Project Performance Audit Report - World Bank Document

35

Document of The World Bank FOR OFFICIAL USE ONLY Report No. 2324 Project Performance Audit Report INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT (Credit 194-IND) December 29, 1978 Operations Evaluation Department This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Project Performance Audit Report - World Bank Document

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 2324

Project Performance Audit Report

INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT

(Credit 194-IND)

December 29, 1978

Operations Evaluation Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

Project Performance Audit Report

INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT

(Credit 194-IND)

TABLE OF CONTENTS

Page

Preface iiBasic Data Sheet iii

Highlights V

PROJECT PERFORMANCE AUDIT MEMORANDUM

I. Summary 1

IT. Cost Overruns 4

Annex I - Highlights of the PPAR on the First 7

and Second North Sumatra Estates Projects,Report No. 2033, April 20, 1978

PROJECT COMPLETION REPORT (Abbreviated)

I. Introduction 8

II. Summary 8

Annex A-1 - Economic Rate of Return Analyses 11

Annex A-2 - Rubber Processing Facilities - PTP IV 13

Annex A-3 - Oil Palm Processing Facilities - PNP VI 21

Map

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

Project Performance Audit Report

INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT

(Credit 194-IND)

PREFACE

This report presents the second part and the final resultsof an audit of the Second North Sumatra Estates Project, partly financedby Credit 194-IND for US$17.0 million. The credit was signed in June1970 and closed with minor cancellations in December 1977. Since thisproject was implemented and supervised simultaneously with the FirstNorth Sumatra Estates Project (Credit 155-IND of June 1969) all aspectsexcept costs and economic issues were analyzed in a joint audit (ReportNo. 2033) which was distributed to the Board on April 20, 1978. At thattime the PCR providing the required financial and economic evaluation wasnot available.

The supplementary audit was based on interviews with Bankstaff and on a reading of the appraisal reports, supervision reports,project files and the abbreviated Completion Report, issued in June1978.

The Audit Report consists of a Memorandum prepared by OEDand the abbreviated PCR prepared by the East Asia and Pacific RegionalOffice. The present Memorandum focusses on the cost overrun issuewhich deserves further elaboration.

- iii -

PROAET : I' MAl.t.1NCE A11111T I1W:1C 1DATA :4111

SECOND NORTH SUMATRA ESTATES PROJE.CT (CREDT 194-IND)

KEY PROJECT DATA

Appraisal Actual orExpectation Current Estimate

Total Project Cost (US$ million) 31.6 73.86Ov4xErun ( 13.51

Loan/Credit Amount (US$ million) 17.

Disbursed 16.Cancelled

Date Physical Components Completed 6/75 6/77Proportion Plantings Completed by Above Date (%) 100 105Proportion of Time Overrun on Plantings (%) - 20Economic Rate of Return (%) 13-31 L3 17-53%

OTHER PROJECT DATA

OriginalItem Plan Revisions Actual

First Mention in Files or Timetable 2/68Government's Application 10/69NegotiationsBoard Approval 5/26/70Loan/Credit Agreement Date 6/15/70Effectiveness Date 9/01/70 2/09/71Closing Date 6/30/75 6/30/76, 6/30/77 12/31/77Borrower Government of Indonesia

Executing Agency PNPs IV and VIFiscal Year of Borrower April 1-March 31Follow-on Project Name Fourth Agricultural Estates Project

Loan/Credit Number Cr 319-INDAmount (US$ million) 11.0Loan/Credit Agreement Date 6/28/72

MISSION DATA

Month, No. of No. of Date ofItem Sent by Year WeekaA Persons Manweeks-/4 Repor

Preparation GOI/RSI 8-9/69Appraisal IDA/RSI 11-12/69 7 5/12/70

Supervision- I IDA 11-12/70 4 3 6 (2/25/71) (2)Supervision II " 3-4/71 3 1 1-1/2 6/7/71 (2)Supervision III " 7-8/71 4 3 6 11/15/71 (2)Supervision IV " 2-4/72 5 2 5 5/17/72 (2)Supervision V " 1-2/73 3 3 2-1/2 4/27/73 (4)Supervision VI IDA/RSI 8-9/73 2 3 2 9/28/73 (3)Supervision VII " 2/74 3 4 3-1/2 3/21/74 (3)Supervision VIII RSI 7-8/74 3 2 2-1/2 8/20/74 (2)Supervision IX 3-4/75 1 1 1/2 4/30/75 (2)Supervision X 10/75 1 2 1 3/18/76 (2)Supervision Xl 8/76 1-1/2 2 1 10/05/76 (2)

Total (to 11/77) T1 177

COUNTRY EXCHANGE RATES

Name of Currency (Abbreviation) Rupiah (Rp)Year: Appraisal Year Average (1970) Exchange Rate: US$1 - Rp 378

Intervening Years Average (1971-1977) US$1 - Rp 416

/1 Plus exchange adjustment of US$0.5 million./2 US$O.1 million cancelled.T3 Rubber fertilization: appraisal 28.4!, actual 17.1%; replanting: appraisal 13.32, actual

20.2%; oll palm: fertilization appraisal 22%, actual 33%; replanting: appraisal 31%,actual 53%.

/4 All missions supervised 2 to 4 projects, always including First N. Sumatra Estates. No. of

Weeks gives total interval on supervision. Manweeks is No. of weeks times No. of Persons,

divided by number of projects supervised. Date of Report is followed by figure in paren-

thesis showing number of project supervised by the mission.

VERNON McMItLANINCFLIZABEIHNJ07 之08 No 專90610 膩R24才010C)10MIllimelers 矓oaCen 暱jme電er.MadelnUSA

ESTIHATED AND ACTUAL IDA DISBDRSEH 胞NTSmillion 一

17 。

16 。

15 。

14 。

13 。

12 。

11 。

10 。

9 。

8 。

7 。

6 。

5 。

4 。

3 。

2 。

1 。

6/30/71 6130172 6130/73 61301746/30/756/301766/30/12/31177 77

- v -

Project Performance Audit Report

INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT

(Credit 194-IND)

HIGHLIGHTS

The second of the estate rehabilitation projects in Indonesia

was signed in 1970 for US$17.0 million. The Credit supported the

rehabilitation and expansion of two groups of rubber and oil palm

estates in North Sumatra. The total area planted or replanted under

the project reached 23,000 ha, about 2,400 ha (10.4%) above appraisal

estimates. While the area under rubber was about 36% below appraisal,

this shortfall was more than compensated by increased oil palm plantings

and replantings. Yields at present are only slightly below and at

full maturity may reach appraisal estimates.

With the exception of the cost-benefit aspects, the project

has been the subject of an audit conjointly with the First North

Sumatra Estates Project (Credit 155-IND) and a PPAR (Report No. 2033)

was issued on April 20, 1978. Due to favorable world market prices

for palm oil and a shift from rubber plantings to oil palm, the project

benefits are higher than anticipated at appraisal. The rate of return

has been recalculated and ranges from 17 to 53% for the various sub-

components as compared to 13-31% estimated at appraisal.

Points of special interest are:

- Cost overrun for oil mill component (PPAR paras. 13 to 16,

PCR, para 2.1, Annex 3);

- Similar inadequacies in cost estimates of components in other

agro-industrial projects raise a larger question about the

adequacy of the appraisal of these components. (PPAR paras. 17

to 19).

Project Performance Audit Memorandum

INDONESIA SECOND NORTH SUMATRA ESTATES PROJECT

(Credit 194-IND)

I. SUMMARY

1. The second project supported the rehabilitation and expansionof two groups of rubber and oil palm estates in North Sumatra. The

estates had been expropriated by Government in 1958 along with other

Dutch properties. All expatriate managers and technicians were then

replaced by Indonesians, mostly employees of the Dutch firms.

2. The plantation economy of Sumatra had been developed during

the colonial period into one of the world's leading centers for rubber

and oil palm production and export. That position was surrenderedin the decade following expropriation, a consequence of (1) assumption

of authority by unprepared Indonesian staff, (2) breaking of technical

contacts with Malaysia and other producing countries and overseas

research stations, (3) heavy export duties and other taxes, which left

the estates with little capital to reinvest, and (4) uncertainties

about Government's financial policies, which discouraged new invest-ment by the estate managements. Technical progress in the rubber and

oil palm enterprises slowed significantly, and estate production and

productivity levels declined in response to reduced fertilization,excessive tapping, and the near cessation of new and replacement plant-

ings. The estate labor force was politicized, further undermining

efficient management. The estates and estate group headquarters

continued to function, of course, and there were some signs of reform.

