POOR 2 PROGRESSIVE- - SIDBI

26

POOR 2 PROGRESSIVE- DECODING LEARNINGS Knowledge Series 2

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of POOR 2 PROGRESSIVE- - SIDBI

POOR 2 PROGRESSIVE- DECODING LEARNINGS

Knowledge Series 2

ABOUT THIS KNOWLEDGE PRODUCT

We are happy to present this document to you as a Knowledge Product that captures successes, strategies

and approaches adopted during the implementation of Poorest States Inclusive Growth (PSIG)

programme. PSIG programme was supported by UKAid through the Department for International

Development (DFID) and implemented by Small Industries Development Bank of India (SIDBI). It aimed

to enhance income and employment opportunities for poor women and men by enabling them to

participate and benefit from wider economic growth in India. The programme targeted improving access

for poor women and men to a variety of financial services in four low income states namely Bihar,

Madhya Pradesh, Odisha and Uttar Pradesh.

The programme, in its 8 years of implementation made significant strides in increasing the financial

institutions’ ability to reach difficult geographies and excluded groups including women. It made a

substantive contribution in improving access to credit for poor households and capacity building of

women on financial literacy and gender issues.

The programme throughout its period of implementation attempted to adopt a comprehensive approach

to strengthen the financial inclusion ecosystem both on the demand and the supply side. It is important

that you are able to see the efficacy of these approaches including from the eyes of multiple stakeholders.

These stakeholders include first and foremost the communities PSIG program worked with, as also

different partners that helped us reach those communities. We also present key lessons we learnt both

from our independent evaluations and continuous rigorous reviews by DFID.

While we may not have been successful at every approach we adopted but we did draw important lessons

from some of these not so successful attempts. These learnings transformed our strategies to fulfill the

needs of the sector in subsequent engagements.

A constructive approach of working in collaboration with private sector and Government stakeholders

was the hallmark of our approach to sustain and institutionalize the positive impacts of the programme

The diversity and scale of programming under the PSIG umbrella was unique and one of its kind in the

sector. We hope that this document is of value to policy makers, development practitioners, donors and

implementers alike on the issue of looking at social and economic inclusion of the last mile.

SIDBI Vision 2.0 of inclusive, innovative & impact oriented engagements gave new dimensions to our

strategies. We could evolve end to end solutions transitioning from Fin Lit to Credit & Market Connect

for aspirant Bharat.

We hope that through PSIG we were able to contribute our two cents to the UN SDGs mandate to

“LEAVE NO ONE BEHIND!”

Background & Objective

SIDBI implemented Poorest State Inclusive Growth

(PSIG) Programme funded by UK Govt. through

Department for International Development (DFID), UK.

The programme aimed to ensure poor and vulnerable

people in low income states (especially women) benefit

from economic growth through better access to financial

services. This project aimed to reach 12 million poor

households with financial services and support 5 million

women clients to testify improvements in social status and

mobility.

PSIG Focus Areas

PSIG program has created a strong legacy in all the

three areas of its work viz., Policy Advocacy,

Access to Finance and Financial Literacy & Women

Empowerment

(i) Policy Advocacy - PSIG’s advocacy initiatives

combined with direct support to MFIs (funding and

capacity building) have contributed to stabilization

and expansion of the sector in the PSIG States and

to the emergence of Small Finance Banks (SFBs).

PSIG has created strong State Microfinance

Associations and helped in strengthening

Responsible Finance in the sector. There has been

substantial growth in the outreach of PSIG-

supported partner Financial Institutions (PFIs) –

MFIs and SFBs – from 3.8 million borrowers at

baseline to 9.7 million borrowers at endline in the

four PSIG states. This translates to a compound

annual growth rate of 26.3% which is significantly

higher than the 10-15% growth of outreach in the

microfinance sector nationwide.

Overall, the program reached out to 13.27 million

beneficiaries in the four poorest states.

(ii) Access to Finance - PSIG has deepened access to

finance in all the four states, by helping MFIs with

branch expansion in unserved and underserved

areas, strengthening digitization of operations and

institutionalizing focus on poorest of the poor by

using tools such as PPI. PSIG has helped 12 MFI

partners transition into next scale category and has

reached 5 million people with other financial

services such as savings, pension, payments &

insurance.

(iii) Financial Literacy and Women Empowerment

(FLWE) - PSIG has successfully catalyzed systemic

change that is significant in scale and sustainable

beyond the timeframe of the program. More than

10 partners have institutionalized FLWE approach in

their operations and 22 institutions have started to

integrate a gender lens in their policies & products.

Two of the largest livelihood missions of the Govt.

have scaled-up PSIG demonstrated approaches of

FLWE and deepening alternate banking services

through Bank Sakhis. PSIG’s microenterprise

development program for women has demonstrated

the viability of scaling-up businesses of more than

9000 “barefoot” entrepreneurs who often lack access

to technical support and capital to expand and

formalize.

PSIG programme was implemented in the 4 states of

UP, MP, Bihar and Odisha. The programme duration

was 6 years starting from April 2012-March 2018,

which was further extended for 2 years till March

2020.

2012-13

PSIG Program

Launch

2013-14

CB Support to

MFIs (1st phase)

Policy Advocacy

for Differentiated

Banking

100 cr Liquidity

Fund set up

2014-15

CB Support to

MFIs (2nd Phase)

Technology

Advisory Board

Studies on Poverty

Outreach, BC model

& Governance

Pilots on Financial

Literacy & Women

Empowerment in

4 states

2015-16

65 cr Debt Fund set up

FIWE Challenge Funds

launched

Programs with RRBs,

SHPIs and BC model

related interventions

PSIG works with partners

for institutional gender

mainstreaming

On lending support to

Wholesale lenders to

lend to small MFIs

2016-17

Handholding to small MFIs

SCI-FI launched for

Fin- tech Incubation

Partnerships with Government March 2020

Livelihood Missions

Setting up of Regional MFI

industry Associations

Support to the sector to

deal with Demonetization

Demonstrable Models to

Work with Ultra Poor

4 PSIG partners

transitioned from

MFIs to SFBs

PSIG moves from

Financial Literacy to

Financial Linkages

& tech based models

of delivering FLWE

PSIG moves from

capacity building

of MFIs to building

capacity for

Enterprise promotion

development, market

& Credit Connect

PSIG partners reach out

to 13.27 million people

in 4 poorest states

Endline shows significant

gains from the program in

terms of Women

Empowerment &

improvement in access

to microfinance for low

income HHs

2017-19

Programs to support women

enterprises’ credit & market

connect Integration with

SIDBI’s Swavalamban Mission

for entrepreneurship promotion

Support to SIDBI National

Microfinance Congress as first

govt. led platform for sector

related policy dialogue

KEY ACHIEVEMENTS AT A GLANCE: POOR 2 PROGRESSIVE STATES

POLICY ADVOCACY ACCESS TO FINANCE FINANCIAL LITERACY & WOMEN’S EMPOWERMENT

PSIG INDEPENDENT ENDLINE FINDING

2 microfinance associations in UP & Odisha set up by PSIG helped strengthen responsible finance & manage fallout of policy shocks like demonetization & loan waivers

