PROSPECTUS - Oslo Børs

66

PROSPECTUS Jack-Up InvestCo 3 Plc. (Registration number: C 57037) (Issuer) DBB Jack-Up Services A/S (Registration number: 24620417) (Guarantor) Listing on Oslo Børs 11 per cent Jack-Up InvestCo 3 Ltd. Senior Secured Callable Bond Issue 2014/2018 ISIN NO 0010699887 ________________________________________________________ THIS PROSPECTUS SERVES AS A LISTING PROSPECTUS ONLY AS REQUIRED BY NORWEGIAN LAW AND REGULATIONS. THIS PROSPECTUS DOES NOT CONSTITUTE AN OFFER TO BUY, SUBSCRIBE OR SELL ANY OF THE SECURITIES DESCRIBED HEREIN, AND NO SECURITIES ARE BEING OFFERED OR SOLD PURSUANT TO IT. THIS PROSPECTUS HAS NOT BEEN APPROVED BY THE U.S. SECURITIES AND EXCHANGE COMMISSION. ________________________________________________________ 16 December 2014

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of PROSPECTUS - Oslo Børs

PROSPECTUS

Jack-Up InvestCo 3 Plc. (Registration number: C 57037) (Issuer)

DBB Jack-Up Services A/S (Registration number: 24620417) (Guarantor)

Listing on Oslo Børs

11 per cent Jack-Up InvestCo 3 Ltd. Senior Secured Callable Bond Issue 2014/2018

ISIN NO 0010699887 ________________________________________________________

THIS PROSPECTUS SERVES AS A LISTING PROSPECTUS ONLY AS REQUIRED BY

NORWEGIAN LAW AND REGULATIONS. THIS PROSPECTUS DOES NOT CONSTITUTE AN

OFFER TO BUY, SUBSCRIBE OR SELL ANY OF THE SECURITIES DESCRIBED HEREIN,

AND NO SECURITIES ARE BEING OFFERED OR SOLD PURSUANT TO IT. THIS

PROSPECTUS HAS NOT BEEN APPROVED BY THE U.S. SECURITIES AND EXCHANGE

COMMISSION.

________________________________________________________

16 December 2014

2

Important information

This Prospectus has been prepared by Jack-Up InvestCo 3 Plc. (the "Company" or the "Issuer") in order to provide information about the Company, its subsidiaries and its business in connection with the listing on the Oslo Stock Exchange of the bonds issued under the 11 per cent Jack-Up InvestCo 3 Ltd. Senior Secured Callable Bond Issue (the "Bonds"). DBB Jack-Up Services A/S is a guarantor for the Bond Issue (the "Guarantor" or the "Parent"). The term "Group" refers to the Guarantor and its subsidiaries, including the

Issuer.

For the definitions of terms used throughout this Prospectus, see Section 10 "Definitions and Glossary of Terms".

_______________________

The Company has furnished the information in this Prospectus and accepts responsibility for the information contained herein. No other party makes any representation or warranty, expressed or implied, as to the accuracy or completeness of such information, and nothing contained in this Prospectus is, nor shall be relied upon as, a promise or representation by another party than the Company. This Prospectus does not contain any offer to subscribe and/or purchase the Bonds. The Norwegian Financial Supervisory Authority has reviewed

and approved this Prospectus in accordance with Sections 7-7 and 7-8 of the Norwegian Securities Trading Act. The Norwegian Financial Supervisory Authority has however not reviewed and/or approved whether the information provided is correct or complete. The Norwegian Financial Supervisory Authority's control and approval in this respect is limited to whether the Issuer has included descriptions according to a pre-defined list of content requirements. The Norwegian Financial Supervisory Authority has not in any way verified or approved company or corporate matters described in or otherwise comprised by the Prospectus. It is the Company's responsibility to ensure that the information in this Prospectus is accurate and complete.

All inquiries relating to this Prospectus should be directed to the Company. No other person has been authorized to give any information about, or make any representation on behalf of, the Company in connection with the listing of the Bonds, and, if given or made, such other information or representation must not be relied upon as having been authorized by the Company.

The information contained herein is as of the date hereof and subject to change, completion or amendment without notice. There may have been changes affecting the Company or its subsidiaries subsequent to the date of this Prospectus. The delivery of this Prospectus at any time after the date hereof will not, under any circumstances, create any implication that there has been no change in the Company’s affairs since the date hereof or that the information set forth in this Prospectus is correct as of any time since its date. However, in accordance with Section 7-15 of the Norwegian Securities Trading Act, every new factor, material mistake or inaccuracy which may have significance for the assessment of the Bonds and which is brought to light between the publication of this Prospectus and the listing of the Bonds, respectively, on Oslo Børs, will to the extent required be included in a supplement to this Prospectus.

The distribution of this Prospectus in certain jurisdictions may be restricted by law. The Company requires persons in possession of this Prospectus to inform themselves about and to observe any such restrictions. This Prospectus serves as a listing prospectus as required by applicable laws and regulations. This Prospectus does not constitute an offer to buy, subscribe or sell any of the securities described herein, and no securities are being offered or sold pursuant to it.

The Bonds have not been and will not be registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act") and may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and applicable state securities laws.

NO APPLICATION HAS BEEN MADE UNDER MALTESE LAW TO PUBLICLY MARKET THE BONDS IN OR OUT OF MALTA. THE BONDS MAY NOT BE OFFERED, SOLD OR DELIVERED IN MALTA OR TO ANY PERSON RESIDENT IN MALTA AND NO PERSON RESIDENT IN MALTA SHALL BE ELIGIBLE TO PURCHASE, ACQUIRE OR HOLD ANY BONDS ISSUED BY ISSUER.

The contents of this Prospectus shall not be construed as legal, business or tax advice. Each reader of this Prospectus should consult its own legal, business or tax advisor as to legal, business or tax advice. If investors are in any doubt about the contents of this Prospectus, they should consult their stockbroker, bank manager, lawyer, accountant or other professional adviser.

Investing in the Bonds involves certain inherent risks. Each potential investor in the Bonds must determine the suitability of that investment in light of its own circumstances. In particular, each potential investor should:

have sufficient knowledge and experience to make a meaningful evaluation of the Bonds, the merits and risks of investing in the Bonds and the information contained or incorporated by reference in this Prospectus or any applicable supplement;

have access to, and knowledge of, appropriate analytical tools to evaluate, in the context of its particular financial situation, an investment in the Bonds and the impact the Bonds will

3

have on its overall investment portfolio;

have sufficient financial resources and liquidity to bear all of the risks of an investment in the Bonds;

understand thoroughly the terms of the Bonds; and

be able to evaluate (either alone or with the help of a financial adviser) possible scenarios for economic, interest rate and other factors that may affect its investment and its ability to bear the applicable risks.

Potential investors are also encouraged to read Section 2 "Risk Factors" of this Prospectus.

4

TABLE OF CONTENTS

1 SUMMARY ....................................................................................................................................... 7

2 RISK FACTORS .............................................................................................................................. 14 2.1 General ............................................................................................................................ 14 2.2 Market Risk....................................................................................................................... 14 2.2.1 Regulations governing operations ........................................................................................ 14 2.2.2 Competition ...................................................................................................................... 14 2.2.3 Technological progress might render the technologies used by the Group obsolete .................... 14 2.3 Operational Risk ................................................................................................................ 14 2.3.1 Operational risks associated with offshore operations ............................................................. 15 2.3.2 The Group may assume substantial responsibilities ................................................................ 15 2.3.3 Intellectual Property Rights ................................................................................................. 15 2.3.4 Dependence on key executives and personnel ....................................................................... 15 2.3.5 Dependence on employment of the Group’s vessels ............................................................... 15 2.3.6 Dependence on services from third parties to complete some of the employment contracts ........ 15 2.3.7 The outcome of future claims and litigation could have a material adverse impact on the

business, results of operation and financial condition of the Group ........................................... 15 2.3.8 Risks associated with upgrade, refurbishment and repairs ...................................................... 16 2.3.9 Risks related to vessels under construction ........................................................................... 16 2.4 Financial Risk .................................................................................................................... 16 2.4.1 Financial covenants............................................................................................................ 16 2.4.2 Foreign exchange risk ........................................................................................................ 16 2.4.3 Credit risk ........................................................................................................................ 16 2.4.4 Liquidity risk – cost of funding ............................................................................................. 16 2.4.5 Borrowing and leverage ...................................................................................................... 17 2.4.6 Related party transactions .................................................................................................. 17 2.4.7 Value of secured assets ...................................................................................................... 17 2.4.8 Overall tax structure .......................................................................................................... 17 2.5 Risks related to the Bonds .................................................................................................. 17 2.5.1 General risks related to the Bonds ....................................................................................... 17 2.5.2 Ability to service indebtedness ............................................................................................ 17 2.5.3 Bond Agreement will impose significant operating and financial restrictions .............................. 17 2.5.4 The Bonds are subject to optional redemption by the Issuer ................................................... 18 2.5.5 Change of control - The Issuer’s ability to redeem the Bonds with cash may be limited .............. 18 2.5.6 Mandatory prepayment events ............................................................................................ 18 2.5.7 The Issuer relies on payments from the Group to redeem the Bonds ........................................ 19 2.5.8 There may only be a limited trading market for the Bonds. ..................................................... 19 2.5.9 The market price of the Bonds may be volatile ...................................................................... 19 2.6 Other Risks ....................................................................................................................... 19 2.6.1 Risks associated with disputes ............................................................................................. 19 2.6.2 Requisition or arrest of assets ............................................................................................. 19

3 STATEMENT OF RESPONSIBILITY FOR THE PROSPECTUS .................................................................... 20 3.1 Persons responsible for the information ................................................................................ 20 3.2 Declaration by persons responsible ...................................................................................... 20

4 THE BOND ISSUE AND THE BONDS .................................................................................................. 21 4.1 Purpose of the Bond Issue and use of the proceeds ............................................................... 21 4.2 Terms of the Bonds............................................................................................................ 21 4.3 Conflicts of Interests .......................................................................................................... 24 4.4 Manager ........................................................................................................................... 25 4.5 Subscription of the Bonds ................................................................................................... 25 4.6 Cash sweep waterfall and accounts ...................................................................................... 25

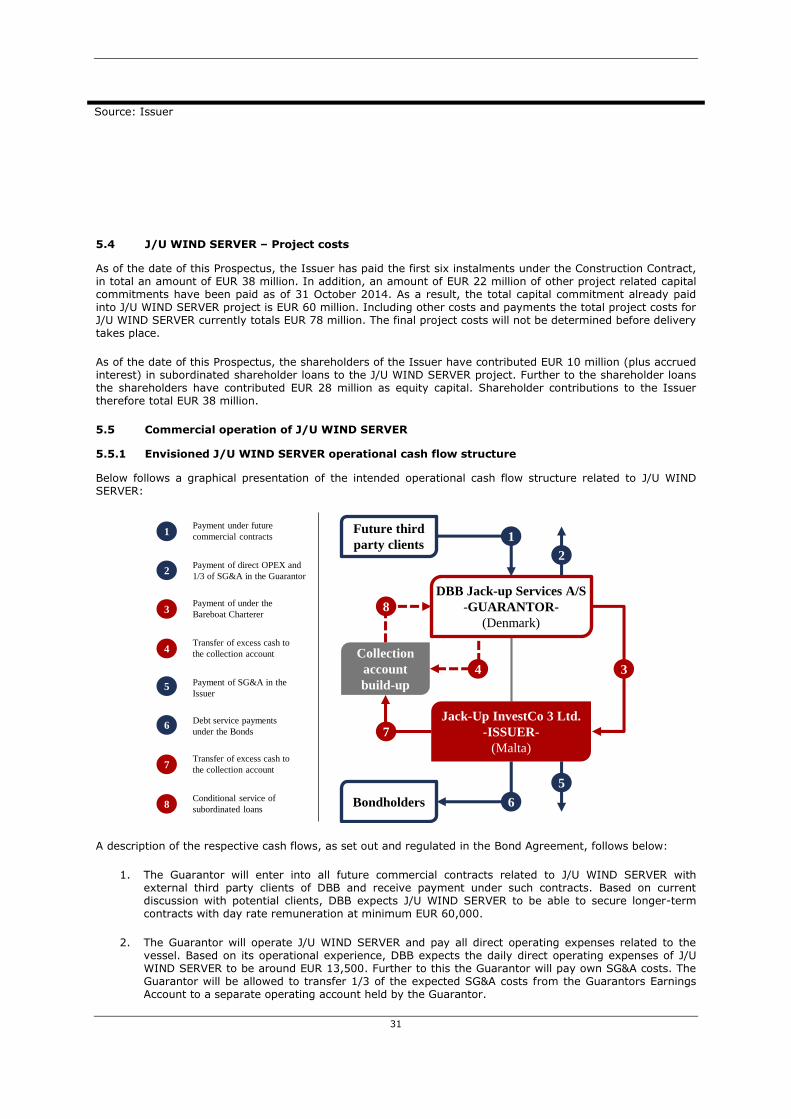

5 THE ISSUER .................................................................................................................................. 27 5.1 General ............................................................................................................................ 27 5.2 Group legal structure ......................................................................................................... 28 5.3 J/U WIND SERVER ............................................................................................................. 29 5.3.1 Introduction ...................................................................................................................... 29 5.3.2 Technical specifications overview ......................................................................................... 29 5.4 J/U WIND SERVER – Project costs........................................................................................ 31 5.5 Commercial operation of J/U WIND SERVER .......................................................................... 31 5.5.1 Envisioned J/U WIND SERVER operational cash flow structure ................................................. 31 5.5.2 Charter Agreements and Current tender processes ................................................................ 32 5.5.3 The Bareboat Agreement .................................................................................................... 32 5.5.4 OPEX related to J/U WIND SERVER ...................................................................................... 32 5.6 Management and Board of Directors of the Issuer.................................................................. 33 5.7 Issuer ownership structure ................................................................................................. 34 5.7.1 The Guarantor ................................................................................................................... 34 5.7.2 BWC ................................................................................................................................ 34

5

5.7.3 Issuer Shareholders Agreement........................................................................................... 34 5.7.4 Post-delivery insurances ..................................................................................................... 34 5.8 Related party agreements of the Issuer ................................................................................ 34 5.9 Issuer debt overview.......................................................................................................... 35 5.10 Legal disputes involving the Issuer ...................................................................................... 35