For example rubber and oil palm research stations were establishedin 1963/64 in North Sumatra to serve the Government estates. But by

the time of the violence of 1965 and the change in political administra-tion early the next year, the conditions of the estates were properlydescribed as in need of massive capital and technical support and more

progressive management.

3. In 1968 the Government regrouped all nationalized Dutch estates

in Indonesia into 28 independent units, referred to as PNPs (PerusahaanNegara Perkebunan). Each PNP was to report directly to the Minister

of Agriculture, though they were collectively serviced by a special

agency of the Ministry, the BKU.(Badan Khusus Urusan - PNP), until thatagency was abolished in 1976 and its functions transferred to a new

advisory staff attached to the office of the Minister. By 1968 a change

in the operating policies on most of the PNPs could have already beendetected. Contacts abroad had been re-established and rehabilitation

investments begun. Thus the Bank was to accelerate a process of recovery

already getting underway.

- 2 -

4. The Bank appraised the project dealing with PNP IV and VI

in November 1969, the mission leading to a credit agreement within

six months. The two PNPs comprise nineteen estates. PNP IV has a

planted area of 29,000 ha rubber and PNP VI manages 44,000 ha oil palm

(1976 figures).

5. The second project was intended to finance the rehabilitation

and development of PNP IV and VI, including planting, replanting and

bringing to maturity or rehabilitating areas already planted with

rubber and oil palm. Productivity increases were to be achieved by

bringing fertilizer rates up again to accepted standards, importing

and breeding better seeds, and applying chemical stimulants, new tapping

systems, and other improved technology. An important issue at appraisal

was the justification of Bank finance of fertilizer imports in view of

(a) the likelihood that some bilateral fertilizer aid would be displaced

and (b) the difficulty of marking the line between fertilizer for reha-

bilitation (and investment cost) and for maintenance (a recurrent cost).

There was no experience in the oil palm sector of South East Asia with

modern, large-scale plantations that had been deprived of fertilizer for

a decade: forecasts of the level of yield response to refertilization

were largely guesswork. The project provided also for rehabilitating or

building of new factories, mills, buildings and roads and for maintenance

and workshop services. A technical assistance component was included in

the project, in recognition of the urgent need to re-establish highmanagement and technical standards.

6. The actual area planting and replanting differed from appraisaltargets. Instead of 7,700 ha of oil palm PNP VI succeeded in expanding

the project area to 14,000 ha. However, due to the decline in rubber

prices in 1971 and the worsening cash flow management deferred the rubber

planting program. While the appraisal had anticipated a project area of

13,000 ha of rubber for PNP IV only 8,300 ha were accomplished.

7. The project got off to a slow start. One cause of delay

was slow progress in appointing the Board of Directors and recruiting

expatriate staff. The planting program of the oil palm group was also

set back, but for a different reason. PNP VI had continued to plant

unproven material after appraisal, in contradiction to the provisions of

the Credit Agreement.l/ Another reason for delay was the difficulty

encountered in procurement of imported goods, a problem attributable to

PNP management's unfamiliarity with procedures of international competi-

tive bidding, to the slow processing of documents through local bureau-

cracies, and to occasional transportation problems. The closing date of

the Credit was extended for two-and-a-half years, but this extension is

largely explained by the protracted effort to disburse the last 27% of

the IDA funds. Technical failures in both rubber and oil palm in the

period 1970-71 put the project on the Problem Projects List in 1972 but

it was removed in 1973 when improvement became apparent.

1/ The major part of project plantings at later stages of project

implementation used only proven planting material.

8. At ::pr.isal it was anticipated that PNP TV would shoulder

about 69% of total project costs and PNP VI only 33%. The remaining

costs would be financed by IDA and Government. In other words, the

rubber estates were expected to cover the major burden of their own

recovery, while the oil palm component with a higher foreign exchange

component would receive a higher share of the project credit. During

project execution, however, the roles of self-finance were to be reversed.

The principal reason was the shift in export prices. At appraisal, it

was expected that the rubber price would decline gradually over the next

six years to a level roughly 20% below its 1968 value, and the palm oil

price would decline by about 10%. But by 1971 the rubber price was

slipping much faster than the forecast, while the palm oil price was

rising. However, later during project implementation, rubber prices

recovered from the low levels of the early 1970s and brought some measure

of prosperity also to PNP IV.

9. The higher palm oil export prices conceal yield improvements

smaller than anticipated. The latter result is due partly to the fact

that the plantings before 1972 were not the high yielding progenies

that were expected, a factor that will depress averages throughout the

life of those trees by about 10-15%. The fertilization program has

been quite successful on the oil palm estates, however, and this, plus

the better quality of plantings since 1972, promises high productivity

levels in the future. PNP VI is now compared favorably with all oilpalm estates in North Sumatra, including the private estates and a

large Belgian/Government joint enterprise (SOCFINDO). Technical stan-

dards on the rubber plantations of PNP IV are also now considered

better than those of Harrisons & Crosfield, Goodyear, Uniroyal and

the other private producers. Fall in prices would of course again

expose the vulnerability of both oil palm and rubber operations.

10. On both PNPs total cumulative production is below appraisalprojections; nevertheless, the recovery of production levels is already

quite apparent. Output of rubber reached 134,000 tons during the proj-

ect period as compared to 145,000 tons assumed at appraisal (7.6% below)l/and palm oil production reached 2.59 million tons as compared to theappraisal estimate of 2.74 million tons (5.5% below). Yields at maturity

of trees planted under the project can only be estimated, but earlyindications are they will nearly reach appraisal estimates except for

some plantings of the 1970-72 period. Latest reports indicate that

average oil palm yields on all estates were up 32% from 1969 to 1976.The rubber picture is a little less impressive. The last supervision

report noted that rubber yields had not improved much to date (improve-

ments made having been offset by the mistakes cited earlier), and that

the full impact of the superior project plantings would show up only

after 1980. The overall impression is that progress to date in tree crop

productivity on the two PNP groups, although less than expected at

appraisal, has been significant nonetheless, with the major advances yet

to come.

1/ The Region indicates that pre-project yield assumptions were

too optimistic. Consequently, actual yield increases amounted toabout 29% for the 1970-1975 period (1,002 kg/ha to 1,293 kg/ha).

-4-

11. The economic rate of return for the project was recalculated

for the PCR (PCR para. 2.2). Higher commodity prices for both rubber

and palm oil more than compensated for cost increases estimated at 84%

for the project investment period. For rubber the rates of return are

17.1% (appraisal 28.4%) for the fertilizer program and 20.2% (appraisal

13.3%) for replanted rubber.1/ The results of the fertilizer subcompo-

nent confirm the empirical findings that old rubber shows little response

to fertilizer application. For oil palm the rates of return range

from 33% (appraisal 22%) for the fertilizer programs to 53% (appraisal

30%) for the replanting scheme.

II. COST OVERRUNS

12. At the time of appraisal it was assumed that one new block

rubber factory would be constructed, one existing sheet factory would

be converted to block rubber production, drying facilities would be

added to two factories and seven existing palm oil mills would be

rehabilitated. It was then estimated that total cost of the rubber

processing facilities would amount to US$0.833 million (including

10% contingencies) and palm oil mills to US$2.993 million (including

10% contingencies). The actual investments, however, included con-

struction of one rubber factory, expansion of three factories and

rehabilitation works of several other rubber plants, as well as

rehabilitation of only six oil mills.

13. While costs for the rubber processing components increased

moderately2/ due to inflation and changes in processing concepts (see

PCR, Annex 2, page 2), costs for the palm oil mill increased dramati-

cally and would therefore merit closer scrutiny. At appraisal costs

of rehabilitating the six mills under the project were estimated at

US$2.432 million, as compared to the final cost of US$8.613 million.

The PCR attributes this increase mainly to expenditures on providing

additional capacity, change in equipment design, inflation, and to

some extent to under-estimation of costs during appraisal.

14. Questions could be raised how the three factors which con-

tributed to a cost overrun of 254% are to be weighted. Capacity had

to be increased because PNP VI expanded oil palm plantations at a

faster pace than anticipated during appraisal and at the same time

wanted to continue with its profitable contractor processing for out-

lying producers. The more rapid increase of oil palm plantings can be

seen in the following table.

1/ It should be noted that fertilizer prices peaked in 1974/75

coinciding with low rubber prices.

2/ From US$757,000 at appraisal to US$1,259. During implementation

rehabilitation of one factory (appraisal estimated cost US$204,000)

was dropped in favor of investing in two other factories (final

cost US$608,000).