Regular Policy dialogues, policy papers (8), policy level flyers (13) and studies (16) highlighted elements that policy makers needed to address

SCI – FI Fintech incubator set up, promoting innovation in financial products

Supported creation of India’s first Self- regulatory institution for Business Correspondents - (BCFI)

Support to the BCs led to deepening and widening of BC model in the PSIG States

Promoting product diversification through loans for solar products, water & sanitation. 5732 solar energy loans and more than 600 water & sanitation loans given to the women entrepreneurs

Built capacities of 51 Microfinance Institutions in India

Our supported partners/MFIs have reached out to 8.28 million clients (mostly women) with credit services & 5 million people with other financial services

12 MFI partners have increased operations into the next scale category within PSIG States & additional 10 MFIs have expanded entry into PSIG States

Supported graduation of 4000 ultra-poor out of extreme poverty through establishment of micro enterprises

Built financial capability of 6 lakh women

Scalable models created in partnership with Govt. Livelihood Missions ready for replication by others ---E.g. Partnership with Government Livelihood Missions JEEViKA (Bihar‘s SRLM) to help 500 SHG members become financially sustainable banking correspondents. The model has been scaled up by JEEViKA from 4 to 25 districts in Bihar

Supported establishment of more than 9000 women led microenterprises though Business Skills & Financial Literacy trainings, handholding, credit and market connect

Evaluation points towards significant improvement in women’s agency in PSIG geographies and reduction in domestic violence

Small but significant reduction in poverty rates by 9 percentage points for the rural areas and by 13 percentage points for the urban areas on the Poverty Probability Index (PPI)

The benefit-cost ratio (BCR) of 11 indicates that for every rupee spent, benefits were accrued to the tune of 11 times which suggests a very high level of efficiency for the PSIG program

There was a statistically significant increase (from 38.0 to 47.1) in Financial Inclusion Index (FII) and a reduction in the rural/urban and SC ST/ other social groups’ gap. Overall 68% of households showed increase in their FII score (70% of the rural sample, 65% of the urban)

S DEMAND

PSIG SUPPORT TO STRENGTHEN THE FINANCIAL INCLUSION ECOSYSTEM

POLICY ADVOCACY

CAPACITY BUILDING OF MICROFINANCE

LENDERS

FINANCIAL LITERACY & WOMEN EM- POWERMENT APPROACH

INSTITUTIONALIZED

TECHNOLOGY ADVISORY BOARD TO

SUPPORT MFIs PROMOTING WOMEN ENTERPRISES & THEIR

CREDIT & MARKET CONNECT

STRENGTHENING SUPPLY SIDE

STRENGTHENING DEMAND SIDE

DEBT FUND, RISK FUND & LIQUIDITY

FUND

CHALLENGE FUND PROJECTS TO TEST INNOVATIVE MODELS AND SUPPORT TO SHPIS LIKE AGA KHAN, CHAITANYA & SEWA HANDHOLDING

SUPPORT TO SMALL MFIs

STRENGTHENING CAPACITY OF STATE

LIVELIHOOD MISSIONS SETTING UP OF STATE

INDUSTRY ASSOCIATIONS & SCI-FI FINTECH INCUBATOR

RESEARCH MONITORING &

EVALUATION

N

L

SU

`

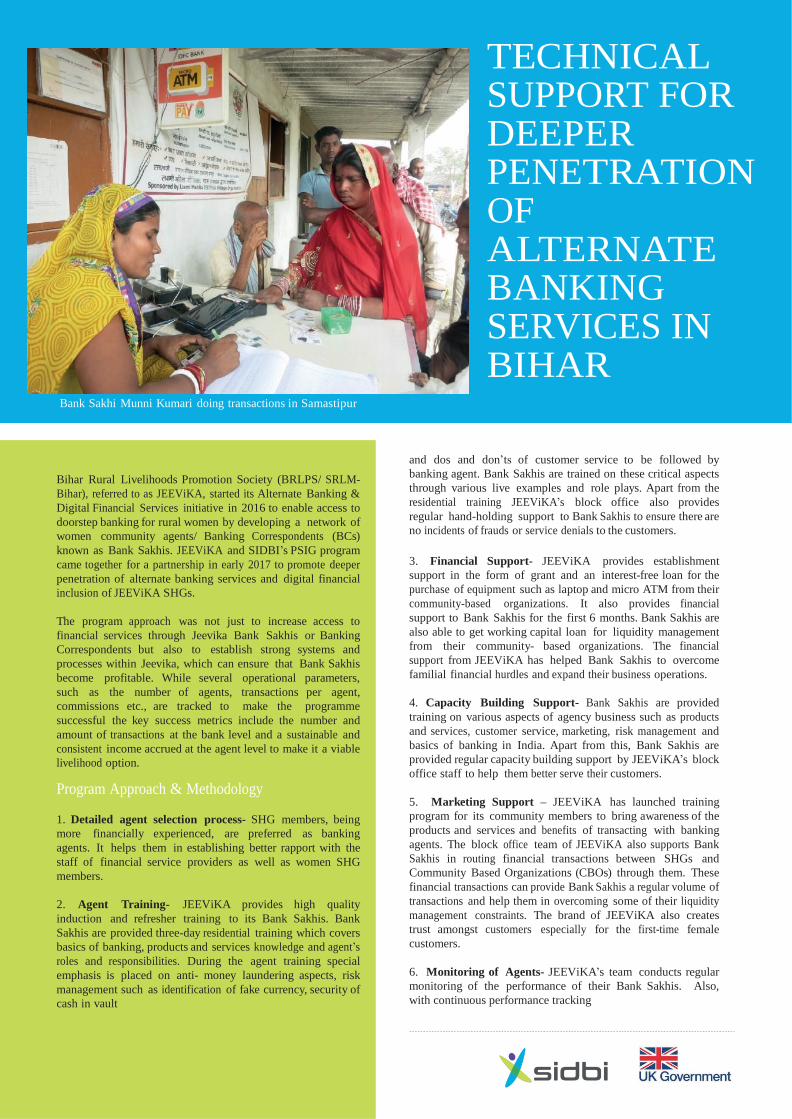

Bank Sakhi Munni Kumari doing transactions in Samastipur

TECHNICAL SUPPORT FOR DEEPER PENETRATION OF ALTERNATE BANKING SERVICES IN BIHAR

Bihar Rural Livelihoods Promotion Society (BRLPS/ SRLM-

Bihar), referred to as JEEViKA, started its Alternate Banking &

Digital Financial Services initiative in 2016 to enable access to

doorstep banking for rural women by developing a network of

women community agents/ Banking Correspondents (BCs)

known as Bank Sakhis. JEEViKA and SIDBI’s PSIG program

came together for a partnership in early 2017 to promote deeper

penetration of alternate banking services and digital financial

inclusion of JEEViKA SHGs.