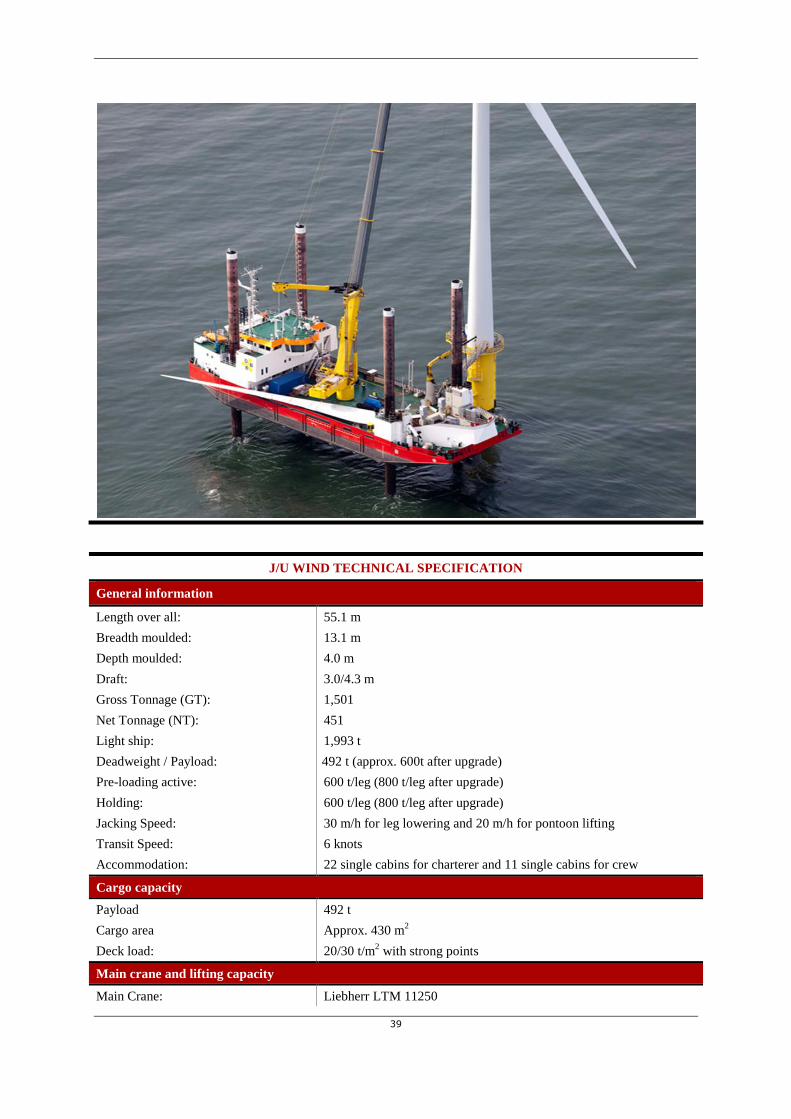

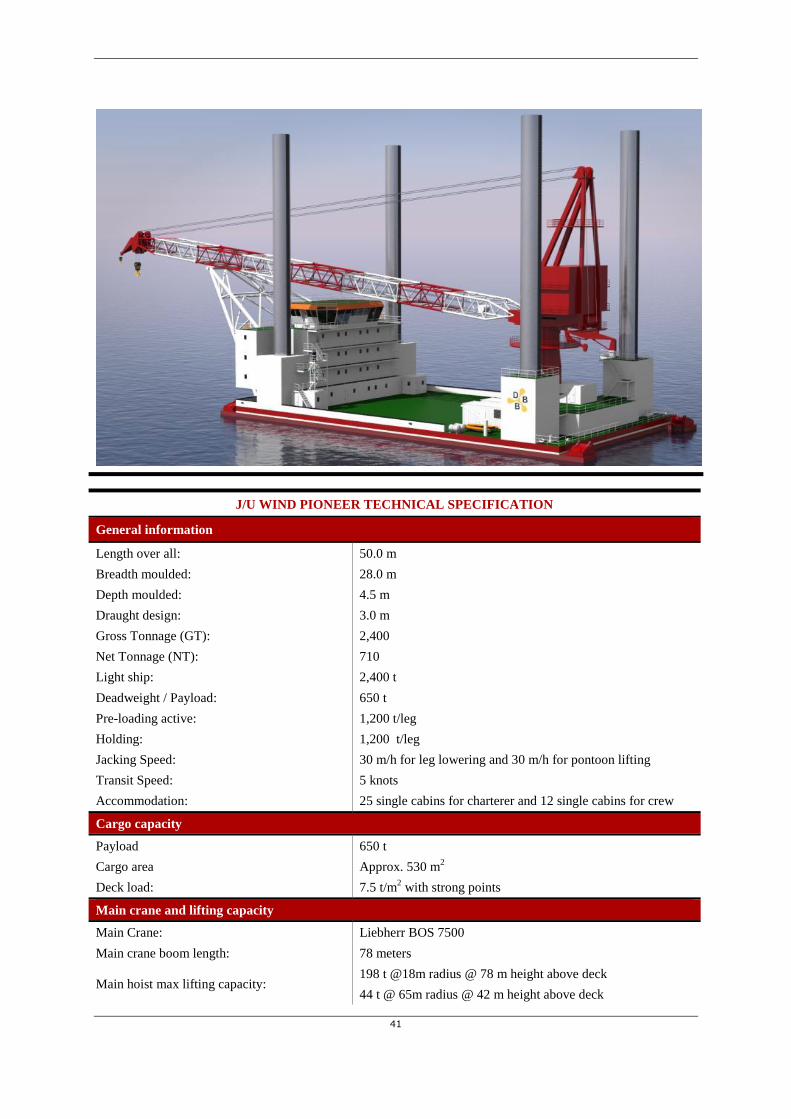

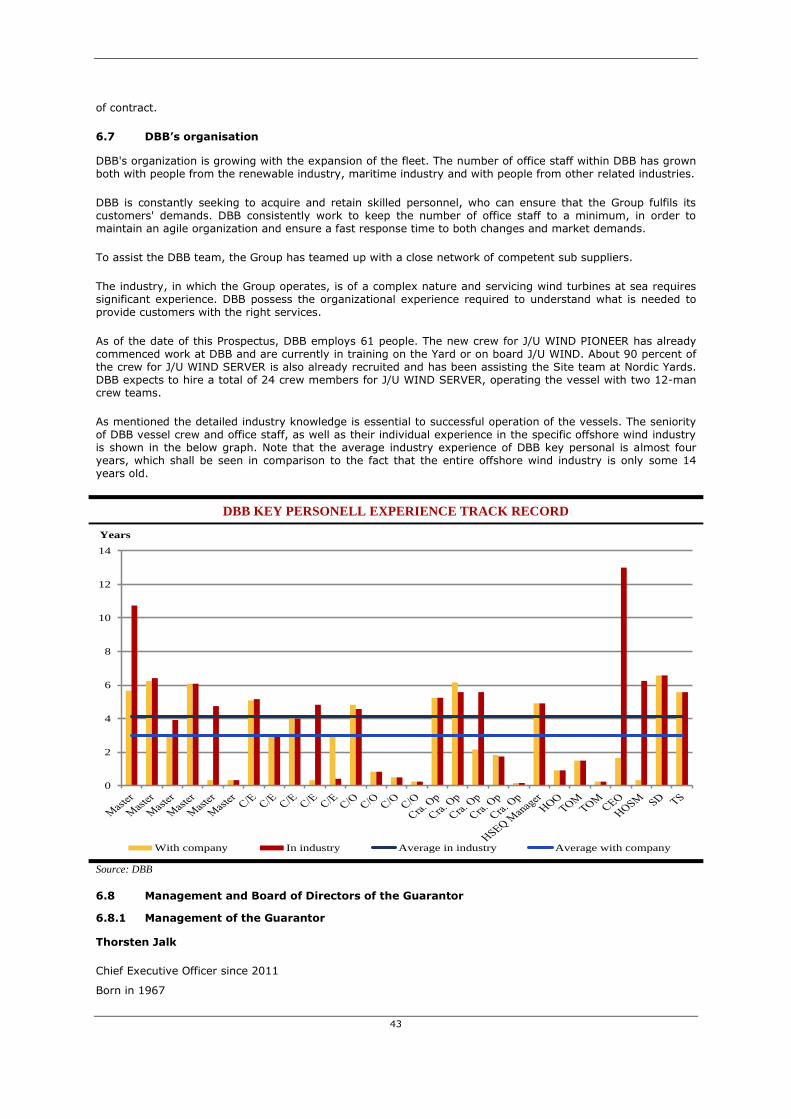

6 THE GUARANTOR AND THE GROUP .................................................................................................. 36 6.1 The Guarantor ................................................................................................................... 36 6.2 DBB's business .................................................................................................................. 36 6.3 History and development of the Group ................................................................................. 37 6.4 DBB Strategy .................................................................................................................... 37 6.5 J/U WIND ......................................................................................................................... 38 6.5.1 Vessel description .............................................................................................................. 38 6.5.2 J/U WIND's charter contract ................................................................................................ 40 6.5.3 J/U WIND's commercial track-record .................................................................................... 40 6.6 J/U WIND PIONEER ............................................................................................................ 40 6.6.1 Vessel description .............................................................................................................. 40 6.6.2 J/U WIND PIONEER conversion, capital expenditure and financing ........................................... 42 6.6.3 J/U WIND PIONEER conversion progress ............................................................................... 42 6.6.4 J/U WIND PIONEER servicing contract .................................................................................. 42 6.7 DBB’s organisation............................................................................................................. 43 6.8 Management and Board of Directors of the Guarantor ............................................................ 43 6.8.1 Management of the Guarantor ............................................................................................. 43 6.8.2 Key Employees .................................................................................................................. 44 6.8.3 Board of Directors of DBB ................................................................................................... 45 6.8.4 Corporate Governance ....................................................................................................... 46 6.9 DBB ownership structure .................................................................................................... 46 6.9.1 Overview of shareholders ................................................................................................... 46 6.9.2 Jack-up Holding A/S - Odin Equity Partners........................................................................... 47 6.9.3 Danske Bjergning og Bugsering Holding ApS ......................................................................... 47 6.9.4 OY Finans ApS .................................................................................................................. 47 6.10 DBB debt overview ............................................................................................................ 47 6.10.1 PenSam subordinated loan ................................................................................................. 48 6.10.2 J/U WIND bank facility ....................................................................................................... 48 6.10.3 J/U WIND crane financial lease ............................................................................................ 48 6.10.4 J/U WIND PIONEER bank facility .......................................................................................... 48 6.10.5 Revolving credit facility ...................................................................................................... 49 6.10.6 Guarantor shareholder loans ............................................................................................... 49 6.11 Related party agreements of DBB ........................................................................................ 49 6.12 Legal disputes of DBB ........................................................................................................ 49

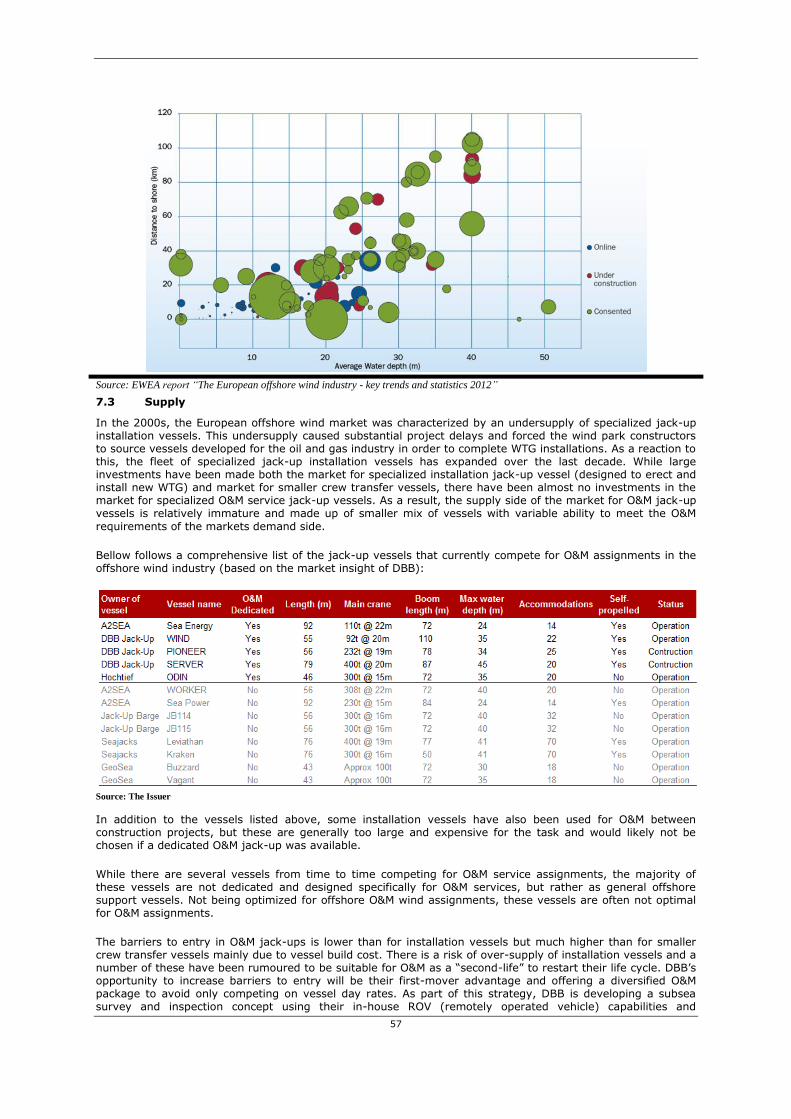

7 THE MARKET ................................................................................................................................. 50 7.1 Industry introduction ......................................................................................................... 50 7.2 Demand ........................................................................................................................... 50 7.2.1 European offshore wind industry ......................................................................................... 50 7.2.2 European O&M jack-up vessel demand ................................................................................. 55 7.3 Supply ............................................................................................................................. 57

8 TAXATION ..................................................................................................................................... 59 8.1 Certain Norwegian tax matters ............................................................................................ 59 8.1.1 Introduction ...................................................................................................................... 59 8.1.2 Taxation on distributions to the bondholder .......................................................................... 59 8.1.3 Taxation on sale and redemption of the Bonds ...................................................................... 59 8.1.4 Norwegian withholding tax .................................................................................................. 59 8.1.5 Net wealth tax .................................................................................................................. 59 8.1.6 Foreign taxes .................................................................................................................... 60 8.1.7 Inheritance tax .................................................................................................................. 60 8.2 Certain Maltese tax matters ................................................................................................ 60 8.2.1 Introduction ...................................................................................................................... 60 8.2.2 Taxation on interest from Bonds .......................................................................................... 60 8.2.3 Taxation on sale and redemption of Bonds ............................................................................ 60