- 5-

Table 1

PNP VI Oil Palm Plantings

Targets and Achievements ('000 ha)

Appraisal Actual

1970 1.3 0.7

1971 2.7 0.3

1972 1.8 2.1

1973 0.9 3.4

1974 1.0 2.8

1975 - 4.7

Total 7.7 14.8

Source: Supervision Report, November 30, 1976, Annex 5, Table 8.

15. To cope with the expected increased output appraisal hadestimated that processing capacity due to rehabilitation should beincreased from 77 fresh fruit bunches/hour (ffb/h) to 124 ffb/h.Actually the project expanded the hourly throughput capacity to 200ffb/h, an increase of 61% above appraisal estimates. This capacityshould adequately cope with total ffb output of PNP VI once plantingswill reach full maturity and allow for processing of outgrowers'production.

16. Although inflation during project execution in the seventiesreached extremely high levels, its impact on the project should notbe exaggerated. Investments in oil mills have a high foreign exchange

component, 72% according to appraisal estimates and cost escalation dueto inflation cannot be linked to Indonesia's inflation index but shouldbe measured against the indices of major supplier countries. In thecase of this project the main suppliers were firms from Germany andthe Netherlands; countries which had the lowest rates of inflationduring the seventies. Bearing in mind that considerable investments(about US$3 million) in oil mill rehabilitation took place during thefirst two years of project implementation, the cost increase due toinflation is unlikely to have exceeded 40%. This leaves a cost overrunof at least 150% due to unrealistic cost estimates at appraisal.

- 6 -

17. The under-estimation of costs for agro-industrial projectcomponents does not seem to be restricted to this particular project.Substantial deviations from appraisal cost estimates were found by OED ina number of projects. An audit report on Tunisia First AgriculturalCredit (Loan 779, Credit 263-TUN) at present under preparation, analyzesa cost increase from US$ 7.5 million to US$ 15.0 million for a dairy plantwhich was mainly due to a more costly water supply system, an aspect notproperly studied at appraisal. Two audit reports circulated: BeninHinvi Agricultural Project (Report No. 2053 of May 1978) and BeninZou-Borgou Cotton (Report No. 2034 of April 1978), both mentioned costincreases due to difficulties in obtaining adequate water supplies fora palm-oil mill and a cotton ginnery, respectively. Similar increasesin costs due to water supply problems are known to OED to exist for theShinyanga abatoir, assisted by the Tanzania Livestock II Project (Credit382-TA) and some cashewnut factories constructed under the CashewnutDevelopment Project (Loan 1014-TA). In all these cases, underestimatedproject costs point to insufficient attention being paid by projectpreparation and appraisal to the water supply problem. A more recent case inpoint is the Nigeria Rice Project (Loan 1103-UNI). The October 1978Supervision report mentions the cost of a rice mill at US$ 6.45 millionas compared to an appraisal estimate of US$ 0.5 million.

18. These cases raise a general question about the adequacy of Bankappraisal of agro-industrial projects. The Bank spends considerable timeand manpower on analyzing and verifying cost estimates of irrigationprojects which, by their complexity, are the type of project which canbe best compared with agro-industry schemes. A large number of engineers,irrigation agronomists/economists and soil experts are on the staffof the Bank. An irrigation adviser has been assigned to CPS, Agriculture.He and other irrigation staff carefully evaluate the preparation as wellas check the appraisal of irrigation projects. Feasibility studies anddetailed engineering studies are required prior to borrowers obtainingBank assistance. However, when it comes to agro-industrial componentsof Bank-financed projects, the number of Bank staff with detailed knowledgeof agro-industries seems to be extremely limited. There is no advisoron agro-industries on the staff of CPS at present, although CPS had such anexpert on its staff for a few years.l/

19. The difficulties borrowers are likely to encounter in securingadditional finance in cases of substantial cost overruns are only oneaspect of this problem. Inadequacies in the analysis of technicalaspects in Bank-financed agro-industry schemes constitute a shortfall inBank technical assistance to borrowers for this type of project.

1/ CPS considers the value of an agro-industries advisor on its staff asdoubtful in view of the wide range of engineering and processing experiencewhich would be required; CPS would prefer ensuring the employment of top levelconsultants during preparation, appraisal and supervision. This audit wouldonly note that cost overruns, and also apparent inadequacies in the technicalsupervision of construction and operation of some agro-industry processingfacilities, suggest that the current arrangements, or budgets, for recruitingspecialized consultants for the preparation, appraisal and supervision ofthese projects merit review.

-7-

Annex 1

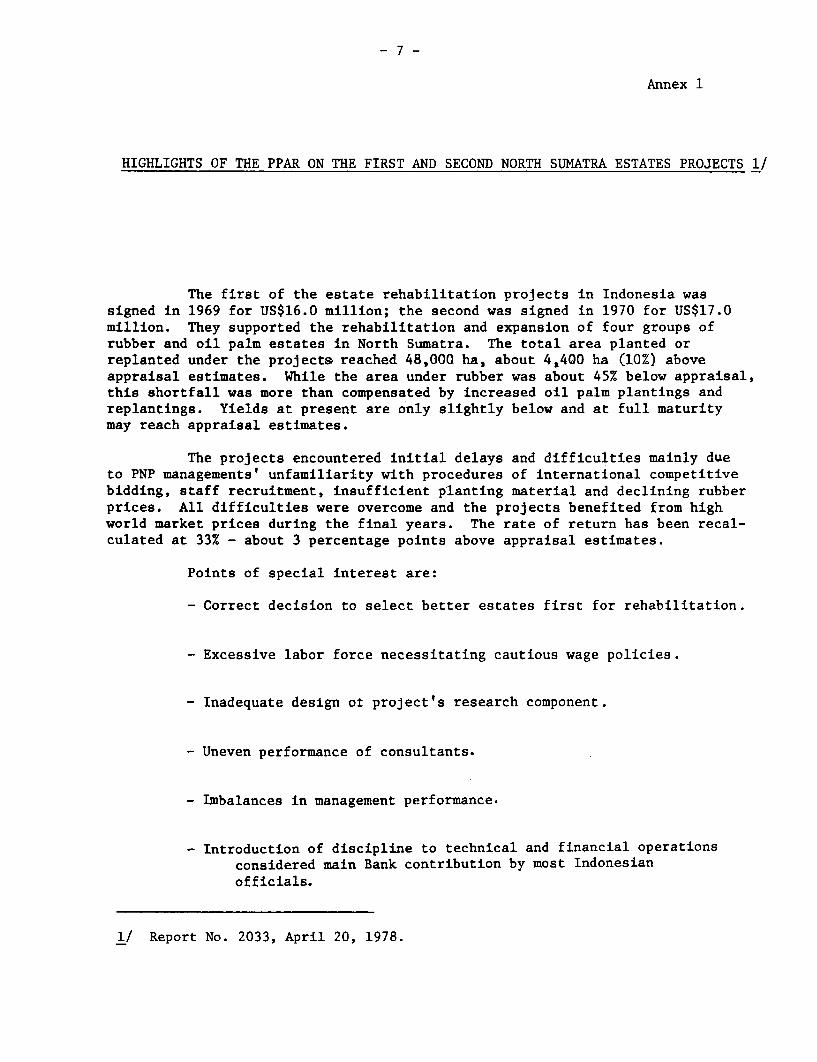

HIGHLIGHTS OF THE PPAR ON THE FIRST AND SECOND NORTH SUMATRA ESTATES PROJECTS 1/

The first of the estate rehabilitation projects in Indonesia wassigned in 1969 for US$16.0 million; the second was signed in 1970 for US$17.0million. They supported the rehabilitation and expansion of four groups ofrubber and oil palm estates in North Sumatra. The total area planted orreplanted under the project& reached 48,000 ha, about 4,400 ha (10%) aboveappraisal estimates. While the area under rubber was about 45% below appraisal,this shortfall was more than compensated by increased oil palm plantings andreplantings. Yields at present are only slightly below and at full maturitymay reach appraisal estimates.

The projects encountered initial delays and difficulties mainly dueto PNP managements' unfamiliarity with procedures of international competitivebidding, staff recruitment, insufficient planting material and declining rubberprices. All difficulties were overcome and the projects benefited from highworld market prices during the final years. The rate of return has been recal-culated at 33% - about 3 percentage points above appraisal estimates.

Points of special interest are:

- Correct decision to select better estates first for rehabilitation.

- Excessive labor force necessitating cautious wage policies.

- Inadequate design ot project's research component.

- Uneven performance of consultants.

- Imbalances in management performance.

- Introduction of discipline to technical and financial operations

considered main Bank contribution by most Indonesian

officials.

1/ Report No. 2033, April 20, 1978.

