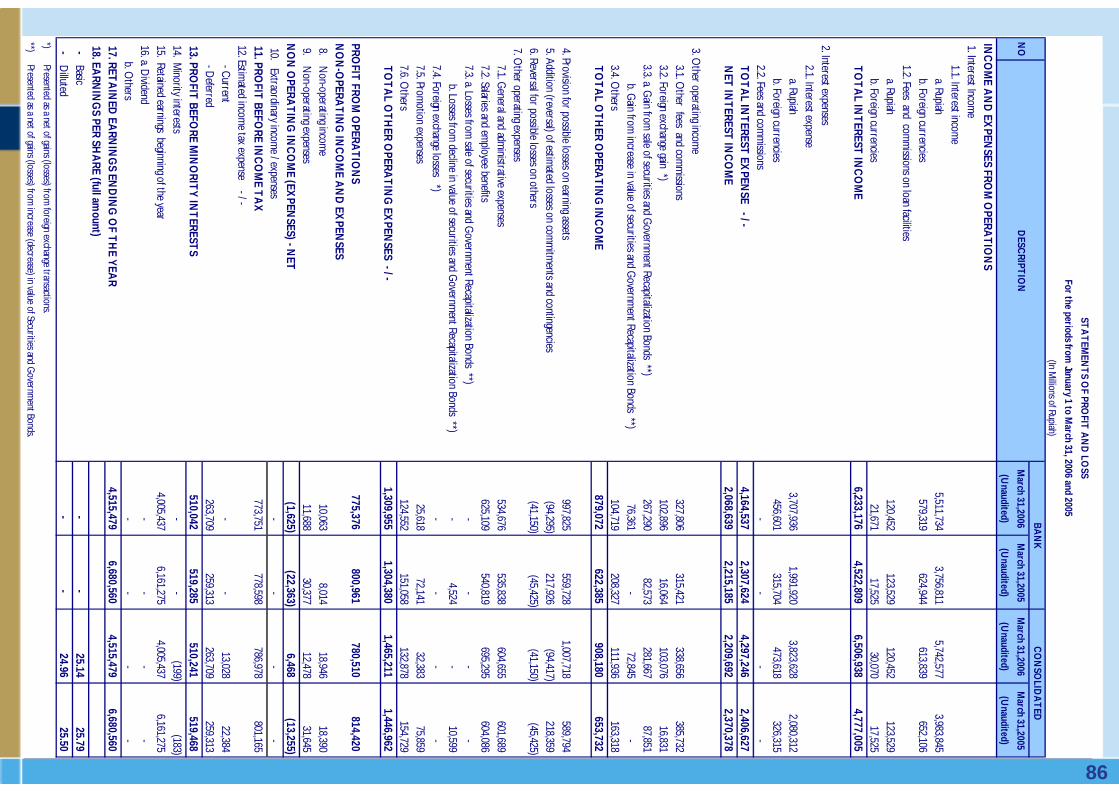

Summary P&L Information – Q1 2006

0.9

1.3

0.0

1.4

(0.3)

(1.1)

(1.0)

(1.3)

0.1

0.9

4.0

(4.0)

8.0

% of Av.Assets*

519

801

(13)

814

(165)

(678)

(604)

(763)

88

566

2,370

(2,407)

4,777

Rp (Billions)

Q1 2005

(808.0)0.5354 (0.1)(50)Gain from Increase in Value & Sale of Bonds

(90.5)0.06 0.163 Non Operating Income

(4.3)(0.2)(133)(0.2)(139)Other Operating Expenses**

(206.9)1.2787 (1.1)(736)Net Income Before Tax

(24.5)(1.0)(636)(1.3)(842)G & A Expenses

(44.0)(1.1)(695)(1.9)(1,241)Personnel Expenses

(23.0)(1.3)(873)(1.8)(1,134)Provisions, Net

(181.9)0.8510 (1.0)(623)Net Income After Tax

(197.7)1.2781 (1.2)(799)Profit from Operations

28.20.9554 0.7432 Other Operating Income

6.73.42,210 3.22,071 Net Interest Income

8.7(6.6)(4,297)(6.2)(3,952)Interest Expense

8.010.06,507 9.46,023 Interest Income

(%)% of Av.Assets

Rp (Billions)

% of Av.Assets*

Rp (Billions)

Q-o-Q Change

Q1 2006Q4 2005

* % of Average Assets on an annualized basis** primarily premiums paid under the blanket guarantee scheme