The program approach was not just to increase access to

financial services through Jeevika Bank Sakhis or Banking

Correspondents but also to establish strong systems and

processes within Jeevika, which can ensure that Bank Sakhis

become profitable. While several operational parameters,

such as the number of agents, transactions per agent,

commissions etc., are tracked to make the programme

successful the key success metrics include the number and

amount of transactions at the bank level and a sustainable and

consistent income accrued at the agent level to make it a viable

livelihood option.

Program Approach & Methodology

1. Detailed agent selection process- SHG members, being

more financially experienced, are preferred as banking

agents. It helps them in establishing better rapport with the

staff of financial service providers as well as women SHG

members.

2. Agent Training- JEEViKA provides high quality

induction and refresher training to its Bank Sakhis. Bank

Sakhis are provided three-day residential training which covers

basics of banking, products and services knowledge and agent’s

roles and responsibilities. During the agent training special

emphasis is placed on anti- money laundering aspects, risk

management such as identification of fake currency, security of

cash in vault

and dos and don’ts of customer service to be followed by

banking agent. Bank Sakhis are trained on these critical aspects

through various live examples and role plays. Apart from the

residential training JEEViKA’s block office also provides

regular hand-holding support to Bank Sakhis to ensure there are

no incidents of frauds or service denials to the customers.

3. Financial Support- JEEViKA provides establishment

support in the form of grant and an interest-free loan for the

purchase of equipment such as laptop and micro ATM from their

community-based organizations. It also provides financial

support to Bank Sakhis for the first 6 months. Bank Sakhis are

also able to get working capital loan for liquidity management

from their community- based organizations. The financial

support from JEEViKA has helped Bank Sakhis to overcome

familial financial hurdles and expand their business operations.

4. Capacity Building Support- Bank Sakhis are provided

training on various aspects of agency business such as products

and services, customer service, marketing, risk management and

basics of banking in India. Apart from this, Bank Sakhis are

provided regular capacity building support by JEEViKA’s block

office staff to help them better serve their customers.

5. Marketing Support – JEEViKA has launched training

program for its community members to bring awareness of the

products and services and benefits of transacting with banking

agents. The block office team of JEEViKA also supports Bank

Sakhis in routing financial transactions between SHGs and

Community Based Organizations (CBOs) through them. These

financial transactions can provide Bank Sakhis a regular volume of

transactions and help them in overcoming some of their liquidity

management constraints. The brand of JEEViKA also creates

trust amongst customers especially for the first-time female

customers.

6. Monitoring of Agents- JEEViKA’s team conducts regular

monitoring of the performance of their Bank Sakhis. Also,

with continuous performance tracking

done through MIS and subsequent data analytics and dashboard

compilation. This way, JEEViKA is able to provide the required support

to non-performing Bank Sakhis. It has also helped in keeping the number

of dormant/inactive Bank Sakhis to less than 5% which is much less than the

general attrition level in the sector.

Ethical Customer Service & Empowerment

Incidents of frauds through BCs are very common in rural areas and they erode

trust over banking agent channel and build a perception that money is not

safe in bank account. Going to bank branch for transactions is an

inconvenient and costly option for most women and men in rural areas

resulting into their financial exclusion.

Common Frauds Committed by Agents

• Use of customer biometrics to open their bank accounts without their

knowledge

• Use of customer biometrics to conduct withdrawal transactions or higher

withdrawal amount without their knowledge

• Remote transactions - Not conducting deposit/fund transfer transactions

in the customers’ presence

• Imposition of unauthorized charges

• Un-authorized access to customers’ pin number for ATM cards

To preserve trust of its community members in the agency banking, JEEViKA

has put in place simple and speedy grievance redressal mechanism, risk

management structures, fraud prevention systems and is constantly working

towards improving financial capability of its community members. Exhibit 1

lists down JEEViKA’s initiatives to achieve customer empowerment and

ethical approach to customer service

Exhibit 1: Key initiatives of JEEViKA under this program to create safe banking

environment

Inclusion through Bank Sakhis

Bank Sakhis have been able to facilitate better social inclusion by

motivating first-time women customers who are usually illiterate,

semi-literate or still in their teens and yet to earn any income of their

own.

Data from one of the partner banks shows that around 74% of the

accounts opened by the Bank Sakhis are of women. They are also

providing doorstep banking to the neediest and otherwise excluded

segment in the community such as the elderly and the disabled for

account opening and distribution of DBT payments. Currently, around

2 million people in rural areas of Bihar are being covered by

JEEViKA Bank Sakhis placed through this program.

Bank Sakhis playing critical role in digitizing SHG transactions Bank

Sakhis are also supporting digitization of financial transactions

between SHGs and CBOs by visiting the SHG meetings to conduct

financial transactions for the members. This has reduced the cash-

carrying risk for SHG members and improved timely repayment of

loan in addition to creating a digital trail for SHG members.

As on December 2019, more than 552 Bank Sakhis are operational in

25 districts of Bihar with cumulative value of transactions more

thanRs.1000 crore done by these Bank Sakhis across a range of

services such as savings, deposits, withdrawals and remittances.

Employing SHG members as banking agents has benefitted the

community and at the same time provided gainful employment to many

of them for the first time. The SIDBI Jeevika partnership has helped them

become more respected in their family and community. They are able

to earn the epithet of ‘Banker Didi’ for themselves. Once begun, these

SHG members are more likely to continue with the bank agency

business as they are less likely to migrate for lucrative employment

opportunities.

As on March 2019, in India, on an average 1 BC outlet serves around

1,225 people whereas in Bihar, on an average, 1 BC outlet serves

around 5,710people. Bihar needs additional 66,000 BC outlets to be

on par with the national average density of BC outlets. These

additional 66,000 BC outlets have a huge potential to generate livelihood

opportunities especially for women.

PSIG’S PILOT OF TARGETING ULTRA POOR

Brief about the Program Targeting the Hard-core Poor (THP) program

model is a well-tested model aimed at

improving the socio-economic condition of the

poorest-of-the-poor and socially disadvantaged

women through sustainable livelihood

opportunities. Bandhan Konnagar

implemented the THP program in Satna

district of Madhya Pradesh since 2017 with

support from SIDBI’s PSIG Programme.