-8-

INDONESIA

SECOND NORTH SUMATRA ESTATES PROJECT

PROJECT COMPLETION REPORT

I. Introduction

The Operations Evaluations Department (OED) has already issued its

Project Performance Audit report on the First and Second North Sumatera

Estates Projects (Credits 155-IND and 194-IND) to the Board. This report

was distributed to the Board on April 20, 1978. An abbreviated PCR has

been prepared, focussing on two issues, namely: (i) the economic analysis,

including total costs and benefits; and (ii) the effieiency of and problems

related to the investments in the palm oil, and rubber mills. The attached

report sets out the findings of the mission which visited North Sumatra

in March 1978.

II. Summary

2.1 Total project costs are estimated at Rp 24.9 billion as against an

appraisal estimate of Rp 12.0 billion. The details are:

PNP's/PCR

Appraisal estimates estimate of actuals----------------- (Rp million)-------------

PTP IV Group 3,847 9,405

PNP VI Group 7,740 15,089

RISPA f1 378 378

11,965 24,872

Due to the longer than anticipated period of the project (1970-77 as against

1970-74 as anticipated at appraisal) and due to changes in investment

components it was difficult to separate project- specific costs._L The

/1 Research Institute of the Sumatra Planters' Association.

/2 See comment in supervision report dated October 5, 1976 which states

that it was impossible to determine total project costs.

-9-

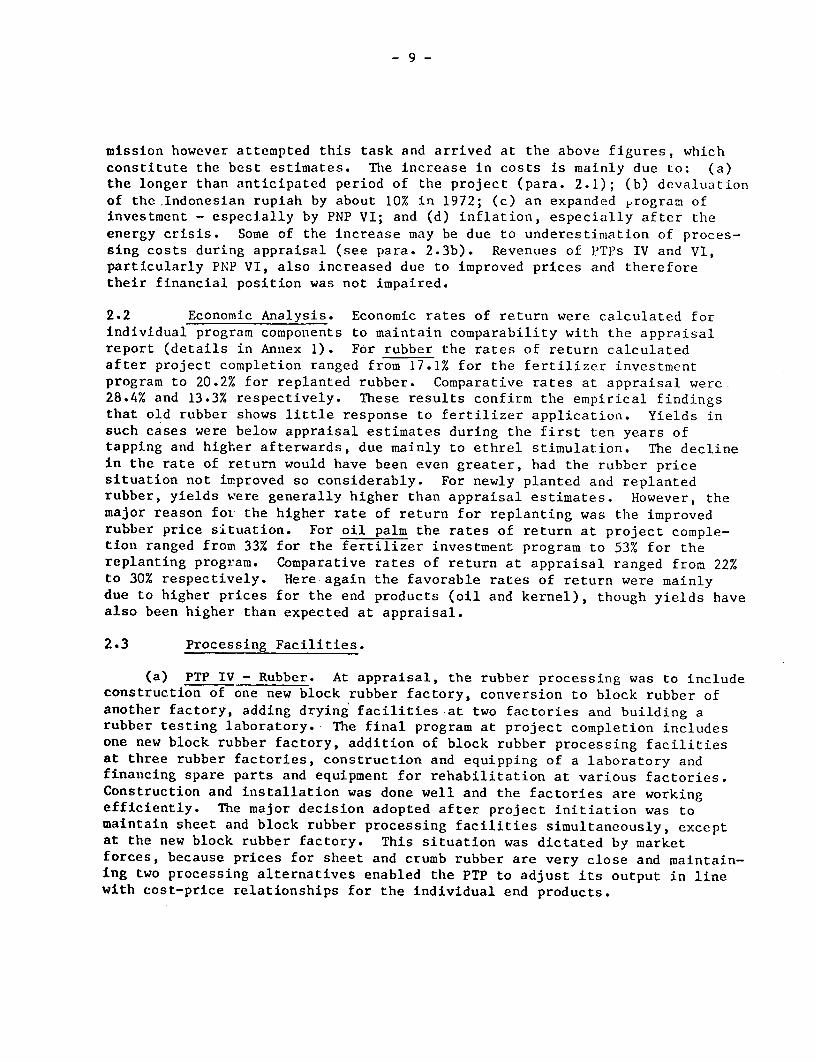

mission however attempted this task and arrived at the above figures, whichconstitute the best estimates. The increase in costs is mainly due to: (a)the longer than anticipated period of the project (para. 2.1); (b) devaluationof the .Indonesian rupiah by about 10% in 1972; (c) an expanded program ofinvestment - especially by PNP VI; and (d) inflation, especially after theenergy crisis. Some of the increase may be due to underestimation of proces-sing costs during appraisal (see para. 2.3b). Revenues of PTPs IV and VI,particularly PNP VI, also increased due to improved prices and thereforetheir financial position was not impaired.

2.2 Economic Analysis. Economic rates of return were calculated forindividual program components to maintain comparability with the appraisalreport (details in Annex 1). For rubber the rates of return calculatedafter project completion ranged from 17.1% for the fertilizer investmentprogram to 20.2% for replanted rubber. Comparative rates at appraisal were.28.4% and 13.3% respectively. These results confirm the empirical findingsthat old rubber shows little response to fertilizer application. Yields insuch cases were below appraisal estimates during the first ten years oftapping and higher afterwards, due mainly to ethrel stimulation. The declinein the rate of return would have been even greater, had the rubber pricesituation not improved so considerably. For newly planted and replantedrubber, yields were generally higher than appraisal estimates. However, themajor reason for the higher rate of return for replanting was the improvedrubber price situation. For oil palm the rates of return at project comple-tion ranged from 33% for the fertilizer investment program to 53% for thereplanting program. Comparative rates of return at appraisal ranged from 22%to 30% respectively. Here again the favorable rates of return were mainlydue to higher prices for the end products (oil and kernel), though yields havealso been higher than expected at appraisal.

2.3 Processing Facilities.

(a) PTP IV - Rubber. At appraisal, the rubber processing was to includeconstruction of one new block rubber factory, conversion to block rubber ofanother factory, adding drying facilities at two factories and building arubber testing laboratory. The final program at project completion includesone new block rubber factory, addition of block rubber processing facilitiesat three rubber factories, construction and equipping of a laboratory andfinancing spare parts and equipment for rehabilitation at various factories.Construction and installation was done well and the factories are workingefficiently. The major decision adopted after project initiation was tomaintain sheet and block rubber processing facilities simultaneously, exceptat the new block rubber factory. This situation was dictated by marketforces, because prices for sheet and crumb rubber are very close and maintain-ing two processing alternatives enabled the PTP to adjust its output in linewith cost-price relationships for the individual end products.

- 10 -

(b) PNP VI - Oil Palm. At appraisal it was planned to rehabilitateseven palm oil factories and increase their capacities by 57 tons ffb/h./l Achange in the program during project execution resulted in the construction ofone -new factory and rehabilitation of the six other factories increasingprocessing capacity by 102 tons ffb/h or 80%. The increase in capacity waswarranted because PNP VI had acquired additional land which was planted withoil palm. This expansion in processing created excess capacity which is nowbeing fully used to process fruit from third parties, but will eventually be

required to process fruit from PNP VI estates. Construction and rehabilitationwas done satisfactorily and efficient use is made of machinery and labor.While the increase in actual processing capacity exceeded appraisal estimates

by about 80%, costs of such installation increased by about 200% (Annex.3,para. 1). The major cause of the cost over-run can be explained by expenditureson the additional capacity, change in equipment design compared with appraisal(Annex 3, para. 3) and inflation. Some proportion of this over-ru, however,may be due to under-estimation of cost during appraisal.

/1 Fresh fruit bunches per hour.

- 11 -

ANNEX A-1Page 1

INDONESIA

SECOND NORTH SUMATRA ESTATES PROJECT

Economic Rate of Return Analysis

1. The project comprises a number of separate programs which are

distinct in terms of costs and benefits. Under these circumstances the

appraisal mission considered it advisable to calculate individual rates of

return for these individual program components. To achieve comparability the

mission adopted the same approach. The analysis in the appraisal report was

based on constant 1970 prices. For palm oil appraisal estimates assumed a

price of $160/ton/c.i.f. Europe and for palm kernels a price of $136/ton was

applied. For rubber appraisal estimates assumed a fall in selling price from

204/lb (c.i.f. New York RSS1) in 1970 to 164/lb in 1975 and thereafter.