9 FINANANCIAL INFORMATION OF THE ISSUER AND THE GUARANTOR ................................................... 61 9.1 Introduction ...................................................................................................................... 61 9.2 Financial information for the Guarantor ................................................................................ 61 9.2.1 Annual Accounts ................................................................................................................ 61 9.2.2 Interim accounts ............................................................................................................... 62 9.3 Key financial information for the Issuer ................................................................................ 63 9.3.1 Annual accounts ................................................................................................................ 63 9.3.2 Interim accounts ............................................................................................................... 64

10 DEFINITIONS AND CROSS REFERENCE LIST ..................................................................................... 65

6

10.1 Definitions ........................................................................................................................ 65 10.2 Cross-reference list ............................................................................................................ 66 10.3 Documents on display ........................................................................................................ 66

7

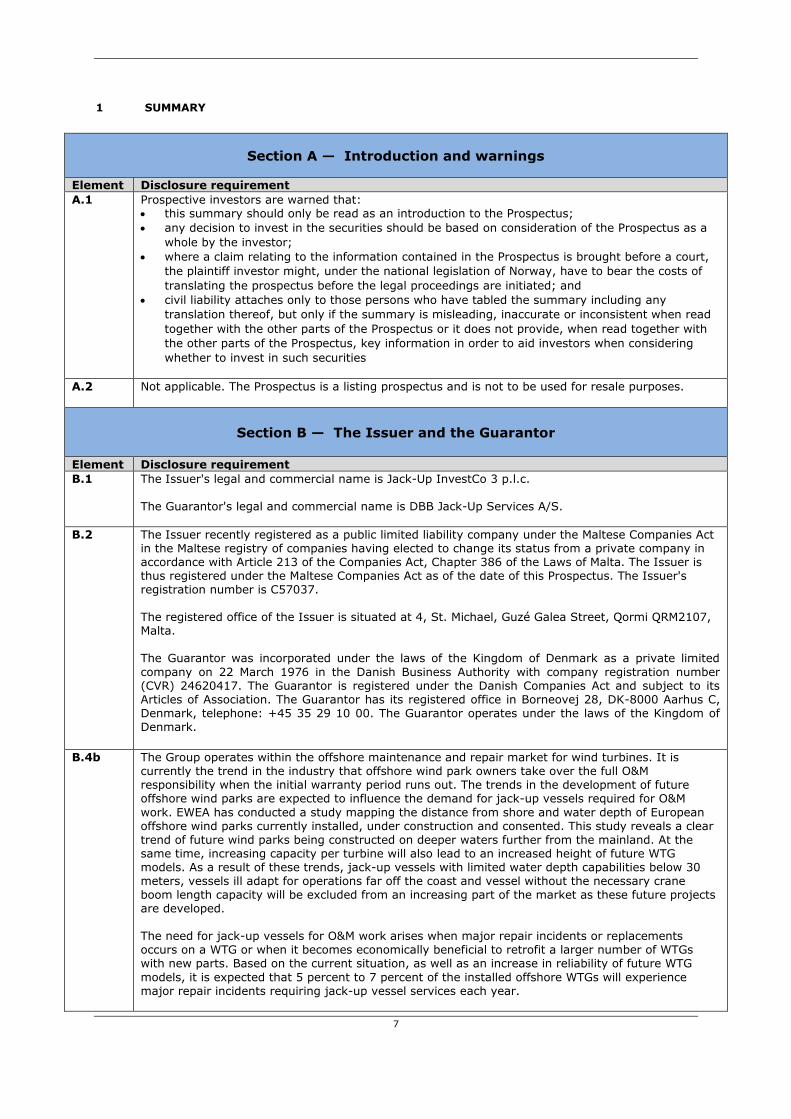

1 SUMMARY

Section A — Introduction and warnings

Element Disclosure requirement

A.1 Prospective investors are warned that: this summary should only be read as an introduction to the Prospectus;

any decision to invest in the securities should be based on consideration of the Prospectus as a

whole by the investor;

where a claim relating to the information contained in the Prospectus is brought before a court,

the plaintiff investor might, under the national legislation of Norway, have to bear the costs of

translating the prospectus before the legal proceedings are initiated; and

civil liability attaches only to those persons who have tabled the summary including any

translation thereof, but only if the summary is misleading, inaccurate or inconsistent when read

together with the other parts of the Prospectus or it does not provide, when read together with

the other parts of the Prospectus, key information in order to aid investors when considering

whether to invest in such securities

A.2 Not applicable. The Prospectus is a listing prospectus and is not to be used for resale purposes.

Section B — The Issuer and the Guarantor

Element Disclosure requirement

B.1 The Issuer's legal and commercial name is Jack-Up InvestCo 3 p.l.c. The Guarantor's legal and commercial name is DBB Jack-Up Services A/S.

B.2 The Issuer recently registered as a public limited liability company under the Maltese Companies Act in the Maltese registry of companies having elected to change its status from a private company in accordance with Article 213 of the Companies Act, Chapter 386 of the Laws of Malta. The Issuer is thus registered under the Maltese Companies Act as of the date of this Prospectus. The Issuer's registration number is C57037. The registered office of the Issuer is situated at 4, St. Michael, Guzé Galea Street, Qormi QRM2107, Malta. The Guarantor was incorporated under the laws of the Kingdom of Denmark as a private limited

company on 22 March 1976 in the Danish Business Authority with company registration number (CVR) 24620417. The Guarantor is registered under the Danish Companies Act and subject to its Articles of Association. The Guarantor has its registered office in Borneovej 28, DK-8000 Aarhus C, Denmark, telephone: +45 35 29 10 00. The Guarantor operates under the laws of the Kingdom of Denmark.

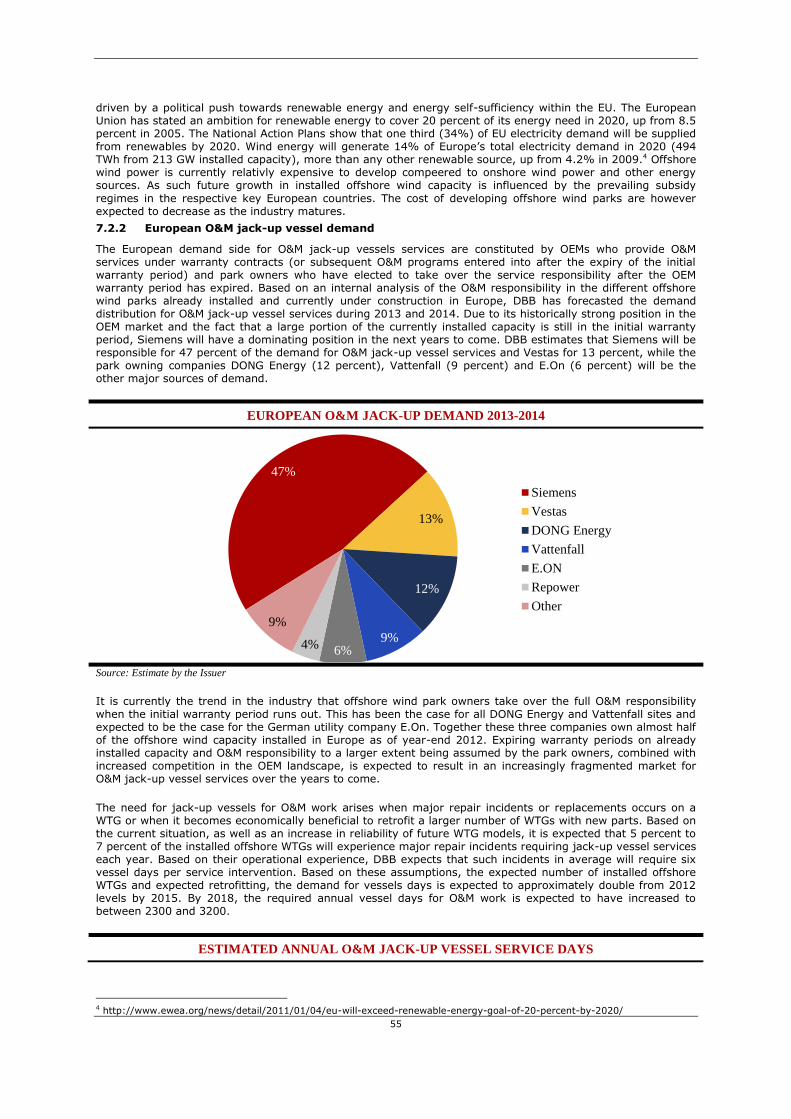

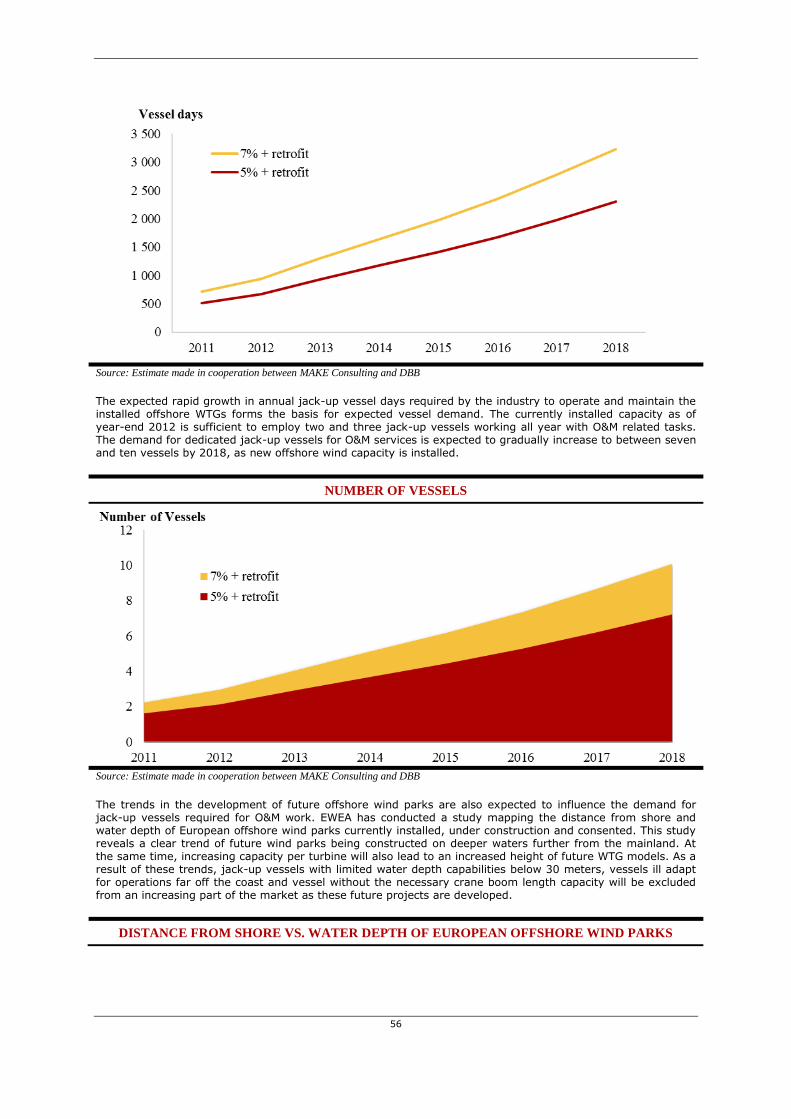

B.4b The Group operates within the offshore maintenance and repair market for wind turbines. It is currently the trend in the industry that offshore wind park owners take over the full O&M responsibility when the initial warranty period runs out. The trends in the development of future offshore wind parks are expected to influence the demand for jack-up vessels required for O&M

work. EWEA has conducted a study mapping the distance from shore and water depth of European offshore wind parks currently installed, under construction and consented. This study reveals a clear trend of future wind parks being constructed on deeper waters further from the mainland. At the same time, increasing capacity per turbine will also lead to an increased height of future WTG models. As a result of these trends, jack-up vessels with limited water depth capabilities below 30 meters, vessels ill adapt for operations far off the coast and vessel without the necessary crane boom length capacity will be excluded from an increasing part of the market as these future projects are developed. The need for jack-up vessels for O&M work arises when major repair incidents or replacements occurs on a WTG or when it becomes economically beneficial to retrofit a larger number of WTGs with new parts. Based on the current situation, as well as an increase in reliability of future WTG

models, it is expected that 5 percent to 7 percent of the installed offshore WTGs will experience major repair incidents requiring jack-up vessel services each year.