41

Trading AFS HTM Trading AFS HTMFixed Rate

FR0002 15-Jun-09 14.00% 68 105.85 72 FR0005 15-Jul-07 12.25% 500 100.66 503 FR0010 15-Mar-10 13.15% 1,350,000 100.00 1,350,000 FR0014 15-Nov-10 15.58% 2,947 112.71 3,321 FR0019 15-Jun-13 14.25% 1,101,133 110.21 1,213,547 FR0020 15-Dec-13 14.28% 518,538 538,491 110.67 573,850 595,932 Sub Total 519,106 1,642,571 1,350,000 574,426 1,812,801 1,350,000

Variable RateVR0010 25-Oct-06 12.92% 1,342,361 100.03 1,342,710 VR0011 25-Feb-07 12.92% 5,000 100.01 5,001 VR0012 25-Sep-07 12.73% 44,000 190,000 100.00 43,998 189,992 VR0013 25-Jan-08 12.92% 155,000 1,198,384 99.98 154,961 1,198,084 VR0014 25-Aug-08 12.92% 40,000 99.84 39,936 VR0016 25-Jul-09 12.92% 20,000 99.18 19,837 VR0017 25-Jun-11 12.73% 30,000 328,270 99.21 29,762 325,670 VR0019 25-Dec-14 12.73% 5,050,000 1,114,300 99.19 5,009,196 1,114,300 VR0020 25-Apr-15 12.92% 4,100,000 391,029 99.08 4,062,362 391,029 VR0021 25-Nov-15 12.92% 2,400,000 690 99.07 2,377,656 690 VR0022 25-Mar-16 12.73% 692,844 6,796,813 99.06 686,352 6,796,813 VR0023 25-Oct-16 12.92% 659,738 4,086,068 98.91 652,534 4,086,068 VR0024 25-Feb-17 12.69% 8,210,550 100.00 8,210,550 VR0025 25-Sep-17 12.83% 5,210,550 100.00 5,210,550 VR0026 25-Jan-18 12.09% 3,475,267 100.00 3,475,267 VR0027 25-Jul-18 12.09% 3,475,267 100.00 3,475,267 VR0028 25-Aug-18 12.92% 1,696,428 3,475,267 98.88 1,677,377 3,475,267 VR0029 25-Aug-19 12.92% 5,344,421 3,475,267 98.80 5,280,235 3,475,267 VR0030 25-Dec-19 12.83% 8,016,765 100.00 8,016,765 VR0031 25-Jul-20 12.92% 5,597,343 12,016,765 98.65 5,521,555 12,016,765 Sub Total 1,636,361 27,257,428 59,744,598 1,636,206 26,981,013 59,744,598 Grand Total 2,155,467 28,899,999 61,094,598 2,210,631 28,793,814 61,094,598

2.34% 31.36% 66.30% 2.40% 31.26% 66.34%92,150,064 92,099,043

SeriesFair ValueNominal

Total Fair ValueTotal Nominal Value

Maturity Date

Interest Rate (%)

Mark to Market

Recap Bond Portfolio Details, 31 Mar 2006 – Bank Only

(Stated in Rp Millions)

42

Bank Mandiri’s Credit Ratings

BShort Term Local Currency Debt

idnAA

BB-

B+

B

BB-

Stable

NR

NR

BB-

Stable

Fitch

B2BBLong Term Local Currency Debt

Subordinated Debt

BShort Term Foreign Currency Debt

idA+BB-Long Term Local Currency Debt

NPBShort Term Foreign Currency Debt

B3Long Term Bank Deposits

BShort Term Local Currency Debt

Bank Mandiri Ratings

B2B+Long Term Foreign Currency Debt

PositivePositiveOutlook

Sovereign Ratings

StableLong Term Local Currency Outlook

B3Long Term Bank Deposits

WRBB-Long Term Foreign Currency Debt

PositiveStableLong Term Foreign Currency Outlook

BNational Rating

E+Bank Financial Strength

PefindoMoody’sS&P

43

Reconciliation to IFRS

5,166

(90)

38

-

-

75

10

25

-

70

(309)

5,256

Rp (Billions)

FY ’04 FY ’05FY ’03FY ’02

(1,405)4,395 3,176 Net profit in accordance with IFRS

--293 Securities & Gov. Bond (trading portfolio)

25199 -De-recognition of revaluation of premises & equipment

86182 (184)Deferred income taxes

955 -Accretion on deferred inc. arising from loan purchase from IBRA

-(21)10Employee benefits

(223)104 351Allow. for possible losses on commitments & contingencies

(2,008)(191)430Net Adjustment

--(995) De-recognition of allowances

-52 -Change in fair value of derivatives

(2,681) (662)955Allow. for possible losses on earning assets

IFRS Adjustments

603 4,586 2,746 Net profit under Indonesian GAAP

Rp (Billions)Rp (Billions)Rp (Billions)