The THP program was in line with

PSIG’s mission to enhance economic

opportunities and empowerment of the rural

poor and targeted women headed households

in rural and slum locations with minimum or

no sources of income. Over the period of two

years, selected ultra-poor1 women beneficiaries

received a sequence of supports, including an

asset grant (livestock or goods for initiating

small enterprise), entrepreneurship training,

1 As per C Rangarajan Committee, ultra-poor are classified as those with per

capita income below Rs 32 per head/day.

temporary consumption support, weekly

personal mentoring, awareness on social issues,

health and sanitation and aspects of financial

education such as savings and maintenance of

accounts.

The support from SIDBI PSIG was crucial to

carry out this evidence based model in the Satna

district of Madhya Pradesh. This was done by

identifying such 1,000 poorest and deprived

households in blocks of Satna, Unchehara,

Maihar and Rampur and moving them out of

extreme poverty and destitution towards

sustainable livelihood and social mainstreaming.

Approach & Methodology The THP model targeted a specific population

type with an aim to create significant and

sustained positive impact by providing various

income generating assets and enterprise

training. The process map and implementation

model is represented below:

THP Model

Beneficiary Life Cycle

Impact The target of the THP program was to achieve at least

INR 4,000 per month income for its beneficiaries through

introduction of enterprises such as kirana stores, readymade

garments, livestock rearing, tailoring, garment selling etc.

93% of the respondents achieved this target by utilizing the

primary income generating assets given to them under the

program. The remaining 7% have also achieved this target

by income accrued from secondary and tertiary income

generating avenues.

The average annual gross income of the beneficiaries was

found to be INR 2,30,069. This is a significant increase of

INR 2,18,034 from their baseline average annual gross

income of INR 12,035.

The average annual net income of the beneficiaries was INR

85,861as average annual input cost of the enterprise was

calculated at INR 1,44,208.

The beneficiaries also reported an average annual saving of

INR 15,230.

The per month average gross income of the beneficiaries was

found to be INR 19,172and average net income was

calculated at INR 7,155against a target of INR 4,000.

The average cost of enterprise per month was found to be

INR 12,017and the beneficiaries reported an average per

month saving of INR 1,269.

95% beneficiary household had an individual household

latrine (IHHL).

Improved awareness of relevant government schemes and

policies for women, with many beneficiaries getting benefits

from schemes like PM Awas Yojana (80% renovated their

houses either through their own scheme), PM Suraksha Bima

Yojana (100%), Rashtriya Swasthya Bima Yojana, PM Jeevan

Jyoti Bima Yojana (37%) and PM Ujjwala Yojana.

Increased awareness, entrepreneurship traits and resulting

financial independence.

`

GENDER MAINSTREAMING IN MICROFINANCE

PSIGs Program with

Microfinance Partners

About the Intervention As the microfinance sector predominantly works

with women, it is usually assumed that there is

little need for gender mainstreaming in the

sector. However, it is crucial to examine if

microfinance promotes gender equality

especially empowerment of women in its true

sense. PSIG implemented a project to

understand the level of institutional gender

integration within its 26 partner institutions,

build institutional capacity on gender

mainstreaming in policies, products and

people. The project has helped gain critical

insights into how successful microfinance has

been in empowering women, whether and

how gender bias operates within the sector

and how power relations within and beyond

the household shape the context and outcomes

of microfinance initiatives.

Approach

This project therefore began with the premise that,

having a gender perspective will enable MFIs to be

more inclusive and responsive to the needs of

women clients, whose lives are impacted by

unequal and discriminatory gender relations, roles

and responsibilities.

Project started with assessing institutional gender

gaps in terms of policies, products & people. A

gender integration report was compiled

highlighting gaps & good practices in terms of

institutional gender integration. After assessing the

gender gaps, the project worked with partners on

enhancing partner’s capacities on gender

mainstreaming.

The project also developed tools like “Engendering

Microfinance – A Capacity Building Toolkit for

Microfinance Institutions”, “the Gender Integration

Index” that serves as a detailed evaluation as well

as rating tool for institutional gender integration. A

simpler and do-it-yourself monitoring or self-

assessment tool has also been developed for use by

MFIs— titled the ‘Gender Equity Quotient’.

Some of the interesting findings from the

project indicate to the exclusion of single

women and women with difficult circumstances in

the priority client group, monitoring and

evaluation of performance is mostly limited to

financial performance with little attention to

social performance. Gender ratio in most MFIs

decline at the top and bottom with most women

concentrated at office and middle level positions.

In terms of loan products most organizations do

not consider women’s rights over family assets

I MPAC T

IMPAC T

Policy

21 out of 26 Partner Institutions (PIs) included

Gender Objectives in their Vision, Mission

and Human Resource Policy

Project team jointly developed revised

Vision and Mission statement for 14 PIs

21 PIs integrated gender indicators in to their

complaint redressal mechanism

Product

PIs have introduced more products for

different genders like product for unmarried

girls, transgenders, products to purchase land

and house by women

Several PIs have agreed to introduce loan

products with condition of women’s name

in house / land ownership title after 2nd or 3rd

loan cycle

as legitimate. In fact, some practices like

requirement of NOC from male member of the

family strengthen patriarchal controls. The

project also documented good practices in

some partner institutions like flexi timings,

special hostel facilities for women staff,

insurance cover for women and her spouse, all

women branches, loan products for drudgery

reduction like smokeless chulha, other clean

energy products and recognizing female family

members as “guarantors”.

Practice

5 out of 26 PIs have inducted women

for inclusion at the Board level and senior

level management

All PIs are involved in non-financial

programs such as financial literacy. During

the project many of them have started

including men in financial literacy classes,

to ensure support of men for the women

borrowers

This work helps in building a strong, stable and

gender sensitive microfinance sector which is

crucial for enabling access to finance for

millions of poor households in the country. It

also builds an understanding among key

stakeholders that gender inequality cannot be

simply eliminated by recruiting more women, it

requires targeted efforts across all levels of the

organization and developing a critical mass of

support for furthering inclusion through

organizational culture and its work.

The Microfinance sector is increasingly

recognizing that a gendered approach to design

and delivery of financial services will help them

better serve different client segments and tap the

untapped opportunity of bringing many more

unbanked clients into the folds of formal

financial services.

FINANCIAL LITERACY TO ENTREPRENEURSHIP PROMOTION AND CREDIT CONNECT

Approach & Methodology

The program has directly improved financial

capabilities of more than 6 lakh women in

these 4 states. The program provided 30

hours of intensive training to each client. In

addition to client level trainings, deploying

various interesting modes of training, the

program also organized 404 Mass Awareness

Camps (MACs) creating awareness of 1.19 lakh

community members in the 4 states.

About the Intervention

PSIG has pioneered an integrated

approach to financial literacy wherein

financial literacy trainings are integrated

with social and gender issues, rights

and entitlements. The program has

implemented demonstration models with

implementing agencies for strengthening

financial capability of poor women;

PSIG went beyond financial literacy to

financial linkages for clients. Partners

included MFIs, SHPIs and collaboration

and convergence with public institutions

like the State Rural Livelihood Missions

(SRLMs) for promoting equitable access

to financial services. Further PSIG has

tested and implemented innovative

technology-based approaches for

financial & digital literacy and women

empowerment. PSIG has implemented

targeted Financial Literacy & Women

Empowerment (FLWE) programs in Bihar,

MP, Odisha and UP.