8

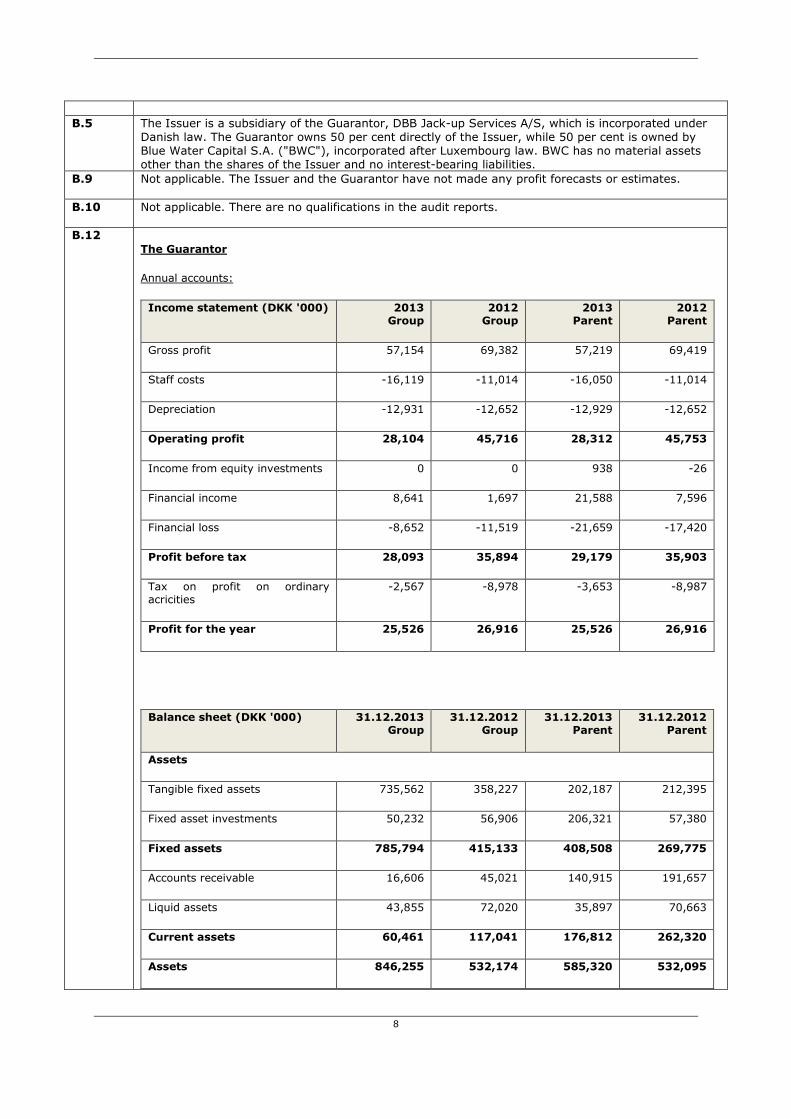

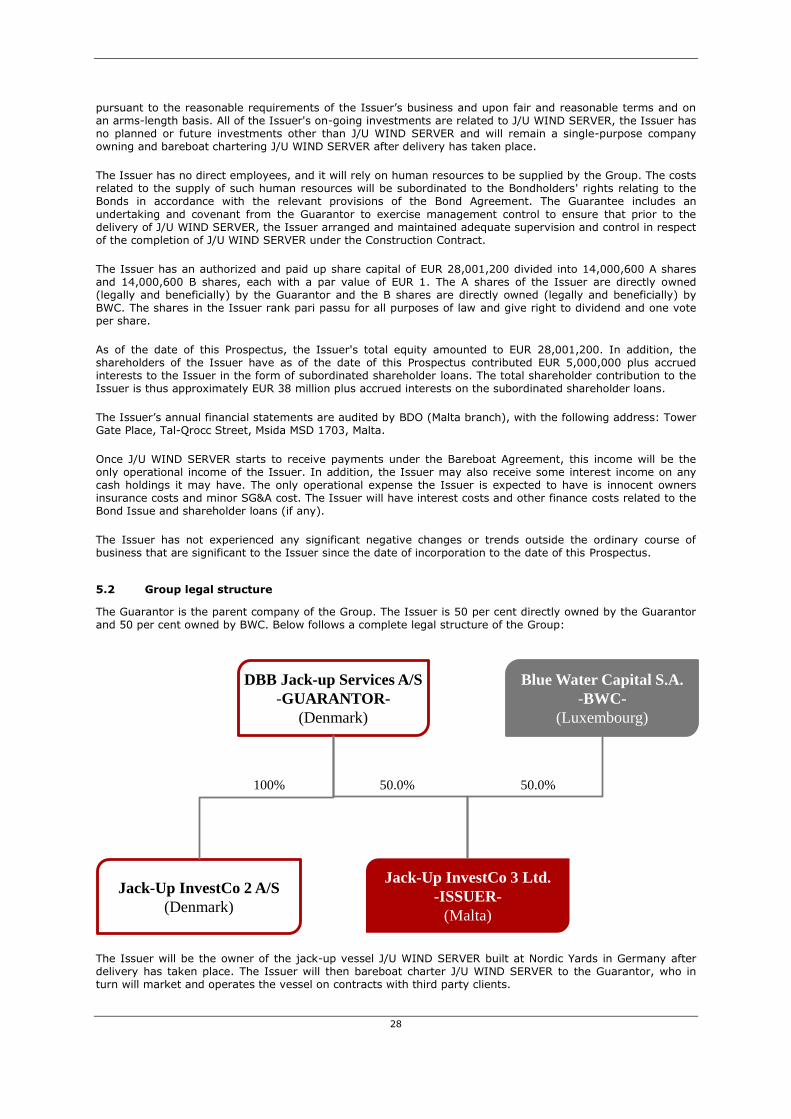

B.5 The Issuer is a subsidiary of the Guarantor, DBB Jack-up Services A/S, which is incorporated under Danish law. The Guarantor owns 50 per cent directly of the Issuer, while 50 per cent is owned by Blue Water Capital S.A. ("BWC"), incorporated after Luxembourg law. BWC has no material assets other than the shares of the Issuer and no interest-bearing liabilities.

B.9 Not applicable. The Issuer and the Guarantor have not made any profit forecasts or estimates.

B.10 Not applicable. There are no qualifications in the audit reports.

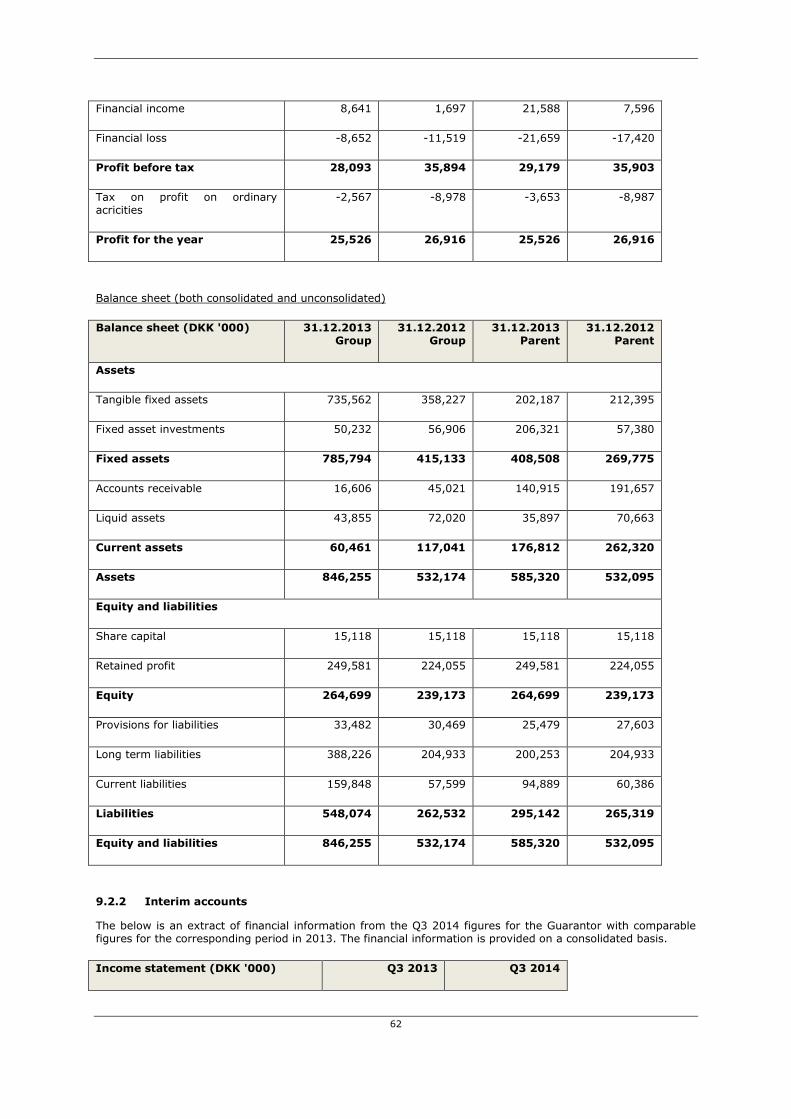

B.12 The Guarantor

Annual accounts:

Income statement (DKK '000) 2013 Group

2012 Group

2013 Parent

2012 Parent

Gross profit 57,154 69,382 57,219 69,419

Staff costs -16,119 -11,014 -16,050 -11,014

Depreciation -12,931 -12,652 -12,929 -12,652

Operating profit 28,104 45,716 28,312 45,753

Income from equity investments 0 0 938 -26

Financial income 8,641 1,697 21,588 7,596

Financial loss -8,652 -11,519 -21,659 -17,420

Profit before tax 28,093 35,894 29,179 35,903

Tax on profit on ordinary acricities

-2,567 -8,978 -3,653 -8,987

Profit for the year 25,526 26,916 25,526 26,916

Balance sheet (DKK '000) 31.12.2013 Group

31.12.2012 Group

31.12.2013 Parent

31.12.2012 Parent

Assets

Tangible fixed assets 735,562 358,227 202,187 212,395

Fixed asset investments 50,232 56,906 206,321 57,380

Fixed assets 785,794 415,133 408,508 269,775

Accounts receivable 16,606 45,021 140,915 191,657

Liquid assets 43,855 72,020 35,897 70,663

Current assets 60,461 117,041 176,812 262,320

Assets 846,255 532,174 585,320 532,095

9

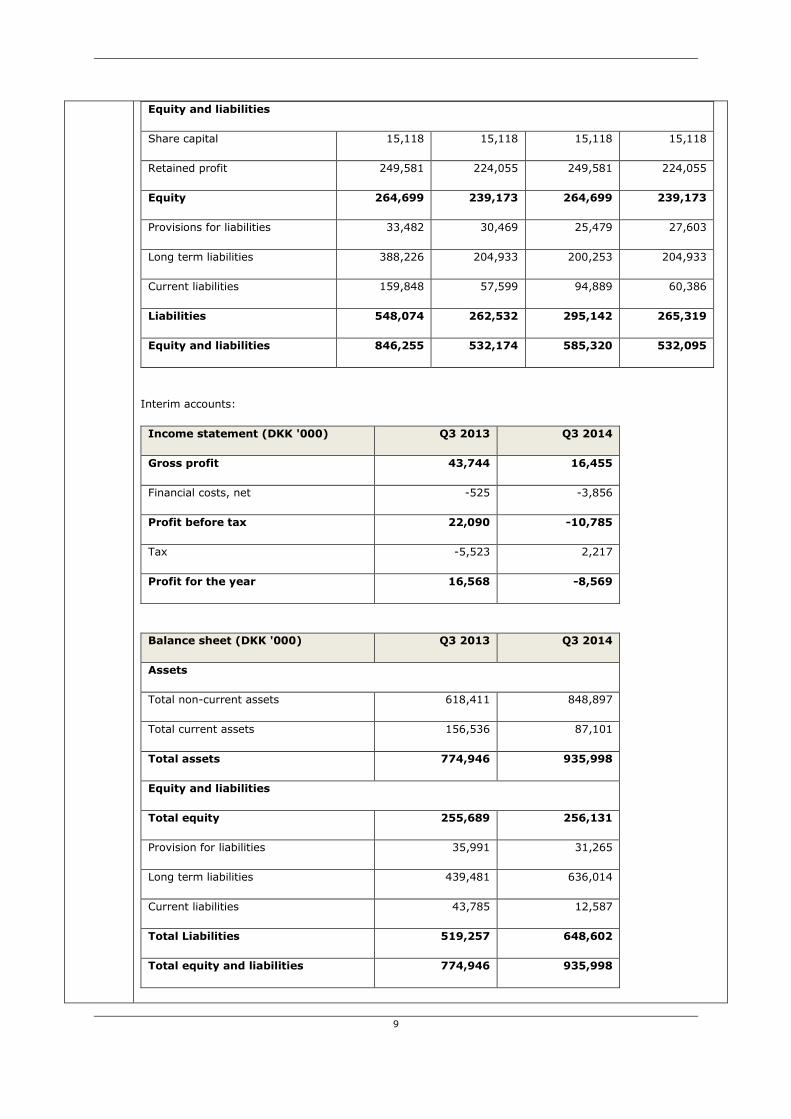

Equity and liabilities

Share capital 15,118 15,118 15,118 15,118

Retained profit 249,581 224,055 249,581 224,055

Equity 264,699 239,173 264,699 239,173

Provisions for liabilities 33,482 30,469 25,479 27,603

Long term liabilities 388,226 204,933 200,253 204,933

Current liabilities 159,848 57,599 94,889 60,386

Liabilities 548,074 262,532 295,142 265,319

Equity and liabilities 846,255 532,174 585,320 532,095

Interim accounts:

Income statement (DKK '000) Q3 2013 Q3 2014

Gross profit 43,744 16,455

Financial costs, net -525 -3,856

Profit before tax 22,090 -10,785

Tax -5,523 2,217

Profit for the year 16,568 -8,569

Balance sheet (DKK '000) Q3 2013 Q3 2014

Assets

Total non-current assets 618,411 848,897

Total current assets 156,536 87,101

Total assets 774,946 935,998

Equity and liabilities

Total equity 255,689 256,131

Provision for liabilities 35,991 31,265

Long term liabilities 439,481 636,014

Current liabilities 43,785 12,587

Total Liabilities 519,257 648,602

Total equity and liabilities 774,946 935,998

10

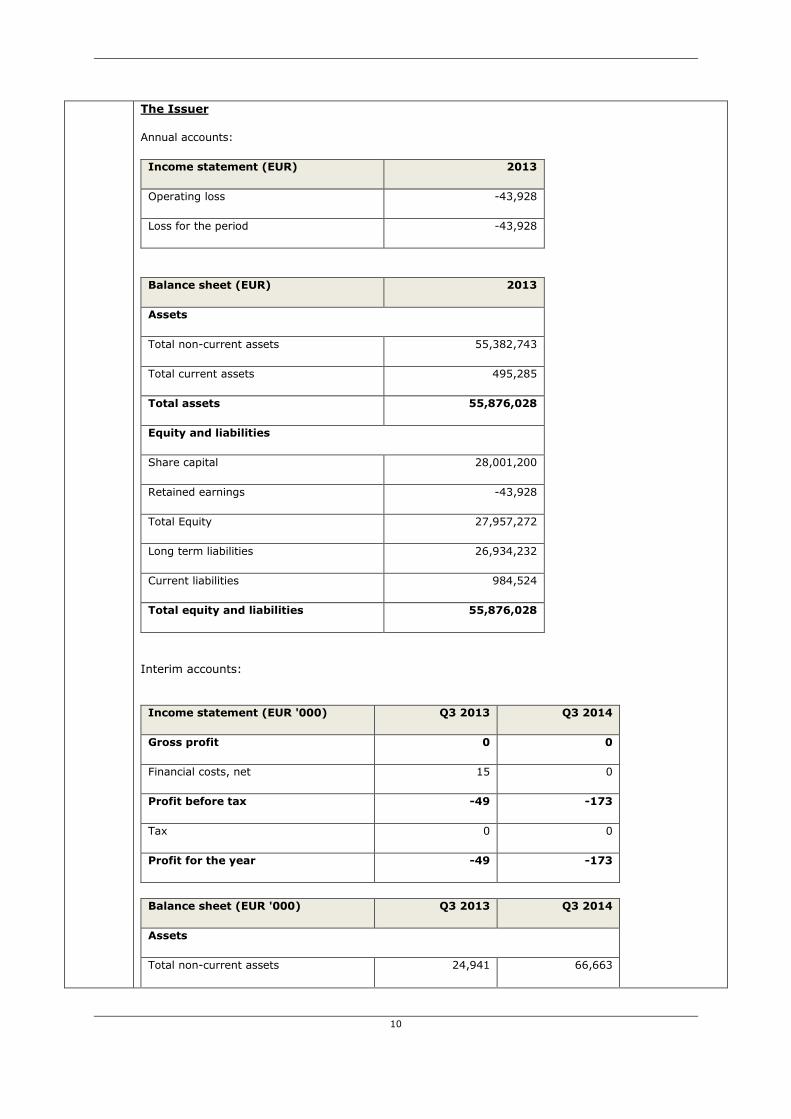

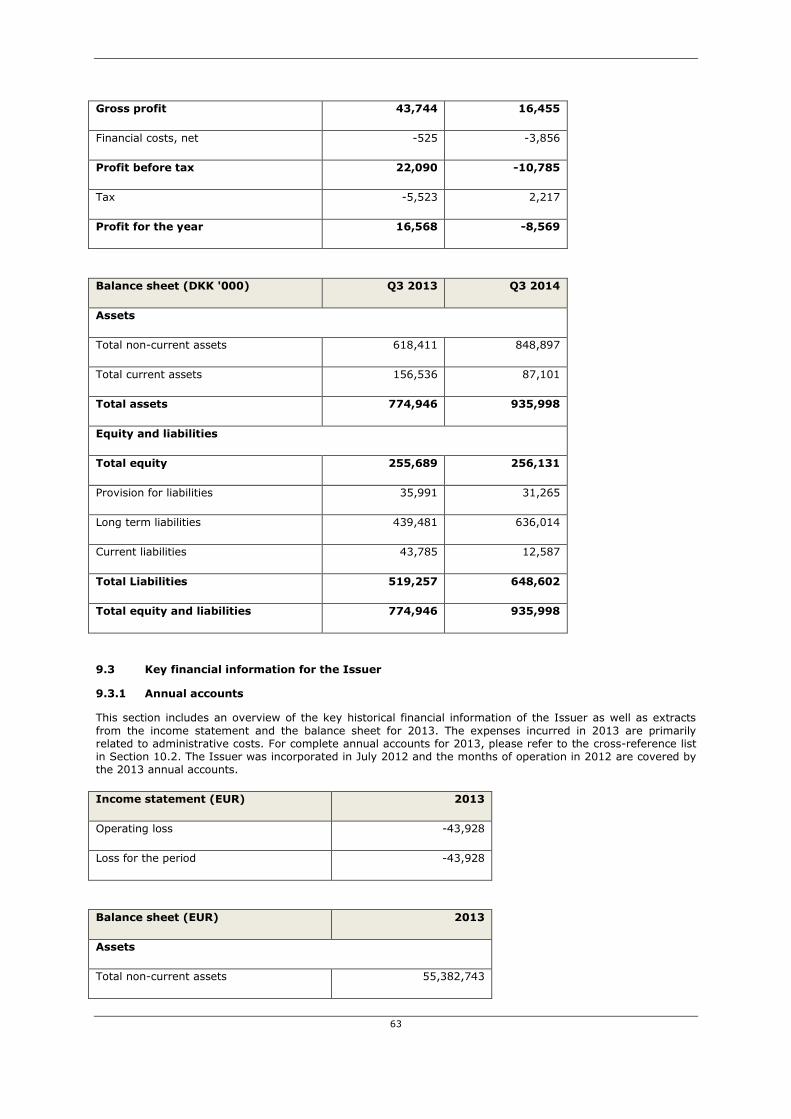

The Issuer

Annual accounts:

Income statement (EUR) 2013

Operating loss -43,928

Loss for the period -43,928

Balance sheet (EUR) 2013

Assets

Total non-current assets 55,382,743

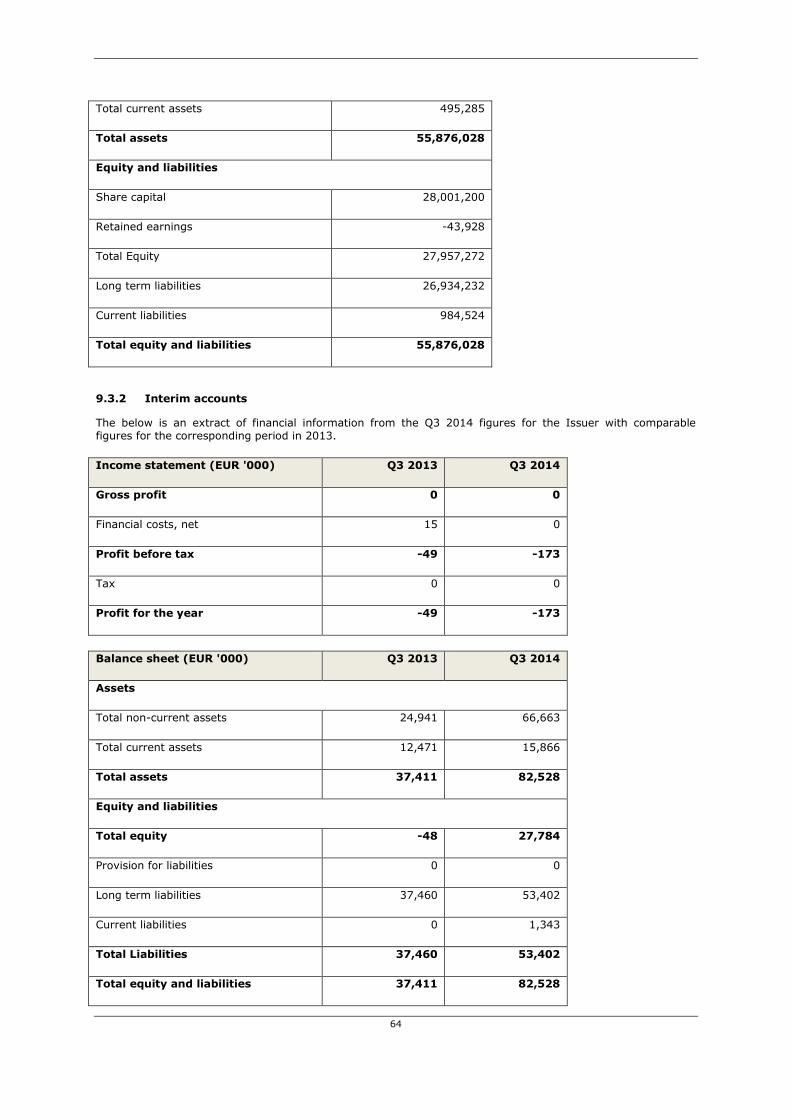

Total current assets 495,285

Total assets 55,876,028

Equity and liabilities

Share capital 28,001,200

Retained earnings -43,928

Total Equity 27,957,272

Long term liabilities 26,934,232

Current liabilities 984,524

Total equity and liabilities 55,876,028

Interim accounts:

Income statement (EUR '000) Q3 2013 Q3 2014

Gross profit 0 0

Financial costs, net 15 0

Profit before tax -49 -173

Tax 0 0

Profit for the year -49 -173

Balance sheet (EUR '000) Q3 2013 Q3 2014

Assets

Total non-current assets 24,941 66,663

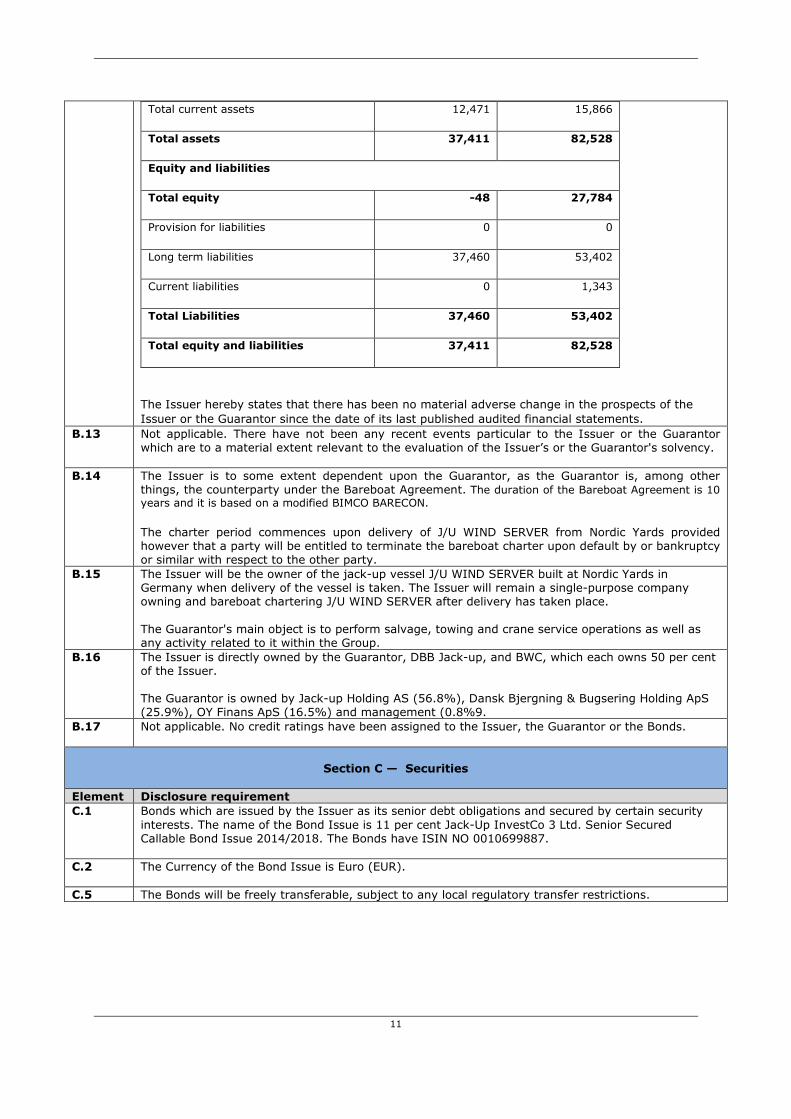

11

Total current assets 12,471 15,866

Total assets 37,411 82,528

Equity and liabilities

Total equity -48 27,784

Provision for liabilities 0 0

Long term liabilities 37,460 53,402

Current liabilities 0 1,343

Total Liabilities 37,460 53,402

Total equity and liabilities 37,411 82,528

The Issuer hereby states that there has been no material adverse change in the prospects of the

Issuer or the Guarantor since the date of its last published audited financial statements.

B.13 Not applicable. There have not been any recent events particular to the Issuer or the Guarantor which are to a material extent relevant to the evaluation of the Issuer’s or the Guarantor's solvency.

B.14 The Issuer is to some extent dependent upon the Guarantor, as the Guarantor is, among other things, the counterparty under the Bareboat Agreement. The duration of the Bareboat Agreement is 10

years and it is based on a modified BIMCO BARECON.

The charter period commences upon delivery of J/U WIND SERVER from Nordic Yards provided however that a party will be entitled to terminate the bareboat charter upon default by or bankruptcy or similar with respect to the other party.

B.15 The Issuer will be the owner of the jack-up vessel J/U WIND SERVER built at Nordic Yards in Germany when delivery of the vessel is taken. The Issuer will remain a single-purpose company owning and bareboat chartering J/U WIND SERVER after delivery has taken place.

The Guarantor's main object is to perform salvage, towing and crane service operations as well as any activity related to it within the Group.

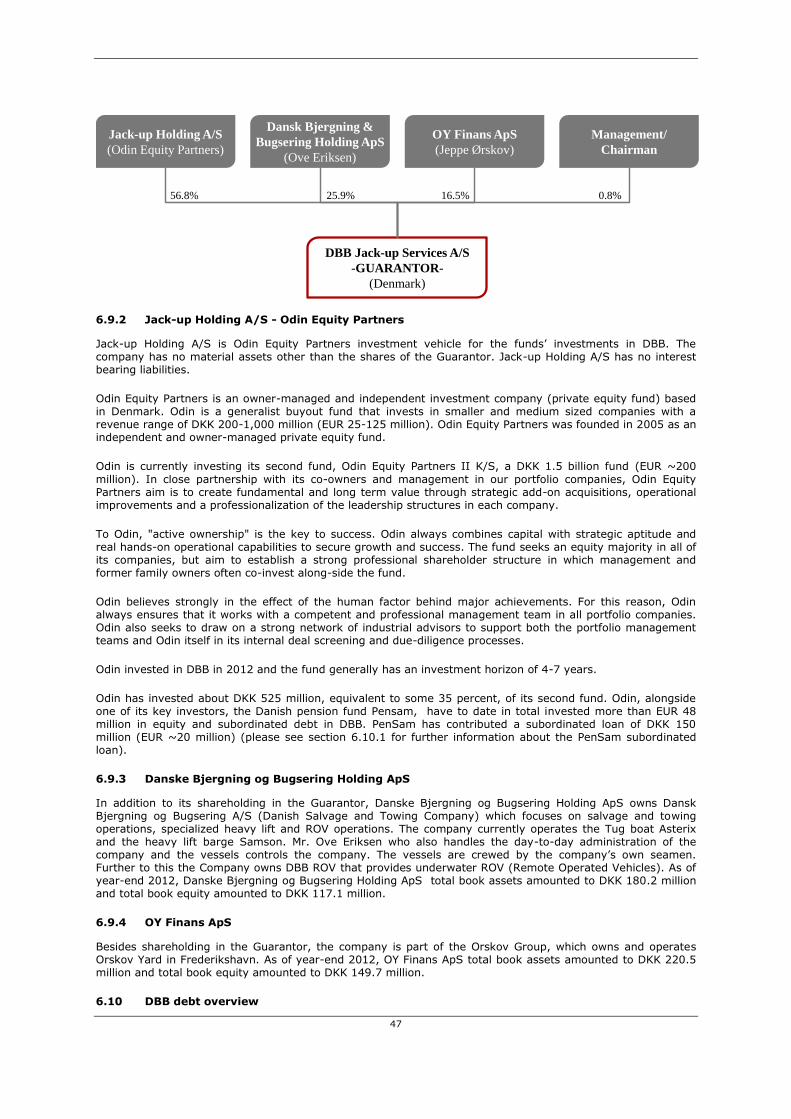

B.16 The Issuer is directly owned by the Guarantor, DBB Jack-up, and BWC, which each owns 50 per cent of the Issuer. The Guarantor is owned by Jack-up Holding AS (56.8%), Dansk Bjergning & Bugsering Holding ApS (25.9%), OY Finans ApS (16.5%) and management (0.8%9.