2. The rates of return calculated by the mission assume constant 1977

c.i.f. Europe prices of US$430 and US$220 per ton for palm oil and kernel

respectively for the period 1978 to 2000 and actual prices for the period 1972

to 1977. For rubber, a constant 1977 c.i.f. price for RSS 1 New York was

assumed to rise from 40.Oi/lb in 1977 to 43.84/lb in 1980 and onward. Labor

and staff salaries are costed fully and it was assumed that real rates would

rise by 2% yearly (compounded). The actual increase in real wages between

1970 and 1977 was about 1.7% per year. Since a considerable expansion in palm

oil mill capacity took place under the project, the mission also determined

the rate of return for the investment of this incremental capacity. This was

not done during appraisal. The comparison between economic rates of return

calculated at appraisal and after project completion is indicated below:

Rates of return (%)At appraisal After project

completion

PTP IV: RubberFertilizer investment program 28.4 17.1

Replanting old rubber-land clearing 13.3 20.2

PNP VI: Oil PalmFertilizer investment program 22.2 33.0

Replanting old oil palm 30.2 52.7

Incremental capacity of oil palm - 36.8

factories

3. The analyses indicate considerably higher economic rates of return than

projected at appraisal, except for the rubber fertilizer investment program.

The relatively low response of old rubber trees to fertilizer application has

been recognized during execution of the project and the rate of return

analysis confirms the empirical findings. In its planning PTP IV took

- 12 -

ANNEX A-1

Page 2

account of this fact and reduced fertilizer applications accordingly. Themajor reasons for the higher rates are the improved price situation forrubber and oil palm products which developed after appraisal as the followingcomparison shows:

Projected price assumptions At appraisal At project completion

Rubber (c.i.f. RSSI New York) US 6//lb US 40-43.8/lbPalm oil (c.i.f. Europe) US$160/ton US$ 430/tonPalm kernels US$136/ton US$220/ton

- 13 -

ANNEX A-2

Page 1

INDONESIA

SECOND NORTH SUMATRA AGRICULTURAL ESTATES PROJECT

Rubber Processing - PTP IV

1. Rubber Processing Capacity

At appraisal the project was projected to include the following:

(a) construction of a new block rubber factory at Bandar Betsy;

(b) conversion to block rubber of an existing sheet rubber factory at

Bangun;

(c) establishment of a rubber testing laboratory at PTP IV; and

(d) additional drying facilities at Bandar Negeri and Sarang Giting.

Funds were also provided for general rehabilitation not involving specific

factories. At appraisal, total costs for processing facilities were estimated

at US$0.83 million. Actual cost at project completion amounted to US$1.26

million. Part of the cost increase is explained by inflation. The major

proportion of the cost increase is explained by a larger physical expansion

of the investment program. The program at project completion, as indicated

in Tables 1 and 2, includes one new crumb rubber factory (Bandar Betsy),

addition of crumb processing facilities at three factories (Sarang Giting,

Gunung Para, Hapesoug), construction and equipping of a laboratory and

financing spare parts and equipment for rehabilitation at various factories.

The factory at Bangun was not rehabilitated as projected at appraisal since

subsequent reviews of processing strategy established that it would be

cheaper and easier to transport rubber from the Bangun area to Gunung Para.

Consequently, crumb rubber processing facilities were added to existing sheet

rubber facilities at the Gunung Para factory.

- 14 -

ANNEX A-2

Page 2

Table 1: CAPITAL INVESTMENT IN PTP IV RUBBER FACTORIES($'000)

Appraisal Actualtotal cost Local

Factory estimate IDA cost Total

Bandar Betsy /a 313 156 102 258

Bangun /b 204 - - -

Bandar Negeri & Sarang Giting Ie 14 358 j 358

Test laboratory 35 35 1 35

Gunung Para - 306 133 439

Hapesong (Tapauuli) - 118 51 169

Equipment for other factories

& spare parts 191 306 - 306

757 973 286 1,259

Contingencies 76

Total 833 973 286 1,259

/a New block rubber factory.

/b Conversion to block rubber factory./c Funds have been used for Sarang Giting only.1d Built with estate labor.

Table 2: PROCESSING CAPACITY OF THE FACTORIES(TONS DRY RUBBER/DAY)

Latex crumb Lower grades

Factories Sheet rubber rubber crumb rubber Total

Gunung Para 14 or 15 + 15 29/30

Gunung Pamela 9 - - 9Gunung Monaco 6.5 6.5

Bandar Bejabu 5 - - 5

Sarang Giting 5.5 or 10 + 14 19.5/24

Bandar Negeri 6.5 - - 6.5

Bangun 9 - 9

Bandar Betsy - 16 - 16

Hapesong - 8 + 2 10

- 15 -ANNEX A-2Page 3

2. The processing program as it was finally instituted (and approvedby consultants while they were engaged by the PTP) is sound and the instal-lation of the machinery and equipment was done satisfactorily. Details arein Appendix A.

3. Except for the new factory at Bandar Betsy which processes latexinto crumb rubber only, none of the other factories is solely geared to crumbrubber production. Sheet rubber processing facilities were maintained andare used together with crumb rubber processing. This situation was dictatedby market forces, since during the last six years prices received by PTP IVfor sheet and crumb were very close and certainly did not show a definiteadvantage for crumb rubber. The PTP therefore adapted a flexible processingpolicy adjusting production in line with market prices.

4. Processing costs of sheet rubber amounting to about 4.52V/kg arelower than those for crumb rubber of about 6.24 /kg. The cost differentialis explained by higher packing costs for crumb rubber and only if this pricedifference is compensated by higher market prices for crumb rubber, does thePTP produce this product.

1L -ANNEX A-2Appendix APage 1

INDONESIA

SECOND NORTH SUMATRA AGRICULTURAL ESTATES PROJECT

CREDIT 194-IND

Rubber Processing Facilities in PTP IV

Gunung Pamela Area

1. Gunung Para Factory. Initially the factory comprised processingfacilities for latex up to 4 t sheet rubber/day and for lower grades up'to4 t crepe/day. While the sheet processing facilities have been maintainedat the same capacity the creping facilities have been phased out. Starting1973 two lines for the manufacture of crumb rubber have been installed oneeach for the processing of latex and lower grades.

2. For the latex processing line the existing bulking and coagulationtanks are used at will either for the reception and coagulation of concentratedlatex for crumb rubber preparation or for the dilution and coagulation ofdiluted latex for sheet rubber preparation.

3. The method of sheet preparation and processing has not changed.

4. The latex crumb rubber line has been completed through addition of:

2 KGSB bulking taium agirators US$ 2,0591 KGSB coagulum slicer US$ 6,1253 KGSB calender extractors cap. 250 kg D.R/h/each US$19,3631 KGSB twin box drier cap. 750 kg D.R/h + cooling fans US$43,7831 KGSB baling press cap. 1000 kg D.R/h US$ 7,9331 Avery weighing scale US$ 8421 KGSB grinding machine US$ 2,3343 High pressure pumping units U$$ 3,241

5. The lower grade crumb rubber line has been completed through additionof:

1 Promoci T72 TD hammermill cap. 750-1000 kg DR/h US$12,1651 KGSB turbo mill cap. 750-1000 KG DR/h (stand by) US$ 9,6811 promoci trio machine US$22,5436 Rehabilitated crepers break cap 700-750 kg/h (local)1 Promoci granulator 15x30 S cap 600-700 kg DR/h US$ 5,7192 Hydrocyclone pump with static separators 90 cu m/h US$ 3,951KGSB high pressure water unit US$ 9841 9 stage mecomb drier cap. 750 kg DR/h (incl. design supervision US$21,802

comm.)1 KGSB baling press cap 1000 kg DR/h US$ 7,1021 Avery weighing scale US$ 1,412

- 17 -ANNEX A-2

Appendix A

Page 2

6. Machinery and equipment used for both lines:

3 Cummins V12-500 GC-262 KVA diesel gensets inclusive

of optional equipment US$ 53,340

1 Cummins VT12-800 6C - 412 KVA (install-including) US$ 33,288

electrical equipment US$ 30,720Laboratory equipment US$ 11,730

1 Forklift yale FC20PM US$ 3,922

7. The total investment for their equipment all

financed by IDA amounts to: US$306,069

8. The additional local cost in equivalent US$ is

respectively for:

Installation cost of macomb drier: US$ 21,007

Installation of electrical equipment US$ 7,258

Rehabilitation and extension of factory buildingsand installation of machinery and equipment US$ 84,976

Installation of an arthesian well US$ 10,791

Rehabilitation and installation of 5 shaw crepers US$ 9,050

9. The total investment cost (IDA and self-generatedfunds) was: US$436,151

10. The rated capacity of each latex and lower gradecrumb rubber lines is 15-16 t/day assuming a 20 working hour/day

Gunung Pamela, Gunung Monaco and Bandar Bejambre Factories

11. All of these factories with sheet processing facilities of

respectively 9, 6.5 and 5 tons sheet per day are still in runningcondition and in operation.