FLWE Program with Microfinance Institutions

Methodology Outreach Cost

18 implementing MFI partners 6 lakh women trained 20% cost shared by partners

ToT approach

Mass Awareness Camps Mobile Phone based IVR Platform for Financial Literacy

A cadre of 522 master trainers created 80% cost borne by PSIG

Gender integrated FL modules 8 Films in Hindi/Odiya

63,508 financial linkages Per client cost was Rs 318/-

15-30 hrs. of client training 108 community women leaders trained

Smart phone enabled MIS

Baseline & end-line evaluation

FLEP Program with SHPIs

PSIG worked with three large SHPI’s in UP,

Bihar and MP to enhance financial

literacy, access to financial services,

better use of technology and book

keeping for SHG members.

FLWE programs in the SHG space

strengthened financial capability, book

keeping and credit linkage for SHG groups

in all 4 states. The program has trained 7.2

lakh SHG members on basic financial

literacy, book keeping, audit of SHGs and

credit linked more than 2,500 SHGs.

Methodology Outreach

3 large SHPI Promoting Institutions 7.2 lakh SHG members

TOT Approach with Credit plus services 18,000 financial linkages

Collaborations with State Govt.

for Financial Literacy

Odisha Livelihood Mission

PSIG worked in partnership with Odisha

Livelihood Mission (OLM) for Training and

Strengthening Capacities of their Financial

Literacy - Community Resource Persons

(FL-CRPs). The project has trained a cadre

of 50 Master Trainers and 300 FL-CRPs for

the OLM in 10 blocks of 10 districts who in

Bihar Livelihood Mission – JEEViKA

PSIG partnered with JEEViKA (which is

Bihar Govt. Rural Livelihood Mission

working with 8 million Rural families) in

Sept 2017 to provide them technical

assistance for deeper penetration of

alternate banking and digital financial

services in Bihar. The project trained SHG

members as Bank Sakhis, streamlined

JEEViKA’s processes for identifying,

training and on-boarding Bank Sakhis,

supported to build an MIS system and app

for monitoring Bank Sakhis’ financial

performance and transactions and also

build capacity of the demand side through

Digital Financial Literacy to 60,000 SHG

members.

Impact

Independent endline evaluations show

substantial improvements in women’s lives

in terms of better financial planning, higher

awareness of their rights & entitlements,

savings, increased mobility & better access

to sanitation. The involvement of clients in

the decision-making process, in both the

project and the control areas, witnessed

an overall positive change during endline.

turn built financial capabilities of 86,000 SHG

members.

Key achievements

• OLM has now up-scaled the program to

1000 additional Gram Panchayats (GPs) in

the State of Odisha by positioning the

trained FL-CRPs and Master Trainers and

setting up Gram Panchayat level Aarthik

Saksharta Kendras.

• Odiya Modules developed under the

programme being used across the State by

OLM.

The project area witnessed 84% of the

clients participating in the decision to take

up a job, while 87% of the clients

participated in the decision-making

regarding children’s education. 90% of the

women in the project group practiced

household budgeting during endline against

17% at baseline. Household budgeting

witnessed a significant differential increase of

50%. Awareness level of insurance and

pension increased from 41% to 93% and from

24% to 94% respectively. There was a

significant differential increase of 18% from

baseline to endline in the access to toilet

with water. Overall, the degree of mobility of

women showed a statistically significant

(p<0.05), positive shift in the endline, as

compared to the baseline.

At the institutional level, FLWE program has

created a successful business case for

financial institutions to invest in building

financial capability of poor women. The

integrated approach of empowering women

along with building their financial capability

has been adopted by partners. The training

content created by FLWE program (both

films & training modules) are being used

widely by more than 10 institutions.

Methodology Outreach

TOT & FLWE Films

Odisha Livelihood Mission

• 86000 SHG members

• Cadre of 50 Master Trainers trained

• 300 FL-CRPs

TOT & FLWE Films

Bihar Rural Livelihood Mission – JEEViKA

• 60,000 SHG members trained on Digital Financial Literacy

• Cadre of 200 FL-CRPs Trained for JEEViKA

MUSP (Mahila Udyami

Sashaktikaran Program)

Project Objective: Women

entrepreneurs establish/scale-

up/diversify their micro enterprises

with reported increased income and

employment of the household over

baseline.

Period and location of the Project:

August 2018–October 2019 / Varanasi

& Ghazipur

Impact:

• 16,000 women entrepreneurs

screened using Screening Tool

prepared for MUSP program

• 15,500 women trained in 12 hrs. of

Grass- roots Management Training

(GMT) including concepts like

enterprise selection, planning, value

addition, income & cash flow, break

even, profits, pricing and costing etc.

• 9,832 credit linked through different

channels and Prayas scheme of SIDBI

• 10,673 business plans prepared, 7000+ of

them were tracked monthly. All women

being provided handholding services to

upscale, diversify and set up their

enterprises.

• 6300 women provided market linkages.

• 7 key trades identified and value chain

analysis completed for these trades

• 25 buyer seller meets organized for women

entrepreneurs for market linkages

• Client feedback sought via direct

messages, 7400 messages received from

clients with 97.0% positive feedback for

the program

• IVR platform launched to strengthen

feedback and peer exchange

• Convergence with skill training institutes

for women who need advanced skills

• 9661 micro-enterprises grounded.

PSIG INTERVENTIONS IN BIHAR

THEMATIC AREA

KEY ENGAG E ME N T S & O U T R E A CH

Capacity Building support to

5 MFIs (CDOT, Arohan,

Jagran, Saija and Sahyog)

which impacted more than

21 lakh beneficiaries

CB support to Sewa Bharat

which impacted 20,000

women and their families

Capacity Building support to

Regional Rural Banks (RRBs)

which impacted 5.6 lakh

beneficiaries

Support to Aga Khan

Foundation for strengthening

SHG program enabling

reaching out to 20,000 SHG

members, support to 1,883

persons (PMJDY) and 10,982

persons (Micro Insurance &

Pension Scheme)

Quarterly State Financial

Inclusion Forum (SFIF) for

cross learning in the state

Debt funding for onlending

to small MFIs and their

capacity building through

Ananya and Sa-Dhan

FLWE - 3 MFIs (Saija, Cashpor, Utkarsh)- financial literacy trainings in 10 districts leading to direct training of 25,867 women, and awareness raising of 24,000 members through Mass Awareness Camps

Program with Sewa Bharat and Gram Vani - improving financial and digital literacy in 5 districts leading to direct on-boarding of 14,846 users on the IVR system - engagement with 74,230 community members

Support to Save Solutions - digital financial literacy in 5 clusters, covering more than 10,000 artisans and their family members

Support to Save Solutions - Customer Service Points (CSPs), leading to 44.5 lakh banking customers being provided better service delivery

An MFI-led Swavalamban Enterprise Development Program (SEDP) for around 1000 women micropreneurs for establishing/scaling-up their micro enterprises (ME)

Support to FWWBI - Solar Energy & Sanitation products extended to more than 5,000 disadvantaged people

Scalable model for WE & ME development - created in partnership with Jeevika (SRLM, Bihar), which has so far trained 552 Bank Sakhis and made them financially profitable who are now providing doorstep delivery of banking services to 3.1 million beneficiaries in rural Bihar.