B.17 Not applicable. No credit ratings have been assigned to the Issuer, the Guarantor or the Bonds.

Section C — Securities

Element Disclosure requirement

C.1 Bonds which are issued by the Issuer as its senior debt obligations and secured by certain security

interests. The name of the Bond Issue is 11 per cent Jack-Up InvestCo 3 Ltd. Senior Secured Callable Bond Issue 2014/2018. The Bonds have ISIN NO 0010699887.

C.2 The Currency of the Bond Issue is Euro (EUR).

C.5 The Bonds will be freely transferable, subject to any local regulatory transfer restrictions.

12

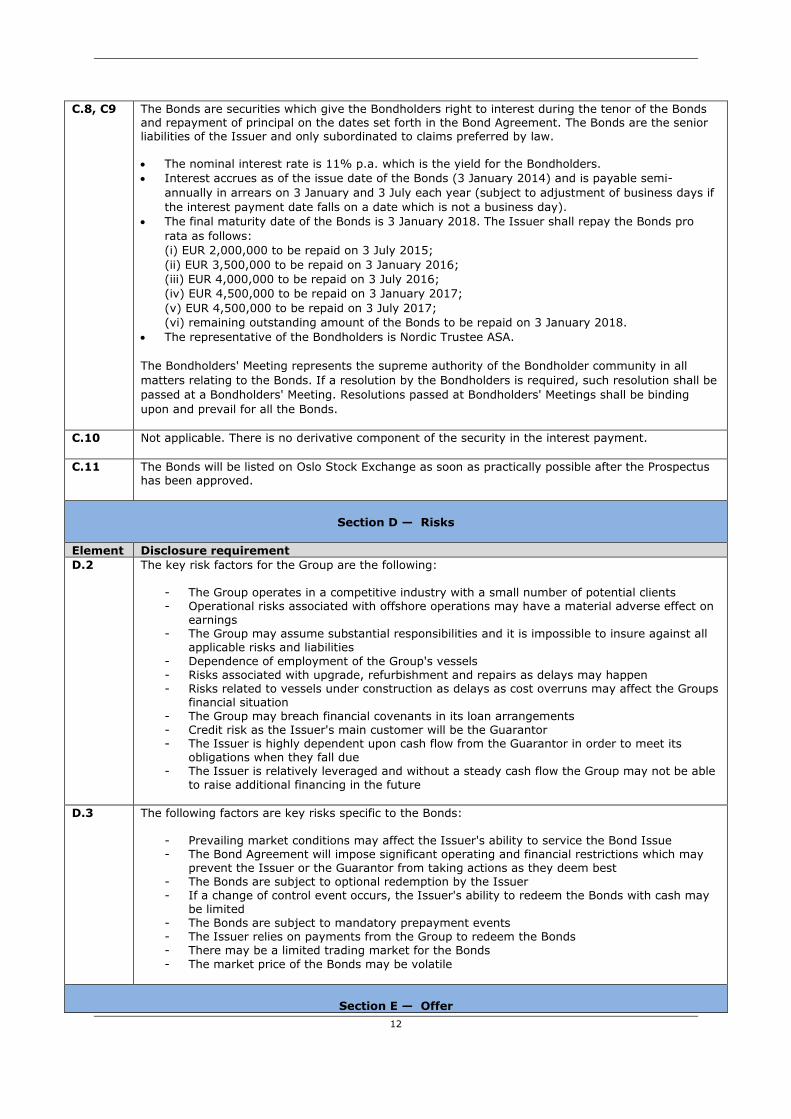

C.8, C9 The Bonds are securities which give the Bondholders right to interest during the tenor of the Bonds and repayment of principal on the dates set forth in the Bond Agreement. The Bonds are the senior liabilities of the Issuer and only subordinated to claims preferred by law. The nominal interest rate is 11% p.a. which is the yield for the Bondholders.

Interest accrues as of the issue date of the Bonds (3 January 2014) and is payable semi-

annually in arrears on 3 January and 3 July each year (subject to adjustment of business days if

the interest payment date falls on a date which is not a business day).

The final maturity date of the Bonds is 3 January 2018. The Issuer shall repay the Bonds pro

rata as follows:

(i) EUR 2,000,000 to be repaid on 3 July 2015;

(ii) EUR 3,500,000 to be repaid on 3 January 2016;

(iii) EUR 4,000,000 to be repaid on 3 July 2016;

(iv) EUR 4,500,000 to be repaid on 3 January 2017;

(v) EUR 4,500,000 to be repaid on 3 July 2017;

(vi) remaining outstanding amount of the Bonds to be repaid on 3 January 2018.

The representative of the Bondholders is Nordic Trustee ASA.

The Bondholders' Meeting represents the supreme authority of the Bondholder community in all

matters relating to the Bonds. If a resolution by the Bondholders is required, such resolution shall be

passed at a Bondholders' Meeting. Resolutions passed at Bondholders' Meetings shall be binding

upon and prevail for all the Bonds.

C.10 Not applicable. There is no derivative component of the security in the interest payment.

C.11 The Bonds will be listed on Oslo Stock Exchange as soon as practically possible after the Prospectus has been approved.

Section D — Risks

Element Disclosure requirement

D.2 The key risk factors for the Group are the following:

- The Group operates in a competitive industry with a small number of potential clients - Operational risks associated with offshore operations may have a material adverse effect on

earnings - The Group may assume substantial responsibilities and it is impossible to insure against all

applicable risks and liabilities

- Dependence of employment of the Group's vessels - Risks associated with upgrade, refurbishment and repairs as delays may happen - Risks related to vessels under construction as delays as cost overruns may affect the Groups

financial situation - The Group may breach financial covenants in its loan arrangements - Credit risk as the Issuer's main customer will be the Guarantor - The Issuer is highly dependent upon cash flow from the Guarantor in order to meet its

obligations when they fall due - The Issuer is relatively leveraged and without a steady cash flow the Group may not be able

to raise additional financing in the future

D.3 The following factors are key risks specific to the Bonds:

- Prevailing market conditions may affect the Issuer's ability to service the Bond Issue - The Bond Agreement will impose significant operating and financial restrictions which may

prevent the Issuer or the Guarantor from taking actions as they deem best - The Bonds are subject to optional redemption by the Issuer - If a change of control event occurs, the Issuer's ability to redeem the Bonds with cash may

be limited - The Bonds are subject to mandatory prepayment events - The Issuer relies on payments from the Group to redeem the Bonds - There may be a limited trading market for the Bonds

- The market price of the Bonds may be volatile

Section E — Offer

13

Element Disclosure requirement

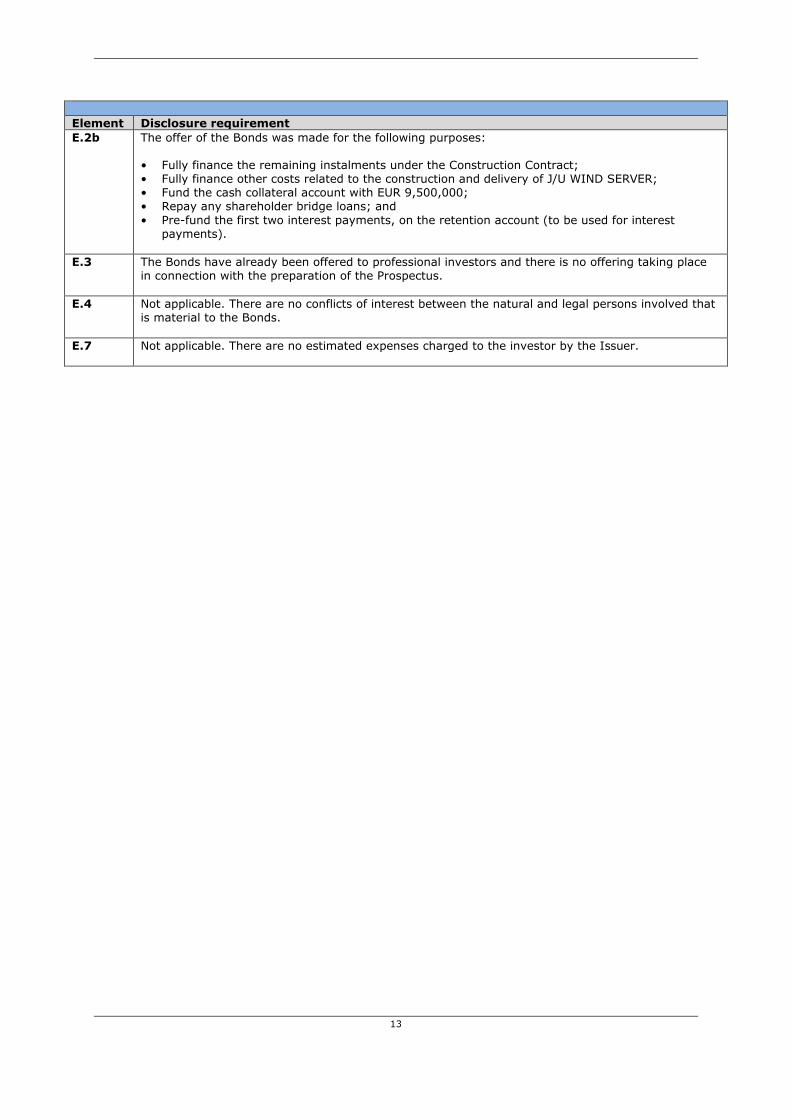

E.2b The offer of the Bonds was made for the following purposes: • Fully finance the remaining instalments under the Construction Contract; • Fully finance other costs related to the construction and delivery of J/U WIND SERVER; • Fund the cash collateral account with EUR 9,500,000; • Repay any shareholder bridge loans; and

• Pre-fund the first two interest payments, on the retention account (to be used for interest payments).

E.3 The Bonds have already been offered to professional investors and there is no offering taking place in connection with the preparation of the Prospectus.

E.4 Not applicable. There are no conflicts of interest between the natural and legal persons involved that is material to the Bonds.

E.7 Not applicable. There are no estimated expenses charged to the investor by the Issuer.

14

2 RISK FACTORS

Investing in the Bonds involves inherent risks. A number of risk factors and uncertainties may adversely affect the Group. These risk factors include, but are not limited to, financial risks, technical risks, risks related to the business operations of the Group, environmental and regulatory risks. If any of these or other risks or uncertainties actually occurs, the business, operating results and financial condition of the Group could be materially and adversely affected, which could have a material adverse effect on the Group's ability to meet its obligations (including repayment of the principal amount and payment of interest) under the Bonds. The risks presented in this Prospectus contain all material risk factors for the Issuer and the Group which are known to the Issuer. Prospective investors should consider carefully the information contained in this Prospectus and make an independent evaluation before making an investment decision.

2.1 General

Investing in the Issuer involves inherent risks. Prospective investors should carefully consider, among other things, the risk factors set out below before making an investment decision. The risks described below are not the only ones facing the Issuer. Additional risks not presently known to the Issuer, or that the Issuer currently deems immaterial, may also impair the Issuer’s business operations and adversely affect the price of the Issuer’s Bonds and ability to service its debt obligations. If any of the following risks actually occur, the Issuer’s business, financial position and operating results could be materially and adversely affected. A prospective investor should carefully consider all of the information set forth in this Prospectus and particularly the risk factors set forth below, and should consult his or her own expert advisors as to the suitability of an investment in the Issuer. An investment in the bonds is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment.

2.2 Market Risk

2.2.1 Regulations governing operations

The Group is subject to the laws and regulations governing the offshore industry. The Group is required to comply with the various regulations introduced by the authorities where the operations take place, various flag states and the guidelines introduced by the International Maritime Organisation (IMO) where applicable.

In the event that the Group is unable at any time to comply with the existing regulations or any changes in such regulations, or any new regulations introduced by local or international bodies, the operations may be adversely affected. Any change in or introduction of new regulations, may increase the costs of operations, which could have an adverse effect on the Group’s profitability. Furthermore, if the Group’s vessels do not comply with the extensive regulations applicable from time to time, the consequence may be that vessels are refused to continue their operations.

2.2.2 Competition

The Group’s equipment and services are provided in an open market characterized by a relatively small number of potential clients and a relatively small number of suppliers. The demand for the Group’s services may be volatile and is subject to variations for a number of reasons, including such factors as:

– Uncertainty in demand for, or timing of, service programs;

– Competition from other suppliers; and

– Regulatory changes.

Should a situation occur where demand is reduced which makes the operation of the Group’s assets unprofitable, there are limited prospects to employ the Group’s assets profitably in other businesses. The failure of the Group to maintain competitive equipment and services offering could have a material adverse effect on the Group’s business, operating results or financial condition.

2.2.3 Technological progress might render the technologies used by the Group obsolete

The market for the services and products of the Group is characterized by continual technological developments to provide better and more reliable performance and services. If the Group is not able to offer commercially competitive products and to implement commercially competitive services in response to changes in technology, the business, results of operations and financial condition of the Group could be materially and adversely affected, and the value of the intellectual property of the Group reduced.

2.3 Operational Risk

15

2.3.1 Operational risks associated with offshore operations

The Issuer will be exposed to operational risks associated with offshore operations, such as breakdowns, bad weather, technical problems, environmental pollution, force majeure situations (nationwide strikes etc.), collisions and groundings, that may have a material adverse effect on the earnings and value of the Issuer. There are several factors that could contribute to an accident, including, but not limited to, human errors, weather conditions and faulty constructions.

2.3.2 The Group may assume substantial responsibilities

It should be emphasized that contracts in the offshore sector of the nature that the Group expects to enter into for its vessels require high standards of safety, and it is important to note that all offshore contracts are associated with considerable risks and responsibilities. These include technical, operational, commercial and political risks. The Group will obtain insurances deemed adequate for its business, but it is impossible to insure against all applicable risks and liabilities.