IFRS = International Financial Reporting Standards

44

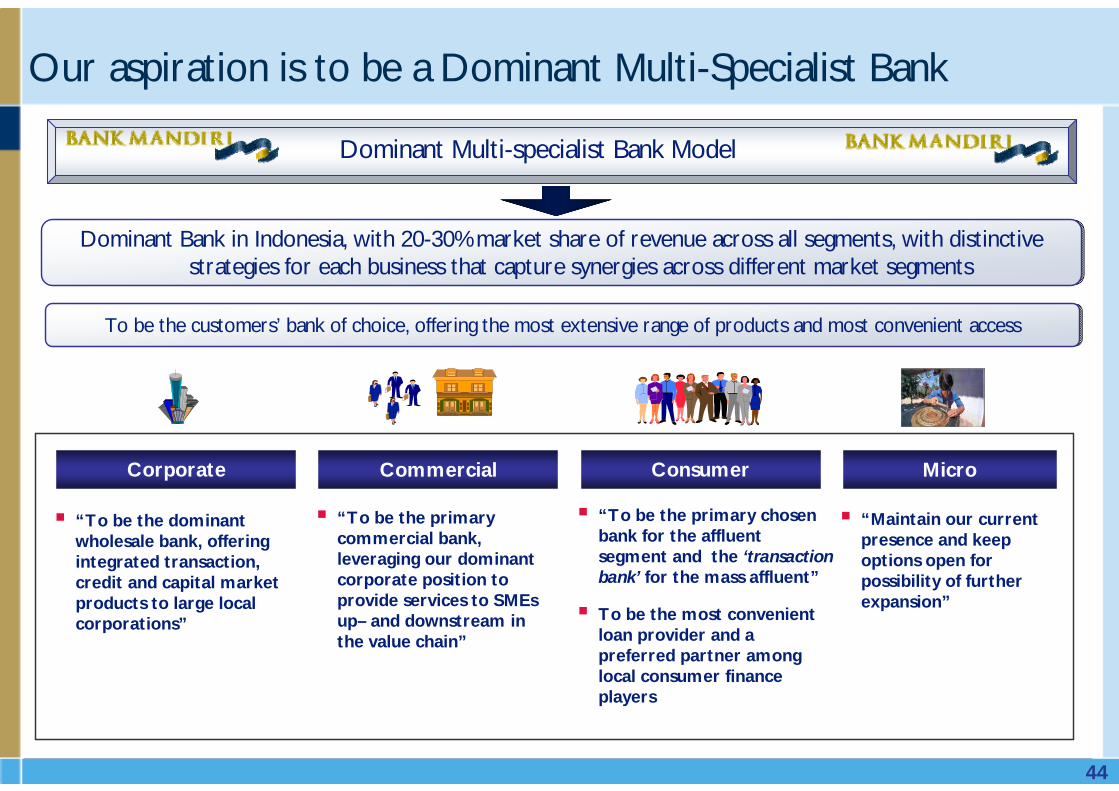

Corporate Consumer

Dominant Bank in Indonesia, with 20-30% market share of revenue across all segments, with distinctive strategies for each business that capture synergies across different market segments

Dominant Bank in Indonesia, with 20-30% market share of revenue across all segments, with distinctive strategies for each business that capture synergies across different market segments

Commercial Micro

Our aspiration is to be a Dominant Multi-Specialist Bank

“To be the dominant wholesale bank, offering integrated transaction, credit and capital market products to large local corporations”

“To be the primary commercial bank, leveraging our dominant corporate position to provide services to SMEsup– and downstream in the value chain”

“To be the primary chosen bank for the affluent segment and the ‘transaction bank’ for the mass affluent”

To be the most convenient loan provider and a preferred partner among local consumer finance players

“Maintain our current presence and keep options open for possibility of further expansion”

Dominant Multi-specialist Bank Model

To be the customers’ bank of choice, offering the most extensive range of products and most convenient accessTo be the customers’ bank of choice, offering the most extensive range of products and most convenient access

45

Maintaining our position as market leader and focusing our effort to shift into a more profitable product mix (e.g. fee-based products)Leveraging our strength in wholesale and investment banking through Mandiri SekuritasEnsuring profitability of our loan book by fundamentally reworking risk management processes Exiting non profitable businesses by reducing our exposure to relationships and sectors which do not offer sufficient returns for the risk