Scaled up from 4 to 20 districts - being further scaled-up to 5 additional districts - 60,000 SHG members have been imparted digital financial literacy.

INTEGRATING WITH STATE LIVELIHOOD

MISSION

FINLIT TO ENTREPRENEURSHIP

EASE OF ACCESS TO CREDIT AND RESPONSIBLE

FINANCE

`

03 02 01

PSIG INTERVENTIONS IN B I H A R

PSIG INTERVENTIONS IN MADHYA PRADESH

KEY ENGAG E ME N T S & O U T R E A CH

CB support to 7 MFIs (Sahyog, Samhita, Disha, Shakti Mahila Sangh, Mahila Chetna Manch, Pratigya, Sanghmitra) which impacted more than 4.4 lakh beneficiaries. (Disha has since converted into Small Finance Bank (SFB)).

Support to RRB (Narmada Jhabua Gramin Bank) which impacted 3.5 lakh beneficiaries (283352 saving bank accounts opened, operations of 276 BCAs made financially viable in all 6 districts (Khargone, Khandwa, Burhanpur, Jhabua, Alirajpur, Barwani) of the project, 10,374 OD facilities made available, 23631 NPS/ APY accounts opened and 2681 SHGs linked to branch).

State Financial Inclusion Forum (SFIF) for cross-learning SFIF- Regular quarterly forums convened to bring together key FI stakeholders of the state.

Support to Self Help Promoting Institution (SHPI) (Chaitanya) - A BC aggregator model in MP for enhancing SHG bank linkage programme and building institutional capacities of smaller SHPIs/MFIs. The support helped develop integrated software named Micro Lekha for SHGs and SHG federations. The intervention has capacitated 4 smaller SHPIs and 16 federations, which consisted around 10,000 SHGs in 2 districts. The efforts were mainly focused on quality of SHGs and financial management of SHG and federations, which included BC operations. Overall, they have impacted 1.6 lakh beneficiaries.

Combination of Debt Fund and Grant Support for onlending to small MFIs and their capacity building initiatives. While the Debt fund was provided to MFIs for on-lending to poor women at the bottom of pyramid, the Grant Support was provided for confidence building through rating, portfolio audit, Code of conduct /social performance and compliance with regulatory guidelines. Technical assistance is provided for new age technology, MIS automation for greater transparency and cost effectiveness. Strengthening governance, risk management, data submission to Credit Information Companies, HR development and promoting other financial services such as Micro Pension & Insurance.

FLWE - 6 MFIs (Disha, Shakti Mahila

Sangh, Pratigya, Mahila Chetna

Manch, Samhita, Sahayog) - financial

literacy trainings in 13 districts.

Directly trained 29,000 women and

raised awareness of around 22,000

members through 72 Mass

Awareness Camps.

Scale-up of FLWE Program with 4

MFIs (Shakti Mahila Sangh, Pratigya,

Mahila Chetna Manch, Samhita).

Directly trained 48,000 women and

raised awareness of around 11,000

members through 94 Mass Awareness

Camps. 18,359 financial linkages

done.

An MFI-led Swavalamban Enterprise

Development Program (SEDP).

Around 1000 women micropreneurs

for establishing/ scaling-up their

micro enterprises (ME).

Bandhan Konnagar (in Satna). A

comprehensive model of

targeting hard core ultra-poor

was piloted in MP benefitting

1,000 women single-headed

households to graduate out of

extreme poverty through

establishment of small

enterprises.

Humana People to People India

(HPPI) (in Sheopur and Gwalior).

The project worked with 40,000

ultra-poor women and built their

capacities on FL, gender & health

issues and developed their

entrepreneurship skills. 3,409

women established their own

micro enterprises after this

support.

Empowering women to access

improved sanitation facilities

and participate as active

entrepreneurs to promote

sanitation (in Sehore, Raisen and

Panna) through Samarthan –

Centre for Development Support.

Capacities of 323 SHGs built on

sanitation and gender issues.

2678 families were benefited

directly from construction/repair

of toilets. Women’s employment

in non-traditional occupations

encouraged by training 450

women to become masons.

Further, these women were linked

to Prime Ministers Awas Yojana

(PMAY) and other construction

opportunities in their respective

villages. 150 women were linked

to school and panchayats for

maintenance of schools toilets.

60 women/groups were trained as

grassroots entrepreneurs or

vendor for taking the contract for

construction of toilets.

PSIG INTERVENTIONS IN MP

FINANCIAL INCLUSION

AND WOMEN

EMPOWERMENT

CHALLENGE FUND

(FIWECF) SUPPORT

ON INNOVATIVE

IDEAS

TARGETING HARD CORE ULTRA POOR

FINLIT TO

ENTREPRENEURSHIP

EASE OF ACCESS

TO CREDIT AND RESPONSIBLE

FINANCE

`

04 03 02 01

THEMATIC AREA

PSIG INTERVENTIONS IN ODISHA

KEY ENGAG E ME N T S & OU TR E A CH

CB support to 7 MFIs (Annapurna, Mahashakti, Sambandh, GU Financial Services, Swayamshree Micro Credit Services, Swayamshree Mahila Samabaya Samiti Limited, Adhikar) impacting 6.07 lakh beneficiaries

State Financial Inclusion Forum (SFIF) for cross learning - Regular quarterly forums convened to bring together key FI stakeholders of the state.

Microfinance State Association- Odisha State Association for Financial Inclusion (OSAFI) - OSAFI organized trainings and district level meetings with the stakeholders reaching out to 60,000 MFI staffs through direct capacity building programs.

Technology Innovation Fund (TIF) support to 2 MFIs (Sambandh, Annapurna) - The TIF was used to enable MFIs to undertake technology based initiatives such as introduction of document management systems, faster credit delivery mechanism, system digitization, hardware support, development of MIS etc. which improved institutions ability to effectively reach out to the poor.

Soft loan support to 2 MFIs (Annapurna, Mahashakti) for improving partners’ capacity to open more branches in unserved/ underserved areas in the State.