2.3.3 Intellectual Property Rights

The Group must observe third parties’ patent rights and intellectual property rights. There is always an inherent risk of third parties claiming that the technology being utilized in the construction of the Group’s vessels or in its operations infringes third parties’ patents or intellectual property rights, and any such claim, if successful, could have a material adverse effect on the Group’s results of operation.

2.3.4 Dependence on key executives and personnel

The Group’s development and prospects are dependent upon the continued services and performance of its senior management and other key personnel. The loss of the services of any of the senior management or key personnel may have an adverse impact on the Group.

2.3.5 Dependence on employment of the Group’s vessels

All or a considerable portion of the Group’s income will be dependent on employment contracts and employment of the Group's vessels. There is a risk that it may be difficult for the Group to achieve employment contracts, or employment contracts on terms projected by the Issuer, resulting in a material adverse impact on the financial condition of the Issuer and the Group and their ability to serve their debts when due.

There could be considerable uncertainty as to the duration of employment contracts because the agreements may give the operator both extension and early cancellation options. The Group’s vessels may work in environments where the season makes it difficult for customers to conduct their normal work and operations. Consequently, the Group’s vessels may be idle during such periods. There can also be off-hire periods between employment contracts and as a consequence of defects and non-performance. The cancellation or postponement of one or more employment contracts can have a material adverse impact on the earnings of the Guarantor and may thus affect the Issuer's ability to serve its debts when due.

2.3.6 Dependence on services from third parties to complete some of the employment contracts

Part of the work performed under the employment contracts of the Group is performed by third-party subcontractors and service providers. The Group also relies on third-party equipment manufacturers or suppliers to provide equipment and materials used in projects. If the Group is unable to hire qualified subcontractors or service partners, or find qualified equipment manufacturers or suppliers, its ability to successfully complete a project could be impaired. If the amount the Group is required to pay for subcontractors or equipment and supplies exceeds what has been estimated, the Group may suffer losses on these contracts. If a subcontractor, supplier, or manufacturer fails to provide services, supplies or equipment as required under a contract for any reason, the Group may be required to source these services, equipment or supplies to other third parties on a delayed basis or at a higher price than anticipated, which could impact contract profitability.

During periods of wide-spread economic slowdowns, third-parties may find it difficult to obtain sufficient financing to help fund their operations. The inability to obtain financing could adversely affect a third party’s ability to provide materials, equipment or services which could materially and adversely impact the business, results of operations or financial condition of the Group.

2.3.7 The outcome of future claims and litigation could have a material adverse impact on the

business, results of operation and financial condition of the Group

The nature of the business of the Group sometimes may result in clients, subcontractors, or vendors presenting claiming for, among other things, recovery of costs related to certain contracts and projects. Similarly, the Group may present change orders and other claims to its clients, subcontractors, and vendors. In the event that the Group fails to document properly the nature of the claims and change orders or are otherwise

16

unsuccessful in negotiating reasonable settlements with its clients, subcontractors, or vendors, the Group could incur cost overruns, reduced profits or, in some cases, a loss for a project or a service contract. Additionally, irrespective of how well the nature of the claims and change orders is documented, the cost to prosecute and defend claims and change orders can be significant.

Further future claims against the Group could result in professional liability, product liability, criminal liability, warranty obligations, and other liabilities which, to the extent the Group is not insured against a loss or the insurer fails to provide coverage, could have a material adverse impact on the business, results of operation

and financial condition of the Group.

2.3.8 Risks associated with upgrade, refurbishment and repairs

The Group will incur upgrade, refurbishment and repair expenditures for the Group’s vessels from time to time, including when repairs or upgrades are required by law, in response to an inspection by a governmental authority, or when damaged. These upgrades, refurbishment and repair projects are subject to risks, including delays and cost overruns, which could have an adverse impact on the Group’s available cash resources and results of operations.

2.3.9 Risks related to vessels under construction

The Group has currently J/U WIND PIONEER and J/U WIND SERVER under construction, currently scheduled to be delivered in January/February 2015 and November/December 2014, respectively. There are certain risks related to construction that may impact the Group's financial situation. For example, Nordic Yards might have a right to terminate the Construction Contract in the event of e.g. a payment default. There is also a risk for delay in construction resulting in delayed delivery. Furthermore, amendments to the Construction Contract in order to comply with regulations or the needs of potential future customers may result in additional construction costs and additional capital needs for the Issuer or the Guarantor. Depending on the severity of the incidents related to the construction, the financial consequences may have an impact on the operations and financial condition of the entire Group.

2.4 Financial Risk

2.4.1 Financial covenants

The Group’s ability to fulfil the covenants will depend on the Group’s results, which is dependent on the prevailing economic and competitive conditions in addition to financial, operational and other factors outside the control of the Group. There can be no guarantee given that the Group is able to fulfil all the conditions in loan agreements associated with current or future debt or that its lenders will waive or amend the conditions in order to avoid a breach of the Group’s debt commitments.

2.4.2 Foreign exchange risk

The Group operates internationally and is exposed to currency risk on commercial transactions, assets and liabilities and investments in foreign operations. Commercial transactions and assets and liabilities are subject to currency risk when payments are denominated in a currency other than the respective functional currency of the relevant group company. The Group’s exposure to currency risk is primarily to EUR and DKK but could also be to other currencies depending on employment contract locations and executions.

2.4.3 Credit risk

The Issuer's main customer will be the Guarantor under the 10 year Bareboat Agreement and accordingly the financial standing of the Issuer is dependent on the profitability and financial standing of the Guarantor, including its ability to secure customers for its vessels and secure payments from its customers. There is a risk that the customers of the Group are delayed or fails to pay invoices. For example, in weak economic environments, the Group may experience increased delays and failures due to, among other reasons, a reduction in the customer’s cash flow from operations and access to the credit markets. Further, from time to time, the Group will be in disagreement with customers in respect of allocation of costs and losses in connection with cost overruns or delays in projects; which could cause such customers to delay payment of disputed or undisputed amounts. If the customers, or any one of them, delay or fail in paying significant amounts of outstanding receivables, for any reason, this could have a material adverse effect on the liquidity position, and on the business, results of operations and financial condition of the Group.

2.4.4 Liquidity risk – cost of funding

The Issuer is highly dependent on cash flow from the Guarantor's operations in order to be able to meet its debt obligations as and when they fall due. As there are many factors affecting the Issuer's liquidity, prospective investors should carefully assess each such factor before making an investment in the Issuer. The bank facilities related to J/U WIND and J/U WIND PIONEER and the revolving bank facility of the Guarantor may be terminated by the bank lender with 14 days' notice. The interest accruing on these facilities is set by the bank lender. A termination of any of these facilities may have a significant negative effect on the liquidity

17

and profitability of the Group, and there can be no assurance that the Guarantor will be able to replace the facilities with new financing on satisfactory terms.

2.4.5 Borrowing and leverage

The Issuer is relatively leveraged and its ability to service its indebtedness as and when it falls due is dependent upon the Group generating sufficient cash from its operations. Should the Group’s operations not generate sufficient cash flow to satisfy future liquidity requirements and/or to finance future operations, the Group may not be able to obtain new loans and/or secure other financing due to its current level of leverage.

2.4.6 Related party transactions

The Group has engaged and will continue to engage in a variety of transactions with related parties. While the Group believes that such transactions have been conducted on an arm's length basis, the Group cannot provide assurance that the tax or other relevant authorities will not challenge these transactions in the future, which may have a material adverse effect on the Group's business, revenues, financial condition and results of operations.

2.4.7 Value of secured assets

Although the Bonds are secured, there can be no assurance that the value of J/U WIND SERVER and/or the Issuer’s and Guarantor’s other assets will be sufficient to cover all the outstanding Bonds together with accrued interest and expenses in case of a default and/or if the Issuer and/or the Guarantors go into bankruptcy.

2.4.8 Overall tax structure

The Issuer is established in Malta and may directly or indirectly operate in numerous countries throughout the world. Consequently, the Group will be subject to changes in tax laws, treaties or regulations or the interpretation or enforcement thereof in various jurisdictions. Tax laws and regulations are highly complex and subject to interpretation. The Group's income tax expense will be based upon its interpretation of the tax laws in effect in various countries at the time that the expense will be incurred. If applicable laws, treaties or regulations change or other taxing authorities do not agree with the Issuer's and/or any subsidiaries’ assessment of the effects of such laws, treaties and regulations, this could have a material adverse effect on the Issuer.

2.5 Risks related to the Bonds

2.5.1 General risks related to the Bonds

Following the issuance of the Bonds described in this Prospectus, the Issuer has substantial indebtedness, which could have negative consequences for the bondholders as:

- the Issuer may be more vulnerable to general adverse economic and industry conditions; - the Issuer may be at a competitive disadvantage compared to its competitors with less indebtedness

or comparable indebtedness at more favourable interest rates and as a result, it may not be better positioned to withstand economic downturns;

- the Issuer’s ability to refinance indebtedness may be limited or the associated costs may increase; and

- the Issuer’s flexibility to adjust to changing market conditions and ability to withstand competitive pressures could be limited, or the Issuer could be prevented from carrying out capital expenditures that are necessary or important to the Issuer’s growth strategy and efforts to improve operating margins for the Issuer’s business.

The above may negatively affect the future income of the Issuer, which again may lead to the Issuer not being able to repay interest and/or principal under the Bond Issue when due.

2.5.2 Ability to service indebtedness

The Issuer’s ability to make scheduled payments on, or to refinance its obligations under, the Bonds will depend upon the Issuer’s financial and operating performance, which, in turn, will be subject to prevailing economic and competitive conditions and to financial and business factors, many of which may be beyond the Issuer’s control. If such conditions negatively affect the Issuer's ability to repay its debt, the Issuer may not be able to repay interest and/or principal under the Bond Issue when due.

2.5.3 Bond Agreement will impose significant operating and financial restrictions

The terms and conditions of the Bond Agreement contains restrictions on the Issuer’s and Guarantor's activities, including, but not limited to, covenants that limit its ability to:

18

transfer or sell assets or use asset sale proceeds other than in or towards prepayment of the Bonds;

incur or guarantee additional debt;

amend certain documents;

make certain investments or acquisitions;

create or permit security interests on the Issuer’s assets;

pay dividends or make other payments;

enter into transactions with affiliates; and

dispose of the Group’s vessels.

The restrictions in the terms and conditions of the Bond Agreement may prevent the Issuer and the Guarantor from taking actions that it believes would be in the best interest of the Issuer’s business, and may make it difficult for the Issuer to execute its business strategy successfully or compete effectively with companies that are not similarly restricted. The Issuer cannot assure investors that it will be granted waivers or amendments to these agreements if for any reason it is unable to comply with these agreements. The breach of any of these covenants and restrictions could result in an event of default under the Bond Agreement which may lead to the investors losing parts or all of their investment.

2.5.4 The Bonds are subject to optional redemption by the Issuer

In accordance with the terms and conditions of the Bond Agreement, the Bonds are subject to optional redemption by the Issuer at their outstanding principal amount, plus accrued and unpaid interest to the date of redemption, plus in some events an amount calculated in accordance with the terms and conditions of the Bond Agreement. This feature is likely to limit the market value of the Bonds. During any period when the Issuer may elect to redeem the Bonds, the market value of the Bonds generally will not rise substantially above the price at which they can be redeemed. This may also be true prior to any redemption period. The Issuer may be expected to redeem the Bonds when its cost of borrowing is lower than the interest rate on the Bonds. At those times, there is a risk that an investor generally would not be able to reinvest the redemption proceeds at an effective interest rate as high as the interest rate on the Bonds and may only be able to do so at a significantly lower rate. Potential investors should consider reinvestment risk in light of other investments available at that time.

2.5.5 Change of control - The Issuer’s ability to redeem the Bonds with cash may be limited

Upon the occurrence of a Change of Control Event (as defined in the Bond Agreement), each individual

bondholder has a right of pre-payment of the Bonds at a price of 101 per cent of par value plus all accrued and unpaid interest to the date of redemption. However, it is possible that the Issuer will not have sufficient funds at the time of the Change of Control Event to make the required redemption of Bonds. The Issuer’s failure to redeem tendered Bonds would constitute an event of default under the Bond Agreement and may lead to the Bondholders losing parts or all of their investment.

2.5.6 Mandatory prepayment events

In accordance with the terms and conditions of the Bond Agreement, the Bonds are subject to mandatory prepayment by the Issuer on the occurrence of certain specified events, individually referred to as a Mandatory Prepayment Event, including:

(a) the Issuer's rights under the Construction Contract or J/U WIND SERVER is sold or disposed of;

(b) the Construction Contract is terminated;

(c) J/U WIND SERVER is not delivered on or prior to 10 February 2015;

(d) the Guarantor ceases to own directly 50 percent or more of the outstanding shares and/or voting capital of the Issuer;

(e) there is an actual or constructive total loss of J/U WIND SERVER; or

(f) an Event of Default occurs.

19

Upon the occurrence of a Mandatory Prepayment Event, the Issuer shall redeem 100 per cent of the outstanding Bonds at a price equal to the prevailing call price set out in the Bond Agreement. Following any early redemption after the occurrence of a Mandatory Prepayment Event, it may not be possible for Bondholders to reinvest such proceeds at an effective interest rate as high as the interest rate on the Bonds and may only be able to do so at a significantly lower rate. It is further possible that the Issuer will not have sufficient funds at the time of the Mandatory Prepayment Event to make the required redemption of Bonds. Consequently the occurrence of a Mandatory Prepayment Event may lead to a loss of parts or all of the

Bondholders investment.

2.5.7 The Issuer relies on payments from the Group to redeem the Bonds

The Issuer relies on payments and transfers from the Guarantor and other Group companies in order to redeem the Bonds. However, the Group may not have sufficient funds to provide such payments. The breach of the Issuer's payment obligations could result in an event of default under the Bond Agreement. Such default may lead to a loss of parts or all of the Bondholders investment.

2.5.8 There may only be a limited trading market for the Bonds.

There is no existing market for the Bonds, and there can be no assurance given regarding the future development of a market for the Bonds even though the Bonds will be listed. Consequently investors in the Bonds may find it difficult to sell the Bonds. The potential limited trading market may damage the financial position of the Bondholders in a situation where they are trying to raise additional funds through selling the Bonds in the market.