Expand our engagement in the consumer segmentBoost our efforts to build Mandiri Prioritas by building our sales capabilities, while refocusing our list of initiatives on acquisition and retention of the mass affluent segmentAspire to have the largest share in terms of primary banking relationships based on the largest branch and ATM network in the country and expansion of EDCs Play a major role in certain consumer finance segments eg. mortgage and cardsIncrease and optimize integration with Bank Syariah Mandiri and AXA Mandiri to provide complete solutions

Accessing and integrating the financial flows across the value chain to better understand the risks and price accordinglyProviding innovative fee-based products around cash management and working capital arrangements to dominate fee businessesFocusing on mid-caps and larger small companies with transaction intensive businessesCapturing wealth management opportunities of operator-owner entities

Focus of this year is to maintain our presence in this segmentLeveraging our in-branch capacity to serve the customersKeep an option for possibility of further expansion later in 2006

Corporate Banking

Corporate Banking

Commercial Banking

Commercial Banking

Consumer Banking

Consumer Banking

Micro BankingMicro

Banking

Individual segment strategies

46

Transformation themes for achieving these aspirations

Revamp alliance program

Revamp alliance program

Build winning organization and

performance culture

Build winning organization and

performance culture

Strategic Aspiration: Dominant Multi-Specialist Bank

Strengthen risk management and

operations

Strengthen risk management and

operations

Re-structure the organization

Revamp performance management system

Reinforce high ethical standards

Implement new corporate culture in the bank

Establish a Leadership and talent development program

Implement new coverage models for wholesale banking

Design and implement an optimal retail channel network configuration

Embed stronger service and sales culture in branches

Develop and launch a lower affluent retail offering

Acquire ethnic banks and multi-finance companies

Improve current NPL position : Bad bank and quick liquidation

Design and implement a strong CRM based loan monitoring system

Enhance effectiveness of current loan approval processes

Optimize end-to-end operations, e.g. significantly reduce TAT for consumer loans

Specify focus of alliance management program

Aggressively launch 2-3 high opportunity programs

“Culture”“Strategic Alliances”

“Control NPLs”

“Boost Sales”

Deliver tailored proposition for

priority segments

Deliver tailored proposition for

priority segments

47

Vision of Bank Mandiri Implementation Roadmap

Source: Team Analysis

“Back on Track” “Outperform the Market” “Shaping the End Game”

~12 months ~12-24 months ~12-24 months

Build winning organization & performance culture

Strengthen risk management & operations

Deliver tailored proposition for priority segments

Revamp alliance program

“Bad Bank” up and running to resolve NPL issuesKey operational improvements well-underway

New BU structure and Performance Management System in place to drive performance cultureHigher professional standards embedded

Piloted and implementing CST model for large corporatesNew commercial business model in place for medium and small commercial

NPLs down to 5% gross

Dominant corporate bank built on CST modelAmong top commercial players with strong penetration in target segmentsCompleted acquisition of specialized bank and multifinance companyMarket-leading position for affluent and lower affluent bankingMost convenient and service-oriented retail bank

Among most desired employers in Indonesia due to best people development program

NPLs fully resolved and Bad Bank dissolved

Alliance program up and running, creating synergies across segments

Completed acquisition and integration of major domestic bank

Overall Bank C/I ratio of ~76% with ~15% market share

C/I ratio of ~59% with ~16-17% market share

C/I ratio of ~54-55% with ~20-30% market shareP/B ratio 2.2 Exploring regional expansion options

Top 3 alliance program up and running, creating synergies across segments

Horizon 1:Fix the leaks and lay foundations

Horizon 2: Consolidate and build momentum

Horizon 3: Accelerate and grow

48

Regulations on Asset Classification: PBI No. 7/2/PBI/2005)

Classificationby Aging of

Interest Payments#

Classificationby Aging of

Interest Payments#

BI Collectibility takes precedence#

BI Collectibility takes precedence#

One Debtor, One Project Concept*One Debtor, One Project Concept*

Completeness of Financial Report*Completeness of Financial Report*

DetailedClassification Guidance#

DetailedClassification Guidance#

Business OutlookBusiness growth potentialMarket condition & debtor position in the marketManagement qualityGroup supportEnvironmental factors

Financial ConditionProfitabilityCapital structureCash flow Sensitivity to market risk

Payment AbilityOn time paymentAvailability of debtor’s financial informationCompleteness of credit documentationCompliance toward credit agreementNature of payment sourceAppropriateness of funds usage

In instances where there is disagreement in the determination of earning asset collectibility between the bank, its external auditors and BI, the bank must adopt BI’s determination