Sarang Giting Area

Sarang Giting Factory

13. The original sheet processing facilities with capacity of 5.5 t

sheet/day have been maintained from 1976 to 1977, two lines of crumb rubber

processing have been added.

14. The latex crumb rubber line has been combined with the existing

3 bulking and 64 coagulation tanks of the sheet processing itne, so that

these tanks can be used either for sheet or crumb rubber processing.

15. The latex crumb rubber line has been completed with:

3 bulking tank agitators US$ 3,2382 crepers 14"x28" US$ 19,367

1 shredder US$ 13,993

1 hydrocyclone pump and static separator US$ 1,749

- 18 - ANNEX A-2

Appendix A

Page 3

16. For the lower grades crumb rubber line the existing lower grades

reception tanks have been adapted. Furthermore the line comprises:

I Hammermill 23" 75 H1P cap 750-1000 kg DR/h US$ 6,628

4 Crepers 14"x28" cap. up to 650 kg DR/h US$ 38,734

1 Shredder US$ 13,993

1 Hydrocyclone pump plus static separator US$ 1,749

17. For the lower grades crumb rubber line the existing lower

grades reception tanks have been adapted. Furthermore the line comprises:

1 B1ammermill 23" 75 HP cap 750-1000 DR/h US$ 6,628

4 Crepers 14"x28 cap. up to 650 kg DR/h US$ 38,734

1 Shredder US$ 13,993

1 Hydrocyclone pump and static separator US$ 1,749

18. The following equipment is shared by the 2 lines

3 Single box KGSB driers cap 500 kg DR/h each US$101,382

2 Hydraulic pressure cap 1000 kg DR/h US$ 13,782

1 Weighing scale US$ 10,530

1 Forklift komatsn cap 5000 lbs. US$ 16,745

1 Party laboratory equipment US$ 1,289

19. Power is provided by:

1. Deutz diesel alternator VT'12 800GC 412 KVA US$ 54,601

1. Deutz diesel alternator VT'12 G356C 333 KVA US$ 47,938

20. The electrical installation has been renewed costing US$37,942. The

total investment from IDA Credit amounts to US$385,903. The 2 lines have been

installed in the existing buildings. Though the installation has been done

neatly the area, especially in the vicinity of the crepes in the lower-grades

crumb line, might prove to be a little overpopulated during the peak production

period. The rated present capacity is 10 t latex and 14 t lower grades crumb

rubber/day.

Bandar Negeri Factory

21. Whereas the Silan Dunia and Serbajadi factories have been phased

out during 1971-72, the Bandar Negeri factory sheet processing facilities

have been maintained and are still used with a processing capacity of 6.5 t

sheet/day.

Bangun Factory

22. The factory has been converted to block rubber production, but

sheet processing facilities have been maintained and are still used with an

output capacity of 9 t/day. The crop of Smibolon estate, though belonging

to the Bangun group, is processed at Gunung Para because of lower transpor-

tation cost.

- 19 -

ANNEX A-2

Appendix A

Page 4

Bandar Betsy Factory

23. Durinq 1973-76 a complete new crumb rubber factory has been erected

at Bandar Betsy.

24. The factory consists of one latex crumb line which, in 1977, had a

maximum processing capacity of 50 t latex i.e. 16 t. Crumb Rubber/day.

2 Bulking receptions tanks with KGSB tank agitators(agitators only) - 104 coagulation tanks US$ 2,059

1 Coagulum slicer US$ 6,1.25

3 Extruders with conveyors cap. 250 kg DR each/h US$ 23,6332 KGSB box drier cap. 450-500 kg DR/h/each US$ 63,6981 Baling press KGSB 1000 kg/h US$ 7,9333 Weighing scales US$ 3,6002 High pressure water units US$ 2,5881 Yale FD20 PM forklift 45HP US$ 4,4603 Caterpillar 3306 turbocharged diesel gen. sets 157/KVA US$ 32,7631 Paddy electrical equipment US$ 9,266

25. The total investment from IDA credit amounted to US$ 156,125. Localcost -amounted to equivalent US$101,847 as follows:

Installation of an artesian well US$ 10,791

Procurement of 1 Emu submersible pump US$ 2,498

Installation of electrical equipment US$ 4,472Factory buildings and erection and installation of

machinery and equipment US$ 84,081

Hence the total cost of the project amounts to US$265,967.

26. The quality of the factory building is fair. The quality of theconcrete factory floor is rather poor.

Hapesong Area Factory

27. The Hapesong factory (also known as Tapanuli factory) has beenrehabilitated and extended to install a combined line for the separateprocessing of crumb rubber from latex and from lower-grades.

28. Machinery and equipment which have been supplied and installedare as follows:

For lower-grades processing:

1 T44TD Hammermill 75 HP with cap. 700 kg/h US$ 7,8911 Blending unit pronoci of 3 crepers 700 kg/h US$ 20,2171 Pump static separator US$ 1,9751 KSGB high power water unit US$ 984

- 20 -

ANNEX A-2Appendix APage 5

29. For latex processing:1 Coagulum testing equipment US$ 3302 Crepers (rehabilitated)

30. Alternatively for latex and lower grades line:

1 Cranulator 15 x 30 S, 404P,1 Hydraulic pump and1 KGSB single box drier capacity 500 kg DR/h1 KGSB baling pressI Forklift Yale FD 20 PM

for power and electricity:3 Cummin's NT 310GC - 157KVA diesel gensetsElectrical equipment

40. The total investment from IDA Credit amounts to US$117,749.

41. The local expenses amount to the equivalent of US$150,632.The capacity is conditioned by the throughput capacity of the drier i.e.500 kg DR x 20 working hours/day = 10 t DR/day which is sufficient to copewith the present productions of this area.

Spare Parts

42. A substantial amount of spare parts for the factories comprisingelectromotors,- parts for the box driers, burners, shredders, pumps, fork lift,aluminum sheets, etc. for nearly US$160,000 has been provided with IDAcredit. Another US$120,000 from the credit has been used to provide sparesfor general technical purposes.

- 21 - ANNEX A-3

Page 1

INDONESIA

SECOND NORTH SUMATRA AGRICULTURAL ESTATES PROJECT

Oil Palm Processing Capacity - PNP VI

1. The objective of the processing component of the project was torehabilitate the seven palm oil factories of PTP VI and increase their proces-sing capacity from its low practical level 1l of 82 tons ffb/h /2 to itstheoretical level of 139 ton ffb/h. This implied an increase in capacity ofabout 57 tons ffb/h (see Table 1). Actual developments were different. Thepractical capacity, which is relevant, was actually increased by 102 tonsffb/h and only six factories were rehabilitated but the old factory atTindjowan was replaced by a new factory including buildings and machinery.Because of this expansion and inflation, costs for the processing componentincreased to US$8.6 million compared with an appraisal estimate of aboutUS$3.0 million (Table 2). Rehabilitation and construction of the new factoryhave been concluded. The processing capacity is sufficient to process about800,000 tons ffb per year. This is in excess of the PTP crop which, atpresent, is about 677,000 tons.ffb year. The spare capacity is used toprocess fruit bunches from other PTPs, private estates and smallholders.

2. The increase in processing capacity beyond PTP VI requirements in1977 was not planned during appraisal. However, it was profitable for thecorporation since the excess capacity was used to process third party crops,which help to recover investment expenditures. The expanding volume of thePTP's own crops will eventually absorb this excess capacity. Yet long-termdevelopment plans include further expansion in capacity which will enable theenterprise to continue processing third party crops, which will be to theadvantage mainly for private estates and smallholders who are not in a positionto provide processing facilities on their own. The decision to build a newfactory at Tindjowan rather than rehabilitate the old one was right. The oldequipment and machinery were not usable; nor could the existing buildingbe adapted to expansion and housing of modern processing facilities withoutgreat expense. In this case, the decision, often difficult to make inrehabilitation projects involving factories - -ew or rehabilitation/replacement - was definitely in favor of a new factory.

At_ For explanation see footnote, Table 1.

I Fresh fruit bunches per hour.

- 22 -ANNEX A-3

Page 2

Table 1: COMPARATIVE THROUGHPUT CAPACITY OF PNP VI PALM OIL

MILLS BEFORE AND AFTER REHABILITATION

Throughput capacity (tons ffb/h)

1970 1977Theor. Pract. Theor. Pract.