2.5.9 The market price of the Bonds may be volatile

The market price of the Bonds could be subject to significant fluctuations in response to actual or anticipated variations in the Issuer’s operating results and those of its competitors, adverse business developments, changes to the regulatory environment in which the Issuer operates, changes in financial estimates by securities analysts and the actual or expected sale of a large number of Bonds, as well as other factors. In addition, in recent years the global financial markets have experienced significant price and volume fluctuations, which, if repeated in the future, could adversely affect the market price of the Bonds without regard to the Issuer’s operating results, financial condition or prospects.

2.6 Other Risks

2.6.1 Risks associated with disputes

The Issuer might become subject to disputes with its suppliers, contractors and other third parties. Such disputes could result in a loss of revenue and/or claims from such third parties.

2.6.2 Requisition or arrest of assets

The Group’s vessels could be requisitioned by a government in the case of war or other emergencies or become subject to arrest. This could significantly and adversely affect the earnings of the Guarantor as well as the Guarantor's and the Issuer’s liquidity.

20

3 STATEMENT OF RESPONSIBILITY FOR THE PROSPECTUS

3.1 Persons responsible for the information

The persons responsible for the information given in this Prospectus are the Board of Directors of the Issuer.

3.2 Declaration by persons responsible

The board of directors of the Issuer confirms that, having taken all reasonable care to ensure that such is the case, the information contained in this Prospectus is, to the best of their knowledge, in accordance with the facts and contains no omission likely to affect its import.

___ December 2014

_____________________________ Carmelo Borg

_____________________________ Slim Bouricha

_____________________________ Vagn Lehd Møller

21

4 THE BOND ISSUE AND THE BONDS

4.1 Purpose of the Bond Issue and use of the proceeds

The Issuer has applied and shall apply the net proceeds from the Bond Issue to:

(i) fully finance the remaining instalments under the Construction Contract;

(ii) fully finance other costs related to the construction and delivery of J/U WIND SERVER;

(iii) fund the cash collateral account with EUR 9,500,000;

(iv) repay any shareholder bridge loans; and

(v) pre-fund the first two interest payments, on the retention account (to be used for interest payments).

The net proceeds from the Bond Issue which currently funds the cash collateral account (and the further funds in such account) will be released from such account and employed to finance the seventh, eighth and ninth instalments under the Construction Contract.

4.2 Terms of the Bonds

ISIN: NO 0010699887

The reference name of the Bonds: 11 per cent Jack-Up InvestCo 3 Ltd. Senior Secured Callable Bond Issue 2014/2018

Issuer: Jack-Up InvestCo 3 p.l.c., incorporated and registered under the Companies Act, Chapter 386, The Laws Malta as a public limited liability company, with registered number C 57037

Currency: EUR

Issue size: EUR 40,000,000

Nominal value: Each Bond has a nominal value of EUR 1

Registration: The Bonds are electronically registered in book-entry form with the Securities Depository (VPS), Fred. Olsens gate 1. Postboks 4, 0051 Oslo, Norway.

Issue Date: 3 January 2014

Interest bearing from and including: Issue Date

Interest bearing to: Final Maturity Date

Final Maturity Date: 3 January 2018

Trustee: Nordic Trustee ASA, which represents the Bondholders. The role and authority of the Trustee is regulated in Section 17.1 in the Bond Agreement which can be obtained as set out in Section 10.2.

Amortization: The Issuer shall repay the Bonds pro rata as follows;

(i) EUR 2,000,000 to be repaid on 3 July 2015;

(ii) EUR 3,500,000 to be repaid on 3 January 2016;

(iii) EUR 4,000,000 to be repaid on 3 July 2016;

(iv) EUR 4,500,000 to be repaid on 3 January 2017;

(v) EUR 4,500,000 to be repaid on 3 July 2017;

22

(vi) remaining outstanding amount of the Bonds to be repaid on 3 January 2018

All scheduled redemptions herein will be at 100% of nominal value (plus accrued interest on redeemed amount).

Interest Payment Dates: Interest on the Bonds accrues from (and including) the Issue Date and is payable semi-annually in arrears on 3 January and 3 July each year, or if not a banking day in Norway and Denmark on the first

subsequent banking day. Daycount fraction is 30/360 unadjusted.

Coupon Rate: 11% p.a., semi-annual interest payments

As the interest rate is fixed, the issue price is 100% and the Bondholders do not have any costs related to the interest payments, the yield for the Bondholders equals the Coupon Rate (11% p.a.).

Time limitation: The time limit on the validity of claims is three years for interest and ten years for repayment of principal.

Issue Price: 100% (nominal value)

Status of the Bonds: The Bonds are the senior debt of the Issuer and rank at least pari passu with the claims of its other creditors, except for obligations which are mandatorily preferred by law.

Taxation: The Company shall pay any stamp duty and other public fees accruing in connection with the Bonds, but not in respect of trading in the secondary market (except to the extent required by applicable laws), and shall deduct at source any applicable withholding tax payable pursuant to law.

Payment mechanics: Interest and principal due for payment will be credited the bank account nominated by each Bondholder in connection with its securities account in VPS.

Guarantee: The Bond Issue is guaranteed by an unconditional guarantee under Norwegian law from the Guarantor securing the Issuer's obligations under the Bond Agreement and any related liabilities, including interests, costs and expenses.

Pursuant to the Guarantee the Guarantor guarantees the due and punctual fulfilment of the Issuer's obligations under the Bond Agreement. The Guarantor undertakes that whenever the Issuer does not pay any amount when due under or in connection with the Bond Agreement, the Guarantor will immediately and on demand pay that amount as if it was a principal obligor. The Guarantor's aggregate liability under the Guarantee is limited to the aggregate amount of EUR 40 million plus interest thereon and fees, costs, expenses and indemnities as set out in the Bond Agreement.

The Guarantee is effective until all the obligations of the Issuer towards the Trustee and the Bondholders under the Bond Agreement have been unconditionally and irrevocably paid and discharged in full in cash.

The Guarantee may be inspected as set out in Section 10.2.

Security: All amounts outstanding under the Bond Agreement are secured by:

(i) a pledge over the Issuer's claim against the bank for the amount from time to time standing to the credit of the Issuer in the escrow account;

(ii) an assignment of the rights of the Issuer under the Construction Contract and the Refund Guarantee;

23

(iii) a pledge over the Issuer's claim against the bank for the amount from time to time standing to the credit of the Issuer in the retention account (according to Norwegian law); and

(iv) an assignment of the Issuer's entitlements under the insurances related to J/U WIND SERVER under construction (other than third party liability insurances);

(v) an unconditional and irrevocable on-demand guarantee;

(vi) a pledge over all the shares in the Issuer; and

(vii) an assignment by way of security from the shareholders of the Issuer of their rights under any shareholder loans provided by them to the Issuer.

Subsequent Security (will be established in connection and right after the delivery of J/U WIND SERVER):

(viii) a mortgage over J/U WIND SERVER;

(ix) an assignment of the Issuer's entitlements under the insurances related to J/U WIND SERVER after delivery (other than third party liability insurances);

(x) a pledge over the Issuer's claim against the bank for the amount from time to time standing to the credit of the Issuer in the Issuer's earnings account, operating account and collection account

(xi) to the extent permitted by applicable law and the terms of the relevant Charter Contract, an assignment of the rights of the Guarantor under any Charter Contracts with a duration of three months or more (including all earnings payable and security granted by the customer thereunder);

(xii) an assignment of the Guarantor's entitlements under the insurances related to J/U WIND SERVER after delivery (other than third party liability insurances); and

(xiii) a pledge over the Guarantor’s claim against the bank for the amount from time to time standing to the credit of the Guarantor in the Guarantor's operating and earnings account.

The Security ranks on a first priority basis.

Issuer's Call Options: The Issuer may redeem (call) the Bonds (all or nothing) from:

(i) 3 January 2014 to, but not including, 3 January 2016 at a price equivalent to the sum of:

a. the present value of 109.00 % of par value as if such payment originally should have taken place on 3 January 2016; and

b. the present value of the remaining coupon payments (less any accrued but unpaid interest) through to and including 3 January 2016; and

c. accrued but unpaid interest on the redeemed amount,

both a. and b. above calculated by using a discount rate of 50 basis points over the comparable German government bond rate (i.e. comparable to the remaining duration of the Bonds until 3 January 2016) on the 10th Business Day prior to the repayment date. The call notice shall be provided no later than 10 business days prior to the repayment date;

(ii) 3 January 2016 to, but not including, 3 July 2016 at a price

24

equal to 109.00% of par value (plus accrued interest on redeemed amount);

(iii) 3 July 2016 to, but not including, 3 January 2017 at a price equal to 107.00% of par value (plus accrued interest on redeemed amount);

(iv) 3 January 2017 to, but not including, 3 July 2017 at a price equal to 105.50% of par value (plus accrued interest on

redeemed amount); and

(v) 3 July 2017 to, but not including, 3 January 2018 at a price equal to 104.00% of par value (plus accrued interest on redeemed amount).

Exercise of the call option shall be notified by the Issuer in writing to the Bond Trustee and the Bondholders at least ten business days prior to the settlement date of the call option.

Optional redemption for tax purposes: In the event of certain developments affecting taxation, the Company may redeem the Bonds in whole, but not in part, at any time, at a redemption price of 100% of the nominal value, plus accrued and unpaid interest, if any, and additional amounts, if any, to the date of redemption. Please refer to Clause 14.7 of the Bond Agreement for further information on this tax call redemption.

Asset sales: The Company will be required to offer to purchase the Bonds with excess proceeds, if any, following certain asset sales at a purchase price equal to 100% of the nominal value, and accrued and unpaid interest to the date of purchase.

Change of control: Upon the occurrence of certain events constituting a change of control event, or if the Company sells all or substantially all of the assets, the Company will be required to offer to repurchase the Bonds at a purchase price equal to 101% of nominal value, plus accrued and unpaid interest and additional amounts, if any, to the date of the purchase. Please refer to Clause 10.3 of the Bond Agreement for further information on change of control and the put option for the Bondholders upon the occurrence of a change of control event.

Listing and admission to trading: The Bonds will be listed on the Oslo Stock Exchange.

Listing will take place as soon as possible after the requirements for listing have been fulfilled.

Bondholders' Meeting: The Bondholders' Meeting represents the supreme authority of the Bondholders community in all matters relating to the Bonds. If a resolution by the Bondholders is required, such resolution shall be passed at a Bondholders' Meeting. Resolutions passed at Bondholders' Meetings shall be binding upon and prevail for all the Bonds. Please refer to Clause 16 of the Bond Agreement for additional information.

Paying agent: The Oslo branch of Skandinaviska Enskilda Banken (publ) AB, reg. no. 971 049 944 and address Filipstad Brygge 1, 0252 Oslo. The paying agent is responsible for registering the owners of the Bonds in the Securities Depository.

Market-making: There is no market-making arrangement entered into in connection with the Bonds.

Governing Laws: The Bonds and the Bond Agreement are governed by Norwegian Law.

4.3 Conflicts of Interests

There are no conflicts of interest between the natural and legal persons involved that is material to the issue.

25

4.4 Manager

Pareto Securities AB ("Pareto") was manager for the Bond Issue. Pareto is a Swedish private limited company, with reg. no. 556206-8956, having its business address at Berzelii Park 9, 103 91 Stockholm.

4.5 Subscription of the Bonds

The minimum subscription amount was EUR 100,000 and higher amounts were allowed to be subscribed in integral multiples of EUR 100,000. The subscription period has ended as the Bonds have been issued.

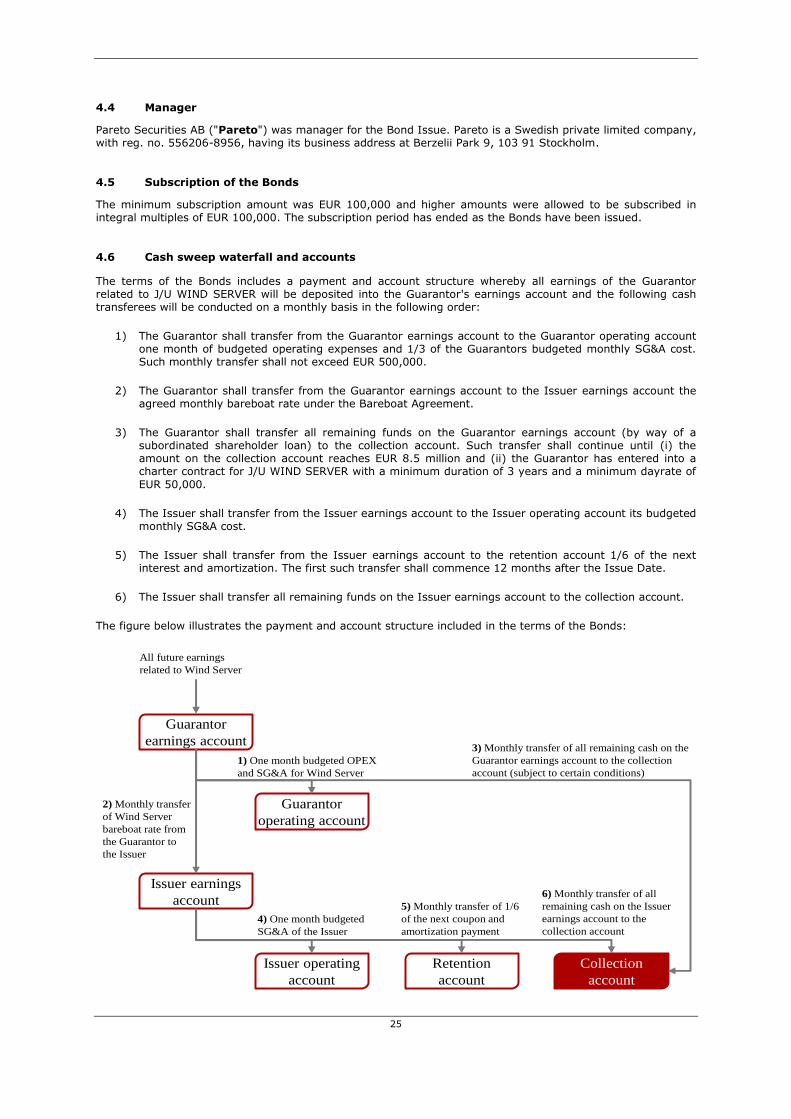

4.6 Cash sweep waterfall and accounts