POR QUE MUDAR O MODELO DO SETOR ELÉTRICO NO BRASIL?

43

BRAZIL BIOFUELS EXPERIENCE Ministry of Science and Technology José Miguez Ministry of Science and Technoloy May - 2007

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of POR QUE MUDAR O MODELO DO SETOR ELÉTRICO NO BRASIL?

BRAZIL BIOFUELS EXPERIENCE

Ministry of Science and Technology

José MiguezMinistry of Science and Technoloy

May - 2007

Brazil Biofuels Experience: Summary

1. A Brief World Energy Outlook

2. Brazil and Biofuels

3. Ethanol

4. Biodiesel

5. H-Bio: a New Brazilian Technology

A BRIEF ENERGY OUTLOOK

WORLD ENERGY CONSUMPTION

Source: BP Statistical Review (June/2006)

Energy consumption - Per capita Tones oil equivalent (toe)

WORLD ENERGY CONSUMPTION

Equator

Cancer Tropic

Consumo de energia per capita(em toneladas de óleo equivalente)

Capricorn Tropic

Tropical Area Biofuels

The greater consumption per capita is outside the tropics!

Source: BP Statistical Review (June/2006)

WORLD ENERGY CONTEXT

World economy growth

Demand growth

Climate change reality

High prices for energy

Refining capacity in the limit

Geopolitical instability and conflict at important energy supplier countries

Strong dependency on non-renewable energy sources

0

10

20

30

40

50

60

70

80

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

JAN

-JU

L 20

06JU

L 20

06

US$

/ ba

rrel

Oil - Brent Dated

CRUDE OIL PRICES

Source: BP Statistical Review (June/2006) e Petrobras (August/2006)

1998 a Jul-2006

+ 475%

THE CHALLENGE FOR ENERGY POLICY

Long term energy supply security

Cheaper prices for energy sources

Keeping the local energy competitiveness

Dealing with climate change and environment

BIOFUELSBIOFUELS

BRAZIL AND BIOFUELS

RENEWABLESOURCES

44.7 %

218.6 MILLIONS

TOE

Hydroelectricity15.0%

Uranium1.2%

Natural Gas9.3%

Petroleum and Derivatives

38.4%

Other Renewables

Sources2.7%

Sugarcane13.9%Wood and other

Biomass13.1%

Coal6.4%

BRAZILIAN ENERGY MATRIX - 2005

RENEWABLENON-RENEWABLE

Brazil0

20406080

100

World

14

86

45 55

%

Source: Brazilian Energy Balance (2006)

Ministry of Mines and Energy

Gasoline A25.6%

Anhydrous Ethanol8.5% Hydrated Ethanol

8.4%

VNG2.9%

Diesel 54.5%

CURRENT MATRIX OF VEHICLE FUELS - 2005

Gasoline C 25.6 + 8.5 = 34.1%

35.3% (2004)

Total Ethanol8.5 + 8.4 = 16.9%

15.4% (2004)

55.7% (2004)

2.4% (2004)

6.6% (2004)

8.8% (2004)

26.5% (2004)

Fuel Production and Dependency on Imports - 2005

Source: National Petroleum Agency, Ministry of Agriculture, Livestock and Food SupplyMinistry of Development, Industry and Foreign Trade(elaborated by Ministry of Mines and Energy (MME)

Production Net Imports

% of demand

% of production

PURE GASOLINE 19.978 - 2.760 14%

DIESEL 38.396 2.070 - 5%

ETHANOL 16.030 - 2.592 16%

NATURAL GAS(million m³/day) 48,5 24,4 - 33%

Fuel

Dependency

Self-sufficiency

thousand m³ thousand m³ thousand m³

Net Exports

Net Imports

Net Exports

Brazilian Energy PolicyLaw nº 9.478/1997

ObjectivesTo promote energy security with

lesser external dependency.

To protect the consumer best interests through regulation mechanisms and surveillance at the Regulatory Agencies

To increase the share of biofuels in the national energy matrix

To promote free competition

To protect the environment

Biofuels ConcernsGuarantee of internal supply

Specific taxation model in order to stimulate its usage

Expansion of production in order to supply the growing internal and external demand for ethanol and biodiesel