Adolina 24 12 40 32Pabatu 36 18 30 24Tanah Itam Ulu 11 5 10 8

Tinjowan 20 20 60 48Air Batu 36 10 40 32

Pulu Raja 20 12 30 24Ajamu 12 5 20 16

Total 139 82 230 184

Note: Theoretical capacity implies ideal working condition where

machinery and equipment is used to its full capacity and supply

of fruit bunches is constantly available to feed the factory toits full capacity. Local condition are usually such that theseideal conditions are not met and, consequently, practical capacityis below theoretical capacity.,

Table 2: INVESTMENT IN PALM OIL FACTORIES

Investment ($'000)

Name of factory Appraisal Completion of projectestimate IDA PTP VI Total

Adolina 83 599 822 1,421Pabatu 292 219 317 536Tanah Itam Ulu .147 - -

Tindjowan 831 2,173 450 2,623

Air Batu 183 127 222 349Pulu Raja 591 858 1,675 2,533Adjamu 452 409 742 1,151Incinerators, bunch conveyor 235Storage tanks 55Weigh bridges 15

Laboratory 49Workshops 60

Total 2,993 4,385 4,228 8,613

Source: Appraisal Report, Mission estimate.

- 23 -

ANNEX A-3Page 3

3. On the whole, 51% of the rehabilitation costs have been paid with

the IDA loan whereas 49% of the expenses.have been covered by PTP VI's own

funds. Generally, the rehabilitation works and the new installations have

been executed in a very satisfactory way. The supplied equipment and machinery

is of known and experienced manufacture. Some basic equipment such as

digester/presses units, continuous oil separators, kernel recovery plants

have been chosen, on purpose, of different design. In these cases the loss

of the advantage of standardization is outweighed by the possibility of

accurate comparison of quantitative and qualitative palm oil and kernel

extraction as well as of the respective efficiency and processing cost when

milling FFB of the same origin with different equipment or processing methods.

4. The average use of labor has been reduced from 0.53 man-days per

ton FFB in 1971 to 0.35 man-days per ton FFB in 1977, i.e. by 33% as a

result of the rehabilitation of the mills. This reduction is not only a side

effect of the technical rehabilitation part but it is also due to a considerable

extent to the improvement of technical know-how of the staff. Although daily

wages of the labor (representing 30% of total processing cost) increased by

62% (from Rp 427.10/day to Rp 694.74/day) from 1975 to 1977, the average total

processing cost decreased slightly during the same period from Rp 9.36/kg FFB

to Rp 9.27/kg FFB processed. Taking into account the benefit resulting from

processing the FFB of third parties during 1977, the realized processing

cost for processing PNP VI's own crops is reduced to about Rp 6.04/kg

FFB processed.

5. Details of the processing rehabilitation are in Appendix A.

Table 3: LABOR EFFICIENCY IN PTP VI PALM OIL MILLS, 1971-77

(Man-days per ton FFB)

Factories 1971 1972 1973 1974 1975 1976 1977

Adolina 0.307 0.391 0.340 0.320 0.290 0.294 0.299

Pabatu 0.408 0.352 0.340 0.270 0.270 0.285 0.276

T. Itam Ulu 0.668 0.637 0.609 0.490 0.439 0.468 0.559

Tindjowan 0.646 0.609 0.570 0.560 0.388 0.311 0.301

Air Batu 0.443 0.419 0.348 0.340 0.377 0.398 0.319

Pulu Raja 0.526 0.559 0.547 0.660 0.624 0.567 0.419

Adjamu 1.143 1.010 1.032 0.520 0.382 0.397 0.308

Total PNP VI 0.534 0.507 0.465 0.410 0.376 0.368 0.354

- 24 -

ANNEX A-3

Appendix APage 1

INDONESIA

SECOND NORTH SUMATRA AGRICULTURAL ESTATES PROJECT

CREDIT 194-IND

PTP VI - Processing Facilities

1. The rehabilitation and expansion program of the palm oil mills

started in 1972 to be complete by end-1977. Details of the rehabilitation at

each factory are following.

(a) Adolina Ilir1 Water treatment plant PCM, cap. 30 tons water/hr comprising sand

filter, anion and cation exchanger, deaerator, etc.

1 Weighbridge, 30 tons.

1 FFB sterilizer cap 9 x 2.5 tons FFB.

1 Oil extraction line comprising hoisting crane, thresher, 2 screw

presses, elevators, pumps, etc.

1 Oil purification station with vertical settling tanks, strainer,

precleaner, sludge separators, purifiers, vacuum drier, cooler,

auxiliary tanks, pumps, etc.

1 Kernel recovery station complete with crackers, separators,

driers, winnowers, etc.

1 Watertube boiler Takuma N 325, cap. 10,000 kg/h superheated steam

to 280 degrees C at 18 kg/sq cm working pressure.

The total cost has been US$1,417,496 of which US$598,969 was

financed by IDA and US$818,527 by TPT VI.

The capacity which was theoretically 24 tons FFB/h before rehabili-

tation (practical 12 t/h), is now 40 tons FFB/h (practical 32 t/h)

when both lines are in operation.

(b) Pabatu - The rehabilitation of this mill has been limited to:

Replacement of the old kernel recovery plant by a new station

identical to that supplied to Adolina.

Completion of the water treatment plant by addition of booster

pumps, anion exchangers and a thermal deaerator with capacity of

15 t/h.

- 25 -

ANNEX A-3AP-PndI x- APage 2

Addition of 1 Takuma N 325 boiler for 10,000 kg/ha saturated steamevaporation at 200 degrees C and working pressure of 16 kg/sq cm.

The total cost has been US$f34,887 of which US$219,422 were IDAfinanced imported items and US$315,465 financed by PTP VI.

The throughput capacity which was theoretically 36 t FFB/h,practically about 18 t/h, before the rehabilitation is now30 t FFB/h, practical 24 t/h.

(c) Tanah Itam Ulu - The rehabilitation of this factory has been doneby reconditioning and subsequent installation of discarded machineryfrom other factories of the group.

One of the 2 L&C Steinmuller boilers has been provided with a newboiler drum and superheater pipes.

The cost of US$443,134 covered by own funds has not been includedin the rehabilitation program.

The practical capacity, which was less than 6 t FFB/h beforerehabilitation, is estimated to be 10 t FFB/h now.

(d) Tindlowon - The old factory has been replaced by a new mill fromwhich the first line with throughput capacity of 30 tons FFB/h hasbeen supplied by Humphrey & Glasgow. The supply consisted of:

A processing and kernel storage buiding measuring respectively18 x 73 m and 11 x 30 m.

The equipment of this line consist of:

The threshing station with 2 hoisting cranes, 2 threshers, onefruit elevator, bottom and top cross conveyors, digester feed andoverflow return conveyors.

The pressing station with 3 continuous units U.W. digester/screwpresses vibrating screens, oil tank and pumps.

The clarification station of the horizontal 3-section type continuoussettling tanks, strainer, sludge separators, purifiers, vacuumdrier, oil basculator, all necessary pumps, tanks and piping.

The depericarping station with all conveyors, depericarper, fibercyclone and duct, one nut bin with cap. 100 tons in 4 equal sections,etc.

The kernel station with cap. 6 t nuts/h with all necessaryconveyors, crackers, separators, driers, etc.

- 26 -

ANNEX A-3

Appendix APage 3

The power plant comprising 2 Allen KKK CF 5 GS type steam turbines500 KW/each, 2 diesel Gensets Ruston Paxman 150 KW/each, etc.

The complete electrical installation, piping, valves, etc. accordingto requirements.

For the realization of the second line separate tenders have beenissued for the several stations while the erection/installation hasbeen entrusted to a single contractor.

The equipment added for this second line comprises:

Threshing station: 1 hoist and thresher.

Pressing station: 3 units Stork digesters/screwpresses plus

tanks and pumps.

Clarification station: doubling of the existing equipment.

Depericarping station: doubling of the existing equipment.

Kernel recovery station: a complete station, but usingself-grading crackers.

Power plant: Addition of one Turbo Alternator: Worthington500 KW.

A complete PCM water treatment plant with capacity of 30 cu m/h hasbeen installed, comprising: dosing equipment, sand filters, anionand cation exchangers, deaerator, booster pumps, etc.

Imported items with IDA Credit amounted to US$2,172,976 while localcost was US$448,005.

The practical capacity which was a maximum of 20 t FFB/h beforerehabilitation is estimated to be 60 t FFB/h now.

(e) Air Batu - The rehabilitation of Air Batu palm oil mill has beenlimited to the supply and installation of:

1 Kernel recovery station similar in all points to the plantsinstalled at Adoline Ilir and Pabatu.

1 Water treatment plant PCM with capacity of 30 tons water/hsimilar to the plants installed at Adolina and Tindjowan factories.

The cost of the rehabilitation amounts to US$127,281 for theimported items paid for with IDA Credit and US$220,913 paid forwith own PTP funds.