The Bank must classify all of its earning assets to a single debtor at the level of the lowest quality assetFor debtors with exposures to more than one bank, all banks must adopt the lowest classification applied by any one bank to the debtor.All earning assets related to a particular project must be classified at the same level

Banks must require debtors to submit current financial statementsFailure to submit financial statements must result in an automatic downgrade of collectibility by one level, or to a maximum classification of sub-standard

No change to BI Prov. Req.CurrentPreviouslyClassification by Payment History

100%181+ days271+ daysCategory 5 - Loss

50%121 – 180 days181 – 270 daysCategory 4 - Doubtful

15%91 – 120 days91 – 180 daysCategory 3 – Sub-Standard

5%1 – 90 days1 – 90 daysCategory 2 – Special Mention

1%CurrentCurrentCategory 1 - Current

# Implemented in Q1 2005 * Implemented in Q2 2005

49

Accounting for Interest, Provisions and Collateral

Recognition of Interest IncomeRecognition of Interest Income

Booking of Payments from

Borrowers

Booking of Payments from

Borrowers

Valuation of Collateral & Provisioning

Valuation of Collateral & Provisioning

ProvisioningProvisioning

IBRA LoansRestructured LoansRegular LoansClassification

Cash BasisCash BasisCash BasisCat. 5 - Loss

Cash BasisCash BasisCash BasisCat. 4 - Doubtful

Cash BasisCash BasisCash BasisCat. 3 – Sub-Standard

Cash BasisCash BasisAccrual BasisCat. 2 – Special Mention

Cash BasisAccrual BasisAccrual BasisCat. 1 - Current

IBRA Loans(w/o new agreement)Restructured LoansRegular LoansClassification

PrincipalPrincipalPrincipalCat. 5 - Loss

PrincipalPrincipalPrincipalCat. 4 - Doubtful

PrincipalInterestInterestCat. 3 – Sub-Standard

PrincipalInterestInterestCat. 2 – Special Mention

PrincipalInterestInterestCat. 1 - Current

IBRA LoansRestructured LoansRegular LoansClassification

100%Cat. 5 - Loss

50%Cat. 4 - Doubtful

15%Cat. 3 – Sub-Standard

5%Cat. 2 – Special Mention

As per BI regulations, except:− Difference between principal and

purchased value book as − Provisions, or− Deferred income if a new

agreement has been made

As per BI regulations, except:− Not reversed by upgrading − Reversed by principal repayment − Beginning provisions determined at

31 Dec. 2004− Based on net book value after

restructuring loss

1%Cat. 1 - Current

All LoansCollateralClassification

Cat. 5 - Loss

Cat. 4 - Doubtful

Cat. 3 – Sub-Standard

−Can be credited against cash provisions for Cat. 2-5

Cat. 2 – Special Mention

Collateral valuation for provisioning is determined by the aging of the most recent independent appraisal (for assets over Rp 5bn):−70% of appraised value within the initial 12 months−50% of appraised value within 12 to 18 months−30% of appraised value within 18 to 24 months−No value after 24 months from appraisal

Not valuedCat. 1 - Current

50

Q4 2005#Q3 2005#Q2 2005# Q1 2006#

84,768

1,973

59,006

903

4,124

18,763

41,694

95

34,444

645

621

5,890

43,073

1,878

24,562

258

3,503

12,873

Value (Rp bn)

4.5%

3.6%

5.1%

1.2%

4.8%

2.9%

6.3%

3.3%

6.5%

0.1%

2.7%

6.6%

2.9%

3.6%

3.3%

6.1%

5.2%

1.1%

Net

2.0%

0.4%

1.4%

0.1%

0.5%

4.5%

1.7%

9.2%

2.5%

0.2%

1.7%

1.9%

5.5%

0.8%

6.9%

-

0.9%

5.7%

Net

8.0%

1.8%

8.2%

0.1%

3.4%

10.0%

7.3%

-

5.4%

0.1%

3.0%

17.9%

8.7%

1.4%

12.0%

0.2%

3.5%

6.1%

Net

0.1%

0.3%

0.1%

0.1%

-

0.1%

0.1%

-

0.1%

0.1%

-

0.3%

0.0%

0.3%

-

-

-

-

UG to PL

1.8%

0.4%

2.3%

0.2%

0.3%

0.9%

2.2%

4.3%

2.5%

0.3%

1.8%

1.0%

1.5%

0.2%

2.1%

-

-

0.8%

DG to NPL

Total

Overseas

Post-Merger

Pre-Merger

IBRA

Restructured

Total Loans

Total

Overseas

Post-Merger

Pre-Merger

IBRA

Restructured

Commercial & Small Business Loans

Total

Overseas

Post-Merger

Pre-Merger

IBRA

Restructured

Corporate Loans

Loan Background

1.8%

0.2%

2.3%

0.2%

0.3%

0.8%

2.1%

4.3%

2.4%

0.3%

1.8%

0.7%

1.4%

0.0%

2.1%

-

-

0.8%

Net

Quarterly Analysis of NPL and PL changes

* Corporate, Commercial & Small Business Loans Only# % downgrades and upgrades are quarterly figures