Private investments

Free prices in the whole chain production

ETHANOL

Ethanol in Brazil: 81 Years of Experience

1925: First tests using ethanol blends with gasoline

1979: Manufacturers begin to sell 100% Ethanol Vehicle

First Results for a 100% Ethanol Vehicle: 1979

April, 1979: Publication in a

technical magazine of the first test-drive of a 100% ethanol vehicle

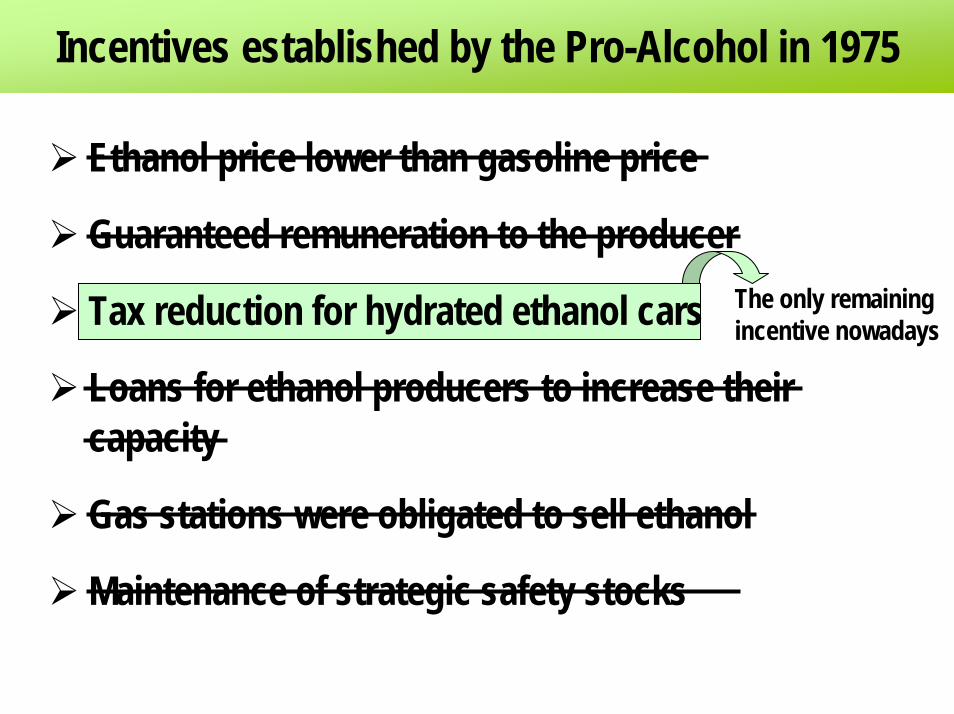

The only remaining incentive nowadays

Incentives established by the Pro-Alcohol in 1975

Ethanol price lower than gasoline price

Guaranteed remuneration to the producer

Tax reduction for hydrated ethanol cars

Loans for ethanol producers to increase their capacity

Gas stations were obligated to sell ethanol

Maintenance of strategic safety stocks

Ethanol World ProductionEthanol World Production

45,9 milhões Kl (2005)

China8%

Others13%

Brasil35%

India4%

USA35%

UE5%

Source: FO Licht

45,9 billion liters (2005)

2005 to 2020: Ethanol World Production Forecast

0

20000

40000

60000

80000

100000

120000

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

mln

lit

res

Brazil USA Canada Central AmericaPeru Colombia Venezuela ChinaIndia Philippines Thailand AustraliaEU

2010: 4%

Today: 1.5%

2020: 6%

Fonte: Berg, C. – Amsterdam, Novembro/05

Fonte: Berg, Cristoph, Ethanol World Market; F.O.Licht 2nd Sugar and Ethanol Brazil, SP 21- 23/03/06

Brasil: Produção de Álcool Hidratado e Anidro

-

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

16.000.000

18.000.000

75/7677/7879/8081/8283/8485/8687/8889/9091/9293/9494/9595/9696/9797/9898/9999/00

2000/01

2001/02

2002/03

2003/04

2004/05

2005/06

(Em

m³)

Álcool Hidratado Álcool Anidro Álcool TotalHydrated Ethanol Anhydrous Et. Total Ethanol

Brazil: Hydrated and Anhydrous Ethanol Productionm

3

Share of Flex Fuel and Gasoline Vehicles in the Light Vehicles Brazilian Market..