Term loan support to 6 MFIs (Annapurna, Mahashakti, Sambandh, Swayamshree Micro Credit Services, Swayamshree Mahila Samabaya, Adhikar) - for expanding their portfolio for on-lending to unserved and underserved clients which impacted/supported around 50,000 beneficiaries.

FLWE Pilot - 7 MFIs (Swayamshree Cuttack, GU Finance, Mahashakti Foundation, Adhikar, Annapurna, Sambandh, Swayamshree Bhubaneswar) - financial literacy trainings in 13 districts. Directly trained 49,500 women and raised awareness of around 35000 members through 132 Mass Awareness Camps

Scale-up of FLWE Program with 6 MFIs (Swayamshree Cuttack, GU Finance, Mahashakti Foundation, Adhikar, Annapurna, Sambandh) - Directly trained 1.06 lakh women and raised awareness of 45,647 members through 220 Mass Awareness Camps. 45,149 financial linkages done.

An MFI-led Swavalamban Enterprise Development Program (SEDP) - Around 1000 women micropreneurs for establishing/ scaling-up their micro enterprises (ME).

Scalable model for imparting FLWE at scale demonstrated in partnership with Odisha Livelihood Mission - Trained a cadre of 50 Master Trainers and 300+ financial literacy resource persons for Odisha Livelihood Mission (OLM). The FL-CRPs further trained 86,010 women members from 8,053 SHGs on FLWE issues. The pilot up-scaled by OLM from 10 blocks to 1000 Gram Panchayats.

Project on inclusion and old age income security through contributory pension schemes: Increasing enrolments through Nudges, Mobile Payments and Online Crowd Funding in 2 blocks of Jagatsinghpura district-Crosslinks Foundation- Testing behavioural solutions to encourage Atal Pension Yojana (APY) enrolments and for measuring the effectiveness of the interventions by applying Randomized Controlled Trial (RCT).

PSIG INTERVENTIONS IN ODISHA

CHALLENGE

FUND SUPPORT

ON INNOVATIVE

IDEAS

INTEGRATING WITH STATE LIVELIHOOD

MISSION

FINLIT TO

ENTREPRENEURSHIP

EASE OF ACCESS

TO CREDIT AND RESPONSIBLE

FINANCE

`

04 03 02 01

THEMATIC AREA

PSIG INTERVENTIONS

IN UTTAR PRADESH

THEMATIC AREA

K E Y E N G A G E M E N T S & O U T R E A C H

Mahila Udyami Sashaktikaran Program (MUSP), a 15-month pilot, in Varanasi and Ghazipur provided end-to-end support (training, handholding, credit and market linkage) to women micro-entrepreneurs for establishing, scaling-up and diversifying their enterprises under which 15,000 women were trained on business skills; 9,000 women-led micro enterprises helped to set-up/scale-up/diversify their respective businesses.

Swavalamban Enterprise Development Program (SEDP) started in Gorakhpur and Raibareily for creation/up-scaling of livelihood activities by way of skill and entrepreneurship development leading to set-up of 1,000 micro-enterprises.

Udyam Saarthi - An intensive digital financial literacy project in the form of a self-contained Mobile Literacy Lab which sensitized over 60,000 individuals on digital financial literacy and handheld about 12,000 individuals for digital transactions in select 9 blocks of Ghazipur & Varanasi districts covering 344 villages.

An intensive financial inclusion programme through community-based institution for poverty reduction undertook Bank Linkage, Financial Literacy, nurturing and promoting young women SHGs and other related activities in 200 backward blocks of Uttar Pradesh reaching out to a total of around 5 lakh SHG members.

Financial Literacy (FL)

Partnered with 5 MFIs for financial literacy trainings in 25 districts in UP.

1.65 lakh women trained on Financial and Digital Literacy across the State.

SIDBI Centre for Innovation in Financial Inclusion (SCI-FI):

SIDBI has supported IIM-Lucknow for setting- up of SCI-FI at IIM-Lucknow, for development of new age financial products, innovative business models and build FinTech in India.

This would also support new start-ups, thereby helping in setting standards and best practices for a more responsible growth in the sector.

The centre is presently incubating 9 diversified FinTechs and has engaged 15 industry mentors. Out of these, 3 FinTech Start-ups have been acknowledged for their solutions at the different fora. “

Microfinance Association of Uttar Pradesh (UPMA)

SIDBI has been instrumental in setting-up of Microfinance Association of Uttar Pradesh (UPMA), a State-level MFI association.

UPMA is promoting responsible lending, client protection, good governance and a supportive regulatory environment in the state.

UPMA is achieving this via activities like organizing FI conclave, awareness generation for digital financial literacy program, mass awareness campaigns towards confidence building post- demonetization, conducting various theme-based workshops and trainings for the MFI officials and other stakeholders etc.

Green Micro Credit

Cashpor Micro Credit was supported to undertake a pilot on modified microfinance loan product called ‘Green Micro Credit’ to promote tree plantation (suitable for GHS sequestration) among matured income generating loan borrowers and suitably incentivize them by way of interest subvention and in meeting initial plantation and upkeep cost. The initiative helped in mitigating carbon emission and is a kind of long-term economic investment for the client.

Capacity building support was sanctioned to 10 MFIs for conducting Loan Portfolio Audit, Social Performance Ratings, System Audit, Software Up-gradation and expansion in underserved/unserved pockets of UP and promotion of other financial services such as pension and insurance. This capacity building support helped MFIs to serve over 41 lakh (4.1 million) clients in UP.

Debt Fund support extended to 8 MFIs, helping in on-lending to 6.35 lakh beneficiaries.

Innovative support mechanisms like Risk Fund improved MFIs capacity

Pradhan Mantri Ujjwala Yojna

(PMUY)

SIDBI supported an MFI- led intervention for awareness generation and switching over to cleaner methods of cooking under PMUY in 8 districts, viz., Azamgarh, Ballia, Chitrakoot, Gorakhpur, Jaunpur, Kushinagar, Mirzapur and Sonebhadra.

In addition to awareness generation of around 70,000 BPL members, more than 7,500 BPL households have been linked with PMUY by way of Energy Loans.

MAJOR PSIG INITIATIVES IN UTTAR PRADESH

01 02 03

`

`

FINANCIAL LITERACY & WOMEN ENTREPRENEURSHIP

(FLWE)

POLICY ADVOCACY

INSTITUTIONAL CAPACITY BUILDING

Key Highlights of Independent Endline Evaluation Independent evaluation of the program points towards

significant improvement in women’s agency captured

through Women’s Agency Index (WAI) in PSIG

geographies and reduction in domestic violence.

There was a small but significant reduction in poverty rates

as measured by the Poverty Probability Index – by 9

percentage points for the rural sample and by 13 percentage

points for the urban households.