- 27 -

ANNEX A-3Appendix APage 4

The throughput capacity which was theoretically not more than 36 t

FFB/h be ore rehabilitation (10 t FFB/h in practice) is

estimated to be 40 t FFB/h now (32 t/FFB/h practical).

(f) Pulu Raja - The layout of the factory has been redesigned to allow

for the installation of 2 lines with a theoretical capacity of 30 t

FFB, practical 24 t FFB.

Presently the first of these lines has been relocated/installed

comprising:

1 weighbridge with capacity 30 tons.

1 threshing station with 2 hoists and 1 thresher.

1 pressing station with 3 units U.W. digesters/screw presses, fruit

elevator and conveyors, screens, oil tank and pumps.

1 complete clarification station with vertical settling tank and

auxiliary tanks, strainer, precleaner, sludge centrifuges, purifiers,

vacuum drier and the necessary pumps, valves and pipes.

1 unit depericarping and kernel recovery station comprising of

vertical column depericarper with fiber cyclone and duct, nut bins,

crackers, separators, driers, winnowers, etc.

1 power plant with 2 Allen KK CF 5 GS steam turbines 500 KW.

1 complete water treatment plant with sand filter, softener,

deaerator, booster pumps, etc.

An amount of US$857,687 from IDA Credit has been used for the

supply of imported machinery while another US$2,524,414 equivalentRp currency from PTP VI funds has been used for the supply of a

Takuma boiler, electrical equipment, buildings, erection, spare

parts, etc.

The throughput capacity which was a bare 10 t FFB/h (practical)

before the rehabilitation is estimated to be now 32 t FFB/h .(practical) and will be 60 t FFB/h when the second line of 30 t

FFB/h is installed in 1979.

(g) Adjamu - The main equipment which has been supplied and installed/

relocated consists of:

One new pressing station comprising 2 units U.W. digester/screw

presses with vibrating screens, crude oil tank and slurry pumps.

Rehabilitation, relocation and completion of the clarification

station through addition of a vertical continuous settling tank,

sludge and water tank, self-cleaning strainer, sludge centrifuge,

purifier, vacuum drier and oil transfer pumps.

- 28 -

ANNEX A-3Appendix A

Page 5

One unit depericarping and kernel recovery of similar design andorigin as supplied at Pulu Raja (procured with PTP VI funds).

One watertube boiler Takuma evaporating capacity 6,000 kg steam/h

superheated to 280 degrees C at 16 kg/sq cm working pressure.

One Allen KKK CF 4 GS steam turbine 350 KW.

One water treatment plant capacity 20 cu m/h, inclusive of 8 km 6"bore asbestos cement pipe, dosing equipment, pressure sand filter,softener, deaerator, 2 each water and booster pump sets.

The total cost amounts to US$1,147,194 of which US$409,179 werepaid for imported materials by IDA and US$738,015 partly forimported goods and partly to cover local expenses with PTP VIfunds. Local expenses include also cost of one motorboat tankerwith capacity 300 t for the transport of palm oil and kernelsvia river and sea to Belawan harbor (cost US$407,675).

The practical throughput capacity of the mill which was about 5 tFFB/h before the rehabilitation is estimated to be 20T FFB/h now.

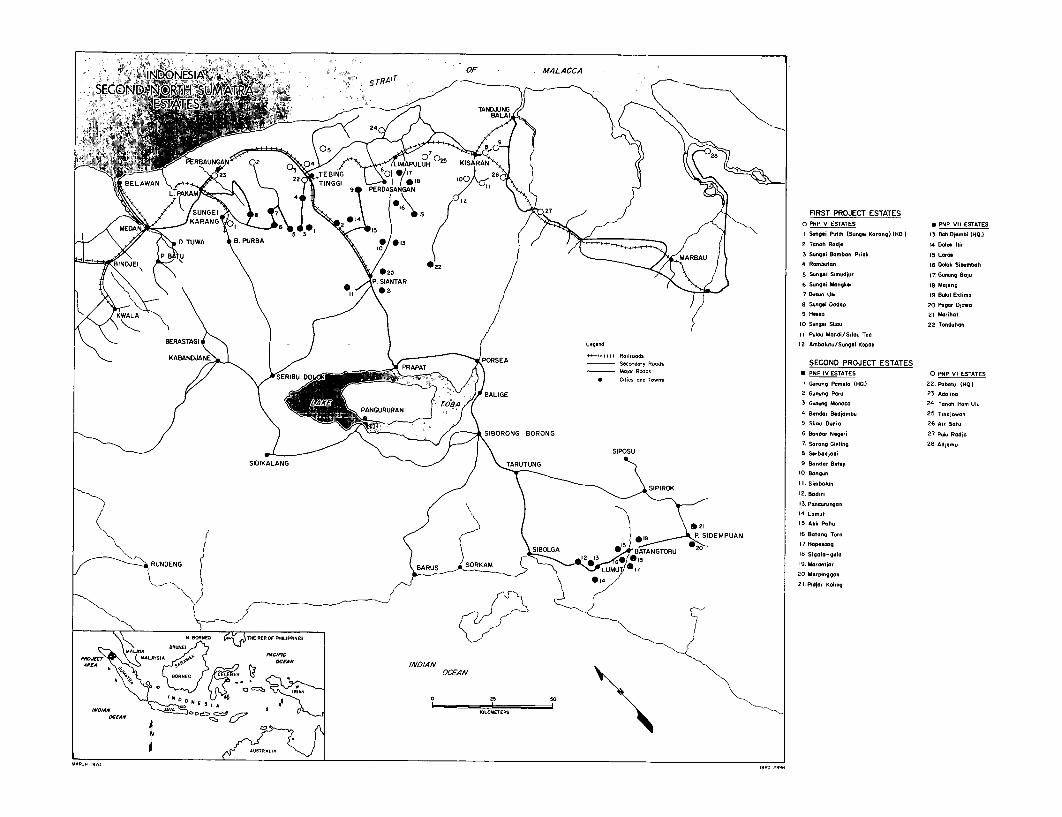

ES|F M ALACCAIN~DONESIA-O AAGSTRASSECONDX NýRTH SUMTR"-

0ý,,T -ES SATS*PPVI SAE

TA~N

., 28

2nAN ?4 LIMAPUH 4 KISARAN

i23 3 TEBnNGOO15L26EELAWAN 22 TINGøl

L. PAKAM 9ý PERDAGANGAN

4 16 S2S5UINGEI 7 19 27 FIRST PROJECT ESTATESMDNKARANG O 2 PNP3 V ESTATES PINP Vil ESTATIES

MEDAN 6 5 3 01 i Sungi Pulih (SIgi Karag) (HO.) 13. Bh D~bi (HO.)D.TUWA B PURBA 13 2 Tnah R«dj. 4 ~ol 11lir

P. MARBAU 3 Sung.i Baban Priok 15 Lar-BINDJEI 22 4. Rabua ,Is D1ok Sin~mb1h

020 5 Sungei Simudjur IT. nng BajuP. SIANTAR

6 Sung.i M.ngkei l8 M.i.ng11 021 7 Du-u Ubu 19 BukM E.lim.

8 Sung.i D.d.p 20 Pagar Dj.M.KWALA9 H-ss 21 M~ih.t

0 SungeA Si1a 22 Tonduhan

I1 Pulou M.ndi/SI-a TuaBERASTAGI

12 Ambalutu/Sung.i K.p..

KABANDANE PRAPAT PORSEA S.dy RoOd, SECOND PROJECT ESTATES-_ MaOr, R.cds 0 PNP IV ESTATES 0 PNP VI ESTATES

SERIBU DO 0l T.l i Gunung Pamelo (HQ.) 22, Pob"tu (HO.)

BALIGE 2 G.n-ng Par- 23 Ad.lino3 Gun.ng Mon-ca 24 Tonak Ita, Ulu

PANGURURN 4 Bnd Ajo 25 Tndjawan

5 Sil.. Ounia 26 Air B.tuSIBORONG BORONG 6 Banda, N.geri 27 Pu%. R.dj.

7. Srang Glnting 28 Adj~muSIPOSU 8 S.,bdj.di

SIDIKALANG TARUTUNG 9 Bad, B.tsy10 BangnS .SimbolanS12. B.diri

13. P.nd.rng.n

14 Lumut

g 19 P. SIDEM PUAN 1 B tng Ta 7l Hopesang

SIBOLGA ANGTORU8 Sgl-go

RUNDENG B8U 0 ORA 120i13 LU6998 ý9LUMU 720 Mororoggon

14 21. Pidjor Kol,ng

80 NEO c L ESN

00a000K<ILO TERSEA

ARC00170 1BD 289