Source: ANFAVEA

82

19,0

68,3

21,9

66

35,7

72,8

76,6

58,9

26,924,4

11,8

0

20

40

60

80

100

jan/04 Jul jan/05 Jul jan/06 Jul

Gasolina Flex FuelGasoline Flex-Fuel

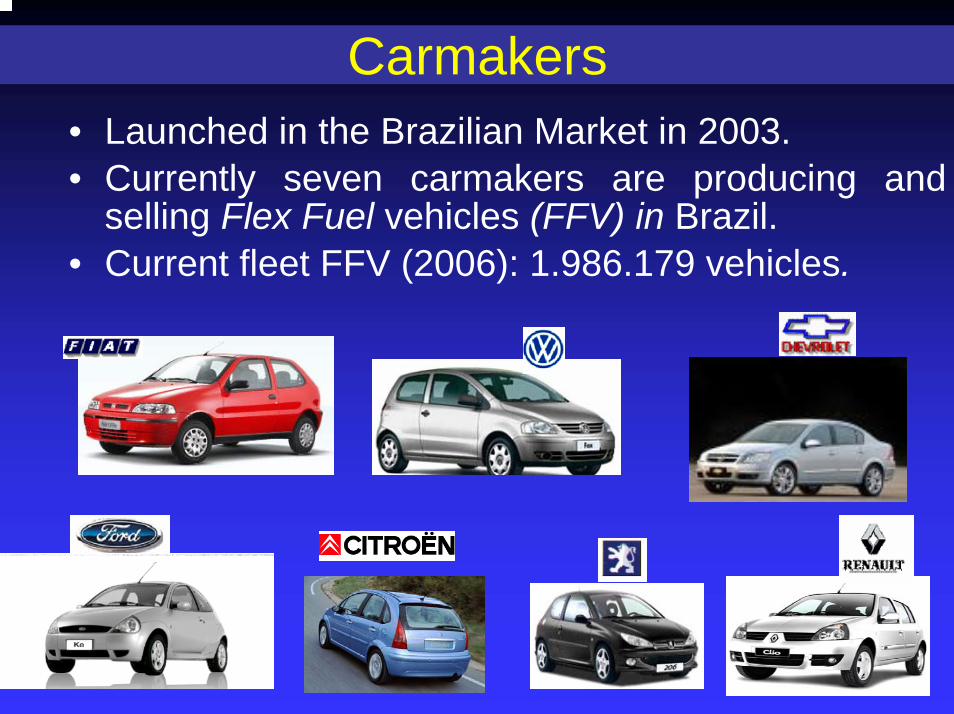

Carmakers• Launched in the Brazilian Market in 2003.• Currently seven carmakers are producing and

selling Flex Fuel vehicles (FFV) in Brazil.• Current fleet FFV (2006): 1.986.179 vehicles.

Benefits for the Consumers• Vehicles can be fueled with a mix

gasoline/hydrated ethanol in any proportion at any point in time.

• Possibility to choose the fuel in each refueling in accordance with the price at that particular pump station, availability, performance and consumption.

Competitividade do álcool hidratado vis a vis com a gasolina (%) – junho 2006

Hydrated ethanol competitiveness vis a visgasoline (%) – June 2006

≤ 70% – competitive> 70% – non competitive

87 75

56

71

72

65

59

78

76

69

51

79

81

77

54

75

88

60

72

77

57

72

Gasoline means gasohol with 25% anhydrous ethanol

Ethanol Competitiveness R$ 2,20/US$

20212426272527283029

2630

333633

2828313132

2830313234353737 38

4546 4943

4748

545350

5659

6562

5859

656263

70

40 41

53

65

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

jan/

02 fev

mar ab

rm

ai jun jul

ago

set

out

nov

dez

jan/

03 fev

mar ab

rm

ai jun jul

ago

set

out

nov

dez

jan/

04 fev

mar ab

rm

ai jun jul

ago

set

out

nov

dez

jan/

05 fev

mar ab

rm

ai jun jul

ago

set

out

nov

dez

jan/

06fe

v/06

mar

/06

abr/0

6

(*) Preço máximo do álcool em função das diferenças de eficiência energética entre álcool e gasolina (75% gasolina).Elaboração: MB Agro.

0

10

20

30

40

50

60

70

80Estímulo Produção Álcool

Álcool: Preço Equivalente*/Custo de Produção

Preço do Petróleo WTI (US$/barril)

Ethanol: Price equivalent to production costs

Oil Prices WTI (US$/bbl)

Incentive to ethanol production

Source: MB Agro

Ethanol in Brazil: Oil economy and environmental benefits

Source: Ministry of Mines and Energy - Brazilian Energy Balance – 2006and Laura Tetti – USP – 2002

106 BEP

FUEL DEMAND FOR LIGHT VEHICLES IN BRAZIL

0

20

40

60

80

100

120

140

160

180

1970 1975 1980 1985 1990 1995 2000 2005

YEAR

TOTAL DEMAND FOR LIGHT VEHICLES (GNV INCLUDED)

GASOLINE PRODUCTIONGASOLINE CONSUMPTION

TOTAL DEMAND FOR LIGHT VEHICLES (WITHOUT GNV)

This curve shows how much gasoline would be necessary to satisfy the fuel demand for light vehicles supposing the non-existence of the

Brazilian Ethanol Program

Total economy of 778 million boeor 15 months of the present Brazilian

petroleum production.

Accumulated economy of 7 years and 9 months of pure gasoline consumption.