There was a statistically significant increase (from

38.0 to 47.1) in Financial Inclusion Index (FII) and a

reduction in the rural/urban and SC ST/ other social groups’

gap. Overall, 68% of households showed increase in their

FII score.

The benefit-cost ratio (BCR) of 11 indicates that for every

rupee spent, benefits were accrued to the tune of 11 times

which suggests a very high level of efficiency for the PSIG

programme.

PSIG Key Learnings

1. Policy Level

PSIG played a critical role in helping the sector absorb

shocks such as 2010 crisis and demonetization

Policy dialogues and position papers highlighted elements

that policy makers needed to address

Important state level role by setting up of MFI

associations in UP & Odisha where these agencies were

instrumental in creating stakeholder awareness and

managing the fallout of policy shocks such as

demonetization and loan waivers in UP and the potential

collateral effects of the collapse of chit funds in Odisha

Strengthened SHGs by supporting the engagement of

SHPIs in the low-income states.

Supported the emergence of the Business

Correspondent model as a para-banking channel to

intensify the engagement of commercial banks with low

income clients and to increase their depth of outreach in the

four poorest states

Lessons

Despite all efforts, limited effect on non-traditional

products like pension & insurance

PSIG could have addressed the knowledge gap through

creating evidence on cost of operations in poor areas that

could have informed policy better.

2. PFI Level

Effectively supported growth & capacity building for MFIs

working at different scales

Supported better institutional readiness for client

protection, gender integration and responsible finance

Strengthened many aspects of operations especially

Governance, IT, Audit & Technology

Lessons

Objectives for product development & diversification only

partially achieved – limited to some adaptation of credit for

WASH and alternative energy – and systematic MIS and

reporting beyond standard portfolio analysis still needs

more attention from MFIs.

Small MFIs had received significant portfolio support from

PSIG, this facilitated some of them to graduate to large or

medium MFI status; whilst others – perhaps inevitably -

failed to make significant progress.

3. Client Level

Contributed to the availability of credit services through

MFIs/SFBs and the ability of MFIs to provide larger loans

Considerable improvement over the baseline on client

understanding of the terms of credit and credit insurance.

Those who attended financial literacy training showed a

marginal increase in use of different services.

In terms of welfare, significant positives changes were

observed in poverty reduction, housing facilities and

ownership of durable assets. Some decrease in dependency

on non-farm casual labour and home- based piece rate

work. Borrowing from moneylenders reduced.

Improvements across geographies and social groups

(including SC/ST, Muslims and women headed

households).

Lessons

On the less positive side, there was a high level of reported

shocks/difficulties with illness/accident followed by

agriculture related difficulties in rural areas.

Non-farm business difficulties were higher for those

borrowing for business use.

4. Women’s Empowerment

Significant improvements for women across all

categories.

Microcredit for women had given some low-income women

the opportunity to start micro non-farm businesses that they

manage themselves. Their reported profits increased since

baseline, but turnover and profits remained lower than for

joint or men managed businesses

Percentage of women saying they experience domestic

violence has fallen significantly to 17.5% (rural & urban)

from 31% at baseline

Endline also reported significant increase in women

reporting better say in family decisions, with this gap also

narrowing between rural and urban women.

Lessons

Work on institutional gender integration remains critical for

the sector to become more client-centred and inclusive.

TEAM MEMOIRS

While considering financial support to an organization

catering to this particular segment of the population, going

deep into the organization’s Balance Sheet is of secondary

importance. In fact, we should look beyond the Balance

Sheet and take a call on the support-worthiness of the

project in terms of the field-level reputation/feedback about

the organization and it’s connect to the roots.

Abhijit Das, DGM, PSIG

The diversity and scale of programming under the PSIG

umbrella helped us make a dent in how gender is perceived

across the spectrum of partners, communities, financial sector

and banks themselves. We learnt to be persistent in our

efforts to integrate a gender lens and learnt a lot ourselves

through this process.

Sonal Jaitly, Theme Leader, Gender & FL, PSIG

I feel privileged and honoured for having

been associated with one of the most

impactful and cost-effective programs of

the development sector catering to the

bottom-of-the pyramid in the

underserved/unserved districts of the 4

PSIG states which was implemented

through a network of NBFCs, MFIs,

corporate BCs, state associations, SRLMs

etc. My biggest learning is that impactful

programs can be implemented in a cost-

effective way; it does not necessarily

require huge quantum of money, it just

requires concerted efforts, dedicated and

meticulous planning and concurrent

monitoring &evaluation of the programs.

Nikhil Raj, Theme Leader, M&E, PSIG

FLWE pilot was my major learning of integrating gender into

financial literacy trainings. 6 months long discussions and

back n forth with resource agency finally led to development

of FLWE modules which tried to imbibe gender analysis tools

in the sessions, calls for prioritizing women’s health and

assets while decision making on savings, investment &

insurance. The pilot gave us a window to directly reach out to

women clients of MFIs. PSIG used micro credit as an

opportunity to further empower women through FLWE and

build their financial well-being.

Archana Ale, Manager, Gender & FL

The provision of debt based financial assistance

mainly at subsidized rates for branch expansion

of MFIs in PSIG States, their technology

upgradation and on lending to their clients

fulfilled the twin objective of promoting financial

inclusion as well as ensuring judicious use &

ownership in the game of financial

intermediaries/implementing partners. PSIG

ensured 100% realization of assistance(s)

extended under debt fund/risk fund, which

ultimately augmented the Institutionalizing of

PSIG Legacy by making the availability of PSIG

residual funds –

Chandan Bajaj, AGM, PSIG

I joined PSIG Project in 2014 when Capacity Building

support to MFI -II, Risk Fund, Debt Fund-II and

Technology Advisory Body was set up. I was involved in

gearing to start these activities being a part of Access

to Finance team.

Indu Rawat, Manager, PSIG

Entering the project in the last phases, our efforts to align it

to SIDBI Vision 2.0 bore fruit. We could, with DFID support,

set-up Legacy Fund for taking forward the pilots &

integrating with Mission Swavalamban-the umbrella

programme which caters to entrepreneurs, enterprise and

entrepreneurship.

Dr. R.K.Singh, GM, PSIG

PSIG TEAM MEMBERS

Involved in the preparation of this Knowledge Product

Dr. R. K Singh, General Manager

Shri Abhijit Das, Dy. General Manager

Ms. Sonal Jaitly, Theme Leader – Gender & Financial Literacy

Shri Nikhil Raj, Theme Leader - Monitoring & Evaluation

DISCLAIMER: The information presented in this document is based on the experience and learnings from DFID supported SIDBI’s interventions under the PSIG program. The document is intended as a knowledge product only, for the purpose of replication of the relevant models by the institutions/organizations who are interested to do so and also as a showcase of the magnitude of the impacts created. SIDBI will not be liable for any damages or loss, direct or indirect, arising out of such use of information provided within this document.