51

Q1 2006 Loan Detail: Collectibility by Business UnitLoan Profile: Q1 Collectibility (%) by BU - Bank Only

50.1%

60.0%

88.4%

76.8%

11.1%

13.1%

8.4%

14.4%16.6%

5.3%

5.5%

9.1%

4.4%

24.4%17.1%

4.5%

78.9%

0.9% 1.0%

1.0%

1.5% 1.4%3.2%

0.8% 2.1%

Corp Comm Small Micro Cons

5

4

3

2

1

0

10,000

20,000

30,000

40,000

50,000

Corp Comm Small Micro Cons

5

4

3

2

1

Loan Profile: Q1 Collectibility (Rp bn) by BU - Bank Only

52

13.5% were still current on interest payments with a further 21.0% less than 30 days overdue

46.4% were Commercial borrowers

10.3% were loans previously restructured

0.7% were loans purchased from IBRA

Largest downgrades by sector:

Textile Manufacturing

Wood Manufacturing

Agriculture

59.6% were Rupiah loans

45.7% were Working Capital loans

1st time downgrades from Textile and Wood Manufacturing, Agriculture & Retail Trade

Corp

Com

m

Small

Organic

Restr

IBRA O/S

Mfg-Text

Mfg-Wood

Mfg-Oth

Agri

Trading-Ret

Constr

Trading-H&R

Trading-Oth

Oth<5%

IDR

US

D

WC

Invest.

Export

Program

Current

< 30 Days

31-60 Days

61-90 Days

90+ Days

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GAS Backgrnd Sector Currency Purpose Int. Aging