US$ 61billions

IN THIS PERIOD, WITH THE ETHANOL USAGE, THE EMISSION OF 644 MILLION TONNES OF CO2 WAS AVOIDED

+ US$ 16billions

Ethanol Perspectives: Aviation Industry

• Brazilian Aviation Industry sells the first 100% ethanol aircraft, the Ipanema (EMB-202) a single-seat agricultural utility .

• Embraer, in partnership with an Italian company, announces the development of the first aircraft with Flex-Fuel technology.

The EMB-202 was awarded with the prizes

"Flight International Aerospace Industry

Award" General Aviation category (June /2005) in Paris and The Scientific

American 50 (December/2005) as one of the best inventions of

the year in the world.

BIODIESEL

0

10

20

30

40

50

60

70

80

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

JAN-

JUL/

06

US$

/ ba

rrel

Oil - Brent Dated

Biodiesel versus Ethanol: Different ReasonsEthanol (1975): basically economics. Reasons for biodiesel (today):

Economic: high crude oil prices again, but Brazilian dependence is now very low

Social: needs for jobs and permanent settlement of families in countryside

Environmental: to introduce another renewable and friendly fuel

1975: Pro-Alcohol is launched

Crude Oil Prices

2003: Biodiesel Program

First bus using Biodiesel – October 1980

Law 11.097/2005: Establishes minimum percentages to mix biodiesel to diesel, besides the monitoring on the introduction of this new fuel into the market.

Biodiesel: Regulatory Framework

2005to

2007

Authorized

Potential Market: 840 million Liters/year

2%

2008to

2012

Mandatory

Sound Market:1 billion Liters/year

2%

From 2013on

Mandatory

Sound Market:2,4 billion Liters/year

5%

Castor Beans Sunflower Palm Oil CottonSoy

Average Agriculture Productivity1.500 kg/ha 1.500 kg/ha 3.000 kg/ha 20.000 kg/ha 3.000 kg/ha

Percentage of Vegetable Oil

47% 42% 18% 20% 15%

Vegetable Oil Production (kg/ha)

705 630 540 4.000 450

Brazilian Production in 2005 m3/year90.000 23.000 5.600.000 151.000 315.000

Raw material diversity for production of Biodiesel

Biokerosene for Aviation Use

• Biokerosene Conception – 1980• Application Tests in Brazil – 1981 to 1984• First Flight (São José dos Campos – Brasília), in a airplane

EMBRAER (Bandeirante) on 23 October 2004 (“Aviator’s Day”)

• International launching of biokerosene in na event promoted by United Nations in China – December 2005

• Tests for international homologation started – August 2006. Homologation foreseen by 2008.

MME/SPG2006MME/SPG2006

BIODIESEL: Producers in Commercial Operation and Projects Forecast (As of Dec/2007)

(*) Elaborated with obtained information of producing potentials and investors. ANP: National Petroleum AgencySRF: IRS (Internal Revenue Service)

Legend:

Under Construction or Project

In Commercial Operation

New Project Intentions

In Authorization Process (ANP / SRF)

Number of Plants

Installed Capacity (MM L/year)

• IN COMMERCIAL OPERATION 7 123

• IN AUTHORIZATION PROCESS (ANP / SRF) 14 466

• UNDER CONSTRUCTION OR PROJECT 16 1,150

• NEW PROJECTS 20 842TOTAL 57 2,581

Industrial Biodiesel plant in Floriano, PiauíOperating with 120,000 l/d castor beans oil

or 180,000 l/d when operating with soya or cotton

Owner Company:

Brasil Ecodiesel – Deutsch Bank

H-BIO: A NEW BRAZILIAN TECHNOLOGY

Diesel oil production process that uses vegetable oils as raw materials in a petroleum refinery.

H-Bio = Hydrogenation of the mixture: diesel fractions + vegetable oil.

H-BIO AND BIODIESEL: COMPLEMENTARY PROCESSES

BiodieselBiodiesel

Glycerin Glycerin OthersOthers

Refinery

Hydrogen Fractions of diesel

Gas Station

Distributors

Agribusiness

Plantation Oil Crushing

Grains

RefinedOil

DieselDiesel

H-BIO

B2 or B5mixture

DieselOR

TransesterificationUnitEthanol Ethanol

or

MethanolMethanol

OROR

BIOFUELS PRODUCTION

BIOFUELS FORUM

• Big producers and big consumers• Brazil, China, European Union, India, South Africa,

United States • Working to transform biofuels into international

commodities• Business like initiative: informal, short term, oriented to

concrete results• Sustainable development • Improving the standard of living of poor countries

Main areas

• Transforming ethanol and biodiesel into international commodities

• Standards• Regulations• Infrastructure• Research and Development

Second Semester 2007

INTERNATIONAL CONFERENCE ON BIOFUELS IN BRAZIL