Q1 2006 Loan Detail*: Downgrades to NPL

* Excluding Micro & Consumer Loans Only

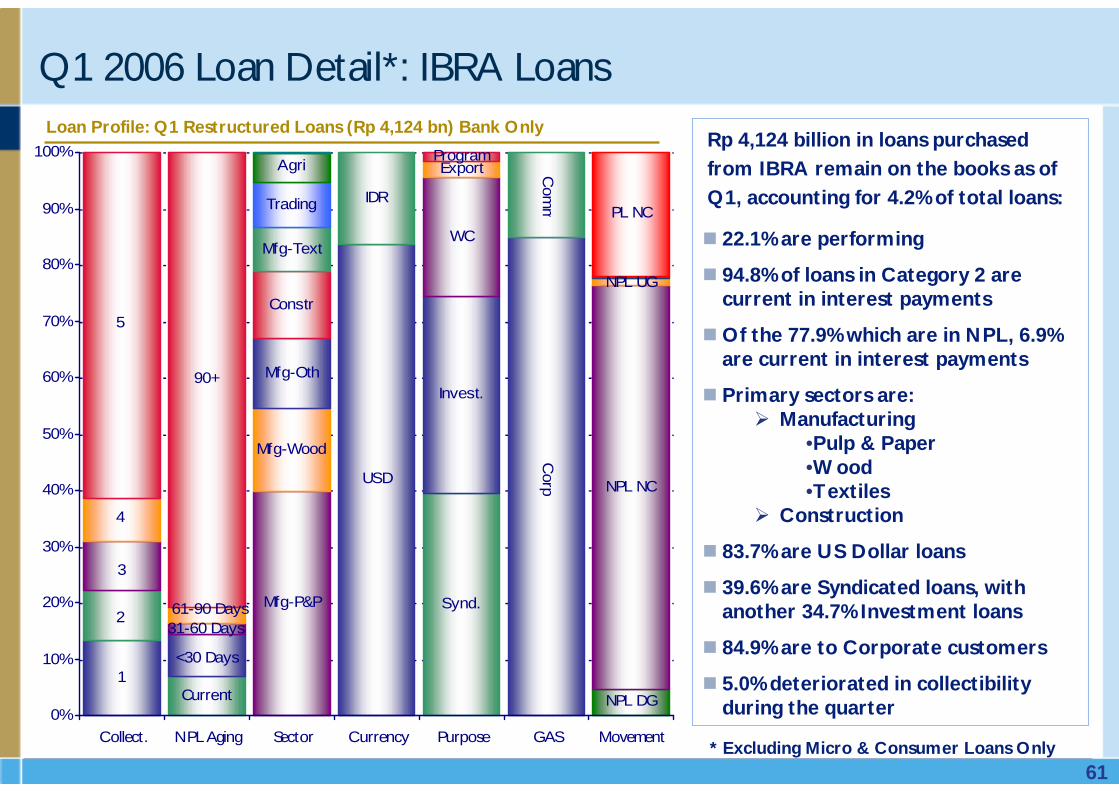

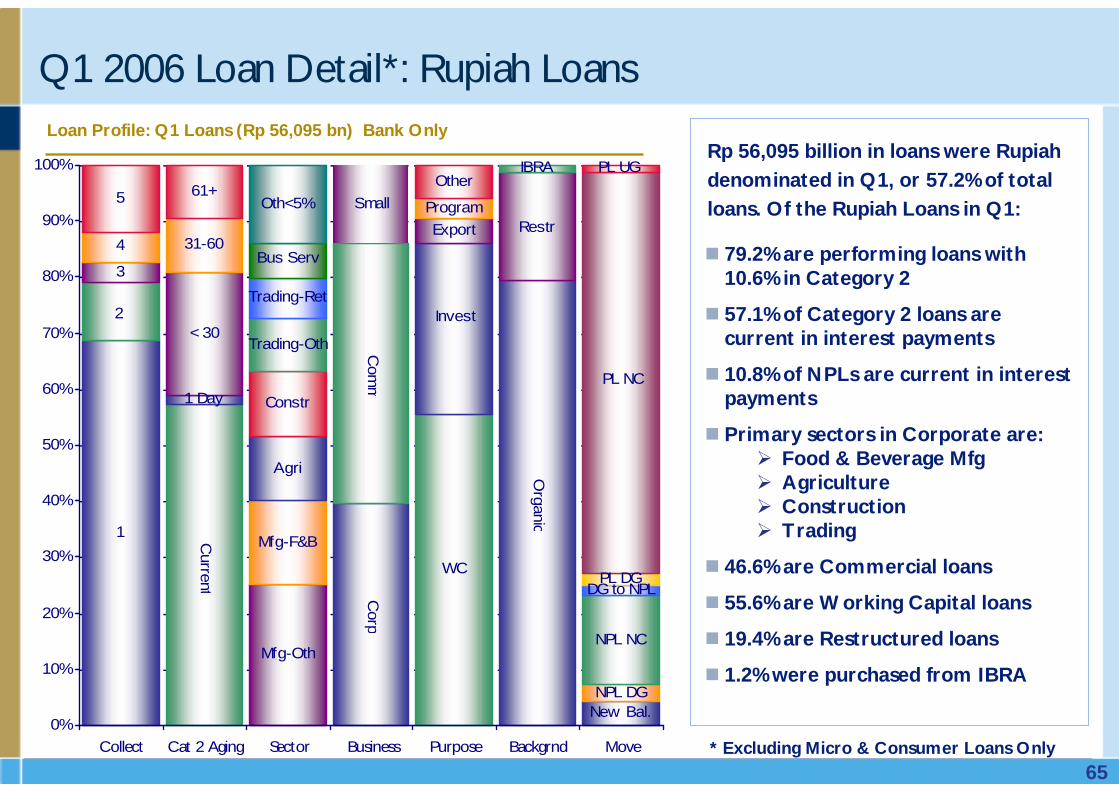

Corporate, Commercial & Small Business loans downgraded to NPL in Q1 totaled Rp 1,558 billion (1.6% of total loans). Of these loans:

Loan Profile: Q1 Downgrades to NPL (Rp 1,558 bn) - Bank Only

53

Q1 2006 Loan Detail*: Non-Performing LoansLoan Profile: Q1 NPLs (Rp 26,424 bn) Bank Only

22.1% remain current on interest payments and 13.7% are less than 90 days overdue

63.3% are to Corporate customers

37.3% are Investment loans

Primary sectors are:Manufacturing

•Textiles•Pulp & Paper•Wood

ConstructionTrading

55.8% are US Dollar loans

33.4% were previously restructured

12.2% were loans purchased from IBRA

16.2% are Cat. 3 & 21.1% are Cat. 4

Corporate, Commercial & Small Business NPLs totaled Rp26,424 billion in Q1, or 26.9% of total loans. Of these NPLs in Q1:

3

4

5

Organic

Restr

IBR

A

O/S

Mfg-Text

Mfg-P&P

Mfg-Oth

Constr

Mfg-Wood

Trading

Agri

Mfg-Chem

Mfg-NonM

Oth<5%

USD

IDR

Invest

WC

Synd

Export

Program

Current

< 30 Days

31-60 Days61-90 Days

90+ Days

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Collectibility Backgrnd Sector Currency Purpose Int. Aging* Excluding Micro & Consumer Loans Only

54

NPL Loan Detail*: Quarterly by Interest Days Past DueQuarterly Downgrades to NPL & Interest DPD - Bank Only

976

665

474

1,108

11,161

6,901

1,177

4,106

1,558

11.8%

43.8%

14.2%

21.0%

65.5%

53.0%

32.8%

38.3%

13.5%

26.0%

10.6%

22.7%

0.5%

25.1%

21.1%

15.9%

10.2%

21.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

Q1 '04Q2 '04Q3 '04Q4 '04Q1 '05Q2 '05Q3 '05Q4 '05Q1 '06

0.0%

12.5%

25.0%

37.5%

50.0%

62.5%

75.0%

Rp Value

Current (%)

<30 Days (%)

Quarterly NPL Stock & Interest DPD - Bank Only

Rp tn

6,196

6,451

5,925

6,334

17,456

24,962

24,193

26,248

26,424

18.7%

22.5%

26.3%

51.9%

60.0%

51.3%

33.0%

28.7%

22.1%

5.3%3.3%

4.5%2.8%

17.2%

10.2%8.5% 7.7% 6.6%

0

5,000

10,000

15,000

20,000

25,000

30,000

Q1 '04Q2 '04Q3 '04Q4 '04Q1 '05Q2 '05Q3 '05Q4 '05Q1 '06

0%

10%

20%

30%

40%

50%

60%

Rp Value

Current (%)

<30 Days (%)

* Excluding Micro & Consumer Loans Only

55

Q1 2006 Loan Detail*: New Downgrades to Category 2Loan Profile: Q1 Downgrades to Cat. 2 loans (Rp 1,492 bn) - Bank Only

62.5% are for Commercial & 23.8% are for Small Business customers

44.1% are current & 1.1% are 1 day overdue

Primary sectors downgraded are:AgricultureTransportationConstructionRetail Trading

78.7% are Rupiah loans

52.8% are Working Capital loans

11.9% are Restructured loans

0.3% were purchased from IBRA

Rp 1,492 billion (1.5% of total loans) in Corporate, Commercial & Small Business loans were downgraded to Category 2 in Q1. Of the downgraded Special Mention Loans in Q1:

Corp

Com

m

Small

Current

1 Day

< 30

31-60

61+

Agri

Trans

Mfg-Oth

Trading-Oth

Constr

Trading-Ret

Mfg-Chem

Oth<5%

IDR

USD

WC

Invest.

ExportProgram

Organic

Restr

IBRA O/S

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GAS Days Aging Sector Currency Purpose Backgrnd * Excluding Micro & Consumer Loans Only

56

Q1 2006 Loan Detail*: Category 2 Loans

Loan Profile: Q1 Category 2 Loans (Rp 9,928 bn) Bank Only

48.1% are to Corporate customers

70.0% are current or 1 day overdue

Primary sectors in Category 2 are:Chemical Manufacturing AgricultureConstructionTrading, Hotels & Restaurants

59.8% are Rupiah loans

54.1% are Investment loans

34.0% are Restructured loans

3.7% were purchased from IBRA

78.1% saw no change in collectibility

Rp 9,928 billion (10.1% of total loans) in Corporate, Commercial & Small Business loans were in Category 2 in Q1. Of these Special Mention loans in Q1:

Corp

Com

m

Small

Current

1 Day

< 30

31-60

61+

Mfg-Chem

Mfg-Oth

Agri

Constr

Trading-H&R

Trading-Oth

Mass Trans

Comm

Oth<5%

IDR

USD

Invest.

WC

ExportSynd.

Program

Organic

Restr

IBRA

PL NC

1 to 2

New Bal.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GAS Days Aging Sector Currency Purpose Backgrnd Move. * Excluding Micro & Consumer Loans Only

57

51.1% were to Commercial borrowers

68.4% were loans with no previous restructuring history

31.6% were loans previously restructured

Largest upgrades by sector:

Agriculture

Retail Trading

Mining

79.4% were Rupiah loans

58.6% were Working Capital loans

63.3% of upgrades to PL were NPLs moving to Category 2

36.7% of upgrades to PL were NPLs moving to Category 1

Corp

Comm

Small

Organic

Restr

O/S

Agri

Trading-Ret

Mining

Trading-Oth

Oth<5%

IDR

US

D

WC

Invest.

Program

1

2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%